Embed Size (px)

Citation preview

IndiaResearch

HDFC Securities Limited, Trade World, C. Wing, 1st Floor, Kamala Mills Compound, Senapati Bapat Marg,Lower Parel, Mumbai 400 013 Phone: (022) 66611700 Fax: (022) 2496 5066

Sanju VermaExecutive Director& Head - Institutional [email protected] 1859

Mukesh [email protected] 1753

June 20, 2008

Pipes & Tubes’ Sector

Pipes & Tubes’ Sector

Pipes ...Beyond the Hype

COMPANIES COVERED

Welspun Gujarat Stahl Rohren

PSL

Jindal Saw

Man Industries

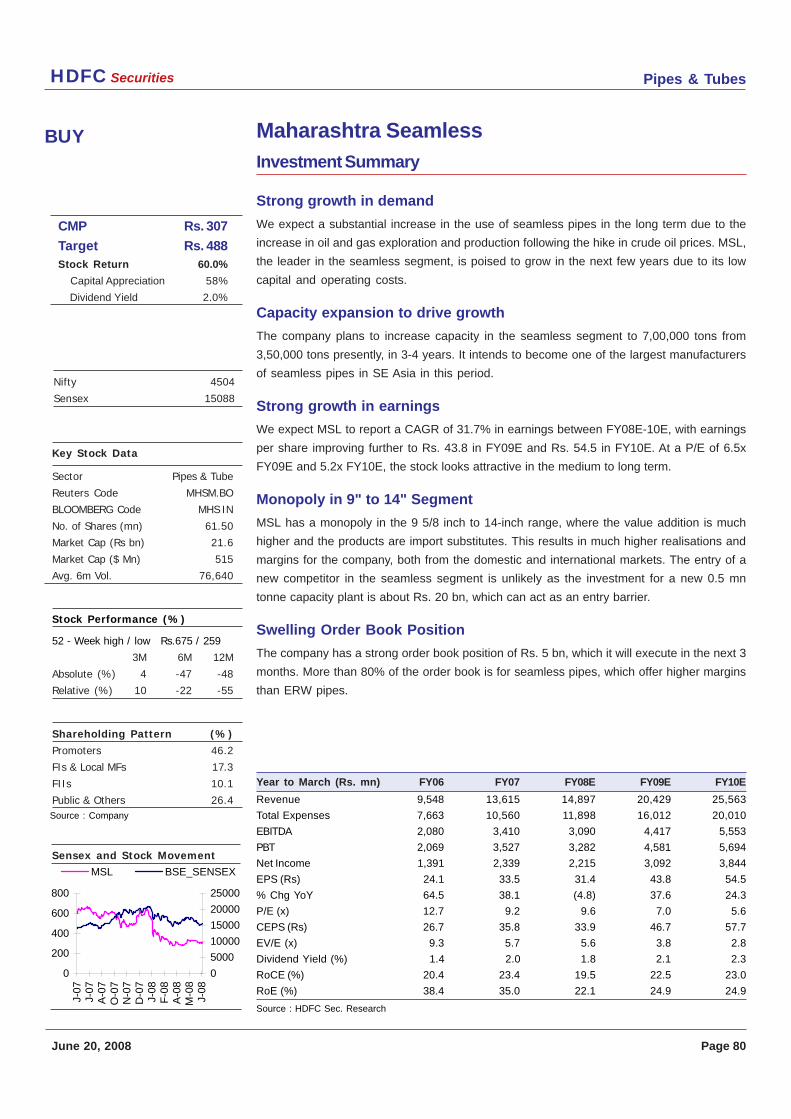

Maharashtra Seamless

Ratnamani Metals & Tubes

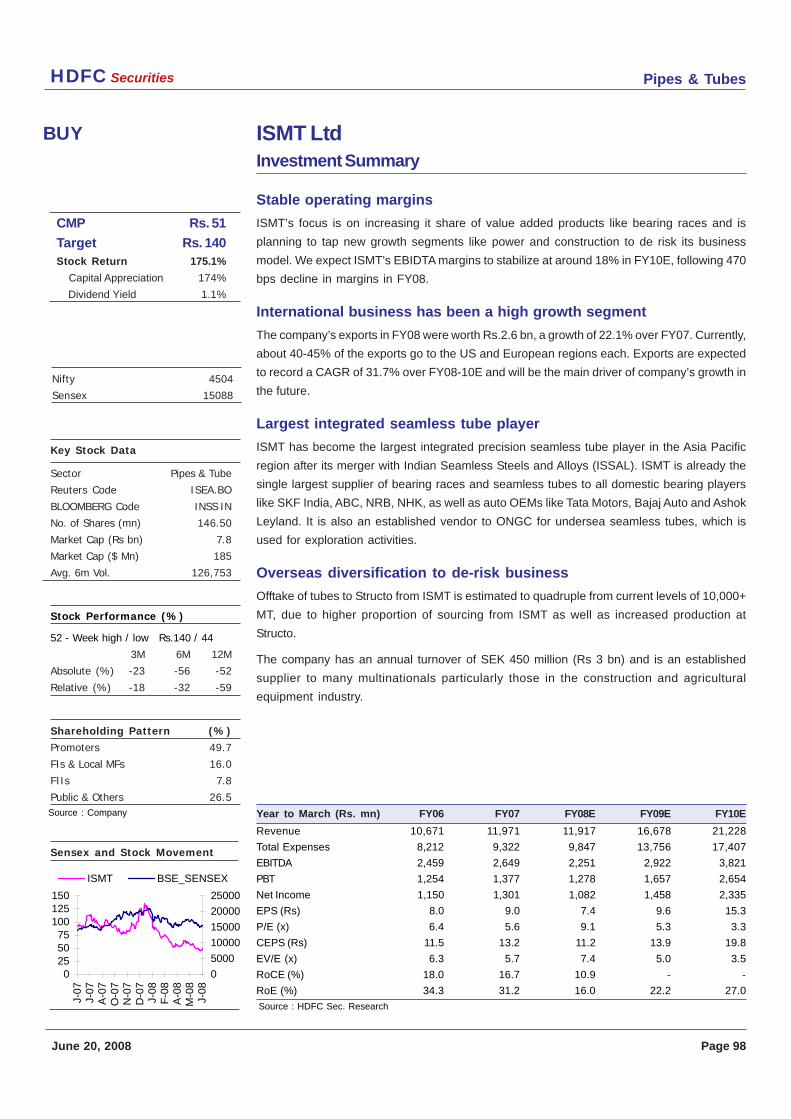

ISMT

Pipes & TubesHDFC Securities

June 20, 2008 Page 2

FOREWORD

Worldwide, about 13 million metric tons of large diameter pipes were produced in 2007. But demand over the next few

years is expected to be about 60 million tons. Most industry observers agree that this is a strong market and will remain so

for the near future. Many mills are sold out through this year and well into the next. Ipsco and Sumitomo are reportedly sold

out through 2009. In fact, some predict that major pipeline projects could be delayed or called off because of high costs and

the difficulty of obtaining material.

So why is the market so strong? It’s not a mystery really. Energy prices are high. The rig count may have leveled off recently,

but it is still strong compared to historical levels. Oil and gas prices may drop from today’s highs. But oil is expected to

remain at or about $80 a barrel for at least the next ten years. Natural gas should hover at least at about $6-7 per million

British thermal units. Strong worldwide GDP growth is expected to support those prices, in the long run. Even if growth trails

off in Europe and North America, it should remain firm in developing and emerging markets. And with energy prices and

demand strong, massive pipeline projects are in the works around the world.

In Russia, for example, projects are underway to connect Siberia to energy markets on the Pacific Coast. China is laying

thousands of miles of pipes to connect natural gas in western provinces to coastal areas like Shanghai. In North America

alone, the Rockies Express pipeline is expected to gobble up almost 1,700 miles of pipe to run natural gas from Wyoming

to Ohio. Billions are also being spent on pipelines to transport crude from the oil sands of Western Canada to the U.S.

Midwest. The U.S. claims to be intent on cutting back dependence on supplies of foreign crude. And if it does, Canada’s oil

sands could be natural replacement. And while projects like the Rockies Express get a lot of attention, there are many

smaller projects underway that taken together will consume a lot of pipe. For example, there are five liquefied natural gas

terminals in the U.S. But there are already five more under construction. And several more will likely be built within the next

twenty years. And all of those projects will mean running steel pipe from local LNG terminals to Interstate pipelines like the

Rockies Express

Then there are also a few wild cards out there to consider. Legislation under consideration in the U.S. calls for the sequestration

of emissions like C02 by 2020. If those new restrictions are put into law, it could create demand for a whole new pipeline

infrastructure. If the laws go into effect in 2020, the pipelines would have to be in place beforehand. It’s a huge potential

market of over & above USD 200 bn approx.

We are confident that the main fundamentals behind the Pipes and Tubes sector remain ¨seamless¨. For the short to

medium term, this is reflected in the sector’s order book, which covers the sectoral activity for close to nine months. For the

longer term, one of the main drivers behind this industry is the development of hydrocarbon reserves; oil reserves represent

around 40 years of consumption and natural gas around 60 years. However, this is not a complete view of the resources: by

adding technical progress which should allow for improvements in recovery rates and discoveries in non explored zones

and non conventional oil and gas as the extra heavy oil from Canada and Venezuela, one can at least double these figures.

The development of these resources will be progressive as the time frame in energy is typically around ten years for

exploration and production projects, but also for transport infrastructure. Hence, the development of these resources will

require very high level of capital expenditure, and also great amounts of pipes and tubes.

Technical innovation is the key for the future of oil and gas development. Hence, supplying high quality and specialised

products will continue to be a differentiating factor in this industry. This is why Indian players will continue to improve their

product mix by introducing new products through ongoing investments allowing them to optimise their integrated production

process. With likely market of USD 100 bn and above for the period 2008-13E, we have raised our estimates for the coming

years based on the strength of the cycle due to ongoing investments in the sector. Along with this, companies are looking

to increase their operating leverage to further fuel growth in the energy cycle by supplying higher value added products

which will lead to higher returns and margins.

By Mukesh Agarwal

Pipes & TubesHDFC Securities

June 20, 2008 Page 3

Table of Contents

Page No.

Executive Summary .......................................................................................................................................................................... 4

Earnings Watch ................................................................................................................................................................................ 6

Comparative Valuation ..................................................................................................................................................................... 7

Swot Analysis .................................................................................................................................................................................... 8

Industry Matrix ................................................................................................................................................................................... 9

Porter’s Five Forces Model ............................................................................................................................................................. 10

Investment Case ............................................................................................................................................................................. 11

Industry Overview ............................................................................................................................................................................ 14

Overview of Global Capacities ....................................................................................................................................................... 17

Demand for API Pipe ...................................................................................................................................................................... 24

Upcoming Pipeline Investment ...................................................................................................................................................... 30

Key Future Projects ........................................................................................................................................................................ 32

API Mill Capacity ............................................................................................................................................................................. 33

Companies

Welspun Gujarat Stahl Rohren ...................................................................................................................................................... 39

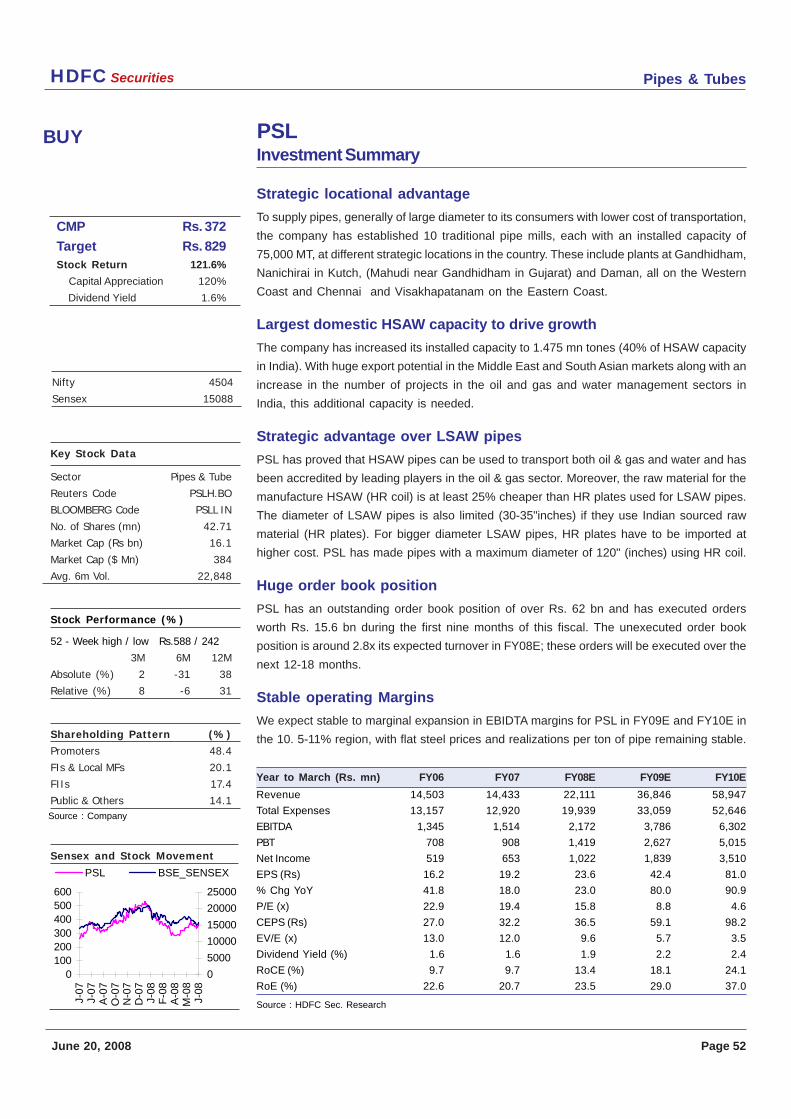

PSL ................................................................................................................................................................................................. 52

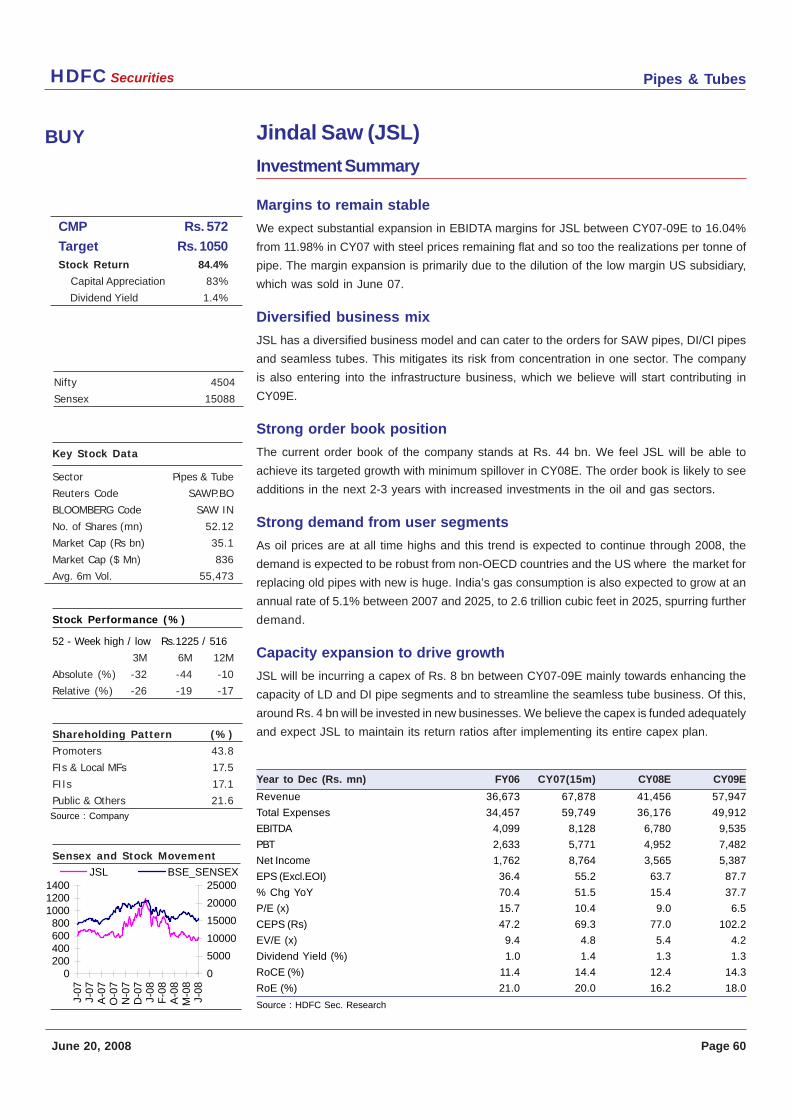

Jindal Saw ...................................................................................................................................................................................... 60

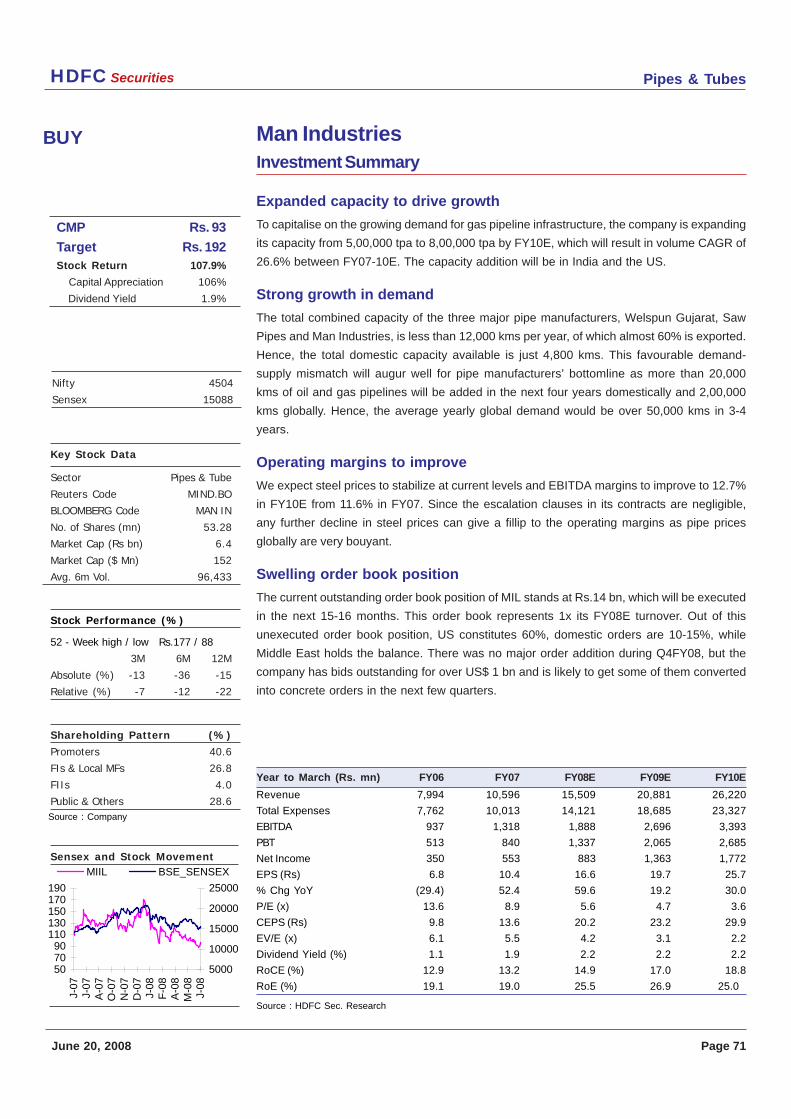

Man Industries ................................................................................................................................................................................ 71

Maharashtra Seamless ................................................................................................................................................................. 80

Ratnamani Metals & Tubes ........................................................................................................................................................... 89

ISMT ................................................................................................................................................................................................ 98

Pipes & TubesHDFC Securities

June 20, 2008 Page 4

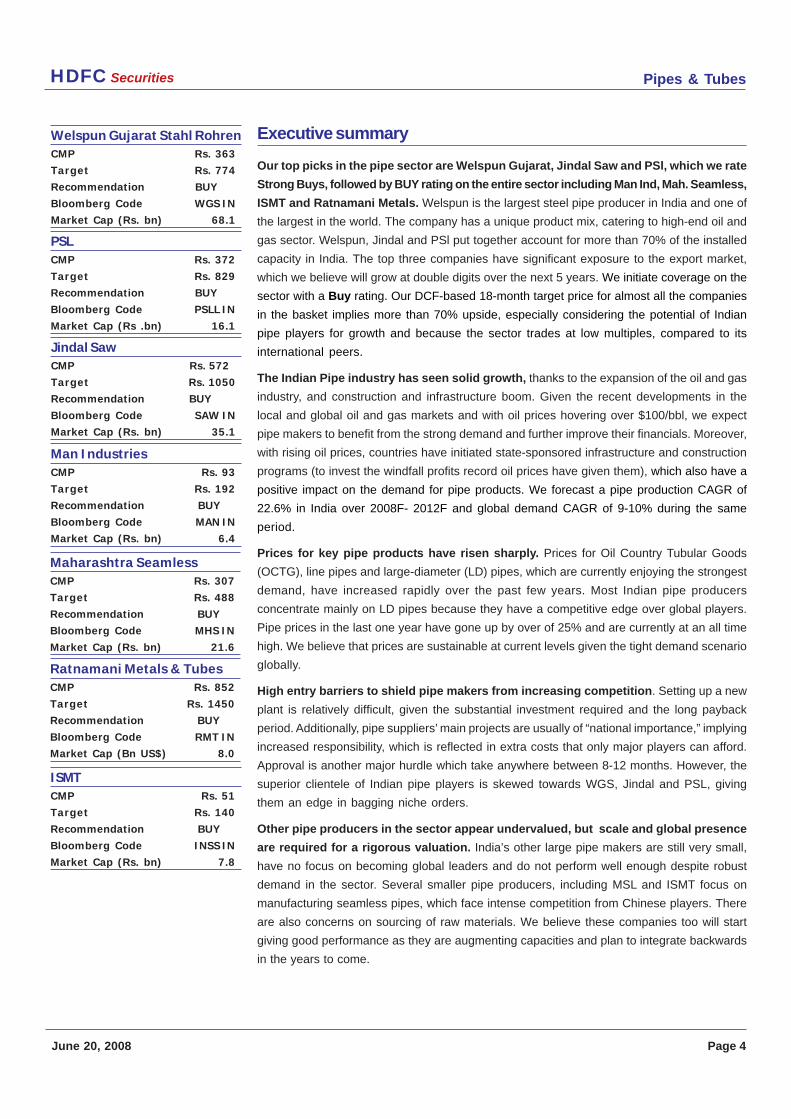

Executive summary

Our top picks in the pipe sector are Welspun Gujarat, Jindal Saw and PSl, which we rate

Strong Buys, followed by BUY rating on the entire sector including Man Ind, Mah. Seamless,

ISMT and Ratnamani Metals. Welspun is the largest steel pipe producer in India and one of

the largest in the world. The company has a unique product mix, catering to high-end oil and

gas sector. Welspun, Jindal and PSl put together account for more than 70% of the installed

capacity in India. The top three companies have significant exposure to the export market,

which we believe will grow at double digits over the next 5 years. We initiate coverage on the

sector with a Buy rating. Our DCF-based 18-month target price for almost all the companies

in the basket implies more than 70% upside, especially considering the potential of Indian

pipe players for growth and because the sector trades at low multiples, compared to its

international peers.

The Indian Pipe industry has seen solid growth, thanks to the expansion of the oil and gas

industry, and construction and infrastructure boom. Given the recent developments in the

local and global oil and gas markets and with oil prices hovering over $100/bbl, we expect

pipe makers to benefit from the strong demand and further improve their financials. Moreover,

with rising oil prices, countries have initiated state-sponsored infrastructure and construction

programs (to invest the windfall profits record oil prices have given them), which also have a

positive impact on the demand for pipe products. We forecast a pipe production CAGR of

22.6% in India over 2008F- 2012F and global demand CAGR of 9-10% during the same

period.

Prices for key pipe products have risen sharply. Prices for Oil Country Tubular Goods

(OCTG), line pipes and large-diameter (LD) pipes, which are currently enjoying the strongest

demand, have increased rapidly over the past few years. Most Indian pipe producers

concentrate mainly on LD pipes because they have a competitive edge over global players.

Pipe prices in the last one year have gone up by over of 25% and are currently at an all time

high. We believe that prices are sustainable at current levels given the tight demand scenario

globally.

High entry barriers to shield pipe makers from increasing competition. Setting up a new

plant is relatively difficult, given the substantial investment required and the long payback

period. Additionally, pipe suppliers’ main projects are usually of “national importance,” implying

increased responsibility, which is reflected in extra costs that only major players can afford.

Approval is another major hurdle which take anywhere between 8-12 months. However, the

superior clientele of Indian pipe players is skewed towards WGS, Jindal and PSL, giving

them an edge in bagging niche orders.

Other pipe producers in the sector appear undervalued, but scale and global presence

are required for a rigorous valuation. India’s other large pipe makers are still very small,

have no focus on becoming global leaders and do not perform well enough despite robust

demand in the sector. Several smaller pipe producers, including MSL and ISMT focus on

manufacturing seamless pipes, which face intense competition from Chinese players. There

are also concerns on sourcing of raw materials. We believe these companies too will start

giving good performance as they are augmenting capacities and plan to integrate backwards

in the years to come.

PSLCMP Rs. 372

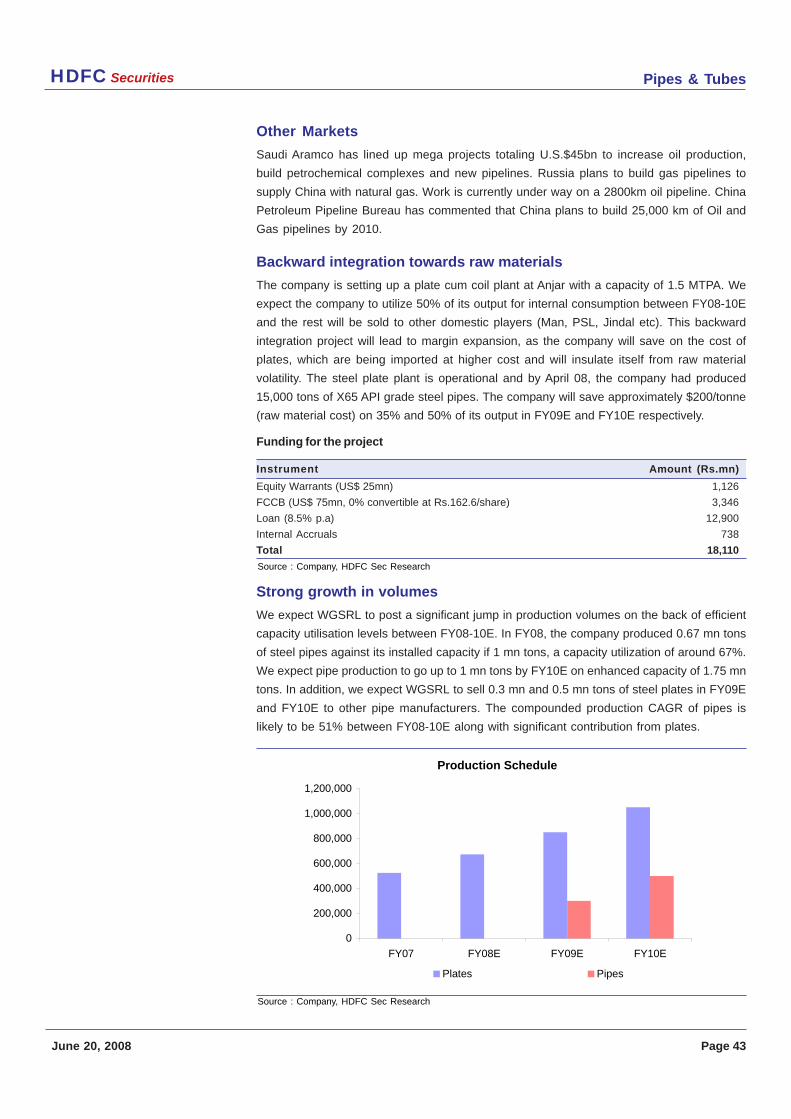

Target Rs. 829

Recommendation BUY

Bloomberg Code PSLL IN

Market Cap (Rs .bn) 16.1

Jindal SawCMP Rs. 572

Target Rs. 1050

Recommendation BUY

Bloomberg Code SAW IN

Market Cap (Rs. bn) 35.1

Man IndustriesCMP Rs. 93

Target Rs. 192

Recommendation BUY

Bloomberg Code MAN IN

Market Cap (Rs. bn) 6.4

ISMTCMP Rs. 51

Target Rs. 140

Recommendation BUY

Bloomberg Code INSS IN

Market Cap (Rs. bn) 7.8

Maharashtra SeamlessCMP Rs. 307

Target Rs. 488

Recommendation BUY

Bloomberg Code MHS IN

Market Cap (Rs. bn) 21.6

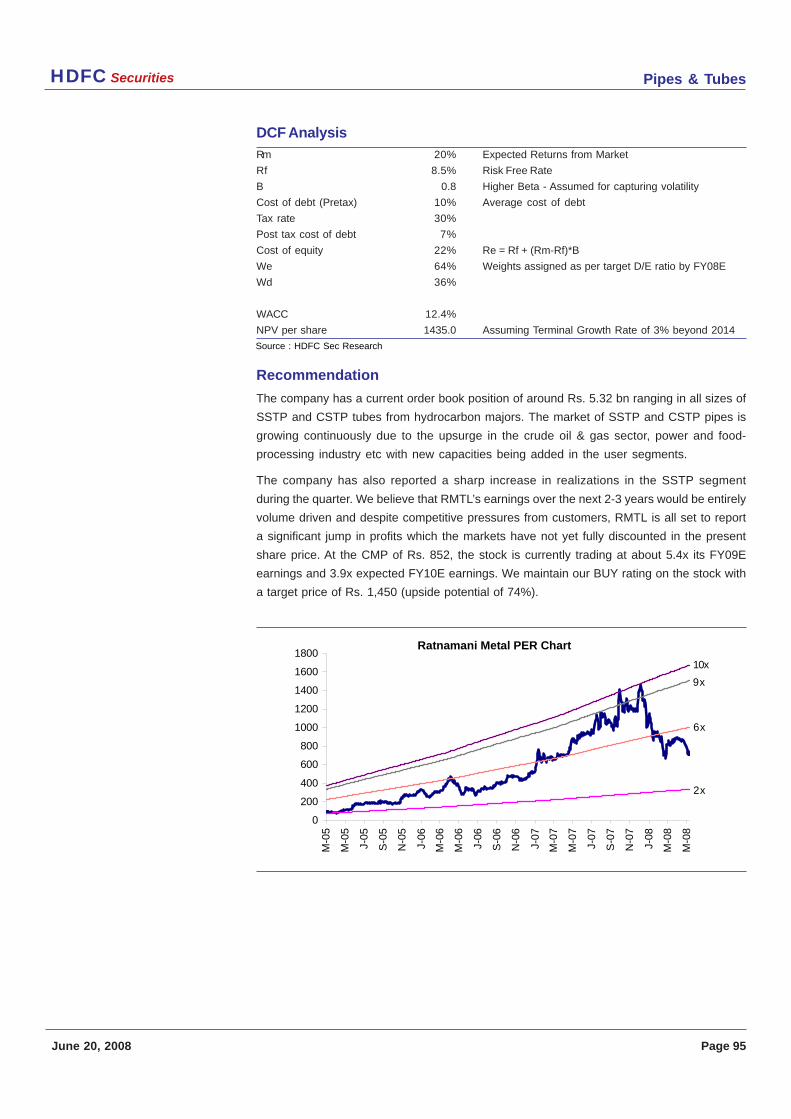

Ratnamani Metals & TubesCMP Rs. 852

Target Rs. 1450

Recommendation BUY

Bloomberg Code RMT IN

Market Cap (Bn US$) 8.0

Welspun Gujarat Stahl RohrenCMP Rs. 363

Target Rs. 774

Recommendation BUY

Bloomberg Code WGS IN

Market Cap (Rs. bn) 68.1

Pipes & TubesHDFC Securities

June 20, 2008 Page 5

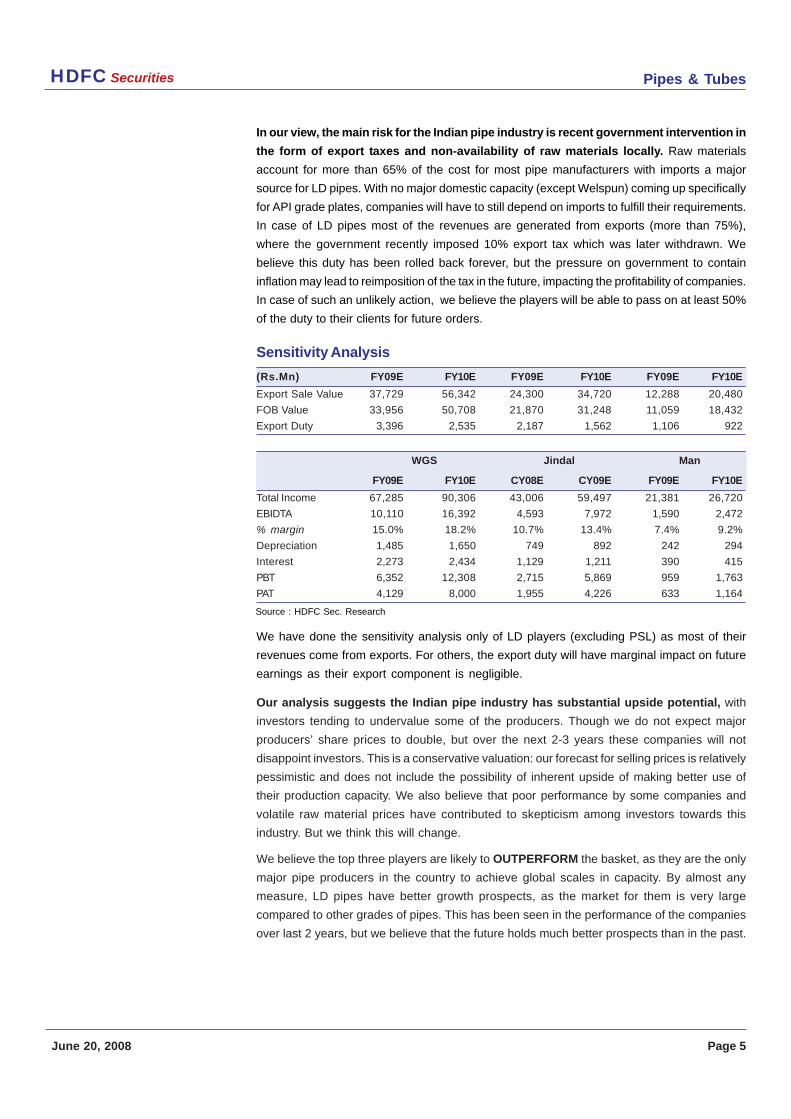

In our view, the main risk for the Indian pipe industry is recent government intervention in

the form of export taxes and non-availability of raw materials locally. Raw materials

account for more than 65% of the cost for most pipe manufacturers with imports a major

source for LD pipes. With no major domestic capacity (except Welspun) coming up specifically

for API grade plates, companies will have to still depend on imports to fulfill their requirements.

In case of LD pipes most of the revenues are generated from exports (more than 75%),

where the government recently imposed 10% export tax which was later withdrawn. We

believe this duty has been rolled back forever, but the pressure on government to contain

inflation may lead to reimposition of the tax in the future, impacting the profitability of companies.

In case of such an unlikely action, we believe the players will be able to pass on at least 50%

of the duty to their clients for future orders.

We have done the sensitivity analysis only of LD players (excluding PSL) as most of their

revenues come from exports. For others, the export duty will have marginal impact on future

earnings as their export component is negligible.

Our analysis suggests the Indian pipe industry has substantial upside potential, with

investors tending to undervalue some of the producers. Though we do not expect major

producers’ share prices to double, but over the next 2-3 years these companies will not

disappoint investors. This is a conservative valuation: our forecast for selling prices is relatively

pessimistic and does not include the possibility of inherent upside of making better use of

their production capacity. We also believe that poor performance by some companies and

volatile raw material prices have contributed to skepticism among investors towards this

industry. But we think this will change.

We believe the top three players are likely to OUTPERFORM the basket, as they are the only

major pipe producers in the country to achieve global scales in capacity. By almost any

measure, LD pipes have better growth prospects, as the market for them is very large

compared to other grades of pipes. This has been seen in the performance of the companies

over last 2 years, but we believe that the future holds much better prospects than in the past.

Sensitivity Analysis

(Rs.Mn) FY09E FY10E FY09E FY10E FY09E FY10E

Export Sale Value 37,729 56,342 24,300 34,720 12,288 20,480

FOB Value 33,956 50,708 21,870 31,248 11,059 18,432

Export Duty 3,396 2,535 2,187 1,562 1,106 922

WGS Jindal Man

FY09E FY10E CY08E CY09E FY09E FY10E

Total Income 67,285 90,306 43,006 59,497 21,381 26,720

EBIDTA 10,110 16,392 4,593 7,972 1,590 2,472

% margin 15.0% 18.2% 10.7% 13.4% 7.4% 9.2%

Depreciation 1,485 1,650 749 892 242 294

Interest 2,273 2,434 1,129 1,211 390 415

PBT 6,352 12,308 2,715 5,869 959 1,763

PAT 4,129 8,000 1,955 4,226 633 1,164

Source : HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 6

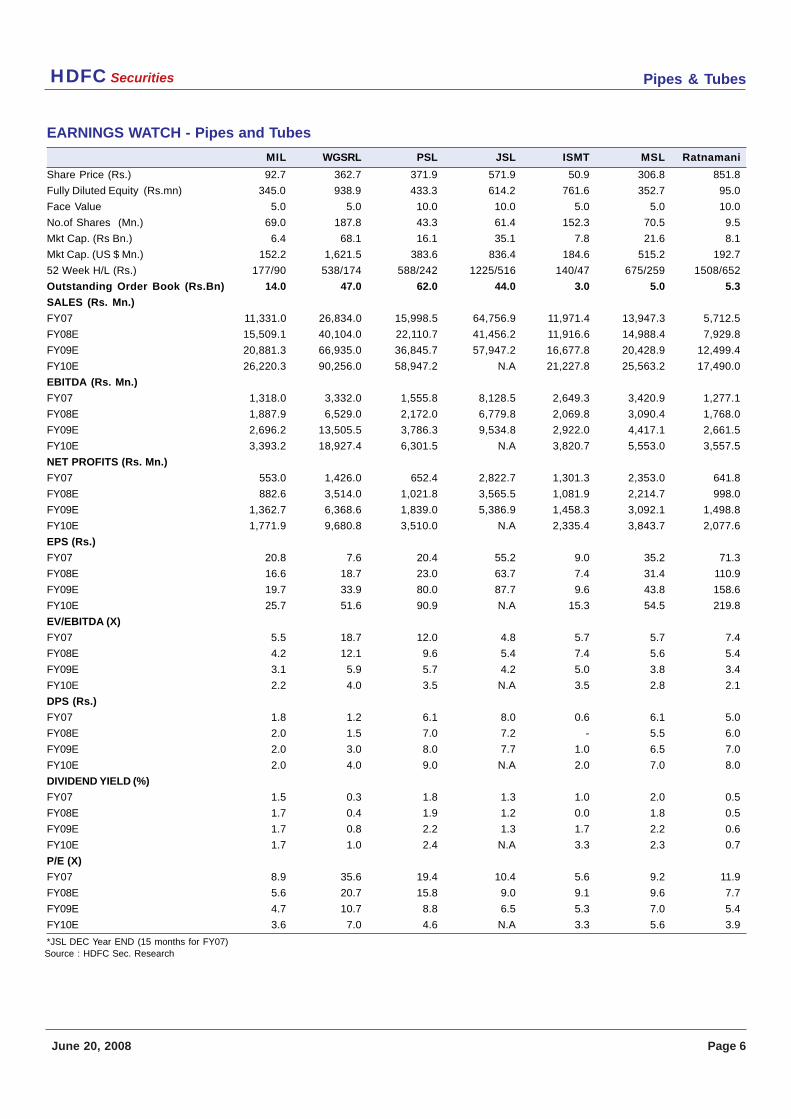

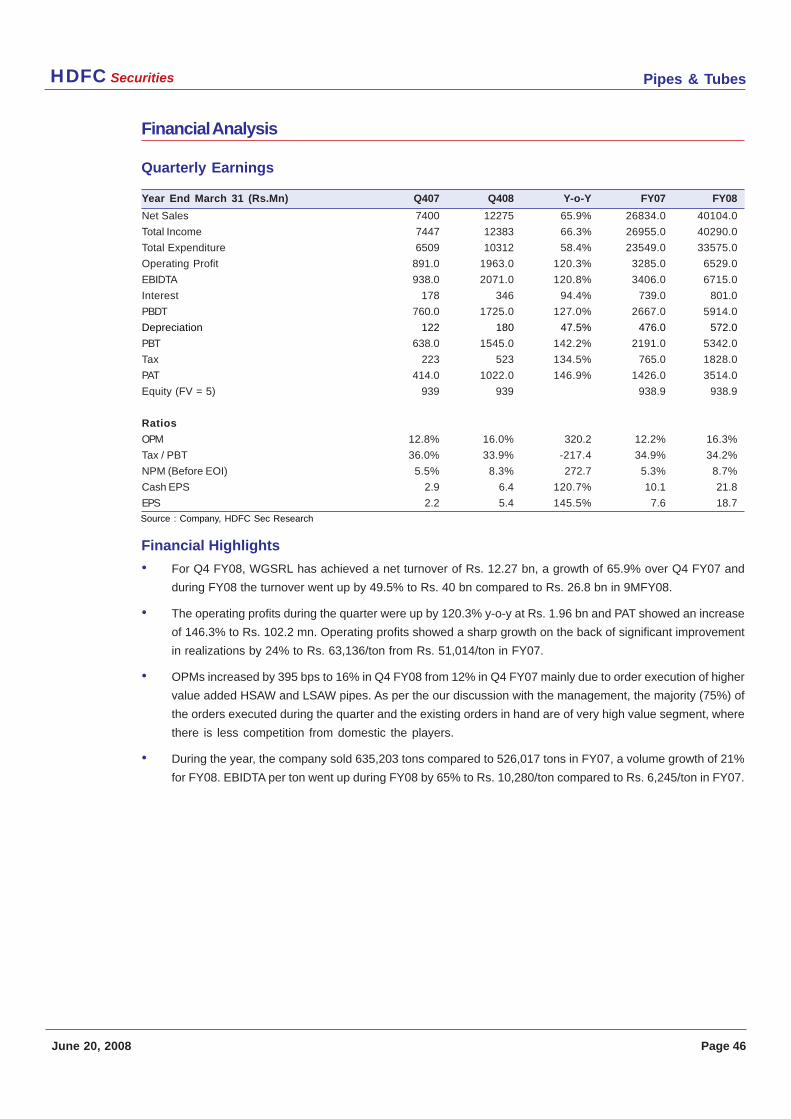

EARNINGS WATCH - Pipes and Tubes

MIL WGSRL PSL JSL ISMT MSL Ratnamani

Share Price (Rs.) 92.7 362.7 371.9 571.9 50.9 306.8 851.8

Fully Diluted Equity (Rs.mn) 345.0 938.9 433.3 614.2 761.6 352.7 95.0

Face Value 5.0 5.0 10.0 10.0 5.0 5.0 10.0

No.of Shares (Mn.) 69.0 187.8 43.3 61.4 152.3 70.5 9.5

Mkt Cap. (Rs Bn.) 6.4 68.1 16.1 35.1 7.8 21.6 8.1

Mkt Cap. (US $ Mn.) 152.2 1,621.5 383.6 836.4 184.6 515.2 192.7

52 Week H/L (Rs.) 177/90 538/174 588/242 1225/516 140/47 675/259 1508/652

Outstanding Order Book (Rs.Bn) 14.0 47.0 62.0 44.0 3.0 5.0 5.3

SALES (Rs. Mn.)

FY07 11,331.0 26,834.0 15,998.5 64,756.9 11,971.4 13,947.3 5,712.5

FY08E 15,509.1 40,104.0 22,110.7 41,456.2 11,916.6 14,988.4 7,929.8

FY09E 20,881.3 66,935.0 36,845.7 57,947.2 16,677.8 20,428.9 12,499.4

FY10E 26,220.3 90,256.0 58,947.2 N.A 21,227.8 25,563.2 17,490.0

EBITDA (Rs. Mn.)

FY07 1,318.0 3,332.0 1,555.8 8,128.5 2,649.3 3,420.9 1,277.1

FY08E 1,887.9 6,529.0 2,172.0 6,779.8 2,069.8 3,090.4 1,768.0

FY09E 2,696.2 13,505.5 3,786.3 9,534.8 2,922.0 4,417.1 2,661.5

FY10E 3,393.2 18,927.4 6,301.5 N.A 3,820.7 5,553.0 3,557.5

NET PROFITS (Rs. Mn.)

FY07 553.0 1,426.0 652.4 2,822.7 1,301.3 2,353.0 641.8

FY08E 882.6 3,514.0 1,021.8 3,565.5 1,081.9 2,214.7 998.0

FY09E 1,362.7 6,368.6 1,839.0 5,386.9 1,458.3 3,092.1 1,498.8

FY10E 1,771.9 9,680.8 3,510.0 N.A 2,335.4 3,843.7 2,077.6

EPS (Rs.)

FY07 20.8 7.6 20.4 55.2 9.0 35.2 71.3

FY08E 16.6 18.7 23.0 63.7 7.4 31.4 110.9

FY09E 19.7 33.9 80.0 87.7 9.6 43.8 158.6

FY10E 25.7 51.6 90.9 N.A 15.3 54.5 219.8

EV/EBITDA (X)

FY07 5.5 18.7 12.0 4.8 5.7 5.7 7.4

FY08E 4.2 12.1 9.6 5.4 7.4 5.6 5.4

FY09E 3.1 5.9 5.7 4.2 5.0 3.8 3.4

FY10E 2.2 4.0 3.5 N.A 3.5 2.8 2.1

DPS (Rs.)

FY07 1.8 1.2 6.1 8.0 0.6 6.1 5.0

FY08E 2.0 1.5 7.0 7.2 - 5.5 6.0

FY09E 2.0 3.0 8.0 7.7 1.0 6.5 7.0

FY10E 2.0 4.0 9.0 N.A 2.0 7.0 8.0

DIVIDEND YIELD (%)

FY07 1.5 0.3 1.8 1.3 1.0 2.0 0.5

FY08E 1.7 0.4 1.9 1.2 0.0 1.8 0.5

FY09E 1.7 0.8 2.2 1.3 1.7 2.2 0.6

FY10E 1.7 1.0 2.4 N.A 3.3 2.3 0.7

P/E (X)

FY07 8.9 35.6 19.4 10.4 5.6 9.2 11.9

FY08E 5.6 20.7 15.8 9.0 9.1 9.6 7.7

FY09E 4.7 10.7 8.8 6.5 5.3 7.0 5.4

FY10E 3.6 7.0 4.6 N.A 3.3 5.6 3.9

*JSL DEC Year END (15 months for FY07)Source : HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 7

Co

mp

an

y N

am

eM

ark

et

Ca

p(B

n)

S

ale

s (B

n)

E

BIT

DA

Ma

rgin

E

V/E

BIT

DA

P

/E

Cu

rre

nt

20

07

20

08

20

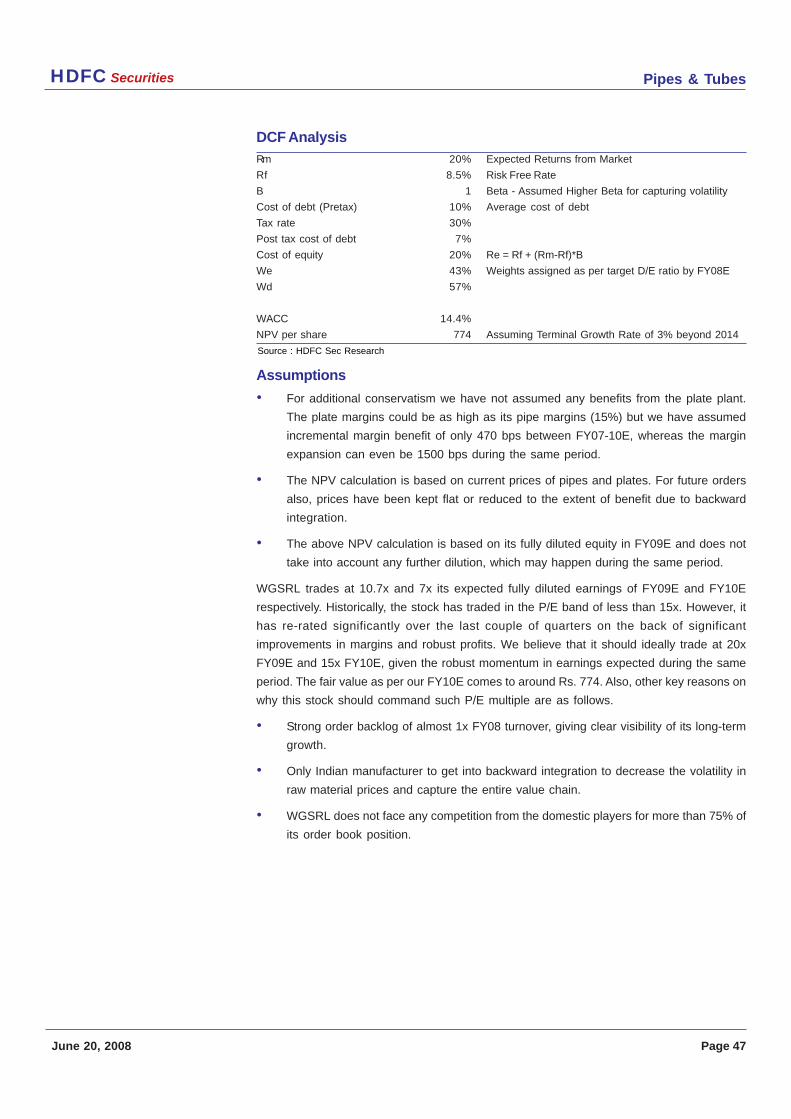

09

E2

01

0E

20

07

20

08

20

09

(E)

20

10

(E)

20

07

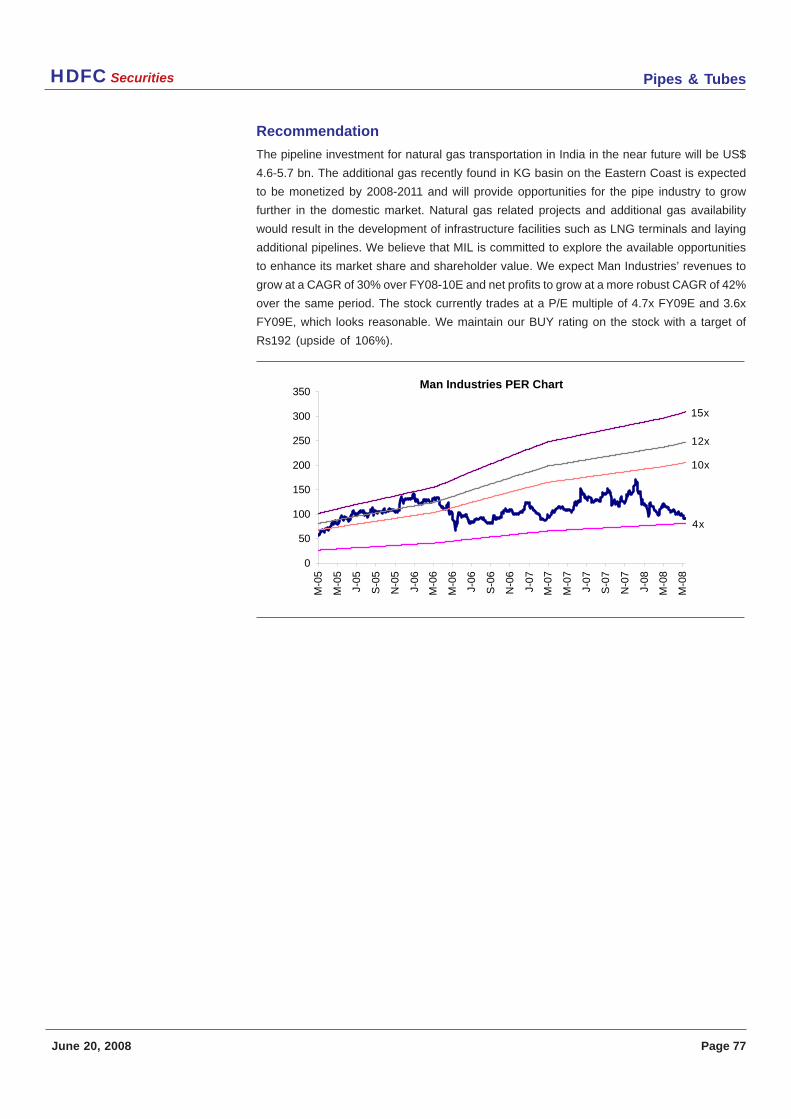

20

08

20

09

(E)

20

10

(E)

20

07

20

08

20

09

(E)

20

10

(E)

De

ve

lop

ed

ma

rke

ts

TM

K2

94

.22

16

2.0

52

17

.88

25

3.2

12

74

.14

19

.5%

23

.1%

23

.0%

23

.2%

9.2

17

.17

6.1

95

.67

8.1

65

.17

7.0

75

.73

Ten

ari

s1

62

6.6

54

10

.97

48

4.5

35

06

.16

54

7.2

33

4.2

%3

4.2

%3

3.2

%3

2.7

%11

.62

10

.73

10

.56

9.9

31

9.0

81

7.5

81

5.8

91

5.3

1

Va

llou

rec

73

2.0

63

76

.31

41

8.4

54

32

.94

45

9.0

82

8.6

%2

4.4

%2

4.9

%2

5.6

%6

.15

7.0

76

.70

6.1

41

0.8

51

2.4

411

.70

10

.58

Gra

nt

Pri

de

co2

72

.34

84

.83

91

.50

96

.04

NA

39

.7%

40

.2%

49

.4%

NA

NA

NA

NA

NA

NA

NA

NA

NA

Tu

ba

ce

x6

5.9

74

1.0

84

8.5

85

1.0

85

1.5

91

5.0

%1

6.9

%1

8.7

%1

8.6

%11

.07

9.4

48

.09

8.0

61

7.3

911

.44

11.3

711

.63

Ste

elm

ak

ers

wit

h p

ipe

Pro

du

cti

on

Arc

elo

r M

itta

l6

41

9.6

64

09

6.7

05

28

9.8

65

42

8.8

85

57

8.2

31

8.9

%1

8.4

%1

8.0

%1

8.8

%9

.33

8.0

28

.00

7.4

51

4.1

611

.38

10

.98

9.6

7

US

Ste

el

93

0.7

66

58

.06

98

0.6

81

02

0.3

41

03

9.3

911

.2%

13

.9%

14

.2%

14

.4%

13

.25

7.6

37

.26

6.9

81

9.5

71

2.6

211

.59

13

.02

Sa

lzg

itte

r5

24

.56

62

2.0

28

00

.06

79

5.7

78

09

.41

14

.8%

12

.4%

12

.7%

12

.1%

4.1

94

.21

4.1

34

.22

9.1

38

.66

8.8

88

.99

Sa

nd

vik

78

7.5

35

31

.81

65

2.3

16

87

.75

70

0.3

62

0.7

%2

0.4

%2

0.6

%2

1.3

%7

.77

7.3

46

.89

6.5

111

.68

11.4

91

0.3

59

.91

Vo

est

alp

ine

57

5.9

43

96

.88

69

7.1

08

03

.84

83

0.8

41

8.7

%1

6.1

%1

8.1

%1

8.0

%9

.30

6.4

05

.74

5.5

511

.41

9.2

88

.87

8.3

5

Ind

ian

Pla

ye

rs

Jin

da

l S

aw

35

.13

64

.76

41

.46

57

.95

NA

12

%1

6%

16

.0%

NA

4.8

25

.45

4.2

5N

A1

0.3

68

.98

6.5

2N

A

Ra

tna

ma

ni

Me

tals

an

d T

ub

es

Ltd

.8

.09

5.7

17

.93

12

.50

17

.49

22

%2

2%

21

%2

0%

7.3

65

.43

3.3

82

.14

11.9

57

.68

5.3

73

.87

PS

L L

imit

ed

16

.11

16

.00

22

.11

36

.85

58

.95

10

%1

0%

10

%11

%11

.96

9.5

95

.71

3.5

11

9.4

01

5.7

78

.76

4.5

9

ISM

T7

.75

11.9

711

.92

16

.68

21

.23

22

%1

7%

18

%1

8%

5.6

67

.40

4.9

73

.46

5.6

59

.09

5.3

23

.32

Ma

ha

rash

tra

Se

am

less

21

.64

13

.95

14

.90

20

.43

25

.56

24

%2

1%

22

%2

2%

5.6

65

.63

3.8

02

.77

9.1

79

.63

7.0

05

.63

We

lsp

un

Gu

jara

t S

tah

l R

oh

ren

68

.10

26

.83

40

.10

66

.94

90

.26

12

%1

7%

20

%2

1%

18

.74

12

.14

5.9

24

.02

35

.57

20

.70

10

.69

7.0

3

Ma

n I

nd

ust

rie

s6

.39

11.3

31

5.5

12

0.8

92

6.2

21

2%

12

%1

3%

13

%5

.51

4.2

33

.13

2.2

38

.93

5.5

94

.69

3.6

1

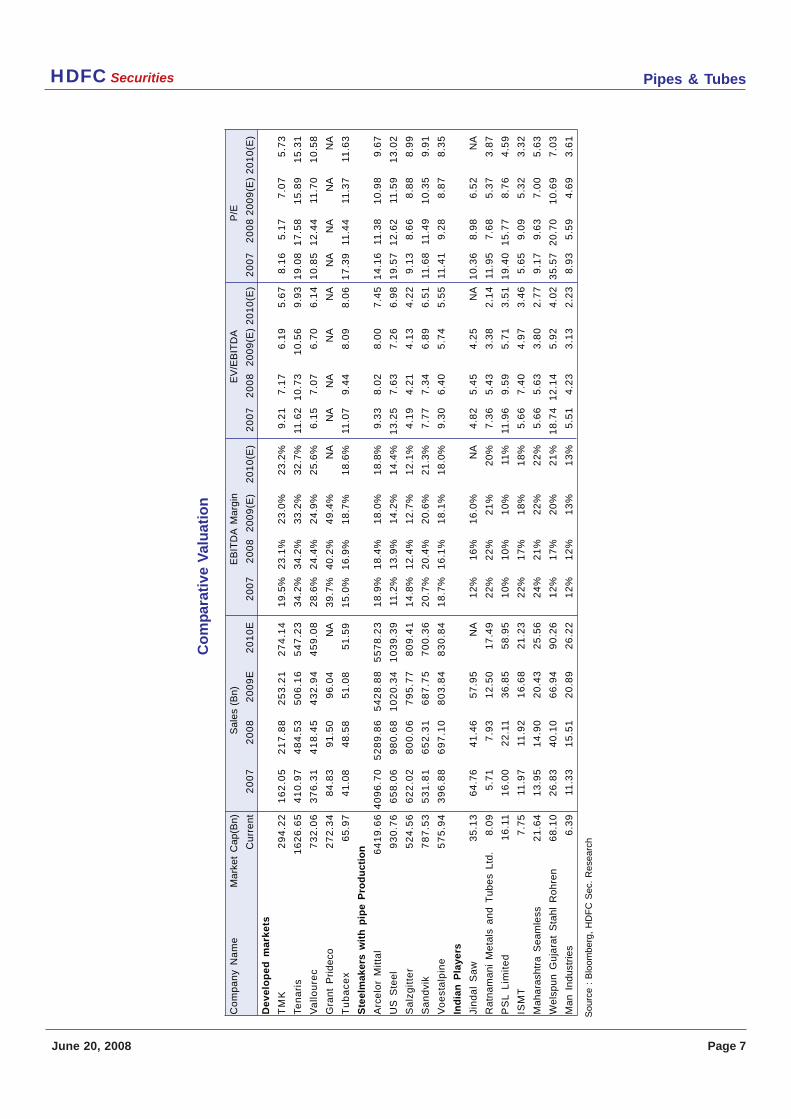

Co

mp

arat

ive

Val

uat

ion

Sou

rce

: B

loom

berg

, H

DF

C S

ec.

Res

earc

h

Pipes & TubesHDFC Securities

June 20, 2008 Page 8

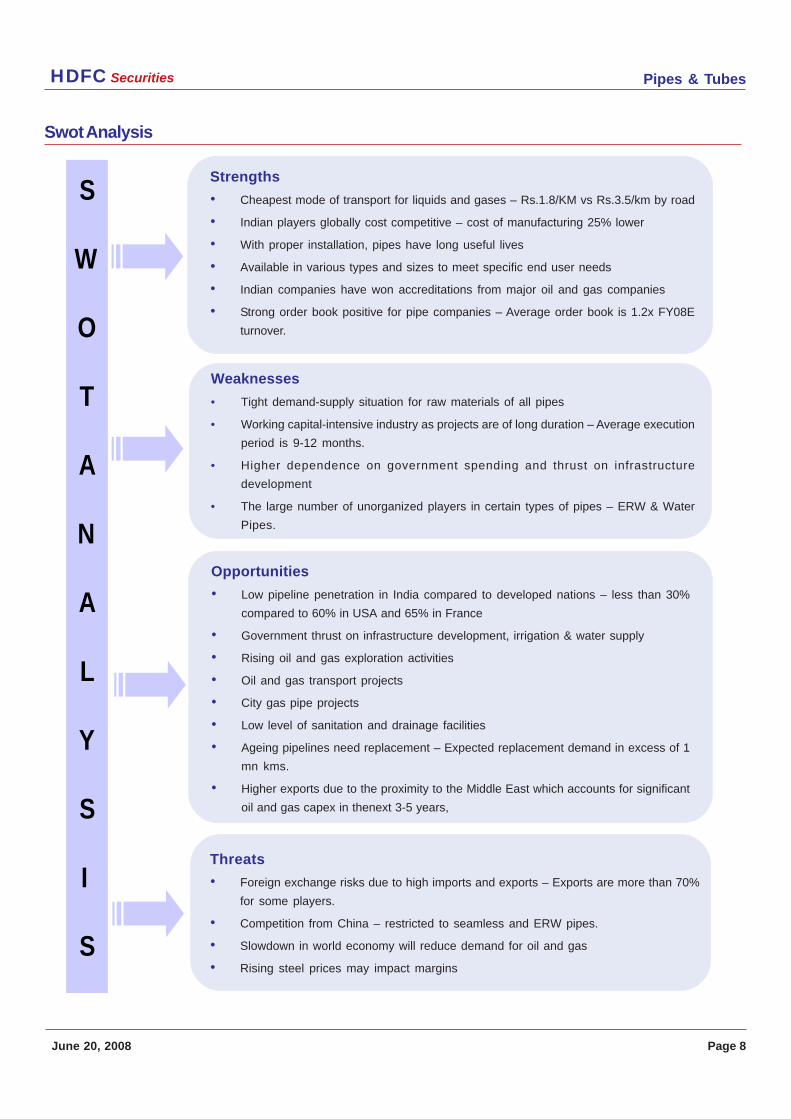

Swot Analysis

S

W

O

T

A

N

A L

Y

S I

S

Weaknesses

• Tight demand-supply situation for raw materials of all pipes

• Working capital-intensive industry as projects are of long duration – Average execution

period is 9-12 months.

• Higher dependence on government spending and thrust on infrastructure

development

• The large number of unorganized players in certain types of pipes – ERW & Water

Pipes.

Strengths

• Cheapest mode of transport for liquids and gases – Rs.1.8/KM vs Rs.3.5/km by road

• Indian players globally cost competitive – cost of manufacturing 25% lower

• With proper installation, pipes have long useful lives

• Available in various types and sizes to meet specific end user needs

• Indian companies have won accreditations from major oil and gas companies

• Strong order book positive for pipe companies – Average order book is 1.2x FY08E

turnover.

Opportunities

• Low pipeline penetration in India compared to developed nations – less than 30%

compared to 60% in USA and 65% in France

• Government thrust on infrastructure development, irrigation & water supply

• Rising oil and gas exploration activities

• Oil and gas transport projects

• City gas pipe projects

• Low level of sanitation and drainage facilities

• Ageing pipelines need replacement – Expected replacement demand in excess of 1

mn kms.

• Higher exports due to the proximity to the Middle East which accounts for significant

oil and gas capex in thenext 3-5 years,

Threats

• Foreign exchange risks due to high imports and exports – Exports are more than 70%

for some players.

• Competition from China – restricted to seamless and ERW pipes.

• Slowdown in world economy will reduce demand for oil and gas

• Rising steel prices may impact margins

Pipes & TubesHDFC Securities

June 20, 2008 Page 9

Industry Matrix

*Avg EDITDA/ton for the sector

Jindal Saw Man Industries PSL WGSRL Mah Seamless ISMT Total

Capacity (tonnes)

2007 1,250,000 600,000 1,100,000 930,000 550,000 158,000 4,588,000

2008E 1,400,000 1,000,000 1,175,000 1,000,000 550,000 158,000 5,283,000

2009E 2,000,000 1,000,000 1,475,000 1,300,000 600,000 475,000 6,850,000

2010E 2,000,000 1,000,000 1,475,000 1,750,000 700,000 475,000 7,400,000

CAGR (%) 18.4%

Production (tonnes)

2007 644,101 246,424 271,075 500,969 314,149 408,532 2,385,250

2008E 1,038,666 330,000 329,000 650,000 343,000 391,000 3,081,666

2009E 765,000 420,000 545,750 850,000 410,000 440,000 3,430,750

2010E 1,100,000 500,000 811,250 1,050,000 500,000 510,000 4,471,250

CAGR (%) 20.5%

EBITDA (Rs.Mn)

2007 4,099 1,318 1,514 3,285 3,421 2,649 16,286

2008E 8,128 1,888 2,172 6,529 3,090 2,101 23,909

2009E 6,780 2,696 3,786 13,506 4,417 2,922 34,107

2010E 9,535 3,393 6,302 18,927 5,553 3,821 47,531

CAGR (%) 41.0%

EBITDA/Tonne (Rs)

2007 6,364 5,348 5,584 6,557 10,889 6,485 6,871

2008E 7,826 5,721 6,602 10,045 9,010 5,373 7,429

2009E 8,863 6,420 6,938 15,889 10,773 6,641 9,254

2010E 8,668 6,786 7,768 18,026 11,106 7,492 9,974

CAGR (%) 15.9%

Source : HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 10

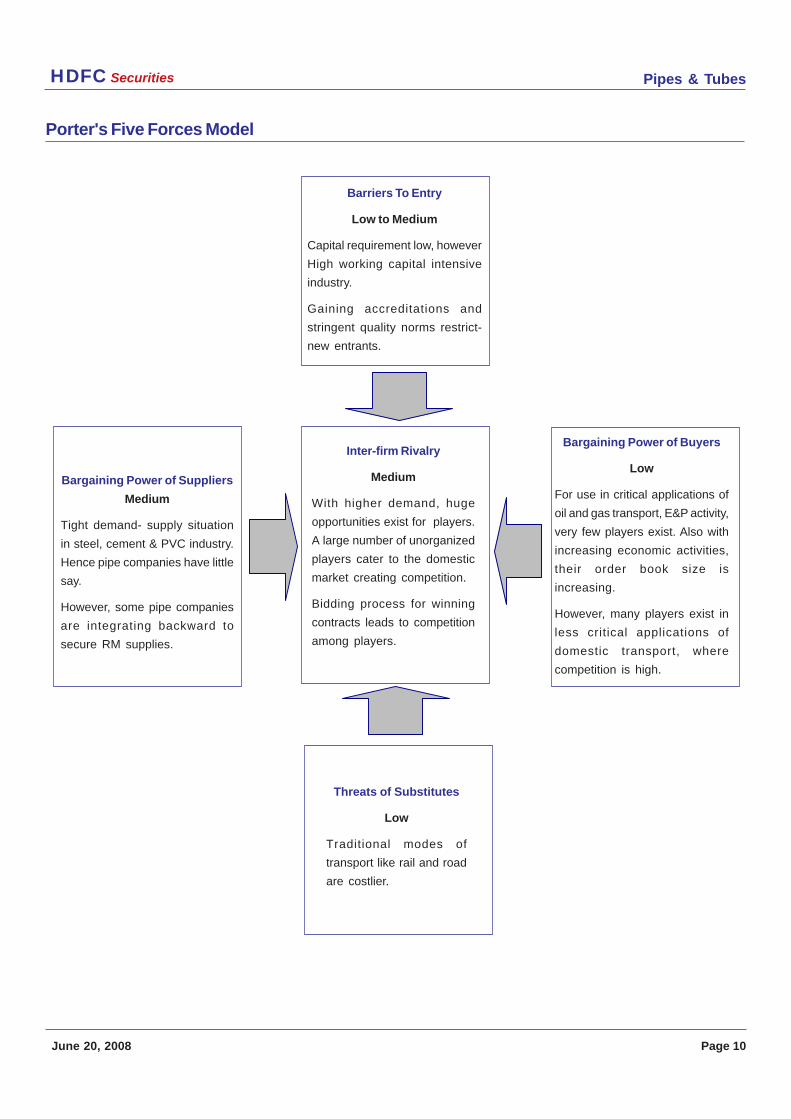

Porter's Five Forces Model

Barriers To Entry

Low to Medium

Capital requirement low, however

High working capital intensive

industry.

Gaining accreditations and

stringent quality norms restrict-

new entrants.

Bargaining Power of Suppliers

Medium

Tight demand- supply situation

in steel, cement & PVC industry.

Hence pipe companies have little

say.

However, some pipe companies

are integrating backward to

secure RM supplies.

Inter-firm Rivalry

Medium

With higher demand, huge

opportunities exist for players.

A large number of unorganized

players cater to the domestic

market creating competition.

Bidding process for winning

contracts leads to competition

among players.

Bargaining Power of Buyers

Low

For use in critical applications of

oil and gas transport, E&P activity,

very few players exist. Also with

increasing economic activities,

their order book size is

increasing.

However, many players exist in

less critical applications of

domestic transport, where

competition is high.

Threats of Substitutes

Low

Traditional modes of

transport like rail and road

are costlier.

Pipes & TubesHDFC Securities

June 20, 2008 Page 11

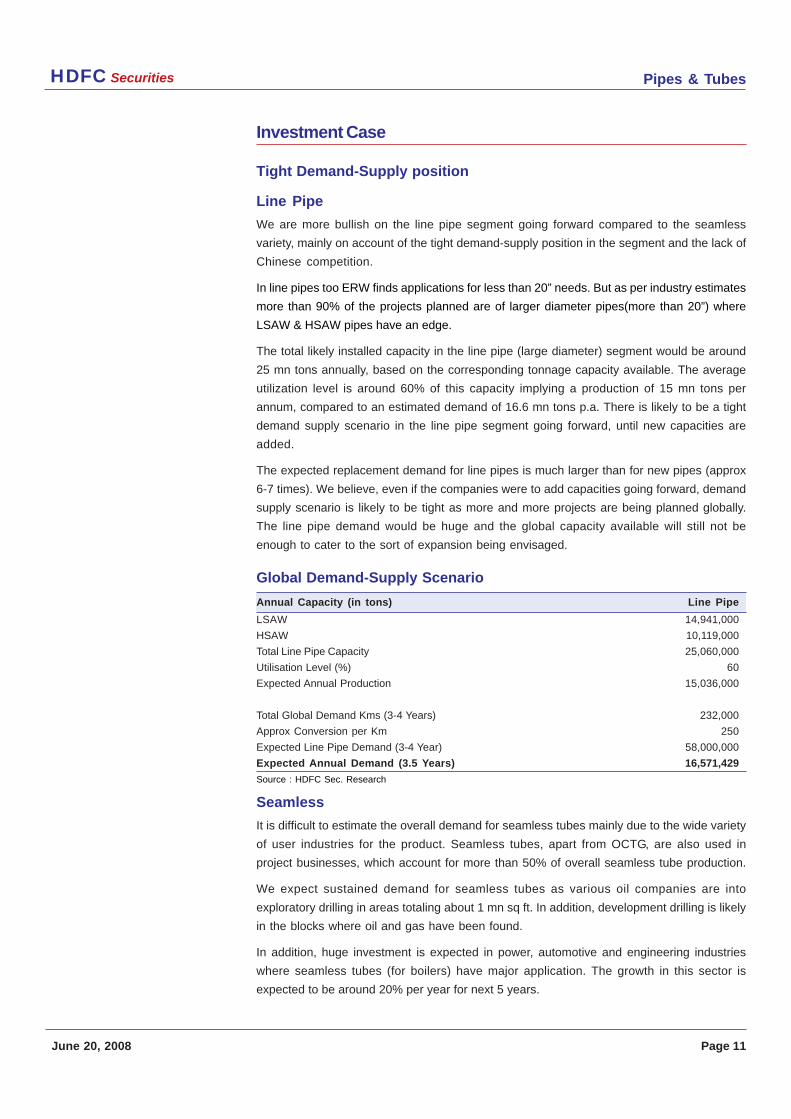

Investment Case

Tight Demand-Supply position

Line Pipe

We are more bullish on the line pipe segment going forward compared to the seamless

variety, mainly on account of the tight demand-supply position in the segment and the lack of

Chinese competition.

In line pipes too ERW finds applications for less than 20” needs. But as per industry estimates

more than 90% of the projects planned are of larger diameter pipes(more than 20”) where

LSAW & HSAW pipes have an edge.

The total likely installed capacity in the line pipe (large diameter) segment would be around

25 mn tons annually, based on the corresponding tonnage capacity available. The average

utilization level is around 60% of this capacity implying a production of 15 mn tons per

annum, compared to an estimated demand of 16.6 mn tons p.a. There is likely to be a tight

demand supply scenario in the line pipe segment going forward, until new capacities are

added.

The expected replacement demand for line pipes is much larger than for new pipes (approx

6-7 times). We believe, even if the companies were to add capacities going forward, demand

supply scenario is likely to be tight as more and more projects are being planned globally.

The line pipe demand would be huge and the global capacity available will still not be

enough to cater to the sort of expansion being envisaged.

Global Demand-Supply Scenario

Annual Capacity (in tons) Line Pipe

LSAW 14,941,000

HSAW 10,119,000

Total Line Pipe Capacity 25,060,000

Utilisation Level (%) 60

Expected Annual Production 15,036,000

Total Global Demand Kms (3-4 Years) 232,000

Approx Conversion per Km 250

Expected Line Pipe Demand (3-4 Year) 58,000,000

Expected Annual Demand (3.5 Years) 16,571,429

Seamless

It is difficult to estimate the overall demand for seamless tubes mainly due to the wide variety

of user industries for the product. Seamless tubes, apart from OCTG, are also used in

project businesses, which account for more than 50% of overall seamless tube production.

We expect sustained demand for seamless tubes as various oil companies are into

exploratory drilling in areas totaling about 1 mn sq ft. In addition, development drilling is likely

in the blocks where oil and gas have been found.

In addition, huge investment is expected in power, automotive and engineering industries

where seamless tubes (for boilers) have major application. The growth in this sector is

expected to be around 20% per year for next 5 years.

Source : HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 12

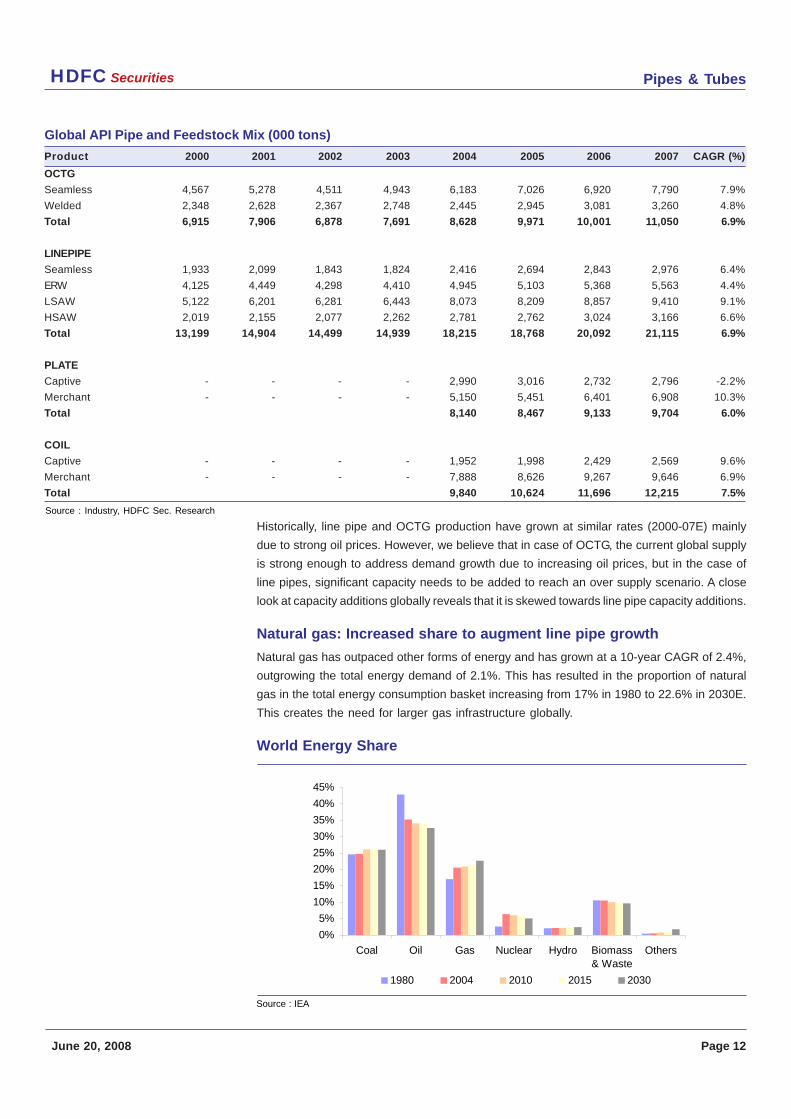

Product 2000 2001 2002 2003 2004 2005 2006 2007 CAGR (%)

OCTG

Seamless 4,567 5,278 4,511 4,943 6,183 7,026 6,920 7,790 7.9%

Welded 2,348 2,628 2,367 2,748 2,445 2,945 3,081 3,260 4.8%

Total 6,915 7,906 6,878 7,691 8,628 9,971 10,001 11,050 6.9%

LINEPIPE

Seamless 1,933 2,099 1,843 1,824 2,416 2,694 2,843 2,976 6.4%

ERW 4,125 4,449 4,298 4,410 4,945 5,103 5,368 5,563 4.4%

LSAW 5,122 6,201 6,281 6,443 8,073 8,209 8,857 9,410 9.1%

HSAW 2,019 2,155 2,077 2,262 2,781 2,762 3,024 3,166 6.6%

Total 13,199 14,904 14,499 14,939 18,215 18,768 20,092 21,115 6.9%

PLATE

Captive - - - - 2,990 3,016 2,732 2,796 -2.2%

Merchant - - - - 5,150 5,451 6,401 6,908 10.3%

Total 8,140 8,467 9,133 9,704 6.0%

COIL

Captive - - - - 1,952 1,998 2,429 2,569 9.6%

Merchant - - - - 7,888 8,626 9,267 9,646 6.9%

Total 9,840 10,624 11,696 12,215 7.5%

Global API Pipe and Feedstock Mix (000 tons)

Historically, line pipe and OCTG production have grown at similar rates (2000-07E) mainly

due to strong oil prices. However, we believe that in case of OCTG, the current global supply

is strong enough to address demand growth due to increasing oil prices, but in the case of

line pipes, significant capacity needs to be added to reach an over supply scenario. A close

look at capacity additions globally reveals that it is skewed towards line pipe capacity additions.

Natural gas: Increased share to augment line pipe growth

Natural gas has outpaced other forms of energy and has grown at a 10-year CAGR of 2.4%,

outgrowing the total energy demand of 2.1%. This has resulted in the proportion of natural

gas in the total energy consumption basket increasing from 17% in 1980 to 22.6% in 2030E.

This creates the need for larger gas infrastructure globally.

World Energy Share

Source : Industry, HDFC Sec. Research

Source : IEA

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Coal Oil Gas Nuclear Hydro Biomass& Waste

Others

1980 2004 2010 2015 2030

Pipes & TubesHDFC Securities

June 20, 2008 Page 13

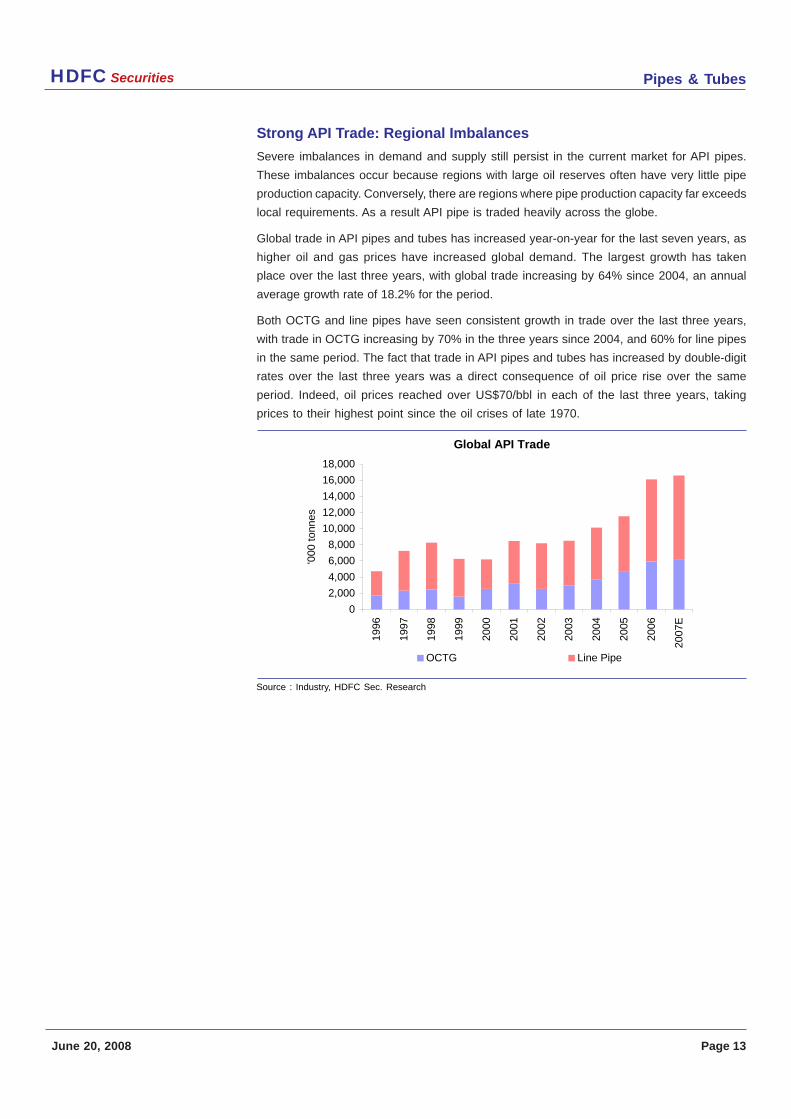

Strong API Trade: Regional Imbalances

Severe imbalances in demand and supply still persist in the current market for API pipes.

These imbalances occur because regions with large oil reserves often have very little pipe

production capacity. Conversely, there are regions where pipe production capacity far exceeds

local requirements. As a result API pipe is traded heavily across the globe.

Global trade in API pipes and tubes has increased year-on-year for the last seven years, as

higher oil and gas prices have increased global demand. The largest growth has taken

place over the last three years, with global trade increasing by 64% since 2004, an annual

average growth rate of 18.2% for the period.

Both OCTG and line pipes have seen consistent growth in trade over the last three years,

with trade in OCTG increasing by 70% in the three years since 2004, and 60% for line pipes

in the same period. The fact that trade in API pipes and tubes has increased by double-digit

rates over the last three years was a direct consequence of oil price rise over the same

period. Indeed, oil prices reached over US$70/bbl in each of the last three years, taking

prices to their highest point since the oil crises of late 1970.

Global API Trade

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

E

'000

ton

nes

OCTG Line Pipe

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 14

Industry Overview

The industry classified for pipes and tubes for our study includes

• Oil Country Tubular Goods (OCTG) Seamless & ERW.

• Line Pipes (LSAW/HSAW/ERW).

• Flat-rolled steel feedstock (Plate & Coil).

The basic distinction between OCTG and line pipe is one of end-use. OCTG consists of oil

and gas well tubing and casing, as well as drill pipe. Line pipe is fabricated into pipelines for

the transportation of oil, gas, and petroleum products. Together, these two families of products

are termed “API grade” pipes, because the American Petroleum Institute provides the

internationally accepted quality benchmark for such products and awards its certification to

most producers worldwide of these pipes.

Apart from API products, pipe mills globally may also produce a portion of their output as

pipes of different quality and for differing end-uses, from structural pipe to line pipe for the

transportation of water.

API Certifications

The primary certification obtained by most API product manufacturers across different products

includes.

• API 5CT for OCTG Tubing and Casing.

• API 5D for Drill Pipes.

• API 5L for Line Pipes.

Beyond the basic API 5CT, 5D or 5L standards, there are a variety of quality grades recognised

by the market, an increasing share of which have been developed by leading manufacturers

of API tubular products. The standard grade range for both OCTG and line pipes is based on

a number denoting the yield strength in thousands of pounds per square inch (ksi). Thus,

common OCTG grades range from H-40 to P-110, while line pipes range from X42 to X80,

apart from newer higher-strength grades such as X100 and X120.

OCTG

By application, OCTG subdivides into tubing, casing and drill pipes. Most mills manufacture

both tubing and casing.

Tubing is used to conduct the extracted oil and gas to the surface after drilling, while casing

provides an outside protection cover. Hence tubing has the smaller diameter. The common

steel industry definition is to classify as tubing OCTG up to 4.5", although some offshore oil

operators see the cut-off at 5".

Casing encompasses diameters above this, extending up to around 20" for the larger-

diameter OCTG. Drill Pipe is used to transmit rotary motion to the drill bit, and is the only type

of OCTG that is reusable. It is produced by a small number of mills and accounts for well

under 5% of overall OCTG output.

For casing and tubing, welded pipe competes with seamless, offering a generally lower cost

product, despite welded OCTG’s increased acceptance by the oil industry. Seamless products

still account for approximately two-thirds of the OCTG market. Unlike casing and tubing, drill

pipe is exclusively seamless because of the much greater strength required of this product.

Pipes & TubesHDFC Securities

June 20, 2008 Page 15

Line Pipe

Small Diameter

A very approximate distinction can be made between a “small-diameter” line pipe market,

up to around 20”, and the “large-diameter” market extending from 20” up to around 80”.

Broadly speaking, the two key types of pipes most suitable for the small-diameter segment

are seamless line pipes and electro-resistance welded (ERW) line pipes. It is worth noting

that ERW is also the manufacturing method used to make welded OCTG, and in a similar

way a seamless pipe mill is likely to be active both in OCTG and line pipe manufacture. The

presence of ERW and seamless pipes begin to decrease as the diameter rises above 20”

because of constraints inherent in the manufacturing method, and also because in the

welding of these pipes, coil width sets the limit on the diameter of the pipe. Until relatively

recently, 16” was the upper limit for ERW pipes, but the increasing availability of wide coils

has prompted an upgrade in ERW diameter capabilities.

Currently, many ERW pipe mills worldwide can produce to diameters of 20”; some mills’

range extend to 24” and in two cases– JFE in Japan and Hysco (formerly known as Hyundai

Pipe) in South Korea – pipes can be produced up to 26”. To further stress upon the absence

of clear boundaries, one of the key large diameter pipe technologies, LSAW, can be used to

make pipes as small as 16”. Indeed, within a crossover band of diameters around 20” all

seamless and welded pipe techniques can compete.

Large Diameter

Most of the large diameter market for over 20” falls under two different welded pipe-

manufacturing techniques. The first of these is longitudinal submerged-arc welded (LSAW)

pipe, which uses reversing mill plate as the feedstock. The alternative is Spiral Welding

(HSAW), which gets around the limitations of coil width by welding the coil helicoidally.

LSAW pipe consists in turn of three competing technologies. By far, the most widely used to

date is the “UOE” process, denoting three major steps in the pipe’s forming, namely the

bending of the plate into a U shape, then a roughly circular section, with welding prior to the

pipe’s final expansion. The UOE process is considered the most efficient operationally, but

has relatively high capital costs and thus requires a minimum operating scale of some

500,000 tpy.

UOE thus competes as a solution with the Three-Roll-Bending Process, which is a popular

choice in some Asian and Middle Eastern countries. Roll-bending’s lower fixed costs allow

economical operation at much lower volumes than for UOE. A third, and much less widely

used alternative is Press Bending, a powerful but low-throughput process whose niche is to

be found in the manufacture of technically difficult sections of pipe.

Spiral-welded’s competitive position relative to LSAW, is in some ways akin to welded OCTG’s

to seamless. Coil-based manufacture of spiral-welded pipe can enjoy a cost advantage over

LSAW, which requires discrete plates. But for high pressure (typically offshore) applications,

LSAW pipe is generally preferred on performance grounds, but even so there is a segment

of the market, particularly for onshore oil and gas pipelines, where the two types of pipes can

compete. Even in such applications, however, the perception of some project specifiers that

spiral-welded’s larger seam area represents an increased risk will tend to offset its cost

advantage. There is no universally accepted method for measuring this risk, and regional

and company preferences will heavily influence the choice of material that is eventually used.

Pipes & TubesHDFC Securities

June 20, 2008 Page 16

LSAW vs. HSAW

So what will it be? Longitudinal welded (LSAW) or spiral welded (HSAW)? According to most

product users, LSAW is still the king. It’s made from plate, it’s thicker, and therefore can

handle the higher pressures often needed for natural gas pipelines. And many believe that

there will be more demand for natural gas than oil in the long term, especially if oil stays at

$100 a barrel.

The problem, of course, is that LSAW is much more expensive than HSAW. Let’s say

commodity plate sells on an average for about $1,400 a ton. HSAW pipe is made from hot

rolled coil, which sells for roughly $1,100 a ton.

HSAW has much thinner walls than LSAW, which increases the risk of ruptures and other

problems. But to reduce costs, some are willing to take on those added risks. And there have

also been reports that safety waivers could be approved for some new pipeline projects. By

reducing pressure requirements, the waivers may in effect allow producers to use HSAW

instead of LSAW for some pipeline projects.

HSAW also has other advantages. It can be made with a larger outside diameter than LSAW,

which means it can push more product through. And it can be made in longer sections. With

lower costs and potentially relaxed regulations, HSAW appears to be gaining traction globally.

Pipes & TubesHDFC Securities

June 20, 2008 Page 17

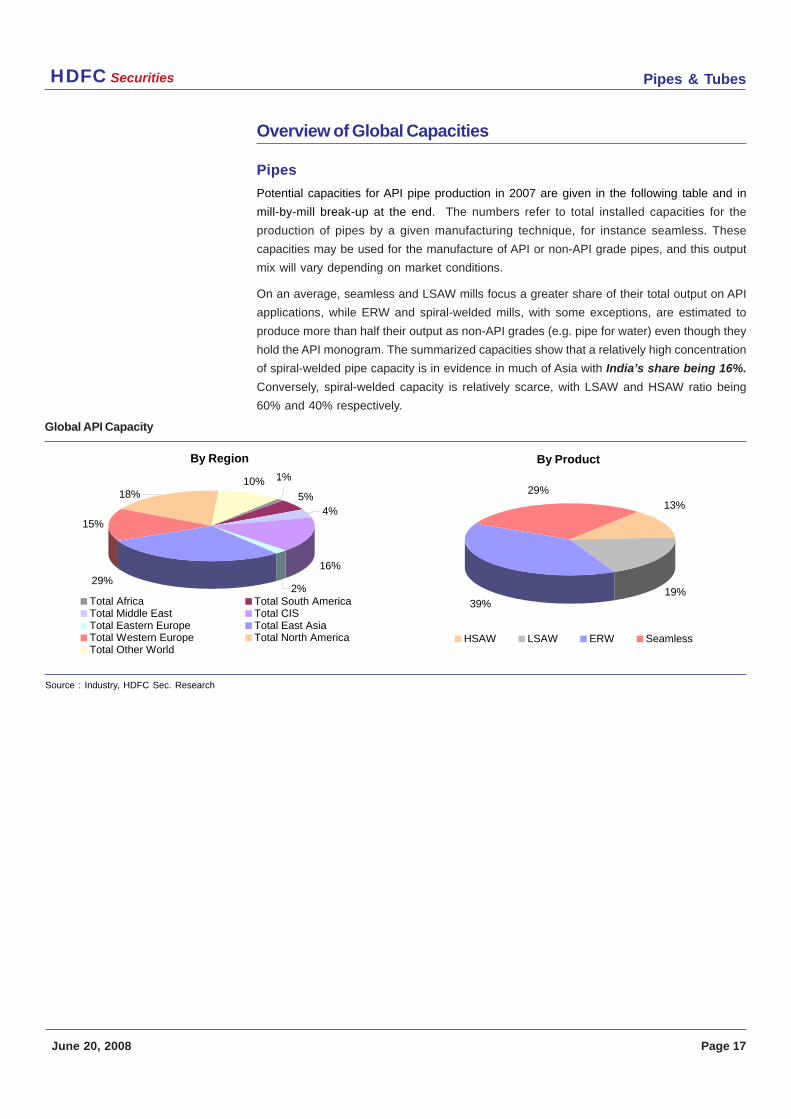

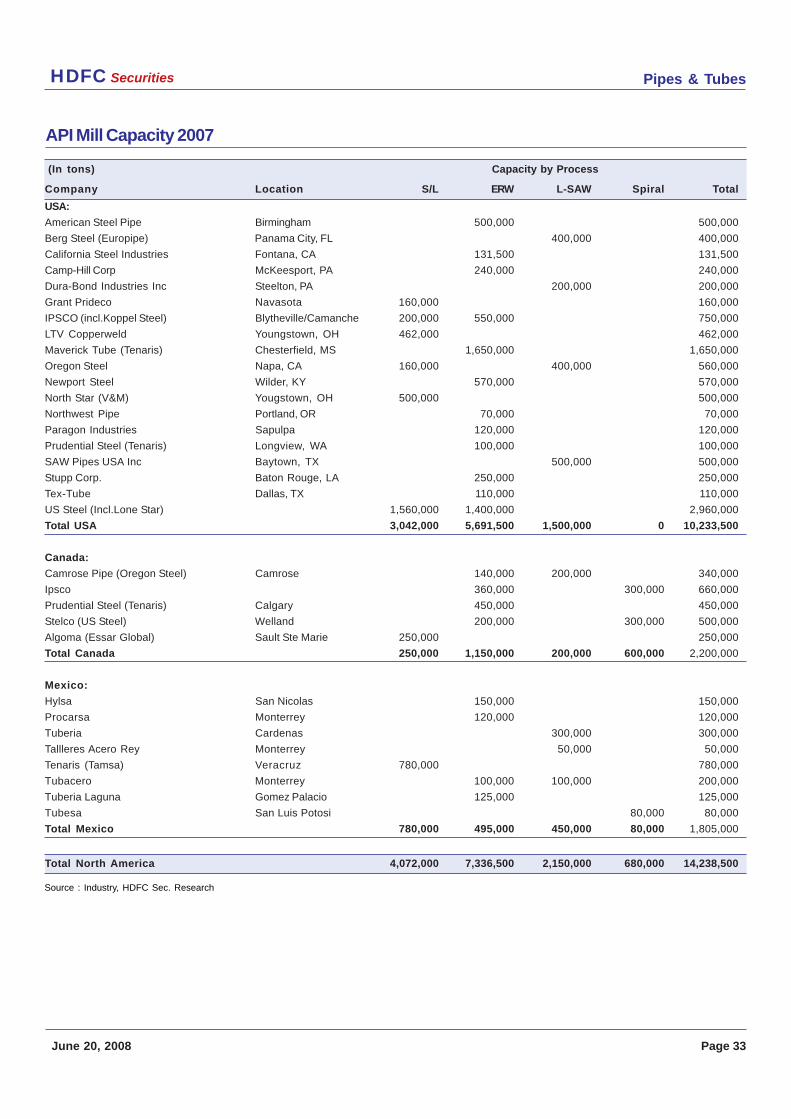

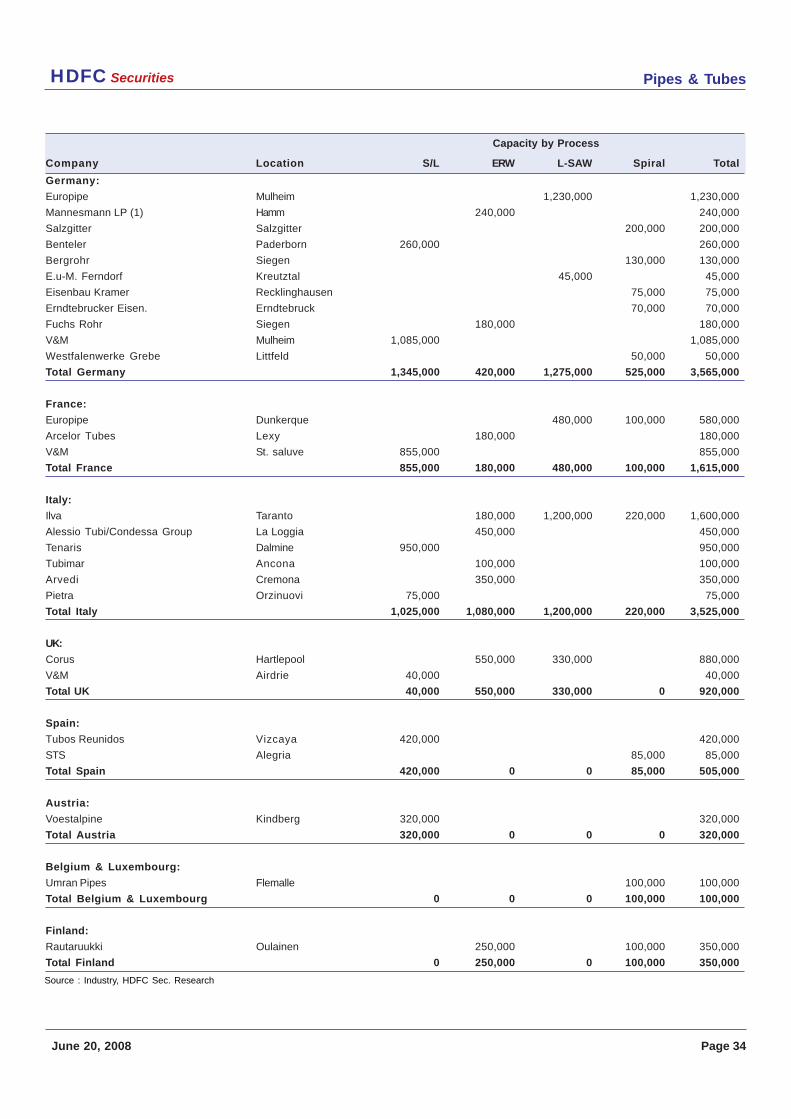

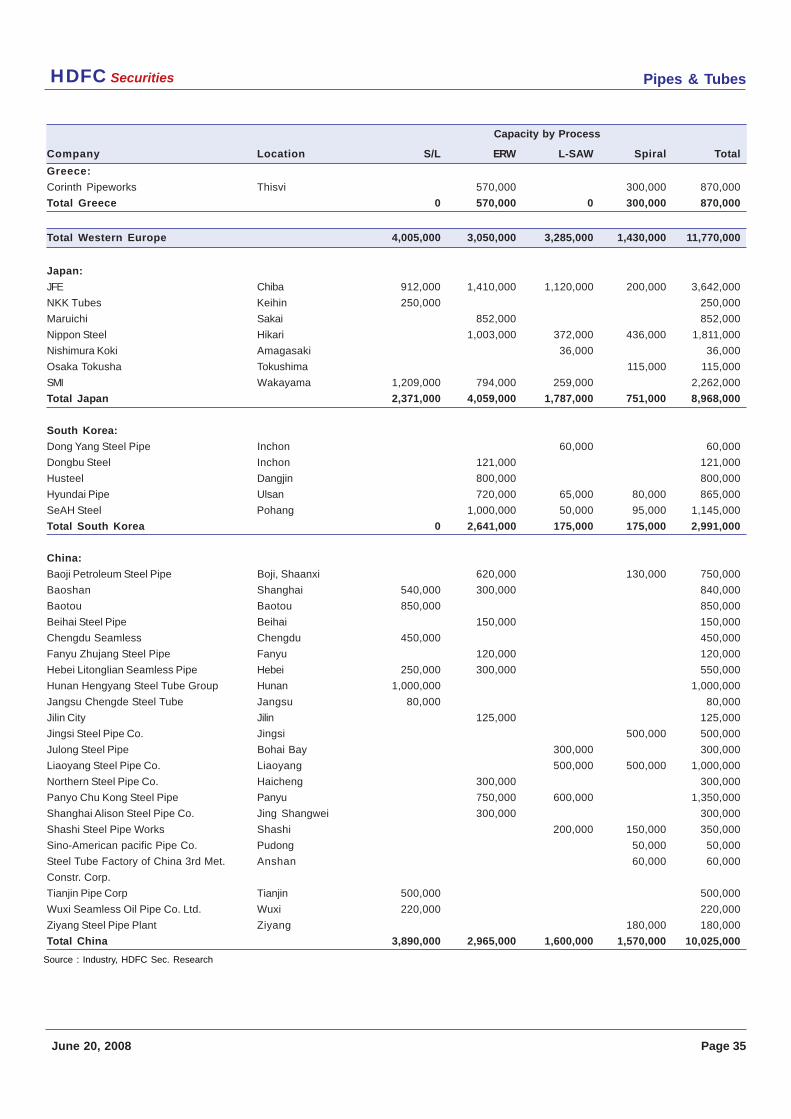

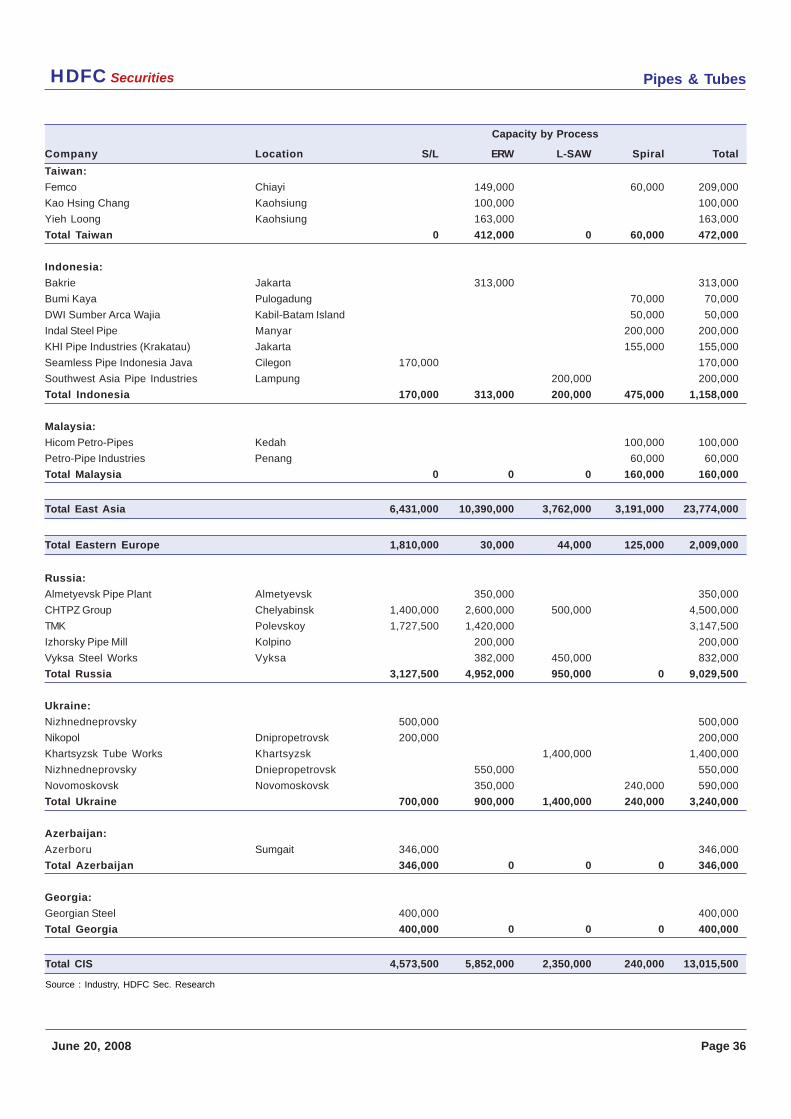

Overview of Global Capacities

Pipes

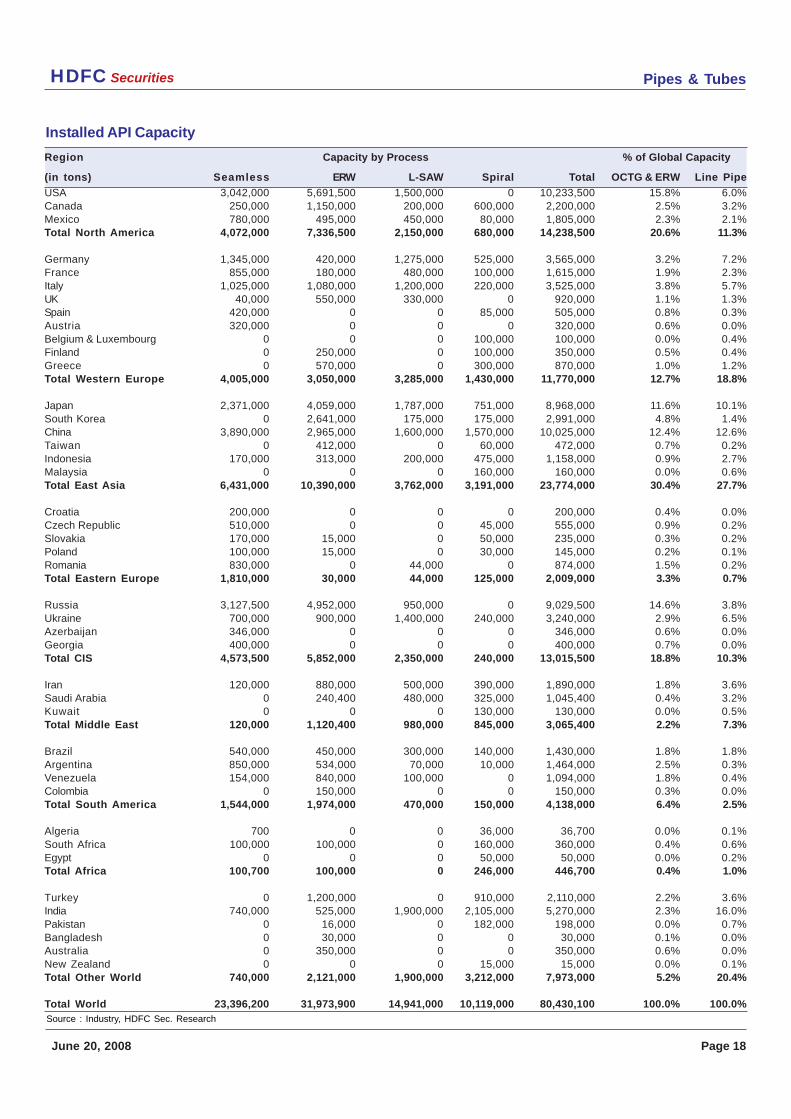

Potential capacities for API pipe production in 2007 are given in the following table and in

mill-by-mill break-up at the end. The numbers refer to total installed capacities for the

production of pipes by a given manufacturing technique, for instance seamless. These

capacities may be used for the manufacture of API or non-API grade pipes, and this output

mix will vary depending on market conditions.

On an average, seamless and LSAW mills focus a greater share of their total output on API

applications, while ERW and spiral-welded mills, with some exceptions, are estimated to

produce more than half their output as non-API grades (e.g. pipe for water) even though they

hold the API monogram. The summarized capacities show that a relatively high concentration

of spiral-welded pipe capacity is in evidence in much of Asia with India’s share being 16%.

Conversely, spiral-welded capacity is relatively scarce, with LSAW and HSAW ratio being

60% and 40% respectively.

By Region

15%

5%

1%

4%

16%

2%

10%18%

29%

Total Africa Total South AmericaTotal Middle East Total CISTotal Eastern Europe Total East AsiaTotal Western Europe Total North AmericaTotal Other World

By Product

29%

39%

13%

19%

HSAW LSAW ERW Seamless

Global API Capacity

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 18

Region Capacity by Process % of Global Capacity

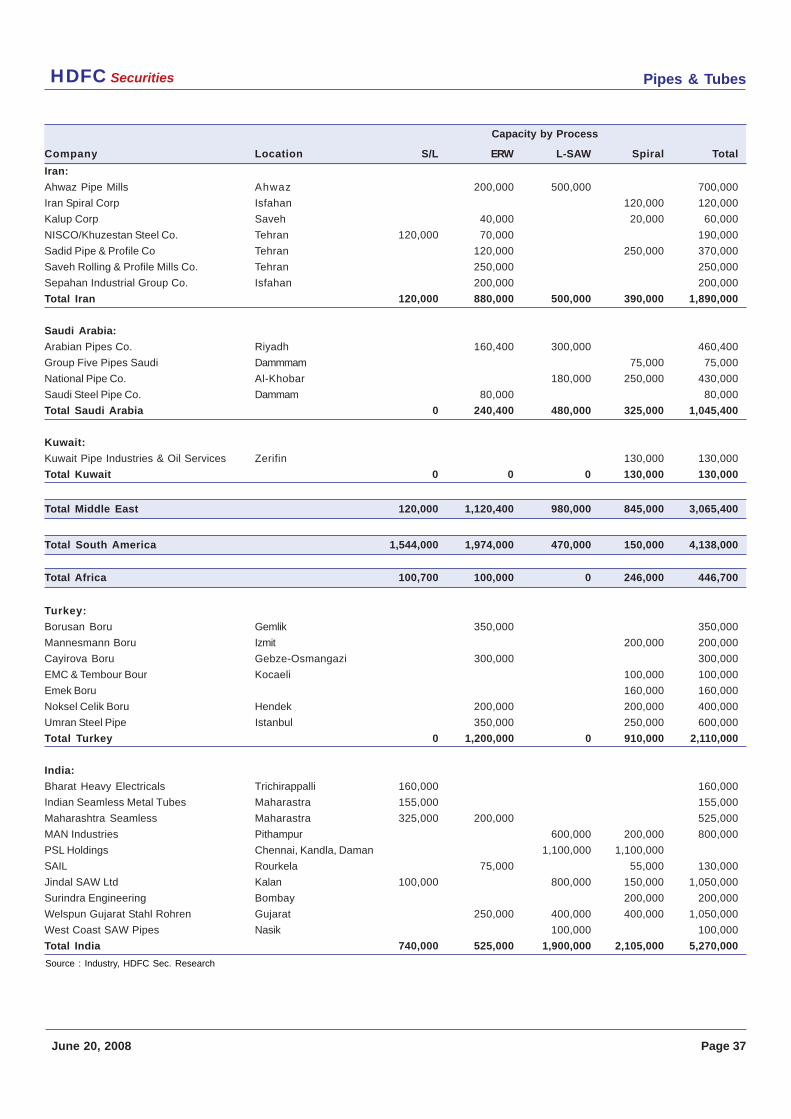

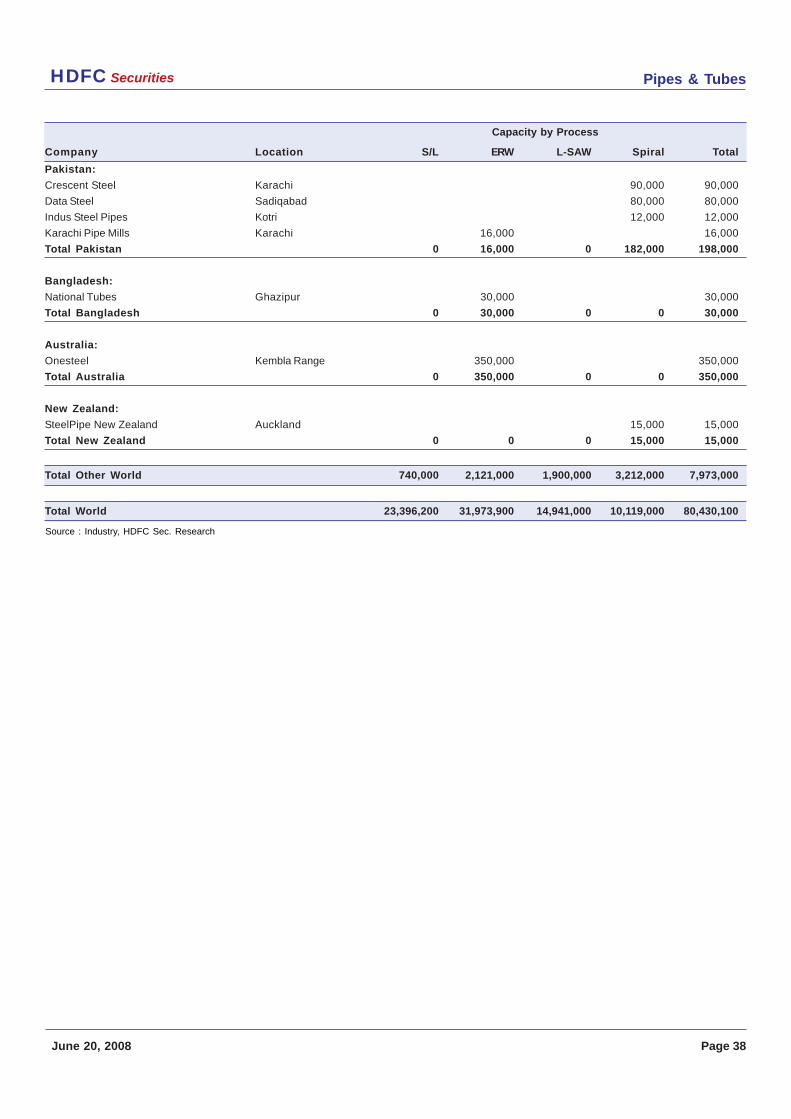

(in tons) Seamless ERW L-SAW Spiral Total OCTG & ERW Line Pipe

USA 3,042,000 5,691,500 1,500,000 0 10,233,500 15.8% 6.0%Canada 250,000 1,150,000 200,000 600,000 2,200,000 2.5% 3.2%Mexico 780,000 495,000 450,000 80,000 1,805,000 2.3% 2.1%Total North America 4,072,000 7,336,500 2,150,000 680,000 14,238,500 20.6% 11.3% Germany 1,345,000 420,000 1,275,000 525,000 3,565,000 3.2% 7.2%France 855,000 180,000 480,000 100,000 1,615,000 1.9% 2.3%Italy 1,025,000 1,080,000 1,200,000 220,000 3,525,000 3.8% 5.7%UK 40,000 550,000 330,000 0 920,000 1.1% 1.3%Spain 420,000 0 0 85,000 505,000 0.8% 0.3%Austria 320,000 0 0 0 320,000 0.6% 0.0%Belgium & Luxembourg 0 0 0 100,000 100,000 0.0% 0.4%Finland 0 250,000 0 100,000 350,000 0.5% 0.4%Greece 0 570,000 0 300,000 870,000 1.0% 1.2%Total Western Europe 4,005,000 3,050,000 3,285,000 1,430,000 11,770,000 12.7% 18.8% Japan 2,371,000 4,059,000 1,787,000 751,000 8,968,000 11.6% 10.1%South Korea 0 2,641,000 175,000 175,000 2,991,000 4.8% 1.4%China 3,890,000 2,965,000 1,600,000 1,570,000 10,025,000 12.4% 12.6%Taiwan 0 412,000 0 60,000 472,000 0.7% 0.2%Indonesia 170,000 313,000 200,000 475,000 1,158,000 0.9% 2.7%Malaysia 0 0 0 160,000 160,000 0.0% 0.6%Total East Asia 6,431,000 10,390,000 3,762,000 3,191,000 23,774,000 30.4% 27.7% Croatia 200,000 0 0 0 200,000 0.4% 0.0%Czech Republic 510,000 0 0 45,000 555,000 0.9% 0.2%Slovakia 170,000 15,000 0 50,000 235,000 0.3% 0.2%Poland 100,000 15,000 0 30,000 145,000 0.2% 0.1%Romania 830,000 0 44,000 0 874,000 1.5% 0.2%Total Eastern Europe 1,810,000 30,000 44,000 125,000 2,009,000 3.3% 0.7% Russia 3,127,500 4,952,000 950,000 0 9,029,500 14.6% 3.8%Ukraine 700,000 900,000 1,400,000 240,000 3,240,000 2.9% 6.5%Azerbaijan 346,000 0 0 0 346,000 0.6% 0.0%Georgia 400,000 0 0 0 400,000 0.7% 0.0%Total CIS 4,573,500 5,852,000 2,350,000 240,000 13,015,500 18.8% 10.3% Iran 120,000 880,000 500,000 390,000 1,890,000 1.8% 3.6%Saudi Arabia 0 240,400 480,000 325,000 1,045,400 0.4% 3.2%Kuwait 0 0 0 130,000 130,000 0.0% 0.5%Total Middle East 120,000 1,120,400 980,000 845,000 3,065,400 2.2% 7.3% Brazil 540,000 450,000 300,000 140,000 1,430,000 1.8% 1.8%Argentina 850,000 534,000 70,000 10,000 1,464,000 2.5% 0.3%Venezuela 154,000 840,000 100,000 0 1,094,000 1.8% 0.4%Colombia 0 150,000 0 0 150,000 0.3% 0.0%Total South America 1,544,000 1,974,000 470,000 150,000 4,138,000 6.4% 2.5% Algeria 700 0 0 36,000 36,700 0.0% 0.1%South Africa 100,000 100,000 0 160,000 360,000 0.4% 0.6%Egypt 0 0 0 50,000 50,000 0.0% 0.2%Total Africa 100,700 100,000 0 246,000 446,700 0.4% 1.0% Turkey 0 1,200,000 0 910,000 2,110,000 2.2% 3.6%India 740,000 525,000 1,900,000 2,105,000 5,270,000 2.3% 16.0%Pakistan 0 16,000 0 182,000 198,000 0.0% 0.7%Bangladesh 0 30,000 0 0 30,000 0.1% 0.0%Australia 0 350,000 0 0 350,000 0.6% 0.0%New Zealand 0 0 0 15,000 15,000 0.0% 0.1%Total Other World 740,000 2,121,000 1,900,000 3,212,000 7,973,000 5.2% 20.4% Total World 23,396,200 31,973,900 14,941,000 10,119,000 80,430,100 100.0% 100.0%

Installed API Capacity

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 19

Capacity Investments

With the exception of North America, API pipe capacity additions are more in LSAW pipes with

the product attracting the most investment. By region, the principal investments include:

North America - Expected capacity addition 1.7 mn tons

Berg Steel, part of the German Europipe, is to build a new large diameter spiral-weld

manufacturing unit in Mobile, Alabama. The new company, Berg Spiral Pipes, is due to be up

and running by mid 2008, at a cost of US$575m. The facility will have the capacity to produce

200,000tpy of 24 to 56 inch diameter pipes, with a maximum length of 80 feet.

IPSCO is set to expand its large diameter pipe mill at its Saskatchewan mill, Regina at a cost

of US$53m. Due on stream in mid 2008, capacity will be increased to 125,000tpy, and will

include a pipe forming mill and finishing equipment. At the same time, the company has also

announced its intention to increase its spiral weld capacity to 500,000tpy.

US Steel is set to form a spiral-weld producing joint venture in California. With annual

capacity expected at 300,000tpy, the new joint venture will be able to produce pipes of 24 to

64 inch diameter, with production expected to start in 2008.

It is expected that around 1 million tons of additional HSAW capacity will be added by Indian

manufactures Welspun, Man and PSL. These are all green field capacities and are expected

to start operations between mid Sept 08 and Sept 09.

Latin America - Expected capacity addition 0.7 mn tons

Tubos Soldados Atlantico (TSA), a joint venture led by Europipe, has began operating a

90,000tpy welded pipe mill in South Eastern Brazil. The joint venture between Europipe, V&M

do Brasil and Interoil is expected to increase the mill’s capacity to 180,000tpy, which will

include the production of SAW pipes.

French producer Vallourec, together with Sumitomo of Japan, is set to take part in a joint

venture in Brazil. Based in Minas Gerais state, the mill is expected to cost US$600m, and will

have the capacity to produce 600,000tpy.

Europe - Expected capacity addition 0.2 mn tons

A joint venture, Borusan Mannesmann, between Turkish company Borusan and Germany’s

Mannesmann Röhrenwerke, is installing a 50,000tpy spiral weld tube line in Albacete,

Spain. The equipment will come from a Europipe operation in Jouef, France, which was shut

down in March 2004. The mill will be transferred to Spain, where it will produce 100,000tpy, at

a cost of €15m.

In Italy, Arvedi Tubi Acciaio (ATA) plans to add 100,000tpy to its welded capacity at its Cremona

site. At a cost of €40m, the new capacity is due on line by mid 2008, and will produce 12 inch

diameter pipes.

Pipes & TubesHDFC Securities

June 20, 2008 Page 20

Asia - Expected capacity addition 0.7 mn tons

Chinese producer Shandong Lubao, a Baosteel subsidiary, is due to start building a

500,000tpy seamless pipe mill this year. The new mill, Shandong Lubao Steel Pipe, is

expected to produce OCTG and boiler pipes, among other commercial pipes, with diameter

range of 6 to 17 inches.

In Japan, Sumitomo Metal Industries (SMI) has announced plans to invest US$85m at its

Kashima works in order to prepare a system for the mass production of ultra high strength

steel pipes. Due to begin production in 2011, the company intends to supply pipes for an

increasing share of gas transportation projects.

Middle East - Expected capacity addition 1 mn tons

Jubail Energy Services Company of Saudi Arabia, is set to build the country’s first seamless

pipe plant in Al Jubail. With a planned capacity of 400,000tpy, the mill will be able to produce

pipes of 5 to 14 inch diameter. With production due to start in 2008, the plant will include a

heat treatment line, a finishing line and a coupling workshop.

Arcelor Mittal has signed a joint venture with the Bin Jarallah Group of companies in Saudi

Arabia for the construction of a seamless tube mill. With annual capacity of 500,000tpy, the

company will concentrate on OCTG products, and will have the capacity to produce 4 to 14

inch pipes. Due to start production in 2010, the project is an attempt by Arcelor Mittal to tap

into the Middle East market.

India - Expected capacity addition 1.7 mn tons

Indian Seamless Metal Tubes (ISMT) is planning a US$55m expansion project at its

Maharashtra facility. Set to increase capacity by 320,000tpy, the new capacity, expected to be

operational by the end of 2008, will make the company India’s largest producer.

Maharashtra Seamless is adding 400,000 tons of seamless capacity over the next 12-18

months. This includes the Romanian acquisition of 200,000 tons.

Jindal Saw, Welspun Gujarat, Man Inds each are adding capacity anywhere in the range of

300,000 – 400,000 tons of HSAW/LSAW, which are slated to commence operations by

H2CY08.

Pipes & TubesHDFC Securities

June 20, 2008 Page 21

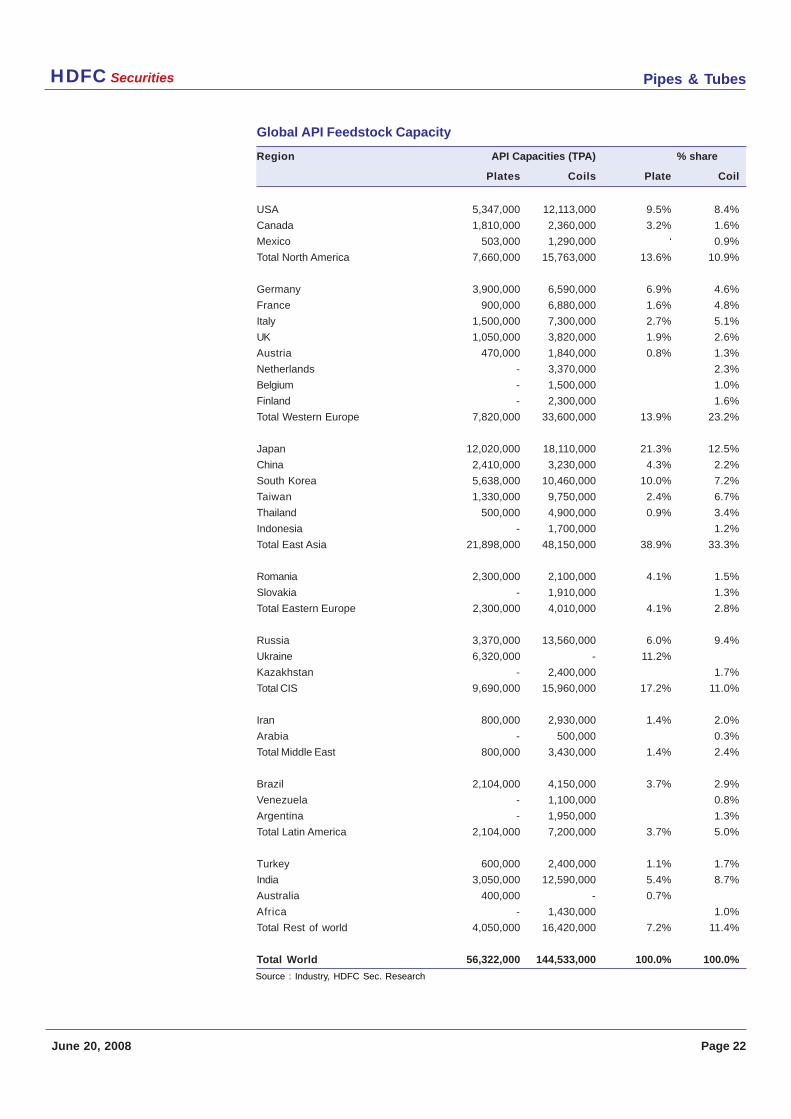

Feedstock (Plate & Coil)

The American Petroleum Institute does not award a monogram to certify production of flat-

rolled feedstock (Plate & Coil) for API 5L or API 5CT pipes. The flat-rolled mills produce hot-

rolled strips or plates. A percentage of overall production will then be of API line pipe or OCTG

grade. Actual production depends on the production levels of welded pipes. As per industry

estimates, for an average configuration strip mill capable of API quality production, actual

output in these grades would typically not exceed 5% of the total gross HR coil output.

For plate mills, the assumed limits to API grade output will be the following:

• For mills known to be ideally equipped for line pipe grades (controlled rolling and

accelerated cooling), a maximum of 40% of total plate production will be the upper limit

for API grade output.

• For plate mills known to lack controlled rolling and accelerated cooling facilities, API

grade output has an upper limit of 10% of total production.

By some estimates, plate demand is expected to grow at about three percent a year. And

there aren’t many API/Heavy Plate grade plate producers globally. Driving that demand is not

only pipes and tubes but also other energy applications like drill rigs and windmills. Wind

mill towers, in particular, consume enormous amounts of plate and represent a strong

growth market.

Heavy equipment and transportation—such as railcars and barges—also account for a big

chunk of plate demand. Freight costs are spiraling in part because there does not seem to

be enough tankers out there. In South Korea, for example, most plates produced go into

shipbuilding and not into pipe markets.

And infrastructure demand in the developing world is booming. It is booming not only in

obvious places like India, China and Russia but also in Vietnam and formerly war-torn

countries such as Serbia and Croatia.

Infrastructure demand is also expected to pick up in the U.S., where the Minneapolis bridge

collapse will probably put more pressure on politicians to spend more and spend it faster.

And of course it’s not just the price of plate that is increasing. Upstream raw material costs

are also rising with global demand, especially demand from China. Iron ore prices are

expected to increase by as much as 20 percent to 30 percent over the next year. Coking coal,

scrap, alloy and electricity costs are also predicted to increase.

Mills may absorb smaller raw material increases of five percent or less. But most experts say

that if they get hit with increases of 30 percent or more, all bets are off. In fact, some argue that

the higher the cost increases, the more likely they are to be passed along to consumers.

Pipes & TubesHDFC Securities

June 20, 2008 Page 22

Global API Feedstock Capacity

Region API Capacities (TPA) % share

Plates Coils Plate Coil

USA 5,347,000 12,113,000 9.5% 8.4%

Canada 1,810,000 2,360,000 3.2% 1.6%

Mexico 503,000 1,290,000 ‘ 0.9%

Total North America 7,660,000 15,763,000 13.6% 10.9%

Germany 3,900,000 6,590,000 6.9% 4.6%

France 900,000 6,880,000 1.6% 4.8%

Italy 1,500,000 7,300,000 2.7% 5.1%

UK 1,050,000 3,820,000 1.9% 2.6%

Austria 470,000 1,840,000 0.8% 1.3%

Netherlands - 3,370,000 2.3%

Belgium - 1,500,000 1.0%

Finland - 2,300,000 1.6%

Total Western Europe 7,820,000 33,600,000 13.9% 23.2%

Japan 12,020,000 18,110,000 21.3% 12.5%

China 2,410,000 3,230,000 4.3% 2.2%

South Korea 5,638,000 10,460,000 10.0% 7.2%

Taiwan 1,330,000 9,750,000 2.4% 6.7%

Thailand 500,000 4,900,000 0.9% 3.4%

Indonesia - 1,700,000 1.2%

Total East Asia 21,898,000 48,150,000 38.9% 33.3%

Romania 2,300,000 2,100,000 4.1% 1.5%

Slovakia - 1,910,000 1.3%

Total Eastern Europe 2,300,000 4,010,000 4.1% 2.8%

Russia 3,370,000 13,560,000 6.0% 9.4%

Ukraine 6,320,000 - 11.2%

Kazakhstan - 2,400,000 1.7%

Total CIS 9,690,000 15,960,000 17.2% 11.0%

Iran 800,000 2,930,000 1.4% 2.0%

Arabia - 500,000 0.3%

Total Middle East 800,000 3,430,000 1.4% 2.4%

Brazil 2,104,000 4,150,000 3.7% 2.9%

Venezuela - 1,100,000 0.8%

Argentina - 1,950,000 1.3%

Total Latin America 2,104,000 7,200,000 3.7% 5.0%

Turkey 600,000 2,400,000 1.1% 1.7%

India 3,050,000 12,590,000 5.4% 8.7%

Australia 400,000 - 0.7%

Africa - 1,430,000 1.0%

Total Rest of world 4,050,000 16,420,000 7.2% 11.4%

Total World 56,322,000 144,533,000 100.0% 100.0%

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 23

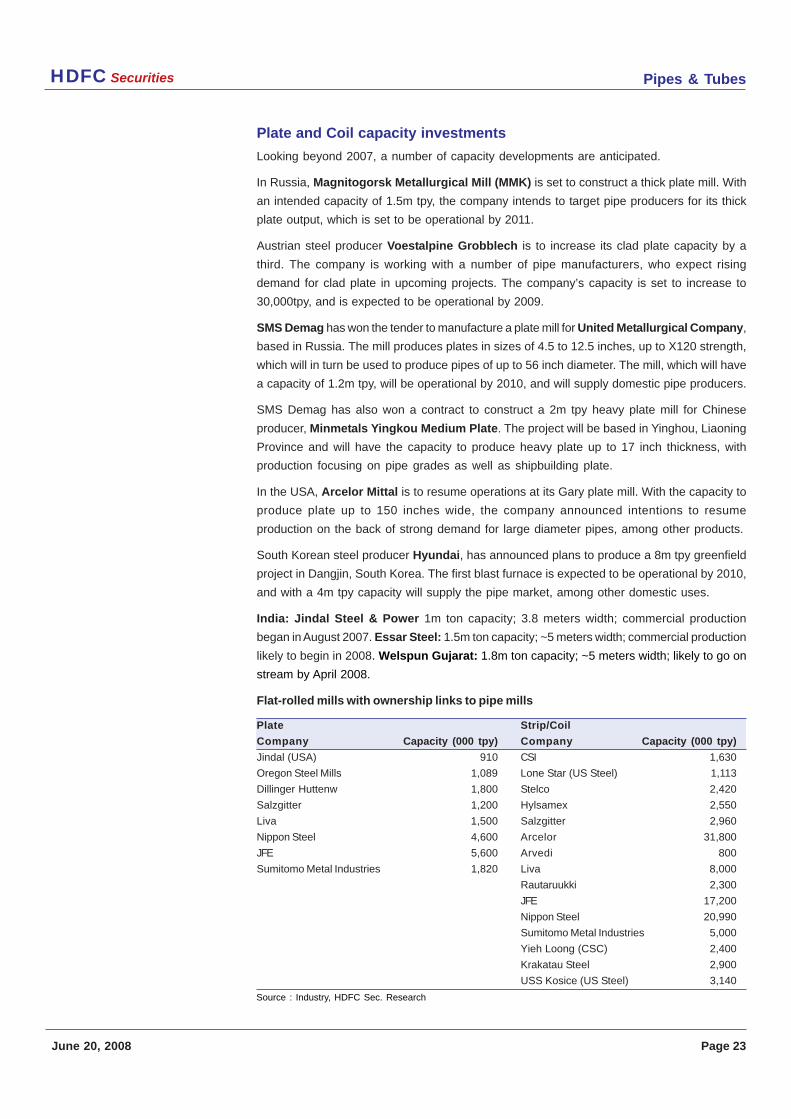

Plate and Coil capacity investments

Looking beyond 2007, a number of capacity developments are anticipated.

In Russia, Magnitogorsk Metallurgical Mill (MMK) is set to construct a thick plate mill. With

an intended capacity of 1.5m tpy, the company intends to target pipe producers for its thick

plate output, which is set to be operational by 2011.

Austrian steel producer Voestalpine Grobblech is to increase its clad plate capacity by a

third. The company is working with a number of pipe manufacturers, who expect rising

demand for clad plate in upcoming projects. The company’s capacity is set to increase to

30,000tpy, and is expected to be operational by 2009.

SMS Demag has won the tender to manufacture a plate mill for United Metallurgical Company,

based in Russia. The mill produces plates in sizes of 4.5 to 12.5 inches, up to X120 strength,

which will in turn be used to produce pipes of up to 56 inch diameter. The mill, which will have

a capacity of 1.2m tpy, will be operational by 2010, and will supply domestic pipe producers.

SMS Demag has also won a contract to construct a 2m tpy heavy plate mill for Chinese

producer, Minmetals Yingkou Medium Plate. The project will be based in Yinghou, Liaoning

Province and will have the capacity to produce heavy plate up to 17 inch thickness, with

production focusing on pipe grades as well as shipbuilding plate.

In the USA, Arcelor Mittal is to resume operations at its Gary plate mill. With the capacity to

produce plate up to 150 inches wide, the company announced intentions to resume

production on the back of strong demand for large diameter pipes, among other products.

South Korean steel producer Hyundai, has announced plans to produce a 8m tpy greenfield

project in Dangjin, South Korea. The first blast furnace is expected to be operational by 2010,

and with a 4m tpy capacity will supply the pipe market, among other domestic uses.

India: Jindal Steel & Power 1m ton capacity; 3.8 meters width; commercial production

began in August 2007. Essar Steel: 1.5m ton capacity; ~5 meters width; commercial production

likely to begin in 2008. Welspun Gujarat: 1.8m ton capacity; ~5 meters width; likely to go on

stream by April 2008.

Flat-rolled mills with ownership links to pipe mills

Plate Strip/Coil

Company Capacity (000 tpy) Company Capacity (000 tpy)

Jindal (USA) 910 CSI 1,630

Oregon Steel Mills 1,089 Lone Star (US Steel) 1,113

Dillinger Huttenw 1,800 Stelco 2,420

Salzgitter 1,200 Hylsamex 2,550

Liva 1,500 Salzgitter 2,960

Nippon Steel 4,600 Arcelor 31,800

JFE 5,600 Arvedi 800

Sumitomo Metal Industries 1,820 Liva 8,000

Rautaruukki 2,300

JFE 17,200

Nippon Steel 20,990

Sumitomo Metal Industries 5,000

Yieh Loong (CSC) 2,400

Krakatau Steel 2,900

USS Kosice (US Steel) 3,140

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 24

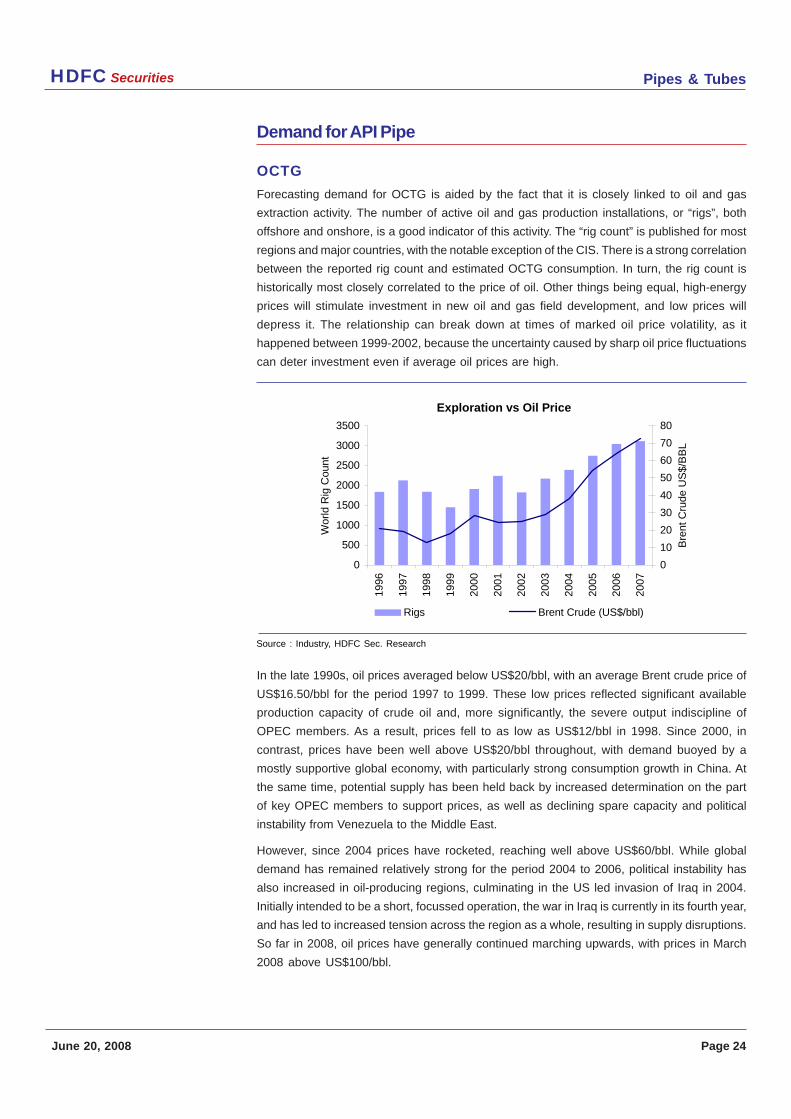

Demand for API Pipe

OCTG

Forecasting demand for OCTG is aided by the fact that it is closely linked to oil and gas

extraction activity. The number of active oil and gas production installations, or “rigs”, both

offshore and onshore, is a good indicator of this activity. The “rig count” is published for most

regions and major countries, with the notable exception of the CIS. There is a strong correlation

between the reported rig count and estimated OCTG consumption. In turn, the rig count is

historically most closely correlated to the price of oil. Other things being equal, high-energy

prices will stimulate investment in new oil and gas field development, and low prices will

depress it. The relationship can break down at times of marked oil price volatility, as it

happened between 1999-2002, because the uncertainty caused by sharp oil price fluctuations

can deter investment even if average oil prices are high.

In the late 1990s, oil prices averaged below US$20/bbl, with an average Brent crude price of

US$16.50/bbl for the period 1997 to 1999. These low prices reflected significant available

production capacity of crude oil and, more significantly, the severe output indiscipline of

OPEC members. As a result, prices fell to as low as US$12/bbl in 1998. Since 2000, in

contrast, prices have been well above US$20/bbl throughout, with demand buoyed by a

mostly supportive global economy, with particularly strong consumption growth in China. At

the same time, potential supply has been held back by increased determination on the part

of key OPEC members to support prices, as well as declining spare capacity and political

instability from Venezuela to the Middle East.

However, since 2004 prices have rocketed, reaching well above US$60/bbl. While global

demand has remained relatively strong for the period 2004 to 2006, political instability has

also increased in oil-producing regions, culminating in the US led invasion of Iraq in 2004.

Initially intended to be a short, focussed operation, the war in Iraq is currently in its fourth year,

and has led to increased tension across the region as a whole, resulting in supply disruptions.

So far in 2008, oil prices have generally continued marching upwards, with prices in March

2008 above US$100/bbl.

Exploration vs Oil Price

0

500

1000

1500

2000

2500

3000

3500

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Wor

ld R

ig C

ount

0

10

20

30

40

50

60

70

80

Bre

nt C

rude

US

$/B

BL

Rigs Brent Crude (US$/bbl)

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 25

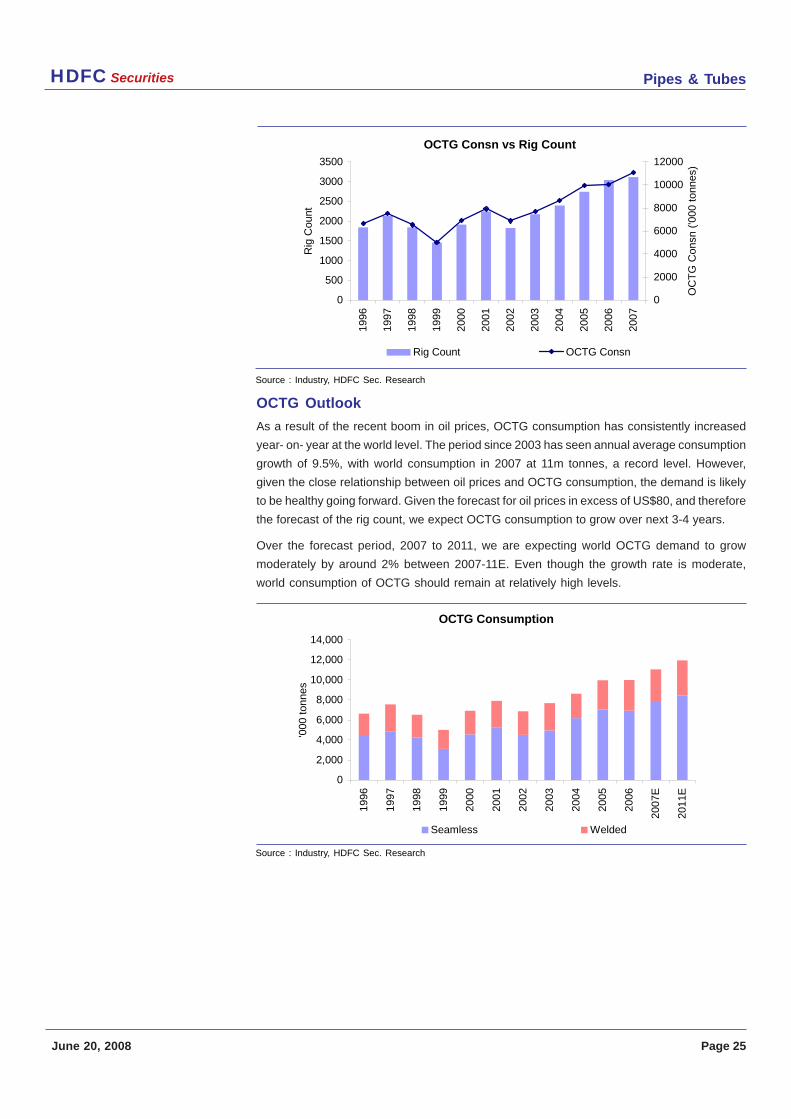

OCTG Outlook

As a result of the recent boom in oil prices, OCTG consumption has consistently increased

year- on- year at the world level. The period since 2003 has seen annual average consumption

growth of 9.5%, with world consumption in 2007 at 11m tonnes, a record level. However,

given the close relationship between oil prices and OCTG consumption, the demand is likely

to be healthy going forward. Given the forecast for oil prices in excess of US$80, and therefore

the forecast of the rig count, we expect OCTG consumption to grow over next 3-4 years.

Over the forecast period, 2007 to 2011, we are expecting world OCTG demand to grow

moderately by around 2% between 2007-11E. Even though the growth rate is moderate,

world consumption of OCTG should remain at relatively high levels.

OCTG Consn vs Rig Count

0

500

1000

1500

2000

2500

3000

3500

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Rig

Cou

nt0

2000

4000

6000

8000

10000

12000

OC

TG

Con

sn (

'000

ton

nes)

Rig Count OCTG Consn

OCTG Consumption

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

E

2011

E

'000

ton

nes

Seamless Welded

Source : Industry, HDFC Sec. Research

Source : Industry, HDFC Sec. Research

Pipes & TubesHDFC Securities

June 20, 2008 Page 26

One of the competitive battlegrounds in the API pipe market is that between welded and

seamless OCTG, with the former’s advantage arising from lower average costs of

manufacturing, and the latter’s from a widespread perception that any weld in casing or

tubing (drill pipe is always seamless) would increase the risk of pipe failure. Seamless has

traditionally been the dominant product solution, but in the 1990s welded OCTG increased

its market share, owing in part to successful efforts to market the reliable performance of

welded pipe. Welded pipe’s share of the overall market for OCTG was around 30% in 2006,

having fallen from the record level of 38% seen in 1999. The share going forward most likely

will remain stable over the forecast period, with any cost advantages for welded pipe proving

insufficient to allow it to capture a substantially higher share of the market from seamless.

Regional product preferences remain entrenched, with the share of welded in the particularly

risk averse Middle East currently estimated to be only 16%, compared to almost 40% in

North America.

OCTG by Product Grade

There has undoubtedly been an underlying trend towards the customization of API pipe

qualities over the past several years, and pressure will continue for the development of

higher-performance products. Some higher-specification requirements, such as severe

pressure resistance, or low- temperature “arctic service” pipe, could however be reduced if

proportionately more exploration and production activity shifts to the (onshore) Middle East

region. However sour service pipe will be in high demand in the Middle East, owing to the

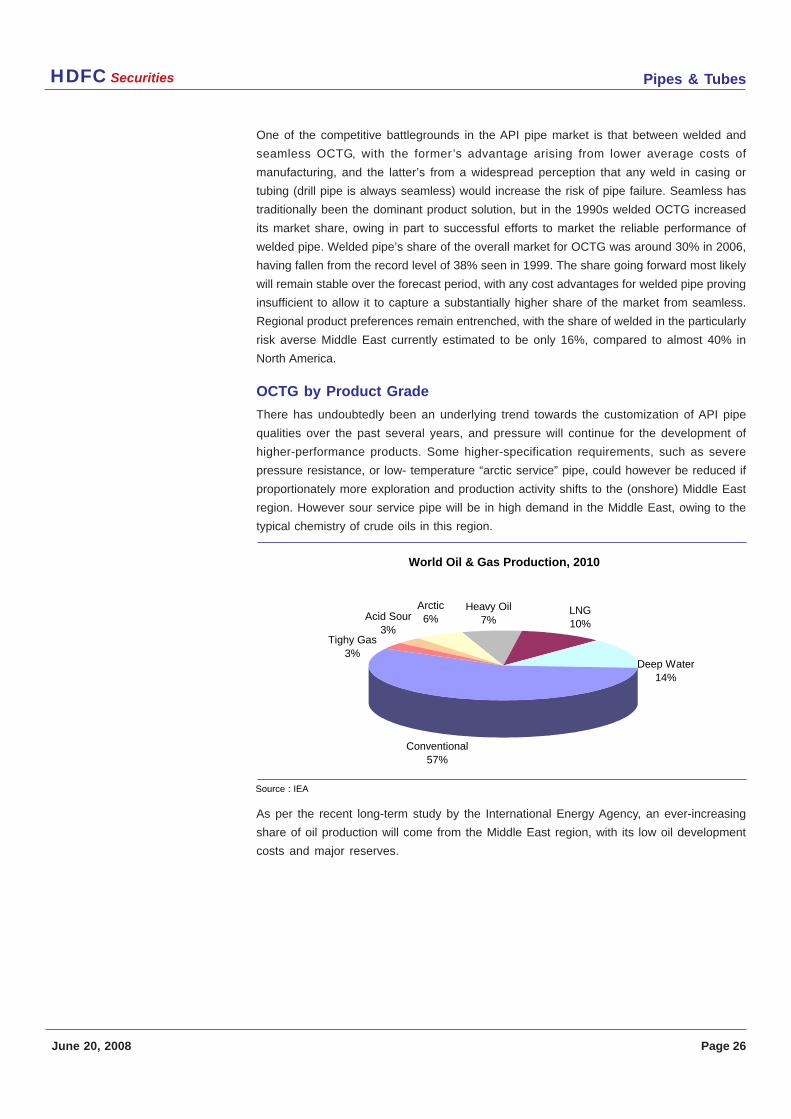

typical chemistry of crude oils in this region.

As per the recent long-term study by the International Energy Agency, an ever-increasing

share of oil production will come from the Middle East region, with its low oil development

costs and major reserves.

World Oil & Gas Production, 2010

Conventional57%

Acid Sour3%

Arctic6%

Heavy Oil7%

LNG10%

Tighy Gas3%

Deep Water14%

Source : IEA

Pipes & TubesHDFC Securities

June 20, 2008 Page 27

World Oil Supply (Million barrels per day)

2005 2010 2015 2030

North America 10 9 9 8

OECD Europe 5 4 3 2

OECD Australasia/pacific 1 1 1 0

Transition economies 11 14 15 16

China 4 4 4 3

Other Asia 3 4 3 3

Latin America 6 7 8 10

Africa 9 11 11 12

Middle East 33 36 41 55

Total 82 90 95 109

World Oil Supply (Regional share of world total)

2005 2010 2015 2030

North America 12% 11% 10% 7%

OECD Europe 6% 4% 3% 1%

OECD Australasia/pacific 1% 1% 1% 0%

Transition economies 14% 16% 15% 15%

China 4% 4% 4% 3%

Other Asia 4% 4% 4% 3%

Latin America 7% 8% 9% 9%

Africa 11% 12% 12% 11%

Middle East 41% 40% 44% 51%

Total 100% 100% 102% 100%

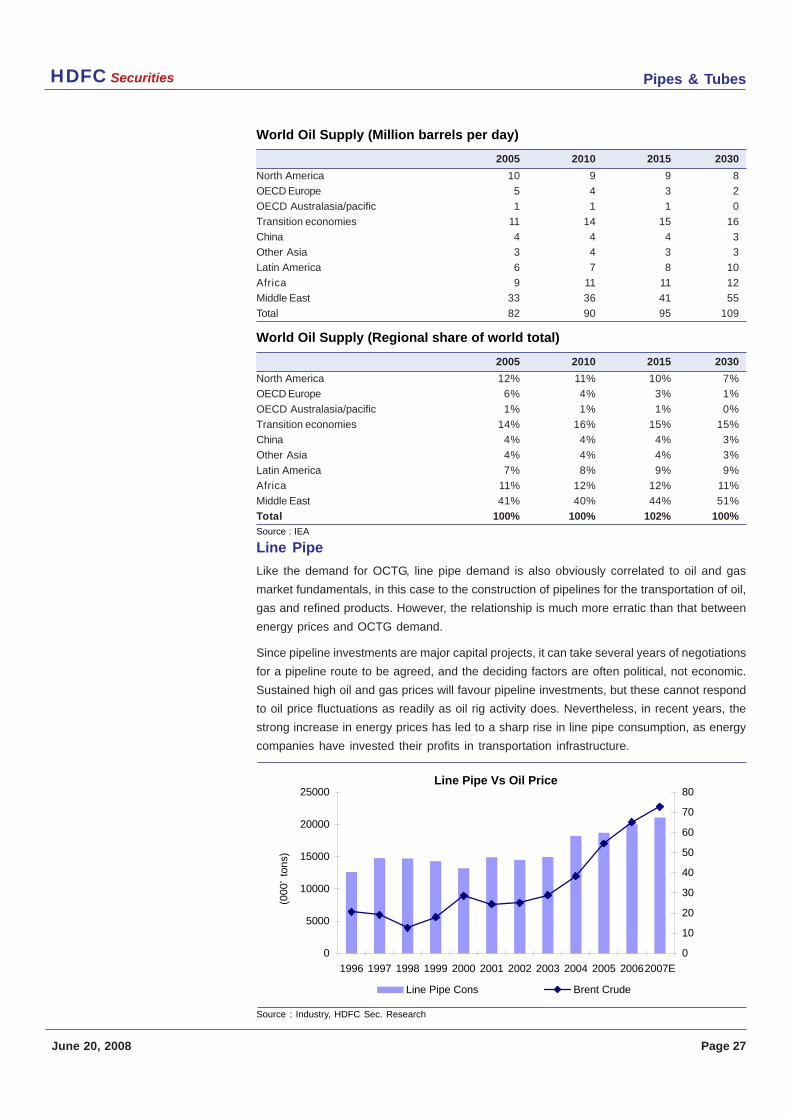

Line Pipe

Like the demand for OCTG, line pipe demand is also obviously correlated to oil and gas

market fundamentals, in this case to the construction of pipelines for the transportation of oil,

gas and refined products. However, the relationship is much more erratic than that between

energy prices and OCTG demand.

Since pipeline investments are major capital projects, it can take several years of negotiations

for a pipeline route to be agreed, and the deciding factors are often political, not economic.

Sustained high oil and gas prices will favour pipeline investments, but these cannot respond

to oil price fluctuations as readily as oil rig activity does. Nevertheless, in recent years, the

strong increase in energy prices has led to a sharp rise in line pipe consumption, as energy

companies have invested their profits in transportation infrastructure.

Line Pipe Vs Oil Price

0

5000

10000

15000

20000

25000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 20062007E

0

10

20

30

40

50

60

70

80

Line Pipe Cons Brent Crude

Source : IEA

Source : Industry, HDFC Sec. Research

(000

’ to

ns)

Pipes & TubesHDFC Securities

June 20, 2008 Page 28

Consumption of line pipe has been rising in recent years, with an increase in construction of

pipeline projects leading the way forward. The line pipe market did suffer from a drop in

consumption in 2000, due to a corresponding fall in pipeline construction projects in 2001.

However, since this decline, construction of pipelines has been increasing year-on-year in

line with increasing oil and gas prices.

Line Pipe: Best Yet to Come

Since 2003, the total line pipe market grew at annual average rate of 10.4%, compared to an

annual average rate of 2.4% for the period 1996 to 2003. However, the fact that growth has

been strong over the last few years is not surprising given the increases in the price of oil and

gas. Indeed, line pipe consumption has in fact grown rather conservatively compared to oil

prices, which have risen by an annual average rate of 31.4% for the three years since 2003,

dwarfing the growth seen in line pipe consumption. Looking ahead, we are expecting

consumption to increase further, given the number of planned and announced pipeline

construction projects and oil above US$ 100/bbl will stimulate newer projects.

A study by analysts Douglas-Westwood titled The World Onshore Pipelines Report 2008-

2012 forecasts that $180 billion will be spent on onshore pipeline projects worldwide

through 2012. The report estimates a 16% increase in the pipeline mileage installed from

2008-2012 compared to the historic five-year period 2003-2007. Nearly 75% of this

expenditure is expected to be spent in Asia, Eastern Europe, the FSU and North America.

Almost 70% is projected to be spent on gas pipelines. Asia stands out as the largest forecast

market — by length of pipeline construction — accounting for $42 billion of forecast capital

expenditure. The status of forecast pipeline projects shows a split between planning (47%),

under construction or ordered (40%) and approved (13%).

Much of this expected growth is based on modest increases in energy consumption. The

International Energy Outlook for 2007 suggests that world demand for primary energy will

increase by an average 2.3% per year for the period 2004 to 2010, before slowing to 1.8% per

year for the period 2010 to 2015.

The longer-term outlook: strongest for gas

Although decisions on individual pipeline projects are extremely unpredictable, the economic

fundamentals point to a sustained level of pipeline investment in the coming years because

of the forecast growth in inter-regional trade in hydrocarbons. In a continuation of recent

years’ trends, the strongest prospects are for larger-diameter natural gas pipelines. The

International Energy Agency forecasts a sharp increase in the requirement for imported

natural gas in major consuming regions such as North America, Europe and China. There

are relatively few physical connections between the major regional markets, but current and

planned pipeline projects are expected to rectify this situation.

Competition for the large-diameter market: LSAW vs HSAW

Although demand prospects are in principle supportive of large-diameter line pipe as a

whole, the degree to which the two key competing pipe solutions – LSAW and spiral-welded

– can capitalise on this may differ. This, in turn, has implications for the relative fortunes

respectively of RM plate and coil as the feedstocks for each of these two types of pipes.

Pipes & TubesHDFC Securities

June 20, 2008 Page 29

There is an ongoing debate in the industry about whether spiral-welded pipes, which enjoy

a production-cost advantage, has an unrecognised potential to compete for a wider range of

API pipeline projects. However strong evidences have not been found that suggests advances

in spiral-welding technology have fundamentally changed the competitive balance, which

largely rests on spiral-welded’s cost advantage versus its – real or perceived – lesser

reliability relative to LSAW. This standoff has capped spiral-welded’s market share to 25-

30% (15% overall line pipe) of the large diameter API line pipe over the past ten years, with

little sign of a durable breakthrough.

Just as in the seamless versus welded OCTG debate, there are entrenched regional

preferences, with US project specifiers traditionally distrustful of spiral-welded for energy

pipeline use, in contrast to the strong use of spiral-welded in the realisation of recent Turkish

and Chinese long-distance pipelines.

Leading North American plate, coil and pipe producer Ipsco has been making efforts to