Embed Size (px)

Citation preview

PICTET BRIEFING

NOVEMBER 2013

THE FAMILY CONSILIUM ASIA PICTET WEALTH MANAGEMENT

SHARING PERSPECTIVES IN A CONVERGING WORLD

CHINA TODAY: CONCEPTIONS AND MISCONCEPTIONS JACQUES DE WATTEVILLE XIANG BING

THE GLOBAL MACROECONOMIC CONTEXTYVES BONZON BHASKAR LAXMINARAYAN MARY MCBAIN JIM WALKER

BUILDING A GREAT BUSINESSMARKUS AKERMANN WILLIAM K FUNG HARALD LINK

BUILDING A GREAT ART COLLECTIONULI SIGG BUDI TEK WILLIAM ZHAO

REPORTING FROM THE TOPMARCUS BRAUCHLI STEPHEN BARBER

OPTIMAL STRATEGIES IN ASSET ALLOCATIONYVES BONZON

THE CHALLENGES OF GLOBAL FAMILY BUSINESSESRICHARD EU

FAMILY ENTERPRISE GOVERNANCE: THEORY AND PRACTICERANDEL CARLOCK

COACHING THE NEXT GENERATION RANDEL CARLOCK

TASTING EAST AND WEST IN HANGZHOU EDOUARD MIAILHE JUDY LEISSNER

UNDERSTANDING EAST AND WESTChina Today: Conceptions and Misconceptions p2The Global Macroeconomic Context p6Building a Great Business p10Building a Great Art Collection p14

SPECIAL TALKReporting from the Top p18

INVESTMENT STRATEGIESOptimal Strategies in Asset Allocation p24

BUSINESS AND FAMILY GOVERNANCEThe Challenges of Global Family Businesses p28Family Enterprise Governance: Theory and Practice p30Coaching the Next Generation p32

POSTSCRIPTTasting East and West in Hangzhou p34

‘

CONTENTS

Front cover: scene from Impression West Lake, a theatrical spectacle performed on the lake at Hangzhou and directed by the celebrated Chinese film director Zhang Yimou, portraying the local folk legend of the so-called Butterfly Lovers. Pages 17 and 36: Four Seasons West Lake. Page 23: Buddha carving at the grotto Feilai Feng before Lingyin Temple, Hangzhou, dating from the Southern Sung Dynasty (1127–1279). Pages 28–29: viewing pavilion on West Lake.

Rapporteur – Stephen Barber Photography – Alan Chow Additional images – Stephen Barber (Cover/pages 23, 28, 36) Proof-reading – Havard Davies Design – Together Design

SHARING PERSPECTIVES IN A CONVERGING WORLD

We have great pleasure in introducing this summary of the proceedings of our Sixth Family Consilium, the second in Asia, here in the historic city of Hangzhou, an outstanding

centre of culture and one-time capital of the Southern Song Dynasty. In some ways we were fortunate to be able to open without

mishap, having already had to postpone from March owing to an outbreak of avian flu in the Shanghai region. And then, on the verge of opening, typhoon Usagi struck Hong Kong and the Chinese mainland, which probably accounted for the heavy rain!

Still, we gathered here, 60 guests, 24 families from across Asia, Europe and Latin America, many with two generations, to experience the special atmosphere of the Consilium.

This is not a classic investment conference. Our intention has been to bring together like-minded people in a spirit of openness and informality, to inform, entertain and discuss things that matter to wealthy families.

To do that we have a group of specialists – experts in their field – from both Pictet and from outside. We begin with a look at the impact of China’s transformation on Asia and the rest of the world. Then we consider more closely global macroeconomic trends and opportunities, before listening to fascinating stories of business-building from Asian and Western family business leaders.

Later on we move away from business to hear about how to build a great art collection. On the second day, the focus is on investment and then on an in-depth examination of the challenges of global business families, before wrapping up with a session on the governance and management of family enterprises. On the last morning we have a special coaching session for the next generation.

We very much hope you will find this summary both fascinating and worthwhile reading.’

Nicolas Pictet & Philippe BertheratPartners of Pictet & Cie

PICTET WEALTH MANAGEMENT The Family Consilium 2013 3PICTET WEALTH MANAGEMENT The Family Consilium 2013 2

UNDERSTANDING EAST AND WEST

CHINA TODAY CONCEPTIONS AND MISCONCEPTIONSJacques de Watteville, Swiss Ambassador to China, and Professor Xiang Bing give two contrasting perspectives on China’s emergence as a world economic power

JACQUES DE WATTEVILLE

I arrived in Beijing from Brussels just twelve months ago, and I can tell you the mood is not high in Europe. Externally, we often think of

China as an industrial machine, a threat to world markets, flooding the West with products—an economic giant on the world scene.

‘I am struck by the immensity and diversity of the country’

But what I found is very different. I have travelled all over the country, from Yunnan to Shanghai, and I am struck by the immensity and diversity of the country. There are 52 ethnic minorities for example. China is not monolithic.

I am struck too, by the huge dynamism, and the enormity of the achievement in lifting 600 million people out of poverty in just thirty years. This is something unparalleled in human history.

The Western media often does not reflect this positive side of China. Our media seems to concentrate on the negative—on environmental damage, on abuse of human rights, on corruption. Our European culture is used to a critical media, but my Chinese friends find it difficult to understand.

survey suggests that 55 per cent will increase investment, 85 per cent intend to add staff and two-thirds expect to raise market share. Now that’s optimism.

Switzerland ranks highest in many global surveys for competitiveness and innovation. But a century ago Switzerland was a very poor country. So China may have things to learn from us.

‘China and Europe are not in competition,

but complementary allies’

If China can learn how to become more efficient and how to grow sustainably while reducing its environmental impact, then the potential is huge. One must keep moving forwards, otherwise one goes into reverse. In this respect China and Europe are not in competition, but complementary allies.

As you may know, I have been recalled to Bern to take on the role of chief negotiator

for tax and banking with the US and the EU, and so I’d like to leave you with a few parting impressions. I have been very impressed with the importance attached to personal relations here, more than in Europe. I have also found Chinese people very expressive, very communicative. It has been an intense and lively experience.

XIANG BINGBefore I talk about the future, let’s look at where China came from under Mao Zedong. His four great achievements were, first, to reunite the country after the civil war; second, with peace to create a great population dividend; third, to liberate women; and fourth, to establish Putonghua (Mandarin) as the common spoken language, building incidentally on the standardisation of the written language by the first Ching emperor. Not that everything was rosy under Mao. My father was sent to the countryside for re-education. For him as for many, this experience was not pleasant, but it increased social mobility.

At the same time, it is true that China is facing a huge task in maintaining the integrity of the country as urban and rural disparities grow. Among the challenges, I would identify three: first, the pressure to stay competitive as labour costs rise and social demands increase; second, growing environmental pollution; and third, state corruption, exemplified by the recent prosecution of Bo Shi Lai. And all this at a time when the world economy is weak.

I believe the new leadership recognises these challenges, and when I see what has been achieved in these thirty years, I am confident about the future of China.

The leadership is aiming at sustainable growth of 7.5 per cent, yet China has a rapidly ageing population, while the working population has been shrinking for two years now. As labour costs rise, China will have to improve product quality, raise domestic consumption and create a genuine middle class. The great migration from the countryside will have to continue—there’s far too much building in rural areas.

One encouraging sign is foreign direct investment. Novartis is building a USD1 billion facility near Shanghai, while 400 Swiss companies operate over 900 facilities. Of these, a recent

PICTET WEALTH MANAGEMENT The Family Consilium 2013 4 PICTET WEALTH MANAGEMENT The Family Consilium 2013 5

Next came Deng Xiaoping. He began the great opening up. In the past, when China was open, it was number one in the world. Today, over 50 per cent of China’s exports are made by foreign companies, who draw on global expertise. This is not the Korean or the Japanese model, it’s the UK, US, German model. Consider for example that Samsung exports over USD30 billion of goods from China, while Cisco has a 75 per cent market share in routing networks. That’s openness.

Many foreigners think of China as the supreme example of state capitalism. It’s true that state-owned enterprises (SOEs) are prominent in over 20 sectors, but the private sector accounts for over 60 per cent of GDP compared with the SOEs, which have a 20 per cent share. China has succeeded despite state capitalism.

‘China’s leadership isn’t based on Communism today, it’s Confucian’

What about the political culture? In the West, China is considered Communist, so no good. But is democracy good? China’s leadership isn’t based on Communism today, it’s Confucian, with two basic principles. First, rule by the elite. Confucius wrote that the highest honour was to serve your community as an official. In a democracy, the best don’t go into government. The second principle is that leaders must rise up the ranks—from local mayor, to regional leader and finally to the politburo. To become an official you must have qualifications and experience. You cannot leapfrog.

As an example of the importance attached to leadership, take the Shanghai Executive Academy of the Communist Party. Here they send their top cadre to France’s ENA, to the Kennedy School of Government and so on. They are developing leaders for the future.

I concede that corruption is a problem, because power and money always attract each other. Here we can learn from the West in how to deal with this.

UNDERSTANDING EAST AND WEST

HE Jacques de Watteville was appointed State Secretary for International Financial and Tax Matters in the Federal Department of Finance of Switzerland on 1 November. From September 2012 he had been Ambassador of Switzerland to the People’s Republic of China, the Democratic People’s Republic of Korea and Mongolia. Previously he was Ambassador and Head of Mission to the EU in Brussels, and before that Ambassador to the Syrian Arab Republic.

Prof. Xiang Bing is the Founding Dean and a Professor of China Business and Globalisation at the Beijing-based Cheung Kong Graduate School of Business (CKGSB), established in November 2002 as China’s first privately funded and faculty-governed business school. Dr Xiang received his PhD in Business Administration from the University of Alberta in Canada and his Bachelor’s degree in Engineering from Xi’an Jiaotong University in China.

Let’s turn to the international context. China has been peaceful for thirty years. There’s no advantage to China in getting involved in conflict; we have so far to catch up. Our GDP per capita is one-eighth of America’s, while even if current growth rates continue, it will still be only half of the US in 2040. China is the biggest beneficiary of peace.

‘There’s no advantage to China in getting involved in conflict’

Consider also that in fact, while Chinese companies will become global, China has no interest in taking global leadership. As Confucius said, you live your way, I live my way. We have so much to do at home. Urbanisation is only 53 per cent compared with the US at 83 per cent; our service sector is only 43 per cent of GDP against 82 per cent in the US. We need to keep on deregulating.

To understand the potential, consider that China is already the largest workshop in the world. Car sales are 19 million a year against only 11 million in the US. And we are willing to learn: we absorbed Buddhism, Islam, Taoism... we have had Communism, socialism, extreme capitalism.

In 1820 China’s share of world GDP stood at 30 per cent. It fell to a low of 1.7 per cent in 1978. Today it’s 11.5–12 per cent, while our share of world population is 17 per cent.

For the past 20 years I have always been the most optimistic of my peers, but my expectations have always been exceeded.

For the past 500 years, all innovation in science, politics, culture has come from the West. China’s Confucian tradition was forgotten. Confucius said that unity is a precondition for humanity, but in the US the saying is, ‘if you are not with me, you are against me’. The Greeks said, ‘man is the measure of all things’, but Confucius spoke of the unity of Man and Heaven. We need to redefine our relationship with Heaven (Nature) and I think that China can play an important role in that dialogue with the West.

PICTET WEALTH MANAGEMENT The Family Consilium 2013 7PICTET WEALTH MANAGEMENT The Family Consilium 2013 6

THE GLOBAL MACROECONOMIC

CONTEXTYves Bonzon and Bhaskar Laxminarayan of Pictet Wealth Management discuss today’s big picture with Jim Walker of Asianomics and Mary McBain of Ruffer

YVES BONZON

I’ll begin with a high-level view—one with which I am much in sympathy—laid out in Niall Ferguson’s latest book. He identifies

four key trends that lead to the degeneration of institutions.1 First, he cites polarisation: the growing divide between rich and poor inside countries; second, the rule of lawyers; third, who regulates the regulators? Fourth, the decline of civil society; and finally, the broken social contract between generations. I believe this is a very powerful prism through which to view longer- term geopolitical and economic prospects for the West.

In the economic sphere, the four big variables in the world’s biggest economy are in monetary policy, house prices, energy and profits. Since early 2009, the Fed’s balance sheet has expanded four times, but still, contrary to expectations, inflation remains dormant. House prices meanwhile, which had fallen by 50 per cent peak to trough, have begun to recover, suggesting the end of the balance sheet recession. On the energy front, the exploitation of shale gas has led to an extraordinary rise in US production and a sharp fall in prices. Finally, as a share of GDP, corporate profits have continued to rise at the expense of employee income.

In Europe, the labour market is still in decline, in contrast to the sharp recovery in US employment since late 2009. Car sales remain very depressed, while Euro bond yields are higher than nominal GDP growth, which means high financing costs impede recovery. In Spain, Greece and Portugal, nominal GDP is still below pre-crisis levels, but the Euro regime prevents a currency break-up that would lead to recovery.

In China meanwhile, nominal GDP has grown at 15 per cent compound for 20 years, which means a doubling every 6–7 years. GDP reached half that of the US last year, boosted by the massive stimulus measures of 2010 which pushed credit growth to 35 per cent and investment as a share of GDP to an astonishing 46 per cent. Even Japan reached only 36 per cent at its peak in 1973. But demography is an issue,

1 The Great Degeneration: How Institutions Decay and Die, Allan Lane, London 2012

UNDERSTANDING EAST AND WEST

as competitiveness begins to be undermined by a decline in the working population.

In Europe, for a common currency area to work in the long term there must be free flows of capital and labour. But what happens is that certain centres, such as London or Bavaria, attract all the talent and capital, leaving other areas very poor. Successful currency union must involve transfers, and this is something Mrs Merkel—a physicist with a Protestant upbringing—is reluctant to concede. As she points out, Europe has 7 per cent of the global population, 25 per cent of the GDP and 50 per cent of social expenses. These ratios are unsustainable.

‘for a common currency area to work in the long term there must

be free flows of capital and labour’

I did think Greece would exit the euro, but it’s clear now that this was not the right policy for Germany—and the longer Greece stays in the more likely it is to stay, as the country empties of its abler citizens, while the pensioners and government employees who are left are perfectly happy with deflation.

In Europe generally, we have stagflation and financial repression. It’s scary, but a crisis is the best time to deploy capital because you have forced sellers.

JIM WALKERWhen asked about the impact of ‘the French revolution’ Chou Enlai famously replied, ‘it’s too early to tell’. This 1971 remark is usually cited as evidence of China’s long-term perspective. Yet he wasn’t referring to the 1789 convulsion, but to the student riots in Paris in 1968. My contention is twofold: that it is too early to tell if China will take global leadership, and that it is too early to tell if the past 40-year experiment in paper money can be sustained.

The world is driven by the perception of profitable opportunities: entrepreneurs invest, create products, employ and pay people who spend. Policymakers miss this obvious fact, and concentrate on credit and government spending. That’s why the jury is still out on China.

Look at the facts. India has 15 per cent nominal GDP growth and a 20 per cent return on equity (ROE). In China, ROE struggles to get to 10 per cent. Why is Indian ROE superior? Because interest rates are higher and this forces companies to focus on higher growth opportunities.

In the US, rates of capex growth have peaked at much lower levels than China, so interest rates have fallen to rock bottom levels. Near zero interest rates send a powerful message: that investment opportunities are bleak.

We are now in the midst of a massive experiment in quantitative easing, and central bankers have no idea how to land the plane, or ‘taper’ as they call it. In 2000 Bob Woodward wrote a book about Alan Greenspan called Maestro. By 2008, as it became clear that he had failed to grasp the disastrous developments in the mortgage market, he was the clown. Bernanke continued his policy emphasis on credit and now —don’t let me scare you—we are entering a new super-typhoon.

Let me extend the metaphor: for the past 20 years, every time they’ve tried to land the plane, they’ve had to take off again. Interest rates are such an important signal to the economy. Current rates say, ‘keep your money in your pocket’. As soon as rates normalise, the economy will begin to recover.

Jim Walker (left), Yves Bonzon

PICTET WEALTH MANAGEMENT The Family Consilium 2013 9PICTET WEALTH MANAGEMENT The Family Consilium 2013 8

The European crisis is not like the Asian crisis of the late 1990s. Then, the IMF imposed major changes that forced huge devaluations—the Thai baht fell from 25 to 55 to the dollar for example—which produced astonishing adjustments. By 2002, Thailand had paid back all its external debt.

But Europe has chosen the very different path of deflation, which is socially very divisive. While devaluation hits the rich, the poor get jobs very quickly, whereas deflation kills the poor. Look at Spain’s 26 per cent unemployment.

BHASKAR LAXMINARAYANLet me begin with India. The economy is faltering, policymaking is paralysed, the rupee is weak and the trade deficit is expanding. There’s a progressive slowdown. Previously, you could always refer to India’s higher rates of return, but now that’s in question. A lot of these problems are self-created. Still, the demographics remain positive compared to China, and this is what policymakers have to focus on.

There are major limitations on Chinese growth and this is critical for the rest of Asia. You need twice the capital to get the same level of growth. This cannot continue. Credit intensity has to come down. We are at the end of a cycle of over-investment that needs to transform into higher domestic consumption. It’s true that China is quite open, but the financial markets are still very regulated: that’s why banking is the most profitable sector.

‘there are lots of opportunities to invest in value-creating enterprises’

Asia has been a big recipient of the flood of easy money since 2009. Foreign banks have lent US700 billion to Asia—three times more than the other direction—and this will reverse.

But I don’t want to depress you. At the micro level we’ve had three decades of good data. Companies have evolved and matured and there are lots of opportunities to invest in value-creating enterprises.

UNDERSTANDING EAST AND WEST

Yves Bonzon is Chief Investment Officer of Pictet Wealth Management (See page 27 for full biography).

Bhaskar Laxminarayan is Chief Investment Officer for Pictet Wealth Management in Asia, based in Singapore. Before joining Pictet in 2007, he was Chief Investment Officer with Shinsei Asset Management. A qualified accountant, Bhaskar holds a management degree from the Indian Institute of Management, Ahmadabad, India and a Bachelor’s degree in Commerce from the Vivekananda College, Madras, India.

Mary McBain has spent most of her life either living or working in Asia. After graduating from Brasenose College, Oxford in 1985 with a degree in Modern History and Economics, she joined the Asian investment team at MIM (now Invesco Perpetual). She currently runs the Hong Kong office of Ruffer LLP and manages the CF Ruffer Pacific Fund, an absolute return fund.

Jim Walker is the founder and Managing Director of Asianomics Limited, an economic research and consul-tancy company. Until 2007 he was chief economist at CLSA Asia-Pacific Markets. He became best known for predicting the 2007 downturn and meltdown in the US financial sector in a series of ‘Apocalypse’ reports. He holds a BA (Hons) and a PhD in Economics from the University of Strathclyde, Glasgow.

MARY MCBAINI’m not sure what I’m doing on a macro panel— I spend most of my time looking at micro opportunities. But I do need to keep a close watch on the macro. Consider QE, which has exported a lot of problems to Asia. Many jobs have been lost as a result of the Western financial crisis. Take one consequence: the new regulation in Hong Kong to dampen property speculation. It’s taken the fun out of speculation, which is the lifeblood of a market economy.

So when I look for interesting stocks, I look for ‘Bernanke-proof’ or ‘QE-proof’ investments. It’s a really interesting time in China for sectors such as travel, health, tourism, even agriculture.

When I first came to China, people told me that Chinese people wouldn’t drink wine, eat cheese, drink milk, go to the beach, wouldn’t ride bicycles for pleasure, don’t care about the environment. Today my portfolio is full of these ideas.

The other day, I went to a funfair. There were two middle-aged women who wouldn’t get off the roller-coaster, they were enjoying it so much. Take education. The children of the rich are going to all the top schools abroad. That will translate into innovation and growth. People are having the chance to do things they’ve never done before. So I continue to see lots of change and opportunity.

I see a little less opportunity in India. Investors have covered India much more than China, where there are a myriad of undiscovered companies and where I still think I can get an edge. So I’m positive, while still expecting things to blow up.

HOW LONG WILL IT TAKE TO GET OUT OF THIS CRISIS? Mary I’d say 10–15 years to escape the Eurozone debacle. Bhaskar At least a decade. Jim Hong Kong is tied to the dollar and after the 1998 Asian crisis it took until 2002, after property prices had fallen by 75–90 per cent. In Spain, property prices have much further to fall. Yves I see major social tensions ahead, especially in France. Europe’s structural policies are leading to deindustrialisation.

WHAT IS THE PSYCHOLOGY OF THE CENTRAL BANKERS?Jim Our analysis is based on the Austrian school—don’t act, let the markets shake out the bad capital. Governments always have a bias towards action. But central bankers can only print money and governments can only spend money. They’re all aligned in this and they keep going because they fear the alternative. In Japan, the consequences haven’t been too bad because most people benefit from deflation, but what happens when Japanese government bonds fall? Yves I have a lot of sympathy for the Austrian school. The combination of free capital flows and local regulation creates a system that is unstable. Monetary union in Europe created a bubble. What we need is not more regulation but better regulation. Jim Supporting banks during and after the crisis is the biggest exercise in institutionalised theft in history.

HOW DO THE DEMOGRAPHICS PLAY OUT?Mary There are still 600 million living in the Chinese countryside, which leaves huge scope for productivity growth to counteract the ageing population. Bhaskar There’s no way round it. Productivity will have to rise. Jim By 2030 China will have a higher percentage over 65 than Japan today. But South East Asia still has a great demographic profile. Thailand, Indonesia, India, Vietnam still have a tremendously bright future.

From the audience WHAT ARE YOUR BEST BETS?

Mary I'd buy China A shares.

If there’s a blow-up you’re invested in a closed market.

Bhaskar I believe in long-term value creation over cycles rather

than near-term growth stories.

Jim I’d be long ASEAN banks,

short European banks.

Yves I’d do the opposite.

Mary McBain (left), Bhaskar Laxminarayan

PICTET WEALTH MANAGEMENT The Family Consilium 2013 10 PICTET WEALTH MANAGEMENT The Family Consilium 2013 11

BUILDING A GREAT BUSINESSLeading businessmen Markus Akermann, former CEO of Holcim, William K Fung of Li & Fung and Harald Link of B. Grimm talk about their achievements

Professor Randel Carlock, TFC moderator, opened the session by noting that on stage were three remarkable, family-related, yet

contrasting businesses: a listed Swiss company with global interests and a non-family CEO, a Chinese family business that recovered from post-war adversity and went public, and a 125-year old, 100% private company that began as a joint venture between a German and a Thai family. MARKUS AKERMANNToday we are a global company spanning 70 countries and 2000 locations. Our turnover is USD23 billion and we have 80,000 employees. We were founded in 1912 and we are the largest cement and aggregates business in the world. The founding family still has a 20 per cent shareholding and though they’re not involved in the business—I was the first non-family CEO—that holding is an important anchor for stability. It limits the risk of takeover and encourages a long-term view in a very cyclical business.

I joined in 1978 and after several years in LATAM I took responsibility for Central American and Andean business. In 1993 I joined the main board and now LATAM is 35 per cent of turnover. I took over as CEO in 1992. Asia Pacific accounts for 30 per cent of sales, while two-thirds of turnover arises from emerging markets (including places like Russia and Central Asia).

The world construction market accounts for 13 per cent of global GDP and it’s growing at 5 per cent annually. The three main drivers are population growth, GDP per capita and urbanisation. Replacement is also potentially significant—just look at the state of US infrastructure.

How did we become a global business? The founders had a vision of building a sustainable business and understood that our future could not lie in Switzerland alone. We have also always operated on the principle of decentralisation, giving strong empowerment to the local employees. This is very different from our competitors. While they made acquisitions and required control, we didn’t have the cash flow, so we opted for minority participation, joint ventures and supply of technical knowhow.

‘We have also always operated on the principle of decentralisation’

When you take a stake in a local business, how do you gain the trust of the local families? It takes a long time. You have to look for a good fit, for common values, business model, environment and social aspects. Once you have agreement, only then do you talk about pricing. In the wake of the Asian crisis, therefore, we were able to help local companies, rather than take a short termist, investment banker type approach.

UNDERSTANDING EAST AND WEST

In 2001 we introduced the Holcim brand across the whole group. A common brand implies common values and common standards that are non-negotiable. Our principles are based on cost leadership, market leadership, people management and local focus.

We believe in corporate social responsibility.It’s a business case, not philanthropy. For each location, we ask what are the local needs. We discuss with the local community. For some years we have been in the top ten of the Dow Jones Sustainability Index and we are one of the most economical in terms of our environmental footprint.

In terms of financing, we regard it as critical that we maintain an investment grade rating. In good times, it’s easy to find credit; in bad, it’s impossible. Our competitors have not done that.

Let me say something about people. Worldwide we want to be a preferred employer. You can’t pick up good cement people off the street. At any one time, 90 per cent of our employees are in training. In many factories we have even installed an apprentice scheme. The graduates may not stay with us, but it’s a contribution to development.

Holcim’s principles

123

4

COST LEADERSHIP From quarry to market

MARKET LEADERSHIP – to be at the top of the pricing curve

TO EXCEL IN HR MANAGEMENT How much is each manager contributing?

TO BE EMBEDDED IN THE LOCAL ENVIRONMENT

From left: Randel Carlock, Marcus Akermann, William Fung, Harald Link

PICTET WEALTH MANAGEMENT The Family Consilium 2013 12 PICTET WEALTH MANAGEMENT The Family Consilium 2013 13

WILLIAM FUNGI’m the third generation in the business, founded by my grandfather in 1906. He was the first in his family to speak English. Until 1949 we were Canton-based China traders in tea, silk, porcelain, fireworks, that kind of thing. It was a thriving business, and my mother always says, you’ve done well, but your grandfather...

In 1949 with the Communist revolution, the Bamboo Curtain came down and we lost everything. My father moved to Hong Kong and we had to reinvent the company as a manufacturer — of plastic flowers, garments and so on.

China evolves in eras of thirty years: from 1949–1979 the country was closed; 1979–2009 was the era of opening up. In the early 70s, Victor and I came back into the business, after Harvard Business School, and began to export Chinese manufactures. Now I don’t like nepotism: we have 36 cousins and we are the only Fungs in the company.

We began to expand into other countries when my friends began to ask, why are you doing labour-intensive manufacturing? You’re losing competitiveness to Taiwan. So we moved into Taiwan... then Korea... and now we’re in 40 countries.

More recently, we embarked on a second engine: the consumer. We talk of the billion toothbrush syndrome: if you can sell a

toothbrush to every Chinese... Well, it’s happening now, as we enter the third thirty-year era. This will be the era of the Chinese consumer.

Chinese GDP, already US8 trillion, will exceed USD40 trillion in today’s dollars by 2039, and if you consider that domestic consumption is only 35 per cent of GDP compared with the US rate of 70 per cent, you can imagine the potential. This is definitely the future.

‘I don’t like nepotism: we have 36 cousins and we are

the only Fungs in the company’

Let me say something about the third generation. In China they say wealth never passes beyond three generations. But the key is rejuvenation, reinvention. When I told my father I didn’t want to work in the company, he said, so what do you want to do? I said, if you go public and install proper corporate governance, I’ll join you. Corporate governance is crucial as a guardrail in a family-controlled business.

HARALD LINKOur business was started in 1878 by Bernard Grimm, an Austrian pharmacist, in a joint venture with a Thai family. My grandfather, also a pharmacist, joined in 1903 and soon bought out the other partners. He was a very resilient man. As a German, he was interned in 1917 and

also in 1945. Later my uncle and father joined the company, with business principles that focused first on customers, then employees and then on suppliers. They believed that what was good for society was good for business—and we continue to operate on this belief today.

My father was the Thai consul-general in Hamburg, and he was exporting medicines in Europe under the B. Grimm name. After the war we reinvented ourselves as distributors. We survived many crises.

The first crisis I remember was when a senior manager left. My father told me, you have to deal with it. I thought I couldn’t handle the responsibility, yet I got through it. But our management was entirely German; they had no long-term commitment to Thailand. So I told my uncle, let me have a go.

I became CEO in 1978 and replaced German management with Thai management. But our model of distributing foreign products wasn’t sustainable, so we focused on joint ventures with companies like Siemens, Mitsubishi, Mercedes and so on. We also moved into financing and power plants, which is now our main business.

When the Asian financial crisis hit in 1997, we suffered non-payments problems. So I went to our joint venture partners, who told us they were committed to Asia and believed in the Grimm franchise, and that got us through.

UNDERSTANDING EAST AND WEST

Markus Akermann has been a board member of Holcim Ltd since 2013. From 2002 until 2012, he was the CEO of Zurich-based Holcim Group, the largest global cement, aggregates and ready-mixed concrete company. He was a member of the Executive Board of the World Business Council for Sustainable Development from 2008 until 2011.

Dr William K Fung, SBS, OBE, JP joined the Li & Fung Ltd Group in 1972 and was appointed Group Chairman in 2012. He holds a BSc degree in Engineering from Princeton University. He also holds an MBA from the Harvard Graduate School of Business and a Doctor of Business Administration, honoris causa, from the Hong Kong University of Science & Technology. He is the co-author of the book Competing in a Flat World.

Harald Link has been a Managing Partner of B. Grimm & Co ROP and Chairman of B Grimm Group of Companies since 1987. He is Chairman of Amata Power Ltd and other companies. He is also a Vice Chairman of Siemens Ltd and holds a number of directorships of both Thai and European companies. He is a qualified lawyer and holds an MBA from St Gallen University, Switzerland.

Three keys to long-term success

PEOPLE DEVELOPMENT Marcus Akermann

REENGINEERING THE BUSINESS MODEL William Fung

REPUTATION AND LEGACY Harald Link

My daughter Caroline joined in 2008. Now the Western way of business is to ask, what business are you in, what is your purpose? But she asked me, what are our values? It says nothing about that on our website. What does B. Grimm stand for?

‘the Western way is to ask, what business are you in, what is your purpose?’

We define ourselves by the way we do business: positivity, professionalism and partnership. Our purpose is not to maximise shareholder value, which is just a by-product of always thinking about how we can contribute to society.

As for succession, I always thought that the way to avoid conflict was to tell my children about my plans. But it’s the opposite! My son loves meditation and doesn’t want to go into the family business. So he will manage the family castle. In three years I will halve my activities and concentrate on the social side—education, culture and religion, environment and sports.

14 PICTET WEALTH MANAGEMENT The Family Consilium 2013 15

UNDERSTANDING EAST AND WEST

due for completion in 2017. ‘It was a difficult decision to avoid China. Contemporary art is about reflecting and commenting on society, while in China the authorities subscribe to the traditional view—that it’s about beauty and harmony. There are no clear rules on what can and can’t be shown, but censorship is widespread, and this is just the tip of the iceberg.’

‘Shanghai’s becoming really exciting culturally’

Budi’s Jakarta museum is five storeys, shortly to move next door to his business head-quarters. ‘My Shanghai space will be 9,000m2 and I plan to add another 12 to 15,000m2. There will be many big install-

ations. Art is my calling and this museum is my lifetime mission.’ A grand opening is planned for next May, before Hong Kong Basel.

He’d prefer it wasn’t a private museum, and intends eventually to establish it as a foundation. ‘I would just like my name attached to it, so that my descendants will know that I was someone who did something good.’

Why did he settle on Shanghai rather than Beijing? ‘Shanghai’s the future centre. It’s becoming really exciting culturally, with the develop-ment of the West Bank Cultural Corridor in the Xuhui District. The city will be like New York, with business and culture together: museums, concert halls, Chelsea, Wall Street, and the like. And China,

with Hong Kong, is now the world’s largest art market.’

In the end, though, Uli thinks their visions will converge. ‘Public museums should represent cultural heritage, not private taste. We need the strength of

Swiss-born Uli Sigg enjoyed a rich career in journalism, business and diplomacy, culminating in a stint as Swiss ambassador to China from 1995–98. But he is best known for his extraordinary collection of contemporary Chinese art. Budi Tek is a Chinese-Indonesian businessman with major interests in agribusiness. He has one of the biggest collections of Chinese, Asian and Western contemporary art. In 2008 he built the first private museum in Jakarta. Introduced by Philippe Bertherat partner of Pictet & Cie and moderated by art curator William Zhao.

Building a great art collection

From left: Budi Tek, Uli Sigg, William Zhao

Left: Philippe Bertherat'

ULI ON M+ A new contemporary art museum in Hong Kong ‘So far the Hong Kong government has invested HK$23 billion in this new cultural project in Kowloon. The M+ space alone is costing USD800 million. The whole complex will be run by Western curators, with a long-term strategy and complete freedom of expression. It won’t be closed to mainland Chinese–40 million visit Hong Kong every year. The museum will be 60,000m2, which is about the size of the MoMA in New York.’

William Zhao began by asking the panellists to describe what

motivated them to collect art.Uli responded that his

original vision was to collect Chinese contemporary art as a bridge into China. ‘But at that time, in the 80s, Chinese contemporary art was deriva-tive of western art. And no-one was collecting systematically. It was all underground.’ So he decided to collect like a museum, representatively, rather than indulging his

personal tastes, with

the eventual aim of bringing

it to the public.Budi’s impulse is

diametrically opposite. ‘I have the DNA of a collector.

In 2005, after recovering from

the Asian crisis, I decided to do something I liked.’ He visited galleries, auction houses, studios. ‘For the first few years I collected rubbish, but it was necessary.’ In time, travelling widely, he began to take an interest in Western artists like Anselm Kiefer, who were influencing Chinese art. His collection expanded to include installations, photography, videos and so on. So he established the Yuz Foundation. ‘I never intended to do this, but it’s an addiction, a drug. Everybody says that.’

‘You can’t buy directly from artists these days, but it’s crucial to visit their studios to understand the purpose of their art, their philosophy,’ says Uli. Recently he pledged a gift of 1,400 works to the M+ museum in Hong Kong,

PICTET WEALTH MANAGEMENT The Family Consilium 2013 16 PICTET WEALTH MANAGEMENT The Family Consilium 2013 17

UNDERSTANDING EAST AND WEST

Uli Sigg was born and grew up in Switzerland. He holds a PhD from the University of Zurich Law Faculty. In 1997 he established the Chinese Contemporary Art Award (CCAA) for Chinese artists living in China, and the Art Critic Award (ACA) in 2007. He is a member of the International Council of New York’s MOMA and the International Advisory Council of the Tate Gallery London.

Budi Tek is a Chinese-Indonesian entrepreneur, art philan-thropist and collector. In 2007 he established the Yuz Foundation, a non-profit organisation dedicated to the promotion of contemporary art and artists. He was named one of the Top 10 most powerful figures in the art world by the international art magazine Art+Auction in late 2011. He will open the Yuz Museum in Shanghai in 2014.

William Zhao was born and grew up in China. He holds an MBA, acquired in France. After an early career in finance, he returned to Asia in 2003 to devote himself to advising collectors and writing on contemporary Chinese art. He contributes regularly to Modern Weekly, Bazaar Art (China edition) and the South China Morning Post.

public institutions as a system-atic memory of our time. After all, traditional art was once contemporary art.’

Philippe Bertherat asked about art as an investment. ‘I never thought about money,’ says Uli, even though pictures he bought for hundreds of dollars are now worth hundreds of thousands.

‘Chinese contemporary art will become the most expensive in the world’

‘Is it an asset class? Of course it is. But it’s not very transparent, even though today excess liquidity drives up art prices along with financial markets. But when that liquidity dries up, watch out. Art requires deep knowledge if you are to treat it as an asset class.’

‘I wasn’t so lucky,’ says Budi. ‘I started buying late and paid

dearly.’ But he observes that Chinese contemporary art is still undervalued relative to Chinese purchasing power, and still a fraction of the price of western equivalents like Warhol. ‘It was the same with Western contemporary. Sotheby’s offered me a Basquiat at USD5 million. Museum quality, they said. Too much, I said. A few years later I was offered the same work for USD45 million.’

He believes that Chinese contemporary art will become the most expensive in the world. ‘There are so few museums collecting today. The Chinese economy produces a dozen new billionaires a year, but not even one good artist a year.’

How does one begin to collect? ‘Surround yourself with art, good or bad,’ says Uli. ‘Bad art is better than no art at all. Go to galleries, art fairs, buy what you like. It’s better than

owning something abstract, like a bank account.’ Budi suggests two alternative approaches. ‘You can buy the cover—what’s on the cover of the catalogue, what everyone is buying—or you can buy the best, the most expensive. But do go to the best galleries.’

And the future? ‘Great art is born out of tension, out of political repression. Maybe that impulse is weakening in China these days, maybe not,’ says Uli. ‘The show goes on,’ says Budi. ‘The first generation of free- market Chinese artists were symbolic, political. Now they’re more personal, creating from the heart. Art forms change with the evolution of society.’

SOME ARTISTS IN THEIR COLLECTIONS

BUDI TEK Maurizio Cattelan

Fred Sandback Ai Weiwei

Adel Abdessemed Mona Hatoum

Huang Yong Ping Yutaka Sone Chen Zhen Wang Jin

Piotr Uklanski

ULI SIGG Wang Keping Geng Jianyi

Wang Guangyi Fang Lijun Yue Minjun

Zhang Xiaogang Zeng Fanzhi Feng Mengbo

SPECIAL TALK

REPORTING FROM THE TOP

Stephen Barber talks with Marcus Brauchli about a media career that has spanned three continents and reached the commanding heights of two of the world’s leading newspapers

SDB Good morning, Marcus. We first met in 1987 during the later days of the Japanese Bubble, in Tokyo, where Tim Geithner was then the Financial Attaché in the US Embassy. It was one of the first financial crises you reported on, before the Asian Crisis and then the great financial crash in the US. By this time you had reached the pinnacle of journalism as the chief editor of the Wall Street Journal. Soon after, Murdoch bought the paper and installed his own man. Then you became the editor of the Washington Post, which became world famous during the Watergate crisis. The Post has just been sold to Jeff Bezos of Amazon.

Let me begin by asking you about the virtues of Confucian leadership, as Dean Xiang mentioned yesterday—which certainly reminded me of Tokyo in the late 1980s when some Western commentators seriously thought that the US Treasury would be better run by the elite bureaucrats of Japan’s Ministry of Finance.

MB It was interesting to hear Dean Xiang talk about Confucian government as a model. When I was covering Japan and SE Asia in the 80s and 90s there was a lot of talk by leaders like Lee Kuan Yew, like Kishore Mahbubani—who’s now head of the Lee Kuan Yew School of Public Policy—about the strength of Asian government models vis-à-vis the West. They predicted that democratic forms of government would be inadequate to deal with the sort of crises we now have. China’s ascent in the past twenty years has given some support to that argument. But I think it’s too early to write off a system of government that’s been so successful for over two centuries.

I first started covering China in 1984. You would never have imagined the scale of China’s ascent then, even in the light of Japan’s and Korea’s earlier achievements. I went into Shenzhen in 1985 to cover the agreement to install the first telephone exchange there. Shenzhen was a city of 400,000 and hardly a building above three storeys. Today it’s a city of 10 million and skyscrapers. In the following decade China went through the Tiananmen

massacre but was continuing rapid reform. We sceptical journalists would always ask whether the country was truly committed to reform.

SDB Moving on, it’s interesting that you worked for three family businesses: the Dow Jones group, News Corp and now the Post Group.

MB US media businesses like these tend to be family-controlled, nowadays usually listed and controlled with the use of restricted voting structures. The New York Times, Axel Springer in Germany, the Hindustan Times, the South China Morning Post among others are also family-controlled. Over the past century these newspaper companies became very powerful and even semi-monopolistic, as they took over competitors—and therefore enormously profitable franchises. The disruptive technology of the internet means that maintaining them as viable family businesses has become increasingly difficult.

The three companies I worked for were very different. The Bancroft family, who controlled Dow Jones, had nothing to do with the day-to-day management of the paper. The ownership

structure of interlocking trusts worked pretty well until Rupert Murdoch came along. He picked the lock of the family ownership by offering a huge premium to the market price. So then I worked for Rupert Murdoch—News Corp—for several months. He is an extraordinary man. He follows every aspect of his businesses closely, especially the newspapers, which is his background, and brings family members into—and out of—the company.

‘Don felt the business and the employees, for whom he cares deeply,

would be secure with Bezos’

The Washington Post company is run by Don Graham, grandson of Eugene Meyer who bought the paper in 1933, and son of Katherine Graham, who famously ran the Post during Watergate, and who for over thirty years was the matriarch of US media. A family member has always held the position of Publisher; they also expanded the company into other areas—education (Kaplan), TV stations, and so on— fortunately, as the profitability of print has declined. The courageous and selfless decision

PICTET WEALTH MANAGEMENT The Family Consilium 2013 19PICTET WEALTH MANAGEMENT The Family Consilium 2013 18

‘He picked the lock of the family ownership by offering

a huge premium to the market price’

Stephen Barber (left), Marcus Brauchli

PICTET WEALTH MANAGEMENT The Family Consilium 2013 21PICTET WEALTH MANAGEMENT The Family Consilium 2013 20

SPECIAL TALK

to sell the newspaper, the soul of the company, to Jeff Bezos of Amazon was only possible because of the strength of these other businesses. Don felt the business and the employees, for whom he cares deeply, would be secure with Bezos—and it’s no coincidence that it was sold to the Bezos family, not to Amazon. Incidentally, Katherine Graham was very close to Warren Buffett, who served on our board until a couple of years ago, and he had argued forcefully in favour of diversification.

Bezos has said he feels that the Post needs the resources, the ‘runway’ as he puts it, he can provide to remain as an important public institution in the US. I think Jeff Bezos has a civic mission. But I also think that Bezos, having built up Amazon selling content produced by others, has become very focused on how content is created and consumed and how people interact with news content, and with the Post—which he bought at a knockdown price of $250 million—he gets a window into that.

I don’t think he comes to it with a mission, with a certain agenda. In fact Don went to Bezos; he chose his successor. I’m sure Don said to him, one day there’ll be a piece of legislation going through Congress that’s bad for Amazon, and by

chance on the day of the vote, there’ll be a front page story detailing the sexual peccadilloes of the committee chairman. And there’ll be not a damn thing you can do about it. You can control a US newspaper, but you can’t really control its newsroom and if you are serious about protecting its integrity and independence you can’t control its news agenda. I think he understands that.

SDB Were there any occasions when businesses or politicians tried to influence your news agenda?

MB When Alan Greenspan wrote his memoir, due to come out on a Monday, I assigned reporters to go to bookstores all over and try and get a copy. As in the film The Devil Wears Prada, at least one male bookstore assistant suggested to a female reporter that if the conditions were right, he could get her a copy. Anyway, we got one, and told Greenspan. He called me and said, ‘Marcus, if you publish an extract before the launch, our relationship is over’. I said, ‘Well, Alan, this is

only our second call, and you’re not the Fed chairman any more’. We’ve subsequently become friends.

More interesting are the conversations on national security. In 2009 Bob Woodward—of Watergate fame—got an advance copy of a report that Stanley McChrystal, the commander in Afghanistan, was due to submit to the President, covering policy and a request for more troops. Woodward wrote a story, which I read on a Saturday morning and instead decided to publish the entire document on our website—one of the ways in which the internet changes journalism. So I got a call saying, could you please hold for the Secretary of Defense, the National Security Adviser, the White House Counsel, the Vice Chairman of the Joint Chiefs of Staff. They basically said, you can’t publish this. After a long conversation I agreed to go to the Pentagon and go through the document line by line to identify anything damaging to national security. In the end we redacted only three lines, which covered specific operations, and published.

SDB What about the White House? Weren’t you at college with Barack Obama? Did he pick you out as a future editor of the Washington Post?

MB No, nor did I pick him out as a future president. This White House is extraordinarily controlling of information, much more so than the Bush White House. Everybody thought the Bush White House were a bunch of troglodytes who came in and just wanted to bomb other countries, control everyone, send people to Guantanamo never to be seen again.

‘If you get within Clinton’s field of vision, first there’s a visual and

then possibly a physical embrace’

But the Obama administration has been every bit as tough on national security and tougher on journalists. Take Rahm Emanuel, the former chief of staff under Obama, now mayor of Chicago—he’s famously missing a crucial finger on one hand that causes Obama to call him rhetorically challenged. He’s profane, rude, demanding; whenever we threatened to publish something he didn’t like he would call up and start swearing and sometimes hang up. Which turns out not to be the most effective approach, because you never finish the conversation and so we end up publishing anyway. The Obama administration does not like talking to mainstream press. In my four and-a-half years as editor we had one extended interview with Obama, and that was in the week before he became president. He prefers television because he can control what is said and he knows TV interviewers will ask about his dog, about Michelle, about the kids.

In person he’s very much as he appears in the media. He’s got a good sense of humour, he’s quick, he’s smart, he’s impatient with people who waste his time and he doesn’t have the charm of Bill Clinton. If you get within Clinton’s field of vision, first there’s a visual and then possibly a physical embrace. He has this incredible ability to read an audience. I was

MB Stephen called the Washington Post a liberal newspaper and I would take issue with that. The editorial page is not as liberal as it used to be—many people in Washington consider it centre-right—but the news department, we like to think we’re not liberal or conservative.

SDB I said that because you write editorials against banking secrecy.

MB Just that one guy. He’s a liberal. I took Stephen to lunch with the guy and this is what happens.

IS THE WASHINGTON POST A LIBERAL NEWSPAPER?

SPECIAL TALK

Marcus Brauchli is an adviser to Donald Graham, Chairman and CEO of The Washington Post Co., the parent company of Kaplan Inc, CableONE and Post-Newsweek Stations. Previously he was executive editor of The Washington Post. Before The Post, he was The Wall Street Journal’s top editor. He spent 15 years as a Journal correspondent and bureau chief in Hong Kong, Shanghai, Tokyo and Stockholm. Marcus is a graduate of Columbia University. Stephen Barber is Head of Group Communications for the Pictet Group. He also runs the global photography prize, the Prix Pictet, whose subject is sustainability. Stephen began his career as an investment manager in 1977 with Samuel Montagu & Co Ltd, the now extinct British merchant bank. He holds a double honours degree (MA) in Mathematics & Philosophy from St John’s College, Oxford.

with him in China 1998 or ‘99 and he met with a bunch of students at Beijing University—hand-picked by the Communist party—and he took their questions, tough questions, and he won them over completely. They would have all voted for him. Obama doesn’t have a way to engage that isn’t cerebral and aloof. He keeps very close counsel. The source of a lot of the problems in the US at the moment is that Obama doesn’t ask anybody else what they think. The way he made the decision to seek Congressional approval on Syrian intervention was just the wrong way to do it. You don’t dither in public for three weeks, and then the day after your top officials have been telling foreign allies there’ll be a strike on Syria, announce you’ve changed your mind after consulting no-one except, well, maybe Michelle and the dog, or maybe Valerie Jarrett, his closest adviser. People think you’re unreliable.

His predecessor, George W Bush—‘the Decider’—was far more charming with a self-deprecating style. I suppose there are people who would say there’s a lot to deprecate, but he was at ease with himself. His greatest moment in my view was during the financial crisis. He’d been bludgeoned for seven years, his image had got worse and worse, the Iraq and Afghanistan wars were a morass, and it was mid 2008. He’s a lame duck, he’s going to be out in six months, and this thing happens.

‘It’s been said that our political system is designed by geniuses and run by idiots’

He completely empowered Hank Paulson, Tim Geithner, Ben Bernanke, and he said, look, you tell me what I need to do. I think the world will never fully appreciate these three as much as it should. These are guys who did really difficult things and stretched the laws to do what was necessary to enable the US and the world economy to stabilise. This wouldn’t have happened if Bush hadn’t empowered them, and in doing so abandoned core principles of his party, the Republicans. It couldn’t happen today.

The hardcore Republicans that we have now— the Tea Party—won’t compromise on anything the Democrats want unless they win their battle to get rid of Obamacare. And since Obama’s not going to give way on that, it’s not impossible that the Republicans might force a default on the debt ceiling.

It’s been said that our political system is designed by geniuses and run by idiots. From 1978, the Republicans changed their strategy. They’d been out of power in Congress for a long time. A history professor from Georgia, a buffoonish loud-mouth, was elected to Congress for the first time. He had the idea that the way for the Republicans to get into power was to destroy the credibility of the Democratic members of the House so that they wouldn’t get re-elected, which is normally almost automatic. And the way to do that was to tear down the credibility of the institution, so that its leaders would be seen as corrupt and venal. That was Newt Gingrich. And he was right. Congress became a deeply unpopular institution. Whenever Republicans were elected, they were told, sleep in your office, and go back to your district every weekend. Never hang out in Washington. You have to be against Washington and against Congress. Culturally what happened is that the Republicans became the party of ‘No’. And today the Republican Party is full of nihilists. They think that if you can just shut down Congress and prevent any legislation from passing, government will cease to be effective, it won’t get funded, people will turn on government, it will get smaller and finally you can reduce the level of taxation – thus, in their view, get a government closer to fundamental American values than what we have today. There are about 87 members of this core group of nihilists, the Tea Party. They can block legislation by attaching whatever amendments they want—reduce taxes, abolish Obamacare and so on. The Democrats allow them to do this, because it makes the Republicans look bad, and so we have a very dysfunctional government. Obama doesn’t handle it well. Joe Manchin, senator for West Virginia, once told me

that in his first year in office he had never heard from Obama or any of his senior staff since he was elected in 2010.

This stuff matters. The US still plays such a central role in the global economy. This fight over who should succeed Bernanke—Summers or Yellen—which Obama handled so badly was completely unnecessary. And now the Fed chairmanship is politicised. It matters if they default on the debt, even for 15 minutes, because interest rates around the world will go haywire. The US may not get involved in Syria, but not because there’s a thoughtful decision-making process, but because they can’t get their act together. It matters because Obama’s relationship with Putin is borderline hostile.

SDB What’s the future for you, another editorship, or maybe a book?

MB I’m setting up a company to invest in journalism-related and media technology companies in emerging markets. My theory is that the disruptive power of digital technology is even larger in countries where there hasn’t been strong non-state or oligarch-controlled media. I think there’s a big opportunity to arbitrage how people interact with information in the digital world and the capital that we can bring, to help companies already in media to be more effective. Media is changing so fast, and every country is different, everyone is finding new models. People who bemoan the decline of mainstream newspapers say they can’t find out what the new model is, as if there’s one model. There isn’t. It’s an exciting time to be in journalism and media, but to find new ways of delivering to people the information that they most care about and is valuable to them.

PICTET WEALTH MANAGEMENT The Family Consilium 2013 22 PICTET WEALTH MANAGEMENT The Family Consilium 2013 23

PICTET WEALTH MANAGEMENT The Family Consilium 2013 25PICTET WEALTH MANAGEMENT The Family Consilium 2013 24

OPTIMAL STRATEGIES IN ASSET ALLOCATIONYves Bonzon, Pictet Wealth Management’s chief investment officer, explains his latest thinking on asset allocation principles

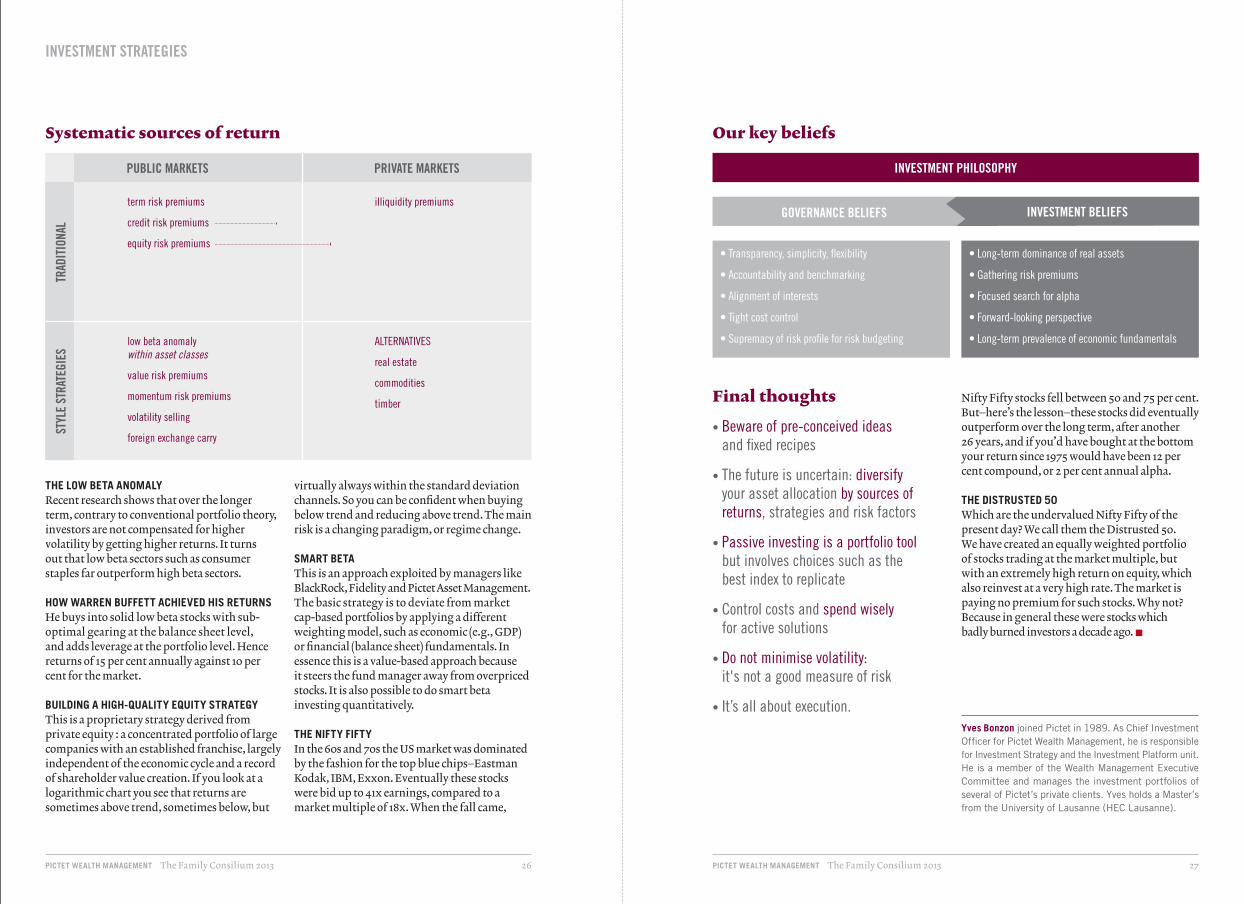

WHERE DO INVESTMENT RETURNS COME FROM? There are two basic sources of return: returns from the market (beta), which can be divided into secular and strategic, and returns from skill (alpha), which are either tactical or entrepreneurial. The table (overleaf ) shows how these returns break down into public and private, and traditional and style strategies.

ESTIMATED TEN-YEAR MARKET RETURNS Our estimates of nominal returns (dividends included) between now and 2023 under a standard growth and inflation model fall between 3 per cent (USD cash) and 15 per cent (private equity), and on average around 4 per cent annually. With an innovation shock (see opposite), returns would be higher by 1–1.5 per cent annually.

WHAT ABOUT ALPHA? The first rule is alpha is not scalable. So you should always measure excess returns in absolute dollars. A dollar of alpha gained by one investor is one dollar less for another investor. You can

gain alpha from market timing (TAA1) and from security selection. To succeed, you need either an information edge (more likely in private markets since insider dealing is mostly illegal) and/or an information processing edge (e.g., from quantitative strategies). Up to a limit, you can also get a deal flow edge, or a capital stickiness edge. Warren Buffett gets first call because he always has capital in times of trouble.

SECULAR TRENDS The 1970s were the years of small caps, oil stocks, gold, the Swiss franc and the yen. The 80s was the decade of government bonds, the Nikkei and the Hang Seng. In the 90s indexation, tech and the US dollar held sway. The 2000s were dominated by hedge funds, emerging equities, commodities and the euro. Now, under conditions of managed deleveraging in the West, we have believed that no government would allow deflation to prevail. In the current decade the strategy focus is TAA plus risk-based asset allocation, emerging debt and the US dollar.

INVESTMENT STRATEGIES

1 tactical asset allocation

MYOPIC LOSS AVERSIONOne interesting insight from behavioural psychology is the phenomenon known as myopic loss aversion (see especially the work of Richard H. Thaler). This well known research finding shows that investors suffer more pain from losses than pleasure from gains, even when the monetary amount is the same. Not only does this tendency lead us to look at the value of our portfolios more frequently than we need to, but it means that as a result, we inevitably suffer from net pain (since in the medium term, the balance of up and down days will tend towards zero). Conclusion: you shouldn’t check your portfolio values more than, say, once a quarter.

SOURCES OF INNOVATION SHOCK'Innovation shocks' are shocks that lead to a positive shift in the economic regime, expressed through two main variables: real GDP growth and inflation. In our opinion, there are three main sources of innovation shock:

Technological Nanotechnology, neuroscience, biotechnology, new IT/communications technology, shale oil & gas

Regulatory Much greater degree of entrepreneurship worldwide and an extension of democracy (demand for economic and social justice; equitable treatment)

Cognitive A shift in monetary-policy stances (move from inflation targeting to targeting of price levels or asset pricing) and new supply-side economic policies.

PICTET WEALTH MANAGEMENT The Family Consilium 2013 27PICTET WEALTH MANAGEMENT The Family Consilium 2013 26

STYL

E ST

RATE

GIES

PUBLIC MARKETS

illiquidity premiums

PRIVATE MARKETS

Systematic sources of return

ALTERNATIVES

real estate

commodities

timber

• Beware of pre-conceived ideas and fixed recipes

• The future is uncertain: diversify your asset allocation by sources of returns, strategies and risk factors

• Passive investing is a portfolio tool but involves choices such as the best index to replicate

• Control costs and spend wisely for active solutions

• Do not minimise volatility: it's not a good measure of risk

• It’s all about execution.

INVESTMENT STRATEGIES

virtually always within the standard deviation channels. So you can be confident when buying below trend and reducing above trend. The main risk is a changing paradigm, or regime change.

SMART BETA This is an approach exploited by managers like BlackRock, Fidelity and Pictet Asset Management. The basic strategy is to deviate from market cap-based portfolios by applying a different weighting model, such as economic (e.g., GDP) or financial (balance sheet) fundamentals. In essence this is a value-based approach because it steers the fund manager away from overpriced stocks. It is also possible to do smart beta investing quantitatively.

THE NIFTY FIFTY In the 60s and 70s the US market was dominated by the fashion for the top blue chips—Eastman Kodak, IBM, Exxon. Eventually these stocks were bid up to 41x earnings, compared to a market multiple of 18x. When the fall came,

THE LOW BETA ANOMALY Recent research shows that over the longer term, contrary to conventional portfolio theory, investors are not compensated for higher volatility by getting higher returns. It turns out that low beta sectors such as consumer staples far outperform high beta sectors.

HOW WARREN BUFFETT ACHIEVED HIS RETURNS He buys into solid low beta stocks with sub-optimal gearing at the balance sheet level, and adds leverage at the portfolio level. Hence returns of 15 per cent annually against 10 per cent for the market.

BUILDING A HIGH-QUALITY EQUITY STRATEGY This is a proprietary strategy derived from private equity : a concentrated portfolio of large companies with an established franchise, largely independent of the economic cycle and a record of shareholder value creation. If you look at a logarithmic chart you see that returns are sometimes above trend, sometimes below, but

Our key beliefs

Final thoughts

INVESTMENT PHILOSOPHY

• Transparency, simplicity, flexibility

• Accountability and benchmarking

• Alignment of interests

• Tight cost control

• Supremacy of risk profile for risk budgeting

• Long-term dominance of real assets

• Gathering risk premiums

• Focused search for alpha

• Forward-looking perspective

• Long-term prevalence of economic fundamentals

Yves Bonzon joined Pictet in 1989. As Chief Investment Officer for Pictet Wealth Management, he is responsible for Investment Strategy and the Investment Platform unit. He is a member of the Wealth Management Executive Committee and manages the investment portfolios of several of Pictet’s private clients. Yves holds a Master’s from the University of Lausanne (HEC Lausanne).

Nifty Fifty stocks fell between 50 and 75 per cent. But—here’s the lesson—these stocks did eventually outperform over the long term, after another 26 years, and if you’d have bought at the bottom your return since 1975 would have been 12 per cent compound, or 2 per cent annual alpha.

THE DISTRUSTED 50 Which are the undervalued Nifty Fifty of the present day? We call them the Distrusted 50. We have created an equally weighted portfolio of stocks trading at the market multiple, but with an extremely high return on equity, which also reinvest at a very high rate. The market is paying no premium for such stocks. Why not? Because in general these were stocks which badly burned investors a decade ago.

TRAD

ITIO

NAL

low beta anomaly within asset classes

value risk premiums

momentum risk premiums

volatility selling

foreign exchange carry

term risk premiums

credit risk premiums

equity risk premiums

GOVERNANCE BELIEFS INVESTMENT BELIEFS

BUSINESS AND FAMILY GOVERNANCE

The Challenges of Global Family Businesses

Richard Eu, CEO of the Eu Yan Sang traditional Chinese medicine group, tells how he rescued the group from oblivion

My great great grandfather, Eu He Sang, was a geomancer, or feng shui expert, from Foshan in China. It was he who

established the principle of continuity in the family, writing a 20 character poem (opposite), binding his descendants to use each character in the poem, successively, for each succeeding generation. We are now on the sixth character.

His son, Eu Kong, went into tin-mining in Penang before opening a medicine shop in 1879 – Yan Sang – to care for his drug-addicted mining coolies. He began importing medicinal herbs. His son, my grandfather Eu Tong San (1877–1941), built up the mining business and went into rubber, becoming known as the King of Tin and Rubber. As a philanthropist and community leader he campaigned for the abolition of the opium trade in the 1930s. By the beginning of the war he was a tycoon with interests across industry, including banking and finance.

But the problems always begin in the third generation. My grandfather had 13 sons and 11 daughters (too many wives?). He left equal shares in the business to each of the sons. Death duties took 55% of the estate at the end of the war, and it took 50 years to wind up his estate—rivalling the fictional case of Jarndyce v Jarndyce!

I came into the business soon after the vestige of the group was listed on the Singapore exchange in 1973. We were soon taken over by Lum Chang, a real shock but probably a good

thing because they kept me on and after three years I managed to do a buyout. Then my uncles, who had a listed business in Hong Kong, decided to sue me because I owned all the trademarks. Eventually I managed to acquire their stake, buying out the rest of the shares in 2000 and relisting on the Singapore market.

In the late 1980s we were a small-scale business in traditional Chinese medicine (TCM), a sunset industry with a poor image. Since then we have established a clear mission, a strong vision and core values. We have completely redesigned our outlets (now 217 in Singapore, Malaysia, Hong Kong, Macao and China), rationalised our products and gone a long way to improving the reputation of TCM. We have 1,665 employees. We have acquired a chain of 53 healthcare shops in Australia. We also have 27 clinics and 2 medical centres, while exporting to Chinese communities abroad.

Richard Eu is Group CEO of Eu Yan Sang International Ltd, a healthcare and wellness company founded on Traditional Chinese Medicine. He graduated in law from London University and began his career as a merchant banker. He was Ernst & Young Entrepreneur of the Year 2011, and recognised in the Singapore Corporate Awards 2010 as CEO of the Year for SGX-listed companies with under S$300 million market value.

HOW TO SUSTAIN A FAMILY BUSINESS

Align family interest with business longevityDecide: family-run or family owned?

Set up good governanceBalance family values and growth

Attract outside talent – professional managementSuccession must be clear and defined – the leader must be given authority to act

Family politics are destructive to sound business decisions – is it family first or business first?

The Eu family poem

In Guangdong, there is a crane from the kingdom

It bears in its chest a sense of righteousness

It builds its family through the righteous path

For its steadfastness, it will be rewarded with success.

PICTET WEALTH MANAGEMENT The Family Consilium 2013 29PICTET WEALTH MANAGEMENT The Family Consilium 2013 28

PICTET WEALTH MANAGEMENT The Family Consilium 2013 31PICTET WEALTH MANAGEMENT The Family Consilium 2013 30

Family enterprise governance theory and practice

Professor Randel Carlock, a trained family therapist, businessman and specialist in family enterprise at INSEAD, explains how to manage the conflict between family and business interests

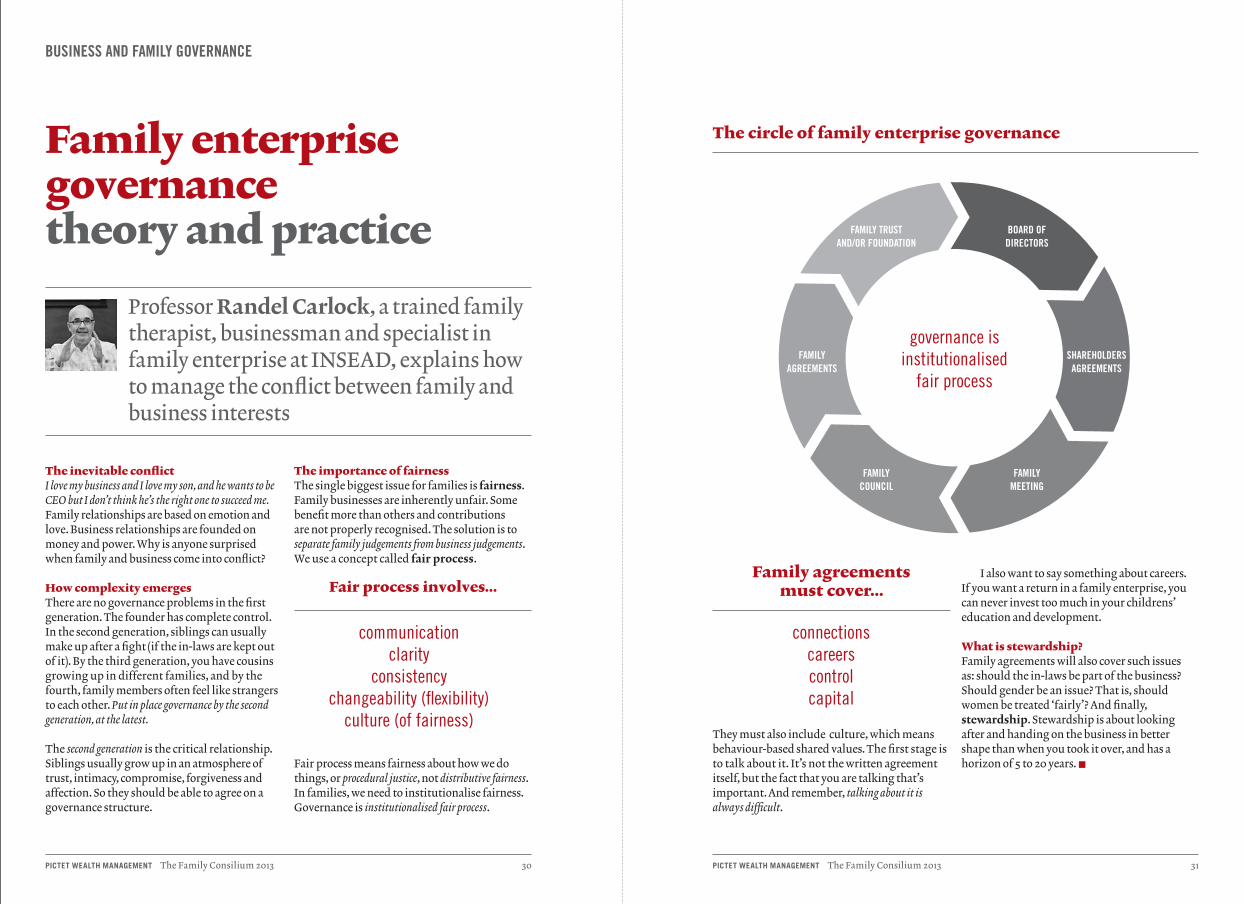

They must also include culture, which means behaviour-based shared values. The first stage is to talk about it. It’s not the written agreement itself, but the fact that you are talking that’s important. And remember, talking about it is always difficult.

BUSINESS AND FAMILY GOVERNANCE

I also want to say something about careers. If you want a return in a family enterprise, you can never invest too much in your childrens’ education and development.

What is stewardship?Family agreements will also cover such issues as: should the in-laws be part of the business? Should gender be an issue? That is, should women be treated ‘fairly’? And finally, stewardship. Stewardship is about looking after and handing on the business in better shape than when you took it over, and has a horizon of 5 to 20 years.

The inevitable conflictI love my business and I love my son, and he wants to be CEO but I don’t think he’s the right one to succeed me. Family relationships are based on emotion and love. Business relationships are founded on money and power. Why is anyone surprised when family and business come into conflict?

How complexity emergesThere are no governance problems in the first generation. The founder has complete control. In the second generation, siblings can usually make up after a fight (if the in-laws are kept out of it). By the third generation, you have cousins growing up in different families, and by the fourth, family members often feel like strangers to each other. Put in place governance by the second generation, at the latest.

The second generation is the critical relationship. Siblings usually grow up in an atmosphere of trust, intimacy, compromise, forgiveness and affection. So they should be able to agree on a governance structure.

The importance of fairnessThe single biggest issue for families is fairness. Family businesses are inherently unfair. Some benefit more than others and contributions are not properly recognised. The solution is to separate family judgements from business judgements. We use a concept called fair process.

The circle of family enterprise governance

Fair process involves...

communicationclarity

consistencychangeability (flexibility)

culture (of fairness)

BOARD OF DIRECTORS

SHAREHOLDERS AGREEMENTS

FAMILY MEETING

FAMILY AGREEMENTS

FAMILY COUNCIL

FAMILY TRUST AND/OR FOUNDATION

Family agreements must cover...

connectionscareerscontrol capital

Fair process means fairness about how we do things, or procedural justice, not distributive fairness. In families, we need to institutionalise fairness. Governance is institutionalised fair process.

governance is institutionalised

fair process

PICTET WEALTH MANAGEMENT The Family Consilium 2013 32

COACHING THE NEXT GENERATIONRandel Carlock gives a seminar for the next generation, with some surprising conclusions

What are the common factors in the career development of a successful leader? First, says Randel, get a tough boss. ‘With my first boss, I did nothing right for three years,’ he comments. ‘But boy did I learn.’ Get a mentor too, he adds, someone senior you don’t report to who can advise you. And when you mature, get a coach, someone you hire to help you think about your career or can give you insights.

He talks also about insights from his experience as a family therapist. ‘Sibling position matters. The middle child always has to negotiate, to manage up and manage down. The youngest has to fight for his position. Men are different from women. Men think of tasks (“How can I fix this?”), women think about relationships (“Let’s work together to fix this”). All this needs to be understood.’

For everyone present, it was an intense, stimulating and enjoyable session, compressing a whole semester’s learning into two hours, to which this summary scarcely does credit.

It turns out that a number of the group score highly on security, which seems appropriate for the next generation. But many of us score quite evenly across the board.

The task of the family is to develop the next generation’s talent in the interests of business—to identify different family members for different roles. Randel calls the process GPRI—goals, processes, roles and individuals. Or, Ferrari Career Planning for the Next Generation of Owners, Directors and Leaders. As Enzo Ferrari said, ‘Only those who dare, truly live’.

If you don’t fit into the family business, says Randel, then think how you can contribute to the family business. Then, when it comes to retirement, don’t retire, just find a new role. Be used, so that the next generation can learn as much as they can from you.

Reinvent yourself ‘As your career develops, remember, it may be all about reinventing the business, but it’s also about reinventing yourself. Sam Walton started Walmart when he was 49.’

FAMILY BUSINESS AND GOVERNANCE

GETTING AHEAD

THEY JUST WANT TO BE AT THE TOP

GETTING SECURE

THEY WANT LIFELONG, OR CONTINUOUS, EMPLOYMENT

GETTING FREE

STEVE JOBS. ALL TECH PEOPLE ARE LIKE THAT. YOU MANAGE

THEM LIKE SQUIRRELS

GETTING HIGH

JOHN GALLIANO. THEY ENJOY BEING AT THE

CENTRE OF ACTION. GET BORED EASILY. TECHNICAL, ENTREPRENEURIAL, FULL

OF IDEAS. A REAL CHALLENGE TO MANAGE

GETTING BALANCED

HAPPY TO GET HIGH, BUT DON’T LIKE BEING OUT OF

BALANCE FOR LONG

The five factors in career motivation

PICTET WEALTH MANAGEMENT The Family Consilium 2013 33