Embed Size (px)

Citation preview

0

OPPORTUNITIES IN A GROWING ECONOMY

PHILIPPINES

29 July 2016, Singapore

1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

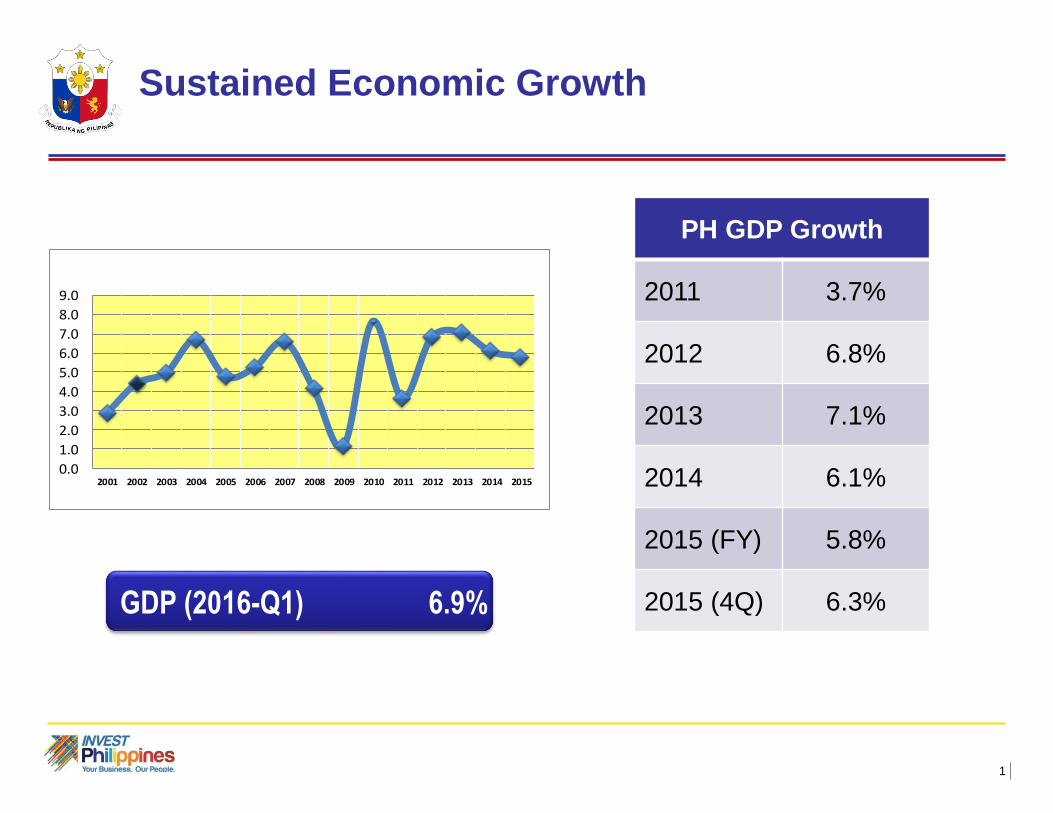

PH GDP Growth

2011 3.7%

2012 6.8%

2013 7.1%

2014 6.1%

2015 (FY) 5.8%

2015 (4Q) 6.3%

Sustained Economic Growth

GDP (2016-Q1) 6.9%

2

2015 Full Year GDP Growth Rates

BY INDUSTRIAL ORIGIN

BY EXPENDITURE SHARES

Source: NEDA

Sustained Economic Growth

3

Total Imports

Imports of Capital Goods

Imports of Consumer Goods

8%

22%

36%

Strong Growth of Import Demand (1Q-2016)

4

Bicol 4.2%

NCR 5.9%

Ctrl Luzon 9.0%

Davao 9.4%

Caraga 7.8%

Ilocos 5.7%

Ctrl Visayas 8.8%

CaLaBaRZon 5.1%

Cagayan Valley 6.4%Regional Economic

Growth Rates, 2014

Source: National Statistical Coordination Board & National Statistics Office

5

5.9

5.9

5.5

5.1

4.7

4.1

3.6

3.1

2.7

2.4

2

1.7

1.1

0.8

0.6

0.4

0.2

0.1

0.1

0.3

0.4

0.7

1

1.5

1.9

2.3

2.7

3.1

3.6

4.2

4.8

5.3

5.8

6.2

6.2

8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8

102 million

Source: United Nations, Department of Economic and Social Affairs, Population Division (2011). World Population Prospects: The 2010 Revision.

Percent of total population

25-29

50-54

40-44

30-34

15-19

4-9

55-59

45-49

35-39

20-24

10-14

0-5

60-6465-69

Working age

population:

50.5%

(51M)Male

Female

Young dependents:

46%

(47M)

Aged dependents:

3.5%

Main Source of Competitive Advantage:

Young and growing population

6

Growing Market (100 Million)

Population Projections

PH will enter the Demographic Sweet Spot

(UN)2015

PH will enter Growth Sweet Spot

(Ernst & Young)2019

80 % will have Middle-Class Incomes

or Higher (ADB)2030

Growing Philippine Market

7

Steady Investment Flows

8

Growth of Total Approved Foreign Investments

Share of Manufacturing

Growth over 2014

+31.2%

55%

+23%

Netherlands, Japan, South Korea, USA, Singapore (up 21%)

Approved Foreign Investments, 2015

9

Steady Investment Flows

10

Philippine IT-BPM industry size 2006–2014; Revenue in US$ billion

x% YoY Growth

1 Philippines IT-BPM market as percentage of global offshore services market, in revenue terms Sources: IBPAP, ACPI, CCAP, GDAP, HIMOAP, PSIA, GICC

# FTEs (~‘000)

236 371 424 527

Global share1 5% 6% 6% 7% 8%

3.44.5

6.17.1

8.9

11.0

13.2

16.1

19.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

34% 17%

25% 24%

CAGR:

24%

Copyright ©2015: BPAP. All rights reserved.

FTEs Revenue (US$M)

Rev % inc.

fr ’13

Voice BPO 685,000 11,700 17%

Non-voice BPO/KPO

186,800 3,440 18%

ITO 85,500 2,122 20%

Health Info Mgt & Care

86,867 1,304 32%

Engineering Services

13,112 227 5%

Animation 10,304 142 8%

Game Development

3,850 55 10%

TOTAL 1,071 18,989 18%

19%

298 640

9.5%

777

31% 45%

10.4%

22%

917

11%

1

18%

1,071

13%

Philippine IT-BPM Performance

11

Centers of Excellence

• Metro Manila

• Metro Cebu

• Metro Clark

• Metro Bacolod

Next Wave Cities

ü Baguio City

ü Davao City

ü Dumaguete

ü Iloilo

ü Lipa City

ü Metro Bulacan

ü Metro Cavite

ü Metro Laguna

ü Metro Naga

ü Metro Rizal Next Wave Cities

Centers of Excellence

Next Wave Cities

12

Continuous Inflow of Foreign Exchange

US$ 1.4 B from Singapore, 19% increase

13

TOP 10

Countries

2015

Volume in

Thousand

% Share

1. Korea 1,339.68 24.99

2. USA 779.22 14.54

3. Japan 495.66 9.25

4. China 490.84 9.16

5. Australia 241.19 4.50

6.Singapore 181.18 3.38

7. Canada 177.67 3.31

8. Taiwan 156.36 2.92

9. Malaysia 155.81 2.91

10. UK 154.59 2.88

Increasing Tourist Arrivals

14

Local Tourists

Projected room gap of 32,023 in critical

destination clusters by 2016

44.1M

in 201456.1Mby 2016

Source: DOT (2015)

Booming Local Tourism

15

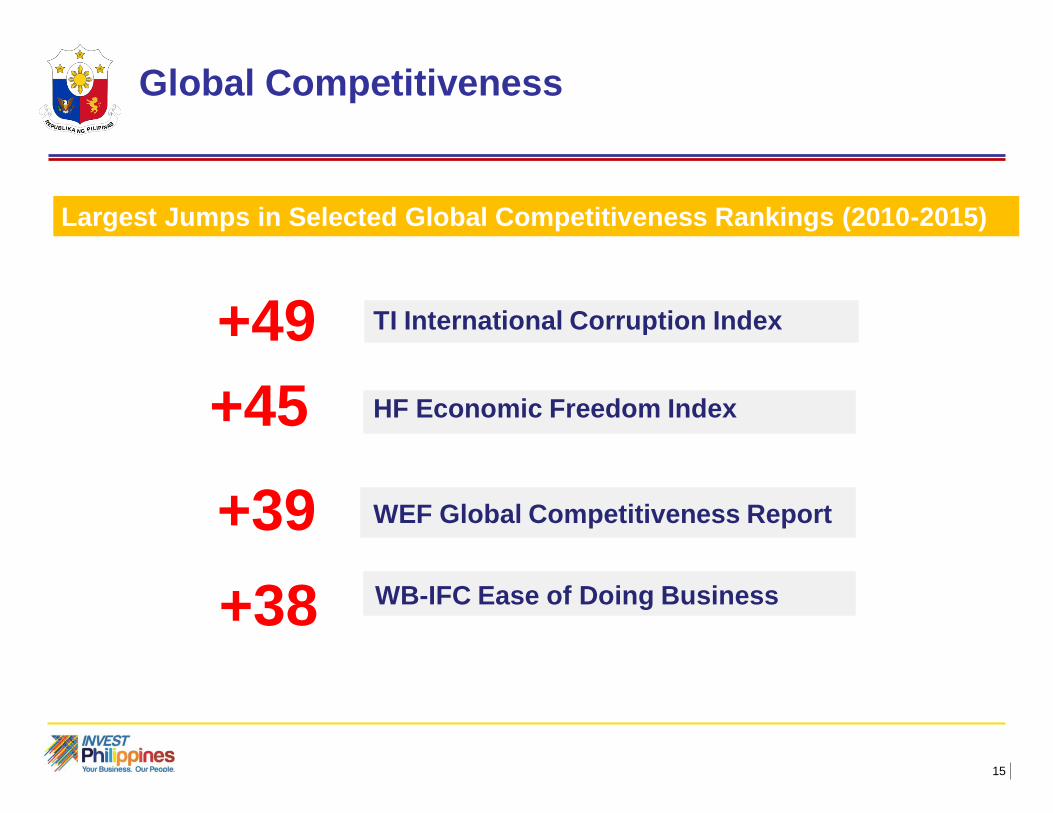

TI International Corruption Index

HF Economic Freedom Index

WEF Global Competitiveness Report

WB-IFC Ease of Doing Business

+49

+39

+38

+45

Largest Jumps in Selected Global Competitiveness Rankings (2010-2015)

Global Competitiveness

16

Global Competitiveness Index (2015/2016)

By World Economic Forum

Economic Freedom Index 2015

By Heritage Foundation

World Competitiveness Report 2015

By International Institute for Management

Global Innovation Index 2015

By World Intellectual Property Organization

+1Out of 60 countries:

From #42 to 41

+5 Out of 140 countries:

From #52 to 47

+17Out of 141 countries:

From #100 to 83

+13Out of 178 countries:

From #89 to 76

Ease of Doing Business

17

World Bank (2015)

Control of Corruption +18

Strengthened Governance

and Anti-Corruption Measures

Most Improved Campaign PERC Report on Corruption 2016

18

BBB-

Baa2

BBB-

Outlook:

Positive

Baa2

Outlook:

Stable

BBBBBB

Outlook:

Stable

Credit Rating Confirms Trust in Economy

19

1. Manufacturing

2. Agribusiness & Fishery

3. Services

4. Economic & Low Cost Housing

5. Hospitals

6. Energy

7. Public Infrastructure & Logistics

8. PPP Projects

I. Preferred Activities

Investment Priorities Plan 2014-2016

20

Manufacture of export products

Services exports

Activities in support of exporters

II. Export Activities

Investment Priorities Plan 2014-2016

21

III. Mandatory List

Investment Priorities Plan 2014-2016

Industrial Tree Plantations

Exploration, Mining & Processing of Minerals

Publication or Printing of Books

Refining, Storage, Marketing & Distribution of

Petroleum Products

Rehabilitation, Self-Development and Self-Reliance

of Persons with Disability

Renewable Energy

Tourism

22

Priority Products/Services

1. Food Products• Premium food products

• Ingredients (industrial, food service)

• Halal

2. Engineering Services (Engineering, Architecture, and

Maintenance, Repair and Overhaul or

MRO of aircraft)

3. IT Services (BPM particularly in finance and

accounting, animation)

Priority Sectors

1. Agribusiness & Food Processing• Plantations

• Value-added Processing (Ingredients)

• Halal

2. Services * IT BPM (Finance & Accounting,

Customer Relations Management,

Animation, Gaming, Health Information

Management)

* Engineering Services (MRO)

3. Infrastructure & PPP Projects

4. Start Ups

Exports Investments

PRIORITY SECTORS FOR PROMOTION

23

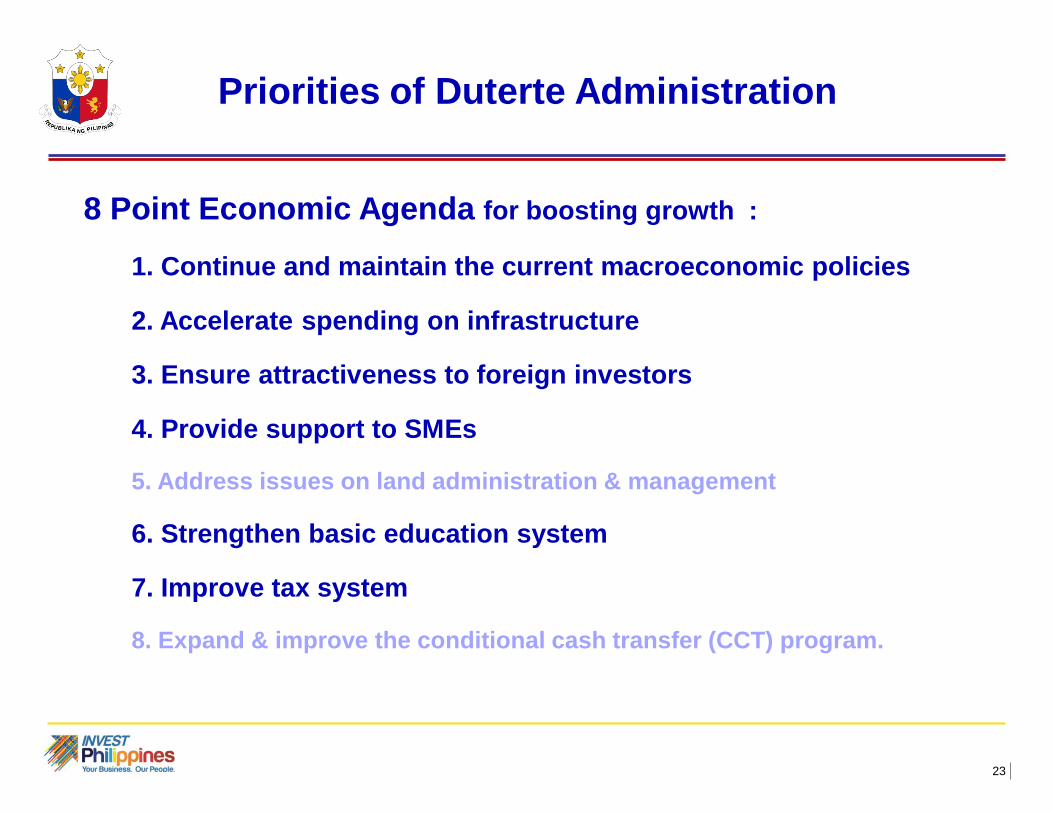

8 Point Economic Agenda for boosting growth :

1. Continue and maintain the current macroeconomic policies

2. Accelerate spending on infrastructure

3. Ensure attractiveness to foreign investors

4. Provide support to SMEs

5. Address issues on land administration & management

6. Strengthen basic education system

7. Improve tax system

8. Expand & improve the conditional cash transfer (CCT) program.

Priorities of Duterte Administration

24

TRADING PARTNER IN ASEANSOURCE OF INVESTMENTS IN ASEAN

SOURCE OF INVESTMENTS WORLDWIDE

TOURISTS, GROWING 18%

#5

181,000

Singapore is part of Philippine Growth Story

The Philippines can be your Growth Story!

25

WHO Glenn G. Peñaranda Commercial Counsellor

WHERE

Your link to opportunities in ASEAN...

07-234 Faber House, 230 Orchard Road, Singapore 238854

(+65) 6887 3186

PhilTradeSG

PhilippineTradeSG philtradesg

www.philippine-embassy.org.sg

-> Doing BusinessThank you!

Philippine Trade & Investment Centre -Singapore

Philippine Trade and Investment Centre - Singapore