Embed Size (px)

Citation preview

Deutsche Bank

Philippine Strategy:External outlook, and Raising potential growthRafael Garchitorena

December 2010

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Rafael [email protected]

+632 894 6644

Deutsche Bank

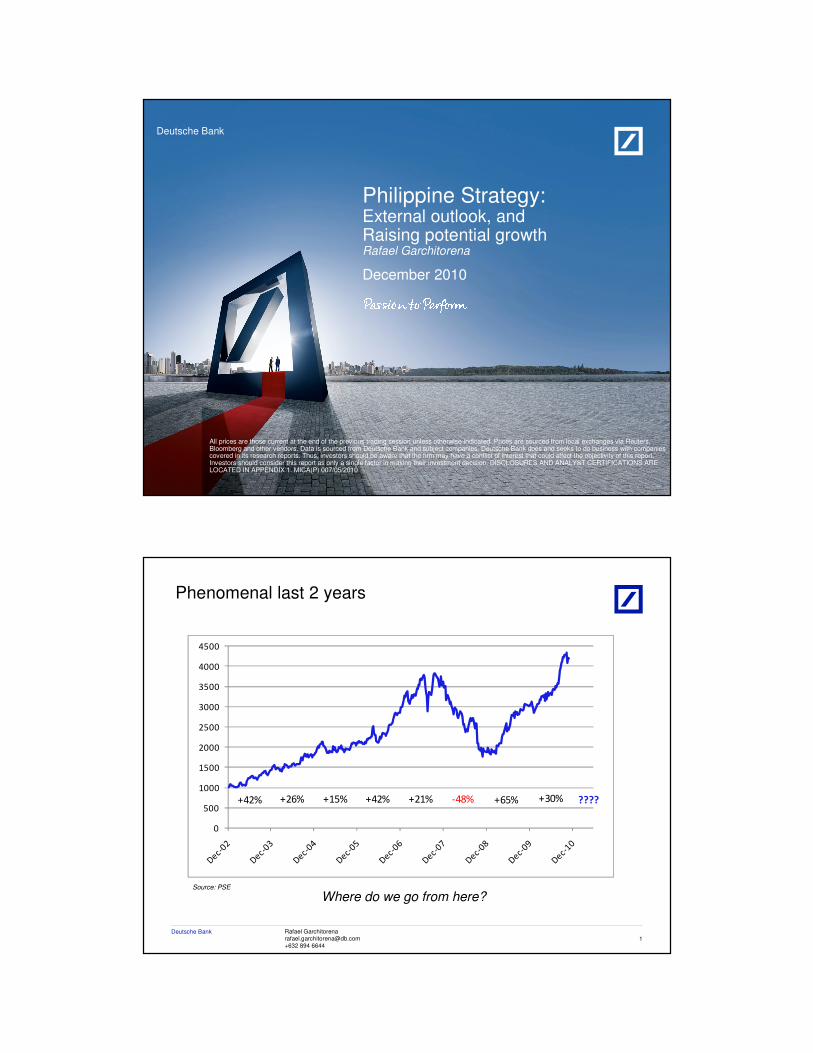

Phenomenal last 2 years

2/1/2011 2010 DB Blue template

1

Source: PSE

0

500

1000

1500

2000

2500

3000

3500

4000

4500

+42% +26% +15% +42% +21% -48% +65% +30% ????

Where do we go from here?

Rafael [email protected]

+632 894 6644

Deutsche Bank

The bull lives pa rin• We are long-term bullish

• Economy structurally more sound than 10/20/30 yrs ago

• Companies are in good shape

• Confidence is high

• Valuations are not excessive

2/1/2011 2010 DB Blue template

2

Rafael [email protected]

+632 894 6644

Deutsche Bank

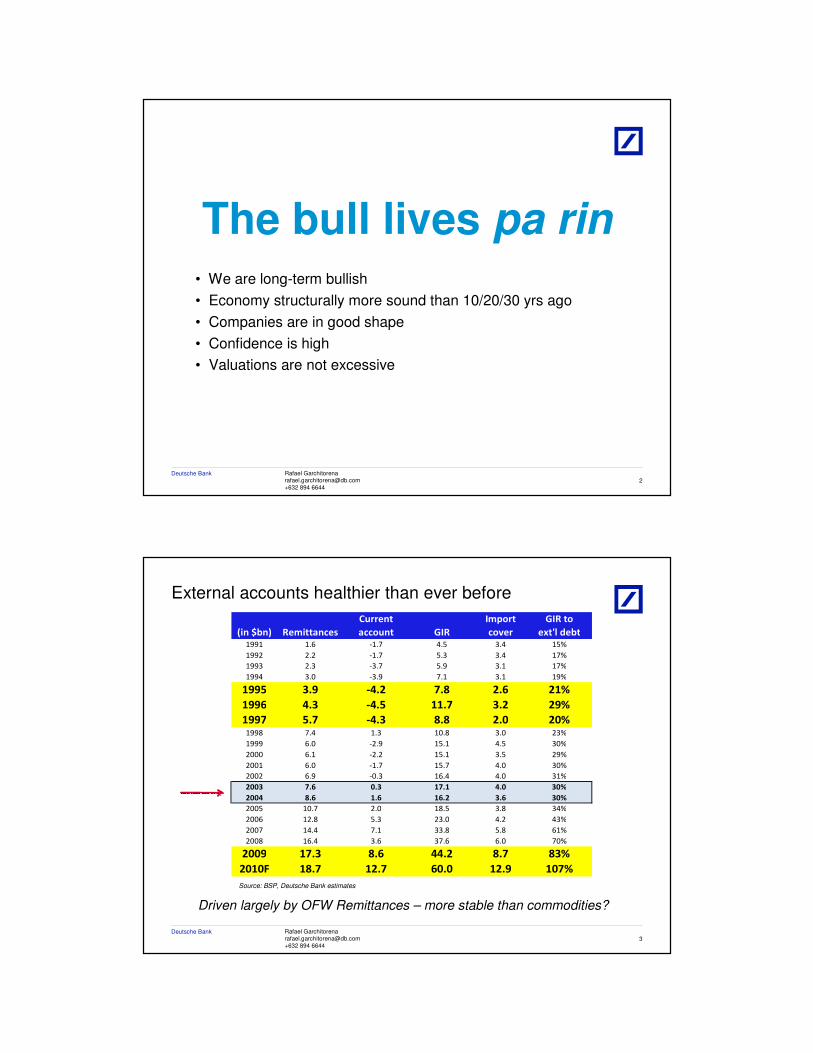

External accounts healthier than ever before

2/1/2011 2010 DB Blue template

3

Source: BSP, Deutsche Bank estimates

Driven largely by OFW Remittances – more stable than commodities?

Current Import GIR to

(in $bn) Remittances account GIR cover ext'l debt1991 1.6 -1.7 4.5 3.4 15%

1992 2.2 -1.7 5.3 3.4 17%

1993 2.3 -3.7 5.9 3.1 17%

1994 3.0 -3.9 7.1 3.1 19%

1995 3.9 -4.2 7.8 2.6 21%

1996 4.3 -4.5 11.7 3.2 29%

1997 5.7 -4.3 8.8 2.0 20%1998 7.4 1.3 10.8 3.0 23%

1999 6.0 -2.9 15.1 4.5 30%

2000 6.1 -2.2 15.1 3.5 29%

2001 6.0 -1.7 15.7 4.0 30%

2002 6.9 -0.3 16.4 4.0 31%

2003 7.6 0.3 17.1 4.0 30%

2004 8.6 1.6 16.2 3.6 30%

2005 10.7 2.0 18.5 3.8 34%

2006 12.8 5.3 23.0 4.2 43%

2007 14.4 7.1 33.8 5.8 61%

2008 16.4 3.6 37.6 6.0 70%

2009 17.3 8.6 44.2 8.7 83%

2010F 18.7 12.7 60.0 12.9 107%

Rafael [email protected]

+632 894 6644

Deutsche Bank

Structurally more able to withstand global stress

2/1/2011 2010 DB Blue template

4

No recession in 2008/09

Source: Bangko Sentral ng Pilipinas, Deutsche Bank

0%

20%

40%

60%

80%

100%

120%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000 GIR

Gross International Reserves (US$mn) GIR / Ext debt

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

F

Current account ($bn)

Rafael [email protected]

+632 894 6644

Deutsche Bank

Growing pool of domestic savings

2/1/2011 2010 DB Blue template

5

Provides cheap source of long-term Peso funding

Source: Bangko Sentral ng Pilipinas, Deutsche Bank

0

200

400

600

800

1,000

1,200

SDAs (Pbn)P1.2trn

at mid-Nov

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Banks' Trust AUMs (Pbn)

Rafael [email protected]

+632 894 6644

Deutsche Bank

Yield curve down c1,500bps since the 1990s

2/1/2011 2010 DB Blue template

6

Source: BSP, Deutsche Bank estimates

Long-term, capital intensive projects are now feasible

0

4

8

12

16

20

24

Oct-

98

Oct-

99

Oct-

00

Oct-

01

Oct-

02

Oct-

03

Oct-

04

Oct-

05

Oct-

06

Oct-

07

Oct-

08

Oct-

09

Oct-

10

10yr PDSF

0

4

8

12

16

20

24

1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 20Y

(%)

Yield Curve

1997 2000 2005 2009 Sept'10 Nov'10

1997

2000

2005

2009

2010

Rafael [email protected]

+632 894 6644

Deutsche Bank

Growth levels already above 10-yr averages

2/1/2011 2010 DB Blue template

7

Source: NSCB, Meralco, CAMPI, CEMAP, Deutsche bank estimates

-20%

-10%

0%

10%

20%

30%

40% Car sales

-10%

-5%

0%

5%

10%

15%Cement sales

0%

2%

4%

6%

8%

10%

12%

14%Electricity sales

0%

1%

2%

3%

4%

5%

6%

7%

8%GDP growth

But is 5% GDP growth good enough?

Rafael [email protected]

+632 894 6644

Deutsche Bank

Investments crucial to raising growth trajectory

2/1/2011 2010 DB Blue template

8

Source: National Statistical Coordination Board, Bangko Sentral ng Pilipinas

5%

11%

24%

14%

0%

5%

10%

15%

20%

25%Investments as % of GDP

Remittances as % of GDP

Akin to an airplane running on only one engine = Consumption

Rafael [email protected]

+632 894 6644

Deutsche Bank

The “lost decade” of under-investment

2/1/2011 2010 DB Blue template

9

Cement, car sales just now beating 1996 levels, despite 30% more people

Source: Various government and industry agencies, Deutsche Bank

Population Investments Construction Cement Car sales Loans

(mn) to GDP (%) to GDP (%) (mn tons) ('000 units) to GDP (%)

1997 72 25 6.4 15 144 59

1998 73 20 5.9 13 80 51

1999 75 19 5.5 12 74 45

2000 77 21 6.5 12 63 43

2001 79 19 4.9 12 77 39

2002 80 18 4.8 13 86 37

2003 82 17 4.5 12 92 35

2004 84 17 4.4 12 88 32

2005 85 15 3.9 12 97 30

2006 87 14 4 11 100 28

2007 89 15 4.5 13 118 31

2008 90 15 4.7 13 124 33

2009 91 14 4.9 14 132 33

2010 93 20 6.1 16 169 35

Rafael [email protected]

+632 894 6644

Deutsche Bank

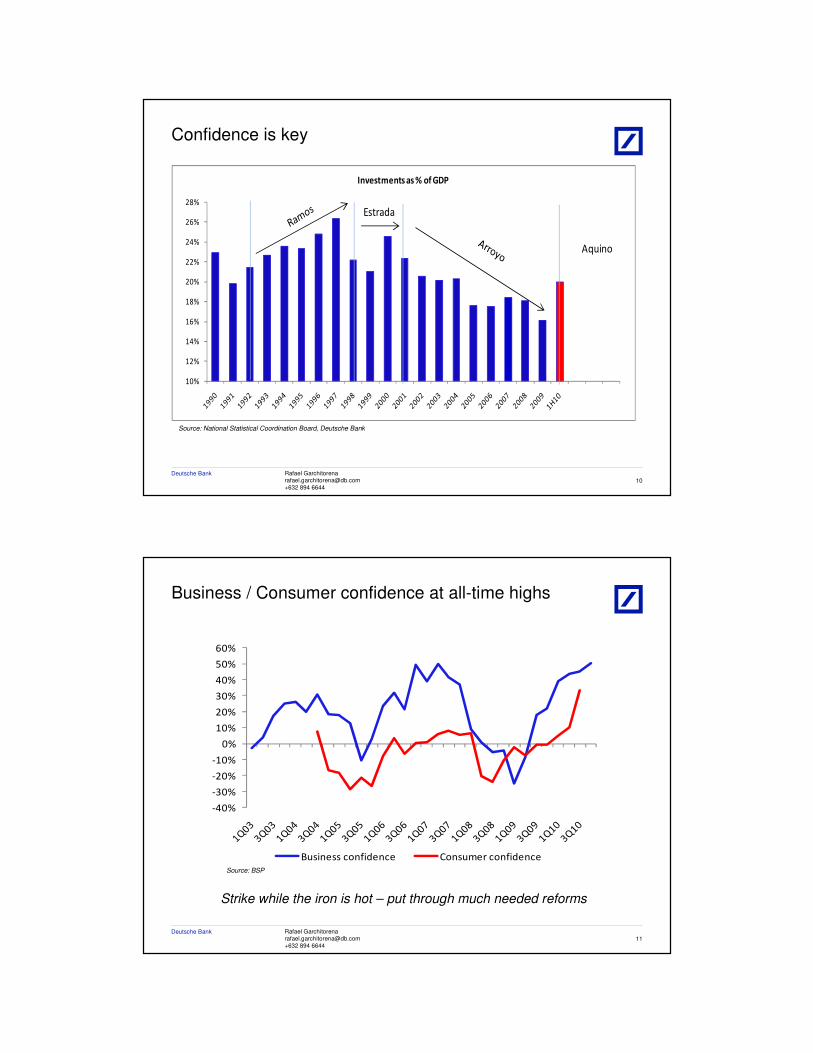

Confidence is key

2/1/2011 2010 DB Blue template

10

Source: National Statistical Coordination Board, Deutsche Bank

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

Investments as % of GDP

Estrada

Aquino

Rafael [email protected]

+632 894 6644

Deutsche Bank

Business / Consumer confidence at all-time highs

2/1/2011 2010 DB Blue template

11

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Business confidence Consumer confidence

Source: BSP

Strike while the iron is hot – put through much needed reforms

Rafael [email protected]

+632 894 6644

Deutsche Bank

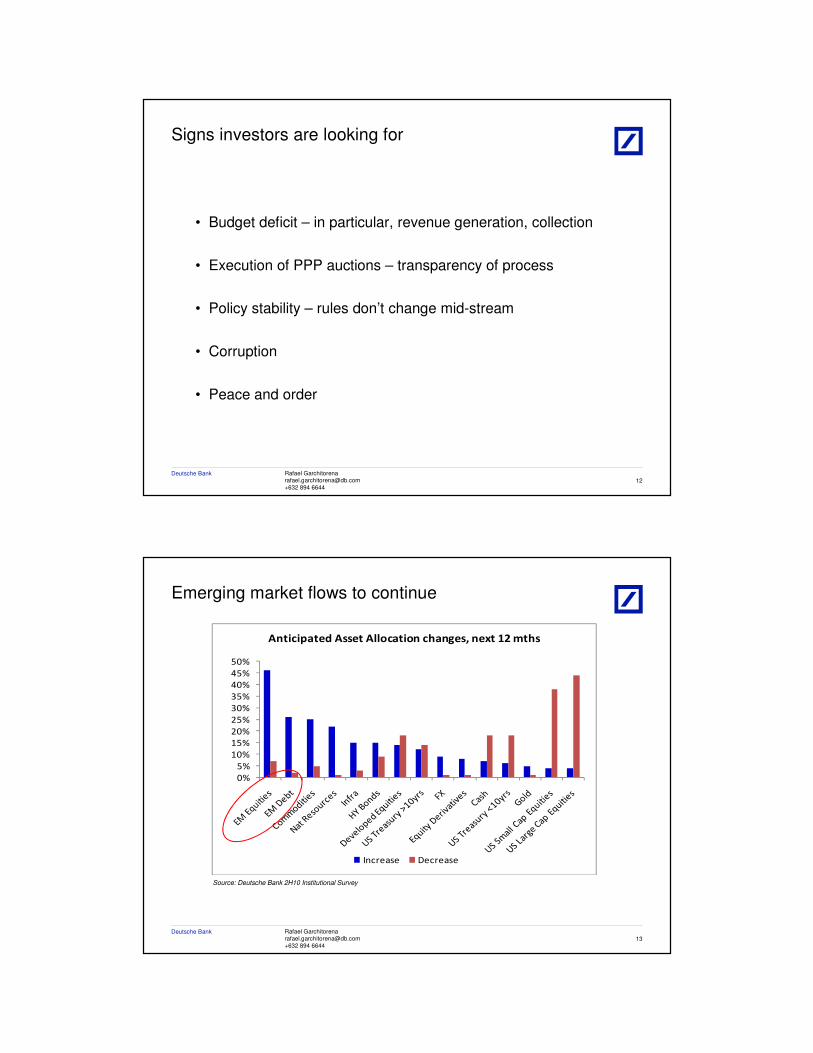

• Budget deficit – in particular, revenue generation, collection

• Execution of PPP auctions – transparency of process

• Policy stability – rules don’t change mid-stream

• Corruption

• Peace and order

Signs investors are looking for

2/1/2011 2010 DB Blue template

12

Rafael [email protected]

+632 894 6644

Deutsche Bank

Emerging market flows to continue

2/1/2011 2010 DB Blue template

13

Source: Deutsche Bank 2H10 Institutional Survey

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Anticipated Asset Allocation changes, next 12 mths

Increase Decrease

Rafael [email protected]

+632 894 6644

Deutsche Bank

Asia is the preferred destination

2/1/2011 2010 DB Blue template

14

Source: Deutsche Bank 2H10 Institutional Survey

57%

23%

11%7%

2% 1%

0%

10%

20%

30%

40%

50%

60%

Asia Latin America US Eastern

Europe

Western

Europe

Other EM

Region expected to show the best growth/value (5yrs)

Rafael [email protected]

+632 894 6644

Deutsche Bank

PSE foreign buying not yet at 2006/07 levels

2/1/2011 2010 DB Blue template

15

Source: Philippine Stock Exchange, Deutsche Bank; * Excluding CEB IPO

1000

1500

2000

2500

3000

3500

4000

4500

(15.0)

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

Ma

r-0

5

Jun

-05

Se

p-0

5

De

c-0

5

Ma

r-0

6

Jun

-06

Se

p-0

6

De

c-0

6

Ma

r-0

7

Jun

-07

Se

p-0

7

De

c-0

7

Ma

r-0

8

Jun

-08

Se

p-0

8

De

c-0

8

Ma

r-0

9

Jun

-09

Se

p-0

9

De

c-0

9

Ma

r-1

0

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-1

1

Foreign net buying/(selling) in Pbn, lhs PCOMP, rhs

|------- Jan'06 - Aug'07 -------|

$2.3bn

|------ Sep'07 - Jun'09 ------|

($1.8bn)

|-- Jul'09 - Jul'10 --|

$0.4bn

|Aug-Nov'10 |

$0.7bn*

Rafael [email protected]

+632 894 6644

Deutsche Bank

Client visits

2/1/2011 2010 DB Blue template

16

9

23

39

58

70

55

44

54

0

10

20

30

40

50

60

70

80

2003 2004 2005 2006 2007 2008 2009 2010

Foreign client visits with DB Regis

Source: Deutsche Bank

Rafael [email protected]

+632 894 6644

Deutsche Bank

Lots of catching up to do

2/1/2011 2010 DB Blue template

17

Source: National Statistical Coordination Board, CEIC, Deutsche Bank

0

5

10

15

20

25

30

35

Investments to GDP (%)

Philippines Indonesia

0

500

1,000

1,500

2,000

2,500

3,000

3,500

GDP per Capita (US$)

Philippines Indonesia

Rafael [email protected]

+632 894 6644

Deutsche Bank

01/02/2011 16:20:53 2010 DB Blue template

Appendix 1Important DisclosuresAdditional Information Available upon Request

7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.

8. Deutsche Bank and/or its affiliate(s) expects to receive or intends to seek compensation for investment banking services from this company in the next three months.

14. Deutsche Bank and/or its affiliate(s) has received non-investment banking related compensation from this company within the past year.

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com.

D isclo su r e Ch eck l i st

Co m pan y T ick e r Pr ice D isc lo su r e

Rafael [email protected]+632 894 6644

Deutsche Bank

01/02/2011 16:20:53 2010 DB Blue template

Special Disclosures

Please also refer to disclosures in the “Important Disclosures Required by US Regulators” and the Explanatory Notes.

7.Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr.

Analyst CertificationThe views expressed in this report accurately reflect the personal views of the undersigned lead analyst about the subject issuers and the securities of those issuers. In addition, the undersigned lead analyst has not and will not receive any compensation for providing a specific recommendation or view in this report. Gio Dela-Rosa

Rafael [email protected]+632 894 6644

Deutsche Bank

01/02/2011 16:20:53 2010 DB Blue template

Buy: Based on a current 12-month view of total shareholder return (TSR = percentage change in share price from current price to projected target price plus projected dividend yield), we recommend that investors buy the stock.

Sell: Based on a current 12-month view of total shareholder return, we recommend that investors sell the stock.

Hold: We take a neutral view on the stock 12 months out and, based on this time horizon, do not recommend either a Buy or Sell.

Notes:

1. Newly issued research recommendations and target prices always supersede previously published research.

2. Ratings definitions prior to 27 January, 2007 were:

Buy: Expected total return (including dividends) of 10% or moreover a 12-month period

Hold: Expected total return (including dividends) between -10%and 10% over a 12-month period

Sell: Expected total return (including dividends) of -10% orworse over a 12-month period

Equity Rating Key Equity Rating Dispersion and Banking

Relationships

Rafael [email protected]+632 894 6644

Deutsche Bank

01/02/2011 16:20:53 2010 DB Blue template

Regulatory Disclosures

1. Important Additional Conflict Disclosures

Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the “Disclosures Lookup” and “Legal” tabs. Investors are strongly encouraged to review this information before investing.

2. Short-Term Trade Ideas

Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are consistent or inconsistent with Deutsche Bank’s existing longer term ratings. These trade ideas can be found at the SOLAR link at http://gm.db.com.

3. Country-Specific Disclosures

Australia: This research, and any access to it, is intended only for “wholesale clients” within the meaning of the Australian Corporations Act.

EU countries: Disclosures relating to our obligations under MiFiD can be found at http://globalmarkets.db.com/riskdisclosures.

Japan: Disclosures under the Financial Instruments and Exchange Law: Company name – Deutsche Securities Inc. Registration number –Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, The Financial Futures Association of Japan. Commissions and risks involved in stock transactions – for stock transactions, we charge stock commissions and consumption tax by multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming from foreign exchange fluctuations.

New Zealand: This research is not intended for, and should not be given to, “members of the public” within the meaning of the New Zealand Securities Market Act 1988.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian Federation.

Rafael [email protected]+632 894 6644

Deutsche Bank

Global DisclaimerThe information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively "Deutsche Bank"). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Deutsche Bank makes no representation as to the accuracy or completeness of such information.

Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research report. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view that is inconsistent with that taken in this research report.

Opinions, estimates and projections in this report constitute the current judgement of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Prices and availability of financial instruments are subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently imprecise and a product of the analyst judgement.

As a result of Deutsche Bank’s recent acquisition of BHF-Bank AG, a security may be covered by more than one analyst within the Deutsche Bank group. Each of these analysts may use differing methodologies to value the security; as a result, the recommendations may differ and the price targets and estimates of each may vary widely.

Deutsche Bank has instituted a new policy whereby analysts may choose not to set or maintain a target price of certain issuers under coverage with a Hold rating. In particular, this will typically occur for "Hold" rated stocks having a market cap smaller than most other companies in its sector or region. We believe that such policy will allow us to make best use of our resources. Please visit our website at http://gm.db.com to determine the target price of any stock.

The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed investment decisions. Stock transactions can lead to losses as a result of price fluctuations and other factors. If

a financial instrument is denominated in a currency other than an investor's currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities covered by this report, sell to or buy from customers on a principal basis, and consider this report in deciding to trade on a proprietary basis.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a

member of the NYSE, the NASD, NFA and SIPC. In Germany this report is approved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange and regulated by the Financial Services Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch, and recipients in Singapore of this report are to contact Deutsche Bank AG, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch accepts legal responsibility to such person for the contents of this report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in

this report and consider the PDS before making any decision about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any person for any purpose without Deutsche Bank's prior written consent. Please cite source when quoting.

Copyright © 2010 Deutsche Bank AG