Embed Size (px)

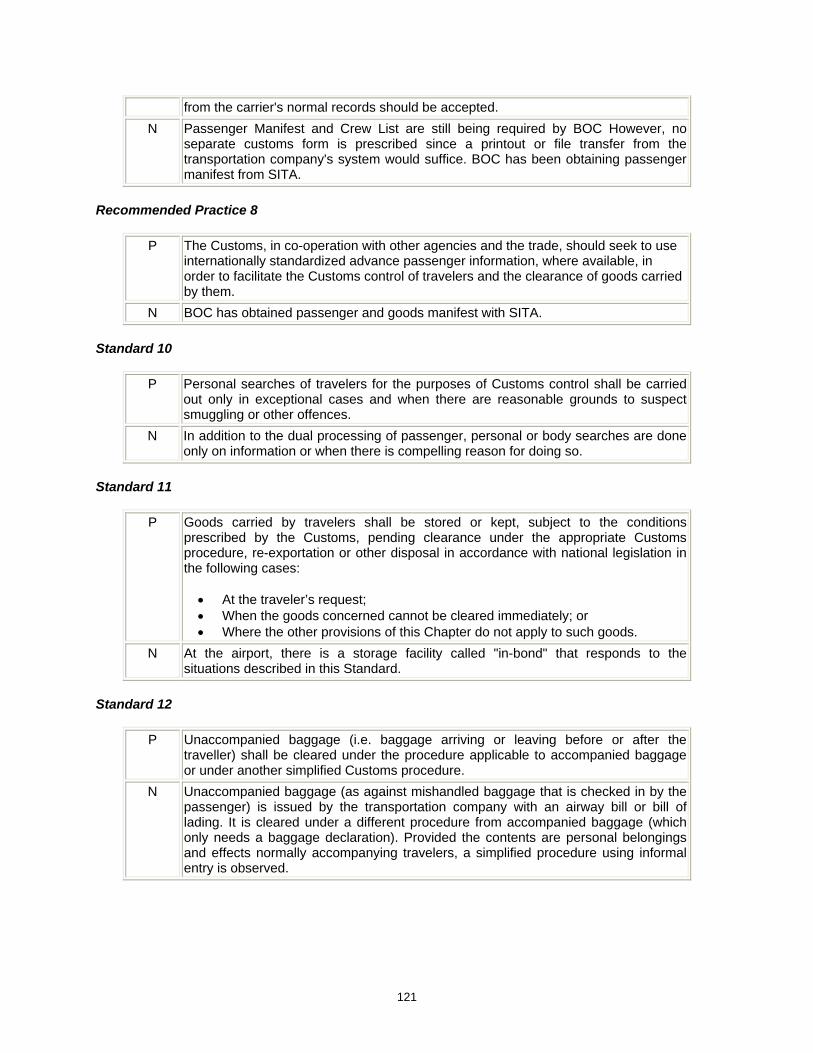

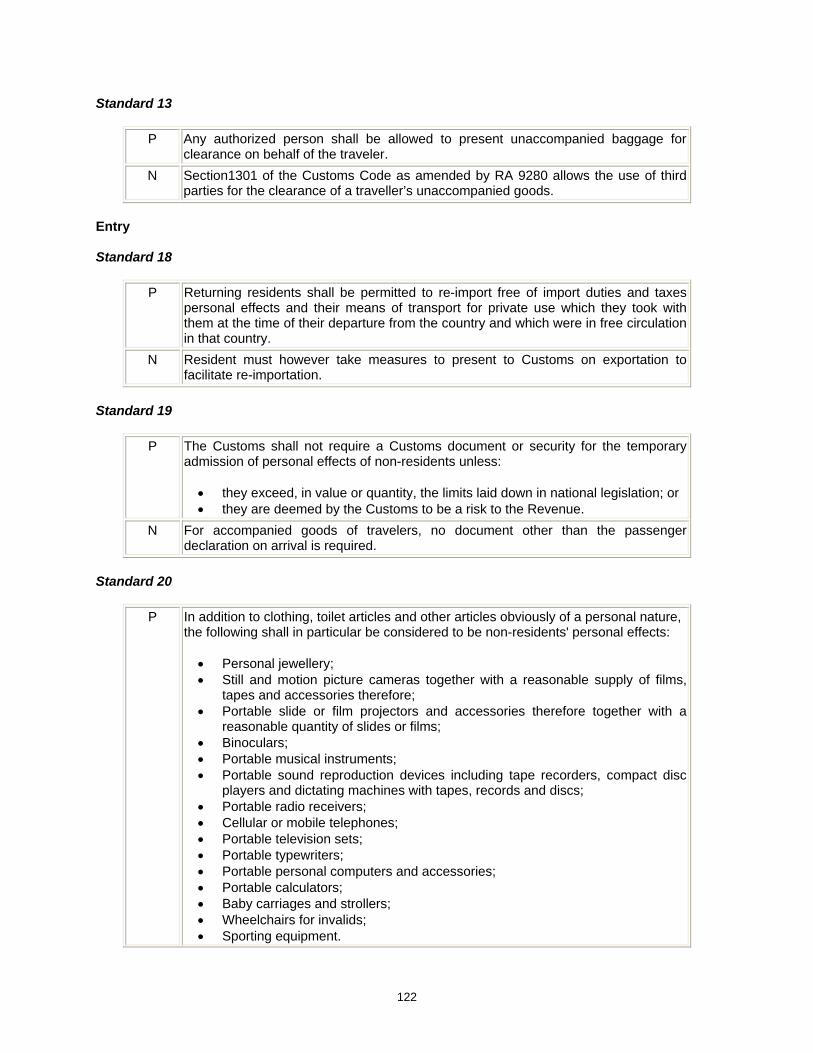

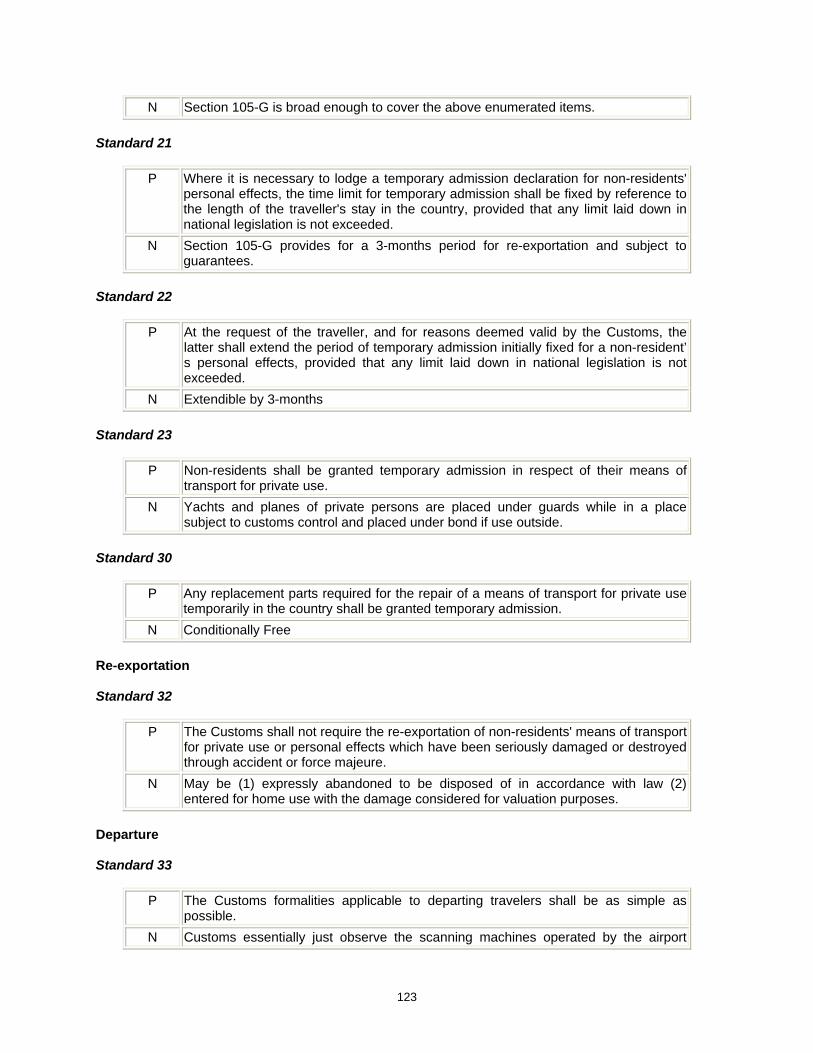

Citation preview

Economic Modernization through Efficient Reforms and Governance Enhancement (EMERGE) Unit 2003 139 Corporate Center 139 Valero St Salcedo Village Makati City 1227 Philippines

Tel No (632) 752 0881 Fax No (632) 752 2225

Technical Report Philippine Compliance with the Revised Kyoto Convention by Parayno Consultancy Services

Prepared for

Fernando P Cala II Executive Director Export Development Council (EDC)

Republic of the Philippines Submitted for review to USAIDPhilippines OEDG

February 28 2007

EMERGE Preface

This report is the result of technical assistance provided by the Economic Modernization through Efficient Reforms and Governance Enhancement (EMERGE) Activity under contract with the CARANA Corporation Nathan Associates Inc and The Peoples Group (TRG) to the United States Agency for International Development Manila Philippines (USAIDPhilippines) (Contract No AFP-I-00-00-03-00020 Delivery Order 800) The EMERGE Activity is intended to contribute towards the Government of the Republic of the Philippines (GRP) Medium Term Philippine Development Plan (MTPDP) and USAIDPhilippinesrsquo Strategic Objective 2 ldquoInvestment Climate Less Constrained by Corruption and Poor Governancerdquo The purpose of the activity is to provide technical assistance to support economic policy reforms that will cause sustainable economic growth and enhance the competitiveness of the Philippine economy by augmenting the efforts of Philippine pro-reform partners and stakeholders By letter dated 25 November 2005 Fernando P Cala II Executive Director of the Philippine Export Development Council (EDC) requested assistance from EMERGE and the Partnership and Advocacy for Competitiveness and Trade (PACT) which is a grant project implemented for USAID by the DLSU-Angelo King Institute for Economic and Business Studies in partnership with Philippine Exporters Confederation Inc (PhilExport) for research and advocacy about Philippine compliance with the Revised Kyoto Convention (RKC) which was to enter into force on February 3 2006 PACT and EMERGE engaged the Parayno Consultancy Services for this purpose in June 2006 The views expressed and opinions contained in this publication are those of the authors and are not necessarily those of USAID the GRP EMERGE or the latterrsquos parent organizations

PROJECT RESEARCH AND ADVOCACY SUPPORT FOR TRADE FACILITATION PHILIPPINE COMPLIANCE WITH THE REVISED KYOTO CONVENTION (ldquoRKCrdquo)

PROPOSED NATIONAL STRATEGY FOR PHILIPPINE COMPLIANCE TO THE INTERNATIONAL CONVENTION ON THE SIMPLIFICATION AND

HARMONIZATION OF CUSTOMS PROCEDURES OTHERWISE KNOWN AS THE REVISED KYOTO CONVENTION (ldquoRKCrdquo)

Submitted by

PARAYNO CONSULTANCY SERVICES

February 2007

Abbreviation

AFTA ASEAN Free Trade Agreement AO Administrative Order APEC Asian Pacific Economic Cooperation ASEAN Association of South East Asian Nations ATA BOC Bureau of Customs BOI Board of Investments CAO Customs Administrative Order CCC Customs Cooperation Council CEPT CMBW Customs Manufacturing Bonded Warehouse CMO Customs Memorandum Order CO Certificate of Origin DOF Department of Finance DSWD Department of Social Welfare and Development EO Executive Order GRP Government of the Republic of the Philippines ICAO ICT Information and Communication Technology IFM IRR Implementing Rules and Regulations KC International Convention on the Simplification and

Harmonization of Customs Procedures or Kyoto Convention

KCMT Kyoto Convention Management Team MOA Memorandum of Agreement MOU Memorandum of Understanding NAIA Ninoy Aquino International Airport NIRC National Internal Revenue Code PACT Partnership and Advocacy for Competitiveness and

Trade PD Presidential Decree PEZA Philippine Economic Zone Authority PHILEXPORT Philippine Exporters Confederation Inc RA Republic Act RKC Revised Kyoto Convention SAD Single Administrative Document SARO Special Allotment Release Order Sec Section SITA TCCP Tariff and Customs Code of the Philippines TWM Trade World Management UN United Nations UNECE VASP Value Added Service Provider VAT Value Added Tax WCO World Customs Organization WTO World Trade Organization

TABLE OF CONTENT

Preface Executive Summary 10 Introduction

11 The World Customs Orgnization 12 Kyoto Convention (ldquoKCrdquo) 13 Rationale for Revising the KC 14 Revised Kyoto Convention (ldquoRKCrdquo) 15 Philippines vis-agrave-vis the KC 16 Consequence of Philippine Non-accession of the KC 17 Compliance versus Accession Differences 18 Accession 19 Benefits Expected from Trading With Countries that are RKC Compliant 110 RKC Structure

1101 General Annex 1102 Specific Annexes and their Chapters

111 RKC Management Committee

20 APEC Recommended Pathway to Accession 30 Tabular Summary of Applicability and Gap Analysis

31 Applicability Analysis 311 Applicability Defined 312 Non-applicable Provisions of the General Annex 313 Non-applicable Provisions of the Specific Annex

32 Gap Analysis 321 Components of Gap Analysis

33 Summary of Applicability and Gap Analysis ndash Including Recommendation on Accession Thereto

40 Proposed National Strategy for Compliance

41 Background 42 Stages of RKC Compliance 43 1ST Stage Activities 44 2nd Stage Activities 45 3rd Stage Activities 46 Endorsement to the President of the RKC National Strategy 47 Required Executive Actions

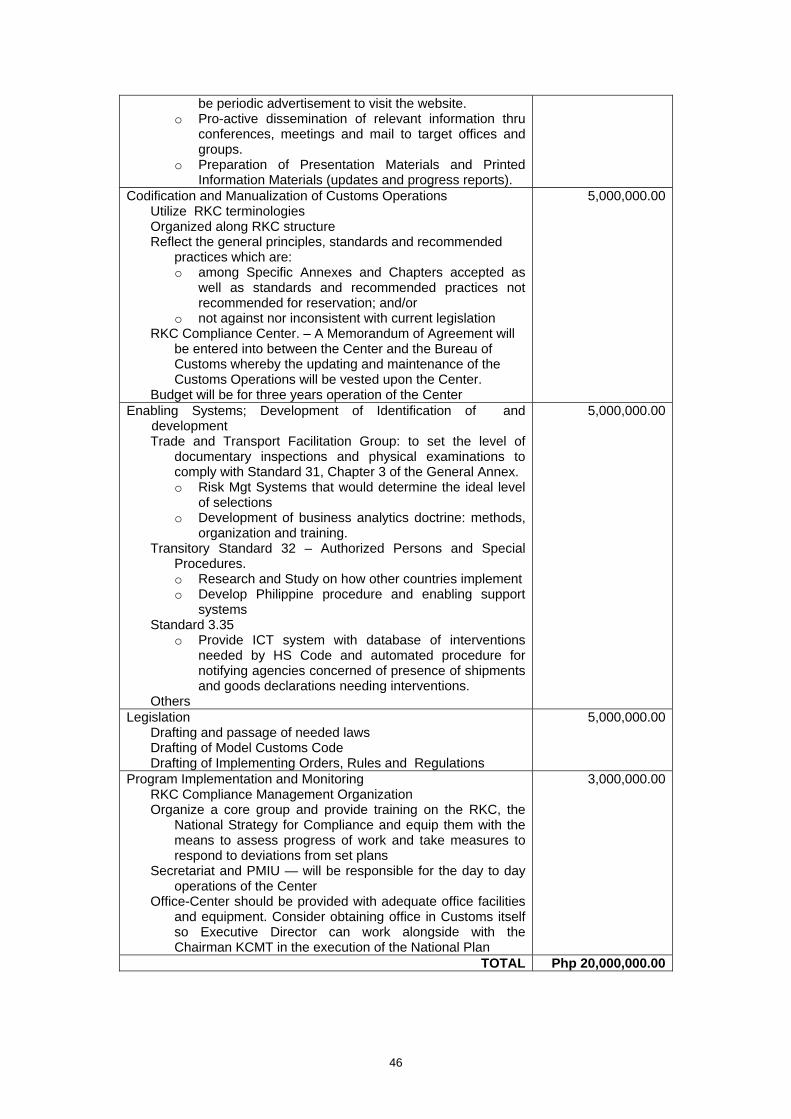

50 Investment Plan 51 Objective 52 Investment Components

Annexes

Annex A ndash Standards and Transitory Standards of the General Annex that Philippine National Legislations are compliant with Annex B ndash Standards and Transitory Standards of the General Annex that Philippine National Legislations are not compliant with Annex C ndash Standards and Recommended Practices of the Specific Annexes that Philippine National Legislations are compliant with Annex D ndash Standards and Recommended Practices of the Specific Annexes that Philippine National Legislations are not compliant with Annex E ndash Private Sector Group endorsement to President Gloria Macapagal Arroyo encouraging accession and compliance to the provisions of the RKC Annex F ndash Customs Report on the Benefits of Accession the Specific Annexes recommended for Acceptance and the Reservations to particular provisions Annex G ndash Department of Finance letter of endorsement of the Customs Report to the Department of Foreign Affairs with the Stakeholder Groups Endorsements Annex H ndash Department of Foreign Affairs Draft Instrument of Accession for the signature of the President Annex I ndash Draft Letter of the President to the Senate requesting advice and concurrence to accession to the Convention

PREFACE

In June 2006 the Partnership and Advocacy for Competitiveness and Trade (PACT) Project a project being implemented by the DLSU-Angelo King Institute for Economic and Business Studies in partnership with Philippine Exporters Confederation Inc (PHILEXPORT) and the Economic Modernization through Efficient Reforms and Governance Enhancement (EMERGE) engaged the Parayno Consultancy Services for the project ldquoResearch and Advocacy Support for Trade Facilitation Philippine Compliance with the Revised Kyoto Convention (ldquoRKCrdquo) hereinafter referred to as the ldquoProjectrdquo The Project was in response to the need to identify a clear path on how the Philippines should respond to the RKCrsquos imminent entry into force and to accelerate the pace and institutionalize the gains of trade facilitation and customs reforms and modernization and involves among others the conduct of a study on the current status of Philippine compliance with the RKC

The main deliverables of the Project are a draft National Strategy for RKC compliance as well as

a workplan for the implementation of the National Strategy The Project Team in coordination with the Philippine Bureau of Customs and concerned private

sector groups undertook a gap analysis to ascertain the measures needed to make Philippine national legislation compliant with the RKC

A pre-summit followed by a national summit was organized and held on 30 January 2007 and 5

February 2007 respectively to arrive at a National Strategy for RKC compliance The draft was presented and subsequently adopted and endorsed by concerned private sector groups Thereafter it was presented to President Gloria Macapagal-Arroyo through Secretary of Finance Margarito V Teves during the 105th Founding Anniversary celebration of the Philippine Customs Service on 6 February 2007

The Project Team wish to thank officials of the Bureau of Customs for their participation in the

gap analysis as well as the pre-summit and the summit We wish to express our gratitude especially to the following without whom the pre-summit and the summit would not have been successfully held

Bureau of Customs (BOC)

o Deputy Commissioner Reynaldo Nicolas o Collector John Simon o Members of the Bureau of Customs Kyoto Convention Management Team who acted as

Lead Shepherds o Officers of the Bureau of Customs who acted as lead facilitators in the pre-summit

Philippine Exporters Confederation Inc (PHILEXPORT) o Dr Ponciano Intal Jr o Gerardo Anigan o Jennifer Tan

AIM Policy Center o Dr Federico Macaranas o Rommella M Denopol

We would also like to express our gratitude to the Project Proponents and Funders for giving

Parayno Consultancy Services the opportunity for spearheading in this very important project that promises to upgrade significantly the global competitiveness of the country

Our deepest gratitude to retired Customs Collector Manual B Dionaldo who graciously welcomed

all refused telephone calls and personal visits to discuss highly technical and legal issues in the course of the gap analysis And who generously shared his knowledge and library of Customs laws rules and regulations

i

EXECUTIVE SUMMARY

Philippine Customs administrations past and present have implemented programs to simplify and harmonize Customs procedures even without having acceded to the World Customs Organizationrsquos (ldquoWCOrdquo) formerly the CCC International Convention on the Simplification and Harmonization of Customs Procedure (Kyoto Convention)

Several of the reform measures introduced from 1992 to 1998 by Philippine Customs in its

operation have in fact pre-dated some of the standards transitory standards and recommended practices agreed upon in 1999 by the WCO countries when they completed the review of the KC and opened for accession of the RKC

However several of these reform measures were not sustained partly because of the absence of

a holistic framework that can serve both a legally binding guidepost and framework for action to harmonizing Philippine Customs procedures with the rest of the world

Customs Administrations in Asian Pacific Economic Cooperation (APEC) and Association of

South East Asian Nations (ASEAN) have long recognized the importance of such a guidepost and framework and have committed as a group to reform and modernize their respective administrations along the standards and recommended practices of the RKC

A guidebook for APEC Economies to assist them to become Contracting Parties to the RKC

entitled The Revised Kyoto Convention a Pathway to Accession and Implementation was issued An important component of the guidebook is the examination of the gaps or differences between the countryrsquos national legislation and the RKC

The gap analysis conducted by the Project would show that the countryrsquos national legislation is

compliant to fifty five percent (55) of the standards transitory standards and recommended practices contained in the RKC ie we can find in our national legislation specific provisions expressly complying with the said standards transitory standards and recommended practices However a significant percentage all not reflected in the legislation Fortunately only sixteen percent (16) of the provisions contained in the RKC requires an amendment of our law Still other provisions of the RKC which may be important for facilitation of trade may however have an adverse impact on our countryrsquos other objectives such as the collection of revenues and the prevention of smuggling and other Customs violations

A national strategy for RKC compliance was therefore crafted that aims to immediately implement

most of the trade facilitation standards transitory standards and recommended practices of the RKC while giving time for the Customs administration to put in place measures that will not erode Customs capacity to effectively enforce their other control objectives

The national strategy proposed a schedule of acceptance and implementation of the RKC

provisions It proposed the immediate acceptance of the Body of the Convention the General Annex eight (8) Specific Annexes consisting of eighteen different chapters while making an express reservation on 27 recommended practices contained in these chapters of the eight Specific Annexes recommended for acceptance Furthermore it proposed that further studies be conducted on 7 Chapters contained in four (4) Specific Annexes A detailed discussion may be found in Annex ldquoGrdquo The national strategy also includes a package of investment measures and proposals which are needed not only to support the soonest accession of the Philippines to the RKC but also to insure quality compliance to most if not all of the modern systems and method of the convention

ii

PROPOSED NATIONAL STRATEGY FOR PHILIPPINE COMPLIANCE TO THE INTERNATIONAL CONVENTION FOR THE SIMPLIFICATION AND

HARMONIZATION 10 Introduction

11 The World Customs Organization (WCO) The Customs Cooperation Council (CCC) which is the forerunner of the WCO has since its

inception in 1952 been working to develop modern principles that would buttress effective customs administrations One of its major outputs is the 1973 Kyoto Convention (KC) which came into force in 1974 The WCO improved on the KC with the entry into force of the Revised Kyoto Convention (RKC) in 2006

12 Kyoto Convention (ldquoKCrdquo)

The early efforts of the CCC for simplifying and harmonizing customs procedures culminated

in the International Convention on the Simplification and Harmonization of Customs Procedures otherwise known as the Kyoto Convention (ldquoKCrdquo) or hereinafter referred to also as the ldquoConventionrdquo The KC was adopted by the Council in 1973 and enforced in 1974

13 Rationale for Revising the KC

Globalization rapid transformation of international trade patterns and advances in

information technology since then compelled the WCO and its members to review and update the KC

14 Revised Kyoto Convention (RKC)

The review and update of the KC resulted in the revision of the convention to reflect economic and technological changes that have occurred and incorporate best practices of the member customs administrations of the WCO The resultant revision is known as the Revised Kyoto Convention (ldquoRKCrdquo) RKC was adopted by 114 customs administrations attending the WCOs 94th Session in June 1999 It came into force on February 3 2006 three months after India became the 40th signatory to the Protocol of Amendment

The RKC contains necessary tools for facilitating trade that will ensure economic growth and

improve the security of the international trading system It seeks to answer the global call for professionalism and integrity in all customs administration The RKC serves as the blueprint for modern and efficient customs procedures in the 21st century The RKC is a key to anti-corruption initiative mdash by promoting the integrity and professionalism of customs administrations worldwide and reducing the susceptibility of businesses and citizens to corrupt customs practices

15 Philippines vis-agrave-vis the KC

The Philippines was not a contracting party to the KC However in the various reforms and modernization programs undertaken by the Philippine Bureau of Customs particularly during the 1992-98 Customs Reform and Modernization Program several national legislation were issued and systems and procedures developed that made many of its Customs operations compliant with the major provisions not just of the KC but also with the RKC which was then being deliberated about

16 Consequences of Philippine Non-accession of the KC

Although many of its Customs operations under the 1992-1998 Customs Reforms and

Modernization Program were compliant with the major provisions of the KC and also of the RKC it was a purely administrative initiative This administrative initiative was subsequently changed or ignored by succeeding Customs management Reforms were not sustained and worst in some fronts there were even reversals This could have been minimized if not all together prevented if the Philippines were a contracting party to the KC or has acceded to the KC

3

17 Compliance vs Accession Differences Being Kyoto Compliant means accepting the responsibility to construct regulatory policies and

practices in a manner that is consistent with the principles laid down in the Convention conforming to the standards set forth in the Convention Being compliant is something that can be done at any time by any country whether or not it accedes to the Convention It does not create rights and responsibilities relative to contracting parties

18 Accession Accession is a step beyond being compliant It is a legal act through which one recognizes

that one is or intends to be compliant that one accepts the obligations of the Convention as being legally binding It creates rights and responsibilities relative to other contracting parties

Accession would send a clear message that the public and private sector truly can work

together to facilitate trade and that trade and security are not mutually exclusive Accession presents a significant step forward in the promotion of economic growth national security and customs integrity at both the national and international level

Accession sends a clear message to both the international trade community and governments

around the world that the Philippines stands firmly behind customs procedures that facilitate the secure movement of legitimate trade across national borders

Accession will bring the following benefits

bull Protection against passage or issuance of National Legislation [revision of Customs Code Issuance of Presidential Decrees (PDs) and Executive Orderrsquos (EOrsquos) and Administrative Orders (AOs) Customs Administrative Orders (CAOs) and Customs Memorandum Orders (CMOs)] that are against the principles and provisions of the RKC Moves to legislate measures that are anti trade facilitation can out rightly be rejected if we are a signatory to the RKC

bull Provide a solid foundation for reforming and strengthening our Legislative Base which

is a very important first step in reforming Customs and related institutions Eliminating the gaps between RKC and National Legislation can be the Action Program of a Joint Business-Congressional-DOF-BOC Reform Agenda

bull Provide benchmark for assessing the status of the Philippinersquos Trade Efficiency and

Competitiveness

bull Provide a mechanism the RKC Management Committee to which foreign companies and countries can express their grievances against Customs administration which does not properly implement RKC

bull Provide the training ground and human resources such as the Lead Shepherds and

the members of the Team of Technical Experts involved in analyzing compliance of national legislation to the provisions of the RKC who can drive the reform process

19 Benefits Expected from Trading with Countries that are RKC Compliant

bull Reduce cost of clearing customs in other countries bull Minimize if not eliminate delays in getting the goods into the country

4

bull Individual companies do not have to learn 140 separate sets of customs procedures

bull Reduce if not eliminate inefficient customs procedures and policies that impede access to markets and unnecessarily increase costs

bull Facilitate product market introduction bull More efficient customs procedures overall bull Standardize customs implementation and administrative procedures worldwide -

across participating countries bull Reduce cycle time due to more predictability in the customs entry and release

process which will result in inventory savings (inventory costs can run as high as $20 million per day)

bull Promote greater understanding of compliance requirements resulting from increased transparency so that industry is better able to meet ldquotime-to-marketrdquo objectives

bull Promote the implementation of special procedures for low-risk importers bull Reduce opportunities for extortion of facilitationgrease payments thereby

paving the smooth transition to increased transparency and automation

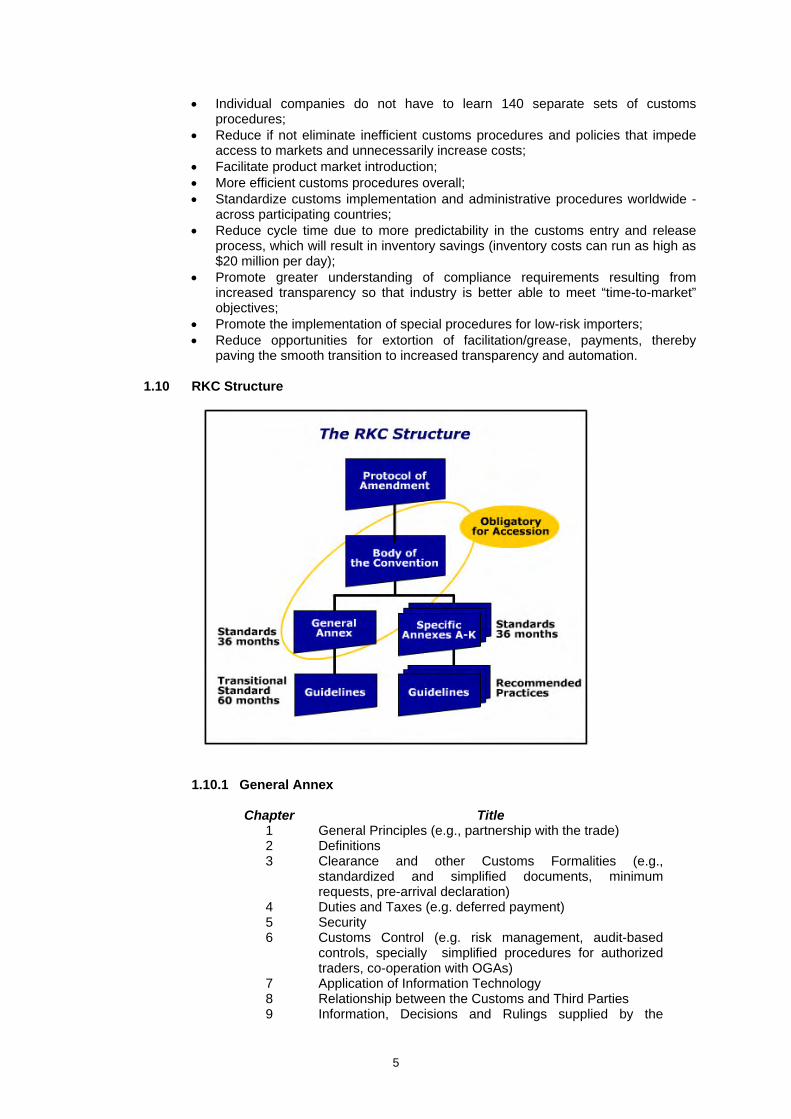

110 RKC Structure

1101 General Annex

Chapter Title 1 General Principles (eg partnership with the trade) 2 Definitions 3 Clearance and other Customs Formalities (eg

standardized and simplified documents minimum requests pre-arrival declaration)

4 Duties and Taxes (eg deferred payment) 5 Security 6 Customs Control (eg risk management audit-based

controls specially simplified procedures for authorized traders co-operation with OGAs)

7 Application of Information Technology 8 Relationship between the Customs and Third Parties 9 Information Decisions and Rulings supplied by the

5

Customs (eg publication of information advance rulings) 10 Appeals in Customs Matters

1102 Specific Annexes and their Chapters

Specific Annex Chapter Title

A Arrival of Goods in a Customs Territory 1 Formalities Prior to the Lodgement of the

Goods Declaration 2 Temporary Storage of Goods

B Importation 1 Clearance for Home Use 2 Re-importation in the Same State 3 Relief from Import Duties and Taxes

C Exportation 1 Outright Exportation

D Customs Warehouses and Free Zones 1 Customs Warehouses 2 Free Zones

E Transit 1 Customs Transit 2 Transhipment 3 Carriage of Goods Coastwise

F Processing 1 Inward Processing 2 Outward Processing 3 Drawback 4 Processing of Goods for Home Use

G Temporary Admission 1 Temporary Admission

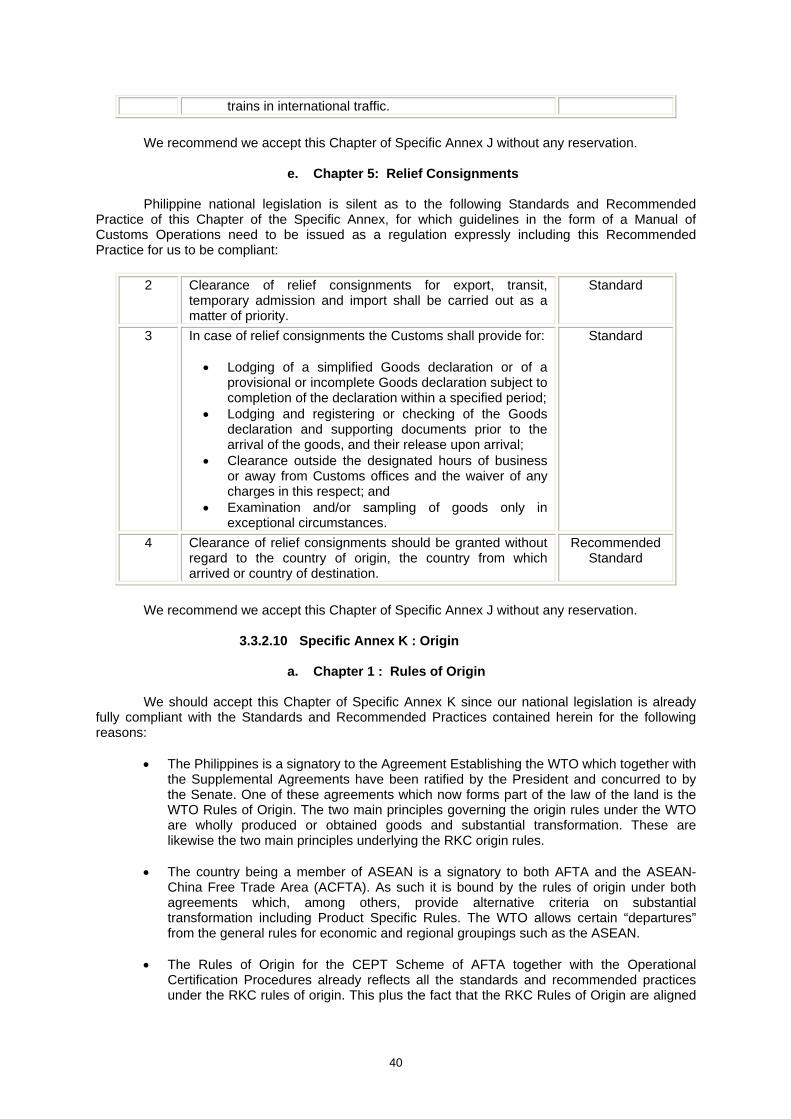

H Offences 1 Customs Offences J Special Procedures 1 Travellers 2 Postal Traffic 3 Means of Transport for Commercial use 4 Stores 5 Relief Consignments

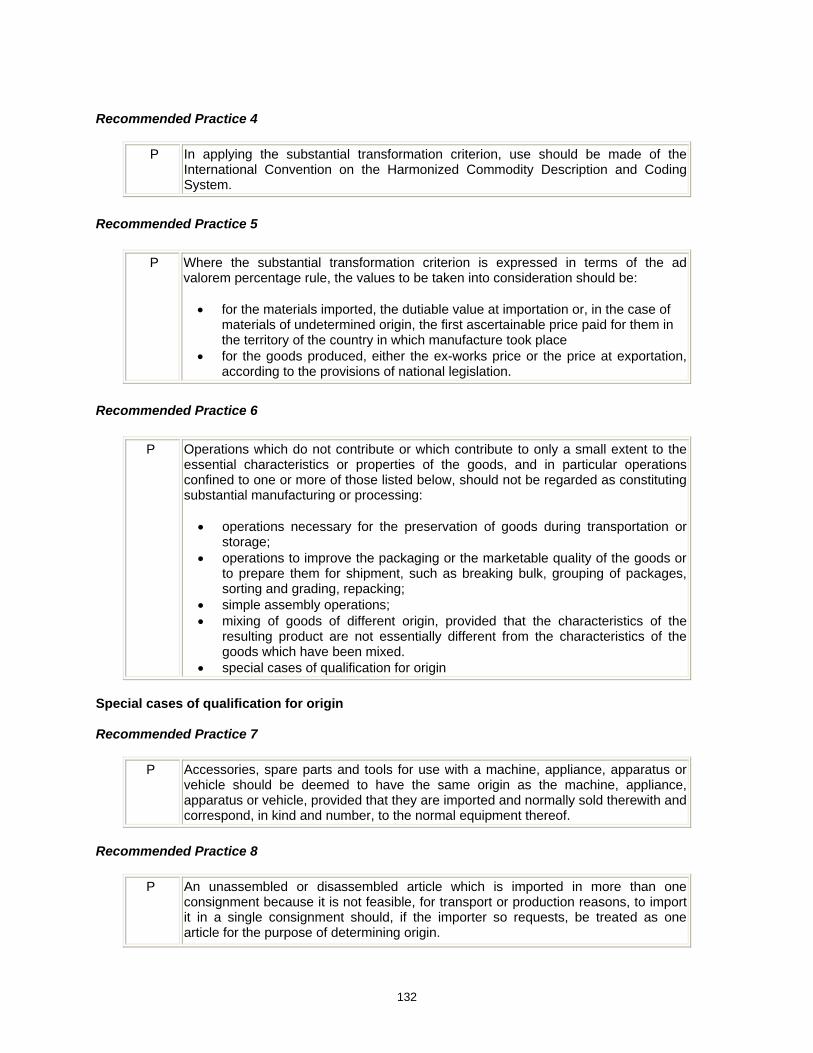

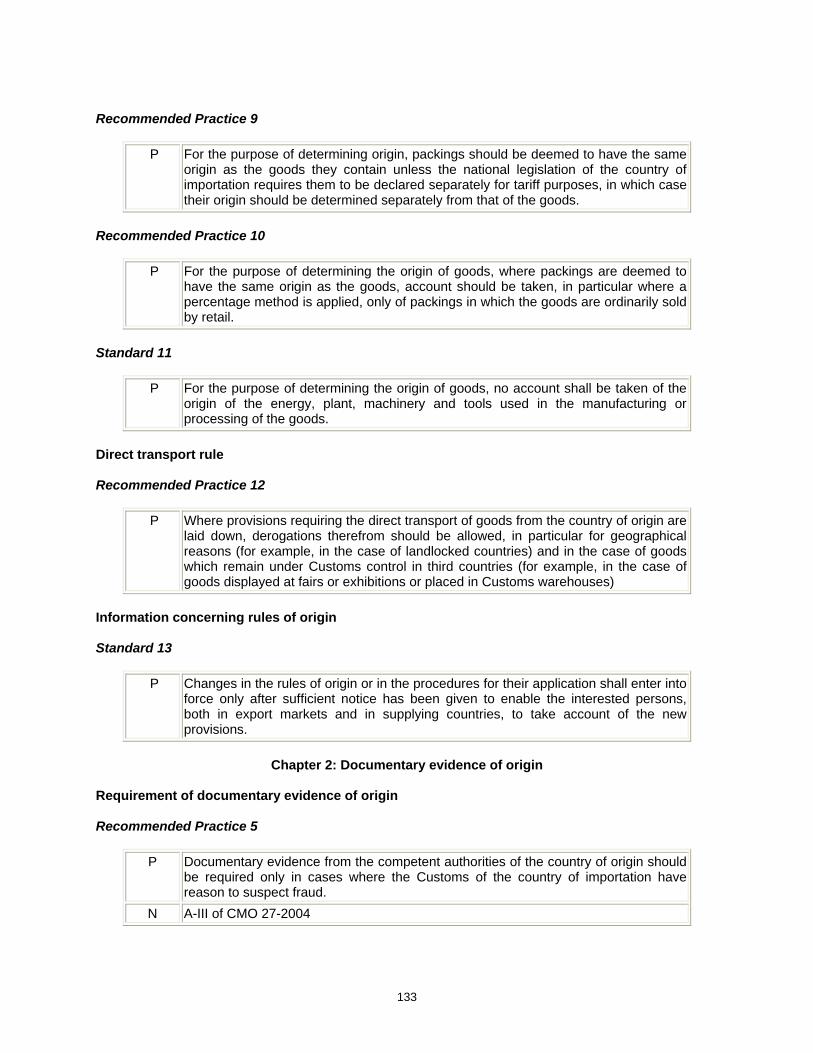

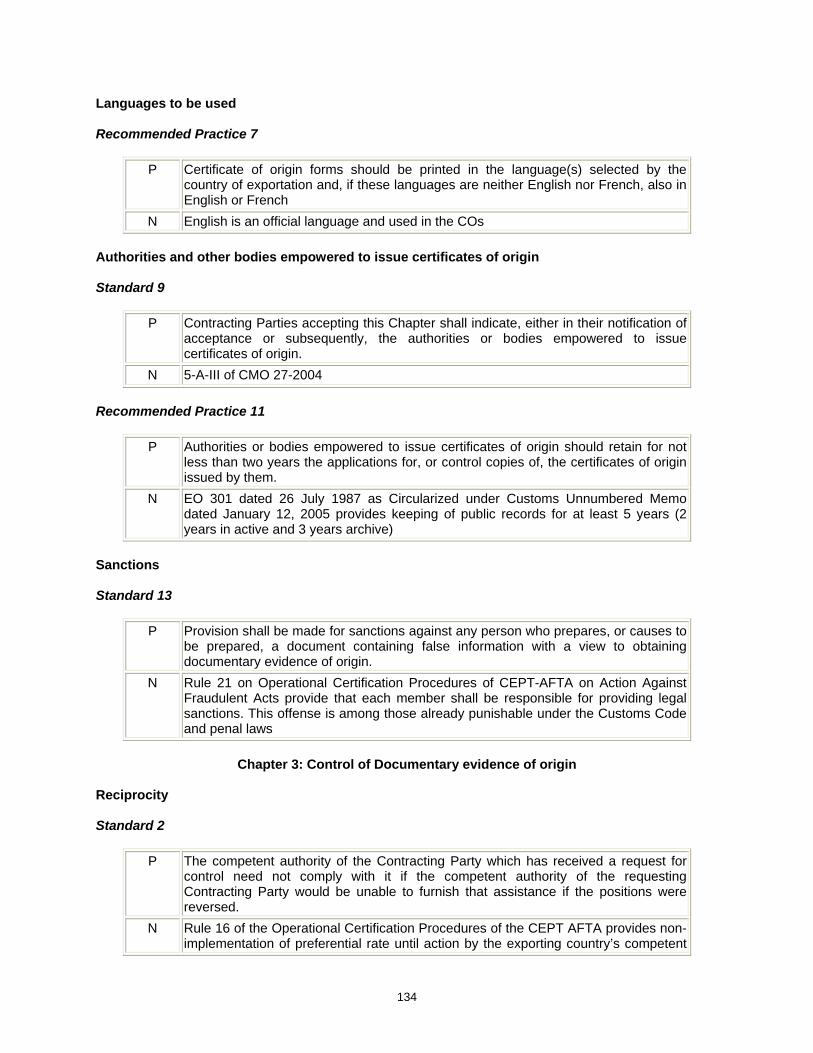

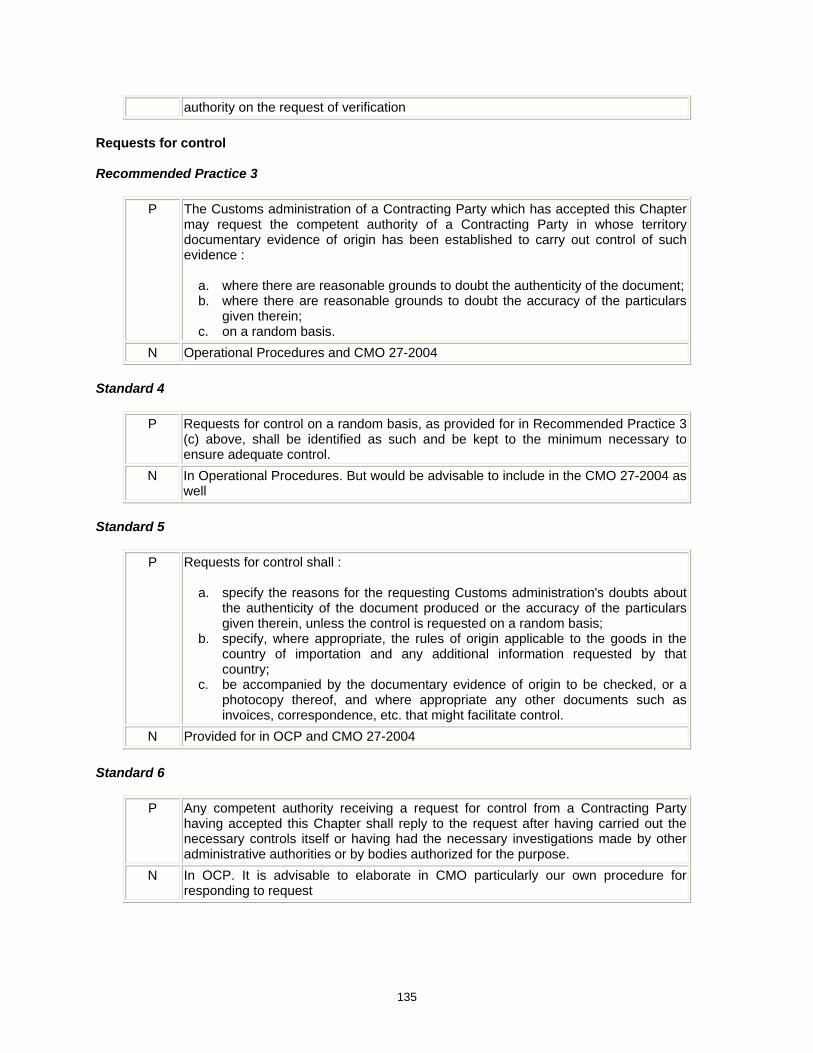

K Origin 1 Rules of Origin 2 Documentary Evidence of Origin 3 Control of Documentary Evidence of Origin

111 RKC Management Committee

The RKC provides for the creation of a RKC Management Committee composed of the

Contracting Parties as members The functions of the RKC Management Committee are to administer the RKC to recommend amendments to the RKC to make decision on amendments to Recommended Practices to make decisions with respect to a request of extension of the implementation period and to review and update the Guidelines The first meeting of the RKC Management Committee was held on 6-7 March 2006 20 APEC Recommended Pathway to Accession

When a new Contracting Party accedes to the RKC it must signify that it is accepting the

Body of the convention and the General Annex It need not accept any of the Specific Annexes However it may do so in whole or in part A country did not feel compelled to be compliant with the Specific Annex at the outset For as long as it is compliant with the Body of the Convention and the General Annex a country can begin to consider accession to the RKC When a country accepts a

6

chapter of a Specific Annex or a Specific Annex it is deemed to have accepted all the Standards contained therein It may only make reservations to the Recommended Practice contained in a chapter or Specific Annex accepted However any reservation to any Recommended Practices must be expressly made by the country in their Instrument of Accession

The guideline issued by APEC entitled The Revised Kyoto Convention A Pathway to

Accession and Implementation recommends as a first step to become RKC compliant undertaking a comparison of the provisions of the General Annex and subsequently of the provisions of the Specific Annexes with a countryrsquos existing national legislation (whether administered by Customs or by any other government agency which has an official regulatory responsibility relating to international trade in goods and the collection of duties and taxes) This will identify the provisions of the General Annex and the Specific Annexes with which a country is already in compliance with and those with which it will need to become compliant This process is referred to as a situational analysis

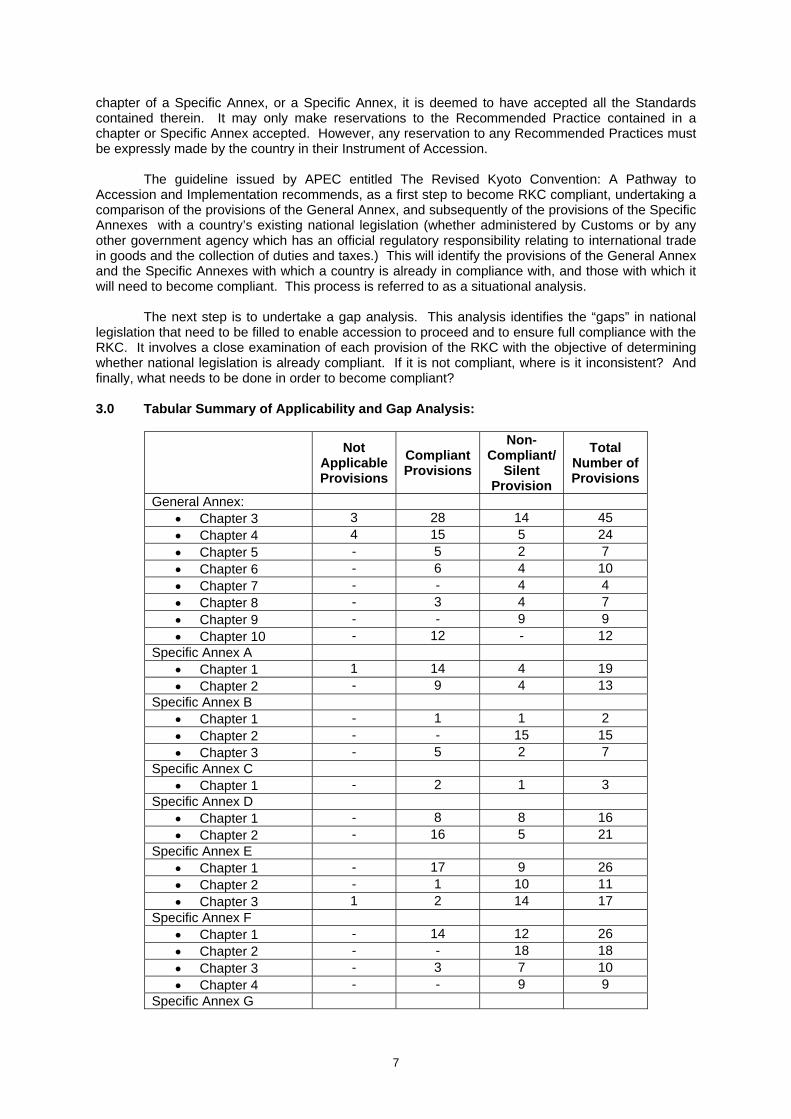

The next step is to undertake a gap analysis This analysis identifies the ldquogapsrdquo in national

legislation that need to be filled to enable accession to proceed and to ensure full compliance with the RKC It involves a close examination of each provision of the RKC with the objective of determining whether national legislation is already compliant If it is not compliant where is it inconsistent And finally what needs to be done in order to become compliant 30 Tabular Summary of Applicability and Gap Analysis

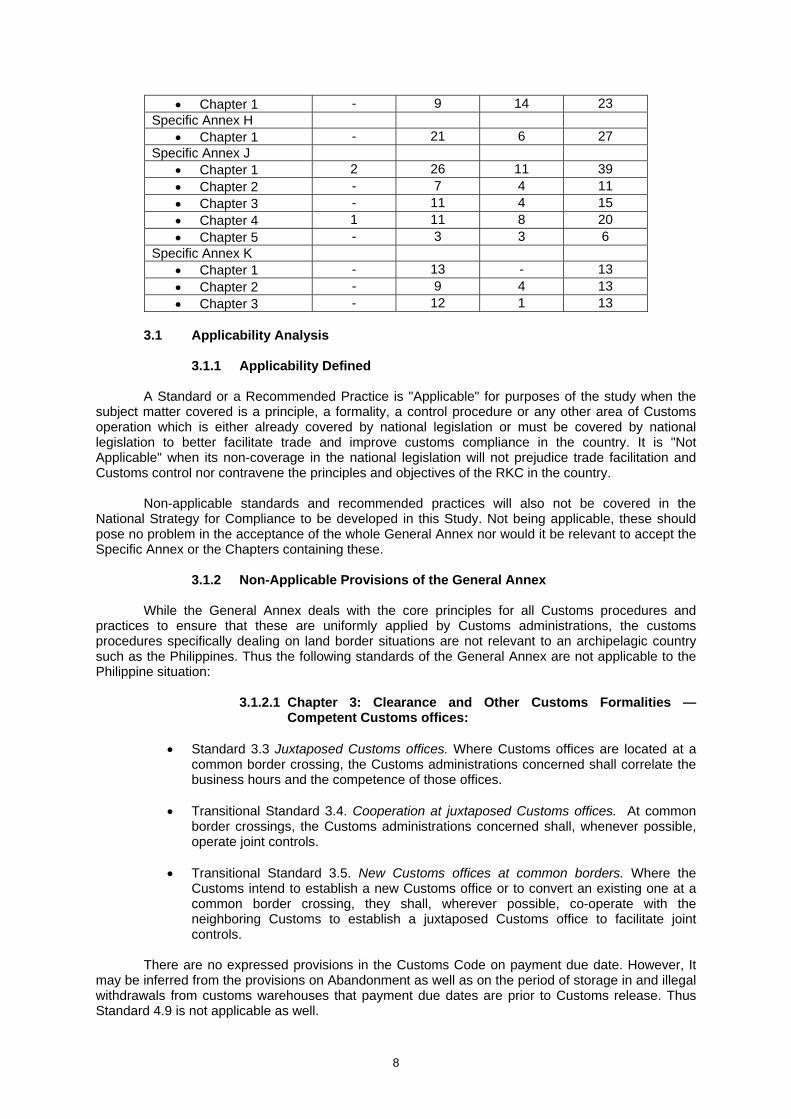

Not

Applicable Provisions

Compliant Provisions

Non-Compliant

Silent Provision

Total Number of Provisions

General Annex bull Chapter 3 3 28 14 45 bull Chapter 4 4 15 5 24 bull Chapter 5 - 5 2 7 bull Chapter 6 - 6 4 10 bull Chapter 7 - - 4 4 bull Chapter 8 - 3 4 7 bull Chapter 9 - - 9 9 bull Chapter 10 - 12 - 12

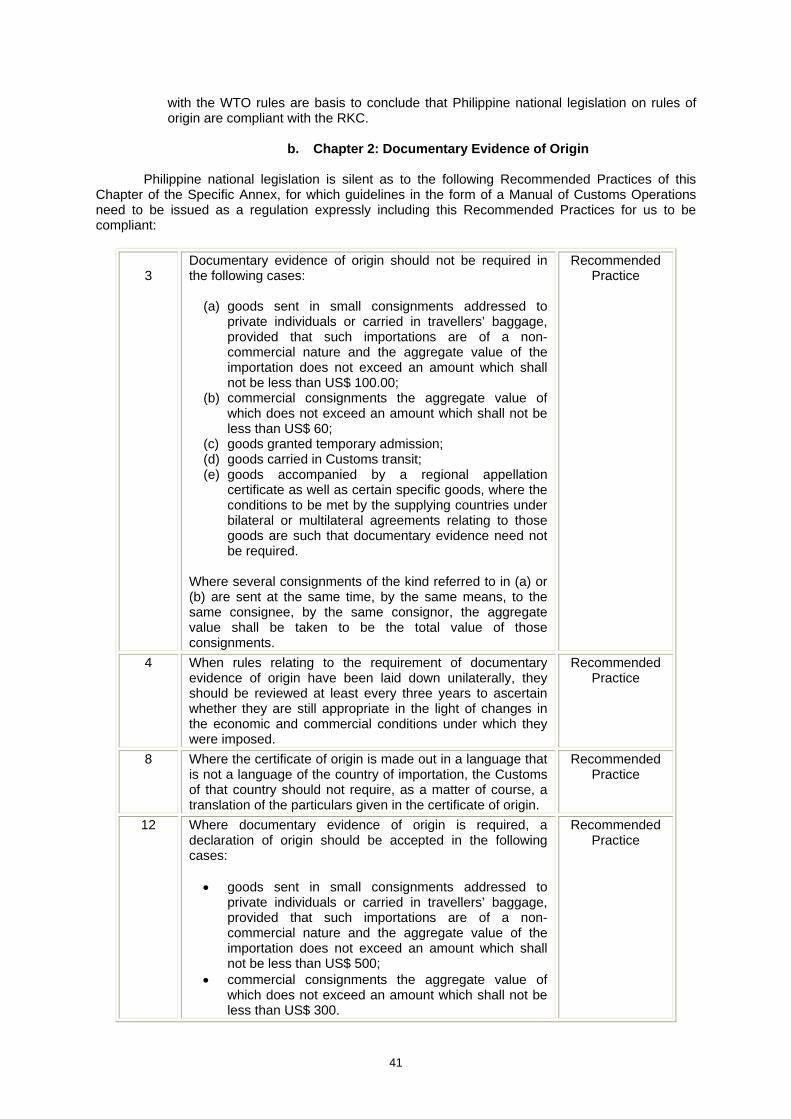

Specific Annex A bull Chapter 1 1 14 4 19 bull Chapter 2 - 9 4 13

Specific Annex B bull Chapter 1 - 1 1 2 bull Chapter 2 - - 15 15 bull Chapter 3 - 5 2 7

Specific Annex C bull Chapter 1 - 2 1 3

Specific Annex D bull Chapter 1 - 8 8 16 bull Chapter 2 - 16 5 21

Specific Annex E bull Chapter 1 - 17 9 26 bull Chapter 2 - 1 10 11 bull Chapter 3 1 2 14 17

Specific Annex F bull Chapter 1 - 14 12 26 bull Chapter 2 - - 18 18 bull Chapter 3 - 3 7 10 bull Chapter 4 - - 9 9

Specific Annex G

7

bull Chapter 1 - 9 14 23 Specific Annex H

bull Chapter 1 - 21 6 27 Specific Annex J

bull Chapter 1 2 26 11 39 bull Chapter 2 - 7 4 11 bull Chapter 3 - 11 4 15 bull Chapter 4 1 11 8 20 bull Chapter 5 - 3 3 6

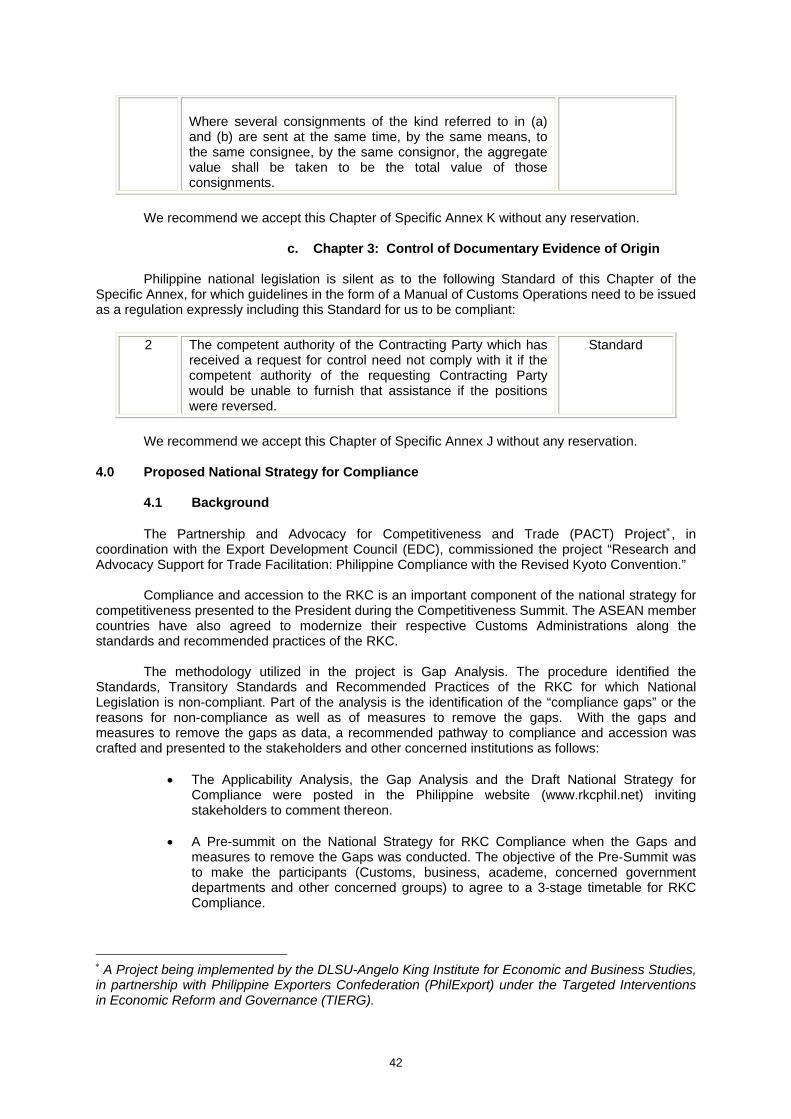

Specific Annex K bull Chapter 1 - 13 - 13 bull Chapter 2 - 9 4 13 bull Chapter 3 - 12 1 13

31 Applicability Analysis

311 Applicability Defined

A Standard or a Recommended Practice is Applicable for purposes of the study when the subject matter covered is a principle a formality a control procedure or any other area of Customs operation which is either already covered by national legislation or must be covered by national legislation to better facilitate trade and improve customs compliance in the country It is Not Applicable when its non-coverage in the national legislation will not prejudice trade facilitation and Customs control nor contravene the principles and objectives of the RKC in the country

Non-applicable standards and recommended practices will also not be covered in the

National Strategy for Compliance to be developed in this Study Not being applicable these should pose no problem in the acceptance of the whole General Annex nor would it be relevant to accept the Specific Annex or the Chapters containing these

312 Non-Applicable Provisions of the General Annex

While the General Annex deals with the core principles for all Customs procedures and

practices to ensure that these are uniformly applied by Customs administrations the customs procedures specifically dealing on land border situations are not relevant to an archipelagic country such as the Philippines Thus the following standards of the General Annex are not applicable to the Philippine situation

3121 Chapter 3 Clearance and Other Customs Formalities mdash Competent Customs offices

bull Standard 33 Juxtaposed Customs offices Where Customs offices are located at a

common border crossing the Customs administrations concerned shall correlate the business hours and the competence of those offices

bull Transitional Standard 34 Cooperation at juxtaposed Customs offices At common

border crossings the Customs administrations concerned shall whenever possible operate joint controls

bull Transitional Standard 35 New Customs offices at common borders Where the

Customs intend to establish a new Customs office or to convert an existing one at a common border crossing they shall wherever possible co-operate with the neighboring Customs to establish a juxtaposed Customs office to facilitate joint controls

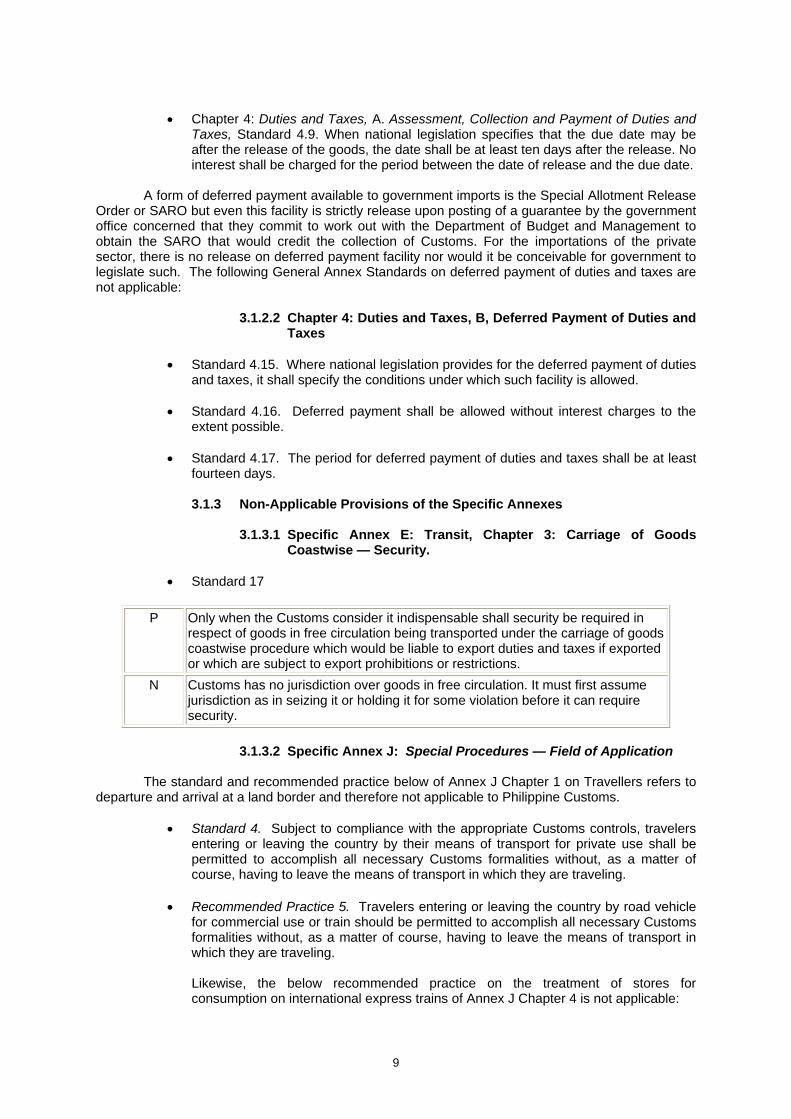

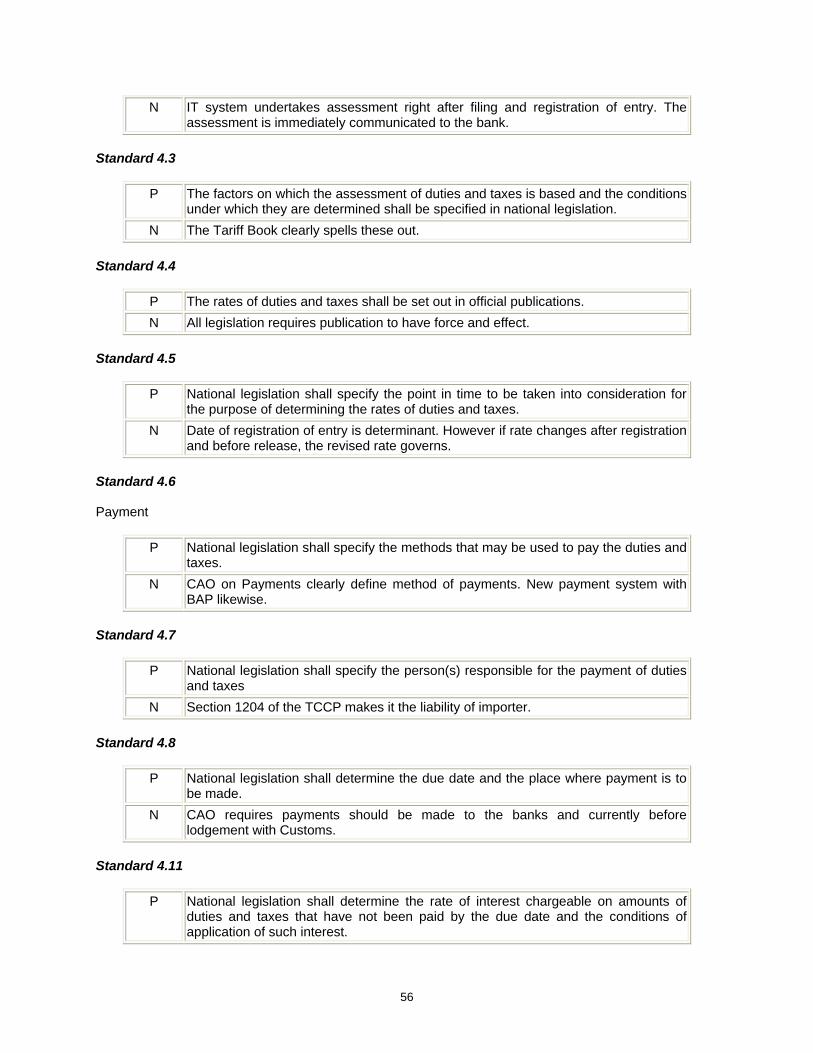

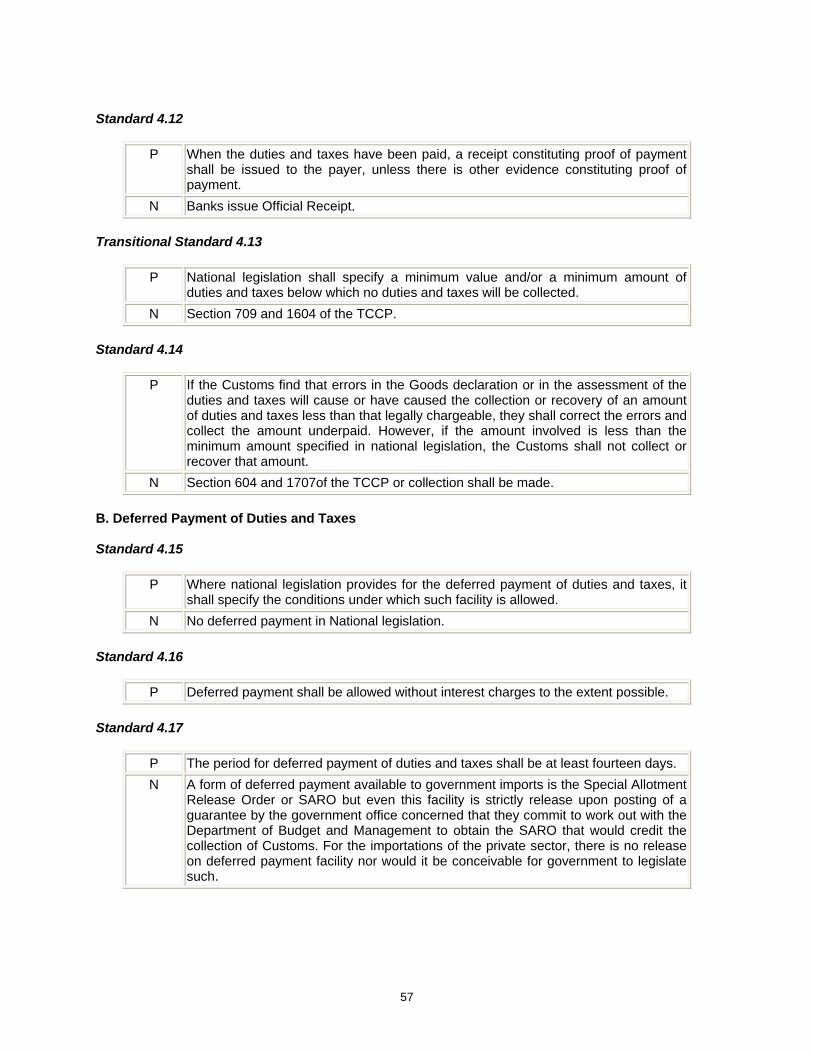

There are no expressed provisions in the Customs Code on payment due date However It may be inferred from the provisions on Abandonment as well as on the period of storage in and illegal withdrawals from customs warehouses that payment due dates are prior to Customs release Thus Standard 49 is not applicable as well

8

bull Chapter 4 Duties and Taxes A Assessment Collection and Payment of Duties and

Taxes Standard 49 When national legislation specifies that the due date may be after the release of the goods the date shall be at least ten days after the release No interest shall be charged for the period between the date of release and the due date

A form of deferred payment available to government imports is the Special Allotment Release Order or SARO but even this facility is strictly release upon posting of a guarantee by the government office concerned that they commit to work out with the Department of Budget and Management to obtain the SARO that would credit the collection of Customs For the importations of the private sector there is no release on deferred payment facility nor would it be conceivable for government to legislate such The following General Annex Standards on deferred payment of duties and taxes are not applicable

3122 Chapter 4 Duties and Taxes B Deferred Payment of Duties and Taxes

bull Standard 415 Where national legislation provides for the deferred payment of duties

and taxes it shall specify the conditions under which such facility is allowed bull Standard 416 Deferred payment shall be allowed without interest charges to the

extent possible

bull Standard 417 The period for deferred payment of duties and taxes shall be at least fourteen days

313 Non-Applicable Provisions of the Specific Annexes

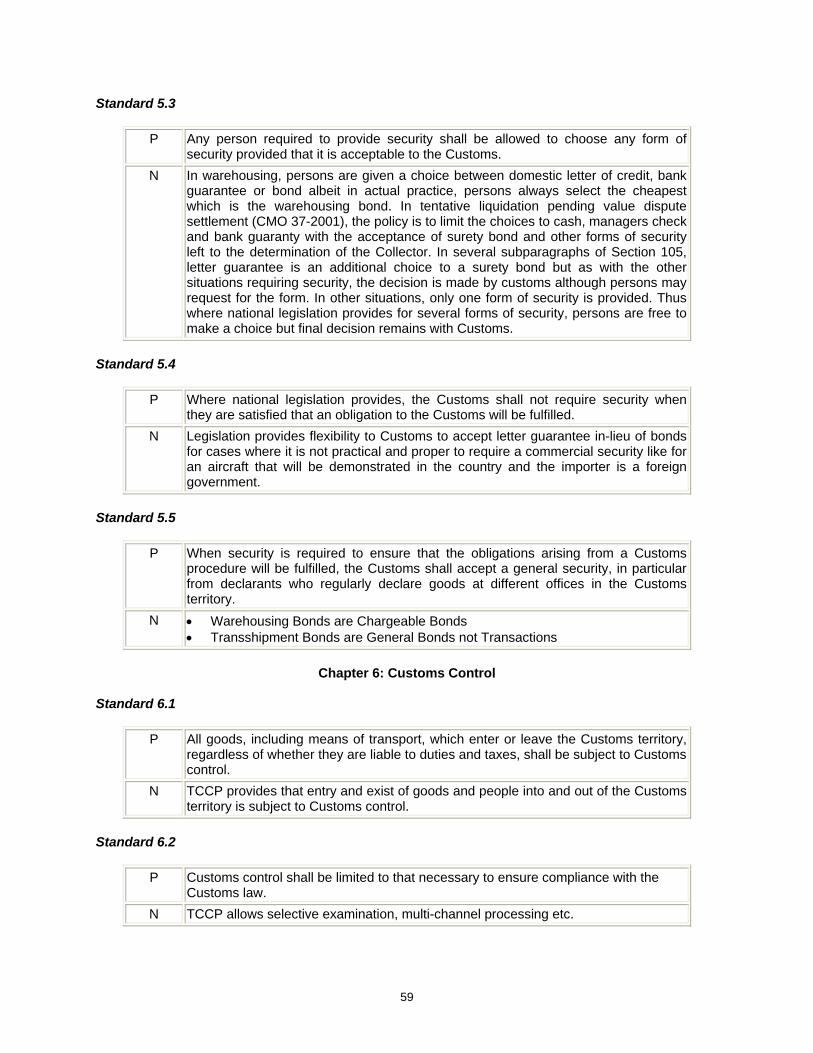

3131 Specific Annex E Transit Chapter 3 Carriage of Goods Coastwise mdash Security

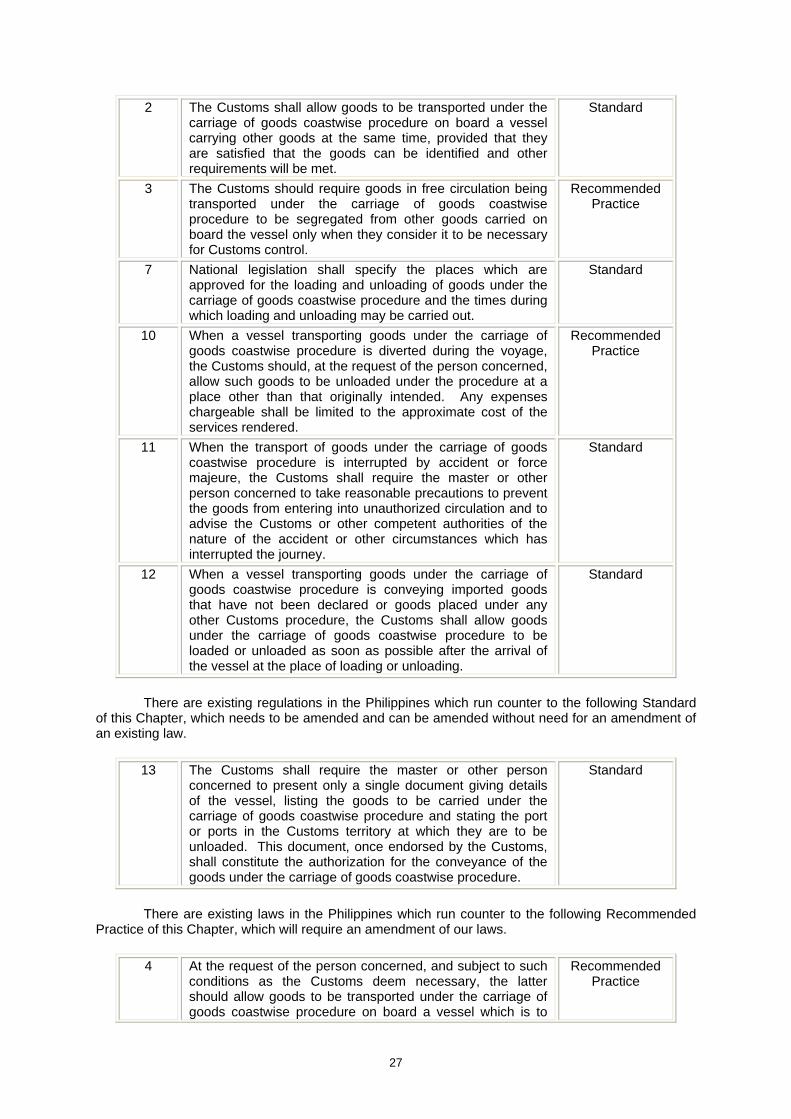

bull Standard 17

P Only when the Customs consider it indispensable shall security be required in respect of goods in free circulation being transported under the carriage of goods coastwise procedure which would be liable to export duties and taxes if exported or which are subject to export prohibitions or restrictions

N Customs has no jurisdiction over goods in free circulation It must first assume jurisdiction as in seizing it or holding it for some violation before it can require security

3132 Specific Annex J Special Procedures mdash Field of Application

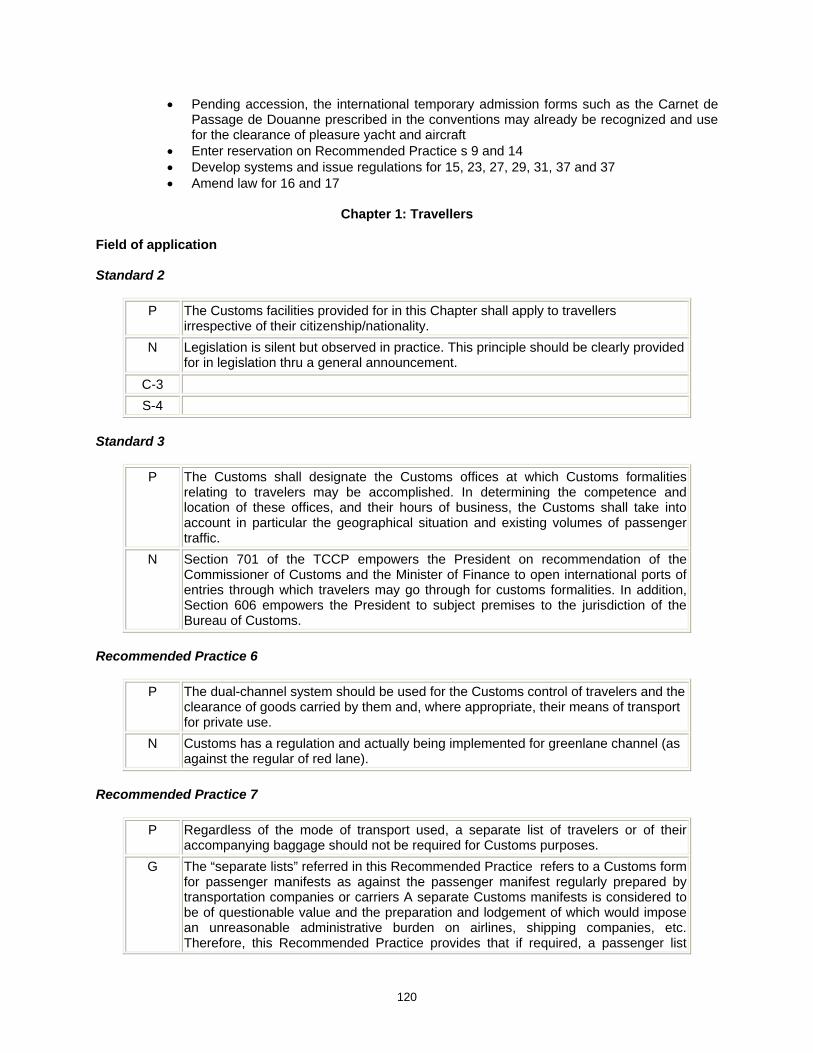

The standard and recommended practice below of Annex J Chapter 1 on Travellers refers to departure and arrival at a land border and therefore not applicable to Philippine Customs

bull Standard 4 Subject to compliance with the appropriate Customs controls travelers

entering or leaving the country by their means of transport for private use shall be permitted to accomplish all necessary Customs formalities without as a matter of course having to leave the means of transport in which they are traveling

bull Recommended Practice 5 Travelers entering or leaving the country by road vehicle

for commercial use or train should be permitted to accomplish all necessary Customs formalities without as a matter of course having to leave the means of transport in which they are traveling

Likewise the below recommended practice on the treatment of stores for consumption on international express trains of Annex J Chapter 4 is not applicable

9

3133 Chapter 4 Stores Stores on board arriving vessels aircraft or trains mdash a Exemption from import duties and taxes

bull Recommended Practice 4 Stores for consumption by the passengers and the crew imported

as provisions on international express trains should be exempted from import duties and taxes provided that

1 Such goods are purchased only in the countries crossed by the international train

in question and 2 Any duties and taxes chargeable on such goods in the country where they were

purchased are paid

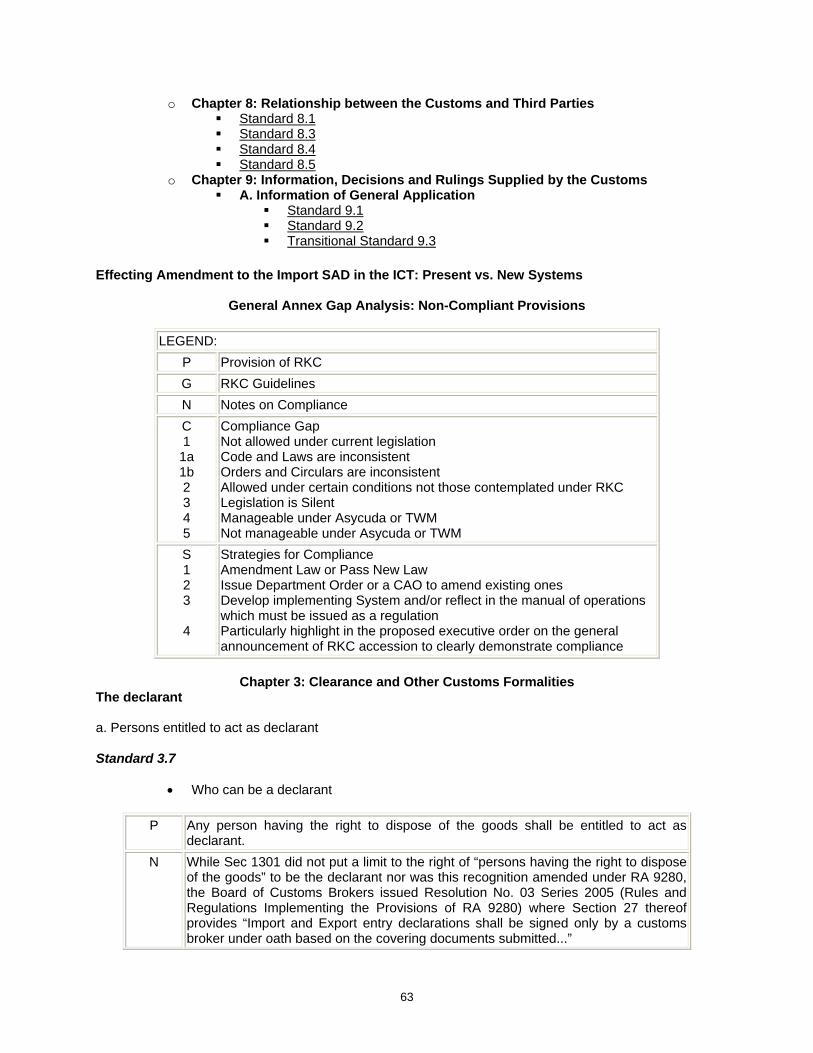

32 Gap Analysis

321 Components of Gap Analysis

The Gap Analysis identified the following

a Standards Transitory Standards and Recommended Practices that are compliant with National Legislation

b Provisions or specific National Legislation that support the Standards Transitory

Standards and Recommended Practices we are compliant with

c Standards Transitory Standards and Recommended Practices that are not compliant with National Legislation for the following reasons

1 It is not allowed under our current legislation 2 Our Code laws administrative orders andor circulars are inconsistent with

the standards transitory standards and recommended practices

3 It is allowed under certain conditions which are not those contemplated by the RKC

4 Our Code laws administrative orders andor circulars are silent with regard

to the said standards transitory standards andor recommended practice 5 Contrary to the present rules or procedure as designed under the Asycuda or

TWM Aside from identifying Standards Transitory Standards and Recommended Practices for which National Legislation is non-compliant part of the analysis was to identify the reason for the gap and to recommend measures needed to remove the gap

The result of the gap analysis and a discussion thereof are contained in the following annexes attached hereto

bull Annex A ndash Standards and Transitory Standards of the General Annex that Philippine

National Legislations are compliant with bull Annex B ndash Standards and Transitory Standards of the General Annex that Philippine

National Legislations are not compliant with

bull Annex C ndash Standards and Recommended Practices of the Specific Annexes that Philippine National Legislations are compliant with

bull Annex D ndash Standards and Recommended Practices of the Specific Annexes that

Philippine National Legislations are not compliant with

10

33 Summary of Applicability and Gap Analysis mdash Including Recommendation on

Accession Thereto

331 General Annex

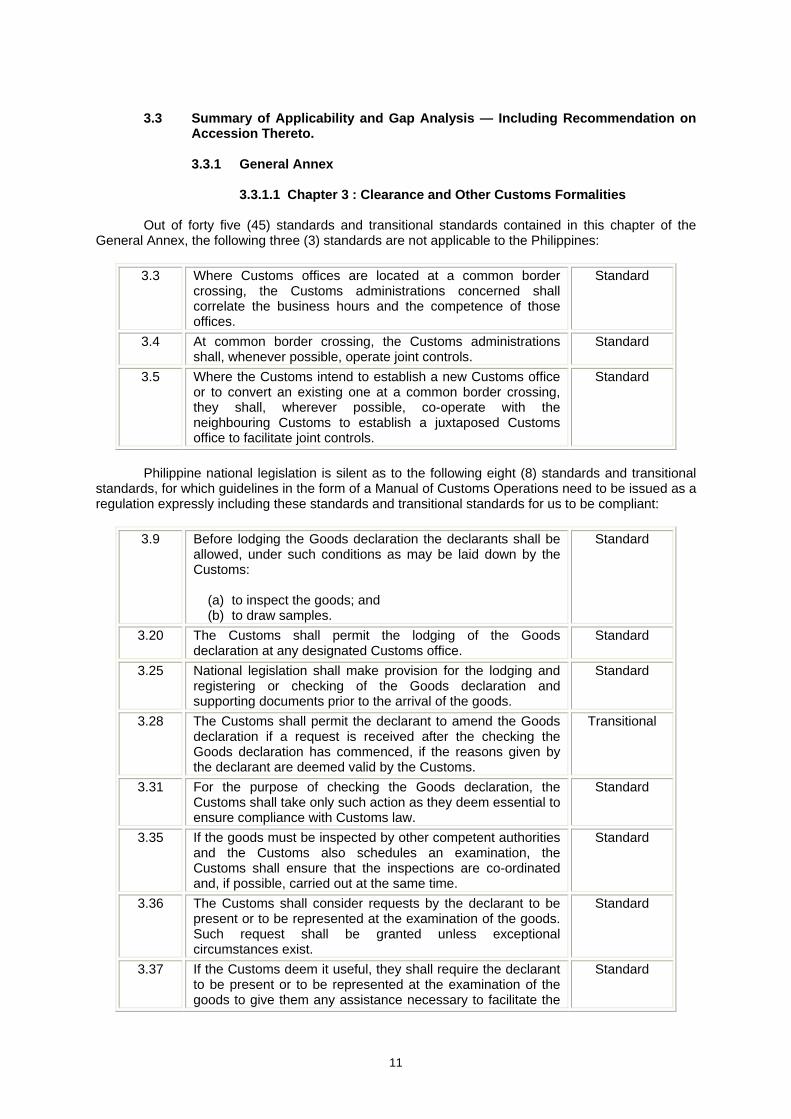

3311 Chapter 3 Clearance and Other Customs Formalities

Out of forty five (45) standards and transitional standards contained in this chapter of the General Annex the following three (3) standards are not applicable to the Philippines

33 Where Customs offices are located at a common border crossing the Customs administrations concerned shall correlate the business hours and the competence of those offices

Standard

34 At common border crossing the Customs administrations shall whenever possible operate joint controls

Standard

35 Where the Customs intend to establish a new Customs office or to convert an existing one at a common border crossing they shall wherever possible co-operate with the neighbouring Customs to establish a juxtaposed Customs office to facilitate joint controls

Standard

Philippine national legislation is silent as to the following eight (8) standards and transitional

standards for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including these standards and transitional standards for us to be compliant

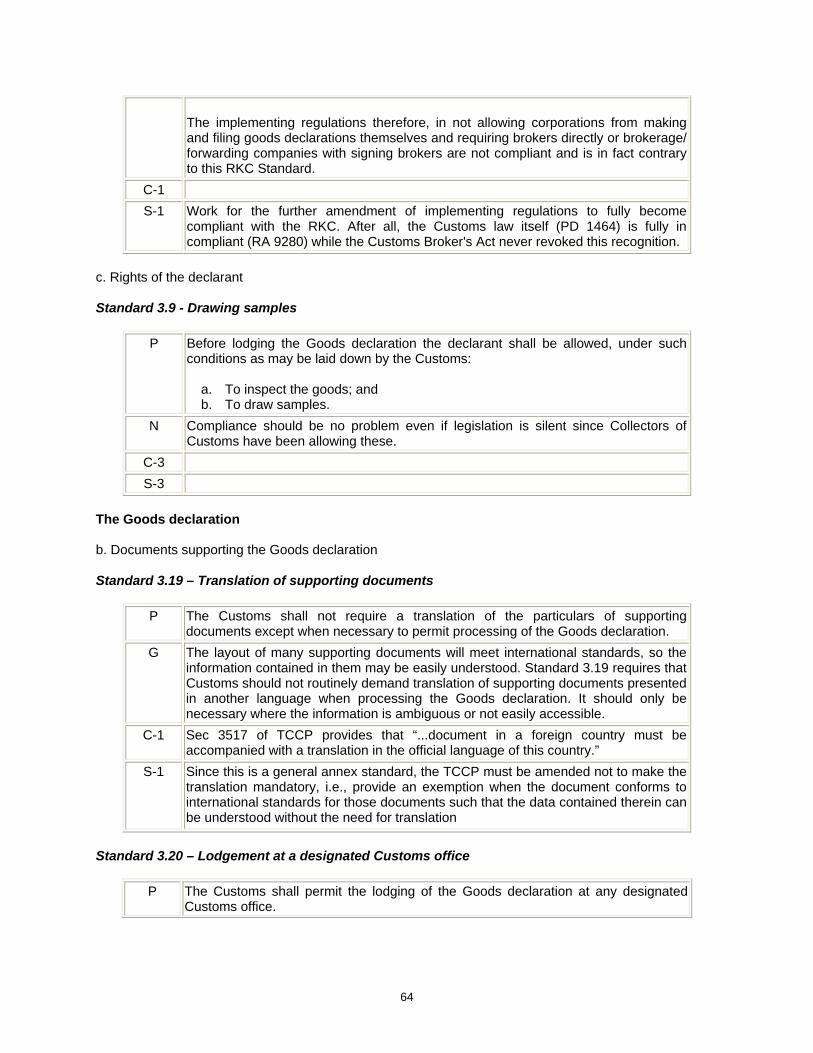

39 Before lodging the Goods declaration the declarants shall be allowed under such conditions as may be laid down by the Customs

(a) to inspect the goods and (b) to draw samples

Standard

320 The Customs shall permit the lodging of the Goods declaration at any designated Customs office

Standard

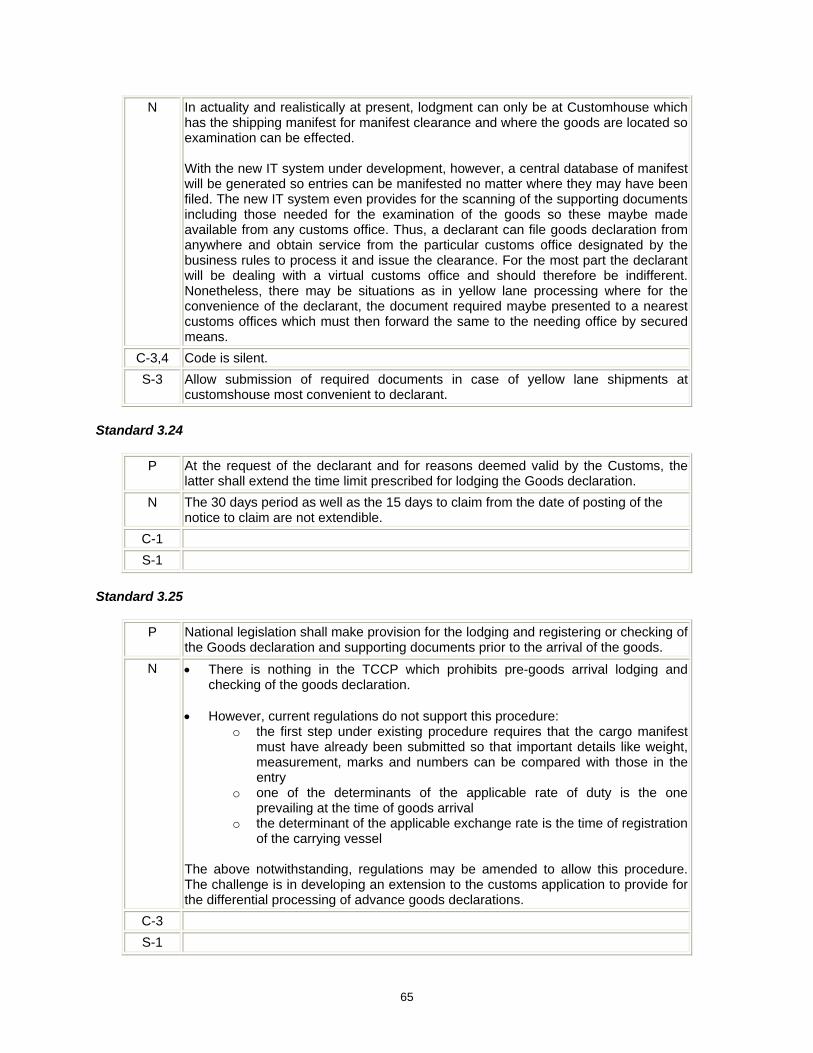

325 National legislation shall make provision for the lodging and registering or checking of the Goods declaration and supporting documents prior to the arrival of the goods

Standard

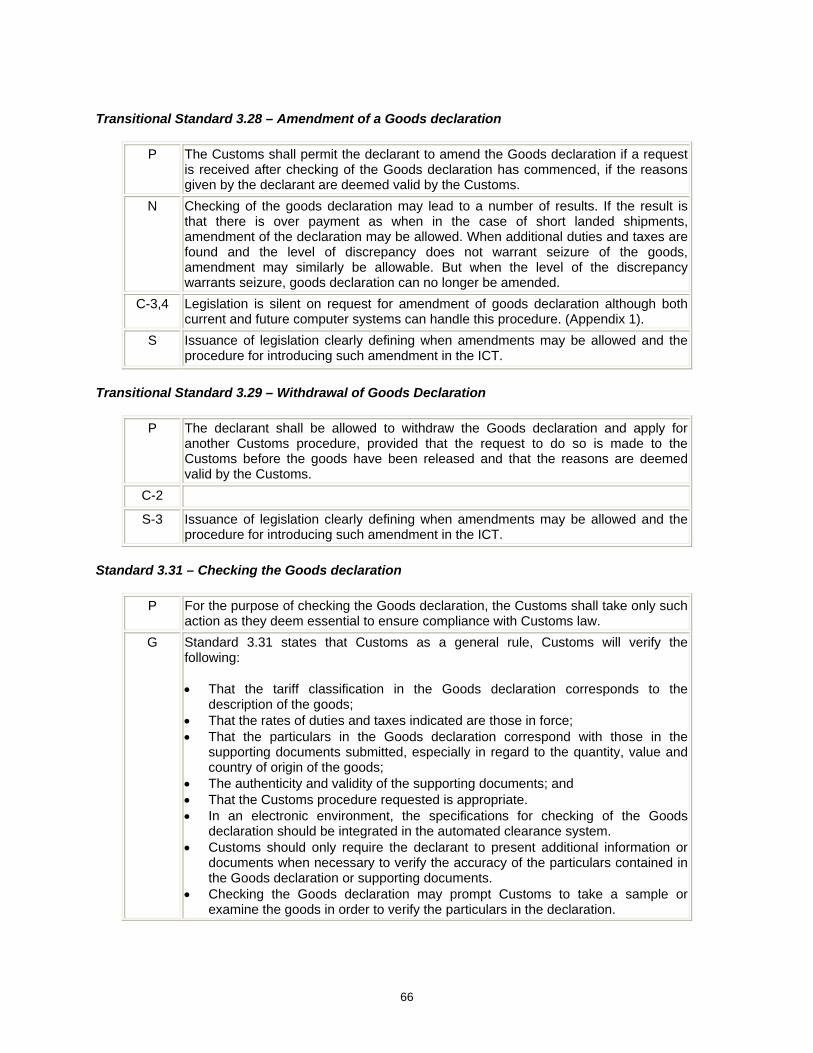

328 The Customs shall permit the declarant to amend the Goods declaration if a request is received after the checking the Goods declaration has commenced if the reasons given by the declarant are deemed valid by the Customs

Transitional

331 For the purpose of checking the Goods declaration the Customs shall take only such action as they deem essential to ensure compliance with Customs law

Standard

335 If the goods must be inspected by other competent authorities and the Customs also schedules an examination the Customs shall ensure that the inspections are co-ordinated and if possible carried out at the same time

Standard

336 The Customs shall consider requests by the declarant to be present or to be represented at the examination of the goods Such request shall be granted unless exceptional circumstances exist

Standard

337 If the Customs deem it useful they shall require the declarant to be present or to be represented at the examination of the goods to give them any assistance necessary to facilitate the

Standard

11

examination

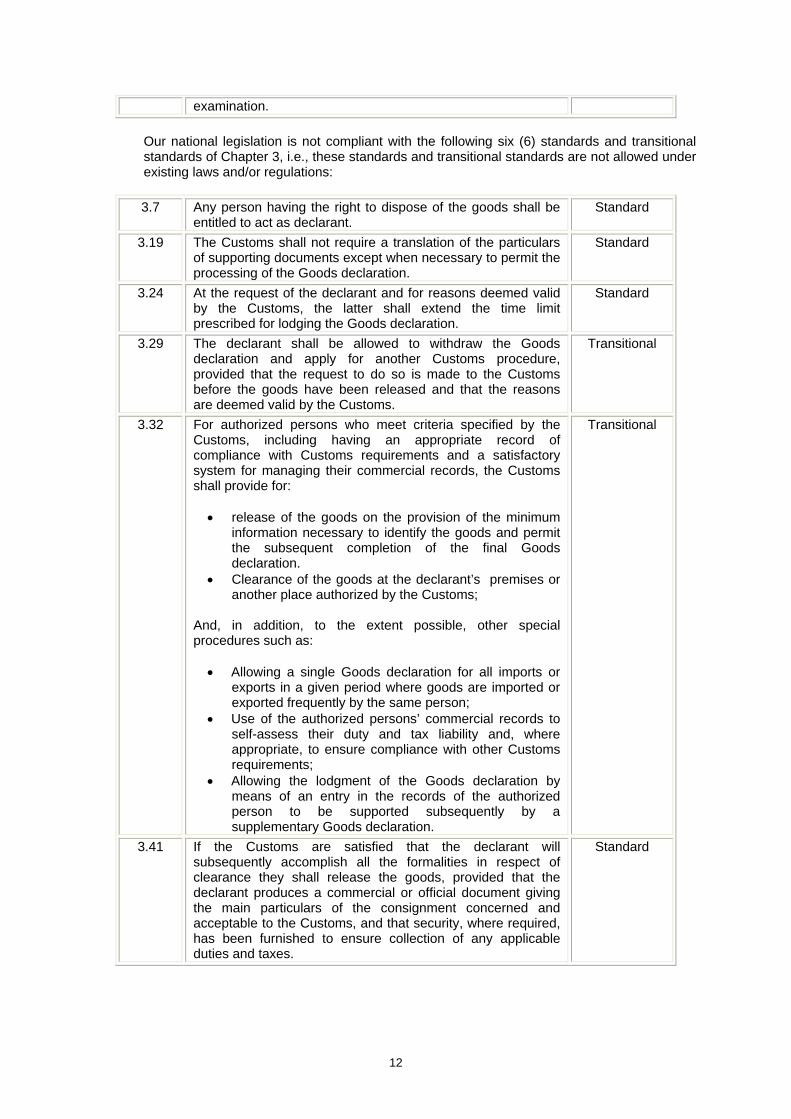

Our national legislation is not compliant with the following six (6) standards and transitional standards of Chapter 3 ie these standards and transitional standards are not allowed under existing laws andor regulations

37 Any person having the right to dispose of the goods shall be

entitled to act as declarant Standard

319 The Customs shall not require a translation of the particulars

of supporting documents except when necessary to permit the processing of the Goods declaration

Standard

324 At the request of the declarant and for reasons deemed valid by the Customs the latter shall extend the time limit prescribed for lodging the Goods declaration

Standard

329 The declarant shall be allowed to withdraw the Goods declaration and apply for another Customs procedure provided that the request to do so is made to the Customs before the goods have been released and that the reasons are deemed valid by the Customs

Transitional

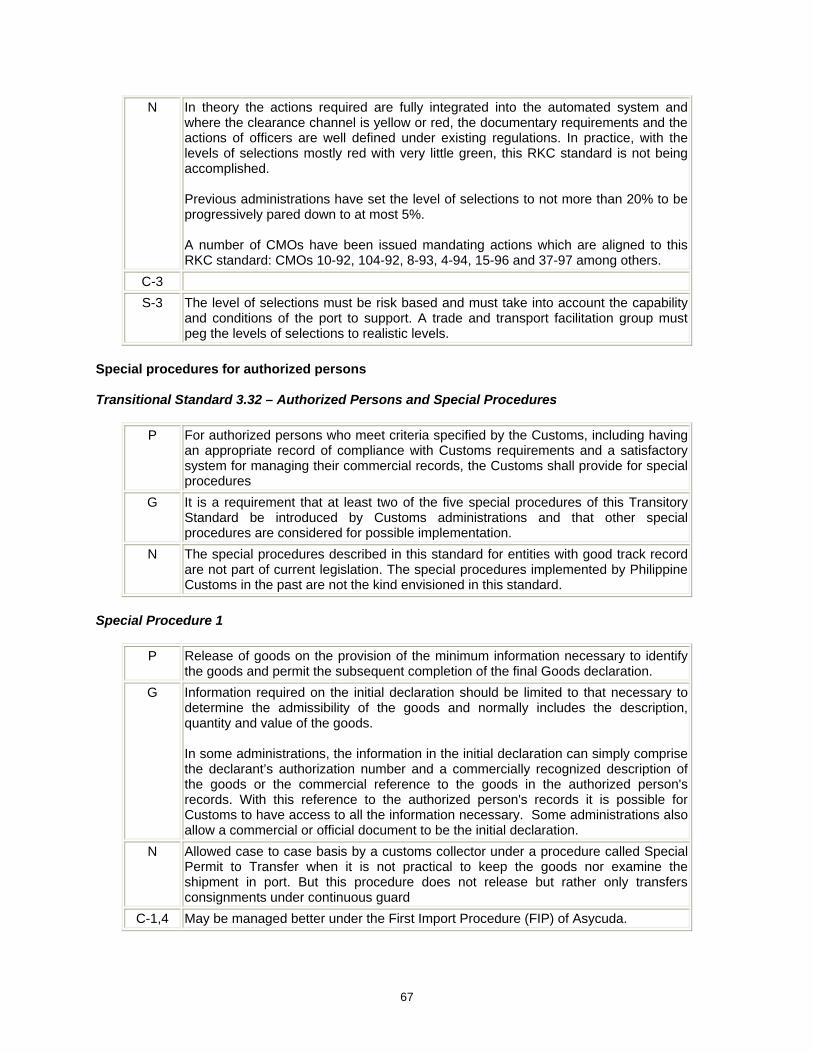

332 For authorized persons who meet criteria specified by the Customs including having an appropriate record of compliance with Customs requirements and a satisfactory system for managing their commercial records the Customs shall provide for bull release of the goods on the provision of the minimum

information necessary to identify the goods and permit the subsequent completion of the final Goods declaration

bull Clearance of the goods at the declarantrsquos premises or another place authorized by the Customs

And in addition to the extent possible other special procedures such as bull Allowing a single Goods declaration for all imports or

exports in a given period where goods are imported or exported frequently by the same person

bull Use of the authorized personsrsquo commercial records to self-assess their duty and tax liability and where appropriate to ensure compliance with other Customs requirements

bull Allowing the lodgment of the Goods declaration by means of an entry in the records of the authorized person to be supported subsequently by a supplementary Goods declaration

Transitional

341 If the Customs are satisfied that the declarant will subsequently accomplish all the formalities in respect of clearance they shall release the goods provided that the declarant produces a commercial or official document giving the main particulars of the consignment concerned and acceptable to the Customs and that security where required has been furnished to ensure collection of any applicable duties and taxes

Standard

12

3312 Chapter 4 Duties and Taxes

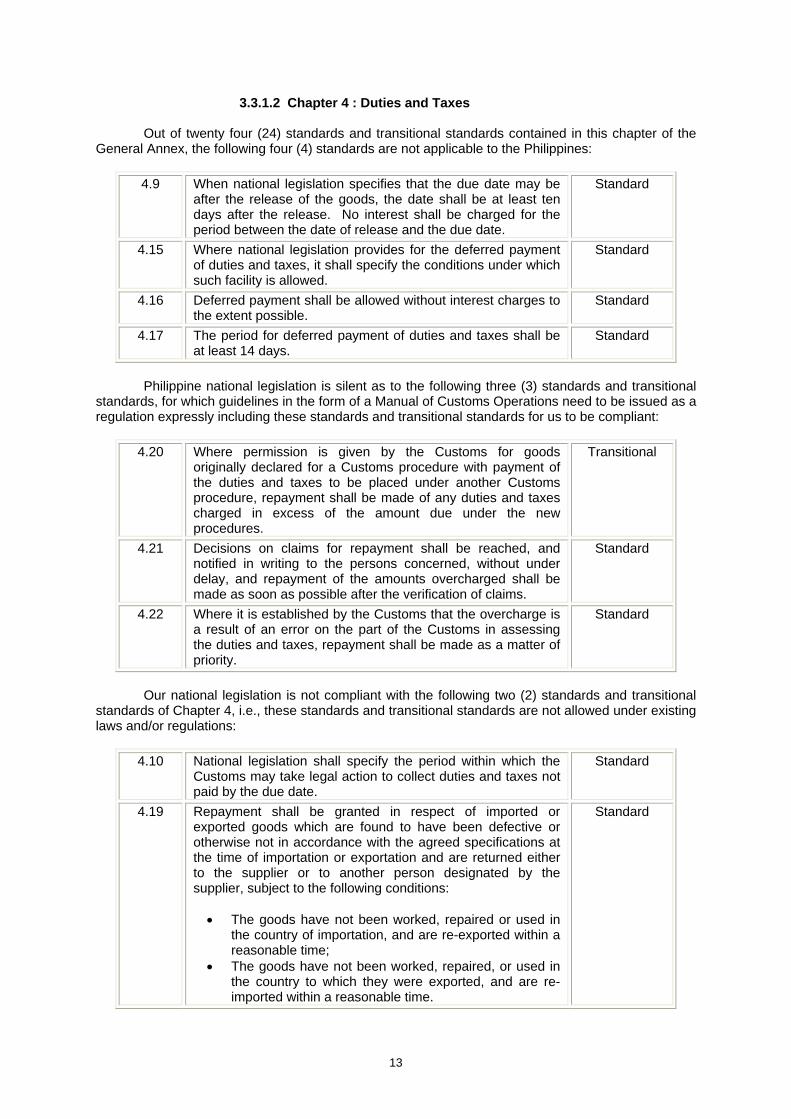

Out of twenty four (24) standards and transitional standards contained in this chapter of the General Annex the following four (4) standards are not applicable to the Philippines

49 When national legislation specifies that the due date may be after the release of the goods the date shall be at least ten days after the release No interest shall be charged for the period between the date of release and the due date

Standard

415 Where national legislation provides for the deferred payment of duties and taxes it shall specify the conditions under which such facility is allowed

Standard

416 Deferred payment shall be allowed without interest charges to the extent possible

Standard

417 The period for deferred payment of duties and taxes shall be at least 14 days

Standard

Philippine national legislation is silent as to the following three (3) standards and transitional

standards for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including these standards and transitional standards for us to be compliant

420 Where permission is given by the Customs for goods originally declared for a Customs procedure with payment of the duties and taxes to be placed under another Customs procedure repayment shall be made of any duties and taxes charged in excess of the amount due under the new procedures

Transitional

421 Decisions on claims for repayment shall be reached and notified in writing to the persons concerned without under delay and repayment of the amounts overcharged shall be made as soon as possible after the verification of claims

Standard

422 Where it is established by the Customs that the overcharge is a result of an error on the part of the Customs in assessing the duties and taxes repayment shall be made as a matter of priority

Standard

Our national legislation is not compliant with the following two (2) standards and transitional

standards of Chapter 4 ie these standards and transitional standards are not allowed under existing laws andor regulations

410 National legislation shall specify the period within which the Customs may take legal action to collect duties and taxes not paid by the due date

Standard

419 Repayment shall be granted in respect of imported or exported goods which are found to have been defective or otherwise not in accordance with the agreed specifications at the time of importation or exportation and are returned either to the supplier or to another person designated by the supplier subject to the following conditions bull The goods have not been worked repaired or used in

the country of importation and are re-exported within a reasonable time

bull The goods have not been worked repaired or used in the country to which they were exported and are re-imported within a reasonable time

Standard

13

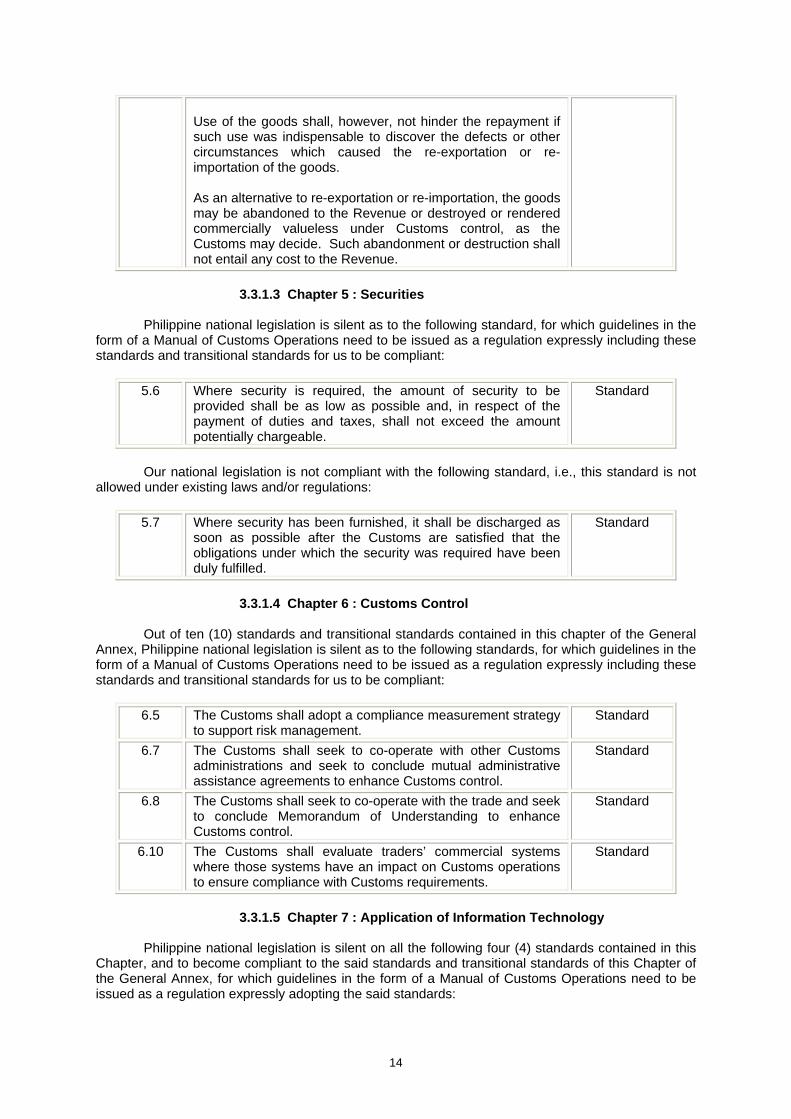

Use of the goods shall however not hinder the repayment if such use was indispensable to discover the defects or other circumstances which caused the re-exportation or re-importation of the goods As an alternative to re-exportation or re-importation the goods may be abandoned to the Revenue or destroyed or rendered commercially valueless under Customs control as the Customs may decide Such abandonment or destruction shall not entail any cost to the Revenue

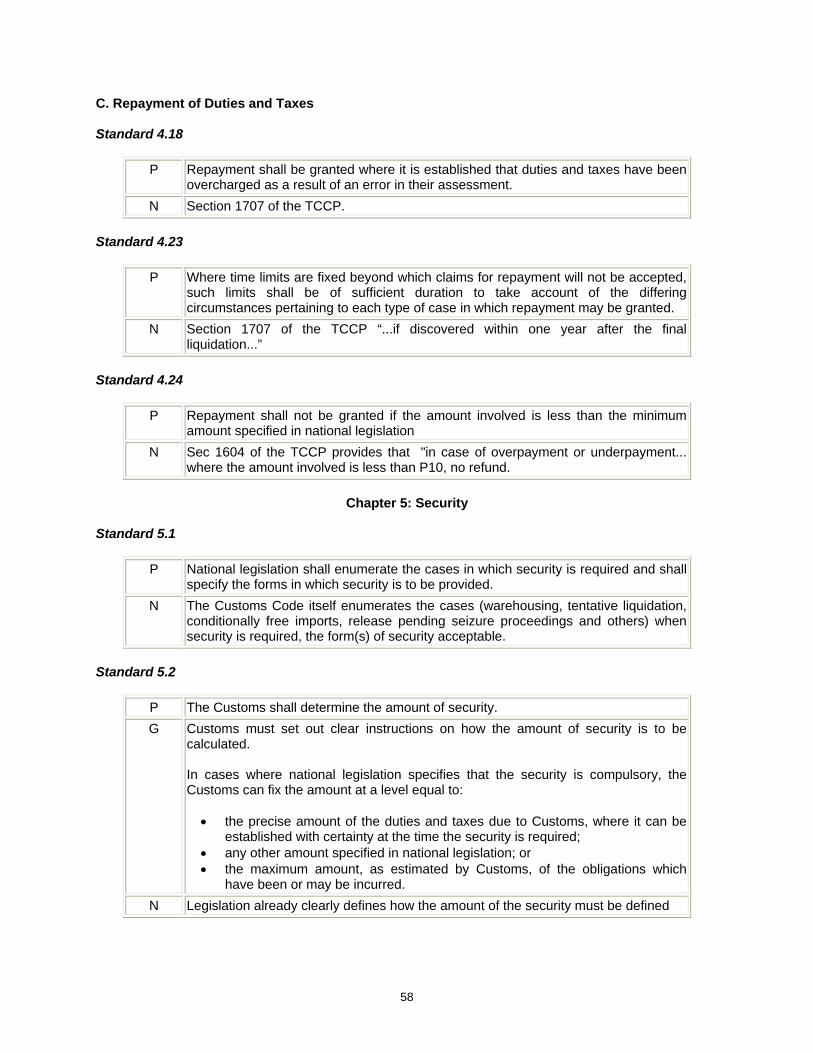

3313 Chapter 5 Securities

Philippine national legislation is silent as to the following standard for which guidelines in the

form of a Manual of Customs Operations need to be issued as a regulation expressly including these standards and transitional standards for us to be compliant

56 Where security is required the amount of security to be provided shall be as low as possible and in respect of the payment of duties and taxes shall not exceed the amount potentially chargeable

Standard

Our national legislation is not compliant with the following standard ie this standard is not

allowed under existing laws andor regulations

57 Where security has been furnished it shall be discharged as soon as possible after the Customs are satisfied that the obligations under which the security was required have been duly fulfilled

Standard

3314 Chapter 6 Customs Control

Out of ten (10) standards and transitional standards contained in this chapter of the General

Annex Philippine national legislation is silent as to the following standards for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including these standards and transitional standards for us to be compliant

65 The Customs shall adopt a compliance measurement strategy to support risk management

Standard

67 The Customs shall seek to co-operate with other Customs administrations and seek to conclude mutual administrative assistance agreements to enhance Customs control

Standard

68 The Customs shall seek to co-operate with the trade and seek to conclude Memorandum of Understanding to enhance Customs control

Standard

610 The Customs shall evaluate tradersrsquo commercial systems where those systems have an impact on Customs operations to ensure compliance with Customs requirements

Standard

3315 Chapter 7 Application of Information Technology

Philippine national legislation is silent on all the following four (4) standards contained in this

Chapter and to become compliant to the said standards and transitional standards of this Chapter of the General Annex for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly adopting the said standards

14

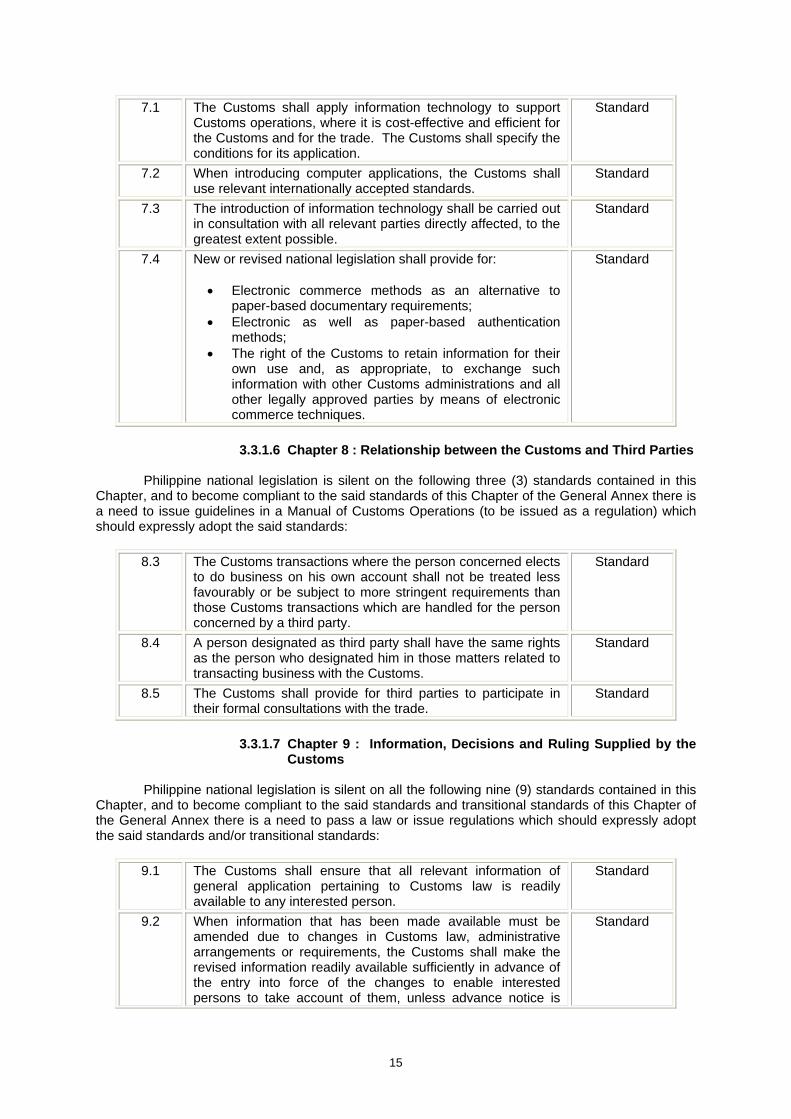

71 The Customs shall apply information technology to support Customs operations where it is cost-effective and efficient for the Customs and for the trade The Customs shall specify the conditions for its application

Standard

72 When introducing computer applications the Customs shall use relevant internationally accepted standards

Standard

73 The introduction of information technology shall be carried out in consultation with all relevant parties directly affected to the greatest extent possible

Standard

74 New or revised national legislation shall provide for bull Electronic commerce methods as an alternative to

paper-based documentary requirements bull Electronic as well as paper-based authentication

methods bull The right of the Customs to retain information for their

own use and as appropriate to exchange such information with other Customs administrations and all other legally approved parties by means of electronic commerce techniques

Standard

3316 Chapter 8 Relationship between the Customs and Third Parties

Philippine national legislation is silent on the following three (3) standards contained in this

Chapter and to become compliant to the said standards of this Chapter of the General Annex there is a need to issue guidelines in a Manual of Customs Operations (to be issued as a regulation) which should expressly adopt the said standards

83 The Customs transactions where the person concerned elects to do business on his own account shall not be treated less favourably or be subject to more stringent requirements than those Customs transactions which are handled for the person concerned by a third party

Standard

84 A person designated as third party shall have the same rights as the person who designated him in those matters related to transacting business with the Customs

Standard

85 The Customs shall provide for third parties to participate in their formal consultations with the trade

Standard

3317 Chapter 9 Information Decisions and Ruling Supplied by the

Customs

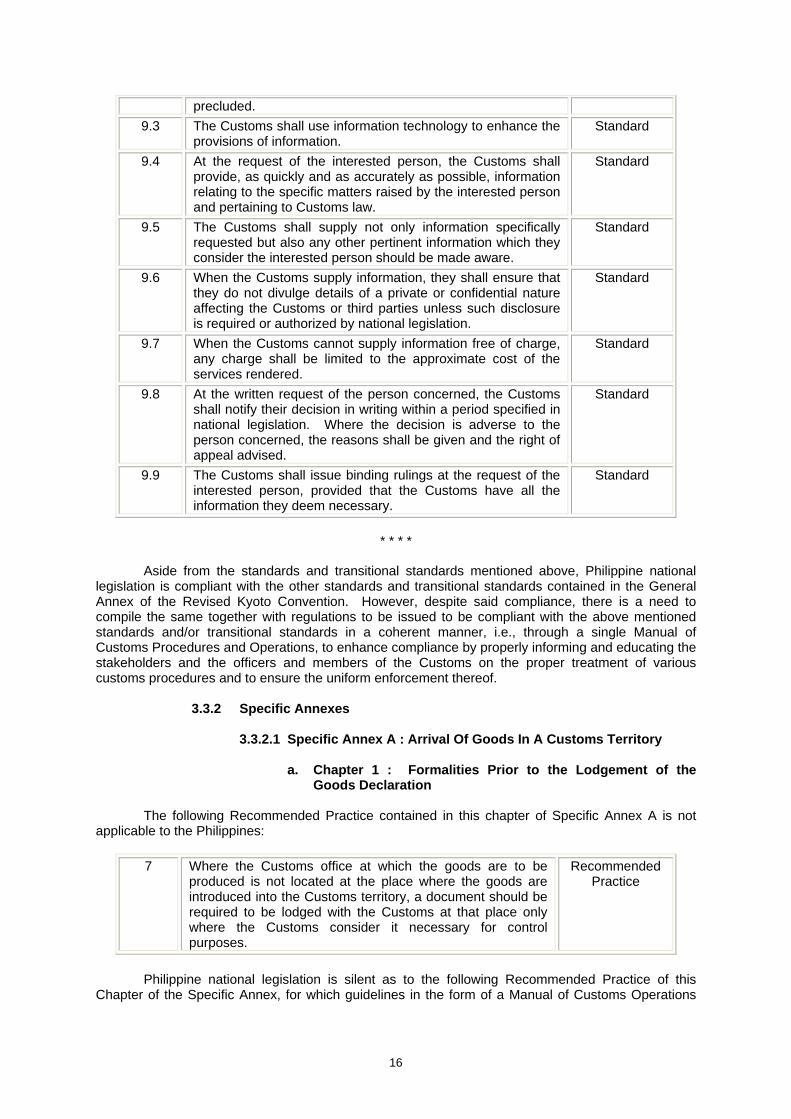

Philippine national legislation is silent on all the following nine (9) standards contained in this Chapter and to become compliant to the said standards and transitional standards of this Chapter of the General Annex there is a need to pass a law or issue regulations which should expressly adopt the said standards andor transitional standards

91 The Customs shall ensure that all relevant information of general application pertaining to Customs law is readily available to any interested person

Standard

92 When information that has been made available must be amended due to changes in Customs law administrative arrangements or requirements the Customs shall make the revised information readily available sufficiently in advance of the entry into force of the changes to enable interested persons to take account of them unless advance notice is

Standard

15

precluded 93 The Customs shall use information technology to enhance the

provisions of information Standard

94 At the request of the interested person the Customs shall

provide as quickly and as accurately as possible information relating to the specific matters raised by the interested person and pertaining to Customs law

Standard

95 The Customs shall supply not only information specifically requested but also any other pertinent information which they consider the interested person should be made aware

Standard

96 When the Customs supply information they shall ensure that they do not divulge details of a private or confidential nature affecting the Customs or third parties unless such disclosure is required or authorized by national legislation

Standard

97 When the Customs cannot supply information free of charge any charge shall be limited to the approximate cost of the services rendered

Standard

98 At the written request of the person concerned the Customs shall notify their decision in writing within a period specified in national legislation Where the decision is adverse to the person concerned the reasons shall be given and the right of appeal advised

Standard

99 The Customs shall issue binding rulings at the request of the interested person provided that the Customs have all the information they deem necessary

Standard

Aside from the standards and transitional standards mentioned above Philippine national legislation is compliant with the other standards and transitional standards contained in the General Annex of the Revised Kyoto Convention However despite said compliance there is a need to compile the same together with regulations to be issued to be compliant with the above mentioned standards andor transitional standards in a coherent manner ie through a single Manual of Customs Procedures and Operations to enhance compliance by properly informing and educating the stakeholders and the officers and members of the Customs on the proper treatment of various customs procedures and to ensure the uniform enforcement thereof

332 Specific Annexes

3321 Specific Annex A Arrival Of Goods In A Customs Territory

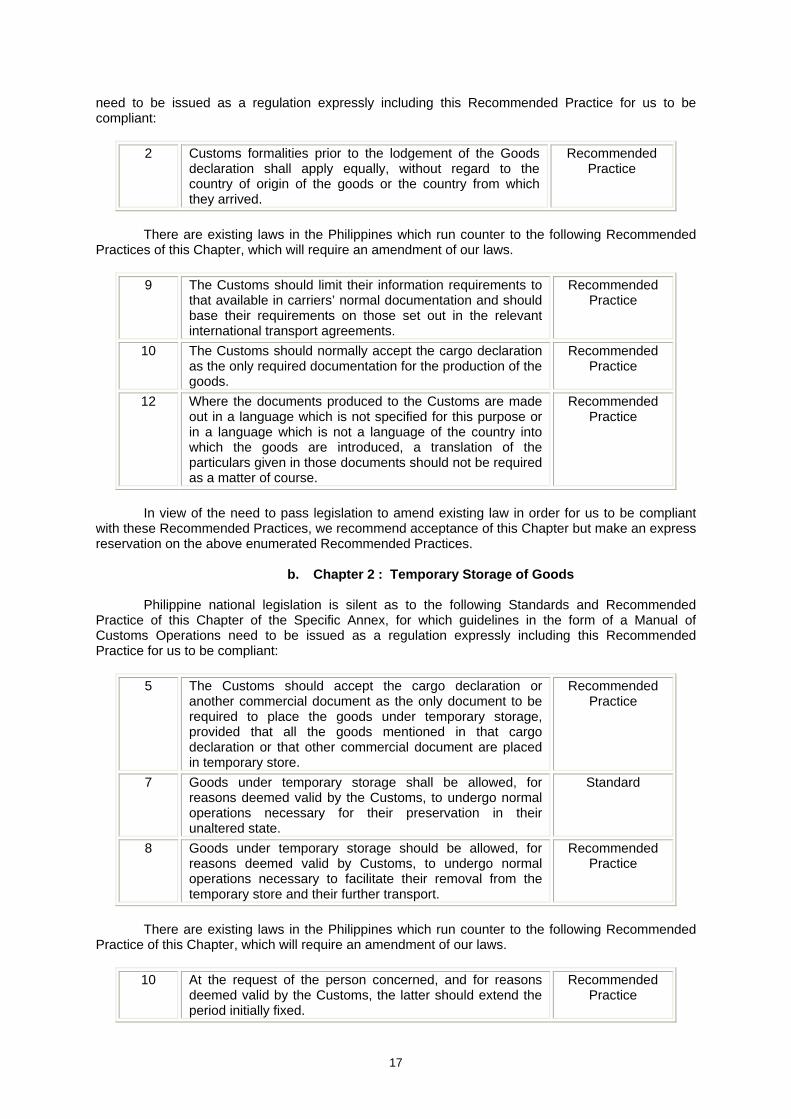

a Chapter 1 Formalities Prior to the Lodgement of the Goods Declaration

The following Recommended Practice contained in this chapter of Specific Annex A is not applicable to the Philippines

7 Where the Customs office at which the goods are to be

produced is not located at the place where the goods are introduced into the Customs territory a document should be required to be lodged with the Customs at that place only where the Customs consider it necessary for control purposes

Recommended Practice

Philippine national legislation is silent as to the following Recommended Practice of this

Chapter of the Specific Annex for which guidelines in the form of a Manual of Customs Operations

16

need to be issued as a regulation expressly including this Recommended Practice for us to be compliant

2 Customs formalities prior to the lodgement of the Goods

declaration shall apply equally without regard to the country of origin of the goods or the country from which they arrived

Recommended Practice

There are existing laws in the Philippines which run counter to the following Recommended

Practices of this Chapter which will require an amendment of our laws 9 The Customs should limit their information requirements to

that available in carriersrsquo normal documentation and should base their requirements on those set out in the relevant international transport agreements

Recommended Practice

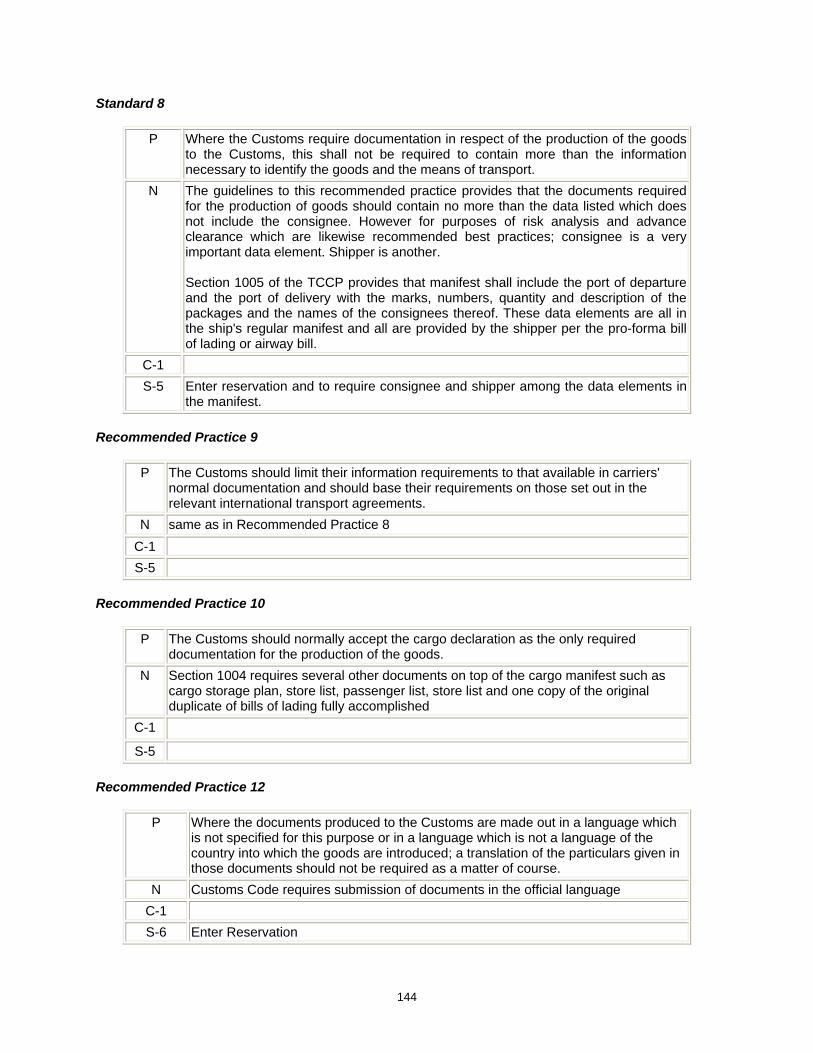

10 The Customs should normally accept the cargo declaration as the only required documentation for the production of the goods

Recommended Practice

12 Where the documents produced to the Customs are made out in a language which is not specified for this purpose or in a language which is not a language of the country into which the goods are introduced a translation of the particulars given in those documents should not be required as a matter of course

Recommended Practice

In view of the need to pass legislation to amend existing law in order for us to be compliant

with these Recommended Practices we recommend acceptance of this Chapter but make an express reservation on the above enumerated Recommended Practices

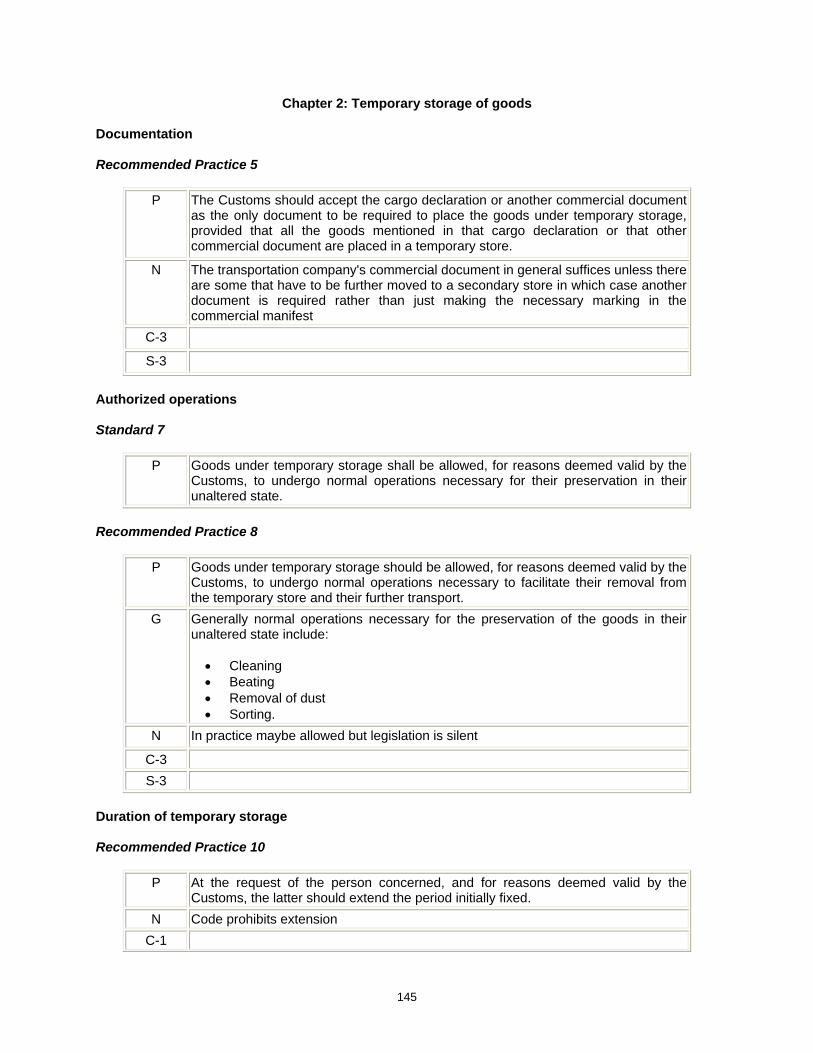

b Chapter 2 Temporary Storage of Goods

Philippine national legislation is silent as to the following Standards and Recommended

Practice of this Chapter of the Specific Annex for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including this Recommended Practice for us to be compliant

5 The Customs should accept the cargo declaration or

another commercial document as the only document to be required to place the goods under temporary storage provided that all the goods mentioned in that cargo declaration or that other commercial document are placed in temporary store

Recommended Practice

7 Goods under temporary storage shall be allowed for reasons deemed valid by the Customs to undergo normal operations necessary for their preservation in their unaltered state

Standard

8 Goods under temporary storage should be allowed for reasons deemed valid by Customs to undergo normal operations necessary to facilitate their removal from the temporary store and their further transport

Recommended Practice

There are existing laws in the Philippines which run counter to the following Recommended

Practice of this Chapter which will require an amendment of our laws 10 At the request of the person concerned and for reasons

deemed valid by the Customs the latter should extend the period initially fixed

Recommended Practice

17

In view of our non-compliance with the above Recommended Practice which will require an

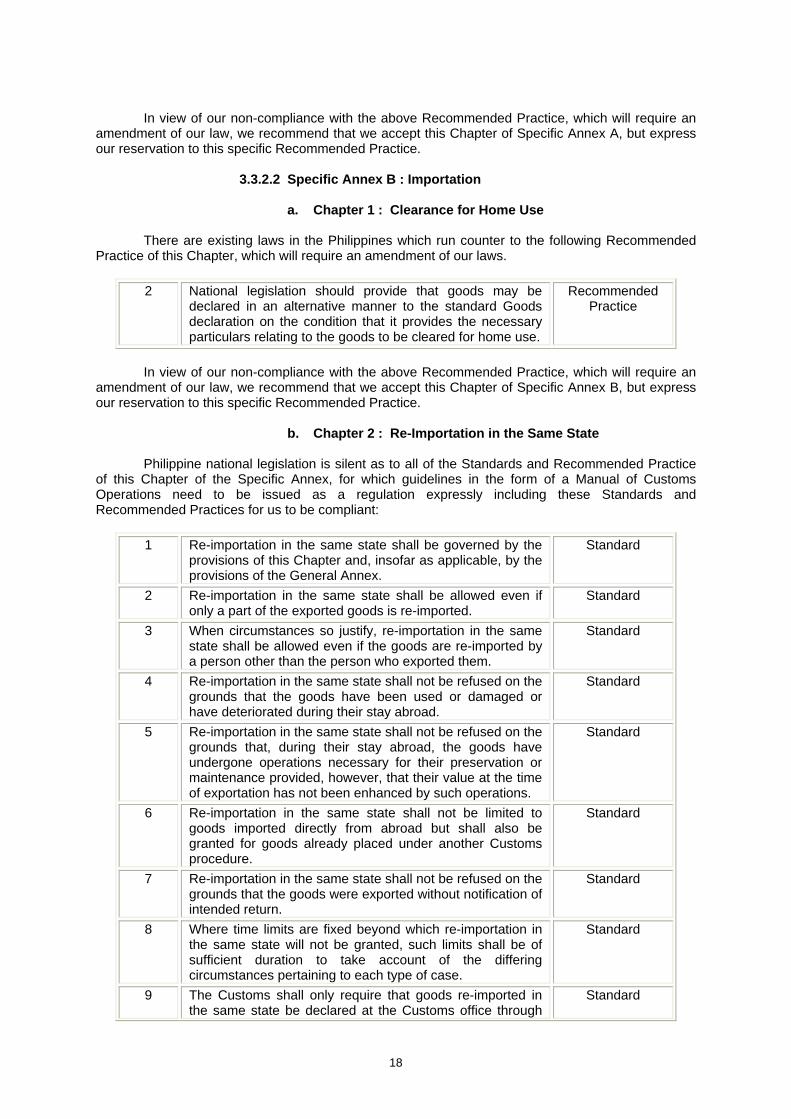

amendment of our law we recommend that we accept this Chapter of Specific Annex A but express our reservation to this specific Recommended Practice

3322 Specific Annex B Importation

a Chapter 1 Clearance for Home Use

There are existing laws in the Philippines which run counter to the following Recommended Practice of this Chapter which will require an amendment of our laws

2 National legislation should provide that goods may be

declared in an alternative manner to the standard Goods declaration on the condition that it provides the necessary particulars relating to the goods to be cleared for home use

Recommended Practice

In view of our non-compliance with the above Recommended Practice which will require an

amendment of our law we recommend that we accept this Chapter of Specific Annex B but express our reservation to this specific Recommended Practice

b Chapter 2 Re-Importation in the Same State Philippine national legislation is silent as to all of the Standards and Recommended Practice

of this Chapter of the Specific Annex for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including these Standards and Recommended Practices for us to be compliant

1 Re-importation in the same state shall be governed by the

provisions of this Chapter and insofar as applicable by the provisions of the General Annex

Standard

2 Re-importation in the same state shall be allowed even if only a part of the exported goods is re-imported

Standard

3 When circumstances so justify re-importation in the same state shall be allowed even if the goods are re-imported by a person other than the person who exported them

Standard

4 Re-importation in the same state shall not be refused on the grounds that the goods have been used or damaged or have deteriorated during their stay abroad

Standard

5 Re-importation in the same state shall not be refused on the grounds that during their stay abroad the goods have undergone operations necessary for their preservation or maintenance provided however that their value at the time of exportation has not been enhanced by such operations

Standard

6 Re-importation in the same state shall not be limited to goods imported directly from abroad but shall also be granted for goods already placed under another Customs procedure

Standard

7 Re-importation in the same state shall not be refused on the grounds that the goods were exported without notification of intended return

Standard

8 Where time limits are fixed beyond which re-importation in the same state will not be granted such limits shall be of sufficient duration to take account of the differing circumstances pertaining to each type of case

Standard

9 The Customs shall only require that goods re-imported in the same state be declared at the Customs office through

Standard

18

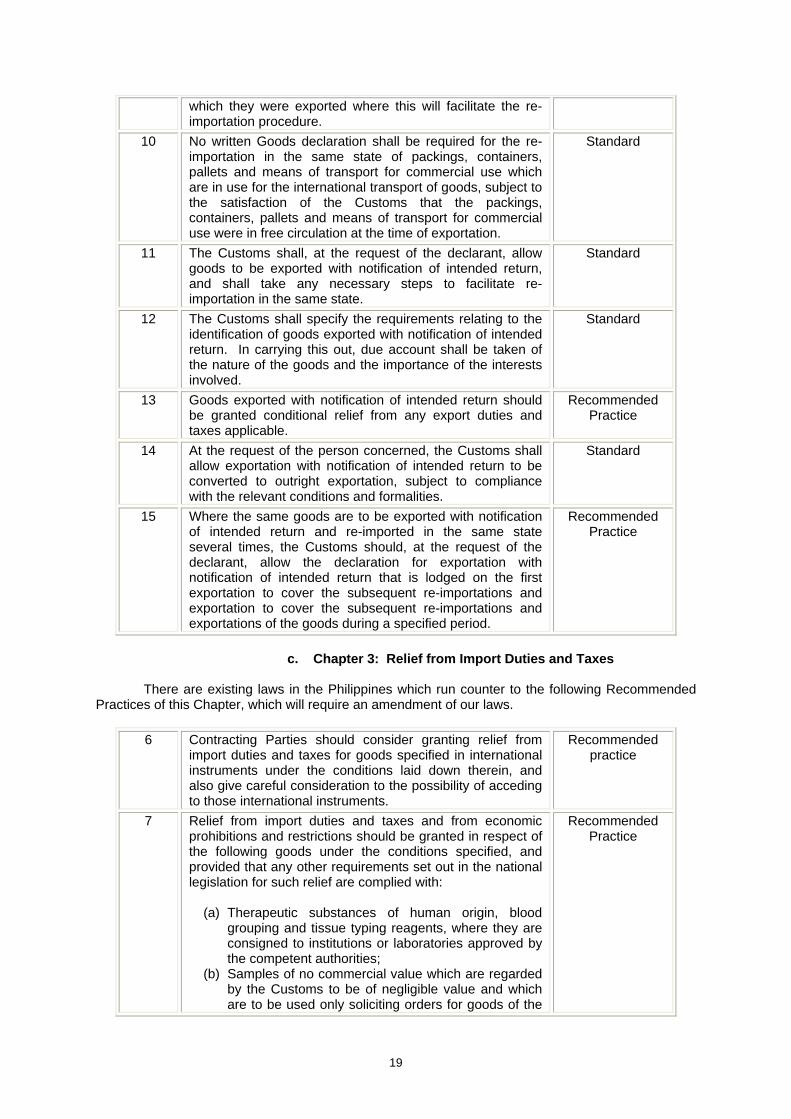

which they were exported where this will facilitate the re-importation procedure

10 No written Goods declaration shall be required for the re-importation in the same state of packings containers pallets and means of transport for commercial use which are in use for the international transport of goods subject to the satisfaction of the Customs that the packings containers pallets and means of transport for commercial use were in free circulation at the time of exportation

Standard

11 The Customs shall at the request of the declarant allow goods to be exported with notification of intended return and shall take any necessary steps to facilitate re-importation in the same state

Standard

12 The Customs shall specify the requirements relating to the identification of goods exported with notification of intended return In carrying this out due account shall be taken of the nature of the goods and the importance of the interests involved

Standard

13 Goods exported with notification of intended return should be granted conditional relief from any export duties and taxes applicable

Recommended Practice

14 At the request of the person concerned the Customs shall allow exportation with notification of intended return to be converted to outright exportation subject to compliance with the relevant conditions and formalities

Standard

15 Where the same goods are to be exported with notification of intended return and re-imported in the same state several times the Customs should at the request of the declarant allow the declaration for exportation with notification of intended return that is lodged on the first exportation to cover the subsequent re-importations and exportation to cover the subsequent re-importations and exportations of the goods during a specified period

Recommended Practice

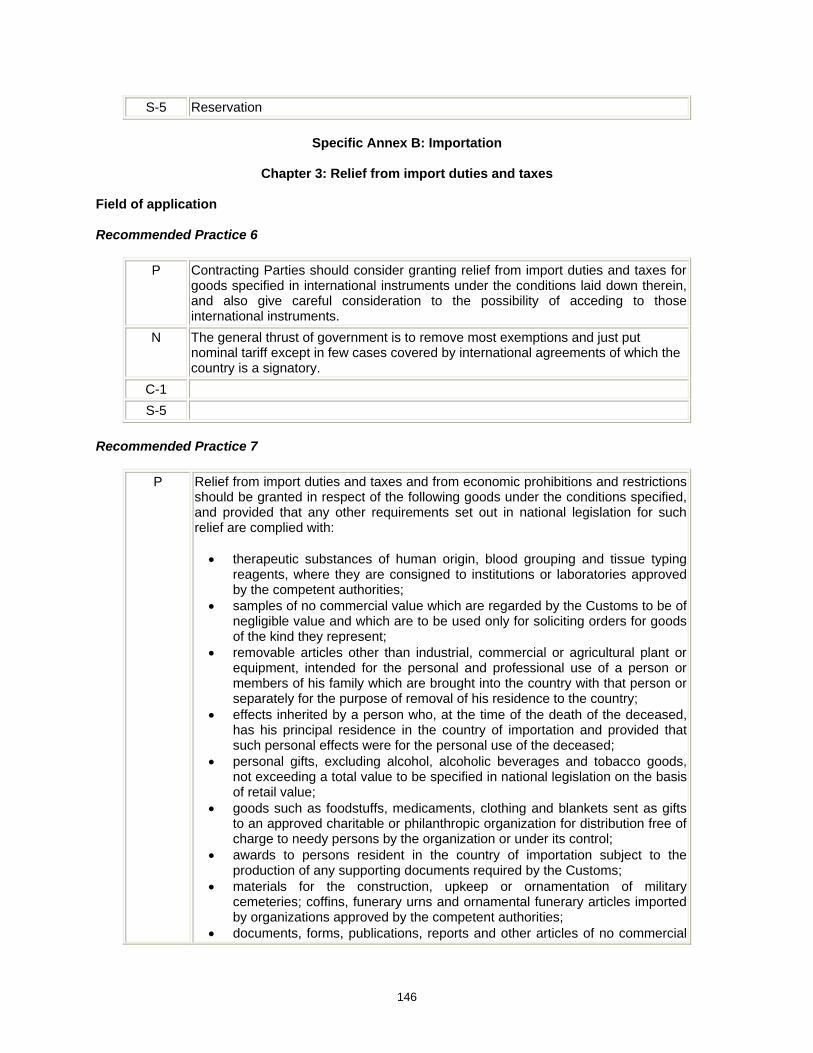

c Chapter 3 Relief from Import Duties and Taxes

There are existing laws in the Philippines which run counter to the following Recommended

Practices of this Chapter which will require an amendment of our laws 6 Contracting Parties should consider granting relief from

import duties and taxes for goods specified in international instruments under the conditions laid down therein and also give careful consideration to the possibility of acceding to those international instruments

Recommended practice

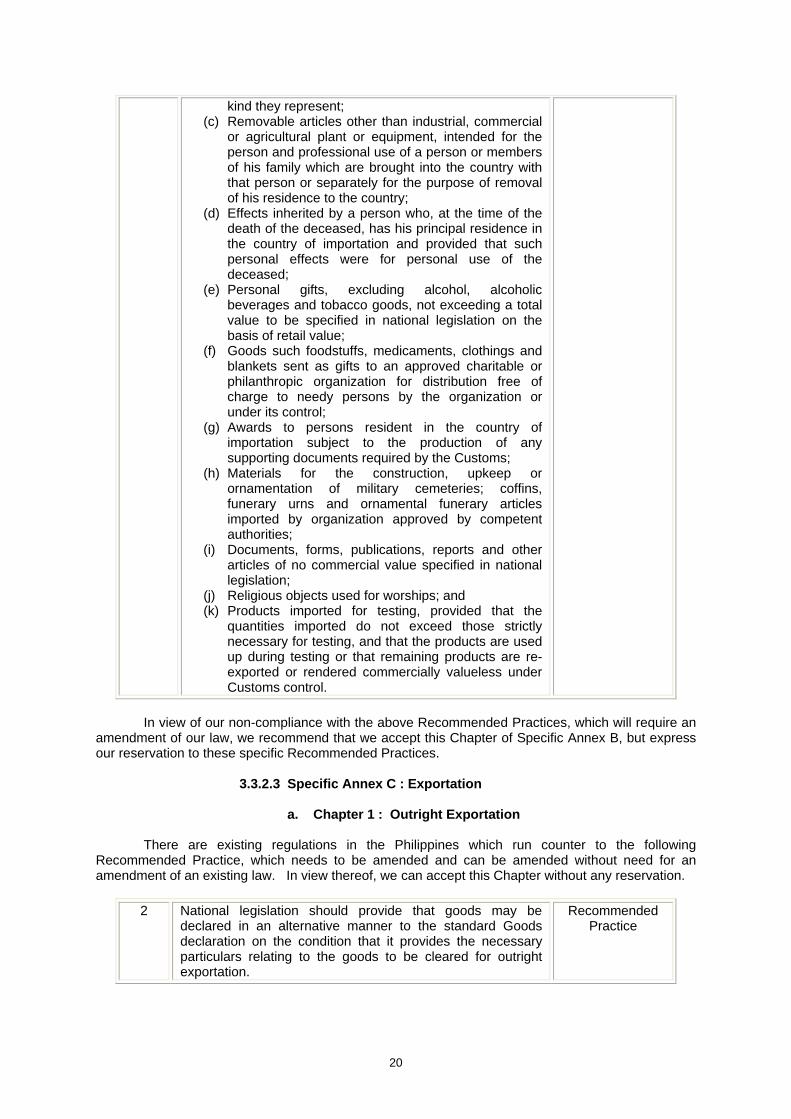

7 Relief from import duties and taxes and from economic prohibitions and restrictions should be granted in respect of the following goods under the conditions specified and provided that any other requirements set out in the national legislation for such relief are complied with

(a) Therapeutic substances of human origin blood grouping and tissue typing reagents where they are consigned to institutions or laboratories approved by the competent authorities

(b) Samples of no commercial value which are regarded by the Customs to be of negligible value and which are to be used only soliciting orders for goods of the

Recommended Practice

19

kind they represent (c) Removable articles other than industrial commercial

or agricultural plant or equipment intended for the person and professional use of a person or members of his family which are brought into the country with that person or separately for the purpose of removal of his residence to the country

(d) Effects inherited by a person who at the time of the death of the deceased has his principal residence in the country of importation and provided that such personal effects were for personal use of the deceased

(e) Personal gifts excluding alcohol alcoholic beverages and tobacco goods not exceeding a total value to be specified in national legislation on the basis of retail value

(f) Goods such foodstuffs medicaments clothings and blankets sent as gifts to an approved charitable or philanthropic organization for distribution free of charge to needy persons by the organization or under its control

(g) Awards to persons resident in the country of importation subject to the production of any supporting documents required by the Customs

(h) Materials for the construction upkeep or ornamentation of military cemeteries coffins funerary urns and ornamental funerary articles imported by organization approved by competent authorities

(i) Documents forms publications reports and other articles of no commercial value specified in national legislation

(j) Religious objects used for worships and (k) Products imported for testing provided that the

quantities imported do not exceed those strictly necessary for testing and that the products are used up during testing or that remaining products are re-exported or rendered commercially valueless under Customs control

In view of our non-compliance with the above Recommended Practices which will require an

amendment of our law we recommend that we accept this Chapter of Specific Annex B but express our reservation to these specific Recommended Practices

3323 Specific Annex C Exportation

a Chapter 1 Outright Exportation

There are existing regulations in the Philippines which run counter to the following Recommended Practice which needs to be amended and can be amended without need for an amendment of an existing law In view thereof we can accept this Chapter without any reservation

2 National legislation should provide that goods may be

declared in an alternative manner to the standard Goods declaration on the condition that it provides the necessary particulars relating to the goods to be cleared for outright exportation

Recommended Practice

20

3324 Specific Annex D Customs Warehouses and Free Zones

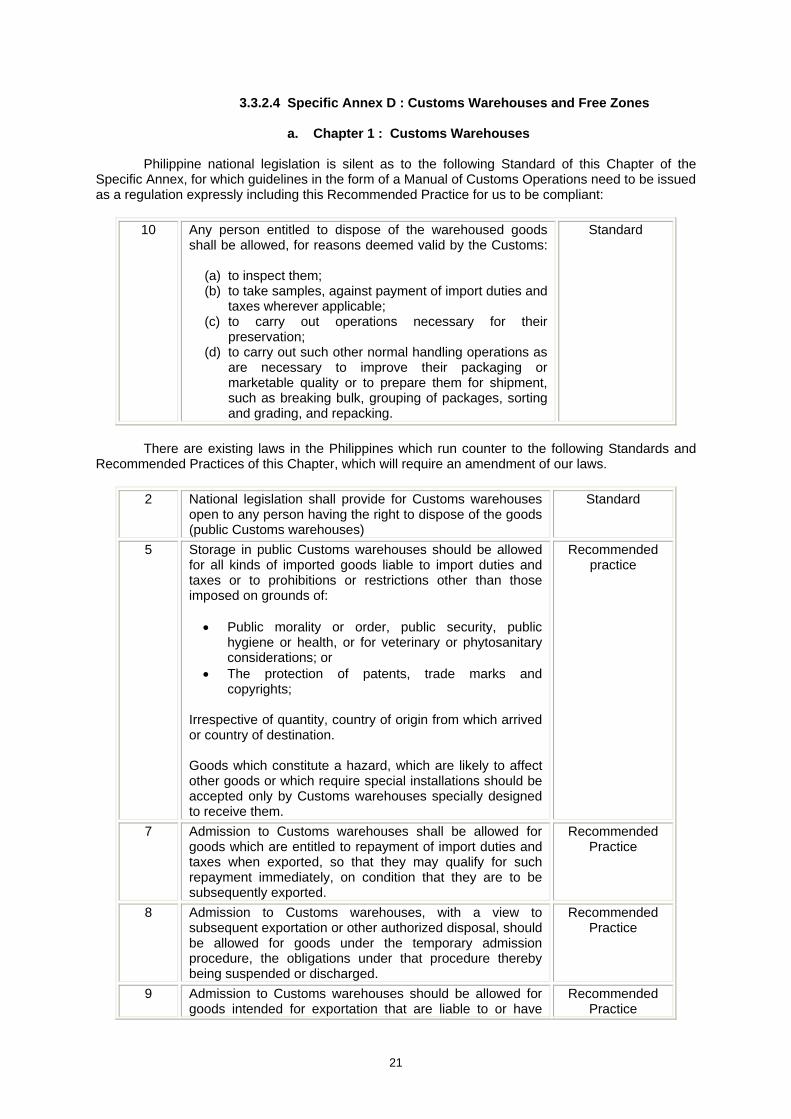

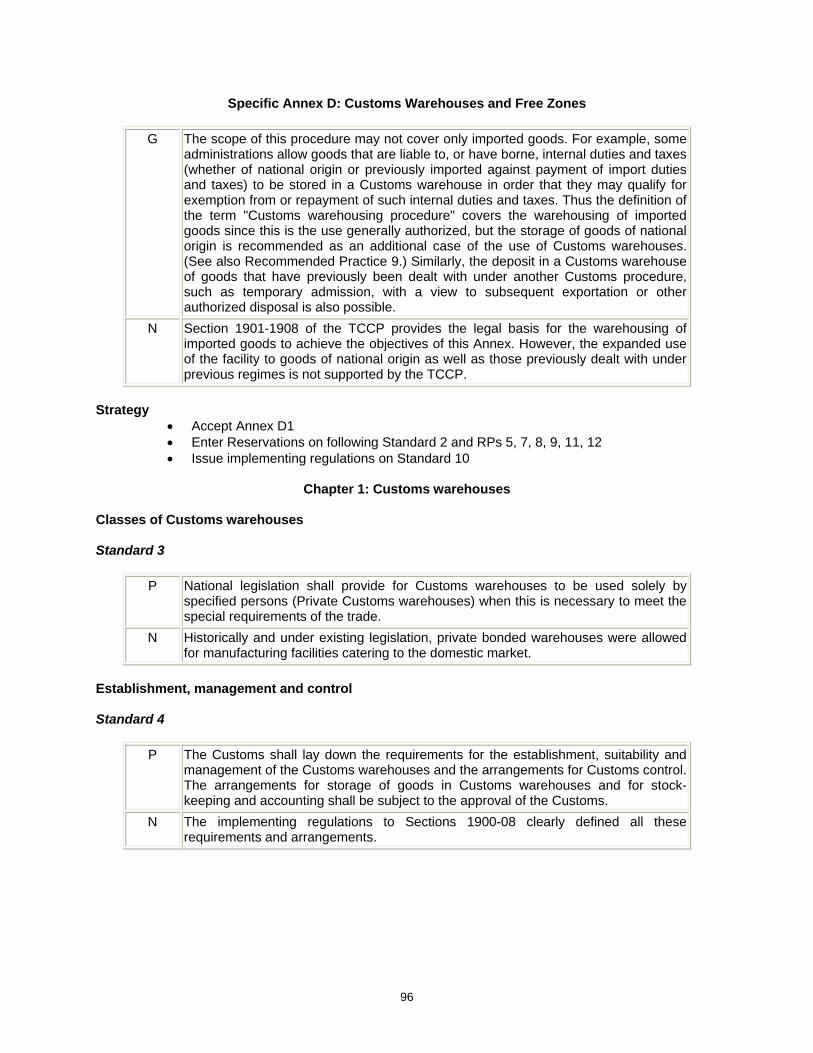

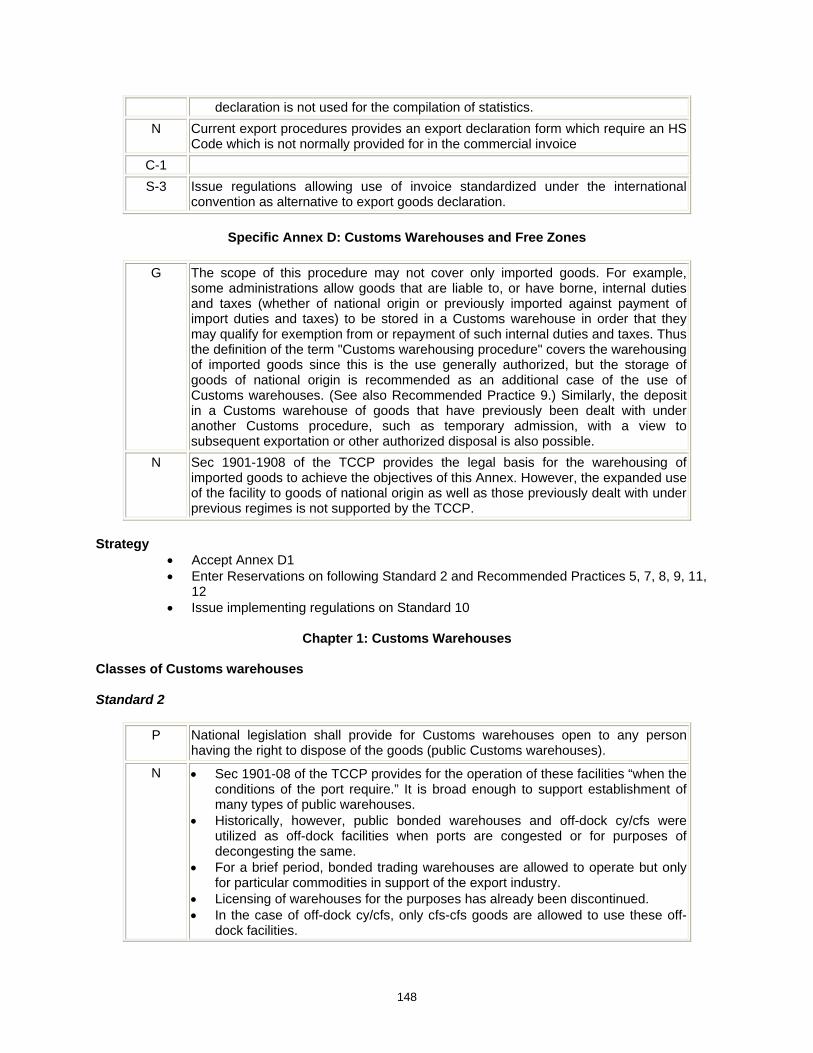

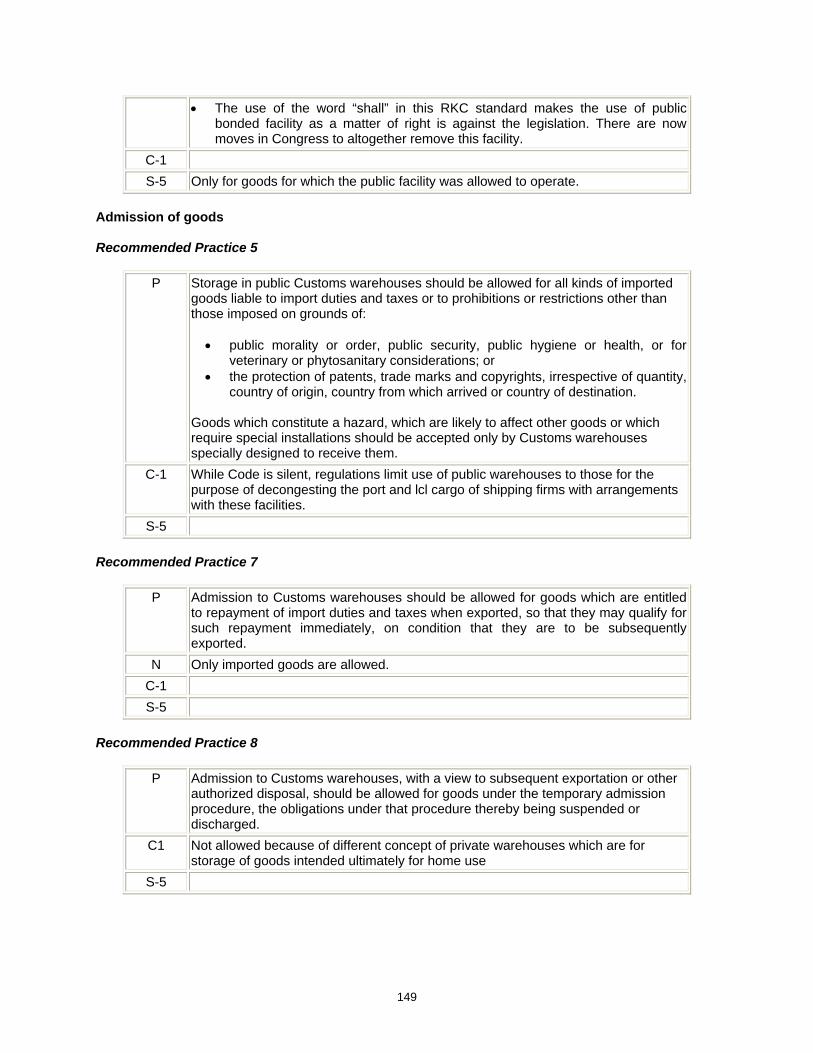

a Chapter 1 Customs Warehouses

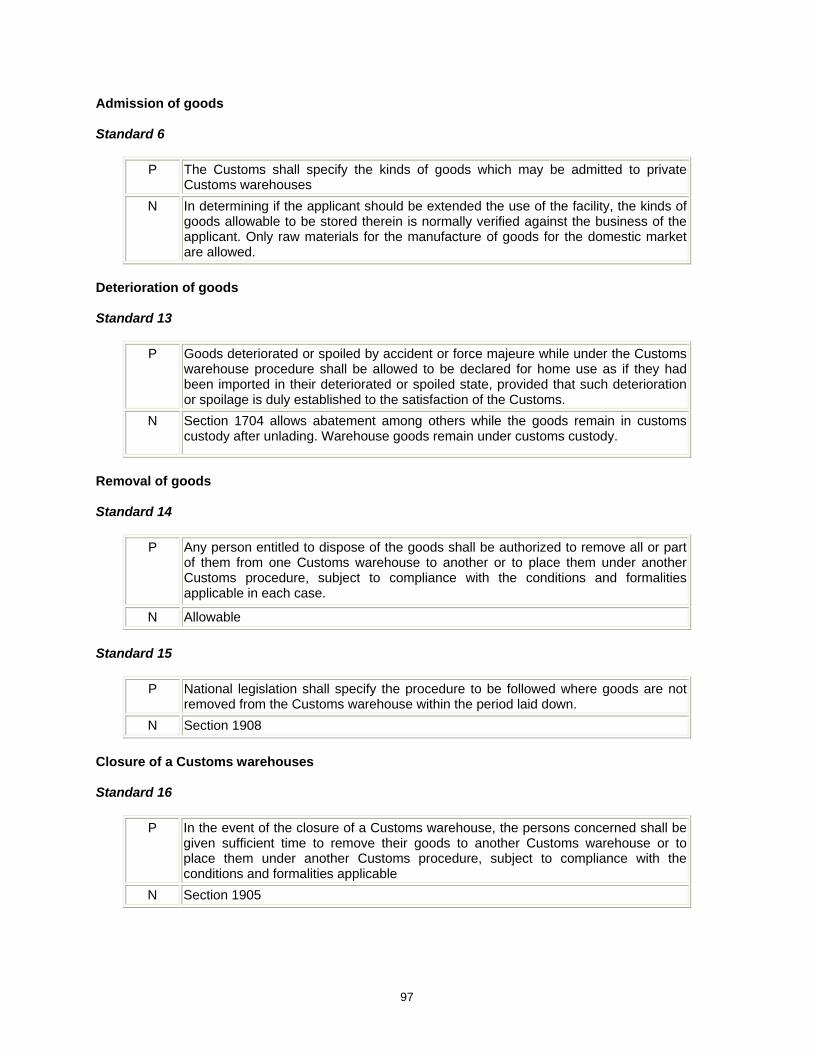

Philippine national legislation is silent as to the following Standard of this Chapter of the Specific Annex for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including this Recommended Practice for us to be compliant

10 Any person entitled to dispose of the warehoused goods

shall be allowed for reasons deemed valid by the Customs

(a) to inspect them (b) to take samples against payment of import duties and

taxes wherever applicable (c) to carry out operations necessary for their

preservation (d) to carry out such other normal handling operations as

are necessary to improve their packaging or marketable quality or to prepare them for shipment such as breaking bulk grouping of packages sorting and grading and repacking

Standard

There are existing laws in the Philippines which run counter to the following Standards and

Recommended Practices of this Chapter which will require an amendment of our laws 2 National legislation shall provide for Customs warehouses

open to any person having the right to dispose of the goods (public Customs warehouses)

Standard

5 Storage in public Customs warehouses should be allowed for all kinds of imported goods liable to import duties and taxes or to prohibitions or restrictions other than those imposed on grounds of bull Public morality or order public security public

hygiene or health or for veterinary or phytosanitary considerations or

bull The protection of patents trade marks and copyrights

Irrespective of quantity country of origin from which arrived or country of destination Goods which constitute a hazard which are likely to affect other goods or which require special installations should be accepted only by Customs warehouses specially designed to receive them

Recommended practice

7 Admission to Customs warehouses shall be allowed for goods which are entitled to repayment of import duties and taxes when exported so that they may qualify for such repayment immediately on condition that they are to be subsequently exported

Recommended Practice

8 Admission to Customs warehouses with a view to subsequent exportation or other authorized disposal should be allowed for goods under the temporary admission procedure the obligations under that procedure thereby being suspended or discharged

Recommended Practice

9 Admission to Customs warehouses should be allowed for goods intended for exportation that are liable to or have

Recommended Practice

21

borne internal duties or taxes in order that they may qualify for exemption from or repayment of such internal duties and taxes on condition that they are to be subsequently exported

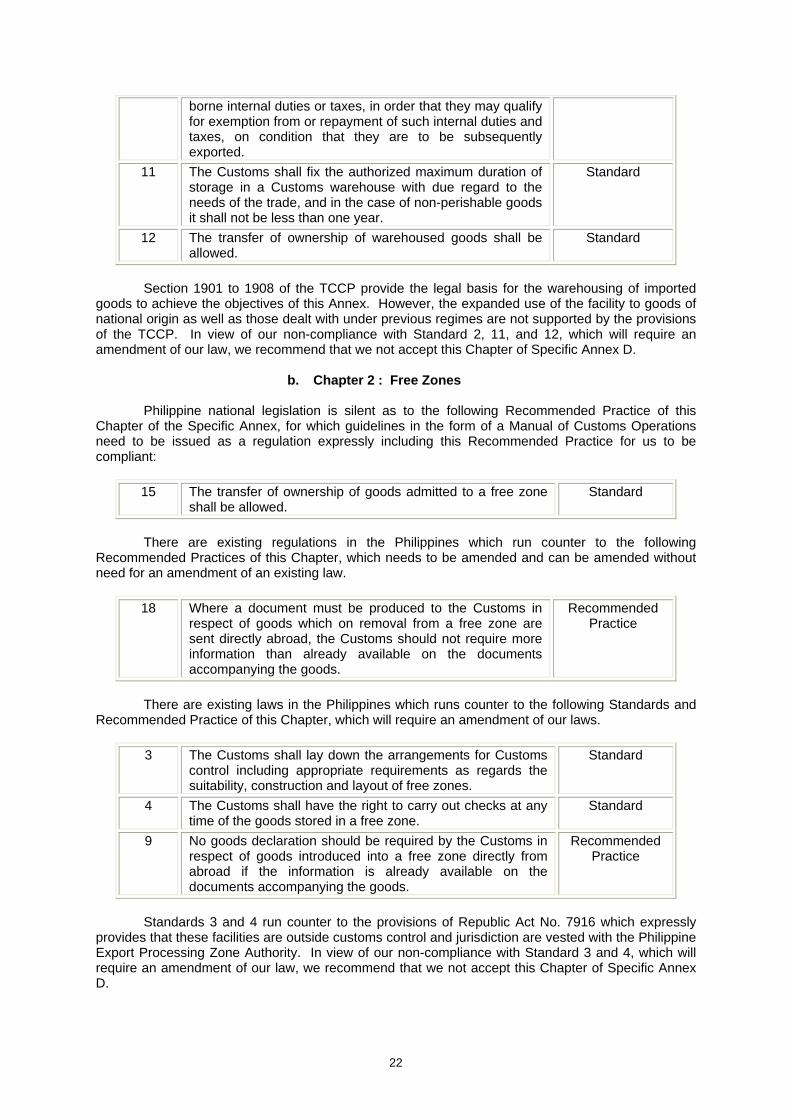

11 The Customs shall fix the authorized maximum duration of storage in a Customs warehouse with due regard to the needs of the trade and in the case of non-perishable goods it shall not be less than one year

Standard

12 The transfer of ownership of warehoused goods shall be allowed

Standard

Section 1901 to 1908 of the TCCP provide the legal basis for the warehousing of imported

goods to achieve the objectives of this Annex However the expanded use of the facility to goods of national origin as well as those dealt with under previous regimes are not supported by the provisions of the TCCP In view of our non-compliance with Standard 2 11 and 12 which will require an amendment of our law we recommend that we not accept this Chapter of Specific Annex D

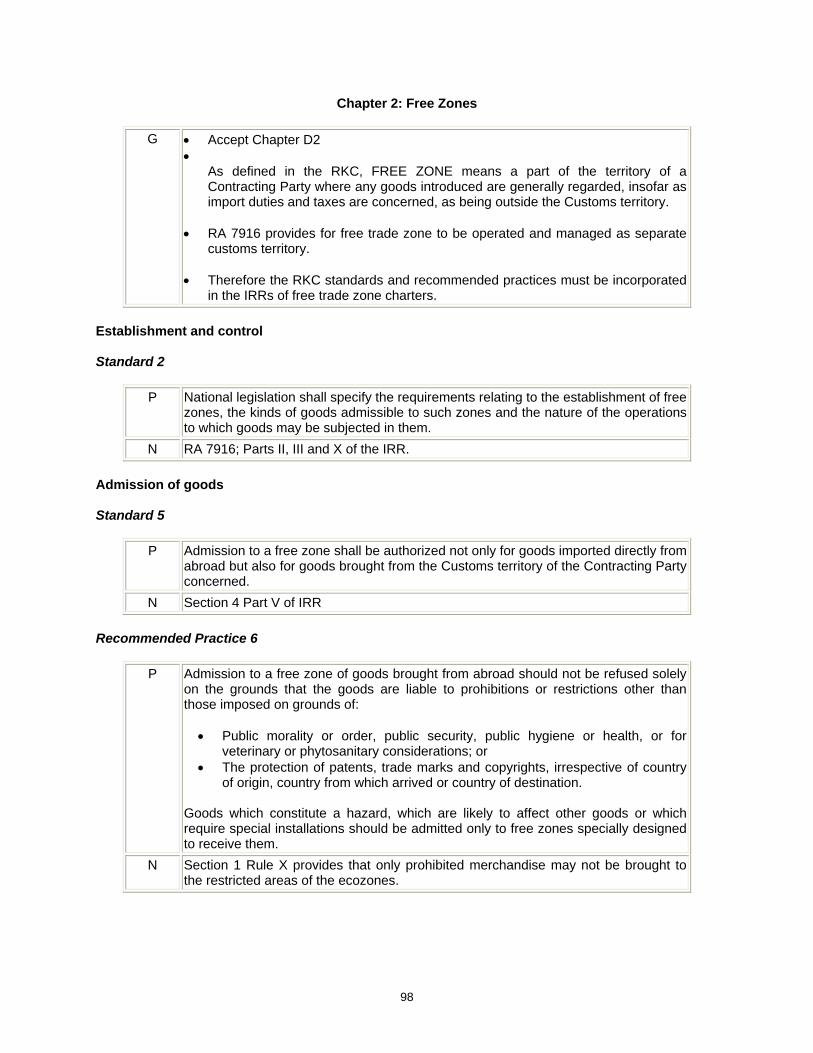

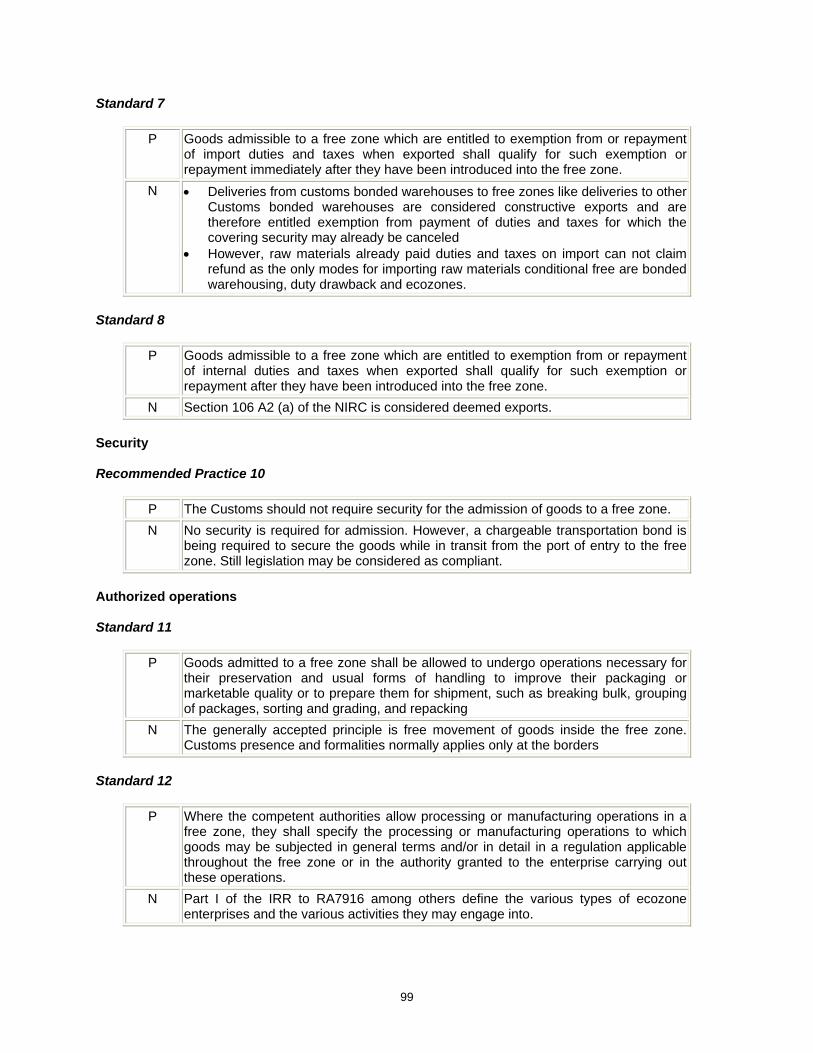

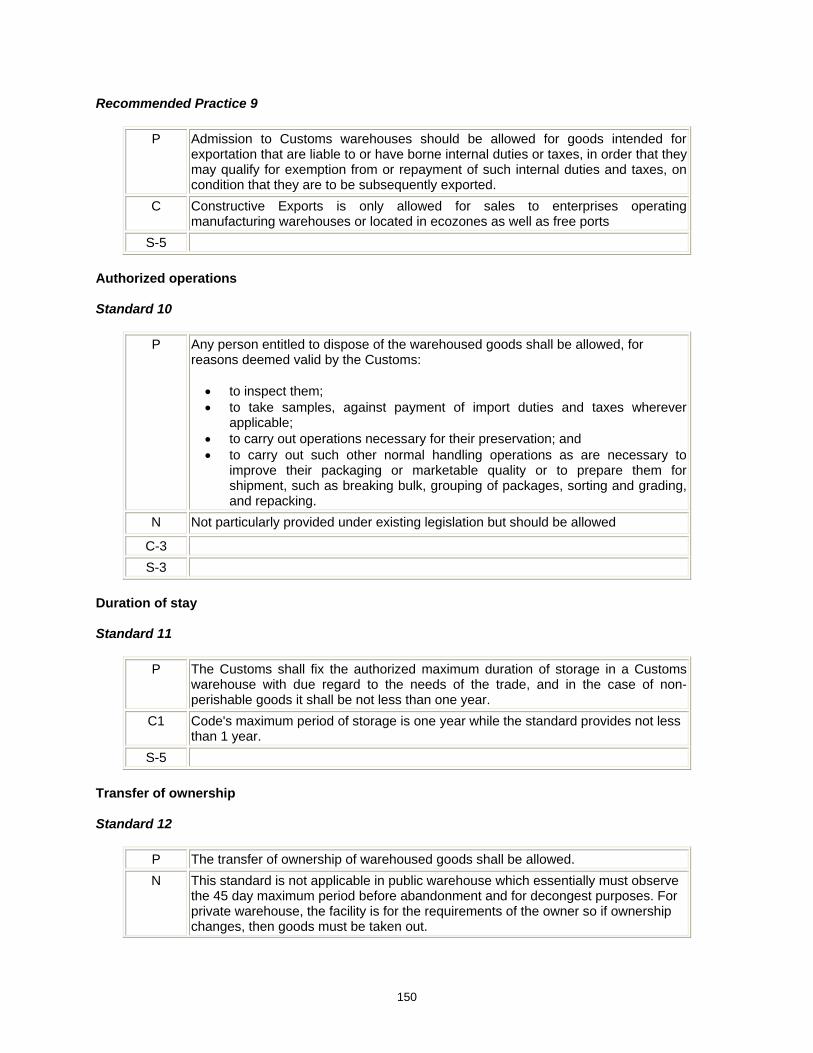

b Chapter 2 Free Zones

Philippine national legislation is silent as to the following Recommended Practice of this

Chapter of the Specific Annex for which guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including this Recommended Practice for us to be compliant

15 The transfer of ownership of goods admitted to a free zone

shall be allowed Standard

There are existing regulations in the Philippines which run counter to the following

Recommended Practices of this Chapter which needs to be amended and can be amended without need for an amendment of an existing law

18 Where a document must be produced to the Customs in

respect of goods which on removal from a free zone are sent directly abroad the Customs should not require more information than already available on the documents accompanying the goods

Recommended Practice

There are existing laws in the Philippines which runs counter to the following Standards and

Recommended Practice of this Chapter which will require an amendment of our laws 3 The Customs shall lay down the arrangements for Customs

control including appropriate requirements as regards the suitability construction and layout of free zones

Standard

4 The Customs shall have the right to carry out checks at any time of the goods stored in a free zone

Standard

9 No goods declaration should be required by the Customs in respect of goods introduced into a free zone directly from abroad if the information is already available on the documents accompanying the goods

Recommended Practice

Standards 3 and 4 run counter to the provisions of Republic Act No 7916 which expressly

provides that these facilities are outside customs control and jurisdiction are vested with the Philippine Export Processing Zone Authority In view of our non-compliance with Standard 3 and 4 which will require an amendment of our law we recommend that we not accept this Chapter of Specific Annex D

22

3325 Specific Annex E Transit

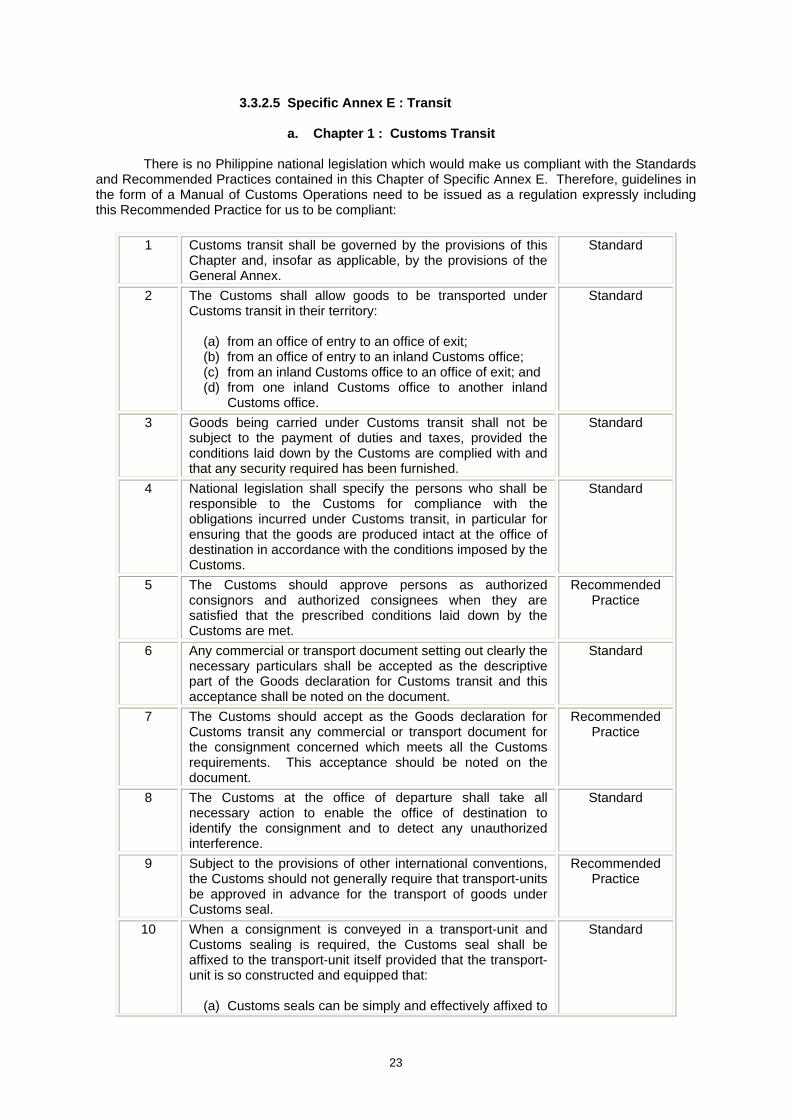

a Chapter 1 Customs Transit

There is no Philippine national legislation which would make us compliant with the Standards and Recommended Practices contained in this Chapter of Specific Annex E Therefore guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including this Recommended Practice for us to be compliant

1 Customs transit shall be governed by the provisions of this Chapter and insofar as applicable by the provisions of the General Annex

Standard

2 The Customs shall allow goods to be transported under Customs transit in their territory

(a) from an office of entry to an office of exit (b) from an office of entry to an inland Customs office (c) from an inland Customs office to an office of exit and (d) from one inland Customs office to another inland

Customs office

Standard

3 Goods being carried under Customs transit shall not be subject to the payment of duties and taxes provided the conditions laid down by the Customs are complied with and that any security required has been furnished

Standard

4 National legislation shall specify the persons who shall be responsible to the Customs for compliance with the obligations incurred under Customs transit in particular for ensuring that the goods are produced intact at the office of destination in accordance with the conditions imposed by the Customs

Standard

5 The Customs should approve persons as authorized consignors and authorized consignees when they are satisfied that the prescribed conditions laid down by the Customs are met

Recommended Practice

6 Any commercial or transport document setting out clearly the necessary particulars shall be accepted as the descriptive part of the Goods declaration for Customs transit and this acceptance shall be noted on the document

Standard

7 The Customs should accept as the Goods declaration for Customs transit any commercial or transport document for the consignment concerned which meets all the Customs requirements This acceptance should be noted on the document

Recommended Practice

8 The Customs at the office of departure shall take all necessary action to enable the office of destination to identify the consignment and to detect any unauthorized interference

Standard

9 Subject to the provisions of other international conventions the Customs should not generally require that transport-units be approved in advance for the transport of goods under Customs seal

Recommended Practice

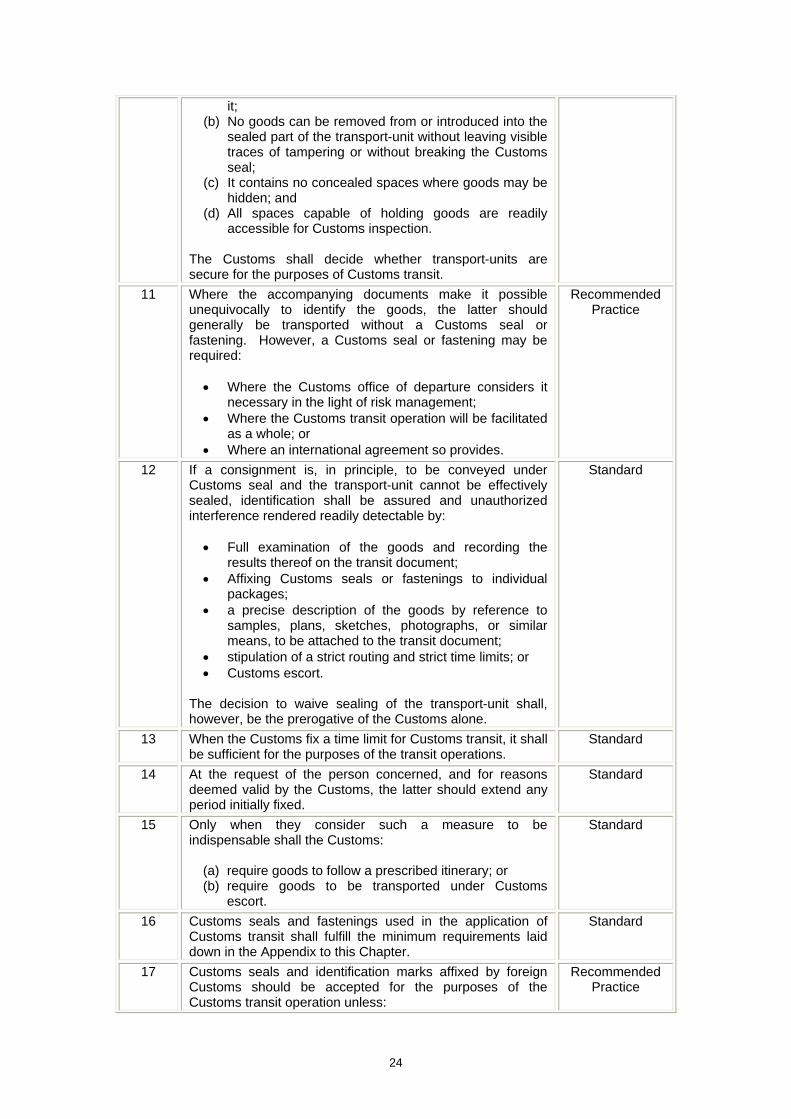

10 When a consignment is conveyed in a transport-unit and Customs sealing is required the Customs seal shall be affixed to the transport-unit itself provided that the transport-unit is so constructed and equipped that

(a) Customs seals can be simply and effectively affixed to

Standard

23

it (b) No goods can be removed from or introduced into the

sealed part of the transport-unit without leaving visible traces of tampering or without breaking the Customs seal

(c) It contains no concealed spaces where goods may be hidden and

(d) All spaces capable of holding goods are readily accessible for Customs inspection

The Customs shall decide whether transport-units are secure for the purposes of Customs transit

11 Where the accompanying documents make it possible unequivocally to identify the goods the latter should generally be transported without a Customs seal or fastening However a Customs seal or fastening may be required bull Where the Customs office of departure considers it

necessary in the light of risk management bull Where the Customs transit operation will be facilitated

as a whole or bull Where an international agreement so provides

Recommended Practice

12 If a consignment is in principle to be conveyed under Customs seal and the transport-unit cannot be effectively sealed identification shall be assured and unauthorized interference rendered readily detectable by bull Full examination of the goods and recording the

results thereof on the transit document bull Affixing Customs seals or fastenings to individual

packages bull a precise description of the goods by reference to

samples plans sketches photographs or similar means to be attached to the transit document

bull stipulation of a strict routing and strict time limits or bull Customs escort

The decision to waive sealing of the transport-unit shall however be the prerogative of the Customs alone

Standard

13 When the Customs fix a time limit for Customs transit it shall be sufficient for the purposes of the transit operations

Standard

14 At the request of the person concerned and for reasons deemed valid by the Customs the latter should extend any period initially fixed

Standard

15 Only when they consider such a measure to be indispensable shall the Customs

(a) require goods to follow a prescribed itinerary or (b) require goods to be transported under Customs

escort

Standard

16 Customs seals and fastenings used in the application of Customs transit shall fulfill the minimum requirements laid down in the Appendix to this Chapter

Standard

17 Customs seals and identification marks affixed by foreign Customs should be accepted for the purposes of the Customs transit operation unless

Recommended Practice

24

bull they are considered not to be sufficient bull they are not secure or bull the Customs proceed to an examination of the goods

When foreign Customs seals and fastenings have been accepted in a Customs territory they should be afforded the same legal protection in that territory as national seals and fastenings

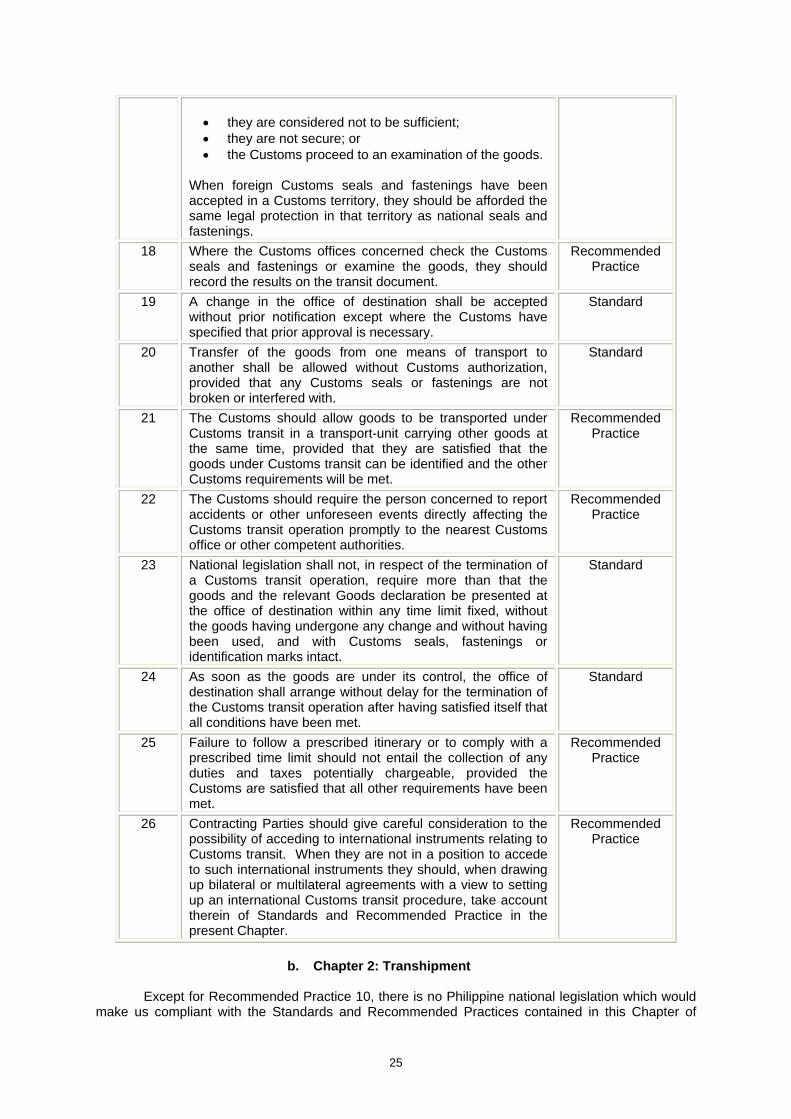

18 Where the Customs offices concerned check the Customs seals and fastenings or examine the goods they should record the results on the transit document

Recommended Practice

19 A change in the office of destination shall be accepted without prior notification except where the Customs have specified that prior approval is necessary

Standard

20 Transfer of the goods from one means of transport to another shall be allowed without Customs authorization provided that any Customs seals or fastenings are not broken or interfered with

Standard

21 The Customs should allow goods to be transported under Customs transit in a transport-unit carrying other goods at the same time provided that they are satisfied that the goods under Customs transit can be identified and the other Customs requirements will be met

Recommended Practice

22 The Customs should require the person concerned to report accidents or other unforeseen events directly affecting the Customs transit operation promptly to the nearest Customs office or other competent authorities

Recommended Practice

23 National legislation shall not in respect of the termination of a Customs transit operation require more than that the goods and the relevant Goods declaration be presented at the office of destination within any time limit fixed without the goods having undergone any change and without having been used and with Customs seals fastenings or identification marks intact

Standard

24 As soon as the goods are under its control the office of destination shall arrange without delay for the termination of the Customs transit operation after having satisfied itself that all conditions have been met

Standard

25 Failure to follow a prescribed itinerary or to comply with a prescribed time limit should not entail the collection of any duties and taxes potentially chargeable provided the Customs are satisfied that all other requirements have been met

Recommended Practice

26 Contracting Parties should give careful consideration to the possibility of acceding to international instruments relating to Customs transit When they are not in a position to accede to such international instruments they should when drawing up bilateral or multilateral agreements with a view to setting up an international Customs transit procedure take account therein of Standards and Recommended Practice in the present Chapter

Recommended Practice

b Chapter 2 Transhipment

Except for Recommended Practice 10 there is no Philippine national legislation which would

make us compliant with the Standards and Recommended Practices contained in this Chapter of

25

Specific Annex E Therefore guidelines in the form of a Manual of Customs Operations need to be issued as a regulation expressly including these Standards and Recommended Practices for us to be compliant

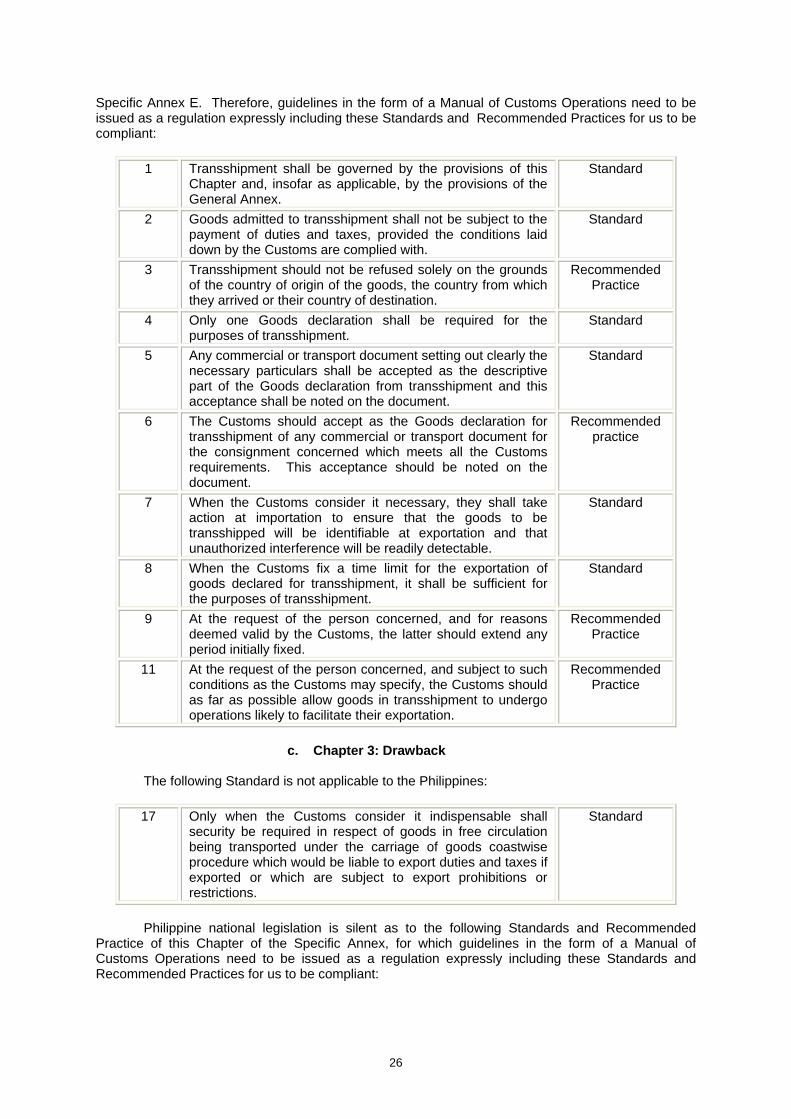

1 Transshipment shall be governed by the provisions of this Chapter and insofar as applicable by the provisions of the General Annex

Standard

2 Goods admitted to transshipment shall not be subject to the payment of duties and taxes provided the conditions laid down by the Customs are complied with

Standard

3 Transshipment should not be refused solely on the grounds of the country of origin of the goods the country from which they arrived or their country of destination

Recommended Practice

4 Only one Goods declaration shall be required for the purposes of transshipment

Standard

5 Any commercial or transport document setting out clearly the necessary particulars shall be accepted as the descriptive part of the Goods declaration from transshipment and this acceptance shall be noted on the document

Standard