Embed Size (px)

Citation preview

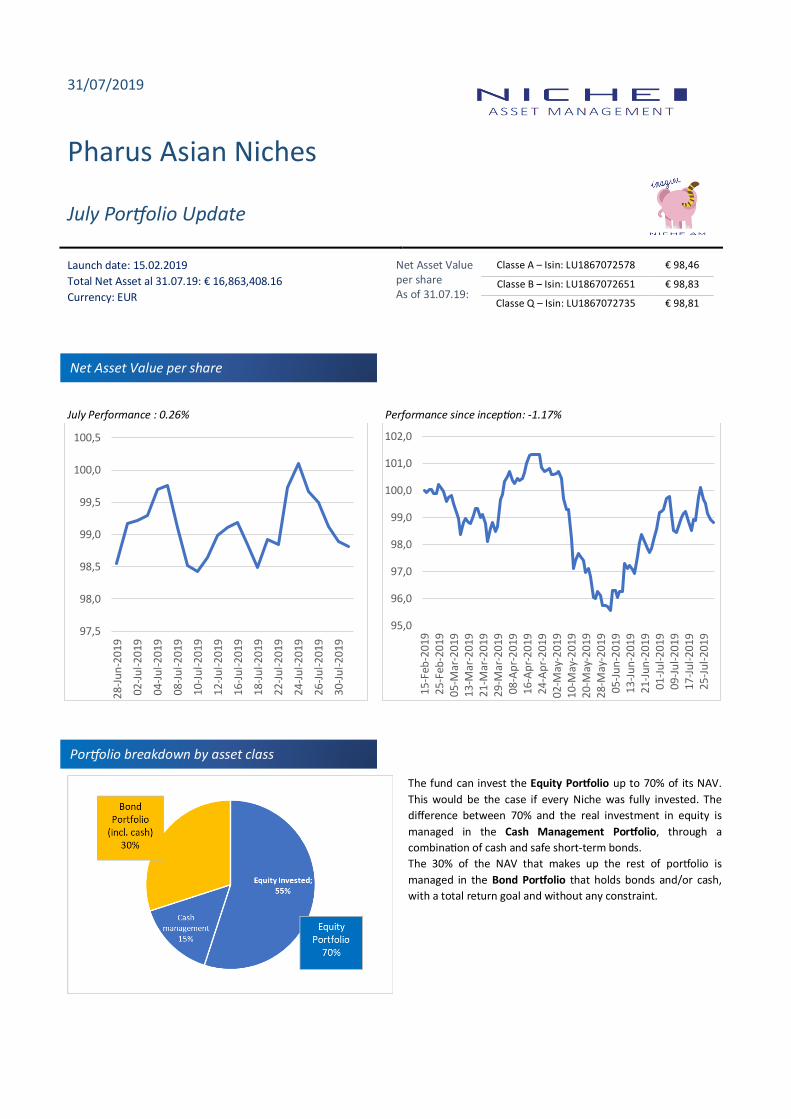

31/07/2019

Pharus Asian Niches

July Portfolio Update

Launch date: 15.02.2019

Total Net Asset al 31.07.19: € 16,863,408.16

Currency: EUR

Net Asset Value per share As of 31.07.19:

Classe A – Isin: LU1867072578 € 98,46

Classe B – Isin: LU1867072651 € 98,83

Classe Q – Isin: LU1867072735 € 98,81

July Performance : 0.26% Performance since inception: -1.17%

The fund can invest the Equity Portfolio up to 70% of its NAV.

This would be the case if every Niche was fully invested. The

difference between 70% and the real investment in equity is

managed in the Cash Management Portfolio, through a

combination of cash and safe short-term bonds.

The 30% of the NAV that makes up the rest of portfolio is

managed in the Bond Portfolio that holds bonds and/or cash,

with a total return goal and without any constraint.

97,5

98,0

98,5

99,0

99,5

100,0

100,5

28-J

un

-201

9

02-J

ul-

2019

04-J

ul-

2019

08-J

ul-

2019

10-J

ul-

2019

12-J

ul-

2019

16-J

ul-

2019

18-J

ul-

2019

22-J

ul-

2019

24-J

ul-

2019

26-J

ul-

2019

30-J

ul-

2019

95,0

96,0

97,0

98,0

99,0

100,0

101,0

102,015

-Feb

-201

925

-Feb

-201

905

-Mar

-201

913

-Mar

-201

921

-Mar

-201

929

-Mar

-201

90

8-A

pr-

2019

16-

Ap

r-20

192

4-A

pr-

2019

02-

May

-201

91

0-M

ay-2

019

20-M

ay-2

019

28-

May

-201

90

5-Ju

n-2

019

13-J

un

-201

92

1-Ju

n-2

019

01-J

ul-

2019

09-J

ul-

2019

17-J

ul-

2019

25-J

ul-

2019

Portfolio breakdown by asset class

Net Asset Value per share

2

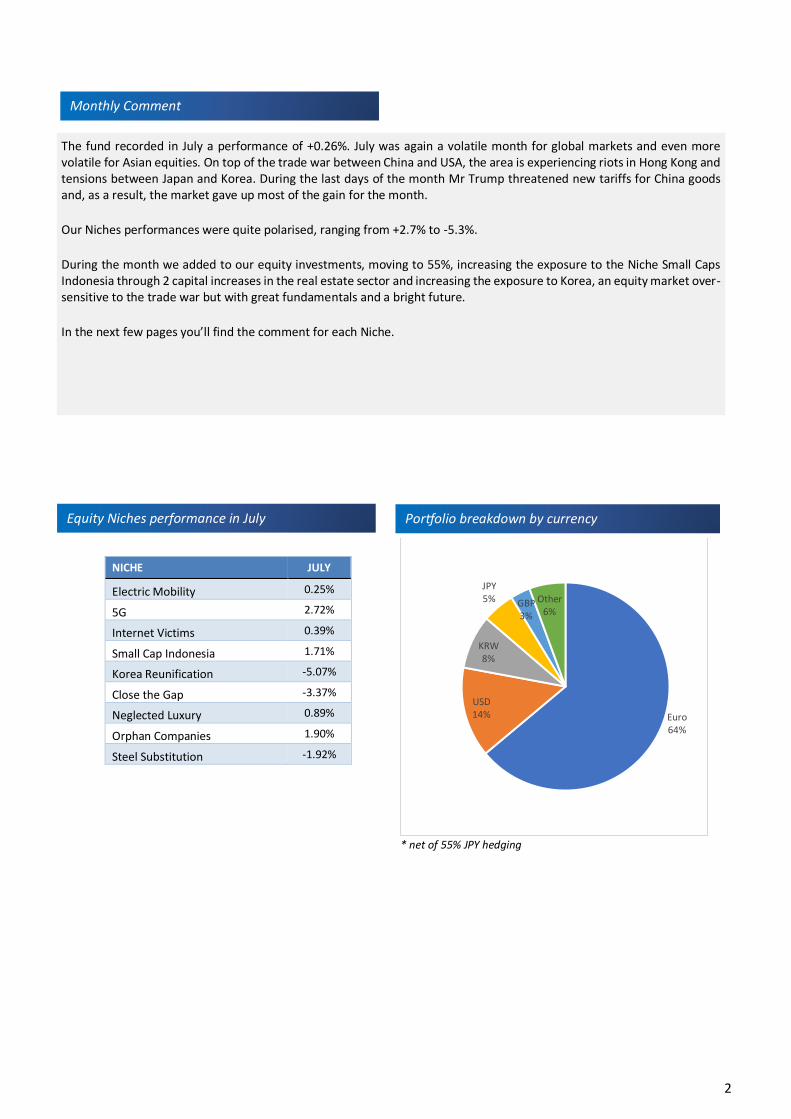

NICHE JULY

Electric Mobility 0.25%

5G 2.72%

Internet Victims 0.39%

Small Cap Indonesia 1.71%

Korea Reunification -5.07%

Close the Gap -3.37%

Neglected Luxury 0.89%

Orphan Companies 1.90%

Steel Substitution -1.92%

* net of 55% JPY hedging

Euro64%

USD14%

KRW8%

JPY5% GBP

3%

Other6%

Monthly Comment

The fund recorded in July a performance of +0.26%. July was again a volatile month for global markets and even more volatile for Asian equities. On top of the trade war between China and USA, the area is experiencing riots in Hong Kong and tensions between Japan and Korea. During the last days of the month Mr Trump threatened new tariffs for China goods and, as a result, the market gave up most of the gain for the month.

Our Niches performances were quite polarised, ranging from +2.7% to -5.3%.

During the month we added to our equity investments, moving to 55%, increasing the exposure to the Niche Small Caps Indonesia through 2 capital increases in the real estate sector and increasing the exposure to Korea, an equity market over-sensitive to the trade war but with great fundamentals and a bright future.

In the next few pages you’ll find the comment for each Niche.

Equity Niches performance in July

Portfolio breakdown by currency

3

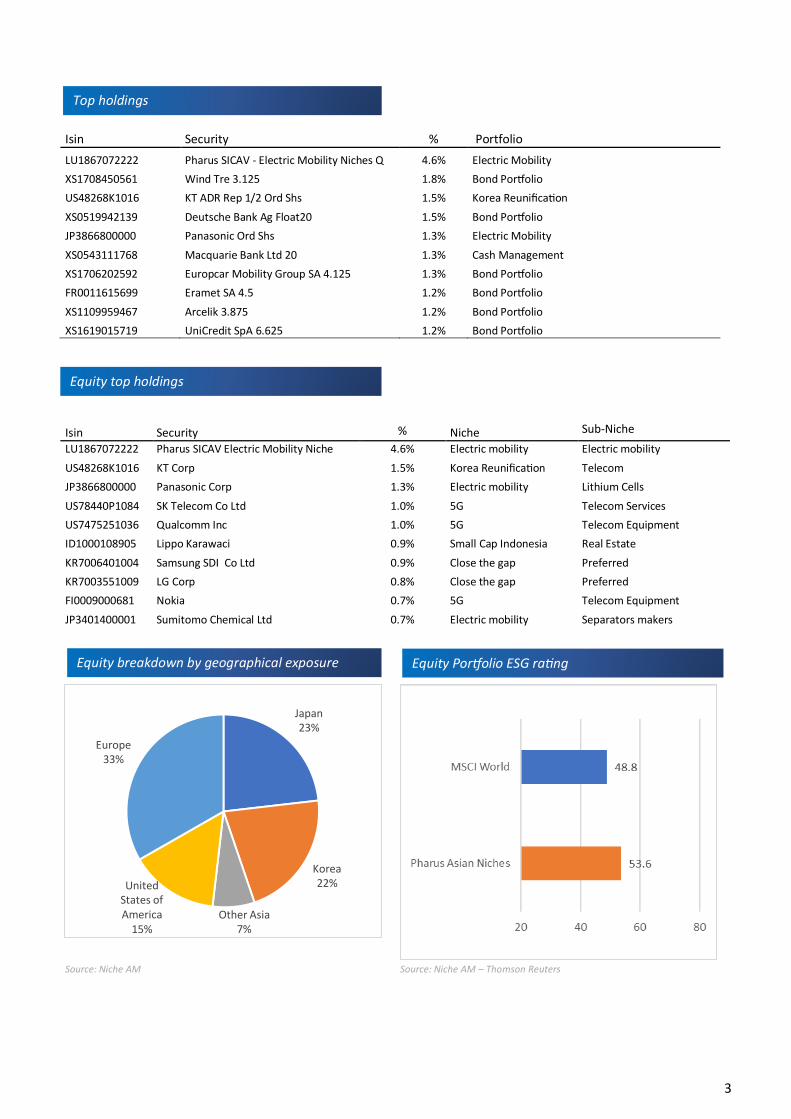

Isin Security % Portfolio

LU1867072222 Pharus SICAV - Electric Mobility Niches Q 4.6% Electric Mobility

XS1708450561 Wind Tre 3.125 1.8% Bond Portfolio

US48268K1016 KT ADR Rep 1/2 Ord Shs 1.5% Korea Reunification

XS0519942139 Deutsche Bank Ag Float20 1.5% Bond Portfolio

JP3866800000 Panasonic Ord Shs 1.3% Electric Mobility

XS0543111768 Macquarie Bank Ltd 20 1.3% Cash Management

XS1706202592 Europcar Mobility Group SA 4.125 1.3% Bond Portfolio

FR0011615699 Eramet SA 4.5 1.2% Bond Portfolio

XS1109959467 Arcelik 3.875 1.2% Bond Portfolio

XS1619015719 UniCredit SpA 6.625 1.2% Bond Portfolio

Isin Security % Niche Sub-Niche

LU1867072222 Pharus SICAV Electric Mobility Niche 4.6% Electric mobility Electric mobility

US48268K1016 KT Corp 1.5% Korea Reunification Telecom

JP3866800000 Panasonic Corp 1.3% Electric mobility Lithium Cells

US78440P1084 SK Telecom Co Ltd 1.0% 5G Telecom Services

US7475251036 Qualcomm Inc 1.0% 5G Telecom Equipment

ID1000108905 Lippo Karawaci 0.9% Small Cap Indonesia Real Estate

KR7006401004 Samsung SDI Co Ltd 0.9% Close the gap Preferred

KR7003551009 LG Corp 0.8% Close the gap Preferred

FI0009000681 Nokia 0.7% 5G Telecom Equipment

JP3401400001 Sumitomo Chemical Ltd 0.7% Electric mobility Separators makers

Source: Niche AM

Source: Niche AM – Thomson Reuters

Japan23%

Korea22%

Other Asia7%

United States of America

15%

Europe33%

Equity top holdings

Top holdings

Equity breakdown by geographical exposure Equity Portfolio ESG rating

4

Electric Mobility ................................................................................................................................................................... 5

5G ........................................................................................................................................................................................ 7

Internet Victims ................................................................................................................................................................... 9

Small Cap Indonesia ........................................................................................................................................................... 11

Korea Reunification ........................................................................................................................................................... 13

Close the Gap ..................................................................................................................................................................... 15

Neglected Luxury ............................................................................................................................................................... 17

Orphan Companies ............................................................................................................................................................ 19

Steel Substitution .............................................................................................................................................................. 21

Bond Portfolio …………………………………………………………………………………………………………………………………………………………………….23

5

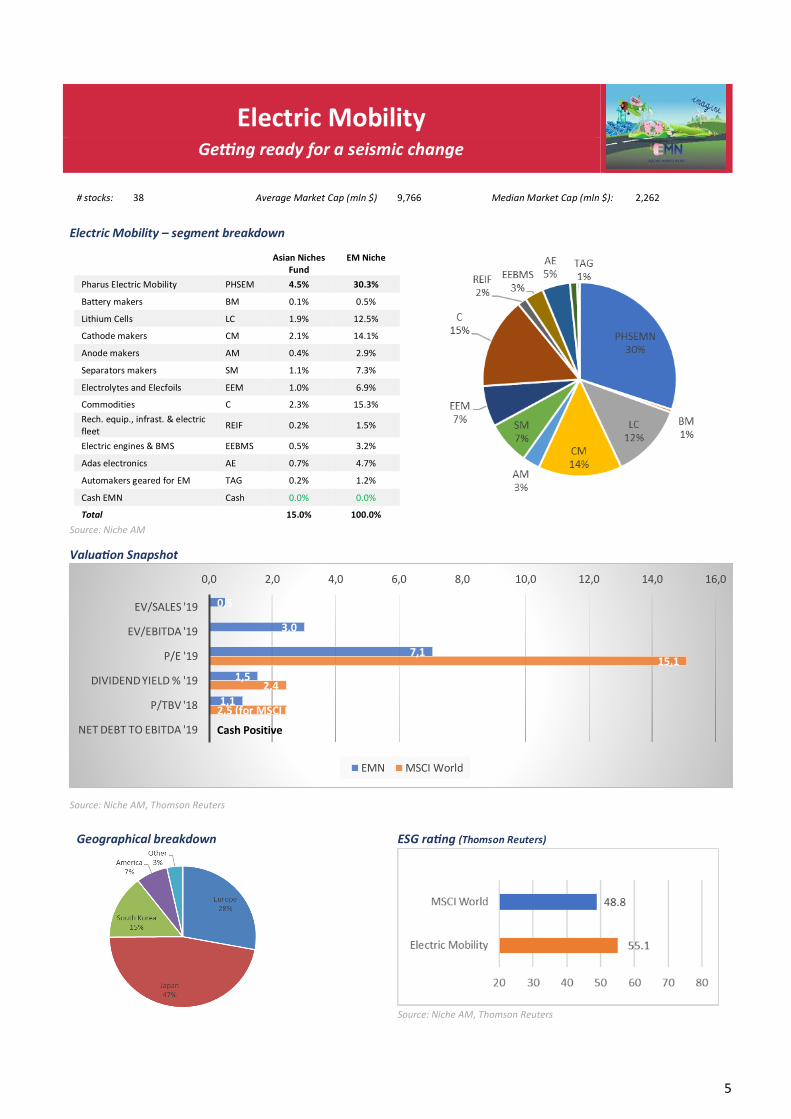

Electric Mobility

Getting ready for a seismic change

# stocks: 38 Average Market Cap (mln $) 9,766 Median Market Cap (mln $): 2,262

Electric Mobility – segment breakdown

Asian Niches

Fund EM Niche

Pharus Electric Mobility PHSEM 4.5% 30.3%

Battery makers BM 0.1% 0.5%

Lithium Cells LC 1.9% 12.5%

Cathode makers CM 2.1% 14.1%

Anode makers AM 0.4% 2.9%

Separators makers SM 1.1% 7.3%

Electrolytes and Elecfoils EEM 1.0% 6.9%

Commodities C 2.3% 15.3%

Rech. equip., infrast. & electric fleet

REIF 0.2% 1.5%

Electric engines & BMS EEBMS 0.5% 3.2%

Adas electronics AE 0.7% 4.7%

Automakers geared for EM TAG 0.2% 1.2%

Cash EMN Cash 0.0% 0.0%

Total

15.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM, Thomson Reuters

0,5

3,0

7,1

1,5

1,1

Cash Positive

15,1

2,4

2,5 (for MSCI P/BV)

0,0 2,0 4,0 6,0 8,0 10,0 12,0 14,0 16,0

EV/SALES '19

EV/EBITDA '19

P/E '19

DIVIDEND YIELD % '19

P/TBV '18

NET DEBT TO EBITDA '19

EMN MSCI World

6

Electric Mobility

Getting ready for a seismic change

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

Electric Mobility was stable (+0.2%), with the Japanese lithium cells and electrolytes makers offsetting the dreadful contribution from

the commodities. During the month of July, the sub-Niche Commodities (nickel, graphite, cobalt and lithium) was deeply down (-9%),

depressed by the fears of an extended trade war. The Niche Cathodes was also negative (-3.6%), affected by the floundering Korean

market where many players are based. On the other hand, the Niche Separators was positive due to a few good earnings reports and

the Niche Electrolytes was the outperformer (+23.2%) thanks to a shortage of components from Japan following a trading spat with

Korea.

The today investment environment, characterised by anxiety and depressed valuations throughout the industrial sector, offers the

ideal background to increase gradually the equity exposure into this promising area.

Niche description Electric mobility will grow dramatically in the next few years, with a speed still unexpected by most and changing the world for good. The electric mobility will be pervasive, affecting land, air and water transportation. The batteries stocks, just a part of the broader electric mo bility sector, will overcome the semiconductor sector by total sales in few years. We deem the sector a great opportunity for those who have a firm understanding of it, and potentially hazardous for those who do not. Niche Asset Management team boasts a long and successful experience in the electric mobility investing. Niche aims to give the investor exposure to this exciting sector through its value approach.

7

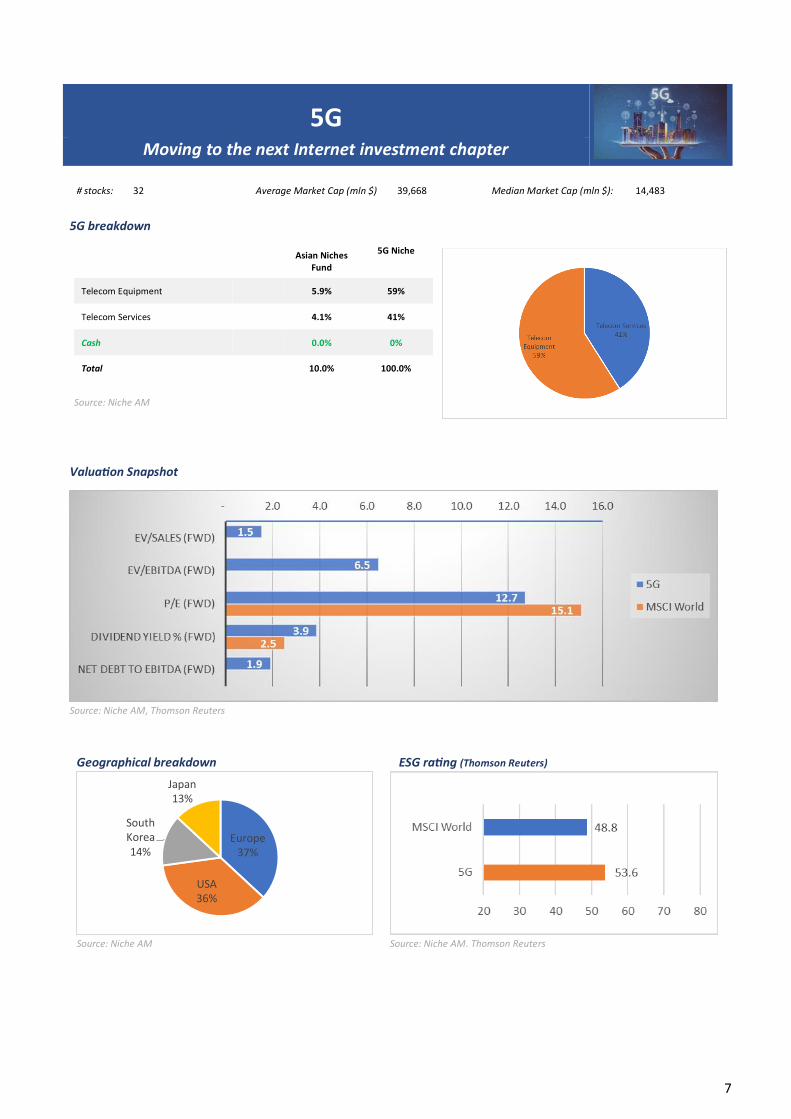

5G Moving to the next Internet investment chapter

# stocks: 32 Average Market Cap (mln $) 39,668 Median Market Cap (mln $): 14,483

5G breakdown

Asian Niches Fund

5G Niche

Telecom Equipment 5.9% 59%

Telecom Services 4.1% 41%

Cash 0.0% 0%

Total 10.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

Europe37%

USA36%

South Korea14%

Japan13%

8

5G

Moving to the next Internet investment chapter

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

The 5G Niche was the top performer in July (+2.7%); the release of the first 5G-related revenues from Nokia and the spin-off and listing

announcement for the mast business of Vodafone were the catalysts. The Finnish telecom equipment vendor now has 45 commercial

5G contracts and the CEO sounded very positive on the outlook. The first lay out of the 5G networks continues, with Korea and USA on

top. However, at this stage the 5G can be hardly tested. There won’t be any real functioning 5G networks before 2020. The first networks

will tap into the 600 MHz low-band spectrum. This low-band deployment strategy will enable the rapid expansion of its 5G network by

allowing the carriers to easily leverage existing 4G LTE assets and infrastructure. Furthermore, in order to better appreciate the first

networks, we’ll need the arrival of the Qualcomm X55 modem that should be available in the new mobile devices at the end of the year.

Niche description The 5G is coming

•This starts a 5 to 10 years journey leading to full 5G connectivity

•The 5G will shape this century and will change the way we live for good

•The 5G will open the gates to new business models, will greatly improve the productivity and will make the world smaller and safer

5G will make a broad and disruptive array of new technologies reality. IoT, AI, VR, AU, block chain, self -driving cars, smart living, smart homes, remote healthcare won’t be possible without 5G. Nonetheless the companies that will make 5G possible are still neglected and offer great value.

The niche aims to give the investors an exposure to these 5G players.

9

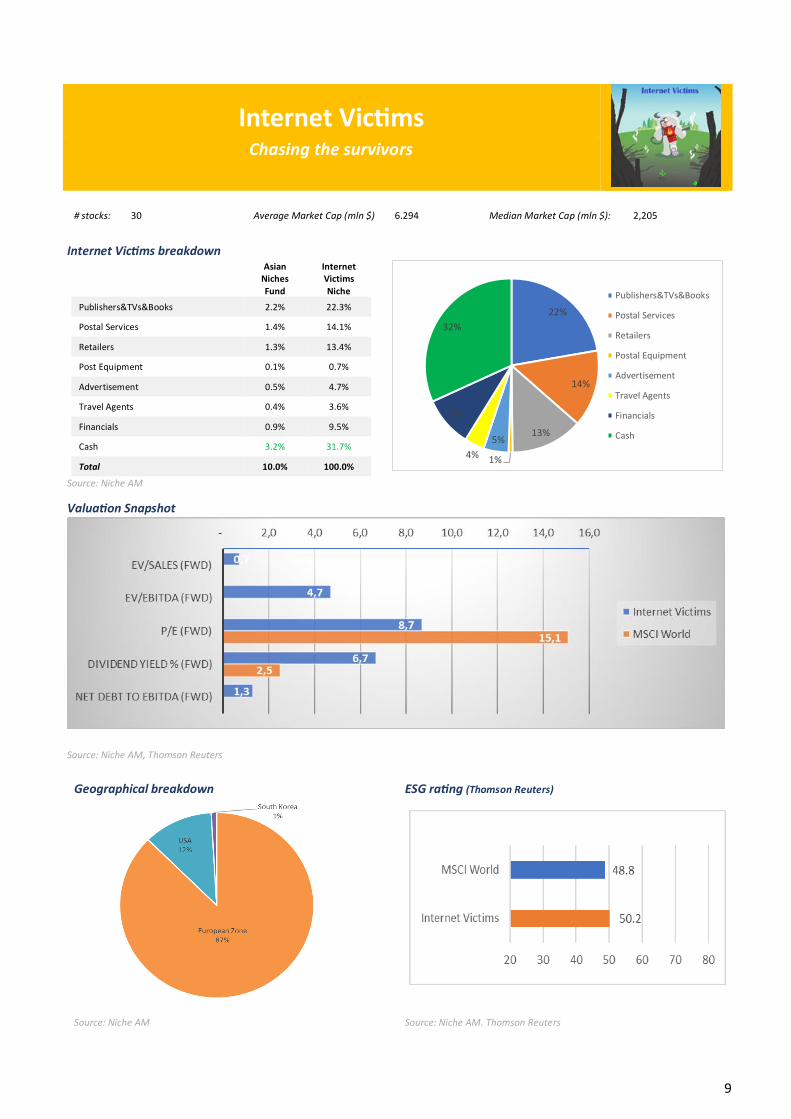

Internet Victims

Chasing the survivors

# stocks: 30 Average Market Cap (mln $) 6.294 Median Market Cap (mln $): 2,205

Internet Victims breakdown

Asian

Niches

Fund

Internet Victims

Niche

Publishers&TVs&Books 2.2% 22.3%

Postal Services 1.4% 14.1%

Retailers 1.3% 13.4%

Post Equipment 0.1% 0.7%

Advertisement 0.5% 4.7%

Travel Agents 0.4% 3.6%

Financials 0.9% 9.5%

Cash 3.2% 31.7%

Total 10.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

22%

14%

13%

1%

5%

4%

9%

32%

Publishers&TVs&Books

Postal Services

Retailers

Postal Equipment

Advertisement

Travel Agents

Financials

Cash

10

Internet Victims

Chasing the survivors

Monthly comment Commento mensile

Chart July (28/06-31/07)

Chart since inception (21/02-31/07)

Source: Niche AM

The Niche Internet Victims was slightly positive (+0.4%). While the broadcasters are still bleeding, we are seeing the first indications of a change of sentiment in the publishers, with Independent News bought out by the media group Mediahuis and Gannet being acquired by GateHouse. The retailers produced again frail performances, while postal services were positive and started to stabilise after a good set of results.

Niche description

Every technology revolution, and the ongoing huge internet revolution is no exception, makes corporate victims; business models are replaced; many of the old players fail to adapt early, while new players are ushered in, thriving and gaining market share. This slow and cruel process is well known by investors, who, however, normally tend to be late in fully understanding the depth and the breath of the shift. Once the trend is established most of the investors sell the old players and gain exposure to the new ones. The old players have to live through a prolonged period of restructuring and reinvention; valuations are squeezed, failures and consolidation are common. We call them the (internet revolution) VICTIMS At the end of a technology revolution a new class of companies emerges; this class is composed by the old players which have learnt to live through the change, thriving in a less competitive environment and/or through an adapted business model. We call them the (internet revolution) SURVIVORS. Finding survivors can be even more rewarding than finding winners. The niche aims to gain exposure to the survivors of the internet revolution.

11

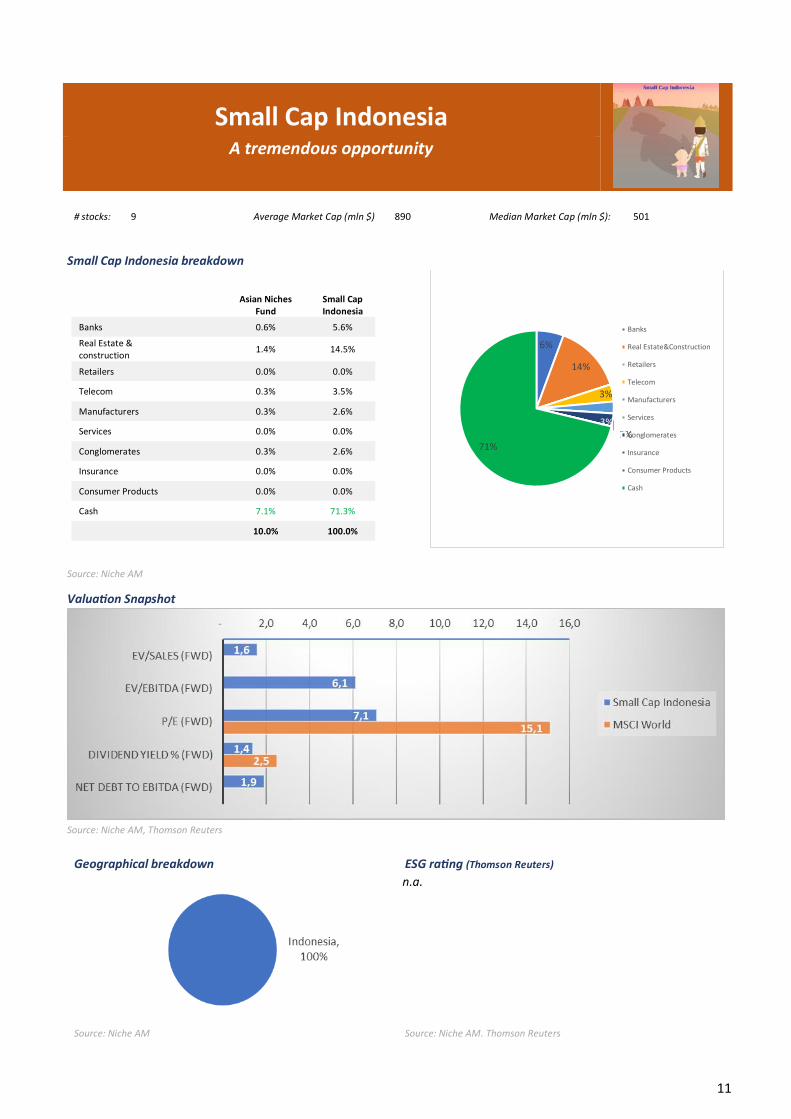

Small Cap Indonesia

A tremendous opportunity

# stocks: 9 Average Market Cap (mln $) 890 Median Market Cap (mln $): 501

Small Cap Indonesia breakdown

Asian Niches

Fund Small Cap Indonesia

Banks 0.6% 5.6%

Real Estate & construction

1.4% 14.5%

Retailers 0.0% 0.0%

Telecom 0.3% 3.5%

Manufacturers 0.3% 2.6%

Services 0.0% 0.0%

Conglomerates 0.3% 2.6%

Insurance 0.0% 0.0%

Consumer Products 0.0% 0.0%

Cash 7.1% 71.3%

10.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

n.a.

Source: Niche AM Source: Niche AM. Thomson Reuters

6%

14%

3%

3%3%

71%

Banks

Real Estate&Construction

Retailers

Telecom

Manufacturers

Services

Conglomerates

Insurance

Consumer Products

Cash

12

Small Cap Indonesia

A tremendous opportunity

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

The Niche small caps Indonesia fared well during the month (+1.7% and +7.5% excluding the cash held in the Niche), supported by the real estate. The Niche greatly overperformed the main Indonesian Index (JKSE) that was only slightly positive (+0.36%). Foreign tourist arrivals in Indonesia rose 9.9% from a year earlier to 1.45 million in June 2019, mostly heading to Bali from the nearby regions (Malaysia, Singapore, Philippines and Thailand). As reference, Thailand recorded about 4.5 million of tourist over the same period, despite being much smaller. In July the World Bank published a report where anticipates that tourism is projected to become the largest ocean-related sector by 2030, surpassing the slower-growing offshore oil and gas sector. Pivotal to this progress will be the development of tourism in the coastal areas. Today out of all overnight stays of international, cruise, and domestic visitors in Indonesia, only an estimated 29 percent are in coastal and non-urban destinations. Containing the world’s highest coral diversity, or 76 percent of the world’s coral species and 37 percent of the world’s coral reef fish species, Indonesia seaside areas are well-positioned to capture a large share of this growth. The same report forecasts healthy GDP growth for 2019 (5.1%) and for 2020 (5.2%), driven by private consumption, as inflation remains low and labour market strong. In this scenario we are increasing the exposure to the small Indonesian banks, that trade a modest multiples and with a huge discount to their bigger peers.

Niche description Indonesia is a land with incredible potential. Its territory is huge, highly fertile and beautiful. The weather is ideal for agriculture and tourism. There are plenty of natural resources. The population is tame and friendly. Corporate governance is decent by emerging markets standards. The Central Bank is independent and from a political perspective the democracy system is maturing rapidly, while corruption is decreasing. The pu blic debt is very low, inflation under control and growth is healthy. While this is well reflected in the valuation of big caps, it is not in small caps’. The discount of Indonesian small caps vs big caps is stunning, which is a legacy of the low visibility and reliability of those stocks in the past. Things have changed, and we expect a rapid catch up in the next few years, as it has happened in India. Through this niche NAM aims to give the investor exposure to this resourceful country through an actively managed small caps portfolio that offers absolute low valuations and a huge discount versus the Indonesia big caps.

13

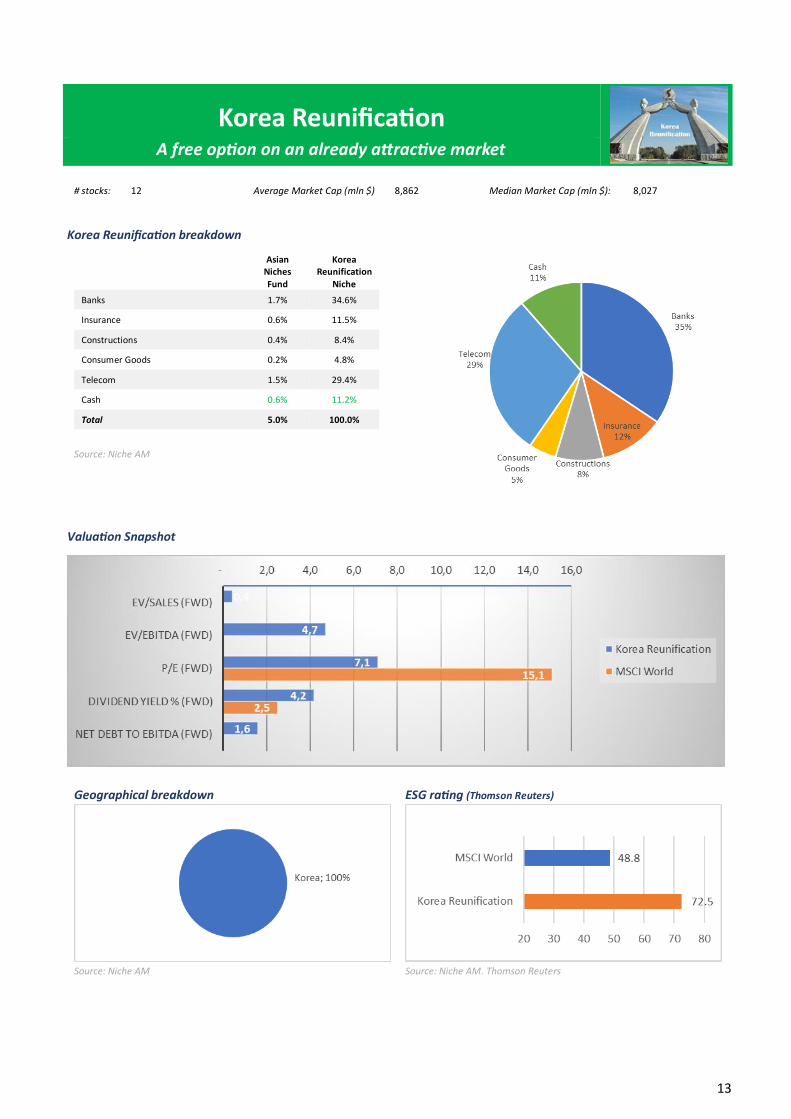

Korea Reunification

A free option on an already attractive market

# stocks: 12 Average Market Cap (mln $) 8,862 Median Market Cap (mln $): 8,027

Korea Reunification breakdown

Asian Niches

Fund

Korea Reunification

Niche

Banks 1.7% 34.6%

Insurance 0.6% 11.5%

Constructions 0.4% 8.4%

Consumer Goods 0.2% 4.8%

Telecom 1.5% 29.4%

Cash 0.6% 11.2%

Total 5.0% 100.0%

Source: Niche AM

Valuation Snapshot

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

14

Korea Reunification

A free option on an already attractive market

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

Korea Reunification did badly (-5.1%), reflecting the negative sentiment on this country significantly exposed to the global trade war; a trade spat with Japan during the month did not help either. However, the second quarter GDP that came out in July was better than expected, at +2.1% from a year ago. Growth was not only firmer than the consensus estimate, but also marked an acceleration from the 1.7% YoY rate recorded in 1Q19. More importantly, the economy avoided a recession with QoQ growth back in positive territory. Private and public consumption persisted as the key expenditure-side drivers of GDP growth. The contribution of private consumption to GDP growth rose to 1.0 percentage point (ppt) from 0.9ppt in 1Q and that of government consumption was up to 1.2ppt from 1.0ppt. Investments remained a drag albeit smaller than in 1Q. And all this more than offset a significant narrowing in the net trade contribution. However, it is unlikely that the country could be able to grow at 2% this year and a modest 1.2% looks a better guess. Despite numbers far from terrible the Korean market is experiencing a deep rout. This is down to its historical volatility and to a widespread positive sentiment towards this region that is broadly overweighed among investors. On the reunification side, just after the end of the month of July, during his liberation day address on Thursday, the South Korea PM Moon said he envisioned a future of close economic cooperation, denuclearisation and the unification of the two Koreas by 2045 – a century after the peninsula was liberated from Japanese colonial rule.

Niche description

South Korea is the ideal market to play through a value approach, as it is cheap, and its economy is growing healthy. Beside this, it has a terrific catalyst, this being a reunification or some form of rapprochement, with its half (North Korea). This event could be able to increase the long-term growth potential of the country and to free the market animal spirits. The Korea reunification is a way to add a free option to an already attractive market. The niche aims to give the investor an exposure to the main beneficiaries of the reunification or of a rapprochement between the South and the North Korea.

15

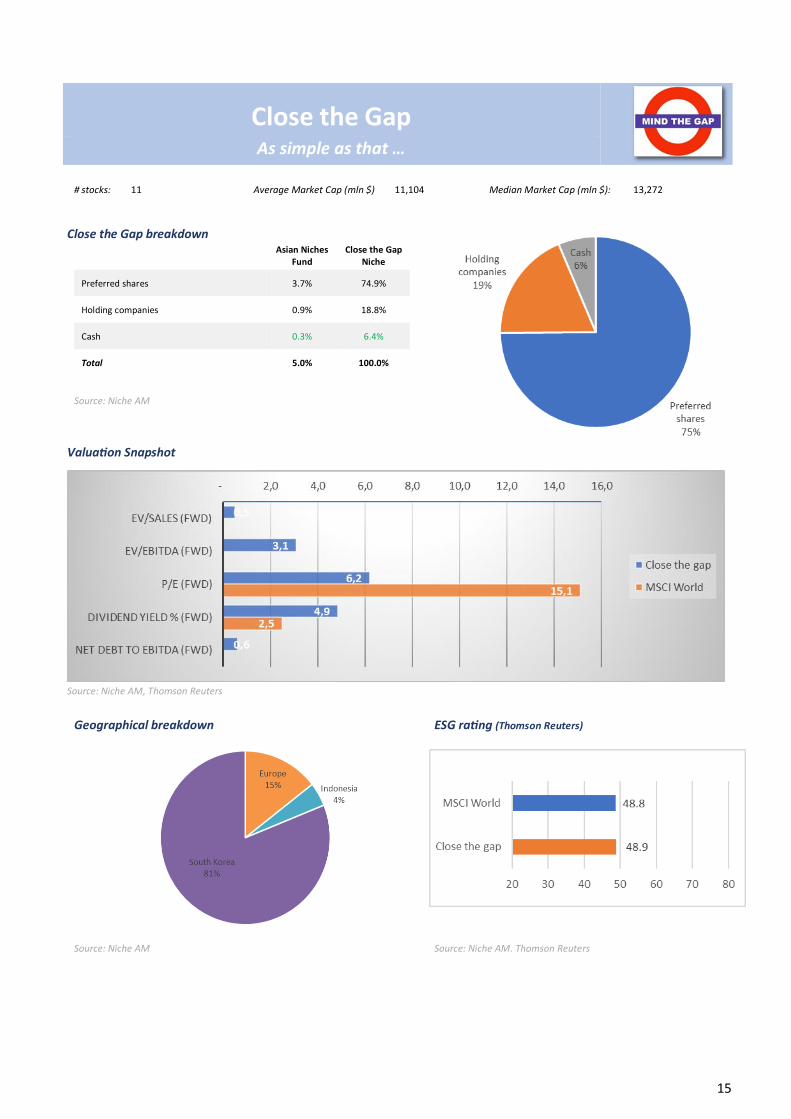

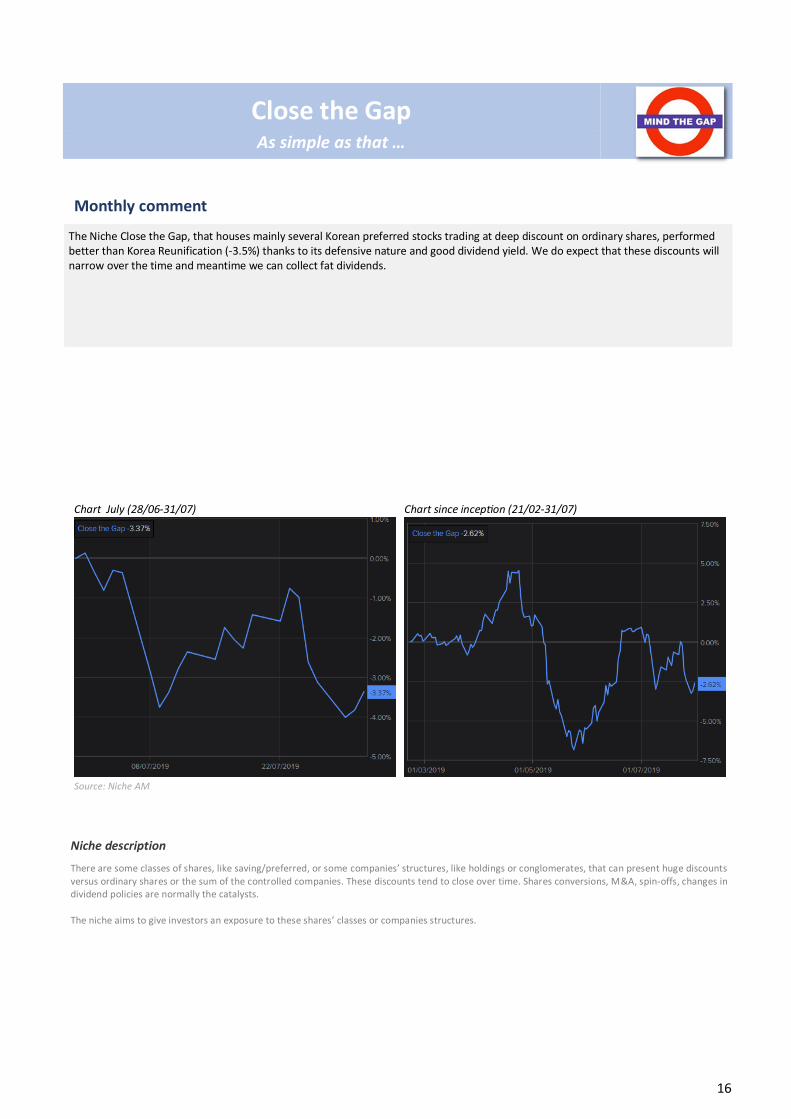

Close the Gap

As simple as that …

# stocks: 11 Average Market Cap (mln $) 11,104 Median Market Cap (mln $): 13,272

Close the Gap breakdown

Asian Niches

Fund Close the Gap

Niche

Preferred shares 3.7% 74.9%

Holding companies 0.9% 18.8%

Cash 0.3% 6.4%

Total 5.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

16

Close the Gap

As simple as that …

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

The Niche Close the Gap, that houses mainly several Korean preferred stocks trading at deep discount on ordinary shares, performed better than Korea Reunification (-3.5%) thanks to its defensive nature and good dividend yield. We do expect that these discounts will narrow over the time and meantime we can collect fat dividends.

Niche description

There are some classes of shares, like saving/preferred, or some companies’ structures, like holdings or conglomerates, that can present huge discounts versus ordinary shares or the sum of the controlled companies. These discounts tend to close over time. Shares conversions, M&A, spin-offs, changes in dividend policies are normally the catalysts. The niche aims to give investors an exposure to these shares’ classes or companies structures.

17

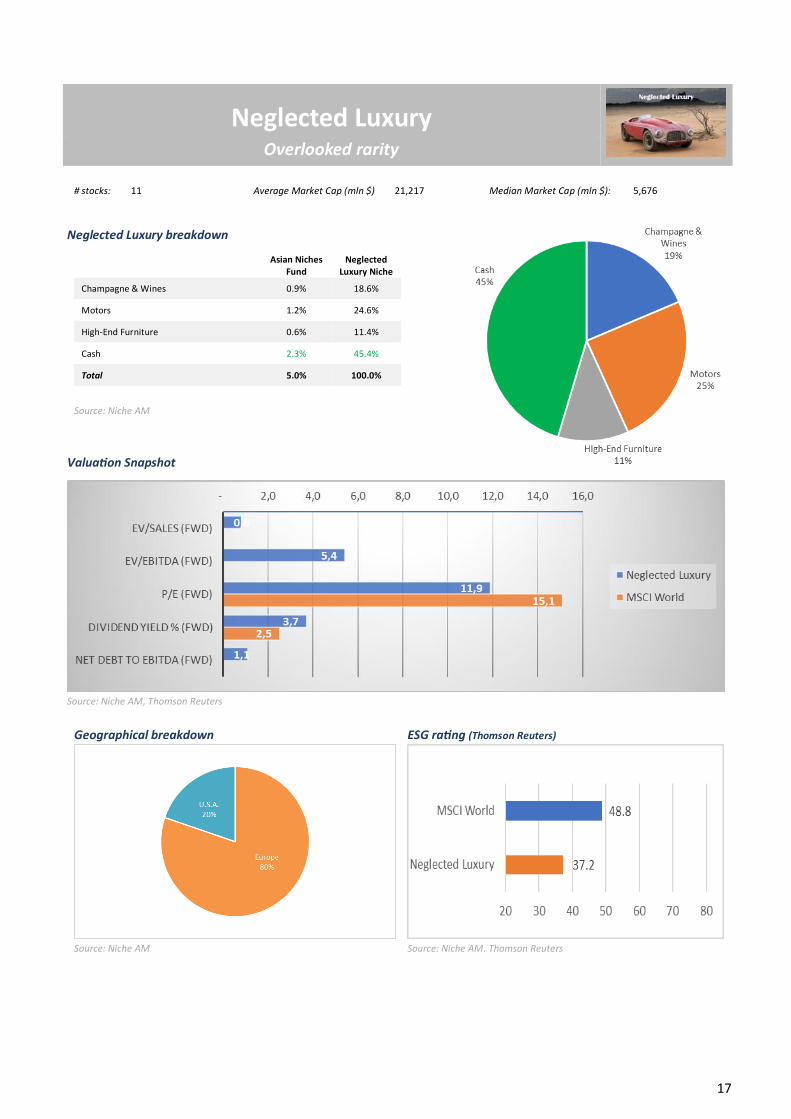

Neglected Luxury

Overlooked rarity

# stocks: 11 Average Market Cap (mln $) 21,217 Median Market Cap (mln $): 5,676

Neglected Luxury breakdown

Asian Niches Fund

Neglected Luxury Niche

Champagne & Wines 0.9% 18.6%

Motors 1.2% 24.6%

High-End Furniture 0.6% 11.4%

Cash 2.3% 45.4%

Total 5.0% 100.0%

Source: Niche AM

Valuation Snapshot

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

18

Neglected Luxury

Overlooked rarity

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

The Niche surged by 0.9%, being invested at around 55% (2,8% of the fund vs 5% maximum). The “Champagne&Wines” sub-Niche was weak, the sub-Niche “Luxury Cars” was stable and the sub-Niche “High-End Furnitures” was again the outperformer. During the month Vranken-Pommery published the semi-annual sales that came out below expectation at 87 mln euro vs 94.8 mln in 2018. The decrease is concentrated in France where a change in the promotion’s regulation (EGalim act) shifted part of the sales into the second half. However, export, pivotal to margins expansion, was up 4.2% and went up to 56.5% of global sales. The furniture maker Knoll reported strong second quarter results, with a growth y/y in sales and EPS, respectively, of 13% and 14% and a reduced leverage ratio (2.4x vs 2.9x EBITDA).

Niche description The luxury sector has been one of the winners of the last 2 decades. Globalisation, growing inequality, emerging markets and westernisation have been at the root of its growth. Luxury means not just quality, but also exclusivity and recognisability. Selling prices or supply constraints determine and warrant the rarity effect that encompass the concept of luxury. Although the market generously prices these luxury stocks, it sometimes does not recognise some companies as belonging to the luxury sector. There could be many reasons for this: low profitability; being part of a conglomerate; short term imbalance between supply and demand; corporate governance issues, etc. The niche aims to give the patient investor the opportunity to gain exposure to these unique stock at valuations that are extremely attractive.

19

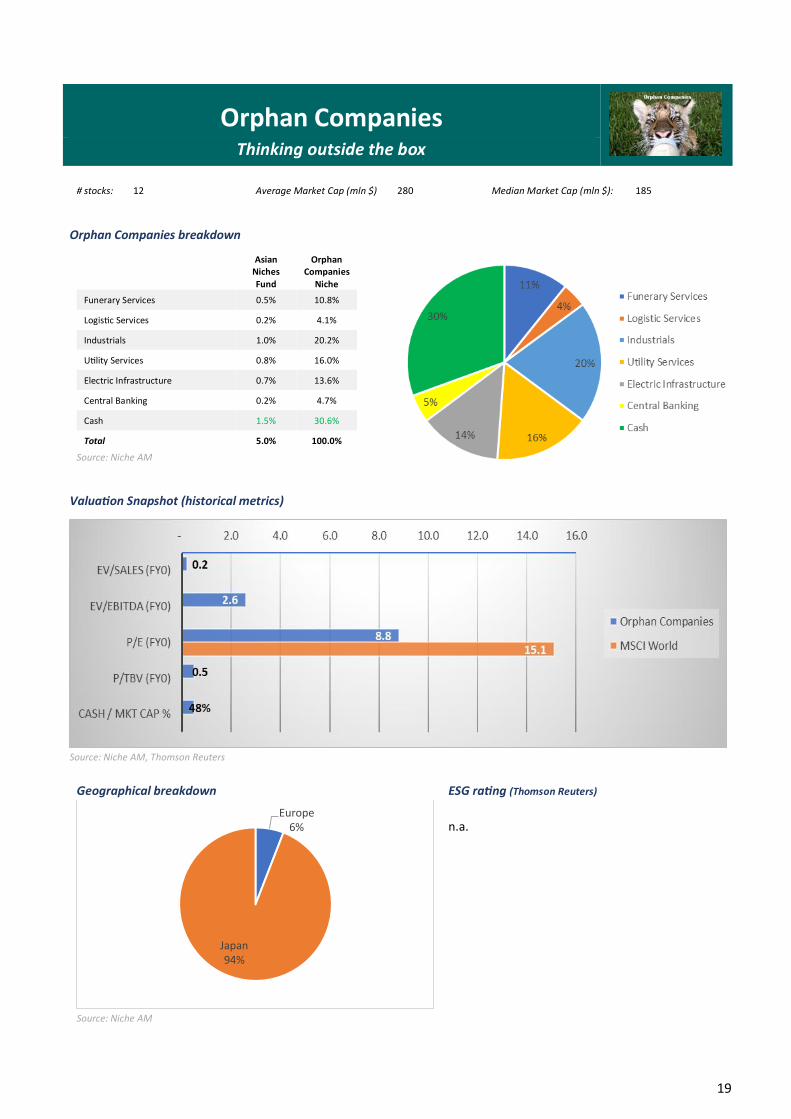

Orphan Companies

Thinking outside the box

# stocks: 12 Average Market Cap (mln $) 280 Median Market Cap (mln $): 185

Orphan Companies breakdown

Asian Niches

Fund

Orphan Companies

Niche

Funerary Services 0.5% 10.8%

Logistic Services 0.2% 4.1%

Industrials 1.0% 20.2%

Utility Services 0.8% 16.0%

Electric Infrastructure 0.7% 13.6%

Central Banking 0.2% 4.7%

Cash 1.5% 30.6%

Total 5.0% 100.0%

Source: Niche AM

Valuation Snapshot (historical metrics)

Source: Niche AM, Thomson Reuters

Geographical breakdown ESG rating (Thomson Reuters)

n.a.

Source: Niche AM

Europe6%

Japan94%

20

Orphan Companies

Thinking outside the box

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

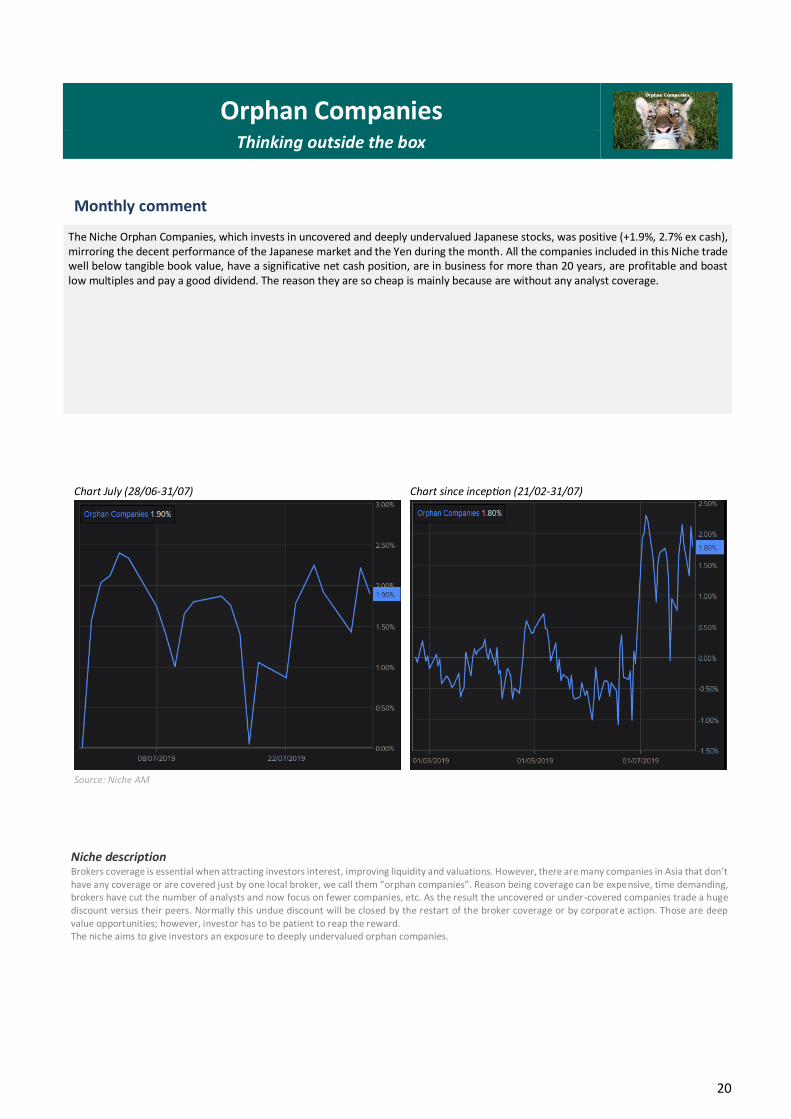

The Niche Orphan Companies, which invests in uncovered and deeply undervalued Japanese stocks, was positive (+1.9%, 2.7% ex cash), mirroring the decent performance of the Japanese market and the Yen during the month. All the companies included in this Niche trade well below tangible book value, have a significative net cash position, are in business for more than 20 years, are profitable and boast low multiples and pay a good dividend. The reason they are so cheap is mainly because are without any analyst coverage.

Niche description Brokers coverage is essential when attracting investors interest, improving liquidity and valuations. However, there are many companies in Asia that don’t have any coverage or are covered just by one local broker, we call them “orphan companies”. Reason being coverage can be expensive, time demanding, brokers have cut the number of analysts and now focus on fewer companies, etc. As the result the uncovered or under-covered companies trade a huge discount versus their peers. Normally this undue discount will be closed by the restart of the broker coverage or by corporat e action. Those are deep value opportunities; however, investor has to be patient to reap the reward. The niche aims to give investors an exposure to deeply undervalued orphan companies.

21

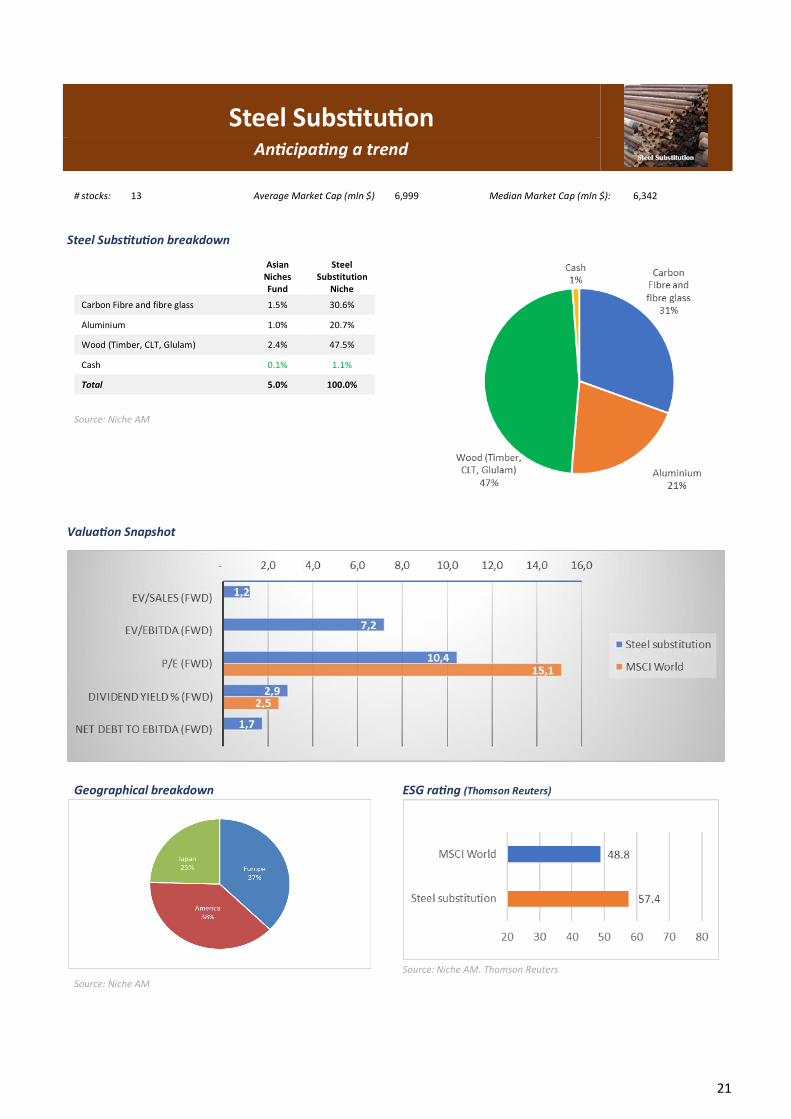

Steel Substitution

Anticipating a trend

# stocks: 13 Average Market Cap (mln $) 6,999 Median Market Cap (mln $): 6,342

Steel Substitution breakdown

Asian Niches Fund

Steel Substitution

Niche

Carbon Fibre and fibre glass 1.5% 30.6%

Aluminium 1.0% 20.7%

Wood (Timber, CLT, Glulam) 2.4% 47.5%

Cash 0.1% 1.1%

Total 5.0% 100.0%

Source: Niche AM

Valuation Snapshot

Geographical breakdown ESG rating (Thomson Reuters)

Source: Niche AM Source: Niche AM. Thomson Reuters

22

Steel Substitution

Anticipating a trend

Monthly comment Commento mensile

Chart July (28/06-31/07) Chart since inception (21/02-31/07)

Source: Niche AM

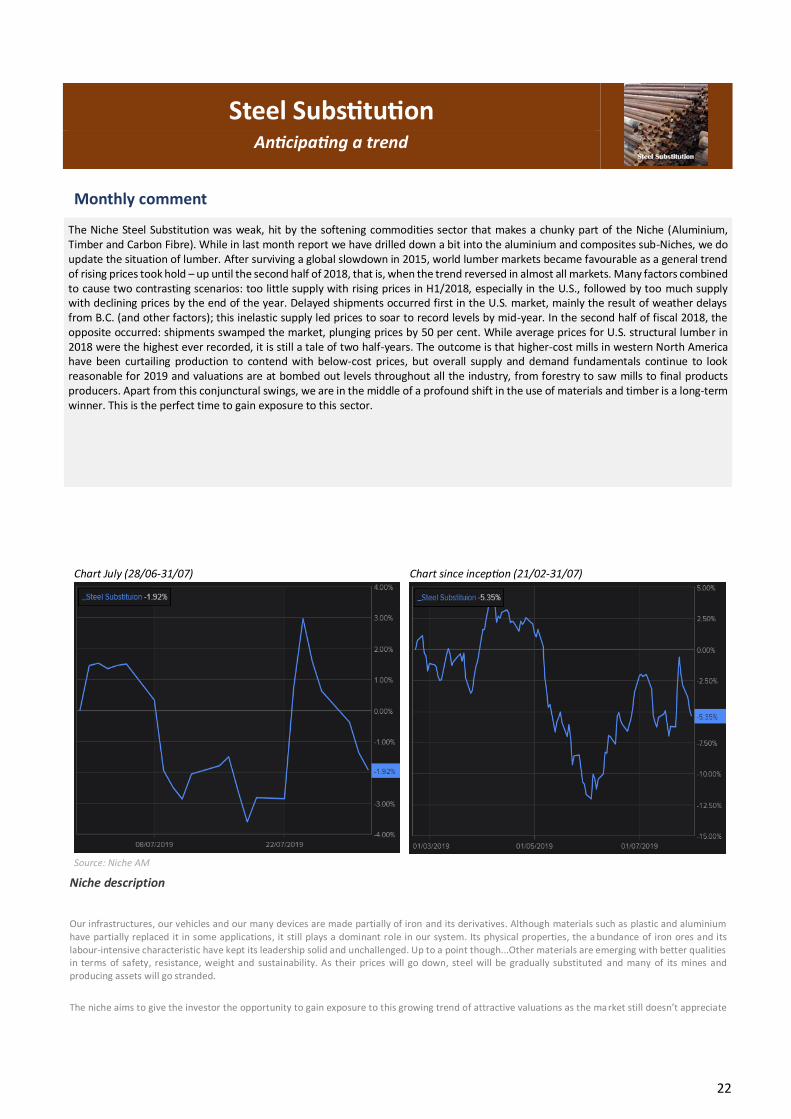

The Niche Steel Substitution was weak, hit by the softening commodities sector that makes a chunky part of the Niche (Aluminium, Timber and Carbon Fibre). While in last month report we have drilled down a bit into the aluminium and composites sub-Niches, we do update the situation of lumber. After surviving a global slowdown in 2015, world lumber markets became favourable as a general trend of rising prices took hold – up until the second half of 2018, that is, when the trend reversed in almost all markets. Many factors combined to cause two contrasting scenarios: too little supply with rising prices in H1/2018, especially in the U.S., followed by too much supply with declining prices by the end of the year. Delayed shipments occurred first in the U.S. market, mainly the result of weather delays from B.C. (and other factors); this inelastic supply led prices to soar to record levels by mid-year. In the second half of fiscal 2018, the opposite occurred: shipments swamped the market, plunging prices by 50 per cent. While average prices for U.S. structural lumber in 2018 were the highest ever recorded, it is still a tale of two half-years. The outcome is that higher-cost mills in western North America have been curtailing production to contend with below-cost prices, but overall supply and demand fundamentals continue to look reasonable for 2019 and valuations are at bombed out levels throughout all the industry, from forestry to saw mills to final products producers. Apart from this conjunctural swings, we are in the middle of a profound shift in the use of materials and timber is a long-term winner. This is the perfect time to gain exposure to this sector.

Niche description

Our infrastructures, our vehicles and our many devices are made partially of iron and its derivatives. Although materials such as plastic and aluminium have partially replaced it in some applications, it still plays a dominant role in our system. Its physical properties, the a bundance of iron ores and its labour-intensive characteristic have kept its leadership solid and unchallenged. Up to a point though...Other materials are emerging with better qualities in terms of safety, resistance, weight and sustainability. As their prices will go down, steel will be gradually substituted and many of its mines and producing assets will go stranded.

The niche aims to give the investor the opportunity to gain exposure to this growing trend of attractive valuations as the market still doesn’t appreciate it yet.

23

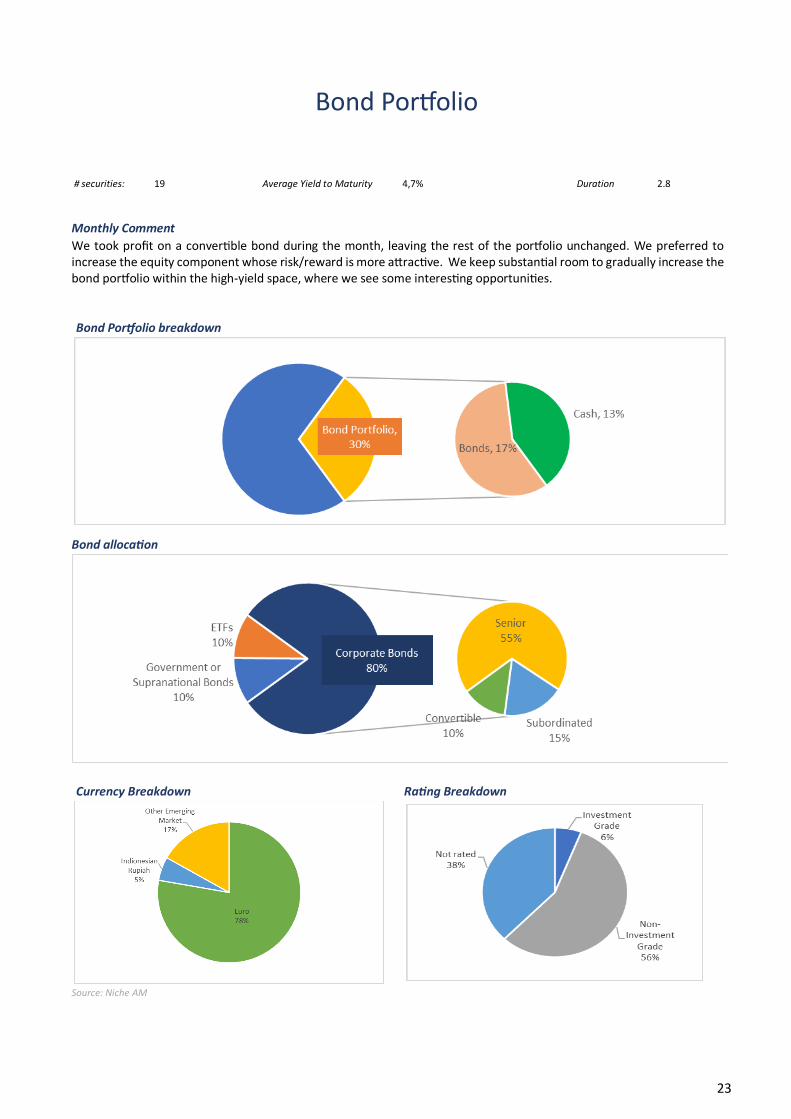

Bond Portfolio

# securities: 19 Average Yield to Maturity 4,7% Duration 2.8

Monthly Comment

We took profit on a convertible bond during the month, leaving the rest of the portfolio unchanged. We preferred to increase the equity component whose risk/reward is more attractive. We keep substantial room to gradually increase the bond portfolio within the high-yield space, where we see some interesting opportunities.

Bond Portfolio breakdown

Bond allocation

Currency Breakdown Rating Breakdown

Source: Niche AM

24

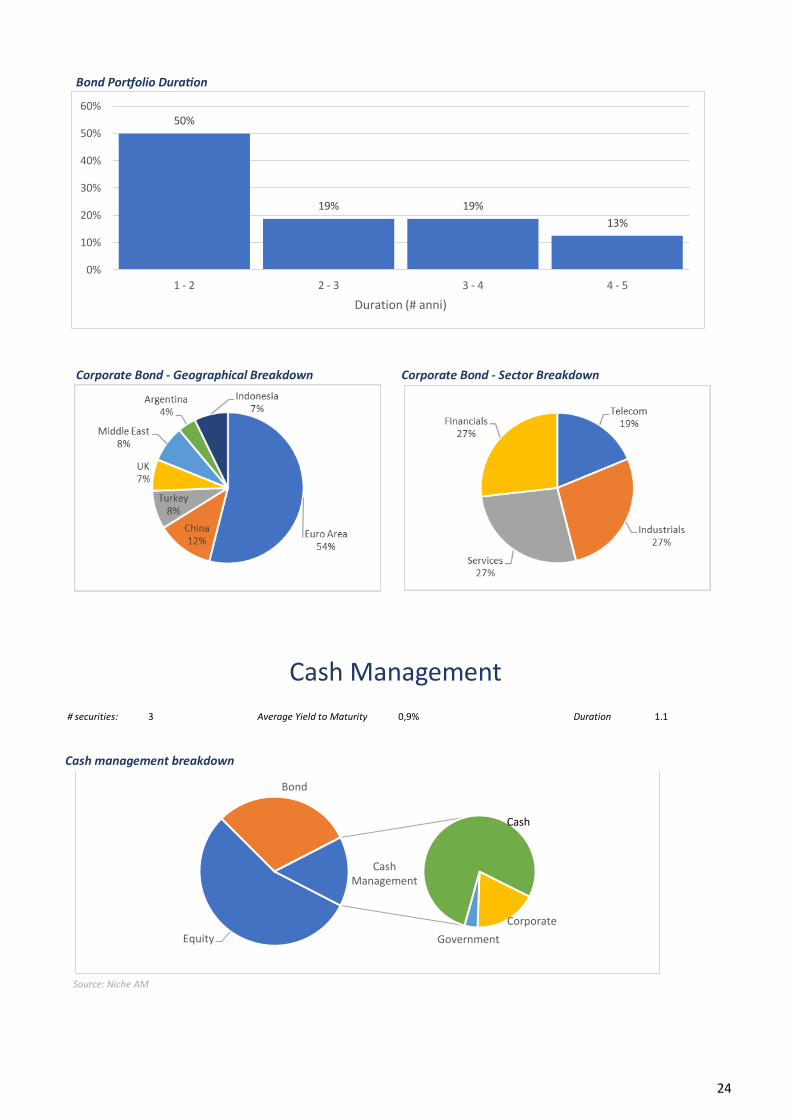

# securities: 3 Average Yield to Maturity 0,9% Duration 1.1

Cash management breakdown

Source: Niche AM

Equity

Bond

Corporate

Government

Cash

Cash Management

Bond Portfolio Duration

Corporate Bond - Geographical Breakdown Corporate Bond - Sector Breakdown

Cash Management

50%

19% 19%

13%

0%

10%

20%

30%

40%

50%

60%

1 - 2 2 - 3 3 - 4 4 - 5

Duration (# anni)

25

DISCLAIMER

This document, any presentation made in conjunction herewith and any accompanying materials are preliminary and for information only. They are not an offering memorandum, do not contain any representations and do not constitute or form part of an offer or invitation to subscribe for any of Niche's funds (each, the ”Fund”). Further they do not constitute or form part of any solicitation of any such offer or invitation, nor do they (or any part of them) or the fact of their distribution, form the basis of, or can they be relied on, in connection with any contract therefor. The information contained in this report has been compiled exclusively by Niche Asset Management Ltd which is authorised and regulated by the Financial Conduct Authority (RN783048) and is registered in England & Wales 10805355. The information and views contained in this document are not intended to be complete and may be subject to change at any time. No representation, warranty or undertaking, stated or implied, is given as to the accuracy of the information or views in this document and no liability for the accuracy and completeness of information is accepted by Niche Asset Management Ltd and/or its partners. The investment strategy of the Fund is speculative and involves a substantial degree of risk of losing some or all of the capital invested. Market, political, counterparty, liquidity and other risk factors may have a significant impact on the investment objectives of the Fund, while past performance is not a guide or otherwise indicative of future results. The distribution of this document and the offering of the Fund's shares in certain jurisdictions may be restricted by law and therefore persons into whose possession this document comes should inform themselves about and observe any such restrictions. The Fund is not yet available for distribution in all countries, it will be only subject to registration with the local supervisory Authority. Potential investors are invited to contact Niche Asset Management Ltd. in order to check registration countries. Any failure to comply with these restrictions could result in a violation of the laws of such jurisdiction. Any reproduction of this information, in whole or in part, without the prior consent of Niche Asset Management Ltd is also prohibited. This document may only be communicated or passed to persons to whom Niche Asset Management Ltd is permitted to communicate financial promotions pursuant to an exemption available in Chapter 4.12 of the Financial Conduct Authority’s Conduct of Business Sourcebook (“COBS”) (“Permitted Recipients”). In addition, no person who is not an authorised person may communicate this document or otherwise promote the Fund or shares therein to any person it the United Kingdom unless such person is both (a) a Permitted Recipient and (b) a person to whom an authorised person is permitted to communicate financial promotions relating to the Fund or otherwise promote the Fund under the rules in COBS 4.12 applicable to such authorised person. The securities referenced in this document have not been registered under the Securities Act of 1933 (the “1933 Act”) or any other securities laws of any other US jurisdiction. Such securities may not be sold or transferred to US persons unless such sale or transfer is registered under the 1933 Act or exemption from such registration. This document is intended for professional investors only. Potential investors are recommended to read carefully the Prospectus and the Key Investor Information Document (KIID) before subscribing.