Embed Size (px)

Citation preview

Global | Healthcare

Pharmaceuticals September 12, 2013

PharmaceuticalsRespiratory Market 2025: Taking A DeepBreath And A Deep Dive

EQU

ITY R

ESEARC

H G

LOB

AL

Jeffrey Holford, PhD, ACA *Equity Analyst

(212) 336-7409 [email protected] McManus, PhD §

Equity Analyst44 (0) 20 7029 8274 [email protected]

Ian Hilliker §Equity Analyst

44 (0) 20 7029 8672 [email protected] Ramakanth, PhD, MBA *

Equity Associate(212) 336-7054 [email protected]

David Gu, PhD *Equity Associate

(212) 336-7459 [email protected]

* Jefferies LLC § Jefferies International Limited

Key TakeawayWe present a deep dive on the respiratory market through to 2025, duringwhich we will see multiple new competitors, treatment modalities andincreased pressure from value brands and generics. We see near to mid termupside for GSK from new product launches, but a devastating hit from US Advairgenerics if launched by 2017. AZN's franchise is likely to be hit by increasedcompetition and generics, whilst NOVN looks only able to build a modestbranded franchise.

Taking a deep breath and a deep dive on the respiratory market: We have builta new Global Respiratory Model out to 2025, which primarily focuses on the inhaledrespiratory market for COPD and asthma. Our work includes input from the results of ourproprietary survey of 52 US based pulmonologists, physician consultations and discussionswith key market players. This market is critical to a number of companies under our coverage,with GlaxoSmithKline being particularly exposed as the market leader, with 19% of Grouprevenues in Advair/ Seretide alone. Other branded players such as AstraZeneca and Novartis(and Sandoz) also remain committed to this market in the long term.

We expect sluggish growth despite multiple new launches and positivedemographics: We forecast that the Global inhaled respiratory maintenance market willshow volume growth of just 2% over the period 2012A-2025E as combination therapiesbecome more prevalent, reducing the number of individual prescriptions per patient,despite positive demographic changes in Emerging Markets. We forecast only 1% revenuegrowth over the same period, reaching a peak of c$22bn in 2016E before the expectedcombined impact of non-substitutable generics for key products in Europe from 2014E andAB-rated substitutable Advair generics in the US from 2017E. However, we do expect thatthe market will return to revenue growth thereafter, driven by premium pricing for triplecombination therapy products in particular.

LABA/ ICS market set for the most change: The LABA/ ICS market for asthma andCOPD is dominated by GlaxoSmithKline's Advair and AstraZeneca's Symbicort. Our surveypredicts that GlaxoSmithKline's Breo Ellipta will become the leading LABA/ ICS brand forCOPD as soon as five years after launch. Despite some near term upside from new productlaunches and aggressive price increases for Advair (and Symbicort in parallel) to force theswitch onto Breo Ellipta, we forecast that the LABA/ ICS class will come under intensepressure from the launch of value brands and non-substitutable generics in Europe andsubstitutable Advair generics in the US (from late 2016E). Further pressure will likely comefrom the launch of the LABA/ LAMA class in the near term and then from LABA/ LAMA/ ICStriple combination products in the longer term.

New LABA/ LAMA class offers some switching potential and pricing upside: Ourproprietary physician survey and interviews indicate that pulmonologists are enthusiasticabout new fixed dose LABA/ LAMA offerings, such as GlaxoSmithKline's Anoro Ellipta,expecting this class to be prescribed to c20% of COPD patients five years after launch. Muchof the market share for this class is expected be gained from the LAMA class (e.g. BoehringerIngelheim's Spiriva). GlaxoSmithKline appears very well positioned in this class with likelyfirst-to-market status in the US, once-daily dosing and a premium device.

Stock implications: Company notes published in parallel and taking the implicationsof this report into account show a positive impact (3%-8%) to our GlaxoSmithKline EPSestimates between 2014E-16E, whilst our 2017E EPS estimate falls by 14% when US Advairgenerics are brought into the equation. Our AstraZeneca EPS estimates fall by 3%-12% across2014E-17E based on our work in this report (see separate company note), whilst our Novartisestimates are not impacted and we have made no formal changes to estimates.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflictof interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 40 to 43 of this report.

Executive Summary The $31bn Global respiratory market is likely to see a number of significant changes over

the next five to ten years as new players enter the market either with new branded or

generic products and existing players broaden their product offerings with new

combination products and devices. This market is critical to a number of companies under

our coverage, with GlaxoSmithKline (GSK LN, 1,629p, Hold) being particularly exposed as

the market leader, with 19% of Group revenues in Advair/ Seretide alone. Other branded

players such as AstraZeneca (AZN LN, 3,190p, Hold) and Novartis (NOVN VX, CHF71.35,

Buy) also remain committed to this market in the long term, whilst generics companies,

such as Mylan (MYL, $38.05, NC) and Novartis’ own Sandoz unit see significant potential

in virgin markets for generic products in the US and Europe.

Guided by a survey of 52 US based pulmonologists conducted in August 2013, we have

built out what we believe is the most contemporary and forward thinking Global

respiratory market models available to investors. The market is extremely complex and the

large number of moving pieces that we have had to consider have led us to make some

significant changes to our thinking on several key respiratory franchises as described in

detail in this report.

It is worth noting specifically at this point that we have mostly considered and evaluated

the Global inhaled maintenance respiratory market for COPD and asthma for the

purposes of this report (total value c$18bn in 2012A), which does exclude some product

classes. However, all of our company models reflect the entirety of their respiratory

franchises including other classes such as oral leukotriene D4 antagonists, corticosteroids,

antibody-based injectable therapeutics and short-acting beta-agonists.

The key implications for the respiratory market and individual companies considered

within this report are as follows:

We expect that the Global inhaled respiratory maintenance market will show

volume growth of just 2% over the period 2012A-2025E as combination

therapies become more prevalent, reducing the number of individual

prescriptions per patient. This driver is likely to be somewhat offset by price

increases for new combination products as well as positive demographics in

Emerging Market countries, where increased prevalence of smoking may act as a

strong volume driver over time. However, it remains unclear as to how well high

value branded products will fair in these markets,

We expect that the Global inhaled respiratory maintenance market will show

only 1% value growth over this period, reaching a peak of c$22bn in 2016E

before we anticipate the combined impact of non-substitutable generics for key

products in Europe from 2014E and AB-rated substitutable generics in the US

from 2017E. However, we do expect the market to begin to recover some value

growth thereafter, driven by premium pricing for triple combination therapy

products in particular,

We anticipate a strong shift towards fixed dose combination products such as

LABA/ LAMA and eventually LABA/ LAMA/ ICS (or MABA/ ICS) with patient

compliance, potential for increased efficacy and a better overall deal for payors

being strong drivers of this,

Healthcare

Pharmaceuticals

September 12, 2013

page 2 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

GlaxoSmithKline should see value growth in its respiratory franchise out to

2016E at least driven by strong US pricing behind Advair to help force switching

over to Breo Ellipta, as well as the launch of Anoro Ellipta. We expect that Anoro

Ellipta will gain significant share from the LAMA class in COPD, while putting

limited pressure on the LABA/ ICS and LABA alone classes. However, we see

significant destruction of value should substitutable generics launch in the US by

2017E, compounded by price referencing pressure from non-substitutable

generics in Europe from 2014E. As a result we have increased our key respiratory

combination franchise (Advair, Anoro Ellipta, Breo Ellipta) revenue estimates for

GlaxoSmithKline by 2%-17% from 2013E-16E, but have then reduced our 2017E

estimate by 25% due to the impact of US generics. From the Group context, this

and other updates (e.g. FX [negative impact of [1%-2%] and the setback on the

MAGE-A3 program) have led us to increase group revenue estimates by 0%-2%

from 2014E-16E and cut 2017E by 6%. From the perspective of Group EPS, we

have increased 2014E-16E EPS by 3%-8%, whilst lowering our 2017E EPS by

14%. We have cut our PT for GlaxoSmithKline to 1,750p from 1,800p and

reiterate our Hold rating (see separate company note also published today for

more details),

AstraZeneca should see slowing growth for its respiratory franchise from 2014E

as Symbicort volume is pressured by in-class competitors (Breo for COPD in the

US, value brands and potentially generics ex-US), and new class launches (LABA/

LAMA class). We expect AstraZeneca to increase the price of Symbicort in the US,

following expected Advair price increases by GlaxoSmithKline, which should

ensure franchise value growth through to 2016E. Volume pressure in the US and

ex-US, and price pressure ex-US will likely push the franchise into decline from

2016E, with the launch of Novartis’ LABA/ ICS QMF149 further adding to the

pressure on the franchise. We see significant pressure on Symbicort revenues

due should a substitutable generic of Advair launch in the US by 2017E,

compounded by price referencing pressure from non-substitutable LABA/ ICS

generics in Europe from 2014E. Whilst the launch of AstraZeneca’s LABA/ LAMA

PT003 will provide a new leg to the franchise, this will be a comparatively late

entrant to the class in 2016E. Revising our company model to reflect this and

other fine tuning, including updated FX, lowers our Group revenue

expectations by 0% to 7% and our CORE EPS numbers by 0% to 12% over the

forecast period. We have cut our PT for AstraZeneca to 2,850p from 3,200p and

reiterate our Hold rating (see separate company note also published today for

more details),

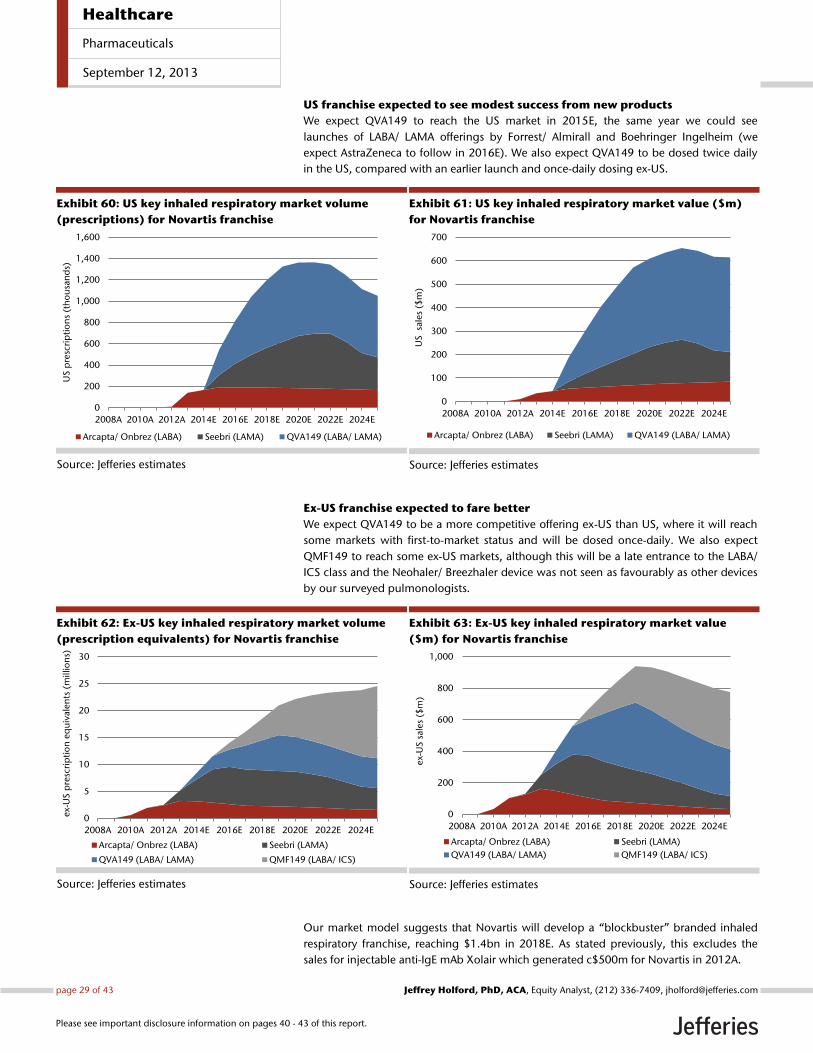

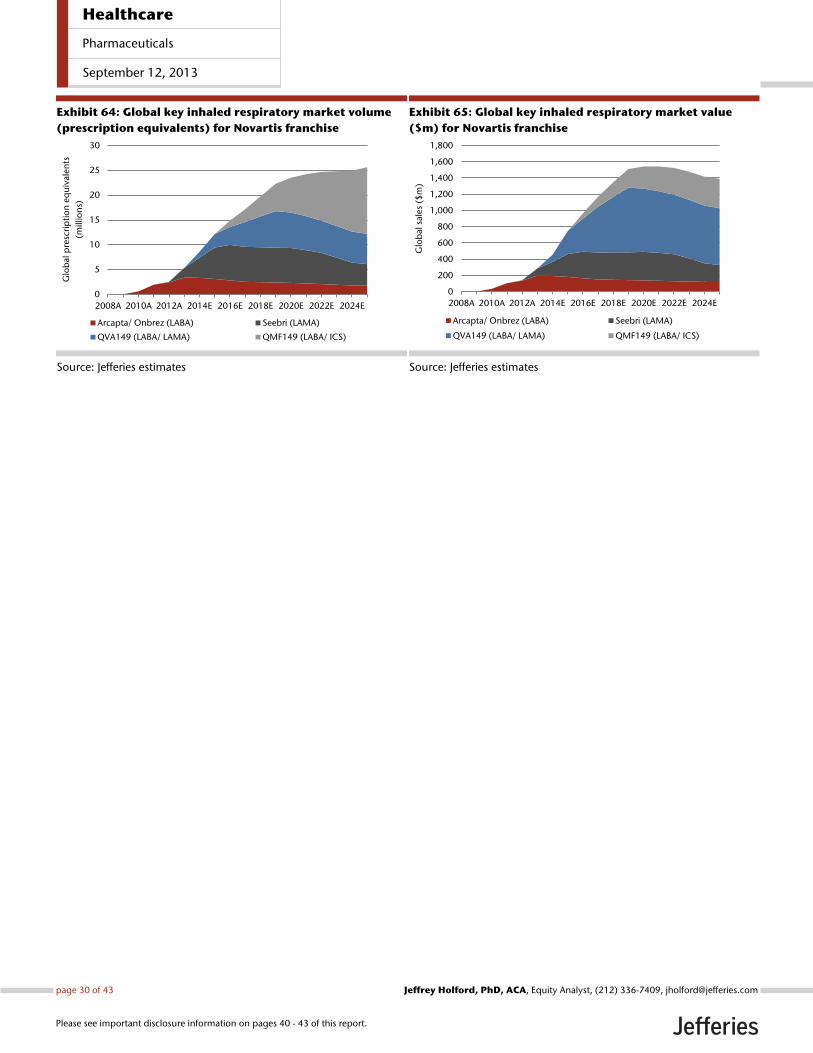

Novartis is a relative new market entrant in the inhaled respiratory market, with

its only significant marketed respiratory product to date being the injectable

anti-IgE mAb Xolair. We expect Novartis’ inhaled respiratory franchise to reach

‚blockbuster‛ status in 2017E. Our global therapy model and proprietary

pulmonologist survey suggests Novartis’ inhaled respiratory franchise (QVA149,

Arcapta, Seebri, QMF149) will struggle to meet current consensus expectations

which are looking for 2017E sales of $1.7bn. Regulatory delays in the US and an

inferior device (according to pulmonologists) will make it difficult for Novartis to

compete successfully in what has become a competitive market. At only 3% of

group sales in 2017E (including Xolair), we do not see the company’s

respiratory franchise as being a significant driver for investor sentiment in either

direction.

Healthcare

Pharmaceuticals

September 12, 2013

page 3 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

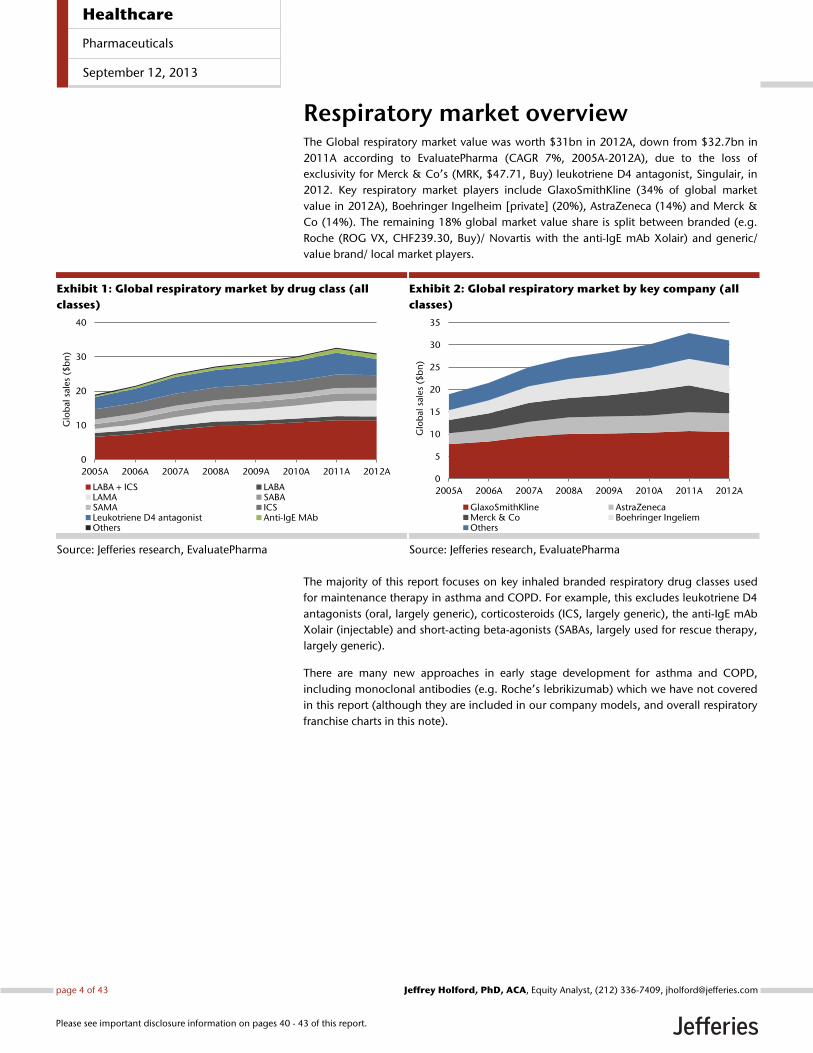

Respiratory market overview The Global respiratory market value was worth $31bn in 2012A, down from $32.7bn in

2011A according to EvaluatePharma (CAGR 7%, 2005A-2012A), due to the loss of

exclusivity for Merck & Co’s (MRK, $47.71, Buy) leukotriene D4 antagonist, Singulair, in

2012. Key respiratory market players include GlaxoSmithKline (34% of global market

value in 2012A), Boehringer Ingelheim [private] (20%), AstraZeneca (14%) and Merck &

Co (14%). The remaining 18% global market value share is split between branded (e.g.

Roche (ROG VX, CHF239.30, Buy)/ Novartis with the anti-IgE mAb Xolair) and generic/

value brand/ local market players.

Exhibit 1: Global respiratory market by drug class (all

classes)

Source: Jefferies research, EvaluatePharma

Exhibit 2: Global respiratory market by key company (all

classes)

Source: Jefferies research, EvaluatePharma

The majority of this report focuses on key inhaled branded respiratory drug classes used

for maintenance therapy in asthma and COPD. For example, this excludes leukotriene D4

antagonists (oral, largely generic), corticosteroids (ICS, largely generic), the anti-IgE mAb

Xolair (injectable) and short-acting beta-agonists (SABAs, largely used for rescue therapy,

largely generic).

There are many new approaches in early stage development for asthma and COPD,

including monoclonal antibodies (e.g. Roche’s lebrikizumab) which we have not covered

in this report (although they are included in our company models, and overall respiratory

franchise charts in this note).

0

10

20

30

40

2005A 2006A 2007A 2008A 2009A 2010A 2011A 2012A

Glo

bal

sale

s ($

bn

)

LABA + ICS LABALAMA SABASAMA ICSLeukotriene D4 antagonist Anti-IgE MAbOthers

0

5

10

15

20

25

30

35

2005A 2006A 2007A 2008A 2009A 2010A 2011A 2012A

Glo

bal

sale

s ($

bn

)

GlaxoSmithKline AstraZenecaMerck & Co Boehringer IngeliemOthers

Healthcare

Pharmaceuticals

September 12, 2013

page 4 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

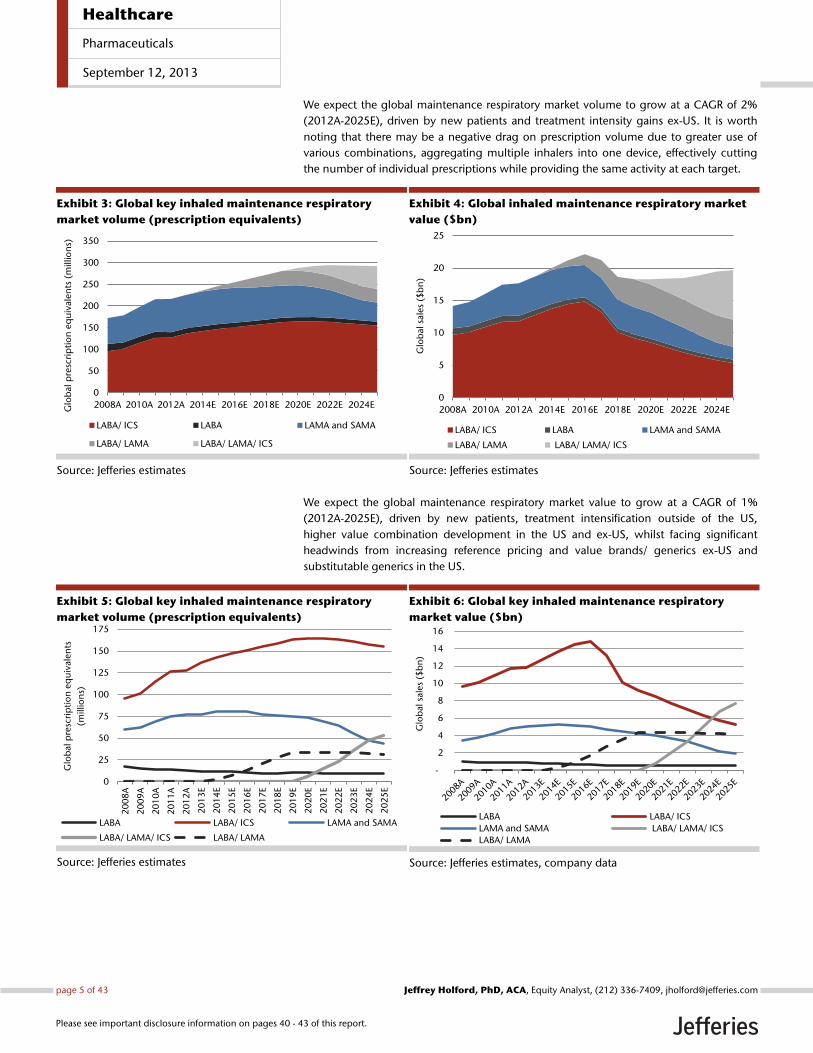

We expect the global maintenance respiratory market volume to grow at a CAGR of 2%

(2012A-2025E), driven by new patients and treatment intensity gains ex-US. It is worth

noting that there may be a negative drag on prescription volume due to greater use of

various combinations, aggregating multiple inhalers into one device, effectively cutting

the number of individual prescriptions while providing the same activity at each target.

Exhibit 3: Global key inhaled maintenance respiratory

market volume (prescription equivalents)

Source: Jefferies estimates

Exhibit 4: Global inhaled maintenance respiratory market

value ($bn)

Source: Jefferies estimates

We expect the global maintenance respiratory market value to grow at a CAGR of 1%

(2012A-2025E), driven by new patients, treatment intensification outside of the US,

higher value combination development in the US and ex-US, whilst facing significant

headwinds from increasing reference pricing and value brands/ generics ex-US and

substitutable generics in the US.

Exhibit 5: Global key inhaled maintenance respiratory

market volume (prescription equivalents)

Source: Jefferies estimates

Exhibit 6: Global key inhaled maintenance respiratory

market value ($bn)

Source: Jefferies estimates, company data

0

50

100

150

200

250

300

350

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024EGlo

bal

pre

scri

pti

on

eq

uiv

alen

ts (

mill

ion

s)

LABA/ ICS LABA LAMA and SAMA

LABA/ LAMA LABA/ LAMA/ ICS

0

5

10

15

20

25

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024EG

lob

al s

ale

s ($

bn

)LABA/ ICS LABA LAMA and SAMA

LABA/ LAMA LABA/ LAMA/ ICS

0

25

50

75

100

125

150

175

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Glo

bal

pre

scri

pti

on

eq

uiv

ale

nts

(mill

ion

s)

LABA LABA/ ICS LAMA and SAMA

LABA/ LAMA/ ICS LABA/ LAMA

-

2

4

6

8

10

12

14

16

Glo

bal

sale

s ($

bn

)

LABA LABA/ ICS

LAMA and SAMA LABA/ LAMA/ ICS

LABA/ LAMA

Healthcare

Pharmaceuticals

September 12, 2013

page 5 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

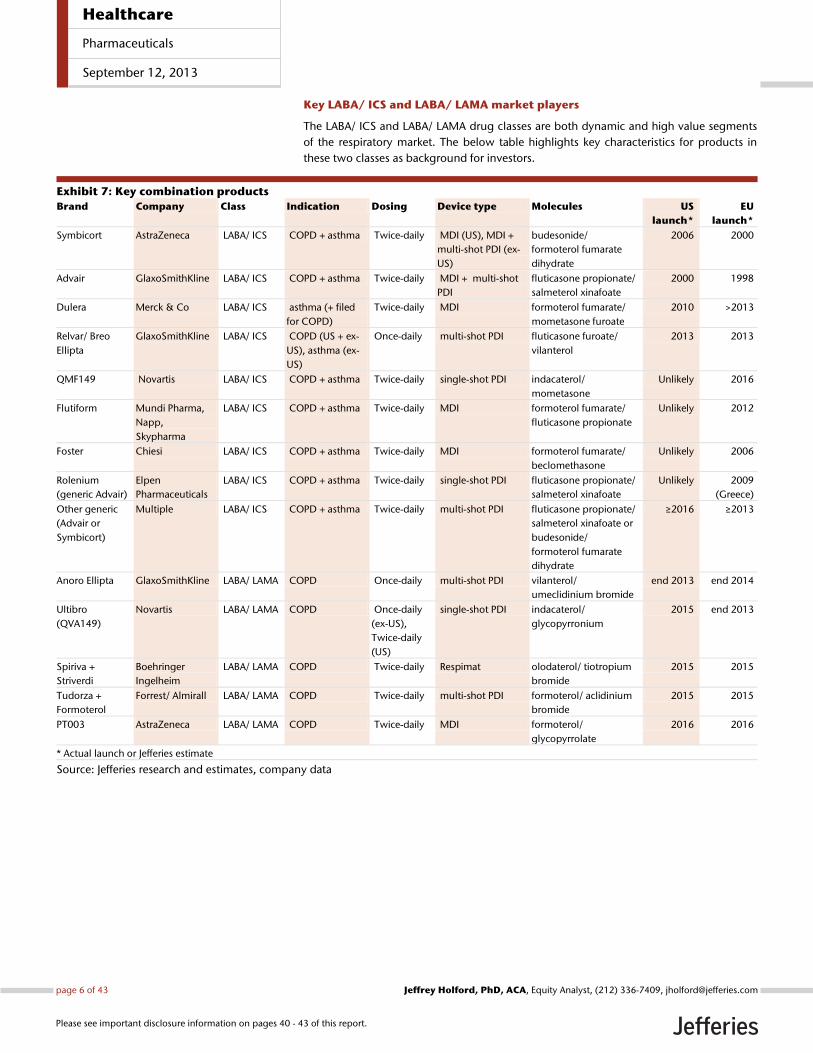

Key LABA/ ICS and LABA/ LAMA market players

The LABA/ ICS and LABA/ LAMA drug classes are both dynamic and high value segments

of the respiratory market. The below table highlights key characteristics for products in

these two classes as background for investors.

Exhibit 7: Key combination products

Brand Company Class Indication Dosing Device type Molecules US

launch*

EU

launch*

Symbicort AstraZeneca LABA/ ICS COPD + asthma Twice-daily MDI (US), MDI +

multi-shot PDI (ex-

US)

budesonide/

formoterol fumarate

dihydrate

2006 2000

Advair GlaxoSmithKline LABA/ ICS COPD + asthma Twice-daily MDI + multi-shot

PDI

fluticasone propionate/

salmeterol xinafoate

2000 1998

Dulera Merck & Co LABA/ ICS asthma (+ filed

for COPD)

Twice-daily MDI formoterol fumarate/

mometasone furoate

2010 >2013

Relvar/ Breo

Ellipta

GlaxoSmithKline LABA/ ICS COPD (US + ex-

US), asthma (ex-

US)

Once-daily multi-shot PDI fluticasone furoate/

vilanterol

2013 2013

QMF149 Novartis LABA/ ICS COPD + asthma Twice-daily single-shot PDI indacaterol/

mometasone

Unlikely 2016

Flutiform Mundi Pharma,

Napp,

Skypharma

LABA/ ICS COPD + asthma Twice-daily MDI formoterol fumarate/

fluticasone propionate

Unlikely 2012

Foster Chiesi LABA/ ICS COPD + asthma Twice-daily MDI formoterol fumarate/

beclomethasone

Unlikely 2006

Rolenium

(generic Advair)

Elpen

Pharmaceuticals

LABA/ ICS COPD + asthma Twice-daily single-shot PDI fluticasone propionate/

salmeterol xinafoate

Unlikely 2009

(Greece)

Other generic

(Advair or

Symbicort)

Multiple LABA/ ICS COPD + asthma Twice-daily multi-shot PDI fluticasone propionate/

salmeterol xinafoate or

budesonide/

formoterol fumarate

dihydrate

≥2016 ≥2013

Anoro Ellipta GlaxoSmithKline LABA/ LAMA COPD Once-daily multi-shot PDI vilanterol/

umeclidinium bromide

end 2013 end 2014

Ultibro

(QVA149)

Novartis LABA/ LAMA COPD Once-daily

(ex-US),

Twice-daily

(US)

single-shot PDI indacaterol/

glycopyrronium

2015 end 2013

Spiriva +

Striverdi

Boehringer

Ingelheim

LABA/ LAMA COPD Twice-daily Respimat olodaterol/ tiotropium

bromide

2015 2015

Tudorza +

Formoterol

Forrest/ Almirall LABA/ LAMA COPD Twice-daily multi-shot PDI formoterol/ aclidinium

bromide

2015 2015

PT003 AstraZeneca LABA/ LAMA COPD Twice-daily MDI formoterol/

glycopyrrolate

2016 2016

* Actual launch or Jefferies estimate

Source: Jefferies research and estimates, company data

Healthcare

Pharmaceuticals

September 12, 2013

page 6 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

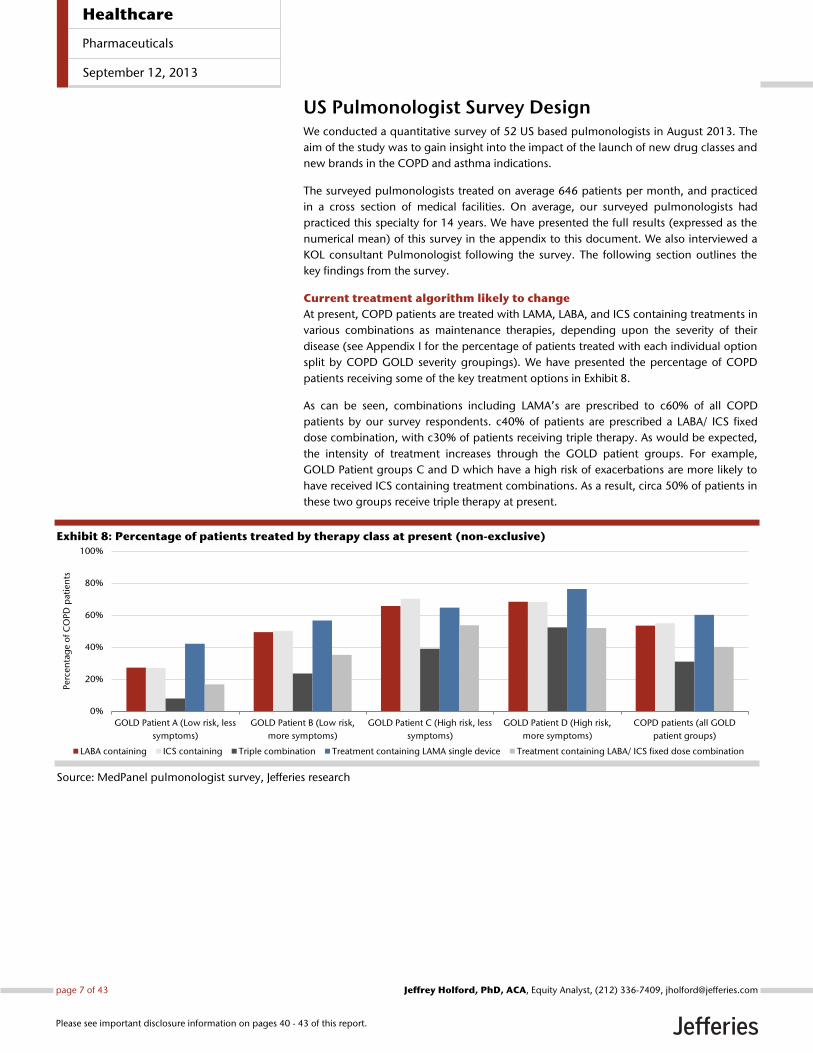

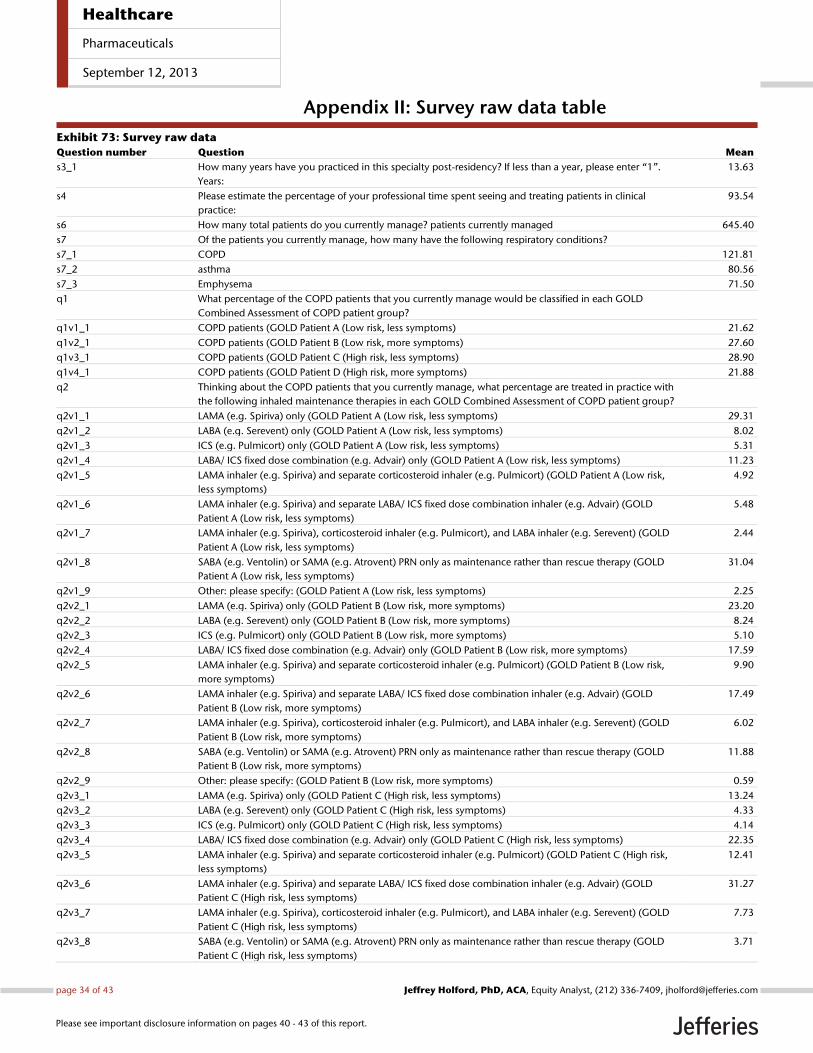

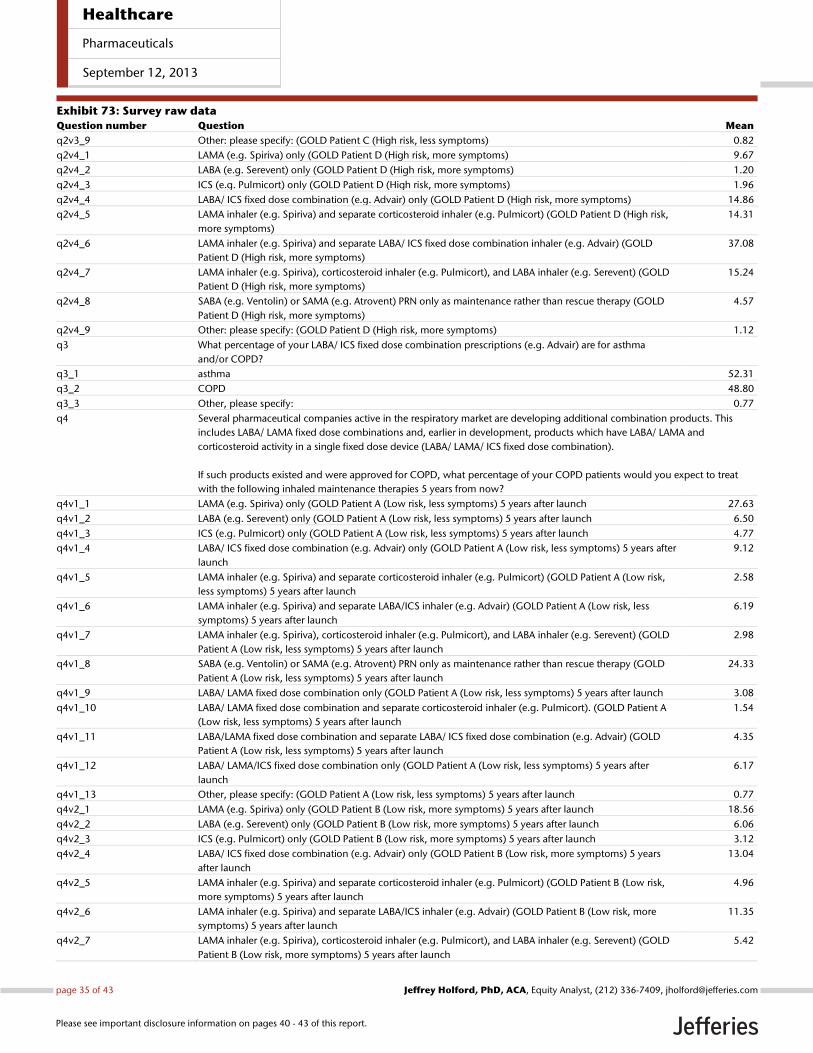

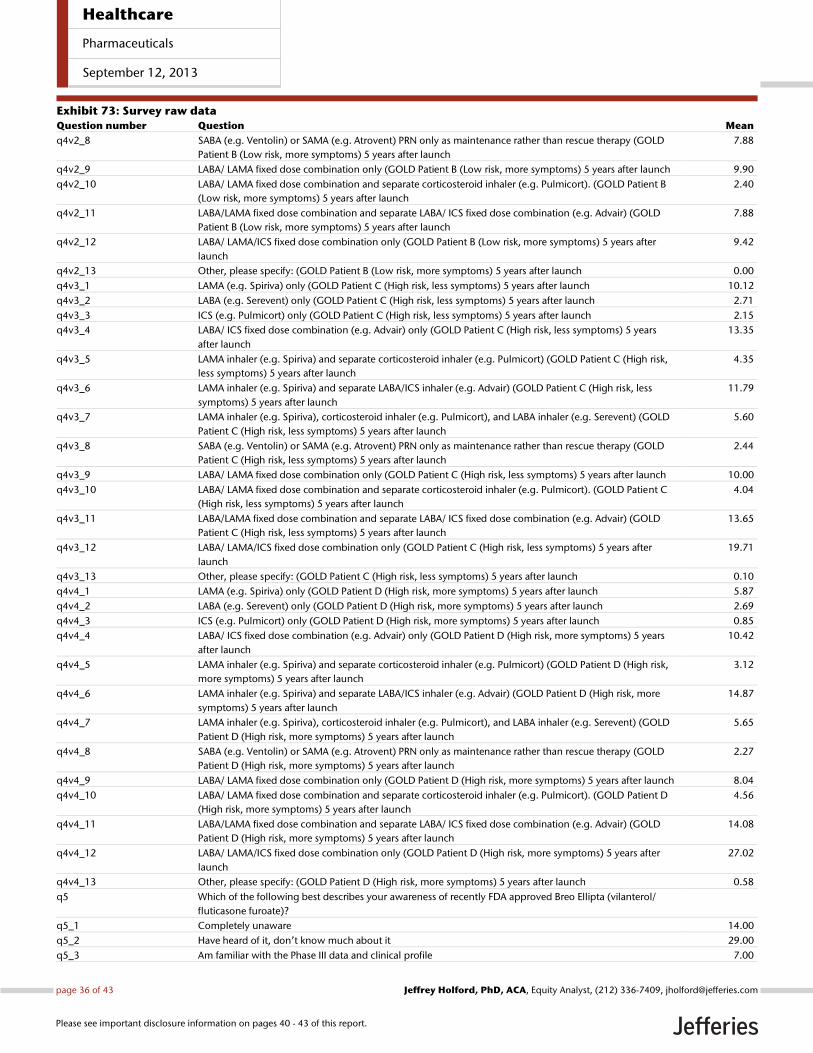

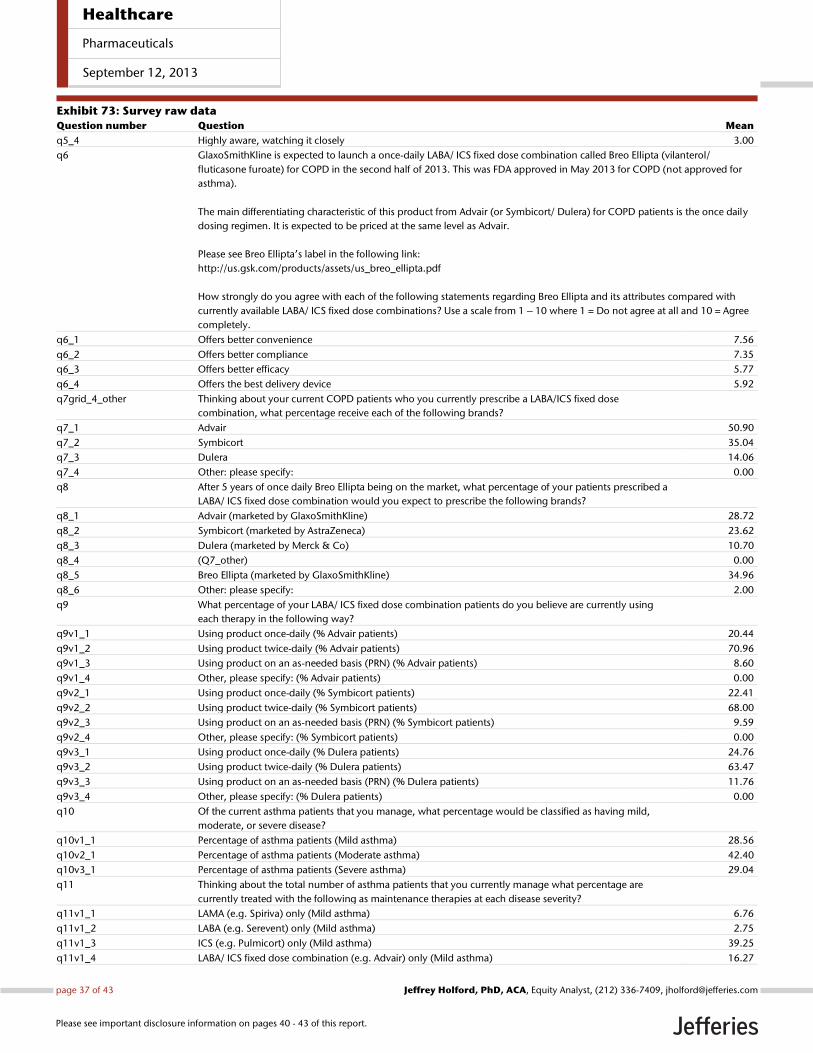

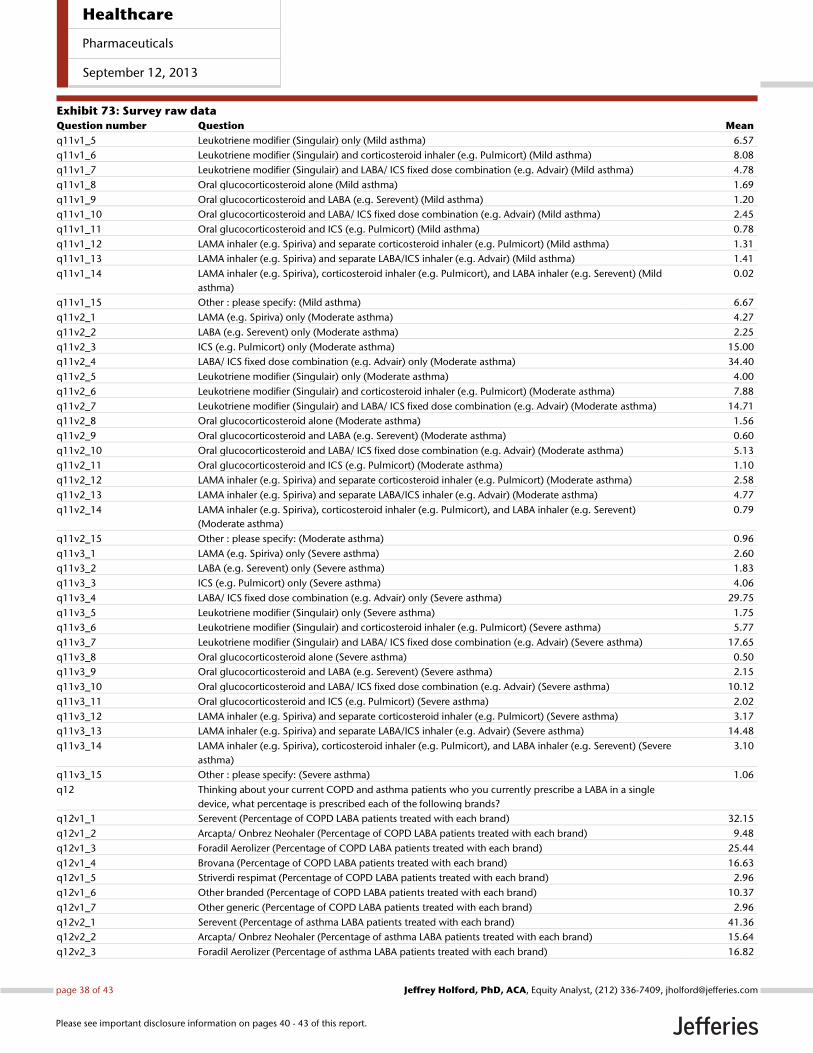

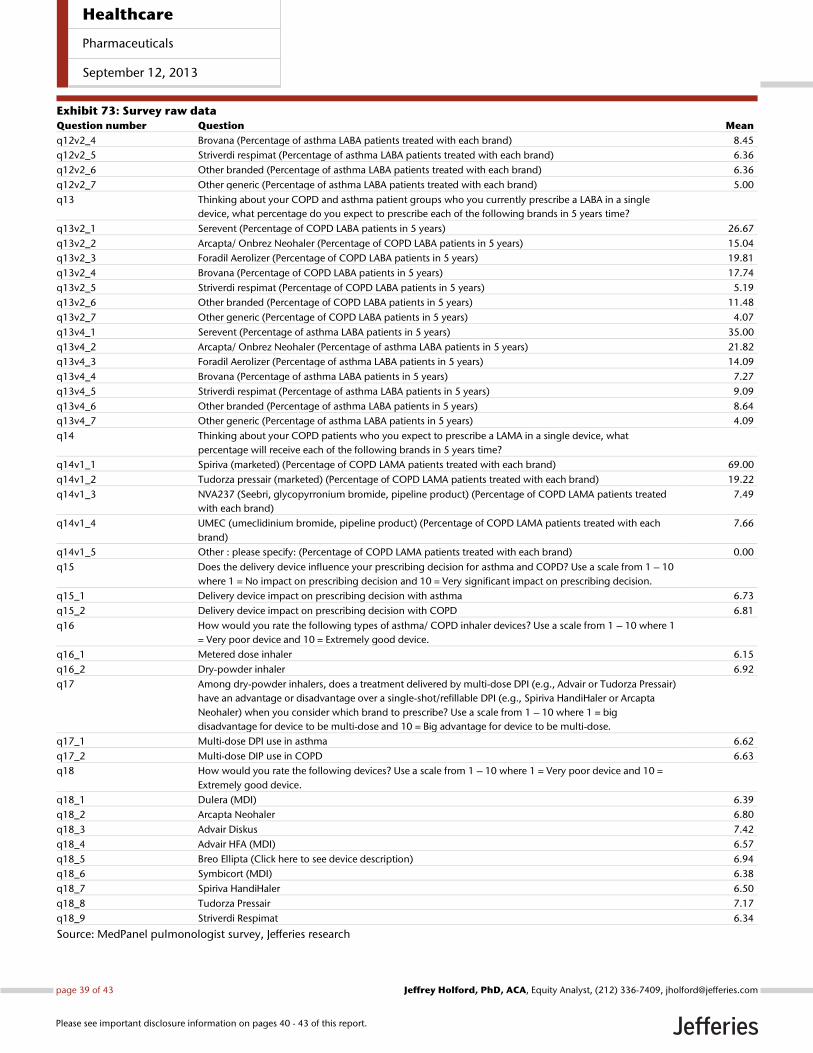

US Pulmonologist Survey Design We conducted a quantitative survey of 52 US based pulmonologists in August 2013. The

aim of the study was to gain insight into the impact of the launch of new drug classes and

new brands in the COPD and asthma indications.

The surveyed pulmonologists treated on average 646 patients per month, and practiced

in a cross section of medical facilities. On average, our surveyed pulmonologists had

practiced this specialty for 14 years. We have presented the full results (expressed as the

numerical mean) of this survey in the appendix to this document. We also interviewed a

KOL consultant Pulmonologist following the survey. The following section outlines the

key findings from the survey.

Current treatment algorithm likely to change

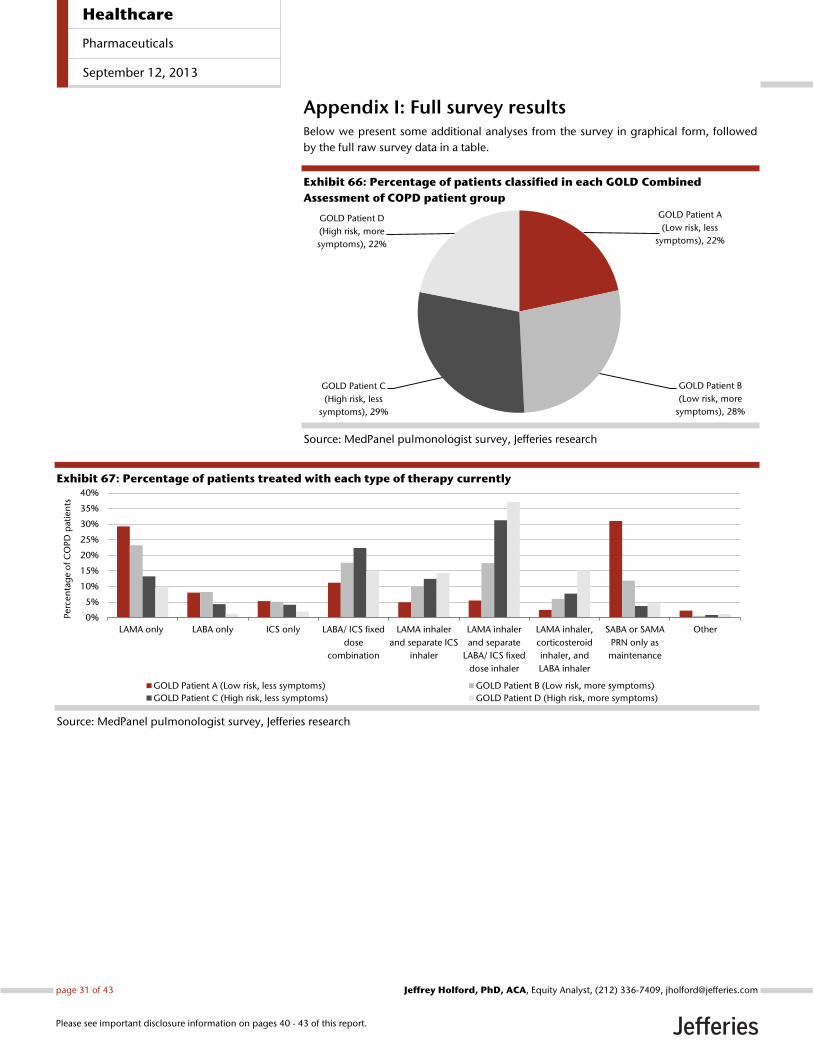

At present, COPD patients are treated with LAMA, LABA, and ICS containing treatments in

various combinations as maintenance therapies, depending upon the severity of their

disease (see Appendix I for the percentage of patients treated with each individual option

split by COPD GOLD severity groupings). We have presented the percentage of COPD

patients receiving some of the key treatment options in Exhibit 8.

As can be seen, combinations including LAMA’s are prescribed to c60% of all COPD

patients by our survey respondents. c40% of patients are prescribed a LABA/ ICS fixed

dose combination, with c30% of patients receiving triple therapy. As would be expected,

the intensity of treatment increases through the GOLD patient groups. For example,

GOLD Patient groups C and D which have a high risk of exacerbations are more likely to

have received ICS containing treatment combinations. As a result, circa 50% of patients in

these two groups receive triple therapy at present.

Exhibit 8: Percentage of patients treated by therapy class at present (non-exclusive)

Source: MedPanel pulmonologist survey, Jefferies research

0%

20%

40%

60%

80%

100%

GOLD Patient A (Low risk, less

symptoms)

GOLD Patient B (Low risk,

more symptoms)

GOLD Patient C (High risk, less

symptoms)

GOLD Patient D (High risk,

more symptoms)

COPD patients (all GOLD

patient groups)

Perc

en

tag

e o

f C

OP

D p

ati

en

ts

LABA containing ICS containing Triple combination Treatment containing LAMA single device Treatment containing LABA/ ICS fixed dose combination

Healthcare

Pharmaceuticals

September 12, 2013

page 7 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

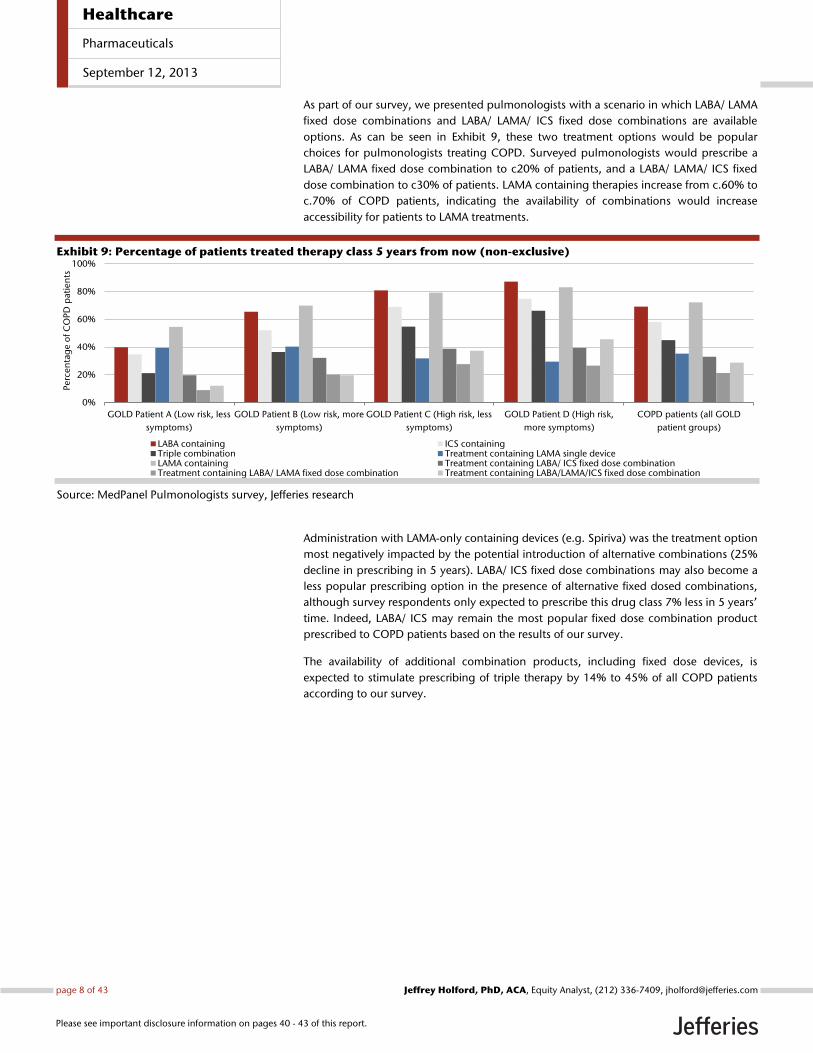

As part of our survey, we presented pulmonologists with a scenario in which LABA/ LAMA

fixed dose combinations and LABA/ LAMA/ ICS fixed dose combinations are available

options. As can be seen in Exhibit 9, these two treatment options would be popular

choices for pulmonologists treating COPD. Surveyed pulmonologists would prescribe a

LABA/ LAMA fixed dose combination to c20% of patients, and a LABA/ LAMA/ ICS fixed

dose combination to c30% of patients. LAMA containing therapies increase from c.60% to

c.70% of COPD patients, indicating the availability of combinations would increase

accessibility for patients to LAMA treatments.

Exhibit 9: Percentage of patients treated therapy class 5 years from now (non-exclusive)

Source: MedPanel Pulmonologists survey, Jefferies research

Administration with LAMA-only containing devices (e.g. Spiriva) was the treatment option

most negatively impacted by the potential introduction of alternative combinations (25%

decline in prescribing in 5 years). LABA/ ICS fixed dose combinations may also become a

less popular prescribing option in the presence of alternative fixed dosed combinations,

although survey respondents only expected to prescribe this drug class 7% less in 5 years’

time. Indeed, LABA/ ICS may remain the most popular fixed dose combination product

prescribed to COPD patients based on the results of our survey.

The availability of additional combination products, including fixed dose devices, is

expected to stimulate prescribing of triple therapy by 14% to 45% of all COPD patients

according to our survey.

0%

20%

40%

60%

80%

100%

GOLD Patient A (Low risk, less

symptoms)

GOLD Patient B (Low risk, more

symptoms)

GOLD Patient C (High risk, less

symptoms)

GOLD Patient D (High risk,

more symptoms)

COPD patients (all GOLD

patient groups)

Perc

en

tag

e o

f C

OP

D p

ati

en

ts

LABA containing ICS containingTriple combination Treatment containing LAMA single deviceLAMA containing Treatment containing LABA/ ICS fixed dose combinationTreatment containing LABA/ LAMA fixed dose combination Treatment containing LABA/LAMA/ICS fixed dose combination

Healthcare

Pharmaceuticals

September 12, 2013

page 8 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

Exhibit 10: Absolute change in prescribing for COPD therapies (non-exclusive) over the next 5 years

Source: MedPanel pulmonologist survey, Jefferies research

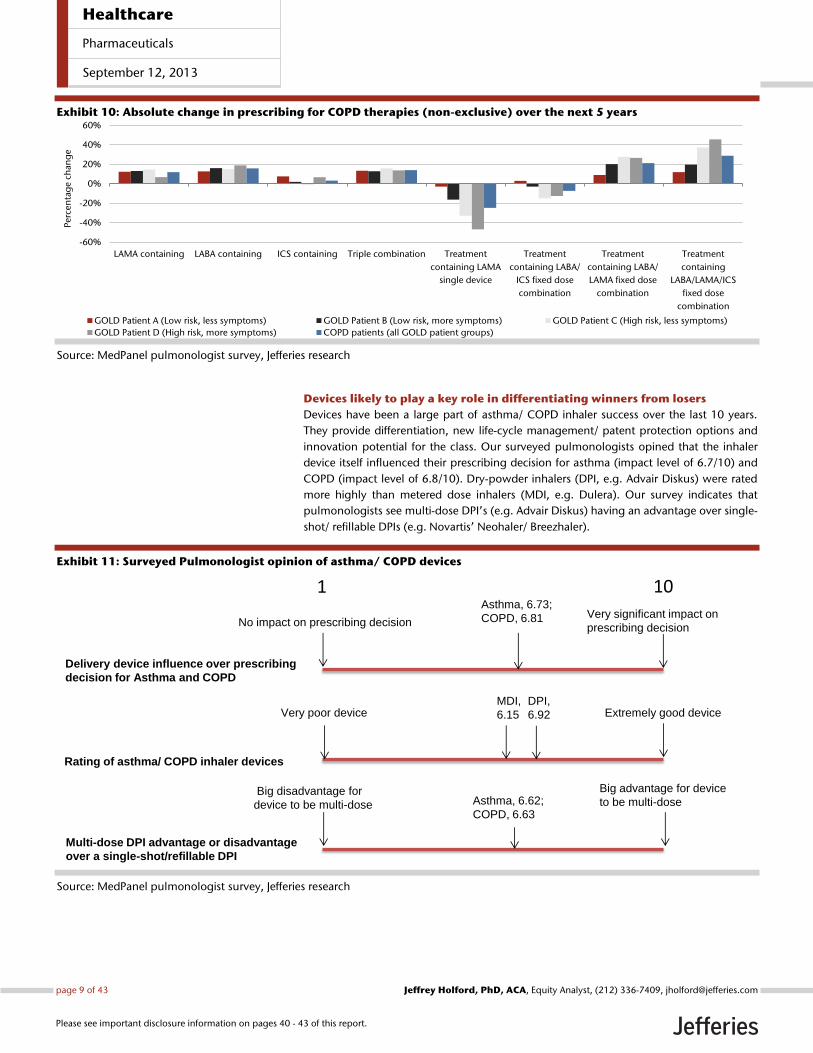

Devices likely to play a key role in differentiating winners from losers

Devices have been a large part of asthma/ COPD inhaler success over the last 10 years.

They provide differentiation, new life-cycle management/ patent protection options and

innovation potential for the class. Our surveyed pulmonologists opined that the inhaler

device itself influenced their prescribing decision for asthma (impact level of 6.7/10) and

COPD (impact level of 6.8/10). Dry-powder inhalers (DPI, e.g. Advair Diskus) were rated

more highly than metered dose inhalers (MDI, e.g. Dulera). Our survey indicates that

pulmonologists see multi-dose DPI’s (e.g. Advair Diskus) having an advantage over single-

shot/ refillable DPIs (e.g. Novartis’ Neohaler/ Breezhaler).

Exhibit 11: Surveyed Pulmonologist opinion of asthma/ COPD devices

Source: MedPanel pulmonologist survey, Jefferies research

-60%

-40%

-20%

0%

20%

40%

60%

LAMA containing LABA containing ICS containing Triple combination Treatment

containing LAMA

single device

Treatment

containing LABA/

ICS fixed dose

combination

Treatment

containing LABA/

LAMA fixed dose

combination

Treatment

containing

LABA/LAMA/ICS

fixed dose

combination

Perc

en

tag

e c

han

ge

GOLD Patient A (Low risk, less symptoms) GOLD Patient B (Low risk, more symptoms) GOLD Patient C (High risk, less symptoms)

GOLD Patient D (High risk, more symptoms) COPD patients (all GOLD patient groups)

Delivery device influence over prescribing

decision for Asthma and COPD

Rating of asthma/ COPD inhaler devices

Multi-dose DPI advantage or disadvantage

over a single-shot/refillable DPI

No impact on prescribing decisionVery significant impact on

prescribing decision

1 10

Very poor device Extremely good device

Big disadvantage for

device to be multi-dose

Big advantage for device

to be multi-dose

Asthma, 6.73;

COPD, 6.81

MDI,

6.15

DPI,

6.92

Asthma, 6.62;

COPD, 6.63

Healthcare

Pharmaceuticals

September 12, 2013

page 9 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

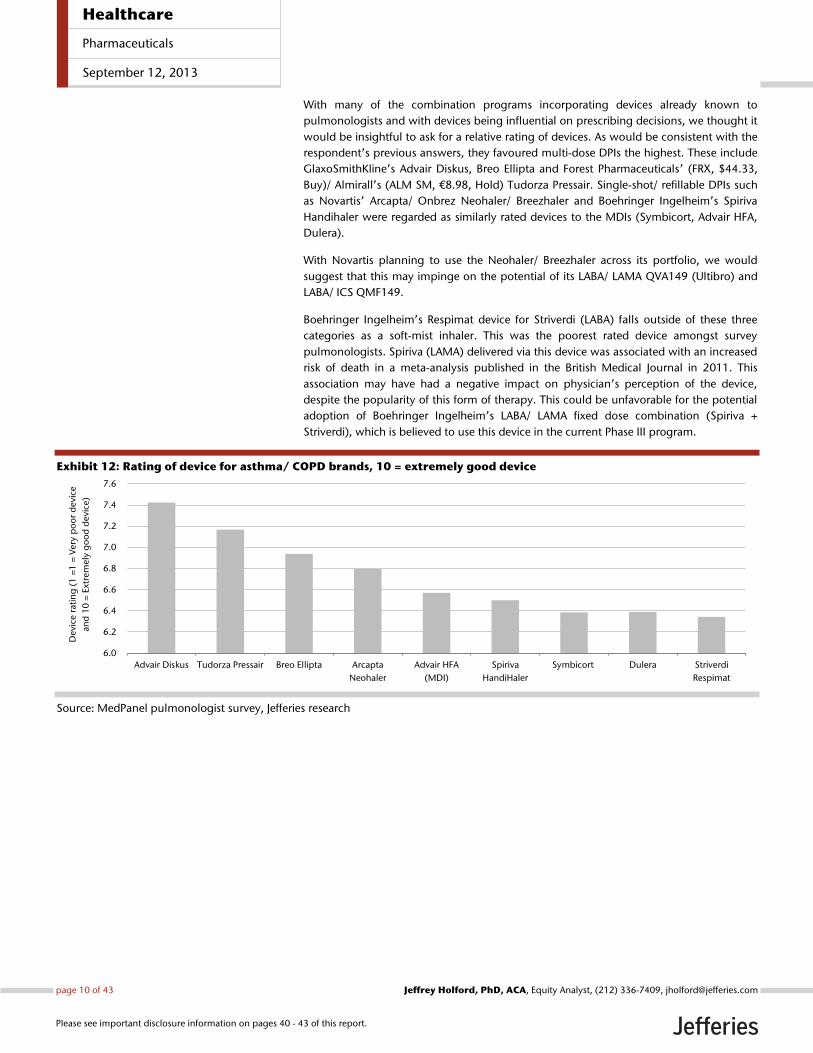

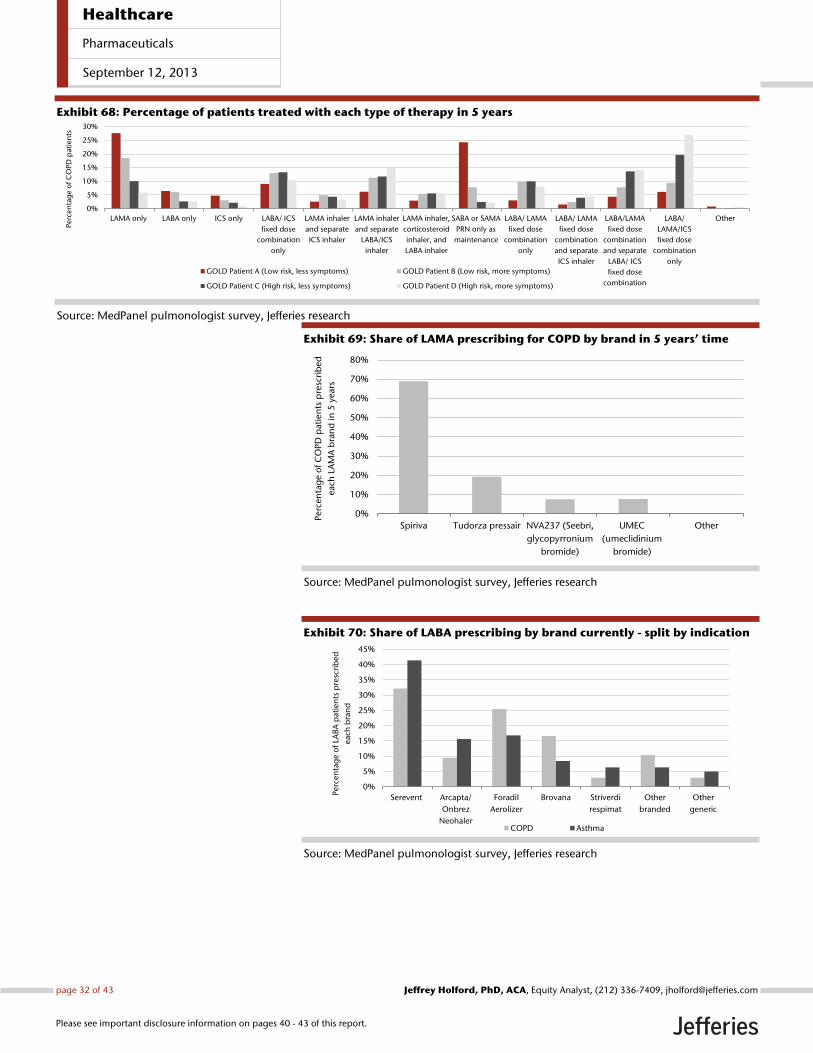

With many of the combination programs incorporating devices already known to

pulmonologists and with devices being influential on prescribing decisions, we thought it

would be insightful to ask for a relative rating of devices. As would be consistent with the

respondent’s previous answers, they favoured multi-dose DPIs the highest. These include

GlaxoSmithKline’s Advair Diskus, Breo Ellipta and Forest Pharmaceuticals’ (FRX, $44.33,

Buy)/ Almirall’s (ALM SM, €8.98, Hold) Tudorza Pressair. Single-shot/ refillable DPIs such

as Novartis’ Arcapta/ Onbrez Neohaler/ Breezhaler and Boehringer Ingelheim’s Spiriva

Handihaler were regarded as similarly rated devices to the MDIs (Symbicort, Advair HFA,

Dulera).

With Novartis planning to use the Neohaler/ Breezhaler across its portfolio, we would

suggest that this may impinge on the potential of its LABA/ LAMA QVA149 (Ultibro) and

LABA/ ICS QMF149.

Boehringer Ingelheim’s Respimat device for Striverdi (LABA) falls outside of these three

categories as a soft-mist inhaler. This was the poorest rated device amongst survey

pulmonologists. Spiriva (LAMA) delivered via this device was associated with an increased

risk of death in a meta-analysis published in the British Medical Journal in 2011. This

association may have had a negative impact on physician’s perception of the device,

despite the popularity of this form of therapy. This could be unfavorable for the potential

adoption of Boehringer Ingelheim’s LABA/ LAMA fixed dose combination (Spiriva +

Striverdi), which is believed to use this device in the current Phase III program.

Exhibit 12: Rating of device for asthma/ COPD brands, 10 = extremely good device

Source: MedPanel pulmonologist survey, Jefferies research

6.0

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

Advair Diskus Tudorza Pressair Breo Ellipta Arcapta

Neohaler

Advair HFA

(MDI)

Spiriva

HandiHaler

Symbicort Dulera Striverdi

Respimat

Devi

ce r

atin

g (

1 =

1 =

Very

po

or

devi

ce

and

10

= E

xtre

mely

go

od

devi

ce)

Healthcare

Pharmaceuticals

September 12, 2013

page 10 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

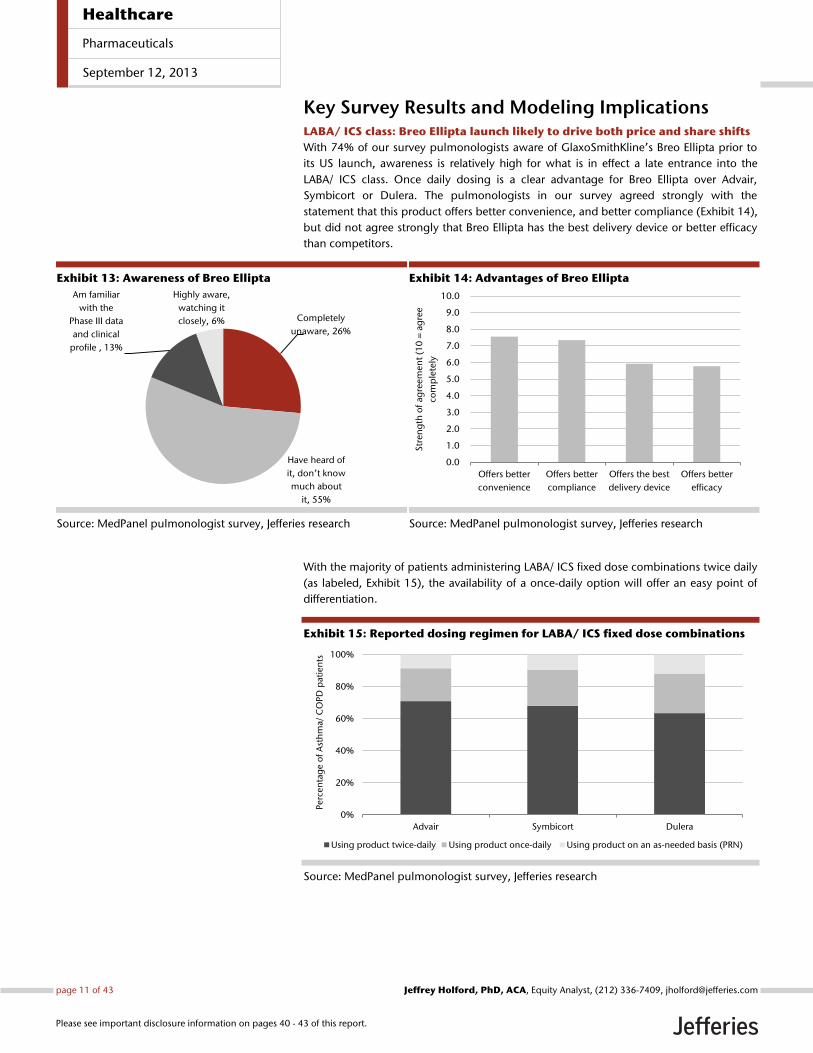

Key Survey Results and Modeling Implications LABA/ ICS class: Breo Ellipta launch likely to drive both price and share shifts

With 74% of our survey pulmonologists aware of GlaxoSmithKline’s Breo Ellipta prior to

its US launch, awareness is relatively high for what is in effect a late entrance into the

LABA/ ICS class. Once daily dosing is a clear advantage for Breo Ellipta over Advair,

Symbicort or Dulera. The pulmonologists in our survey agreed strongly with the

statement that this product offers better convenience, and better compliance (Exhibit 14),

but did not agree strongly that Breo Ellipta has the best delivery device or better efficacy

than competitors.

Exhibit 13: Awareness of Breo Ellipta

Source: MedPanel pulmonologist survey, Jefferies research

Exhibit 14: Advantages of Breo Ellipta

Source: MedPanel pulmonologist survey, Jefferies research

With the majority of patients administering LABA/ ICS fixed dose combinations twice daily

(as labeled, Exhibit 15), the availability of a once-daily option will offer an easy point of

differentiation.

Exhibit 15: Reported dosing regimen for LABA/ ICS fixed dose combinations

Source: MedPanel pulmonologist survey, Jefferies research

Completely

unaware, 26%

Have heard of

it, don’t know

much about

it, 55%

Am familiar

with the

Phase III data

and clinical

profile , 13%

Highly aware,

watching it

closely, 6%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Offers better

convenience

Offers better

compliance

Offers the best

delivery device

Offers better

efficacy

Str

en

gth

of

agre

em

en

t (1

0 =

ag

ree

com

ple

tely

0%

20%

40%

60%

80%

100%

Advair Symbicort Dulera

Perc

en

tag

e o

f A

sth

ma/

CO

PD

pati

en

ts

Using product twice-daily Using product once-daily Using product on an as-needed basis (PRN)

Healthcare

Pharmaceuticals

September 12, 2013

page 11 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

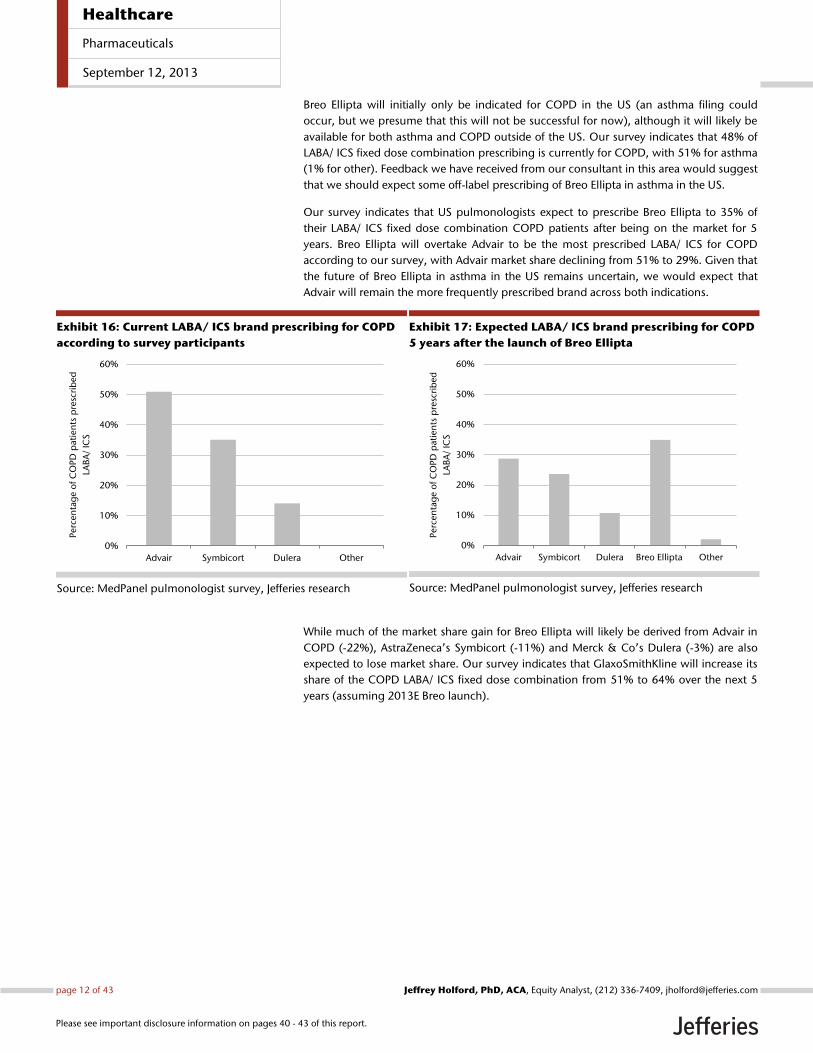

Breo Ellipta will initially only be indicated for COPD in the US (an asthma filing could

occur, but we presume that this will not be successful for now), although it will likely be

available for both asthma and COPD outside of the US. Our survey indicates that 48% of

LABA/ ICS fixed dose combination prescribing is currently for COPD, with 51% for asthma

(1% for other). Feedback we have received from our consultant in this area would suggest

that we should expect some off-label prescribing of Breo Ellipta in asthma in the US.

Our survey indicates that US pulmonologists expect to prescribe Breo Ellipta to 35% of

their LABA/ ICS fixed dose combination COPD patients after being on the market for 5

years. Breo Ellipta will overtake Advair to be the most prescribed LABA/ ICS for COPD

according to our survey, with Advair market share declining from 51% to 29%. Given that

the future of Breo Ellipta in asthma in the US remains uncertain, we would expect that

Advair will remain the more frequently prescribed brand across both indications.

Exhibit 16: Current LABA/ ICS brand prescribing for COPD

according to survey participants

Source: MedPanel pulmonologist survey, Jefferies research

Exhibit 17: Expected LABA/ ICS brand prescribing for COPD

5 years after the launch of Breo Ellipta

Source: MedPanel pulmonologist survey, Jefferies research

While much of the market share gain for Breo Ellipta will likely be derived from Advair in

COPD (-22%), AstraZeneca’s Symbicort (-11%) and Merck & Co’s Dulera (-3%) are also

expected to lose market share. Our survey indicates that GlaxoSmithKline will increase its

share of the COPD LABA/ ICS fixed dose combination from 51% to 64% over the next 5

years (assuming 2013E Breo launch).

0%

10%

20%

30%

40%

50%

60%

Advair Symbicort Dulera Other

Perc

en

tag

e o

f C

OP

D p

ati

en

ts p

resc

rib

ed

LAB

A/

ICS

0%

10%

20%

30%

40%

50%

60%

Advair Symbicort Dulera Breo Ellipta Other

Perc

en

tag

e o

f C

OP

D p

ati

en

ts p

resc

rib

ed

LAB

A/

ICS

Healthcare

Pharmaceuticals

September 12, 2013

page 12 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

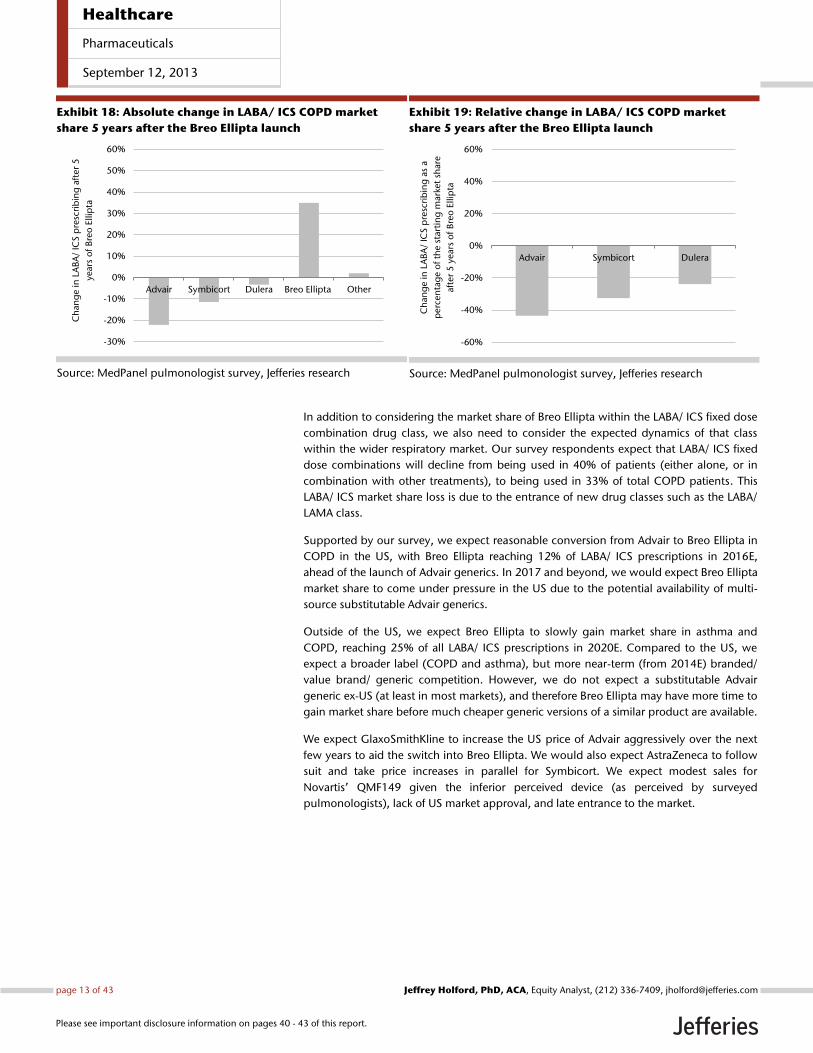

Exhibit 18: Absolute change in LABA/ ICS COPD market

share 5 years after the Breo Ellipta launch

Source: MedPanel pulmonologist survey, Jefferies research

Exhibit 19: Relative change in LABA/ ICS COPD market

share 5 years after the Breo Ellipta launch

Source: MedPanel pulmonologist survey, Jefferies research

In addition to considering the market share of Breo Ellipta within the LABA/ ICS fixed dose

combination drug class, we also need to consider the expected dynamics of that class

within the wider respiratory market. Our survey respondents expect that LABA/ ICS fixed

dose combinations will decline from being used in 40% of patients (either alone, or in

combination with other treatments), to being used in 33% of total COPD patients. This

LABA/ ICS market share loss is due to the entrance of new drug classes such as the LABA/

LAMA class.

Supported by our survey, we expect reasonable conversion from Advair to Breo Ellipta in

COPD in the US, with Breo Ellipta reaching 12% of LABA/ ICS prescriptions in 2016E,

ahead of the launch of Advair generics. In 2017 and beyond, we would expect Breo Ellipta

market share to come under pressure in the US due to the potential availability of multi-

source substitutable Advair generics.

Outside of the US, we expect Breo Ellipta to slowly gain market share in asthma and

COPD, reaching 25% of all LABA/ ICS prescriptions in 2020E. Compared to the US, we

expect a broader label (COPD and asthma), but more near-term (from 2014E) branded/

value brand/ generic competition. However, we do not expect a substitutable Advair

generic ex-US (at least in most markets), and therefore Breo Ellipta may have more time to

gain market share before much cheaper generic versions of a similar product are available.

We expect GlaxoSmithKline to increase the US price of Advair aggressively over the next

few years to aid the switch into Breo Ellipta. We would also expect AstraZeneca to follow

suit and take price increases in parallel for Symbicort. We expect modest sales for

Novartis’ QMF149 given the inferior perceived device (as perceived by surveyed

pulmonologists), lack of US market approval, and late entrance to the market.

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Advair Symbicort Dulera Breo Ellipta Other

Ch

ang

e in

LA

BA

/ IC

S p

resc

rib

ing

aft

er

5

year

s o

f B

reo

Ellip

ta

-60%

-40%

-20%

0%

20%

40%

60%

Advair Symbicort Dulera

Ch

an

ge in

LA

BA

/ IC

S p

resc

rib

ing

as

a

perc

en

tag

e o

f th

e s

tart

ing

mark

et

share

aft

er

5 y

ears

of

Bre

o E

llip

ta

Healthcare

Pharmaceuticals

September 12, 2013

page 13 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

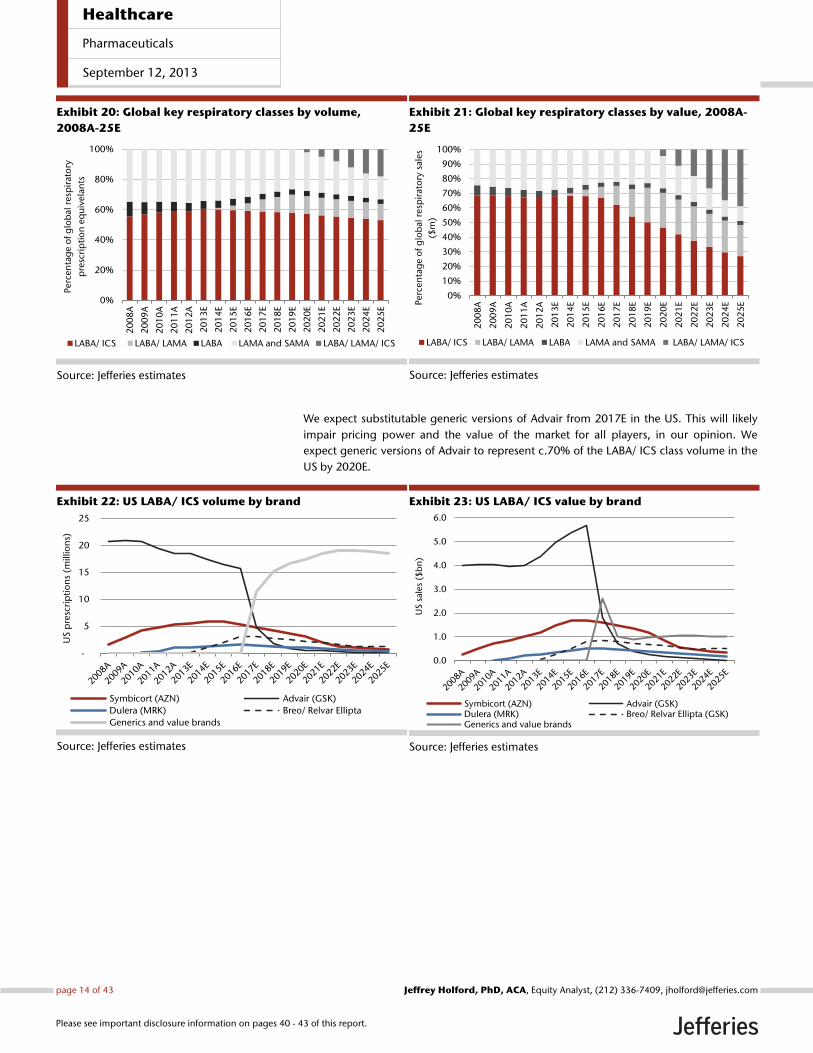

Exhibit 20: Global key respiratory classes by volume,

2008A-25E

Source: Jefferies estimates

Exhibit 21: Global key respiratory classes by value, 2008A-

25E

Source: Jefferies estimates

We expect substitutable generic versions of Advair from 2017E in the US. This will likely

impair pricing power and the value of the market for all players, in our opinion. We

expect generic versions of Advair to represent c.70% of the LABA/ ICS class volume in the

US by 2020E.

Exhibit 22: US LABA/ ICS volume by brand

Source: Jefferies estimates

Exhibit 23: US LABA/ ICS value by brand

Source: Jefferies estimates

0%

20%

40%

60%

80%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Perc

en

tag

e o

f g

lob

al r

esp

irat

ory

pre

scri

pti

on

eq

uiv

ela

nts

LABA/ ICS LABA/ LAMA LABA LAMA and SAMA LABA/ LAMA/ ICS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

EPerc

en

tag

e o

f g

lob

al

resp

irato

ry s

ale

s

($m

)

LABA/ ICS LABA/ LAMA LABA LAMA and SAMA LABA/ LAMA/ ICS

-

5

10

15

20

25

US

pre

scri

pti

on

s (m

illio

ns)

Symbicort (AZN) Advair (GSK)

Dulera (MRK) Breo/ Relvar Ellipta

Generics and value brands

0.0

1.0

2.0

3.0

4.0

5.0

6.0

US

sale

s ($

bn

)

Symbicort (AZN) Advair (GSK)Dulera (MRK) Breo/ Relvar Ellipta (GSK)Generics and value brands

Healthcare

Pharmaceuticals

September 12, 2013

page 14 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

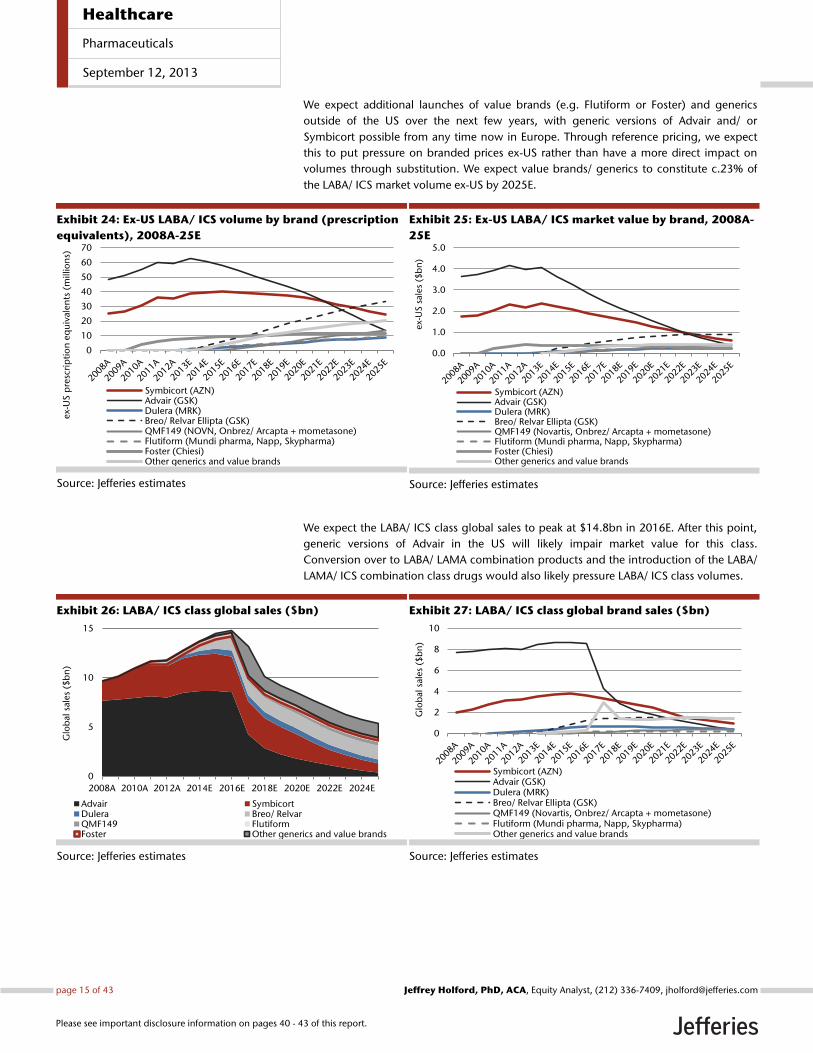

We expect additional launches of value brands (e.g. Flutiform or Foster) and generics

outside of the US over the next few years, with generic versions of Advair and/ or

Symbicort possible from any time now in Europe. Through reference pricing, we expect

this to put pressure on branded prices ex-US rather than have a more direct impact on

volumes through substitution. We expect value brands/ generics to constitute c.23% of

the LABA/ ICS market volume ex-US by 2025E.

Exhibit 24: Ex-US LABA/ ICS volume by brand (prescription

equivalents), 2008A-25E

Source: Jefferies estimates

Exhibit 25: Ex-US LABA/ ICS market value by brand, 2008A-

25E

Source: Jefferies estimates

We expect the LABA/ ICS class global sales to peak at $14.8bn in 2016E. After this point,

generic versions of Advair in the US will likely impair market value for this class.

Conversion over to LABA/ LAMA combination products and the introduction of the LABA/

LAMA/ ICS combination class drugs would also likely pressure LABA/ ICS class volumes.

Exhibit 26: LABA/ ICS class global sales ($bn)

Source: Jefferies estimates

Exhibit 27: LABA/ ICS class global brand sales ($bn)

Source: Jefferies estimates

0

10

20

30

40

50

60

70

ex-

US

pre

scri

pti

on

eq

uiv

alen

ts (

mill

ion

s)

Symbicort (AZN)Advair (GSK)Dulera (MRK)Breo/ Relvar Ellipta (GSK)QMF149 (NOVN, Onbrez/ Arcapta + mometasone)Flutiform (Mundi pharma, Napp, Skypharma)Foster (Chiesi)Other generics and value brands

0.0

1.0

2.0

3.0

4.0

5.0

ex-

US

sale

s ($

bn

)

Symbicort (AZN)Advair (GSK)Dulera (MRK)Breo/ Relvar Ellipta (GSK)QMF149 (Novartis, Onbrez/ Arcapta + mometasone)Flutiform (Mundi pharma, Napp, Skypharma)Foster (Chiesi)Other generics and value brands

0

5

10

15

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

Glo

bal

sal

es

($b

n)

Advair SymbicortDulera Breo/ RelvarQMF149 FlutiformFoster Other generics and value brands

0

2

4

6

8

10

Glo

bal

sale

s ($

bn

)

Symbicort (AZN)Advair (GSK)Dulera (MRK)Breo/ Relvar Ellipta (GSK)QMF149 (Novartis, Onbrez/ Arcapta + mometasone)Flutiform (Mundi pharma, Napp, Skypharma)Other generics and value brands

Healthcare

Pharmaceuticals

September 12, 2013

page 15 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

LABA/ LAMA class: Enter Anoro Ellipta

The pulmonologists included in our survey expect to prescribe a LABA/ LAMA fixed dose

combination to c20% of COPD patients in five years’ time. This would either be as a

standalone product, or in combination with an ICS to produce an alternative form of

triple therapy. The majority of patients at low risk of exacerbation (GOLD patient groups A

and B) do not receive ICS treatment at present according to pulmonologists (c.60%).

Feedback from our consultant suggests that treatment with an ICS adds little or no benefit

in these patients, but offers the potential for side effects. Therefore in these patients, a

once-daily LABA/ LAMA could offer a safer, convenient, and effective alternative. Indeed,

this would be in line with the current GOLD recommendations.

At present our survey suggests that c27% and 50% of GOLD patient group A and B

patients, respectively, are receiving an ICS, the majority of which is through use of a

LABA/ ICS fixed dose inhaler. Our consultant suggests that in order to achieved LAMA and

LABA therapy, combining a LABA/ ICS and LAMA is sometimes conducted because of a

lack of good LABA single device options. He also mentioned that the recent launch of

Novartis’ Arcapta/ Onbrez Neohaler/ Breezhaler has meant that combination use with

Spiriva to achieve LABA/ LAMA therapy has become an alternative option in GOLD patient

group A and B patients which do not require ICS treatment. We therefore believe that the

availability a LABA/ LAMA fixed dose combination (starting with GlaxoSmithKline’s Anoro

Ellipta in the US, and Novartis’ QVA149 ex-US) will be welcomed by pulmonologists

because it offers a convenient route to dual therapy in a single modern device.

Triple combination could also be achieved with Anoro Ellipta and potentially a generic

ICS. This would offer potentially a much cheaper option than the most popular route to

achieving this outcome at present which is Advair/ Symbicort + Spiriva. In addition, triple

therapy could be achieved by combining Anoro Ellipta with GlaxoSmithKline’s new ICS

fluticasone furoate (although likely off-label, currently in Phase III for Asthma only), to

achieve triple therapy with once-daily dosing.

The potential to achieve cheaper and more convenient triple therapy, and the formation

of this new class, underpins our expectation for a price premium for Anoro Ellipta over

Advair/ Breo Ellipta (c40% premium to Advair in 2014).

GlaxoSmithKline may have to tread carefully when launching Anoro Ellipta. It would be

potentially damaging to market Anoro as a ‚safer‛ alternative to triple therapy when it

has so much at stake in the LABA/ ICS class. Nevertheless, our survey suggests that a clear

role for LABA/ LAMA monotherapy is present and formation of an alternative triple

therapy regime is also a possibility in the future for patients with different stages of COPD.

We would expect Anoro Ellipta to be the market leading LABA/ LAMA due to its once-daily

dosing, first-to-market status (in the US), and multi-dose DPI device. Novartis’ QVA149 is

likely to be administered twice daily in the US, as is Forest/ Almirall’s Tudorza +

Formoterol, AstraZeneca’s PT003, and Boehringer Ingelheim’s Spiriva + Striverdi.

We would expect aggressive marketing from Forest/ Almirall and Boehringer Ingelheim in

the LABA/ LAMA class. Unlike GlaxoSmithKline/ AstraZeneca, they will potentially be able

to describe ICS use in low exacerbation risk patients as inappropriate when detailing

LABA/ LAMA as a safer option to triple therapy in this patient group. Novartis would also

potentially be able to employ this strategy in the US where it is not expected to file

QMF149 for approval.

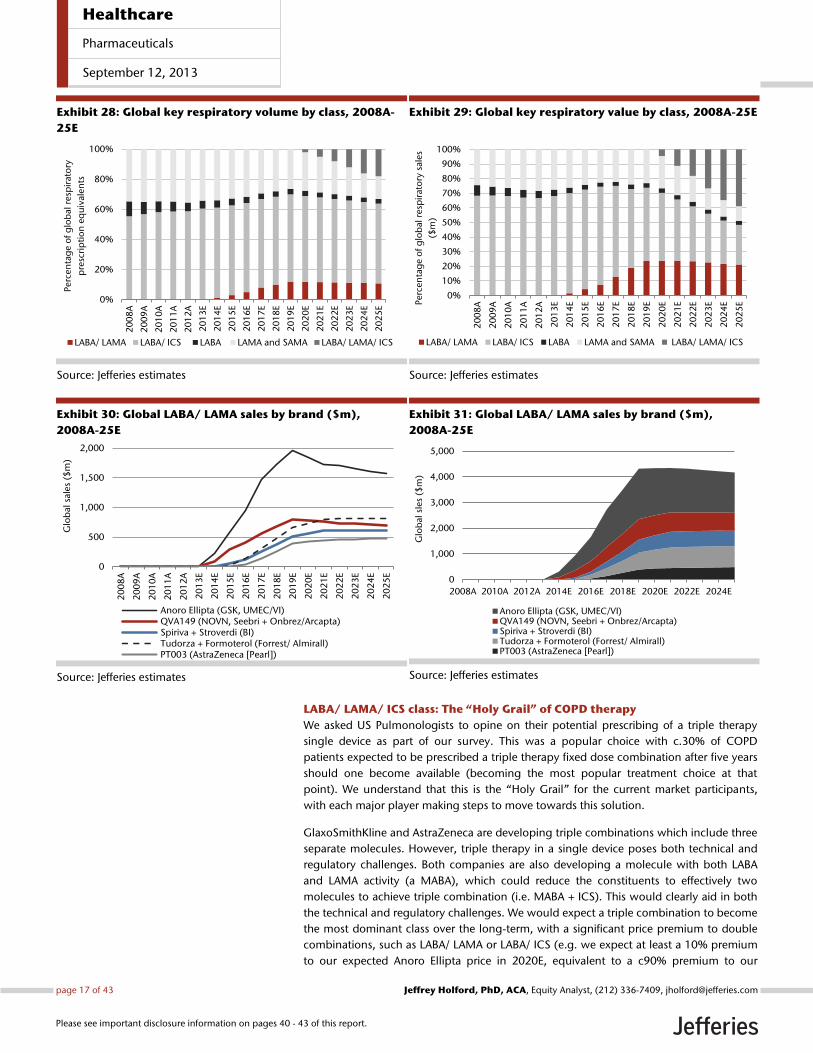

We expect the LABA/ LAMA class to peak at 12% of global prescriptions in 2019, and 24%

of global value in the same year. After this point the introduction of LABA/ LAMA/ ICS

class drugs would likely impinge on the LABA/ LAMA class.

Healthcare

Pharmaceuticals

September 12, 2013

page 16 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

Exhibit 28: Global key respiratory volume by class, 2008A-

25E

Source: Jefferies estimates

Exhibit 29: Global key respiratory value by class, 2008A-25E

Source: Jefferies estimates

Exhibit 30: Global LABA/ LAMA sales by brand ($m),

2008A-25E

Source: Jefferies estimates

Exhibit 31: Global LABA/ LAMA sales by brand ($m),

2008A-25E

Source: Jefferies estimates

LABA/ LAMA/ ICS class: The “Holy Grail” of COPD therapy

We asked US Pulmonologists to opine on their potential prescribing of a triple therapy

single device as part of our survey. This was a popular choice with c.30% of COPD

patients expected to be prescribed a triple therapy fixed dose combination after five years

should one become available (becoming the most popular treatment choice at that

point). We understand that this is the ‚Holy Grail‛ for the current market participants,

with each major player making steps to move towards this solution.

GlaxoSmithKline and AstraZeneca are developing triple combinations which include three

separate molecules. However, triple therapy in a single device poses both technical and

regulatory challenges. Both companies are also developing a molecule with both LABA

and LAMA activity (a MABA), which could reduce the constituents to effectively two

molecules to achieve triple combination (i.e. MABA + ICS). This would clearly aid in both

the technical and regulatory challenges. We would expect a triple combination to become

the most dominant class over the long-term, with a significant price premium to double

combinations, such as LABA/ LAMA or LABA/ ICS (e.g. we expect at least a 10% premium

to our expected Anoro Ellipta price in 2020E, equivalent to a c90% premium to our

0%

20%

40%

60%

80%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Perc

en

tag

e o

f g

lob

al r

esp

irat

ory

pre

scri

pti

on

eq

uiv

alen

ts

LABA/ LAMA LABA/ ICS LABA LAMA and SAMA LABA/ LAMA/ ICS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

EPerc

en

tag

e o

f g

lob

al r

esp

irat

ory

sale

s

($m

)

LABA/ LAMA LABA/ ICS LABA LAMA and SAMA LABA/ LAMA/ ICS

0

500

1,000

1,500

2,000

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Glo

bal

sale

s ($

m)

Anoro Ellipta (GSK, UMEC/VI)QVA149 (NOVN, Seebri + Onbrez/Arcapta)Spiriva + Stroverdi (BI)Tudorza + Formoterol (Forrest/ Almirall)PT003 (AstraZeneca [Pearl])

0

1,000

2,000

3,000

4,000

5,000

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

Glo

bal

sle

s ($

m)

Anoro Ellipta (GSK, UMEC/VI)QVA149 (NOVN, Seebri + Onbrez/Arcapta)Spiriva + Stroverdi (BI)Tudorza + Formoterol (Forrest/ Almirall)PT003 (AstraZeneca [Pearl])

Healthcare

Pharmaceuticals

September 12, 2013

page 17 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

expected Breo Ellipta price in the same year). This class would likely cannibalize product

offerings from other players, however a higher price premium should ensure significant

franchise value gains.

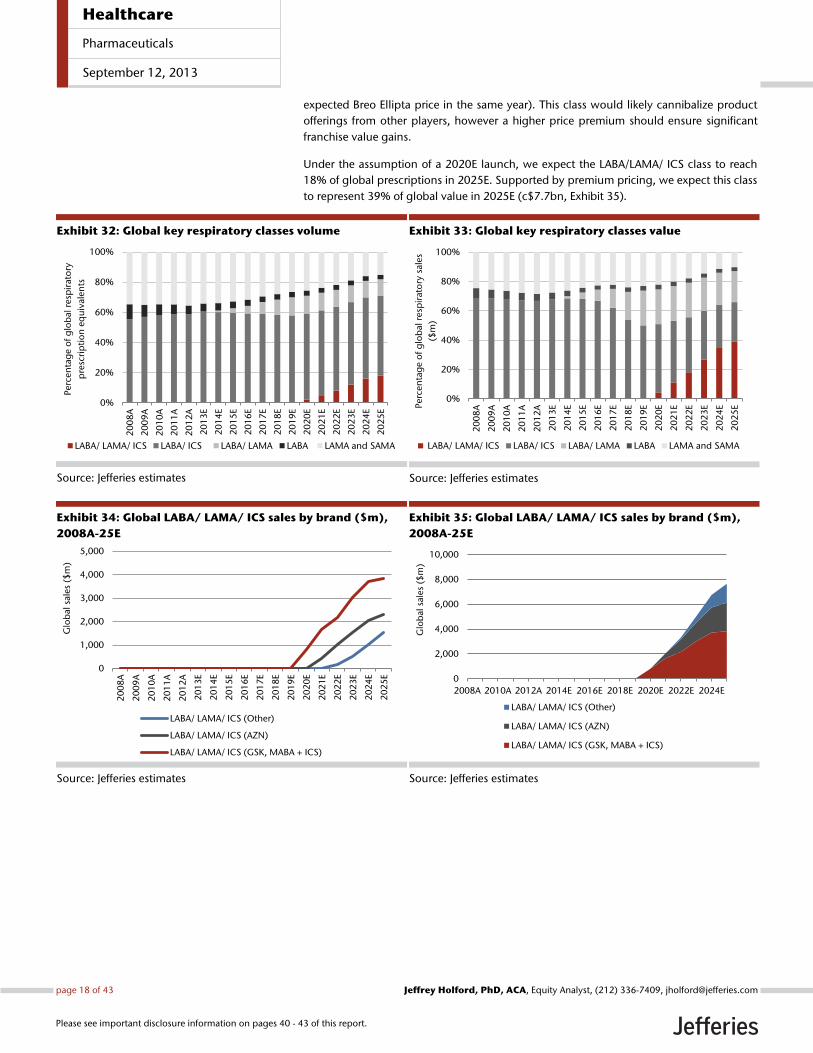

Under the assumption of a 2020E launch, we expect the LABA/LAMA/ ICS class to reach

18% of global prescriptions in 2025E. Supported by premium pricing, we expect this class

to represent 39% of global value in 2025E (c$7.7bn, Exhibit 35).

Exhibit 32: Global key respiratory classes volume

Source: Jefferies estimates

Exhibit 33: Global key respiratory classes value

Source: Jefferies estimates

Exhibit 34: Global LABA/ LAMA/ ICS sales by brand ($m),

2008A-25E

Source: Jefferies estimates

Exhibit 35: Global LABA/ LAMA/ ICS sales by brand ($m),

2008A-25E

Source: Jefferies estimates

0%

20%

40%

60%

80%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Perc

en

tag

e o

f g

lob

al r

esp

irat

ory

pre

scri

pti

on

eq

uiv

alen

ts

LABA/ LAMA/ ICS LABA/ ICS LABA/ LAMA LABA LAMA and SAMA

0%

20%

40%

60%

80%

100%

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

EPerc

en

tag

e o

f g

lob

al r

esp

irat

ory

sale

s

($m

)

LABA/ LAMA/ ICS LABA/ ICS LABA/ LAMA LABA LAMA and SAMA

0

1,000

2,000

3,000

4,000

5,000

20

08

A

20

09

A

20

10

A

20

11

A

20

12

A

20

13

E

20

14

E

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

20

21

E

20

22

E

20

23

E

20

24

E

20

25

E

Glo

bal

sale

s ($

m)

LABA/ LAMA/ ICS (Other)

LABA/ LAMA/ ICS (AZN)

LABA/ LAMA/ ICS (GSK, MABA + ICS)

0

2,000

4,000

6,000

8,000

10,000

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

Glo

bal

sale

s ($

m)

LABA/ LAMA/ ICS (Other)

LABA/ LAMA/ ICS (AZN)

LABA/ LAMA/ ICS (GSK, MABA + ICS)

Healthcare

Pharmaceuticals

September 12, 2013

page 18 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

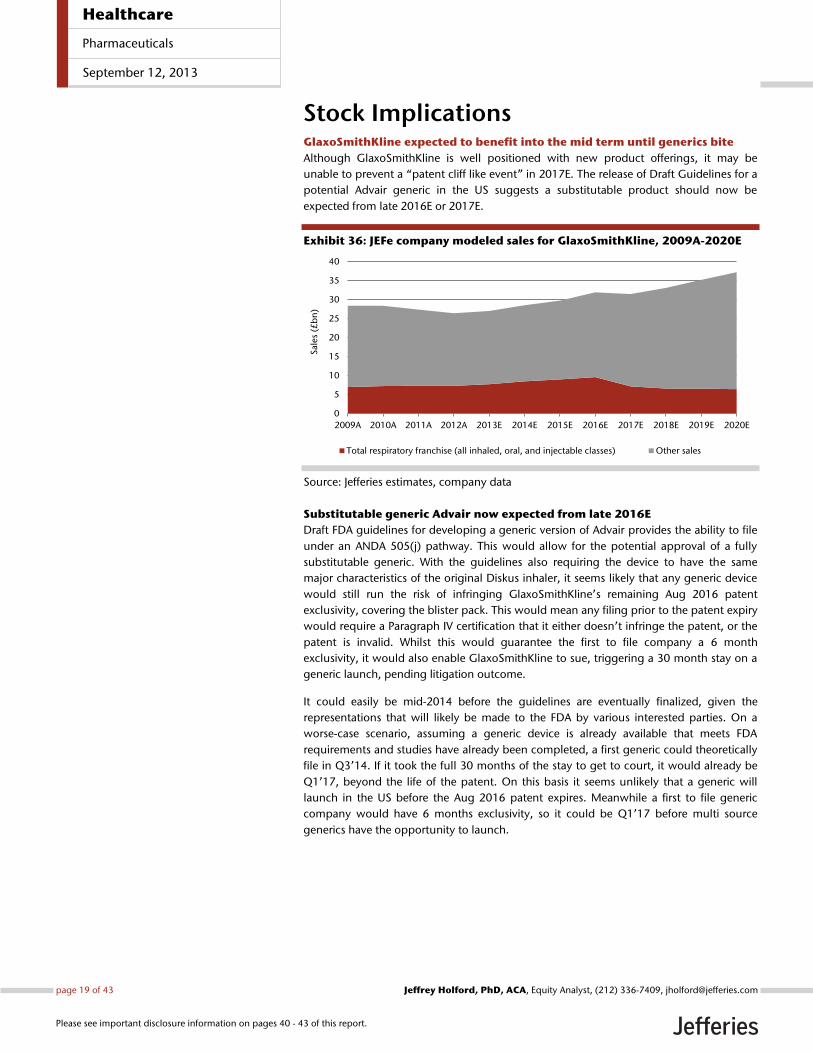

Stock Implications GlaxoSmithKline expected to benefit into the mid term until generics bite

Although GlaxoSmithKline is well positioned with new product offerings, it may be

unable to prevent a ‚patent cliff like event‛ in 2017E. The release of Draft Guidelines for a

potential Advair generic in the US suggests a substitutable product should now be

expected from late 2016E or 2017E.

Exhibit 36: JEFe company modeled sales for GlaxoSmithKline, 2009A-2020E

Source: Jefferies estimates, company data

Substitutable generic Advair now expected from late 2016E

Draft FDA guidelines for developing a generic version of Advair provides the ability to file

under an ANDA 505(j) pathway. This would allow for the potential approval of a fully

substitutable generic. With the guidelines also requiring the device to have the same

major characteristics of the original Diskus inhaler, it seems likely that any generic device

would still run the risk of infringing GlaxoSmithKline’s remaining Aug 2016 patent

exclusivity, covering the blister pack. This would mean any filing prior to the patent expiry

would require a Paragraph IV certification that it either doesn’t infringe the patent, or the

patent is invalid. Whilst this would guarantee the first to file company a 6 month

exclusivity, it would also enable GlaxoSmithKline to sue, triggering a 30 month stay on a

generic launch, pending litigation outcome.

It could easily be mid-2014 before the guidelines are eventually finalized, given the

representations that will likely be made to the FDA by various interested parties. On a

worse-case scenario, assuming a generic device is already available that meets FDA

requirements and studies have already been completed, a first generic could theoretically

file in Q3’14. If it took the full 30 months of the stay to get to court, it would already be

Q1’17, beyond the life of the patent. On this basis it seems unlikely that a generic will

launch in the US before the Aug 2016 patent expires. Meanwhile a first to file generic

company would have 6 months exclusivity, so it could be Q1’17 before multi source

generics have the opportunity to launch.

0

5

10

15

20

25

30

35

40

2009A 2010A 2011A 2012A 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Sale

s (£

bn

)

Total respiratory franchise (all inhaled, oral, and injectable classes) Other sales

Healthcare

Pharmaceuticals

September 12, 2013

page 19 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

A number of generic companies have been looking at developing inhaled generic DPI

products for some time now, including Novartis’ Sandoz and Mylan. Following disclosure

of the draft guidelines John Sheehan, the CFO of Mylan, was quoted at the Morgan

Stanley Global Healthcare Conference on 10th September 2013, saying:

“…the guidance…is exactly in line with what we had indicated our discussions with the FDA –

were, and so, fully anticipated from our side”. “Our device…..has been examined by the FDA.

Our program has been validated as a AB-rated program, generically substitutable program.

And so, we are definitely moving down the path for a generic form of Advair.”

This implies that as long as the final guidelines do not have any major changes in them,

Mylan would appear to be well advanced. Sheehan went on to say;

“….this is going to be a hard to formulate product, hard to manufacture that's where

Mylan's expertise has typically been and therefore we believe that this will be a market that

still have a small number of players and as a result that there will be significant value….”.

He later clarified that Mylan expected “the launch of a generic Advair in 2016”.

This further confirms the expectation that we could have a US generic shortly after the

remaining Advair patent expires. Even if the assertion that it is hard to formulate and

manufacture is correct, even a ‘small number of players’ will still have a devastating effect

on pricing as they fight for market share. Lovenox would serve as a good example to

prove the point here, in our view.

Positive Anoro AdCom vote and supportive class expectations from our survey

Following the near unanimous vote for approval by the FDA’s Advisory committee panel

on September 10th, Anoro Ellipta is very likely to offer first-to-market status in the US, will

likely be the only once-daily LABA/ LAMA on the US market and uses a best-in-class

device, in our opinion. Novartis will present competition ex-US, where QVA149 (Ultibro)

will be first-to-market and once-daily, although our surveyed pulmonologists appeared

less convinced regarding the Neohaler/ Breezhaler device it uses.

We expect GlaxoSmithKline to price Anoro Ellipta at a significant premium to Advair or

Breo Ellipta and our surveyed pulmonologists expect to prescribe a LABA/ LAMA fixed

dose combination to c20% of COPD patients in five years’ time. Much of the market share

for Anoro Ellipta will be gained from patients who would have been prescribed two

branded products (Advair + Spiriva for example), therefore a higher price should be

justified. Some market share for GlaxoSmithKline’s LABA/ ICSs’ Advair and Breo Ellipta

may be lost to Anoro Ellipta in COPD, but this should be a positive event given our

expected higher price point for Anoro Ellipta.

Breo Ellipta offers a chance to protect some of the franchise, but not enough

Breo Ellipta offers once-daily LABA/ ICS therapy for COPD patients in the US, and

potentially for both COPD and asthma patients ex-US. 74% of surveyed pulmonologists

were aware of Breo Ellipta prior to the product’s launch, and noted convenience and

compliance as key attributes. We expect GlaxoSmithKline to employ a price-driven

switching strategy from Advair, helping to protect the franchise from potential Advair

generics and value brands. We expect a key part of this strategy to include significant

price increases for Advair from the point of launch, encouraging switching and providing

a near term boost to overall franchise sales. GlaxoSmithKline is also well positioned to

reach the COPD ‚holy grail‛ of triple therapy in a single device. This could be through its

new LABA, LAMA, and ICS molecules or through development of MABA in combination

with an ICS.

Healthcare

Pharmaceuticals

September 12, 2013

page 20 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

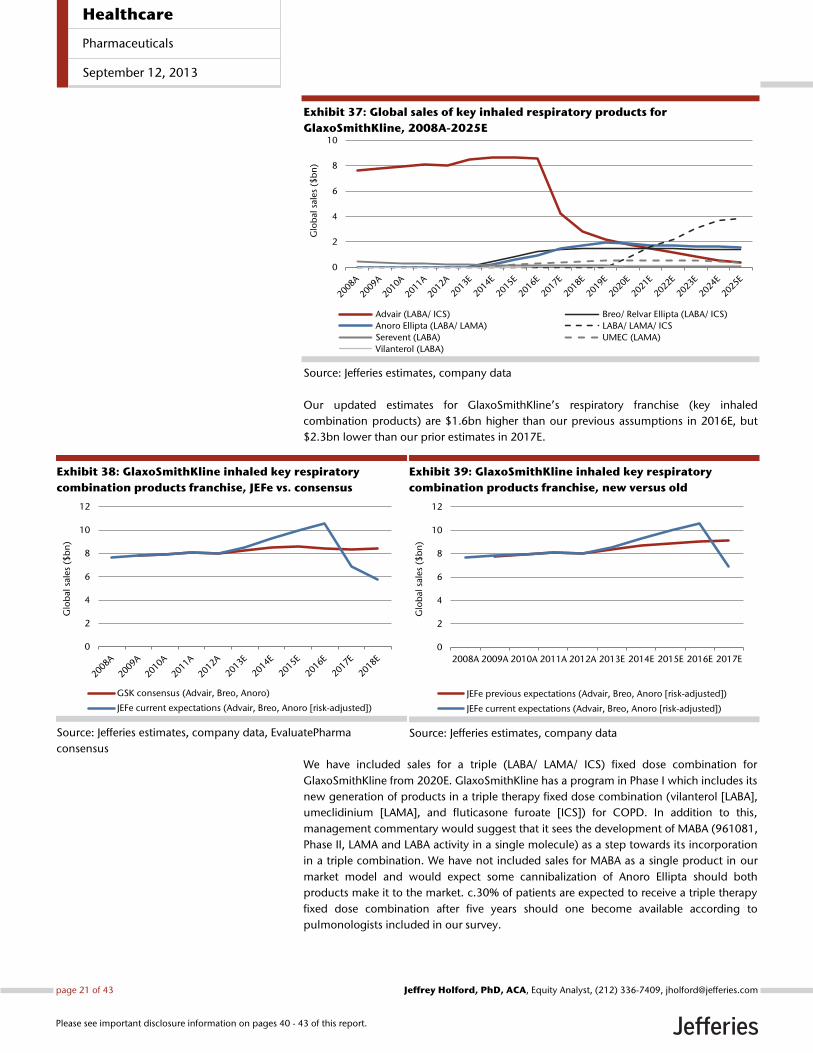

Exhibit 37: Global sales of key inhaled respiratory products for

GlaxoSmithKline, 2008A-2025E

Source: Jefferies estimates, company data

Our updated estimates for GlaxoSmithKline’s respiratory franchise (key inhaled

combination products) are $1.6bn higher than our previous assumptions in 2016E, but

$2.3bn lower than our prior estimates in 2017E.

Exhibit 38: GlaxoSmithKline inhaled key respiratory

combination products franchise, JEFe vs. consensus

Source: Jefferies estimates, company data, EvaluatePharma

consensus

Exhibit 39: GlaxoSmithKline inhaled key respiratory

combination products franchise, new versus old

Source: Jefferies estimates, company data

We have included sales for a triple (LABA/ LAMA/ ICS) fixed dose combination for

GlaxoSmithKline from 2020E. GlaxoSmithKline has a program in Phase I which includes its

new generation of products in a triple therapy fixed dose combination (vilanterol [LABA],

umeclidinium [LAMA], and fluticasone furoate [ICS]) for COPD. In addition to this,

management commentary would suggest that it sees the development of MABA (961081,

Phase II, LAMA and LABA activity in a single molecule) as a step towards its incorporation

in a triple combination. We have not included sales for MABA as a single product in our

market model and would expect some cannibalization of Anoro Ellipta should both

products make it to the market. c.30% of patients are expected to receive a triple therapy

fixed dose combination after five years should one become available according to

pulmonologists included in our survey.

0

2

4

6

8

10

Glo

bal

sale

s ($

bn

)Advair (LABA/ ICS) Breo/ Relvar Ellipta (LABA/ ICS)

Anoro Ellipta (LABA/ LAMA) LABA/ LAMA/ ICS

Serevent (LABA) UMEC (LAMA)

Vilanterol (LABA)

0

2

4

6

8

10

12

Glo

bal

sale

s ($

bn

)

GSK consensus (Advair, Breo, Anoro)

JEFe current expectations (Advair, Breo, Anoro [risk-adjusted])

0

2

4

6

8

10

12

2008A 2009A 2010A 2011A 2012A 2013E 2014E 2015E 2016E 2017E

Glo

bal

sale

s ($

bn

)

JEFe previous expectations (Advair, Breo, Anoro [risk-adjusted])

JEFe current expectations (Advair, Breo, Anoro [risk-adjusted])

Healthcare

Pharmaceuticals

September 12, 2013

page 21 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

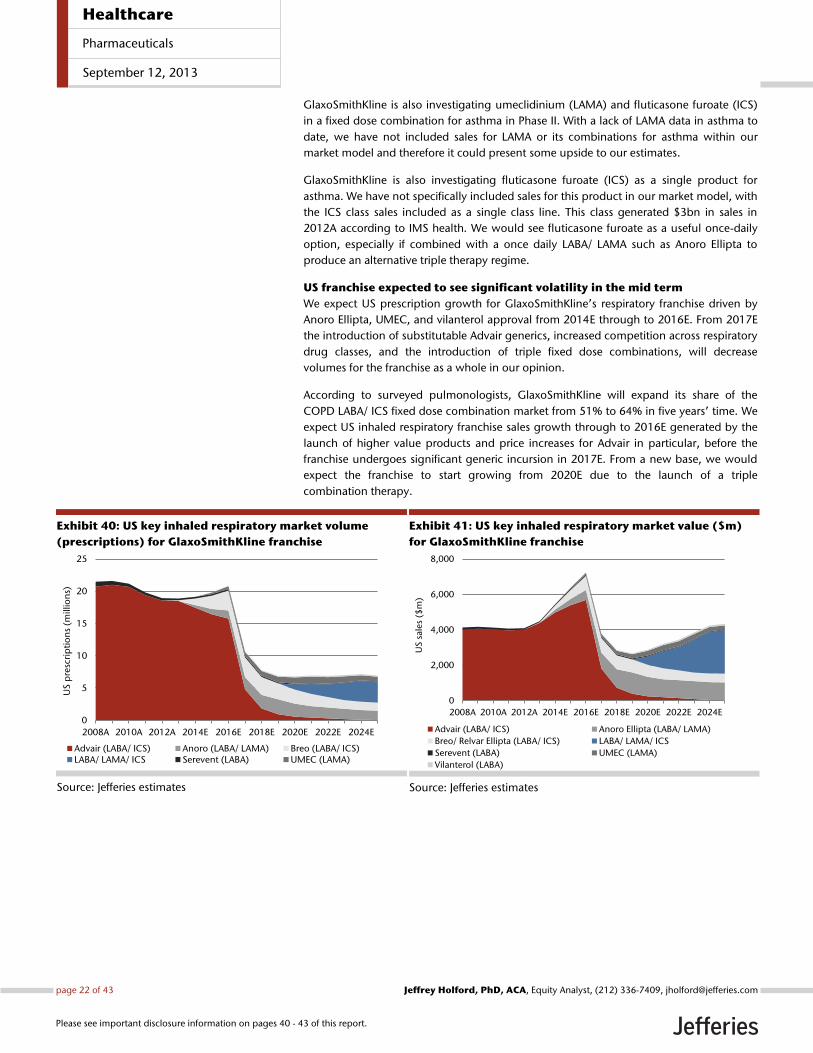

GlaxoSmithKline is also investigating umeclidinium (LAMA) and fluticasone furoate (ICS)

in a fixed dose combination for asthma in Phase II. With a lack of LAMA data in asthma to

date, we have not included sales for LAMA or its combinations for asthma within our

market model and therefore it could present some upside to our estimates.

GlaxoSmithKline is also investigating fluticasone furoate (ICS) as a single product for

asthma. We have not specifically included sales for this product in our market model, with

the ICS class sales included as a single class line. This class generated $3bn in sales in

2012A according to IMS health. We would see fluticasone furoate as a useful once-daily

option, especially if combined with a once daily LABA/ LAMA such as Anoro Ellipta to

produce an alternative triple therapy regime.

US franchise expected to see significant volatility in the mid term

We expect US prescription growth for GlaxoSmithKline’s respiratory franchise driven by

Anoro Ellipta, UMEC, and vilanterol approval from 2014E through to 2016E. From 2017E

the introduction of substitutable Advair generics, increased competition across respiratory

drug classes, and the introduction of triple fixed dose combinations, will decrease

volumes for the franchise as a whole in our opinion.

According to surveyed pulmonologists, GlaxoSmithKline will expand its share of the

COPD LABA/ ICS fixed dose combination market from 51% to 64% in five years’ time. We

expect US inhaled respiratory franchise sales growth through to 2016E generated by the

launch of higher value products and price increases for Advair in particular, before the

franchise undergoes significant generic incursion in 2017E. From a new base, we would

expect the franchise to start growing from 2020E due to the launch of a triple

combination therapy.

Exhibit 40: US key inhaled respiratory market volume

(prescriptions) for GlaxoSmithKline franchise

Source: Jefferies estimates

Exhibit 41: US key inhaled respiratory market value ($m)

for GlaxoSmithKline franchise

Source: Jefferies estimates

0

5

10

15

20

25

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

US

pre

scri

pti

on

s (m

illio

ns)

Advair (LABA/ ICS) Anoro (LABA/ LAMA) Breo (LABA/ ICS)LABA/ LAMA/ ICS Serevent (LABA) UMEC (LAMA)

0

2,000

4,000

6,000

8,000

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

US

sale

s ($

m)

Advair (LABA/ ICS) Anoro Ellipta (LABA/ LAMA)

Breo/ Relvar Ellipta (LABA/ ICS) LABA/ LAMA/ ICS

Serevent (LABA) UMEC (LAMA)

Vilanterol (LABA)

Healthcare

Pharmaceuticals

September 12, 2013

page 22 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

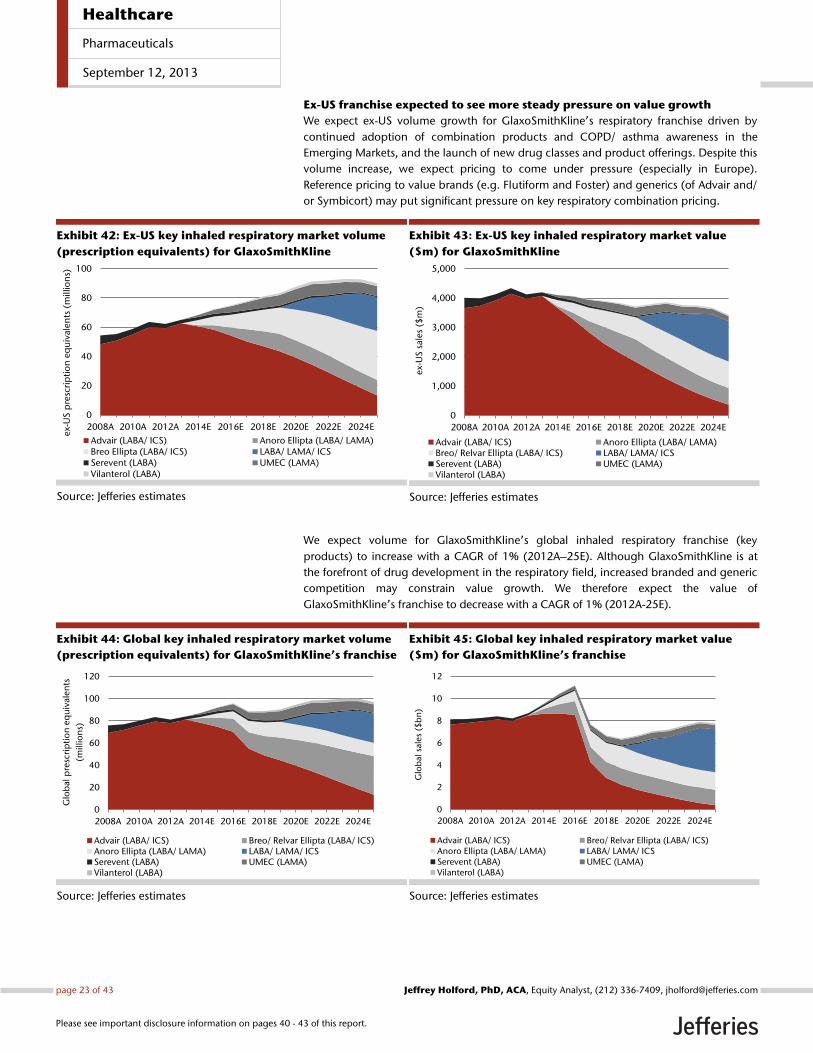

Ex-US franchise expected to see more steady pressure on value growth

We expect ex-US volume growth for GlaxoSmithKline’s respiratory franchise driven by

continued adoption of combination products and COPD/ asthma awareness in the

Emerging Markets, and the launch of new drug classes and product offerings. Despite this

volume increase, we expect pricing to come under pressure (especially in Europe).

Reference pricing to value brands (e.g. Flutiform and Foster) and generics (of Advair and/

or Symbicort) may put significant pressure on key respiratory combination pricing.

Exhibit 42: Ex-US key inhaled respiratory market volume

(prescription equivalents) for GlaxoSmithKline

Source: Jefferies estimates

Exhibit 43: Ex-US key inhaled respiratory market value

($m) for GlaxoSmithKline

Source: Jefferies estimates

We expect volume for GlaxoSmithKline’s global inhaled respiratory franchise (key

products) to increase with a CAGR of 1% (2012A–25E). Although GlaxoSmithKline is at

the forefront of drug development in the respiratory field, increased branded and generic

competition may constrain value growth. We therefore expect the value of

GlaxoSmithKline’s franchise to decrease with a CAGR of 1% (2012A-25E).

Exhibit 44: Global key inhaled respiratory market volume

(prescription equivalents) for GlaxoSmithKline’s franchise

Source: Jefferies estimates

Exhibit 45: Global key inhaled respiratory market value

($m) for GlaxoSmithKline’s franchise

Source: Jefferies estimates

0

20

40

60

80

100

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

ex-

US

pre

scri

pti

on

eq

uiv

alen

ts (

mill

ion

s)

Advair (LABA/ ICS) Anoro Ellipta (LABA/ LAMA)Breo Ellipta (LABA/ ICS) LABA/ LAMA/ ICSSerevent (LABA) UMEC (LAMA)Vilanterol (LABA)

0

1,000

2,000

3,000

4,000

5,000

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024Eex-

US

sale

s ($

m)

Advair (LABA/ ICS) Anoro Ellipta (LABA/ LAMA)Breo/ Relvar Ellipta (LABA/ ICS) LABA/ LAMA/ ICSSerevent (LABA) UMEC (LAMA)Vilanterol (LABA)

0

20

40

60

80

100

120

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

Glo

bal

pre

scri

pti

on

eq

uiv

alen

ts

(mill

ion

s)

Advair (LABA/ ICS) Breo/ Relvar Ellipta (LABA/ ICS)Anoro Ellipta (LABA/ LAMA) LABA/ LAMA/ ICSSerevent (LABA) UMEC (LAMA)Vilanterol (LABA)

0

2

4

6

8

10

12

2008A 2010A 2012A 2014E 2016E 2018E 2020E 2022E 2024E

Glo

bal

sale

s ($

bn

)

Advair (LABA/ ICS) Breo/ Relvar Ellipta (LABA/ ICS)Anoro Ellipta (LABA/ LAMA) LABA/ LAMA/ ICSSerevent (LABA) UMEC (LAMA)Vilanterol (LABA)

Healthcare

Pharmaceuticals

September 12, 2013

page 23 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

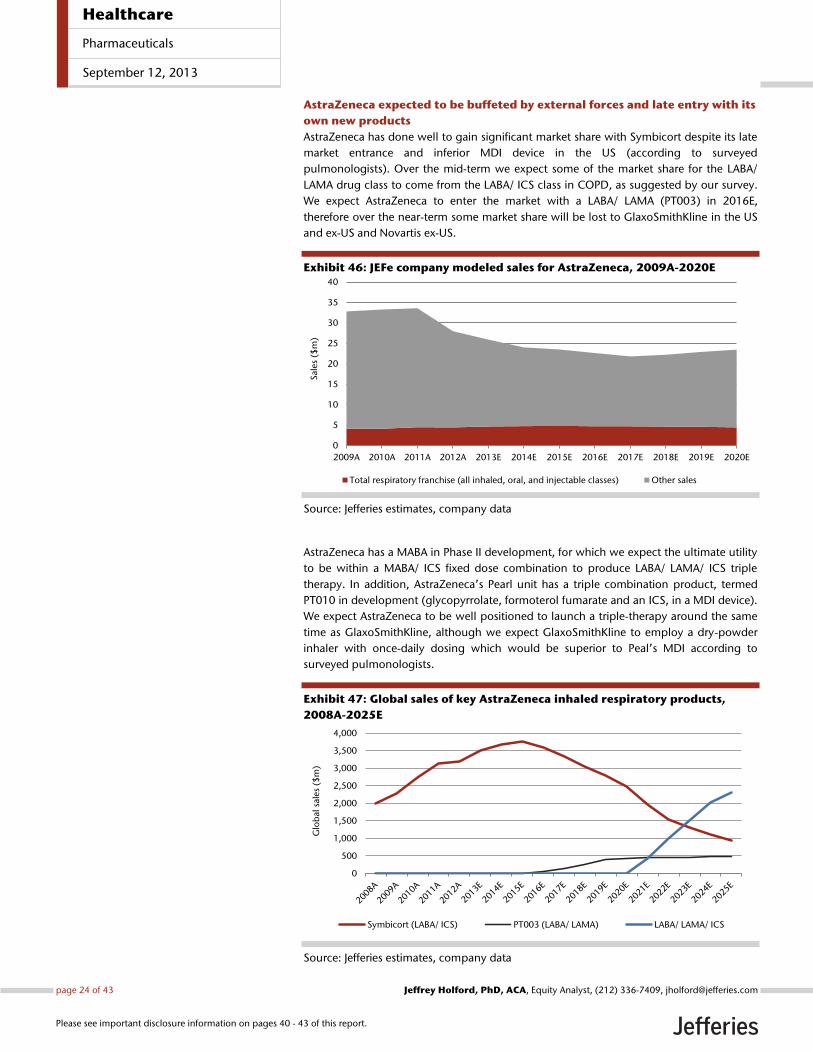

AstraZeneca expected to be buffeted by external forces and late entry with its

own new products

AstraZeneca has done well to gain significant market share with Symbicort despite its late

market entrance and inferior MDI device in the US (according to surveyed

pulmonologists). Over the mid-term we expect some of the market share for the LABA/

LAMA drug class to come from the LABA/ ICS class in COPD, as suggested by our survey.

We expect AstraZeneca to enter the market with a LABA/ LAMA (PT003) in 2016E,

therefore over the near-term some market share will be lost to GlaxoSmithKline in the US

and ex-US and Novartis ex-US.

Exhibit 46: JEFe company modeled sales for AstraZeneca, 2009A-2020E

Source: Jefferies estimates, company data

AstraZeneca has a MABA in Phase II development, for which we expect the ultimate utility

to be within a MABA/ ICS fixed dose combination to produce LABA/ LAMA/ ICS triple

therapy. In addition, AstraZeneca’s Pearl unit has a triple combination product, termed

PT010 in development (glycopyrrolate, formoterol fumarate and an ICS, in a MDI device).

We expect AstraZeneca to be well positioned to launch a triple-therapy around the same

time as GlaxoSmithKline, although we expect GlaxoSmithKline to employ a dry-powder

inhaler with once-daily dosing which would be superior to Peal’s MDI according to

surveyed pulmonologists.

Exhibit 47: Global sales of key AstraZeneca inhaled respiratory products,

2008A-2025E

Source: Jefferies estimates, company data

0

5

10

15

20

25

30

35

40

2009A 2010A 2011A 2012A 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Sale

s ($

m)

Total respiratory franchise (all inhaled, oral, and injectable classes) Other sales

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Glo

bal

sale

s ($

m)

Symbicort (LABA/ ICS) PT003 (LABA/ LAMA) LABA/ LAMA/ ICS

Healthcare

Pharmaceuticals

September 12, 2013

page 24 of 43 , Equity Analyst, (212) 336-7409, [email protected] Holford, PhD, ACA

Please see important disclosure information on pages 40 - 43 of this report.

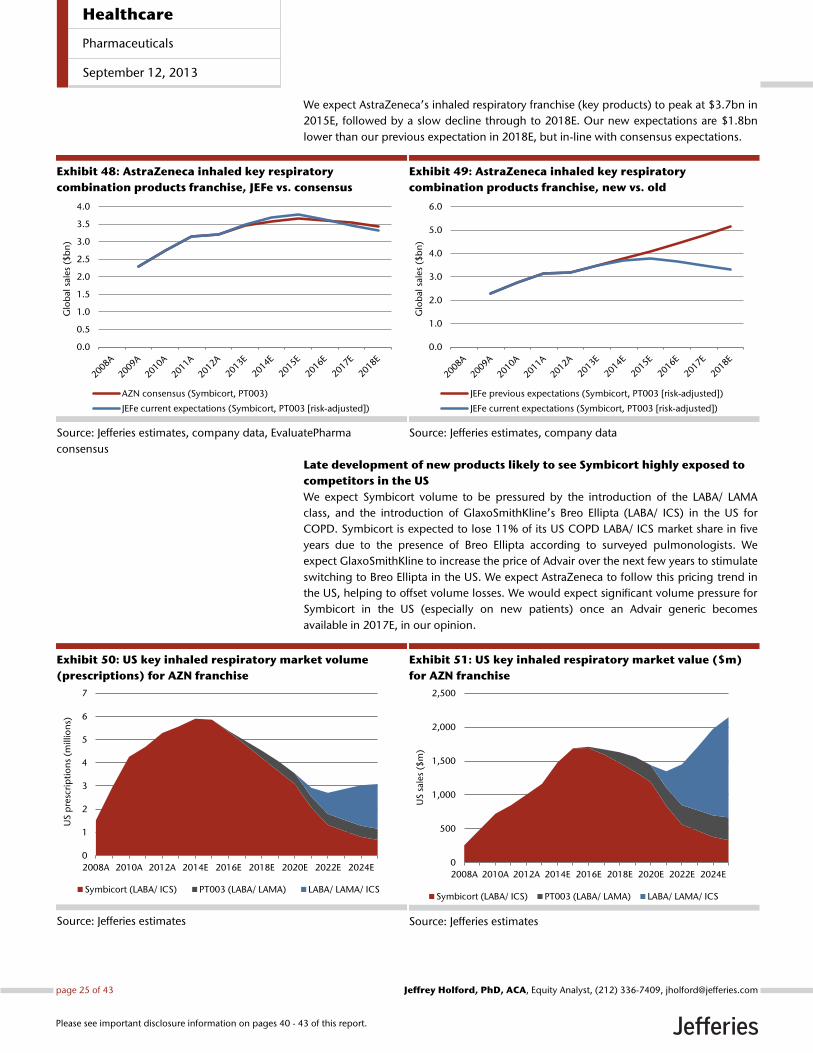

We expect AstraZeneca’s inhaled respiratory franchise (key products) to peak at $3.7bn in

2015E, followed by a slow decline through to 2018E. Our new expectations are $1.8bn

lower than our previous expectation in 2018E, but in-line with consensus expectations.

Exhibit 48: AstraZeneca inhaled key respiratory

combination products franchise, JEFe vs. consensus

Source: Jefferies estimates, company data, EvaluatePharma

consensus

Exhibit 49: AstraZeneca inhaled key respiratory

combination products franchise, new vs. old

Source: Jefferies estimates, company data

Late development of new products likely to see Symbicort highly exposed to

competitors in the US

We expect Symbicort volume to be pressured by the introduction of the LABA/ LAMA

class, and the introduction of GlaxoSmithKline’s Breo Ellipta (LABA/ ICS) in the US for

COPD. Symbicort is expected to lose 11% of its US COPD LABA/ ICS market share in five