Embed Size (px)

Citation preview

Pharmaceutical industry changes and market insights Survey of leaders in the pharma value chain

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

II | Parthenon-EY

Ernst & Young LLP and YourEncore alliance overviewErnst & Young LLP and YourEncore have formed a strategic alliance to help life sciences and consumer products clients accelerate product development, strengthen regulatory compliance and improve productivity.

This first-of-its-kind relationship unites EY advisory, transaction advisory and tax services with the real-world experience of YourEncore’s 10,000 on-demand industry experts to help clients innovate, drive growth, manage risk and comply with increasing regulatory challenges.

About YourEncoreIndianapolis-based YourEncore, named a “100 Most Brilliant Company” by Entrepreneur Magazine, is a leading provider of proven expertise, delivering flexible resourcing and consulting services to the biopharma, medical devices and diagnostics and consumer goods industries.

With its network of highly experienced subject matter experts, including MDs, PhDs, regulators and scientists, YourEncore mobilizes the wisdom and know-how of its experts to help companies out-think, out-pace and outperform.

For more information, visit www.yourencore.com.

Parthenon-EY | 1

Introduction

Parthenon-EY and YourEncore recently conducted a nationwide survey of life sciences experts to query them on recent market trends, uncover their points of view on potential regulations, refine their current business models and gain insights into what discovery efforts might yield better results. With all the rhetoric surrounding the drug industry from political, news and personal channels, we wanted to know what “those who know” think of various ways to improve the system.

We asked 10 simple questions, soliciting input from more than 50 past and present industry executives and experts from pharmaceutical, consulting and pharmacy backgrounds. What we heard was informative, provocative and in some cases unsurprising — but important to consider.

Here is what we have learned.

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

2 | Parthenon-EY

Q1 Which top regulations could have the greatest impact on accelerating discovery and getting breakthrough products to market faster?

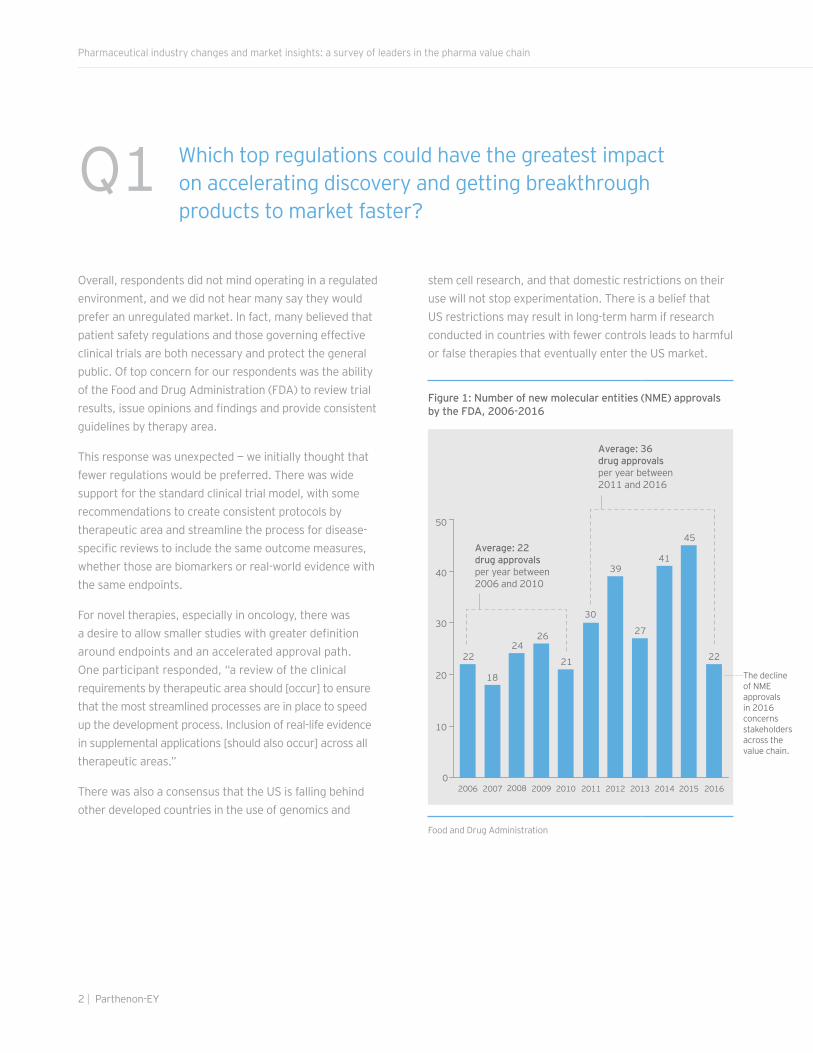

Overall, respondents did not mind operating in a regulated environment, and we did not hear many say they would prefer an unregulated market. In fact, many believed that patient safety regulations and those governing effective clinical trials are both necessary and protect the general public. Of top concern for our respondents was the ability of the Food and Drug Administration (FDA) to review trial results, issue opinions and findings and provide consistent guidelines by therapy area.

This response was unexpected — we initially thought that fewer regulations would be preferred. There was wide support for the standard clinical trial model, with some recommendations to create consistent protocols by therapeutic area and streamline the process for disease-specific reviews to include the same outcome measures, whether those are biomarkers or real-world evidence with the same endpoints.

For novel therapies, especially in oncology, there was a desire to allow smaller studies with greater definition around endpoints and an accelerated approval path. One participant responded, “a review of the clinical requirements by therapeutic area should [occur] to ensure that the most streamlined processes are in place to speed up the development process. Inclusion of real-life evidence in supplemental applications [should also occur] across all therapeutic areas.”

There was also a consensus that the US is falling behind other developed countries in the use of genomics and

stem cell research, and that domestic restrictions on their use will not stop experimentation. There is a belief that US restrictions may result in long-term harm if research conducted in countries with fewer controls leads to harmful or false therapies that eventually enter the US market.

Figure 1: Number of new molecular entities (NME) approvals by the FDA, 2006-2016

0

10

20

30

40

50

22

18

2426

21

30

39

27

41

45

22

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average: 22 drug approvals per year between 2006 and 2010

Average: 36 drug approvals per year between 2011 and 2016

Food and Drug Administration

The decline of NME approvals in 2016 concerns stakeholders across the value chain.

Parthenon-EY | 3

Q2 Which top regulations or agency reform would have the biggest impact on lowering the cost of drugs?

Our respondents named several potential changes that could help lower the cost of drugs. Mentioned quite often was reforming how the US uses generic drugs. For many years, payers and pharmacy benefit managers (PBMs) have driven the “generic conversion rate” — mandating that patients switch from branded drugs to generics — with the belief that costs would decline.

Role of genericsDrug prices have continued to rise due to how drugs are placed on formularies, the use of non-transparent incentives, and the lack of generics in high-cost disease states. Several respondents indicated that the role of generics may be limited as new therapies and biologics hit the market. Others believed that generics still have a long way to go and can be lower-cost alternatives for the right disease states. These respondents believed that payers need better guidelines for how products are reimbursed, such as comparing the net retail costs between a generic and brand after all incentives are included. Affordability for the patient should be the priority, not unit costs of a single product.

Accelerating generic drugs to market through improved processes was seen as one path to less-expensive alternatives making it to market faster. There was a belief that introducing competition to the pioneer product earlier can impact overall drug costs. Rapid approval of biosimilars was another category believed to lower costs as brand patents expire. One respondent said savings could be realized if Code of Federal Regulations Part 314 were to require third-line drug approvals to be superior to the first two products on the market and have the same or better safety and efficacy profile.

Medicare/Medicaid price negotiationsSome said that Medicare, Medicaid and other government programs should be able to negotiate prices similar to

those in European countries where list prices are public and competition is more open. There was a broad consensus that pricing needs to be transparent, not only for manufacturers, but for everyone in the value chain — particularly PBMs and pharmacies — that profits from unit price arbitrage vs. services provided.

Patient and provider educationMarketing and direct-to-consumer advertising is the one area that most respondents agreed is a huge cost to manufacturers and drives up the wholesale price of the drug to recover investment for capturing patients. Use of paper for product inserts, packaging and marketing materials, rather than moving to electronic labeling were also considered to drive up unit cost. Patients’ lack of allowed time with physicians creates both a greater burden to educate the public and costs associated with paper-based materials.

Formulary reviewsOther respondents believed that formularies need to be overhauled and that exclusions, substitutions, and non-preferred products need to be thoroughly reviewed with new guidelines and clinical protocols, not just price comparisons. There was a consensus that payers need to apply more clinical rigor in making decisions and focus on outcomes instead of unit price.

Figure 2: Year-over-year growth of branded drug prices in US, 2012-2015

0.0

2.5

5.0

7.5

10.0

12.5%

2012

7.5%

2013

8.0%

2014

8.3%

2015

10.1%

EY analysis, Morgan Stanley and UBS industry analyst reports

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

4 | Parthenon-EY

Q3 Which top regulations or agencies create the largest barrier to collaboration (research or otherwise)?

In looking at the regulatory environment, we had to ask whether current legislation and agencies were a barrier to clinical collaboration between pharmaceutical manufacturers. We heard that there is significant concern about collusion, patent protection and sharing of information. However, when we queried the market, many told us that these fears are overblown, and that internal legal and leadership risk tolerance represent the largest barrier.

One respondent said that “regulations and agencies are not a meaningful barrier to collaboration among companies or between companies and medical institutions/universities/NIH (National Institutes of Health). The barriers are far more related to the diverging interests of these organizations.” Another responded, “Much could be done on the industry side to encourage collaboration, especially in therapeutic areas that are advancing cures in areas of unmet medical need. This has always been a problem due to competitive environment and patent enforcement but is worthy of a dialog session to discuss solutions.”

Other respondents believed that the FDA and NIH can do more to foster collaboration, but that the current complexity of different departments with different processes makes it seem as though they are dealing with multiple agencies. Every submission and request seems to be a “first” or “one-time exception” rather than a standard operating procedure.

Several respondents felt that funding should be directed to small start-ups and innovative companies that are willing to partner. These respondents suggested government assistance in identifying partners and financing or, alternatively, private equity and smaller investors could

assume this role. Supporting biotech incubators and helping fund partnership creation were seen as a way to increase competition and collaboration.

One respondent indicated Hatch-Waxman Amendments (patent reform and generic drug regulations) may help with price, but they also favor generic drug companies. Moreover, the respondent indicated patent protections for new chemical entities should be extended so larger pharmaceutical companies have the money needed for additional research.

Lastly, there is also a belief that PBMs and payers have not fostered collaboration when they could have largely helped reconcile inconsistencies in the industry around common practices and data sharing. One respondent said insurance companies could have implemented clearer requirements for routine standards of care and covered the increased frequency of testing to capture data on valuable health outcomes.

Parthenon-EY | 5

Q4 What components of the value chain (discovery, manufacture, distribution) contribute the most to drug prices?

Unsurprisingly, research and development (R&D) was most often cited as the most expensive component and contributor to drug prices. Obviously, the sunk cost of failed trials was the primary driver, as these investments need to be incorporated into the cost for successful programs.

According to one respondent, “In my opinion, manufacturing (i.e., cost of goods) has a major impact on the ultimate drug price. Having said that, however, the cost of development is very high and very risky. Numbers of studies, numbers of patients, late-stage failures all contribute to the soaring cost of drug development and therefore drug prices.”

Phase 3 or late-stage clinical trials were also cited because of the number of endpoints that need to be evaluated and the manual process by which data is collected and evidence is submitted to the FDA for approvals. Several respondents indicated the clinical trial process heavily depends on inefficient processes that are not automated or consistent and even incremental improvements could yield significant savings to the industry.

Other components cited were product recalls, packaging, destruction costs and labor associated with the management of product in the channel. Of course, also on the list was marketing, especially direct-to-consumer advertising, which is more expensive than a sales force that calls on physicians. Recent rules on how much time a drug rep can spend with a physician have shifted marketing expenses into digital and media advertising, which requires significant investment and constant updating.

There was, however, a new category that has emerged recently as a contentious element in the cost of drugs: the expenses associated with “middlemen.” This includes prescription benefit managers (PBMs) and wholesalers that are using their dominant positions in the value chain to drive up profits by demanding more rebates or “discounts” for products that are not passed on to consumers and do not add value to the process. One respondent called the distribution chain an “antiquated model” that involves far too many middlemen. Restrictions around distribution have created excessive handoffs before a product reaches the consumer.

The issue with the middleman has become very prominent in recent national conversations, as the market asks why there is still a need for handoffs in a highly consolidated sector. One respondent indicated “distribution, insofar as insurance companies and PBMs increase their profits at the expense of patient choice and co-pay/co-insurance increases … also leads to increased noncompliance to prescribed therapies.”

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

6 | Parthenon-EY

Q5 What changes to regulations would lower prices the most?

While respondents indicated many diverse approaches to lowering prices, many were in agreement that the quantity and complexity of regulations can contribute to higher drug prices. One respondent said, “The relationship between regulatory expansion and higher prices cannot be ignored. Price increases caused by regulation have a disproportionately negative effect on low-income households. The poorest households tend to spend a larger proportion of their income on goods that are heavily regulated and are subject to both high and volatile prices. This cost should be recognized in policymakers’ efforts to consider the costs and benefits of new and existing regulations.”

Other respondents focused significantly on the manual, inefficient compliance processes that require documentation by requesting a “commonsense approach to documentation requirements.” “Eliminating the requirement for printed packaging and physician leaflets

and transitioning that information to electronic labeling” could reduce costs. One respondent indicated “lowering the preclinical burden and opportunity potential for approval with one pivotal trial (or counting a good Phase II as a pivotal in some cases)” could also lower costs. This is done now in some orphan indications but “should be allowed more generally.”

Some respondents believe that allowing Medicare and Medicaid to negotiate prices or limiting prices to a ceiling based on European price lists will have an impact. The topic of value-based pricing came up quite a bit, and one respondent said, “Regulators should allow for more value-based pricing innovation. The current minimum discounts and best price rules around Medicaid, Department of Defense (DoD), and the bloating of 340b (the federal drug discount program used by hospitals to benefit lower income and vulnerable populations), [and]the complex negotiations with PBMs all conspire to cause

Figure 3: Percentage of respondents indicating type of reform

0

10

20

30

40%

31%

19% 19%

12%8%

4% 4% 4%

No changeneeded

Value–basedpricing

Documentationreform

Drugpackaging

Patentreform

Physician/consumercommunication

Clinical trialreform

CMS negotiation

of prices

Parthenon-EY and YourEncore pharmaceutical survey results, 2017

inflated list prices. Changing the rules to allow for more innovation and more simplified market competition would be beneficial. Allow drug companies to share information with payers, including Medicaid, about future drugs so that health systems can plan better.”

Others discussed the rise of direct-to-consumer advertising in response to tight restrictions around profiling and educating physicians directly. One respondent said that we should “limit direct-to-consumer advertising and sales calls to physicians. Information on medicines should be provided to physicians from objective, peer-reviewed sources, funded publicly or by the industry as a whole — not by individual companies.”

Some respondents indicated a preference for limits to direct-to-consumer advertising and rebalancing those with physician education and the establishment of “an industry-wide, peer-reviewed resource as a central depository for drug information.”

Many respondents want to see more rapid approval of biosimilars and shortening of the time allowed before generic approvals. Respondents generally do not want to see broad decreases in FDA oversight, and they mentioned patient safety as a critical issue that the FDA should continue to oversee.

Parthenon-EY | 7

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

8 | Parthenon-EY

Q6 What changes to the value chain (discovery, manufacture, distribution) need to occur to eliminate unnecessary costs or reduce prices?

The responses to questions #5 and #6 had subtle differences. Responses to this question focused more on R&D, price transparency and stakeholder collaboration across the entire health care value chain. One respondent indicated incentive structures are misaligned for some players in the value chain and questioned whether drug companies should be publicly traded with Wall Street’s financial performance expectations imposed.

One respondent said R&D is a long, risky process and collaborations are needed to enable greater value delivery in product discovery. The respondent further indicated there is a need for the public to differentiate between a small number of “bad actors” that create a negative public perception of pharma, and the majority of honest companies that invest in research and development.

There was also a willingness to work within an environment with greater price transparency for the market to see relative pricing/value along the entire distribution channel and know who really profits from drug delivery. Many respondents believe there are too many players profiting from low-value services, such as distribution and price triaging by intermediaries.

Some respondents also referenced inefficient internal practices within pharma, such as excess production capacity in manufacturing plants that is not well-utilized. If fewer studies and patients studied were required, cost

savings could potentially be realized, some respondents said, especially if trials could be conducted in a collaborative environment, reducing redundancies for similar trials.

One interesting observation is that there may be issues with near monopolies in the distribution channel as secondary and tertiary wholesalers and payers/PBMs retain deep discounts they receive from the pharmaceutical manufacturers. Respondents said that all discounts and savings, including rebates, should be passed on to consumers in the form of lower co-pays and co-insurance rates. One respondent said product liability expenses are a hidden form of costs as well.

Parthenon-EY | 9

Q7 What should providers be doing that they are not doing today to improve prescribing patterns or therapy outcomes?

When asked specifically about providers, respondents commented on how the physicians’ role has changed and how critical their attention to the details surrounding appropriate drugs matters to overall clinical outcomes. Most respondents believe that physicians have a significant responsibility to better understand how drugs work in the body, when it is medically necessary to prescribe a drug and how it will interact with other agents. Several respondents commented about how most treatments are now a prescription vs. a procedure and that not allotting enough time to educate physicians may detrimentally affect their efficacy in treating disease.

Respondents want more time for physicians to learn about new therapies/products and assess and ensure the appropriateness of their use after initial availability. There were comments about bringing more physicians into trials to better understand how investigations are conducted and suggest improvements to the process. Many physicians are never a part of trials and often don’t understand how to enable patient therapies, so only a small pool of physicians shapes how trials are conducted.

A common barrier noted was the shortage of physicians in primary care and payer pressure to see more patients. This pressure leaves little time for continuing medical education and patient counseling, thought to majorly impact clinical outcome improvement. Compliance and adherence were mentioned repeatedly as a responsibility of both the patient and the physician, who should check in to evaluate the progress and efficacy of the therapy.

Respondents want to see payers take more responsibility in enabling physicians and electronic medical record (EMR) standards rather than delegating those standards to a fragmented provider market. A specific comment around EMRs was that “electronic medical records must be reorganized to capture therapeutic outcomes so they can be a tool for real-world evidence (value) — and not just for cost assessment (price).”

Many buzzwords were also mentioned, such as value- and outcome-based reimbursements, real-world evidence and evidence-based medicine. However, there were some specific recommendations for more head-to-head trials between competitor products in the same therapy class, especially with interchangeable products — the goal being to gather more data on the drivers for efficacy and better understanding of clinical performance vs. patient behavior.

Other respondents wanted to see more pressure on physicians to stop overprescribing, especially antibiotics and to polypharmacy patients, without doing more research into the patients’ history.

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

10 | Parthenon-EY

Q8 What improvements need to be made in the prescribing process to balance costs, access to therapies and patient safety?

Many respondents indicated that the physician, being on the front lines of medical care, can drive change in prescribing trends. Improving continuing medical education of physicians can position physicians to prescribe the most effective medicine, either branded or generic, that provides for improved clinical and financial outcomes.

Continuing medical education and the need to integrate electronic medical records with pharma databases was cited as critical for physicians to immediately access important information around drugs and their impact on patient physiology. Once again, the topic of polypharmacy patients and the “sickest of the sick” came up as a specific area requiring much greater coordination, especially as these patients are the highest cost claimants.

Some respondents also advocated for simplified national policies from regulators and guidelines from payers around how care should be triaged. One respondent said, “The US should adopt NICE-like (National Institute for Health and Care Excellence) reviews of therapies.” Others said that payers need to start making the hard trade-offs between products to rationalize the number of treatment options without denying care and reviewing it after the fact. Respondents want to see payers hold physicians accountable to complying with safety requirements and not just prescribe off label without the existence of a standardized protocol.

Another respondent said the US can combat the shortage of physicians by allowing pharmacists to prescribe, as

they are best educated about pharmaceuticals and better understand how drugs work and how they affect patients: “I would like to see pharmacists prescribe, based on physician diagnosis. Pharmacists are the most underutilized brain trust in the US.”

Lastly, one respondent made a bold statement that we need to “change the system totally. Insurance companies have no value, they only add cost. The best system I’ve heard of has the care of each patient managed by a team that includes providers and patient advocates. Without that, we have people who go to a doctor because they are bored or because they heard an ad on TV. The present system including ACA [Affordable Care Act] will not work nor will Medicare for all.”

Parthenon-EY | 11

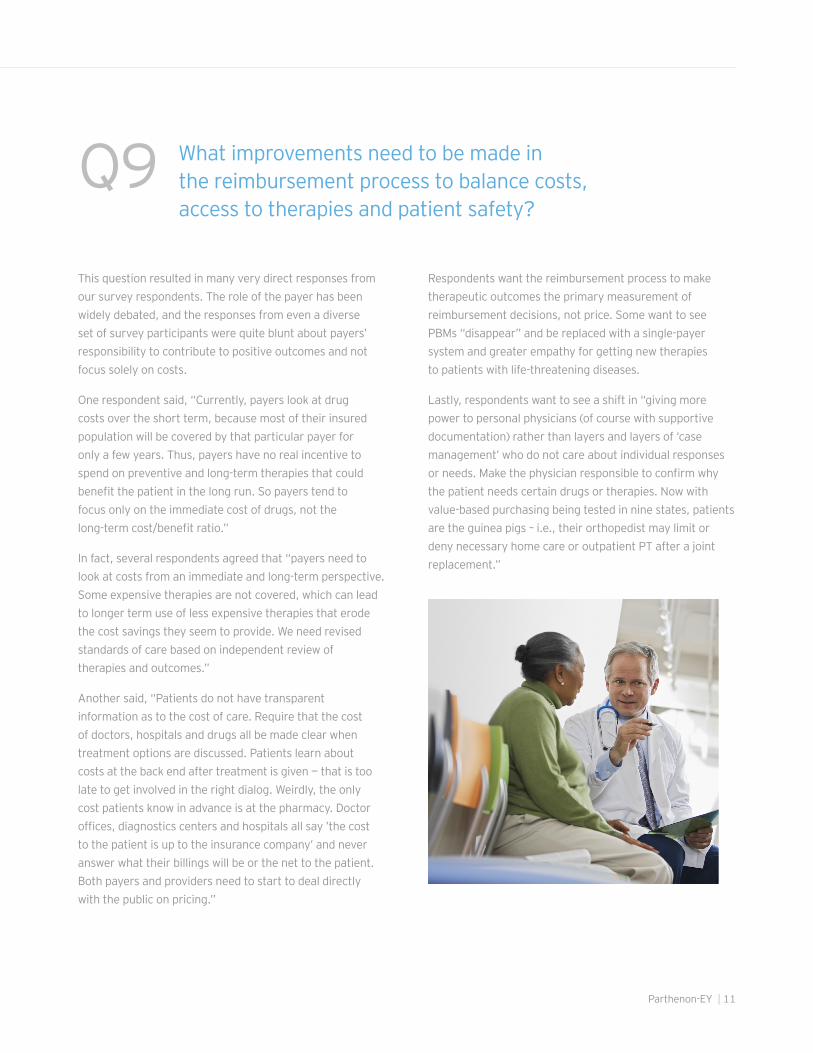

Q9 What improvements need to be made in the reimbursement process to balance costs, access to therapies and patient safety?

This question resulted in many very direct responses from our survey respondents. The role of the payer has been widely debated, and the responses from even a diverse set of survey participants were quite blunt about payers’ responsibility to contribute to positive outcomes and not focus solely on costs.

One respondent said, “Currently, payers look at drug costs over the short term, because most of their insured population will be covered by that particular payer for only a few years. Thus, payers have no real incentive to spend on preventive and long-term therapies that could benefit the patient in the long run. So payers tend to focus only on the immediate cost of drugs, not the long-term cost/benefit ratio.”

In fact, several respondents agreed that “payers need to look at costs from an immediate and long-term perspective. Some expensive therapies are not covered, which can lead to longer term use of less expensive therapies that erode the cost savings they seem to provide. We need revised standards of care based on independent review of therapies and outcomes.”

Another said, “Patients do not have transparent information as to the cost of care. Require that the cost of doctors, hospitals and drugs all be made clear when treatment options are discussed. Patients learn about costs at the back end after treatment is given — that is too late to get involved in the right dialog. Weirdly, the only cost patients know in advance is at the pharmacy. Doctor offices, diagnostics centers and hospitals all say ’the cost to the patient is up to the insurance company’ and never answer what their billings will be or the net to the patient. Both payers and providers need to start to deal directly with the public on pricing.”

Respondents want the reimbursement process to make therapeutic outcomes the primary measurement of reimbursement decisions, not price. Some want to see PBMs “disappear” and be replaced with a single-payer system and greater empathy for getting new therapies to patients with life-threatening diseases.

Lastly, respondents want to see a shift in “giving more power to personal physicians (of course with supportive documentation) rather than layers and layers of ‘case management’ who do not care about individual responses or needs. Make the physician responsible to confirm why the patient needs certain drugs or therapies. Now with value-based purchasing being tested in nine states, patients are the guinea pigs – i.e., their orthopedist may limit or deny necessary home care or outpatient PT after a joint replacement.”

Pharmaceutical industry changes and market insights: a survey of leaders in the pharma value chain

12 | Parthenon-EY

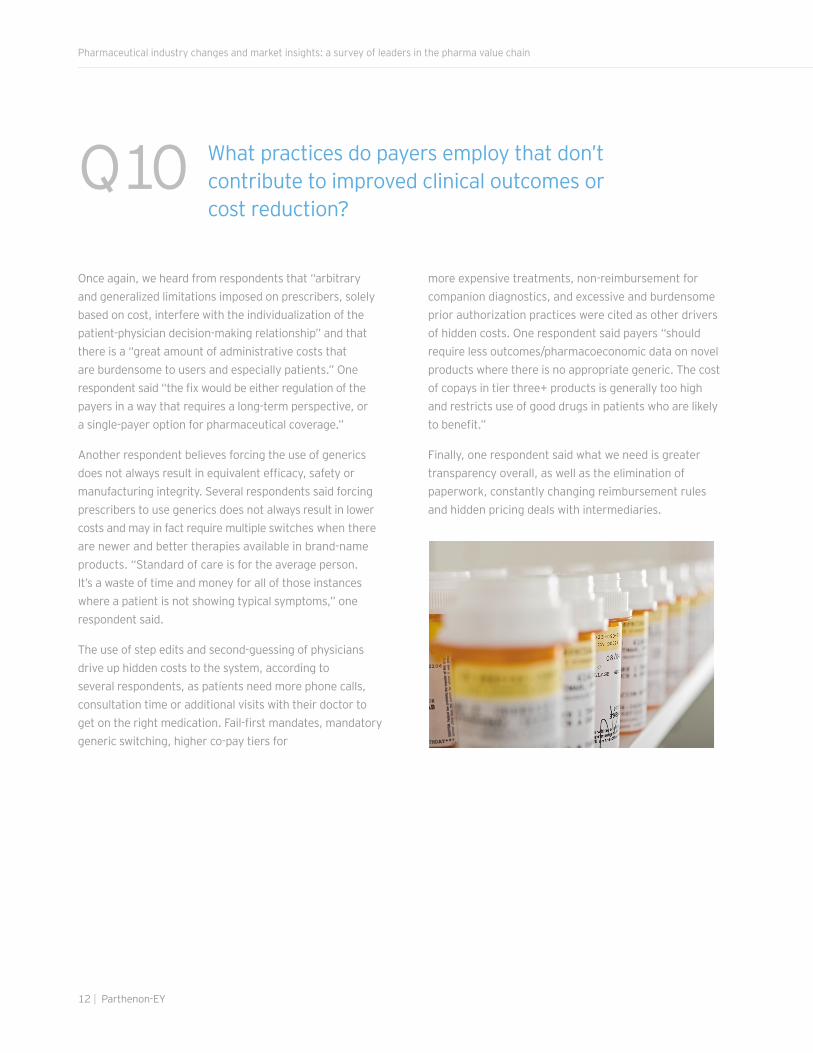

Q10 What practices do payers employ that don’t contribute to improved clinical outcomes or cost reduction?

Once again, we heard from respondents that “arbitrary and generalized limitations imposed on prescribers, solely based on cost, interfere with the individualization of the patient-physician decision-making relationship” and that there is a “great amount of administrative costs that are burdensome to users and especially patients.” One respondent said “the fix would be either regulation of the payers in a way that requires a long-term perspective, or a single-payer option for pharmaceutical coverage.”

Another respondent believes forcing the use of generics does not always result in equivalent efficacy, safety or manufacturing integrity. Several respondents said forcing prescribers to use generics does not always result in lower costs and may in fact require multiple switches when there are newer and better therapies available in brand-name products. “Standard of care is for the average person. It’s a waste of time and money for all of those instances where a patient is not showing typical symptoms,” one respondent said.

The use of step edits and second-guessing of physicians drive up hidden costs to the system, according to several respondents, as patients need more phone calls, consultation time or additional visits with their doctor to get on the right medication. Fail-first mandates, mandatory generic switching, higher co-pay tiers for

more expensive treatments, non-reimbursement for companion diagnostics, and excessive and burdensome prior authorization practices were cited as other drivers of hidden costs. One respondent said payers “should require less outcomes/pharmacoeconomic data on novel products where there is no appropriate generic. The cost of copays in tier three+ products is generally too high and restricts use of good drugs in patients who are likely to benefit.”

Finally, one respondent said what we need is greater transparency overall, as well as the elimination of paperwork, constantly changing reimbursement rules and hidden pricing deals with intermediaries.

Parthenon-EY | 13

Conclusion

There are many conversations taking place in both public and private forums around the current state of pharmaceuticals, drug prices and public policy changes. Parthenon-EY and YourEncore decided to conduct a survey to ask leaders in the industry value chain what they thought of the regulatory environment and how changes may impact the industry. What we heard was both interesting and affirming of many of the sentiments being reported by the general press. Everyone seems to want change and there is still widespread support around patient safety and efficacy as a priority. The types of changes needed range from simplification of rules and guidelines to wholesale changes around the economic models to usher in greater transparency. The myriad of models and processes that have evolved over the years are putting additional burdens and costs on a constrained system, so thoughtful restructuring of business and economic

models is needed and welcomed by the community of leaders in the industry.

Parthenon-EY has been helping clients across the entire life sciences value chain assess whether they need to change their business, operating and economic models to help them be better positioned in the future. There is broad openness to doing things differently, but many clients are looking for guidance from regulatory authorities to help them design more optimal solutions. There are many ideas but little clarity around expectations and desired outcomes, much less how success will be measured. Restrictions around sharing information make it difficult for companies to innovate and change their infrastructure, so there is considerable stasis around wholesale change. The will exists, the way needs to be paved.

EY | Assurance | Tax | Transactions | AdvisoryAbout EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

Parthenon-EY refers to the combined group of Ernst & Young LLP and other EY member firm professionals providing strategy services worldwide. Visit parthenon.ey.com for more information.

©2017 Ernst & Young LLPAll Rights Reserved. SCORE No. 03522-171US ED None This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.ey.com

About Parthenon-EYParthenon joined Ernst & Young LLP on 29 August 2014. Parthenon-EY is a strategy consultancy, committed to bringing unconventional yet pragmatic thinking together with our clients’ smarts to deliver actionable strategies for real impact in today’s complex business landscape. Innovation has become a necessary ingredient for sustained success. Critical to unlocking opportunities is Parthenon-EY’s ideal balance of strengths — specialized experience with broad executional capabilities — to help you optimize your portfolio of businesses, uncover industry insights to make investment decisions, find effective paths for strategic growth opportunities and make acquisitions more rewarding. Our proven methodologies along with a progressive spirit can deliver intelligent services for our clients, amplify the impact of our strategies and make us the global advisor of choice for business leaders.

About the Parthenon-EY Life Sciences practiceThe Parthenon-EY Life Sciences practice has dedicated life sciences professionals across member firms in 17 countries spanning the Americas, Europe, Middle East and Asia-Pacific. Our global hub is based in the US and has life science leaders in Boston, New York, Chicago and San Francisco. All Parthenon-EY Life Sciences professionals have extensive experience in life sciences strategy consulting and academic degrees in science, clinical and business disciplines. The practice coordinates with the Parthenon-EY Health care and Consumer practices as well, bringing the full gamut of convergence in consumer, health care and life sciences offerings to clients in companies, investor groups, payers and providers worldwide.

Parthenon-EY Life Sciences practice

For more information on our Life Sciences practice and our team, please visit parthenon.ey.com.

Our team

Alex Jung Managing Director Parthenon-EY Ernst & Young LLP 1 312 879 2778 [email protected]

YourEncore contributors

Kyle FenstermakerManaging Director, YourEncoreBio-Pharmaceutical Practice1 609 240 [email protected]

Joseph LamendolaSenior Vice President, YourEncoreBio-Pharmaceutical Practice1 609 937 [email protected]

Daniel MaterConsultant Parthenon-EY Ernst & Young LLP 1 312 879 3345 [email protected]