Embed Size (px)

Citation preview

Pharma & Life Science Get Together

May 2017

Introduction

PwC

Your contacts

Monica Cohen-Dumani

Partner – Corporate Tax

PricewaterhouseCoopers SA, Geneva SwitzerlandPhone: +41 58 792 97 18Email: [email protected]

Dr. Sandra Ragaz

Director - Leader Pharma & Life Science VAT Switzerland

PricewaterhouseCoopers AG, Zurich SwitzerlandPhone: +41 58 792 44 69E-mail: [email protected]

Patricia More

Partner – Indirect Taxes

PricewaterhouseCoopers SA, Geneva SwitzerlandPhone: +41 58 792 95 07Email: [email protected]

May 2017Pharma & Life Science Get Together

PwC

1.

Sales of pharmaceutical products within Europe by Swiss established companies – hurdles and opportunities

3.

Agenda

Toll manufacturing in the pharma & life science sector2.

CTR III: three months after the popular vote, US Tax Reform and European Tax latest developments

Pharma & Life Science Get Together May 2017

1 CTR III, US Tax Reform and European Tax latest developments

2 Toll manufacturing

PwC

2 Toll manufacturing hurdles and opportunities

Toll Manufacturing / Toll Processing VS Contract manufacturing

May 2017Pharma & Life Science Get Together

• The Principal retains title of the goods throughout themanufacturing process

• The Principal will buy and hold legal title to the raw material,but the goods will be shipped to the Toll Manufacturer

• The toll manufacturer performs processing services, and iscompensated by manufacturing principal through a tollmanufacturing fee

• The manufacturing principal bears the risks associated withholding raw materials and finished goods inventory, as wellas final demand and price risks

• Toll manufacturer‘s supplies are treated as services for VATpurposes in most of the countries

• The contract manufacturer produces goods formanufacturing principal that directly bears demand and finalcustomer pricing risk

• The contract manufacturer comply with the principal’sguidelines, standards, products and quality specifications

• The contract manufacturer owns plant and equipment andpurchase raw material according to the standards agreed withthe Principal

• The contract manufacturer bears the risks associated withholding fixed assets and inventory

• Contract manufacturer’s supplies are treated as supply ofgoods for VAT purposes

Contract ManufacturingWhat is Toll Manufacturing/Toll Processing?

PwC

2 Toll manufacturing hurdles and opportunities

Pharma & Life Science Get Together

Toll manufacturing Contract manufacturing

Toll manufacturer

ManufacturingPrincipal

Suppliers

Customers

Payment for raw materials and semi-finished goods

Payment for finished goods

Finished goods

Goods legal ownership

Goods physical flow

Finished goods

Toll manufacturing fee (markupon manufacturing costs)

Contractmanufacturer

ManufacturingPrincipal

Suppliers

Customers

Payment for finished goods

Finished goods

Goods legal ownership

Goods physical flow

Finished goods

Manufacturing compensation (consideration for finished goods)

Payment for raw materials and semi-finished goods

Raw materials and semi-finished goods

VAT TechnicalToll Manufacturing / Toll Processing VS Contract manufacturing

May 2017

PwC

2 Toll manufacturing hurdles and opportunities

Reporting

Issues EU Member States:• Typically toll manufacturer‘s supplies are treated

as services for VAT purposes (Basic place of supplyrule in EU)

• Physical movement of goods must be reported (aswell as the supply of services)

- By Principal/ toll manufacturer?

- Key to distinguish from Contractmanufacturing

Issues Switzerland:• Typically toll manufacturer‘s transactions are

treated as supply of goods for VAT purposes (i.e. place of taxation is where the goods are going to be processed)

• Physical movement of goods must be reported (as well as the manufacturers' transaction)

• The following two processes are possible for the physical movement of goods;

- Definitive import into Switzerland, toll manufacturing of the products and definitive export of the processed goods

- Inward processing in Switzerland: special procedure and documentation are required

Pharma & Life Science Get Together

Reporting EU Member States:• EU reporting requirements

- VAT returns

- Intrastat

- EC Sales List

- EC services List

- Registers of the goods processed

May 2017

PwC

2 Toll manufacturing hurdles and opportunities

Point of attention

Pharma & Life Science Get Together

• Qualification of toll manufacturing VS contract manufacturing:

Qualification of supplies depends on type of goods which are supplied by manufacturer; if e. g. these goods qualify as mainmaterial, supply would qualify as supply of goods; if goods are rather ancillary then the supply would qualify as supply of service; r/c procedure might apply. Customs duty reliefs may be applied where raw materials for manufacture are sourced from non-EU location.

• Physical flows of raw material & finished products:

Bilateral work on goods / triangular / other

• Who is liable for the reporting ?:

Principal or toll manufacturer

May 2017

PwC

2 Toll manufacturing hurdles and opportunities

Fixed establishment

Pharma & Life Science Get Together

Why does it matter?

• Determination of place of supply

◦ B2B (Article 44 EU VAT Directive 112/2006) – services taxable where the recipient has established his business.

◦ Article 11 Council Implementing Regulation no. 282/2011: A fixed establishment means:

any place, other than the taxpayer's place of establishment of a business,

which is characterized by a sufficient degree of permanence and

a suitable structure in terms of human and technical resources

• to enable it to receive and use the services supplied to it for its own needs (passive FE)

• to enable it to provide the services which it supplies (active FE)

• Determination of person liable to pay/ account for VAT

◦ VAT liability for local supply of goods might be in some countries shifted to the recipient if he is established in that country

• Input VAT refund

◦ The way how local VAT should be recovered will depend on the fact if company is or is not VAT registered (local VAT return vs VAT refund claim)

May 2017

PwC

2 Toll manufacturing hurdles and opportunities

Fixed establishment = The Polish “Cans case” (I FSK 1379/15) – main arguments of the court

Literal reading

Optimisation Undefined period

Exclusive relationship

All infrastructure necessary to run the

business

Managed from abroad

Actions taken by SwissCo aiming at diminishing its tax burden (lower VAT rate in Switzerland –depending on the product)

Specific for SwissCo

Steering can be done on long distance, it however means that the external personnel in Poland was controlled and managed in an analogic way as own employees.

Place of management

The resources in Poland were sufficient to allow to conduct business permanently and in some sense independently from the Swiss headquarter

Footprint

FE

Fixed = related to determined place, unchangeable, still and not temporary nor occasionally”

.

Interpretation method

Undefined period of the tolling agreement (e.g. packaging

services) supports the fact that the structure is not temporary

Contractual terms

The fact that SwissCo was the only customer of the Polish tolled

supported the fact that the latter was dependent on SwissCo and

therefore should be considered as SwissCo’s own infrastructure

Dependency

Pharma & Life Science Get Together May 2017

PwC

2 Toll manufacturing hurdles and opportunities

Reporting and IT

Your ERP coding process must enable you to classify each transaction so that the tax determination logic within yourERP system applies the correct VAT treatment.

Pharma & Life Science Get Together

Challenges:

• ERP systems native capabilities may be limited

• ERP set up may not be optimal. Limited resources

• Deadlines and time limits: on time reporting

• New reporting obligations

Action steps:

• Improve your existing ERP set up or review your ITorganisation

• Enhance your existing VAT and statistical reports

• Automate your reconciliation process

• Automate report testing and return preparation

May 2017

1 ITX Strategy 3 Sales of pharmaceutical products – hurdles and opportunities

PwC

3 Indirect Taxes: sales of pharmaceutical & life science products

Sale of pharmaceutical products within the EU by non established companies - background 1/2

• Recent developments show that health authorities increase audits and prevent the sale of pharmaceutical products within the EU under certain circumstances by companies located outside of the EU

• Legal basis: The pharmaceutical legislation, Art. 76 of the directive 2001/83EG, the anti-counterfeiting directive 2011/62 and correspondent legal acts implemented in 2015 in different EU Member States

• Consequences: Stricter controls of the sales channels in the EU member states by the health authorities and tighter implemented regulations (e.g. para. 52 of the pharmaceutical legislation in Germany). The sale of pharmaceutical products of a non EU established business is prohibited within the EU in case a wrong wholesaler license is used

Pharma & Life Science Get Together May 2017

PwC

3 Indirect Taxes: sales of pharmaceutical & life science products

Sale of pharmaceutical products within the EU by non established companies - background 2/2

• Major challenges:- Restructuring the current Swiss business model- Significant changes in the supply chain- Direct and indirect tax implications in Switzerland

and in the European Union- ERP system and contract adaptions - etc.

• Action steps: It is crucial to ensure that the pharmaceutical companies are prepared to the new developments resp. have a solution at hand if already affected

Pharma & Life Science Get Together May 2017

PwC

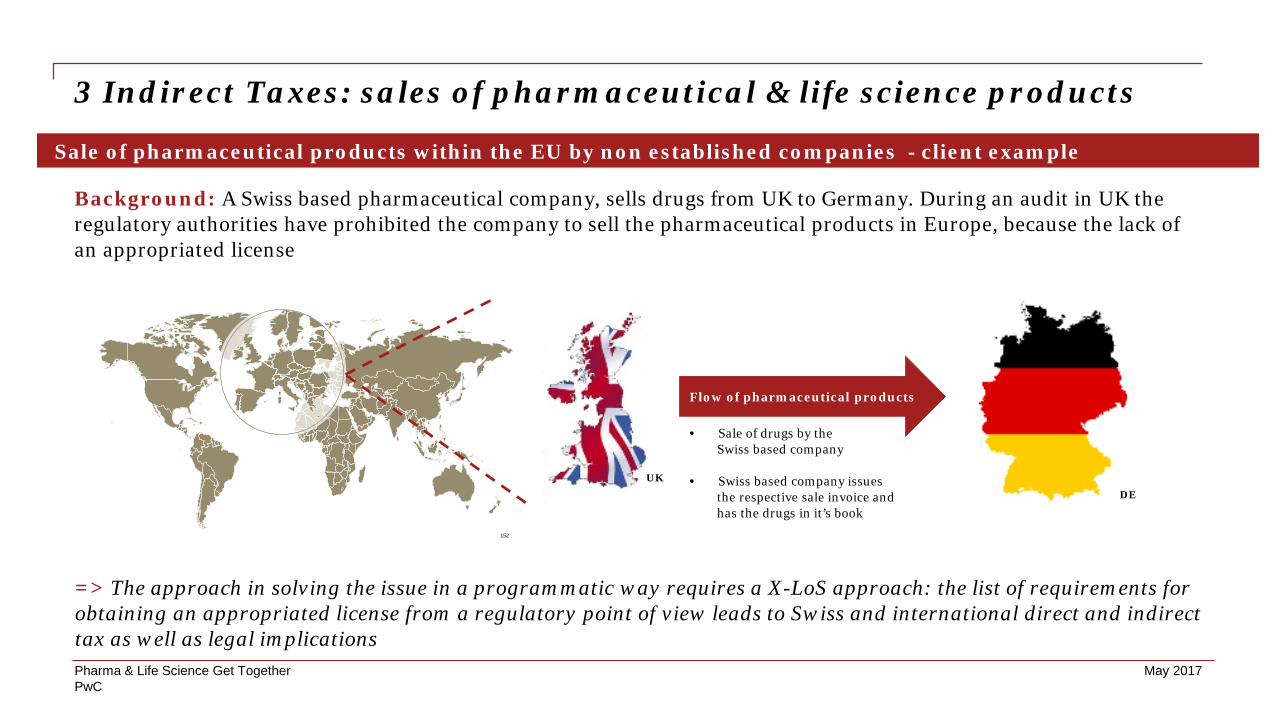

3 Indirect Taxes: sales of pharmaceutical & life science products

Sale of pharmaceutical products within the EU by non established companies - client example

Background: A Swiss based pharmaceutical company, sells drugs from UK to Germany. During an audit in UK the regulatory authorities have prohibited the company to sell the pharmaceutical products in Europe, because the lack of an appropriated license

152

DE

Flow of pharmaceutical products

UK

• Sale of drugs by the Swiss based company

• Swiss based company issues the respective sale invoice and has the drugs in it’s book

=> The approach in solving the issue in a programmatic way requires a X-LoS approach: the list of requirements for obtaining an appropriated license from a regulatory point of view leads to Swiss and international direct and indirect tax as well as legal implicationsPharma & Life Science Get Together May 2017

PwC

Case Study

Pharma & Life Science Get Together

3 Indirect Taxes: sales of pharmaceutical & life science products

May 2017

PwC

Excurs: Indirect Taxes: Clinical Trials – Are you ready for transparency?

<<<<<<<<<<<The new regulation for clinical trials – Annex 6 and 16 and impact on processes

Impact on core processes/data of pharmaceutical companies

• Requirements for compliance and for sharing sensitive information (Annex 6 & 16)

• Company data will be disclosed in a new EU database (Annex 6)

• Data includes scientific and financial information (financial set-up and arrangements for rewarding or compensating subjects i.e. investigators and patients)

Sponsors should prepare themselves for new transparency requirements that make them disclose, either directly or indirectly, information on the financial and tax position

Pharma & Life Science Get Together May 2017

PwC

How do we can assist you?

Some examples

• PwC Data analytics & Reporting tools help also identify risks and opptimizethe transaction structure (e.g. electronic health-check)

1. STARS (Strategic Tax Accounting & Reporting Solutions)

2. Customised- Import tool

3. Healtcheck and machine learningPwC

4. SAP Cockpit

5. SmartTools

Pharma & Life Science Get Together May 2017

PwCMay 2017Pharma & Life Science Get Together

Discussion and Q&A

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication withoutobtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extentpermitted by law, PricewaterhouseCoopers AG, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, orrefraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2017 PwC. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers AG which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Thank you for attending the Get Together