Embed Size (px)

Citation preview

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 1/9

www.synerzys.com

Pharma Business dynamics in ROW marketsChallenges & opportunities for Indian Pharma SME manufacturers

a) Introduction

From an era (Pharma 1.0) of “blockbuster” drugs, global Pharma market has moved into the

current era (Pharma 2.0) that is focussing on emerging markets opportunity and Genericisation.

Many factors are driving this change. Western economies are decelerating and a large chunk

of Healthcare costs are public funded. Though governments acknowledge healthcare provision

to be strategically important, their willingness and ability to pay for it is subject to the current

economic slowdown. Simultaneously R&D productivity at global pharma giants has been at

historic lows leaving them grappling with a patent cliff and need to discover newer avenues of

growth.

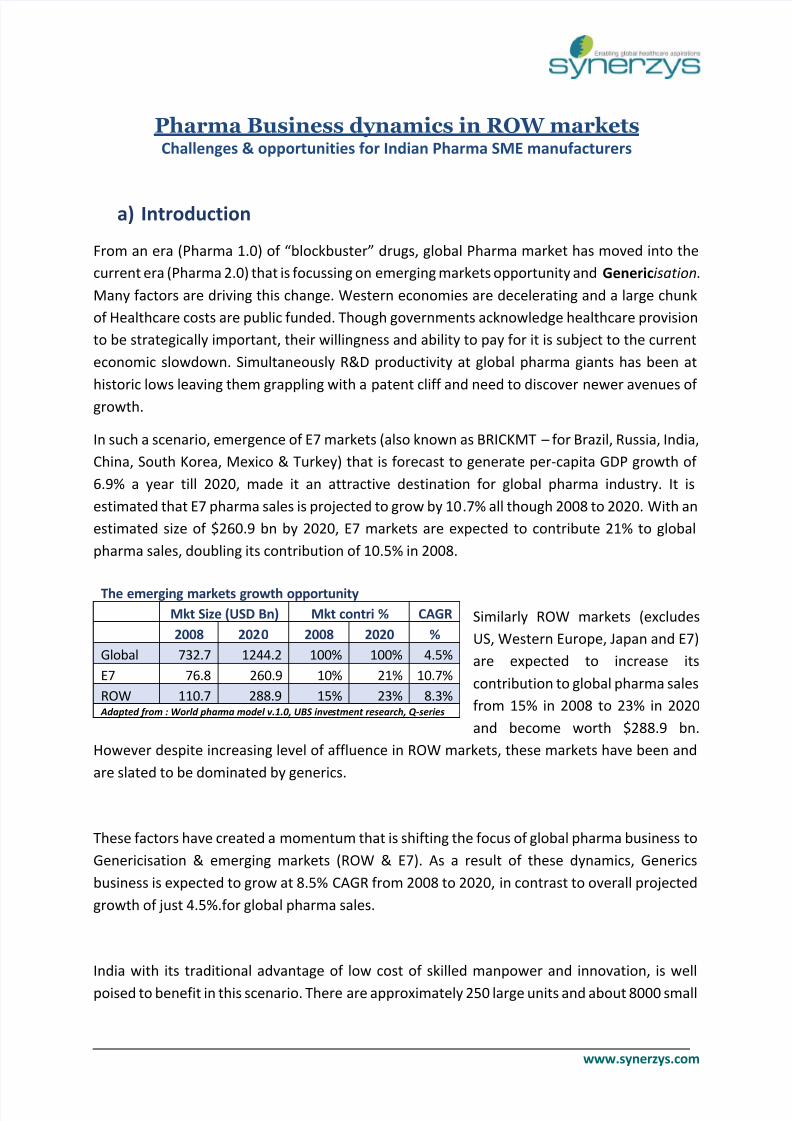

In such a scenario, emergence of E7 markets (also known as BRICKMT – for Brazil, Russia, India,

China, South Korea, Mexico & Turkey) that is forecast to generate per-capita GDP growth of

6.9% a year till 2020, made it an attractive destination for global pharma industry. It is

estimated that E7 pharma sales is projected to grow by 10.7% all though 2008 to 2020. With an

estimated size of $260.9 bn by 2020, E7 markets are expected to contribute 21% to global

pharma sales, doubling its contribution of 10.5% in 2008.

Similarly ROW markets (excludes

US, Western Europe, Japan and E7)

are expected to increase its

contribution to global pharma sales

from 15% in 2008 to 23% in 2020

and become worth $288.9 bn.

However despite increasing level of affluence in ROW markets, these markets have been and

are slated to be dominated by generics.

These factors have created a momentum that is shifting the focus of global pharma business to

Genericisation & emerging markets (ROW & E7). As a result of these dynamics, Generics

business is expected to grow at 8.5% CAGR from 2008 to 2020, in contrast to overall projected

growth of just 4.5%.for global pharma sales.

India with its traditional advantage of low cost of skilled manpower and innovation, is well

poised to benefit in this scenario. There are approximately 250 large units and about 8000 small

The emerging markets growth opportunity

Mkt Size (USD Bn) Mkt contri % CAGR

2008 2020 2008 2020 %

Global 732.7 1244.2 100% 100% 4.5%

E7 76.8 260.9 10% 21% 10.7%

ROW 110.7 288.9 15% 23% 8.3% Adapted from : World pharma model v.1.0, UBS investment research, Q-series

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 2/9

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 3/9

www.synerzys.com

c.1) Increased focus on indigenisation

Many governments in ROW countries are realizing the strategic importance of Pharmaceuticalindustry. Pharma industry not only is a key component of their welfare agenda to provide basic

level of healthcare to local population but also can be a significant drain on limited foreign

currency reserves. Thus governments are setting up tariff and non-tariff barriers to protect and

promote local pharmaceutical industry.

For example in Algeria, in last few years, government has implemented following measures

leading to a significant increase in local manufacturing activity.

Tariff barriers

o

Increased tax rates for imported products

Non-Tariff barriers

o Banning import of products with more than 2 local manufacturers

o Preferential interest rates for new manufacturing projects

o Differential regulatory requirements for imported and locally produced

products. Bioequivalence is required for imported formulations and formulated

bulk premix but not for locally produced formulations

c.2) Increased regulatory stringency

With the rising reach of low-cost generic medicines, regulators across many ROW markets are

opting for stricter norms to focus on quality. With the distinction between regulated and semi

/ non-regulated market thinning by the day, CTD format with minor country specific

customizations is becoming increasingly common. More countries insist on plant audits for

GMP approval.

For eg. Peru MOH now insists for GMP plant audits for those plants that do not have approvals

from any one of the Stringent regulatory authorities like USFDA, EMEA, TGA etc

Many African countries like Kenya, Uganda & Tanzania authorities have also mandated GMP

Plant audits.

c.3) Move towards a harmonized regulatory environment

A cluster of countries come together to create a uniform regulatory environment, provide

mutual recognition to product approvals and in many cases also provide an unified market forthe manufacturers

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 4/9

www.synerzys.com

ASEAN(Indonesia, Cambodia, Malaysia, Laos, Myanmar, Philippines, Singapore, Thailand, Vietnam & Brunei Darussalam)

Its major objectives includes the harmonisation of technical guidelines and regulatory

requirements applicable to the ASEAN pharmaceutical industry & development of Common

Technical Documents with a view to arriving at Mutual Recognition Arrangement (MRAs).

GCC(KSA, UAE, Qatar, Kuwait, Oman, Bahrain..)

The GCC countries agreed to adopt the Common Technical Document (CTD) framework in 2009

and have since progressively moved towards its implementation. They also have a unified

streamline approach for plant and product registrations.

d)

Key Aspects for success in ROW markets

The above trends can be managed and even leveraged by Indian formulation manufacturers to

build their export business in ROW markets.

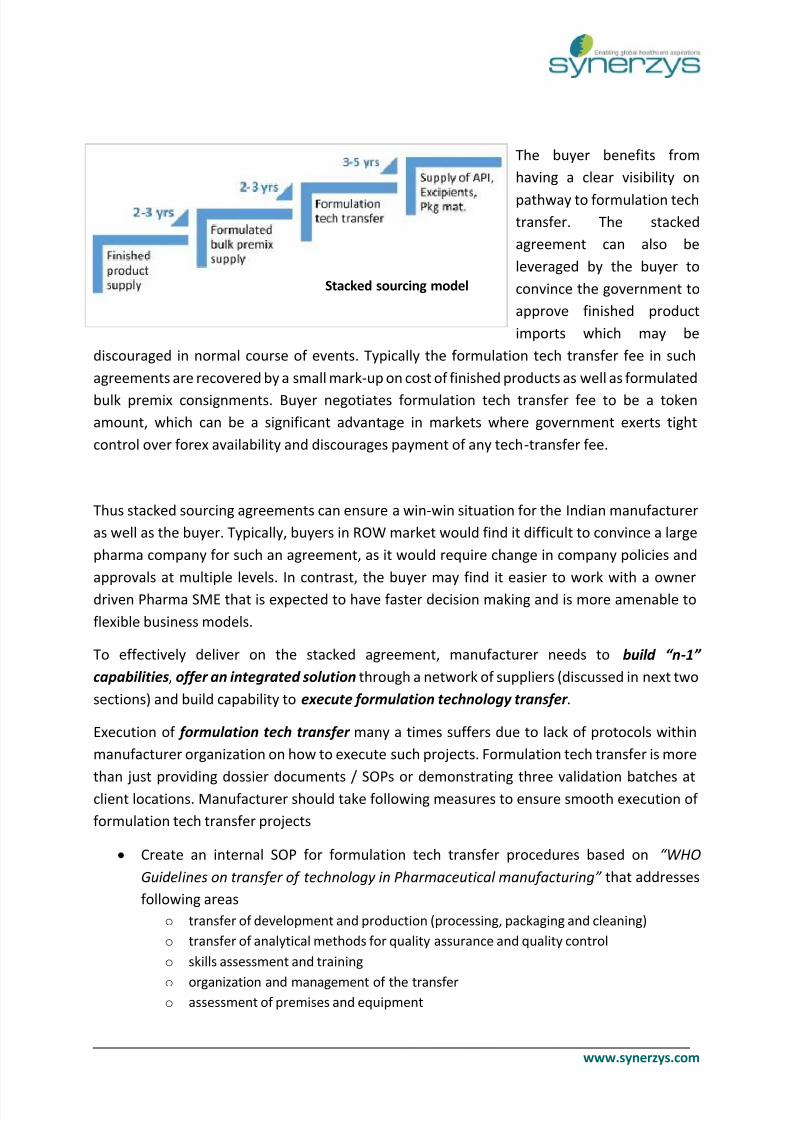

d.1) Newer business models – Stacked sourcing agreements

A stacked agreement is a long term supply commitment that progressively moves from supply

of finished formulation supply of formulated bulk premix formulation technology transfer

followed by supply of API / excipients / packaging material for a specified period. Typically

formulation tech transfer occurs after fulfilment of volume commitment by buyer over a period

of 3 to 5 years.

Historically manufacturers have been reluctant to adopt stacked sourcing model as they are

not keen to part with the intellectual property. However it is slowly gaining acceptance as this

model aids manufacturer to open up a market for their finished products, which in normal

course of events was unavailable due to local government policy of promoting “local

manufacturing”. The manufacturer gets a long term commitment for revenues and is able to

generate significant revenues before actual formulation tech transfer.

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 5/9

www.synerzys.com

The buyer benefits from

having a clear visibility on

pathway to formulation tech

transfer. The stacked

agreement can also be

leveraged by the buyer to

convince the government to

approve finished product

imports which may be

discouraged in normal course of events. Typically the formulation tech transfer fee in such

agreements are recovered by a small mark-up on cost of finished products as well as formulated

bulk premix consignments. Buyer negotiates formulation tech transfer fee to be a token

amount, which can be a significant advantage in markets where government exerts tight

control over forex availability and discourages payment of any tech-transfer fee.

Thus stacked sourcing agreements can ensure a win-win situation for the Indian manufacturer

as well as the buyer. Typically, buyers in ROW market would find it difficult to convince a large

pharma company for such an agreement, as it would require change in company policies and

approvals at multiple levels. In contrast, the buyer may find it easier to work with a owner

driven Pharma SME that is expected to have faster decision making and is more amenable to

flexible business models.

To effectively deliver on the stacked agreement, manufacturer needs to build “n-1”

capabilities, offer an integrated solution through a network of suppliers (discussed in next two

sections) and build capability to execute formulation technology transfer .

Execution of formulation tech transfer many a times suffers due to lack of protocols within

manufacturer organization on how to execute such projects. Formulation tech transfer is more

than just providing dossier documents / SOPs or demonstrating three validation batches at

client locations. Manufacturer should take following measures to ensure smooth execution of

formulation tech transfer projects

Create an internal SOP for formulation tech transfer procedures based on “WHO

Guidel ines on transfer of technology in Pharmaceutical manufacturing” that addresses

following areas

o transfer of development and production (processing, packaging and cleaning)

o transfer of analytical methods for quality assurance and quality control

o skills assessment and training

o

organization and management of the transfero assessment of premises and equipment

Stacked sourcing model

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 6/9

www.synerzys.com

o documentation

o Qualification and validation.

These formulation tech transfer projects, should have a project manager to drive the whole

initiative towards timely successful completion. Ideally the project manager should have crossfunctional reach across the manufacturing organization.

d.2) Build “n-1” capabilities

Whether as a part of stacked sourcing agreements or as a stand-alone product, supply of

formulated bulk premix (“n-1” in API parlance) can be a quick mode of entry into many markets

for a SME Pharma manufacturer. This strategy has advantage of circumventing “Local

manufacturing” requirements as discussed in previous section, without actually needing to ever

share formulation technology. This strategy may also translate into lower upfront expenses like

product registration & GMP plant audit costs.

However companies need to view formulated bulk premix as an independent revenue source

and not just an extension of finished product. Manufacturers are advised to generate following

data specifically for formulated bulk premix,

Stability studies – Accelerated and long term stability studies to be generated for formulated

bulk as well as for finished product.

Shipment validation – Stability in the container intended to be used for delivery of formulated

bulk premix to client for a period and temp/humidity conditions simulating the shipment period

& conditions, builds confidence among the buyers and regulators.

d.3) Offer an integrated solutionMany a times ROW markets have less developed ecosystem for supply of API, packaging

material or excipients. In such cases, stacked agreement not only allows extending the revenue

stream for the Indian manufacturer beyond formulation tech transfer, but also assures the

buyer of continued long term support.

While Buyers generally prefer an integrated supply source rather than deal with multiple

partners, manufacturer organization is not structured to provide the seamless experience. A

manufacturer can benefit immensely from a networked model wherein manufacturer has pre-

negotiated agreements with their vendors to provide seamless sourcing experience for the

buyer. If needed a unified invoicing option can also be negotiated with the vendors as well as

the buyer.

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 7/9

www.synerzys.com

d.4) Improve compliance with regulatory norms

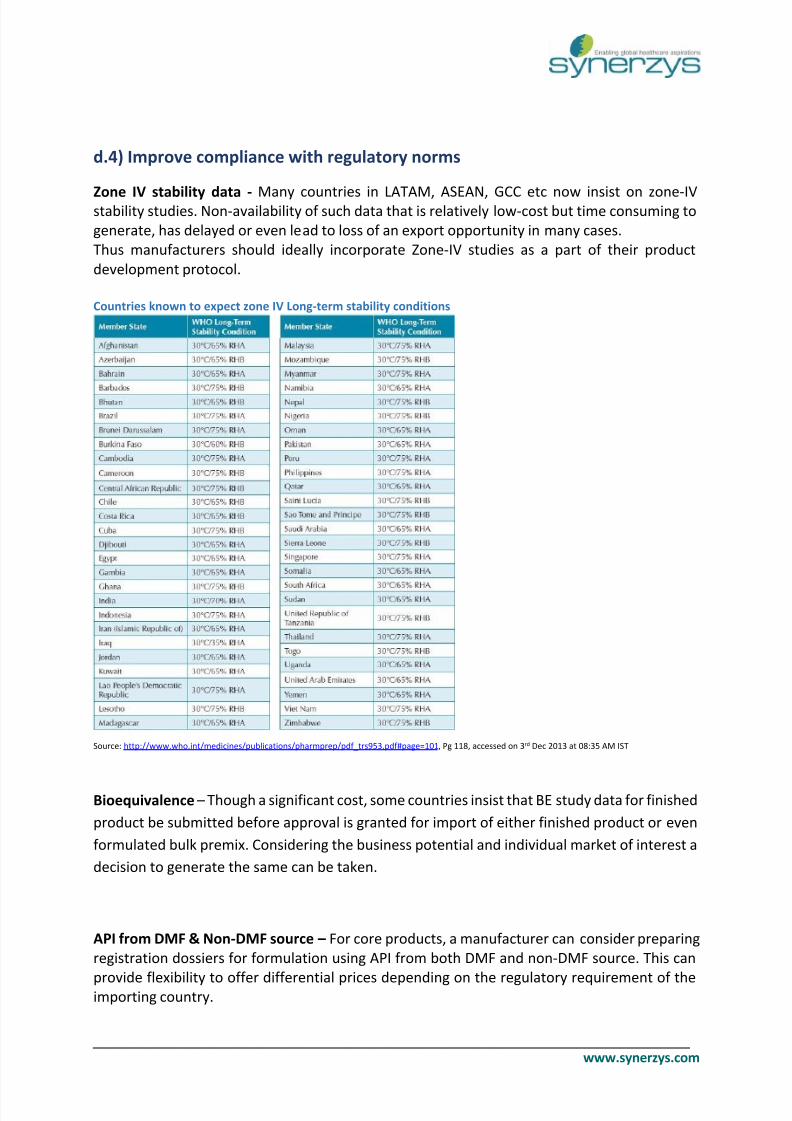

Zone IV stability data - Many countries in LATAM, ASEAN, GCC etc now insist on zone-IVstability studies. Non-availability of such data that is relatively low-cost but time consuming to

generate, has delayed or even lead to loss of an export opportunity in many cases.

Thus manufacturers should ideally incorporate Zone-IV studies as a part of their product

development protocol.

Countries known to expect zone IV Long-term stability conditions

Source: http://www.who.int/medicines/publications/pharmprep/pdf_trs953.pdf#page=101, Pg 118, accessed on 3rd Dec 2013 at 08:35 AM IST

Bioequivalence – Though a significant cost, some countries insist that BE study data for finished

product be submitted before approval is granted for import of either finished product or even

formulated bulk premix. Considering the business potential and individual market of interest a

decision to generate the same can be taken.

API from DMF & Non-DMF source – For core products, a manufacturer can consider preparing

registration dossiers for formulation using API from both DMF and non-DMF source. This can

provide flexibility to offer differential prices depending on the regulatory requirement of theimporting country.

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 8/9

www.synerzys.com

Reference NRA approval - Plant approval from stringent regulatory authorities like USFDA, TGA

Australia, UK MHRA, can enable exemption from plant audits in large number of countries.

However typically this route entails high cost, huge efforts and in many cases manufacturer’s

infrastructure may not be geared to face audit from such SRA.

However similar strategy can be employed with lower resources, within regional clusters. In

many cases, an approval of reference NRA makes approval from other countries within that

cluster significantly easy.

For example, if a manufacturer is targeting Middle East markets than approval by Jordan NRA

(JFDA) provides automatic approval in Syria and facilitates approval within Middle East.

Similarly, for a manufacturer targeting LATAM markets approval by any one of the four

reference NRAs can facilitate approvals in other countries. The four reference NRAs for LATAMare ANVISA Brazil, ANMAT Argentina, COFEPRIS Mexico, INVIMA Colombia,

d.5) Super GenericsIndian pharma industry is known globally for its formulation development prowess.

Supergenerics (Mouth Dissolving tabs/ Effervescent /Granules) or fixed dose combinations

approved by USFDA / EMEA enables pharma SMEs to build competitive advantage. Regulatory

pathway for approvals of such products may be slightly longer compared to normal products,however it can lead to significant improvement in margins, especially when the improvement

fulfils a genuine patient need. For example, Ahmedabad based Lincoln Pharma has developed

a novel Ondansetron nasal spray which has been granted a patent in 2011.

e) What can Pharma SMEs do better?

e.1) Well thought out comprehensive contract documentso Certified Bilingual contracts

o Focus on scenario planning.

All possible “what if” scenarios & remedial measures to be clearly defined

o Embassy legalized

o Choose Neutral venue of arbitration

8/10/2019 Pharma business dynamics in ROW markets

http://slidepdf.com/reader/full/pharma-business-dynamics-in-row-markets 9/9

www.synerzys.com

e.2) Partner identification & assessment processPharma SMEs would need a partner in local countries to register, distribute and market their

products. Choosing a partner arguably can be the most important decision a manufacturer will

make that will determine the success in particular market. Hence most companies pay asignificant amount of time and energy to whet the prospective partners on a matrix of

capability, financial strength, strategic fit and reputation.

Equally important in our opinion is to assess the partner on softer areas like cultural fit, business

principles, personal comfort, organizational culture etc. This issues are particularly important

wherein a manufacturer envisages a long term relations with the partner.

f)

Conclusion

ROW markets can offer a comparatively easier learning curve for exports market access to

Indian Pharma SMEs. ROW markets offer higher margins compared to domestic markets and

can become a significant contributor to a Pharma SME’s top line and bottom line. Indian

Pharma SMEs can leverage their relatively nimble decision making process to create

organizational processes that endow competitive advantage to it compared to its bigger peers.

Profitable growth of Pharma SMEs is necessary not only to ensure continued self-reliance of

India in healthcare segment