Embed Size (px)

Citation preview

© Grant Thornton India LLP. All rights reserved.© Grant Thornton India LLP. All rights reserved.

Pharma and Manufacturing Industry - Analysis & Methodology for Benchmarking and Documentation (including Domestic Transfer Pricing)

23 March 20133rd Intensive Course on Transfer Pricing

Grant Thornton India LLPKarishma R. PhatarphekarPartner & Practice Leader, Transfer Pricing Services

© Grant Thornton India LLP. All rights reserved.

Agenda

• Pharmaceutical Industry

• Overview• Types of International Transactions• Other Pharma TP Issues• Comparison of Relevant Decisions

• Manufacturing Industry

• Types of Manufacturer• Typical and Specific TP Issues• Challenges for Contract Manufacturers• Management Payouts

• Backdrop & Coverage of Specified Domestic Transactions (SDTs)

• SDTs – through case studies and case laws

• Way Forward

© Grant Thornton India LLP. All rights reserved. 3

PHARMACEUTICAL

INDUSTRY

© Grant Thornton India LLP. All rights reserved.

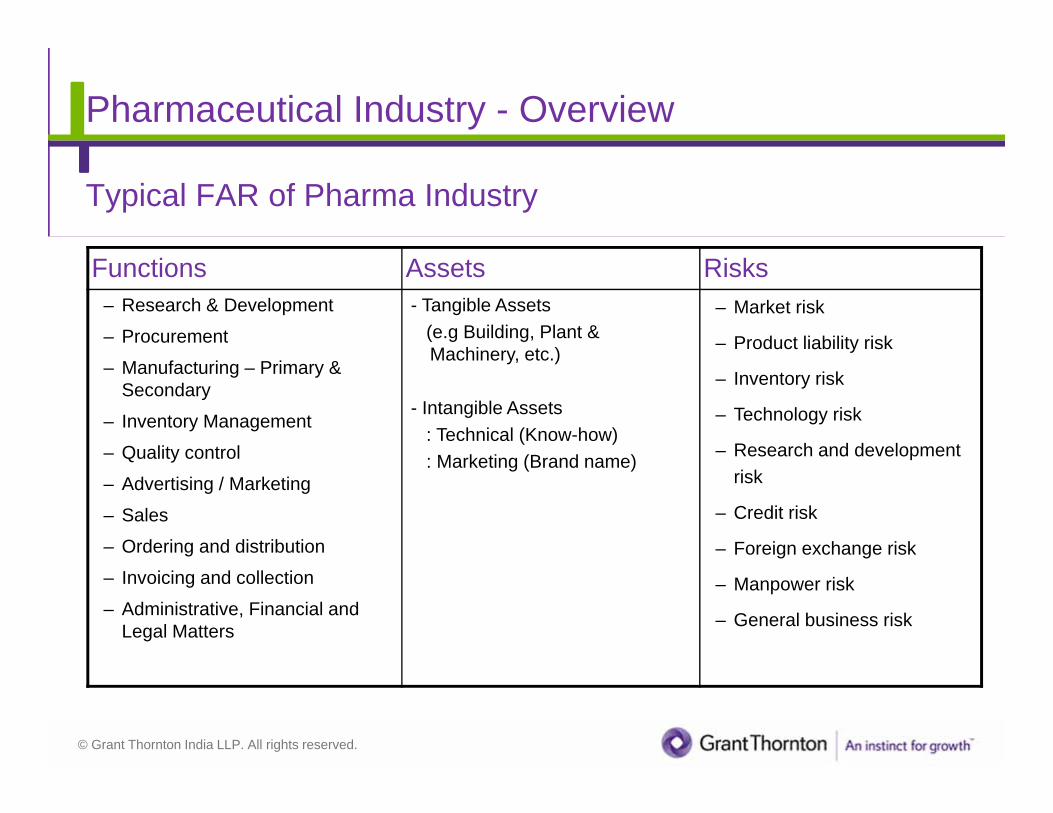

Pharmaceutical Industry - Overview

Typical FAR of Pharma Industry

Functions Assets Risks– Research & Development

– Procurement

– Manufacturing – Primary & Secondary

– Inventory Management

– Quality control

– Advertising / Marketing

– Sales

– Ordering and distribution

– Invoicing and collection

– Administrative, Financial and Legal Matters

- Tangible Assets(e.g Building, Plant & Machinery, etc.)

- Intangible Assets: Technical (Know-how): Marketing (Brand name)

– Market risk

– Product liability risk

– Inventory risk

– Technology risk

– Research and development risk

– Credit risk

– Foreign exchange risk

– Manpower risk

– General business risk

© Grant Thornton India LLP. All rights reserved.

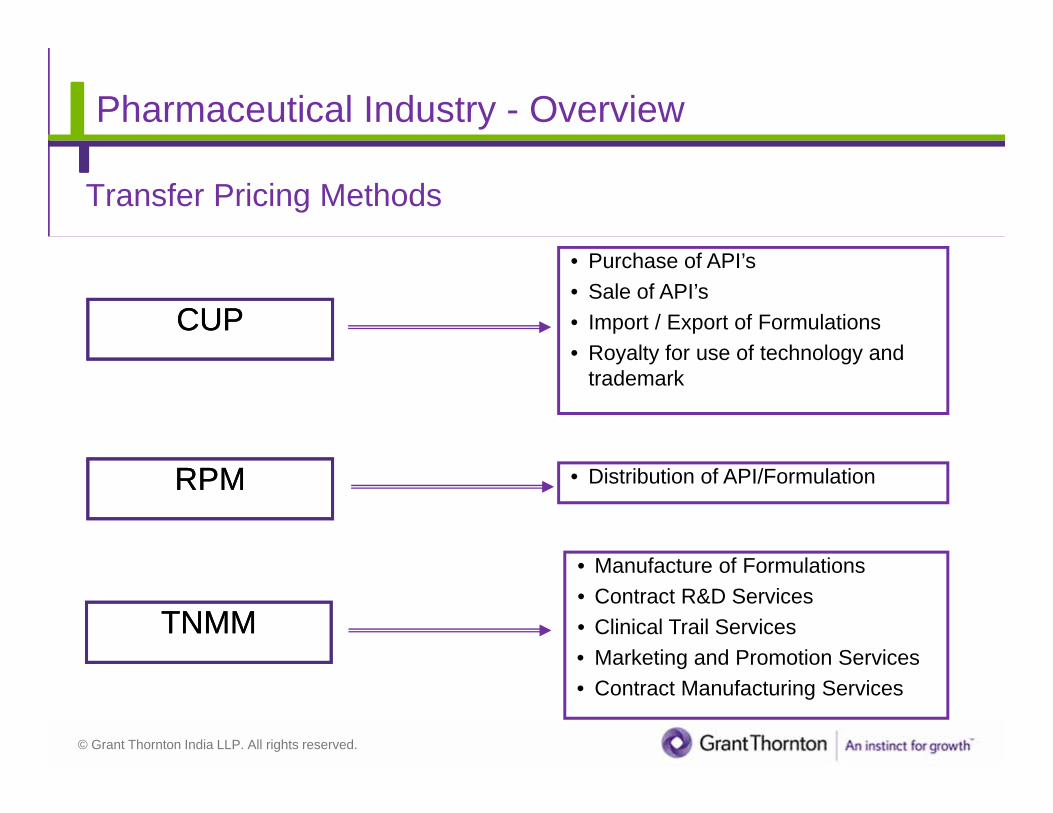

Pharmaceutical Industry - Overview

Transfer Pricing Methods

CUPCUP

• Purchase of API’s• Sale of API’s• Import / Export of Formulations• Royalty for use of technology and

trademark

TNMMTNMM

• Manufacture of Formulations• Contract R&D Services• Clinical Trail Services• Marketing and Promotion Services• Contract Manufacturing Services

RPMRPM • Distribution of API/Formulation

© Grant Thornton India LLP. All rights reserved.

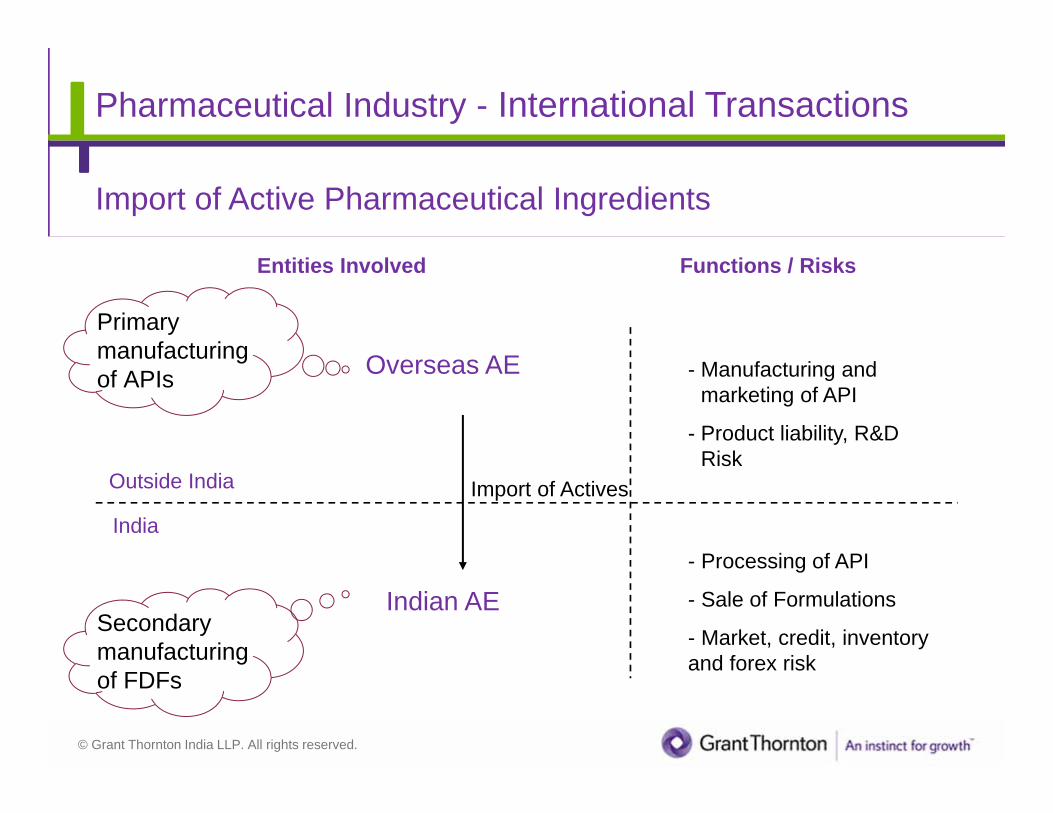

Entities Involved Functions / Risks

Overseas AE - Manufacturing and marketing of API

- Product liability, R&D Risk

- Processing of API

- Sale of Formulations

- Market, credit, inventory and forex risk

Import of ActivesOutside India

India

Indian AE

Pharmaceutical Industry - International Transactions

Import of Active Pharmaceutical Ingredients

Primary manufacturing of APIs

Secondary manufacturing of FDFs

© Grant Thornton India LLP. All rights reserved.

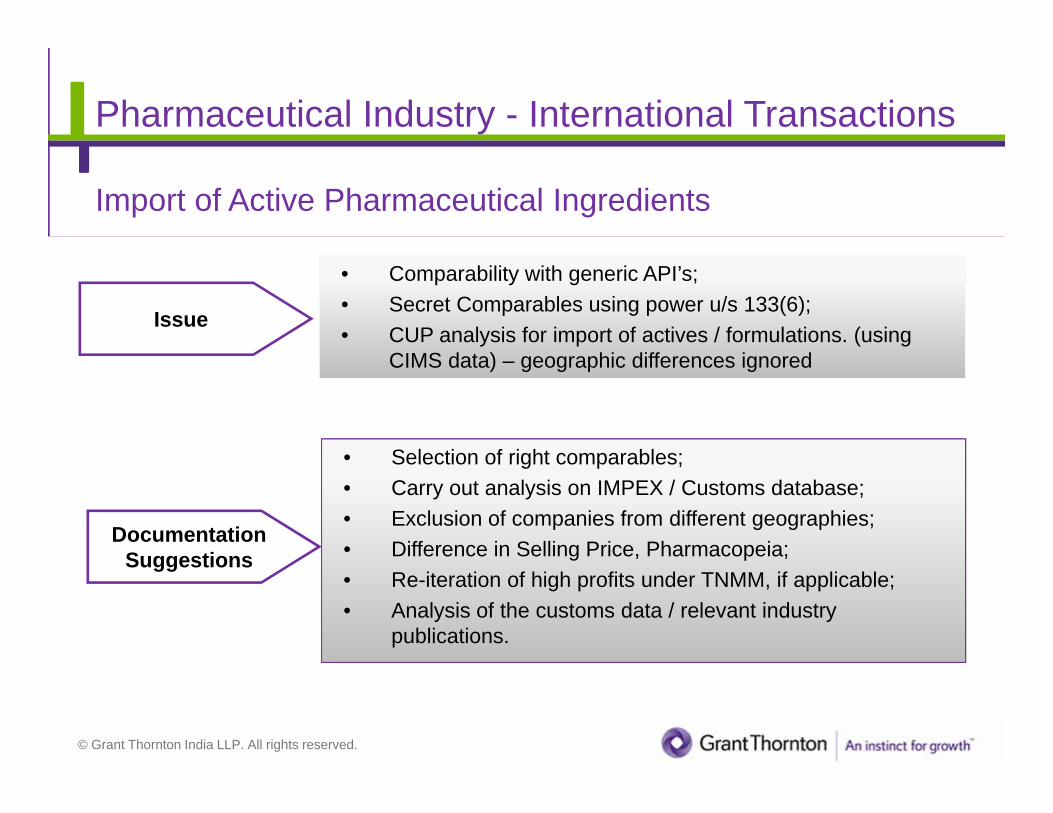

Pharmaceutical Industry - International Transactions

Import of Active Pharmaceutical Ingredients

Issue

DocumentationSuggestions

• Comparability with generic API’s;• Secret Comparables using power u/s 133(6);• CUP analysis for import of actives / formulations. (using

CIMS data) – geographic differences ignored

• Selection of right comparables;• Carry out analysis on IMPEX / Customs database;• Exclusion of companies from different geographies;• Difference in Selling Price, Pharmacopeia;• Re-iteration of high profits under TNMM, if applicable;• Analysis of the customs data / relevant industry

publications.

© Grant Thornton India LLP. All rights reserved.

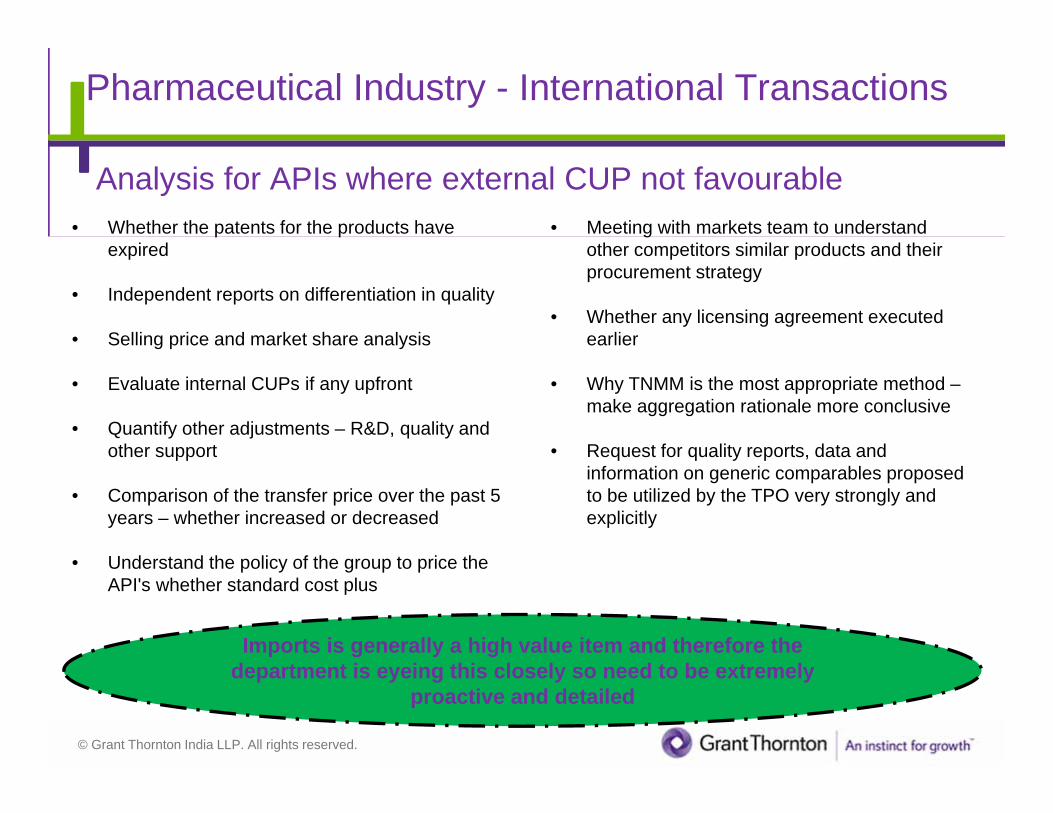

Pharmaceutical Industry - International Transactions

Analysis for APIs where external CUP not favourable• Whether the patents for the products have

expired

• Independent reports on differentiation in quality

• Selling price and market share analysis

• Evaluate internal CUPs if any upfront

• Quantify other adjustments – R&D, quality and other support

• Comparison of the transfer price over the past 5 years – whether increased or decreased

• Understand the policy of the group to price the API's whether standard cost plus

Imports is generally a high value item and therefore the department is eyeing this closely so need to be extremely

proactive and detailed

• Meeting with markets team to understand other competitors similar products and their procurement strategy

• Whether any licensing agreement executed earlier

• Why TNMM is the most appropriate method –make aggregation rationale more conclusive

• Request for quality reports, data and information on generic comparables proposed to be utilized by the TPO very strongly and explicitly

© Grant Thornton India LLP. All rights reserved.

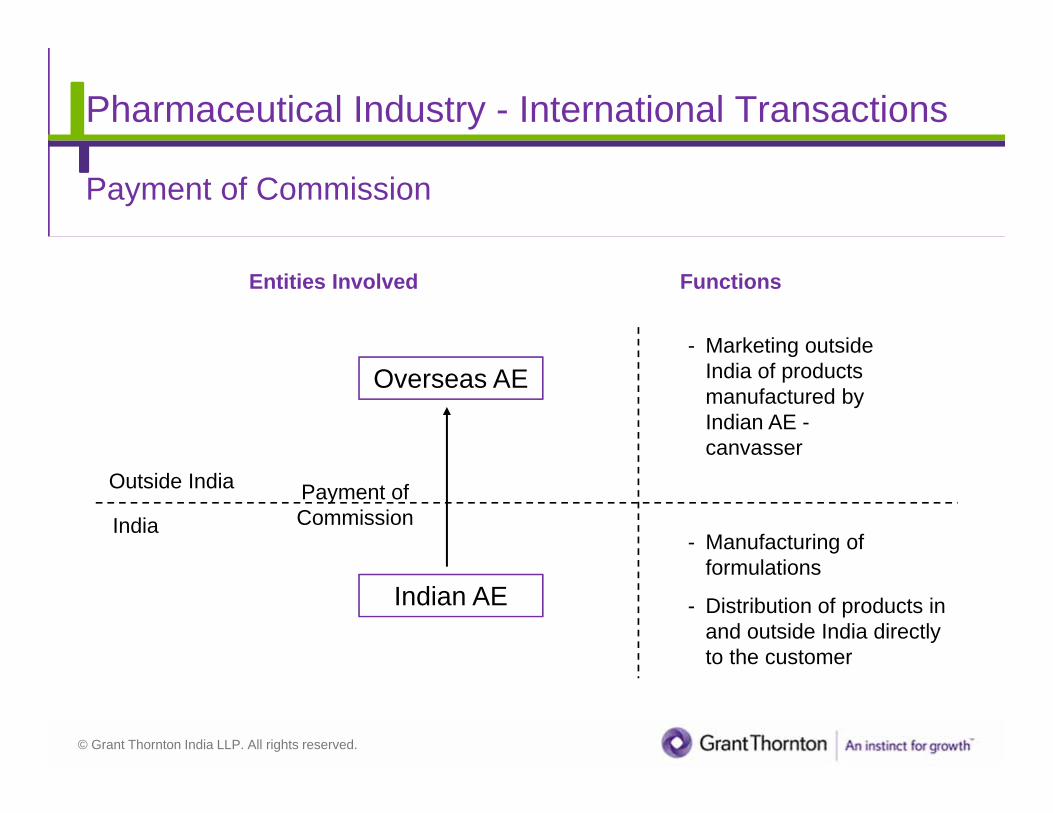

Pharmaceutical Industry - International Transactions

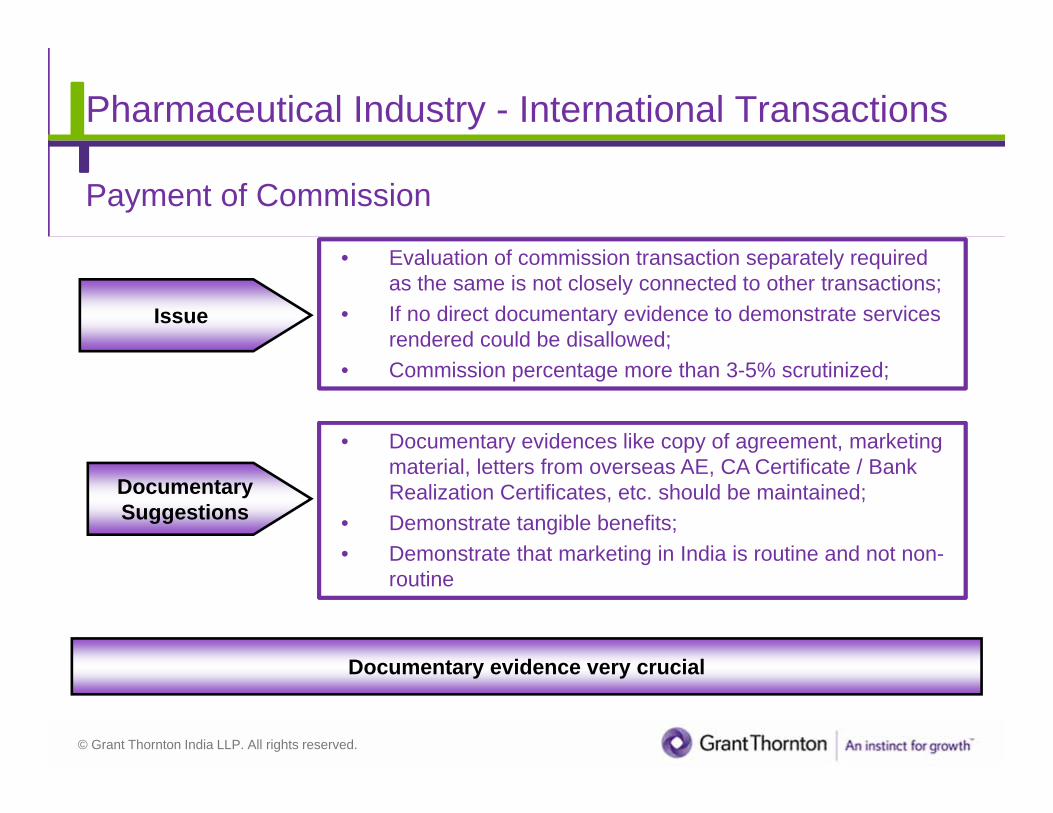

Payment of Commission

Entities Involved Functions

Overseas AEOverseas AE- Marketing outside

India of products manufactured by Indian AE -canvasser

- Manufacturing of formulations

- Distribution of products in and outside India directly to the customer

Payment of Commission

Outside India

India

Indian AEIndian AE

© Grant Thornton India LLP. All rights reserved.

Issue

DocumentarySuggestions

• Evaluation of commission transaction separately required as the same is not closely connected to other transactions;

• If no direct documentary evidence to demonstrate services rendered could be disallowed;

• Commission percentage more than 3-5% scrutinized;

• Documentary evidences like copy of agreement, marketing material, letters from overseas AE, CA Certificate / Bank Realization Certificates, etc. should be maintained;

• Demonstrate tangible benefits;• Demonstrate that marketing in India is routine and not non-

routine

Documentary evidence very crucial

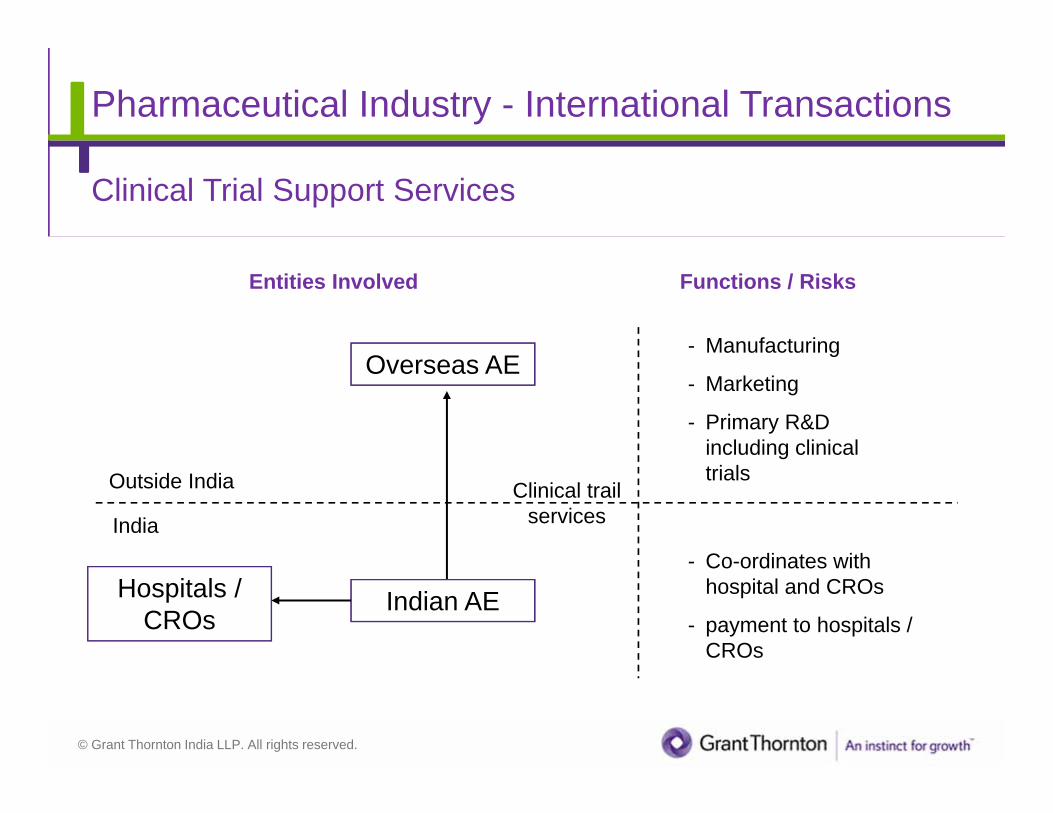

Pharmaceutical Industry - International Transactions

Payment of Commission

© Grant Thornton India LLP. All rights reserved.

Entities Involved Functions / Risks

Overseas AEOverseas AE- Manufacturing

- Marketing

- Primary R&D including clinical trials

- Co-ordinates with hospital and CROs

- payment to hospitals / CROs

Outside India

India

Indian AEIndian AE

Clinical trail services

Pharmaceutical Industry - International Transactions

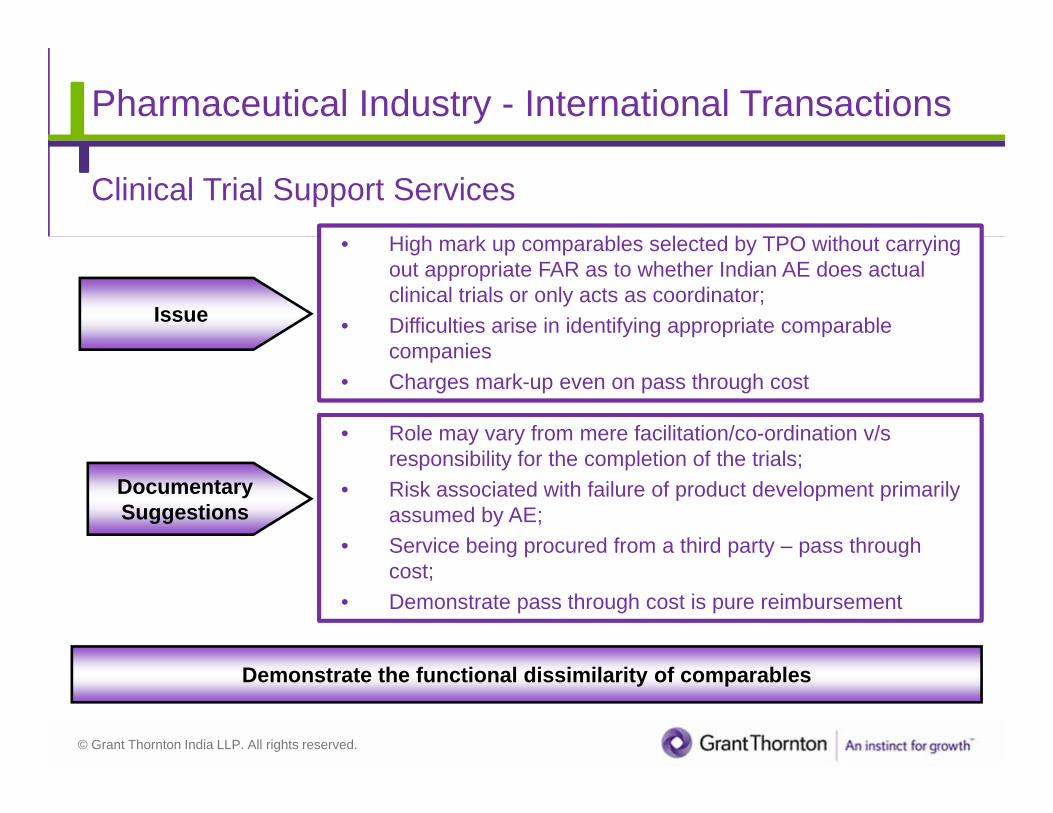

Clinical Trial Support Services

Hospitals / CROs

Hospitals / CROs

© Grant Thornton India LLP. All rights reserved.

Issue

DocumentarySuggestions

• High mark up comparables selected by TPO without carrying out appropriate FAR as to whether Indian AE does actual clinical trials or only acts as coordinator;

• Difficulties arise in identifying appropriate comparable companies

• Charges mark-up even on pass through cost

• Role may vary from mere facilitation/co-ordination v/s responsibility for the completion of the trials;

• Risk associated with failure of product development primarily assumed by AE;

• Service being procured from a third party – pass through cost;

• Demonstrate pass through cost is pure reimbursement

Demonstrate the functional dissimilarity of comparables

Pharmaceutical Industry - International Transactions

Clinical Trial Support Services

© Grant Thornton India LLP. All rights reserved.

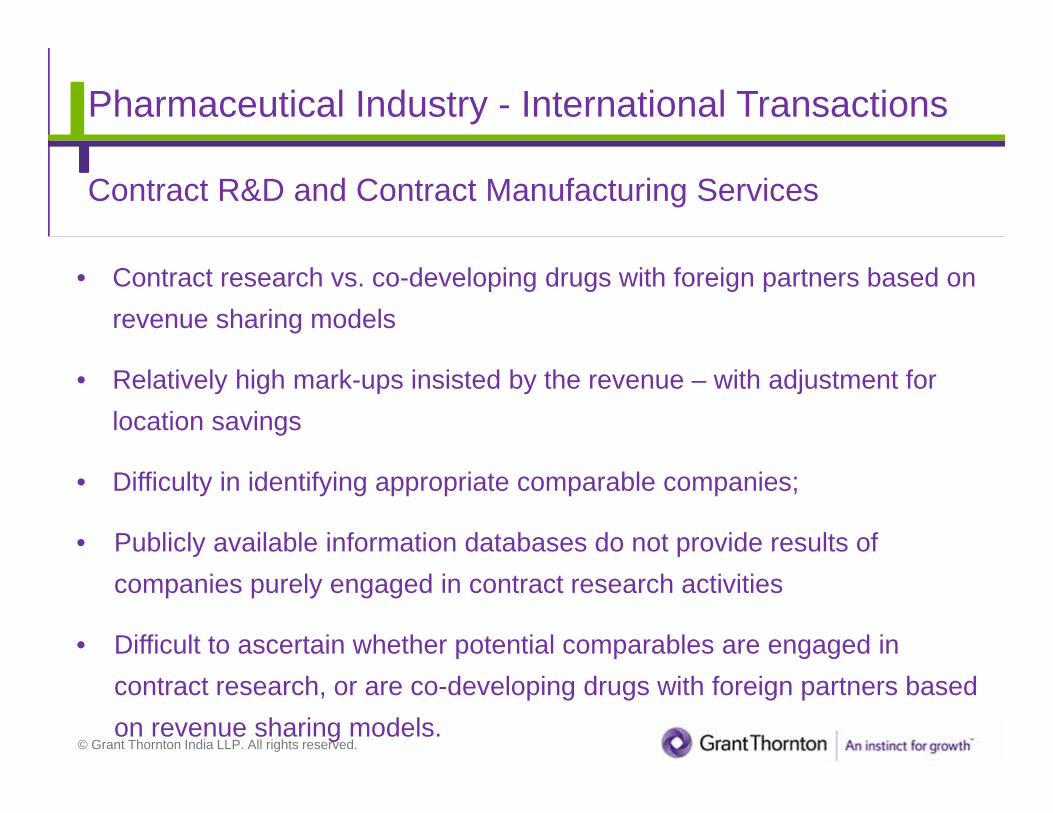

• Contract research vs. co-developing drugs with foreign partners based on revenue sharing models

• Relatively high mark-ups insisted by the revenue – with adjustment for location savings

• Difficulty in identifying appropriate comparable companies;

• Publicly available information databases do not provide results of companies purely engaged in contract research activities

• Difficult to ascertain whether potential comparables are engaged in contract research, or are co-developing drugs with foreign partners based on revenue sharing models.

Pharmaceutical Industry - International Transactions

Contract R&D and Contract Manufacturing Services

© Grant Thornton India LLP. All rights reserved.

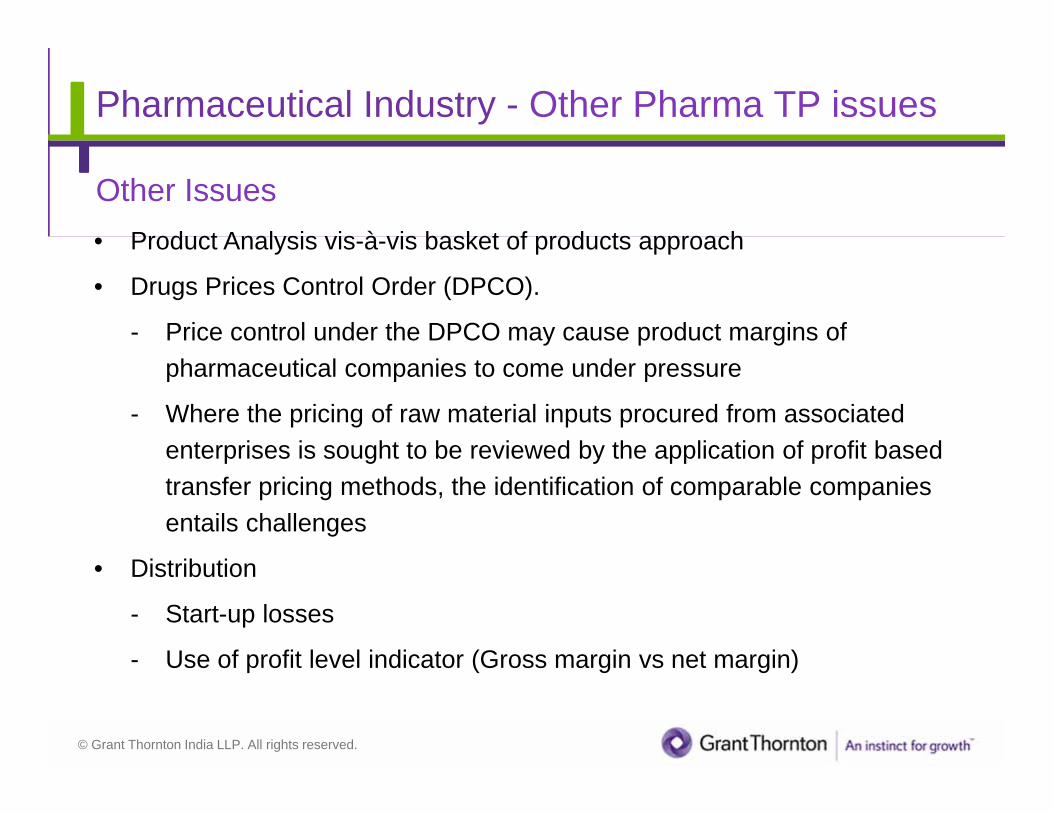

Pharmaceutical Industry - Other Pharma TP issues

Other Issues• Product Analysis vis-à-vis basket of products approach

• Drugs Prices Control Order (DPCO).

- Price control under the DPCO may cause product margins of pharmaceutical companies to come under pressure

- Where the pricing of raw material inputs procured from associated enterprises is sought to be reviewed by the application of profit based transfer pricing methods, the identification of comparable companies entails challenges

• Distribution

- Start-up losses

- Use of profit level indicator (Gross margin vs net margin)

© Grant Thornton India LLP. All rights reserved.

Pharmaceutical Industry - Comparison of Other

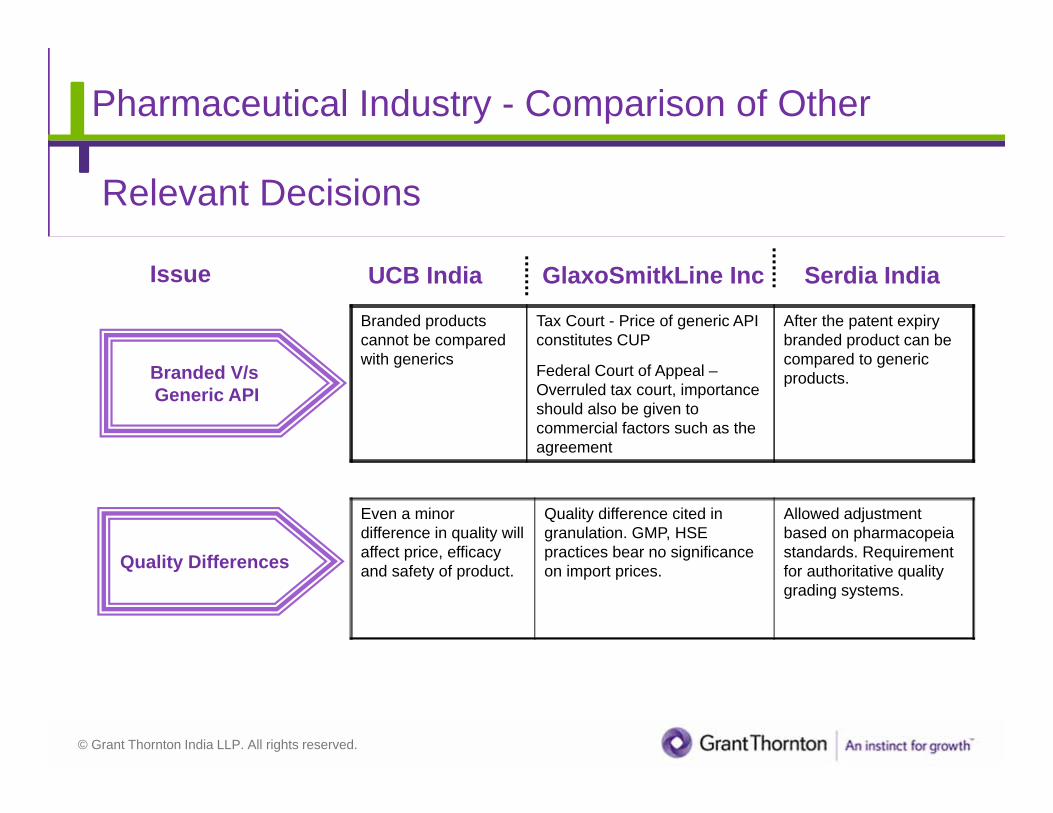

Relevant Decisions

UCB India GlaxoSmitkLine Inc Serdia India

Branded products cannot be compared with generics

Tax Court - Price of generic API constitutes CUP

Federal Court of Appeal –Overruled tax court, importance should also be given to commercial factors such as the agreement

After the patent expiry branded product can be compared to generic products.

Issue

Branded V/s Generic API

Quality Differences

Even a minor difference in quality will affect price, efficacy and safety of product.

Quality difference cited in granulation. GMP, HSE practices bear no significance on import prices.

Allowed adjustment based on pharmacopeia standards. Requirement for authoritative quality grading systems.

© Grant Thornton India LLP. All rights reserved.

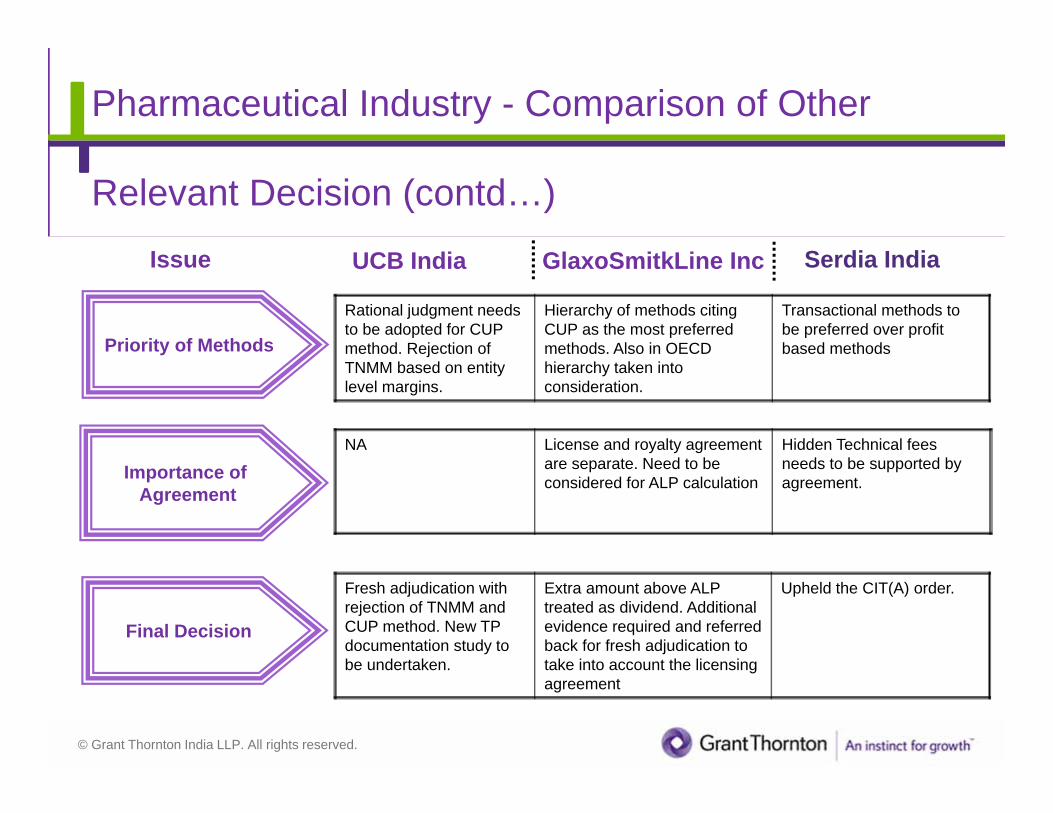

Pharmaceutical Industry - Comparison of Other

Relevant Decision (contd…)

UCB India GlaxoSmitkLine Inc Serdia India

Rational judgment needs to be adopted for CUP method. Rejection of TNMM based on entity level margins.

Hierarchy of methods citing CUP as the most preferred methods. Also in OECD hierarchy taken into consideration.

Transactional methods to be preferred over profit based methods

Issue

Priority of Methods

Final Decision

Importance of Agreement

NA License and royalty agreement are separate. Need to be considered for ALP calculation

Hidden Technical fees needs to be supported by agreement.

Fresh adjudication with rejection of TNMM and CUP method. New TP documentation study to be undertaken.

Extra amount above ALP treated as dividend. Additional evidence required and referred back for fresh adjudication to take into account the licensing agreement

Upheld the CIT(A) order.

© Grant Thornton India LLP. All rights reserved.

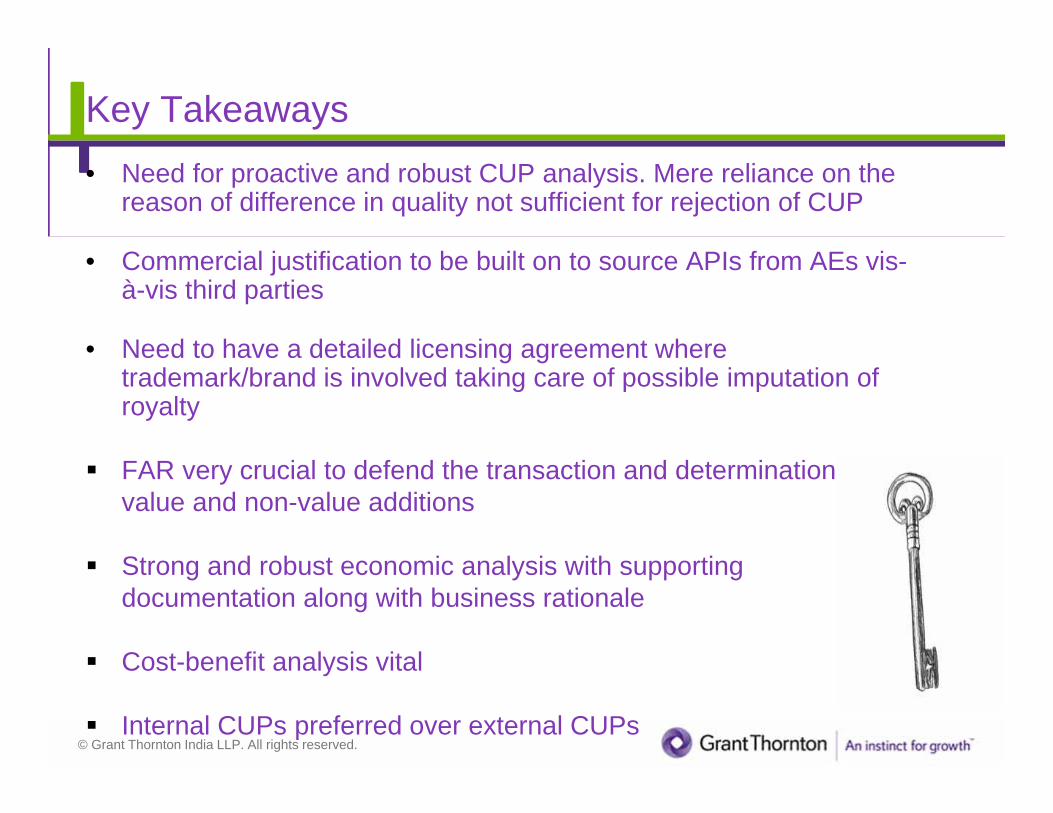

Key Takeaways• Need for proactive and robust CUP analysis. Mere reliance on the

reason of difference in quality not sufficient for rejection of CUP

• Commercial justification to be built on to source APIs from AEs vis-à-vis third parties

• Need to have a detailed licensing agreement where trademark/brand is involved taking care of possible imputation of royalty

FAR very crucial to defend the transaction and determination of value and non-value additions

Strong and robust economic analysis with supporting documentation along with business rationale

Cost-benefit analysis vital

Internal CUPs preferred over external CUPs

© Grant Thornton India LLP. All rights reserved.

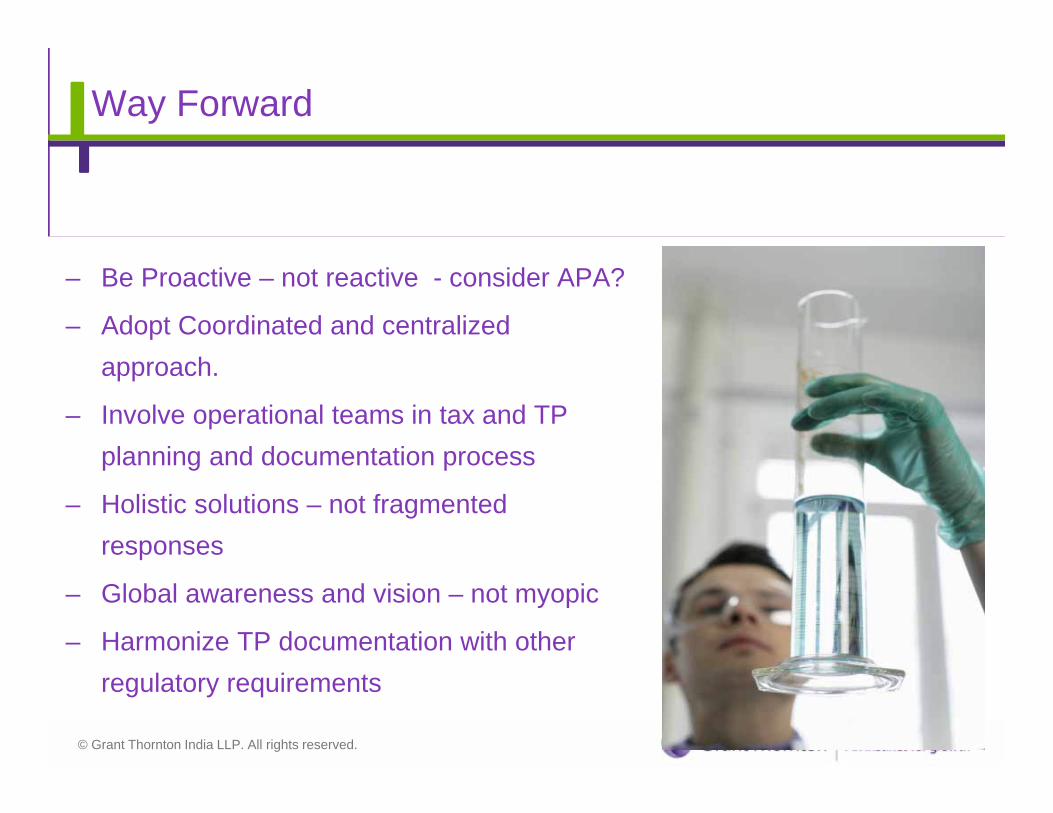

Way Forward

– Be Proactive – not reactive - consider APA?

– Adopt Coordinated and centralized approach.

– Involve operational teams in tax and TP planning and documentation process

– Holistic solutions – not fragmented responses

– Global awareness and vision – not myopic

– Harmonize TP documentation with other regulatory requirements

© Grant Thornton India LLP. All rights reserved. 19

MANUFACTURING

INDUSTRY

© Grant Thornton India LLP. All rights reserved. 20

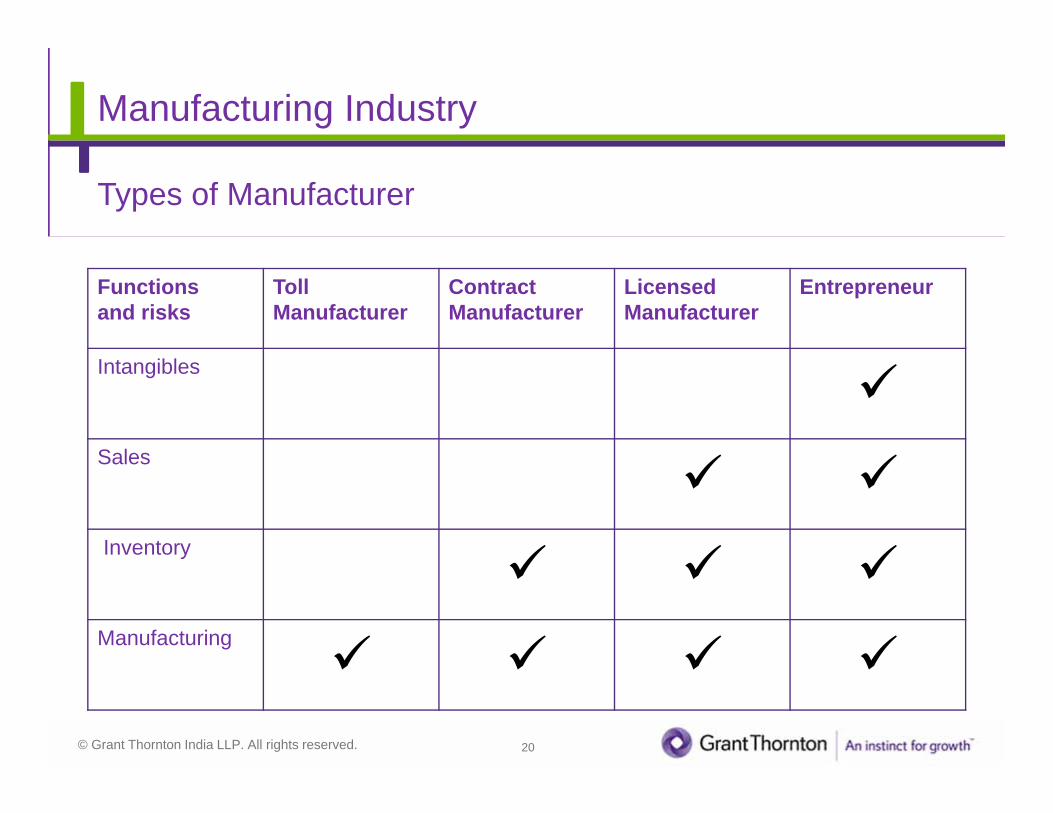

Manufacturing Industry

Types of Manufacturer

Functions and risks

Toll Manufacturer

Contract Manufacturer

Licensed Manufacturer

Entrepreneur

Intangibles

Sales

Inventory

Manufacturing

© Grant Thornton India LLP. All rights reserved. 21

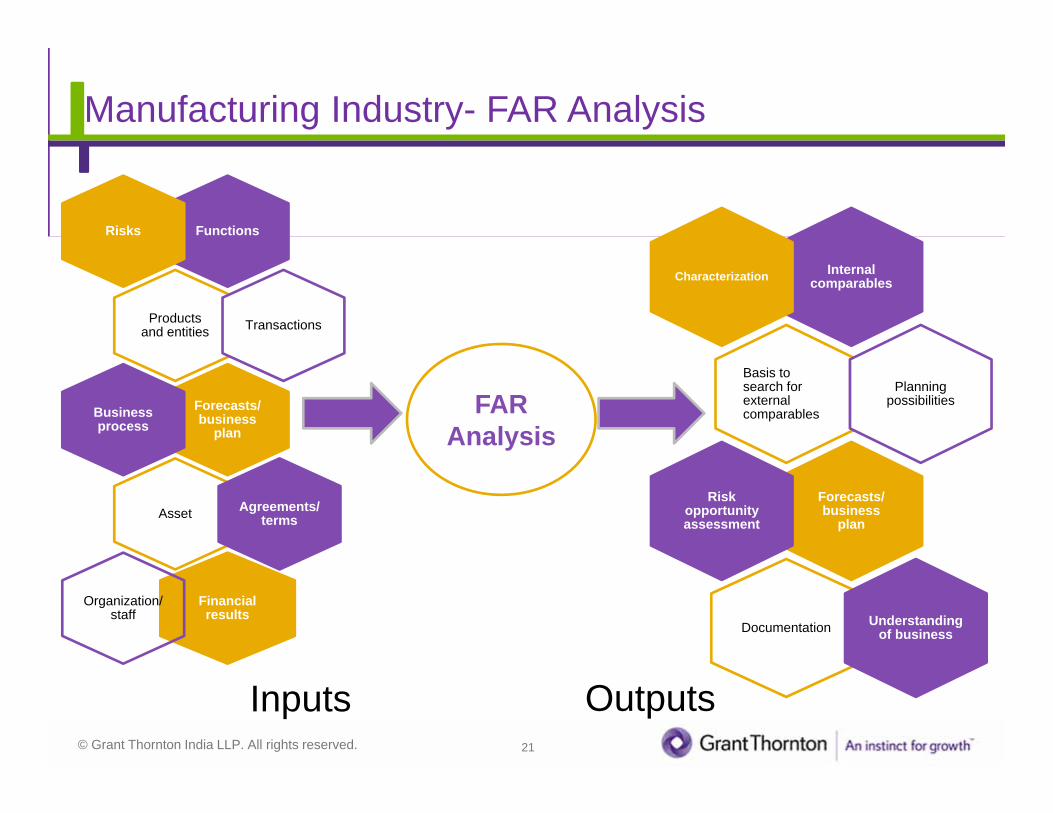

Manufacturing Industry- FAR Analysis

FunctionsRisks

Products and entities Transactions

Forecasts/ business

planBusiness process

Asset Agreements/ terms

Financial results

Organization/ staff

FAR Analysis

Internal comparablesCharacterization

Basis to search for external comparables

Planning possibilities

Forecasts/ business

plan

Risk opportunity assessment

Documentation Understanding of business

Inputs Outputs

© Grant Thornton India LLP. All rights reserved. 22

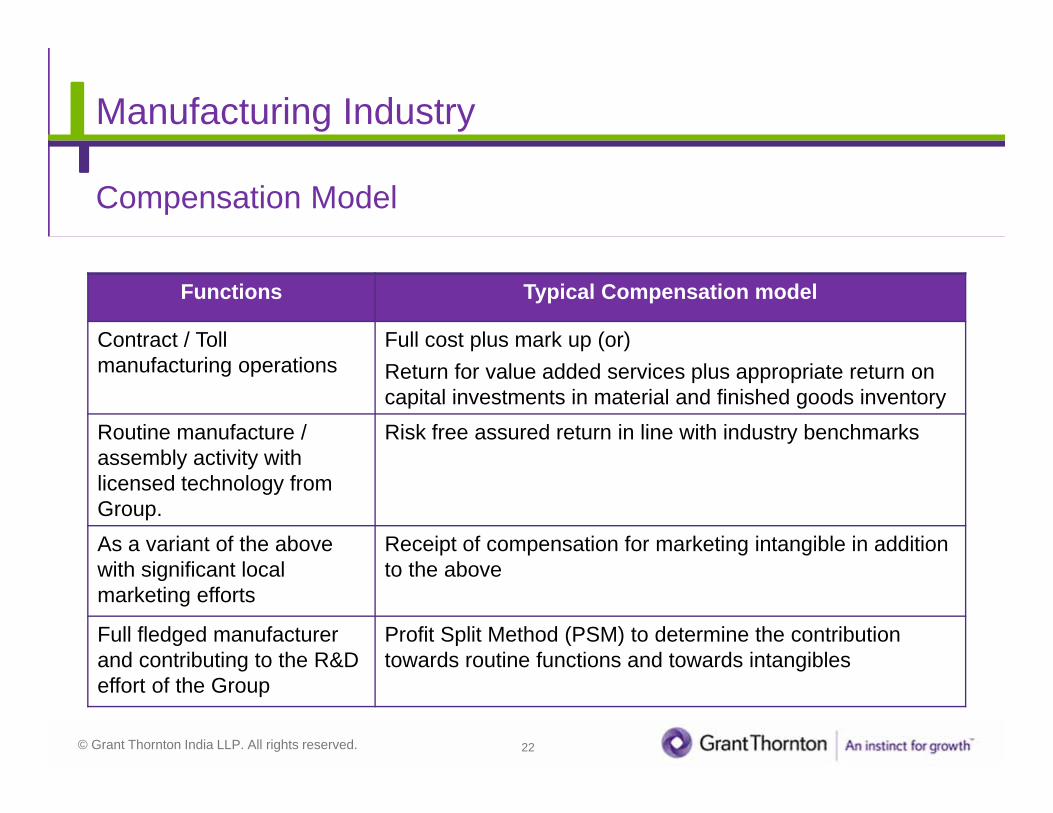

Manufacturing Industry

Compensation Model

Functions Typical Compensation model

Contract / Toll manufacturing operations

Full cost plus mark up (or) Return for value added services plus appropriate return on capital investments in material and finished goods inventory

Routine manufacture / assembly activity with licensed technology from Group.

Risk free assured return in line with industry benchmarks

As a variant of the above with significant local marketing efforts

Receipt of compensation for marketing intangible in addition to the above

Full fledged manufacturer and contributing to the R&D effort of the Group

Profit Split Method (PSM) to determine the contribution towards routine functions and towards intangibles

© Grant Thornton India LLP. All rights reserved. 23

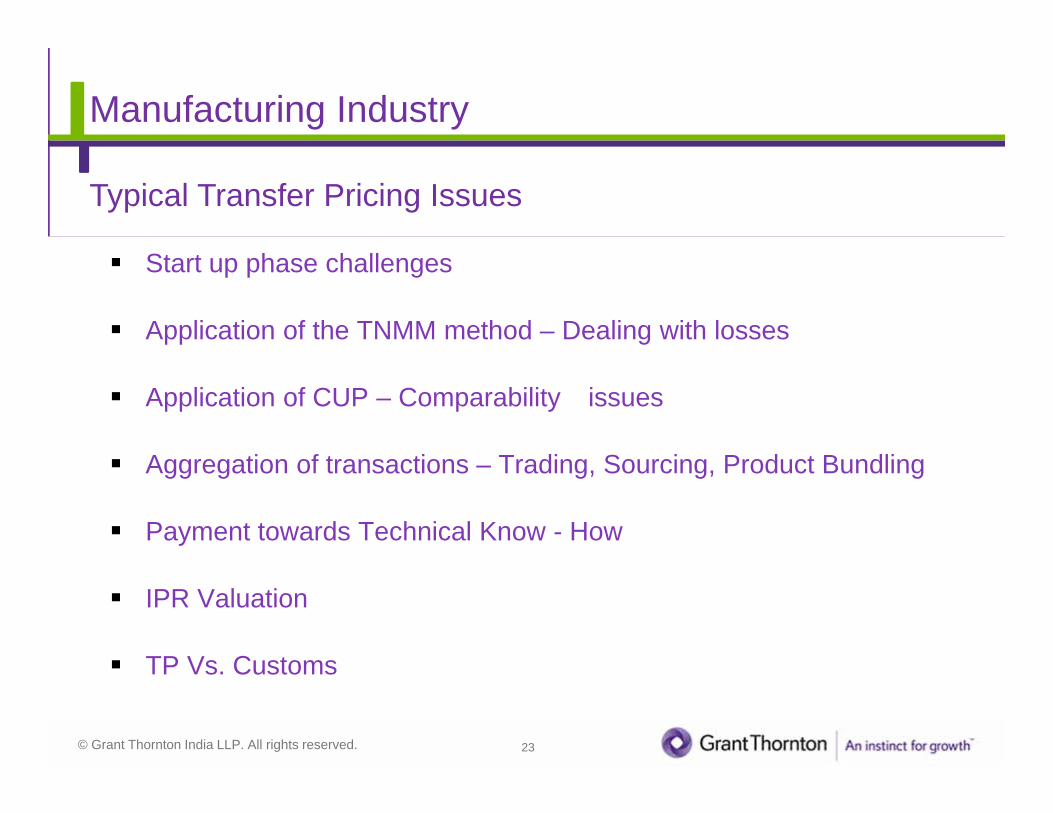

Manufacturing Industry

Typical Transfer Pricing Issues

Start up phase challenges

Application of the TNMM method – Dealing with losses

Application of CUP – Comparability issues

Aggregation of transactions – Trading, Sourcing, Product Bundling

Payment towards Technical Know - How

IPR Valuation

TP Vs. Customs

© Grant Thornton India LLP. All rights reserved. 24

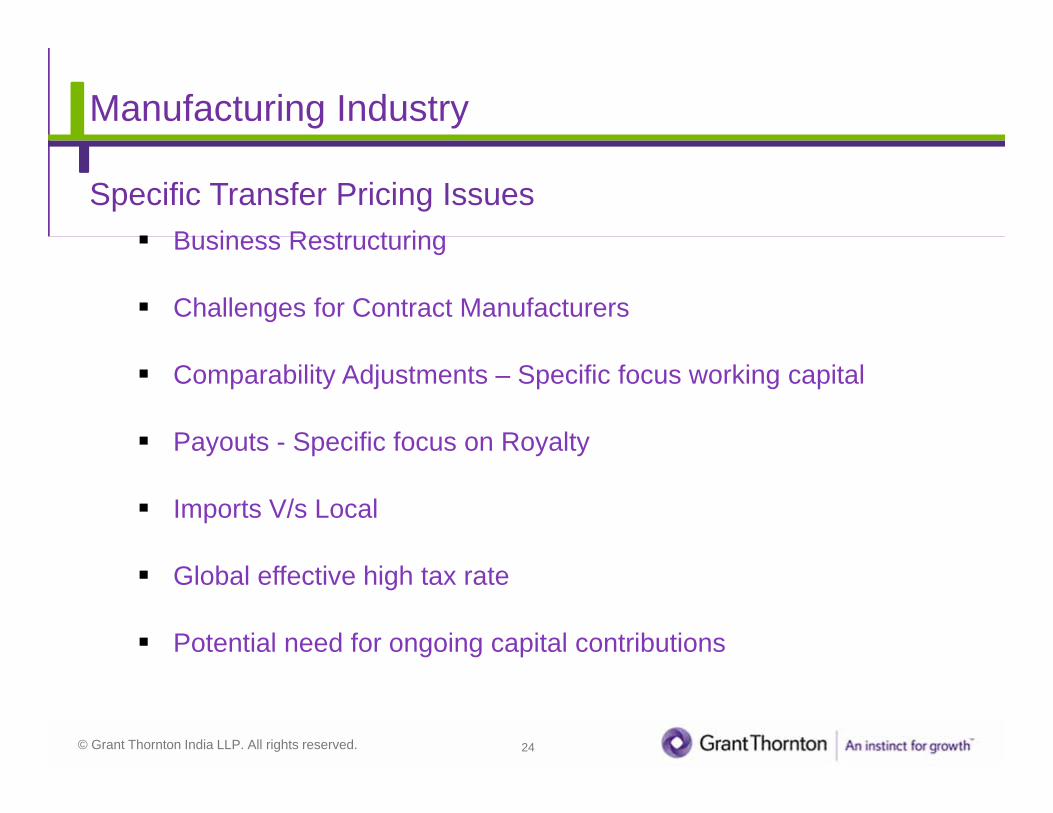

Manufacturing Industry

Specific Transfer Pricing Issues Business Restructuring

Challenges for Contract Manufacturers

Comparability Adjustments – Specific focus working capital

Payouts - Specific focus on Royalty

Imports V/s Local

Global effective high tax rate

Potential need for ongoing capital contributions

© Grant Thornton India LLP. All rights reserved. 25

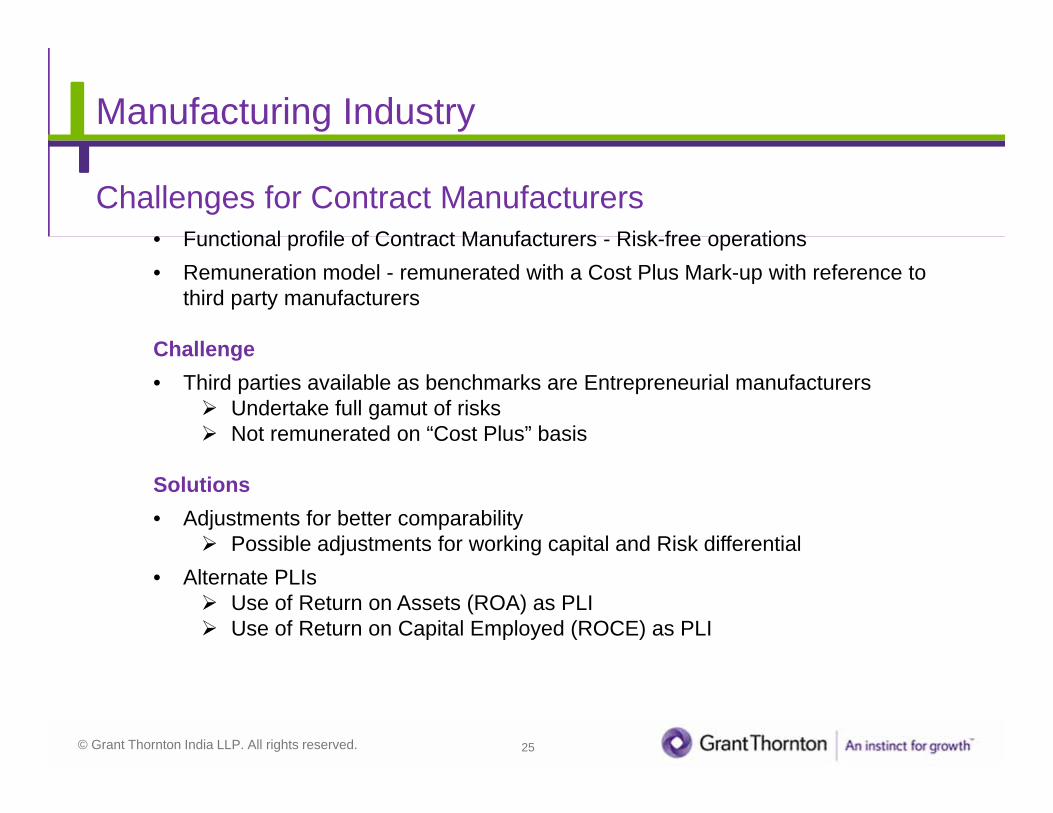

Manufacturing Industry

Challenges for Contract Manufacturers• Functional profile of Contract Manufacturers - Risk-free operations• Remuneration model - remunerated with a Cost Plus Mark-up with reference to

third party manufacturers

Challenge• Third parties available as benchmarks are Entrepreneurial manufacturers

Undertake full gamut of risks Not remunerated on “Cost Plus” basis

Solutions• Adjustments for better comparability

Possible adjustments for working capital and Risk differential• Alternate PLIs

Use of Return on Assets (ROA) as PLI Use of Return on Capital Employed (ROCE) as PLI

© Grant Thornton India LLP. All rights reserved. 26

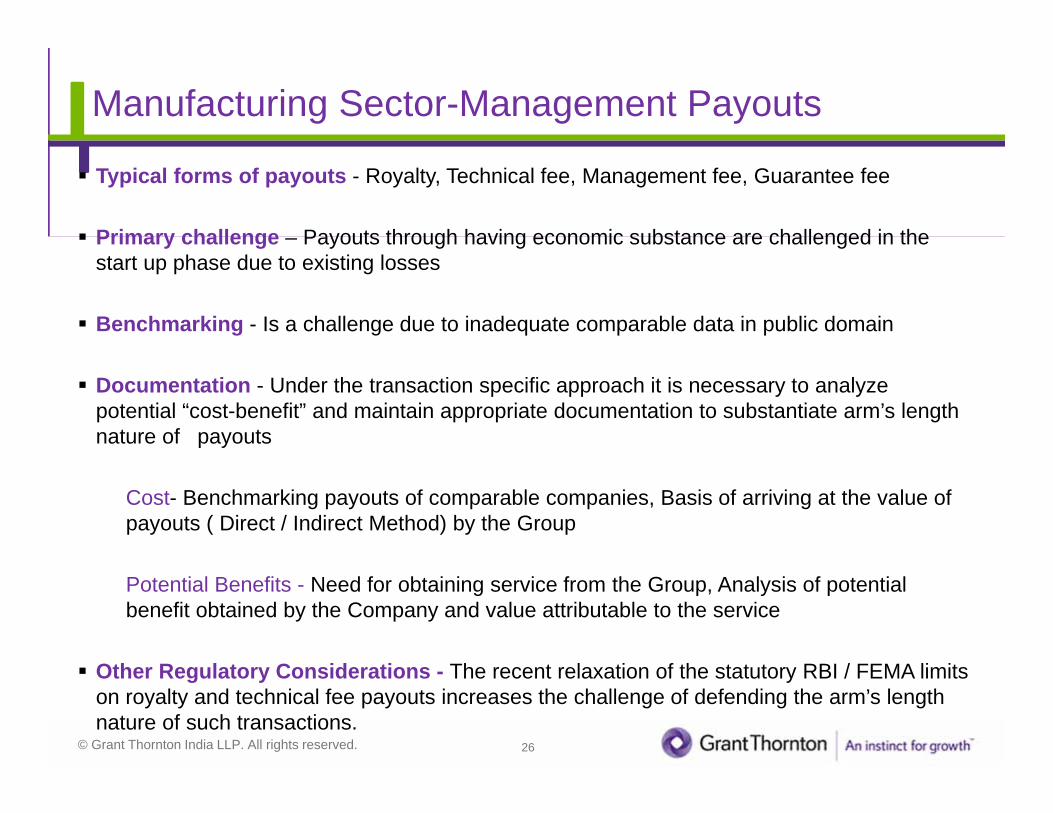

Manufacturing Sector-Management Payouts

Typical forms of payouts - Royalty, Technical fee, Management fee, Guarantee fee

Primary challenge – Payouts through having economic substance are challenged in the start up phase due to existing losses

Benchmarking - Is a challenge due to inadequate comparable data in public domain

Documentation - Under the transaction specific approach it is necessary to analyze potential “cost-benefit” and maintain appropriate documentation to substantiate arm’s length nature of payouts

Cost- Benchmarking payouts of comparable companies, Basis of arriving at the value of payouts ( Direct / Indirect Method) by the Group

Potential Benefits - Need for obtaining service from the Group, Analysis of potential benefit obtained by the Company and value attributable to the service

Other Regulatory Considerations - The recent relaxation of the statutory RBI / FEMA limits on royalty and technical fee payouts increases the challenge of defending the arm’s length nature of such transactions.

© Grant Thornton India LLP. All rights reserved. 27

SPECIFIED

DOMESTIC

TRANSACTIONS

© Grant Thornton India LLP. All rights reserved.

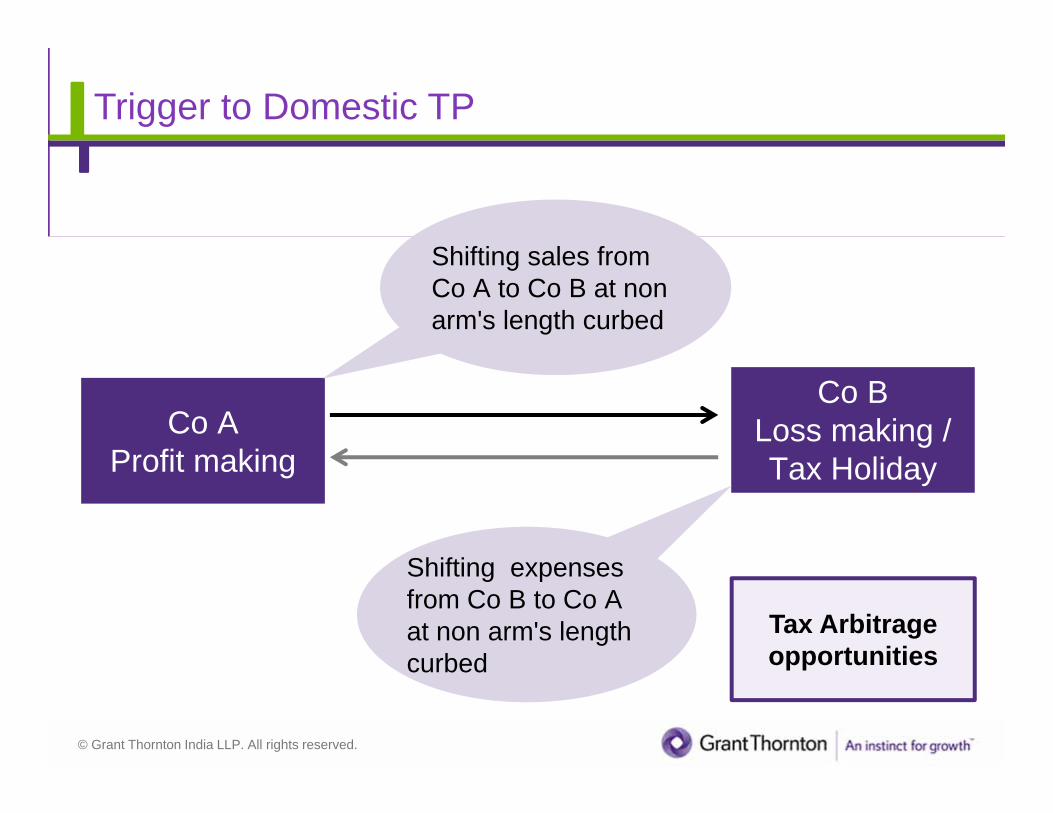

Trigger to Domestic TP

Co A Profit making

Co B Loss making / Tax Holiday

Shifting expenses from Co B to Co A at non arm's length curbed

Shifting sales from Co A to Co B at non arm's length curbed

Tax Arbitrage opportunities

© Grant Thornton India LLP. All rights reserved.

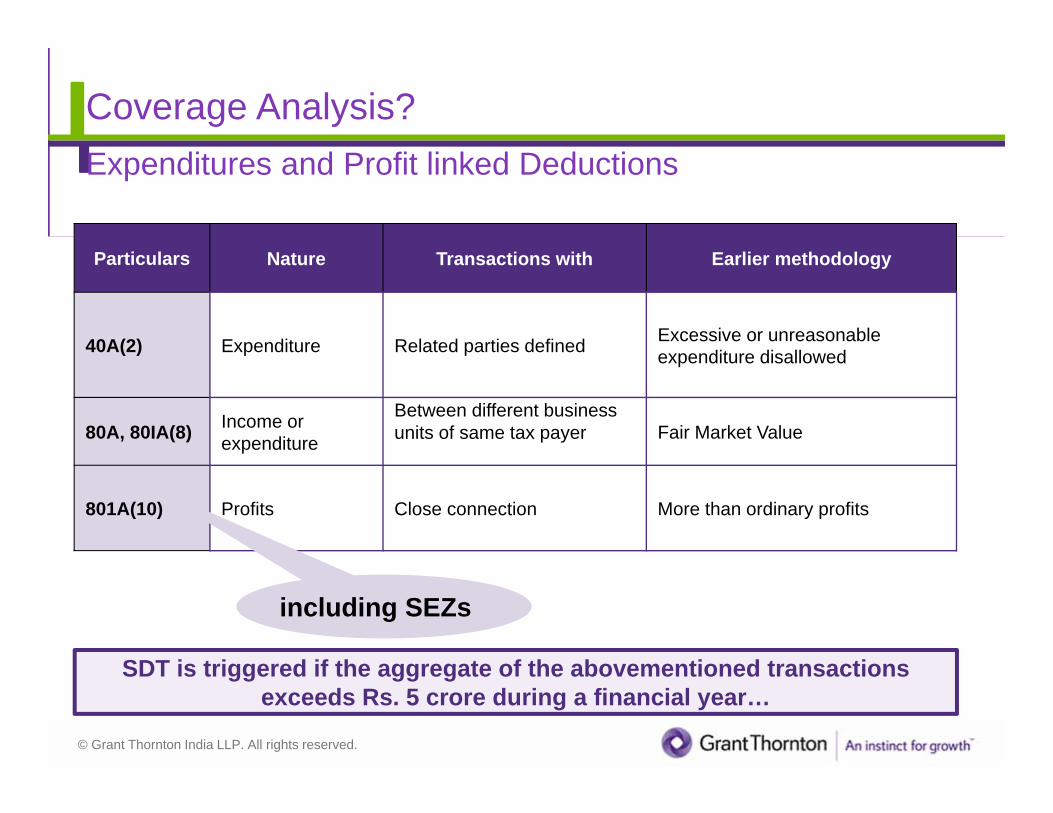

Coverage Analysis?Expenditures and Profit linked Deductions

SDT is triggered if the aggregate of the abovementioned transactions exceeds Rs. 5 crore during a financial year…

Particulars Nature Transactions with Earlier methodology

40A(2) Expenditure Related parties defined Excessive or unreasonable expenditure disallowed

80A, 80IA(8) Income or expenditure

Between different business units of same tax payer Fair Market Value

801A(10) Profits Close connection More than ordinary profits

including SEZs

© Grant Thornton India LLP. All rights reserved.

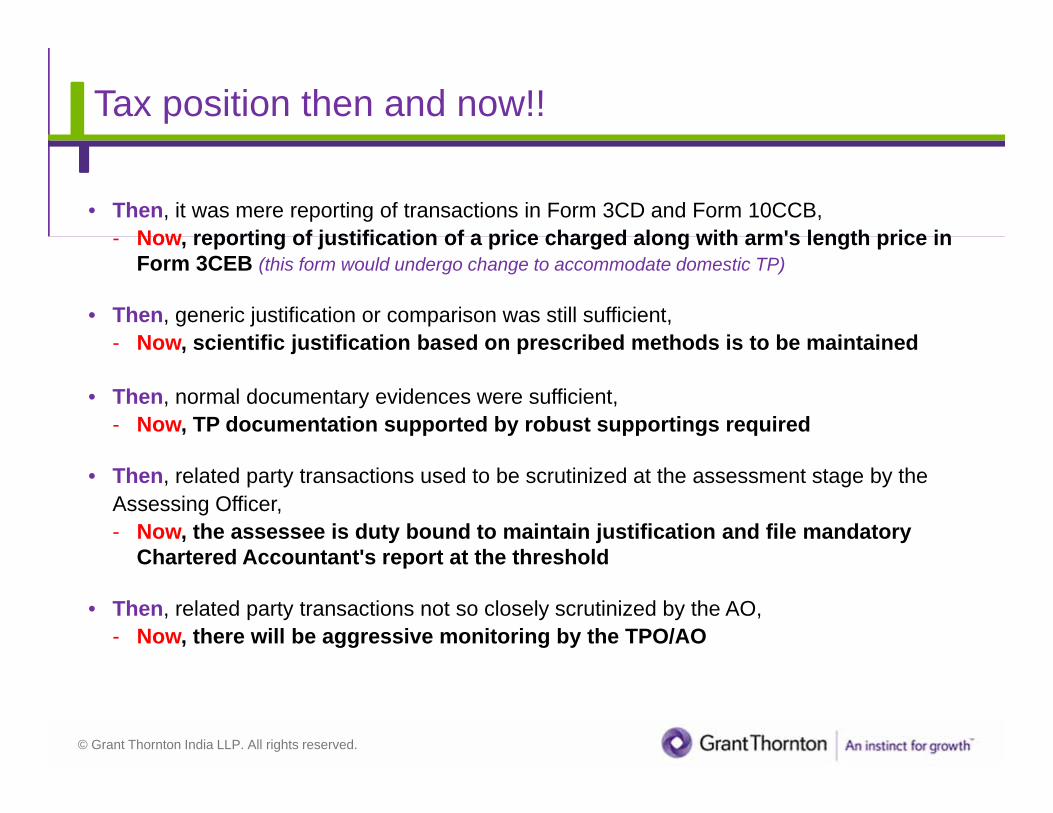

Tax position then and now!!

• Then, it was mere reporting of transactions in Form 3CD and Form 10CCB, - Now, reporting of justification of a price charged along with arm's length price in

Form 3CEB (this form would undergo change to accommodate domestic TP)

• Then, generic justification or comparison was still sufficient, - Now, scientific justification based on prescribed methods is to be maintained

• Then, normal documentary evidences were sufficient, - Now, TP documentation supported by robust supportings required

• Then, related party transactions used to be scrutinized at the assessment stage by the Assessing Officer, - Now, the assessee is duty bound to maintain justification and file mandatory

Chartered Accountant's report at the threshold

• Then, related party transactions not so closely scrutinized by the AO, - Now, there will be aggressive monitoring by the TPO/AO

© Grant Thornton India LLP. All rights reserved.

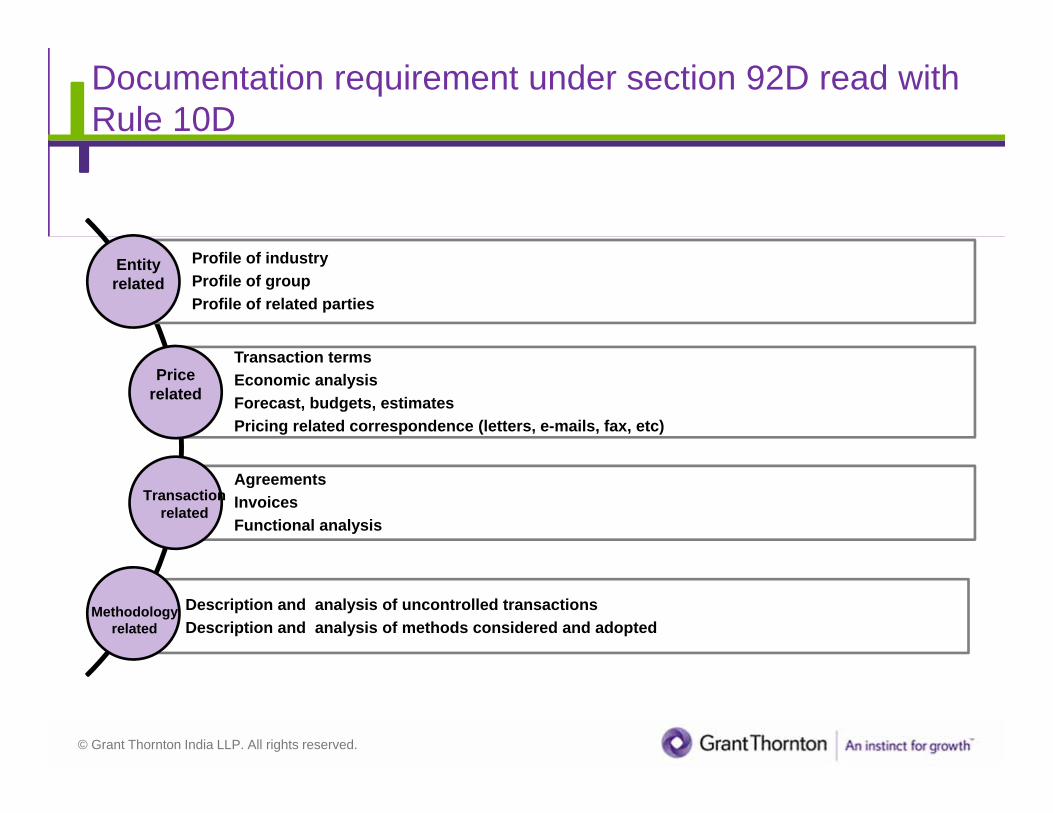

Documentation requirement under section 92D read with Rule 10D

Profile of industryProfile of groupProfile of related parties

Transaction termsEconomic analysisForecast, budgets, estimatesPricing related correspondence (letters, e-mails, fax, etc)

AgreementsInvoicesFunctional analysis

Description and analysis of uncontrolled transactionsDescription and analysis of methods considered and adopted

Entity related

Price related

Methodology related

Transactionrelated

© Grant Thornton India LLP. All rights reserved.

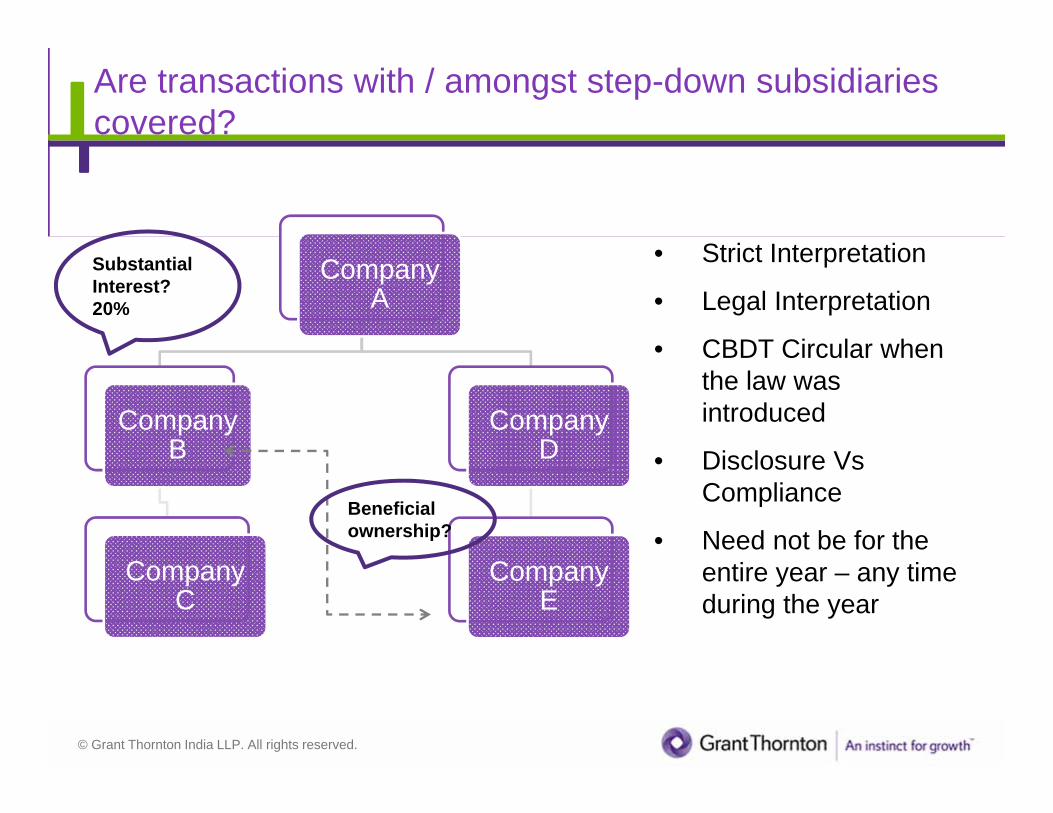

Are transactions with / amongst step-down subsidiaries covered?

Company A

Company B

Company C

Company D

Company E

Beneficial ownership?

Substantial Interest? 20%

• Strict Interpretation

• Legal Interpretation

• CBDT Circular when the law was introduced

• Disclosure Vs Compliance

• Need not be for the entire year – any time during the year

© Grant Thornton India LLP. All rights reserved.

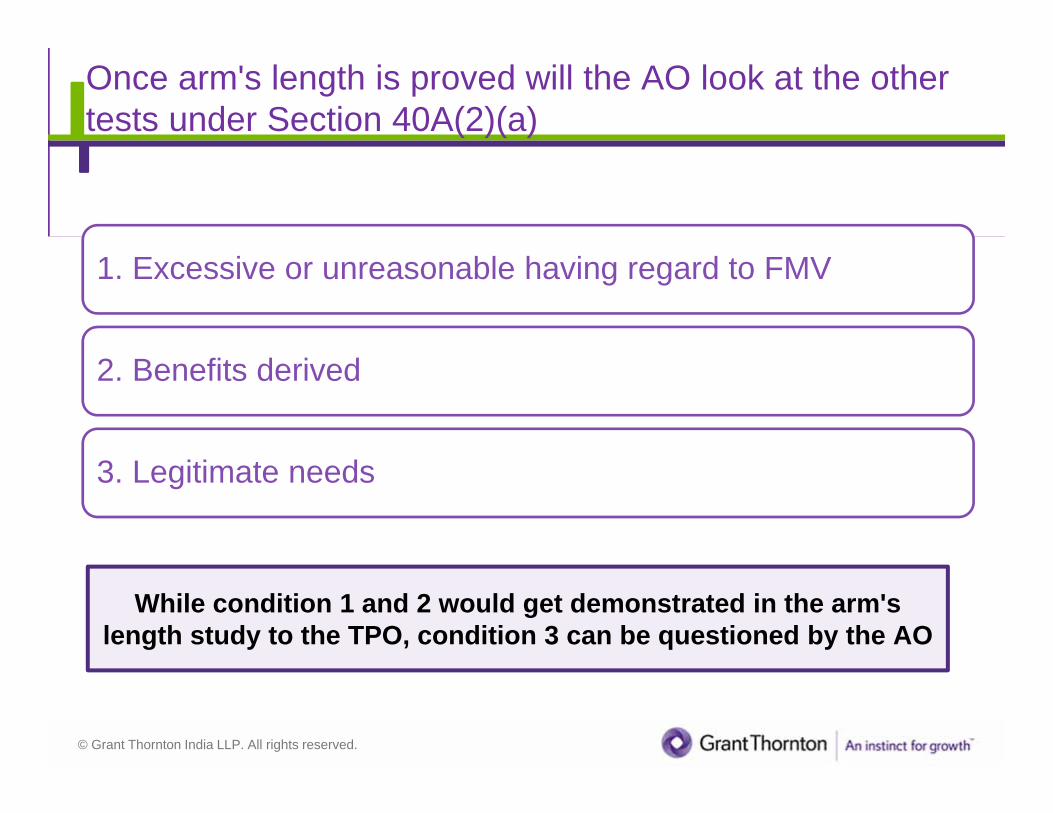

Once arm's length is proved will the AO look at the other tests under Section 40A(2)(a)

1. Excessive or unreasonable having regard to FMV

2. Benefits derived

3. Legitimate needs

While condition 1 and 2 would get demonstrated in the arm's length study to the TPO, condition 3 can be questioned by the AO

© Grant Thornton India LLP. All rights reserved.

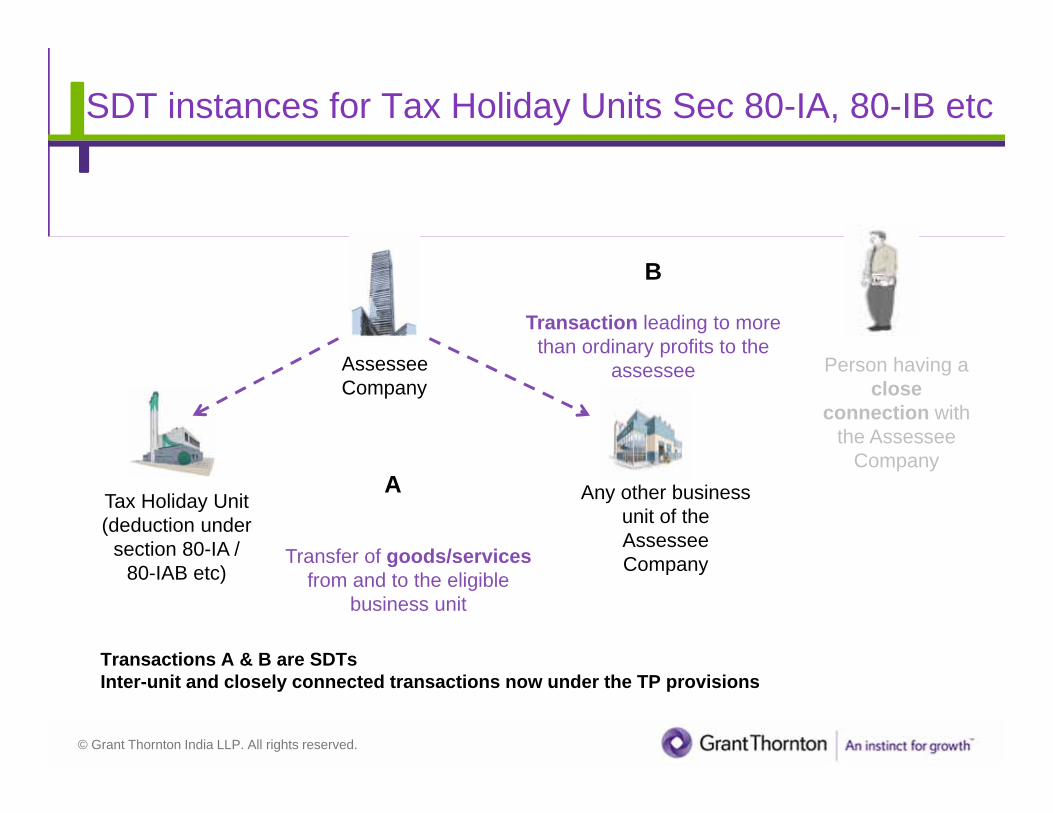

SDT instances for Tax Holiday Units Sec 80-IA, 80-IB etc

Tax Holiday Unit (deduction under

section 80-IA / 80-IAB etc)

Any other business unit of the Assessee CompanyTransfer of goods/services

from and to the eligible business unit

Assessee Company

Transaction leading to more than ordinary profits to the

assessee

Transactions A & B are SDTsInter-unit and closely connected transactions now under the TP provisions

Person having a close

connection with the Assessee

CompanyA

B

© Grant Thornton India LLP. All rights reserved.

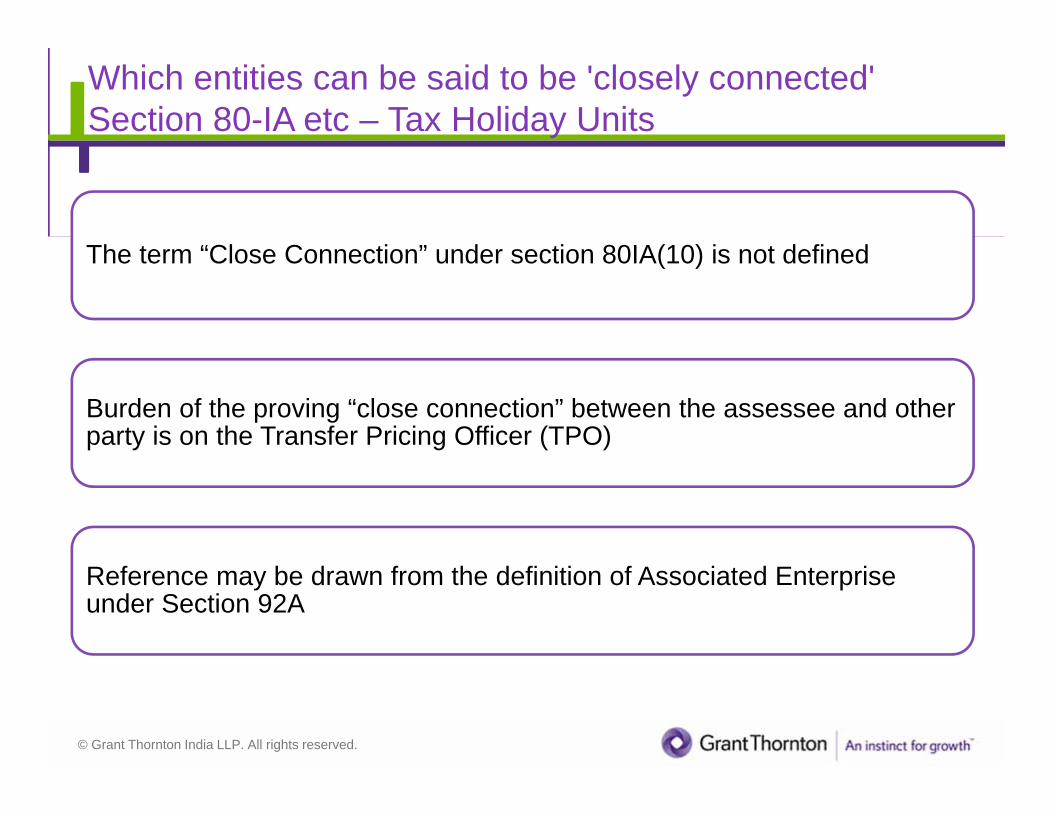

Which entities can be said to be 'closely connected'Section 80-IA etc – Tax Holiday Units

The term “Close Connection” under section 80IA(10) is not defined

Burden of the proving “close connection” between the assessee and other party is on the Transfer Pricing Officer (TPO)

Reference may be drawn from the definition of Associated Enterprise under Section 92A

© Grant Thornton India LLP. All rights reserved.

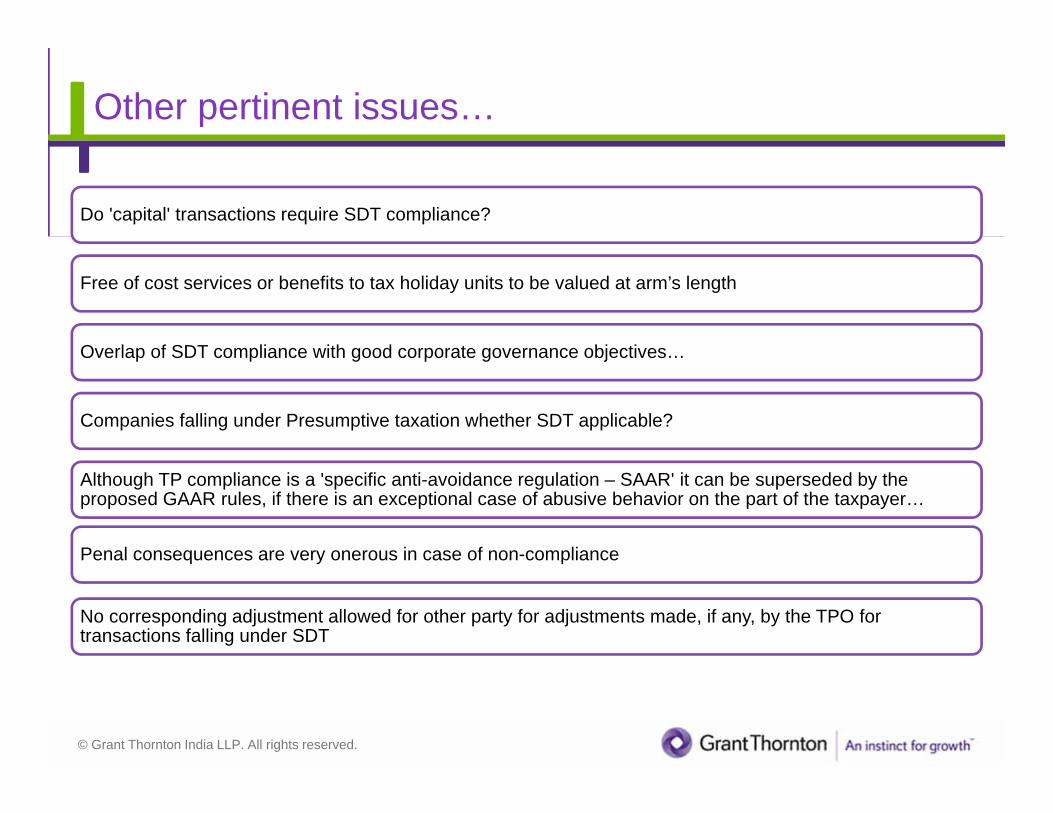

Other pertinent issues…

Do 'capital' transactions require SDT compliance?

Free of cost services or benefits to tax holiday units to be valued at arm’s length

Overlap of SDT compliance with good corporate governance objectives…

Companies falling under Presumptive taxation whether SDT applicable?

Although TP compliance is a 'specific anti-avoidance regulation – SAAR' it can be superseded by the proposed GAAR rules, if there is an exceptional case of abusive behavior on the part of the taxpayer…

Penal consequences are very onerous in case of non-compliance

No corresponding adjustment allowed for other party for adjustments made, if any, by the TPO for transactions falling under SDT

© Grant Thornton India LLP. All rights reserved.

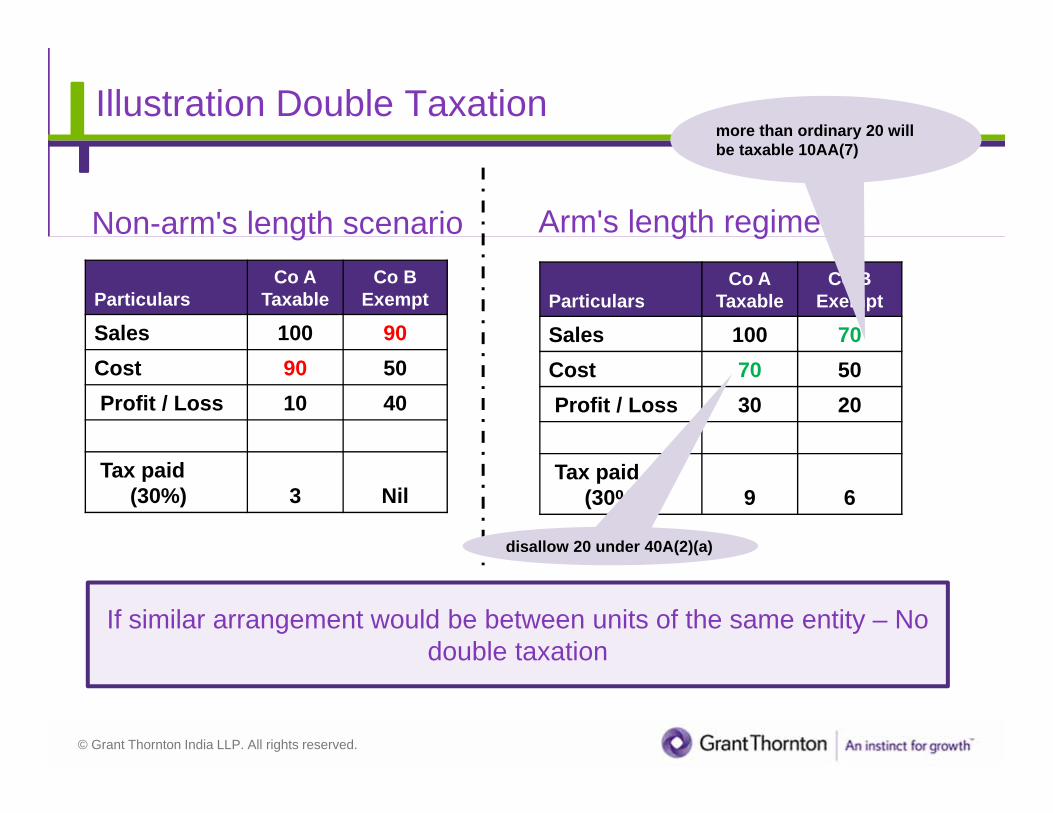

Illustration Double Taxation

ParticularsCo A

TaxableCo B

Exempt

Sales 100 90Cost 90 50Profit / Loss 10 40

Tax paid (30%) 3 Nil

Non-arm's length scenario Arm's length regime

ParticularsCo A

TaxableCo B

Exempt

Sales 100 70Cost 70 50Profit / Loss 30 20

Tax paid (30%) 9 6

If similar arrangement would be between units of the same entity – No double taxation

disallow 20 under 40A(2)(a)

more than ordinary 20 will be taxable 10AA(7)

© Grant Thornton India LLP. All rights reserved. 38

SDT – Case Study

© Grant Thornton India LLP. All rights reserved.

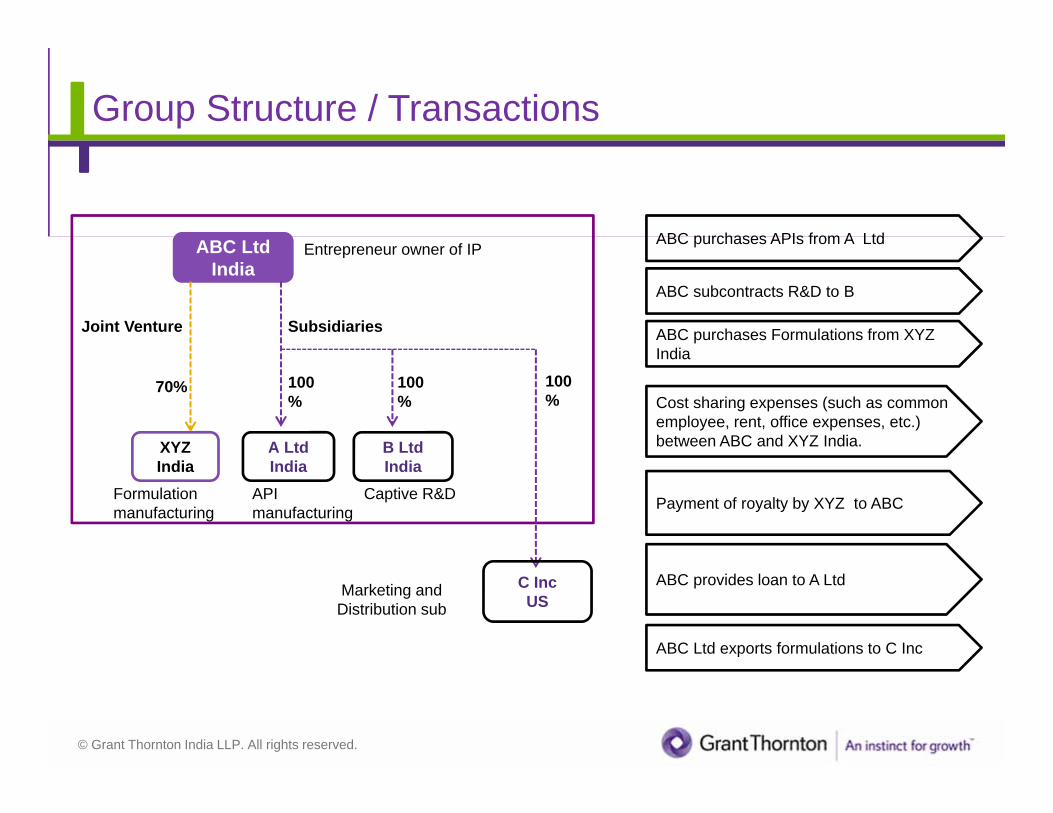

Group Structure / Transactions

A LtdIndia

ABC LtdIndia

XYZIndia

B LtdIndia

C IncUS

SubsidiariesJoint Venture

100%

100%

100%

70%

Entrepreneur owner of IP

Formulation manufacturing

Marketing and Distribution sub

API manufacturing

Captive R&D

ABC purchases APIs from A Ltd

Cost sharing expenses (such as common employee, rent, office expenses, etc.) between ABC and XYZ India.

ABC subcontracts R&D to B

ABC purchases Formulations from XYZ India

Payment of royalty by XYZ to ABC

ABC provides loan to A Ltd

ABC Ltd exports formulations to C Inc

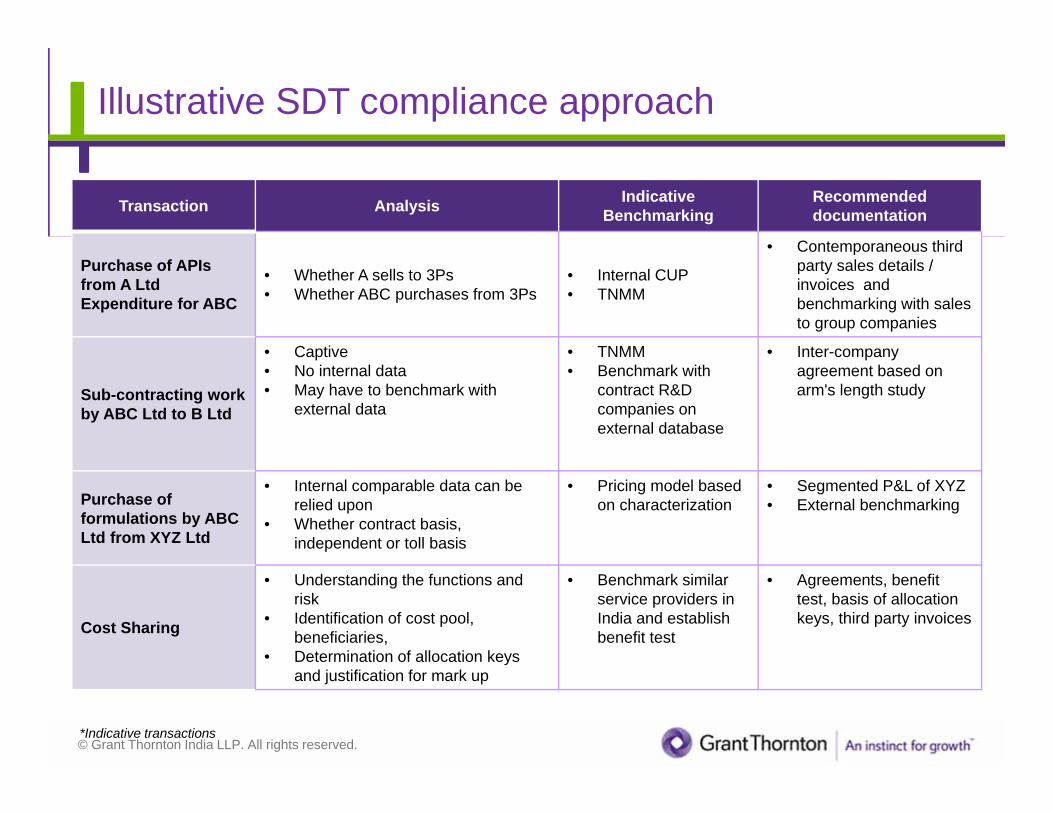

© Grant Thornton India LLP. All rights reserved.

Transaction Analysis Indicative Benchmarking

Recommendeddocumentation

Purchase of APIs from A Ltd Expenditure for ABC

• Whether A sells to 3Ps• Whether ABC purchases from 3Ps

• Internal CUP• TNMM

• Contemporaneous third party sales details / invoices and benchmarking with sales to group companies

Sub-contracting work by ABC Ltd to B Ltd

• Captive• No internal data• May have to benchmark with

external data

• TNMM• Benchmark with

contract R&D companies on external database

• Inter-company agreement based on arm's length study

Purchase of formulations by ABC Ltd from XYZ Ltd

• Internal comparable data can be relied upon

• Whether contract basis, independent or toll basis

• Pricing model based on characterization

• Segmented P&L of XYZ• External benchmarking

Cost Sharing

• Understanding the functions and risk

• Identification of cost pool, beneficiaries,

• Determination of allocation keys and justification for mark up

• Benchmark similar service providers in India and establish benefit test

• Agreements, benefit test, basis of allocation keys, third party invoices

*Indicative transactions

Illustrative SDT compliance approach

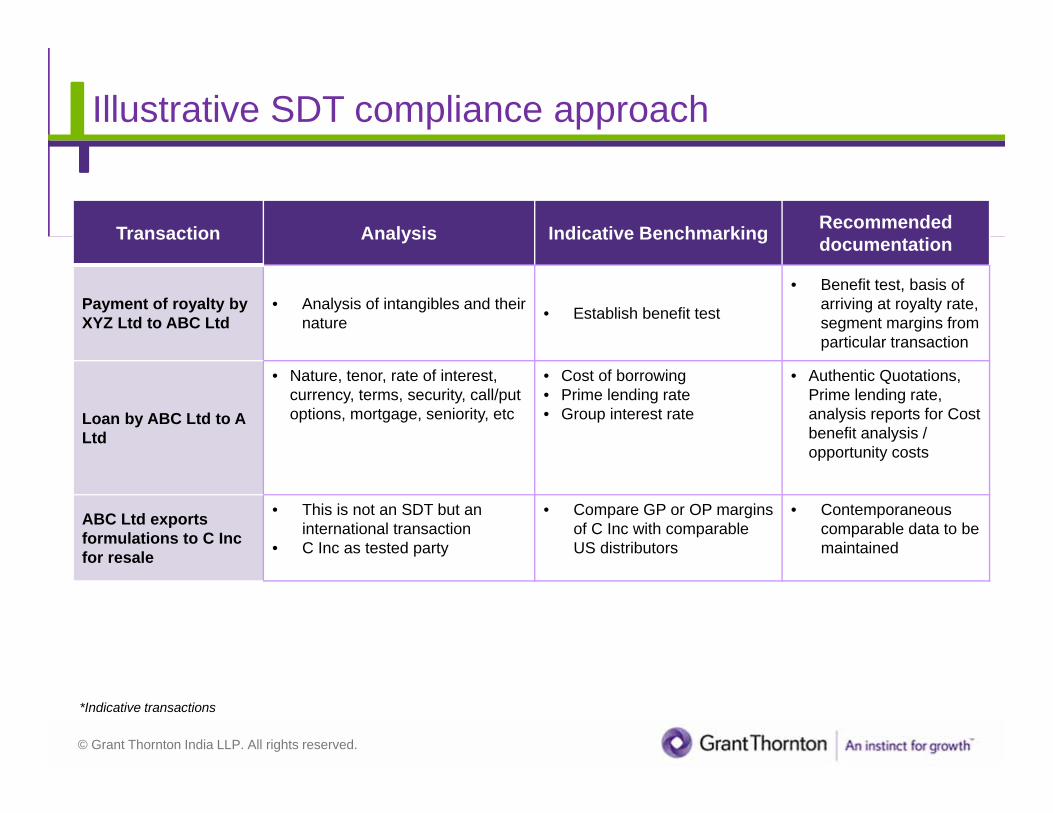

© Grant Thornton India LLP. All rights reserved.

Transaction Analysis Indicative Benchmarking Recommendeddocumentation

Payment of royalty by XYZ Ltd to ABC Ltd

• Analysis of intangibles and their nature • Establish benefit test

• Benefit test, basis of arriving at royalty rate, segment margins from particular transaction

Loan by ABC Ltd to A Ltd

• Nature, tenor, rate of interest, currency, terms, security, call/putoptions, mortgage, seniority, etc

• Cost of borrowing• Prime lending rate• Group interest rate

• Authentic Quotations, Prime lending rate, analysis reports for Cost benefit analysis / opportunity costs

ABC Ltd exports formulations to C Inc for resale

• This is not an SDT but an international transaction

• C Inc as tested party

• Compare GP or OP margins of C Inc with comparable US distributors

• Contemporaneouscomparable data to be maintained

*Indicative transactions

Illustrative SDT compliance approach

© Grant Thornton India LLP. All rights reserved.

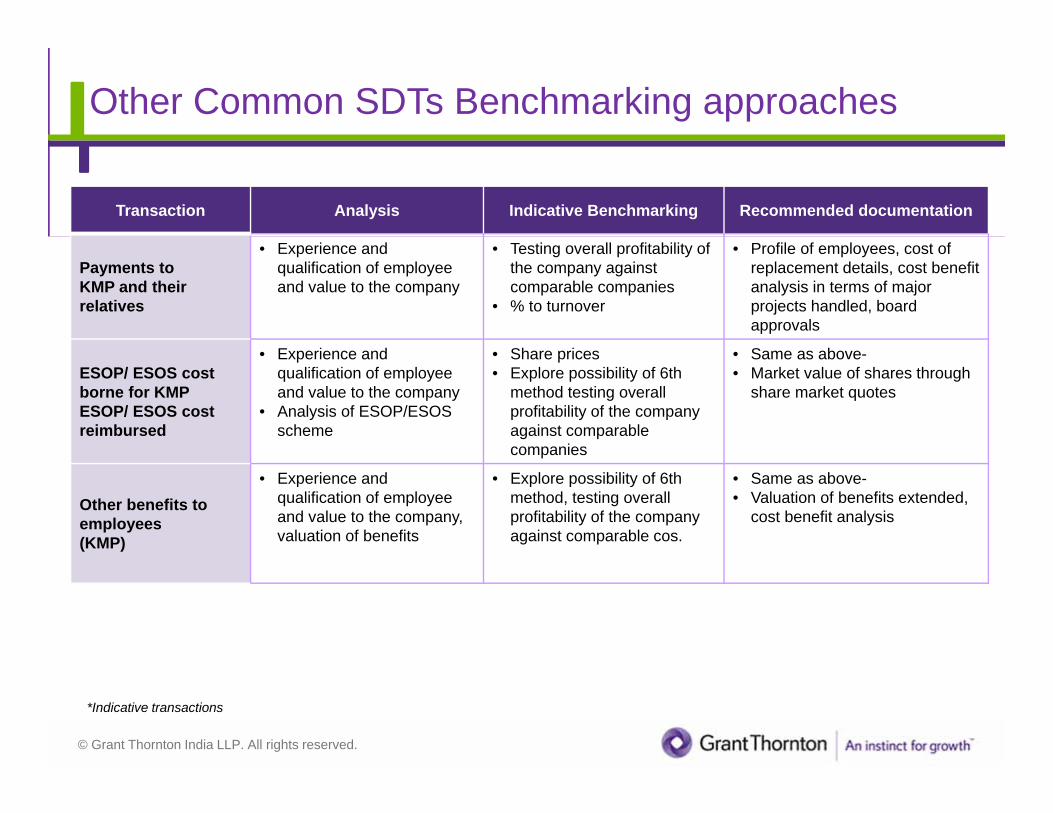

Transaction Analysis Indicative Benchmarking Recommended documentation

Payments to KMP and their relatives

• Experience and qualification of employee and value to the company

• Testing overall profitability of the company againstcomparable companies

• % to turnover

• Profile of employees, cost of replacement details, cost benefit analysis in terms of major projects handled, board approvals

ESOP/ ESOS cost borne for KMP ESOP/ ESOS cost reimbursed

• Experience and qualification of employee and value to the company

• Analysis of ESOP/ESOS scheme

• Share prices• Explore possibility of 6th

method testing overall profitability of the company against comparable companies

• Same as above-• Market value of shares through

share market quotes

Other benefits to employees(KMP)

• Experience and qualification of employee and value to the company, valuation of benefits

• Explore possibility of 6th method, testing overall profitability of the company against comparable cos.

• Same as above-• Valuation of benefits extended,

cost benefit analysis

*Indicative transactions

Other Common SDTs Benchmarking approaches

© Grant Thornton India LLP. All rights reserved.

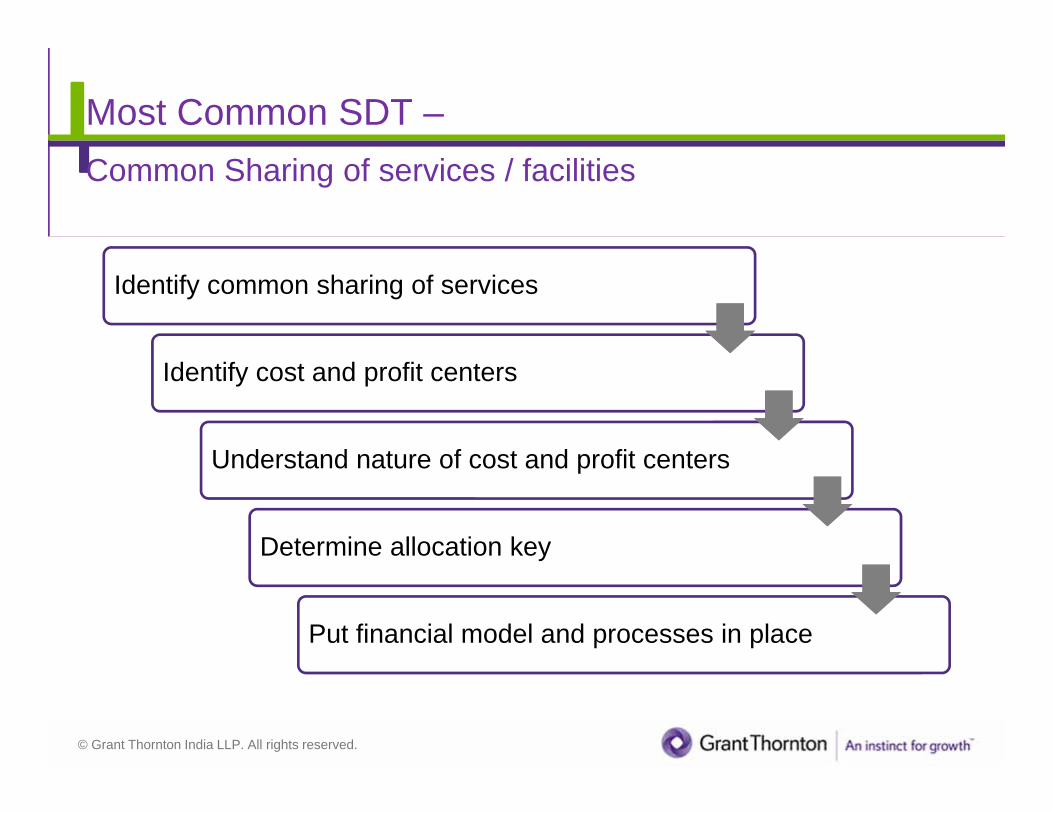

Most Common SDT –Common Sharing of services / facilities

Identify common sharing of services

Identify cost and profit centers

Understand nature of cost and profit centers

Determine allocation key

Put financial model and processes in place

© Grant Thornton India LLP. All rights reserved.

Specific Action steps / Supporting documents tocollate on a real time basis

• Close tracking of covered transactions - clear communication to the management of each company to track covered transaction and maintain supporting documents, illustrated (not exhaustive) as under:

- Supporting invoices (including third party invoices for similar transaction, if any)- Relevant agreements, contracts, written/documented understanding- Cost allocation calculations along with justification of allocation keys wherever cost is

being shared- Valuation reports- Rationale for any mark up and price charged- Documentation to support benefits derived- Deliverables obtained- Qualification and experience for KMP, where transacted with- Comparative details of third party, where transacted with for similar situation or where

evaluated for a particular transaction- Quotes received from third parties- Competitor/ industry data as available in public domain- Computation of transactional / segmental / company level margin

© Grant Thornton India LLP. All rights reserved.

Q & A

Karishma R. PhatarphekarPartner & Practice Leader, Transfer Pricing ServicesGrant Thornton India LLPM +91 98202 38577 D +91 22 6626 2625E [email protected]

© Grant Thornton India LLP. All rights reserved.

Contact usNEW DELHINational OfficeOuter CircleL 41 Connaught CircusNew Delhi 110 001T +91 11 4278 7070

CHANDIGARHSCO 172nd floorSector 17 E Chandigarh 160 017T +91 172 4338 000

GURGAON21st floor, DLF SquareJacaranda MargDLF Phase IIGurgaon 122 002T +91 124 462 8000

HYDERABAD7th floor, Block IIIWhite HouseKundan Bagh, BegumpetHyderabad 500 016T +91 40 6630 8200

MUMBAI16th Floor, Tower IIIndiabulls Finance CentreS B Marg, Elphinstone (W)Mumbai 400013T +91 22 6626 2600

PUNE401 Century ArcadeNarangi Baug RoadOff Boat Club RoadPune 411 001T +91 20 4105 7000

CHENNAIArihant Nitco Park, 6th floorNo.90, Dr. Radhakrishnan Salai MylaporeChennai 600 004T +91 44 4294 0000

BENGALURU“Wings”, 1st floor16/1 Cambridge RoadUlsoorBengaluru 560 008T +91 80 4243 0700

KOLKATA10C Hungerford Street5th floorKolkata 700 017T +91 33 4050 8000

© Grant Thornton India LLP. All rights reserved.

Grant Thornton India LLP (formerly Grant Thornton India) is registered with limited liability with identity number AAA-7677 and its registered office at L-41 Connaught Circus, New Delhi, 110001

Grant Thornton India LLP is a member firm within Grant Thornton International Ltd (‘Grant Thornton International’). Grant Thornton International and the member firms are not a worldwide partnership. Services are delivered by the member firms independently.

For more information or for any queries, write to us at [email protected]