Embed Size (px)

Citation preview

IBM Business Consulting Services

ibm.com/bcs

An IBM Institute for Business Value executive brief

Pharma 2010: The threshold of innovation

The IBM Institute for Business Value develops fact-based strategic insights for senior

business executives around critical industry-specific and cross-industry issues. This executive

brief is based on an in-depth study created by the IBM Institute for Business Value. This

research is a part of an ongoing commitment by IBM Business Consulting Services to provide

analysis and viewpoints that help companies realize business value. You may contact the

authors or send an e-mail to [email protected] for more information.

Pharma 2010: The threshold of innovation IBM Business Consulting Services3

Pharma 2010: The threshold of innovation – an updateIt has been almost two years since we originally published the 2010 story told in

Pharma 2010: The threshold of innovation. It has received wide coverage in the

media; we have presented at numerous industry conferences in North America,

Europe and Asia; and we have taken the story to major pharmaceutical companies

around the globe, many of whom have asked us to come back repeatedly to

present the story to other groups within their organizations. The story has met with

overwhelming support, and the general response has confi rmed our assessment

of industry conditions. We have entered lively discussions about many of our “ways

forward” approaches, but they are invariably centered on when a particular trend

will occur, not whether it will occur. Our defi nition of the problem statement is now

well accepted by the industry, to the point where several CEOs have waived off the

fi rst part of the presentation, proclaiming, “We buy the problem now, now design

solutions that meet our needs.”

Since publishing Pharma 2010, the passage of time has added facts and

experiences, which have substantiated our original premises, namely, that the

industry still does not generate enough innovation, will miss its growth targets and

needs a new model for meeting emerging realities.

We have seen additional consolidation with Pfi zer’s acquisition of Pharmacia and

Sanofi ’s acquisition of Aventis, and analysts have adjusted their forecasts, coming

closer to our own compounded annual growth forecast of 5.2 percent. There is,

today, little question that the industry has entered an era of much lower returns.

Further, the premise of the “threshold of innovation” – that pressure from managed

care providers will make it increasingly diffi cult to bring products to market if they

do not add signifi cant value through improved effi cacy, safety, delivery or cost

– has been borne out with products like AstraZeneca’s Crestor, that has, to date,

experienced disappointing sales. And yet another blockbuster, Merck’s Vioxx, has

been withdrawn due to safety concerns identifi ed almost fi ve years after marketing

approval was fi rst granted.

The focus on cost reduction is intense today, and we expect this trend to continue

as the industry manages the near-term trough and attempts to build a future based

on product innovation and cost effective, streamlined operations. To enhance cost

containment strategies and improve responses to market conditions, companies

are broadening their outsourcing of key enterprisewide processes, such as HR,

Pharma 2010: The threshold of innovation IBM Business Consulting Services4

fi nance, procurement and customer care. This adds fuel to a burgeoning trend which

is prompting companies industrywide to search for a new business model, one

that looks strikingly similar to the Targeted Treatment Solutions model described in

Pharma 2010. New business models, based on business transformation outsourcing

for example, represent one way the industry can refocus its resources.

What have we learned during the past two years? First, business models already

exist that this industry can borrow from others to drive down costs and increase

innovation. Second, although it has been diffi cult for large fi rms to make the kinds of

changes called for, interest in doing so has simply grown over time. That is why we

are republishing Pharma 2010.

The report is essentially the same as published two years ago; however, we have

updated information where appropriate. Since the new data reinforced the paper’s

original concepts, we have not revised its key points. Since 2002, we have also

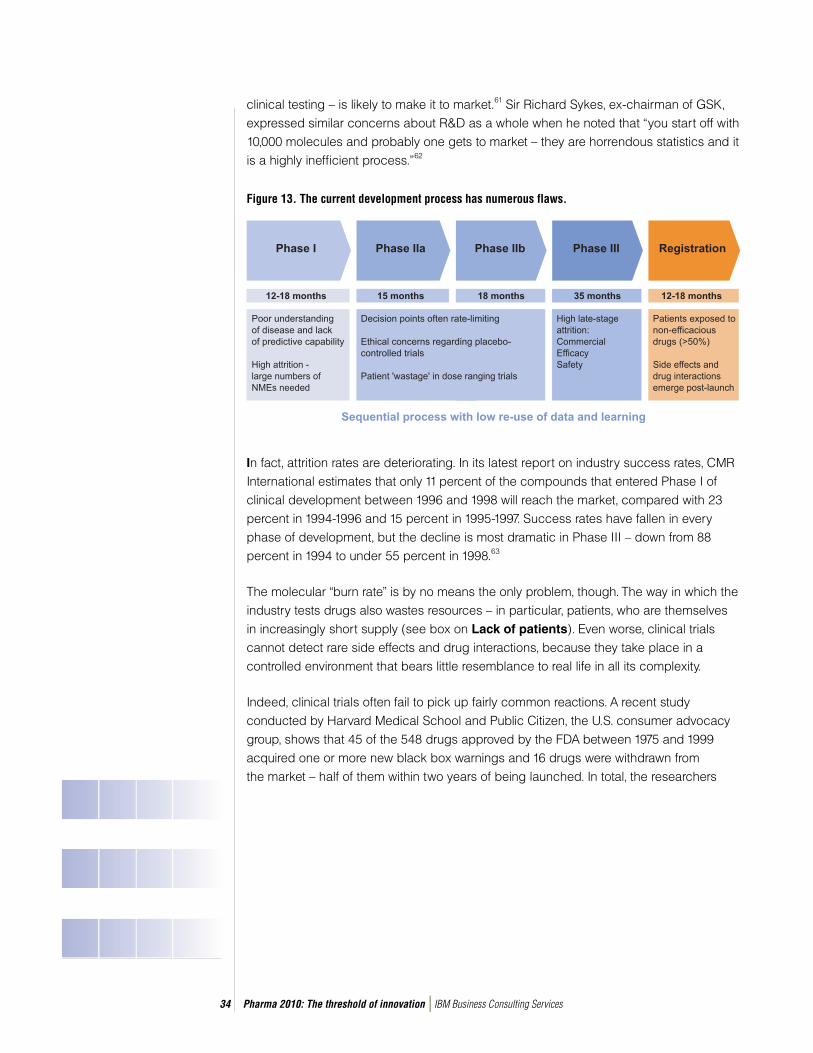

examined facets of the story in more detail, publishing additional studies related to the

use of information technology, supply chain transformation and a wide mix of other

industry-specifi c issues. These papers can be accessed at http://www.ibm.com/bcs/

pharma2010.

We want to thank all of the industry executives and analysts who worked with us and

endorsed our assessment. We are continuing to identify ways that fi rms can meet

the twin challenges of cost control and profi table growth, and we will publish those

ideas as they mature. But in the meantime, thank you for making Pharma 2010 an

industry “best seller!”

– The 2010 Team

Pharma 2010: The threshold of innovation IBM Business Consulting Services1

On target: The future of medicinesIn 2010, the pharmaceutical industry (Pharma) will not only make white powders; it will sell a variety of products and therapeutic healthcare packages that include diagnostic tests, drugs and monitoring devices and mechanisms, as well as a wide range of services to support patients. Companies that learn how to make “targeted treatment solutions”, as we call them, will deliver bigger shareholder returns than they have ever delivered before. This is what our vision of the future looks like.

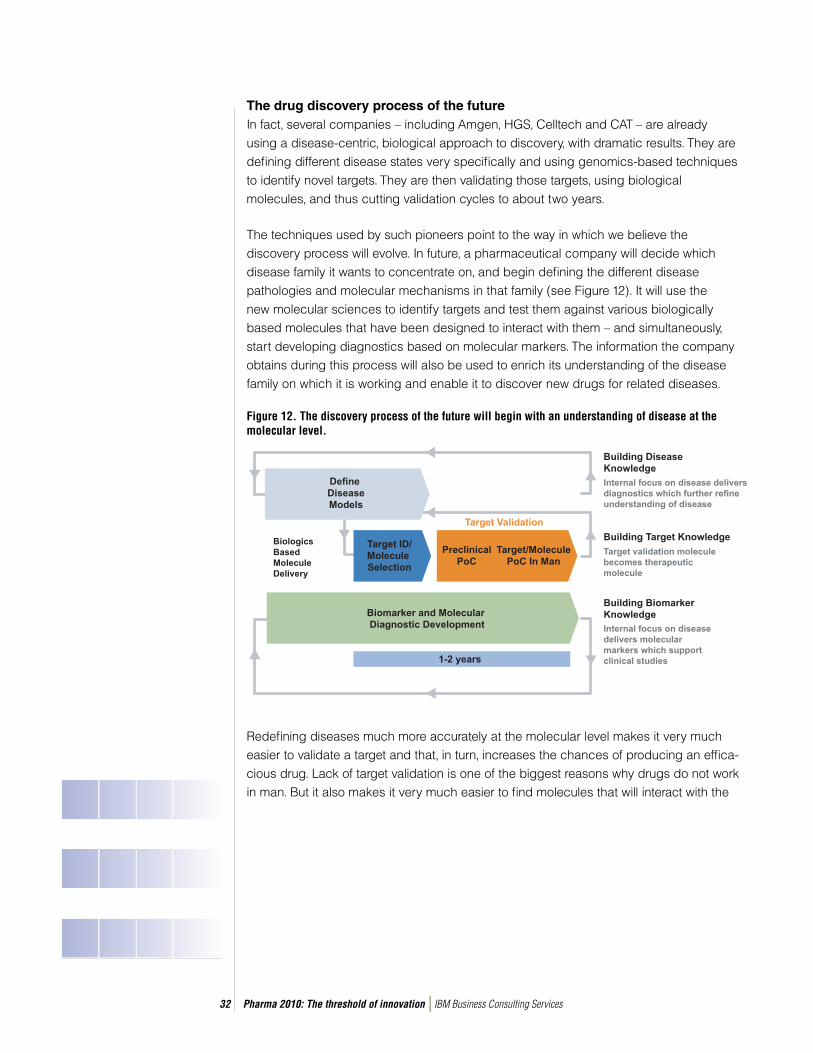

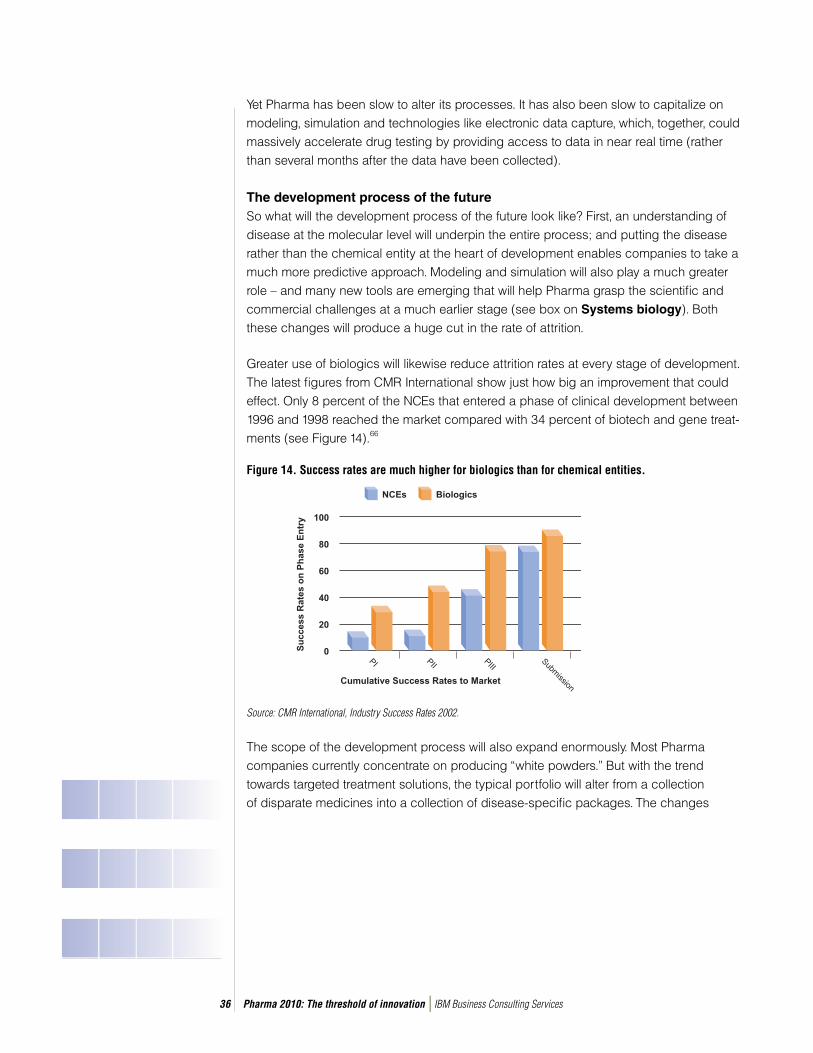

Discovery and developmentDrug discovery and development will be underpinned by an understanding of how different diseases function both at a molecular level and as part of a biological system. The molecular sciences will enable the industry to defi ne diseases much more accurately – and to create a collection of treatments and services for patients with specifi c disease subtypes, rather than making one-size-fi ts-all drugs for patients with similar symptoms but essentially different diseases.

Many of these new medicines will be based on biology rather than chemistry, because biologics are typically less toxic than chemical entities and behave more predictably. They will be made using biological methods of discovery and research, which are easier and faster than traditional methods. And they will be available in a variety of formulations that patients fi nd convenient, rather than having to be delivered by injection.

Modeling, simulation and high-performance computing will play a vital role in the way such medicines are discovered and developed. They will enable the industry to model how drugs act in whole body systems, organs and at a sub-cellular level; to design accurate trials; and to conduct adaptive trials, where information acquired during a particular trial is used to modify the course of the same trial without compromising its statistical validity.

Promising new drugs will fi rst be tested in man during late-stage discovery, to prove their safety and effi cacy. They will be tested still further in Phase II trials and submitted to the regulators for conditional approval. They will then be launched on the market and subjected to additional “in-life testing,” using a variety of remote monitoring devices that exploit advances in bandwidth, networking, mobile telecoms, radio frequency technologies and miniaturization – thereby obviating the need to expose patients to placebos or dosing levels that are pharma-cologically ineffective.

Contents

1 On target: The future of medicines

4 Introduction

6 Drivers of change

6 Chapter 1: Tough times

14 Chapter 2: The old ways don’t work

19 The road to the future

19 Chapter 3: The rise of the targeted treatment solution

29 Recommendations

29 Chapter 4: A disease-driven approach to drug discovery

33 Chapter 5: The transformation of drug development

42 Chapter 6: The potential for global blockbusters

48 Chapter 7: Targeted marketing for targeted treatments

56 Summary and implications

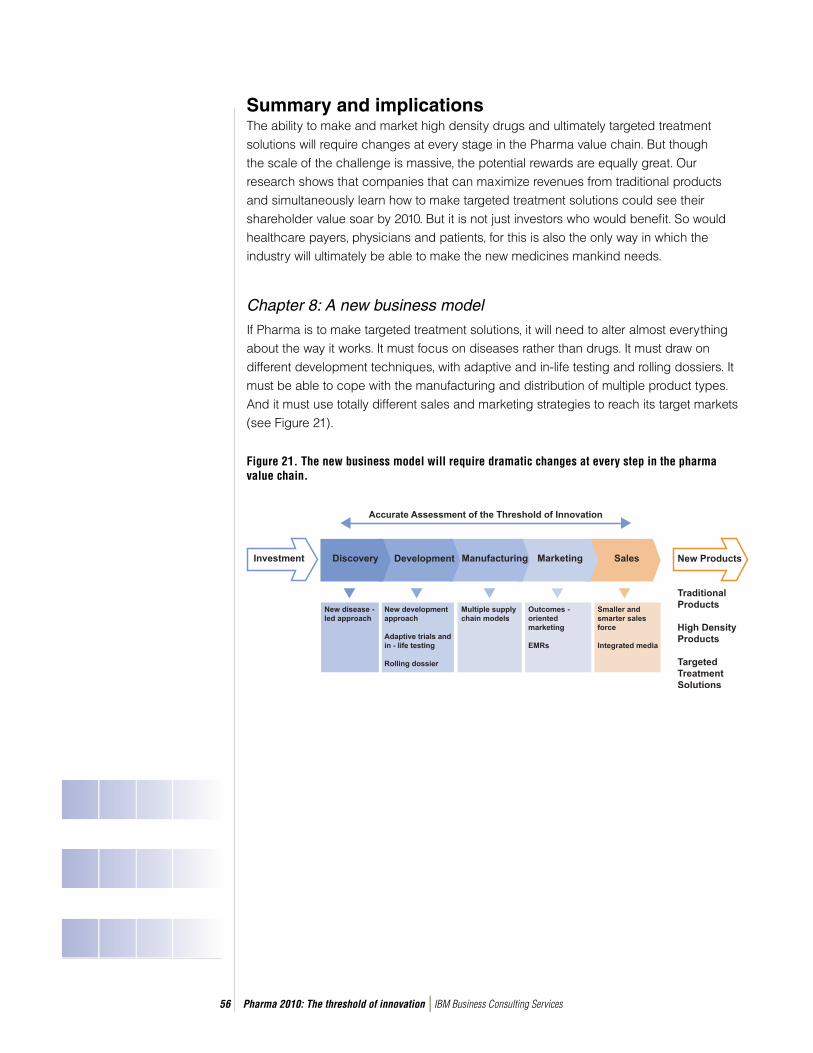

56 Chapter 8: A new business model

59 About the authors

59 About IBM Business Consulting Services

60 References

Pharma 2010: The threshold of innovation IBM Business Consulting Services2

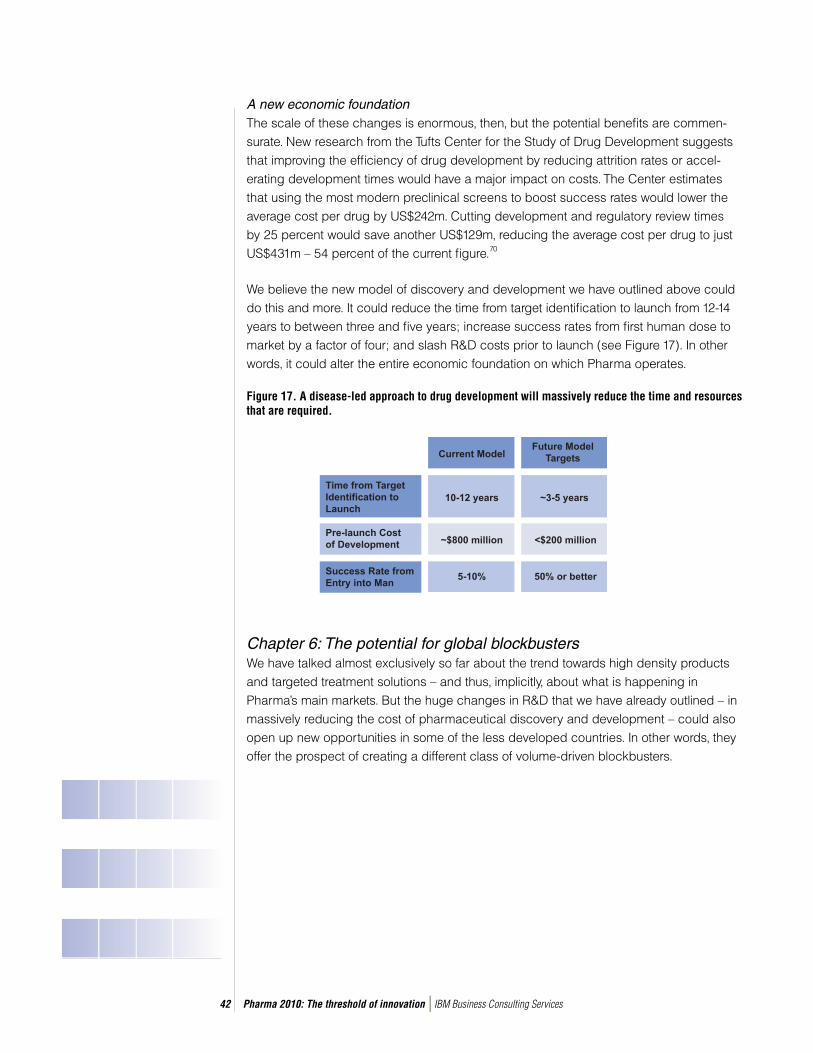

Collectively, these changes will blur the boundaries between discovery, development and the marketplace – creating a fully integrated model. They will also massively reduce the time and cost of making new drugs. In 2010, the discovery and development process will take half as long as it does now, and costs per drug will fall to a quarter of the current average.

Regulation Pharma companies will initiate contact with the regulatory authorities regarding the devel-opment of a particular treatment while it is still in the early stages of discovery. They will submit clinical data to the regulators on an ongoing automated basis via rolling dossiers. And they will work much more closely in partnership with the regulators throughout the entire discovery and development process.

The very basis on which the regulators grant permission to sell a drug will also change. The traditional one-off endorsement will be replaced by continuous evaluation. The right to market a drug will be granted and re-confi rmed subject to regular reviews of its safety and effi cacy – reviews that are even more stringent than the checks involved in adverse-event reporting.

In 2010, Pharma will engage much more fully with healthcare payers, physicians and patients as well. In this way, it will get better feedback – both clinical and commercial – at a much earlier point in the development process. It will also be able to promote accurate diagnosis and treatments, and support medical practitioners.

Sales and marketing Many of the new medicines that are made will cover secondary rather than primary care, so they will be marketed differently – using smaller sales teams, trained to converse with specialists. But all new medicines will be promoted on the basis of the specifi c disease states they address, rather than whether or not they work better than competing products. They will be supported by objective evidence and priced according to the medical results they deliver, not the price of rival drugs that are already on the market. And a substantial part of their value will lie in the services that come with them.

These services will form the backbone of a comprehensive support network that helps individual patients to identify when they really need to see a doctor; to manage the particular disease states from which they suffer; and to understand why they should keep taking the medicines they have been prescribed. In conjunction with targeted treatments and remote monitoring, better persistence will improve the healthcare patients receive. It will also boost the industry’s revenues.

Pharma 2010: The threshold of innovation IBM Business Consulting Services3

The future of Pharma Our research shows that these changes will be driven by the shifting balance of power between Pharma and its customers. Governments, healthcare insurers and patients are increasingly dictating the sort of new drugs they want and the prices they are willing to pay. In short, it is the healthcare payers – not the drug makers – that are now defi ning the threshold of innovation. They are also squeezing every ounce of value out of products that are already available, so they are raising the threshold of innovation ever higher.

But a much better grasp of the biological sciences and a massive increase in computing power will equip the industry with the tools to rise to this challenge. In 2010, we believe Pharma will be able to develop products and therapeutic packages that demonstrably surpass the drugs that are already on the market – the hurdle governments and healthcare insurers will set in deciding when to pay premium prices.

Pharma 2010: The threshold of innovation IBM Business Consulting Services4

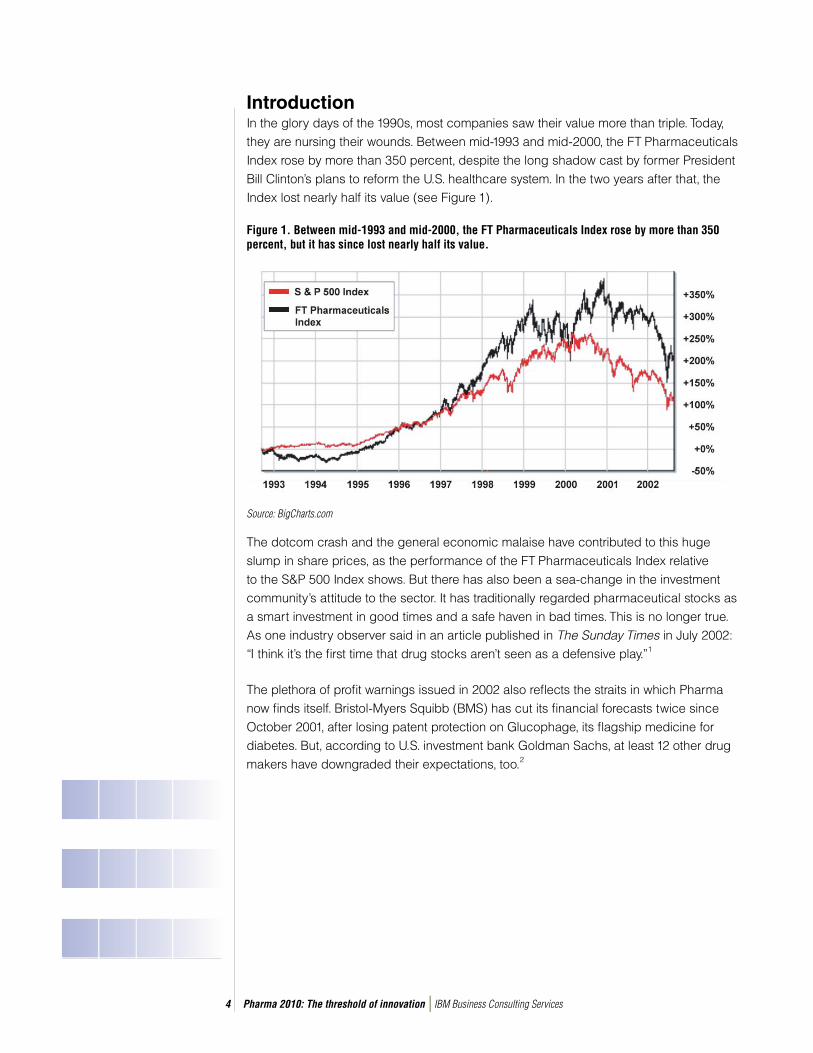

IntroductionIn the glory days of the 1990s, most companies saw their value more than triple. Today, they are nursing their wounds. Between mid-1993 and mid-2000, the FT Pharmaceuticals Index rose by more than 350 percent, despite the long shadow cast by former President Bill Clinton’s plans to reform the U.S. healthcare system. In the two years after that, the Index lost nearly half its value (see Figure 1).

Figure 1. Between mid-1993 and mid-2000, the FT Pharmaceuticals Index rose by more than 350 percent, but it has since lost nearly half its value.

The dotcom crash and the general economic malaise have contributed to this huge slump in share prices, as the performance of the FT Pharmaceuticals Index relative to the S&P 500 Index shows. But there has also been a sea-change in the investment community’s attitude to the sector. It has traditionally regarded pharmaceutical stocks as a smart investment in good times and a safe haven in bad times. This is no longer true. As one industry observer said in an article published in The Sunday Times in July 2002: “I think it’s the fi rst time that drug stocks aren’t seen as a defensive play.”1

The plethora of profi t warnings issued in 2002 also refl ects the straits in which Pharma now fi nds itself. Bristol-Myers Squibb (BMS) has cut its fi nancial forecasts twice since October 2001, after losing patent protection on Glucophage, its fl agship medicine for diabetes. But, according to U.S. investment bank Goldman Sachs, at least 12 other drug makers have downgraded their expectations, too.2

Source: BigCharts.com

Pharma 2010: The threshold of innovation IBM Business Consulting Services5

The shifting balance of power A potent mix of problems, including lack of productivity in the laboratory, patent expiries and intense therapeutic competition, has made it increasingly diffi cult for Pharma to make good new medicines. The situation has been compounded by a gradual shift in the balance of power. Where once the industry could command a good return on investment, governments and healthcare insurers are now beginning to stipulate the sort of improve-ments they want and the prices they are willing to pay. They are not just defi ning the threshold of innovation; they are using much more quantitative measures of innovation than they did previously, and squeezing every ounce of value out of drugs that are already on the market, so they are raising the threshold of innovation ever higher.

Pharma has also incurred growing criticism for concentrating primarily on the chronic degenerative illnesses of the developed world and failing to address the needs of the billions of people living in less developed countries, although some companies have done more on this front than is widely recognized. Pfi zer has, for example, launched an initiative to deal with trachoma, while Aventis has focused on African trypanosomiasis and Novartis on leprosy. Similarly, GlaxoSmithKline (GSK) is trying to tackle malaria.3 It is also cutting prices yet again.4

A totally different perspective Yet, bleak though the current outlook is, we believe there are grounds for great optimism. A better grasp of the molecular sciences and a better electronic infrastructure will give Pharma some of the tools it needs to meet these challenges. Those tools will ultimately enable the industry both to surmount the rising threshold of innovation in the developed world and to reduce the cost of pharmaceutical discovery and development so signifi -cantly that it can serve some of the world’s poorer markets, profi tably.

But if Pharma is to realize the full potential of these scientifi c and technological advances, it will need to alter its perspective. Rather than focusing on the search for new one-size-fi ts-all drugs, it will need to focus on defi ning diseases much more precisely – and that will, in turn, enable it to develop treatments for specifi c disease states. Looking through the opposite end of the telescope to the one on which the industry has relied for so many decades will entail massive changes in the way it makes and markets new medicines. It will also require that companies forge much closer links with the regulators, healthcare payers, doctors and patients, to ensure that they make the sort of drugs people really want.

Pharma 2010: The threshold of innovation IBM Business Consulting Services6

We shall discuss all these changes in much greater detail in the rest of this paper, which follows up on the work we published in the “Pharma 2005” series. We shall also discuss the fi nancial implications they carry. We have modeled the impact of various scenarios on the industry’s shareholder value.5 Our model shows that, regardless of what happens over the next eight years – the landmark we have set – Pharma cannot stand still.

Companies that fail to respond to the market conditions which are now emerging – and those that are currently most successful may well be those that most resist making the requisite changes – will see their value continue to plummet. But even those that are most successful in using traditional techniques to maximize revenues from traditional products will not be able to generate suffi cient growth. At best, they will do little more than double their current value by 2010 – a performance that falls far short of the increase in shareholder value the industry provided in the 1990s.

It is only by entering totally new terrain that Pharma companies can hope to produce the truly innovative medicines for which people will readily pay, but if they succeed, the rewards will be huge. We estimate that, even if the market for “targeted treatment solutions” (as we have called them) is slow to get started, companies that learn how to make such medicines could triple their shareholder value by 2010. If the market for such medicines takes off more rapidly, they could enjoy almost twice the growth the industry enjoyed in its heyday – a prize well worth the effort required.

Drivers of changeThe shortage of good new drugs in the pipeline; the imminent expiry of the patents on numerous blockbusters; intense competition; a more demanding market that has begun to specify the sort of innovations it wants, and what it is willing to pay for them – all these challenges are making life very much harder for Pharma than it was a few years ago. The industry has responded with several strategies that have previously proved successful. It has shopped around for new leads in the biotechnology sector, exploited its consid-erable marketing clout, and consolidated rapidly. Yet the evidence suggests that none of these tried and tested techniques will be suffi cient to close the fi nancial gap.

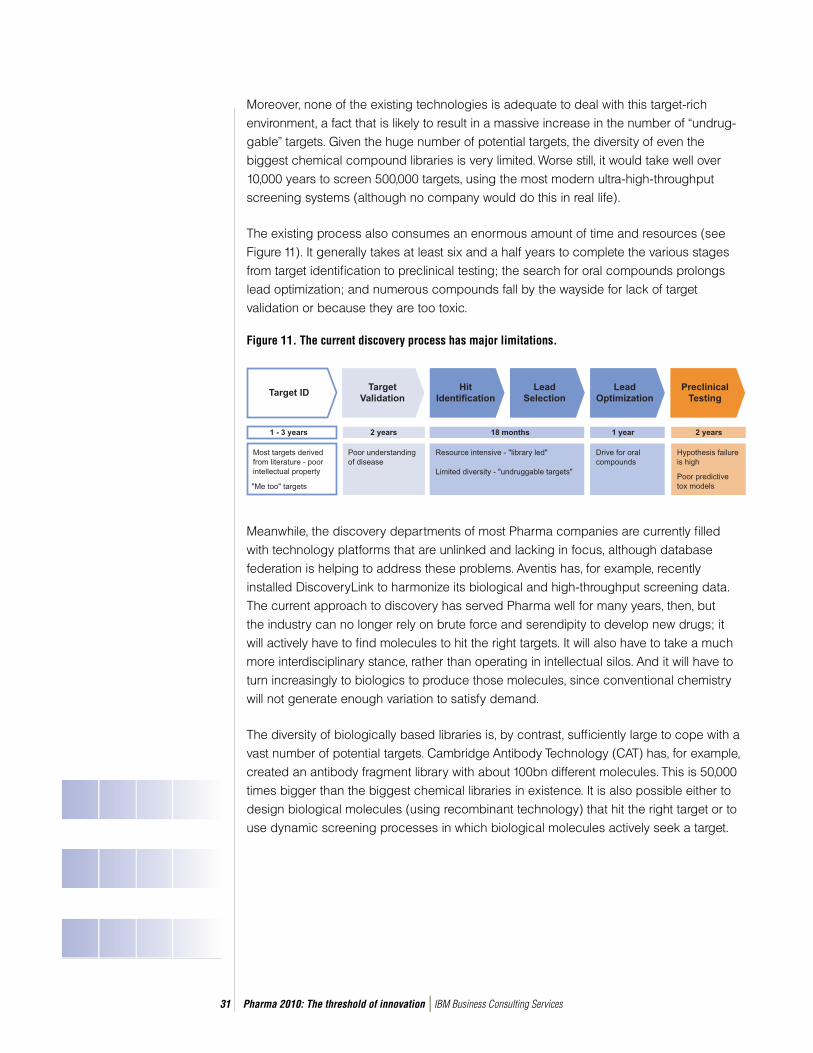

Chapter 1: Tough timesOver the years Pharma has developed a very successful model for making new medicines. The world’s leading companies have collectively validated about 500 targets – the biological mechanisms (usually receptors or enzymes in human cells) through which drugs work.6 They have created large compound libraries, containing as many as two million molecules apiece. They have evolved a phased development process that includes large-scale trials to establish the safety and effi cacy of their products, and they have patented those products to protect their huge investment.

Pharma 2010: The threshold of innovation IBM Business Consulting Services7

They have become equally profi cient at marketing and selling new medicines. They have acquired the expertise to launch new drugs rapidly across a wide range of territories; built big sales forces to promote those drugs; and secured premium prices to generate the revenues they need for further research and development (R&D). They have also tapped the potential of direct-to-consumer (DTC) advertising; managed the lifecycle of their products to maximize returns on investment; and in-licensed new products to sustain their therapeutic franchise.

The results of this approach speak for themselves. During the past two decades, sales of new drugs and new formulations of older drugs have consistently outstripped the fall in income from products that have come off patent. And that has enabled Pharma to reward investors very handsomely: between 1993 and 1998, some of the industry leaders provided total shareholder returns of more than 40 percent a year. But for a variety of reasons the current model has recently come under growing pressure.

The dearth of good new drugsOne of the main reasons why Pharma has failed to meet shareholders’ expectations is lack of R&D productivity. In 1998, the biggest drug makers each announced that they aimed to produce three new chemical entities (NCEs) a year; indeed, some companies now claim they need to produce three or more billion-dollar blockbusters a year, just to maintain their sales growth. Yet they are far from fulfi lling this promise.

Goldman Sachs estimates that, in 2001, the industry leaders spent about US$35bn, roughly double the sum they spent in 1997 and three times the sum they spent in 1992.7 And in 2003 the 15 major pharmaceutical companies spent US$48bn on R&D.8 Even so, the output of new drugs has declined. In 2003, 30 new active substances (NASs) were launched on to the world market – the lowest number for 25 years – and this downward trend seems set to continue.9 (The number of NME fi lings has also dropped substantially, so longer approval times may have contributed to the fall in productivity, but they are certainly not the sole explanation.)

This is only one sign of how diffi cult it has become to create good new drugs using tradi-tional sciences and technologies. The incidence of post-marketing product withdrawals and late-stage failures in the pipeline is further evidence of the challenges the industry is facing. Between 1997 and 2001, 12 drugs with combined peak sales potential of more than US$11bn were removed from the market. Late-stage failures cost even more; in the three years to 2001, the industry leaders terminated 28 products, with potential peak sales of more than US$20bn, in Phases II or III.

Pharma 2010: The threshold of innovation IBM Business Consulting Services8

The ticking bomb of patent expiriesMeanwhile, Pharma’s existing revenues are exposed as never before. Between 2002 and 2007, the U.S. patents on 35 drugs with global sales of more than US$73bn will expire (see Figure 2).10

Figure 2. Patent expiries will make a huge hole in future revenues.

Experience shows that when a drug comes off patent, sales drop very sharply. Take one recent case: the dramatic erosion in sales of Prozac, Lilly’s well-known antidepressant, which came off patent in the U.S. in August 2001. As soon as the fi rst generic version hit the market, Merck-Medco started switching its mail order patients to the new product. Within a week, it had converted 80 percent of them. Express Scripts did the same and, by December 2001, almost 90 percent of its mail order patients were taking the generic alternative. As a result, sales of Prozac fell by 22 percent, in 2001.11

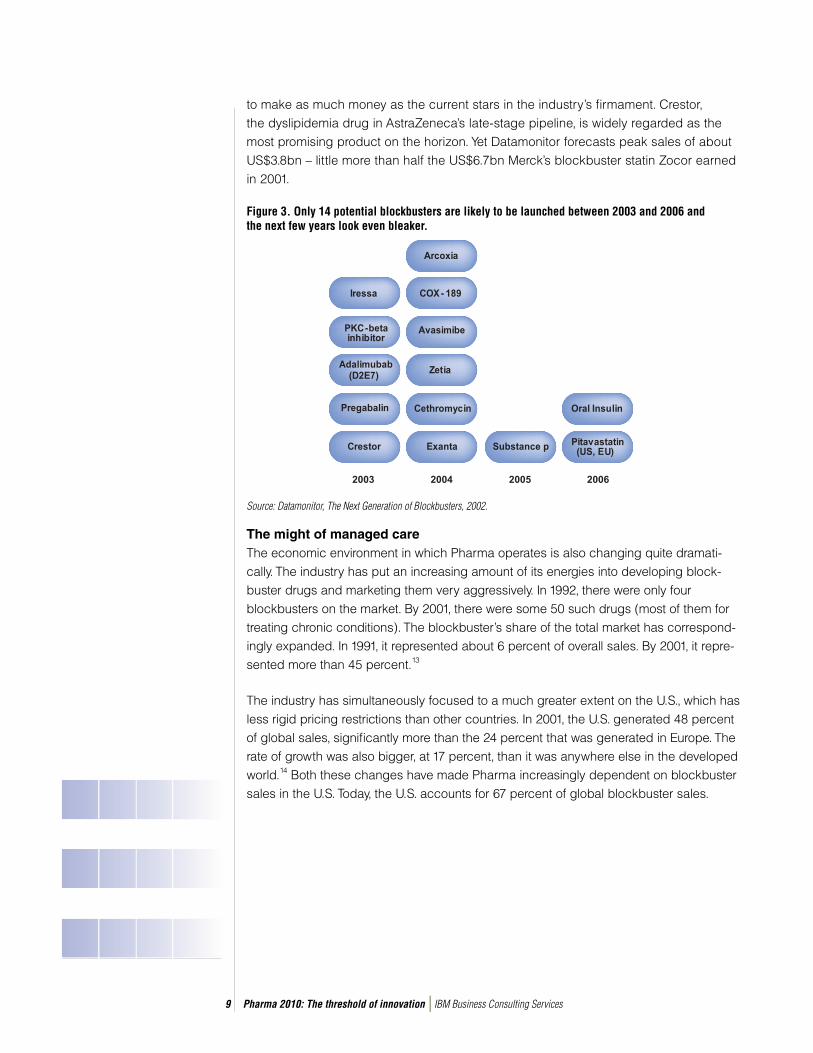

Pharma will fi nd it hard to replace much of this revenue. In a report published in 2002, Datamonitor estimated that there were four potential blockbusters in the industry’s pipeline in 2002, and another 14 such drugs in the pipeline between 2003 and the end of 2008 – excluding products that have already been launched in different indications or in any part of the world (see Figure 3).12 But none of these new medicines is expected

Source: Datamonitor, 2002.

Blockbuster U.S. Patent expires, 2002 - 2007

Pharma 2010: The threshold of innovation IBM Business Consulting Services9

to make as much money as the current stars in the industry’s fi rmament. Crestor, the dyslipidemia drug in AstraZeneca’s late-stage pipeline, is widely regarded as the most promising product on the horizon. Yet Datamonitor forecasts peak sales of about US$3.8bn – little more than half the US$6.7bn Merck’s blockbuster statin Zocor earned in 2001.

Figure 3. Only 14 potential blockbusters are likely to be launched between 2003 and 2006 and the next few years look even bleaker.

The might of managed careThe economic environment in which Pharma operates is also changing quite dramati-cally. The industry has put an increasing amount of its energies into developing block-buster drugs and marketing them very aggressively. In 1992, there were only four blockbusters on the market. By 2001, there were some 50 such drugs (most of them for treating chronic conditions). The blockbuster’s share of the total market has correspond-ingly expanded. In 1991, it represented about 6 percent of overall sales. By 2001, it repre-sented more than 45 percent.13

The industry has simultaneously focused to a much greater extent on the U.S., which has less rigid pricing restrictions than other countries. In 2001, the U.S. generated 48 percent of global sales, signifi cantly more than the 24 percent that was generated in Europe. The rate of growth was also bigger, at 17 percent, than it was anywhere else in the developed world.14 Both these changes have made Pharma increasingly dependent on blockbuster sales in the U.S. Today, the U.S. accounts for 67 percent of global blockbuster sales.

Source: Datamonitor, The Next Generation of Blockbusters, 2002.

Pharma 2010: The threshold of innovation IBM Business Consulting Services10

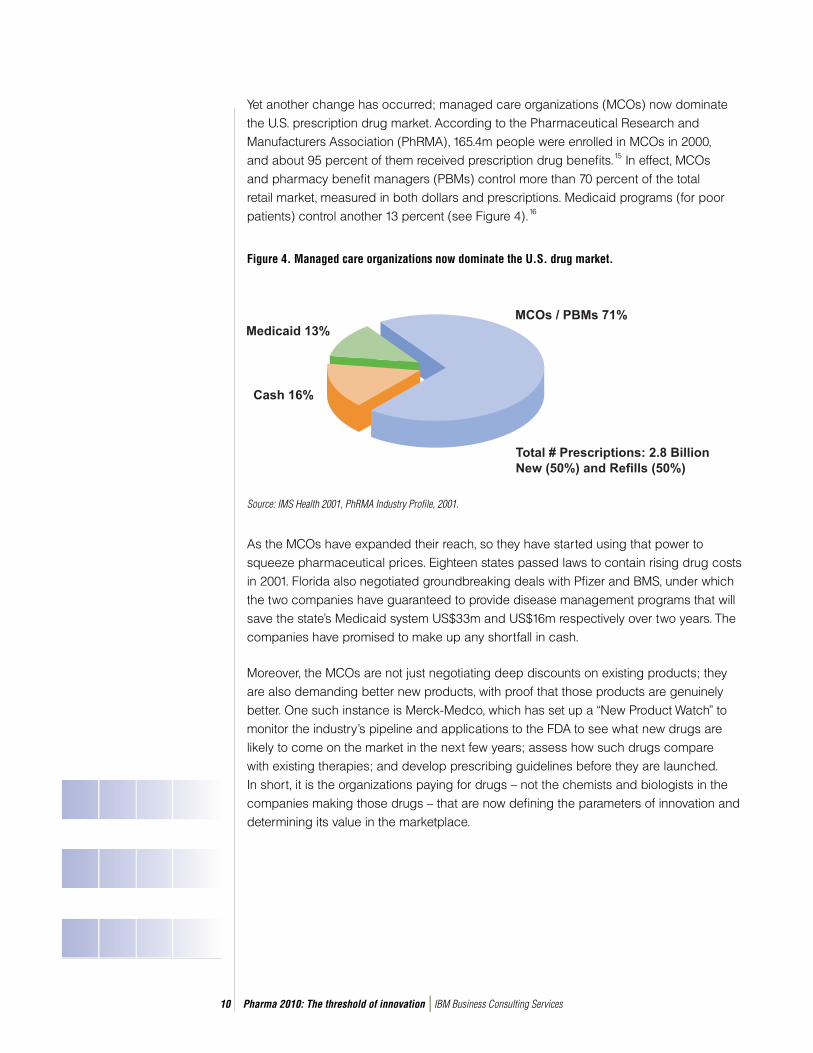

Yet another change has occurred; managed care organizations (MCOs) now dominate the U.S. prescription drug market. According to the Pharmaceutical Research and Manufacturers Association (PhRMA), 165.4m people were enrolled in MCOs in 2000, and about 95 percent of them received prescription drug benefi ts.15 In effect, MCOs and pharmacy benefi t managers (PBMs) control more than 70 percent of the total retail market, measured in both dollars and prescriptions. Medicaid programs (for poor patients) control another 13 percent (see Figure 4).16

Figure 4. Managed care organizations now dominate the U.S. drug market.

As the MCOs have expanded their reach, so they have started using that power to squeeze pharmaceutical prices. Eighteen states passed laws to contain rising drug costs in 2001. Florida also negotiated groundbreaking deals with Pfi zer and BMS, under which the two companies have guaranteed to provide disease management programs that will save the state’s Medicaid system US$33m and US$16m respectively over two years. The companies have promised to make up any shortfall in cash.

Moreover, the MCOs are not just negotiating deep discounts on existing products; they are also demanding better new products, with proof that those products are genuinely better. One such instance is Merck-Medco, which has set up a “New Product Watch” to monitor the industry’s pipeline and applications to the FDA to see what new drugs are likely to come on the market in the next few years; assess how such drugs compare with existing therapies; and develop prescribing guidelines before they are launched. In short, it is the organizations paying for drugs – not the chemists and biologists in the companies making those drugs – that are now defi ning the parameters of innovation and determining its value in the marketplace.

Source: IMS Health 2001, PhRMA Industry Profile, 2001.

Pharma 2010: The threshold of innovation IBM Business Consulting Services11

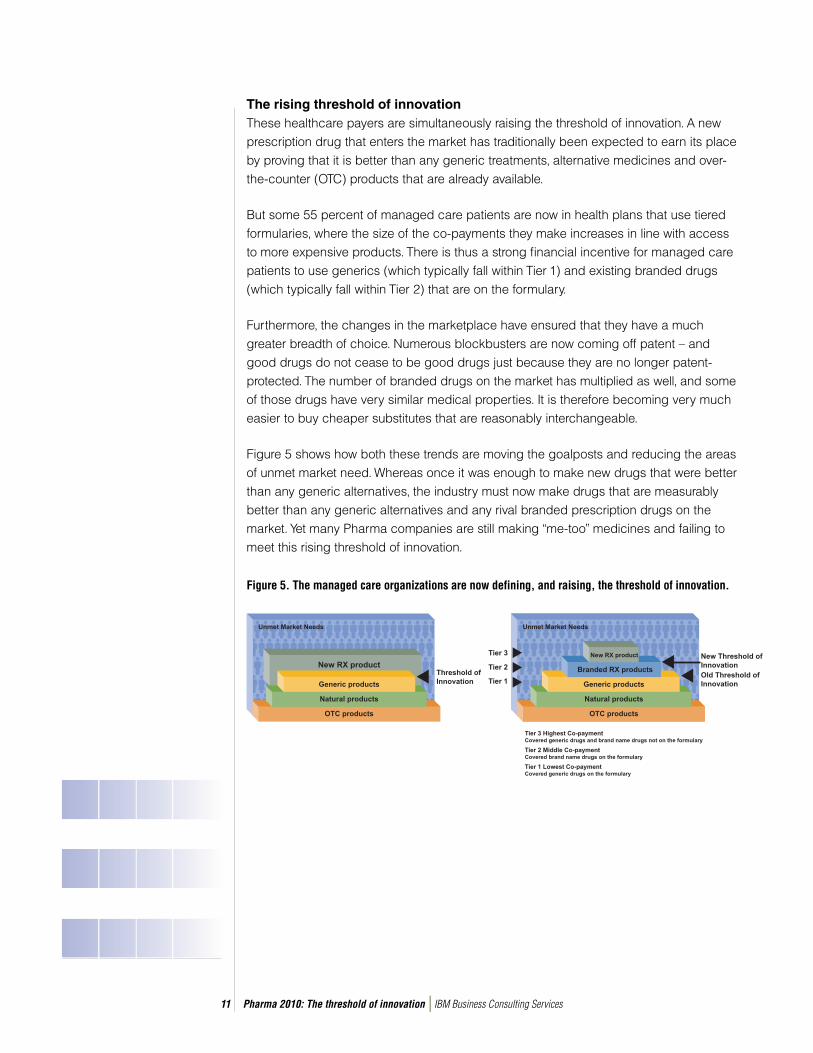

The rising threshold of innovation These healthcare payers are simultaneously raising the threshold of innovation. A new prescription drug that enters the market has traditionally been expected to earn its place by proving that it is better than any generic treatments, alternative medicines and over-the-counter (OTC) products that are already available.

But some 55 percent of managed care patients are now in health plans that use tiered formularies, where the size of the co-payments they make increases in line with access to more expensive products. There is thus a strong fi nancial incentive for managed care patients to use generics (which typically fall within Tier 1) and existing branded drugs (which typically fall within Tier 2) that are on the formulary.

Furthermore, the changes in the marketplace have ensured that they have a much greater breadth of choice. Numerous blockbusters are now coming off patent – and good drugs do not cease to be good drugs just because they are no longer patent-protected. The number of branded drugs on the market has multiplied as well, and some of those drugs have very similar medical properties. It is therefore becoming very much easier to buy cheaper substitutes that are reasonably interchangeable.

Figure 5 shows how both these trends are moving the goalposts and reducing the areas of unmet market need. Whereas once it was enough to make new drugs that were better than any generic alternatives, the industry must now make drugs that are measurably better than any generic alternatives and any rival branded prescription drugs on the market. Yet many Pharma companies are still making “me-too” medicines and failing to meet this rising threshold of innovation.

Figure 5. The managed care organizations are now defining, and raising, the threshold of innovation.

.

That’s not all. The decision as to whether a new drug is better than rival brands rests with the MCOs, which have a vested interest in putting as many new drugs as possible in Tier 3 (where patients pick up a big portion of the bill), unless such drugs are demon-strably better than their rivals. This is making it more diffi cult than ever for drug makers to achieve the prices and volumes required to produce a blockbuster – the very model on which they have become increasingly dependent.

The worldwide spread of cost controlsThe situation in the U.S. is getting tougher, then, but there are no easy alternatives anywhere else. The European Union (EU) has introduced various measures for reducing drug prices – including reference-pricing rules that mean prices can only go down – and individual member states have taken other steps to cut the bill. A similar drive to contain costs is taking place in Japan. Moreover, although some governments are willing to pay for products they regard as genuinely new, they are becoming much more vociferous in their demands for a quid pro quo in the form of lower prices for drugs that are already on the market.

Several countries have also adopted new prescribing criteria. They have set up “gatekeepers” for evaluating products and therapies in terms of their cost-effectiveness as well as their safety and effi cacy – the two conventional measures for assessing a drug. The UK’s National Institute of Clinical Excellence (NICE) and the Canadian Coordi-nating Offi ce for Health Technology Assessment are two such instances, as is the center for evidence-based medicine at Kyoto University in Japan. But during the last decade almost every country in the developed world has introduced stringent measures to contain soaring healthcare costs, and these measures are becoming increasingly sophis-ticated. So the industry needs to become much more proactive in pointing out that drugs constitute a relatively small percentage of overall healthcare costs.

As if this were not bad enough, the therapeutic competition is also becoming much fi ercer. Just one example illustrates the point. In 1999, Searle (now part of Pharmacia) launched Celebrex, the fi rst of the new class of Cox-2 inhibitors. Merck followed hard on its heels with Vioxx. Today, Pharmacia has another two Cox-2 inhibitors on the market: Bextra, which was approved by the FDA in November 2001; and Dynastat, which was approved by the European Medicines Evaluation Agency in March 2002. There are at least another nine similar products in late-stage development in other companies – and it is hard to see how all these medicines will be able to surmount the rising threshold of innovation.

Pharma 2010: The threshold of innovation IBM Business Consulting Services12

The slowdown in sales growthIn sum, the outlook is bleak. R&D productivity and shareholder value are falling, much as we predicted in “Pharma 2005: An Industrial Revolution,” the report we published in 1998.17 Revenues from existing products are highly exposed, with a very large number of top-selling products due to come off patent over the next few years. Opportunities to make conventional blockbusters are shrinking, as control over the defi nition of innovation moves from the laboratory to the marketplace, and it is becoming increasingly diffi cult to differen-tiate products that treat common chronic conditions on therapeutic grounds alone.

Our research suggests that all these problems will substantially reduce the pace at which sales of branded products grow. We have estimated probable revenues from drugs that are already on the market and from drugs that are likely to be launched over the next eight years. Our fi gures indicate that they will collectively deliver compound annual growth of just 5.3 percent between 2001 and 2010 (see Figure 6).

Figure 6. The growth in sales of branded pharmaceuticals is expected to be very much slower Figure 6. The growth in sales of branded pharmaceuticals is expected to be very much slower between 2002 and 2010. between 2002 and 2010.

This is signifi cantly lower than the 9 percent per annum at which the industry was growing just a few years ago, and massively below the double-digit growth it enjoyed in the early 1990s. A recent analysis of 26 leading pharmaceutical companies by Goldman Sachs confi rms this gloomy picture.18 So it is clearly time for a fundamental review of the way in which Pharma works.

Pharma 2010: The threshold of innovation IBM Business Consulting Services13

Pharma 2010: The threshold of innovation IBM Business Consulting Services14

Chapter 2: The old ways don’t workMost Pharma companies have made strenuous efforts to improve the effi ciency of their R&D, without much success; the odds of getting a molecule to market remain as slim as they did a decade ago. Most companies have also tried to close the fi nancial gap by resorting to three traditional strategies for improving their bottom line:

• They have acquired new products from biotechnology and genomics companies – but this is now becoming very expensive and increasingly difficult, as biotech companies come of age.

• They have maximized revenues from existing products by increasing their market penetration, extending their product lines and raising prices.

• And they have tried to cut costs, usually in the wake of a merger or acquisition.

But although these strategies can reduce the gap between what investors expect and what Pharma can deliver, there is little to suggest they can eliminate it.

A big bill for biotechBiotech and genomics companies currently perform nearly a fi fth of all pharmaceutical R&D, a fi gure that is set to double within the next 10 years.19 Indeed, William Haseltine, chairman and chief executive of Human Genome Sciences (HGS), predicted at a conference in February 2002 that over half of all the New Active Substances (NASs) developed in the next 10 to 15 years will result from research into antibodies.20 Recog-nizing the importance of this work, the industry leaders have been actively shopping around to fi ll the gaps in their pipelines.

But as the competition for drug candidates increases, so prices go up – and there is no guarantee that such money will be well spent, as BMS recently learned. BMS paid ImClone Systems more than US$2bn for the cancer drug Erbitux in a part-cash, part-equity deal, only to see the FDA fi nd fault with ImClone’s trial data in January 2002.

The choice is also becoming more restricted, as the biotech industry matures. A number of the biotech companies that began life by selling technology have evolved into producers in their own right because they are now big enough to go it alone and the capital markets value the direct sales of drugs more highly than royalties from a pharmaceutical partner. Millennium Pharmaceuticals and HGS have products in the clinic, and Genentech has bought back the licensing rights to some of its own drugs. Other companies have benefi ted from the collapse of the dotcom bubble, when investors moved heavily, albeit briefl y, into biotech stocks. In 2000, the biotech industry raised more

Pharma 2010: The threshold of innovation IBM Business Consulting Services15

capital than ever before – and some fi rms were able to raise enough funds to cover their cash requirements for the next four or fi ve years.21

When it comes to stocking the pipeline, then, biotech is in a much stronger position than it was a short while ago. The economic downturn may make some biotech companies more vulnerable, and it is likely that the biggest pharmaceutical companies will still be able to exert a considerable degree of market control. Even so, many companies may well end up paying more than they expected to get their hands on the most promising leads.

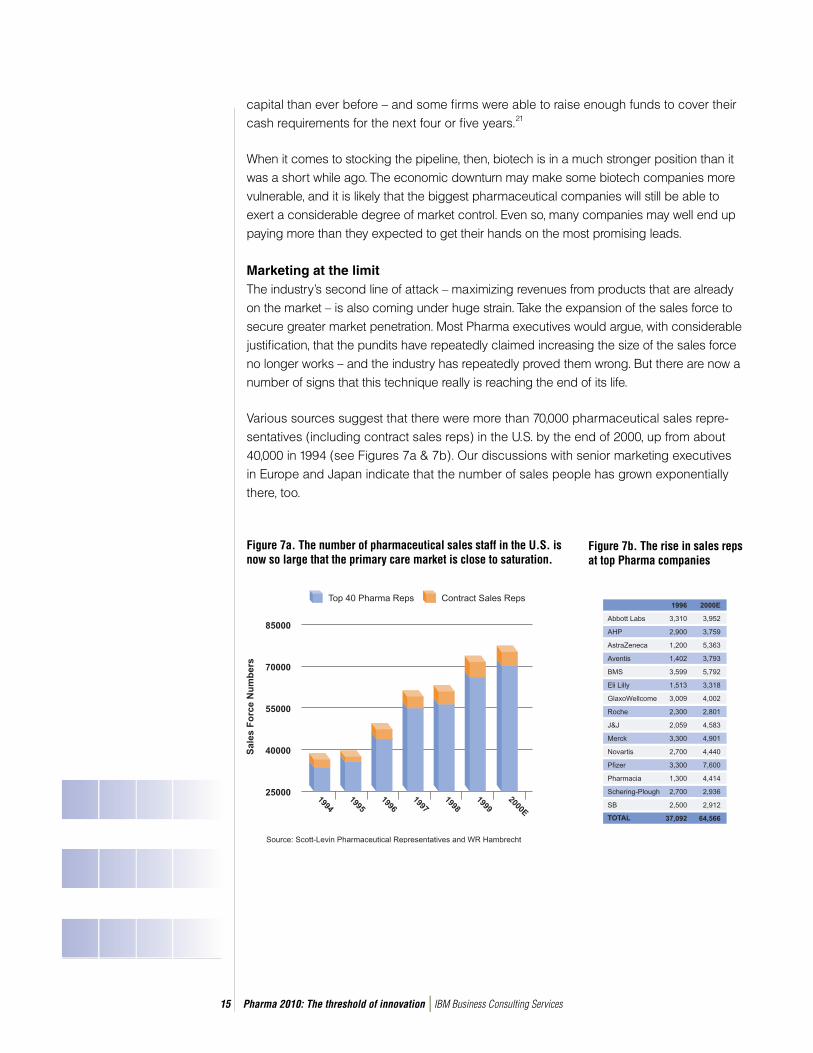

Marketing at the limitThe industry’s second line of attack – maximizing revenues from products that are already on the market – is also coming under huge strain. Take the expansion of the sales force to secure greater market penetration. Most Pharma executives would argue, with considerable justifi cation, that the pundits have repeatedly claimed increasing the size of the sales force no longer works – and the industry has repeatedly proved them wrong. But there are now a number of signs that this technique really is reaching the end of its life.

Various sources suggest that there were more than 70,000 pharmaceutical sales repre-sentatives (including contract sales reps) in the U.S. by the end of 2000, up from about 40,000 in 1994 (see Figures 7a & 7b). Our discussions with senior marketing executives in Europe and Japan indicate that the number of sales people has grown exponentially there, too.

Figure 7a. The number of pharmaceutical sales staff in the U.S. is now so large that the primary care market is close to saturation.

Figure 7b. The rise in sales reps at top Pharma companies

Pharma 2010: The threshold of innovation IBM Business Consulting Services16

But research by Lehman Brothers, the U.S. investment bank, shows that the primary care market in the U.S. at least is now close to saturation. There are only 400,000 practicing physicians in the whole country – and 250,000 of them write four-fi fths of all prescriptions. Moreover, most companies put most of their efforts into targeting the top 150,000 physi-cians, so each top physician would need to see a sales rep every two hours to justify such a large sales force.22 Further expansion of the sales force therefore seems likely to yield diminishing returns – and some companies may have recognized this already. It would certainly explain the growing level of interest in e-detailing, as a means of reaching doctors as effectively and economically as possible.

The situation is very different when it comes to DTC advertising; the more the industry spends, the more it sells. But the sheer enthusiasm with which consumers have responded has begun to elicit alarm. Expenditure on DTC advertising in the U.S. reached US$3.3bn in 2003.23 The EU is also testing the waters; it recently loosened the constraints on DTC advertising of products for HIV/AIDS, diabetes and asthma.

However, a survey conducted by the FDA in 1999 found that when patients asked their doctors for a specifi c product, 82 percent got a prescription – and 50 percent got the particular brand they requested.24 Similarly, Merck-Medco estimates that expenditure on the most heavily promoted drugs is rising three times more than it is on those drugs that are not advertised at all.25 There may thus be something of a backlash against DTC advertising, if it proves as powerful a weapon as some people suspect.

Many companies are also trying to extend the economic life span of drugs that are already on the market by spinning off new formulations or versions of them. Indeed, 65 percent of the new drug applications (NDAs) the FDA approved between 1989 and 2000 were for drugs containing existing active ingredients.26 This practice is certain to continue, although it carries several dangers. First, the attempt may backfi re, as it did for BMS when it failed to persuade U.S. Congress to extend the monopoly on Glucophage. Second, it may prove diffi cult to migrate patients to newer formulations that do not offer genuine medical advances. Several industry sources have, for example, expressed doubts that the discount Schering-Plough is offering on Clarinex, the follow-up drug to Claritin, will be enough to persuade patients to switch products, given that generic versions of Claritin will retail at half the price of the branded drug.

Aggressive promotion of new, more expensive versions of existing medicines has boosted revenue. Pharma has also lifted prices, in common with other industry sectors. But though each of these factors has contributed to the rise in prescription

Pharma 2010: The threshold of innovation IBM Business Consulting Services17

The splurge to merge

In November 1998, we predicted that financial constraints

would fuel a spate of M&As, leaving as few as 13 industry

giants by 2005.33 Since then, Hoechst and Rhône Poulenc

have amalgamated to create Aventis; Astra and Zeneca

have joined forces, as have Glaxo Wellcome and SmithKline

Beecham; Sanofi and Synthélabo have united; Pharmacia &

Upjohn has merged with Monsanto; and Pfizer has pulled

off the industry’s biggest hostile bid with the acquisition of

Warner-Lambert. It also plans to buy Pharmacia, creating a

combined group with annual revenues of more than US$48bn.

Serious money is involved. The merger of Glaxo Wellcome

and SmithKline Beecham was valued at US$76bn and the

purchase of Warner-Lambert at US$87bn. But these are just

the deals that have garnered the bulk of the headlines, partly

because of their size. In 2001, the industry completed 334

M&As – only seven less than it completed the year before.

The trend towards consolidation has been driven by several

factors – including the desire to secure economies of scale;

boost tired pipelines; get a stronger foothold in the most

important geographic and therapeutic markets; and strip out

surplus capacity. It has also concentrated market share. Data

from IMS Health shows that in 2000 the top 20 companies,

measured by pharmaceutical revenues, accounted for 64.6

percent of audited sales worldwide. The next 20 companies

accounted for just 11.3 percent.34

drug spending, increasing drug utilization accounts for a bigger share. Merck-Medco estimates that, between 1996 and 2000, the average U.S. drug spend per member per year nearly doubled. Greater use of drugs was responsible for almost half this additional sum; higher prices accounted for only 22 percent of the overall increase.27 Prices went up more in 2001. Nevertheless, it is clear that the main reason the drugs bill is climbing is because more people are taking more medicines for a wider array of conditions than ever before, not because Pharma has been especially successful in making and selling innovative new medicines.

Big but not always betterSo have mergers and acquisitions (M&As) proved any better a route? The rate of consoli-dation has certainly been frenetic. During the past four years alone there have been six “mega-mergers” and many hundreds of smaller transactions (see box on The splurge to merge). In July 2002, Pfi zer also announced plans to buy Pharmacia in a US$60bn, all-stock deal that will make it by far the world’s largest drug maker with 11 percent of the global market, and Roche is currently completing the friendly takeover of Chugai, Japan’s tenth biggest pharmaceutical company.

There is some evidence that size counts when it comes to licensing in good new medicines. However, critics say that there is little sign of greater productivity in the industry giants that have consolidated. In its latest assessment of pipeline valuations, for example, Goldman Sachs has measured the productivity of the industry leaders by comparing the net present value (NPV) of their late-stage pipelines with their capitalized R&D. Between 1997 and 1999, 29 top-selling drugs were in-licensed – and Pharma’s heavyweights secured the rights to four times as many of these drugs as the middleweights did.28 This shows that three of the fi ve companies with the highest pipeline NPVs, in absolute terms, score below the global sector average on productivity (as do half the top 10 companies).29

Moreover, M&As are notoriously diffi cult to manage, and many actually destroy shareholder value. In a study of 193 mergers conducted by Southern Methodist University in the U.S., 89 percent of the target companies had experienced a slowdown in revenue growth by the third quarter after the deal was announced. Additional research by McKinsey on more than 160 acquisitions suggests that only 12 percent of acquiring companies manage to accelerate their growth signifi cantly over the next three years, while 42 percent lose ground.30

Pharma 2010: The threshold of innovation IBM Business Consulting Services18

In short, the strategies to which Pharma has historically resorted are no longer suffi cient. They are reducing the gap between the fi nancial expectations of investors and the actual performance of the industry leaders, but they are certainly not eradicating it.

The global challengeTo make matters worse, the industry has also come under growing social and political pressure both at home and abroad. Economic, demographic and political changes are sweeping through the world (see box on The global picture). These changes will open up new markets, but they will simultaneously compound the diffi culties the leading drug makers face.

Pharma’s traditional expertise lies in making medicines for people who live in the developed world and selling them at premium prices. However, it has attracted increasing criticism in the media for failing to tackle the plight of the very poor. In fact, some companies have made much more active efforts in this respect than the press coverage might suggest, but their efforts have been individual rather than co-ordinated with those of other industry players and governments. The World Health Organization (WHO) Commission on Macroeco-nomics and Health concluded in a report published in December 2001: “The corporate principles that have spurred recent and highly laudable programs of drug donations and price discounts need to be generalized to support the scaling up of health interventions in the poor countries.”31

If the industry is to preserve its reputation and provide better healthcare for everyone, then, it must simultane-ously develop more innovative products and make a bigger effort to serve the needs of people in the less and least developed regions – although it certainly cannot, and should not be expected to, solve the health problems bedeviling these populations by itself.

The global picture

About 1.2bn people live in the developed countries.35 The population

is also becoming more diverse, as political and economic migration

redraw the global map. But the biggest change of all is the gray factor.

Thirteen percent of the people living in North America, 15 percent

of those living in Europe and 17 percent of those living in Japan are

now over 65 – compared with a global average of just 7 percent.36 In

all, the WHO estimates that there are some 355m elderly people in

the key Pharma markets today.37 Mass longevity and the increasing

expectations of aging “Baby Boomers” – spurred on by the information

they have gleaned from DTC advertising and the Internet – are

stimulating demand for more and better healthcare. But they are also

straining already over-stretched healthcare budgets to breaking point.

The less developed world is likewise struggling to curb soaring

healthcare bills. The problem is especially acute in Asia, where

AIDS may become an even bigger killer than it is in Africa.38 But the

population is growing very rapidly, too. About 4.2bn people live in Latin

America and the Caribbean, Asia Pacific and the Indian sub-continent;

and the UN predicts that the numbers will reach 6.3bn over the next 50

years. Many of these people do not have very much money, but most

less developed countries are effectively multiple markets, with different

financial and educational attributes, medical problems and expectations

for healthcare provision. China, for example, can be divided into two

distinct segments: the rural and urban. About 455m people – 35

percent of the country’s 1.3bn inhabitants – now live in cities, enjoy

increasing prosperity and rely to a growing extent on the branded

pharmaceuticals produced by the big Western drug makers rather than

local generics, so the urban market is starting to look very attractive.

Moreover, the population is aging; according to the national census in

2000, 88.1m people are 65 or older.39

The situation is different again in the least developed world. About

700m people live in sub-Saharan Africa and the population is also

growing very rapidly. However, AIDS has wreaked havoc on its health

and the vast majority of people cannot afford the drug prices that

prevail in the developed world. In fact inadequate infrastructure is an

even bigger barrier than poverty, and the shortage of medicines goes

much further than treatments for AIDS; many of the diseases from

which these populations suffer are not prevalent in developed countries

and so drugs have not been produced to treat them (although Pharma

has been successful in developing vaccines for some conditions). But

it is clear that the industry will never be able to make any money in the

very poorest parts of the world, and this is why it gives drugs away in

such areas.

Pharma 2010: The threshold of innovation IBM Business Consulting Services19

As PhRMA, the leading U.S. trade body, states: “The tremendous challenges facing developing countries demand continued and concerted efforts from both the private and public sectors – and we stand ready to participate in effective partnerships to help improve public health.”32

The road to the futureThe industry has traditionally produced “one-size-fi ts-all” drugs that share certain thera-peutic and economic features, but a new type of product is now beginning to emerge. A growing number of these products are also biological in nature, and most biologically based molecules are both safer than chemical entities and easier to develop (although they are more diffi cult to formulate). Meanwhile, the molecular sciences are providing the tools with which to acquire a much more accurate understanding of disease. Together, these trends will enable Pharma to develop highly profi table healthcare packages for patients suffering from specifi c disease states.

Chapter 3: The rise of the targeted treatment solutionMany of the most successful medicines Pharma has produced have a similar thera-peutic profi le. They are typically fi rst-line treatments; come in a single, one-size-fi ts-all form; are aimed at a mass population; are easy to take (often orally); treat a chronic condition; and ameliorate the symptoms of the disease rather than changing the way in which it progresses.

These medicines have similar economic features, too. They are typically very expensive to research and develop; the Tufts Center for the Study of Drug Development estimates that average costs per drug are now US$802m (including the cost of capital).40 They take about 10-12 years to progress from the laboratory to launch.41 They require an intensive marketing and sales push to promote them; rely on premium pricing; and are expected to cover their costs within a few years of being approved. However, the rising threshold of innovation will make it increasingly diffi cult for such drugs to attain blockbuster status in the future.

The development of high density productsA growing number of what we have called “high density” products are also coming onto the market. These have a different therapeutic profi le. They are typically second-line treatments; designed for a clinically defi ned population; and administered by specialists. But like conventional blockbusters, they come in a single, one-size-fi ts-all form and (with the exception of oncology drugs) generally treat a chronic condition – albeit that they sometimes modify the disease as distinct from just alleviating the symptoms.

Pharma 2010: The threshold of innovation IBM Business Consulting Services20

High density products share some of the economic characteristics of conventional block-busters. They are, for example, expensive and time-consuming to develop. That said, they usually face less intense competition and have lower sales costs because they are marketed to specialists rather than general practitioners and consumers. There is also some evidence to suggest that high density products that modify the progression of a disease now have the potential to generate greater revenues than traditional drugs.

Our analysis of the top 200 prescription medicines, measured by revenues in 2001, shows that 31 percent of them are high density products. They are predominantly oncology drugs but they also include Remicade and Enbrel, both pioneering treatments for rheumatoid arthritis; Neupogen, which maintains the white blood cell count in patients undergoing chemotherapy; Procrit, which boosts the production of red cells in patients suffering from anaemia; and Risperdal, the fi rst truly new anti-psychotic in 20 years.

The beauty of biologicsIf the number of high density products is increasing, so is the number of biologi-cally based drugs (biologics) – large molecules such as soluble proteins, monoclonal antibodies and antibody fragments, as well as smaller molecules such as antisense RNA. IMS Health reports that biotechnology products (predominantly biologics) accounted for more than 35 percent of the 37 NASs that were launched in 2001.42

This is no accident. The biological approach rests on a fundamental understanding of disease. In addition, biologics possess several advantages over chemical entities. They are increasingly derived from human proteins or antibodies (as opposed to those of mice, pigs or other animals) and are therefore less likely to trigger an immune response; it is generally much easier to predict how they will be distributed, metabolized and eliminated; and they typically have much faster development cycles. Indeed, research from CMR International shows that biologics have a four-fold greater chance than chemical entities of making it to market from the point at which they fi rst get tested in man.43

Further evidence of the growing importance of biologics comes from the fact that the FDA now plans to bring the review of such products under the auspices of its main drug division, the Center for Drug Evaluation and Research (CDER). The biologics division has attracted criticism for being slower than CDER. In September 2002, the agency responded to these complaints by announcing that it would consolidate oversight of chemical and biological drugs to improve the effi ciency and consistency of the process.44

Pharma 2010: The threshold of innovation IBM Business Consulting Services21

But though biologics offer considerable promise, that promise has so far been limited and the fault lies mainly within the industry itself. This is not to say that all diseases will be amenable to treatment with biologics. However, Pharma lacks experience in dealing with the problems of discovering, developing and manufacturing large molecules. It is also wary of making drugs that must generally be delivered by injection – believing they will generate lower revenues than medicines that can be taken orally – and has therefore tended to steer clear of such research opportunities. The new challenge is thus to formulate biologics so that they can be delivered in more acceptable forms.

The molecular mazeThe new molecular sciences will enable the industry to change its approach, but they will not do so in the way it originally hoped. The sequencing of the human genome has revealed about 25,000-50,000 new targets, although not all of them are suitable for treating with drugs. And, as scientists readily acknowledge, very little is known about these targets precisely because they are so new. The average number of academic citations per target fell from about 100 in 1990 to almost none in 2002, refl ecting the degree to which the industry has been moving into uncharted territory.

Moreover, the scale of the challenge has proved much greater than anyone initially envisaged, with the dawning realization that it is proteins and their interactions – rather than the mapping of our genes – which hold the key to understanding and treating disease. The human body may contain as many as 500,000 different proteins, so the number of points at which pharmaceutical intervention is possible could increase by a factor of 1,000.

Fortunately, a number of technologies are now emerging that should eventually enable Pharma both to come to grips with genomics and proteomics, and to understand biological systems as coherent entities. For example, the U.S. National Institutes of Health (NIH) has launched the Protein Structure Initiative, which aims to identify 10,000 protein structures over the next decade. And the supercomputer Blue Gene, which should be built by 2005, will be 30 times faster than the fastest machine available today. This enormous computing power will help biologists explore how proteins fold themselves up into their distinctive shapes, and drugs can be more easily directed at particular proteins when their characteristics are known. It will also be used to improve homology searching and pattern recognition, and in systems biology – the study of living systems, using biological models that simulate the behavior of organs and cell tissues.

Pharma 2010: The threshold of innovation IBM Business Consulting Services22

Two other major classes of molecule – carbohydrates (simple and complex sugars) and lipids (fats) – likewise play a big part in the way the body works. In fact, sugars perform multiple jobs: they modify many proteins and fats on cell surfaces; they also affect cell-to-cell communication, the operation of the immune system, the impact of certain infec-tious agents, and the progression of cancer. Recognition of the importance of sugars has spurred a growing number of academics and biotech companies to look into this area more closely.45

In short, exploration into fi elds such as genomics, proteomics and metabonomics will provide Pharma with plenty of new biological targets, but researchers will know very little about which targets are relevant or which diseases they are associated with. So, unless the industry makes radical changes in the way it conducts R&D, the direct benefi ts of the new molecular sciences are likely to be fairly restricted in the short to medium term. They will certainly not facilitate the development of a stream of new drugs.

A disease-centric approachNevertheless, they will effect two major changes. First, they will put an end to the current one-size-fi ts-all approach. It is widely recognized that most drugs only work for between 40 percent and 60 percent of the patients for whom they are prescribed, and that drugs which work well for some patients cause intolerable side effects in others. This is sometimes because drugs act in unexpected ways. But it is often because Pharma’s understanding of many common diseases is so limited that it can only defi ne them in very simplistic terms – and patients who do not respond, or do not respond well, to a particular drug actually suffer from a different disease.

However, thanks to genomics, researchers are gradually acquiring a much better grasp of the factors involved in a particular disease state, including its severity, how it progresses, and why particular individuals are susceptible in the fi rst place. They are also beginning to devise genetic tests that will predict which drugs would work best on which patients, and which would not. So, for example, GSK is working on a test for Ziagen – one of the components in Trizivir, its three-drug treatment for HIV, which some 20 percent of patients cannot take because they have an allergic reaction to Ziagen.

The ability to segment patients on the basis of their probable responses to a particular drug will inevitably fragment the market and end the monolithic approach that has characterized past blockbusters. But it could also give some products a new lease of life; drugs that cause serious side effects in a small percentage of the patient population could then be administered to the “right” patients without causing any harm (see box on One size doesn’t fi t all).

Pharma 2010: The threshold of innovation IBM Business Consulting Services23

One size doesn’t fi t all

Under the current “one-size-fi ts-all” approach, patients are treated in the same manner, even

though complex biomolecular and genetic variations in individuals, as well as the different environ-

mental infl uences to which they are exposed, mean that many drugs do not work for a signifi cant

percentage of the patient population. Beta-blockers, for example, do not work for between 15

percent and 35 percent of the patients for whom they are prescribed; tricyclic antidepressants

do not work for between 20 percent and 50 percent; and interferons do not work for between 30

percent and 70 percent.

Some drugs also cause serious side effects in some people (without necessarily doing them any

good). In fact, an article recently published in the Journal of the American Medical Association

suggests that more than half the 27 drugs frequently cited for causing adverse reactions are linked

to at least one enzyme with a variant allele (one of two or more forms of a gene that may occur

alternatively at a given site on a chromosome) that is known to cause poor metabolism.48 Moreover,

most medicines for adult patients (with the exception of oncology products) are prescribed without

regard for variations in body size, even though there is a roughly three-fold difference between the

biggest and smallest adults.

These differences in genetic make-up and body size cause numerous problems. Research

conducted at University College, London, shows that every year more than 800,000 patients using

the UK National Health Service (NHS) experience adverse drug reactions (ADRs). As a result, about

68,000 patients die and 50,000 are permanently disabled.49 Similarly, one U.S. study estimates

that in 1994 over two million patients were admitted to hospital because they had been prescribed

inappropriate drugs or had experienced adverse effects from drugs that had been correctly

prescribed. Over 100,000 died as a result – suggesting that ADRs are between the fourth and sixth

leading cause of death in the U.S.50

The human cost of such injuries is clearly considerable, but so is the economic cost. Three U.S.

studies, conducted between 1995 and 1997, put the bill for medication-related problems in nursing

homes, hospitals and the community at almost US$85bn.51 But the number of adverse events

is rising, as drugs get steadily more powerful and as aging Baby Boomers take more medicines

– especially drugs for long-term use on chronic conditions. Indeed, it is widely thought that for

every dollar the U.S. spends on drugs, it spends another correcting the problems caused by drugs.

Given that retail expenditure on prescription drugs reached US$154.5bn in 2001, this sum would

be enough to cover the cost of treating every patient with cardiovascular disease in the country.52

Pharma 2010: The threshold of innovation IBM Business Consulting Services24

Genomics and proteomics will not only enable the industry to develop tests that distin-guish between patients with different genetic features, though; they will enable Pharma to defi ne diseases much more accurately and make commercially viable drugs for smaller patient populations. Researchers will eventually be able to separate diseases that currently get lumped together as if they were the same disease, and treat them as different diseases within a particular disease family (or collection of related diseases).

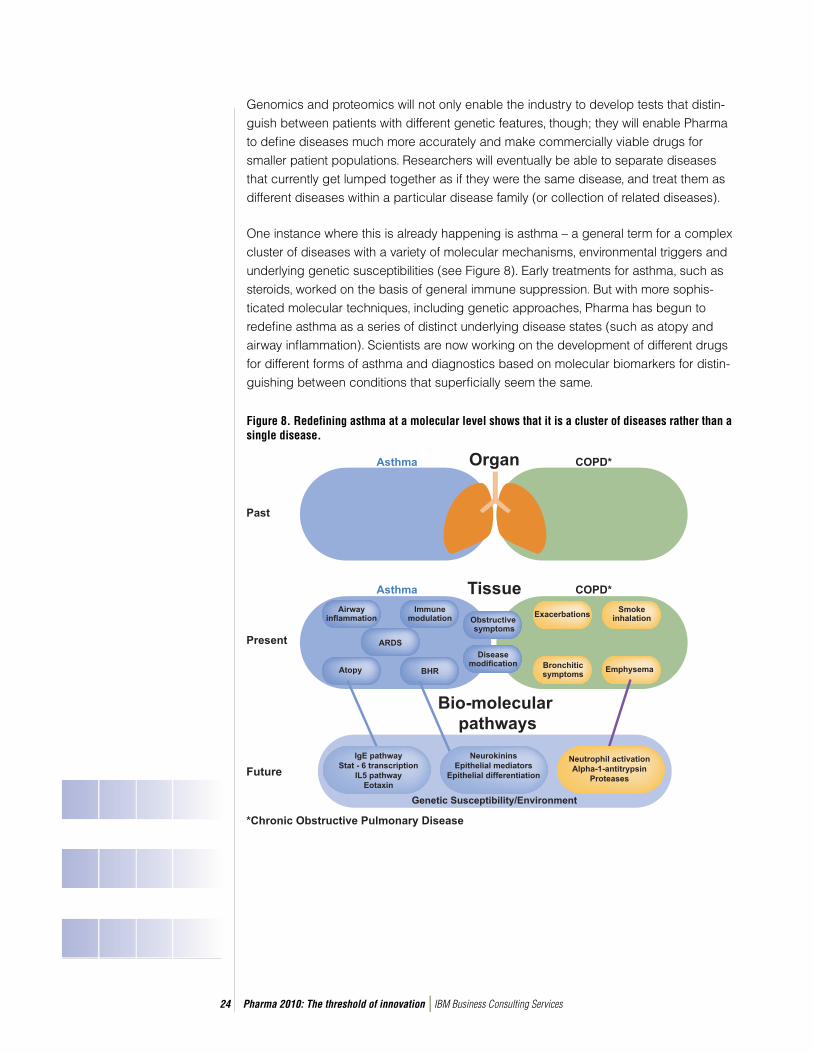

One instance where this is already happening is asthma – a general term for a complex cluster of diseases with a variety of molecular mechanisms, environmental triggers and underlying genetic susceptibilities (see Figure 8). Early treatments for asthma, such as steroids, worked on the basis of general immune suppression. But with more sophis-ticated molecular techniques, including genetic approaches, Pharma has begun to redefi ne asthma as a series of distinct underlying disease states (such as atopy and airway infl ammation). Scientists are now working on the development of different drugs for different forms of asthma and diagnostics based on molecular biomarkers for distin-guishing between conditions that superfi cially seem the same.

Figure 8. Redefining asthma at a molecular level shows that it is a cluster of diseases rather than a single disease.

Pharma 2010: The threshold of innovation IBM Business Consulting Services25

A similar trend is evident in the fi eld of cancer. The Winship Cancer Institute at Emory University has joined forces with NuTec Sciences and IBM to develop a system that will segment breast, prostate, lung and other forms of cancer into sub-types. The system will pinpoint the genes and gene combinations that cause cancer in individual patients, and enable doctors to treat such patients according to their specifi c genetic make-up. As Jonathan Peck, Vice President of the U.S. Institute for Alternative Futures, notes: “We will probably go from the roughly 200 forms of cancer that are known today to 2,000 recognized forms of the disease by 2010. Pathologists have historically defi ned cancers according to where they are located, but that scheme is already being challenged by the emerging molecular taxonomy.”46

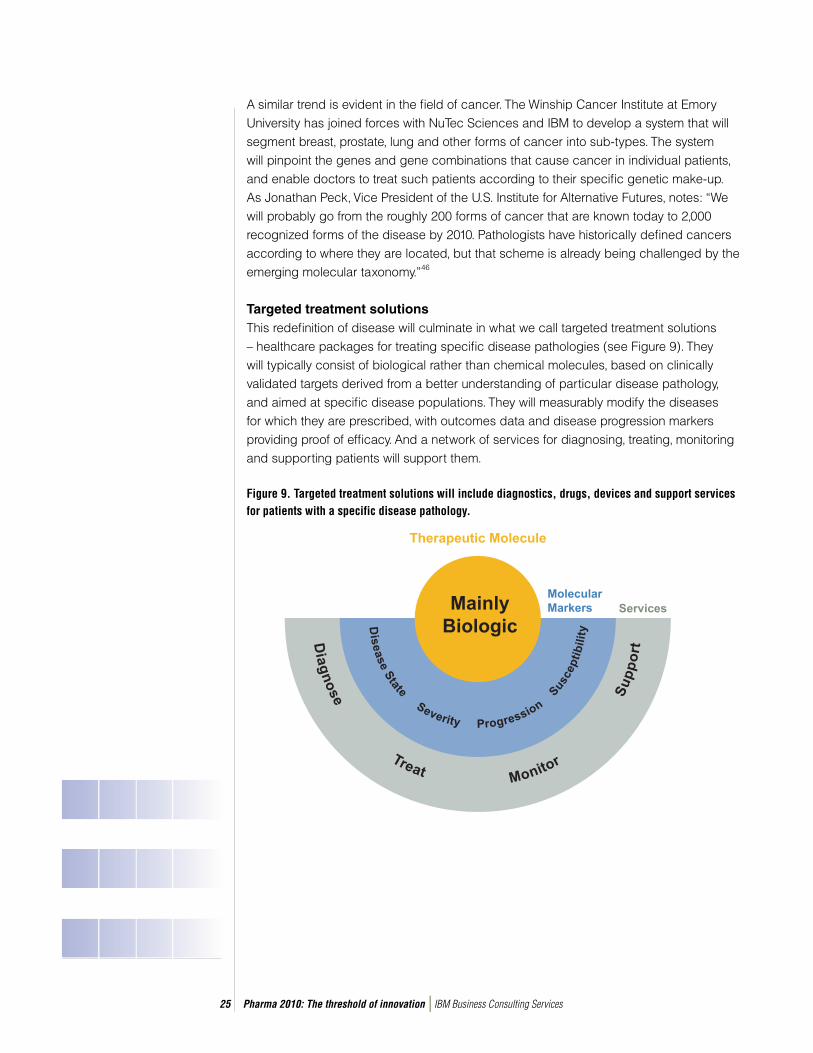

Targeted treatment solutions This redefi nition of disease will culminate in what we call targeted treatment solutions – healthcare packages for treating specifi c disease pathologies (see Figure 9). They will typically consist of biological rather than chemical molecules, based on clinically validated targets derived from a better understanding of particular disease pathology, and aimed at specifi c disease populations. They will measurably modify the diseases for which they are prescribed, with outcomes data and disease progression markers providing proof of effi cacy. And a network of services for diagnosing, treating, monitoring and supporting patients will support them.

Figure 9. Targeted treatment solutions will include diagnostics, drugs, devices and support services for patients with a specific disease pathology.

Pharma 2010: The threshold of innovation IBM Business Consulting Services26

Advances in web-based and mobile technologies will play a big part in facilitating the development of these wrap around services and enabling the industry to generate additional revenues. They will also allow individual pharmaceutical companies to generate more intellectual capital and get closer to patients, which will in turn help them to establish a dominant position in the treatment of particular disease pathologies.

Similarly, new forms of data management will help the industry to handle the vast quantities of outcomes data it will need to support the development of targeted treatment solutions. One such technique is “database federation” – where users can access data sources independently, in their original format, as well as searching all the opera-tional databases in the system. The UK Department of Health has just commissioned a massive distributed computing grid for the screening and diagnosis of breast cancer, which operates on this basis. eDiamond, as it is called, will be used to build a massive digital “photo album” of mammogram scans, which medical experts throughout the country will then be able to search, no matter where or how they were created.

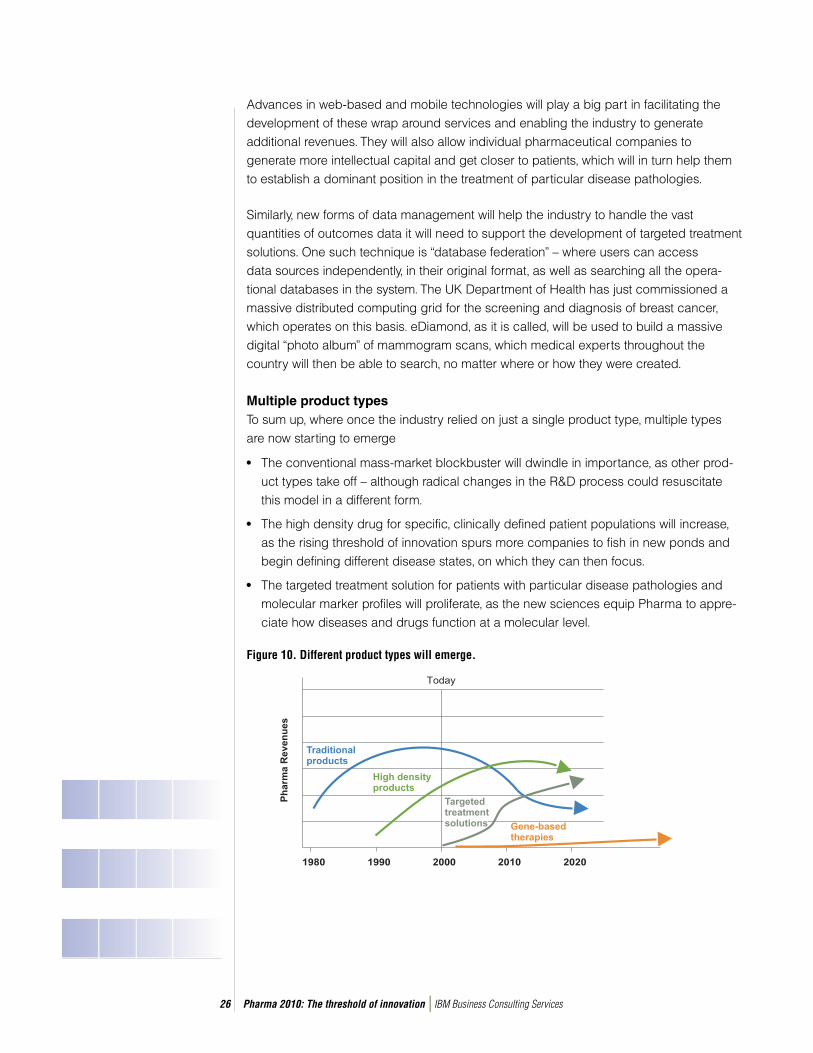

Multiple product typesTo sum up, where once the industry relied on just a single product type, multiple types are now starting to emerge

• The conventional mass-market blockbuster will dwindle in importance, as other prod-uct types take off – although radical changes in the R&D process could resuscitate this model in a different form.

• The high density drug for specific, clinically defined patient populations will increase, as the rising threshold of innovation spurs more companies to fish in new ponds and begin defining different disease states, on which they can then focus.

• The targeted treatment solution for patients with particular disease pathologies and molecular marker profiles will proliferate, as the new sciences equip Pharma to appre-ciate how diseases and drugs function at a molecular level.

Figure 10. Different product types will emerge.

Pharma 2010: The threshold of innovation IBM Business Consulting Services27

We believe it is this last product type that offers the industry the greatest opportunities to improve the quality of healthcare, generate new revenues for the long term and protect its intellectual capital (See Figure 10). It is already clear that concentrating on a few intensely competitive therapeutic areas for which there are already many good drugs on the market will produce diminishing returns. It is equally clear that making high density drugs for therapeutic areas which are clearly defi ned but poorly treated may well produce some additional growth. However, the development of targeted treatment solutions for specifi c disease states will create new market spaces. It will also benefi t patients, healthcare professionals and payers, and the industry alike.

It will ultimately give patients comprehensive therapies that work for them – diagnostics for evaluating their susceptibility to a particular disease; prophylactics for those at risk; molecular markers for defi ning the disease state from which they suffer, and for measuring its severity and progression; and monitoring mechanisms that help them to comply with their individual medical regimens. It will also give doctors the means with which to provide better medical care and healthcare payers better value for money – by enabling them to get the right drugs to the right patients and eliminating the cost of treating people with adverse drug reactions.

Similarly, it will enable Pharma to charge premium prices for treatments that demon-strably work for particular disease states, even though the target market may be smaller; to add value with the provision of diagnostics, biomarkers and monitoring devices; and to increase drug utilization with better compliance and persistence (see box on Persis-tence pays off). In addition, the industry will have numerous opportunities to exploit the same research, because it can build on its expertise in one disease state by moving onto other disease states in the same disease family, and developing entire treatment packages as distinct from single drugs.

It may also help Pharma to stave off a danger that is just beginning to emerge. In August 2002, a German bill on product liability reversed the burden of proof. Under the old rules, a patient had to prove that a drug had harmed him; under the new rules, the pharma-ceutical company must prove that its drug did not cause the injury.47 So any company that wants to defend itself from such allegations will need to be able to show that any treatment it has developed is appropriate for the particular disease state and patient for whom it has been prescribed, or that it was incorrectly used.

Pharma 2010: The threshold of innovation IBM Business Consulting Services28

Persistence pays off

Many patients do not stick to their treatment regimen, even when they risk becoming seriously ill. In a

study of Canadian patients with hypertension, 82 percent of those who had been diagnosed before the

program began were still taking their medicine 4.5 years afterwards. But only 46 percent of those who had

been newly diagnosed at the start of the program were still doing so.53 Persistence levels in another study

of patients with high cholesterol were even lower. Only 33 percent of patients were still using a statin at the

end of 12 months, and only 13 percent were still doing so at the end of five years.54

Predictably, persistence and compliance rates are lower for preventative medications than for drugs for acute

symptomatic illnesses. However, outcomes data on patients with adult hypertension are similar in all Western

countries, despite wide variations in the financing of medical care and the reimbursement of prescription

drugs. So the issue is not simply money. Fear of drugs, denial of illness, confusion, forgetfulness and the

belief that a disease has been cured when the symptoms fade are also contributing factors.55

Yet failure to persist with a medication or comply with the conditions under which it should be taken

increases the risk to individual patients and the overall cost to healthcare providers in terms of

hospitalization and surgery. A landmark study conducted in 1994 shows, for example, that simvastatin

(marketed under the brand name Zocor) can reduce the risk of a fatal heart attack by 40 percent, and the

risk of a non-fatal heart attack by 33 percent, over a period of six years.56

Furthermore, short-term withdrawal of some drugs produces a “rebound” phenomenon that actually leaves

patients more vulnerable. In one piece of research, patients with stable coronary heart disease experienced

a three-fold increase in thrombosis after treatment with simvastatin was stopped and replaced with lower

doses of fluvastatin.57 Another more recent study shows that giving people statins before a major cardiac

event can reduce the risk of a heart attack by as much as half, but withdrawing statin therapy after the onset

of symptoms completely abrogates the beneficial effects.58

Greater persistence in taking drugs that treat chronic conditions would improve the health of many patients,

then, but it also represents a huge opportunity for Pharma. Over 85 percent of patients enrolled in the

big, multi-year trials that have been used to test statins persisted with their treatment for the full five-year

duration. So, if persistence levels in everyday use of such drugs equated with those in clinical trials, and

prices and patient numbers remained the same, the revenues they earned would be roughly 2.7 times

higher. (If 90 percent of patients take a statin for five years, persistence is 2.7 times greater than it is with

a median persistence of 25 weeks, with only 33 percent patients persisting for 12 months, and only 13

percent persisting for five years.) To put it another way, sales of Zocor would be US$18bn a year instead of

US$6.7bn.

In fact, it is far more likely that there would be some sort of trade-off between volume and pricing, not

least because few (if any) countries could afford to pick up such a sudden surge in the drugs bill. But with

a two- or three-fold increase in demand for medicines that treat such conditions, Pharma would certainly

not suffer. As John Urquhart, Professor of Pharmacoepidemiology at Maastricht University and Professor

of Biopharmaceutical Sciences, at UCSF, San Francisco, points out: “Finding a cost-effective solution to the

persistence problem with drugs for chronic use has enormous economic potential. It is comparable with

tripling the pipeline for new drugs.”59

Pharma 2010: The threshold of innovation IBM Business Consulting Services29

RecommendationsAny pharmaceutical company that wants to capitalize on these advances in the under-standing of disease will need to alter its entire scientifi c and commercial model. It will have to start by acquiring an in-depth knowledge of particular diseases. It will also have to use modeling, simulation and the molecular sciences to a much greater extent in the early stages of research. It will have to call on the most sophisticated web-based technol-ogies and data management systems to support both discovery and development. It will have to collaborate much more closely with the regulators, healthcare payers, physicians and patients. And it will have to ensure that it has the requisite marketing, sales and manufacturing infrastructure to support multiple product types.

These are huge changes, but they have the potential to cut attrition rates, cycle times and costs dramatically. Indeed, they could collectively transform the economic founda-tions of drug discovery and development so greatly that they not only enable the industry to make very profi table targeted treatment solutions for affl uent patients in the developed world, but also to make mass-market blockbusters for dealing with some of the big infec-tious diseases that beset people in the less developed world.

Chapter 4: A disease-driven approach to drug discovery

Flipping the telescope around and looking at pharmaceutical R&D in terms of redefi ning diseases much more precisely not only provides opportunities for developing different treatments for different pathologies, it also provides opportunities for cracking medical problems that have previously proved intractable. One such instance is rheumatoid arthritis.