Embed Size (px)

Citation preview

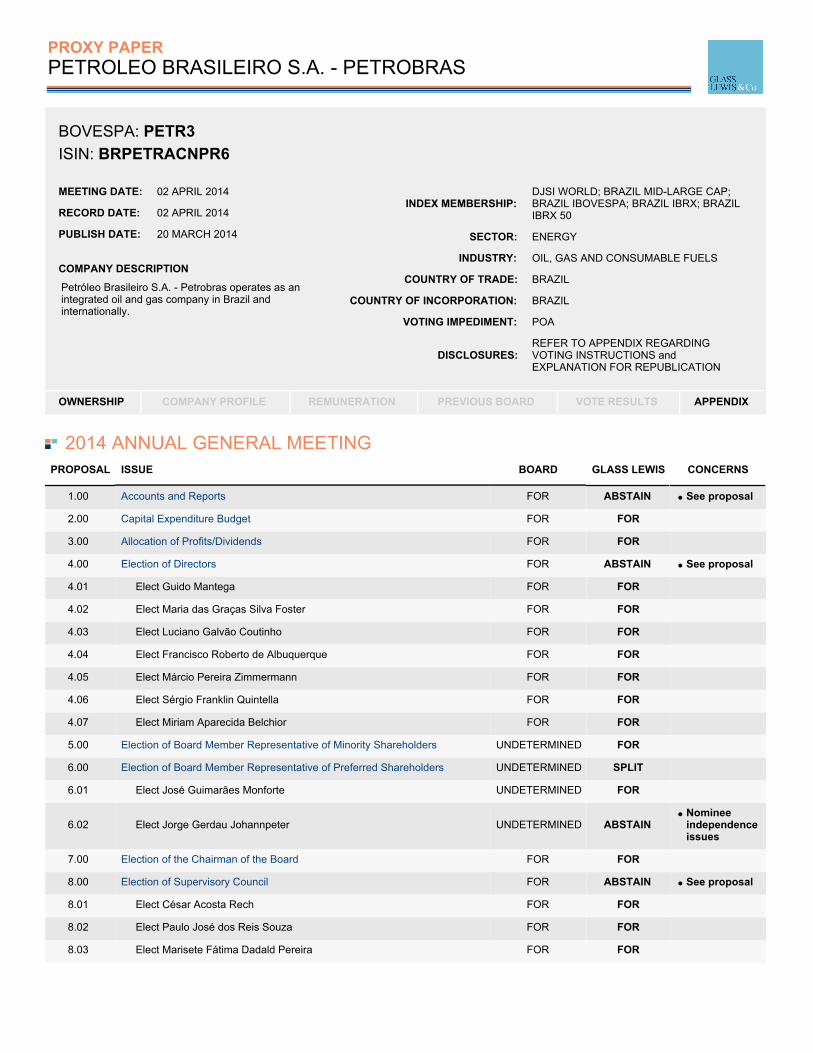

PROXY PAPERPETROLEO BRASILEIRO S.A. - PETROBRAS

BOVESPA: PETR3 ISIN: BRPETRACNPR6

MEETING DATE: 02 APRIL 2014

RECORD DATE: 02 APRIL 2014

PUBLISH DATE: 20 MARCH 2014

COMPANY DESCRIPTION

Petróleo Brasileiro S.A. - Petrobras operates as anintegrated oil and gas company in Brazil andinternationally.

INDEX MEMBERSHIP:DJSI WORLD; BRAZIL MID-LARGE CAP;BRAZIL IBOVESPA; BRAZIL IBRX; BRAZILIBRX 50

SECTOR: ENERGY

INDUSTRY: OIL, GAS AND CONSUMABLE FUELS

COUNTRY OF TRADE: BRAZIL

COUNTRY OF INCORPORATION: BRAZIL

VOTING IMPEDIMENT: POA

DISCLOSURES:REFER TO APPENDIX REGARDINGVOTING INSTRUCTIONS andEXPLANATION FOR REPUBLICATION

OWNERSHIP COMPANY PROFILE REMUNERATION PREVIOUS BOARD VOTE RESULTS APPENDIX

2014 ANNUAL GENERAL MEETING PROPOSAL ISSUE BOARD GLASS LEWIS CONCERNS

1.00 Accounts and Reports FOR ABSTAIN See proposal

2.00 Capital Expenditure Budget FOR FOR

3.00 Allocation of Profits/Dividends FOR FOR

4.00 Election of Directors FOR ABSTAIN See proposal

4.01 Elect Guido Mantega FOR FOR

4.02 Elect Maria das Graças Silva Foster FOR FOR

4.03 Elect Luciano Galvão Coutinho FOR FOR

4.04 Elect Francisco Roberto de Albuquerque FOR FOR

4.05 Elect Márcio Pereira Zimmermann FOR FOR

4.06 Elect Sérgio Franklin Quintella FOR FOR

4.07 Elect Miriam Aparecida Belchior FOR FOR

5.00 Election of Board Member Representative of Minority Shareholders UNDETERMINED FOR

6.00 Election of Board Member Representative of Preferred Shareholders UNDETERMINED SPLIT

6.01 Elect José Guimarães Monforte UNDETERMINED FOR

6.02 Elect Jorge Gerdau Johannpeter UNDETERMINED ABSTAINNomineeindependenceissues

7.00 Election of the Chairman of the Board FOR FOR

8.00 Election of Supervisory Council FOR ABSTAIN See proposal

8.01 Elect César Acosta Rech FOR FOR

8.02 Elect Paulo José dos Reis Souza FOR FOR

8.03 Elect Marisete Fátima Dadald Pereira FOR FOR

9.00 Election of Supervisory Council Member Representative of MinorityShareholders

UNDETERMINED FOR

10.00 Election of Supervisory Council Member Representative of PreferredShareholders

UNDETERMINED FOR

2014 EXTRAORDINARY GENERAL MEETING PROPOSAL ISSUE BOARD GLASS LEWIS CONCERNS

1.00 Remuneration Policy FOR FOR

2.00 Capitalization of Reserves w/o Share Issuance FOR FOR

3.00 Merger by Absorption (Termoaçu) FOR FOR

3.01 Ratification of Appointment of Appraiser (Termoaçu) FOR FOR

3.02 Valuation Report (Termoaçu) FOR FOR

3.03 Merger Agreement (Termoaçu) FOR FOR

3.04 Merger by Absorption (Termoaçu) FOR FOR

3.05 Authority to Carry Out Merger by AbsorptionFormalities (Termoaçu) FOR FOR

4.00 Merger by Absorption (Termoceará) FOR FOR

4.01 Ratification of Appointment of Appraiser (Termoceará) FOR FOR

4.02 Valuation Report (Termoceará) FOR FOR

4.03 Merger Agreement (Termoceará) FOR FOR

4.04 Merger by Absorption (Termoceará) FOR FOR

4.05 Authority to Carry Out Merger by AbsorptionFormalities FOR FOR

5.00 Merger by Absorption (CLEP) FOR FOR

5.01 Ratification of Appointment of Appraiser (CLEP) FOR FOR

5.02 Valuation Report (CLEP) FOR FOR

5.03 Merger Agreement (CLEP) FOR FOR

5.04 Merger by Absorption (CLEP) FOR FOR

5.05 Authority to Carry Out Merger by AbsorptionFormalities FOR FOR

PETR3 April 02, 2014 Annual Meeting 2 Glass, Lewis & Co., LLC

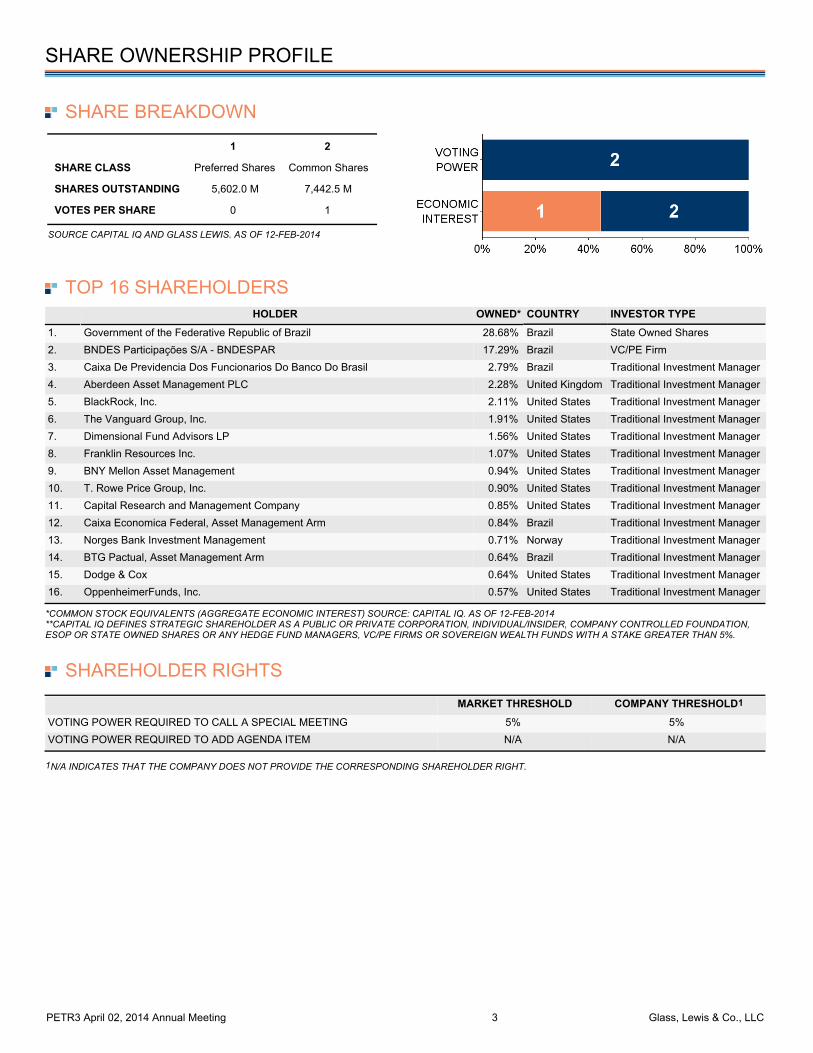

SHARE OWNERSHIP PROFILE

SHARE BREAKDOWN

1 2

SHARE CLASS Preferred Shares Common Shares

SHARES OUTSTANDING 5,602.0 M 7,442.5 M

VOTES PER SHARE 0 1

SOURCE CAPITAL IQ AND GLASS LEWIS. AS OF 12-FEB-2014

TOP 16 SHAREHOLDERS HOLDER OWNED* COUNTRY INVESTOR TYPE

1. Government of the Federative Republic of Brazil 28.68% Brazil State Owned Shares 2. BNDES Participações S/A - BNDESPAR 17.29% Brazil VC/PE Firm 3. Caixa De Previdencia Dos Funcionarios Do Banco Do Brasil 2.79% Brazil Traditional Investment Manager 4. Aberdeen Asset Management PLC 2.28% United Kingdom Traditional Investment Manager 5. BlackRock, Inc. 2.11% United States Traditional Investment Manager 6. The Vanguard Group, Inc. 1.91% United States Traditional Investment Manager 7. Dimensional Fund Advisors LP 1.56% United States Traditional Investment Manager 8. Franklin Resources Inc. 1.07% United States Traditional Investment Manager 9. BNY Mellon Asset Management 0.94% United States Traditional Investment Manager 10. T. Rowe Price Group, Inc. 0.90% United States Traditional Investment Manager 11. Capital Research and Management Company 0.85% United States Traditional Investment Manager 12. Caixa Economica Federal, Asset Management Arm 0.84% Brazil Traditional Investment Manager 13. Norges Bank Investment Management 0.71% Norway Traditional Investment Manager 14. BTG Pactual, Asset Management Arm 0.64% Brazil Traditional Investment Manager 15. Dodge & Cox 0.64% United States Traditional Investment Manager 16. OppenheimerFunds, Inc. 0.57% United States Traditional Investment Manager

*COMMON STOCK EQUIVALENTS (AGGREGATE ECONOMIC INTEREST) SOURCE: CAPITAL IQ. AS OF 12-FEB-2014 **CAPITAL IQ DEFINES STRATEGIC SHAREHOLDER AS A PUBLIC OR PRIVATE CORPORATION, INDIVIDUAL/INSIDER, COMPANY CONTROLLED FOUNDATION,ESOP OR STATE OWNED SHARES OR ANY HEDGE FUND MANAGERS, VC/PE FIRMS OR SOVEREIGN WEALTH FUNDS WITH A STAKE GREATER THAN 5%.

SHAREHOLDER RIGHTS MARKET THRESHOLD COMPANY THRESHOLD1

VOTING POWER REQUIRED TO CALL A SPECIAL MEETING 5% 5% VOTING POWER REQUIRED TO ADD AGENDA ITEM N/A N/A

1N/A INDICATES THAT THE COMPANY DOES NOT PROVIDE THE CORRESPONDING SHAREHOLDER RIGHT.

PETR3 April 02, 2014 Annual Meeting 3 Glass, Lewis & Co., LLC

1.00: ACCOUNTS AND REPORTS

PROPOSAL REQUEST: Approval of financial statements and related reports forthe past fiscal year.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A ABSTAIN- The Company's director and supervisory council reservationsregarding the financial statements are absent fromindependent auditor's report.BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

Shareholders will be presented with the Company's financial statements, management report and supervisory council'sreport.

MARKET PRACTICE

In Brazil, unanimous shareholder approval of a company's financial statements exempts management and supervisorycouncil members from liability for their actions during the corresponding fiscal year, with exceptions in instances of error,bad faith, fraud or misrepresentations of accounting, as explained in article 134 of Brazilian Corporations Law 6.404.

GLASS LEWIS ANALYSIS

We believe that all of the necessary financial statements and reports are present in the Company's annual report. We notethat in the opinion of PricewaterhouseCoopers, the Company's independent auditor, the financial statements have beenproperly prepared in accordance with generally accepted accounting principles in Brazil and International FinancialReporting Standards.

We note that in its unqualified opinion, PricewaterhouseCoopers places an emphasis of matter on the accountingstandards which were used to prepare the Company's individual financial statements, generally accepted accountingprinciples in Brazil, which differ from IFRS in the manner investments in subsidiaries are valued.

However, we highlight that the Company has electronically disclosed through BM&FBOVESPA that director MauroRodrigues da Cunha (representative of minority shareholders), voted against the approval of the aforementioned financialstatements during a board meeting, held on February 25, 2014. Mr. Cunha highlighted the following reasons for hisobjection: (i) lack of timely distribution of financial statements for analysis; (ii) disagreement about the hedge accountingpolicy; (iii) lack of information and the apparent inadequacy of accounting investments in refineries. Further, in ameeting held on the same day, the supervisory council expressed concerns regarding the possible deterioration of theCompany's credit rating, which may affect volumes and costs for future borrowings to finance the investment plans of theCompany.

We believe shareholders should exercise caution in evaluating the Company's financial statements given Mr. Cunha'sobjection. However, in the absence of an auditor's qualified opinion regarding these concerns, we do not believe thatshareholders have sufficient information to make a well-informed judgment regarding this matter at this time. Although it isunusual for Glass Lewis to recommend that shareholders abstain from voting on a company's accounts in Brazil, theuncertainty regarding the integrity of the Company's financial statements does not warrant support for this proposal at thistime.

Accordingly, we recommend that shareholders ABSTAIN from voting on this proposal.

PETR3 April 02, 2014 Annual Meeting 4 Glass, Lewis & Co., LLC

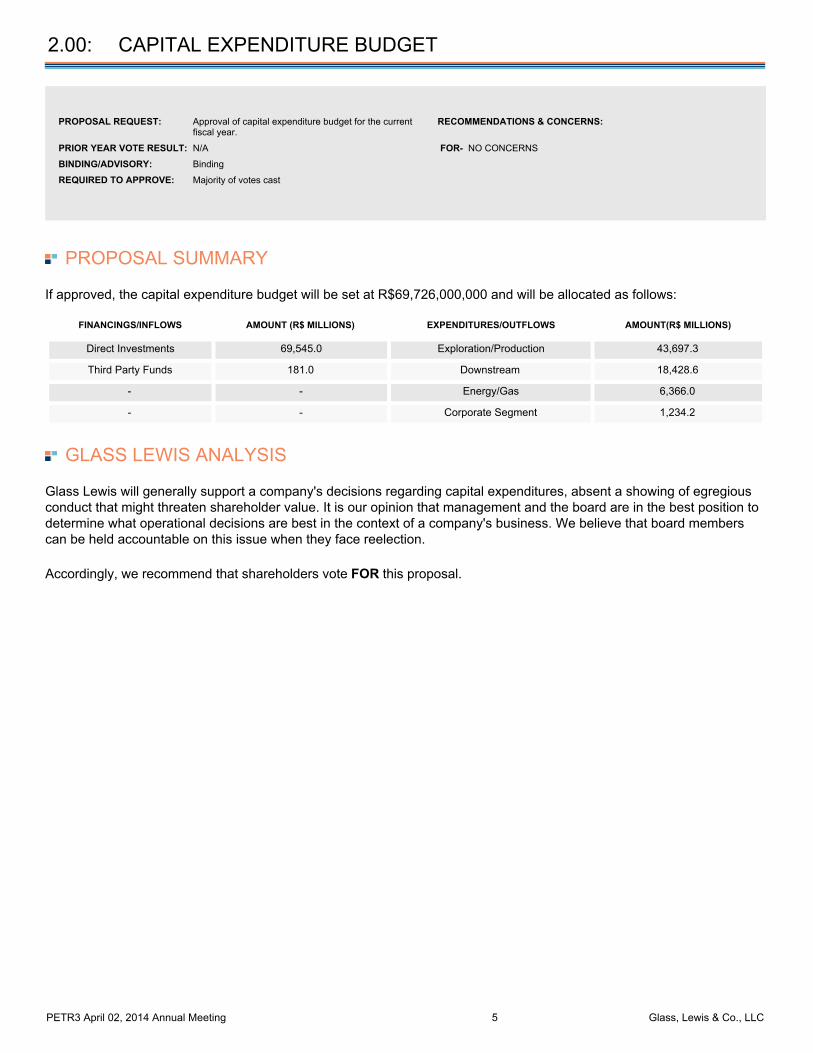

2.00: CAPITAL EXPENDITURE BUDGET

PROPOSAL REQUEST: Approval of capital expenditure budget for the currentfiscal year.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, the capital expenditure budget will be set at R$69,726,000,000 and will be allocated as follows:

FINANCINGS/INFLOWS AMOUNT (R$ MILLIONS) EXPENDITURES/OUTFLOWS AMOUNT(R$ MILLIONS)

Direct Investments 69,545.0 Exploration/Production 43,697.3

Third Party Funds 181.0 Downstream 18,428.6

- - Energy/Gas 6,366.0

- - Corporate Segment 1,234.2

GLASS LEWIS ANALYSIS

Glass Lewis will generally support a company's decisions regarding capital expenditures, absent a showing of egregiousconduct that might threaten shareholder value. It is our opinion that management and the board are in the best position todetermine what operational decisions are best in the context of a company's business. We believe that board memberscan be held accountable on this issue when they face reelection.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 5 Glass, Lewis & Co., LLC

3.00: ALLOCATION OF PROFITS/DIVIDENDS

PROPOSAL REQUEST: Approval of the allocation of profits and distribution ofdividends for the most recently completed fiscal year.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, the Company will distribute its profits as follows:

FUNDS AND ALLOCATIONS AMOUNT (R$ MILLIONS)

Net Profit 23,407.6

Legal Reserve 1,170.4

Retained Earnings 11,744.4

Interest on Capital and Dividends 9,301.0

PERCENTAGE

Payout Ratio 42%

GLASS LEWIS ANALYSIS

With limited exceptions, Glass Lewis will generally support the dividend policy proposed by a company. In Brazil,companies are required by law to distribute a mandatory dividend equal to at least 25% of their profits for the previousfiscal year, subsequent to the allocation of 5% to the legal reserve. Moreover, in addition to, in lieu of, or as part of themandatory dividend, shareholders in Brazil may be entitled to the payment of interest from their investments.

In our view, paying interest on capital allows a company to benefit from accrued interest collected on its own capital, andtreat such payments as fiscal expenses for income tax and social contribution purposes. Generally, the interest is limitedto the daily pro rata variation of a nominal long-term interest rate (“TJLP”) determined by the federal government thatincludes an inflation factor and cannot exceed the greater of 50% of net income for the period in which the payment ismade, or 50% of the sum of retained earnings and profit reserves.

Given that the Company complies with the aforementioned Brazilian requirements, we do not see any cause for concernin terms of the board's process in making this determination.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 6 Glass, Lewis & Co., LLC

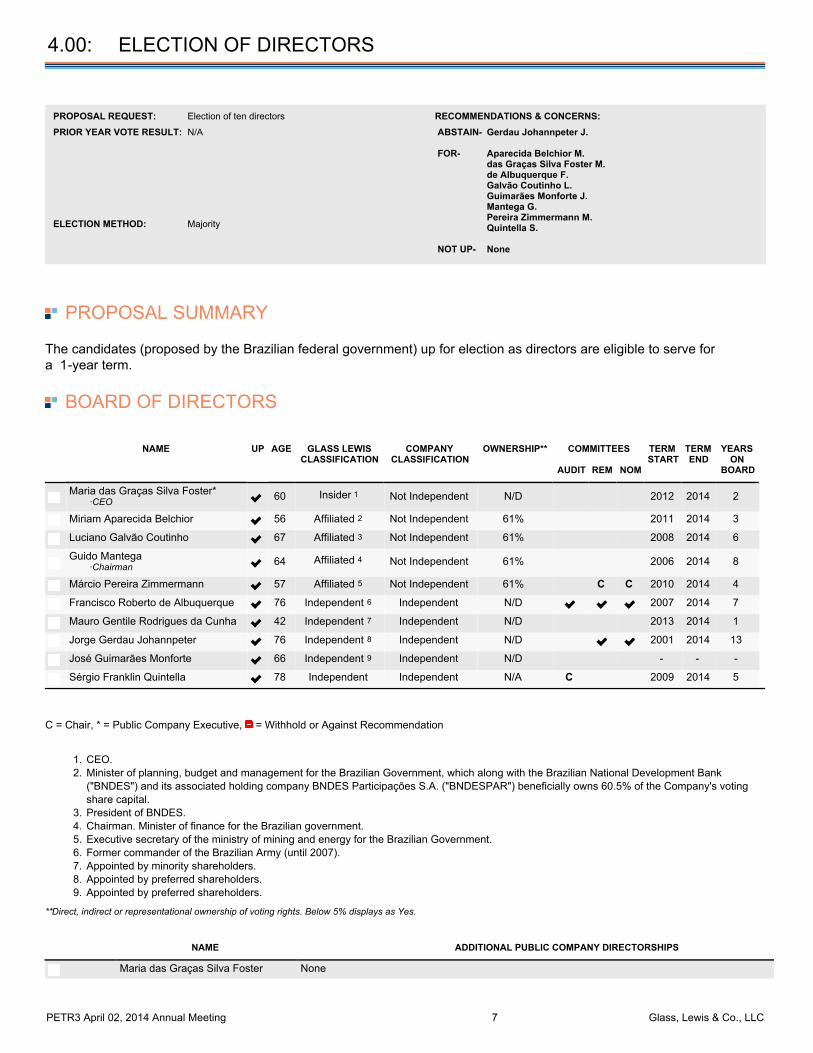

4.00: ELECTION OF DIRECTORS

PROPOSAL REQUEST: Election of ten directors RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A ABSTAIN- Gerdau Johannpeter J.

FOR- Aparecida Belchior M.

das Graças Silva Foster M.de Albuquerque F.Galvão Coutinho L.Guimarães Monforte J.Mantega G.Pereira Zimmermann M.Quintella S.

NOT UP- None

ELECTION METHOD: Majority

PROPOSAL SUMMARY

The candidates (proposed by the Brazilian federal government) up for election as directors are eligible to serve fora 1-year term.

BOARD OF DIRECTORS

NAME UP AGE GLASS LEWISCLASSIFICATION

COMPANYCLASSIFICATION

OWNERSHIP** COMMITTEES TERMSTART

TERMEND

YEARSON

BOARDAUDIT REM NOM

Maria das Graças Silva Foster* ·CEO 60 Insider 1 Not Independent N/D 2012 2014 2

Miriam Aparecida Belchior 56 Affiliated 2 Not Independent 61% 2011 2014 3

Luciano Galvão Coutinho 67 Affiliated 3 Not Independent 61% 2008 2014 6

Guido Mantega ·Chairman 64 Affiliated 4 Not Independent 61% 2006 2014 8

Márcio Pereira Zimmermann 57 Affiliated 5 Not Independent 61% C C 2010 2014 4

Francisco Roberto de Albuquerque 76 Independent 6 Independent N/D 2007 2014 7

Mauro Gentile Rodrigues da Cunha 42 Independent 7 Independent N/D 2013 2014 1

Jorge Gerdau Johannpeter 76 Independent 8 Independent N/D 2001 2014 13

José Guimarães Monforte 66 Independent 9 Independent N/D - - -

Sérgio Franklin Quintella 78 Independent Independent N/A C 2009 2014 5

C = Chair, * = Public Company Executive, = Withhold or Against Recommendation

CEO. 1.Minister of planning, budget and management for the Brazilian Government, which along with the Brazilian National Development Bank("BNDES") and its associated holding company BNDES Participações S.A. ("BNDESPAR") beneficially owns 60.5% of the Company's votingshare capital.

2.

President of BNDES. 3.Chairman. Minister of finance for the Brazilian government. 4.Executive secretary of the ministry of mining and energy for the Brazilian Government. 5.Former commander of the Brazilian Army (until 2007). 6.Appointed by minority shareholders. 7.Appointed by preferred shareholders. 8.Appointed by preferred shareholders. 9.

**Direct, indirect or representational ownership of voting rights. Below 5% displays as Yes.

NAME ADDITIONAL PUBLIC COMPANY DIRECTORSHIPS

Maria das Graças Silva Foster None

PETR3 April 02, 2014 Annual Meeting 7 Glass, Lewis & Co., LLC

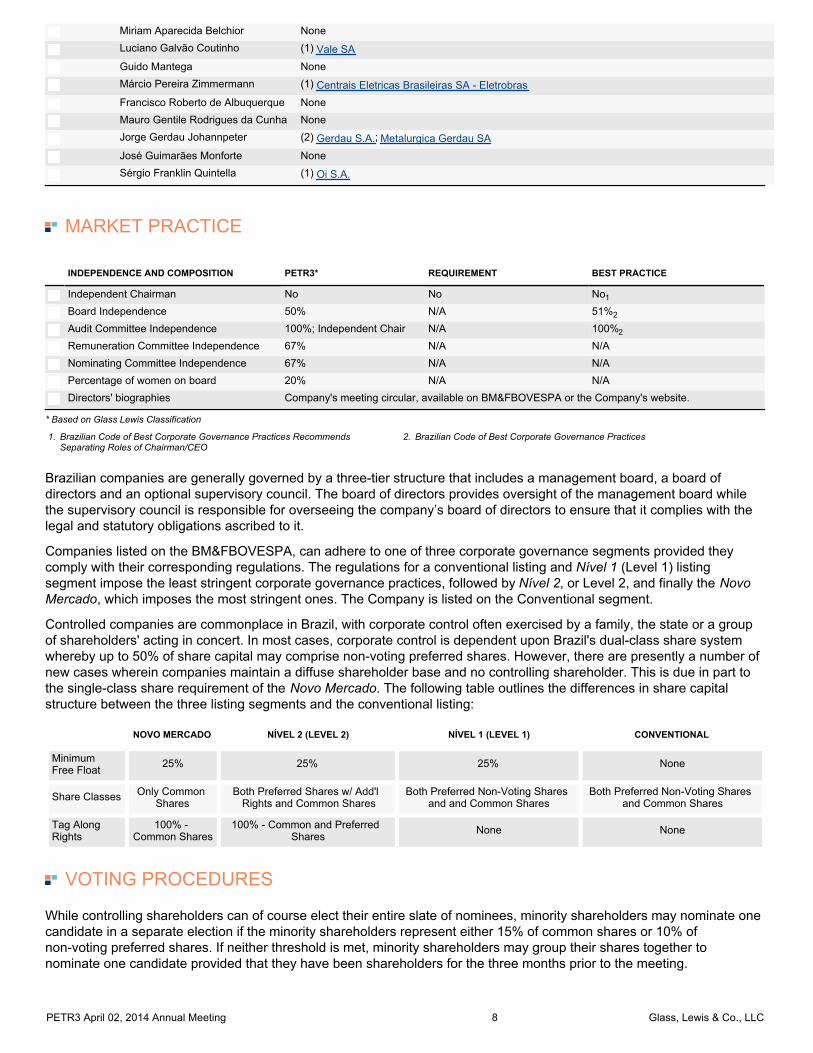

Miriam Aparecida Belchior None

Luciano Galvão Coutinho (1) Vale SA

Guido Mantega None

Márcio Pereira Zimmermann (1) Centrais Eletricas Brasileiras SA - Eletrobras

Francisco Roberto de Albuquerque None

Mauro Gentile Rodrigues da Cunha None

Jorge Gerdau Johannpeter (2) Gerdau S.A.; Metalurgica Gerdau SA

José Guimarães Monforte None

Sérgio Franklin Quintella (1) Oi S.A.

MARKET PRACTICE

INDEPENDENCE AND COMPOSITION PETR3* REQUIREMENT BEST PRACTICE

Independent Chairman No No No1

Board Independence 50% N/A 51%2

Audit Committee Independence 100%; Independent Chair N/A 100%2

Remuneration Committee Independence 67% N/A N/A

Nominating Committee Independence 67% N/A N/A

Percentage of women on board 20% N/A N/A

Directors' biographies Company's meeting circular, available on BM&FBOVESPA or the Company's website.

* Based on Glass Lewis Classification

Brazilian Code of Best Corporate Governance Practices RecommendsSeparating Roles of Chairman/CEO

1. Brazilian Code of Best Corporate Governance Practices 2.

Brazilian companies are generally governed by a three-tier structure that includes a management board, a board ofdirectors and an optional supervisory council. The board of directors provides oversight of the management board whilethe supervisory council is responsible for overseeing the company’s board of directors to ensure that it complies with thelegal and statutory obligations ascribed to it.

Companies listed on the BM&FBOVESPA, can adhere to one of three corporate governance segments provided theycomply with their corresponding regulations. The regulations for a conventional listing and Nível 1 (Level 1) listingsegment impose the least stringent corporate governance practices, followed by Nível 2, or Level 2, and finally the NovoMercado, which imposes the most stringent ones. The Company is listed on the Conventional segment.

Controlled companies are commonplace in Brazil, with corporate control often exercised by a family, the state or a groupof shareholders' acting in concert. In most cases, corporate control is dependent upon Brazil's dual-class share systemwhereby up to 50% of share capital may comprise non-voting preferred shares. However, there are presently a number ofnew cases wherein companies maintain a diffuse shareholder base and no controlling shareholder. This is due in part tothe single-class share requirement of the Novo Mercado. The following table outlines the differences in share capitalstructure between the three listing segments and the conventional listing:

NOVO MERCADO NÍVEL 2 (LEVEL 2) NÍVEL 1 (LEVEL 1) CONVENTIONAL

MinimumFree Float 25% 25% 25% None

Share Classes Only CommonShares

Both Preferred Shares w/ Add'lRights and Common Shares

Both Preferred Non-Voting Sharesand and Common Shares

Both Preferred Non-Voting Sharesand Common Shares

Tag AlongRights

100% -Common Shares

100% - Common and PreferredShares None None

VOTING PROCEDURES

While controlling shareholders can of course elect their entire slate of nominees, minority shareholders may nominate onecandidate in a separate election if the minority shareholders represent either 15% of common shares or 10% ofnon-voting preferred shares. If neither threshold is met, minority shareholders may group their shares together tonominate one candidate provided that they have been shareholders for the three months prior to the meeting.

PETR3 April 02, 2014 Annual Meeting 8 Glass, Lewis & Co., LLC

In Brazil directors are elected by a majority vote. However, Brazilian Companies Law allows for the adoption of cumulativevoting if minority shareholders representing at least 5% of common shares (unless otherwise stated in the articles ofassociation) make such a request 48 hours in advance of the meeting. In this case, the controlling shareholder ispermitted to elect one more director than the number nominated by minority shareholders.

GLASS LEWIS ANALYSIS

We believe shareholders should be mindful of the following issues:

MINORITY SHAREHOLDER ACTIVISM

On February 24, 2014 the Company announced on its website that a group of shareholders (Aberdeen do Brasil Gestãode Recuros, APG Asset Management, British Colombia Investment Management Corporation, AMUNDI AssetManagement, MN Services N.V., USS Investments Management, Hermes Equity Ownership Services Ltd., F&CManagement Ltd., State of Board Administration of Florida) representing 0.5% of the Company's issued sharecapital, have nominated two independent directors (nominee Rodrigues da Cunha, representative of minorityshareholders and nominee Monforte representative of common shareholders). The group claims that the Company'spolicy regarding the pricing of gas and diesel has been harmful to shareholders and requires more transparency regardingthe Company's internal practices in order to guarantee the capacity of investments and Company expansion ("Foreignshareholders unite to ask 'improvement' of the federal administration." Estadão. March 19, 2014).

Further, on February 28, 2014 it was also announced that BRAM - Bradesco Asset Management S.A., representing0.63% of the Company's issued share capital, has also nominated two independent directors (also nominee Rodrigues daCunha and nominee Gerdau , representative of preferred shareholders). The public release of this information marks theCompany's second anniversary of disclosing candidates nominated by minority and preferred shareholders and isdiscussed further in Proposals 5 and 6.

SIGNIFICANT BENEFICIAL OWNERSHIP

We note that the Brazilian federal government, together with BNDESPar, BNDES, FPS and FIFE, beneficially owns 60.5%of the Company's voting share capital. We suspect that most, if not all, shareholders both understand and accept thenature and the extent of the majority shareholder's control over the Company.

ATTENDANCE NOT DISCLOSED

To the best of our knowledge, the Company has not disclosed the director attendance records for the board andcommittee meetings held during the past fiscal year. We believe attendance at board and committee meetings is a vitalelement of a director's performance and that companies have a responsibility to disclose this information to itsshareholders. In cases where a director fails to attend at least 75% of the meetings held by the board and the committeeson which he or she served during a given fiscal year, we view it as a failure by the director to fulfill his or her duty toshareholders. Accordingly, we believe the board should provide greater transparency with regard to the attendance recordof the Company's directors at board and committee meetings going forward.

BRIBERY INVESTIGATIONS WITH SBM OFFSHORE NV

Nominee Graças Silva Foster, the Company's CEO, is currently leading an internal investigation regarding allegations thatthe Company accepted USD$139.2 million in bribes from the Netherlands-based ship leaser, SBM Offshore NV. SBMOffshore NV claims a former employee seeking to extort money from the company is responsible. The employeereportedly circulated parts of documents from the early stages of an internal audit on "potentially improper payments"made in several nations between 2007 and 2011 ("Brazil's Petrobras Bribery Investigation Continues." Wall StreetJournal. March 17, 2014). While nominee Graças Silva Foster states that the Company hopes to conclude itsinvestigation soon, as of March 19, 2014, we have not found any additional information surrounding this issue. Wesuspect news regarding the outcome of this internal investigation will be delayed until after the meeting. We will monitorthis issue going forward.

RECOMMENDATION

Having reviewed the board's nominees, we do not believe there are substantial issues for shareholder concern.

However, we note that holders of common shares may only cast votes on this proposal or Proposal 5, not both. While we

PETR3 April 02, 2014 Annual Meeting 9 Glass, Lewis & Co., LLC

would ordinarily support this proposal, we recommend shareholders abstain from voting on the slate of candidatesproposed by the Brazilian federal government, given that common shareholders will have the rare opportunity to vote forcandidates representative of minority and preferred shareholder interests. Further, holders of preferred shares may notcast votes on this agenda item, but rather may vote on Proposal 6.

Accordingly, we recommend that shareholders ABSTAIN from voting on this proposal.

PETR3 April 02, 2014 Annual Meeting 10 Glass, Lewis & Co., LLC

5.00:

ELECTION OF BOARD MEMBER REPRESENTATIVE OF MINORITYSHAREHOLDERS

PROPOSAL REQUEST: Election of one minority shareholder representatives toserve on the board of directors.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast by minority common shareholders

PROPOSAL SUMMARY

If approved, one candidate representative of minority shareholders will be elected to serve on the board of directors for a1-year term.

MARKET PRACTICE

In accordance with Brazilian corporate law, minority common shareholders representing at least 15% of acompany’s common shares and preferred shareholders representing at least 10% of a company’s non-voting preferredshares may each nominate one candidate to the board of directors in a separate election. If neither threshold is met,minority/preferred shareholders may group their shares together to nominate one candidate. Further, CVM Instruction 481expressly requires the inclusion in a company's proxy solicitation materials of any candidates to the board of directorsand supervisory council nominated by shareholders owning at least 0.5% of the Company's total share capital.

Moreover, shareholders individually or jointly representing between at least 5% and 10% of a company’s votingshare capital may request the adoption of cumulative voting, provided the request is received at least 48 hours prior tothe shareholder meeting. However, since requests for a separate election are generally made at the meeting, andrequests for cumulative voting are made after the instructions from those voting by proxy have been sent, shareholdersvoting by proxy are generally unable to participate in the election of minority/preferred shareholder-nominated candidates.

VOTING PROCEDURES

Shareholders should note that the election of the candidates proposed by minority shareholders will take place afterthe election of the board's candidates. That is, in addition to voting on this proposal, shareholders who wish to vote infavor of the currently known candidate should submit a separate power of attorney to an authorized representative whowill be present at the meeting.

Further, common shareholders should note that a vote in favor or against the board's proposed slate discussed inProposal 4.0 will automatically disqualify them from voting on this proposal. As such, common minority shareholders mayonly vote on Proposal 4.0 or this proposal, but not both.

GLASS LEWIS ANALYSIS

As of March 19, 2014, Mauro Rodrigues da Cunha is the only announced nominee for the seat reserved for directorsrepresentative of minority shareholders. However, we note that additional candidates for the minority shareholderrepresentative position on the board may be presented up to and during the meeting.

Glass Lewis generally recommends that shareholders abstain from voting on these elections given that the names ofcandidates are rarely disclosed by an issuer and that additional candidates may be nominated. Therefore, a definitiverecommendation to vote for this proposal may allow for a vote in favor of unknown candidates proposed by minorityshareholders who meet the minimum ownership threshold at the general meeting, or a default candidate proposed by acompany's management, who therefore may not independently represent the best interest of minority shareholders.

In this case, however, we believe the proposed candidate has relevant skills and experience which would bring a

PETR3 April 02, 2014 Annual Meeting 11 Glass, Lewis & Co., LLC

necessary and independent perspective to the board. Moreover, as this proposal represents one of the few times aBrazilian issuer has opened the door for participation among its minority shareholders, particularly foreign shareholderswho are generally excluded from participating in these elections unless present at the meetings, we believe thatshareholders should actively participate, rather than abstain, from voting on this significant proposal.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 12 Glass, Lewis & Co., LLC

6.00:

ELECTION OF BOARD MEMBER REPRESENTATIVE OFPREFERRED SHAREHOLDERS

PROPOSAL REQUEST: Election of one preferred shareholder representative toserve on the board of directors.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A SPLIT- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast by preferred shareholders

PROPOSAL SUMMARY

If approved, one candidate representative of preferred shareholders will be elected to serve on the board of directors for a1-year term.

MARKET PRACTICE

In accordance with Brazilian corporate law, minority common shareholders representing at least 15% of acompany’s common shares and preferred shareholders representing at least 10% of a company’s non-voting preferredshares may each nominate one candidate to the board of directors in a separate election. If neither threshold is met,preferred shareholders may group their shares together to nominate one candidate. Further, CVM Instruction 481expressly requires the inclusion in a company's proxy solicitation materials of any candidates to the board of directorsand supervisory council nominated by shareholders owning at least 0.5% of the Company's total share capital.

Moreover, shareholders individually or jointly representing between at least 5% and 10% of a company’s votingshare capital may request the adoption of cumulative voting, provided the request is received at least 48 hours prior tothe shareholder meeting. However, since requests for a separate election are generally made at the meeting, andrequests for cumulative voting are made after the instructions from those voting by proxy have been sent, shareholdersvoting by proxy are generally unable to participate in the election of preferred shareholder-nominated candidates.

VOTING PROCEDURES

Shareholders should note that the election of the candidates proposed by preferred shareholders may only result in theelection of one director and will take place after the election of the board's candidates. That is, in addition to voting on thisproposal, shareholders who wish to vote in favor of one the currently known candidates should submit a separate powerof attorney to an authorized representative who will be present at the meeting.

Further, preferred shareholders should note they may not cast a vote in favor or against the board's proposed slatediscussed in Proposal 4.0. Rather, this proposal is preferred shareholders' only opportunity to elect nominees for theboard of directors.

GLASS LEWIS ANALYSIS

Glass Lewis generally recommends that shareholders abstain from voting on these elections given that the names ofcandidates are rarely disclosed by an issuer and that additional candidates may be nominated. Therefore, a definitiverecommendation to vote for this proposal may allow for a vote in favor of unknown candidates proposed by preferredshareholders who meet the minimum ownership threshold at the general meeting, or a default candidate proposed by acompany's management, who therefore may not independently represent the best interest of preferred shareholders.

As of March 19, 2014, José Guimarãres Monforte and Jorge Gerdau Johanpeter are the announced nominees for theseat reserved for directors representative of preferred shareholders. However, we note that additional candidates for thepreferred shareholder representative position on the board may be presented up to and during the meeting.

We highlight that Mr. Gerdau is president of the Chamber of Management Policies, Performance and Competitiveness

PETR3 April 02, 2014 Annual Meeting 13 Glass, Lewis & Co., LLC

(CGDC), an organization linked to the Dilma Rousseff presidency of Brazil. We do not believe a vote in favor of thiscandidate best represents the interests of minority preferred shareholders, as the Brazilian federal governmentbeneficially owns 33.11% of the Company's preferred share capital. As such, we recommend shareholders vote for theactual independent nominee, Monforte, who we believe will better represent the interests of minority preferredshareholders.

RECOMMENDATIONS

Accordingly, we recommend that shareholders vote:

FOR: Monforte

ABSTAIN: All other nominees.

The Company discloses biographical details for its newly proposed nominees; however, the biographies are not availablein English.

PETR3 April 02, 2014 Annual Meeting 14 Glass, Lewis & Co., LLC

7.00: ELECTION OF THE CHAIRMAN OF THE BOARD

PROPOSAL REQUEST: Election of the board's chairman. RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, Guido Mantega will be appointed as chairman of the board.

GLASS LEWIS ANALYSIS

Having reviewed the background of the proposed candidate for chairman and given our favorable recommendations forthe proposed candidate discussed in Proposal 4, we do not believe there are substantial issues for shareholder concern.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 15 Glass, Lewis & Co., LLC

8.00: ELECTION OF SUPERVISORY COUNCIL

PROPOSAL REQUEST: Election of supervisory council members. RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A ABSTAIN- Shareholders may only vote on Proposals 6.04 and 6.05

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

Three candidates (proposed by the Brazilian federal government) are up for election to serve on the supervisory councilfor a 1-year term.

SUPERVISORY COUNCIL

NAME UP AGE GLASS LEWISCLASSIFICATION

COMPANYCLASSIFICATION

OWNERSHIP** TERMSTART

TERMEND

YEARSON

BOARD

César Acosta Rech 46 Independent 1 Independent N/D 2008 2014 6

Walter Luis Bernardes Albertoni 45 Independent 2 Independent N/D - - -

Marisete Fátima Dadald Pereira 58 Independent 3 Independent N/D 2011 2014 3

Paulo José dos Reis Souza 51 Independent 4 Independent N/D 2012 2014 2

Reginaldo Ferreira Alexandre 54 Independent 5 Independent N/D - - -

C = Chair, * = Public Company Executive, = Withhold or Against Recommendation

Appointed by the controlling shareholder. 1.Appointed by preferred shareholders. 2.Appointed by the controlling shareholder. 3.Appointed by the controlling shareholder. 4.Appointed by minority shareholders. 5.

**Direct, indirect or representational ownership of voting rights. Below 5% displays as Yes.

MARKET PRACTICE

Brazilian companies generally have a supervisory council that is independent of management and the external auditor. Inthe absence of a permanent supervisory council, shareholders representing 10% of a company's common shares or 5%of its non-voting preferred shares may request that one be established. According to Article 162 of the BrazilianCompanies Law, the supervisory council must be comprised of three to five members, none of whom can be (i) anexecutive, director or employee of the company, of a subsidiary or of any affiliate thereof; or (ii) a spouse or relative of anyofficer, director or employee of the company, of a subsidiary or of any affiliate thereof, up to the third degree. We believethat this provision ensures that the current council has a certain minimal level of independence.

In most cases, the controlling shareholder typically elects a majority of the supervisory council's members. Shareholderswith restricted or no voting rights (i.e. preferred shares) and minority shareholders who jointly represent at least 10% ofthe voting share capital (i.e. common shares) are each entitled to elect one member and his/her alternate to thesupervisory council.

GLASS LEWIS ANALYSIS

We find that the board's nominees comply with the aforementioned independence standards and do not believe there aresubstantial issues for shareholder concern.

PETR3 April 02, 2014 Annual Meeting 16 Glass, Lewis & Co., LLC

However, we note that minority common shareholders and preferred shareholders may only vote on Proposals 9 and 10,respectively. A vote in favor of the slate proposed by the Brazilian federal government will not be counted and renderminority common shareholders and preferred shareholders ineligible to vote on Proposals 9 and 10 .

RECOMMENDATION

Accordingly, we recommend that shareholders ABSTAIN from voting on this proposal.

PETR3 April 02, 2014 Annual Meeting 17 Glass, Lewis & Co., LLC

9.00:

ELECTION OF SUPERVISORY COUNCIL MEMBERREPRESENTATIVE OF MINORITY SHAREHOLDERS

PROPOSAL REQUEST: Election of one minority shareholder representative toserve on the supervisory council.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, one candidate representative of minority shareholders will be elected to serve on the supervisory council for a1-year term.

MARKET PRACTICE

Brazilian companies generally have a supervisory council that is independent of management and the external auditor.In the absence of a permanent supervisory council, shareholders representing 10% of a company's common shares or5% of its non-voting preferred shares may request that one be established. According to Article 162 of theBrazilian Companies Law, the supervisory council must be comprised of three to five members, none of whom can be (i)an executive, director or employee of the company, of a subsidiary or of any affiliate thereof; or (ii) a spouse or relative ofany officer, director or employee of the company, of a subsidiary or of any affiliate thereof, up to the third degree. Webelieve that this provision ensures that the current council has a certain minimal level of independence.

In most cases, the controlling shareholder typically elects a majority of its members. However, in accordancewith Brazilian corporate law, shareholders with restricted or no voting rights (i.e. preferred shares) and minorityshareholders who jointly represent at least 10% of the voting share capital (i.e. common shares) are each entitled to electone member and his/her alternate to the supervisory council. Further, CVM Instruction 481 expressly requires theinclusion in a company's proxy solicitation materials of any candidates to the board of directors and supervisory councilnominated by shareholders owning at least 0.5% of the Company's total share capital.

VOTING PROCEDURES

Shareholders should note that the election of the proposed minority shareholders will take place after the election of theboard's supervisory council candidates. In addition to voting on this proposal, shareholders who wish to vote in favor ofthe currently known candidate should submit a separate power of attorney to an authorized representative who will bepresent at the meeting.

Further, common shareholders should note that a vote in favor or against the board's proposed slate for the supervisorycouncil discussed in Proposal 8 will not be counted. As such, we recommend holders of common shareholders only voteon this proposal.

GLASS LEWIS ANALYSIS

As of March 19, 2014, Reginaldo Ferreira Alexandre and alternate Mario Cordeiro Filho are the only known candidates forthe supervisory council. Moreover, we note that additional candidates for the minority shareholder representativepositions on the supervisory council may be presented up to and during the meeting.

Glass Lewis generally recommends that shareholders abstain from voting on these elections given that the names ofcandidates are rarely disclosed by an issuer and that additional candidates may be nominated. Therefore, a definitiverecommendation to vote for this proposal may allow for a vote in favor of unknown candidates proposed by minorityshareholders who meet the minimum ownership threshold at the general meeting, or a default candidate proposed by acompany's management, who therefore may not independently represent the best interest of minority shareholders.

PETR3 April 02, 2014 Annual Meeting 18 Glass, Lewis & Co., LLC

In this case, however, we believe the proposed candidates have relevant skills and experience which would bring anecessary and independent perspective to the supervisory council. Moreover, as this proposal represents one of the fewtimes a Brazilian issuer has opened the door for participation among its minority and preferred shareholders, particularlyforeign shareholders who are generally excluded from participating in these elections unless present at the meetings, webelieve that shareholders should actively participate, rather than abstain, from voting on this significant proposal.

RECOMMENDATION

Accordingly, we recommend that shareholders vote FOR this proposal.

The Company discloses biographical details for its newly proposed nominees; however, the biographies are not availablein English.

PETR3 April 02, 2014 Annual Meeting 19 Glass, Lewis & Co., LLC

10.00:

ELECTION OF SUPERVISORY COUNCIL MEMBERREPRESENTATIVE OF PREFERRED SHAREHOLDERS

PROPOSAL REQUEST: Election of one preferred shareholder representative toserve on the board of directors

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast by preferred shareholders

PROPOSAL SUMMARY

If approved, one candidate and one alternate member representative of preferred shareholders will be elected to serve onthe supervisory council for a 1-year term.

MARKET PRACTICE

Brazilian companies generally have a supervisory council that is independent of management and the external auditor.In the absence of a permanent supervisory council, shareholders representing 10% of a company's common shares or5% of its non-voting preferred shares may request that one be established. According to Article 162 of theBrazilian Companies Law, the supervisory council must be comprised of three to five members, none of whom can be (i)an executive, director or employee of the company, of a subsidiary or of any affiliate thereof; or (ii) a spouse or relative ofany officer, director or employee of the company, of a subsidiary or of any affiliate thereof, up to the third degree. Webelieve that this provision ensures that the current council has a certain minimal level of independence.

In most cases, the controlling shareholder typically elects a majority of its members. However, in accordancewith Brazilian corporate law, shareholders with restricted or no voting rights (i.e. preferred shares) and preferredshareholders who jointly represent at least 10% of the voting share capital (i.e. common shares) are each entitled to electone member and his/her alternate to the supervisory council. Further, CVM Instruction 481 expressly requires theinclusion in a company's proxy solicitation materials of any candidates to the board of directors and supervisory councilnominated by shareholders owning at least 0.5% of the Company's total share capital.

VOTING PROCEDURES

Shareholders should note that the election of the proposed preferred shareholders will take place after the election of theboard's supervisory council candidates. In addition to voting on this proposal, shareholders who wish to vote in favor ofthe currently known candidates should submit a separate power of attorney to an authorized representative who will bepresent at the meeting.

Further, preferred shareholders should note that a vote in favor or against the board's proposed slate for the supervisorycouncil discussed in Proposal 8 will not be counted. As such, we recommend holders of preferred shareholders only voteon this proposal.

GLASS LEWIS ANALYSIS

As of March 19, 2014, Walter Luis Bernardes Albertoni and alternate Robert Lamb are the only known candidates for thesupervisory council. Moreover, we note that additional candidates for the preferred shareholder representative positionson the supervisory council may be presented up to and during the meeting.

Glass Lewis generally recommends that shareholders abstain from voting on these elections given that the names ofcandidates are rarely disclosed by an issuer and that additional candidates may be nominated. Therefore, a definitiverecommendation to vote for this proposal may allow for a vote in favor of unknown candidates proposed by preferredshareholders who meet the minimum ownership threshold at the general meeting, or a default candidate proposed by acompany's management, who therefore may not independently represent the best interest of preferred shareholders.

PETR3 April 02, 2014 Annual Meeting 20 Glass, Lewis & Co., LLC

In this case, however, we believe the proposed candidates have relevant skills and experience which would bring anecessary and independent perspective to the supervisory council. Moreover, as this proposal represents one of the fewtimes a Brazilian issuer has opened the door for participation among its preferred and preferred shareholders, particularlyforeign shareholders who are generally excluded from participating in these elections unless present at the meetings, webelieve that shareholders should actively participate, rather than abstain, from voting on this significant proposal.

RECOMMENDATION

Accordingly, we recommend that shareholders vote FOR this proposal.

The Company discloses biographical details for its newly proposed nominees; however, the biographies are not availablein English.

PETR3 April 02, 2014 Annual Meeting 21 Glass, Lewis & Co., LLC

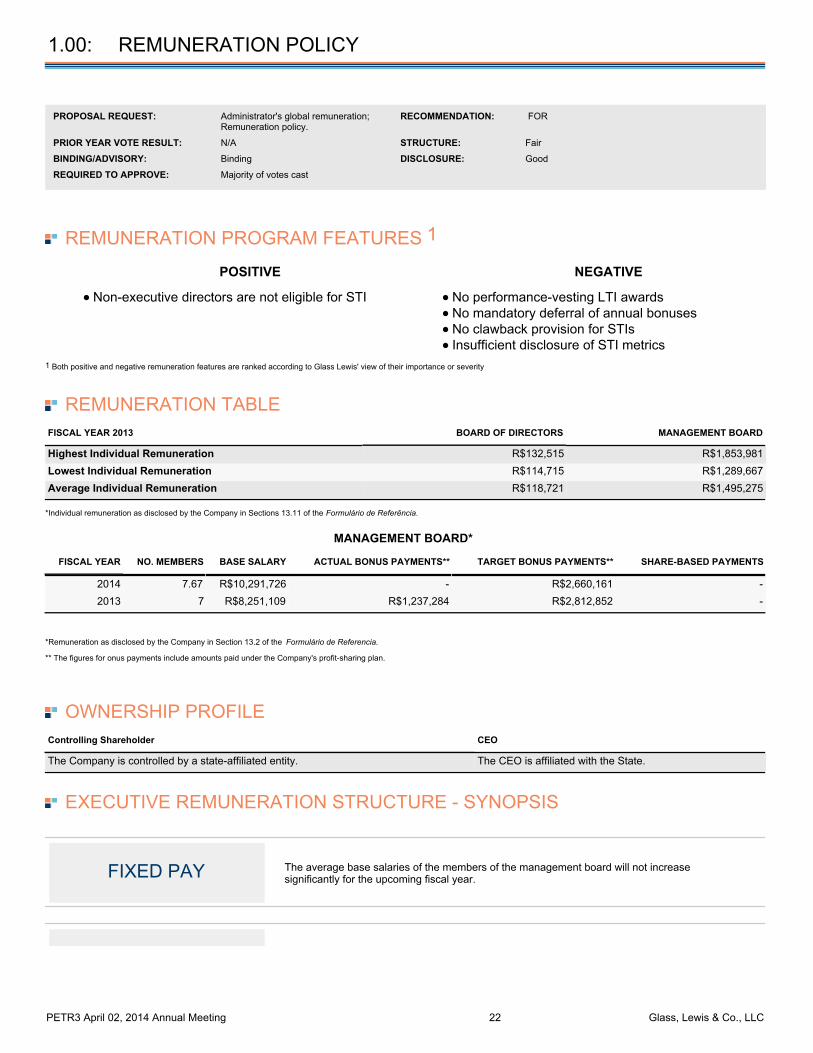

1.00: REMUNERATION POLICY

PROPOSAL REQUEST: Administrator's global remuneration;Remuneration policy.

RECOMMENDATION: FOR

PRIOR YEAR VOTE RESULT: N/A STRUCTURE: Fair

BINDING/ADVISORY: Binding DISCLOSURE: Good

REQUIRED TO APPROVE: Majority of votes cast

REMUNERATION PROGRAM FEATURES 1

POSITIVE

Non-executive directors are not eligible for STI

NEGATIVE

No performance-vesting LTI awardsNo mandatory deferral of annual bonusesNo clawback provision for STIsInsufficient disclosure of STI metrics

1 Both positive and negative remuneration features are ranked according to Glass Lewis' view of their importance or severity

REMUNERATION TABLEFISCAL YEAR 2013 BOARD OF DIRECTORS MANAGEMENT BOARD

Highest Individual Remuneration R$132,515 R$1,853,981Lowest Individual Remuneration R$114,715 R$1,289,667Average Individual Remuneration R$118,721 R$1,495,275

*Individual remuneration as disclosed by the Company in Sections 13.11 of the Formulário de Referência.

MANAGEMENT BOARD*

FISCAL YEAR NO. MEMBERS BASE SALARY ACTUAL BONUS PAYMENTS** TARGET BONUS PAYMENTS** SHARE-BASED PAYMENTS

2014 7.67 R$10,291,726 - R$2,660,161 -2013 7 R$8,251,109 R$1,237,284 R$2,812,852 -

*Remuneration as disclosed by the Company in Section 13.2 of the Formulário de Referencia.

** The figures for onus payments include amounts paid under the Company's profit-sharing plan.

OWNERSHIP PROFILEControlling Shareholder CEO

The Company is controlled by a state-affiliated entity. The CEO is affiliated with the State.

EXECUTIVE REMUNERATION STRUCTURE - SYNOPSIS

FIXED PAY The average base salaries of the members of the management board will not increasesignificantly for the upcoming fiscal year.

PETR3 April 02, 2014 Annual Meeting 22 Glass, Lewis & Co., LLC

SHORT-TERMINCENTIVES

Annual Bonus Plan

Annual bonuses were awarded in the form of cash.The Company says that the criteria it may consider in determining bonuses includesnegotiations with regulators, relevant legislation and market practices.

Profit-Sharing Plan

Awards are based on the following criteria:battainment of performance conditionsnegotiated with the Department of Coordination and Governance of Public Companies(DEST) such as national oil processing, oil and natural gas production and unit cost ofextraction without government participation.Beneficiaries are entitled to an undisclosed percentage of the Company's net incomeunder a profit-sharing plan.

LONG-TERMINCENTIVES

The Company did not have a long-term incentive plan in the past fiscal year.

GLASS LEWIS ANALYSIS

This proposal seeks shareholder approval to set the aggregate remuneration for the Company's non-executive directors(NEDs), executives, and supervisory council members (the administrators) for the current fiscal year at R$19,355,282.According to Brazilian Companies Law, shareholders must approve the aggregate or individual remuneration of theadministrators at the annual general meeting.

Further, according to CVM Instruction 481, when the general meeting is called to resolve on this issue, the Company mustprovide the information required under Section 13 of the Reference Form, or annual report, which details its remunerationpolicy. Glass Lewis takes Section 13 into account when analyzing these proposals. This resolution is legally binding.

STRUCTURE : GOOD

We note the following concerns with the structure of the Company's remuneration programs:

No Long-Term Incentive Plan While the Company has failed to implement a long-term incentive plan, the Company's CEO is also affiliated with itscontrolling shareholder. As such, there is a natural alignment between the interests of management and shareholders.Consequently, we believe the lack of long-term incentives for the CEO to be acceptable and in minority shareholders' bestinterest.

DISCLOSURE : FAIR

We note the following concerns with the disclosure of the Company's remuneration programs:

STI Performance Metrics Not Disclosed

The Company has failed to disclose its process for determining awards granted under its annual bonus plan.Without such disclosure, shareholders are unable to evaluate the extent to which the Company strives to alignexecutive remuneration with short-term performance. We believe the Company should provide substantially more detailregarding the determination of awards under the annual bonus plan.

SUMMARY

While we do not believe these concerns are sufficiently grave to warrant voting against this proposal at this time, we urgethe Company to take corrective measures to address each of these issues in due course. In the aggregate,however, considering that the chief executive officer is a controlling shareholder, we do not consider any of theCompany's remuneration practices to be particularly contentious and find the interests of executives and shareholders tobe appropriately aligned.

PETR3 April 02, 2014 Annual Meeting 23 Glass, Lewis & Co., LLC

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 24 Glass, Lewis & Co., LLC

2.00: CAPITALIZATION OF RESERVES W/O SHARE ISSUANCE

PROPOSAL REQUEST: Approval to increase share capital via capitalization ofreserves without the issuance of new shares.

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, the Company will increase its share capital by R$21,055,260.02, from R$205,410,905,230.50 toR$205,431,960,490.52, via the capitalization of the Company's tax incentive revenue reserve.

Article 4 of the Company's articles of association will be amended to reflect the Company's new share capital following thecapitalization.

GLASS LEWIS ANALYSIS

The Brazilian Companies Law establishes that the balance of all profit reserves, excluding reserves for contingencies andfor unrealized profits, may not exceed its paid-in capital. If this occurs, the company is required to either capitalize theexcess reserves or distribute them as dividends.

In this case, the Company has decided to capitalize its excess reserves so as to comply with the requirements set forth byBrazilian law. We believe that the proposed transaction will benefit shareholders by allowing the Company to increasepaid-in capital through a series of alternatives, above and beyond the issuance of shares. Moreover, when companiescapitalize reserves or retained earnings, there is no risk of dilution. This procedure merely transfers wealth toshareholders and does not impact share value.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 25 Glass, Lewis & Co., LLC

3.00: MERGER BY ABSORPTION (TERMOAÇU)

PROPOSAL REQUEST: Approval of merger by absorption. RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, Termoaçu S.A. ("Termoaçu") will be absorbed into the Company. Subsequent to the merger, any and all ofthe assets and liabilities held by Termoaçu will be absorbed by the Company and Termoaçu will cease to exist.

Further, shareholders must ratify the appointment of Apsis Consultoria e Avaliações Ltda., who prepared the valuation ofTermoaçu at book value, as well as approve the valuation itself and the merger agreement. The board will be granted thepower to complete any formalities, such as required filings and registrations, needed to give full force and effect to themerger.

In the merger agreement filed with the BM&FBOVESPA, the Company states that the proposed merger is intended toreduce administrative and operating costs as well as to simplify the Company's corporate structure.

GLASS LEWIS ANALYSIS

We believe that shareholders should support the proposed transaction. Given that the Company currently controlsTermoaçu, the proposed transaction will not have any adverse impact on shareholders. Moreover, as a subsidiary of theCompany, the financial results of Termoaçu are already consolidated with those of the group.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 26 Glass, Lewis & Co., LLC

4.00: MERGER BY ABSORPTION (TERMOCEARÁ)

PROPOSAL REQUEST: Approval of merger by absorption. RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, Termoceará Ltda. ("Termoceará") will be absorbed into the Company. Subsequent to the merger, any and allof the assets and liabilities held by Termoceará will be absorbed by the Company and Termoceará will cease to exist.

Further, shareholders must ratify the appointment of Apsis Consultoria e Avaliações Ltda., who prepared the valuation ofTermoceará at book value, as well as approve the valuation itself and the merger agreement. The board will be grantedthe power to complete any formalities, such as required filings and registrations, needed to give full force and effect to themerger.

In the merger agreement filed with the BM&FBOVESPA, the Company states that the proposed merger is intended toreduce administrative and operating costs as well as to simplify the Company's corporate structure.

GLASS LEWIS ANALYSIS

We believe that shareholders should support the proposed transaction. Given that the Company currently controlsTermoceará, the proposed transaction will not have any adverse impact on shareholders. Moreover, as a subsidiary of theCompany, the financial results of Termoceará are already consolidated with those of the group.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 27 Glass, Lewis & Co., LLC

5.00: MERGER BY ABSORPTION (CLEP)

PROPOSAL REQUEST: Approval of merger by absorption. RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority of votes cast

PROPOSAL SUMMARY

If approved, Companhia Locadora de Equipamentos Petrolíferos – CLEP (“CLEP”) will be absorbed into the Company.Subsequent to the merger, any and all of the assets and liabilities held by CLEP will be absorbed by the Company andCLEP will cease to exist.

Further, shareholders must ratify the appointment of PricewaterhouseCoopers, who prepared the valuation of CLEP atbook value, as well as approve the valuation itself and the merger agreement. The board will be granted the power tocomplete any formalities, such as required filings and registrations, needed to give full force and effect to the merger.

In the merger agreement filed with the BM&FBOVESPA, the Company states that the proposed merger is intended toreduce administrative and operating costs as well as to simplify the Company's corporate structure.

GLASS LEWIS ANALYSIS

We believe that shareholders should support the proposed transaction. Given that the Company currently controls CLEP,the proposed transaction will not have any adverse impact on shareholders. Moreover, as a subsidiary of the Company,the financial results of CLEP are already consolidated with those of the group.

Accordingly, we recommend that shareholders vote FOR this proposal.

PETR3 April 02, 2014 Annual Meeting 28 Glass, Lewis & Co., LLC

APPENDIX

Questions or comments about this report, GL policies, methodologies or data? Contact your client service representative or go towww.glasslewis.com/issuer/ for information and contact directions.

NOTE

Shareholders should note that the elections of directors and supervisory council members representative of minority and preferred shareholders will takeplace after the slate elections of directors and supervisory council members proposed by management. Minority common and preferred shareholderswho cast votes on Proposals 4 and 8 will be disqualified from participating in Proposals 5, 6, 9 and 10. As such, we recommend common shareholderscast votes on Proposals 5 and 9 and that preferred shareholders cast votes on Proposals 6 and 10. In addition to voting on these proposal, shareholders who wish to vote in favor of the currently known candidates should submit a separate power ofattorney to an authorized representative who will be present at the meeting.

Second Update: March 21, 2014. We have revised our analysis in Proposal 1 to state that the approval of the Company's financial statements releasesmanagement and supervisory council members from liability for their actions during the past fiscal year. In Proposal 1, we had previously stated thatshareholders were only approving the receipt of the statements and reports, not their substance or content. As such, we have revised ourrecommendation from FOR to ABSTAIN in light of the conflicting information regarding the integrity of the Company's financial statements. No otherchanges have been made to the report at this time.

Update: March 21, 2014. We have revised our analysis in Proposal 6.0 to reflect that Mr. Gerdau is president of the Chamber of Management Policies,Performance and Competitiveness (CGDC) in Brazil. The proxy paper published on March 20, 2014 originally stated that Mr. Monforte holds thisposition. None of our voting recommendations have changed as a result of this clarification.

DISCLOSURES

Glass, Lewis & Co., LLC is not a registered investment advisor. As a result, the proxy research and vote recommendations included in this report shouldnot be construed as investment advice or as any solicitation, offer, or recommendation to buy or sell any of the securities referred to herein. Allinformation contained in this report is impersonal and is not tailored to the investment strategy of any specific person. Moreover, the content of this reportis based on publicly available information and on sources believed to be accurate and reliable. However, no representations or warranties, expressed orimplied, are made as to the accuracy, completeness, or usefulness of any such content. Glass Lewis is not responsible for any actions taken or nottaken on the basis of this information.

This report may not be reproduced or distributed in any manner without the written permission of Glass Lewis.

DOW JONES SUSTAINABILITY INDEXThe Dow Jones Sustainability World Index, Dow Jones Sustainability North America Index, Dow Jones Sustainability Europe Index and Dow JonesSustainability Asia Pacific Index are a joint product of S&P Dow Jones Indices LLC and/or its affiliates and SAM Sustainable Asset Management AG(“SAM”). Dow Jones® and DJ® are trademarks of Dow Jones Trademark Holdings LLC. UBS® is a registered trademark of UBS AG. S&P® is aregistered trademark of Standard & Poor’s Financial Services LLC. All content of the DJSI World © S&P Dow Jones Indices LLC or its affiliates andSAM Sustainable Asset Management AG.

For information on Glass Lewis' policies and procedures regarding conflicts of interests, please visit: http://www.glasslewis.com/

LEAD ANALYSTS Governance & Remuneration: Madeleine Moore

PETR3 April 02, 2014 Annual Meeting 29 Glass, Lewis & Co., LLC

![Petromec v Petroleo 2004 - NADR v... · Petromec Inc v Petroleo Brasileiro SA Petrobras [2004] APP.L.R. 02/02](https://img.pdfslide.us/doc/110x75/5bab9aeb09d3f2e74b8c776e/petromec-v-petroleo-2004-v-petromec-inc-v-petroleo-brasileiro-sa-petrobras.jpg)

![Petroleo v Kos - The Supreme Court · Easter Term [2012] UKSC 17 On appeal from: [2010] EWCA Civ 772 JUDGMENT Petroleo Brasileiro S.A. (Respondent) v E.N.E. Kos 1 Limited (Appellant)](https://img.pdfslide.us/doc/110x75/5bab9aeb09d3f2e74b8c7720/petroleo-v-kos-the-supreme-court-easter-term-2012-uksc-17-on-appeal-from.jpg)