Embed Size (px)

Citation preview

1

PETROBRASBrazilian Oil and Gas Exploration &

ProductionChallenges and Opportunities

IBSEN FLORES LIMA

June/2011

Seoul, Korea

2Cluster blocks

Houston

Colombia

Argentina

Angola

United Kingdom

USA

BRASIL

BoliviaRio de

Janeiro

Nigeria

Venezuela

Equador

Peru

Mexico

Tanzania

Iran

New York

Tokio

Beijing

Singapure

Libia

Mozambique

Uruguay

Turkey

Senegal

Jordan

Pakistan

India

Portugal

Paraguay

Okinawa

Trading

Upstream

Head Office

Downstream

Representative Offices

Petrobras 2010

3

Proven Reserves : 16

billion boe (SPE)

Refineries: 15

- Installed Capacity: 2.223 million bpd

- Output of Oil Products: 2.034 million bpd

Service stations- Brazil: 5,998- Abroad: 1,223

Net Operating

Revenues:

US$ 91.9 billion

Total Investments

- 2010-2014: US$ 224.1 billion

Natural Gas Sales: 37 million m3/d

Vessels- Own fleet: 52

- Chartered: 120

Power Plants- Thermoelectric: 18- Installed Capacity : 6,136 MW

Pipelines : 29,398 km

Terminals: 47- Storage capacity: 10 million m³

Average O&G

Production:

2.3 million boed

- Oil: 2.0 million bpd

- Gas: 0.3 million boed

Producing Platforms

- Fixed: 86

- Floating: 47

Producing Wells:

- Onshore: 14,115

- Offshore: 790

Fertilizer Plants: 2

Drilling Rigs (domestic)

- Onshore: 34

- Offshore: 53

LNG Terminals- Pecém: 7 million m3/d- Rio de Janeiro: 14 million m3/d

Petrobras Overview*: An integrated oil major

*As of Nov/2010

4

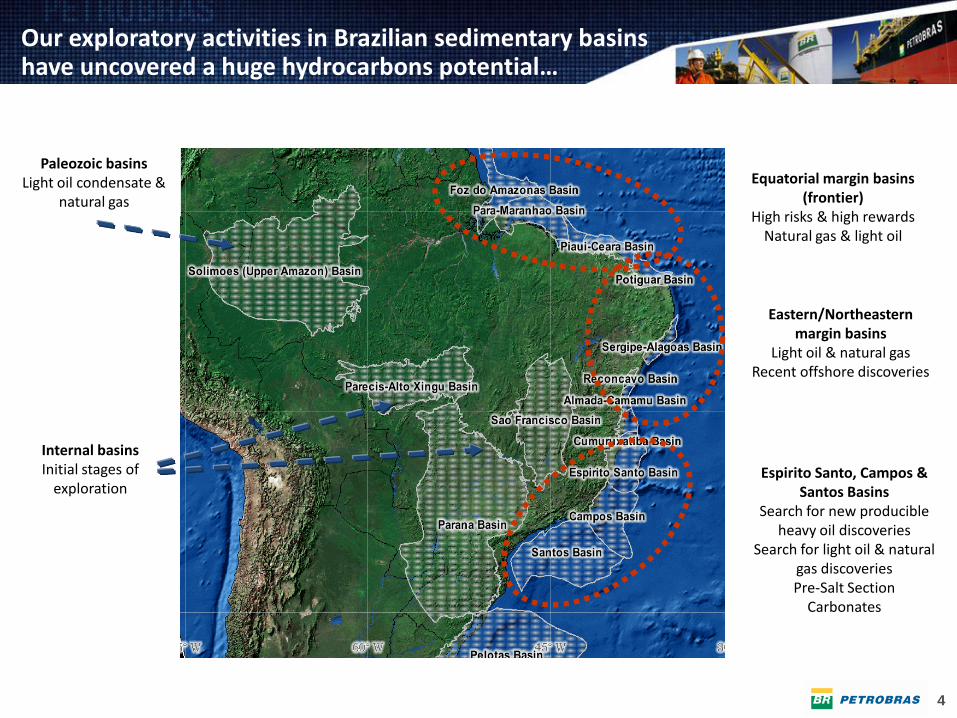

Our exploratory activities in Brazilian sedimentary basinshave uncovered a huge hydrocarbons potential…

Paleozoic basinsLight oil condensate &

natural gas

Eastern/Northeastern margin basins

Light oil & natural gas Recent offshore discoveries

Equatorial margin basins(frontier)

High risks & high rewardsNatural gas & light oil

Espirito Santo, Campos &Santos Basins

Search for new producible heavy oil discoveries

Search for light oil & natural gas discoveriesPre-Salt Section

Carbonates

Internal basinsInitial stages of

exploration

6

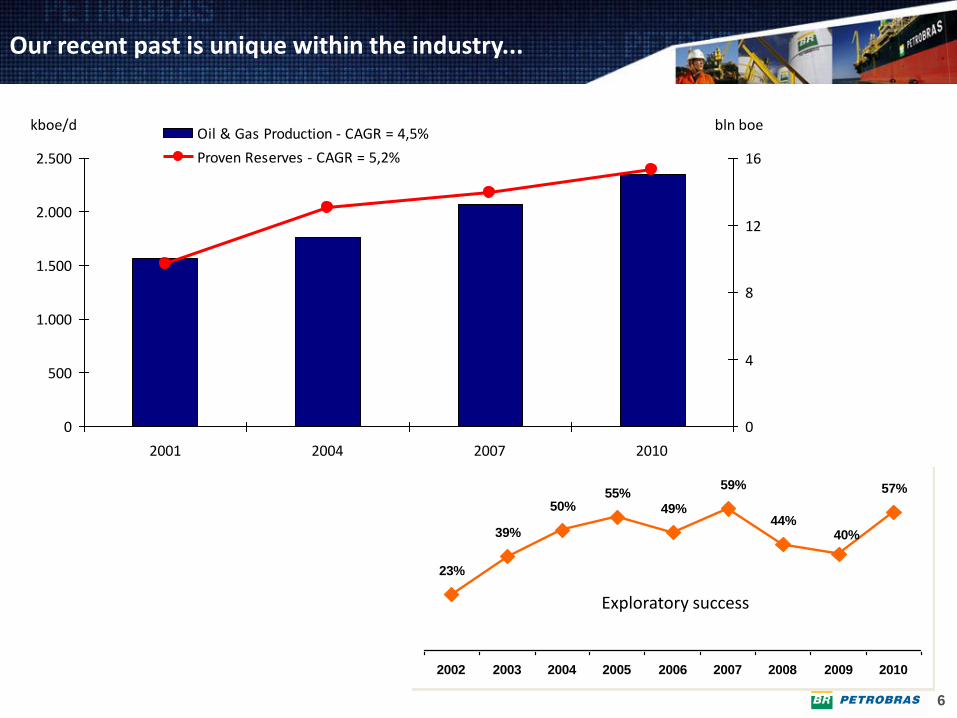

Our recent past is unique within the industry...

23%

39%

50%55%

49%44%

57%

40%

59%

2002 2003 2004 2005 2006 2007 2008 2009 2010

Exploratory success

0

500

1.000

1.500

2.000

2.500

2001 2004 2007 2010

0

4

8

12

16

Oil & Gas Production - CAGR = 4,5%

Proven Reserves - CAGR = 5,2%

kboe/d bln boe

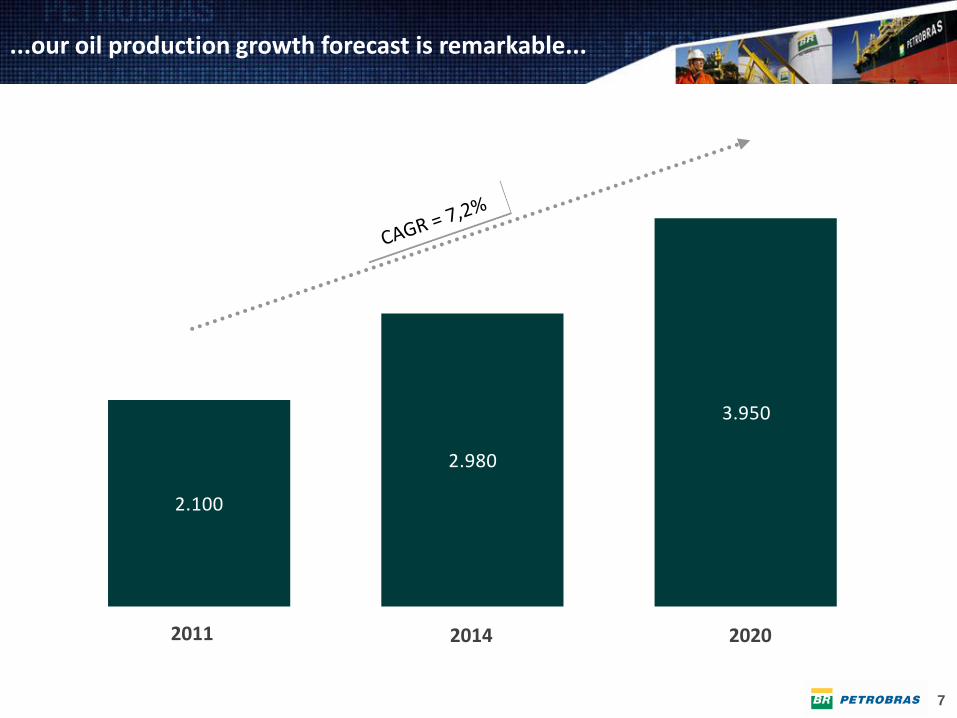

7

2.100

2.980

3.950

2011

...our oil production growth forecast is remarkable...

2014 2020

8

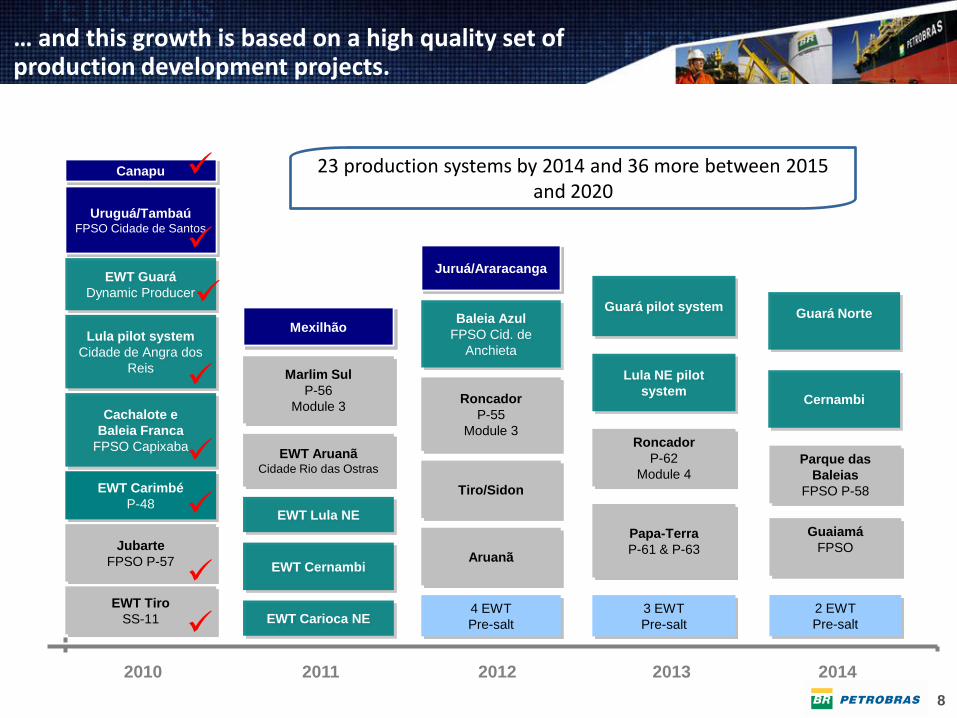

… and this growth is based on a high quality set of production development projects.

EWT Cernambi

EWT Guará

Dynamic Producer

Lula pilot system

Cidade de Angra dos

Reis

Cachalote e

Baleia Franca

FPSO Capixaba

Marlim Sul

P-56

Module 3

Jubarte

FPSO P-57

Baleia Azul

FPSO Cid. de

Anchieta

Roncador

P-55

Module 3

Papa-Terra

P-61 & P-63

Guará pilot system

Parque das

Baleias

FPSO P-58

Lula NE pilot

system

Tiro/Sidon

EWT AruanãCidade Rio das Ostras

EWT Tiro

SS-11

Mexilhão

Aruanã

Guaiamá

FPSO

Uruguá/TambaúFPSO Cidade de Santos

4 EWT

Pre-salt

3 EWT

Pre-salt

2 EWT

Pre-salt

Juruá/Araracanga

Canapu

EWT Carimbé

P-48

Cernambi

Guará Norte

Roncador

P-62

Module 4

EWT Lula NE

EWT Carioca NE

2010 2011 2012 2013 2014

8

6

23 production systems by 2014 and 36 more between 2015 and 2020

9

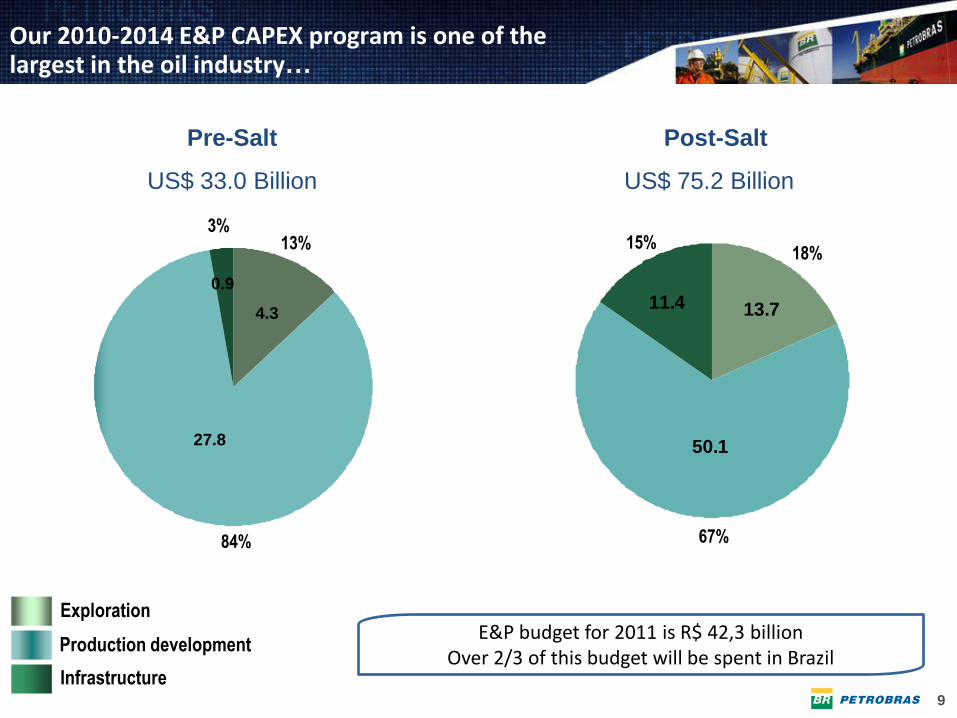

Our 2010-2014 E&P CAPEX program is one of the largest in the oil industry…

Exploration

Production development

Infrastructure

27.8

0.9

4.3

84%

3%13%

Pre-Salt

US$ 33.0 Billion

Post-Salt

US$ 75.2 Billion

50.1

11.4 13.7

15%18%

67%

E&P budget for 2011 is R$ 42,3 billion Over 2/3 of this budget will be spent in Brazil

10

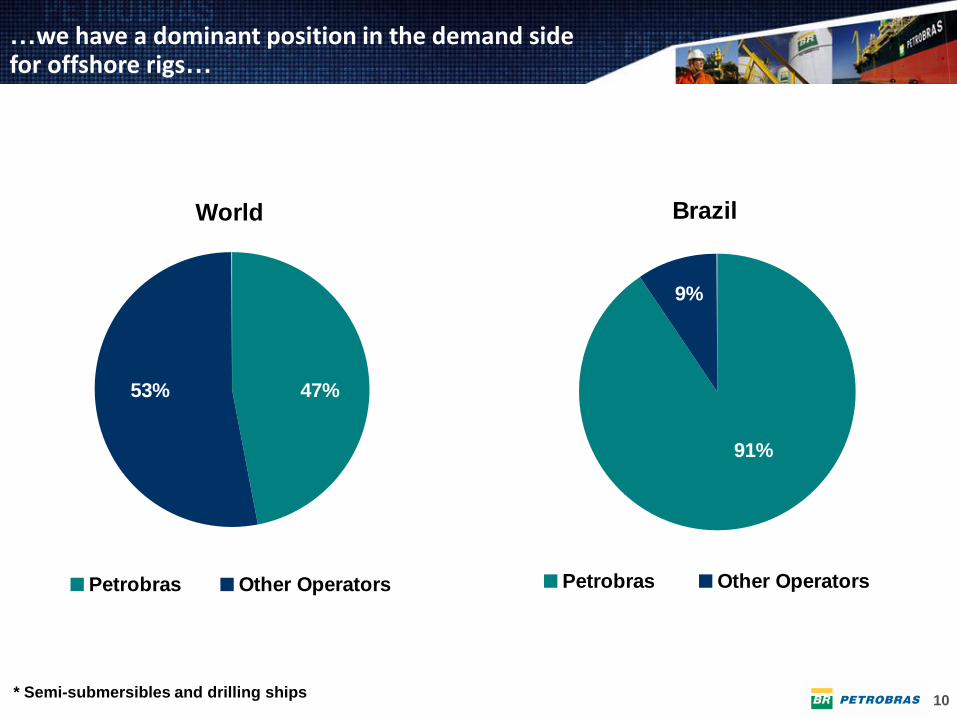

World

53% 47%

Petrobras Other Operators

Brazil

91%

9%

Petrobras Other Operators

* Semi-submersibles and drilling ships

…we have a dominant position in the demand side for offshore rigs…

11

Critical ResourcesDelivery Plan - Accumulated Value

By 2013 By 2015 By 2020

Drilling Rigs Water Depth Above 2.000 m 26 31 53*

Supply and Special Vessel 465 491 504

Production Platforms SS e FPSO 53 63 84

Others (Jacket and TLWP) 81 83 85

Production

Platform (FPSO)Drilling RigsSupply Vessel

…and we have a firm demand for several critical resources that is not yet contracted…

12

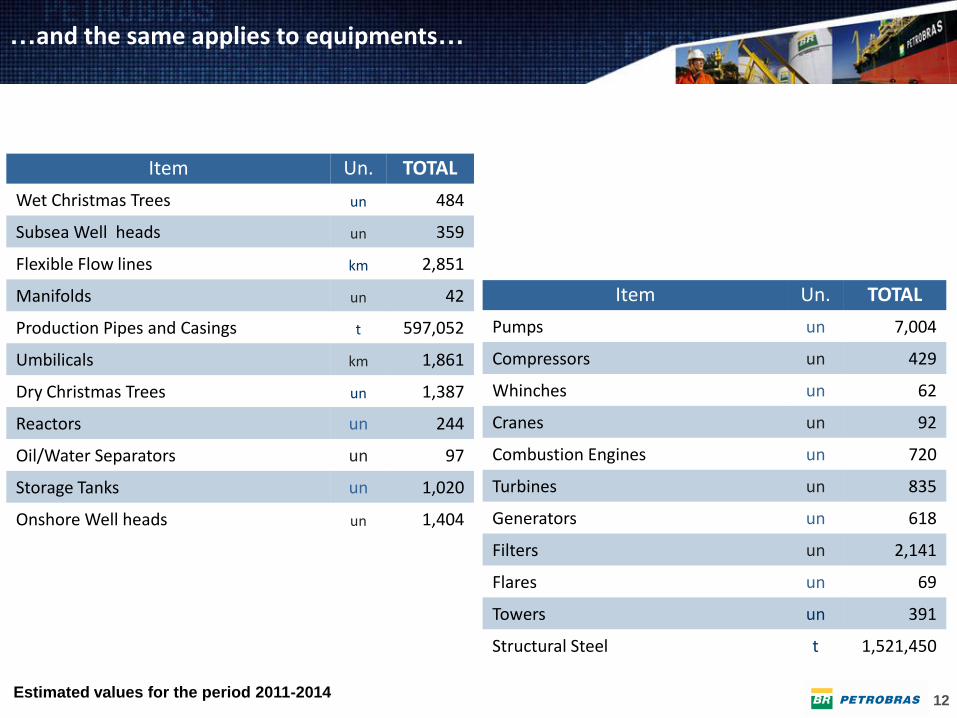

Item Un. TOTAL

Wet Christmas Trees un 484

Subsea Well heads un 359

Flexible Flow lines km 2,851

Manifolds un 42

Production Pipes and Casings t 597,052

Umbilicals km 1,861

Dry Christmas Trees un 1,387

Reactors un 244

Oil/Water Separators un 97

Storage Tanks un 1,020

Onshore Well heads un 1,404

Item Un. TOTAL

Pumps un 7,004

Compressors un 429

Whinches un 62

Cranes un 92

Combustion Engines un 720

Turbines un 835

Generators un 618

Filters un 2,141

Flares un 69

Towers un 391

Structural Steel t 1,521,450

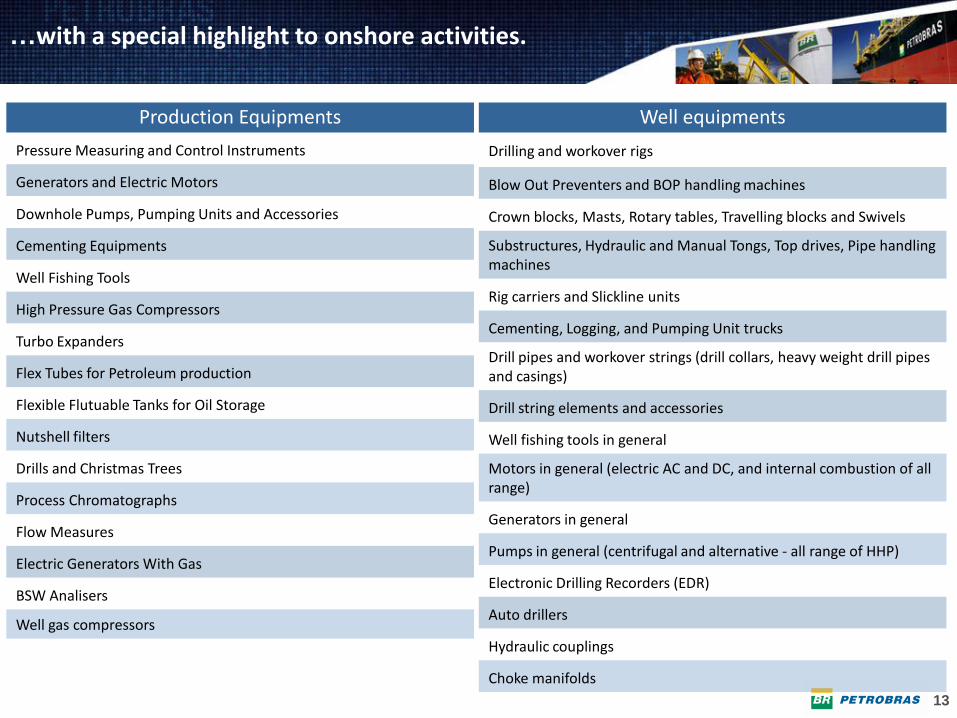

…and the same applies to equipments…

Estimated values for the period 2011-2014

13

Production Equipments

Pressure Measuring and Control Instruments

Generators and Electric Motors

Downhole Pumps, Pumping Units and Accessories

Cementing Equipments

Well Fishing Tools

High Pressure Gas Compressors

Turbo Expanders

Flex Tubes for Petroleum production

Flexible Flutuable Tanks for Oil Storage

Nutshell filters

Drills and Christmas Trees

Process Chromatographs

Flow Measures

Electric Generators With Gas

BSW Analisers

Well gas compressors

…with a special highlight to onshore activities.

Well equipments

Drilling and workover rigs

Blow Out Preventers and BOP handling machines

Crown blocks, Masts, Rotary tables, Travelling blocks and Swivels

Substructures, Hydraulic and Manual Tongs, Top drives, Pipe handling machines

Rig carriers and Slickline units

Cementing, Logging, and Pumping Unit trucks

Drill pipes and workover strings (drill collars, heavy weight drill pipes and casings)

Drill string elements and accessories

Well fishing tools in general

Motors in general (electric AC and DC, and internal combustion of all range)

Generators in general

Pumps in general (centrifugal and alternative - all range of HHP)

Electronic Drilling Recorders (EDR)

Auto drillers

Hydraulic couplings

Choke manifolds

14

ENGINEERING CHALLENGES

Reduction in the complexity

of the projects, using

standard solutions

Contributing for the consolidation

of Brazil as a supplying hub with

international competitive level

Using international engineering

patterns and metrics in our

facility projects

Simplification and

Standardization

Competitiveness/

Sustainability

Brazilian ContentTechnology &

Engineering

Drivers

On the engineering and supply chain sideswe have a clear framework…

15

…and Petrobras has crafted a program to help replicating this success…

Local content requirements in

contracts

Cooperation agreements to

develop new products and

technologies

Long term contracts

Cooperation agreements for

imports substitution

Examples

Platforms Rigs Refineries

Ships (PROMEF) Vessels

(PSV, AHTS, ORSV)

Oil-water subsea separation Umbilical, Special xmas tree (BCS)

Lifeboats Steam turbine Flexible pipes - monitoring

New plants in Brazil Shipyards Offshore cranes Pumping units Pumps and valves

Expansions Umbilical Wet xmas tree Pressure vases.

Strategies

16

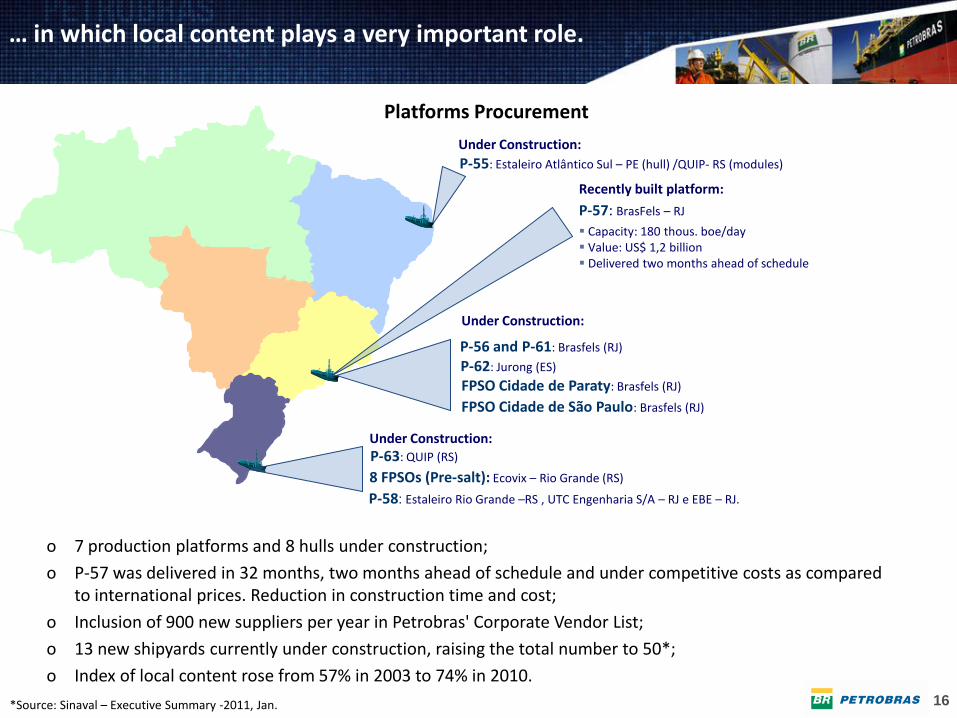

o 7 production platforms and 8 hulls under construction;

o P-57 was delivered in 32 months, two months ahead of schedule and under competitive costs as compared to international prices. Reduction in construction time and cost;

o Inclusion of 900 new suppliers per year in Petrobras' Corporate Vendor List;

o 13 new shipyards currently under construction, raising the total number to 50*;

o Index of local content rose from 57% in 2003 to 74% in 2010.

Recently built platform:

P-57: BrasFels – RJ

Capacity: 180 thous. boe/day Value: US$ 1,2 billion Delivered two months ahead of schedule

8 FPSOs (Pre-salt): Ecovix – Rio Grande (RS)

P-56 and P-61: Brasfels (RJ)

P-62: Jurong (ES)

P-63: QUIP (RS)

FPSO Cidade de Paraty: Brasfels (RJ)

FPSO Cidade de São Paulo: Brasfels (RJ)

Under Construction:

Under Construction:

Platforms Procurement

Under Construction:

P-55: Estaleiro Atlântico Sul – PE (hull) /QUIP- RS (modules)

P-58: Estaleiro Rio Grande –RS , UTC Engenharia S/A – RJ e EBE – RJ.

*Source: Sinaval – Executive Summary -2011, Jan.

… in which local content plays a very important role.

1717

THANK YOU