Embed Size (px)

Citation preview

Perspectives

on Indian VC

Ecosystem, 2018

December, 2018

2IVCA Bain India VC report 2018_PPTBOS

Context

• This report is a comprehensive assessment of the Indian VC industry – includes key trends shaping the industry with

respect to VC investment landscape, India’s start-up ecosystem and the supporting regulatory framework

• The primary sources used for this report include Bain Deals Database, AVCJ, Venture Intelligence, VCCEdge, Tracxn,

NASSCOM, WorldBank Data and Euromonitor

• For the purpose of this report, we define a VC investment as follows:

o Investments with deal size <$20M at Seed/Series A/Series B/Series C round of investment

o Investments with deal size between $20-100M at Seed/Series A/Series B/Series C/Series D round of investment by typical VC firms (such

as Sequoia, Lightspeed, etc.) as well as other companies that typically engage in VC activity (such as Softbank, Naspers, Tiger, etc.)

3IVCA Bain India VC report 2018_PPTBOS

Summary

• India Venture Capital landscape

– Fund-raising environment in India is positive with ~$10B worth India-focused funds raised since 2014; momentum to continue and expected to be stronger in

future, with multiple global LPs viewing India as an attractive VC investment destination

– VC deal value grew 5x in last 10 years with 2017 deal value at ~$3.4B; the VC investment ecosystem in India is now maturing with focus shifting to a few high

quality deals vs. larger volume of deals

– Multiple trends that affected the Indian VC landscape over the last few years are expected to continue being relevant in the future as well. These include increasing

focus of larger VCs on late stage investment deals, increasing quantum of investment by corporate VCs and diversification of investment in terms of industry

segments (albeit within consumer technology)

– VCs in India have seen some early success with 5-15% of start-ups funded by the larger VCs going on to raise >$100M; exit momentum has also picked up in the

last few years - ~$4B worth of exits in 2017 with the industry seeing multiple, recent big ticket exits

– With increasing maturity of start-up ecosystem - exits are expected to increase in future with ~80% start-up founders expecting investor exits by 2024

• Startup ecosystem in India

– India is among one of the top startup ecosystems in the world - housing ~3.5K+ funded start-ups growing rapidly at 30%+

– Multiple drivers that have been at play in building a flourishing start-up ecosystem in India – 1) Access to abundant, high quality talent (e.g. second highest number

of annual engineering grads), 2) Strong underlying macroeconomic growth (e.g. growing internet users), 3) Holistic ecosystem enablers (e.g. co-working spaces,

incubators, global initiatives, etc.) and 4) Supportive regulatory framework - are expected to drive further growth in future

– While Bangalore is the startup capital of India followed by Delhi-NCR and Mumbai, smaller cities such as Hyderabad, Pune and Chennai are emerging hubs

witnessing a lot of recent start-up activity - indicating maturity of the overall start-up ecosystem

• Regulatory framework

– Regulatory Framework in India has been increasingly conducive to the start-up ecosystem with multiple government policies and initiatives launched over the last

few years committed to the success of start-ups in India

– Initiatives such as Startup India, SIDBI Fund-of-Funds, Atal Innovation Mission, Make In India, SEBI AIPAC recommendations for VC funds, expected to

continue to foster the ecosystem in India over the next few years; more initiatives such as ease of closing a company are though needed to further turbocharge growth

4IVCA Bain India VC report 2018_PPTBOS

A G E N D A

India Venture Capital landscape

Startup ecosystem in India

Regulatory framework

5IVCA Bain India VC report 2018_PPTBOS

Venture Capital – Key Messages

VCs in India are Well Funded with ~$10B capital raised over the last 4-5 years by a mix of large and small VCs – 80-85% total capital raised by 10-15 large

VCs, while the rest has been raised by smaller, domestic VCs (fund-raising by smaller VCs significantly increased over this period)

VC landscape in India is moving from its Scale-up Phase to Maturing Phase with shift in focus from quantity of deals to quality of deals - secular increase

in round sizes across investment stages over the past 3-4 years; future outlook for investments in India is positive

Number of VCs with investments in India grew rapidly from ~130 in 2013 to ~270 in 2018; additionally, bigger funds are increasingly focusing on later stage,

higher ticket size deals (largest 10 VCs account for ~50% of all Seed B/ C/ D deals in 2017 vs. 30% in 2012) while multiple, smaller funds are dominant in the

seed/ series A stages

Investment by Corporate VCs has increased 4x over the past 4-5 years; expected to increase further in future given traction from funds set-up by

mature start-ups such as Flipkart/ PayTM as well as from top international corporate VCs such as Google Ventures

Consumer Technology accounts for ~60% of total VC investments in India with SaaS accounting for another ~20%; most large funds have presence across

segments (consumer tech./ IT accounting for 60-80% of the portfolio) with very few funds having any vertical-specific focus

Investments within Consumer Technology have diversified (more verticalized/ niche vs. horizontal investments) over the past few years - trend is expected to

continue in future with emergence of new verticals in e-tailing and rising prominence of vernacular web content; IT investments also expected to be increasingly focused

on SaaS/ Analytics B2B Products (vs. services focus till a few years ago)

VC investments is India have seen reasonable success - 5-15% of start-ups funded by large funds have gone on to cumulatively raise >$100M; 30% of

VC seed investments and ~50% of VC Series A+ investments have raised follow-up capital in subsequent rounds

Exit Momentum in India has been picking up over the past few years (~$4.2B net VC exit value in 2017, vs. ~$1.3B in 2014), and is expected to acceleratein the future as the start-up ecosystem matures; ~80% of start-up founders expect exits by 2024

1

2

3

4

5

6

7

8

6IVCA Bain India VC report 2018_PPTBOS

Quantum of fund-raising for focused Indian VC investments has increased

significantly since 2014

Note: (*) Only includes funds that are earmarked for India – whether raised by Indian or global VCs Source: Venture Intelligence

Number of

funds raised

Value of funds raised in 2017 considerably

lower because (a) Highest quantum of funds

raised in 2016 (vs. previous years), (b) 40%

drop in investments in 2016 vs. 2015 leading to

higher than expected availability of funds , (c)

Smaller seed/ series A focused funds led fund-

raising in 2017 → low value raised per fund

1 . F U N D I N G F U N D S E A R M A R K E D F O R I N D I A

7IVCA Bain India VC report 2018_PPTBOS

~$10B capital raised by VCs for India-focused investments over the past 4 years

Others includes smaller, domestic

funds raised by VCs such as Prime

Venture Partners, Pi ventures and

Fireside that primarily focus on

seed/early stage startups

1 . F U N D I N G

Multiple smaller series/ seed A

focused raised capital in 2017,

while participation of larger VCs in

fund-raising was limited

Note: (*) Only includes funds that are earmarked for India – whether raised by Indian or global VCs Source: Venture Intelligence

F U N D S E A R M A R K E D F O R I N D I A

~20% of total funds raised

by Sequoia deployed ex-

India in SEA

8IVCA Bain India VC report 2018_PPTBOS

Significant fund-raising activity also seen by smaller, seed/ series A focused VCs

11 . F U N D I N G

VC Firm

Funds raised

(’14 -’18, in

$M)

Prime Venture Partners 109

IvyCap Ventures 100

SRI Capital 100

Ventureast 83

Fireside Ventures 79

DSG Consumer Partners 75

Pi Ventures 58

IIM-A-CIIE 57

Saama Capital 57

Alteria Capital 55

Lightbox 54

Indus Age 50

Montane Ventures 50

VC Firm

Funds raised

(’14 -’18, in

$M)

Stellaris Ventures 50

Unitus Seed Fund 46

Exfinity Fund 45

Lok Capital 40

Omnivore Partners 40

Blume Ventures 30

Kae Capital 30

Ganesh Ventures 30

Trifecta Capital 30

Zodius Capital 30

Endiya Partners 26

Indian Angel Network 26

Note: (*) Includes all funds above $50M raised from 2014-18

Source: Venture Intelligence; Bain Analysis

9IVCA Bain India VC report 2018_PPTBOS

VC industry in India has evolved to a more “mature” phase in the last couple of years

Source: Venture Intelligence; AVCJ; VCCEdge; Bain Analysis

• Scale-up Phase for VCs in India with multiple new VCs setting up funds to benefit from a

booming start-up environment

• Focus on doing more deals given high number of start-ups seeking investment and aggressive

competition among VCs

• Maturing Phase for VCs in India as VCs now

more focused on placing select bets on fewer

investments - given their initial portfolios are

already in place

Scale-up Phase Maturing Phase

2 . I N V E S T M E N T S

10IVCA Bain India VC report 2018_PPTBOS

Focus has shifted to fewer, higher quality deals

Number of Deals Average Deal Size

Source: Venture Intelligence; Bain Analysis

Scale-up Phase(VC focus on doing more

deals and building initial

portfolio)

Maturing Phase(VC focus on doing select deals

to holistically grow portfolio)

2 . I N V E S T M E N T S

Scale-up Phase(VC focus on making

multiple, smaller

investments)

Maturing Phase(Focus on placing select bets

on fewer investments)

11IVCA Bain India VC report 2018_PPTBOS

With increasing focus on quality – number of deals has declined and deal size has

increased across all investment stages

Number of Deals per Round Round Size

2 . I N V E S T M E N T S

Source: Venture Intelligence; Bain Analysis

Classification of rounds

as Seed/ Series A/

Series B/ Series C per

investment

announcements

Classification of rounds

as Seed/ Series A/

Series B/ Series C per

investment

announcements

12IVCA Bain India VC report 2018_PPTBOS

India is well positioned to attract high quantum of investments in future

Source: Coller Capital’s Global Private Equity Barometer, 2018; EY Report; Bain Analysis

India VC Market Attractiveness – LP Perspective

Key Drivers

“Better growth opportunities, more exits taking place and improved choices in fund managers make India very attractive”

EMPEA 2018 Global Limited Partners’ survey

“We believe that the strong exits seen in the past 3 years

have played a material role in ‘rerating’ the India VC sector in

the eyes of Global LPs. These exits have underlined the ability

of the Indian market to return foreign capital to LPs”

PE/VC Agenda 2018, EY

Strong

exits in

the last

3 years

Positive

macro

outlook “Limited Partners are attracted to the Indian market because it’s

relatively young and because of the sheer volume of consumer demand that the country generates”

Former AVP, Sequoia Capital

“Limited partners are more positive today about India’s macroeconomic environment than they were in the past.

Partner, Indian Fund manager

2 . I N V E S T M E N T S

13IVCA Bain India VC report 2018_PPTBOS

Number of active VCs have grown significantly from 2013 but have plateaued out

recently

Source: Venture Intelligence; Bain Analysis

Decreasing annual deals per

VC given focus on quality deals

vs. quantity of deals post 2015

3 . V C F I R M S

14IVCA Bain India VC report 2018_PPTBOS

Bigger VCs have shifted their focus to late investment stages with smaller VCs

dominant in the seed/ series A stages

Investment Break-Down of Large Funds Seed/ Series A VC Examples

VC Fund

Year

Founded Investments

Pi Ventures 2016

Exfinity

Ventures2013

Unitus

Ventures2012

Omnivore

Ventures 2011

2015,Series A

2018, Seed

2016,Seed 2016, Seed

2018,Series A

2017, Series A

2016, Series A

2017, Series A

Note: Top 10 funds include Sequoia, Accel India, Nexus, Matrix, IDG, SAIF, Kalaari, Lighspeed, Lightbox, Saama Capital

Source: Tracxn; Venture Intelligence; Bain Analysis

3 . V C F I R M S

Top 10 based on

funds raised

between ’14 and ‘18

15IVCA Bain India VC report 2018_PPTBOS

Investment by Indian corporate VCs has grown 4x since 2013 – quantum of

investment expected to further increase in future

Corporate VC Investments in India Drivers of Future Growth

Source: CBInsights; Bain Analysis

Increasing

number of

mature start-ups

expected to start

own funds

Leading Global

CVCs doubling

down on

investments in

India

• Flipkart and PayTM are active VC investors

• Aim to further integrate in the start-up

ecosystem, and strengthen own presence

through VC investments

• Global Corporate VCs such as Google, and

Intel increasing direct investments in India

• Google made first direct investment in India in

Dunzo in ’17, second investment in Fynd in ’18

4 . C O R P O R A T E V C S

Investment include

Blackbuck, and Tinystep

Investments include Jugnoo

and Big Basket

16IVCA Bain India VC report 2018_PPTBOS

Consumer Technology has dominated VC investments over the past few years

VC Investments ($) in India by Industry Segment

VC Number of Deals in India by Industry

Segment

5 . S E G M E N T S

Source: Venture Intelligence; AVCJ; VCCEdge; Bain Analysis

Average deal size of ~$7M

for Consumer Technology

Investments; ~ $5.5-7M for

other segments

17IVCA Bain India VC report 2018_PPTBOS

Most funds have diversified portfolios with only a few having vertical focus

Consumer Technology and IT/ ITeS dominate investments of large funds Funds with vertical-specific focus

8 investments in

Healthcare

30 investments in

BFSI

18 investments in

BFSI

10+ investments in

Consumer Goods

10+ investments in

Consumer Goods

5 . S E G M E N T S

15 investments in

Healthcare

Source: Venture Intelligence; AVCJ; VCCEdge; Bain Analysis

Investments of all large funds are diversified across sectors almost mirroring the

market mix - all funds have exposure to consumer technology/ IT

18IVCA Bain India VC report 2018_PPTBOS

Even within Consumer Tech., VC investments have diversified - shifting away from

General e-tailing/ OTAs

Sub-segments Sample Companies

EdTech

HealthTech

FoodTech

FinTech

Verticalized e-tailing

Online Travel

Aggregators (OTAs)

Horizontal e-tailing

Top Consumer Tech investments

T O P 5 0 0 C O N S U M E R T E C H D E A L S

Diversification of Consumer Tech Investments

6 . D I V E R S I F I C A T I O N

Source: Venture Intelligence; AVCJ; VCCEdge; Bain Analysis

19IVCA Bain India VC report 2018_PPTBOS

Going ahead - multiple new areas within Consumer Technology expected to gain

traction

Source: Forrester; Bain Analysis

Multiple categories within e-tailing that are sizeable globally are likely to see traction

in India over the next few years (such as Beauty, Sports, Toys, Auto Parts, etc.)

New verticals in E-tailing Vernacular Content

• Rapid increase in web

only and vernacular

content driven by growth

in consumers spending

more time online to be

another theme of growth;

Models emerging across

text, messaging, music,

gaming and video

6 . D I V E R S I F I C A T I O N

20IVCA Bain India VC report 2018_PPTBOS

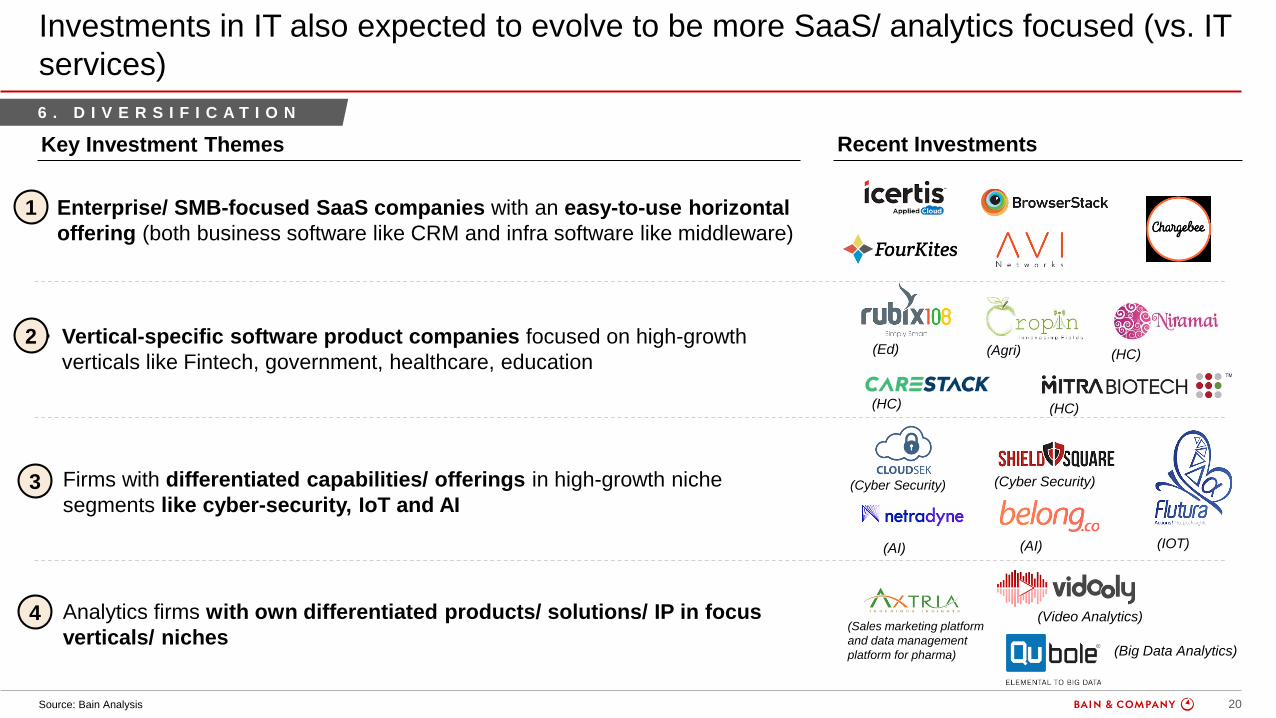

Investments in IT also expected to evolve to be more SaaS/ analytics focused (vs. IT

services)

• Enterprise/ SMB-focused SaaS companies with an easy-to-use horizontal

offering (both business software like CRM and infra software like middleware)

1

(AI)

(Sales marketing platform

and data management

platform for pharma)

(Cyber Security) (Cyber Security)

(AI)

• Vertical-specific software product companies focused on high-growth

verticals like Fintech, government, healthcare, education

• Firms with differentiated capabilities/ offerings in high-growth niche

segments like cyber-security, IoT and AI

• Analytics firms with own differentiated products/ solutions/ IP in focus

verticals/ niches

(IOT)

(Video Analytics)

(Big Data Analytics)

(HC)

(HC)(Agri)(Ed)

(HC)

2

3

4

Source: Bain Analysis

Key Investment Themes Recent Investments

6 . D I V E R S I F I C A T I O N

21IVCA Bain India VC report 2018_PPTBOS

VCs in India have seen reasonable success - 5-15% portfolio companies of large

funds went on to cumulatively raise >$100M funding (1/3)

VC Name

Funds

raised,

2014-18

(in $M)

# of deals

participated

2014-18 (total

deal value)

Typical investment

Partners

% Portfolio

companies

that raised

further

funding1

% of Portfolio

companies with

total funding

>$100M

Portfolio

companies

with total

funding

>$500M

Exits

(2006)~3000

~190

(~$5.4B)

• 80-85% deals in

partnership

• Frequent Partners:

Accel, Lightspeed,

Matrix, SAIF, Nexus

~80% 15-16%

3/190 • 40-50 exits in last 5 years (total

exit value2 of ~$3B)

• Marquee exits (company

valuation >$500M) include Star

Health Insurance, Freecharge

(2008)~800

~150

(~$3.8B)

• 80-85% deals in

partnership

• Frequent Partners:

Sequoia, IDG, SAIF

~70% 6-7%

2/150 • ~20 exits in last 5 years (total

exit value of ~$2B)3

• Marquee exits (company

valuation >$500M) include

Flipkart, Myntra, Ola

(2006)~750

~85

(~$1.3B)

• 80-85% deals in

partnership

• Frequent Partners:

Sequoia, Blume, Helion

~65% 5-6%

1/85

• 10-12 exits last 5 years (total

exit value of ~$0.2B)

• Top 2 exits (by total exit value)

include Mezi.com, What’s on

India

7 . P E R F O R M A N C E

Note: (1) Further funding also includes subsequent rounds raised/participated by the same funds; (2) Total exit value includes combined exit value for all participating firms

Source: Tracxn, Venture Intelligence; Bain Analysis

22IVCA Bain India VC report 2018_PPTBOS

VCs in India have seen reasonable success - 5-15% portfolio companies of large

funds went on to cumulatively raise >$100M funding (2/3)

VC Name

Funds

raised,

2014-18

(in $M)

# of deals

participated

2014-18 (total

deal value)

Typical investment

Partners

% Portfolio

companies

that raised

further

funding1

% of Portfolio

companies with

total funding

>$100M

Portfolio

companies

with total

funding

>$500M

Exits

(2006)

~700~70

(~$1.1B)

• 75-80% deals in

partnership

• Frequent partners:

Sequoia, Nexus, Tiger

~60% 10-11%

1/70

• 15-16 exits in last 5 years (total

exit value2 of ~$0.4B)

• Top 3 exits (by total exit value)

include ItzCash, TCNS Clothing,

Quikr

(2006)

~420~90

(~$0.9B)

• 95-100% deals in

partnership

• Frequent Partners:

Accel, Kalari, Inventus

~70% 6-7% ---

• ~16 exits in last 5 years (total

exit value of $1.1-1.2B3)

• Marquee exits (company

valuation >$500M) nclude

Myntra, Lenskart

(2000)

~350~100

(~$1.1B)

• 65-70% deals in

partnership

• Frequent Partners:

Accel, India Quotient

Fund, Sequoia

~70% 11-12%

1/100

• ~15 exits in last 5 years (total

exit value of ~$1.0B)

• Marquee exits (company

valuation >$500M) include

PayTM, Just Dial

7 . P E R F O R M A N C E

Note: (1) Further funding also includes subsequent rounds raised/participated by the same funds; (2) Total exit value includes combined exit value for all participating firms

Source: Tracxn, Venture Intelligence; Bain Analysis

23IVCA Bain India VC report 2018_PPTBOS

VCs in India have seen reasonable success - 5-15% portfolio companies of large

funds went on to cumulatively raise >$100M funding (3/3)

VC Name

Funds

raised,

2014-18

(in $M)

# of deals

participated

2014-18 (total

deal value)

Typical investment

Partners

% Portfolio

companies

that raised

further

funding1

% of Portfolio

companies with

total funding

>$100M

Portfolio

companies

with total

funding

>$500M

Exits

(2006)

~290~90

(~$1.0B)

• 80-85% deals in

partnership

• Frequent Partners:

IDG, Accel, India

Quotient Fund

~70% 4-5%

1/90• 7-8 exits in the past 5 years

(total exit value2 of ~$0.3B)

• Top exits (by total exit value)

include Embibe, VisionaryRCM

and Zivame

(2007)

~290~40

(~$2.4B)

• 85-90% deals in

partnership

• Frequent Partners:

Sequoia, Matrix, Helion,

Nexus

~70% 13-14%

1/40• 3-4 exits in the past 5 years

(total exit value of $0.2-0.3B)

• Top 2 exits (by total exit value)

include ItzCash, India Energy

Exchange

7 . P E R F O R M A N C E

Note: (1) Further funding also includes subsequent rounds raised/participated by the same funds; (2) Total exit value includes combined exit value for all participating firms

Source: Tracxn; Venture Intelligence; Bain Analysis

24IVCA Bain India VC report 2018_PPTBOS

Overall, ~30% of all VC seed investments in India and ~50% series A/ B/ C

investments continued to raise subsequent rounds of capital

Funding post Seed stage Funding post Series A Funding post Series B Funding post Series C

7 . P E R F O R M A N C E

~30%

~47% ~49%~50%

Note: Classification of rounds as Seed/ Series A/ Series B/ Series C per investment announcements

Source: Bain Analysis

Classification of rounds

as Seed/ Series A/

Series B/ Series C per

investment

announcements

Includes start-ups that

directly raised Series A

funding

25IVCA Bain India VC report 2018_PPTBOS

Exit momentum in India has been strong with increasing exit value per deal

Note: Exits with undisclosed deal amounts have not been included

Source: Venture Intelligence; AVCJ; VCCEdge; Bain Analysis

~$16B Walmart-

Flipkart deal

contributes ~80%

to exits in 2018

High Transaction Value per deal

driving higher total VC Exit value

even as the number of annual exits

is consistent at 100-150

8 . E X I T S

Increasing % of strategic exits driven

by higher number of exits from

consumer technology deals (~25%

of all exits in 2018 vs. 1% in 2013);

these deals are almost all primarily

top-line growth driven - need further

seasoning pre-IPO (especially in

terms of profitability)

Exits in early 2010s were from

primarily from IT deals done in

late 2000s – more IPO exits given

more mature investment profile

26IVCA Bain India VC report 2018_PPTBOS

Multiple big ticket exits in recent years have contributed to a stark increase in

average exit value per deal

Startup/Asset VC/Investor name Year

Exit Value

(in $M)

Kalaari Capital, Tiger Global, IDG Ventures India, Accel India, SoftBank Corp, Greenoaks Capital,

Naspers, Others

Tiger Global

2018

2017

16,000

800

Tata Capital, Sequoia Capital India, ICICI Venture, Apis Partners, Tata Capital Growth Fund, Others 2018 930

Tiger Global2017 500

Sequoia Capital, Sofina Societe, Tybourne Capital, Valiant Capital, ru-Net,2015 450

SAIF Partners2017 400

SAIF Partners

Reliance Capital Ventures Ltd., Saama Capaital (SVB), SAP ventures

2017

2017

400

250

Citi Venture Capital, Infrastructure Development Finance, Baring Asia Private, Samara Capital2015 340

Kalaari Capital, IDG Ventures India, Accel India; Tiger Global, Others2014 240

Sequoia Capital India, Saama Capital, Madison India 2018 240

Source: Venture Intelligence; Tracxn; Bain Analysis

8 . E X I T S

27IVCA Bain India VC report 2018_PPTBOS

Exits are expected to further accelerate - 80% founders expecting exit by 2024

“Going ahead, number of strategic exits are likely to grow given

increasing corporate interest in startups in adjacent spaces. For

instance, TVS might be interested to acquire an electric scooter

company, which has seen significant VC investments in the past.”

- Former Investment Lead, Accel Partners

“The number of buyers in the market has increased. It is not

difficult to find a buyer in the industry even for a moderately

attractive asset.”

- Former AVP, Sequoia Capital

80%550+ deals due for

immediate exit based on

investments before 2013

(assuming 5 year holding

period)

Multiple impending exits Founders’ expectation

• 35% of founders expect an exit between

2019 and 2021; a further 41% expect exits

by 2024

Source: Innoven Start-up Outlook Report; Bain Analysis

8 . E X I T S

28IVCA Bain India VC report 2018_PPTBOS

A G E N D A

India Venture Capital landscape

Startup ecosystem in India

Regulatory framework

29IVCA Bain India VC report 2018_PPTBOS

Start-up Ecosystem – Key Messages

India is among one of the top startup ecosystems in the world housing 50K+ total start-ups and 3.5K+ funded start-ups

Start-up ecosystem in India has been recording rapid growth with number of total start-ups and funded start-ups growing at ~30% CAGR;

multiple factors have contributed in building this flourishing start-up ecosystem in India - key factors include:

Access to abundant, high quality talent – India has the largest young (i.e. age group 20-39 in the world) working population (~440 M), second highest

college enrollments in the world (~32M), and a healthy mix of STEM and Business graduates; also boasts of more than 1M annual engineering graduates -

second only to China

Strong underlying macroeconomic growth - Disposable income & consumer expenditure per capita have grown at ~10% CAGR over past 5 years

leading to increased consumer demand, while rapid growth (20%+ CAGR) in number of internet users and high smartphone penetration has increased access

Holistic ecosystem enablers – Access to (1) Sprawling base of co-working spaces simplifying start-up setting up process (both domestic & International

companies), (b) ~140 private and government incubators (across different models) providing funding/ networking/ knowledge-exchange opportunities, and (c)

multiple global partnerships with other start-up ecosystems such as France (French Tech ticket) & UK (London’s IE20 Program) leading to increased exposure

Supportive Regulatory framework - Multiple government schemes and initiatives such as Startup India, SIDBI Fund of Funds, initiatives by NITI Aayog

fostering the entrepreneurial ecosystem in India by providing financial (e.g. reduced tax burden) and operational (e.g. procedural simplification) benefits

Bangalore is the startup capital of India housing 800+ funded tech startups, followed by Delhi-NCR and Mumbai with 700 and 450 start-

ups respectively; Bangalore’s lead driven by access to large talent base and lower cost of living (commercial rent lower vs. Mumbai/ NCR)

With increasing maturity of the ecosystem – smaller cities such as Hyderabad, Pune and Chennai (each housing 100+ funded tech

startups) are seeing increased start-up activity, primarily driven by their cost advantage and growing talent base

30IVCA Bain India VC report 2018_PPTBOS

India houses 50K+ total start-ups, of which ~3.5K+ are funded – growing rapidly at

~30% CAGR

Number of startups

Note: Startups are companies founded post 2005; as reported by Tracxn

Source: Tracxn

Number of funded startups

28%33%

31IVCA Bain India VC report 2018_PPTBOS

India is considered among one of the top startup ecosystems in the world

Total funded tech startup*

base (2017), Growth (2013-

2017)

Total number of unicorns

(2018)*

Source: NASSCOM; Tracxn; Euromonitor

Total engineering grads

(2017, M)

Total number of incubators

(2017)

~20100, 19% ~4800, 48% ~2800, 39% ~3000, 26% ~1150, 23%

126 77 18 15 3

0.25 4.5 1.1 0.07 0.007

~240 ~740 ~399 ~59 ~6.5

~1500 ~2400 ~140 ~50 ~130

8 46 77 9 49Ease of doing business

rank (2018)

Total number of internet

users (M) (2018)

US China India UK Israel

32IVCA Bain India VC report 2018_PPTBOS

Availability of tech talent and a strong macroeconomic base are top factors

contributing to India’s startup boom

Availability of talentStrong underlying

macroeconomic growthRegulatory push

Other ecosystem

enablers

1 2 3 4

• Significant presence of both

International (e.g. - WeWork,

SpacesWorks) and domestic

(Awfis, 91-Springboard, etc.) co-

working spaces

• Multiple Incubation programs

across sectors and segments

• Global partnerships with other

mature startup ecosystems like

Israel, France UK and S. Korea

• Multiple schemes and initiatives

to give boost to start-up

ecosystem such as Startup

India, SIDBI Fund of Funds,

initiatives by NITI Aayog

• Financial and operational

benefits for VCs investing in

India facilitated by SEBI’s recent

revamping of regulations for

VCs

• Disposable income &

consumer expenditure per

capita have grown at ~10%

CAGR over past 5 years

• Access to consumer tech

products and services has grown

- rapid growth in number of

internet users and high

smartphone penetration

• Largest young (i.e. age group

20-39 in the world) working

population (~440 M)

• 50% of India’s college graduates

are STEM and business

students

• More than 1 million annual

engineering graduates

Covered in detail in the

next section

33IVCA Bain India VC report 2018_PPTBOS

India is one of the largest base for quantity and quality of talent

Largest young, working population

Second highest annual college

enrollments

Healthy mix of STEM and Business

graduates

Note: STEM education degrees in includes, Science, Technology, Engineering and Mathematics

Source: World Bank Data

1

34IVCA Bain India VC report 2018_PPTBOS

India produces more than 1M engineering graduates each year - second only to

China

Annual engineering graduates in India Comparison vs. other countries

CAGR

(’13’-17)

Note: Engineering graduates include Construction and Manufacturing graduates too

Source: Euromonitor

1

35IVCA Bain India VC report 2018_PPTBOS

Growing consumer demand and increased tech penetration are top macro factors

driving growth in India’s start-up ecosystem2

Disposable income & consumer expenditure per capita Internet users and smartphone penetration

Source: Euromonitor; Bain Analysis

DEMAND ENABLERS

36IVCA Bain India VC report 2018_PPTBOS

There are multiple ecosystem enablers that have contributed immensely to India’s

startup story

Incubation centers Co-working spaces Global Programs

Source: Indian Tech Start-up ecosystem, NASSCOM;

N O N E X H A U S T I V E

3

37IVCA Bain India VC report 2018_PPTBOS

Incubation programs have delivered successful startups in India

Corporate Government University Social Private

• Bangalore (2017) • Hyderabad (2015) • Chennai (2013) • Delhi (2011) • Bangalore (2015)

• Advanced Tech- IoT,

Cloud, Virtualization,

Analytics, Machine

learning

• FoodTech, EdTech,

HealthTech, Finance

• Biotech, HealthTech,

Hardware and Software

start-ups

• AgriTech • ConsumerTech, FinTech,

Deep-tech, HealthTech,

Enterprise solutions

• Financial: Equity-free

grant of $15,000

• Access: Technology

and business

mentorship

• Support System:

NetApp platforms/ tools,

co-working space, HR,

marketing, legal and

tech support

• Access: Extensive

network of CXOs, serial

entrepreneurs, senior

executives

• Support System:

Financial advisory, legal

and HR/recruiting services

• Financial: Connections

with angel investors/VCs

for funding

• Access: Extensive alumni

network & industry

connects

• Operational: Access to

R&D infrastructure

• Financial: Up to $50,000

equity investment in 1 to 3

businesses of each cohort

• Access: 4-month

workshops with mentors

followed by investor

showcase

• Financial: Seed funding

for early stage start-ups;

Initial investment of up to

$450-500K

• Access: 50+ VCs, 200+

founders in Axilor’s

network

Source: Indian Tech Start-up ecosystem, NASSCOM

Location

Key Offerings

Focus Area

3

38IVCA Bain India VC report 2018_PPTBOS

Co-working spaces have simplified setting up process for startups

Inception Year• Launched in 2015 in Delhi NCR • Launched in 2013 in Delhi • Entered India in 2017

• 55 facilities with 25,000 seats

• Present in 9 cities – Delhi,

Bangalore, Mumbai, Hyderabad,

Gurgaon, Noida, Pune, Kolkata

• 19 facilities

• Present in 8 cities - Bangalore,

Delhi, Goa, Gurgaon, Hyderabad,

Mumbai, Navi Mumbai and Noida

• 9 facilities in India with 12,000 seats

• Present in 3 cities- Mumbai, Bangalore and Gurgaon

• Raised ~50M till date from

Sequoia and InnoVen

• Raised ~$20M till date from

Sandway Investment, AMA

Holdings, 33 Investments etc.

• Raised $4.4B from Softbank in 2017, out of which $1.4B

would go into Asia Pacific subsidiaries

No. of facilities

Funding

Indian co-working spaces International co-working spaces

3

Source: Indian Tech Start-up ecosystem, NASSCOM

39IVCA Bain India VC report 2018_PPTBOS

India has forged collaborative programs with other top global startup ecosystems

Overview

Israel France South Korea United Kingdom

India Israel Global

Innovation challengeFrench Tech ticket

K start-up Grand

Challenge

Mayor of London’s IE20

Program

• Collaboration between

Start-up India and Israel

Innovation

• Focus Area: Agriculture,

Water and Digital Health

• Initiative to attract entrepreneurs

to create tech start-ups in France

• Initiative to invite foreign start-

ups to Korea and cooperate

with VCs and

• Initiative to discover 20 of

India’s most innovative and

high-growth start-ups that are

considering international

expansion

• INR 2-5 lakh cash prize;

additional INR 10-25 lakh

cash prize in water-tech

• Cross-border mentorship

and incubation/acceleration

support

• Connection to

investors/corporates to

explore piloting solutions

• €45,000 per team; French

residence permit

• 1 year incubation; Office space

and mentoring in France

• Networking events, demo days

with investors

• Access to early tech

adopting Korean population;

Govt. support for launch in S.

Korea

• $11,300 funding support

• 3.5 months accelerator

program

• Free office space in Seoul;

Corporate support and

sponsorship

• Opportunity to set up or

expand business in London

• 6 months free office

membership

• Expert advice on marketing,

access to finance and local

market analysis

• 18 Indian start-ups selected• 11 Indian start-ups won (Total 70

winners)

• 10 of the 80 start-ups selected

from India

• 20 Indian start-ups out of 300

applications selected

Key Offerings

Impact

3

Source: Indian Tech Start-up ecosystem, NASSCOM

40IVCA Bain India VC report 2018_PPTBOS

Bengaluru is the startup capital of India, followed by Delhi NCR and Mumbai

Bengaluru Delhi NCR Mumbai

~840 ~710 ~450

~320 ~180 ~270

• Talent – 24 universities, ~135

engineering colleges; abundant tech

talent given proximity to IT campuses

and captives (highest in India)

• Low cost of commercial real estate

for grade A rentals compared to NCR/

Mumbai (INR 70 sq. ft vs. INR 80-100

sq. ft.)

• Supportive state government:

Launched a dedicated startup cell aimed

to provide mentorship, regulatory advice

and corporate exposure to startups

• Talent – 26 universities, 34 engineering

colleges

• One of the fastest growing urban

centers of India – highest vacant grade

A commercial real estate stock (~30

MSF) and as well as upcoming supply

(~42 MSF) across all metros

• Rising number of

incubators/accelerators set up by

govt., corporates & educational

institutions

• Talent – 14 universities, 46 engineering

colleges

• India’s commercial capital – highest

contribution to India’s GDP and

highest share of disposable income

• Highest number of VC headquartered

in Mumbai vs. other hubs

Number of funded tech

startups

Number of

Co-working spaces

Top funded startups

headquartered in locations

Key growth drivers

Note: Includes only funded companies founded after 2005 – excludes deadpooled startups

Source: NASSCOM; Tracxn; Euromonitor

41IVCA Bain India VC report 2018_PPTBOS

In addition to the 3 hubs, Indian startup ecosystem has expanded to newer cities

Hyderabad Pune Chennai

~150 ~120 ~110

~110 ~90 ~30

• Talent – 15 universities, ~42

engineering colleges

• House captives of global tech giants

like Microsoft, Facebook & Google –

attracts top tech talent

• Very low cost of grade A commercial

real estate rentals @ INR 50 sq. ft

• Proactive state government – set up

“T-Hub” (India’s fastest growing

incubation center) and launched

Innovation Policy – offering tax

incentives to startups & incubators

• Talent – 17 universities, ~129

engineering colleges

• Low cost of grade A commercial real

estate rentals @ INR 60 sq. ft

• Presence of major IT hubs like Infosys,

TCS, Wipro, Accenture leading to large

pool of IT resources

• Abundant product engineering/

design talent given proximity to

automotive/ manufacturing captives

• Talent – 25 universities, ~29

engineering colleges

• Low cost of grade A commercial real

estate rentals @ INR 55 sq. ft

• Large number of Special Economic

Zones (~20)

Number of funded tech

startups

Number of

Co-working spaces

Top funded startups

headquartered in locations

Key growth drivers

Note: Includes only funded companies founded after 2005 – excludes deadpooled startups

Source: NASSCOM; Tracxn; Euromonitor

A G E N D A

India Venture Capital landscape

Startup ecosystem in India

Regulatory framework

43IVCA Bain India VC report 2018_PPTBOS

Government’s recent programs and policies aim to boost the Indian startup

ecosystem by benefiting both Start-ups and Venture Capital firms

Policies and Schemes benefitting Startups Policies and Schemes benefitting VCs

• Securities and Exchange Board of India

(SEBI) constituted a standing committee

‘Alternative Investment Policy Advisory

Committee’ (AIPAC)

• Aim of committee is to at help domestic

financial institutions access appropriate

investment opportunities to earn risk-

adjusted returns

• Since setting up of AIPAC, SEBI observed:

– >3x growth in total capital raised by VC firms

(AIF category 1 funds)

– ~33% growth in total registered VCs with SEBI

• Flagship initiative by govt. of India aimed at promoting

growth of startups and generate large scale job opportunities

• Key initiatives include setting up incubation centers, tax

exemptions for startups, easier patent filing, etc.

• Intent of supporting startups at different stages of their

lifecycle – incubation, seed funding and growth

• Key initiative is setting up of a INR. 10,000 Cr. fund of

funds – capital to be deployed in startups through VCs

• Founded by NITI Aayog, key initiative is setting up of Atal

Incubation Centers (AICs) for support to startups across

sectors

• Launched in 2014 to encourage companies to manufacture in

India and increase investment in manufacturing sector

• Key initiatives include making collateral-free credit available

to Micro and Small Enterprises engaged in manufacturing

activities

1

2

3

4

5

Source: Bain Analysis

44IVCA Bain India VC report 2018_PPTBOS

Startup India is the government’s flagship initiative to extend operational and

financial support to startups

“Startups, technology and innovation will be effective and exciting instruments for India’s transformation.”

Shri Narendra Modi, Prime Minister of India

Procedural Simplifications

for setting of entities

Providing tax relaxation

to financially incentivizestartups

1

2

3Providing incubation

and funding assistance

MA

IN F

OC

US

AR

EA

S

1

45IVCA Bain India VC report 2018_PPTBOS

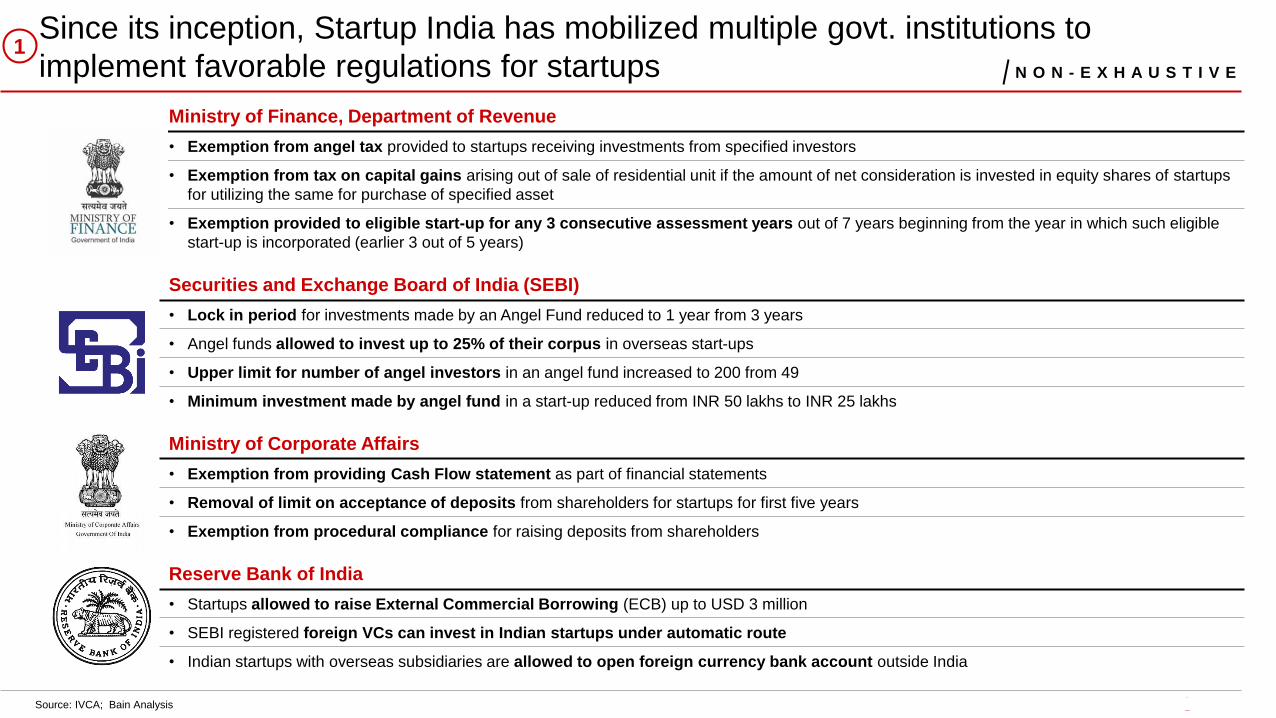

Since its inception, Startup India has mobilized multiple govt. institutions to

implement favorable regulations for startups 1

N O N - E X H A U S T I V E

Source: IVCA; Bain Analysis

Ministry of Finance, Department of Revenue

• Exemption from angel tax provided to startups receiving investments from specified investors

• Exemption from tax on capital gains arising out of sale of residential unit if the amount of net consideration is invested in equity shares of startups

for utilizing the same for purchase of specified asset

• Exemption provided to eligible start-up for any 3 consecutive assessment years out of 7 years beginning from the year in which such eligible

start-up is incorporated (earlier 3 out of 5 years)

Securities and Exchange Board of India (SEBI)

• Lock in period for investments made by an Angel Fund reduced to 1 year from 3 years

• Angel funds allowed to invest up to 25% of their corpus in overseas start-ups

• Upper limit for number of angel investors in an angel fund increased to 200 from 49

• Minimum investment made by angel fund in a start-up reduced from INR 50 lakhs to INR 25 lakhs

Ministry of Corporate Affairs

• Exemption from providing Cash Flow statement as part of financial statements

• Removal of limit on acceptance of deposits from shareholders for startups for first five years

• Exemption from procedural compliance for raising deposits from shareholders

Reserve Bank of India

• Startups allowed to raise External Commercial Borrowing (ECB) up to USD 3 million

• SEBI registered foreign VCs can invest in Indian startups under automatic route

• Indian startups with overseas subsidiaries are allowed to open foreign currency bank account outside India

46IVCA Bain India VC report 2018_PPTBOS

• Small Industries Development Bank of

India (SIDBI) aims to provide

government support to the VC

ecosystem of India

• An initiative by NITI Aayog, the policy think

tank of government of India, AIM acts as an

umbrella organization that aligns innovation

policies between central and state

governments

• Make in India was launched in 2014 with

the objective of job creation and "to

transform India into a “global design and

manufacturing hub“

• Establishment of a Fund of Funds for

Startups (FFS) with a corpus of INR.

10,000 Cr. to be deployed through

SEBI registered VC funds

• ASPIRE Fund of corpus INR. 200 Cr.

focusing on rural and agri-based

startups

• Atal Incubation Centers (AIC): Provides a

grant-in-aid of INR. 10 Cr. for a maximum

period of 5 years

• Atal Tinkering Labs (ATL): Dedicated work

spaces aimed at imparting additional

skillset to school students – computational

thinking, adaptive learning, etc.

• Credit Linked Capital Subsidy Scheme

assists in technological and machinery

upgradation of manufacturing startups

• Stepping up of credit line for Small and

Medium Enterprises (SMEs)

• INR 600 Cr. of funds already deployed

by SIDBI across 75 startups in India

• 13 AICs approved across India with INR. 10

Cr. grant each

• 2441 schools across the country selected for

setting up ATLs

• Procedural simplifications like complete

digitization of Industrial Entrepreneur

Memorandum (IEM)

Several other government schemes have created tangible impact for startups

Overview

Key Initiatives

Impact

2 3 4

Source: Bain Analysis

47IVCA Bain India VC report 2018_PPTBOS

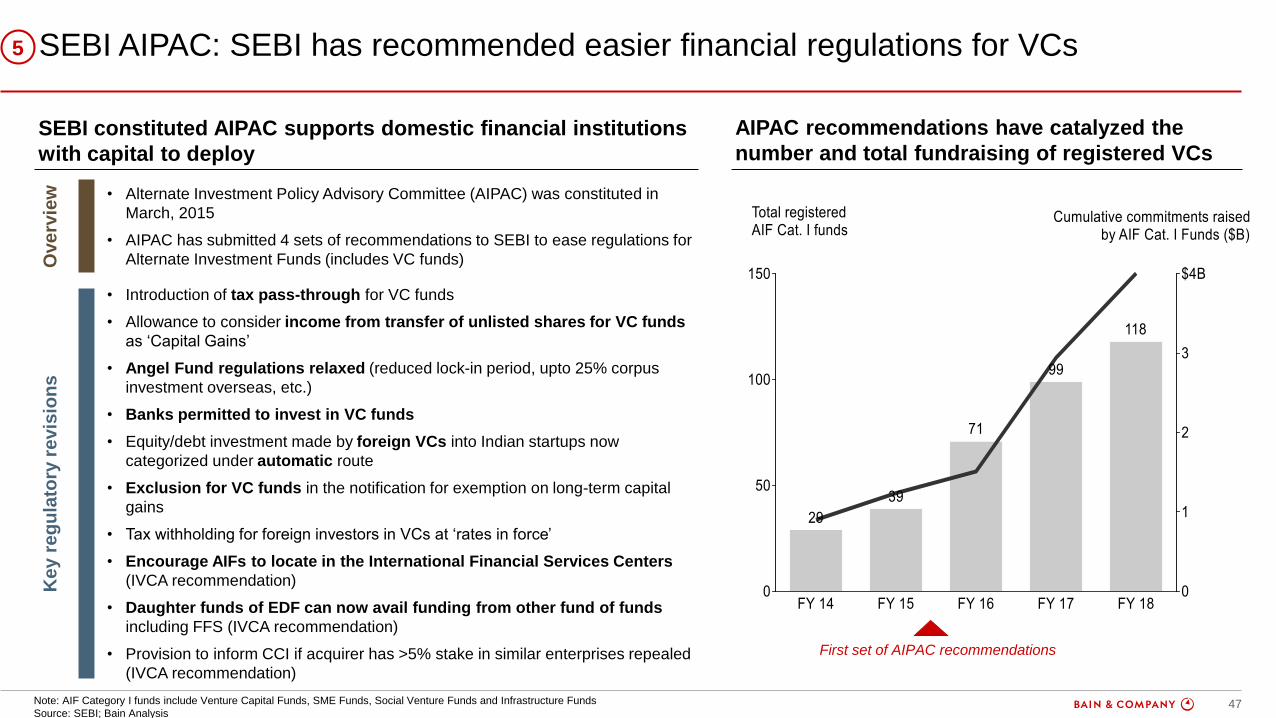

SEBI AIPAC: SEBI has recommended easier financial regulations for VCs5

SEBI constituted AIPAC supports domestic financial institutions

with capital to deploy

AIPAC recommendations have catalyzed the

number and total fundraising of registered VCs

Ove

rvie

wK

ey r

eg

ula

tory

re

vis

ion

s

• Alternate Investment Policy Advisory Committee (AIPAC) was constituted in

March, 2015

• AIPAC has submitted 4 sets of recommendations to SEBI to ease regulations for

Alternate Investment Funds (includes VC funds)

• Introduction of tax pass-through for VC funds

• Allowance to consider income from transfer of unlisted shares for VC funds

as ‘Capital Gains’

• Angel Fund regulations relaxed (reduced lock-in period, upto 25% corpus

investment overseas, etc.)

• Banks permitted to invest in VC funds

• Equity/debt investment made by foreign VCs into Indian startups now

categorized under automatic route

• Exclusion for VC funds in the notification for exemption on long-term capital

gains

• Tax withholding for foreign investors in VCs at ‘rates in force’

• Encourage AIFs to locate in the International Financial Services Centers

(IVCA recommendation)

• Daughter funds of EDF can now avail funding from other fund of funds

including FFS (IVCA recommendation)

• Provision to inform CCI if acquirer has >5% stake in similar enterprises repealed

(IVCA recommendation)

First set of AIPAC recommendations

Note: AIF Category I funds include Venture Capital Funds, SME Funds, Social Venture Funds and Infrastructure Funds

Source: SEBI; Bain Analysis

48IVCA Bain India VC report 2018_PPTBOSSource: World Bank Data

Ease of doing business: India jumped 23 places globally on World Bank’s Ease of

Doing Business Index in 2018 – highest rank in last 10 years

49IVCA Bain India VC report 2018_PPTBOS

Disclaimer

• This material and the analysis contained herein (the “Report”) was prepared by Bain & Company India Pvt Ltd (“Bain”), in

cooperation with Indian Private Equity and Venture Capital Association (“IVCA”), over a limited time period to provide a

perspective on the VC Industry in India.

• The Report is intended solely for the use of the recipient to whom the Report has been provided directly (e.g. by email), and

is not to be disclosed in whole or in part to any third party without Bain’s explicit prior written permission. In the event Bain

does grant permission for this Report to be disclosed to a third party, Bain will not permit the third party to rely on this

Report.

• No representation or warranty, either expressed or implied, is made as to the reliability, completeness or accuracy of this

Report. Due to lack of sufficient internal data on any particular company, the Report contains some estimates based on

outside-in assessments and comparisons within the industry and the experience base. Bain does not have any duty to

update or supplement any information in this Report.

• No responsibility or liability whatsoever is accepted by any person including Bain or its affiliates and their respective officers,

employees or agents for any errors or omissions in this Report.

• Projected market and financial information, analyses and conclusions contained herein are based (unless sourced

otherwise) on the information described above and Bain’s judgment and should not be construed as definitive forecasts or

guarantees of future performance or results.

• This paper is not to be considered as a recommendation for investment in all or any part of the industry.