Embed Size (px)

DESCRIPTION

OIS

Citation preview

PAPER - PERSPECTIVES IN MODELLING OF PRICING OF INTEREST RATE SWAPS W.R.T INDIAN MARKETS

________________________________________________________________________ By Prof. Deepak Tandon

Professor . (Finance) IILM Institute for Higher Education

Plot No 69 Sector 53 IILM GURGAON

Abstract

Swaps are an integral part of the world of international finance. Their use has permeated almost every aspect of domestic and international capital and money markets. Banks use them to reduce their exposure to the risk of changes in interest rates and currency movements, thereby reducing the potential tax burden on the public which results from the failure of the banks. The existence of swaps creates greater choice for consumers and in the provision of fixed rate finance for mortgages, or even of loans with caps or other embedded options. The arbitrage opportunities which are capitalized in the swap markets have resulted in a narrowing of the capital markets bid/offer spread. This means that the institutional investors get a better return on their investments and international borrowers pays lower financing costs. This in turn, results in more competitively priced goods for consumers and in enhanced returns for pensioners. Swaps therefore have an effect on almost all of us yet they remain in arcane derivatives risk management tool, sometimes suspected of providing the international banking system with the tools required to bring about its destruction. This Paper covers the basic understanding of Swap Markets in India and also emphasizes the pricing aspects of Interest Rate Swaps Interest rate swaps are over-the-counter contracts, in which one party agrees to pay a fixed interest rate in exchange to receiving a floating interest rate from the other counterparty, on a given notional principal during a certain time period. The amount of the principal, however, never changes hands. Both rates are specified when the contract is initialized. These instruments are widely used in the management of interest rate risks in a wide range of fields of business, e.g the acquisition of funds and asset management. KEY WORDS - IRS ( Interest Rate SWAPS ), OIS(Overnight Indexed Swaps ) MIBOR ( Mumbai Inter Bank Offered Rate ) ,IN BMK rate- derived from rate on the benchmark Indian Government Securities _____________________________________________________________________

- - - 1 -

INTRODUCTION

SWAPS are arrangements between two firms to exchange a series of future payments .

A SWAP is necessarily is a long dated forward contract between two parties through the

intermediation of a third party , such as a Bank . Through the Interest rate Swaps two

parties agree to exchange interest with each other over an agreed period .

In the early days the interest rate market was driven by bonds. However, during the last

decades the interest rate market has expanded immensely and the contracts traded tends

to get more complicated every day. This has implied a need for sophisticated models in

order to price and hedge these contracts, normally called interest rate swaps. Banks

undertake both Cross-Currency-Swaps and Interest-Rate-Swaps with an average of 2-

receive and 1-pay deals per day. Seeing the liquidity and the standardization of the

product Swaps are quite popular at the Bank.But, in the journey of Swap at the time of

initiation of swap the present value of all future cash flows (both fixed and floating) are

equal. But due to dynamic nature of interest rates there is change in the benchmark rate to

which the floating leg payment rests. As the benchmark rate changes the floating rate

payments also undergoes a change. Now with the change in benchmark interest rates the

Present value of all future cash flows also undergoes a change. The spot rate also

undergoes a change. With change in benchmark interest rates the value of swap also

changes after initiation. Due to this dynamic nature of the Swap products it becomes

quite imperative to study the short term interest rate forecasting. This helps in developing

the view (as to increase or decrease in the interest rates) and subsequently makes the

decision to go for the type of structure i.e. trading, hedging or back-to-back deals.

- - - 2 -

Also as per the RBI guidelines for valuations the bank has to Mark-To-Market their

portfolios on daily basis, calculate the hedge effectiveness and estimate the asset-liability

mismatches. For this purpose the bank valuates its swap portfolio on the Reuters and

records them on their swap book.

Thus a need was identified at the bank for having there own model for daily MTM of the

swap deal which would return the same values as returned by Reuters and also

incorporates the investment objectives of the bank.

A>INTEREST RATE SWAPS :

A. Characteristics - An Interest Rate Swap is an off-balance sheet contract between two

counterparties to exchange a stream of payments on specified dates based on a notional

principal. In a plain vanilla interest rate swap, a series of payments calculated by applying

a fixed rate of interest to the notional principal amount is exchanged for a stream of

payments calculated by using a floating rate of interest on the same principal. This is a

standard fixed-for-floating interest rate swap.

Alternatively, both series of cash flows could be calculated using floating rates of interest

that are based upon different benchmarks. Floating rate benchmarks include MIBOR, the

91 day T-Bill rate, the Reuters CP reference rate, the Bank Rate etc. Further, the interest

payments are not grossed-up like in call money transactions but are net settled on

periodic payment dates.

- - - 3 -

B. Participants

The following participants are allowed to undertake IRS/FRAs -Scheduled Commercial

Banks, Primary Dealers, All India Financial Institutions, Corporates, Mutual Funds and

Corporates Corporates and mutual funds can use these products only to hedge existing

assets/liabilities while the first three types of participants may do market making. RBI has

currently allowed transactions only in plain vanilla IRS/FRA. Swaps having explicit or

implicit options such as cap, floors or collars are not permitted.

C Overnight Indexed Swaps (OIS)

Currently, the most common form of Interest Rate Swaps in the Indian market is the

Overnight Indexed Swap (OIS). An OIS or call money swap is a fixed to floating interest

rate swap with the floating leg linked to the overnight borrowing rate (call money rate).

The tenor of the swap ranges typically from 2 days to one year.

D.Pricing an IRS

Pricing an IRS refers to ascertaining the fixed rate of the swap, also called swap rate.

First, the credit of the borrower is priced into the swap rate (whether inter-bank or

corporate). Further refinements to the term money rate are added to account for notional

principal, payment frequency and basis risk. The above would require the swap curve to

lie between the T-Bill curve and inter-bank Term Money curve or Commercial Paper

curve. However, expectation of overnight rates (floating leg) weighs heavily in the final

pricing. OIS are quoted on a bid/offer basis with the bid referring to the quoting party’s

willingness to pay the fixed rate and offer referring to the party’s willingness to receive

- - - 4 -

the fixed rate. In developed markets however, swaps are quoted as a spread over the

sovereign curve signifying the credit risk.

B >Advantages of interest rate swaps

The primary advantage offered by Interest Rate Swaps is the facility to hedge interest rate

exposure in a flexible and easy manner. Further, due to netting off of interest payments,

credit exposure is minimal. However, swaps may also be used to execute interest rate

views. Specifically, banks, primary dealers and institutions may use Interest Rate Swaps

for the following:

Asset Management: Swaps may be used to lock-in to a fixed rate, which may be higher

than the average floating rate while still maintaining liquidity by receiving the fixed rate

in an IRS·

Hedging: A short period of volatility in the interest rates may be hedged by paying the

fixed rate in an IRS and removing the risk of floating rates shooting up·

Liability Management: Raising term deposits can be replicated by overnight borrowing

and paying fixed in an IRS. This is cheaper and more flexible route than term deposits.

- - - 5 -

Execution of Interest Rate View: Portfolio size can be expanded without putting a

strain on funding by receiving the fixed rate in an IRS. Also IRS allows a rising interest

rate view to be executed by paying fixed in an IRS.

Reducing Asset Liability Mismatch: Banks can use swaps of specific tenors to reduce

the mismatch between assets and liabilities Corporates may use swaps to hedge interest

rate exposure on their liabilities or assets whether fixed or floating. Most corporates in

India have PLR linked (and hence floating rate) loans from financial institutions or banks.

These may be hedged by receiving the floating rate (PLR, Bank Rate, MIBOR etc) and

paying a fixed rate. This way the corporate can fix its cost of funds in an uncertain or

tightening scenario. Additionally, there are corporates which have issues fixed rates

bonds or debentures. Such corporates may wish to receive fixed and thereby convert their

liabilities to floating rates (MIBOR, Bank rates etc). In a liquid scenario this swap allows

corporate to benefit from lower rates by converting high cost fixed rates debt into a

floating rate.Corporate desiring to borrow through floating rate instruments may find it

difficult to do so owing to the low investor appetite for such products. They may now

borrow funds through fixed rate instruments and swap it into floating by received fixed

and pay floating. This way they effectively simulate the desired floating rate instrument.

Corporates can also convert high cost fixed deposits to floating rate if it reduces their cost

of funds by receiving the fixed rate in an OIS.

Open ended mutual funds maintain a certain portion of their corpus in call money for

liquidity management. On this they earn a variable return. They may wish to remove this

uncertainty by receiving a fixed rate in an OIS (paying the overnight rate). The key

- - - 6 -

advantage of this strategy is that the amount so hedged continues to be maintained in call

money and can be used to meet an unexpected redemption. Floating rate debentures

currently held by a mutual fund may similarly be effectively converted to fixed rate

instruments. In a bearish or Uncertain market, a fund may use swaps to hedge its

portfolio by paying the fixed rate (receiving the floating rate) thus offsetting the losses on

its portfolio with gains on the swaps.

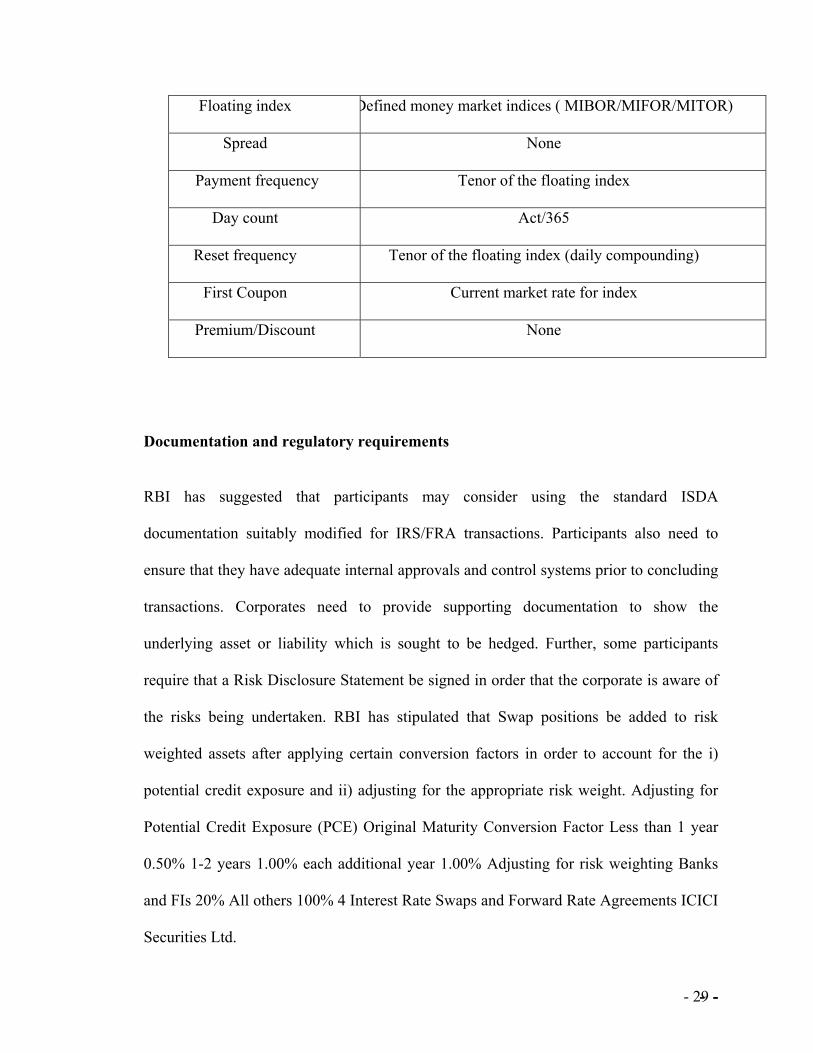

C>Documentation and regulatory requirements

RBI has suggested that participants may consider using the standard ISDA

documentation suitably modified for IRS/FRA transactions. Participants also need to

ensure that they have adequate internal approvals and control systems prior to concluding

transactions. RBI has stipulated that Swap positions be added to risk weighted assets after

applying certain conversion factors in order to account for the i) potential credit exposure

and ii) adjusting for the appropriate risk weight. Adjusting for Potential Credit Exposure

(PCE) Original Maturity Conversion Factor Less than 1 year 0.50% 1-2 years 1.00% each

additional year 1.00% Adjusting for risk weighting Banks and FIs 20% All others 100%

4 Interest Rate Swaps and Forward Rate Agreements ICICI Securities Ltd.

D>Valuation of an IRS

A swap can be decomposed into two parts - Accrual and Mark-to Market (MTM).

Accrual refers to the difference between the interests’ payments on both legs from the

start date till the valuation date. MTM value of a swap would be the replacement value of

an existing swap on the valuation date

- - - 7 -

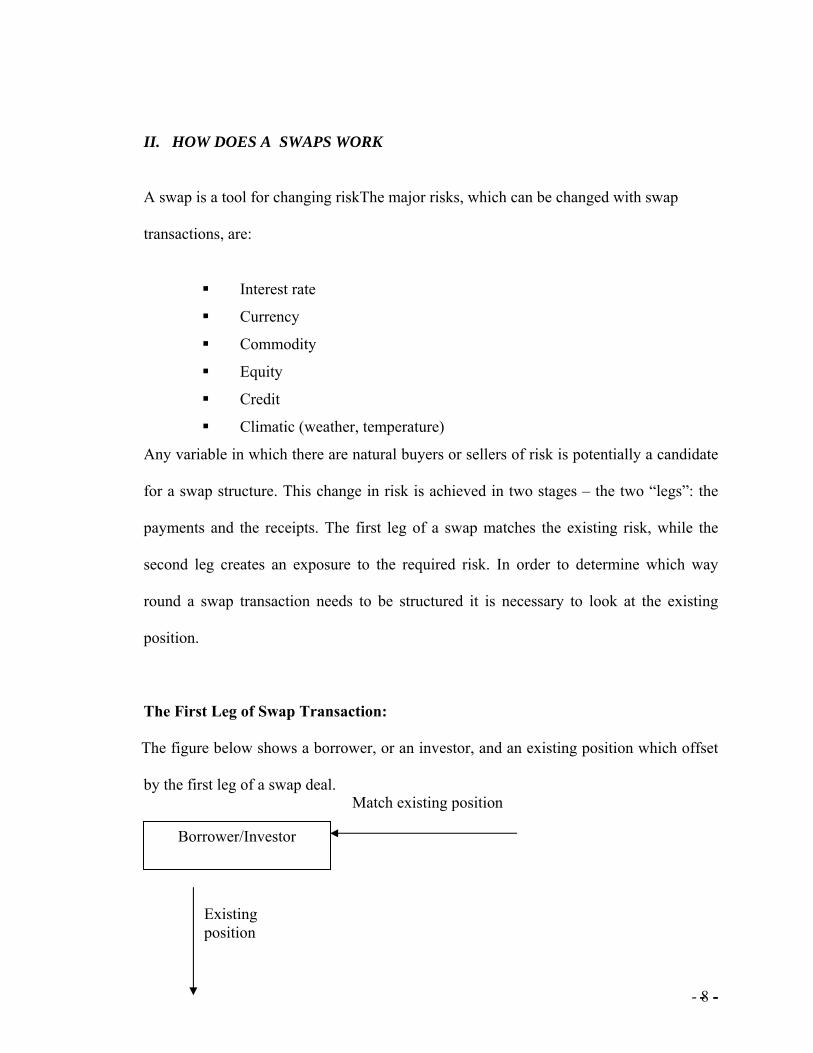

II. HOW DOES A SWAPS WORK

A swap is a tool for changing riskThe major risks, which can be changed with swap

transactions, are:

Interest rate

Currency

Commodity

Equity

Credit

Climatic (weather, temperature)

Any variable in which there are natural buyers or sellers of risk is potentially a candidate

for a swap structure. This change in risk is achieved in two stages – the two “legs”: the

payments and the receipts. The first leg of a swap matches the existing risk, while the

second leg creates an exposure to the required risk. In order to determine which way

round a swap transaction needs to be structured it is necessary to look at the existing

position.

The First Leg of Swap Transaction:

The figure below shows a borrower, or an investor, and an existing position which offset

by the first leg of a swap deal. Match existing position

Borrower/Investor

Existing position

- - - 8 -

So in all interest rate swaps where the existing position is debt, the first leg of the swap is

interest income which matches the interest payments of the debt.

The Second Leg of Swap Transaction:

Having matched the existing exposure with the first leg of the Swap, the borrower creates

the required exposure with the second leg of the swap.

Match existing position: fixed rate YEN

Borrower/Investor

Scenario - An Interest Rate Swap is a method for managing Debt:

Interest rate swaps allow users to switch from one basis to another, for example, from a

fixed-rate export credit to a floating-rate bank borrowing (say 3-month Libor), or to

switch within a specific interest rate type, e.g.: from 6-month Libor to 3-month Libor.

Scenario 1: Interest rates are expected to rise significantly. A floating-rate

borrower could consider fixing the cost of debt for whatever time horizon is

deemed prudent.

Scenario 2: Interest rates are expected to fall significantly. A fixed-rate

borrower could consider receiving a fixed rate and paying a floating rate in a swap

transaction.

- - - 9 -

RATIONALE OF INTEREST RATE SWAPS

A Single Currency Interest Rate Swap (IRS) is an exchange of cash flows between two

counter parties at predetermined specifications. It is an obligation between them for

exchange of interest payments or receipts on investments, in the same currency on an

agreed amount of notional principal at regular intervals, over an agreed period of time.

Swaps can broadly be classified into two types:

(a) Fixed to Floating-In this type of a swap the customer receives cash flows at a

fixed rate of interest and simultaneously pays cash flows at a floating rate of

interest or vice versa. The cash flows are calculated on a Notional Principal

amount. The floating rate of interest is usually determined by reference to a

transparent benchmark

(b) Floating to Floating - In this kind of a swap, both the counter-parties exchange

interest amounts based on two different floating reference rates, through the life

of the swap.

Dealing and Quotations:

Trade date is the date the counterparties agree on the swap conditions. Effective date is

the date that the swap becomes effective, i.e. when the interest obligations start to accrue.

Maturity date is the date the swap stops accruing interest and terminates.

Market quotations for swaps are usually quoted against standard benchmark / index rates

and non-amortising national principal, free from the margin actually payable in the cash

market by the relevant counterparties. The rate is thus quoted flat and any amortising

structure that envisages a customised rate is adjusted accordingly.

A quote of 9.75% - 10.25% against 3 month MIBOR means that the market maker:

(i)Pays (bid) 9.75% fixed and receives INR 3 month MIBOR

- - - 10 -

(ii) Receives (ask/offer) 10.5% fixed and pays INR 3 month MIBOR

Overnight Trade rate or MIBOR ,Treasury Bills and Term Money rate are examples

of floating rate benchmarks

REGULATIONS FOR IRS :

RBI regulations for Swaps are as under:

a. Banks can offer these derivatives to corporates for hedging underlying genuine

exposures

b. No specific permission is required from the RBI to undertake FRAs/IRS

c. Benchmark can be any rate from the domestic money or debt

d. market, or any rate implied in the forward foreign exchange markets, provided

that the methodology of calculating the rate is objective, transparent and mutually

acceptable

e. There are no restrictions on size or tenor for interest rate swaps, though there are

some limits on currency swaps

f. Banks are allowed to deal without underlying exposure for market

making activity (within prudential internal limits)

II> OBJECTIVES AND RATIONALE OF STUDY

(a) The main objective of this paper to make the treasurer to understand the company”s

Interest rate risk exposure . , how it is likely to change over time , and where any of

the exposures are compensating , how they can be netted against each other

(b) As heavy dependence upon short term borrowing not only increases risk of insolvency

from funding long term assets with short term borrowings but also exposes a Corporate

to short term interest rate increases .IRS are hedging tools to reduce Interest rate risk . It

- - - 11 -

has therefore become pertinent and inevitable to study the approaches to manage

interest rates .

METHODOLOGY FOR PRICING IRS :

The methodology adopted is to develop the model for pricing and valuation of plain

vanilla interest rate swap is as follows:

The project has parts:

PART I : undertakes the study of the Pricing and Valuation of Plain Vanilla Interest

Rates Swaps in India and formulates the model for the same on Microsoft

Excel.Literature survey was made to understand the different theoretical concepts of

Pricing and Valuation of Plain Vanilla Interest Rate swaps. This process was extended to

understand and conceptualize the structure used by Reuters for pricing and valuation of

the Swaps. This was finally modeled in the excel sheet which generates the same value as

returned by Reuters for Generic Swaps

THE APPLICATIONS OF INTEREST RATE SWAPS:

Changing A Borrower’s Mix Of Fixed-And-Floating Rate Debt:

The three most commonly used techniques, which change floating-rate debt to fixed-rate

basis, are:

Pay a fixed rate and receive a floating rate in an interest rate swap.

- - - 12 -

Buy FRAs (Forward Rate Agreements).

Sell three-month Eurodollar futures.

It would be possible to change floating-rate debt to fixed-rate debt by borrowing fixed-

rate money and using the proceeds of the fixed-rate loan to repay the floating-rate debt.

This technique is administratively burdensome and often very costly as there are likely

fees charged on both loans. There are other difficulties. It may not be possible to prepay

the existing floating-rate debt and it may be difficult to source fixed-rate money.

Liquidity in the fixed-ate markets varies with currency, maturity, the borrower’s credit

quality and the economic

cycle. Many borrowers therefore use Swaps or FRAs or futures as a cost effective

alternative.

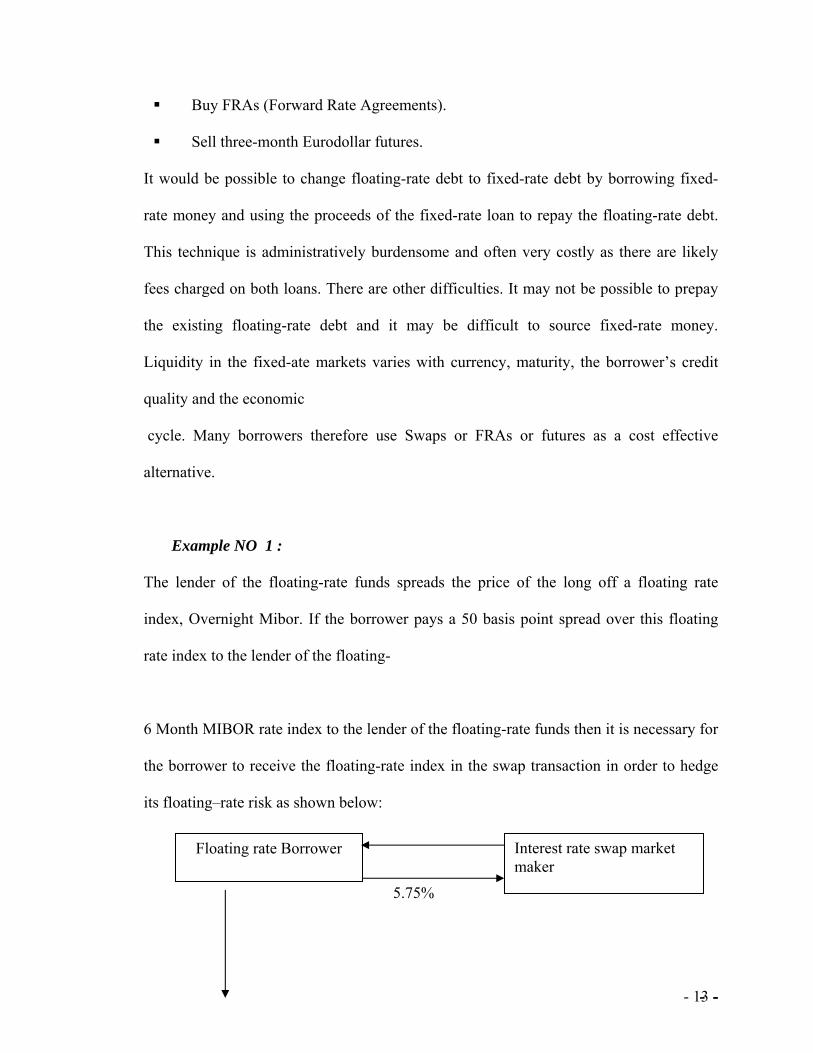

Example NO 1 :

The lender of the floating-rate funds spreads the price of the long off a floating rate

index, Overnight Mibor. If the borrower pays a 50 basis point spread over this floating

rate index to the lender of the floating-

6 Month MIBOR rate index to the lender of the floating-rate funds then it is necessary for

the borrower to receive the floating-rate index in the swap transaction in order to hedge

its floating–rate risk as shown below:

5.75%

Interest rate swap market maker

Floating rate Borrower

- - - 13 -

The floating rate borrower’s net floating-rate position is now fixed at a cost of 50 basis

points. O matter what the level of Mibor, the borrower is hedged from changes in the

floating rate because it’s both payer and a receiver of Mibor. So if the daily Mibor is 6%

the borrower will pay 6.50% for the loan and receive 6.0% in the swap: net cost 50 basis

points.

6-month Mibor + 0.50%

Credit Arbitrage, Reducing The Cost Of Floating-Rate Money

Credit arbitrage exists because there is no universal price for credit. This helps to

contribute to inefficiencies in the credit markets.

Example No 2 :

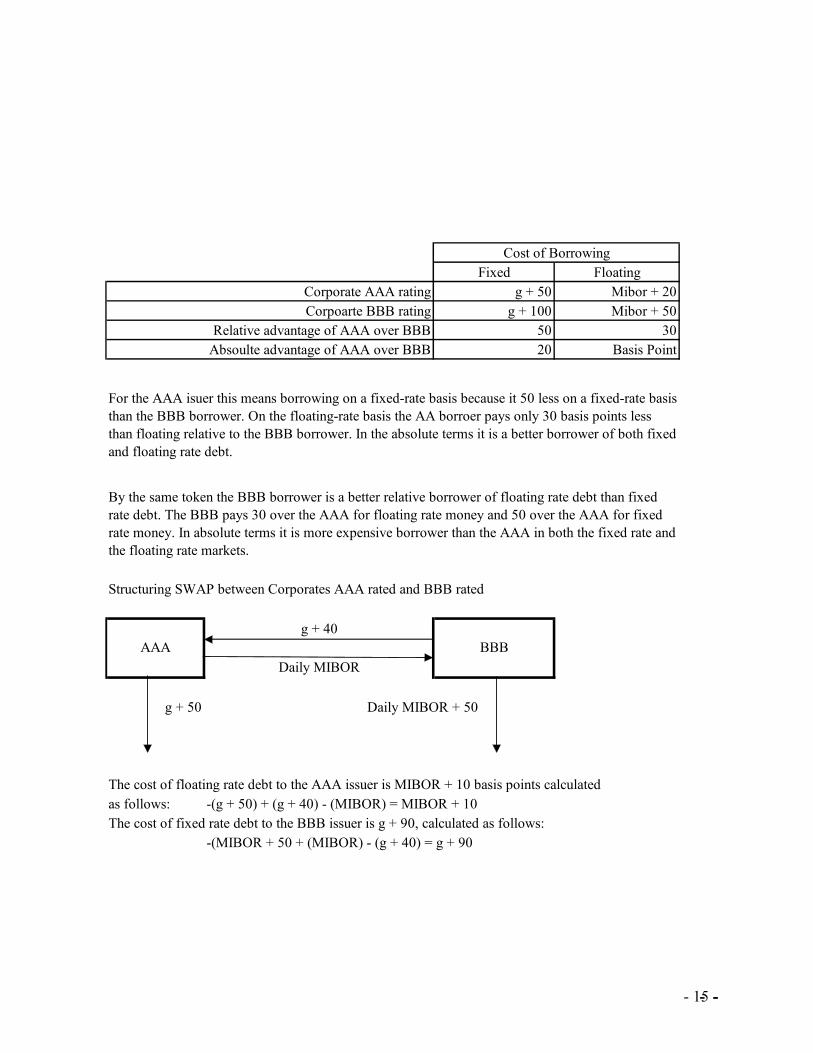

Let there be two corporates with different credit ratings (AAA and BBB). Investor

preferences and the relative demand for the fixed-rate credits will determine the

fluctuations in the spread between the cost of borrowing on a fixed-rate basis for the

AAA and the BBB rated companies. In a market, where credit suddenly becomes major

concern, it would be evidenced in a widening of the spread between these two particular

credit.

- - - 14 -

Fixed Floatingg + 50 Mibor + 20

g + 100 Mibor + 5050 3020 Basis Point

Structuring SWAP between Corporates AAA rated and BBB rated

g + 50

The cost of floating rate debt to the AAA issuer is MIBOR + 10 basis points calculated as follows: -(g + 50) + (g + 40) - (MIBOR) = MIBOR + 10The cost of fixed rate debt to the BBB issuer is g + 90, calculated as follows:

-(MIBOR + 50 + (MIBOR) - (g + 40) = g + 90

Daily MIBOR

Absoulte advantage of AAA over BBB

For the AAA isuer this means borrowing on a fixed-rate basis because it 50 less on a fixed-rate basis than the BBB borrower. On the floating-rate basis the AA borroer pays only 30 basis points less than floating relative to the BBB borrower. In the absolute terms it is a better borrower of both fixed and floating rate debt.

Daily MIBOR + 50

Corporate AAA ratingCorpoarte BBB rating

Cost of Borrowing

Relative advantage of AAA over BBB

By the same token the BBB borrower is a better relative borrower of floating rate debt than fixed rate debt. The BBB pays 30 over the AAA for floating rate money and 50 over the AAA for fixed rate money. In absolute terms it is more expensive borrower than the AAA in both the fixed rate and the floating rate markets.

AAA BBBg + 40

- - - 15 -

So the AAA issuer saves 10 basis points by swapping from the fixed to floating by paying

MIBOR + 10 rather than MIBOR + 20, and the BBB issuer also saves 10 basis points by

paying g + 90 rather than g + 100. The combined savings are equal to the difference

between the differences in their respective cost of credit on a fixed and a floating rate

basis. So, the credit arbitrage is created by the different prices of credit in different

markets. This happens as a result of the different motivations of institutional and retail

investors in the bond markets and the competitive forces of syndicated loan pricing

amongst banks in the loan market.

Example 3

Consider two companies, rated AAA and BBB. AAA has a higher credit rating than BBB. Both companies can raise funds either by issuing fixed-interest bonds or by taking bank loans (at a floating interest rate). Their borrowing costs are:

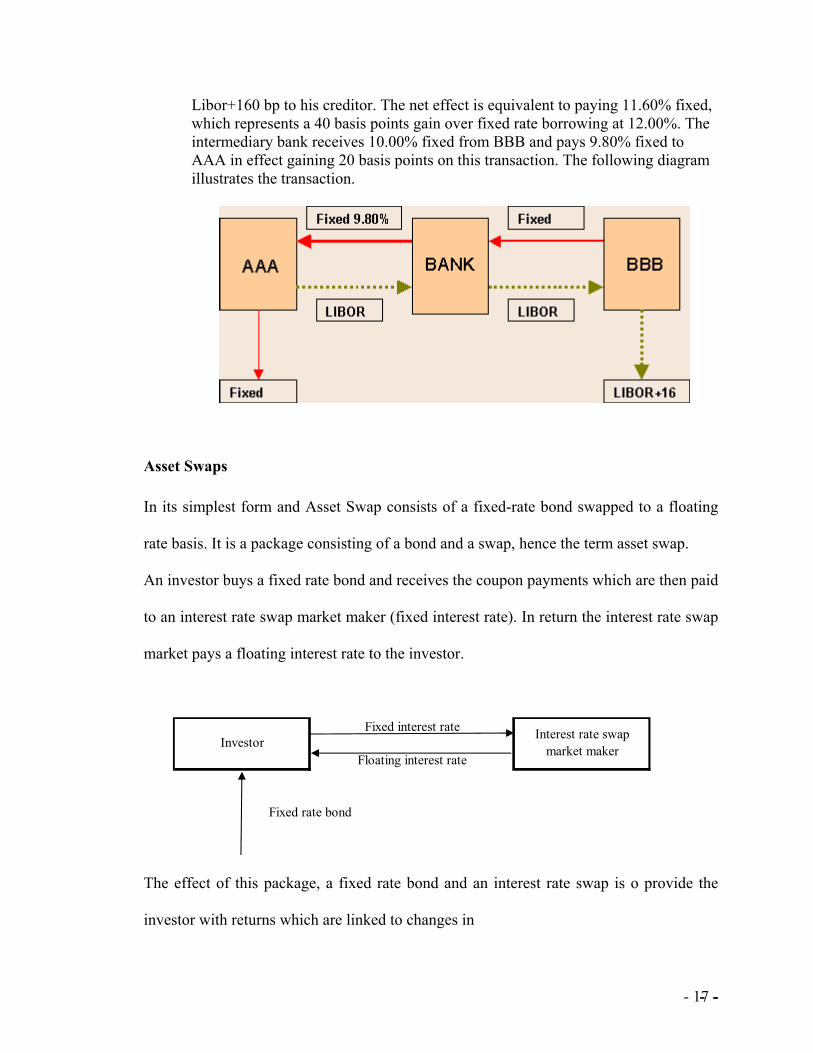

Cost of Funds to AAA and BBB Fixed rate bonds Floating rate loans AAA 10.00% p.a. Libor+100bp BBB 12.00% pa Libor+160bp Differential 200 bps 60bps

Assume now that AAA wants to raise floating rate money and BBB wants to raise fixed rate money. It will be realized that the advantage (200 basis points) of AAA raising fixed rate money in the bond market as against BBB, which is, is greater than the disadvantage (60 basis points) of letting BBB raise floating rate money in the credit market. There is a comparative advantage of 140(200-60) basis points. Both the parties can share the difference and reduce their borrowing costs. A Banker normally acts as an intermediary and arranges most of these deals. A share of the advantage is passed on to the banker. In this case, if the three parties agree to share the difference as 80:40:20 basis points, then AAA will receive 9.80% fixed from the bank in exchange for Libor, while paying 10.00% on his bonds. The net outcome for AAA is a floating rate liability at Libor+20 bps. This represents a gain of 80 basis points, than if he had borrowed at Libor+100 bp. Similarly Borrower BBB receives Libor in lieu of 10.00% fixed while paying

- - - 16 -

Libor+160 bp to his creditor. The net effect is equivalent to paying 11.60% fixed, which represents a 40 basis points gain over fixed rate borrowing at 12.00%. The intermediary bank receives 10.00% fixed from BBB and pays 9.80% fixed to AAA in effect gaining 20 basis points on this transaction. The following diagram illustrates the transaction.

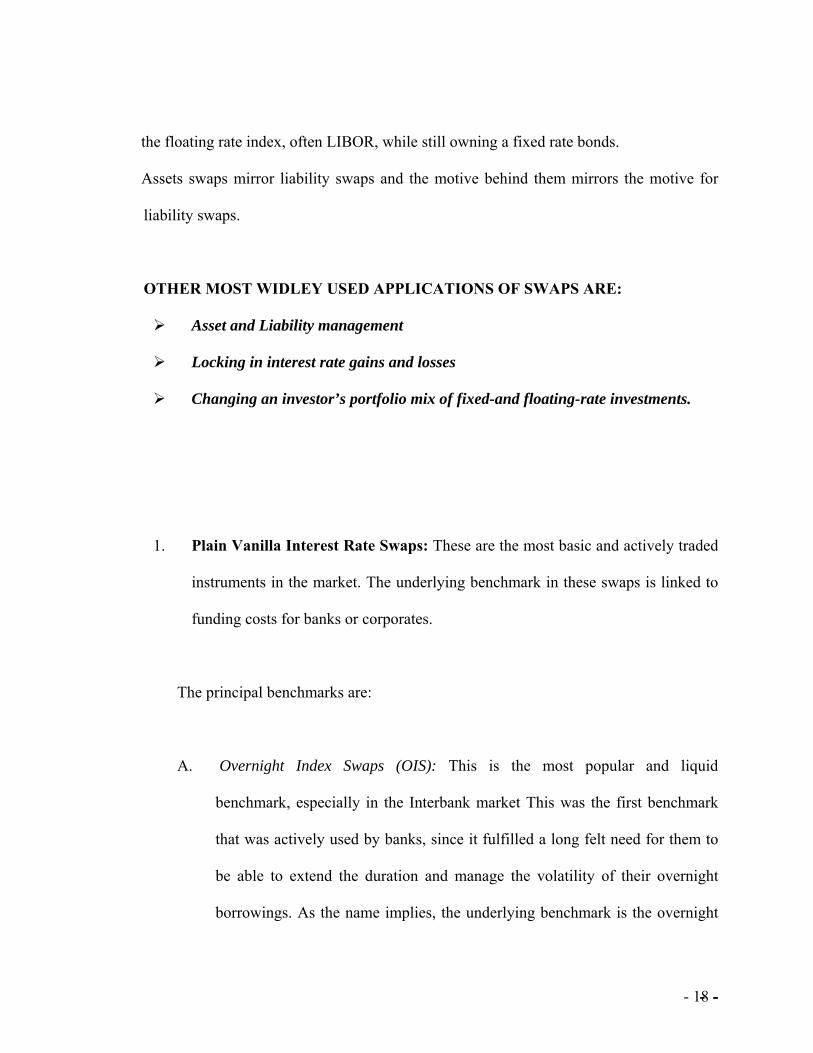

Asset Swaps

In its simplest form and Asset Swap consists of a fixed-rate bond swapped to a floating

rate basis. It is a package consisting of a bond and a swap, hence the term asset swap.

An investor buys a fixed rate bond and receives the coupon payments which are then paid

to an interest rate swap market maker (fixed interest rate). In return the interest rate swap

market pays a floating interest rate to the investor.

Investor Interest rate swap market maker

Fixed rate bond

Floating interest rate

Fixed interest rate

The effect of this package, a fixed rate bond and an interest rate swap is o provide the

investor with returns which are linked to changes in

- - - 17 -

the floating rate index, often LIBOR, while still owning a fixed rate bonds.

Assets swaps mirror liability swaps and the motive behind them mirrors the motive for

liability swaps.

OTHER MOST WIDLEY USED APPLICATIONS OF SWAPS ARE:

Asset and Liability management

Locking in interest rate gains and losses

Changing an investor’s portfolio mix of fixed-and floating-rate investments.

1. Plain Vanilla Interest Rate Swaps: These are the most basic and actively traded

instruments in the market. The underlying benchmark in these swaps is linked to

funding costs for banks or corporates.

The principal benchmarks are:

A. Overnight Index Swaps (OIS): This is the most popular and liquid

benchmark, especially in the Interbank market This was the first benchmark

that was actively used by banks, since it fulfilled a long felt need for them to

be able to extend the duration and manage the volatility of their overnight

borrowings. As the name implies, the underlying benchmark is the overnight

- - - 18 -

call money rate. The floating

benchmark is known as MIBOR, which is a daily fixing done by the National

Stock Exchange (NSE) against which the swap is settled. Although the

floating rate is reset daily, for the sake of convenience, it is compounded and

settled only at a frequency which can be chosen by the swap counter parties

(e.g., every month, quarter or half year). Although OIS swaps are quoted out

to five years, the maximum liquidity is for tenor’s upto two years.

FIXED vs NSE Overnight MIBOR Index

B. MITOR Swaps: These are similar to OIS swaps, with the difference being that

the underlying overnight floating rupee rate is derived from the USD Fed

Funds Rate and the USD/INR C/T Premia, rather than being directly derived

from the actual call rate in the Indian market. This benchmark is not as

popular as the preceding OIS benchmark.

C. MIFOR Swaps : This is another popular benchmark that has developed into a

proxy for the AAA corporate funding cost in India. Since India does not have

a fully developed term money market, it is derived from USD Libor and the

USD/INR Forward Premia, both of which are extremely deep and liquid

markets. Although the popular perception is that MIFOR might be subject to

sudden swings on account of the fact that it is derived from the forex forwards

market, this is a misplaced fear − it is simply the Indian equivalent of USD

Libor and the USD Interest Rate Swaps market, and behaves like an interest

rate benchmark, not a forex benchmark. There are a large number of Indian

- - - 19 -

Corporates who now regularly use this benchmark to actively manage the

interest rate risk on their debt portfolios, and access funding at better rates.

Fixed vs Implied INR yield derived from USD /INR

2. Currency Swaps: These are interest rate derivatives whereby Rupee debt held by

banks or corporate can be swapped into debt in another currency or vice versa. As

expected, the most popular currency for swapping debt is the US Dollar, with the

Japanese Yen coming in second. It is especially useful for companies having

raised forex debt who wish to hedge all or part of the foreign exchange risk and

interest rate risk by swapping into Rupees. Similarly, companies holding rupee

debt who wish to either lower funding costs or diversify the currency mix of their

debt portfolios often choose to swap from rupee debt into forex debt. An

interesting point to note is that while no optionality is permitted on the Rupee leg

of the currency swap, there is substantial scope for employing more sophisticated

hedging strategies by embedding options on the forex leg of the swap.

There are also many variants of currency swaps, like coupon swaps and Principal

Only swaps (POS) which are popular amongst Indian corporates.

3. G−Sec Linked Swaps: While the first category of benchmarks like OIS and

MIFOR are linked to corporate/bank funding costs in India, this category of

benchmarks is linked to the Government of India’s borrowing cost, viz. yields on

Government Securities (G−Sec). Just as a company can enter into a swap where

the benchmark for the floating leg is 6 month MIFOR, it can also enter into a

- - - 20 -

swap where the benchmark is the yield on the 1−Year G−Sec. The daily setting

for G−Sec yields for different tenors is exhibited on a Reuter’s page known as

INBMK.

IN BMK SWAP =Fixed vs 1 year IN BMK rate

These swaps are important as they allow banks and corporates to take views on the

relative movements of GOI yields and corporate spreads, without necessarily actually

taking positions in the securities themselves. Apart from these basic products, there are

a variety of complex products that can be built from these underlying benchmarks. e.g.

a popular variant in India has been the Constant Maturity Treasury (CMT) swap, where

the underlying floating rate, instead of being a 3−month or 6−month rate, is the 5− Year

G−Sec Yield. There are also forward rate agreements, rate locks, spread locks, quanto

swaps etc which all use these basic building blocks to allow the swap counter parties to

take more sophisticated views on not only the future movement of interest rates, but

also the shape and slope of the yield curve and the widening or narrowing of spreads

between different benchmarks, to name just a few.

PRICING OF INTEREST RATE SWAP

GENERIC INTEREST RATE SWAP

A generic or “Plain Vanilla” interest rate swap is the simplest form of medium-term IRS.

A contract which involves two counterparties to exchange over an agreed price streams

of interest payments during the period of swap contract, each based on a different kind on

interest rate, on a notional amount which is not exchanged during the period of contract.

- - - 21 -

Interest rate swaps are used to hedge interest rate risks as well as to take interest rate

risks. If a bank is of the view that interest rates will fall, it may convert its fixed interest

liability into a floating interest liability and also his floating rate into fixed rate assets. If

it expects the interest rate to go up then it may convert its floating rate liability into fixed

liability and fixed rate assets into floating rate assets.

The characteristics of Interest Rate Swaps:-

1. The principal amount is only notional.

2. Opposing payments through the swap are normally netted.

3. The frequency of payment reflects the tenor of the floating rate index.

These constitute the vast bulk of inter-bank trading.

Definition

An interest rate swap is a financial contract between two parties exchanging or swapping

a stream of interest payments for a 'notional principal' amount on multiple occasions

during a specified period. Such contracts generally involve exchange of a ‘fixed to

floating’ or ‘floating to floating’ rate of interest. Accordingly, on each payment date - that

occurs during the swap period - cash payments based on fixed/floating and floating rates,

are made by the parties to one another.

Features

• Minimum Notional Principal Amount: The minimum notional principal amount

for which market makers will stand committed to their two-way quote is Rs. 5

crores.

- - - 22 -

• Tenor: The swap can be flexible in tenor i.e. there are no restrictions on the tenor

of the swap. Unless stated otherwise, a rupee interest rate swap shall be assumed

to have a day count basis of Actual/365.

• Trading Hours: The trading hours will be 9.00 am -5.30 p.m. for all swaps

wherein the benchmark is based on the money market or the fixed income market.

In respect of swaps, wherein the benchmark is based on the foreign exchange

market, the trading hours will be in accordance with the trading hours for foreign

exchange transactions. Currently the trading hours for foreign exchange is from

9.00/10.00 a.m. to 4.00p.m.

• Effective Date: The Effective Date will be the first Mumbai Business Day

(excluding Saturday) after the Trade Date, except for interest rate swaps against

which payments are based upon the “INR-MIFOR” Floating Rate Option, for

which the Effective Date will be the second Mumbai Business Day (excluding

Saturday) after the Trade Date.

• Business Day Convention: The Business Day Convention applicable to all INR

interest rate swaps shall be the Modified Following Business Day Convention,

unless otherwise specified in the confirmation.

- - - 23 -

• Business Day: Unless otherwise specified in the Confirmation, Saturdays shall

not be Business Days for any purpose, except in relation to INR-MIBOR-OIS-

COMPOUND for which Saturday shall be deemed to be a Business Day.

It is recommended that regardless of the centre where the deal is transacted, the

benchmark and the holiday calendar for the purposes of computation of interest

streams be as that in Mumbai, except in case of interest rate swaps wherein the

benchmark is based on the foreign exchange market, for which the holiday calendar

of the relevant centre for that currency will also be applicable.

• Reset dates: No fixing of rates and compounding of interest will be done on a

Saturday.

• Day count fraction: The Day Count Fraction applicable to all INR interest rate

swap transitions shall be Actual / 365 Fixed.

• Broken or short calculation periods: The rate for any Calculation Period which

is shorter than the Designated Maturity set forth in the Confirmation will be

determined by the Calculation Agent based upon straight line interpolation

between the Floating Rate Option with a Designated Maturity that is immediately

shorter than the Calculation Period and the Floating Rate Option with a

Designated Maturity that is immediately longer than the Calculation Period.

• Floating Rates: The definitions of the various floating rates that are currently

dealt with in respect of interest swaps and their definitions are given below:

- - - 24 -

INR-MIBOR-OIS-COMPOUND

“INR-MIBOR-OIS-COMPOUND “ means that the rate for a Reset Date, calculated in

accordance with the formula set forth below, will be the rate of return of a daily

compound interest investment (it being understood that the reference rate for the

calculation of interest is the arithmetic mean of the daily rates of the day to day inter-

bank INR offered rate).

Formula for calculation of the floating rate

“INR-MIBOR-OIS-COMPOUND” will be calculated as follows, and the resulting

percentage will be rounded in accordance with method set forth in Section 8.1(a) of

the 2000 ISDA Definitions, but to the nearest one ten-thousandth of a percentage

point (0.0001%)

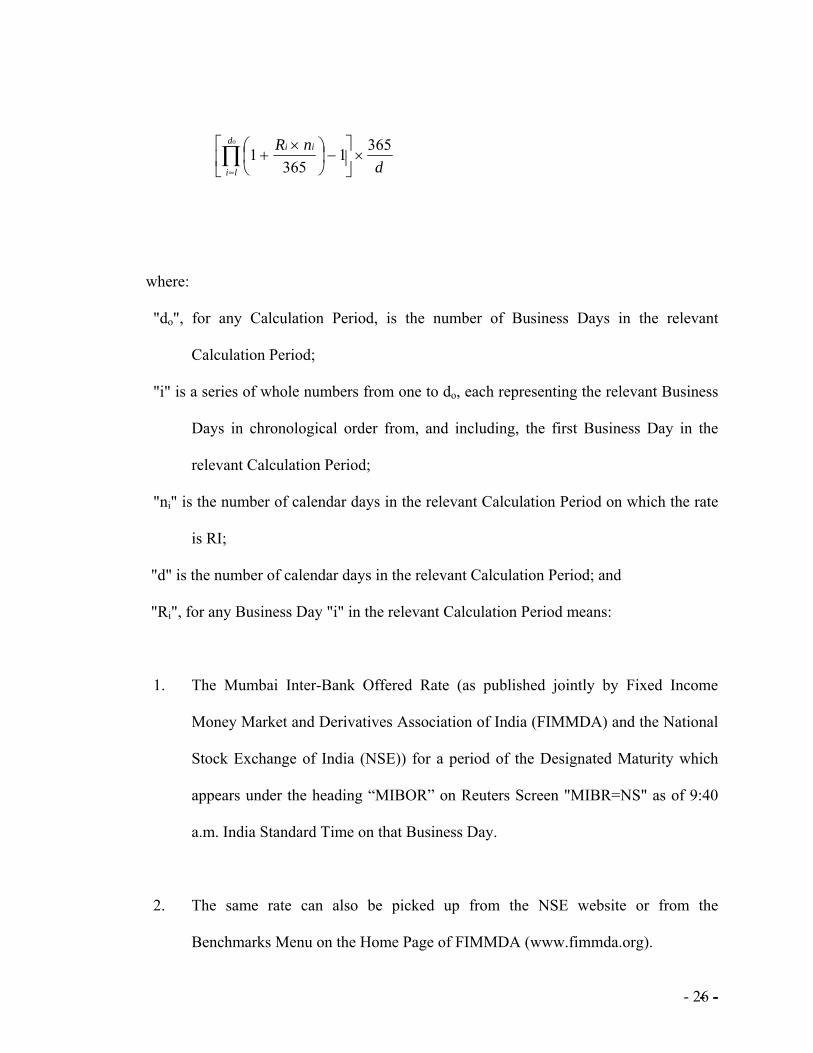

- - - 25 -

dnRod

li

ii 3651365

1 ×⎥⎦

⎤⎢⎣

⎡−⎟

⎠⎞

⎜⎝⎛ ×+∏

=

where:

"do", for any Calculation Period, is the number of Business Days in the relevant

Calculation Period;

"i" is a series of whole numbers from one to do, each representing the relevant Business

Days in chronological order from, and including, the first Business Day in the

relevant Calculation Period;

"ni" is the number of calendar days in the relevant Calculation Period on which the rate

is RI;

"d" is the number of calendar days in the relevant Calculation Period; and

"Ri", for any Business Day "i" in the relevant Calculation Period means:

1. The Mumbai Inter-Bank Offered Rate (as published jointly by Fixed Income

Money Market and Derivatives Association of India (FIMMDA) and the National

Stock Exchange of India (NSE)) for a period of the Designated Maturity which

appears under the heading “MIBOR” on Reuters Screen "MIBR=NS" as of 9:40

a.m. India Standard Time on that Business Day.

2. The same rate can also be picked up from the NSE website or from the

Benchmarks Menu on the Home Page of FIMMDA (www.fimmda.org).

- - - 26 -

3. If such rate does not appear on the Reuters Screen “MIBR=NS” or on the website

of FIMMDA / NSE, as of 9:40 a.m. India Standard Time, the rate for that

Business Day will be the Fixing Rate which appears on Reuters Screen "MIBR="

as of 9:40 a.m. India Standard Time on that Business Day.

4. If such rate does not appear on Reuters Screen "MIBR=" prior to 10:40 a.m. India

Standard Time on that Business Day then the rate for that Business Day shall be

determined as if the parties had specified “INR-Reference Banks” as the

applicable Floating Rate Option for purposes of determining Ri.

Confirmations to include

Floating Rate Option: INR-MIBOR-OIS-COMPOUND

Designated Maturity: Overnight

Spread: +/- [ ]% per annum

Floating Rate Day Count Fraction: Actual / 365 Fixed

- - - 27 -

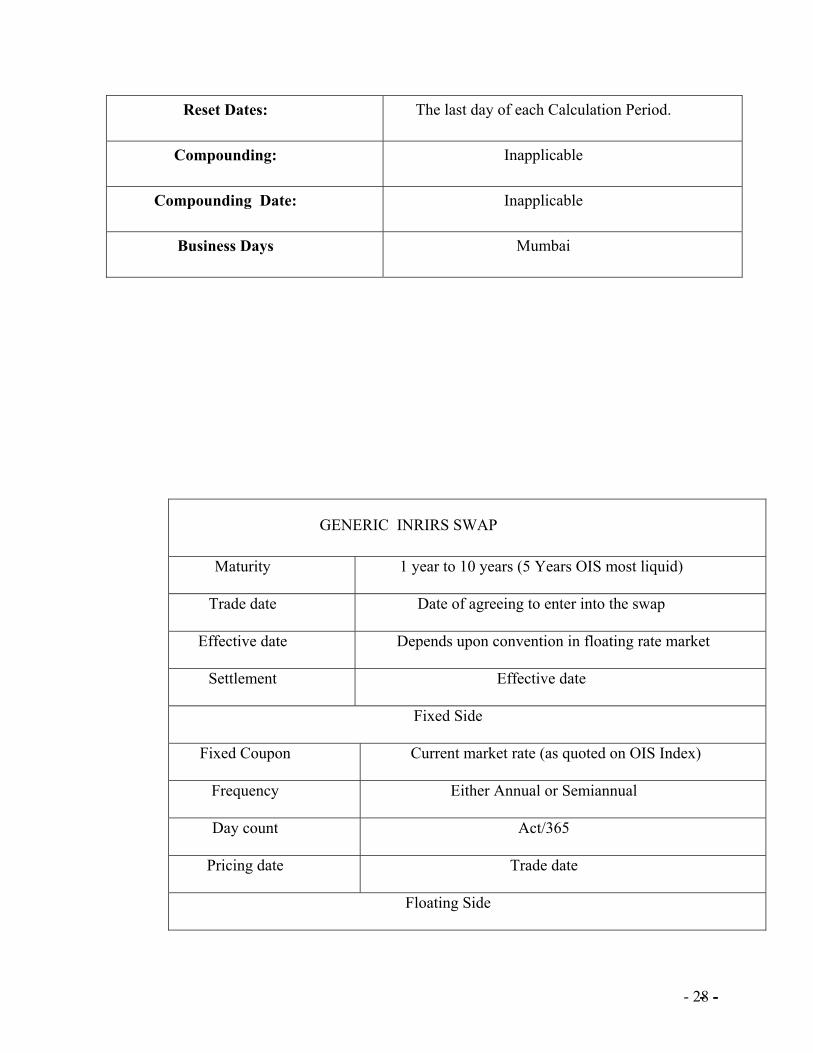

Reset Dates: The last day of each Calculation Period.

Compounding: Inapplicable

Compounding Date: Inapplicable

Business Days Mumbai

GENERIC INRIRS SWAP

Maturity 1 year to 10 years (5 Years OIS most liquid)

Trade date Date of agreeing to enter into the swap

Effective date Depends upon convention in floating rate market

Settlement Effective date

Fixed Side

Fixed Coupon Current market rate (as quoted on OIS Index)

Frequency Either Annual or Semiannual

Day count Act/365

Pricing date Trade date

Floating Side

- - - 28 -

Floating index Defined money market indices ( MIBOR/MIFOR/MITOR)

Spread None

Payment frequency Tenor of the floating index

Day count Act/365

Reset frequency Tenor of the floating index (daily compounding)

First Coupon Current market rate for index

Premium/Discount None

Documentation and regulatory requirements

RBI has suggested that participants may consider using the standard ISDA

documentation suitably modified for IRS/FRA transactions. Participants also need to

ensure that they have adequate internal approvals and control systems prior to concluding

transactions. Corporates need to provide supporting documentation to show the

underlying asset or liability which is sought to be hedged. Further, some participants

require that a Risk Disclosure Statement be signed in order that the corporate is aware of

the risks being undertaken. RBI has stipulated that Swap positions be added to risk

weighted assets after applying certain conversion factors in order to account for the i)

potential credit exposure and ii) adjusting for the appropriate risk weight. Adjusting for

Potential Credit Exposure (PCE) Original Maturity Conversion Factor Less than 1 year

0.50% 1-2 years 1.00% each additional year 1.00% Adjusting for risk weighting Banks

and FIs 20% All others 100% 4 Interest Rate Swaps and Forward Rate Agreements ICICI

Securities Ltd.

- - - 29 -

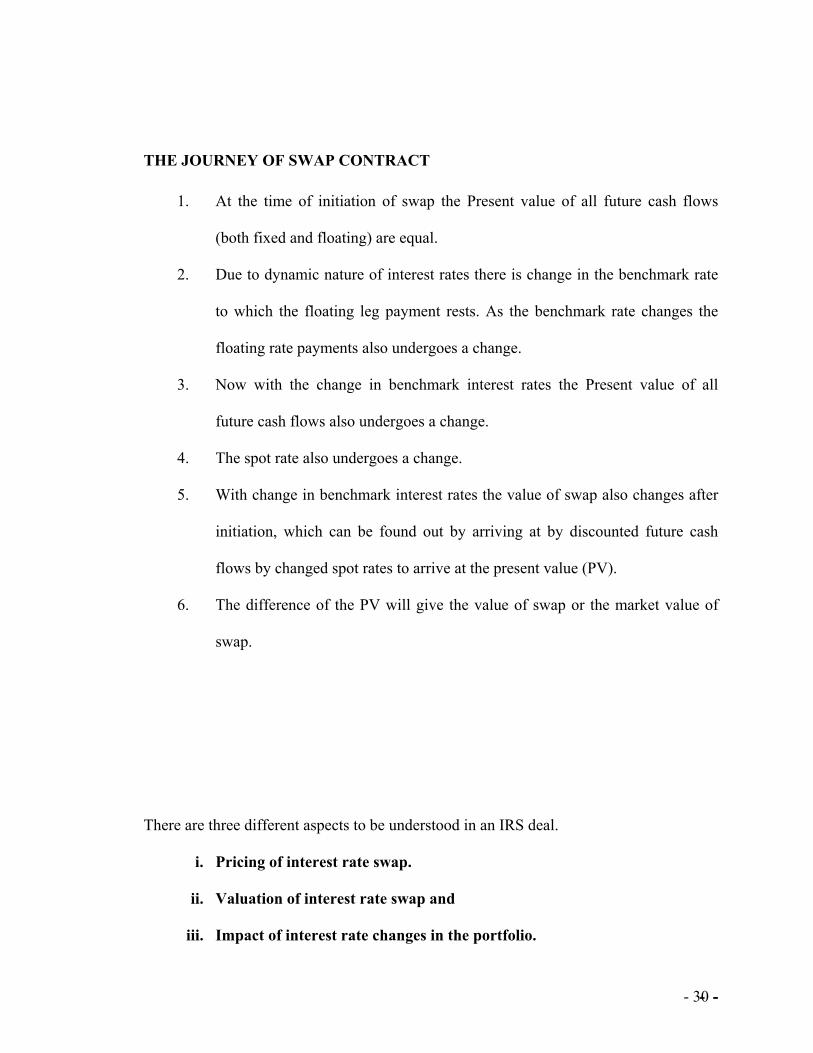

THE JOURNEY OF SWAP CONTRACT

1. At the time of initiation of swap the Present value of all future cash flows

(both fixed and floating) are equal.

2. Due to dynamic nature of interest rates there is change in the benchmark rate

to which the floating leg payment rests. As the benchmark rate changes the

floating rate payments also undergoes a change.

3. Now with the change in benchmark interest rates the Present value of all

future cash flows also undergoes a change.

4. The spot rate also undergoes a change.

5. With change in benchmark interest rates the value of swap also changes after

initiation, which can be found out by arriving at by discounted future cash

flows by changed spot rates to arrive at the present value (PV).

6. The difference of the PV will give the value of swap or the market value of

swap.

There are three different aspects to be understood in an IRS deal.

i. Pricing of interest rate swap.

ii. Valuation of interest rate swap and

iii. Impact of interest rate changes in the portfolio.

- - - 30 -

Pricing:-

In a fixed` floating interest rate swap, one party agrees to make a series of fixed payments

and receive a series of floating or variable payments. Thus the goal of swap pricing is to

determine the fixed interest rate that makes the present value of fixed payments equal to

the present value of the floating receipts. At its origination the theoretically correct swap

price will create a swap with zero value.

The pricing of interest rate swaps will depend on the price of a package of forward

contracts with the same settlement dates in which the underlying for the forward contract

is the same reference rate. The pricing of swap will depend upon the fixed rate and the

forward interest rate as on date on the basis of which we will arrive at the floating rate

payments. The pricing will be done on the basis in which the PV of both the legs (fixed

and floating) is equal at the time of initiation.

At the time of initiation of swap: -

Expected fixed payment PV = Expected floating payment PV

Valuation:-

Interest rate being dynamic in nature will change after swap initiation. Valuing swaps

after they have been originated is important for many related reasons. First the

organizations wish to know their current financial position by estimating the true value of

their assets and liabilities. Secondly, firms wishes to know the default risk they face. If a

swap has become a net asset for them they will become more concerned about the ability

- - - 31 -

of the counter party to make the payments. Thirdly swaps are marked to market. This

requires valuing of swap after they have been originated. After the initiation of swap deal

there is always a change in interest rates and as such the spot and the corresponding

forward rate also undergo a change.

Thus there is a difference in future forward rates estimated at the initiation of swap and

the current forward rates. In a Fixed Floating swap the fixed coupons for the tenure of

swap is known at the time of origination and the first floating cash flow is known, but the

remaining cash flows are unknown. With a change in interest rates the future floating

cash flows also undergoes a change. The detailed calculation is placed in Annexure- B

Value of swap (Short position) = PV of remaining Fixed cash flows – PV of

remaining floating cash flows.

Value of swap (Long position) = PV of remaining floating cash flows - PV of

remaining fixed cash flows.

- - - 32 -

Approaches to Interest Rate Risk:-

Two approaches to IRR are:-

1. Earning approach.

2. Economic value approach.

Earnings approach: - The earnings approach otherwise known as accounting approach.

The main focus of the approach is on the impact of interest rate changes on Net Interest

Income. NII is an important top line performance indicator of a bank and is computed as

under:-

NII = Interest Income - Interest Expenses.

NII in monetary terms can be expressed as a percentage in the form of Net Interest

Margin (NIM) and impact of interest rate change can be analysed on NIM. The earnings

approach concentrates on accrual income proxies of NII and has a short term focus as the

analysis of interest rate impact is restricted to maximum of a year as the accounting cycle

has a period of one year.

As the derivative portfolio of bank mainly includes Interest Rate Swaps (IRS). NII

approach to assess the impact of interest rate changes on IRS include bucketing of

notional principal amounts according to time to repricing. IRS could be considered as a

combination of a short position and long position. The notional of the fixed and floating

- - - 33 -

leg of an interest rate swap could be shown in the respective maturity bucket based on the

maturity date for the fixed leg and the reset date for the floating leg. e.g. Suppose bank

receives 5 year fixed rate of 5% and pays MIBOR on a notional principal of 10 lacs, then

the fixed leg of swap could be shown on asset side as positive in the 5-7 year bucket and

the floating leg would be shown as a negative in <1month bucket. The gap in the

respective bucket can be measured and the interest rate sensitivity can be measured.

Economic value approach (EVE): - Earnings approach of IRR has a short term focus

and covers only a shorter period with a max of one year whereas the Economic value

approach considers the long term impact of interest rate changes by covering the entire

life.

EVE = Economic value of assets - Economic value of liability.

This approach calls for the valuation of each rate sensitive asset and liability to arrive at

EVE. The approach to the valuation includes estimating the present value of future cash

flows.

This approach recognizes the fact that changes in interest rates not only affect the NII but

also the economic value also which in turn is reflected in the value of equity.

- - - 34 -

III. METHODOLOGY :

PERSPECTIVES IN IRS PRICING AND MODELLING - CASE STUDIES :

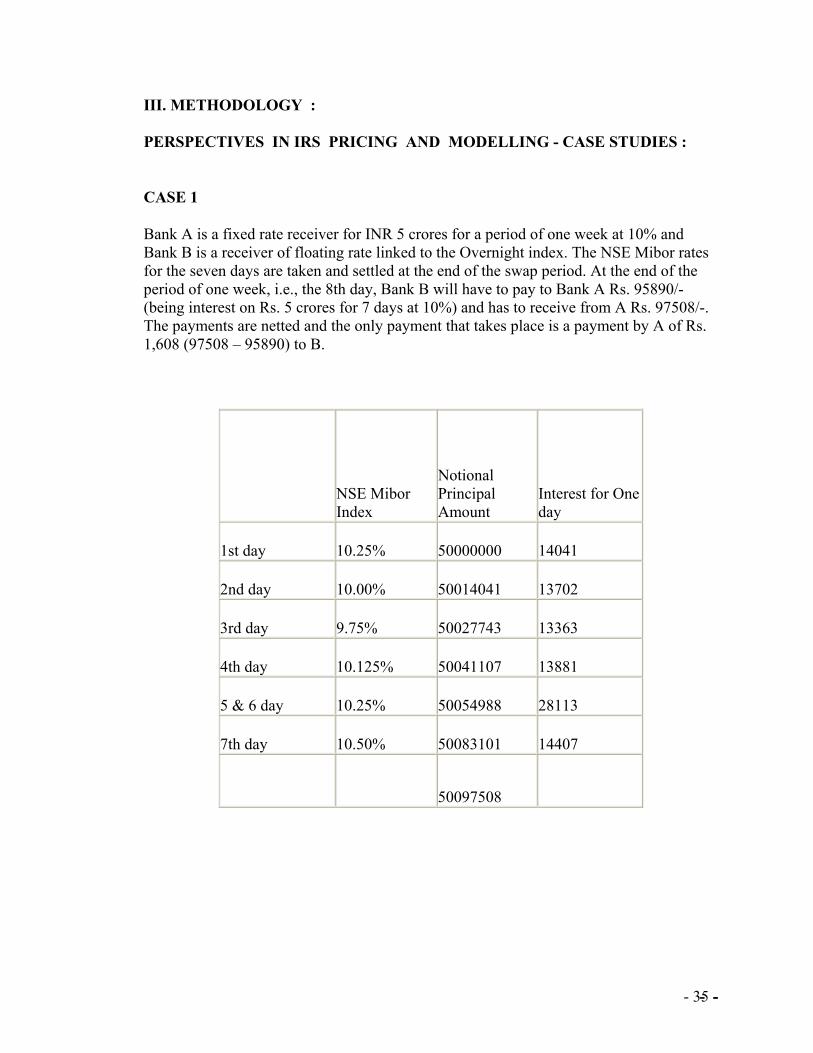

CASE 1

Bank A is a fixed rate receiver for INR 5 crores for a period of one week at 10% and Bank B is a receiver of floating rate linked to the Overnight index. The NSE Mibor rates for the seven days are taken and settled at the end of the swap period. At the end of the period of one week, i.e., the 8th day, Bank B will have to pay to Bank A Rs. 95890/- (being interest on Rs. 5 crores for 7 days at 10%) and has to receive from A Rs. 97508/-. The payments are netted and the only payment that takes place is a payment by A of Rs. 1,608 (97508 – 95890) to B.

NSE Mibor Index

Notional Principal Amount

Interest for One day

1st day 10.25% 50000000 14041

2nd day 10.00% 50014041 13702

3rd day 9.75% 50027743 13363

4th day 10.125% 50041107 13881

5 & 6 day 10.25% 50054988 28113

7th day 10.50% 50083101 14407

50097508

- - - 35 -

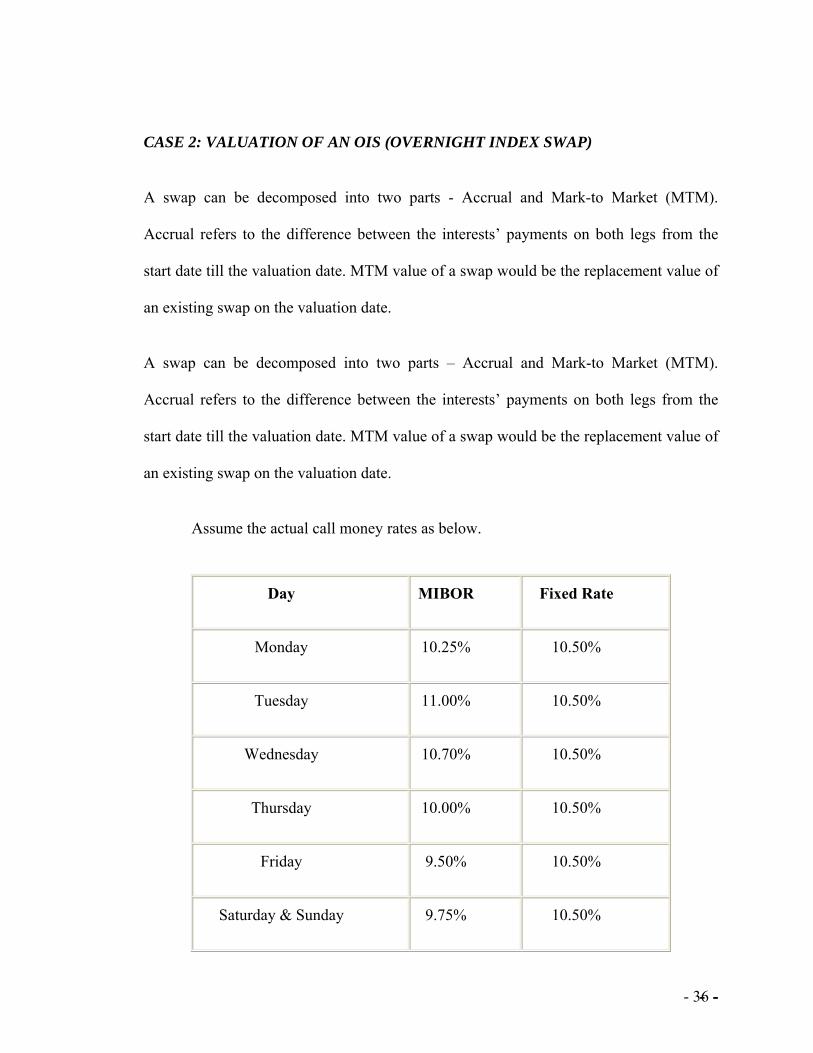

CASE 2: VALUATION OF AN OIS (OVERNIGHT INDEX SWAP)

A swap can be decomposed into two parts - Accrual and Mark-to Market (MTM).

Accrual refers to the difference between the interests’ payments on both legs from the

start date till the valuation date. MTM value of a swap would be the replacement value of

an existing swap on the valuation date.

A swap can be decomposed into two parts – Accrual and Mark-to Market (MTM).

Accrual refers to the difference between the interests’ payments on both legs from the

start date till the valuation date. MTM value of a swap would be the replacement value of

an existing swap on the valuation date.

Assume the actual call money rates as below.

Day MIBOR Fixed Rate

Monday 10.25% 10.50%

Tuesday 11.00% 10.50%

Wednesday 10.70% 10.50%

Thursday 10.00% 10.50%

Friday 9.50% 10.50%

Saturday & Sunday 9.75% 10.50%

- - - 36 -

If a Bank has entered into an OIS wherein it receive a fixed rate of 10.50% (and pays the

floating rate, i.e., MIBOR) for 6 months, then the valuation at the end of the week would

be done as follows.

The bank would have received interest (notionally) at the fixed rate of 10.50% p.a. for the

past week. Thus, it would have an accrued interest receivable of

Rs 25, 00, 00,000*0.1050*7/365= 5, 03,424.66

As far as the payment of the floating interest is concerned, the notional interest payable

will be equal to ((1+r1/365)*(1+r2/365)…1+r6*2/365)-1)*365= Rs 4, 86,345.90. The

rates r1, r2, etc. are the daily MIBOR rates. A key point to be noted is that the interest

payable on the floating side here is compounded daily, as the floating benchmark is

overnight MIBOR. Similarly, for other floating benchmarks, the compounding frequency

will vary. As a market convention, the interest payable for Sunday or a holiday is taken to

be the same as the previous working day (in this case, Saturday). In other words, the

interest is obtained through simple interest calculation across holidays and not on daily

compounded basis. Thus, the principal for calculation of interest payment applicable to a

non-working day (Sunday) is the same as the previous working day.

Netting the notional payments from the notional receipts, i.e. the fixed interest accrued

less floating interest payable, the accrued profit works out to Rs 17,078.76 (Rs 5,

03,424.66 less Rs 4, 86,345.90).

- - - 37 -

Now for MTM purpose, the bank has to check quotes for a 173-day tenure contract,

which is the residual maturity of the swap. If the quotes available are 10.00%/10.25%p.a.,

the bank has the option to pay 10.25%p.a. fixed rate (and receive MIBOR) and unwind

the existing swap. This way the bank may lock-in to a profit, irrespective of movements

in the overnight rate from then till maturity of the swap. The MTM value then is derived

as follows:

On a notional principal of Rs 25 crore, the bank pays interest under the new contract of

Rs 25,00,00,000*0.1025*173/365= Rs 1,21,45,547.95. On the earlier contract, the bank

continues to receive at the rate of 10.50% p.a., which for the next 173 days equals Rs 1,

24, 41,780.83. Thus, the bank will have a net gain of Rs 2, 96,232.88, which is termed as

the Mark to Market (MTM) gain. Actually, the MTM gain will be a tad lower than this.

This is because of the different notional principals on which the bank receives (new

contract) and pays MIBOR (old contract). Under the new contract, while it receives

MIBOR for the next 173 days on a principal of Rs 25 crore, under the old contract, it

pays MIBOR for the residual 173 days effectively on a higher principal, because of

continuous compounding done over the first seven days.

- - - 38 -

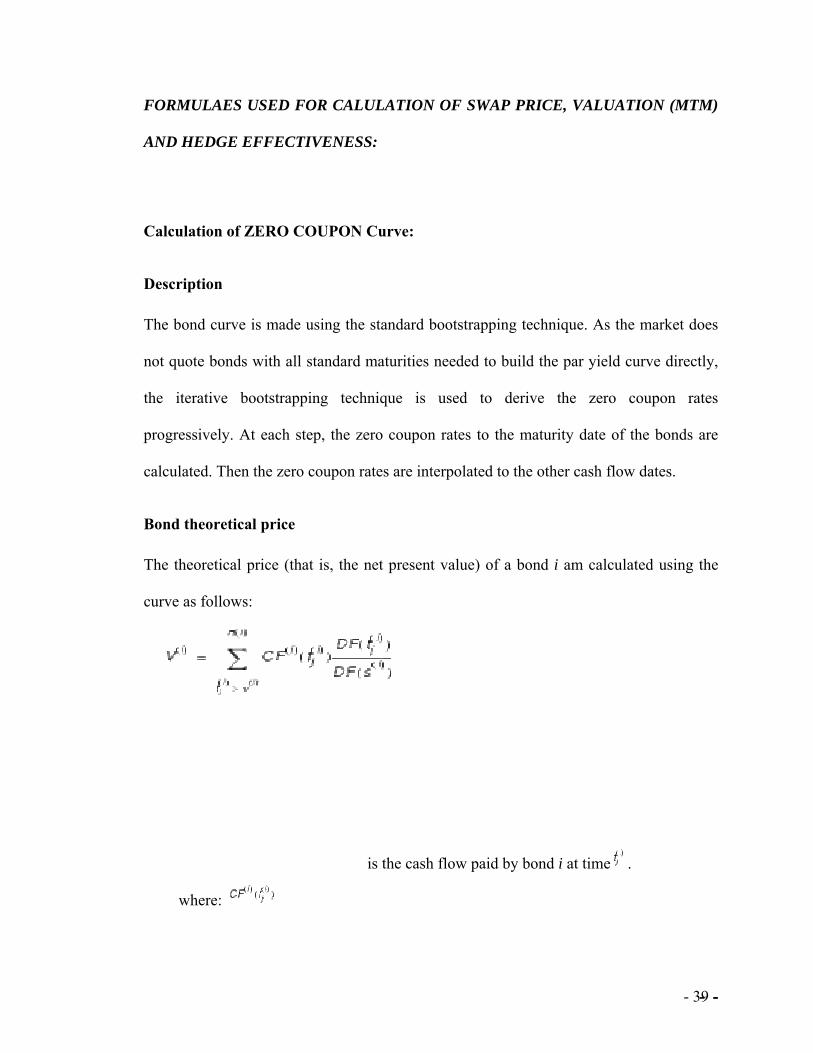

FORMULAES USED FOR CALULATION OF SWAP PRICE, VALUATION (MTM)

AND HEDGE EFFECTIVENESS:

Calculation of ZERO COUPON Curve:

Description

The bond curve is made using the standard bootstrapping technique. As the market does

not quote bonds with all standard maturities needed to build the par yield curve directly,

the iterative bootstrapping technique is used to derive the zero coupon rates

progressively. At each step, the zero coupon rates to the maturity date of the bonds are

calculated. Then the zero coupon rates are interpolated to the other cash flow dates.

Bond theoretical price

The theoretical price (that is, the net present value) of a bond i am calculated using the

curve as follows:

where:

is the cash flow paid by bond i at time .

- - - 39 -

is the discount function.

is the number of cash flows paid by bond i.

is the settlement date of bond i.

is the value date of bond i.

Then the Adjusted bootstrapping is calculated as follows

Compound interest form

Once the discount curve is calculated, then the zero coupons curve can be derived by first

determining the discount factor and then using the result as follows:

- - - 40 -

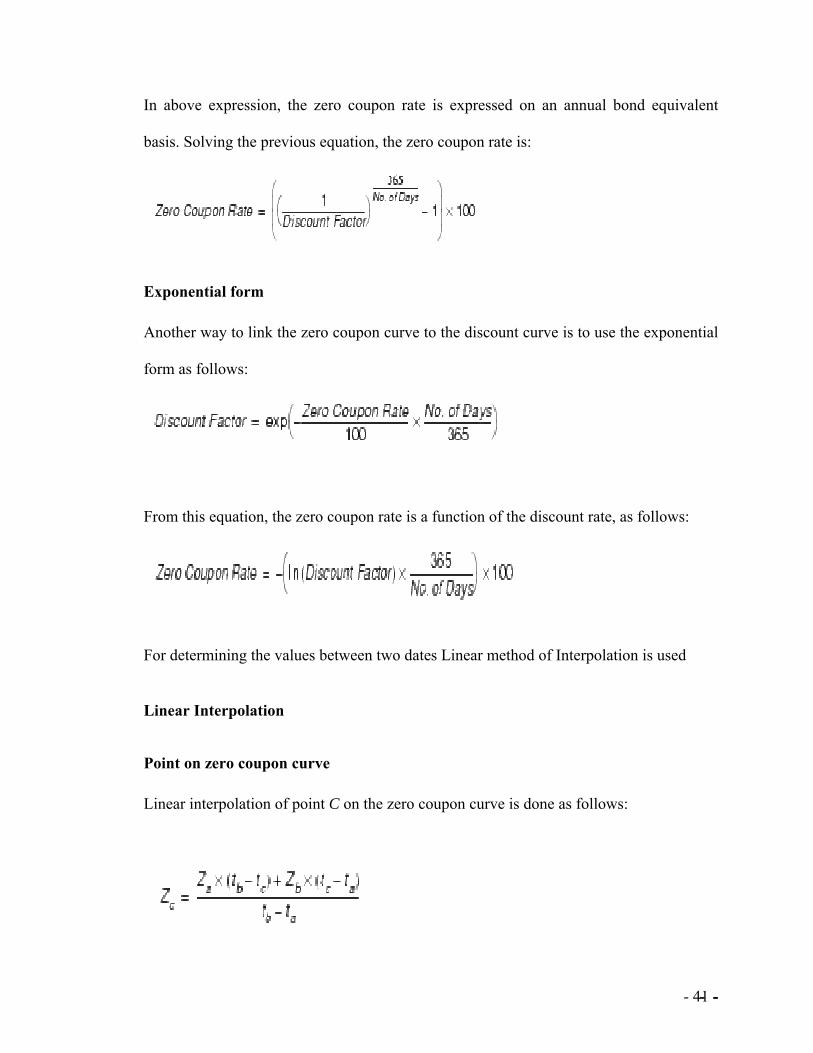

In above expression, the zero coupon rate is expressed on an annual bond equivalent

basis. Solving the previous equation, the zero coupon rate is:

Exponential form

Another way to link the zero coupon curve to the discount curve is to use the exponential

form as follows:

From this equation, the zero coupon rate is a function of the discount rate, as follows:

For determining the values between two dates Linear method of Interpolation is used

Linear Interpolation

Point on zero coupon curve

Linear interpolation of point C on the zero coupon curve is done as follows:

- - - 41 -

Exponential form

Using the exponential form of the discount curve, the preceding equation can be

expressed using the discount factor on points A and B. Solving the previous equation for

the time interval, y, and results in:

Discount factors

Then substituting y in the first equation, the discount factor at point C is:

or:

This equation can be rewritten using the discount factors for A and B:

- - - 42 -

or:

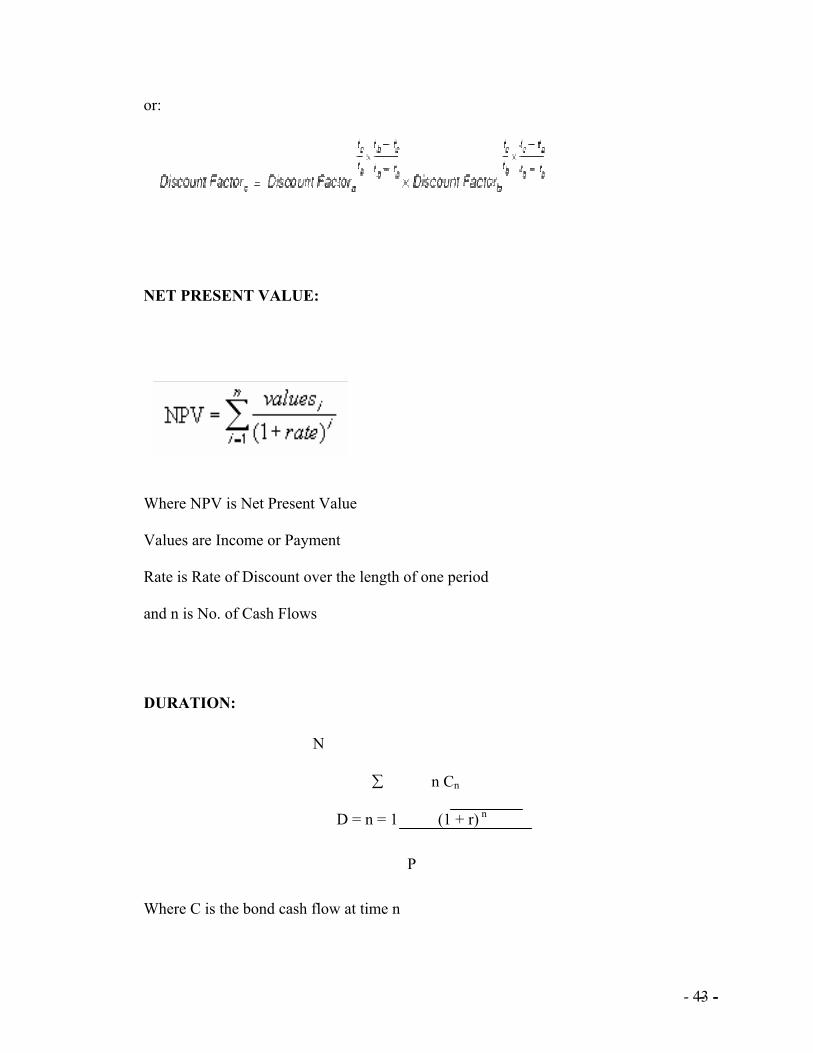

NET PRESENT VALUE:

Where NPV is Net Present Value

Values are Income or Payment

Rate is Rate of Discount over the length of one period

and n is No. of Cash Flows

DURATION:

N

∑ n Cn

D = n = 1 (1 + r) n

P

Where C is the bond cash flow at time n

- - - 43 -

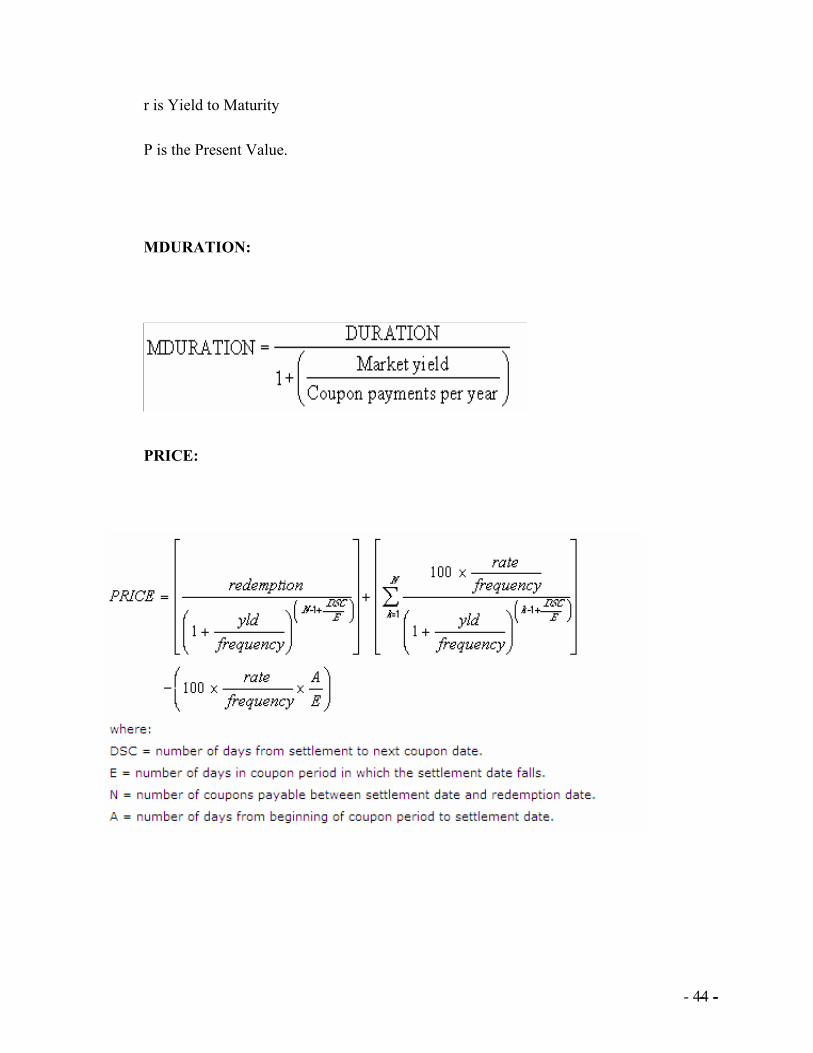

r is Yield to Maturity

P is the Present Value.

MDURATION:

PRICE:

- - - 44 -

- - - 45 -

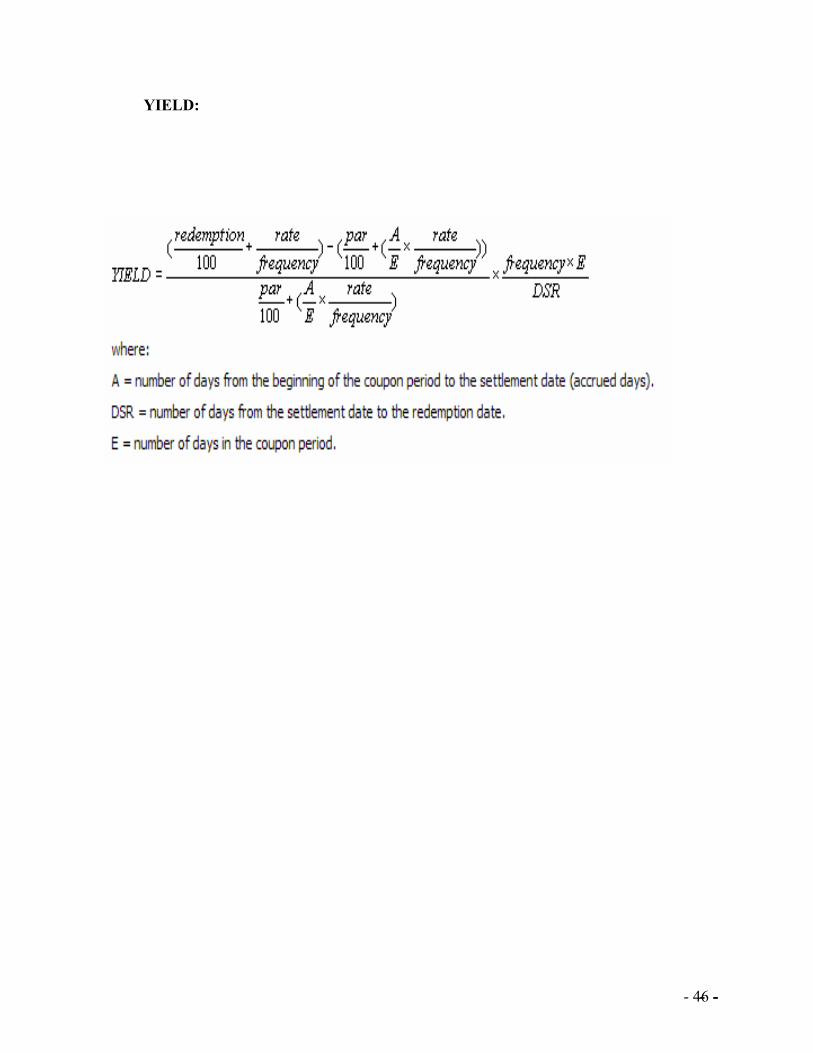

YIELD:

- - - 46 -

IV. CONCLUSIONS:

This paper examines recently developed class of models to price interest rate swaps, the

so-called model plain vanilla interest rates swaps. This class of models has several

advantages over the traditional approach.

(a)These models are based directly on observable market rates, such as Mibor rates and

swap rates, instead of instantaneous (forward) interest rates.

(b) The models yield pricing formulas for caplets or swaptions that correspond to the

Black pricing formulas that are used in practice.

(c ) As a consequence, these models can easily be calibrated to market prices of caps or

swaptions.

V. OBSERVATIONS & RECOMMENDATIONS: (a) There is heterogeneity seen across banks. In India, banks holding

similar portfolios of government securities seem to have rather different interest rate risk

exposures. This suggests that the RBI’s ‘investment fluctuation reserve,’ which is

computed as a fraction of the investment portfolio without regard for the extent to which

risk is hedged,is an unsatisfactory approach to addressing interest rate risk.

(b) As a result of the above many banks have twisted RBI regulations to sell leveraged

products to corporate clients This has resulted in a situation where corporates have taken

currency bets where the amount at stake is a few multiples of the actual underlying. Say,

an exporter eager to protect its income has cut a deal where an adverse movement in the

euro or dollar could expose it to an amount which may be twice or thrice its export

- - - 47 -

income. Companies have entered into such deals since the exchange rate the bank offers

is more attractive than in a plain vanilla forward contract.

( c ) India already has interest rate swaps and over-the-counter forwards and options for

currency trading but needs more hedging tools as the country integrates more with the

global economy and because it has moved to more market-driven interest rates. The

Reserve Bank of India (RBI) expects the broad framework for currency futures trading to

be finalised by the end of May and senior dealers say trading could start within the year.

(d) More liberalized norms for IRS ( borrowing in fixed Rate basis ) and Exchanges the

periodical interest payments be on floating rate terms be made available to the Banks .

VI. REFERENCES:

1. Flavell Richard -Swaps and Other Derivates-, John Wiley & Sons Ltd, 2002,

Wiley Finance Series.

2. Choudhury Moorad- Bond Market Securities-, Pearson Education Ltd, 2001,

Financial Times Prentice Hall Professional Finance Series.

3. Choudhury Moorad - Analyzing & Interpreting the YIELD CURVE-, John Wiley

& Sons (Asia) Pte Ltd, 2004, Wiley Finance Series.

4. McDougall Alan - Mastering Swaps Markets A step-by-step guide to products,

applications and risks-, Pearson Education Ltd, 2000, Financial Times Prentice

Hall Market Editions.

5. Eales Brian - Financial Engineering-, MACMILLAN PRESS LTD 2000,

MACMILLAN Business Series

- - - 48 -

6. Hull John C. - Options, Futures and Other Derivatives-, Fifth Edition Pearson

Education Inc, 2003, Prentice Hall Finance Series

7. Marshall J.F. and Kapner K.R- Understanding Swaps-, John Wiley & Sons Ltd,

1999, Wiley Finance Series.

8. De Lurgio Stephen A.- Forecasting Principles and Applications- Tata Mc Graw

Hill, 1998

9. Levine, Krehbiel, Berenson- Business Statistics A First Course, 3rd Edition

Pearson Education Ltd, 2003

10. Hank John E, Wichern Dean W., Reitsch Arthur G.- Business Forecasting 7th

Edition Pearson Education Ltd, 2002

Journals and Publications

1. Overnight Indexed Swap Rates- Reserve Bank of Australia Bulletin- June 2002.

2. Financial Markets- Banque DeFrance Bulletin Digest – No. 136 – April 2005

3. “The determinants of the Overnight interest rate in the Euro area” by J. Moschitz,

September 2004- European Central Working Paper Series – 393

4. “Inferring market interest rate expectations from money market rates” by Martin

Brooke of the Bank’s Gilt-edge and Money Markets Division, and Neil Cooper

and Cedric Scholtes of the

Bank’s Monetary Instruments and Markets Division- Bank of England, 2002

5. “Estimating a ‘bank liability’ forward curve using the Bank’s VRP curve-fitting

technique” by Anderson and Sleath- Bank of England, 1999.

- - - 49 -

6. Fixed Income Derivatives in India- Citibank 2005

7. “Fixed income derivatives for India “ by Vijayan Subramani and Ananth Narayan

G.

8. “Fiscal policy Events and Interest rate Swap spreads:Evidence From the EU”- By

António Afonso and Rolf Strauch working paper series No. 303 / february 2004

European central bank

9. Product Training – Module VII Swaps – Morgan Stanley

Master circulars and notifications:

1. FIMCIR/2005-06/69, March 28, 2006- “Valuation of Investments as on 31st

March 2006- FIXED INCOME MONEY MARKET AND DERIVATIVES

ASSOCIATION OF INDIA

2. Circular MPD BC. 187/07.01.279- “Usage of Fixed Income Derivatives by

banksFIs/PDs – Reserve Bank of India.

3. Handbook of Market Practices- January 2003 FIXED INCOME MONEY

MARKET AND DERIVATIVES ASSOCIATION OF INDIA

- - - 50 -

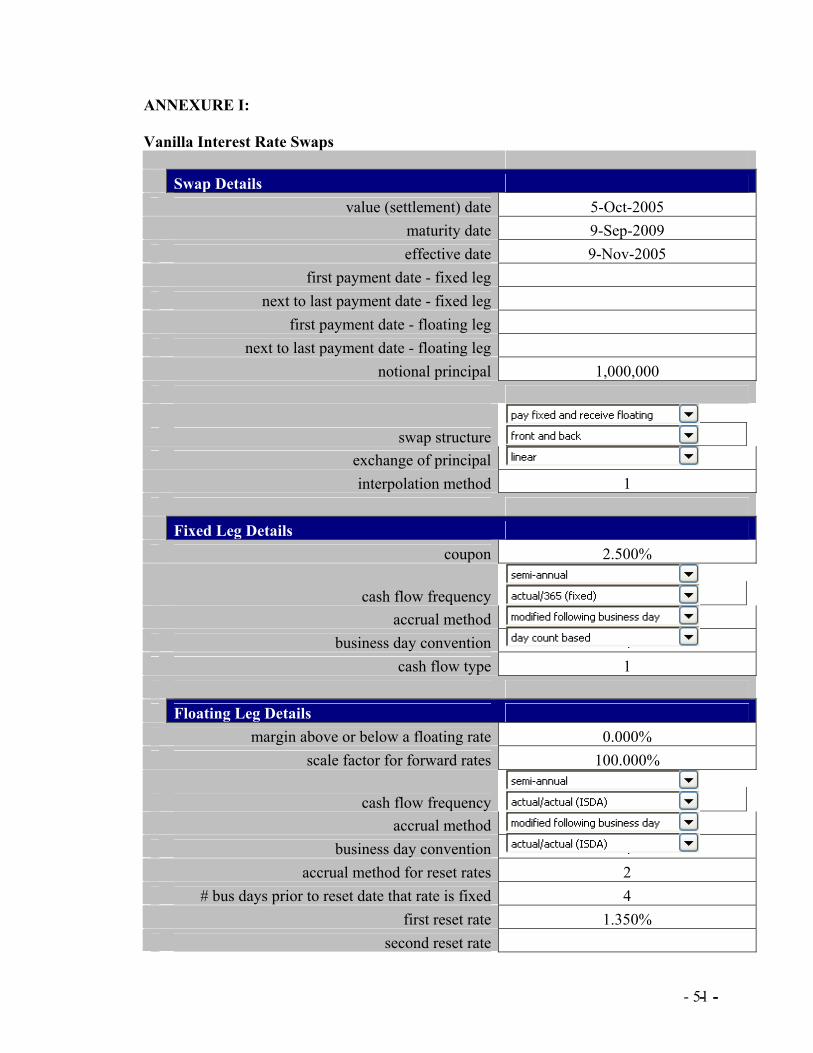

ANNEXURE I:

Vanilla Interest Rate Swaps Swap Details value (settlement) date 5-Oct-2005 maturity date 9-Sep-2009 effective date 9-Nov-2005 first payment date - fixed leg next to last payment date - fixed leg first payment date - floating leg next to last payment date - floating leg notional principal 1,000,000

swap structure

2 exchange of principal 2 interpolation method 1 Fixed Leg Details coupon 2.500%

cash flow frequency

2 accrual method 4 business day convention 4 cash flow type 1 Floating Leg Details margin above or below a floating rate 0.000% scale factor for forward rates 100.000%

cash flow frequency

2 accrual method 2 business day convention 4 accrual method for reset rates 2 # bus days prior to reset date that rate is fixed 4 first reset rate 1.350% second reset rate

- - - 51 -

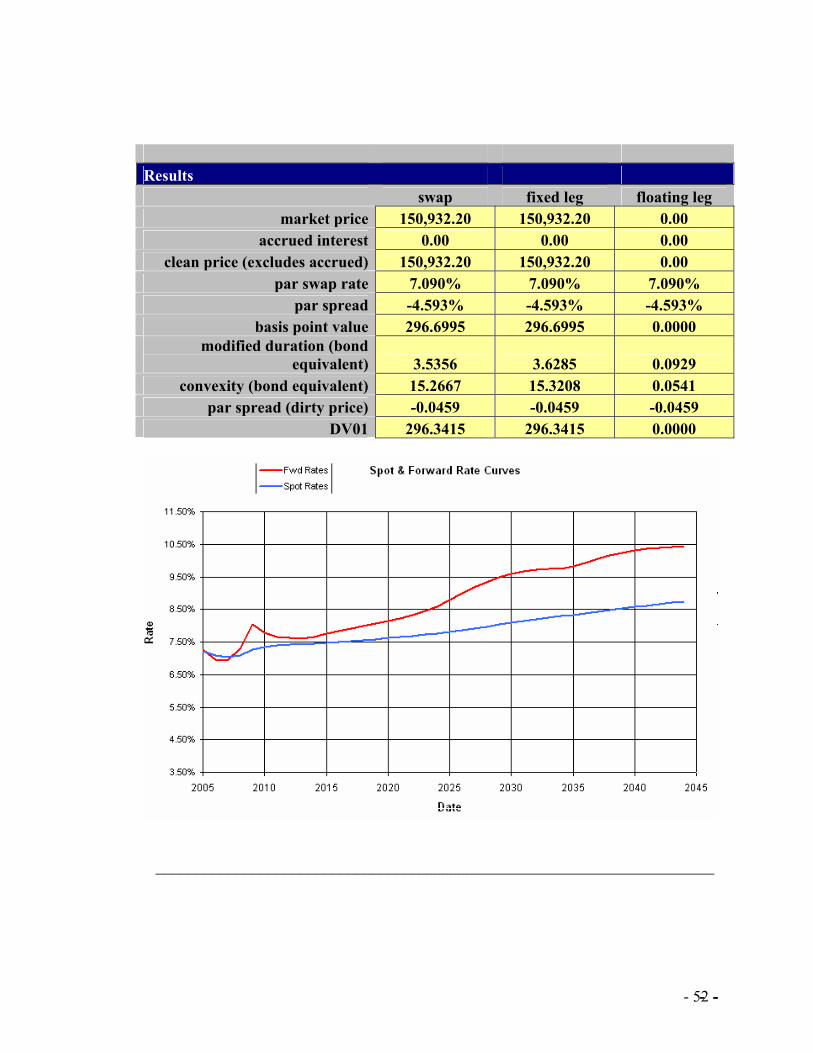

Results swap fixed leg floating leg

market price 150,932.20 150,932.20 0.00 accrued interest 0.00 0.00 0.00

clean price (excludes accrued) 150,932.20 150,932.20 0.00 par swap rate 7.090% 7.090% 7.090%

par spread -4.593% -4.593% -4.593% basis point value 296.6995 296.6995 0.0000

modified duration (bond equivalent) 3.5356 3.6285 0.0929

convexity (bond equivalent) 15.2667 15.3208 0.0541 par spread (dirty price) -0.0459 -0.0459 -0.0459

DV01 296.3415 296.3415 0.0000

______________________________________________________________________

- - - 52 -