Embed Size (px)

Citation preview

The Quantity Surveying International Convention 2011

Penang, Malaysia, 11th -12th October

1

PERSPECTIVE OF QUANTITY SURVEYORS TOWARDS THE ACCURACY OF PRELIMINARY COST ESTIMATES IN PUBLIC PROJECTS OF MALAYSIA

First and corresponding author: Mohd Azrai Azman1

Second author: Sr Dr. Zulkiflee Abdul Samad2

1 Postgraduate student - Master of Science (Building)

2 Senior Lecturer

Department of Quantity Surveying, Faculty of Built Environment, University of Malaya

E-mail (corresponding author): [email protected]

ABSTRACT

Preliminary Cost Estimate is prepared at early stage of development to decide the cost limit for projects.

Sometimes, public agency uses approved preliminary cost estimate to select a suitable bidder. A Quantity

Surveyor prepares an estimate before the completion of tender document. Therefore, he has to make

assumptions to incorporate the important variables. Factors affecting the accuracy of Preliminary Cost Estimate

and methods to improve the accuracy are indentified through literatures. 157 questionnaires were received from

the respondents. Findings of this study show almost all variables are important. Design scope, cost data, location

and experience are the most important factors affecting the accuracy. Meanwhile, the quality of information

supplied to Quantity Surveyors the main concern to improve the current practice. Investing in human resource,

sharing cost data and introduction of standardized rules for estimating are important in order to improve the

accuracy in the near future.

KEYWORDS

Accuracy, Preliminary Cost Estimate, Quantity Surveyor, Public Works Department, Peninsular Malaysia

Introduction

This paper reports the initial research by the authors about the accuracy of the preliminary estimates prepared by

both Public and Private Quantity Surveyors for Public Works Department (PWD) projects in Peninsular

Malaysia. Quantity Surveyors in this respect are QS officers working in PWD and private Quantity Surveyors

hired by PWD. The comments and suggestions will be incorporated in the main study.

The government often considers preliminary cost estimates as the cost limit of the projects. The estimates are

provided from the size of buildings and functional unit using cost indicators of similar projects (Morton &

Jaggar, 1995). It depends on information gathered at early design stages. It ensures the projects is built

according to desired quality, in the allowed time and within budget (Karlsen & Lereim, 2005).

Chappell, Marshall, Power-Smith, & Cavender (2001, p. 149) describes the general term of early estimates as:

“Colloquially and in the industry generally it means „probable cost‟ and is then a judged amount,

approximate rather than precise”

Seeley (1996, p.154) describes the QS consultants’ standpoint on preliminary cost estimates:

“The primary role of estimated or preliminary estimating is to produce a forecast of probable cost of a

future project, before the building has been designed in detail and contract particulars prepared. In this

way the building client is made aware of his likely financial commitments before extensive design is

undertaken”

The difference between QS consultants’ estimates and Contractors’ bidding (Skitmore, 1988, p.2):

“Estimating is the process of working out likely costs and bidding is the process of converting an

estimate into a tender price”.

2

The estimates are prepared based on standard and cost guideline to ensure value for money. This standard states

the general requirements and features for planning i.e. space per pupil as the standard for school buildings

(Morton & Jaggar, 1995). This ensures the user’s needs are established unlike in private the needs are defined

by profit (Kirkham, 2007).

Normally, the Public Works Department supervised the public projects in Malaysia. The PWD is the largest

construction management organisation in Malaysia (Abdul-Rashid Abdul-Aziz & Normah Ali, 2004). This

department may appoint private consultants to provide drawings and cost estimates. The design and planning

must use Standard and Cost Guideline prepared by Standard and Cost Sub-committee of Economic Planning

Unit (EPU) under the Prime Minister Department. This guideline provides the standard of practice for land use,

schedule of accommodation and standard general spaces (Prime Minister Department, 2005). However, not all

projects are required to use this guideline. Projects exceed RM 5.0 million for alteration of buildings and

buildings for rental exceed 465m2GFA are not required to follow the guideline. The purpose of this guideline is

to appreciate cost saving from planning, design and implementation of the projects. It provides maximum

benefits within reasonable cost (Prime Minister Department, 2005).

Preliminary Cost Estimates are prepared according to initial design forwarded by the Ministries or other

government agencies. The estimates are prepared to ensure the project’s budget is sufficient. Currently, there are

two (2) types of estimating methods used by PWD. These methods are Single Rate Method and Estimated

Quantities The estimates will be prepared using Preliminary Detailed Abstract Form PWD142 (Ministry of

Finance, 1958; Public Works Department, 2010).

Cost estimates are not an exact science, but it needs construction knowledge and common sense to have accurate

estimates (Peurifoy & Oberlender, 2006). Different method of procurement and lack of basic information can

also influence the accuracy of estimates (Hughes, Hillebrandt, Greenwood, & Kwawu, 2006).

In summary, the function of preliminary cost estimates is essential to government procurement activity.

Therefore, an acceptable level of accuracy in the estimates is important. Estimates can influence the selection of

contractors because of government budget constraint. The factors influence the accuracy of estimates will be

studied. In addition, this study will look into the ways to improve the accuracy of estimates.

Problems related to inaccurate Preliminary Cost Estimate

The early cost advice of public funded projects is essential because budget constraint will limit the capacity of

government to spend (Morton & Jaggar, 1995). In addition, estimates will provide the basis for budgeting and

cost control for construction projects. If the estimates are too low, the project design could be abandoned, and it

may lead to a lawsuit (Ashworth, 2010). Overestimation will lead lesser funds available for other projects and

underestimation will result in unviable figures during tender award stage (Odusami & Onukwube, 2008). To

overcome these problems, Public Works Department could take two (2) possible solutions, which are design

amendment, or additional budget will be requested (Public Works Department, 2010). Nevertheless, clients are

more tolerated to overestimation of preliminary cost estimates (Cheung, Wong, & Skitmore, 2008).

Even so, these recommendations will not resolve the problems of inaccurate estimation. Preliminary cost

estimates must be prepared using reliable estimating methods and procedures. Budget must be ready before

project implementation. Thus, inaccurate estimates could result in resource mismanagement

Estimates provided to PWD could be from internal and external sources. PWD may engage private consultants

QS to provide the department with estimates (Ministry of Finance, 1958). The main reason for outsourcing is the

restriction to employ more staff while public expenditure is growing (Abdul-Rashid Abdul-Aziz & Normah Ali,

2004). Cost estimates could be influenced by different management and firms’ competencies (Morrison, 1999).

The use of different sources of estimates could provide the PWD with a different quality of estimates. The PWD

on client behalf could hire consultants to provide preliminary cost estimates. Nevertheless, only 57.8 % of QS

consultants met the expectation to complete this task (Abdul-Rashid Abdul-Aziz & Normah Ali, 2004).

A study made in Australia shows the accuracy of QS’ estimates has not improved over time (Aibinu & Pasco,

2008). According to Jackson (2002) quoted by Fortune (2006), most clients are not satisfied with the service

provided by QS for budget cost estimates. Therefore, the objectives of this study are:

a) To investigate the accuracy of Preliminary Cost Estimates in Public Works Department

3

b) To indentify the factors affecting the Quantity Surveyors in preparing accurate estimates.

a) To indentify the ways that can enhance the accuracy of the estimates.

Definition of accuracy

The meaning of accuracy is a lack of error. Lack of error results more accurate estimate. Accuracy is measured

according to bias and consistency (Skitmore, 1991). Bias concerns with the average differences between

estimates and tender bids and consistency is the degree of variation around the average. The greater the mean

differences, the greater the estimates said to be biased. Lesser error estimate is associated with more accurate

forecast. The lesser the degree of variation gained the greater the consistency of the forecast. It explains the

efficiency of a quantity surveyor performance over the number of estimates. The accuracy of estimates can be

measured using the percentage differences of estimates and tender bids (Gunner & Skitmore, 1999a; Skitmore,

1991; Skitmore, Stradling, Tuohy, & Mkwezalamba, 1990). These are as follows:

a) Estimate and lowest bid

b) Estimate and accepted bid

c) Estimate and mean of the bids

Factors affecting the Preliminary Cost Estimates

The estimates are influenced by a number of variables (Ashworth, 2010; Morton & Jaggar, 1995). These

variables are inter-correlated by other factors (Gunner & Skitmore, 1999b). Limited time to prepare estimates

and incomplete design scopes could result in inaccurate estimates (Aibinu & Pasco, 2008; Akintoye, 2000).

Nature of target, information, forecasting methods, feedback mechanism and the person who prepared the

forecast will decide the accuracy of early estimates (Skitmore, 1991). Serpell (2004) says scope, information,

uncertainty level, estimator and estimating procedure will influence the accuracy of estimates. The factors on

early cost estimate defined by these two authors are similar. The contractors’ estimates are for profit based

business while QS consultants are towards budget certainty (Skitmore, 1988). Sinclair et al. (2002) says 100%

estimating accuracy will not be achievable since it involves assessment of probabilities and risks.

Gunner and Skitmore (1999b) describes building type, type of contract, project value, price intensity,

construction period, number of bidders, economy condition, procurement basis, sector and location will

contribute to accuracy of estimates. Accuracy is also depending on progress of design works (Ashworth, 2010;

Chappell, et al., 2001; Park & Jackson, 1984; Potts, 2008). Estimating method used could also influence the

accuracy (Boussabaine, 2007; Skitmore & Patchell, 1999). By combining the literatures from numerous authors

the factors affecting the accuracy are defined as follows:

Table 1: The factors affecting accuracy of estimates

Scope quality Design scope (Plan shape, size m2, height, specification and

performance)

Design team experience (architect, engineers and etc)

Unclear documentation (project brief / drawings)

Location of project (site and soil conditions and extent of services)

Type and condition of contract

Basis of selection (open, selective and direct negotiation)

Commitment of client to project

Information

quality Cost data (historical and current information)

Uncertainty

level Project technology and complexity level

Market conditions and sentiments

Estimator

performance QS’ experience

Ability of QS to cope with stress (work pressure)

Communication barrier

Familiarity of QS with the type of projects

Perception of estimating importance

4

Quality of

estimating

procedure

Expected level of error in estimates

Limited time to prepare estimate due to dateline

Estimating method use in the preparation of estimates

Application of alternative methods by organisation

Organization’s estimating procedure

The accuracy of Preliminary Cost Estimates

Chappell et al. (2001) has decided the accuracy in term of error should be around +/-15% in early estimate and

5% in final estimate. Park and Jackson (1984) indicate the accuracy will improve from early design at +/-15%,

semi-detailed design at +/-10% and detailed design +/- 5%. Ashworth (2010) suggests the accuracy of estimates

on average is about +13% from contract sums. Morrison and Steven (1999) conclude the general consistency

should be around 15% to 20% for early design and 13% to 18% to detailed design stage. Refer Table 2.

Table 2: Summary of accuracy for early cost estimates (abstracted from Aibinu & Pasco, 2008;

Skitmore & Ng, 2003; Skitmore & Picken, 2000)

Rank Organization Location Period N Mean

Bias (%)

Coefficient

of variation

1 Hanscomb USA 1973-75 62 7.71

2 Hanscomb USA 1980-92 217 +5.19 7.82

3 Levett and Bailey Singapore 1980-91 86 +3.47 8.46

4 QS Office UK pre1984 55 +3.72 9.37

5 PW QS Office Australia 1970s 153 +5.85 9.73

6 QS Firm Australia 1999-2007 56 +4.29 10.17

7 QS Office UK pre1984 62 +2.89 10.88

8 County Council UK 1980s 61 +12.77 11.00

9 QS Office UK pre1984 89 -0.33 11.29

10 QS Office UK pre1984 222 +2.61 11.50

11 QS Office UK pre1984 62 -5.76 11.68

12 QS Office UK pre1984 115 +4.38 12.22

13 County Council8 UK 1971-77 63 c12.50

14 QS Firm Hong

Kong

1995-97 89 -1.78 12.95

15 PW Dept Belgium 1971-74 132 -5.17 13.13

16 QS Office Singapore 1980s 88 -0.18 14.13

17 County Council UK 1975-78 103 +11.50 c15.00

18 QS Office UK 1978 310 +5.86 15.52

19 City Council UK 1983-87 33 -4.91 18.11

20 PW Dept Belgium 1971-74 168 -1.45 18.37

21 Govt Agency USA 1975-84 292 +9.22 23.99

22 Levett and Bailey Singapore 1980-91 181 +10.32 28.30

*positive value of mean bias shows overestimated

The ways to improve the accuracy of Preliminary Cost Estimates

The preliminary cost estimates are needed to progress as the construction industry becomes more complicated. It

happens because the introduction of new technology and procurement options into the industry. The PWD and

QS consultants hired under them need to take action, so that they can enhance their estimating policies and

procedures. This ensures the estimates are in tolerable quality, more accurate and acceptable to clients. Some

researchers say the current estimating process should be improved and introduction of approaches should take

place in QS practices for sustainable approaches.

5

Improvement methods to current estimating practice

A number of authors have discussed about their concerns on estimates’ accuracy. There are a number of

researches on the factors which influence the estimating accuracy and the steps to improve it. However, these

researches are based on the procurement scenario and working systems of their respective countries. Ling and

Boo (2001) and Aibinu and Pasco (2008) analyzed the current estimating processes to prepare cost estimates as

the method to improve the accuracy which is practised in Singapore and Australia. Lin and Boo (2001) found

that a proper design documentation and information management are the most accepted method to improve the

current estimating process. QS should also check all assumptions and provide a realistic estimating period.

However, Aibinu and Pasco (2008) stressed that, sufficient information, all assumptions checked and use of cost

control and cost planning are the priority. As this research is done in Malaysia and focused on Public Works

Departments, the outcome of the research might be different from previous studies by Aibinu and Pasco (2008)

and Ling and Boo (2001). The methods used by them are as follows:

a) Proper design documentation and information management.

b) Effective communication and coordination between designers.

c) Sufficient design information from the designers.

d) Ascertained assumptions from designers and client.

e) Establish formal feedback for design and estimating activities.

f) Realistic time for estimating activity.

g) Use more rigorous estimating method.

h) Incorporate market sentiments and economic conditions into estimates.

i) Tender documents used as estimates.

j) Quantification of design and construction risks.

k) Cost planning and cost control during design stage.

l) Subdivided the large item into small items to reduce pricing errors.

m) Improve methods of selection, adjustments and application of cost data.

n) Update cost data with new cost and create feedback system for improving estimating accuracy.

Introduction of approaches to estimating procedures and policies

The Building Research Board (BRB) had been asked by Federal Construction Council of United States (NRC)

to review the current estimating practices for federal projects. The committee found that the use of faulty

estimating methods and procedures are not the primary reasons for budgets related problems. They have

suggested a number of steps should be taken by both government and private practices (BRB & NRC, 1990). In

addition, Royal Institution of Chartered Surveyors has introduced standardized guideline to reduce the practices

inconsistencies (Lee & Smith, 2010). These are as follows:

a) Invest and collaborating in cost estimate research between PWD and consultants.

b) Sharing of Cost Data among consultants and PWD.

c) Introduction of scientific based estimating methods i.e. Mathematical, Knowledge based, Value-related

and Neural models as alternative tools for decision making.

d) Introduction of value engineering.

e) Investing in estimating training for QS officers / consultants’ executives.

f) Introduction of standardize rules of measurement for estimating and cost planning in detail.

Research methodology

The quantitative method was employed to address the objective of this study. Questionnaires are designed for

data collection. In addition, project estimates and tender bids from Public Works Department (PWD) were used

to examine the accuracy of PCE. Questionnaires were sent to PWD QS officers and Private QS Consultants in

Peninsular Malaysia. This could give a different level of agreement. All QS in private consultants are hired by

PWD to provide cost advices. Questionnaires are intended to be answered by experience QS who are working

for 5 years or more. Information regarding respondents is provided by Cawangan Kontrak dan Ukur Bahan

(CKUB), PWD. 344 questionnaires were sent for this survey. Elhag et al. (2005) suggests the ideal return

responses is about 30% out of total questionnaires sent. Therefore, the sample collection should be at least 103

from both PWD QS officers and QS private practices combined. Accuracy of PCE is analyzed from samples of

6

completed projects. These samples are from Preliminary Detailed Abstract (PDA) and As Tendered Detailed

Abstract (ATDA).

Data Analysis

The questionnaire is designed to examine QS observation on factors affecting the QS in preparing accurate

estimates. In addition, questions are designed to identify the ways to improve the accuracy of preliminary cost

estimates. Data from projects are collected to investigate the accuracy of estimates. These are as follows:

a) Questionnaire survey analysis

b) Project data analysis (comparison between estimates and tender bids) for estimates’ accuracy

Questionnaire survey analysis

The following are the quantitative data analyses used for questionnaire survey analysis:

a) Cronbach’s Alpha (Reliability test)

b) The relative importance index

c) Mann-Whitney test

d) Kendall’s Coefficient of Concordance

Cronbach’s Alpha (reliability of the question)

This is for instrument reliability. It means the questionnaire should be consistent to reflect the construct that is

being measured. It measures the reliability of a scale. It is based on the idea that individual items or set of items

should produce consistent results with overall questionnaires (Field, 2009).

Alpha value varies from 0 to 1. The closer the Alpha values to 1, the greater the internal consistency of items for

the instrument being assumed. The acceptable value is 0.60 (Moss, et al., 1998). If more than 0.70 it is

considered as excellent in social sciences research (Nunnally & Bernstein, 1994). The formula for the

standardized Cronbach’s alpha:

α = k r

1 + (k-r)

k is number of items

r is average inter-item covariance among items

The relative importance index

Likert’s scale is used to measure levels of agreement. Each scale represents the following:

1 = not important

2 = little important

3 = somewhat important

4 = important

5 = very important

Then, relative importance index is used to rank the variables. This test was used by several researchers i.e.

Akintoye (2000) Elhag et al. (2005) and Odusami and Onukwube (2008). The relative importance index is as

follows:

∑ W = 5n5 + 4n4 + 3n3 + 2n2 + 1n1

AN 5N

W is the weighting given to each factor by the respondent, from 1 to 5

A is the highest weight (5 in the study)

N is the total number of samples

n1 to n5 is the number respondents answered each likert‟s scale

7

One-sample t-test

One sample t-test examines the mean score of a hypothesis value. The value of the mean for 5-point Likert’s

scale is 3. It was assumed that the mean score of 3 is the mean usefulness. The score below 3 is not considered

important. This test determines the difference between the expected and the actual score.

Mann-Whitney test

Mann-Whitney test is a nonparametric statistic used to look for differences in the ranks between two

independent samples. It tests whether the populations from two samples are drawn from the same distribution

(Field, 2009). This test is equivalent to parametric independent t-test. Mann-Whitney test is used to determine

whether there is a significant difference between the two (2) groups of respondents that is the PWD officers and

QS consultants. The following is the formula for Mann-Whitney test:

Ux = n1n2 + n1 (n1 + 1) - Tx

2

Uy = n1n2 + n1 (n1 + 1) - Ty

2

U = min (Ux,Uy), Tx and Ty : Rank sum of x and y

n1 is the sample size for example 1, n2 is the sample size for sample 2

Kendall’s coefficient of concordance

Kendall coefficient of concordance (W) is a nonparametric statistic used to evaluate the strength of agreement

between QS officers in PWD and QS in Private Sector regarding their opinions on each ranking for related

factors. It measures the extent of agreement between respondents. In social sciences, the variables are often

people assessing different subjects or situations (Legendre, 2010). Kendall’s (W) ranges 0 ≤ W ≤ 1. One (1) is in

perfect concordance (agreement). If the test statistic (W) is one (1), it means all respondents unanimously agree,

if W is zero, no agreement among respondents (Elhag, et al., 2005). Refer Table 3 for the interpretation of

Kendall’s W score.

The formula is as follows:

W = 12S

p2(n

3− n) − pT

Where, n

S = ∑ (∑Ri - R) 2

i=1

S is a sum-of-squares statistic over the row sums of ranks Ri

R is the mean of the Ri values

n is the number of objects,

p the number of judges (respondents).

T is a correction factor for tied values

Table 3: The interpretation of Kendall’s W score (abstracted from Schmidt, 1997)

Kendall's W Interpretation Confidence in Ranks

0.1 Very weak agreement None

0.3 Weak agreement Low

0.5 Moderate agreement Fair

0.7 Strong agreement High

0.9 Unusually strong agreement Very high

1 Complete agreement Highest

8

Project data analysis

The following calculation is used to examine the accuracy of the PCE. It examines the mean bias and the

consistency of the PCE.

The following formula calculates the accuracy of an estimate:

Bias (%) = Forecast - Accepted bid x 100%

Accepted bid

Therefore, the mean bias of ( ) =

x = estimate bias; n= number of projects

Standard Deviation (s) of the estimates is as the following:

- ) 2/n

x = estimate bias; = mean estimate bias; n= number of project

Then, coefficient of variation measures the consistency of the estimates

CV =

Results

Questionnaires were sent to senior executives and senior officers of PWD and private consultants. All

respondents from PWD have at least 5 years experience. Respondents from private consultants which have at

least 5 years experience are 75.5%. Overall 92% of the respondents (PWD + private consultants) have at least 5

years experience. Out of this, 40.1% of the respondents have more than 15 years experience. So, questionnaire

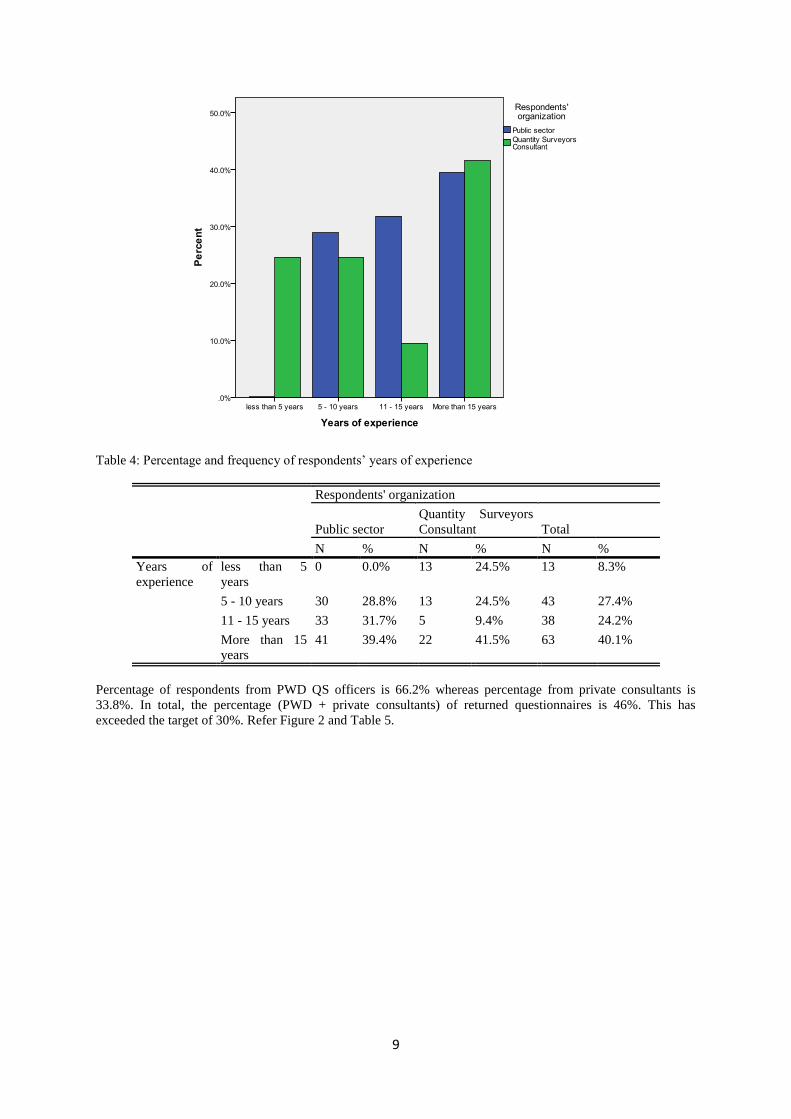

survey has achieved its target to have experience respondents. Refer Figure 1 and Table 2.

Figure 1: Percentage of respondents’ years of experience

∑x

N

Standard deviation of ratio forecast / tender bid x 100%

Mean estimate ratio forecast / tender bid

9

Table 4: Percentage and frequency of respondents’ years of experience

Respondents' organization

Public sector

Quantity Surveyors

Consultant Total

N % N % N %

Years of

experience

less than 5

years

0 0.0% 13 24.5% 13 8.3%

5 - 10 years 30 28.8% 13 24.5% 43 27.4%

11 - 15 years 33 31.7% 5 9.4% 38 24.2%

More than 15

years

41 39.4% 22 41.5% 63 40.1%

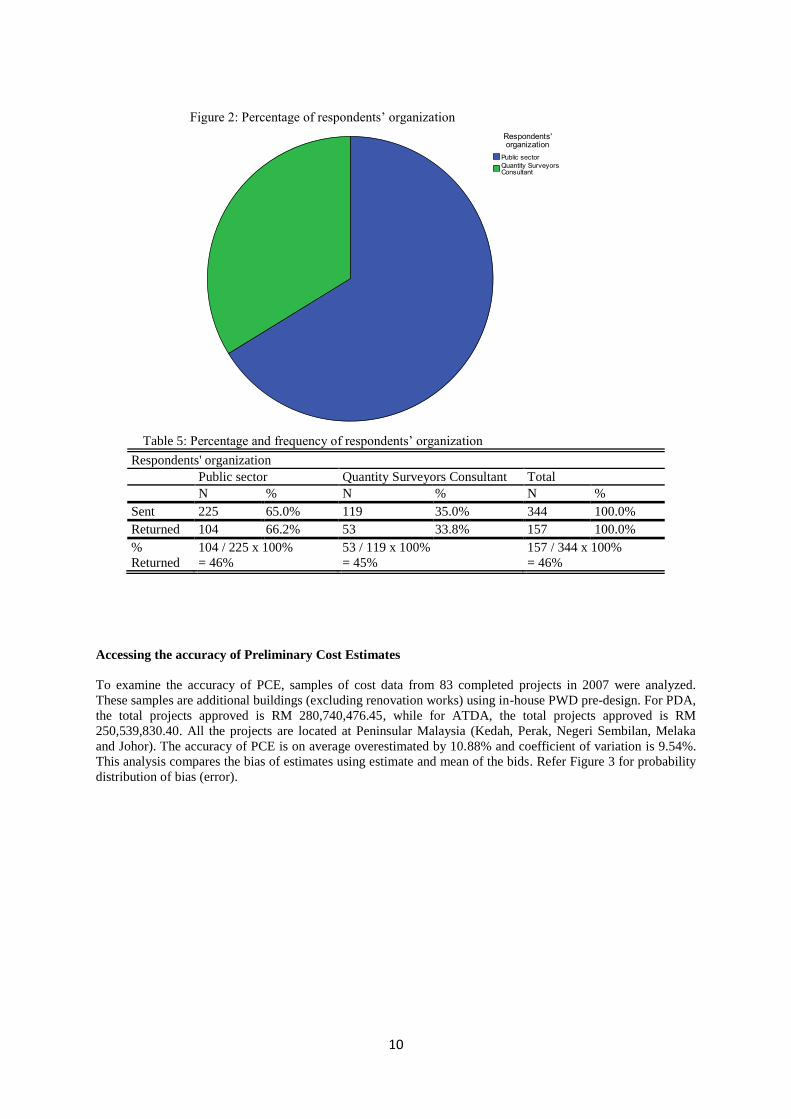

Percentage of respondents from PWD QS officers is 66.2% whereas percentage from private consultants is

33.8%. In total, the percentage (PWD + private consultants) of returned questionnaires is 46%. This has

exceeded the target of 30%. Refer Figure 2 and Table 5.

10

Figure 2: Percentage of respondents’ organization

Table 5: Percentage and frequency of respondents’ organization

Respondents' organization

Public sector Quantity Surveyors Consultant Total

N % N % N %

Sent 225 65.0% 119 35.0% 344 100.0%

Returned 104 66.2% 53 33.8% 157 100.0%

%

Returned

104 / 225 x 100%

= 46%

53 / 119 x 100%

= 45%

157 / 344 x 100%

= 46%

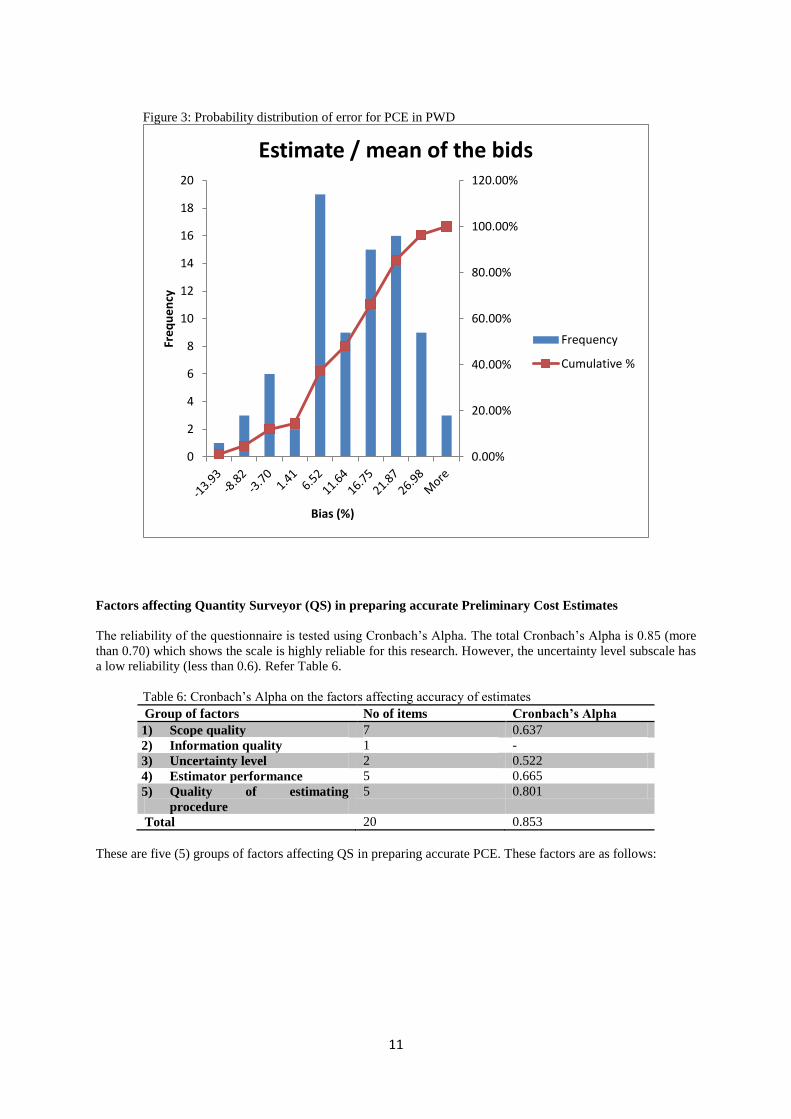

Accessing the accuracy of Preliminary Cost Estimates

To examine the accuracy of PCE, samples of cost data from 83 completed projects in 2007 were analyzed.

These samples are additional buildings (excluding renovation works) using in-house PWD pre-design. For PDA,

the total projects approved is RM 280,740,476.45, while for ATDA, the total projects approved is RM

250,539,830.40. All the projects are located at Peninsular Malaysia (Kedah, Perak, Negeri Sembilan, Melaka

and Johor). The accuracy of PCE is on average overestimated by 10.88% and coefficient of variation is 9.54%.

This analysis compares the bias of estimates using estimate and mean of the bids. Refer Figure 3 for probability

distribution of bias (error).

11

Figure 3: Probability distribution of error for PCE in PWD

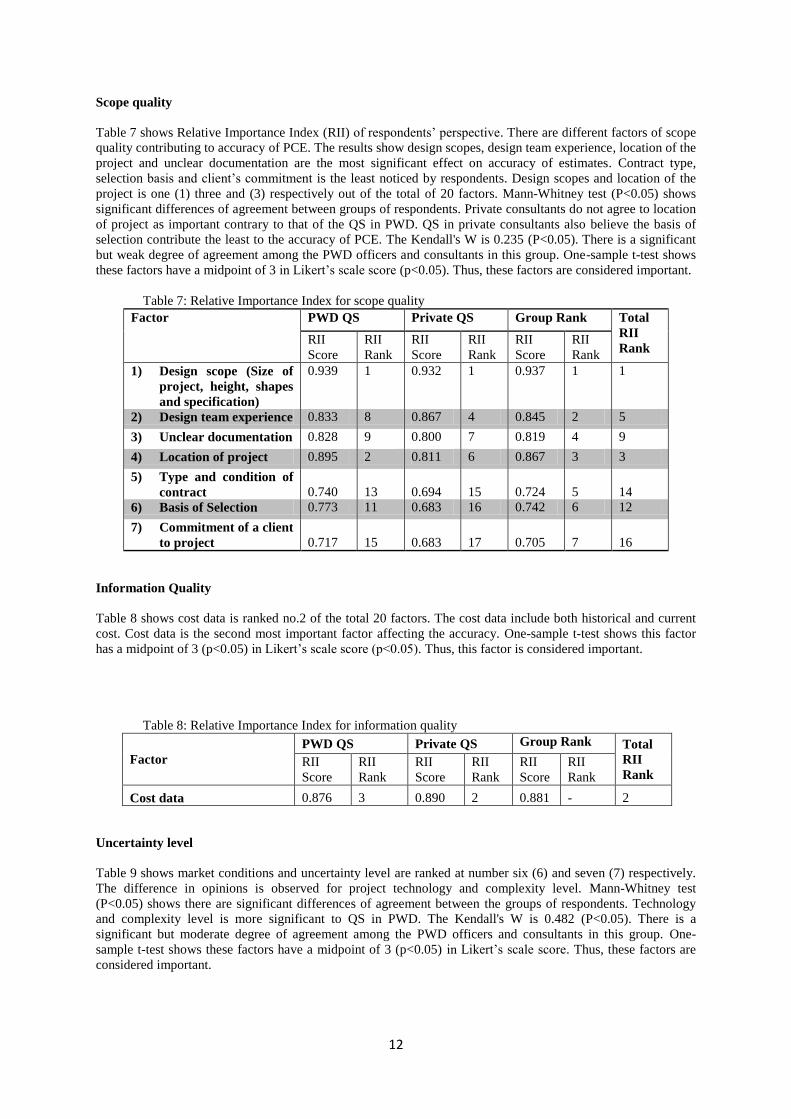

Factors affecting Quantity Surveyor (QS) in preparing accurate Preliminary Cost Estimates

The reliability of the questionnaire is tested using Cronbach’s Alpha. The total Cronbach’s Alpha is 0.85 (more

than 0.70) which shows the scale is highly reliable for this research. However, the uncertainty level subscale has

a low reliability (less than 0.6). Refer Table 6.

Table 6: Cronbach’s Alpha on the factors affecting accuracy of estimates

Group of factors No of items Cronbach’s Alpha

1) Scope quality 7 0.637

2) Information quality 1 -

3) Uncertainty level 2 0.522

4) Estimator performance 5 0.665

5) Quality of estimating

procedure

5 0.801

Total 20 0.853

These are five (5) groups of factors affecting QS in preparing accurate PCE. These factors are as follows:

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

0

2

4

6

8

10

12

14

16

18

20 Fr

eq

ue

ncy

Bias (%)

Estimate / mean of the bids

Frequency

Cumulative %

12

Scope quality

Table 7 shows Relative Importance Index (RII) of respondents’ perspective. There are different factors of scope

quality contributing to accuracy of PCE. The results show design scopes, design team experience, location of the

project and unclear documentation are the most significant effect on accuracy of estimates. Contract type,

selection basis and client’s commitment is the least noticed by respondents. Design scopes and location of the

project is one (1) three and (3) respectively out of the total of 20 factors. Mann-Whitney test (P<0.05) shows

significant differences of agreement between groups of respondents. Private consultants do not agree to location

of project as important contrary to that of the QS in PWD. QS in private consultants also believe the basis of

selection contribute the least to the accuracy of PCE. The Kendall's W is 0.235 (P<0.05). There is a significant

but weak degree of agreement among the PWD officers and consultants in this group. One-sample t-test shows

these factors have a midpoint of 3 in Likert’s scale score (p<0.05). Thus, these factors are considered important.

Table 7: Relative Importance Index for scope quality

Factor PWD QS Private QS Group Rank Total

RII

Rank RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) Design scope (Size of

project, height, shapes

and specification)

0.939 1 0.932 1 0.937 1 1

2) Design team experience 0.833 8 0.867 4 0.845 2 5

3) Unclear documentation 0.828 9 0.800 7 0.819 4 9

4) Location of project 0.895 2 0.811 6 0.867 3 3

5) Type and condition of

contract

0.740

13

0.694

15

0.724

5

14

6) Basis of Selection 0.773 11 0.683 16 0.742 6 12

7) Commitment of a client

to project

0.717

15

0.683

17

0.705

7

16

Information Quality

Table 8 shows cost data is ranked no.2 of the total 20 factors. The cost data include both historical and current

cost. Cost data is the second most important factor affecting the accuracy. One-sample t-test shows this factor

has a midpoint of 3 (p<0.05) in Likert’s scale score (p<0.05). Thus, this factor is considered important.

Table 8: Relative Importance Index for information quality

Factor

PWD QS Private QS Group Rank Total

RII

Rank RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

Cost data 0.876 3 0.890 2 0.881 - 2

Uncertainty level

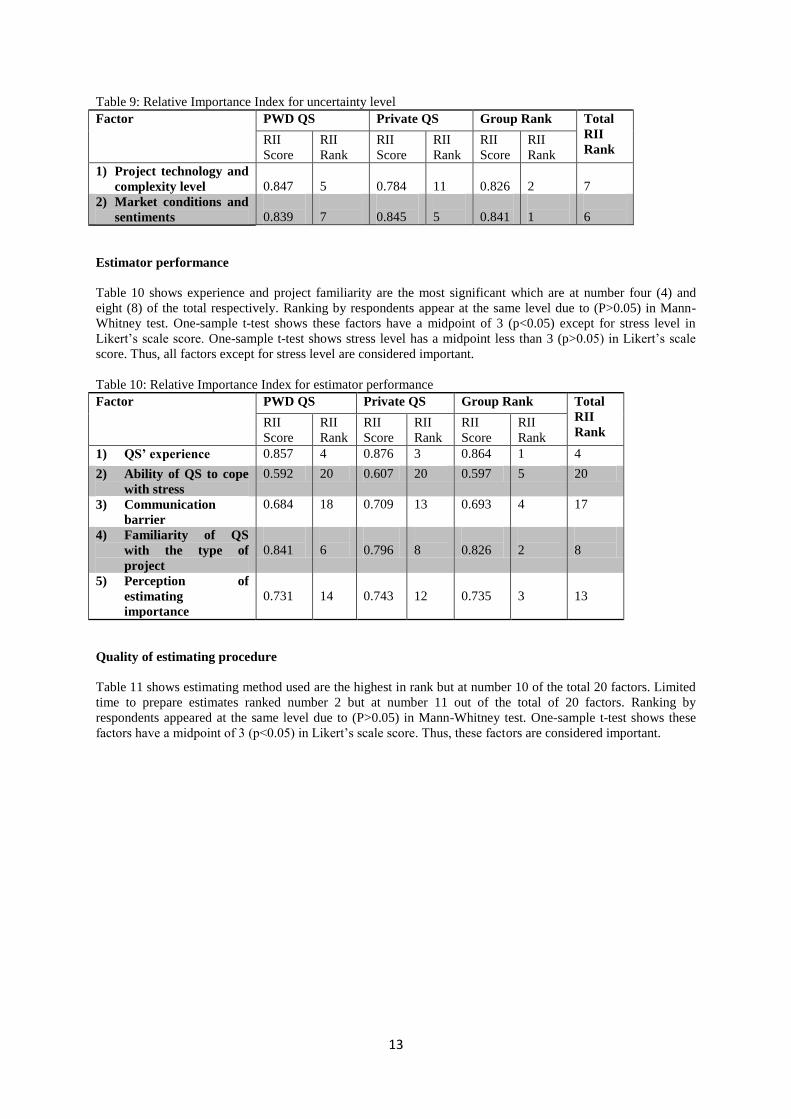

Table 9 shows market conditions and uncertainty level are ranked at number six (6) and seven (7) respectively.

The difference in opinions is observed for project technology and complexity level. Mann-Whitney test

(P<0.05) shows there are significant differences of agreement between the groups of respondents. Technology

and complexity level is more significant to QS in PWD. The Kendall's W is 0.482 (P<0.05). There is a

significant but moderate degree of agreement among the PWD officers and consultants in this group. One-

sample t-test shows these factors have a midpoint of 3 (p<0.05) in Likert’s scale score. Thus, these factors are

considered important.

13

Table 9: Relative Importance Index for uncertainty level

Factor PWD QS Private QS Group Rank Total

RII

Rank RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) Project technology and

complexity level

0.847

5

0.784

11

0.826

2

7

2) Market conditions and

sentiments

0.839

7

0.845

5

0.841

1

6

Estimator performance

Table 10 shows experience and project familiarity are the most significant which are at number four (4) and

eight (8) of the total respectively. Ranking by respondents appear at the same level due to (P>0.05) in Mann-

Whitney test. One-sample t-test shows these factors have a midpoint of 3 (p<0.05) except for stress level in

Likert’s scale score. One-sample t-test shows stress level has a midpoint less than 3 (p>0.05) in Likert’s scale

score. Thus, all factors except for stress level are considered important.

Table 10: Relative Importance Index for estimator performance

Factor PWD QS Private QS Group Rank Total

RII

Rank RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) QS’ experience 0.857 4 0.876 3 0.864 1 4

2) Ability of QS to cope

with stress

0.592 20 0.607 20 0.597 5 20

3) Communication

barrier

0.684 18 0.709 13 0.693 4 17

4) Familiarity of QS

with the type of

project

0.841

6

0.796

8

0.826

2

8

5) Perception of

estimating

importance

0.731

14

0.743

12

0.735

3

13

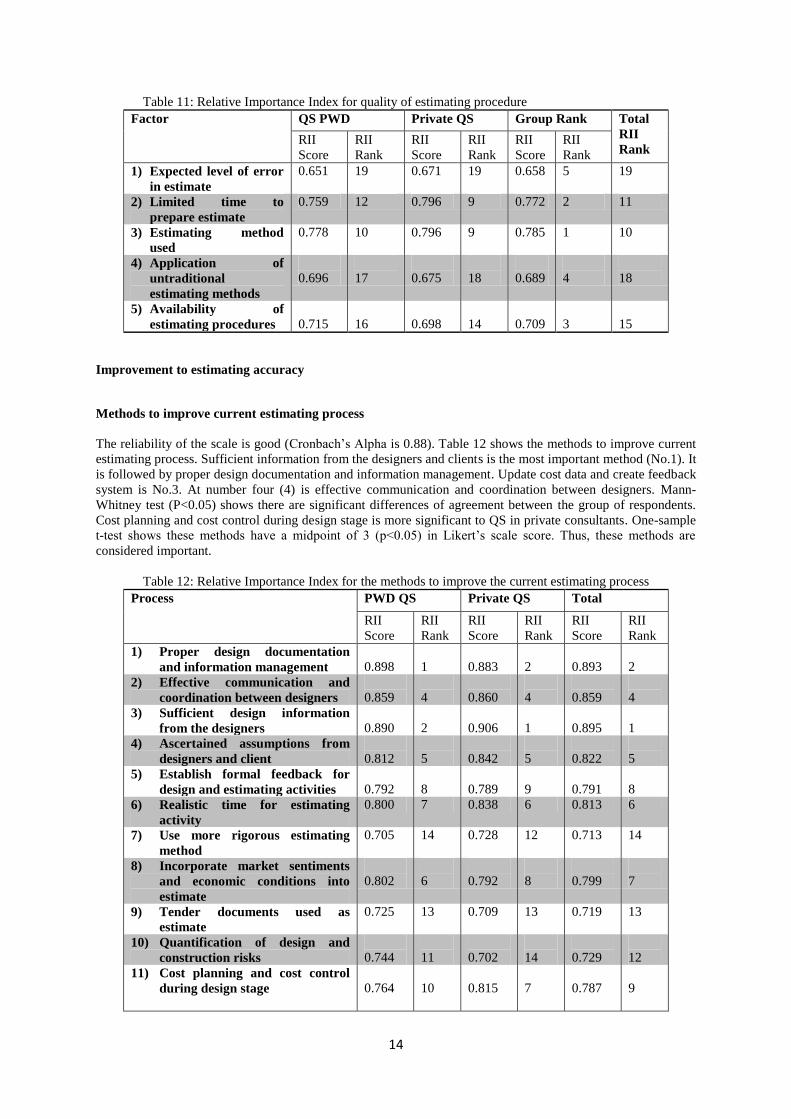

Quality of estimating procedure

Table 11 shows estimating method used are the highest in rank but at number 10 of the total 20 factors. Limited

time to prepare estimates ranked number 2 but at number 11 out of the total of 20 factors. Ranking by

respondents appeared at the same level due to (P>0.05) in Mann-Whitney test. One-sample t-test shows these

factors have a midpoint of 3 (p<0.05) in Likert’s scale score. Thus, these factors are considered important.

14

Table 11: Relative Importance Index for quality of estimating procedure

Factor QS PWD Private QS Group Rank Total

RII

Rank RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) Expected level of error

in estimate

0.651 19 0.671 19 0.658 5 19

2) Limited time to

prepare estimate

0.759 12 0.796 9 0.772 2 11

3) Estimating method

used

0.778 10 0.796 9 0.785 1 10

4) Application of

untraditional

estimating methods

0.696

17

0.675

18

0.689

4

18

5) Availability of

estimating procedures

0.715

16

0.698

14

0.709

3

15

Improvement to estimating accuracy

Methods to improve current estimating process

The reliability of the scale is good (Cronbach’s Alpha is 0.88). Table 12 shows the methods to improve current

estimating process. Sufficient information from the designers and clients is the most important method (No.1). It

is followed by proper design documentation and information management. Update cost data and create feedback

system is No.3. At number four (4) is effective communication and coordination between designers. Mann-

Whitney test (P<0.05) shows there are significant differences of agreement between the group of respondents.

Cost planning and cost control during design stage is more significant to QS in private consultants. One-sample

t-test shows these methods have a midpoint of 3 (p<0.05) in Likert’s scale score. Thus, these methods are

considered important.

Table 12: Relative Importance Index for the methods to improve the current estimating process

Process PWD QS Private QS Total

RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) Proper design documentation

and information management

0.898

1

0.883

2

0.893

2

2) Effective communication and

coordination between designers

0.859

4

0.860

4

0.859

4

3) Sufficient design information

from the designers

0.890

2

0.906

1

0.895

1

4) Ascertained assumptions from

designers and client

0.812

5

0.842

5

0.822

5

5) Establish formal feedback for

design and estimating activities

0.792

8

0.789

9

0.791

8

6) Realistic time for estimating

activity

0.800 7 0.838 6 0.813 6

7) Use more rigorous estimating

method

0.705 14 0.728 12 0.713 14

8) Incorporate market sentiments

and economic conditions into

estimate

0.802

6

0.792

8

0.799

7

9) Tender documents used as

estimate

0.725 13 0.709 13 0.719 13

10) Quantification of design and

construction risks

0.744

11

0.702

14

0.729

12

11) Cost planning and cost control

during design stage

0.764

10

0.815

7

0.787

9

15

12) Subdivided the large item into

small items to reduce pricing

errors

0.731

12

0.747

11

0.736

11

13) Improve methods of selection,

adjustments and application of

cost data

0.782

9

0.777

10

0.781

10

14) Update cost data with new cost

and create feedback system

0.865

3

0.875

3

0.869

3

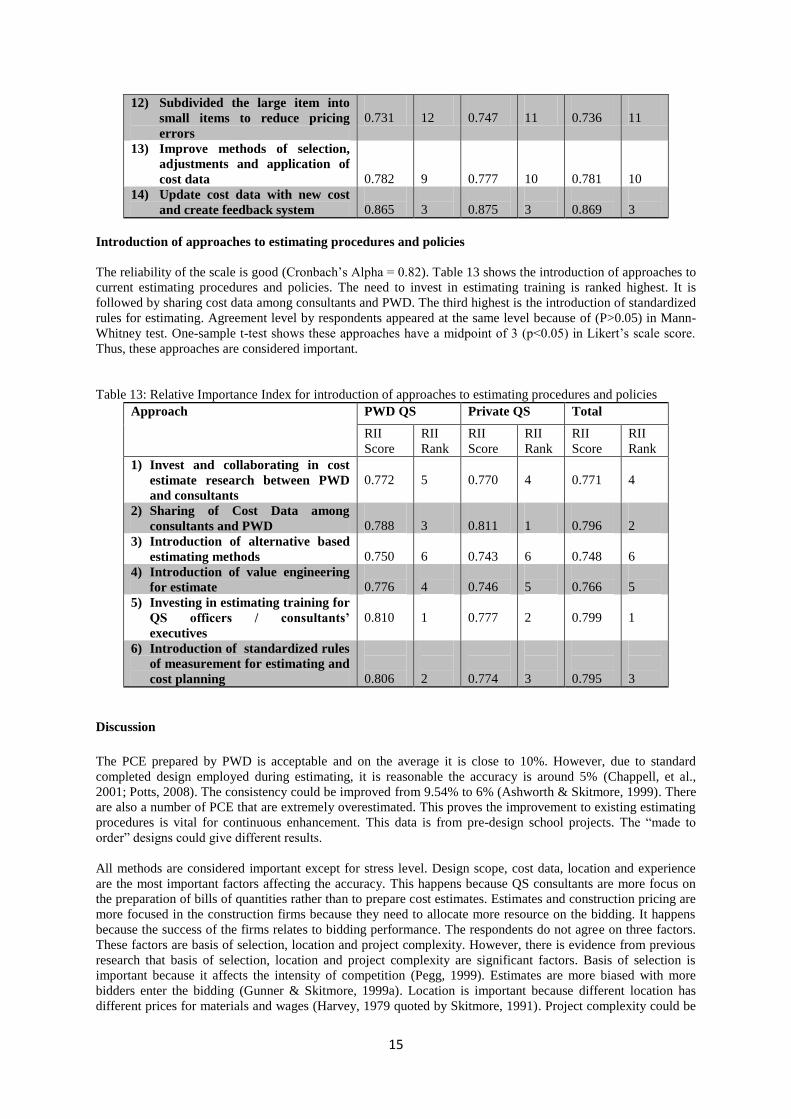

Introduction of approaches to estimating procedures and policies

The reliability of the scale is good (Cronbach’s Alpha = 0.82). Table 13 shows the introduction of approaches to

current estimating procedures and policies. The need to invest in estimating training is ranked highest. It is

followed by sharing cost data among consultants and PWD. The third highest is the introduction of standardized

rules for estimating. Agreement level by respondents appeared at the same level because of (P>0.05) in Mann-

Whitney test. One-sample t-test shows these approaches have a midpoint of 3 (p<0.05) in Likert’s scale score.

Thus, these approaches are considered important.

Table 13: Relative Importance Index for introduction of approaches to estimating procedures and policies

Approach PWD QS Private QS Total

RII

Score

RII

Rank

RII

Score

RII

Rank

RII

Score

RII

Rank

1) Invest and collaborating in cost

estimate research between PWD

and consultants

0.772

5

0.770

4

0.771

4

2) Sharing of Cost Data among

consultants and PWD

0.788

3

0.811

1

0.796

2

3) Introduction of alternative based

estimating methods

0.750

6

0.743

6

0.748

6

4) Introduction of value engineering

for estimate

0.776

4

0.746

5

0.766

5

5) Investing in estimating training for

QS officers / consultants’

executives

0.810

1

0.777

2

0.799

1

6) Introduction of standardized rules

of measurement for estimating and

cost planning

0.806

2

0.774

3

0.795

3

Discussion

The PCE prepared by PWD is acceptable and on the average it is close to 10%. However, due to standard

completed design employed during estimating, it is reasonable the accuracy is around 5% (Chappell, et al.,

2001; Potts, 2008). The consistency could be improved from 9.54% to 6% (Ashworth & Skitmore, 1999). There

are also a number of PCE that are extremely overestimated. This proves the improvement to existing estimating

procedures is vital for continuous enhancement. This data is from pre-design school projects. The “made to

order” designs could give different results.

All methods are considered important except for stress level. Design scope, cost data, location and experience

are the most important factors affecting the accuracy. This happens because QS consultants are more focus on

the preparation of bills of quantities rather than to prepare cost estimates. Estimates and construction pricing are

more focused in the construction firms because they need to allocate more resource on the bidding. It happens

because the success of the firms relates to bidding performance. The respondents do not agree on three factors.

These factors are basis of selection, location and project complexity. However, there is evidence from previous

research that basis of selection, location and project complexity are significant factors. Basis of selection is

important because it affects the intensity of competition (Pegg, 1999). Estimates are more biased with more

bidders enter the bidding (Gunner & Skitmore, 1999a). Location is important because different location has

different prices for materials and wages (Harvey, 1979 quoted by Skitmore, 1991). Project complexity could be

16

explained by the project value. Finding by Aibinu and Pasco (2008) shows project value is the significant factor

which explains the bias in the estimates. Only uncertainty level has a moderate degree of agreement. This

explains why QS experience is subjective rather than specific in general (Ashworth & Skitmore, 1999). This

shows data analysis on project data is the best to determine these factors in future research. It happens because

QS could not see the persistent error trend that developed during estimation (Morrison, 1999).

All methods are considered important. The most important methods suggested by most respondents are

sufficient design information, ensure proper documentation and cost data update. This indicates they are more

concerned with information supplied to QS from designers. These outcomes are slightly different when

compared to Ling and Boo (2001) and Aibinu and Pasco (Aibinu & Pasco, 2008). They suggest the need of QS

to be proactive in ensuring sufficient design information, the use of cost control and cost planning and sufficient

estimating time. The concern about information quality during estimation could be one of the reasons why the

estimates are overestimated (Soo & Oo, 2007). A QS provided with insufficient information will see his

estimate most likely to be overestimated due to bias as he fills the gap with inappropriate mark-ups and

construction items.

All approaches are considered important. However, the best approach to improve the estimating procedures and

policies are for QS in both public agencies and private consultants to invest more in estimating training. A

rigorous estimating syllabus could be used to enhance the knowledge of new recruits. It is because most

universities and colleges are more focused towards training the graduates with the knowledge to prepare bills of

quantities (Hackett & Hicks, 2007). QS in both public agencies and private consultants should share cost data

among themselves. There are many buildings that shared the same contextual requirements built by different

government departments. Then, there is a need to introduce standardized rules of measurement for estimating

and cost planning. This could be the ways to reduce the inconsistencies voiced by private consultants (Abdul-

Rashid Abdul-Aziz & Normah Ali, 2004). They found that the use of different terminologies affects private

consultants when they take-up government projects. This standard could define the level of information based

on the completeness of design. As for know, the estimates are prepared using limited information. However,

there must be acceptable level of information to be supplied by the designers to QS.

Conclusion and Recommendation

Preliminary Cost Estimate is one of the most important services offered by both Public and Private Quantity

Surveyors (PPQS). Therefore, continuous improvement can increase the quality of the estimates prepared for

public projects. PPQS has to be vigilant and take necessary action when preparing the estimates as there are a

number of factors that will affect the accuracy of estimates. These five (5) factors are design scopes, cost data,

location, PPQS experience and design team experience. PPQS should make necessary effort using various

scientific and good approaches while preparing PCE in order to recognize these important factors. Follow up

studies should be done on the factors. Thus, we can understand precisely on how it will affect the accuracy of

PCE as perception could lead to bias. Consequently the data analysis on project data could remove this

uncertainty. The current estimating process could also improve if problems related to insufficient information

are overcome. PPQS need to decide the acceptable level of information from designers.

Some introduction of good approaches into the policies and procedures could improve the accuracy of PCE. The

improvement in estimating might be done if PPQS are willing to invest in employees’ continuous training.

Knowledge for estimating are transferable as it can be learnt over time. There is a need to have a proper

estimating syllabus in their training. QS in both public agencies and private consultants could also share their

cost data as some projects do share similar contextual requirements. It is a good initiative if an information

sharing system among PWD and private consultants is available. The introduction of standardized rules for

estimating and cost planning could also be introduced. This could point out the acceptable level of information

needed by PPQS. The use of standard terminologies may reduce ambiguities and increase common

understanding among PPQS.

Finally, all these improvements could contribute to Public-Private Partnerships through the Government

Transformation Program (GTP). To remain sustainable in the challenging world today, continuous improvement

in estimating will equip PPQS with knowledge and skills for them to adapt in this dynamic world. This could

increase the efficiency of public project management and delivery.

17

Authors’ comment on this paper according to convention theme

Estimating is a dry subject, but it is one of the most important specializations to QS. Transformation is to adapt

to the new environments and challenges. Adaptation requires improvement on current ways of working and

introduction of new things to suit the need of the trends. The old ways of working may need to improve because

more countries have moved forward to benchmark themselves against world standard. To sustain in knowledge

based economy the improvement of QS core services like estimating is necessary for retooling.

REFERENCES

1. Abdul-Rashid Abdul-Aziz, & Normah Ali. (2004). Outsourcing and quality performance: Malaysia's

public works department. Structural Survey, 22(1), 53-60.

2. Aibinu, A. A., & Pasco, T. (2008). The accuracy of pre-tender building cost estimates in Australia.

Construction Management and Economics, 26(12), 1257 - 1269.

3. Akintoye, A. (2000). Analysis of factors influencing project cost estimating practice. Construction

Management and Economics, 18(1), 77 - 89.

4. Ashworth, A. (2010). Cost studies of buildings (5 ed.). Essex: Pearson Education Limited.

5. Ashworth, A., & Skitmore, M. (1999). Accuracy in estimating. In M. Skitmore & V. Marston (Eds.),

Cost modelling (pp. 412-437). London: E & FN Spon.

6. Boussabaine, A. (2007). Cost planning of PFI and PPP building projects. Oxford: Taylor & Francis.

7. BRB, & NRC. (1990). Improving the accuracy of early cost estimates for federal construction projects.

Washington DC: National Academic Press.

8. Chappell, D., Marshall, D., Powell-Smith, V., & Cavender, S. (2001). Building contract dictionary.

Oxford: Blackwell Science Ltd.

9. Cheung, F. K. T., Wong, M. W. L., & Skitmore, M. (2008). A study of clients' and estimators'

tolerance towards estimating errors. Construction Management and Economics, 26(4), 349 - 362.

10. Elhag, T. M. S., Boussabaine, A., & Ballal, T. M. A. (2005). Critical determinants of construction

tendering costs: Quantity surveyors' standpoint. International Journal of Project Management, 23(7),

538-545.

11. Field, A. (2009). Discovering statistics using SPSS (2nd ed.). London: Sage Publications Ltd.

12. Fortune, C. (2006). Process standardisation and the impact of professional judgement on the

formulation of building project budget price advice. Construction Management and Economics, 24(10),

1091 - 1098.

13. Gunner, J., & Skitmore, M. (1999a). Comparative analysis of pre-bid forecasting of building prices

based on Singapore data. Construction Management and Economics, 17(5), 635-646.

14. Gunner, J., & Skitmore, M. (1999b). Pre-bid building price forecasting accuracy: price intensity theory.

Engineering, Construction and Architectural Management, 6(3), 267 - 275.

15. Hackett, J. A., & Hicks, C. M. (2007). Estimating as a profession in UK construction. Engineering

Construction and Architectural Management, 14(1), 26-51.

16. Hughes, W., Hillebrandt, Greenwood, D., & Kwawu, W. (2006). Procurement in the construction

industry – the impact and cost of alternative market and suppy processes. London: Taylor & Francis.

17. Karlsen, J. T., & Lereim, J. (2005). Management of project contingency and allowance. Cost

Engineering, 47(9), 24-29.

18. Kirkham, R. (2007). Ferry and Brandon's cost planning of buildings (8th ed.). Oxford: Blackwell

Publishing.

19. Lee, S., & Smith, A. (2010). New rules of measurement – order of cost estimating and elemental cost

planning. London: The College of Estate Management, Royal Institute of Chartered Surveyors.

20. Legendre, P. (2010). Coefficient of concordance. In N. J. Salkind (Ed.), Encyclopedia of Research

Design. California: SAGE Publications, Inc.

21. Ling, Y. Y., & Boo, J. H. S. (2001). Improving the accuracy of approximate estimates of building

projects. Building Research & Information, 29(4), 312-318.

22. Ministry of Finance. (1958). Federal government building projects - Treasury circular no.3 year 1958.

Kuala Lumpur: Ministry of Finance.

23. Morrison, N. (1999). The accuracy of quantity surveyor's cost estimating. In M. Skitmore & V.

Marston (Eds.), Cost modelling (pp. 438-459). London: E & FN Spon.

24. Morton, R., & Jaggar, D. (1995). Design and the Economics of Building: Spon Press.

25. Moss, S., Prosser, H., Costello, H., Simpson, N., Patel, P., Rowe, S., et al. (1998). Reliability and

validity of the PAS-ADD Checklist for detecting psychiatric disorders in adults with intellectual

disability. Journal of Intellectual Disability Research, 42(2), 173-183.

18

26. Nunnally, J., & Bernstein, I. (1994). Pyschometric theory (3rd ed.). New York: McGraw-Hill.

27. Odusami, K. T., & Onukwube, H. N. (2008). Factors affecting the accuracy of pre-tender cost estimate

in nigeria. Paper presented at the The Construction and Building Research Conference of the Royal

Institution of Chartered Surveyors, Dublin Institute of Technology.

28. Park, W. R., & Jackson, D. E. (1984). Cost engineering analysis: A guide to economic evaluation of

Engineering projects. New York: John Wiley & Sons, Inc.

29. Pegg, I. (1999). The effect of location and other measureable parameters on tender levels. In M.

Skitmore & V. Marston (Eds.), Cost modelling (pp. 293-306). London: E & FN Spon.

30. Peurifoy, R., & Oberlender, G. (2006). Estimating construction costs (5th ed.). New York.: McGraw-

Hill Higher Education.

31. Potts, K. (2008). Construction cost management: learning from case studies. Oxford: Taylor & Francis

Group.

32. Prime Minister Department. (2005). General circular no.4. Putrajaya: Prime Minister Department.

33. Public Works Department. (2010). Guideline for public works' contract management (3rd ed.). Kuala

Lumpur: Public Works Department.

34. Schmidt, R. C. (1997). Managing Delphi Surveys Using Nonparametric Statistical Techniques.

Decision Sciences, 28(3), 763–774.

35. Seeley, I. H. (1996). Building economics: appraisal and control of building design cost and efficiency

36. (4th ed.). London: Macmillan Press.

37. Serpell, A. (2004). Towards a knowledge-based assesment of conceptual cost estimates. Building

Research & Information, 32(2), 157-164.

38. Sinclair, N., Artin, P., & Mulford, S. (2002). Construction cost data workbook. Paper presented at the

Conference on the International Comparison Program, Washington, D.C.

39. Skitmore, M. (1988). Fundamental research in bidding and estimating. Paper presented at the

British/Israeli Seminar on Building Economics: The International Council for Building Research

Studies and Documentation CIB W-55, Haifa, Israel.

40. Skitmore, M. (1991). Early stage construction price forecasting: A review of performance. London:

RICS.

41. Skitmore, M., & Ng, T. (2003). Forecast models for actual construction time and cost. Building and

Environment, 38(2003), 1075-1083.

42. Skitmore, M., & Patchell, B. R. T. (1999). Developments in contract price forcecasting and bidding

technique. In M. Skitmore & V. Marston (Eds.), Cost modelling (pp. 53-84). London: E & FN Spon.

43. Skitmore, M., & Picken, D. H. (2000). The accuracy of pre-tender building price forecasts: an analysis

of USA data. Australian Institute of Quantity Surveyors Refered Journal, 4(1), 33-39.

44. Skitmore, M., Stradling, S. G., Tuohy, A. P., & Mkwezalamba, H. (1990). The accuracy of

construction price forecasts A study of quantity surveyors' performance in early stage estimating:

Department of Surveying, University of Salford.

45. Soo, A., & Oo, B. L. (2007). The effect of information feedback in construction bidding. Australasian

Journal of Construction Economics and Building, 10(1/2), 65‐75.

![[Act 487] Quantity Surveyors Act 1967](https://img.pdfslide.us/doc/110x75/577cc9c41a28aba711a4900f/act-487-quantity-surveyors-act-1967.jpg)