Embed Size (px)

Citation preview

ADVERTISING SUPPLEMENT | SUNDAY, APRIL 6, 2014

Personal loans & finance

n New credit bureau will shake up the UAE’s financial sector

Planning for the futurePage 2

Beware the fine printPage 4

InsideUnlocking the true potential for credit

Borrowing money from banks relatively cheaply has never been difficult for consumers in the UAE. Due

to the absence of a formal credit rating system, consumers have al-ways been able to receive loans or credit cards easily, often leveraging themselves beyond their means. However, things are set to change soon with the UAE’s new credit bu-reau, which will make consumers’ financial history available to banks.

The bureau, widely reported to become fully operational this year, is expected to provide cru-cial regulation in curbing excess lending and rise in consumer debt. Nikola Kosutic, Research Manager

at business information provider Euromonitor International, says, “A group of 12 banks have already started collecting data and running trials ahead of the full introduction. However, one point of controversy that is still looming is whether banks should ask consumers’ consent to probe their credit his-tory, something that banks argue should be compulsory.”

The overall consumer lending environment is projected to undergo a positive transformation when the official credit bureau begins opera-tions. Credit reports will make in-dividuals more aware of financial management and should make them more cautious about getting into debt.

By Chiranti SenguptaFeatures Writer

See Lead on page 2

Online: www.gulfnews.com/GN-Focus Facebook.com/GNFocus

Gulf News Archives

Personal loan solutionsPage 3

Personal loans & FInancePersonal loans & FInance 32Gulf News | Sunday, April 6, 2014 | Advertising SupplementAdvertising Supplement | Sunday, April 6, 2014 | Gulf News

It will go some way to en-suring individuals borrow within their limits and main-tain a good repayment profile. “In time, the bureau will have an impact on retail borrowing in the UAE, since it will help lenders make more accurate lending decisions and, there-fore, better manage risk and reduce credit defaults,” says a spokesperson for Al Etihad Credit Bureau.

Formal system in placeBankers in the UAE also

point out that the formal cred-it rating system will have a positive impact in helping the UAE’s retail borrowing sec-tor mature in a way that will allow for long-term growth, while at the same time, avoid-ing the debt-related vulner-abilities witnessed during the financial crisis.

Devendar Agarwal, Cards and Loans Business Head, Citi-bank, says, “The credit bureau is good for both customers as well as banks and it is a wel-

come move forward.” He adds, “The absence of a credit bureau has impacted the sector ad-versely with some customers getting overleveraged beyond their means. In addition, there is a challenge with recovery in case a customer leaves the country without settling his debts. The launch of a cred-it bureau will help stabilise the sector.”

Consumer credit in the UAE grew from Dh217.5 billion in 2012 to Dh224.9 billion in 2013. It is expected to reach Dh242.3 billion in 2015, according to a recent study on the consumer finance sector in the UAE by Euromonitor International.

Since 2011 — as the UAE began to recover from a 5 per cent drop in real GDP, decline in construction and property sales from the 2008-2010 economic downturn and burst of the Dubai property bubble — several factors have been driving growth in the consumer lending segment. During the downturn, lenders and borrowers, not knowing if or when economic recov-ery would come, shied away from lending and spending, preferring to remain cautious

by mainly turning to sav-ing. However, this scenario is changing with current growth in consumer lending being fuelled by an increase in bank competition, a rising number of expatriates returning to the UAE in response to a surge in job opportunity, particularly in the construction and real estate sectors, and a strong, stable economy, the report highlights.

Growing risk appetiteBanks reported strong

growth in the personal loan segment in 2013 and are upbeat about the health of the indus-try this year.

“The personal loans segment has seen a tremendous resur-gence in the past two years with business increasing at a rate of 25 per cent year-on-year. We expect a similar growth this year,” says a spokesperson for ADCB. “Along with the eco-nomic growth in the UAE and increased job security, which is strengthening the risk appetite of borrowers, the depreciating Indian rupee is also fuelling increased uptake of personal loans from the Indian expatri-ate community.”

Jamal Alvi, Head of Retail Assets, ADIB, is also looking at

a strong re-vival in the

personal loan segment. He

says, “The demand for personal loans has been fairly high this year, as the economy has recovered signifi-

cantly. This has led to a rise in customers’ con-

fidence.” ADIB’s customer financ-

ing category grew above market average by 20 per cent in 2013.

The Al Etihad Credit Bureau (AECB) will produce your financial health report card, says Sandi Saksena, Financial Counselor, Nexus Insurance Brokers. “It will flag things such as unclosed bank accounts, non-cancelled credit cards that have been mailed but are not in use, outstanding pay-ment and loans on several credit cards, plus overdraft facilities.” Sadi Has-souneh, CEO, wealth management firm Mahal Thqa, says, “ A credit report is designed to encourage individuals and companies not to get into debt that they will find difficult to manage and to act as a gauge to lenders of how trustworthy an individual or company is in regard to paying back debt.” Maintaining confidentiality: An AECB spokesperson says data protec-tion is of the utmost importance. Credit reports will be available to lending institutions, utility companies, landlords, telecoms and insurance compa-nies, subject to written consent from consumers. Making life tougher: Saksena says, “The report is important for con-sumers as it will help them to better understand their debt level and cred-itworthiness, and will provide a full picture of their financial obligations. In addition, it will assist them in managing their credit and future borrowing responsibly,” adds the AECB spokesperson.Getting bank loans: AECB is quick to point out the ultimate lending de-cision is the responsibility of the financial institution. “Also, having access to individuals’ and corporations’ payment history and current debt status will ensure that lenders fund customers appropriately, helping consumers to avoid becoming trapped by debts,” says the spokesperson. Overseas impact: The credit report issued by the bureau will have no relevance overseas. The bureau will not have access to credit histories in other countries.

— sanaya Pavri/Features Writer

AL ETIhAD CREDIT BUREAU

How will the move affect my life?

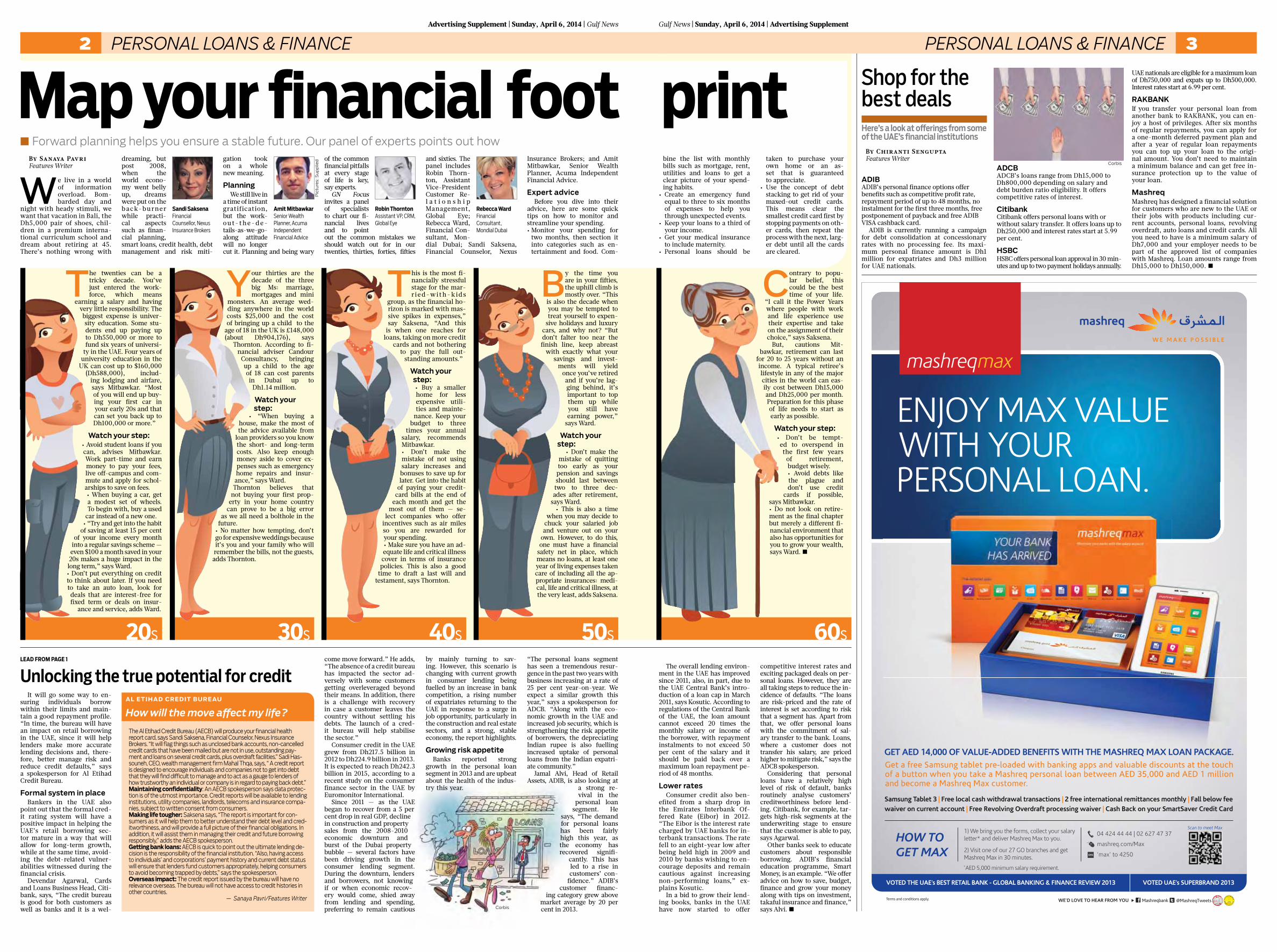

The twenties can be a tricky decade. You’ve just entered the work-force, which means

earning a salary and having very little responsibility. The biggest expense is univer-sity education. Some stu-dents end up paying up to Dh550,000 or more to fund six years of universi-

ty in the UAE. Four years of university education in the

UK can cost up to $160,000 (Dh588,000), includ-

ing lodging and airfare, says Mitbawkar. “Most of you will end up buy-ing your first car in your early 20s and that can set you back up to Dh100,000 or more.”

Watch your step: • Avoid student loans if you can, advises Mitbawkar. Work part-time and earn money to pay your fees, live off-campus and com-mute and apply for schol-arships to save on fees. • When buying a car, get a modest set of wheels. To begin with, buy a used

car instead of a new one. • “Try and get into the habit

of saving at least 15 per cent of your income every month

into a regular savings scheme — even $100 a month saved in your 20s makes a huge impact in the long term,” says Ward.• Don’t put everything on credit to think about later. If you need to take an auto loan, look for deals that are interest-free for fixed term or deals on insur-

ance and service, adds Ward.

Map your financial foot print

This is the most fi-nancially stressful stage for the mar-rie d-wi t h - kid s

group, as the financial ho-rizon is marked with mas-sive spikes in expenses,” say Saksena, “And this

is when one reaches for loans, taking on more credit

cards and not bothering to pay the full out-

standing amounts.”

Watch your step: • Buy a smaller home for less expensive utili-ties and mainte-

nance. Keep your budget to three

times your annual salary, recommends Mitbawkar. • Don’t make the mistake of not using salary increases and bonuses to save up for later. Get into the habit

of paying your credit-card bills at the end of

each month and get the most out of them — se-

lect companies who offer incentives such as air miles so you are rewarded for your spending.• Make sure you have an ad-equate life and critical illness cover in terms of insurance policies. This is also a good

time to draft a last will and testament, says Thornton.

By the time you are in your fifties, the uphill climb is mostly over. “This

is also the decade when you may be tempted to treat yourself to expen-

sive holidays and luxury cars, and why not? “But don’t falter too near the finish line, keep abreast

with exactly what your savings and invest-

ments will yield once you’ve retired and if you’re lag-ging behind, it’s important to top them up while you still have earning power,”

says Ward.

Watch your step:

• Don’t make the mistake of quitting too early as your pension and savings should last between two to three dec-ades after retirement,

says Ward.• This is also a time

when you may decide to chuck your salaried job and venture out on your

own. However, to do this, one must have a financial

safety net in place, which means no loans, at least one year of living expenses taken care of including all the ap-propriate insurances: medi-cal, life and critical illness, at the very least, adds Saksena.

ADIB ADIB’s personal finance options offer benefits such as competitive profit rate, repayment period of up to 48 months, no instalment for the first three months, free postponement of payback and free ADIB VISA cashback card.

ADIB is currently running a campaign for debt consolidation at concessionary rates with no processing fee. Its maxi-mum personal finance amount is Dh1 million for expatriates and Dh3 million for UAE nationals.

ADCB ADCB’s loans range from Dh15,000 to Dh800,000 depending on salary and debt burden ratio eligibility. It offers competitive rates of interest.

Citibank Citibank offers personal loans with or without salary transfer. It offers loans up to Dh250,000 and interest rates start at 5.99 per cent.

HSBCHSBC offers personal loan approval in 30 min-utes and up to two payment holidays annually.

UAE nationals are eligible for a maximum loan of Dh750,000 and expats up to Dh500,000. Interest rates start at 6.99 per cent.

RAkBAnkIf you transfer your personal loan from another bank to RAKBANK, you can en-joy a host of privileges. After six months of regular repayments, you can apply for a one-month deferred payment plan and after a year of regular loan repayments you can top up your loan to the origi-nal amount. You don’t need to maintain a minimum balance and can get free in-surance protection up to the value of your loan.

Mashreq Mashreq has designed a financial solution for customers who are new to the UAE or their jobs with products including cur-rent accounts, personal loans, revolving overdraft, auto loans and credit cards. All you need to have is a minimum salary of Dh7,000 and your employer needs to be part of the approved list of companies with Mashreq. Loan amounts range from Dh15,000 to Dh150,000. 7

n Forward planning helps you ensure a stable future. Our panel of experts points out how

We live in a world of information overload. Bom-barded day and

night with heady stimuli, we want that vacation in Bali, the Dh5,000 pair of shoes, chil-dren in a premium interna-tional curriculum school and dream about retiring at 45. There’s nothing wrong with

dreaming, but post 2008, when the world econo-my went belly up, dreams were put on the b ack- bu rner while practi-cal aspects such as finan-cial planning, smart loans, credit health, debt management and risk miti-

gation took on a whole new meaning.

PlanningWe still live in

a time of instant gratification, but the work-o u t- t h e - d e -tails-as-we-go-along attitude will no longer cut it. Planning and being wary

of the common financial pitfalls at every stage of life is key, say experts.

GN Focus invites a panel of specialists to chart our fi-nancial lives and to point out the common mistakes we should watch out for in our twenties, thirties, forties, fifties

and sixties. The panel includes Robin Thorn-ton, Assistant Vice-President Customer Re-l a t i o n s h i p Management, Global Eye; Rebecca Ward, Financial Con-sultant, Mon-dial Dubai; Sandi Saksena, Financial Counselor, Nexus

By Sanaya Pavri Features Writer

amit MitbawkarSenior Wealth Planner, Acuma Independent Financial Advice

Rebecca WardFinancial Consultant, Mondial Dubai

Robin ThorntonAssistant VP, CRM, Global Eye

Shop for the best dealsHere’s a look at offerings from some of the UAE’s financial institutions

Contrary to popu-lar belief, this could be the best time of your life.

“I call it the Power Years where people with work and life experience use their expertise and take on the assignment of their choice,” says Saksena.

But, cautions Mit-bawkar, retirement can last

for 20 to 25 years without an income. A typical retiree’s lifestyle in any of the major cities in the world can eas-ily cost between Dh15,000 and Dh25,000 per month. Preparation for this phase of life needs to start as early as possible.

Watch your step: • Don’t be tempt-ed to overspend in the first few years

of retirement, budget wisely.• Avoid debts like the plague and don’t use credit

cards if possible, says Mitbawkar.• Do not look on retire-ment as the final chapter but merely a different fi-nancial environment that also has opportunities for you to grow your wealth, says Ward. 7

The overall lending environ-ment in the UAE has improved since 2011, also, in part, due to the UAE Central Bank’s intro-duction of a loan cap in March 2011, says Kosutic. According to regulations of the Central Bank of the UAE, the loan amount cannot exceed 20 times the monthly salary or income of the borrower, with repayment instalments to not exceed 50 per cent of the salary and it should be paid back over a maximum loan repayment pe-riod of 48 months.

Lower ratesConsumer credit also ben-

efited from a sharp drop in the Emirates Interbank Of-fered Rate (Eibor) in 2012. “The Eibor is the interest rate charged by UAE banks for in-terbank transactions. The rate fell to an eight-year low after being held high in 2009 and 2010 by banks wishing to en-courage deposits and remain cautious against increasing non-performing loans,” ex-plains Kosutic.

In a bid to grow their lend-ing books, banks in the UAE have now started to offer

competitive interest rates and exciting packaged deals on per-sonal loans. However, they are all taking steps to reduce the in-cidence of defaults. “The loans are risk-priced and the rate of interest is set according to risk that a segment has. Apart from that, we offer personal loans with the commitment of sal-ary transfer to the bank. Loans, where a customer does not transfer his salary, are priced higher to mitigate risk,” says the ADCB spokesperson.

Considering that personal loans have a relatively high level of risk of default, banks routinely analyse customers’ creditworthiness before lend-ing. Citibank, for example, tar-gets high-risk segments at the underwriting stage to ensure that the customer is able to pay, says Agarwal.

Other banks seek to educate customers about responsible borrowing. ADIB’s financial education programme, Smart Money, is an example. “We offer advice on how to save, budget, finance and grow your money along with tips on investment, takaful insurance and finance,” says Alvi. 7

20s 40s

Your thirties are the decade of the three big Ms: marriage, mortgages and mini

monsters. An average wed-ding anywhere in the world costs $25,000 and the cost of bringing up a child to the

age of 18 in the UK is £148,000 (about Dh904,176), says

Thornton. According to fi-nancial adviser Candour

Consultancy, bringing up a child to the age of 18 can cost parents in Dubai up to

Dh1.14 million.

Watch your step:

• “When buying a house, make the most of the advice available from

loan providers so you know the short- and long-term costs. Also keep enough money aside to cover ex-penses such as emergency home repairs and insur-ance,” says Ward.

• Thornton believes that not buying your first prop-

erty in your home country can prove to be a big error

as we all need a bolthole in the future.

• No matter how tempting, don’t go for expensive weddings because it’s you and your family who will remember the bills, not the guests, adds Thornton.

30s 50s 60s

Sandi SaksenaFinancial Counsellor, Nexus Insurance Brokers

Insurance Brokers; and Amit Mitbawkar, Senior Wealth Planner, Acuma Independent Financial Advice.

Expert adviceBefore you dive into their

advice, here are some quick tips on how to monitor and streamline your spending.• Monitor your spending for

two months, then section it into categories such as en-tertainment and food. Com-

bine the list with monthly bills such as mortgage, rent, utilities and loans to get a clear picture of your spend-ing habits.

• Create an emergency fund equal to three to six months of expenses to help you through unexpected events.

• Keep your loans to a third of your income.

• Get your medical insurance to include maternity.

• Personal loans should be

taken to purchase your own home or an as-set that is guaranteed to appreciate.

• Use the concept of debt stacking to get rid of your maxed-out credit cards. This means clear the smallest credit card first by stopping payments on oth-er cards, then repeat the process with the next, larg-er debt until all the cards are cleared.

By Chiranti Sengupta Features Writer

Corbis

Pic

ture

s: S

uppl

ied

Unlocking the true potential for creditLead fRoM page 1

Corbis