Embed Size (px)

Citation preview

Personal FinancePersonal Finance

Unit 1Unit 1

PlanningPlanning

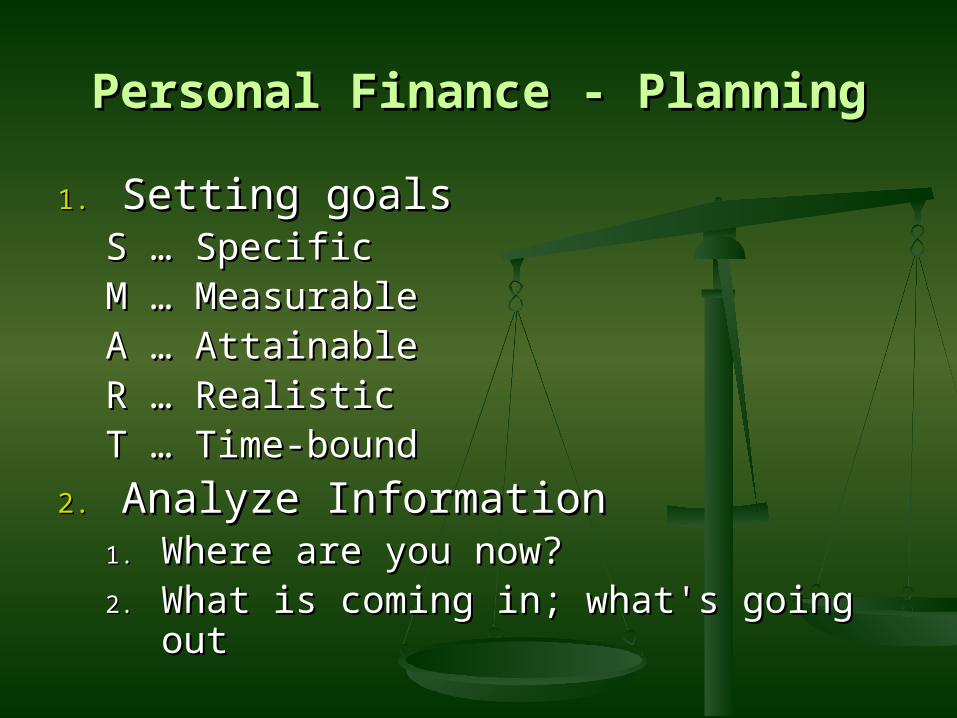

Personal Finance - PlanningPersonal Finance - Planning

1.1. Setting goalsSetting goalsS … SpecificS … SpecificM … MeasurableM … MeasurableA … AttainableA … AttainableR … RealisticR … RealisticT … Time-boundT … Time-bound

2.2. Analyze InformationAnalyze Information1.1. Where are you now?Where are you now?2.2. What is coming in; what's going outWhat is coming in; what's going out

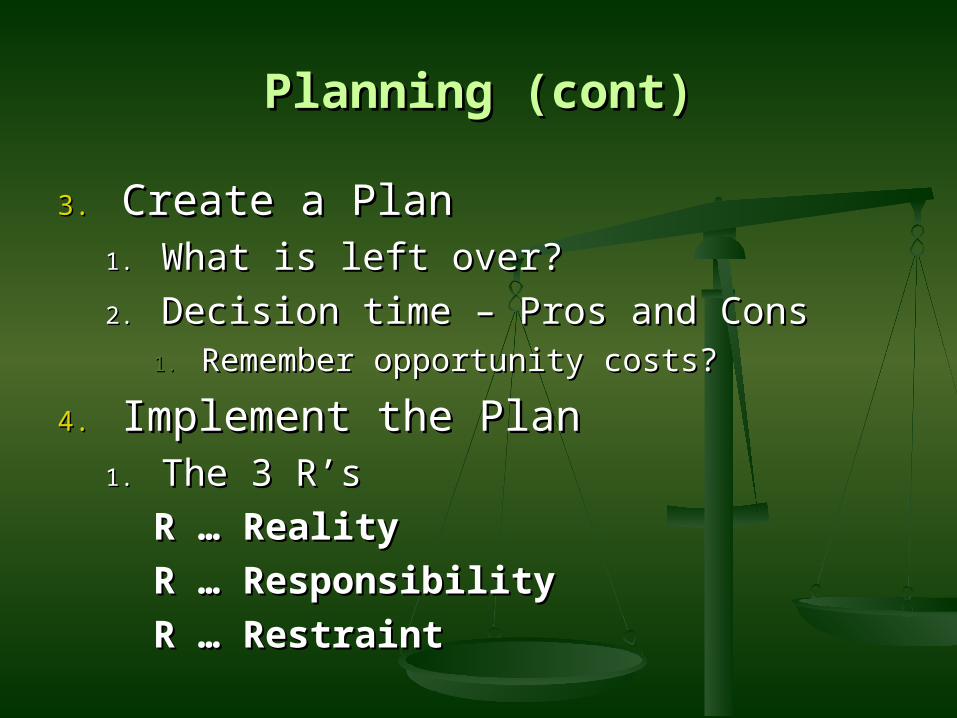

Planning (cont)Planning (cont)

3.3. Create a PlanCreate a Plan1.1. What is left over?What is left over?

2.2. Decision time – Pros and ConsDecision time – Pros and Cons1.1. Remember opportunity costs?Remember opportunity costs?

4.4. Implement the PlanImplement the Plan1.1. The 3 R’sThe 3 R’s

R … RealityR … Reality

R … ResponsibilityR … Responsibility

R … RestraintR … Restraint

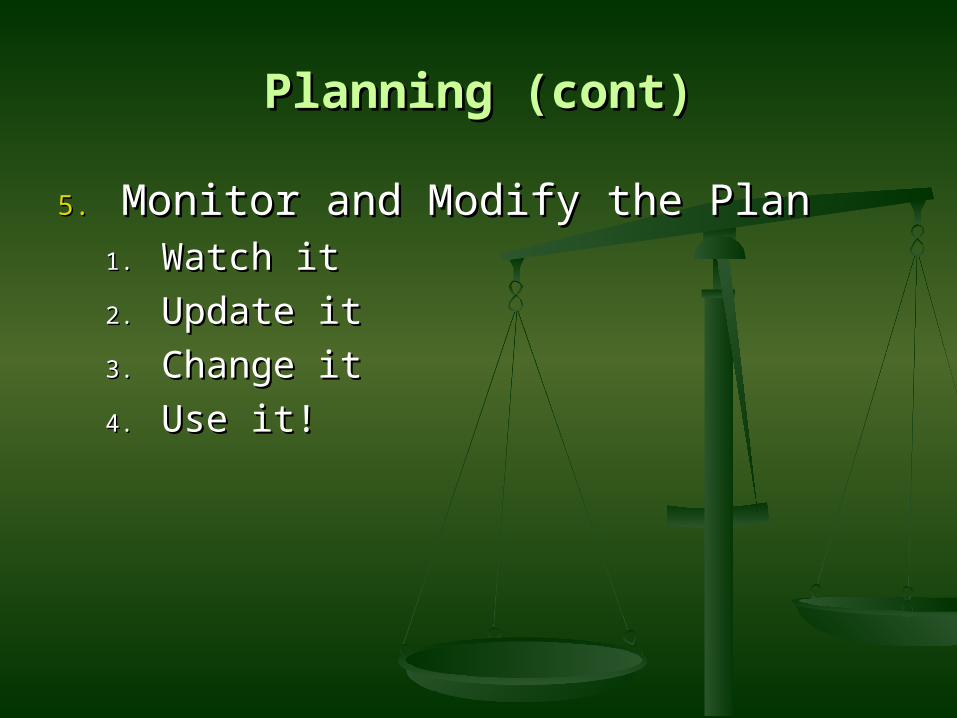

Planning (cont)Planning (cont)

5.5. Monitor and Modify the PlanMonitor and Modify the Plan1.1. Watch itWatch it

2.2. Update itUpdate it

3.3. Change itChange it

4.4. Use it!Use it!

Personal FinancePersonal Finance

Unit 3Unit 3

BudgetBudget

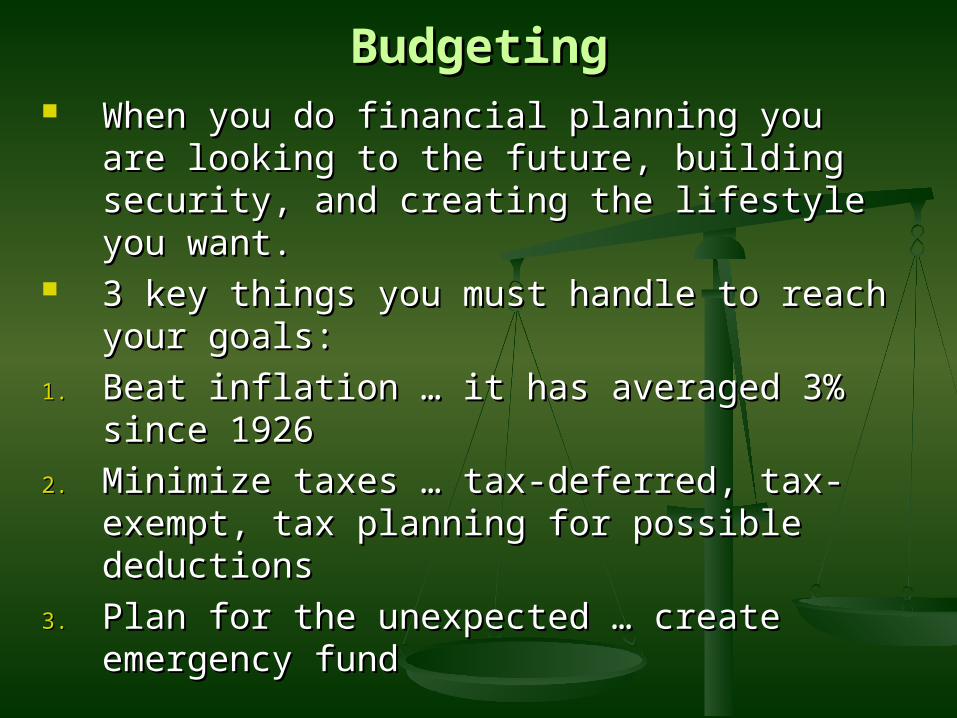

BudgetingBudgeting When you do financial planning you are When you do financial planning you are

looking to the future, building security, looking to the future, building security, and creating the lifestyle you want.and creating the lifestyle you want.

3 key things you must handle to reach 3 key things you must handle to reach your goals:your goals:

1.1. Beat inflation … it has averaged 3% since Beat inflation … it has averaged 3% since 19261926

2.2. Minimize taxes … tax-deferred, tax-Minimize taxes … tax-deferred, tax-exempt, tax planning for possible exempt, tax planning for possible deductionsdeductions

3.3. Plan for the unexpected … create Plan for the unexpected … create emergency fundemergency fund

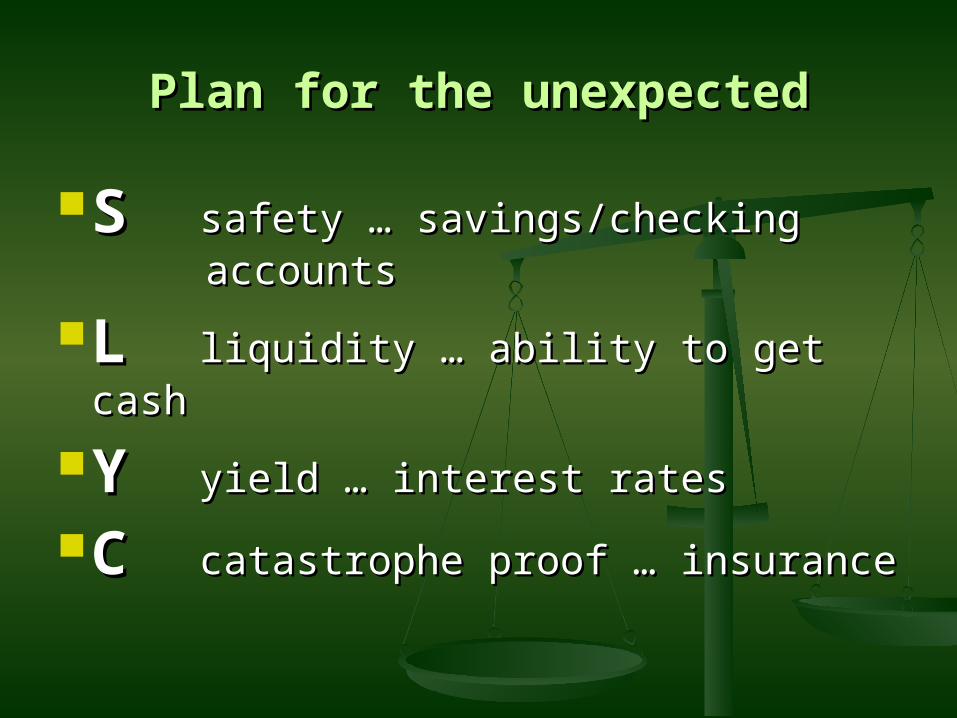

Plan for the unexpectedPlan for the unexpected

S S safety … savings/checking safety … savings/checking accounts accounts

L L liquidity … ability to get cashliquidity … ability to get cash

Y Y yield … interest ratesyield … interest rates

C C catastrophe proof … insurancecatastrophe proof … insurance

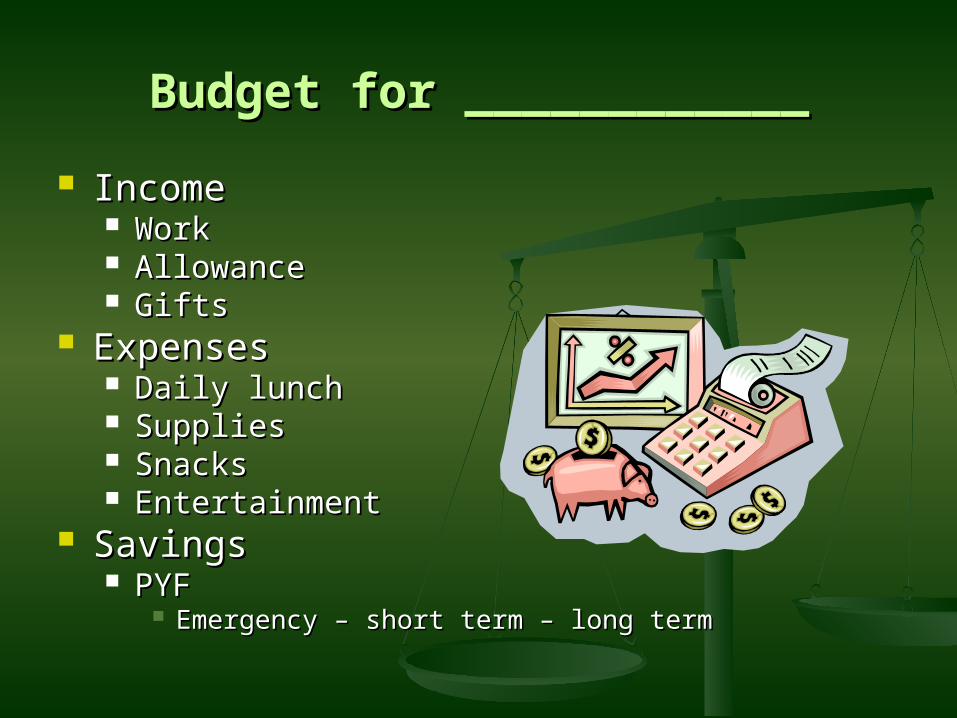

Budget for ____________Budget for ____________

IncomeIncome WorkWork AllowanceAllowance GiftsGifts

ExpensesExpenses Daily lunchDaily lunch SuppliesSupplies SnacksSnacks EntertainmentEntertainment

SavingsSavings PYFPYF

Emergency – short term – long termEmergency – short term – long term

Personal Property InventoryPersonal Property Inventory

A list of all valuable items you ownA list of all valuable items you own Examples: furniture, clothing, Examples: furniture, clothing,

appliances, books, collectionsappliances, books, collections Important for insurance claimsImportant for insurance claims Best if you use photographs of the Best if you use photographs of the

itemsitems Helps you see your spending patternsHelps you see your spending patterns

Item - Year purchased – Price – ValueItem - Year purchased – Price – Value

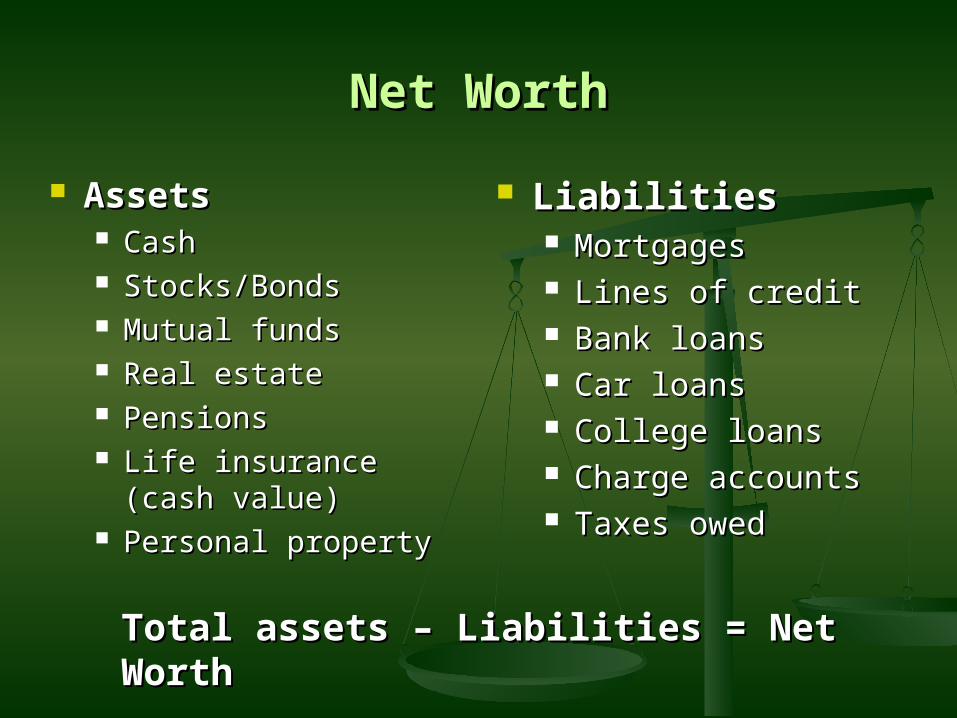

Net WorthNet Worth

AssetsAssets CashCash Stocks/BondsStocks/Bonds Mutual fundsMutual funds Real estateReal estate PensionsPensions Life insurance (cash Life insurance (cash

value)value) Personal propertyPersonal property

LiabilitiesLiabilities MortgagesMortgages Lines of creditLines of credit Bank loansBank loans Car loansCar loans College loansCollege loans Charge accountsCharge accounts Taxes owedTaxes owed

Total assets – Liabilities = Net Total assets – Liabilities = Net WorthWorth

Net Worth (cont)Net Worth (cont)

When do you need it?When do you need it?

College financial aidCollege financial aid LoansLoans MortgagesMortgages Lines of creditLines of credit

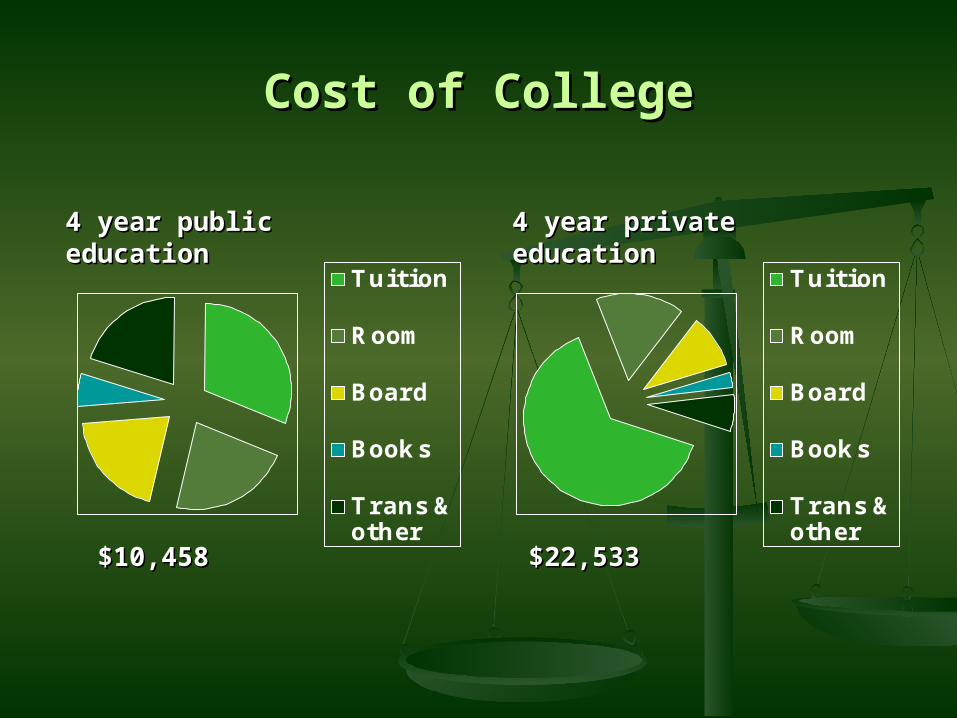

Cost of CollegeCost of College

Tuition

Room

Board

Books

Trans &other

Tuition

Room

Board

Books

Trans &other

4 year public 4 year public educationeducation

$10,458$10,458

4 year private 4 year private educationeducation

$22,533$22,533

Personal FinancePersonal Finance

Unit 4Unit 4

Savings and InvestmentsSavings and Investments

SavingsSavings

Why save?Why save? To ensure you have enough money To ensure you have enough money

for special purchases & future for special purchases & future expensesexpenses Money set aside for short-term goalsMoney set aside for short-term goals

Savings accountSavings account Money Market accountMoney Market account Time deposit (CD)Time deposit (CD)

InvestmentsInvestments Why risk your money?Why risk your money? To grow your money and combat To grow your money and combat

inflation riskinflation risk Money set aside for long-term goalsMoney set aside for long-term goals

Decision – own or loan?Decision – own or loan?

1.1. Stocks: capital gains + dividendsStocks: capital gains + dividends Common vs. preferred stockCommon vs. preferred stock

2.2. Bonds: right to receive fixed amount at a Bonds: right to receive fixed amount at a future date + interestfuture date + interest

3.3. Mutual fundsMutual funds Benefit – diversification + pro mgmtBenefit – diversification + pro mgmt Money Market, bonds, stocks, indexMoney Market, bonds, stocks, index

Growing your MoneyGrowing your Money What do you need?What do you need?

1.1. MoneyMoney

2.2. TimeTime

DecisionsDecisions

1.1. Do you own or loan?Do you own or loan?

2.2. Risk vs. RewardRisk vs. Reward

Understand the time-valueUnderstand the time-valueof moneyof money

StocksStocks BondsBonds

Risk vs. RewardRisk vs. RewardRiskRisk

SafetySafety

InsuranceInsurance

Savings Savings accountaccount

Mutual fundsMutual funds

Stocks/Stocks/BondsBonds

CommoditieCommoditiess

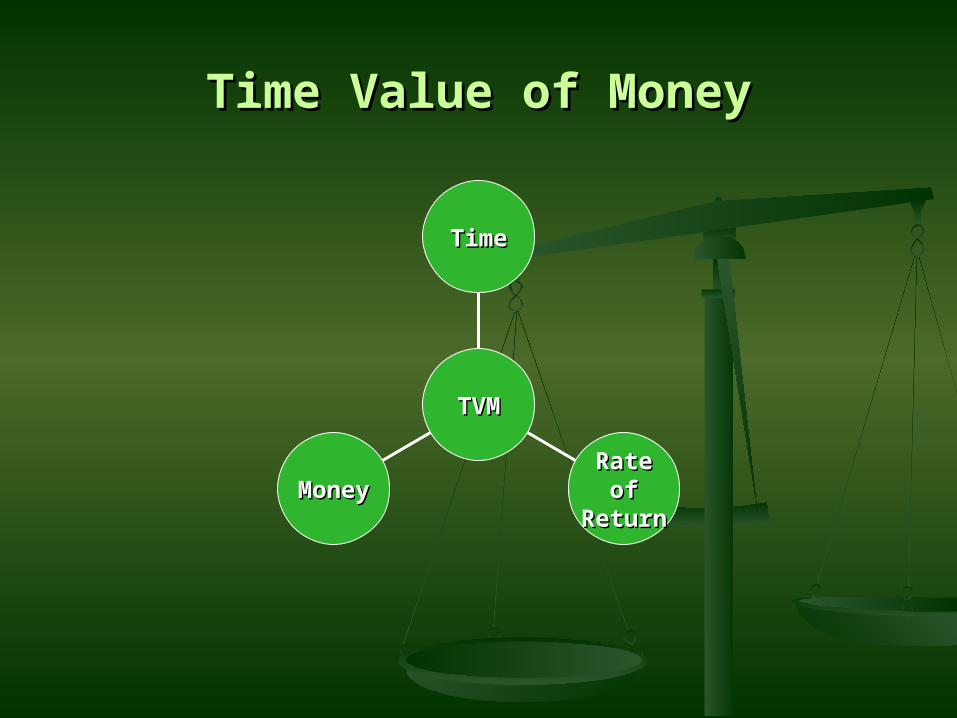

Time Value of MoneyTime Value of Money

MoneyMoney Rate Rate

of of ReturnReturn

TimeTime

TVMTVM

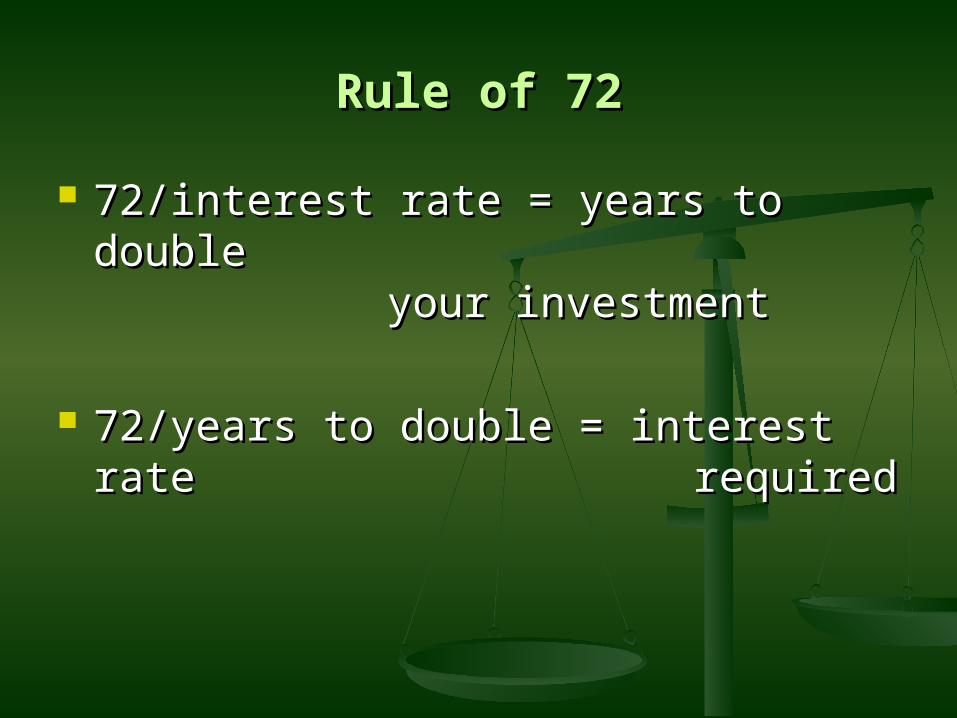

Rule of 72Rule of 72

72/interest rate = years to double 72/interest rate = years to double your your investmentinvestment

72/years to double = interest rate 72/years to double = interest rate required required

Personal FinancePersonal FinanceUnit 5Unit 5

CreditCredit

CreditCredit Loans, credit cards, and other deferred Loans, credit cards, and other deferred

payments. You are renting money.payments. You are renting money. Steps to establish credit:Steps to establish credit:

1.1. Maintain savings and checking accountsMaintain savings and checking accounts Shows money mgmtShows money mgmt

2.2. Get a department store credit cardGet a department store credit card Responsible use gives you good creditResponsible use gives you good credit

3.3. Use your savings as collateralUse your savings as collateral

4.4. Have someone with good credit cosignHave someone with good credit cosign

CreditCredit Are you credit worthy?Are you credit worthy? The four C’s:The four C’s:1.1. CapacityCapacity

Your ability to repay (job? How long? How Your ability to repay (job? How long? How much?)much?)

2.2. CapitalCapital Your regular income + savings and checkingYour regular income + savings and checking

3.3. CharacterCharacter Your willingness to repay. Your credit report.Your willingness to repay. Your credit report.

4.4. CollateralCollateral Property to secure a loan.Property to secure a loan.

CreditCredit Types of creditTypes of credit

Loans – either single-payment or Loans – either single-payment or installmentinstallment

Loans with collateral are called secured loansLoans with collateral are called secured loans Loans without collateral are unsecured or Loans without collateral are unsecured or

signature loanssignature loans Credit cards – revolving or open-ended Credit cards – revolving or open-ended

creditcredit Bank cards – Mastercard, VisaBank cards – Mastercard, Visa Travel & Entertainment – American Express, Travel & Entertainment – American Express,

Diners ClubDiners Club Pay total each monthPay total each month

Credit ProtectionCredit Protection Truth in Lending LawsTruth in Lending Laws

Require lenders to disclose certain information:Require lenders to disclose certain information: Exact finance charges on an loansExact finance charges on an loans Credit cards – monthly interest rate, APR, method of Credit cards – monthly interest rate, APR, method of

finance charge calculationfinance charge calculation Fair Credit Reporting ActFair Credit Reporting Act

Protects you from errors on credit reportsProtects you from errors on credit reports Entitled to know the reason for negative reportEntitled to know the reason for negative report

Fair Credit Billing ActFair Credit Billing Act Lets you dispute and correct billing informationLets you dispute and correct billing information

Equal Credit Opportunity ActEqual Credit Opportunity Act Protects you from being discriminated againstProtects you from being discriminated against

Comparing OffersComparing Offers

What is the APR?What is the APR? Is the APR fixed or Is the APR fixed or

variable?variable? What is the periodic What is the periodic

rate?rate? How are finance How are finance

charges computed?charges computed? Is there a grace period?Is there a grace period? What fees does the What fees does the

creditor charge?creditor charge? Annual, late payment, Annual, late payment,

cash advance, exceeding cash advance, exceeding the credit limitthe credit limit

Personal FinancePersonal FinanceUnit 6Unit 6

InsuranceInsurance

InsuranceInsurance

The concept of insuranceThe concept of insurance A method of spreading individual A method of spreading individual riskrisk

among a large group to make losses among a large group to make losses more affordable to allmore affordable to all Risk is the chance of financial loss from Risk is the chance of financial loss from

perils to people or propertyperils to people or property Terms:Terms:

Insurer – policy – premium - policyholder -Insurer – policy – premium - policyholder - deductibledeductible

InsuranceInsurance Insurance is not meant to enrichInsurance is not meant to enrich Insurance is meant to compensate for Insurance is meant to compensate for

actual losses. To put you back into actual losses. To put you back into the same financial condition you were the same financial condition you were in before the loss.in before the loss. IndemnificationIndemnification

Statistical probability is the root of Statistical probability is the root of indemnificationindemnification Higher probability = higher premiumHigher probability = higher premium

RisksRisks What risks do you face?What risks do you face? Reference poster Reference poster 3 major insurable risks:3 major insurable risks:1.1. PersonalPersonal

Job, health, disability, deathJob, health, disability, death2.2. PropertyProperty

Home, car, possessionsHome, car, possessions3.3. LiabilityLiability

Errors, neglect, accidentErrors, neglect, accident

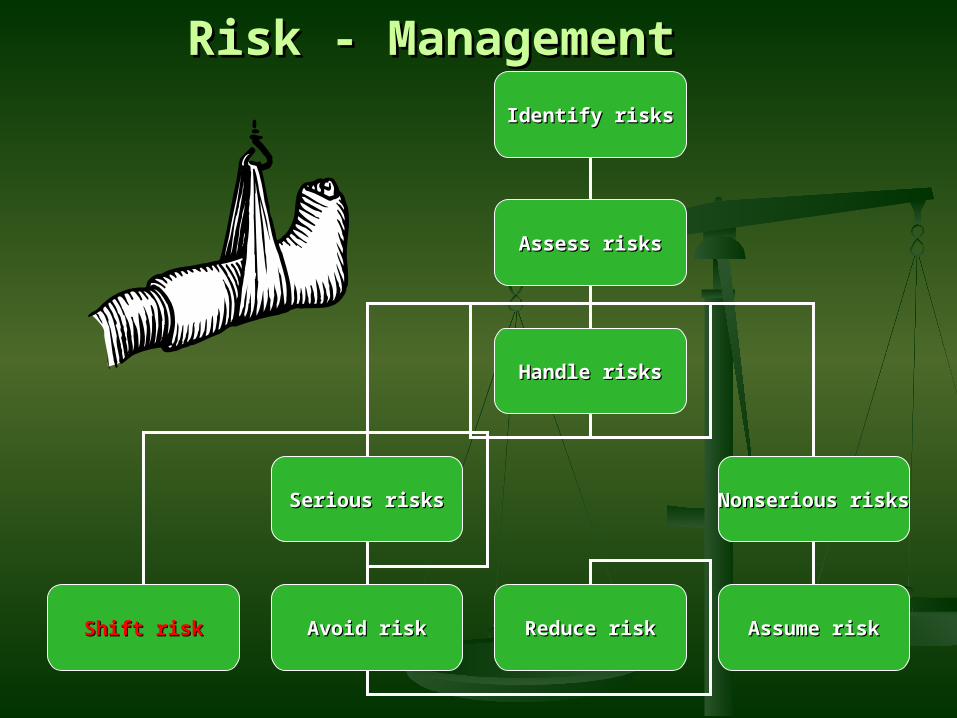

Risk - ManagementRisk - ManagementIdentify risksIdentify risks

Assess risksAssess risks

Handle risksHandle risks

Serious risksSerious risks Nonserious risksNonserious risks

Shift riskShift risk Avoid riskAvoid risk Reduce riskReduce risk Assume riskAssume risk

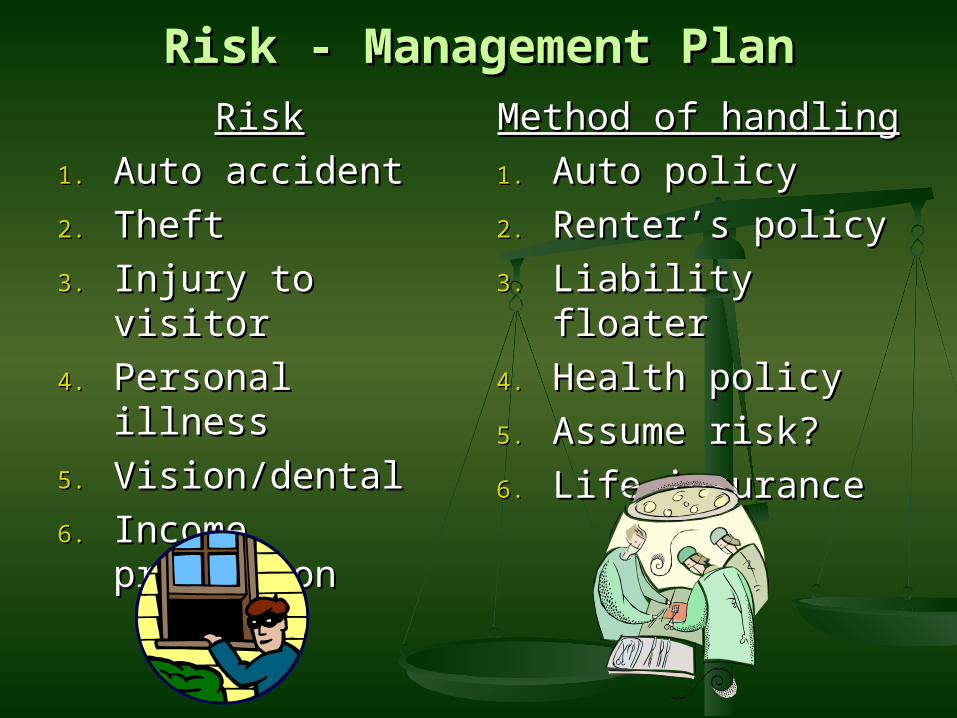

Risk - Management PlanRisk - Management PlanRiskRisk

1.1. Auto accidentAuto accident

2.2. TheftTheft

3.3. Injury to visitorInjury to visitor

4.4. Personal illnessPersonal illness

5.5. Vision/dental Vision/dental

6.6. Income protectionIncome protection

Method of handlingMethod of handling

1.1. Auto policyAuto policy

2.2. Renter’s policyRenter’s policy

3.3. Liability floaterLiability floater

4.4. Health policyHealth policy

5.5. Assume risk?Assume risk?

6.6. Life insuranceLife insurance

Auto InsuranceAuto Insurance

Types of coverage:Types of coverage:1.1. LiabilityLiability

Bodily injury, Property damageBodily injury, Property damage1.1. Medical paymentsMedical payments2.2. Uninsured motoristUninsured motorist3.3. Underinsured motorist Underinsured motorist 4.4. CollisionCollision5.5. comprehensivecomprehensive

Auto Insurance Auto Insurance

Cost factors:Cost factors:1.1. Car modelCar model

+ sports car; - safety features+ sports car; - safety features2.2. Driver classificationDriver classification

+ male teenager+ male teenager3.3. LocationLocation

+ cities; - rural areas+ cities; - rural areas4.4. Miles driven and purposeMiles driven and purpose5.5. Your recordYour record

Health InsuranceHealth Insurance Managed care plans:Managed care plans:

1.1. HMO – health maintenance org.HMO – health maintenance org. Primary care physicianPrimary care physician Care from within the networkCare from within the network No co-insurance or deductibleNo co-insurance or deductible

2.2. PPO – preferred provider org.PPO – preferred provider org. Wider choiceWider choice Pay deductible & co-insurancePay deductible & co-insurance Reduced rates within networkReduced rates within network

Managed Care (cont)Managed Care (cont)3.3. POS – point of servicePOS – point of service

Coverage less restrictiveCoverage less restrictive Pay co-payPay co-pay Referrals outside network still coveredReferrals outside network still covered

4.4. Indemnity plansIndemnity plans Broader choice of doctorsBroader choice of doctors Must pay deductibles (80/20)Must pay deductibles (80/20)

Government HelpGovernment Help

1.1. Workers compensationWorkers compensation Employers required to carry this Employers required to carry this

insuranceinsurance Covers job related injuries & illnessCovers job related injuries & illness

2.2. COBRA – consolidated omnibus COBRA – consolidated omnibus reconciliation actreconciliation act

For employees who lose their For employees who lose their insurance at workinsurance at work

Short term (while you find new Short term (while you find new insurance)insurance)

Government Help (cont)Government Help (cont)

3.3. MedicareMedicare Part of social securityPart of social security For people over 65 & those receiving For people over 65 & those receiving

social security disabilitysocial security disability

4.4. MedicaidMedicaid Insurance for low income familiesInsurance for low income families

Life InsuranceLife Insurance ““Anytime someone else depends on your Anytime someone else depends on your

income . . . You need life insurance.”income . . . You need life insurance.” Terms: beneficiary – mortality tables –Terms: beneficiary – mortality tables –

rider – cash valuerider – cash value Types:Types:

1.1. Term insuranceTerm insurance

““pure” insurance – level – decreasing – pure” insurance – level – decreasing – renewablerenewable

2.2. Permanent insurancePermanent insurance

combines savings with lifetime protectioncombines savings with lifetime protection Many combinations of protectionMany combinations of protection

Property InsuranceProperty Insurance Insurance to protect your personal Insurance to protect your personal

possessionspossessions Renter’s insuranceRenter’s insurance

Household inventory (best of video taped)Household inventory (best of video taped) Room – item – cost – date of purchase – Room – item – cost – date of purchase –

receiptreceipt Cash value vs. replacement valueCash value vs. replacement value

Homeowner’s insuranceHomeowner’s insurance Basic – Broad – Special – ComprehensiveBasic – Broad – Special – Comprehensive Does not cover floods, animals, motor Does not cover floods, animals, motor

vehicles, business propertyvehicles, business property Liability coverageLiability coverage