Embed Size (px)

Citation preview

NEW MILFORD PUBLIC SCHOOLSNew Milford, Connecticut

PERSONAL FINANCE

August 2011

Approved by the Board of Education

December 13, 2011

2

New Milford Board of Education

Wendy Faulenbach, ChairpersonDaniel Nichols, Vice Chairperson

Daniele Shook, SecretaryLynette Celli Rigdon, Assistant Secretary

Tom BrantDavid Lawson

Thomas McSherryDavid R. ShafferWilliam Wellman

Superintendent of SchoolsJeanAnn C. Paddyfote, Ph.D.

Assistant SuperintendentMaureen E. McLaughlin, Ph.D.

New Milford High School PrincipalGreg P. Shugrue

Authors of Course GuideDaryl Daniels

Janice Perrone

3

New Milford’s Mission Statement

The mission of the New Milford Public Schools, a collaborative partnership of students,

educators, family and community, is to prepare each and every student to compete and

excel in an ever-changing world, embrace challenges with vigor, respect and appreciate

the worth of every human being, and contribute to society by providing effective

instruction and dynamic curriculum, offering a wide range of valuable experiences, and

inspiring students to pursue their dreams and aspirations.

4

Personal Finance

This semester course provides a foundation for studying and using personal financial

planning techniques in the 21st century. Students learn applicable skills necessary to

manage personal finances and become smart consumers. They learn how personal

choices can affect goals and one’s earning potential. A variety of instructional practices

and assessments will be used to cover topics such as money management, income,

spending and credit, saving, and investing. Group work, discussions, projects, and

simulation video games will be used to authenticate the learning process.

5

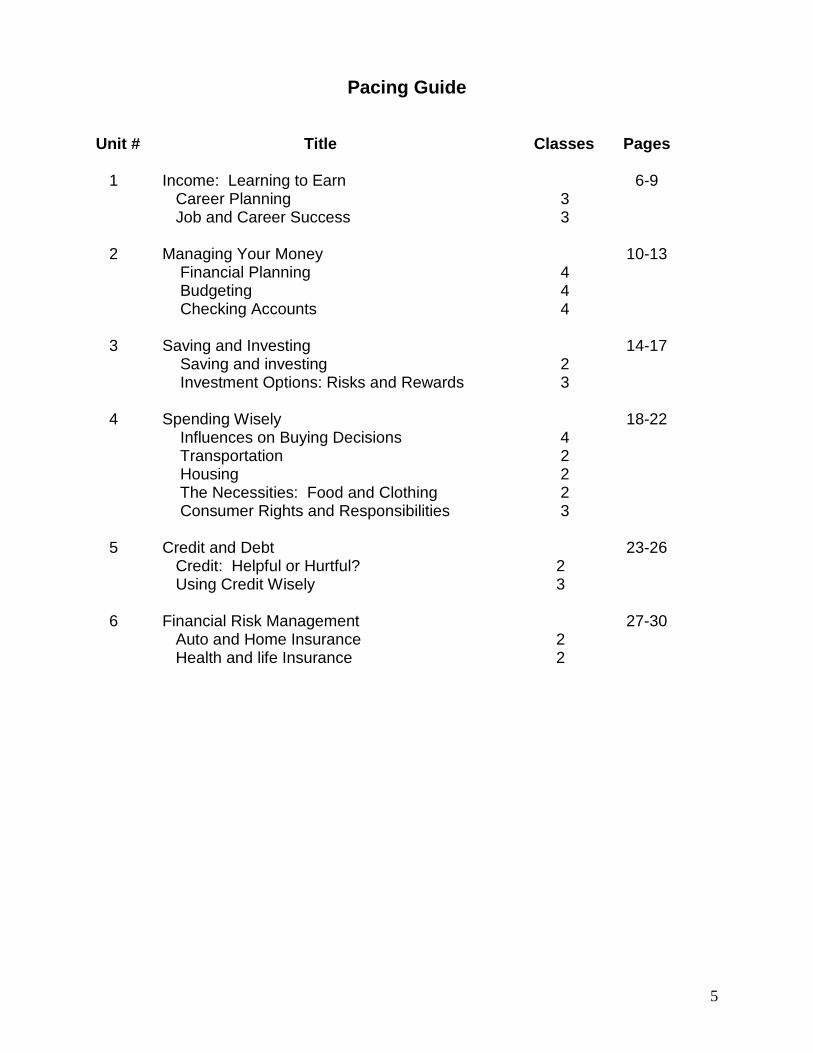

Pacing Guide

Unit # Title Classes Pages

1 Income: Learning to EarnCareer PlanningJob and Career Success

33

6-9

2 Managing Your MoneyFinancial PlanningBudgetingChecking Accounts

444

10-13

3 Saving and InvestingSaving and investingInvestment Options: Risks and Rewards

23

14-17

4 Spending WiselyInfluences on Buying DecisionsTransportationHousingThe Necessities: Food and ClothingConsumer Rights and Responsibilities

42223

18-22

5

6

Credit and DebtCredit: Helpful or Hurtful?Using Credit Wisely

Financial Risk ManagementAuto and Home InsuranceHealth and life Insurance

23

22

23-26

27-30

6

New Milford Public Schools

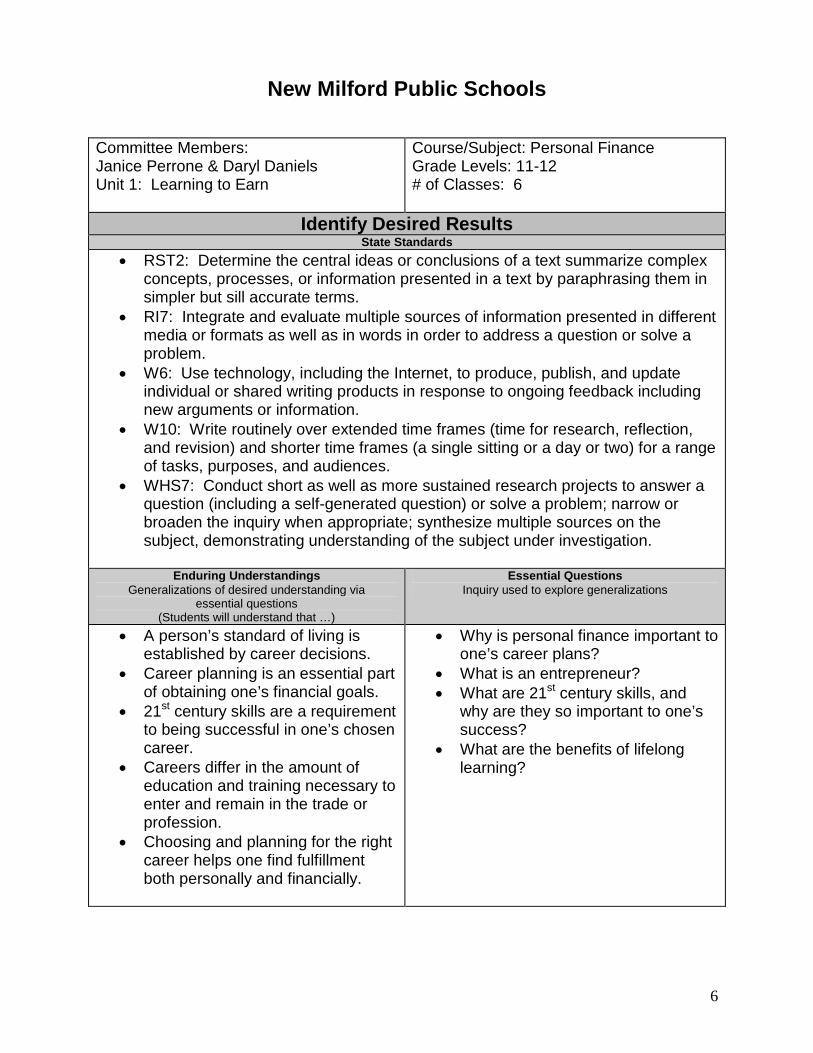

Committee Members:Janice Perrone & Daryl DanielsUnit 1: Learning to Earn

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 6

Identify Desired ResultsState Standards

RST2: Determine the central ideas or conclusions of a text summarize complexconcepts, processes, or information presented in a text by paraphrasing them insimpler but sill accurate terms.

RI7: Integrate and evaluate multiple sources of information presented in differentmedia or formats as well as in words in order to address a question or solve aproblem.

W6: Use technology, including the Internet, to produce, publish, and updateindividual or shared writing products in response to ongoing feedback includingnew arguments or information.

W10: Write routinely over extended time frames (time for research, reflection,and revision) and shorter time frames (a single sitting or a day or two) for a rangeof tasks, purposes, and audiences.

WHS7: Conduct short as well as more sustained research projects to answer aquestion (including a self-generated question) or solve a problem; narrow orbroaden the inquiry when appropriate; synthesize multiple sources on thesubject, demonstrating understanding of the subject under investigation.

Enduring UnderstandingsGeneralizations of desired understanding via

essential questions(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

A person’s standard of living isestablished by career decisions.

Career planning is an essential partof obtaining one’s financial goals.

21st century skills are a requirementto being successful in one’s chosencareer.

Careers differ in the amount ofeducation and training necessary toenter and remain in the trade orprofession.

Choosing and planning for the rightcareer helps one find fulfillmentboth personally and financially.

Why is personal finance important toone’s career plans?

What is an entrepreneur? What are 21st century skills, and

why are they so important to one’ssuccess?

What are the benefits of lifelonglearning?

7

Expected PerformancesWhat students should know and be able to do

Students will know the following: How key words can help in obtaining a job The steps necessary to secure a job How work can affect family and friends What a credit score is and how they can check it Common expectations employers have of new employees The basics of legal documents associated with employment such as a Form W4

and a Company Policy Handbook The differences among the three forms of business What an entrepreneur is and the advantages and disadvantages of being one The personal issues one should consider when choosing and planning a career

Students will be able to do the following: Identify and complete the necessary documentation that is associated with

employment, such as a Form W4 or a Pay Stub Demonstrate their understanding of an employee evaluation form and correlate

this with the courses “Business Attitude Rubric” and their own manner, workethic, and performance demonstrated in class

Establish a plan necessary to obtain an entry level position in their chosen career Describe effective strategies to obtain employment Associate the advantages to being an entrepreneur and the skills necessary for

their success Identify the four components of the U.S. economy Identify sources of income Identify the basic forms of business organizations and their differences Recognize different forms of income Utilize three online job sites Create a resume Write a cover letter Differentiate the parts of a paycheck stub Fill out a tax return form Participate and communicate with a guest speaker regarding career planning and

decisions Create and maintain a reflective journal regarding one’s new thoughts,

understandings, and connections to past knowledge of personal finance

Character Attributes

Citizenship Responsibility

8

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

Develop Teaching and Learning PlanSuggested Teaching Strategies:

Teacher uses PowerPoint presentation summarizing the content of the unit. Teacher leads discussion about career planning and how employment affects

personal finances. Teacher reviews vocabulary using a Prezi presentation. Teacher assigns pretest to be self-corrected and discussed with a partner. Teacher places students into groups of 3-4 to discuss open-ended questions and

future responses. Teacher shows video clips regarding planning for a successful career. Teacher shows video clips regarding the forms of business organizations.

Suggested Learning Activities: Students will self-evaluate pretest performance identifying needs from the unit

content. Students will respond to open-ended questions. Students will collaboratively develop a structure for a resume and cover letter. Students will explore electronic options of posted jobs. Students will create a career growth chart realizing the importance of lifelong

learning. Students will share their thoughts on questions regarding career opportunities

and choices with group members. Students will use the Internet to complete workbook exercises regarding income

and income potential. Students will complete math exercises incorporating percentages and routine

expenses. Students will use word processing software to complete a chart and respond to

questions referring to payroll deductions. Students will use spreadsheet software and the Internet to research and develop

a graph comparing education to employment and income levels.

9

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Test and quiz results Student’s ability to research topics

given and create charts and graphs Discussions and questions with guest

speaker and teacher Reflective writing

Suggested Resources Money.Tips.Net – Tips for Controlling Your Financial Destiny. Sharon Parq

Associates, 2011. Web. Summer 2011. <http://money.tips.net/>. Family Economics and Financial Education. University of Arizona. Web.

<http://www.fefe.arizona.edu/>.Forbes.com Video Network – Personal Finance.” Forbes.com Video Network |

ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills – Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.

10

New Milford Public Schools

Committee Members:Janice Perrone & Daryl DanielsUnit 2: Managing Your Money

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 12

Identify Desired ResultsState Standards

W6: Use technology, including the Internet, to produce, publish, and updateindividual or shared writing products in response to ongoing feedback includingnew arguments or information.

W10: Write routinely over extended time frames (time for research, reflection,and revision) and shorter time frames (a single sitting or a day or two) for a rangeof tasks, purposes, and audiences.

Enduring UnderstandingsGeneralizations of desired understanding via

essential questions(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

Budgeting is important to asuccessful, fulfilling life.

The role of a bank is essential toone’s personal financial plan andgoals.

Many healthy money habits areformed when people are young.

How does setting financial goalshelp people maintain their personalfinances?

What does it mean to plan forsuccess and how can it impact yourfinances?

Why should one plan for retirementas young as possible?

What are consequences of havingfinancial debt?

What do you value?

Expected PerformancesWhat students should know and be able to do

Students will know the following: A budget is a plan for how to use one’s money

Financial planning should include how one can help others Financial decisions are to be made based on one’s personal goals and values There are many forms of taxationReasonable percentages for sharing, saving, and spending Qualities of a good budget What a credit score is and why it is important to maintain a satisfactory score The difference between fixed and variable expenses How a checking account worksThe difference between a bank and a credit union Recognize banking terms and how they apply to one’s banking needs

11

The difference between a bank card and a credit card How to protect one’s banking account information

Students will be able to do the following: Set up a budget Keep track of income and expenses Calculate the true cost of the educational loan they will need to meet the

requirements of their desired profession Compare options from differing financial institutions and determine which best fits

diverse situations Open a checking account Write a check Complete a bank deposit transaction Read a bank statement Reconcile a checking account Bank online

Character Attributes

Citizenship Compassion Honesty Responsibility

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

Develop Teaching and Learning PlanSuggested Teaching Strategies:

Teacher uses PowerPoint presentation summarizing the content of the unit. Teacher leads discussion about budgets and how they are determined by

individual values using a PowerPoint presentation. Teacher reviews vocabulary using a Prezi presentation. Teacher assigns pretest to be self-corrected and discussed with a partner. Teacher places students into groups of 3-4 to discuss open-ended questions and

future responses. Teacher places students into groups of two to collaboratively choose, explore,

and discuss the financial activities of two charitable organizations.

12

Suggested Learning Activities: Students will complete an expense tracker worksheet. Students will self-evaluate pretest performance identifying needs from the unit

content. Students will complete an example 1040EZ tax form using necessary resources. Students will create a goal chart and planning worksheet. Students will collaboratively create charts comparing the financial activities of two

charitable organizations. Students will respond to open-ended questions. Students will complete a monthly budget using spreadsheet software. Students will reconcile a bank statement using spreadsheet software. Students will create graphs to present data from a budget in a visual format.

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Reflective writing

Suggested Resources "Managing Debt and Credit | MyMoney." Home - English | MyMoney. Web. Summer

2011. <http://www.mymoney.gov/category/topics/managing-debt-and-credit.html>.

Money.Tips.Net - Tips for Controlling Your Financial Destiny. Sharon ParqAssociates, 2011. Web. Summer 2011. <http://money.tips.net/>.

Family Economics and Financial Education. University of Arizona. Web.<http://www.fefe.arizona.edu/>.

Forbes.com Video Network - Personal Finance." Forbes.com Video Network |ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

13

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills - Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.

14

New Milford Public Schools

Committee Members:Janice Perrone & Daryl DanielsUnit 3: Saving and Investing

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 5

Identify Desired ResultsState Standards

RI1: Cite strong and thorough textual evidence to support analysis of what thetext says explicitly as well as inferences drawn from the text, includingdetermining where the text leaves matters uncertain.

RI4: Determine the meaning of words and phrases as they are used in a text,including figurative, connotative, and technical meanings; analyze how an authoruses and refines the meaning of a key term or terms over the course of a text.

RI3: Analyze a complex set of ideas or sequence of events and explain howspecific individuals, ideas, or events interact and develop over the course of thetext.

W4: Produce clear and coherent writing in which the development, organization,and style are appropriate to task, purpose, and audience.

W7: Conduct short, as well as more sustained research projects, to answer aquestion (including a self-generated question) or solve a problem, narrow orbroaden the inquiry when appropriate, synthesize multiple sources on the subjectdemonstrating understanding of the subject under investigation.

Enduring UnderstandingsGeneralizations of desired understanding via

essential questions(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

Saving success starts with a plan Setting short and long term goals is

essential to successful savingsplans

Many saving and investing toolsshould be evaluated to matchspecific circumstances

Investing in stocks, bonds, andmutual funds carry varying degreesof risk and return

Saving and investment advice canbe obtained from many sources

Why does one need financial goals? How do individuals determine which

saving and investing tools are bestsuited to meet their goals?

What are the advantages anddisadvantages of each type ofinvestment?

15

Expected PerformancesWhat students should know and be able to do

Students will know the following: The difference between saving and investing There are several types of savings accounts with varying rates of interest There is some element of risk involved in all investment activity Stock is an investment that represents ownership in a company Stocks are bought and sold on various stock exchanges Bonds represent a promise from a company or government to pay a certain

amount of money on a specific date A mutual fund is an investment where people pool their money to buy other

investments collectively The value of money changes over time Strategies for evaluating investments Investments can also take the form of real estate or collectibles

Students will be able to do the following: Evaluate the characteristics of different types of investments and match them to

specific financial goals Develop their own financial goals Differentiate between short and long term goals Monitor success in their saving and investing activities Calculate simple and compound interest Describe the characteristics of various commercial savings products Read and interpret a stock market listing Explain how the stock market works Analyze the performance of stocks and mutual funds over time Detail reasons why savings and investing plans change over time Explain the importance of planning for retirement Examine the Social Security System and its effects on retirement planning

Character Attributes

Responsibility Integrity Honesty Courage Perseverance Cooperation

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

16

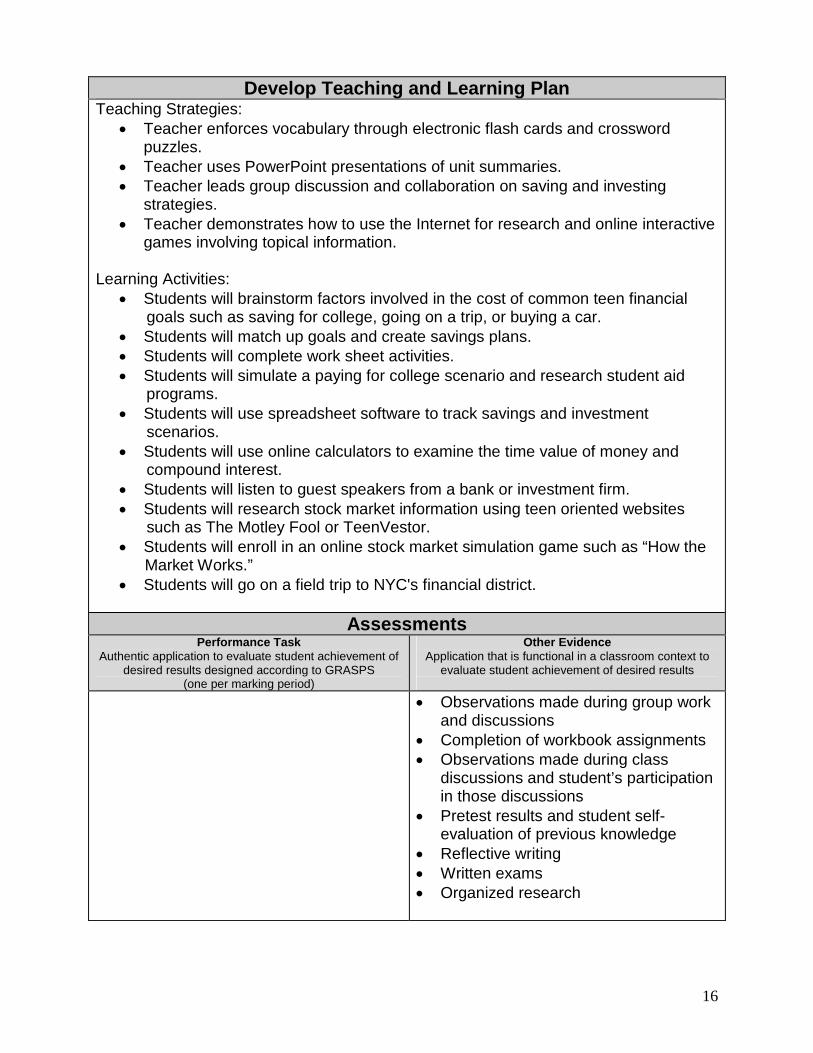

Develop Teaching and Learning PlanTeaching Strategies:

Teacher enforces vocabulary through electronic flash cards and crosswordpuzzles.

Teacher uses PowerPoint presentations of unit summaries. Teacher leads group discussion and collaboration on saving and investing

strategies. Teacher demonstrates how to use the Internet for research and online interactive

games involving topical information.

Learning Activities: Students will brainstorm factors involved in the cost of common teen financial

goals such as saving for college, going on a trip, or buying a car. Students will match up goals and create savings plans. Students will complete work sheet activities. Students will simulate a paying for college scenario and research student aid

programs. Students will use spreadsheet software to track savings and investment

scenarios. Students will use online calculators to examine the time value of money and

compound interest. Students will listen to guest speakers from a bank or investment firm. Students will research stock market information using teen oriented websites

such as The Motley Fool or TeenVestor. Students will enroll in an online stock market simulation game such as “How the

Market Works.” Students will go on a field trip to NYC's financial district.

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Reflective writing Written exams Organized research

17

Suggested Resources "Saving and Investing | MyMoney." Home - English | MyMoney. Web. Summer 2011.

<http://www.mymoney.gov/category/topic1/saving-and-investing.html>. Money.Tips.Net - Tips for Controlling Your Financial Destiny. Sharon Parq

Associates, 2011. Web. Summer 2011. <http://money.tips.net/>. Family Economics and Financial Education. University of Arizona. Web.

<http://www.fefe.arizona.edu/>.Forbes.com Video Network - Personal Finance." Forbes.com Video Network |

ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills - Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.

18

New Milford Public Schools

Committee Members:Janice Perrone & Daryl DanielsUnit 4: Spending Wisely

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 13

Identify Desired ResultsState Standards

W6: Use technology, including the Internet, to produce, publish, and updateindividual or shared writing products in response to ongoing feedback includingnew arguments or information.

W1: Write arguments to support claims in an analysis of substantive topics ortexts, using valid reasoning and relevant and sufficient evidence.a. Introduce precise, knowledgeable claims; establish the significance of the

claims; distinguish the claims from alternate or opposing claimscounterclaims, reasons, and evidence.

b. Develop claims and counterclaims fairly and thoroughly, supplying the mostrelevant evidence for each while pointing out the strength and limitations ofboth in a manner that anticipates the audience’s knowledge level, concerns,values, and possible biases.

c. Use words, phases, and clauses as well as varied syntax to link the majorsections of the text, create cohesion, and clarity the relationships betweenclaims and reasons, between reasons and evidence, and between claims andcounterclaims.

d. Establish and maintain a formal style and objective tone while attending to thenorms and conventions of the discipline in which they are writing.

e. Provide a concluding statement or section that follows from and supports theargument presented.

W10: Write routinely over extended time frames (time for research, reflection,and revision) and shorter time frames (a single sitting or a day or two) for a rangeof tasks, purposes, and audiences.

RI1: Cite strong and thorough textual evidence to support analysis of what thetext says explicitly as well as inferences drawn from the text, includingdetermining where the text leaves matters uncertain.

RI3: Analyze a complex set of ideas or sequence of events and explain howspecific individuals, ideas, or events interact and develop over the course of thetext.

19

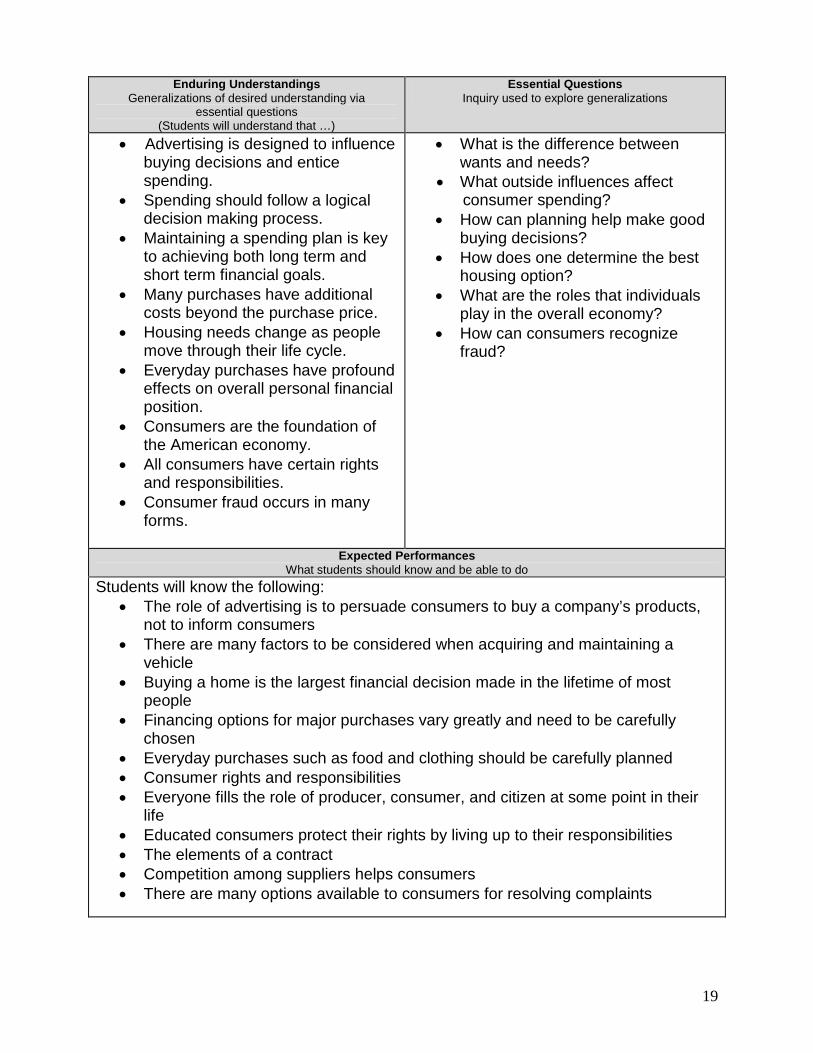

Enduring UnderstandingsGeneralizations of desired understanding via

essential questions(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

Advertising is designed to influencebuying decisions and enticespending.

Spending should follow a logicaldecision making process.

Maintaining a spending plan is keyto achieving both long term andshort term financial goals.

Many purchases have additionalcosts beyond the purchase price.

Housing needs change as peoplemove through their life cycle.

Everyday purchases have profoundeffects on overall personal financialposition.

Consumers are the foundation ofthe American economy.

All consumers have certain rightsand responsibilities.

Consumer fraud occurs in manyforms.

What is the difference betweenwants and needs?

What outside influences affectconsumer spending?

How can planning help make goodbuying decisions?

How does one determine the besthousing option?

What are the roles that individualsplay in the overall economy?

How can consumers recognizefraud?

Expected PerformancesWhat students should know and be able to do

Students will know the following: The role of advertising is to persuade consumers to buy a company’s products,

not to inform consumers There are many factors to be considered when acquiring and maintaining a

vehicle Buying a home is the largest financial decision made in the lifetime of most

people Financing options for major purchases vary greatly and need to be carefully

chosen Everyday purchases such as food and clothing should be carefully planned Consumer rights and responsibilities Everyone fills the role of producer, consumer, and citizen at some point in their

life Educated consumers protect their rights by living up to their responsibilities The elements of a contract Competition among suppliers helps consumers There are many options available to consumers for resolving complaints

20

Students will be able to do the following: Follow a logical decision-making process for spending decisions including major

purchases as well as everyday spending Comparison shop using a variety of reliable consumer resources Identify marketing techniques used by companies to persuade consumers Analyze and evaluate factors related to acquiring a vehicle or other mode of

transportation Analyze and evaluate factors related to housing options Compare financing options available from a variety of sources Compare costs and benefits related to rent/lease/buy decisions Evaluate features and benefits of everyday purchases Identify reasons for price variation among similar products Describe consumer rights and responsibilities Increase awareness of Internet scams Evaluate product guarantees, warrantees, and other certifications Identify public and private consumer advocacy groups Identify ways to resolve customer disputes

Character Attributes

Integrity Perseverance Citizenship Cooperation Honesty Responsibility

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

Develop Teaching and Learning PlanSuggested Teaching Strategies:

Teacher uses PowerPoint presentation summarizing the content of the unit. Teacher leads discussion about budgets and how they are determined by

individual values using a PowerPoint presentation. Teacher invites guest speakers from marketing firms, auto dealerships, and

lending institutions to speak to the class. Teacher assigns pretest to be self corrected and discussed with a partner. Teacher places students into groups of 3-4 to discuss open-ended questions and

future responses.

21

Teacher places students into groups of two to collaboratively choose, explore,and discuss advertising techniques.

Suggested Learning Activities: Students will keep a journal or blog documenting the advertisements to which

they have been exposed and rate their persuasive factor. Students will use current auto availability resources to make a car purchasing

decision. Students will examine and prepare real world documents such as rental

agreements, car loan and mortgage applications, warranties, and guarantees. Students will compare food ingredient and nutrition labels of brand names and

house brands. Students will conduct blind taste tests of brand names and house brand foods. Students will research instances of consumer scams and discuss the role of the

Internet in these. Students will discuss case studies identifying consumer complaints. Students will research consumer rights in Connecticut.

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Goal: Students research a consumer rightsissue and write a persuasive essay to takea position on it.

Role: Consumer

Audience: Peers and teacher

Situation: Through the study of currentcases of consumer rights issues, studentsidentify both sides of the issue and defendone position with facts they have gathered.

Product: Persuasive essay

Standard for Success: School-widerubric for information literacy

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Reflective writing Organized research

22

Suggested Resources Money.Tips.Net - Tips for Controlling Your Financial Destiny. Sharon Parq

Associates, 2011. Web. Summer 2011. <http://money.tips.net/>. Family Economics and Financial Education. University of Arizona. Web.

<http://www.fefe.arizona.edu/>.Forbes.com Video Network - Personal Finance." Forbes.com Video Network |

ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills - Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.

23

New Milford Public Schools

Committee Members:Janice Perrone & Daryl DanielsUnit 5: Credit and Debt

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 5

Identify Desired ResultsState Standards

RI4: Determine the meaning of words and phrases as they are used in a text,including figurative, connotative, and technical meanings; analyze how an authoruses and refines the meaning of a key term or terms over the course of a text.

RI7: Integrate and evaluate multiple sources of information presented in differentmedia or formats as well as in words in order to address a question or solve aproblem.

W6: Use technology, including the Internet, to produce, publish, and updateindividual or shared writing products in response to ongoing feedback includingnew arguments or information.

Enduring Understandings

Generalizations of desired understanding viaessential questions

(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

When used properly, credit can bean essential tool in managingfinances.

Abuse of credit privileges can leadto serious financial problems.

Examining the costs and benefits ofcredit is essential to making soundfinancial decisions.

How can using credit help managefinances?

What are the costs of credit? What are the factors that determine

creditworthiness? Why is it important to establish good

credit?

Expected PerformancesWhat students should know and be able to do

Students will know the following: Credit as a privilege Types of consumer credit falling into the categories of short term credit and loans How credit scores and credit history affect a person’s ability to obtain future credit Predatory lenders exist and should be avoided How to determine the cost of credit The components of a credit score Strategies to solve credit issues The implications of bankruptcy

24

Students will be able to do the following: Identify the advantages and disadvantages of using consumer credit Recognize the characteristics of different types of credit Evaluate credit options for varying purchasing situations Acquire information about their own credit history Identify methods of establishing good credit Explain the components of a credit report and the uses of this information Determine ways to safeguard information and to avoid credit fraud and identity

theft Explain the difference between secured and nonsecured loans Recognize predatory lending practices Identify types of loans that should be avoided Calculate interest Analyze and reconcile a credit card statement Determine the factors involved in bankruptcy and explain its implications

Character Attributes

Cooperation Honesty Integrity Perseverance Responsibility

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

Develop Teaching and Learning PlanSuggested Teaching Strategies:

Teacher uses PowerPoint presentation summarizing the content of the unit. Teacher leads discussion about credit and how it is determined by individual

values using a PowerPoint presentation. Teacher demonstrates how to use the Internet for research and online interactive

games involving topical information. Teacher assigns pretest to be self-corrected and discussed with a partner. Teacher places students into groups of 3-4 to discuss open-ended questions and

future responses. Teacher invites guest speakers from a consumer credit counseling agency to

speak to the class.

25

Suggested Learning Activities: Students will bring in ‘junk mail’ credit card offers that have been delivered to

their homes. Students will compare credit card offerings available with online applications and

make a decision about the best credit card. Students will examine and prepare real world documents such as credit card

applications. Students will research and analyze bankruptcy statistics and trends in

Connecticut. Students will research instances of predatory lending practices and discuss the

role of the internet in these. Students will read case studies identifying credit abuse. Students will examine actual credit reports. Students will research consumer rights in Connecticut.

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Reflective writing Organized research

26

Suggested Resources "Getting Insured | MyMoney." Home - English | MyMoney. Web. Summer 2011.

<http://www.mymoney.gov/category/topic1/getting-insured.html>. Money.Tips.Net - Tips for Controlling Your Financial Destiny. Sharon Parq

Associates, 2011. Web. Summer 2011. <http://money.tips.net/>. Family Economics and Financial Education. University of Arizona. Web.

<http://www.fefe.arizona.edu/>.Forbes.com Video Network - Personal Finance." Forbes.com Video Network |

ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills - Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.

27

New Milford Public Schools

Committee Members:Janice Perrone & Daryl DanielsUnit 6: Financial Risk Management

Course/Subject: Personal FinanceGrade Levels: 11-12# of Classes: 4

Identify Desired ResultsState Standards

RST2: Determine the central ideas or conclusions of a text; summarize complexconcepts, processes, or information presented in a text by paraphrasing them insimpler but sill accurate terms.

RI7: Integrate and evaluate multiple sources of information presented in differentmedia or formats as well as in words in order to address a question or solve aproblem.

Enduring UnderstandingsGeneralizations of desired understanding via

essential questions(Students will understand that …)

Essential QuestionsInquiry used to explore generalizations

Insurance programs help managefinancial risk.

A risk management plan forpersonal holdings such as a homeare very important, and goalsshould be set to appropriatelyprotect one’s assets at the lowestcost.

Knowing how to determine the besthealth plan necessary to furnishone’s needs is important.

What does it mean to protect “one’sassets” and why is it necessary?

Why should one be concerned withhealth care and the latest trendsand laws associated with it?

Expected PerformancesWhat students should know and be able to do

Students will know the following: How an insurance program can manage risk Types of insurance coverage and policies available Factors that affect the cost of motor vehicle insurance Difference between private and government health plans Importance of disability insurance in a financial planning Key provisions in a life insurance policy What insurance companies consider “high risk” Cost of unethical claims and practices that are passed on to the consumer

28

Students will be able to do the following: Describe the importance of property and liability insurance Analyze the factors that influence the amount of coverage and cost of home

insurance Identify the important types of motor vehicle coverage Explain the importance of health insurance in financial planning Describe various types of life insurance programs Explain why renters need property insurance Create a risk management plan

Character Attributes

Citizenship Responsibility

Technology Competencies

Students use content specific tools, software, and simulations to support learningand research.

Students use telecommunications and collaboration tools to work with peers andothers to investigate information and to develop solutions or products.

Students apply productivity/ multimedia tools and peripherals to support personalproductivity, group collaboration, and learning.

Develop Teaching and Learning PlanSuggested Teaching Strategies:

Teacher uses PowerPoint presentation summarizing the content of the chapter. Teacher leads discussion about facts and fiction regarding insurance. Teacher reviews vocabulary using a Prezi presentation. Teacher assigns pretest to be self-corrected and discussed with a partner. Teacher places students into groups of 3-4 to discuss open-ended questions and

future responses. Teacher places students into groups of two to discuss why and what insurance is

important to have. Teacher provides a step-by-step scenario of what one should do if s/he is

involved in an accident. Teacher examines and explains a sample employer insurance benefits overview. Teacher poses questions regarding authentic situations and the insurance

coverage necessary to alleviate risk.

Suggested Learning Activities: Students will complete the “Look Before You leap” exerciser regarding the cost of

car insurance. Students will self-evaluate pretest performance identifying needs from the unit

content. Students will use the Internet to research quotes for auto insurance for various

situations

29

Students will research the pros and cons of differing insurance coverage forindividuals in the twenties.

Students will collaboratively create responses to situations regarding insuranceand advice (given in text).

Students will respond to open-ended questions regarding authentic situationsand the necessary insurance plans.

Students will complete a monthly insurance cost analysis spreadsheet and graphelectronically.

Students will respond to end-of-chapter questions regarding key terms. Students will collaboratively respond to questions regarding the main ideas of the

chapter. Students will share their responses to the unit questions with other groups. Students will respond to workbook questions regarding assessing risk and then

collaborate with a group member to increase their comprehension of the activity. Students will participate and communicate with a guest speaker regarding risk

management.

AssessmentsPerformance Task

Authentic application to evaluate student achievement ofdesired results designed according to GRASPS

(one per marking period)

Other EvidenceApplication that is functional in a classroom context to

evaluate student achievement of desired results

Goal: Find the best insurance for thegiven scenario

Role: A citizen engaged in an activesearch for insurance

Audience: Teacher and classmates

Situation: You have certain standardsand a profile which you must use to findthe best insurance for your case. Studentswill be placed in groups of two, given thesame scenario as another group. Eachscenario will involve two types of insuranceand a profile for the person activelysearching.

Presentation: Presentation that outlinesthe steps taken to research the situationand the conclusions drawn.

Standard for Success: School-wide rubricfor oral presentations

Observations made during group workand discussions

Completion of workbook assignments Observations made during class

discussions and student’s participationin those discussions

Pretest results and student self-evaluation of previous knowledge

Completion of workbook “AssessingRisk” activity

Students ability to research andcollaborate with group member to gainacceptable insurance policies

Discussions and questions with guestspeaker and teacher

Reflective writing

30

Suggested Resources "Knowing Your Consumer Rights | MyMoney." Home - English | MyMoney. Web.

Summer 2011. <http://www.mymoney.gov/category/topic1/knowing-your-consumer-rights.html>.

Money.Tips.Net - Tips for Controlling Your Financial Destiny. Sharon ParqAssociates, 2011. Web. Summer 2011. <http://money.tips.net/>.

Family Economics and Financial Education. University of Arizona. Web.<http://www.fefe.arizona.edu/>.

Forbes.com Video Network – “Personal Finance." Forbes.com Video Network |ForbesLife: Custom Jeans The 3x1 Way. Forbes.com, LLC, 2011. Web.<http://video.forbes.com/personal-finance/guide>.

Kimbrell, Grady, and Nathan Dungan. Personal Finance: a Lifetime Responsibility.St. Paul, MN: EMC, 2009. Print.

Personal Finance: a Lifetime Responsibility, Student Activities Book St. Paul, MN:EMC, 2009. Print.

Kapoor, Jack R., Les R. Dlabay, and Robert James Hughes. Glencoe PersonalFinance. Woodland Hills, CA: Glencoe/McGraw-Hill, 2007. Print.

Campbell, Sally R., and Sally R. Campbell. Foundations of Personal Finance. TinleyPark, IL: Goodheart-Willcox, 2010. Print

Practical Money Skills - Financial Literacy for Everyone. VISA, 2011. Web.<http://www.practicalmoneyskills.com/>.