Embed Size (px)

DESCRIPTION

The principle of objective of the study is to performance evaluation of investment management of three Islamic Banks namely, Islamic Bank Bangladesh Limited, Al Arafah Islami Bank Limited and Shahjalal Islami Bank Limited.

Citation preview

Performance Evaluation of Investment Management of Three Islamic Banks (IBBL, AIBL & SJIBL)

SUBMITTED TO

Mohammad Hasmat Ali

Associate Professor

Department of Finance & Banking

University Of Chittagong

SUBMITTED BY

Group 11

2

GROUP MEMBER

MEMBER ID NO

Shanku Biswas © 07303093

Sultan Ahammad Khan 07303099

Md. Minjar Hossain 07303115

Estiuque Uddin 07303045

Mohammad Ashik Rubaet 07303090

Md. Syed Alam 05303146

Iqbal Hossain 07303077

3

TABLE OF CONTENT

PARTICULARS PAGE NOChapter 1INTRODUCTION 4-19

1.1 Prelude 5-61.2 Statement Of The Problem 71.3 Objective Of The Study 81.4 Literature Review 9-111.5 Bangladesh Bank Guidelines 12-161.6 Methods Of Analysis 17-181.7 Limitation Of The Study 19

Chapter 2OVERVIEW OF INVESTMENT MANAGEMENT OF IBBL, AIBL & SJIBL 20-49

2.1 Islami Bank Bangladesh Limited 21-282.2 Al Arafah Islami Bank Limited 29-302.3 Shahjalal Islami Bank Limited 31-49

Chapter 3PERFORMANCE MEASUREMENT 50-61

3.1 Sector Wise Investment 51-52

3.2 Trend Analysis Of The IBBL, AIBL & SJIBL 53-55

3.3 Financial Indicator 56-61

Chapter 4SWOT ANALYSIS 62-68

4.1 SWOT Analysis Of Islami Bank Bangladesh Limited 64 4 . 2 S W O T A n a l y s i s O f A l A r a f a h I s l a m i B a n k L i m i t e d

65-66

4.3 SWOT Anaylsis Of Shahjalal Islami Bank Limited 67

Chapter 5FINDINGS, SUGGESTION AND CONCLUSION

69-72

5.1 Findings 705.2 Suggestion 715.3 Conclusion 72

REFERENCES 73-74

4

CHAPTER 1INTRODUCTION

5

1.1 PRELUDE

Investment management is the professional asset management of various securities (shares, bonds and other securities) and assets (e.g., real estate) in order to meet specified investment goals for the benefit of the investors. Investors may be institutions (insurance companies, pension funds, corporations, charities, educational establishments etc.) or private investors (both directly via investment contracts and more commonly via collective investment schemes e.g. mutual funds or exchange-traded funds).

The provision of investment management services includes elements of financial statement analysis, asset selection, stock selection, plan implementation and ongoing monitoring of investments. Coming under the remit of financial services many of the world's largest companies are at least in part investment managers and employ millions of staff.

The goal of investment/credit management is to maximize a bank's risk-adjusted rate of return by maintaining lending/credit risk exposure within acceptable parameters. Banks need to manage the credit risk inherent in the entire portfolio as well as the risk in individual credits or transactions. Banks should also consider the relationships between credit risk and other risks. The effective management of credit/lending risk is a critical component of a comprehensive approach to risk management and essential to the long-term success of any banking organization. Institutions manage it in different ways. In assessing credit risk from a single counterparty, an institution must consider three issues: Default Probability, Credit Exposure, and Recovery Rate. While financial institutions have faced difficulties over the years for a multitude of reasons, the major cause of serious banking problems continues to be directly related to lax credit standards for borrowers and counterparties, poor portfolio risk management, or a lack of attention to changes in economic or other circumstances that can lead to a deterioration in the credit standing of a bank's counterparties. Credit analysis refers lending/credit risk in which a loan officer attempts to evaluate a borrower’s ability and willingness to repay. Generally through lending/ credit analysis the loan officer analyze all available information to determine whether the loan meets the bank’s risk-return objectives. To analyze credit three techniques are used: Qualitative analysis, Quantitative analysis and Credit Risk Grading. In the qualitative analysis the bank usually analyze the 5 C’s of the customer Character, Capacity, Cash, and Condition & Collateral. Knowledge and learning become perfect when it is associated with theory and practice. Theoretical knowledge gets its perfection with practical application. As our educational system predominantly text based, inclusion practical orientation program, as an academic component is as exception to the norm. As the parties, educational institution and the organization substantially benefit from such a program, it seems a “win-win situation”. It establishes contracts and networking contracts. Contracts may help to get a job. That is,

6

students can train and prepare themselves for the job market. My report will discuss the comparisons between Islami Bank Bangladesh Limited & National Bank Limited, shows how islami banks perform better in spite of being interest free banks. The purpose of this report is to evaluate its performance through ratio analysis; trend analysis, regression etc.

7

1.2 STATEMENT OF THE PROBLEM

Investment management is the professional asset management of various securities and assets in order to meet specified investment goals for the benefits of the investors. If a bank can’t properly manage its investment than its recovery rate will be low due to which a bank needs to maintain increasing amount of provision against this NPI that ultimately locks the money of a bank to maintain its sustainability. The main mission of this report is to identify the problems associated with investment management of selected Islamic banks of Bangladesh and to suggest some pragmatic solution to overcome these problems. So far we know, there have conducted a little study on investment management of investment management of Islamic banks of Bangladesh. The researchers firmly believed that the suggestions provided will help the banks to some extent and the academician as well.

8

1.3 OBJECTIVE OF THE STUDY

The principle of objective of the study is to performance evaluation of investment management of three Islamic Banks Namely, Islamic Bank Bangladesh Limited, Al Arafah Islami Bank Limited and Shahjalal Islami Bank Limited.

In order to accomplish the ultimate objective the following specific objectives are taken into consideration:

To have a clear understanding of the investment management of IBBL, AIBL and SJIBL.

To find out the sector wise investment performance of the three banks.

To find the investment forecasting via trend analysis.

To get a clear perception of the strength, weakness, opportunities and threats of the three banks via SWOT analysis.

To find out the problems of investment management of the selected banks.

To provide some probable suggestions for overcoming the problems.

9

1.4 LITERATURE REVIEW

Kym Brown & Michael Skully have conducted a study on “Ethical Investment & Performance Of Islamic Banks” in 2003 to know the profitability and economic efficiency of Islamic Banks and then compares these results with their involvement in Islamic finance by using non-parametric cost efficiency analysis, data envelopment analysis(DEA) and ratio analysis and the finding is that average efficiency of listed banks is slightly higher than non-listed banks at 75.2% as compared to 71.87%.

Muhammad Jaffar & Irfan Manarvi have run a study on “Performance Comparison Of Islamic And Conventional Banks In Pakistan” in 2011 to examine and compare the performance of Islamic and conventional banks operating inside Pakistan during 2005 to 2009 by analyzing CAMEL test standard factors such as capital adequacy, asset quality, management quality, earning ability and liquidity position and the finding is that Islamic banks performed poorly in earning on their assets with records of 1.37% in 2005 and -68.55% in 2006 and overall return on asset ratio of -13.47% during the period 2005 to 2009. Conventional banks had a mean ratio of 1.53% marking better investment decision and more profit for the banks and shareholders.

Mahmood Ahmed have conducted an study on “Practice of Mudaraba and Musharaka in Islamic Banking” to find ways of effecting Mudaraba and Musharaka modes of investment in Islamic banking, where neither the capital nor return is guaranteed by using the method of purposive random sampling and the finding is financing social projects through Mudaraba and Musharaka by commercial banks is especially important on account of its immediate relevance to the majority of the people living in rural Bangladesh.

Muhamad Abduh & Nazreen T. Chowdhury have run an study on “Does Islamic Banking Matter for Economic Growth in Bangladesh?”, to investigate the long run and dynamic relationship between Islamic banking development and economic growth in Bangladesh by using quarterly time-series data of economic growth, total financing and total deposit of Islamic banking from Q1:2004 to Q2:2011 and co-integration and Granger’s causality method and the finding is that Islamic bank financing has shared long run positive relationship with economic growth.

Mohammad Saif Noman Khan, M. Kabir Hassan & Abdullah Ibneyy Shahid have conducted a study on “Banking Behavior of Islamic Bank Customers in Bangladesh” to investigate the banking behavior of Islamic bank customers in Bangladesh by using comprehensive profile analysis, a number of chi-square tests, and t tests on a sample of 100 customers of Islamic banks. The findings are: 1. most of the customers of Islamic

10

banks fall in the age category of 25-35 years. Islamic bank customers are highly educated and have durable relationships with the banks; 2. High customer awareness and usage exist for various deposit mobilization instruments but there is not high awareness and usage of any individual financing facilities of Islamic banks; 3. Income category and education have a significant role in customers’ usage of various Islamic bank products/services; 4. Customers seem to be satisfied with a number of products/services of Islamic banks; 5. Among the service delivery elements, ‘employees’ deserve an immediate attention for improving customer satisfaction; 6. ‘Religious principles’ is the key bank selection criterion of the Islamic bank customers, while customers’ demography plays some role in determining which selection criteria matter more than others do.

Abdus Samad has run a study on, “Performance Of Interest-Free Islamic Banks Vis-À-Vis Interest-Based Conventional Banks Of Bahrain” in 2004 to know the comparative performance of Bahrain’s interest-free Islamic banks and the interest-based conventional commercial banks during the post Gulf War period with respect to (a) profitability, (b) liquidity risk, and (c) credit risk by using t-test to financial ratios for Islamic and conventional commercial banks in Bahrain for the period 1991-2001and concludes that there is no major difference in performance between Islamic and conventional banks with respect to profitability and liquidity.

Muhammad Shehzad Moin have run an study on “Performance of Islamic Banking and Conventional Banking in Pakistan” to examine and to evaluate the performance of the first Islamic bank in Pakistan, i.e. Meezan Bank Limited (MBL) in comparison with that of a group of 5 Pakistani conventional banks by using profitability, liquidity, risk, financial ratios such as Return on Asset (ROA), Return on Equity (ROE), Loan to Deposit ratio (LDR), Loan to Assets ratio (LAR), Debt to Equity ratio (DER), Asset Utilization (AU) and Income to Expense ratio (IER), T-test and F-test and the findings are: conventional banks are more profitable and are significantly different from Islamic bank in Return on Equity (ROE) and Profit Expense Ratio (PER); Islamic bank is getting closer to conventional banks in an upward trend.

Jill Johnes, Marwan Izzeldin and Vasileios Pappas, have studied on,” A comparison of performance of Islamic and conventional banks 2004 to 2009” in April 2012 to know the performance of Islamic and conventional banks prior to, during and immediately after the 2008 financial crisis (2004-2009) by using ratio measures and find that there are no significant differences in gross efficiency (on average) between conventional and Islamic banks.

Bishnu Kumar Adhikary, has conducted an study on “Nonperforming Loans in the Banking Sector of Bangladesh: Realities and Challenges” to discusses the magnitude of

11

Nonperforming Loans (“NPLs”) in the banking sector of Bangladesh since the adoption of prudential norms in the loan classification and provisioning system in 1990.The finding is that NPLs in Bangladesh reveals that the banking sector of Bangladesh is yet to get out of its NPL mess, although substantial improvement has been noticed recently.

Ezaz Ahmed, Ziaur Rahman and Rubina I. Ahmed, have run a study on “Comparative Analysis Of Loan Recovery Among Nationalized, Private And Islamic Commercial Banks of Bangladesh” to analyze and determine the reasons behind the better recovery position of ICBs compared to PCBs and NCBs. The finding is that the advance structure of the Islamic Banks are greatly skewed to the comparatively safer modes of financing like Murabaha, Bai Muajjal, Ijara, Ijara wa Iqtina. On the other hand, Conventional Banks’ asset portfolios are less skewed to the short term financing (compared to the ICBs).

1.5 BANGLADESH BANK GUIDELINES

12

Islamic Banking has experienced a phenomenal growth and expansion in Bangladesh in the backdrop of strong public demand and support for the system along with its gradually increasing popularity across the world. As a result, a number of full-fledged Islamic Banks has been established, while a good number of conventional banks have come forward to offer services compliant with Islamic Shariah through opening of Islamic branches along with conventional ones. There is also a trend of conversion of conventional banks into Islamic bank.

It has, therefore, become necessary to ensure that activities of the fast growing Islamic Banks are carried out properly and uniformly according to the principles of Islamic Shariah. With this end in view, Bangladesh Bank constituted a Focus group comprising representatives of the central Bank, a number of Islamic Banks and the Central Shariah Board for Islamic Banks of Bangladesh to formulate an integrated guideline for conducting banking business of the Islamic Bank/Islamic bank branches of conventional banks. Based on the recommendations of the Focus group this guideline embodying different terminologies used in Islamic Banking operations, definitions of the terminologies, the principles and modes of deposits and investments has been prepared. It also dwelt upon the issues of liquidity, maintenance of books of accounts and preparation of financial statements and other related issues. This guideline has been prepared mainly on the basis of Banking Companies Act 1991, Companies Act 1994 and Prudential Regulations of Bangladesh Bank. However, this guideline should be treated as supplementary, not a substitute, to the existing banking laws, rules and regulations. In case of any point not covered under this Guideline as also in case of any contradiction, the instructions issued under the Banking Companies Act and CompaniesAct will prevail.

Islamic banks do not directly deal in money. They run business with money. The funds of Islamic banks are mainly invested in the following modes:

Mudaraba;Musharaka;Bai-Murabaha (Murabaha to the purchase orders);Bai-Muajjal;Salam and parallel Salam;Istisna and parallel Istisna;Ijara;Ijarah Muntahia Bittamleek (Hire Purchase);Hire Purchase Musharaka Mutanaqisa (HPMM);Direct Investment;Investment Auctioning etc.QuardQuard Hassan etc.

13

1. Mudaraba: Mudaraba is a shared venture between labour and capital. Here Bank provides with entire capital and the investment client conducts the business. The Bank, provider of capital, is called Sahib-Al-Maal and the client is called Mudarib. The profit is to be distributed between the Bank and the investment client at a predetermined ratio while the bank has to bear the entire loss, if any.

2. Musharaka: Musharaka means partnership business. Every partner has to provide more or less equity funds in this partnership business. Both the Bank and the investment client reserve the right to share in the management of the business. But the Bank may opt to permit the investment client to operate the whole business. In practice, the investment client normally conducts the business. The profit is divided between the bank and the investment client at a predetermined ratio. Loss, if any, is to be borne by the bank and the investment client according to capital ratio.

3. Bai-Murabaha: Contractual buying and selling at a mark-up profit is called Murabaha. In this case, the client requests the Bank to purchase certain goods for him. The Bank purchases the goods as per specification and requirement of the client. The client receives the goods on payment of the price which includes mark-up profit as per contract. Under this mode of investment the purchase/ cost price and profit are to be disclosed separately.

4. Bai-Muajjal: "Bai-Muajjal" means sale for which payment is made at a future fixed date or within a fixed period. In short, it is a sale on Credit. It is a contract between a buyer and a seller under which the seller sells certain specific goods (permissible under Shariah and Law of the Country), to the buyer at an agreed fixed price payable at a certain fixed future date in lump sum or within a fixed period by fixed installments. The seller may also sell the goods purchased by him as per order and specification of the buyer. In Bank's perspective, Bai-Muajjal is treated as a contract between the Bank and the Client under which the bank sells to the Client certain specified goods, purchased as per order and specification of the Client at an agreed price payable within a fixed future date in lump sum or by fixed installments.

5. Salam and Parallel Salam: Salam means advance purchase. It is a mode of business under which the buyer pays the price of the goods in advance on the condition that the goods would be supplied / delivered at a particular future time. The seller supplies the goods within the fixed time.

Parallel Salam:Parallel Salam is a Salam contract whereby the seller depends, for executing his obligation, on receiving what is due to him - in his capacity as purchaser from a sale in a

14

previous Salam contract, without making the execution of the second Salam contract dependent on the execution of the first one. The following conditions are essential in the contracts of Murabaha, Bai-Muajjal and Salam. The respective contracts must include the following aspects regarding the goods:

Number/QuantityQualitySamplePrice and amount of profitDate of supply/time limitPlace of supplyWho will bear the cost of supply?Timeframe for payment in case of Bai-Murabaha and Bai-Muajjal.

6. Istisna and parallel Istisna: A contract executed between a buyer and a seller under which the seller pledges to manufacture and supply certain goods according to specification of the buyer is called Istisna. An Istisna agreement is executed when a manufacturer or a factory owner accepts a proposal placed to him by a person or an Institution to produce/manufacture certain goods for the latter at a certain negotiated price. Here, the person giving the order is called Mustasni, the receiver of the order is called Sani and the goods manufactured as per order is called Masnu. An order placed for manufacturing or producing those goods which under prevailing customs and practice are produced or manufactured will be treated as Istisna contract.

Parallel Istisna:If it is not stipulated in the contract that the seller himself would produce/provide the goods or services, then the seller can enter into another contract with third party for getting the goods or services produced/ provided by the third party. Such a contract is called Parallel Istisna. This may be treated as a sub-contract. The main features of this contract are:-

The original Istisna contract remains valid even if the Parallel Istisna contract fails and the seller will be legally liable to produce/ provide the goods or services mentioned in the Istisna contract.Istisna and Parallel Istisna contracts are treated as two separate contracts.The seller under the Istisna contract will remain liable for failure of the sub-contract.

7. Ijara: The mode under which any asset owned by the bank, by creation, acquirement or building-up is rented out is called Ijara or leasing. In this mode, the leasee pays the Bank rents at a determined rate for using the assets/properties and returns the same to the Bank at the expiry of the agreement. The Bank retains absolute ownership of the

15

assets/properties in such a case. However, at the end of the leased period, the asset may be sold to the client at an agreed price.

8. Ijarah Muntahia Bittamleak (Hire-Purchase): Under this mode, the bank purchases vehicles, machineries and instruments, building, apartment etc. and allowed clients to use those on payment of fixed rents in installments with the ultimate objective to sell the asset to the client at the end of the rental period . The client acquires the ownership/ title of the assets/ properties subject to full payment/ adjustment of all the installments.

9. Hire-purchase Musharaka Mutanaqasa (HPMM): Hire-purchase Musharaka Mutanaqasa means purchasing and acquiring ownership by one party by sharing in equity and paying rents for the rest of the equity held by the Bank/or other party. Under this mode, the Bank and the client on contract basis jointly purchase vehicles, machineries, building, apartment etc. The client uses the portion of the assets owned by the bank on rental basis and acquires the ownership of the same assets by way of paying banks portion of the equity on the assets in installments together with its rents as agreed upon.

10. Direct Investment: Under this mode, the bank can under its full proprietorship conduct business by directly investing in the industries, trading, transports etc. In these cases, the profit/loss fully goes to the bank.

11. Investment Auctioning: Selling by auction of those assets/goods acquired by the bank through direct investment is called Investment auctioning. Generally, the bank establishes industrial units by direct investment, makes the same operationally profitable and then sells out on auction. This mode of investment is very helpful for industrialization of the country.

12. Quard:It is a mode to provide financial assistance/ loan with the stipulation to return the principal amount in the future without any increase thereon.

13. Quard Hassan:This is a benevolent loan that obliges a borrower to repay the lender the principal amount borrowed on maturity. The borrower, however, has the discretion to reward the lender for his loan by paying any amount over and above the amount of the principal provided there will be no reference (explicit or implicit) in this regard. If a bank provides its client any loan, it can receive actual expenditure relating to the loan as service charge only once. It cannot charge annually at a percentage rate. If a loan is provided against the money deposited by a client in the bank, it has the right not to pay any profit

16

against the amount of money given as loan. But profit should be paid on the rest of the amount deposited as per previous agreement.

1.6 METHODS OF ANALYSIS

Technique of analysis:

17

In this part, we have made various types of analysis as per the guideline of honorable course instructor as well utilizing our prudence if we have any. Four different types of analysis have been done, these are-

SWOT AnalysisCore indicator & Ratio analysisLeast Squares Method for Time series Analysis

To conduct the Analysis part I have chosen the most widely used techniques of analysis. These are Least Squares method for Time Series Analysis and Regression Analysis.

Time series analysis

The first step in making estimates for the future consists of gathering information from the past data. In this connection, one usually deals with statistical data which are collected, observed or recorded at successive lest of time. Such data are generally referred as Time Series data.

Least squares method for straight line trend

Here the researchers have used Least squares method for measuring a straight line trend by using time series data. This method is most widely used in practice. When this method is applied, a trend line is fitted to data in such a manner that the following two conditions are satisfied-

1. ∑(Y-Yc) = 0; it means the sum of deviations of the actual values of Y and the computed value of Y is zero.

2. ∑(Y-Yc)2 is least; it means the sum of the squares of the deviations of the actual and computed values is last from the line. That is why this method is called the method of Least square. The line obtained by this method is known as the line of “Best Fit”.

Series data for straight line trend:

The straight line trend is represented by the equation-

Yc = a +bX;

Where-

Yc = The trend (computed) values to distinguish them from the actual Y values,

18

a= The Y intercept on the value of the Y variable when X=0,

b= Slope of the line or the amount of change in Y variable.

Source of data:

Data, for this research report, is collected from only the secondary sources, as of the nature of research; no primary data have been used for conducting the analysis and deducting findings

Secondary Sources

The data which has already been collected by others, such data are called Secondary data. For this report, the secondary data are collected from the below sources-

Annual reports of the Islami Bank Bangladesh Limited from year 2007-2011,Official website of the Islami Bank Bangladesh Limited Annual reports of the Al-Arafah Islami Bank from year 2007-2011Official website of the Al-Arafah Islami Bank Annual reports of Shahjalal Islami Bank Limited from year 2007-2011Official website of Shahjalal Islami Bank Limited

1.7 LIMITATION OF THE STUDY

Every report or research proposal consists of various limitations. Ours also has a few. This report is extensively dependent on secondary data such as annual report of bank,

19

published materials, different internet sources. Primary information in investigating the report findings is difficult for time constraints. Though we tried our level best in preparing this report some limitations were yet present there:

Fund

Preparing a quality report vast requires investigation & thorough explanation which needs a big amount of money to collect enough research materials & quality research papers. But the fund for the preparation of this report is too much limited. We couldn’t just afford it. If more funds would be available, the report could be more accurate & informative.

Time

The preparation time for this report was too much limited - around two weeks. It is very difficult to prepare a quality report within this time. If more time would be available, then we could make a better report.

Skills

We do not have enough skills to prepare a quality report. The lacks of skills are computing knowledge, business knowledge, analytical knowledge and linguistic skills.

CHAPTER 2

20

OVERVIEW OF INVESTMENT MANAGEMENT OF IBBL, AIBL & SJIBL

21

2.1 ISLAMI BANK BANGLADESH LIMITED

Introduction:

Islami Bank Bangladesh limited was incorporation on 13.03.1983 and received its Banking License on 28.03.1983. IBBL started functioning on 30.03.1983. The authorized capital of the Bank is TK. 20000.00 million.

Business Philosophy of the IBBL

The philosophy of the IBBL is to the principles of Islamic Shariah. The organization of Islamic conference (OIC) defines an Islamic bank as “A financial institution whose status, rules and procedures expressly state its commitment to the principles of Islamic Shariah and to the banning of the receipt and payment of interest on any of its operations. The sponsor, perception is that IBBL should be quite different from other privately owned and managed commercial bank operating in Bangladesh, IBBL to grow as a leader in the industry rather than a follower. The leadership will be in the area of service, constant effort being made to add new dimensions so that clients can get “Additional” in the matter of services commensurate with the needs and requirements of the country’ growing society and developing economy.

Mission and objective of the IBBL

To establish Islamic Banking through introduction of welfare oriented banking system.To ensure equity and justice in the field of economic activity.To achieve balance growth and equitable development through diversified investment operation particularly in the priority sector and less developed areas.To encourage socio economic up-liftmen and provide financial services to the rural and low income community.To establish a welfare-oriented banking system.To extend co-operation to the poor, the helpless and the low-income group for their economic uplift.To pay a vital role in human development and employment generation.To contribute towards balanced growth and development of the country through investment operations particularly in the less developed area.To contribute in achieving the ultimate goal of Islamic economic system.

22

Functions of Islami Bank Bangladesh Limited:

The IBBL is quite different from other privately owned and managed commercial bank operating in Bangladesh; it grows as a leader in the industry rather than a follower. The leadership will be in the area of service, constant effort being made to add new dimensions so that clients can get “Additional” in the matter of services commensurate with the needs and requirements of the country’ growing society and developing economy.

The main functions of Islami Bank Bangladesh Limited are as under:

To maintain all types of deposit accounts.To make investment. To conduct foreign exchange business. To extend other banking services. To Conduct Social welfare activities through Islami bank foundation.

Shariah CouncilShariah Council of the Bank is playing a vital role in guiding and supervising the implementation and compliance of Islamic Shariah principles in all activities of the Bank since its very inception. The Council, which enjoys a high status in the structure of the Bank, consists of prominent Ulema, reputed banker, renowned lawyer and eminent economist.Members of the Shariah Council meet frequently and deliberate on different issues confronting the Bank on Shariah matters. They also conduct Shariah inspection of branches regularly so as to-ensure that the Shariah principles are implemented and complied with meticulously by the branches of the Bank.

Investment Mechanism of IBBL:

Investment operation of a Bank is vital importance the greatest share of total revenue is generated from it, maximum risk is centered in it and the very existence of a Bank mostly depends on prudent management of its investment Portfolio. As such, for efficient deployment of mobilized resources in profitable, safe and liquid investments, a sound, well-defined, well-planned and appropriate Investment Policy framework is necessary prerequisite for achieving the goal of the Bank.

The special feature of the investment policy of the Bank is to invest on the basis of profit-loss sharing system in accordance with the tenets and principles of lslami Shariah Earning of profit is not the only motive and objective of the Bank’s investment policy rather emphasis is given in attaining social good and in creating employment opportunities

23

Objectives and Principles of investment:

The objectives and principles of investment operations of the Bank are:

To invest fund strictly in accordance with the principles of Islami Shariah.To diversity its investment portfolio by size of investment, by sectors (public and private) by economic purpose, by securities and by geographical area including industrial, commercial & agricultural.To ensure mutual benefit both for the Bank and the investment client by professional appraisal of investment proposals, judicious sanction of investment close and constant supervision and monitoring thereof.To make investment keeping the socio economic requirement of the country in view.To increase the number of potential investors by making participatory and productive investment.To finance various development schemes for poverty alleviation, income and employment generation with a view to accelerate sustainable soico-economic growth and for upliftment of the society.To invest in the form of goods and commodities rather than give out cash money to the investment clients.To encourage social up liftman enterprises.To shun even highly profitable investment in fields forbidden under Islamic Shariah and are harmful for the society.The Bank extends investments under the principles of Bai-Murabaha, Bai-Muazzal, Hire Purchase under Shirkatul Meelk and Mudaraba. The bank is making sincere efforts to go for investment under Mudaraba principle in near future.

Investment Policy of the IBBL:

Strict observance of Islamic Shariah principles.Investment to national priority sectors.Diversified investment portfolio: Diversification by size, sector, geographical area, economic purpose, securities and mode of investment.Preference to short-term Investments.Preference to investment of small size.To ensure safety & security of investmentsTo look profitability of investments.To give support to government denationalization industrial program.Investment to trade and commerce sector.Investment to industrial sectors.Investment to Foreign Trade (import & export).

24

Exploration of the possibility of investment in the existing Money & capital Market and help organization of Islamic Money & Capital Market

Investment Strategy of the IBBL:

Investment strategy of Islamic Bank and interest-based bank are contradictory. The investment strategies of Islamic Bank are:

To check exodus of investment clients. To induct new investment clients. To induct good investment clients of other Banks.To enhance existing limits of good investment clients. Extension of investment transport sector.Extension of investment to backward as well as forward linkage industries.Extension of investment to real Estate Sector. Extension of investment to Jute sector; particularly for trading and export purpose.Strengthening supervision, control and monitoring mechanism.

A brief description of investment mechanisms of the IBBL

The IBBL invests its money in various sectors of the economy through different modes permitted by Islamic Shariah and approved by the Bangladesh Bank. The Modes of Investment are as follows:

1) Bai Mechanism:

Bai-MurabahaBai-MuazzalBai-SalamBai-Istishana

2) Ijara Mechanism:

Hire Purchase (HP)Hire Purchase under Shirkatul Melk (HPSM)

3) Shirkat Mechanism:

Mudaraba Musharaka

25

Bai-Mechanism

Murabaha:

Bai- Murabaha may be defined as a contract between a buyer and a seller under which the sells certain specific goods (permissible under Islamic Shariah and the law of the land) to the buyer at a cost plus agreed profit payable in cash or on any fixed future data in lump sum or by installments. The marked up profit may be fixed in lump sum or in percentage of the cost price of the goods.

Bai-Muazzal:

Bai-Muajjal may be defined as a contract between a Buyer and a Seller under which the Seller sells certain specific goods (permissible under Shariah and Law of the Country), to the Buyer at an agreed fixed price payable at a certain fixed future date in lump sum or within a fixed period by fixed installments. The seller may also sell the goods purchased by him as per order and specification of the Buyer.

In this Bank, Bai-Muajjal is treated as a contract between the Bank and the Client under which the Bank sells to the Client certain specified goods, purchased as per order and specification of the Client at an agreed price payable within a fixed future date in lump sum or by fixed installments.

Bai-Salam:

Bai-Salam may be defined as a contract between a Buyer and a Seller under which the Seller sells in advance the certain commodity (ies)/product(s) permissible under Islamic Shariah and the law of the land to the Buyer at an agreed price payable on execution of the said contract and the commodity (ies)/product(s) is/are delivered as per specification, size, quality, quantity at a future time in a particular place.

In other words, Bai-Salam is a sale whereby the seller undertakes to supply some specific Commodity (ies) /Product(s) to the buyer at a future time in exchange of an advanced price fully paid on the spot. Here the price is paid in cash, but the delivery of the goods is deferred.

Bai-Istishna’a:

A contract between a manufacturer/ seller and a buyer under which the manufacturer/ seller sells specific product(s) after having manufactured, permissible under Islamic Shariah and Law of the Country after having manufactured at an agreed price payable a advance or by installments within a fixed period or on/within a fixed future date on basis of the order placed by the buyer. In contract the buyer is called ‘Al-Mustasni’, the seller ‘Al-Sani’ and the goods or the subject matter of the contract ‘Al-Masnoon’.

26

If the ultimate buyer does not stipulate in the contract that the seller will manufacture the product(s) by himself, then the seller may enter into a second Istisna'a contract in order to fulfil his contractual obligations in the first contract. This new contract is known as Parallel Istisna'a, whereby the obligations of the seller in the first contract are carried out.

Ijara Mechanism

a) Hire purchase:

It is practiced for procurement of goods which are mainly of fixed nature. Here purchaser purchases the assets from the seller by paying the price gradually or in lump sum after the rent period and pay for the assets up until making the full payment.

In this type of contract the hire has the full ownership of the goods. The ownership is only transferred to the hirer after the price of the goods is fully paid to the Bank. It means ownership has to be manually transferred in this type of contract. Up until ownership of the assets is transferred the client has to pay a fixed rental to the Bank according to the schedule specified in the contract.

b) Hire Purchase under Shirkatul Melk:

Hire Purchase under Shirkatul Melk is a Special type of contract which has been developed through practice. Actually, it is a synthesis of three contracts:

i) Shirkatii) Ijarah; and iii) Sale

These may be defined as follows

Shirkat:

Shirkat means partnership and Shirkatul Melk means share in ownership. When two or more persons supply equity, purchase an asset, own the same jointly, and share the benefit as per agreement and bear the loss in proportion to their respective equity, the contract is called Shirkatul Melk contract.

Ijarah

27

Ijarah has been defined as a contract between two parties, the Hiree and Hirer where the Hirer enjoys or reaps a specific service or benefit against a specified consideration or rent from the asset owned by the Hiree.

Sale

Sale is a sale contract against which the buyer gets the ownership of the goods from the seller by paying agreed upon price or by agreeing to pay the price at a later date

Share Mechanism:

a) Mudaraba:

Mudaraba is a partnership in profit whereby one party provides capital and the other party provides skill and labour. The provider of capital is called "Shahib Al-Maal" while the provider of skill and labour is called "Mudarib".

So, Mudaraba may be defined as a contract of partnership where the Shahib al-maal provides capital to the Mudarib for investing it in a commercial enterprise by applying his labour and endeavor. Both the parties share the profit as per agreed upon ratio and the losses, if any, being borne by the provider of funds i.e. Shahib al-maal except if it is due to breach of trust i.e. misconduct, negligence or violation of the conditions agreed upon by the Mudarib. If there is any loss incurred due to the reasons mentioned above, the Mudarib becomes liable for that.

Types of MudarabaMudaraba Contracts may be divided into 2 types:

# Restricted Mudaraba (Al-Mudaraba Al-Muqayyadah)

A restricted Mudaraba (Al-Mudaraba Al-Muqayyadah) is a contract in which the Shahib al-maal impose any restrictions on the actions of the Mudarib but not in a manner that would unduly constrain the Mudarib in his operations.

Restricted Mudaraba may further be divided into three types:

a. Restriction in respect of time or period:In this type of Mudaraba, the Mudaraba contract includes a clause on duration of the business. After expiry of such period, the Mudaraba shall become void

b. Restriction in respect of place or location:

28

In this type of Mudaraba, the Mudaraba contract includes a clause on place or location of the business. The Mudarib shall bind to do the business within the area of such place or location.

c. Restriction in respect of business:

In this type of Mudaraba, the Shahib al-maal restricts the actions of the Mudarib to a particular type of business as he (Shahib al-maal) considers appropriate.

# Unrestricted Mudaraba (Al-Mudaraba Al-Mutlaqah)

An unrestricted Mudaraba (Al Mudaraba Al Mutlaqah) is a contract in which Shahib al-maal permits the Mudarib to administer the Mudaraba capital without any restrictions. In this case, the Mudarib has a wide range of trade or business freedom on the basis of trust and the business expertise he has acquired. Such unrestricted business freedom must be exercised only in accordance with the interests of the parties and the objectives of the Mudaraba contract.

But, if Mudarib wants to have an extraordinary work, which is beyond the normal course of business, he cannot do so without express permission from Shahib al-maal. He is also not authorized to:

Keep another Mudarib or a partnerMix his own capital in that particular Mudaraba without the consent of the Shahib al-maal

b) Musharaka:

Musharaka may be defined as a contract of partnership between two or more individuals or bodies in which all the partners contribute capital, participate in the management, and share the profit in proportion to their capital or as per pre-agreed ratio and bear the loss, if any, in proportion to their capital/equity ratio.

In Islami Bank Bangladesh Limited (IBBL), the Bank may take part in a business with its Client(s), where both the Client(s) and the Bank provide capital in fixed proportions, take part in the management of business and share the profit in proportion to their respective capital ratio or at pre-agreed ratio and bear the loss, if any, in proportion to their respective capital/ equity ratio.

2.2 AL ARAFAH ISLAMI BANK LIMITED

29

Al-Arafah Islami Bank incorporated in Bangladesh as a banking company in 1995 with limited liability by shares. It started business on 27 September of that year with an authorised capital of Tk 1,000 million. At inception, its paid up capital was Tk 101.20 million divided into 101,200 ordinary shares of Tk 1,000 each. 23 sponsors of the bank subscribed the total issued capital.

Al-Arafah Bank is an interest-free shariah bank and its modus operandi is substantially different from those of regular commercial banks. The bank however, renders all types of commercial banking services under the regulation of the Bank Companies Act 1991. It conducts its business on the principles of musharaka, Bai-murabaha, Bai-muajjal and Hire Purchase transactions. A Shariah Council of the bank maintains constant vigilance to ensure that the activities of the bank are being conducted according to the precepts of Islam.

The management of the bank is vested in a 23-member board of directors, who oversee the affairs of the bank through a managing director, the chief executive officer of the bank.

A group of dedicated and pious personalities entrepreneurs are the architects and directors of the bank. Noted Islamic scholar, economist, writer and ex-bureaucrat of Bangladesh government AZM Shamsul Alam is the founder chairman of the bank. His progressive leadership and continuous inspiration provided a boost for the bank in getting a foothold in the financial market of Bangladesh. A group of 13 dedicated and noted Islamic personalities of Bangladesh are the members of Board of Directors of Al-Arafa Islami Bank (AIBL).

AIBL believe in providing dedicated services to the clients imbued with Islamic spirit of brotherhood, peace and fraternity. The bank is committed towards establishing a welfare-oriented banking system to meet the needs of low income and underprivileged class of people and upholds the Islamic values of establishment of a justified economic system through social emancipation and equitable distribution of wealth.

The bank has established AIBL English Medium Madrasha and AIBL Library. The bank provides a bunch of state-of-art banking services within the wide bracket of shariah. It has a number of unique products.

INVESTMENT POLICIES

30

All activities of AIBL are conducted under an profit/loss based system according to Islamic Shariah. Its investment policies under different modes are fully Shariah compliant and well monitored by the board of Shariah Council. During the year 2007, 70% of the investment incomes were distributed among the Mudaraba depositors.

In 2008, AIBL has included online banking in its wide range of services. AIBL regularly arranges its AGMs (Annual General Meeting). Whenever needed EGMs (Extraordinary General Meeting) are also arranged.

In 2007, the bank declared 20% bonus dividend to our shareholders.

SPECIAL FEATURES OF THE BANK

All activities of the Bank are conducted under an interest-free system according to Islamic Shariah.

Its investment policies under different modes are fully Shariah compliant.

During the year 2003, 70% of the investment income has been distributed among the Mudaraba depositors.

It believes in providing dedicated services to the clients imbued with Islamic spirit of brotherhood, peace and fraternity.

The bank is committed towards establishing a welfare-oriented banking system to meet the needs of low income and under privileged class of people.

The Bank upholds the Islamic values of establishment of a just economic system through social emancipation and equitable distribution of wealth.

Following the Islamic traditions, it is assisting in the economic progress of the socially disadvantage people; in the creation of employment opportunities and in up-liftment of rural areas to ensure a balance development of the country.

The Bank believes in social and philanthropic activities and has established AIBL English Medium Madrasha and AIBL library.

2.3 SHAHJALAL ISLAMI BANK LIMITED

31

Investment operation of a bank is of vital importance. The greatest share of total

revenue is generated from it, maximum risk is centered in it and the very existence of a

bank mostly depends on prudent management of its investment Portfolio. As such, for

efficient deployment of mobilized resources in profitable, safe and liquid investments, a

sound, well-defined, well-planned and appropriate Investment Policy framework is

necessary prerequisite for achieving the goal of the bank.

The special feature of the investment policy of the bank is to invest on the basis of

profit-loss sharing system in accordance with the tenets and principles of lslami Shariah.

Earning of profit is not the only motive and objective of the Bank’s investment policy

rather emphasis is given in attaining social good and in creating employment

opportunities.

AIMS OF SHAHJALAL ISLAMI BANK LIMITED

To be the unique modern Islami Bank in Bangladesh and to make significant

contribution to the national economy and enhance customers' trust & wealth, quality

investment, employees' value and rapid growth in shareholders' equity.

OBJECTIVES OF SHAHJALAL ISLAMI BANK LIMITED

To provide quality services to customers.

To set high standards of integrity.

To make quality investment.

To ensure sustainable growth in business.

To ensure maximization of Shareholders' wealth.

To extend our customers innovative services acquiring state-of-the-art

technology blended with Islamic principles.

To ensure human resource development to meet the challenges of the time.

MODES OF INVESTMENTS

32

To provide interest-free Banking Shahjalal Islami Bank has adopted the following modes

of investment:

Musharaka (equity participation on the basis of sharing profit and loss)

Mudaraba (sharing of profit and loss in business where one of the partners

provides expertise and management and other partner provides capital

remaining inactive)

Murabaha (buying and selling of commodities goods etc. with profit)

Bai-Muajjal (credit sale with profit)

Ijara (leasing for rent)

Hire purchase or Shirkatul Melk

Bi-Salam (purchasing of agricultural products while in production and providing

advance oney to the producers)

Istisna (purchasing of industrial products while in production and providing

advance money to the producers).

INVESTMENT SCHEMES

Small & Medium Enterprise Investment program

Small Business Investment Scheme

Housing Investment Scheme

Household Durable Scheme

Car Investment Scheme

CNG Conversion Investment Scheme

Overseas Employment Investment Scheme

Investment Scheme for Doctors

Investment Scheme for Executives

Investment Scheme for Marriage

Investment Scheme for Education

A BRIEF DESCRIPTION OF INVESTMENT MECHANISMS OF THE SJIBL

33

BAI MECHANISM:

Bai means purchase and sale of goods in cash or on credit or in advance at an agreed

upon profit, which may or may not be disclosed to the client. Majority of investments of

Islamic banks are extended through this mechanism. A good number of investment

products have been designed to facilitate mainly working capital financing which goes

as follows:

Bai-Murabaha

Murabaha LC(Sight/Deferred):

Through this mode of indirect facility, the bank facilitates import of goods of the client at

fixed rate of service charge (LC commission) on invoice value. LC may be opened at

100% cash or at a different ratio.

Murabaha Post Import TR :

This is a post import finance under the principle of “Bai”, extended to retire Shipping

Documents under LC opened. We buy the imported goods and sell the same to the

importer at a cost plus an agreed upon profit repayable today or on some date in the

future in lumpsum or by installments. Usually payment is made by lumpsum from the

sale proceeds of the consignment. Possession of goods remains with the client.

Collateral security is usually obtained to secure the finance.

Murabaha Post Import Pledge :

As like as Murabaha Post Import TR with an exception to security. Goods remain under

the control of the Bank. Collateral security may or may not be obtained.

Bai-Muajjal

Bai-Muajjal Commercial TR:

It is an agreement between bank and client whereby bank delivers goods to the client

upon deferred payment, i.e. the client shall pay the price at some future date at a time,

by lumpsum or by installment. Under this mode of investment, bank is not supposed to

34

disclose cost price and profit separately. Goods are delivered on trust and Trust Receipt

is obtained for legal implication.

Bai-Muajjal (Real Estate):

Mode of operation and principle of this product are alike Bai-Mujjal Commercial TR.

Difference is with the purpose, i.e. the facility is only extended against construction or

purchase of building, apartment etc.

Bai-Muajjal (WES Bill):

Investment facility under this Mode is extended to liquidate ABP liability at maturity,

when the client cannot liquidate the liability as a result of non-repatriation of the related

export proceeds.

Bai-Muajjal (Term):

Under this mode of investment, term facility is given to meet client’s requirement, which

is repaid by a specific repayment schedule. Purpose is a bit different, such as to meet

BG claim, etc.

Bai-Salam

Bai-Salam (PC):

This is export finance. Bai-Salam is a term used to define a sale in which the buyer

makes advance payment, but the delivery is delayed until sometime in the future.

Usually the seller is an individual or business and the buyer is the bank.

The Bai-Salam sales serve the interest of both parties:

The seller- receives advance payment in exchange for the obligation to deliver

the commodity at some later date. He benefits from the salam sale by locking in

a price for his commodity, thereby allowing him to cover his financial needs

whether they are personal expenses, family expenses or business expenses.

35

The purchaser benefits because he receives delivery of the commodity when it is

needed to fulfill some other agreement, without incurring storage costs. Second,

a Bai-Salam sale is usually less expensive than a cash sale. Finally a Bai-Salam

agreement allows the purchase to lock in a price, thus protecting him price

fluctuation.

SMALL & MEDIUM ENTERPRISE INVESTMENT PROGRAM

The SME Sector has been declared by the Government as a priority sector. In our

country, Small and Medium Enterprises (SMEs) play the pivotal role for employment

generation, poverty alleviation and overall economic growth of the country. It has been

observed that fund is the major constraint of this sector. Therefore, we need to inject

more funds into this sector in a very planned manner to boost-up this sector for the sake

of overall economic development of the country. Our country is labour abundant and

SMEs are typically labour intensive. So, the sector deserves more investment facility for

smooth functioning of the existing enterprises and expansion of the same with a view to

retain the workforce active as well as creating more employment opportunities. Further,

investment in SMEs can be very effective in reducing poverty as well as ensuring long

term economic growth.

Shahjalal Islami Bank Limited (SJIBL) is a modern commercial bank governed by the

principles of Islamic Shariah, which is committed to implement and materialize the

economic and financial principles of Islam in the banking sector. It has undertaken

initiatives for investment in SME sector by introducing a number of SME products in the

market gradually with a view to patronizing the trade, commerce and industrial entities

with equity & justice and to make effective contribution for creating employment

opportunities, which will ultimately help the nation for poverty alleviation from the

society.

SME investment Products:

36

Prottasha for Small Enterprises

Shahjalal Islami Bank Limited (SJIBL) is firmly committed to implement and materialize

the economic and financial principles of Islam in the Banking Arena. The very essence

of Islamic mode of banking is to remove the disparity through establishing equity justice

in trade, commerce and industry sector, creating opportunities for employment, boosting

up income generation which ultimately helps alleviation of poverty from the society.

Keeping the view and as an active contributor in the economic growth of Bangladesh,

Shahjalal Islami Bank Ltd. has initiated SME Investment throughout the country.

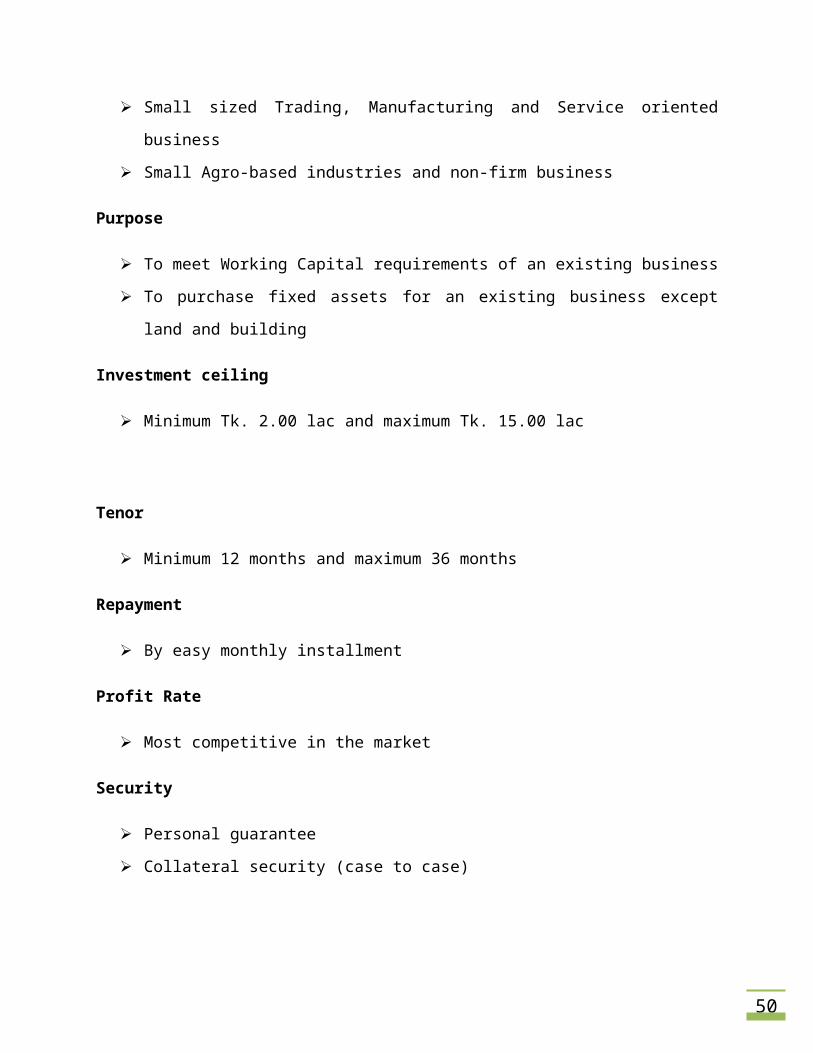

Target Group

Small sized Trading, Manufacturing and Service oriented business

Small Agro-based industries and non-firm business

Purpose

To meet Working Capital requirements of an existing business

To purchase fixed assets for an existing business except land and building

Investment ceiling

Minimum Tk. 2.00 lac and maximum Tk. 30.00 lac

Tenor

Minimum 12 months and maximum 36 months

Repayment

By easy monthly installment

Profit Rate

Most competitive in the market

Security

37

Personal guarantee

Collateral security (case to case)

Prottasha for Women Entrepreneur

It is well-known that women's empowerment and economic development go hand-in-

hand. Now a day’s Women Entrepreneurs are receiving greater attention from

policymakers and experts in developed and developing countries. In our country,

Women Entrepreneurs are also encouraged to contribute to the national economy

through establishing and expanding small & medium enterprises all over the country.

Shahjalal Islami Bank Limited (SJIBL) is extending investment to Women Entrepreneurs

for their business all over the country through its Small & Medium Enterprise (SME)

Investment program on easy terms and conditions.

Target Group

Small sized Trading, Manufacturing and Service oriented business

Small Agro-based industries and non-firm business

Purpose

To meet Working Capital requirements of an existing business

To purchase fixed assets for an existing business except land and building

Investment ceiling

Minimum Tk. 2.00 lac and maximum Tk. 15.00 lac

Tenor

Minimum 12 months and maximum 36 months

Repayment

38

By easy monthly installment

Profit Rate

Most competitive in the market

Security

Personal guarantee

Collateral security (case to case)

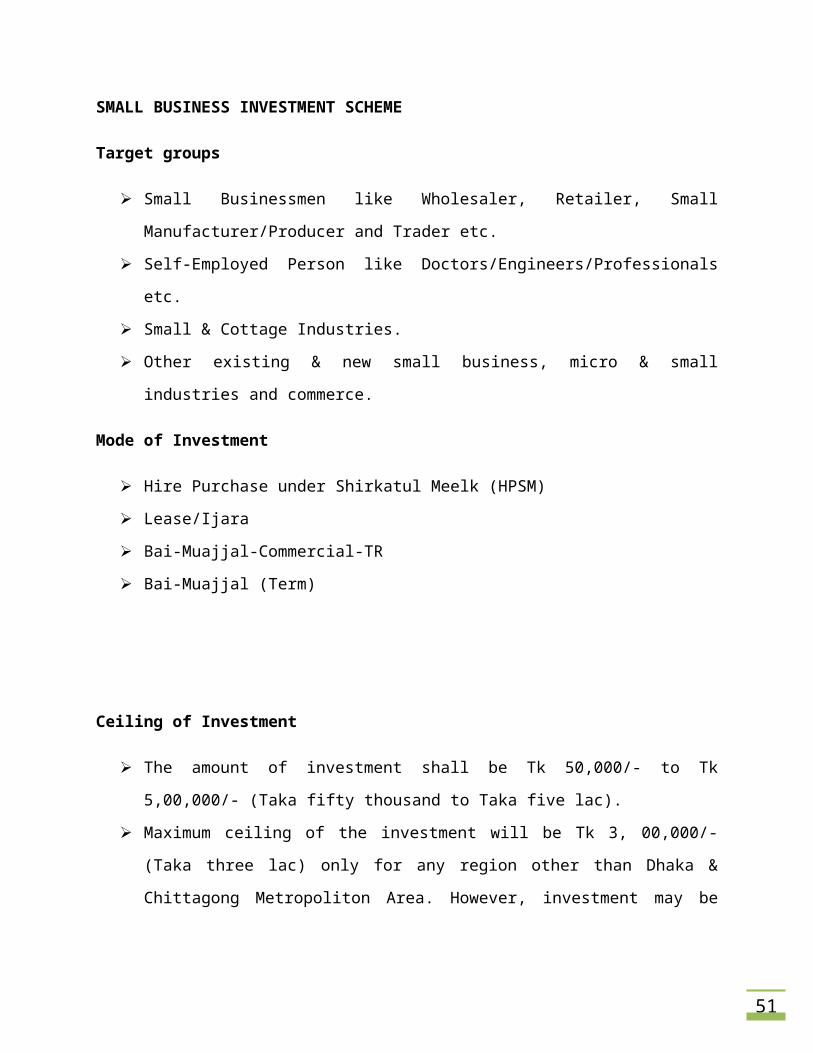

SMALL BUSINESS INVESTMENT SCHEME

Target groups

Small Businessmen like Wholesaler, Retailer, Small Manufacturer/Producer and

Trader etc.

Self-Employed Person like Doctors/Engineers/Professionals etc.

Small & Cottage Industries.

Other existing & new small business, micro & small industries and commerce.

Mode of Investment

Hire Purchase under Shirkatul Meelk (HPSM)

Lease/Ijara

Bai-Muajjal-Commercial-TR

Bai-Muajjal (Term)

Ceiling of Investment

The amount of investment shall be Tk 50,000/- to Tk 5,00,000/- (Taka fifty

thousand to Taka five lac).

39

Maximum ceiling of the investment will be Tk 3, 00,000/- (Taka three lac) only for

any region other than Dhaka & Chittagong Metropoliton Area. However,

investment may be extended beyond the ceiling at the discretion of the

Management.

Bank investment-Client equity ratio where applicable shall be 60:40.

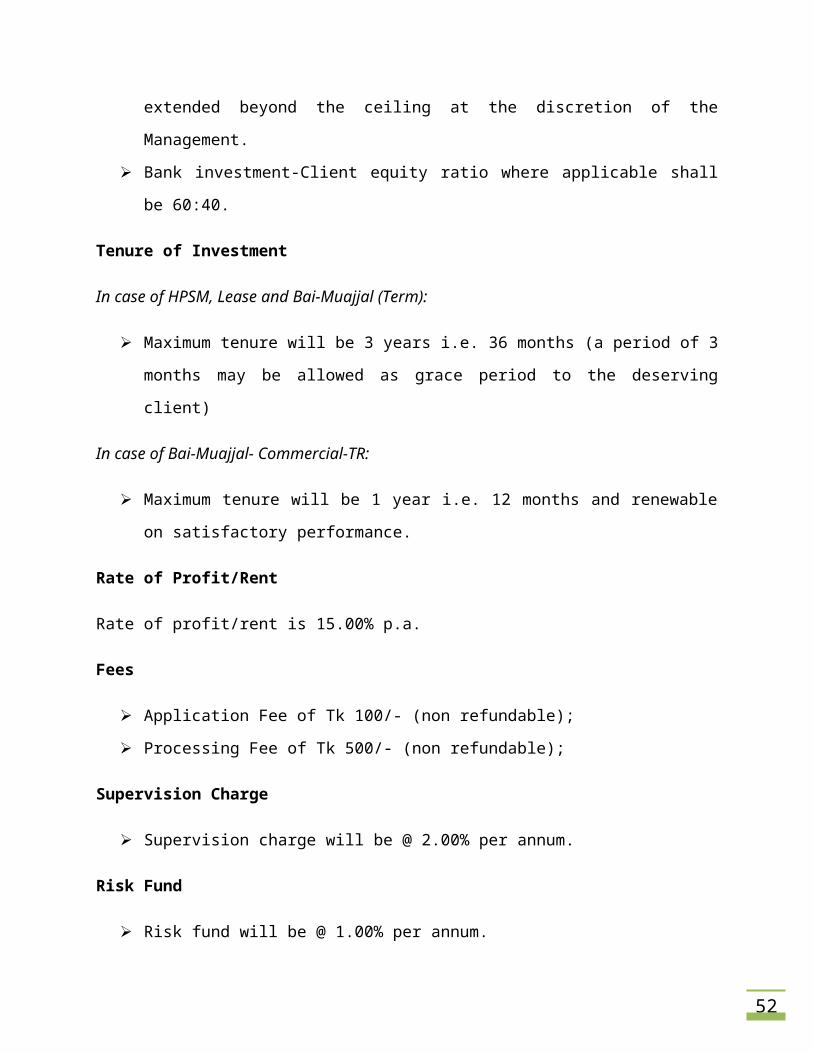

Tenure of Investment

In case of HPSM, Lease and Bai-Muajjal (Term):

Maximum tenure will be 3 years i.e. 36 months (a period of 3 months may be

allowed as grace period to the deserving client)

In case of Bai-Muajjal- Commercial-TR:

Maximum tenure will be 1 year i.e. 12 months and renewable on satisfactory

performance.

Rate of Profit/Rent

Rate of profit/rent is 15.00% p.a.

Fees

Application Fee of Tk 100/- (non refundable);

Processing Fee of Tk 500/- (non refundable);

Supervision Charge

Supervision charge will be @ 2.00% per annum.

Risk Fund

Risk fund will be @ 1.00% per annum.

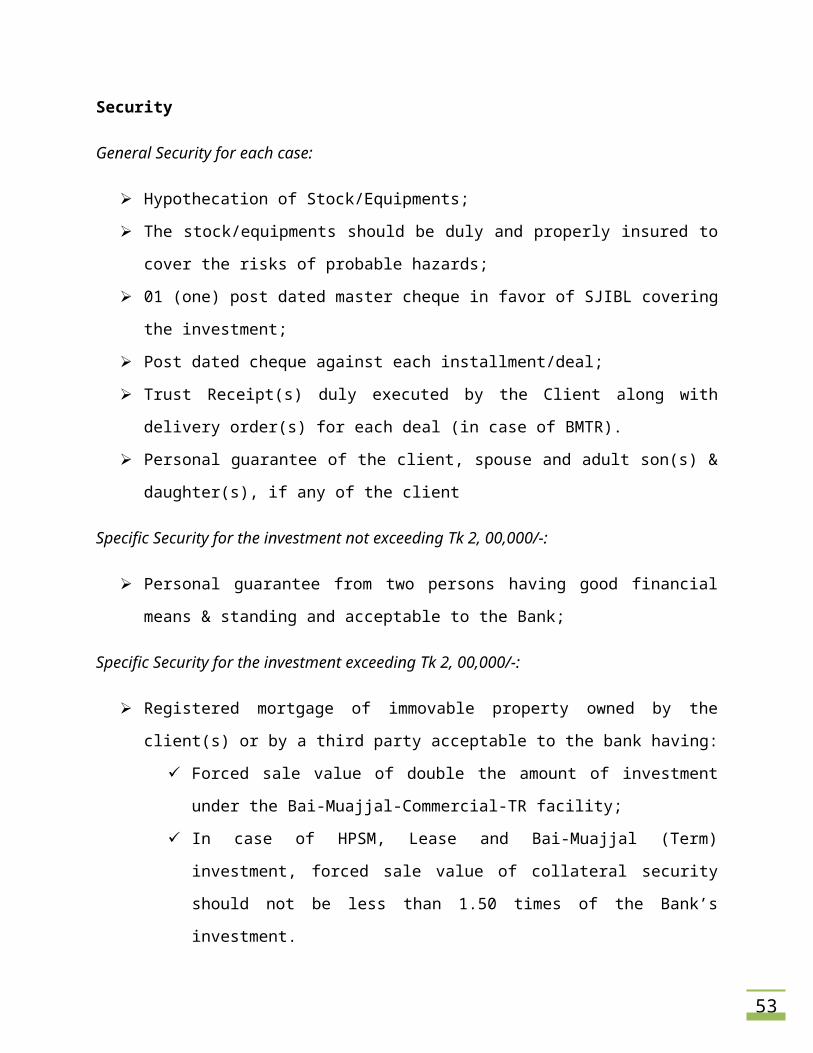

Security

General Security for each case:

40

Hypothecation of Stock/Equipments;

The stock/equipments should be duly and properly insured to cover the risks of

probable hazards;

01 (one) post dated master cheque in favor of SJIBL covering the investment;

Post dated cheque against each installment/deal;

Trust Receipt(s) duly executed by the Client along with delivery order(s) for each

deal (in case of BMTR).

Personal guarantee of the client, spouse and adult son(s) & daughter(s), if any of

the client

Specific Security for the investment not exceeding Tk 2, 00,000/-:

Personal guarantee from two persons having good financial means & standing

and acceptable to the Bank;

Specific Security for the investment exceeding Tk 2, 00,000/-:

Registered mortgage of immovable property owned by the client(s) or by a third

party acceptable to the bank having:

Forced sale value of double the amount of investment under the Bai-

Muajjal-Commercial-TR facility;

In case of HPSM, Lease and Bai-Muajjal (Term) investment, forced sale

value of collateral security should not be less than 1.50 times of the

Bank’s investment.

HOUSEHOLD DURABLES INVESTMENT SCHEME

Purpose

41

Facilitate investment to purchase household durables to the different low &

medium income honest businessman/professionals.

Socio-economic improvement of the country through improvement of life style of

the low & medium income people

Target groups

The permanent employees working in the following organizations aged between 20 to

55 years and willing to avail investment under the scheme:

Government Organizations.

Semi-Government & Autonomous Organizations.

Different Corporations.

Multi-national Companies.

Different local renowned Non-governmental Organizations.

Different Banks and Financial Institutions (Including Shahjalal Islami Bank Ltd.).

Different Insurance Companies.

Different renowned University, College, School & Madrasha besides Government

University, College, School & Madrasha.

The persons serving in Military and Paramilitary.

Acceptable persons to the Bank's Management.

Genuine businessman having valid Trade license, VAT certificate, TIN certificate

and Monthly Income evidenced by relevant documents may be included as client.

Note

In case of service holder minimum service length requirement is 3 years which

may be relaxed for the client having banking service;

In case of businessmen minimum business experience requirement is 5 years

that may be relaxed on special consideration.

Household Items

Air-Conditioner/Air-Cooler Electrical/Electronic goods IPS/UPS/Stabilizer/FAX/Cell-Phone

42

Crockery Items Computer Washing Machine

Knitting Machine (Home

useable)Furniture and Fixtures Non-Commercial Generator

Photo Copier Oven Refrigerator

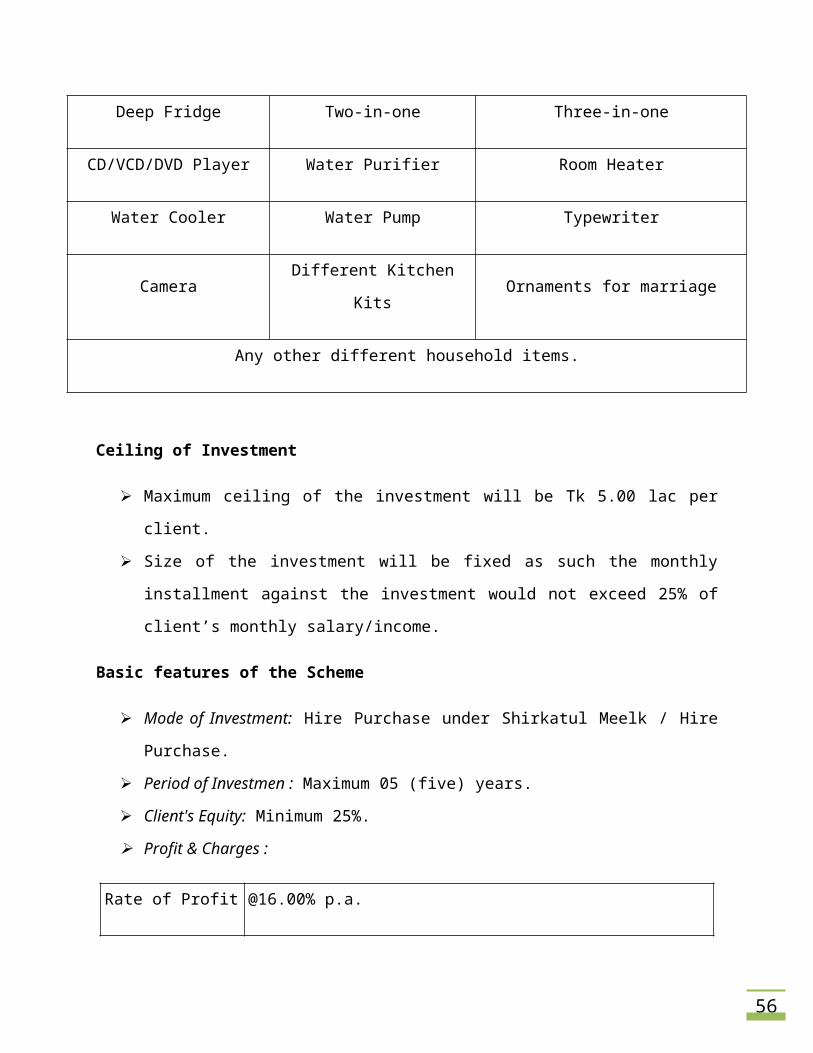

Deep Fridge Two-in-one Three-in-one

CD/VCD/DVD Player Water Purifier Room Heater

Water Cooler Water Pump Typewriter

Camera Different Kitchen Kits Ornaments for marriage

Any other different household items.

Ceiling of Investment

Maximum ceiling of the investment will be Tk 5.00 lac per client.

Size of the investment will be fixed as such the monthly installment against the

investment would not exceed 25% of client’s monthly salary/income.

Basic features of the Scheme

Mode of Investment: Hire Purchase under Shirkatul Meelk / Hire Purchase.

Period of Investmen : Maximum 05 (five) years.

Client's Equity: Minimum 25%.

Profit & Charges :

Rate of Profit @16.00% p.a.

Service Charge @1.00% p.a. on approved limit to be realized upfront.

43

Risk Fund @1.00% to be realized at the time of disbursement.

Repayment Procedure: Monthly Installment basis.

Securities:

The ownership of the item(s) shall be in the name of the Bank.

One post dated master cheque, covering the facility amount (with profit).

Post-dated cheques against each monthly installment.

Personal guarantee from two persons having good financial means &

standing and acceptable to the Bank.

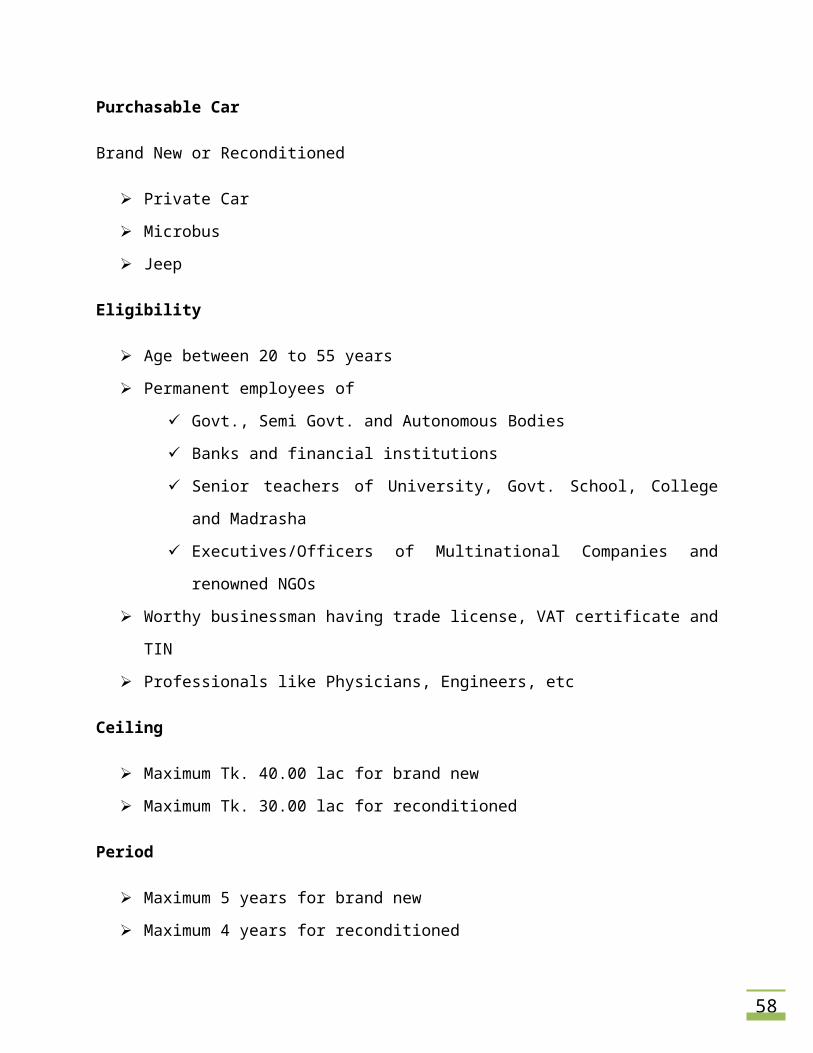

CAR PURCHASE INVESTMENT SCHEME

Maintaining a car now a day is no more a luxury, but an essential part of daily working

life to add speed to its performance and taking this as view Shahjalal Islami Bank has

introduced Car Purchase Investment Scheme. Potential users of personal cars are

requested to contact any of the branches of the bank for availing the facility within

shortest possible time at very easy terms.

Purchasable Car

Brand New or Reconditioned

Private Car

Microbus

Jeep

Eligibility

Age between 20 to 55 years

Permanent employees of

44

Govt., Semi Govt. and Autonomous Bodies

Banks and financial institutions

Senior teachers of University, Govt. School, College and Madrasha

Executives/Officers of Multinational Companies and renowned NGOs

Worthy businessman having trade license, VAT certificate and TIN

Professionals like Physicians, Engineers, etc

Ceiling

Maximum Tk. 40.00 lac for brand new

Maximum Tk. 30.00 lac for reconditioned

Period

Maximum 5 years for brand new

Maximum 4 years for reconditioned

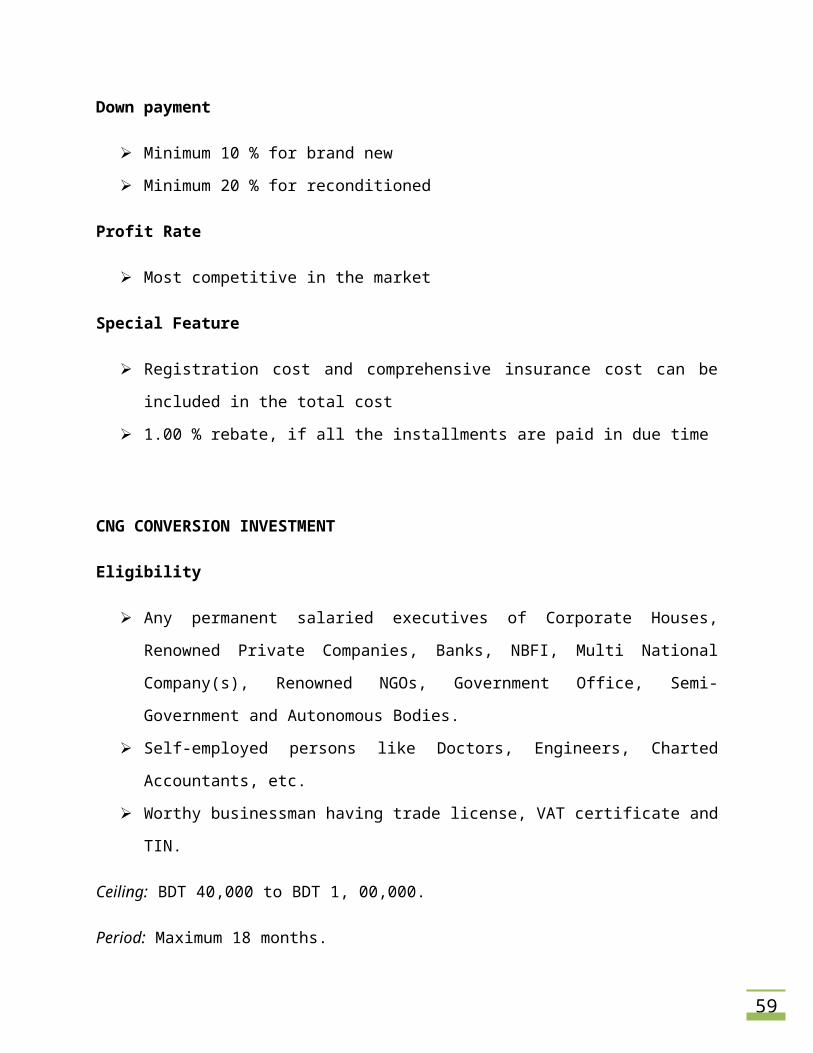

Down payment

Minimum 10 % for brand new

Minimum 20 % for reconditioned

Profit Rate

Most competitive in the market

Special Feature

Registration cost and comprehensive insurance cost can be included in the total

cost

1.00 % rebate, if all the installments are paid in due time

CNG CONVERSION INVESTMENT

Eligibility

45

Any permanent salaried executives of Corporate Houses, Renowned Private

Companies, Banks, NBFI, Multi National Company(s), Renowned NGOs,

Government Office, Semi-Government and Autonomous Bodies.

Self-employed persons like Doctors, Engineers, Charted Accountants, etc.

Worthy businessman having trade license, VAT certificate and TIN.

Ceiling: BDT 40,000 to BDT 1, 00,000.

Period: Maximum 18 months.

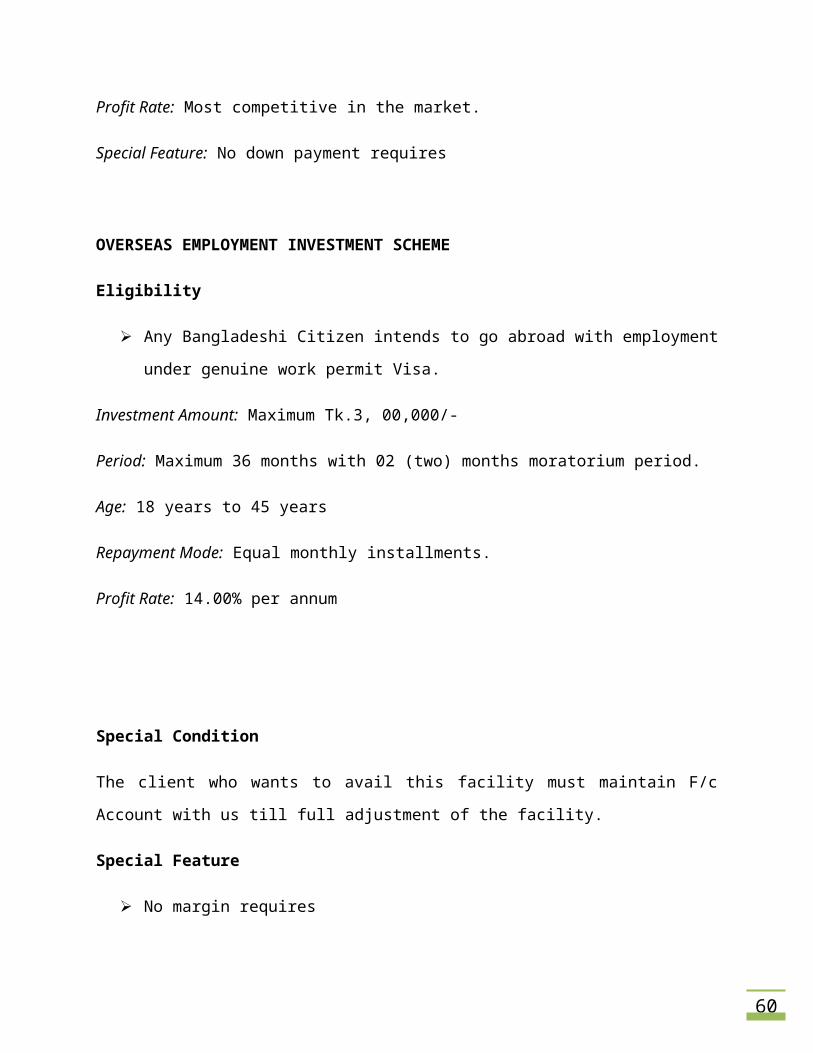

Profit Rate: Most competitive in the market.

Special Feature: No down payment requires

OVERSEAS EMPLOYMENT INVESTMENT SCHEME

Eligibility

Any Bangladeshi Citizen intends to go abroad with employment under genuine

work permit Visa.

Investment Amount: Maximum Tk.3, 00,000/-

Period: Maximum 36 months with 02 (two) months moratorium period.

Age: 18 years to 45 years

Repayment Mode: Equal monthly installments.

Profit Rate: 14.00% per annum

Special Condition

46

The client who wants to avail this facility must maintain F/c Account with us till full

adjustment of the facility.

Special Feature

No margin requires

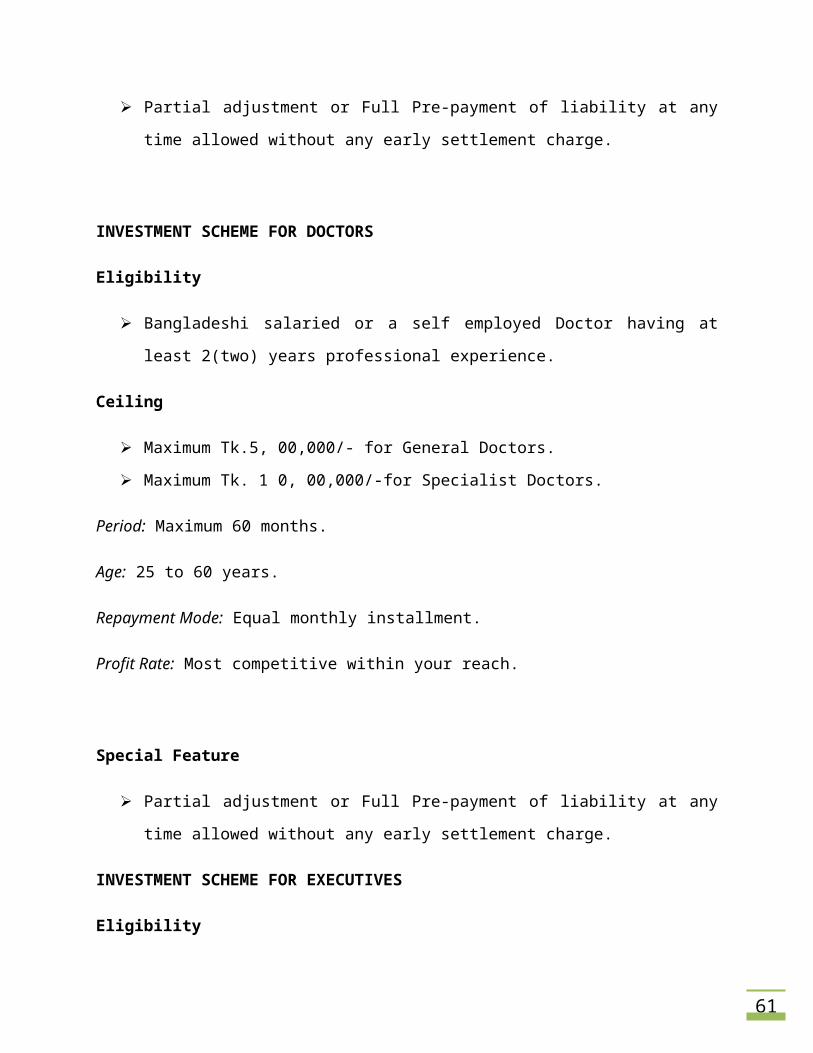

Partial adjustment or Full Pre-payment of liability at any time allowed without any

early settlement charge.

INVESTMENT SCHEME FOR DOCTORS

Eligibility

Bangladeshi salaried or a self employed Doctor having at least 2(two) years

professional experience.

Ceiling

Maximum Tk.5, 00,000/- for General Doctors.

Maximum Tk. 1 0, 00,000/-for Specialist Doctors.

Period: Maximum 60 months.

Age: 25 to 60 years.

Repayment Mode: Equal monthly installment.

Profit Rate: Most competitive within your reach.

Special Feature

Partial adjustment or Full Pre-payment of liability at any time allowed without any

early settlement charge.

INVESTMENT SCHEME FOR EXECUTIVES

47

Eligibility

Any Bangladeshi salaried executives of Corporate Houses, Banks, NBFI, Multi

National Company(s), Government Office & Semi-Government Office can avail

this facility.

Investment Amount: Maximum Tk. 10, 00,000/-

Period: Maximum 36 months.

Age: 22 years to 60 years

Repayment Mode: Equal monthly installments.

Profit Rate: Most competitive within your reach.

Special Condition

Salary A/c & end service benefit. will be lien till full adjustment of the liability.

Special Feature

Partial adjustment or Full Pre-payment of liability at any time allowed without any

early settlement charge.

INVESTMENT SCHEME FOR MARRIAGE

Eligibility

Any Bangladeshi salaried or a self employed person having 2 (Two) years

professional experience

Investment Amount: Maximum Tk. 3, 00,000/-

Period: Maximum 48 months.

Age: 25 years to 60 years.

48

Repayment Mode: Equal monthly installments.

Profit Rate: Most competitive within your reach.

Special Feature

Partial adjustment or Full Pre-payment of liability at any time allowed without any

early settlement charge.

INVESTMENT SCHEME FOR EDUCATION

Eligibility

Any Bangladeshi credit worthy salaried or a self-employed person can avail this

facility for their Children.

Purpose of Investment

To pay the Tuition fees.

To pay the Hostel fees.

To meet Travel expenses.

Purchase of computer, books etc.

Investment Amount

In Bangladesh: Maximum Tk. 7,00,000/-

In Abroad: Maximum Tk. 15,00,000/-

Period: Maximum 60 months.

Margin: - In Bangladesh: 10% margin.

- In Abroad: 20% margin.

Repayment Mode: Equal monthly installments.

Profit Rate: 14.00% per annum

49

Special Condition

Student file must be maintained with Shahjalal Islami Bank Ltd.

Special Feature

Partial adjustment or Full Pre-payment of liability at any time allowed without any

early settlement charge.

50

CHAPTER 3PERFORMANCE MEASUREMENT

51

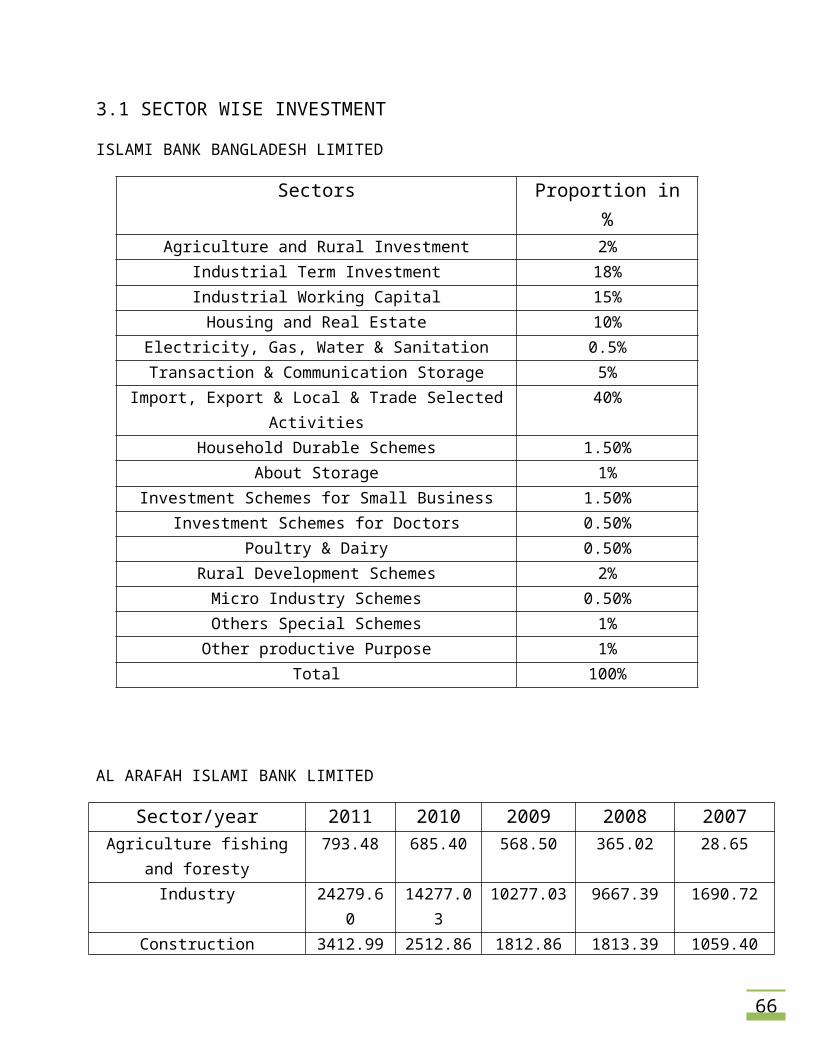

3.1 SECTOR WISE INVESTMENT

ISLAMI BANK BANGLADESH LIMITED

Sectors Proportion in %Agriculture and Rural Investment 2%

Industrial Term Investment 18%Industrial Working Capital 15%Housing and Real Estate 10%

Electricity, Gas, Water & Sanitation 0.5%Transaction & Communication Storage 5%

Import, Export & Local & Trade Selected Activities 40%Household Durable Schemes 1.50%

About Storage 1%Investment Schemes for Small Business 1.50%

Investment Schemes for Doctors 0.50%Poultry & Dairy 0.50%

Rural Development Schemes 2%Micro Industry Schemes 0.50%Others Special Schemes 1%Other productive Purpose 1%

Total 100%

AL ARAFAH ISLAMI BANK LIMITED

Sector/year 2011 2010 2009 2008 2007Agriculture fishing and

foresty793.48 685.40 568.50 365.02 28.65

Industry 24279.60 14277.03 10277.03 9667.39 1690.72Construction 3412.99 2512.86 1812.86 1813.39 1059.40

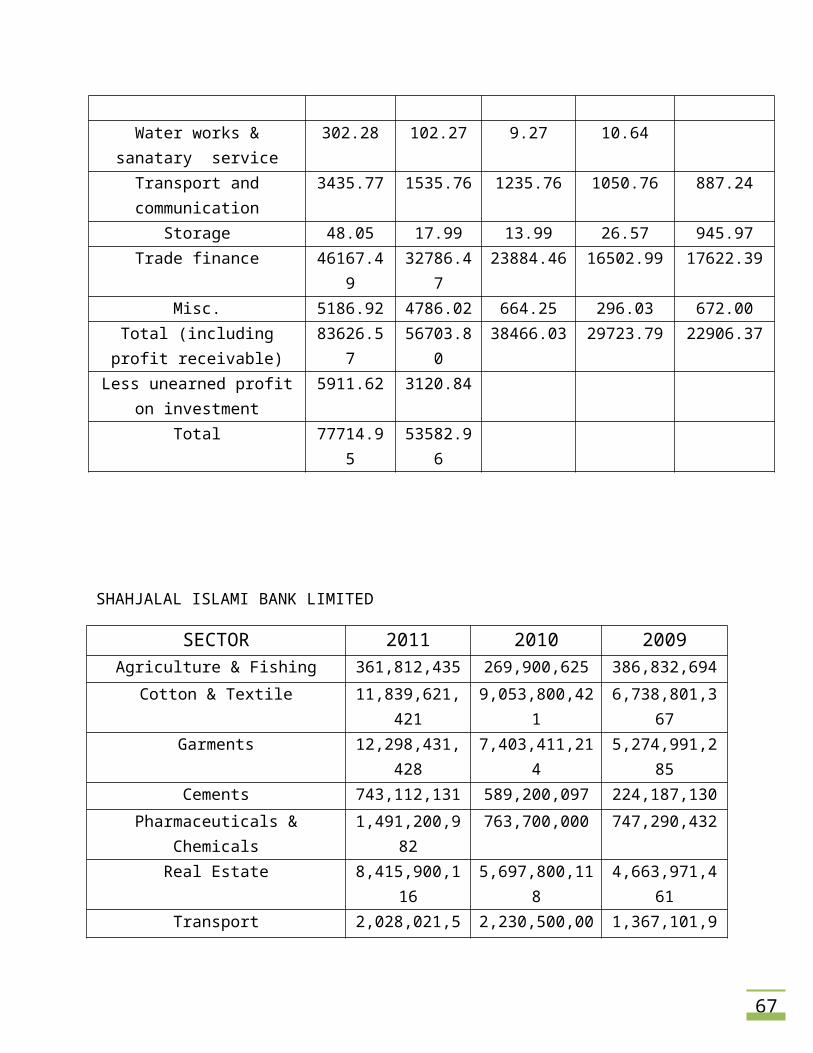

Water works & sanatary service

302.28 102.27 9.27 10.64

Transport and communication

3435.77 1535.76 1235.76 1050.76 887.24

Storage 48.05 17.99 13.99 26.57 945.97Trade finance 46167.49 32786.47 23884.46 16502.99 17622.39

Misc. 5186.92 4786.02 664.25 296.03 672.00

52

Total (including profit receivable)

83626.57 56703.80 38466.03 29723.79 22906.37

Less unearned profit on investment

5911.62 3120.84

Total 77714.95 53582.96

SHAHJALAL ISLAMI BANK LIMITED

SECTOR 2011 2010 2009Agriculture & Fishing 361,812,435 269,900,625 386,832,694

Cotton & Textile 11,839,621,421 9,053,800,421 6,738,801,367

Garments 12,298,431,428 7,403,411,214 5,274,991,285

Cements 743,112,131 589,200,097 224,187,130

Pharmaceuticals & Chemicals 1,491,200,982 763,700,000 747,290,432

Real Estate 8,415,900,116 5,697,800,118 4,663,971,461

Transport 2,028,021,543 2,230,500,000 1,367,101,908

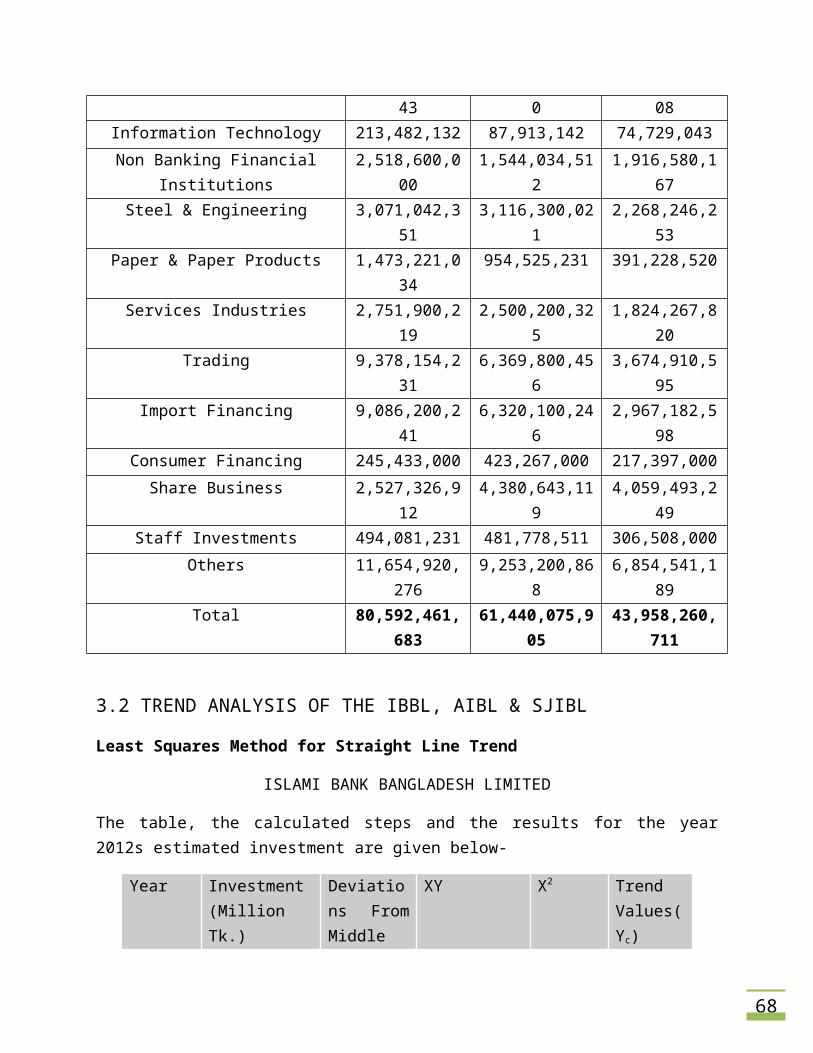

Information Technology 213,482,132 87,913,142 74,729,043

Non Banking Financial Institutions 2,518,600,000 1,544,034,512 1,916,580,167

Steel & Engineering 3,071,042,351 3,116,300,021 2,268,246,253

Paper & Paper Products 1,473,221,034 954,525,231 391,228,520

Services Industries 2,751,900,219 2,500,200,325 1,824,267,820

Trading 9,378,154,231 6,369,800,456 3,674,910,595

Import Financing 9,086,200,241 6,320,100,246 2,967,182,598

Consumer Financing 245,433,000 423,267,000 217,397,000

Share Business 2,527,326,912 4,380,643,119 4,059,493,249

Staff Investments 494,081,231 481,778,511 306,508,000

Others 11,654,920,276 9,253,200,868 6,854,541,189

Total 80,592,461,683 61,440,075,905 43,958,260,711

53

3.2 TREND ANALYSIS OF THE IBBL, AIBL & SJIBL

Least Squares Method for Straight Line Trend

ISLAMI BANK BANGLADESH LIMITED

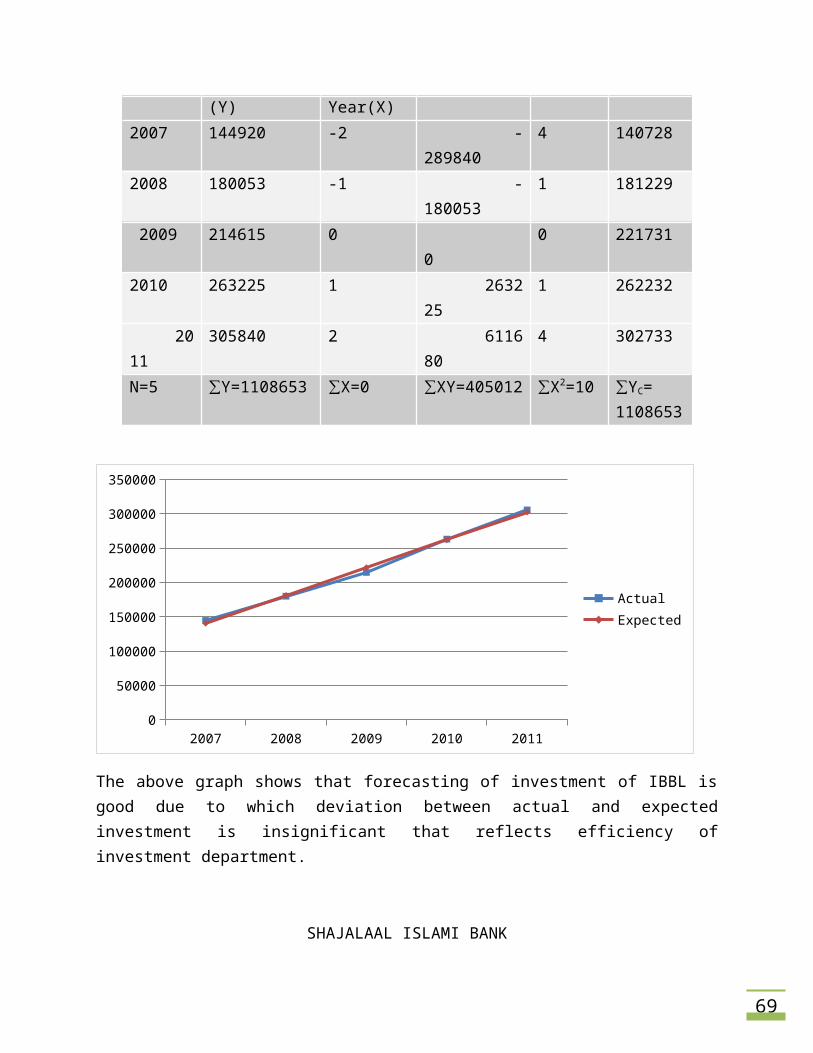

The table, the calculated steps and the results for the year 2012s estimated investment are given below-

Year Investment (Million Tk.)(Y)

Deviations From Middle Year(X)

XY X2 Trend Values(Yc)

2007 144920 -2 - 289840 4 140728

2008 180053 -1 -180053 1 181229

2009 214615 0 0 0 221731

2010 263225 1 263225 1 262232

2011 305840 2 611680 4 302733N=5 ∑Y=1108653 ∑X=0 ∑XY=405012 ∑X2=10 ∑YC=

1108653

2007 2008 2009 2010 20110

50000

100000

150000

200000

250000

300000

350000

ActualExpected

The above graph shows that forecasting of investment of IBBL is good due to which deviation between actual and expected investment is insignificant that reflects efficiency of investment department.

54

SHAJALAAL ISLAMI BANK

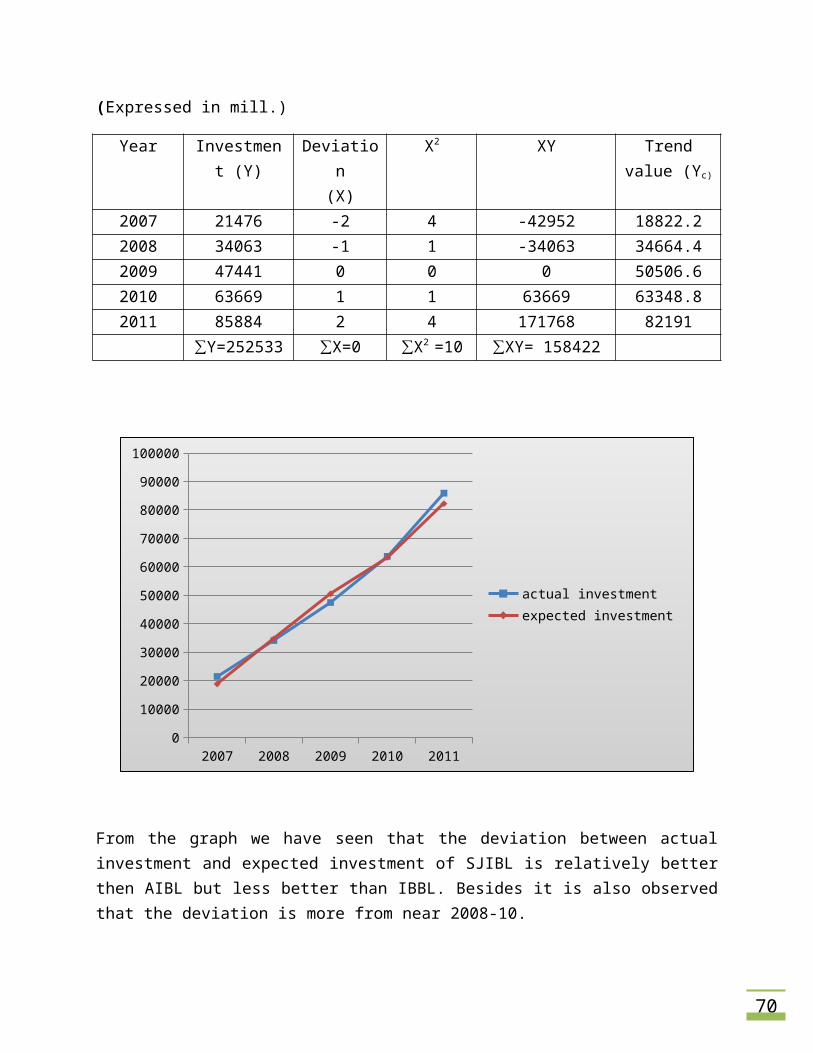

(Expressed in mill.)

Year Investment (Y)

Deviation(X)

X2 XY Trend value (Yc)

2007 21476 -2 4 -42952 18822.22008 34063 -1 1 -34063 34664.42009 47441 0 0 0 50506.62010 63669 1 1 63669 63348.82011 85884 2 4 171768 82191

∑Y=252533 ∑X=0 ∑X2 =10 ∑XY= 158422

2007 2008 2009 2010 20110

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

actual investment expected investment

From the graph we have seen that the deviation between actual investment and expected investment of SJIBL is relatively better then AIBL but less better than IBBL. Besides it is also observed that the deviation is more from near 2008-10.

55

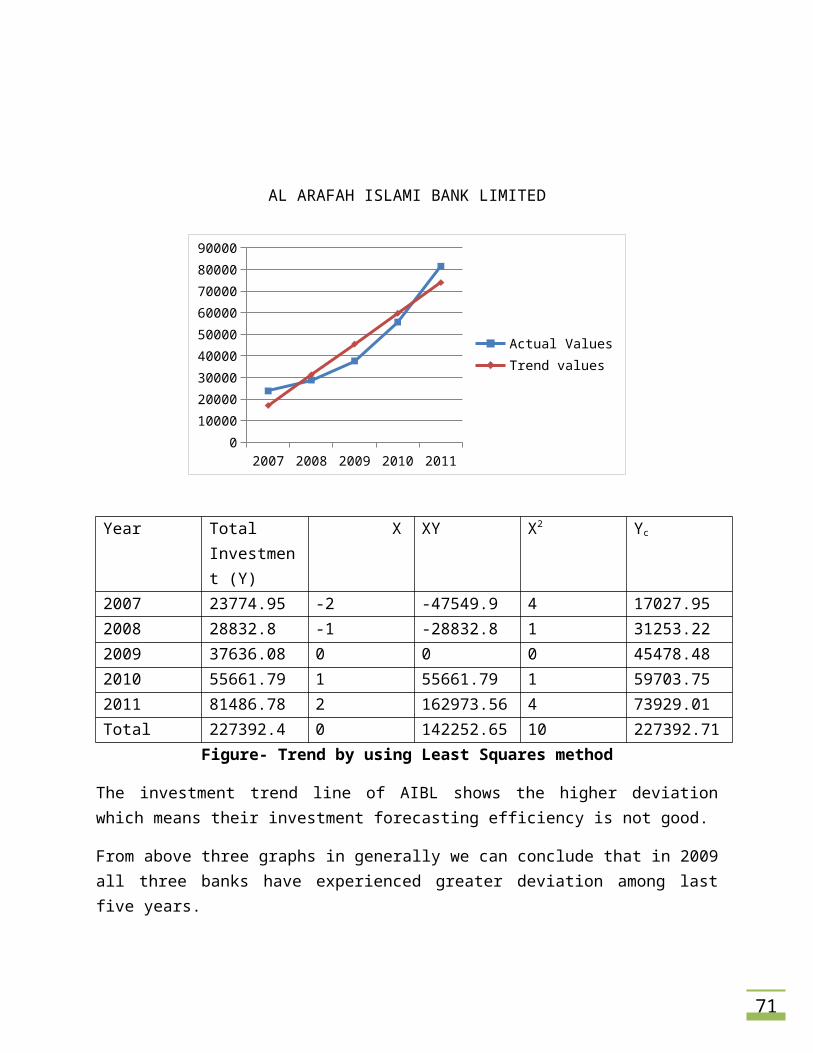

AL ARAFAH ISLAMI BANK LIMITED

2007 2008 2009 2010 20110

10000

20000

30000

40000

50000

60000

70000

80000

90000

Actual ValuesTrend values

Year Total Investment (Y)

X XY X2 Yc

2007 23774.95 -2 -47549.9 4 17027.952008 28832.8 -1 -28832.8 1 31253.222009 37636.08 0 0 0 45478.482010 55661.79 1 55661.79 1 59703.752011 81486.78 2 162973.56 4 73929.01Total 227392.4 0 142252.65 10 227392.71

Figure- Trend by using Least Squares method

The investment trend line of AIBL shows the higher deviation which means their investment forecasting efficiency is not good.

From above three graphs in generally we can conclude that in 2009 all three banks have experienced greater deviation among last five years.

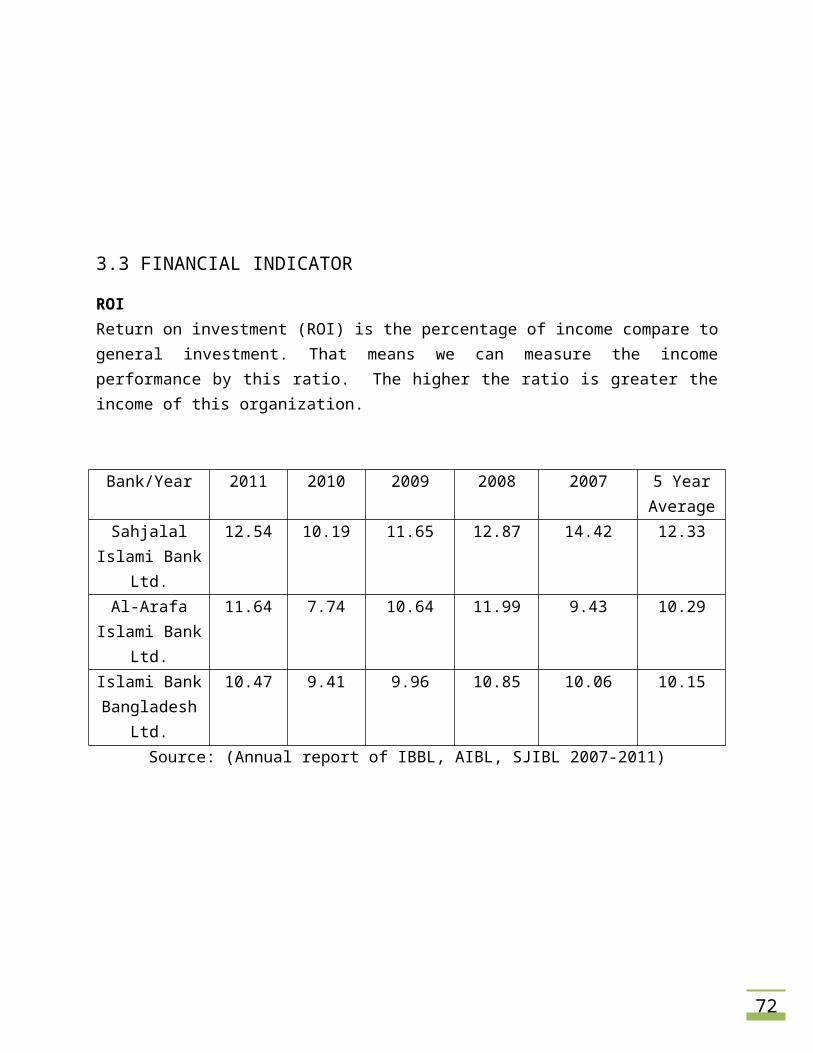

3.3 FINANCIAL INDICATOR

56

ROIReturn on investment (ROI) is the percentage of income compare to general investment. That means we can measure the income performance by this ratio. The higher the ratio is greater the income of this organization.

Bank/Year 2011 2010 2009 2008 2007 5 Year Average

Sahjalal Islami Bank Ltd.

12.54 10.19 11.65 12.87 14.42 12.33

Al-Arafa Islami Bank Ltd.

11.64 7.74 10.64 11.99 9.43 10.29

Islami Bank Bangladesh

Ltd.

10.47 9.41 9.96 10.85 10.06 10.15

Source: (Annual report of IBBL, AIBL, SJIBL 2007-2011)

2011 2010 2009 2008 20070

2

4

6

8

10

12

14

16

Sahjalal Islami Bank Ltd.Al-Arafa Islami Bank Ltd.Islami Bank Bangladesh Ltd.

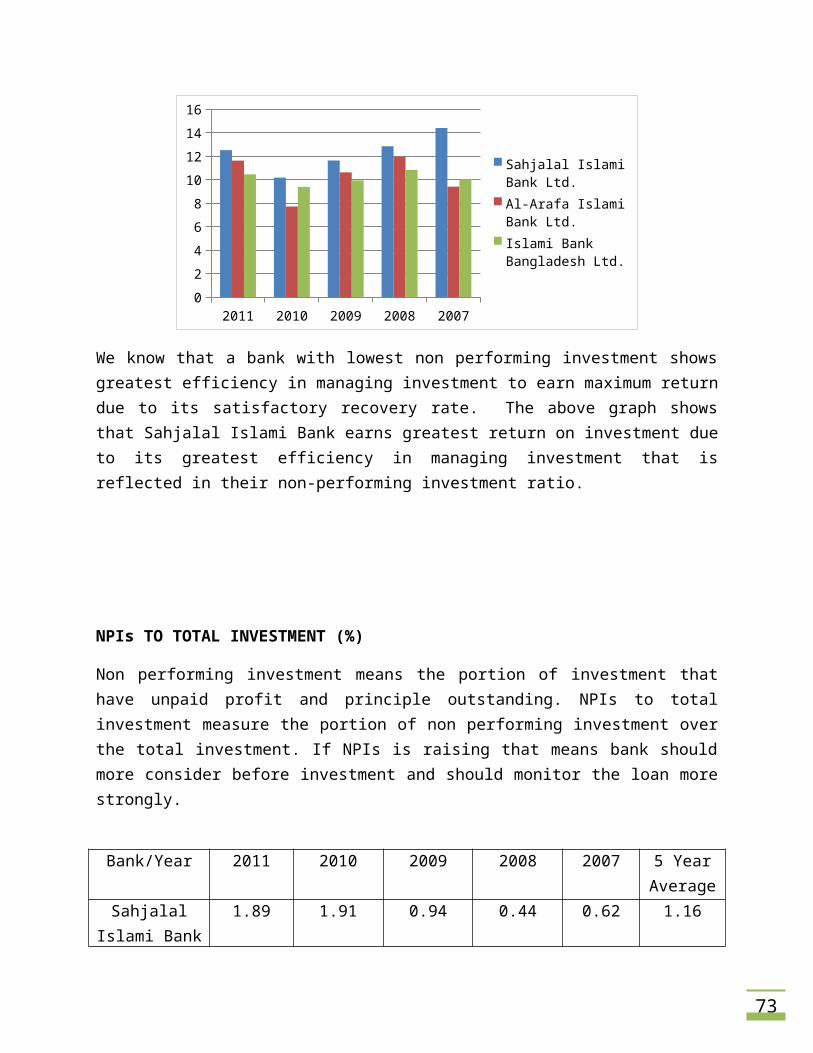

We know that a bank with lowest non performing investment shows greatest efficiency in managing investment to earn maximum return due to its satisfactory recovery rate. The above graph shows that Sahjalal Islami Bank earns greatest return on investment due to its greatest efficiency in managing investment that is reflected in their non-performing investment ratio.

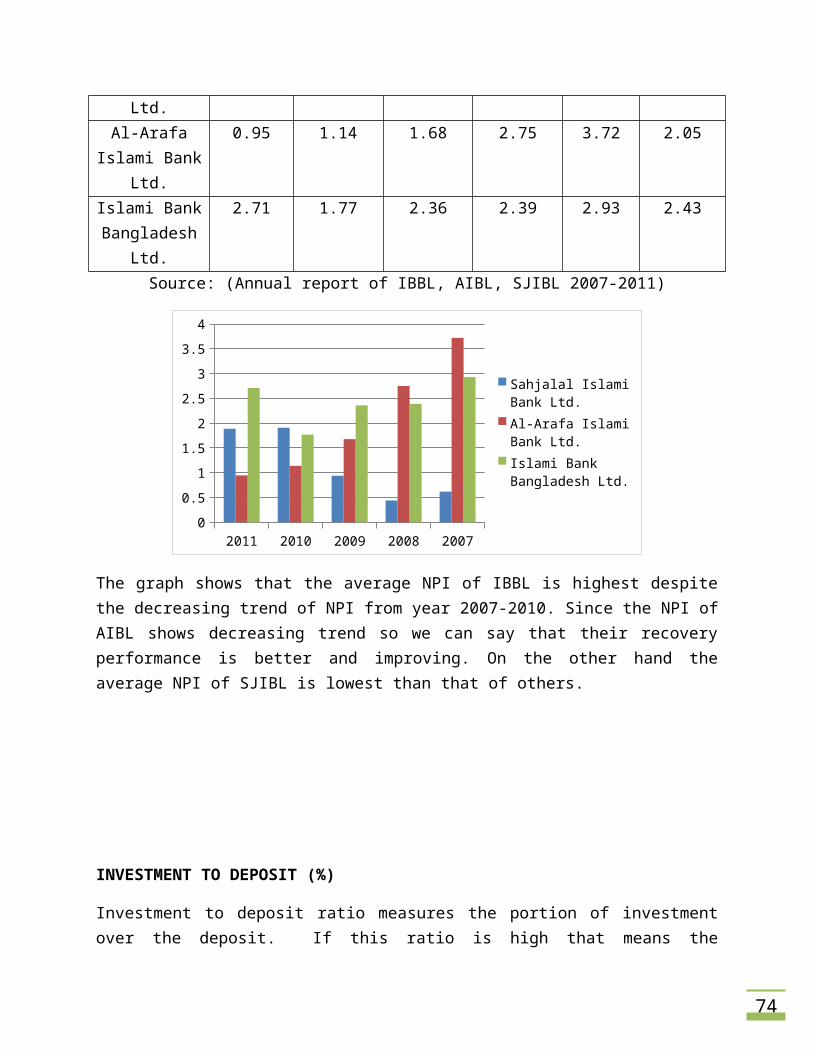

NPIs TO TOTAL INVESTMENT (%)

57

Non performing investment means the portion of investment that have unpaid profit and principle outstanding. NPIs to total investment measure the portion of non performing investment over the total investment. If NPIs is raising that means bank should more consider before investment and should monitor the loan more strongly.

Bank/Year 2011 2010 2009 2008 2007 5 Year Average

Sahjalal Islami Bank Ltd.

1.89 1.91 0.94 0.44 0.62 1.16

Al-Arafa Islami Bank Ltd.

0.95 1.14 1.68 2.75 3.72 2.05

Islami Bank Bangladesh

Ltd.

2.71 1.77 2.36 2.39 2.93 2.43

Source: (Annual report of IBBL, AIBL, SJIBL 2007-2011)

2011 2010 2009 2008 20070

0.5

1

1.5

2

2.5

3

3.5

4

Sahjalal Islami Bank Ltd.Al-Arafa Islami Bank Ltd.Islami Bank Bangladesh Ltd.

The graph shows that the average NPI of IBBL is highest despite the decreasing trend of NPI from year 2007-2010. Since the NPI of AIBL shows decreasing trend so we can say that their recovery performance is better and improving. On the other hand the average NPI of SJIBL is lowest than that of others.

INVESTMENT TO DEPOSIT (%)

58

Investment to deposit ratio measures the portion of investment over the deposit. If this ratio is high that means the organization may earn greater profit but the organization may face the liquidity problem. Because higher investment creates lower cash balance.

Bank/Year 2011 2010 2009 2008 2007 5 Year Average

Sahjalal Islami Bank Ltd.

93.00 96.34 92.62 90.23 91.15 92.67

Al-Arafa Islami Bank Ltd.

89.07 93.43 94.21 93.44 99.55 93.94

Islami Bank Bangladesh

Ltd.

89.47 90.17 87.88 89.08 87.13 88.75

Source: (Annual report of IBBL, AIBL, SJIBL 2007-2011)

2011 2010 2009 2008 200780

85

90

95

100

105

Sahjalal Islami Bank Ltd.Al-Arafa Islami Bank Ltd.Islami Bank Bangladesh Ltd.

The above calculation and graph shows that the investment to deposit ratio of AIBL is higher than that of SJIBL but we have seen a reverse situation of that two with respect to ROI as the NPI of SJIBL is comparatively lower than AIBL. On the contrary, although the average investment to deposit ratio of IBBL is the lowest one but their average NPI is highest that reflect in their lowest average ROI.

ROA (%)

59