Embed Size (px)

Citation preview

Strategic Management JournalStrat. Mgmt. J., 28: 681–706 (2007)

Published online 16 March 2007 in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/smj.589

Received 10 November 2004; Final revision received 27 July 2006

PERFORMANCE CONSEQUENCES OF NEW CEO‘OUTSIDERNESS’: MODERATING EFFECTS OF PRE-AND POST-SUCCESSION CONTEXTS

AYSE KARAEVLI*Faculty of Management, Sabanci University, Istanbul, Turkey

This study seeks to reconcile inconsistent findings on the performance consequences of newCEO origin. Drawing on five decades of empirical research on CEO succession outcomes, Idevelop a more refined theoretical conceptualization and a finer-grained measurement of theunderlying construct of the insider vs. outsider CEO, and build and test a more comprehensiveand nuanced framework of the succession context. A longitudinal investigation of the U.S. airlineand chemical industries (1972–2002) indicates that new CEO ‘outsiderness,’ conceptualizedas a continuum raging from new CEOs who have a greater combination of firm and industrytenure to those who have no experience in the firm and the industry, has no main effecton post-succession firm performance. However, significant moderating effects are found whenenvironmental munificence, pre-succession firm performance, and concomitant strategic andsenior executive team changes are considered. Together, these findings highlight the need toconsider both pre- and post-succession contextual factors for evaluating the performance effectsof new CEO outsiderness. Copyright 2007 John Wiley & Sons, Ltd.

Since taking over as CEO (of IBM) on April 1,1993, Louis V. Gerstner, Jr., has made it clear thathe has no intention of restructuring IBM. For themoment, Gerstner is determined to carry out a setof policies put in place by his predecessor. (Arnst,1993)

Rather,

. . . the first item on his (Gerstner’s) agenda was tolearn everything he could about the troubled techgiant’s business, staff, and customers. (Lavelle,2005)

On the other hand, although Fiorina was hiredby the HP board to initiate major changes in the

Keywords: CEO successions; CEO origin; outsider suc-cessions; succession context; performance change∗ Correspondence to: Ayse Karaevli, Faculty of Management,Sabanci University, Orhanli, Tuzla 34956, Istanbul, Turkey.E-mail: [email protected]

firm, some of the immediate changes she made,without connecting to people first, alienated theengineering-rooted culture of the company. Hence,one of the major reasons for her forced turnoverwas identified as:

collision with the celebrated and deeply rooted‘HP Way’ . . . Some longtime employees said ‘theythought she failed to understand what she had setout to transform.’ (Rivlin and Markoff, 2005)

Both Lou Gerstner and Carly Fiorina came to IBM(a data-processing equipment and services com-pany) and Hewlett-Packard (HP: a printer, per-sonal computer, and server maker) respectively, ata time when both firms lost momentum and neededa clear turnaround. Both successors, who by thetime of the succession had been characterized bytheir high profile and successful careers, were out-siders in their respective new firms and industries.Gerstner was hired from RJR Nabisco, a tobacco

Copyright 2007 John Wiley & Sons, Ltd.

682 A. Karaevli

and food company in 1993, and Fiorina was hiredfrom Lucent Technologies, a telecommunicationscompany that was a spin-off of AT&T, in 1999.In the early years of her tenure as Chief Execu-tive Officer (CEO), Fiorina did things that popularbusiness press characterizes as typical expectationsfrom new outsider successors, such as efforts atmaking a ‘fresh start’ and providing ‘new blood’(Anabtawi and Stout, New York Times, 2005). Ourprevious theories have also predicted that outsiderCEOs would be brought in with the purpose ofinitiating swift changes (Shen and Cannella, 2002;Zajac, 1990). On the other hand, as can be under-stood from the opening statement, Gerstner sur-prised everyone by deciding not to embark onradical changes at IBM right away. In the end,however, while Gerstner has been considered asa legendary CEO or ‘savior’ of IBM by turn-ing the poor-performing computer giant into aninnovative, service-oriented, and high-performingindustry leader, Carly Fiorina was ousted by theHP board in early 2005 after a disappointing per-formance record.

The paradoxical nature of the Gerstner and Fio-rina successions is not an exception and can alsobe seen in a Booz Allen Hamilton study, whichwas conducted in the world’s largest 2,500 corpo-rations and reports that although the average rateof external successions doubled between 1995 and2003, 55 percent of outsider CEOs in North Amer-ica, and 70 percent of outsider CEOs in Europe,were forced to resign for performance-related rea-sons in 2003 (Lucier, Schuyt, and Handa, 2003).In other words, firms are both hiring and firingoutsider CEOs at an increased rate, and thereforeit is not clear how outsider CEOs influence theirfirms.

Five decades of empirical research (1954–2005)does not, unfortunately, provide much insight intothis apparent paradox on outsider successions.Scholars have failed to reach a consensus onwhether succession events in general, and insidervs. outsider successions in particular, affect firmperformance positively, negatively, or insignifi-cantly (see Table 1).

Since it is important to reconcile inconsistentfindings concerning the performance consequencesof new CEO origin (whether the new CEO is hiredfrom within or outside the firm) from both theoret-ical and practical standpoints, it is critical to iden-tify the sources of inconsistencies in prior empiri-cal research. First, one of the major reasons for the

mixed findings is the lack of agreement regardingwhat has been captured by the insider vs. out-sider dichotomy (Finkelstein and Hambrick, 1996;Kesner and Sebora, 1994; Shen and Cannella,2002; Zajac and Westphal, 1996). Although suc-cessor origin was identified by Carlson (1961) overfour decades ago as a ‘gross and unrefined’ vari-able (p. 227), CEO successions are still viewed inbinary terms. Others have also regarded the notionof the insider/outsider dichotomy as an oversimpli-fication, and suggested that the focus be redirectedto consider fine-grade theoretical conceptualiza-tions and empirical analyses of the successor ori-gin (Finkelstein and Hambrick, 1996; Zajac andWestphal, 1996), which will bring, in Finkelsteinand Hambrick’s (1996) terms, ‘the biggest break-throughs in the study of insider versus outsidersuccession’ (p. 183). Second, although successionevents do not happen in a vacuum, and the fac-tors precipitating the succession and the actionsof the successors affect the outcomes (Finkelsteinand Hambrick, 1996), a review of prior empiricalstudies of CEO succession outcomes (see Table 1)suggests that there has been lack of a compre-hensive theoretical conceptualization and empiricaltesting of the simultaneous effects of these pre- andpost-succession contextual factors on CEO succes-sion consequences.

This study attempts to overcome these issues bybuilding and testing a more complete and nuancedframework of how the succession context influ-ences the performance consequences of new CEOorigin. First, the study offers a more refined theo-retical conceptualization and a finer-grained mea-surement of the underlying construct of the insidervs. outsider CEO. Responding to Finkelstein andHambrick’s (1996) call, the underlying constructof successor origin is conceptualized here as acontinuum of new CEO ‘outsiderness,’1 which isconceptually defined as the extent to which a newCEO brings different leadership style, knowledge,skills, and perspective to a firm based on his or herprevious experience in other firms and industries.A new CEO’s fresh knowledge, skills, and per-spective have traditionally been considered as pre-requisites for his or her ability to manage changeeffectively (Finkelstein and Hambrick, 1996).

1 I use the term ‘outsiderness’ to be consistent with the vastamounts of research on CEO successions, and to acknowledgeFinkelstein and Hambrick’s (1996) intellectual leadership on theissue.

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 683

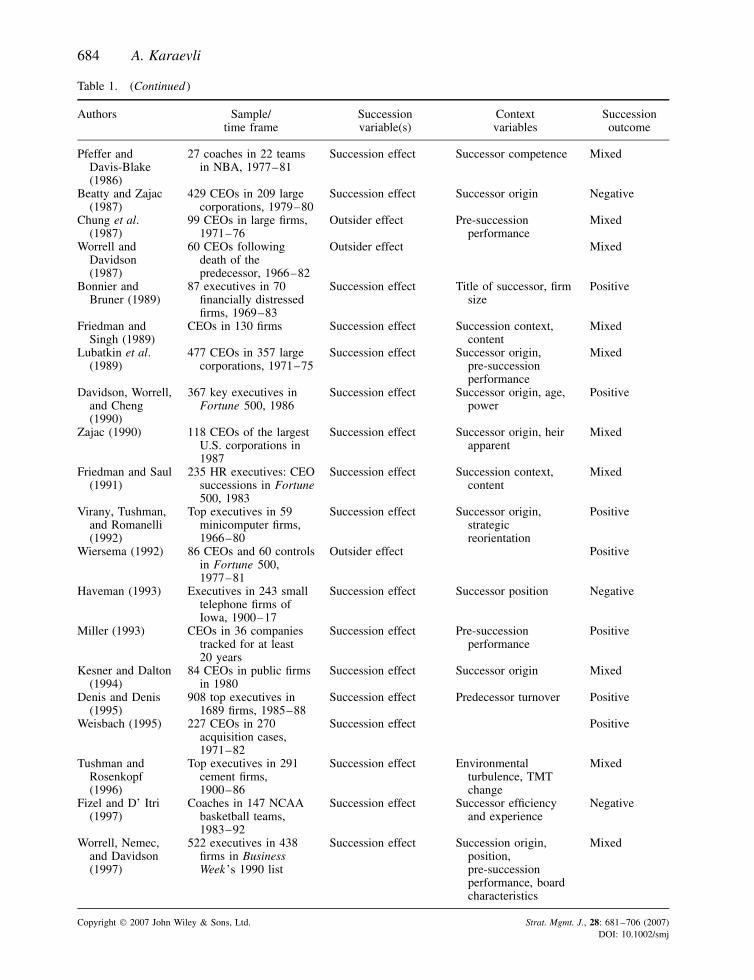

Table 1. Consequences of CEO successions: published empirical research (1954–2005)

Authors Sample/time frame

Successionvariable(s)

Contextvariables

Successionoutcome

Gouldner (1954) A plant manager in agypsum miningcorp.

Succession effect Successor actions Negative

Carlson (1961) 782 schoolsuperintendents,over 30 years

Outsider effect Positive

Trow (1961) Presidents in 108smallmanufacturingcompanies

Succession effect Heir apparent ornot

Mixed

Guest (1962) A plant manager in alarge automobileplant, 3 years

Succession effect Successor actions Positive

Grusky (1963) 135 coaches in 16baseball teams,1921–41; 1951–58

Succession frequency Negative

Gamson and Scotch(1964)

Managers in 22baseball teams,1954–61

Succession effect Not significant

Grusky (1964) Managers in 21baseball teams,1954–61

Outsider effect Negative

Eitzen and Yetman(1972)

657 coaches in 129NCAA basketballteams, 1930–70

Succession effect Successor tenure Not significant

Helmich and Brown(1972)

204 presidents in 208chemical firms,1959–69

Outsider effect Positive

Lieberson andO’Connor (1972)

Chairman/Presidentsin 167 largecorporations,1946–65

Succession effect Not significant

Helmich (1974) Presidents in 29manufacturingfirms, 1964–72

Outsider effect Positive

Allen, Panian, andLotz (1979)

283 coaches inbaseball teams,1920–73

Succession frequency,timing, type

Mixed

Brown (1982) Coaches in 26 NFLteams, 1970–1978

Succession andoutsider effects

Not significant

Carroll (1984) 662 publishers in2137 localnewspapers,1800–1975

Succession effect Control structure Negative

Smith, Carson, andAlexander (1984)

Ministers in UnitedMethodist Church,Ohio, 1961–80

Succession effect Not significant

Reinganum (1985) 842 Chair-man/Presidents in667 public firms,1978–79

Successioncharacteristics

Size, successororigin,predecessorcharacteristics

Mixed

Samuelson,Galbraith, andMcGuire (1985)

102 CEOs in 61corporations vs.controls, 1970–76

Succession effect Successor origin Mixed

(continued overleaf )

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

684 A. Karaevli

Table 1. (Continued )

Authors Sample/time frame

Successionvariable(s)

Contextvariables

Successionoutcome

Pfeffer andDavis-Blake(1986)

27 coaches in 22 teamsin NBA, 1977–81

Succession effect Successor competence Mixed

Beatty and Zajac(1987)

429 CEOs in 209 largecorporations, 1979–80

Succession effect Successor origin Negative

Chung et al.(1987)

99 CEOs in large firms,1971–76

Outsider effect Pre-successionperformance

Mixed

Worrell andDavidson(1987)

60 CEOs followingdeath of thepredecessor, 1966–82

Outsider effect Mixed

Bonnier andBruner (1989)

87 executives in 70financially distressedfirms, 1969–83

Succession effect Title of successor, firmsize

Positive

Friedman andSingh (1989)

CEOs in 130 firms Succession effect Succession context,content

Mixed

Lubatkin et al.(1989)

477 CEOs in 357 largecorporations, 1971–75

Succession effect Successor origin,pre-successionperformance

Mixed

Davidson, Worrell,and Cheng(1990)

367 key executives inFortune 500, 1986

Succession effect Successor origin, age,power

Positive

Zajac (1990) 118 CEOs of the largestU.S. corporations in1987

Succession effect Successor origin, heirapparent

Mixed

Friedman and Saul(1991)

235 HR executives: CEOsuccessions in Fortune500, 1983

Succession effect Succession context,content

Mixed

Virany, Tushman,and Romanelli(1992)

Top executives in 59minicomputer firms,1966–80

Succession effect Successor origin,strategicreorientation

Positive

Wiersema (1992) 86 CEOs and 60 controlsin Fortune 500,1977–81

Outsider effect Positive

Haveman (1993) Executives in 243 smalltelephone firms ofIowa, 1900–17

Succession effect Successor position Negative

Miller (1993) CEOs in 36 companiestracked for at least20 years

Succession effect Pre-successionperformance

Positive

Kesner and Dalton(1994)

84 CEOs in public firmsin 1980

Succession effect Successor origin Mixed

Denis and Denis(1995)

908 top executives in1689 firms, 1985–88

Succession effect Predecessor turnover Positive

Weisbach (1995) 227 CEOs in 270acquisition cases,1971–82

Succession effect Positive

Tushman andRosenkopf(1996)

Top executives in 291cement firms,1900–86

Succession effect Environmentalturbulence, TMTchange

Mixed

Fizel and D’ Itri(1997)

Coaches in 147 NCAAbasketball teams,1983–92

Succession effect Successor efficiencyand experience

Negative

Worrell, Nemec,and Davidson(1997)

522 executives in 438firms in BusinessWeek ’s 1990 list

Succession effect Succession origin,position,pre-successionperformance, boardcharacteristics

Mixed

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 685

Table 1. (Continued )

Authors Sample/time frame

Successionvariable(s)

Contextvariables

Successionoutcome

Datta andRajagopalan(1998)

134 CEOs inmanufacturing firms,1977–87

Successorcharacteristics

Industry characteristics,pre-successionperformance

Not significant

Lauterbach, Vu,and Weisberg(1999)

165 top managers inpublic firms, 1989–91

Outsider effect Positive

Sakano and Lewin(1999)

CEOs in 81 Japanesecompanies, 1988–93

Succession andoutsider effects

Governance structures Not significant

Smith andAmoako-Adu(1999)

124 managers inCanadian family firms,1962–96

Successorcharacteristics

Mixed

Boyne, Ashworth,and Powell(2001)

CEOs in 402 Englishlocal authorities,1981–96

Succession effect Not significant

Davidson, Nemec,and Worrell(2001)

421 CEOs in 332 firmsin Business Week ’s1992 list

Succession effect Heir apparent Mixed

Bigley andWiersema(2002)

61 CEOs in firms inForbes 500 list,1990–94

Heir apparent Mixed

Davidson et al.(2002)

55 outsiders in largefirms, 1982–92

Outsider effect Relatedness of industryorigin of successor

Mixed

Shen and Cannella(2002)

228 CEOs in 300 publicorganizations,1988–94

Successor type TMT turnover Mixed

Bailey and Helfat(2003)

36 external CEOs inlarge public firms,1978–87

Outsider effect Relatedness of industryorigin of successor

Not significant

Shen and Cannella(2003)

193 CEOs in largecorporations, 1988–97

Succession effect Heir apparent exit andpromotion,succession origin

Mixed

Davidson et al.(2004)

173 duality-creatingsuccessions in publicfirms, 1982–92

Succession effect Successor duality,pre-successionperformance

Mixed

Haveman andKhaire (2004)

Successions in early U.S.magazine industry,1741–1860

Succession effect Successorcharacteristics (role,ideology, affiliation)

Negative

Huson, Malatesta,and Parrino(2004)

1344 CEOs at largefirms, 1971–94

Succession effect Successor, firm, andpredecessorcharacteristics

Positive

Zhang andRajagopalan(2004)

204 CEOs innondiversified firms,1993–98

Succession type Pre-successionperformance;environmental andstrategic instability

Mixed

The concept of new CEO outsiderness offeredhere strives to be a significant improvement on pre-vious constructs of successor origin (the insider/outsider dichotomy and the outsiderness contin-uum of Finkelstein and Hambrick, 1996). First,previous constructs take an executive’s ‘currentfirm membership’ as the basis of theoretical cat-egorization of new CEOs as insiders and out-siders. This may add to conceptual confusion by

possibly conveying an impression that outsider-ness is a reflection of someone’s in- or out-groupmembership, rather than the extent of changein important leadership characteristics, such asleadership style, knowledge, skills, and perspec-tive.2 Second, previous constructs do not make

2 This also creates problems in measurement. For example, a newCEO who has 3 years of tenure with the firm, but who had spent

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

686 A. Karaevli

a theoretical distinction between the extent towhich a board of directors signals change withthe selection of an outsider and that of changea firm achieves based on a new CEO’s previousexperiences. This may have greatly contributed totheoretical confusion and empirical inconsistencyregarding the outcomes of insider vs. outsider suc-cession. More recent research indeed suggests thatinside successions do not always reflect a boardof directors’ intent to maintain strategic direction(Shen and Cannella, 2002), and outside succes-sions do not necessarily signal changes because ofa myriad of sociopolitical forces and institutional-ization processes within organizations (Zajac andWestphal, 1996) as well as in external labor mar-kets (Khurana, 2002). Therefore, drawing upon thetheoretical salience of executives’ firm and indus-try tenure for their leadership style, knowledge,skills, and perspective, and therefore for firms’strategic inertia or change, the outsiderness con-ceptualization offered here mainly builds on theupper echelon theory by attempting to capture theconsequences of change in important leadershipcharacteristics rather than the internal and exter-nal ‘signaling’ effects of inside vs. outside succes-sion.

In addition, after reviewing five decades ofempirical research on executive successions (seeTable 1) and vast amounts of research on topmanagement teams (TMTs), I model and simul-taneously test the most theoretically salient fac-tors of the pre- and post-succession contexts thataffect the performance consequences of new CEOoutsiderness. Building on the strategic leader-ship, and organizational learning and change lit-erature, the main thesis of this paper is thatnew CEO outsiderness will have—by itself—nodirect effect on post-succession firm performance.Rather, I suggest that the performance effects ofnew CEO outsiderness are contingent on the turbu-lence and the munificence of the external environ-ment, pre-succession firm performance, and con-comitant changes in strategy and senior executiveteam that take place during early years of the newCEO’s tenure.

all of his or her career in a very different industry before joiningthe firm 3 years ago, would be coded as less of an outsider thana new CEO who was hired directly from outside the firm, butwho had been working in the focal firm’s industry for decades.

THEORETICAL BACKGROUND

Top executives and firm performance

Given its emphasis on CEOs’ demographic char-acteristics, investigation of the implications of newCEO outsiderness for the firm is a natural progres-sion in the extant research on TMTs. According toresearch tradition inspired by the upper echelontheory of Hambrick and Mason (1984), exec-utives’ demographic characteristics significantlyaffect strategic decision making and organizationaloutcomes. While one stream of TMT research hasfocused on the ‘team’ level of analysis in investi-gating the organizational implications of executivebackgrounds (e.g., TMT demographic heterogene-ity), the other research stream has focused on theoutcomes of change in key leadership, mostly thechange in CEO position.

The selection of a new CEO has been widelythought to be a critical decision that influences afirm’s future direction and effectiveness. The ori-gins of succession research go back to two earlycase studies, which yielded contrasting outcomeson succession events (Gouldner, 1954; Guest,1962). There have been at least 50 other pub-lished empirical studies on the firm consequencesof top executive successions (see Table 1). How-ever, as Table 1 suggests, mixed findings on theperformance implications of succession events inthose studies have led scholars to move from theunpromising question of whether executive succes-sion helps or hurts firm performance to investigatethe effects of succession context, in other words,under what circumstances succession benefits ordisrupts firm performance (Finkelstein and Ham-brick, 1996: 164).

This latter group of succession research hasidentified successor origin as an important compo-nent of the succession context, which has signif-icant implications for organizational performance.These theories have predicted that outsiders wouldbe selected when organizations perform poorlyand need a strategic change, and insiders wouldbe selected when organizations desire continu-ity (Boeker, 1997; Boeker and Goodstein, 1993;Brady and Helmich, 1984; Zajac, 1990). However,the performance consequences of new CEO originhave also been characterized by mixed results. Asdiscussed earlier, the lack of consistency in whatthe insider vs. outsider CEO dichotomy captures

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 687

may have greatly contributed to the mixed find-ings on the performance consequences of successororigin reported throughout the research (Kesnerand Sebora, 1994: 356). To overcome this issue,the next section seeks to spell out the implica-tions of the underlying construct of the insider vs.outsider CEO with the concept of new CEO out-siderness.

New CEO outsiderness and post-successionperformance

Advantages of new CEO outsiderness

Both resource dependence (Pfeffer and Salancik,1978) and upper echelon (Hambrick and Mason,1984) perspectives highlight the advantages of hir-ing a CEO from outside the firm and the indus-try. The resource-dependence theory-based adap-tive view advocates the replacement of top man-agers with those hired from outside the firm asa remedy for organizational difficulties, such aspoor performance (Boeker and Goodstein, 1993;Datta and Guthrie, 1994; Helmich and Brown,1972; Kosnik, 1987) and resistance to change inresponse to shifting environmental demands (Pfef-fer and Salancik, 1978; Thompson, 1967; Virany,Tushman, and Romanelli, 1992).

The upper echelon perspective has identifiedexecutives’ firm and industry tenure as two of themost prominent sources of strategic inertia in thefirm. According to the upper echelon perspective,tenure in the organization is the most salient char-acteristic of a new CEO’s insiderness to that firm(Finkelstein and Hambrick, 1996). Research sug-gests that because of socialization processes insidethe firm, long-tenured executives are more likely tohave narrow perspectives, psychological commit-ments to the status quo (Hambrick, Geletkanycz,and Fredrickson, 1993; March and March, 1977;Katz, 1982), and a declined amount and qualityof information processing (Finkelstein and Ham-brick, 1996; Tushman and Romanelli, 1985). Fur-thermore, due to their psychological commitmentto the status quo and entrenched social relation-ships within firms, executives with long organiza-tional tenure tend not to make necessary changesin their organizations (Finkelstein and Hambrick,1990; Gabarro, 1987; Wiersema and Bantel, 1993).Another source of an executive’s commitment tothe status quo has been identified as his or her longtenure in the industry (Hambrick et al., 1993). Sig-nificant homogeneity of perceptions exists within

industries (Spender, 1989), and therefore execu-tives’ long industry tenure results in a social con-struction of reality and difficulty in conceivingalternative logics (Sutcliffe and Huber, 1998). Inother words, a CEO’s industry background influ-ences his or her cognitive representations (Prahaladand Bettis, 1986) and choice of strategy (Gunzand Jalland, 1996), and therefore industry tenureof a new CEO is expected to affect firm perfor-mance.

Based on all of the theoretical discussions ofFinkelstein and Hambrick (1996: 184) on thebenefits of new CEO outsiderness, and previousempirical research inspired by the upper eche-lon perspective (e.g., Hambrick et al., 1993), as anew CEO’s outsiderness increases, the new CEObecomes more cognitively open-minded, less com-mitted to the status quo, and better able to see newcourses of actions. Furthermore, such CEOs willbe less hesitant to make major changes, since theyare less likely to be socially connected to inter-nal executives and are less committed to currentstrategic direction. However, despite all of theseadvantages of new CEO outsiderness, there areforces that may prevent firms from benefiting fromnew CEO outsiderness. These are described in thefollowing section.

Disadvantages of new CEO outsiderness

According to the ‘continuity’ view of successions,the main goal of succession is to ensure lead-ership continuity in the organization. This viewfocuses attention on succession from within theorganization, highlighting the importance of insid-ers’ greater knowledge of the firm and estab-lished networks for achieving continuity (Lauter-bach, Vu, and Weisberg, 1999). At the sametime, the economic rents of human capital (Bai-ley and Helfat, 2003) and upper echelon (e.g.,Shen and Cannella, 2002) perspectives identifyseveral disadvantages of hiring CEOs from out-side the firm and the industry. For instance, asa new CEO’s outsiderness increases, it is morelikely that he or she will lack critical firm- andindustry-specific skills. Since outsider CEOs aremore likely to be hired under poor performance cir-cumstances, when their lack of firm and industry-specific skills combines with pressure from theboard of directors to turn performance around,such CEOs are more likely to take premature

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

688 A. Karaevli

actions rather than make well-formulated, appro-priate changes in strategy, structure, and internalprocesses (Gabarro, 1987).

Furthermore, there is often more uncertaintyregarding an external candidate’s skills and person-ality traits, and whether he or she fits well with theculture of an organization and the strategic needsof the firm. A board of directors usually inter-acts with an insider candidate on many occasions,and therefore has a chance to observe his or herbehavior and personality traits under different cir-cumstances. On the other hand, boards usually facegreater difficulties in acquiring this type of diverseinformation about external candidates (Harris andHelfat, 1997). This may result in an adverse selec-tion, in that the successor may not be the rightperson for the strategic demands facing the firm(Zajac, 1990). The risk of adverse selection willprobably be higher in cases of more outsider CEOselections, because a board of directors does notusually have a large amount of information aboutthe best-managed firms in a different industry,although they usually have that benchmark infor-mation about the firms in their own industry (Bai-ley and Helfat, 2003). Therefore, these combinedinformation asymmetries negatively influence aboard’s ability to effectively assess the fit betweenmore outsider candidates and the needs of thefirm.

Lastly, current senior executives who wereappointed by the predecessor CEO often have anegative attitude toward the selection of some-one from outside the firm, and they tend to eitherleave the firm or resist the significant changesinitiated by the new CEO (Helmich and Brown,1972; Shen and Cannella, 2002). If the new CEOis hired from outside the industry, the importanceof an experienced and supportive team is evenhigher until the new CEO gets to know the firm’sbusiness and competitive environment. Hence, allof these factors work against the potential bene-fits that successor outsiderness brings to a firm inthe early years of the new CEO’s tenure. There-fore, based on these discussions of the advan-tages and the disadvantages associated with newCEO outsiderness, when a new CEO is selectedit is hard to predict the direction of the maineffect of his or her outsiderness on post-successionfirm performance (controlling for the environmen-tal and performance contexts in which he or she isselected).

Hypothesis 1: Controlling for the environmen-tal and performance contexts in which a newCEO is selected, new CEO outsiderness will notbe significantly associated with post-successionfirm performance.

MODERATING INFLUENCES

One productive strategy to solve the theoreti-cal indeterminacy on the effects of new CEOoutsiderness is to specify the conditions underwhich successor outsiderness will have its differenteffects. As Table 1 presents, in the evolution ofempirical succession research, several studies haveattempted to use the same strategy by using contin-gency variables on the effects of succession eitherat the individual (successor origin and character-istics), team (TMT change), organizational (size,pre-succession firm performance, strategic reori-entation), or environmental (environmental turbu-lence, industry characteristics) level. Therefore,it is understood from Table 1 that the condi-tions under which a successor is selected (pre-succession context) and the successor’s actions,in other words, what happened after the succes-sion (post-succession context), are both importantin terms of the consequences of succession eventand successor origin. However, no studies havemodeled and tested a comprehensive and nuancedframework that includes the most theoreticallysalient factors of pre- and post-succession contextssimultaneously. Building on the prior research onCEO successions, TMTs, and organizational learn-ing and adaptation, as the following sections aim toexplain in detail, such a complete theoretical con-ceptualization is necessary to make more accuratepredictions on the effects of new CEO outsider-ness.

Pre-succession context

External environment

Previous theory has identified CEO succession asa key adaptation mechanism in response to shift-ing environmental demands (Pfeffer and Salan-cik, 1978; Tushman and Romanelli, 1985). How-ever, the implications of the specifics of theseenvironmental changes for the performance con-sequences of succession events and successor ori-gin remain unknown (Finkelstein and Hambrick,

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 689

1996). Environments can be characterized alongseveral dimensions. In this study I focus on theirdegree of turbulence or stability, and munificence,since these are directly associated with uncertainty,which is important for the strategic decision-making process (Dess and Beard, 1984). Earlierresearch has also identified their effects on the firmoutcomes of top executive characteristics (e.g.,Haleblian and Finkelstein, 1993).

Turbulence refers to instability, or difficult-to-predict changes in the environment (Aldrich, 1979;Dess and Beard, 1984; Wholey and Brittain, 1989).Relatively speaking, in stable industries where thegrowth rate is typically low and product or ser-vice demand is quite predictable, the dominantrole of leadership is to maintain values, culture,and the current strategic direction (Pfeffer, 1981;Tushman and Romanelli, 1985). In stable environ-ments, top managers’ information and decision-making requirements are more ‘standardized androutine’ (Kotter, 1982: 29), and problem solv-ing is more systematic (Eisenhardt, 1989). Hence,the exploitation of established capabilities that areassociated with firm and industry-specific knowl-edge is valued (Finkelstein and Hambrick, 1996;March, 1991).

As the rate of turbulence increases, the impor-tance of exploration capability also increases(McGrath, 2001). In turbulent environments, man-agers need a wide range of multidimensional capa-bilities (Volberda, 1996) and abilities to envisionand implement a broad range of strategic options(Carpenter and Westphal, 2001). Turbulent envi-ronments are also characterized by frequent envi-ronmental shifts, or discontinuities, which require‘second-order learning’ (March, 1991), associatedwith an ability to make fundamental changes inorganizational strategy, structure, and processes(Virany et al., 1992). Norburn and Birley (1988)indeed found that executives’ firm tenures werepositively associated with firm performance in sta-ble industries but negatively associated with firmperformance in turbulent industries.

For instance, in the turbulent U.S. airline indus-try, very different CEO choices of Delta andUnited Airlines in the late 1990s resulted invery different performance outcomes. In mid-1997Delta Airlines chose Leo Mullin, a former bankerand electric utility executive who had no previ-ous airline experience. Substantial improvementsin employee morale and company performancewere observed at Delta Airlines within a 3-year

performance window after Mullin took the helm ofthe company (Bond, 2003). On the other hand, atUnited Airlines, the unions’ choice, Jim Goodwin,who was a 32-year-veteran of the company, wonthe race to become the new CEO against the othertop candidate, Louis Hughes, an outsider exec-utive from General Motors Company. AlthoughGoodwin had extensive firm and industry-specificknowledge, company performance continued todeteriorate in the turbulent context of the airlineindustry, and Goodwin had to resign only 2 yearsafter he took over as CEO. Given these discus-sions, the following hypothesis is suggested:

Hypothesis 2: New CEO outsiderness will bemore positively associated with post-successionfirm performance in turbulent environments thanin stable environments.

Based on the premises of the adaptive view oforganizations and the upper echelons theory, themunificence of the external environment also influ-ences CEO succession outcomes. Environmentalmunificence refers to the ability or capacity ofthe environment to permit organizational growth(Aldrich, 1979; Dess and Beard, 1984). Munificentenvironments help organizations buffer themselvesfrom external threats and enable them to accumu-late slack resources (Aldrich, 1979; Finkelstein andHambrick, 1996). Therefore, top managers have awider breadth of options, and greater discretion,or latitude of action, in making strategic choices(Hambrick and Finkelstein, 1987). Furthermore,in munificent environments firms are expected tomaintain or expand their market share under con-ditions of strong competitive forces. This requirestop executives to take risks in entrepreneurial deci-sion making (Palmer and Wiseman, 1999). Forinstance, Motorola, a large telecom equipmentmaker, was no longer a market leader in manyof its biggest business segments in late 2003. Thecompany was losing market share particularly inits cell phone business, which accounted for abouthalf of the company’s revenues, when the boardof directors decided to hire Ed Zadner, who wasa longtime computer industry executive, from SunMicrosystems. About one and a half years afterZadner took over as CEO, Motorola has gainedsignificant market share in its cell phone business,and the net income of the company jumped 14percent (Rhoads, 2005).

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

690 A. Karaevli

On the other hand, under conditions of con-straining forces in less munificent environments,top managers do not usually have a high degree ofcontrol over firm outcomes (Hambrick and Finkel-stein, 1987). Therefore, environmental and orga-nizational contexts have a greater effect on firmperformance than does executive leadership (Hale-blian and Finkelstein, 1993). Based on these dis-cussions, the following hypothesis is suggested:

Hypothesis 3: New CEO outsiderness will bemore positively associated with post-successionfirm performance in munificent environmentsthan in less munificent environments.

Firm performance

Among the factors triggering the succession eventand the selection of an outsider CEO, poor pre-succession firm performance has probably receivedthe most attention (e.g., Boeker and Goodstein,1993; Datta and Guthrie, 1994; Helmich andBrown, 1972; Kosnik, 1987). While there is abun-dant empirical evidence supporting the greaterlikelihood of outsiders being selected in the poorfirm performance context, the post-succession per-formance consequences of outsider successions,which occurred under poor performance condi-tions, are less clear (Finkelstein and Hambrick,1996).

Research implies that poor performance acts asa catalyst to organizational adaptation by signalingthat the existing way of operating is inappropri-ate and that leadership needs to achieve a moresuccessful alignment with the external environ-ment (Boeker and Goodstein, 1993; Tushman andRomanelli, 1985). If a firm’s performance is con-sistently declining, incremental changes to existingoperating procedures will probably not be suffi-cient; indeed, reinforcement of the status quo ismore likely to exacerbate the performance decline(D’Aveni, 1989; Tushman and Rosenkopf, 1996).The experiences of Leo Mullin and Jim Goodwin,which were described earlier, illustrate this point aswell. Both Mullin and Goodwin were hired whentheir respective firms were suffering from poorfirm performance conditions. Although an outsiderto both the firm and the airline industry when hebecame CEO of Delta Airlines, Leo Mullin wasable to turn around Delta’s performance in thelate 1990s. Jim Goodwin’s experience during the

same time period, however, was markedly differ-ent. Goodwin had risen through the ranks at UnitedAirlines and was thus both a firm and airline indus-try veteran when becoming CEO of United Air-lines, yet during his tenure United Airlines’ perfor-mance continued to deteriorate rapidly. Therefore,under poor firm performance conditions, more out-sider successors who can initiate major changes inthe firm and alter standards of performance fortheir team are more likely to turn performancearound. Poor pre-succession firm performance isalso likely to make it easier for the new outsiderCEO to overcome resistance to his or her changeinitiatives (Boeker, 1997). Given these arguments,the following hypothesis is suggested:

Hypothesis 4: New CEO outsiderness will bemore positively associated with post-successionfirm performance when pre-succession firm per-formance is low.

Post-succession context

Strategic change

Most research implies that changes in strategy,structure, and internal processes introduced by newoutsider CEOs mediate the relationship betweenthe succession and the subsequent performance. Itis beyond the scope of this study to investigate allof the changes, which follow a succession event.However, prior research regarding the performanceeffects of swift strategic changes following CEOsuccessions has been characterized by theoreticalindeterminacy and empirical inconsistency. Thismay have greatly contributed to the mixed find-ings on the outcomes of CEO succession eventsand successor origin. Therefore, it is important toclarify the role of swift strategic changes intro-duced by new external CEOs in post-successionperformance change.

Although theoretical advancement and empiricalevidence are both very limited, previous researchimplies that swift changes in important compo-nents of a firm’s strategy triggered by some CEOsuccessions may cause a decline in organizationalperformance (Friedman and Singh, 1989; Viranyet al., 1992). Some in-depth case studies in the1980s suggest that while facing pressure from theboard of directors to take quick actions, new out-sider CEOs are at risk of formulating and imple-menting inappropriate strategies (Gabarro, 1987;

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 691

Kotter, 1982). More recently, it has been discussedthat outsider CEOs’ increased likelihood of initiat-ing strategic changes does not necessarily implythat such changes improve post-succession per-formance (Zhang and Rajagopalan, 2004: 497).However, there has been no large-sample empir-ical study to directly test the implications of swiftpost-succession strategic changes initiated by out-sider CEOs for subsequent firm performance.

In the meantime, with the increasing rate of out-sider successions, this problem has gained momen-tum in the business environment and has recentlybeen identified by popular business media as out-sider CEOs’ ‘revolving door phenomenon’ (Lucieret al., 2003). The underlying idea is that new out-sider CEOs assume that they have a mandate fromthe board to initiate major changes in a shortperiod of time; otherwise their contract will mostlikely to be terminated. Because of this pressure,the changes they make can be more like quickfixes rather than real transformations. The qual-ity of these changes is questionable as well, sincesuch new CEOs usually lack cultural understand-ing, personal networks, and a deep knowledge ofthe firm’s internal and external environment to suc-cessfully formulate and implement major changesin early years of their tenure. In a sense, this is aparadox, since very often such CEOs are broughtin with the purpose of initiating massive changesin a relatively short amount of time.

Although it is beyond the scope of this paper toresolve this paradox, the contrasting approachesof Louis Gerstner at IBM and Carly Fiorina atHP in initiating swift strategic changes, whichwas explained earlier, suggests some useful hintsregarding the performance implications of swiftstrategic changes introduced by new outsider CEOs.Gerstner critically evaluated the existing policiesand strategies before making any attempt to changethem (Arnst, 1993). This approach not only gavehim the necessary time to gain expertise aboutseveral aspects of the firm and its business, butalso helped him gain the necessary power base,and social and political capital to make effec-tive massive changes a couple of years later. Onthe other hand, before she tried to get to knowHP inside out, Carly Fiorina turned immediatelyto the outside and started to work on the exte-rior image of the company by initiating severalswift changes (Lavelle, 2005). She made theseimmediate changes without getting the necessaryknowledge and sociopolitical support, which set

the ground for her forced turnover in early 2005(Rivlin and Markoff, 2005).

Therefore, although outsiders are selected whena transformation is most needed, swift changesin core dimensions of a firm’s strategic profilewhen initiated by new CEOs who are less familiarwith the firm’s internal operations and businessenvironment will likely hurt firm performance.Given these arguments, the following hypothesisis suggested:

Hypothesis 5: New CEO outsiderness in thepresence of fewer swift strategic changes will bemore positively associated with post-successionfirm performance than new CEO outsiderness inthe presence of more swift strategic changes.

Senior executive team change

Research tradition inspired by the upper echelontheory of Hambrick and Mason (1984) predictsthat it is not the CEO alone, but the whole exec-utive team, who influence strategic decision mak-ing and firm performance (e.g., Hambrick, Cho,and Chen, 1996; Shen and Cannella, 2002; Tush-man and Rosenkopf, 1996). Senior executive teamchange affects composition of the team (Wagner,Pfeffer, and O’Reilly, 1984) and team dynam-ics (Shen and Cannella, 2002). As a result, priorresearch concluded that ‘focusing on the CEO suc-cessor alone without considering other personnelchanges within top management can not fully andaccurately capture the performance consequencesof CEO succession’ (Shen and Cannella, 2002:728). However, the exact nature of the theoreti-cal and empirical relationships between CEO suc-cessions, post-succession senior executive teamchanges, and subsequent firm performance, has notbeen established clearly (Tushman and Rosenkopf,1996).

The degree of the senior executive team changeis not only important in terms of triggering dif-ferent modes of organizational learning (Tushmanand Rosenkopf, 1996; Virany et al., 1992), but it iscritical for enabling a new CEO to establish cred-ibility, and to gain the social and political supportrequired to make necessary changes (Helmich andBrown, 1972; Shen and Cannella, 2002). However,prior research has yielded inconsistent findingsregarding the performance effects of the degreeof senior executive team change following a CEOsuccession event. For example, while Tushman and

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

692 A. Karaevli

Rosenkopf (1996) found a negative effect, Kesnerand Dalton (1994) reported a curvilinear effect,and Virany et al. (1992) showed no direct effectof post-succession senior executive team changeon subsequent firm performance. The inconsistentfindings may have resulted from the fact that seniorexecutive team change has different causes andeffects in different succession contexts (e.g., Shenand Cannella, 2002). Empirical evidence is partic-ularly limited with regard to performance effectsof executive team changes following insider vs.outsider successions.

While Shen and Cannella (2002) found a nega-tive impact of senior executive team turnover afteran outside succession on subsequent performance,a majority of the previous research highlightsthe benefits of significant senior executive teamchanges following external CEO successions. Forinstance, as discussed earlier, current senior exec-utives who were appointed by the previous CEOoften have a negative attitude toward the selectionof an outsider, and resist the significant changesinitiated by the new CEO (Helmich and Brown,1972). Fondas and Wiersema (1997) also discussthat while newcomer CEOs’ interactions with old-timers in the executive team elicit a more statusquo definition of the right strategy, new CEOs’interactions with newly appointed team memberswill probably result in a more innovative response.Furthermore, empirical evidence suggests that thescope of executive team changes triggers differ-ent modes of learning within the organization:while CEO succession is associated with incre-mental changes, or first-order learning, sweepingexecutive team changes have been considered asa more fundamental source of change within theorganization, associated with second-order learn-ing (Tushman and Rosenkopf, 1996; Virany et al.,1992). Greater degrees of post-succession seniorexecutive team change result in decreased teamtenure and increased team heterogeneity. These arelikely to be associated with more open problemsolving, new communication networks, and newintra-group processes, which alter bases of com-petence and power within the team, and can helpthe team take substantive action (Tushman andRosenkopf, 1996).

If we go back to the comparative case of the Ger-stner and Fiorina successions, we see that a majordifference between Gerstner and Fiorina is in theirapproach toward their senior executive team. Lessthan 2 years after Gerstner took the CEO office at

IBM, he completed a major reshuffling in the TMTby replacing the previous management’s seniorexecutives with new ones whom Gerstner trustedand thought could deliver results (Hays, 1995). Onthe other hand, one of Fiorina’s major mistakes,which contributed to her dismissal, was identifiedas her

failure to bring with her a team of effective andloyal key subordinates. Without such a supportgroup from below, she laid herself open to havingher legs cut off by the hostile old guard that sheinherited (Bill Deibel, letter to the editor, WallStreet Journal, 15 February 2005).

Given these arguments, I suggest the followinghypothesis:

Hypothesis 6: New CEO outsiderness withgreater senior executive team change will bemore positively associated with post-successionfirm performance than new CEO outsidernesswith less senior executive team change.

METHOD

Sample and data sources

The population for this study is middle- andlarge-sized, publicly traded corporations, existingbetween the years 1972 and 2002, in the U.S. Air-line industry (SIC 4512) and the two branchesof the Chemical industry: Paints, Varnishes, Lac-quers, Enamels, and Allied products (SIC 2851),and Industrial Inorganic Chemicals (SIC 2819).The industries selected afford several contrasts andcomparisons in environmental context. This is nec-essary in order to assess the hypothesized differ-ences on the effects of environmental turbulenceand munificence, and to generalize the findingsof this study to different contexts. The industry-based sampling logic is also aimed at controllingfor as many industry-related potentially confound-ing factors as possible, enabling me to capture theeffects of environmental aspects that are of theo-retical interest in this study more adequately.3

3 During the study period, the airline industry has gone throughmajor structural changes. The Deregulation Act of Airlinersin 1978, which removed governmental control of routes andpricing, resulted in a proliferation of new players both at theregional and the national level. The competition grew fierce,and the industry witnessed a wave of mergers, acquisitions, and

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 693

The final sample includes all firms that reached$100 million in sales at any point between theyears 1972 and 2002 in the U.S. airline industry,and all firms whose primary business was paintor industrial inorganic chemicals in the chemi-cal industry for which data were available. Therelationship between organizational environment,executive characteristics, and firm outcomes canbe more directly assessed for nondiversified firms(Gupta, 1988). Therefore, by applying the defi-nition of Rumelt’s (1982) product-dominant cat-egory of firm strategy, in the chemical industryfirms that diversified into different industries wherethey derived, more than 30 percent of their saleswere dropped from the sample. Choosing primarilysingle-business firms has been a common prac-tice in previous succession research (e.g., Dattaand Rajagopalan, 1998; Zhang and Rajagopalan,2003). Accordingly, in the final sample there werea total of 90 firms, including 52 airline, 25 indus-trial inorganic chemicals, and 13 paint firms. Out

bankruptcies, which resulted in the consolidation of the industryby mid-1980. The jolts caused by the Gulf War in 1991 andthe attacks on 11 September 2001 were other major sourcesof turbulence and bankruptcies in the industry. While industryentries are related to growth rate or the level of munificencein an industry (Porter, 1980), industry exits are more affectedby uncertainty caused by turbulence (Anderson and Tushman,2001). Therefore, environmental turbulence and munificencemeasures, which have cross-industry applicability, also aim tocapture the effects of the structural changes that occurred in theairline industry.

More specifically, during the study period, from 1972 to2002, the U.S. airline industry had shorter periods of stabil-ity (i.e., before the deregulation in 1978) and longer periods ofturbulence caused by continuously high demand instability andunpredictability, competitive rivalry, and various discontinuouschanges, as compared to the U.S. industrial inorganic chemicalsindustry which had relatively longer periods of stability, andshorter periods of turbulence caused by technological innova-tions, demand instability, and unpredictability. Furthermore, themunificence of the environment was considered generally low inthe airline industry, except for short periods of high growth (e.g.,1979–85, and 1994–98). In the industrial inorganic chemicalsindustry the most munificent period was the early 1990s, wherethe annual growth jumped to 11 percent. Otherwise, the indus-try was considered as a moderately munificent context, wherethe average annual growth was about 4 percent. Throughout thewhole period, the U.S. paint industry was a relatively stable andmoderately munificent environment characterized by slow andsteady growth, with incremental process innovations.

The sources for the airline industry: Air Transport AssociationAnnual Reports, 1972–2002, Encyclopedia of American Indus-tries, various editions; Morrison and Winston (1995); Standardand Poor’s industry surveys; Value Line investment analyses.The sources for the chemical industry: Encyclopedia of Amer-ican Industries, various editions; Standard and Poor’s industrysurveys; Value Line investment analyses; see also Fredricksonand Iaquinto (1989) and Benner and Tushman (2002) for thepaint industry.

of data for 1436 firm-years (689 airline firm-years,747 chemical firm-years), 163 successions (106 inairline firms, and 57 in chemical firms) have beenobserved. Because of missing data, 15 airline andeight chemical observations were dropped from thedata. Therefore, the final sample included 140 suc-cession observations.

This study used secondary data from publishedand Web-based resources. The information onCEO successions and biographies and from seniorexecutive team lists was gathered from Standard& Poor’s Register of Corporations, Directors, andExecutives, Dun & Bradstreet’s Reference Book ofCorporate Managements, Who’s Who in Financeand Industry, Wall Street’s CEO change announce-ments, and corporate annual reports. The datafor computing strategic change, environmental tur-bulence and munificence, firm operational andmarket-based performance indicators, and firm sizewere collected from COMPUSTAT and severalpublished sources, such as the U.S. Industry Out-look and the U.S. Census of Manufacturers. Addi-tional airline firm performance measures were col-lected from the annual reports of the Air TransportAssociation.

Measures

Dependent variable

Post-succession firm performance change wasmeasured as a composite measure by summingthe standardized (Z-score) change in a firm’stwo operational performance indicators—industry-adjusted return on assets (ROA) and industry-adjusted return on sales (ROS)—and a market-based performance indicator—industry-adjustedtotal shareholder return (TSR)—from the time ofsuccession until 3 years later. The performanceimplications of executive successions have beenstudied by using both market (e.g., Beatty andZajac, 1987; Friedman and Singh, 1989; Daily,Certo, and Dalton, 2000) and accounting (e.g.Datta and Rajagopalan, 1998; Shen and Cannella,2002) indicators. This study combines the two,since assessing performance with a multidimen-sional measure has generally been considered asmore desirable in strategic management research,particularly when firms in the sample are gen-erally undiversified (Venkatraman and Ramanu-jam, 1986). A similar composite firm performancemeasure, the sum of the standardized (Z-score)

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

694 A. Karaevli

ROA and TSR, has also been used in previ-ous succession research (e.g., Zajac and Westphal,1996). Additional analyses were also conductedwith changes in adjusted accounting (combinedstandardized ROA and ROS) and market-based(TSR) measures as separate dependent variables(and with pre-succession adjusted accounting-basedand market-based measures as separate control andmoderating variables in respective analyses). Thefindings of these additional analyses are reportedas a footnote at the end of the Results section.

A 3-year time frame in firm performance hasbeen widely used in previous succession research(e.g., Datta and Rajagopalan, 1998; Shen and Can-nella, 2002). Furthermore, Datta and Rajagopalan(1998) argue that ‘the change in performance canbe more directly related to the succession event;in contrast, absolute measures of post successionperformance are more likely to reflect enduringperformance effects carried over from the pre-succession period’ (p. 843). Therefore, I used thechange in composite firm performance rather thanthe absolute measure of composite firm perfor-mance as the dependent variable.

Independent variable

The new CEO outsiderness is operationally definedas a continuum ranging from new CEOs who havea greater combination of firm and industry tenureto those who have no experience in the firm and theindustry, and was measured as an index variable bysumming the inversed standardized (Z-score) firmand industry tenure of the new CEO. As discussedin the Theory section, although firm and indus-try tenure have both been identified as importantsources of executives’ psychological commitmentto the status quo and consequential strategic per-sistence (Hambrick et al., 1993), the concept ofsuccessor origin puts heavier weight on firm expe-rience for a new CEO’s ‘insiderness’ (Finkelsteinand Hambrick, 1996). Therefore, in order to beable to capture the underlying construct of succes-sor origin, firm tenure carries more weight in theoutsiderness measure that I offer in this paper aswell. For example, a new CEO who has a 10-yearindustry tenure, but has no firm tenure, is twice asmuch an outsider as another new CEO who has a10-year firm tenure, and has no additional indus-try tenure (since in the latter case the new CEOis regarded as having a 10-year industry tenure

as well). The standardization of firm and industrytenure also normalizes the distribution.4

Moderating variables

Environmental turbulence was measured by thevolatility of demand across time, by regressing avariable for each year (time) on a variable for rev-enue per available seat miles in the airline indus-try, and for value of shipments in the chemicalindustry. Five years of data were used for eachequation (for instance, revenue from 1994 to 1998was used to predict dynamism in 1999). Follow-ing the equation yt = b0 + b1t + at , where y is therevenue per available seat miles or value of ship-ments, t is year, and a is the residual, the volatilityof demand across time measure is the standarderror of the regression slope coefficient divided bythe mean value of the dependent variable (e.g.,Carpenter and Fredrickson, 2001). Environmen-tal munificence was measured by using the sameregression model, where munificence is the regres-sion slope coefficient divided by the mean value ofthe dependent variable, indicating a growth-basedmeasure (e.g., Boyd, 1995; Palmer and Wiseman,1999; Wiersema and Bantel, 1993).5

4 As a robustness check of my outsiderness measure, I alsotested the hypotheses by using the ‘outsiderness’ measure offeredby Finkelstein and Hambrick (1996: 185), where I measurednew CEO outsiderness on a seven-point ordinal scale, rangingfrom extreme insiders (long firm tenure category) to extremeoutsiders (a new hire from unrelated industry). The results ofthe hypotheses testing were very similar, with a reduction in theR2 of the models.5 To address the reviewer suggestion for a robustness check onthe effects of external environment, I also investigated the impli-cations of industry structure for the new CEO outsiderness–post-succession performance relationship. Based on previous research(e.g., Porter, 1980), industry concentration is an important aspectof industry structure. However, researchers (e.g., Datta andRajagopalan, 1998) have also discussed the ambiguity of the the-oretical effects of industry concentration on competition. First,it has been discussed that a lower level of concentration isrelated to higher uncertainty and a greater range of competitiveactions (e.g., Hambrick and Finkelstein, 1987). Therefore, newCEO outsiderness is expected to be more positively associatedwith post-succession performance in lower levels of industryconcentration. Secondly, based on Pfeffer and Salancik (1978),competitive uncertainty is highest at intermediate concentrationlevels. According to this rationale, there is relatively little scopefor managerial discretion at very low and very high levels ofconcentration. Therefore, new CEO outsiderness is expected tobe more positively associated with post-succession performanceat the intermediate levels of industry concentration. I measuredindustry concentration by two alternative established measures:the market share of four largest firms, and the Gibbs–Martinindex (the inverse of the Herfindahl index). The coefficients ofthe interaction effects of the new CEO outsiderness with any

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 695

To measure pre-succession firm performance,I constructed a composite measure by summingthe standardized (Z-score) average growth (ordecline) in a firm’s industry-adjusted ROA, ROS,and TSR for 2 years before the succession eventoccurred. The main effect of pre-succession firmperformance also served to control the potentialthreat of ‘regression-to-the-mean’ effect (Brown,1982; Shen and Cannella, 2002; Tushman andRosenkopf, 1996), and therefore, it was includedas a control variable.

Treating t as the year succession occurred, thepost-succession strategic change was defined asthe extent to which a firm’s strategy changes fromthe last year of the previous CEO’s tenure (t − 1)to the end of the year that follows the successionyear (t + 1). The composite strategic change mea-sure that I used is a variation of Finkelstein andHambrick’s (1990) strategic persistence measure.First, I used six strategic indicators used by Finkel-stein and Hambrick (1990) to create a compositemeasure of strategic change. Those indicators wereadvertising intensity (advertising/sales), researchand development intensity (R&D/sales),6 plant andequipment newness (net P&E/gross P&E), nonpro-duction overhead (SGA expenses/sales), inventorylevels (inventories/sales), and financial leverage(debt/equity) (for a detailed explanation of the jus-tification behind using these six indicators, seeFinkelstein and Hambrick, 1990: 491). The com-posite strategic change measure was calculated asfollows: the firm’s three year (for t − 1 throught + 1, inclusive) variance �(xi − X)2/(n − 1) foreach strategic dimension was computed. Next, theindustry average variance was subtracted from thefirm’s variance score for each dimension in orderto control industry effects.7 Finally, the industry-adjusted variance scores for each of the six indi-cators were summed to yield an overall strategicchange measure.

of the industry concentration measure (the market share of fourlargest firms, Gibbs–Martin index, and square-Herfindahl index)were all nonsignificant, and did not affect the other results pre-sented in the paper.6 Since R&D expenditures were almost nonexistent in the airlineindustry, I used the acquisition/sales ratio as a replacement toR&D intensity. Acquisitions have been identified as an importantdimension of a firm’s strategy in the airline industry (Morrisonand Winston, 1995).7 Instead of Finkelstein and Hambrick’s (1990) practice of cod-ing changes that are above industry average as 1 and the othersas 0, I used the actual value of the industry-adjusted changescore. The ratios that were above 1 (they were very rare) werecoded as 1.

The senior executive team is defined here as allexecutives who report directly to the CEO (thus theCEO is not included in the count of senior execu-tive team). This operationalization has been widelyused in prior studies of TMT (e.g., Keck and Tush-man, 1993; Tushman and Rosenkopf, 1996). Fol-lowing the practice of Tushman and Rosenkopf(1996), taking t as the year of the CEO succession,I measured the post-succession senior executiveteam change as follows. First, the percentage ofentering executives was calculated by counting thenumber of executives per firm who were not onthe team the last year the predecessor held office(t − 1) but on the team the following two years(t , and t + 1), and dividing this number by teamsize. The percentage of exiting executives was cal-culated by counting the number of executives whowere listed the last year the predecessor held office(t − 1) but not in the following 2 years the suc-cessor started to hold office (t , and t + 1), anddividing this number by team size. As an indica-tion of the overall percentage of change in teams, Iaveraged the percentages of team entries and exitsfollowing the CEO succession.

Control variables

Previous research on executive successions hasconsistently identified the role of organizationalage and size on firm performance (e.g., Haleblianand Finkelstein, 1993; Tushman and Rosenkopf,1996). Therefore, organization age, measured asthe number of years since the firm’s founding,and organizational size, measured as the loga-rithm of the number of employees (and the log-arithm of sales, alternatively) were controlled.Furthermore, there are certain CEO-level demo-graphic variables that might confound the effectsof new CEO outsiderness on subsequent firm per-formance. Therefore, a successor CEO’s age, edu-cational background, and functional backgroundwere controlled. Age was measured as the num-ber of years from birth to the year of succes-sion. Educational background was measured bya seven-point ordinal scale adopted from Finkel-stein (1988): (1) High school; (2) Some college;(3) Undergraduate degree; (4) Some graduateschool; (5) Masters degree; (6) Attended doctoralprogram; and (7) Doctorate degree. Functionalbackground (longest tenure in a functional areain a person’s employment history) category was

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

696 A. Karaevli

adopted from Ocasio and Kim (1999). Accord-ingly, I used five categories of the functionalbackground of CEOs: (a) production and techni-cal (manufacturing, engineering, and R&D); (b)marketing and sales; (c) finance; (d) legal; (e)operations and other. Results did not change signif-icantly when I used Hambrick and Mason’s (1984)categorization, where core functional areas aredefined by output (marketing and sales), through-put (operations, R&D, and engineering), andperipheral (law, finance, and accounting) func-tions. Several other control variables were includedin equations predicting the succession event; thesevariables are described in the following section.

Analysis

Since a succession event is more likely to occurin more poorly performing firms, it is necessary tocorrect for selection bias in analyzing the changein post-succession firm performance. Therefore,I used the Heckman selection model (Heckman,1979), which is a two-staged procedure that cor-rects for selection bias in regression analysis (for amore detailed explanation of the Heckman selec-tion model, see Zajac and Westphal, 1996: 72).Specifically, I first estimated the likelihood of suc-cession with a discrete-time event history modelfor the full sample (N = 1436). I then incorpo-rated the parameter for the likelihood of successionevent from that model to a second-stage ordinary-least-squares (OLS) hierarchical regression modelto predict the performance change for those firmsexperiencing succession events. Although the coef-ficients from discrete-time event history model arenot displayed in this paper, it took the followingform:

Successiont = a + b1roa + b2tsr + b3volatility

+ b4 log(sales) + b5independent directors

+ b6boardsize + b7separate CEO/board chair

+ b8length prior interval + b9time since last event

+ b10number of prior events + [b11industry

dummies] + [b12year dummies] + e

(independent variables were lagged 1 year as inZajac and Westphal, 1996).

I controlled for industry by including two indus-try dummy variables in the full model, and a cate-gorical variable with three values in the second

model (because of the smaller sample size anddegrees of freedom in my second model, I useddifferent operationalizations of the time and indus-try control variables). To ensure that results werenot affected by unspecified, time-specific factors, Iincluded dummy variables for the first 30 years inthe first model, and a single categorical time vari-able in the second model (Allison, 1984). Further-more, given that firms were at risk of successionduring the study’s time period, it was necessaryto minimize the consequences of potentially vio-lating the assumption of the independence of afirm’s likelihood of succession in a given yearfrom its prior event history (Allison, 1984; Yam-aguchi, 1991). Therefore, I included three controlvariables in the first model suggested by Allison(1984) for repeated event models, which have beenused in previous succession research (e.g., ZajacWestphal, 1996): (1) the length of the prior intervalbetween successions, measured in years; (2) thelength of the time since the prior succession, mea-sured in years; (3) the number of prior successionsobserved during the time period. To measure thefirst two variables, I used data on CEO successionsfor all sample firms during the prior 20-year timeperiod.

The other control variables that were includedin equations predicting the succession event (fullmodel) are as follows. The CEO separate/chairvariable was measured by a dummy variable indi-cating whether the chairman of the board and CEOwere different individuals (1) or not (0). The ratioof outside directors was calculated from the ratioof outside (nonemployee) directors to total direc-tors in the year preceding the succession event.Finally, board size, the total number of inside andoutside directors, was included as a control vari-able. Table 2 provides the means, standard devia-tions, and bivariate correlations for the OLS mod-els.

RESULTS

The hypotheses were tested using OLS hierar-chical regression analysis with change in post-succession firm performance as the dependent vari-able. The results are reported in Table 3. Model1 reports the results with only the control vari-ables included. Model 2 reports the results withthe addition of the main effect of new CEO out-siderness. Given the time order of their occurrence,

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 697

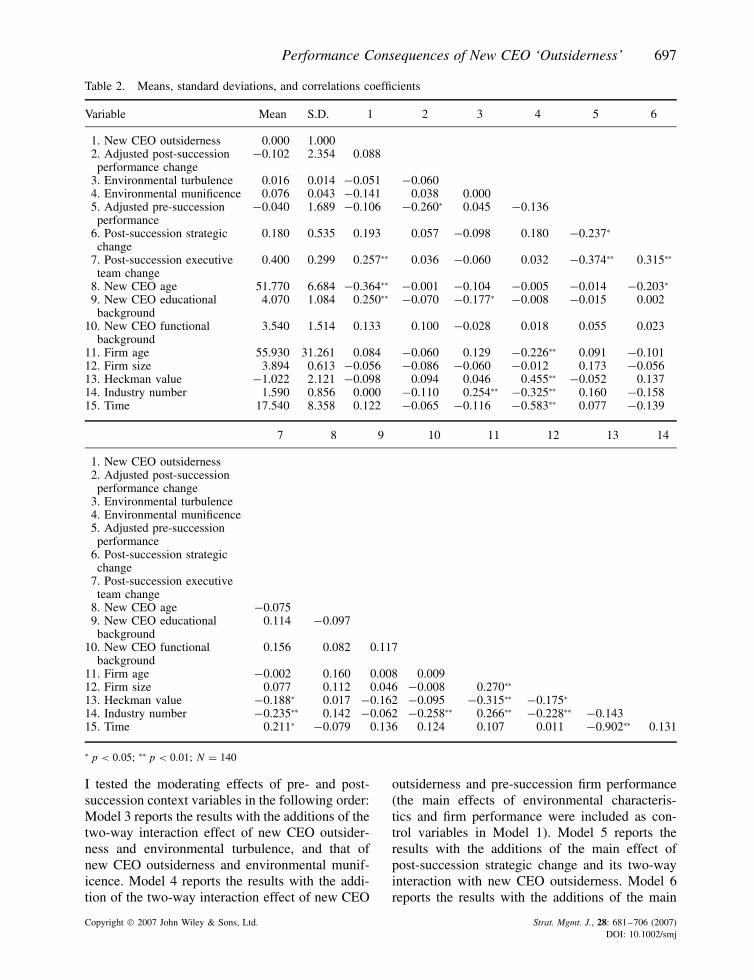

Table 2. Means, standard deviations, and correlations coefficients

Variable Mean S.D. 1 2 3 4 5 6

1. New CEO outsiderness 0.000 1.0002. Adjusted post-succession

performance change−0.102 2.354 0.088

3. Environmental turbulence 0.016 0.014 −0.051 −0.0604. Environmental munificence 0.076 0.043 −0.141 0.038 0.0005. Adjusted pre-succession

performance−0.040 1.689 −0.106 −0.260∗ 0.045 −0.136

6. Post-succession strategicchange

0.180 0.535 0.193 0.057 −0.098 0.180 −0.237∗

7. Post-succession executiveteam change

0.400 0.299 0.257∗∗ 0.036 −0.060 0.032 −0.374∗∗ 0.315∗∗

8. New CEO age 51.770 6.684 −0.364∗∗ −0.001 −0.104 −0.005 −0.014 −0.203∗

9. New CEO educationalbackground

4.070 1.084 0.250∗∗ −0.070 −0.177∗ −0.008 −0.015 0.002

10. New CEO functionalbackground

3.540 1.514 0.133 0.100 −0.028 0.018 0.055 0.023

11. Firm age 55.930 31.261 0.084 −0.060 0.129 −0.226∗∗ 0.091 −0.10112. Firm size 3.894 0.613 −0.056 −0.086 −0.060 −0.012 0.173 −0.05613. Heckman value −1.022 2.121 −0.098 0.094 0.046 0.455∗∗ −0.052 0.13714. Industry number 1.590 0.856 0.000 −0.110 0.254∗∗ −0.325∗∗ 0.160 −0.15815. Time 17.540 8.358 0.122 −0.065 −0.116 −0.583∗∗ 0.077 −0.139

7 8 9 10 11 12 13 14

1. New CEO outsiderness2. Adjusted post-succession

performance change3. Environmental turbulence4. Environmental munificence5. Adjusted pre-succession

performance6. Post-succession strategic

change7. Post-succession executive

team change8. New CEO age −0.0759. New CEO educational

background0.114 −0.097

10. New CEO functionalbackground

0.156 0.082 0.117

11. Firm age −0.002 0.160 0.008 0.00912. Firm size 0.077 0.112 0.046 −0.008 0.270∗∗

13. Heckman value −0.188∗ 0.017 −0.162 −0.095 −0.315∗∗ −0.175∗

14. Industry number −0.235∗∗ 0.142 −0.062 −0.258∗∗ 0.266∗∗ −0.228∗∗ −0.14315. Time 0.211∗ −0.079 0.136 0.124 0.107 0.011 −0.902∗∗ 0.131

∗ p < 0.05; ∗∗ p < 0.01; N = 140

I tested the moderating effects of pre- and post-succession context variables in the following order:Model 3 reports the results with the additions of thetwo-way interaction effect of new CEO outsider-ness and environmental turbulence, and that ofnew CEO outsiderness and environmental munif-icence. Model 4 reports the results with the addi-tion of the two-way interaction effect of new CEO

outsiderness and pre-succession firm performance(the main effects of environmental characteris-tics and firm performance were included as con-trol variables in Model 1). Model 5 reports theresults with the additions of the main effect ofpost-succession strategic change and its two-wayinteraction with new CEO outsiderness. Model 6reports the results with the additions of the main

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

698 A. Karaevli

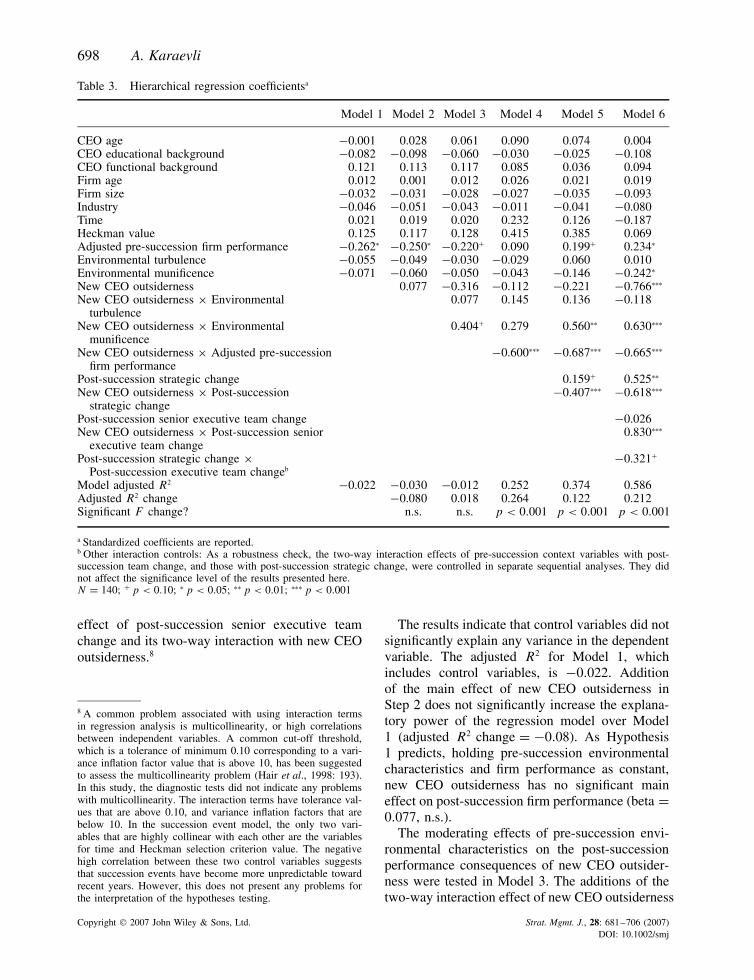

Table 3. Hierarchical regression coefficientsa

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6

CEO age −0.001 0.028 0.061 0.090 0.074 0.004CEO educational background −0.082 −0.098 −0.060 −0.030 −0.025 −0.108CEO functional background 0.121 0.113 0.117 0.085 0.036 0.094Firm age 0.012 0.001 0.012 0.026 0.021 0.019Firm size −0.032 −0.031 −0.028 −0.027 −0.035 −0.093Industry −0.046 −0.051 −0.043 −0.011 −0.041 −0.080Time 0.021 0.019 0.020 0.232 0.126 −0.187Heckman value 0.125 0.117 0.128 0.415 0.385 0.069Adjusted pre-succession firm performance −0.262∗ −0.250∗ −0.220+ 0.090 0.199+ 0.234∗

Environmental turbulence −0.055 −0.049 −0.030 −0.029 0.060 0.010Environmental munificence −0.071 −0.060 −0.050 −0.043 −0.146 −0.242∗

New CEO outsiderness 0.077 −0.316 −0.112 −0.221 −0.766∗∗∗

New CEO outsiderness × Environmentalturbulence

0.077 0.145 0.136 −0.118

New CEO outsiderness × Environmentalmunificence

0.404+ 0.279 0.560∗∗ 0.630∗∗∗

New CEO outsiderness × Adjusted pre-successionfirm performance

−0.600∗∗∗ −0.687∗∗∗ −0.665∗∗∗

Post-succession strategic change 0.159+ 0.525∗∗

New CEO outsiderness × Post-successionstrategic change

−0.407∗∗∗ −0.618∗∗∗

Post-succession senior executive team change −0.026New CEO outsiderness × Post-succession senior

executive team change0.830∗∗∗

Post-succession strategic change ×Post-succession executive team changeb

−0.321+

Model adjusted R2 −0.022 −0.030 −0.012 0.252 0.374 0.586Adjusted R2 change −0.080 0.018 0.264 0.122 0.212Significant F change? n.s. n.s. p < 0.001 p < 0.001 p < 0.001

a Standardized coefficients are reported.b Other interaction controls: As a robustness check, the two-way interaction effects of pre-succession context variables with post-succession team change, and those with post-succession strategic change, were controlled in separate sequential analyses. They didnot affect the significance level of the results presented here.N = 140; + p < 0.10; ∗ p < 0.05; ∗∗ p < 0.01; ∗∗∗ p < 0.001

effect of post-succession senior executive teamchange and its two-way interaction with new CEOoutsiderness.8

8 A common problem associated with using interaction termsin regression analysis is multicollinearity, or high correlationsbetween independent variables. A common cut-off threshold,which is a tolerance of minimum 0.10 corresponding to a vari-ance inflation factor value that is above 10, has been suggestedto assess the multicollinearity problem (Hair et al., 1998: 193).In this study, the diagnostic tests did not indicate any problemswith multicollinearity. The interaction terms have tolerance val-ues that are above 0.10, and variance inflation factors that arebelow 10. In the succession event model, the only two vari-ables that are highly collinear with each other are the variablesfor time and Heckman selection criterion value. The negativehigh correlation between these two control variables suggeststhat succession events have become more unpredictable towardrecent years. However, this does not present any problems forthe interpretation of the hypotheses testing.

The results indicate that control variables did notsignificantly explain any variance in the dependentvariable. The adjusted R2 for Model 1, whichincludes control variables, is −0.022. Additionof the main effect of new CEO outsiderness inStep 2 does not significantly increase the explana-tory power of the regression model over Model1 (adjusted R2 change = −0.08). As Hypothesis1 predicts, holding pre-succession environmentalcharacteristics and firm performance as constant,new CEO outsiderness has no significant maineffect on post-succession firm performance (beta =0.077, n.s.).

The moderating effects of pre-succession envi-ronmental characteristics on the post-successionperformance consequences of new CEO outsider-ness were tested in Model 3. The additions of thetwo-way interaction effect of new CEO outsiderness

Copyright 2007 John Wiley & Sons, Ltd. Strat. Mgmt. J., 28: 681–706 (2007)DOI: 10.1002/smj

Performance Consequences of New CEO ‘Outsiderness’ 699

and environmental turbulence, and that of newCEO outsiderness and environmental munificencein Model 3, did not significantly increase theexplanatory power of the regression equation overModel 2 (adjusted R2 change = 0.018, n.s.).Hypothesis 2, which predicts that new CEO out-siderness will be more positively associated withpost-succession firm performance in turbulent envi-ronments than in stable environments, is not sup-ported. The interaction effect of new CEO out-siderness and environmental turbulence on post-succession firm performance is in the expecteddirection, but is not statistically significant whenit is entered into the regression equation in Step3 (beta = 0.077, n.s.), and it stays insignificant inthe rest of the models.

Hypothesis 3 predicts that new CEO outsider-ness will be more positively associated with post-succession firm performance in munificent envi-ronments than in less munificent environments.Although the interaction effect of new CEO out-siderness and environmental munificence on post-succession firm performance is in the expecteddirection, but is only marginally statistically signif-icant when it is entered into the regression equation(beta = 0.404, p < 0.10), this interaction effect isstrongly significant in the final model where theother main and interaction effects are included(beta = 0.630, p < 0.001). Therefore, Hypothesis3 is supported.