Embed Size (px)

Citation preview

Pension Reform in Latin America

Experience & Lessons (*)

Guillermo Arthur E.FIAP President September, 2005

* Presented at the 2005 Pension Seminar 2005 – Netherland Antilles, September 1, 2005

Contents

I. Reforms in Latin America

II. Why were the reforms necessary?

III. Characteristics of the reforms

IV. Findings

V. Lessons from the experience

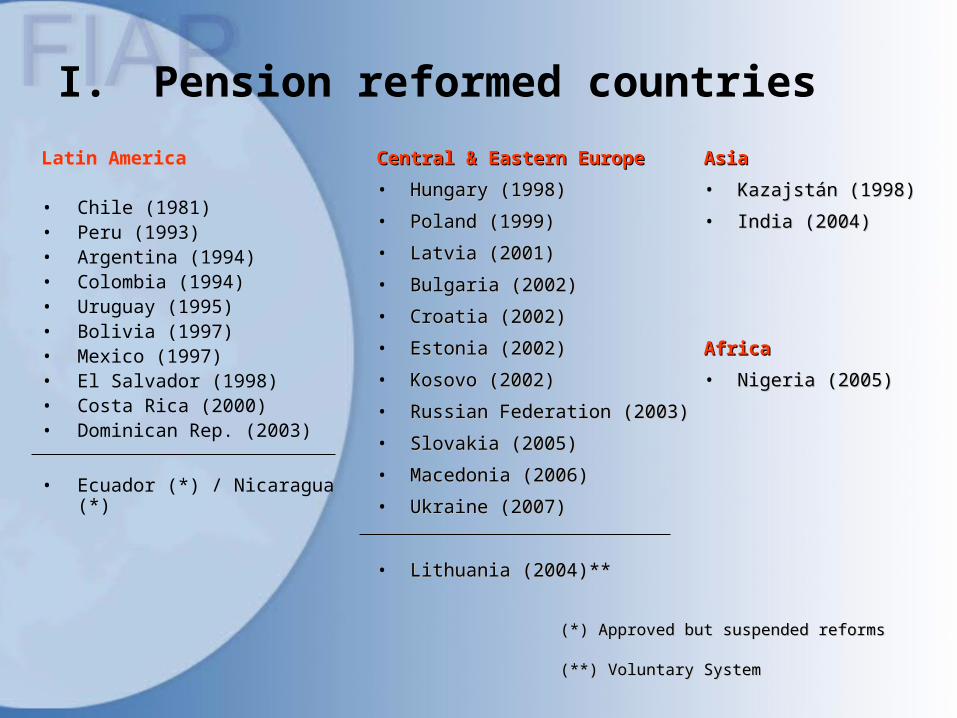

Latin America

• Chile (1981)• Peru (1993)• Argentina (1994)• Colombia (1994)• Uruguay (1995)• Bolivia (1997)• Mexico (1997)• El Salvador (1998)• Costa Rica (2000)• Dominican Rep. (2003)

• Ecuador (*) / Nicaragua (*)

Central & Eastern EuropeCentral & Eastern Europe

• Hungary (1998)Hungary (1998)

• Poland (1999)Poland (1999)

• Latvia (2001)Latvia (2001)

• Bulgaria (2002)Bulgaria (2002)

• Croatia (2002)Croatia (2002)

• Estonia (2002)Estonia (2002)

• Kosovo (2002)Kosovo (2002)

• Russian Federation (2003)Russian Federation (2003)

• Slovakia (2005)Slovakia (2005)

• Macedonia (2006)Macedonia (2006)

• Ukraine (2007)Ukraine (2007)

• Lithuania (2004)** Lithuania (2004)**

AsiaAsia

• Kazajstán (1998)Kazajstán (1998)

• India (2004)India (2004)

AfricaAfrica

• Nigeria (2005)Nigeria (2005)

I. Pension reformed countries

(*) Approved but suspended reforms(*) Approved but suspended reforms

(**) Voluntary System(**) Voluntary System

II. Why were the reforms necessary?

The financial situation of the traditional systems deteriorated mainly because of the

impact of three (3) phenomena:

Population aging Inefficient public management of pension funds

Sharp salary & employment cycles as a result of successive economic crises

continues...continues...

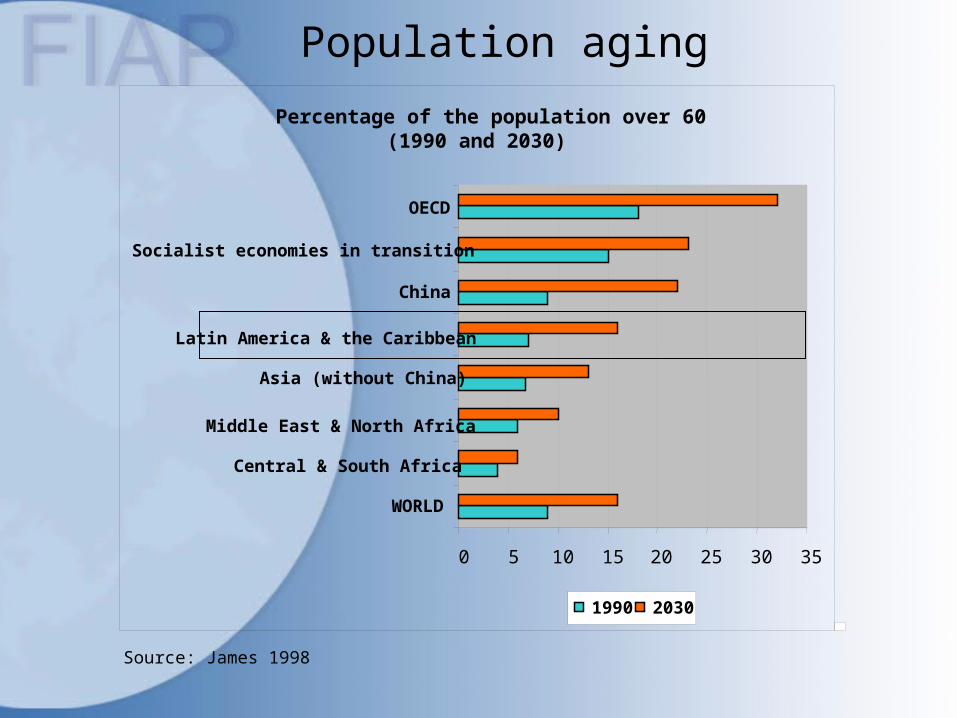

Population aging

Percentage of the population over 60 (1990 and 2030)

0 5 10 15 20 25 30 35

WORLD

Central & South Africa

Middle East & North Africa

Asia (without China)

Latin America & the Caribbean

China

Socialist economies in transition

OECD

1990 2030

Source: James 1998

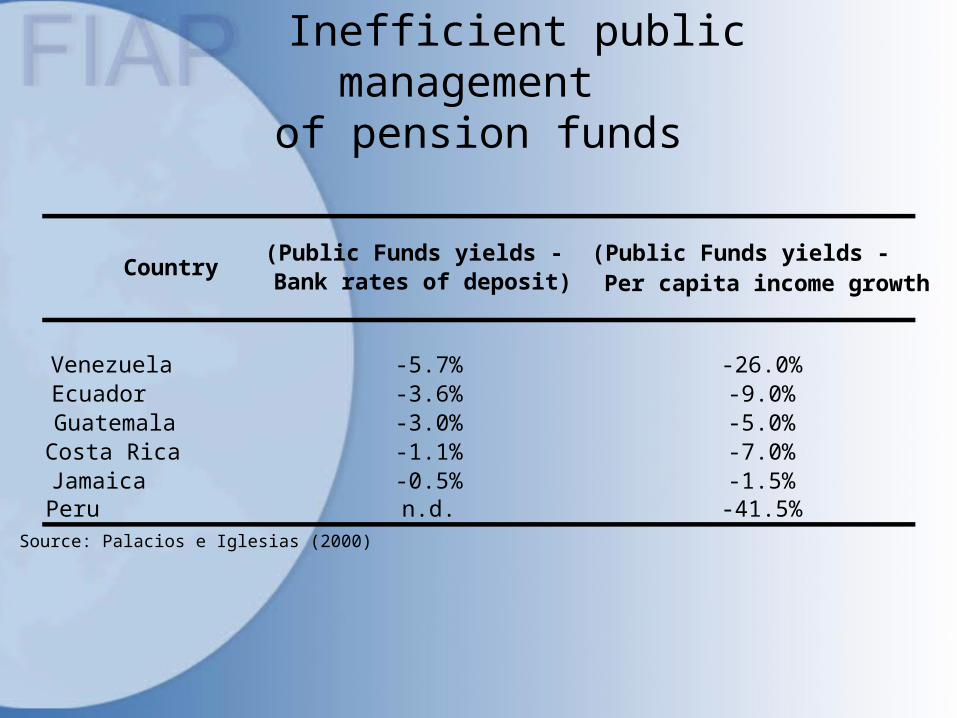

Inefficient public management of pension funds

Venezuela -5.7% -26.0%Ecuador -3.6% -9.0%Guatemala -3.0% -5.0%Costa Rica -1.1% -7.0%Jamaica -0.5% -1.5%Peru n.d. -41.5%Source: Palacios e Iglesias (2000)

Country(Public Funds yields -Bank rates of deposit)

(Public Funds yields - Per capita income growth

II. Why were the reforms necessary?

As a consequence of the deterioration of the traditional financial systems, one observed:

Increased public spending for pensions Increased social security debt High level of membership contribution rates

continues...continues...

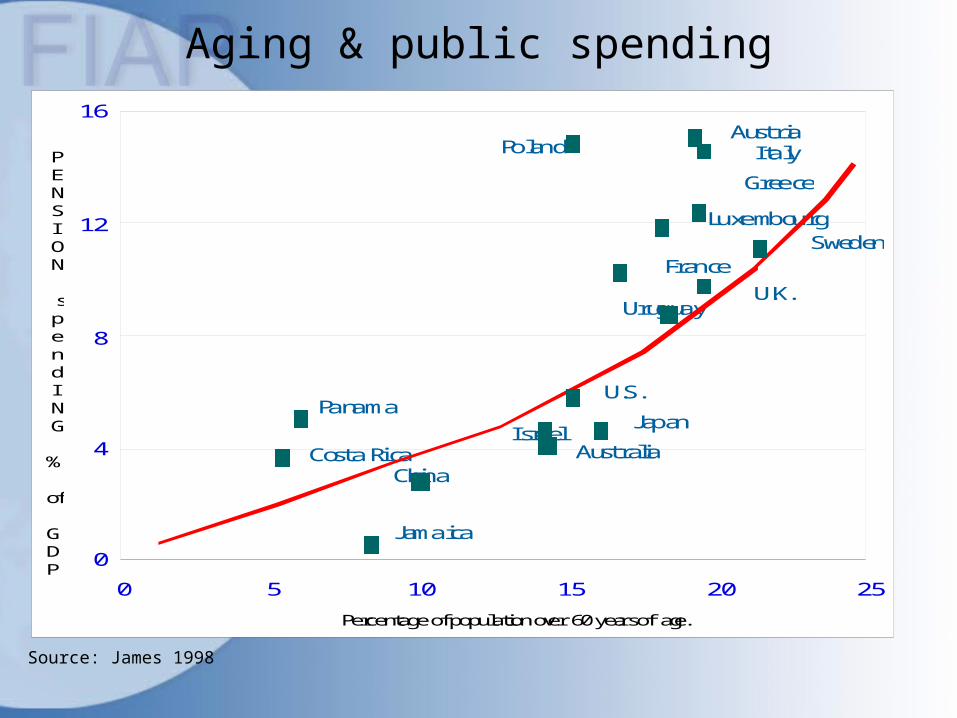

Aging & public spending

Panama

Costa Rica China

Jamaica

Israel Australia

Japan

U.S.

Uruguay U.K.

France Sweden

Luxembourg

Greece

Italy Austria

Poland

0 5 10 15 20 25

Percentage of population over 60 years of age.

0

4

8

12

16

P E N S I O N s p e n d I N G % of GD P

Source: James 1998

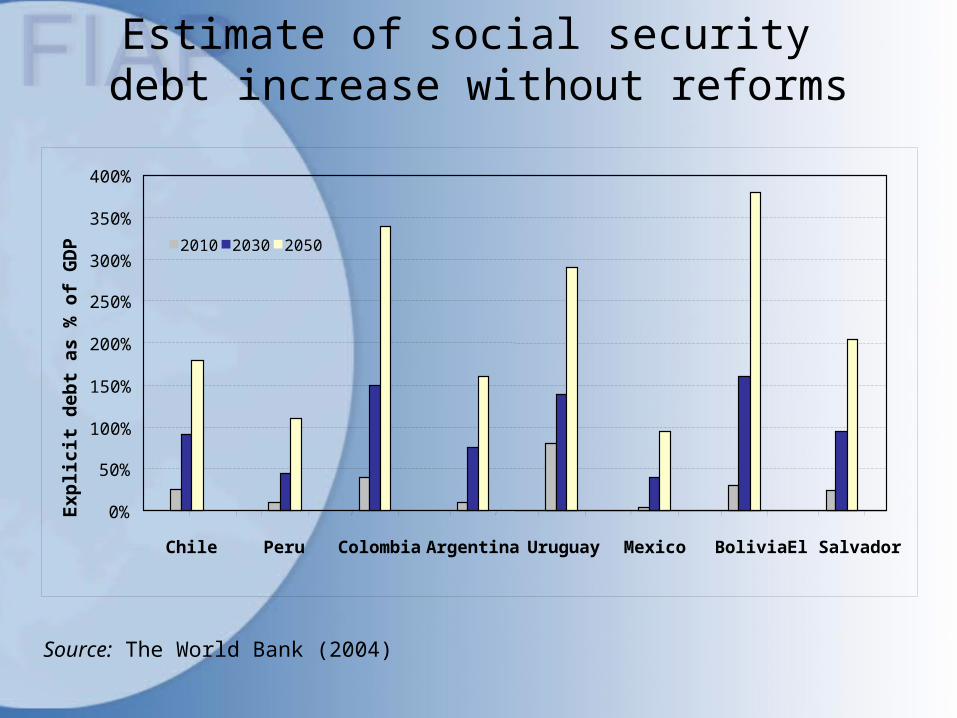

Estimate of social security debt increase without reforms

0%

50%

100%

150%

200%

250%

300%

350%

400%

Chile Peru Colombia Argentina Uruguay Mexico Bolivia El Salvador

Exp

lici

t d

ebt

as %

of

GD

P

2010 2030 2050

Source: The World Bank (2004)

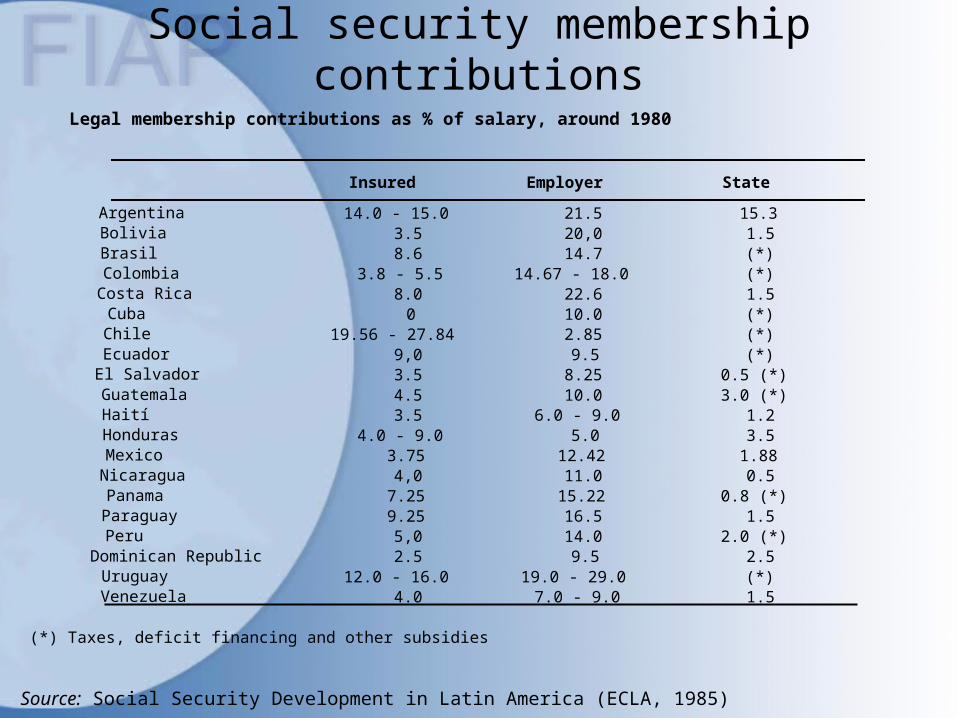

Social security membership contributions

Insured Employer State

Argentina 14.0 - 15.0 21.5 15.3Bolivia 3.5 20,0 1.5Brasil 8.6 14.7 (*)Colombia 3.8 - 5.5 14.67 - 18.0 (*)Costa Rica 8.0 22.6 1.5Cuba 0 10.0 (*)Chile 19.56 - 27.84 2.85 (*)Ecuador 9,0 9.5 (*)El Salvador 3.5 8.25 0.5 (*)Guatemala 4.5 10.0 3.0 (*)Haití 3.5 6.0 - 9.0 1.2Honduras 4.0 - 9.0 5.0 3.5Mexico 3.75 12.42 1.88Nicaragua 4,0 11.0 0.5Panama 7.25 15.22 0.8 (*)Paraguay 9.25 16.5 1.5Peru 5,0 14.0 2.0 (*)Dominican Republic 2.5 9.5 2.5Uruguay 12.0 - 16.0 19.0 - 29.0 (*)Venezuela 4.0 7.0 - 9.0 1.5

(*) Taxes, deficit financing and other subsidies

Legal membership contributions as % of salary, around 1980

Source: Social Security Development in Latin America (ECLA, 1985)

II. Why were the reforms necessary?

• Additionally, the traditional systems proved to be “soft” when confronted with sector interest group pressures. All of this translated into:

Program fragmentation

Inequity (discrimination) between worker groups

Negative impact over income distribution

continues...continues...

II Why were the reforms necessary?

• Consequently, the objectives of the reforms were:

To stop the growth of social security deficit & pension debt.

To improve pensions (without increasing contributions or minimizing whatever increase might be necessary).

To eliminate the inequities of the social security systems.

To shield social security systems from “political risks”.

To minimize the economic distortions generated by the operation of a mandatory pension system.

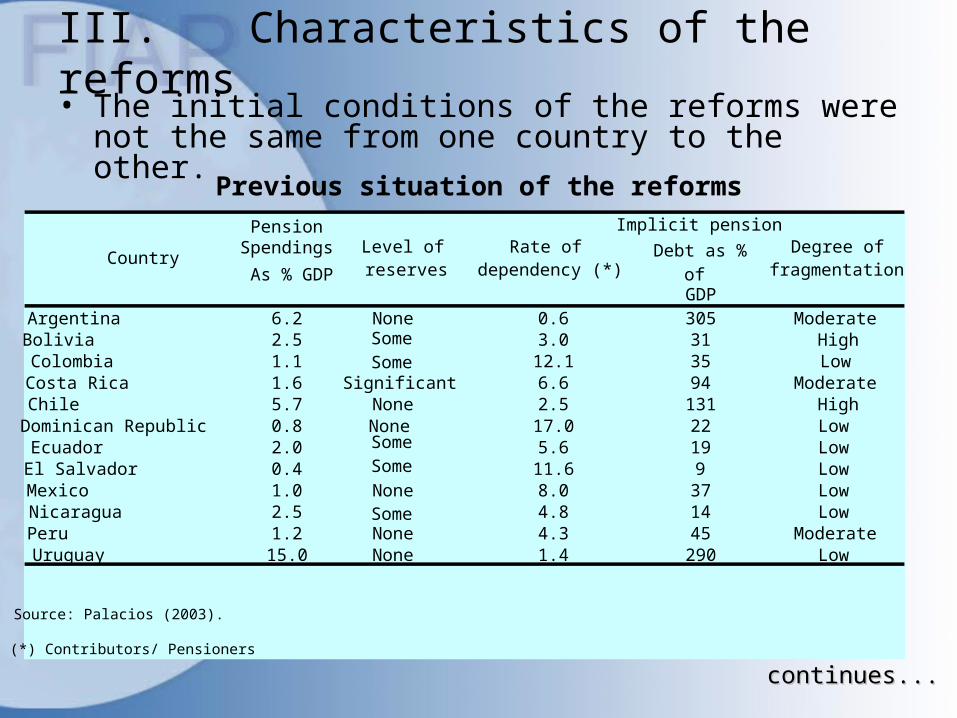

III. Characteristics of the reforms• The initial conditions of the reforms were not the

same from one country to the other.

Pension Spendings

Implicit pension

Debt as %As % GDP of

GDPArgentina 6.2 None 0.6 305 ModerateBolivia 2.5 Some 3.0 31 HighColombia 1.1 Some 12.1 35 LowCosta Rica 1.6 Significant 6.6 94 ModerateChile 5.7 None 2.5 131 HighDominican Republic 0.8 None 17.0 22 LowEcuador 2.0 Some 5.6 19 LowEl Salvador 0.4 Some 11.6 9 LowMexico 1.0 None 8.0 37 LowNicaragua 2.5 Some 4.8 14 LowPeru 1.2 None 4.3 45 ModerateUruguay 15.0 None 1.4 290 Low

(*) Contributors/ Pensioners

Source: Palacios (2003).

CountryLevel of reserves

Rate of dependency (*)

Degree of fragmentation

continues...continues...

Previous situation of the reforms

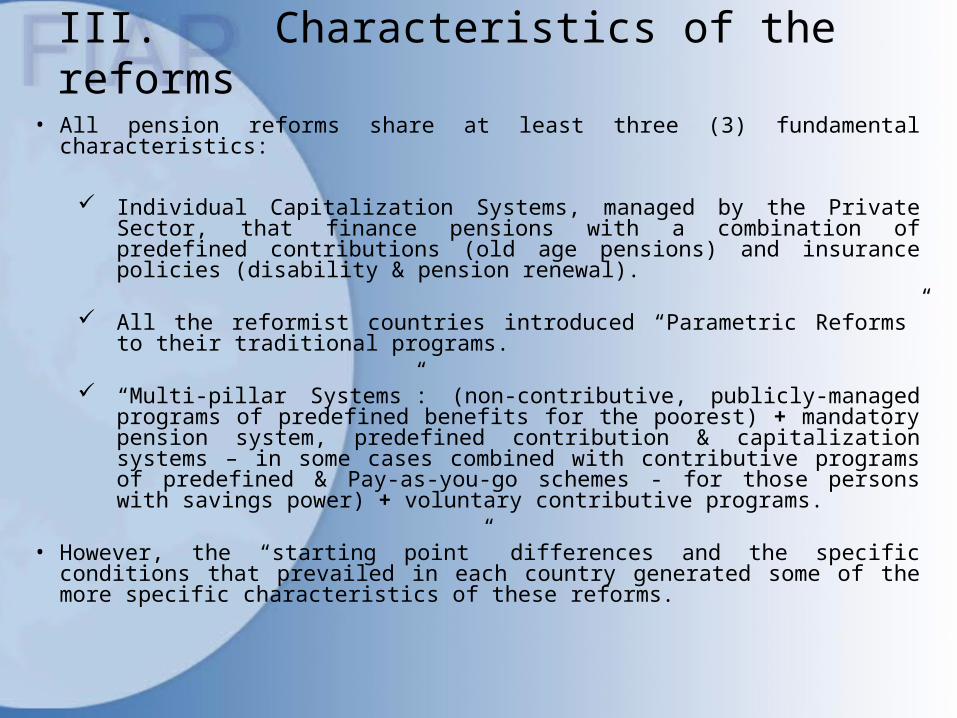

III. Characteristics of the reforms

• All pension reforms share at least three (3) fundamental characteristics:

Individual Capitalization Systems, managed by the Private Sector, that finance pensions with a combination of predefined contributions (old age pensions) and insurance policies (disability & pension renewal).

All the reformist countries introduced “Parametric Reforms” to their traditional programs.

“Multi-pillar Systems”: (non-contributive, publicly-managed programs of predefined benefits for the poorest) + mandatory pension system, predefined contribution & capitalization systems – in some cases combined with contributive programs of predefined & Pay-as-you-go schemes - for those persons with savings power) + voluntary contributive programs.

• However, the “starting point” differences and the specific conditions that prevailed in each country generated some of the more specific characteristics of these reforms.

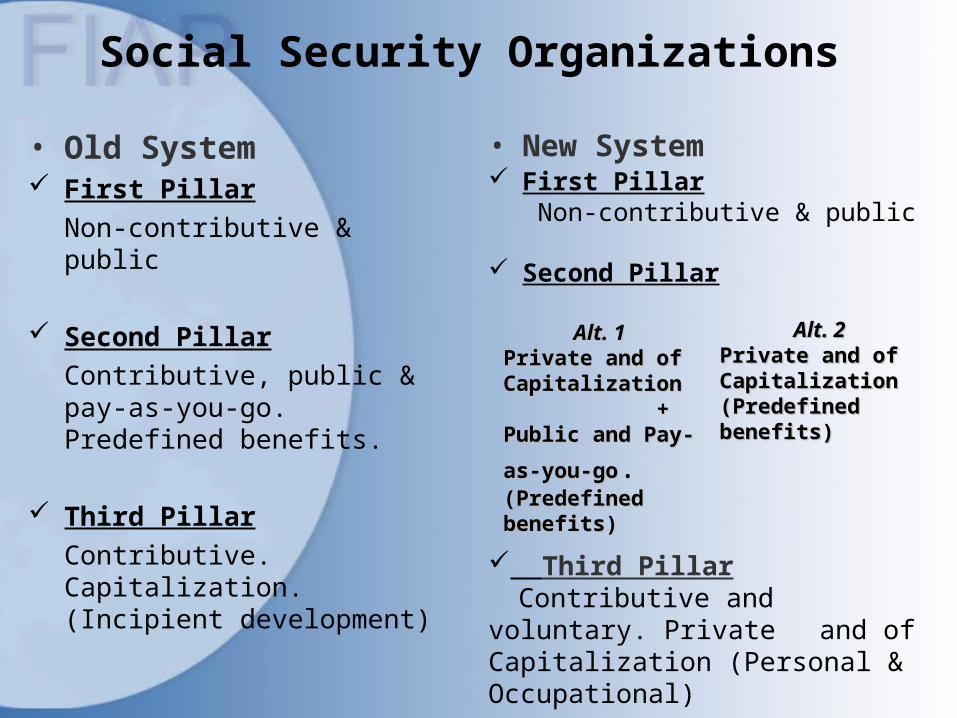

Social Security Organizations

• Old System First Pillar

Non-contributive & public

Second PillarContributive, public & pay-as-you-go. Predefined benefits.

Third PillarContributive. Capitalization. (Incipient development)

• New System First Pillar

Non-contributive & public

Second Pillar

Alt. 1Alt. 1Private and of Private and of CapitalizationCapitalization ++Public and Pay-Public and Pay-

as-you-goas-you-go.(Predefined (Predefined benefits)benefits)

Alt. 2Alt. 2Private and of Private and of CapitalizationCapitalization(Predefined (Predefined benefits)benefits)

Third Pillar Contributive and voluntary.

Private and of Capitalization (Personal & Occupational)

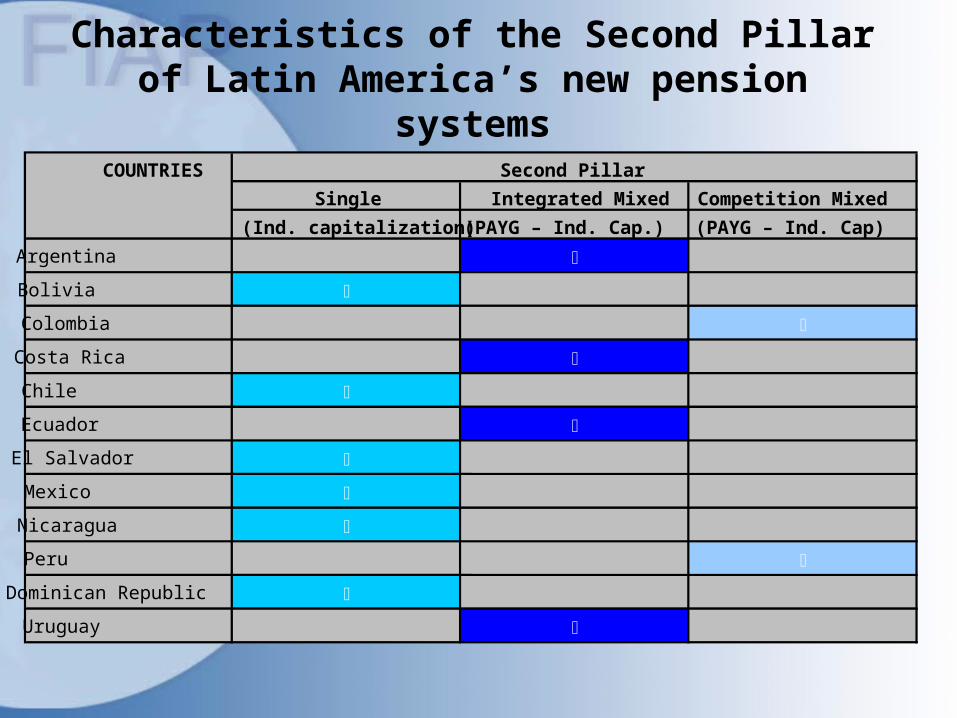

Characteristics of the Second Pillar of Latin America’s new pension systems

COUNTRIES

Single Integrated Mixed Competition Mixed

(Ind. capitalization) (PAYG – Ind. Cap.) (PAYG – Ind. Cap)

Argentina

Bolivia

Colombia

Costa Rica

Chile

Ecuador

El Salvador

Mexico

Nicaragua

Peru

Dominican Republic

Uruguay

Second Pillar

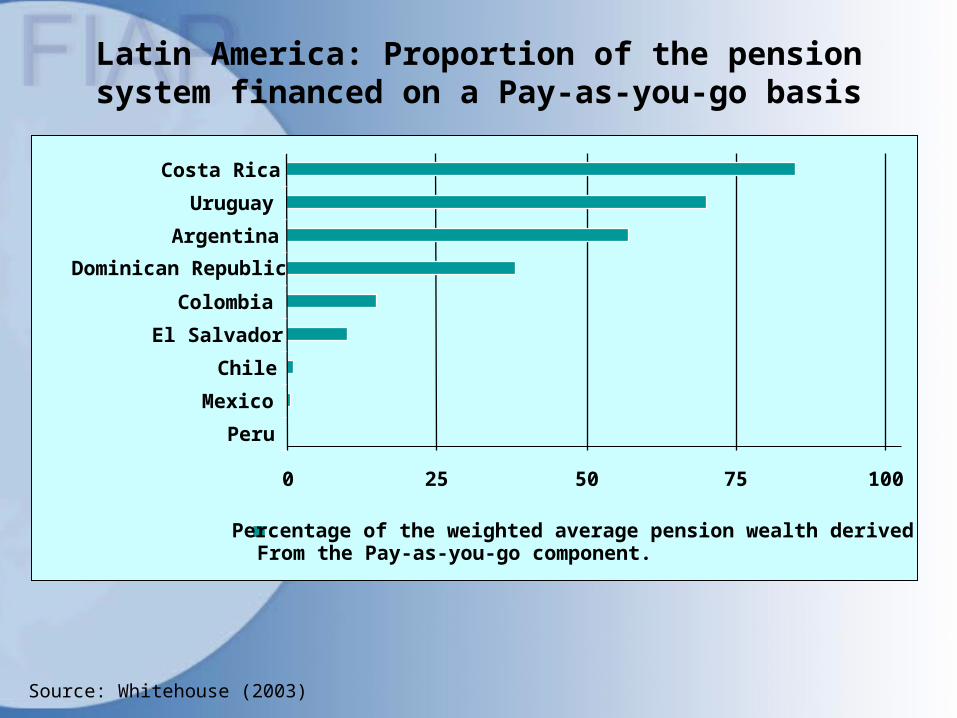

Latin America: Proportion of the pension system financed on a Pay-as-you-go basis

Source: Whitehouse (2003)

0 25 50 75 100

Peru

Mexico

Chile

El Salvador

Colombia

Dominican Republic

Argentina

Uruguay

Costa Rica

Percentage of the weighted average pension wealth derivedFrom the Pay-as-you-go component.

IV. Findings

• Pensions must be evaluated over a long period of time. Consequently, one cannot yet arrive at final conclusions.

• Nevertheless, there are three (3) very significant findings:

1. The Fund’s rates of return exceed the rate of growth of real salaries and per capita incomes.

continues...continues...

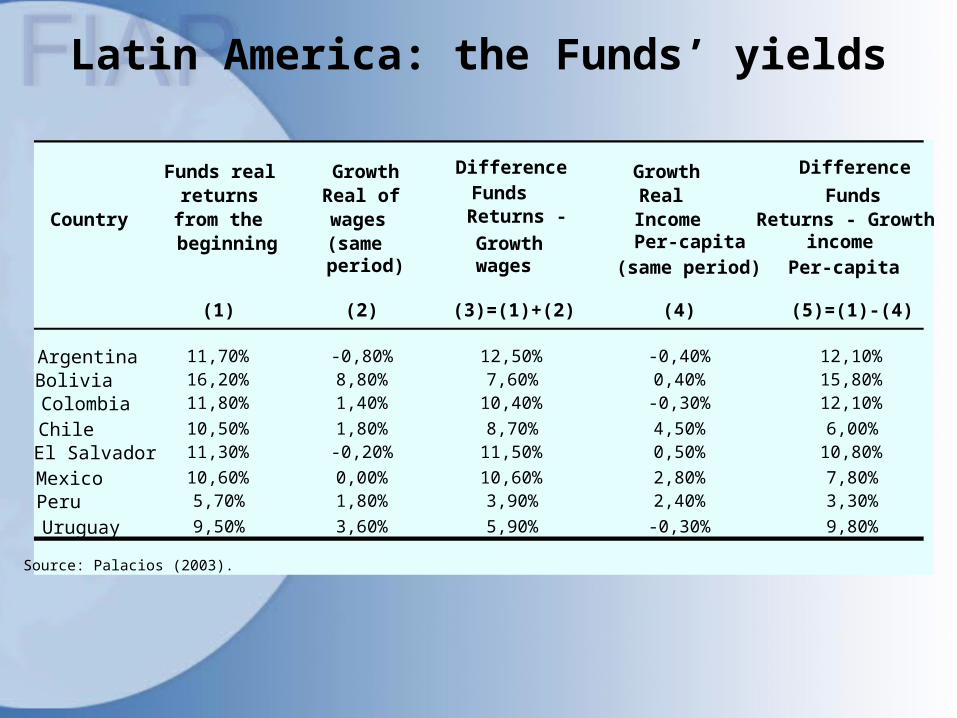

Latin America: the Funds’ yields

Country

Funds real returns

from the beginning

GrowthReal of wages (sameperiod)

Difference Funds Returns -

Growthwages

Growth RealIncomePer-capita

(same period)

Difference

FundsReturns - Growth

income Per-capita

(1) (2) (3)=(1)+(2) (4) (5)=(1)-(4)

Argentina 11,70% -0,80% 12,50% -0,40% 12,10%Bolivia 16,20% 8,80% 7,60% 0,40% 15,80%Colombia 11,80% 1,40% 10,40% -0,30% 12,10%

Chile 10,50% 1,80% 8,70% 4,50% 6,00%El Salvador 11,30% -0,20% 11,50% 0,50% 10,80%

Mexico 10,60% 0,00% 10,60% 2,80% 7,80%Peru 5,70% 1,80% 3,90% 2,40% 3,30%

Uruguay 9,50% 3,60% 5,90% -0,30% 9,80%

Source: Palacios (2003).

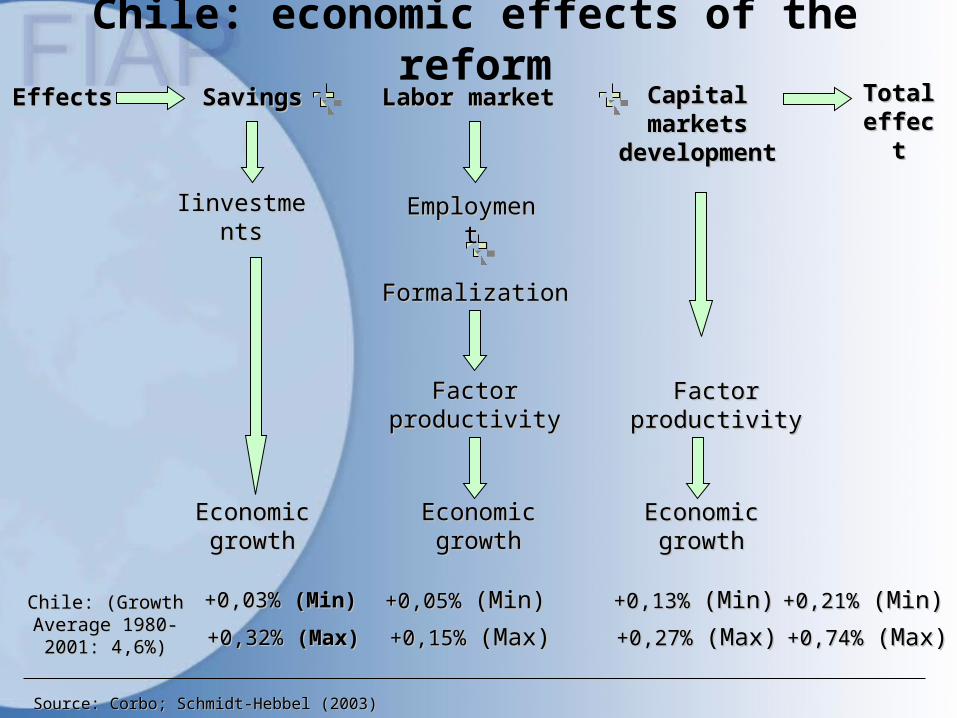

IV. Findings

2. The economic impact of the reforms has been very positive. Particularly, the accumulation of pension funds (and of the reserves of life insurance companies) has directly affected:

Savings The development of capital markets The labor market

As a result of these effects, the reforms have contributed to economic growth.

continues...continues...

Chile: economic effects of the reformEffectsEffects SavingsSavings Labor marketLabor market CapitalCapital

marketsmarketsdevelopmedevelopme

ntnt

TotalTotaleffeceffec

tt

IinvestmenIinvestmentsts

EconomicEconomicgrowthgrowth

Chile: (Growth Chile: (Growth Average 1980-Average 1980-2001: 4,6%)2001: 4,6%)

+0,03% +0,03% (Min)(Min)

+0,32% +0,32% (Max)(Max)

EmploymeEmploymentnt

FormalizationFormalization

FactorFactorproductivityproductivity

EconomicEconomicgrowthgrowth

+0,05% +0,05% (Min)(Min)

+0,15% +0,15% (Max)(Max)

FactorFactorproductivityproductivity

EconomicEconomicgrowthgrowth

+0,13% +0,13% (Min)(Min)

+0,27% +0,27% (Max)(Max)

+0,21% +0,21% (Min)(Min)

+0,74% +0,74% (Max)(Max)

Source: Corbo; Schmidt-Hebbel (2003)Source: Corbo; Schmidt-Hebbel (2003)

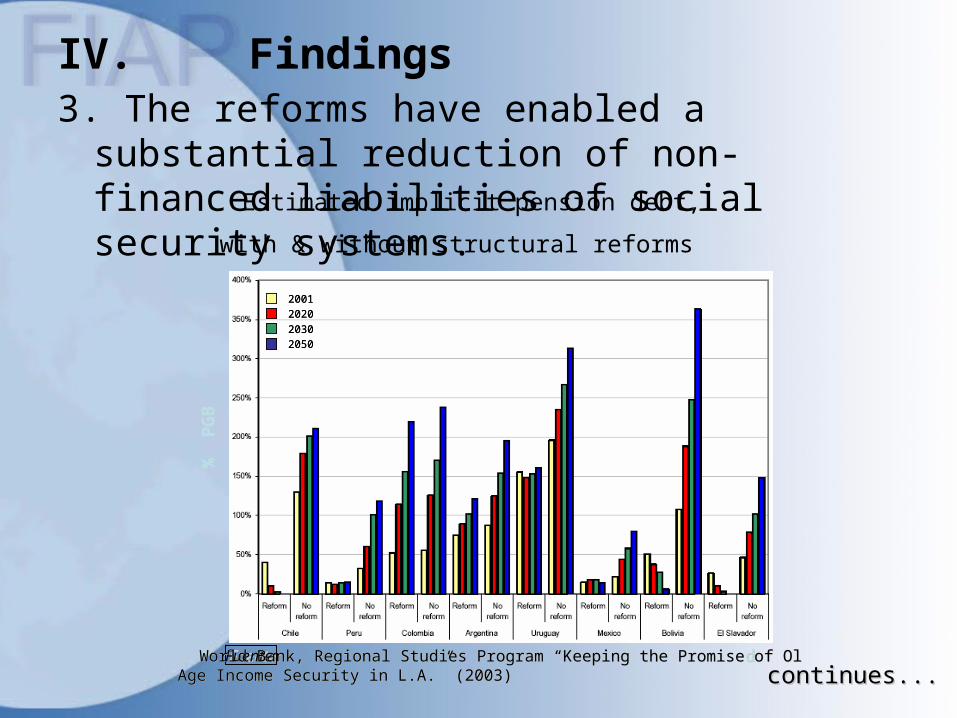

IV. Findings3. The reforms have enabled a substantial reduction of

non-financed liabilities of social security systems.

2001202020302050

Fuente:Fuente:World Bank, Regional Studies Program “Keeping the Promise of OlWorld Bank, Regional Studies Program “Keeping the Promise of Ol d d Age Income Security in L.A.” (2003)Age Income Security in L.A.” (2003)

% P

GB

2001202020302050

2001202020302050

Fuente:Fuente: World Bank, Regional Studies Program “Keeping the Promise of OlWorld Bank, Regional Studies Program “Keeping the Promise of Ol d d Age Income Security in L.A.” (2003)Age Income Security in L.A.” (2003)

% P

GB

Estimated implicit pension debt,

with & without structural reforms

continues...continues...

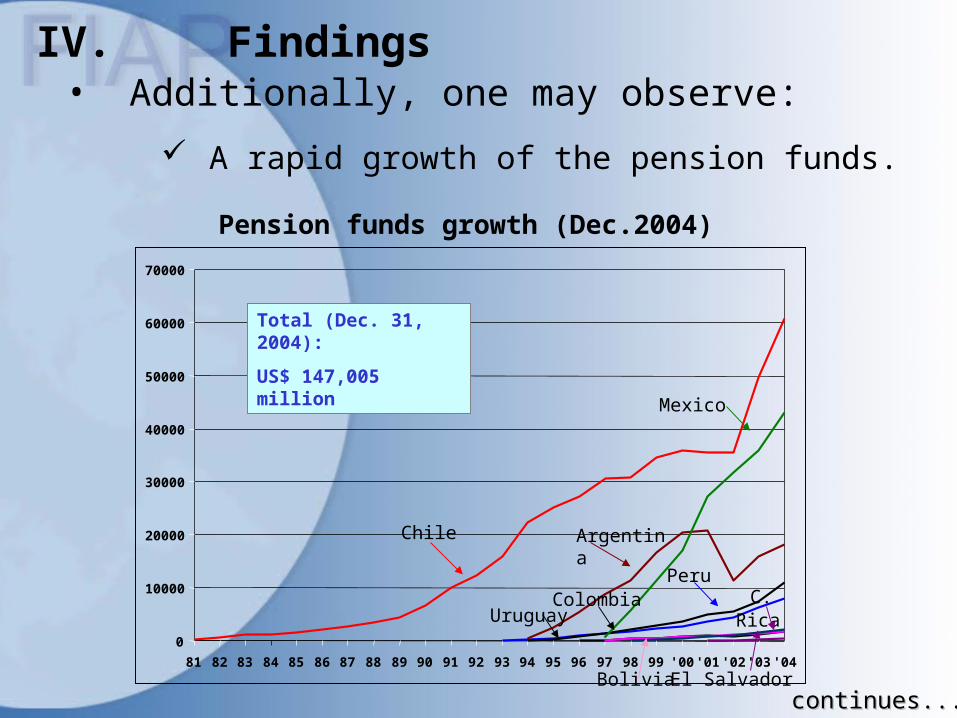

IV. Findings• Additionally, one may observe:

A rapid growth of the pension funds.

0

10000

20000

30000

40000

50000

60000

70000

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04

Total (Dec. 31, 2004):

US$ 147,005 million

Chile Argentina

Mexico

PeruColombia

Uruguay C. Rica

El SalvadorBolivia

Pension funds growth (Dec.2004)

continues...continues...

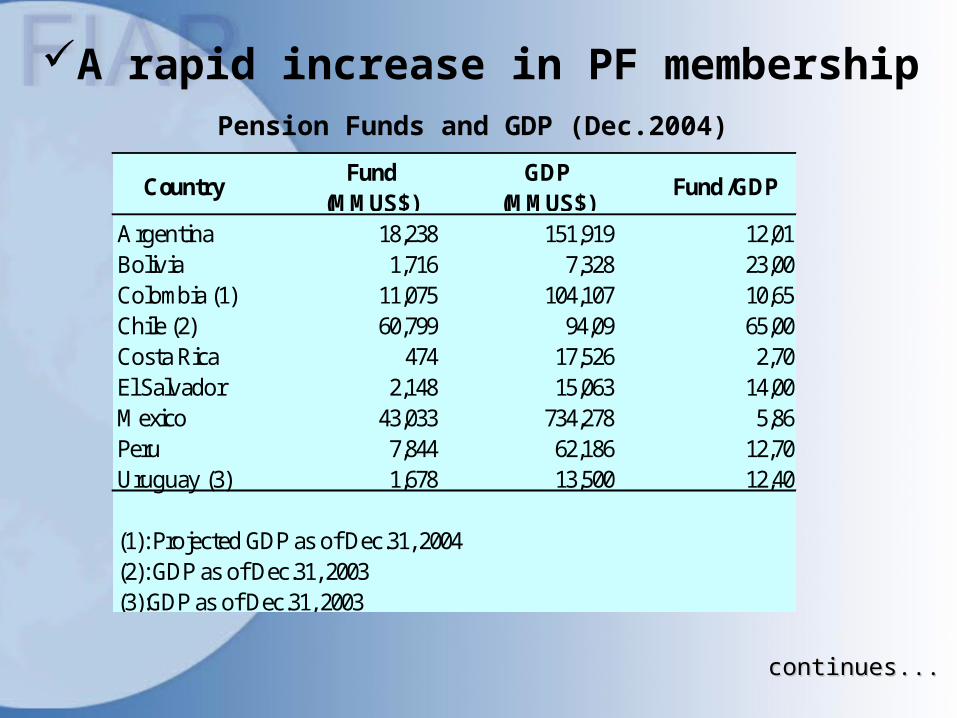

A rapid increase in PF membershipPension Funds and GDP (Dec.2004)

CountryFund

(MMUS$)GDP

(MMUS$)Fund /GDP

Argentina 18,238 151,919 12,01Bolivia 1,716 7,328 23,00Colombia (1) 11,075 104,107 10,65Chile (2) 60,799 94,09 65,00Costa Rica 474 17,526 2,70El Salvador 2,148 15,063 14,00Mexico 43,033 734,278 5,86Peru 7,844 62,186 12,70Uruguay (3) 1,678 13,500 12,40

(1): Projected GDP as of Dec.31, 2004(2): GDP as of Dec.31, 2003(3):GDP as of Dec.31, 2003

continues...continues...

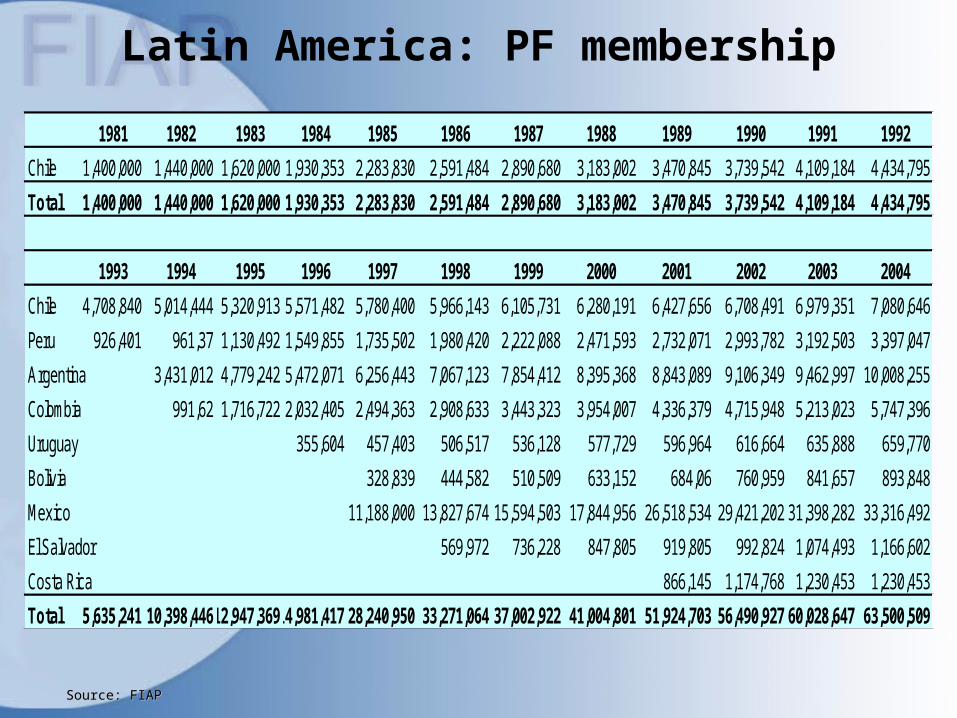

Latin America: PF membership

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

Chile 1,400,000 1,440,000 1,620,000 1,930,353 2,283,830 2,591,484 2,890,680 3,183,002 3,470,845 3,739,542 4,109,184 4,434,795

Total 1,400,000 1,440,000 1,620,000 1,930,353 2,283,830 2,591,484 2,890,680 3,183,002 3,470,845 3,739,542 4,109,184 4,434,795

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Chile 4,708,840 5,014,444 5,320,913 5,571,482 5,780,400 5,966,143 6,105,731 6,280,191 6,427,656 6,708,491 6,979,351 7,080,646

Peru 926,401 961,37 1,130,492 1,549,855 1,735,502 1,980,420 2,222,088 2,471,593 2,732,071 2,993,782 3,192,503 3,397,047

Argentina 3,431,012 4,779,242 5,472,071 6,256,443 7,067,123 7,854,412 8,395,368 8,843,089 9,106,349 9,462,997 10,008,255

Colombia 991,62 1,716,722 2,032,405 2,494,363 2,908,633 3,443,323 3,954,007 4,336,379 4,715,948 5,213,023 5,747,396

Uruguay 355,604 457,403 506,517 536,128 577,729 596,964 616,664 635,888 659,770

Bolivia 328,839 444,582 510,509 633,152 684,06 760,959 841,657 893,848

Mexico 11,188,000 13,827,674 15,594,503 17,844,956 26,518,534 29,421,202 31,398,282 33,316,492

El Salvador 569,972 736,228 847,805 919,805 992,824 1,074,493 1,166,602

Costa Rica 866,145 1,174,768 1,230,453 1,230,453

Total 5,635,241 10,398,44612,947,36914,981,417 28,240,950 33,271,064 37,002,922 41,004,801 51,924,703 56,490,927 60,028,647 63,500,509

Source: FIAPSource: FIAP

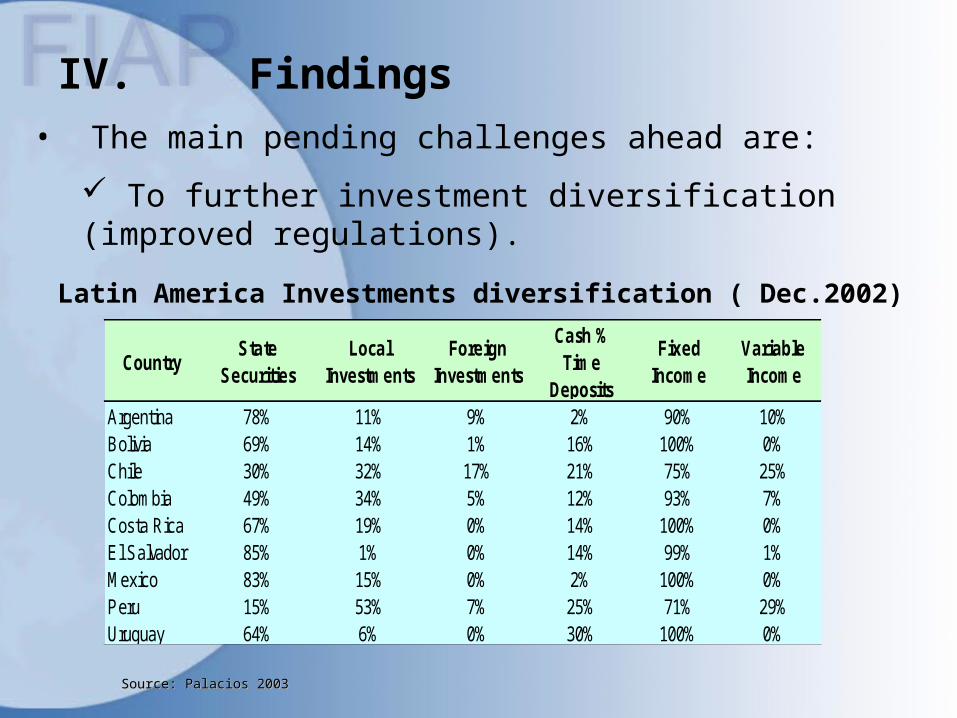

IV. Findings• The main pending challenges ahead are:

To further investment diversification (improved regulations).

Latin America Investments diversification ( Dec.2002)

CountryState

SecuritiesLocal

InvestmentsForeign

Investments

Cash % Time

Deposits

Fixed Income

Variable Income

Argentina 78% 11% 9% 2% 90% 10%Bolivia 69% 14% 1% 16% 100% 0%Chile 30% 32% 17% 21% 75% 25%Colombia 49% 34% 5% 12% 93% 7%Costa Rica 67% 19% 0% 14% 100% 0%El Salvador 85% 1% 0% 14% 99% 1%Mexico 83% 15% 0% 2% 100% 0%Peru 15% 53% 7% 25% 71% 29%Uruguay 64% 6% 0% 30% 100% 0%

Source: Palacios 2003Source: Palacios 2003

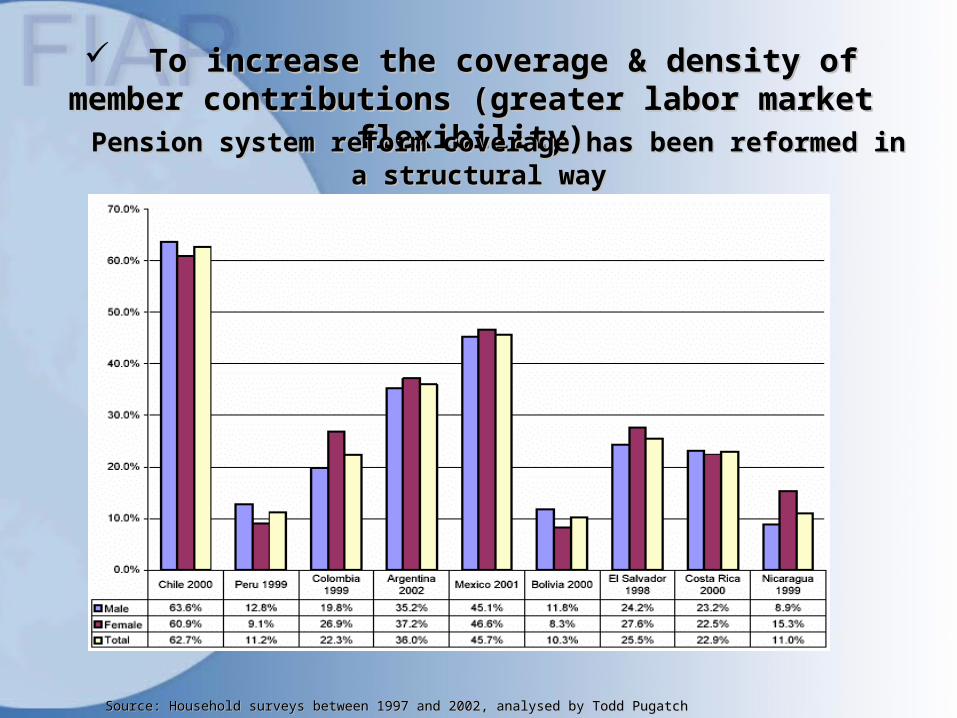

To increase the coverage & density of To increase the coverage & density of member contributions (greater labor market member contributions (greater labor market

flexibility)flexibility) Pension system reform coverage has been reformed in Pension system reform coverage has been reformed in a structural waya structural way

Source: Household surveys between 1997 and 2002, analysed by Todd PugatchSource: Household surveys between 1997 and 2002, analysed by Todd Pugatch

V. Lessons derived from the experience…

• Lesson 1:In the long-run, the purely Pay-as-you-go pension systems are not sustainable. The solution to this crisis lies in introducing a capitalization component into social security systems.

• Lesson 2:Introducing capitalization programs is not only necessary – it is also possible.

• Lesson 3:The decisions regarding the design of each Pillar, the relative size of each Program within the Second Pillar; and the Manner in which the new Capitalization Program is introduced are indeed crucial (the gradualism of the reform; a greater relative size of the capitalization program; and the non-competition between programs appear to have been beneficial in most cases).

continues...continues...

V. Lessons derived from the experience.

• Lesson 4:The detailed design of the Capitalization Program requires the maximum attention (although capitalization programs can be designed in many forms, not all of them yield the same results).

• Lesson 5:Pension fund investment regulations must promote the diversification of portfolios and avoid forced investments (or “earmarked investments”).

• Lesson 6:In order to maximize the positive economic impact of a pension system reform, it should be closely coordinated with a capital markets reform (and, eventually, tax and labor market reforms).

• Lesson 7:An effective & independent supervision of the various programs is crucial for the success of all pension reforms.