Embed Size (px)

Citation preview

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 1

General Comments The overall performance of candidates was again disappointing. The lack of ability of candidates to apply knowledge to questions that are slightly different from those they have seen before is a major issue. Students appear to have learned how to reconcile actual and budget figures using variance analysis but do not understand what they are doing. This was highlighted by the fact that a large proportion of candidates did not know what flexible budgeting is, despite the fact that the technique is applied in variance analysis. Learning how to do a particular type of question by rote is a risky strategy to apply to a management accounting examination paper. Many candidates were unable to apply fundamental concepts such as flexible budgeting and the high low method for estimating costs, both of which are part of the Certificate Level syllabus. Candidates must ensure, particularly if they have been exempted from the Certificate Level, that they are able to apply the techniques covered by that syllabus since many of these techniques will be used throughout the Performance pillar. Candidates should also be aware that the full range of the syllabus will be examined and that they should not rely on speculation in student magazines and by tutors about what topics will be included in any particular diet. There is still evidence of lack of preparation for the examination and a general lack of knowledge in some areas. A number of questions were poorly answered, in particular Q2(a) on the conflicts in budgeting and Q2(e) on export financing methods. The performance on the narrative budgeting question that has been set in every diet of the new syllabus has been very poor which suggests that candidates have made a conscious decision to ignore this area of the syllabus perhaps because the weighting is only 10%. As the exam papers reflect the weighting of the syllabus this could mean that candidates have forgone 10% of the marks before the exam begins. All questions in the paper are compulsory therefore it is important that candidates’ knowledge covers the full range of the syllabus.

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 2

Section A – 20 marks ANSWER ALL EIGHT SUB-QUESTIONS IN THIS SECTION

Question 1.1 Which of the following is NOT a feature of an agreed overdraft facility? A The borrower may draw funds, up to the agreed overdraft limit, as and when required. B Interest is payable on the total amount of the agreed overdraft limit rather than on the amount

borrowed. C There is no fixed repayment date for the amount borrowed.

D The borrowing is repayable on demand.

(2 marks)

The correct answer is B

Question 1.2 A marketing manager is deciding which of four potential selling prices to charge for a new product. Market conditions are uncertain and demand may be good, average or poor. The contribution that would be earned for each of the possible outcomes is shown in the payoff table below:

Demand level Selling price

$40 $60 $80 $100

Good $50,000 $60,000 $40,000 $30,000

Average $20,000 $30,000 $30,000 $20,000

Poor $30,000 $30,000 $20,000 $10,000

If the manager applies the maximin criterion to make decisions, which selling price would be chosen? A $40 B $60

C $80

D $100

(2 marks)

The correct answer is B

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 3

Workings The minimum contribution at a selling price of $40 is $20,000 The minimum contribution at a selling price of $60 is $30,000 The minimum contribution at a selling price of $80 is $20,000 The minimum contribution at a selling price of $100 is $10,000 Therefore if the manager wants to maximise the minimum contribution, a selling price of $60 will be selected.

Question 1.3 A company is considering whether to develop and market a new product. The cost of developing the product is estimated to be $150,000. There is a 70% probability that the development will succeed and a 30% probability that the development will be unsuccessful. If the development is successful the product will be marketed. There is a 50% chance that the marketing will be very successful and the product will make a profit of $250,000. There is a 30% chance that the marketing will be reasonably successful and the product will make a profit of $150,000 and a 20% chance that the marketing will be unsuccessful and the product will make a loss of $80,000. The profit and loss figures stated are after taking account of the development costs of $150,000. The expected value of the decision to develop and market the product is: A $154,000 B $4,000

C $107,800

D $62,800

(2 marks)

The correct answer is D

Workings ((50% x 70% x $250k) + (30% x 70% x $150k) + (20% x 70% x - $80k) + (30% x -$150k) = $62,800

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 4

Question 1.4 If a traditional contribution approach is used, the ranking of products, in order of priority, for the profit maximising product mix will be: A D, E, F B E, D, F C F, D, E

D D, F, E

(2 marks)

The correct answer is C Workings D E F Contribution per unit $12 $14 $10 Units of limiting factor 20 mins 25 mins 15 mins Contribution per unit of limiting factor $0.60 $0.56 $0.667 Ranking 2nd 3rd 1st

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 5

Question 1.5 If a throughput accounting approach is used, the ranking of products, in order of priority, for the profit maximising product mix will be: A D, E, F B E, D, F C F, D, E

D D, F, E

(2 marks)

The correct answer is D

Workings D E F Throughput contribution per unit $22 $20 $16 Units of limiting factor 20 mins 25 mins 15 mins Throughput contribution per unit of limiting factor

$1.10 $0.80 $1.07

Ranking 1st 3rd 2nd

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 6

Question 1.6 GS has budgeted sales for the next two years of 24,000 units per annum spread evenly throughout both years. The estimated opening inventory of finished goods at the start of the next year is 500 units but GS now wants to maintain inventory of finished goods equivalent to one month’s sales. Each unit uses 2kg of material. The estimated opening raw material inventory at the start of the next year is 300kg but GS now wants to hold sufficient raw material inventory at the end of each month to cover the following month’s production. The change in the policy for inventory holding for both raw materials and finished goods will take effect in the first month of next year and will apply for the next two years. The budgeted material cost is $12 per kg. Required: Calculate the material purchases budget for the next year in $.

(3 marks) Workings

Budgeted sales 24,000 units Plus closing inventory 2,000 units Less opening inventory units (500) Budgeted production 25,500 units Raw material required 25,500 units x 2 kg = 51,000 kg Plus closing inventory 2,000 units x 2 kg = 4,000 kg Less opening inventory Raw material purchases

(300) kg 54,700 kg

Raw material purchases budget

54,700 kg x $12 = $656,400

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 7

Question 1.7 DB’s latest estimate for trade payables outstanding at the end of this year is 45 days. Estimated purchases for this year are $474,500. DB is preparing the budget for next year and estimates that purchases will increase by 10%. The trade payables amount, in $, outstanding at the end of next year is estimated to be the same as at the end of this year. Required: Calculate the budgeted trade payable days at the end of next year.

(3 marks)

Workings Trade payables outstanding at end of this year = $474,500 / 365 x 45 = $58,500 Purchases budget for next year = $474,500 x 1.1 = $521,950 Trade payable days at end of next year = $58,500 / $521,950 x 365 = 40.9 days

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 8

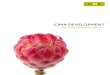

Question 1.8

A company is considering whether to invest in a new project. The probability distribution of the net present value of the project is as follows:

Net present value Probability $2,800 0.25 $3,900 0.40 $4,900 0.35

Required: Calculate the expected value of the net present value of the project and its standard deviation.

(4 marks) Note:

Workings

NPV Probability Expected value

Deviation from expected value

Squared deviation

Weighted amounts

$2,800 0.25 $700 -1,175 1,380,625 345,156.25

$3,900 0.40 $1,560 -75 5,625 2,250

$4,900 0.35 $1,715 925 855,625 299,468.75

$3,975 646,875 The expected value of the project is $3,975 The standard deviation is √646,875 = $804.29

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 9

Section B – 30 marks ANSWER ALL SIX SUB-QUESTIONS. YOU SHOULD SHOW YOUR WORKINGS AS MARKS ARE AVAILABLE FOR THE METHOD YOU USE

Question 2(a) “Different budgets should be used for different purposes. The budget used for planning purposes should be different from the budget used to set performance targets.” Required: Explain the above statement and the conflicts that may arise when a single budget is used for both purposes.

(5 marks)

Rationale This question assesses learning outcome B1(b) explain the purposes of budgeting, including planning, communication, co-ordination, motivation, authorisation, control and evaluation, and how these may conflict. It examines candidates’ ability to explain the behavioural consequences of budgeting and the difficulties and conflicts that can arise. Suggested Approach Candidates should first consider the use of the budget for planning and control purposes and the need for realistically achievable targets. They should then consider the use of the budget to motivate managers and optimise their performance and how this can result in a conflict since tight budgets are needed to motivate managers. The use of two different budgets should be considered and the impracticability of doing this in practice. Marking Guide

Marks

• Explanation of use of budgeting for planning purposes • Explanation of use of budgeting as a control mechanism • Need for realistically achievable targets

• Explanation of use of budgets to motivate managers and optimise their

performance • Effect of attainability of target on motivation and management performance • Need for tight budgets to motivate managers

• Need for two separate budgets to be produced but unrealistic in practice

1 mark per valid point

Maximum marks awarded 5 marks Examiner’s comments This question was particularly badly done with few candidates scoring highly. Answers included activity based budgeting, zero based budgeting and a lot of discussion of planning and operational variances. Every budgeting question that has been set under the new syllabus has been badly answered with disappointingly few candidates being able to apply their knowledge to address the question that was set and many answering the question that was set the time before. Poor exam technique was used in answering this question. The question asks for an explanation of the

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 10

statement therefore marks were available for candidates explaining the two purposes of budgeting and then explaining why they conflict. Common errors

• Failure to answer the question • Failure to explain the statement as required by the question • Discussion of a wide variety of budgeting techniques which were irrelevant to the question

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 11

Question 2(b) A company has to decide which of three mutually exclusive projects to invest in during the next year. The directors believe that the success of the projects will vary depending on consumer demand. There is a 20% chance that consumer demand will be above average; a 45% chance that consumer demand will be average and a 35% chance that consumer demand will be below average. The net present value for each of the possible outcomes is as follows:

Consumer demand Project A Project B Project C

$000s $000s $000s

Above average 400 300 800

Average 500 400 600

Below average 700 600 300 A market research company believes it can provide perfect information on potential consumer demand in this market. Required: Calculate, on the basis of expected value, the maximum amount that should be paid for the information from the market research company.

(5 marks)

Rationale The question assesses learning outcome D1(e) calculate the value of information. It examines candidates’ ability to calculate the expected value of projects given a range of outcomes and their associated probabilities and then to calculate the value of perfect information about the projects.

Suggested Approach Candidates should firstly calculate the expected value of the net present value without perfect information. They should then select the best outcome for each of the possible consumer demands and apply the probabilities to these to calculate the expected value with perfect information. The value of perfect information can then be calculated as the difference between the expected value with perfect information and the best of the expected values without perfect information. Marking Guide

Marks

Expected value without perfect information Expected value with perfect information Value of perfect information

1½ mark 2½ mark 1 mark

Maximum marks awarded 5 marks Examiner’s comments This question was well done with many candidates obtaining full marks whereas others were awarded only 1 ½ marks for calculating the expected value of the projects. Some candidates misunderstood how to

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 12

apply the perfect information, selecting by project rather than by consumer demand or adding together all of the expected values. Common errors

• Calculating the expected value of the consumer demand rather than the expected value of the projects

• Comparing the total of the expected values of the projects to the total of the three best outcomes • Lack of understanding of how to calculate the expected value with perfect information

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 13

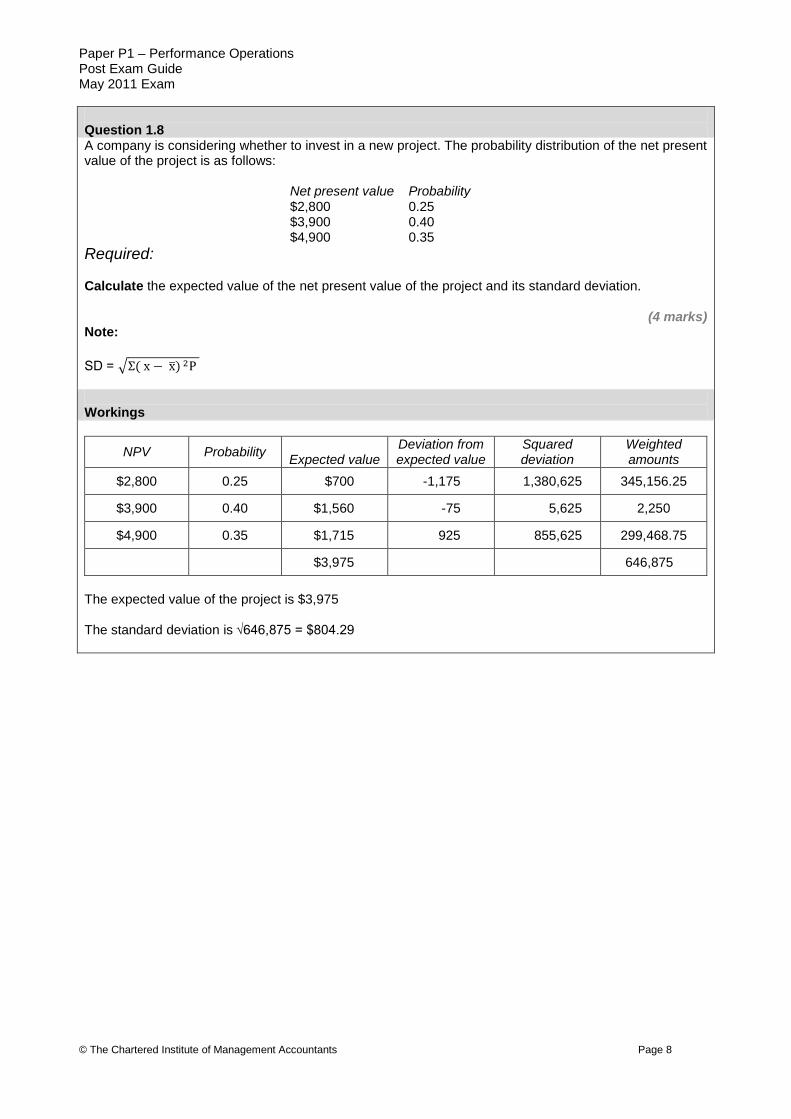

Question 2(c) TS operates a fleet of vehicles and is considering whether to replace the vehicles on a 1, 2 or 3 year cycle. Each vehicle costs $25,000. The operating costs per vehicle for each year and the resale value at the end of each year are as follows:

Year 1 $

Year 2 $

Year 3 $

Operating costs 5,000 8,000 11,000 Resale value 18,000 15,000 5,000

The cost of capital is 6% per annum. Required: Calculate the optimum replacement cycle for the vehicles. You should assume that the initial investment is incurred at the beginning of year 1 and that all other cash flows arise at the end of the year.

(5 marks)

Rationale The question assesses learning outcome C1(g) prepare decision support information for management, integrating financial and non-financial considerations. It examines candidates’ ability to calculate the optimum replacement cycle for an asset.

Suggested Approach Candidates should firstly calculate the net present value if the vehicles were replaced after each of 1 year, 2 years or 3 years. They should then divide the present value of the cash flows by the cumulative discount factor for 1 year, 2 years and 3 years respectively. The selection of the optimum replacement cycle should then be based on the lowest annualised equivalent cost. Marking Guide

Marks

Calculation of net present value for each cycle Use of cumulative discount factor Annualised equivalent Choice of replacement cycle

3 marks 1 mark ½ mark ½ mark

Maximum marks awarded 5 marks Examiner’s comments This question was not particularly well done. Few candidates knew the correct approach to take. Although most recognised the need to calculate the net present value for each of the alternatives they did not know what to do once they had calculated the NPV. Many went no further and selected the replacement cycle based on the NPV. Some decided on a basic approach and divided by 1, 2 and 3 years. Surprisingly few knew that the cumulative discount factor needed to be used to find the annualised equivalent cost. The more ambitious candidates tried to do rolling cycles but most who did this went for a three year approach rather than a more sensible six year cycle so the results were not comparable. Common errors

• Including the cost of the vehicle in year 1 rather than in year 0

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 14

• Allocating the cost to the wrong years • Failure to calculate an annualised equivalent cost

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 15

Question 2(d) Discuss the advantages AND disadvantages of factoring as a method of managing trade receivables.

(5 marks) Rationale The question assesses learning outcome E1(f) analyse the impacts of alternative debtor and creditor policies. It examines candidates’ ability to discuss the advantages and disadvantages of factoring as a method of managing a company’s trade receivables. Suggested Approach Candidates should firstly consider the potential benefits to a company of using factoring and then contrast with the potential disadvantages that can arise from its use. Marking Guide

Marks

1 mark for each advantage or disadvantage Up to 3 marks for either advantages or disadvantages

5 marks

Maximum marks awarded 5 marks Examiner’s comments This question was very well answered with candidates showing a good knowledge of both the advantages and disadvantages of factoring. The majority of candidates scored full marks for this question. Common errors

• Failure to explain points clearly

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 16

Question 2(e)

Describe the following methods of export financing:

(i) Bills of exchange (ii) Forfaiting (iii) Documentary credits

(5 marks)

Rationale The question assesses learning outcome E2(c) identify appropriate methods of finance for trading internationally. It examines candidates’ ability to describe three suggested methods of export financing. Suggested Approach

Candidates should consider each of the methods in turn describing the main features of each method and how they operate. Marking Guide

Marks

1 mark per valid point Up to 3 marks for each method

5 marks

Maximum marks awarded 5 marks Examiner’s comments This question demonstrated a lack of knowledge in some areas of the syllabus. Candidates showed some knowledge of bills of exchange but few candidates had any knowledge whatsoever of forfaiting and documentary credits. This question examines an important learning outcome and yet has obviously been considered a peripheral part of the syllabus and not studied by candidates. Common errors

• Inability to answer the question due to lack of knowledge • Making general statements for all three methods in a vain hope of gaining some marks

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 17

Question 2(f)

A bond has a coupon rate of 6% and will repay its nominal value of $100 when it matures after four years. The bond will be purchased today for $103 ex-interest and held until maturity. Required: Calculate, to 0.01%, the yield to maturity for the bond based on today’s purchase price.

(5 marks) Rationale The question assesses learning outcome E2(d) Illustrate numerically the financial impact of short-term funding and investment methods. It examines candidates’ ability to calculate the yield to maturity on a bond given the current market value and the coupon rate of the bond. Suggested Approach Candidates should identify the cash flows if the bond is purchased today and then held until maturity. They should then discount the cash flows using two different discount rates to determine a positive and a negative net present value. Candidates should then use interpolation to calculate the IRR of the cash flows.

Marking Guide

Marks

Calculation of present value of cash flows ½ mark each 3 marks 1 mark 1 mark

Calculation of net present value ½ mark each Interpolation Maximum marks awarded 5 marks Examiner’s comments Generally this question was well done although candidates continue to make simple mistakes. Most candidates recognised the need to perform two net present value calculations and then use interpolation to calculate the IRR. Common errors

• Using $100 rather than $103 as a cash outflow in year 0 • Applying 6% interest to $103 rather than to $100 • Assuming only three years of interest rather than four years

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 18

Section C – 50 marks ANSWER BOTH THE TWO QUESTIONS

Question 3

(a) Calculate, for the original budget, the budgeted fixed overhead costs, the budgeted variable overhead cost per tray and the budgeted total overheads costs.

(3 marks)

(b) Prepare, for last year, a budget control statement on a marginal cost basis for the

Premium product.

The statement should show the original budget, the flexed budget and the total budget variances for sales revenue and each cost element.

(5 marks)

(c) Discuss the benefits of flexible budgeting for planning and control purposes.

You should use the figures calculated in (b) above to illustrate your answer.

(6 marks)

(d) The company has previously calculated only a sales volume variance but has now decided

that valuable management information will be provided by further analysis of this variance.

(i) Calculate the sales quantity contribution variance. (3 marks)

(ii) Calculate the sales mix contribution variance.

(3 marks)

(e) Explain why the analysis of the sales volume variance into the sales quantity and sales mix variances will provide valuable management information.

Your answer should refer to the figures calculated in (d) above.

(5 marks)

(Total for Question Three = 25 marks)

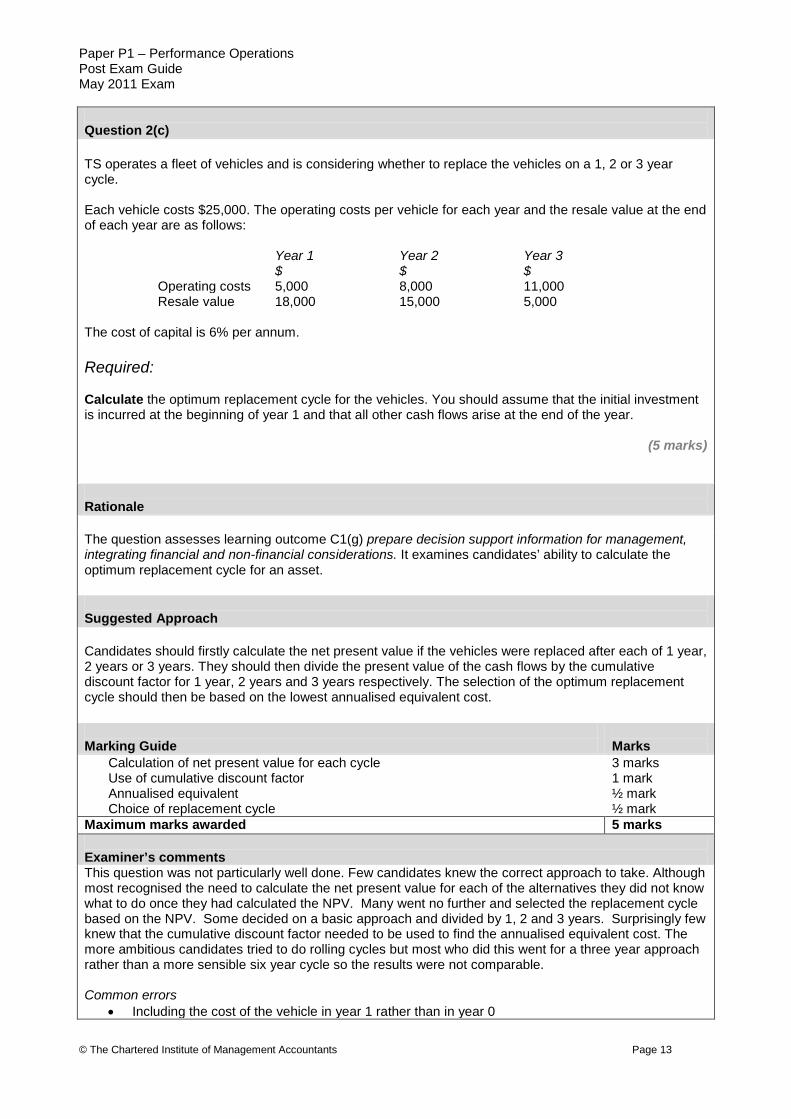

Rationale The question assesses a number of learning outcomes. Part (a) assesses learning outcome B2(b) calculate projected revenues and costs based on product/service volumes; pricing strategies and cost structures. It examines candidates’ ability to calculate projected overhead costs using the high-low method. Part (b) assesses learning outcome A1(d) apply standard costing methods, within costing systems, including the reconciliation of budgeted and actual profit margins. It examines candidates’ ability to prepare a flexible budget statement and calculate variances using information regarding cost behaviour. Part (c) assesses learning outcome A1(b) discuss a report which reconciles budget and actual profit using absorption and/or marginal costing principles. It examines candidates’ ability to discuss the benefits of flexible budgeting when producing a report that reconciles budget and actual contribution. Part (d) also assesses learning outcome A1(d) apply standard costing methods, within costing systems, including the reconciliation of budgeted and actual profit margins. It examines candidates’ ability to

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 19

calculate sales mix and sales quantity variances. Part (e) assesses learning outcome A1(f) interpret material, labour, variable overhead, fixed overhead and sales variances, distinguishing between planning and operational variances. It examines candidates’ ability to explain why the analysis of the sales volume variance into the sales mix and sales quantity variance provides useful management information. Suggested Approach Candidates should firstly apply the high-low method in part (a) to calculate the variable overhead cost per unit and use this to then calculate the total variable overheads and fixed overheads. They should then use these figures in part (b) to produce a flexed budget statement showing the flexed budget for the actual volume of production and sales and compare this to the actual results to calculate the variances for sales and each cost element. In part (c) they should use the figures calculated in part (b) to discuss the benefit of comparing actual results with a flexed budget rather than with the original budget which was based on a different level of output. In part (d) they should calculate the sales mix contribution variance and sales quantity contribution variance. In part (e) they should explain use the figures calculated in part (d) to demonstrate why this analysis provides management with more useful information.

Marking Guide Marks

Part (a) Budgeted variable cost per unit Budgeted fixed overheads Budgeted total overheads

1 mark 1 mark 1 mark

Part (b) Flexed budget ( ½ mark each element) Variances from flexed budget ( ½ mark each variance)

2 ½ marks 2 ½ marks

Part (c) 1 mark per valid point Part (d) Sales quantity contribution variance

6 marks 3 marks

Sales mix contribution variance 3 marks Part (e) 1 mark per valid point

5 marks

Maximum marks awarded 25 marks Examiner’s comments

This question was generally poorly done. Disappointingly few candidates scored highly on this question despite the fact that part (a) and part (b) are at Certificate level standard. Flexible budgeting is a fundamental concept but it was obvious from the answers to part (c) that some candidates had never heard the term despite the fact that the technique is used in variance analysis. In part (a) many candidates decided not to use the high-low method but instead to perform a medium-high or medium-low calculation of their own invention. Candidates did usually manage to follow through with their own incorrect variable cost per unit to derive at least one of the fixed or variable overheads. In part (b) most candidates did not produce a flexible budget statement despite being asked for one.

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 20

However, most did attempt to reconcile what ended up to be the flexible figures against the actuals. The weaker candidates gave the variances for the flexible budget against the original budget and some, despite using the heading flexible budget, gave the actual figures and calculated the variances just between the actual and the original budget. Candidates obviously expected a variance analysis question that required them to reconcile the original budgeted profit with the actual profit and, despite the fact that this was not what was asked, decided to do this anyway. The result was lot of unnecessary work for only 5 marks. Candidates who did not produce a flexible budget statement in part (b) struggled in part (c) to explain the benefits of flexible budgeting. Many candidates discussed changing budgets for movements in prices and other external factors but few discussed the flexing in terms of activity level. In part (d) most candidates were unable to calculate the sales quantity contribution variance with the majority clearly not knowing what it was. Many candidates calculated a volume variance but even this was badly done since the variance was calculated using sales price rather than contribution. The sales mix contribution variance was tackled much better with candidates usually deriving correctly the actual sales at budget mix. Quite a few then got the signs of the variances the wrong way round and many used incorrect contribution figures (or sales prices). In part (e) candidates were able to discuss the mix variances and how the change in the mix had affected the contribution. A number of candidates however decided to explain why a material mix variance was calculated. Common errors

• Inability to apply the high-low method to cost estimation • Failure to produce a budget control statement • Comparison of original budget with actual figures to calculate variances • Comparison of flexed budget with the original budget to calculate variances • Lack of knowledge of the purposes of flexible budgeting • Assuming the budget was changed for a number of different variables rather than just volume • Calculation of sales volume contribution variance rather than sales quantity contribution variance • Using sales price to evaluate sales volume and sales mix variances • Using actual contribution rather than standard contribution to evaluate variances • Lack of knowledge of reasons to calculate a sales mix and sales quantity contribution variance • Discussion of material mix variances rather than sales mix variances

.

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 21

Question 4

(a) Calculate the net present value (NPV) of the project. Workings should be shown in $millions.

(12 marks)

(b)

(i) Calculate the internal rate of return (IRR) of the project.

(ii) Calculate the discounted payback period of the project. (5 marks)

(c) Discuss the reasons why a company may want to calculate the IRR and discounted payback period of a project even though NPV is the theoretically superior method of investment appraisal.

(4 marks)

(d) Explain the benefits to a company of carrying out a post-completion audit of a project. (4 marks)

Total for Question Four = 25 marks)

Rationale Part (a) assesses learning outcomes C1(b) apply the principles of relevant cash flow analysis to long-run projects that continue for several years and learning outcome C2(a) evaluate project proposals using the techniques of investment appraisal. It examines candidates’ ability to identify the relevant costs of a project and then apply discounted cash flow analysis to calculate the net present value of the project. Part (b) also assesses learning outcome C2(a) evaluate project proposals using the techniques of investment appraisal. It examines candidates’ ability to calculate the IRR and discounted payback period of a project. Part (c) assesses learning outcome C2(b) compare and contrast the alternative techniques of investment appraisal. It examines the candidates’ ability to discuss why certain investment appraisal techniques might be used in practice despite their theoretical disadvantages. Part (d) assesses learning outcome C1(a) explain the processes involved in making long-term decisions. It examines candidates’ ability to explain the benefits of carrying out a post-completion audit of a project. Suggested Approach In part (a) candidates should identify the relevant cash flows for each year of the project including the loss of contribution from the 4G model. They should then calculate the tax depreciation and tax payments. The net cash flows after tax should be discounted at the discount rate of 8% to calculate the NPV of the project. In part (b) the same cash flows should then be discounted at a higher discount rate and the IRR calculated using interpolation. The discounted payback period should also be calculated using the discounted cash flows from part a). In part (c) candidates should discuss the reasons why IRR and discounted payback may be used in investment appraisal despite the theoretical superiority of NPV.

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 22

In part (d) candidates should clearly explain the potential benefits to a company of carrying out a post-completion audit. Marking Guide

Marks

Part (a) Contribution from 5G sales ( ½ mark each year) Loss of contribution from 4G sales Other fixed costs Initial investment Residual value Tax depreciation Year 1-3 Tax depreciation Year 4 Tax at 30% Phasing of tax payments Present value of cash flows Net present value of cash flows Part (b)(i) Correct use of own cash flows Use of an appropriate discount factor Net present value Interpolation Part (b)(ii) Cumulative discounted cash flows Discounted payback period Part (c) 1 mark per valid point Part (d) 1 mark per valid point

2 marks 1 mark 1 mark 1 mark 1 mark 1 mark 1 mark 1 mark 1 mark 1 mark 1 mark ½ mark 1 mark ½ mark 1 mark 1 mark 1 mark 4 marks 4 marks

Maximum marks awarded 25 marks

Examiner’s comments Overall this question was well done and showed some improvement in candidates’ ability to deal with project appraisal questions. Most candidates scored well in part (a) although too many candidates are still showing the initial investment occurring in Year 1 of the project. The weakest area was in the tax calculations with many candidates being unable to deal with a taxable loss arising on the project. Part (b) (i) was fairly well done but it is surprising how many candidates are unable to calculate an IRR. The weaker candidates performed two further calculations, with different discount rates, which was a poor use of time given that they had already calculated the net present value using one discount rate in part (a). In part (b) (ii) most candidates knew what was required although many candidates used undiscounted cash flows and again the weaker candidates looked at the payback from just the revenue rather than from the present value of the cash flows. A significant percentage of candidates were unable to calculate the correct payback period despite having correctly calculated the cumulative cash flows. In part (c) candidates stated that IRR was easy to understand and that payback was useful in explaining when the investment would be returned. Few candidates discussed risk. Many candidates relied on providing definitions of IRR and discounted payback and explaining why NPV was superior –

Paper P1 – Performance Operations Post Exam Guide May 2011 Exam

© The Chartered Institute of Management Accountants Page 23

unfortunately these details were not relevant to the question. Part (d) on post completion audits was very well answered with many candidates scoring full marks. Common errors

• $600m initial investment included in Year 1 rather than in Year 0 • Treating $100m residual value as working capital • Inclusion of $35m sunk costs as a cash outflow • Failure to treat the $200m lost contribution from 4G sales as a cash outflow • Calculation of tax before all costs had been included • Including $100m residual value in calculation of corporation tax payable • Treating the tax on a taxable loss as zero rather than as a tax credit • Calculating net present value at a different discount rate using already discounted cash flows • Calculating discounted payback using undiscounted cash flows • Counting year 0 as one year when calculating payback period • Defining discounted payback and IRR rather than explaining why they are used in practice