Embed Size (px)

Citation preview

WELCOME TO

PEARLMAN 2018

1

Pearlman 2018

Building Relationships – Keeping Them Strong

Special Recognition 2

Schedule of Events 3

Program Co-Chairs 8

Presenters/Biographies 9

Sustaining Members 32

Board of Directors/Officers 60

Pearlman 2018 Attendees 61

Driving Directions 80

Notes 82

Papers 84

On behalf of the Board of Directors and Sustaining Members of the Pearlman Association, I want to express our sincere appreciation to you for choosing to attend the Pearlman events this year. Whether you traveled across the country or across town, whether this is your first visit or your 25th, we have worked hard to make your time with us a rewarding and memorable experience and we hope we surpass your every expectation.

Pearlman is an organization designed, built and managed exclusively by company-side surety professionals. Its close, continuous access to the collective heartbeat of a large number of surety companies makes for a unique, targeted perspective on the needs, goals and challenges facing the industry – a perspective available to no other similarly situated organization. Our annual events draw from this special vantage point as we design our curriculum, training and recreational events.

As you take part in our events this year, please keep in mind that Pearlman has but one mission; to strengthen and enhance the talent, professionalism and career prospects of the surety professional. We will accomplish this mission through our scholarship distribution, our educational programs and our commitment to building industry relationships and keeping them strong.

Thank you, again, for joining us this year.

All the best –

R. Jeffrey Olson Chairman/Director Pearlman Association

2

SpecialRecognition

ThePearlmanwouldliketogivespecialrecognitiontothefolkswhoworktirelesslybehindthescenestomakeeachPearlmanconferenceareality.SpecialthankstoLihHudsonwhotrulydoesallthework.Shespendshoursuponhoursmakingsurethateverylittledetailisthoughtofanddealtwith.Lihworkstirelesslytomakeeachconferencethebestintheindustryandtoensurethateverythingrunssmoothly.Whenyouseeher,pleasegiveheraheart‐felt“thankyou.”Shedeservesit.SpecialthanksalsotoChristineBrakman.Chrisusuallypullsall‐nighterstoputalltheconferencematerialstogether,formattedcorrectly,andtrulyuseable.Wecan’tthankherenoughforherhardworkinpreparingThePearlman“packet”forprinting.Thankyou,Chris!AbigthankstoDavidStryjewskiforgraciouslyvolunteeringhistimetodothebooksandkeepingthePearlmanfinancesinorder.Lastly,aspecialthankstoCourtneyCarronandCherieMcCalmonwhohelpputtogetherthenametags,downloadthematerialstothumbdrives,andlotsofothertasksthathelpmakePearlmangreat.Thankyou,CourtneyandCherie.

3

ScheduleofEvents

Wednesday,September5th4:30‐7:30 HospitalityReception–WillowsLodge,Woodinville

HostedbyTheVertexCompanies,Inc.,Langley,LLP,SageAssociates,Inc.,andTheHusteadLawFirm

HospitalityReceptionEntertainmentHostedbyFauxLawGroupandWilliamsKastner

Thursday,September6th7:00‐8:00 RegistrationandBreakfast–ColumbiaWinery,Woodinville

HostedbyAlberFrank,PC,PCAConsultingGroup,andForconInternationalCorporation

AllDayCoffee/BeverageServiceHostedbyStewartSokol&Larkin,LLC

8:00‐8:15 Welcome/IntroductoryRemarks

R.JeffreyOlsonCo‐Chairs:RichardTasker,JimCurran,PaulHarmon

8:15‐9:00 Scollickv.Narula:IndustryPanelReviewofRecentReportedDecision

onFRCP15(a)Motion RobertNiesley,DanPope,MaureenO’Connell,TiffanySchaak9:00‐9:30 HiddenRisksinSpecifications,LEED,DesignandOtherPitfalls

MikeSpinelli,EllenCavallero,KurtFaux9:30‐10:00 SubcontractorDefaultInsuranceandExpeditedResolutionBonds

JonBondy,ChrisMorkan,BryceHolzer10:00‐10:15Break10:15‐10:30ThePearlmanCase

GregSmith

4

10:30‐11:15 Underwriting101 KeithLangley,BryanBullinger,GeorgeCrittenden11:15‐12:00 InternationalBondsandForeignContractorsComingtotheU.S. RichardTasker,JohnMcDevitt,LuisAragon,GinaShearer12:00‐1:15 Lunch

HostedbyWolkinCurran,LLP,SageConsultingGroupandWeinsteinRadcliffPipkin,LLP

1:15‐1:50 DealingwithBadCasesStacieBrandt,LarryRothstein,Keri‐AnnBaker

1:50‐2:35 ExperiencesatNationalInsuranceCrimeBureau MikeTimpane,DaleZlock,BillHealy,JohnFallat2:35‐3:00 Bankruptcy:What’sChanging JanSokol,ChadSchexnayder,JohnFouhy,NinaDurante3:00‐3:15 Break3:15‐3:55 ExtraContractualClaimsandHowtoAvoidThem MeredithDishaw,PaulFriedrich,AndrewTorrance,TomDuke,JohnEgbert3:55‐4:45 Supplementation:HowtoRespond WilliamMcConnell,DarrellLeonard,PatrickHustead,JenniferFiore5:00 WelcomeReception/Cocktails–ColumbiaWinery,Woodinville

HostedbyStewart,Sokol,andLarkin,LLC6:00 Dinner–ColumbiaWinery,Woodinville

HostedbyWatt,Tieder,Hoffar&Fitzgerald,LLPandJ.S.Held,LLCSPECIALENTERTAINMENTMikePipkin,SamBarker

7:15 Hold‘EmTournament–ColumbiaWinery,Woodinville

DealersSponsoredbyBenchmarkConsultingServices,LLCandWeinsteinRadcliffPipkin,LLP

CocktailsHostedbyKrebsFarley,PLLC

5

Friday,September7th7:30‐8:30 RegistrationandBreakfast–ColumbiaWinery,Woodinville

HostedbyCashinSpinelli&Ferretti,LLC,andSnow,Christensen&Martineau

AllDayCoffee/BeverageServiceHostedbyGuardianGroup,Inc.

BloodyMaryBarHostedbySMTDLawLLPEspressoBarHostedbyPartnerEngineeringandScience,Inc.

8:30‐8:40 Welcome/ProgramIntroduction

R.JeffreyOlson,RichardTasker,JimCurran,PaulHarmon8:40‐9:10 WhentoSettleAroundYourPrincipal TrishWager,GregWeinstein,R.JeffreyOlson,MarcBrown,RodTompkins9:10‐9:40 ProductivityLoss:CalculationandProof JasonFair,BillSchwartzkopf,JimCarlson9:40‐10:05 RiskAssessmentinLitigationandPre‐Litigation:EmphasisonFee

ShiftingShaunaSzczechowicz,BrittanyRose,MarlaThompson,LeighAnneHenican,RosaMartinez‐Genzon

10:05‐10:20 Break10:20‐10:35 UCCArticle9:RightsoftheSurety EdRubacha,DavidPinkston10:35‐10:50 OverviewoftheNewAIAA201(2007v.2017):

EmphasisonDisputeResolution GeneZipperle,JackCostenbader,KenHumphrey10:50‐11:05 WhenYourPrincipalisDe‐Barred,NowWhat DavidKash,ToddBauer,ChristineBartholdt

6

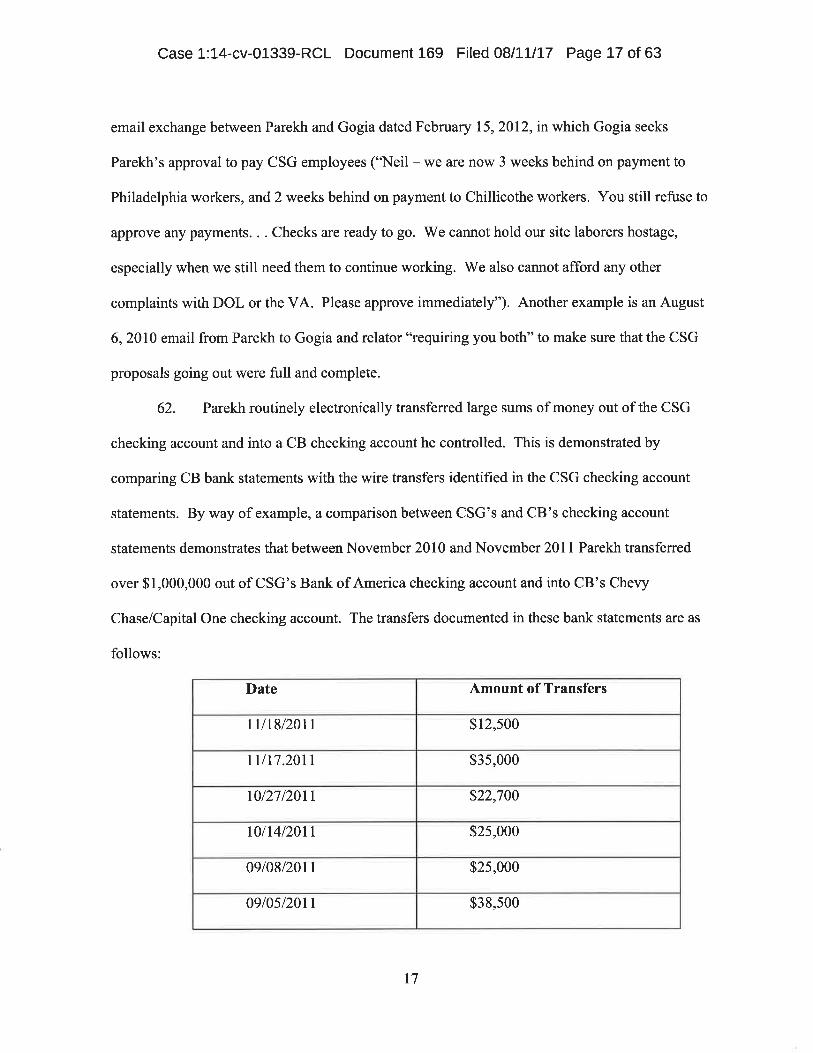

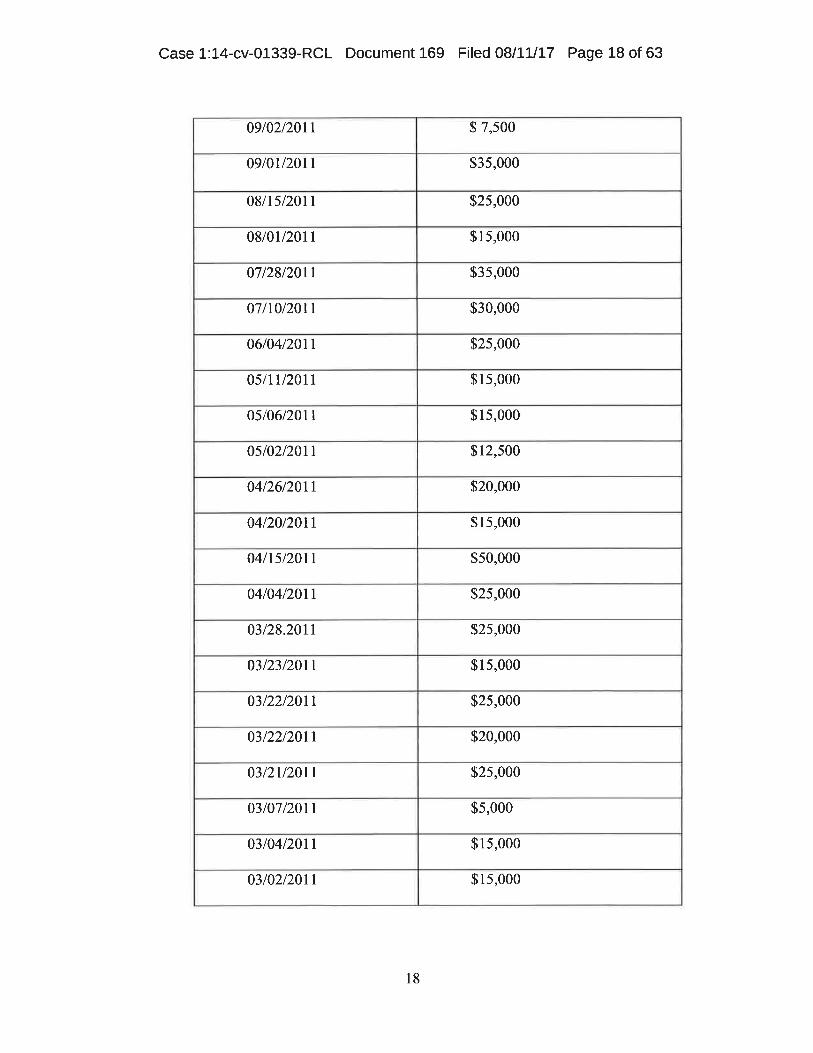

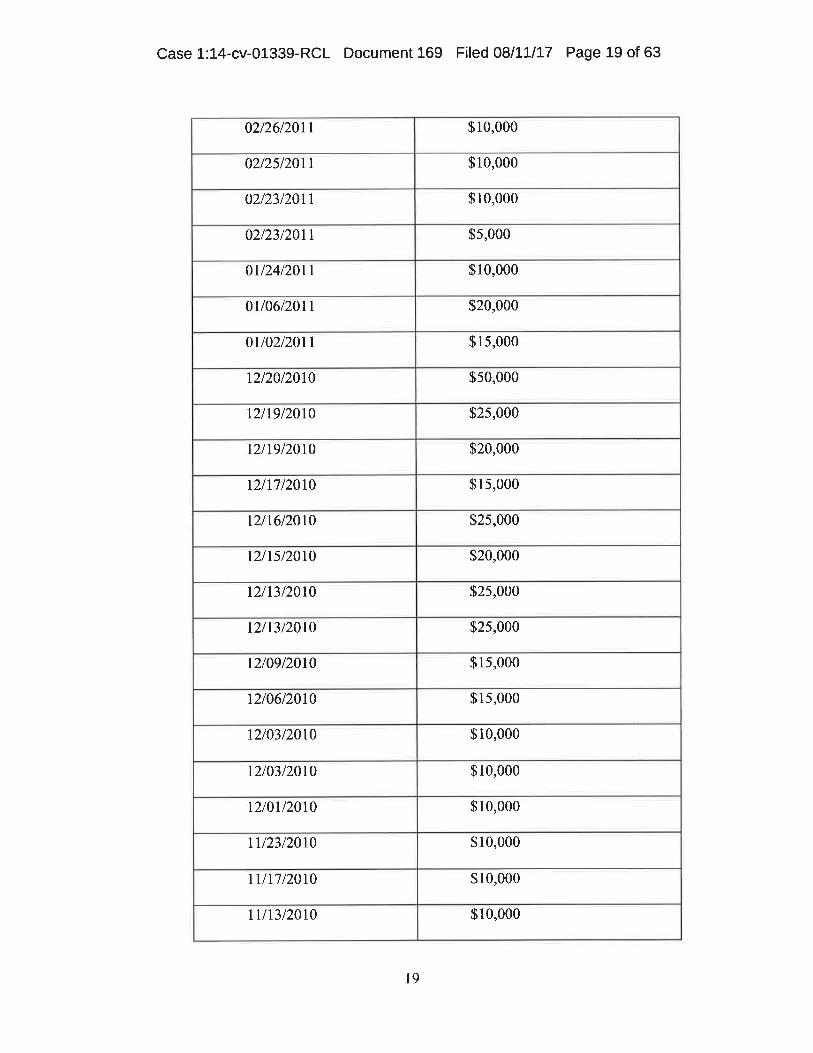

11:05‐11:45 Fees,Costs,andInterestUndertheGAI CassandraHewlings,SunnyLee,RanaeSmith11:45‐12:00 ClosingComments R.JeffreyOlson12:00 Lunch–OnYourOwn12:15 BusServiceto/fromHarbourPointeGolfClub

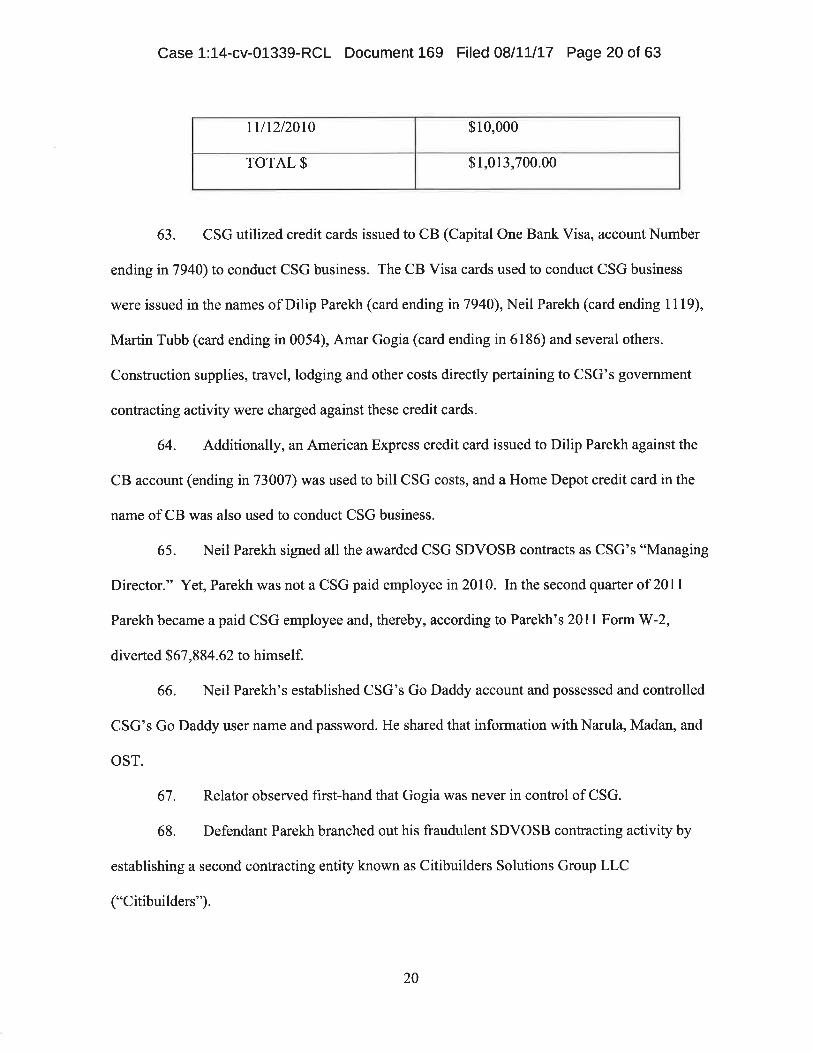

HostedbyLawOfficesofLarryRothstein BusleavesWillowsLodgeat12:15PM 1:00 SignIn/WarmUp–HarbourPointeGolfClub1:30 ScrambleTournament–ShotgunStart

HarbourPointeGolfClub,11817HarbourPointeBlvd,Mukilteo,WA98275

BeverageCartHostedbyWatt,Tieder,Hoffar&Fitzgerald,LLP,BenchmarkConsultingServices,LLC,andTheSutorGroup

7:00 Dinner–HarbourPointeGolfClubHostedbyWard,Hocker&Thornton,PLLC,ChiesaShahinian&GiantomasiPC,andKerrRussellandWeber,PLC

CocktailsHostedbyStewartSokol&Larkin,LLC

7:45 Awards–Scholarships–Closing8:00 BusesreturntoColumbiaWineryandWillowsLodge

7

Saturday,September8th‐“OnYourOwn”

WewouldliketoextendoursincerestappreciationtoourSustainingMembersandfriendsofPearlmanwhograciouslyvolunteeredtheirtimetocoordinateandchaperoneSaturday’s“onyourown”event.

Forthoseofyouwhosignedupforanyoftheelectiveevent,youwillhavereceivedbynowane‐mailmessagefromyourrespective“chaperone”alertingyoutothelogisticsofyourevent.

WoodinvilleWineTour

Torre,Lentz,Gamell,Gary&Rittmaster,LLPJ.S.HeldLLCLawOfficesofT.ScottLeo,P.C.

SMTDLawLLP JenningsHaugCunninghamLLP

8

ProgramCo‐Chairs

JAMESD.CURRANJamesD.CurranisapartnerwithWolkinCurran,LLP,locatedinSanFranciscoandSanDiego,California.Heworkswithsuretiesininvestigatingandlitigatingcommercialandcontractsuretyclaims,takingoverandcompletingpublicandprivateworksprojects,resolvingperformanceandpaymentbondclaims,pursuingindemnitors,findingassets,andobtainingrecoveriesinstate,federal,bankruptcy,andappellatecourts.RICHARDE.TASKERRichardE.TaskerisPresidentofSageAssociates,Inc.,aswellasSageConsultingAssociates,Inc.,andSageContractorServices.HehasbeenaConstructionandSuretyConsultantsincethemid‐1970’sandhasbeeninvolvedwithhundredsofcontractordefaultsandconstructiondisputes.HebeganhiscareerintheNortheast,workingforatimeintheMidwestandRockyMountainregion,andforthepast+15yearshasresidedinCalifornia.Mr.Taskerhasrepresentedmostofthetop20largestsuretiesandmanysmallervolumesuretycompanies.Hehasbeendesignatedinmanyareasofconstructionincludingforensicscheduleanalysis,efficiencyandproductivity,constructionaccounting,procurement,meansandmethods,andstandardsofcare.HeisactiveandhasoftenpresentedatindustryfunctionsincludingABA,NBCA,SCI,NASBP,andWSSC,andishonoredtoseehismanyfriendsandspeakagainatthe2018Pearlman.PAULHARMONPaulHarmonhasbeenwithTravelersBond&SpecialtyInsurancesince2007,handlingperformance,paymentandcommercialsuretyclaims.Mr.HarmonalsoprovidesbusinesssupporttoTravelersunderwritersthroughcontractreviewandriskanalysis.PriortojoiningTravelers,Mr.Harmonreceivedhisbachelor’sdegreefromtheUniversityofCalifornia,SanDiegoin2004andreceivedhisJ.D.fromtheUniversityofOregonSchoolofLawin2007.Mr.HarmonisamemberoftheWashingtonStateBarAssociation.

9

Presenters/Biographies

Wewouldliketothankeachofourco‐chairsandpresentersforthesignificanttimeandtalentthateachofthemhaveselflesslyinvestedintothesuccessofoureducationalprograms.LUISARAGONLuisAragonisSuretyClaimCounselforLibertyMutualInsuranceCompany.PriortoLibertyMutual,LuisspentovertwoyearsasasuretyattorneyintheSeattleofficeofWattTiederHoffar&Fitzgerald.LuishasaB.A.inHistorywithHonorsandaB.S.inBiochemistry,bothfromtheUniversityofWashington.LuisalsoreceivedhisJ.D.fromtheUniversityofWashington.LuissimplycannotfinditinhimselftoleaveSeattle.Outsideofwork,Luishasawifewhoisabetterlawyerthanheis,andtwoamazingyoungdaughters.Whentheladieslethimoutofthehouse,heenjoysplayingsoccer.Heisanexceptionallymediocregolfer.KERI‐ANNC.BAKERKeri‐AnnC.BakerisanofcounselattorneywiththeLawOfficesofCharlesG.Evans.Shespecializesinrealestate,environmental,tribalandsuretylaw.Keri‐AnnfoundherwaytothelastfrontieraftertwelveyearsofpracticeinsouthFlorida.SheworkswithnumerousclientsonchallengingconstructionprojectsinremotelocationsthroughoutthestateofAlaska.Shelovestosolvetrickyproblems,helpherclientslimittheirexposureandcapturerepaymentquicklyandefficiently.Keri‐Annisavidreader,lovestofish,hikeandcamp.Whensheisnotatworkyoucanfindhersomewhereoutsidehiking,paddleboardingorskiing.CHRISTINEBARTHOLDTChristineBartholdtisSeniorSuretyClaimsCounselwithLibertyMutualSuretyintheSeattleclaimsoffice.Sheisa1994graduateofWilliamMitchellCollegeofLaw.AfterrelocatingfromMinneapolis,shepracticedlawinSeattlepriortojoiningSafecoSuretyin1999.

10

TODDM.BAUERToddM.BauerisExecutiveVicePresidentofGuardianGroup,Inc.andhasmorethan30yearsofconstructionandgeneralmanagementexperience.ToddreceivedhisBachelorofSciencedegreefromtheUniversityofSouthernCaliforniaandreceivedhisgraduatedegreefromtheUniversityofTexasatAustin.Heisaffiliatedwithnumerousindustryorganizations.Toddassistsnumerousclientswithclaimsinvestigationandsettlement,forensicaccounting,takeoverandcompletionofdefaultedcontracts,bondclaimanalysis,affirmativeclaimpreparation,delayclaimanalysis,scheduling,andaccountingauditsaswellasprovidedlitigationsupportandhasactedasanexpertwitness.Inaddition,Mr.Bauer’sexpertiseincludesprojectmanagementofschools,residentialhousing,airports,highways,undergroundconduit,hospitals,powerplants,subdivisions,gasprocessingplants,prisons,landscaping,computersystems,manufacturingprocesses,aswellasroofing,glazingandelectricalprojects.Mr.BauerisalsothePresidentofCompletionContractors,Inc.,Guardian’sgeneralcontractingsubsidiary,andholdsaCommercialCaliforniaContractors“B”license.HeisalsolicensedbyTheU.S.TreasuryasaU.S.CustomsBroker,andprovidesexpertiseintheinvestigationandresolutionofU.S.CustomsandFMCbondclaims.Mr.BauerhasalsoactedasleadonClaimDepartmentoutsourcingandclaimsrunoffassignmentsforsuretycompaniesandstate’sDepartmentsofInsurance.JONATHANBONDYJonathanBondyisamemberofChiesaShahinian&GiantomasiPC,whichmaintainsofficesinNewYorkCityandWestOrange,NewJersey.HereceivedhisBachelorofScienceinEconomicsfromtheWhartonSchoolofBusinessoftheUniversityofPennsylvaniain1988,andaJurisDoctordegreein1991fromtheBenjaminN.CardozoSchoolofLaw,YeshivaUniversity,wherehewasamemberoftheMootCourtHonorSociety.Mr.BondypreviouslyservedasanAssistantDistrictAttorneyinKingsCounty(Brooklyn),NewYork.Heconcentrateshispracticeinsuretyandfidelitylaw,andcommercialandconstructionlitigation.HeisamemberoftheNewYorkandNewJerseyStateBarAssociationsandtheFidelityandSuretyLawCommitteeoftheTort,TrialandInsurancePracticeSectionoftheAmericanBarAssociation.HeisadmittedtopracticeinNewYorkandNewJersey,theUnitedStatesCourtofAppealsfortheSecondCircuit,andtheUnitedStatesDistrictCourtsfortheSouthernandEasternDistrictsofNewYorkandtheDistrictofNewJersey.HehaspreviouslyspokenonsuretyandconstructionlawissuesbeforetheFidelityandSuretyLawCommitteeoftheAmericanBarAssociation’sTort,TrialandInsurancePracticeSection,theSuretyClaimsInstitute,theNortheastSurety&FidelityClaimsConference,andtheCommercialFinanceAssociation.

11

STACIEL.BRANDTStacieL.BrandtisapartnerintheOrangeCountyofficeofBooth,Mitchel&StrangeLLP.Shespecializesinsuretylitigation,emphasizingconstruction,prevailingwage,andprobatematters.SheisamemberoftheCaliforniaBarAssociationandadmittedtopracticebeforeallstateandfederalcourtsinCalifornia.Ms.Brandtreceivedherjurisdoctoratein1993fromtheUniversityofSanDiegoSchoolofLawwhereshewasamemberoftheSanDiegoLawReviewandeditor‐in‐chiefofthelawschoolnewspaper.ShereceivedaBachelorofSciencedegreeinmechanicalengineeringfromCornellUniversityin1979.Ms.Brandtworkedforanumberofyearsformajorchemicalcompanies,andlongagowasamemberoftheSocietyofWomanEngineers(1975‐1979)andtheSocietyofPlasticsEngineers(1979‐1990).MARCBROWNMarcBrownispresentlyManagingDirector&CounselintheWesternRegionofTravelersBond&SpecialtyInsuranceClaim,whereheoverseesateamofattorneysandclaimrepresentativesandprovidesbusinesssupporttotheWesternRegionunderwritingteam.Marchas25yearsofexperienceinSuretyClaims.PriortoembarkingonhisSuretycareer,hewasinprivatepracticeintheSeattlearea,representinggeneralcontractors,subcontractors,andownersinconstructiondisputes.HeisagraduateoftheSeattleUniversitySchoolofLawandBrighamYoungUniversityandisadmittedtopracticeintheStateofWashington.BRYANBULLINGERBryanreceivedhisBachelor’sandMBAatGonzaga,graduatingin2006and2009respectively.HiscareerbeganatTravelersinmid‐2006ontheP&Csideinthecallcenter,butafterayearandahalfhemovedovertounderwritingforGuardianLifeInsuranceinSpokanewherehespentthenext4years.In2012hestumbledacrossthesuretyworldandlandedaroleasatraineeintheTravelersFederalWayhomeoffice.Afterabout2yearsinFedWayhewastransferredtotheTravelersSouthernCaliforniaregionwherehehandledabookrangingfromSanDiegotoElCentrotoPalmdale.HealsomethiswifewhilelivinginOrangeCounty,andinlate2016convincedhertomovewithhimbacktoSeattlewhentheopportunitysurfaced.TheyhavebeenlivingintheNorthgateareanowsinceJanuary2017,andhejustpassedhis6yearanniversaryworkinginthesuretyworld.Finallyhe’saTaurusthatenjoyslongwalksonthebeach.

12

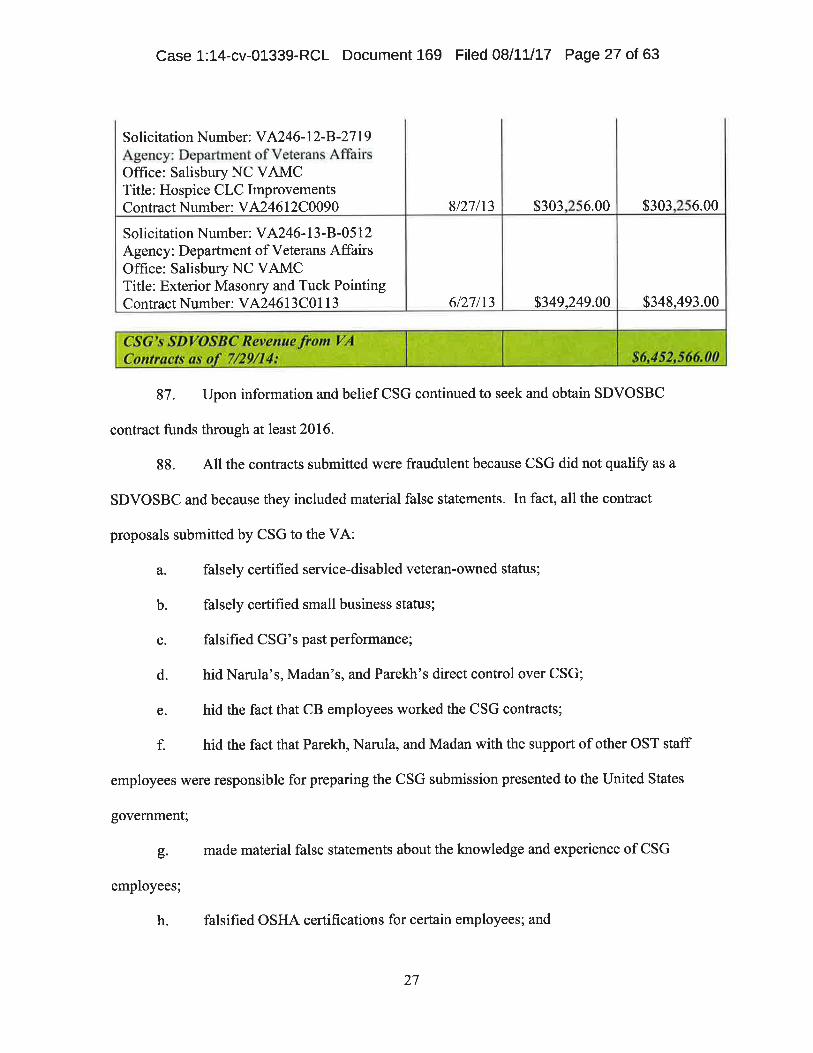

JIMCARLSONJimCarlson,TechnicalDirectorofOwner’sRepresentativeandSuretyServices,worksoutofPartnerEngineeringandScience,Inc.’sSantaAnaoffice.HeisaCalPolyPomonaandUniversityofLaVernegraduatewithaBachelorofScience,aMasterofBusinessAdministration,andaJurisDoctorate.Mr.Carlsonhasover15yearsofexperienceinexecutive‐leveltechnicalanalysisofmechanicalsystemsandcontrols,electricalandplumbingsystems,andstrategicplanning.Hehasworkedonpublicandprivateprojectscopesthatrangefromminorrepairstolarge‐scaleandtechnicallycomplex,bothlocallyandinternationally,including:militarybases,industrialsites,heavyhighwayandcivildesign,residential,andcommercialtenantimprovement.ELLENCAVALLAROEllenCavallaroisanAssistantVicePresidentofBerkleySuretyGroupLLC.ShehasaBAfromFordhamUniversity,anMAfromColumbiaUniversity,andJDfromFordhamUniversitySchoolofLaw.SheisadmittedtothepracticeoflawinNewYork.SheisaformerViceChairoftheSuretyandFidelityLawCommitteeoftheAmericanBarAssociation,andSecretaryoftheSuretyClaimsInstitute.JACKCOSTENBADERJackCostenbaderisPresidentofPCAConsultingGroup,aSanFranciscobasedconstructionconsultingfirmandPCADisbursements,Inc.aCalifornialicensedFundsControlAgent.Jackhas40yearsofdirectexperienceincontractsurety,andpropertyinsuranceclaimsconsultingthroughoutthecountry.Inaddition,Jackhas11yearsofhands‐on,buildforprofitconstructionexperience.Hisprofessionaltradeorganizationsinclude:AmericanArbitrationAssociation EscrowAgent’sFidelityCorporationAmericanInstituteofConstructors NationalBondClaimsAssociationAmericanConcreteInstitute PearlmanAssociationAmericanBarAssociation‐Associate PhiladelphiaSuretyClaimsAssociationAtlantaSuretyClaimsAssociation SuretyClaimsAssociationofLosAngelesConstructionSpecificationInstitute SuretyClaimsInstituteChicagoSuretyClaimsAssociation

13

GEORGECRITTENDENGeorgeCrittendenisAssistantVicePresidentUnderwritingOfficerforCoreContractSuretyintheWesternRegionforLibertyMutualSuretyhandlingtheSeattleandSpokaneoffices.GeorgebeganhiscareerwithUSF&GinKansasCityin1985.In1989GeorgewenttoAmericanStatesInsuranceservingvariousfieldofficesinKansas,AlabamaandMinnesotaoveran8yearperiod.In1997SafecopurchasedAmericanStates.In2006whileatSafecoGeorgewaspromotedfromcontractmanagerinKansasCitytoAssistantVicePresidentUnderwritingOfficerintheSeattleHomeOffice.In2008LibertypurchasedSafeco.AsaHomeOfficeUnderwritingOfficer,GeorgehasworkedwithofficesinBoston,Philadelphia,SanFrancisco,Cincinnati,St.Louis,KansasCity,Richmond,SeattleandSpokane.GeorgegraduatedfromEmporiaStateUniversity(KS)in1984withaB.S.inBusinessAdministration,andhehasearnedhisCPCU,AFSBandAIMdesignations.JAMESD.CURRANJamesD.CurranisapartnerwithWolkinCurran,LLP,locatedinSanFranciscoandSanDiego,California.Heworkswithsuretiesininvestigatingandlitigatingcommercialandcontractsuretyclaims,takingoverandcompletingpublicandprivateworksprojects,resolvingperformanceandpaymentbondclaims,pursuingindemnitors,findingassets,andobtainingrecoveriesinstate,federal,bankruptcy,andappellatecourts.MEREDITHDISHAWMeredithDishawisanassociateintheSeattleofficeofWilliamsKastnerandpartoftheConstructionandSuretyPracticeTeams.Herpracticefocusesonrepresentingpublicandprivateowners,contractors,andsuretiesthroughouttheconstructionprocess,withaparticularfocusoncommercialconstructionlitigation.Ms.Dishawhasrepresentedclientsinfederalandstatecourtsthroughoutthecountryandinprivatearbitrationproceedingsinvariousconstruction‐relatedmatters,includingpayment,performanceandsupplybondclaims,promptpaymentclaims,mechanic’slienclaims,indemnityissues,latentandpatentdefectsinconstructionanddesign,andcontractandwarrantyclaims.Ms.Dishaw’spracticealsofocusesondefendingsuretiesandinsurersfromcommonlawandstatutorybadfaithandextra‐contractualclaims.

14

THOMASH.DUKEThomasH.DukeisSeniorSuretyClaimsCounselforAmTrustSuretyintheClaimsDepartmentandislicensedtopracticelawintheStateofTexas.Hehasmorethan25yearsofcombinedlegalexperienceasanAssistantUnitedStatesAttorneyintheSouthernDistrictofFloridaandinprivatepracticeasaciviltrialattorney.BeforejoiningAmTrust,Tomwasinprivatepracticefor16yearsspecializinginsuretylaw.TomreceivedhisJurisDoctorfromtheFredricG.LevinSchoolofLawandBachelorofArtsinEnglishfromtheUniversityofFlorida.HealsohasaMastersofDivinitywithLanguagesdegreefromSoutheasternBaptistTheologicalSeminary.TomismarriedtoSuzanne,hiswifeof36years.Theyhavetwochildren,RachelandHaden,bothofwhomaremarried,andonegrand‐daughter,JulietFaye.NINAM.DURANTENinaM.DuranteisSeniorSuretyClaimsCounselwithLibertyMutualInsuranceCompanyinitsCommercialClaimsDepartment.SheisbasedinSeattle,WA.Formostofherprofessionalcareer,Ninahasworkedinthesuretyindustryhandlingavarietyofclaims,includingcontract,fidelityandmiscellaneousmatters.In2013,NinajoinedLiberty’snewlycreatedCommercialClaimsRegionwhereshehandlesavarietyoflargecommercialclaims,bankruptcies,andcontractclaims.

NinareceivedherB.A.inPoliticalSciencefromSeattleUniversityandherJ.D.fromtheUniversityofPugetSoundSchoolofLaw(now,SeattleUniversitySchoolofLaw).SheisanactivememberoftheWashingtonStateBarAssociationandtheAmericanBarAssociation‐TIPSsection.JOHNT.EGBERTJohnT.EgbertistheownerofGlobalConstructionServices,Inc.,acompanywhichspecializesinconstructionconsultingandsuretyclaims.Servicesprovidedtothesuretyindustryincludeevaluatingperformancebondclaims,estimatingthecosttocompete,preparationofre‐letpackages,evaluatingpaymentbondclaims,monitoringtheworkofacompletioncontractor,andassistingwithprojectcloseoutandwarrantyissues.Johnalsoperformsprojectscheduling,evaluatesscheduledelaysandimpacts,preparesTimeImpactAnalyses,calculatesdamages,preparesconstructionclaims,andoffersexpertwitnessservicesatmediations,arbitrationsandtrials.JohngraduatedfromtheU.S.CoastGuardAcademyandholdstwograduatedegreesinengineeringfromStanfordUniversity.

15

JASONFAIRJasonR.FairisanAssociateintheLosAngelesofficeofRobinsKaplanLLP.Mr.Fair’spracticefocusesonassistingclientsintheconstruction,fidelity,andsuretyfields.Mr.Fairguidesandcounselssureties,generalcontractors,subcontractors,andowner/developersthroughcomplexdefaultscenariosandhestrivestoapplypragmaticandcost‐effectivestrategiestomitigatelossesandcompletetroubledprojectswhileresolvingprojectdisputes.Mr.Fairisexperiencedinhandlingfederal,state,andprivateconstructionprojects,includingissuesrangingfrombiddingprocessesandproteststogeneraldelay,productivity,andefficiencyclaims,aswellastermination,takeover,andcompletionagreementsandsuretyfinancingagreements.Mr.Fairalsoassistsclientsingenerallitigationmatters,includingbusiness,commercial,andpropertydisputes.Hehandlesallstagesoflitigationinbothstateandfederalcourtandhecounselsclientsthroughthealternativedisputeresolutionprocess.Mr.FairreceivedhisB.A.fromUniversityofCalifornia,LosAngelesandhisJ.D.fromLoyolaLawSchoolwherehewasamemberoftheSt.ThomasMoreLawHonorSociety.Mr.FairisadmittedtopracticeinCaliforniaandU.S.DistrictCourt,CentralDistrictofCalifornia.Mr.FairisamemberofABATortTrial&InsurancePracticeSection,FidelityandSuretyLawCommittee,CenturyCityBarAssociation,RiversideCountyBarAssociation,andSanBernardinoCountyBarAssociation.JOHNL.FALLATJohnL.FallatwasadmittedtotheCaliforniaBaraftergraduatingcumlaudefromtheCaliforniaWesternSchoolofLawin1984.Hehasbeenpracticingsuretybonddefensesince1986whenhejoinedtheOaklanddefensefirmofBennett,Samuelson,Reynolds,andAllardindefendingamongnotarypublicsuretybondsfortheKirbybrotherswhothenownedWesternSuretyCompany,nowpartofCNA.HethenjoinedWilliams&MartinetinSanFranciscowhereheexpandedhissuretybondpracticetoincludealltypesofclaimandlawsuits.Hestartedhisownpracticein1989representingsuretiesthroughoutCaliforniawithanemphasisoncommercialclaims.Thefirmcurrentlyhastwoassociatesandthreeparalegals.HeconsidershimselfveryfortunatetohavestumbledintothisfieldwhichhasenabledhimtoraiseafamilyinMarinCountyandbefreetorepresentclientsinothercivillitigationsuchasconsumerclassactions,employmentlitigation,andrealestatedisputes.

16

KURTFAUXKurtFauxisthepresidentandfounderoftheFauxLawGroup,practicinginNevada,Utah,andIdaho.Mr.FauxreceivedaB.A.fromBrighamYoungUniversity‐Hawaii,magnacumlaude,in1982.HeobtainedaJ.D.fromBrighamYoungUniversity,J.ReubenClarkLawSchoolin1986,wherehewasaneditorfortheLawReview.Mr.Fauxhasrepresentedsuretiesforover30years,andisafrequentpresentertovariousgroupsregardingsuretyandconstructionissues.JENNIFERFIOREAsaprincipalinDunlapFiore,LLC,Ms.Fiorespecializesinconstructionlaw,businesslaw,litigation,publicfinanceaswellasFederalandStateregulatoryandadministrativelawmatters.Ms.Fiore’spracticeencompassesthefullbreadthofprivateandpublicconstructionandsuretylaw.Sherepresentsclientsinthedraftingandnegotiationofcontracts;theadministrationofprojectobligations;andthepreparation,prosecutionanddefenseofclaims.Shealsohasextensiveexperienceinperformanceandpaymentguaranty‐relatedmatters,bonding,andindemnityissuesgivingheranexperienced,educatedperspectiveonallaspectsofconstruction,andsuretylaw.Ms.Fiorehasrepresentedcontractors,owners,andsuretiesandhasexperienceincontractingissuesinvolvingtheFederalAcquisitionRegulation.ShehasassistedclientswithcomplianceoftheFederalContractorethicsrulesinawidevarietyofconstruction‐relatedmatters.Ms.FioreisaVice‐ChairoftheFidelityandSuretyLawCommitteeoftheTortTrialandInsurancePracticeSectionoftheAmericanBarAssociation,amemberofAmericanBarAssociation,ConstructionLawForum,theLouisianaBarAssociation,thePearlmanAssociationandtheNationalBondClaimsAssociation.JOHNM.FOUHYJohnM.FouhyisaClaimCounselforTravelersCasualty&SuretyCompanyofAmericainFederalWay,WA,wherehehasworkedsince2010.HegraduatedwithaB.B.A.fromPacificLutheranUniversityin2005,andreceivedhisJ.D.fromtheUniversityofOregonSchoolofLawin2009.HeisadmittedtopracticeinWashingtonState.

17

PAULK.FRIEDRICH

PaulK.FriedrichisanattorneywithWilliamsKastnerandisamemberofthefirm’sConstructionLitigation&SuretyPracticeTeam.Hispracticeinvolvesrepresentingsuretiesandinsurersinallaspectsofbondclaimswithaparticularemphasisonconstructionlaw.Asignificantportionofhispracticeisdevotedtoprosecutingindemnityandsubrogationmattersonbehalfofhissuretyclients.Mr.Friedrichhasaproventrackrecordofsuccessforhisclientsatboththetrialcourtlevelandonappeal.PAULC.HARMONPaulC.HarmonhasbeenwithTravelersBond&SpecialtyInsurancesince2007,handlingperformance,paymentandcommercialsuretyclaims.Mr.HarmonalsoprovidesbusinesssupporttoTravelersunderwritersthroughcontractreviewandriskanalysis.PriortojoiningTravelers,Mr.Harmonreceivedhisbachelor’sdegreefromtheUniversityofCalifornia,SanDiegoin2004andreceivedhisJ.D.fromtheUniversityofOregonSchoolofLawin2007.Mr.HarmonisamemberoftheWashingtonStateBarAssociation.BILLHEALYBillHealyisacontractsuretyUnderwritingDirectorinTravelers’westernregionalhomeofficeinFederalWay,Washington.Billstartedhissuretycareerin1992inSanFranciscowithFidelity&DepositCompanyaftergraduatingfromU.C.Davis.HejoinedTravelersinSanFranciscoinMarchof1998andthentransferredtotheFederalWayofficeinJuly,2011.LEIGHANNEHENICANLeighAnneHenicanistheSuretyClaimsManageratTheGrayCasualty&SuretyCompanyinNewOrleans,Louisiana.Shehasovernineyearsofexperienceininsurancedefense,withmorethanfiveyearsofexperiencesolelydevotedtohandlingsuretybondclaims.SincebecomingtheClaimsManageratGrayin2015,shehasreengineeredtheentireecosystemofclaimshandlingattheorganization.Hereffortshaveincludedafocusonnegotiationratherthanlitigation,whichhasledtoadramaticdecreaselossratios,includingareductioninthenumberofopenclaimsbymorethan50%andareductioninthirdpartylegalexpensesbymorethan35%inthepastthreeyears.LeighAnneearnedherB.A.inPoliticalScienceandPublicRelationsfromtheUniversityofAlabamain2005andherJ.D.fromLoyolaUniversityNewOrleansCollegeofLawin2009.

18

CASSANDRAR.HEWLINGSCassieHewlingsisanassociatewithKrebsFarley,PLLCinNewOrleans,Louisiana,havingjoinedthefirmin2015.Cassieprimarilyfocusesherpracticeoncomplexcommerciallitigation,constructionlitigation,andsuretyandfidelitylaw.Shealsohasexperienceinprofessionalmalpractice,securitieslitigation,generaltortlitigation,andrepresentingattorneysindisciplinarymatters.CassiegraduatedsummacumlaudeandOrderofCoiffromTulaneUniversityLawSchoolin2013.Whileinlawschool,sheservedasArticlesandOnlineEditorfortheTulaneLawReviewandwasapublishedmemberaswell.Priortoattendinglawschool,CassieworkedinjournalismforvariousmediacompaniesinColorado.BRYCEHOLZERBryceHolzerisClaimCounselforTravelersBondandSpecialtyInsuranceinFederalWay,WA.BrycegraduatedfromWashingtonStateUniversitywithaB.A.inEconomics,summacumlaude,inMay,2007.AfterworkingfortheBoingCompanyasanIndustrialEngineer,BryceattendedtheUniversityOfWashingtonSchoolOfLawandgraduatedinMarchof2011.BryceworkedinprivatepracticepriortojoiningTravelersinAugust2012.BryceisamemberoftheWashingtonStateBarAssociation.KENHUMPHREYKenHumphrey,borninPasadena,California,graduatedfromUCSantaBarbara,andreceivedhisJDatLoyolaLawSchoolLosAngelesin1990.HeworkedasatriallawyerforBolton,Dunn&Yatesfrom1990to1999performingallaspectsofcivillitigationincludingconstructiondefects,insurancebadfaith,insurancecoverageissues,premisesandproductliability,andpersonalinjuryactions.Herepresentedpublicentities,self‐insuredentities,insurancecompanies,aswellascorporationsandindividuals.In1999hejoinedAmwestInsuranceGroup,Inc.’sin‐houselawfirmasaSeniorLitigatorbeforestartinghisownfirmin2002.Inthattime,hehandledhundredsofsuretydefenseandcomplexlitigationmattersincludingthoseinvolvingcontractandcommercialbonds,licenseandpermitbonds,probatebonds,andcollectionandsubrogationcases.Healsohassignificantexperienceininsurancecompanyliquidationandrehabilitationlaw.Hehastakenover25casestotrialorarbitration,andarguedmattersbeforetheCaliforniaCourtofAppeal.

19

PATRICKQ.HUSTEADPatrickQ.HusteadisthefounderofTheHusteadLawFirminDenver,Colorado.HehasaregionalpracticecenteredintheRockyMountainregion.HeisafounderoftheABAFidelityandSuretyExtra‐ContractualLiabilityCommitteeandhasrepresentedsuretiesandinsurersforover30years.HehastriedmanycasesintheRockyMountains,ontopicsrangingfrombadfaithtobraininjuriesandconstructiondefaults.HegraduatedfromBostonCollegeLawSchool,cumlaude,andisadmittedtopracticeinallcourtsinColorado,Montana,Wyoming,NebraskaandtheDakotas.Patrickhasspokenin18statesandtheUKonavarietyofinsurancerelatedtopics.Hehasover70publishedopinionsinsixstatesandhaspennedover20piecespublishedbytheABAandDRI.HegraduatedfromtheUniversityofColoradoLeedsSchoolofBusiness(BS)1981,attendedtheUniversityofParisattheSorbonne(CP)1984andgraduatedcumlaudefromBostonCollege(JD),1987.DAVIDW.KASHDavidW.KashisapartnerinthefirmofKoellerNebekerCarlson&Haluck,LLPinitsPhoenix,Arizonaoffice.Mr.KashreceivedhisBSCwithhonors(Accounting)fromDePaulUniversityin1977andhisJDfromChicago‐KentCollegeofLawwithhonorsin1981.HeisadmittedtopracticeinbothArizonaandIllinois,heisAVratedbyMartindaleHubbell,heisamemberofArizonaFinestLawyers,isrecognizedasaSouthwestSuperLawyer,andselectedtoTheBestLawyersinAmerica.Heisatrialattorneyandhispracticeincludesconstructionandsuretylaw.Mr.KashisapastChairoftheInternationalAssociationofDefenseCounsel(IADC)Fidelity&SuretyandADRCommittees.HeisapastboardmemberandpastPresidentofTheFoundationoftheIADC.Hehasauthoredavarietyoflegalarticlesandgivenseveralpresentations.HehasbeenafrequentspeakeratPearlmanAssociationGatherings.ManyofhisarticlescanbeaccessedonlineorbyrequesttoDavid.Kash@knchlaw.com.

20

KEITHA.LANGLEYFor30yearsofpractice,KeithLangleyhasfocusedonunderstandingtheclient’sbusinesswhileseekingtheearliestresolutionofissuesbystartingwithearlycomprehensiveevaluation.Hefocuseshispracticeoncomplexworkout,litigation,andbankruptcymatters.Keithisalsoexperiencedatcounselinghisclientsondisputeavoidance.HistrialexperienceincludesservingasleadcounselonfederalandstatetrialsinTexasandotherjurisdictions,aswellasasuccessfulrecordinarbitrationsandappeals.Keithstaysonthecuttingedgeofthelatesttechnologyinpresentingevidencetothesophisticatedjurorsintoday’scourtrooms.Keith’spracticeincludesconstructionandsuretylawfocusingonconstruction‐relatedclaims,lawsuits,mediations,andarbitrations.Hisexperienceinclaims,trials,arbitrations,andmediationsincludesprojectssuchashighwaysandbridges,publicworksprojects,commercialandretailconstruction,industrialandwarehousefacilities,healthcarefacilities,powerplants,pipelines,petrochemicalplants,refineries,chemicalplants,gasprocessingplants,schools,andmulti‐familyhousing.Heisafrequentauthorandspeakeronavarietyoflitigation,bankruptcy,constructionlaw,suretyandfidelitytopics.KeithislicensedinTexas,Florida,Arkansas,andOklahoma.SUNNYLEESunnyLeeisapartneratBronsterFujichakuRobbinsinHonolulu,Hawaii.AdmittedtopracticeinWashingtonandHawaii,hehasabroadlitigationbackgroundbutfocusesonSuretyandConstructionlitigation.SunnyexternedfortheHonorableKevinS.C.Chang,Magistrate,U.S.DistrictCourtfortheDistrictofHawaiiandclerkedforHawaiiSupremeCourtJusticeSabrinaS.McKennaattheCircuitCourt.Hewaspreviouslyin‐housecounselforatitleandescrowcompanybeforejoiningthefirmin2008.HereceivedaB.A.fromtheUniversityofHawaiiin1999andhisJ.D.fromSeattleUniversityin2003.Sunnyisalsoactivelyinvolvedinseveralnon‐profitboards.DARRELLLEONARDDarrellLeonardisTeamLeadandSeniorClaimsCounselforZurichAmericanInsuranceCompany.Mr.LeonardgraduatedwithhonorsfromTheUniversityofTexasSchoolofLawandcurrentlyservesasChair‐ElectoftheFidelity&SuretyLawCommitteeforABATIPS.

21

ROSAMARTINEZ‐GENZONRosaMartinez‐GenzonisapartneratAnderson,McPharlin&ConnersinLosAngeles.Herpracticefocusesontherepresentationofsuretiesinclaimsinvolvingcontractandcommercialbonds.Shehasextensiveexperienceinclaimsinvestigation,defaultanalysisandnegotiation,consultation,claimshandlingandresolutionofbondclaimsthroughlitigation,mediationandarbitration.Shehassuccessfullyhandledawiderangeofcasesonconstructionprojects,includingbiddisputes,wageandlaborclaims,delay,defaultandcompletionofprojects.Sheisknowledgeableandhaspresentedandwrittenarticlesregardingtheinterplayofinsurancepoliciesandconstructionbonds.Ms.Martinez‐Genzonisalsoexperiencedinthepursuitofsalvagerecoveriesthroughadverselitigationinbothcivilandbankruptcyproceedings.Shealsorepresentstheinterestsofsuretiesinadministrativehearings,includinghearingsbeforetheCaliforniaLaborCommissioninvolvingnonpaymentofwagesandfringebenefits.BILLMCCONNELLBillMcConnellisaco‐founderandCEOofTheVertexCompanies,Inc.,aglobalforensicconsulting,designengineering,environmental,andconstructioncompanythathascompletednearly50,000projectssince1995.Vertexcurrentlyhasover20officesandnearly500employee‐owners.BillearnedaBachelorofSciencedegreeinCivilEngineeringfromtheUniversityofMaine,aJurisDoctordegreefromtheUniversityofDenver,aMasterofScienceinCivilEngineeringDegreefromColumbiaUniversity,andheisworkingonhisDoctorofPhilosophydegreeinEngineeringandAppliedSciencefromtheUniversityofColorado.Heislicensedprofessionalengineerinmanystates.Billhasworkedintheconstructionindustryfornearlyhisentirelifeandhastestifiedapproximately150timesasanexpertonconstructiondisputes,mostnotablyforcost,allocation,scheduling,andstandardofcareopinions.JOHNA.MCDEVITTJohnA.McDevittistheRegionalVicePresidentforGlobalandSpecialtyClaimsforLibertyMutualInsuranceCompany.Priortohiscurrentrole,hewasSeniorSuretyCounselintheNortheastRegionforLibertyMutualInsuranceCompany,BondClaimsCounselforHanoverInsuranceCompany,andrepresentedcontractorandsubcontractorsinprivatepractice.HereceivedaB.A.inHistoryfromBatesCollegeinLewiston,Maine,andaJ.D.fromSuffolkUniversityLawSchoolinBoston,Massachusetts.Althoughhecanfrequentlybefoundworshipping#12athisTomBradyshrine,JohnissecretlyaSeattleSeahawksfanandhasahugecollectionofRussellWilsonjerseys.

22

CHRISMORKANChrisMorkanoverseestheclaimactivitiesofHudson’sSubcontractDefaultInsuranceproductaswellasitsotherconstructionandpropertyrelatedinsurancelines,includingsurety.HeisalsoresponsibletheoperationsofNapaRiverInsuranceServiceswhichprovidesfeebasedclaimmanagementsolutions,riskmanagement,andfundscontrolservices.ROBERTC.NIESLEYRobertC.NiesleyisaSeniorPartnerintheIrvine,CaliforniaofficeofWatt,Tieder,Hoffar&Fitzgerald,LLP.Robhasspecializedinsuretyandconstructionlawforover30years,representingfirmclientsthroughouttheUnitedStatesandinternationally.Robhastriedcasesinbothstateandfederalcourts,theCourtofFederalClaims,andmanyarbitrationforums.Robhasextensivegovernmentcontractsexperiencerepresentingsureties,andtheirprincipals,intheirdealingswithmanybranchesofthefederalgovernment,butmostlytheUnitedStatesArmyCorpsofEngineers.Sincemostcasesgetsettled,Robhasmediatedand/ornegotiatedtosettlementthousandsofcases.WithofficesinVirginia,California,Illinois,WashingtonandFlorida,WattTieder’snationalsuretyandconstructionpracticeaggressivelyrepresentsitsclientswithskilledlawyersinalmostanyforumintheUnitedStates.MAUREENO’CONNELLMaureenhasoverthirtyyearsofexperienceinthesuretyindustry,sixteenyearsworkingforsuretycompaniesasanunderwriter/managerandsixteenyearsasasuretybrokerforArthurJ.Gallagher.PriortojoiningGallagher,MaureenwastheRegionalSuretyManageroftheSanFranciscoofficesforFireman’sFundandKemperSurety.ShebeganhersuretycareerwithSafecoInsuranceCompany.InadditiontohermanagementroleatGallagher,MaureenisaSuretyProducerandAccountExecutive.Maureenhandlesmanylargeconstructionaccountsincluding,generalbuilders,generalengineeringcontractorsanddevelopersthroughouttheWesternUnitedStates.MaureenreceivedaBachelorofArtsdegreeinPoliticalEconomyofIndustrialSocietiesfromtheUniversityofCalifornia,BerkeleyandaMastersofBusinessAdministrationfromSt.Mary’sCollegeofCalifornia.

23

MaureenisontheBoardofDirectorsoftheCaliforniaSuretyFederation,NationalAssociationofSuretyBondProducersandWomeninConstruction,WestCoastandisanactivememberofCFMA,AGC,UnitedContractorsandSuretyandFidelityAssociationofAmerica.R.JEFFREYOLSONJeffOlsonisaSeniorSuretyClaimsCounselforLibertyMutual.Jeffhasworkedinthesuretyclaimsfieldsince2000,handlingprimarilyperformanceandpaymentbondclaims.JeffalsobecamethePresidentofthePearlmanAssociationin2015.Jeffenjoysspendingtimewithhisfamilyandgettinginaroundofgolfeverysooften.Heclaimsa10handicap.JeffhasbeenalicensedattorneyinthestateofWashingtonsince1996.DAVIDL.PINKSTONDavidL.PinkstonisashareholderinthefirmofSnow,Christensen&MartineauinSaltLakeCity,Utah.OriginallyanativeofSouthernCalifornia,hegraduatedcumlaudein1993fromtheJ.ReubenClarkLawSchoolatBrighamYoungUniversity,whereheservedastheLeadArticlesEditoroftheB.Y.U.LawReviewfrom1992‐93.HewasalsoamemberoftheAmericanInnsofCourtI.HereceivedaB.A.(cumlaudeandUniversityHonors)fromBrighamYoungUniversityin1990.Aftergraduationfromlawschool,hewasadmittedtotheUtahStateBarandjoinedSnow,Christensen&Martineauin1993.HeisalsoadmittedtopracticebeforetheUnitedStatesCourtofAppealsfortheTenthCircuit,aswellastheUteIndianTribalCourtoftheUintahandOurayReservation.Inadditiontobeingamemberofthefirm’sConstructionpracticegroup,heisalsoamemberofSnowChristensen’sBankruptcyandCreditors’Rightspracticegroup,representingprimarilycreditorsinbankruptcyandrelatedlitigation.Mr.Pinkston’spracticealsoinvolvescontractandothercomplexcommerciallitigation.DANIELPOPEDanielPopeisVicePresident/SeniorUnderwritingOfficerwithZurich.Hehasmorethan25yearsinthesuretyindustry,12ofthoseyearswithZurich.Dancurrentlyhasleadunderwritingresponsibilityforadiverseportfolioofnationalcontractorsinthewesternregion.Danhasheldvarioushomeofficeandfieldunderwritingrolesinadditiontosuretyclaimsandprojectmanagementrolesthroughouthissuretycareer.Danhasunderwrittenthefullspectrumofsuretyproductsbutspentthemajorityofhiscareerincontractsurety.DanearnedaJurisDoctorfromClevelandMarshallCollegeofLawandaBachelorofArtsfromtheCollegeofWooster.

24

BRITTANYROSEBrittanyRoseisaClaimCounselforTravelersBond&SpecialtyInsuranceinFederalWay,Washington.ShegraduatedfromLoyolaMarymountUniversityin2005withaB.A.inEnglish,andshereceivedherJ.D.fromSeattleUniversitySchoolofLawin2011.SheisadmittedtopracticelawinWashingtonState.LARRYA.ROTHSTEINLarryA.Rothsteinhaspracticedsuretyandconstructionlitigationforfortyyears.Hehastakenadozensuretytrialstojuryverdict,winningallofthem.In2008,hewasafeaturedparticipantinamocksuretybadfaithtrialpresentedattheABASuretyandFidelityLawmid‐wintermeeting.Hehasauthorednumerousarticlesonsuretyclaimsandrecentdevelopmentsandisafrequentpresenteratnumeroussuretyconferences.Mr.RothsteinreceivedhisundergraduatedegreefromUCLAandJ.D.fromSouthwesternUniversitySchoolofLaw.HehasbeenselectedasaSuperLawyer®sevenstraightyears.HepracticesinWestlakeVillage,CA.EDWARDRUBACHAEdwardRubachaisapartnerwiththePhoenix,ArizonalawfirmofJenningsHaugCunningham,practicinginthefirm’sSuretySection.EdhasaB.S.E.E.fromPurdueUniversity,anM.B.A.fromArizonaStateUniversity,andaJ.D.,cumlaude,fromArizonaState.EdjoinedJennings,Haugin1987.Ed’spracticeincludesrepresentingsuretiesinallphasesofbonding,includingunderwritingandclaimslitigation,includingissuesconcerningbondingonIndianreservations.EdrepresentsanumberofsuretiesinArizona,California,Colorado,andonvariousreservationsthroughoutthewesternUnitedStates.Edisadmittedtopracticeeachofthosestates,inbothstateandfederalcourt,andinanumberoftribalcourts.Edhaspublishedthreearticlesonthetopicofbondingandcontractingonthereservationandisafrequentspeakeronthatuniqueareaofthelaw.

25

TIFFANYSCHAAKTiffanySchaakbegunhersuretycareerintheclaimsdepartmentforAmericanBondingCompanyin1994andisnowtheWesternRegionalHomeOfficeCounselforLibertyMutualGroupinSeattle,WA.Ms.SchaakearnedaBachelorofArtsdegreeinFinancefromtheUniversityofPugetSoundandaJurisDoctorate,cumlaude,fromSeattleUniversitySchoolofLaw.Ms.SchaakalsohasreceivedtheAssociateinFidelityandSuretyBondingdesignationfromTheInstitutesaswellastheCharteredPropertyCasualtyUnderwritingdesignation.CHADSCHEXNAYDERChadL.Schexnayderisacommercialandsuretylitigator.Hisfirm,Jennings,Haug&Cunningham,LLPbasedinPhoenix,Arizonahasrepresentedthesuretyindustryformorethan80years.HeisagraduateofWashingtonUniversityinSt.Louis,(A.B.,cumlaude,1981)andtheSandraDayO’ConnorCollegeofLawatArizonaStateUniversity(J.D.,cumlaude,1984).HecurrentlyservesintheLawDivision(BankruptcyCo‐Chair)oftheABA/TIPSFidelityandSuretyLawCommittee.Chadisafrequentauthorandspeakertosuretyandconstructionindustrygroups,andhasmostrecentlyspokenattheSpring2018FSLCmeetinginSantaFe,NewMexicoandco‐authoredChapter12,NavigatingInandAroundBankruptcy,intheThirdEditionofManagingandLitigatingTheComplexSuretyCase(ABA2018).WILLIAMSCHWARTZKOPFWilliamSchwartzkopfheadstheconstructiondisputespracticeatSageConsultingGroup,aconsultingfirmbasedinDenver,Colorado,thatspecializesinconstructionclaimsandcontractsuretydefaults.HehastestifiedasanexpertwitnessinvariouscourtsandarbitrationforumsthroughouttheUnitedStates,Canada,Mexico,andIceland.WithintheUnitedStates,hehastestifiedinmanystateandfederalcourts,aswellasinvariousboardsofcontractappeals,disputereviewboards,andarbitrationpanels.Previously,hewasaVicePresidentandGeneralManagerofanEngineeringNews‐RecordTop150buildingcontractor,VicePresidentandGeneralCounselforanEngineeringNews‐RecordTop10specialtycontractor,aswellastheVicePresidentofOperationsforaregionalcommercialdevelopmentcompany.Mr.SchwartzkopfisalsotheauthorofCalculatingLostLaborProductivityinConstructionClaimsandPracticalGuidetoConstructionContractSuretyClaims,bothpublishedbyWoltersKluwerConstructionLawLibrary.

26

AsaregisteredProfessionalEngineer,Mr.SchwartzkopfisamemberoftheNationalSocietyofProfessionalEngineers.Heislicensed(inactive)intheNebraskaStateBarandisamemberoftheAmericanBarAssociationandbothitsForumCommitteeontheConstructionIndustryandtheSuretyandFidelitySectionoftheTortandInsurancePracticeSection.HereceivedbothaBachelorofScienceinElectricalEngineeringandaJurisDoctoratefromtheUniversityofNebraska.GINAD.SHEARERGinaShearerisanAssociateAttorneyatClarkHill|Strasburger.Shedevotesherpracticeprimarilytoconstructionandsuretymatters,withparticularemphasisonbankruptcy,oilandgaspluggingandabandonmentobligations,paymentandperformancebondobligations,constructiondefectdisputes,andenforcingrightsagainstindemnitors.Shealsorepresentspartiesincomplexcommerciallitigationinfederalandstatetrialandappellatecourts,aswellasbeforetribunalsandfederalagencies.GinaisadisplacedChicagoanwhofoundherselfinTexasfifteenyearsagoforwhatshethoughtwasashortstaytocompletehereducation.ShereceivedaBachelorofScienceinBusinessAdministrationfromtheUniversityofTexasatDallas,magnacumlaude,in2007,andthenobtainedherJ.D.fromSouthernMethodistUniversityin2010.WhileinlawschoolshestudiedatUniversityCollege,OxfordduringthesummerandwaspresidentoftheCorporateLawAssociation.Shestumbledintothesuretyindustrybychance,buthashappilyspentherwholecareerimmersedinsurety.Onceshegottoknowherfellowsuretyindustryprofessionalsbetter,shefeltcompelledtojointhecircustomaintainhersanity.Shenowhasabackupcareerasanamateuraerialacrobatandregularlyperformssilks,rope,contortion,staticandduotrapezeacts.GREGORYH.SMITHGregoryH.SmithisapartnerintheOrangeCountyofficeofBooth,Mitchel&StrangeLLP.Mr.Smith'spracticefocusesonbusinesslitigationmattersandsuretylawmattersinstateandfederalcourts.Mr.SmithgraduatedfromtheUniversityofCaliforniaBerkeleyin2003andobtainedhislawdegreefromWhittierLawSchoolin2005.HejoinedBooth,Mitchel&StrangeLLPin2012.Priortojoiningthefirm,Mr.SmithworkedasanEqualJusticeWorks/AmeriCorpsAttorneyandlaterasaStaffAttorneyatthePublicCounselLawCenterwherehispracticefocusedonconsumerlitigation.HeisanavidsurferandrunnerandlivesinLagunaBeachCaliforniawithhiswifeanddaughter.

27

RANAESMITHRanaeSmithisaSeniorSuretyClaimsSpecialistforLibertyMutualSurety’sClaimDepartment/WesternRegioninSeattle.RanaeJoinedLibertyin2014.HerpriorsuretyexperienceincludedworkingasaParalegal/LegalAssistantwithacommercialcollectionagencyforover20+years,whereshehandledthelegalaspectsagainstcontractorslicensingbonds.JAND.SOKOLJanD.SokolisoneofthefoundersandtheManagingMemberofStewartSokol&Larkin,LLC.Herepresentsprimecontractors,subcontractors,realpropertymanagers,smallcorporations,suretiesandfidelityinsurers.Hispracticeincludesadvisingandorganizingbusinesses,aswellasthepreparationofconstructionclaims.HealsohasanextensivepracticerepresentingcreditorsinbankruptcycourtsthroughouttheUnitedStates.Mr.Sokolhandlescomplexcorporate,commercial,constructionandrealpropertylitigation,arbitrationsandmediations.Mr.SokolisafrequentspeakerattheWesternStatesSuretyConferenceandthePearlmanaddressingwiderangingtopicsintheconstructionandsuretyindustry.OregonSuperLawyersMagazinelistedJanasoneofthetoplawyersinthestateforthelastelevenconsecutiveyears:2006to2016.MICHAELW.SPINELLI,ESQ.,AIAMr.Spinelliisafoundingpartnerintheconstruction‐consultingfirmofCashinSpinelli&Ferretti,LLC.HavingreceivedaB.S.inArchitecturalTechnologyfromtheNewYorkInstituteofTechnology,Mr.SpinelliisaRegisteredArchitectlicensedtopracticeinthestatesofNewYork,ConnecticutandTexas.Mr.SpinelliisPast‐PresidentoftheLongIslandChapteroftheAmericanInstituteofArchitects,andthePast‐VicePresidentofGovernmentAffairsforAIANewYorkState.Mr.SpinelliisalsoanattorneyadmittedtopracticeintheStateofNewYork.HavingearnedhisJ.D.summacumlaudefromTouroCollegeJacobD.FuchsbergLawCenterwherehewasanHonorsProgramscholar,Mr.SpinelliisanadjunctprofessorofgraduatestudiesattheStateUniversityofNewYork(SUNY),FarmingdaleCollege,whereheteachesTheLegalAspectsofEngineering,Architecture,andtheConstructionProcess.Mr.SpinellialsoservesastheCo‐EditoroftheNewYorkStateBarAssociation’sMunicipalLawyernewsletter.

28

SHASHAUNASZCZECHOWICZShashaunaSzczechowicz,apartneratWolkinCurran,primarilypracticesoutofWolkinCurran’sSanDiegooffice.Shespecializesinrepresentingsuretyclientsinallaspectsoflitigationinvolvingsuretybondclaims.Ms.Szczechowiczassistssuretieswithdevelopingcosteffectivestrategiestominimizeriskandloss.Ms.Szczechowiczregularlyrepresentssuretyclientsinthedefenseofcomplexconstructionsuretybondclaims.Herexperienceincludeslitigatingpublicandprivateconstructiondisputesinvolvingsureties,suchasnegotiatingcompletionobligationsinbonddefaultsituations,analyzinganddefendingagainstpublicworkswageclaims,enforcingpaymentdefenses,securingcollateral,andpursuingindemnityrights.Ms.Szczechowiczhassignificantexperiencewithcommercialbondsinvolvingprobateestates,trusts,conservatorshipsandguardianships.ShehasrepresentedsuretiesthroughoutCaliforniainavarietyofprobatematters,includingdefendingagainstsurchargeactions,locatingandsecuringassets,preparinginventoriesandaccountings,andobtainingordersdischargingthebond.Ms.Szczechowicz’spracticealsoincludesbankruptcyexperiencerepresentingsuretiesinpursuingsecuredclaims,liftingtheautomaticstayandprotectingcashcollateral,andlitigatingadversaryproceedings,includingobjectionstodebtor’sdischarge.RICHARDE.TASKERRichardE.TaskerisPresidentofSageAssociates,Inc.,aswellasSageConsultingAssociates,Inc.andSageContractorServices.HehasbeenaConstructionandSuretyConsultantsincethemid‐1970’sandhasbeeninvolvedwithhundredsofcontractordefaultsandconstructiondisputes.HebeganhiscareerintheNortheast,workingforatimeintheMidwestandRockyMountainregion,andforthepast+15yearshasresidedinCalifornia.Mr.Taskerhasrepresentedmostofthetop20largestsuretiesandmanysmallervolumesuretycompanies.Hehasbeendesignatedinmanyareasofconstructionincludingforensicscheduleanalysis,efficiencyandproductivity,constructionaccounting,procurement,meansandmethods,andstandardsofcare.HeisactiveandhasoftenpresentedatindustryfunctionsincludingABA,NBCA,SCI,NASBP,andWSSC,andishonoredtoseehismanyfriendsandspeakagainatthe2018Pearlman.

29

MARLAD.THOMPSONMarlaD.Thompsonbeganhercareerinsuretyunderwritingin1988,transitionedtosuretyclaimsin1989andhasspentthepast30yearswithsuretycompaniesinpositionsofclaimsmanagement,collectionandcollateralmanagement,subrogationandlossmitigationmanagement.Overtheyearsshedevelopedresearchmethodsandtoolsforskiptracing,dataverificationandassetsearches.InFebruary2017shefoundedandlaunchedhercompanySuretySolutionstoprovidesuretycompanieswithcommercialsuretyclaimsmanagement,deliveringextraordinaryexpertisewithCaliforniaContractorsLicenseBondclaimsinparticular,recovery&ARprograms,skiptracing,dataverificationandassetsearches.In2018MarladesignedandformulatedVIPER[Verify‐Identify‐Pursue]anonlineinstantsearchtoolandprovidescustomizedsearchesandreports.SuretySolutionsservicessuretycompanies,attorneys,homesecurityfirms,privateinvestigators,andothergroupsandindustrieswithfirst‐partyrecovery&ARprogramsaswellasdataverification,assetandotherrecordsearchesthroughVIPERReports.MICHAELJ.TIMPANEMikeTimpaneisapartnerwithSMTDLaw,LLP,andmanagesSMTD’sNorthernCaliforniaofficelocatedinOakland.Mikebeganhiscareerin1984,andhasfocusedhispracticeonlitigatingsuretyandconstructionmattersfor34years.MikeisalsoanactiveprivatemediatorandisaAAAarbitratoraswell.RODNEYJ.TOMPKINS,SR.,CCPRodneyJ.TompkinsSr.isamanagingpartnerandPresidentofRJTConstructionInc.,ConsultingServices.Rodbringsover48yearsofexperienceinavarietyoftypesofConstruction,SuretyclaimsandConstructionConsultingtotheindustry.RJTfocusesonSuretyclaimsandcompletion,complexprojectandsuretylossmitigation,casemanagement,scheduling,estimating,accounting,litigation,andconstructionprocessesandmethodology.RodhasalsobeenqualifiedasanExpertandhastestifiedinStateCourts,FederalCourts,AAAArbitrationsandMediations.RodisthequalifierforRJT’sGeneralEngineeringandBuildingContractorsLicensesinCalifornia,OregonandLouisiana.RJThasalsobeentherecipientoftheAGCCConstructorAward,CaliforniaPreservationFoundationAward,andtheAGCCSafetyAwardofExcellence.RodalsohascompletedvariousadvancedtrainingprogramsfromtheAGC,FMI,AAA,andholdsclassificationofCertifiedCostProfessional(CCP)fromtheAmericanAssociationofCostEngineersInternational(AACEi).

30

ANDREWW.TORRANCEAndrewW.Torranceisanattorneywith30yearsofexperienceinprivatepracticerepresentingcontractors,insurancecarriersandbondingcompanies.HeislicensedtopracticeinWashingtonandAlaska.ForthepastsevenyearshehasbeenemployedatLibertyMutualasSeniorSuretyCounselfortheWesternRegionmanagingbondclaims.PATRICIAWAGERPatriciaWagerisaPartnerwithTorre,Lentz,Gamell,Gary&Rittmaster,LLP.ShereceivedherundergraduatedegreeinPoliticalSciencefromVassarCollegeandherlawdegree,fromAlbanyLawSchoolofUnionUniversity.Triciaisresponsibleforhandlinglitigationmatterswithanemphasisoncomplexsuretyclaims,paymentandperformancebonddefense,andallaspectsofconstructiondefaults.Inaddition,shecurrentlyservesasaco‐chairoftheABATIPSFidelityandSuretyLawCommittee’sLawDivision,andisaVice‐ChairoftheABATIPSFidelity&SuretyLawCommittee.GREGORYM.WEINSTEINGregoryM.WeinsteinisafoundingPartnerinthelawfirmWeinsteinRadcliffPipkinLLP.Gregprimarilyrepresentsnationalsureties,contractors,developers,andinsurancecarriersincasesinvolvingawidevarietyofissues,includingcomplexdefaults,constructiondefects,delayclaims,andcoveragedisputes.GregislicensedtopracticelawinTexas,Oklahoma,Arkansas,andnumerousfederalcourtsacrossthecountry.HereceivedaB.A.inhistory,withdistinguishedhonors,fromtheUniversityofPennsylvania,aMastersofScienceinhistoryfromEdinburghUniversity,andaJ.D.fromSouthernMethodistUniversityDedmanSchoolofLaw.GENEF.ZIPPERLEJR.GeneF.ZipperleJr.,isapartneroftheLouisville,Kentucky,officeofthelawfirmofWard,HockerThornton,PLLC.,withofficesinLexingtonandLouisville,Kentucky.HeisadmittedtopracticeinthestateandfederalcourtsinKentuckyandIndiana,andfederalcourtsinOhio,NorthCarolinaandFlorida.Geneconcentrateshispracticeintheareasofsuretyandfidelitylawincludingbid,paymentandperformancebondclaimsandlitigation,aswellasprotectingandprosecutingofthesurety’sindemnityrights.Genealsorepresentssuretiesandinsurersinotherbusinessandcommercialcontexts,includingcoverageissues,estateandprobate,andmiscellaneousbondmatters,particularlytransportationrelatedbonds.GeneisanactivememberoftheDefenseResearchInstitute’sFidelityandSuretyLaw

31

Committee,NationalBondClaimsAssociationandEasternBondClaimsReviewandABATIPSFidelityandSuretyLawCommittee.HehaspresentedatThePearlman,NationalBondClaimsAssociationannualmeeting,theEasternBondClaimsReviewannualmeeting,andtheNationalAssociationofIndependentSureties.Genehasalsowrittenarticlesforseveralindustrypublications.DALEZLOCK

DaleZlockiscurrentlyaSpecialAgentwiththeNationalInsuranceCrimeBureaufocusingontheinvestigationofcommercialclaimsinWashington,OregonandAlaska.HeisalsoassignedasanNICBrepresentativetoPSATT(PugetSoundAutoTheftTaskForce).His39‐yearinvestigatorycareerhasbeenevenlysplitbetweenpublicandprivateservice.Themajorityofthiscareerhasbeenfocusedontheinvestigationoffinancialandorganizedcrime,includingsupervisoryandmanagementpositions.Mr.ZlockhasaBachelorofSciencedegreeinInformationTechnologyManagementandholdscertificationsasCriminalAnalyst,FraudExaminerandFireInvestigator(IFSAC‐WA).HeisalsoapublishedauthorandlecturerintheuseofVisualAnalyticstofurtherinvestigationsasdiverseasGamblingLicensure,AsianOrganizedCrime,InsuranceFraudandFireInvestigations.Aspartofhiscurrentpositionheconductstrainingontheinvestigationofautotheft,stagedaccidents,andinsurancefraudtolawenforcementandinsurancecompanies.

32

SustainingMembers

AlberFrank,PSCisaregionalsurety,fidelityandconstructionlawfirmthatistheproductofrelationshipsforgedbyyearsoftrustandconfidencebetweenitsattorneysandclients.Toeffectivelyservetheinterestsofourclientsinmattersofsuretyandfidelitylaw,constructionlaw,insurancelaw,commerciallaw,bankruptcylaw,andprobatelaw,ourattorneysholdlicensestopracticeinArkansas,Indiana,Kentucky,MichiganandOhio.Furthermore,bypartneringwithlocalcounsel,wehavebeenabletoexpandourgeographicboundariestorepresentourclientsinAlabama,Colorado,FloridaMinnesota,NorthCarolina,Pennsylvania,SouthCarolina,Tennessee,Texas,Virginia,WestVirginiaandWashingtonD.C.Pleasevisitourwebsiteatwww.alberfrank.com.

BenchmarkConsultingServices,LLCisafullserviceconstructionconsultingfirmservingtheWesternUnitedStatesfromofficesinIrvine,California,LasVegas,NevadaandPhoenix,Arizona.Benchmark’s staffofconstruction industry experts consult ourclients intheareasofsurety, construction defectlitigation, property andcasualty evaluations, constructionclaims, scheduling, construction litigation support,constructionmonitoring/fundcontrol,projectmanagementandqualityassuranceservices.Pleasevisitourwebsiteatwww.benchmark‐consulting.com.

33

BerkeleyResearchGroupoffersprofessionalexperienceandcompetenceinfact‐finding,claims/disputeanalysis,andlitigationsupport,alongwithtechnicalexpertiseinengineering,architecture,constructionmanagement,publiccontracting,specificationsandtechnicaldocumentdevelopment,scheduledevelopmentandanalysis,costanalysis,negotiations,andexpertwitnesstestimony.Ourmultidisciplinaryteamhasastrongfoundationinprojectmanagement,scheduling,andaccountingcombinedwithdeepindustryexperience.BRGhasworkedextensivelywithourclientsandtheiroutsidecounseltoassesstheallegationsandfactsatissueanddevelopsophisticatedbutefficientsolutions.Ourexpertsareexperiencedinlitigationanddomesticandinternationalarbitration,andincludeProfessionalEngineers,ProjectManagementProfessionals,AACECertifiedPlanning&SchedulingProfessionals,CertifiedPublicAccountants,CertifiedFraudExaminers,forensicaccountants,andindustryleaders.Pleasevisitourwebsiteatwww.brg‐expert.com.

Since1955,Booth,Mitchel&StrangeLLPhasprovidedexemplarylegalservicetobusinessesandindividualsthroughoutCalifornia.Withoffices inLosAngeles,OrangeCountyandSanDiego,wearepositionedtoefficientlyhandlelitigationandtransactionsthroughoutSouthernCalifornia.Inaddition,overhalfofthefirm’spracticinglawyersarepartnerswhohaveapersonalstakeinthequalityofourwork,thesatisfactionofourclientsintheresultsobtainedandintheprofessionalismwithwhichwerepresentthem.RatedAVbyMartindale‐Hubbell,Booth,Mitchel&StrangeLLPhandlesprivateandcommerciallawsuitsandarbitrationsinvolvingtort,contract,environmental,construction,surety,commercial,employment,professionalliability,landlord‐tenantandrealestatedisputes.Werepresentbothplaintiffsanddefendantsandhavetherebydevelopedabreathofinsightthatfacilitatespromptandaccurateanalysisofourclient’sproblemandanabilitytoobtainthemostfavorableresolutioninthemostefficientandcosteffectiveway.

34

Wearealsoavailabletoconsultintheareasofcommercialandconstructioncontracting,realestatetransactions,leasing,suretyandemployment.Pleasevisitourwebsiteatwww.boothmitchel.com._________________________________________________________________________________________________________

BronsterFujichakuRobbinsisrecognizedasoneofthepremiertriallawfirmsinHawaii,handlingcasesonalloftheislands.Weareanexperiencedlitigationfirmwithanestablishedtrackrecordofsuccessfulsettlements,workouts,andtrialverdictsinawidevarietyofcomplexlitigation,arbitrationsandmediations.Ourfirmisstronglycommittedtoservingthecommunitythroughsignificantpublicandprivateprobonowork.Ourphilosophyistoobtainthebestresultspossibleforourclientsthroughaggressiveadvocacyandefficientmanagementpractices.

Ourareasofpracticeincludecommercial,business,suretyandrealpropertylitigation;consumerprotectionlawinvolvingfinancialfraud,unfairordeceptivebusinesspractices;antitrustandcompetitionlaw;litigationandadvicetotrusteesandtrustbeneficiaries,includingclaimsofbreachoffiduciaryduties;regulatoryandadministrativelawbeforestateandcountyagencies;environmentallitigation;civilrightsemploymentcasesincludingdiscrimination,harassment,andwrongfuldischarge;andarbitration,mediationandotherdisputeresolutionservices.

Pleasevisitourwebsiteatwww.bfrhawaii.com.

CashinSpinelli&Ferretti,LLCisamulti‐disciplinaryfirmprovidingconsultingandconstructionmanagementservicestotheSuretyandconstructionindustries.ThePrincipalsofCashinSpinelli&Ferrettihavemorethan70yearsofexperienceinprovidingexpertadviceandanalysistothenation’sleadingSuretycompanies.Drawingontheexpertiseofits staffofProfessionalEngineers,Architects,Attorneys,CertifiedPublic

35

Accountants,Field Inspectorsand Claimsexperts,CashinSpinelli&FerrettiiswellpoisedtoofferSuretyconsultingandlitigationsupportservicestotheindustry.Operatingfromofficesin:Hauppauge,NewYork(LongIsland);Horsham,Pennsylvania(Philadelphiaarea);Farmington,Connecticut(Hartfordarea);Libertyville,Illinois(Chicagoarea);andMiami,Florida;CashinSpinelli&FerrettiprovidesitsservicestoallareasoftheUnitedStates.Pleasevisitourwebsiteatwww.csfllc.com.

ChiesaShahinian&GiantomasiPC,withofficesinNewYork,NY,WestOrange,NJandTrenton,NJ,iscommittedtoteamingwithourclientstoachievetheirobjectivesinanincreasinglycomplexbusinessenvironment.Thisgoalisasimportanttoustodayasitwaswhenourfirmwasfoundedin1972.Overthepastfourdecades,CSGhasexpandedfromeighttomorethan130membersandassociates,allofwhomarededicatedtothelegalprofessionandtotheclientstheyserve.Asourfirmhasgrown,wehavesteadfastlymaintainedourcommitmenttoexcellence,offeringbusinessesandindividualscomprehensivelegalrepresentationinacost‐effective,efficientmanner.Ourfirmprovidesthehighlevelofservicefoundinthelargestfirmswhilefosteringthetypeofpersonalrelationshipswiththefirm’sclientsoftencharacteristicofsmallfirms.Wetakeprideinourreputationforexcellenceinallourareasofpractice,includingbanking,bankruptcy&creditors’rights,construction,corporate&securities,employment,environmentallaw,ERISA&employeebenefits,fidelity&surety,government®ulatoryaffairs,healthlaw,intellectualproperty,internalinvestigations&monitoring,litigation,media&technology,privateequity,productliability&toxictort,publicfinance,realestate,renewableenergy&sustainability,tax,trusts&estates,andwhitecollarcriminalinvestigations.Pleasevisitourwebsiteat www.csglaw.com.

36

ClarkHill|Strasburgerhasbeenattheforefrontofthefidelityandsuretyindustryforoverfiftyyears.Fromthequietdaysofthe1960’stothemercurial1980’sdealingwiththebankingandrealestatecrisisthroughoutthecountry,totheadventofelectronicbankingandmega‐constructionprojectsof the1990’sand2000’s,the lawyersinClarkHill|Strasburger’sFidelity&Suretygrouphaveworkedinpartnershipwithourclientsineveryaspectoftheindustry.ClarkHill|Strasburger’ssuretylawyersprovideexperiencedrepresentationinallfacetsofthesuretyindustry.Thegroup’slawyershavesignificantexperiencerepresentingsuretiesinconnectionwithalltypesofbonds,includingperformance,payment,probate,publicofficials, subdivision,and variousothermiscellaneouscommercial suretybonds.Ourlawyers havesuccessfullyhandledcountlesscomplexcontractsuretyclaims,expertlyguidingsuretiesthroughpre‐defaultinvestigationsandnegotiationsandcompletionofconstructionprojectsafterdefault,includingdraftingandnegotiatingcompletioncontracts,takeoveragreements,ratificationagreements,financingagreements,andotherpertinentsuretyagreements.Ourlawyerslikewisehaveextensiveexperiencehandlingcomplicatedandvariedcommercialsuretybondclaims,fromtheinitialinvestigationandanalysistoconclusion.Ourexpertiseandexperienceextendstoprotectingthesurety’sinterests in bankruptcyproceedings, includingpre‐bankruptcyand post‐filingnegotiationsof reorganizationplans,conflictsregardingunpaidproceedsofbondedcontracts,negotiationsregardingassumptionofbondedobligations,andotherissuesaffectingthesuretyinbankruptcy.Pleasevisitourwebsiteatwww.clarkhillstrasburger.com.

TheattorneysatDunlapFiore,LLC,representsuretyclientsthroughouttheUnitedStatesandhaveextensiveexperienceinallaspectsoftheconstructionindustryincluding:default,projectcompletion,disputesinvolvingpayment,defectivework,defectivedesign,delayclaims,andclaimsforadditionalwork.Ourattorneysareactivelyinvolvedinnegotiationswithprojectowners,creditorsandfinanciallytroubledcontractorsduringallstagesoftheconstructionprocess.

37

OurfirmhasaparticularfocusinfederalcontractingandissuesinvolvingtheFederalAcquisitionRegulation.Representingsuretiesforgovernmentcontractors,wedrawondecadesofexperienceinresolvinggovernmentcontractcontroversies.Ourapproachtolegalrepresentationinvolvesfullyunderstandingtheneedsofourclients,followedbypersonalizingourrepresentationtoobtainquick,positiveresults.Pleasevisitourwebsiteat:www.dunlapfiore.com

TheErnstrom&Dreste,LLP lawfirm is proud to focus its practiceon the suretyandconstructionindustries.Ourexperienceand in‐depthknowledgeofsuretyandconstructionlawisrecognizedlocally,acrossNewYorkStateandevennationally.Weserveclientsacrossthecountryandaroundtheglobe.Wearemorethanjustalawfirm;ourindustryknowledgehelpsusunderstandwhatisimportanttoourclients.Asleadersinsuretyandconstructionlaw,weareateamofaccomplishedprofessionalswhounderstandthenatureofbothindustriesandtheforceswhichshapethoseindustries.Becausetheindustriesweserveareintertwined,ourunderstandingofthesuretyindustrymeanswecanbetterserveourconstructionclients,andourknowledgeoftheconstructionindustrymeanswecanbetterserveoursuretyclients.Wegotheextramiletomakesureourclientsaresatisfiedwiththelegalservicesweprovide.Pleasevisitourwebsiteatwww.ed‐llp.com.

FasanoAcchione&Associatesprovidesconsultingservicesforavarietyofclientsintheconstructionandsuretyindustries.TheindividualsatFasanoAcchione&Associatesareaccomplishedprofessionalswithexpertiseinsurety,construction,engineering,projectmanagement,anddisputeresolutionincludinglitigationsupport.FA&AmaintainsofficesinNewYork,NY,Philadelphia,PA,MountLaurel,NJ,Seattle,WA,andBaltimore,MD.Ifyouwouldlikemoreinformation,pleasecontactVinceFasanoat(856)273‐0777orTomAcchioneat(212)244‐9588.Pleasevisitourwebsiteatwww.fasanoacchione.com.

38

TheWild‐WildWestisthehomeofFauxLawGroup.FauxLawGrouprepresentssuretiesinNevada,IdahoandUtahregardingclaimsonpublicandprivatepaymentandperformancebonds,subdivisionbonds,commercialbonds,licensebonds,DMVbonds,andmiscellaneousbonds.FauxLawGrouprepresentssuretiesintherecoveryoflossesthroughindemnityandsubrogationactions.Ourattorneysareactivelyinvolvedinthelocalcommunitiesinordertobetterrepresenttheinterestsofoursuretyclients.Pleasevisitourwebsiteatwww.fauxlaw.com.

ForconInternationalisamulti‐dimensionalconsultingandoutsourcingfirmthathasprovidedservicestothesurety,fidelity,insuranceandconstructionservicesindustryformorethantwenty‐nineyears.Oursuretyandconstructionservicesincludebooksandrecordsreview,claimanalysis,thirdpartyclaimsadministrationforsureties,bidprocurement,estimating,projectadministration,schedulingandfundscontrol.WeareabletoofferthesebroadrangesofservicesbecauseFORCONiscomposedofseniorclaimmanagementprofessionals,accountants,professionalengineersandconstructionmanagementexecutives. Forconhasactedas thirdpartyadministratordealingwithbondclaimsandrunoffservicessince its inception. The firmoperatesfromsix (6)offices located throughouttheUnitedStates[FL,GA,MI,MD,PA,VA].Pleasevisitourwebsiteatwww.forcon.com.

39

GlobalConstructionServices,Inc.,locatedinRedmond,Washington,hasprovidedprojectmanagement,claimsconsultingservicesandsuretylossconsultingtovirtuallytheentirespectrumoftheconstructionindustrysince1972.Ourconstructionexpertshaveassistedownersandcontractorsalikewiththepreparationandupdatingofprojectschedules,changeorderpricingandnegotiation,andtimeextensioncalculations.Wehavepreparedand/ordefendedclaimsonbehalfofgeneralcontractors,subcontractors,sureties,publicowners,privateowners,architectsandengineers.Wehave extensiveexperienceprovidingexpert testimonyat deposition,arbitrationand trial.We havedeftlyhandledsuretylossesthroughallphasesofprojectcompletionaswellastheresolutionofrelatedclaimsbothassertedbyanddefendedbythesurety.Pleasevisitourwebsiteatwww.consultgcsi.com.

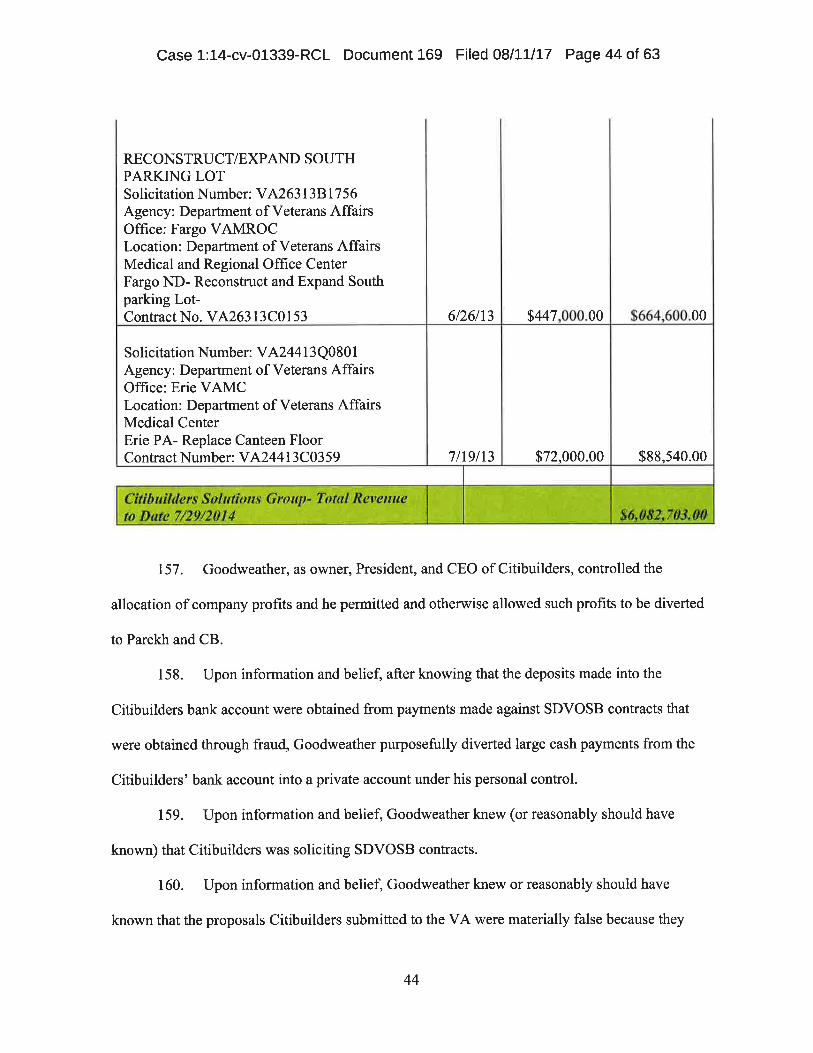

GuardianGroup,Inc.isafull‐serviceconsultingfirmwithofficesnationwidespecializinginsuretyclaims,propertyandcasualtyclaims,constructionmanagementandclaims,constructiondefectclaims,fidelityclaims,constructionriskmanagement,expertwitnessingandlitigationsupport.Whenyouneedexpertconstructionandsuretyclaimssupport,ourdistinguishedtwenty‐fiveyeartrackrecordyieldsconfidence,unprecedentedefficiencyandresults.Guardian’smanagementandstaffconsistsofauniquecombinationofhighlyqualifiedengineers,architects,schedulers,projectestimators,accountants,claimspersonnelandotherprofessionalswithexpertiseinalltypesofconstructionandsuretybondclaims.Thisknowledge,togetherwithfullyautomatedsystems,providesourclientswithexpedientandcosteffectiveclaimsresolutions.Callontheonecompanyengineeredtoexceedyourexpectations.PleaselearnmoreaboutGuardianGroup,Inc.’ssuccessfulapproachtoconsultingbyvisitingourwebsiteatwww.guardiangroup.com.

Global Construction Services, Inc.

40

Foundedin1979,JAMSisthelargestprivateproviderofmediationandarbitrationservicesworldwide. With Resolution Centers nationwide and abroad, JAMS and its nearly 300exclusiveneutralsare responsiblefor resolvingthousandsoftheworld’simportantcases.JAMSmaybereachedat800‐352‐5267.JAMSneutralsare responsible for resolvingawidearrayofdisputes in the constructionindustry, includingmattersinvolvingbreachofcontract,defect,costoverrun,delay,disruption,acceleration,insurancecoverage,surety,andengineeringanddesignissues.TheJAMSGlobalEngineeringandConstructionGroupconsistsofneutralswhoservetheindustrythroughtraditionalADRoptionssuchasmediationandarbitration,andthroughseveralinnovativeapproachestoADRsuchasRapidResolution,InitialDecisionMaker,andProjectNeutralfunctions.Further,JAMSneutralsunderstandthecomplexityofprojectfinancingandthedemandsoflargeinfrastructureandothermega‐projectsandareuniquelyqualifiedtoserveonDisputeReviewBoardsandotherinstitutionalapproachestoconflictresolution.Pleasevisitourwebsiteatwww.jamsadr.com.

Thesurety,construction,andlitigationfirmofJennings,Haug&Cunningham,LLPdeliverseffectivecourtroomrepresentation, capablelegaladvice,andsuperiorpersonalservicetoourclientsintheconstruction andsuretyindustries.Ourexperiencedlawyersproviderepresentationina broadarrayofpracticeareas includingconstructionlaw,surety/fidelitylaw,bankruptcy,Indianlaw,businesslaw,andinsurancedefense.WhatdistinguishesourFirm is thequalityof serviceand the consistent follow‐throughclientscanexpect fromourattorneysand staff.Weprideourselves inprovidingtimely,effective,andefficient legal services to oursuretyandcontractorclients.ThefirmservesbusinessesandindividualclientsthroughoutthestateofArizona,andwecanacceptcasesinthesouthwestUnitedStates,California,NewMexico,Nevadaandinselectbankruptcyactionsnationwide.Pleasevisitourwebsiteatwww.jhc.law.

41

FoundedinPhoenix,Arizonain1942,JenningsStroussisadynamiclawfirmwiththetalentandinsighttoaddressawiderangeofbusinesslegalissues.WithlawofficesinPhoenix,PeoriaandYuma,Arizona,andWashington,D.C.,thefirmleveragesitsresourcesregionallyandnationally.OurlitigationdepartmentstandsasoneofthemostrespectedintheSouthwest,withaproventrackrecordoftrialvictoriesandsuccessfuloutcomesforclients.Thetransactionaldepartmenthandlesanarrayofbusinesslegalmatters,fromthenegotiationandclosingofcomplextransactionstoprovidingcounseloncommonlegalquestions.OneofthemanybenefitsofarelationshipwithJenningsStroussisourpragmaticandresults‐orientedlegaladvicecoupledwithahealthy,well‐managedandfriendlyrelationshipwithourattorneys.Infact,severalofourkeyclientshavebeenwithusfor30+years.Wefeelprivilegedtoenjoylastingrelationshipswiththem,whichwetakeasatestamenttotheirconfidenceinandcomfortwithus.Webelievethattoofferexcellentadviceandservice,weneedtounderstandourclients,aswellastheirbusiness.Excellentservicealsomeanstakingalong‐termviewandinvestinginrelationshipswithclientsaswellasinourownpeople,processes,andservices.Noclientservicecouldbebetterthanthatgivenbyaunitedfirm,whichvaluescollaborationandteamwork.Webelieveeveryoneatthefirmcanmakeadifferenceinservingallofourclients.Pleasevisitourwebsiteatwww.jsslaw.com.

42

J.S.Heldisaleadingconsultingfirmspecializinginconstructionconsulting,propertydamageassessment,suretyservices,projectandprogrammanagement,andenvironmental,health&safetyservices.Ourorganizationisbuiltuponthreefundamentalpillars:toprovidehighqualitytechnicalexpertise;todeliveranunparalleledclientexperience;andtobeacatalystforchangeinourindustry.Ourcommitmenttothesepillarspositionsusasaleadingglobalconsultingfirm,respectedforourexceptionalsuccessaddressingcomplexconstructionandenvironmentalmattersintheworld.Ourteamisagroupofmulti‐talentedprofessionals,bringingtogetheryearsoftechnicalfieldexperienceamongallfacetsofprojectsincludingcommercial,industrial,highrise,specialstructures,governmental,residential,andinfrastructure.Ouruncompromisingcommitmenttoourclientsensuresourpositionasoneofthemostprominentconsultingfirmsinourindustry.Pleasevisitourwebsiteatwww.jsheld.com._________________________________________________________________________________________________________

Established in 1874, Kerr, Russell and Weber, PLC has evolved from asmall practicein Detroit into afirm ofcommitted,resourcefulandrespectedlawyerswithmanytalentsandspecialties.Ourareasofpracticeincludefidelityandsurety. KerrRussellrepresentssuretiesinawiderangeofmatters,includingthehandlingofdefaults;claimsagainstperformancebonds,paymentbonds,probatebondsandothercommercialbondforms;performancetakeovers,tendersandsubcontractratifications;pursuitofindemnification;andallaspectsoflitigation.Ourattorneysalsoincludethosewhose specialties afford oursuretypractice access to a wide arrayof disciplineswhichare often beneficial to ourservicesforsuretyclients,includingcorporate,tax,realestate,bankruptcy,andemploymentpractices.Pleasevisitourwebsiteatwww.kerr‐russell.com.

43

Koeller,Nebeker,Carlson,Haluck,LLP(KNCH)pridesitselfinitshandlingofcomplexlitigationmatters.Ourbroadspectrumofpracticeareasincludeslitigationdefense,businesslaw,employmentlaw,insurancecoverageandbadfaith,environmentallaw,andmosttypesofgeneralpracticeareas.Ourclientsrangefromsmallbusinessownersandtheirinsurancecompanies;tomid‐sizedcommercialcontractors,landlordsandtenants;tolargenationwidehomebuildersandcommercialbuilders.

Overthe30yearsofourexistence,wehavealsobecomearecognizedauthorityinallareasofconstructionlitigationandtransactions,withaparticularspecialtyinrepresentingbuilders,developersandgeneralcontractors.Fromrealestateacquisition,developmentandfinancing,toconstructionandbusinesslitigationforbothresidentialandcommercialprojects,ourbreadthofexperienceandgeographicalcoverageensuresthatourclients'personalbusinessandfinancialconcernsarebeingrepresentedeverystepoftheway.

Asadirectresultofthefaithfulsupportofourclientsandthededicatedserviceofourattorneysandstaff,thefirmhasgrowntoover80attorneys,200employees,withofficesinIrvine,SanDiego,Sacramento,LasVegas,Phoenix,OrlandoandAustin.Indeed,sinceitsinceptionin1986,KNCHhasformedadynamicpresencethroughoutthestatesofCalifornia,Arizona,NevadaandFloridaandhasrecentlyextendeditsreachintoTexas.Welookforwardtodevelopingnewclientrelationshipswhilecontinuingtoexcelatservingtheneedsofexistingclientsbyachievingthehighestlevelofexcellence.

Dedicatedtoservice,anddrivingaheadwithintegrityandcourage,wearethelawfirmyouwantonyourside.www.knchlaw.com

ThenationallyrecognizedattorneysofKrebsFarley,PLLChave litigatedcasesallovertheUnitedStates.Ourattorneys’skillsshownotonlyinthecourtroom,butalsoinnegotiation.Thepersonalcommitmentanddedicatedeffortthatourattorneysputforthmakeadifferenceineverycasewehandle.Wearesmart,pragmaticanddiligent.Andwearededicatedtocreativelypursuingthebestsolutionsforourclients.

44

Weunderstandtheimportanceofprompt,correct,andconciseresponses;foreseeingandaccountingforfuturecontingenciesincontractdrafting;resolvingdisputesthatcanbeamicablyresolved;andpositioningthosemattersthatcannot be settled for a successfuloutcome in litigation.Wedo thiswhile remaining cognizant that litigationoftenimpactsbusiness considerationsbeyond the case at hand.We alsowork closelywithour clientsin developingandoperatingwithinalitigationbudget.Whetheritbeinnegotiation,inmediation,inarbitration,intrialoronappeal,theattorneysatKrebsFarley,PLLCseekpragmaticsolutionsforourclients.Pleasevisitourwebsiteatwww.kfplaw.com.

Langley,LLPisaTexasciviltrial,commercialbankruptcy,andappellatefirmthatrepresentsFortune500andmiddle‐marketindustryleadersindisputesthroughouttheUnitedStates.Ourfirmismadeupofambitiousandsmartlawyerswhodemonstratepassionandzealinrepresentationofthefirm’sclients. Wehelpourclientssolvetheirlegalchallengesthroughaggressivenegotiationorlitigation.Ourareasofspecialtyincludesuretyandconstruction,propertyinsuranceclaims,commerciallitigation,andcommercialbankruptcy.Ourattorneystrycases,handlearbitrations,litigate,negotiate,analyze,andcommunicate.Attheheartofthematter,forus it is all about understandingour clients’businessandkeepingour clients informed.We are strongbelievers increatingaplanforeachmatterdesignedtoarriveatanefficientandeffectiveresolution. MostcasesintheUnitedStatessettle,asdomostofours.Whenacasemustbetried,ourtriallawyersrelishtheopportunity–whetheritisatwodaytrialtothebenchorasixteenweekjurytrial.Whethertheamountincontroversyishundredsofmillionsofdollarsorasmallsum,ourexperience,communicationskills,anduseofcuttingedgetechnologypositionustoachievethewinningresult.Pleasevisitourwebsiteatwww.l‐llp.com.

45

TheLawOfficeofCharlesG.EvanshasrepresentedsuretiesinthelastfrontierofAlaskaformorethanfortyyears.Fromrebidsandcompletionofdefaultedcontractsinremotelocations,tobondedbutbustedroads,schools,hospitals,anddams,wesolveproblemswithlocalknowledgeandexpertise.Weknowtheenvironment.Ourfirmhasaproventrackrecordoflimitingsuretyexposureandquicklycapturingrepaymentforourclients.WecombinepersonalservicewithinnovativetechsolutionsandbigfirmcapabilitiestoachieveresultsanywhereinAlaska.

_________________________________________________________________________________________________________

Law Offices of John L. Fallat Ourfirmhasbeenrepresentingfidelityandsuretycompaniesforover20years.Wefocusonproblemsolving,alwaysattemptingtoresolveconflictsefficientlyinagood‐faithefforttoavoidexpensive,protractedlitigation.However,weare certainlyprepared to defendclaims through the entire judicialprocess, includingappeals.The size of our firmenablesustogivepersonalattentiontoourclients’needs.Pleasevisitourwebsiteatwww.fallat.com.

46

MDDisaworld‐classforensicaccountingfirmthatspecializesineconomicdamagequantificationassessments.Wehavedeeprootedandcomprehensiveexpertiseinmattersrelatedtothesuretyandconstructionindustry.

Ourexpertsspeakover30languagesandwehave42officeson4continents.Ourworkspansmorethan130countriesand800industries,andwefrequentlyworkwithlawfirms,governmententities,multi‐nationalcorporations,smallbusinesses,insurancecompaniesandindependentadjustmentfirms.

FormoreinformationpleasecontactDavidStryjewskiorPeterFasciaat215.238.1919orvisitusatmdd.com.

Manier&Herod,P.C.islocatedinNashville,Tennesseeandprovidesrepresentation,counsel,andadvocacyonbehalfofsuretiesandfidelityinsurersthroughouttheUnitedStates.Manier&Herod’sattorneysareactivelyinvolvedintheFidelityand SuretyCommitteeof the AmericanBar Association (ABA)andfrequentlyaddress the ABA andotherprofessionalorganizationsontopicsrelevanttothefidelityandsuretyindustries.Manier&Herodrepresentsfidelityinsurersandsuretiesinunderwriting,pre‐claimworkouts,coverageanalysisandlitigation,contractordefaultsincludingperformancebondandpaymentbond claims, contractorbankruptcies,surety litigation, indemnityactions, and othermattersandforums.Pleasevisitourwebsiteatwww.manierherod.com.

47

PartnerEngineeringandScience,Inc.(Partner)offersfull‐serviceengineering,environmentalandenergyconsultinganddesignservicesthroughouttheAmericas,Europe,andaroundtheglobe.Ourmulti‐disciplinaryapproachallowsustoprovidecomprehensivesuretyconsultingsolutions,includingclaimsmanagementservicesandcompletioncontracting,frominitialduediligenceanddesigntoprojectclose‐outandexpertwitnesslitigationsupport.Ourdedicatedsuretyconsultingteamhasover20yearsofdomesticandinternationalexperiencemanagingdozensofcomplexfilesandprojectsites.BackedbyPartner’sdeepbenchofregisteredprofessionalsandspecialistsindiversepracticesincludingforensicengineering,constructionmanagement,environmentalconsulting,andcivilandstructuralengineering,thesuretyconsultingteamcanperformathoroughandexpeditiousreviewofadistressedcontractedproject;interfacewithsubcontractors,vendorsandotherstakeholders;isolatecausesandcontributingfactors;andrecommendand/orexecuteaplanforresolution.Pleasevisitourwebsiteatwww.partneresi.com.

PCA ConsultingGroupwas formed in January1989 for the purpose of providing thesurety, insurance, legal andfinancialindustrieswithcosteffectivetechnicalservices.Withover80yearsofaggregateexperience,theconstructionandengineeringprofessionalsofthePCAConsultingGrouphaveservedthesuretyandinsuranceindustriesthroughoutthemajorityofthecontinentalUnitedStatesandhavebeeninvolvedinmattersrequiringknowledgeofeveryconstructionspecialty.PCAhasadapteditsexperienceandsystemstomeettheSurety’srequirements.Fromevaluatingthestatusandcost‐to‐completeprojectionforan individualproject, toanalyzingthe fiscalandoperatingpoint‐in‐timecashpositionofanentire constructioncompany,PCAhasdeveloped the systems, acquired the expertise, and retained thepersonnel toprovideresultsinatimelyandcosteffectivemanner.Pleasevisitourwebsiteatwww.pcacg.com.

48