Embed Size (px)

Citation preview

WithRon Sompels, Richard Kotzen, and Marv Hills

from Crowe Horwath LLC

Moderated byMike Bowers

Executive Editor at DealersEdge

New Directions in Dealership Succession Planning it’s getting more complicated

2

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

www.crowehorwath.com/dealer

Crowe Retail Dealers: Assurance Tax Financial Advisory Risk Consulting Performance

New Directions in Dealership Succession Planning:It’s Getting More ComplicatedRon Sompels, Richard Kotzen, and Marv Hills

3

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

NoticeThese slides for the webcast presentation ("presentation") have been prepared to present general information on selected accounting and reporting subject matter. The content of this presentation, which is the copyrighted work of Crowe Horwath LLP, does not constitute audit, accounting, financial reporting, income tax reporting or any other professional advice and should not be relied upon as such. The content of this presentation should not be duplicated or redistributed. Crowe Horwath LLP shall not be responsible for any loss sustained by any person or entity that places reliance on the content of this presentation. The content of this presentation was not intended to be used, and cannot be used, to avoid any government penalties that may be imposed on a taxpayer.

4

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

PresentersRick Kotzen, CPA: Richard Kotzen has devoted his professional career to performing consulting, merger and acquisition, litigation support, and assurance services to single-point, mega-dealership groups, and publicly traded consolidators. Mr. Kotzen leads our retail dealer litigation support and expert witness practice, and is certified in federal court as an expert in the retail automotive industry. Mr. Kotzen has participated in negotiating, analyzing, and performing due diligence for transactions in excess of $1 billion and for more than 100 dealerships.

He has gained national recognition for both his knowledge and experience in working with dealerships as a lecturer on issues affecting the industry. He is a CPA, member of Florida’s and Pennsylvania’s institute of CPAs societies, AICPA, and the National Association of Dealer Counsel (NADC).

Mr. Kotzen graduated Summa Cum Laude from George Washington University with a Bachelor of Arts (BA) in Accounting.

5

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

PresentersMarv Hills, CPA: Marvin Hills is the partner-in-charge of the private client services practice of tax . He is a member of the American Institute of Certified Public Accountants (AICPA), the Indiana CPA Society, the Personal Financial Planning Division of the AICPA, and the Society of Financial Service Professionals. Mr. Hills is a past president and current member of the Michiana Estate Planning Council.

Mr. Hills is a frequent speaker for professional and civic organizations on estate planning and fiduciary income taxation topics, including seminars taught for PESI, the Notre Dame Tax and Estate Planning Institute, the American Bankers Association, and the Illinois Bankers Association, and presentations to the Indiana Continuing Legal Education Forum, the Young Lawyers Section of The Chicago Bar Association, and the Estate Planning Council of Indianapolis. He has written articles on various topics for publications including The Tax Advisor, Hoosier Banker, Taxes – The Tax Magazine®, and Kentucky Banker.

Mr. Hills graduated Summa Cum Laude from Anderson University.

6

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

PresentersRon Sompels, CPA: Ronald Sompels is a partner at Crowe Horwath LLP, a top 10 public accounting and consulting firm. Mr. Sompels, a CPA and CPIM, is the Partner-in-Charge of Crowe’s Retail Dealer industry horizontal and has more than 30 years experience in providing assurance, tax, risk management, financial advisory, and performance consulting services to more than 600 retail dealerships.

He has conducted courses on many subjects, including inventory control, and is a published writer, with articles featured in trade magazines, periodicals, and business journals.

Mr. Sompels holds a Bachelor of Business Administration in Accounting from Western Michigan University.

7

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Agenda� Rick Kotzen

� Relevancy of this topic in today’s environment� Succession from the manufacturers’ view� Consequences of not addressing this issue now� How to get started

� Marv Hills� Differences between succession and estate planning and importance of integrating these plans

� Importance and urgency of addressing these issues now� Issues to consider

� Ron Sompels� Crowe introduction� Issues to consider in preparing your dealership for sale

8

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

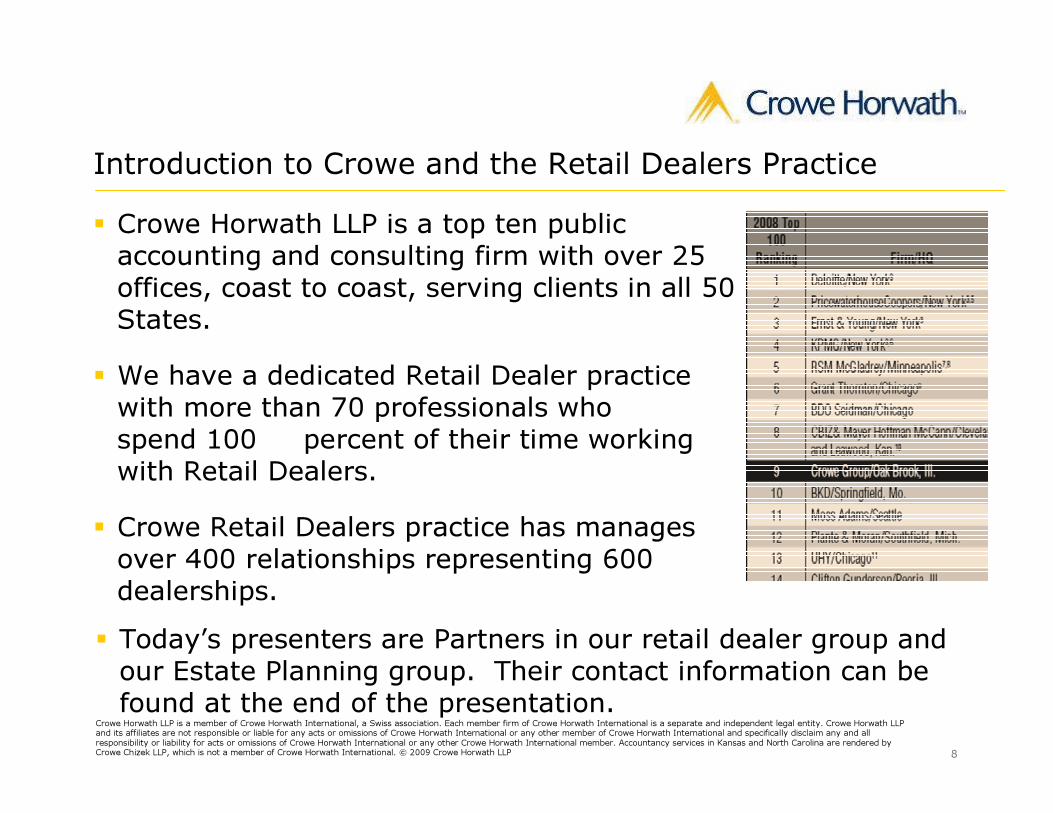

Introduction to Crowe and the Retail Dealers Practice

� Crowe Horwath LLP is a top ten public accounting and consulting firm with over 25 offices, coast to coast, serving clients in all 50 States.

� We have a dedicated Retail Dealer practice with more than 70 professionals who spend 100 percent of their time working with Retail Dealers.

� Crowe Retail Dealers practice has manages over 400 relationships representing 600 dealerships.

� Today’s presenters are Partners in our retail dealer group and our Estate Planning group. Their contact information can be found at the end of the presentation.

9

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Background� Background information

� Combining Crowe’s thought leadership in the Dealer space with expertise in estate and succession planning offers a unique solution to the market place.

� We have met with major manufacturers to understand their concerns and goals related to dealership succession plans. We understand their thinking on the successor’s:

� Individual qualifications� Ownership requirements� Ability to exercise control over major decisions� Structure of organization

� Importance of integrating succession and estate planning in today’s environment.

10

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Succession and Estate Planning� The overall goal is to create a legacy that will continue for many generations.

� Succession Planning: Focus is on the transfer of management (and ultimately control) from the Current Dealer to the Successor Dealer or Operator.

� Estate Planning: Focus is on the transfer of ownership of assets (including businesses) to the intended beneficiaries using the most tax efficient and administratively efficient methods possible.

11

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

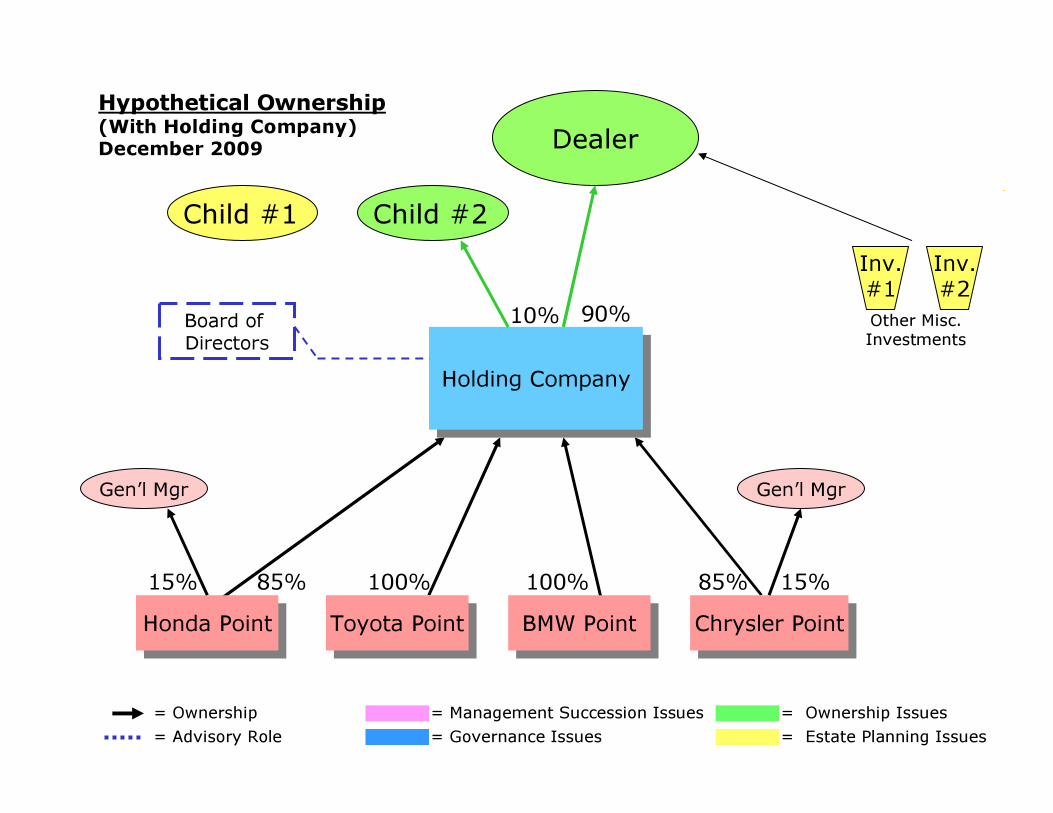

Child #2

Dealer

Gen’l Mgr

Honda PointHonda Point85%15%

90%

Holding CompanyHolding Company

Hypothetical Ownership(With Holding Company)December 2009

Toyota PointToyota Point BMW PointBMW Point Chrysler PointChrysler Point

Inv.#1

Inv.#2

100% 15%85%100%

Board of Directors

10%

Gen’l Mgr

= Management Succession Issues= Governance Issues

= Ownership Issues= Estate Planning Issues

Child #1

Other Misc. Investments

= Ownership= Advisory Role

12

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

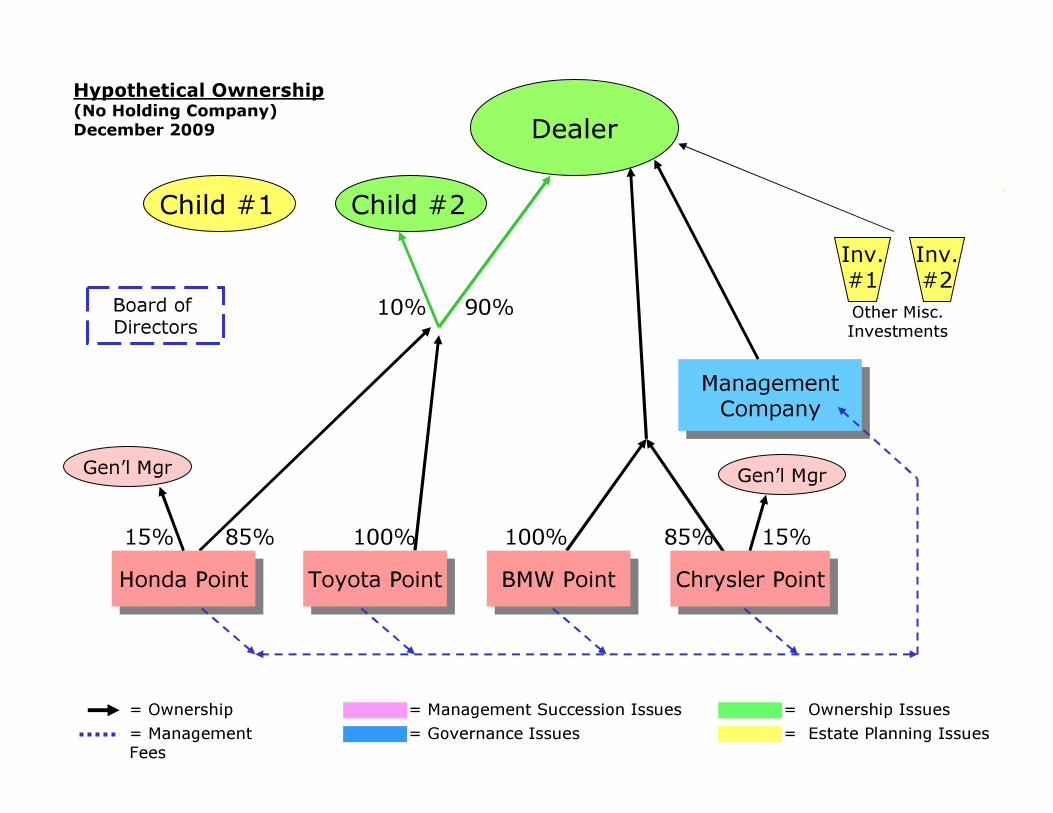

Child #2

Dealer

Gen’l Mgr

Honda PointHonda Point85%15%

90%

ManagementCompany

ManagementCompany

Hypothetical Ownership(No Holding Company)December 2009

Toyota PointToyota Point BMW PointBMW Point Chrysler PointChrysler Point

Inv.#1

Inv.#2

100% 15%85%100%

Board of Directors

Gen’l Mgr

= Management Succession Issues= Governance Issues

= Ownership Issues= Estate Planning Issues

Child #1

Other Misc. Investments

= Ownership= Management Fees

10%

13

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Succession Planning – Aging Dealer Population� As the dealer community ages the turnover in the dealer body will accelerate. � Each month in Automotive News we are seeing dealers receiving 25 30 and 40 Year awards from Manufacturers -- many dealers are now settling into their 70's to 80's.

2 5 Y ear A w ard

5 0 Y e a r A w a r d

14

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Succession Planning is on the Radar of…� Financial Institutions who bank dealers.� Manufacturers who are concerned about their future leadership in their dealership bodies.

� The Dealers who are aging.� Contrary to popular opinion, immortality has NOT been achieved in the Dealer Community.

� Manufacturers and Financial Institutions are increasing their level of scrutiny.

� Mortality statistics show transition is a near- term issue for a high percentage of the aging dealers.

15

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Should You Care?� Should Dealer/Operators care what Manufacturers and Financial Institutions have on their radars screens?????

� Hopefully today's seminar will assist in bringing clarity to those issues!!!!!

16

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

S u cc e s

s ion

P lan

Two Independent Processes� Succession Planning and Estate Planning are two independent processes.

� One over-all plan that fits the Succession and Estate Planning puzzle pieces together will mitigate the risk of a negative impact when a triggering event occurs.

Es t a t e

P l a n

17

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Two Independent Processes� Who is at risk when a triggering event occurs?

� Dealer/Operator; � The Dealership or Dealership(s) Corporations; � Immediate family members; � Key employees;� Other long-term valued employees; � Manufacturers; and� Lending Financial Institutions.

18

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Financial Institution’s Perspective� Today's economic environment is forcing Financial Institutions to mitigate risk.

� Understanding the Succession Planning of their borrower/ customers is now another area of risk mitigation.

19

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Why Are Financial Institutions Concerned?� One of their critical lending criteria is the relationship with the Principal Borrower -- The Dealer.

� The day a triggering event occurs the Financial Institutions loses a portion of the linkage they have with the Corporation.

� This increases the Financial institution’s risk scenario of principal losses.

20

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Impact on Automotive Lenders� Automotive Lenders - the lending due diligence process will be expanded to understand the Succession Plan of their borrower/customers.

� The critical life blood of a dealership: borrowed funds; � Could depend partially on having a viable plan for succession in the case of a triggering event.

21

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

The Manufacturer Perspective� The Manufacturers are particularly concerned by the age of the dealer community and the future leadership of their dealerships.

� As turnover increases in dealer body it becomes a major threat to the brand stability.

� Manufacturers want to protect and grow their brands as the transition to the next generation Dealer/Operators occurs!!!!!

� It’s NOT going to be business as usual for Manufacturer to approve spouses, relatives, GMs or some other designated party or entity to be the successor’s Dealer/Operators.

22

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

The Manufacturer Perspective� Manufacturers are particularly sensitive to prior changes in ownership that have been implemented due to succession and /or estate plans.

� Concern stems from intentional or unintentional lack of required notification of changes in ownership.

� Many Dealers or their beneficiaries may find out they are in violation of their dealership agreements if the ownership structure is not approved by the Manufacturer.

� It could be a catastrophic event forcing a sale of the franchise at in-opportune time.

23

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Ownership Transfers� Such ownership transfers are as follows:

� Family Members;� General Managers; � Holding Companies;� Trusts; and� Charities.

� Holding Companies, Trusts, and Charities present very complicated set of issues to Manufacturer.

� Estate Plans that have transferred ownership should seek the their respective Manufacturers approval.

24

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

The Value of the Succession Plan� No matter whether you are the entrepreneurial dealer who wants to sell or

� See your dealership or dealership’s transition to new leadership:

� A succession plan is extremely valuable to the dealer.

25

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Triggering Event without a Viable Succession Plan� Most, if not all, the following negative scenarios will play outwithin their dealership or dealerships…� Significant drop in CSI and SSI results; � Erosion in service parts and Body Shop operations;� Lower new and used unit volume sales;� Loss of key employees;� Reputation loss in business and customer community;� Drop in lenders confidence leading to alteration in debt; structure;

� Loss in Manufacturer backing and confidence;

26

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Triggering Event without a Viable Succession Plan� Most, if not all, the following negative scenarios will play outwithin their dealership or dealerships…continued:� Significantly weakened financial structure - need for re-capitalization of the business;

� Un-foreseen material expenditures;� Lower profitability or significant Losses; � Significant deterioration in enterprise value; � Litigation among shareholders and or family members;� Forced to sale - many times at a distressed price.

� Winners - Lawyers and future acquirer.� A terrible outcome for the many years of building a successful business .

27

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Why Focus on Estate Planning Now?

� Current economic conditions � Value of assets are depressed. An asset valued at $XX two years ago, may be 50% of $XX today.

� Current interest rates are at historic lows.� Sales to heirs today can be financed at under 2.7% for up to nine-year notes. (Under 4.2% for long-term)

� Current political climate� Proposed legislation threatens to repeal useful estate planning techniques.

� “The Perfect Storm”

28

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

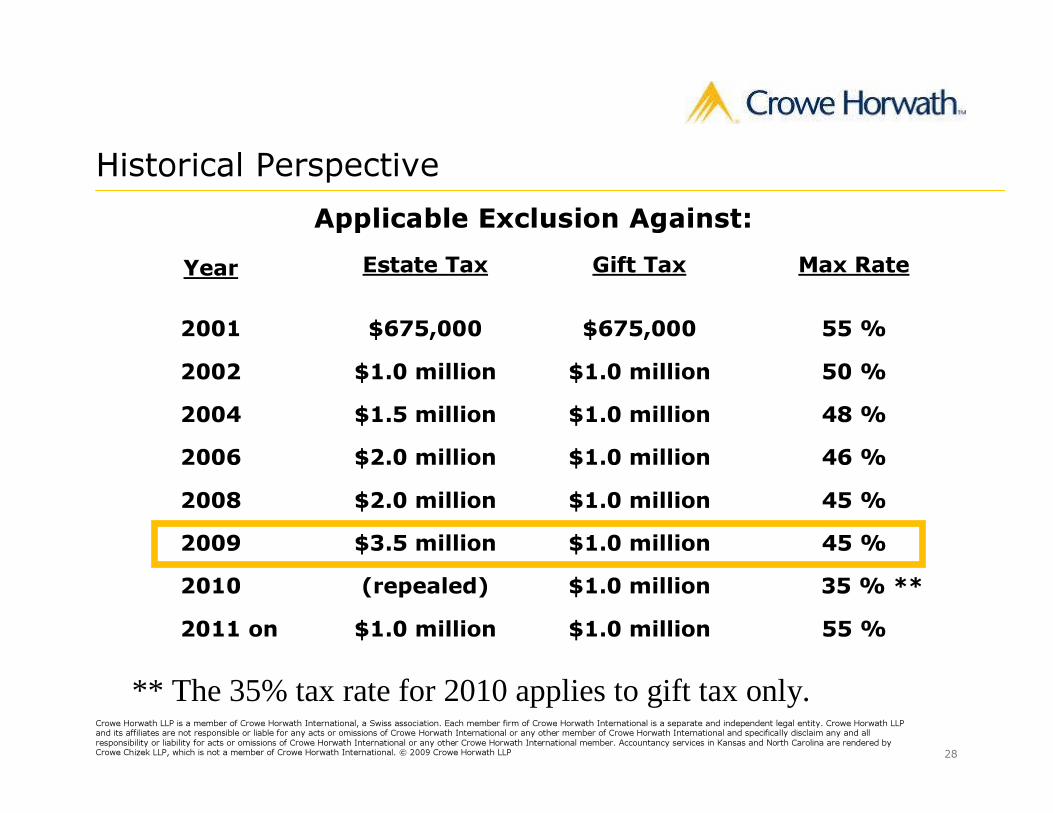

Historical Perspective

Year Estate Tax Gift Tax Max Rate

2001 $675,000 $675,000 55 %2002 $1.0 million $1.0 million 50 %2004 $1.5 million $1.0 million 48 %2006 $2.0 million $1.0 million 46 %2008 $2.0 million $1.0 million 45 %2009 $3.5 million $1.0 million 45 %2010 (repealed) $1.0 million 35 % **2011 on $1.0 million $1.0 million 55 %

Applicable Exclusion Against:

** The 35% tax rate for 2010 applies to gift tax only.

29

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Benefits of Lifetime Transfers

� Tax Benefits:Potential to remove assets from taxable estate now, without increasing future estate tax liability:� Annual Exclusion Gifting� Transfer assets at discounted value� Shift future appreciation to heirs

� Non-Tax Benefits� Recipient has “pride of ownership” (motivation).� Recipient has potential for increased cash flow.

30

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

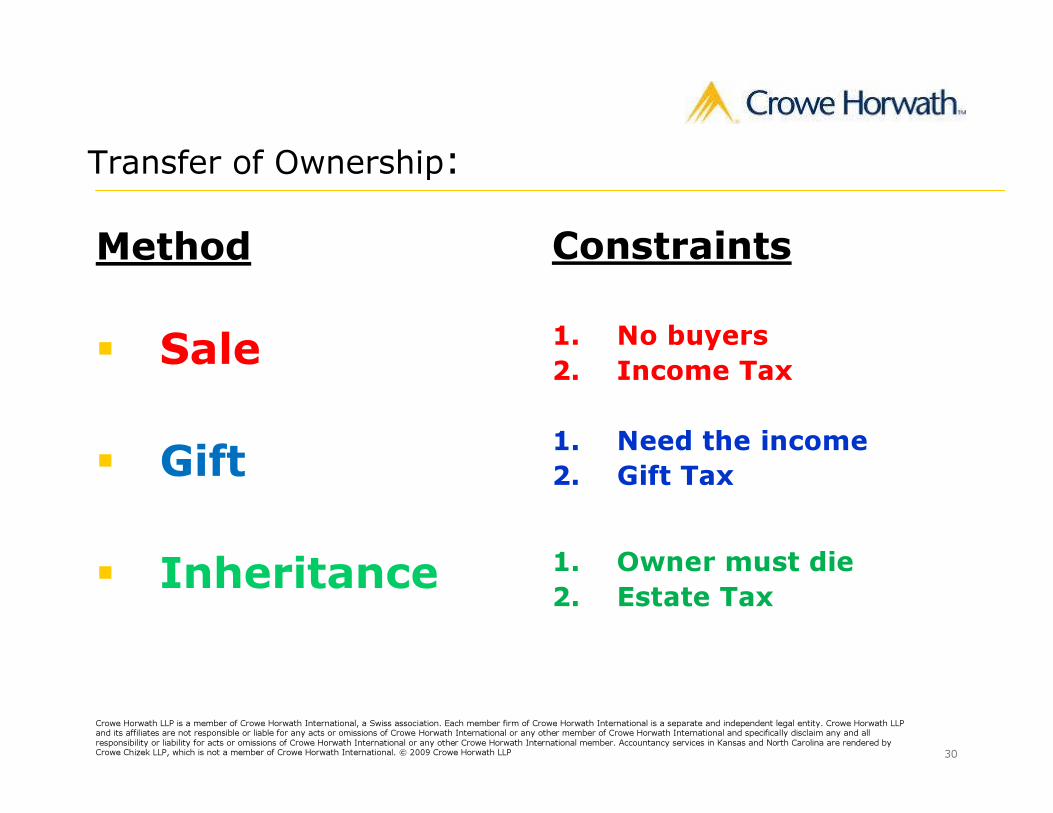

Transfer of Ownership:Method

� Sale

� Gift

� Inheritance

Constraints

1. No buyers2. Income Tax

1. Need the income2. Gift Tax

1. Owner must die2. Estate Tax

31

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

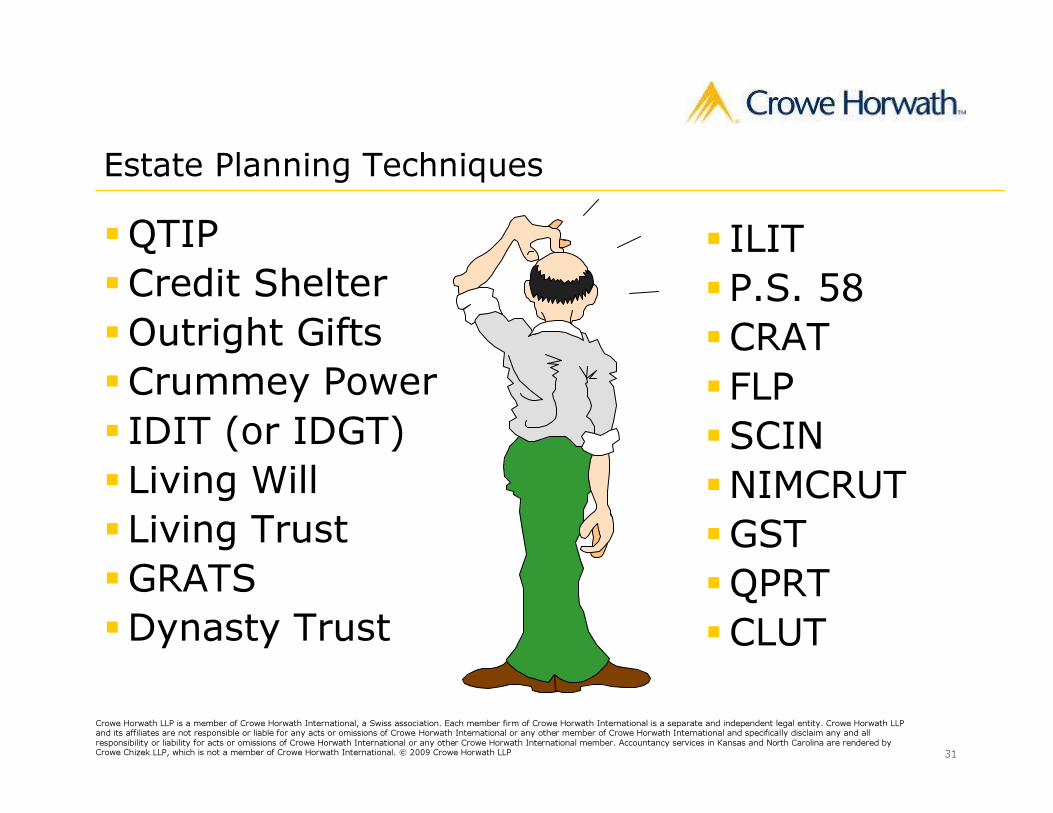

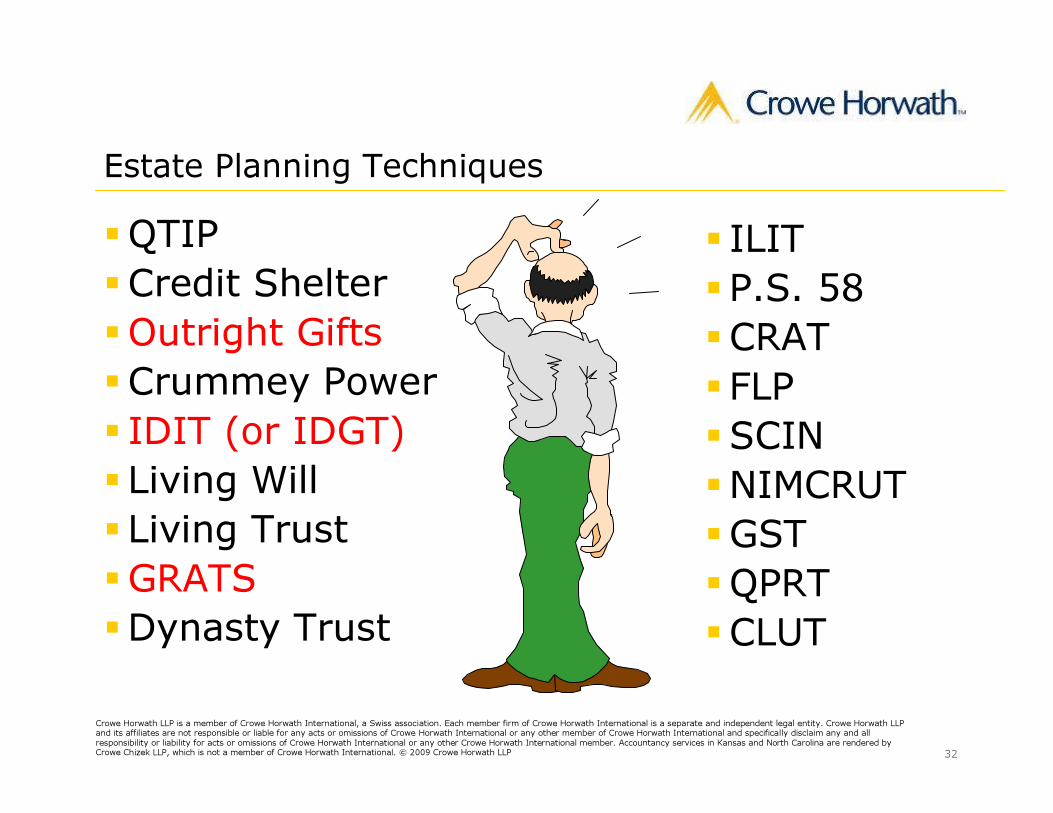

Estate Planning Techniques�QTIP�Credit Shelter�Outright Gifts�Crummey Power� IDIT (or IDGT)� Living Will� Living Trust�GRATS�Dynasty Trust

� ILIT�P.S. 58 �CRAT� FLP�SCIN�NIMCRUT�GST�QPRT�CLUT

32

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Estate Planning Techniques�QTIP�Credit Shelter�Outright Gifts�Crummey Power� IDIT (or IDGT)� Living Will� Living Trust�GRATS�Dynasty Trust

� ILIT�P.S. 58 �CRAT� FLP�SCIN�NIMCRUT�GST�QPRT�CLUT

33

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Lifetime Gifting Strategies� Two Methods of Gifting (Control Issues):

� Outright Direct Gift – Recipient Controls Property� (Less of an issue/concern for Non-Voting Stock)

� Gift to a Trust – Recipient is merely a beneficiary� (Trustee manages the property, and cash received)

� Timing and Amount� Annual exclusion gifting program� Lifetime exemption gifting program

34

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

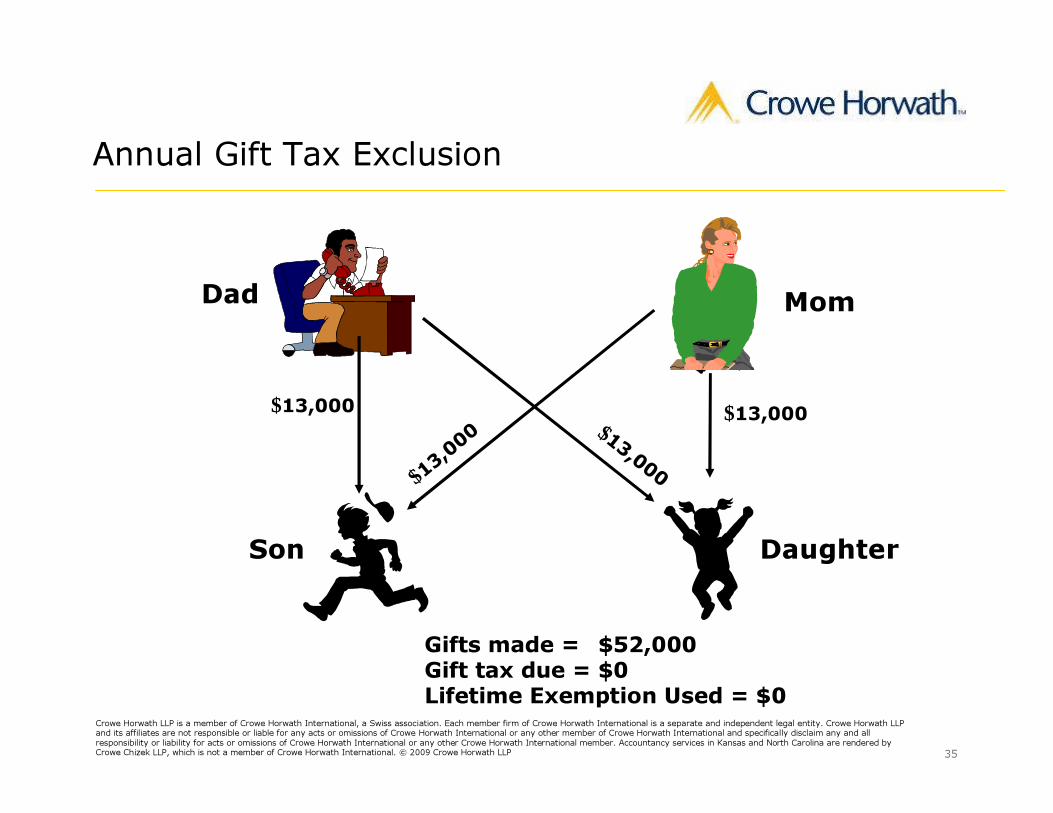

Annual Gift Tax Exclusion

� The first $13,000 of gifts of a present interestmade by a donor to each donee in each calendar year is excluded from the amount of the donor’s taxable gifts.

35

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Annual Gift Tax Exclusion

MomDad

Son Daughter

Gifts made = $52,000Gift tax due = $0Lifetime Exemption Used = $0

$13,000$1 3 ,0 0 0

$13,000

$ 1 3, 0 0

0

36

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

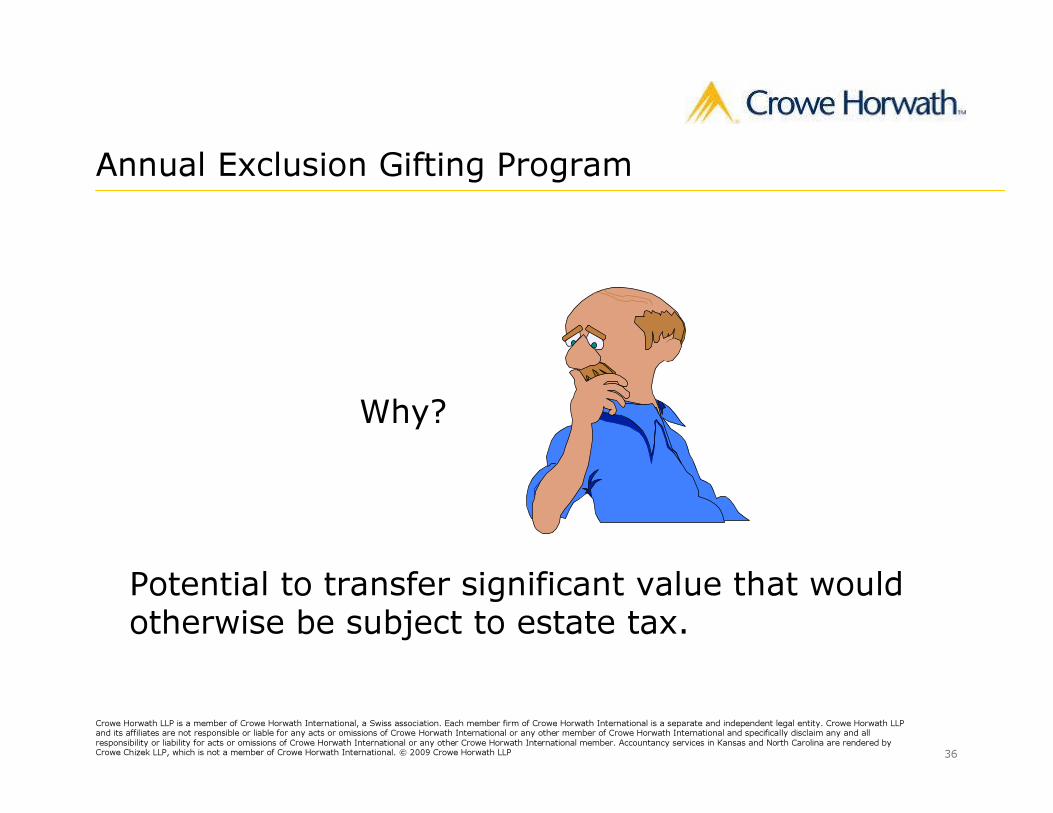

Annual Exclusion Gifting Program

Why?

Potential to transfer significant value that would otherwise be subject to estate tax.

37

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

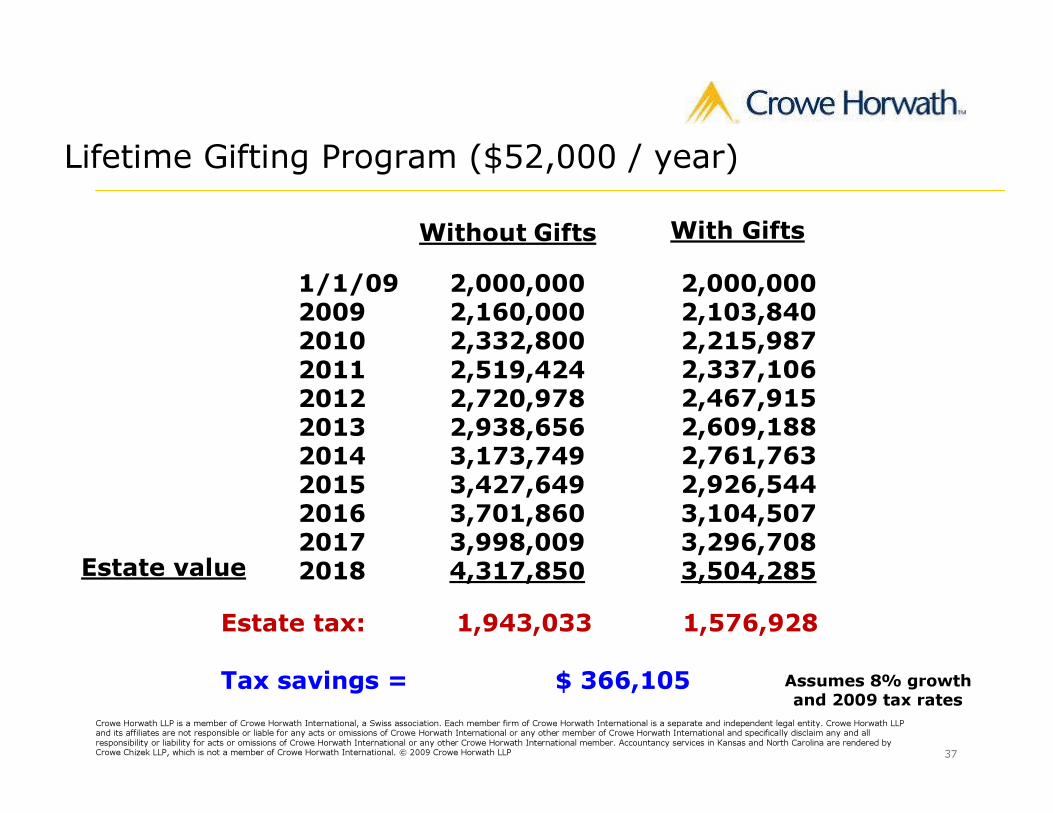

Lifetime Gifting Program ($52,000 / year)

Estate value

Without Gifts

Estate tax: 1,943,033 1,576,928Tax savings = $ 366,105 Assumes 8% growth

and 2009 tax rates

1/1/09 2,000,0002009 2,160,0002010 2,332,8002011 2,519,4242012 2,720,9782013 2,938,6562014 3,173,7492015 3,427,6492016 3,701,8602017 3,998,0092018 4,317,850

2,000,0002,103,8402,215,9872,337,1062,467,9152,609,1882,761,7632,926,5443,104,5073,296,7083,504,285

With Gifts

38

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Additional Gifting to Use Lifetime Exemption

� Make gifts in a year that exceed the $13,000 exclusion, and thus utilize up to $1,000,000 of lifetime gift exclusion.

� No gift tax due, provided that the cumulative gifts are less than the $1 million exemption.

� Total gift/estate tax burden will be reduced by removing future appreciation from estate.

� Use discounted value of assets if possible.

39

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Gift Strategies� Discounting opportunities

� Minority Interest (a/k/a “lack of control”)� What would you pay for 49% of a company?� Rev. Ruling 93-12 requires the IRS to ignore “family attribution”; thus minority discounts authorized

� Lack of Marketability� It takes time to find a buyer for a closely-held Business.

� Professional valuation is important� “What is a business worth?” (Depends who’s asking.)� Providing “adequate disclosure” to IRS will start the three-year gift tax statute of limitations.

40

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

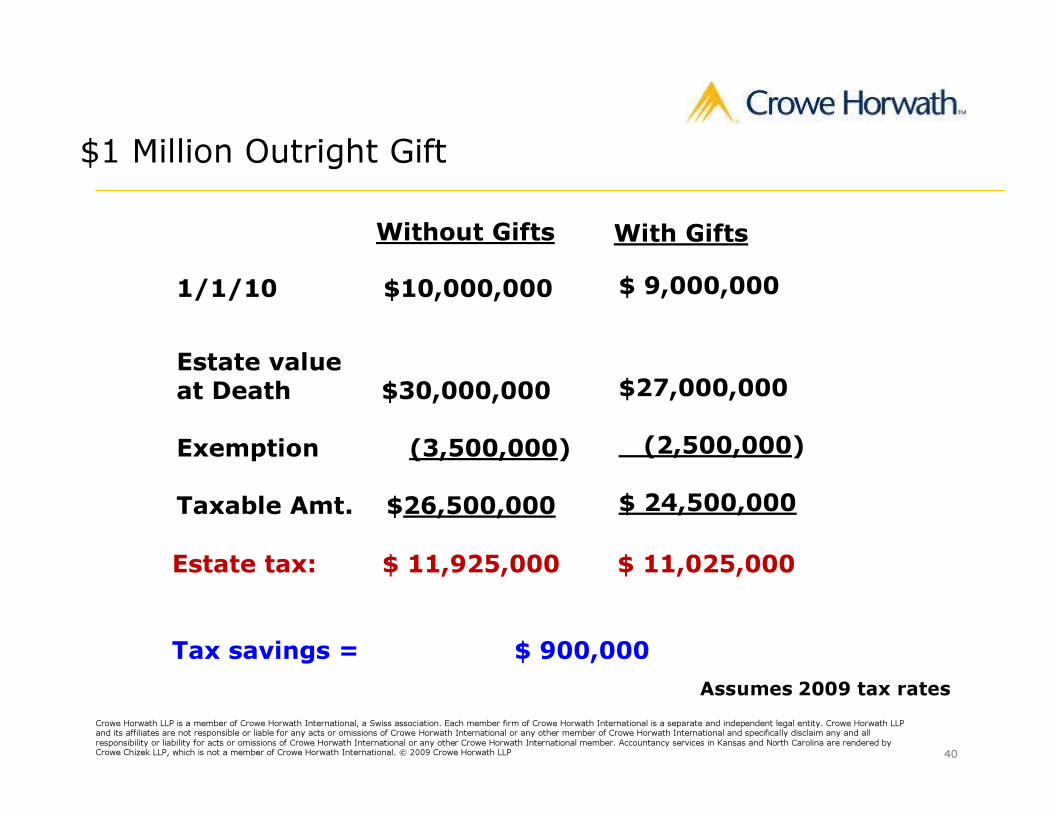

$1 Million Outright GiftWithout Gifts

Estate tax: $ 11,925,000 $ 11,025,000

Tax savings = $ 900,000Assumes 2009 tax rates

1/1/10 $10,000,000

Estate value at Death $30,000,000Exemption (3,500,000) Taxable Amt. $26,500,000

$ 9,000,000

$27,000,000(2,500,000)

$ 24,500,000

With Gifts

41

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

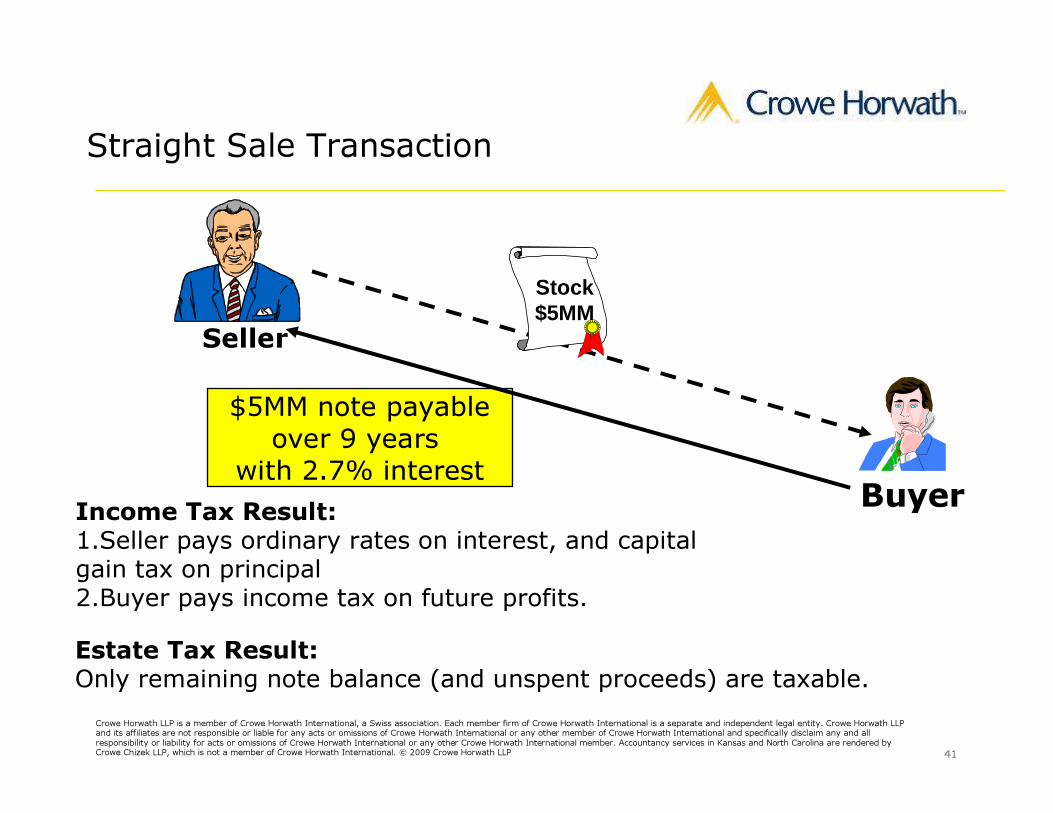

Straight Sale Transaction

Seller

Buyer

$5MM note payableover 9 years

with 2.7% interest

Stock$5MM

Income Tax Result:1.Seller pays ordinary rates on interest, and capital gain tax on principal2.Buyer pays income tax on future profits.Estate Tax Result:Only remaining note balance (and unspent proceeds) are taxable.

42

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Sale to a “Grantor Trust”

� In general, both the income tax and estate tax laws provide thatif a taxpayer transfers property to a trust but continues to “control” either the trust or the property, the IRS will simply ignore the existence of the trust.

� However, the test for what constitutes “control” is different for income tax purposes than it is for estate and gift tax purposes.

43

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

“Intentionally Defective” Trust

� Taxpayers can take advantage of these rules to make the trust intentionally defective for income tax purposes.

� It still is a valid transfer for legal purposes, as well as for estate and gift tax purposes.

44

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

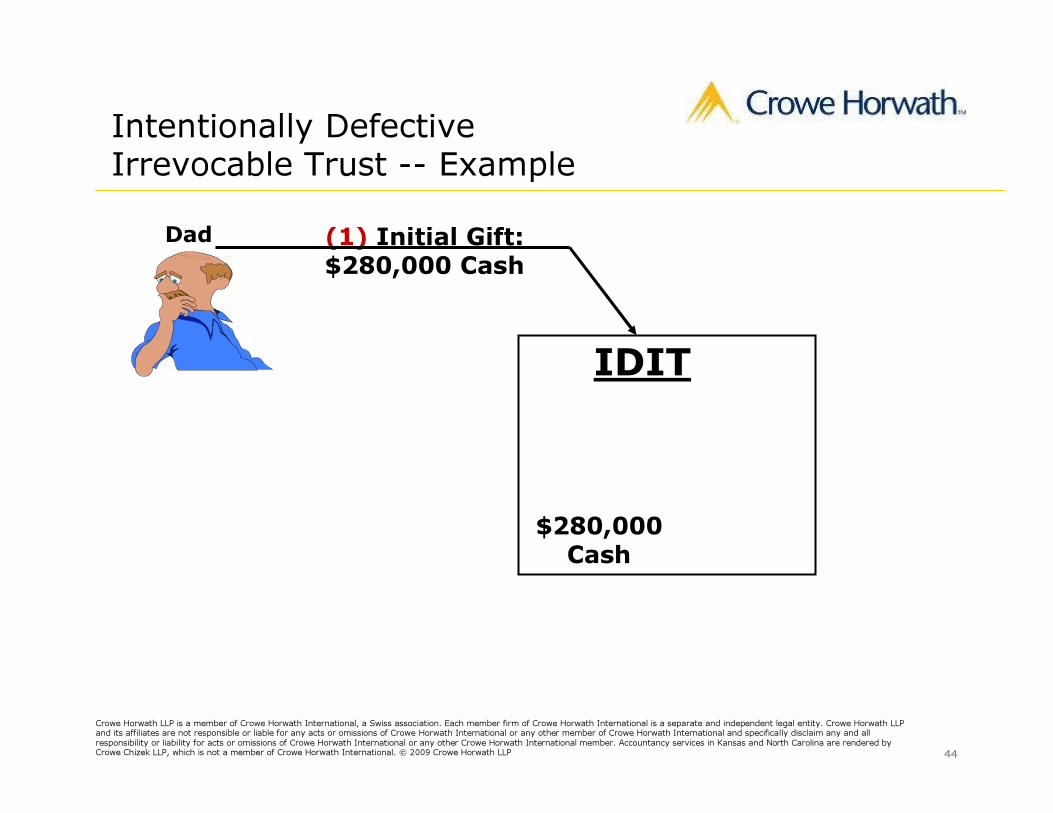

IDIT

Dad (1) Initial Gift:$280,000 Cash

$280,000Cash

Intentionally DefectiveIrrevocable Trust -- Example

45

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

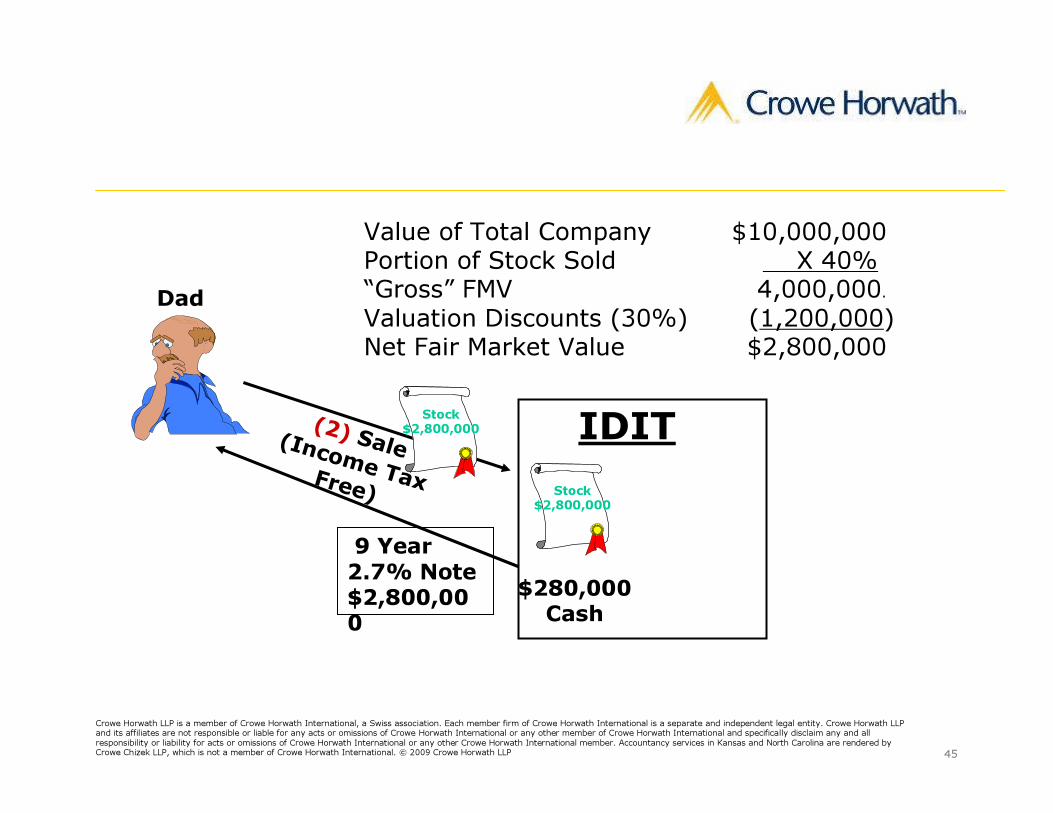

IDIT

Dad

( 2 ) Sal e( I n c o m e T ax F r e e )

9 Year 2.7% Note$2,800,000

Stock$2,800,000

Stock$2,800,000

$280,000Cash

Value of Total CompanyPortion of Stock Sold“Gross” FMVValuation Discounts (30%)Net Fair Market Value

$10,000,000 X 40%

4,000,000.(1,200,000)$2,800,000

46

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

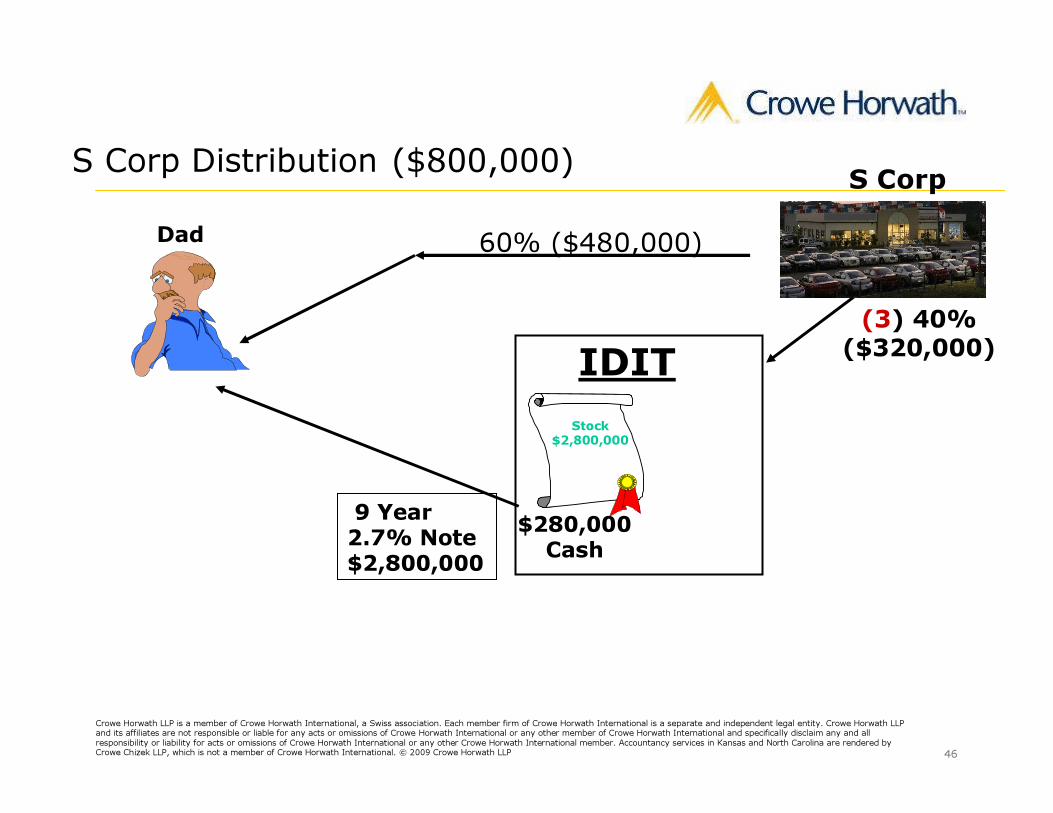

S Corp Distribution ($800,000)

IDIT

Dad

9 Year 2.7% Note$2,800,000

Stock$2,800,000

(3) 40%($320,000)

S Corp

$280,000Cash

60% ($480,000)

47

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

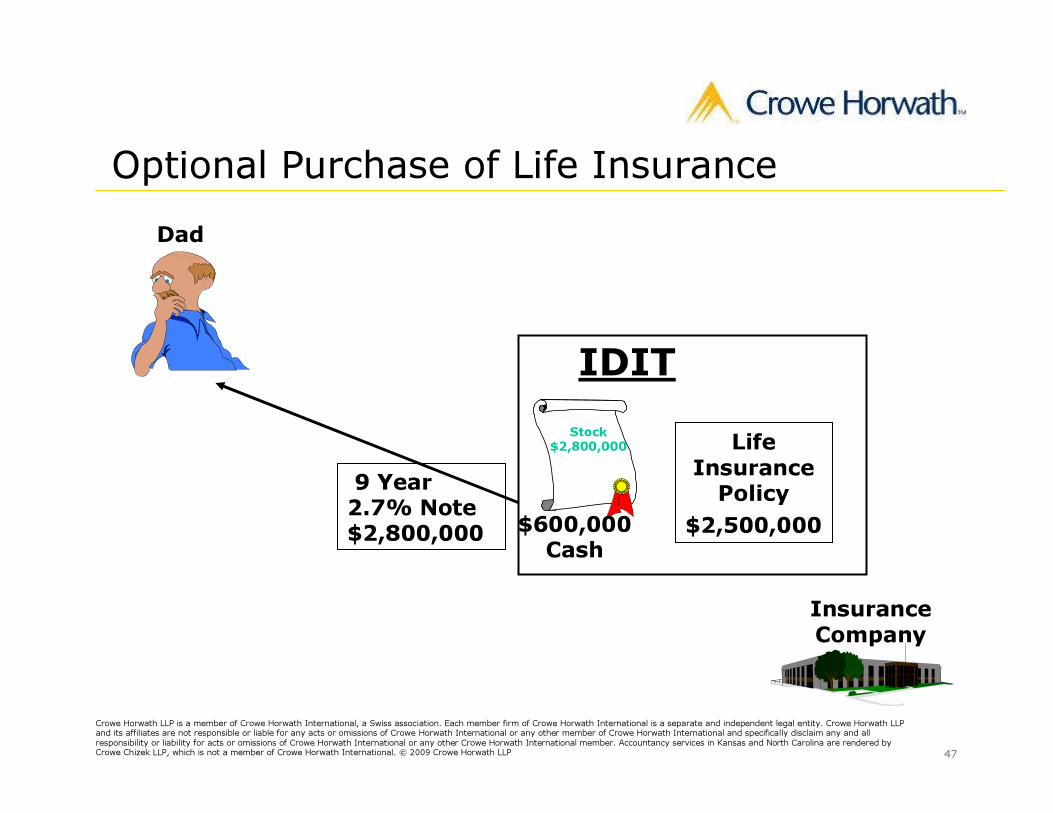

Optional Purchase of Life Insurance

IDIT

Dad

9 Year 2.7% Note$2,800,000

Stock$2,800,000 Life

Insurance Policy

$2,500,000

Insurance Company

$600,000Cash

48

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

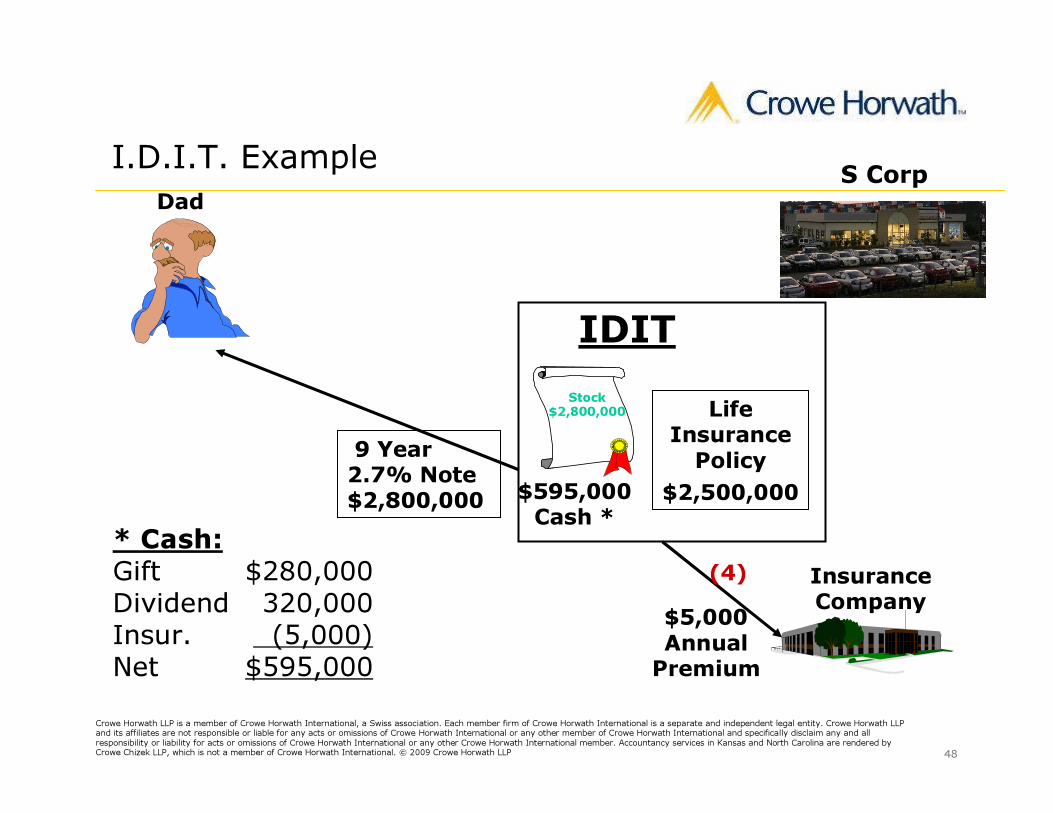

I.D.I.T. Example

IDIT

Dad

9 Year 2.7% Note$2,800,000

Stock$2,800,000 Life

Insurance Policy

$2,500,000

Insurance Company$5,000

AnnualPremium

(4)

S Corp

$595,000Cash ** Cash:

GiftDividendInsur.Net

$280,000320,000(5,000)

$595,000

49

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

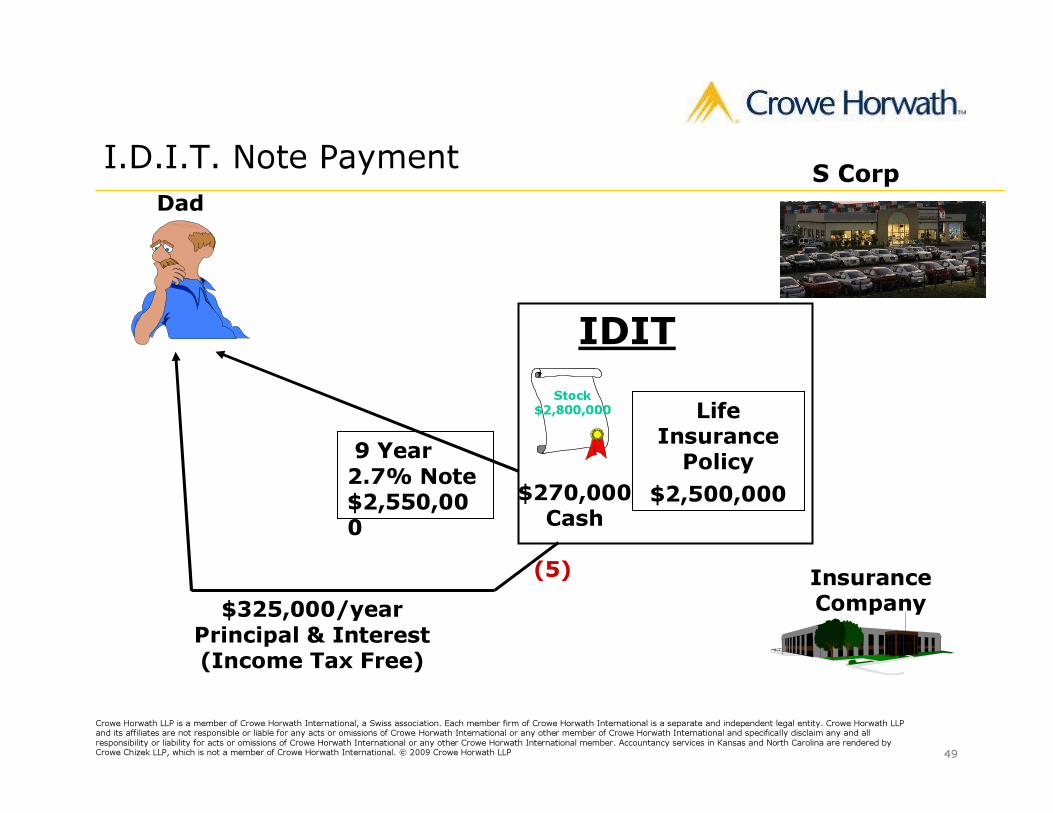

I.D.I.T. Note Payment

IDIT

Dad

9 Year 2.7% Note$2,550,000

Stock$2,800,000 Life

Insurance Policy

$2,500,000

Insurance Company$325,000/year

Principal & Interest(Income Tax Free)

(5)

S Corp

$270,000Cash

50

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

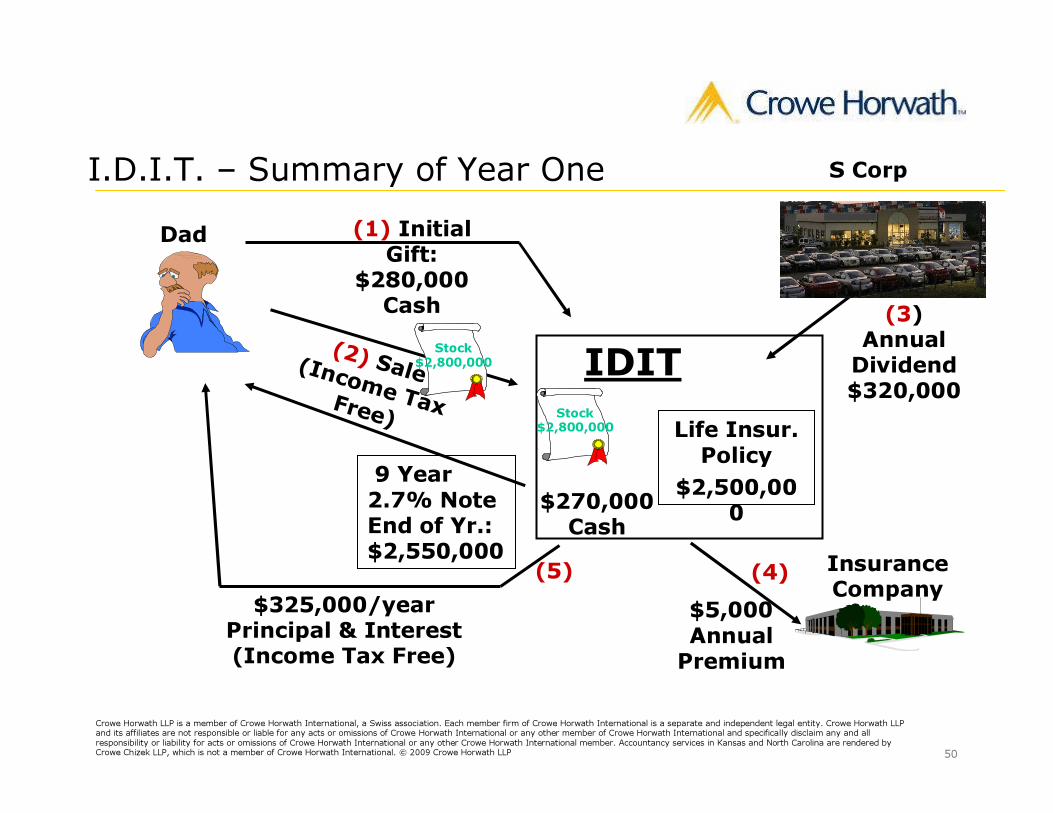

I.D.I.T. – Summary of Year One

IDIT

Dad

( 2 ) Sal e( I n c o m e T ax F r e e )

9 Year 2.7% NoteEnd of Yr.:$2,550,000

Stock$2,800,000

Stock$2,800,000

(1) Initial Gift:

$280,000 Cash

$270,000Cash

(3) AnnualDividend$320,000

Life Insur. Policy

$2,500,000

Insurance Company$5,000

AnnualPremium

(4)$325,000/year

Principal & Interest(Income Tax Free)

(5)

S Corp

51

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

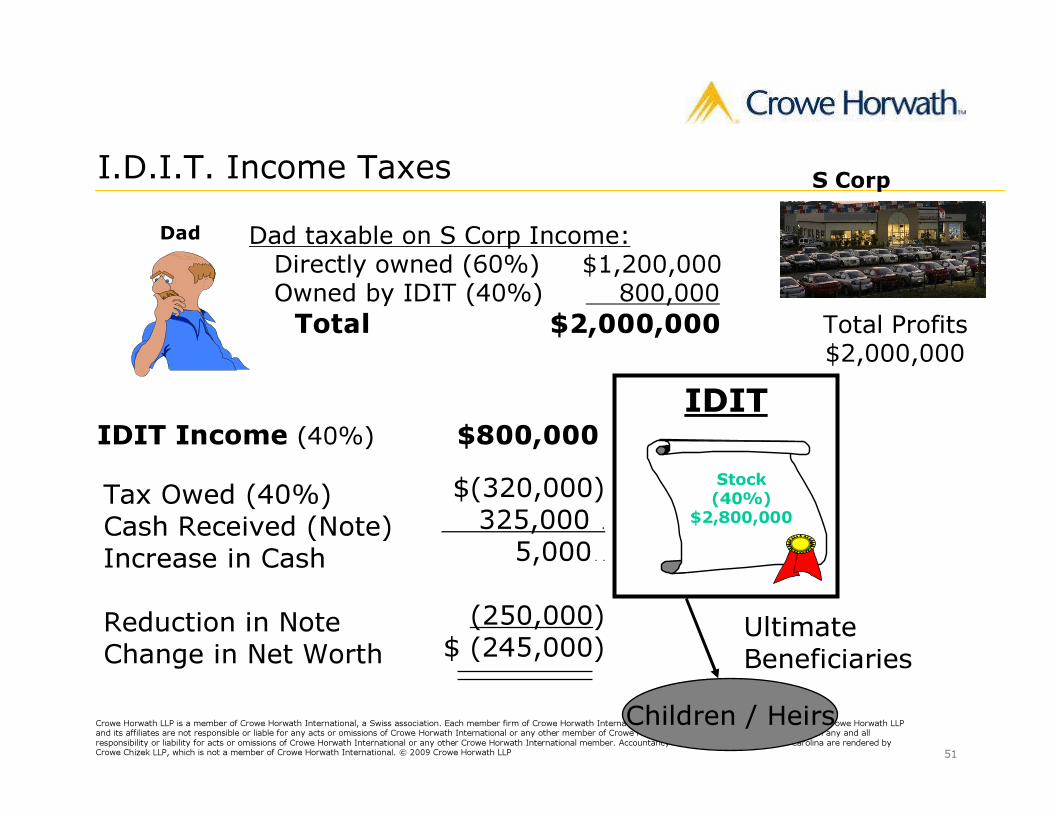

I.D.I.T. Income TaxesDad

IDITStock (40%)

$2,800,000

UltimateBeneficiaries

S Corp

Total Profits$2,000,000

Tax Owed (40%)Cash Received (Note)Increase in CashReduction in NoteChange in Net Worth

$(320,000)325,000 .

5,000 . .

(250,000)$ (245,000)

Children / Heirs

IDIT Income (40%) $800,000

Dad taxable on S Corp Income:Directly owned (60%) $1,200,000Owned by IDIT (40%) 800,000Total $2,000,000

52

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Benefits of IDIT Technique� Selling assets at discounted values.� No income tax on sale, or on note payments.� Any increase in the value of the original asset sold to the trust avoids estate tax.

� The value of the note (included in seller’s estate) does not appreciate, other than for interest earned on the note.

� Grantor pays all income taxes on profits or gains on trust assets, resulting in a further reduction of his estate with no gift tax.

53

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

� Alternative Technique: useful when transferor has previously utilized all gift tax lifetime exemption.

� Transfer assets to an irrevocable trust, in exchange for a series of payments from the trust.

� Taxable gift is difference between value of property and the Present Value of the series of payments.

� You are treated for income tax purposes as if you still own the assets until all payments are made.

� For Estate Tax Purposes, the assets are only taxable if you die before all payments are made as scheduled.

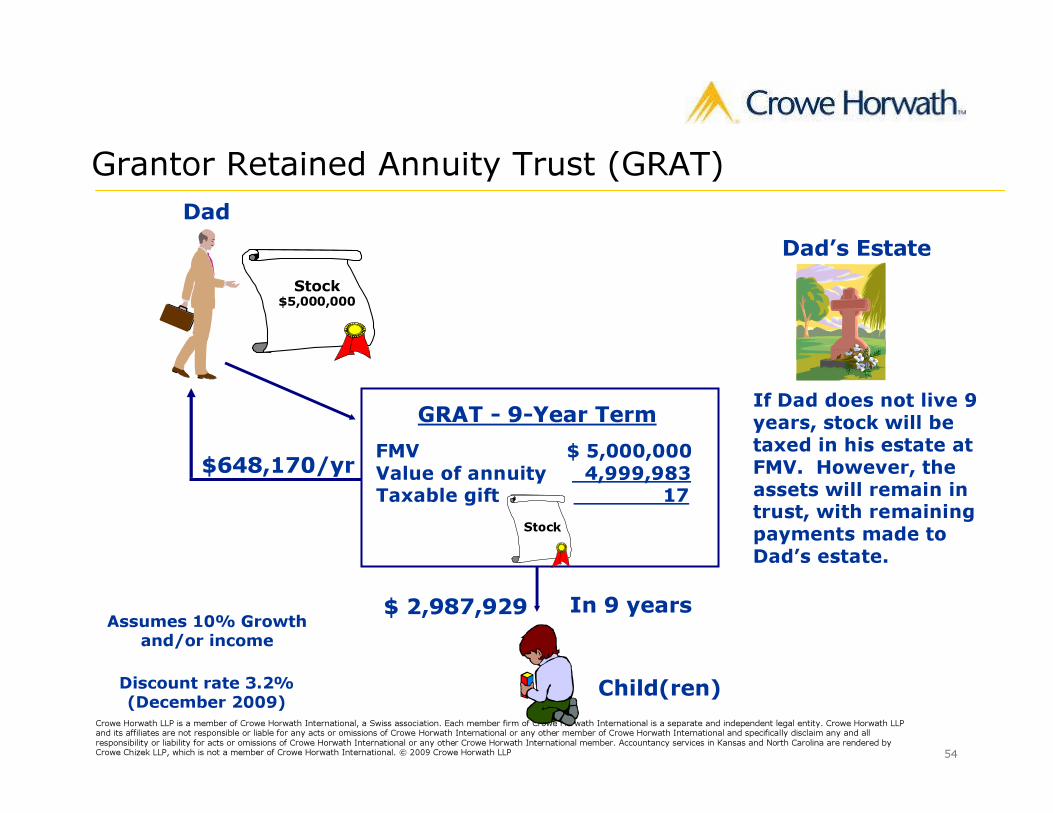

Grantor Retained Annuity Trust (GRAT)

54

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Grantor Retained Annuity Trust (GRAT)Dad

Stock$5,000,000

$648,170/yrGRAT - 9-Year Term

FMV $ 5,000,000Value of annuity 4,999,983Taxable gift 17

Stock

In 9 years$ 2,987,929

Child(ren)Discount rate 3.2% (December 2009)

Dad’s Estate

If Dad does not live 9 years, stock will be taxed in his estate at FMV. However, the assets will remain in trust, with remaining payments made to Dad’s estate.

Assumes 10% Growth and/or income

55

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Fundamental Road Map Questions to be Answered1. Is a Successor Dealer/Operator identified for all dealerships

that will continue after the triggering event? 2. Does that successor candidate have relevant automotive

experience and meet the manufacturer criteria and expectation of a Dealer/Operator; � or how will it be achieved over time?

3. Do any of the following individuals truly meet manufacturers requirements - Be realistic – it’s critical : � Surviving spouses, sons, daughters, other relatives, GM

and other designated person.

56

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Fundamental Road Map Questions Answered4. Who will have the actual operating control of the dealership

and have the authority to assure the dealership is in compliance with Manufacturer’s policies and procedures?

5. Who will have the voting control over the dealership?� Governance issues - Successor Dealer/Operator or the

investor shareholders.6. Will the Successor Dealer/Operator have a significant equity

position? 7. Who has authority to raise capital to meet the Manufacturer

working capital levels - investor shareholders and/or the successor Dealer/Operator?

8. What voting and operating rights do the Non-Dealer Investor shareholders possess?

57

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Fundamental Road Map Questions Answered9. How are OTHER key employees brought into the plan? 10. Is financing in place to achieve the plan?

� Dealer or Corporation funding for buy in or outs;� Financial Institution funding phantom stock plans,

deferred compensation plans, etc... 11.Does the succession plan and estate plan dove tail into one

coordinated plan and are both plans documented?12.Does the succession plan violate any Manufacturer banking

or other critical agreements?Moral of the story get the appropriate

approvals for the plans!!!!!!

58

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Preparing your Business for Sale� Focus on the bottom line, not the top line

� Multiples are based on earnings, not revenue;� Buyers are paying up to 7x profits, so $1 saved is $7 “earned”;� The most recent year is the most important year for Blue Sky.

� Eliminate all “controversial” spending� Don’t make add backs a negotiation point – eliminate them where possible.

� Push managers hard to maximize results� Older dealers get into the “don’t mess it up mode” and may not be demanding on staff.

� If there is an operational problem, take as much expense as possible in one month rather than dragging it forward over future months� Makes identification of normalization item easier.

59

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Preparing your Business for Sale� Negotiate OEM required facility actions pre-sale

� OEMs may be easier on the existing dealer than an entering dealer� Buyers will magnify and over estimate unknown costs� Negotiate and get agreement but don’t necessarily make the expenditures.

� Reduce non-essential cap exp to reduce price to buyers� Capitalize items whenever possible rather than expense.� Clearly document any non-recurring expenses so they can be added back

� MAKE IT EASY FOR A BUYER TO UNDERSTAND THE VALUE IN THE DEALERSHIP

60

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Questions

61

Crowe Horwath LLP is a member of Crowe Horwath International, a Swiss association. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLPand its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2009 Crowe Horwath LLP

Richard Kotzen, CPACrowe Horwath [email protected]

More Information

Marv Hills, CPACrowe Horwath [email protected]

Ron Sompels, CPACrowe Horwath [email protected]

For more information on this subject, or to discuss your specific situation, contact the presenters or your Crowe representative .

Download Dealership Flash article on Estate Planning at

www.crowehorwath.com/dealer

![APPLICATIONSOF PROBABILITY: PHILOSOPHYmatthewkotzen.net/matthewkotzen.net/Research_files/29_Hajek_C29.pdf · “ -Hajek-C ” — / / — : — page — 626 matthew kotzen realistic,since“[t]hereisnoevidencetobelievethatthemindcontainstworepresentational](https://img.pdfslide.us/doc/110x75/5e6ac8aeb31b5f7605604ec4/applicationsof-probability-phi-aoe-hajek-c-a-a-a-a-page-a-626.jpg)

![[Richie Kotzen]-Actual Thing to Play](https://img.pdfslide.us/doc/110x75/5695d5611a28ab9b02a52390/richie-kotzen-actual-thing-to-play.jpg)

![[GUITAR] Richie Kotzen - Rock Chops Tab Book](https://img.pdfslide.us/doc/110x75/54779449b4af9fcd528b4673/guitar-richie-kotzen-rock-chops-tab-book-55845eb7c9b88.jpg)

![(Guitar Book) Richie Kotzen - Shining Virtuocity [Young Guitar]](https://img.pdfslide.us/doc/110x75/551658c44a7959c4028b5445/guitar-book-richie-kotzen-shining-virtuocity-young-guitar.jpg)