Embed Size (px)

Citation preview

155

CHAPTER CHAPTER CHAPTER CHAPTER –––– 4444

INDIA’S TRADE WITH INDIA’S TRADE WITH INDIA’S TRADE WITH INDIA’S TRADE WITH

SAARC COUNTRIES SAARC COUNTRIES SAARC COUNTRIES SAARC COUNTRIES ––––

COUNTRIWISE ANALYSISCOUNTRIWISE ANALYSISCOUNTRIWISE ANALYSISCOUNTRIWISE ANALYSIS

156

CHAPTER – 4

India’s Trade with Saarc countries: Country wise Analysis

This Chapter presents a detailed descriptive analysis of each

member country’s socio, economic and political background of the

SAARC group and India’s trade relations with them.

Indo-Bangla Trade Relations:

Geographical features:

Bangladesh is a low-lying area with 147570sq. k.m. It is

located in South Asia with a largely marshy jungle coastline of 710

kilometers (440 mi.) on northern littoral of the Bay of Bengal.

Bangladesh’s alluvial soil is highly fertile but vulnerable to flood

and drought. Bangladesh has a subtropical monsoonal climate

characterized by heavy seasonal rainfall, moderately warm

temperatures, and high humidity. Natural calamities, such as

floods, tropical cyclones, tornadoes, and tidal bores affect the

country almost every year. Bangladesh also is haunted by major

cyclones on an average of 16 times a decade.

Urbanization is happening fast, and it is estimated that only

30 per cent of the population entering the labor force in the future

will be absorbed into agriculture, although many will likely find

other kinds of work in rural areas. The Sundarbans, an area of

coastal tropical jungle in the southwest and the Chittagong Hill

tracts on the southeastern border with Burma and India, are the

least densely populated.

The area that is now Bangladesh has a rich historical and

cultural past, combining Dravidian, Indo-Aryan, Mongol/Mughul,

Arab, Persian, Turkic, and west European cultures. Majority

157

residents of Bangladesh, about 98 per cent of whom are ethnic

Bengali speak Bangla.

ECONOMY

Being one of the world’s poorest and most densely populated

countries, Bangladesh has stepped up its efforts major to meet the

food needs of its increasing population, by augmenting domestic

production. The land is devoted mainly to rice and jute cultivation

Wheat production has also increased in recent years the country

has attained self-sufficiency in rice production. However, 10 to 15

per cent of the population suffers from high nutritional risk and

erratic monsoon, with high degree occurrence of floods. Although

improving Bangladesh has yet to imports its infrastructure to

support transportation, communications, and energy supply.

Bangladesh’s industrial base is weak with limited reserves of coal

and oil. The country’s main endowments include its vast human

resource base, rich agricultural land, relatively abundant water,

and substantial reserves of natural gas, which can be items of

exchange among the Saarc countries.

Moves towards Market Economy

Bangladesh-began its exercise in the direction of raising the

country’s new industrial capacity and rehabilitating the economy

after he violent events of 1971recovery from the static economic

model adopted by its early leadership, Bangladesh drove its

economy out of the clutches of inefficient public sector to the result

oriented private sector in late 1975, by gradually increasing the

scope to private sector participation in the economy, since 1975; of

course major portions of the banking and jute sector, are kept

remain under government control.

158

Investors viewed favorably steps taken by the interim government

to address corruption, governance, and infrastructure issues,

though most believed it was too early to assess the long-term

impact of those developments.

Predominance of Agriculture:

For majority, agriculture is the main source of livelihood in

Bangladesh in spite of often volatile weather conditions. After rice

and jute, maize and vegetables follow in importance. Expanded

irrigation facilities have, encouraged some wheat producers

switched to cultivation of maize which is used mostly as poultry

feed. Because of Bangladesh’s fertile soil and normally ample water

supply, rice can be grown and harvested three times a year in

many areas. Due to a number of factors, Bangladesh’s labor-

intensive agriculture has achieved steady increases in food grain

production despite the often unfavorable weather conditions.

Under employment remains a serious problem and a growing

concern for Bangladesh’s agricultural sector, Finding alternative

sources of employment will continue to be a challenge problem for

future economy.

Garment export – base

The country’s ready-made garment industry, which made

rapid strides, provides employment to millions of people however;

the country could still done better in expanding garment exports

accounting for more than three-fourths of all exports, even the

country’s cash crop, and jute.

The U.S. and the European Union (EU) market imports

significant amounts of garments and knitwear from Bangladesh.

Bangladesh also has established Export Processing Zones in

159

Chittagong (1983), Dhaka (1994), Comilla (2000), Mongla (2001),

Iswardi (2005), Uttara (2006), and Karnafully (2007).

It is suggested that Bangladesh should privatize state-owned

enterprises deregulate and promote foreign investment in high-

potential industries like energy and telecommunications.

Bilateral Relations with India:

India and Bangladesh are good neighbours. Geographic,

cultural, historic, and commercial ties are strong, and both

countries recognize the importance of good relations. In the

Bangladesh’s struggle for independence from Pakistan in 1971,

India helped in gaining independence of Bangladesh, and furnished

relief and reconstruction aid during the post war period.

Notwithstanding the development that India and Bangladesh

have witnessed in recent years, the two countries together still

contain a large number of extremely poor people living on one

dollar a day, this is the real challenge posed before the two

countries. Although they are situated in a region endowed with

vast resources, they have failed to convert these resources into

productive and collective wealth in an accelerating manner.

Together India and Bangladesh boast a total population of

more than 1 billion, and their rapid domestic economic

development has demonstrated broad prospects for cooperation.

India and Bangladesh are still characterized by a low level of

economic integration, despite the fact that their economies are

complementary to a large extent and stand to benefit substantially

from economic integration. However, compared with their strength,

there still exists much potential for developing trade and economic

relations between the two countries.

160

Indo-Bangladesh relations are often strained and many Bangladesh

feel India likes to play “big brother” to smaller neighbors, including

Bangladesh. Bilateral relations warmed in 1996, due to a softer

India’s foreign policy and the new Awami League government. A 30-

year water-sharing agreement for the Ganges river was signed in

December 1996, after an earlier bilateral water-sharing agreement

for the Ganges River lapsed in 1988. Bangladesh is not happy with

the proposed Indian River Linking Project, which the government

says could turn many parts of Bangladesh into a desert. Indian

army maintains a strong presence in the Hill Tracts. Arms

smuggling and reported opium crop cultivation are concerns in this

area. Occasional exchanges of fire between the two countries flare

up and seriously disrupt bilateral relations. Much to Bangladesh’s

displeasure, India’s erected a barbed-wire fence is an irritant in the

bilateral relations of both the countries.

Former Prime Minister Khaleda Zia of Bangla, however,

visited the Indian capital in March 2006 and reviewed bilateral

relations with her Indian counterpart*. Two agreements viz., the

Revised Trade Agreement and the Agreement on Mutual

Cooperation for Preventing Illicit Drug Trafficking in Narcotic Drugs

and Psychotropic Substances and Related Matters-were signed

between the two countries during this visit. The then Indian

Foreign Minister Pranab Mukherjee met with the Chief Adviser in

Dhaka on February 26, 2007. Mukherjee invited Ahmed to the

April 3-4, 2007, SAARC summit in Delhi, and both sides pledged to

put Bangladesh-India relations on “an irreversible higher

trajectory.

Improving relations with India became a priority with the

return of the Awami League government in January 2009. The new

Prime Minister Hasina herself travelled to New Delhi in January

161

2010 and signed several agreements to further strengthen their

bilateral relationship. India plays an important role in

Bangladesh’s trade since the independence and since nineties,

Indo-Bangla trade increased tremendously.

The importance of Bangladesh to India’s trade can be

understood from the fact that Bangla contributed 0.74 per cent in

1990, 1.59 percent in 1995, per cent and 1.40 per cent of India’s

global exports in 2010-11.

Trend, Structure and Current Picture of Indo - Bangladesh

Trade:

One of the important features of Indo-Bangladesh bilateral

trade to be mentioned is that a large volume of informal or

unrecorded trade, both in commodities and services, occurs every

year, and it is growing despite unilateral or regional or multilateral

trade liberalization in these two countries. The official data on

trade in services between these nations are, in fact, not available at

all. Under this situation of data paucity with regard to illegal trade

and trade in services, our current analysis will depend on mostly

on the official trade data in commodities.

Historical Development of Indo-Bangla Trade Relations

Bangladesh and India signed the ‘Treaty of Friendship’

Cooperation and Peace on March 19, 1972 in Dhaka for 25 years.

In the agreement, fish, raw-jute, newsprint and naphtha were

identified as the principal exports of Bangladesh to India. Bangla’s

major import items from India introduced were cement, coal,

machinery and unmanufactured tobacco. The trade between the

162

two nations was limited to government level.1 This agreement also

provided border trade between Bangladesh and neighboring Indian

states; and within 16 kilometers of both countries border, free

trade was allowed for certain commodities2.

The first trade agreement of 1972 was replaced by another

trade agreement for three years. This agreement was signed on

July 5, 1973 and became effective from 28 September, 1973. This

agreement provided for a system of balanced trade and payment

arrangement and most favored nation treatment to both the

Countries.

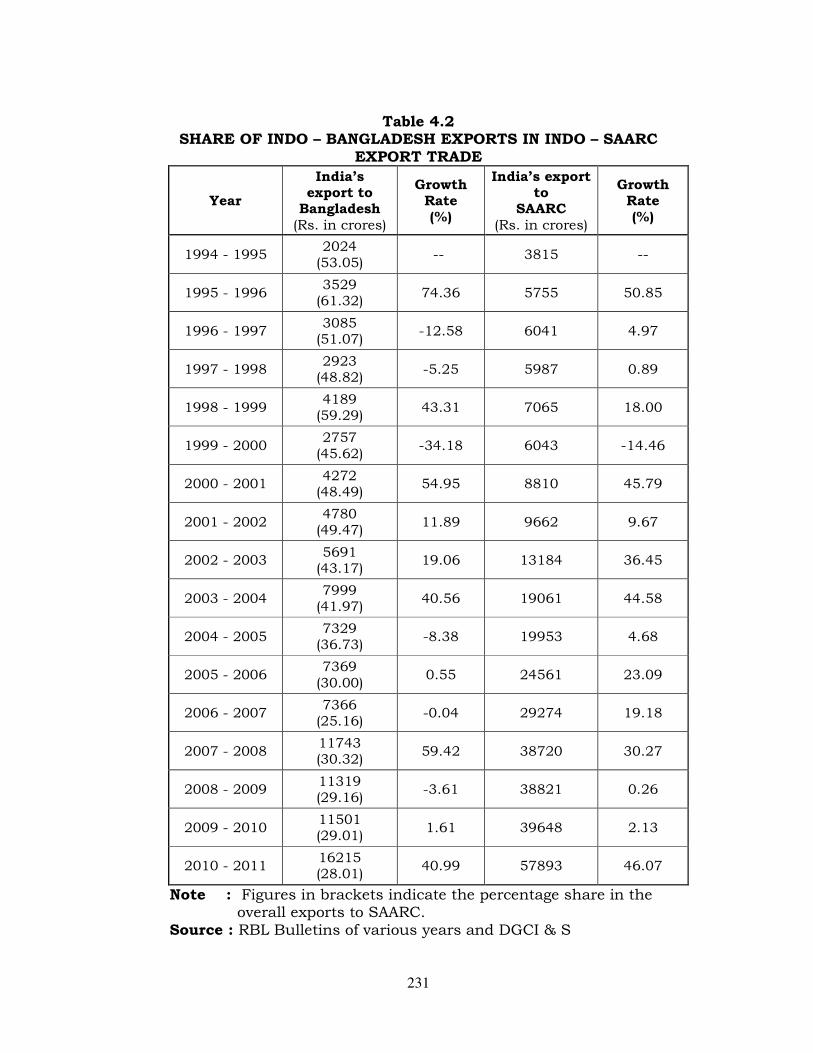

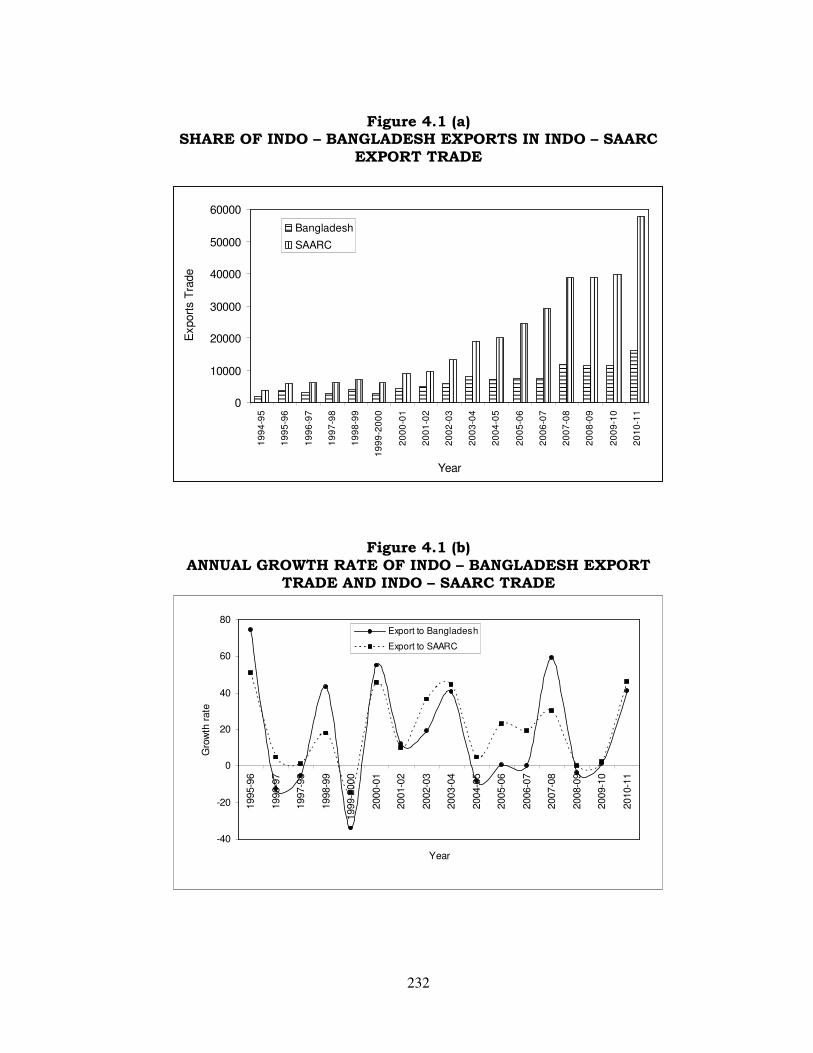

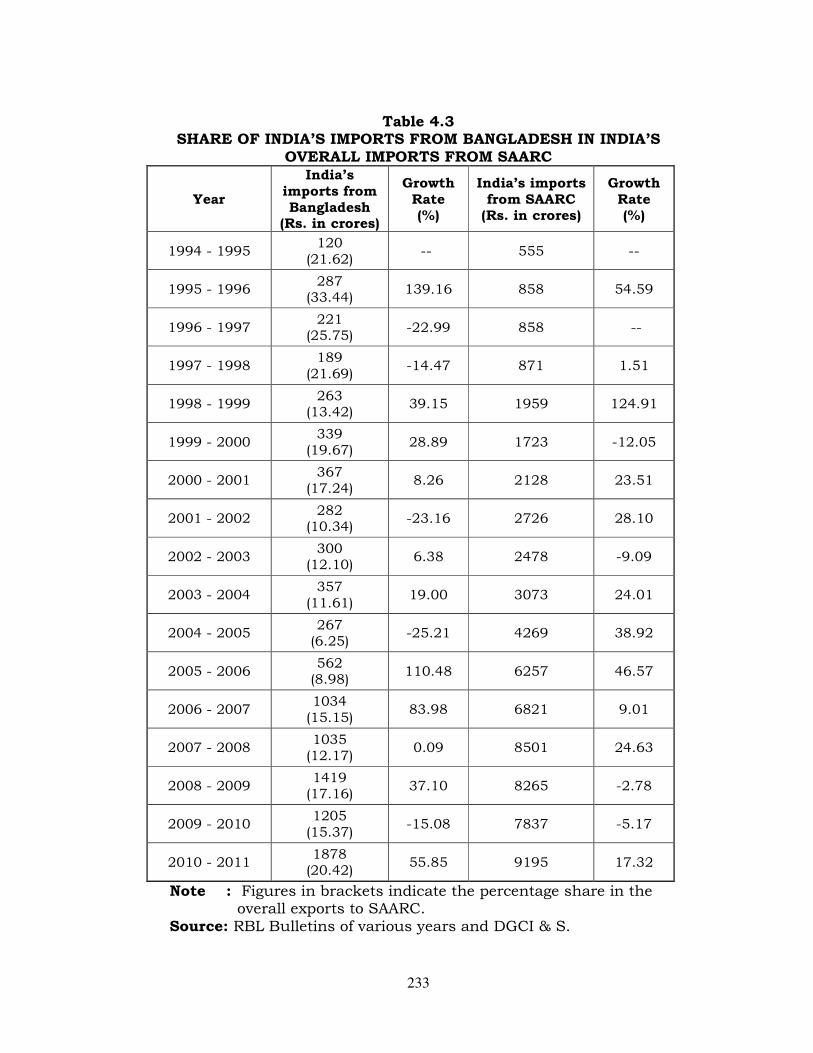

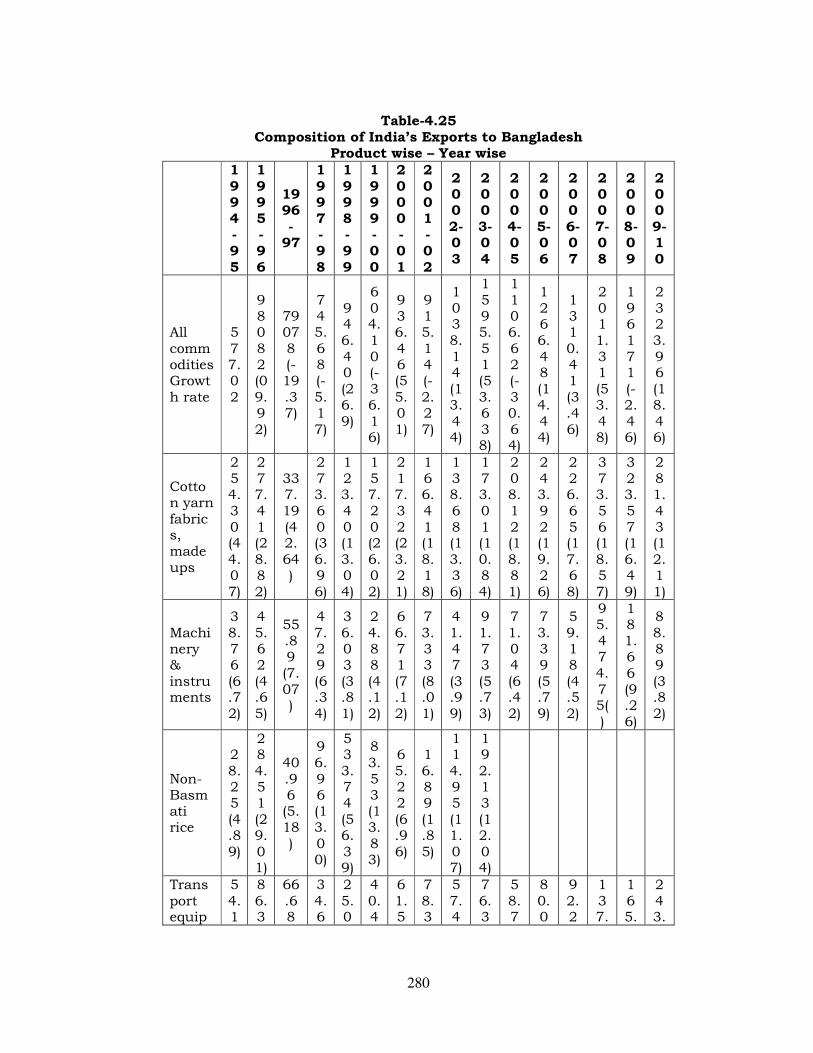

Share of Indo-Bangladesh trade in Indo-SAARC Trade (Table 4.2)

It is evident from table 4.2 that the member country, which

registered the largest percentage share in Indo-SAARC trade, was

Bangladesh. India’s exports to Bangladesh amounted to Rs. 2024

crores in 1994-95, contributing the highest percentage share to

Indo-SAARC trade with 53.05 per cent. The exports to Bangladesh

being amounted Rs. 3529 crores in 1995-96, contributed the

highest ever percentage share to Indo-SAARC trade with 61.32 per

cent in 1995-96. But, in 1998-99, the percentage share was

recorded at 59.29 per cent, (see table 4.2). Since then, the

percentage share exhibited decreasing trend through out the study

period. The lowest percentage share was observed in 2006-07 with

25.16 per cent. With regard to India’s export growth rate with

Bangladesh, the following observation have been noted.

1 Madan, D.K., Indo-Bangladesh Economic Relations and SAARC, (New Delhi: Deep and Deep Pubication), 1996.

2 Hasan, M.K., Trade with India and Trade Policies of Bangladesh, in F.E. Cookson and A.K.M.S. Alam (Eds) Towards Greater sub –regional Economic Cooperation. 2002, chapter 10, 349-401.

163

Between 1994-95 and 2000-01, India’s exports to

Bangladesh had been doubled as the exports worth of Rs. 2024

crores in 1994-95, went up to Rs. 4272 crores in 2000-2001 over

1994-95. However, the compound growth rate of exports recorded

in respect of Bangladesh was not as high as had been registered in

respect of India’s compound growth rate of exports with SAARC,

which was recorded at 130.93 per cent in 2000-01 over 1994-95.

Between 2001-02 and 2005-06, the compound growth rate of

exports, recorded in respect of Bangladesh, was not as large as had

been registered in the previous phase i.e., from 1994-95 to 2000-

01. The compound growth rate of exports, registered during second

phase was 54.16 per cent in 2005-06 over 2001-02. Also, this

compound growth rate of exports, recorded in respect of

Bangladesh, was far lesser than the compound growth rate of

exports, registered in respect of SAARC; the compound growth rate

recorded in respect of SAARC was 154.20 per cent in 2005-06 over

that of 2001-02.

But, the above trend, recorded in II phase was reversed, as

the compound growth rate of exports recorded at 120.13 per cent

in 2010-11 in respect of Bangladesh, far higher than the

compound growth rate of exports, registered at 97.76 per cent in

2010-11 over 2006-07, in respect of exports to other SAARC

Nations.

Share of India’s imports from Bangladesh in the overall India’s

imports from SAARC.

India had substantial trade relations with Bangladesh during

the recent decade. According to table 4.3 the imports from

Bangladesh as a proportion of imports from SAARC had been

registered at 21.62 per cent in 1994-95. The highest percentage

164

share of imports from Bangladesh had been recorded at 33.44 per

cent in 1995-96 and the least percentage share was recorded at

6.25 per cent in 2004-05.

When we considered the growth rate of imports in respect of

Bangladesh, the highest annual growth rate of imports was

recorded at 139.6 per cent in 1995-96 over 1994-95, as the

imports from Bangladesh worth of Rs. 120 crores in 1994-95, had

gone up to 287 crores in 1995-96. Negative annual growth rates of

imports had been observed during 1996-97 with 22.99 per cent,

14.47 per cent in 1997-98, 23.16 per cent in 2001-02 and 25.21

per cent in 2004-05 and with 15.08 per cent in 2009-10. (See table

4.3).

With regard to compound growth in 2000-01, the imports

from Bangladesh had been more than doubled when compared to

1994-95. When we considered the compound growth rate of

imports in respect of SAARC nations during the same period, it

was, registered at 283.42 per cent in 2000-01 over 1994-95.

During 2001-02 and 2005-06, the imports from Bangladesh

had been almost doubled with the compound growth rate of

imports being registered at 99.29 per cent in 2005-06 over 2001-

02. When the compound growth rate of imports was considered in

respect of SAARC during the same period, it was registered at

129.53 per cent in 2005-06 over 2000-01 (more than doubled).

Between 2006-07 and 2010-11, the compound growth rate of

India’s imports in respect of Bangladesh was recorded at 81.62 per

cent in 2010-11 over 2006-07. But, the compound growth rate of

imports, recorded in respect of SAARC was at 34.80 per cent only.

165

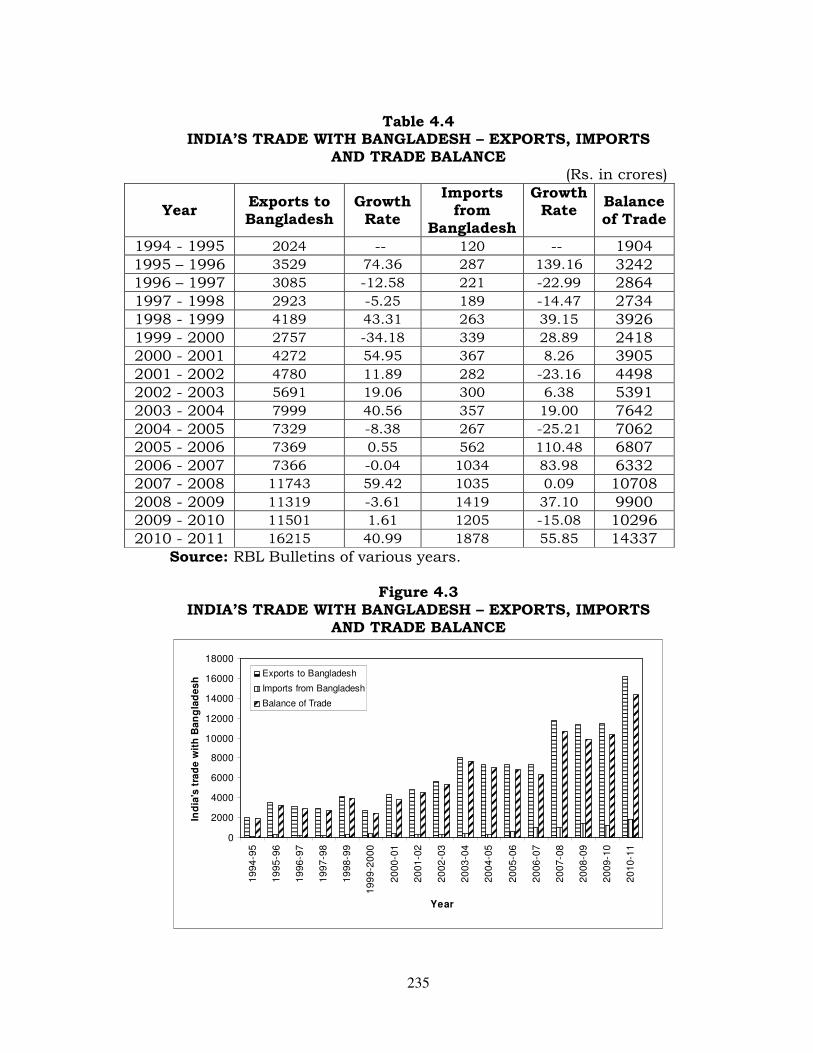

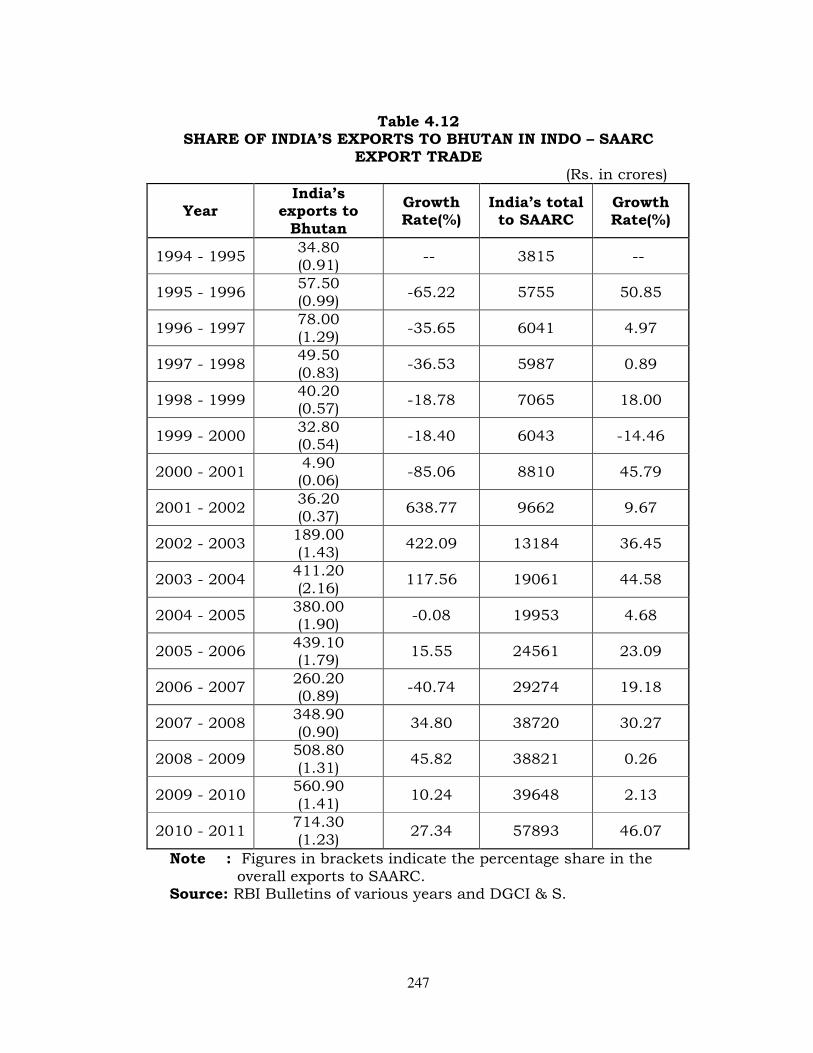

India’s balance of trade with Bangladesh

It is evident from the table 4.4 that India’s exports to

Bangladesh have always surpassed the values of imports. While

the values of exports to Bangladesh were in thousands of crores,

imports from Bangladesh were just in hundreds. Thus, the ±

balance of trade has always been in favour of India. However, the

annual growth rate in balance of trade with Bangladesh had been

widely fluctuating with erratic trends. The ups and downs in the

growth rate could be witnessed in table 4.4.

The Indo-Bangla trade deficit has been increasing

exponentially since the recent past. The data show that compared

to 1994-95, trade deficit is more than three times in 2004-05 and

seven and half times in 2010-11 when compared to 1994-95 (see

table 4.4). Between 1983 and 2003, according to an IMF study, the

trade deficit was increased by 46 times.3

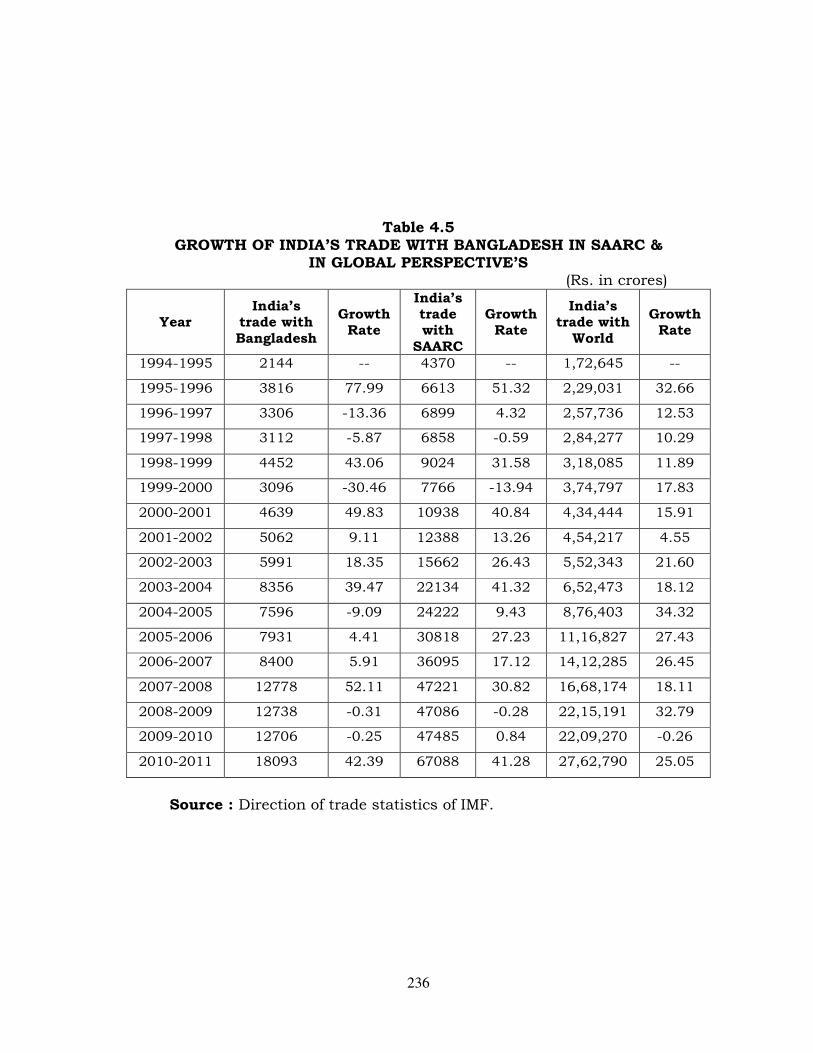

The importance of India in Bangladesh’s trade

India plays an important role in Bangladesh’s trade since

independence. Recently especially in 1990’s, Bangladesh trade with

India increased tremendously. The table 4.5 compares the growth

rates of India’s trade with Bangladesh, with that of SAARC

countries and with world for the period from 1994-95 to 2010-11.

It could be observed from table 4.5 that the annual growth rate of

India’s trade with Bangladesh during 1995-96 was much higher

than those with SAARC and the world. For example during 1998-

99, while annual growth rate of India’s trade with SAARC and the

world were 31.58 per cent and 11.89 per cent respectively, but with

Bangladesh this was 43.06 per cent. During 2000-2001, the

3 IMF (2004). Direction of Trade Statistics Year book, Washington D.C.

166

growth rates with the world, SAARC and Bangladesh were 15.91

per cent, 40.84 per cent and 49.83 per cent respectively. The

growth rate of India’s trade with Bangladesh increased very

significantly during 2007-08. While the growth rates with world

and the SAARC were 18.11 per cent and 30.82 per cent

respectively, the growth rate with Bangladesh was at 52.11 per

cent during the same period. During 2008-09 and 2009-10,

negative growth rates recorded consecutively with Bangladesh, and

also with the world during 2009-10. However, these figures turned

into convincingly positive in 2010-11. (See table 4.5).

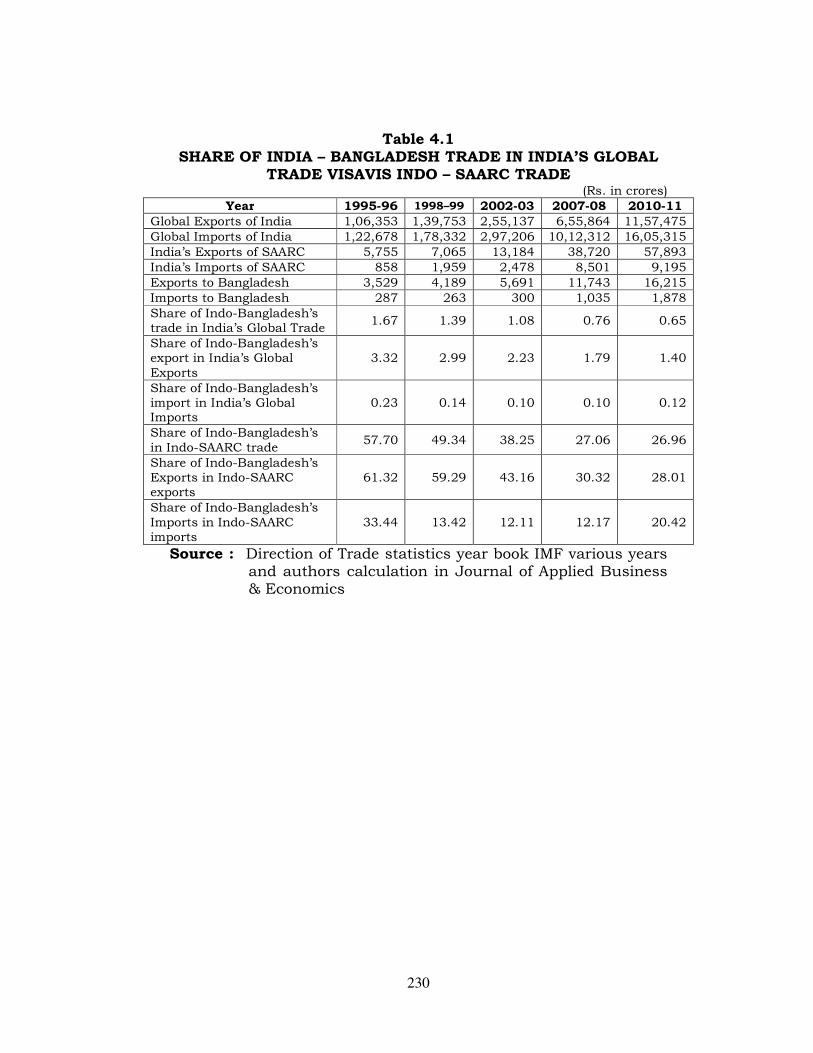

From the table 4.1, it is observed that Bangladesh’s share in

India’s global trade both exports and imports has decreased from

1.67 per cent in 1995-96 to 1.08 per cent in 2002-03 and further

to 0.65 per cent in 2010-11. It is also discouraging that both Indo-

Bangladesh export share and import share have been showing

declining trend in India’s global exports and global imports.

The share of Indo-Bangladesh’s trade in Indo-SAARC trade

also, is not impressive as the trend recorded in respect of Indo-

SAARC trade, displaying a decreasing trend throughout the years.

(see table 4.5). The important feature is that the share of Indo-

Bangladesh’s import trade in India’s global imports slightly went

up from 0.10 per cent in 2007-08 to 0.12 per cent in 2010-11(see

Table 4.1).

INDO-SRI LANKA TRADE RELATIONS:

The area of Srilanka in 65,610 sq.k.m which is about the size

of West Virginia, The population of Sri Lanka is 21.3 millions. The

167

annual growth rate is 0.9 per cent.4 The languages, spoken in

Srilanka are Simhala and Tamil. The natural resources available

are limestone, graphite, mineral sands, gems and phosphate.5

PROFILE

Sri Lanka is ethnically, linguistically, and religiously diverse.

Sinhalese make up 74% of the population and are concentrated in

the densely populated southwest. Sri Lankan Tamils, citizens

whose south Indian ancestors have lived on the island for

centuries, comprise about 0.9 per cent of the population.

Indian Tamils, a distinct ethnic group, represent about 5 per

cent of the population. The British brought them to Sri Lanka in

the 19th century as tea and rubber plantation workers, and they

remain concentrated in the “tea country” of south-central Sri

Lanka. In accordance with a 1964 agreement with India, Sri Lanka

granted citizenship to 230,000 “stateless” Indian Tamils in 1988.

Under the pact, India granted citizenship to the remainder, some

200,000 of whom now live in India.

Other minorities include Mulsims (both Moors and Malays),

at about 7 per cent of the population; Sizable minorities of both

Sinhalese and Tamils are Christians, most of whom are Roman

Catholic. The 1978 constitution-while assuring freedom of religion-

grants primacy to Buddhism. Tamils and most Muslims speak

Tamil. Use of English has declined since independence Both

Sinhala and Tamil are official languages.

4 Various Reports of Bureau of South and Central Asian Affairs, 2010.

5 Ibid.

168

HISTORY

The actual origins of the Sinhalese are shrouded in myth.

Most believe they came to Sri Lanka from northern India during the

6th century BC. Buddhism arrived from the subcontinent 300 years

later and spread rapidly.

Sri Lanka Economy

Sri Lanka is a lower-middle income developing nation. When

compared to India, Bangladesh and Pakistan, Sri Lanka is ahead

with 91 per cent literacy rate in local languages and life

expectancy of 75 years rank well above those of India.

Like many countries in South Asia Sri Lanka shifted away

from a socialist orientation and opened its economy to foreign

investment with aggressive economic reform under the UNP-led

government that ruled from 2002 to 2004.

The economic situation in Sri Lanka received a jolt in 2009

due to the global recession. In the recent past, it was hindered by

large scale hostilities between the government and the LTTE, high

government expenditure, inflation and interest rates. Exports fell

by about 13.5%. In 2008, trade and current accounts recorded

large deficits due to high oil and commodity prices, and an

unsuccessful effort by the government to defend the Sri Lankan

rupee drained Sri Lanka’s exchange reserves, forcing it to turn to

the International Monetary Fund (IMF) in early 2009 for assistance.

The economic strategy as outlined by President Rajapaksa

namely “Mahinda Chintana” (Mahinda’s Thoughts), guides

government economic policy, Presently with a focus on poverty

169

alleviation and steering investment to backward areas; The small

and medium enterprise (SME) sector; promotion of agriculture etc.

The government has also drafted a 10-year long term development

framework to accelerate growth to strengthen big infrastructure

projects in the country. The government is not for privatization of

state enterprises, including “strategic” enterprises such as state-

owned banks, airports and electrical utilities. Instead, it plans to

retain ownership and management of these enterprises and make

them profitable.

The service sector comprising telecom, trading, transport,

and financial services is the largest component of Sri Lanka’s GDP

at around 60 per cent. Financial scarcities arose with the rise in

hostilities, and defense expenditures expansion of public sector

employment, and the expenses associated with the jumbo cabinet

and growing information technology sector, especially information

technology training and software development.

Sri Lanka’s GDP comprises 30 per cent of its volume from

Industry accounts. Like in India, agriculture production of GDP

has lost its relative importance to the Sri Lanka economy in recent

decades with only about 12 per cent of GDP. Sri Lanka gets its

earnings from rice, cereals, tea, rubber, and coconut.

Foreign Trade and Foreign Assistance

Sri Lanka’s exports (mainly apparel, tea, rubber, gems and

jewellery) were estimated at $7.0 billion and imports (mainly oil,

textiles, food, and machinery) were estimated at $9.6 billion for

2009. The trade deficit of Sri Lanka was financed primarily by

remittances from Sri Lankan expatriate workers, foreign aid and,

from public borrowings. Sri Lanka must diversify its exports

170

beyond garments and tea. The tea industry is challenged by a

shortage of plantation labor and by growing competition.

Exports to the United States, Sri Lanka’s most important single-

country market, were estimated to be around $1.54 billion for

2009, or 22% of total exports. For many years, the United States

has been Sri Lanka’s biggest market for garments, taking almost

50% of total garment exports. India is Sri Lanka’s largest source of

imports, accounting for over 20 per cent of imports.

Iran is a major lender to Sri Lanka and has provided

infrastructure project loans and an interest-free credit facility for

oil imports. Iran assistance for modernization of Sri Lanka’s only

oil refinery has come forth though no firm commitments are in

place. China has also become a major lender for infrastructure

projects, such as a new port and a coal power plant.

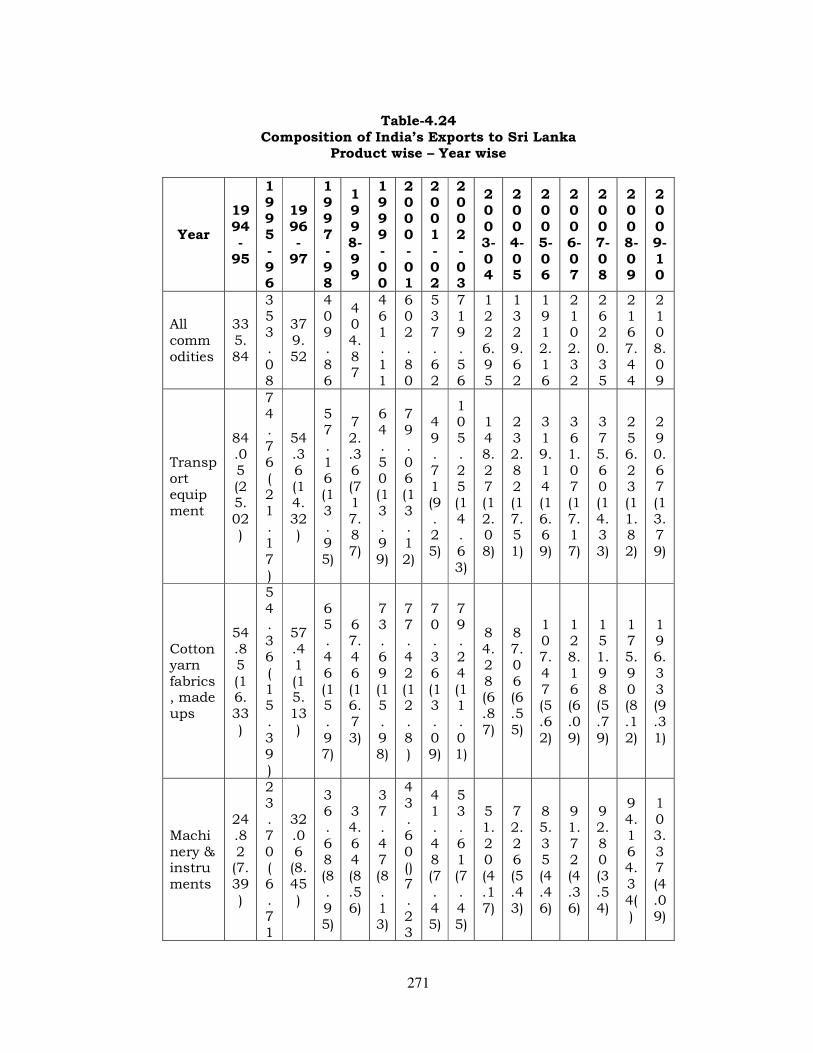

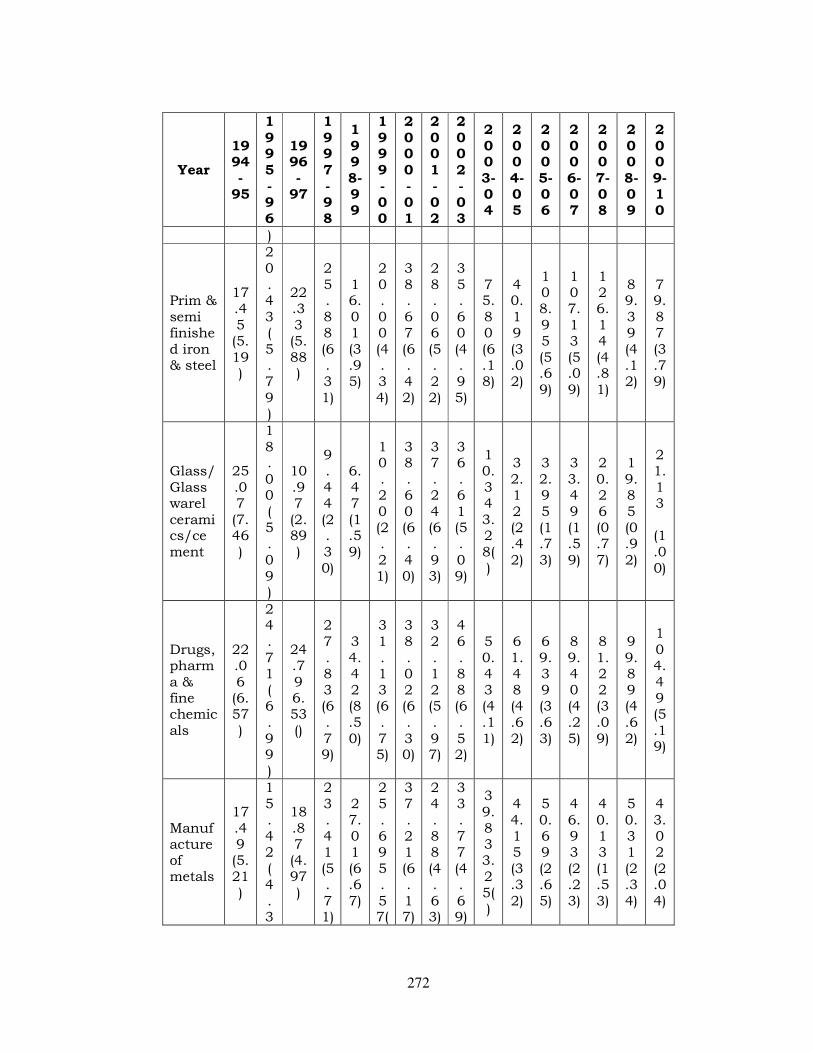

Sri Lanka has traditionally been an important export market

for India and is the second largest trading partner in the region

after Bangladesh (See table 4.22). The bilateral trade is carried out

in accordance with the provisions of the Trade Agreement signed in

1961. The trade is in freely convertible currencies and on MFN

basis. Both the countries are the signatories of WTO, SAARC and

Bangkok Agreement. Within the frame work of SAARC Preferential

Trading Agreement and the Bangkok Agreement, mutual

preferential trade concessions are extended to each other.

India and Sri Lanka have signed a Free Trade Agreement on

28th December, 1998 under which tariff on a large number of items

would be phased out within an agreed time frame.6 While India

would reduce the tariff to zero in three years, Sri Lanka would do

6 Reeta Mathur. International Economics, (Jaipur: Sub Lime Publications, 2002) p. 245.

171

so in eight years.7 Two sides will maintain negative Lists of items

on which no duty concessions are given, where protection to local

industry in considered necessary.

INDO-SRI LANKA RELATIONS:

Bilateral relations between Sri Lanka and India have been

generally friendly, but were affected by the Sri Lankan civil war and

by the failure of Indian intervention during the Sri Lankan civil

war. India is Sri Lanka’s only neighbor, separated by the Palk

Strait; both nations occupy a strategic position in South Asia and

have sought to build a common security umbrella in the Indian

Ocean.

India - Sri Lanka relations have undergone a qualitative and

quantitative transformation in the recent past. Political relations

are close, trade and investments have increased dramatically,

structural linkages are constantly being augmented, defense

collaboration has increased and there is a general, broad-based

improvement across all sectors of bilateral cooperation. India

was first country to respond to Sri Lanka’s request for assistance

after the tsunami in December 2004. In July 2006, India evacuated

430 Sri Lankan nationals from Lebanon, first to Cyprus by Indian

Navy ships and then to Delhi and Colombo by special Air India

flights.

There exists broad consensus within the Sri Lankan polity on

the primacy of India in Sri Lanka’s external relations matrix. Both

the major political parties in Sri Lanka, the Sri Lanka Freedom

Party and the United Nationalist Party have contributed to the

rapid development of bilateral relations in the last ten years. Sri

7 Ibid., p.256

172

Lanka has supported India’s candidature to the permanent

membership of the UN Security Council.

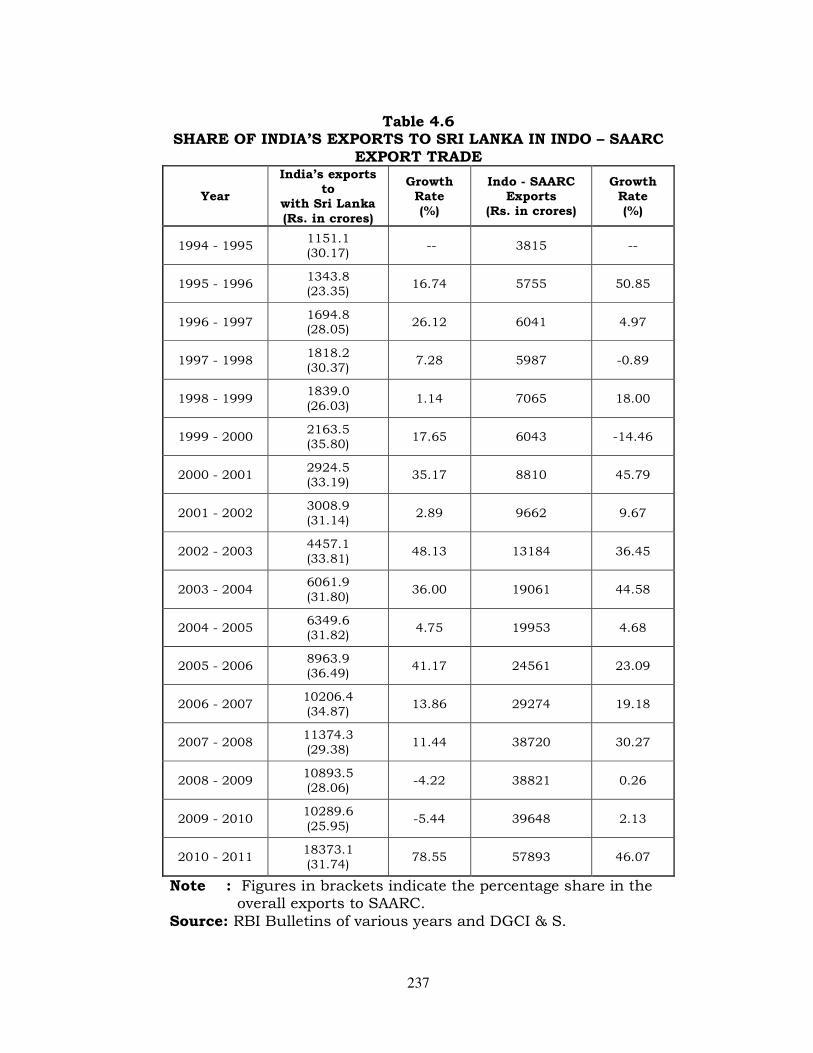

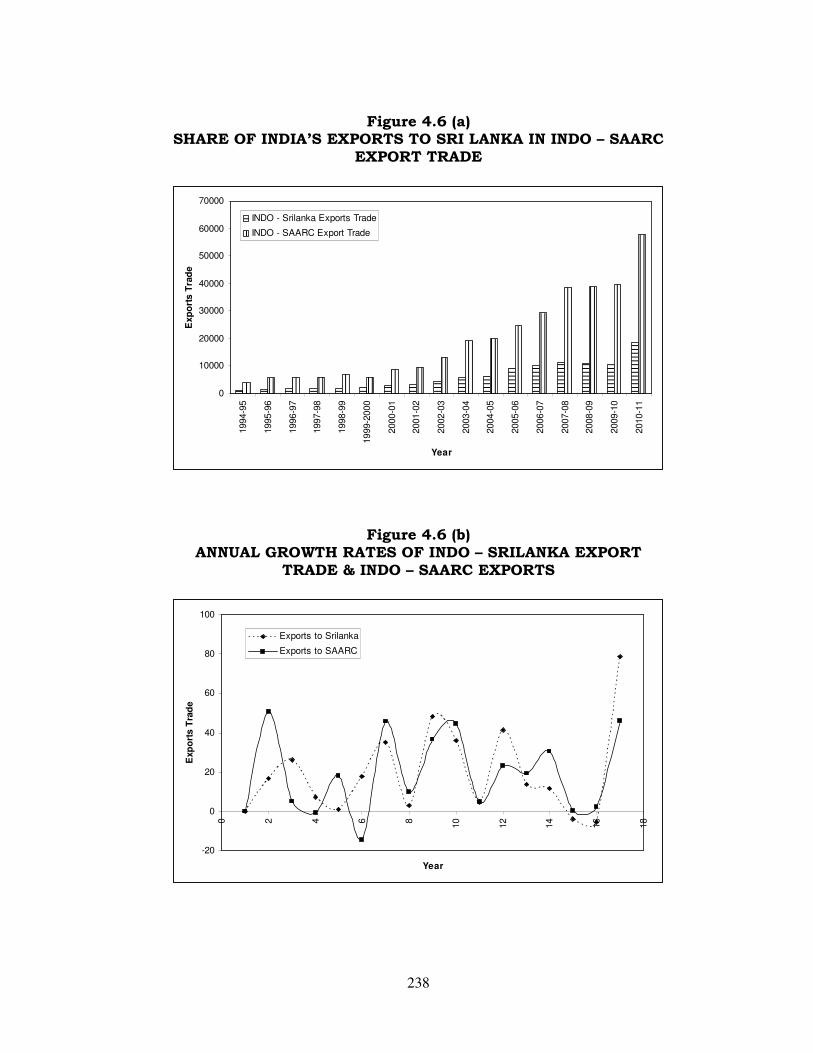

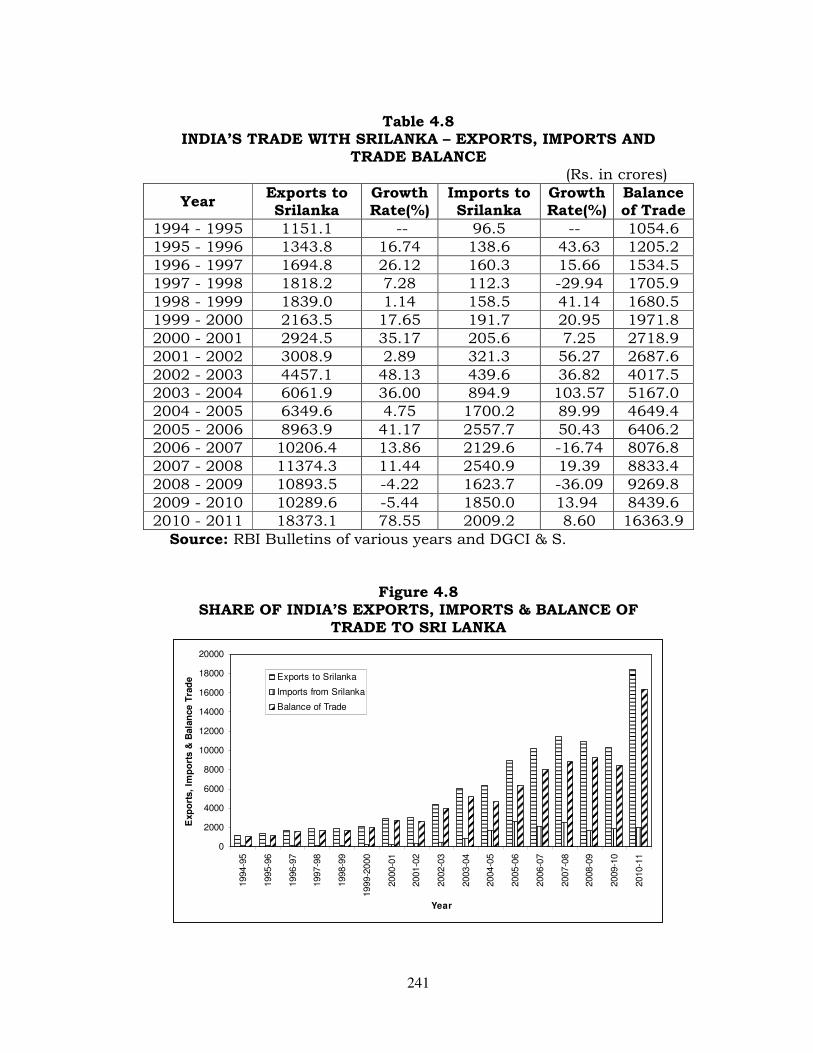

SHARE OF INDO-SRI LANKAN EXPORT TRADE IN INDO -

SAARC EXPORT TRADE:

As indicated by table 4.6, the exports worth of Rs. 2163.5

crores in 1999-2000 as compared to Rs. 1151.1 crores in 1994-95,

reflecting a compound growth rate of 87.95 per cent. On the other

hand, the overall exports to SAARC nations were worth of Rs. 6043

crores in 1999-2000 as compared to Rs. 3815 crores in 1994-5,

contributing the compound growth rate at 50.40 per cent in 1999-

2000 over 1994-95. (See table 4.6).

Between 2000-2001 and 2005-06, there was a remarkable

growth in the compound growth rate of exports with 206.51 per

cent in 2005-06 over 2000-01; in the same way, substantial

compound growth rate of exports had been recorded in respect of

overall exports to SAARC countries with 178.79 per cent in 2005-

06 over 2000-01.

The compound growth rates, which displayed tremendous

records during above period of study, had not been observed

during the last phase of study period that was between 2006-07

and 2010-11.

The compound growth rate of exports, which was registered

at 97.76 per cent in respect of Indo-SAARC trade was more

encouraging than the compound growth rate of exports recorded at

80.02 per cent in 2010-11 over 2006-07, in respect of Sri Lanka. It

was also noteworthy that two consecutive annual negative growth

rates of exports were noted with 4.22 per cent in 2008-09 and also

with 5.44 per cent in 2009-10. In respect of Indo-SAARC trade

173

also, negative annual growth rates had been witnessed with 0.89

per cent in 1997-98 and with 14.46 per cent in 1999-2000.

The share of India’s exports to Sri Lanka as a proportion of

overall exports to SAARC stood at 30.17 per cent in 1994-95. But,

it was declined to 23.35 per cent in 1995-96. During 1997-98, the

percentage share went up to 30.37 per cent as compared to 28.05

per cent in the previous year. The highest percentage share of

exports with Sri Lanka was registered at 36.49 per cent in 2005-

06. (See table 4.6.). This percentage share, however, came down to

25.95 per cent in 2009-10, before it slightly picked up to 31.74 per

cent at the end of 2010-11. The annual growth rates, which were

thus negative during 2008-09, 2009-10, increased to 78.55 per

cent in 2010-11 over the previous year.

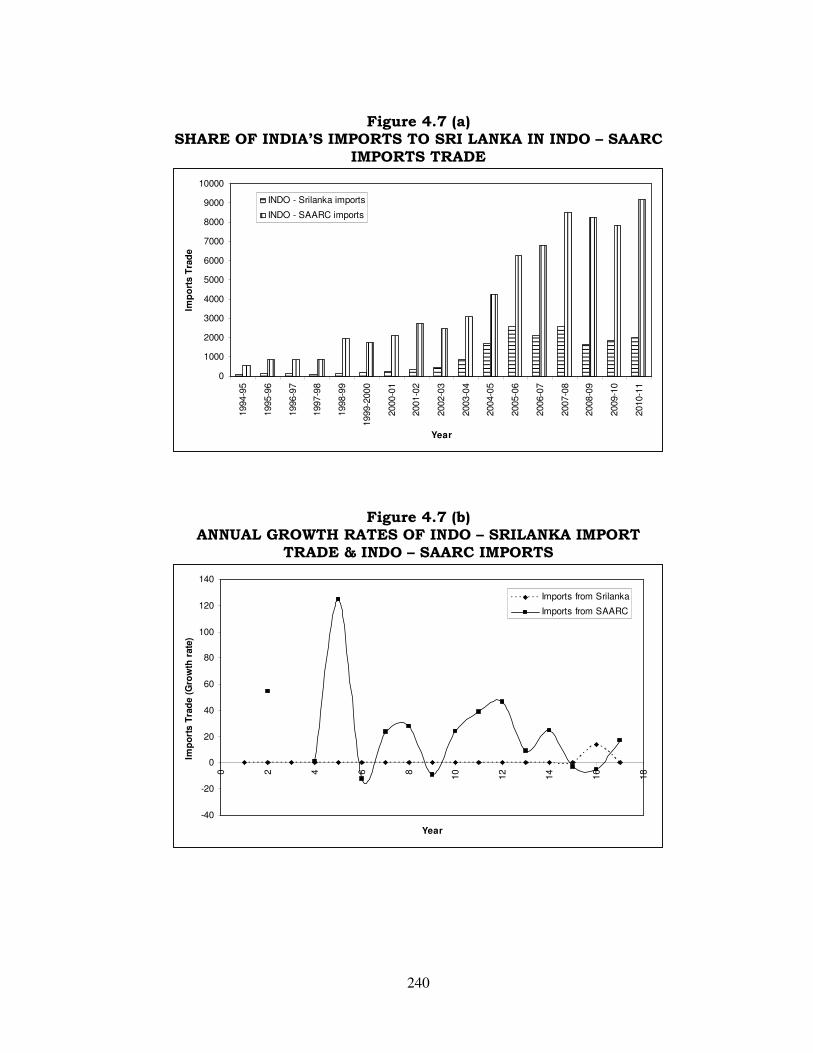

Share of India’s imports from Sri Lanka in Indo-SAARC import

Trade (Table 4.7)

It is evident from table 4.7 that India’s imports from Sri

Lanka have displayed a fluctuating trend through out the study

period.

Between 1994-95 and 1990-2000, the imports from Sri

Lanka were almost doubled with 98.65 per cent in 1999-2000

where as during the same period, in respect of Indo-SAARC trade

there was a remarkable growth in compound growth rate, having

been recorded at 210.45 per cent in 1999-2000 over 1994-95. (see

Table 4.7).

Between 2000-2001 and 2003-04, the imports from Sri

Lanka, which amounted Rs. 205.6 crores in 2000-01 went up

tremendously to Rs. 894.9 crores in 2003-04, contributing a

remarkable growth in the compound growth rate at 335.26 per

174

cent. When we considered the same period in respect of Indo-

SAARC trade, the compound growth rate was just recorded at

44.40 per cent in 2003-04 over 2000-01.

The notable feature during 2002-03 and 2003-04 was that,

the imports from Sri Lanka were more than doubled, with the

Annual growth rate of imports being registered at 103.57 per cent

in 2003-04 over 2002-03.

Between 2004-05 and 2010-11, the compound growth rate of

imports was just recorded at 18.17 per cent in 2010-11 over

2004—05. Further, it was also observed that there were two

negative annual growth rates being recorded at 16.74 per cent in

2006-07 and the other one at 36.09 per cent in 2008-09. But, the

trend was different, if the same period was considered in respect of

Indo-SAARC trade. The imports were more than doubled with the

compound growth rate of imports being registered at 115.39 per

cent in 2010-11 over 2004-05. However, there were two negative

consecutive annual growth rates being registered at 2.78 per cent

in 2008-09 and 5.17 per cent in 2009-10 consecutively.

It was observed that the exports in respect of Sri Lanka have

surpassed the imports through out the study period stretching

from 1994-95 to 2010-11, displaying a favourable balance of trade.

(See table 4.8).

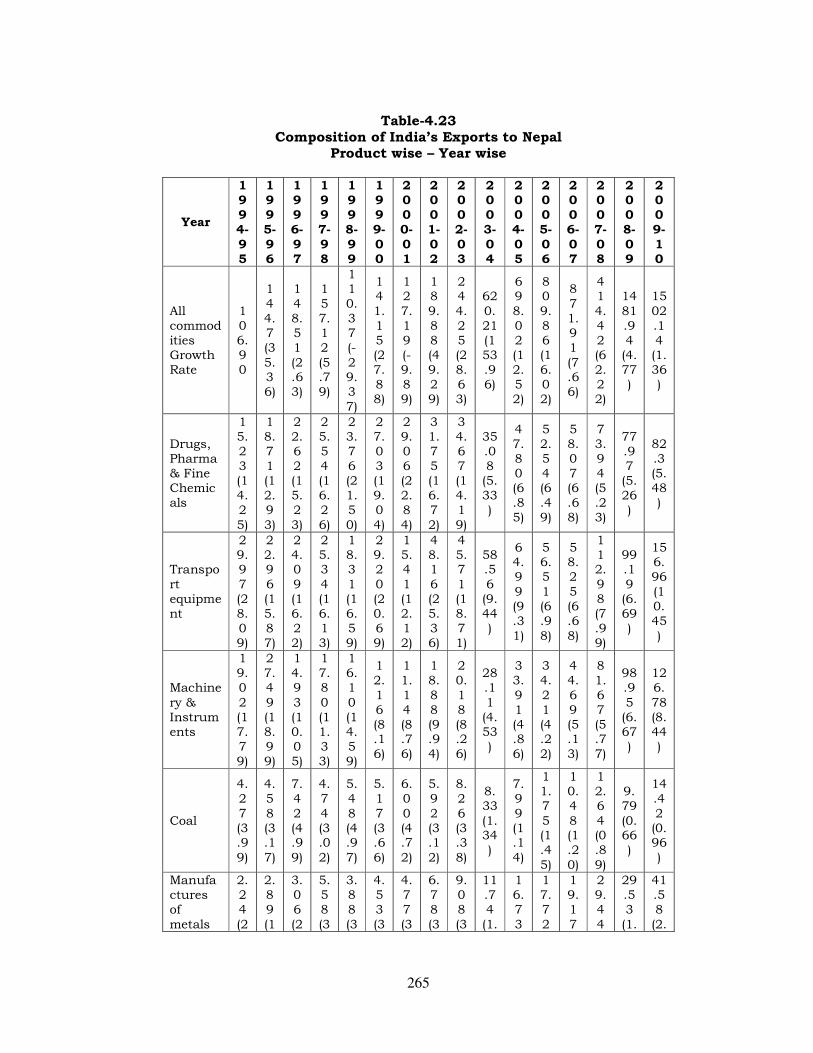

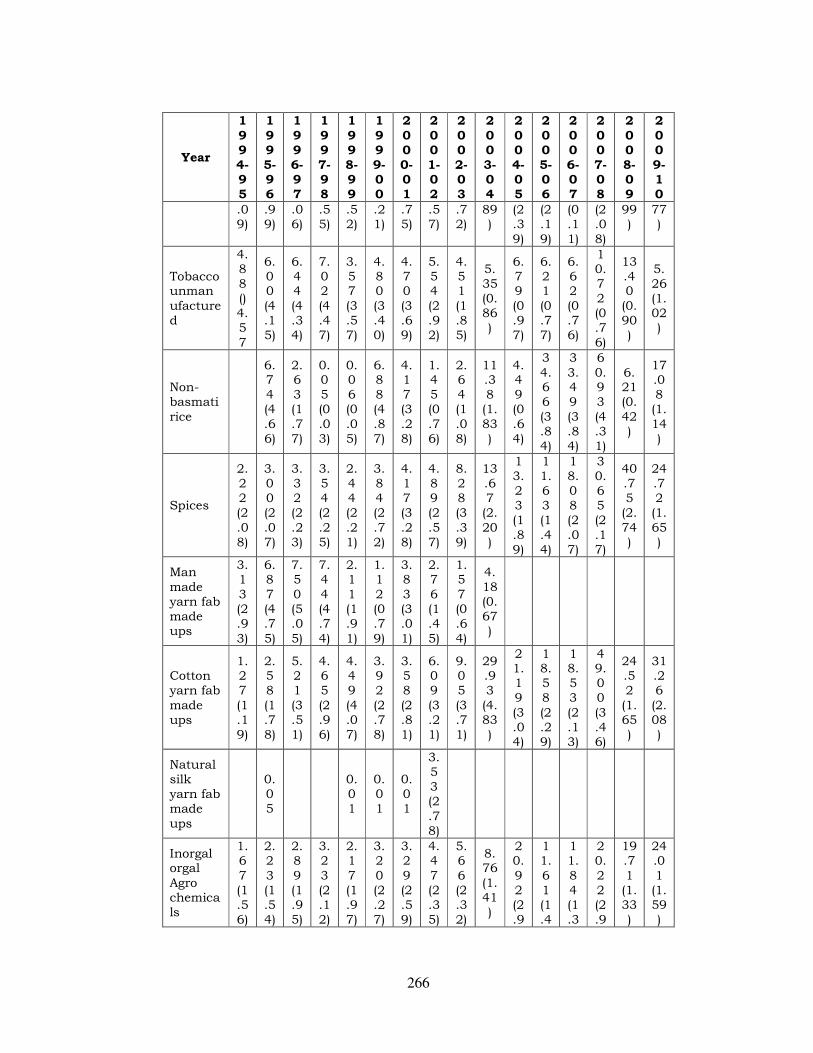

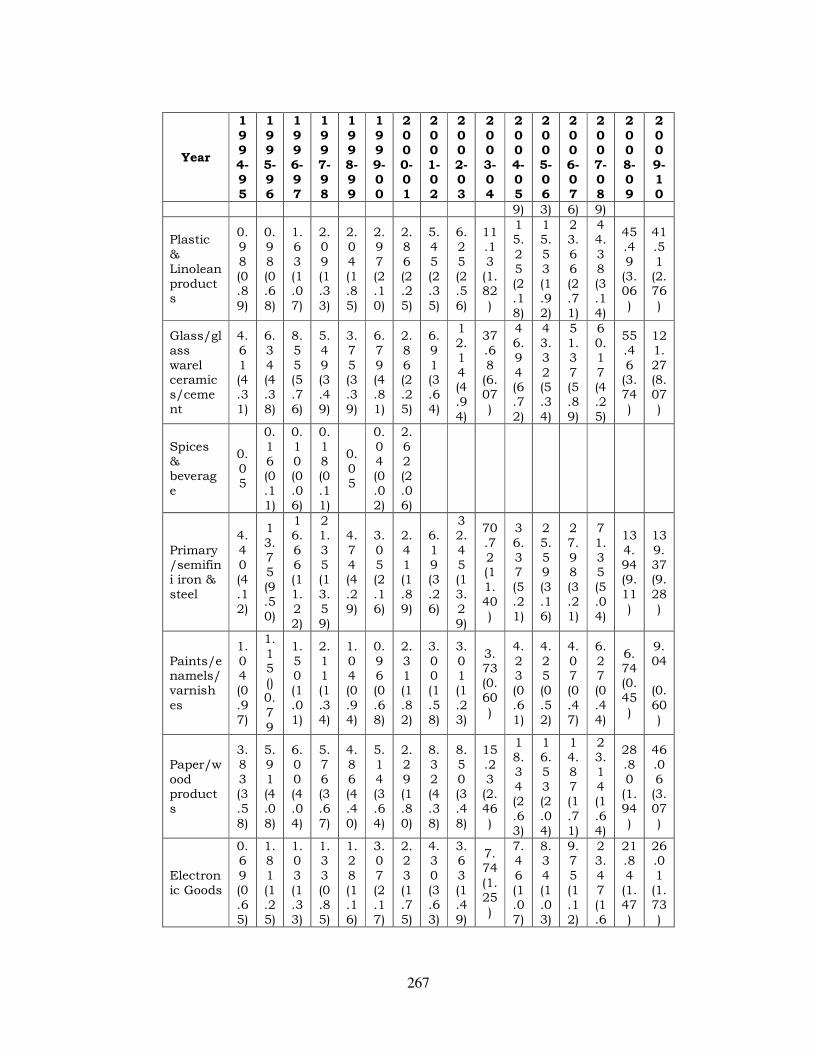

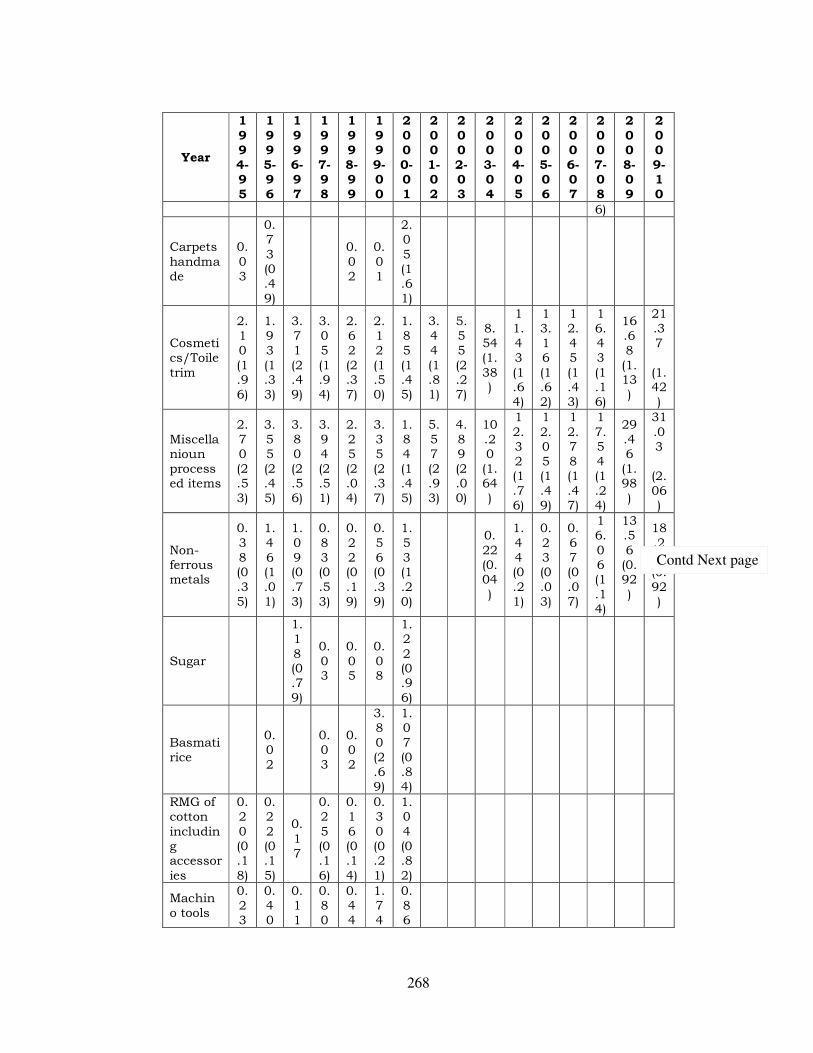

INDO – NEPAL TRADE RELATIONS

Area, People, Religion and Languages:

Nepal with an area of 147.181 sq. k.m. shares borders with

China and India. The capital is Kathmandu. The population of

175

Nepal is about 29.3 million with an annual population growth rate

of 2.132 per cent.8

Religion is important in Nepal; the Kathmandu Valley alone

has more than 2,700 religious shrines which attract a large

number of tourists. According to the 2011 census, Nepal is roughly

81% Hindu. Buddhists account for about 11% of the population.

The interim constitution, promulgated on January 15, 2007,

declared the country a “secular state”.

Nepali is the official language, although over 100 regional

and indigenous languages are spoken throughout the country.

Derived from Sanskrit, Nepal is similar to Hindi and is spoken by

about 90% of the population (although often as a second or third

language). Many Nepalese in government and business also speak

Hindi and English.

Economy, Trade and foreign relations:

Nepal ranks among the world’s poorest countries, with a per

capita income of around $427 in 2009. Based on national

calorie/GNP criteria, an estimated 55% of the population is below

the poverty line of $1.25 per day. An isolated, agrarian society until

the mid-20th century9, Nepal entered the modern era in 1951

without schools, hospitals, roads, telecommunications, electric

power, industry, or a civil service. The country has, however, made

progress toward sustainable economic growth since the 1950s and

is committed to a program of economic liberalization.

Agriculture remain Nepal’s principal economic activity,

employing over 73% of the population and providing 34% of GDP.

8 Ibid. 9 Ibid.

176

Because of Nepal’s dependence on agriculture, the magnitude of

the annual monsoon rain strongly influences economic growth.

In 2009-2010 Nepal’s exports decreased by 6% and imports

grew by 187% in FY when compared to 2007-2008. Exports

constrained by political turmoil and a poor investment climate were

also impacted by the worldwide financial crisis. According to the

revised estimations of the Central Bureau of Statistics, GDP growth

increased marginally to 3.72% in 2005-2006 and slipped to 3.19%

in 2006-2007. In 2009 GDP grew by about 4.7%.

In addition to a growing trade deficit, Nepal faced a balance

of payments (BOP) deficit of $36 million for the first time in 2009-

2010. Nepal receives substantial amounts of external assistance

from India, the United Kingdom, the United States, Japan, and the

European Union (EU).

With eight of the world’s ten highest mountain peaks-

including Mt. Everest at 8,848 m (29,000 ft)-Nepal is a tourist

destination for hikers and mountain climbers. However, the

decade-long insurgency and a global economic slowdown

threatened the tourism industry. But 2007 witnessed a renewed

wave of tourism. Since the political parties and Maoists brokered a

comprehensive peace agreement in November 2006, renewed

tourist arrivals have given relief to the tourism-based hotel,

trekking, mountaineering, and aviation industries during the later

years and in 2011 Nepal celebrated its Year of Tourism.

Swift rivers flowing south through the Himalayas have

massive hydroelectric potential to service domestic power needs

and growing demand from India. Only about 1% to 2% of Nepal’s

hydroelectric potential is currently tapped. Several hydroelectric

177

projects, the Kali Gandaki A (144 megawatts-MW), and a number

of private projects were planned and some completed.

Population pressure on natural resources is increasing.

Overpopulation is already straining the middle hill areas,

particularly the Kathmandu Valley, resulting in the decline of forest

cover. Progress has been achieved in education, health, and

infrastructure, a countrywide primary education system is under

development, and Tribhuvan University has several campuses.

Kathmandu is linked to India and nearby hill regions by an

expanding highway network.

FOREIGN RELATIONS

Nepal’s association with India traditionally has been very

close. Because of strong cultural, religious, linguistic, and

economic ties, India and Nepal restored trade relations in 1990

after a break caused by India’s security concerns over Nepal’s

relations with China.

Nepal played an active role in the formation of SAARC and is

also the headquarters of its secretariat. Nepal is also a signatory of

the agreement on South Asian Free Trade Area (SAFTA), which

came into force on January 1, 2006. A SAFTA Tariff Liberalization

Program (TLP) was scheduled to be implemented from July 1, 2006.

All member countries, except for Nepal, whose TLP started on

August 1, 2006, reduced tariffs for each other∗∗∗∗

* On July 1, 2006, Pakistan officially toughened its stance of not trading with India under the SAFTA

arrangements and did not announce TLP for India. Due to the stalemate between India and Pakistan, the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation free Trade Agreement (BIMSTEC), which was initially scheduled to come into force on July 1, 2006, was deferred indefinitely. The BIMSTEC Summit scheduled for February 8, 2007 in India was also deferred due to political instability in member states, including Nepal, but eventually took place in November 2008. On international issues, Nepal follows a non-aligned policy and often votes with the Non-Aligned Movement in the United Nations. Nepal participates in a number of UN specialized agencies and is a member of the World Trade Organization, World Bank, International Monetary Fund, Colombo Plan, and Asian Development Bank

178

Indo – Nepal Economic Relations

Economic relationship between Nepal and India is unique.

There are historical, geographical, cultural, linguistic, ethnic, social

and family links between people living in India and Nepal.

Institution relating to government and the economic activities are

also more or less similar. Therefore, the trade and other related

relationship between Nepal and India has its own significance.

Trade relationship between these two countries often goes beyond

the economic reason significantly influenced by the social-ethical

norms and values. Research and studies reveal that both the

countries have comparative cost advantages in trading amongst

themselves for several reasons. Historic trade relations,

geographical proximity, identical culture, similar agriculture

productions are cited few examples quite repeatedly. Economical

transport cost is seen as another important factor determining the

volume of trade between these countries. In view of the rising

energy costs, it often considered that the transport costs are likely

to rise so that the transport cost advantage to both these countries

trading with each other is likely to increase in future. This would

further increase the potential for trade between these countries.1

Timilsina (2000), on the other hand, notes that the economic

cooperation between Nepal and India is based on the movements of

goods and services across Nepal-India border of about 1,600 km.

The movement is free and spontaneous. This movement further

accelerated by the movement of people for economic pursuits,

social and marriage relations. The cultural ties and non-existence

of visa system have created better environment for the conduction

of free trade between the two countries.

Indo-Nepal trade has its own importance for the economic

development of both these countries. Trade relation with India is

179

rather crucial to Nepal particularly due to her land-locked

geographic characteristics. Trade statistics show an increasing

trend of trade in both the exports and imports. However, it is

noteworthy that the trade balance is not in favour of Nepal. As

such, it does not present a convincing picture in the macro-

economic performance of Nepal. Both the countries have realized

the significance of bilateral trade. Trade with India is likely to play

further a key role in trade and industrial fronts in the future as

well. Trade and transit treaties held between the two countries are

continuously reflecting the fact. These treaties have increasingly

guided the trade direction, more specifically in the case of Nepal.

ECONOMIC LIBERALIZATION IN NEPAL

Nepal opened up its economy in the early 1990s with the

adoption of economic reform package. The reform measures have

since covered all sectors of the economy including trade and

investment, fiscal and monetary policies, financial and capital

markets and other economic and social sectors. The import

licensing system and quantitative restrictions were eliminated and

tariff rates and structure were reduced and rationalized to make

the trade sector competitive. The trade weighted nominal rate of

protection declined from about 90 per cent in the early 1980s to

about 31 per cent in 1994. Similarly, the average rate of protection

has declined from about 111 per cent in 1989 to 16 per cent in

1992. In a similar manner, the number of slabs subject to

protection fell from more than 100 in the 1980s to 5 in 1996.

Additional measures initiated to promote international trade

include the introduction of a bonded warehouse, duty-drawback

scheme, initiation of the multi-modal facility (dry port) and an

export-processing zone.

180

A new bilateral trade treaty signed with India in 1996

supported the trade reform program of Nepal. The treaty allows

Nepal to export manufactured products to India free of customs

duty and quantitative restrictions. Similarly, in order to improve

the environment for investment, the Industrial Enterprise act, 1992

and the Foreign Investment and Technology Transfer Act (1992)

wee enacted in line with the open, liberal and market-oriented

policy. These Acts have further improved investment incentives. No

license is required for the establishment, expansion and

modernization of industries except for a few related with defense,

public health and environment. In short, the environment was

made more conducive to larger inflows of foreign direct investment

(FDI).

Financial sector reforms have also been carried out to

support the trade and industrial reforms. Interest rates were

deregulated and joint-venture banks were allowed to open up.

Nepal also included full convertibility of the Nepalese rupees on the

current account. The overvalued Nepalese currency was also

corrected to improve export competitiveness of the country.

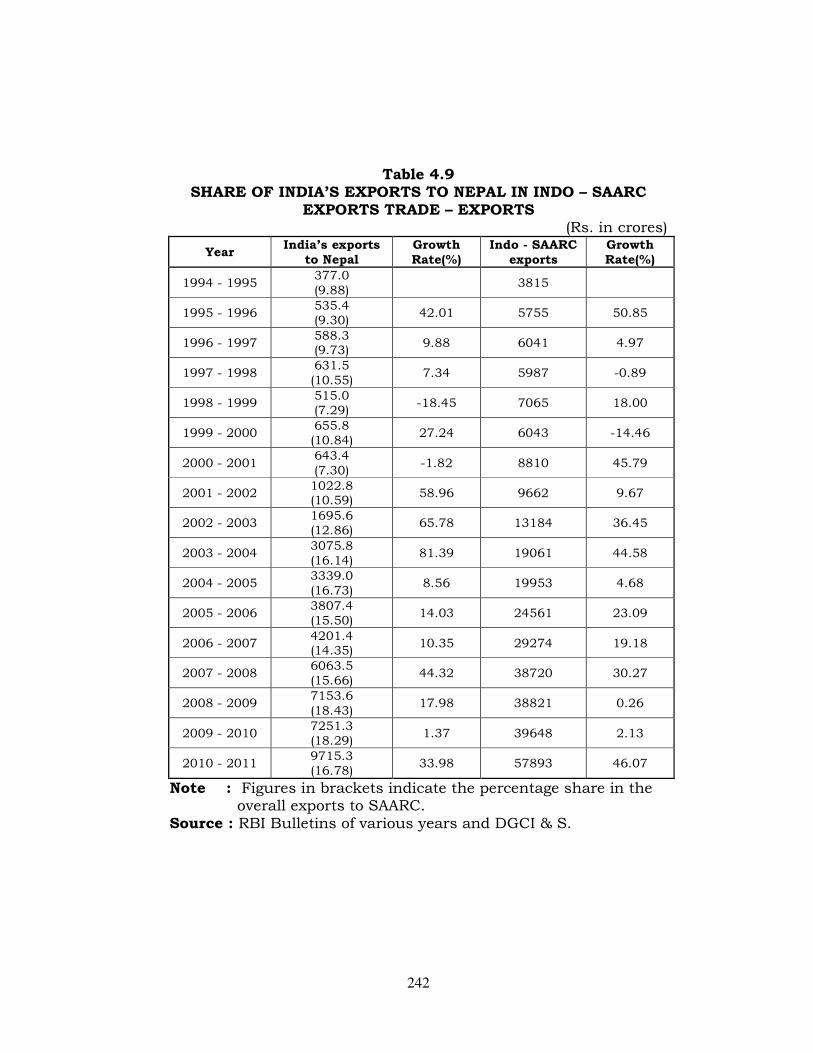

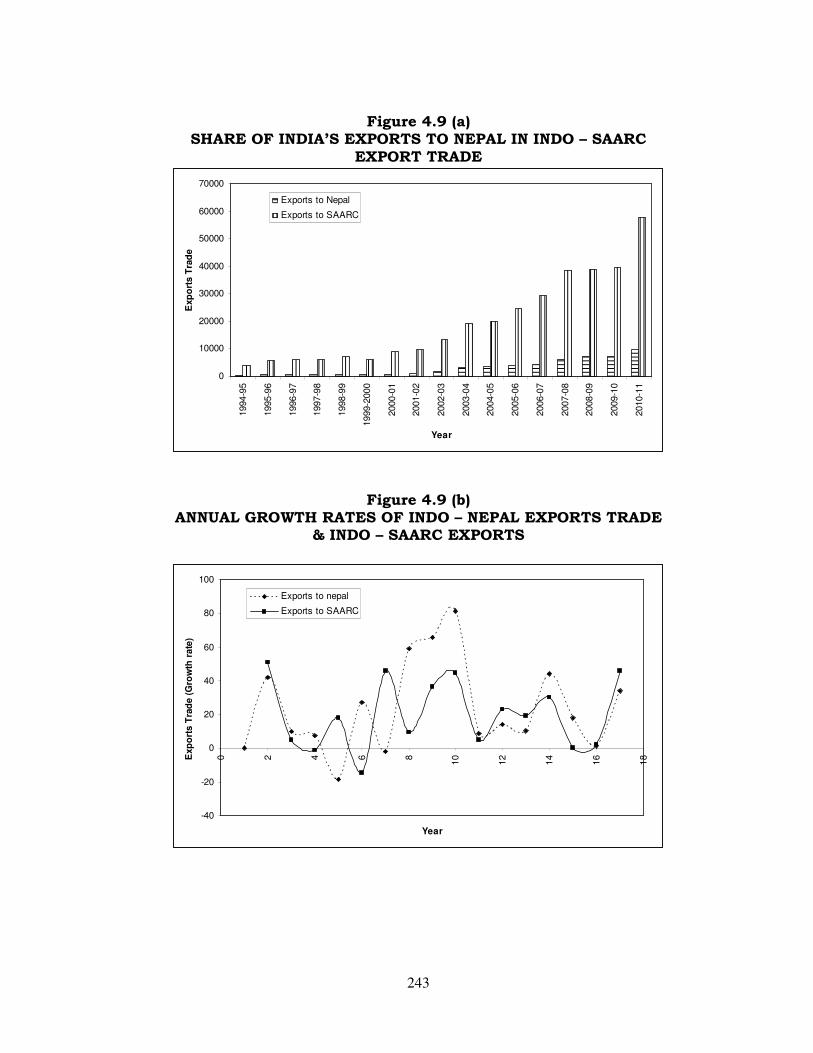

Share of India’s exports to Nepal in Indo-SAARC export trade

It is evident from the table 4.9 that Nepal emerged as the

third largest trading partner of India after Bangladesh and Sri

Lanka during the study period. Indo-Nepal relations in trade and

other related matters are governed by the bilateral treaties of trade

and transit and agreement for cooperation and also to control the

unauthorized trade. The treaty of transit was renewed on 5th

January, 1999.10 Its validity has been made automatically

extendable for a period of seven years at a time, unless either party

10

Reeta Mathur, Op. cit. p. 243.

181

give it to the other, a written notice, six months in advance, of its

intention to terminate the treaty, while the modalities of transit

routes, conditions of transit, customs arrangements as contained

in the protocol and memorandum to the treaty shall be reviewed

and modified every seven years, or earlier if warranted, to meet the

changing conditions before the automatic renewal and such

changes would be the integral part of the treaty.

Though, under the international conventions, Nepal, being a

landlocked country, India is obliged to provide only one transit

route to facilitate Nepal’s trade with third countries and 15 transit

routes have been provided through the Indian territory and more

such routes can be added to the list with mutual agreement.

India’s trade with Nepal has been substantial during the last

decade. According to table 4.9, India’s exports to Nepal during

2000-01 amounted to Rs. 643.4 crores, as compared to Rs. 377

crores in 1994-95, reflecting the compound growth rate of exports,

registered at 70.66 per cent in 2000-01 over 1994-95. But, when

the same period is considered in respect of overall exports to

SAARC nations, the exports were more than doubled with the

compound growth rate being registered at 130.93 per cent in 2000-

01 over 1994-95.

The period between 2001-02 and 2005-06 was observed to be

noteworthy as the annual growth rates of exports displayed a

remarkable performance with 58.96 in 2001-02, 65.78 per cent in

2002-03 and 81.39 per cent in 2003-04, which ultimately resulted

in the tremendous increase in compound growth rate of exports at

272.25 per cent in 2005-06 over 2001-02. (See table 4.9). On the

other hand, the compound growth rate of exports was registered at

182

154.20 per cent, in respect of Indo-SAARC export trade during the

same period.

Between 2006-07 and 2010-11 also, a better trend could be

observed with regard to exports in respect of Nepal. The compound

growth rate of exports was recorded at 131.24 per cent in 2010-11

over 2006-07 in respect of Nepal. When the Indo-SAARC trade was

considered during the same period, the compound growth rate of

exports was registered at 97.76 per cent in 2010-11 over 2006-07.

the present trend is encouraging and this can be further enlarged if

export potential to that country is further identified and tapped.

The per cent share of exports to Nepal as a proportion of

exports to SAARC countries was significant. The share of exports to

Nepal was 9.88 per cent in 1994-95. However, it sharply increased

to 10.55 per cent in 1997-98. As the annual growth rate of exports

in respect of Nepal was negative by 18.45 per cent in 1998-99, the

percent share was less with 7.29 per cent in 1998-99. Another

negative annual growth rate recorded in 2000-01 at 1.82 per cent

resulted in the less percentage share of exports at 7.30 per cent in

respect of Nepal. The highest percent share of exports was observed

at 18.43 per cent in 2008-09. Hence, it is observed that the share

of exports to Nepal as a proportion of over all exports to SAARC

had been impressive and this upward trend in percentage share is

visible through out the study period.

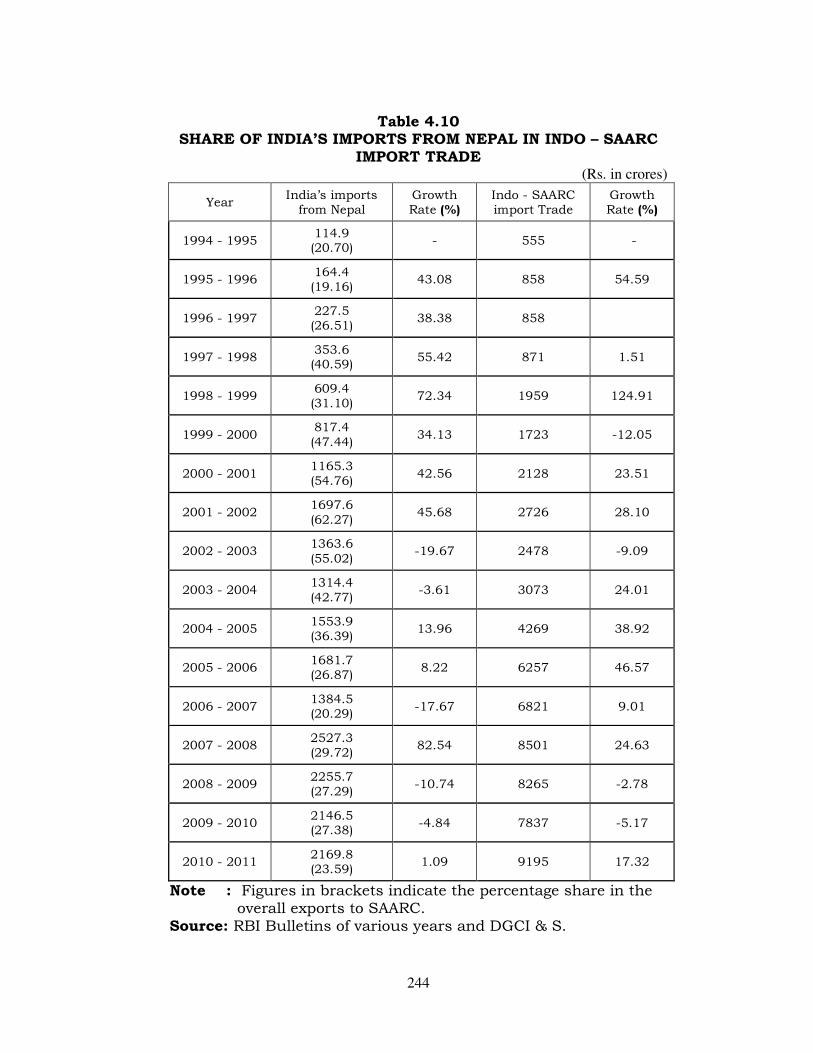

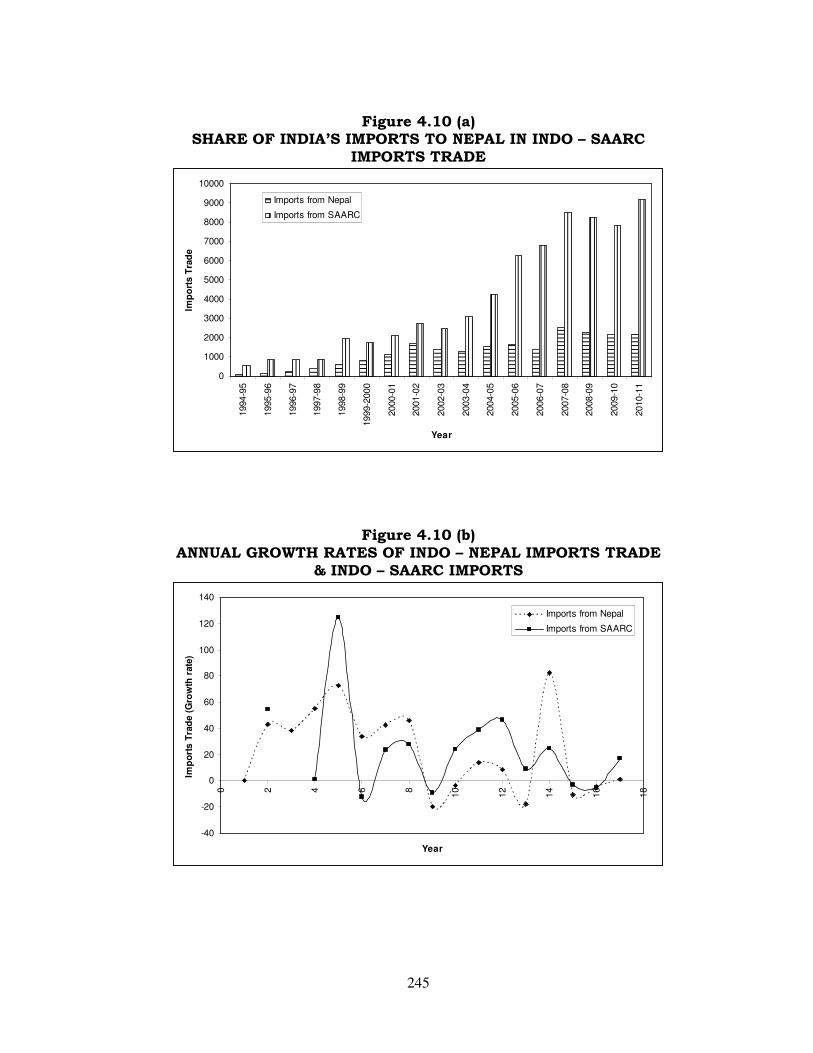

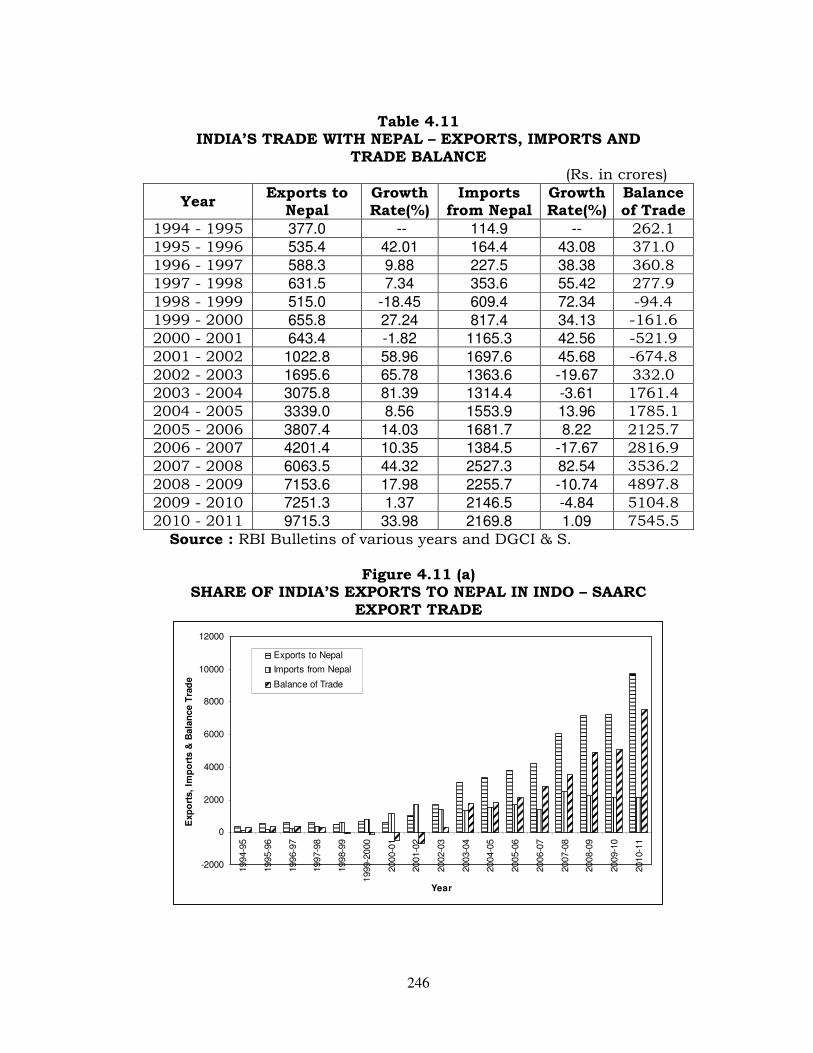

Share of India’s imports from Nepal in Indo-SAARC import

trade

According to table 4.10, the imports from Nepal amounted

Rs. 817.4 crores in 1999-2000 as compared to 114.9 in 1994-95,

reflecting a tremendous compound growth rate at 611.40 per cent

in 1999-00 over 1994-95. When we consider the Indo-SAARC

183

import trade during the same period, the compound growth rate of

imports was recorded at 210.45 per cent in 1999-2000 and 1994-

95.

As two consecutive negative annual growth rates had been

registered between 2000-01 and 2005-06, with 19.67 per cent in

2002-03, and 3.61 per cent in 2003-04, the compound growth rate

of imports was recorded just at 44.31 per cent in 2005-06 over

2000-01. On the other hand, there was a remarkable growth in

respect of Indo-SAARC trade with 194.03 per cent, being recorded

in 2005-06 over 2000-01.

Between 2006-07 and 2010-11, the compound growth rate,

recorded in respect of Indo-Nepal import trade was 56.72 per cent

in 2010-11 over 2006-07 with regard to Indo-SAARC import trade

during the same period, the compound growth rate of imports was

registered at 34.80 per cent in 2010-11 over 2006-07.

The share of imports from Nepal as a proportion of imports

from SAARC nations was very significant. The percent share of

imports from Nepal during 1994-95 was registered at 20.70 per

cent. The highest per cent share of imports in respect of Nepal was

recorded at 62.27 per cent in 2001-02 and the least per cent share

was registered at 19.16 per cent in 1995.96.

When we observe the balance of trade in respect of Nepal,

adverse balance of trade had been registered during the period

from 1998-99 to 2001-02 and the favourable balance of trade was

witnessed with rest of the period. (See table 4.11).

INDO-BHUTAN TRADE RELATION

The area of Bhutan is 46,500 sq. k.m. The capital city of

Bhutan is Thimpu. The population of Bhutan is 6, 72,425 and the

184

annual growth rate of population is 2.082 per cent with a density of

the population in 45 per sq. k.m.

ECONOMY

Bhutan’s economy, one of the world’s smallest and least

developed, is based on hydroelectricity, tourism, agriculture, and

forestry.

Bhutan’s tenth five-year plan (2008-2013) focuses on ways to

manage the country’s new-found wealth with special emphasis on

three development areas: rural, regional and private-sector. India

has pledged to support and plan and promised to double the

amount of aid given to Bhutan in the previous five-year plan.

January 2004, as a member of the South Asian Association

for Regional Cooperation (SAARC), Bhutan also joined the South

Asian Free Trade Agreement (SAFTA).

Bhutan hosted the SAARC summit in Thimphu in April

2010. In February 2004 Bhutan joined the Bangladesh, Indian,

Myanmar, Singapore, and Thailand Economic Cooperation Forum

(BIMSTEC). Bhutan has applied for membership in the World

Trade Organization and is in the process of developing clear legal

and regulatory systems designed to promote business development.

INDIA-BHUTAN BILATERAL RELATIONS

Diplomatic relations between India and Bhutan were

established in 1968 with the appointment of a resident

representative of India in Thimphu. Before this our relations with

Bhutan were looked after by our Political Officer in Sikkim. The

basic framework of India - Bhutan bilateral relations is the Treaty

of Friendship and Cooperation of 1949 between the two countries,

185

which was updated and signed during the visit to India of His

Majesty Jigme Khesar Namgyel Wangchuck in February 2007.

The updated India-Bhutan Treaty not only reflects the

contemporary nature of our relationship but also lays the

foundation for their future development in the 21st century. The

Treaty provides, amongst other things, for perpetual peace and

friendship, free trade and commerce, and equal justice to each

other’s citizens. India’s bilateral political relations with Bhutan

India’s have matured over the years and are characterized by close

trust and understanding and extensive cooperation in the field of

economic development, particularly in the mutually beneficial

sector of hydroelectric power.

Agreements/MOUs

India and Bhutan have signed many agreements and MOUs

during the last few decades. During the visit of His Majesty Jigme

Khesar Namgyel Wangchuck in December 2009, twelve (12)

MOUs/Agreements in areas of hydropower, IT, health/medicine,

narcotics, civil aviation, agriculture and environment were signed

A major step towards this was made when the 336 MW Indo-

Bhutan Friendship Project was commissioned at Chukha. This

hydropower-harnessing project constitutes 30 per cent of Bhutan’s

annual revenue and it’s export to India reached 75.2 per cent in

1998. Bhutan also enjoys 90 per cent of it’s trade with India and

will export more hydropower to India in the coming years.

SAARC

The Kingdom attaches great importance to SAARC. Ever

since the inception of SAARC, Bhutan has firmly supported and

promoted the activities, and worked towards making the South

186

Asian Region self-reliant. This is in consistent with its policy of

developing friendly relations with all the neighboring countries. It

has also displayed a keen interest in economic cooperation and

various peacemaking efforts in South Asia.

Reflecting growing congruence in their relationship, India

and Maldives today decided to intensify bilateral cooperation in

diverse fields including trade, commerce, security, combating

piracy and terrorism as well as enhancing people-to-people contact

GOI has issued notification allowing Bhutanese passengers duty

free access at Indian airports, as well as exempting exports to

Bhutan from any export bans in India on some essential items

subject to limits.

Economic Cooperation

Mutually beneficial economic inter-linkages between India

and Bhutan have been an important element in our bilateral

relations. India continues to be the largest trade and development

partner of Bhutan. Planned development efforts in Bhutan began

in the early 1960s. The first Five Year Plan (FYP) of Bhutan was

launched in 1961. Since then, India has been extending financial

assistance to Bhutan’s FYPs. So far, nine Five Year Plans of

Bhutan have been completed.

Some of the major projects in Bhutan carried out with Indian

assistance in the past include 1020 MW Tala Hydroelectric Project,

336 MW Chukha Hydroelectric Project, 60 MW Kurichhu

Hydroelectric Project, Penden Cement Plant, Paro Airport, Bhutan

Broadcasting Station, Major Highways, Electricity Transmission

and Distribution System, Indo-Bhutan Microwave Link,

Exploration of Mineral Resources, and Survey and Mapping.

187

Trade with India

India is not only Bhutan’s main development partner but

also its leading trade partner. A free trade regime exists between

India and Bhutan. The India-Bhutan Trade and Commerce

Agreement which expired in March 2005, has been renewed for a

period of 10 years. Currently, the major items of exports from

Bhutan to India are electricity (from Tala, Chikha and Kurichhu

Hydroelectric Project), base metals and articles, minerals, vegetable

fat and oils, alcoholic beverages, chemicals, cement, timber and

wood products, cardamom, fruit products, potatoes, oranges and

apples, raw silk, spices, processed food and animal products,

chemicals, wood, plastic and rubber. The Agreement on Trade and

Commerce also provides for duty free transit of Bhutanese

merchandise for trade with third countries. Sixteen exit/entry

points in India identified in the Protocol for Bhutan’s third country

trade are: Jaigaon, Chamurchi, Ulta Pani, Hathisar (Gelephu),

Darranga, Kolkata, Haldia, Dhubri, Raxaul, Panitanki,

Changrabandh, Phulbari, Dawki, New Delhi, Chennai and Mumbai.

Of these, Kolkata, Haldia, Mumbai and Kolkata are the air routes

and Raxaul is the rail route. The others are the designated road

routes.

India is not only Bhutan’s main development partner but

also its largest trade partner. During 2010, imports from India

were of the order of Rs. 2930 crores and constituted 75% of

Bhutan’s total imports. Bhutan’s exports to India in 2010

amounted to Rs. 2600 crores and constituted 90% of its total

exports. Total trade in 2010 grew by about 26% from 2009.

Trade Talks

188

The India Bhutan Bilateral Trade Talks were held in New Delhi on 18-19 August 2011∗.

At the request of RGOB, Gol has agreed to the use of Dalu

LCS (land custom station) and Ghasuapara LCS (both in

Meghalaya) as additional exit/entry points for Bhutan’s trade with

Bangladesh. Ghusuapara LCS will be used only as exit point for

Bhutan for the present till the necessary infrastructure in place for

it to be used as entry point also. In addition, 4 entry/exit points for

India-Bhutan bilateral trade viz., Upper Khogla (West Bengal),

Dalmore or Birpara (West Bengal). Bokajuli (Assam) and Rangapani

(Assam) would also be notified by government of India.

Share of India’s exports to Bhutan in Indo-SAARC export trade

There are bilateral trade agreements of which provides for

free trade and commerce, between India and Bhutan. Commercial

transactions are carried out in Indian rupees and Bhutanese

regulations. India provides unhindered transit facilities to

landlocked Bhutan to facilitate her trade with third countries.

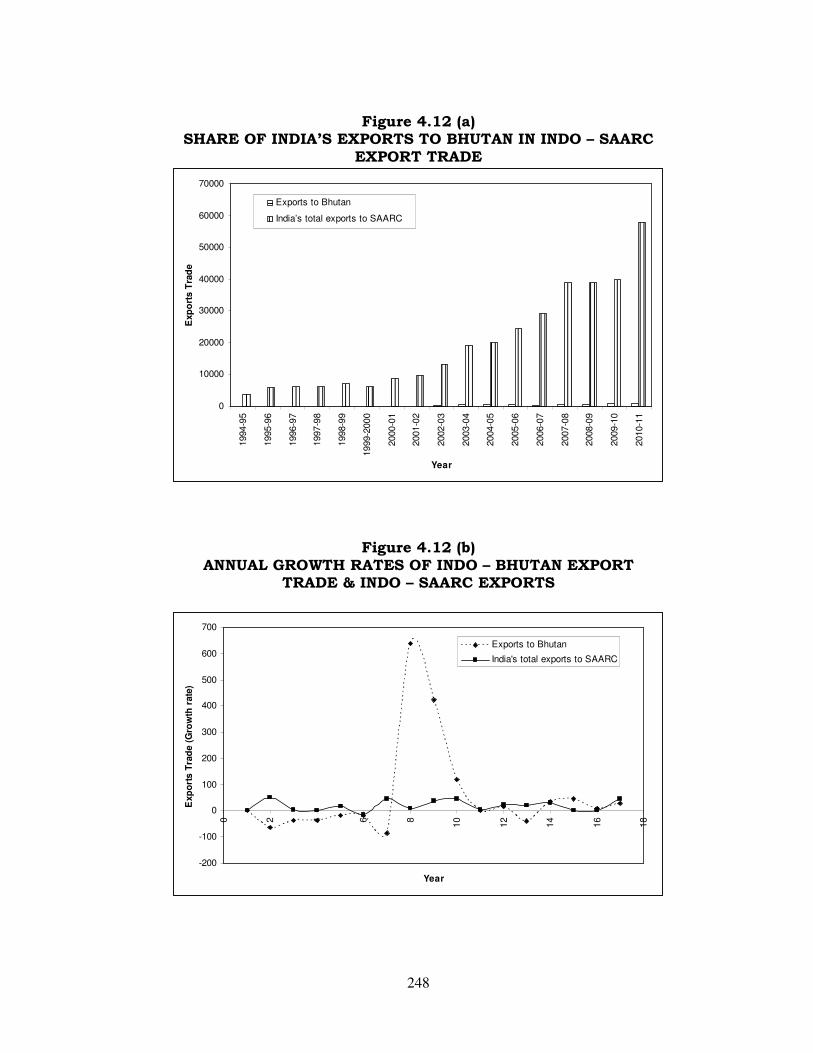

It is evident from table 4.12 that India’s exports to Bhutan

were very insignificant and less substantial. According to table

4.12, India’s exports to Bhutan which amounted Rs. 34.80 crores

in 1994-95, went up to Rs. 36.20 contributing the least compound

growth rate at 4.02 per cent in 2001-02 over 1994-95. On the other

hand there was a remarkable growth in respect of India’s exports to

SAARC, with the compound growth rate of exports being recorded

at 153.26 per cent in 2001-02 over 1994-95.

* The Bhutanese delegation was led by Mr. Sonam P. Wangdi, Director General, Department of Trade

and included representatives from Ministries of Economic Affairs, Finance and Foreign Affairs. Indian delegation was led by Joint Secretary, Ministry of Commerce and included representatives from Ministries of Commerce, External Affairs and Finance.

189

Between 2002-03 and 2006-07 also, not much growth was

noticed in respect of India’s exports to Bhutan. The compound

growth rate of exports was recorded just at 37.7 per cent in 2006-

07 over 2003-04. But, in respect of Indo-SAARC trade, similar

trend had been repeated with exports being doubled, contributing

the compound growth by 122.04 per cent in 2006-07 over 2003-04.

The trends in exports, which were observed during the two

earlier phases, in respect of Bhutan, had not been repeated

between 2007-08 and 2010-11. The items which India exported to

Bhutan during this period were more than doubled with the

compound growth rate being recorded at 104.73 per cent in 2010-

11 over 2007-08. Similar change in respect of Indo-SAARC trade

had been witnessed during the same period. The remarkable trends

n exports, observed in respect of Indo-SAARC trade during the

earlier two phases had not been repeated in this last phase of the

study period. The compound growth rate of exports, recorded in

respect of Indo-SAARC trade was 49.52 per cent in 2010-11 over

2007-08.

When we considered the percentage share of exports to

Bhutan in Indo-SAARC export trade, the following facts have been

noticed.

According to table 4.12, India’s exports to Bhutan, as a

proportion of exports to SAARC nations was less than 1 per cent

during period from 1994-95 to 2001-02 except 1996-97.

From 2002-03 onwards, there was a slight increase in

percentage share, in respect of Indo-SAARC export trade. Highest

percentage of share was recorded at 2.16 per cent in 2003-04.

190

Share of India’s imports from Bhutan in Indo-SAARC import

trade

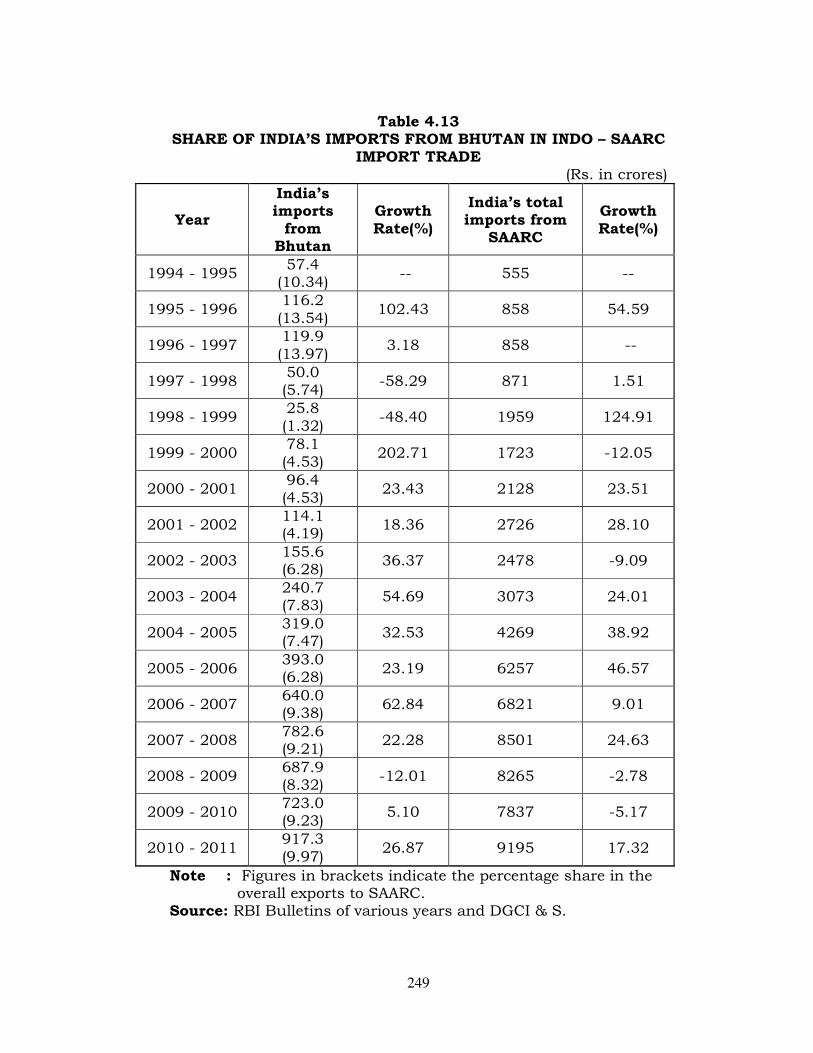

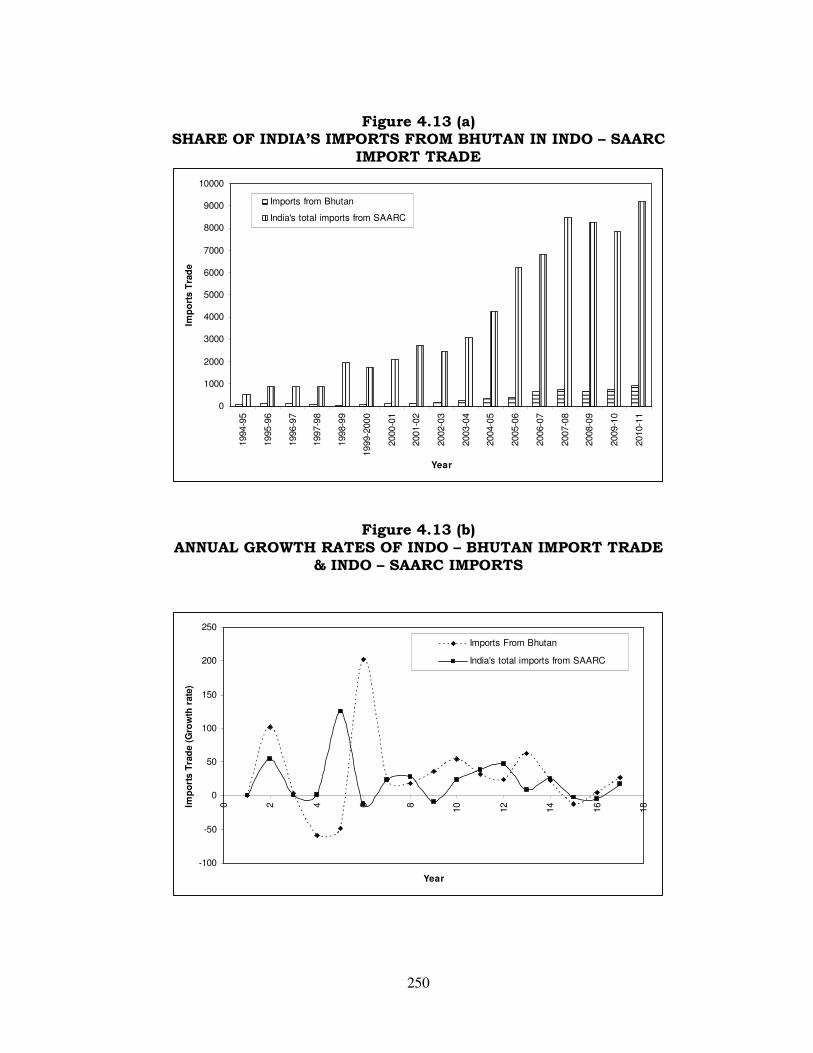

It is evident from table 4.13 that India’s import trade from

Bhutan also was insignificant. India’s imports from Bhutan during

1999-2000 amounted Rs. 78.1 crores as compared to 57.4 crores

in 1994-95, reflecting a compound growth rate at 36.06 per cent in

1999-2000 over 1994-95. On the other hand, there was a

remarkable growth, in respect of Indo-SAARC import trade with the

compound growth rate of imports being recorded at 210.45 per

cent in 1999-2000 over 1994-95.

Between 2000-01 and 2005-06, there was a tremendous

growth, in respect of Indo-Bhutan import trade, with the

compound growth rate of imports being registered at 307.67 per

cent in 2005-06 over 2000-01. Similar trend can be noticed in

respect of Indo-SAARC import trade with the compound growth

rate of imports being recorded at 194.03 per cent in 2005-06 over

2000-01.

The export trend which was registered in the earlier phase

with both Indo-Bhutan import trade and Indo-SAARC import trade

had not been observed during the last phase of the study period

i.e., 2006-07 act 2010-11. The compound growth rate of imports,

recorded in respect of Indo-Bhutan import trade was at 43.32,

while that of the compound growth rate, recorded in respect of

Indo-SAARC import trade was at 34.80 per cent in 2010-11 over

2006-07.

The share of imports from Bhutan as a proportion of overall

imports from SAARC was also less substantial. The percentage

share of imports in respect of Bhutan was recorded at 10.34 per

cent in 1994-95. However, this percentage share went up to 13.97

191

per cent in1996-97; but declined to 5.74 per cent in 1997-98 and

further decreased to at 1.32 per cent in 1998-99. The percentage

share of imports, recorded in respect of Bhutan in 2010-11 was at

9.97 per cent.

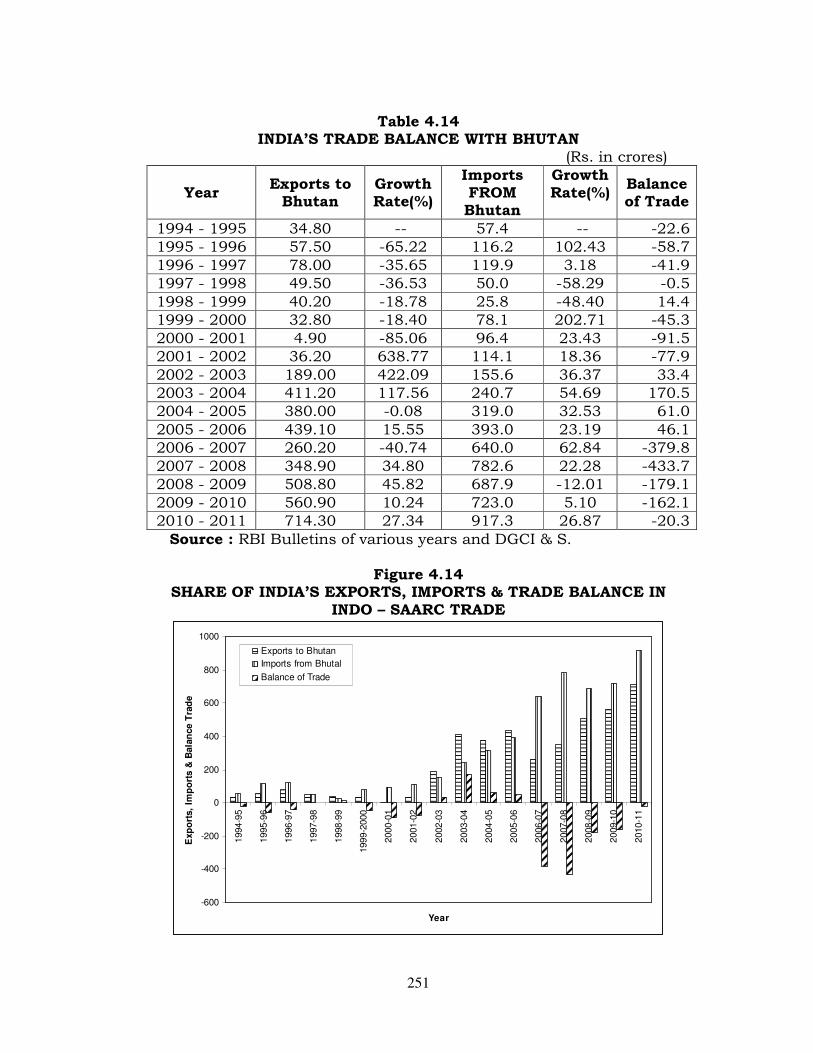

Balance of trade with Bhutan

It is evident from the table 4.14 that the trade balance

between India and Bhutan was not in favour of India as India’s

imports from Bhutan outweighed the exports to that country.

Excepting the year 1998-99 as the years from 2002 to 2005, India

had always trade deficit with Bhutan.

INDO-PAKISTAN TRADE

The area of Pakistan is 803.943 sq. k.m. almost twice the

size of California. The capital city of Pakistan is Islamabad. The

other cities are Ravalpindi, Karachi, Lahore, Faisalabad and

Hyderabad. The population of Pakistan is 16,77,62,040 with an

annual growth rate of 1.81 per cent.

Economy

Pakistan had a GDP growth rate of 2.7 per cent. Its Per

capita GDP was $2600 by the end of 2009. Pakistan has natural

resources like arable land, natural gas, substantial hydropower

potential, coal, iron ore, copper, salt, limestone. Its agriculture:

products-are wheat, cotton, rice, sugarcane, eggs, fruits,

vegetables, milk, beef, and mutton.

Industrial sector comprises and apparel, food processing,

pharmaceuticals, construction materials, shrimp, fertilizer, and

paper products. Pakistan foreign trade amounted to $17.87 billion.

at the end of 2009. Textiles (garments, bed linen, cotton cloth, and

192

yarn), rice, leather goods, sports goods, carpets, rugs, chemicals

and manufactures are the major export items. Major partners are

U.S. 16%, United Arab Emirates 11.7%, Afghanistan 8.6% U.K.

4.5%, and China 4.2%. Imports are worth arround-$28.31 billion.

Major import items are petroleum, petroleum products, machinery,

plastics, paper and paper board, transportation equipment, edible

oils, pulses, iron and steel, tea. Major partners in Pakistan imports

are China 14.1%, Saudi Arabia 12%, U.A.E. 11.2%, Kuwait 5.4%,

India 4.8%, U.S. 4.7%, and Malaysia 4.1%.

ECONOMY

The World Bank considers Pakistan a low-income country.

GDP is around $166 billion at the official exchange rate. The

population numbered some 167 million in 2008 with a 1.81%

growth rate. Not more than 55.0% of adults are literate, and life

expectancy is about 64 years. In 2008-2009, the GDP growth rate

was 3.7%, and unemployment was estimated at 14%. Year-over-

year consumer price inflation averaged 13.6% in 2009. Main

inflation drivers include food and utility prices. Low levels of

spending in the social services and high population growth have

contributed to persistent poverty and unequal income distribution.

Pakistan’s extreme poverty and underdevelopment are key

concerns, especially in rural areas. The country’s economy remains

vulnerable to internal and external shocks due to internal security

concerns and the global financial crises.

Industry

Pakistan’s manufacturing sector accounts for about 25% of

GDP. Cotton textile production and apparel manufacturing are

Pakistan’s largest industries, accounting for about 51.4% of total

exports. Other major industries include food processing, beverages,

193

construction materials, clothing, and paper products.

Manufacturing sector growth has slowed in the recent years due to

energy shortages and capacity constrains. However, the sector is

forecast to grow 5.5% for FY 2010. Despite government efforts to

privatize large-scale units, the public sector continues to account

for a significant proportion of industry. The government seeks to

diversify the country’s industrial base and bolster export

industries. Net foreign investment in Pakistani industries is only

0.5% of GDP, Pakistan’s search for additional foreign direct

investment has been hampered by concerns about the security

situation, domestic and regional political uncertainties, and

questions about judicial transparency.

Foreign Trade

Weak world demand for its exports and domestic political

uncertainty has contributed to Pakistan’s high trade deficits. In

major imports, which fell to $28.4 billion in 2009, include

petroleum products, edible oil, wheat, chemicals, fertilizer, capital

goods, industrial raw materials, and consumer products. Energy

imports account for nearly 30% of Pakistan’s imports, and the total

gap between electricity supply and demand in Pakistan is over

4,800 megawatts (MW). The ongoing energy crisis and security

concerns, together with a decline in global demand, have hampered

Pakistan’s textile-reliant export base. Pakistan’s exports continue

to be dominated by cotton textiles and apparel, despite government

diversification efforts.

FOREIGN RELATIONS

After September 11, 2001, Pakistan’s prominence in the

international community increased significantly, as it pledged its

alliance with the U.S. in countering terrorism efforts and made a

194

commitment to eliminate terrorist camps on its territory.

Historically, Pakistan has had difficult and volatile relations with

India, long-standing close relations with China, extensive security

and economic interests in the Persian Gulf, and wide-ranging

bilateral relations with the United States and other Western

countries. It expresses a strong desire for a stable Afghanistan.

Trade cooperation between India and Pakistan was a direct

outcome of the partition of Indian sub-continent on August 14,

1947. At that time, India and Pakistan were highly dependent on

each other for trade. Thereafter, both resorted to deliberate

measures to minimize their trade dependence on each other.

India’s share in Pakistan’s global exports and imports was 23.6 per

cent and 50.6 per cent, respectively, in 1948-49. These shares

went down to 1.3 per cent and 0.06 per cent in 1975.76. Similarly,

Pakistan’s share in India’s global exports and imports was 2.2 per

cent and 1.1 per cent respectively, in 1951-52. These shares went

down to 0.02 per cent and 0.4 per cent, in 1975-76, and 0.7 per

cent and 0.13 per cent in 2005-06. This shows that the trade

between these two neighboring countries has been much below the

potential.

Economic Structure of India and Pakistan

Before we discuss the potentialities of trade between India

and Pakistan, it would be better to have a glance at the economic

structure of India and Pakistan. India and Pakistan are the

neighboring and developing countries of the SAARC region. India is

comparatively larger in terms of her size, population, GDP etc.,

Since partition, relations between Pakistan and India have

been characterized by rivalry and suspicion. Although many issues

195

divide the two countries, the most sensitive one since

independence has been the status of Kashmir.∗∗∗∗

In fact, the period between 1965 and 1971 witnessed two

wars between India and Pakistan. Immediately after the war,

Pakistan imposed official embargo on her trade with India. The

trade relations between the two neighboring countries remained

suspended for nine years and created problems for both the

countries. Both were forced to import many items from the world

market at much higher prices. The same could have been imported

from each other at much lower prices involving substantially lower

transport and transshipment costs.

In July 1972, following the 1971 Indo-Pakistan war, which resulted

in the creation of an independent Bangladesh, President Zulfiqar

Ali Bhutto and the then Indian Prime Minister Indira Gandhi met

in the hill station of Shimla and agreed to a line of control in

Kashmir. Both leaders endorsed the principle of settlement of

bilateral disputes through peaceful means. In 1974, Pakistan and

India agreed to resume postal and telecommunications linkages

and to enact measures to facilitate travel. Trade and diplomatic

relations were restored in 1976 after a hiatus of 5 years.

The resumption of trade relations between them took place with

the signing of bilateral trade agreement on January 23, 1975. But

∗∗∗∗ At the time of partition, the princely state of Kashmir, though ruled by a Hindu king, had an

overwhelmingly Muslim population. When the king hesitated in acceding to either Pakistan or India in 1947, some of his Muslim subjects revolted in favor of joining Pakistan. In

exchange for military assistance in containing the revolt, the Kashmir ruler offered his allegiance to India. Indian troops occupied the eastern portion of Kashmir, including its capital, while the western part came under Pakistani control India submitted this dispute to the United Nations on January 1, 1948. One year later, the UN arranged a cease-fire along a line dividing Kashmir but leaving the northern end of the line not demarcated and the Valley of Kashmir (with the majority of the population) under Indian control. India and Pakistan agreed to a UN-supervised plebiscite to determine the State’s future. This plebiscite has not occurred because the main precondition, withdrawal of both nations’ forces from Kashmir, has failed to take place. Pakistan has since fought three wars with India on Kashmir issue, in 1948, 1965, and the Kargil conflict in 1999.

196

the flow of trade was restricted to government levels. This trade

agreement expired on January 22, 1978 and thereafter trade has

continued without any agreement. In July 1982, Pakistan declared

a list of 40 items in which private sectors of the two countries

could trade11. The mutual trade has grown significantly since

1989, when Pakistan expanded the list of approved imports from

India to 571 items, and further enhanced it to 600 items on July

17, 2000, and 1075 items on November 3, 2006. But this list is

just 10 per cent of the total number of classified tariff lines, and

does not include items like consumer durables, computer software,

textiles machinery, automobiles, two wheelers, cars etc.,

Share of India’s exports to Pakistan in Indo-SAARC trade

The role of external sector, mainly of trade, assumes

significance in the development of India and Pakistan economies

since the partition in 1947. Foreign trade registered a phenomenal

increase in India and Pakistan during 1950-51 to 2010-11.

India’s trade with Pakistan is constrained by the

discriminatory policy adopted by Pakistan against imports from

India. While we accord MFN treatment to imports from Pakistan,

they allow their private sector to import only selected items from

India. Despite bilateral discussions and our diplomatic demarches

in this regard, Pakistan is yet to allow its trade with India on free

trade and MFN basis.

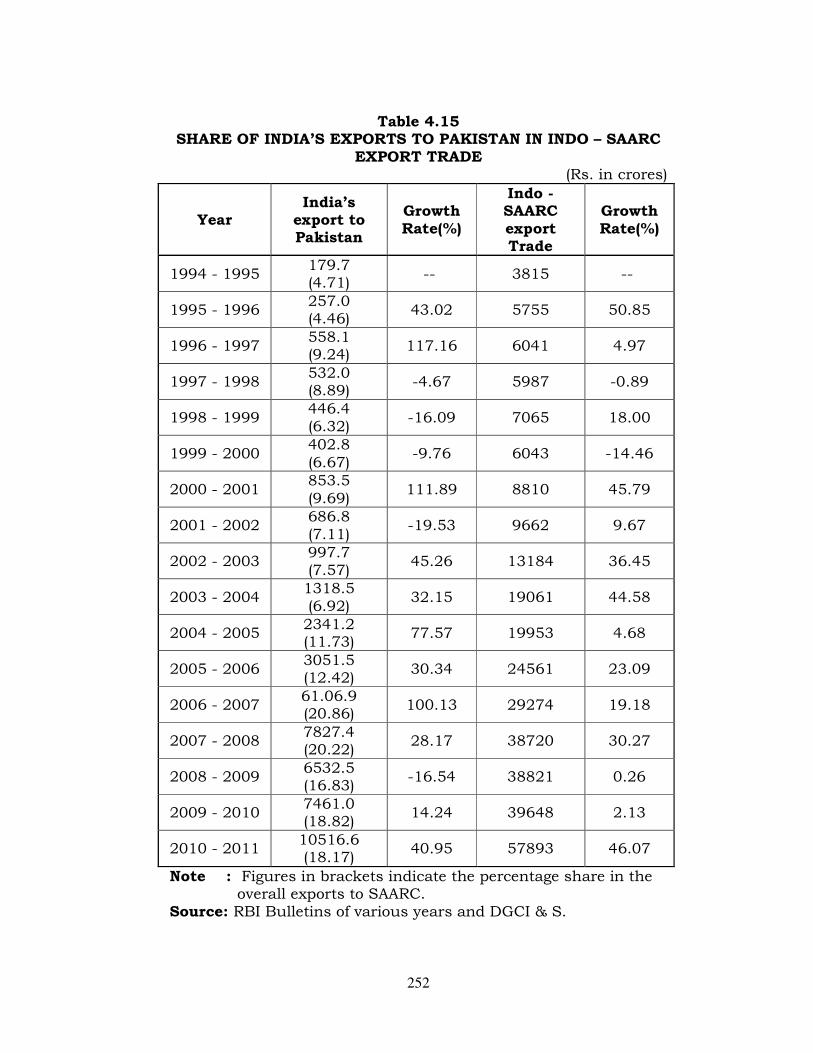

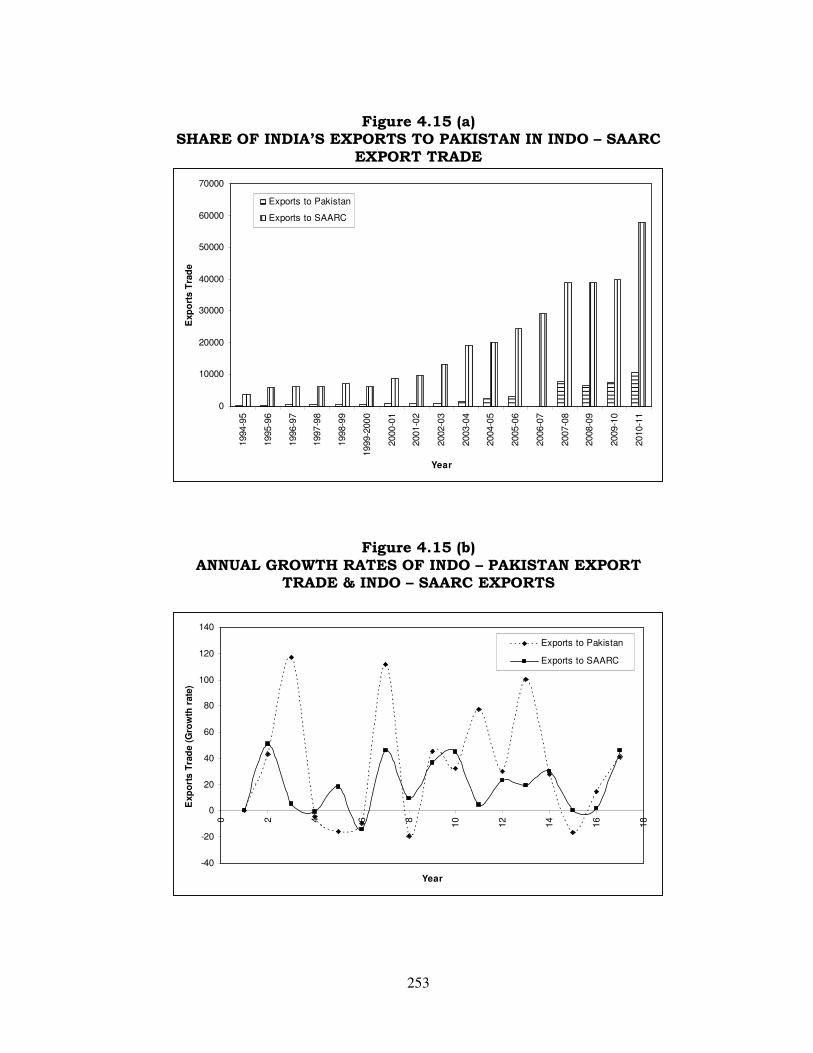

According to table 4.15, India’s exports to Pakistan during

1999-2000, amounted Rs. 402.8 crores, as compared to Rs. 179.70

crores in 1994-95, reflecting a compound growth rate at 124.15 per

cent in 1999-2000 over 1994-95. On the other hand, the

11 Ranjit Singh Ghuman, Indo-Pakistan Trade Cooperation and Saarc, Peace and Democracy in

South Saia, Volume 2, Nos.1& 2 p.72

197

compound growth rate of exports recorded in respect of Indo-

SAARC export trade was at 58.40 per cent in 1999-2000 over

1994-95.

Between 2000-01 and 2005-06, remarkable growth had been

witnessed in respect of both Indo-Pakistan export trade and Indo-

SAARC trade. The compound growth rate of exports, recorded in

respect of Indo-Pak export trade was at 257.53 per cent in 2005-06

over 2000-01, while it was registered at 178.79 per cent, in respect

of Indo-SAARC trade during the same period.

Between 2006-07 and 2010-11, the compound growth rate of

exports, recorded in respect of Indo-SAARC export trade was higher

than the compound growth rate of exports recorded, in respect of

Indo-Pak export trade. The compound growth rate of exports,

recorded in respect of Indo-Pak export trade was at 72.21 per cent,

while it was at 97.70 per cent in 2010-11 over 2006-07, in respect

of Indo-SAARC export trade.

With regard to India’s share of exports to Pakistan in Indo-

SAARC export trade, it was observed that the percentage share was

not only less substantial but also insignificant. The percentage

share of exports stood well below 10 per cent till 2003-04.

Thereafter, the percentage share exhibited an upward trend. The

highest percentage share was recorded at 20.86 per cent in 2006-

07.

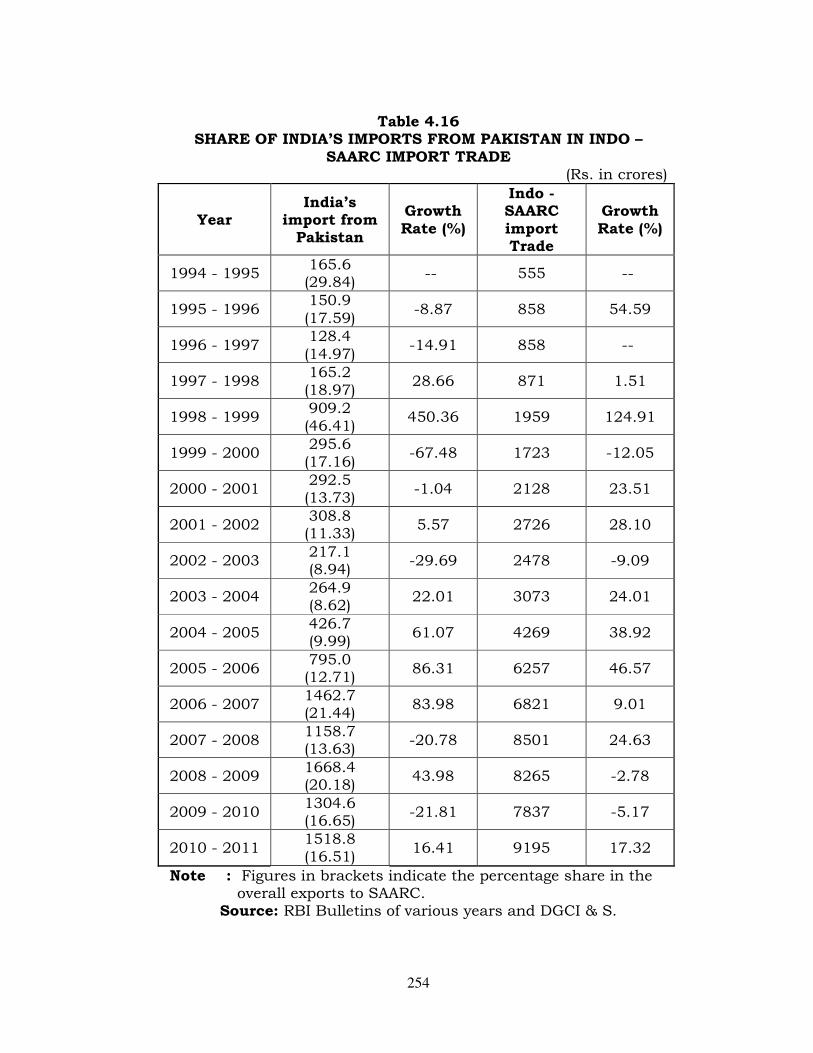

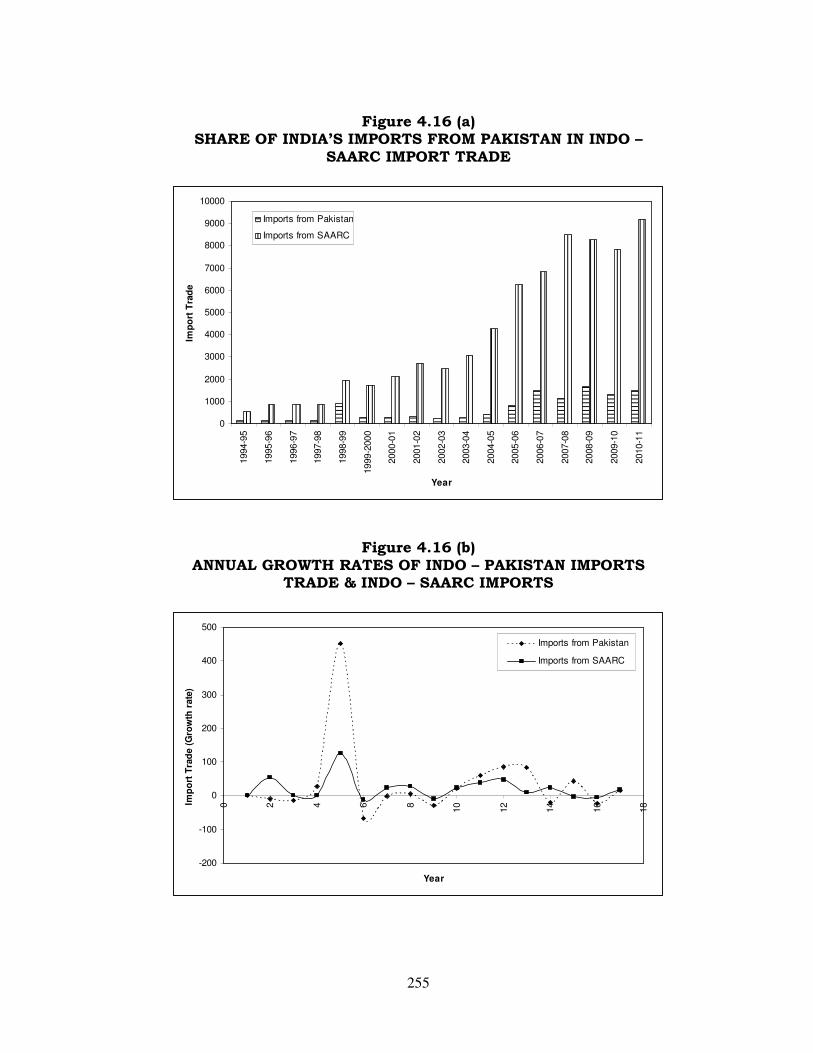

Share of India’s imports from Pakistan in Indo-SAARC import

trade.

The imports from Pakistan had exhibited a fluctuating trend

through out the study period. According to table 4.16, the imports

from Pakistan during 1999-2000 amounted Rs. 295.6 crores as

198

compared to 165.6 crores in 1994-95, contributing a compound

growth rate at 78.50 per cent in 1999-2000 over 1994-95.

On the other hand, the compound growth rate of exports was

very high at 210.45 per cent in respect of Indo-Pak import trade

during the same period.

The period between 2000-01 and 2005-06, was very

encouraging for exports in respect of Indo-Pak import trade as well

as Indo-SAARC import trade. The compound growth rate of

imports, recorded in respect of Indo-Pak import trade was at

171.79 per cent, while that of the compound growth rate, recorded

in respect of Indo-SAARC trade was at 194.03 per cent in 2005-06

over 2000-01.

The rate at which, the compound growth, recorded in respect

of Indo-Pak import trade, was very low at 3.83 per cent in 2010-11

over 2006-07. But, it was a little bit batter in respect of Indo-

SAARC import trade, with the compound growth rate being

recorded at 34.80 per cent in 2010-11 over 2006-07.

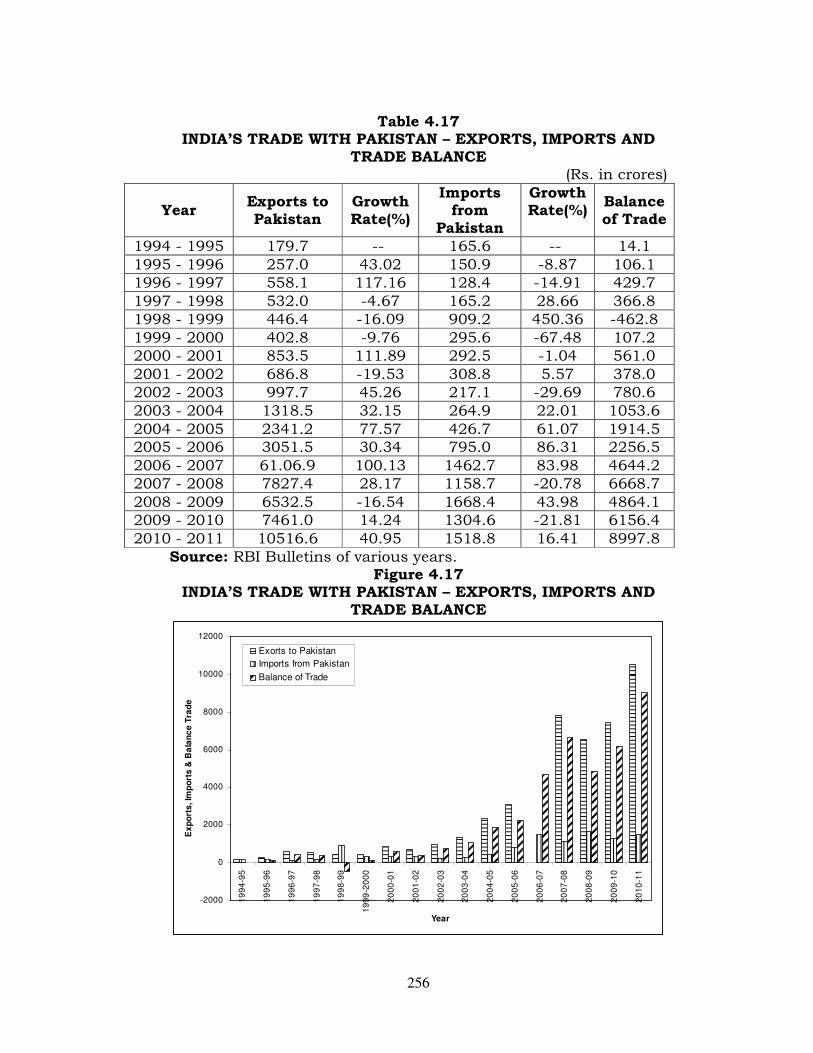

India’s balance of trade with Pakistan

India’s exports to Pakistan were higher as compared to her

imports. The balance of trade was unfavorable to India during

1979-93, but it became favorable during 1993-2006, except

1998=99, when India imported a large quantity of sugar from

Pakistan.

It is evident from the table 4.17 that the balance of trade

with Pakistan had been favorable to India through out the study

period except 1998-99 with the adverse balance of trade being

registered at Rs. 462.8 crores. Balance of trade had exhibited an

upward trend from 2002-03 onwards.

199

Gains from mutual trade to India and Pakistan

It is gainful to India and Pakistan to promote mutual trade

as both are neighboring countries and can have trade by land

route, which would save a lot in terms of transportation and

transshipment costs. At present, major portion of trade between

India and Pakistan is through the ports of Karachi and Mumbai.

From economic point of view, it is illogical to confine trade to ports

only, when a large common land border is shared by both the

countries. Land route is cheaper, faster and safe. In fact, there is a