Embed Size (px)

Citation preview

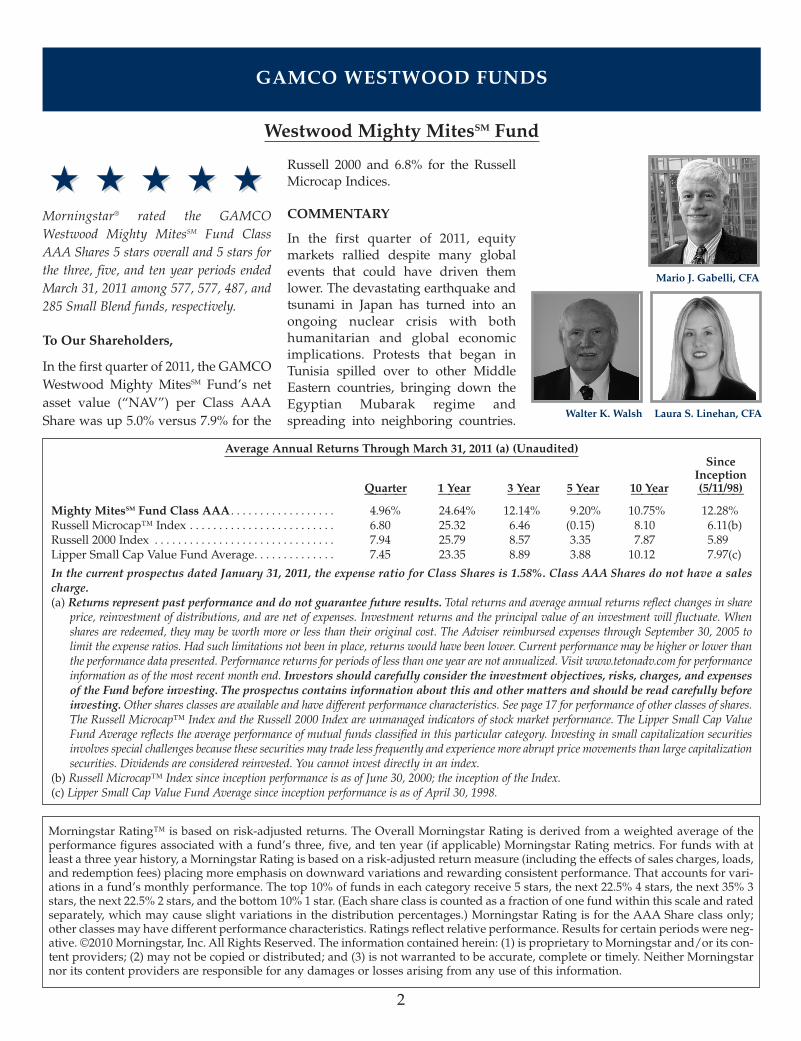

GAMCO WESTWOOD FUNDS

CommentaryMarch 31, 2011

Mighty MitesSM Fund

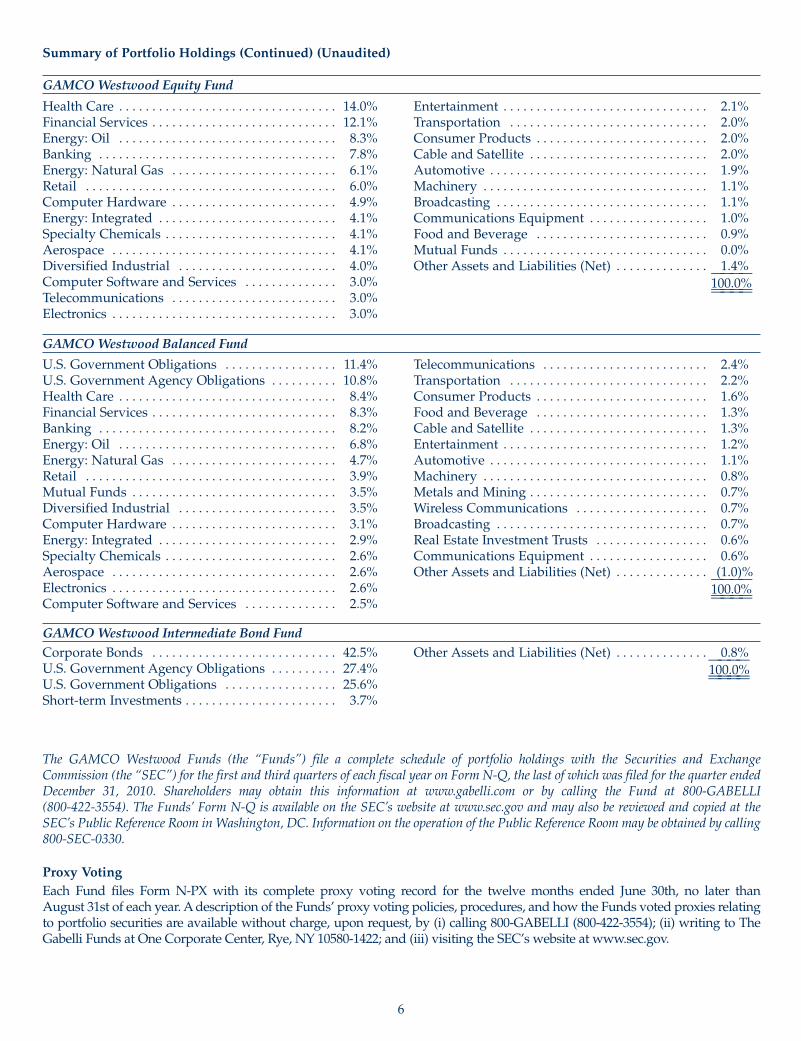

SmallCap Equity Fund

Income Fund

Equity Fund

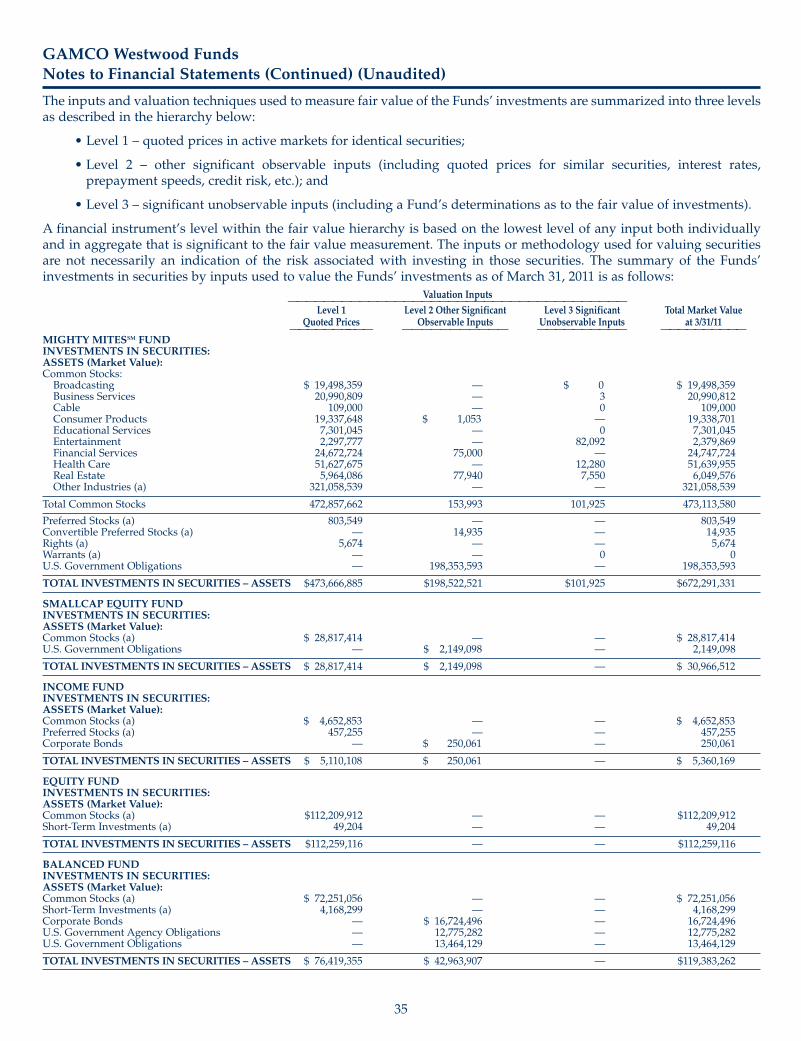

Balanced Fund

Intermediate Bond Fund

́́ ́ ́ ́ ́́ ́ ́ ́Morningstar® rated the GAMCOWestwood Mighty MitesSM Fund ClassAAA Shares 5 stars overall and 5 stars forthe three, five, and ten year periods endedMarch 31, 2011 among 577, 577, 487, and285 Small Blend funds, respectively.

To Our Shareholders,

In the first quarter of 2011, the GAMCOWestwood Mighty MitesSM Fund’s netasset value (“NAV”) per Class AAAShare was up 5.0% versus 7.9% for the

Russell 2000 and 6.8% for the RussellMicrocap Indices.

COMMENTARY

In the first quarter of 2011, equitymarkets rallied despite many globalevents that could have driven themlower. The devastating earthquake andtsunami in Japan has turned into anongoing nuclear crisis with bothhumanitarian and global economicimplications. Protests that began inTunisia spilled over to other MiddleEastern countries, bringing down theEgyptian Mubarak regime andspreading into neighboring countries.

2

GAMCO WESTWOOD FUNDS

Average Annual Returns Through March 31, 2011 (a) (Unaudited)Since

InceptionQuarter 1 Year 3 Year 5 Year 10 Year (5/11/98)———— ——— ——— ——— ——–— ——–——

Mighty MitesSM Fund Class AAA . . . . . . . . . . . . . . . . . . 4.96% 24.64% 12.14% 9.20% 10.75% 12.28% Russell Microcap™ Index . . . . . . . . . . . . . . . . . . . . . . . . . 6.80 25.32 6.46 (0.15) 8.10 6.11(b)Russell 2000 Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.94 25.79 8.57 3.35 7.87 5.89Lipper Small Cap Value Fund Average. . . . . . . . . . . . . . 7.45 23.35 8.89 3.88 10.12 7.97(c)

In the current prospectus dated January 31, 2011, the expense ratio for Class Shares is 1.58%. Class AAA Shares do not have a salescharge. (a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. Whenshares are redeemed, they may be worth more or less than their original cost. The Adviser reimbursed expenses through September 30, 2005 tolimit the expense ratios. Had such limitations not been in place, returns would have been lower. Current performance may be higher or lower thanthe performance data presented. Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performanceinformation as of the most recent month end. Investors should carefully consider the investment objectives, risks, charges, and expensesof the Fund before investing. The prospectus contains information about this and other matters and should be read carefully beforeinvesting. Other shares classes are available and have different performance characteristics. See page 17 for performance of other classes of shares.The Russell Microcap™ Index and the Russell 2000 Index are unmanaged indicators of stock market performance. The Lipper Small Cap ValueFund Average reflects the average performance of mutual funds classified in this particular category. Investing in small capitalization securitiesinvolves special challenges because these securities may trade less frequently and experience more abrupt price movements than large capitalizationsecurities. Dividends are considered reinvested. You cannot invest directly in an index.

(b) Russell Microcap™ Index since inception performance is as of June 30, 2000; the inception of the Index.(c) Lipper Small Cap Value Fund Average since inception performance is as of April 30, 1998.

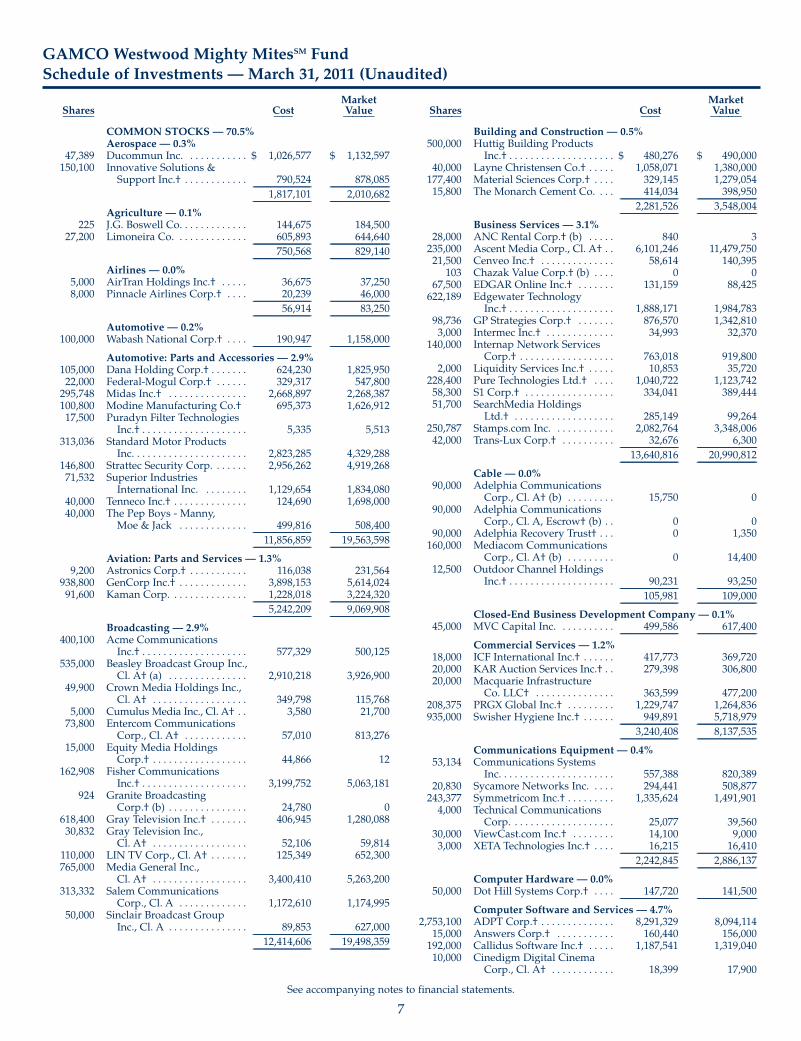

Westwood Mighty MitesSM Fund

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

Walter K. Walsh

Mario J. Gabelli, CFA

Laura S. Linehan, CFA

3

The United States is now involvedmilitarily in establishing a no-fly zonein Libya, preventing a humanitariandisaster and possibly helping to wrestQaddafi from power. Europe continuesto wrestle with budget and bankingcrises, and faces its own protestsregarding austerity measures. Yet themarkets are still up.

Back home, consumer headwindsinclude rising fuel, food, and clothingcosts. The national average price ofgasoline has risen 22% in the past year,and shows no signs of abating. Oilprices are being driven higher by insta-bility in the Middle East and thenuclear crisis in Japan. Higher oil pricesare not just felt at the pump, but affectprices of all goods that require trans-portation – food and clothing, forexample, and those with petroleum-based cost inputs. The consumer walletis definitely pinched by this dynamic.Finally, the housing market has not yetrecovered, with the S&P/Case-Shiller20-City Composite falling 3.1% yearover year.

It appears, however, the markets arefocused on the good news: Real GDProse at an annual rate of 3.1 percent inthe fourth quarter of 2010, up from thethird quarter’s 2.6 percent growth rate.Notably, personal consumption expen-ditures were up 4.4%. The employmentsituation continued to improve, withnonfarm payroll employment increasingby 216,000 in March, and an unem-ployment rate of 8.8 percent, downfrom its peak of 10.1 percent in Octoberof 2009. Lower unemployment spursconsumer spending, which accountsfor 70% of the U.S. economy, and isvital to growth.

In the quarter, three of four portfoliocompanies that received takeoveroffers rejected them. In January, FisherCommunications (0.8% of net assets asof March 31, 2011) rejected a bid worth$23.99 per share from HuntingdonREIT. In February, Bel Fuse made anunsolicited, and ultimately rejected,bid for Pulse Electronics (0.5%) for$6.00 per share. Then on March 17th,Stern Agee offered $6.25 per share forSWS Group (0.1%), but was alsorebuffed. A deal that is in the workswas announced on February 20th,when CSR Corp. (0.2%) agreed toacquire Zoran Corp. (0.2%) for $13.03in stock. We continue to expect mergerand acquisition activity amongst ourportfolio companies going forward.

We are pleased with the resiliency ofthe markets, given the many head-winds. There may be hiccups goingforward. We continue to do what wedo best, which is bottom-up, funda-mental stock picking. We look forstocks that are mispriced by Mr.Market, trading at a discount to ourassessment of their Private MarketValues, adding a margin of safety toexcellent growth opportunities.

Let’s Talk Investments

The following are stock specifics onselected holdings of our Fund.Favorable earnings prospects do notnecessarily translate into higher stockprices, but they do express a positivetrend that we believe will develop overtime. Individual securities mentionedare not necessarily representative ofthe entire portfolio. For the followingholdings, the percentage of net assetsand their share prices are presented asof March 31, 2011.

Top Contributors

• Ascent Media Corp. (1.7% of net assetsas of March 31, 2011) (ASCMA - $48.85 -Nasdaq) We bought Ascent, a spinofffrom Discovery Holding Company,because it was a “net-net,” tradingbelow cash, but with a valuablecollection of businesses. Managementplanned to use the cash to make a large acquisition in the telecom/mediaarea. The company agreed to sellsubstantially all of its operating busi-nesses for $181 million. Then itannounced a transformative acqui-sition of Monitronics International,Inc., a rapidly growing security moni-toring company, for $1.2 billion.

• Swisher Hygiene Inc. (0.9%) (SWI -$6.12 - TSE), a hygiene solutionscompany. Mighty MitesSM originallyowned Eskimo Pie, which wasacquired by CoolBrands in 2000.CoolBrands became bogged down inlitigation in 2006, and sold most of itsbusinesses. During this process, wewere buying shares at prices below thecash on the balance sheet. CoolBrandssettled its litigation and was ultimatelymerged with Swisher International, acommercial cleaning company.Notably, Swisher is controlled byWayne Huizenga, Chairman, and Steve Berrard, CEO, who were instru-mental in transforming Blockbuster,AutoNation, and Waste Managementinto multi-billion dollar companies.Swisher has already announcedseveral acquisitions in the first quarter,continuing its strategy to transformitself and expand its product offerings.

• Dawson Geophysical Co. (0.6%)(DWSN - $43.88 - Nasdaq), a provider ofonshore seismic data acquisitionservices. The company reported very

Top Ten Holdings (Percent of Net Assets)March 31, 2011

Ascent Media Corp. 1.7%Ferro Corp. 1.4%ADPT Corp. 1.2%Schiff Nutrition International Inc. 1.1%Journal Communications Inc. 1.0%

Epoch Holding Corp. 1.0%Biglari Holdings Inc. 1.0%Universal Technical Institute Inc. 0.9%Materion Corp. 0.9%Cantel Medical Corp. 0.9%

4

strong earnings growth in the fourthquarter of 2010, is debt-free, and has astrengthening order book and agrowing number of requests forproposals. Dawson provides higherresolution sub-surface images to explo-ration and production customers, usedto efficiently find and produce oil andgas. The company is active in theBakken, Niobrara, Marcellus,Haynesville , Barnett, and Eagle Fordshales.

• Ferro Corp. (1.4%) (FOE - $16.59 -NYSE), a specialty materials andchemical company whose end marketsinclude consumer and other elec-tronics, solar cells, construction, auto-motive, appliances, and packaging.Continued growth in sales areexpected in 2011, especially driven byconductive metal pastes for solarpanels, inks for digital tile decoration,and compounded materials. Thecompany has spent the last severalyears cutting its cost structure andstrengthening its balance sheet, whichalong with the improving economy ledto substantially improved results in2010. Management is now focused onprofitable growth, with efficiencies andcost control at the forefront.

Bottom Contributors

• IRIS International Inc. (0.7%) (IRIS -$9.02 - Nasdaq), a molecular diagnosticcompany whose core business ofurinalysis has an installed base of over

3,000 systems, and recurring revenueof consumables and service. IRIS isinvesting heavily in NADiA, a systemto identify post-surgical prostatecancer patients with a low risk of recur-rence to prevent overtreatment, and isawaiting key regulatory clearances. Inthe meantime, the company purchasedArista Molecular, a high complexityCLIA-certified laboratory, for a directcommercial channel for NADiA. Aristais estimated to dilute 2011 EPS by$0.20. Although the company’s invest-ments are taking longer than antici-pated to bear fruit, we believe thatNADiA presents a solid growth oppor-tunity.

• Zep Inc. (0.5%) (ZEP - $17.41 - NYSE),a distributor of cleaning and mainte-nance solutions including hand careproducts, cleaners, degreasers, deodor-izers, disinfectants, and sanitizers. Thecompany reported positive organicgrowth in its automotive and food endmarkets, but other customers continueto be negatively impacted by sustainedhigh rates of unemployment andreduced government spending. Zepwill continue to broaden its businessesto help move away from the unem-ployment correlation. We expect signif-icant consolidation in this highly frag-mented market.

• Sonesta International Hotels Corp.(0.6%) (SNSTA - $19.19 - Nasdaq),which owns and operates the 400 roomRoyal Sonesta Hotel Boston in

Cambridge, MA and operates the 500room Royal Sonesta Hotel in NewOrleans, LA under a long-term lease.The company also has a developmentpartnership with Miami-based FortuneInternational for the site of the formerSonesta Beach Resort Key Biscayneand has received approval for a 165unit residential project for a total of625,000 saleable square feet. Underexisting management agreements,Sonesta also operates hotels in CoconutGrove, FL and Egypt.

• Quidel Corp. (0.3%) (QDEL - $11.96 -Nasdaq), a diagnostic testing company.Quidel sells high-margin influenzatests and had a particularly strong2009, as it was a pandemic year withH1N1. Flu activity was much lighter in2010, and sales and margins took a hit.The company is focused on growingsales of Thyretain, a test for Grave’sDisease, which leads to hyperthy-roidism. Quidel also continues to workon new product development.

Conclusion

Our portfolio management teamcontinues to seek inefficiently pricedcompanies selling at a discount to theirprivate market value (PMV). Our goalis to deliver attractive risk adjustedreturns for our investors over the longrun.

We appreciate your confidence andtrust.

Sincerely,

Mario J. Gabelli, CFA Walter K. Walsh Laura S. Linehan, CFACo-Portfolio Manager Co-Portfolio Manager Co-Portfolio Manager

April 11, 2011

5

́́́ ́Morningstar® rated the GAMCOWestwood SmallCap Equity Fund ClassAAA Shares 2 stars overall and 3 stars forthe three year period, 4 stars for the fiveyear period, and 1 star for the ten yearperiod ended March 31, 2011 among 577,577, 487, and 285 Small Blend funds,respectively.

To Our Shareholders,

The GAMCO Westwood SmallCapEquity Fund’s NAV per Class AAAShare appreciated 11.0% during theMarch quarter versus a gain of 7.9% forthe Russell 2000 Index. Our outperfor-mance is attributable to strong gainsamong company holdings in the indus-trial, technology, and energy sectors.Moreover, performance benefited fromannounced acquisitions of four port-folio companies by corporate acquirers.In previous letters, we have highlightedthis major wave of merger and acqui-sition activity sweeping the small caplandscape as fourteen of our companieswere acquired last year by eitherstrategic or financial buyers.

COMMENTARYDuring the March 2011 quarter, thefollowing portfolio companiesannounced plans to merge: DanversBancorp, Inc. (DNBK), was acquired by People’s United Financial, Inc.(PBCT); Genoptix, Inc. (GXDX),acquired by Novartis AG (NVS); PrideInternational, Inc. (PDE), by Ensco PLC(ESV); and Herley Industries, Inc.(HRLY) by Kratos Defense & SecuritySolutions, Inc. (KTOS).We believe the inherent pricing ineffi-ciencies in the small capitalization assetclass have been amplified due to themassive downsizing of Wall StreetResearch during the financial crisis. Notsurprisingly, given the attractive valua-tions, we are witnessing the early stagesof a major wave of merger and acqui-sition activity by both strategic buyersand private equity investors. Ourbottom up, fundamental researchdriven process attempts to identifycompanies selling at a discount to theirintrinsic value. As such, diversifiedsmall cap portfolios stand to benefitfrom this trend. Some 70% of transac-tions last year, for example, were lessthan $5 billion, so smaller companiesare increasingly acquisition targets.

At Teton Advisors,we believe thisconsolidation act-ivity will continuegiven the $3trillion in cash oncorporate balancesheets. Banks havereturned to lend-ing, supportingdeal financing, and the Federal Reserveshould continue to maintain an easymonetary policy which should bringprivate equity players back to dealmaking. As value investors, we concen-trate on buying companies at discountsto their intrinsic value. We also look attheir fundamentals, market positionand business model. As bottom up,research driven investors, we employmany of the same criteria used bystrategic corporate acquirers andprivate equity firms. The near universalrestructuring and cost cuttingthroughout corporate America in late2008 and 2009 lowered the risk profileof many acquisition targets. Therecession’s severity also afforded largerfirms the opportunity to fill gaps intheir product strategies or to acquirestrategic assets.

Westwood SmallCap Equity Fund

Average Annual Returns Through March 31, 2011 (a) (Unaudited)Since

InceptionQuarter 1 Year 3 Year 5 Year 10 Year (4/15/97)———— ——— ——— ——— ——–— ——–——

SmallCap Equity Fund Class AAA . . . . . . . . . . . . . . . . . 11.03% 32.39% 12.31% 6.71% 5.73% 7.75% Russell 2000 Index. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.94 25.79 8.57 3.35 7.87 8.09In the current prospectus dated January 31, 2011, the gross expense ratio for Class AAA Shares is 1.99%. The net expense ratio is 1.50%,after contractual reimbursements by Teton Advisors, Inc. (the “Adviser”) in place through January 31, 2012. Class AAA Shares do nothave a sales charge. (a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. Whenshares are redeemed, they may be worth more or less than their original cost. The Adviser reimbursed expenses to limit the expense ratio. Had suchlimitation not been in place, returns would have been lower. Current performance may be lower or higher than the performance data presented.Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performance information as of the mostrecent month end. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund beforeinvesting. The prospectus contains information about this and other matters and should be read carefully before investing. Othershares classes are available and have different performance characteristics. See page 17 for performance of other classes of shares. The Russell 2000Index is an unmanaged indicator of stock market performance. Investing in small capitalization securities involves special challenges because thesesecurities may trade less frequently and experience more abrupt price movements than large capitalization securities. Dividends are consideredreinvested. You cannot invest directly in an index.

Nicholas F. Galluccio

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

6

From a macro perspective, we believeU.S. economic growth is about to enter aself-sustaining phase as evidenced byimproving corporate earnings andemployment. An abrupt shift inmonetary policy to tighten credit wouldundoubtedly negatively impact equitymarkets and the equities of smaller capi-talization companies. However, giventhe fragile housing and lagging labormarkets, it is more likely that, even witha phasing out of the Federal Reserve’squantitative easing program QE2 thisJune, the Fed will maintain a ratheraccommodative monetary policy whichis typically benign for small capital-ization equities. Federal Reserve policymakers in March differed over whetherto begin removing some stimulus aftercompletion of their $600 billion bond-purchase program. We do not expect anabrupt change in policy. According to theMarch minutes of the Federal OpenMarket Committee (FOMC) “almost all”Fed officials saw no need to “taper”Treasury buying after June, discardingtheir prior language of reducing the paceof purchases. We believe the Fed issingularly focused on using monetarypolicy to elevate inflation and inflationexpectations. As such, we have added toholdings in the metal, mining andenergy sectors which stand to benefitfrom pricing power. Despite theimprovement in non-farm payrollemployment in March to 216K jobsversus, expectations of a 190K gain,(along with a decline in unemploymentto 8.8% from 8.9%), the Fed will bereluctant to tighten until we enter aperiod of self sustaining economicgrowth.

Let’s Talk Investments

The following are stock specifics onselected holdings of our Fund.Favorable earnings prospects do notnecessarily translate into higher stockprices, but they do express a positivetrend that we believe will develop overtime. Individual securities mentionedare not necessarily representative of theentire portfolio. For the followingholdings, the percentage of net assets

and their share prices are presented asof March 31, 2011.Among the best performing stocks thisquarter were: Brigham Exploration Co(1.2% of net assets as of March 31, 2011),LeCroy Corporation (1.1%), and TrinityIndustries, Inc. (1.3%).

Brigham Exploration Co (BEXP - $37.18 -Nasdaq) explores and develops domesticonshore oil and gas formations utilizingtechnologically advanced techniques. Inaddition to rising energy prices in thequarter, BEXP reported strong results,driven by accelerated production of oilfrom the Bakken region of Montana andNorth Dakota. Furthermore, thecompany outlined an increased plan fordrilling activity in 2011.LeCroy Corporation (LCRY - $13.37 -Nasdaq) a niche builder of high-endoscilloscopes and protocol analyzersused by design engineers for industrial,optical network, and consumer elec-tronic end markets. The companyentered the year with an unseasonablystrong order book across all geogra-phies and end markets, an improvingbalance sheet, and receding liquidityconcerns. Given the significant consoli-dation of the space in past years, LCRYcontinues to benefit from both anincreasingly rational competitive setand scarcity value as a technology asset.Trinity Industries, Inc. (TRN - $36.67 -NYSE) is a leading manufacturer ofrailcars and inland barges, both cyclicalindustries. As the domestic economyexits the recession and rail trafficimproves, operators have begun toincrease capital expenditures and placesignificantly improved orders withTRN. Trinity is in the early stages of amultiyear upcycle.Among the worst performing stocks inthe quarter were: Akamai Technologies,Inc. (0.2%), Hudson Valley Holding Corp.(0.6%), and The Jones Group, Inc. (0.9%).Akamai Technologies, Inc. (AKAM -$38.00 - Nasdaq) the developer ofsoftware systems which acceleratedelivery of internet content, declined asa result of diminished expectations thatthe company would be acquired.

Furthermore, a well-known customeropportunistically shifted business tocapture discounted pricing by acompetitor, reigniting a long-runningdebate as to whether AKAM’spremium pricing strategy could be atrisk. Given the company’s dominantmarket share over a long period,breadth in product offering andrational behavior in the past, webelieve this threat is overstated.Hudson Valley Holding Corp. (HUVL -$22.00 - Nasdaq) provides communitybanking services in WestchesterCounty, New York and Connecticut.Hudson Valley’s underperformance inthe quarter was attributable to concernsover its exposure to construction loans.We believe improving credit conditionsshould alleviate the necessity foroutsized loan loss provisions; thisshould result in improved profitability.The Jones Group, Inc. (JNY - $13.75 -NYSE) designs and markets brandedapparel, dresses, footwear, jeans,sportswear, jewelry, and handbagsthrough department stores andbranded specialty retail and outletstores. Excess inventory and risingcotton prices depressed margins in thequarter, causing the stock to decline.We believe the company’s long termprospects are attractive.

Conclusion

Our research team is working dili-gently to deliver attractive risk adjustedreturns for our fund investors. Webelieve the portfolio is well positionedto participate in this next marketrecovery cycle.We appreciate your confidence andtrust.

Sincerely,

Nicholas F. GalluccioPortfolio ManagerPresident and CEOTeton Advisors, Inc.April 11, 2011

Top Ten Holdings (Percent of Net Assets)March 31, 2011

Patterson Cos. Inc. 1.6%Electro Scientific Industries Inc. 1.4%Mine Safety Appliances Co. 1.3%FTI Consulting Inc. 1.3%Trinity Industries Inc. 1.3%

Qlogic Corp. 1.3%Brigham Exploration Co. 1.2%First Niagara Financial Group Inc. 1.1%Lecroy Corp. 1.1%Vishay Intertechnology Corp. 1.0%

7

́́ ́ ́ ́́ ́ ́Morningstar® rated the GAMCOWestwood Income Fund Class AAA Shares4 stars overall and 4 stars for the three andfive year periods and 5 stars for the ten yearperiod ended March 31, 2011 among 1,120,1,120, 945, and 522 Large Value funds,respectively.

To Our Shareholders,The stock market closed on a solid gainin the first quarter, overcoming severenatural, geopolitical, and financialshocks. In January, popular protestssprang up in the Middle East andNorth Africa, surprising everyone asthey developed into full rebellionsagainst long-term incumbent govern-ments and spread widely. In midMarch, the worst earthquake to ever hitJapan combined with the tsunami andsevere damage to a nuclear plant, sentinvestors fleeing. The stock marketgave back all its gains by the middle ofMarch but rose strongly in the last two

weeks of the quarter, taking only thepositive economic news into account.

The nation’s biggest companies increasedtheir dividends by a record amount in thefirst quarter. According to a report fromStandard and Poor’s, 117 companies inthe S&P 500 Index said they wouldraise or start paying dividends, for atotal additional payout amounting to arecord $16.6 billion. This compareswith 78 companies raising their divi-dends in the first quarter a year ago.

We expect the increases in dividends tocontinue for some time. Dividendpolicy lags corporate earnings by a yearto eighteen months, as managementsreassess their experience to determinewhat they can sustain. As evidence ofthis, corporate earnings peaked in 2007and tumbled down in 2008, butdividend cuts were the largest in thefollowing year. Now, with two years ofstrong earnings increases, corporateearnings are approaching record levelsand the payout ratio of earnings in theform of dividends remains low, approx-

imately 34% versusa long term aver-age of 50%. Inaddition, the cashin companies’ cof-fers is at an alltime high.

PerformanceThe GAMCO Westwood Income Fund’s(the “Fund”) net asset value (“NAV”)per Class AAA Shares gained 5.6% inthe first quarter compared with gains of5.9% for the S&P 500 and 5.9% for theLipper Equity Income Fund Average.The S&P 500 is divided into ten sectorsand all had positive gains in the quarter.The strongest was, of course, energy,with the stocks in this sector rising anaverage of 17% as the price of oil rosefrom $90 a barrel to $108, pricing in thepotential for disruption from the MiddleEast. Industrial stocks posted the nexthighest return, with an average of 9%;both of these sectors have had stronggains for the past twelve months, withenergy reflecting oil’s price increase andindustrials benefiting from oil’s price

Westwood Income Fund

Average Annual Returns Through March 31, 2011 (a)(c) (Unaudited) SinceInception

Quarter 1 Year 3 Year 5 Year 10 Year (9/30/97)———— ——— ——— ——— ——–— ——–——Income Fund Class AAA. . . . . . . . . . . . . . . . . . . . . . . . . . 5.64% 14.32% 1.60% 1.23% 8.99% 7.15% S&P 500 Index. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.92 15.65 2.35 2.62 3.29 4.34Lipper Equity Income Fund Average . . . . . . . . . . . . . . . . 5.85 14.93 1.84 2.34 4.10 4.46Blended Index (b). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.22 2.88 1.28 (1.98) (0.09) 0.11 10 Year Treasury Note Index . . . . . . . . . . . . . . . . . . . . . . . 4.51 (9.89) 0.21 (6.57) (3.46) (4.13)In the current prospectus dated January 31, 2011, the gross expense ratio for Class AAA is 3.19%. The net expense ratio is 2.00%, aftercontractual reimbursements by Teton Advisors, Inc. (the “Adviser”) in place through January 31, 2012. Class AAA Shares do not have asales charge. (a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price, reinvestment of dividends, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When sharesare redeemed, they may be worth more or less than their original cost. The Adviser reimbursed expenses to limit the expense ratio. Had suchlimitation not been in place, returns would have been lower. Current performance may be lower or higher than the performance data presented.Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performance information as of the mostrecent month end. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund beforeinvesting. The prospectus contains information about this and other matters and should be read carefully before investing. Othershares classes are available and have different performance characteristics. See page 17 for performance of other classes of shares. The Standard &Poor’s (“S&P”) 500 Index is an unmanaged indicator of stock market performance. The Lipper Equity Income Fund Average includes the 30largest equity funds tracked by Lipper, Inc. The 10 Year Treasury Note Index is an unmanaged index tracking U.S. Treasury Notes with a 10 yearmaturity. Dividends are considered reinvested. You cannot invest directly in an index.

(b) The Blended Index consists of a 50% blend of each of the 10 Year Treasury Note Index and the S&P 500 Index.(c) As per the January 31, 2011 prospectus, the fund’s benchmarks are the S&P 500 Index and the Lipper Equity Income Fund Average.

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

Barbara G. Marcin, CFA

8

gain of 17% in the first quarter accom-panied by more encouraging economicreports and continued manufacturingand export strength. The surprise mightbe from the health care sector, whichwas dormant in 2010 and rose 6% in thefirst quarter. The three sectors with theleast return, all returning about 3%,were the financial, utility, and consumerstaple stocks, apparently not as inter-esting to investors who were looking forstocks with more upside in animproving economy.

Not surprisingly, our stocks in the Fundwith the best performance in the quarter,rising more than 15%, included ourenergy holdings such as Chevron (3.0%of net assets as of March 31, 2011),ConocoPhillips (3.7%), and DevonEnergy (1.7%). Other large holdings withsimilar gains included Pfizer (2.6%),Tupperware (2.2%), and EMC (0.5%).

The Tumultuous Quarter

The first quarter offered a rollercoasterof returns, with the Dow JonesIndustrial Average rising almost 7% bymid-month on an improving economy,giving back all of those returns by mid-March, and then shrugging off theseextraordinary events and concerns toclose up 6.4%. In January, a revolution inTunisia quickly forced out its presidentof 23 years, and then violent demonstra-tions spread to Egypt, Yemen, Bahrain,Jordan, Syria, Libya, and even SaudiArabia over economic grievances,political governance, and corruption.

Governments worldwide struggled toquickly reassess their own self interests,goals, and allies in the region, whilefinancial markets struggled to price inpotential changes in the price of oil andgovernment policies. The United Statesled a coalition of forces to invade Libyain March, in response to ColonelGaddafi’s pronouncements that hewould crush the rebels. However,within two weeks, at quarter end, itbecame clear that this coalition hadunderestimated the amount of muni-tions and help that the rebellion wouldneed to sustain itself, and ColonelGaddafi promised a very long war tokeep his position.

The disaster in Japan thwarted hopesfor its economic recovery this year.Global industries whose manufac-turing would be disrupted due to

sourcing a substantial part of theirproduct in Japan included componentsfor computers and electronic devicesfor cars. Unaccountably, the yen surgedin chaotic trading to an all time high of76.32 yen to the U.S. dollar, promptingthe first concerted effort by the G-7countries to intervene in the currencymarkets since 2000.

In the United States showdownserupted as governors in Wisconsin andOhio, acting upon their newly electedmandates, attempted to pass reformbudgets that would end collectivebargaining and allow workers to optout of paying union dues. Polls showedthat even though Americans expectedcuts to be made and accepted in publicworkers’ pensions and benefits to helpclose state and local budget deficits, themajority supported the right tocollective bargaining, indicating a deepappreciation for these workers’ contri-butions to public service as policeofficers, teachers, and firefighters.

In Europe, the political and financialdrama that has plagued the EuropeanUnion erupted again, causing doubtsover its future as a unified entity. Thegovernment of Portugal resigned whenthe mostly opposition legislaturerefused to pass its austerity budget,leaving it leaderless and in a difficultposition to refinance its debt frominvestors. Not only does this throw upanother country in need of a bailoutfrom the Union, and rekindle questionsabout the size and power of theregion’s bailout funds, but it throwsinto question the ability of the Union toresolve anything, as their strategy hasrevolved around states slashing deficitsand willingly implementing austeritybudgets in return for rescue loans.

This year is setting up to be a blockbusterfor deals and mergers, starting off withthe huge announced acquisitions ofGenzyme by Sanofi Aventis, Bulgari byLVMH, and T-Mobile USA by AT&T inthe first quarter. According to data fromThomson Reuters, worldwide mergersand acquisitions have doubled involume in the United States and Europeand have risen 58% worldwide, makingthis the best start to a year since 2007.The fundamentals of an improvingeconomy, record corporate earnings, andrecord cash on corporate balance sheetsappear to support a continued strongyear for deals.

Let’s Talk Investments

The following are stock specifics onselected holdings of our Fund.Favorable earnings prospects do notnecessarily translate into higher stockprices, but they do express a positivetrend that we believe will develop overtime. Individual securities mentionedare not necessarily representative of theentire portfolio. For the followingholdings, the percentage of net assetsand their share prices are presented asof March 31, 2011.

Air Products and Chemicals Inc. (1.7% ofnet assets as of March 31, 2011 ) (APD -$90.18 - NYSE), an industrial gas supplybusiness, has numerous strengths,including a significant market share, anextensive global production and distri-bution network, and a diverse customerbase. The company has a highproportion of long-term contracts thatcontribute to stable demand andpricing. Secular trends in the industrialgas business include rising energydemand, with growing demand forhydrogen for oil refining and oxygen forcoal gasification; increasing environ-mental regulation, providing opportu-nities that should benefit gas; andgrowth in emerging economies.

International Paper (2.8%) (IP- $30.18 -NYSE) has undergone a dramatic trans-formation over the past few years asmanagement has done as promised,executing on its plan to improve returnon capital and margins, exit non-corebusinesses to deliver a higher return oncapital, pay down debt and return cashto shareholders. The company hasreduced capacity and lowered fixedcosts to improve margins. In the firstquarter, the company announced that itwould acquire the majority of theleading paper manufacturer in India,which is the fastest growing papermarket in the world. InternationalPaper has paid dividends without inter-ruption since 1946, but cut its dividendin March of 2009 to instead reduce debt.The company increased its dividendthree times in the past twelve months,to $1.05 now, above its pre-recessionlevel, indicating its commitment toreturn cash to shareholders.

E.I. du Pont de Nemours & Company(4.1%) (DD - $54.97 - NYSE) continuesto benefit from the improved globaleconomy as well as the restructuring of

9

its businesses to concentrate uponthose with a higher return on capital.The company is experiencing broadbased gains in volumes across itsproducts and geographies, and its agri-cultural products are continuing to gainmarket share. The company has a highdividend yield which we believe is wellsupported by its cash flow and growthoutlook as well as evidence ofmanagement’s commitment to returnearnings to shareholders.

Honeywell International (2.2%) (HON -$59.71 - NYSE) is a leading producer ofavionics, power, and electronic systemsfor the aerospace market, processautomation, and security products forthe industrial, residential, andcommercial building markets. Thecompany also makes turbochargers forthe automotive industry and providestechnologies to the energy market.HON has excellent products, a strongbalance sheet, and generates sub-stantial free cash flow that could beused for internal growth, acquisitions,and stock repurchases. In addition, thecompany is executing on its long-termstrategy to expand in less costly regionsof the world while reducing costs inmore costly countries by closing plants,consolidating facilities, and imple-menting six sigma and lean manufac-turing. These dynamics should positionHON for bigger profitability gains inthe future.

Looking Ahead

As the first quarter ends, consensus isgenerally optimistic for growth in theU.S. economy, with the average of econ-omists projecting 3.7% growth in thegross domestic product for the secondquarter. Manufacturing continues to bestrongly driven by exports. However,the so far mediocre growth has not beenenough as of yet to create enough jobsto absorb workers and lower unem-ployment, particularly as housing andconstruction remain weak.

Still looming as a potential threat togrowth, oil prices continued to soar inthe first quarter, as supportive U.S. jobsdata reinforced economic growthexpectations and Libya’s conflict andMiddle East unrest kept supply threatsin focus. Oil has climbed from $90 at thebeginning of the year to $108 by quarterend, reflecting both a stronger globaleconomy, if not here in the UnitedStates, and the threat of disruption fromthe turmoil in most Middle Easternproducing countries. The rise in oilprice is supported by continuedviolence in Libya as Colonel Gaddafi isnow vowing a long war to keep hisposition. The invasion, initially led bythe United States, France, and Britainand then assumed by NATO, appears tohave misjudged the amount of muni-tions and troops help the rebels wouldneed to sustain their effort.

The administration, which justannounced the creation of the 2012 re-election organization, remains, alongwith the Federal Reserve, determinedto hold rates down and providestimulus as long as the economy is lessthan robust. So we expect this policybehavior to continue, and when thesecond quantitative easing programends as scheduled in June, we expectthe Federal Reserve to remain on hold,and possibly even discuss being readywith more easing policy.

Nevertheless, there is a growingdiscomfort that we are again holdingrates too low too long, and fostering thenext problem of some imbalance that isnot evident now. The chairman of theFederal Reserve, Ben Bernanke, believesthat he does not have to consider thesignificant inflation of raw materials,commodities, and input prices to be aproblem until he sees widespreadinflation in finished goods. This isunlikely to happen in a global economywhere labor is cheap, the consumer isweak, and there is broad transparentpricing and movement of goods.

As the quarter ends, we are once againslipping down the path towardgovernment shut down as Americanpoliticians fight over what to pay forand what to cut from the budget, aproblem exacerbated by one quarter ofthe year already being over.

Stock markets worldwide haveresponded to the accommodation of theFederal Reserve, accompanied, untilthis year, by easing in other countries.The Federal Reserve, holding the riskfree rate down at zero, has pushedinvestors out on the risk curve,evidenced by the strong stock markets,bullish sentiments, record low “junk”or high yield spreads, and tremendousbuyout deal activity. It has become amantra on television and in thefinancial press that dividend payingstocks are a better buy than bonds, andthat stocks are also the right choice toprotect against the rising bond yieldsand inflation that will follow.

We are finding good value in manycompanies that have some combinationof long term growth prospects,exposure to faster growing globalmarkets, good balance sheets to seedgrowth and or make acquisitions, andstrong cash generation. These includeKraft Foods (3.5% of net assets as ofMarch 31, 2011), General Mills (4.4%),Honeywell (2.2%), International Paper(2.8%), Air Products and Chemicals(1.7%), Tupperware (2.2%), AmericanWater Works (3.4%), Mead JohnsonNutrition (2.7%), and DuPont (4.1%).

Sincerely,

Barbara G. Marcin, CFAPortfolio Manager

May 9, 2011

Top Ten Holdings (Percent of Net Assets)March 31, 2011

Bank One Capital Trust VI, 7.200% Pfd. 5.7%American Express Credit Corp., MTN, 0.417%, 06/16/11 4.6%Halliburton Co. 4.6%General Mills Inc. 4.4%E.I. du Pont de Nemours & Co. 4.1%

ConocoPhillips 3.7%Wells Fargo & Co. 3.5%Kraft Foods Inc. 3.5%American Water Works Co. Inc. 3.4%Apple Inc. 3.2%

10

́́́ ́ ´́Morningstar® rated the GAMCO WestwoodEquity Fund Class AAA Shares 3 starsoverall and 2 stars for the three year periodand 3 stars for the five year period and 4stars for the ten year period ended March 31,2011 among 1,757, 1,757, 1,471, and 816Large Blend funds, respectively.

To Our Shareholders,

For the quarter ended March 31, 2011,the net asset value (“NAV”) of theGAMCO Westwood Equity Fund ClassAAA Shares posted a return of 6.0%versus 1.1% for the Lipper Large CapValue Fund Average and 5.9% for theS&P 500 Index.

Market Commentary

Events in the Middle East and Japanwere a key factor in the market’s firstquarter gain but also of importance

were concerns about the potential peakin selected leading economic indicatorsand continued concerns over housing,inflation and the fiscal health of statesand municipalities. January started theyear well with strong earnings andeconomic reports. By month endhowever, protests in Egypt helped pushmarkets lower. Violence in Libya andcrude oil’s surge kept the pressure on inearly February but sentiment wasstrong and corporate earnings reportsand improving employment conditionsfueled the optimism. With events andconcerns weighing on investors, Marchreturns, while still positive, laggedthose of January and February asprotests and natural disasters took theirtoll on investor psyche. The bestperforming sectors were those tied tohigher commodity prices such asEnergy as well as economic optimismsuch as Producer Durables. Sectors thatlagged were the Consumer Staples asinvestors worried about rising foodcosts and Financial Services.

Performance Drivers:

The largest contributor to performancewas stock selection in FinancialServices, Consumer Discretionary andProducer Durables. The largestdetractors to relative performance werestock selection in Energy andTechnology.

Within Financial Services, companiessuch as Franklin Resources (2.1% of netassets as of March 31, 2011), whichbenefit from strong markets overall,posted some of the strongest absoluteperformance in the sector. Holdings inthe insurance segment, with stable cash generation characteristics, alsoperformed well. Performance was

Westwood Equity Fund

Average Annual Returns Through March 31, 2011 (a) (Unaudited)Since

InceptionQuarter 1 Year 3 Year 5 Year 10 Year 15 Year 20 Year (1/2/87)———— ——— ——— ——— ——–— ——–— ——–— ——–——

Equity Fund Class AAA . . . . . . . . . . . . . . . . . . 6.02% 11.89% (1.17)% 2.27% 3.69% 7.62% 9.61% 9.97% S&P 500 Index . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.92 15.65 2.35 2.62 3.29 6.80 8.72 9.75(b)Lipper Large Cap Value Fund Average . . . . . . 1.06 6.68 6.10 5.77 5.34 5.85 6.44 9.08(b)In the current prospectus dated January 31, 2011, the expense ratio for Class Shares is 1.54%. Class AAA Shares do not have a salescharge.(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price, reinvestment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. Whenshares are redeemed, they may be worth more or less than their original cost. Current performance may be lower or higher than the performancedata presented. Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performance information asof the most recent month end. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fundbefore investing. The prospectus contains information about this and other matters and should be read carefully before investing.Other shares classes are available and have different performance characteristics. See page 17 for performance of other classes of shares. The S&P500 Index is an unmanaged indicator of stock market performance, while the Lipper Large Cap Value Fund Average reflects the averageperformance of mutual funds classified in this particular category. Dividends are considered reinvested. You cannot invest directly in an index.

(b) S&P 500 Index and the Lipper Large Cap Value Fund Average since inception performance are as of December 31, 1986.

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

Susan M. Byrne

11

offset by weakness in AFLAC (2.0%),which pulled back as investors tried todigest the impact that the disasters inJapan might have on financialperformance of the company.

In Consumer Discretionary, WaltDisney (2.1%), along with CBS Corp.(1.1%), had a good quarter as strong adrates and demand figures werereleased along with Comcast (2.0%),which reported a positive earningssurprise based on good subscribergrowth in broadband services.Offsetting some of this strength wasweakness in Wal-Mart (1.9%) andGeneral Motors (1.9%) as each fell onthe potential for rising gas prices nega-tively impacting sales.

Producer Durables benefited from topcontributor ITT Corp. (2.0%), whichrose after announcing that they intendto split the company into three publicentities – Water, Defense, andInformation Solutions and IndustrialProducts. By splitting the company,previously hidden value can beuncovered as each unit will likelyreceive multiples appropriate for itssegment rather than as a conglomerateof varied, non-related companies.

Within Energy, overall performancefailed to keep pace with the strength ofthe index sector despite strong priceindividual performance from selectedholdings such as Exxon Mobil (2.0%)and Chevron (2.1%). Natural gas, usedin many electric utility generators, hadits price move higher as the coldweather spread across the countrycausing increased demand for elec-tricity while crude oil prices remainedelevated allowing companies holdingoil and gas assets to perform well.Together, higher energy prices posi-tively impacted the share prices ofmany companies in the sector. NationalOilwell however, detracted fromperformance as the shares were soldbefore the security’s price rise later inthe period.

Our underweight in Technology, a lowperforming sector on an absolute basis,was also a benefit to relativeperformance however, stock selectionfailed to keep pace with thebenchmark. Strong performance wasdelivered by holdings such as EMC,which delivered results that were high-lighted by record core and VMwarerevenues, IBM (2.0%), which reportedearnings that showed it is seeing a

broad based recovery that is beinghelped by new product cycles, andMotorola Mobility, which rose onoptimism surrounding its potential as anewly formed company. This strongperformance however, was offset byweakness in Cisco Systems andMicrosoft Corp (2.0%). Cisco Systemsrecently posted disappointing earningsbased on margin contraction due toswitch and router product transitionsand ongoing consumer weakness whileMicrosoft results disappointed on salesof its Windows product. Lastly,performance of new holding TEConnectivity Ltd. (2.0%) detracted asnear term uncertainty surrounding theimpact to supply and demand funda-mentals from the situation in Japanimpacted performance.

Sincerely,

Susan M. ByrnePortfolio Manager

April 11, 2011

Top Ten Holdings (Percent of Net Assets)March 31, 2011

Metlife Inc. 3.0%Pfizer Inc. 3.0%JPMorgan Chase & Co. 3.0%AT&T Inc. 3.0%Wells Fargo & Co. 3.0%

Johnson & Johnson 3.0%Anadarko Petroleum Corp. 2.2%Abbott Laboratories 2.2%The Walt Disney Co. 2.1%Dominion Resources Inc. 2.1%

12

́́ ́ ́́ ́Morningstar® rated the GAMCO WestwoodBalanced Fund Class AAA Shares 3 starsoverall and 2 stars for the three year periodand 3 stars for the five and ten year periodsended March 31, 2011 among 932, 932, 734,and 408 Moderate Allocation funds, respec-tively.

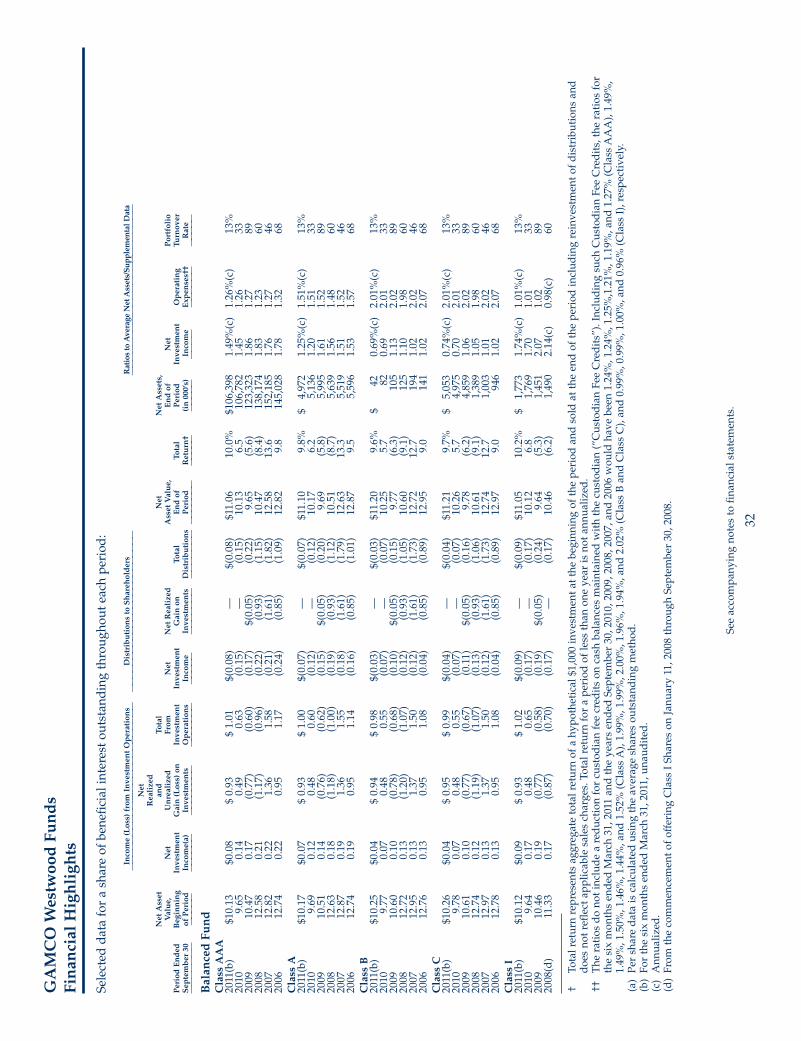

To Our Shareholders,

In the first quarter, the fund return of4.0% , net of fees and expenses,

exceeded the 2.5% return of thebenchmark: 60% S&P 500 StockIndex/40% Barclays CapitalGovernment/Credit Bond Index. Thefund is designed to provide exposure toequities while reducing overall risk viathe inclusion of short-to-intermediatefixed income securities. The EquityFund strategy comments apply to theequity portion of the Balanced Fund.The bond portion typically invests inhigh quality notes with lower interestrate sensitivity than the typical bondindex, with the objective of dampeningthe volatility of equity holdings.

Top and Bottom Fixed IncomeContributors

Recall that the contribution of a security(or a sector) is the product of itspercentage of the portfolio times itsreturn. We discussed in the com-

Westwood Balanced Fund

Average Annual Returns Through March 31, 2011 (a)(d) (Unaudited)Since

InceptionQuarter 1 Year 3 Year 5 Year 10 Year 15 Year (10/1/91)———— ——— ——— ——— ——–— ——–— ——–——

Balanced Fund Class AAA. . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.02% 9.09% 1.37% 3.69% 4.45% 7.13% 8.75% Barclays Capital Government/Credit Bond Index . . . . . . . 0.28 5.26 4.82 5.83 5.53 6.15 6.58(c)S&P 500 Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.92 15.65 2.35 2.62 3.29 6.80 8.67(c)60% S&P 500 Index and 40% Barclays Capital Government/Credit Bond Index (b) . . . . . . . . . . . . . . . . . . 2.54 9.42 3.83 4.55 4.63 6.41 7.42

Lipper Mixed Asset Target Allocation Moderate Fund Average . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.72 11.70 3.30 3.78 4.58 6.35 7.42(c)

Barclays Capital Government/Corporate Bond Index . . . . 0.22 5.27 4.81 5.79 5.47 0.00(e) 5.64(e)60% S&P 500 Index and 40% Barclays Capital Government/Corporate Bond Index (f) . . . . . . . . . . . . . . . 3.64 11.50 3.33 3.89 4.16 4.08 7.46

In the current prospectus dated January 31, 2011, the expense ratio for Class AAA Shares is 1.24%. Class AAA Shares do not have a salescharge.(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price and reinvestment of distributions and are net of expenses. Investment returns and the principal value of an investment will fluctuate. Whenshares are redeemed, they may be worth more or less than their original cost. The Adviser reimbursed expenses in years prior to 1998 to limit theexpense ratio. Had such limitation not been in place, returns would have been lower. Current performance may be lower or higher than theperformance data presented. Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performanceinformation as of the most recent month end. Investors should carefully consider the investment objectives, risks, charges, and expensesof the Fund before investing. The prospectus contains information about this and other matters and should be read carefully beforeinvesting. Other shares classes are available and have different performance characteristics. See page 17 for performance of other classes of shares.The S&P 500 Index is an unmanaged indicator of stock market performance. The Barclays Capital Government/Credit Bond Index and BarclaysCapital Government/Corporate Bond Index are market value weighted indices that track the performance of fixed rate, publicly placed, dollardenominated obligations. The Lipper Mixed Asset Target Allocation Moderate Fund Average reflects the average performance of mutual fundsclassified in this particular category. Dividends are considered reinvested. You cannot invest directly in an index.

(b) The Blended Index consists of a 60% blend of each of the S&P 500 Index and 40% Barclays Capital Government/Credit Bond Index.(c) S&P 500 Index, Barclays Capital Government/Credit Bond Index and the Lipper Mixed Asset Target Allocation Moderate Fund Average since

inception performance are as of September 30, 1991. (d) As per the January 31, 2011 prospectus, the fund’s benchmarks are the 60% S&P 500 and the 40% Barclays Capital Government/Credit Bond

Blended Index.(e) The Barclays Capital Government/Corporate Bond Index since inception performance is as of December 31, 1998.(f) The Blended Index consists of a 60% blend of each of the S&P 500 Index and 40% Barclays Capital Government/Corporate Bond Index.

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

Susan M. Byrne Mark R. Freeman, CFA

13

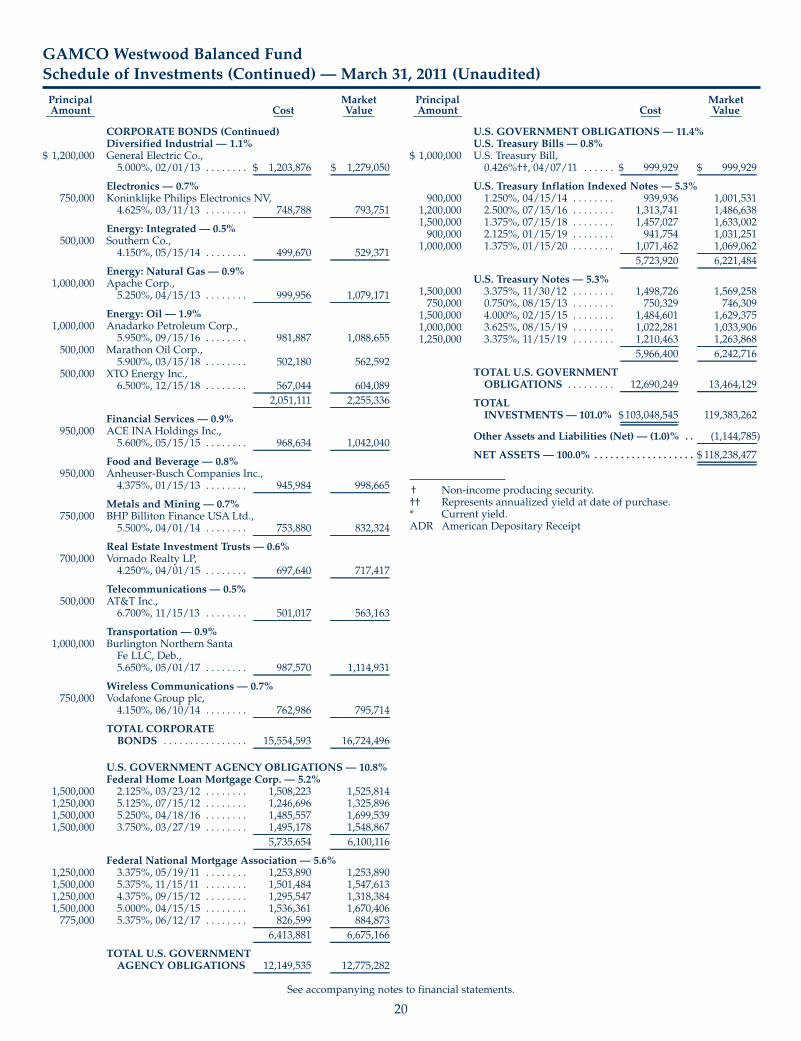

Top Ten Issuers (a) (Percent of Net Assets)March 31, 2011

Fannie Mae Notes 5.6%Freddie Mac Notes 5.1%JPMorgan Chase & Co 2.5%Bank of America Corp. 2.4%AT&T Inc. 2.3%

Apache Corp. 2.3%Anadarko Petroleum Corp. 2.2%Pfizer Inc. 1.8%Johnson & Johnson 1.8%Wells Fargo & Co. 1.7%

mentary on the Intermediate Bond Fundthat U.S. Treasury debt lagged theperformance of U.S. Agency debt, whichlagged the performance of U.S.Corporate and non-corporate debt; andlong-maturity Treasury debt took thebrunt of the hit in a rising rate envi-ronment. This was also the case in theIntermediate Barclays CapitalGovernment/Credit Bond Index, anindex of maturity no longer than 10years and one to which the bond portionin the Balanced Fund is often compared.

The shorter duration of the bonds in theBalanced Fund was also a factor in ourperformance of the fund. Additionalcontributors to out performance weresecurity selection in U.S. Treasuries

(notably TIPs) and in Utility bonds, andover weighting U.S. Credits and Baa-rated corporate debt. The top fixedincome contributors included twosecurities in the Intermediate BondFund – the Bank of America note (1.1%of net assets as of March 31, 2011) andthe TIPs, two additional TIPs - U.S.Treasury Inflation Indexed note 1.375%due 07-15-18 and 1.250% due 04-15-14,and Anadarko 5.950% due 09-15-16(0.9%).

Detracting the most from performanceof the fixed income portion of the fundwere two of the five notes listed for theIntermediate Bond Fund – the JPMorgan and Fannie Mae notes.

Changes in Fixed Income Holdings:

During the quarter there were no salesand a single purchase, U.S. TreasuryInflation Indexed note 1.375% due 01-15-20 (1.4%).Sincerely,

Susan M. ByrneCo-Portfolio Manager

Mark R. Freeman, CFACo-Portfolio Manager

April 11, 2011

(a) Bonds and equity positions have been combined.

14

́́Morningstar® rated the GAMCOWestwood Intermediate Bond Fund ClassAAA Shares 2 stars overall and 2 stars forthe three, five, and ten year periods endedMarch 31, 2011 among 1,021, 1,021, 873,and 563 Intermediate-Term Bond funds,respectively.

To Our Shareholders,

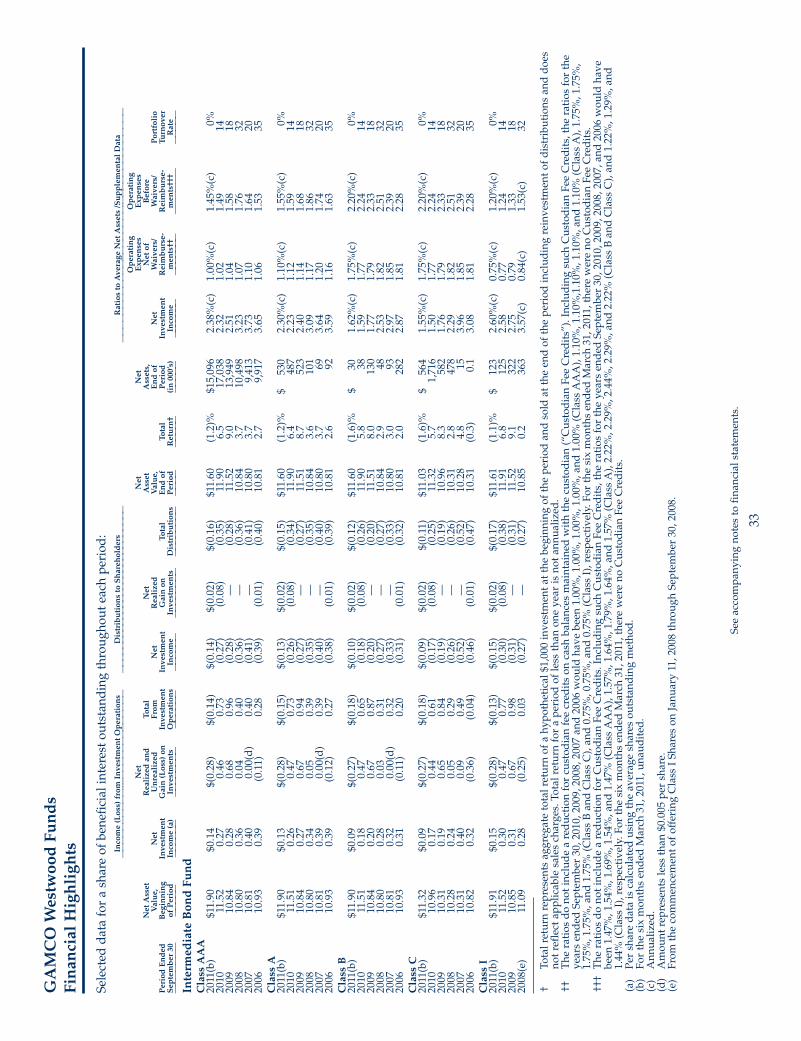

For the quarter ended March 31, 201,the net asset value (“NAV”) of theGAMCO Westwood Intermediate BondFund Class AAA Shares posted a returnof 0.4%, net of fees and expenses,versus 0.2% for the Barclays CapitalGovernment/Credit Bond Index, theFund’s benchmark.

Market Background

As was the case for most asset classes,volatility was a defining characteristicof the bond market in the first quarterof 2011. After a relatively quiet January,bond yields moved sharply higher inFebruary on (1) signs of an improvingeconomic outlook and (2) growingconcerns over inflation in response tosurging commodity prices, especiallyoil. But the rise in rates provedtemporary as the catastrophe in Japanon March 11th prompted a strong bidfor bonds and sharp decline in rates.However, the flight-to-safety Treasurybid proved to be relatively short-livedas investors once again turned theirattention to a steady stream ofeconomic data showing the U.S.recovery remained on track.

After all was saidand done Treasuryyields finished thequarter 0.15– 0.26%higher than at thebeginning of theyear (led by thethree-year note),reflecting expecta-tions for the Federal Reserve to raiseofficial rates earlier than previouslyexpected. Despite the volatility ininterest rates and a steady stream ofnew supply of debt during the quarter,investors continued to show strongdemand for corporate bonds and otherspread sectors, which in turn pushedcredit spreads even lower and pricescorrespondingly higher.The slight increase in yield-to-maturityproduced another quarter of negative

Westwood Intermediate Bond Fund

Average Annual Returns Through March 31, 2011 (a)(c) (Unaudited)Since

InceptionQuarter 1 Year 3 Year 5 Year 10 Year 15 Year (10/1/91)———— ——— ——— ——— ——–— ——–— ——–——

Intermediate Bond Fund Class AAA . . . . . . . . . . . . . . . . . 0.36% 3.97% 4.24% 4.89% 4.44% 5.30% 5.53% Barclays Capital Government/Credit Bond Index . . . . . . 0.28 5.26 4.82 5.83 5.53 6.15 6.58(b)Lipper Intermediate Investment Grade Debt Fund Average . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.06 6.68 6.10 5.77 5.34 5.85 6.22(b)

Barclays Capital Government/Corporate Bond Index . . 0.22 5.27 4.81 5.79 5.47 N/A(d) 5.64(d)In the current prospectus dated January 31, 2011, the gross expense ratio for AAA Shares is 1.49%. The net expense ratio is 1.02%, aftercontractual reimbursements, by Teton Advisors Inc. (the “Adviser”) in place through January 31, 2012. Class AAA Shares do not have asales charge. (a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share

price, investment of distributions, and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When sharesare redeemed, they may be worth more or less than their original cost. The Adviser reimbursed expenses to limit the expense ratio. Had suchlimitation not been in place, returns would have been lower. Current performance may be lower or higher than the performance data presented.Performance returns for periods of less than one year are not annualized. Visit www.tetonadv.com for performance information as of the mostrecent month end. The Fund is subject to interest rate and credit risks. Investors should carefully consider the investment objectives, risks,charges, and expenses of the Fund before investing. The prospectus contains information about this and other matters and should beread carefully before investing. Other shares classes are available and have different performance characteristics. See page 17 for performanceof other classes of shares. The Barclays Capital Government/Credit Bond Index and Barclays Capital Government/Corporate Bond Index aremarket value weighted indices that track the performance of fixed rate, publicly placed, dollar denominated obligations. The Lipper IntermediateInvestment Grade Debt Fund Average reflects the average performance of mutual funds classified in this particular category. Dividends areconsidered reinvested. You cannot invest directly in an index.

(b) The Barclays Capital Government/Credit Bond Index and the Lipper Intermediate Investment Grade Debt Fund Average since inceptionperformance are as of September 30, 1991.

(c) As per the January 31, 2011 prospectus, the fund’s benchmark is the Barclays Capital Government/Credit Bond Index.(d) The Barclays Capital Government/Corporate Bond Index since inception performance is as of December 31, 1998.

Mark R. Freeman, CFA

Morningstar Rating™ is based on risk-adjusted returns. The Overall Morningstar Rating is derived from a weighted average of theperformance figures associated with a fund’s three, five, and ten year (if applicable) Morningstar Rating metrics. For funds with atleast a three year history, a Morningstar Rating is based on a risk-adjusted return measure (including the effects of sales charges, loads,and redemption fees) placing more emphasis on downward variations and rewarding consistent performance. That accounts for vari-ations in a fund’s monthly performance. The top 10% of funds in each category receive 5 stars, the next 22.5% 4 stars, the next 35% 3stars, the next 22.5% 2 stars, and the bottom 10% 1 star. (Each share class is counted as a fraction of one fund within this scale and ratedseparately, which may cause slight variations in the distribution percentages.) Morningstar Rating is for the AAA Share class only;other classes may have different performance characteristics. Ratings reflect relative performance. Results for certain periods were neg-ative. ©2010 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its con-tent providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstarnor its content providers are responsible for any damages or losses arising from any use of this information.

15

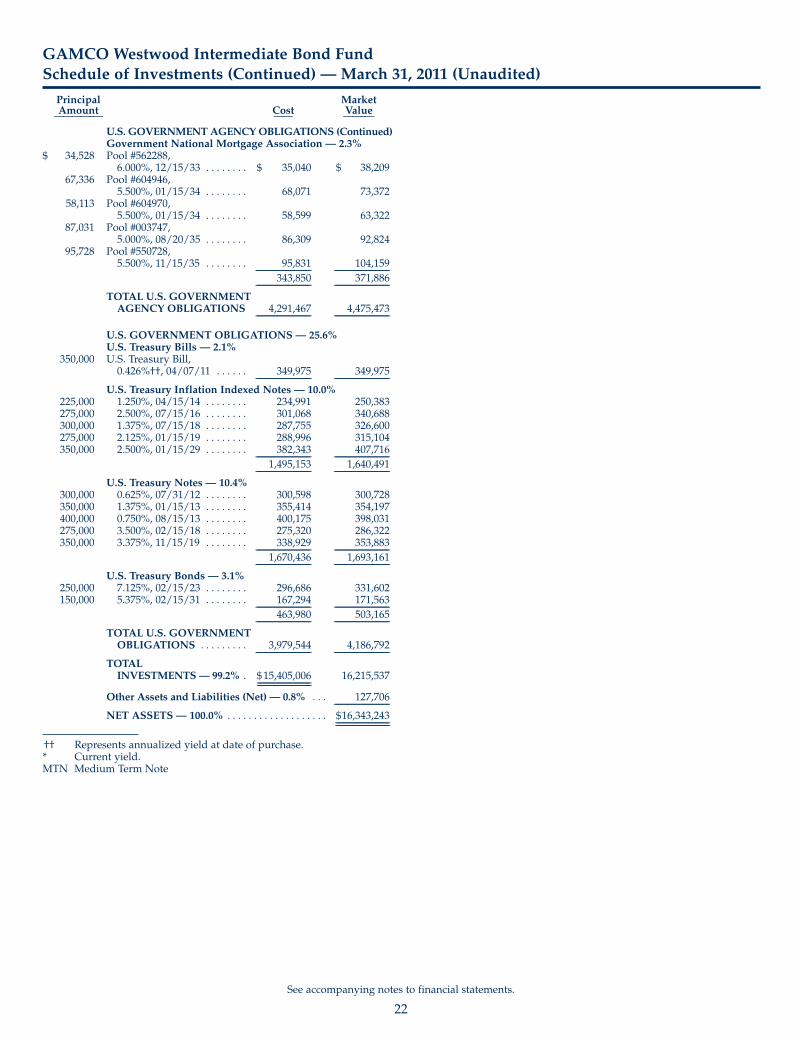

Top Ten Holdings (Percent of Net Assets)March 31, 2011

U.S. Treasury Notes 17.9%Fannie Mae Notes 13.3%Freddie Mac Notes 10.1%U.S. Treasury Bonds 5.6%Ginnie Mae Pools 2.3%

International Bank for Reconstruction & Development, 8.625%, 10/15/16 2.0%Bank of America Corp., 5.375%, 06/15/14 2.0%Berkshire Hathaway Inc., 5.125%, 09/15/12 1.9%Dominion Resources Inc., 6.400%, 06/15/18 1.9%Merrill Lynch & Co Inc., 5.000%, 01/15/15 1.8%

returns for the Treasury market, withthe most interest-rate sensitive secu-rities performing worst: the 30-yearbond returned a loss of 1.7% for theperiod. A notable exception in thissector was U.S. TIPs (TreasuryInflation-Indexed securities, or Treas-ury inflation-protected securities). Thedecline in credit spreads resulted inmodestly positive returns for mostnon-government sectors of the bondmarket. TIPs, securities backed bycommercial real estate, and corporatebonds of financial institutions were thetop performers in the first quarter,posting gains of 2% or more. Within thecredit sector, higher yielding Baa-ratedbonds again strongly outperformed A-,Aa-, and Aaa-rated securities.

Fund Performance Analysis:

The fund’s first quarter return of 0.3%,net of all fees and expenses, exceededthe 0.28% return of the Barclays CapitalGovernment Credit Bond Index

(BCGC). The portfolio’s severalcontributors to out performanceincluded (1) Allocation: the underweight in U.S. Governments, particu-larly in U.S. Treasuries, the over weightin U.S. credits – notably financial insti-tutions and Baa-rated notes – and theinclusion of Mortgage-Backed Securitiesissued by Ginnie Mae and Fannie Mae;and (2) Security Selection: industrialnotes and TIPs. Of importance was thelower interest rate sensitivity of thefund, as measured by duration,achieved by deliberately under-weighting long-maturity debt – thearea of the yield curve more negativelyimpacted by rising rates in mostsectors. Negative factors were an underweight in non-corporate credits andsecurity selection in Utilities and in U.S.Agency debt.

Arrow Electronics 6.000% due 04-01-20(1.3% of net assets as of March 31, 2011)topped individual contributors, joinedby two financial institutions notes:

Bank of America Corp. 5.375% due 06-15-14 (2.0%) and Merrill Lynch &Co. 5.000% due 01-15-15 (1.8%), andU.S. Treasury Inflation Indexed Note2.500% due 07-15-16 (2.1%).

Securities contributing the least, inorder, were: JP Morgan 6.300% due 04-23-19 (1.4%), Fannie Mae 5.000%due 04-15-15 (2.1%), Kraft Foods5.375% due 02-10-20 (1.6%), DominionResources 6.400% due 06-15-18 (1.9%),and U.S. Treasury 5.375% due 02-15-31(1.1%).

Changes in Holdings:

There were no purchases during thequarter. The single sale was Fannie Mae5.375% due 11-15-11.

Sincerely,

Mark R. Freeman, CFAPortfolio ManagerApril 11, 2011

16

Nasdaq Symbols (Cusip) Table

GAMCO Westwood Funds Class AAA Class A Class B Class C Class I—————————————— —————— ———— ———— ———— ————Mighty MitesSM WEMMX WMMAX WMMBX WMMCX WEIMXSmallCap Equity WESCX WESAX 361439821 WWSCX WWSIXIncome WESRX WEIAX — WEICX WESIXEquity WESWX WEECX — WEQCX WEEIXBalanced WEBAX WEBCX WBCBX WBCCX WBBIXIntermediate Bond WEIBX WEAIX WEBIX WECIX WEIIX

Minimum Initial Investment

Each fund, other than the MightyMitesSM Fund, has a minimum initialinvestment requirement for regularaccounts of $1,000; there are no subse-quent investment minimums; no initialminimum is required for those estab-lishing an Automatic Investment Plan;and all of the GAMCO WestwoodFunds are available through financialintermediaries including the no trans-action fee programs at many majorbrokerage firms. The minimum initialinvestment for the Mighty MitesSM

Fund is $10,000 for all accounts. There are no subsequent investmentminimums. The minimum investmentfor each fund’s Class I Shares is$500,000, which shares are purchasedby institutions directly through Gabelli & Company, Inc., the Fund’sdistributor, or brokers that have

entered into selling agreements withthe distributor specifically with respectto Class I Shares.

www.tetonadv.com

Please visit us on the Internet. Ourhomepage at www.tetonadv.comcontains information about theGAMCO Westwood Funds, with linksto information about the GabelliMutual Funds, IRAs, 401(k)s, currentand historical quarterly reports, closingprices, and other current news. Wewelcome your comments and questionsvia e-mail at [email protected].

The Funds’ daily net asset values areavailable in the financial press and eachevening after 7:00 PM (Eastern Time) bycalling 800-WESTWOOD (800-937-8966).Please call us during the business day,between 8:00 AM – 7:00 PM (EasternTime), for further information. Thank

you for investing in the GAMCOWestwood Funds. We look forward toserving your investment objectives in theyears ahead.

e-delivery

We are pleased to offer electronicdelivery of fund documents. Directshareholders of our mutual funds cannow elect to receive their Annual,Semiannual, and Quarterly FundReports, Manager Commentaries, andProspectuses via e-delivery. For moreinformation or to sign up for e-delivery, please visit our website atwww.tetonadv.com. You may also signup for our e-mail alerts and receiveearly notice of quarterly report avail-ability, news events, media sightings,and mutual fund prices and per-formance via our website.

17

GAMCO WESTWOOD FUNDS(Unaudited)

Class AAA Shares Class A Shares——––—–——————––———————————————— ——––—–——————————————————————Average Annual Returns – March 31, 2011 (a) Average Annual Returns – March 31, 2011 (a)(b)(e)

Current CurrentExpense Expense Ratio after Ratio after

Gross Adviser Maximum Gross Adviser MaximumSince Expense Reimburse- Sales Since Expense Reimburse- Sales

1 Year 5 Year 10 Year Inception Ratio ments Charge 1 Year 5 Year 10 Year Inception Ratio ments Charge——––—–——————––———————————————— ——––—–——————————————————————Mighty MitesSM . . . . . 24.64% 9.20% 10.75% 12.28% 1.58% 1.58% None 19.37% 8.10% 10.08% 11.74% 1.83% 1.83% 4.00%SmallCap Equity . . . 32.39 6.71 5.73 7.75 1.99 1.50 None 26.84 5.60 5.13 7.31 2.24 1.75 4.00Income . . . . . . . . . . . . 14.32 1.23 8.99 7.15 3.19 2.00 None 9.57 0.18 8.30 6.65 3.44 2.25 4.00Equity . . . . . . . . . . . . . 11.89 2.27 3.69 9.97 1.54 1.54 None 7.13 1.19 3.00 9.56 1.79 1.79 4.00Balanced . . . . . . . . . . . 9.09 3.69 4.45 8.75 1.24 1.24 None 4.34 2.58 3.76 8.25 1.49 1.49 4.00Intermediate Bond . . 3.97 4.89 4.44 5.53 1.49 1.02 None (0.32) 3.95 3.92 5.26 1.59 1.12 4.00

Class B Shares Class C Shares——––—–——————––———————————————— ——––—–——————————————————————Average Annual Returns – March 31, 2011 (a)(c)(e) Average Annual Returns – March 31, 2011 (a)(d)(e)

Current CurrentExpense Expense Ratio after Ratio after

Gross Adviser Maximum Gross Adviser MaximumSince Expense Reimburse- Sales Since Expense Reimburse- Sales

1 Year 5 Year 10 Year Inception Ratio ments Charge 1 Year 5 Year 10 Year Inception Ratio ments Charge——––—–——————––———————————————— ——––—–——————————————————————Mighty MitesSM . . . . . 18.64% 8.09% 9.94% 11.64% 2.33% 2.33% 5.00% 22.67% 8.42% 9.97% 11.66% 2.33% 2.33% 1.00%SmallCap Equity . . . 26.45 5.61 4.96 7.19 2.74 2.25 5.00 30.48 5.94 4.92 7.16 2.74 2.25 1.00Income . . . . . . . . . . . . Class B Shares have been discontinued. 12.47 0.46 8.37 6.70 3.94 2.75 1.00Equity . . . . . . . . . . . . . Class B Shares have been discontinued. 10.06 1.52 2.93 9.54 2.29 2.29 1.00Balanced . . . . . . . . . . . 3.20 2.52 3.65 8.22 1.99 1.99 5.00 7.27 2.92 3.71 8.25 1.99 1.99 1.00Intermediate Bond . . (1.82) 3.79 3.63 5.12 2.24 1.77 5.00 2.18 4.19 3.70 5.15 2.24 1.77 1.00

Class I Shares——––—–——————––————————————————Average Annual Returns – March 31, 2011 (a)(e)

CurrentExpense Ratio after

Gross Adviser MaximumSince Expense Reimburse- Sales

1 Year 5 Year 10 Year Inception Ratio ments Charge——––—–——————––————————————————Mighty MitesSM . . . . . 24.89% 9.37% 10.84% 12.35% 1.33% 1.33% NoneSmallCap Equity . . . 32.74 6.88 5.81 7.81 1.74 1.25 NoneIncome . . . . . . . . . . . . 14.77 1.41 9.09 7.23 2.94 1.75 NoneEquity . . . . . . . . . . . . . 12.19 2.46 3.79 10.01 1.29 1.29 NoneBalanced . . . . . . . . . . . 9.30 3.84 4.53 8.79 0.99 0.99 NoneIntermediate Bond . . 4.22 5.05 4.52 5.57 1.24 0.77 None

(a) Returns represent past performance and do not guarantee future results. Total returns and average annual returns reflect changes in share priceand reinvestment of distributions and are net of expenses. Investment returns and the principal value of an investment will fluctuate. When sharesare redeemed, they may be worth more or less than their original cost. For the SmallCap Equity, Income, and Intermediate Bond Funds (and for theMighty MitesSM Fund through September 30, 2005), the Adviser reimbursed expenses to limit the expense ratio. Had such limitations not been inplace, returns would have been lower. The contractual expense limitations are in effect through January 31, 2011 and are renewable annually by theAdviser. Current performance may be lower or higher than the performance data presented. Visit www.tetonadv.com for performance information asof the most recent month end. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Funds beforeinvesting. The prospectus contains information about this and other matters and should be read carefully before investing.

(b) Includes the effect of the maximum 4.0% sales charge at the beginning of the period.(c) Assuming payment of the maximum contingent deferred sales charge (CDSC). The maximum CDSC for Class B Shares is 5% and is reduced to 0%

after six years.(d) Assuming payment of the maximum CDSC. A CDSC of 1% is imposed on redemptions made within one year of purchase.(e) The performance of the Class AAA Shares is used to calculate performance for the periods prior to the issuance of Class A Shares, Class B Shares, Class

C Shares, and Class I Shares. The performance for the Class B Shares and Class C Shares would have been lower due to the additional expensesassociated with these classes of shares. The performance for the Class I Shares would have been higher due to the lower expenses associated with thisclass of shares. The inception dates for the Class AAA Shares and the initial issuance dates for the Class A Shares, Class B Shares, Class C Shares, andClass I Shares after which shares remained continuously outstanding are listed below.

Class AAA Shares Class A Shares Class B Shares Class C Shares Class I Shares——————————— ————————— ————————— ————————— —————————Mighty MitesSM . . . . . . . . . . 05/11/98 11/26/01 06/06/01 08/03/01 01/11/08SmallCap Equity . . . . . . . . . 04/15/97 11/26/01 03/27/01 11/26/01 01/11/08Income . . . . . . . . . . . . . . . . . 09/30/97 05/09/01 11/26/01 11/26/01 01/11/08Equity . . . . . . . . . . . . . . . . . . 01/02/87 01/28/94 03/27/01 02/13/01 01/11/08Balanced . . . . . . . . . . . . . . . . 10/01/91 04/06/93 03/27/01 09/25/01 01/11/08Intermediate Bond . . . . . . . 10/01/91 07/26/01 03/27/01 10/22/01 01/11/08

GAMCO Westwood Funds and Your Personal Privacy

Who are we?