Embed Size (px)

Citation preview

PC Makers

Presenters:Oana ConstantinKevin RidingerAdam Svoboda

Cindy Xia

Agenda

• Industry Analysis

• Company Analysis• Dell, Inc.

• Hewlett-Packard Development Company, L.P.

• Gateway, Inc.

Industry Definition

• The personal computer industry consists mostly of assembling and selling:

• Desktops & Notebooks• Servers & Mainframes• Workstations & Thin Clients• Supercomputers• Mass Storage Devices• Network Equipment• Peripherals• Handheld Devices

Nature of Industry

Motherboard

& CPUPower

Source & Cables

Floppy, CD/DVD Drive

Case

Extra Peripherals

Hard-drive

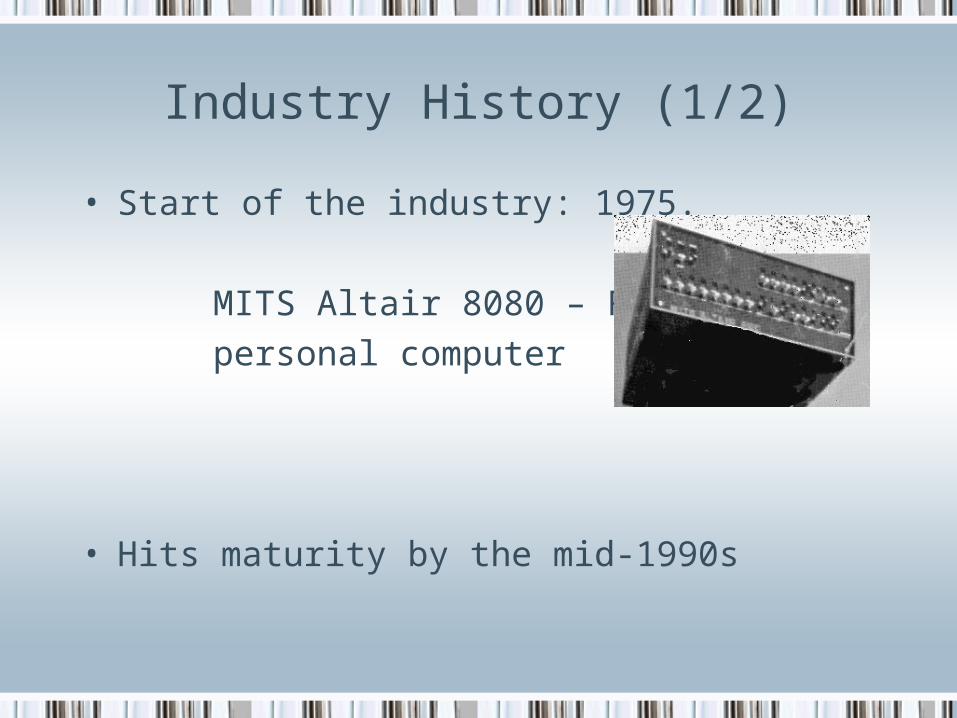

Industry History (1/2)

• Start of the industry: 1975.

MITS Altair 8080 – First

personal computer

• Hits maturity by the mid-1990s

Industry History (2/2)

• New developments beginning with late-1990s:

• Rapid decline in PC prices Consequently decrease in gross profit margins

• Acceleration in the product cycle Faster depreciation of components and finished good inventories

• Success of direct-sales/build-to-order strategy Remodeling of the value chain

• Mergers and Acquisitions HP/Compaq, Lenovo/IBM

1995 Worldwide Market Share

10%8%

3%4%

8%

4%

7%3%3% 3%

47%

CompaqIBMDellHPAppleNECPackard-BellFujitsu/ICLAcerToshibaOther

2004 Worldwide Market Share

16%

6%

18%

1%4%

55%

HP/CompaqIBMDellFujitsu/SiemensAcerOther

PC Market Growth

US and Worldwide PC Market Growth

1985 1990 1995 2000 2003 2005 2010

U.S. PC Unit Sales (#M) 6.6 9.5 21.4 46.0 48.3 56.6 66.7

U.S. PC Dollar Dales ($B) 17.2 24.5 56.8 86.9 78.1 84.5 86.1

Worldwide PC Unit Sales (#M) 11 24.2 70.1 130 149 181 249

Worldwide PC Dollar Sales ($B) 29.5 71.3 155 247 243 270 302

PC Unit Sales by Region (millions)

PC Market Segments (Million Units)

020406080

100120140160

1990 1995 2000 2003 2005 2010

Servers (U.S.) Servers (Worldwide)Desktops (U.S.) Desktops (Worldwide)Mobile PCs (U.S.) Mobile PCs (Worldwide)

PC Market Segment Growth

Worldwide PC Market Segment Growth for Desktops, Mobile PCs, and Servers

1990 1995 2000 2003 2005 2010

Desktops 89.9% 81% 74% 68% 63% 55%

Mobile PCs 9.9% 17% 22% 27% 32% 39%

Servers 0.02% 2% 4% 5% 5% 6%

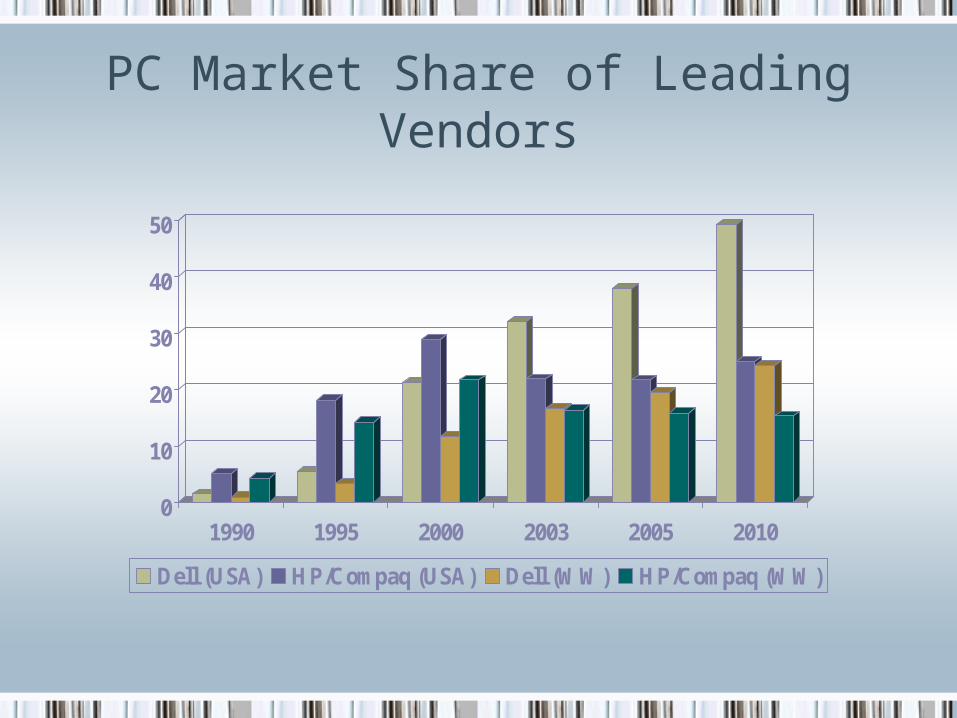

PC Market Share of Leading Vendors

0

10

20

30

40

50

1990 1995 2000 2003 2005 2010

Dell (USA) HP/Compaq (USA) Dell (WW) HP/Compaq (WW)

Business Models

• Big Box

• Direct

• White Box

Big Box Model

• Traditional approach, through “brick and mortar” retailers and own stores

• Distributors purchase assembled, ready-to-use computers

• Allows consumers to touch and feel the product

• Higher cost due to high inventories, longer distribution channel

• Profit margin eroded

Direct Model

• Take customized orders directly from end consumers

• Assemble systems as orders come in

• Ship the product direct to customers

• More efficient, JIT inventory system

• Lower costs due both to inventory savings and distribution by-passing

• Savings are passed to customers

White Box Model

• Combination of Big Box and Direct Sales Strategies

• Own distribution facilities

• Allows consumers to customize their products while giving them a phisical location to purchase

• Highly fragmented, estimated to more than 500 unbranded PC makers

• Often sell directly to small businesses looking for a significant price break rather than a big brand machine.

PC Industry Value Chain, 2004

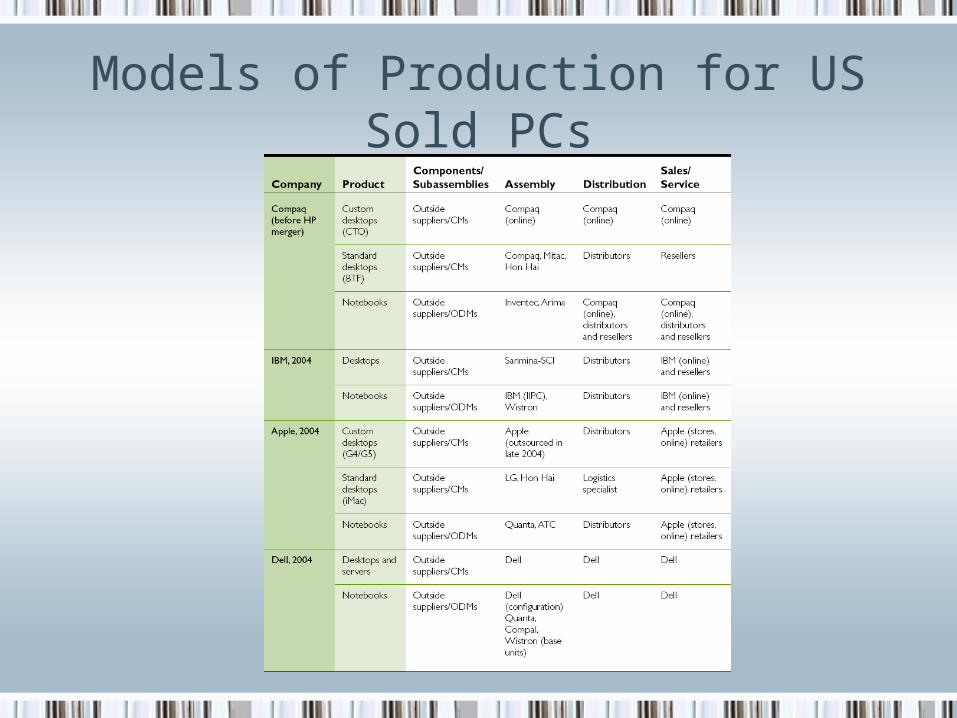

Models of Production for US Sold PCs

Industry Performance

• NASDAQ Computer Index (IXCO)

Includes 603 securities from categories:

Computer HardwareComputer SoftwareSemiconductorsComputer Services

Industry Performance: 1 Year Nasdaq Computer Index (IXCO)

Industry Performance: 10 Year Nasdaq Computer Index (IXCO)

Industry Key Measures

• Profit Margin

• Sales Growth

• Market Share Growth

• Valuation Ratios

• Business Capital Spending

Industry Statistics

Valuation Ratios Financial Strength

P/E 22.96 Quick Ratio 1.34

P/Sales 1.85 Current Ratio 1.61

P/Book 6.83 LT Debt/Equity 0.31

Total Debt/Equity 0.38

Profitability Management Effectiveness

Gross Margin 31.33% ROI 19.28%

Operating Margin 9.22% ROA 9.94%

Net Profit Margin 10.68% ROE 31.35%

Recent Developments

• Lenovo’s buyout of IBM’s PC unit.• Propelled the company on 3rd place in terms of worldwide market

share (7.6%) for the 2nd quarter of 2005

• Apple switches to Intel processors

• Lenovo investing $84m in new R&D center in North Carolina

• Dell lowering earnings forecast, plus a $300m charge to repair faulty circuit boards

• Hewlett-Packard has hired Dell’s CIO, Randy Mott

• Soaring Apple stock price due to strong iPod sales

Apple – One Year Stock Price

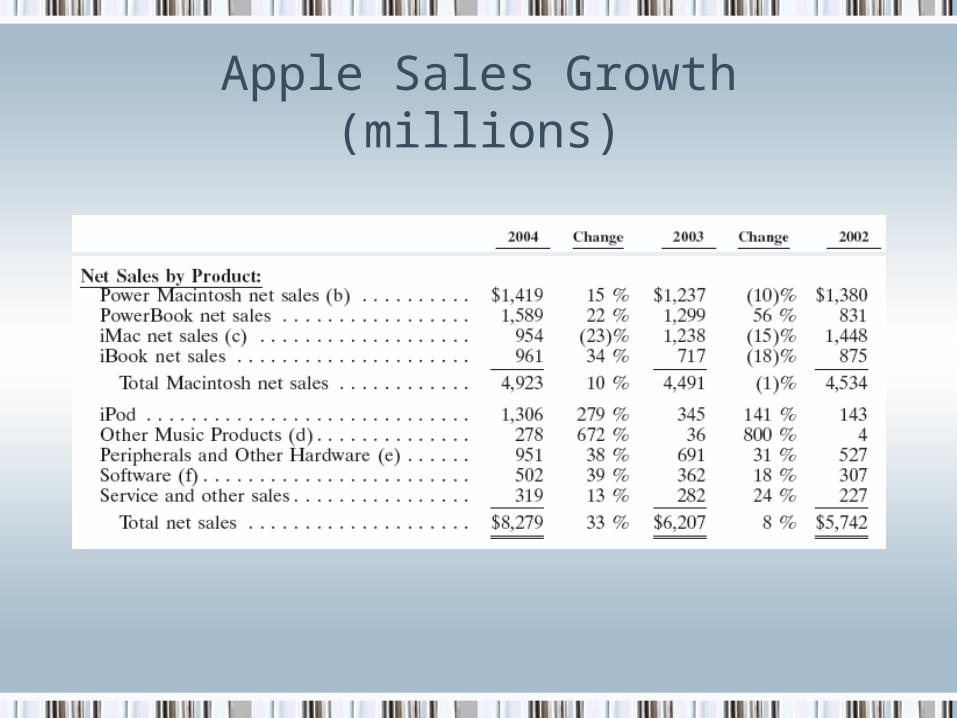

Apple Sales Growth (millions)

Future Trends – Industry

• Pricing competition will become more aggressive Exit by some smaller players Further consolidation through mergers and acquisitions

• PC shipments expected to grow at 6% per year, but revenues will remain almost flat Forces players to further innovate and expand product offering

such as media center computers and tablet PCs

• Faster growth in Europe and Asia segments Build strong marketing strategy targeting these segments to

capture market share

Future Trends – Technology

• Continued shift from desktops to notebooks

• Shift towards wireless devices

• Adaptive hardware technology to support PC virtualization

• Continuous movement toward miniaturization and digital enhancement of portable music players and phones

Dell Inc.

Presented by: Kevin Ridinger

Fast Facts about Dell Inc. Trades on NASDAQ, symbol: DELL One share bought for $8.50 at IPO in 1988 would be worth

$3,800 today. Employs over 61,400 people Revenues totaled over $52.8 billion for the last four quarters Market Position: #1 in U.S., #3 in Japan, #2 in Europe 7 Manufacturing centres spanning the globe, located in United

States(3), Brazil, Europe (Ireland), Malaysia, and China. Nearly one out of every five standards-based computer system

sold in the world today is a Dell.

Dell Timeline

1984: Michael Dell founds Dell Computer Corporation

1987: International expansion begins with opening of subsidiary in United Kingdom

1988: Dell conducts initial public offering of company stock (3.5 million shares at $8.5 each)

1993: Enters into Asia-Pacific region with subsidiaries in Australia and Japan

1996: Company begins major push into the server market

2000: Company sales via Internet reach $50 million per day

2001: For the first time, Dell ranks No. 1 in global market share

2004: Kevin Rollins becomes Dell's next chief executive officer. Michael Dell moves to Chairman of the Board

Management Michael Dell – Chairman of the Board (founded company

in 1984) Kevin B Rollins – President and CEO since July 2004

(prior he was president and COO of Dell Americas – joined in 1994)

William J. Amelio – Sr. VP Asia-Pacific/Japan (since 2001)

Paul D. Bell – Sr. VP Europe, Middle East & Africa (since 1996)

Joseph A. Marengi, Sr. VP, Americas (since 1996, came from Novell)

Many of Dell’s current management came to the company around 1996-97. Based on biographical evidence, many were lured from other high-tech companies, including Novell, HP, Apple, Sun and Texas Instruments.

Strategy Uses the direct business model (reliant on very efficient

manufacturing and supply chain management) Helps turnover inventory every four days (on average) Helps ensure the latest technology is offered without

keeping outdated products on the ‘shelves’. Provides customers with single point of accountability

Standards-based (do not support proprietary technologies)

Collaboration with strategic partners Positively affects both input prices and product leadership

Adding a significant layer of innovation (value-added processes)

Dell’s strategic corporate initiatives for the future

Continued Global Growth Growth outside of U.S. in largest countries at 30%

Product Leadership Ex. integrated solutions to businesses (servers,

desktops, and now printing) Enhancing the Customer Experience

Dell value-added services (anti-spyware and virus software and support)

Developing a Winning Culture: Essential for integrating Dell’s subsidiaries in over 47

countries

Company Structure

Sources of Revenue Dell designs, develops, manufactures, markets,

sells, and supports the follow products:

•Notebook Computers•Desktop Computers•Printing and Imaging•Software and Peripherals

•Servers•Storage•Workstations•Networking

•Dell also offers a variety of services from development and support to professional and fully managed solutions.

Dell also has a financial services division which is a joint venture between Dell and CIT group. It organizes financing alternatives for clients

Sales Mix (by Region & Product line)

Product-specific

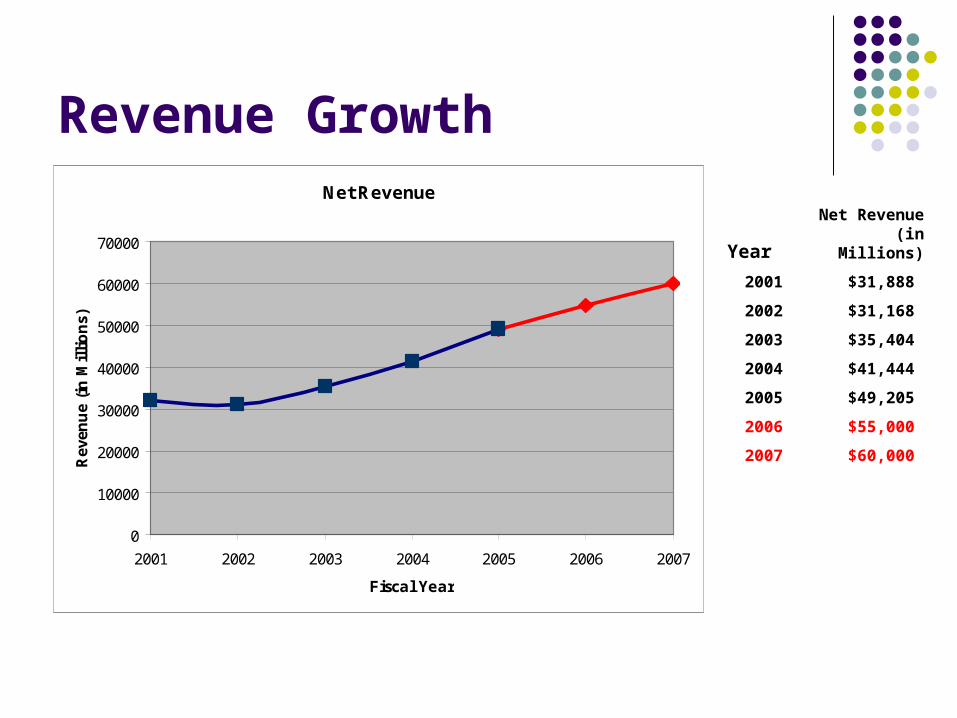

Revenue Growth

Revenue Growth

Year Net Revenue (in

Millions)

2001 $31,888

2002 $31,168

2003 $35,404

2004 $41,444

2005 $49,205

2006 $55,000

2007 $60,000

Net Revenue

0

10000

20000

30000

40000

50000

60000

70000

2001 2002 2003 2004 2005 2006 2007

Fiscal Year

Rev

enu

e (i

n M

illi

on

s)

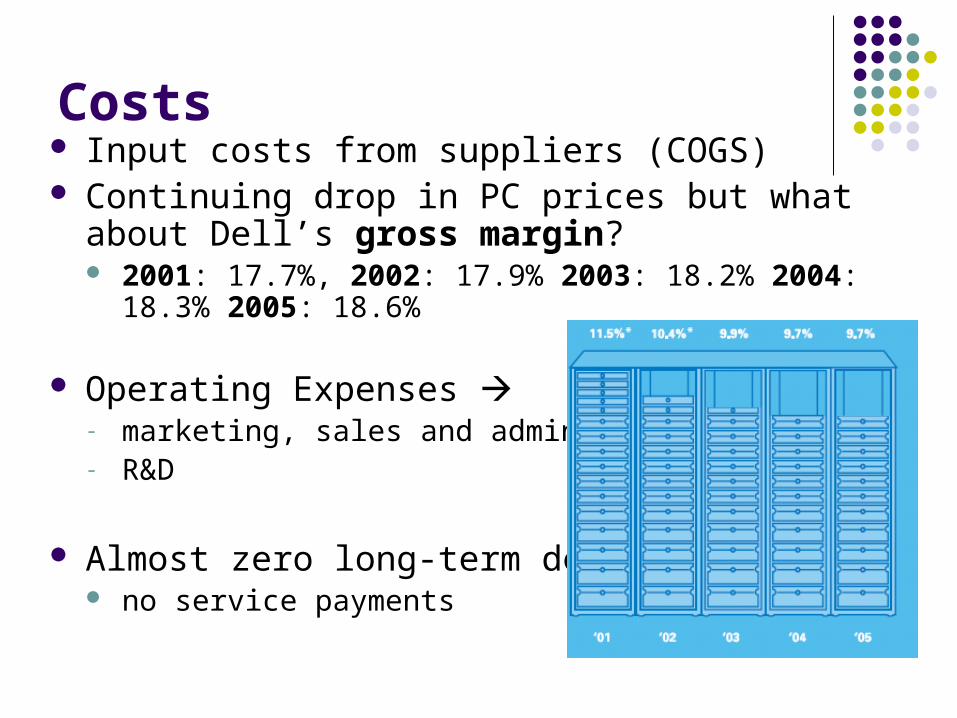

Costs Input costs from suppliers (COGS) Continuing drop in PC prices but what about Dell’s

gross margin? 2001: 17.7%, 2002: 17.9% 2003: 18.2% 2004: 18.3%

2005: 18.6%

Operating Expenses - marketing, sales and admin.- R&D

Almost zero long-term debt no service payments

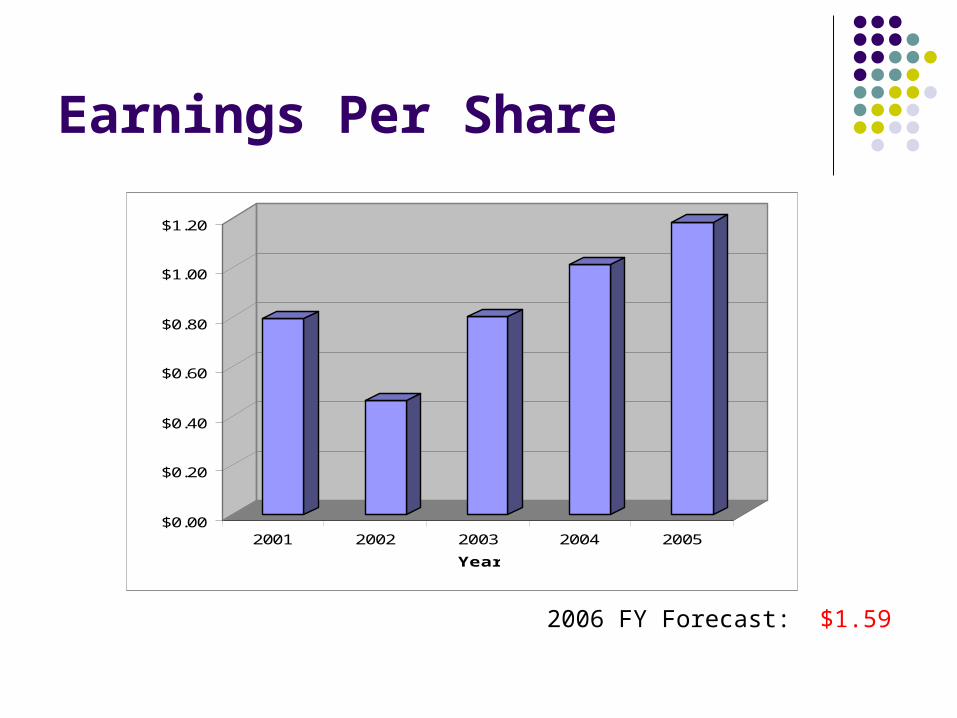

Earnings Per Share

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

2001 2002 2003 2004 2005

Year

2006 FY Forecast: $1.59

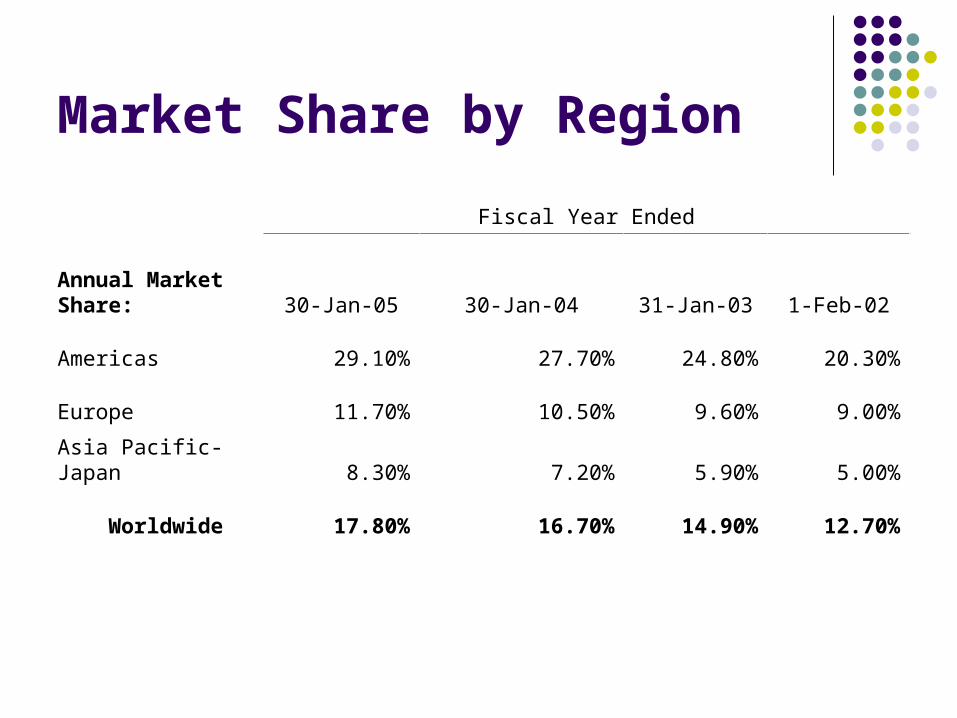

Market Share by Region

Fiscal Year Ended

Annual Market Share: 30-Jan-05 30-Jan-04 31-Jan-03 1-Feb-02

Americas 29.10% 27.70% 24.80% 20.30%

Europe 11.70% 10.50% 9.60% 9.00%

Asia Pacific-Japan 8.30% 7.20% 5.90% 5.00%

Worldwide 17.80% 16.70% 14.90% 12.70%

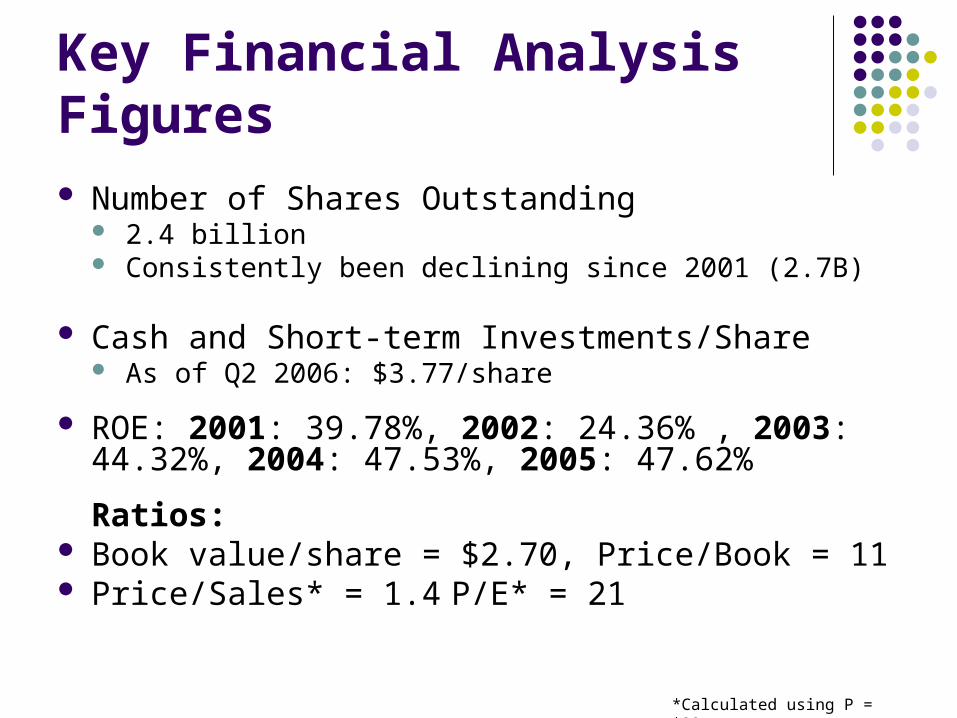

Key Financial Analysis Figures Number of Shares Outstanding

2.4 billion Consistently been declining since 2001 (2.7B)

Cash and Short-term Investments/Share As of Q2 2006: $3.77/share

ROE: 2001: 39.78%, 2002: 24.36% , 2003: 44.32%, 2004: 47.53%, 2005: 47.62%

Ratios: Book value/share = $2.70, Price/Book = 11 Price/Sales* = 1.4 P/E* = 21

*Calculated using P = $29

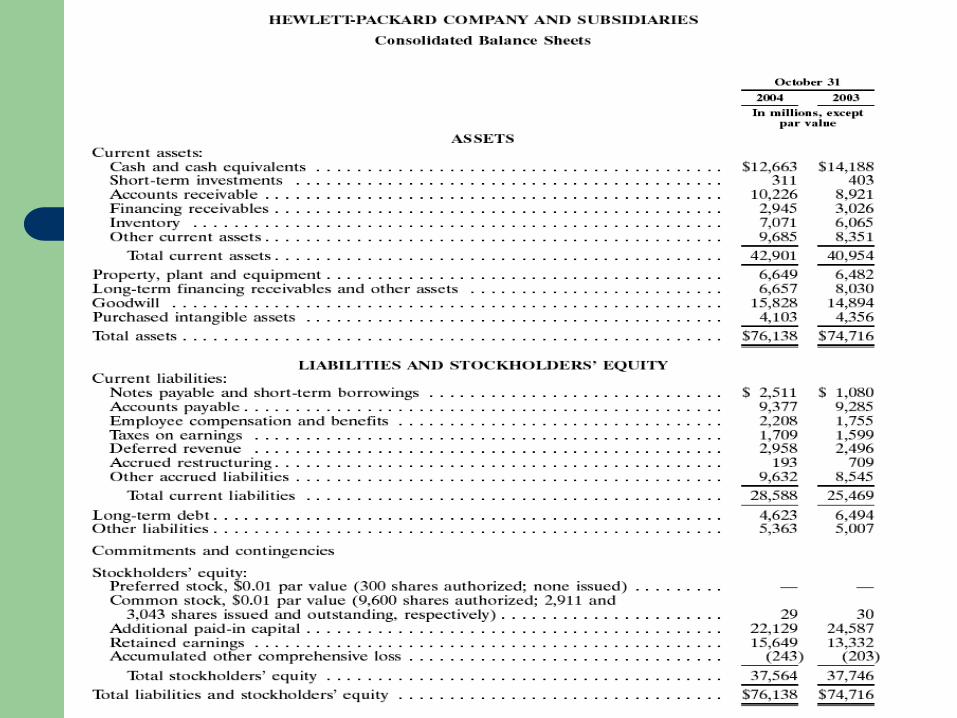

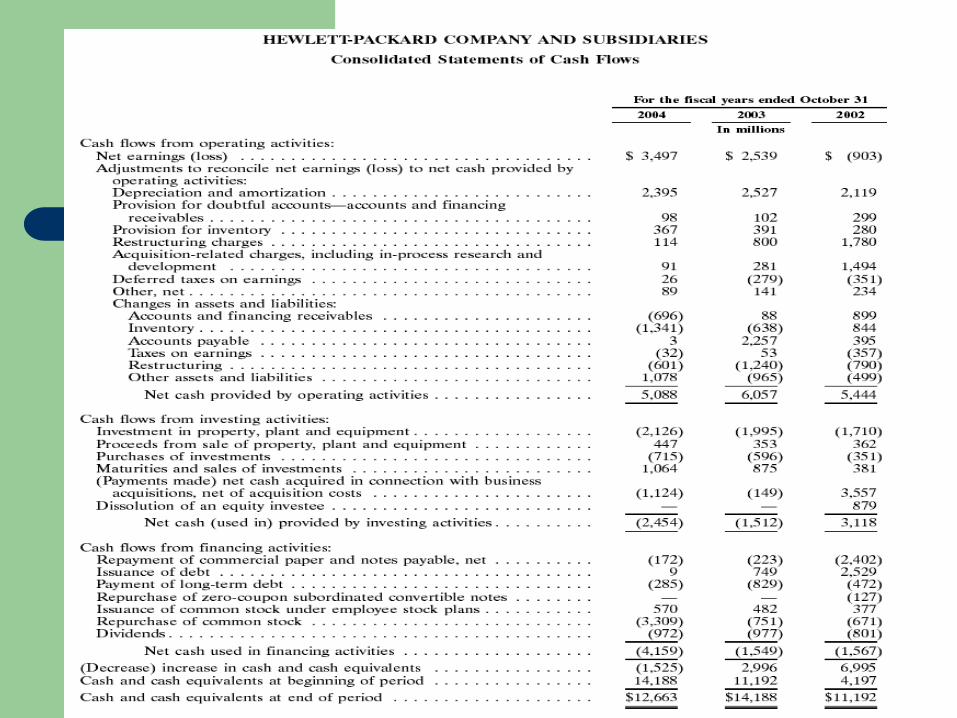

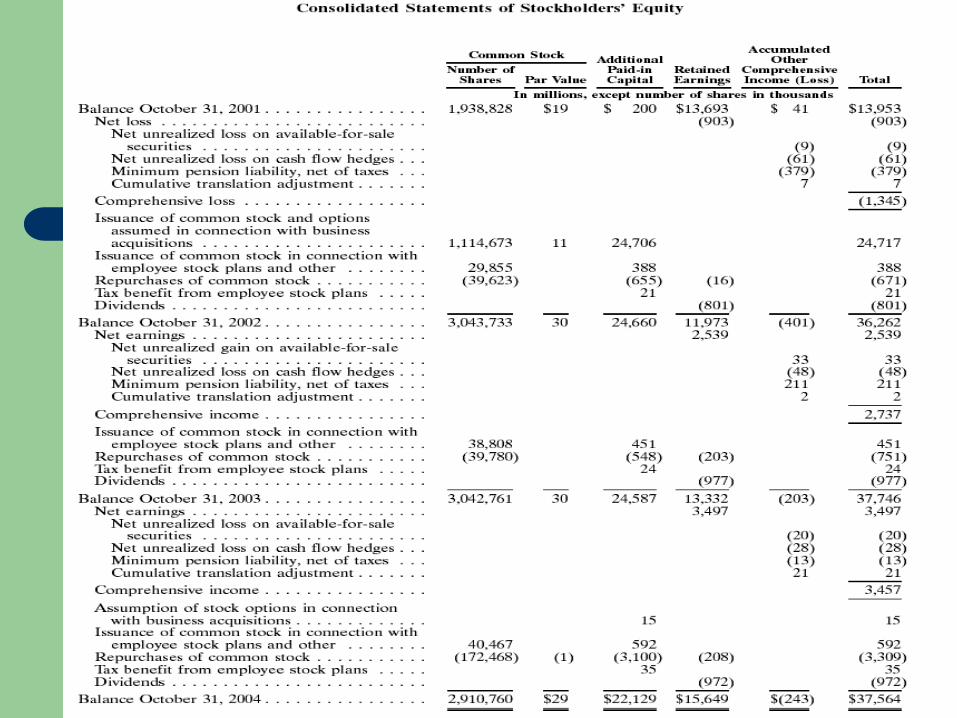

Financial Statements

Balance Sheet Income Statement Cash flow Statement

Stock Options

Average exercise price has steadily been increasing ($28.99 in 2005, compared to $8.78 in 2001)

As of Jan 28, 2005

As of Jan 31, 2003

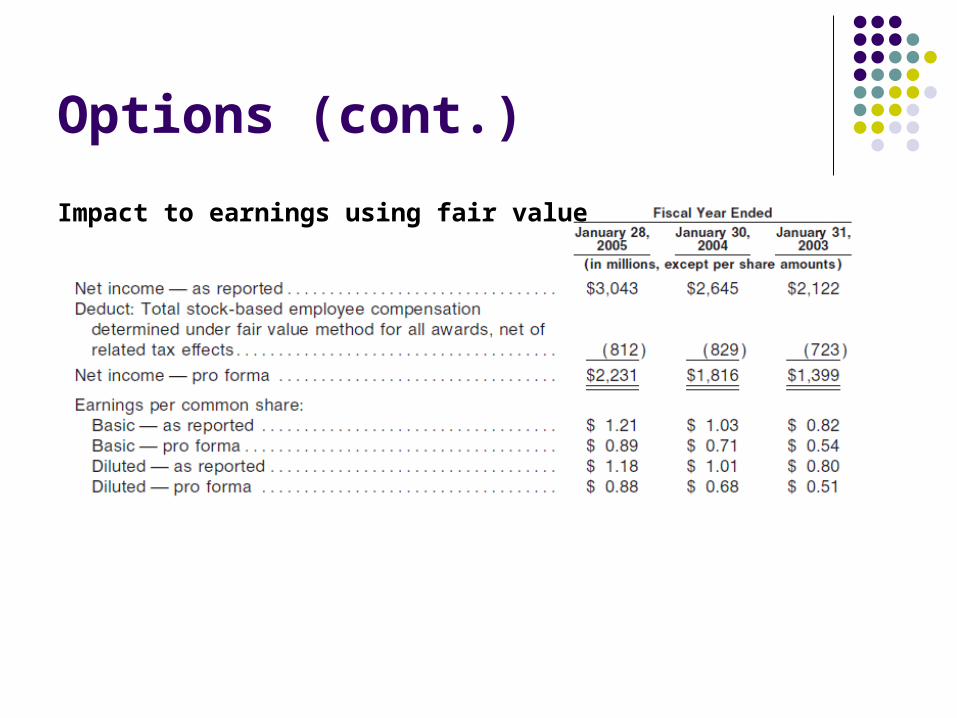

Options (cont.)

Impact to earnings using fair value

One Year Stock Price

10 Year Trading History

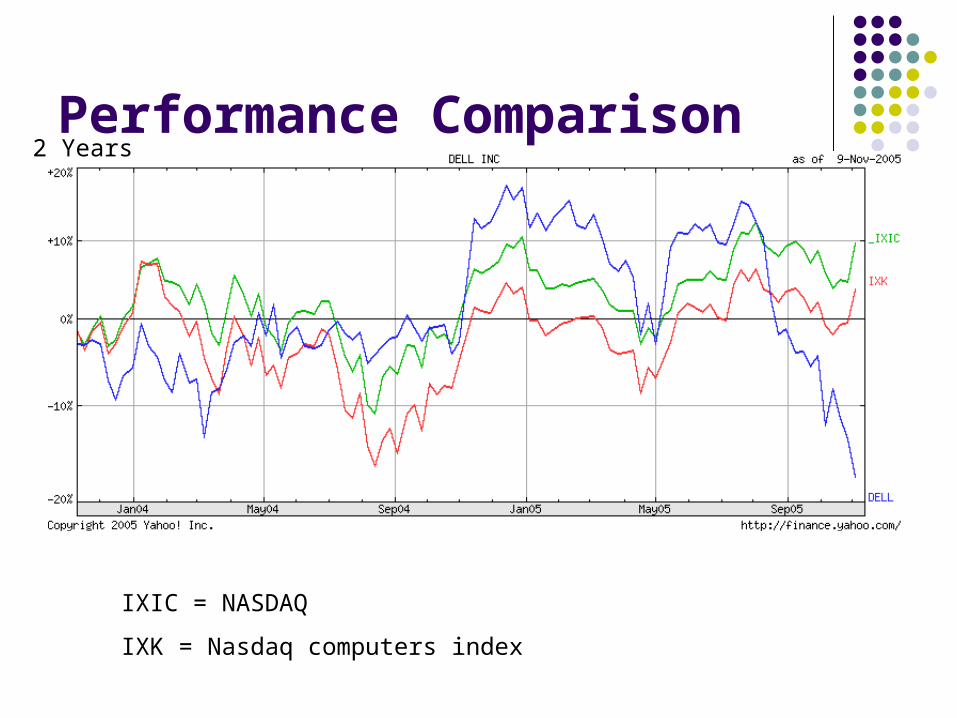

Performance Comparison

IXIC = NASDAQ

IXK = Nasdaq computers index

2 Years

Model Valuation

With the residual income model: Dell’s price should be between $15 and $25

depending on the assumptions used.

Since Dell does not pay a dividend we cannot use dividend models to calculate a price.

The FCFE model also does not work very well with the stocks that are in Dell’s industry Produces a price of $6 if the same k from the RI

model is used.

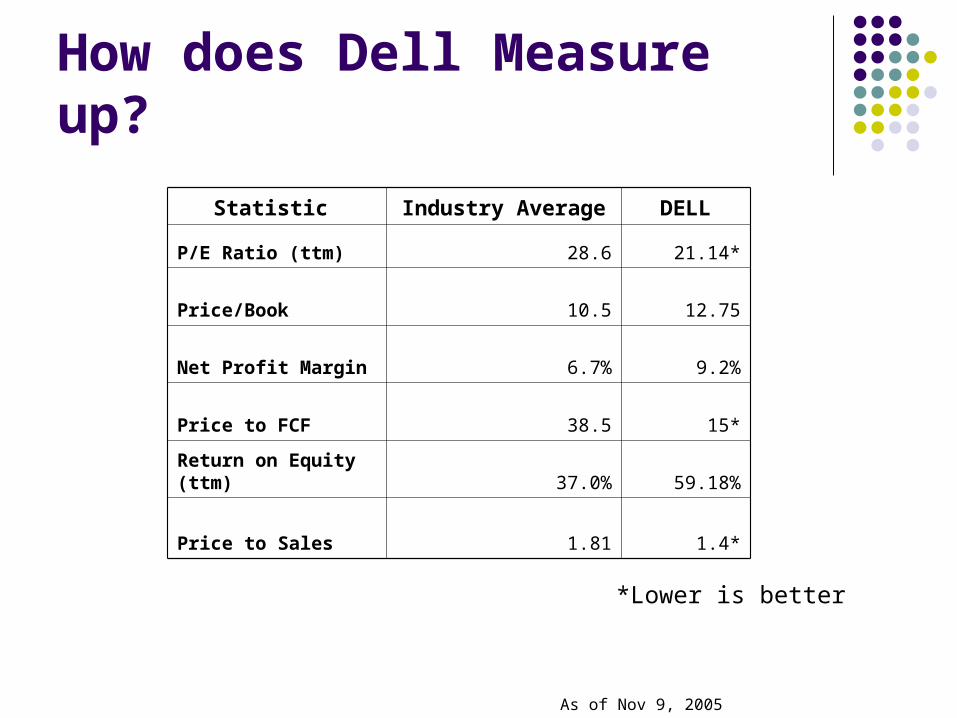

How does Dell Measure up?

Statistic Industry Average DELL

P/E Ratio (ttm) 28.6 21.14*

Price/Book 10.5 12.75

Net Profit Margin 6.7% 9.2%

Price to FCF 38.5 15*

Return on Equity (ttm) 37.0% 59.18%

Price to Sales 1.81 1.4*

As of Nov 9, 2005

*Lower is better

Value Drivers (cont.) Profits

Company has turned a profit year after year. Continued expense reduction and increasing

margins will help contribute to higher profits. Especially as international centres recently expanded

into mature. Share buy back and continued reduction in

gratuitous option issuance to execs Has a growing and already significant international

presence through diversifying it spreads risk of national economic/demand slowdowns

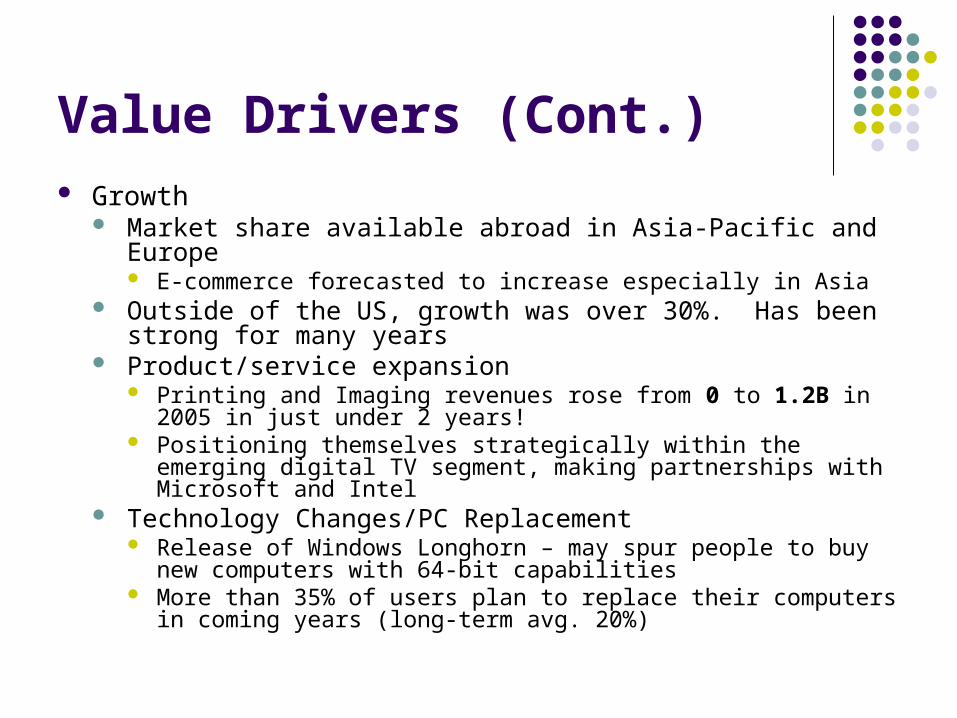

Value Drivers (Cont.) Growth

Market share available abroad in Asia-Pacific and Europe E-commerce forecasted to increase especially in Asia

Outside of the US, growth was over 30%. Has been strong for many years

Product/service expansion Printing and Imaging revenues rose from 0 to 1.2B in 2005 in just

under 2 years! Positioning themselves strategically within the emerging digital TV

segment, making partnerships with Microsoft and Intel Technology Changes/PC Replacement

Release of Windows Longhorn – may spur people to buy new computers with 64-bit capabilities

More than 35% of users plan to replace their computers in coming years (long-term avg. 20%)

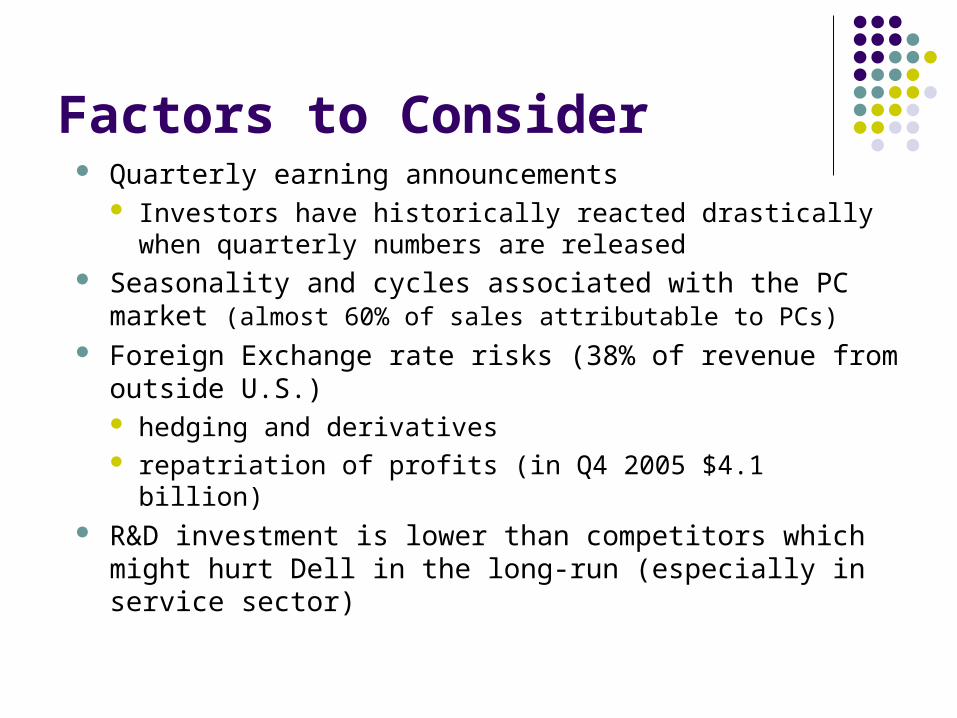

Factors to Consider Quarterly earning announcements

Investors have historically reacted drastically when quarterly numbers are released

Seasonality and cycles associated with the PC market (almost 60% of sales attributable to PCs)

Foreign Exchange rate risks (38% of revenue from outside U.S.) hedging and derivatives repatriation of profits (in Q4 2005 $4.1 billion)

R&D investment is lower than competitors which might hurt Dell in the long-run (especially in service sector)

1.951.65High Estimate

1.801.55Low Estimate

3233No. of Analysts

1.871.59Avg. Estimate

Next Year Jan-07

Current Year Jan-06

Earnings Est

Recommendation

Analysts:

Current Month Last Month Two Months AgoThree Months

Ago

Strong Buy 8 9 9 8

Buy 11 13 12 15

Hold 12 9 9 7

Sell 1 0 0 0

Strong Sell 0 0 0 0

• Recent Price Depression due to one quarter’s earnings forecast is a buying opportunity.

•Attractive price vs. Competitors

• The company continues to make enormous amounts of money

• Limited-Downside potential for price (Share buyback)

•Expansion efforts in Asia-Pacific and Europe continue to show value

•Good management (experienced) have led Dell on a path of continued growth

•Value Drivers (growth & profits) are strong

Adam J Svoboda

Background

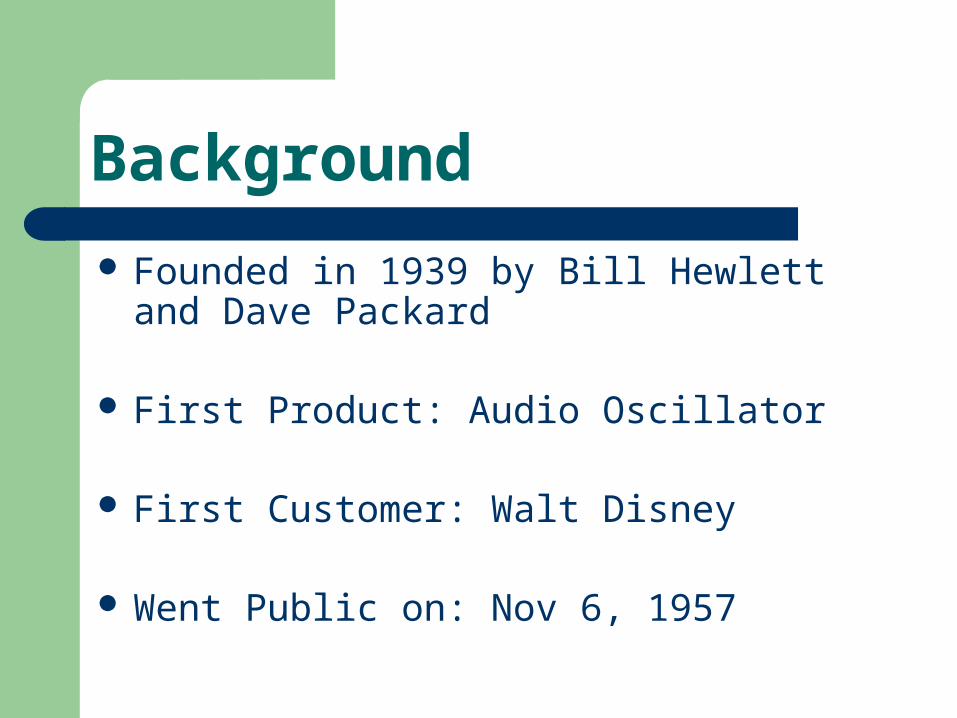

Founded in 1939 by Bill Hewlett and Dave Packard

First Product: Audio Oscillator

First Customer: Walt Disney

Went Public on: Nov 6, 1957

Management/Executives Mark Hurd - 2005 - Chief Executive Officer and

President. President and CEO of NCR since 2003 (25 years of experience)

Gilles Bouchard - Exec Vice President PSG (in Hp since 1989)

Vyomesh Joshi - Exec Vice President IPG since 1980

Randall D. Mott - Exec Vice President since 2005, with dell for 3 years

IN GENERAL: MOSTLY NEW BUT EXPERIENCED

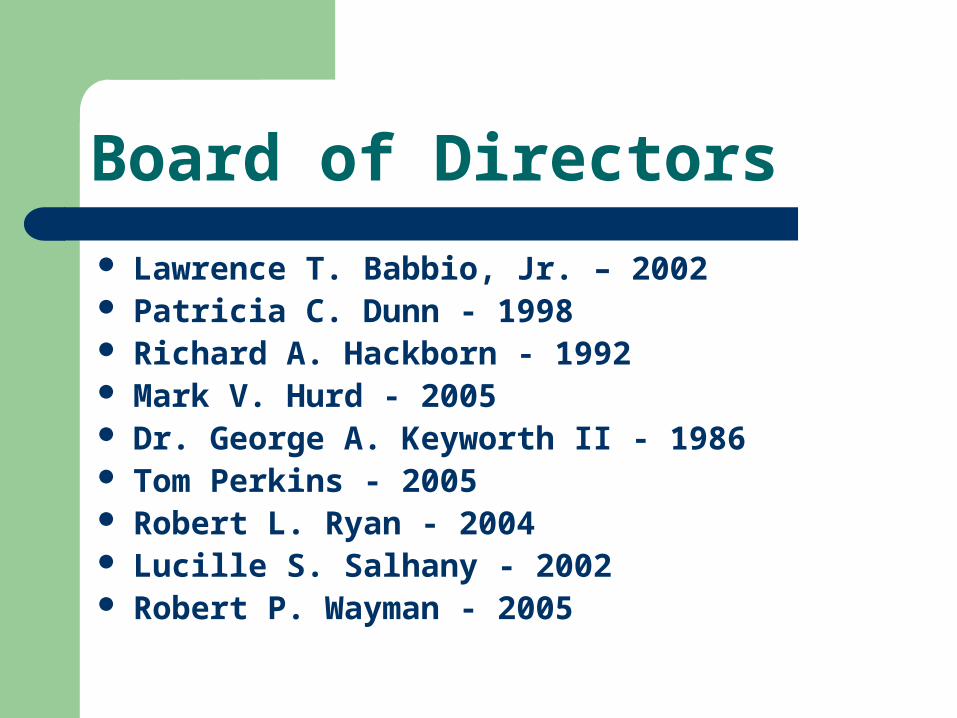

Board of Directors

Lawrence T. Babbio, Jr. – 2002 Patricia C. Dunn - 1998 Richard A. Hackborn - 1992 Mark V. Hurd - 2005 Dr. George A. Keyworth II - 1986 Tom Perkins - 2005 Robert L. Ryan - 2004 Lucille S. Salhany - 2002 Robert P. Wayman - 2005

Current Events

HP takeover of Compaq - $25bn

New CEO – Mark Hurd

2005 – Profits fall

Compaq acquisition complete

Several other acquisitions have taken place

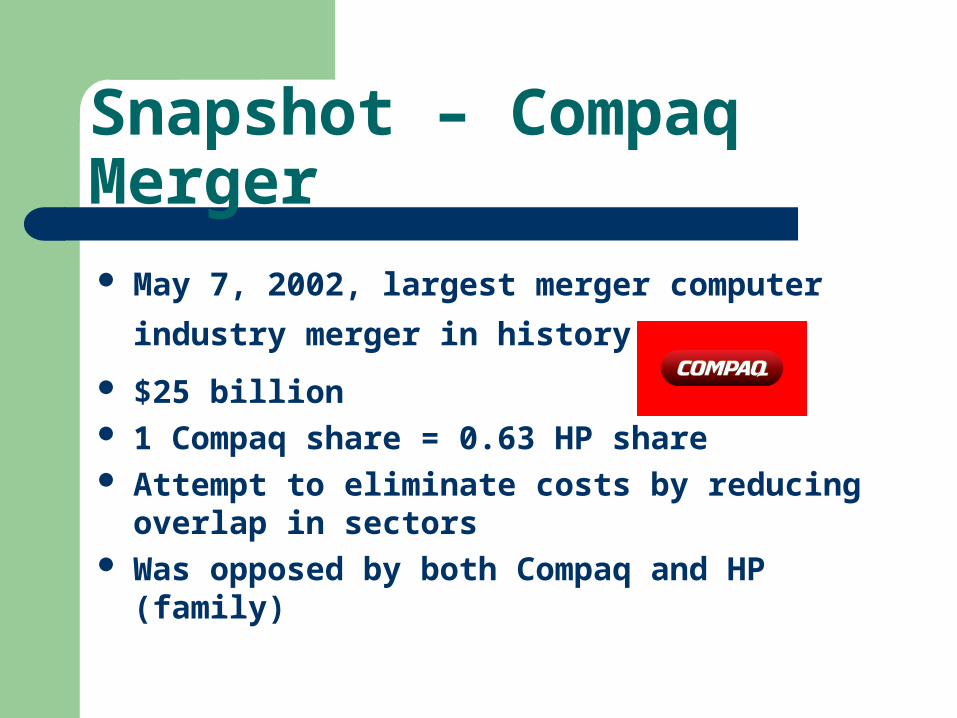

Snapshot – Compaq Merger May 7, 2002, largest merger computer industry

merger in history

$25 billion 1 Compaq share = 0.63 HP share Attempt to eliminate costs by reducing overlap

in sectors Was opposed by both Compaq and HP (family)

Corporate Objectives

Customer loyalty Profit Market leadership Growth Employees Leaders Global citizenship

Products and Services

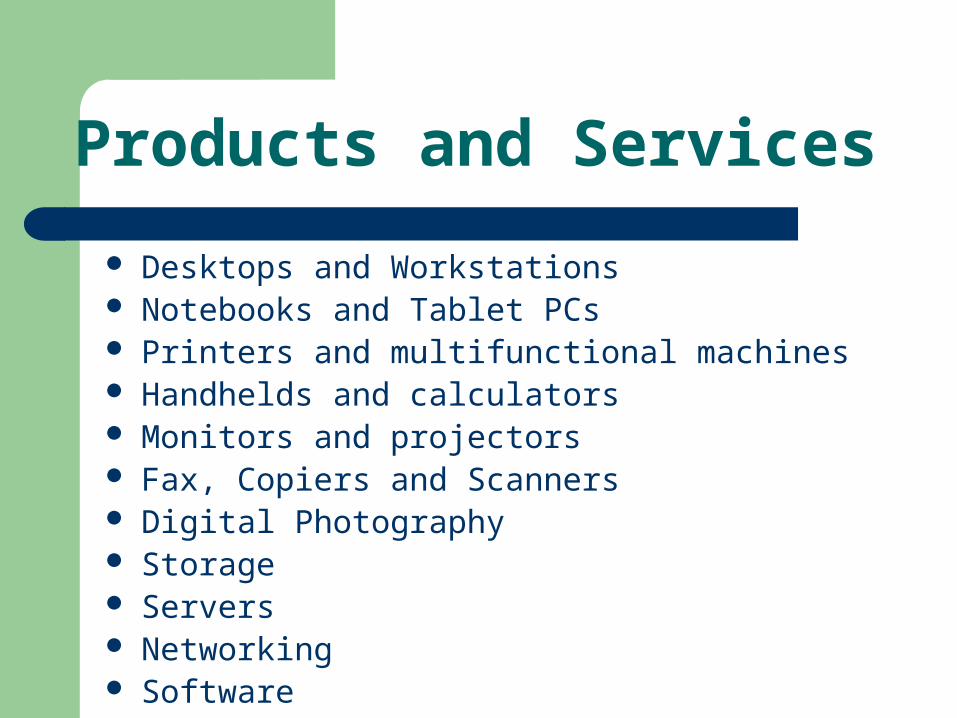

Desktops and Workstations Notebooks and Tablet PCs Printers and multifunctional machines Handhelds and calculators Monitors and projectors Fax, Copiers and Scanners Digital Photography Storage Servers Networking Software

Market Position

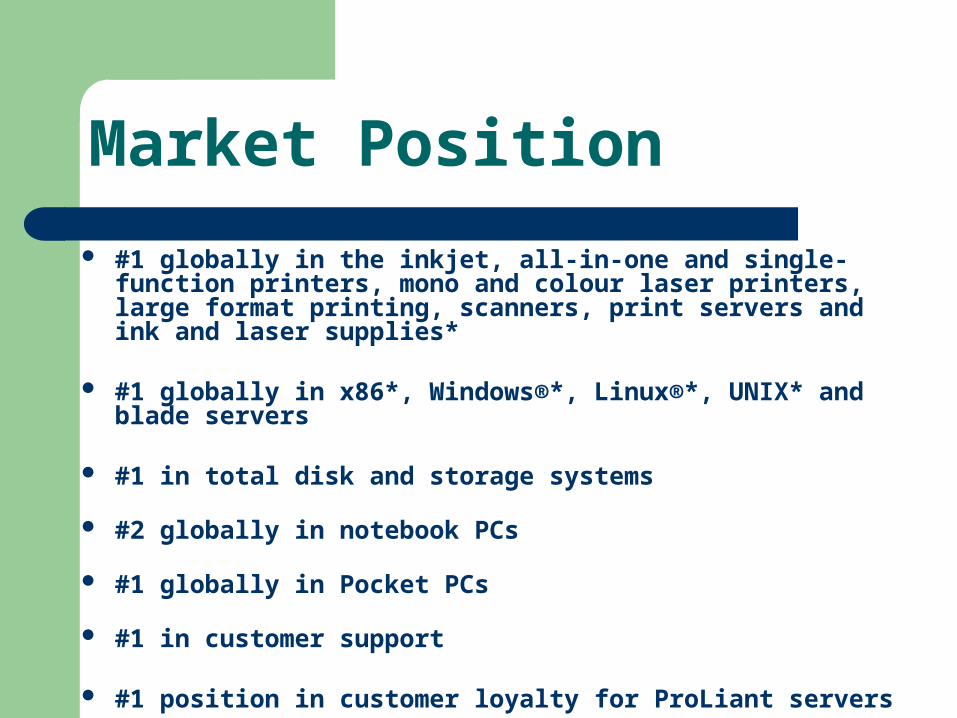

#1 globally in the inkjet, all-in-one and single-function printers, mono and colour laser printers, large format printing, scanners, print servers and ink and laser supplies*

#1 globally in x86*, Windows®*, Linux®*, UNIX* and blade servers

#1 in total disk and storage systems

#2 globally in notebook PCs

#1 globally in Pocket PCs

#1 in customer support

#1 position in customer loyalty for ProLiant servers

HP Business Sectors

(PSG) Personal Systems Group (IPG) Imaging and Printing Group (ESS) Enterprise Storage and Servers (HPFS) HP Financial Services (HPS) HP Services Software Corporate Investments

(PSG) Personal Systems Group Commercial and consumer PC’s

Workstations, handheld computer devices and digital entertainment systems

Calculators

Software services for commercial and consumer markets

(IPG) Imaging and Printing Group

Printing, imaging and publishing devices

Both for home users and businesses

(ESS) Enterprise Storage and Servers

Storage and server products

Low and high end scalable servers e.g. Superdome

Enterprise arrays, storage area networks

(HPFS) HP Financial Services Leasing, financing, utility and asset recovery

services

Specialized financial services for small/medium businesses and educational and governmental entities.

(HPS) HP Services

Technology and consulting

Integration services

Managed services

Software

Software solutions including support

Infrastructure, operations and applications management

Corporate Investments

Labs and ‘business incubation’ projects.

Revenue is from selling network infrastructure products: enhancing computer and enterprise solutions.

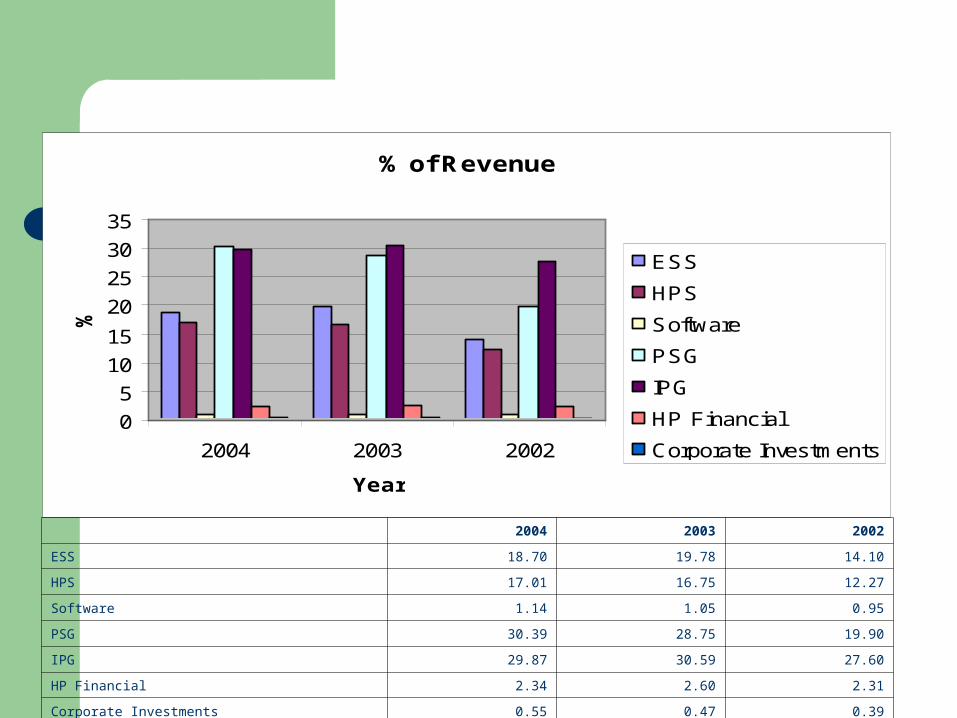

% Revenue by Sector% of Revenue

0

5

10

15

20

25

30

35

2004 2003 2002

Year

%

ESS

HPS

Software

PSG

IPG

HP Financial

Corporate Investments

2004 2003 2002

ESS 18.70 19.78 14.10

HPS 17.01 16.75 12.27

Software 1.14 1.05 0.95

PSG 30.39 28.75 19.90

IPG 29.87 30.59 27.60

HP Financial 2.34 2.60 2.31

Corporate Investments 0.55 0.47 0.39

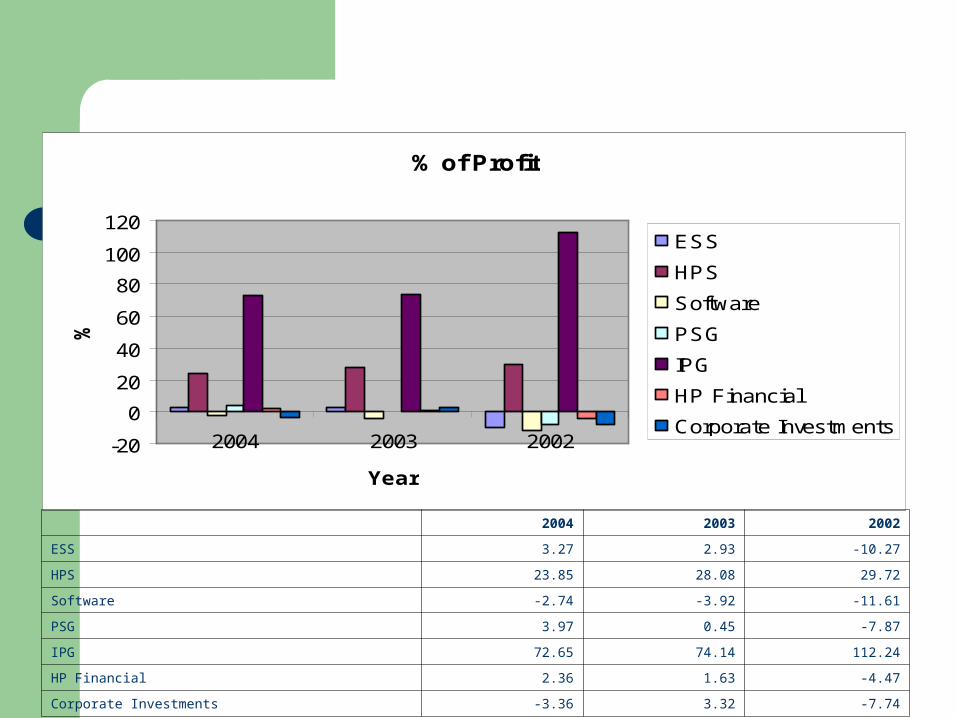

% Profit by Sector% of Profit

-20

0

20

40

60

80

100

120

2004 2003 2002

Year

%

ESS

HPS

Software

PSG

IPG

HP Financial

Corporate Investments

2004 2003 2002

ESS 3.27 2.93 -10.27

HPS 23.85 28.08 29.72

Software -2.74 -3.92 -11.61

PSG 3.97 0.45 -7.87

IPG 72.65 74.14 112.24

HP Financial 2.36 1.63 -4.47

Corporate Investments -3.36 3.32 -7.74

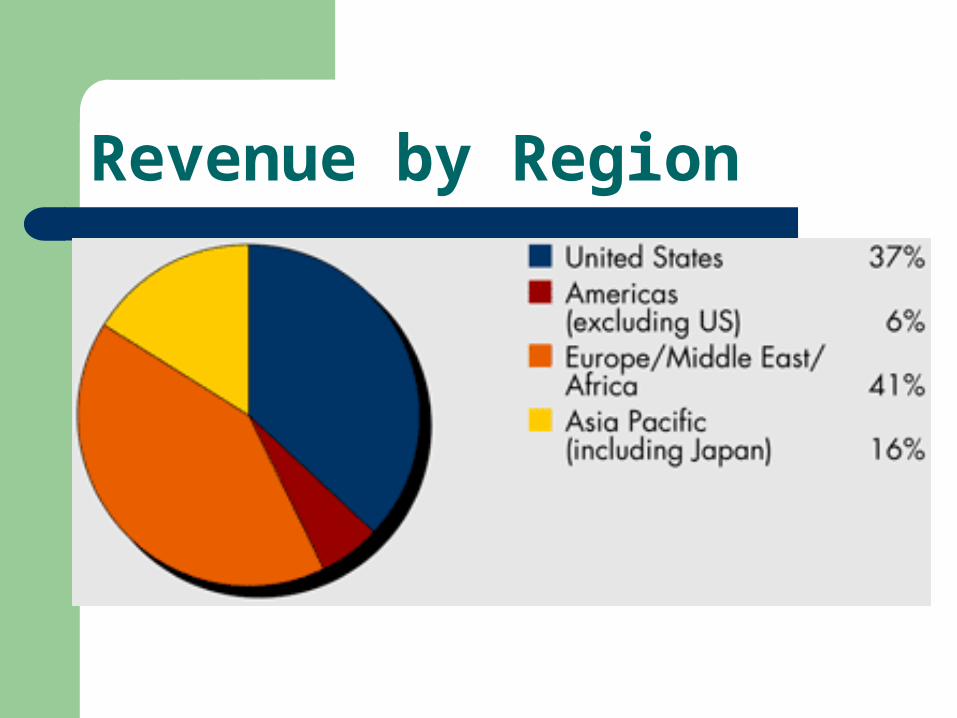

Earnings by Region

Revenue overview by region (in billions, for fiscal year 2003)

Americas (excluding

U.S.)6%

Japan4%

Asia Pacific11%

United States40%

Europe, Middle East,

Africa39%

Revenue by Region

Analysis

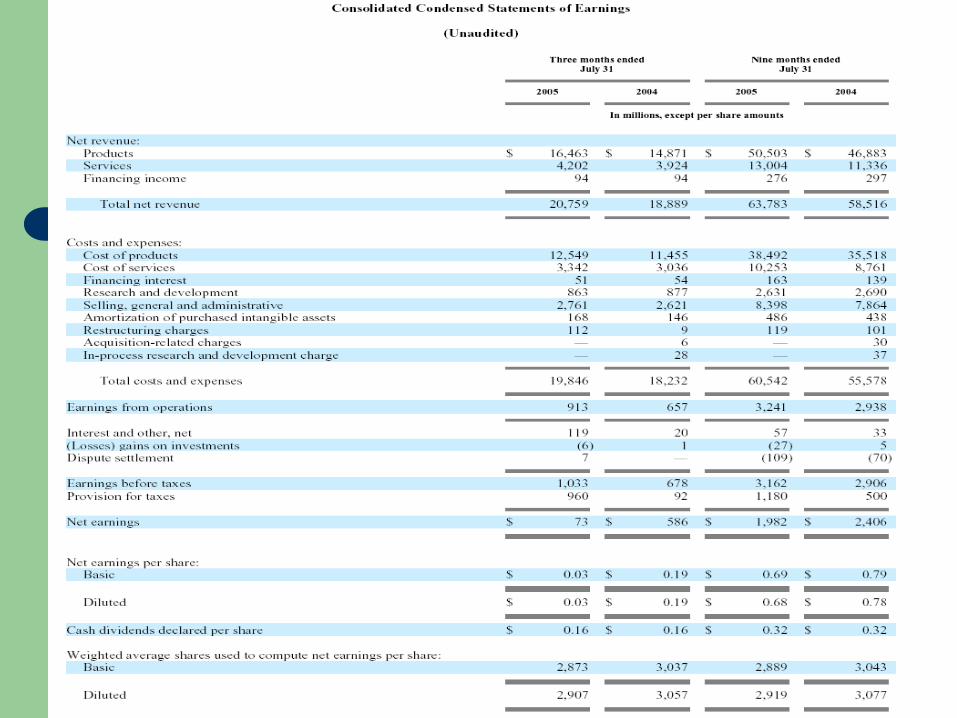

% increase/decrease in 2003-2004 2002-2003

Revenue 9.37 29.11

Costs 7.86 21.81

Earnings on Operations 45.96 386.17

Net Earnings 37.73 381.17

% increase/decrease in 9 months of 2004 - 2005

Net Revenue 9.000957003

Net Expenses 8.931591637

Earnings from Operations 10.31313819

Net Earnings -17.62261014

Shares

000’ 2004 2003 2002 2001

Balance 2,910,760 3,042,761 3,043,733 1,938,828

Issuance 111463

Repurchases 172468 39780 39623

Current – 2,907,000,000

Further $4bn buyback approved

Financials

Dividend - $0.08 per quarter No stock splits since Dec 2000 (2 for 1) Year Est. EPS (10/05) 1.56 Price/Earnings (Trailing)18.695 Earnings Growth Rate17.200 Relative P/E1.053 Estimated P/E18.300

The stock as of 10 Nov 2005

Last 28.23 USD

Change -0.31

% Change (1) -1.09%

High 28.63

Open 28.4

Low 28.21

Net Volume 7,242,200

52 Wk High 29.51

Date 20/09/2005

52 Wk Low 18.85

Date 11/11/2004

Dividend 0.08

Div Date 12/09/2005

Market Cap 80,879 M

P/E Ratio 26.89

EPS 1.05

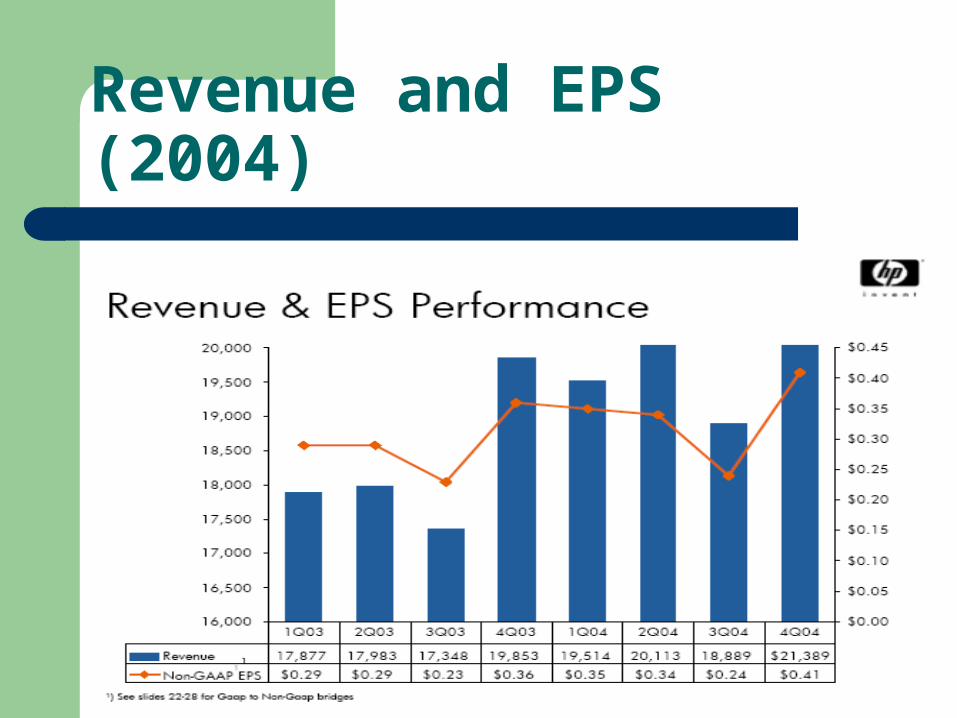

Revenue and EPS (2004)

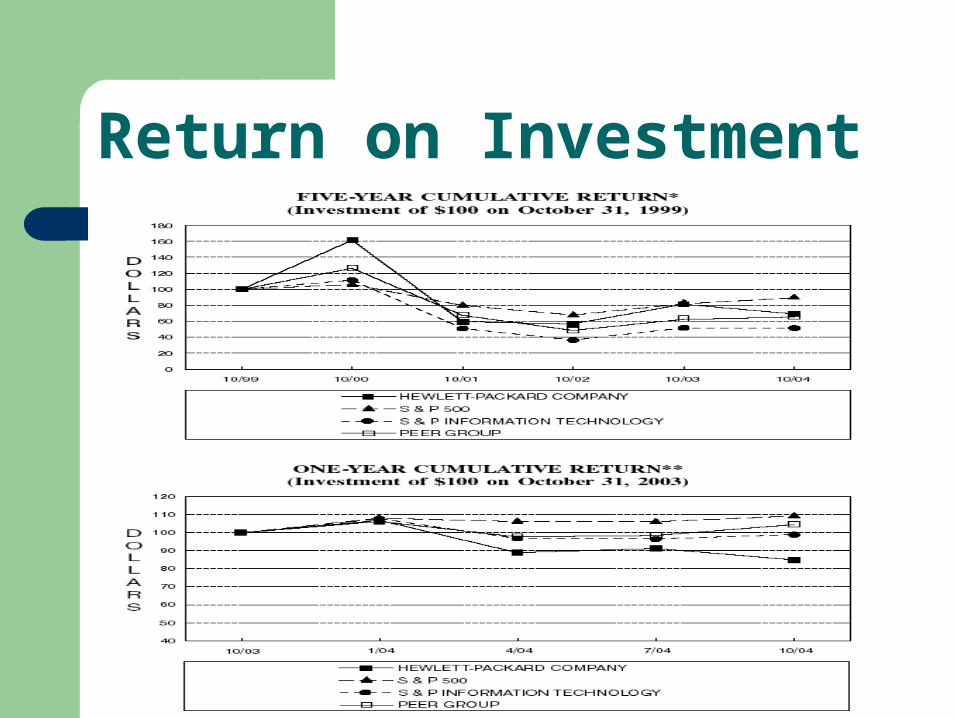

Return on Investment

Stock Performance

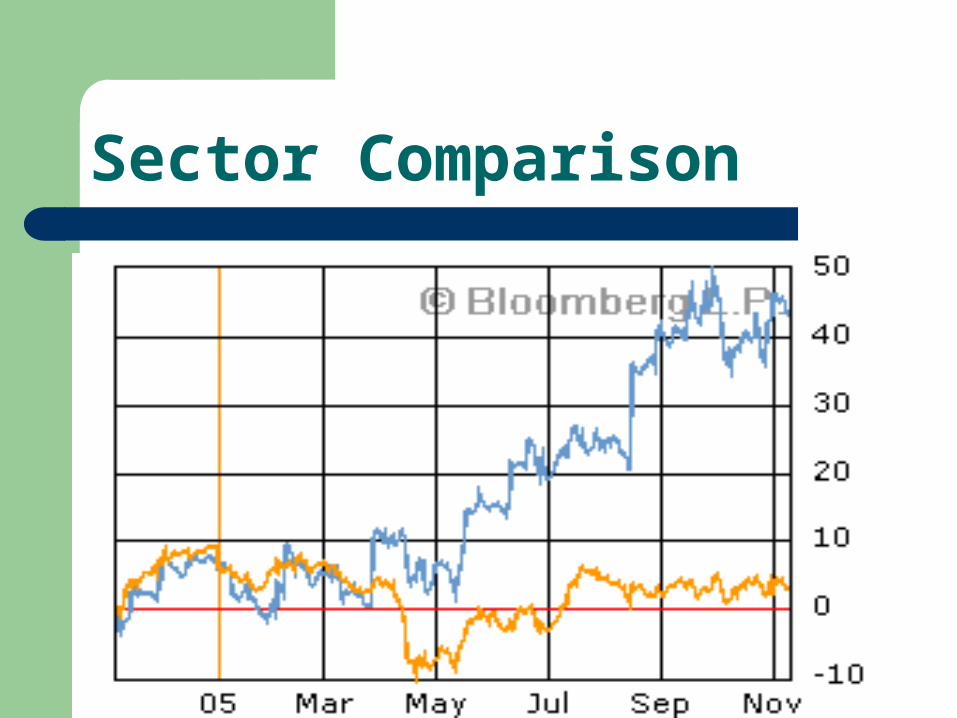

Sector Comparison

Factors affecting future performance Competition Inventory management ‘Staying on top of technological development’ Intellectual property rights Economic uncertainty Terrorism Political changes ‘business disruptions’

Inventory and Distribution

Big Box

BTO and CTO combined

High end and low end sales

Competitors by Sector PSG – Dell, IBM. Acer and Fujitsu (Europe) IPG – Very pricing competitive. Xerox, Epson,

Lexmark ESS – Rapid technological innovation. IBM,

EMC, Sun Micro HPS – IBM, EDS. Competitive in support and

Consulting. Software – BMC, Veritas, Mercury, IBM HPFS – Financing companies: IBM Global

Financing, Banks and Financial Institutions

Moving Forward?

R&D – Constant at $3,500million Revenue increasing BUT so are costs Profits are sensitive to US$ exchange rate Several Business acquisitions $5billion authorized for share repurchases ($3b

remaining) Innovative and popular products Predicted fourth Q $22.2-$22.4bn Revenue – Up

10%

Acquisitions

Snapfish – Online photo service Scitex Vision – Super-wide digital printing RLX Technologies – Software provider Peregrine Systems – Management software Compaq – PC supplier ApplQ – open storage area network management

Market Leaders

The largest consumer IT company

The world's largest SMB IT company

A leading enterprise IT company

Also has a significant presence in the public sector as well as health and education

Philip Fisher

Production, Marketing, Research and Financial skills

Good The People Factor

New and old leaders - experienced Investment characteristics

Very diversified and continually evolving Price of the investment

Medium

Conclusion and Recommendation 2005 is a disappointing year New acquisitions bring a positive light Share buy-back

WEAK BUY (wait till

final results and evaluate!)

Gateway Inc.Technology You Trust

Values

Caring, honesty, teamwork, respect,aggressiveness, efficiency, fun and commonsense.

--- Offering products directly to customers, providing them with the best value for their money and unparalleled service and support

Company Background

Founded in 1985 in a farmhouse by Ted Waitt Went public in 1993 traded on NASDAQ Started trading on NY Stock Ex in 1997 3rd largest PC maker in U.S. In March 2004, acquired eMachines ($235 million) Currently 1,900 employees 6% of US market share in consumer segment

Distribution Channels

Direct distribution: web, phone, retail stores Indirect distribution: retailers like Costco Limited resellers in Canada and Mexico

Products

Computersdesktops, notebooks, all-in-ones, professional PCSystems (networking, servers and storage)

Computer accessoriesMouse, storage, memories, monitors, modems Consumer electronicsdigital TVs, digital camera, MP3 players, DVD

players

Software

Competitive Strategies in the 90’s

Gateway’ big box strategy and JIT

Direct +retail

Competitors:

Dell’s build-to-order, direct only, JIT

Compaq’s Build-to-forecast, retail only

Acquired Advanced Logic Research (ALR) in

1997 and announced its entry into corporate

network server market

Channeled through own retailing stores

Acquired ALR

Strategies in the 21st Century

• Encountered big loss from 2001failure of cost leadership strategyhigher cost and lower marginslow inventory turnover

• “Branded integrator”offered the fullest range of product and service

• B2B 2003

Acquiring eMachines

Acquired eMachines in March 2004

50 million new Gateway shares and $30 million cash

eMachines

Philosophy Build affordable computers for everyone – no

compromise PCs that deliver incredible value and performance.

Market budget-conscious consumers

Products PCs and peripheral displays

Distribution Channels 3rd party retailers: BestBuy, Office Depot

eMachines

2cnd largest vendor of desktop through US retailers

low-cost, full-featured computer systems $1.1 billions of sales in 2003 International market in Japan and UK Wayne Inouye, who joined eMachines in

2001 and quickly turned it into money-making business

What does eMashine bring to GTW

Low cost distribution model and retail relationaship

Highly efficient and profitable operation model

Market shares in consumer desktop sector International growth opportunities Management team

After Acquisition

eMachines CEO Wayne Inouye was named CEO of Gateway, succeeding Ted Waitt, who remains chairman and the company's largest stockholder 28.3% shares and plays an active role in long-term strategic direction, product development and marketing plans.

Combined management team from both Gateway and eMachine

A few new members joined management team

Management

Wayne R. Inouye (eMachine) CEO and President

Former president & CEO of eMachine since 2001

Senior vice president of PC merchandising for BestBuy

Scott Bauhofer, Senior vice president

Former senior vice president of BestBuy

bachelor's in history from San Francisco State University

Management

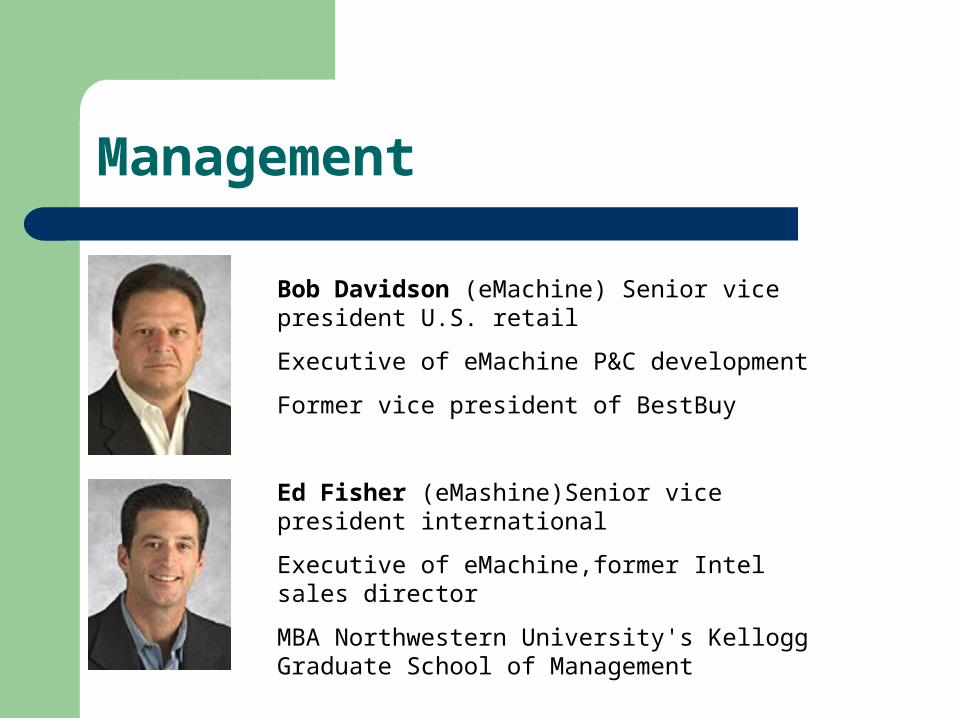

Bob Davidson (eMachine) Senior vice president U.S. retail

Executive of eMachine P&C development

Former vice president of BestBuy

Ed Fisher (eMashine)Senior vice president international

Executive of eMachine,former Intel sales director

MBA Northwestern University's Kellogg Graduate School of Management

Management

John Goldsberry, (eMachine)senior vice president, CFOJoined Gateway in 2004Former CFO of eMachine, leaded the negotiation withGatewaybachelor's degree in Applied Mathematics and a Ph.D. inBusiness Economics from Harvard University

Greg Memo ,(eMachine) Senior Vice President, Products,Marketing &WebFormer president at CompaqMBA degree from San Jose State University and abachelor's degree in industrial engineering from Arizona State University.

Management

Bruce K. Riggs, Senior Vice President, Operations and Customer careFormer senior vice president of Quanta Computer Inc and Dellbachelor's degree in Economics and Spanish at Lawrence University MBA from from Indiana University

Bruce W. Smith, senior vice president, professional lineFormer senior vice president of Equant, a global telecommunications-servicesmaster's degree in history from the University of Virginia bachelor's degree in history from The Johns Hopkins University

Management

Dan Stevenson, Vice President, DirectJoined Gateway in 2004Former senior director at Apple ComputerMBA from Harvard University and a bachelor's in accounting from Purdue University

Mike Zimmerman,(eMachine) Senior Vice President, Customer Care Services & Quality AssuranceFormer vice president and corporate planning at BestBuyBachelor's degree in business administration and marketing from Northwood University.

Corporate Goals

Profitably grow PC business Diversify revenue Increase gross margin with consumer

electronics products Reduce cost structure

Modified Strategies

Multi-branding Keep eMachine’s original marketing strategy Closed 188 Gateway owned retail stores Channel through big retailers New manufacturing model International markets (Japan, Mexico) Consolidated supply base Decrease employees from 7400-1900

Go-to-market strategy

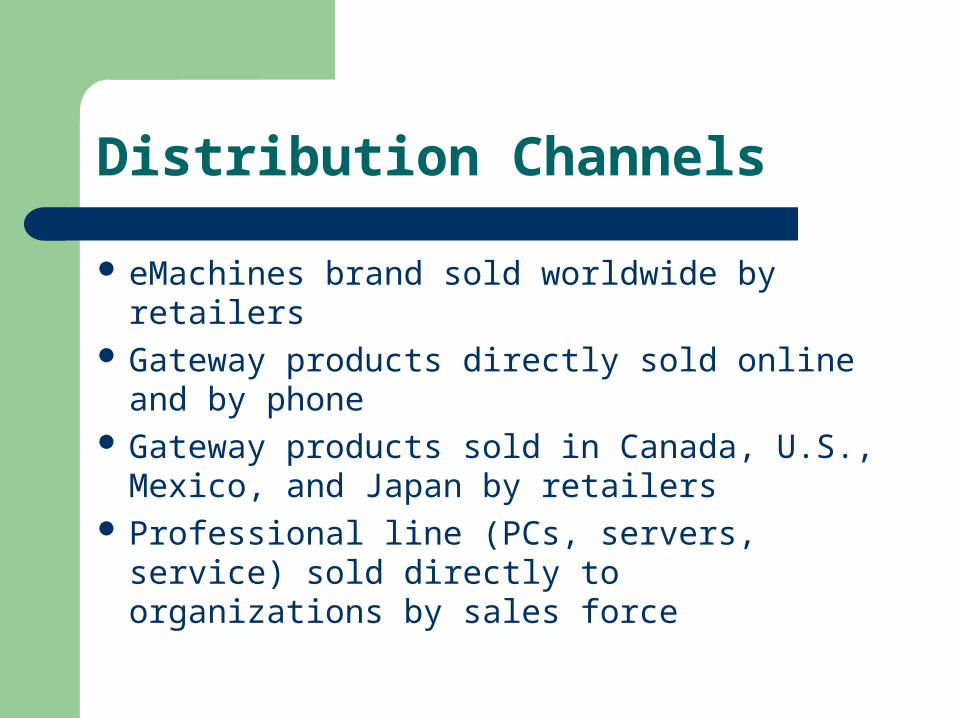

Distribution Channels

eMachines brand sold worldwide by retailers Gateway products directly sold online and by

phone Gateway products sold in Canada, U.S.,

Mexico, and Japan by retailers Professional line (PCs, servers, service) sold

directly to organizations by sales force

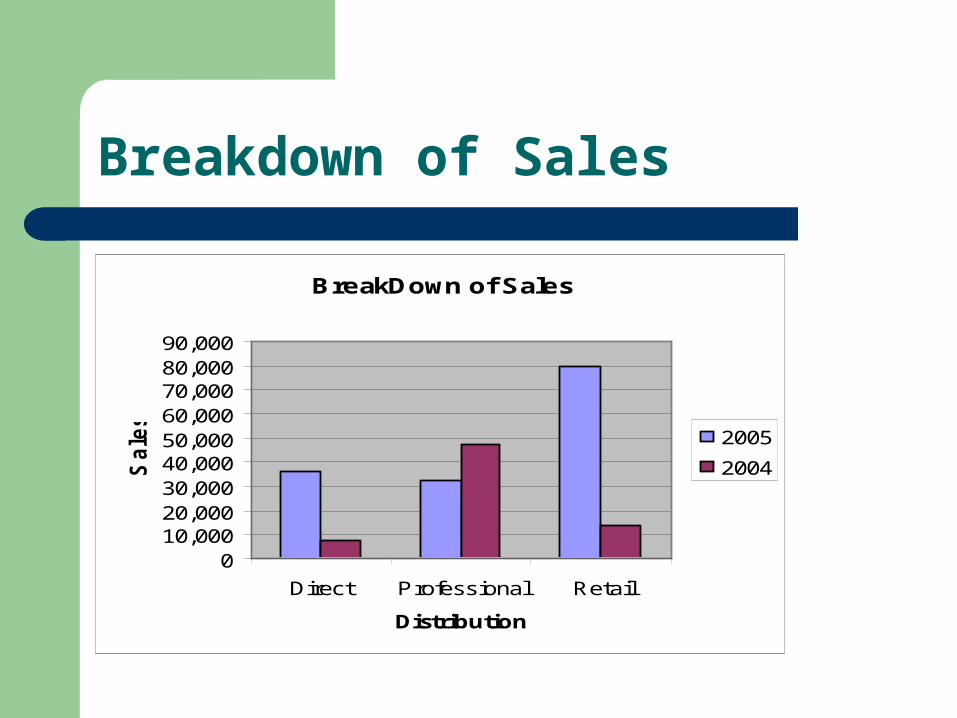

Breakdown of Sales

BreakDown of Sales

010,00020,00030,00040,00050,00060,00070,00080,00090,000

Direct Professional Retail

Distribution

Sale

s

2005

2004

Net Income

Net Income

-1200

-1000

-800

-600

-400-200

0

200

400

600

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Net

Inco

me

Series1

Earning Per Share

EPS

-4

-3

-2

-1

0

1

2

Year

EP

S

Series1

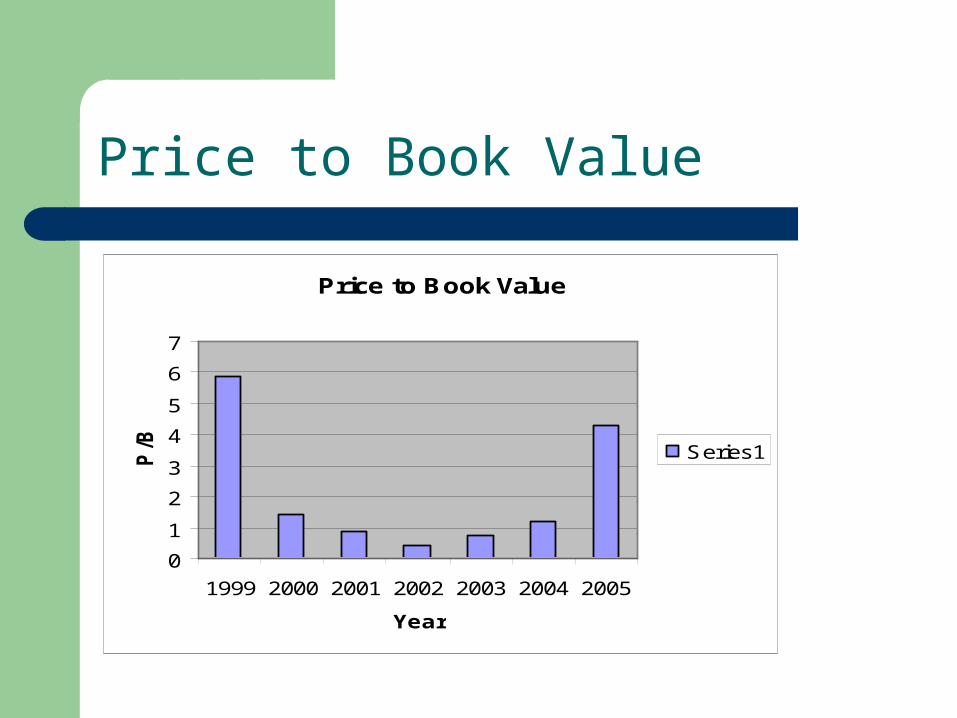

Price to Book Value

Price to Book Value

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004 2005

Year

P/B Series1

Price/Earnings

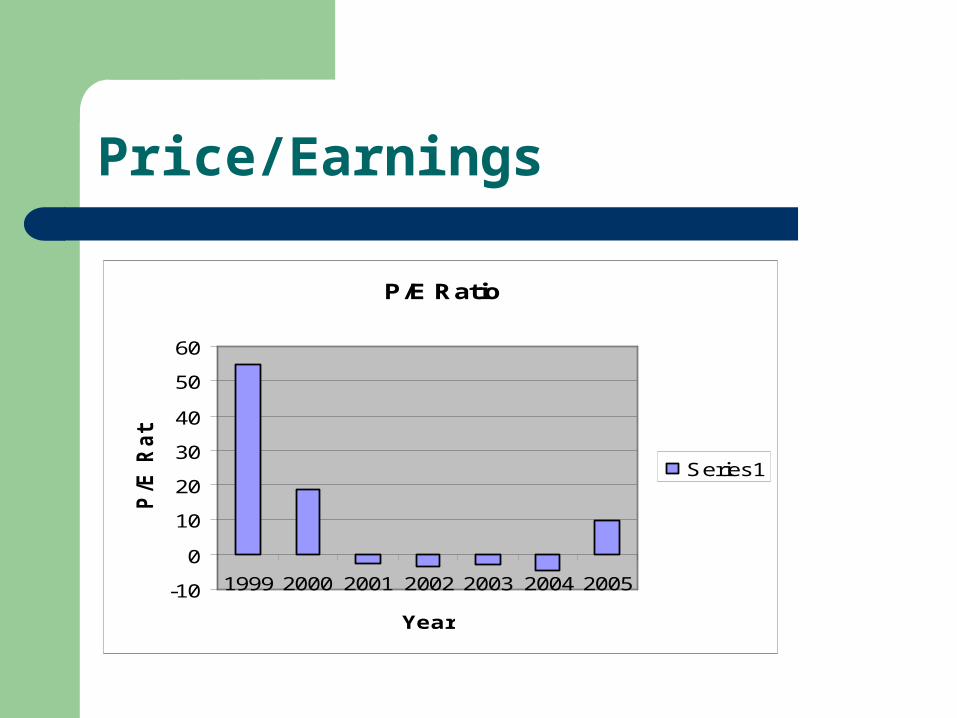

P/E Ratio

-10

0

10

20

30

40

50

60

1999 2000 2001 2002 2003 2004 2005

Year

P/E

Rati

o

Series1

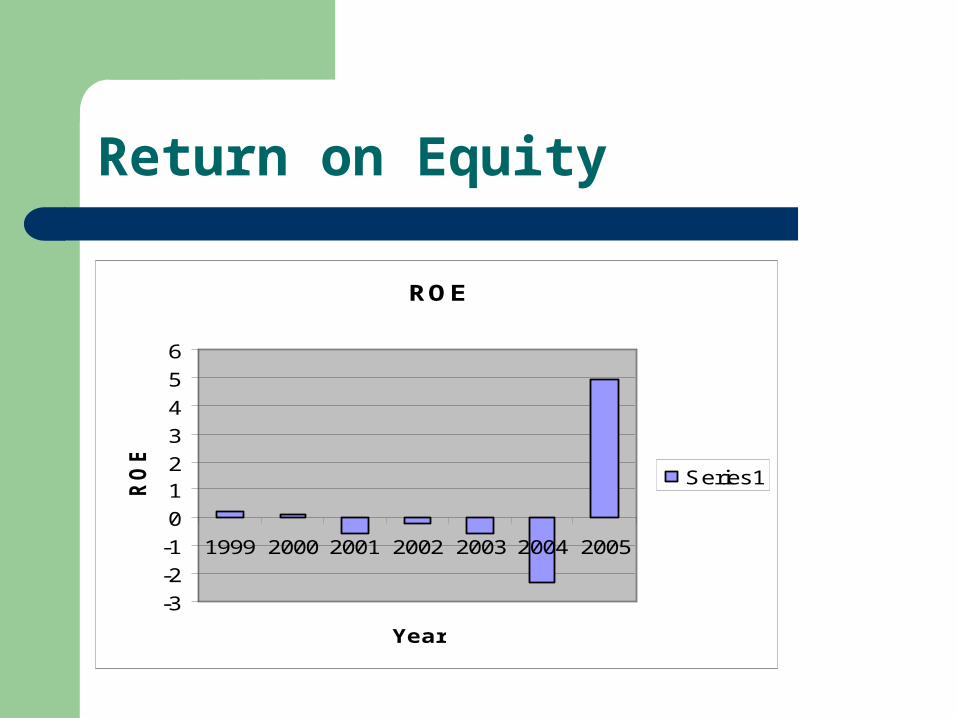

Return on Equity

ROE

-3

-2

-1

0

12

3

4

5

6

1999 2000 2001 2002 2003 2004 2005

Year

RO

E

Series1

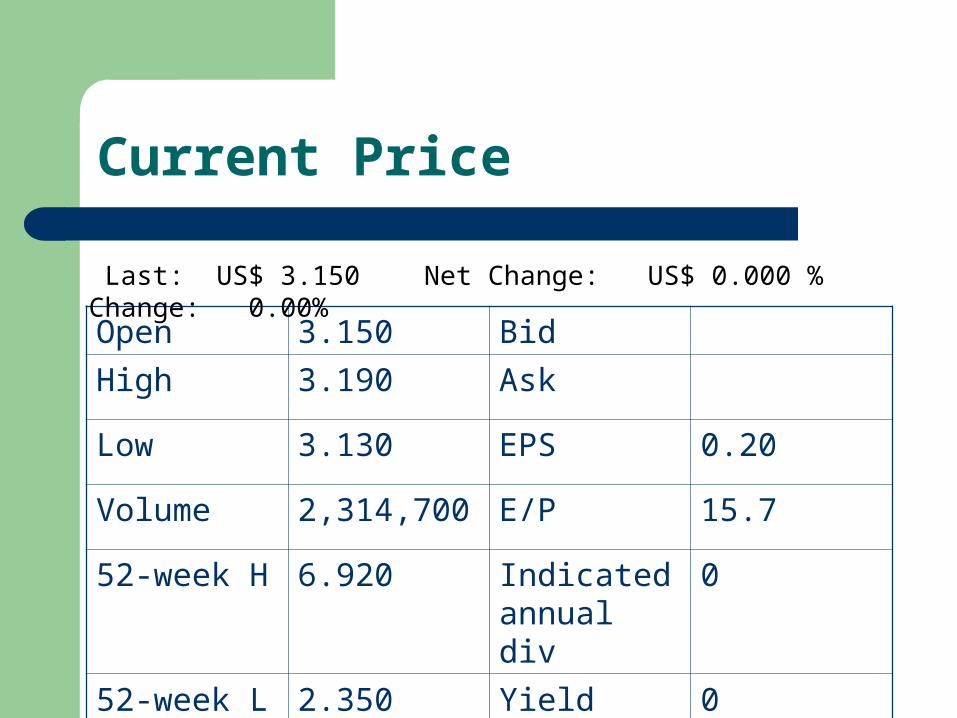

Current Price

Open 3.150 Bid

High 3.190 Ask

Low 3.130 EPS 0.20

Volume 2,314,700 E/P 15.7

52-week H 6.920 Indicated annual div

0

52-week L 2.350 Yield 0

Last: US$ 3.150 Net Change: US$ 0.000 % Change: 0.00%

Current Ratios

P/E Ratio9.26 Beta Coefficient1.87 Earnings per Share0.34 Market Cap (billion)1.17 B Shares Outstanding371,165,000

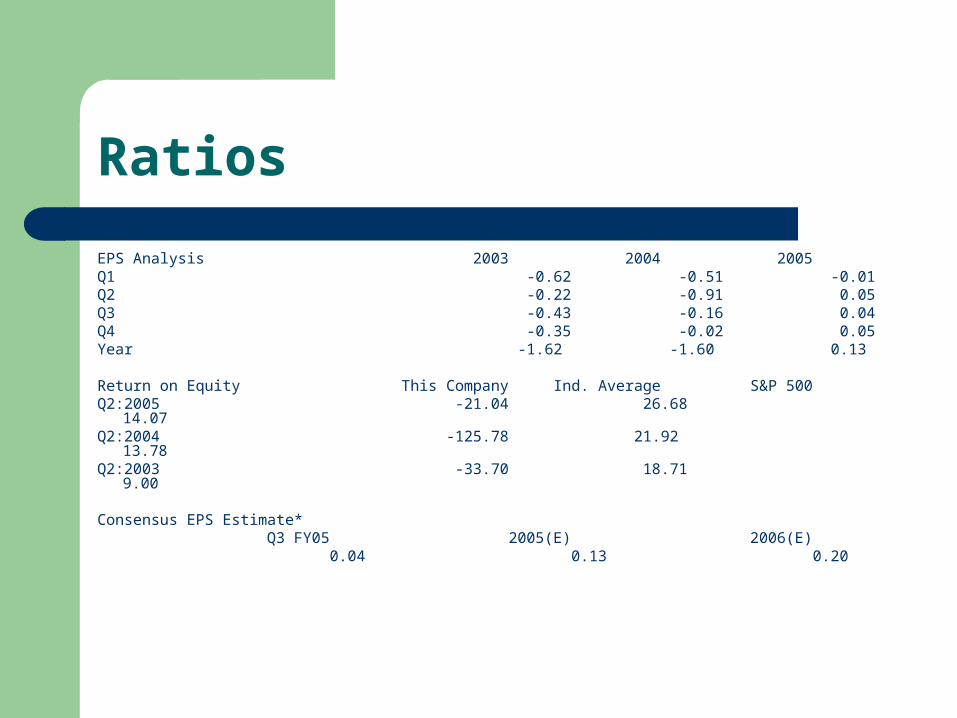

Ratios

EPS Analysis 2003 2004 2005Q1 -0.62 -0.51 -0.01Q2 -0.22 -0.91 0.05Q3 -0.43 -0.16 0.04Q4 -0.35 -0.02 0.05Year -1.62 -1.60 0.13

Return on Equity This Company Ind. Average S&P 500Q2:2005 -21.04 26.68 14.07Q2:2004 -125.78 21.92 13.78Q2:2003 -33.70 18.71 9.00

Consensus EPS Estimate* Q3 FY05 2005(E) 2006(E) 0.04 0.13 0.20

Financial Statement

Income statement Balance sheet Cash flow statement

One-Year Price Chart

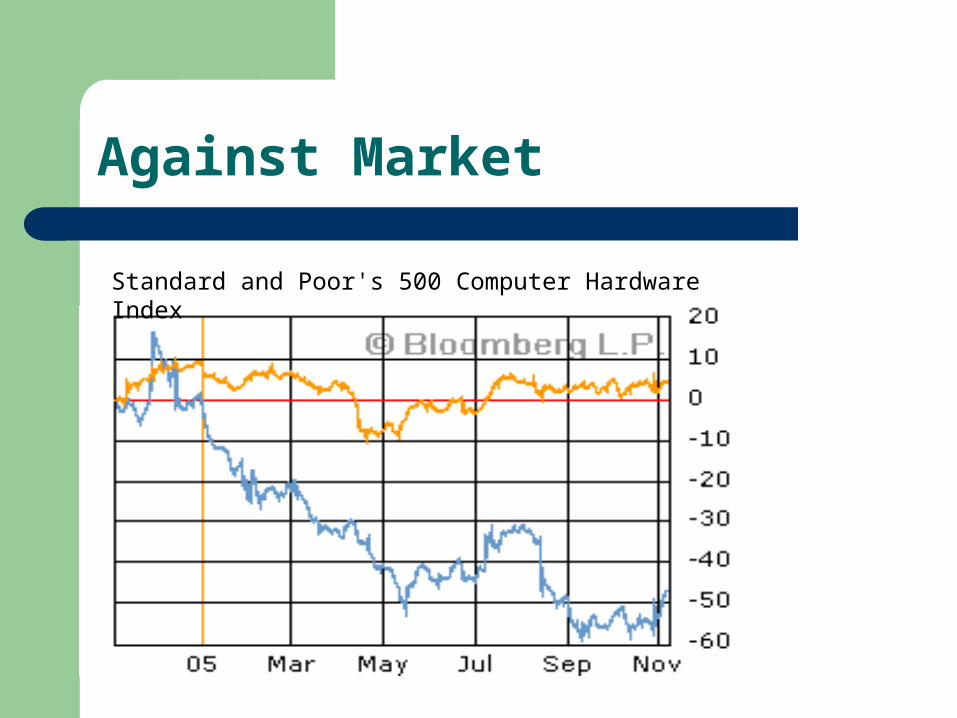

Against Market

Standard and Poor's 500 Computer Hardware Index

Five Year Performance

Share Repurchase

Repurchase of Preferred Stock and Convertible Note 2004 from America Online,

Series A and C Preferred Stock with a par value of $400 million plus 2.7 million common shares, for $315.6 million in cash and credits.

Value Driver

Profitable eMachine brand sector eMashine’s profitable operating model International market

Underminded by Failure of integration of the two companies Competition in international market

Forecasting

Opportunity to grow in international markets Maintain relationship with the big buyers Let us entertain you” is the new mantra of

computer industry. Previously, companies

focused solely on creating technology Competition:

Dell, Apple, HP

Competitive Landscape

Current Events

Closed three federal deals valued more than $20 million

$1.7 million deal with California Highway Patrol (CHP)

Hyper-threaded dual-core added Enters strategic alliance with LEAF Financial

and Merrill Lynch

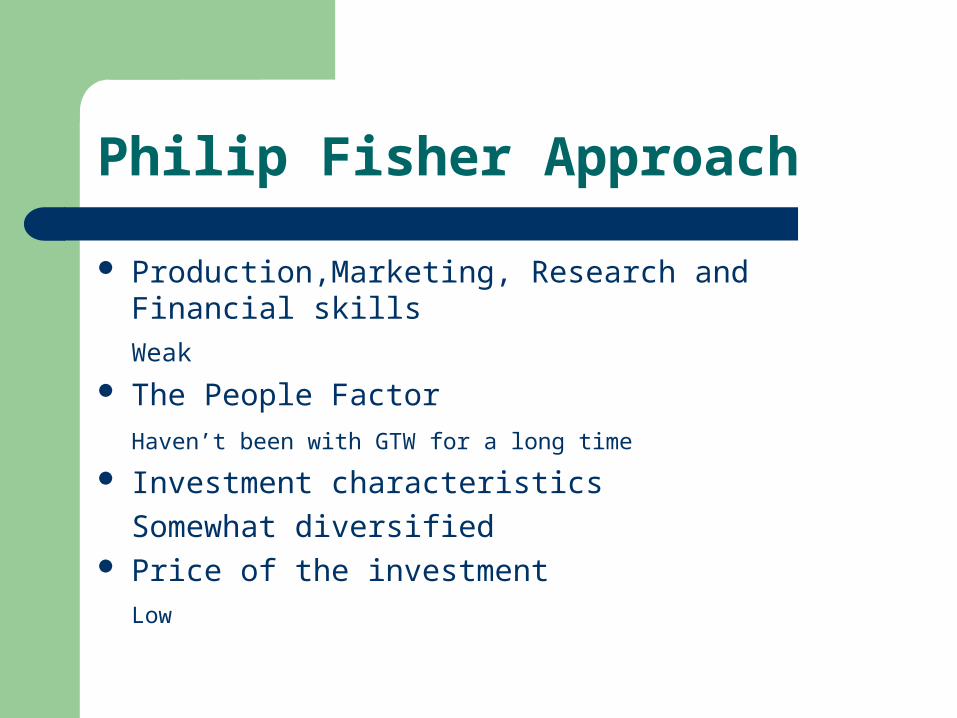

Philip Fisher Approach

Production,Marketing, Research and Financial skills

Weak

The People Factor

Haven’t been with GTW for a long time Investment characteristics

Somewhat diversified Price of the investment

Low

Weak Hold

Conclusion