Embed Size (px)

Citation preview

eSocial The challenges of the new digital environment

What has been done — and what is to come

“It is risky to think that only a few months during 2015 will be enough for a broad discussion of eSocial, its effects on the company, and appropriate adjustmentsto decision-making”

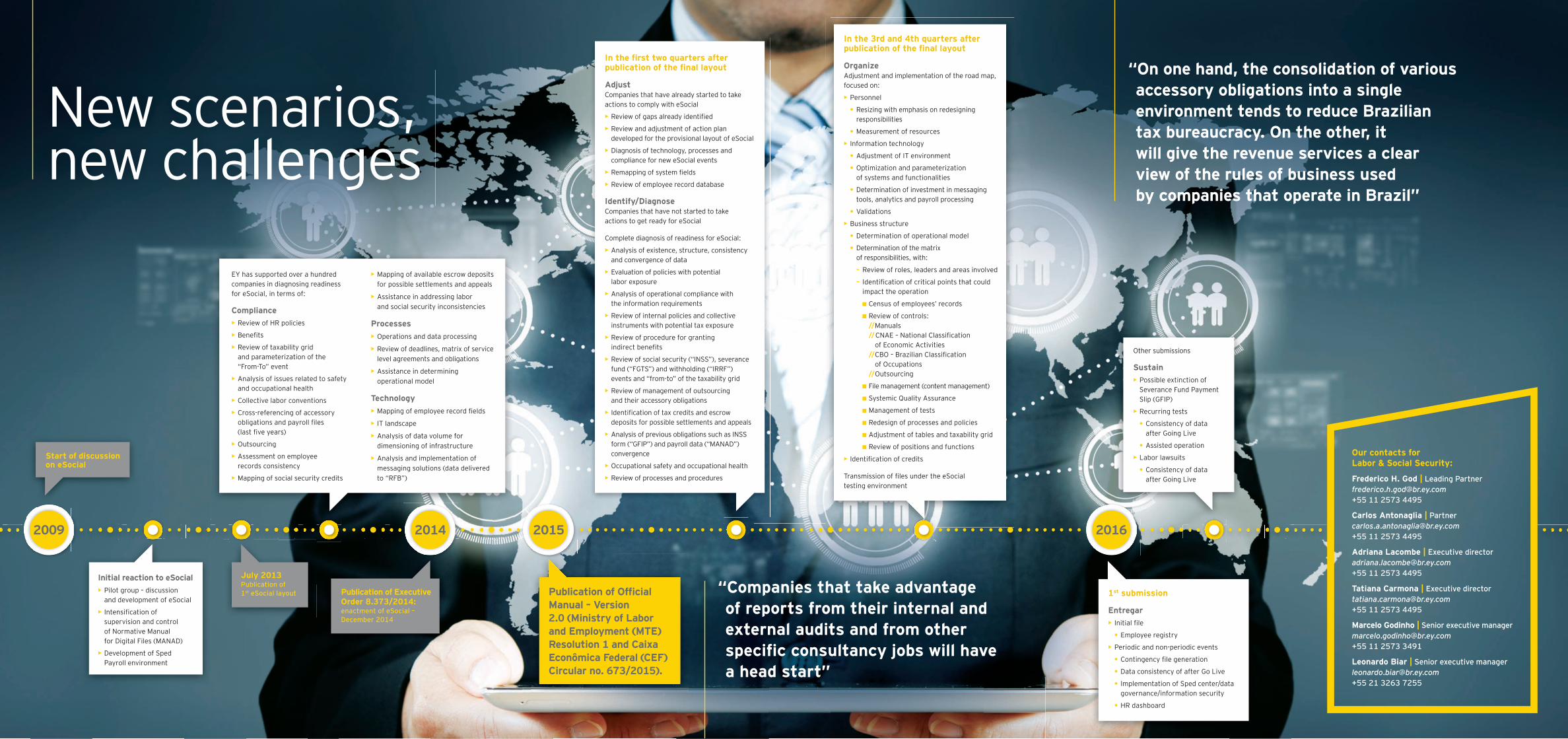

eSocial — originally known as EFD Social or eFopag — is a long awaited and important innovation by the Brazilian Revenue Service in terms of the amount of information consolidated in it and expectations for the extinction, in the long term, of accessory obligations today submitted by companies, such as GFIP, Dirf, Rais, Caged, etc.

If on one hand the consolidation of various accessory obligations into a single environment tends to reduce Brazilian tax bureaucracy — a major bottleneckfor attracting investment — on the other hand it will provide the revenue services with a clear view of the rules of business used by companies that operate in Brazil, in areas such as hiring, management, payment and/or termination of labor contracts.

Preparation by companies sinceJune 2013

Aware of this situation, many companies have anticipated the publication of Decree 8.373/2014, and even the Executive Declaratory Act 17/2013, and begun a long journey of preparing themselves for the new virtual environment, mapping important points that could impact compliance with eSocial and identifying items that, although not obstacles per se, could become the source of labor and pension contingencies.

Almost 5 years has gone by since the initial design of eSocial, but the offi cial layout and manual (version 2.0) were fi nally published on February 24, 2015, in Ministry of Labor and Employment (MTE) Resolution 1. This publication represents a milestone on the road to effective implementation of this new accessory obligation. From here on out, taxpayers have precisely one year to enter into compliance with eSocial.

In the meantime, Brazilian affi liates of multinational companies are asking their headquarters to free up funds for the preparation. Some have even made good progress, by acquiring software and/or changing internal procedures, even amidst the uncertainties of the world economic landscape, permeated by strong cost cutting and — in some cases — even closings and layoffs.

These companies were the fi rst to obtain buy-in from their headquarters, and are certainly in a better position today for having mapped their gaps ahead of time, addressing them through multidisciplinary discussions, as required by eSocial.

The challenges — and howto overcome them2016 is just around the corner — and it is risky to think that only a few months in 2015 will be enough for a broad discussion of eSocial, its effects on the company and appropriate adjustments to decision-making. If the constant delays with regard to the publication of Decree 8.373 raised doubts in the minds of companies, the majority of which delayed the start of preparation for eSocial, it is now certain that, after the publication of the defi nitive manual, a race against time has begun.

The uncertain economic situation continues. Therefore, companies that take advantage of reports from their internal and external audits and from other specifi c consultancy jobs will have a head start: based on a risk matrix, they will be able to quickly identify key initiatives and investments for the delivery of eSocial.

This is the only way the preparation will be completed successfully: with changes and investments considering the real needs of each company.

Start of discussionon eSocial

Initial reaction to eSocial• Pilot group – discussion

and development of eSocial

• Intensifi cation of supervision and controlof Normative Manualfor Digital Files (MANAD)

• Development of Sped Payroll environment

July 2013Publication of1st eSocial layout

EY has supported over a hundred companies in diagnosing readinessfor eSocial, in terms of:

Compliance• Review of HR policies

• Benefi ts

• Review of taxability gridand parameterization of the “From-To” event

• Analysis of issues related to safety and occupational health

• Collective labor conventions

• Cross-referencing of accessory obligations and payroll fi les(last fi ve years)

• Outsourcing

• Assessment on employeerecords consistency

• Mapping of social security credits

Publication of Executive Order 8.373/2014: enactment of eSocial – December 2014

New scenarios, new challenges

20142009

• Mapping of available escrow deposits for possible settlements and appeals

• Assistance in addressing laborand social security inconsistencies

Processes• Operations and data processing

• Review of deadlines, matrix of service level agreements and obligations

• Assistance in determining operational model

Technology• Mapping of employee record fi elds

• IT landscape

• Analysis of data volume for dimensioning of infrastructure

• Analysis and implementation of messaging solutions (data delivered to “RFB”)

Publication of Offi cial Manual – Version2.0 (Ministry of Labor and Employment (MTE) Resolution 1 and Caixa Econômica Federal (CEF) Circular no. 673/2015).

In the fi rst two quarters after publication of the fi nal layout

Adjust�Companies that have already started to take actions to comply with eSocial

• Review of gaps already identifi ed

• Review and adjustment of action plan developed for the provisional layout of eSocial

• Diagnosis of technology, processes and compliance for new eSocial events

• Remapping of system fi elds

• Review of employee record database

Identify/Diagnose�Companies that have not started to takeactions to get ready for eSocial

Complete diagnosis of readiness for eSocial:

• Analysis of existence, structure, consistency and convergence of data

• Evaluation of policies with potentiallabor exposure

• Analysis of operational compliance withthe information requirements

• Review of internal policies and collective instruments with potential tax exposure

• Review of procedure for grantingindirect benefi ts

• Review of social security (“INSS”), severance fund (“FGTS”) and withholding (“IRRF”) events and “from-to” of the taxability grid

• Review of management of outsourcingand their accessory obligations

• Identifi cation of tax credits and escrow deposits for possible settlements and appeals

• Analysis of previous obligations such as INSS form (“GFIP”) and payroll data (“MANAD”) convergence

• Occupational safety and occupational health

• Review of processes and procedures

In the 3rd and 4th quarters after publication of the fi nal layout

OrganizeAdjustment and implementation of the road map, focused on:

• Personnel

ª Resizing with emphasis on redesigning responsibilities

ª Measurement of resources

• Information technology

ª Adjustment of IT environment

ª Optimization and parameterizationof systems and functionalities

ª Determination of investment in messaging tools, analytics and payroll processing

ª Validations

• Business structure

ª Determination of operational model

ª Determination of the matrixof responsibilities, with:

– Review of roles, leaders and areas involved

– Identifi cation of critical points that could impact the operation

Census of employees’ records

Review of controls:// Manuals// CNAE – National Classifi cation

of Economic Activities// CBO – Brazilian Classifi cation

of Occupations// Outsourcing

File management (content management)

Systemic Quality Assurance

Management of tests

Redesign of processes and policies

Adjustment of tables and taxability grid

Review of positions and functions

• Identifi cation of credits

Transmission of fi les under the eSocialtesting environment

“Companies that take advantageof reports from their internal and external audits and from other specifi c consultancy jobs will havea head start”

2015

Other submissions

Sustain• Possible extinction of

Severance Fund Payment Slip (GFIP)

• Recurring tests

ª Consistency of data after Going Live

ª Assisted operation

• Labor lawsuits

ª Consistency of data after Going Live

1st submission

Entregar• Initial fi le

ª Employee registry

• Periodic and non-periodic events

ª Contingency fi le generation

ª Data consistency of after Go Live

ª Implementation of Sped center/data governance/information security

ª HR dashboard

“On one hand, the consolidation of various accessory obligations into a single environment tends to reduce Brazilian tax bureaucracy. On the other, itwill give the revenue services a clearview of the rules of business usedby companies that operate in Brazil”

2016

Our contacts forLabor & Social Security:

Frederico H. God | Leading [email protected]+55 11 2573 4495

Carlos Antonaglia | [email protected]+55 11 2573 4495

Adriana Lacombe | Executive [email protected]+55 11 2573 4495

Tatiana Carmona | Executive [email protected]+55 11 2573 4495

Marcelo Godinho | Senior executive [email protected]+55 11 2573 3491

Leonardo Biar | Senior executive [email protected]+55 21 3263 7255

EYAssurance | Tax | Transactions | Advisory

About EY

EY is a global leader in Assurance, Tax, Transactions and Advisory services. Our insights and the high quality services that we provide help to build confidence in capital markets and economies aroundthe world. We develop exceptional leaders who work in teams tofulfill our commitments to all interested parties. In doing so, we play a fundamental role in the building of a better business world for our people, our clients and our communities.

EY is Brazil’s most complete Assurance, Tax, Transactions and Advisory firm, with 5,000 professionals providing support and service to over 3,400 small, medium and large clients.

EY Brasil is an Official Supporter of the Rio 2016 Olympic and Paralympic Games and exclusive supplier of consulting services for the organizing committee. The alignment of the Olympic movement values with those of Ernst & Young was decisive in this initiative.

EY refers to the global organization and may also refer to oneor more member firms of EY Global Limited (EYG), each of whichis an independent legal entity. EY Global Limited, a private company established in Great Britain and limited by guarantee, does not provide services to clients.

© 2015 Ernst & Young Serviços Tributários. All rights reserved.

This is a publication of the Department of Brand, Marketing and Communication.Reproductionof this content, partially or in full, is permitted as long as the source is cited.

ey.com.br

facebook | EYBrasiltwitter | EY_Brasillinkedin | ernstandyoungapp | ey.com.br/eyinsights

![eSocial - Anexo III - Tabelas do eSocial [OFICIAL]](https://img.pdfslide.us/doc/110x75/55ae12731a28ab8d3b8b476a/esocial-anexo-iii-tabelas-do-esocial-oficial.jpg)