Embed Size (px)

Citation preview

Field Staff Training Dian Mandiri11 August 2006

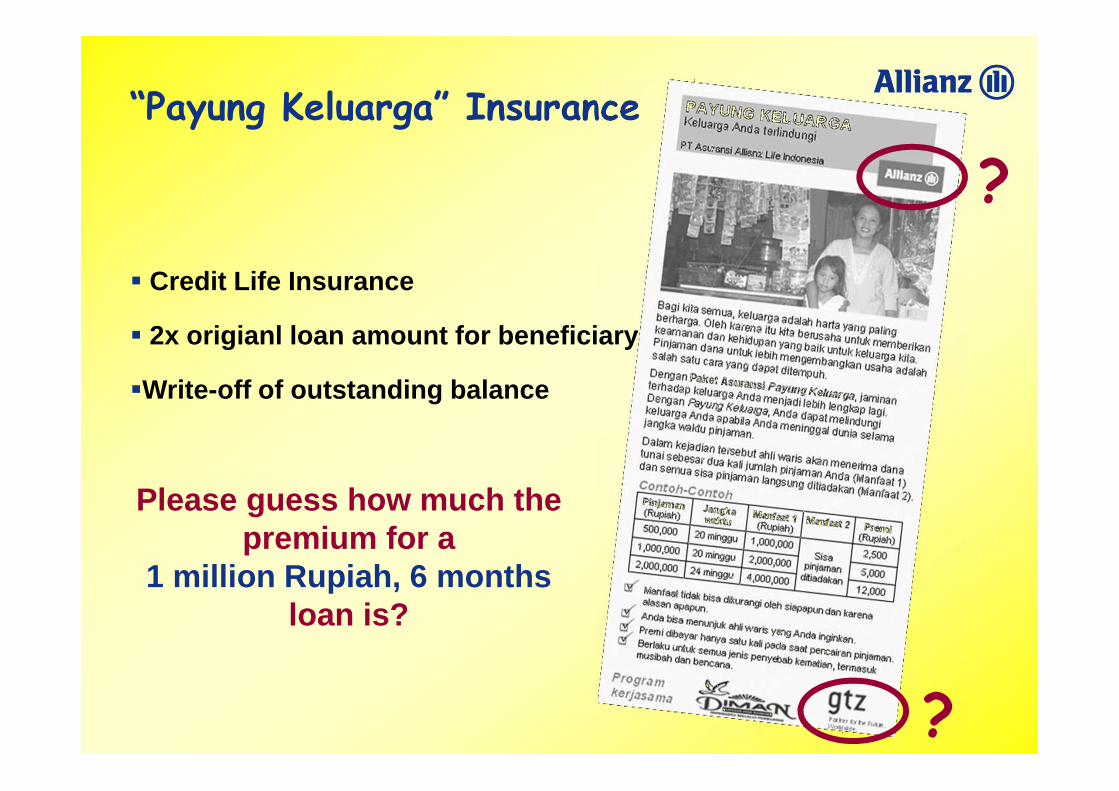

“Payung Keluarga” Insurance

2

3

DRESSED FOR SUCCESS

Tried to make it little by little, tried to make it bit by bit on my own. Quit the job, the grey believers, another town where I get close to the bone.

Whatcha gonna tell your brother? - oh oh oh whatcha gonna tell your father? - I don't know! Whatcha gonna tell your mother? - Let me go...

I'm gonna get dressed for success shaping me up for the big time, baby. Get dressed for success shaping it up for your love,…… yeah yeah yeah.

I'm not afraid, a trembling flower, I'll feed your heart and blow the dust from your eyes and in the dark things happen faster. I love the way you sway your hips next to mine.

Whatcha gonna tell your brother? - oh oh oh... whatcha gonna tell your father? - I don't know! Whatcha gonna tell your mother? - Let me go...

I'm gonna get dressed for success, hitting a spot for the big time, baby. Get dressed for success shaping it up for your love.

Look sharp!

4

5

What is today’s training about?

Today’s training is about Insurance and especially about the insurance product “Payung Keluarga” that you together with Allianz are just about to launch.

What are your expectations towards this training?

� You will have confidence in your insurance knowledge

� You understand the benefits of insurance for you, your organisation and your customers

� You feel ready to distribute and explain about “Payung Keluarga” to your customers.

6

What do you already know about insurance?

� What kind of insurances are there?

� How about benefits and costs of insurance?

� Do you know some insurance principles? For instance, where does the insurance company get the money from that it needs to pay claims?

7

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

8

IntroductionIntroduction

9

“Payung Keluarga” Insurance

� Credit Life Insurance

� 2x origianl loan amount for beneficiary

�Write-off of outstanding balance

?

?

Please guess how much the premium for a

1 million Rupiah, 6 monthsloan is?

10

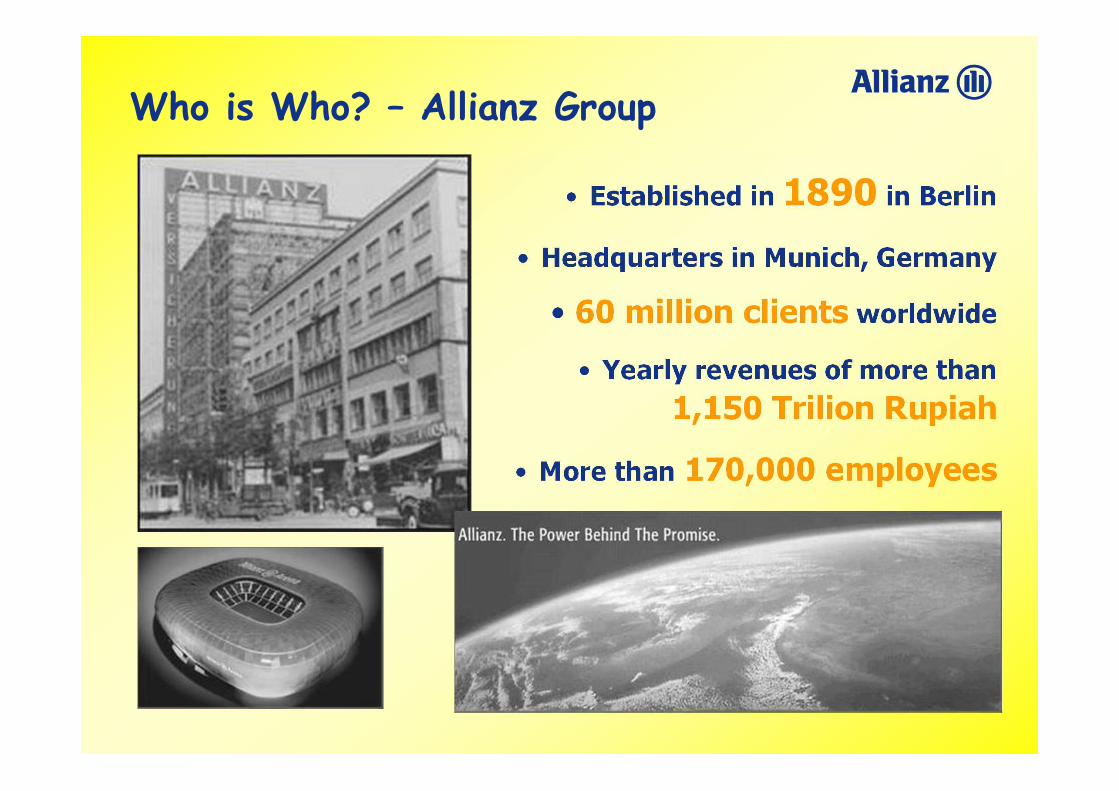

Who is Who? – Allianz Group

Allianz Video

11

Who is Who? – Allianz Group

• Established in 1890 in Berlin

• Headquarters in Munich, Germany

• 60 million clients worldwide

• Yearly revenues of more than

1,150 Trilion Rupiah

• More than 170,000 employees

12

Who is Who? – Allianz Group

• India • Thailand

• China

• Hongkong

• Vietnam

• Korea

• Japan

•Indonesia• Singapore• Malaysia

•Europe

•America

Allianz operates in more than 72 countriesAllianz operates in more than 72 countries

• Pakistan

•Australia

13

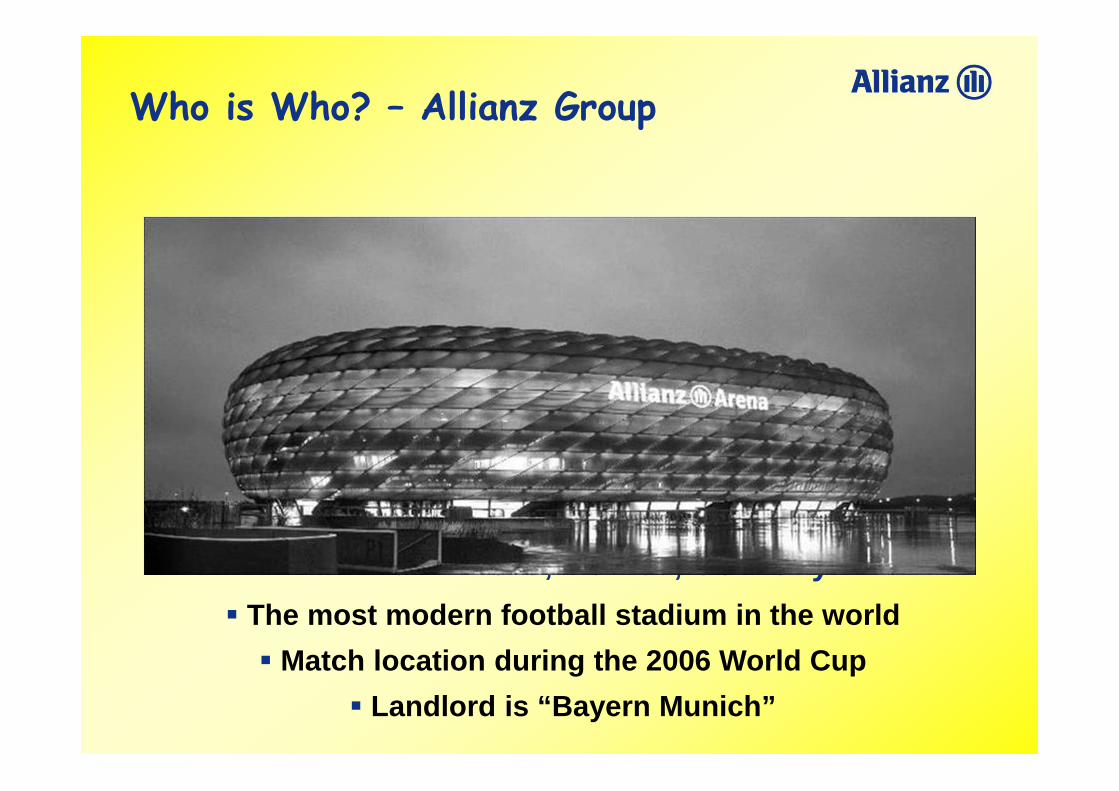

Who is Who? – Allianz Group

� The most modern football stadium in the world

� Match location during the 2006 World Cup

� Landlord is “Bayern Munich”

Allianz Arena, Munich, Germany

14

Who is Who? – Allianz Life Indonesia

� In 1981, Allianz establishes a representative office in Indonesia

� In 1989, PT Asuransi Allianz Utama Indonesia is established as a general insurance company

� In 1996, Allianz establishes PT Asuransi Allianz Life Indonesia as a life and health insurance company that also offers pension plan products

� The headquarters of PT Asuransi Allianz Utama Indonesia and PT Asuransi Allianz Life Indonesia are located in Jakarta

� In Indonesia, Allianz has 778 employees. Currently, PT Asuransi Allianz Utama Indonesia and PT Asuransi Allianz Life Indonesia have more than 8,000 sales agents in more than 80 sales offices in 44 cities.

15

Who is Who? – Allianz Life Indonesia

16

Who is Who? – Allianz Life Indonesia

Allianz Life Indonesia is the first choice for customers, business partners and employees.We build long term relationships based on mutual trust.

Vis

ion

17

Who is Who? – Allianz Life Indonesia

18

Who is Who? – Allianz Life Indonesia

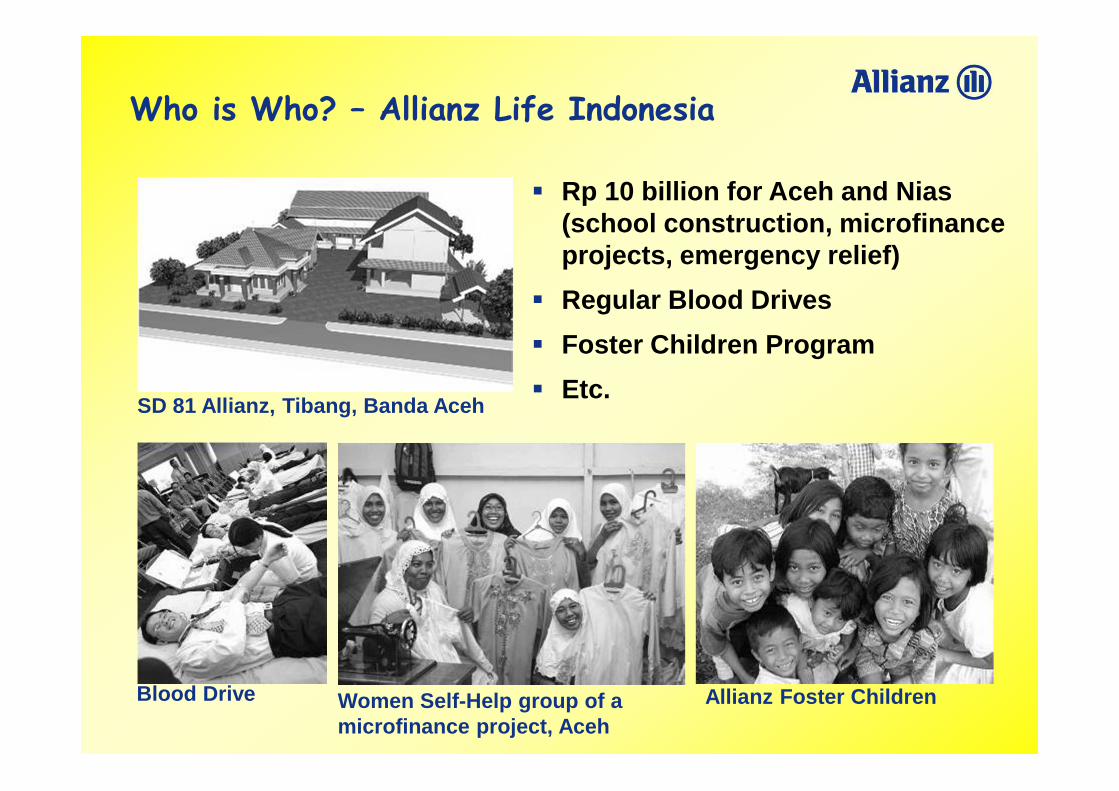

� Rp 10 billion for Aceh and Nias (school construction, microfinance projects, emergency relief)

� Regular Blood Drives

� Foster Children Program

� Etc.SD 81 Allianz, Tibang, Banda Aceh

Allianz Foster ChildrenBlood Drive Women Self-Help group of a microfinance project, Aceh

19

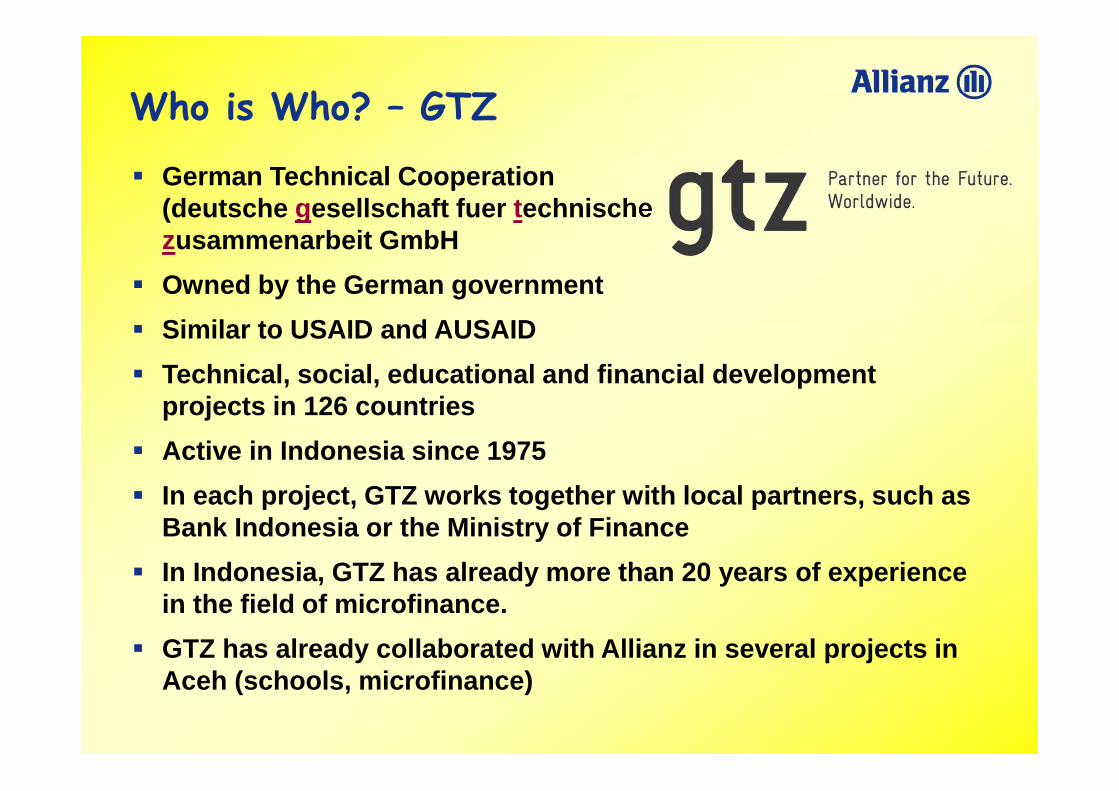

Who is Who? – GTZ

� German Technical Cooperation(deutsche gesellschaft fuer technische zusammenarbeit GmbH

� Owned by the German government

� Similar to USAID and AUSAID

� Technical, social, educational and financial development projects in 126 countries

� Active in Indonesia since 1975

� In each project, GTZ works together with local partners, such as Bank Indonesia or the Ministry of Finance

� In Indonesia, GTZ has already more than 20 years of experience in the field of microfinance.

� GTZ has already collaborated with Allianz in several projects in Aceh (schools, microfinance)

20

You can be proud

� The “Payung Keluarga” insurance program is the first time ever that Allianz Life Indonesia and GTZ are doing an insurance program for low-income households …

� … and we are very happy to be working with you …

� … because

Strong vision and mission

Strong and motivated team

Outstanding performance

21

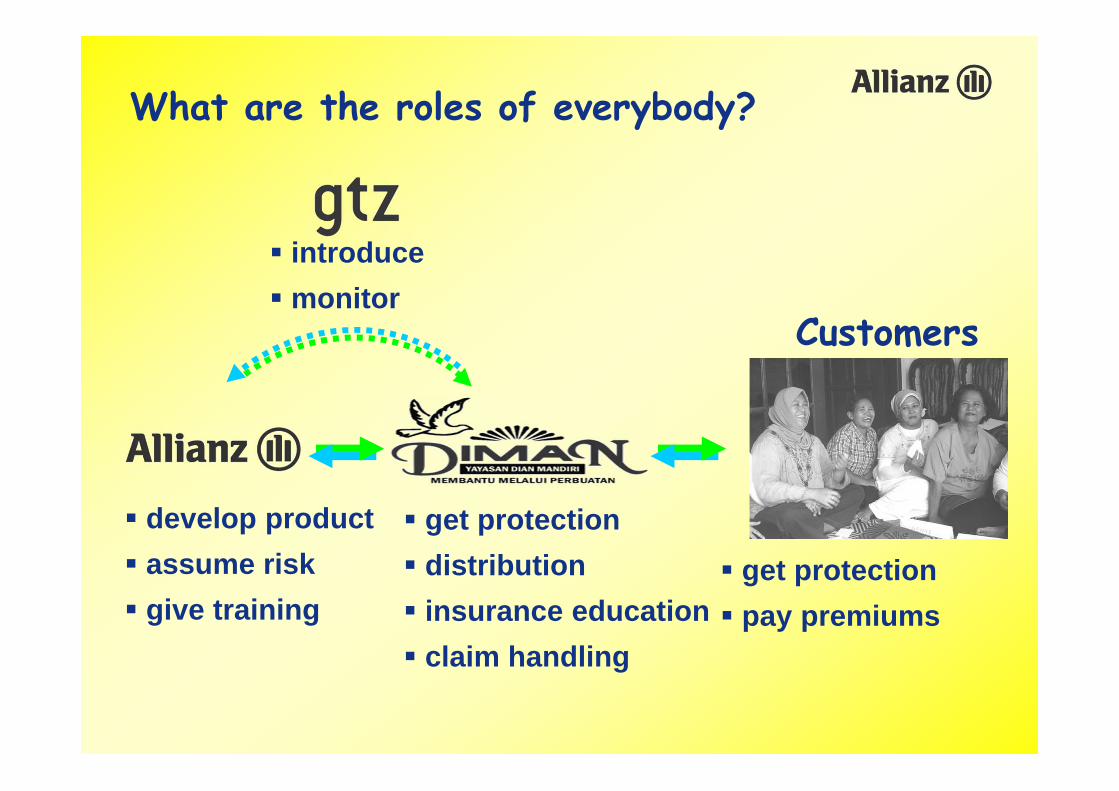

What are the roles of everybody?

� develop product

� assume risk

� give training

Customers

� get protection

� pay premiums

� get protection

� distribution

� insurance education

� claim handling

� introduce

� monitor

22

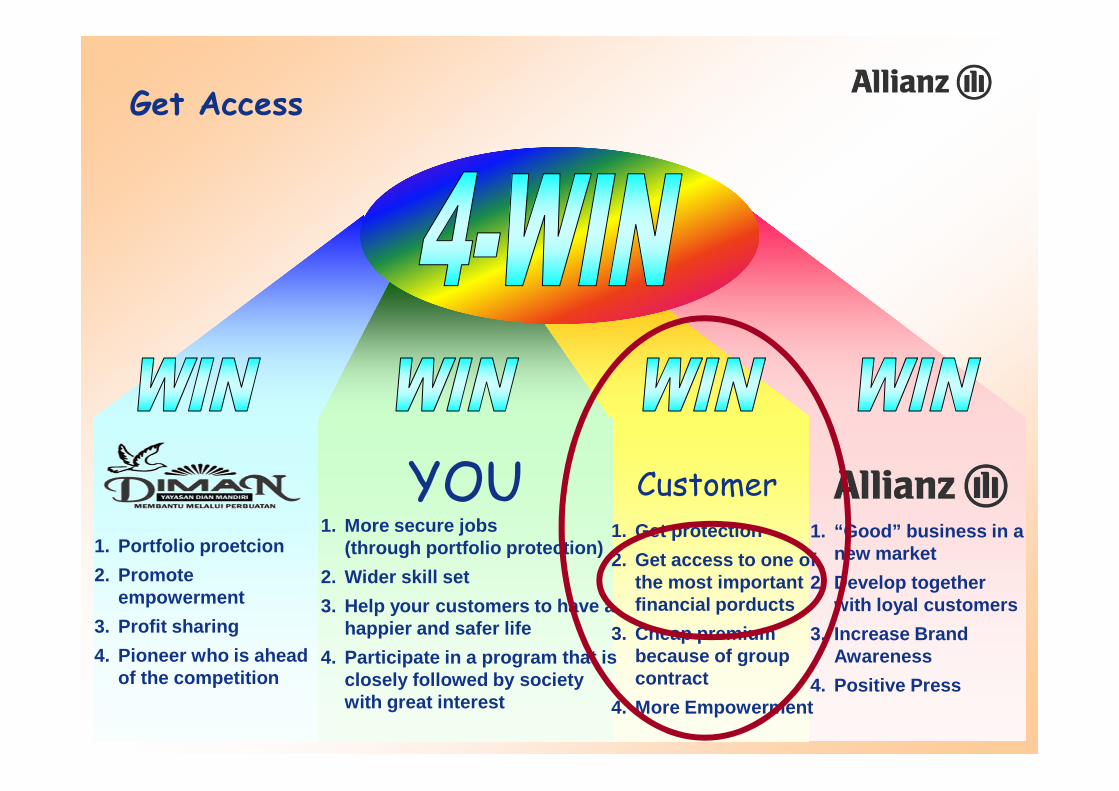

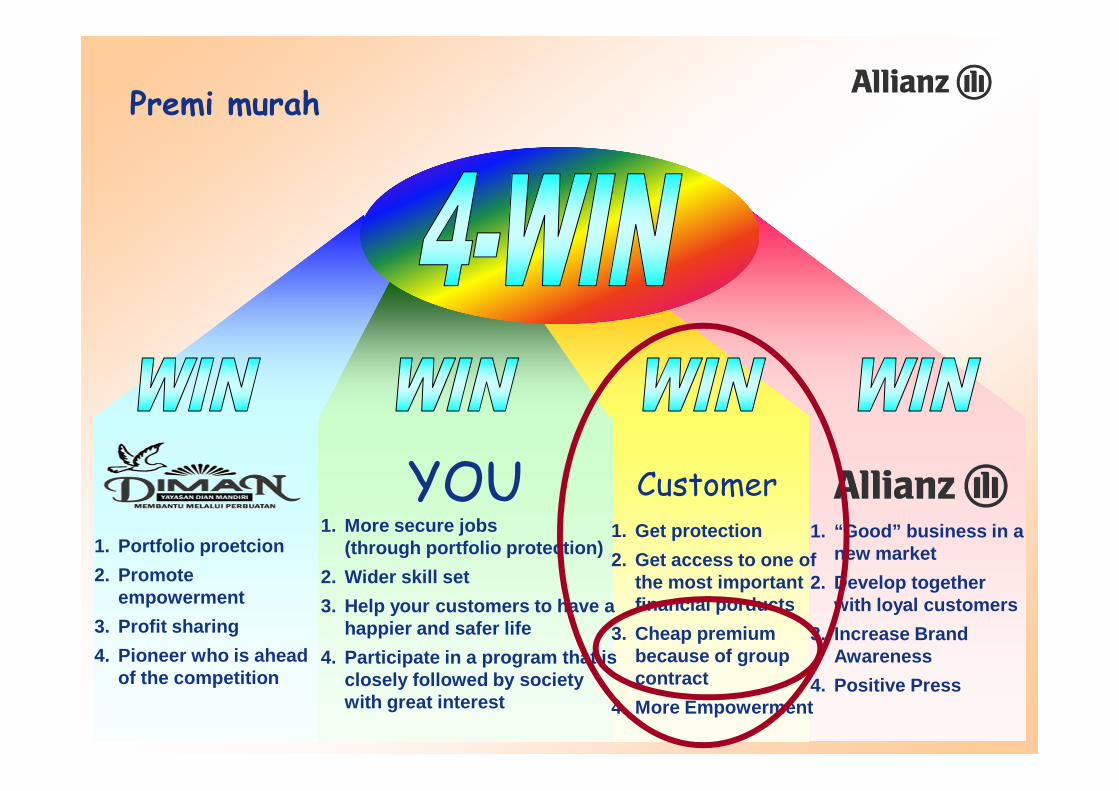

What are the benefits for all of us?

YOU Customer1. Get protection

2. Get access to one of the most important financial porducts

3. Cheap premium because of group contract

4. More Empowerment

1. “Good” business in a new market

2. Develop together with loyal customers

3. Increase Brand Awareness

4. Positive Press

1. Portfolio proetcion

2. Promote empowerment

3. Profit sharing

4. Pioneer who is ahead of the competition

1. More secure jobs(through portfolio protection)

2. Wider skill set

3. Help your customers to have a happier and safer life

4. Participate in a program that is closely followed by society with great interest

23

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

24

InsurancePrinciplesInsurancePrinciples

25

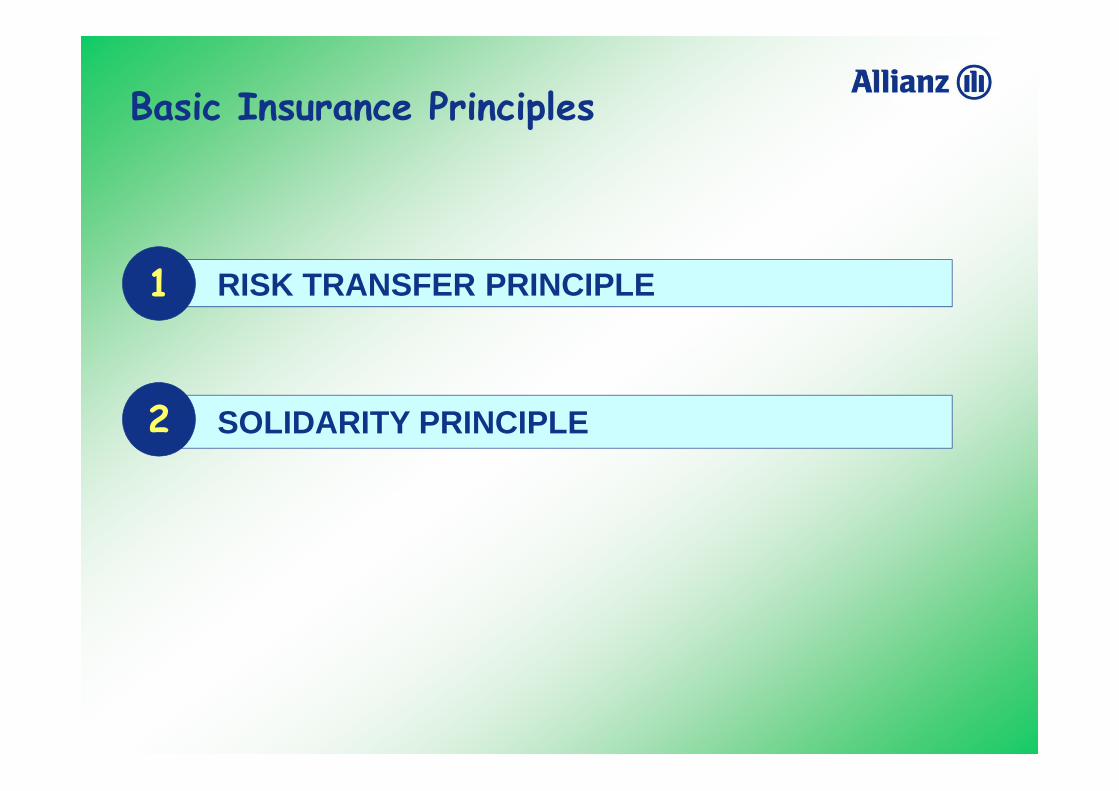

Basic Insurance Principles

1 RISK TRANSFER PRINCIPLE

SOLIDARITY PRINCIPLE2

26

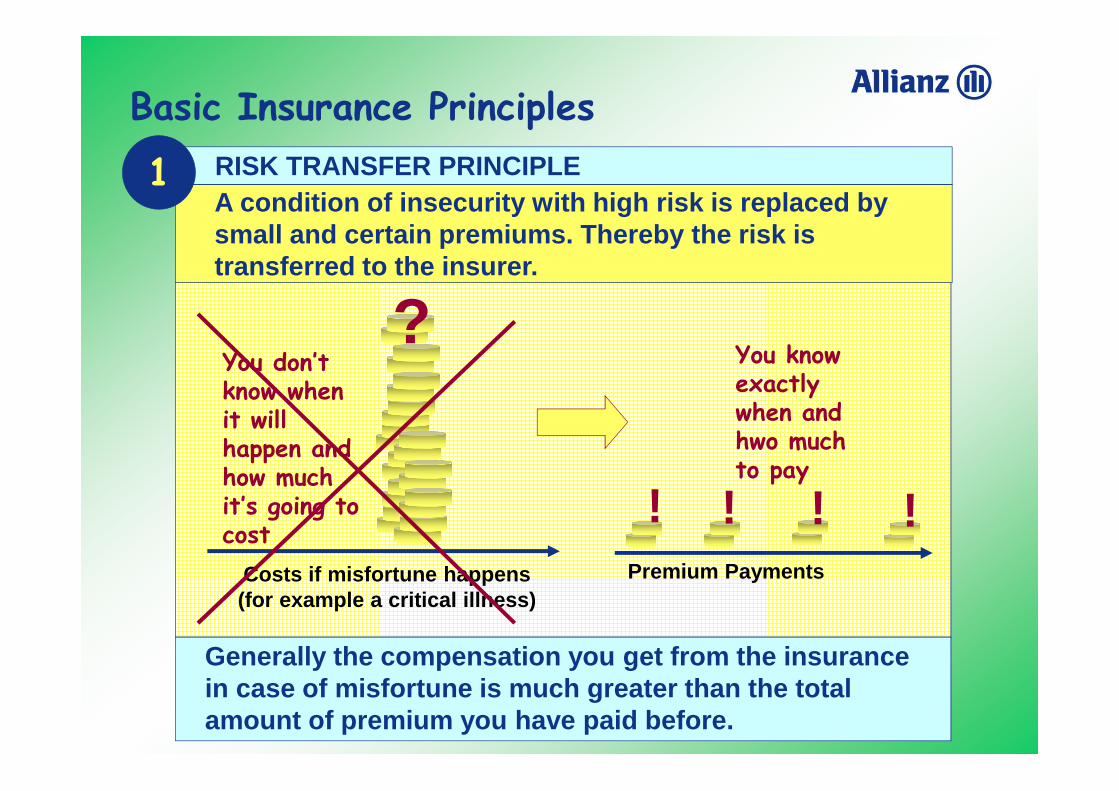

Basic Insurance Principles

A condition of insecurity with high risk is replaced by small and certain premiums. Thereby the risk is transferred to the insurer.

Generally the compensation you get from the insurance in case of misfortune is much greater than the total amount of premium you have paid before.

Costs if misfortune happens (for example a critical illness)

?You don’t know when it will happen and how much it’s going to cost

Premium Payments

! ! ! !

You know exactly when and hwo much to pay

1 RISK TRANSFER PRINCIPLE

27

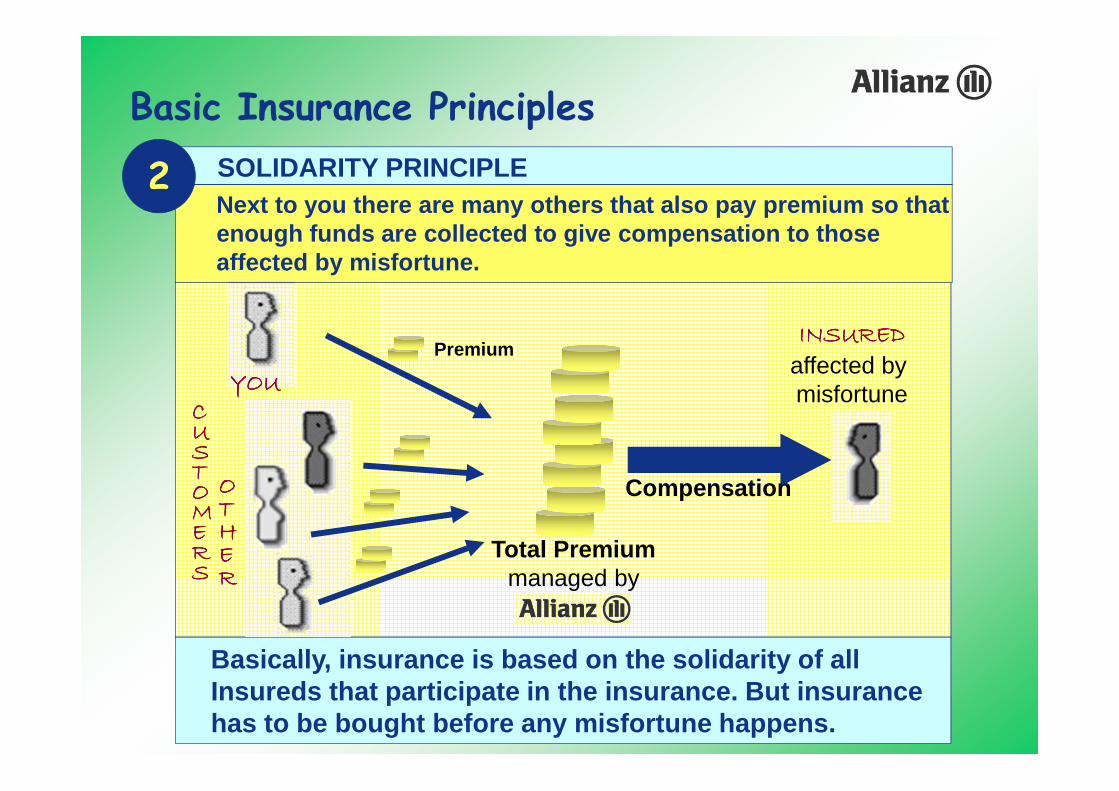

Basic Insurance Principles

Next to you there are many others that also pay premium so that enough funds are collected to give compensation to those affected by misfortune.

Basically, insurance is based on the solidarity of all Insureds that participate in the insurance. But insurance has to be bought before any misfortune happens.

YOUYOUYOUYOUCCCCUUUUSSSSTTTTOOOOMMMMEEEERRRRSSSS

OOOOTTTTHHHHEEEERRRR

Premium

Total Premiummanaged by

Compensation

SOLIDARITY PRINCIPLE2

INSUREDINSUREDINSUREDINSUREDaffected by misfortune

28

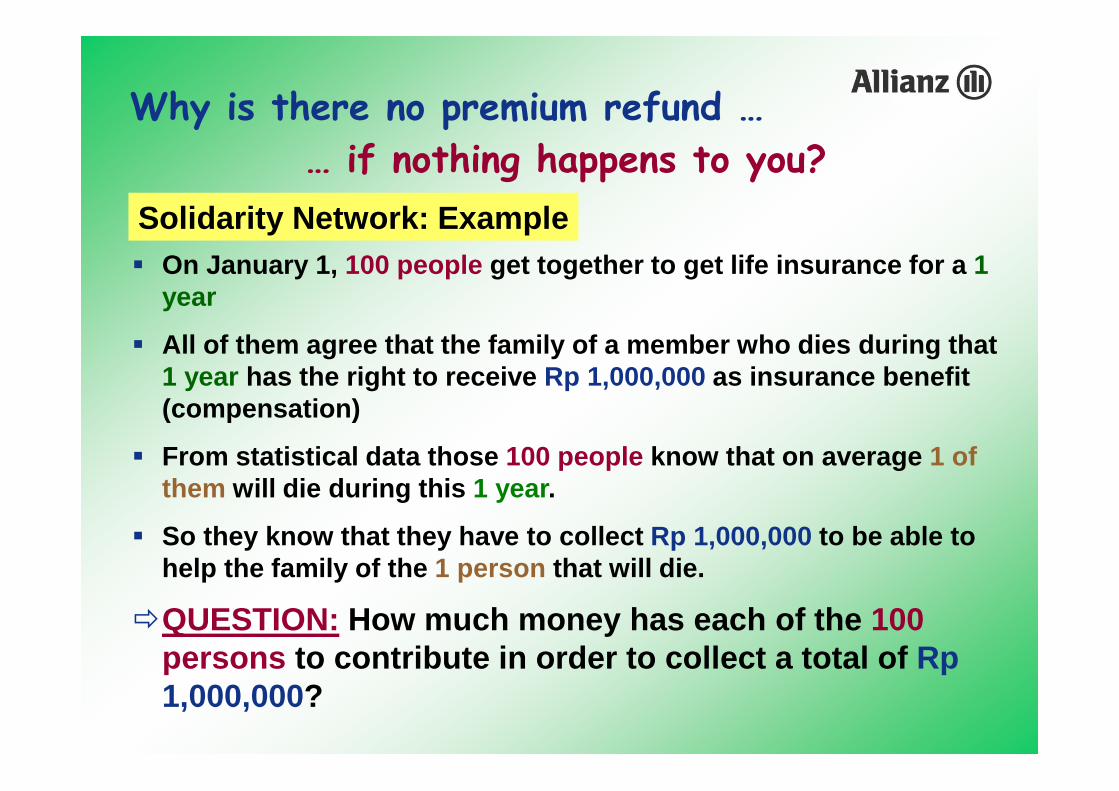

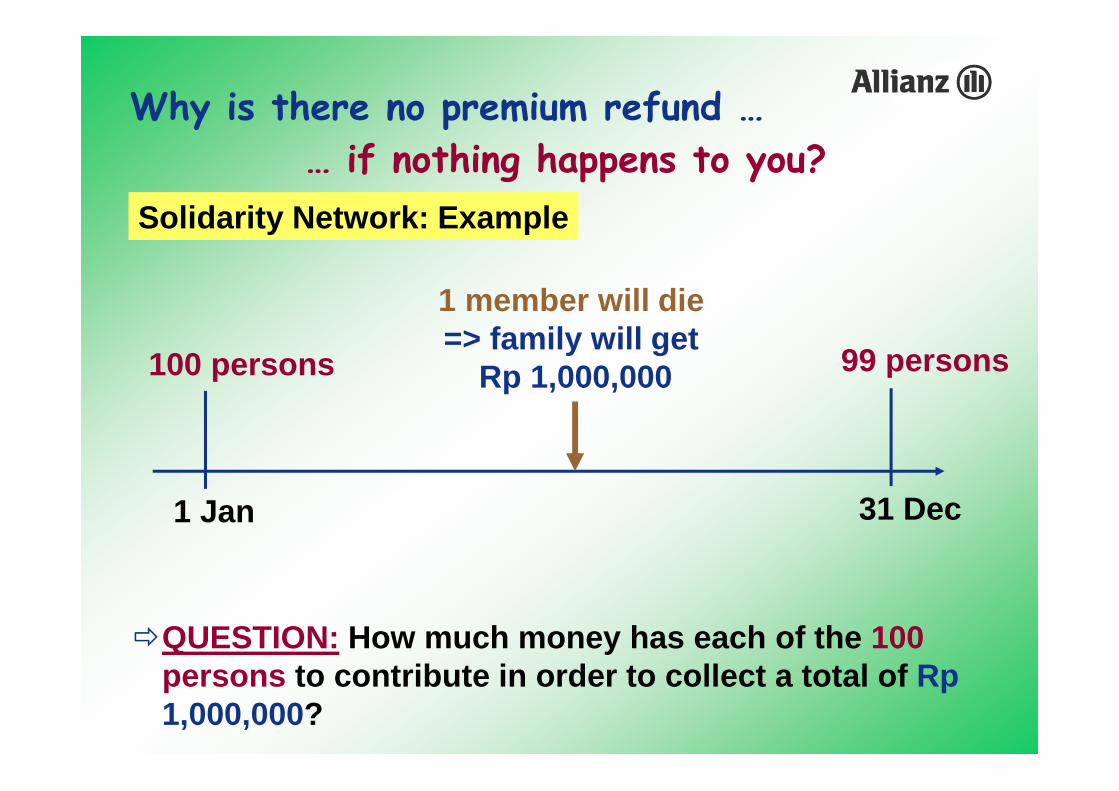

Why is there no premium refund …

… if nothing happens to you?

Solidarity Network: Example� On January 1, 100 people get together to get life insurance for a 1

year

� All of them agree that the family of a member who dies during that 1 year has the right to receive Rp 1,000,000 as insurance benefit (compensation)

� From statistical data those 100 people know that on average 1 of them will die during this 1 year.

� So they know that they have to collect Rp 1,000,000 to be able to help the family of the 1 person that will die.

�QUESTION: How much money has each of the 100 persons to contribute in order to collect a total of Rp 1,000,000?

29

Why is there no premium refund …

… if nothing happens to you?

Solidarity Network: Example

�QUESTION: How much money has each of the 100 persons to contribute in order to collect a total of Rp 1,000,000?

1 Jan

100 persons

31 Dec

1 member will die=> family will get

Rp 1,000,000 99 persons

30

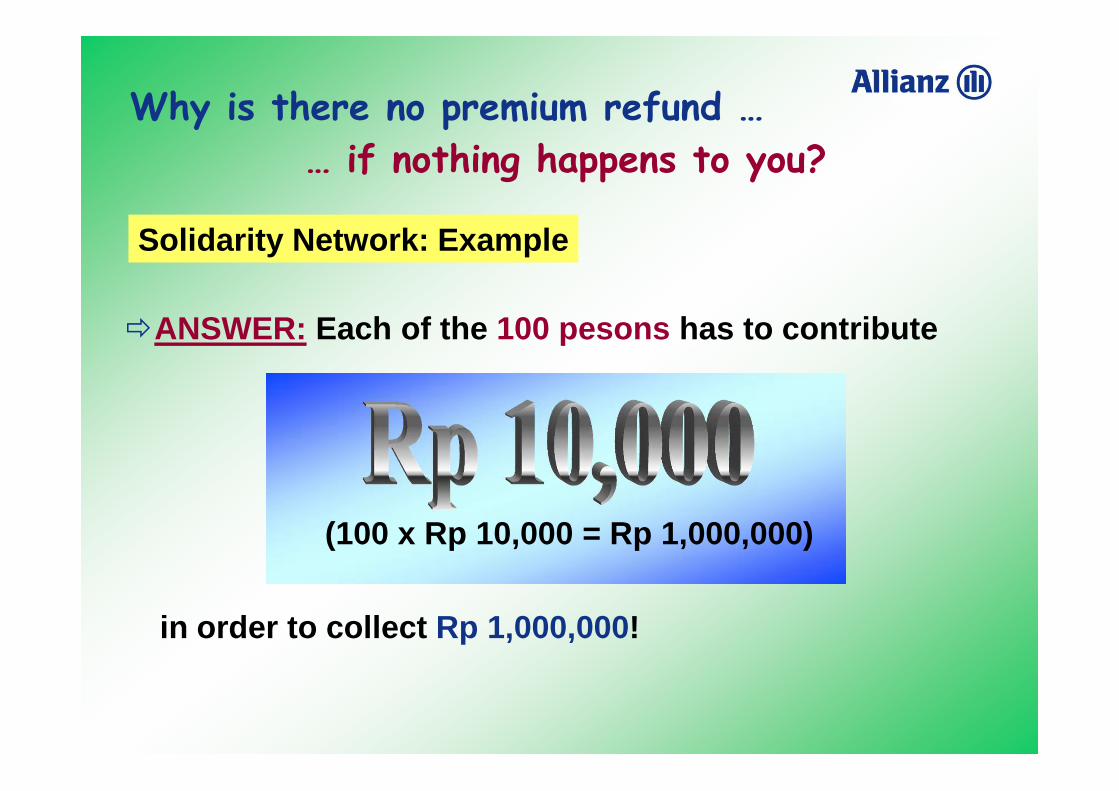

Why is there no premium refund …

… if nothing happens to you?

Solidarity Network: Example

�ANSWER: Each of the 100 pesons has to contribute

in order to collect Rp 1,000,000!

(100 x Rp 10,000 = Rp 1,000,000)

31

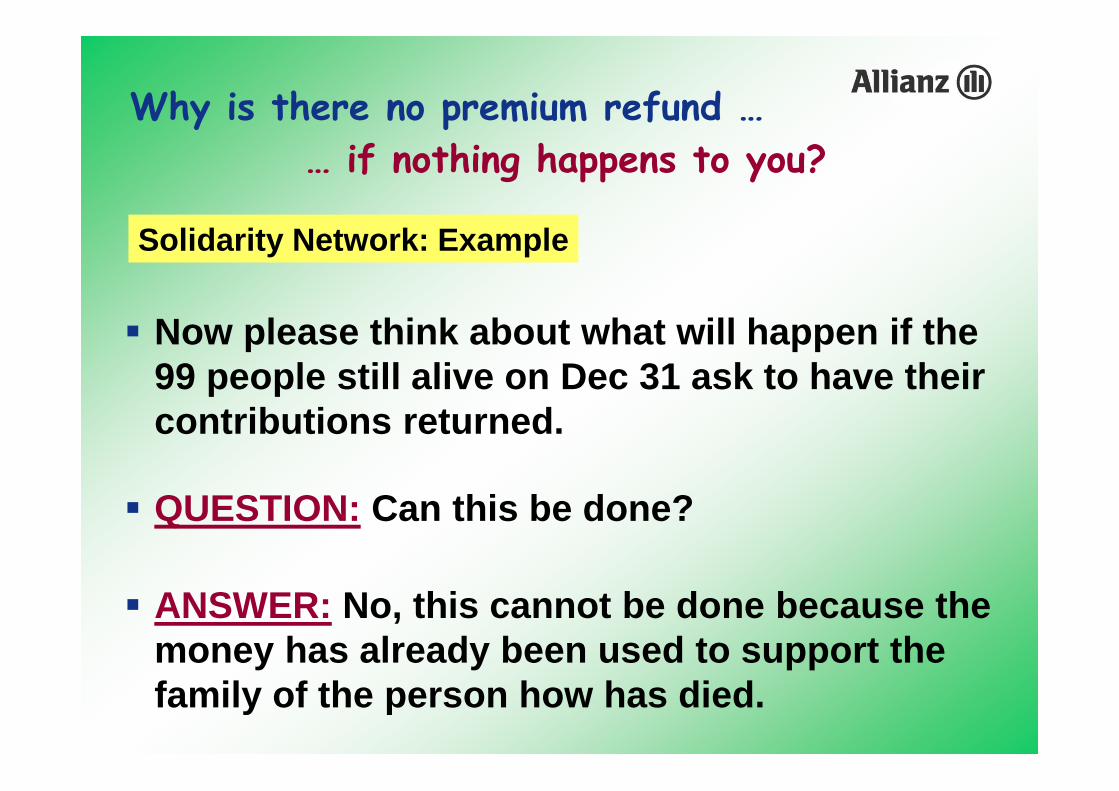

Why is there no premium refund …

… if nothing happens to you?

Solidarity Network: Example

� Now please think about what will happen if the 99 people still alive on Dec 31 ask to have their contributions returned.

� QUESTION: Can this be done?

� ANSWER: No, this cannot be done because the money has already been used to support the family of the person how has died.

32

Basic Insurance Principles

1 RISK TRANSFER PRINCIPLE

SOLIDARITY PRINCIPLE2

Please explain

33

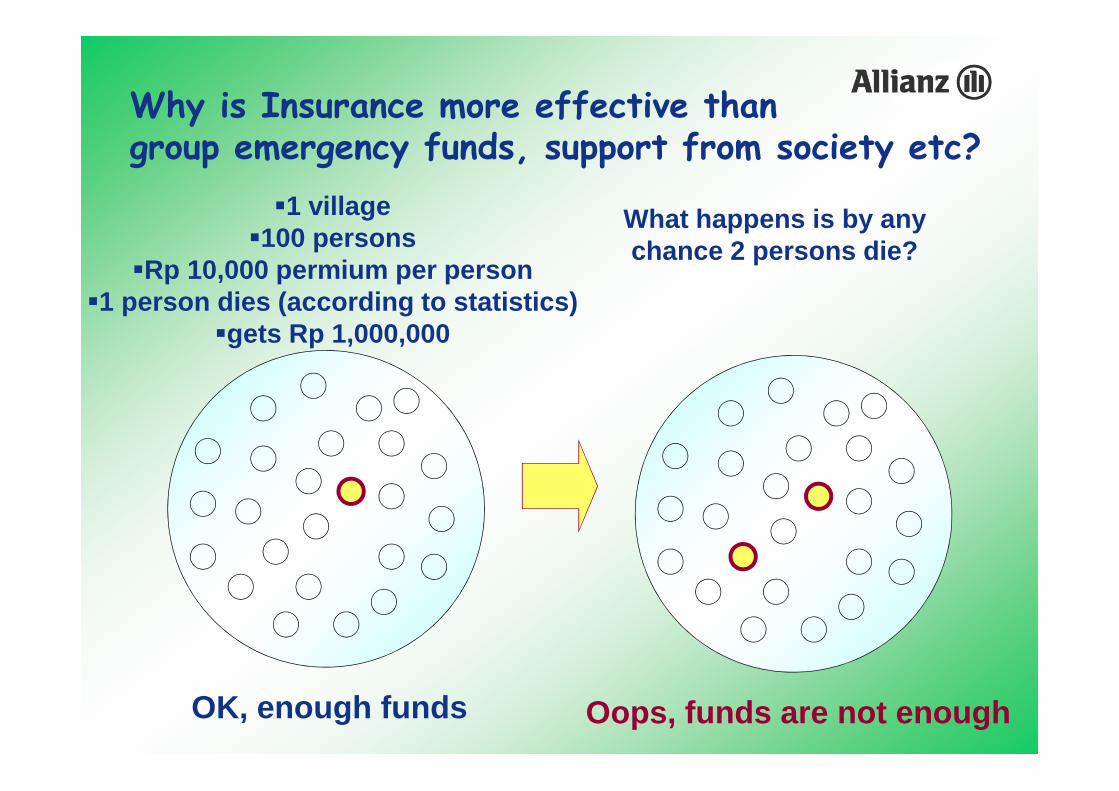

Why is Insurance more effective than group emergency funds, support from society etc?

�1 village�100 persons

�Rp 10,000 permium per person�1 person dies (according to statistics)

�gets Rp 1,000,000

OK, enough funds

What happens is by any chance 2 persons die?

Oops, funds are not enough

34

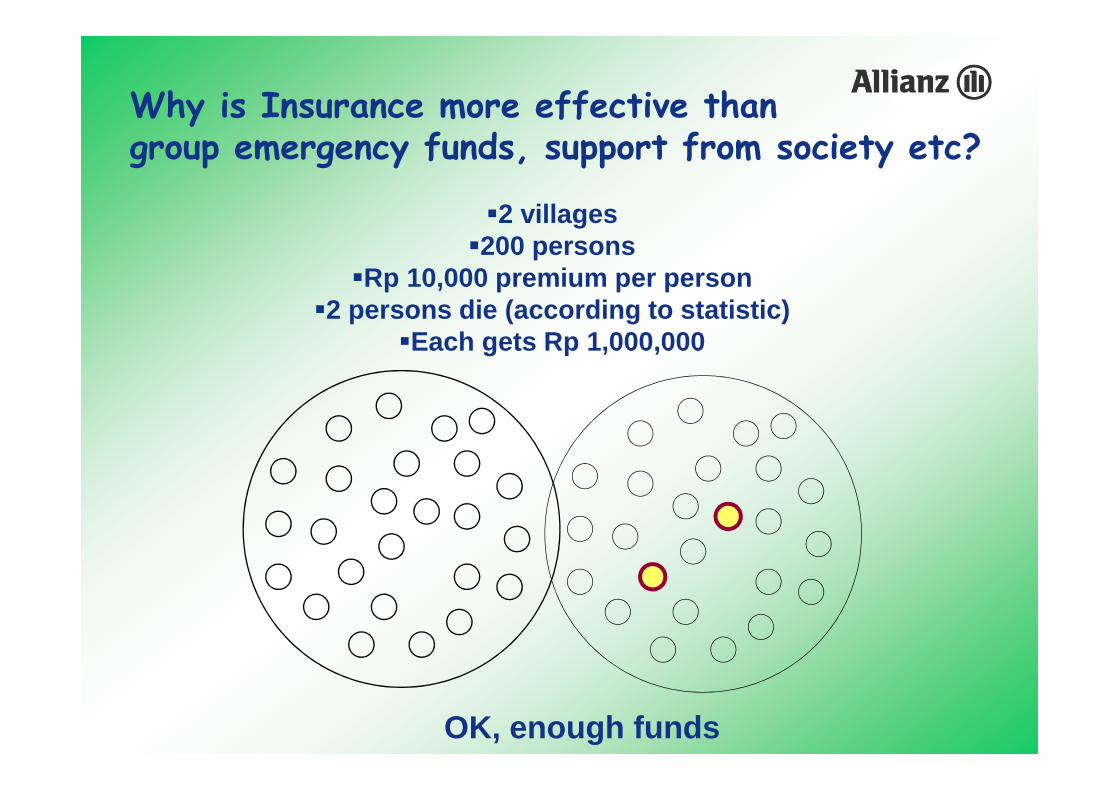

Why is Insurance more effective than group emergency funds, support from society etc?

�2 villages�200 persons

�Rp 10,000 premium per person�2 persons die (according to statistic)

�Each gets Rp 1,000,000

OK, enough funds

35

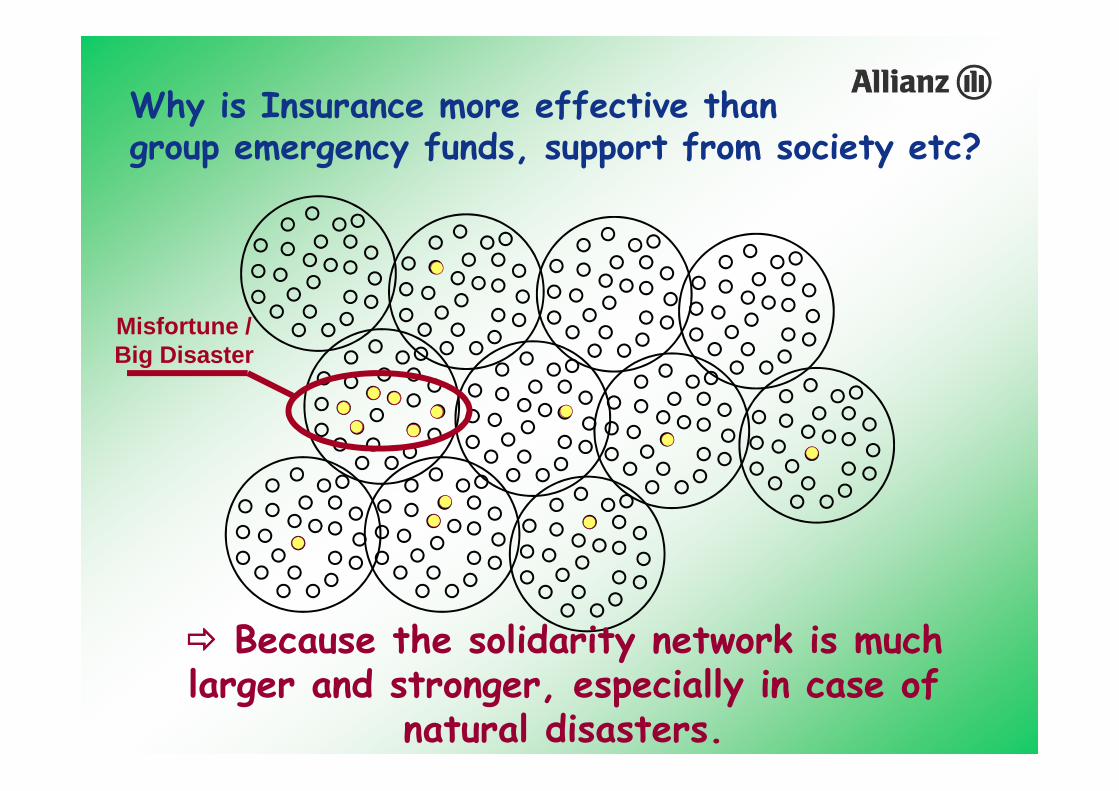

Why is Insurance more effective than group emergency funds, support from society etc?

���� Because the solidarity network is much larger and stronger, especially in case of

natural disasters.

Misfortune / Big Disaster

36

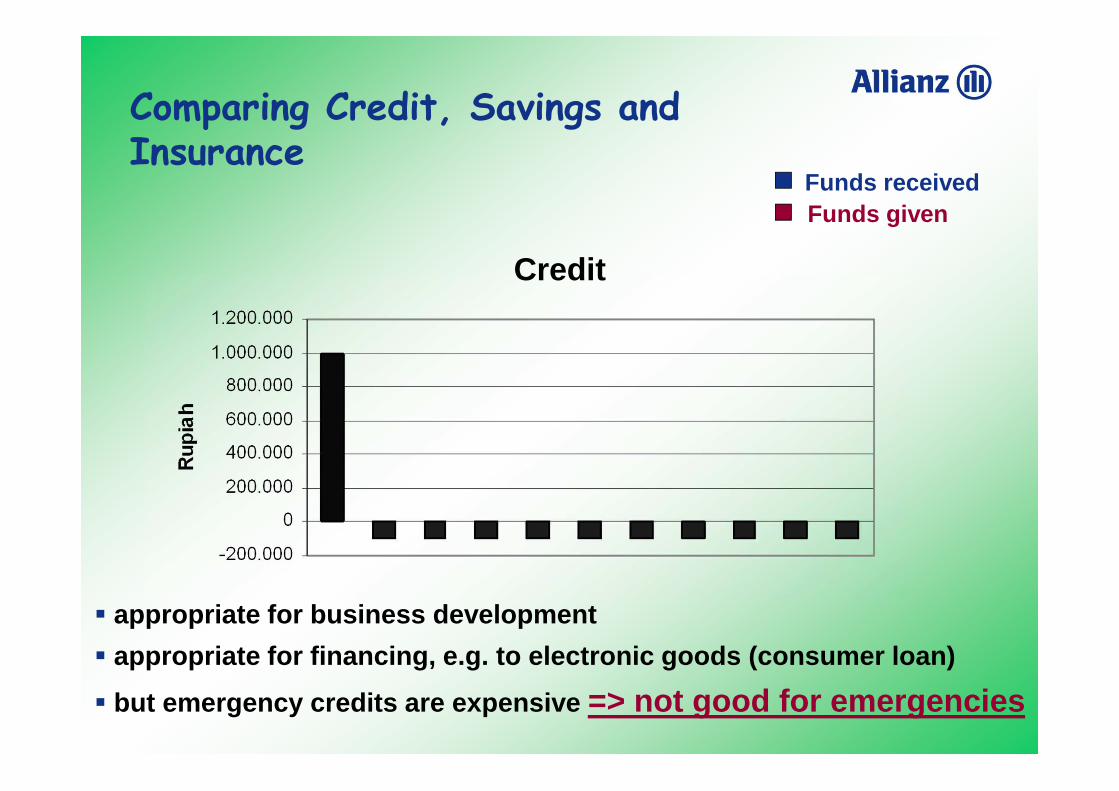

Comparing Credit, Savings and Insurance

Funds receivedFunds given

Credit

� appropriate for business development

� appropriate for financing, e.g. to electronic goods (consumer loan)

� but emergency credits are expensive => not good for emergencies

37

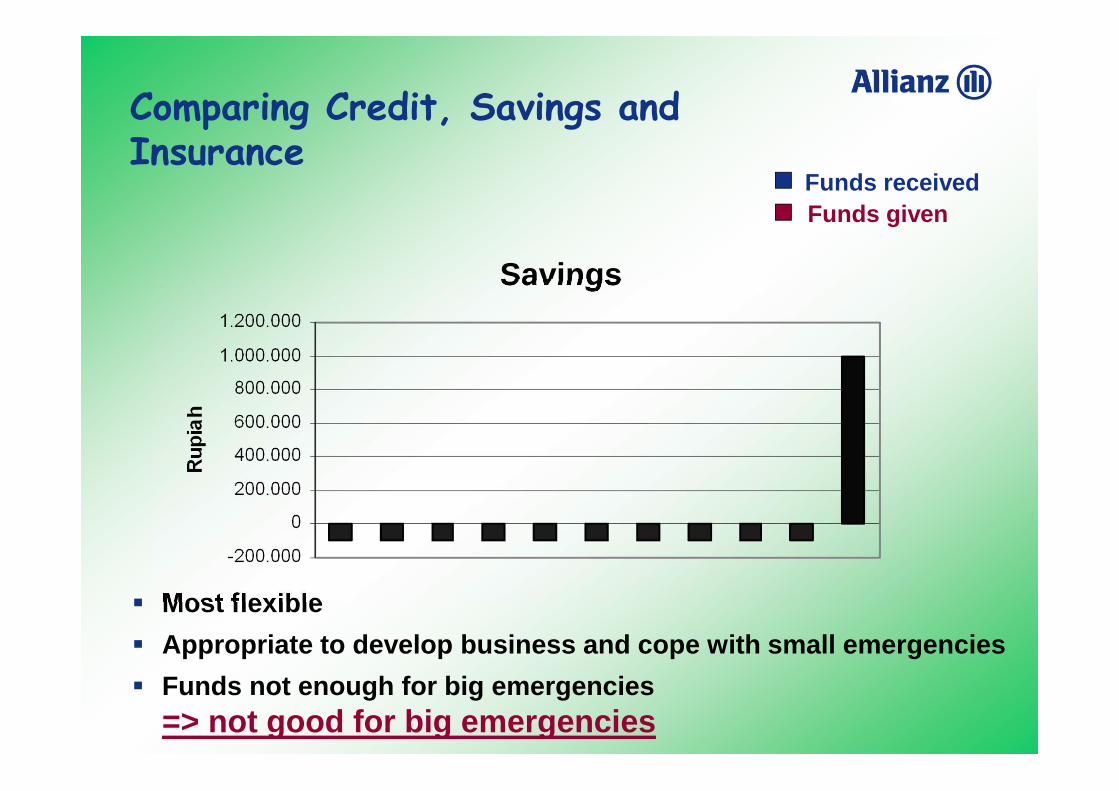

Comparing Credit, Savings and Insurance

Savings

� Most flexible

� Appropriate to develop business and cope with small emergencies

� Funds not enough for big emergencies => not good for big emergencies

Funds receivedFunds given

38

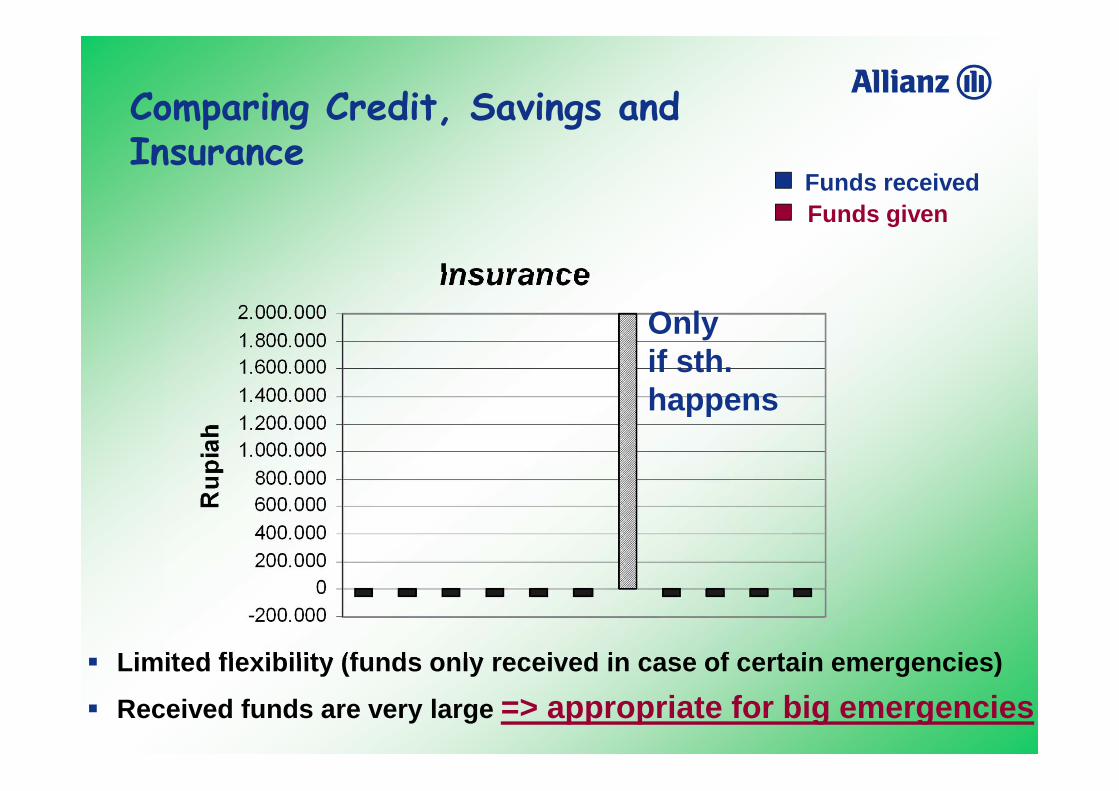

Comparing Credit, Savings and Insurance

� Limited flexibility (funds only received in case of certain emergencies)

� Received funds are very large => appropriate for big emergencies

Funds receivedFunds given

Insurance

Only if sth. happens

39

Comparing Credit, Savings and Insurance

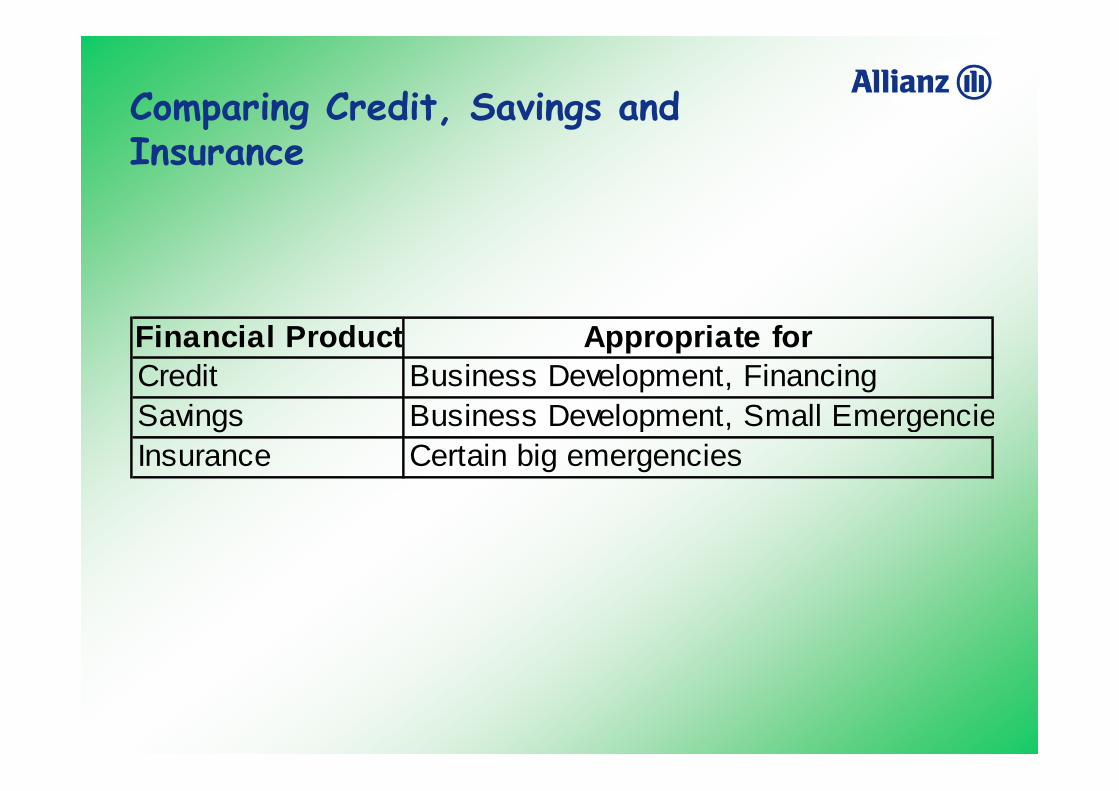

Financial Product Appropriate forCredit Business Development, FinancingSavings Business Development, Small EmergenciesInsurance Certain big emergencies

40

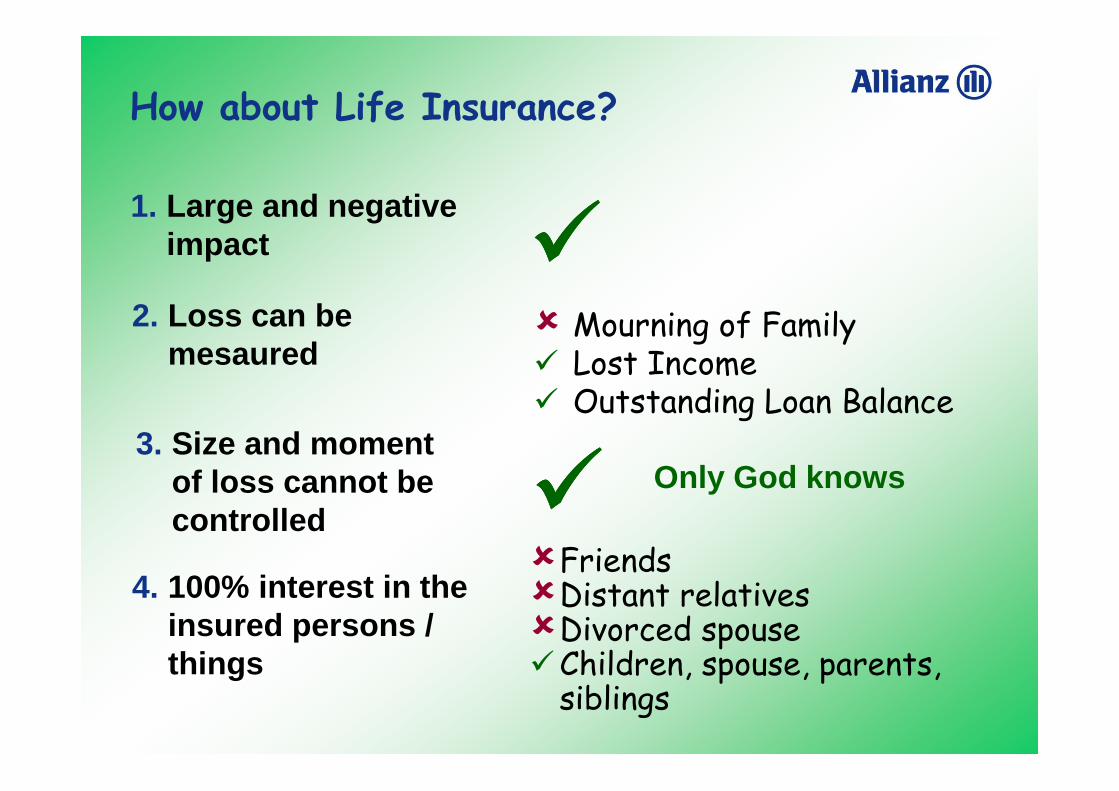

What can be insured?

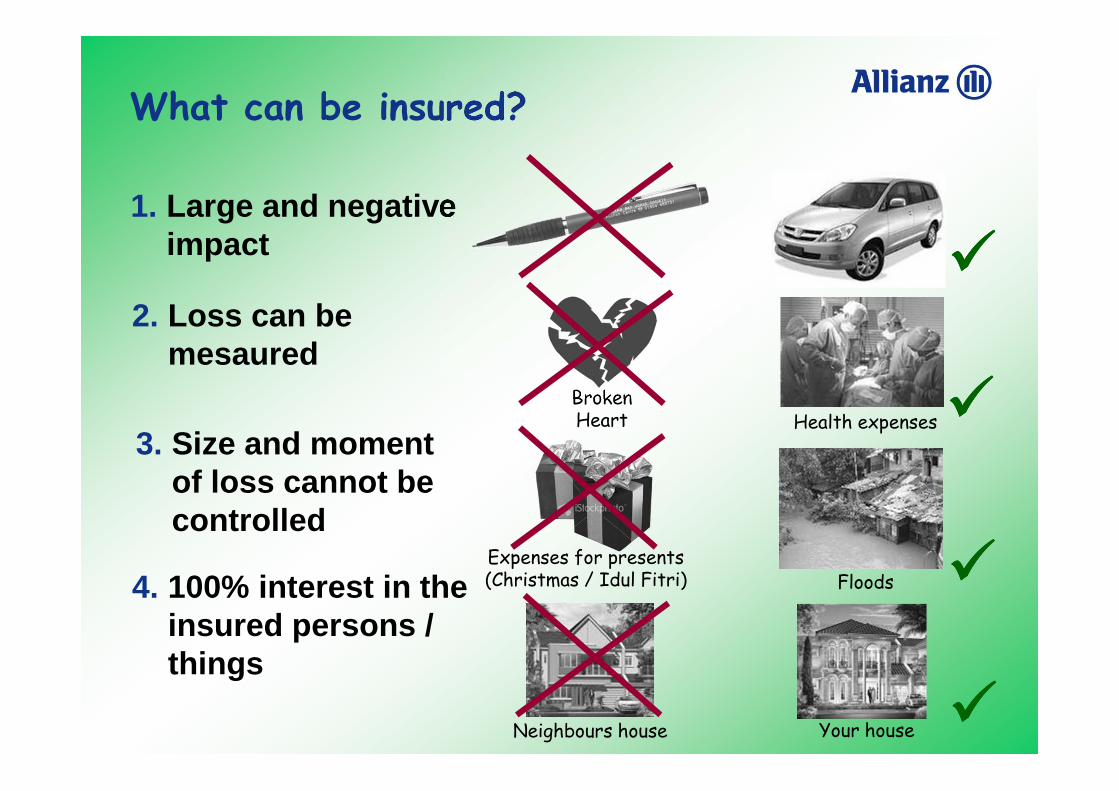

1. Large and negative impact ����

BrokenHeart Health expenses����

Expenses for presents(Christmas / Idul Fitri) ����Floods

Neighbours house Your house ����

2. Loss can be mesaured

3. Size and moment of loss cannot be controlled

4. 100% interest in the insured persons / things

41

How about Life Insurance?

� Mourning of Family� Lost Income� Outstanding Loan Balance

����

�Friends �Distant relatives�Divorced spouse�Children, spouse, parents,

siblings

���� Only God knows

1. Large and negative impact

3. Size and moment of loss cannot be controlled

4. 100% interest in the insured persons / things

2. Loss can be mesaured

42

How about Life Insurance?

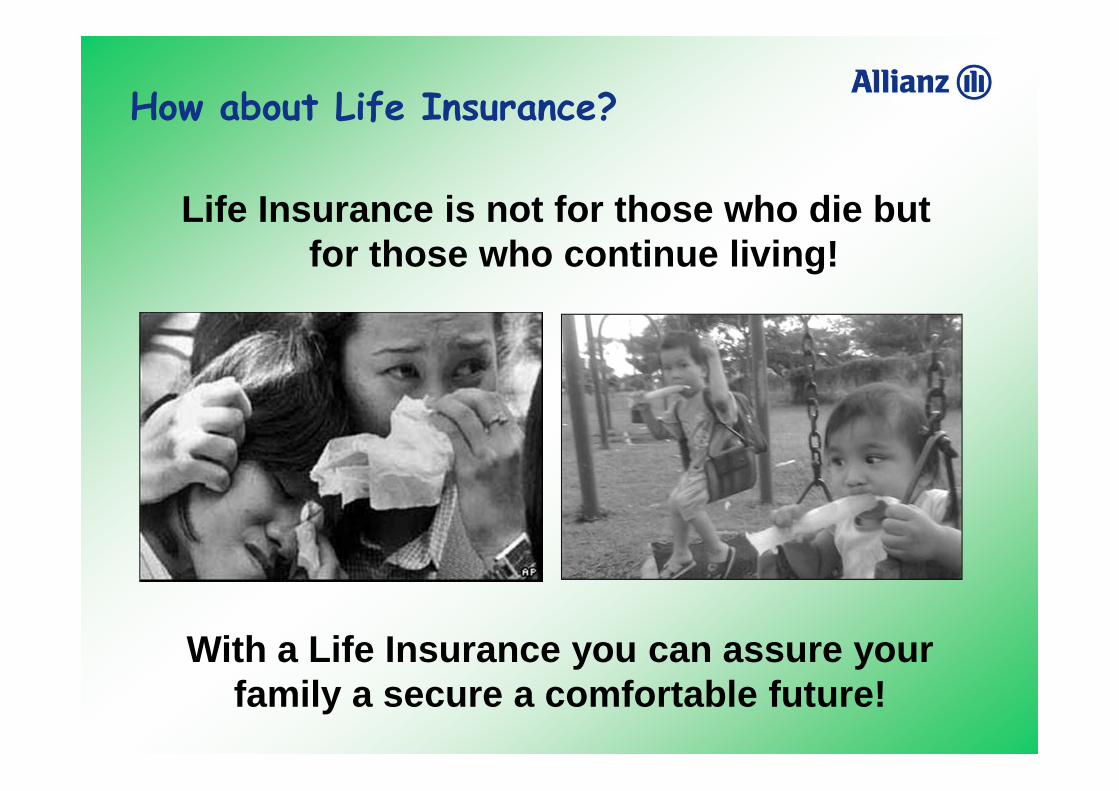

Life Insurance is not for those who die but for those who continue living!

With a Life Insurance you can assure your family a secure a comfortable future!

43

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

44

MotivationMotivation

45

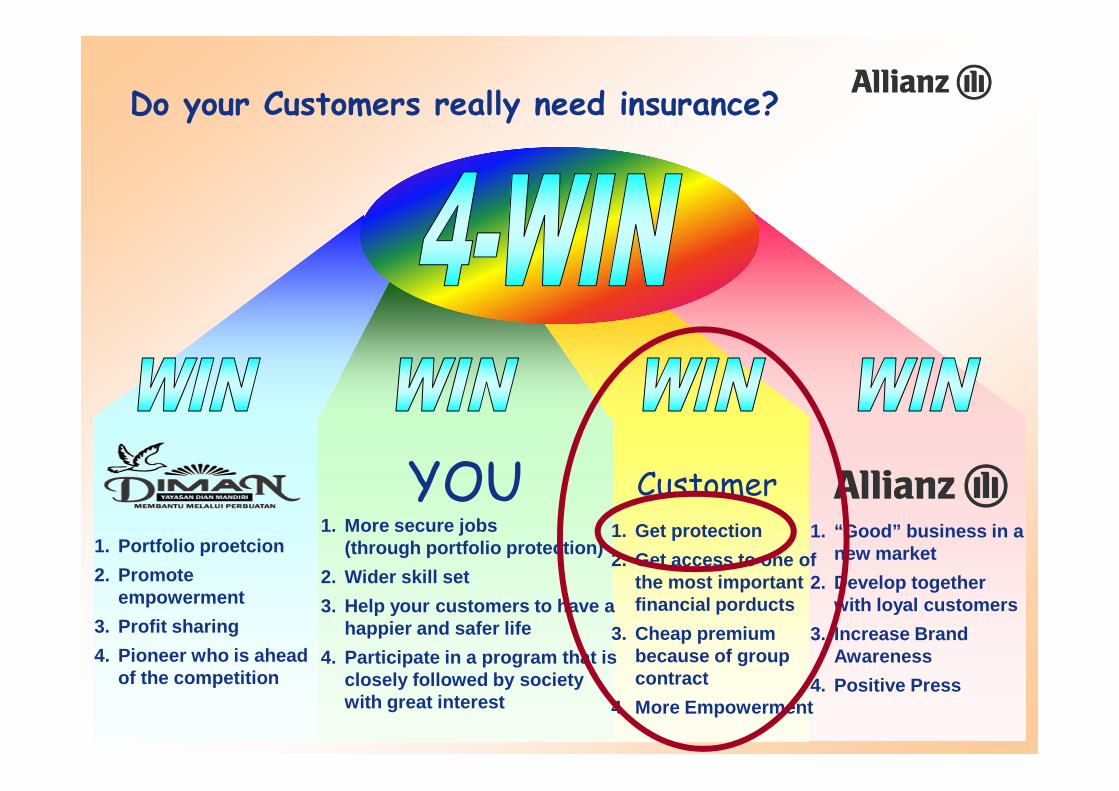

Do your Customers really need insurance?

YOU Customer1. Get protection

2. Get access to one of the most important financial porducts

3. Cheap premium because of group contract

4. More Empowerment

1. “Good” business in a new market

2. Develop together with loyal customers

3. Increase Brand Awareness

4. Positive Press

1. Portfolio proetcion

2. Promote empowerment

3. Profit sharing

4. Pioneer who is ahead of the competition

1. More secure jobs(through portfolio protection)

2. Wider skill set

3. Help your customers to have a happier and safer life

4. Participate in a program that is closely followed by society with great interest

46

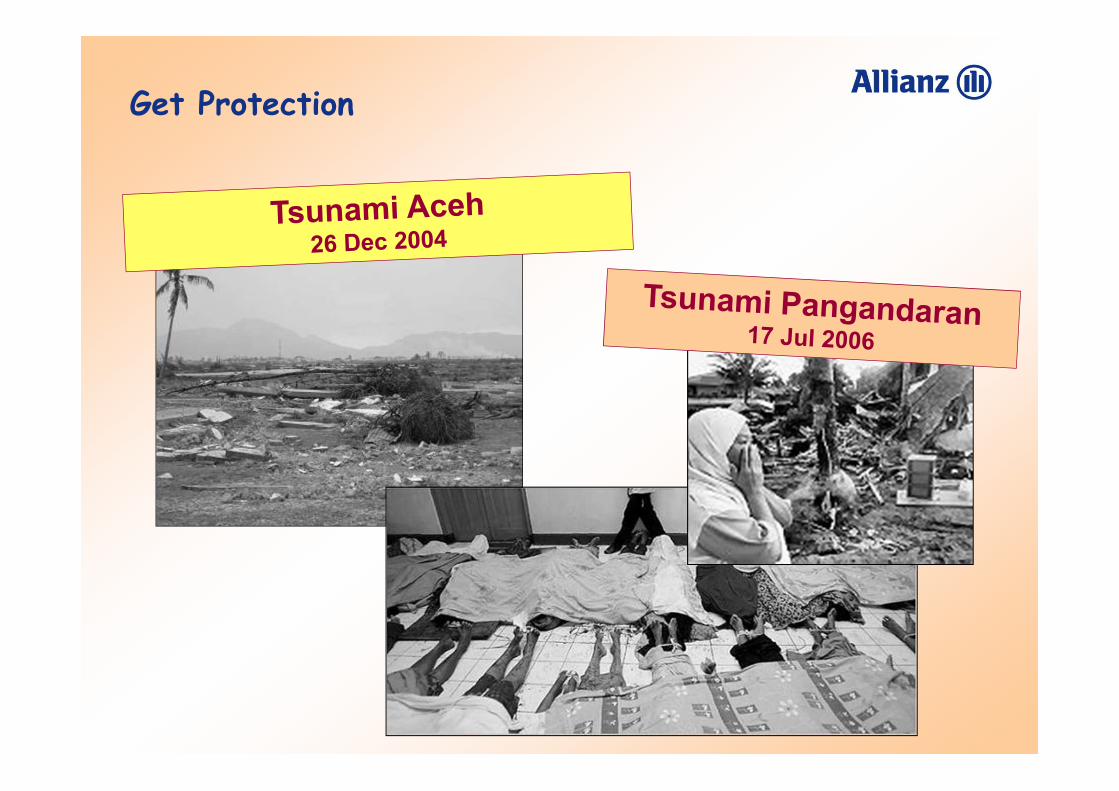

Get Protection

47

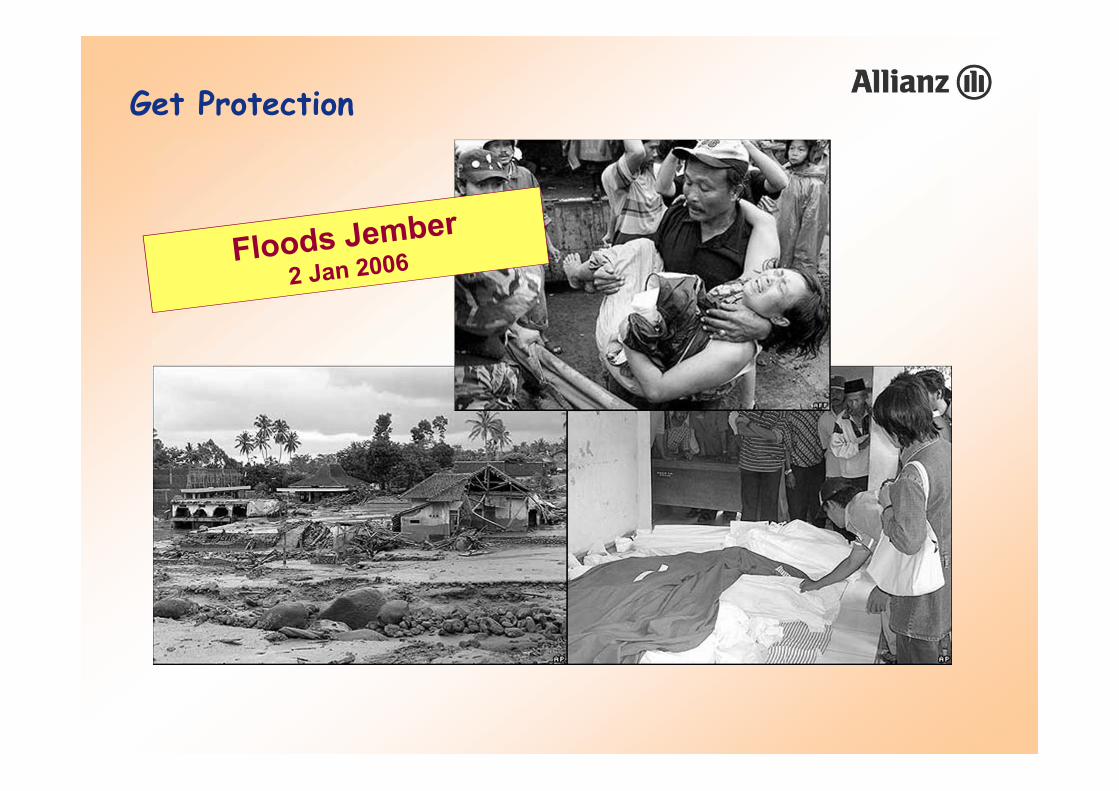

Get Protection

48

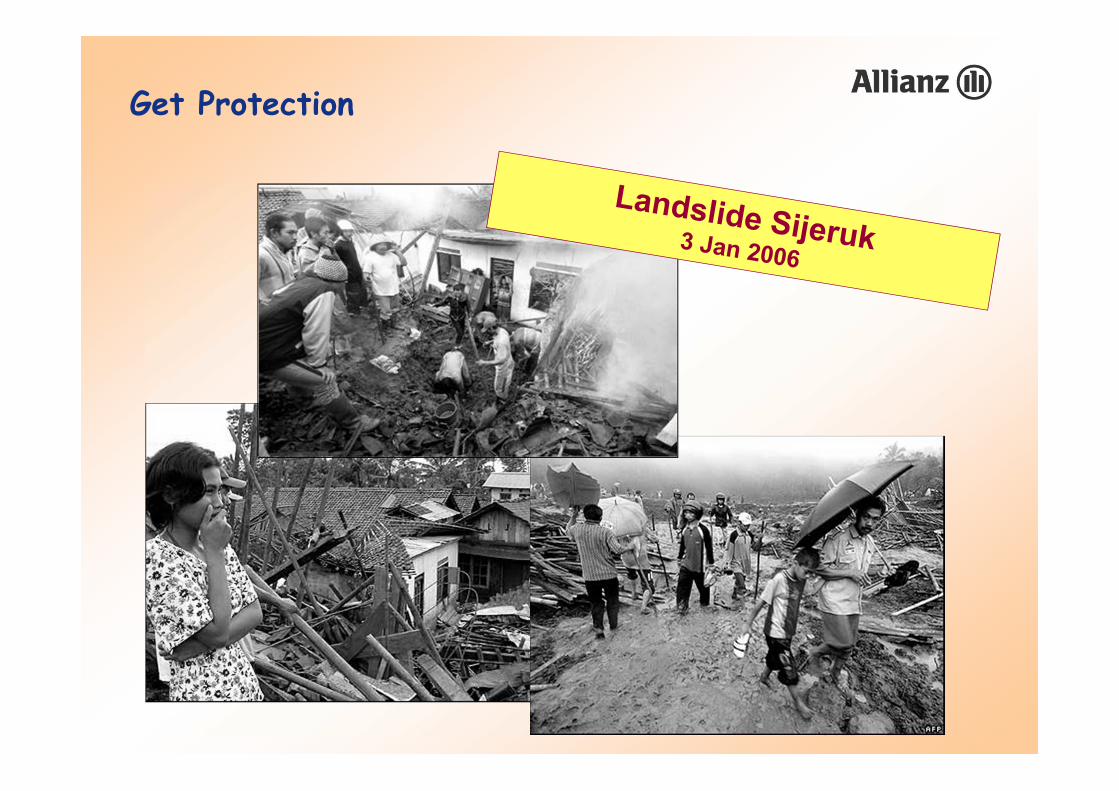

Get Protection

49

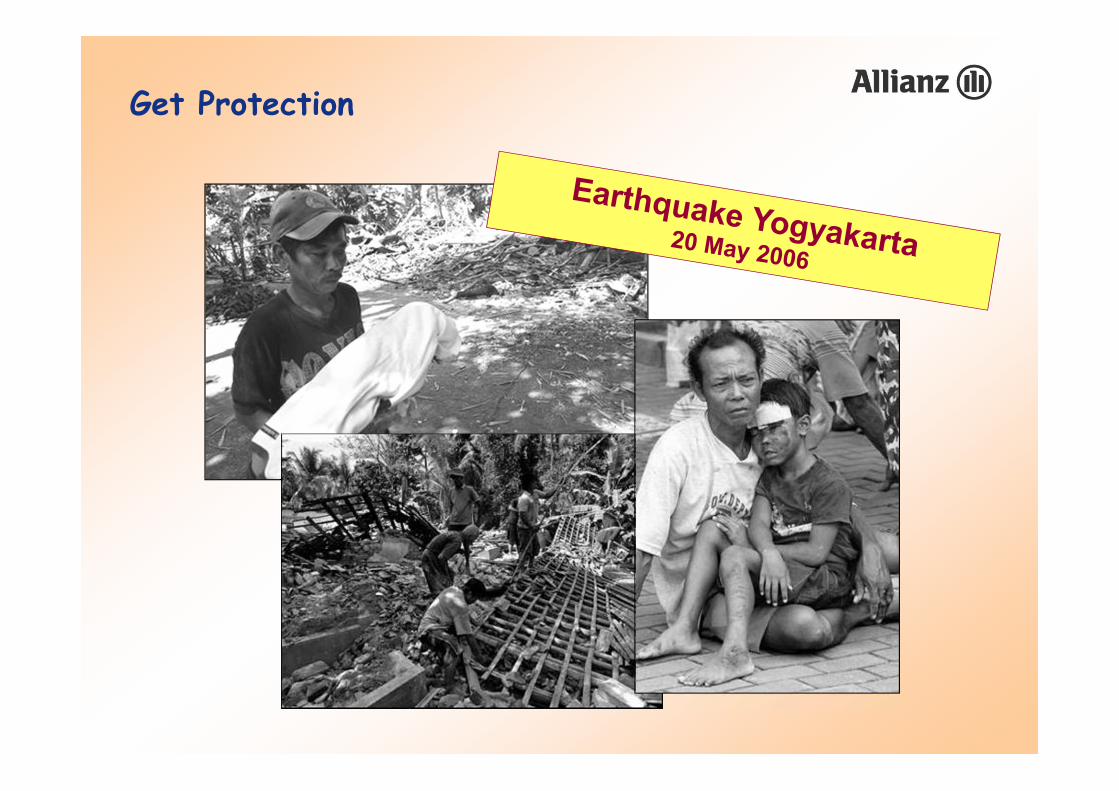

Get Protection

50

Get Protection

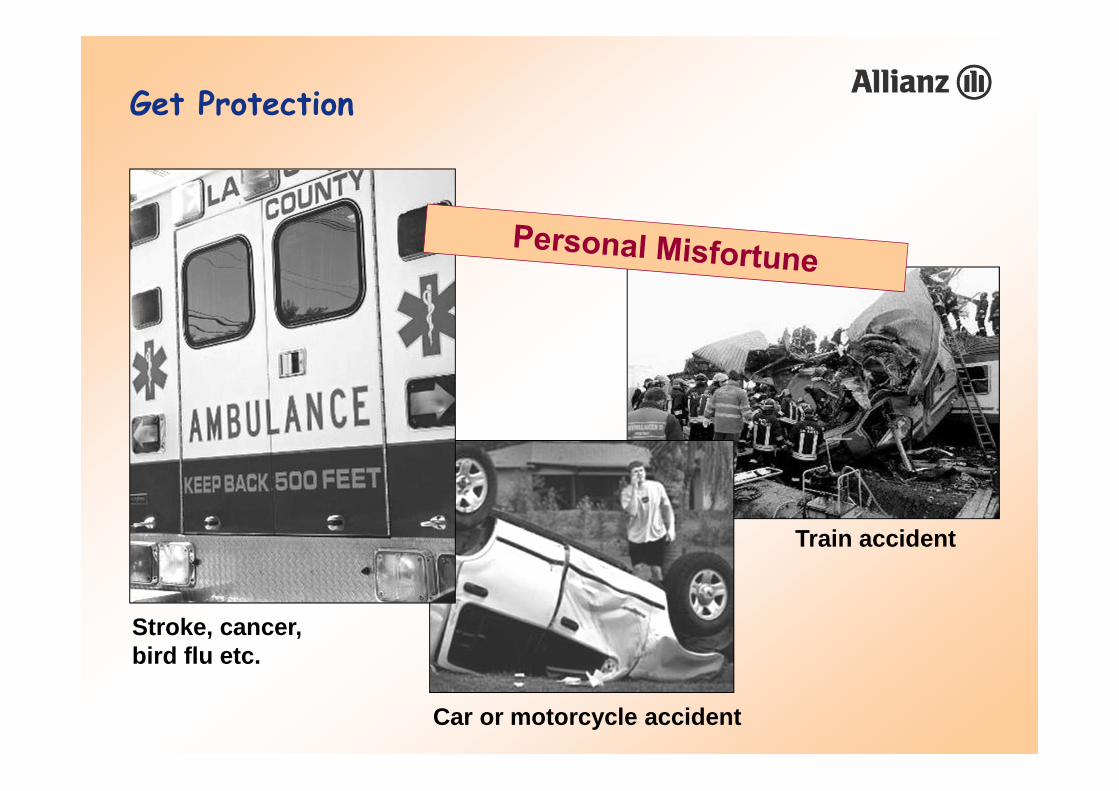

Train accident

Car or motorcycle accident

Stroke, cancer,bird flu etc.

51

Get Protection

� Normally it is low-income households who are most affected by and suffer the most from misfortune.

• they live “closest” to the risk, for instance in houses close to flood prone areas, less strong houses etc.

• They have no assets, savings or insurance to quickly cope with the inflicted losses

52

Get Access

YOU Customer1. Get protection

2. Get access to one of the most important financial porducts

3. Cheap premium because of group contract

4. More Empowerment

1. “Good” business in a new market

2. Develop together with loyal customers

3. Increase Brand Awareness

4. Positive Press

1. Portfolio proetcion

2. Promote empowerment

3. Profit sharing

4. Pioneer who is ahead of the competition

1. More secure jobs(through portfolio protection)

2. Wider skill set

3. Help your customers to have a happier and safer life

4. Participate in a program that is closely followed by society with great interest

53

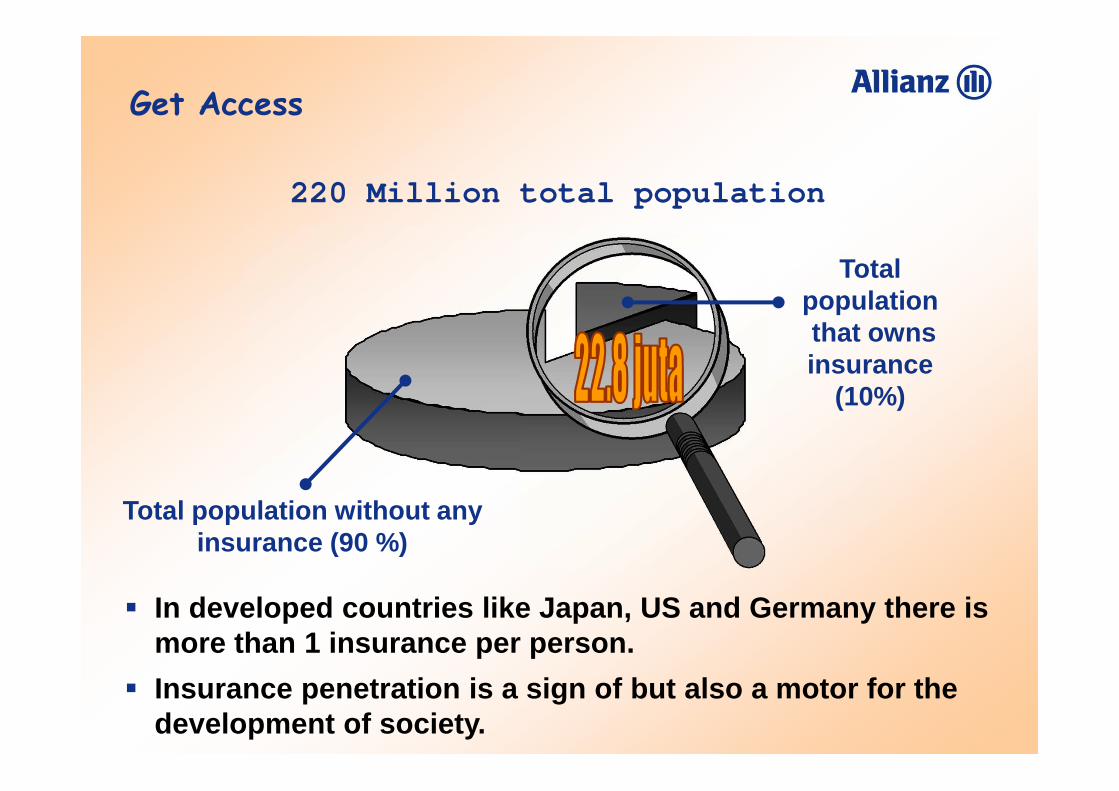

220 Million total population

Total population without any insurance (90 %)

Total populationthat owns insurance

(10%)

� In developed countries like Japan, US and Germany there is more than 1 insurance per person.

� Insurance penetration is a sign of but also a motor for the development of society.

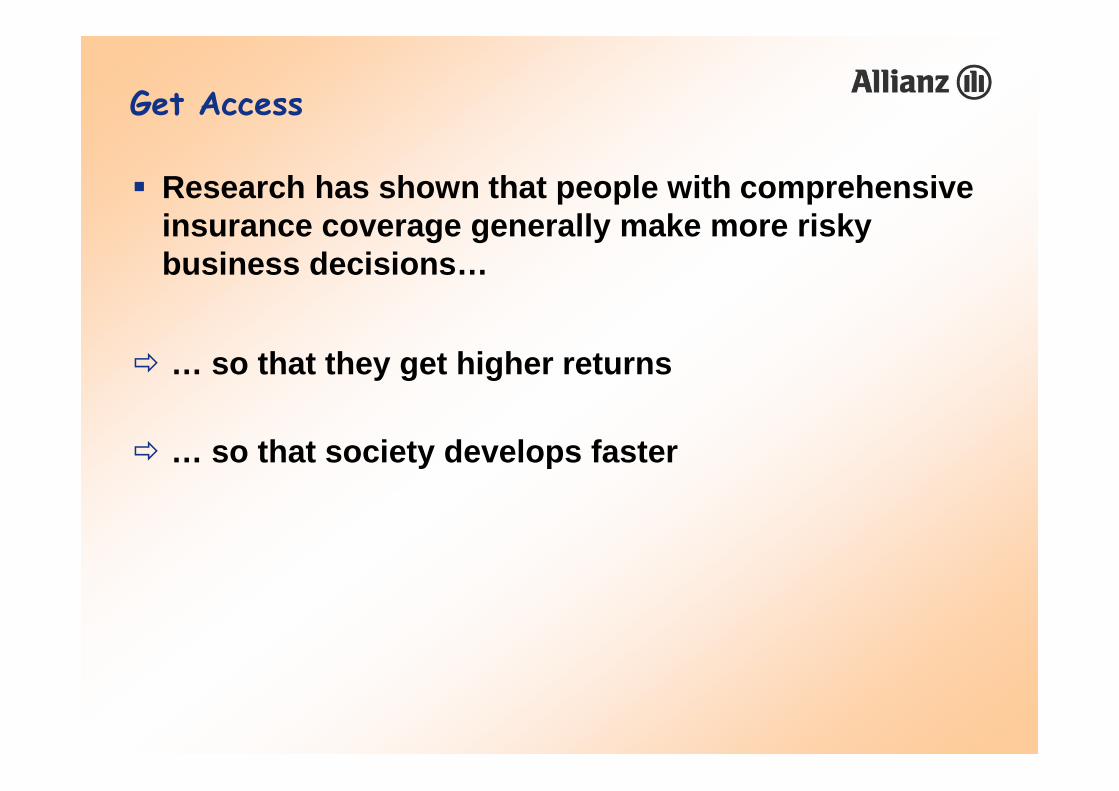

Get Access

54

� Research has shown that people with comprehensive insurance coverage generally make more risky business decisions…

� … so that they get higher returns

� … so that society develops faster

Get Access

55

Premi murah

YOU Customer1. Get protection

2. Get access to one of the most important financial porducts

3. Cheap premium because of group contract

4. More Empowerment

1. “Good” business in a new market

2. Develop together with loyal customers

3. Increase Brand Awareness

4. Positive Press

1. Portfolio proetcion

2. Promote empowerment

3. Profit sharing

4. Pioneer who is ahead of the competition

1. More secure jobs(through portfolio protection)

2. Wider skill set

3. Help your customers to have a happier and safer life

4. Participate in a program that is closely followed by society with great interest

56

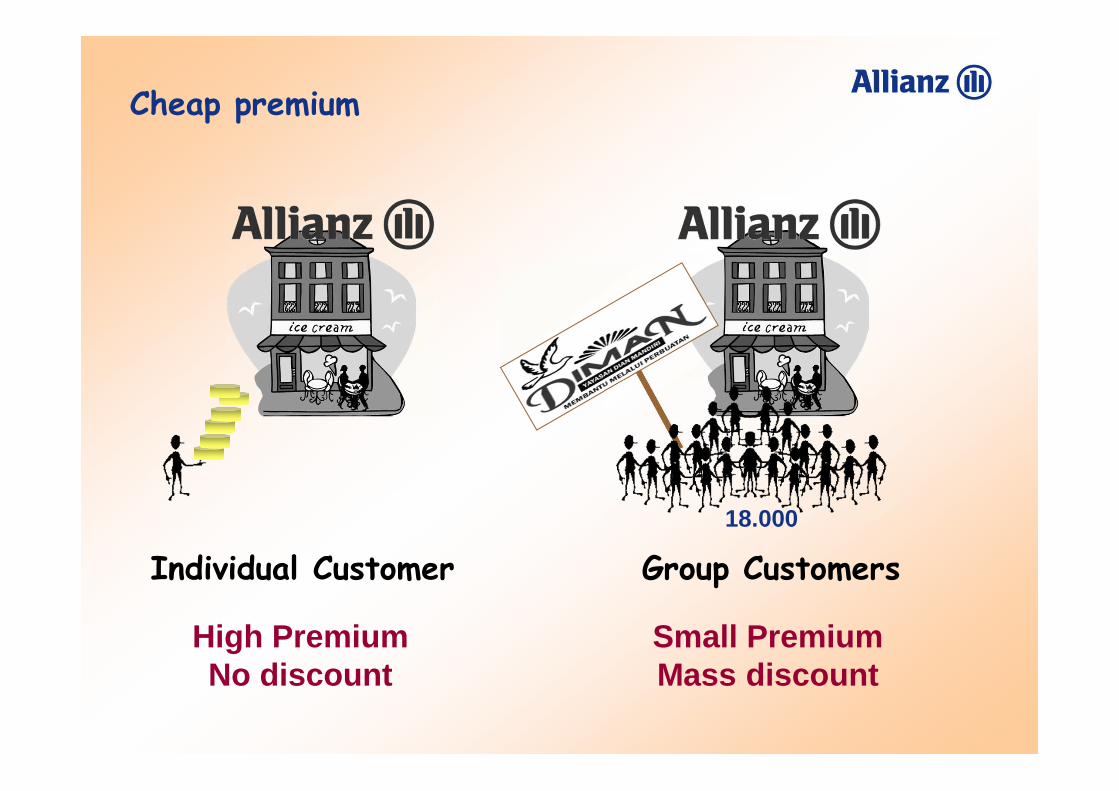

Cheap premium

Individual Customer

High PremiumNo discount

Group Customers

Small PremiumMass discount

18.000

57

Empowerment Naik

YOU Customer1. Get protection

2. Get access to one of the most important financial porducts

3. Cheap premium because of group contract

4. More Empowerment

1. “Good” business in a new market

2. Develop together with loyal customers

3. Increase Brand Awareness

4. Positive Press

1. Portfolio proetcion

2. Promote empowerment

3. Profit sharing

4. Pioneer who is ahead of the competition

1. More secure jobs(through portfolio protection)

2. Wider skill set

3. Help your customers to have a happier and safer life

4. Participate in a program that is closely followed by society with great interest

58

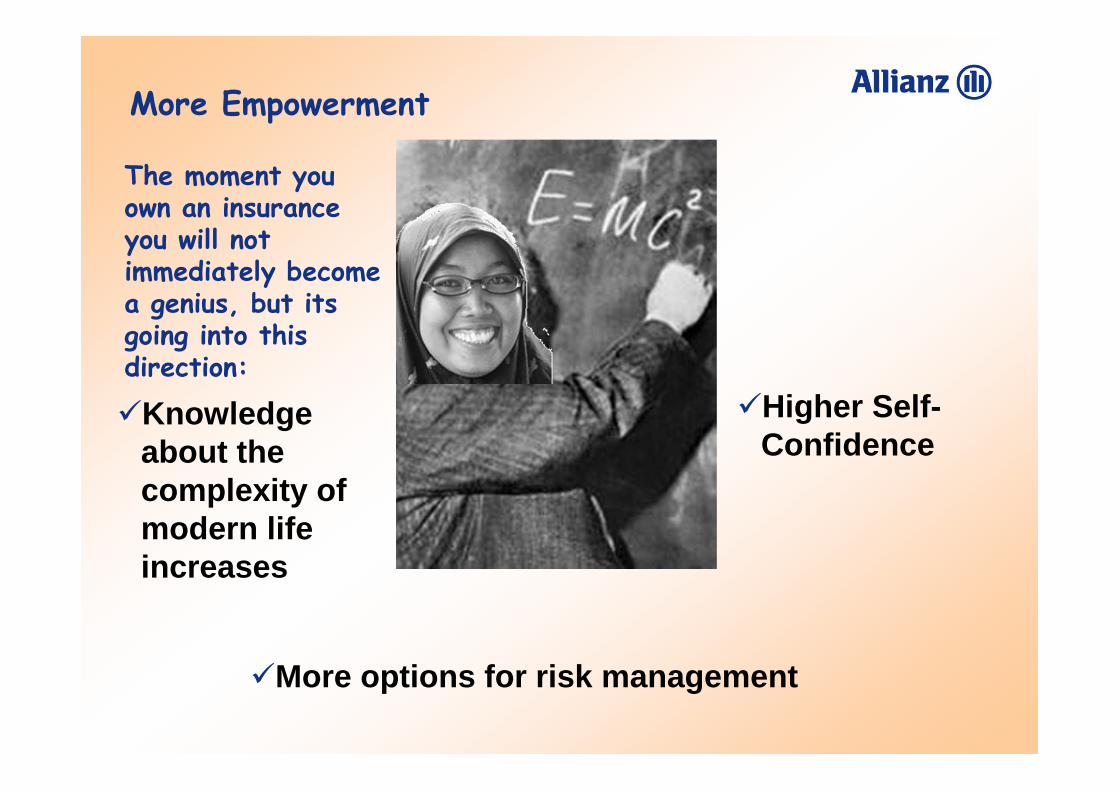

More Empowerment

The moment you own an insurance you will not immediately become a genius, but its going into this direction:

�Knowledge about the complexity of modern life increases

�More options for risk management

�Higher Self-Confidence

59

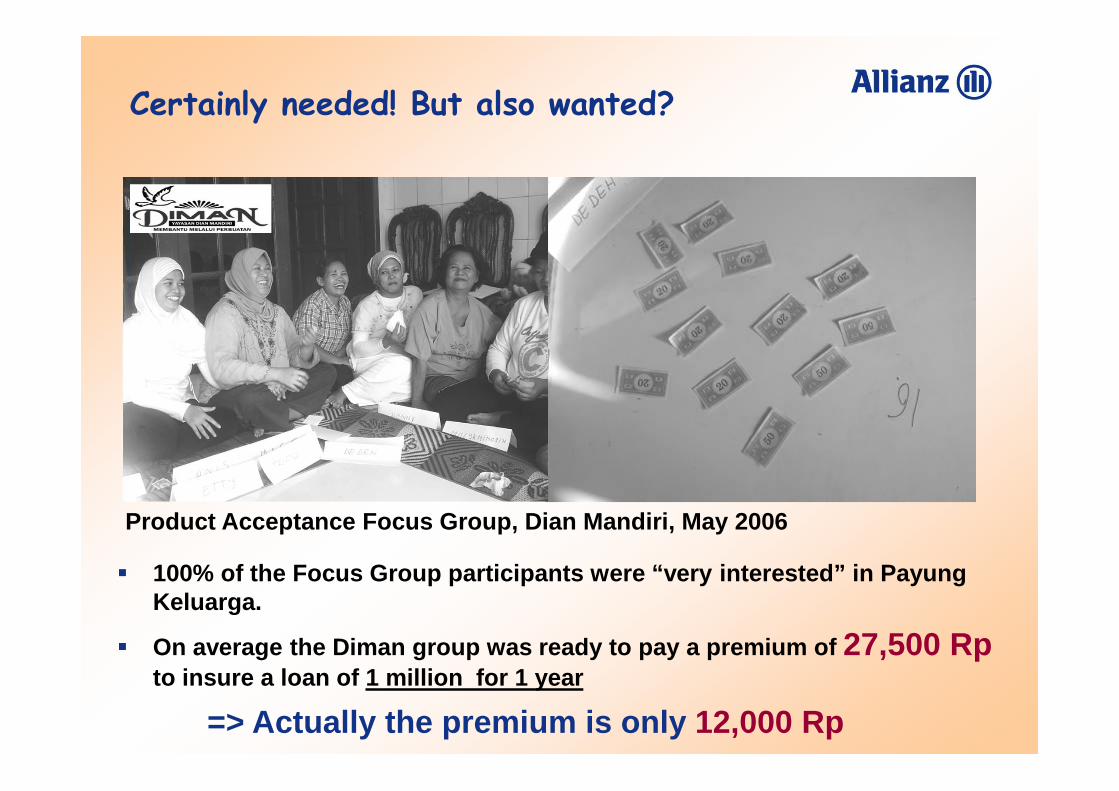

Certainly needed! But also wanted?

� 100% of the Focus Group participants were “very interested” in Payung Keluarga.

� On average the Diman group was ready to pay a premium of 27,500 Rpto insure a loan of 1 million for 1 year

=> Actually the premium is only 12,000 Rp

Product Acceptance Focus Group, Dian Mandiri, May 2006

60

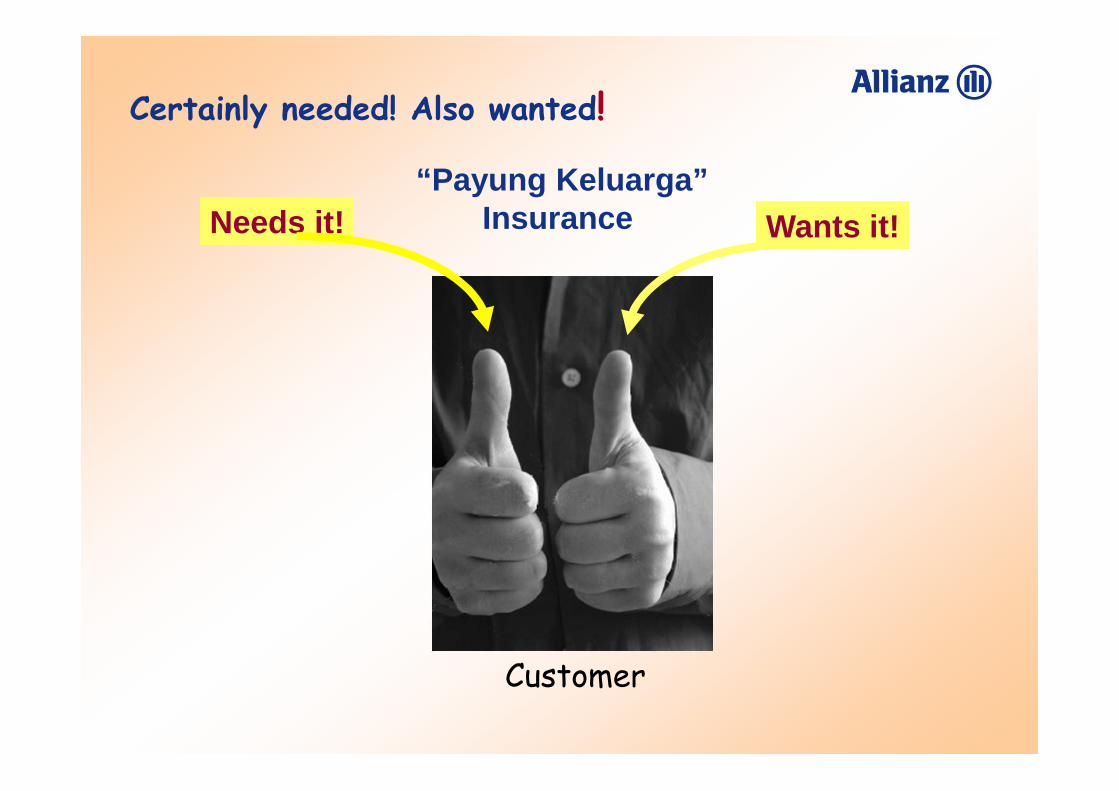

Certainly needed! Also wanted!

“Payung Keluarga”Insurance

Customer

Needs it! Wants it!

61

Even the strongest sometimes need to relax

62

Jangan Buang Waktu

Begitu Indah duniaBerwarna warni ceritaBerikanlah cintaSirami dengan tawaBiar penuh bahagiaBegitu singkat usiaTiada pernah di dugaBerikan senyumanHujani kasih sayangBiar damai terbawa

Buang jauh prasangkamuHilangkanlah rasa cemburuHapus pikiran yang bukan-bukan

Hidup hanya saat ini saja

Hidup Cuma untuk sementara

Jangan buang buang waktumu tiada

berguna

Hidup hanya saat ini saja

Hidup Cuma untuk sementara

Jangan sia-siakan cerita diantara kita

Begitu singkat usia

Tiada pernah diduga

Berikan senyuman

Hujani kasih sayang

Biar damai terbawa

Buang jauh prasangkamu

Hilangkanlah rasa cemburu

Hapus pikiran yang bukan bukan

CHORUS

63

64

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

65

Product DetailsProduct Details

66

PAYUNG KELUARGA

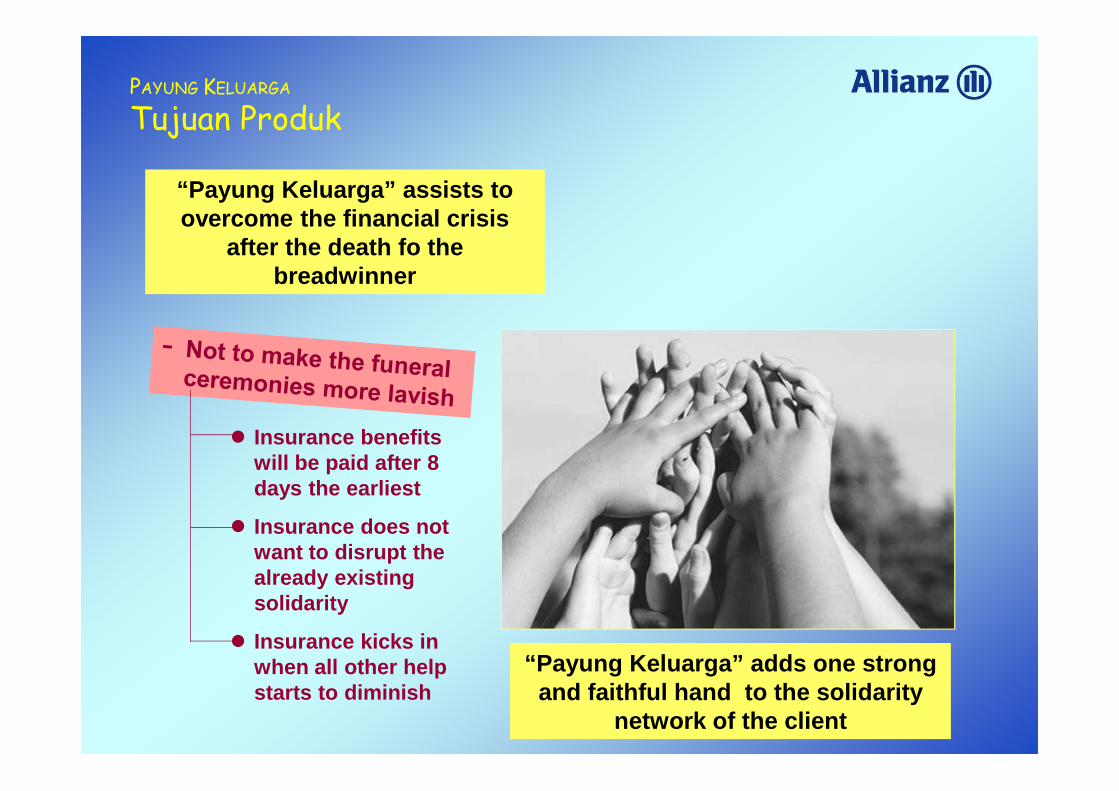

Product Goal

“Payung Keluarga” assists to overcome the financial crisis

after the death fo the breadwinner

+ The family is freed from paying back the loan

67

PAYUNG KELUARGA

Tujuan Produk

� Insurance benefits will be paid after 8 days the earliest

� Insurance does not want to disrupt the already existing solidarity

� Insurance kicks in when all other help starts to diminish

“Payung Keluarga” adds one strong and faithful hand to the solidarity

network of the client

“Payung Keluarga” assists to overcome the financial crisis

after the death fo the breadwinner

68

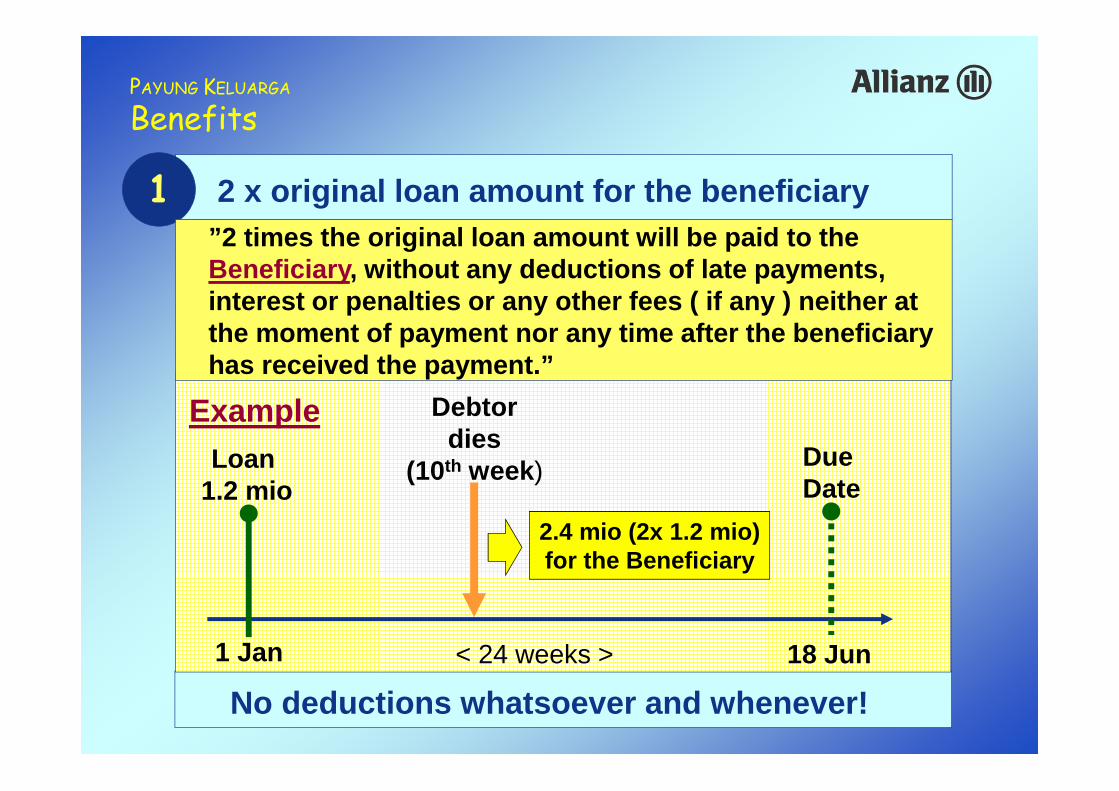

1 2 x original loan amount for the beneficiary

No deductions whatsoever and whenever!

Example

1 Jan

Loan 1.2 mio

18 Jun< 24 weeks >

Due Date

Debtordies

(10th week)

2.4 mio (2x 1.2 mio)for the Beneficiary

PAYUNG KELUARGA

Benefits

”2 times the original loan amount will be paid to the Beneficiary, without any deductions of late payments, interest or penalties or any other fees ( if any ) neither at the moment of payment nor any time after the beneficiary has received the payment.”

69

PAYUNG KELUARGA

Benefits

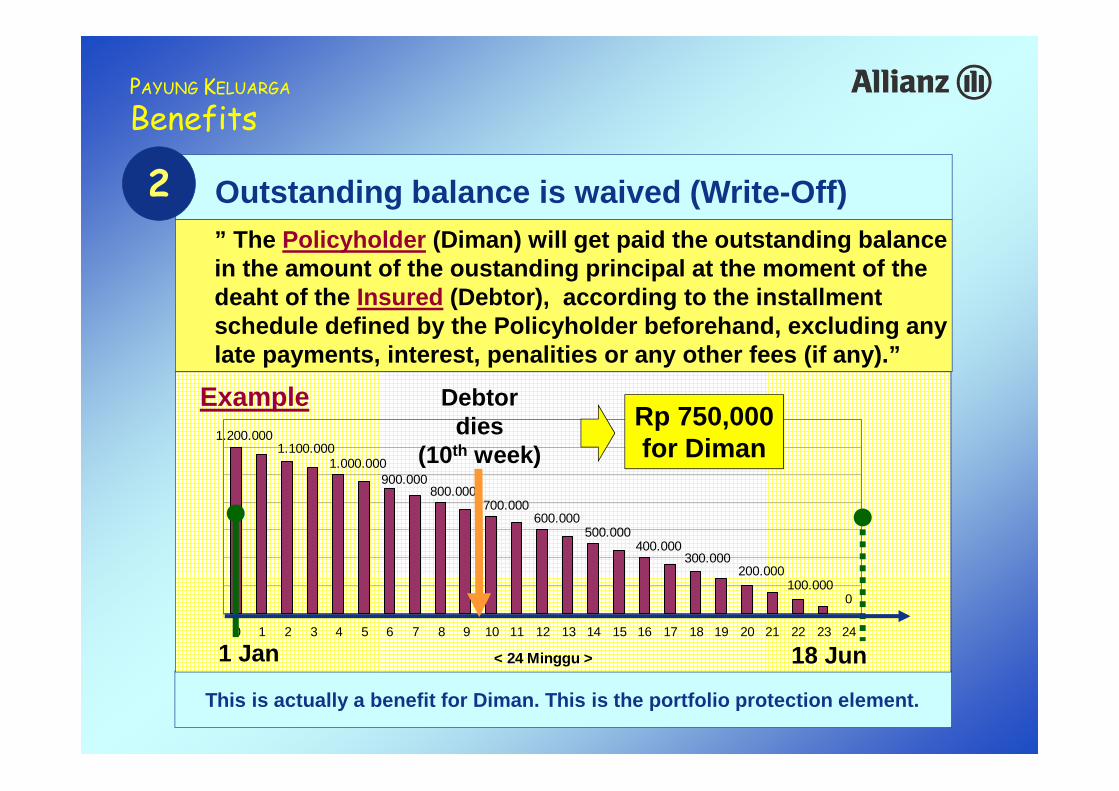

” The Policyholder (Diman) will get paid the outstanding balance in the amount of the oustanding principal at the moment of the deaht of the Insured (Debtor), according to the installment schedule defined by the Policyholder beforehand, excluding any late payments, interest, penalities or any other fees (if any).”

2 Outstanding balance is waived (Write-Off)

This is actually a benefit for Diman. This is the portfolio protection element.

Example

1 Jan 18 Jun

0

1.200.0001.100.000

1.000.000900.000

800.000700.000

600.000500.000

400.000300.000

200.000100.000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

< 24 Minggu >

Debtordies

(10th week)

Rp 750,000for Diman

70

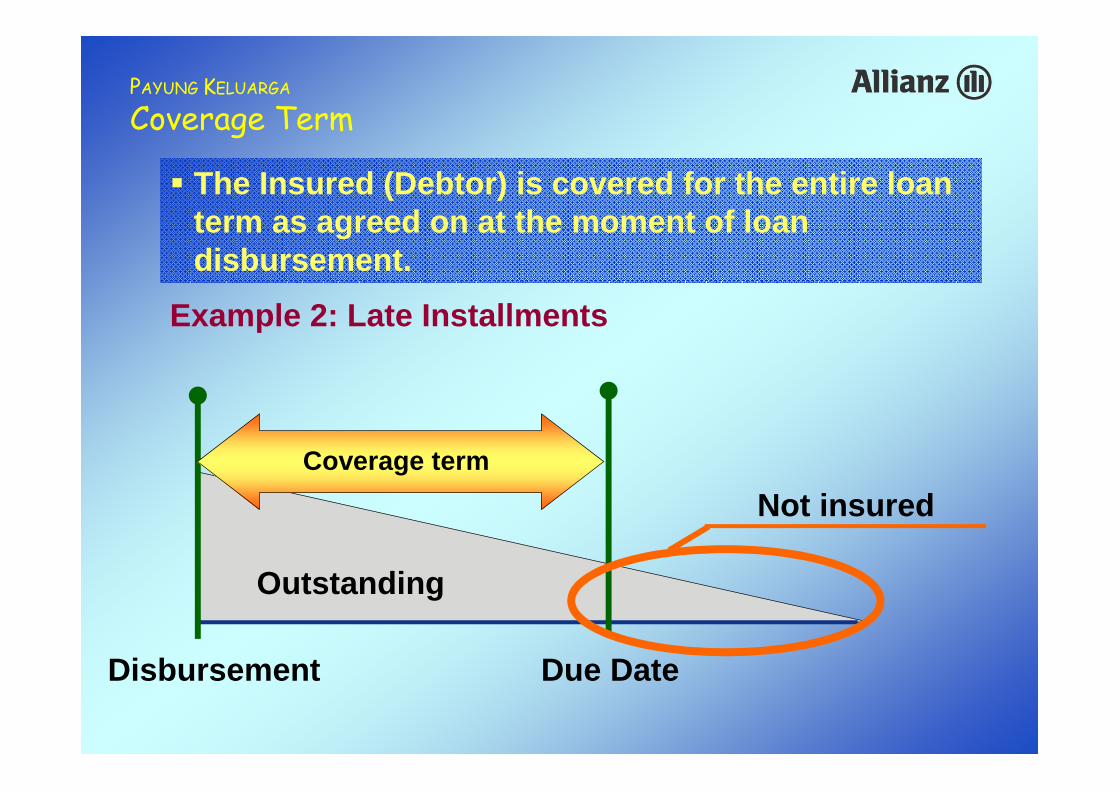

PAYUNG KELUARGA

Coverage Term

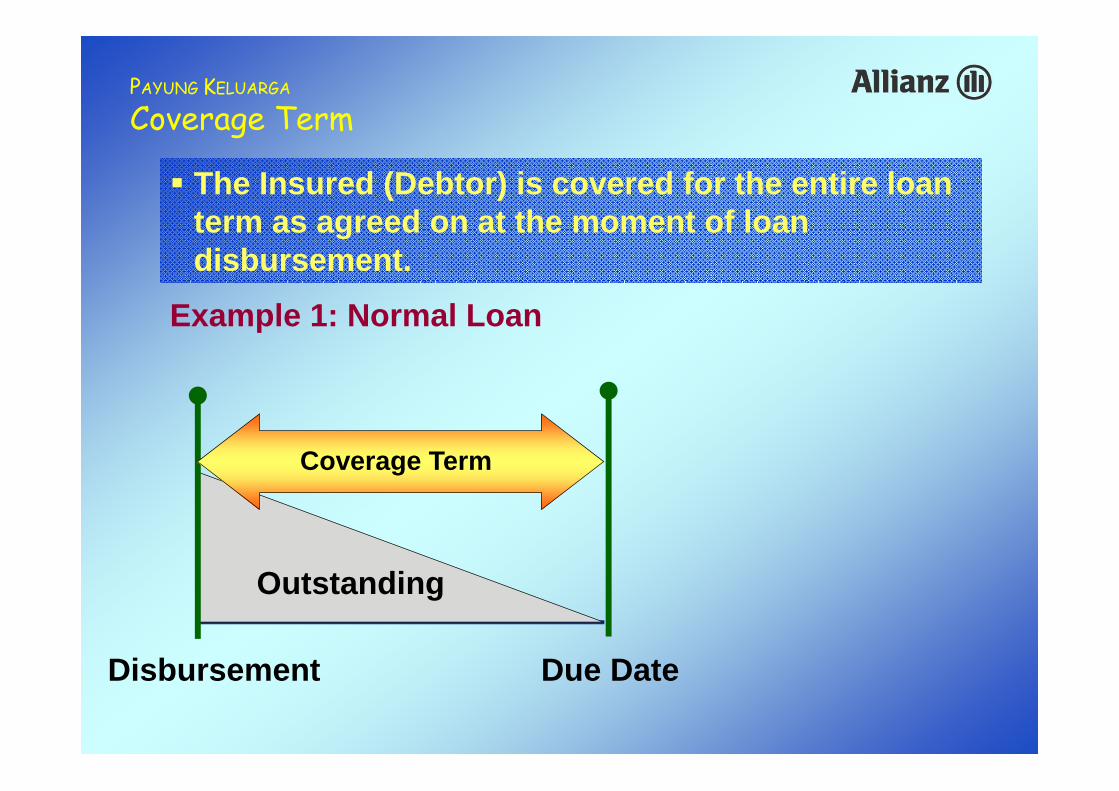

� The Insured (Debtor) is covered for the entire loan term as agreed on at the moment of loan disbursement.

Example 1: Normal Loan

Disbursement Due Date

Outstanding

Coverage Term

71

PAYUNG KELUARGA

Coverage Term

Example 2: Late Installments

Disbursement Due Date

Outstanding

Not insured

� The Insured (Debtor) is covered for the entire loan term as agreed on at the moment of loan disbursement.

Coverage term

72

PAYUNG KELUARGA

Coverage Term

2nd Dis-bursement

Outstanding

2nd Due Date

Coverage Term

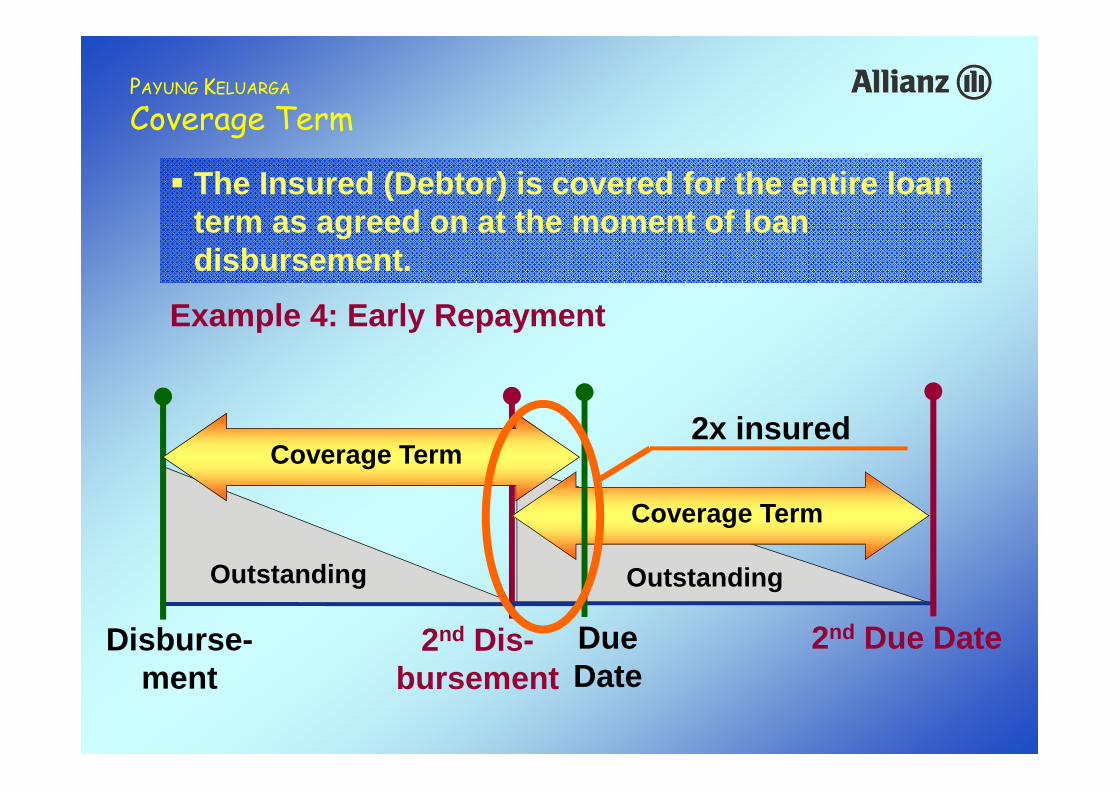

Example 4: Early Repayment

� The Insured (Debtor) is covered for the entire loan term as agreed on at the moment of loan disbursement.

Disburse-ment

DueDate

Coverage Term

Outstanding

2x insured

73

PAYUNG KELUARGA

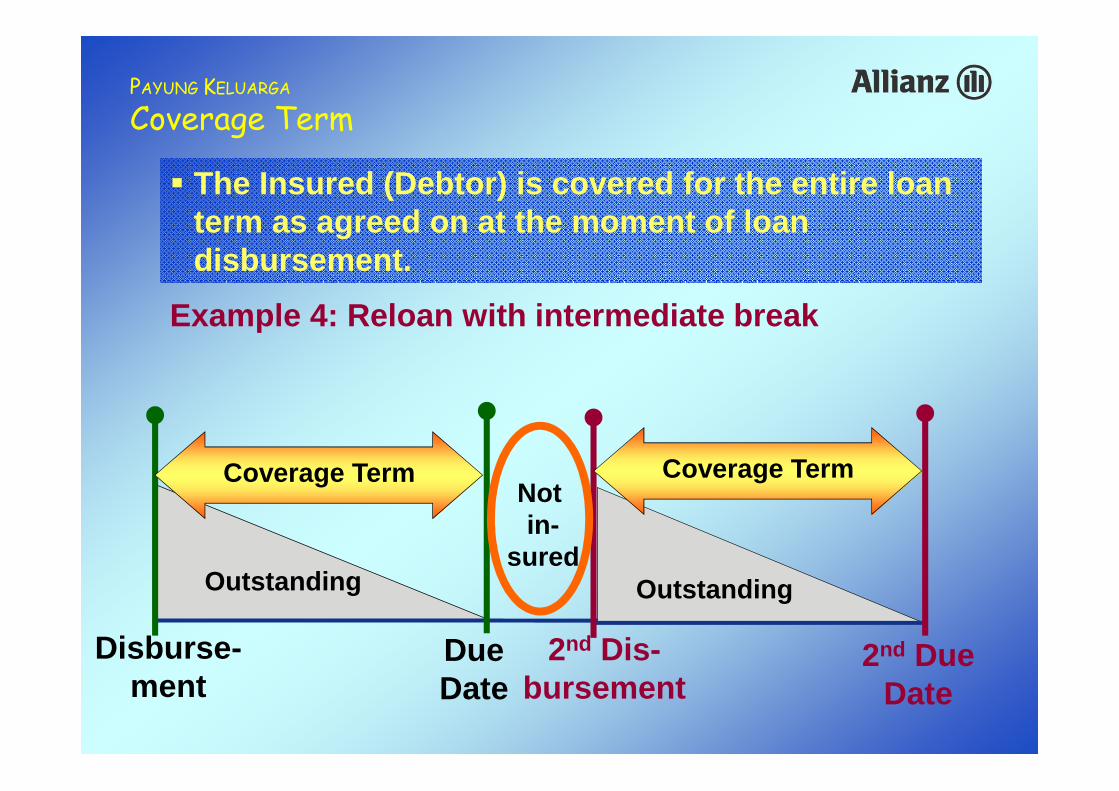

Coverage Term

Disburse-ment

DueDate

Coverage Term

Outstanding

2nd Dis-bursement

Outstanding

2nd Due Date

Coverage TermNot in-

sured

Example 4: Reloan with intermediate break

� The Insured (Debtor) is covered for the entire loan term as agreed on at the moment of loan disbursement.

74

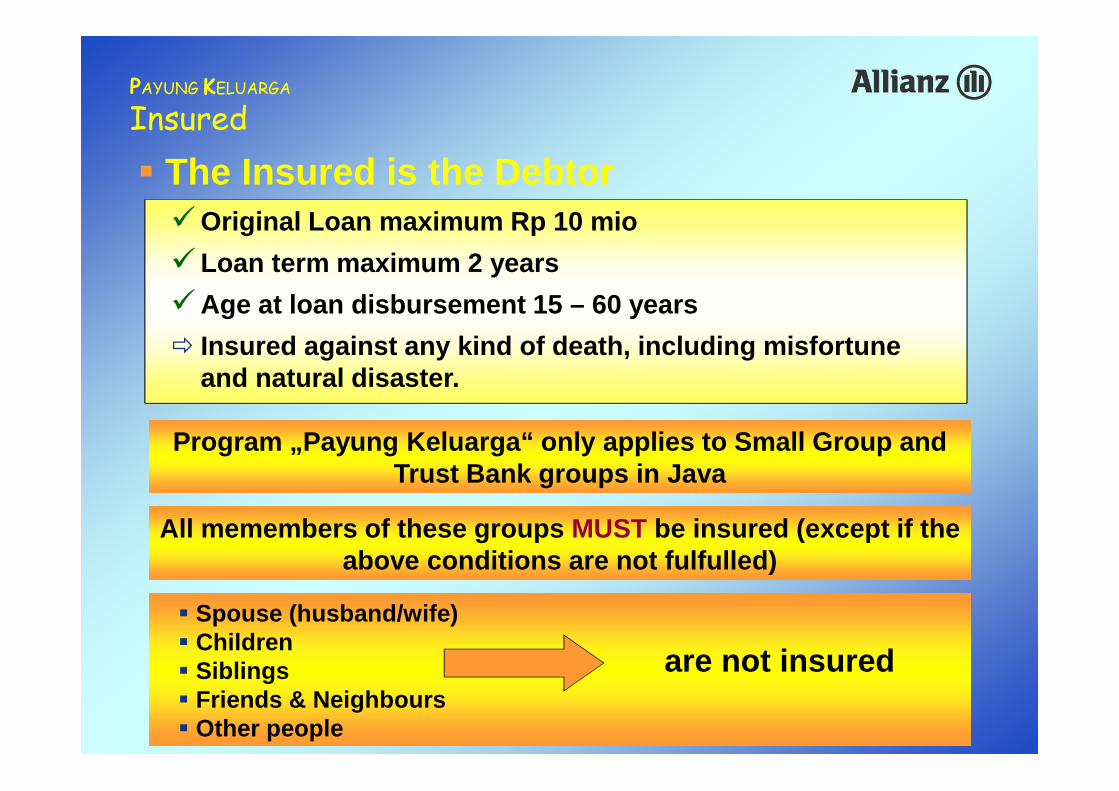

PAYUNG KELUARGA

Insured

Program „Payung Keluarga“ only applies to Small Group and Trust Bank groups in Java

Program „Payung Keluarga“ only applies to Small Group and Trust Bank groups in Java

All memembers of these groups MUST be insured (except if the above conditions are not fulfulled)

All memembers of these groups MUST be insured (except if the above conditions are not fulfulled)

� Spouse (husband/wife)� Children� Siblings� Friends & Neighbours� Other people

� Spouse (husband/wife)� Children� Siblings� Friends & Neighbours� Other people

are not insured

�Original Loan maximum Rp 10 mio

�Loan term maximum 2 years

�Age at loan disbursement 15 – 60 years

� Insured against any kind of death, including misfortune and natural disaster.

� The Insured is the Debtor

75

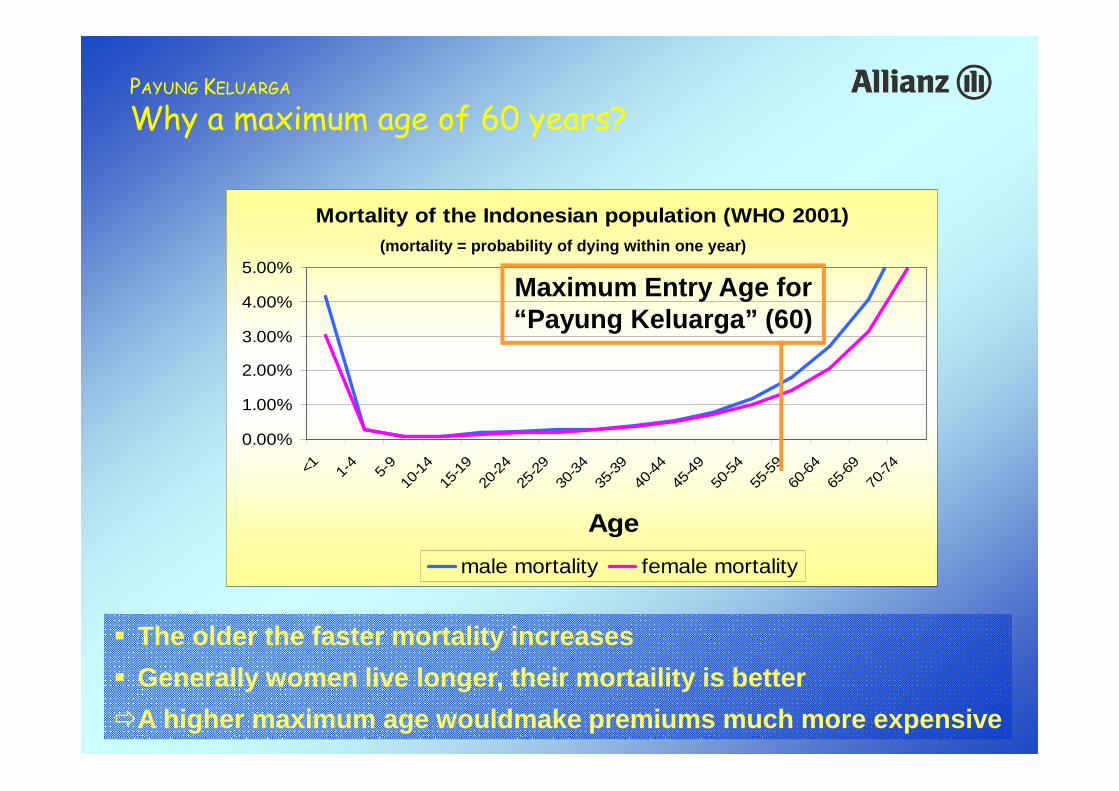

PAYUNG KELUARGA

Why a maximum age of 60 years?

Mortality of the Indonesian population (WHO 2001)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

<1 1-4

5-9

10-1

415

-19

20-2

425

-29

30-3

435

-39

40-4

445

-49

50-5

455

-59

60-6

465

-69

70-7

4

Age

male mortality female mortality

� The older the faster mortality increases

� Generally women live longer, their mortaility is better

�A higher maximum age wouldmake premiums much more expensive

Maximum Entry Age for“Payung Keluarga” (60)

(mortality = probability of dying within one year)

76

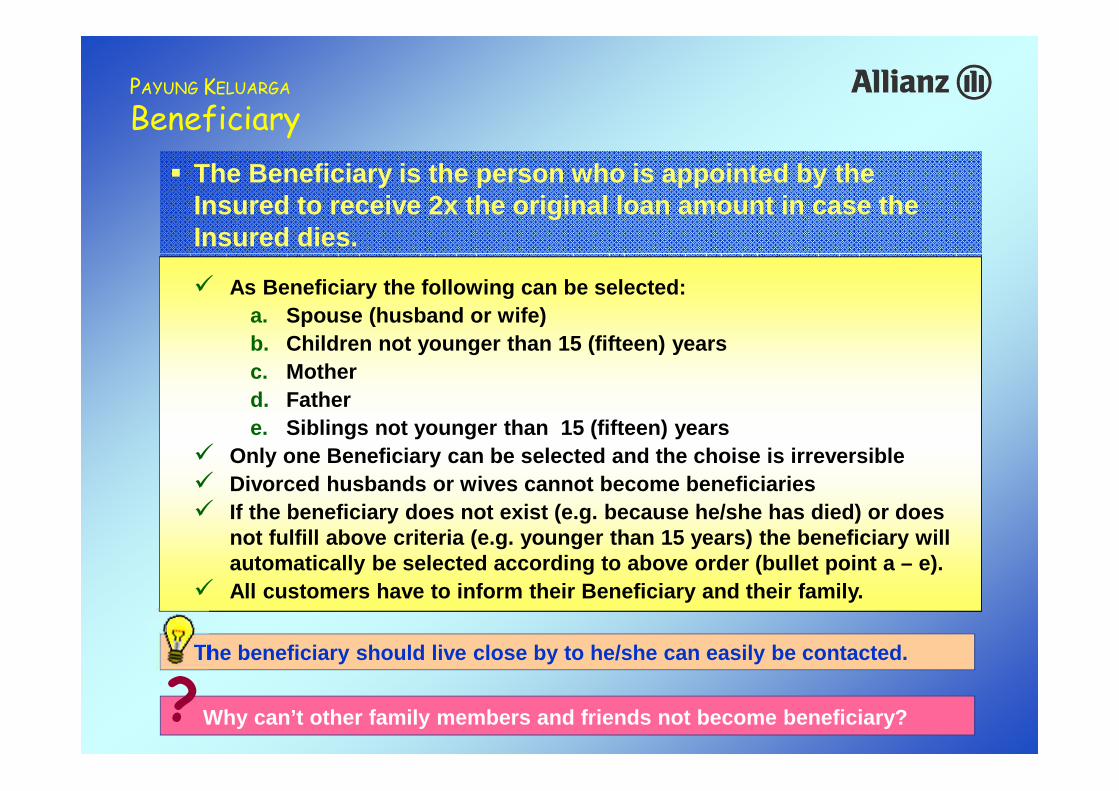

PAYUNG KELUARGA

Beneficiary

� The Beneficiary is the person who is appointed by the Insured to receive 2x the original loan amount in case the Insured dies.

� As Beneficiary the following can be selected:a. Spouse (husband or wife)b. Children not younger than 15 (fifteen) yearsc. Motherd. Fathere. Siblings not younger than 15 (fifteen) years

� Only one Beneficiary can be selected and the choise is irreversible� Divorced husbands or wives cannot become beneficiaries� If the beneficiary does not exist (e.g. because he/she has died) or does

not fulfill above criteria (e.g. younger than 15 years) the beneficiary will automatically be selected according to above order (bullet point a – e).

� All customers have to inform their Beneficiary and their family.

� The beneficiary should live close by to he/she can easily be contacted.

Why can’t other family members and friends not become beneficiary??

77

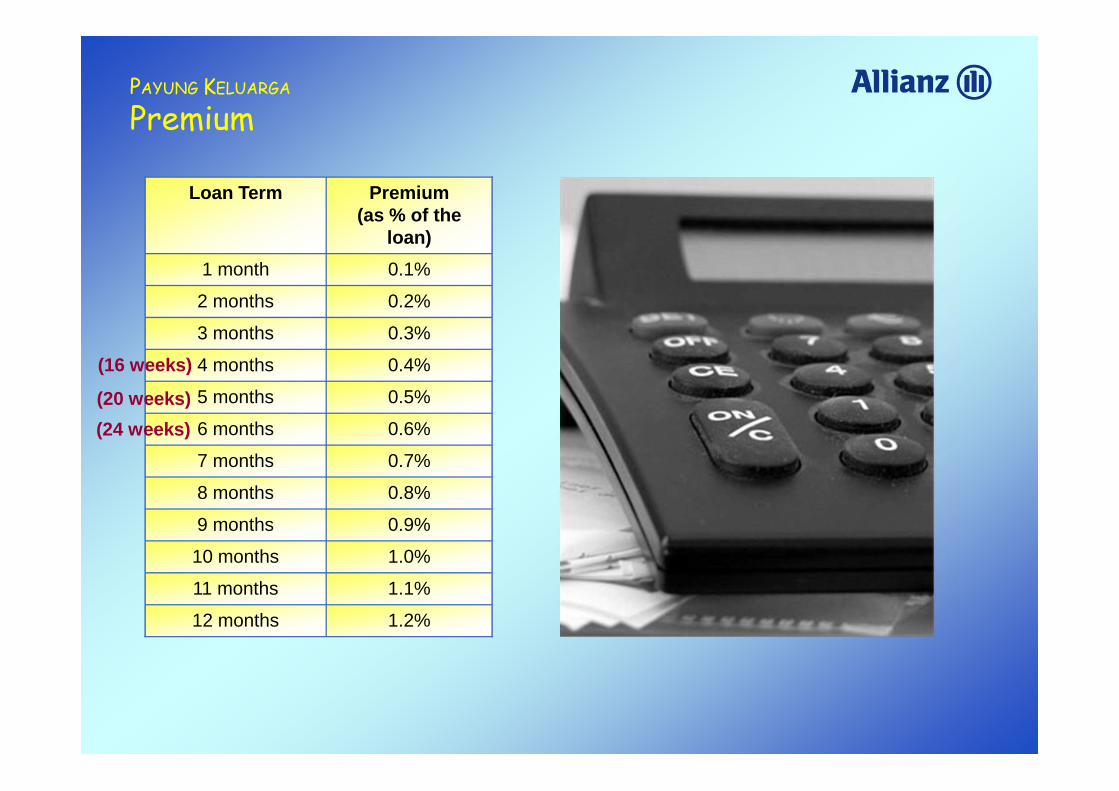

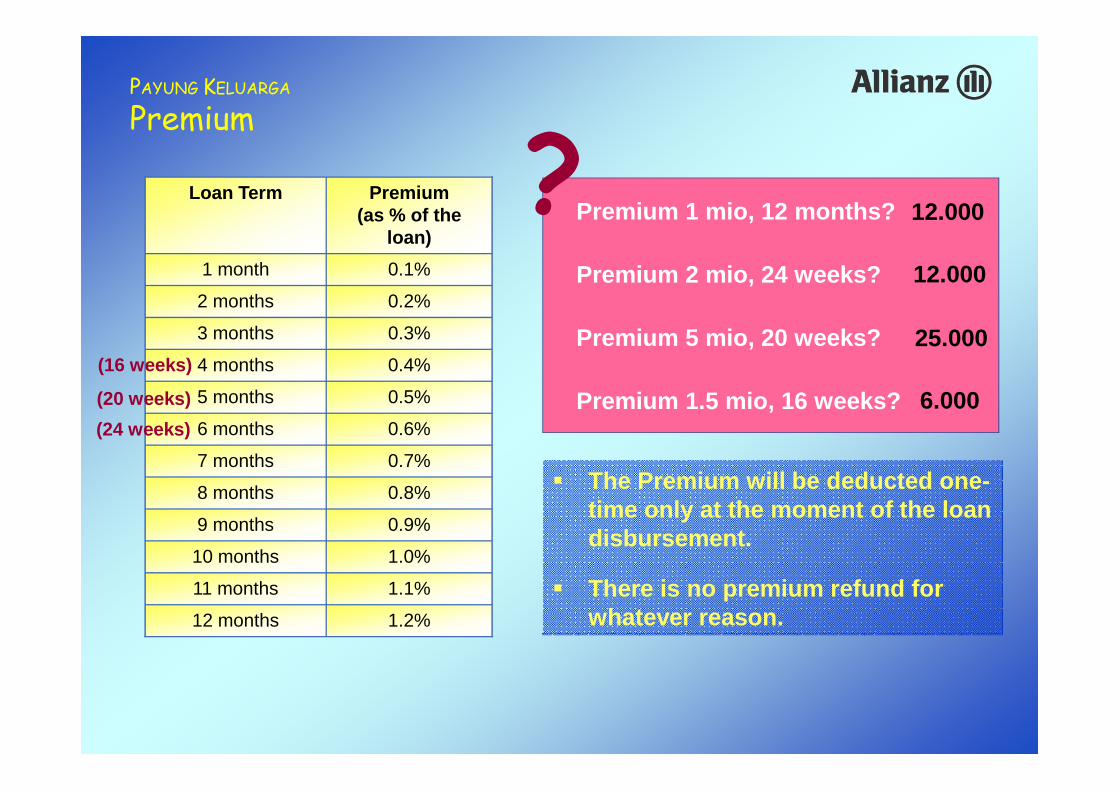

PAYUNG KELUARGA

Premium

1.2%12 months

1.1%11 months

1.0%10 months

0.9%9 months

0.8%8 months

0.7%7 months

0.6%6 months

0.5%5 months

0.4%4 months

0.3%3 months

0.2%2 months

0.1%1 month

Premium(as % of the

loan)

Loan Term

(20 weeks)

(16 weeks)

(24 weeks)

78

PAYUNG KELUARGA

Premium

� The Premium will be deducted one-time only at the moment of the loan disbursement.

� There is no premium refund for whatever reason.

Premium 1 mio, 12 months?

Premium 2 mio, 24 weeks?

Premium 5 mio, 20 weeks?

Premium 1.5 mio, 16 weeks?

? 12.000

12.000

25.000

6.000

1.2%12 months

1.1%11 months

1.0%10 months

0.9%9 months

0.8%8 months

0.7%7 months

0.6%6 months

0.5%5 months

0.4%4 months

0.3%3 months

0.2%2 months

0.1%1 month

Premium(as % of the

loan)

Loan Term

(20 weeks)

(16 weeks)

(24 weeks)

79

PAYUNG KELUARGA

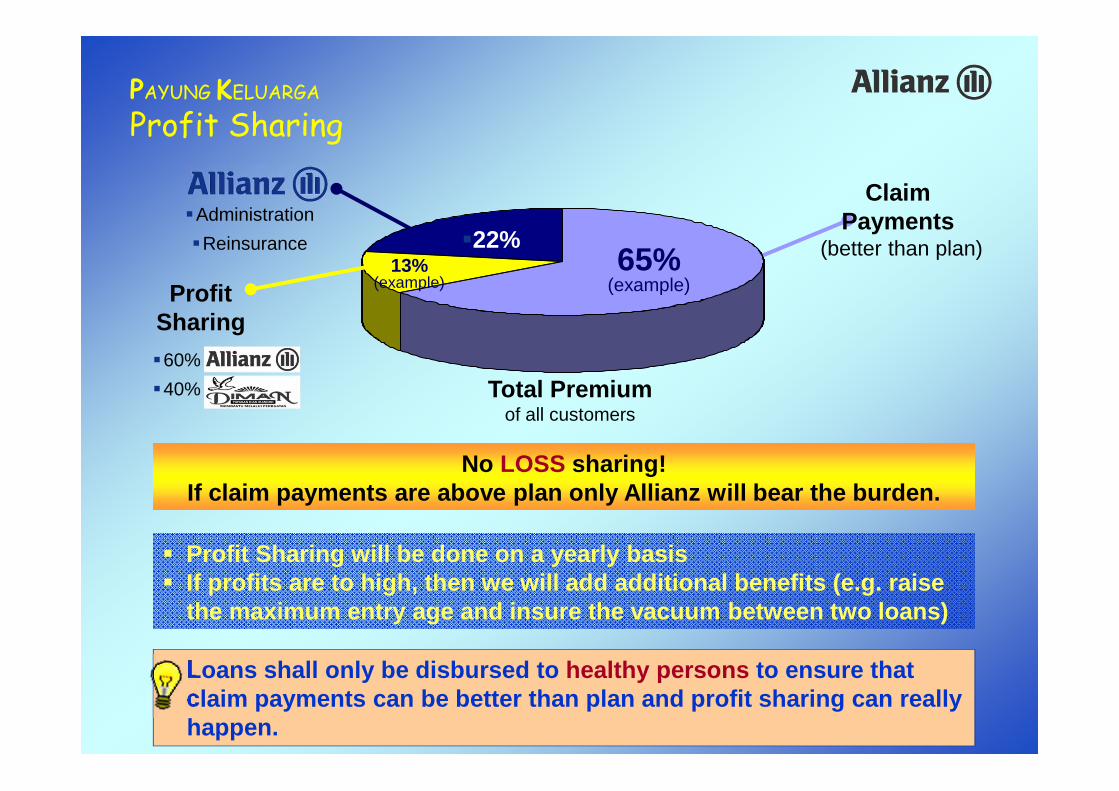

Profit Sharing

Total Premiumof all customers

�Administration

�Reinsurance

ClaimPayments

(better than plan)

� Profit Sharing will be done on a yearly basis� If profits are to high, then we will add additional benefits (e.g. raise

the maximum entry age and insure the vacuum between two loans)

No LOSS sharing!If claim payments are above plan only Allianz will bear the burden.

No LOSS sharing!If claim payments are above plan only Allianz will bear the burden.

� Loans shall only be disbursed to healthy persons to ensure that claim payments can be better than plan and profit sharing can really happen.

78%22%�22%

65%(example)

13%(example)Profit

Sharing

�60%

�40%

80

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

81

DistributionDistribution

82

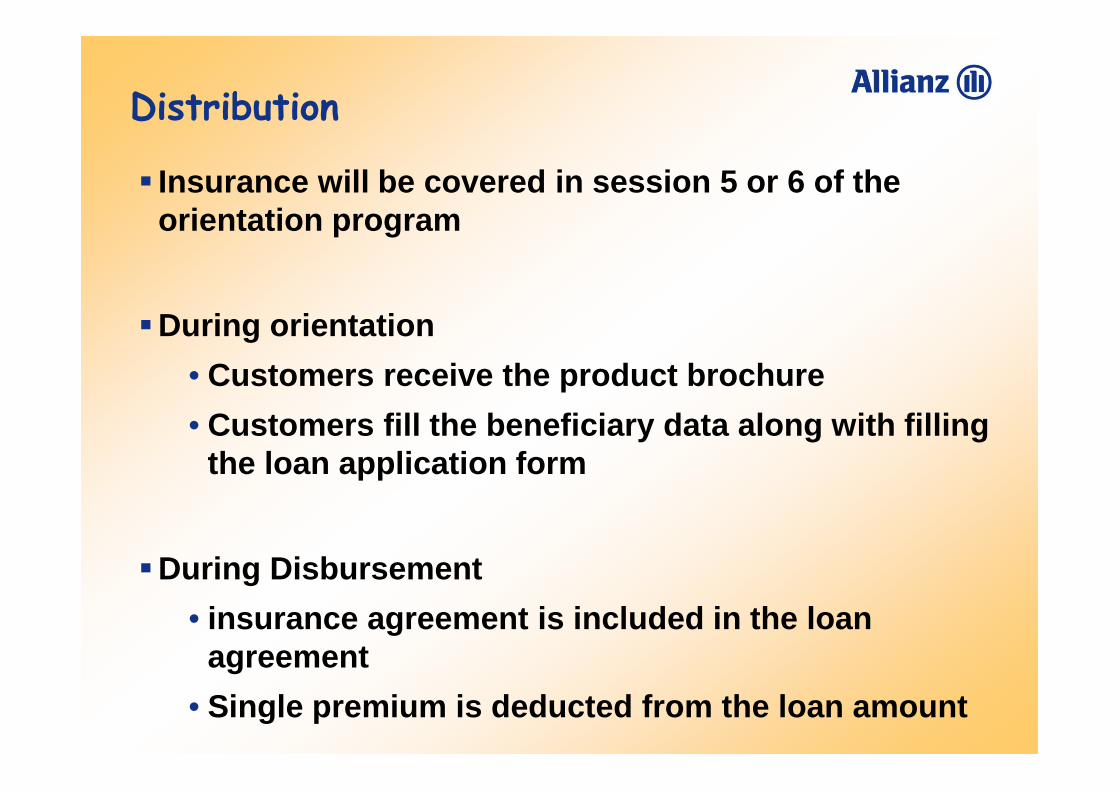

Distribution

� Insurance will be covered in session 5 or 6 of the orientation program

�During orientation

• Customers receive the product brochure

• Customers fill the beneficiary data along with filling the loan application form

�During Disbursement

• insurance agreement is included in the loan agreement

• Single premium is deducted from the loan amount

83

Launch Schedule

� 11 / 18 August - Training of Branch Managers, Program Officers + FAO

� 22 August - Insurance enters the orientation programs (including those already under way)

- brochure already ready at every branch- temporarily the form for selecting the beneficiary will be stamped onto the old loan application forms

� 24 August - „Payung Keluarga“ Launch event at Allianz(in the media 1 day afterwards)

� Start September - First loan disbursement with „Payung Keluarga“

84

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

85

ClaimsClaims

86

Claims

The Moment of Truth

� The claim is the moment to fulfill the promise to the customers

� very sensitive periode

� lots of emotions

Together we have to handle claims with the utmost care !Together we have to handle claims with the utmost care !

87

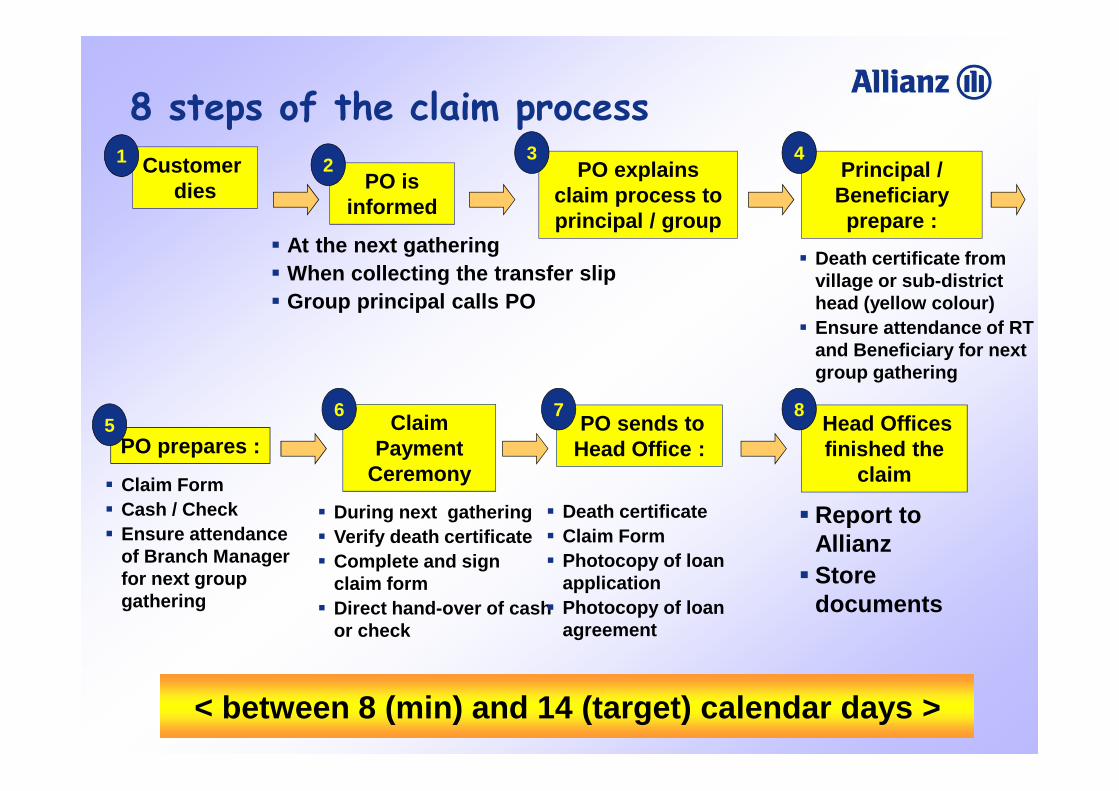

8 steps of the claim process

Customer dies

1

PO prepares :

� Claim Form� Cash / Check � Ensure attendance

of Branch Manager for next group gathering

5

� At the next gathering� When collecting the transfer slip� Group principal calls PO

PO is informed

2 PO explains claim process to principal / group

3Principal /

Beneficiaryprepare :

� Death certificate from village or sub-district head (yellow colour)

� Ensure attendance of RT and Beneficiary for next group gathering

4

Claim Payment

Ceremony

� During next gathering� Verify death certificate� Complete and sign

claim form� Direct hand-over of cash

or check

6PO sends to

Head Office :

� Death certificate� Claim Form� Photocopy of loan

application� Photocopy of loan

agreement

7Head Offices finished the

claim

� Report to Allianz

� Store documents

8

< between 8 (min) and 14 (target) calendar days >< between 8 (min) and 14 (target) calendar days >

88

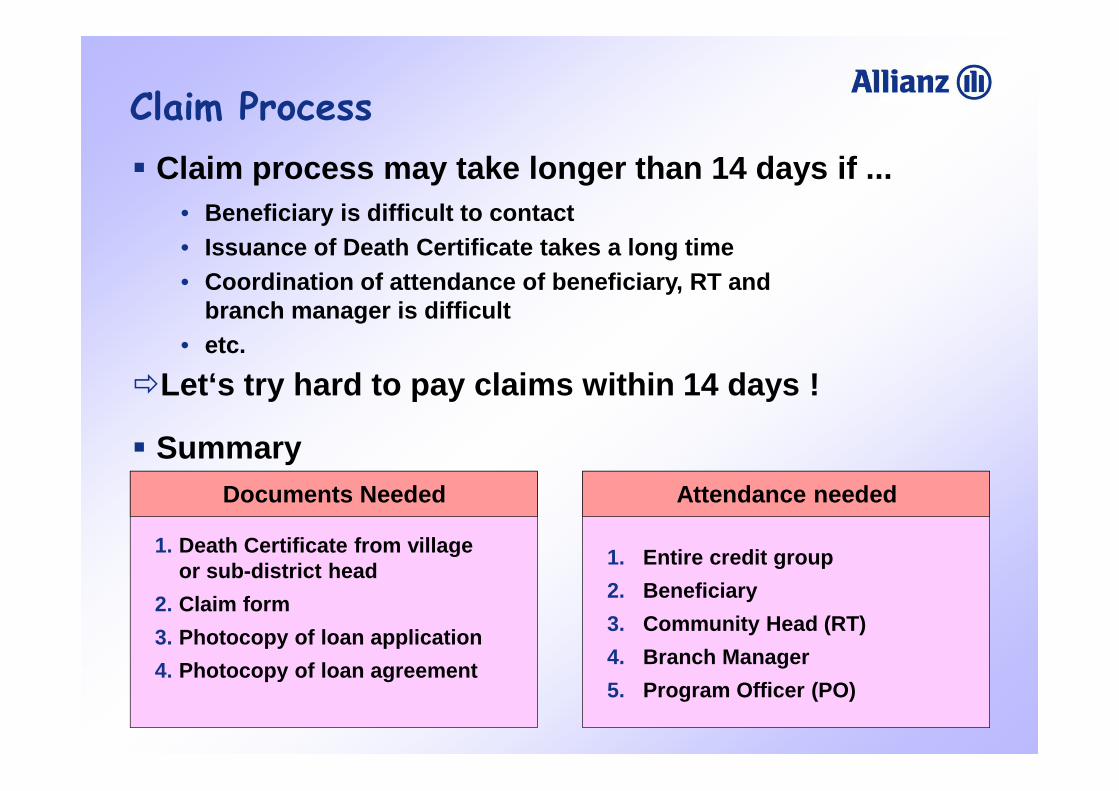

Claim Process

� Claim process may take longer than 14 days if ...• Beneficiary is difficult to contact • Issuance of Death Certificate takes a long time• Coordination of attendance of beneficiary, RT and

branch manager is difficult• etc.

�Let‘s try hard to pay claims within 14 days !

� SummaryDocuments Needed

1. Death Certificate from village or sub-district head

2. Claim form

3. Photocopy of loan application

4. Photocopy of loan agreement

Attendance needed

1. Entire credit group

2. Beneficiary

3. Community Head (RT)

4. Branch Manager

5. Program Officer (PO)

89

Claim Process

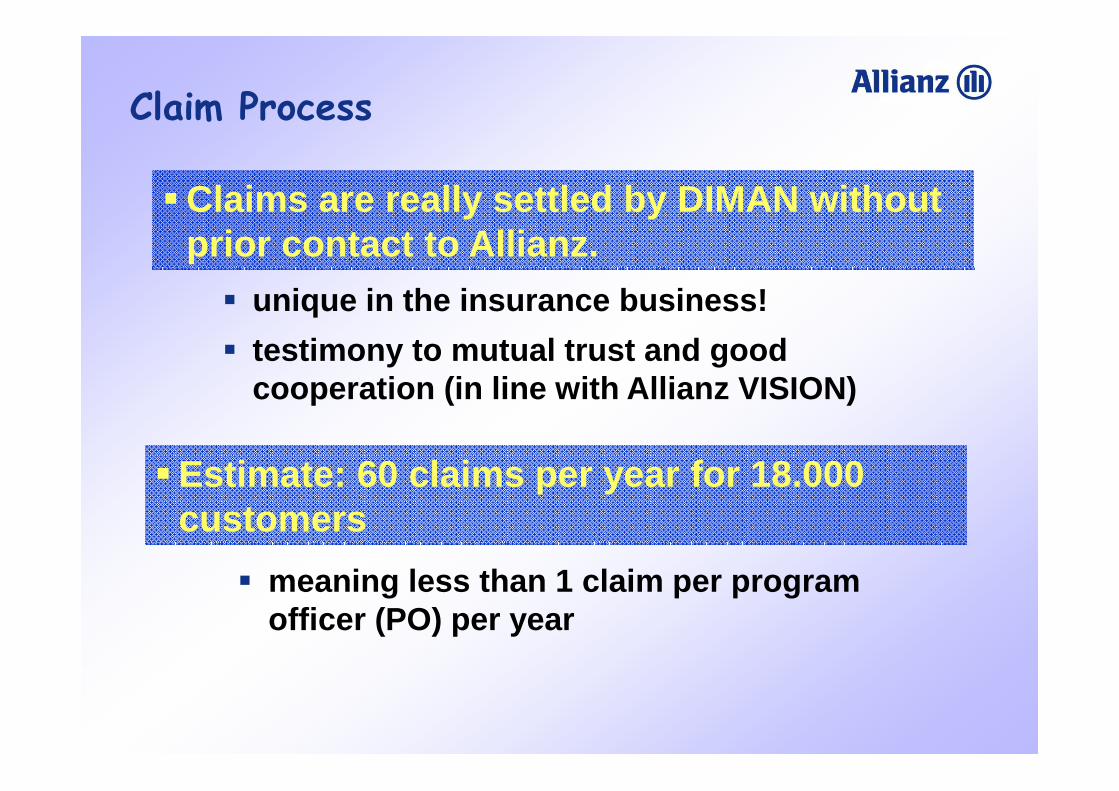

�Claims are really settled by DIMAN without prior contact to Allianz.

� unique in the insurance business!

� testimony to mutual trust and good cooperation (in line with Allianz VISION)

�Estimate: 60 claims per year for 18.000 customers

� meaning less than 1 claim per program officer (PO) per year

90

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

91

Other IssuesOther Issues

92

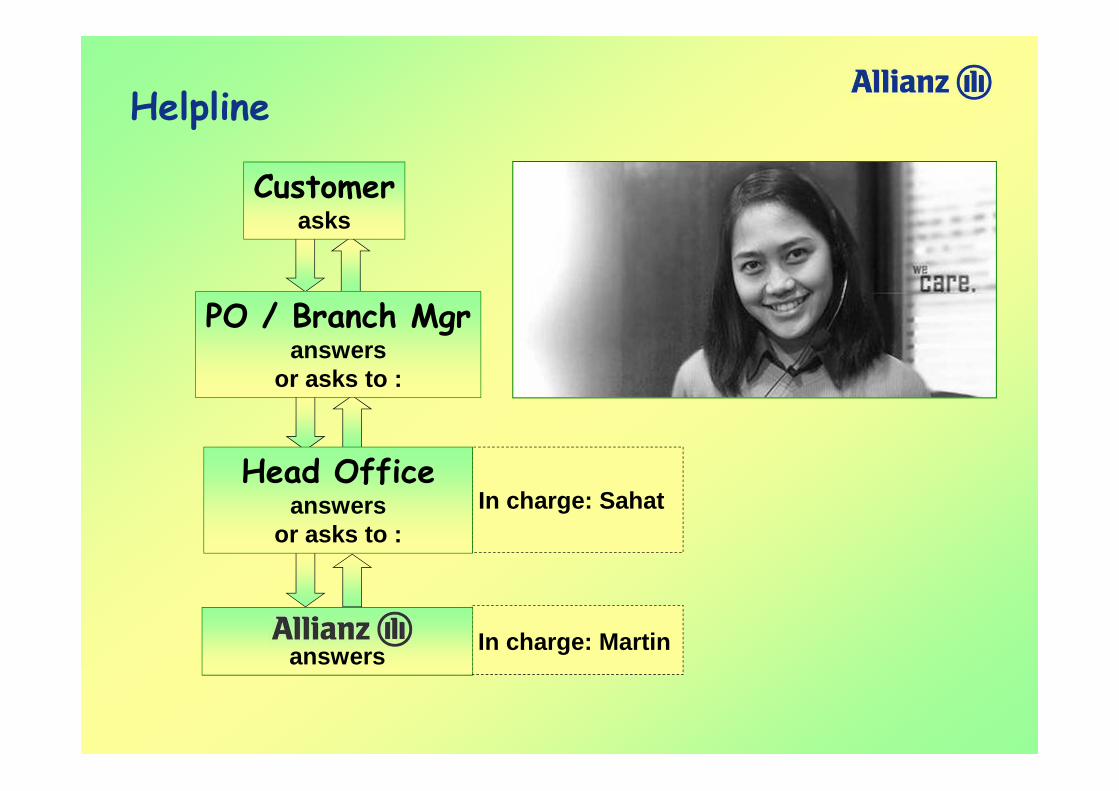

Helpline

In charge: Sahat

In charge: Martin

Customerasks

PO / Branch Mgranswers

or asks to :

Head Office answers

or asks to :

answers

93

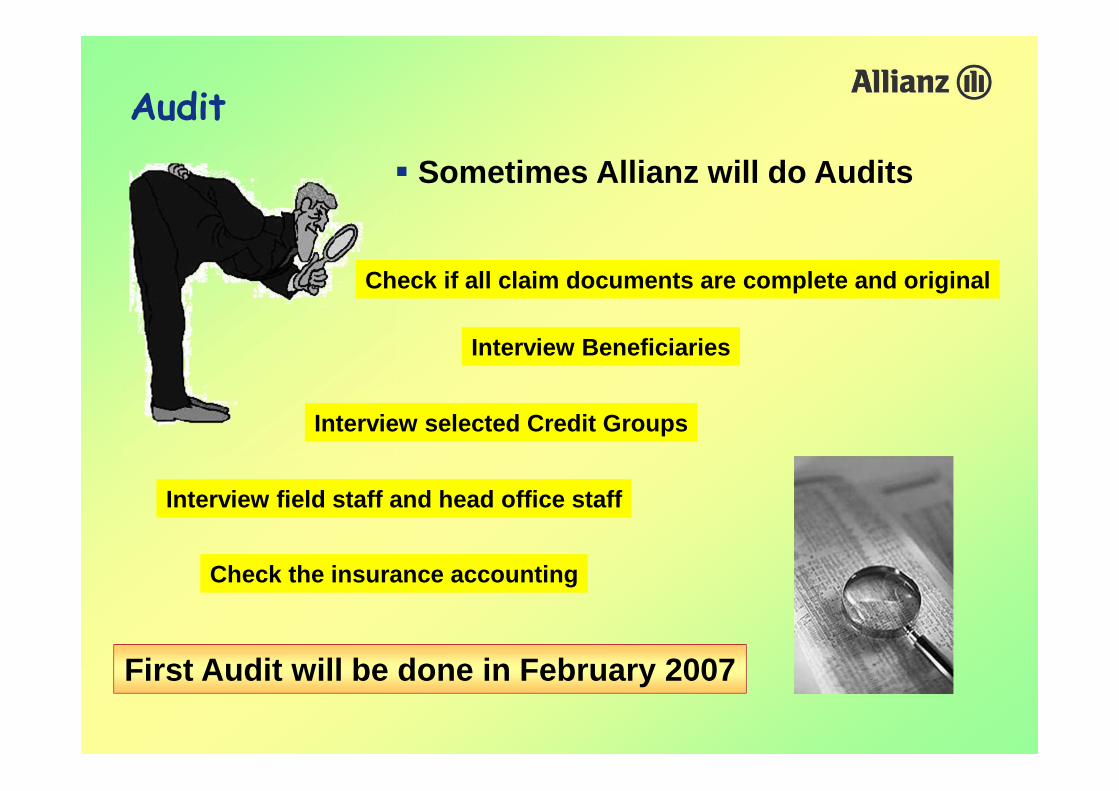

Audit

� Sometimes Allianz will do Audits

Check if all claim documents are complete and original

Interview Beneficiaries

Interview selected Credit Groups

Interview field staff and head office staff

Check the insurance accounting

First Audit will be done in February 2007

94

Even the strongest sometimes need to relax

95

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

96

Question & Answer SessionQuestion & Answer Session

97

Why can the spouse and the children notbe insured as well?

� If two or more people are insured the premium will definitely be higher. For the beginning we want to start with a very simple and cheap product.

� At the moment they cannot be insured but there is already plans to offer this as an optional choice next year.

98

I am young. I don’t need insurance.

� It is true that the probability to die is lower, but if it happens the consequences are more severe than for old people.

� The young normally have children and parents to look after.

� The old normally just support the spouse.

� If only the old take insurance, the premium will be a lot more expensive (SOLIDARITY)

99

Are you as Program Officers also insured?

� Yes, all staff and POs of DIMAN already have life insurance. The premium is paid by DIMAN.

100

What happens if the clients dies at the day of installment payment?

� If the insured dies on the day of installment payment the outstanding balance before the date of death of the insured will be considered as the outstanding balance.

101

Is insurance similar to betting (haram)?

� No, because with insurance you only get compensation for what you have already lost.

� You cannot make a gain with insurance Dengan Asuransi tidak ada kemungkinan profit (except with products that are mixed with savings or investment elements such as education endowments or unit-link products).

� There is no Fatwa that declares insurance to be haram.

102

How long until a claim HAS TO be reported to Allianz?

� DIMAN head offices has to report all claims maximum 70 days after the date of death.

103

ANY OTHER QUESTIONS?

104

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

105

Role PlayRole Play

106

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

107

TestTest

108

Agenda 1. Introduction

2. Insurance Principles

3. Motivation

4. Product Details

5. Distribution

6. Claims

7. Other Issues

8. Question & Answer Session

9. Role Play

10. Test

11. Lucky Draw

109

Lucky DrawLucky Draw

110