Embed Size (px)

Citation preview

Payroll Fraud &

Continuous Monitoring Activities

VLGAA – May 21, 2009

Darlene FitzPatrickDarlene FitzPatrick, CIA, CFE, CCSA, Audit , CIA, CFE, CCSA, Audit Director, Director,

Bon Secours Health System, Inc.Bon Secours Health System, Inc.

BSHSI © 2009BSHSI © 2009 22

Bon Secours Health System, Bon Secours Health System, Inc.Inc.

• $2.4 Billion Company$2.4 Billion Company

• 18 Acute Care Facilities18 Acute Care Facilities

• 1 Psychiatric Facility1 Psychiatric Facility

• 5 Nursing Care Centers5 Nursing Care Centers

• 5 Assisted Living Facilities5 Assisted Living Facilities

BSHSI © 2009BSHSI © 2009 33

Background of Local SystemBackground of Local System

• Acute Care Hospital Acute Care Hospital

• Approximately 1,700 peopleApproximately 1,700 people

• Combination of union and non-unionCombination of union and non-union

• Hospital was losing moneyHospital was losing money

• Discussions for selling and/or closingDiscussions for selling and/or closing

• Consultants brought in to manage Consultants brought in to manage hospitalhospital

• Minimal internal management oversightMinimal internal management oversight

BSHSI © 2009BSHSI © 2009 44

Background – Payroll DepartmentBackground – Payroll Department

• Security person transferred to Payroll Security person transferred to Payroll ClerkClerk

• Conflict between Payroll Manager and Conflict between Payroll Manager and ClerkClerk

• One full time, two part-timeOne full time, two part-time

• Part-time only responsible for time entryPart-time only responsible for time entry

• Processing access locked down to Processing access locked down to ManagerManager

BSHSI © 2009BSHSI © 2009 55

Finance StructureFinance Structure

CFO - Consultant

Controller - Consultant

Accounting Manager Consultant

Payroll Manager

• Payroll Processing• Demand Checks• Quarterly Reporting Prep and Submission• W2 and W4 updates

Bank ReconciliationsReconciling P/R to GL

Oversight

Oversight

BSHSI © 2009BSHSI © 2009 66

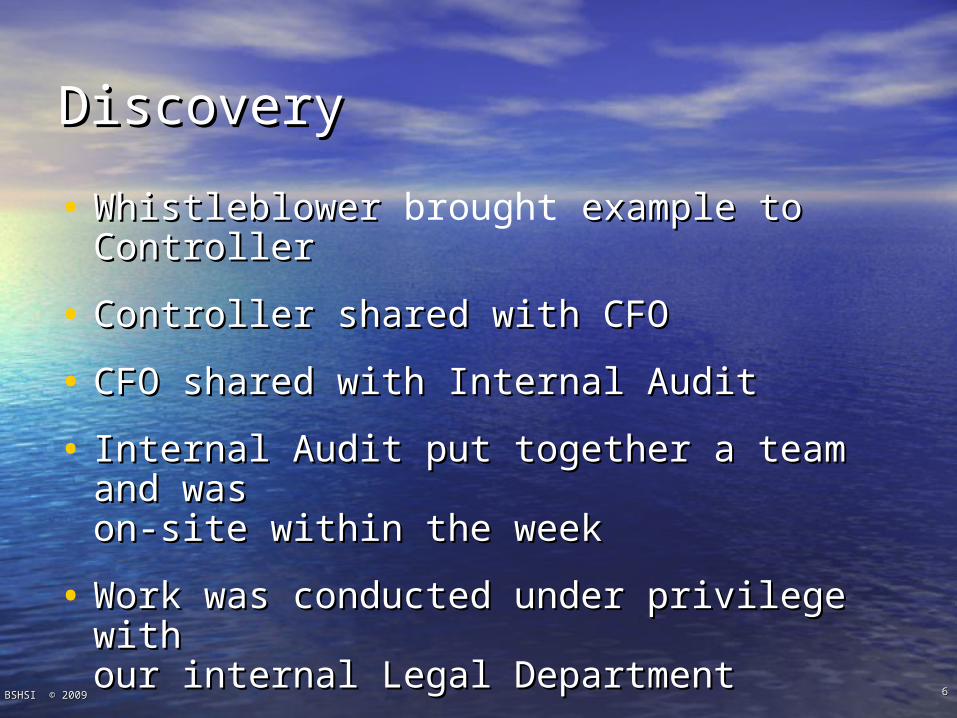

DiscoveryDiscovery

• Whistleblower Whistleblower brought example to example to ControllerController

• Controller shared with CFOController shared with CFO

• CFO shared with Internal AuditCFO shared with Internal Audit

• Internal Audit put together a team and Internal Audit put together a team and was was on-site within the weekon-site within the week

• Work was conducted under privilege with Work was conducted under privilege with our internal Legal Departmentour internal Legal Department

BSHSI © 2009BSHSI © 2009 77

How Was It Perpetrated?How Was It Perpetrated?

Manipulation of the following areasManipulation of the following areas::

• ChecksChecks

• Direct DepositsDirect Deposits

• PTOPTO

• Withholding TaxesWithholding Taxes

• Overtime and Shift DifferentialOvertime and Shift Differential

• Quarterly Tax ReportsQuarterly Tax Reports

• W-2 YTD AmountsW-2 YTD Amounts

BSHSI © 2009BSHSI © 2009 88

Manipulation ProcessManipulation Process

Demand checks with gross pay of $0.01Demand checks with gross pay of $0.01

Federal and State taxes were entered as a Federal and State taxes were entered as a negative amount, resulting in net pay negative amount, resulting in net pay higher than gross higher than gross

Other deductions were used in the same Other deductions were used in the same manner as the bullet abovemanner as the bullet above

Shift differential substantially greater than Shift differential substantially greater than the hours workedthe hours worked

BSHSI © 2009BSHSI © 2009 99

Manipulation Process Cont.Manipulation Process Cont.

Payments to terminated and leave of Payments to terminated and leave of absence employeesabsence employees

Paid regular hours in lieu of PTO hoursPaid regular hours in lieu of PTO hours

Individuals had no taxes withheld in 2005, Individuals had no taxes withheld in 2005, but W-2 was modified to appear as though but W-2 was modified to appear as though taxes were paidtaxes were paid

Individual’s 2006 master file information Individual’s 2006 master file information was adjusted to appear that taxes were was adjusted to appear that taxes were withheldwithheld

BSHSI © 2009BSHSI © 2009 1010

Manipulation Process Cont.Manipulation Process Cont.

Checks were voided on the payroll system Checks were voided on the payroll system but not on the positive pay file held by the but not on the positive pay file held by the bankbank

Standard practice included reimbursement Standard practice included reimbursement for taxes when overtime was combined on for taxes when overtime was combined on a regular bi-weekly payroll checka regular bi-weekly payroll check

Transactions hidden by using word pad to Transactions hidden by using word pad to change reports given to Financechange reports given to Finance

BSHSI © 2009BSHSI © 2009 1111

Effect of Negative Tax Effect of Negative Tax TransactionsTransactions

Gross Pay Net Pay Fed W/H State W/H

Employee A $ 2,500.00 $ 1,550.00 $ 750.00 $ 200.00

Employee B $ 4,000.00 $ 2,250.00 $ 1,250.00 $ 500.00

Employee C $ 1,750.00 $ 1,425.00 $ 250.00 $ 75.00

Employee D (Fraudulent Pymt) $ 0.01 $ 1,000.01 $ (1,000.00) $ -

Total $ 8,250.01 $ 6,225.01 $ 1,250.00 $ 775.00

Example – Effect of Fraud on Withholding Submissions

BSHSI © 2009BSHSI © 2009 1212

Recap of LossesRecap of Losses

Losses due to: Losses due to: 20052005 20062006 TotalTotal

Negative Federal Negative Federal TaxesTaxes

$953.35$953.35 $326,729.22$326,729.22 $327,682.57$327,682.57

Negative State Negative State TaxesTaxes

$165.78$165.78 $29,685.43$29,685.43 $29,851.21$29,851.21

Corrections to Corrections to Direct DepositsDirect Deposits

$36,795.04$36,795.04 $15,799.36$15,799.36 $52,594.40$52,594.40

Other*Other* $18,758.56$18,758.56 $32,286.17$32,286.17 $51,044.73$51,044.73

TOTALTOTAL $56,672.73$56,672.73 $404,500.18$404,500.18 $461,172.91$461,172.91

Misappropriated dollars – BSHSI’s losses due to irregularities were $461,172.91. The table summarizes by year and category the irregularity involved:

BSHSI © 2009BSHSI © 2009 1313

Tax ImplicationsTax Implications

Due to the methodology used to misappropriate funds, BSHSI incurred a sizable tax impact. The table summarizes by year and agency the tax impact:

Tax Impact Tax Impact 20052005 20062006 TotalTotal

Federal TaxesFederal Taxes $2,455$2,455 $273,459$273,459 $275,914$275,914

State TaxesState Taxes $368$368 $39,393$39,393 $39,761$39,761

TotalTotal $2,823$2,823 $312,852$312,852 $315,675$315,675

BSHSI © 2009BSHSI © 2009 1414

Results of InvestigationResults of Investigation

• 9 Individuals terminated9 Individuals terminated

• Prosecution performed by State Prosecution performed by State Attorney GeneralAttorney General

• Results thus far:Results thus far:

– 4 have plea bargained and ordered to pay 4 have plea bargained and ordered to pay restitutionrestitution

– Primary Instigator is pending grand jury Primary Instigator is pending grand jury indictmentindictment

– Remainder are in negotiationsRemainder are in negotiations

BSHSI © 2009BSHSI © 2009 1515

CAATSCAATS

BSHSI © 2009BSHSI © 2009 1616

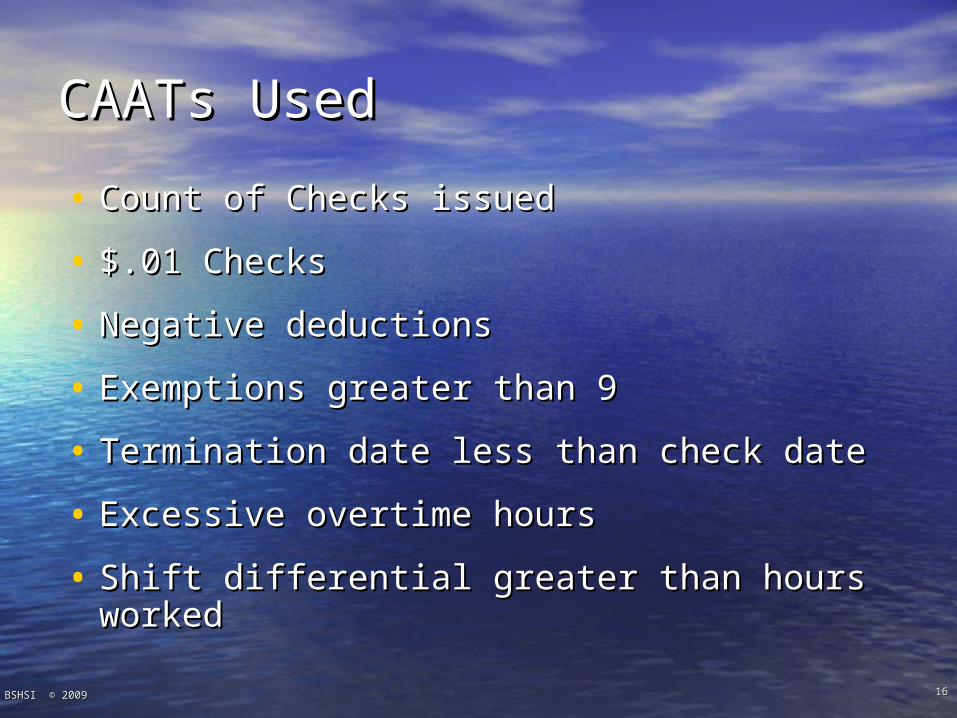

CAATs UsedCAATs Used

• Count of Checks issuedCount of Checks issued

• $.01 Checks$.01 Checks

• Negative deductionsNegative deductions

• Exemptions greater than 9Exemptions greater than 9

• Termination date less than check dateTermination date less than check date

• Excessive overtime hoursExcessive overtime hours

• Shift differential greater than hours Shift differential greater than hours workedworked

BSHSI © 2009BSHSI © 2009 1717

Internal Control BreakdownsInternal Control Breakdowns

• Minimal oversightMinimal oversight

• Segregation of Duties Segregation of Duties

• ReconciliationsReconciliations

• Policies and ProceduresPolicies and Procedures

BSHSI © 2009BSHSI © 2009 1818

Minimal OversightMinimal Oversight

Lack of issue ownershipLack of issue ownership

Cutting CornersCutting Corners

Reducing Staff VolumesReducing Staff Volumes

Missing documentation (copies of tax Missing documentation (copies of tax filings, canceled checks, W-4s, etc.)filings, canceled checks, W-4s, etc.)

BSHSI © 2009BSHSI © 2009 1919

Lack of Segregation of DutiesLack of Segregation of Duties

• Manual calculation and entry of overtimeManual calculation and entry of overtime

• Access to initiate payroll transactions within Access to initiate payroll transactions within the payroll system and the bankthe payroll system and the bank

• Recording payroll transactions in the Recording payroll transactions in the payroll system payroll system

• Custodial access to employer and Custodial access to employer and employee bank accounts, funds, and employee bank accounts, funds, and related employee pay rate and tax recordsrelated employee pay rate and tax records

BSHSI © 2009BSHSI © 2009 2020

ReconciliationsReconciliations

• Federal and/or state quarterly reportingFederal and/or state quarterly reporting

• Actual summation of the appropriate pay Actual summation of the appropriate pay periodsperiods

• Payroll bank accounts, payroll system, and Payroll bank accounts, payroll system, and the general ledger were being performed the general ledger were being performed at a very high levelat a very high level

• The lack of adequate reconciliations was The lack of adequate reconciliations was previously notedpreviously noted

BSHSI © 2009BSHSI © 2009 2121

Lack of Policies and ProceduresLack of Policies and Procedures

Relevant documentation not consistently Relevant documentation not consistently maintainedmaintained

Payroll performing HR tasksPayroll performing HR tasks

HR developed a practice that allowed overtime HR developed a practice that allowed overtime to be paid in a separate payment (Demand to be paid in a separate payment (Demand check)check)

Ad hoc practice allowed employees to request Ad hoc practice allowed employees to request payroll refunds of the tax withholding variancespayroll refunds of the tax withholding variances

BSHSI © 2009BSHSI © 2009 2222

Future Audit ConsiderationsFuture Audit ConsiderationsDocumentation:Documentation:

• Where is it located?Where is it located?

• How current are such items as W4s, benefit How current are such items as W4s, benefit elections, and pay increases?elections, and pay increases?

Policies and procedures: Policies and procedures:

• Are they in place?Are they in place?

• Are they being circumvented?Are they being circumvented?

• Are there ad-hoc procedures?Are there ad-hoc procedures?

BSHSI © 2009BSHSI © 2009 2323

Future Audit ConsiderationsFuture Audit Considerations

Overtime: Overtime:

• How is it approved?How is it approved?

• Is it paid separately?Is it paid separately?

• Are responsibility reports being reviewed Are responsibility reports being reviewed as a verification?as a verification?

BSHSI © 2009BSHSI © 2009 2424

Future Audit ConsiderationsFuture Audit Considerations

Demand checks:Demand checks:

• Are there a large number of them?Are there a large number of them?

• Are “Penny” checks being issued?Are “Penny” checks being issued?

• Who approves demand checks?Who approves demand checks?

• Under what circumstances are they being Under what circumstances are they being issued?issued?

BSHSI © 2009BSHSI © 2009 2525

Future Audit ConsiderationsFuture Audit Considerations

Security:Security:

• Who has the ability to do what?Who has the ability to do what?

• How are checks numbered?How are checks numbered?

Reconciliations:Reconciliations:

• Is the bank account being reconciled to the payroll Is the bank account being reconciled to the payroll information?information?

• Are the payrolls/deductions being reconciled to the GL?Are the payrolls/deductions being reconciled to the GL?

• Are responsibilityAre responsibility reports verified to payroll?reports verified to payroll?

BSHSI © 2009BSHSI © 2009 2626

Future Audit ConsiderationsFuture Audit Considerations

Tax Reporting:Tax Reporting:

• Are the proper forms being filed on a Are the proper forms being filed on a quarterly basis? Electronically?quarterly basis? Electronically?

• Are the forms being reconciled to payroll Are the forms being reconciled to payroll system details?system details?

• Who approves the forms before filing and Who approves the forms before filing and how are the forms verified as to accuracy?how are the forms verified as to accuracy?

BSHSI © 2009BSHSI © 2009 2727

Future Audit ConsiderationsFuture Audit ConsiderationsSystem Integrity:System Integrity:

• Do the W4s, benefit elections, and pay Do the W4s, benefit elections, and pay increases match what is in the hard-copy file?increases match what is in the hard-copy file?

• Is a separate check writing system used?Is a separate check writing system used?

• Who has access to the check, positive pay Who has access to the check, positive pay and direct deposit files?and direct deposit files?

• Are accruals (vacation, sick time, etc) being Are accruals (vacation, sick time, etc) being adjusted accurately?adjusted accurately?

• How are voids handled?How are voids handled?

BSHSI © 2009BSHSI © 2009 2828

Future Audit ConsiderationsFuture Audit Considerations

CAATS:CAATS:

• List of negative deductions (federal, state taxes; List of negative deductions (federal, state taxes; corrections to direct deposits; etc.)corrections to direct deposits; etc.)

• Shift differential or other types of incentives Shift differential or other types of incentives being paid for more hours than workedbeing paid for more hours than worked

• Hours worked not matching hours paidHours worked not matching hours paid

• Net pay greater than gross payNet pay greater than gross pay

• Individuals with no benefitsIndividuals with no benefits

BSHSI © 2009BSHSI © 2009 2929

Future Audit ConsiderationsFuture Audit Considerations

CAATS (continued):CAATS (continued):

• Voids (checks and direct deposits) on systemVoids (checks and direct deposits) on system

• Multiple checks in a pay periodMultiple checks in a pay period

• People terminated in benefits but not in People terminated in benefits but not in payrollpayroll

• People on leave getting checksPeople on leave getting checks

• Checks to same addressChecks to same address

• Duplicate SSNsDuplicate SSNs

BSHSI © 2009BSHSI © 2009 3030

Total Cost of FraudTotal Cost of Fraud

• Amount Misappropriated - $461,173

• Investigation Costs (includes salaries, travel, external attorneys, administration) - $310,868

• TOTAL COST – $772,041

BSHSI © 2009BSHSI © 2009 3131

QuestionsQuestions

BSHSI © 2009BSHSI © 2009 3232

CONTACT INFORMATIONCONTACT INFORMATION

Darlene FitzPatrickDarlene FitzPatrick, CFE, CIA, , CFE, CIA, CCSACCSA

Bon Secours Health System, Inc.Bon Secours Health System, Inc.8555 Magellan Parkway8555 Magellan Parkway

Richmond, VA 23227Richmond, VA 23227

804-289-7479804-289-7479