Embed Size (px)

Citation preview

Payment on account of Remuneration

- Taxability and Remittance ProceduresCA Rutvik Sanghvi

Workshop on Taxation of Foreign Remittances

The Chamber of Tax ConsultantsMaharashtra Chamber of Commerce & Industry

20th January 2017

Contents

Taxability under the Act

Taxability under Double Tax Avoidance Agreements

Employee Stock Options

Leave salary

Tax Equalisation & Hypothetical tax

Social Security contributions

Pensions

Deduction of tax at source

Other areas of concern

2CA Rutvik Sanghvi

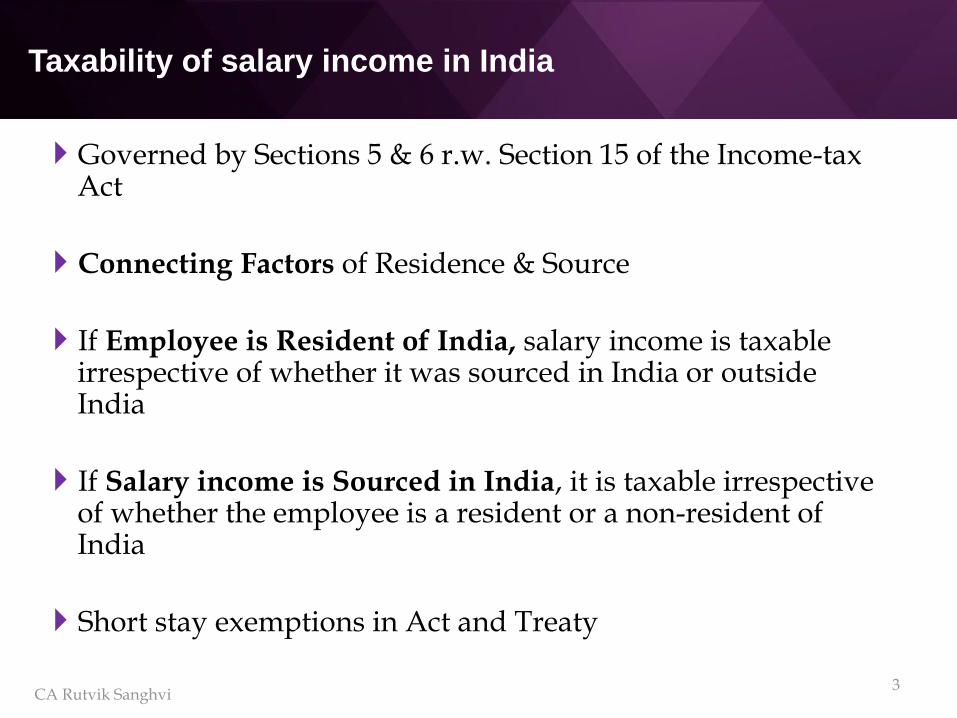

Taxability of salary income in India

Governed by Sections 5 & 6 r.w. Section 15 of the Income-tax Act

Connecting Factors of Residence & Source

If Employee is Resident of India, salary income is taxable irrespective of whether it was sourced in India or outside India

If Salary income is Sourced in India, it is taxable irrespective of whether the employee is a resident or a non-resident of India

Short stay exemptions in Act and Treaty

3CA Rutvik Sanghvi

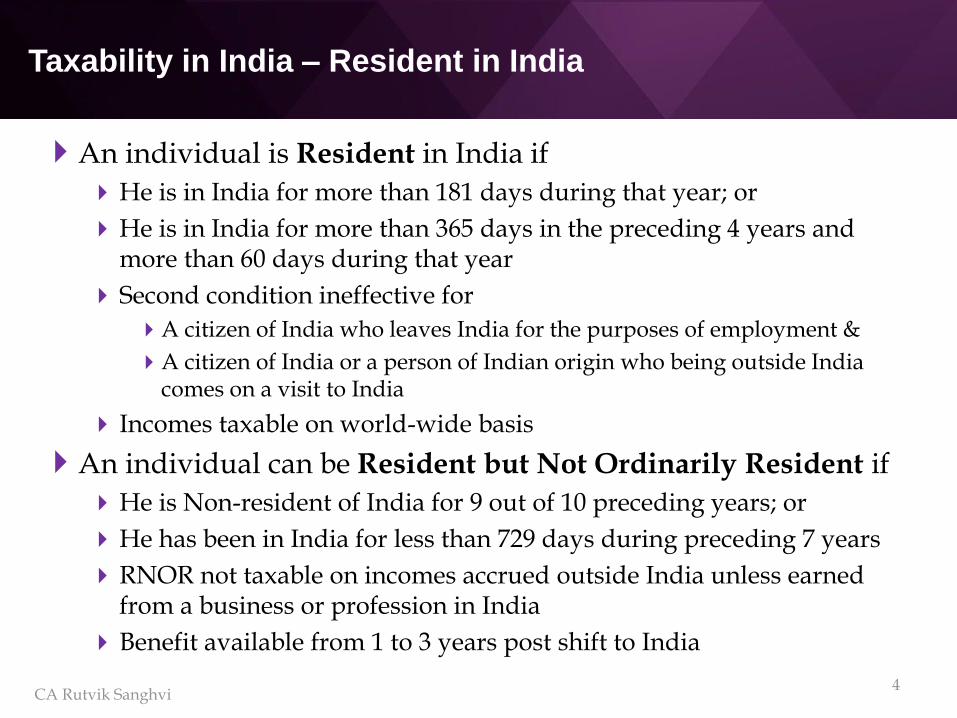

Taxability in India – Resident in India

An individual is Resident in India if

He is in India for more than 181 days during that year; or

He is in India for more than 365 days in the preceding 4 years and more than 60 days during that year

Second condition ineffective for

A citizen of India who leaves India for the purposes of employment &

A citizen of India or a person of Indian origin who being outside India comes on a visit to India

Incomes taxable on world-wide basis

An individual can be Resident but Not Ordinarily Resident if

He is Non-resident of India for 9 out of 10 preceding years; or

He has been in India for less than 729 days during preceding 7 years

RNOR not taxable on incomes accrued outside India unless earned from a business or profession in India

Benefit available from 1 to 3 years post shift to India

4CA Rutvik Sanghvi

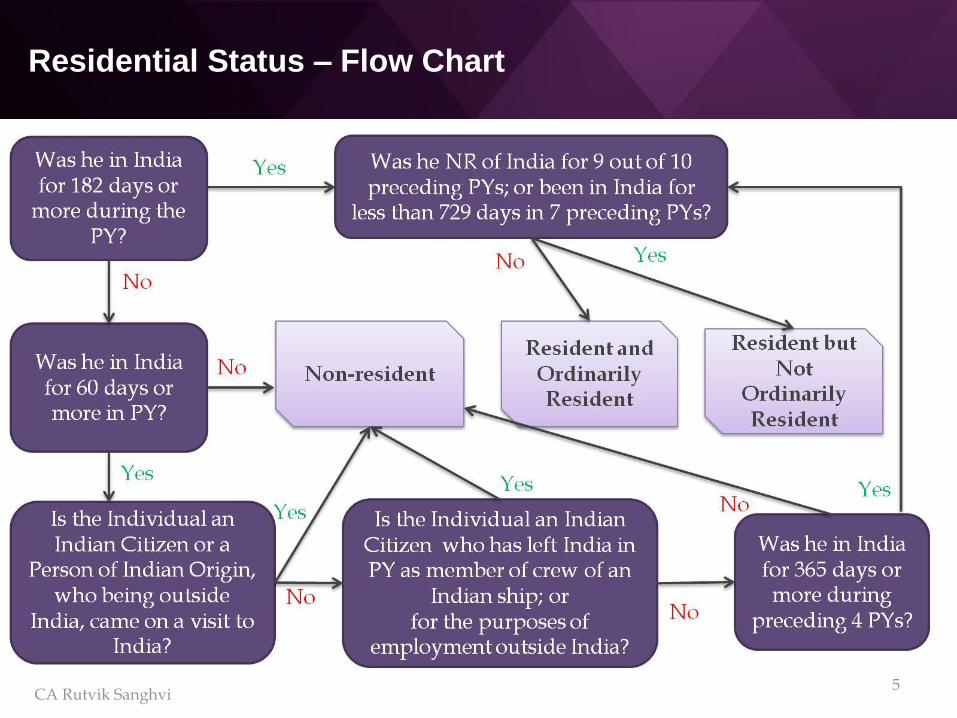

Residential Status – Flow Chart

CA Rutvik Sanghvi5

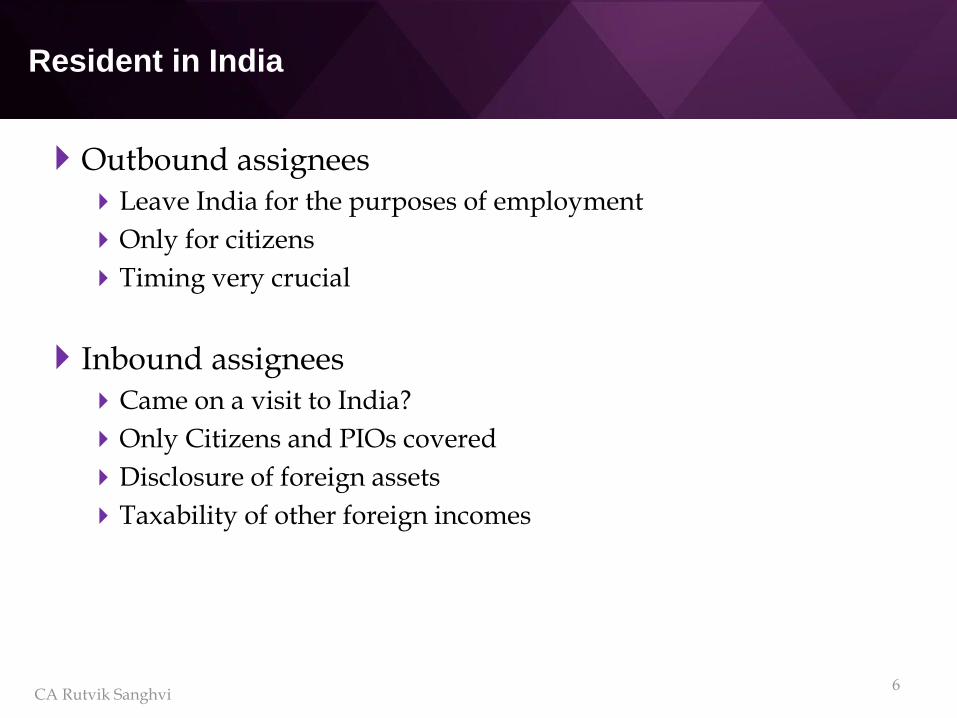

Resident in India

Outbound assigneesLeave India for the purposes of employment

Only for citizens

Timing very crucial

Inbound assigneesCame on a visit to India?

Only Citizens and PIOs covered

Disclosure of foreign assets

Taxability of other foreign incomes

CA Rutvik Sanghvi6

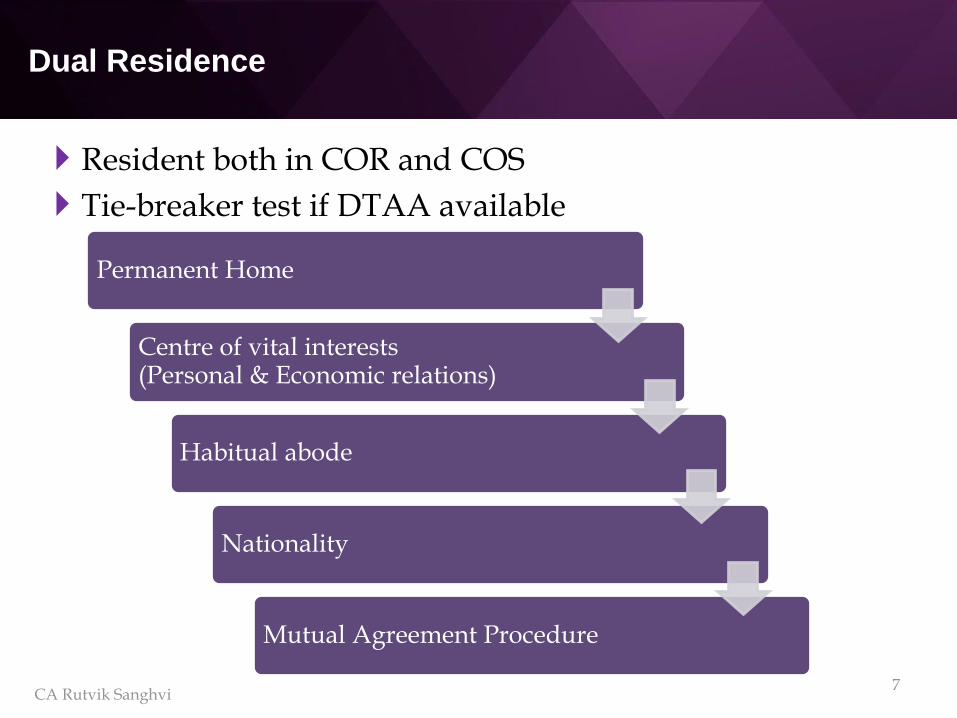

Dual Residence

Resident both in COR and COS

Tie-breaker test if DTAA available

7

Permanent Home

Centre of vital interests (Personal & Economic relations)

Habitual abode

Nationality

Mutual Agreement Procedure

CA Rutvik Sanghvi

Taxability in India – Sourced in India

“Sourced” in India means salary incomes which Accrue or arise in India; or Are Received in India

“Accrue” or “arise” in India (Section 5) if: Involve the concept of receivability or the right to receive in a particular place

and do not refer to income being earned in that place or being derived from a source of income situated in that place

In other words, the “Employment Base” of the employee is in India – where right to receive the salary arises, where the employee’s services functions are supervised; where the employer utilises the employee’s services; takes decisions regarding the employee’s employment; maintains employee records; etc.

Deemed to Accrue in India (Section 9) Salaries “earned” in India, i.e., for services rendered in India Salaries payable by the Government to an Indian citizen for service outside India

“Received” in India means where the first receipt of income happens in India Remittance after first receipt is of money, not income

8CA Rutvik Sanghvi

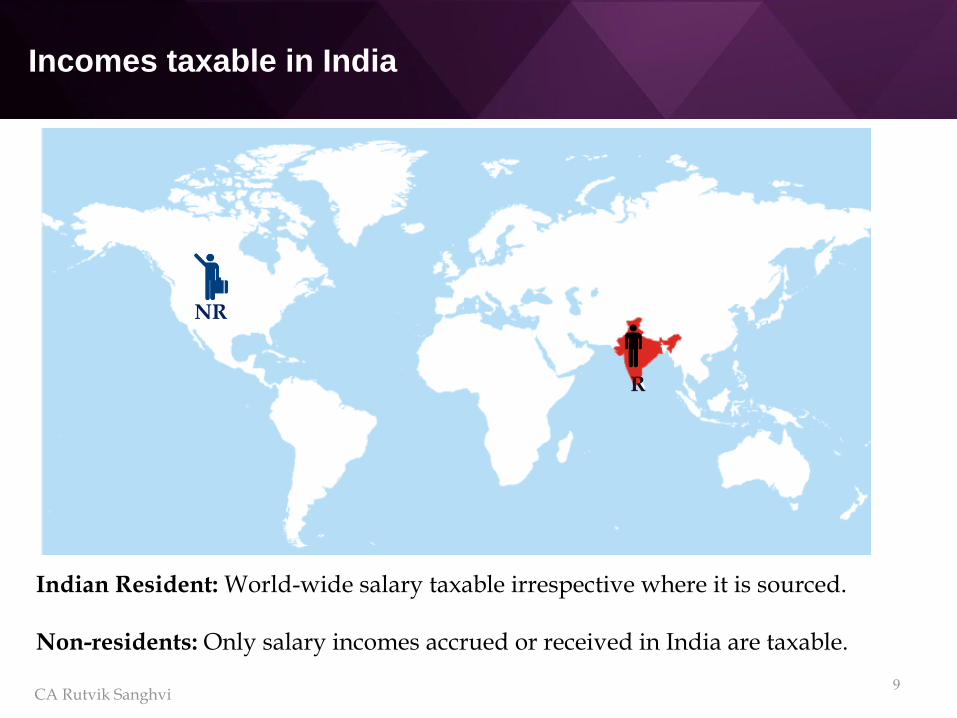

Incomes taxable in India

9

Indian Resident: World-wide salary taxable irrespective where it is sourced.

Non-residents: Only salary incomes accrued or received in India are taxable.

R

NR

CA Rutvik Sanghvi

Taxation of Salary income – Where and When

Section 5

Determines scope of salary income – where it will be taxed

Salary taxable in India for NR only if it accrues or is received or is deemed to accrue in India

Section 15

Determines categorisation & time of taxation – when it will be taxed

Salary income taxable in Previous Year (PY) if:

Salary is due in the Previous Year, whether paid or not

Salary is paid in the PY though not due or before it became due

Arrears of salary paid in PY; if not charged to tax earlier

10CA Rutvik Sanghvi

Salary income - Accrual vs Receipt

Case Study:Mr. X, an NR, employed with a HK Co. renders service in HK,

but salary received in IndiaSalary accrues outside India, but taxable in India on receipt basisSalary taxable in India if first receipt in India

If salary received outside India and then remitted to India - no tax in India

Typical issue faced by employees on board ships in international waters Tapas Kr. Bandopadhyay [70 taxmann.com 50 Kolkata - ITAT] Avtar Singh Wadhwan [247 ITR 260] Prahlad Vijendra Rao [198 taxmann 551] Arvind Singh Chauhan [42 taxmann.com 285 Agra ITAT]

Actual Receipt vs Constructive receipt

Taxability may be different under DTAA situation11

CA Rutvik Sanghvi

Salary income - Accrual vs Receipt

Case StudyMr. Y, an NR, employed with Indian Co., renders service in

HK, and receives salary in HKSalary accrues in India under Section 5(2) as “employment

base” in India Salary taxable in India though earned and received outside

India Similar issue if employment agreement entered into with Indian

Branch of Foreign Co.

Salary accrues in India under Section 5(2) and hence taxable in India, irrespective of where services are rendered, salary is earned or received Phra Phraison Salarak (3 ITC 237) Diwan Bahadur Sir T. Vijayarahavacharya (4 ITR 317) V G Every (5 ITR 216)

However, taxability under DTAA may be different12

CA Rutvik Sanghvi

Taxability under the DTAAs

Article 15 – Dependent Personal Services

The article applies to employment income. Anemployee who is a resident of one country & works inanother country, is covered by this article.

The article is subject to the provisions of other articles ondirector’s remuneration, Government service, pension,artists and sportsperson.

OECD Model commentary uses the words “Incomefrom Employment” after deletion of IPS article.

13CA Rutvik Sanghvi

Article 15 – Dependent Personal Services

Primarily all income is taxable in the country ofresidence

However, if the employment is exercised inthe source country, & some conditions inarticle 15(2) are satisfied, then income istaxable in the source country

Employment exercised on board a ship or aircraftoperated in international traffic taxed in the countrywhere effective management of enterprise is situated

14CA Rutvik Sanghvi

Article 15 – Dependent Personal Services

What kind of employment income is covered?Private individual employment

What is NOT covered by this article? Director’s fees (and Director’s salary, etc. in some cases)

Artist’s & sportsperson’s remuneration

Pension

Payments to students, professors & foreign teachers in some cases

Salary& pension of Government employees.

Does not include employment with Government companies /bodies; and with businesses run by Government – sovereign wealthfund, Railways, etc.

15

Thus only current employment income of “Non-Government” sector employees is covered

CA Rutvik Sanghvi

Article 15 – Dependent Personal Services

Article 15(1):

Salaries, wages & other similar remuneration

derived by a resident of say, UK,

in respect of employment,

shall be taxed only in UK.

unless,

the employment is exercised in India.

Salary is primarily taxable in Country of Residence - UK.

If the employment is exercised in India, thenremuneration may be taxed in India also.

Thus salary can be taxed in UK & India.16

CA Rutvik Sanghvi

Article 15 – Dependent Personal Services

Difference between Independent Services &Employment – not explained.

Where is employment exercised – normally where theemployee is physically present when performing hisactivities. Not where results are exploited.A short visit to India – is employment exercised in India?

Salary includes perquisites.

Time of payment is immaterial. All payment for exerciseof employment is taxable.

17CA Rutvik Sanghvi

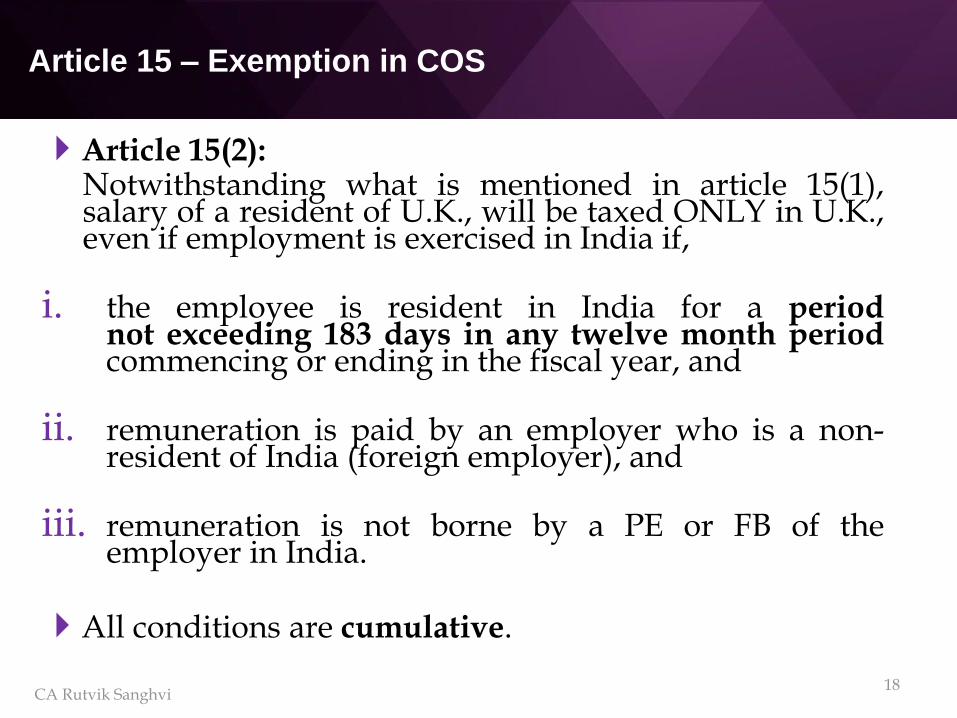

Article 15 – Exemption in COS

Article 15(2):Notwithstanding what is mentioned in article 15(1),salary of a resident of U.K., will be taxed ONLY in U.K.,even if employment is exercised in India if,

i. the employee is resident in India for a periodnot exceeding 183 days in any twelve month periodcommencing or ending in the fiscal year, and

ii. remuneration is paid by an employer who is a non-resident of India (foreign employer), and

iii. remuneration is not borne by a PE or FB of theemployer in India.

All conditions are cumulative.

18CA Rutvik Sanghvi

Article 15 – Exemption in COS

In other words, India can tax the employment income, ifany of converse conditions are satisfied, i.e.,

if number of days of employee in India exceed 183, or

if remuneration is paid by an Indian resident, or

if remuneration is borne by the employer’s PE or FB inIndia.

Purpose - Short duration employment, & where noexpenses are claimed in India (no base erosion in India) –No tax in India

19CA Rutvik Sanghvi

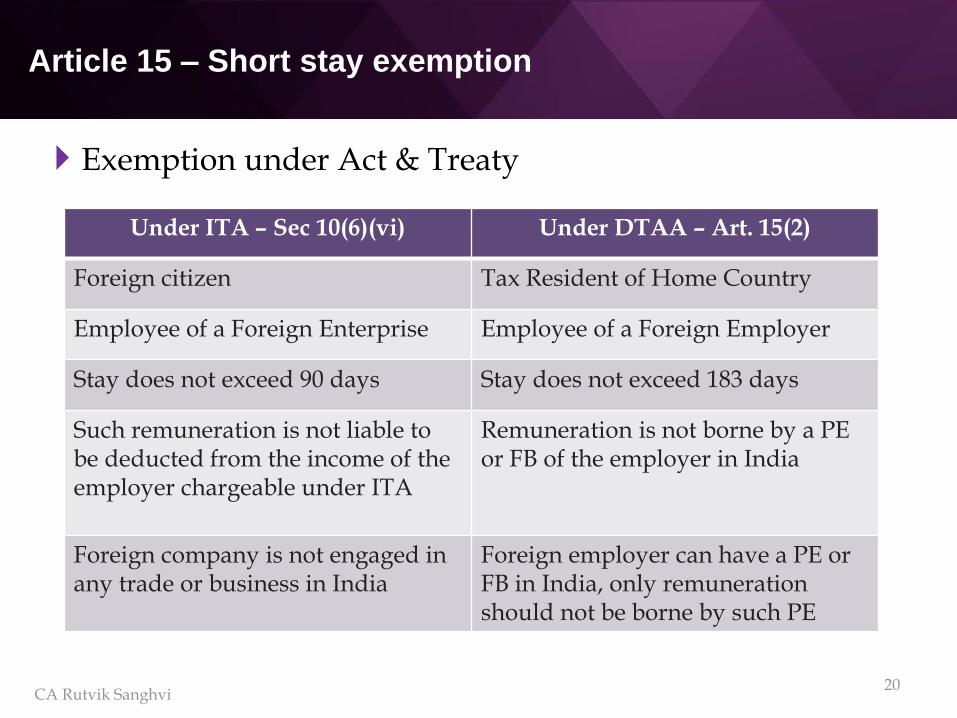

Article 15 – Short stay exemption

Exemption under Act & Treaty

20

Under ITA – Sec 10(6)(vi) Under DTAA – Art. 15(2)

Foreign citizen Tax Resident of Home Country

Employee of a Foreign Enterprise Employee of a Foreign Employer

Stay does not exceed 90 days Stay does not exceed 183 days

Such remuneration is not liable to be deducted from the income of the employer chargeable under ITA

Remuneration is not borne by a PE or FB of the employer in India

Foreign company is not engaged in any trade or business in India

Foreign employer can have a PE or FB in India, only remuneration should not be borne by such PE

CA Rutvik Sanghvi

Article 15 – 183 day test

The test applies to any twelve month periodPhysical presence is considered for counting the

number of days. Following days are included:Part of a dayDay of arrivalDay of departureHolidaysSickness

unless he is prevented to leave the country due to sickness, & hewould otherwise qualify for exemption

Days in transit for trip between 2 points outside India isNOT counted as in India.

21

Thus only full days outside India are not considered in 183 days test

CA Rutvik Sanghvi

Article 15 – Important Terms

Employer should be a non-resident.

An employer with residence in India only due to tie-breaking status is irrelevant. If employer is NR as perIndian law, it is sufficient.

Salary should not be borne by a PE or FB in India of theemployer.

What is the meaning of “borne by”?

Economic concept rather than an accounting concept

Direct and proximate relation

22CA Rutvik Sanghvi

Article 15 –Employment on Ship, etc.

Article 15(3):

Notwithstanding anything contained in articles 15(1) &15(2),

if salary is derived from employment exercised aboard aship or aircraft operated in international traffic, or a boatengaged in inland waterways, it may be taxed in thecountry where the effective management of theenterprise is situated.

This is keeping in line with article 8 on internationaltraffic.

Salary is taxed in the country of effective managementof the enterprise.

Country of Residence of employee can also tax theincome.

23CA Rutvik Sanghvi

Article 15 – Employment on Ship, etc.

If the ship comes to India, can salary of employee betaxed in India?

Only employment “on board” is covered

Generally treaty benefit not available for employees onboard shipsAs employees are not tax resident of any country - Nomads

Is it avoidable?

CA Rutvik Sanghvi24

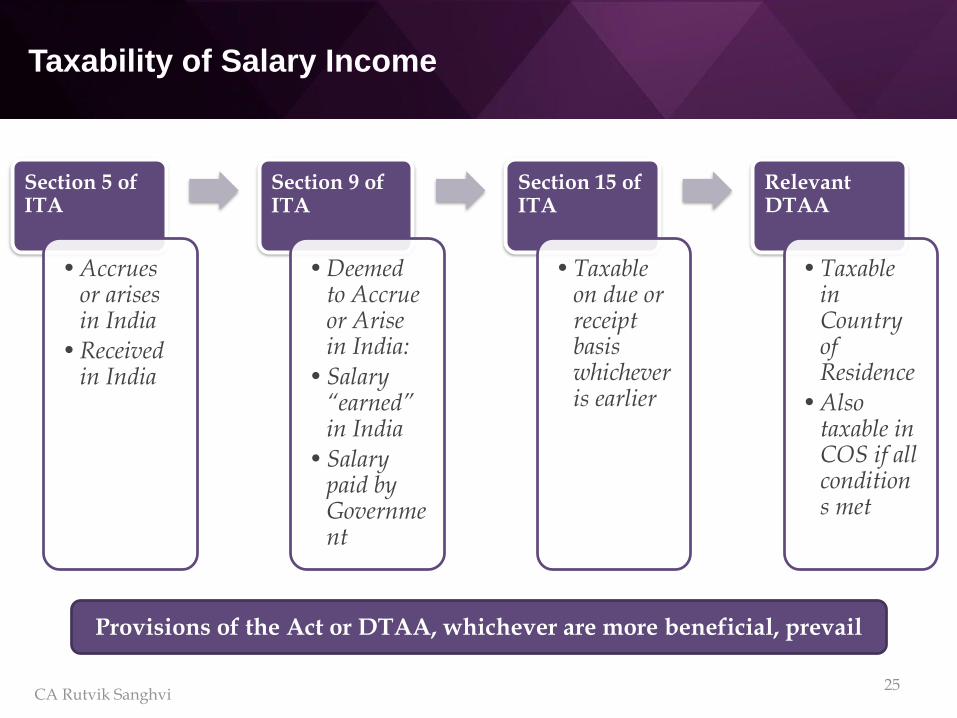

Taxability of Salary Income

Section 5 of ITA

• Accrues or arises in India

• Received in India

Section 9 of ITA

• Deemed to Accrue or Arise in India:

• Salary “earned” in India

• Salary paid by Government

Section 15 of ITA

• Taxable on due or receipt basis whichever is earlier

Relevant DTAA

• Taxable in Country of Residence

• Alsotaxable in COS if all conditions met

25

Provisions of the Act or DTAA, whichever are more beneficial, prevail

CA Rutvik Sanghvi

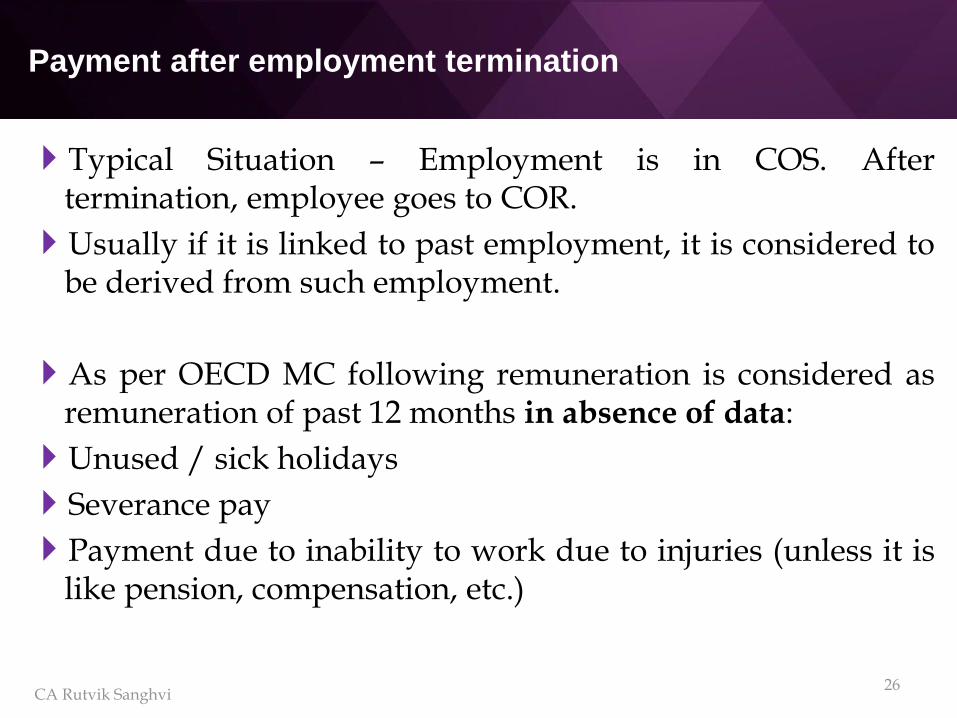

Payment after employment termination

Typical Situation – Employment is in COS. Aftertermination, employee goes to COR.

Usually if it is linked to past employment, it is considered tobe derived from such employment.

As per OECD MC following remuneration is considered asremuneration of past 12 months in absence of data:

Unused / sick holidays

Severance pay

Payment due to inability to work due to injuries (unless it islike pension, compensation, etc.)

26CA Rutvik Sanghvi

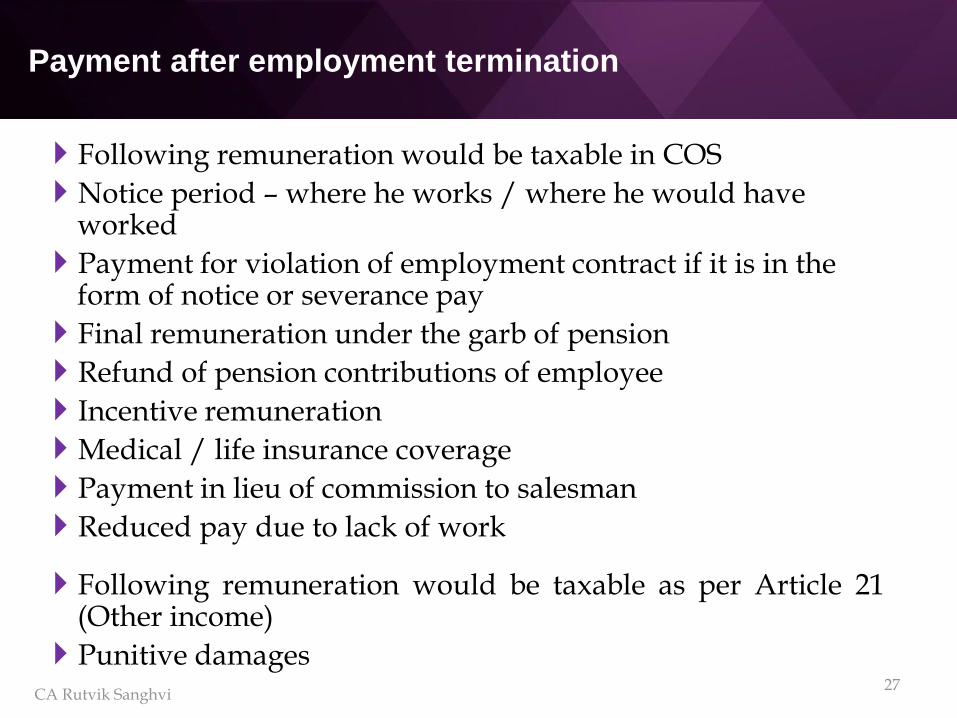

Payment after employment termination

Following remuneration would be taxable in COS

Notice period – where he works / where he would have worked

Payment for violation of employment contract if it is in the form of notice or severance pay

Final remuneration under the garb of pension

Refund of pension contributions of employee

Incentive remuneration

Medical / life insurance coverage

Payment in lieu of commission to salesman

Reduced pay due to lack of work

Following remuneration would be taxable as per Article 21(Other income)

Punitive damages27

CA Rutvik Sanghvi

Payment after employment termination

Following remuneration would be taxable in COR

Payment for not working for employer’s competitor – asit pertains to future employment.However if the payment does not make any real difference to the

ex-employer, it will be taxable in COS.

Difficulties for tax credit in COR in case of timingdifferences

28CA Rutvik Sanghvi

Accrual vs Receipt – Different Years

Case Study:

Mr. A, NR, was employed with HK Co. from 1st April 2015 to 31st March 2016

Renders services in HK during FY 2015-16

Mr. A leaves employment, and returns to India in April 2016

Mr. A is R&OR for FY 2016-17

He receives salary for March 2016 in April 2016 in India

Salary accrued outside India when NR, but received in India when R&OR

Taxability of salary earned for March 2016?29

CA Rutvik Sanghvi

Accrual vs Receipt – Different Years

Salary for March 2016 earned on rendering of services outside India for a foreign employer – salary income accrued outside India - Section 5(2)

Salary taxable on due basis in FY 2015-16 whether paid or not -as per Section 15(a)

Mr. A non-resident of India during FY 2015-16

Hence, salary not taxable in India on accrual basis in FY 2015-16

Salary received in India in FY 2016-17

But salary taxable on due basis and not receipt basis

Once salary considered for scope of taxation on accrual basis, cannot be brought to tax again on receipt basis

Relevant also for incomes from ESOP, leave salary, retirement benefits, etc.

30CA Rutvik Sanghvi

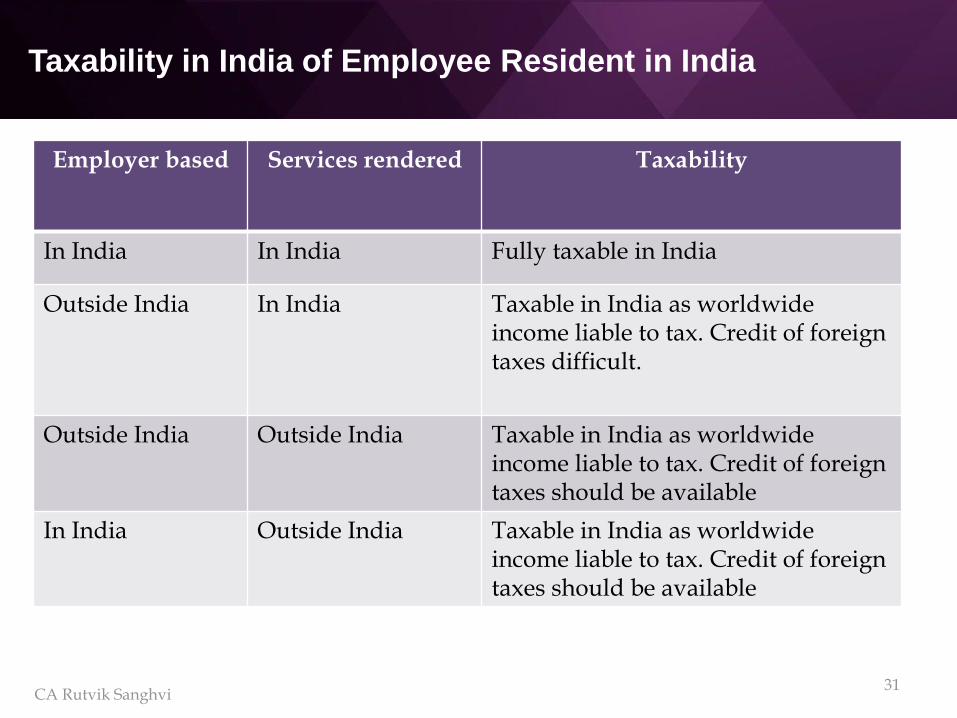

Taxability in India of Employee Resident in India

Employer based Services rendered Taxability

In India In India Fully taxable in India

Outside India In India Taxable in India as worldwide income liable to tax. Credit of foreign taxes difficult.

Outside India Outside India Taxable in India as worldwide income liable to tax. Credit of foreign taxes should be available

In India Outside India Taxable in India as worldwide income liable to tax. Credit of foreign taxes should be available

31CA Rutvik Sanghvi

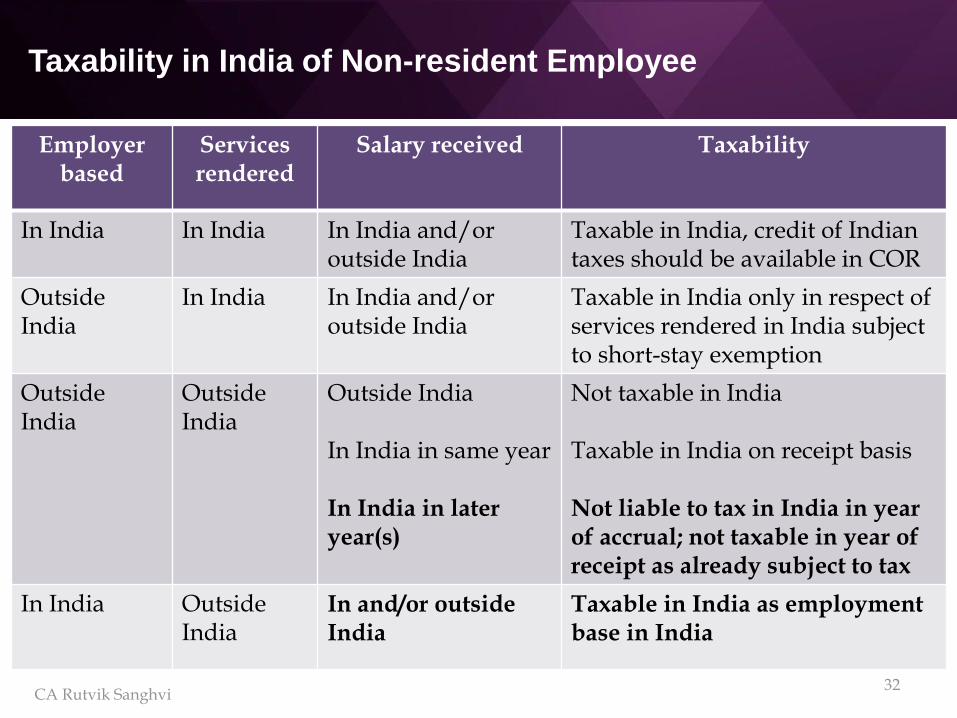

Taxability in India of Non-resident Employee

Employerbased

Services rendered

Salary received Taxability

In India In India In India and/or outside India

Taxable in India, credit of Indian taxes should be available in COR

Outside India

In India In India and/or outside India

Taxable in India only in respect of services rendered in India subject to short-stay exemption

Outside India

Outside India

Outside India

In India in same year

In India in later year(s)

Not taxable in India

Taxable in India on receipt basis

Not liable to tax in India in year of accrual; not taxable in year of receipt as already subject to tax

In India Outside India

In and/or outside India

Taxable in India as employment base in India

32CA Rutvik Sanghvi

International Hiring-out of labour

33

Employer(Employee contractor)

Indian Resident

Employees for less than 183

days

Employees work under supervision of Indian client.All conditions of Article 15(2) satisfied

PaymentContractIndia

Gibraltar

CA Rutvik Sanghvi

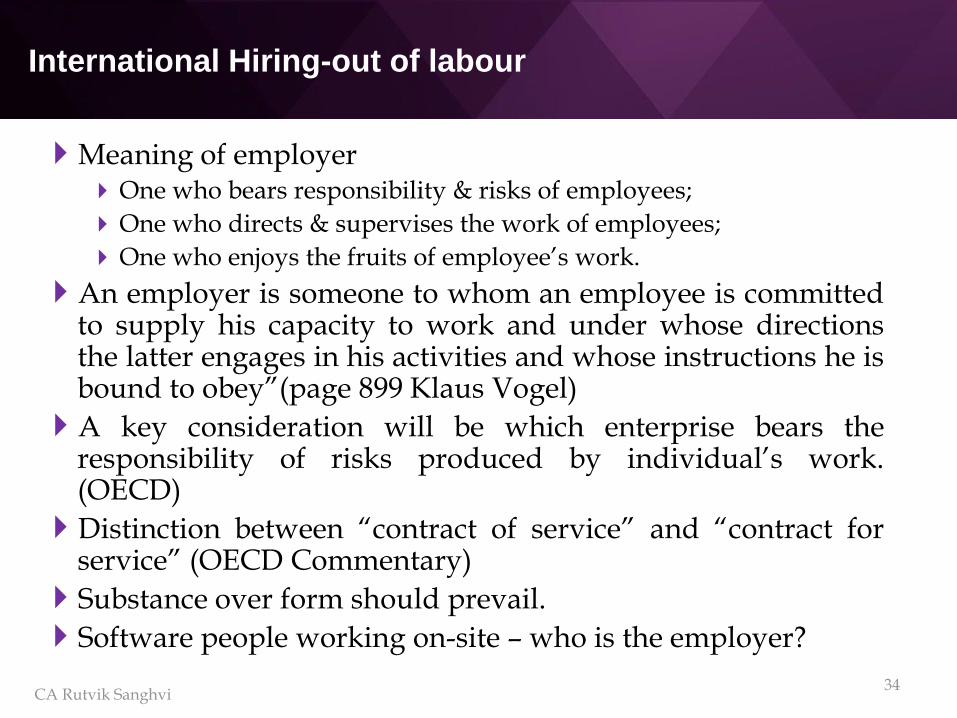

International Hiring-out of labour

Meaning of employer One who bears responsibility & risks of employees;

One who directs & supervises the work of employees;

One who enjoys the fruits of employee’s work.

An employer is someone to whom an employee is committedto supply his capacity to work and under whose directionsthe latter engages in his activities and whose instructions he isbound to obey”(page 899 Klaus Vogel)

A key consideration will be which enterprise bears theresponsibility of risks produced by individual’s work.(OECD)

Distinction between “contract of service” and “contract forservice” (OECD Commentary)

Substance over form should prevail.

Software people working on-site – who is the employer?

34CA Rutvik Sanghvi

Frontier Workers

Employees staying near the border, & going to work inthe country across the border – where is salary taxable?

OECD / UN models do not prescribe anything. It is leftto the countries concerned.

35CA Rutvik Sanghvi

Employee Stock Options

Distinguish employment benefit from capital gains.

Gains up to exercise of option is salary income underArticle 15.

Gain after exercise is capital gain under Article 13.

ESOPs given by foreign holding companies toemployees of Indian subsidiary are taxable.

36CA Rutvik Sanghvi

Employee Stock Options

Option Grant

Option Vest

Option Exercise

Allot Shares

Sell Shares

37

Perquisite taxable as Salary incomeTaxable under Article 15

Capital Gain taxable under Article 13

Key considerations:Time of taxation (left to COS).

Link to employment.

Tax Principles for point of taxation and type of income can differ

Double taxation easily possible

CA Rutvik Sanghvi

ESOPs – Post Exercise Gain

Exercise of Option

Allotment of Shares

Comes to India

Sale of Shares

38

If foreign employees come to India, & become residents; &then sell shares – India can tax Capital Gains.

Home country can tax appreciation post exercise till employeeleaves the country.

Home Country can tax

India can tax

…Appreciation in Value of shares...

CA Rutvik Sanghvi

ESOPs – For Future or Past Employment?

ESOPs are generally for retaining employees, i.e., futureemployment.

Generally after the minimum period of employmentnecessary for ESOPs, the benefit should not be related to theservices after the minimum period is over.

Difference between minimum period of employment (ESOPbenefit), & blocking period (Not ESOP benefit).

ESOPs could be granted for past employment. If pastemployment is in India, ESOP benefit can be taxed in India.

Some ESOPs may suggest that it applies for past employment,& for future services. The benefit should be divided. Division can be pro-rata based on time spent in each country

39CA Rutvik Sanghvi

Leave Salary

Salary for leave periods not utilised during the period of service received on termination of service or on retirement

Income accrues during the period of service; and not when received Not taxable under ITA if at the time of accrual employee was

Non-resident

DTAA benefit results in same tax treatment

Allocation to be done between service rendered in India and outside India

40CA Rutvik Sanghvi

Leave Salary

Case Study:

Mr. A was employed from 1st April 2000 with Co. XYZ, an Australian company

Deputed to India on 1st June 2010 and services rendered in India thereon

Mr. A resigned from Co. XYZ on 31st May 2016

Leave salary accumulated from 2010 paid on retirement

Taxability of leave salary in India?

Leave salary earned in Australia accrued when Mr. A was NR

Not taxable on receipt basis in India on retirement

Only portion relating to services rendered in India taxable in India

CA Rutvik Sanghvi41

Tax Equalisation & Hypothetical tax

Tax EqualisationCompensation method designed to make income taxes a

neutral factor in the expatriates’ compensation package.Expatriates will continue to incur tax burden equal to home

countryLocation agnostic - the employee has no benefit from low host

country taxes; nor is disadvantaged if assigned to a high taxcountry

Hypothetical taxNotional tax that an assignee would have paid if living and

working at homeMany companies limit the tax that an assignee must

personally bear during the assignment to the hypothetical taxHypo tax is deducted from the salary and total tax in host and

home countries are paid by employer

42CA Rutvik Sanghvi

Tax Equalisation & Hypothetical tax

Hypo Tax held deductible in:

Yoshio Kubo (357 ITR 452) (Del)

Jaydev Raja (357 ITR 292) (Bombay)

Dr Percy Batlivala and others (2010 TIOL 175) (Delhi)“In our opinion, the income arising in India in the present case is

actual salary plus the incremental tax liability arising on account of Indian assignment. Hypo Tax never accrued to the assessee and thus is deductible”.

Reliance was placed on E. D. Sasoon & Co. Ltd. (26 ITR 27 (SC)) for meaning of “accrued”

CA Rutvik Sanghvi43

Social Security contributions

Compulsory / mandatory natureThe employer should be authorised to deduct the social security

contribution from the monthly remuneration payable to the employee

Contributions are required to be made by all employees compulsorily

Certain penal implications for default

No vested right conferred on an employee

Overriding title on income from remuneration

Social Security AgreementsApplicable to ‘International Workers’

Provide for Detachment, Exportability and Totalisation

Certificate of Coverage required

44CA Rutvik Sanghvi

Pension income

Employer’s contribution to the Pension Funds is not taxable in the year of contribution as it does not vest in the employee till a much later date

Employer’s contribution would be taxed at the time of receipt of retirement benefits to the extent it relates to services rendered in India as per the ITA

Article 18 of the UN and OECD Models

Primary right of taxation with COR

Pensions received from Government may be taxable only in COS and not COR Check Article 19 – Government Service

Private pensions taxable in COR

45CA Rutvik Sanghvi

Deduction of tax at source

Section 192 applicable for incomes covered under the head “salaries”Section 195 not applicable

Deductible on payment basisTiming difference for salary “due” and “paid”

Tax computation based on Part III of Schedule 1 to the Finance ActTax computed on annual income basis and pro-rata deduction

20% rate if no PAN available; or wrong PAN cited - Sec 206AA

Can DTAA relief be considered while computing TDS?

Can Foreign Tax Credit be considered while computing TDS?

Reimbursement of salary

46CA Rutvik Sanghvi

Deduction of tax at source

Person responsible to deduct tax at sourceEmployer

In case of company – the company and its principal officer

Indian employer to deduct tax at source on salaries received by foreign expatriates deputed to it on the whole amount including portion received abroad – Eli Lilly [312 ITR 225 SC]

Sec. 192(1A) – employer has option to pay tax on non-monetary perquisites without TDSTax to be paid at the time of payment of perquisite

Benefit exempt from tax in hands of employee – Sec 10(10CC)

Tax borne by employer not available as deduction – Sec 40(a)(v)

47CA Rutvik Sanghvi

Deduction of tax at source - Compliance

TDS to be deposited with Government by 7th of next monthFacility for quarterly deposit can be made vide application

Quarterly statements to be submitted to tax authorities

Annual Form 16 to be issued to employee

48CA Rutvik Sanghvi

Deduction of tax at source - Consequences

Consequences on shortfall or non-deduction of tax

Employer deemed to be assessee in default – Sec 201(1)Exemption for Resident employee who pays up tax on own

Rule 31ACB and Form No. 26A

Hindustan Coca Cola Beverage (293 ITR 226)

Circular No. 275/201/95- IT(B) dated 29.1.1997

Interest – Sec 201(1A) and Penalties leviable –Sec 221 & Sec 271C

Prosecution, rare but possible – Sec 276B

Disallowance of salary expense – Sec 40(a)(iii)

Interest under 234B and 234C payable by employee for shortfall in TDS by employer? Ian Peter Morris [2016] 76 taxmann.com 271 (SC)

CA Rutvik Sanghvi49

Remittance of salary

Generally salary paid in India by employerAfter payment of taxes, employee can remit salary to home

country

Direct remittance to employee’s bank account outside India possible for:Foreign or Indian Citizen, resident of India under FEMA, and

employee of a foreign company, deputed to India

Foreign citizen, resident of India under FEMA, employed with an Indian company

Reg. 8 of FEMA Notification 10(R) / 2015-RB

Banks insist on proof of payment of taxesForm 16 – not possible before year-end

Form 26AS

Form 15CA and 15CB?

Employer’s certificate / Board Resolution

50CA Rutvik Sanghvi

Other areas of concern

Change of residence Resident under FEMA from day one

‘Not permanently resident’ Foreign incomes received abroad?

Filing of tax returns in India Submitting full income to tax Claiming correct tax credits Foreign incomes Black Money Act 2015

Service PE for employer Facts vs statements GE Energy Parts Inc.

Deputation/Secondment agreements drafting

Transfer Pricing for outsourced activities where cost plus method is followed

51CA Rutvik Sanghvi