Embed Size (px)

Citation preview

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 1

PAYING, RECORDING, AND

REPORTING PAYROLL AND

PAYROLL TAXES: THE

CONCLUSION OF THE

PAYROLL PROCESS

Chapter 8

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 2

Learning Objectives

1. Recording payroll and payroll taxes

2. Recording the payroll and the paying of the

payroll taxes

3. Recording employer taxes for FICA OASDI, FICA

HI, FUTA, SUTA, and workers’ compensation

insurance

4. Paying FUTA, SUTA, and workers’ compensation

insurance

5. Preparing Forms W-2, W-3, 941, and 940

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 3

Pay, Record, and Report

In Chapter 7, we learned how to calculate:

gross earnings

employee withholding taxes

net pay

employer payroll taxes

We now look at how businesses

pay, record, and report these amounts

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 4

Familiar Payroll Accounts

8 - 5 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Recording payroll and payroll

taxes

Learning Objective 1

8 - 6 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Revie

w A

ccount

s

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 7

Record Salaries Expense

Use Employee’s Payroll Register

Salary/Wages Expense = gross salary of all employees

Salaries/Wages Payable = net pay

Amounts of taxes withheld = “payable” accounts

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 8

Payroll Tax Expense

Different taxes are recorded in separate

liability accounts. These are:

FICA OASDI, FICA Medicare, FUTA, and SUTA

FICA taxes are paid to different government

agencies.

8 - 9 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Recording the payroll and the

paying of the payroll taxes

Learning Objective 2

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 10

Record Payment of Salaries

Record the payment of payroll to

employees

Would occur if the pay date is different from

the payroll recording date

Could occur if the pay date is the same as the

recording date

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 11

Pay Checks with Pay Stub

Pay stubs show the gross earnings, deductions & net pay

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 12

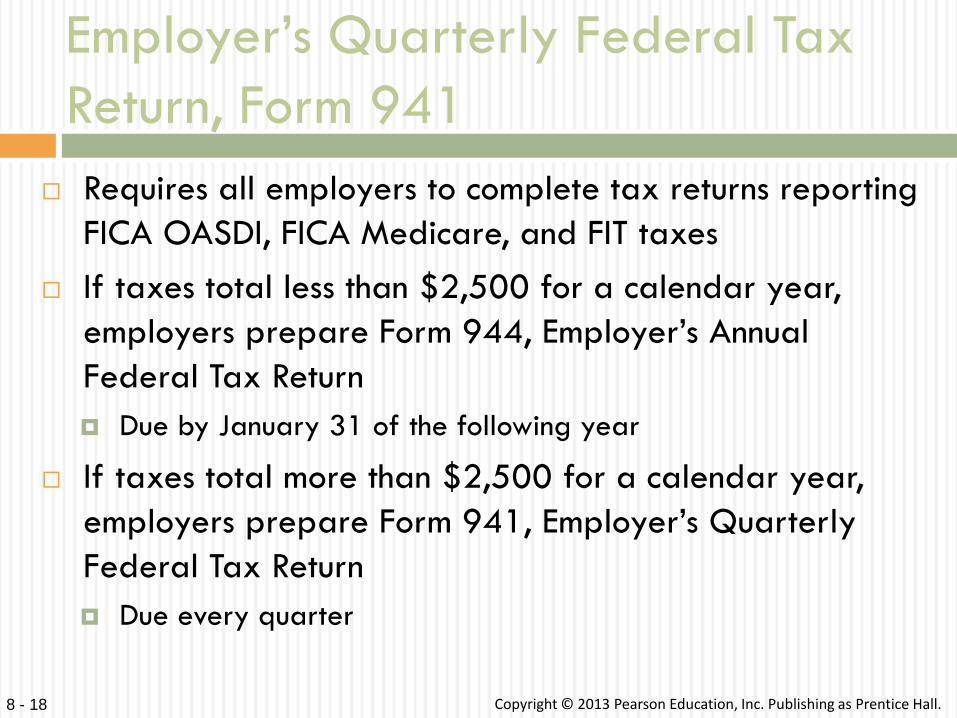

Employer’s Quarterly Federal Tax

Return, Form 941

Taxes withheld from employee checks are

reported and paid to the specific levels of

government

How?

Every employer must get a federal identification

number (EIN)

Form SS-4 to obtain the EIN

Use the EIN to report employee earnings and

payroll taxes

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 13

Form SS-4

Employer

identification

number (EIN)

is like a

Social

Security

number

8 - 14 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Recording employer taxes for

FICA OASDI, FICA HI, FUTA, SUTA,

and workers’ compensation

insurance

Learning Objective 3

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 15

FIT and FICA

First, determine when FIT and FICA taxes need to be paid and make the payment on time

Secondly, report these on Form 941, the Employer’s Quarterly Federal Tax Return

Use worksheet to complete the form

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 16

FIT and FICA

Transmitted to the Treasury Department using the Electronic Federal Tax Payment System (EFTPS)

If company owes < $2,500 in total taxes deposit quarterly

Monthly depositor – deposit taxes on 15th day of every month

Employer pays less than $50,000 of Form 941 taxes during look-back period

Semiweekly depositors – deposit taxes within three banking days

Employer pays more than $50,000 of Form 941 taxes during look-back period

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 17

Record Payment of Taxes

Journal entry to record the payment

of the FIT and FICA taxes

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 18

Employer’s Quarterly Federal Tax

Return, Form 941

Requires all employers to complete tax returns reporting

FICA OASDI, FICA Medicare, and FIT taxes

If taxes total less than $2,500 for a calendar year,

employers prepare Form 944, Employer’s Annual

Federal Tax Return

Due by January 31 of the following year

If taxes total more than $2,500 for a calendar year,

employers prepare Form 941, Employer’s Quarterly

Federal Tax Return

Due every quarter

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 19

Form 941

At the end of the

calendar year,

someone prepares the

Form 941 following

line-by-line instructions.

8 - 20 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Paying FUTA, SUTA, and workers’

compensation insurance

Learning Objective 4

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 21

Paying FUTA Tax

If tax owed for calendar year is < $500, employer

pays to the IRS by end of January of the next year.

If amount owed is > $500, employer pays quarterly

due by the end of the month following the end of the

calendar quarter.

In each case, a journal entry is recorded when the

payment is made.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 22

Form 940, Employer’s Annual Federal

Unemployment (FUTA) Tax Return

Form 940

Prepared at end of calendar year

Filed by January 31 following year

If taxes have be paid in full, then the firm has until February 10

Reports the amount of unemployment tax due for the year

Calculated on total wages, not individual earnings

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 23

Form 940

At the end of the

calendar year,

someone prepares the

Form 940 following

line-by-line instructions.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 24

Paying SUTA Tax

Paid to state government

Typically due by end of month following

each calendar quarter

Usually required to complete a state

unemployment tax form

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 25

Record Payment of Workers’

Compensation Insurance

Paid at the beginning of the year

Will gradually be transferred from the Prepaid

account to Workers’ Compensation Insurance Expense

account

At the end of the year, one could owe more

premiums or receive a refund

8 - 26 Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Preparing Forms W-2, W-3, 941,

and 940.

Learning Objective 5

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 27

W-2: Wage and Tax Statement

Prepared by employer each calendar year

Provides summary of gross earnings and deductions to each employee

Copies provided to:

Employee

IRS

State and Local Governments

Social Security Administration

Company records

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 28

Sample W-2

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 29

Form W-3: Transmittal of Income and

Tax Statements

Reports

Total amounts of wages, tips, and

compensation paid to employees

Total OASDI and Medicare taxes

withheld

Sent to a Social Security Administration

with copies of each employee’s W-2

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 30

Sample W-3

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 31

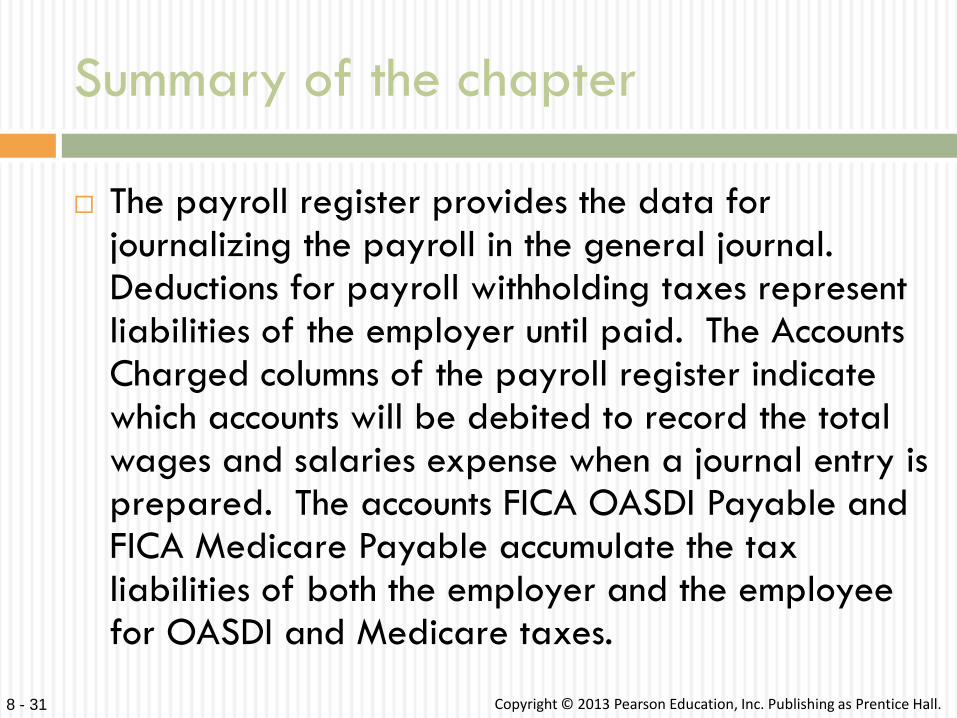

Summary of the chapter

The payroll register provides the data for journalizing the payroll in the general journal. Deductions for payroll withholding taxes represent liabilities of the employer until paid. The Accounts Charged columns of the payroll register indicate which accounts will be debited to record the total wages and salaries expense when a journal entry is prepared. The accounts FICA OASDI Payable and FICA Medicare Payable accumulate the tax liabilities of both the employer and the employee for OASDI and Medicare taxes.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 32

Summary of the chapter

The payroll tax expense is recorded at the same time that the payroll is recorded. Paying a payroll results in debiting Wages and Salaries Payable and crediting Cash or Payroll Cash.

Federal Form 941 is prepared and filed no later than one month after the calendar quarter ends. It reports the amount of FIT, OASDI, and Medicare tax withheld from employees and the OASDI and Medicare taxes due from the employer for the calendar quarter. FIT, OASDI, and Medicare taxes are known as Form 941 taxes.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 33

Summary of the chapter

The total amount of Form 941 taxes paid by a business during a specific period of time determines how often the business will have to make its payroll tax deposits. This time period is called a look-back period.

Businesses will normally make their payroll tax deposits to pay their Form 941 taxes either monthly or semiweekly. Different deposit rules apply to monthly and semiweekly depositors and these rules determine when deposits are due. Form 941 payroll tax deposits must be made—if the payment is less than $2,500 per quarter it is made—by check at the time the Form 941 is submitted.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 34

Summary of the chapter

Information to prepare W-2 forms can be obtained from the individual employee earnings records. Form W-3 is used by the Social Security Administration in verifying that taxes have been withheld as reported on individual employee W-2 forms. Form 940 is prepared by January 31, after the end of the previous calendar year. This form can be filed by February 10 if all required deposits have been made by January 31. If the amount of FUTA taxes is equal to or more than $500 during any calendar quarter, the deposit must be made no later than one month after the quarter ends.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 35

Summary of the chapter

If the amount is less than $500, no deposit is required until the liability reaches the $500 point or until the year ends, when any tax due must be paid by January 31 of the following year. The premium for workers’ compensation insurance based on estimated payroll for the year is paid at the beginning of the year by the employer to protect against potential losses to its employees due to accidental death or injury incurred while on the job.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 36

Questions

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8 - 37

Copyright

All rights reserved. No part of this publication may be reproduced, stored in

a retrieval system, or transmitted, in any form or by any means, electronic,

mechanical, photocopying, recording, or otherwise, without the prior written

permission of the publisher. Printed in the United States of America.