Embed Size (px)

Citation preview

Paula Alves ZaikenVice President

February 3, 2011

presentation to:

The Property and Casualty Initiative, LLC

About PCI

State wide community loan fund

Established in 1999 as the result of state legislation

Funded by fourteen Massachusetts-based property and casualty insurance companies

$85 million in capital

Promotes economic development by providing loans that improve health and welfare of low income communities and residents

Flexible financing for businesses, developers, and community organizations

What we do

affordable

housing

small and medium-sized

businesses

economic

development

community

services

Benefits of PCI relationship to Arranging Bank

Strengthens customer relationship by delivering complete loan solution

Retains depository and service business Drives financing structure to meet internal bank requirements

PCI is:

FlexibleNon-competitive

Relationship orientedEconomic-mission driven

Business and Not-for-Profit Lending

Typically $500M-$3MM “junior” piece of bank-arranged financing package permanent working capital equipment purchases owner occupied real estate/leasehold improvements acquisition/ partner buy-out loan participations as low as $250M

Borrower must meet at least one of the eligibility criteria located in an economic target area minority or woman-owned creating new jobs employ low or moderate-income Massachusetts residents engaged in providing health services, daycare, education, social services

Pricing and terms based upon needs of the transaction

Fixed rate loans usually one to seven years

Economic Target Areas

Affordable Housing Loans

Typically $500M-$5MM loan Acquisition and predevelopment Bridge loans Construction Permanent loans with 7-10 year term

Subordinate loans permitted

Competitive pricing and terms based on transaction

Both for-profit and not-for-profit borrowers welcome

At least 20% of the units must be affordable to households earning no more than 80% of area median income

Customer Case 1 –

Small BusinessFamily Dental Practice

The Problem: A well-established family dental practice had been occupying leased space in a small strip mall for several years. Imbedded in the lease was an option to buy the entire mall for $1. 6MM, a price the business owner considered attractive. Her bank, however, was faced with a number of challenges that had the loan “stuck” in the credit process. Specifically, 1.) no money down, and 2.) bank’s RE group not satisfied with appraisal.

SBA programs were not an option since the borrower occupied only 30% of the real estate.

The PCI Solution: PCI approved a $600M second mortgage behind the bank’s $1MM first mortgage. PCI’s loan brought the transaction to 88% LTV based on the available appraisal and the bank loan, in turn, was well within 75% LTV maximum that was bank policy.

Customer Case 2 –

Special Needs School

The Problem: A regional school for special needs children planned to construct a new 28,000 s.f. two-story building on existing school land to enable the school to expand services and eventually double the current student population. The cost of the project was $5.3MM. The school’s bank obtained approval for the loan at 50% of loan need, or $2,650,000 and sought a participant for the 50% loan balance. They approached a number of small local banks who expressed interest only at insufficient amounts, and then partnered with a quasi-public that subsequently approved the full $2,650,000 amount. A problem arose however, in that neither the Bank nor the Borrower wanted floating rate exposure during the tenor of the loan. The quasi had only floating rate funding to offer.

The PCI Solution: PCI turned around the loan request in 10 business days from initial phone call to full commitment. PCI matched the Bank’s fixed rate pricing, and in addition offered the Borrower the benefit of prepayment without penalty.

Customer Case 3 –

Project with Not-for-Profit Lessee

The Problem: An experienced developer sought a construction loan from one of its relationship banks (25+ years) for the construction and build-out of 32,000 sf of space in an empty Boston building that he had owned for many years. The project’s timing was crucial since the developer had signed a lease with a not-for-profit that had a narrow timing window to relocate. The bank declined the loan partially because of discomfort with the lessee.

The PCI Solution: PCI identified that the project could be split into two phases, only one of which was urgent. We approved a Phase I loan of $4.6MM based on the single lease in place and adequate cashflow for debt service. PCI approved its commitment in under 4 weeks.

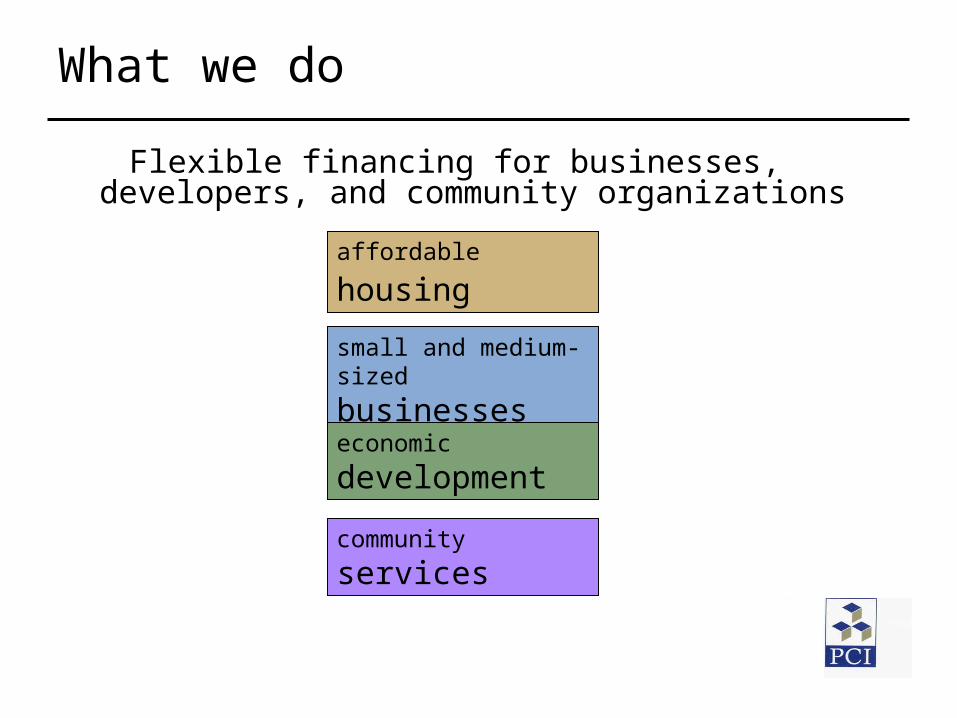

Customer Case 4 –

Tax Exempt Bond - NMTC Deal

The Problem: The relationship bank of an established Boston based college obtained approval of $18MM in financing for the renovation and construction by the college of a new center for the arts. The financing involved New Market Tax Credits and a proprietary loan structure. The bank’s credit committee approved a hold limit of only $10MM, therefore an $8MM participant was needed.

The PCI Solution: The bank invited PCI to take a $5MM participation in the loan based on: our familiarity with New Markets Tax Credit loan structures PCI is a friendly non-bank competitor we have a history of strong partnership – and, in this instance, delivered a

$5MM commitment in 5 business days from initial conversation

Customer Case 5 –

Affordable Housing

The Problem: A neighborhood CDC in partnership with a for profit developer wanted to take advantage of the opportunity to buy a parcel of underutilized industrial land for a mixed income housing development. They needed a patient lender who would stand-by while they arranged for project financing from multiple sources.

The PCI Solution: PCI approved a $2.55 MM interest only acquisition loan and subsequently partnered with a bank to provide construction financing for 109 rental and homeownership housing units. The loan was repaid with proceeds from a Mass Housing Partnership – MHP permanent mortgage.

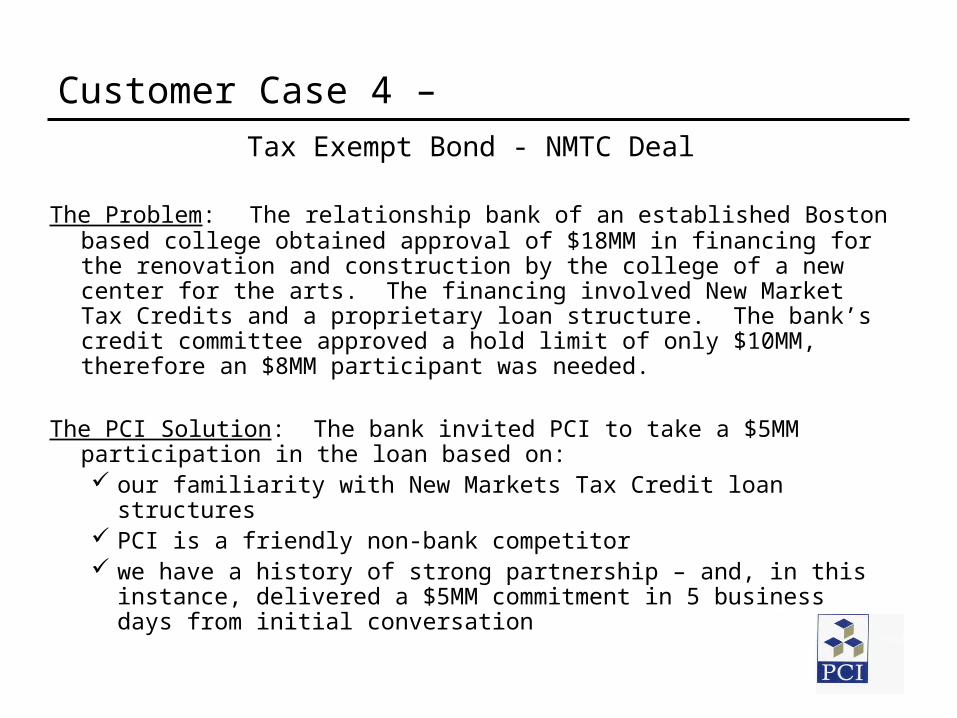

The PCI Process

Project Eligibility

Financial Underwriting

Investment Committee Approval

Loan Commitment

Loan Closing

PCI contacts

Vice President

Business Lending

[email protected] [email protected]

PCI - The Property and Casualty Initiative, LLC

211 Congress Street, 4th Floor

Boston, MA 02110

Tel: 617-723-7878

Fax: 617-723-4411

Vice President

Affordable Housing

Rufus PhillipsStacey Parks TownsendPaula Alves Zaiken