Embed Size (px)

Citation preview

Pass-Through Liabilities and Federal

Tax Treatment: Resolving Complex Issues Reporting Liabilities for General or Limited Partnerships and LLCs Given Tax Code Inconsistencies

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, AUGUST 28, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Carolyn Turnbull, CPA, MST, Consultant, Orlando, Fla.

Belan Wagner, Managing Partner, Wagner Kirkman Blaine Klomparens & Youmans, Mather, Calif.

For this program, attendees must listen to the audio over the telephone.

Sound Quality

Call in on the telephone by dialing 1-866-570-7602 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Pass-Through Liabilities and Federal Tax Treatment: Resolving Complex Issues Seminar

Carolyn Turnbull, CPA, MST, CGMA

Independent Tax Consultant

Aug. 28, 2013

Belan Wagner, Wagner Kirkman Blaine

Komparens & Youmans

Today’s Program

Liability Characterization Under IRC Sect. 1001

[Belan Wagner]

Treatment Of Partnership Liabilities Under IRC Sect. 752

[Carolyn Turnbull, Belan Wagner]

Examples Of Taxpayer Situations

[Belan Wagner, Carolyn Turnbull]

At-Risk Rules Under IRC Sect. 465

[Carolyn Turnbull]

Concluding Remarks

[Carolyn Turnbull, Belan Wagner]

Slide 8 – Slide 10

Slide 11 – Slide 32

Slide 33 – Slide 70

Slide 71 – Slide 79

Slide 80

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

LIABILITY CHARACTERIZATION UNDER IRC SECT. 1001

Belan Wagner, Wagner Kirkman Blaine Komparens & Youmans

9

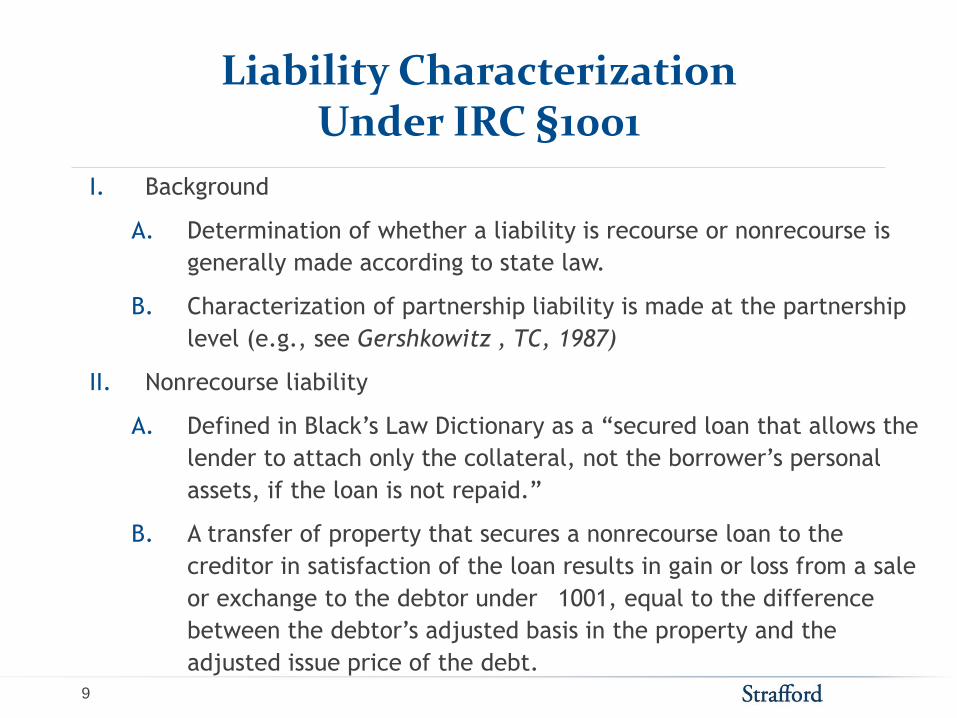

Liability Characterization Under IRC §1001

I. Background

A. Determination of whether a liability is recourse or nonrecourse is

generally made according to state law.

B. Characterization of partnership liability is made at the partnership

level (e.g., see Gershkowitz , TC, 1987)

II. Nonrecourse liability

A. Defined in Black’s Law Dictionary as a “secured loan that allows the

lender to attach only the collateral, not the borrower’s personal

assets, if the loan is not repaid.”

B. A transfer of property that secures a nonrecourse loan to the

creditor in satisfaction of the loan results in gain or loss from a sale

or exchange to the debtor under

1001, equal to the difference

between the debtor’s adjusted basis in the property and the

adjusted issue price of the debt.

10

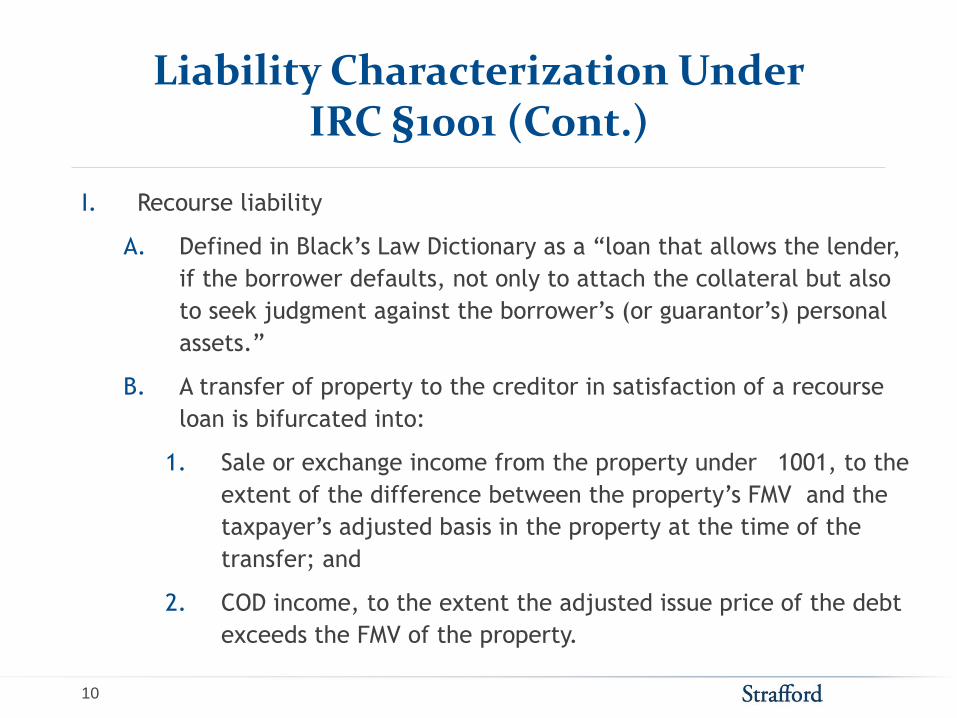

Liability Characterization Under IRC §1001 (Cont.)

I. Recourse liability

A. Defined in Black’s Law Dictionary as a “loan that allows the lender,

if the borrower defaults, not only to attach the collateral but also

to seek judgment against the borrower’s (or guarantor’s) personal

assets.”

B. A transfer of property to the creditor in satisfaction of a recourse

loan is bifurcated into:

1. Sale or exchange income from the property under

1001, to the

extent of the difference between the property’s FMV and the

taxpayer’s adjusted basis in the property at the time of the

transfer; and

2. COD income, to the extent the adjusted issue price of the debt

exceeds the FMV of the property.

TREATMENT OF PARTNERSHIP LIABILITIES UNDER IRC SECT. 752

Carolyn Turnbull, CPA, MST, CGMA, Independent Tax Consultant

Belan Wagner, Wagner Kirkman Blaine Komparens & Youmans

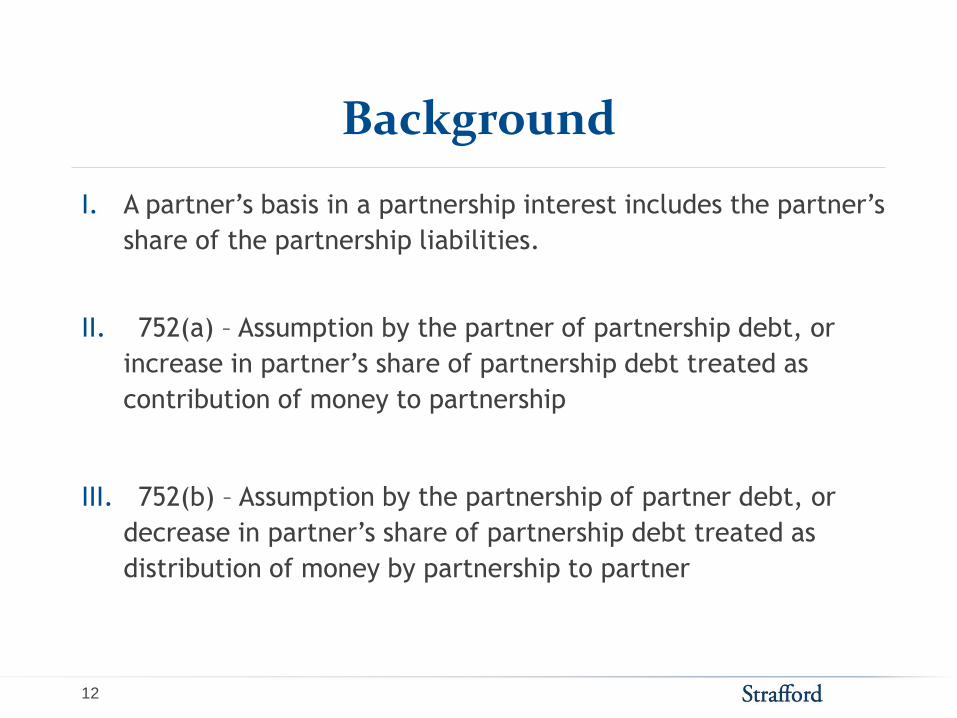

12

Background

I. A partner’s basis in a partnership interest includes the partner’s

share of the partnership liabilities.

II.

752(a) – Assumption by the partner of partnership debt, or

increase in partner’s share of partnership debt treated as

contribution of money to partnership

III.

752(b) – Assumption by the partnership of partner debt, or

decrease in partner’s share of partnership debt treated as

distribution of money by partnership to partner

13

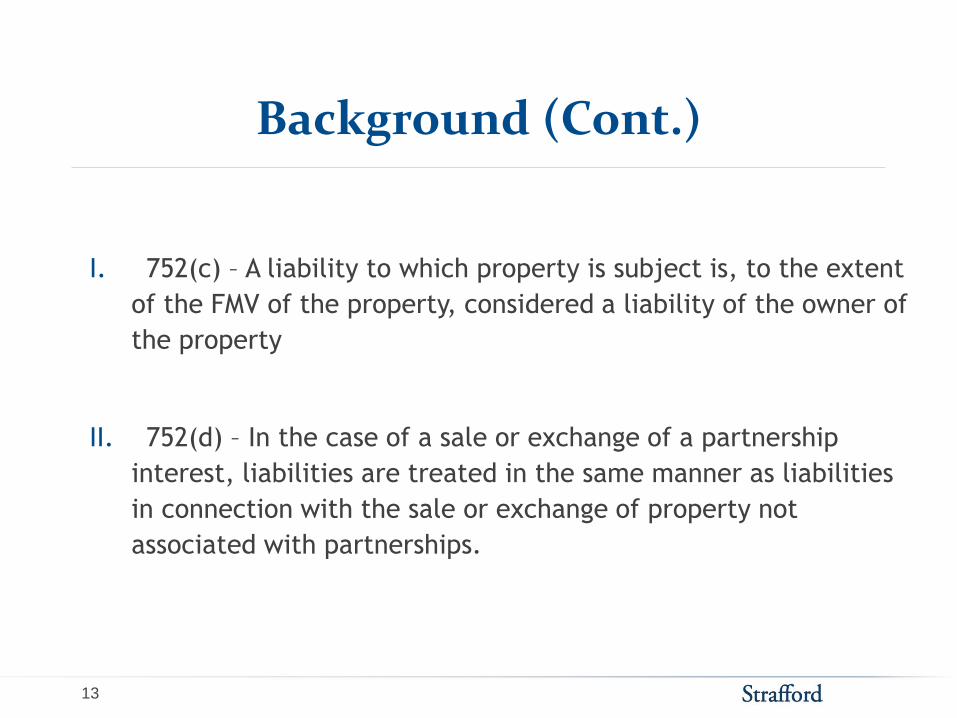

Background (Cont.)

I.

752(c) – A liability to which property is subject is, to the extent

of the FMV of the property, considered a liability of the owner of

the property

II.

752(d) – In the case of a sale or exchange of a partnership

interest, liabilities are treated in the same manner as liabilities

in connection with the sale or exchange of property not

associated with partnerships.

14

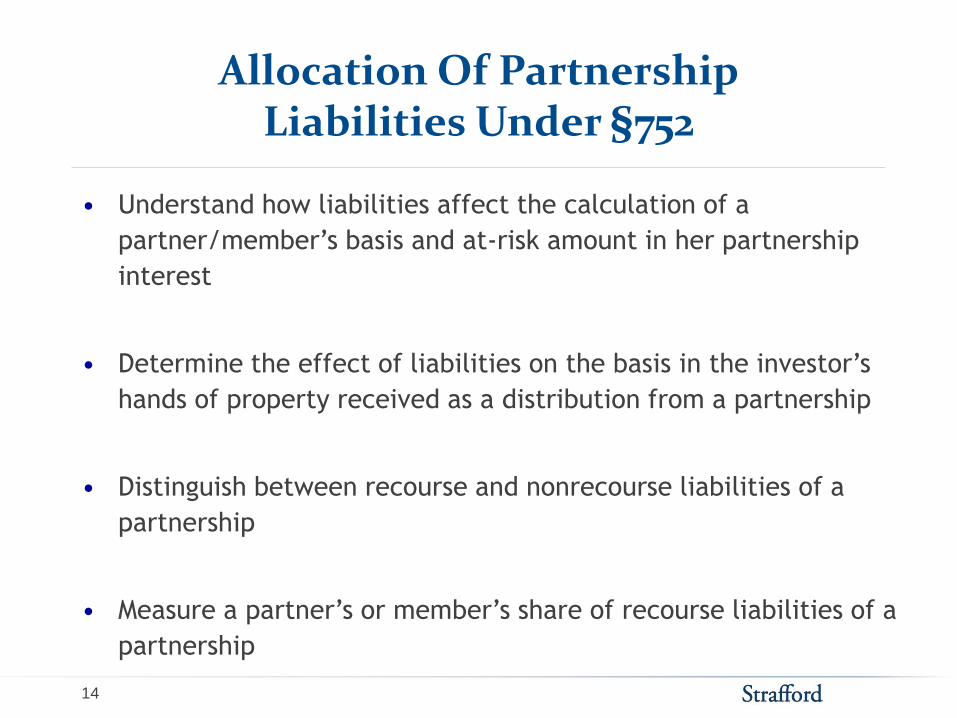

Allocation Of Partnership Liabilities Under §752

• Understand how liabilities affect the calculation of a

partner/member’s basis and at-risk amount in her partnership

interest

• Determine the effect of liabilities on the basis in the investor’s

hands of property received as a distribution from a partnership

• Distinguish between recourse and nonrecourse liabilities of a

partnership

• Measure a partner’s or member’s share of recourse liabilities of a

partnership

15

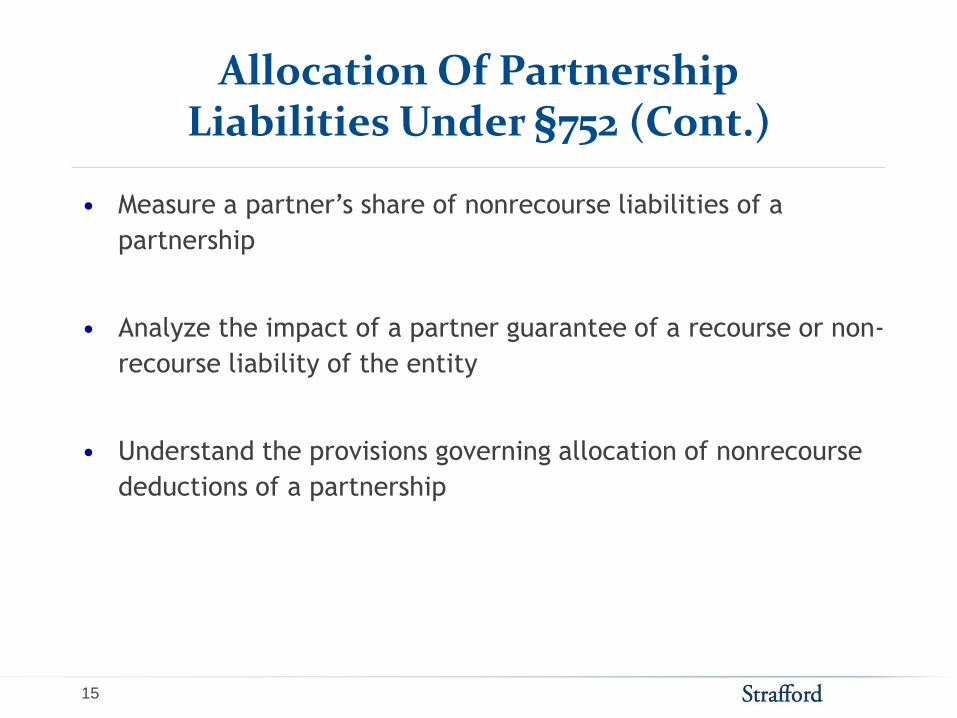

Allocation Of Partnership Liabilities Under §752 (Cont.)

• Measure a partner’s share of nonrecourse liabilities of a

partnership

• Analyze the impact of a partner guarantee of a recourse or non-

recourse liability of the entity

• Understand the provisions governing allocation of nonrecourse

deductions of a partnership

16

Contribution Of Encumbered Property

I. Net relief of liabilities treated as a distribution of cash

II. Will result in gain to contributing partner at partnership

formation, if net relief of liabilities is greater than basis of

property contributed

17

Distribution Of Encumbered Property

I. Net assumption of debt is treated as a contribution of cash to

partnership.

II. Net relief of debt is treated as a distribution of cash.

18

Allocation Of Partnership Liabilities Under §752

I. Recourse liabilities allocated as if partnership lost everything and

then liquidated (i.e., partnership constructively liquidated) –

what partners would have to repay creditors or other partners

II. Same rules do not apply to nonrecourse liabilities, because no

one would have to repay those liabilities.

Slide Intentionally Left Blank

20

Recourse Liabilities

I. If any partner or related person bears risk of loss for debt, it is a

recourse debt.

A. Determined without regard for how the liability is

characterized under state law

II. Partner’s share of partnership recourse debt equals the amount for

which the partner or related person bears the economic risk of

loss.

III. Nonrecourse loans recharacterized if:

A. Loan or interest thereon is guaranteed by one or more

partners

B. Collateralized by property owned by a partner

C. Loan obtained from a partner

21

Constructive Liquidation

I. Constructive liquidation – all of the following events are deemed to occur

simultaneously:

A. All of the partnership liabilities become payable in full.

B. With the exception of property contributed to secure a partnership

liability, all of the partnership’s assets, including cash, have a value

of zero.

C. Partnership disposes of all of its property in a fully taxable

transaction for no consideration (except relief from liabilities for

which the creditor’s right to repayment is limited solely to one or

more assets of the partnership).

D. All items of income, gain, loss and deduction are allocated among

the partners.

E. The partnership liquidates.

22

Constructive Liquidation (Cont.)

I. Partners who have deficit restoration provisions are presumed to

contribute any deficit balance in their capital account to the

partnership.

II. Debt allocations based on book capital accounts (and deficits

therein)

III. If the partnership agreement provides for any special allocations,

liability allocations will change every year.

23

Effect Of Partner Guarantees

I. Guarantee of nonrecourse loan makes that loan recourse for

purposes of

752.

II. Loan guarantee is ignored, however, for purposes of allocating

guaranteed debt, unless the guarantor has no further recourse

against remaining partners.

24

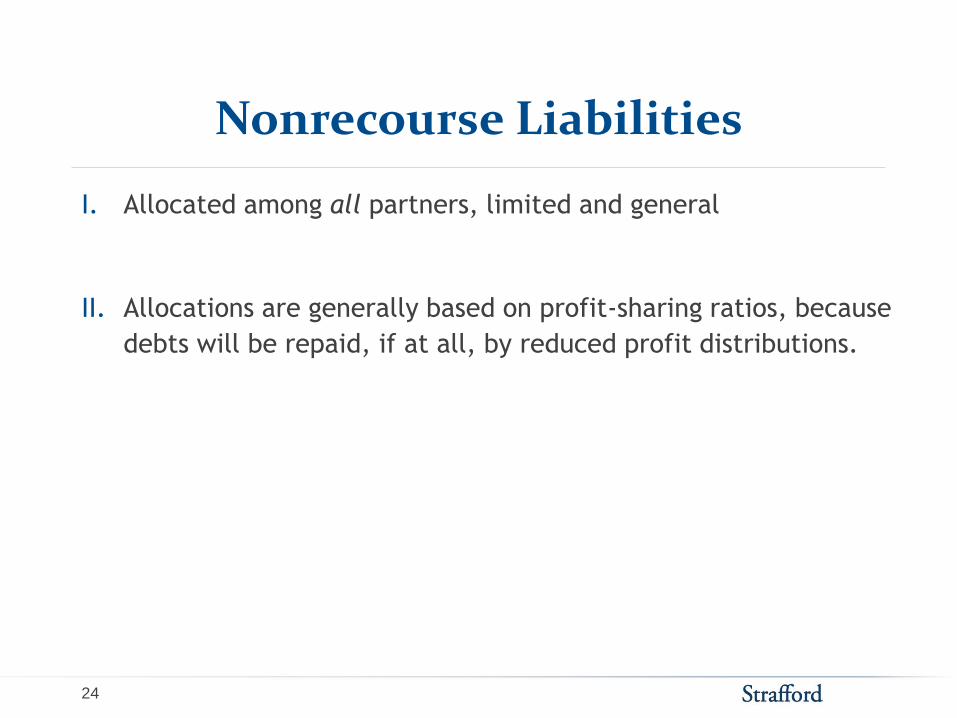

Nonrecourse Liabilities

I. Allocated among all partners, limited and general

II. Allocations are generally based on profit-sharing ratios, because

debts will be repaid, if at all, by reduced profit distributions.

25

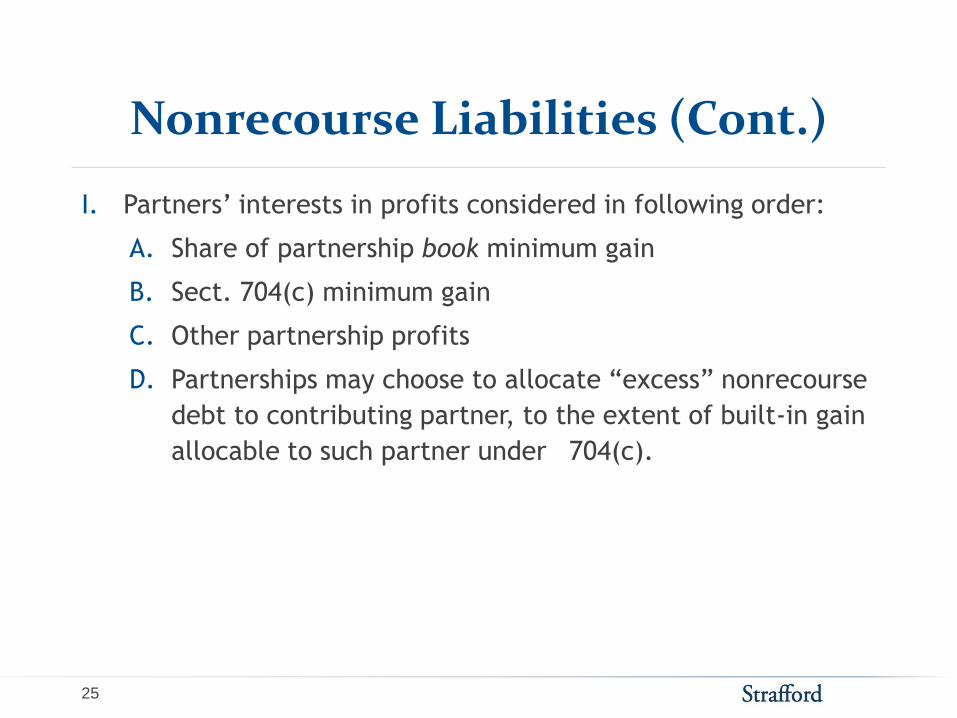

Nonrecourse Liabilities (Cont.)

I. Partners’ interests in profits considered in following order:

A. Share of partnership book minimum gain

B. Sect. 704(c) minimum gain

C. Other partnership profits

D. Partnerships may choose to allocate “excess” nonrecourse

debt to contributing partner, to the extent of built-in gain

allocable to such partner under

704(c).

26

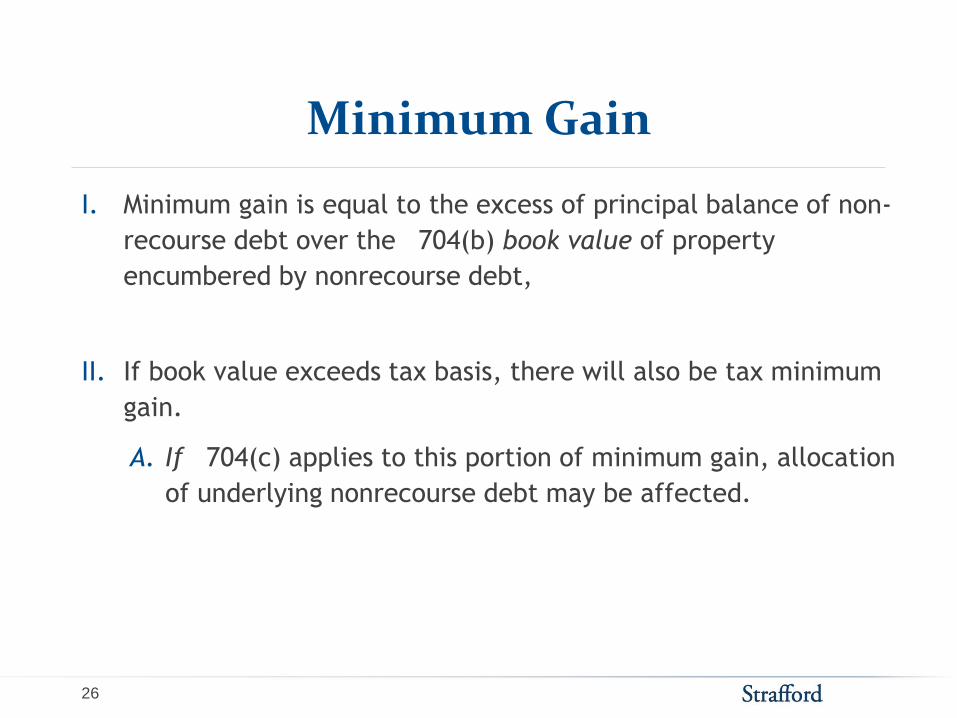

Minimum Gain

I. Minimum gain is equal to the excess of principal balance of non-

recourse debt over the

704(b) book value of property

encumbered by nonrecourse debt,

II. If book value exceeds tax basis, there will also be tax minimum

gain.

A. If

704(c) applies to this portion of minimum gain, allocation

of underlying nonrecourse debt may be affected.

27

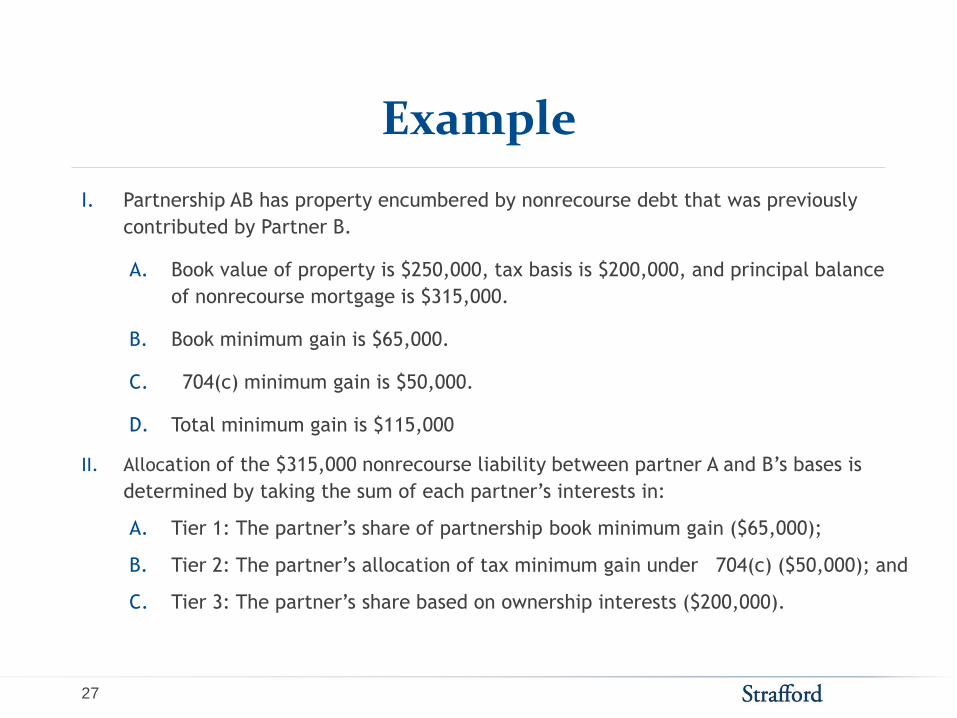

Example

I. Partnership AB has property encumbered by nonrecourse debt that was previously

contributed by Partner B.

A. Book value of property is $250,000, tax basis is $200,000, and principal balance

of nonrecourse mortgage is $315,000.

B. Book minimum gain is $65,000.

C.

704(c) minimum gain is $50,000.

D. Total minimum gain is $115,000

II. Allocation of the $315,000 nonrecourse liability between partner A and B’s bases is

determined by taking the sum of each partner’s interests in:

A. Tier 1: The partner’s share of partnership book minimum gain ($65,000);

B. Tier 2: The partner’s allocation of tax minimum gain under

704(c) ($50,000); and

C. Tier 3: The partner’s share based on ownership interests ($200,000).

28

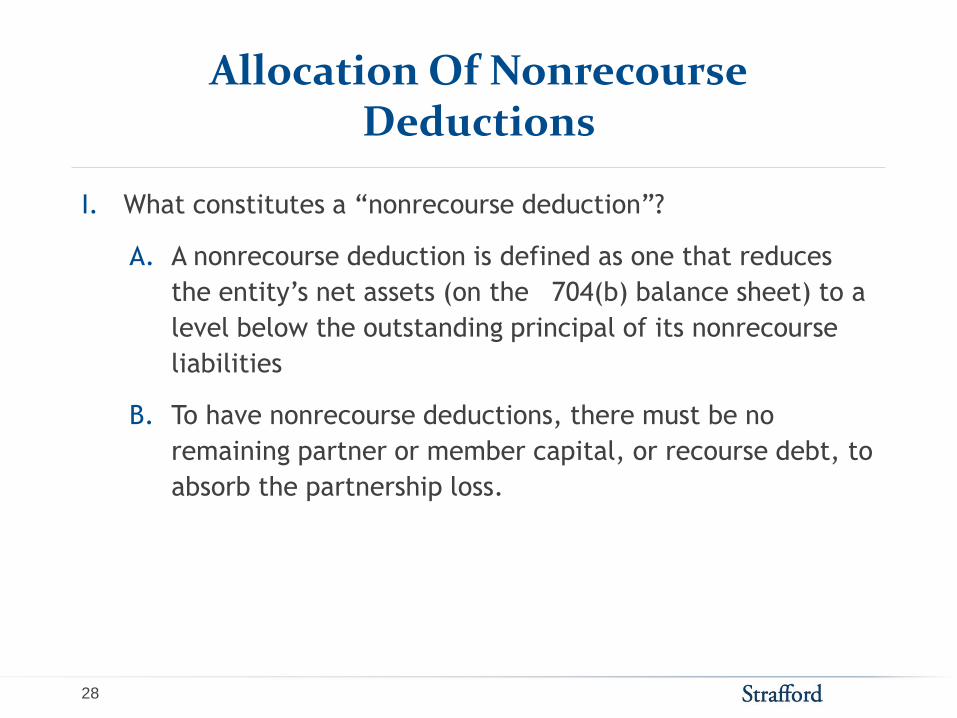

Allocation Of Nonrecourse Deductions

I. What constitutes a “nonrecourse deduction”?

A. A nonrecourse deduction is defined as one that reduces

the entity’s net assets (on the

704(b) balance sheet) to a

level below the outstanding principal of its nonrecourse

liabilities

B. To have nonrecourse deductions, there must be no

remaining partner or member capital, or recourse debt, to

absorb the partnership loss.

29

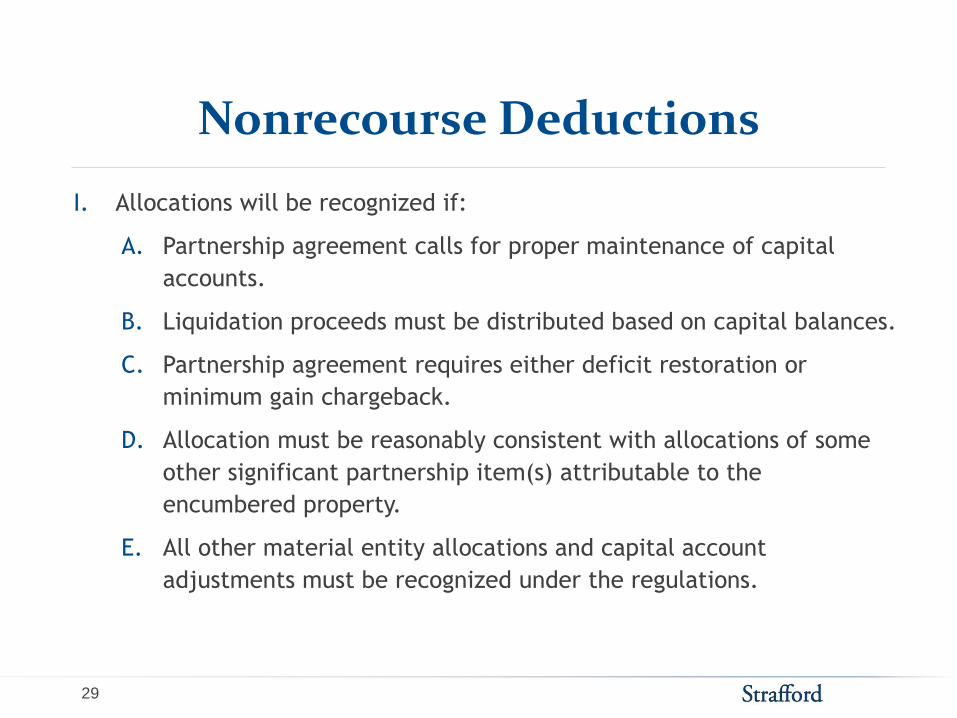

Nonrecourse Deductions

I. Allocations will be recognized if:

A. Partnership agreement calls for proper maintenance of capital

accounts.

B. Liquidation proceeds must be distributed based on capital balances.

C. Partnership agreement requires either deficit restoration or

minimum gain chargeback.

D. Allocation must be reasonably consistent with allocations of some

other significant partnership item(s) attributable to the

encumbered property.

E. All other material entity allocations and capital account

adjustments must be recognized under the regulations.

30

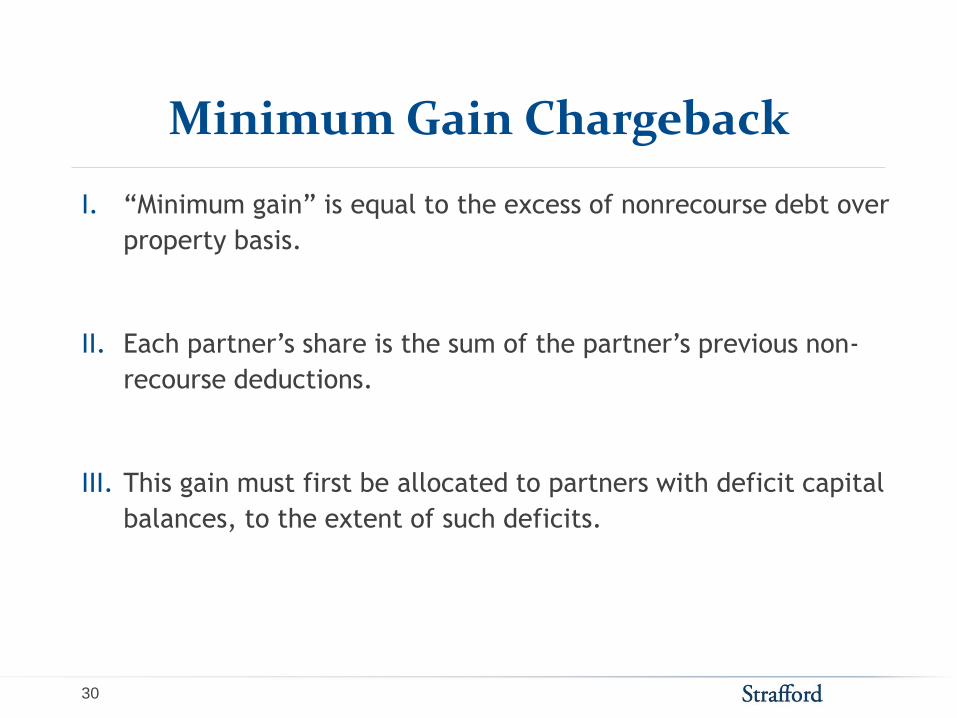

Minimum Gain Chargeback

I. “Minimum gain” is equal to the excess of nonrecourse debt over

property basis.

II. Each partner’s share is the sum of the partner’s previous non-

recourse deductions.

III. This gain must first be allocated to partners with deficit capital

balances, to the extent of such deficits.

Slide Intentionally Left Blank

32

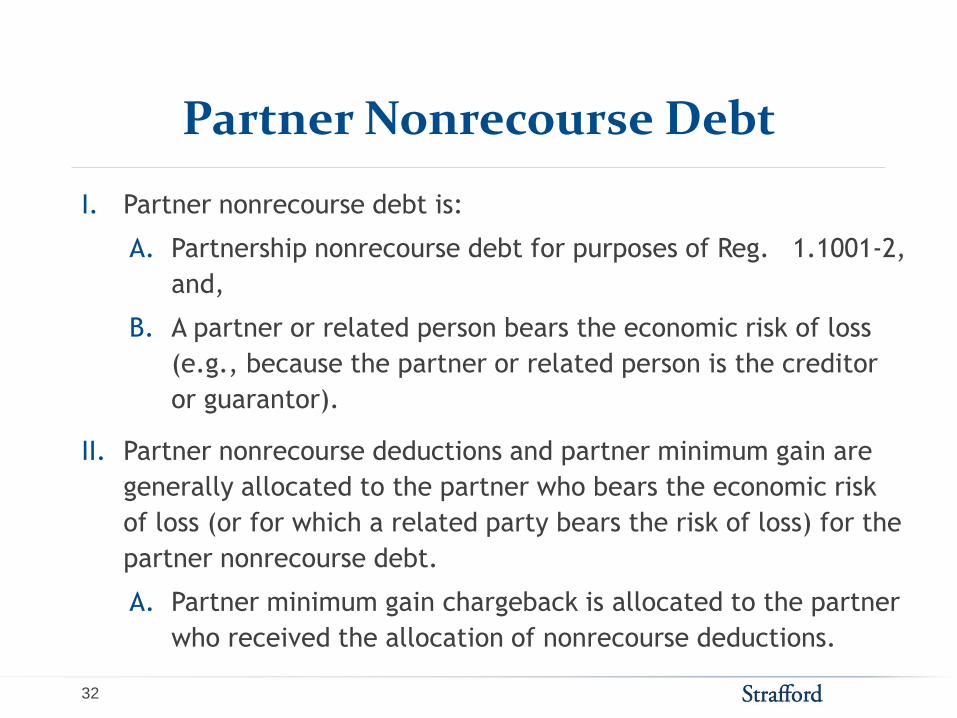

Partner Nonrecourse Debt

I. Partner nonrecourse debt is:

A. Partnership nonrecourse debt for purposes of Reg.

1.1001-2,

and,

B. A partner or related person bears the economic risk of loss

(e.g., because the partner or related person is the creditor

or guarantor).

II. Partner nonrecourse deductions and partner minimum gain are

generally allocated to the partner who bears the economic risk

of loss (or for which a related party bears the risk of loss) for the

partner nonrecourse debt.

A. Partner minimum gain chargeback is allocated to the partner

who received the allocation of nonrecourse deductions.

EXAMPLES OF TAXPAYER SITUATIONS

Belan Wagner, Wagner Kirkman Blaine Komparens & Youmans

Carolyn Turnbull, CPA, MST, CGMA, Independent Tax Consultant

34

Examples based on article from Blake

Rubin, Andrea Macintosh Whiteway,

and Jon G. Finkelstein, “Treatment of

Liabilities as Recourse or Nonrecourse

in a Complex Financial World”,

Journal of Passthrough Entities

(July-August 2010)

35

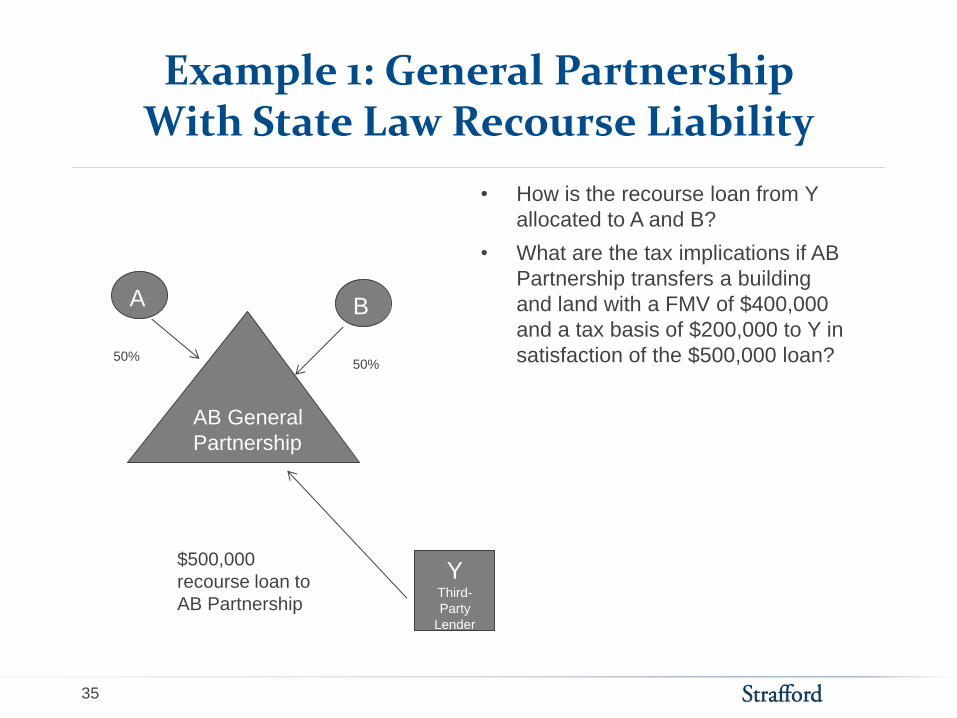

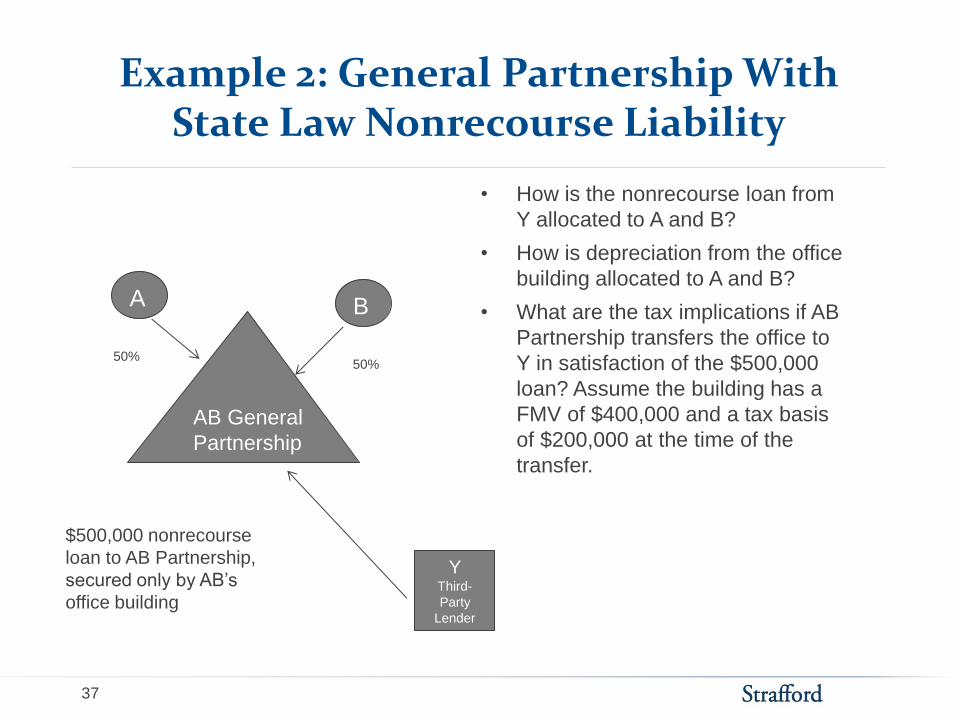

Example 1: General Partnership With State Law Recourse Liability

AB General

Partnership

A B

Y Third-

Party

Lender

$500,000

recourse loan to

AB Partnership

• How is the recourse loan from Y

allocated to A and B?

• What are the tax implications if AB

Partnership transfers a building

and land with a FMV of $400,000

and a tax basis of $200,000 to Y in

satisfaction of the $500,000 loan? 50% 50%

36

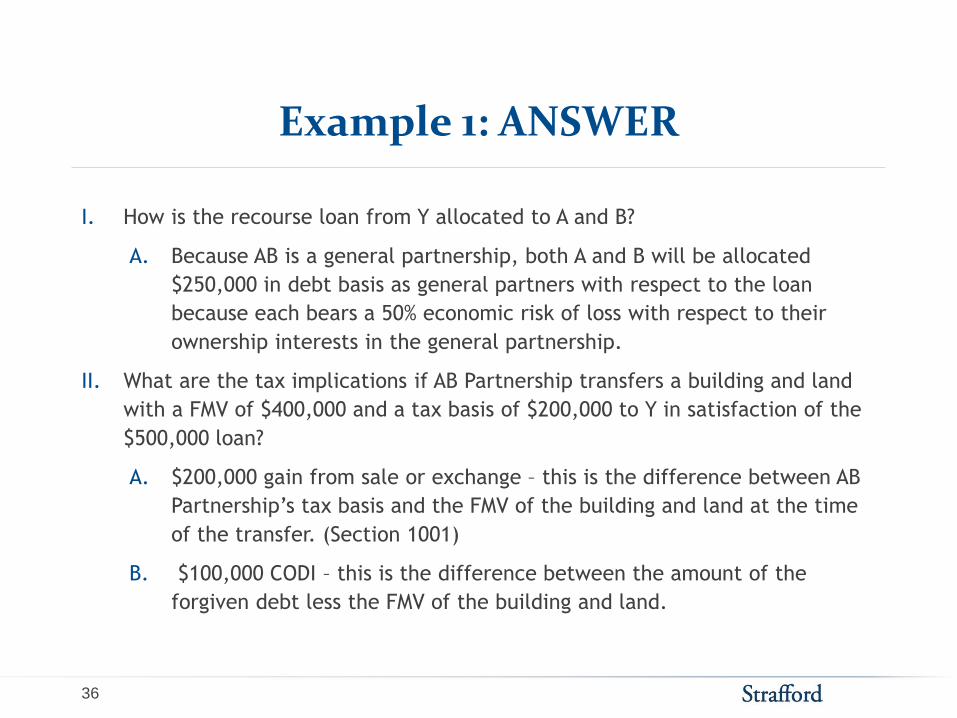

Example 1: ANSWER

I. How is the recourse loan from Y allocated to A and B?

A. Because AB is a general partnership, both A and B will be allocated

$250,000 in debt basis as general partners with respect to the loan

because each bears a 50% economic risk of loss with respect to their

ownership interests in the general partnership.

II. What are the tax implications if AB Partnership transfers a building and land

with a FMV of $400,000 and a tax basis of $200,000 to Y in satisfaction of the

$500,000 loan?

A. $200,000 gain from sale or exchange – this is the difference between AB

Partnership’s tax basis and the FMV of the building and land at the time

of the transfer. (Section 1001)

B. $100,000 CODI – this is the difference between the amount of the

forgiven debt less the FMV of the building and land.

37

Example 2: General Partnership With State Law Nonrecourse Liability

AB General

Partnership

A B

Y Third-

Party

Lender

$500,000 nonrecourse

loan to AB Partnership,

secured only by AB’s

office building

• How is the nonrecourse loan from

Y allocated to A and B?

• How is depreciation from the office

building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to

Y in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50% 50%

38

Example 2: ANSWER

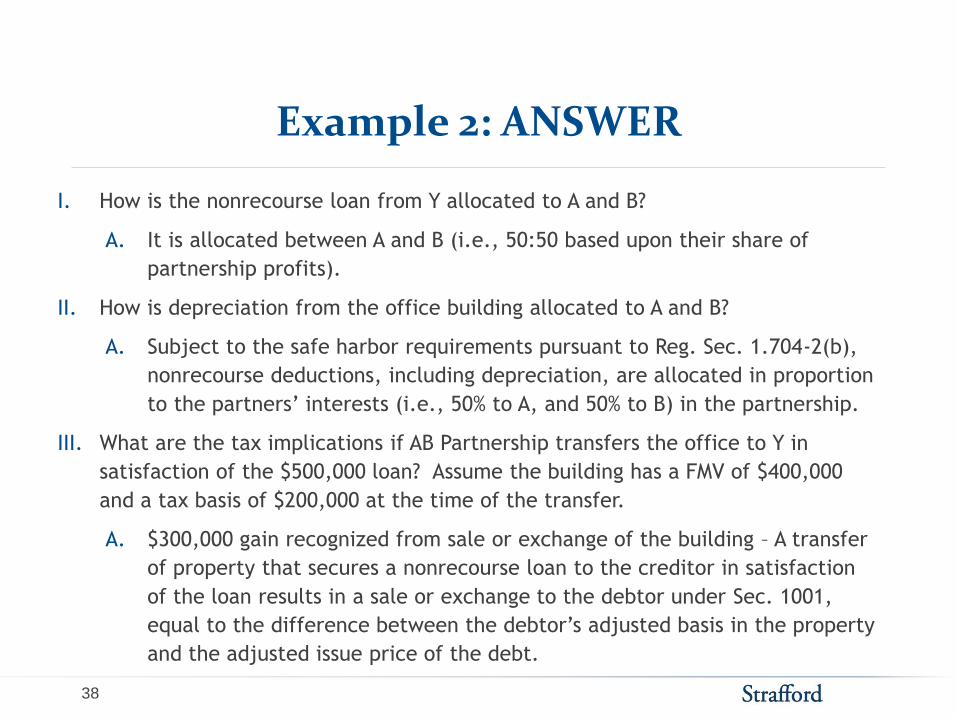

I. How is the nonrecourse loan from Y allocated to A and B?

A. It is allocated between A and B (i.e., 50:50 based upon their share of

partnership profits).

II. How is depreciation from the office building allocated to A and B?

A. Subject to the safe harbor requirements pursuant to Reg. Sec. 1.704-2(b),

nonrecourse deductions, including depreciation, are allocated in proportion

to the partners’ interests (i.e., 50% to A, and 50% to B) in the partnership.

III. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $300,000 gain recognized from sale or exchange of the building – A transfer

of property that secures a nonrecourse loan to the creditor in satisfaction

of the loan results in a sale or exchange to the debtor under Sec. 1001,

equal to the difference between the debtor’s adjusted basis in the property

and the adjusted issue price of the debt.

39

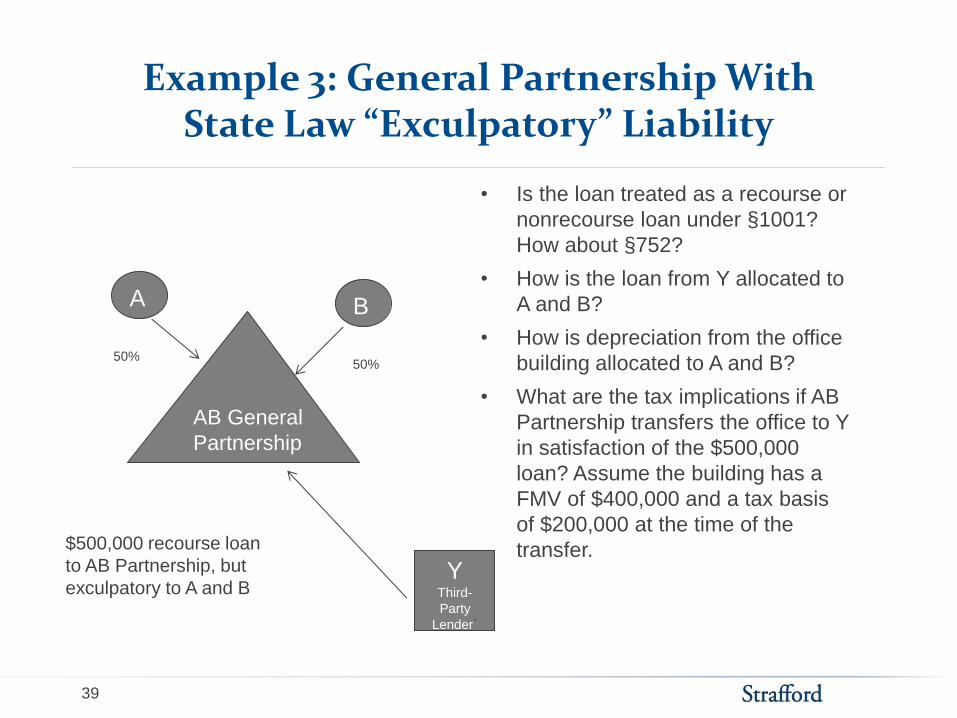

Example 3: General Partnership With State Law “Exculpatory” Liability

AB General

Partnership

A B

Y Third-

Party

Lender`

$500,000 recourse loan

to AB Partnership, but

exculpatory to A and B

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• How is depreciation from the office

building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50% 50%

40

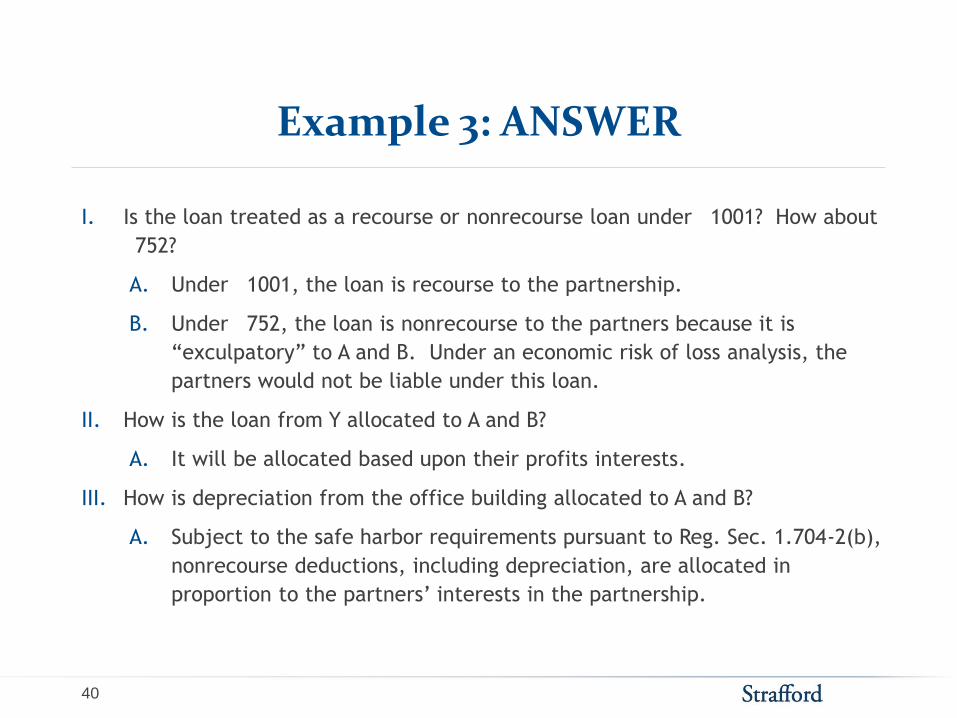

Example 3: ANSWER

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. Under

1001, the loan is recourse to the partnership.

B. Under

752, the loan is nonrecourse to the partners because it is

“exculpatory” to A and B. Under an economic risk of loss analysis, the

partners would not be liable under this loan.

II. How is the loan from Y allocated to A and B?

A. It will be allocated based upon their profits interests.

III. How is depreciation from the office building allocated to A and B?

A. Subject to the safe harbor requirements pursuant to Reg. Sec. 1.704-2(b),

nonrecourse deductions, including depreciation, are allocated in

proportion to the partners’ interests in the partnership.

41

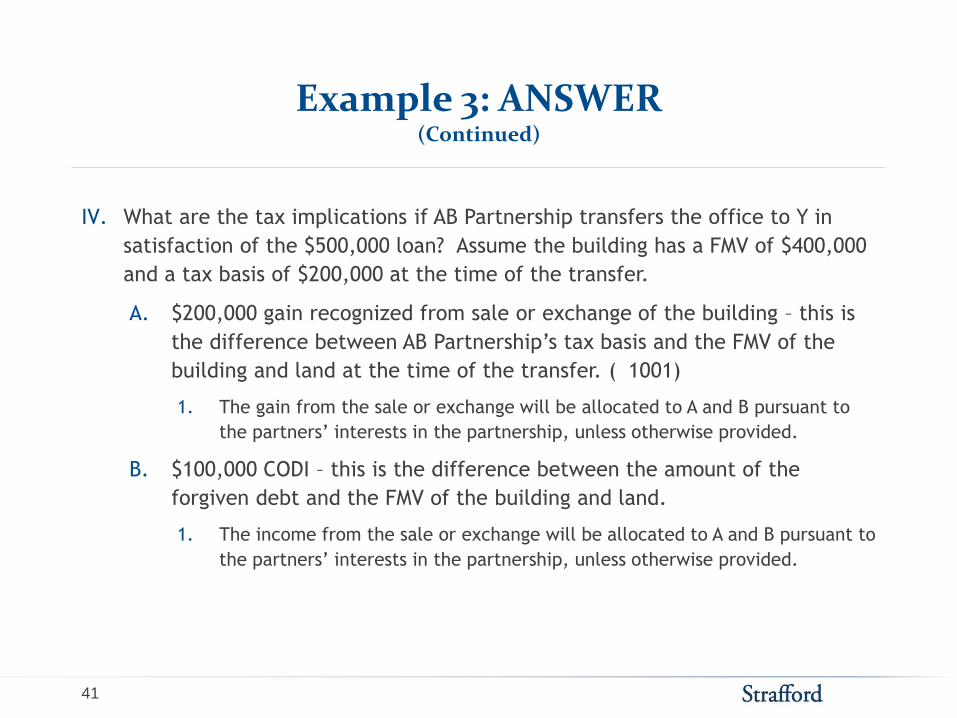

Example 3: ANSWER (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $200,000 gain recognized from sale or exchange of the building – this is

the difference between AB Partnership’s tax basis and the FMV of the

building and land at the time of the transfer. (

1001)

1. The gain from the sale or exchange will be allocated to A and B pursuant to

the partners’ interests in the partnership, unless otherwise provided.

B. $100,000 CODI – this is the difference between the amount of the

forgiven debt and the FMV of the building and land.

1. The income from the sale or exchange will be allocated to A and B pursuant to

the partners’ interests in the partnership, unless otherwise provided.

42

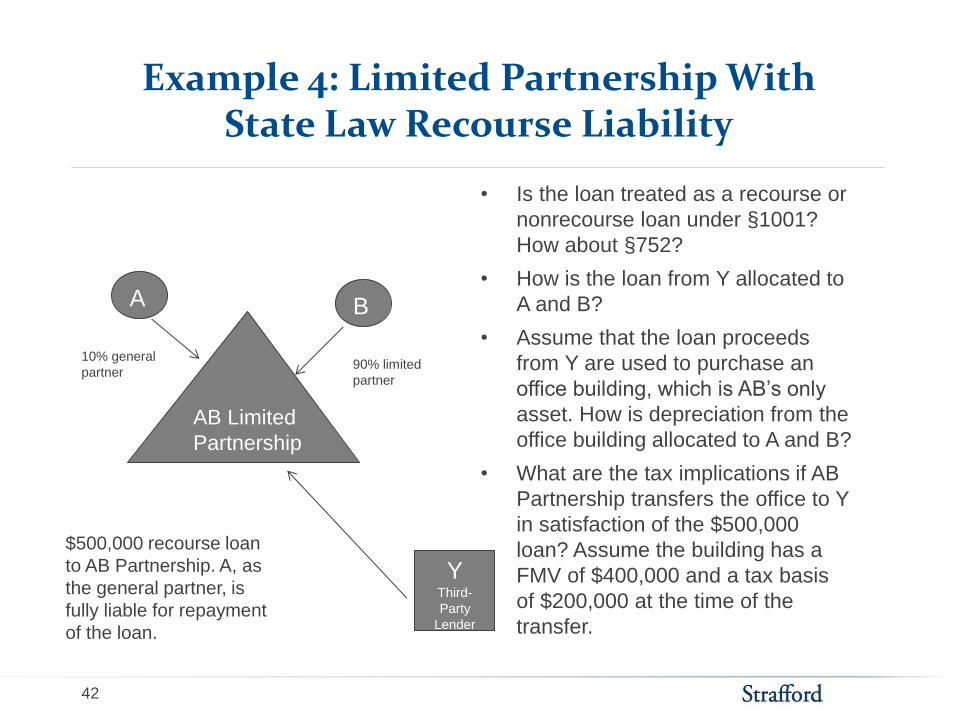

Example 4: Limited Partnership With State Law Recourse Liability

AB Limited

Partnership

A B

Y Third-

Party

Lender

$500,000 recourse loan

to AB Partnership. A, as

the general partner, is

fully liable for repayment

of the loan.

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

10% general

partner 90% limited

partner

43

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. Under

1001, this is a recourse loan to the partnership.

B. Under

752, this is a recourse loan to Partner A because A bears economic

risk of loss.

II. How is the loan from Y allocated to A and B?

A. It is allocated 100% to Partner A because A bears economic risk of loss.

B. None of the loan is allocated to Partner B.

Example 4: ANSWER

44

Example 4: ANSWER (Continued)

III. Assume that the loan proceeds from Y are used to purchase an office building, which is

AB’s only asset. How is depreciation from the office building allocated to A and B?

A. Depreciation is allocated to A and B in accordance with the partnership

agreement provided the allocation has substantial economic effect under Reg. 1.704-1.

B. Based on the facts in this example, an allocation of 10% of the depreciation to

A and 90% of the depreciation to B will likely not have substantial effect if the

allocation would create a deficit balance in B’s capital account.

1. A qualified income offset provision in the partnership agreement will not cause

the allocation to have substantial economic effect because the allocation of

depreciation to B would not unexpectedly cause B’s capital account to go

negative.

2. Neither a partnership minimum gain chargeback nor partner minimum gain

chargeback provision in the partnership agreement would apply because the

debt is neither partnership nonrecourse debt nor partner nonrecourse debt.

45

Example 4: ANSWER (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $200,000 gain from sale or exchange of the office – this is the difference

between AB Partnership’s tax basis and the FMV of the building and land

at the time of the transfer. (

1001)

1. The gain from the sale or exchange of the office will be allocated in

accordance with the partnership agreement provided the allocation has

substantial economic effect.

B. $100,000 CODI – this is the difference between the amount of the

forgiven debt and the FMV of the building and land.

1. The CODI is allocated in accordance with the partnership agreement provided

the allocation has substantial economic effect.

Slide Intentionally Left Blank

47

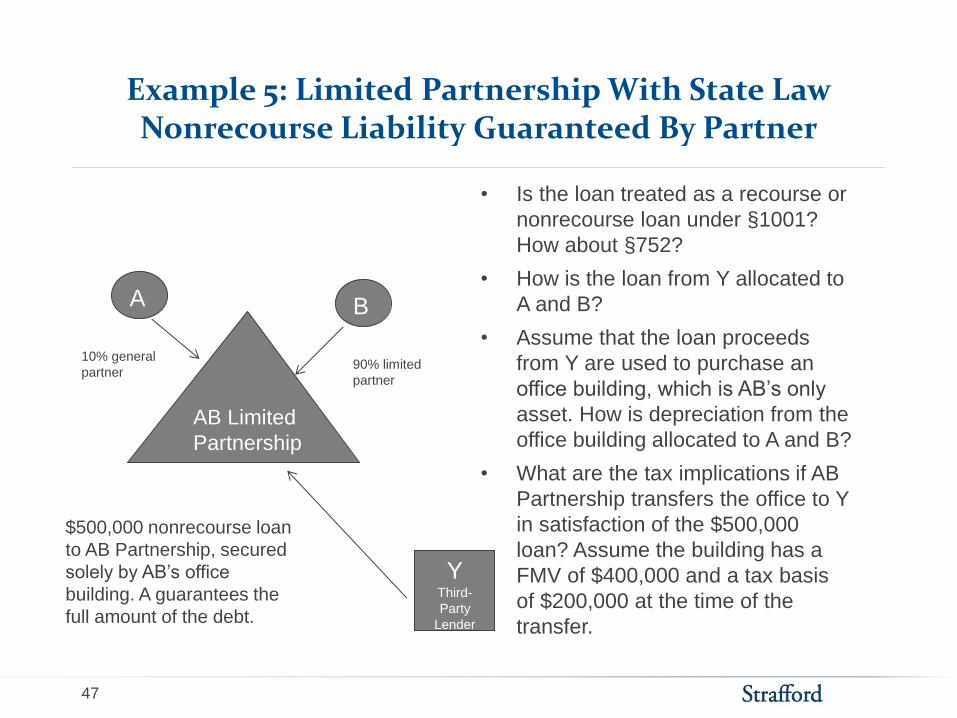

Example 5: Limited Partnership With State Law Nonrecourse Liability Guaranteed By Partner

AB Limited

Partnership

A B

Y Third-

Party

Lender

$500,000 nonrecourse loan

to AB Partnership, secured

solely by AB’s office

building. A guarantees the

full amount of the debt.

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

10% general

partner 90% limited

partner

48

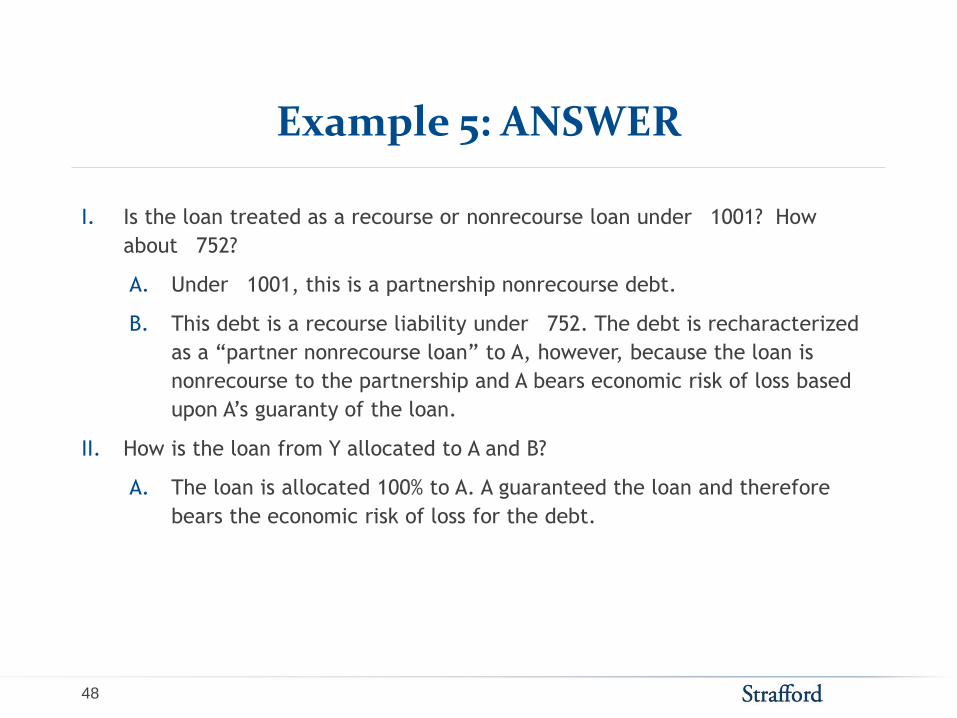

Example 5: ANSWER

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How

about

752?

A. Under

1001, this is a partnership nonrecourse debt.

B. This debt is a recourse liability under

752. The debt is recharacterized

as a “partner nonrecourse loan” to A, however, because the loan is

nonrecourse to the partnership and A bears economic risk of loss based

upon A’s guaranty of the loan.

II. How is the loan from Y allocated to A and B?

A. The loan is allocated 100% to A. A guaranteed the loan and therefore

bears the economic risk of loss for the debt.

49

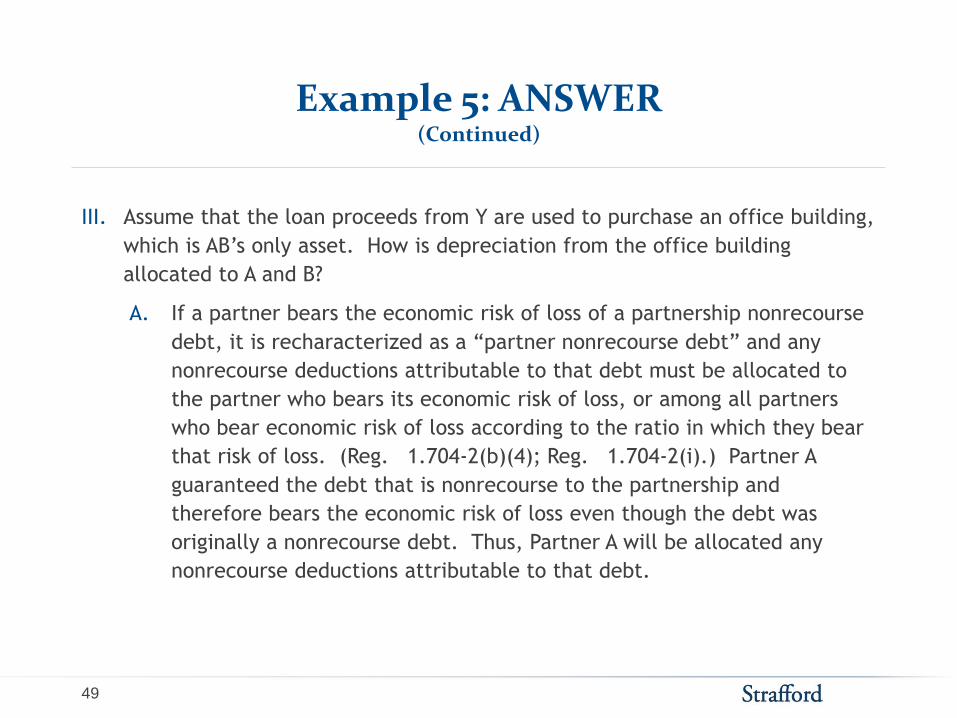

Example 5: ANSWER (Continued)

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building

allocated to A and B?

A. If a partner bears the economic risk of loss of a partnership nonrecourse

debt, it is recharacterized as a “partner nonrecourse debt” and any

nonrecourse deductions attributable to that debt must be allocated to

the partner who bears its economic risk of loss, or among all partners

who bear economic risk of loss according to the ratio in which they bear

that risk of loss. (Reg.

1.704-2(b)(4); Reg.

1.704-2(i).) Partner A

guaranteed the debt that is nonrecourse to the partnership and

therefore bears the economic risk of loss even though the debt was

originally a nonrecourse debt. Thus, Partner A will be allocated any

nonrecourse deductions attributable to that debt.

50

Example 5: ANSWER (Continued)

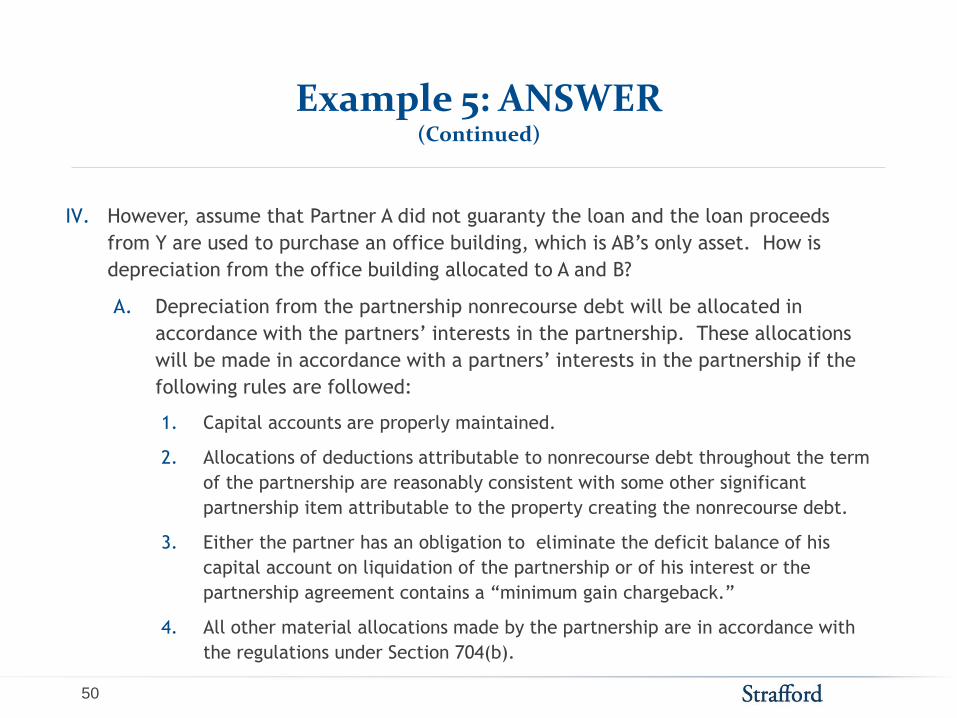

IV. However, assume that Partner A did not guaranty the loan and the loan proceeds

from Y are used to purchase an office building, which is AB’s only asset. How is

depreciation from the office building allocated to A and B?

A. Depreciation from the partnership nonrecourse debt will be allocated in

accordance with the partners’ interests in the partnership. These allocations

will be made in accordance with a partners’ interests in the partnership if the

following rules are followed:

1. Capital accounts are properly maintained.

2. Allocations of deductions attributable to nonrecourse debt throughout the term

of the partnership are reasonably consistent with some other significant

partnership item attributable to the property creating the nonrecourse debt.

3. Either the partner has an obligation to eliminate the deficit balance of his

capital account on liquidation of the partnership or of his interest or the

partnership agreement contains a “minimum gain chargeback.”

4. All other material allocations made by the partnership are in accordance with

the regulations under Section 704(b).

51

Example 5: ANSWER (Continued)

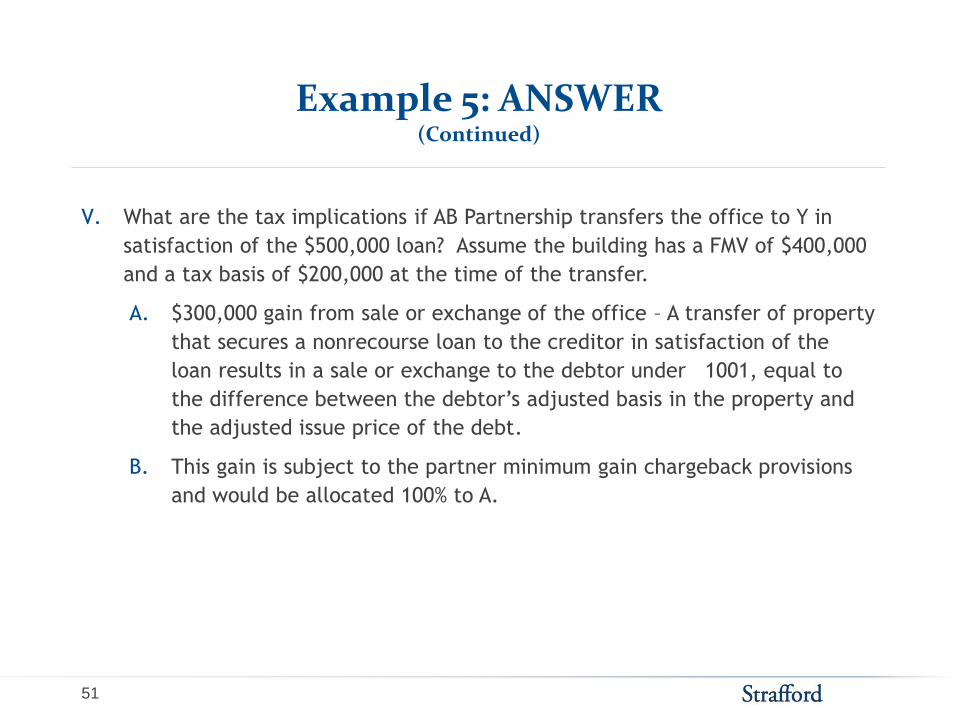

V. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $300,000 gain from sale or exchange of the office – A transfer of property

that secures a nonrecourse loan to the creditor in satisfaction of the

loan results in a sale or exchange to the debtor under

1001, equal to

the difference between the debtor’s adjusted basis in the property and

the adjusted issue price of the debt.

B. This gain is subject to the partner minimum gain chargeback provisions

and would be allocated 100% to A.

52

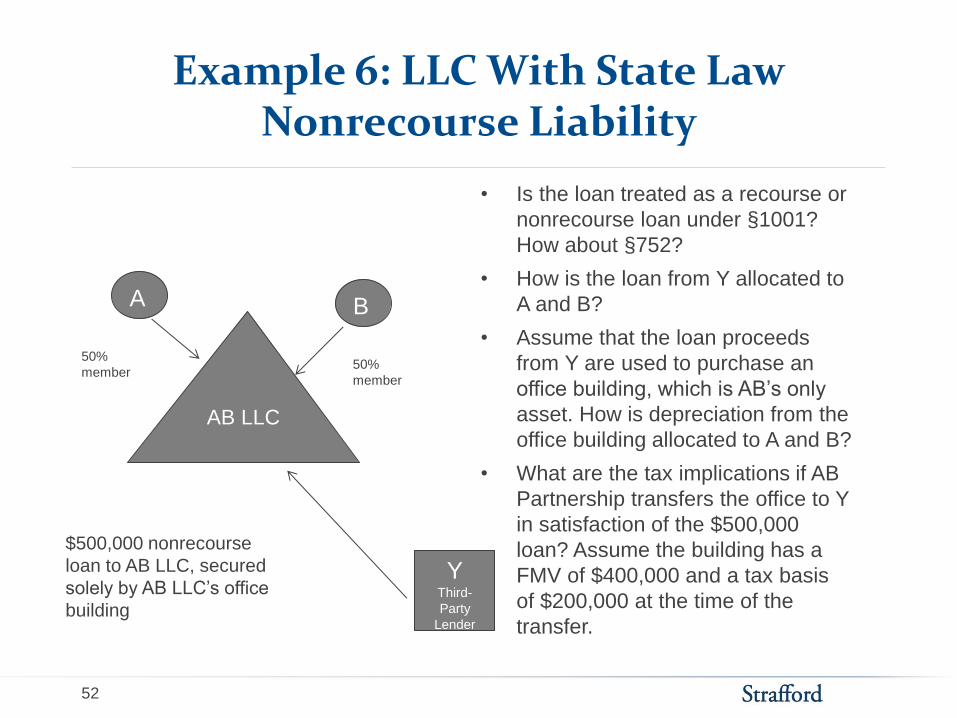

Example 6: LLC With State Law Nonrecourse Liability

AB LLC

A B

Y Third-

Party

Lender

$500,000 nonrecourse

loan to AB LLC, secured

solely by AB LLC’s office

building

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50%

member 50%

member

53

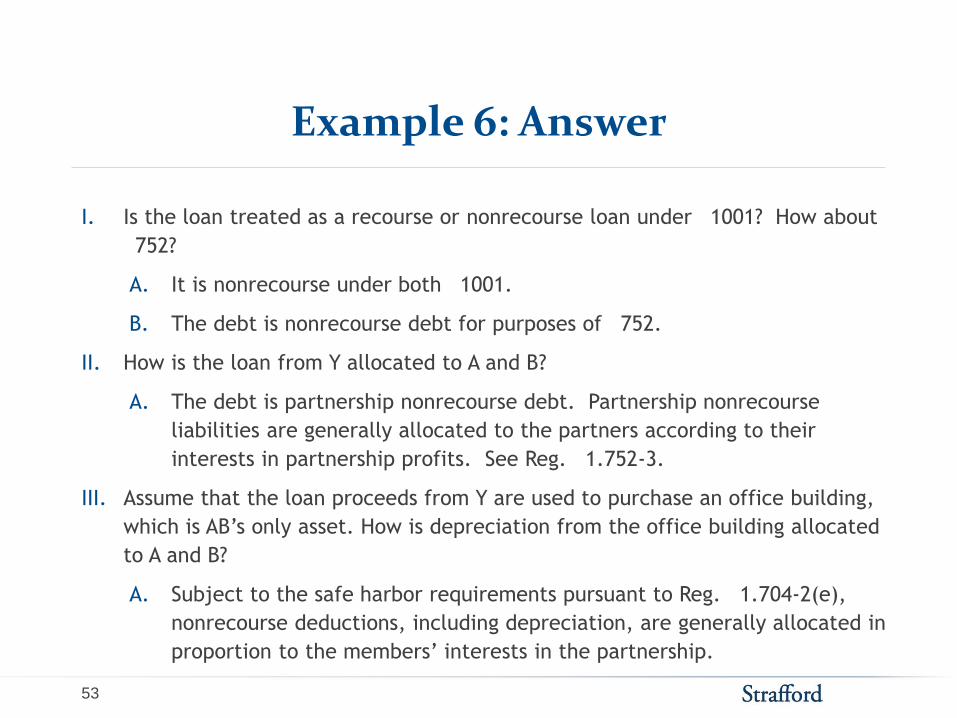

Example 6: Answer

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. It is nonrecourse under both

1001.

B. The debt is nonrecourse debt for purposes of

752.

II. How is the loan from Y allocated to A and B?

A. The debt is partnership nonrecourse debt. Partnership nonrecourse

liabilities are generally allocated to the partners according to their

interests in partnership profits. See Reg.

1.752-3.

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building allocated

to A and B?

A. Subject to the safe harbor requirements pursuant to Reg.

1.704-2(e),

nonrecourse deductions, including depreciation, are generally allocated in

proportion to the members’ interests in the partnership.

54

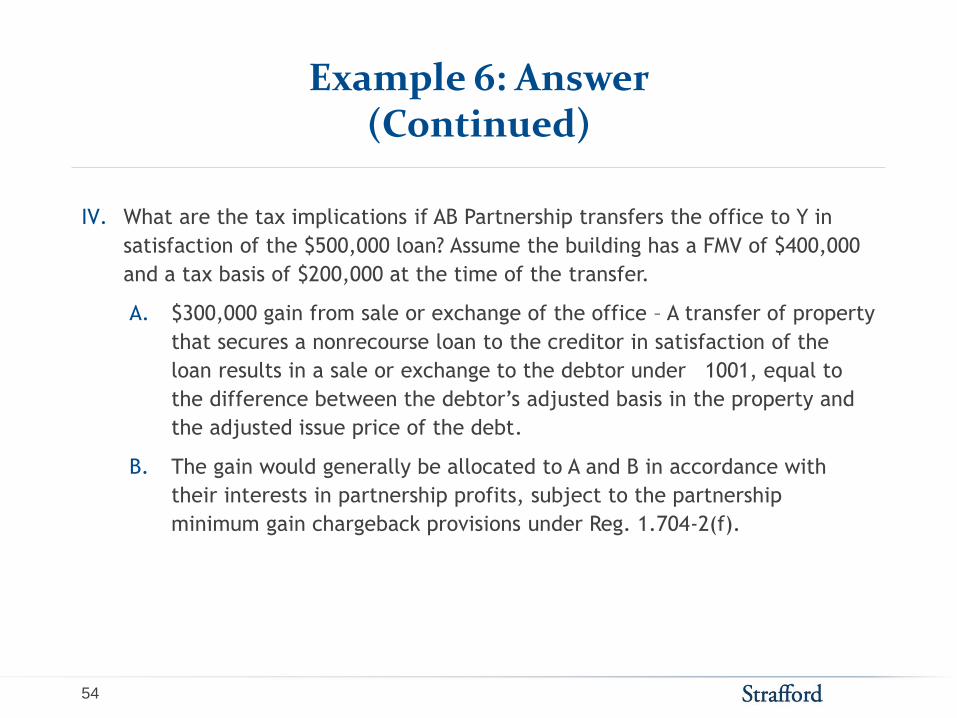

Example 6: Answer (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $300,000 gain from sale or exchange of the office – A transfer of property

that secures a nonrecourse loan to the creditor in satisfaction of the

loan results in a sale or exchange to the debtor under

1001, equal to

the difference between the debtor’s adjusted basis in the property and

the adjusted issue price of the debt.

B. The gain would generally be allocated to A and B in accordance with

their interests in partnership profits, subject to the partnership

minimum gain chargeback provisions under Reg. 1.704-2(f).

55

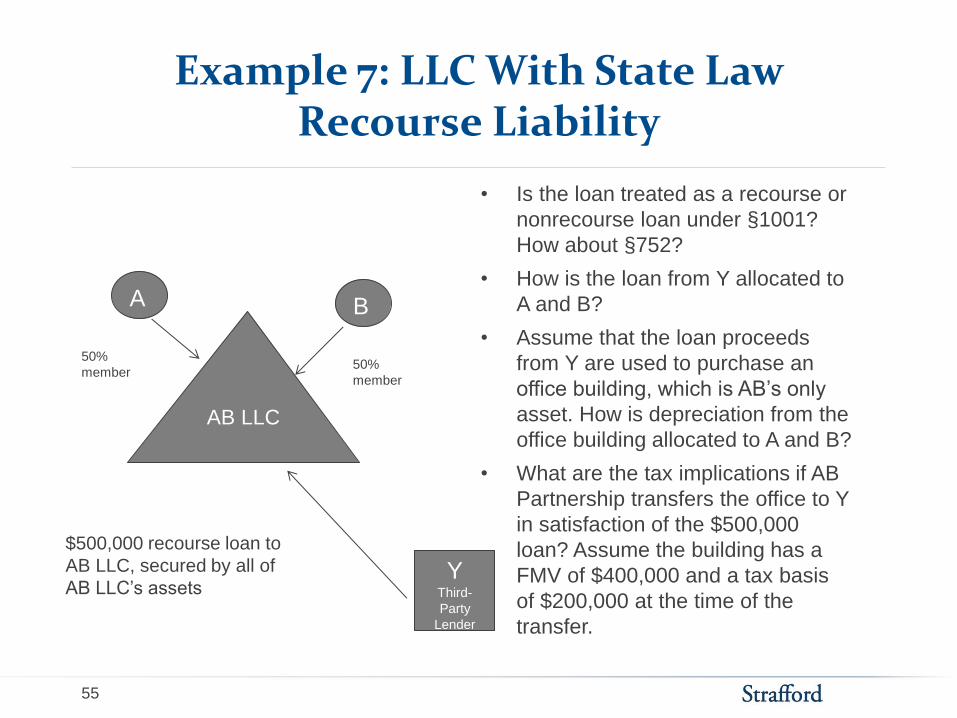

Example 7: LLC With State Law Recourse Liability

AB LLC

A B

Y Third-

Party

Lender

$500,000 recourse loan to

AB LLC, secured by all of

AB LLC’s assets

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50%

member 50%

member

56

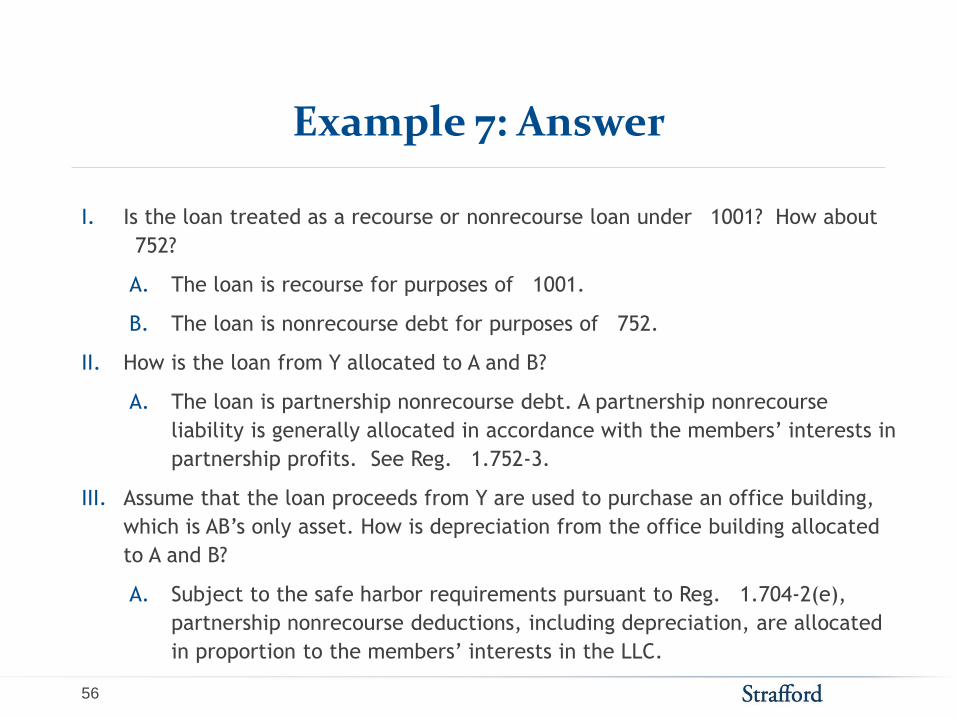

Example 7: Answer

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. The loan is recourse for purposes of

1001.

B. The loan is nonrecourse debt for purposes of

752.

II. How is the loan from Y allocated to A and B?

A. The loan is partnership nonrecourse debt. A partnership nonrecourse

liability is generally allocated in accordance with the members’ interests in

partnership profits. See Reg.

1.752-3.

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building allocated

to A and B?

A. Subject to the safe harbor requirements pursuant to Reg.

1.704-2(e),

partnership nonrecourse deductions, including depreciation, are allocated

in proportion to the members’ interests in the LLC.

57

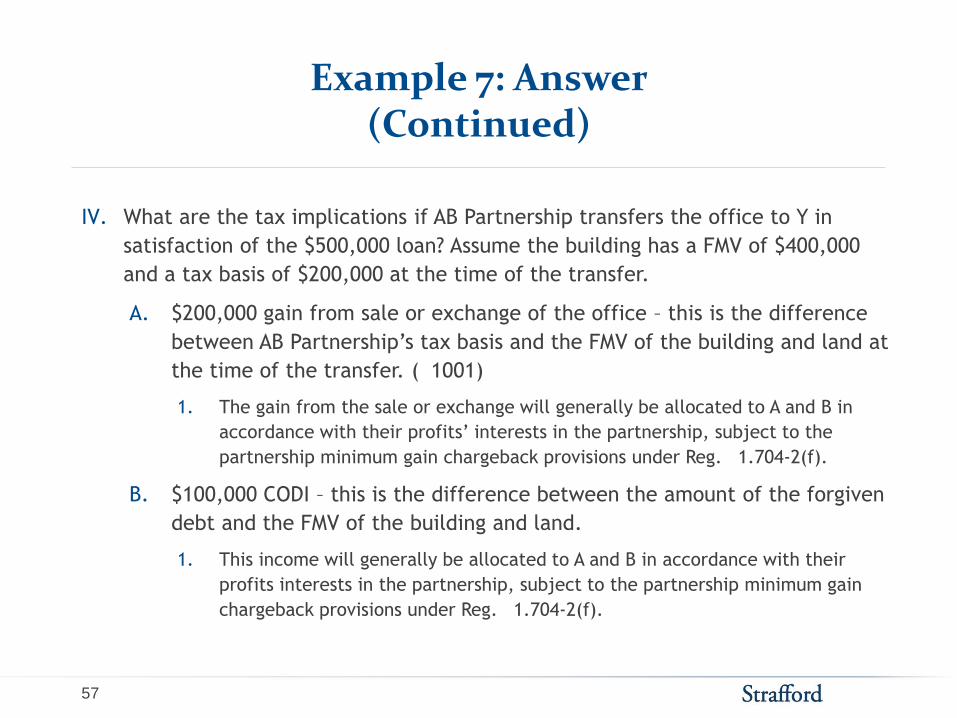

Example 7: Answer (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $200,000 gain from sale or exchange of the office – this is the difference

between AB Partnership’s tax basis and the FMV of the building and land at

the time of the transfer. (

1001)

1. The gain from the sale or exchange will generally be allocated to A and B in

accordance with their profits’ interests in the partnership, subject to the

partnership minimum gain chargeback provisions under Reg.

1.704-2(f).

B. $100,000 CODI – this is the difference between the amount of the forgiven

debt and the FMV of the building and land.

1. This income will generally be allocated to A and B in accordance with their

profits interests in the partnership, subject to the partnership minimum gain

chargeback provisions under Reg.

1.704-2(f).

58

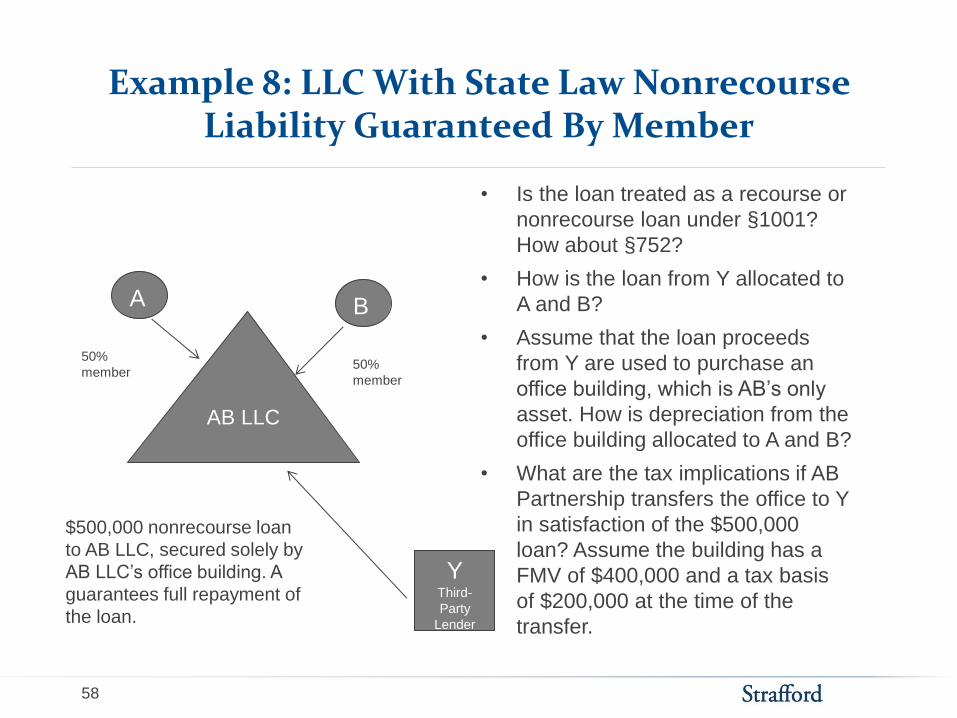

Example 8: LLC With State Law Nonrecourse Liability Guaranteed By Member

AB LLC

A B

Y Third-

Party

Lender

$500,000 nonrecourse loan

to AB LLC, secured solely by

AB LLC’s office building. A

guarantees full repayment of

the loan.

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50%

member 50%

member

59

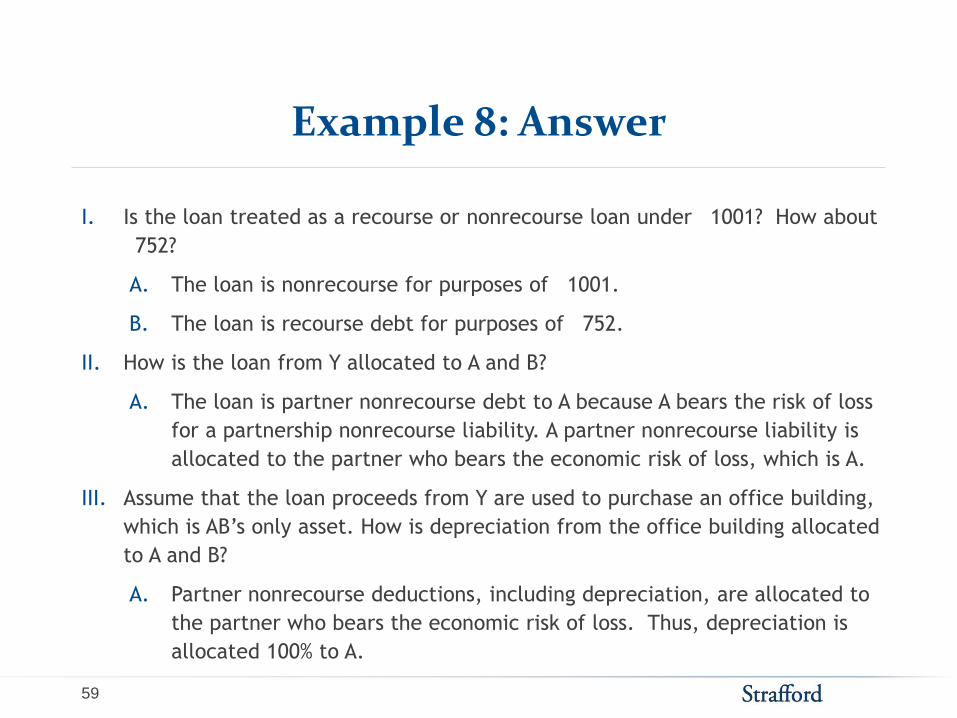

Example 8: Answer

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. The loan is nonrecourse for purposes of

1001.

B. The loan is recourse debt for purposes of

752.

II. How is the loan from Y allocated to A and B?

A. The loan is partner nonrecourse debt to A because A bears the risk of loss

for a partnership nonrecourse liability. A partner nonrecourse liability is

allocated to the partner who bears the economic risk of loss, which is A.

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building allocated

to A and B?

A. Partner nonrecourse deductions, including depreciation, are allocated to

the partner who bears the economic risk of loss. Thus, depreciation is

allocated 100% to A.

60

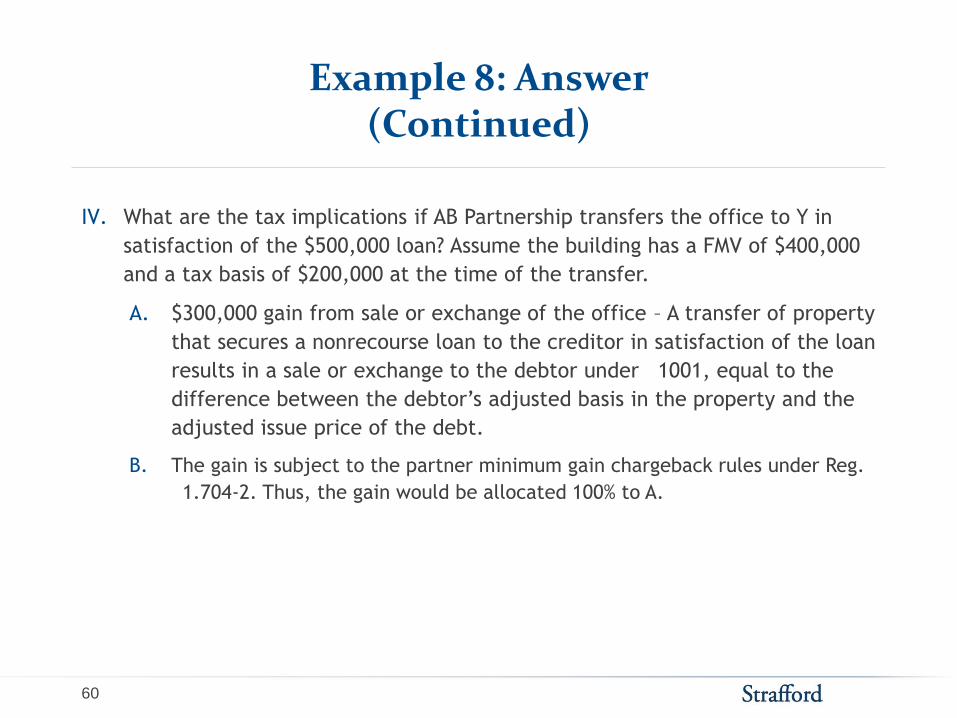

Example 8: Answer (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $300,000 gain from sale or exchange of the office – A transfer of property

that secures a nonrecourse loan to the creditor in satisfaction of the loan

results in a sale or exchange to the debtor under

1001, equal to the

difference between the debtor’s adjusted basis in the property and the

adjusted issue price of the debt.

B. The gain is subject to the partner minimum gain chargeback rules under Reg. 1.704-2. Thus, the gain would be allocated 100% to A.

Slide Intentionally Left Blank

62

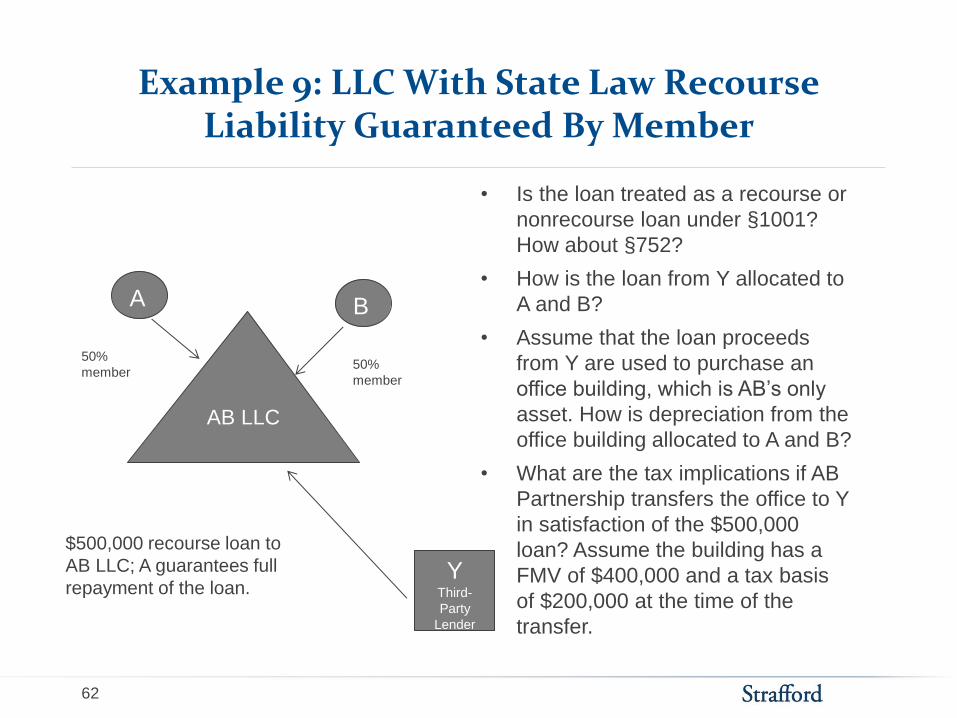

Example 9: LLC With State Law Recourse Liability Guaranteed By Member

AB LLC

A B

Y Third-

Party

Lender

$500,000 recourse loan to

AB LLC; A guarantees full

repayment of the loan.

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50%

member 50%

member

63

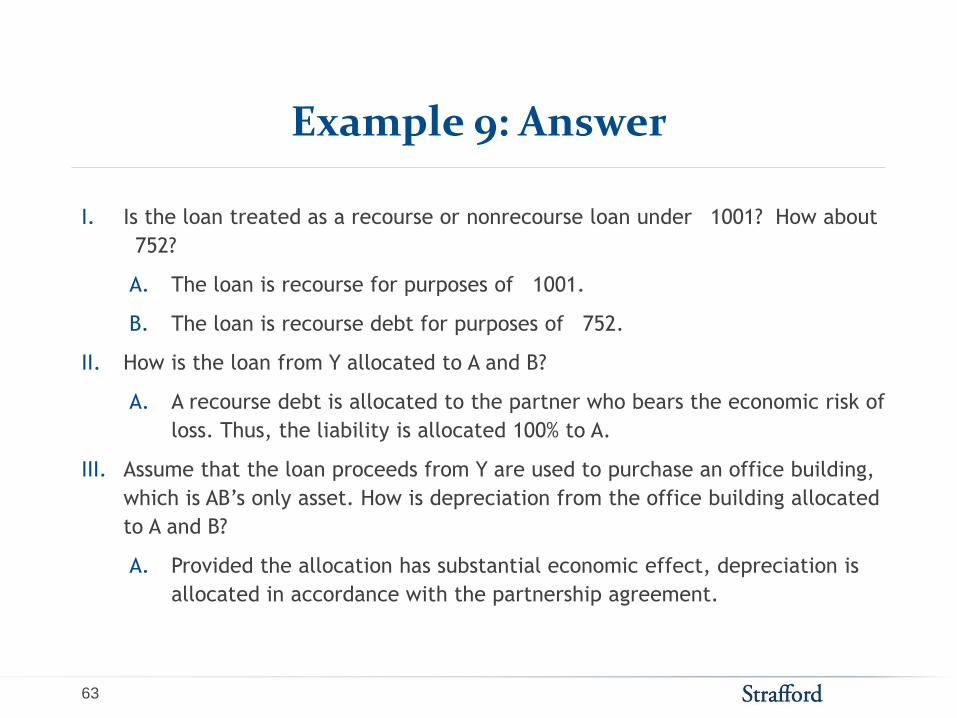

Example 9: Answer

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. The loan is recourse for purposes of

1001.

B. The loan is recourse debt for purposes of

752.

II. How is the loan from Y allocated to A and B?

A. A recourse debt is allocated to the partner who bears the economic risk of

loss. Thus, the liability is allocated 100% to A.

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building allocated

to A and B?

A. Provided the allocation has substantial economic effect, depreciation is

allocated in accordance with the partnership agreement.

64

Example 9: Answer (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. $200,000 gain from sale or exchange of the office – this is the difference

between AB Partnership’s tax basis and the FMV of the building and land at

the time of the transfer. (

1001).

1. The gain would be allocated to A and B in accordance with the partnership

agreement provided such allocation has substantial economic effect.

B. $100,000 CODI – this is the difference between the amount of the forgiven

debt and the FMV of the building and land.

1. The income would be allocated to A and B in accordance with the partnership

agreement provided such allocation has substantial economic effect.

65

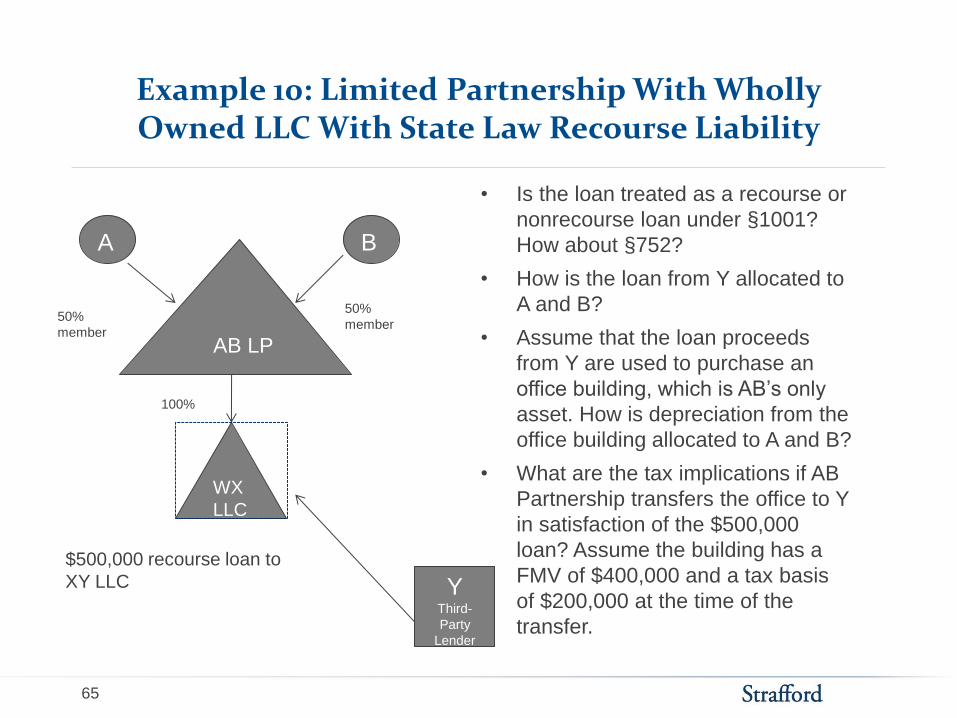

Example 10: Limited Partnership With Wholly Owned LLC With State Law Recourse Liability

AB LP

A B

Y Third-

Party

Lender

$500,000 recourse loan to

XY LLC

• Is the loan treated as a recourse or

nonrecourse loan under §1001?

How about §752?

• How is the loan from Y allocated to

A and B?

• Assume that the loan proceeds

from Y are used to purchase an

office building, which is AB’s only

asset. How is depreciation from the

office building allocated to A and B?

• What are the tax implications if AB

Partnership transfers the office to Y

in satisfaction of the $500,000

loan? Assume the building has a

FMV of $400,000 and a tax basis

of $200,000 at the time of the

transfer.

50%

member

50%

member

WX

LLC

100%

66

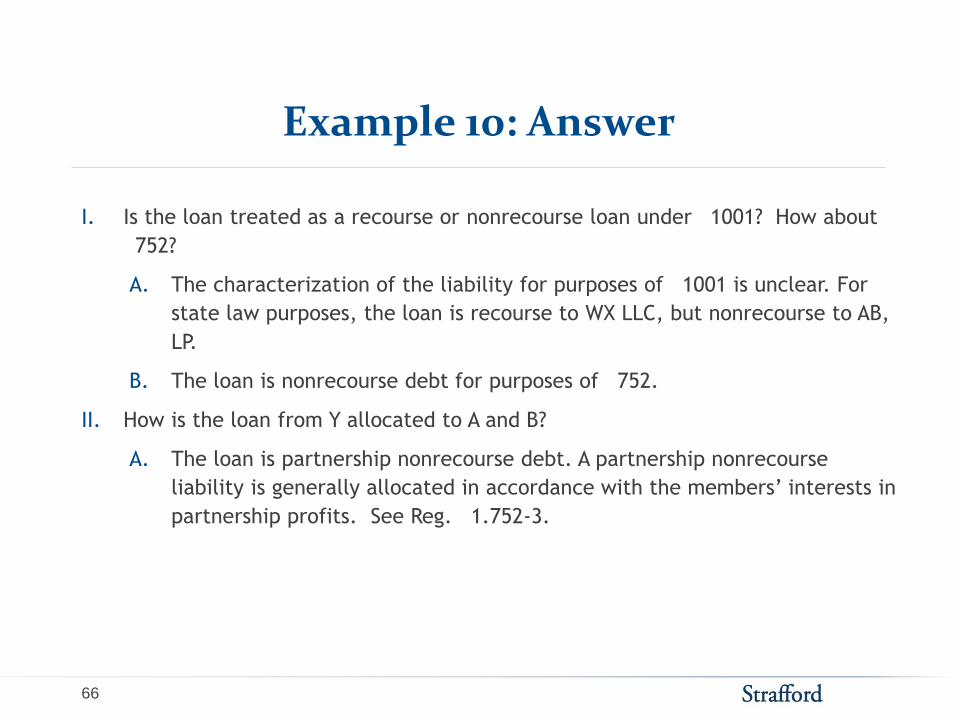

Example 10: Answer

I. Is the loan treated as a recourse or nonrecourse loan under

1001? How about 752?

A. The characterization of the liability for purposes of

1001 is unclear. For

state law purposes, the loan is recourse to WX LLC, but nonrecourse to AB,

LP.

B. The loan is nonrecourse debt for purposes of

752.

II. How is the loan from Y allocated to A and B?

A. The loan is partnership nonrecourse debt. A partnership nonrecourse

liability is generally allocated in accordance with the members’ interests in

partnership profits. See Reg.

1.752-3.

67

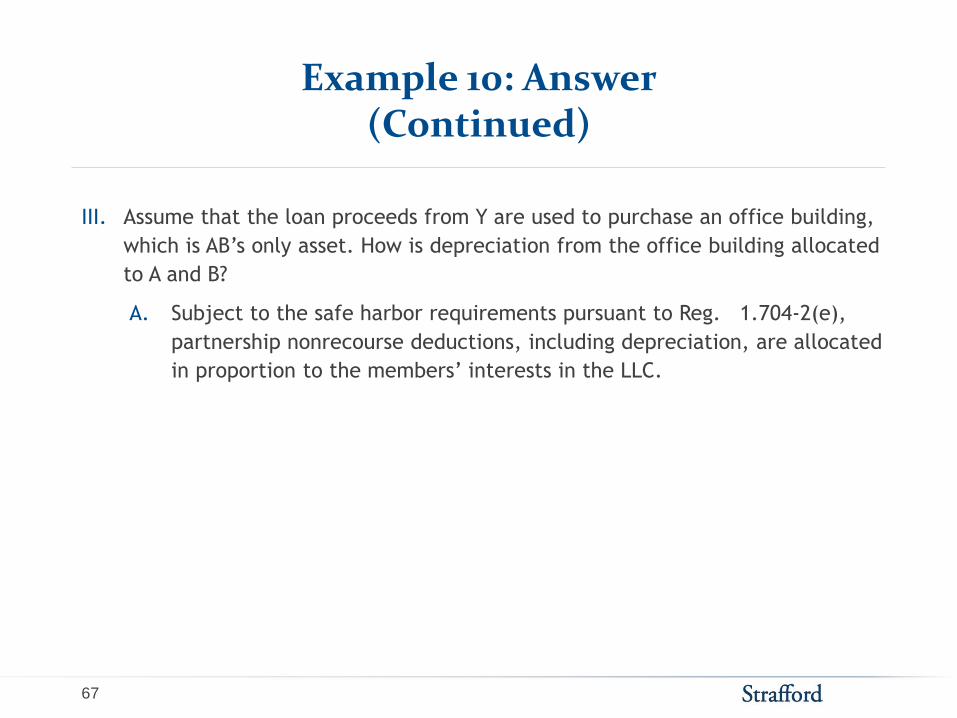

Example 10: Answer (Continued)

III. Assume that the loan proceeds from Y are used to purchase an office building,

which is AB’s only asset. How is depreciation from the office building allocated

to A and B?

A. Subject to the safe harbor requirements pursuant to Reg.

1.704-2(e),

partnership nonrecourse deductions, including depreciation, are allocated

in proportion to the members’ interests in the LLC.

68

Example 10: Answer (Continued)

IV. What are the tax implications if AB Partnership transfers the office to Y in

satisfaction of the $500,000 loan? Assume the building has a FMV of $400,000

and a tax basis of $200,000 at the time of the transfer.

A. The answer will depend on how the liability is treated for purposes of 1001.

69

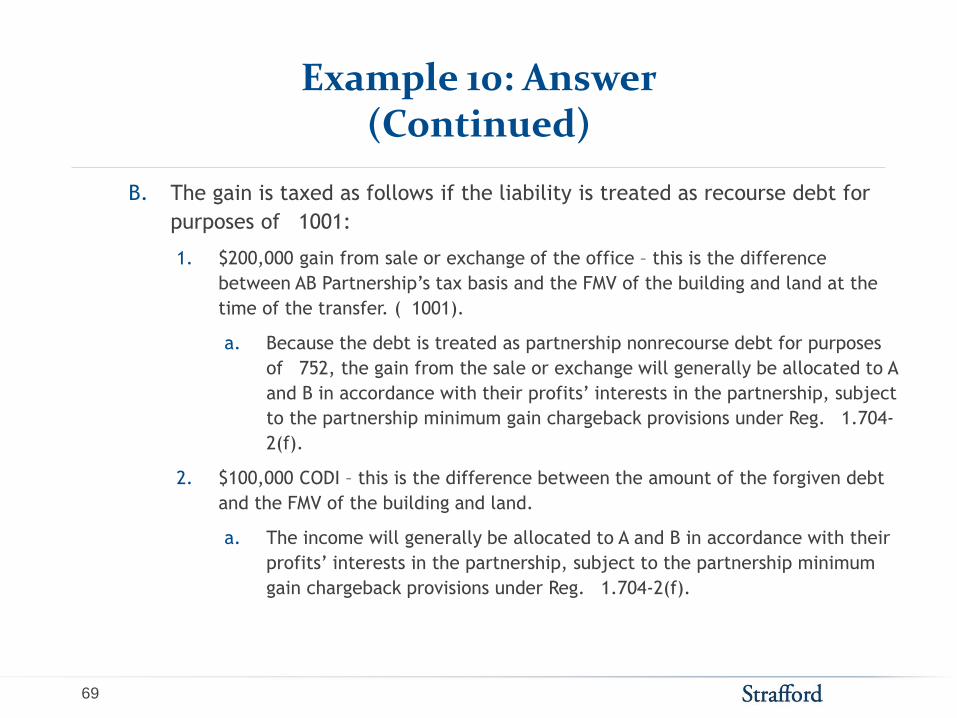

Example 10: Answer (Continued)

B. The gain is taxed as follows if the liability is treated as recourse debt for

purposes of

1001:

1. $200,000 gain from sale or exchange of the office – this is the difference

between AB Partnership’s tax basis and the FMV of the building and land at the

time of the transfer. (

1001).

a. Because the debt is treated as partnership nonrecourse debt for purposes

of

752, the gain from the sale or exchange will generally be allocated to A

and B in accordance with their profits’ interests in the partnership, subject

to the partnership minimum gain chargeback provisions under Reg.

1.704-

2(f).

2. $100,000 CODI – this is the difference between the amount of the forgiven debt

and the FMV of the building and land.

a. The income will generally be allocated to A and B in accordance with their

profits’ interests in the partnership, subject to the partnership minimum

gain chargeback provisions under Reg.

1.704-2(f).

70

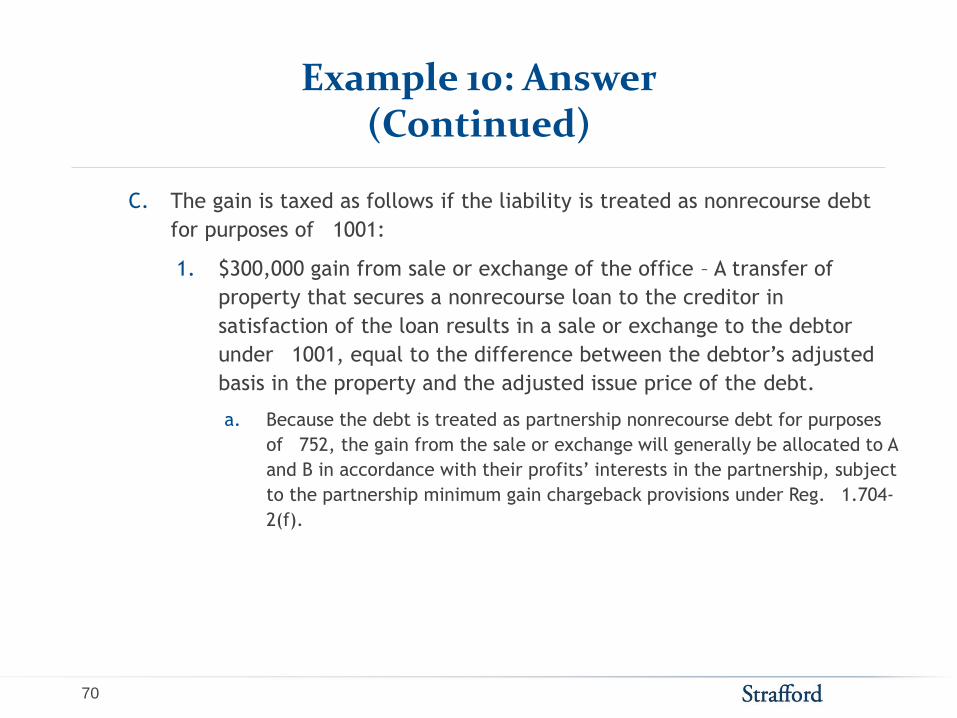

Example 10: Answer (Continued)

C. The gain is taxed as follows if the liability is treated as nonrecourse debt

for purposes of

1001:

1. $300,000 gain from sale or exchange of the office – A transfer of

property that secures a nonrecourse loan to the creditor in

satisfaction of the loan results in a sale or exchange to the debtor

under

1001, equal to the difference between the debtor’s adjusted

basis in the property and the adjusted issue price of the debt.

a. Because the debt is treated as partnership nonrecourse debt for purposes

of

752, the gain from the sale or exchange will generally be allocated to A

and B in accordance with their profits’ interests in the partnership, subject

to the partnership minimum gain chargeback provisions under Reg.

1.704-

2(f).

AT-RISK RULES UNDER IRC SECT. 465

Carolyn Turnbull, McGladrey LLP

72

Sect. 465 At-Risk Amount

I. A taxpayer is considered at risk for an activity with respect to

amounts borrowed with respect to such activity. (

465(b)(1)(B))

II. Amounts borrowed for use in an activity include:

A. Debt for which the taxpayer is personally liable for

repayment, and

B. Debt for which the taxpayer has pledged property (other

than property used in the activity) as security for the

borrowed amount.

1. Amount at risk is limited to the net FMV of the collateral.

73

Sect. 465 At-Risk Amount (Cont.)

I. Taxpayer must be primarily liable on the debt.

A. Guarantees do not increase the taxpayer’s amount at risk

until the taxpayer repays the creditor for the amount

borrowed, and the taxpayer has no remaining legal rights

against the primary obligor. (Prop. Reg.

1.465-6(d))

II. Amounts borrowed for use in an activity do not include:

A. Amounts borrowed from any person who has an interest

(other than as a creditor) in the activity

B. Amounts borrowed from a person related to any person who

has an interest (other than as a creditor) in the activity

(other than the taxpayer)

74

Sect. 465 At-Risk Amount (Cont.)

I. Only “qualified” nonrecourse debts are included in at-risk

amount:

A. Borrowed with respect to activity of holding real estate,

and secured by real estate;

B. Borrowed from a lender in the business of lending money

and who has no interest in the activity in which the funds

are used; and

C. Not convertible into stock or securities.

75

Example: Basis And At-Risk Limitations

Susan is a 10% owner in ABC LLC, which has elected to be treated as

a partnership for federal income tax purposes. Her tax basis in the

LLC is $25,000, consisting of a $10,000 capital contribution and

$15,000 of non-qualified, nonrecourse debt. For 2011, Susan’s

distributive share of the LLC’s loss is ($32,000).

76

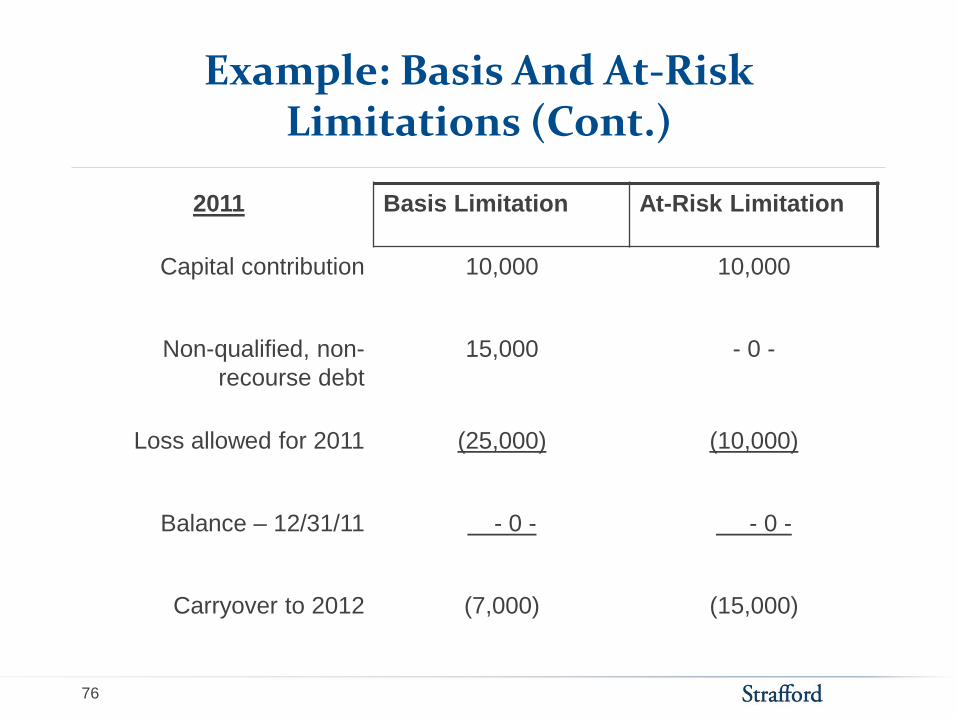

Example: Basis And At-Risk Limitations (Cont.)

2011 Basis Limitation At-Risk Limitation

Capital contribution 10,000 10,000

Non-qualified, non-

recourse debt

15,000 - 0 -

Loss allowed for 2011 (25,000) (10,000)

Balance – 12/31/11 - 0 - - 0 -

Carryover to 2012 (7,000) (15,000)

77

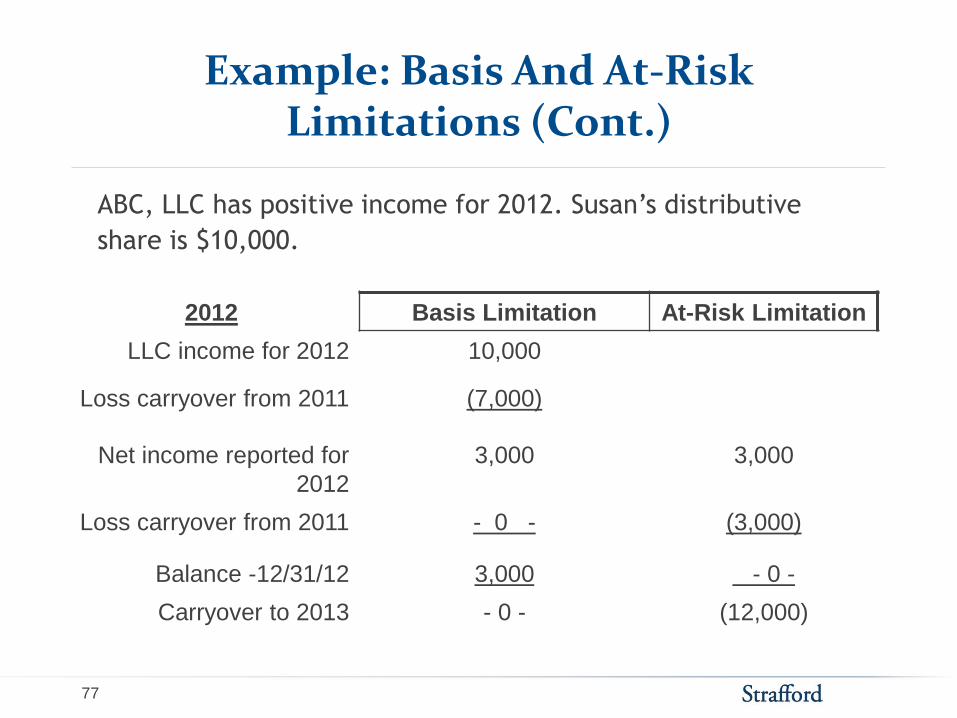

Example: Basis And At-Risk Limitations (Cont.)

2012 Basis Limitation At-Risk Limitation

LLC income for 2012 10,000

Loss carryover from 2011 (7,000)

Net income reported for

2012

3,000 3,000

Loss carryover from 2011 - 0 - (3,000)

Balance -12/31/12 3,000 - 0 -

Carryover to 2013 - 0 - (12,000)

ABC, LLC has positive income for 2012. Susan’s distributive

share is $10,000.

78

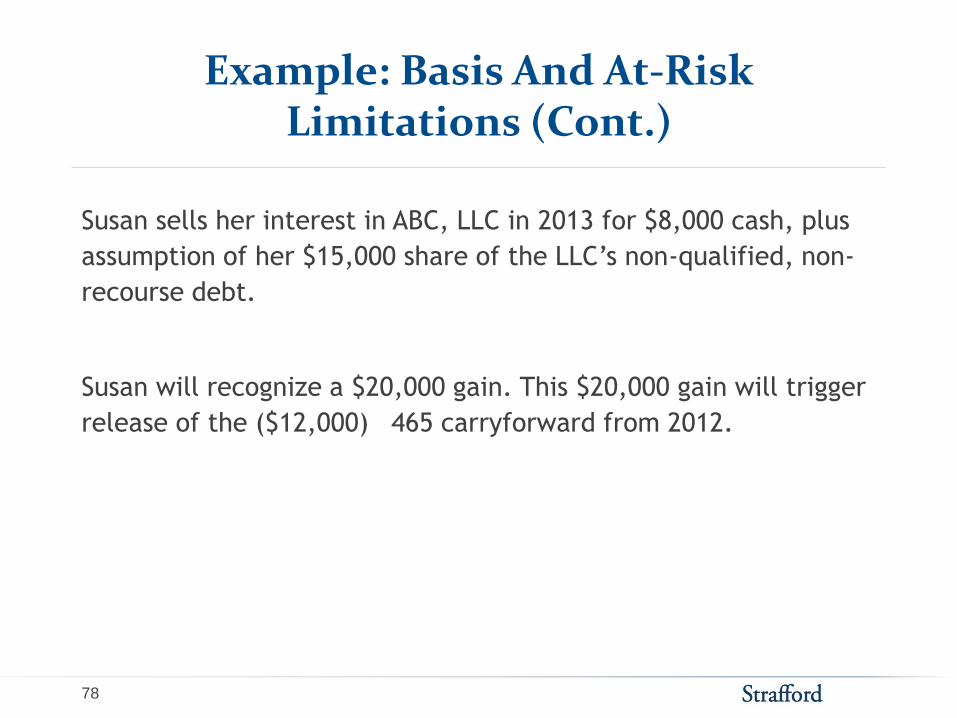

Example: Basis And At-Risk Limitations (Cont.)

Susan sells her interest in ABC, LLC in 2013 for $8,000 cash, plus

assumption of her $15,000 share of the LLC’s non-qualified, non-

recourse debt.

Susan will recognize a $20,000 gain. This $20,000 gain will trigger

release of the ($12,000)

465 carryforward from 2012.

79

Treatment Of Partnership Liabilities For Partnership Income Tax Purposes

Circular 230 Disclosure

These materials are intended for internal discussion purposes only. To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or any other state or local law, or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.

CONCLUDING REMARKS

Carolyn Turnbull, CPA, MST, CGMA, Independent Tax Consultant

Belan Wagner, Wagner Kirkman Blaine Komparens & Youmans