Embed Size (px)

Citation preview

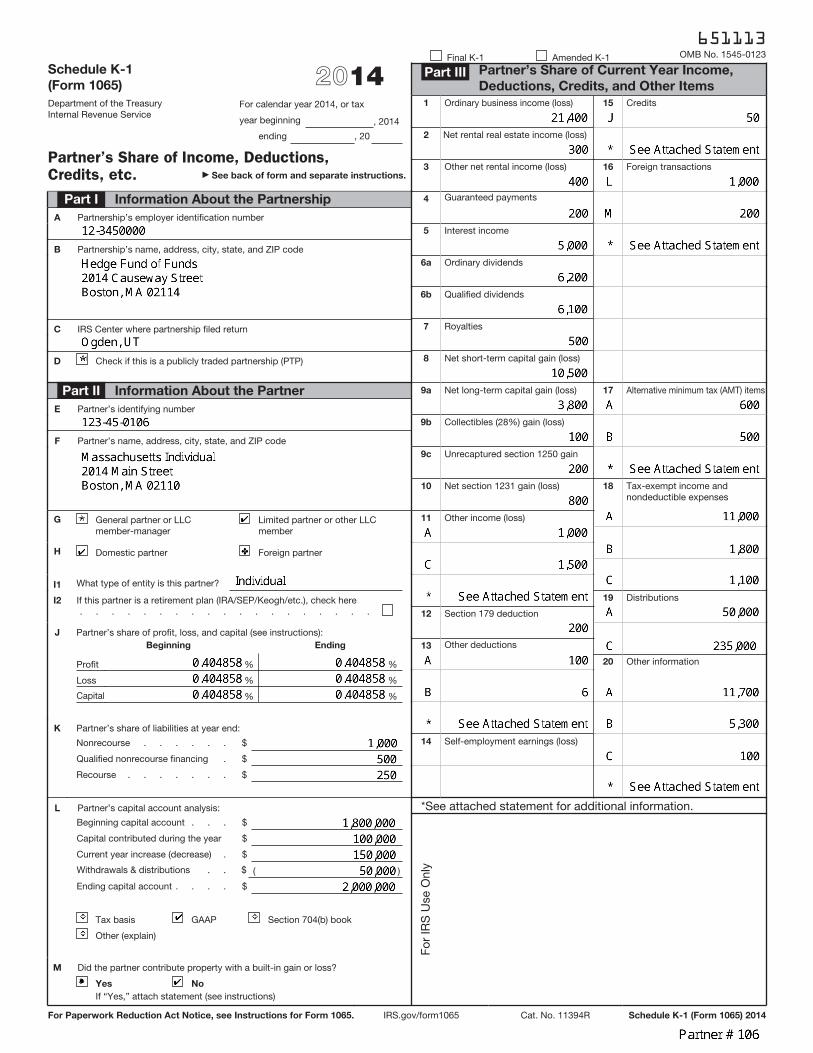

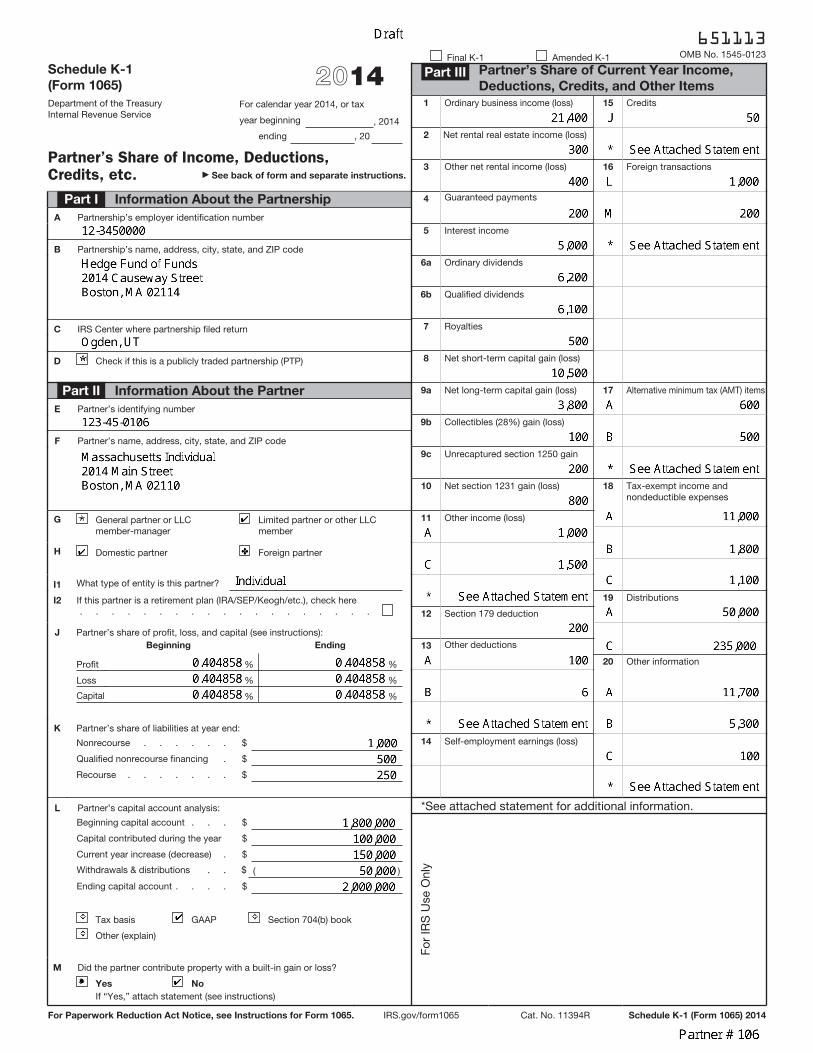

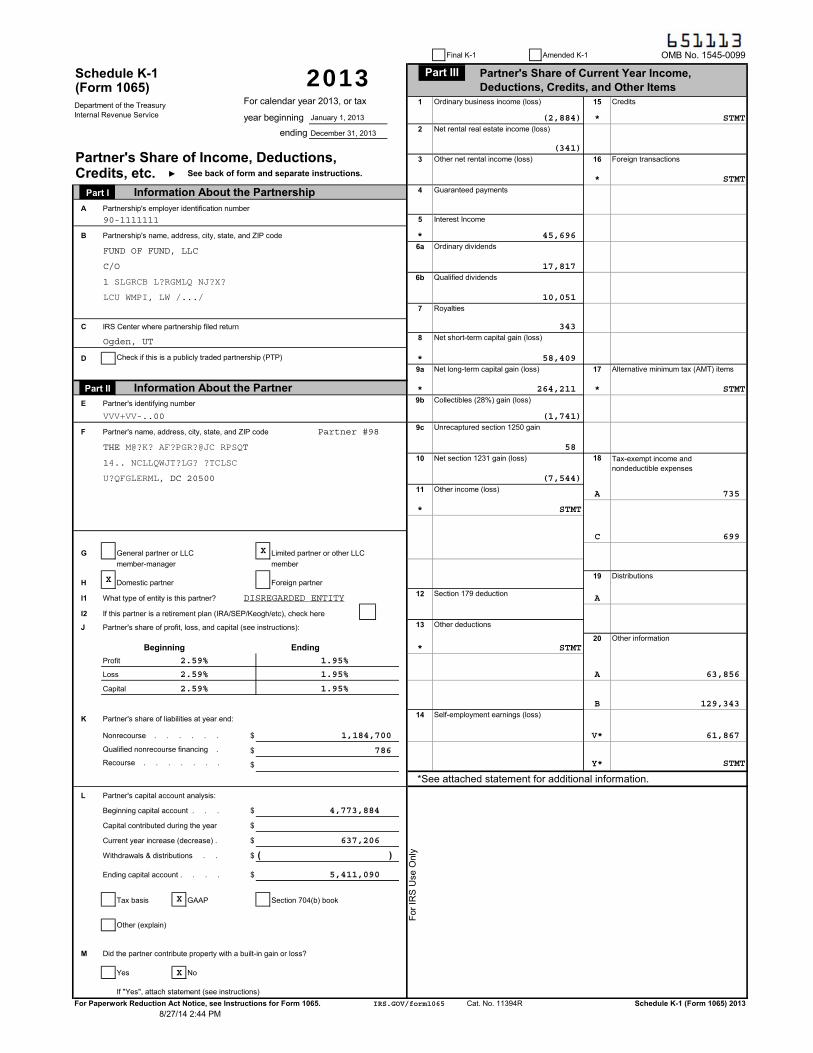

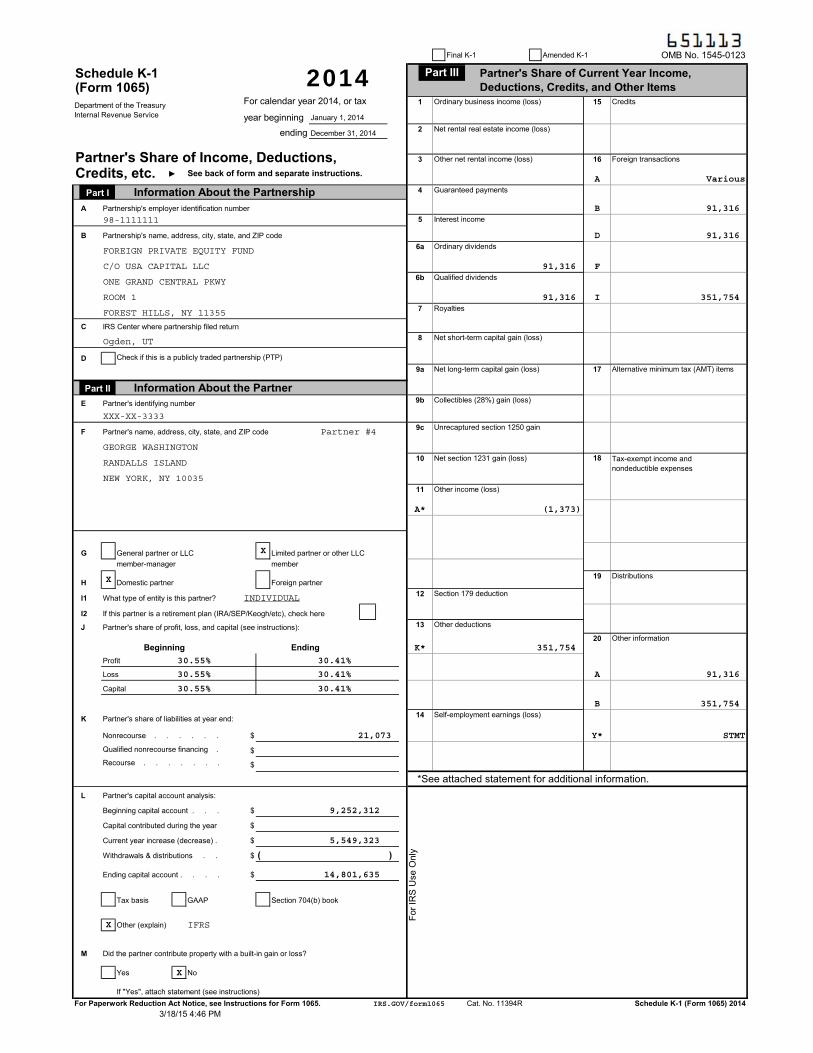

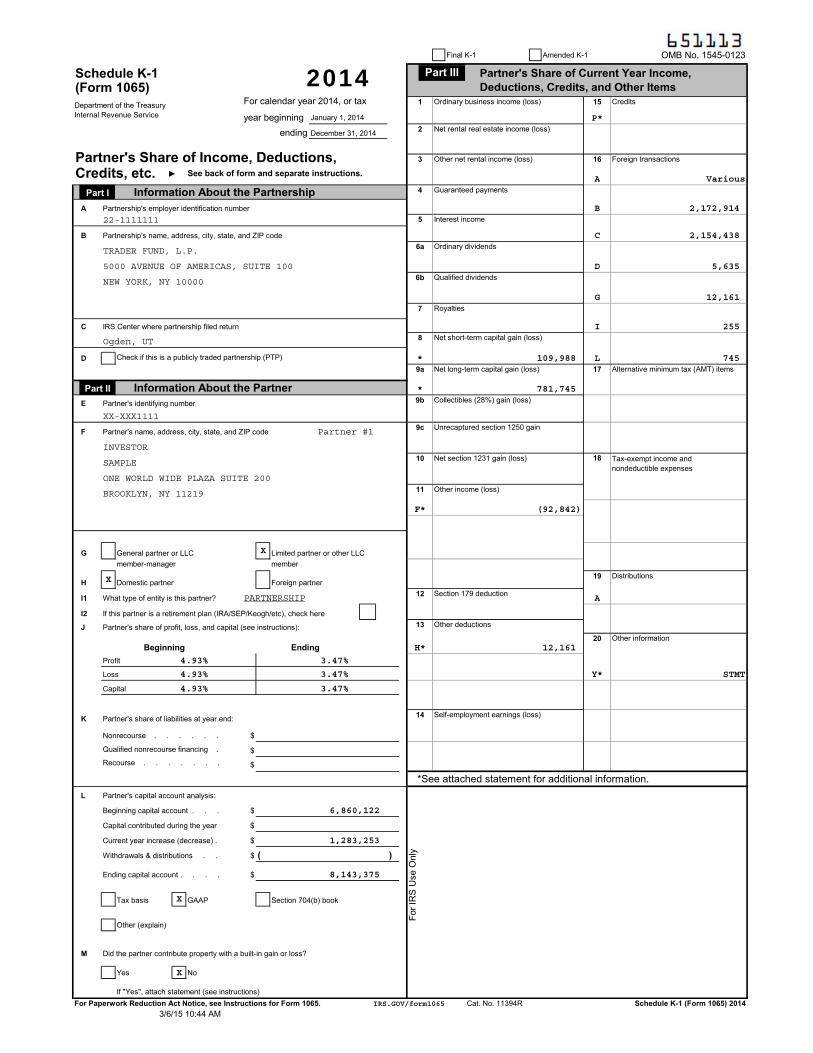

OMB No. 1545-0123

Schedule K-1

(Form 1065) 2014Department of the Treasury Internal Revenue Service

For calendar year 2014, or tax

year beginning , 2014

ending , 20

Partner’s Share of Income, Deductions, Credits, etc. See back of form and separate instructions.

651113 Final K-1 Amended K-1

Information About the Partnership Part I

A Partnership’s employer identification number

B Partnership’s name, address, city, state, and ZIP code

C IRS Center where partnership filed return

D Check if this is a publicly traded partnership (PTP)

Information About the Partner Part II

E Partner’s identifying number

F Partner’s name, address, city, state, and ZIP code

G General partner or LLC member-manager

Limited partner or other LLC member

H Domestic partner Foreign partner

I1 What type of entity is this partner?

I2 If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here . . . . . . . . . . . . . . . . . . .

J Partner’s share of profit, loss, and capital (see instructions): Beginning Ending

Profit % %

Loss % %

Capital % %

K Partner’s share of liabilities at year end:

Nonrecourse . . . . . . $

Qualified nonrecourse financing . $

Recourse . . . . . . . $

L Partner’s capital account analysis:

Beginning capital account . . . $

Capital contributed during the year $

Current year increase (decrease) . $

Withdrawals & distributions . . $ ( )

Ending capital account . . . . $

Tax basis GAAP Section 704(b) book

Other (explain)

M Did the partner contribute property with a built-in gain or loss?

Yes No

If “Yes,” attach statement (see instructions)

Partner’s Share of Current Year Income,

Deductions, Credits, and Other Items Part III

1 Ordinary business income (loss)

2 Net rental real estate income (loss)

3 Other net rental income (loss)

4 Guaranteed payments

5 Interest income

6a Ordinary dividends

6b Qualified dividends

7 Royalties

8 Net short-term capital gain (loss)

9a Net long-term capital gain (loss)

9b Collectibles (28%) gain (loss)

9c Unrecaptured section 1250 gain

10 Net section 1231 gain (loss)

11 Other income (loss)

12 Section 179 deduction

13 Other deductions

14 Self-employment earnings (loss)

15 Credits

16 Foreign transactions

17 Alternative minimum tax (AMT) items

18 Tax-exempt income and nondeductible expenses

19 Distributions

20 Other information

*See attached statement for additional information.

For

IRS

Use

Onl

y

For Paperwork Reduction Act Notice, see Instructions for Form 1065. IRS.gov/form1065 Cat. No. 11394R Schedule K-1 (Form 1065) 2014

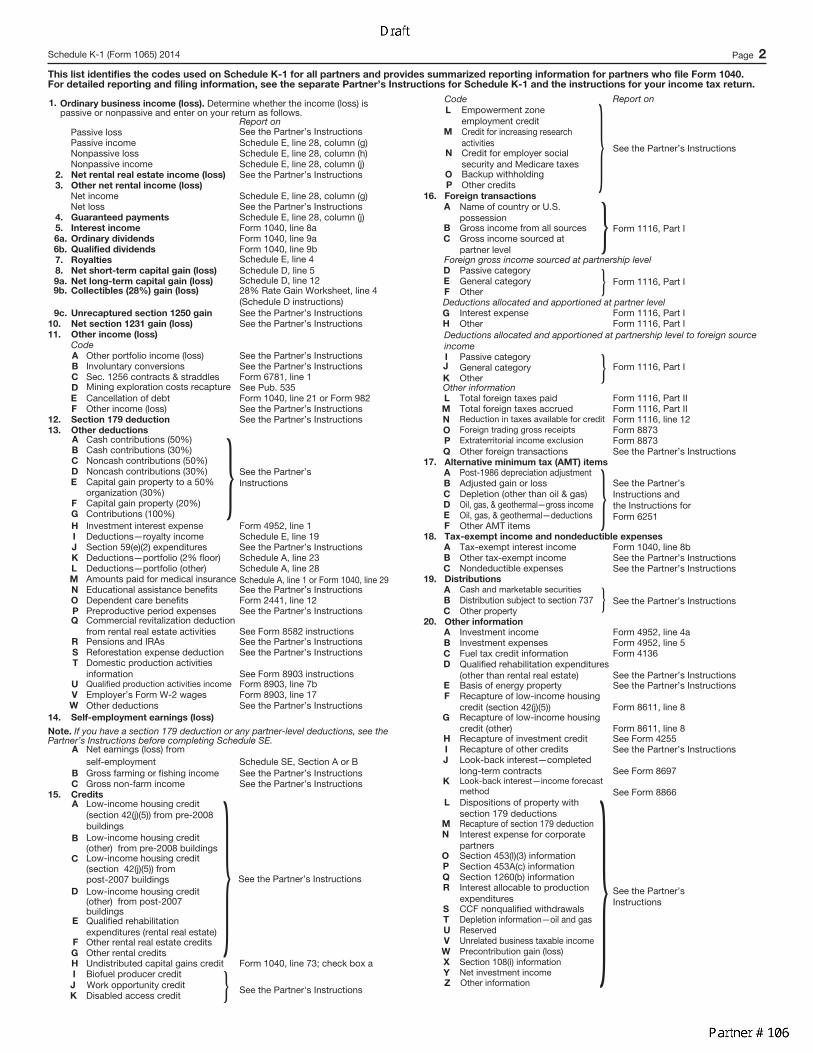

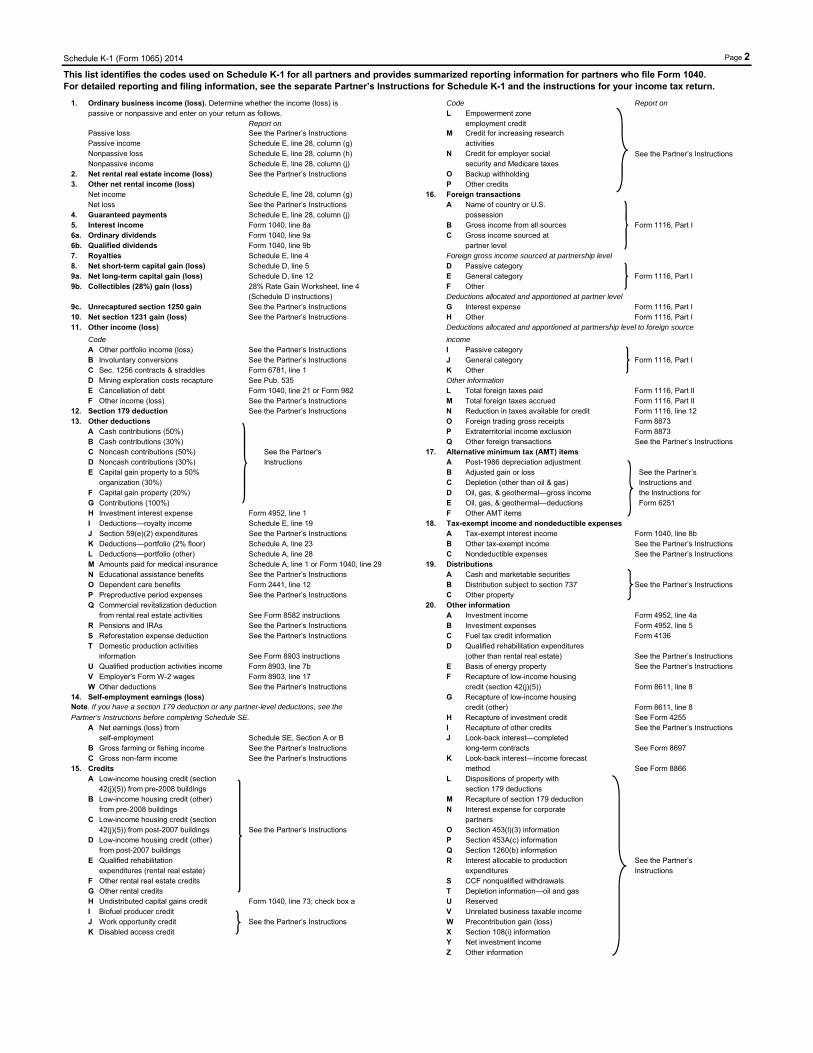

Schedule K-1 (Form 1065) 2014 Page 2

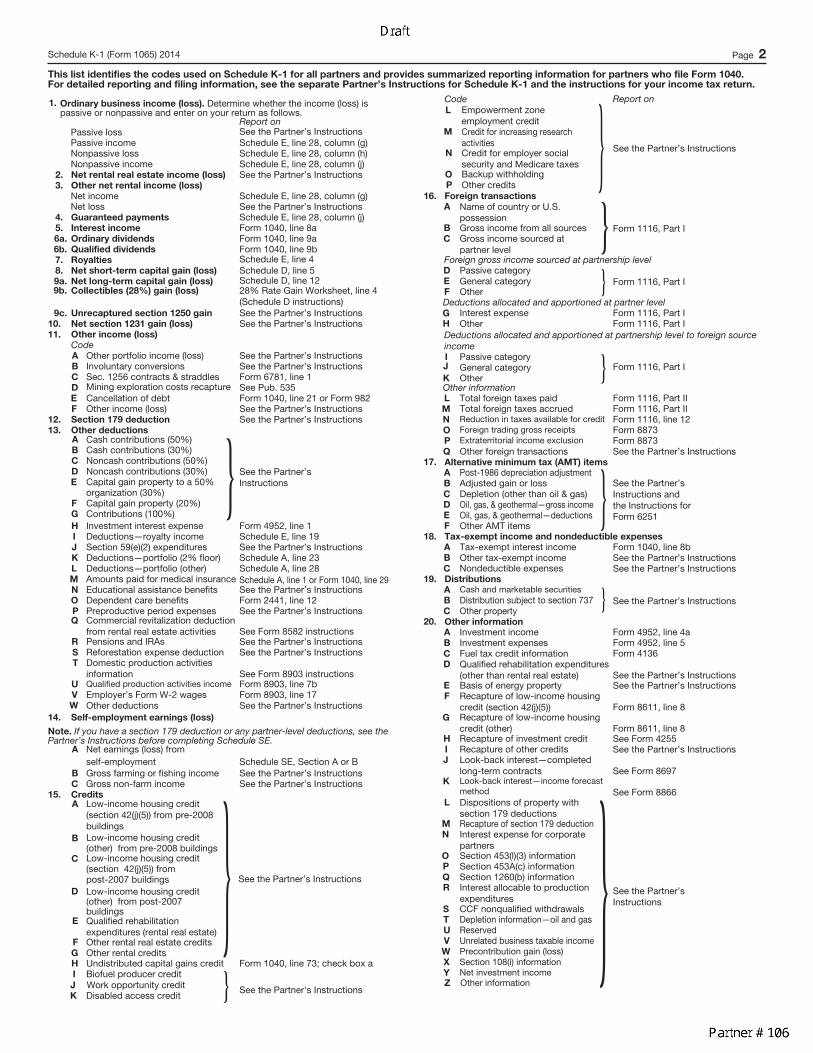

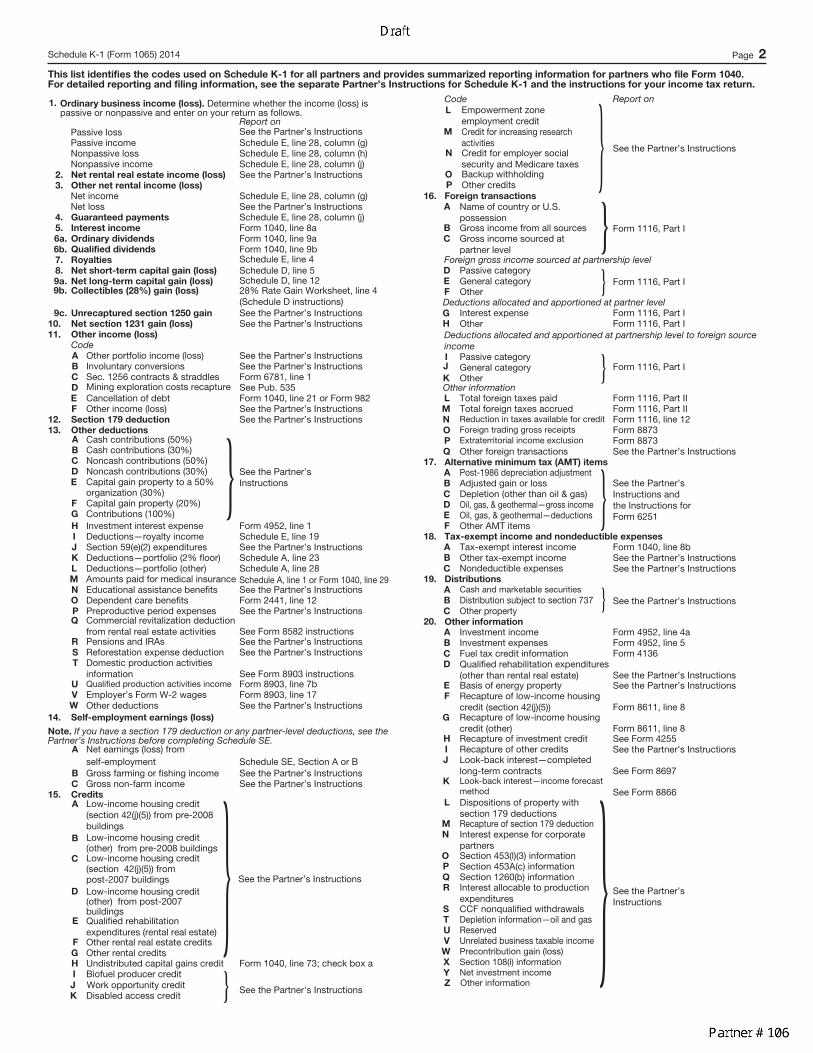

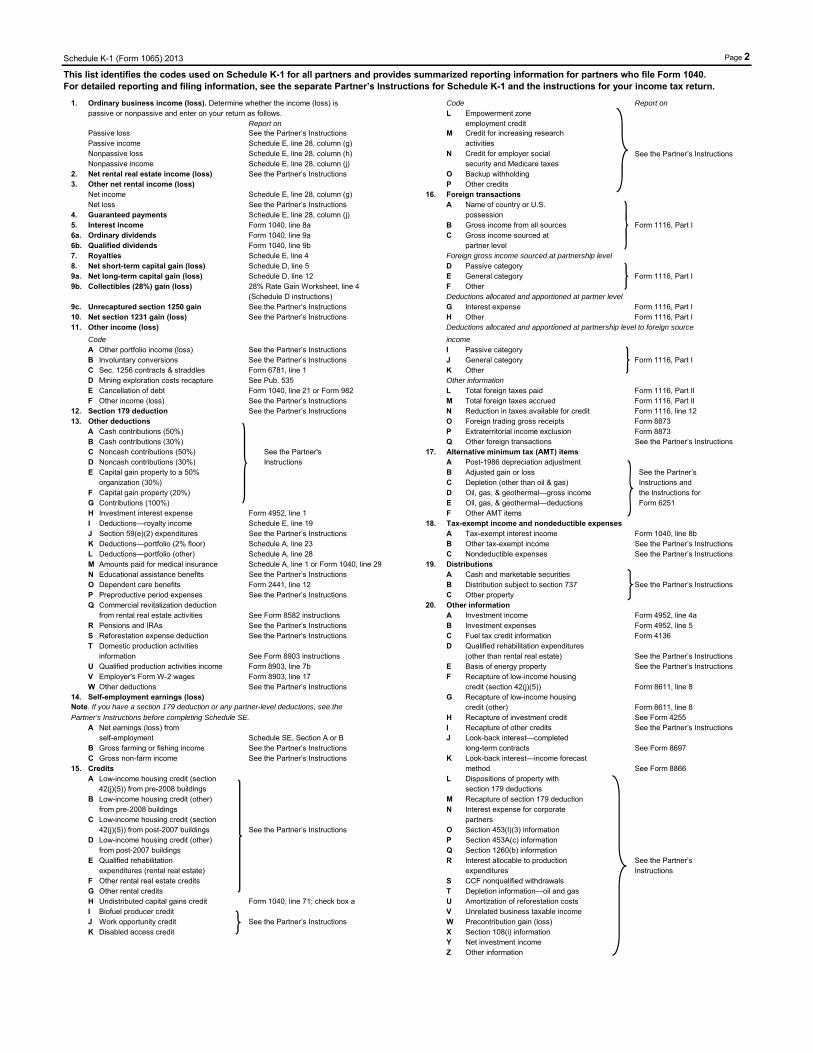

This list identifies the codes used on Schedule K-1 for all partners and provides summarized reporting information for partners who file Form 1040. For detailed reporting and filing information, see the separate Partner’s Instructions for Schedule K-1 and the instructions for your income tax return.

1. Ordinary business income (loss). Determine whether the income (loss) is passive or nonpassive and enter on your return as follows.

Passive loss Report on See the Partner’s Instructions

Passive income Schedule E, line 28, column (g) Nonpassive loss Schedule E, line 28, column (h) Nonpassive income Schedule E, line 28, column (j)

2. Net rental real estate income (loss) See the Partner’s Instructions 3. Other net rental income (loss)

Net income Schedule E, line 28, column (g) Net loss See the Partner’s Instructions

4. Guaranteed payments Schedule E, line 28, column (j) 5. Interest income Form 1040, line 8a 6a. Ordinary dividends Form 1040, line 9a 6b. Qualified dividends Form 1040, line 9b 7. Royalties Schedule E, line 48. Net short-term capital gain (loss) Schedule D, line 59a. Net long-term capital gain (loss) Schedule D, line 129b. Collectibles (28%) gain (loss) 28% Rate Gain Worksheet, line 4

(Schedule D instructions) 9c. Unrecaptured section 1250 gain See the Partner’s Instructions

10. Net section 1231 gain (loss) See the Partner’s Instructions 11. Other income (loss)

Code A Other portfolio income (loss) See the Partner’s Instructions B Involuntary conversions See the Partner’s Instructions C Sec. 1256 contracts & straddles Form 6781, line 1 D Mining exploration costs recapture See Pub. 535E Cancellation of debt Form 1040, line 21 or Form 982 F Other income (loss) See the Partner’s Instructions

12. Section 179 deduction See the Partner’s Instructions 13. Other deductions

A Cash contributions (50%) B Cash contributions (30%) C Noncash contributions (50%) D Noncash contributions (30%) E Capital gain property to a 50%

organization (30%) F Capital gain property (20%) G Contributions (100%)

} See the Partner’s Instructions

H Investment interest expense Form 4952, line 1 I Deductions—royalty income Schedule E, line 19 J Section 59(e)(2) expenditures See the Partner’s Instructions K Deductions—portfolio (2% floor) Schedule A, line 23 L Deductions—portfolio (other) Schedule A, line 28 M Amounts paid for medical insurance Schedule A, line 1 or Form 1040, line 29 N Educational assistance benefits See the Partner’s Instructions O Dependent care benefits Form 2441, line 12P Preproductive period expenses See the Partner’s Instructions Q Commercial revitalization deduction

from rental real estate activities See Form 8582 instructions

R Pensions and IRAs See the Partner’s Instructions S Reforestation expense deduction See the Partner’s Instructions T Domestic production activities

information See Form 8903 instructions

U Qualified production activities income Form 8903, line 7b V Employer’s Form W-2 wages Form 8903, line 17W Other deductions See the Partner’s Instructions

14. Self-employment earnings (loss)

Note. If you have a section 179 deduction or any partner-level deductions, see the Partner’s Instructions before completing Schedule SE.

A Net earnings (loss) from self-employment

Schedule SE, Section A or B

B Gross farming or fishing income See the Partner’s Instructions C Gross non-farm income See the Partner’s Instructions

15. CreditsA Low-income housing credit

(section 42(j)(5)) from pre-2008 buildings

B Low-income housing credit (other) from pre-2008 buildings

C Low-income housing credit (section 42(j)(5)) from post-2007 buildings

D Low-income housing credit (other) from post-2007 buildings

E Qualified rehabilitation expenditures (rental real estate)

F Other rental real estate credits G Other rental credits

} See the Partner’s Instructions

H Undistributed capital gains credit Form 1040, line 73; check box a I Biofuel producer credit J Work opportunity credit K Disabled access credit

See the Partner's Instructions}

Code Report on L Empowerment zone

employment credit M Credit for increasing research

activities N Credit for employer social

security and Medicare taxes O Backup withholding P Other credits

} See the Partner’s Instructions

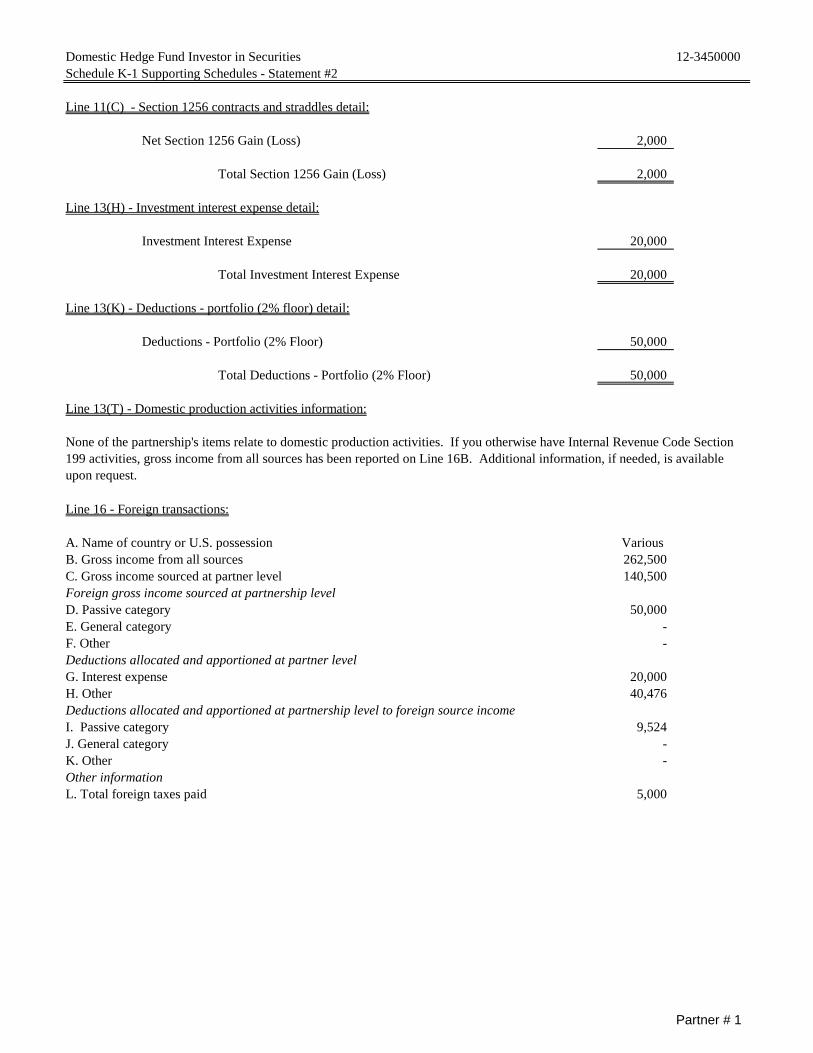

16. Foreign transactions

A Name of country or U.S. possession

B Gross income from all sources C Gross income sourced at

partner level } Form 1116, Part I

Foreign gross income sourced at partnership level D Passive category E General category F Other } Form 1116, Part I

Deductions allocated and apportioned at partner level G Interest expense Form 1116, Part I H Other Form 1116, Part I Deductions allocated and apportioned at partnership level to foreign source income I Passive category J General category K Other } Form 1116, Part I

Other information L Total foreign taxes paid Form 1116, Part II M Total foreign taxes accrued Form 1116, Part II N Reduction in taxes available for credit Form 1116, line 12 O Foreign trading gross receipts Form 8873 P Extraterritorial income exclusion Form 8873 Q Other foreign transactions See the Partner’s Instructions

17. Alternative minimum tax (AMT) items

A Post-1986 depreciation adjustment B Adjusted gain or loss C Depletion (other than oil & gas) D Oil, gas, & geothermal—gross income E Oil, gas, & geothermal—deductions F Other AMT items

} See the Partner’s Instructions and the Instructions for Form 6251

18. Tax-exempt income and nondeductible expenses

A Tax-exempt interest income Form 1040, line 8b B Other tax-exempt income See the Partner’s Instructions C Nondeductible expenses See the Partner’s Instructions

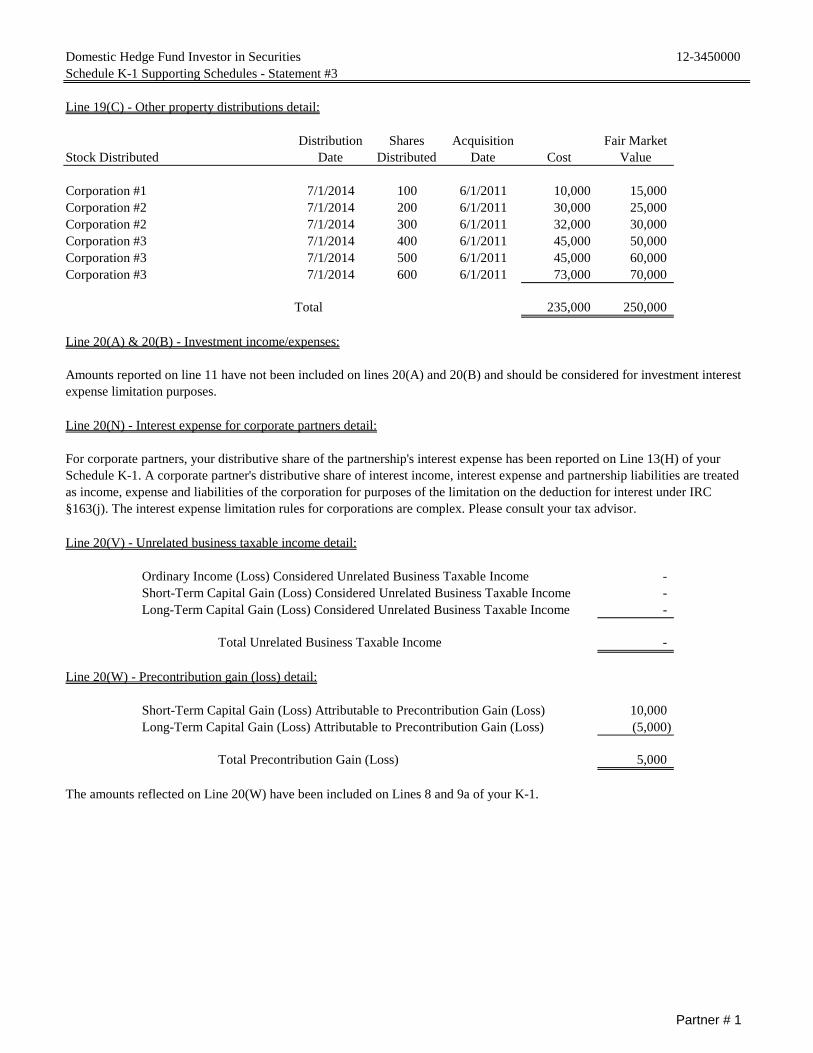

19. Distributions

A Cash and marketable securitiesB Distribution subject to section 737C Other property

} See the Partner’s Instructions

20. Other information

A Investment income Form 4952, line 4a B Investment expenses Form 4952, line 5 C Fuel tax credit information Form 4136 D Qualified rehabilitation expenditures

(other than rental real estate) See the Partner’s Instructions

E Basis of energy property See the Partner’s Instructions F Recapture of low-income housing

credit (section 42(j)(5)) Form 8611, line 8

G Recapture of low-income housing credit (other)

Form 8611, line 8

H Recapture of investment credit See Form 4255 I Recapture of other credits See the Partner’s Instructions J Look-back interest—completed

long-term contracts See Form 8697

K Look-back interest—income forecast method

See Form 8866

L Dispositions of property with section 179 deductions

M Recapture of section 179 deductionN Interest expense for corporate

partners O Section 453(l)(3) information P Section 453A(c) information Q Section 1260(b) information R Interest allocable to production

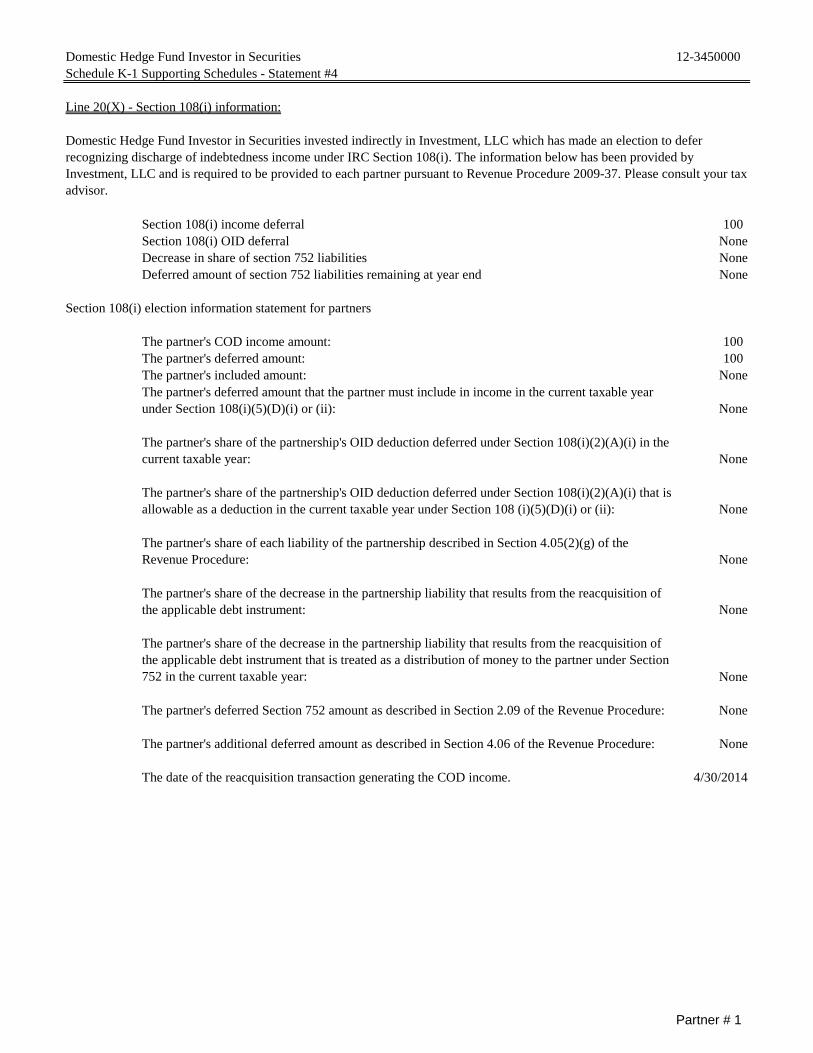

expenditures S CCF nonqualified withdrawals T Depletion information—oil and gas U ReservedV Unrelated business taxable incomeW Precontribution gain (loss) X Section 108(i) informationY Net investment income

} See the Partner’s Instructions

Z Other information

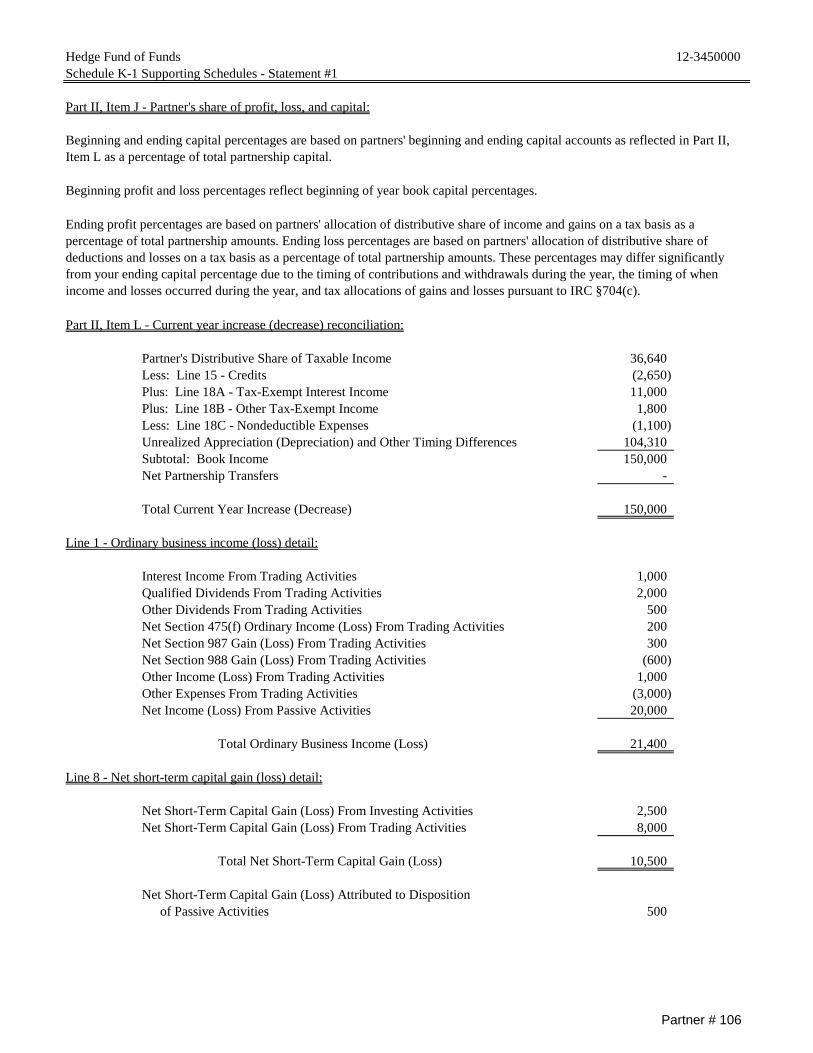

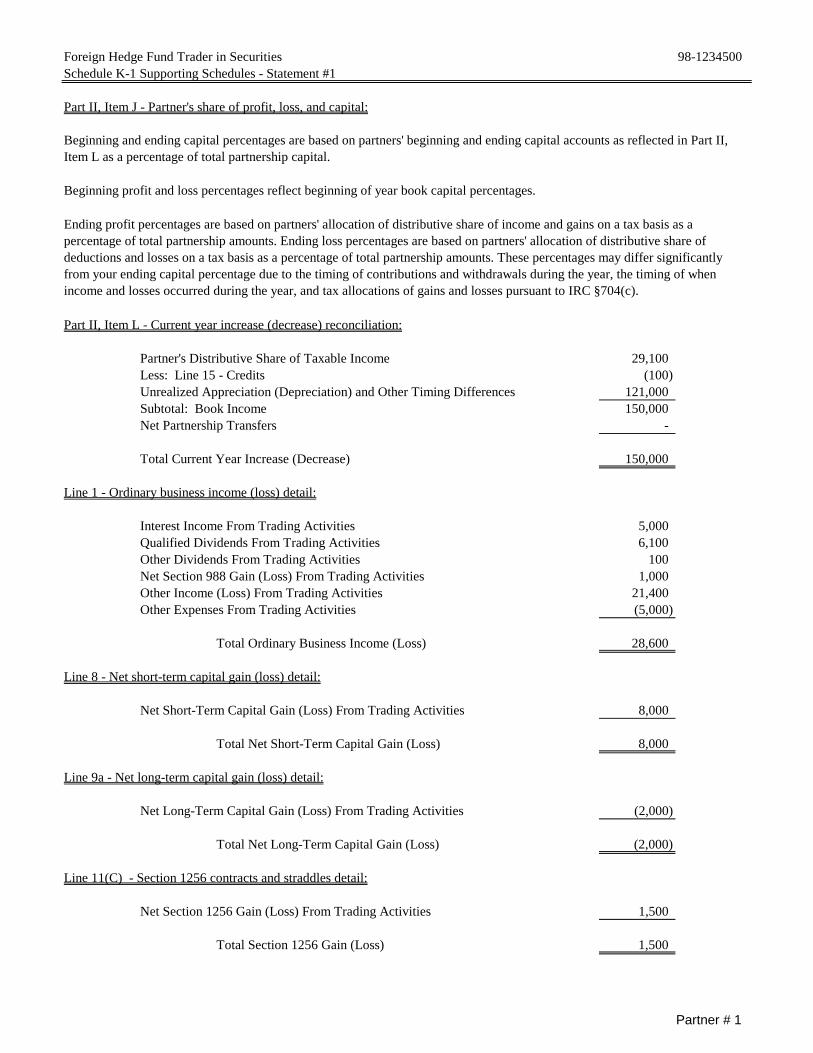

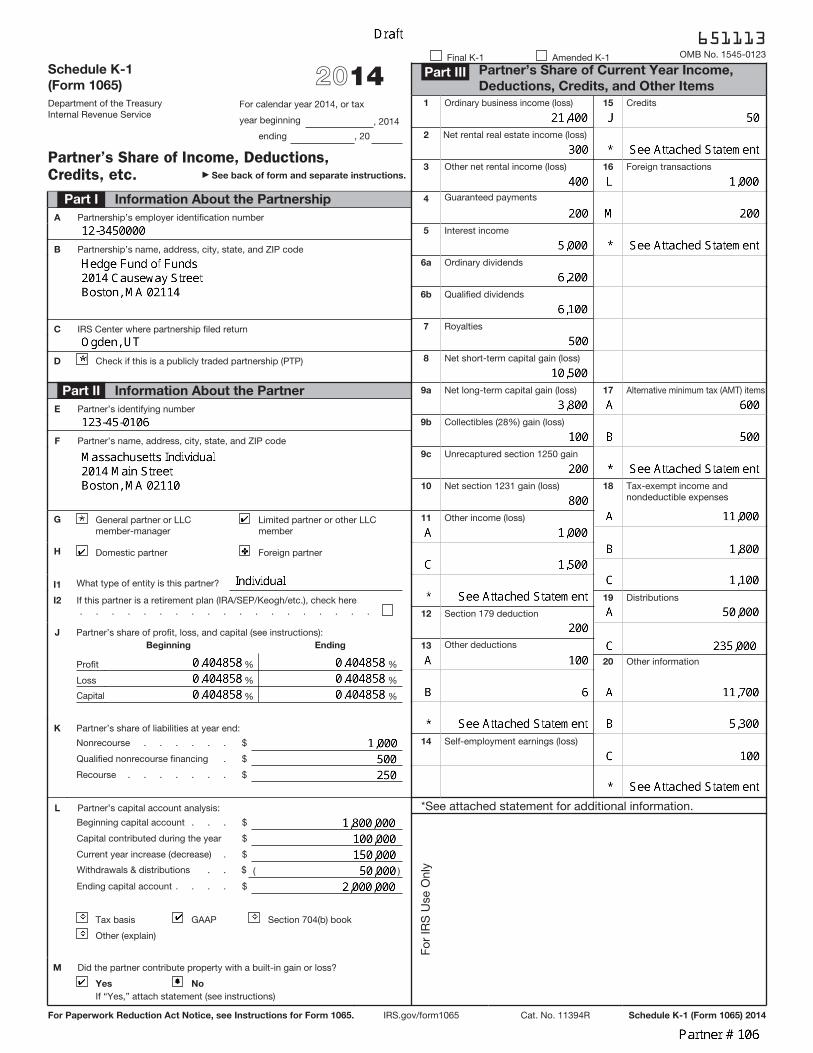

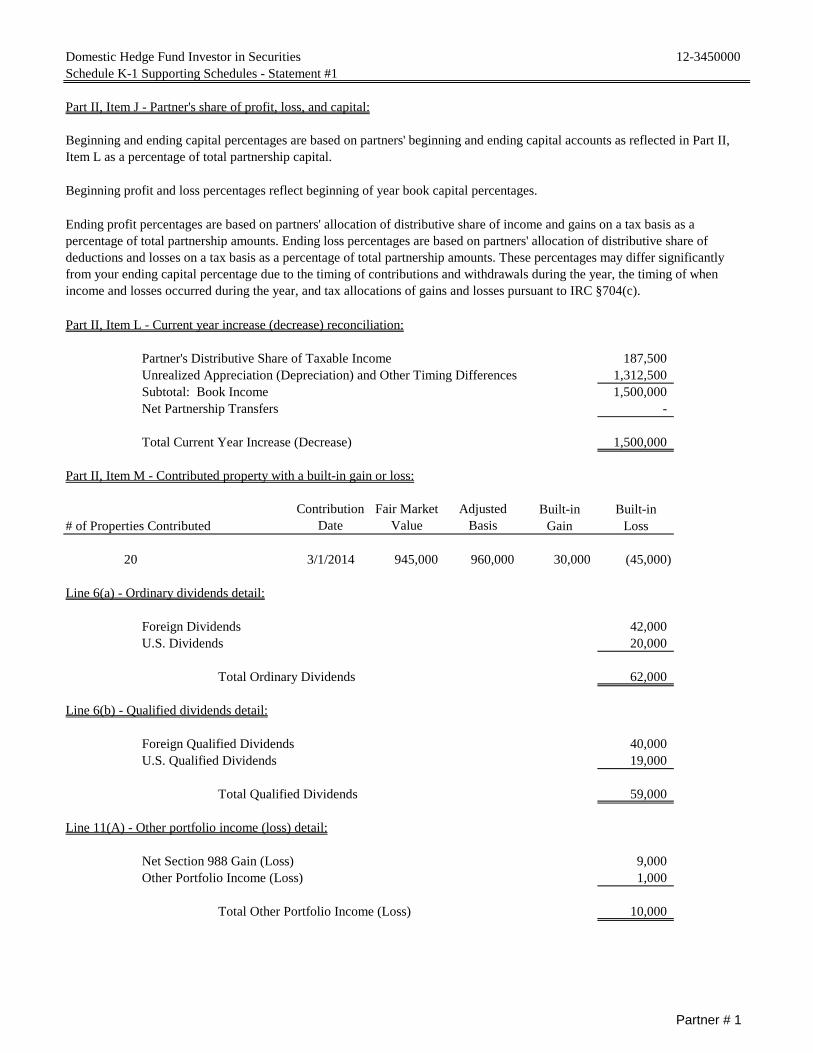

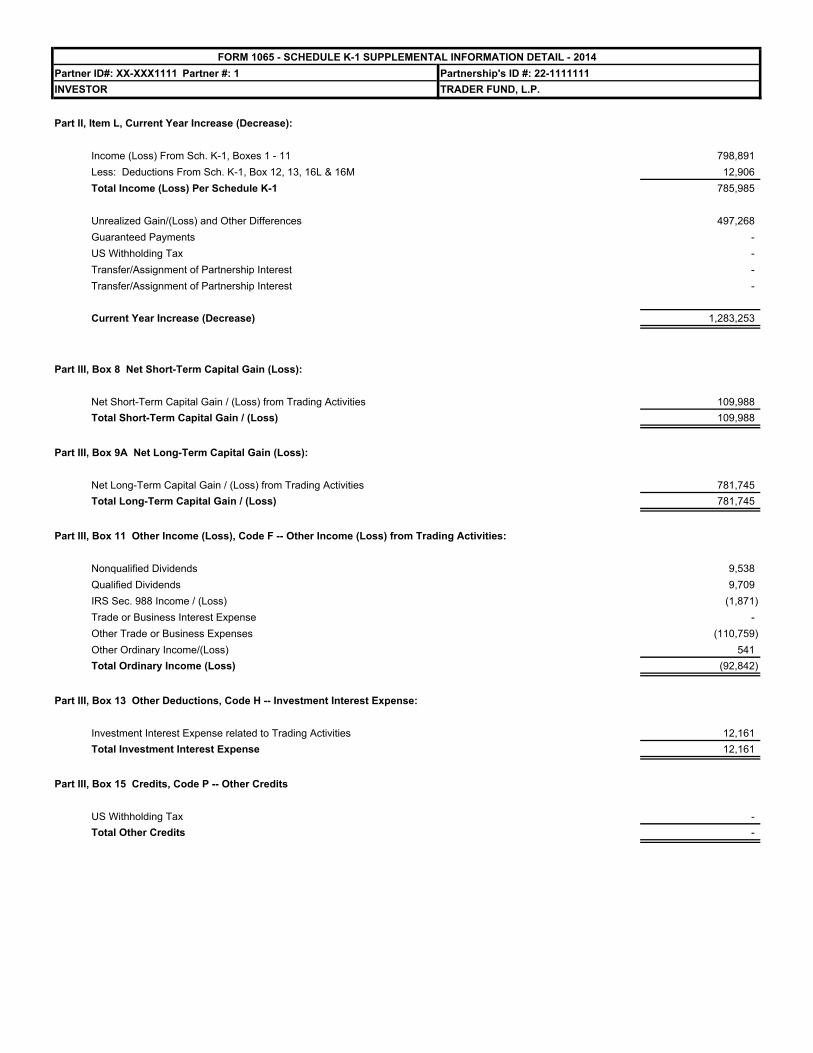

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #1

Part II, Item J - Partner's share of profit, loss, and capital:

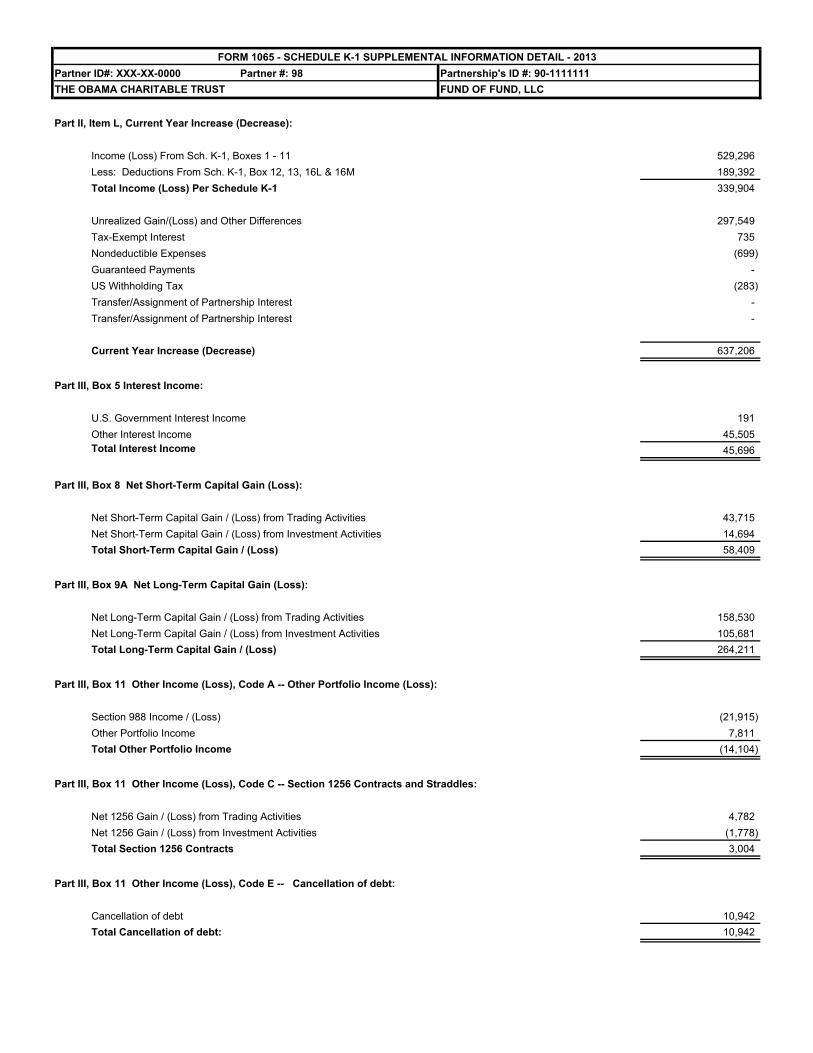

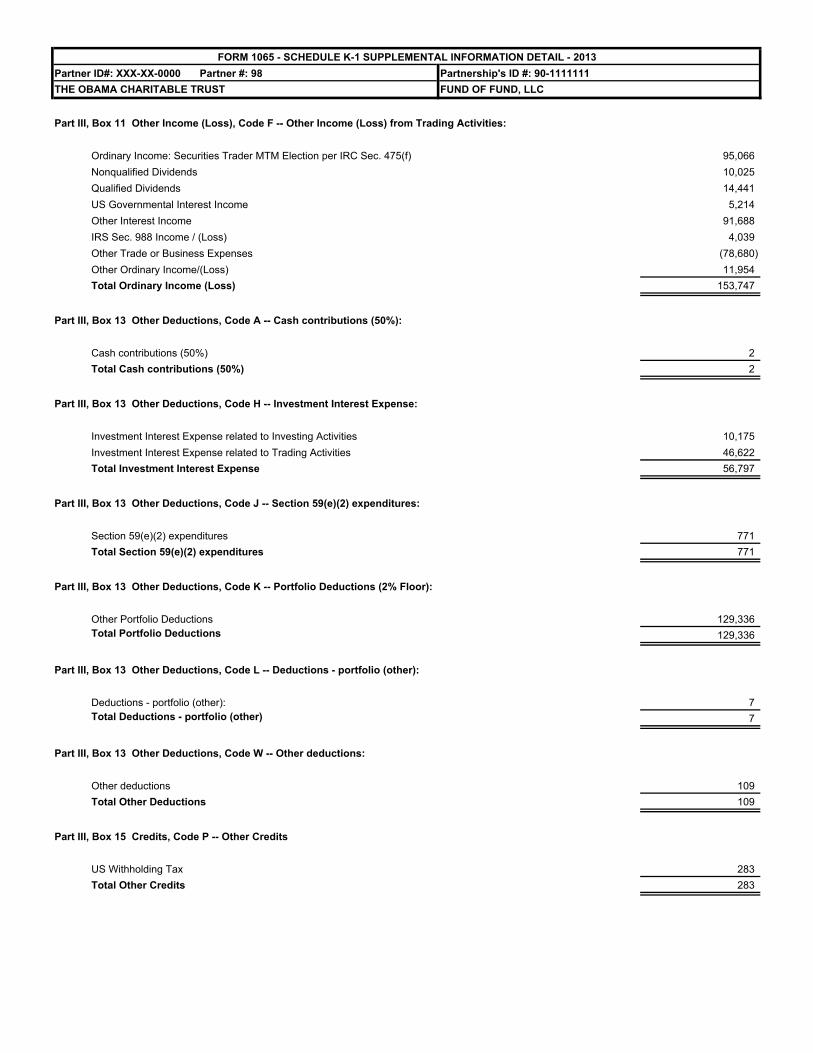

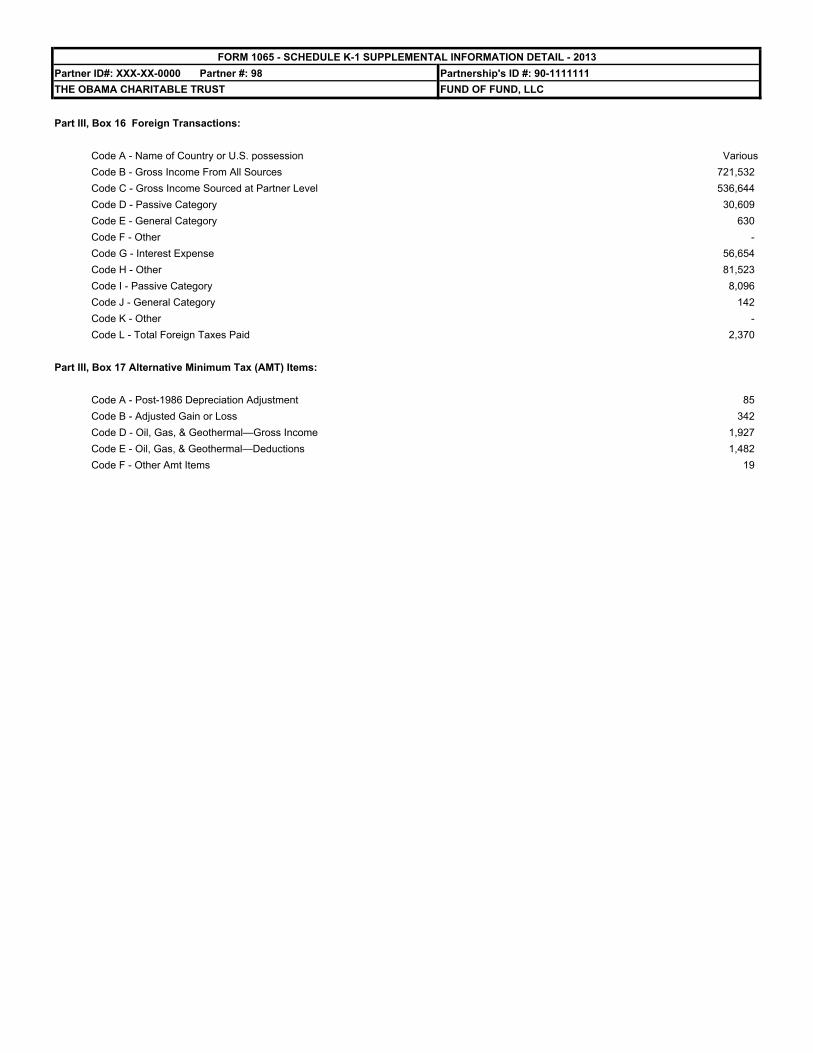

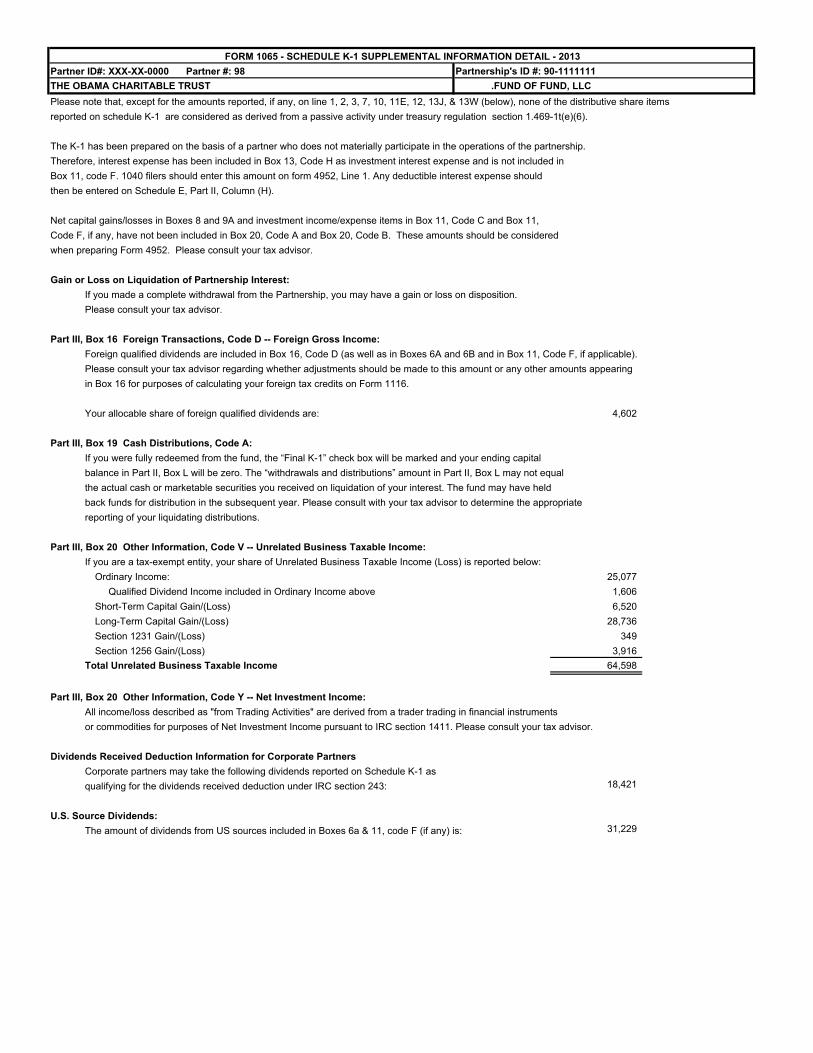

Part II, Item L - Current year increase (decrease) reconciliation:

Partner's Distributive Share of Taxable Income 36,640 Less: Line 15 - Credits (2,650) Plus: Line 18A - Tax-Exempt Interest Income 11,000 Plus: Line 18B - Other Tax-Exempt Income 1,800 Less: Line 18C - Nondeductible Expenses (1,100) Unrealized Appreciation (Depreciation) and Other Timing Differences 104,310 Subtotal: Book Income 150,000 Net Partnership Transfers -

Total Current Year Increase (Decrease) 150,000

Line 1 - Ordinary business income (loss) detail:

Interest Income From Trading Activities 1,000 Qualified Dividends From Trading Activities 2,000 Other Dividends From Trading Activities 500 Net Section 475(f) Ordinary Income (Loss) From Trading Activities 200 Net Section 987 Gain (Loss) From Trading Activities 300 Net Section 988 Gain (Loss) From Trading Activities (600) Other Income (Loss) From Trading Activities 1,000 Other Expenses From Trading Activities (3,000) Net Income (Loss) From Passive Activities 20,000

Total Ordinary Business Income (Loss) 21,400

Line 8 - Net short-term capital gain (loss) detail:

Net Short-Term Capital Gain (Loss) From Investing Activities 2,500 Net Short-Term Capital Gain (Loss) From Trading Activities 8,000

Total Net Short-Term Capital Gain (Loss) 10,500

Net Short-Term Capital Gain (Loss) Attributed to Disposition of Passive Activities 500

Beginning and ending capital percentages are based on partners' beginning and ending capital accounts as reflected in Part II, Item L as a percentage of total partnership capital.

Beginning profit and loss percentages reflect beginning of year book capital percentages.

Ending profit percentages are based on partners' allocation of distributive share of income and gains on a tax basis as a percentage of total partnership amounts. Ending loss percentages are based on partners' allocation of distributive share of deductions and losses on a tax basis as a percentage of total partnership amounts. These percentages may differ significantly from your ending capital percentage due to the timing of contributions and withdrawals during the year, the timing of when income and losses occurred during the year, and tax allocations of gains and losses pursuant to IRC §704(c).

Partner # 106

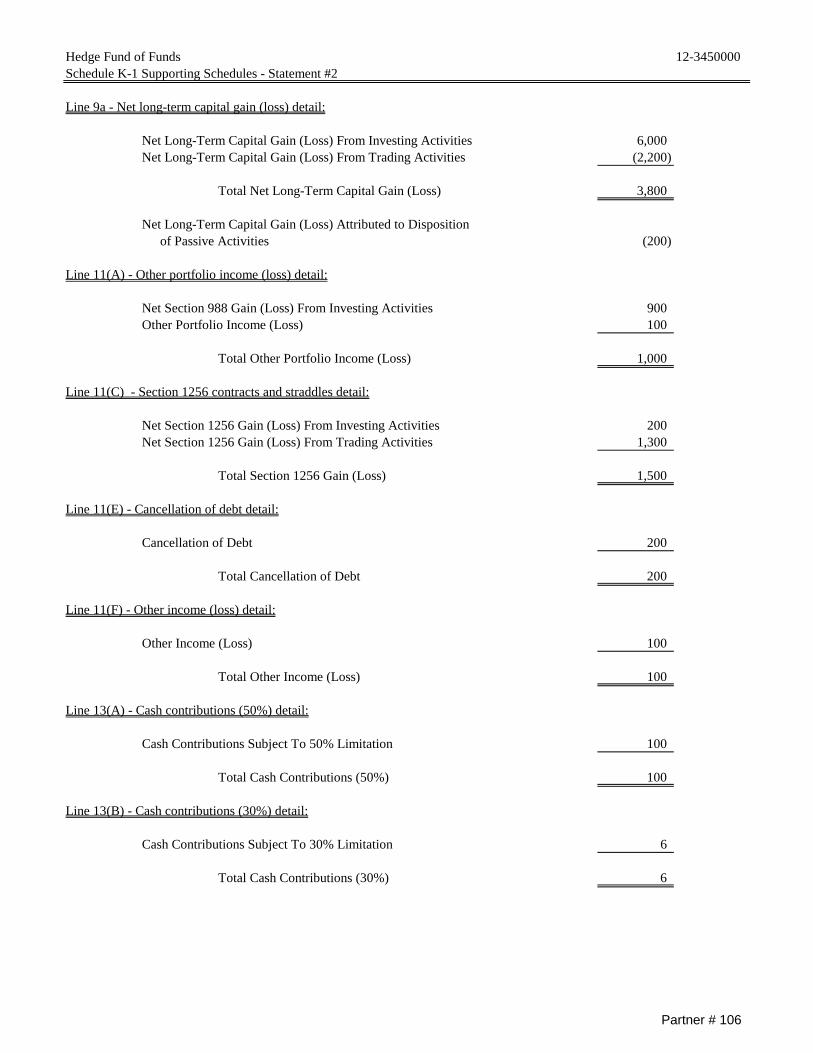

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #2

Line 9a - Net long-term capital gain (loss) detail:

Net Long-Term Capital Gain (Loss) From Investing Activities 6,000 Net Long-Term Capital Gain (Loss) From Trading Activities (2,200)

Total Net Long-Term Capital Gain (Loss) 3,800

Net Long-Term Capital Gain (Loss) Attributed to Disposition of Passive Activities (200)

Line 11(A) - Other portfolio income (loss) detail:

Net Section 988 Gain (Loss) From Investing Activities 900 Other Portfolio Income (Loss) 100

Total Other Portfolio Income (Loss) 1,000

Line 11(C) - Section 1256 contracts and straddles detail:

Net Section 1256 Gain (Loss) From Investing Activities 200 Net Section 1256 Gain (Loss) From Trading Activities 1,300

Total Section 1256 Gain (Loss) 1,500

Line 11(E) - Cancellation of debt detail:

Cancellation of Debt 200

Total Cancellation of Debt 200

Line 11(F) - Other income (loss) detail:

Other Income (Loss) 100

Total Other Income (Loss) 100

Line 13(A) - Cash contributions (50%) detail:

Cash Contributions Subject To 50% Limitation 100

Total Cash Contributions (50%) 100

Line 13(B) - Cash contributions (30%) detail:

Cash Contributions Subject To 30% Limitation 6

Total Cash Contributions (30%) 6

Partner # 106

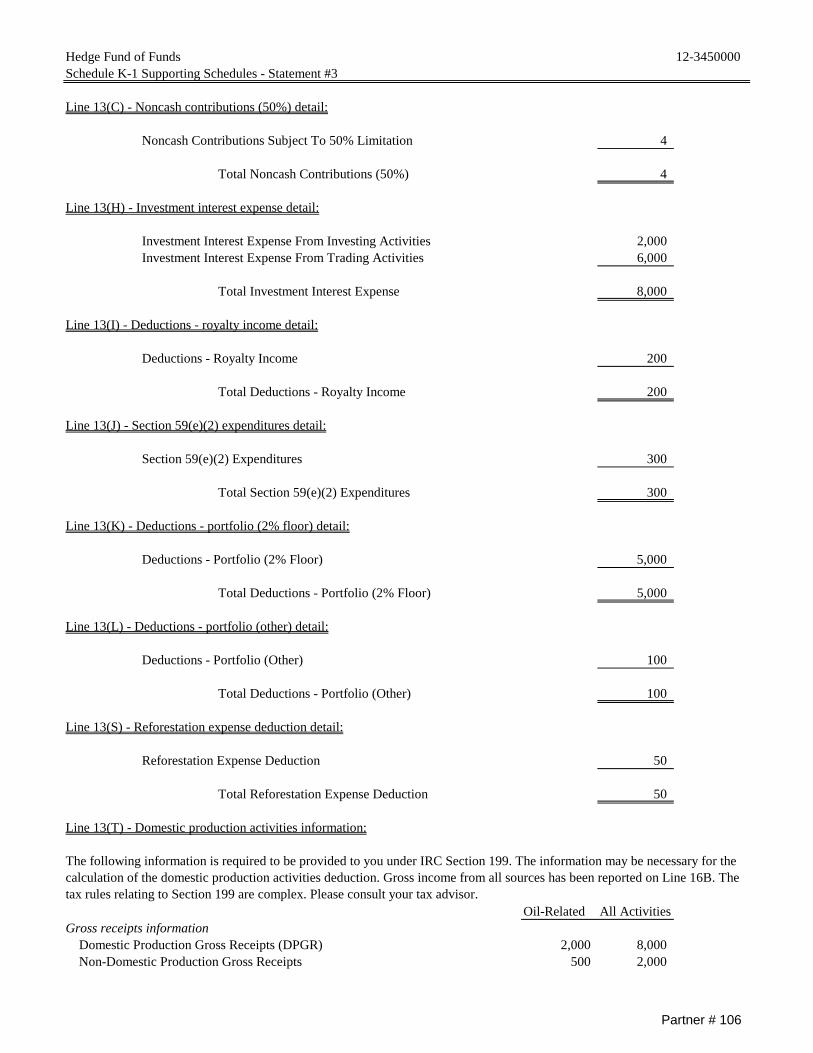

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #3

Line 13(C) - Noncash contributions (50%) detail:

Noncash Contributions Subject To 50% Limitation 4

Total Noncash Contributions (50%) 4

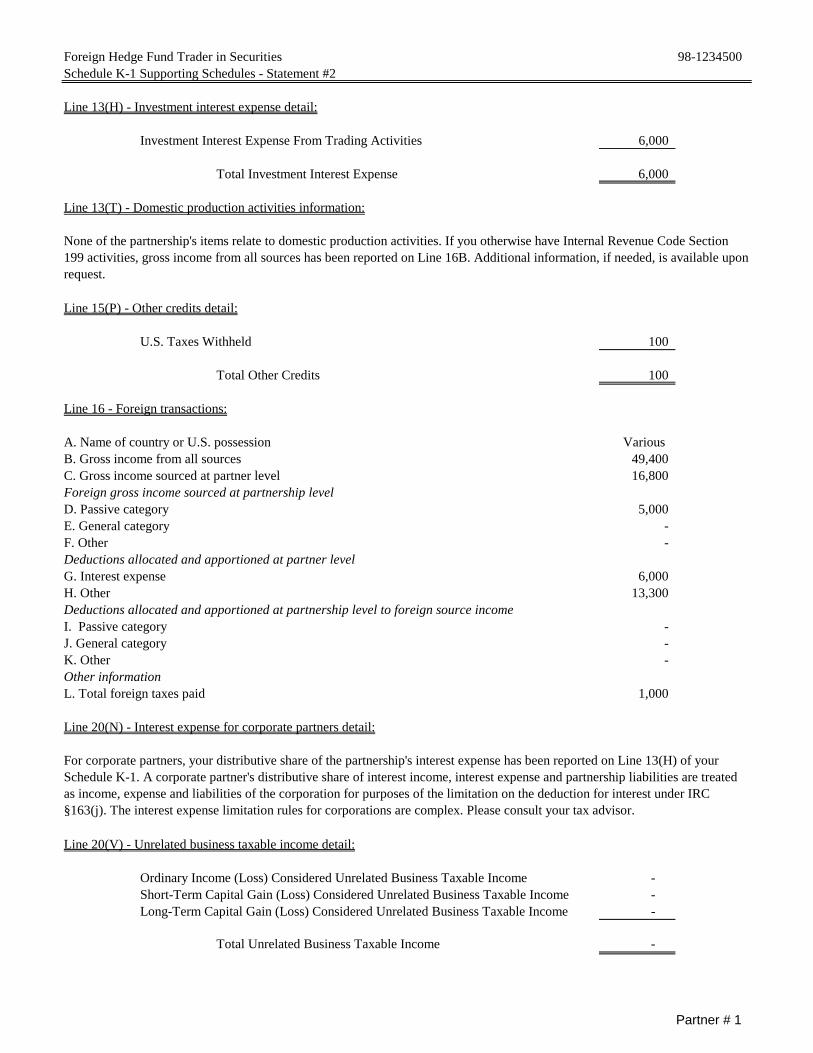

Line 13(H) - Investment interest expense detail:

Investment Interest Expense From Investing Activities 2,000 Investment Interest Expense From Trading Activities 6,000

Total Investment Interest Expense 8,000

Line 13(I) - Deductions - royalty income detail:

Deductions - Royalty Income 200

Total Deductions - Royalty Income 200

Line 13(J) - Section 59(e)(2) expenditures detail:

Section 59(e)(2) Expenditures 300

Total Section 59(e)(2) Expenditures 300

Line 13(K) - Deductions - portfolio (2% floor) detail:

Deductions - Portfolio (2% Floor) 5,000

Total Deductions - Portfolio (2% Floor) 5,000

Line 13(L) - Deductions - portfolio (other) detail:

Deductions - Portfolio (Other) 100

Total Deductions - Portfolio (Other) 100

Line 13(S) - Reforestation expense deduction detail:

Reforestation Expense Deduction 50

Total Reforestation Expense Deduction 50

Line 13(T) - Domestic production activities information:

Oil-Related All ActivitiesGross receipts information Domestic Production Gross Receipts (DPGR) 2,000 8,000 Non-Domestic Production Gross Receipts 500 2,000

The following information is required to be provided to you under IRC Section 199. The information may be necessary for the calculation of the domestic production activities deduction. Gross income from all sources has been reported on Line 16B. The tax rules relating to Section 199 are complex. Please consult your tax advisor.

Partner # 106

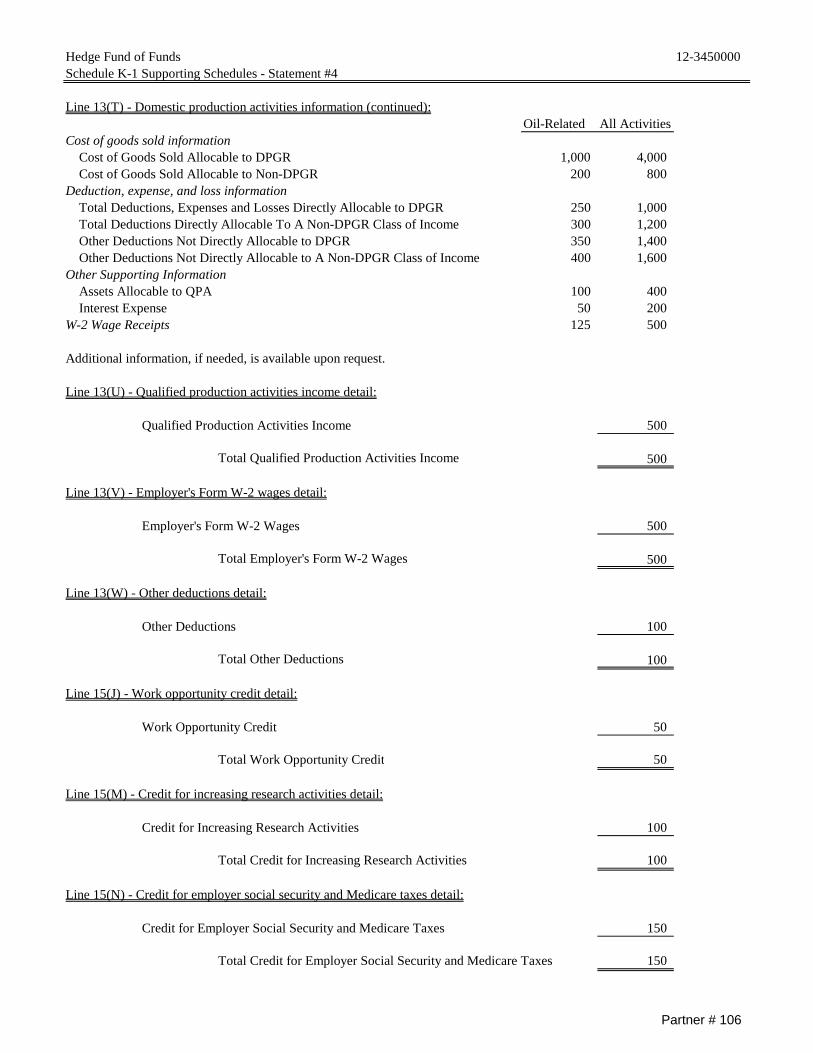

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #4

Line 13(T) - Domestic production activities information (continued):Oil-Related All Activities

Cost of goods sold information Cost of Goods Sold Allocable to DPGR 1,000 4,000 Cost of Goods Sold Allocable to Non-DPGR 200 800 Deduction, expense, and loss information Total Deductions, Expenses and Losses Directly Allocable to DPGR 250 1,000 Total Deductions Directly Allocable To A Non-DPGR Class of Income 300 1,200 Other Deductions Not Directly Allocable to DPGR 350 1,400 Other Deductions Not Directly Allocable to A Non-DPGR Class of Income 400 1,600 Other Supporting Information Assets Allocable to QPA 100 400 Interest Expense 50 200 W-2 Wage Receipts 125 500

Additional information, if needed, is available upon request.

Line 13(U) - Qualified production activities income detail:

Qualified Production Activities Income 500

Total Qualified Production Activities Income 500

Line 13(V) - Employer's Form W-2 wages detail:

Employer's Form W-2 Wages 500

Total Employer's Form W-2 Wages 500

Line 13(W) - Other deductions detail:

Other Deductions 100

Total Other Deductions 100

Line 15(J) - Work opportunity credit detail:

Work Opportunity Credit 50

Total Work Opportunity Credit 50

Line 15(M) - Credit for increasing research activities detail:

Credit for Increasing Research Activities 100

Total Credit for Increasing Research Activities 100

Line 15(N) - Credit for employer social security and Medicare taxes detail:

Credit for Employer Social Security and Medicare Taxes 150

Total Credit for Employer Social Security and Medicare Taxes 150

Partner # 106

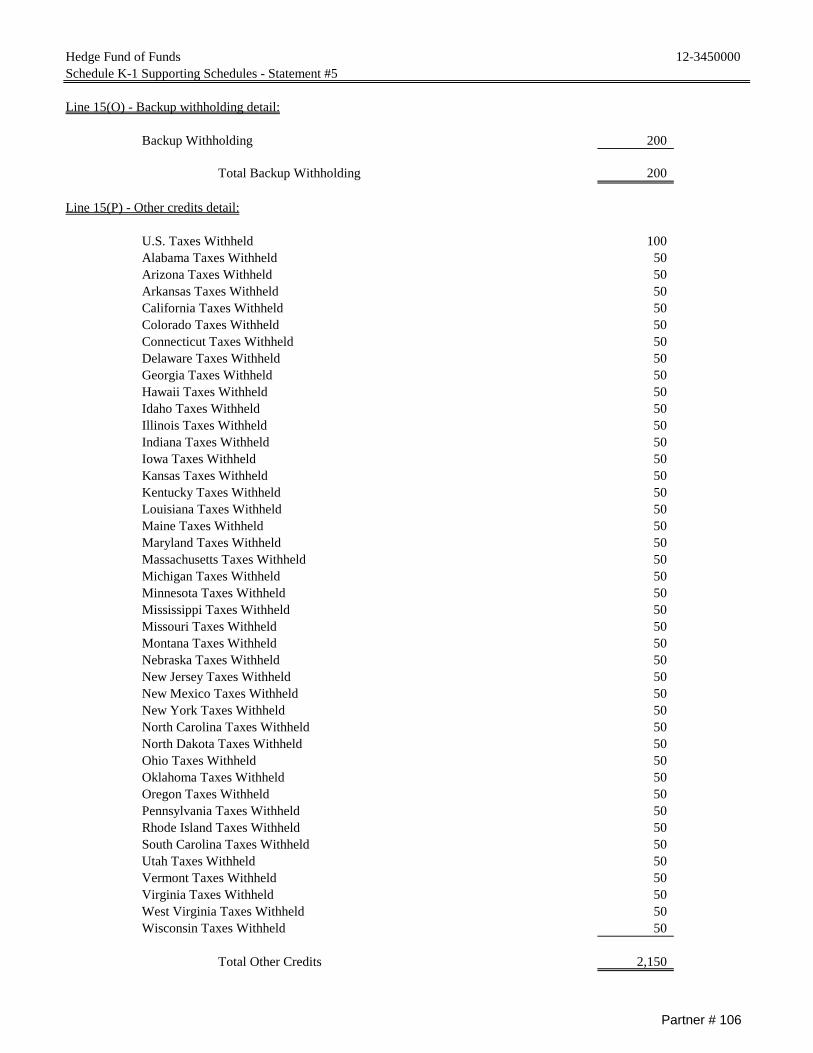

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #5

Line 15(O) - Backup withholding detail:

Backup Withholding 200

Total Backup Withholding 200

Line 15(P) - Other credits detail:

U.S. Taxes Withheld 100 Alabama Taxes Withheld 50 Arizona Taxes Withheld 50 Arkansas Taxes Withheld 50 California Taxes Withheld 50 Colorado Taxes Withheld 50 Connecticut Taxes Withheld 50 Delaware Taxes Withheld 50 Georgia Taxes Withheld 50 Hawaii Taxes Withheld 50 Idaho Taxes Withheld 50 Illinois Taxes Withheld 50 Indiana Taxes Withheld 50 Iowa Taxes Withheld 50 Kansas Taxes Withheld 50 Kentucky Taxes Withheld 50 Louisiana Taxes Withheld 50 Maine Taxes Withheld 50 Maryland Taxes Withheld 50 Massachusetts Taxes Withheld 50 Michigan Taxes Withheld 50 Minnesota Taxes Withheld 50 Mississippi Taxes Withheld 50 Missouri Taxes Withheld 50 Montana Taxes Withheld 50 Nebraska Taxes Withheld 50 New Jersey Taxes Withheld 50 New Mexico Taxes Withheld 50 New York Taxes Withheld 50 North Carolina Taxes Withheld 50 North Dakota Taxes Withheld 50 Ohio Taxes Withheld 50 Oklahoma Taxes Withheld 50 Oregon Taxes Withheld 50 Pennsylvania Taxes Withheld 50 Rhode Island Taxes Withheld 50 South Carolina Taxes Withheld 50 Utah Taxes Withheld 50 Vermont Taxes Withheld 50 Virginia Taxes Withheld 50 West Virginia Taxes Withheld 50 Wisconsin Taxes Withheld 50

Total Other Credits 2,150

Partner # 106

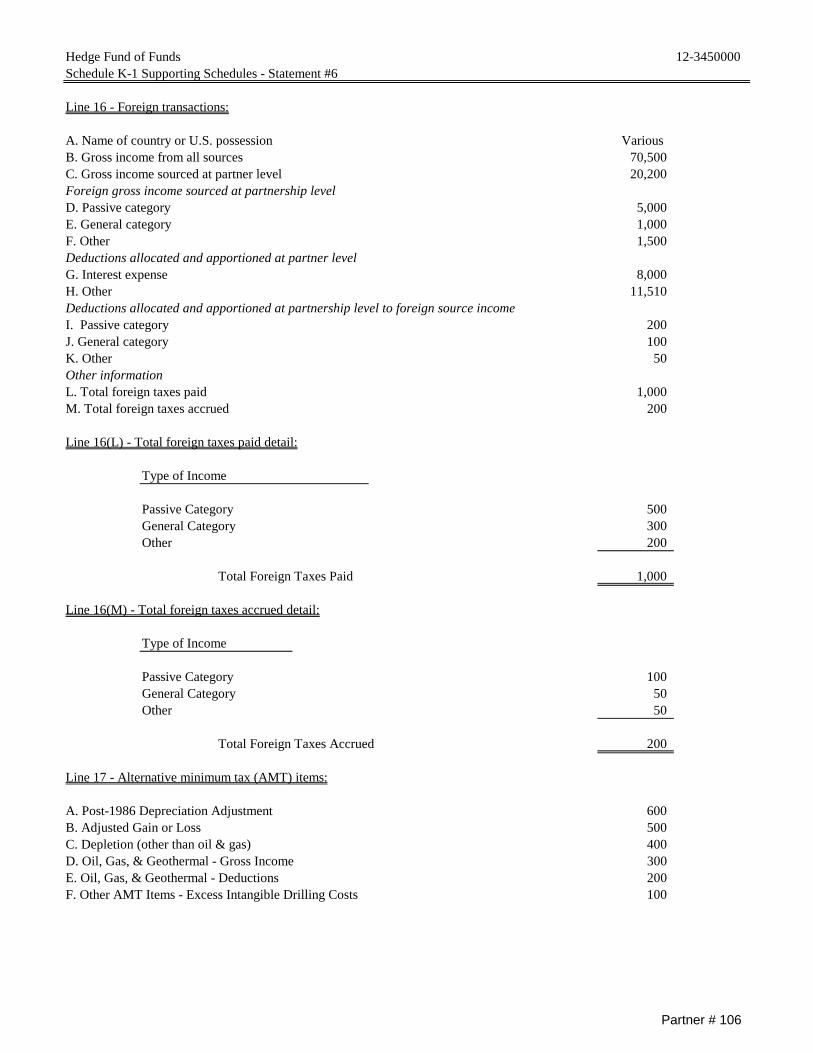

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #6

Line 16 - Foreign transactions:

A. Name of country or U.S. possession Various B. Gross income from all sources 70,500 C. Gross income sourced at partner level 20,200 Foreign gross income sourced at partnership levelD. Passive category 5,000 E. General category 1,000 F. Other 1,500 Deductions allocated and apportioned at partner levelG. Interest expense 8,000 H. Other 11,510 Deductions allocated and apportioned at partnership level to foreign source incomeI. Passive category 200 J. General category 100 K. Other 50 Other informationL. Total foreign taxes paid 1,000 M. Total foreign taxes accrued 200

Line 16(L) - Total foreign taxes paid detail:

Type of Income

Passive Category 500 General Category 300 Other 200

Total Foreign Taxes Paid 1,000

Line 16(M) - Total foreign taxes accrued detail:

Type of Income

Passive Category 100 General Category 50 Other 50

Total Foreign Taxes Accrued 200

Line 17 - Alternative minimum tax (AMT) items:

A. Post-1986 Depreciation Adjustment 600 B. Adjusted Gain or Loss 500 C. Depletion (other than oil & gas) 400 D. Oil, Gas, & Geothermal - Gross Income 300 E. Oil, Gas, & Geothermal - Deductions 200 F. Other AMT Items - Excess Intangible Drilling Costs 100

Partner # 106

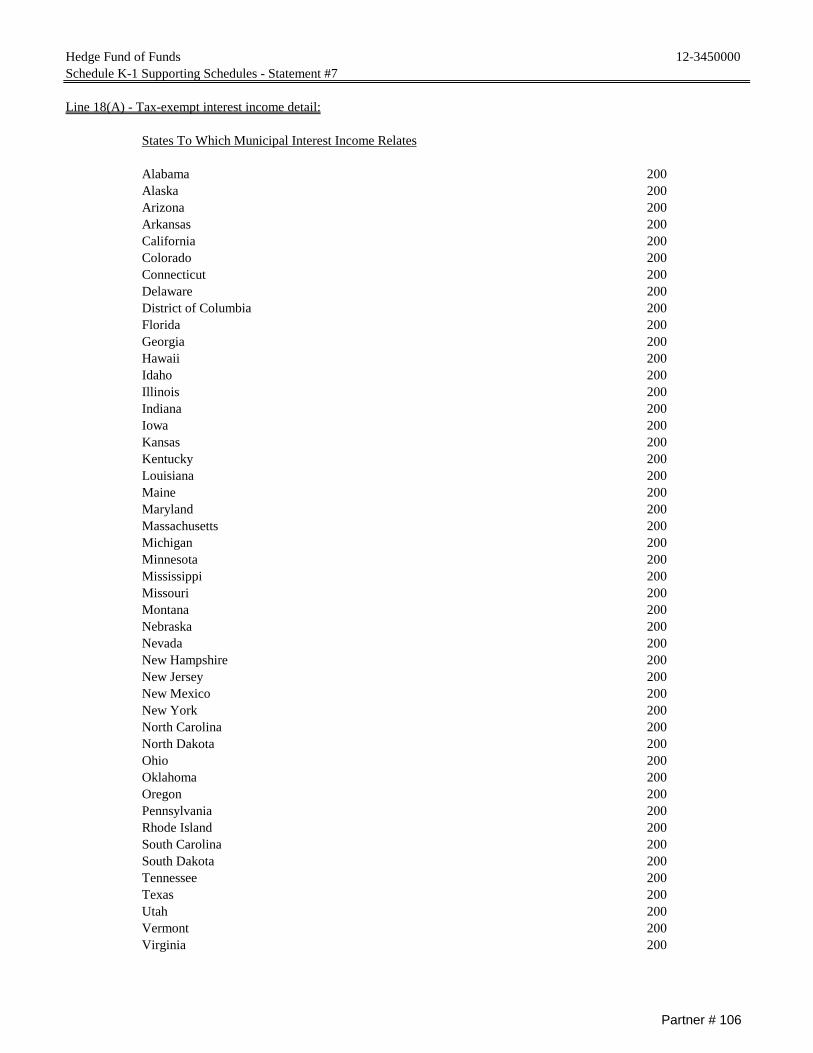

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #7

Line 18(A) - Tax-exempt interest income detail:

States To Which Municipal Interest Income Relates

Alabama 200 Alaska 200 Arizona 200 Arkansas 200 California 200 Colorado 200 Connecticut 200 Delaware 200 District of Columbia 200 Florida 200 Georgia 200 Hawaii 200 Idaho 200 Illinois 200 Indiana 200 Iowa 200 Kansas 200 Kentucky 200 Louisiana 200 Maine 200 Maryland 200 Massachusetts 200 Michigan 200 Minnesota 200 Mississippi 200 Missouri 200 Montana 200 Nebraska 200 Nevada 200 New Hampshire 200 New Jersey 200 New Mexico 200 New York 200 North Carolina 200 North Dakota 200 Ohio 200 Oklahoma 200 Oregon 200 Pennsylvania 200 Rhode Island 200 South Carolina 200 South Dakota 200 Tennessee 200 Texas 200 Utah 200 Vermont 200 Virginia 200

Partner # 106

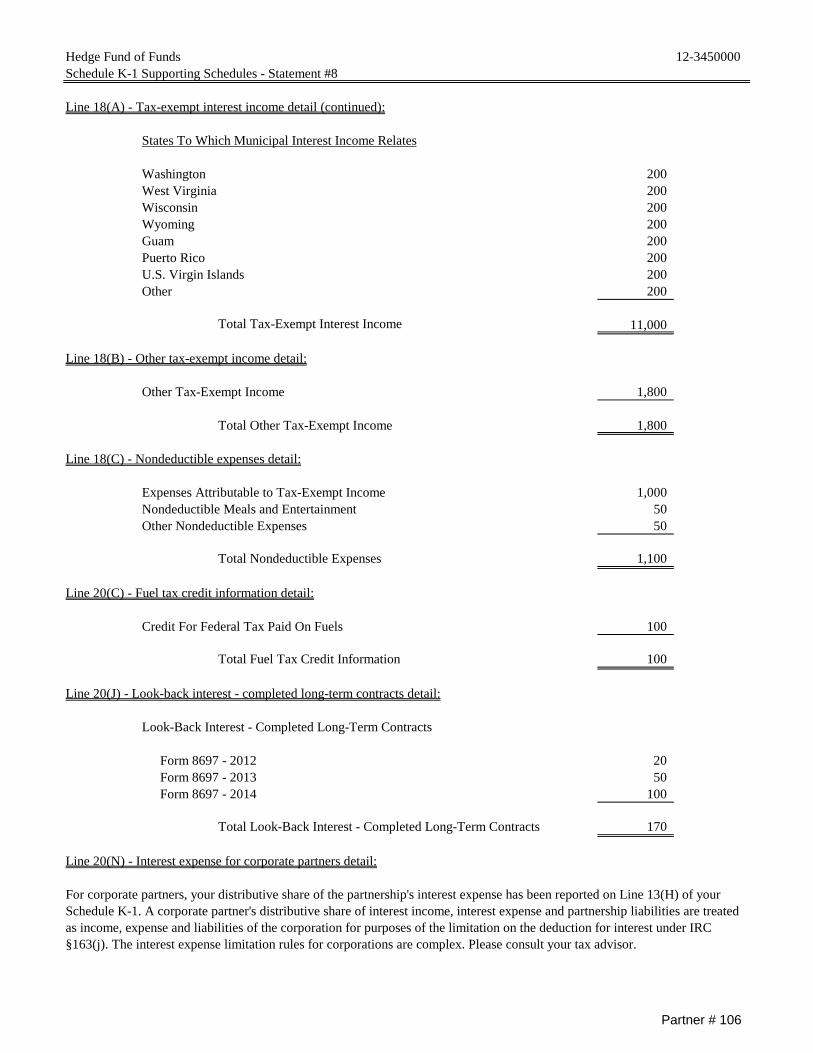

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #8

Line 18(A) - Tax-exempt interest income detail (continued):

States To Which Municipal Interest Income Relates

Washington 200 West Virginia 200 Wisconsin 200 Wyoming 200 Guam 200 Puerto Rico 200 U.S. Virgin Islands 200 Other 200

Total Tax-Exempt Interest Income 11,000

Line 18(B) - Other tax-exempt income detail:

Other Tax-Exempt Income 1,800

Total Other Tax-Exempt Income 1,800

Line 18(C) - Nondeductible expenses detail:

Expenses Attributable to Tax-Exempt Income 1,000 Nondeductible Meals and Entertainment 50 Other Nondeductible Expenses 50

Total Nondeductible Expenses 1,100

Line 20(C) - Fuel tax credit information detail:

Credit For Federal Tax Paid On Fuels 100

Total Fuel Tax Credit Information 100

Line 20(J) - Look-back interest - completed long-term contracts detail:

Look-Back Interest - Completed Long-Term Contracts

Form 8697 - 2012 20 Form 8697 - 2013 50 Form 8697 - 2014 100

Total Look-Back Interest - Completed Long-Term Contracts 170

Line 20(N) - Interest expense for corporate partners detail:

For corporate partners, your distributive share of the partnership's interest expense has been reported on Line 13(H) of your Schedule K-1. A corporate partner's distributive share of interest income, interest expense and partnership liabilities are treated as income, expense and liabilities of the corporation for purposes of the limitation on the deduction for interest under IRC §163(j). The interest expense limitation rules for corporations are complex. Please consult your tax advisor.

Partner # 106

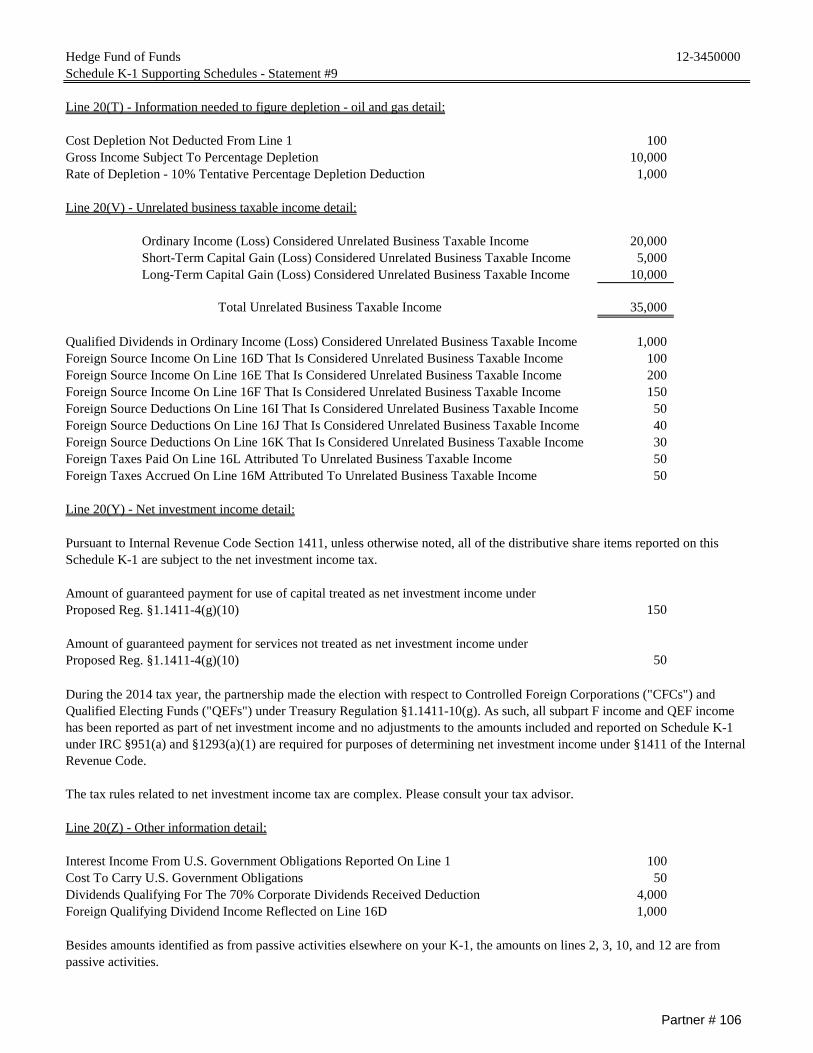

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #9

Line 20(T) - Information needed to figure depletion - oil and gas detail:

Cost Depletion Not Deducted From Line 1 100 Gross Income Subject To Percentage Depletion 10,000 Rate of Depletion - 10% Tentative Percentage Depletion Deduction 1,000

Line 20(V) - Unrelated business taxable income detail:

Ordinary Income (Loss) Considered Unrelated Business Taxable Income 20,000 Short-Term Capital Gain (Loss) Considered Unrelated Business Taxable Income 5,000 Long-Term Capital Gain (Loss) Considered Unrelated Business Taxable Income 10,000

Total Unrelated Business Taxable Income 35,000

Qualified Dividends in Ordinary Income (Loss) Considered Unrelated Business Taxable Income 1,000 Foreign Source Income On Line 16D That Is Considered Unrelated Business Taxable Income 100 Foreign Source Income On Line 16E That Is Considered Unrelated Business Taxable Income 200 Foreign Source Income On Line 16F That Is Considered Unrelated Business Taxable Income 150 Foreign Source Deductions On Line 16I That Is Considered Unrelated Business Taxable Income 50 Foreign Source Deductions On Line 16J That Is Considered Unrelated Business Taxable Income 40 Foreign Source Deductions On Line 16K That Is Considered Unrelated Business Taxable Income 30 Foreign Taxes Paid On Line 16L Attributed To Unrelated Business Taxable Income 50 Foreign Taxes Accrued On Line 16M Attributed To Unrelated Business Taxable Income 50

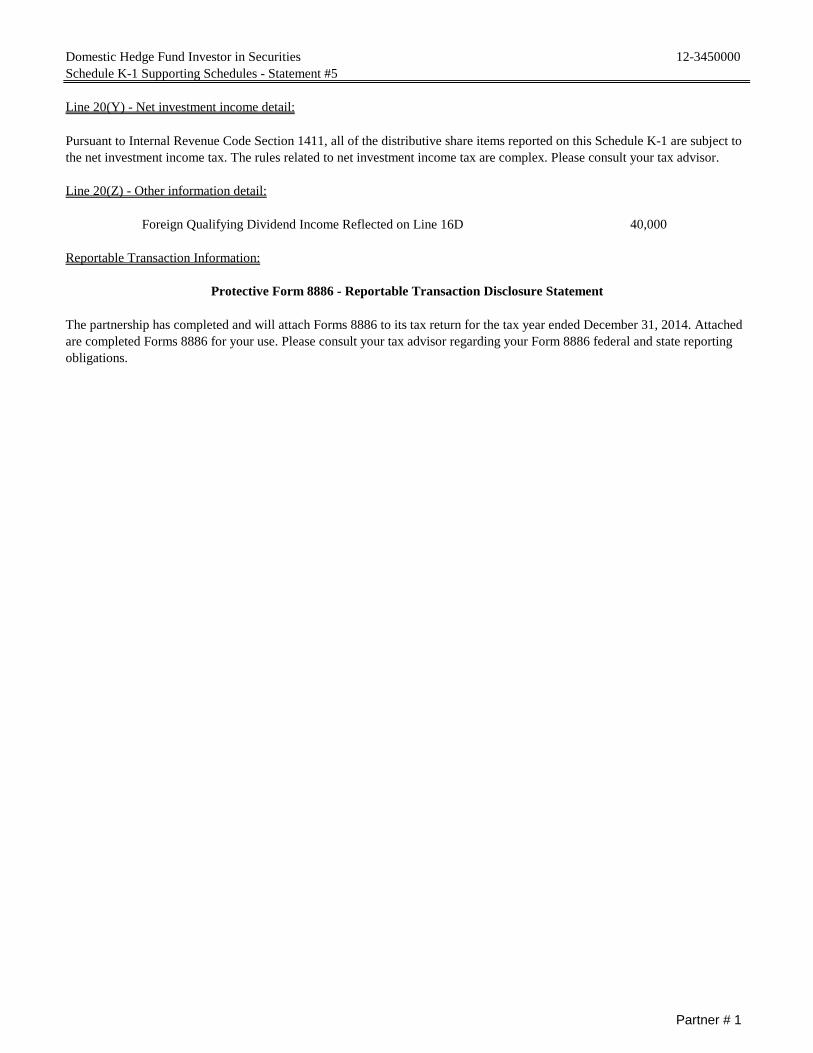

Line 20(Y) - Net investment income detail:

150

50

The tax rules related to net investment income tax are complex. Please consult your tax advisor.

Line 20(Z) - Other information detail:

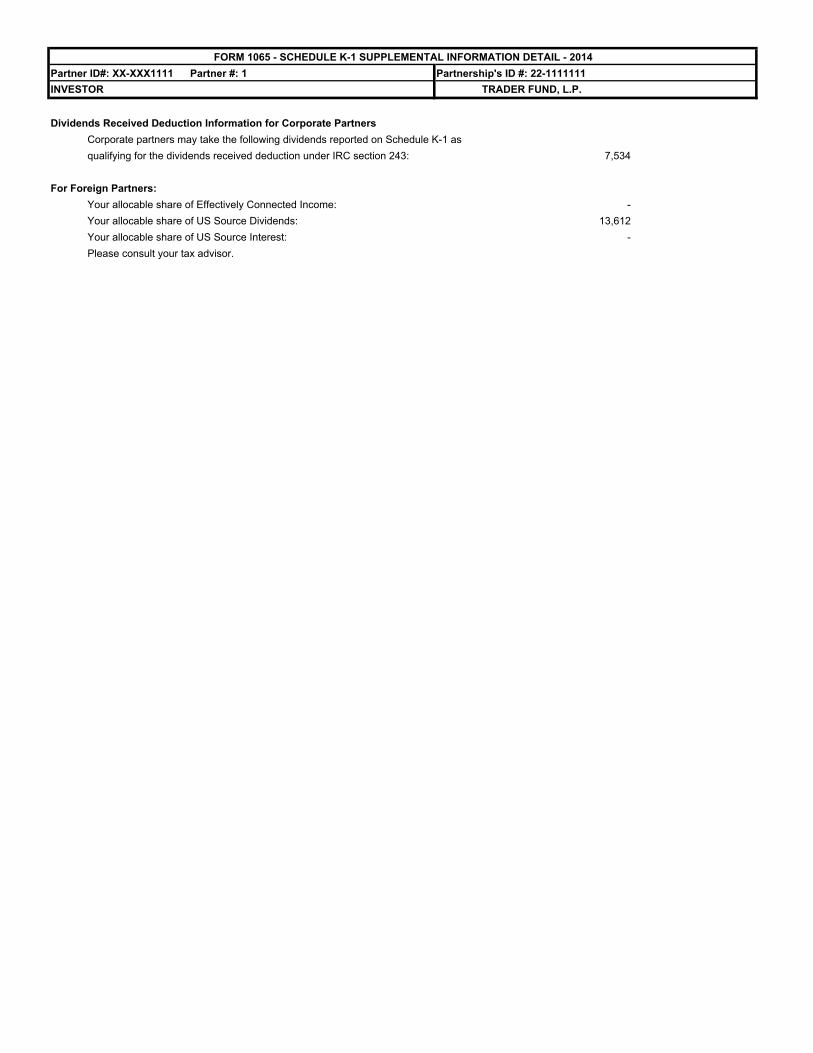

Interest Income From U.S. Government Obligations Reported On Line 1 100 Cost To Carry U.S. Government Obligations 50 Dividends Qualifying For The 70% Corporate Dividends Received Deduction 4,000 Foreign Qualifying Dividend Income Reflected on Line 16D 1,000

Amount of guaranteed payment for use of capital treated as net investment income under Proposed Reg. §1.1411-4(g)(10)

Amount of guaranteed payment for services not treated as net investment income underProposed Reg. §1.1411-4(g)(10)

During the 2014 tax year, the partnership made the election with respect to Controlled Foreign Corporations ("CFCs") and Qualified Electing Funds ("QEFs") under Treasury Regulation §1.1411-10(g). As such, all subpart F income and QEF income has been reported as part of net investment income and no adjustments to the amounts included and reported on Schedule K-1 under IRC §951(a) and §1293(a)(1) are required for purposes of determining net investment income under §1411 of the Internal Revenue Code.

Besides amounts identified as from passive activities elsewhere on your K-1, the amounts on lines 2, 3, 10, and 12 are from passive activities.

Pursuant to Internal Revenue Code Section 1411, unless otherwise noted, all of the distributive share items reported on this Schedule K-1 are subject to the net investment income tax.

Partner # 106

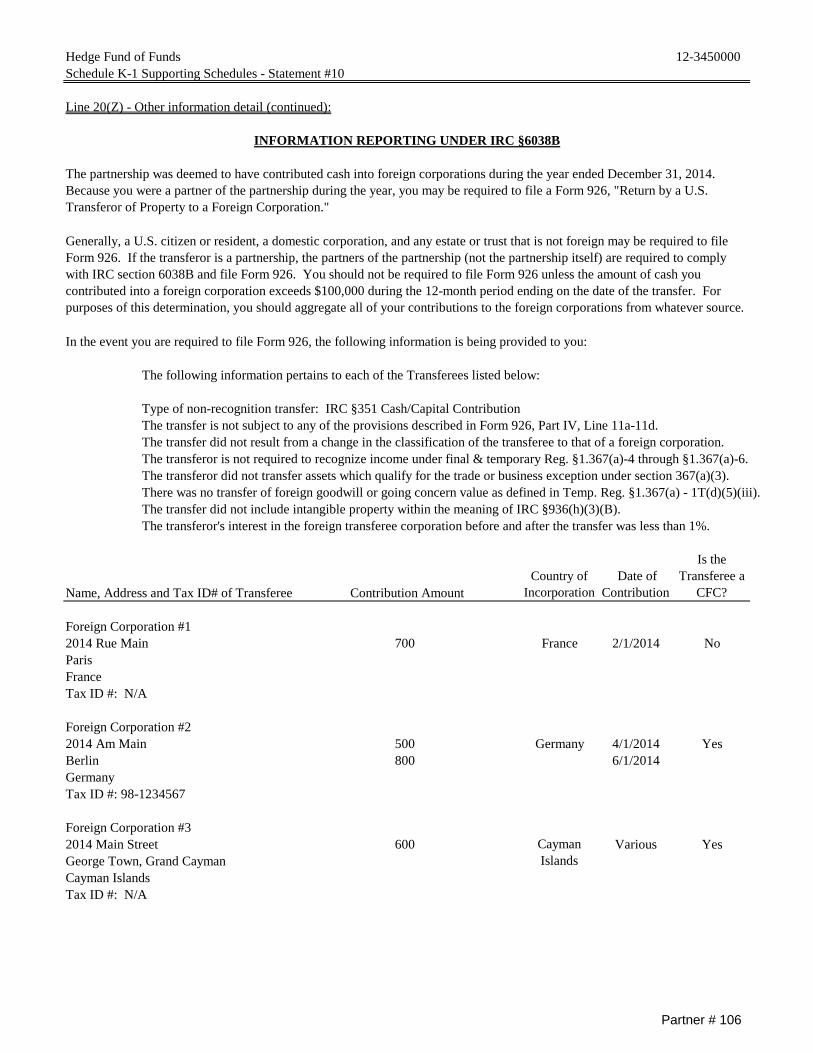

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #10

Line 20(Z) - Other information detail (continued):

In the event you are required to file Form 926, the following information is being provided to you:

The following information pertains to each of the Transferees listed below:

Type of non-recognition transfer: IRC §351 Cash/Capital ContributionThe transfer is not subject to any of the provisions described in Form 926, Part IV, Line 11a-11d.The transfer did not result from a change in the classification of the transferee to that of a foreign corporation. The transferor is not required to recognize income under final & temporary Reg. §1.367(a)-4 through §1.367(a)-6.The transferor did not transfer assets which qualify for the trade or business exception under section 367(a)(3).There was no transfer of foreign goodwill or going concern value as defined in Temp. Reg. §1.367(a) - 1T(d)(5)(iii).The transfer did not include intangible property within the meaning of IRC §936(h)(3)(B).The transferor's interest in the foreign transferee corporation before and after the transfer was less than 1%.

Name, Address and Tax ID# of Transferee Contribution Amount

Foreign Corporation #12014 Rue Main 700 France 2/1/2014 NoParisFranceTax ID #: N/A

Foreign Corporation #22014 Am Main 500 Germany 4/1/2014 YesBerlin 800 6/1/2014GermanyTax ID #: 98-1234567

Foreign Corporation #32014 Main Street 600 Various YesGeorge Town, Grand CaymanCayman IslandsTax ID #: N/A

Generally, a U.S. citizen or resident, a domestic corporation, and any estate or trust that is not foreign may be required to file Form 926. If the transferor is a partnership, the partners of the partnership (not the partnership itself) are required to comply with IRC section 6038B and file Form 926. You should not be required to file Form 926 unless the amount of cash you contributed into a foreign corporation exceeds $100,000 during the 12-month period ending on the date of the transfer. For purposes of this determination, you should aggregate all of your contributions to the foreign corporations from whatever source.

Is the Transferee a

CFC?Country of

Incorporation Date of

Contribution

Cayman Islands

INFORMATION REPORTING UNDER IRC §6038B

The partnership was deemed to have contributed cash into foreign corporations during the year ended December 31, 2014. Because you were a partner of the partnership during the year, you may be required to file a Form 926, "Return by a U.S. Transferor of Property to a Foreign Corporation."

Partner # 106

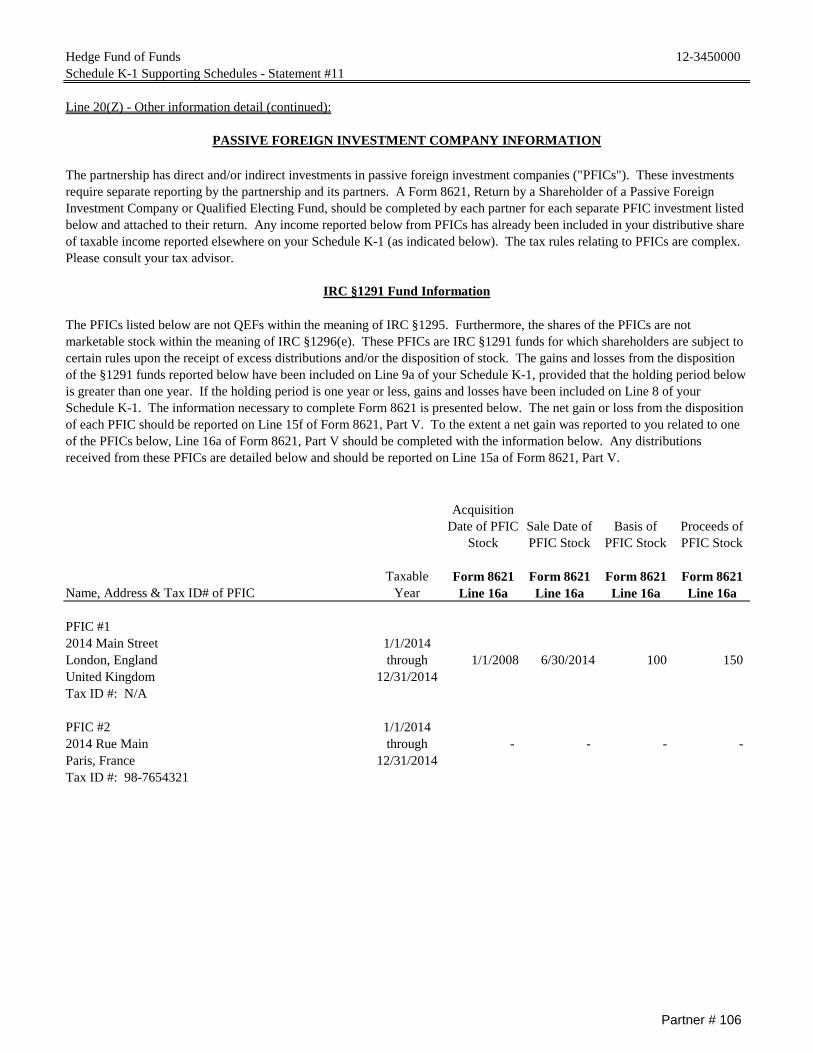

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #11

Line 20(Z) - Other information detail (continued):

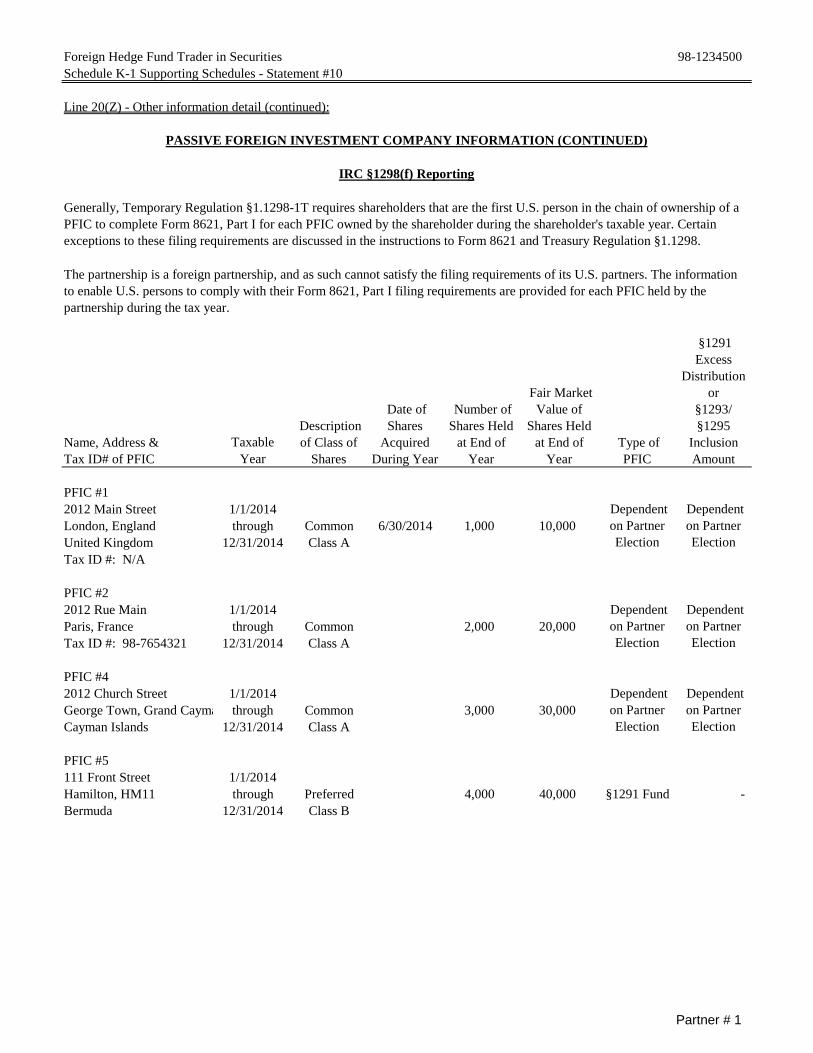

Taxable Form 8621 Form 8621 Form 8621 Form 8621Name, Address & Tax ID# of PFIC Year Line 16a Line 16a Line 16a Line 16a

PFIC #12014 Main Street 1/1/2014London, England through 1/1/2008 6/30/2014 100 150 United Kingdom 12/31/2014Tax ID #: N/A

PFIC #2 1/1/20142014 Rue Main through - - - - Paris, France 12/31/2014Tax ID #: 98-7654321

The partnership has direct and/or indirect investments in passive foreign investment companies ("PFICs"). These investments require separate reporting by the partnership and its partners. A Form 8621, Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund, should be completed by each partner for each separate PFIC investment listed below and attached to their return. Any income reported below from PFICs has already been included in your distributive share of taxable income reported elsewhere on your Schedule K-1 (as indicated below). The tax rules relating to PFICs are complex. Please consult your tax advisor.

IRC §1291 Fund Information

The PFICs listed below are not QEFs within the meaning of IRC §1295. Furthermore, the shares of the PFICs are not marketable stock within the meaning of IRC §1296(e). These PFICs are IRC §1291 funds for which shareholders are subject to certain rules upon the receipt of excess distributions and/or the disposition of stock. The gains and losses from the disposition of the §1291 funds reported below have been included on Line 9a of your Schedule K-1, provided that the holding period below is greater than one year. If the holding period is one year or less, gains and losses have been included on Line 8 of your Schedule K-1. The information necessary to complete Form 8621 is presented below. The net gain or loss from the disposition of each PFIC should be reported on Line 15f of Form 8621, Part V. To the extent a net gain was reported to you related to one of the PFICs below, Line 16a of Form 8621, Part V should be completed with the information below. Any distributions received from these PFICs are detailed below and should be reported on Line 15a of Form 8621, Part V.

Acquisition Date of PFIC

StockSale Date of PFIC Stock

Basis of PFIC Stock

Proceeds of PFIC Stock

PASSIVE FOREIGN INVESTMENT COMPANY INFORMATION

Partner # 106

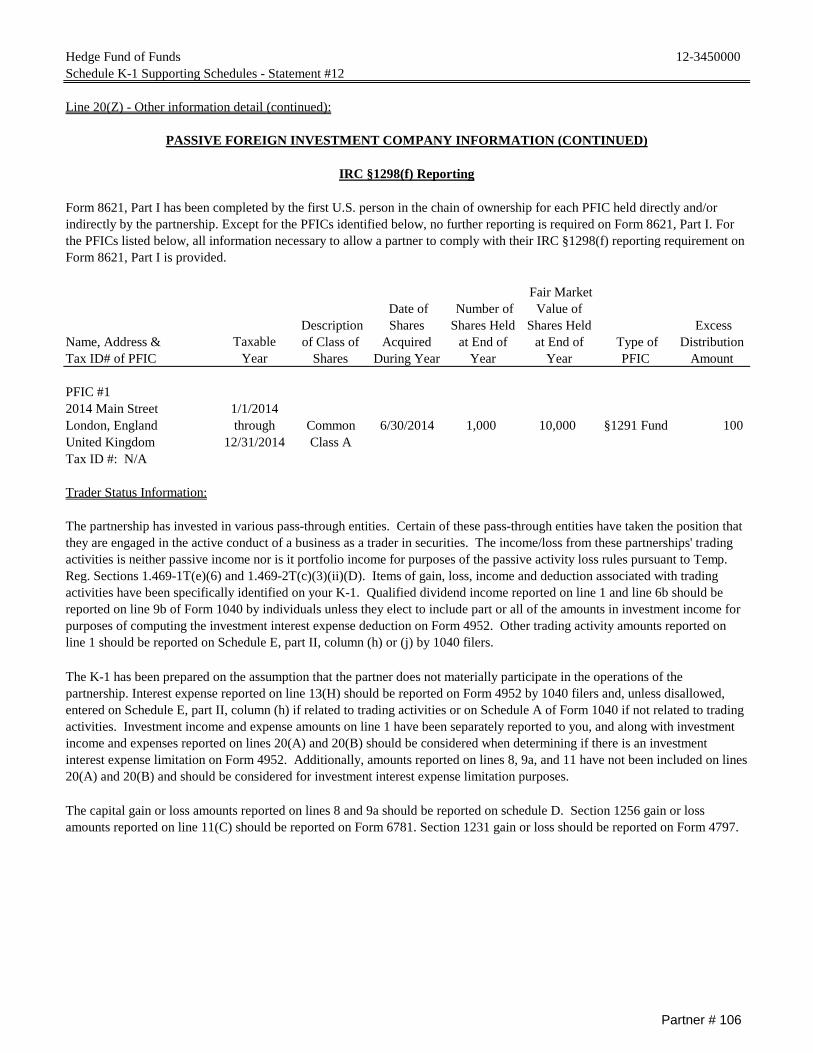

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #12

Line 20(Z) - Other information detail (continued):

TaxableYear

PFIC #12014 Main Street 1/1/2014London, England through Common 6/30/2014 1,000 10,000 §1291 Fund 100 United Kingdom 12/31/2014 Class ATax ID #: N/A

Trader Status Information:

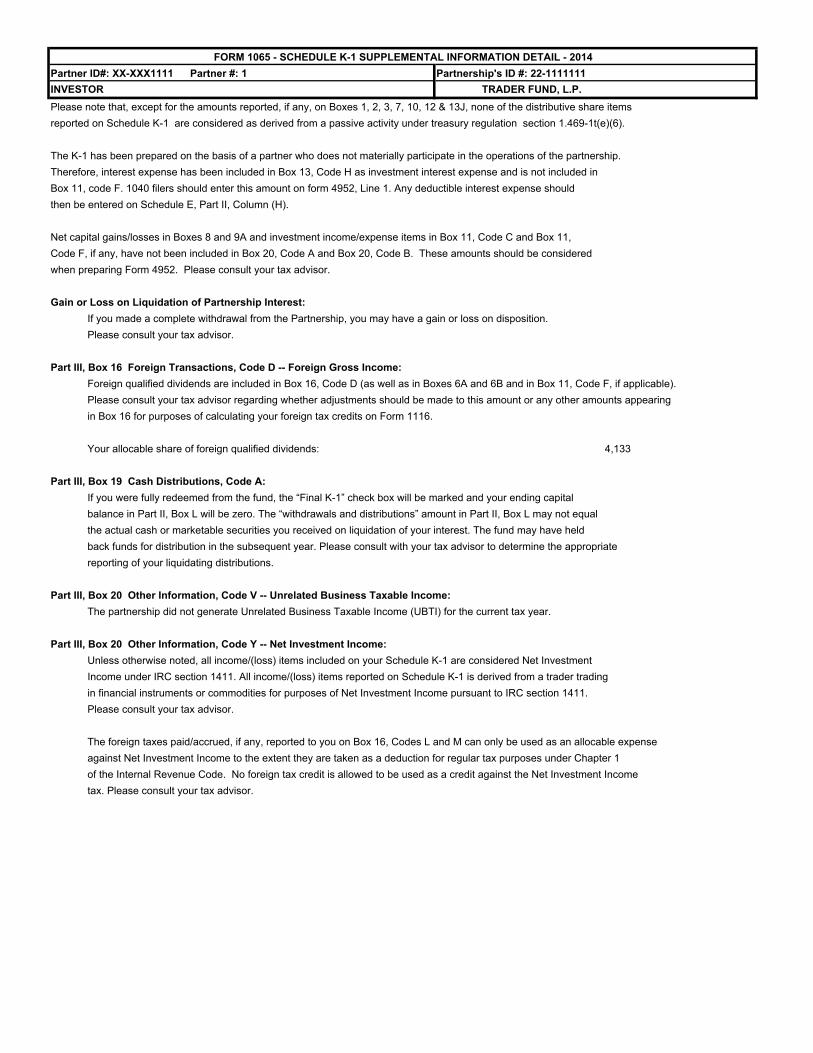

The partnership has invested in various pass-through entities. Certain of these pass-through entities have taken the position that they are engaged in the active conduct of a business as a trader in securities. The income/loss from these partnerships' trading activities is neither passive income nor is it portfolio income for purposes of the passive activity loss rules pursuant to Temp. Reg. Sections 1.469-1T(e)(6) and 1.469-2T(c)(3)(ii)(D). Items of gain, loss, income and deduction associated with trading activities have been specifically identified on your K-1. Qualified dividend income reported on line 1 and line 6b should be reported on line 9b of Form 1040 by individuals unless they elect to include part or all of the amounts in investment income for purposes of computing the investment interest expense deduction on Form 4952. Other trading activity amounts reported on line 1 should be reported on Schedule E, part II, column (h) or (j) by 1040 filers.

The K-1 has been prepared on the assumption that the partner does not materially participate in the operations of the partnership. Interest expense reported on line 13(H) should be reported on Form 4952 by 1040 filers and, unless disallowed, entered on Schedule E, part II, column (h) if related to trading activities or on Schedule A of Form 1040 if not related to trading activities. Investment income and expense amounts on line 1 have been separately reported to you, and along with investment income and expenses reported on lines 20(A) and 20(B) should be considered when determining if there is an investment interest expense limitation on Form 4952. Additionally, amounts reported on lines 8, 9a, and 11 have not been included on lines 20(A) and 20(B) and should be considered for investment interest expense limitation purposes.

The capital gain or loss amounts reported on lines 8 and 9a should be reported on schedule D. Section 1256 gain or loss amounts reported on line 11(C) should be reported on Form 6781. Section 1231 gain or loss should be reported on Form 4797.

PASSIVE FOREIGN INVESTMENT COMPANY INFORMATION (CONTINUED)

IRC §1298(f) Reporting

Form 8621, Part I has been completed by the first U.S. person in the chain of ownership for each PFIC held directly and/or indirectly by the partnership. Except for the PFICs identified below, no further reporting is required on Form 8621, Part I. For the PFICs listed below, all information necessary to allow a partner to comply with their IRC §1298(f) reporting requirement on Form 8621, Part I is provided.

Fair Market Value of

Shares Held at End of

Year Name, Address &Tax ID# of PFIC

Date of Shares

Acquired During Year

Number of Shares Held

at End of Year

Description of Class of

Shares Type of

PFIC

Excess Distribution

Amount

Partner # 106

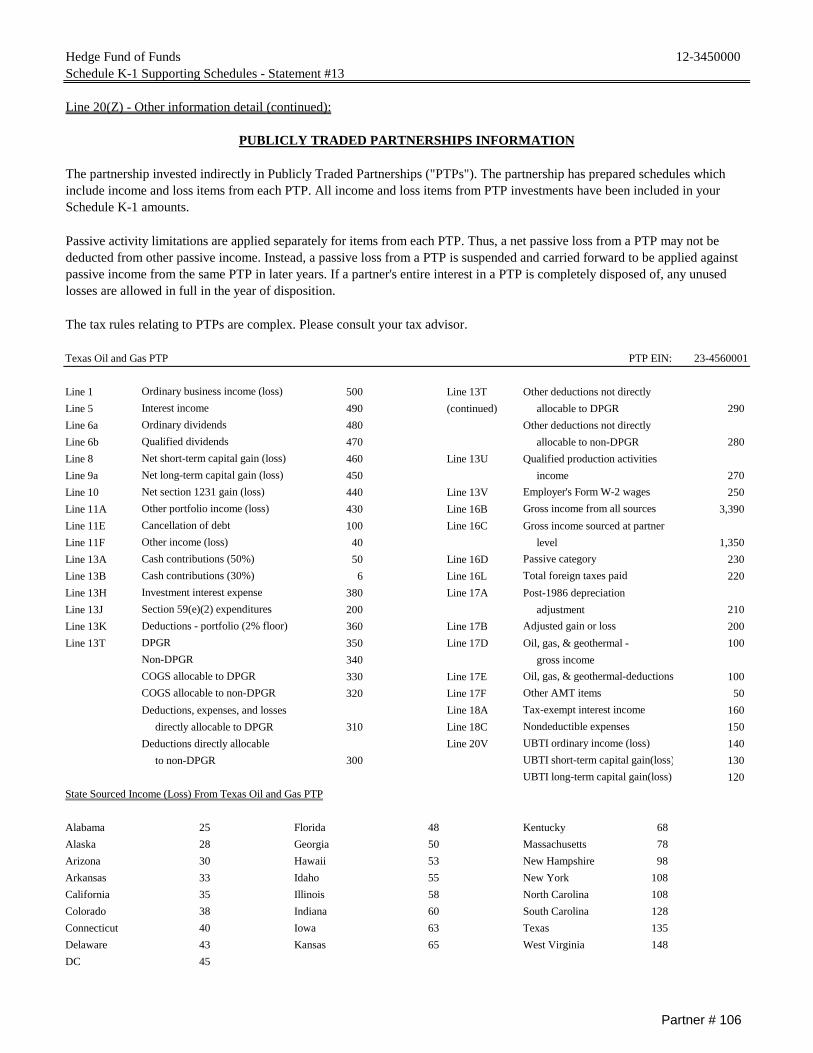

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #13

Line 20(Z) - Other information detail (continued):

Texas Oil and Gas PTP PTP EIN: 23-4560001

Line 1 500 Line 13T Other deductions not directly

Line 5 490 (continued) allocable to DPGR 290

Line 6a 480 Other deductions not directly

Line 6b 470 allocable to non-DPGR 280

Line 8 460 Line 13U Qualified production activities

Line 9a 450 income 270

Line 10 440 Line 13V 250

Line 11A 430 Line 16B 3,390

Line 11E 100 Line 16C Gross income sourced at partner

Line 11F 40 level 1,350

Line 13A 50 Line 16D 230

Line 13B 6 Line 16L 220

Line 13H 380 Line 17A Post-1986 depreciation

Line 13J 200 adjustment 210

Line 13K 360 Line 17B 200

Line 13T 350 Line 17D Oil, gas, & geothermal - 100

340 gross income

330 Line 17E 100

320 Line 17F 50

Deductions, expenses, and losses Line 18A 160

directly allocable to DPGR 310 Line 18C 150

Deductions directly allocable Line 20V 140

to non-DPGR 300 130

120

State Sourced Income (Loss) From Texas Oil and Gas PTP

Alabama 25 Florida 48 Kentucky 68

Alaska 28 Georgia 50 Massachusetts 78

Arizona 30 Hawaii 53 New Hampshire 98

Arkansas 33 Idaho 55 New York 108

California 35 Illinois 58 North Carolina 108

Colorado 38 Indiana 60 South Carolina 128

Connecticut 40 Iowa 63 Texas 135

Delaware 43 Kansas 65 West Virginia 148

DC 45

UBTI long-term capital gain(loss)

COGS allocable to non-DPGR Other AMT items

Tax-exempt interest income

Nondeductible expenses

UBTI ordinary income (loss)

UBTI short-term capital gain(loss)

Section 59(e)(2) expenditures

Deductions - portfolio (2% floor) Adjusted gain or loss

DPGR

Non-DPGR

COGS allocable to DPGR Oil, gas, & geothermal-deductions

Other income (loss)

Cash contributions (50%) Passive category

Cash contributions (30%) Total foreign taxes paid

Investment interest expense

Net long-term capital gain (loss)

Net section 1231 gain (loss) Employer's Form W-2 wages

Other portfolio income (loss) Gross income from all sources

Cancellation of debt

The tax rules relating to PTPs are complex. Please consult your tax advisor.

Ordinary business income (loss)

Interest income

Ordinary dividends

Qualified dividends

Net short-term capital gain (loss)

PUBLICLY TRADED PARTNERSHIPS INFORMATION

The partnership invested indirectly in Publicly Traded Partnerships ("PTPs"). The partnership has prepared schedules which include income and loss items from each PTP. All income and loss items from PTP investments have been included in your Schedule K-1 amounts.

Passive activity limitations are applied separately for items from each PTP. Thus, a net passive loss from a PTP may not be deducted from other passive income. Instead, a passive loss from a PTP is suspended and carried forward to be applied against passive income from the same PTP in later years. If a partner's entire interest in a PTP is completely disposed of, any unused losses are allowed in full in the year of disposition.

Partner # 106

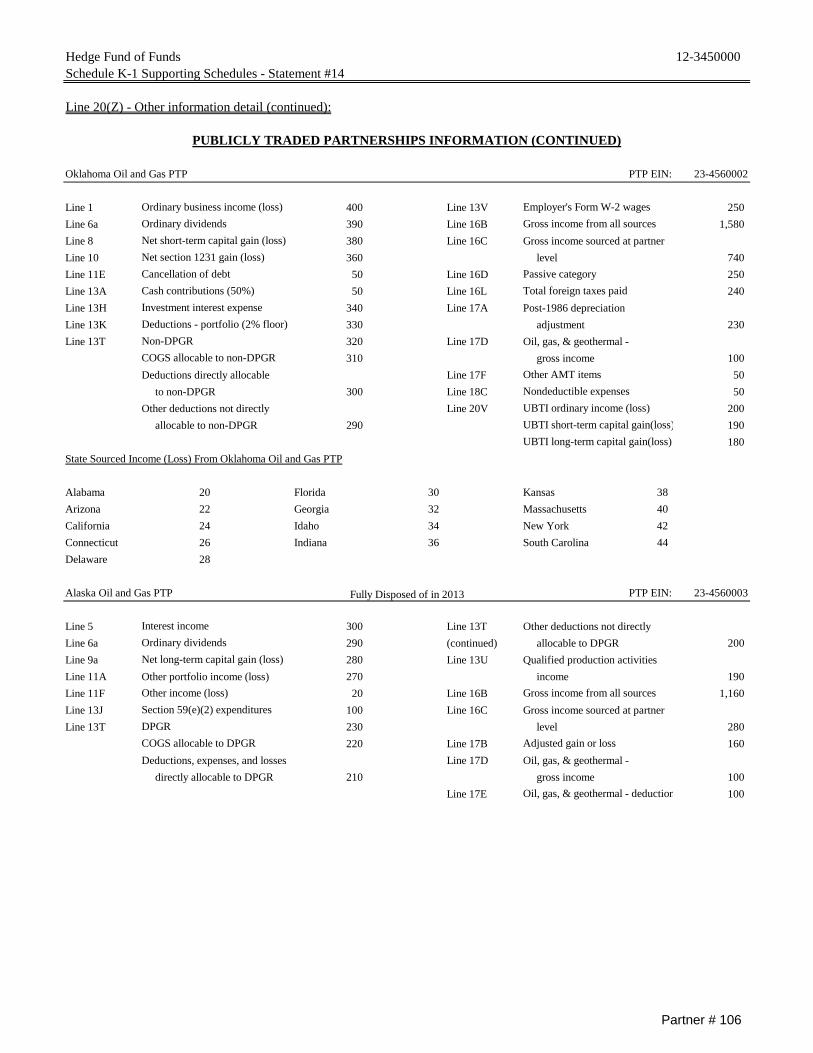

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #14

Line 20(Z) - Other information detail (continued):

Oklahoma Oil and Gas PTP PTP EIN: 23-4560002

Line 1 400 Line 13V 250

Line 6a 390 Line 16B 1,580

Line 8 380 Line 16C Gross income sourced at partner

Line 10 360 level 740

Line 11E 50 Line 16D 250

Line 13A 50 Line 16L 240

Line 13H 340 Line 17A Post-1986 depreciation

Line 13K 330 adjustment 230

Line 13T 320 Line 17D Oil, gas, & geothermal -

310 gross income 100

Deductions directly allocable Line 17F 50

to non-DPGR 300 Line 18C 50

Other deductions not directly Line 20V 200

allocable to non-DPGR 290 190

180

State Sourced Income (Loss) From Oklahoma Oil and Gas PTP

Alabama 20 Florida 30 Kansas 38

Arizona 22 Georgia 32 Massachusetts 40

California 24 Idaho 34 New York 42

Connecticut 26 Indiana 36 South Carolina 44

Delaware 28

Alaska Oil and Gas PTP Fully Disposed of in 2013 PTP EIN: 23-4560003

Line 5 300 Line 13T Other deductions not directly

Line 6a 290 (continued) allocable to DPGR 200

Line 9a 280 Line 13U Qualified production activities

Line 11A Other portfolio income (loss) 270 income 190

Line 11F 20 Line 16B 1,160

Line 13J 100 Line 16C Gross income sourced at partner

Line 13T 230 level 280

220 Line 17B 160

Deductions, expenses, and losses Line 17D Oil, gas, & geothermal -

directly allocable to DPGR 210 gross income 100

Line 17E 100 Oil, gas, & geothermal - deduction

Other income (loss) Gross income from all sources

Section 59(e)(2) expenditures

DPGR

COGS allocable to DPGR Adjusted gain or loss

UBTI ordinary income (loss)

UBTI short-term capital gain(loss)

UBTI long-term capital gain(loss)

Interest income

Ordinary dividends

Net long-term capital gain (loss)

Investment interest expense

Deductions - portfolio (2% floor)

Non-DPGR

COGS allocable to non-DPGR

Other AMT items

Nondeductible expenses

Net short-term capital gain (loss)

Net section 1231 gain (loss)

Cancellation of debt Passive category

Cash contributions (50%) Total foreign taxes paid

PUBLICLY TRADED PARTNERSHIPS INFORMATION (CONTINUED)

Ordinary business income (loss) Employer's Form W-2 wages

Ordinary dividends Gross income from all sources

Partner # 106

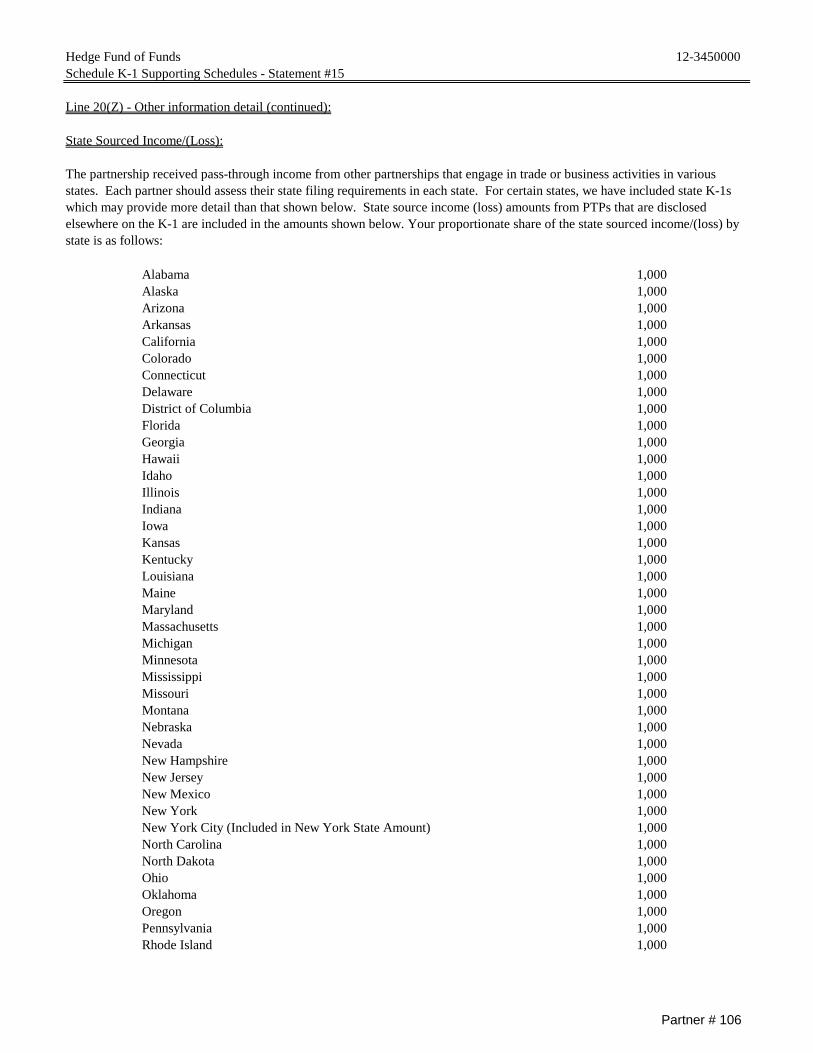

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #15

Line 20(Z) - Other information detail (continued):

State Sourced Income/(Loss):

Alabama 1,000 Alaska 1,000 Arizona 1,000 Arkansas 1,000 California 1,000 Colorado 1,000 Connecticut 1,000 Delaware 1,000 District of Columbia 1,000 Florida 1,000 Georgia 1,000 Hawaii 1,000 Idaho 1,000 Illinois 1,000 Indiana 1,000 Iowa 1,000 Kansas 1,000 Kentucky 1,000 Louisiana 1,000 Maine 1,000 Maryland 1,000 Massachusetts 1,000 Michigan 1,000 Minnesota 1,000 Mississippi 1,000 Missouri 1,000 Montana 1,000 Nebraska 1,000 Nevada 1,000 New Hampshire 1,000 New Jersey 1,000 New Mexico 1,000 New York 1,000 New York City (Included in New York State Amount) 1,000 North Carolina 1,000 North Dakota 1,000 Ohio 1,000 Oklahoma 1,000 Oregon 1,000 Pennsylvania 1,000 Rhode Island 1,000

The partnership received pass-through income from other partnerships that engage in trade or business activities in various states. Each partner should assess their state filing requirements in each state. For certain states, we have included state K-1s which may provide more detail than that shown below. State source income (loss) amounts from PTPs that are disclosed elsewhere on the K-1 are included in the amounts shown below. Your proportionate share of the state sourced income/(loss) by state is as follows:

Partner # 106

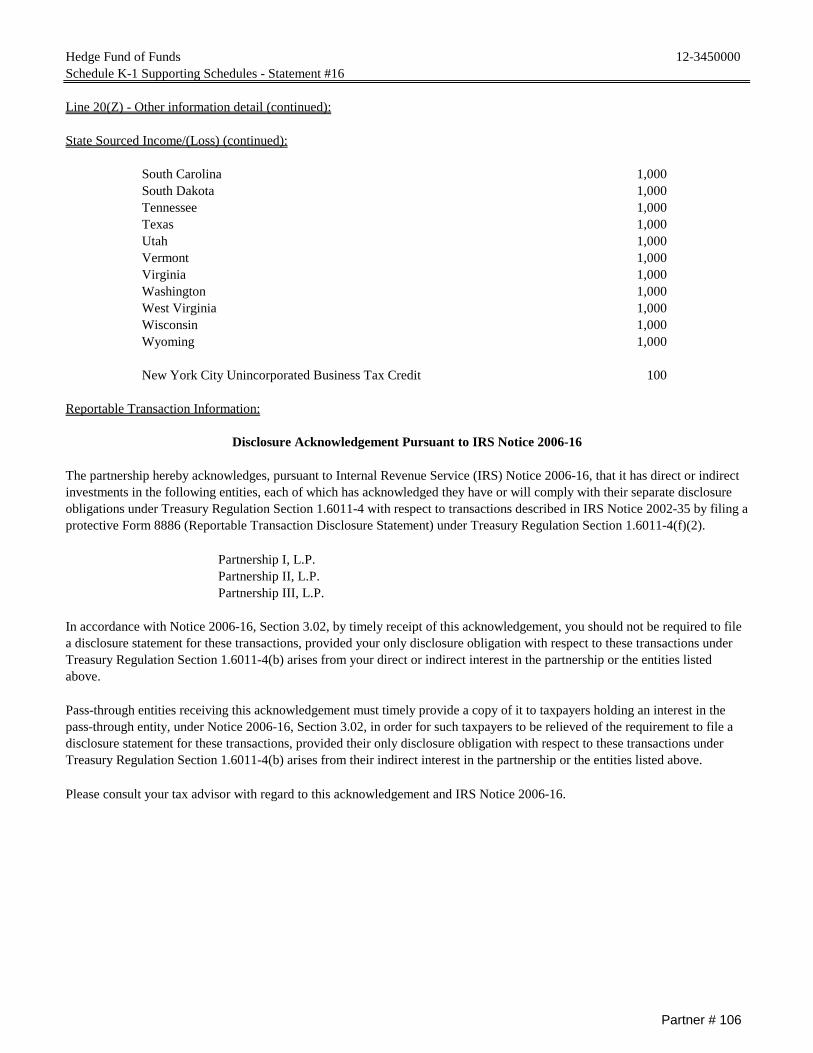

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #16

Line 20(Z) - Other information detail (continued):

State Sourced Income/(Loss) (continued):

South Carolina 1,000 South Dakota 1,000 Tennessee 1,000 Texas 1,000 Utah 1,000 Vermont 1,000 Virginia 1,000 Washington 1,000 West Virginia 1,000 Wisconsin 1,000 Wyoming 1,000

New York City Unincorporated Business Tax Credit 100

Reportable Transaction Information:

Partnership I, L.P.Partnership II, L.P.Partnership III, L.P.

Please consult your tax advisor with regard to this acknowledgement and IRS Notice 2006-16.

Disclosure Acknowledgement Pursuant to IRS Notice 2006-16

The partnership hereby acknowledges, pursuant to Internal Revenue Service (IRS) Notice 2006-16, that it has direct or indirect investments in the following entities, each of which has acknowledged they have or will comply with their separate disclosure obligations under Treasury Regulation Section 1.6011-4 with respect to transactions described in IRS Notice 2002-35 by filing a protective Form 8886 (Reportable Transaction Disclosure Statement) under Treasury Regulation Section 1.6011-4(f)(2).

In accordance with Notice 2006-16, Section 3.02, by timely receipt of this acknowledgement, you should not be required to file a disclosure statement for these transactions, provided your only disclosure obligation with respect to these transactions under Treasury Regulation Section 1.6011-4(b) arises from your direct or indirect interest in the partnership or the entities listed above.

Pass-through entities receiving this acknowledgement must timely provide a copy of it to taxpayers holding an interest in the pass-through entity, under Notice 2006-16, Section 3.02, in order for such taxpayers to be relieved of the requirement to file a disclosure statement for these transactions, provided their only disclosure obligation with respect to these transactions under Treasury Regulation Section 1.6011-4(b) arises from their indirect interest in the partnership or the entities listed above.

Partner # 106

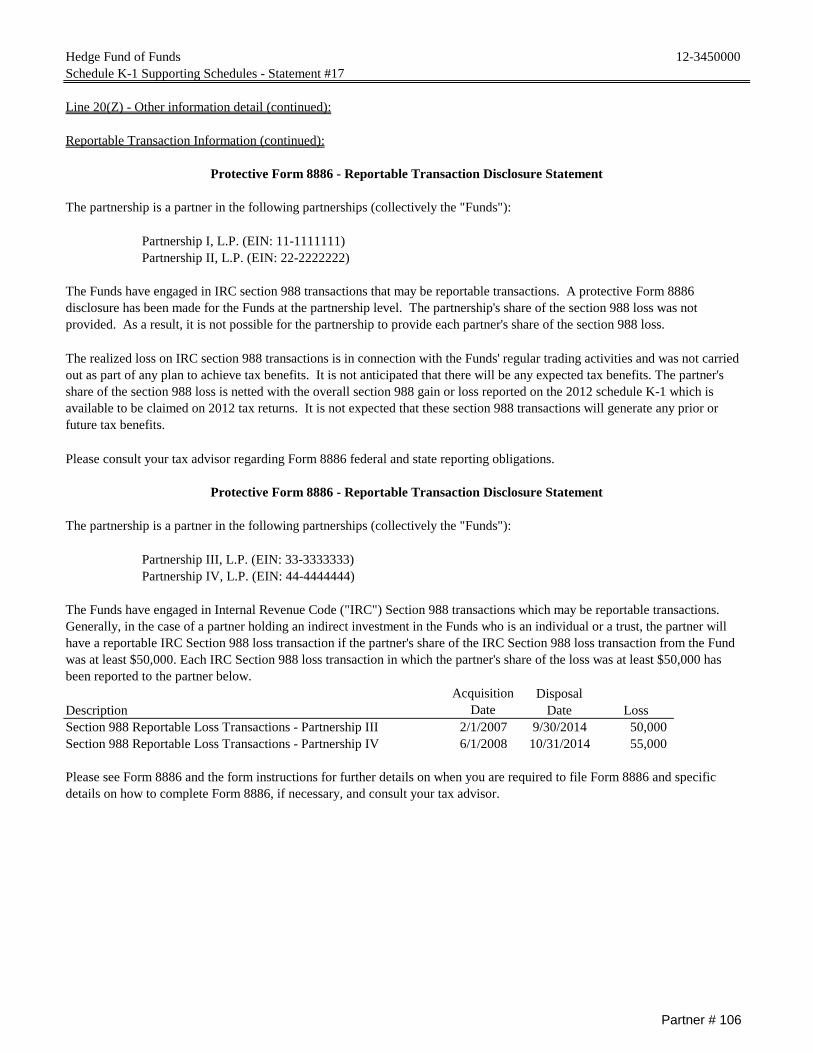

Hedge Fund of Funds 12-3450000Schedule K-1 Supporting Schedules - Statement #17

Line 20(Z) - Other information detail (continued):

Reportable Transaction Information (continued):

Partnership I, L.P. (EIN: 11-1111111)Partnership II, L.P. (EIN: 22-2222222)

Please consult your tax advisor regarding Form 8886 federal and state reporting obligations.

Partnership III, L.P. (EIN: 33-3333333)Partnership IV, L.P. (EIN: 44-4444444)

DisposalDescription Date LossSection 988 Reportable Loss Transactions - Partnership III 2/1/2007 9/30/2014 50,000 Section 988 Reportable Loss Transactions - Partnership IV 6/1/2008 10/31/2014 55,000

The Funds have engaged in Internal Revenue Code ("IRC") Section 988 transactions which may be reportable transactions. Generally, in the case of a partner holding an indirect investment in the Funds who is an individual or a trust, the partner will have a reportable IRC Section 988 loss transaction if the partner's share of the IRC Section 988 loss transaction from the Fund was at least $50,000. Each IRC Section 988 loss transaction in which the partner's share of the loss was at least $50,000 has been reported to the partner below.

Acquisition Date

Please see Form 8886 and the form instructions for further details on when you are required to file Form 8886 and specific details on how to complete Form 8886, if necessary, and consult your tax advisor.

Protective Form 8886 - Reportable Transaction Disclosure Statement

The partnership is a partner in the following partnerships (collectively the "Funds"):

The Funds have engaged in IRC section 988 transactions that may be reportable transactions. A protective Form 8886 disclosure has been made for the Funds at the partnership level. The partnership's share of the section 988 loss was not provided. As a result, it is not possible for the partnership to provide each partner's share of the section 988 loss.

The realized loss on IRC section 988 transactions is in connection with the Funds' regular trading activities and was not carried out as part of any plan to achieve tax benefits. It is not anticipated that there will be any expected tax benefits. The partner's share of the section 988 loss is netted with the overall section 988 gain or loss reported on the 2012 schedule K-1 which is available to be claimed on 2012 tax returns. It is not expected that these section 988 transactions will generate any prior or future tax benefits.

Protective Form 8886 - Reportable Transaction Disclosure Statement

The partnership is a partner in the following partnerships (collectively the "Funds"):

Partner # 106

OMB No. 1545-0123

Schedule K-1

(Form 1065) 2014Department of the Treasury Internal Revenue Service

For calendar year 2014, or tax

year beginning , 2014

ending , 20

Partner’s Share of Income, Deductions, Credits, etc. See back of form and separate instructions.

651113 Final K-1 Amended K-1

Information About the Partnership Part I

A Partnership’s employer identification number

B Partnership’s name, address, city, state, and ZIP code

C IRS Center where partnership filed return

D Check if this is a publicly traded partnership (PTP)

Information About the Partner Part II

E Partner’s identifying number

F Partner’s name, address, city, state, and ZIP code

G General partner or LLC member-manager

Limited partner or other LLC member

H Domestic partner Foreign partner

I1 What type of entity is this partner?

I2 If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here . . . . . . . . . . . . . . . . . . .

J Partner’s share of profit, loss, and capital (see instructions): Beginning Ending

Profit % %

Loss % %

Capital % %

K Partner’s share of liabilities at year end:

Nonrecourse . . . . . . $

Qualified nonrecourse financing . $

Recourse . . . . . . . $

L Partner’s capital account analysis:

Beginning capital account . . . $

Capital contributed during the year $

Current year increase (decrease) . $

Withdrawals & distributions . . $ ( )

Ending capital account . . . . $

Tax basis GAAP Section 704(b) book

Other (explain)

M Did the partner contribute property with a built-in gain or loss?

Yes No

If “Yes,” attach statement (see instructions)

Partner’s Share of Current Year Income,

Deductions, Credits, and Other Items Part III

1 Ordinary business income (loss)

2 Net rental real estate income (loss)

3 Other net rental income (loss)

4 Guaranteed payments

5 Interest income

6a Ordinary dividends

6b Qualified dividends

7 Royalties

8 Net short-term capital gain (loss)

9a Net long-term capital gain (loss)

9b Collectibles (28%) gain (loss)

9c Unrecaptured section 1250 gain

10 Net section 1231 gain (loss)

11 Other income (loss)

12 Section 179 deduction

13 Other deductions

14 Self-employment earnings (loss)

15 Credits

16 Foreign transactions

17 Alternative minimum tax (AMT) items

18 Tax-exempt income and nondeductible expenses

19 Distributions

20 Other information

*See attached statement for additional information.

For

IRS

Use

Onl

y

For Paperwork Reduction Act Notice, see Instructions for Form 1065. IRS.gov/form1065 Cat. No. 11394R Schedule K-1 (Form 1065) 2014

Schedule K-1 (Form 1065) 2014 Page 2

This list identifies the codes used on Schedule K-1 for all partners and provides summarized reporting information for partners who file Form 1040. For detailed reporting and filing information, see the separate Partner’s Instructions for Schedule K-1 and the instructions for your income tax return.

1. Ordinary business income (loss). Determine whether the income (loss) is passive or nonpassive and enter on your return as follows.

Passive loss Report on See the Partner’s Instructions

Passive income Schedule E, line 28, column (g) Nonpassive loss Schedule E, line 28, column (h) Nonpassive income Schedule E, line 28, column (j)

2. Net rental real estate income (loss) See the Partner’s Instructions 3. Other net rental income (loss)

Net income Schedule E, line 28, column (g) Net loss See the Partner’s Instructions

4. Guaranteed payments Schedule E, line 28, column (j) 5. Interest income Form 1040, line 8a 6a. Ordinary dividends Form 1040, line 9a 6b. Qualified dividends Form 1040, line 9b 7. Royalties Schedule E, line 48. Net short-term capital gain (loss) Schedule D, line 59a. Net long-term capital gain (loss) Schedule D, line 129b. Collectibles (28%) gain (loss) 28% Rate Gain Worksheet, line 4

(Schedule D instructions) 9c. Unrecaptured section 1250 gain See the Partner’s Instructions

10. Net section 1231 gain (loss) See the Partner’s Instructions 11. Other income (loss)

Code A Other portfolio income (loss) See the Partner’s Instructions B Involuntary conversions See the Partner’s Instructions C Sec. 1256 contracts & straddles Form 6781, line 1 D Mining exploration costs recapture See Pub. 535E Cancellation of debt Form 1040, line 21 or Form 982 F Other income (loss) See the Partner’s Instructions

12. Section 179 deduction See the Partner’s Instructions 13. Other deductions

A Cash contributions (50%) B Cash contributions (30%) C Noncash contributions (50%) D Noncash contributions (30%) E Capital gain property to a 50%

organization (30%) F Capital gain property (20%) G Contributions (100%)

} See the Partner’s Instructions

H Investment interest expense Form 4952, line 1 I Deductions—royalty income Schedule E, line 19 J Section 59(e)(2) expenditures See the Partner’s Instructions K Deductions—portfolio (2% floor) Schedule A, line 23 L Deductions—portfolio (other) Schedule A, line 28 M Amounts paid for medical insurance Schedule A, line 1 or Form 1040, line 29 N Educational assistance benefits See the Partner’s Instructions O Dependent care benefits Form 2441, line 12P Preproductive period expenses See the Partner’s Instructions Q Commercial revitalization deduction

from rental real estate activities See Form 8582 instructions

R Pensions and IRAs See the Partner’s Instructions S Reforestation expense deduction See the Partner’s Instructions T Domestic production activities

information See Form 8903 instructions

U Qualified production activities income Form 8903, line 7b V Employer’s Form W-2 wages Form 8903, line 17W Other deductions See the Partner’s Instructions

14. Self-employment earnings (loss)

Note. If you have a section 179 deduction or any partner-level deductions, see the Partner’s Instructions before completing Schedule SE.

A Net earnings (loss) from self-employment

Schedule SE, Section A or B

B Gross farming or fishing income See the Partner’s Instructions C Gross non-farm income See the Partner’s Instructions

15. CreditsA Low-income housing credit

(section 42(j)(5)) from pre-2008 buildings

B Low-income housing credit (other) from pre-2008 buildings

C Low-income housing credit (section 42(j)(5)) from post-2007 buildings

D Low-income housing credit (other) from post-2007 buildings

E Qualified rehabilitation expenditures (rental real estate)

F Other rental real estate credits G Other rental credits

} See the Partner’s Instructions

H Undistributed capital gains credit Form 1040, line 73; check box a I Biofuel producer credit J Work opportunity credit K Disabled access credit

See the Partner's Instructions}

Code Report on L Empowerment zone

employment credit M Credit for increasing research

activities N Credit for employer social

security and Medicare taxes O Backup withholding P Other credits

} See the Partner’s Instructions

16. Foreign transactions

A Name of country or U.S. possession

B Gross income from all sources C Gross income sourced at

partner level } Form 1116, Part I

Foreign gross income sourced at partnership level D Passive category E General category F Other } Form 1116, Part I

Deductions allocated and apportioned at partner level G Interest expense Form 1116, Part I H Other Form 1116, Part I Deductions allocated and apportioned at partnership level to foreign source income I Passive category J General category K Other } Form 1116, Part I

Other information L Total foreign taxes paid Form 1116, Part II M Total foreign taxes accrued Form 1116, Part II N Reduction in taxes available for credit Form 1116, line 12 O Foreign trading gross receipts Form 8873 P Extraterritorial income exclusion Form 8873 Q Other foreign transactions See the Partner’s Instructions

17. Alternative minimum tax (AMT) items

A Post-1986 depreciation adjustment B Adjusted gain or loss C Depletion (other than oil & gas) D Oil, gas, & geothermal—gross income E Oil, gas, & geothermal—deductions F Other AMT items

} See the Partner’s Instructions and the Instructions for Form 6251

18. Tax-exempt income and nondeductible expenses

A Tax-exempt interest income Form 1040, line 8b B Other tax-exempt income See the Partner’s Instructions C Nondeductible expenses See the Partner’s Instructions

19. Distributions

A Cash and marketable securitiesB Distribution subject to section 737C Other property

} See the Partner’s Instructions

20. Other information

A Investment income Form 4952, line 4a B Investment expenses Form 4952, line 5 C Fuel tax credit information Form 4136 D Qualified rehabilitation expenditures

(other than rental real estate) See the Partner’s Instructions

E Basis of energy property See the Partner’s Instructions F Recapture of low-income housing

credit (section 42(j)(5)) Form 8611, line 8

G Recapture of low-income housing credit (other)

Form 8611, line 8

H Recapture of investment credit See Form 4255 I Recapture of other credits See the Partner’s Instructions J Look-back interest—completed

long-term contracts See Form 8697

K Look-back interest—income forecast method

See Form 8866

L Dispositions of property with section 179 deductions

M Recapture of section 179 deductionN Interest expense for corporate

partners O Section 453(l)(3) information P Section 453A(c) information Q Section 1260(b) information R Interest allocable to production

expenditures S CCF nonqualified withdrawals T Depletion information—oil and gas U ReservedV Unrelated business taxable incomeW Precontribution gain (loss) X Section 108(i) informationY Net investment income

} See the Partner’s Instructions

Z Other information

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #1

Part II, Item J - Partner's share of profit, loss, and capital:

Part II, Item L - Current year increase (decrease) reconciliation:

Partner's Distributive Share of Taxable Income 29,100 Less: Line 15 - Credits (100) Unrealized Appreciation (Depreciation) and Other Timing Differences 121,000 Subtotal: Book Income 150,000 Net Partnership Transfers -

Total Current Year Increase (Decrease) 150,000

Line 1 - Ordinary business income (loss) detail:

Interest Income From Trading Activities 5,000 Qualified Dividends From Trading Activities 6,100 Other Dividends From Trading Activities 100 Net Section 988 Gain (Loss) From Trading Activities 1,000 Other Income (Loss) From Trading Activities 21,400 Other Expenses From Trading Activities (5,000)

Total Ordinary Business Income (Loss) 28,600

Line 8 - Net short-term capital gain (loss) detail:

Net Short-Term Capital Gain (Loss) From Trading Activities 8,000

Total Net Short-Term Capital Gain (Loss) 8,000

Line 9a - Net long-term capital gain (loss) detail:

Net Long-Term Capital Gain (Loss) From Trading Activities (2,000)

Total Net Long-Term Capital Gain (Loss) (2,000)

Line 11(C) - Section 1256 contracts and straddles detail:

Net Section 1256 Gain (Loss) From Trading Activities 1,500

Total Section 1256 Gain (Loss) 1,500

Beginning and ending capital percentages are based on partners' beginning and ending capital accounts as reflected in Part II, Item L as a percentage of total partnership capital.

Beginning profit and loss percentages reflect beginning of year book capital percentages.

Ending profit percentages are based on partners' allocation of distributive share of income and gains on a tax basis as a percentage of total partnership amounts. Ending loss percentages are based on partners' allocation of distributive share of deductions and losses on a tax basis as a percentage of total partnership amounts. These percentages may differ significantly from your ending capital percentage due to the timing of contributions and withdrawals during the year, the timing of when income and losses occurred during the year, and tax allocations of gains and losses pursuant to IRC §704(c).

Partner # 1

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #2

Line 13(H) - Investment interest expense detail:

Investment Interest Expense From Trading Activities 6,000

Total Investment Interest Expense 6,000

Line 13(T) - Domestic production activities information:

Line 15(P) - Other credits detail:

U.S. Taxes Withheld 100

Total Other Credits 100

Line 16 - Foreign transactions:

A. Name of country or U.S. possession Various B. Gross income from all sources 49,400 C. Gross income sourced at partner level 16,800 Foreign gross income sourced at partnership levelD. Passive category 5,000 E. General category - F. Other - Deductions allocated and apportioned at partner levelG. Interest expense 6,000 H. Other 13,300 Deductions allocated and apportioned at partnership level to foreign source incomeI. Passive category - J. General category - K. Other - Other informationL. Total foreign taxes paid 1,000

Line 20(N) - Interest expense for corporate partners detail:

Line 20(V) - Unrelated business taxable income detail:

Ordinary Income (Loss) Considered Unrelated Business Taxable Income - Short-Term Capital Gain (Loss) Considered Unrelated Business Taxable Income - Long-Term Capital Gain (Loss) Considered Unrelated Business Taxable Income -

Total Unrelated Business Taxable Income -

None of the partnership's items relate to domestic production activities. If you otherwise have Internal Revenue Code Section 199 activities, gross income from all sources has been reported on Line 16B. Additional information, if needed, is available upon request.

For corporate partners, your distributive share of the partnership's interest expense has been reported on Line 13(H) of your Schedule K-1. A corporate partner's distributive share of interest income, interest expense and partnership liabilities are treated as income, expense and liabilities of the corporation for purposes of the limitation on the deduction for interest under IRC §163(j). The interest expense limitation rules for corporations are complex. Please consult your tax advisor.

Partner # 1

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #3

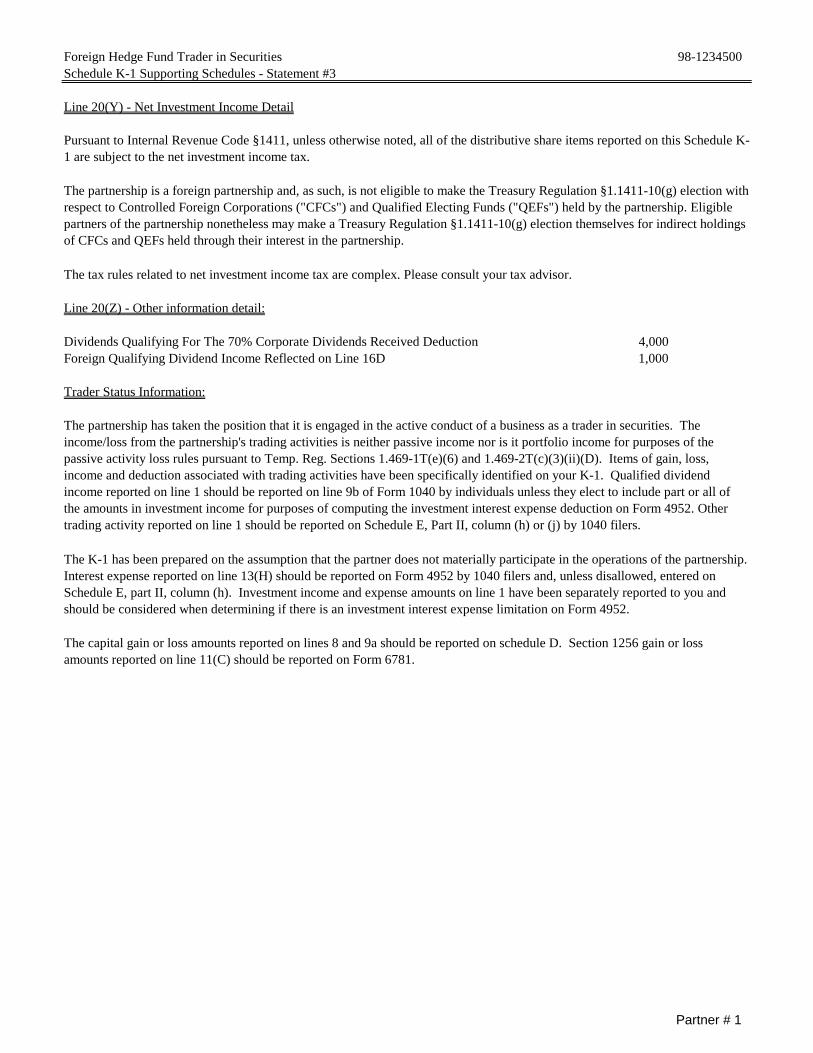

Line 20(Y) - Net Investment Income Detail

The tax rules related to net investment income tax are complex. Please consult your tax advisor.

Line 20(Z) - Other information detail:

Dividends Qualifying For The 70% Corporate Dividends Received Deduction 4,000 Foreign Qualifying Dividend Income Reflected on Line 16D 1,000

Trader Status Information:

The partnership is a foreign partnership and, as such, is not eligible to make the Treasury Regulation §1.1411-10(g) election with respect to Controlled Foreign Corporations ("CFCs") and Qualified Electing Funds ("QEFs") held by the partnership. Eligible partners of the partnership nonetheless may make a Treasury Regulation §1.1411-10(g) election themselves for indirect holdings of CFCs and QEFs held through their interest in the partnership.

The partnership has taken the position that it is engaged in the active conduct of a business as a trader in securities. The income/loss from the partnership's trading activities is neither passive income nor is it portfolio income for purposes of the passive activity loss rules pursuant to Temp. Reg. Sections 1.469-1T(e)(6) and 1.469-2T(c)(3)(ii)(D). Items of gain, loss, income and deduction associated with trading activities have been specifically identified on your K-1. Qualified dividend income reported on line 1 should be reported on line 9b of Form 1040 by individuals unless they elect to include part or all of the amounts in investment income for purposes of computing the investment interest expense deduction on Form 4952. Other trading activity reported on line 1 should be reported on Schedule E, Part II, column (h) or (j) by 1040 filers.

The K-1 has been prepared on the assumption that the partner does not materially participate in the operations of the partnership. Interest expense reported on line 13(H) should be reported on Form 4952 by 1040 filers and, unless disallowed, entered on Schedule E, part II, column (h). Investment income and expense amounts on line 1 have been separately reported to you and should be considered when determining if there is an investment interest expense limitation on Form 4952.

The capital gain or loss amounts reported on lines 8 and 9a should be reported on schedule D. Section 1256 gain or loss amounts reported on line 11(C) should be reported on Form 6781.

Pursuant to Internal Revenue Code §1411, unless otherwise noted, all of the distributive share items reported on this Schedule K-1 are subject to the net investment income tax.

Partner # 1

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #4

Line 20(Z) - Other information detail (continued):

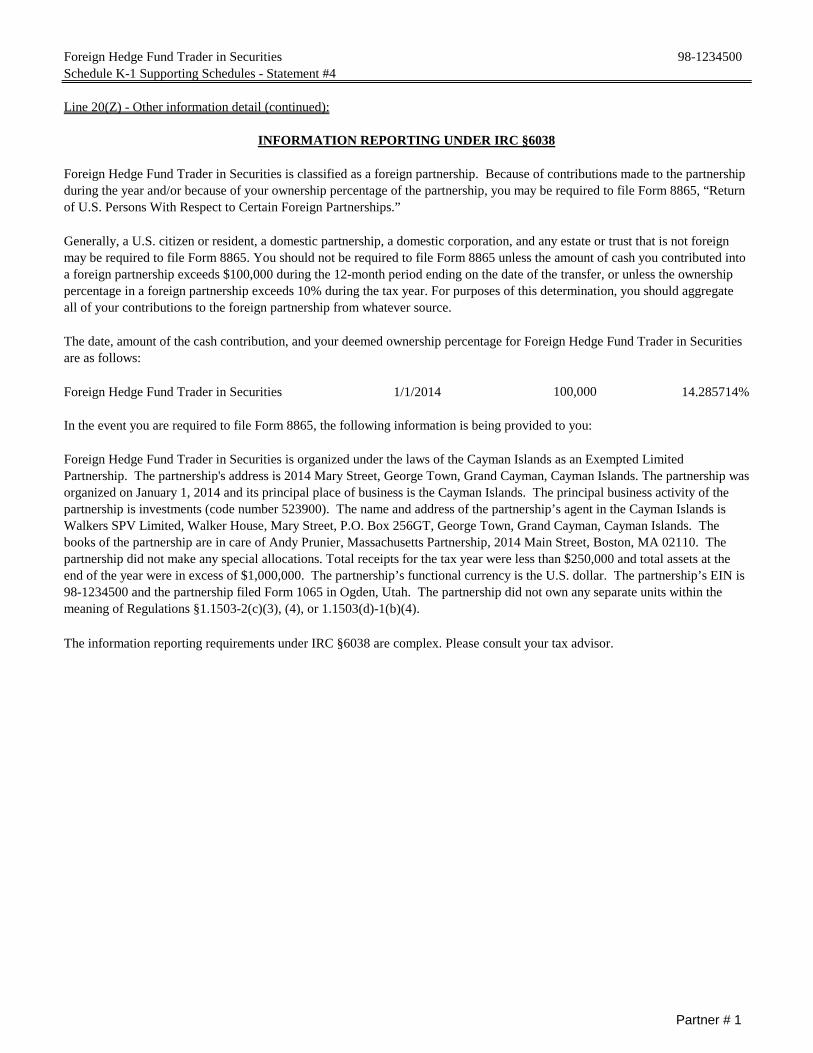

Foreign Hedge Fund Trader in Securities 1/1/2014 14.285714%

In the event you are required to file Form 8865, the following information is being provided to you:

The information reporting requirements under IRC §6038 are complex. Please consult your tax advisor.

Generally, a U.S. citizen or resident, a domestic partnership, a domestic corporation, and any estate or trust that is not foreign may be required to file Form 8865. You should not be required to file Form 8865 unless the amount of cash you contributed into a foreign partnership exceeds $100,000 during the 12-month period ending on the date of the transfer, or unless the ownership percentage in a foreign partnership exceeds 10% during the tax year. For purposes of this determination, you should aggregate all of your contributions to the foreign partnership from whatever source.

The date, amount of the cash contribution, and your deemed ownership percentage for Foreign Hedge Fund Trader in Securities are as follows:

100,000

Foreign Hedge Fund Trader in Securities is organized under the laws of the Cayman Islands as an Exempted Limited Partnership. The partnership's address is 2014 Mary Street, George Town, Grand Cayman, Cayman Islands. The partnership was organized on January 1, 2014 and its principal place of business is the Cayman Islands. The principal business activity of the partnership is investments (code number 523900). The name and address of the partnership’s agent in the Cayman Islands is Walkers SPV Limited, Walker House, Mary Street, P.O. Box 256GT, George Town, Grand Cayman, Cayman Islands. The books of the partnership are in care of Andy Prunier, Massachusetts Partnership, 2014 Main Street, Boston, MA 02110. The partnership did not make any special allocations. Total receipts for the tax year were less than $250,000 and total assets at the end of the year were in excess of $1,000,000. The partnership’s functional currency is the U.S. dollar. The partnership’s EIN is 98-1234500 and the partnership filed Form 1065 in Ogden, Utah. The partnership did not own any separate units within the meaning of Regulations §1.1503-2(c)(3), (4), or 1.1503(d)-1(b)(4).

INFORMATION REPORTING UNDER IRC §6038

Foreign Hedge Fund Trader in Securities is classified as a foreign partnership. Because of contributions made to the partnership during the year and/or because of your ownership percentage of the partnership, you may be required to file Form 8865, “Return of U.S. Persons With Respect to Certain Foreign Partnerships.”

Partner # 1

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #5

Line 20(Z) - Other information detail (continued):

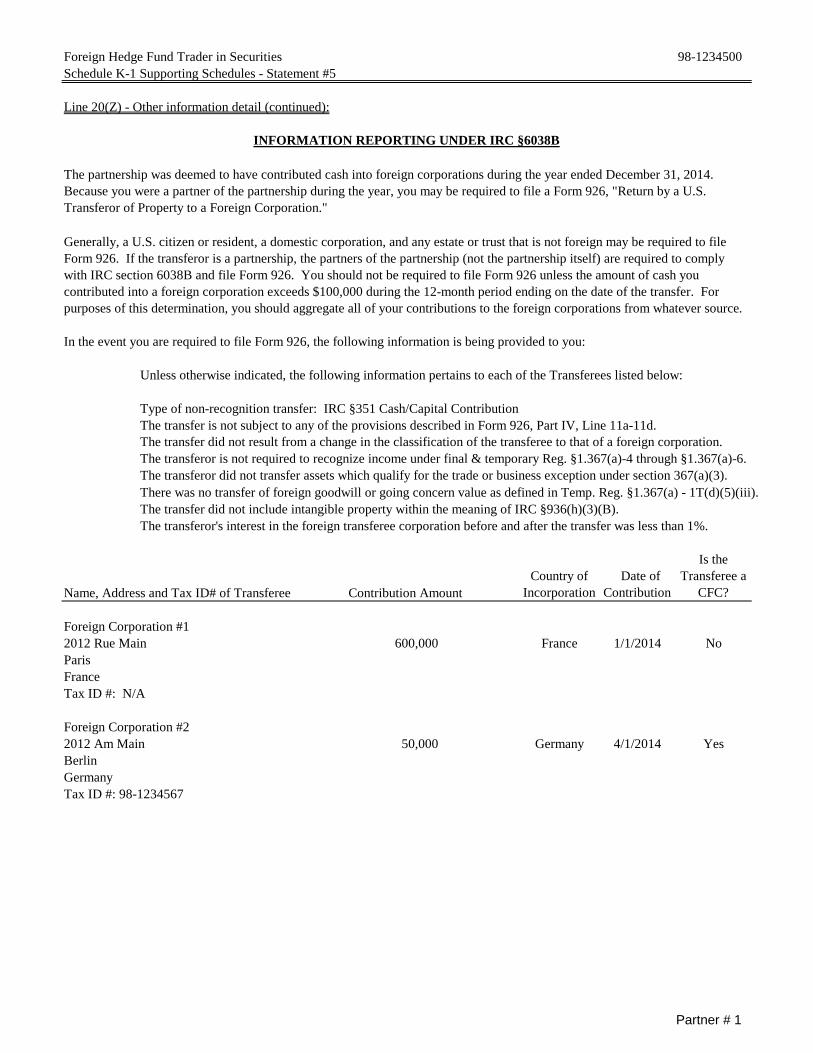

There was no transfer of foreign goodwill or going concern value as defined in Temp. Reg. §1.367(a) - 1T(d)(5)(iii).The transfer did not include intangible property within the meaning of IRC §936(h)(3)(B).The transferor's interest in the foreign transferee corporation before and after the transfer was less than 1%.

Name, Address and Tax ID# of Transferee Contribution Amount

Foreign Corporation #12012 Rue Main 600,000 France 1/1/2014 NoParisFranceTax ID #: N/A

Foreign Corporation #22012 Am Main 50,000 Germany 4/1/2014 YesBerlinGermanyTax ID #: 98-1234567

The transfer is not subject to any of the provisions described in Form 926, Part IV, Line 11a-11d.The transfer did not result from a change in the classification of the transferee to that of a foreign corporation. The transferor is not required to recognize income under final & temporary Reg. §1.367(a)-4 through §1.367(a)-6.The transferor did not transfer assets which qualify for the trade or business exception under section 367(a)(3).

Is the Transferee a

CFC?Country of

Incorporation Date of

Contribution

INFORMATION REPORTING UNDER IRC §6038B

The partnership was deemed to have contributed cash into foreign corporations during the year ended December 31, 2014. Because you were a partner of the partnership during the year, you may be required to file a Form 926, "Return by a U.S. Transferor of Property to a Foreign Corporation."

Generally, a U.S. citizen or resident, a domestic corporation, and any estate or trust that is not foreign may be required to file Form 926. If the transferor is a partnership, the partners of the partnership (not the partnership itself) are required to comply with IRC section 6038B and file Form 926. You should not be required to file Form 926 unless the amount of cash you contributed into a foreign corporation exceeds $100,000 during the 12-month period ending on the date of the transfer. For purposes of this determination, you should aggregate all of your contributions to the foreign corporations from whatever source.

In the event you are required to file Form 926, the following information is being provided to you:

Unless otherwise indicated, the following information pertains to each of the Transferees listed below:

Type of non-recognition transfer: IRC §351 Cash/Capital Contribution

Partner # 1

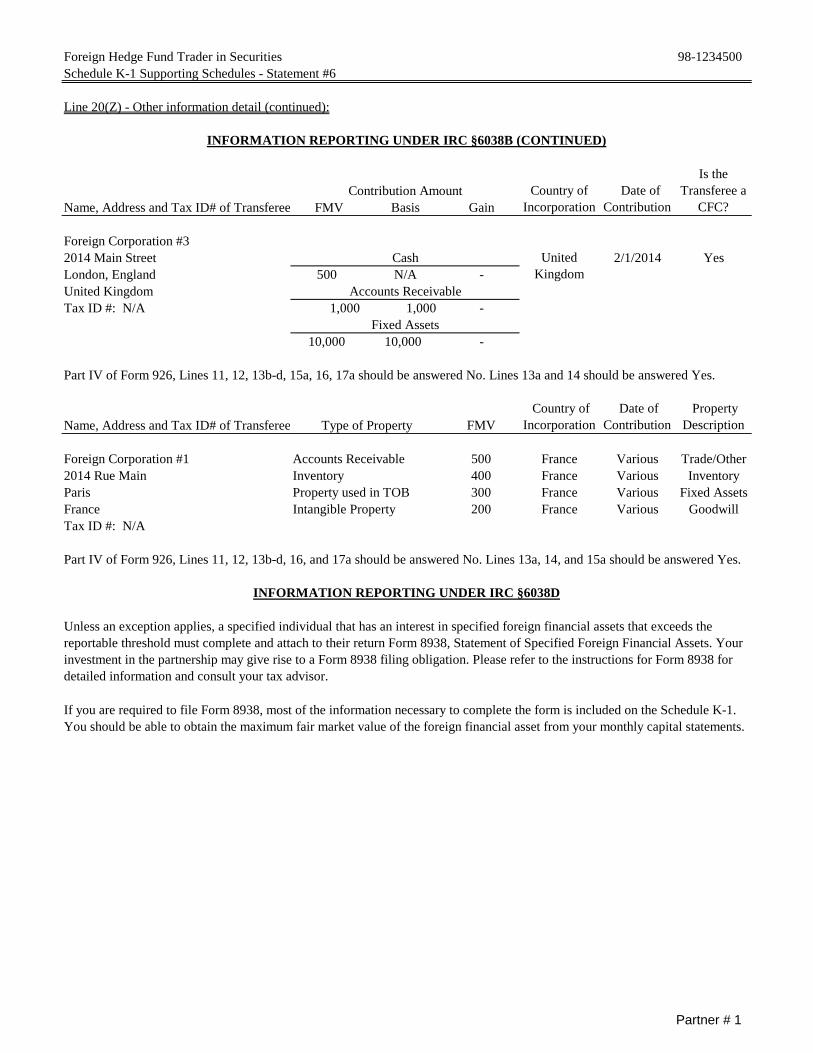

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #6

Line 20(Z) - Other information detail (continued):

Contribution AmountName, Address and Tax ID# of Transferee FMV Basis Gain

Foreign Corporation #32014 Main Street Cash 2/1/2014 YesLondon, England 500 N/A -United Kingdom Accounts ReceivableTax ID #: N/A 1,000 1,000 -

Fixed Assets10,000 10,000 -

Part IV of Form 926, Lines 11, 12, 13b-d, 15a, 16, 17a should be answered No. Lines 13a and 14 should be answered Yes.

Name, Address and Tax ID# of Transferee FMV

Foreign Corporation #1 Accounts Receivable 500 France Various Trade/Other2014 Rue Main Inventory 400 France Various InventoryParis Property used in TOB 300 France Various Fixed AssetsFrance Intangible Property 200 France Various GoodwillTax ID #: N/A

Part IV of Form 926, Lines 11, 12, 13b-d, 16, and 17a should be answered No. Lines 13a, 14, and 15a should be answered Yes.

If you are required to file Form 8938, most of the information necessary to complete the form is included on the Schedule K-1. You should be able to obtain the maximum fair market value of the foreign financial asset from your monthly capital statements.

Country of Incorporation

Date of Contribution

Property Description Type of Property

INFORMATION REPORTING UNDER IRC §6038D

Unless an exception applies, a specified individual that has an interest in specified foreign financial assets that exceeds the reportable threshold must complete and attach to their return Form 8938, Statement of Specified Foreign Financial Assets. Your investment in the partnership may give rise to a Form 8938 filing obligation. Please refer to the instructions for Form 8938 for detailed information and consult your tax advisor.

INFORMATION REPORTING UNDER IRC §6038B (CONTINUED)

Is the Transferee a

CFC?Country of

Incorporation Date of

Contribution

United Kingdom

Partner # 1

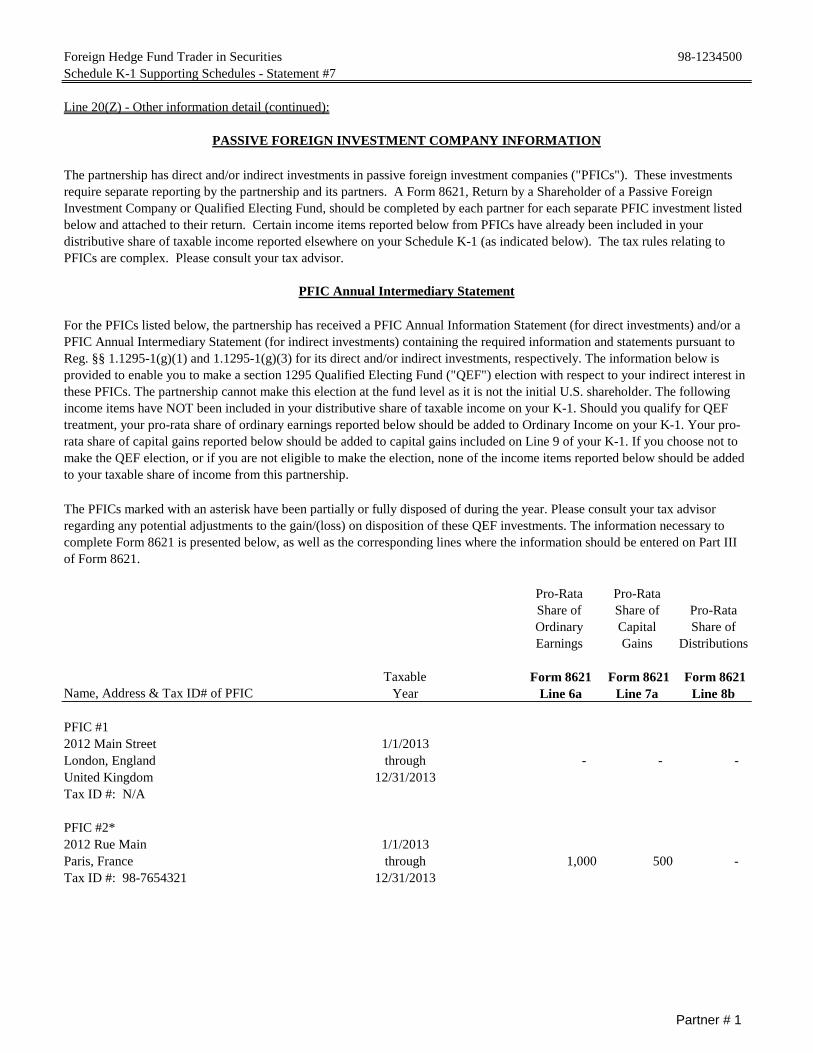

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #7

Line 20(Z) - Other information detail (continued):

Taxable Form 8621 Form 8621 Form 8621 Year Line 6a Line 7a Line 8b

PFIC #12012 Main Street 1/1/2013London, England through - - - United Kingdom 12/31/2013Tax ID #: N/A

PFIC #2*2012 Rue Main 1/1/2013Paris, France through 1,000 500 - Tax ID #: 98-7654321 12/31/2013

The PFICs marked with an asterisk have been partially or fully disposed of during the year. Please consult your tax advisor regarding any potential adjustments to the gain/(loss) on disposition of these QEF investments. The information necessary to complete Form 8621 is presented below, as well as the corresponding lines where the information should be entered on Part III of Form 8621.

Pro-Rata Share of Ordinary Earnings

Pro-Rata Share of Capital Gains

Pro-Rata Share of

Distributions

Name, Address & Tax ID# of PFIC

PASSIVE FOREIGN INVESTMENT COMPANY INFORMATION

The partnership has direct and/or indirect investments in passive foreign investment companies ("PFICs"). These investments require separate reporting by the partnership and its partners. A Form 8621, Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund, should be completed by each partner for each separate PFIC investment listed below and attached to their return. Certain income items reported below from PFICs have already been included in your distributive share of taxable income reported elsewhere on your Schedule K-1 (as indicated below). The tax rules relating to PFICs are complex. Please consult your tax advisor.

PFIC Annual Intermediary Statement

For the PFICs listed below, the partnership has received a PFIC Annual Information Statement (for direct investments) and/or a PFIC Annual Intermediary Statement (for indirect investments) containing the required information and statements pursuant to Reg. §§ 1.1295-1(g)(1) and 1.1295-1(g)(3) for its direct and/or indirect investments, respectively. The information below is provided to enable you to make a section 1295 Qualified Electing Fund ("QEF") election with respect to your indirect interest in these PFICs. The partnership cannot make this election at the fund level as it is not the initial U.S. shareholder. The following income items have NOT been included in your distributive share of taxable income on your K-1. Should you qualify for QEF treatment, your pro-rata share of ordinary earnings reported below should be added to Ordinary Income on your K-1. Your pro-rata share of capital gains reported below should be added to capital gains included on Line 9 of your K-1. If you choose not to make the QEF election, or if you are not eligible to make the election, none of the income items reported below should be added to your taxable share of income from this partnership.

Partner # 1

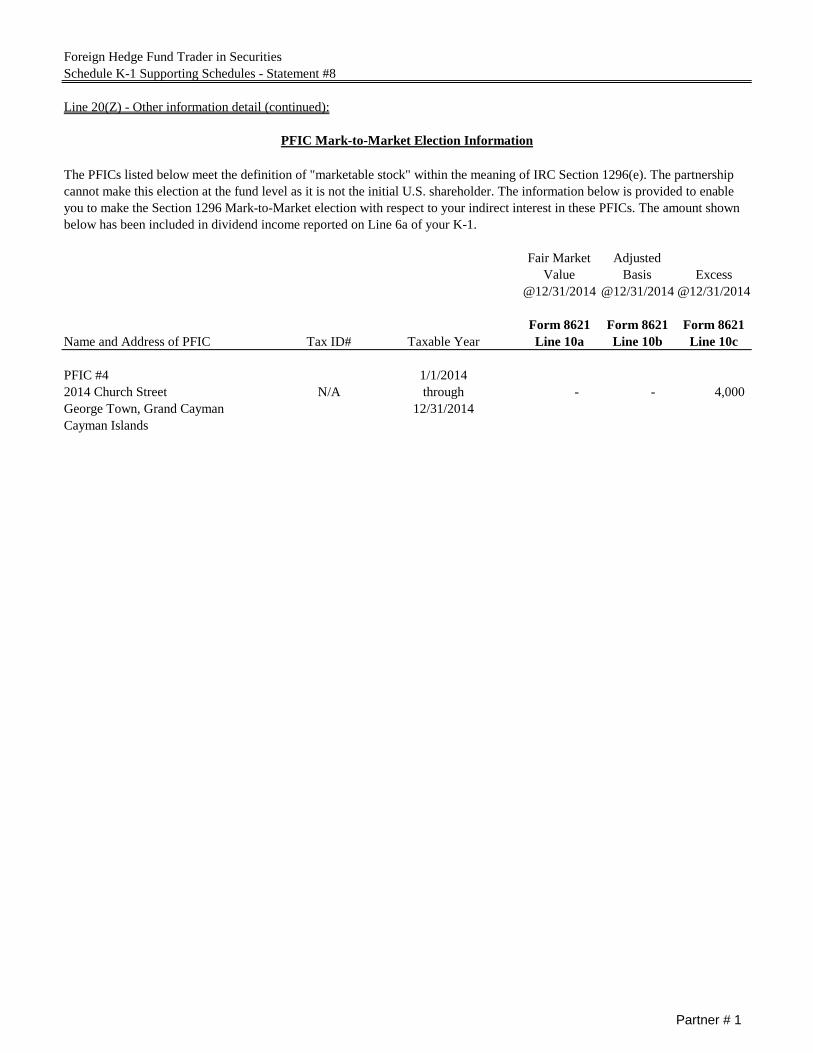

Foreign Hedge Fund Trader in Securities Schedule K-1 Supporting Schedules - Statement #8

Line 20(Z) - Other information detail (continued):

Excess@12/31/2014 @12/31/2014 @12/31/2014

Form 8621 Form 8621 Form 8621Name and Address of PFIC Tax ID# Line 10a Line 10b Line 10c

PFIC #42014 Church Street N/A - - 4,000 George Town, Grand CaymanCayman Islands

12/31/2014

The PFICs listed below meet the definition of "marketable stock" within the meaning of IRC Section 1296(e). The partnership cannot make this election at the fund level as it is not the initial U.S. shareholder. The information below is provided to enable you to make the Section 1296 Mark-to-Market election with respect to your indirect interest in these PFICs. The amount shown below has been included in dividend income reported on Line 6a of your K-1.

Fair Market Value

Adjusted Basis

Taxable Year

1/1/2014through

PFIC Mark-to-Market Election Information

Partner # 1

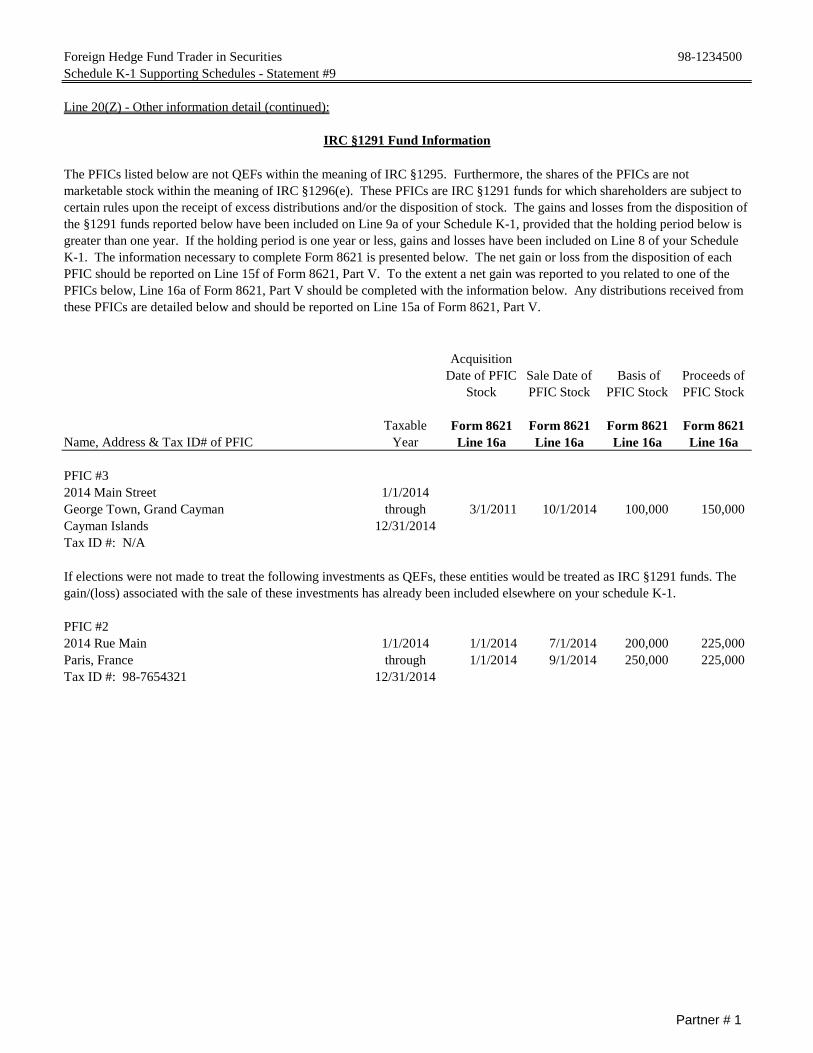

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #9

Line 20(Z) - Other information detail (continued):

Taxable Form 8621 Form 8621 Form 8621 Form 8621 Name, Address & Tax ID# of PFIC Year Line 16a Line 16a Line 16a Line 16a

PFIC #32014 Main Street 1/1/2014George Town, Grand Cayman through 3/1/2011 10/1/2014 100,000 150,000 Cayman Islands 12/31/2014Tax ID #: N/A

PFIC #22014 Rue Main 1/1/2014 1/1/2014 7/1/2014 200,000 225,000 Paris, France through 1/1/2014 9/1/2014 250,000 225,000 Tax ID #: 98-7654321 12/31/2014

If elections were not made to treat the following investments as QEFs, these entities would be treated as IRC §1291 funds. The gain/(loss) associated with the sale of these investments has already been included elsewhere on your schedule K-1.

IRC §1291 Fund Information

The PFICs listed below are not QEFs within the meaning of IRC §1295. Furthermore, the shares of the PFICs are not marketable stock within the meaning of IRC §1296(e). These PFICs are IRC §1291 funds for which shareholders are subject to certain rules upon the receipt of excess distributions and/or the disposition of stock. The gains and losses from the disposition of the §1291 funds reported below have been included on Line 9a of your Schedule K-1, provided that the holding period below is greater than one year. If the holding period is one year or less, gains and losses have been included on Line 8 of your Schedule K-1. The information necessary to complete Form 8621 is presented below. The net gain or loss from the disposition of each PFIC should be reported on Line 15f of Form 8621, Part V. To the extent a net gain was reported to you related to one of the PFICs below, Line 16a of Form 8621, Part V should be completed with the information below. Any distributions received from these PFICs are detailed below and should be reported on Line 15a of Form 8621, Part V.

Acquisition Date of PFIC

StockSale Date of PFIC Stock

Basis of PFIC Stock

Proceeds of PFIC Stock

Partner # 1

Foreign Hedge Fund Trader in Securities 98-1234500Schedule K-1 Supporting Schedules - Statement #10

Line 20(Z) - Other information detail (continued):

TaxableYear

PFIC #12012 Main Street 1/1/2014London, England through Common 6/30/2014 1,000 10,000United Kingdom 12/31/2014 Class ATax ID #: N/A

PFIC #22012 Rue Main 1/1/2014Paris, France through Common 2,000 20,000Tax ID #: 98-7654321 12/31/2014 Class A

PFIC #42012 Church Street 1/1/2014George Town, Grand Cayma through Common 3,000 30,000Cayman Islands 12/31/2014 Class A

PFIC #5111 Front Street 1/1/2014Hamilton, HM11 through Preferred 4,000 40,000 §1291 Fund - Bermuda 12/31/2014 Class B

Dependent on Partner Election

Dependent on Partner Election

Dependent on Partner Election

Dependent on Partner Election

Dependent on Partner Election

Dependent on Partner Election

§1291 Excess

Distribution or

§1293/§1295

Inclusion Amount

Fair Market Value of

Shares Held at End of

Year Name, Address &Tax ID# of PFIC

Date of Shares

Acquired During Year

Number of Shares Held

at End of Year

Description of Class of

Shares Type of

PFIC

PASSIVE FOREIGN INVESTMENT COMPANY INFORMATION (CONTINUED)

IRC §1298(f) Reporting

Generally, Temporary Regulation §1.1298-1T requires shareholders that are the first U.S. person in the chain of ownership of a PFIC to complete Form 8621, Part I for each PFIC owned by the shareholder during the shareholder's taxable year. Certain exceptions to these filing requirements are discussed in the instructions to Form 8621 and Treasury Regulation §1.1298.

The partnership is a foreign partnership, and as such cannot satisfy the filing requirements of its U.S. partners. The information to enable U.S. persons to comply with their Form 8621, Part I filing requirements are provided for each PFIC held by the partnership during the tax year.

Partner # 1

OMB No. 1545-0123

Schedule K-1

(Form 1065) 2014Department of the Treasury Internal Revenue Service

For calendar year 2014, or tax

year beginning , 2014

ending , 20

Partner’s Share of Income, Deductions, Credits, etc. See back of form and separate instructions.

651113 Final K-1 Amended K-1