Embed Size (px)

Citation preview

Benfield v Farebrother [2011] NTSC 65

PARTIES: JULIA BENFIELD

v

JAMIN FAREBROTHER

TITLE OF COURT: SUPREME COURT OF THE

NORTHERN TERRITORY

JURISDICTION: SUPREME COURT OF THE

TERRITORY EXERCISING

TERRITORY JURISDICTION

FILE NO: 36 of 2010 (21013180)

DELIVERED: 30 AUGUST 2011

HEARING DATES: 16, 17, 18, 20 MAY 2011 AND

WRITTEN SUBMISSIONS TO 29 JULY

2011

JUDGMENT OF: MASTER LUPPINO

CATCHWORDS:

De Facto Relationships – Application for adjustive property order – Factors

relevant to determining the duration of the relationship – Principles relevant

to assessment of entitlements – Approach to be taken in determining

entitlements – Time limit for commencing actions under the Act.

Practice and Procedure – Sufficiency of prayer for relief – Seeking relief not

claimed on the pleadings – Request for extension of limitation period made

after closing of evidence.

De Facto Relationships Act ss 3A, 14, 15, 16, 18

Supreme Court Rules r 13.02

Dare v Pulham (1982) 148 CLR 658;

Blay v Pollard [1930] 1 KB 628;

Wicks v Bennett (1921) 30 CLR 80;

Aon Risk Services Australia Ltd v Australian National University (2009) 239

CLR 175.

Kardos v Sarbutt (2006) 34 Fam LR 550.

Evans v Marmont (1997) 21 Fam LR 760.

Parker v Parker (1993) 16 DFC 95-139.

Ottley v Chester [2010] NTSC 38.

Grant, Civil Procedure Northern Territory.

Williams, Civil Procedure.

REPRESENTATION:

Counsel:

Plaintiff: Mr Black

Defendant: Ms Gillies

Solicitors:

Plaintiff: Cecil Black Family Lawyers

Defendant: Ward Keller Lawyers

Judgment category classification: B

Judgment ID Number: LUP1106

Number of pages: 53

1

IN THE SUPREME COURT OF THE NORTHERN TERRITORY OF AUSTRALIA AT DARWIN

Benfield v Farebrother [2011] NTSC 65

No. 36 of 2010 (21013180) BETWEEN:

JULIA BENFIELD

Plaintiff AND:

JAMIN FAREBROTHER Defendant CORAM: MASTER LUPPINO

REASONS FOR DECISION

(Delivered 30 August 2011)

[1] This is an application by the Plaintiff for an adjusting property order

pursuant to section 18 of the De Facto Relationships Act (“the Act”).

[2] The prayer for relief in the Plaintiff’s Statement of Claim sought orders as

follows:-

1. That the Plaintiff retains the property at 45 McInnis Circuit, Driver;

2. That the Defendant settle upon the Plaintiff such other property as it is in the opinion of this Court necessary to effect the principles set out in section 18 of the De Facto Relationships Act; and

3. That the Defendant retain his property interests.

2

[3] When the Plaintiff’s case was opened at trial it was revealed that the

specific orders that the Plaintiff sought were for a payment representing

40% of the net pool on the basis that the Plaintiff retained her house situate

at 45 McInnis Circuit, Driver (“the Driver Property”) and with an

appropriate adjustment on that account. The Defendant opposes any order in

favour of the Plaintiff and seeks orders dismissing the Plaintiff’s claim. The

Defendant asserts that the distribution of assets to date has resulted in a

distribution in favour of the Plaintiff more favourable then she would be

entitled to under the Act.

[4] The first mention that the Plaintiff sought a distribution based on 40% of the

net pool came in the Plaintiff’s opening. The Defendant complains of the

late notice of the precise orders that the Plaintiff seeks. However in my view

the prayer for relief gives sufficient notice of the nature of the Plaintiff’s

claim. Order 13.02(1)(c) of the Supreme Court Rules (“the Rules”), which is

set out in full below, only requires a pleading to “state specifically the relief

or remedy, if any, claimed”. The extant prayer for relief sufficiently

complies.1

[5] There is no dispute that the parties were in a de facto relationship. The

satisfaction of the pre-requisites specified in sections 15 and 16 of the Act

has been admitted. There is a dispute both as to the commencement date and

the termination date of the relationship. The Plaintiff claims that it

1 See generally, Grant, Civil Procedure Northern Territory at para 5.13.112 and Williams, Civil

Procedure at para 13.02.40

3

commenced on 25 August 2002 whereas the Defendant says that it was in

late October or early November of that year. The Plaintiff says that the

relationship ended on 28 November 2008. The Defendant says that the

relationship ended in June 2006.

[6] Much turns on which of the two dates I find was the commencement date

and both parties have made adverse suggestions against the other concerning

motives and possible advantage derived from their versions. Mr Black,

counsel for the Plaintiff submitted that the Defendant’s pre relationship

contributions benefit from a finding of the later date as the evidence reveals

that the Defendant’s savings were then approximately $30,000.00 more. Ms

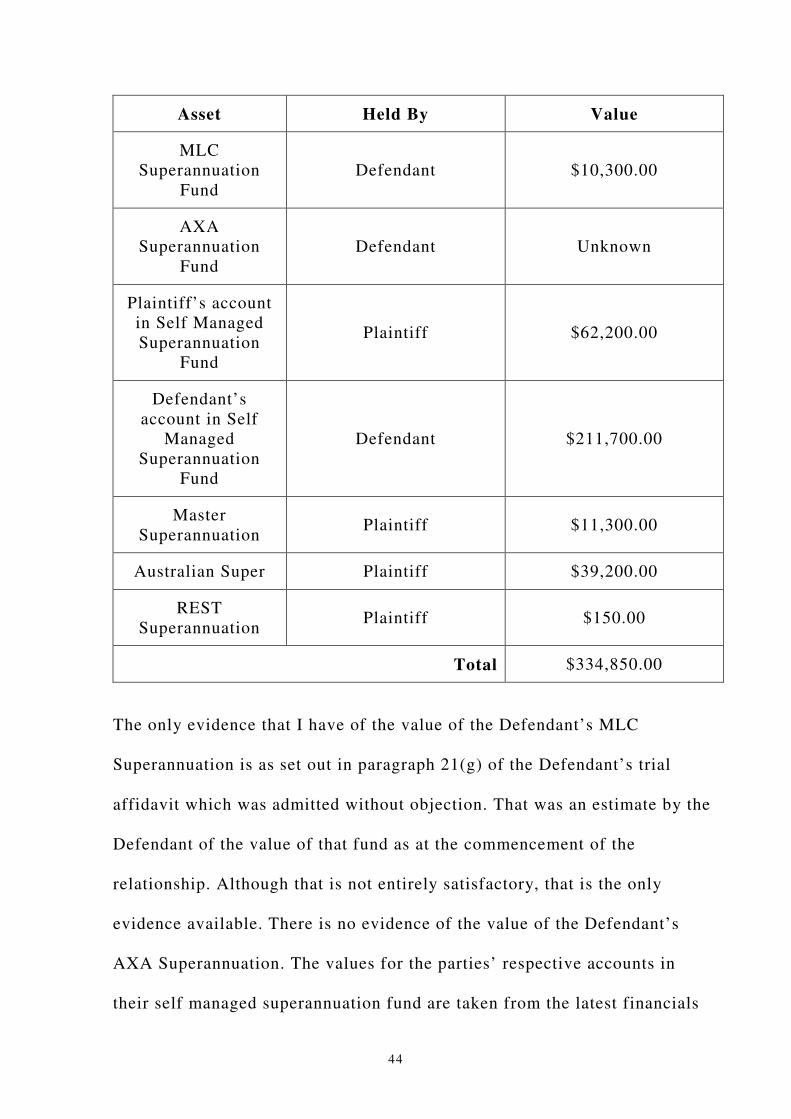

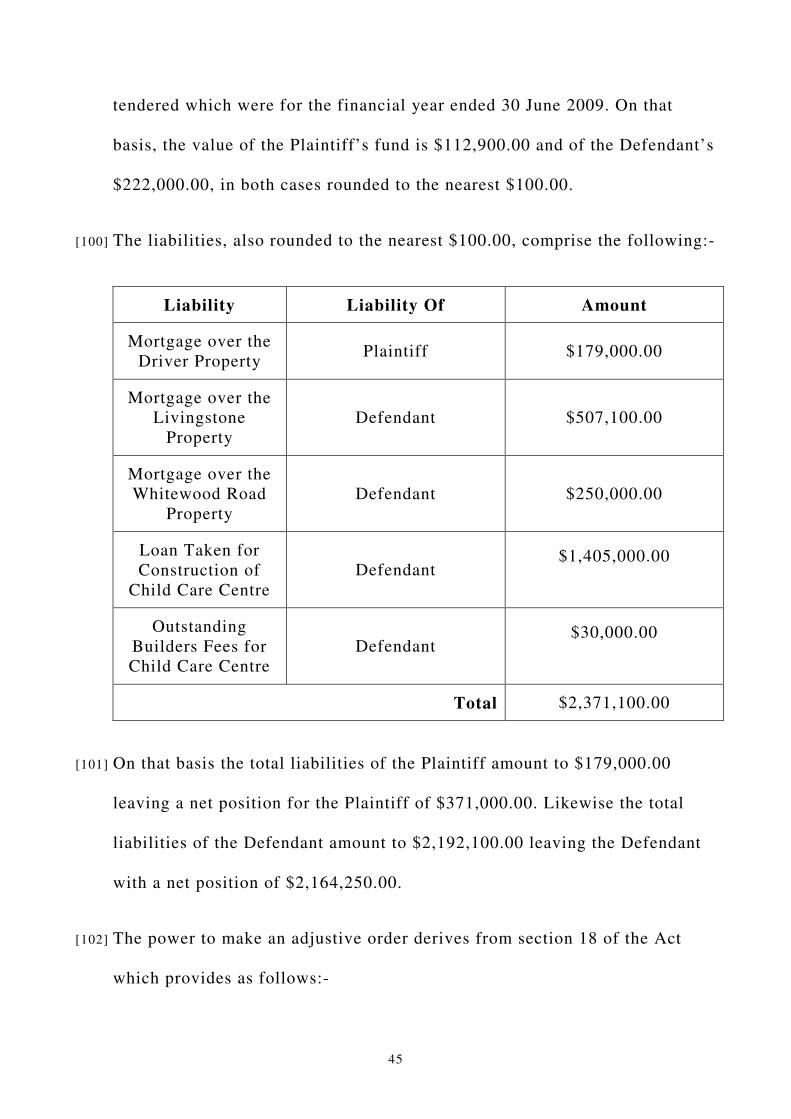

Gillies for the Defendant points out that the basis of the Plaintiff’s claim for

non-financial contribution in respect of the acquisition of the Howard

Springs Veterinary Clinic (“HSVC”) is adversely affected by a finding in

favour of the Defendant’s version. Agreement for the sale and purchase of

that practice was reached in September 2002 with completion occurring in

February 2003. Although the Plaintiff asserts a contribution to that practice

beyond its acquisition, relevant to the issue of the commencement date of

the relationship is that the Plaintiff alleges that the Defendant purchased the

practice as a result of the Plaintiff’s suggestion, the underlying implication

being that absent that suggestion, the Defendant would not have purchased

that practice.

[7] The dispute as to the date that the relationship ended is more significant

however. The proceedings in this matter were commenced on 19 April 2010

4

hence if the relationship ended anytime prior to April 2008 then the

Plaintiff’s application is out of time and requires leave pursuant to section

14(2) of the Act.

[8] The Plaintiff has sought the necessary leave in the event that I find that the

proceedings have not been commenced within the time mandated by section

14(1) of the Act. The request was made late in the proceedings. It was made

in the Plaintiff’s written submissions filed after the Defendant’s submissions

and approximately two months after the evidence closed.

[9] The proceedings were commenced by Originating Motion filed on 19 April

2010. The relief claimed was a declaration as to the existence of a de facto

relationship, an adjusting property order and costs. After I made an order

that the proceeding continues as if commenced by writ, a Statement of Claim

was filed by the Plaintiff on 27 September 2009. There it was pleaded that

the de facto relationship commenced on 25 August 2002 and ended on 28

November 2008. The prayer for relief does not seek the declaration as to the

existence of a de facto relationship which was in the prayer for relief in the

Originating Motion. The Statement of Claim then elaborates on the adjusting

property order sought.

[10] The Defence denied the alleged separation date and asserted a separation

date of November 2006. Moreover the Defence sought an order for dismissal

of the Plaintiff’s claim as being out of time. There has not been an

amendment to the Statement of Claim to seek an order for an extension.

5

[11] The basic purposes of pleadings are to give notice to the other party of the

case they must prepare to meet as well as to define the issues for trial.

Notice ensures procedural fairness and the general rule that follows is that

relief is confined to that available on the pleadings: Dare v Pulham.2 Cases

must be decided on the issues raised on the pleadings and if it is intended to

raise other issues then there must be an amendment: Blay v Pollard.3

[12] Rule 13.02 of the Rules provides as follows:-

13.02 Content of pleading

(1) A pleading shall:

(a) contain in a summary form a statement of all the material facts on which the party relies but not the evidence by which those facts are to be proved;

(b) where a claim, defence or answer of the party arises by or under an Act identify the specific provision relied on; and

(c) state specifically the relief or remedy, if any, claimed.

(2) A party may, by his pleading:

(a) raise a point of law; and

(b) plead a conclusion of law if the material facts supporting the conclusion are pleaded.

[13] Although Rule 13.02(1)(c) allows general relief to be claimed as the

Plaintiff has done in the prayer for relief relative to the adjusting property

order sought, the Court will not grant relief that is not specifically claimed

unless it is consistent with the case made out on the pleadings: Wicks v

2 (1982) 148 CLR 658 3 [1930] 1 KB 628

6

Bennett.4 The rather significant consequence that follows as a result of the

state of the pleadings is that, were I to find that the relationship ended prior

to April 2008, the Plaintiff’s claim stands to be dismissed as there has not

been an amendment to the Statement of Claim.

[14] An application to amend the Statement of Claim made in the course of the

Plaintiff’s written submissions and without a formal application, after the

evidence has closed and after the Defendant has made submissions would

likely be refused. The Defendant clearly made the time point an issue in his

Defence yet no attempt has been made to amend the Statement of Claim.

None of the usual evidence when an application for an extension of time

pursuant to section 14(2) is sought, such as an explanation for the delay has

been led. The Defendant can, in the absence of an amendment to the

pleadings, rightly claim to have foregone calling any relevant evidence on

this issue. The Defendant claims that raising the issue in this way and after

the evidence has closed has the effect of denying procedural fairness. I

agree. The Plaintiff will, in addition to a grant of leave to amend the

pleadings, also require leave to re-open the evidence. In those circumstances

leave would likely be refused in accordance with the principles set out in

Aon Risk Services Australia Ltd v Australian National University.5

[15] The Plaintiff submits that I should decline to make an order which denies

the Plaintiff any substantive relief merely because there has not been a

4 (1921) 30 CLR 80 5 (2009) 239 CLR 175

7

formal application for leave as the result would not be just and equitable as

required by the Act. Presumably that refers to that phrase as it appears in

section 18(1) of the Act. I think that confuses the principles relevant to the

making of an adjusting property order and the procedural principles relative

to claims and pleadings. The former is regulated by the Act whereas the

latter is regulated by the Rules and common law.

[16] Dealing first with the evidence relevant to these issues, the starting point is

section 3A of the Act. This sets out various indicia for determining the

existence of a de facto relationship. It is therefore relevant to both the

commencement and cessation date. That section provides:-

3A De facto relationships

(1) For this Act, 2 persons are in a de facto relationship if they are not married but have a marriage-like relationship.

(2) To determine whether 2 persons are in a de facto relationship, all the circumstances of their relationship must be taken into account, including such of the following matters as are relevant in the circumstances of the particular case:

(a) the duration of the relationship;

(b) the nature and extent of common residence;

(c) whether or not a sexual relationship exists;

(d) the degree of financial dependence or interdependence, and any arrangements for financial support, between them;

(e) the ownership, use and acquisition of property;

(f) the degree of mutual commitment to a shared life;

8

(g) the care and support of children;

(h) the performance of household duties;

(i) the reputation and public aspects of their relationship.

[17] These indicia are not exhaustive. The existence or absence of any one or

more is not determinative. The indicia are a guide to determining whether

the parties are in a marriage-like relationship.

[18] Having regard to those indicia, the relevant background facts are that the

parties met in early July 2002 at a social function. They began sharing a

house in the same month. There is no dispute that initially the relationship

was simply one of housemates. The Plaintiff asserts that a de facto

relationship commenced on or about 25 August 2002. That date apparently

coincides with the time when the parties first had sexual intercourse. The

Defendant says that the change in the relationship from housemates to de

facto partners did not occur until late October or early November 2002.

Although the Defendant initially deposed to sexual relations having

commenced in late September or early October 2002, he conceded in cross

examination that it occurred at the time the Plaintiff said. The Defendant

maintained that until late September or early October 2002 the Plaintiff was

in a relationship with a person named Steve. The Plaintiff however said that

her relationship with that person had ended before she met the Defendant. If

that were correct then it is curious that the Defendant knew anything about

Steve. She was not challenged much about her version in this context.

9

[19] The Defendant was challenged on his version of events and ultimately made

a number of concessions. Although Mr Black submitted that the Defendant

had agreed in cross examination that the Plaintiff had told the Defendant

that her relationship with Steve had ended and at a time consistent with the

Plaintiff’s version, that is not apparent from the transcript, particularly at

the reference cited by Mr Black in his submissions. At best the Defendant

acknowledges that the Plaintiff was attempting to dissuade Steve from

seeing her but it is clear from his evidence that this was within a timeframe

which is consistent with the Defendant’s stated position.

[20] The Plaintiff also relied on being sent flowers by the Defendant in early

September 2002, she claiming it as indicative of the relationship having

commenced by then. The Defendant on the other hand said that it was a

courting gesture only and done in the hope that the Plaintiff would end her

relationship with Steve. Either version is equally plausible.

[21] The Defendant describes the state of affairs between the parties during this

disputed period as being preliminary to a relationship. The Defendant’s

submission is that there is no evidence to show that there was a continuing

sexual relationship beyond the first admitted encounter. That is correct and

although it is a notable omission, it is not conclusive either way.

[22] Equally relevant however is the lack of evidence, other than possibly in the

form of the bare assertion by the Plaintiff that they were in a de facto

relationship, that they presented externally as a de facto couple. What is

10

lacking in the Plaintiff’s case is evidence commonly led when the existence

of a relationship is disputed such as evidence of how others viewed the

relationship between the parties during the disputed period (section

3A(2)(i)). I consider the absence of that evidence to be very relevant. Also

lacking is evidence indicating how the Defendant viewed that relationship

given that mutuality to a certain extent is required. Leaving aside her bare

assertion, the Plaintiff has not led any evidence to challenge the Defendant’s

version in respect of this indicium. Although there is evidence which could

demonstrate that the Plaintiff believed that a de facto relationship had

commenced, there is no evidence which goes to demonstrate that the

Defendant viewed the relationship as marriage-like (section 3A(2)(f)).

[23] As to the termination of the relationship, numerous items of evidence are

relevant in terms of the indicia in section 3A of the Act. The Plaintiff’s

nominated termination date of 28 November 2008 is the date that she moved

out of the home where the parties last resided together namely, at Bradley

Road Livingstone (“the Livingstone Property”). The Defendant accepts that

physical separation occurred at about that time but says that the cohabitation

after June 2006 was one of separation under the same roof.

[24] The indicium of financial interdependence (section 3A(2)(d)) is not

determinative in this case as the parties mostly kept their financial affairs

separate throughout the relationship. The only asset which the parties had

jointly owned was the veterinarian supply business established by the parties

and known as Monsoon Veterinary Supplies Pty Ltd (“Monsoon”) and which

11

was sold early in 2008. However the Defendant established a private

superannuation fund in October 2006, i.e., around, and possibly after, the

date that the Defendant alleges a separation occurred. Both parties were

named as trustees and both parties contributed to the fund. I consider it to be

unlikely that the fund would have been set up in this way if the parties had

been separated at that time.

[25] The purchase of the property at 45 McInnis Circuit Driver (“the Driver

Property”) by the Plaintiff is a very significant factor in my view. It appears

to be the only real estate that the Plaintiff ever purchased. The Plaintiff

purchased that in July 2008 utilising in part some of the funds derived from

the sale of Monsoon. The Plaintiff told the Defendant nothing about that.

Despite that she would have spent time locating and inspecting a number of

properties, negotiating the purchase, arranging finance and attending to

numerous other matters in the lead up to settlement, she failed to tell the

Defendant anything at all about that purchase yet claims to be in a marriage-

like relationship throughout that time. Her explanation was that she feared

the Defendant would have been physically aggressive towards her. That does

not sit well with the evidence and I was most unimpressed with that

explanation having regard to the overall evidence concerning the

relationship. I reject that explanation. The Plaintiff’s failure to disclose that

acquisition is contraindicative of a relationship existing at that time

although that needs to be assessed in light of the evidence that the

12

relationship was fragile by that time and that it occurs less than four months

before the latest conceivable separation date.

[26] The other evidence relevant to this issue is summarised below. It can be

seen that typical evidence concerning public aspects such as socialising with

friends, attending at functions, holidaying together and the like is lacking.

The evidence is:-

1. The Plaintiff and the Defendant spent Christmas 2006 together and

with the Plaintiff’s family interstate;

2. The Plaintiff gave the Defendant a puppy as a gift for Christmas

2006;

3. The Plaintiff participated in the move to the Livingstone Property,

paid for the removalists and purchased an outdoor setting for that

home;

4. The Plaintiff alleges, and the Defendant disputes, an arrangement for

sharing of household chores and expenses at the Livingstone

Property;

5. The Plaintiff alleges (and the Defendant disputes) matters which

were led primarily as evidence of indirect non-financial contributions

but which are also relevant to the question of the existence or extent

of the de facto relationship such as gardening, cleaning, cooking,

laundry and household chores;

13

6. The Defendant bought a new bed for the parties to share at the

Livingstone Property. The Defendant admits to sharing the bed with

the Plaintiff but claims it was a gift for the Plaintiff;

7. The Defendant gave the Plaintiff an expensive watch for Christmas

2007;

8. The Defendant wrote to the Plaintiff’s parents in February 2009. In

that letter he thanked them for their friendship “...over the last 6-7

years since I have been going out with Julia.” He added that “Julia

and I had drifted in the last 3-4 years and we seemed not to be a

couple anymore...”. Both counsel relied on this letter to support their

case. Considering the letter as a whole, I think it is neutral as it is

consistent with both versions;

9. The socialising together by the parties ended towards the end of 2006

or early 2007, albeit that it did not appear to be a significant feature

of their relationship even during the undisputed period of the

relationship.

[27] Relevant also is that throughout the disputed period there were ongoing

sexual relationships. The Defendant’s explanation for the parties sharing a

bed at the Livingstone Property is that neither party wanted to move into the

separate granny flat at that property. Why the Defendant apparently

considered that to be the only alternative to sharing a bedroom was not

explained. That situation persisted for over 18 months which seems unlikely

14

in the context of the evidence as a whole if the parties were separated as the

Defendant claims.

[28] There were also two periods in 2007 when the Plaintiff temporarily moved

from the Livingstone Property and moved in with a friend. The duration was

in dispute and the versions vary from a span of a weekend only up to a

couple of weeks. There is also some controversy regarding the surrounding

circumstances. Both parties agreed that the relationship was fragile at those

times. Ms Gillies submitted that these physical separations were particularly

telling in establishing the separation however I think it is equally telling that

the Plaintiff returned on both occasions. The evidence of counselling is also

evidence which is consistent with both versions.

[29] What is more significant about that in my view is the Defendant’s evidence

in his trial affidavit, that he asked the Plaintiff to return on the occasion of

the last of those separations. The Defendant offers an explanation for that

but I do not consider that to be credible. The Defendant deposes that he said

to the Plaintiff “…I don’t want you to move out like this. Come back and

save money and move out properly…”. I am uncertain what those last words

mean however, given that in cross-examination the Defendant said, more

than once, that the relationship was a big mistake on his part and that he

wished that he had broken it off earlier, it is anomalous that he asked her to

return after she actually left. That claim by the Defendant lacks credit in my

view. It is more consistent with the Plaintiff’s version that the relationship

15

was still on foot albeit that it was fragile and the parties were attempting to

resolve their issues.

[30] The Defendant also gave some unconvincing explanations when matters

which contradicted his claimed separation date were put to him. For

example, when asked why he gave the Plaintiff an expensive watch as a gift

for Christmas in 2007, his explanation was that it was given as a departing

gift, similar in nature to a gift given to a departing employee. If it is a

departing gift, then it is given some 12 months after the separation date he

alleges. Although he agreed it was given at Christmas 2007, he said that it

was not a Christmas gift. I think his explanation is nonsense, particularly as

on his version they had already separated as a couple by then.

[31] The Defendant acknowledged that the move to the Livingstone Property in

February 2007 represented an obvious opportunity to end his cohabitation

with the Plaintiff. However he said he did not do so as he claimed he

“…didn’t have the heart to kick her out.” This precedes the occasion when

he implored her to return after her departure to live with her friend. That

evidence is likewise inconsistent and unconvincing.

[32] Based on the foregoing, overall I am not satisfied, having regard to all of the

circumstances of the case and in particular the indicia in section 3A of the

Act, that the evidence establishes the existence of a de facto relationship as

at the commencement date the Plaintiff nominates. The evidence is not

16

sufficient in my view and I find that the relationship commenced in late

September 2002.

[33] As to the date of the termination of the relationship, there is no dispute that

there was a de facto relationship within the meaning of the Act until at least

late 2006. Beyond that the duration of the relationship falls to be resolved

based on the credibility of the parties given the extent of, or lack of,

objective corroborating evidence. The evidence of both parties on the issue

of the termination date was tainted to some extent. Notwithstanding that I

have rejected the Plaintiff’s evidence as to the commencement date, on the

question of the termination date, I prefer the Plaintiff’s evidence. I find that

the relationship ended on or about 28 November 2008. Clearly there had

been a deterioration of the relationship for approximately one year before

this date but that relates to the quality of the relationship, not its existence.

[34] That largely deals with the significant areas of factual dispute. The asset

pool and financial resources is largely agreed. The areas in dispute relate

largely to indirect and non-financial contributions. Having regard generally

to my assessment of the credibility of witnesses and also for the reasons

which follow, other than the specific instances where I indicate specifically

that I prefer the evidence of the Plaintiff, I prefer the evidence of the

Defendant to that of the Plaintiff wherever the two are in conflict. In

arriving at that I have had regard to the extent that the evidence is

corroborated either by objective evidence or by other evidence which I am

prepared to accept.

17

[35] I start the process of determining what, if any, adjusting order is appropriate

by looking at the assets and liabilities of the parties at the commencement of

the relationship. Leaving aside the dispute about the indirect contribution to

HSVC, there is otherwise no dispute as to the asset position at the

commencement of the relationship. At the time of the commencement of the

relationship the Plaintiff had minimal assets comprising sundry furniture and

household effects of approximately $5,000.00 in value, approximately

$7,000.00 in savings and a superannuation account claimed by the Plaintiff

to be worth less than $10,000.00. This was not proved by any documentary

evidence but was not disputed by the Defendant. Her income for the

financial year ending 30 June 2003 was $32,760.00.

[36] At the time of the commencement of the relationship the Defendant was a

qualified veterinarian and had worked in that capacity for some nine years at

various locations. He was employed at HSVC. He had savings of

approximately $60,000.00, shareholdings worth approximately $120,000.00,

sundry furniture worth approximately $5,000.00 and a motor vehicle

claimed to be of $30,000.00, a value disputed by the Plaintiff. He also had a

superannuation account which he says, had an account balance of the order

of $10,300.00. Although the Plaintiff does not accept that, no evidence

contradicting that claim was produced. His income for the financial year

ending 30 June 2003 was $107,170.00.

[37] The Defendant was extensively cross-examined as to the source of

approximately $21,500.00 of his claimed savings however as I am satisfied

18

that it was part of the Defendant’s assets at the time, I do not consider that

anything turns on the source of those savings.

[38] The dispute as to the then value of the Defendant’s motor vehicle

complicates matters as I have no basis to resolve that. Expert evidence

would be required for that purpose, hence resolving it based on the

credibility of the parties is not an option. But for that, for the reasons which

appear elsewhere in these reasons, I would prefer the evidence of the

Defendant. On that basis, the Plaintiff brought into the relationship 5.3% of

a total pool of some $227,000.00. For comparison only, if I were to reduce

the value of the Defendant’s motor vehicle by one third, that percentage

would change to 5.5%, hence the difference is small in any case.

[39] Clearly the Defendant’s assets at the commencement of the relationship far

outweighed those of the Plaintiff. Similarly in respect of earning capacity.

To the extent that taxation returns were tendered, they indicate that the

parties earnings were:-

19

Financial Year Plaintiff Defendant

2001/2002 - $53,795.00

2002/2003 $32,760.00 $107,170.00

2003/2004 $36,689.00 $144,677.00

2004/2005 $45,371.00 -

2005/2006 $40,838.00 $117,093.00

2006/2007 $83,906.00 -

2007/2008 $163,595.00 $214,639.00

2008/2009 - $258,802.00

[40] The income for the Plaintiff for the financial years 2006/2007 and

2007/2008 were extraordinary in that they reflected the Plaintiff’s

shareholder profits from Monsoon as well as the Defendant’s share of those

profits. Those extraordinary amounts therefore relate directly to issues of

contribution to the Monsoon business and I will discuss that in more detail

below.

[41] The assets acquired by the parties during the course of the relationship

comprise:-

1. HSVC by the Defendant;

2. The property at 16 Smyth Road, Howard Springs (“the Smyth

Road Property”) by the Defendant;

3. The property at 290 Whitewood Road Howard Springs (“the

Whitewood Road Property”) by the Defendant;

20

4. The Livingstone Property by the Defendant;

5. The Monsoon business by both;

6. The Driver Property by the Plaintiff.

In addition, each party made various contributions to their superannuation

accounts.

[42] Commencing with the HSVC, it is conceded and the evidence confirms that

with one relatively insignificant exception which is discussed below, the

Plaintiff made no financial contribution to the acquisition of that practice.

The major claim to contribution to the acquisition of that practice by the

Plaintiff on her case is that she suggested or motivated the Defendant to

acquire that practice. That is disputed by the Defendant. The practice was a

very important asset on my view of the evidence. The income derived from

that funded the acquisition of all other assets by the Defendant and the bulk

of the parties’ living expenses, albeit not exclusively in the case of the

latter.

[43] The Defendant’s evidence in this respect is that he came to Darwin

specifically with the objective of working in a practice and to ultimately

acquire that practice. His evidence is that he commenced working at HSVC

with that objective. He denied that it was the Plaintiff’s idea that he did so.

The valuation report tendered without challenge suggests that process is a

21

usual and established course for anyone wishing to purchase a veterinary

practice in major centres.

[44] The Defendant’s letter of offer of employment at the clinic was tendered. It

is dated 13 July 2002. It provides in part for a remuneration based on an

incentive scheme to be negotiated based on performance and also

acknowledged that “...opportunities for leasing or buying into the practice if

mutually agreed” would also be negotiated.

[45] I accept that as corroboration of the Defendant’s evidence that he

commenced work at HSVC with the intention of acquiring the practice.

Although Mr Black sought to make something of the reference to leasing or

buying into the practice as opposed to buying the practice, I consider that to

be irrelevant to the issue. The issue is whether the Plaintiff suggested,

motivated or inspired the Defendant to acquire the practice and the letter

demonstrates that, in one form or another that was the Defendant’s plan

before he met the Plaintiff. The parties met three days before the date of that

letter, hence the Plaintiff’s version as attested before me cannot be correct. I

therefore reject the Plaintiff’s evidence on this issue.

[46] There is however one undisputed financial contribution by the Plaintiff to

the acquisition of HSVC. Although there was a dearth of evidence as to the

surrounding circumstances, the evidence reveals that the Plaintiff made a

very short term loan to the Defendant of $5,000.00 to enable him to

complete the purchase of HSVC. The loan was made on 20 February 2003

22

and was repaid on 24 February 2003, i.e., a four day loan. It was apparently

interest free. Absent evidence of the surrounding circumstances and of the

value of this contribution, I consider that the appropriate value is what it

would have cost the Defendant to borrow that amount on commercial terms,

with little formality and for a short term. Often higher than usual rates of

interest are charged for such loans. Even so, if an exceptionally high rate of

say 10% per month were to be charged, that would equate to approximately

$60.00, which is insignificant as a financial contribution against a total cost

of approximately $370,000.00.

[47] Therefore I cannot accept Mr Black’s submission that it was a significant

contribution. He based this on an assertion that it was made at a time when

the Defendant needed support. However there is no evidence of the

surrounding circumstances so there is nothing upon which such a conclusion

can be based. On the contrary, the Defendant’s evidence was that he had an

alternative source if necessary namely, his father.

[48] The purchase of HSVC was completed on 20 February 2003. It is agreed the

total purchase price was $369,435.00 which included the Smyth Road

Property. The purchase price was broken up as to $120,000.00 for the

business and $230,000.00 for the land and buildings. The balance is made up

of amounts for plant, equipment and stock. The Defendant financed the

purchase by way a bank loan of $325,000.00, the short term loan of

$5,000.00 from the Plaintiff referred to above and the balance came from his

own funds.

23

[49] The Defendant retains that practice and continues to practice as a

veterinarian. He has plans to relocate the practice to the Whitewood Road

Property and he has made significant post separation acquisitions of plant

and equipment. The bank loan taken out to finance the acquisition of HSVC

has apparently been repaid. Although the submissions of both parties make

reference to this (the Plaintiff’s submissions alleging repayment from the

practice income and from the proceeds from Monsoon and the Defendant’s

submissions acknowledging the former), nonetheless there was no evidence

about that.

[50] The Plaintiff claims non-financial contributions to the practice in various

forms, most notably by way of after hours assistance to the Defendant for

which she was not remunerated. She also claims that she was instrumental in

the Defendant securing work from the Darwin Turf Club which in turn later

secured work from trainers working at the Darwin Turf Club track. She also

claims a contribution by way of special services to HSVC from Monsoon.

The extent of that contribution is disputed.

[51] The claimed unremunerated work relates to assistance on after hours call

outs and with the visiting clinic at Jabiru. The Jabiru clinic was an initiative

commenced after the Defendant acquired the practice and always occurred

on a Saturday. The Plaintiff claims that she attended to assist on a number of

such trips when the Defendant was the veterinarian who travelled to Jabiru.

There is no precision in the evidence as to the exact number of trips. On the

Plaintiff’s evidence it is between four and eight such trips. I think it is odd

24

that the Plaintiff cannot be more precise when a small number and range is

involved. The Defendant concedes two trips. Only one trip can be verified

by objective evidence in that records of the Plaintiff’s mobile phone indicate

calls made from Jabiru on one occasion.

[52] The Plaintiff also claimed to have assisted with the stock take when the

practice was purchased but that proved to be misleading as she conceded in

cross-examination that she did so at the request of the vendors. She claimed

also to have assisted in obtaining quotes for the purchase of new equipment

but gave no details of this and there is little evidence to assess it as a

contribution. I am reluctant to rely on the Plaintiff’s bare assertions given

the number of instances which show her propensity to exaggerate or

embellish her evidence to her benefit.

[53] The Plaintiff also claimed that she assisted with internal painting of the

HSVC premises but the Defendant denied this. Likewise the Plaintiff

appears to claim an indirect contribution by way of her father performing

repairs to the flyscreens at the premises. That work allegedly took two days.

The Defendant says that the Plaintiff’s father commenced that work but had

to stop after a matter of hours due to feeling unwell. I prefer the Defendant’s

evidence as to the extent of the work performed by the Plaintiff’s father but

in any case, in the absence of evidence of the surrounding circumstances I

am not prepared to treat any work by the Plaintiff’s father as a contribution

by the Plaintiff. The letter from the Defendant to the Plaintiff’s parents in

February 2009 referred to above shows that the Defendant had a good

25

relationship with the Plaintiff’s parents and that may account for any

assistance given by the Plaintiff’s father.

[54] The Plaintiff also asserts, and the Defendant agrees, that she lent the

Defendant her work vehicle for dump runs. There was no evidence of any

detriment to the Plaintiff, either by reason of the loan of her work vehicle or

the assistance by her father. The Plaintiff later submitted that any inflated

price charged by Monsoon for its products should be ignored due to the lack

of detriment to the Defendant’s practice and that submission has equal

application here if consistency is to be maintained.

[55] As to the assistance with after hours call outs, the Plaintiff claims this

occurred both during after hours calls at the clinic as well as visits to

clients’ premises. The extent of this claimed assistance is extensive. The

Plaintiff lists many tasks in her affidavit but lacks any useful details as to

the frequency duration and the like. It reads like a job description for a full

time employee and given the propensity of the Plaintiff to exaggerate her

contribution, which was reinforced by the cross-examination on this issue, I

am not prepared to accept her uncorroborated assertions in the face of the

Defendant’s contradictory evidence. The Defendant concedes there were

some attendances but disputes the frequency claimed by the Plaintiff. The

Defendant’s version is corroborated by other evidence including that of his

practice manager which I am prepared to accept.

26

[56] As for attendances at clients’ premises, some of the occasions which the

Plaintiff claimed as after hours assistance were occasions where the client

was a mutual friend of the parties. The Plaintiff conceded in cross-

examination that some of those visits were more for the social visit than for

any need to provide assistance to the Defendant. Her evidence in chief

portrayed a different impression.

[57] Other instances involved claimed call outs where I consider that it was

established sufficiently that a nurse was not required such as attendances to

treat a hoof abscess and cases of horse colic. The Defendant’s evidence,

which the Plaintiff did not effectively challenge and which I accept, was to

the effect that a nurse was not required to assist with such cases. However

the Plaintiff attempted to create a different impression and again I feel this

is another instance of embellishment by her.

[58] The practice accounting and other records do not support the Plaintiff’s

version. The records are used in part for billing purposes. The practice made

a charge for a nurse’s attendance on after hours call outs. When challenged

that the after hours records of the practice where inconsistent with her

claimed after hours attendances, the Plaintiff suggested falsification of those

records on the part of the Defendant. I consider that to be a very serious

allegation made without any apparent or objective basis. It reflects adversely

on the Plaintiff. I reject Mr Black’s submission that the evidence of the

Plaintiff only alleged an oversight by the Defendant. In my view, it was

clear that the Plaintiff suggested falsification.

27

[59] The Plaintiff also sought to take credit for suggesting to the Defendant that

he undertake equine work. Similar to her evidence that she suggested to the

Defendant that he purchase HSVC, she claims that she suggested he

approach the Darwin Turf Club to become the club’s race day veterinarian.

That contrasts the evidence of the Defendant that he always had that interest

in equine work and his version was corroborated by objective evidence that

pre-relationship he attended an equine medicine course. The Defendant’s

evidence is that he had arranged to be the Darwin Turf Club’s race day

veterinarian before he and the Plaintiff commenced house sharing.

Additionally an invoice, the date of which precedes the commencement of

the relationship, disclosed that he had worked as the race day veterinarian at

the Darwin Turf Club. All that again points to embellishment by the Plaintiff

of her evidence.

[60] Lastly the Plaintiff claims non-financial contribution by having made after

hours deliveries from the Monsoon business to the Defendant’s practice.

Cross-examination revealed that was also an embellishment. The Plaintiff

conceded in cross-examination that such a service was provided to all

customers of that business and the Plaintiff conceded that HSVC was a

major customer. There is was no evidence that the service was provided to

any greater extent than to any other customer. I reject that claim by the

Plaintiff.

[61] In general terms, for the reasons given to date relative to the assessment of

the parties’ credit and also for the reasons which follow, on this and other

28

aspects of evidence regarding contributions, I prefer the evidence of the

Defendant. I find that the Plaintiff had no input into the Defendant’s

decision to buy HSVC or to undertake equine work or to work at the Darwin

Turf Club. I find that the Plaintiff assisted the Defendant by accompanying

him for the purpose of Jabiru clinics on two occasions. It is difficult to put

an accurate number on the after hours call outs that the Plaintiff attended. I

do not accept that it was as extensive as she claims. The Defendant says that

it was only one or two but I think that understates it. Such a small number as

the Defendant suggests seems unlikely given the number of after hours calls

the Defendant made and as the Plaintiff was a veterinary nurse. That

convenience lends itself to a likely greater use of the Plaintiff’s skill than

the Defendant concedes. I am prepared to treat the number of attendances by

the Plaintiff to assist with after hours calls as ten in all. The number

involved is therefore small.

[62] The net value of HSVC for current purposes is agreed at $361,350.00. The

net value of the Smyth Road Property from which the practice is conducted

is agreed at $600,000.00 for current purposes.

[63] The next asset is the establishment of Monsoon in March 2005. The business

was established in conjunction with Ross Ainsworth who was involved in

the cattle export industry. The start up costs for the business were met

equally by the Defendant and Mr Ainsworth. There was an initial start up

loan from both and further amounts were subsequently provided. It is agreed

29

that the total contributions by the Defendant were approximately

$124,500.00 and approximately $133,500.00 by Mr Ainsworth.

[64] The Plaintiff concedes that she contributed nothing financially to the

establishment of the business. She claims she was prepared to but “…was

told it was not needed”. That was misleading as she conceded in cross-

examination that she had no funds to enable her to do so and had no realistic

prospect of borrowing funds for that purpose. This is another example of

embellishment by the Plaintiff. Her contribution was non-financial in the

form of her experience in running a similar competing business.

[65] Despite that the Plaintiff referred to her initial salary at Monsoon as being a

“minimal” amount, initially $40,000.00 per annum, the evidence of her tax

returns indicates that her salary was closely comparable to her salary with

her previous employer. In her last full financial year of employment with her

previous employer (2003/2004), according to tax returns put in evidence her

salary was $36,666.00.

[66] The Plaintiff concedes that notwithstanding her lack of any financial

contribution to the start up costs, the Defendant insisted that she be made an

equal shareholder in the business. As a result, and for no financial outlay on

her part, the Plaintiff had not only a salary but she also had a right to an

equal share of the profits as well as an equal share in the equity of that

business.

30

[67] The Defendant gave evidence that the loans he made to Monsoon meant that

he was unable to purchase a property he was otherwise interested in at

Noonamah. Mr Black submits that I should reject that evidence as evidence

of a non-financial contribution by the Defendant as it is not supported by

evidence of probative value. However to the extent that the Defendant was

challenged about this, he was not discredited and if I were to accept this

evidence, as I do, and corroboration not being mandatory, his evidence is

sufficient to support the proposition. The Defendant also claims a

contribution in the form of providing free veterinarian services to the

Plaintiff. The provision of those services was not challenged. Although I

think that both are valid contributions, individually they are not overly

significant and I think they fall conveniently within the approximate

equality that I have provided for in respect of domestic type contributions.

[68] Monsoon was sold four years after the business was established for

$1,100,000.00 exclusive of GST but subject to various adjustments. The

evidence however is unclear as to the amount of the net proceeds of sale or

the amounts distributed to the three shareholders. Figures for these items

have been referred to in the submissions by both parties but it appears that

the tendering of that evidence has been overlooked.

[69] The Plaintiff does not refer to any amounts in her evidence but says that she

paid part of the proceeds of sale she received into the self managed

superannuation fund and that part was also applied to the purchase of the

Driver Property. The difference, on the Plaintiff’s evidence, between the

31

purchase cost of the Driver Property ($431,000.00) and the amount funded

by bank loan ($348,000.00) was approximately $83,000.00. The amount of

that loan as at trial however was agreed to be approximately $179,000.00

which is approximately $169,000.00 less than originally borrowed. No

evidence was given to explain that. On the available evidence, other than for

the routine reduction of the mortgage amount by regular repayments, the

Plaintiff had no source of funds to enable her to make such a significant

reduction other than her share of the net proceeds of sale of Monsoon.

[70] Some guidance to reveal the net proceeds comes from the affidavits of the

parties. The Defendant deposes that he only received the cash component of

the net proceeds of sale sometime in 2010. In her affidavit the Plaintiff says

that her share of the proceeds of sale had not then crystallized. Without

clearer evidence, I assume that the same applied to the Plaintiff’s funds from

the sale of Monsoon. Nonetheless, it does not help in determining the value

of the Defendant’s contribution to those proceeds received by the Plaintiff.

[71] Further complicating the question is the evidence which reveals that Mr

Ainsworth made a gratuitous adjustment in favour of the Plaintiff of

$50,000.00 from the proceeds of sale. There had not been any previous

mention of that. Although the reasons why Mr Ainsworth allowed that

adjustment was not clear on the evidence, I do not think anything turns on it.

Any suggestion that this somehow follows from the Defendant ensuring that

the Plaintiff was to be an equal shareholder in the business and thereby

amounting to a non-financial contribution by the Defendant is fanciful.

32

[72] In comparison the Defendant’s evidence is that he received approximately

$200,000.00 in money or money’s worth from the proceeds of sale of

Monsoon but apparently after payment of capital gains tax. No details are

given of the capital gains tax and I cannot ascertain that from the tax returns

that have been tendered. In any case, I assume that the amounts he refers to

must be in addition to reimbursement of his loans as otherwise the effect

would be that out of a sale price of $1,100,000.00, he only receives

approximately $75,000.00 after his loans funds are repaid. That not only

seems inadequate, it appears to be significantly less than what the Plaintiff

received. Overall the state of the evidence concerning the dispersal of the

net proceeds of sale of Monsoon is unsatisfactory and I will evaluate that as

best I can on the available evidence.

[73] It was a term of the contract of sale of Monsoon that the Plaintiff was to

remain as manager of the business for the purchaser for a period of three

years. The Plaintiff claims that as an indirect contribution. There is no

evidence that her employment terms are any less favourable as a result of

that contractual obligation. The three year period expired in January 2011

and the Plaintiff is still employed in that business, hence the contractual

obligation on sale does not appear to have had any negative impact on her.

The Plaintiff conceded that her current salary arrangements are in excess of

her base salary when employed as the manager of Monsoon. Mr Black

submits that nonetheless it is a contribution as, given it was made as a

33

contractual obligation, it must have had a bearing on achieving the sale

price. That seems self evidently correct.

[74] There was also much evidence concerning the price charged by Monsoon for

veterinary supplies to the Defendant’s practice. There was much evidence

about the pricing of Monsoon’s products and whether the Defendant paid

premium prices and thereby indirectly propped up the Monsoon business.

The evidence was challenged. Mr Ainsworth, who was called by the

Plaintiff, indicated that he sourced some supplies from other companies due

to price considerations.

[75] One of the Defendant’s employees specifically conducted a comparison of

prices charged by Monsoon with other suppliers and made a

recommendation to the Defendant as a result. That evidence was not

successfully challenged in my view. Mr Black submits that it makes no

difference as there was no evidence of detriment to the Defendant’s practice.

I am inclined to agree that there was no detriment to the practice as I expect

that the practice passed on the cost to its customers. However, in my view,

as the Defendant could have sourced supplies from other competitors,

notwithstanding that the Defendant also received a proportionate benefit, the

support of Monsoon by the Defendant’s practice was an indirect contribution

by the Defendant for adjustment order purposes.

[76] In the end the dispute on this issue is largely insignificant. It is clear the

Defendant’s practice was an important customer of Monsoon. The Plaintiff

34

conceded that the Monsoon business would be in trouble without the

business of the Defendant’s practice. Although I am prepared to find that

some supplies were purchased by HSVC at prices higher than might have

been able to be achieved through other suppliers, the converse was also true

in respect of other supplies. I think that it logically follows that it would be

impractical for HSVC to purchase supplies from different suppliers based

entirely on the price differences of individual products. Although the

available evidence favours a finding that overall HSVC paid slightly higher

prices for supplies by dealing with Monsoon, absent a full analysis, the

evidence is insufficient to satisfactorily establish how much the difference

was.

[77] The best evidence called was that of Elisha Horne which indicates that over

one particular month the practice could have saved approximately 10% had

the supplies been sourced form other suppliers. That is selective and there is

no evidence, other than possible inference, to show that the same percentage

could be applied throughout. I am not prepared to draw that inference. The

indirect contribution of the Plaintiff in committing to a three year

employment term is a contribution similar in nature to the contribution of

the Defendant in supporting the Monsoon business. Given that the Plaintiff

has stayed on with that employer after the expiry of the period she

contracted, in assessing these contributions I conclude that the Defendant’s

contribution exceeds that of the Plaintiff.

35

[78] The granting of a one third share of Monsoon to the Plaintiff also gave her

an entitlement to one third of shareholder profits. The profits were extensive

and amounted to $20,000.00 per share in the 2006/2007 financial year and

$50,000.00 per share in the 2007/2008 financial year. In addition the

Defendant allowed the Plaintiff to retain his share of those profits. That is

not disputed but it is unclear how that occurred. The tax returns of the

parties for those years are not clear as to how that was treated and there was

no other evidence to assist in determining that. From the tax returns it

appears to have been treated as if it were salary from Monsoon. Therefore,

irrespective as to how that occurred and the efficacy of that, the net effect is

that the Plaintiff has paid income tax on those amounts and that needs to be

taken into account. Absent expert evidence of that, doing the best I can with

the available evidence and relying on legislated tax scales, the additional tax

payable by the Plaintiff due to her retaining the Defendant’s profit

distribution is $6,900.00 for 2006/2007 and $20,700.00 for 2007/2008. The

adjusted value of this financial contribution by the Defendant is therefore

reduced to $42,400.00 rounded to the nearest $100.

[79] The Whitewood Road Property was purchased in November 2004 by the

Defendant. The purchase price was $892,000.00 including acquisition costs.

This was financed by a loan from National Australia Bank in the amount of

$650,000.00. The Defendant says the balance represents his savings and

shareholdings. The Plaintiff challenges that based on credit issues and

submits that it should be assumed that the balance was also generated

36

through the practice. Although the Defendant provides no details of the

savings and shareholdings that he claims to have contributed (approximately

$240,000.00), there is no evidence to support the Plaintiff’s bare contention.

The Defendant was not effectively challenged on this. I accept the

Defendant’s evidence on this point.

[80] The property was primarily acquired for development as new premises for

the HSVC practice and construction of that has been planned and financed.

The development includes the establishment of a child care centre on the

property which affects the value of the property. The loan has been serviced

from the Defendant’s income generated through the veterinarian practice and

the rental income from the child care centre.

[81] The evidence reveals that the negotiations, meetings and the like to secure a

child care operator for the site, as well as all of the attendance in respect of

the construction of the centre and development of the property were

undertaken by the Defendant to the exclusion of the Plaintiff. The Plaintiff

has not led any evidence indicating any contribution to the acquisition,

improvement and development of that property. The Plaintiff claims that she

was involved in decisions concerning that acquisition. The Defendant says

that he only discussed his plans with her and that she was not involved in

the decision making process. Again I prefer the Defendant’s version. The

nature of the discussions appear to be consistent with typical discussion of

matters relevant to one party in a relationship as opposed to a considered

process of consultation and joint decision making. The Plaintiff’s only

37

possible claim to contribution in respect of that property is to the extent that

any entitlement that she has in respect of her contributions to HSVC filters

through to that property given that the income from the practice was the

partly the source of the funds to meet loan commitments.

[82] The evidence of the valuer, Mr Gore, shows the value of the property differs

by approximately $1,200,000.00 on account of the establishment of the child

care centre on the site. His evidence was that without a childcare centre the

value was $1,500,000.00 and with it, $2,700,000.00. The Defendant has

submitted that the construction of the child care centre has significantly

increased the value of that property as a result. That is self evidently correct

in absolute terms, however it overlooks the cost of construction which on

the evidence is $1,435,000.00. At current values therefore it appears, as Mr

Black submits, that the net value has therefore been reduced by $235,000.00.

[83] I do not think the position is as simple as that. Mr Black’s submission seeks

to treat the child care centre as a separate matter divorced from the rest of

the land and then to apply that back to an overall value. Once the finer

details of the valuation are considered, it appears the valuer puts the value

of the child care centre on a standalone basis at between $1,428,000.00 and

$1,588,000.00 and that exceeds the construction costs. Nonetheless, the

available evidence indicates that as at the date of the valuation the

construction of the child care centre has not significantly added any value to

the Whitewood Road Property.

38

[84] As to the Livingstone Property, it was purchased for $670,000.00 in January

2007. It was purchased by the Defendant alone with a loan of $590,000.00

from the National Australia Bank and the balance from his savings. The

Plaintiff does not challenge the Defendant’s evidence as to the source of the

funds for that acquisition.

[85] The Plaintiff concedes that she has not made any financial contribution to

the acquisition of the property. The Plaintiff however claims an indirect

contribution namely that she claims to have located the property and

thereafter attended with the Defendant to inspect the property.

[86] Cross-examination however shows that the Plaintiff exaggerated the extent

of this intangible contribution. She conceded that the Defendant became

aware of the property by chance when he passed by the property. He agrees

the Plaintiff went with him when the property was inspected. The fact of

merely locating the property as a contribution is of dubious significance in

any case. Other than that, the Plaintiff had no other involvement either in

the negotiations for the purchase of the property or in respect of the

attendances leading up to settlement.

[87] As such I conclude that her indirect contribution is less than that of the

Defendant. Again, to the extent that the source of funds to meet loan

commitments came from the Defendant’s practice, the Plaintiff may be able

to trace indirectly through a contribution based on her indirect contribution

to that practice.

39

[88] The valuation evidence in respect of the Livingstone Property puts the

current value of that property at $695,000.00. The current liability to

National Australia Bank is approximately $507,000.00 resulting in equity of

the order of $188,000.00. This represents an increase in the equity of the

property in the order of $80,000.00 over the period the Defendant has owned

it. However, the Defendant has also expended nearly $50,000.00 on

improvements since acquisition. Additionally the Defendant has met all

outgoings and utilities for the property since acquisition. The evidence

reveals that the Plaintiff has not made any significant financial contribution

in respect of the property.

[89] There was some dispute as to the extent of the non-financial contributions of

the parties both at the Livingstone Property and before that in their rented

accomodation. The Plaintiff says that until the move to the Livingstone

Property, the arrangement was that the Defendant would pay the rent and she

would pay the utilities and groceries. This was not challenged by the

Defendant but no amounts were deposed to so making an assessment of the

relative contributions is difficult. I will treat those as equal. At the

Livingstone Property however all mortgage payments outgoings and utilities

were paid by the Defendant and the costs of groceries were shared, hence

that further skews the financial contributions in favour of the Defendant.

[90] The Defendant claims that he has done nearly all of the work in establishing

the grounds at the Livingstone Property. Although the Plaintiff claims to

have given some assistance in that work, this is disputed by the Defendant

40

who asserts any such work was minimal. The Plaintiff claims that in any

event she performed the bulk of the indoor household tasks during the

course of the relationship. A cleaner was employed from approximately

2005 and ordinarily that would water down the extent of that contribution.

However the cleaner was paid for by the Plaintiff hence that should

nonetheless count as a contribution by the Plaintiff. The Defendant claims

that his excess of contribution to the external areas at least matched the

Plaintiff’s excess of contribution in respect of the internal household chores.

[91] The Plaintiff claims that she did most of the cooking and laundry but the

Defendant disputes that and says those tasks were shared approximately

equally. For the same reasons I have previously given for generally

preferring the evidence of the Defendant over that of the Plaintiff, I accept

the Defendant’s version over that of the Plaintiff. I find that the domestic

type household contributions are approximately equal.

[92] There remains a dispute as to the maintenance of the pool at the property

where the parties first resided together. It appears that both parties

contributed to the maintenance of the pool at the Livingstone Property,

likely more by the Defendant. The Plaintiff claims that she purchased the

chlorinator for the pool on that property. She produced an invoice

evidencing the cost at $1,099.00. The Defendant queries whether the invoice

was paid by the Plaintiff but has no specific recall. On this issue I am

prepared to accept the Plaintiff’s evidence over that of the Defendant.

41

[93] With respect to the superannuation accounts of the parties, I was told during

the course of the evidence that the parties were seeking to agree a position

as to the parties’ superannuation. Nothing however was put to me on that

basis and presumably the parties were not able to reach agreement as

contemplated. However that leaves a shortfall of evidence. The evidence

that was led reveals that both parties had separate superannuation

entitlements as at the commencement of the relationship which were

approximately equal. The parties contributed to superannuation from

earnings and then established a self managed superannuation fund in

October 2006. In terms of contributions to the fund, the Defendant’s income

has been greater throughout the relationship and that is reflected in greater

contributions to the fund. Each of the parties has a separate account within

that fund. Each party contributed to that fund. Both parties said that they

made contributions to the fund from their proceeds of sale of Monsoon but

no details were put in evidence.

[94] The latest available records put into evidence shows that the balance of the

parties’ accounts in the fund as at 30 June 2009, again rounded to the

nearest $100.00, was $62,200.00 for the Plaintiff and $211,700.00 for the

Defendant. I have no other evidence as to the extent of these financial

resources. I have otherwise relied on unchallenged amounts as deposed to by

the parties in their trial affidavits.

[95] The Defendant claims as an indirect contribution in respect of that fund on

the basis that he has been responsible for administering and investing the

42

funds holdings throughout. He has also dealt with the fund managers and

accountants since the separation. He has paid all the expenses of the fund

since the separation. An allowance in favour of the Defendant as an indirect

contribution to the financial resources of the Plaintiff is appropriate. This

evidence was not challenged by the Plaintiff. As the Defendant’s income

from HSVC was the source of his contributions to superannuation, at least in

part, then indirectly the Plaintiff has an indirect contribution to the

Defendant’s superannuation to the extent of her contribution to HSVC. On

my assessment, the Defendant’s indirect contribution to the Plaintiff’s

superannuation exceeds that of the Plaintiff to the Defendant’s

superannuation.

[96] With that background I now turn to apply that evidence to determination of

an appropriate adjustive order.

[97] The pool currently comprises the following. Firstly the assets, with values as

I find them, rounded to the nearest $100.00:-

43

Asset Held By Value

The Livingstone Property

Defendant $695,000.00

HSVC Defendant $361,350.00

The Smyth Road Property

Defendant $600,000.00

The Whitewood Road Property

Defendant $2,700,00.00

The Driver Property Plaintiff $550,000.00

Total $4,906,350.00

Additionally both parties must have furniture and other items of personalty

but there has not been any evidence of those hence I will treat them as equal

and disregard them for current purposes.

[98] Of the aforesaid total the value of assets held by the Plaintiff is $550,000.00

and by the Defendant $4,356,350.00.

[99] Superannuation entitlements, again rounded to the nearest $100.00,

comprise:-

44

Asset Held By Value

MLC Superannuation

Fund Defendant $10,300.00

AXA Superannuation

Fund Defendant Unknown

Plaintiff’s account in Self Managed Superannuation

Fund

Plaintiff $62,200.00

Defendant’s account in Self

Managed Superannuation

Fund

Defendant $211,700.00

Master Superannuation

Plaintiff $11,300.00

Australian Super Plaintiff $39,200.00

REST Superannuation

Plaintiff $150.00

Total $334,850.00

The only evidence that I have of the value of the Defendant’s MLC

Superannuation is as set out in paragraph 21(g) of the Defendant’s trial

affidavit which was admitted without objection. That was an estimate by the

Defendant of the value of that fund as at the commencement of the

relationship. Although that is not entirely satisfactory, that is the only

evidence available. There is no evidence of the value of the Defendant’s

AXA Superannuation. The values for the parties’ respective accounts in

their self managed superannuation fund are taken from the latest financials

45

tendered which were for the financial year ended 30 June 2009. On that

basis, the value of the Plaintiff’s fund is $112,900.00 and of the Defendant’s

$222,000.00, in both cases rounded to the nearest $100.00.

[100] The liabilities, also rounded to the nearest $100.00, comprise the following:-

Liability Liability Of Amount

Mortgage over the Driver Property

Plaintiff $179,000.00

Mortgage over the Livingstone

Property Defendant $507,100.00

Mortgage over the Whitewood Road

Property Defendant $250,000.00

Loan Taken for Construction of

Child Care Centre Defendant

$1,405,000.00

Outstanding Builders Fees for Child Care Centre

Defendant $30,000.00

Total $2,371,100.00

[101] On that basis the total liabilities of the Plaintiff amount to $179,000.00

leaving a net position for the Plaintiff of $371,000.00. Likewise the total

liabilities of the Defendant amount to $2,192,100.00 leaving the Defendant

with a net position of $2,164,250.00.

[102] The power to make an adjustive order derives from section 18 of the Act

which provides as follows:-

46

18 The order for adjustment

(1) The order which a court may make under this Division with respect to the property of de facto partners or either of them is such order adjusting the interests of the partners in the property as the court considers just and equitable having regard to:

(a) the financial and non-financial contributions made directly or indirectly by or on behalf of the partners to the acquisition, conservation or improvement of any of the property or to the financial resources of the partners or either of them; and

(b) the contributions (including any made in the capacity of homemaker or parent) made by either of the partners to the welfare of the other partner, or to the welfare of the family constituted by the partners and one or more of the following:

(i) a child of the partners;

(ii) a child accepted by the partners or either of them into the household of the partners, whether or not the child is a child of either of the partners; or

(iii) any person dependent on the partners who has been accepted by the partners or either of them into the household of the partners.

(2) A court may make an order in respect of property whether or not it has declared the title or rights of a de facto partner in respect of the property.

[103] The exercise of the jurisdiction in section 18 of the Act, per Kardos v

Sarbutt6 and Evans v Marmont,7 involves three main steps. Firstly, the

identification and valuation of the property of the parties which may be

subject to an adjustive property order. Secondly, the evaluation and

balancing of the respective contributions of the parties. This step typically

6 (2006) 34 Fam LR 550 7 (1997) 21 Fam LR 760

47

results in an apportionment between the parties on a percentage basis of

the overall contributions. Thirdly, the determination of the order required

to recognise and compensate the parties for those contributions which is

typically in line with the percentage determined by step two.

[104] In the course of the first step, the identification and valuation of the

property of the parties is usually undertaken at the date of trial (Parker v

Parker8 and Kardos v Sarbutt

9 and Ottley v Chester10). In cases where

there have not been ongoing contributions by one party which have

benefited the other party since separation, it may be appropriate to adopt

the date of separation as the appropriate date. (Kardos v Sarbutt11). Values

are mostly agreed between the parties without apparently demarcating

between trial date and separation date and I will deal with it in that

manner.

[105] Also relevant to the first step is the determination of the approach the

Court takes in that process. The two recognised approaches are

vernacularly referred to as the “global” approach and the “asset-by-asset”

approach. The approach to take is in the discretion of the Court. The

global approach is the approach usually adopted. It typically involves the

Court considering the total net property of the parties and awarding a

percentage to make any adjustment considered necessary. The authorities

say that in exercising the discretion, a major consideration is to ensure 8 (1993) 16 DFC 95-139 9 (2006) 34 Fam LR 550 10 [2010] NTSC 38 11 (2006) 34 Fam LR 550

48

that no distortion results and that a party’s contributions are properly

evaluated. There is particular concern to ensure that use of the asset-by-

asset approach does not distort or undervalue the domestic and non-

financial contributions: Kardos v Sarbutt.12 As I find that those types of

contributions are approximately equal in any event, that concern is not an

issue.

[106] The Plaintiff submits that the global approach should be utilised. The

Defendant argues for the asset-by asset approach and draws support from:

1. The absence of co-mingling of funds;

2. The brevity of the relationship;

3. That there were no children of the relationship;

4. The disproportionately large initial contribution by the Defendant;

5. That a cleaner was employed from 2005;

6. The lack of cross collateralisation of assets;

7. The nature of the contributions.

[107] The employment of a cleaner is said to be relevant to this issue as the

homemaker contribution was thereby decreased. There is insufficient

evidence to make that finding. The evidence reveals that the cleaner was

employed part time and was paid for by the Plaintiff. That payment is

12 (2006) 34 Fam LR 550

49

itself a contribution. There is no evidence of the duties actually performed

by the cleaner.

[108] Whether it is co-mingling in the true sense of the word or not there was

co-mingling of assets to some extent. True the parties maintained separate

bank accounts, however the parties had a jointly owned business in

Monsoon and they had a self managed superannuation fund where they

were both trustees and into which they both contributed. The de facto tax

planning arrangement between them arising from the Defendant allowing

the Plaintiff to retain his share of the profits and deflecting tax liability

for that income to the Plaintiff is an indirect instance of co-mingling of

assets. To the same extent there was cross collateralisation of assets.

[109] I do not consider a relationship of more than six years to be brief. More

important is the extent of the mutuality of the relationship. Likewise I do

not consider the absence of children to be overly significant to this

question.

[110] The global approach is the usual approach adopted and in my view the

global approach is to be utilised.