Embed Size (px)

Citation preview

2014

Annual Regulatory Risk Report of the DZ BANK Group – Partial disclosure of DVB Bank SE

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Annual Regulatory Risk Report 2014 of the DZ BANK Group

Partial disclosure of DVB Bank SE pursuant to article 13 of Regulation (EU) No. 575/2013of the European Parliament and of the Council of 26 June 2013 on prudential requirements for

credit institutions and investment firms and amending Regulation (EU) No. 646/2012 (1).

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

1Contents

Introduction 02

Scope in accordance with article 436 of the CRR 03 – 04

Own funds and capital requirements 05 – 19

05 Own funds

Structure of own funds in accordance

with article 437 (1) (d) and (e) of the CRR

Reconciliation of own funds to statement of financial position

in accordance with article 437 (1) (a) of the CRR

Own funds in accordance with article 437 (1) (b) of the CRR

16 Capital requirements in accordance with article 438 (a) of the CRR

16 Capital requirements in accordance

with article 438 (c) to (f), 445 and 446 of the CRR

Credit risks

Market price risks

Operational risks

19 Total and tier 1 capital ratios

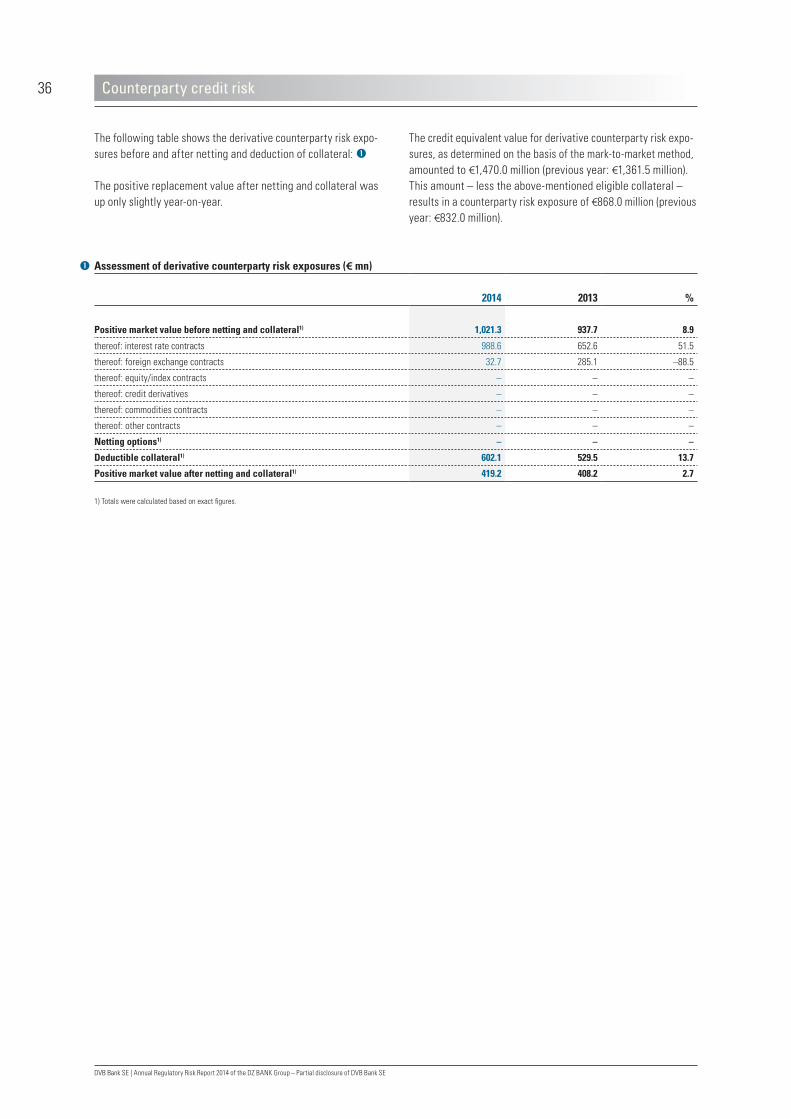

Counterparty credit risk 20 – 36

20 Objectives and principles of credit risk management

in accordance with article 435 of the CRR

20 Lending volume and allowance for credit losses

in accordance with article 442 of the CRR

25 IRBA asset class ratings in accordance

with article 435 (a) to (c) of the CRR

Rating methods used, and transitional arrangements

Internal rating system structure

Additional uses of internal estimates

Rating system controls

Allocation to rating categories

27 CRSA asset class ratings in accordance

with article 444 (a) to (d) of the CRR

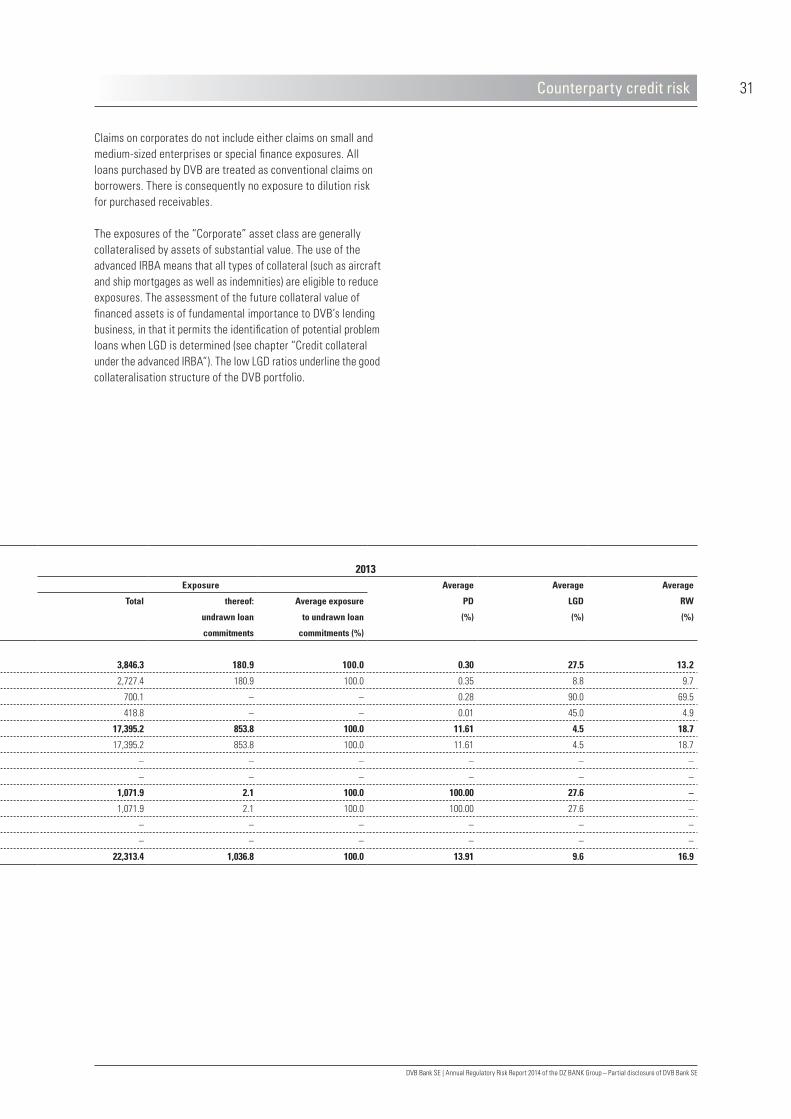

28 Exposures in accordance with article 444 (e) and 452 of the CRR

Exposures before and after CRSA credit risk mitigation

IRBA exposures by asset classes and risk categories

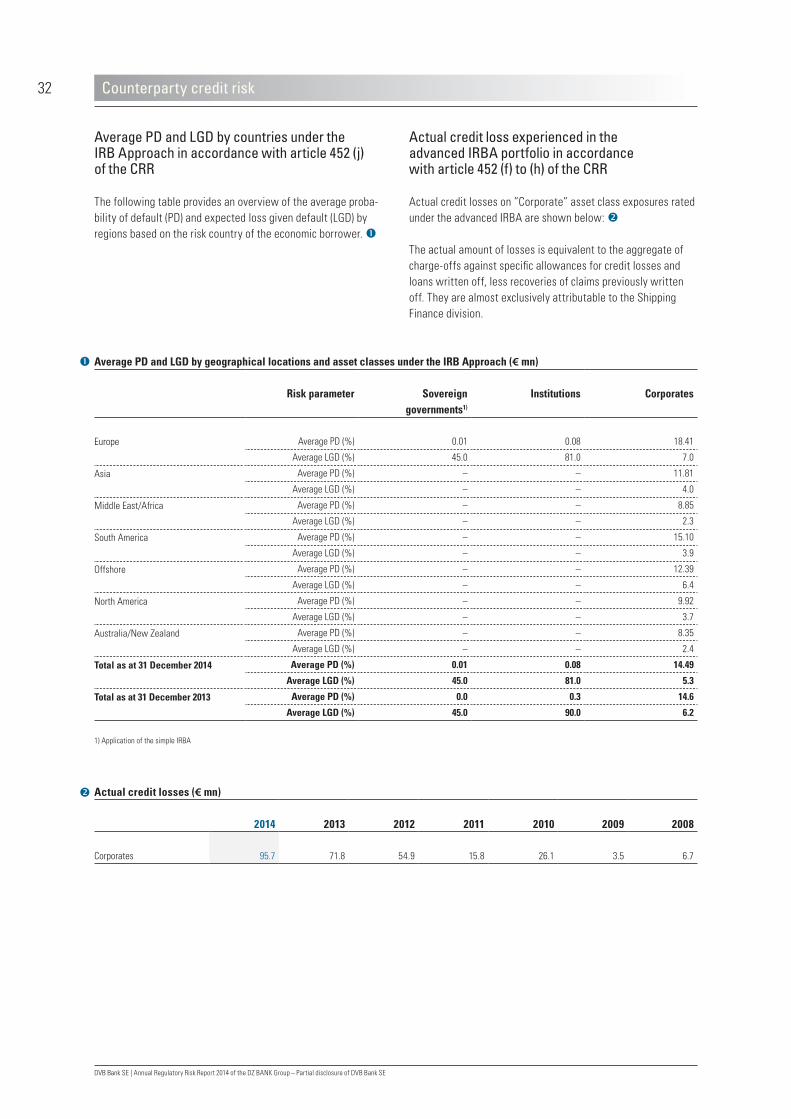

Average PD and LGD by countries under the IRB Approach

in accordance with article 452 (j) of the CRR

Actual credit loss experienced in the advanced IRBA portfolio

in accordance with article 452 (f) to (h) of the CRR

Loss estimates and actual credit loss experienced in the advanced

IRBA portfolio in accordance with article 452 (i) of the CRR

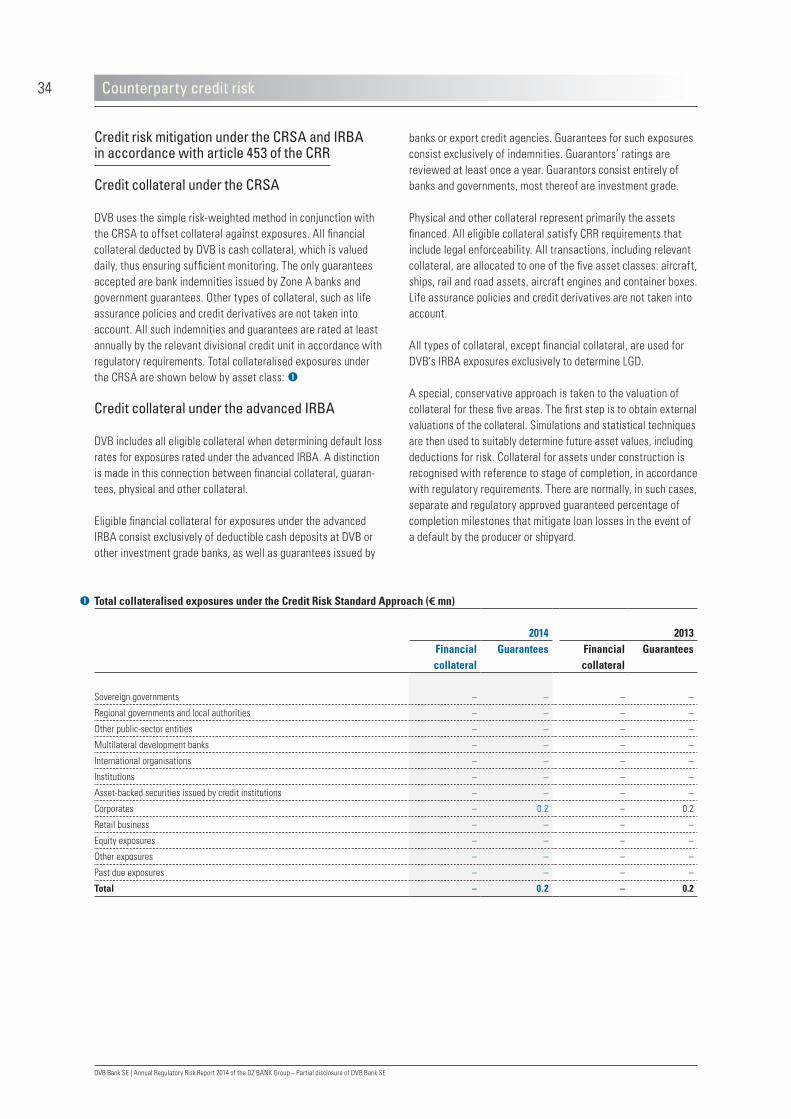

34 Credit risk mitigation under the CRSA and IRBA

in accordance with article 453 of the CRR

Credit collateral under the CRSA

Credit collateral under the advanced IRBA

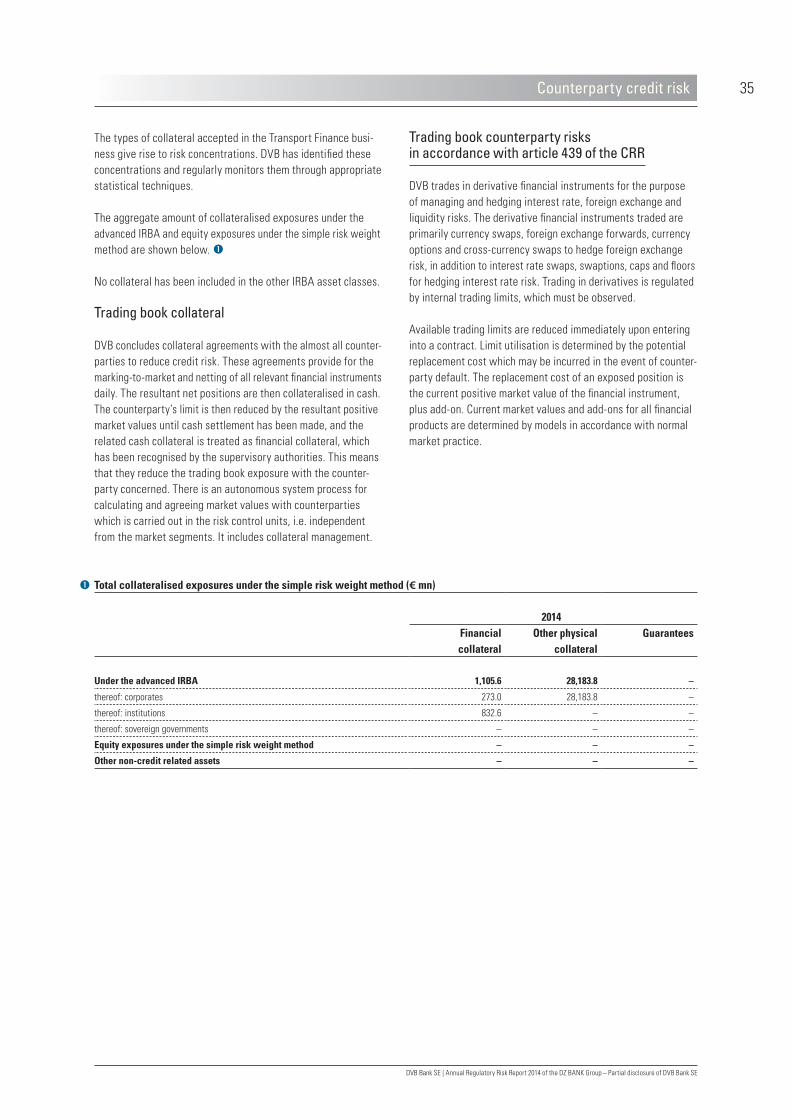

Trading book collateral

34 Trading book counterparty risks in accordance

with article 439 of the CRR

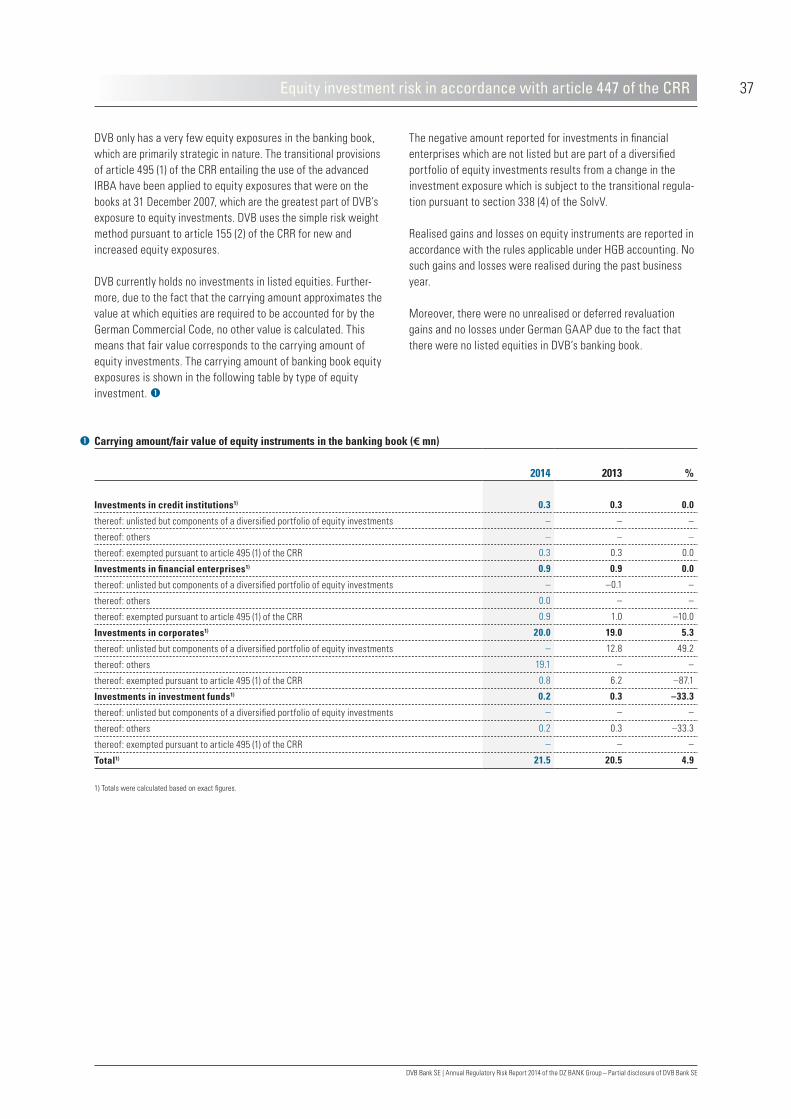

Equity investment risk in accordance with article 447 of the CRR 37

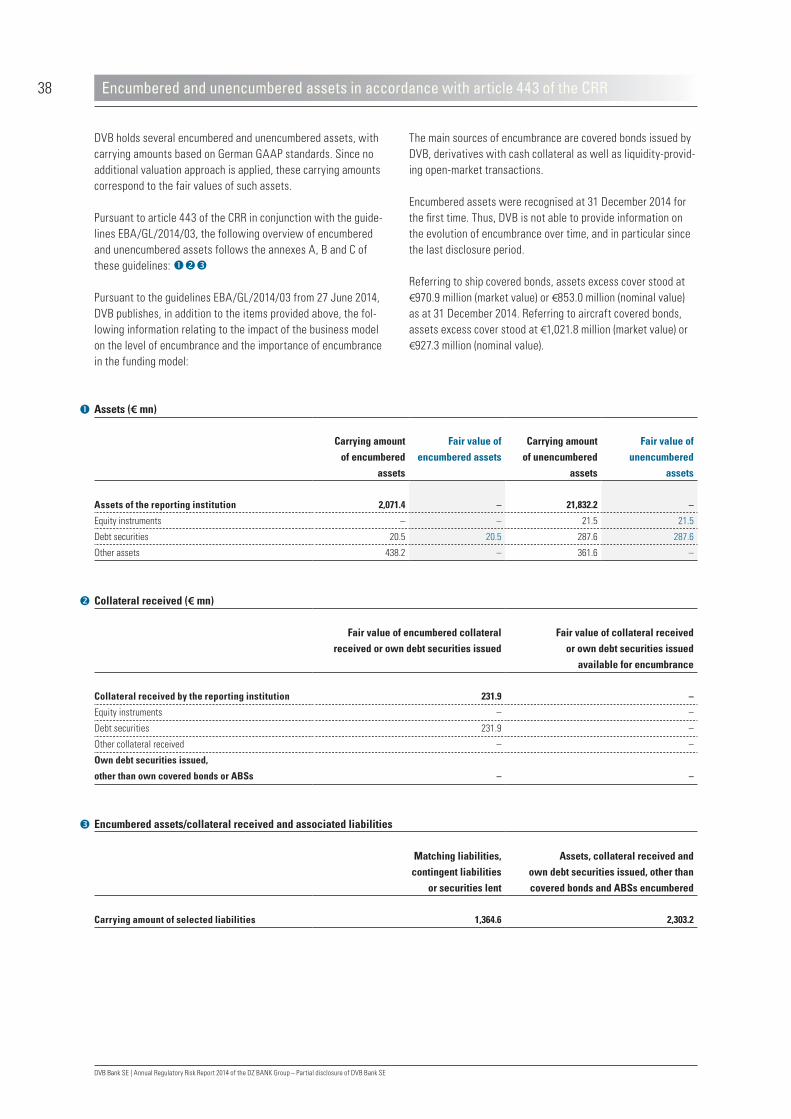

Encumbered and unencumbered assets in accordance with article 443 of the CRR 38

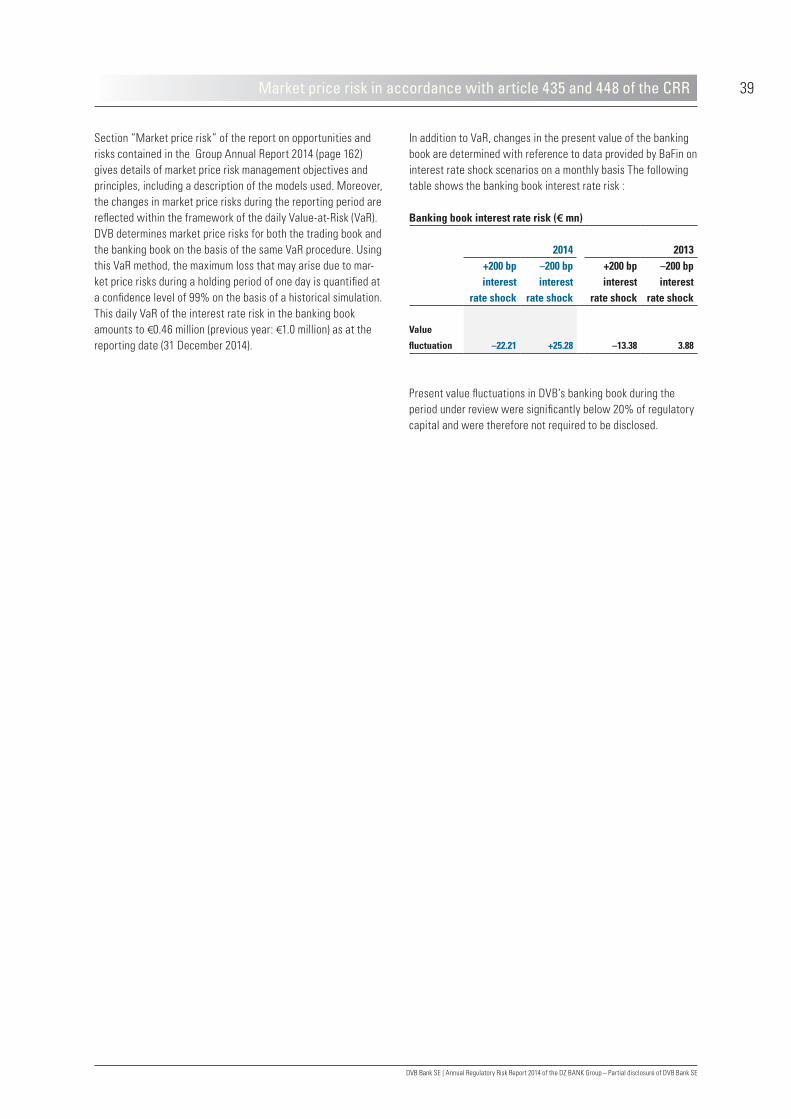

Market price risk in accordance with article 435 and 448 of the CRR 39

Notes 40 – 56

40 Main features of instruments issued by the institution

in accordance with article 437 (1) (b) of the CRR

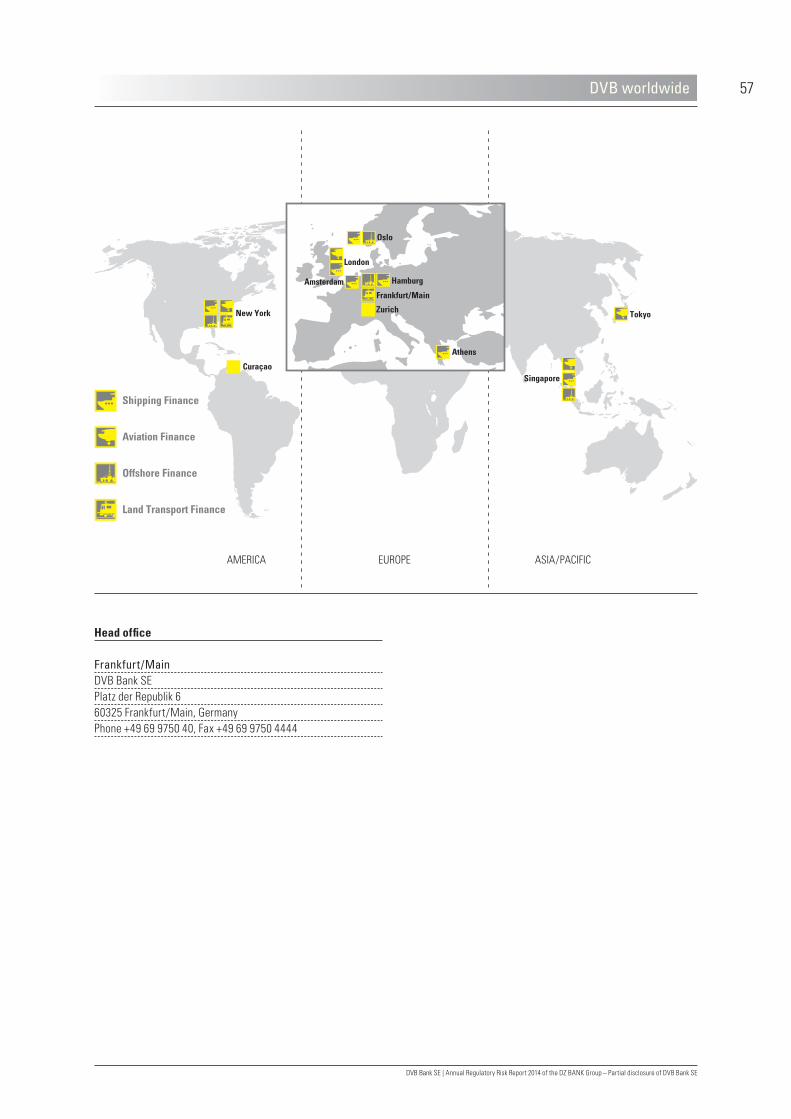

DVB worldwide 57 – 58

Imprint 59

2

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Introduction

All details and figures cited in this report are as at, or pertain to the twelve months ended 31 December 2014. As permitted by article 434 (2) of the CRR, this report incorporates information provided by DVB’s Group Annual Report 2014 to the extent that such information is in compliance with the reporting requirements of the CRR.

DVB is a specialist bank focused on global transport finance, offering integrated financial and advisory services in its Shipping Finance, Aviation Finance, Offshore Finance and Land Transport Finance segments through its network of eleven office locations around the world. Recognising the requirements associated with its focused market presence, and its status having adopted the “Advanced Approach”, DVB provides enhanced transparency at all times, maintaining an active and open financial communi-cations policy. DVB’s strategic focus, and the resulting specific nature of its business areas and products, means that certain disclosure requirements are not applicable. In particular, this refers to some (if not all) disclosures required by article 439 (exposure to counterparty credit risk), article 452 (specialised lending and retail), and article 449 (securitisations) of the CRR, thus reducing the qualitative and quantitative scope of this report.

The macroeconomic and industry-specific conditions of the business year 2014 are described in detail in the Annual Report of DVB Bank SE on pages 3 to 7, as well as in the chapters “Report on the economic position” and “Development of the business divisions” of the Group Annual Report on pages 54 to 55 and 76 to 136. Please refer to these sections for a full description.

Additional disclosure requirements pursuant to the CRR

Pursuant to section 16 of the Regulation, DVB is obliged to disclose information regarding its remuneration policy and practice. DVB’s disclosure duties, as a bank subject to Regulation 575/2013/EU (Capital Requirements Regulation – CRR), as defined in section 1 of the KWG, are based solely on article 450 of the CRR which requires that the Bank discloses certain quan-titative and qualitative details for groups of employees whose activity has a material impact on the Bank’s risk profile (“risk takers”).

We will comply with this disclosure duty in a separate report, which will be made available on our website

www.dvbbank.com > Investors > Corporate Governance during the second quarter of 2015.

In 2004, the Basel Committee on Banking Supervision issued the Basel II framework containing international standards for risk-adjusted capital adequacy. The standard was incorporated into German law (to which DVB is subject) on 1 January 2007 through the adoption of the German Solvency Regulation (SolvV) of 14 December 2006, which was, in turn, the transposition into German law of the European minimum capital standards pre-scribed in the Banking Directive (2006/48/EC) and the Capital Adequacy Directive (2006/49/EC), and the corresponding equiv-alent requirements of the new Basel Capital Accord (Basel II).

In December 2010, the Basel Committee on Banking Super-vision issued an extended framework, known as Basel III. This framework has taken effect from 1 January 2014 based on the requirements of Regulation (EU) No. 575/2013 (Capital Require-ments Regulation – CRR).

DVB has received supervisory approval for the use of the advanced Internal Ratings Based Approach (IRBA), effective 1 January 2008, for the determination of credit risk-related charges against regulatory capital.

With this report, DVB Bank SE, in its capacity as parent company of the DVB Group, complies with the reporting requirements of article 431 to 455 of the CRR in conjunction with section 26a of the German Banking Act (KWG). As a member of the DZ BANK Group, DVB is, in fact, exempt from full disclosure according to article 13 (1) sentence 2 of the CRR. For the reporting period 2014, DVB Bank SE provides as a minimum standard the information required under the Basel II framework applicable so far, in order to facilitate comparability with the previous year’s voluntary disclosures. This exceeds the minimum disclosure requirements pursuant to article 13 (1) sentence 2 of the CRR.

The DVB Group is referred to in this report either as “DVB” or the “DVB Group”, whereas the European public limited- liability company (Societas Europaea) is referred to by its registered name “DVB Bank SE“.

Unless otherwise indicated, all amounts are stated in millions of euros (€ mn or € million). Figures are rounded pursuant to standard business principles. This may result in slight differences when aggregating figures and calculating per-centages. The sums presented generally are rounded figures of exact amounts.

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

3Scope in accordance with article 436 of the CRR

Code (HGB). There are, furthermore, certain differences in accounting methods required by the SolvV in addition to other special CRR requirements. DVB’s risk management is compre-hensive in nature in that it includes all DVB Group entities. The information contained in this risk report relates to all companies in the DVB group of institutions as defined for regulatory purposes. All material companies of DVB are fully consolidated under both regulatory law and commercial law. The companies have been classified by the nature of their operations under headings that correspond to those defined in section 1 of the KWG. (see table on page 4)

DVB Bank SE is subordinated to another credit institution based in Germany, i.e. Deutsche Zentral-Genossenschaftsbank, Frankfurt/Main (in the following “DZ BANK AG”). Pursuant to section 10a (10) of the KWG in conjunction with article 22 of the CRR, DVB Bank SE is subject to a so-called subconsolidation, since another institution based in a third country is subordinated to DVB Bank SE. Consolidation for regulatory purposes pursuant to section 10a (1) of the KWG in conjunction with article 11 et seq. of the CRR differs from the methods and basis of consolidation for accounting purposes as required by International Financial Reporting Standards (IFRS), and supplemented by the statutory requirements of section 315a (1) of the German Commercial

Consolidation matrix – Differences in scope of consolidation of material companies for regulatory law and commercial law purposes

Regulatory treatment Consolidation

under IFRS

Consolidation

Classification

Name

Full

Pro rata

Deduction

treatment

Risk-

weighted

investment

Full

Pro rata

Banks

(credit institutions)

DVB Bank SE,

Frankfurt/Main, Germany• •

DVB Bank America N.V.,

Willemstad, Curaçao• •

DVB Group Merchant Bank (Asia) Ltd,

Singapore• •

ITF International Transport Finance Suisse AG,

Zurich, Switzerland• •

Financial

enterprises

LogPay Financial Services GmbH,

Eschborn, Germany• •

DVB Transport Finance Ltd,

London, United Kingdom• •

DVB Holding GmbH,

Frankfurt/Main, Germany• •

DVB Holding (US) Inc.,

New York City, N.Y., USA• •

4

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Scope in accordance with article 436 of the CRR

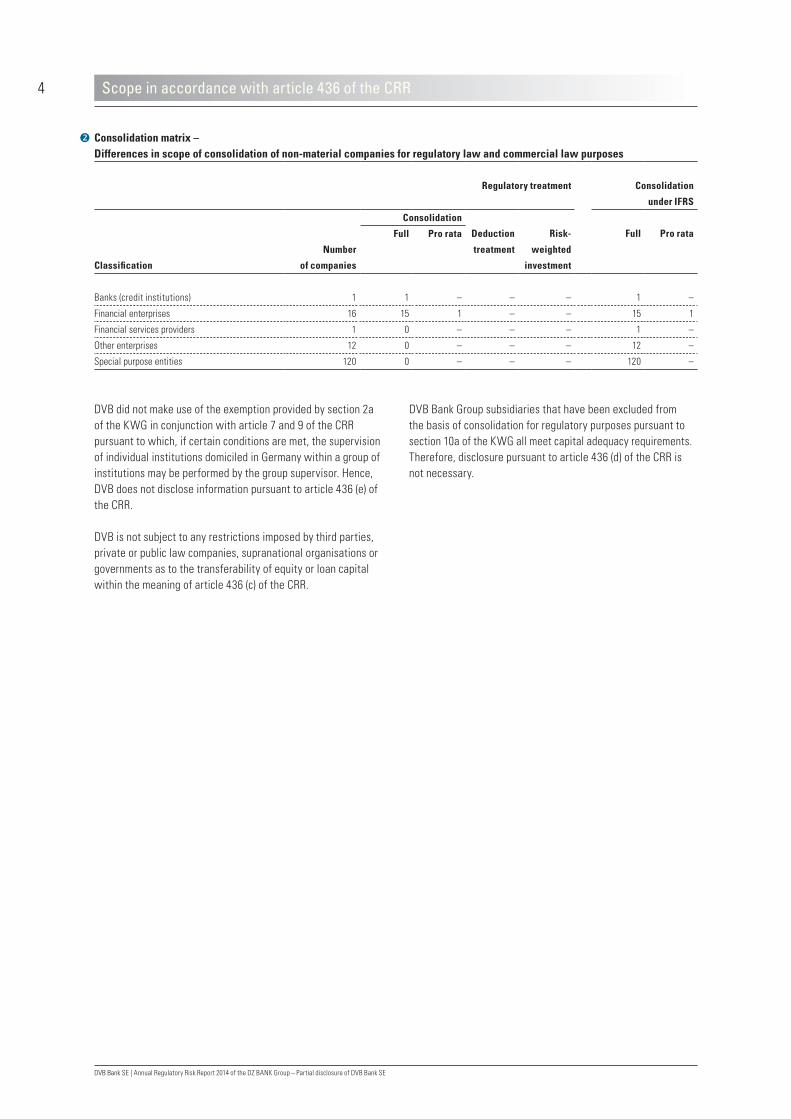

DVB did not make use of the exemption provided by section 2a of the KWG in conjunction with article 7 and 9 of the CRR pursuant to which, if certain conditions are met, the supervision of individual institutions domiciled in Germany within a group of institutions may be performed by the group supervisor. Hence, DVB does not disclose information pursuant to article 436 (e) of the CRR.

DVB is not subject to any restrictions imposed by third parties, private or public law companies, supranational organisations or governments as to the transferability of equity or loan capital within the meaning of article 436 (c) of the CRR.

DVB Bank Group subsidiaries that have been excluded from the basis of consolidation for regulatory purposes pursuant to section 10a of the KWG all meet capital adequacy requirements. Therefore, disclosure pursuant to article 436 (d) of the CRR is not necessary.

Consolidation matrix – Differences in scope of consolidation of non-material companies for regulatory law and commercial law purposes

Regulatory treatment Consolidation

under IFRS

Consolidation

Classification

Number

of companies

Full

Pro rata

Deduction

treatment

Risk-

weighted

investment

Full

Pro rata

Banks (credit institutions) 1 1 – – – 1 –

Financial enterprises 16 15 1 – – 15 1

Financial services providers 1 0 – – – 1 –

Other enterprises 12 0 – – – 12 –

Special purpose entities 120 0 – – – 120 –

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

5Own funds and capital requirements

Own funds

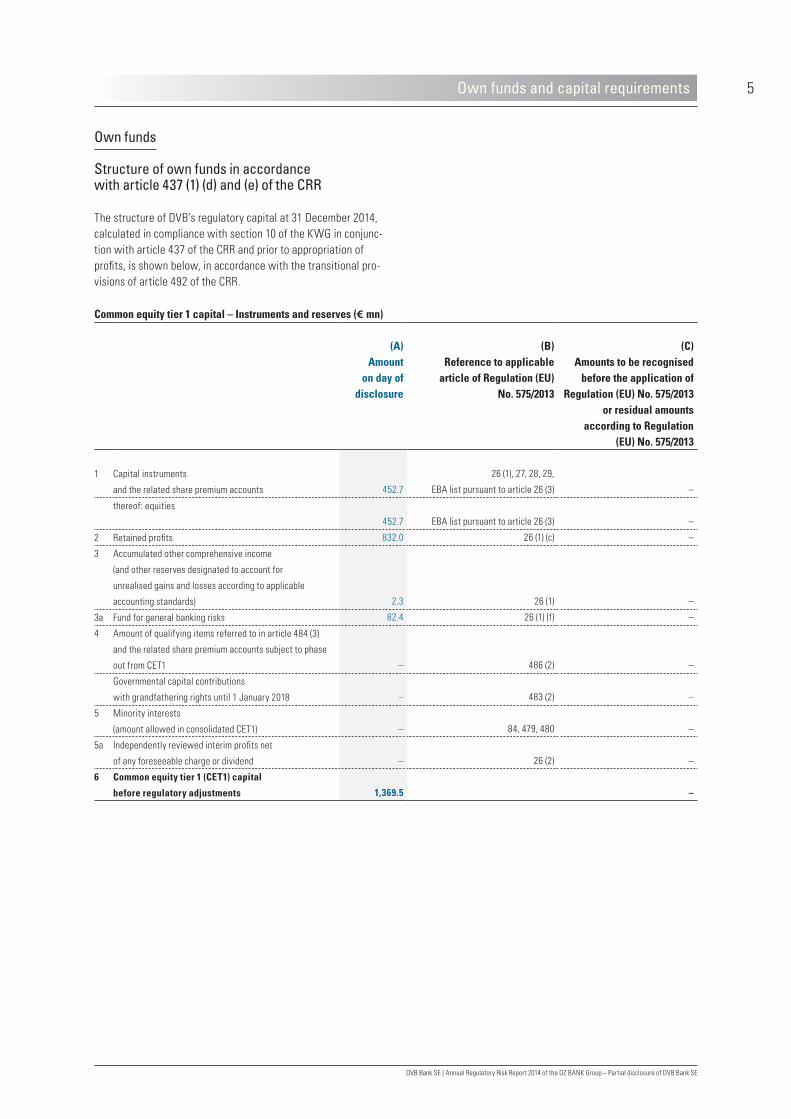

Structure of own funds in accordance with article 437 (1) (d) and (e) of the CRR

The structure of DVB’s regulatory capital at 31 December 2014, calculated in compliance with section 10 of the KWG in conjunc-tion with article 437 of the CRR and prior to appropriation of profits, is shown below, in accordance with the transitional pro-visions of article 492 of the CRR.

Common equity tier 1 capital – Instruments and reserves (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

1 Capital instruments

and the related share premium accounts 452.7

26 (1), 27, 28, 29,

EBA list pursuant to article 26 (3) –

thereof: equities

452.7 EBA list pursuant to article 26 (3) –

2 Retained profits 832.0 26 (1) (c) –

3

Accumulated other comprehensive income

(and other reserves designated to account for

unrealised gains and losses according to applicable

accounting standards) 2.3 26 (1) –

3a Fund for general banking risks 82.4 26 (1) (f) –

4

Amount of qualifying items referred to in article 484 (3)

and the related share premium accounts subject to phase

out from CET1 – 486 (2) –

Governmental capital contributions

with grandfathering rights until 1 January 2018 – 483 (2) –

5 Minority interests

(amount allowed in consolidated CET1) – 84, 479, 480 –

5a Independently reviewed interim profits net

of any foreseeable charge or dividend – 26 (2) –

6 Common equity tier 1 (CET1) capital

before regulatory adjustments 1,369.5 –

6

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Own funds and capital requirements

Common equity tier 1 (CET1) capital – Regulatory adjustments (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

7 Additional value adjustments (negative amount) –1.9 34, 105 –

8 Intangible assets (net of related tax liability)

(negative amount) –16.0 36 (1) (b), 37, 472 (4) –64.1

9 In the EU: empty set

10

Deferred tax assets that rely on future profitability

excluding those arising from temporary differences

(net of related tax liability where the conditions of

article 38 (3) are met) (negative amount) –0.9 36 (1) (c), 38, 472 (5) –3.5

11 Fair value reserves related to gains or losses

on cash flow hedges of financial instruments 25.5 33 (a) –

12 Negative amounts resulting from the calculation

of expected loss amounts –42.8 36 (1) (d), 40, 159, 472 (6) –171.2

13 Increase in equity resulting from securitised assets

(negative amount) – 32 (1) –

14 Gains or losses on liabilities valued at fair value resulting

from changes in own credit standing – 33 (b) –

15 Defined-benefit pension fund assets (negative amount) 0.0 36 (1) (e), 41, 472 (7) –0.1

16 Direct and indirect holdings of own common

equity tier 1 instruments (negative amount) –3.1 36 (1) (f), 42, 472 (8) –12.5

17

Holdings of common equity tier 1 instruments of

financial sector entities where those entities have

reciprocal cross holdings with the institution designed

to artificially inflate the own funds of the institution

(negative amount) – 36 (1) (g), 44, 472 (9) –

18

Direct and indirect holdings of common equity tier 1

instruments of financial sector entities in which

the institution does not hold a material interest

(amount above 10% threshold and net of eligible

short positions) (negative amount) –

36 (1) (h), 43, 45, 46,

49 (2) and (3), 79, 472 (10) –

19

Direct, indirect and synthetic holdings by the institution

of common equity tier 1 instruments of financial sector

entities in which the institution holds a material interest

(amount above 10% threshold and net of eligible short

positions) (negative amount) –

36 (1) (i), 43, 45, 47, 48 (1) (b),

49 (1) to (3), 79, 470, 472 (11) –

(Continued on the next page)

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

7Own funds and capital requirements

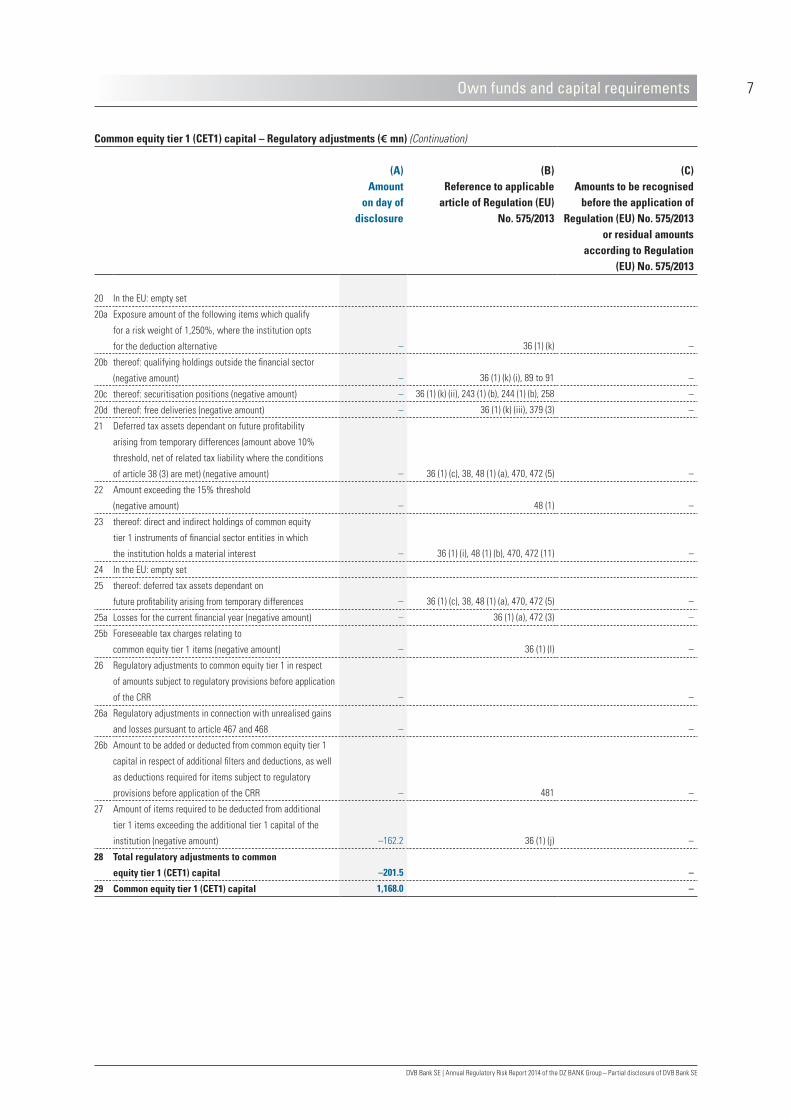

Common equity tier 1 (CET1) capital – Regulatory adjustments (€ mn) (Continuation)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

20 In the EU: empty set

20a

Exposure amount of the following items which qualify

for a risk weight of 1,250%, where the institution opts

for the deduction alternative – 36 (1) (k) –

20b thereof: qualifying holdings outside the financial sector

(negative amount) – 36 (1) (k) (i), 89 to 91 –

20c thereof: securitisation positions (negative amount) – 36 (1) (k) (ii), 243 (1) (b), 244 (1) (b), 258 –

20d thereof: free deliveries (negative amount) – 36 (1) (k) (iii), 379 (3) –

21

Deferred tax assets dependant on future profitability

arising from temporary differences (amount above 10%

threshold, net of related tax liability where the conditions

of article 38 (3) are met) (negative amount) – 36 (1) (c), 38, 48 (1) (a), 470, 472 (5) –

22 Amount exceeding the 15% threshold

(negative amount) – 48 (1) –

23

thereof: direct and indirect holdings of common equity

tier 1 instruments of financial sector entities in which

the institution holds a material interest – 36 (1) (i), 48 (1) (b), 470, 472 (11) –

24 In the EU: empty set

25 thereof: deferred tax assets dependant on

future profitability arising from temporary differences – 36 (1) (c), 38, 48 (1) (a), 470, 472 (5) –

25a Losses for the current financial year (negative amount) – 36 (1) (a), 472 (3) –

25b Foreseeable tax charges relating to

common equity tier 1 items (negative amount) – 36 (1) (l) –

26

Regulatory adjustments to common equity tier 1 in respect

of amounts subject to regulatory provisions before application

of the CRR – –

26a Regulatory adjustments in connection with unrealised gains

and losses pursuant to article 467 and 468 – –

26b

Amount to be added or deducted from common equity tier 1

capital in respect of additional filters and deductions, as well

as deductions required for items subject to regulatory

provisions before application of the CRR – 481 –

27

Amount of items required to be deducted from additional

tier 1 items exceeding the additional tier 1 capital of the

institution (negative amount) –162.2 36 (1) (j) –

28 Total regulatory adjustments to common

equity tier 1 (CET1) capital –201.5 –

29 Common equity tier 1 (CET1) capital 1,168.0 –

8

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

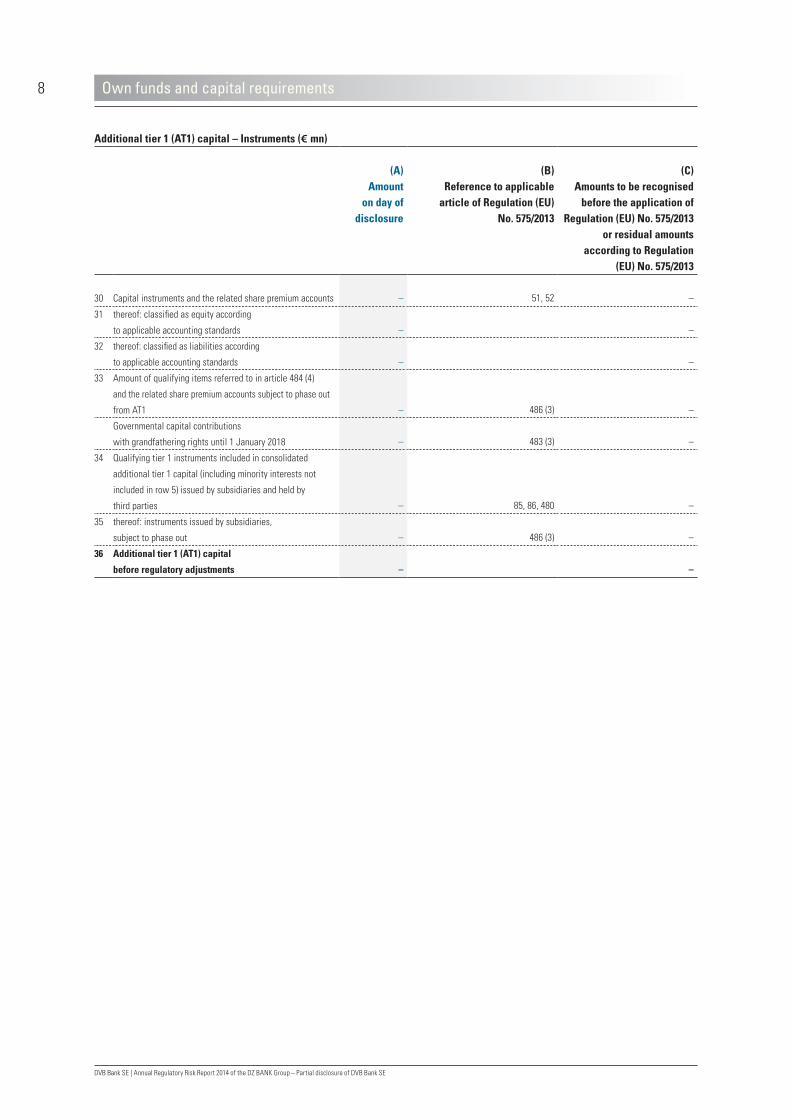

Additional tier 1 (AT1) capital – Instruments (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

30 Capital instruments and the related share premium accounts – 51, 52 –

31 thereof: classified as equity according

to applicable accounting standards – –

32 thereof: classified as liabilities according

to applicable accounting standards – –

33

Amount of qualifying items referred to in article 484 (4)

and the related share premium accounts subject to phase out

from AT1 – 486 (3) –

Governmental capital contributions

with grandfathering rights until 1 January 2018 – 483 (3) –

34

Qualifying tier 1 instruments included in consolidated

additional tier 1 capital (including minority interests not

included in row 5) issued by subsidiaries and held by

third parties – 85, 86, 480 –

35 thereof: instruments issued by subsidiaries,

subject to phase out – 486 (3) –

36 Additional tier 1 (AT1) capital

before regulatory adjustments – –

Own funds and capital requirements

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

9

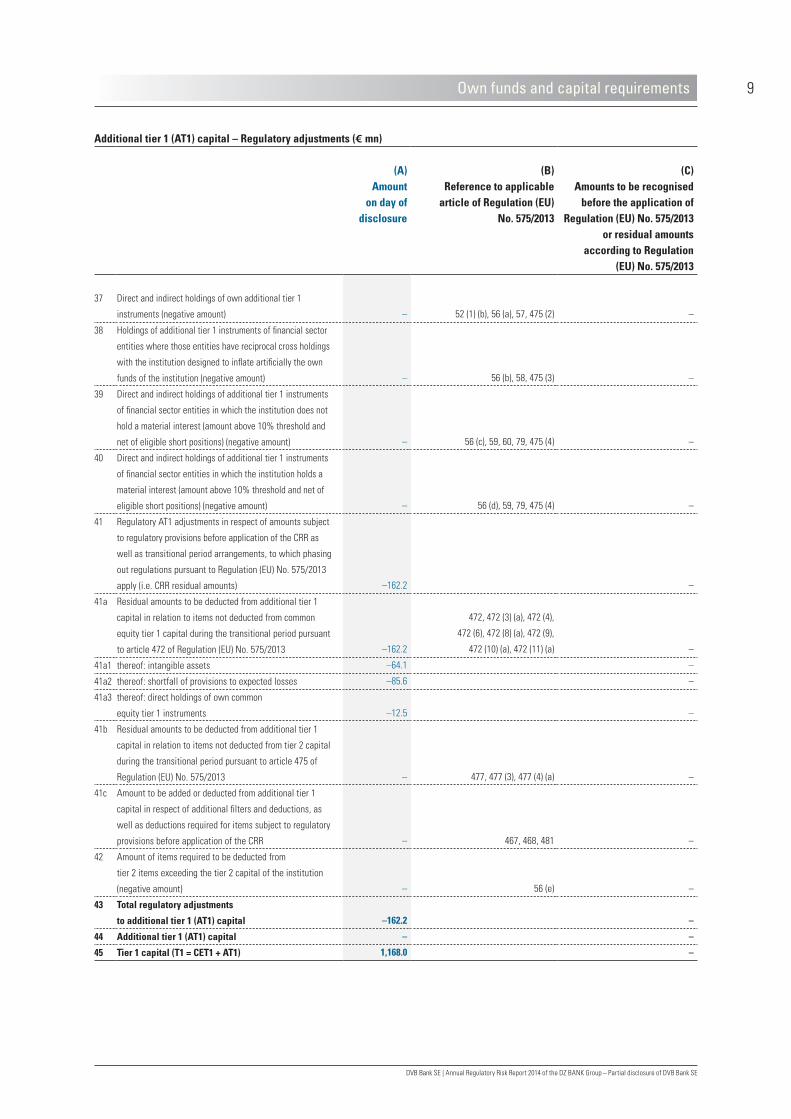

Additional tier 1 (AT1) capital – Regulatory adjustments (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

37 Direct and indirect holdings of own additional tier 1

instruments (negative amount) – 52 (1) (b), 56 (a), 57, 475 (2) –

38

Holdings of additional tier 1 instruments of financial sector

entities where those entities have reciprocal cross holdings

with the institution designed to inflate artificially the own

funds of the institution (negative amount) – 56 (b), 58, 475 (3) –

39

Direct and indirect holdings of additional tier 1 instruments

of financial sector entities in which the institution does not

hold a material interest (amount above 10% threshold and

net of eligible short positions) (negative amount) – 56 (c), 59, 60, 79, 475 (4) –

40

Direct and indirect holdings of additional tier 1 instruments

of financial sector entities in which the institution holds a

material interest (amount above 10% threshold and net of

eligible short positions) (negative amount) – 56 (d), 59, 79, 475 (4) –

41

Regulatory AT1 adjustments in respect of amounts subject

to regulatory provisions before application of the CRR as

well as transitional period arrangements, to which phasing

out regulations pursuant to Regulation (EU) No. 575/2013

apply (i.e. CRR residual amounts) –162.2 –

41a

Residual amounts to be deducted from additional tier 1

capital in relation to items not deducted from common

equity tier 1 capital during the transitional period pursuant

to article 472 of Regulation (EU) No. 575/2013 –162.2

472, 472 (3) (a), 472 (4),

472 (6), 472 (8) (a), 472 (9),

472 (10) (a), 472 (11) (a) –

41a1 thereof: intangible assets –64.1 –

41a2 thereof: shortfall of provisions to expected losses –85.6 –

41a3 thereof: direct holdings of own common

equity tier 1 instruments –12.5 –

41b

Residual amounts to be deducted from additional tier 1

capital in relation to items not deducted from tier 2 capital

during the transitional period pursuant to article 475 of

Regulation (EU) No. 575/2013 – 477, 477 (3), 477 (4) (a) –

41c

Amount to be added or deducted from additional tier 1

capital in respect of additional filters and deductions, as

well as deductions required for items subject to regulatory

provisions before application of the CRR – 467, 468, 481 –

42

Amount of items required to be deducted from

tier 2 items exceeding the tier 2 capital of the institution

(negative amount) – 56 (e) –

43 Total regulatory adjustments

to additional tier 1 (AT1) capital –162.2 –

44 Additional tier 1 (AT1) capital – –

45 Tier 1 capital (T1 = CET1 + AT1) 1,168.0 –

Own funds and capital requirements

10

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

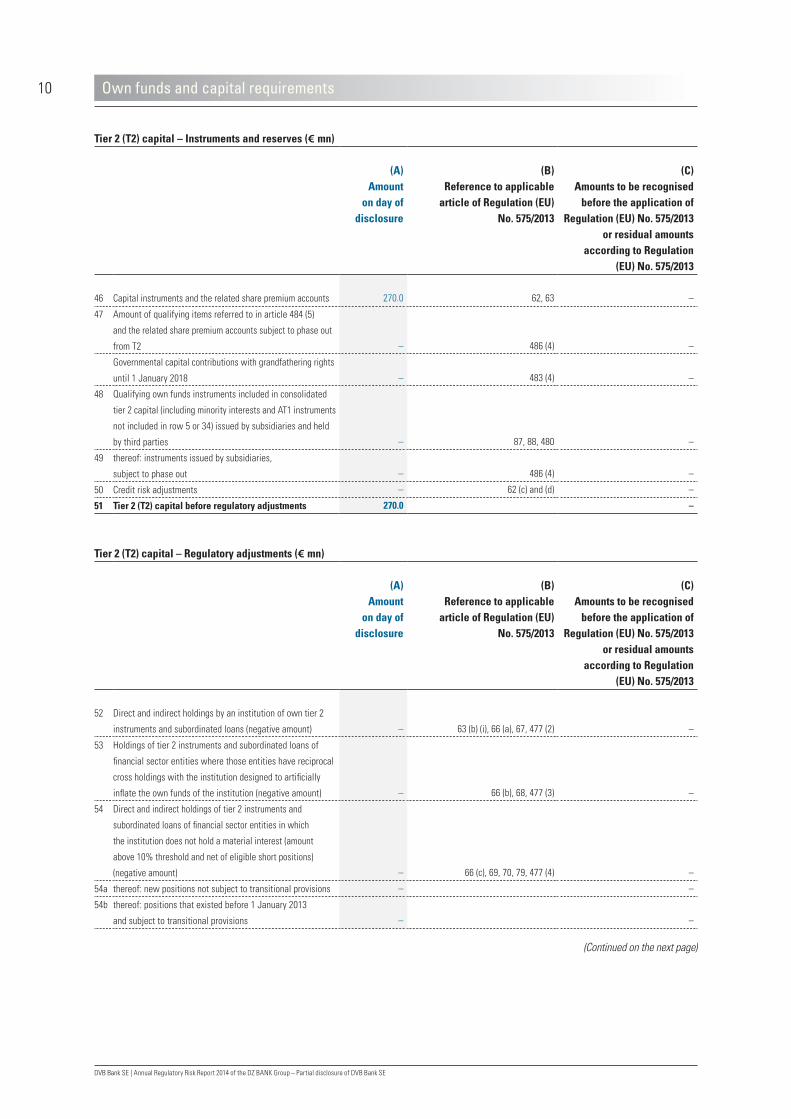

Tier 2 (T2) capital – Instruments and reserves (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

46 Capital instruments and the related share premium accounts 270.0 62, 63 –

47

Amount of qualifying items referred to in article 484 (5)

and the related share premium accounts subject to phase out

from T2 – 486 (4) –

Governmental capital contributions with grandfathering rights

until 1 January 2018 – 483 (4) –

48

Qualifying own funds instruments included in consolidated

tier 2 capital (including minority interests and AT1 instruments

not included in row 5 or 34) issued by subsidiaries and held

by third parties – 87, 88, 480 –

49 thereof: instruments issued by subsidiaries,

subject to phase out – 486 (4) –

50 Credit risk adjustments – 62 (c) and (d) –

51 Tier 2 (T2) capital before regulatory adjustments 270.0 –

Tier 2 (T2) capital – Regulatory adjustments (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

52 Direct and indirect holdings by an institution of own tier 2

instruments and subordinated loans (negative amount) – 63 (b) (i), 66 (a), 67, 477 (2) –

53

Holdings of tier 2 instruments and subordinated loans of

financial sector entities where those entities have reciprocal

cross holdings with the institution designed to artificially

inflate the own funds of the institution (negative amount) – 66 (b), 68, 477 (3) –

54

Direct and indirect holdings of tier 2 instruments and

subordinated loans of financial sector entities in which

the institution does not hold a material interest (amount

above 10% threshold and net of eligible short positions)

(negative amount) – 66 (c), 69, 70, 79, 477 (4) –

54a thereof: new positions not subject to transitional provisions – –

54b thereof: positions that existed before 1 January 2013

and subject to transitional provisions – –

(Continued on the next page)

Own funds and capital requirements

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

11

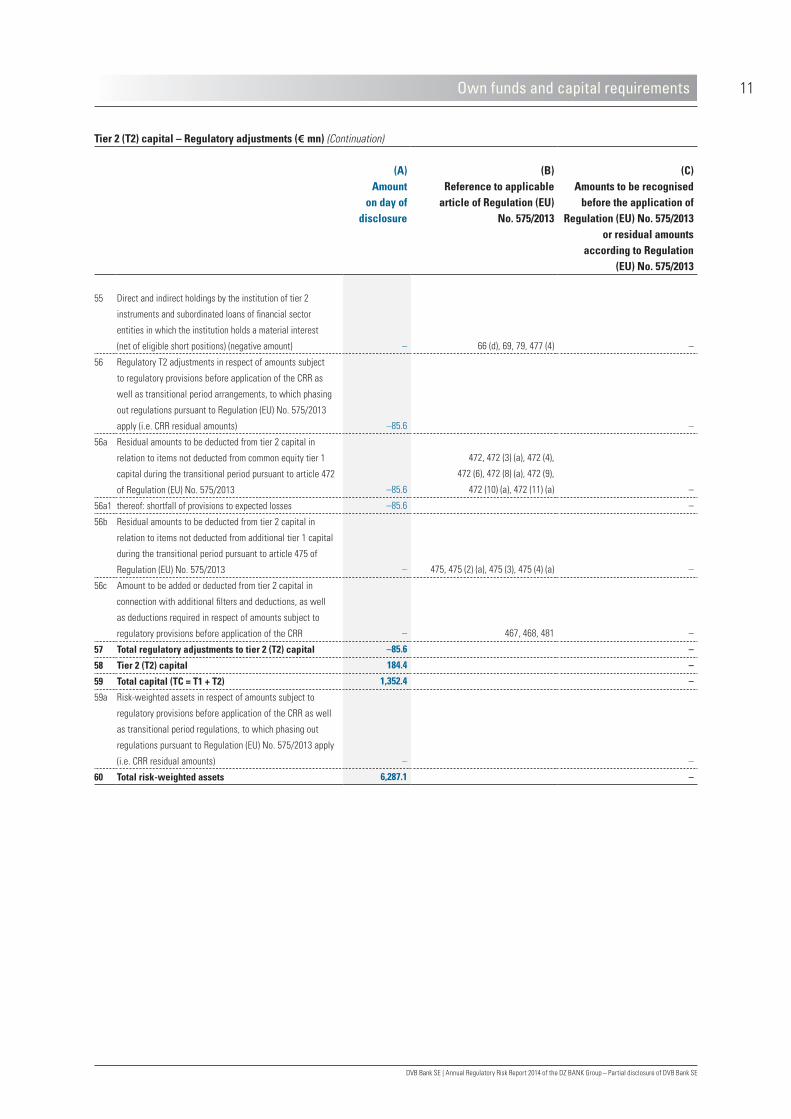

Tier 2 (T2) capital – Regulatory adjustments (€ mn) (Continuation)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

55

Direct and indirect holdings by the institution of tier 2

instruments and subordinated loans of financial sector

entities in which the institution holds a material interest

(net of eligible short positions) (negative amount) – 66 (d), 69, 79, 477 (4) –

56

Regulatory T2 adjustments in respect of amounts subject

to regulatory provisions before application of the CRR as

well as transitional period arrangements, to which phasing

out regulations pursuant to Regulation (EU) No. 575/2013

apply (i.e. CRR residual amounts) –85.6 –

56a

Residual amounts to be deducted from tier 2 capital in

relation to items not deducted from common equity tier 1

capital during the transitional period pursuant to article 472

of Regulation (EU) No. 575/2013 –85.6

472, 472 (3) (a), 472 (4),

472 (6), 472 (8) (a), 472 (9),

472 (10) (a), 472 (11) (a) –

56a1 thereof: shortfall of provisions to expected losses –85.6 –

56b

Residual amounts to be deducted from tier 2 capital in

relation to items not deducted from additional tier 1 capital

during the transitional period pursuant to article 475 of

Regulation (EU) No. 575/2013 – 475, 475 (2) (a), 475 (3), 475 (4) (a) –

56c

Amount to be added or deducted from tier 2 capital in

connection with additional filters and deductions, as well

as deductions required in respect of amounts subject to

regulatory provisions before application of the CRR – 467, 468, 481 –

57 Total regulatory adjustments to tier 2 (T2) capital –85.6 –

58 Tier 2 (T2) capital 184.4 –

59 Total capital (TC = T1 + T2) 1,352.4 –

59a

Risk-weighted assets in respect of amounts subject to

regulatory provisions before application of the CRR as well

as transitional period regulations, to which phasing out

regulations pursuant to Regulation (EU) No. 575/2013 apply

(i.e. CRR residual amounts) – –

60 Total risk-weighted assets 6,287.1 –

Own funds and capital requirements

12

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Own funds and capital requirements

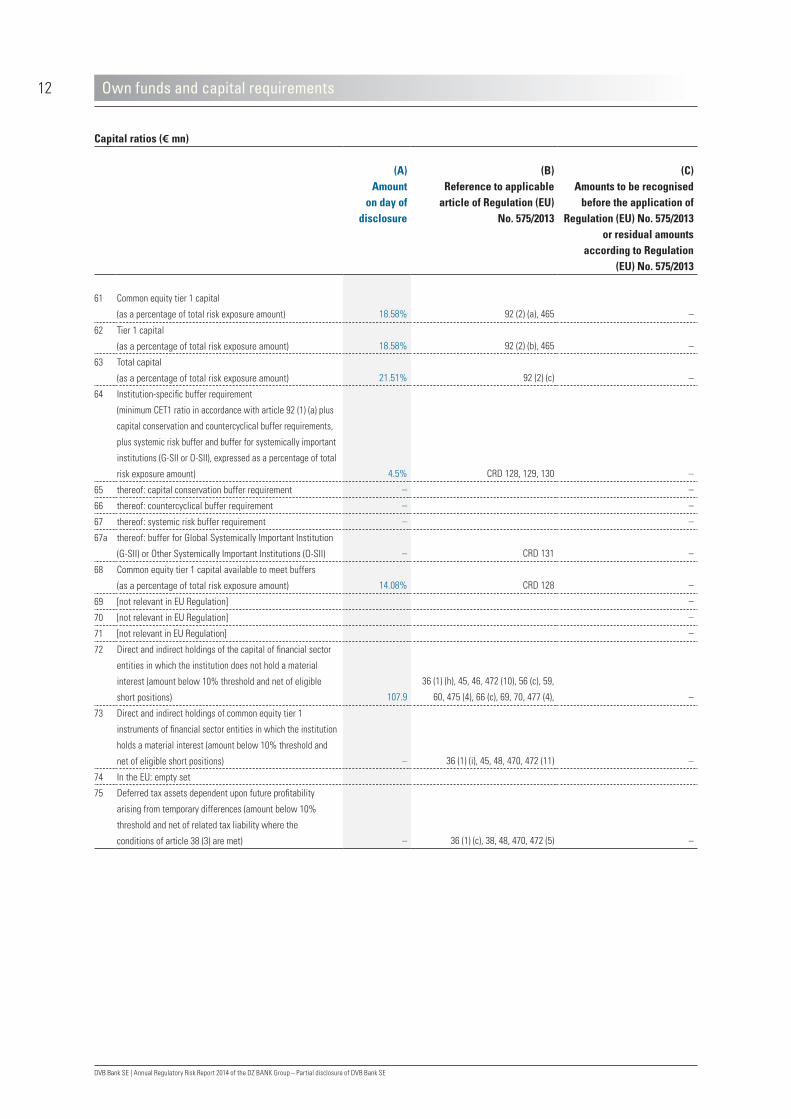

Capital ratios (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

61 Common equity tier 1 capital

(as a percentage of total risk exposure amount) 18.58% 92 (2) (a), 465 –

62 Tier 1 capital

(as a percentage of total risk exposure amount) 18.58% 92 (2) (b), 465 –

63 Total capital

(as a percentage of total risk exposure amount) 21.51% 92 (2) (c) –

64

Institution-specific buffer requirement

(minimum CET1 ratio in accordance with article 92 (1) (a) plus

capital conservation and countercyclical buffer requirements,

plus systemic risk buffer and buffer for systemically important

institutions (G-SII or O-SII), expressed as a percentage of total

risk exposure amount) 4.5% CRD 128, 129, 130 –

65 thereof: capital conservation buffer requirement – –

66 thereof: countercyclical buffer requirement – –

67 thereof: systemic risk buffer requirement – –

67a thereof: buffer for Global Systemically Important Institution

(G-SII) or Other Systemically Important Institutions (O-SII) – CRD 131 –

68 Common equity tier 1 capital available to meet buffers

(as a percentage of total risk exposure amount) 14.08% CRD 128 –

69 [not relevant in EU Regulation] –

70 [not relevant in EU Regulation] –

71 [not relevant in EU Regulation] –

72

Direct and indirect holdings of the capital of financial sector

entities in which the institution does not hold a material

interest (amount below 10% threshold and net of eligible

short positions) 107.9

36 (1) (h), 45, 46, 472 (10), 56 (c), 59,

60, 475 (4), 66 (c), 69, 70, 477 (4), –

73

Direct and indirect holdings of common equity tier 1

instruments of financial sector entities in which the institution

holds a material interest (amount below 10% threshold and

net of eligible short positions) – 36 (1) (i), 45, 48, 470, 472 (11) –

74 In the EU: empty set

75

Deferred tax assets dependent upon future profitability

arising from temporary differences (amount below 10%

threshold and net of related tax liability where the

conditions of article 38 (3) are met) – 36 (1) (c), 38, 48, 470, 472 (5) –

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

13Own funds and capital requirements

Applicable caps on the inclusion of provisions in tier 2 (€ mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

76

Credit risk adjustments included in tier 2 in respect

of exposures subject to standardised approach

(prior to the application of the cap) – 62 –

77 Cap on inclusion of credit risk adjustments in tier 2

under standardised approach 7.2 62 –

78

Credit risk adjustments included in tier 2 in respect

of exposures subject to internal ratings-based approach

(prior to the application of the cap) – 62 –

79 Cap on inclusion of credit risk adjustments in tier 2

under internal ratings-based approach 26.5 62 –

Capital instruments subject to phase-out arrangements (only applicable between 1 January 2013 and 1 January 2022 – € mn)

(A) Amount

on day of disclosure

(B) Reference to applicable

article of Regulation (EU) No. 575/2013

(C) Amounts to be recognised

before the application of Regulation (EU) No. 575/2013

or residual amounts according to Regulation

(EU) No. 575/2013

80 Current cap on CET1 instruments subject

to phase out arrangements – 484 (3), 486 (2) and (5) –

81 Amount excluded from CET1 due to cap

(excess over cap after redemptions and maturities) – 484 (3), 486 (2) and (5) –

82 Current cap on AT1 instruments subject

to phase out arrangements – 484 (4), 486 (3) and (5) –

83 Amount excluded from AT1 due to cap

(excess over cap after redemptions and maturities) – 484 (4), 486 (3) and (5) –

84 Current cap on T2 instruments subject

to phase out arrangements – 484 (5), 486 (4) and (5) –

85 Amount excluded from T2 due to cap

(excess over cap after redemptions and maturities) – 484 (5), 486 (4) and (5) –

14

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

For the first time, DVB disclosure follows article 437 of the CRR. No reference values from the previous year are available.

Please refer to page 64 of the Group Annual Report 2014 for details regarding the structure of DVB’s regulatory capital after appropriation of profits.

Deductions from common equity tier 1 items pursuant to article 36 of the CRR mainly include negative amounts resulting from the calculation of expected loss amounts as well as the amount of items required to be deducted from additional tier 1 items exceeding the additional tier 1 capital of the institution.

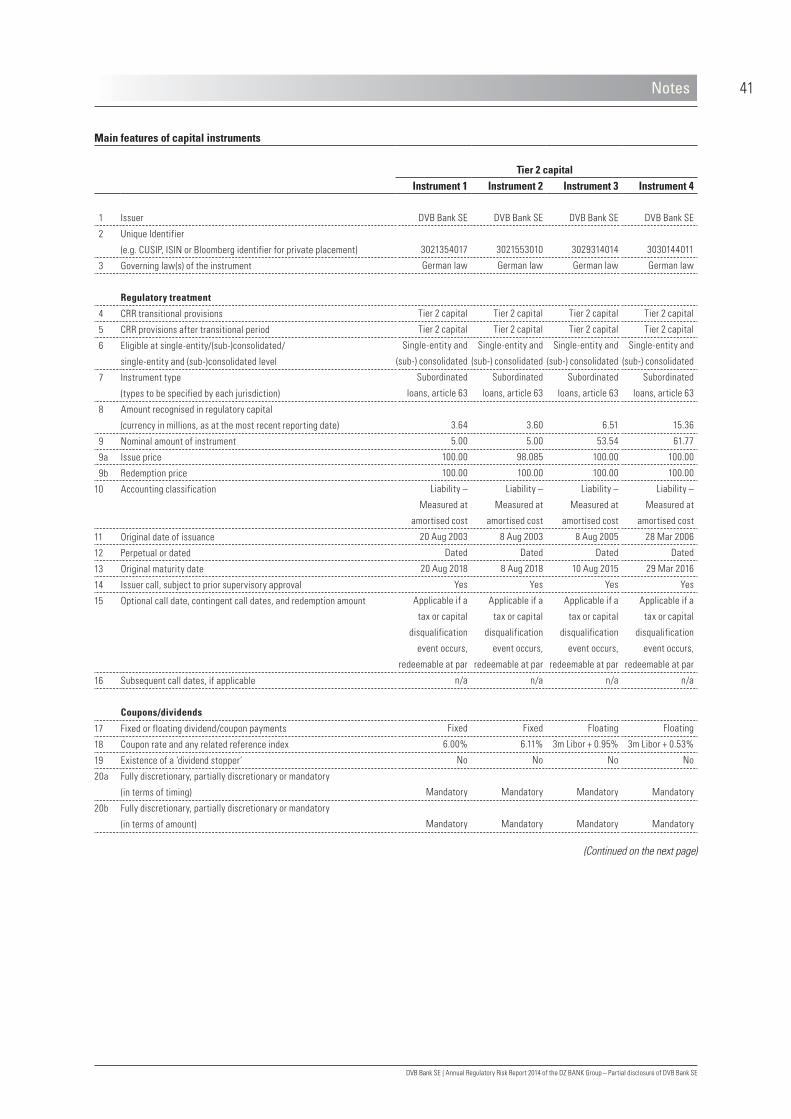

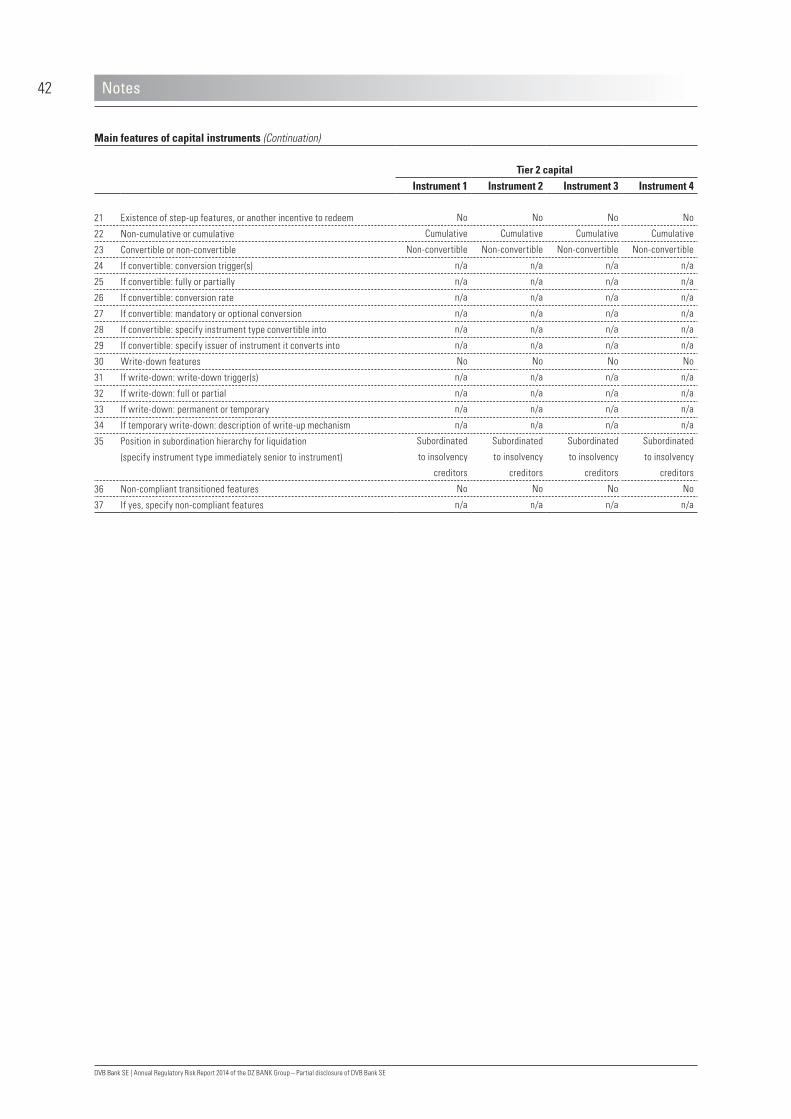

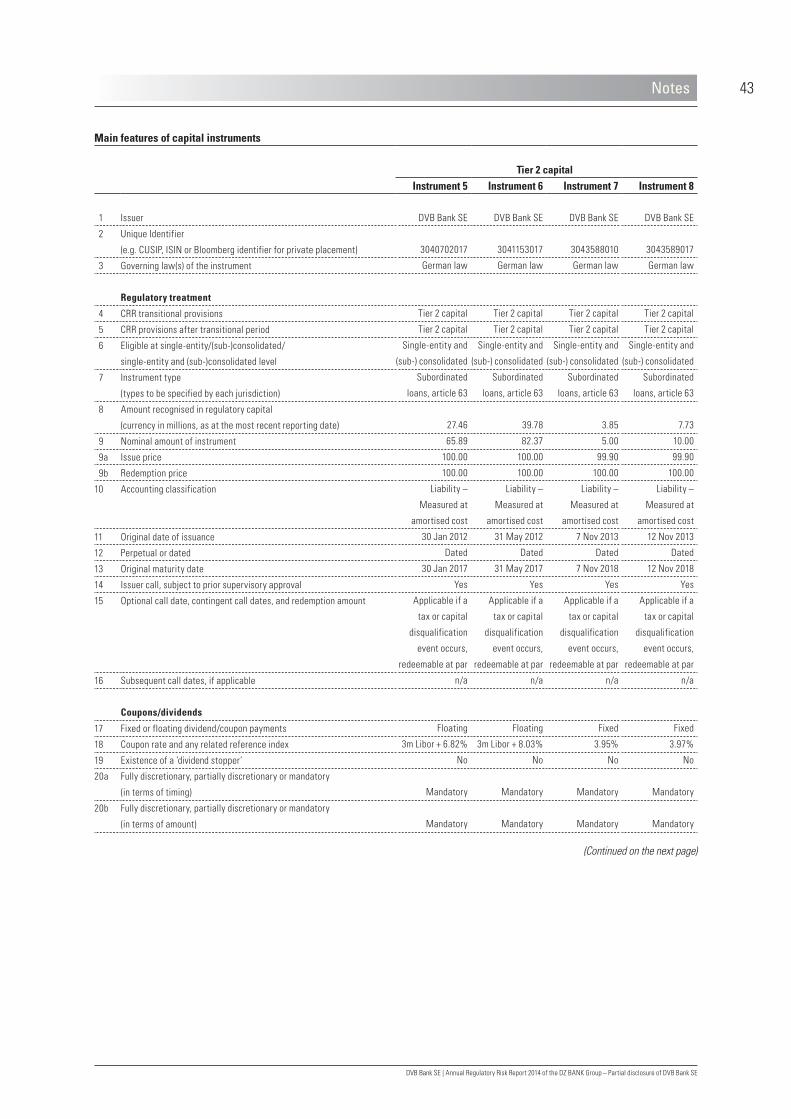

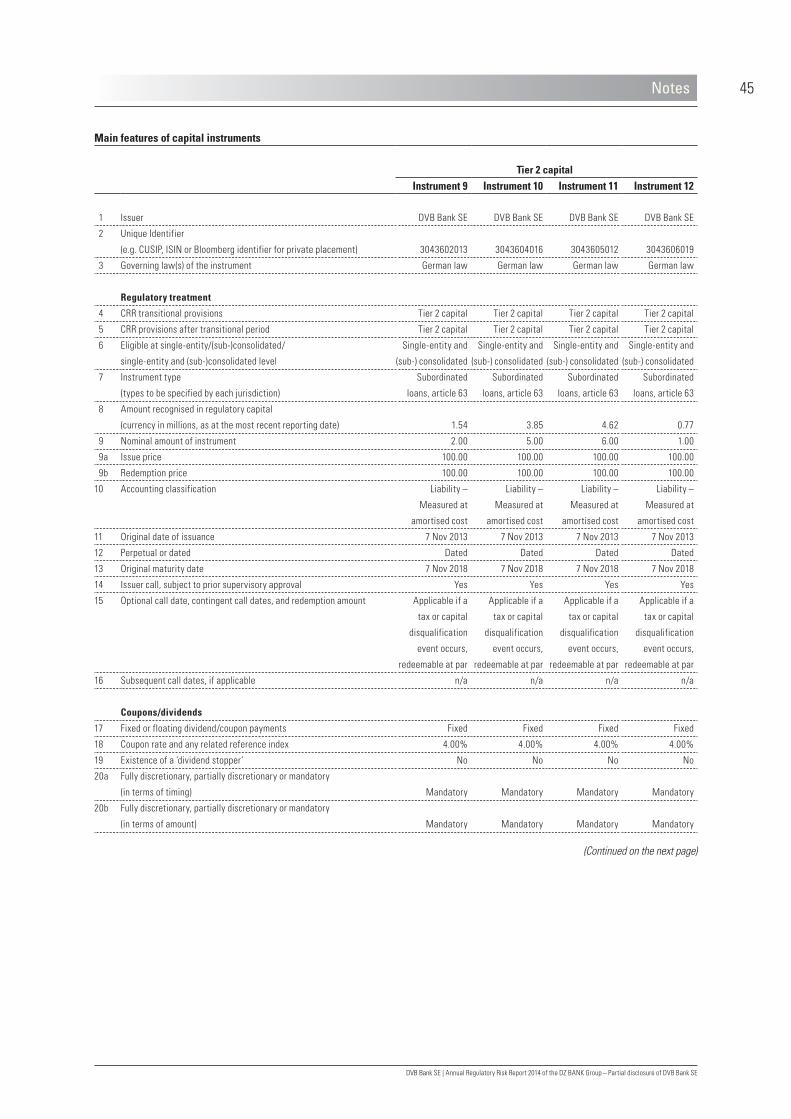

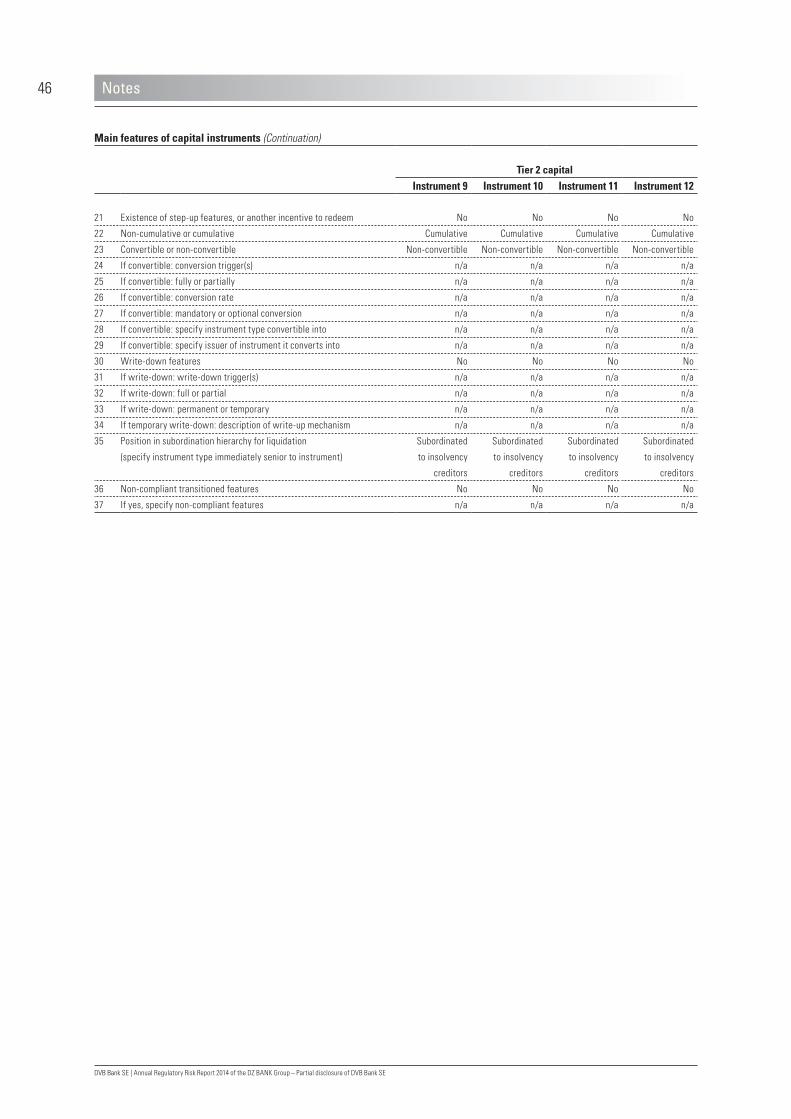

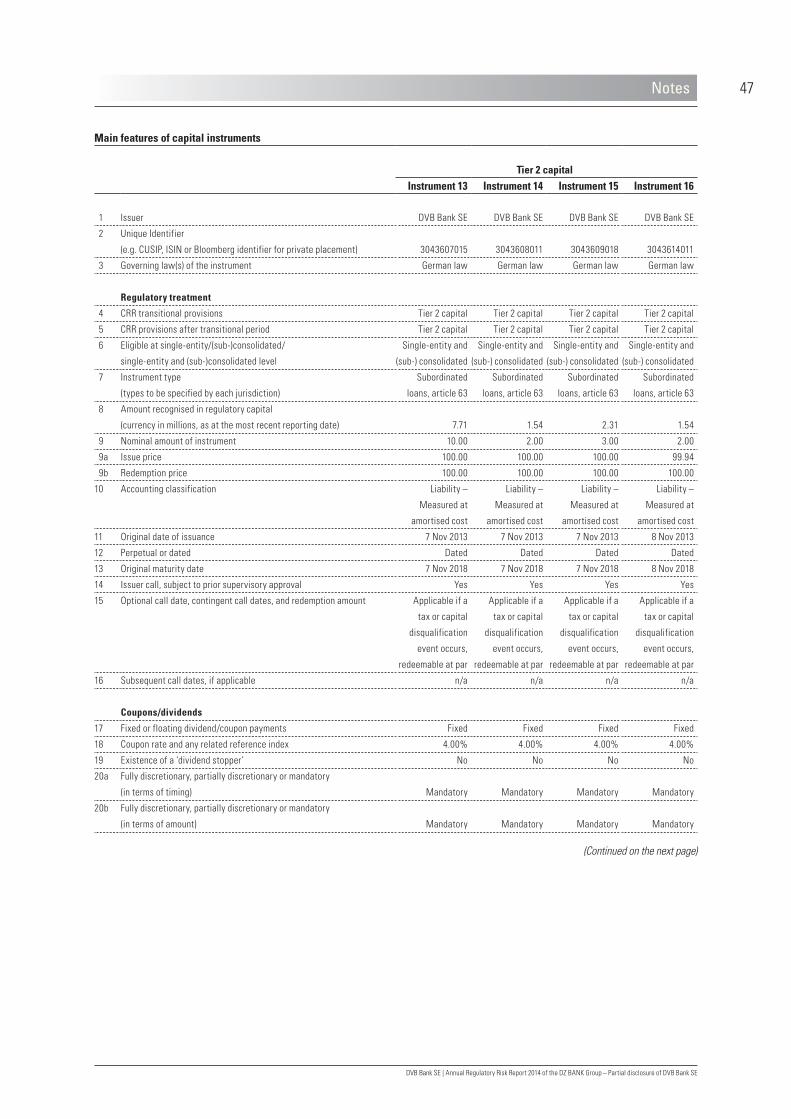

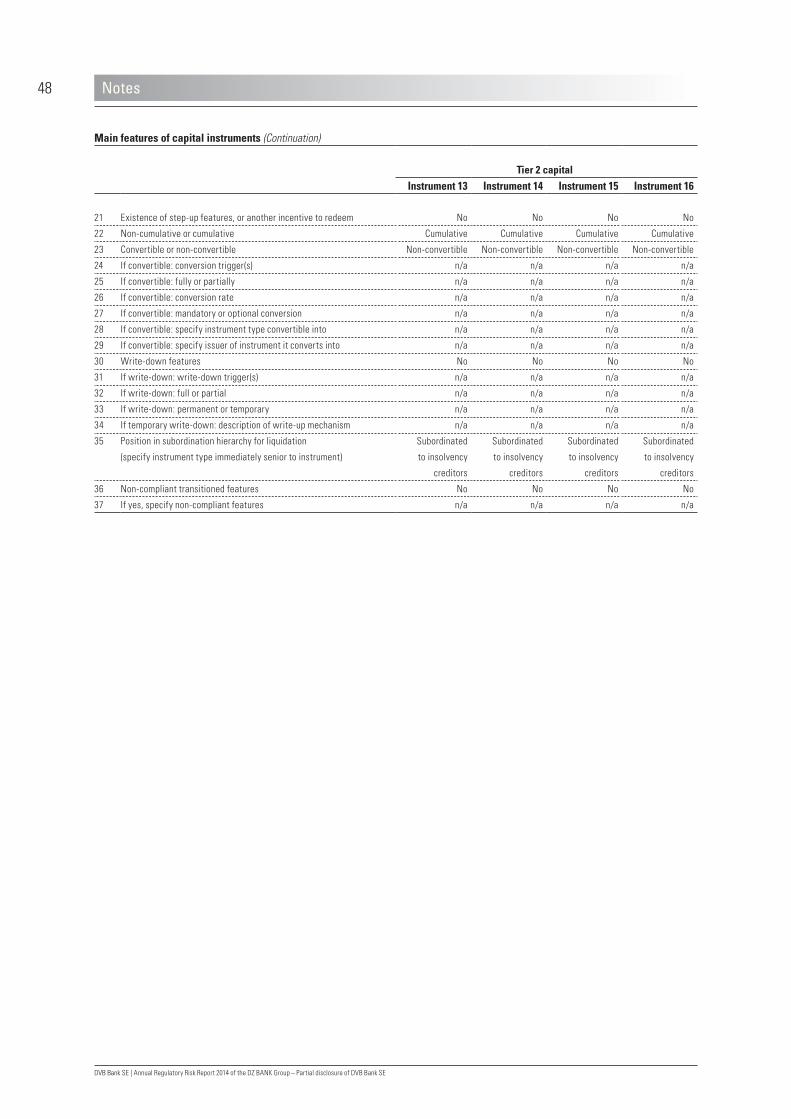

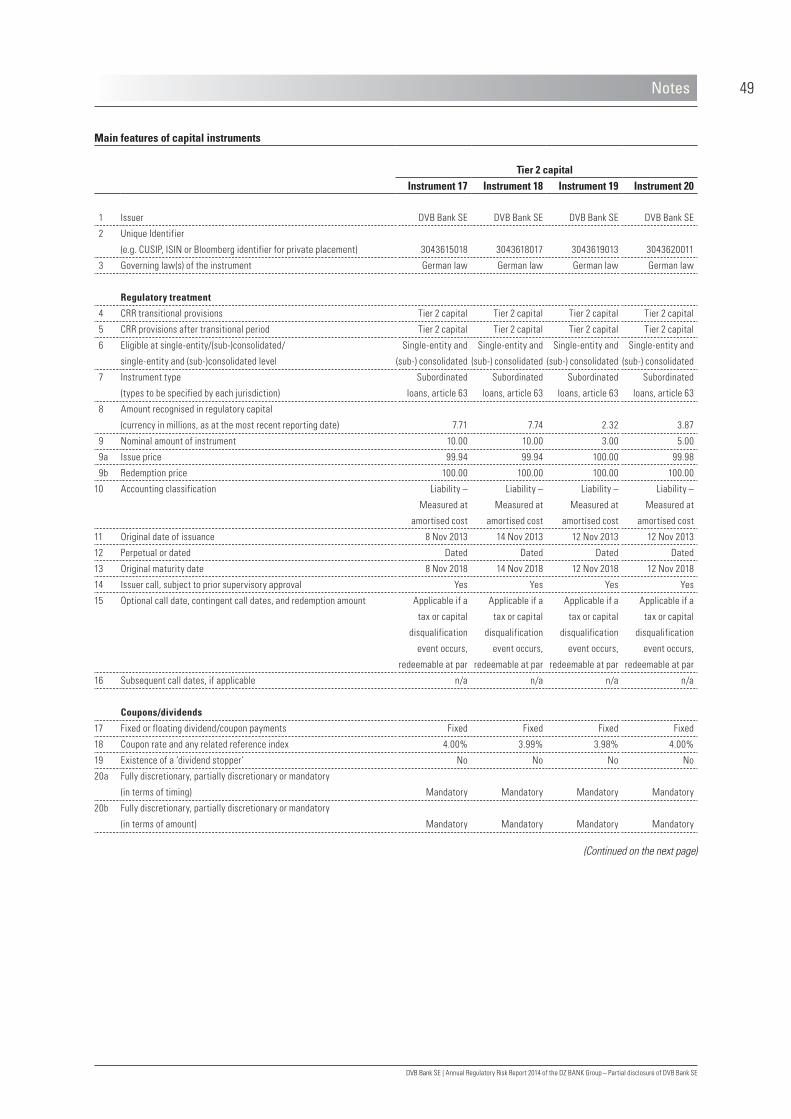

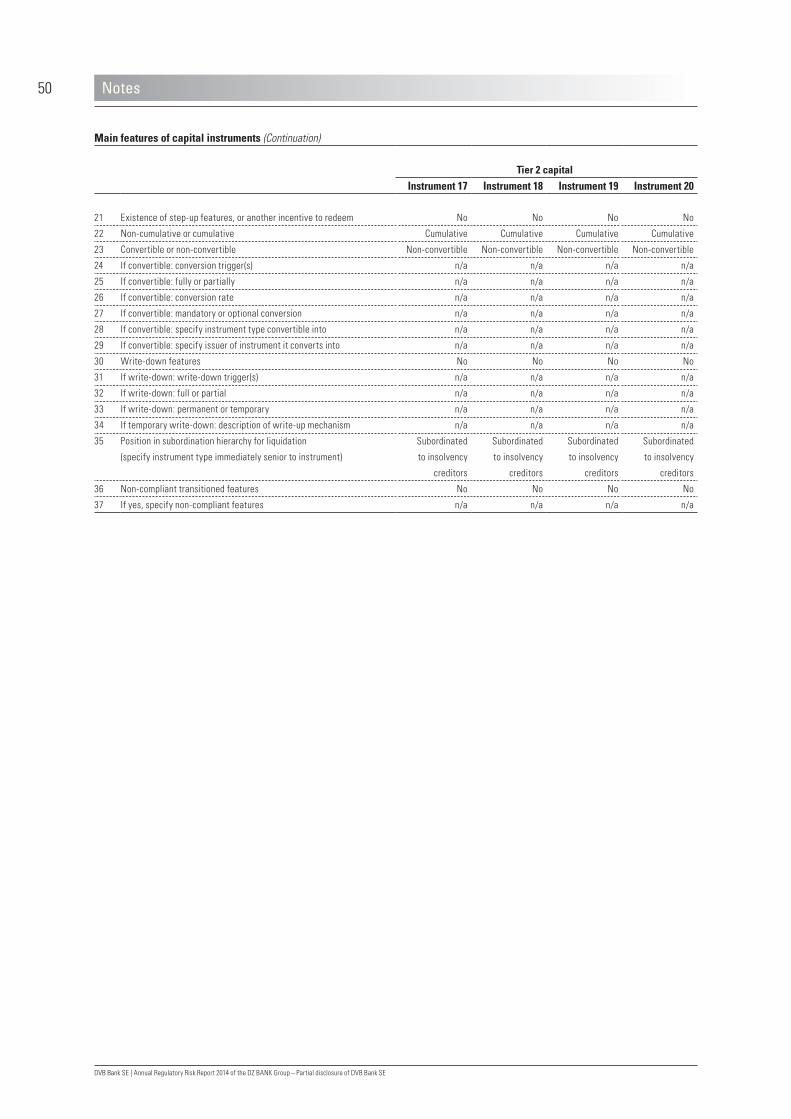

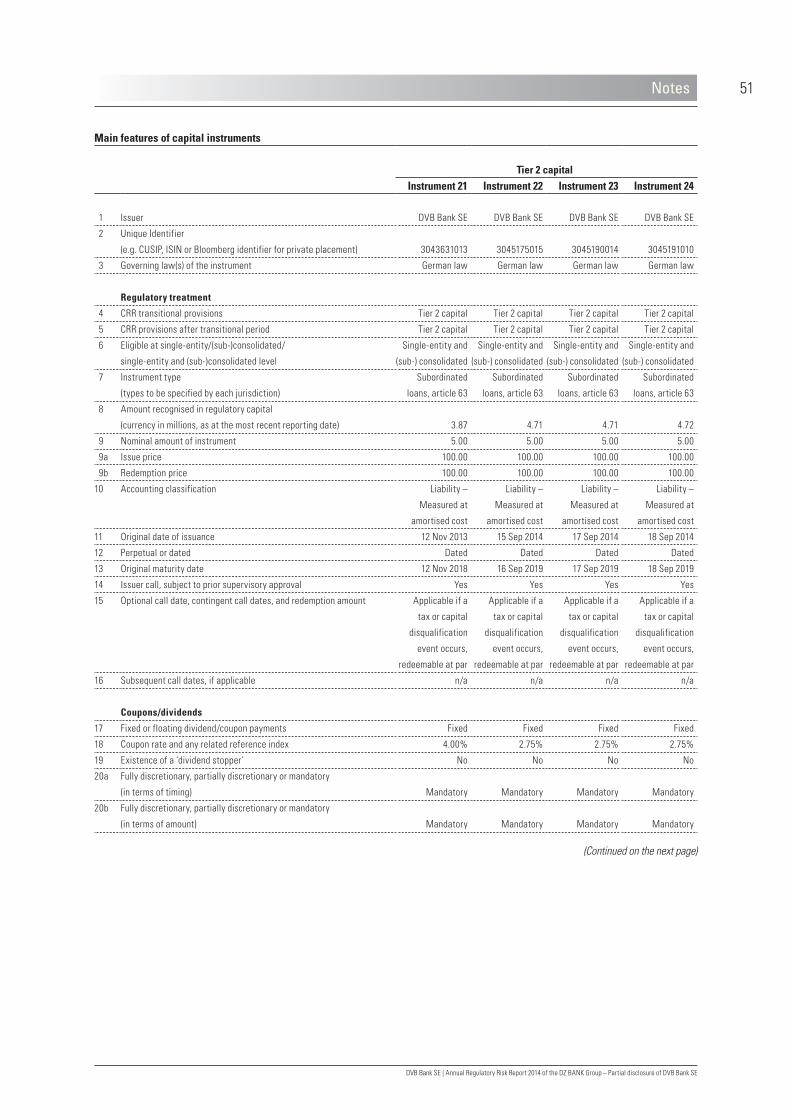

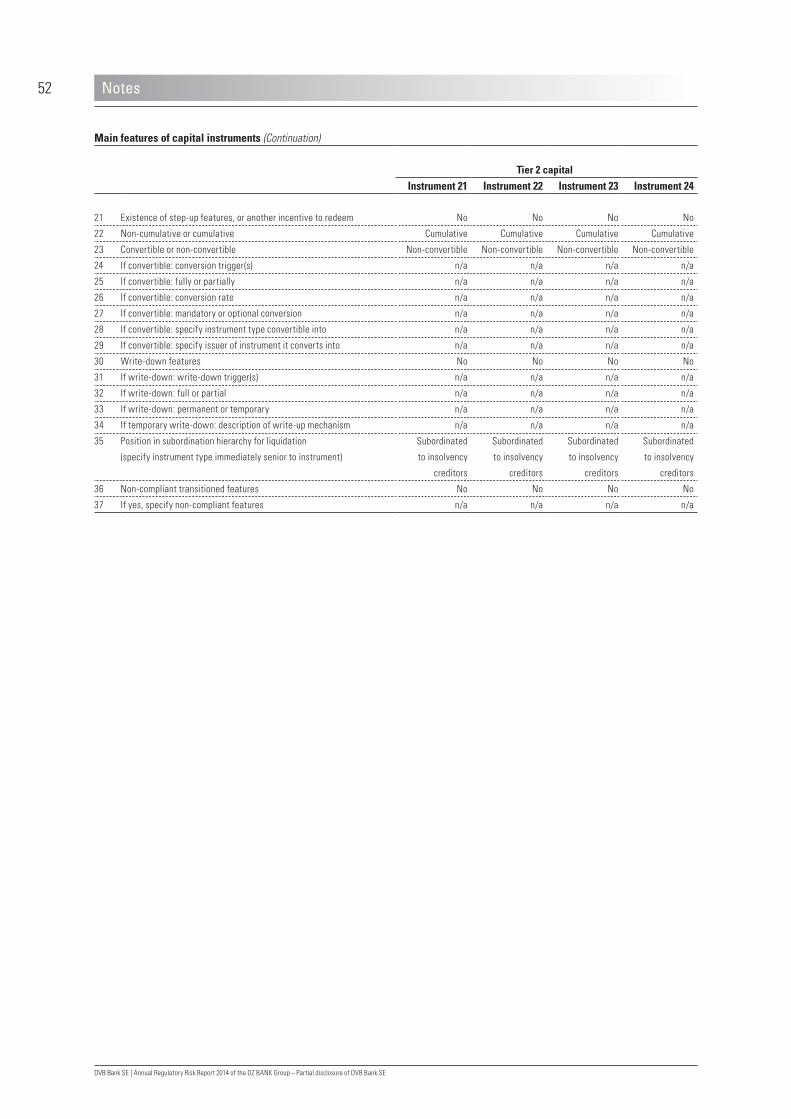

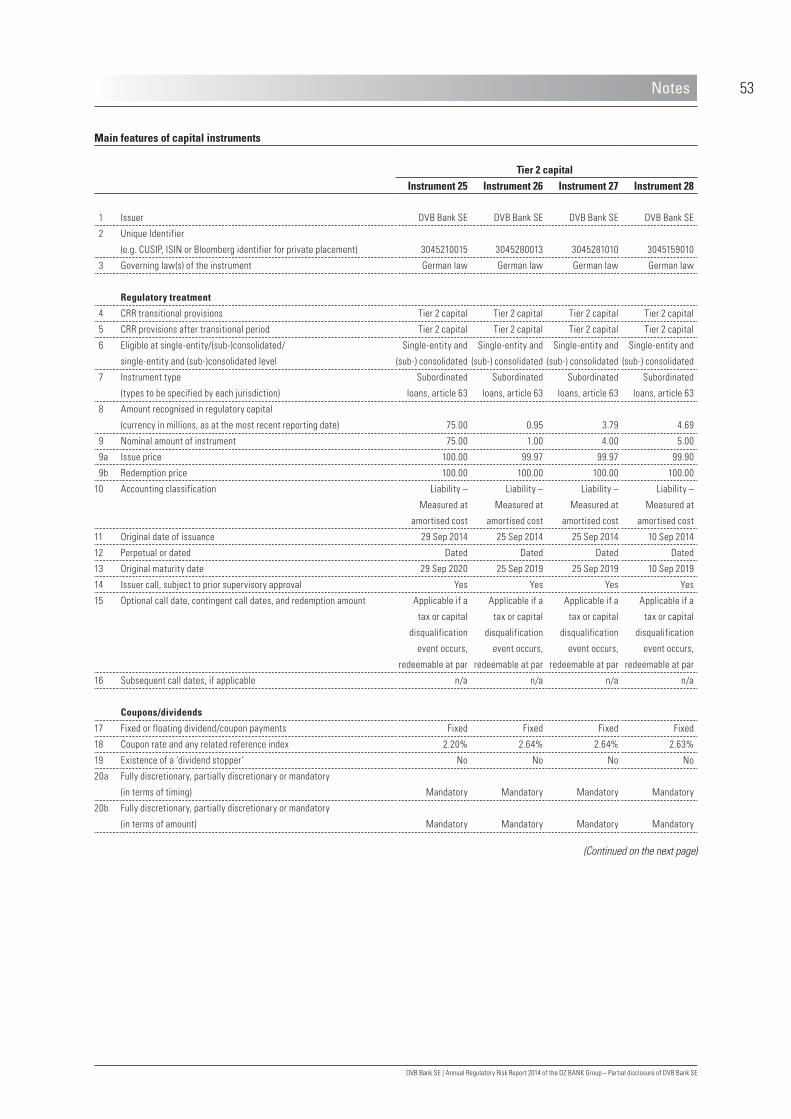

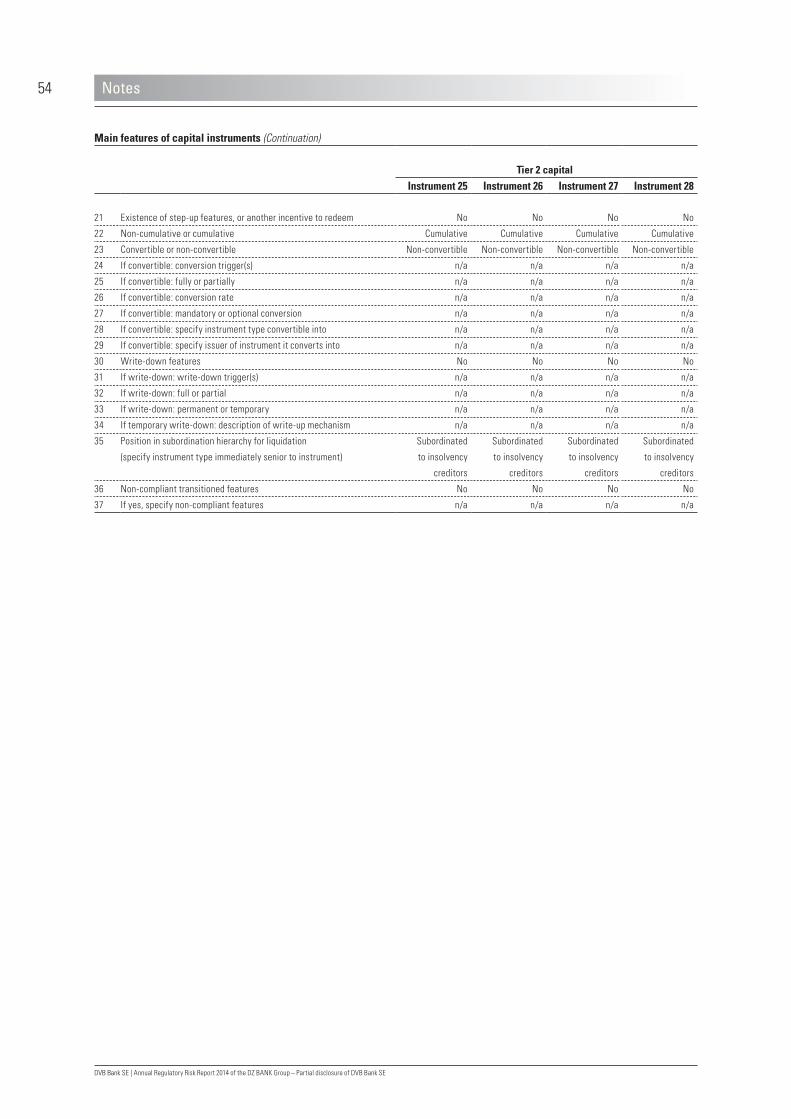

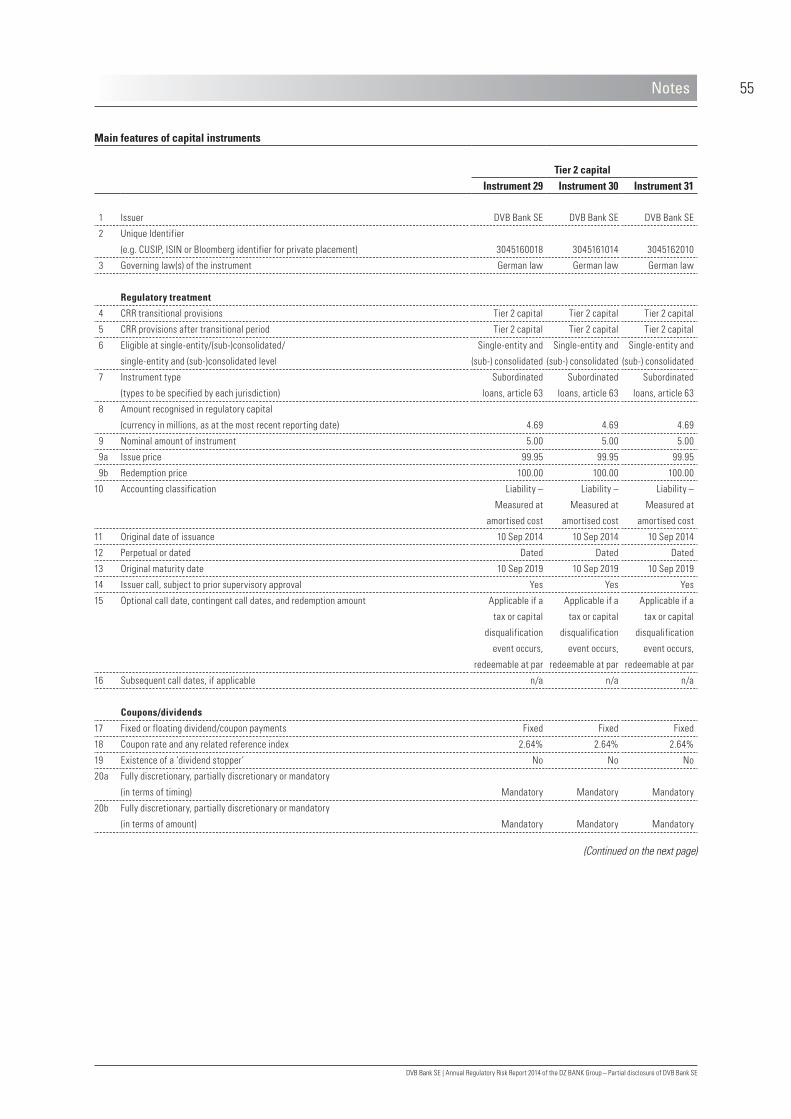

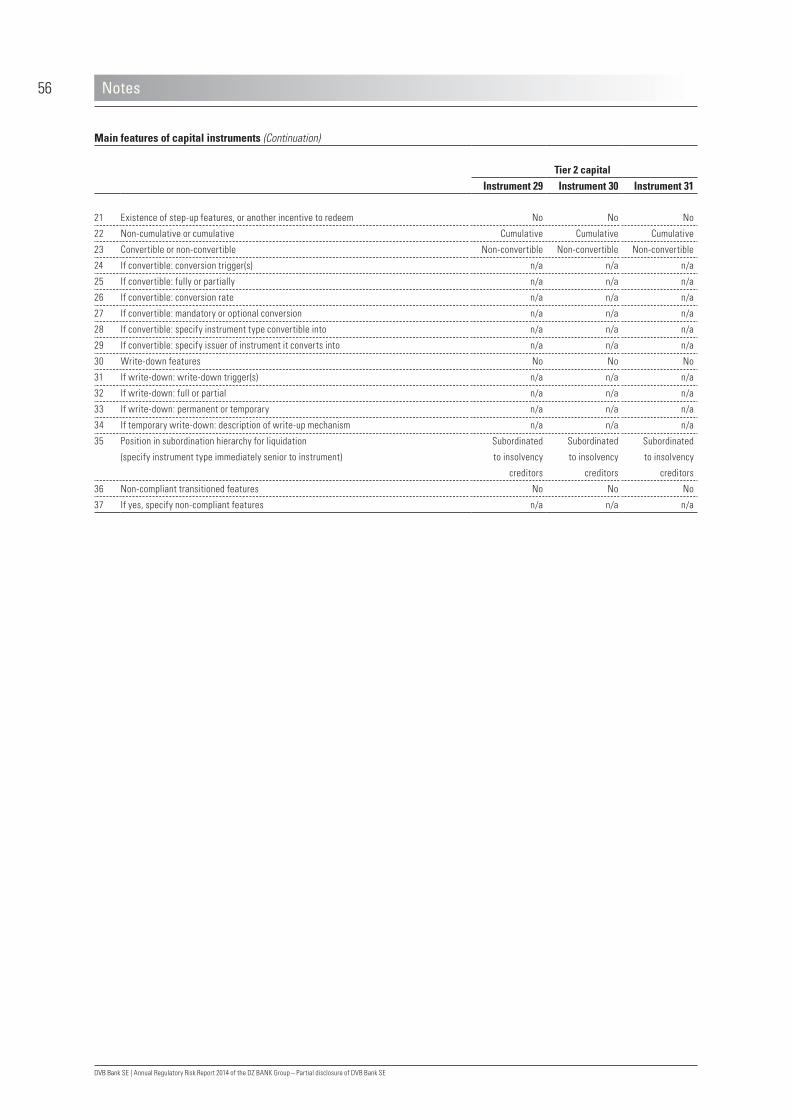

DVB’s tier 2 capital in accordance with article 62 of the CRR consists of subordinated liabilities of €270 million, which includes 29 subordinated promissory notes and two bearer bonds with original maturities ranging between five and 15 years, denomi-nated in either euros or US dollars. Please refer to annex A for a detailed description of such instruments.

Deductions included in tier 2 capital pursuant to article 471 of the CRR consist of CRR residual amounts.

DVB had no tier 3 capital at the reporting date. Items deducted from tier 1 and tier 2 capital pursuant to sections 10 (6) and (6a) of the KWG consist of shortfalls of allowances and expected losses under the IRB Approach for exposures to equity investments pursuant to section 10a (6a) nos. 1 and 2 of the KWG. Upon approval of net income for the year and the specific and portfolio- based allowance for credit losses included in such net income, the shortfall related to allowance for credit losses will be reduced by approximately €6 million.

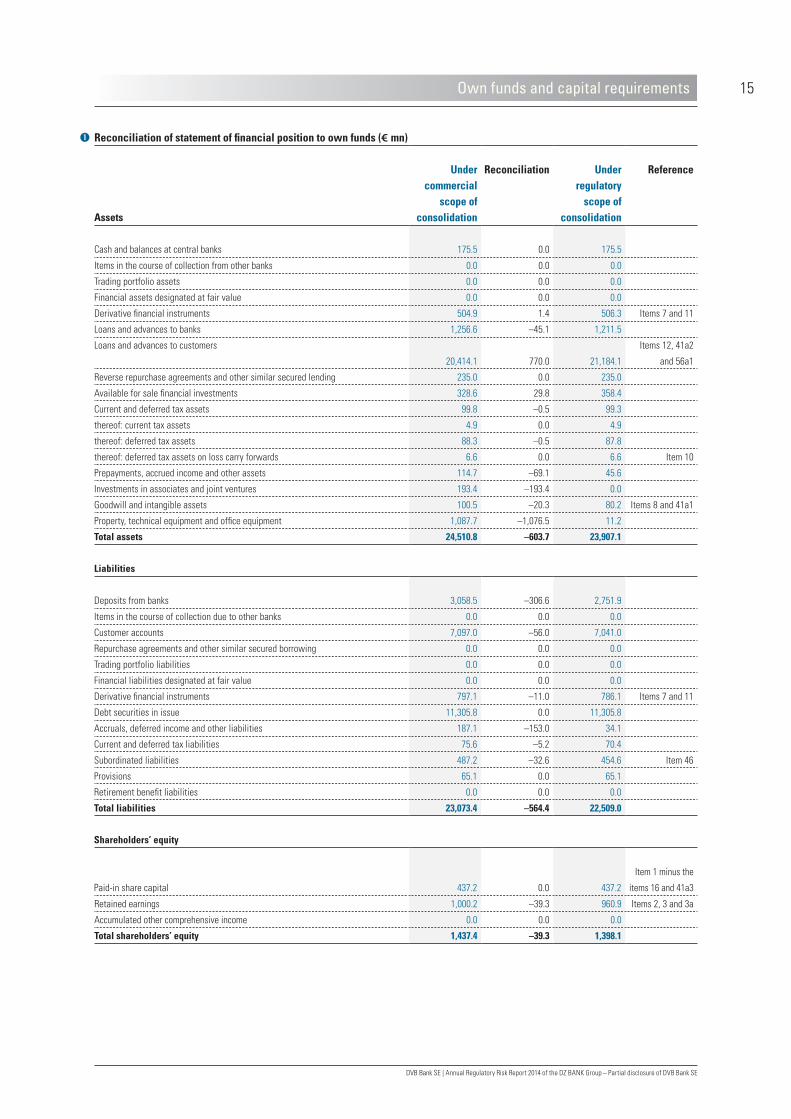

Reconciliation of own funds to statement of financial position in accordance with article 437 (1) (a) of the CRR

The following table features the reconciliation of items in DVB’s statement of financial position as disclosed in the published financial statements to DVB’s own funds.

As a first step, items in the statement of financial position based on the commercial law scope of consolidation are assigned to the corresponding items in the scope of consolidation under regulatory law. These items are then classified into various categories in order to allow the calculation of items to be included in own funds. Reference is made to the corresponding item in DVB’s own funds in the “Reference” column according to article 437 (1) (d) and (e) of the CRR in chapter 2.1.1.

Material differences are due to the implementation of different scopes of consolidation and, in particular, to the different treat-ment of special purpose entities. This mainly affects the struc-ture of assets. The inclusion of special purpose entities in DVB’s consolidated financial statements translates into an increase in tangible fixed assets, while corresponding receivables from such entities have to be included under the regulatory scope of consolidation.

Own funds and capital requirements

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

15

Reconciliation of statement of financial position to own funds (€ mn)

Assets

Under commercial

scope of consolidation

Reconciliation

Under regulatory

scope of consolidation

Reference

Cash and balances at central banks 175.5 0.0 175.5

Items in the course of collection from other banks 0.0 0.0 0.0

Trading portfolio assets 0.0 0.0 0.0

Financial assets designated at fair value 0.0 0.0 0.0

Derivative financial instruments 504.9 1.4 506.3 Items 7 and 11

Loans and advances to banks 1,256.6 –45.1 1,211.5

Loans and advances to customers

20,414.1

770.0

21,184.1

Items 12, 41a2

and 56a1

Reverse repurchase agreements and other similar secured lending 235.0 0.0 235.0

Available for sale financial investments 328.6 29.8 358.4

Current and deferred tax assets 99.8 –0.5 99.3

thereof: current tax assets 4.9 0.0 4.9

thereof: deferred tax assets 88.3 –0.5 87.8

thereof: deferred tax assets on loss carry forwards 6.6 0.0 6.6 Item 10

Prepayments, accrued income and other assets 114.7 –69.1 45.6

Investments in associates and joint ventures 193.4 –193.4 0.0

Goodwill and intangible assets 100.5 –20.3 80.2 Items 8 and 41a1

Property, technical equipment and office equipment 1,087.7 –1,076.5 11.2

Total assets 24,510.8 –603.7 23,907.1

Liabilities

Deposits from banks 3,058.5 –306.6 2,751.9

Items in the course of collection due to other banks 0.0 0.0 0.0

Customer accounts 7,097.0 –56.0 7,041.0

Repurchase agreements and other similar secured borrowing 0.0 0.0 0.0

Trading portfolio liabilities 0.0 0.0 0.0

Financial liabilities designated at fair value 0.0 0.0 0.0

Derivative financial instruments 797.1 –11.0 786.1 Items 7 and 11

Debt securities in issue 11,305.8 0.0 11,305.8

Accruals, deferred income and other liabilities 187.1 –153.0 34.1

Current and deferred tax liabilities 75.6 –5.2 70.4

Subordinated liabilities 487.2 –32.6 454.6 Item 46

Provisions 65.1 0.0 65.1

Retirement benefit liabilities 0.0 0.0 0.0

Total liabilities 23,073.4 –564.4 22,509.0

Shareholders’ equity

Paid-in share capital

437.2

0.0

437.2

Item 1 minus the

items 16 and 41a3

Retained earnings 1,000.2 –39.3 960.9 Items 2, 3 and 3a

Accumulated other comprehensive income 0.0 0.0 0.0

Total shareholders’ equity 1,437.4 –39.3 1,398.1

Own funds and capital requirements

16

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

The same applies to investments in affiliated companies and joint ventures, which are disclosed as receivables from the corresponding entities for regulatory purposes.

The regulatory adjustments to common equity tier 1 capital (items 7 and 11) (table under 2.1.1 “Structure of own funds in accordance with article 437 (1) (d) and (e) of the CRR”) in the amount of –€1.9 million and €25.5 million, respectively, are part of the derivative financial instruments on the assets side and the liabilities side. No further categorisation of the statement of financial position items will be provided.

The shortfall related to allowance for credit risks in the amount of €214 million (items 12, 41a2 and 56a1) (table under 2.1.1 “Structure of own funds in accordance with article 437 (1) (d) and (e) of the CRR”) relates to the calculation of the expected loss based on the statement of financial position item “loans and advances to customers”.

Referring to the line items “deferred tax assets” and “retained earnings”, the differences between the values as disclosed in the statement of financial position and the values as disclosed under DVB’s own funds relate to certain items which had not been audited or had not received regulatory approval as at the reporting date.

Qualifying regulatory capital on subordinated liabilities within tier 2 capital is reduced compared to the statement of financial position. This is due to the amortisation of tier 2 instruments according to article 64 of the CRR. Please refer to annex A for an overview of the eligible amounts.

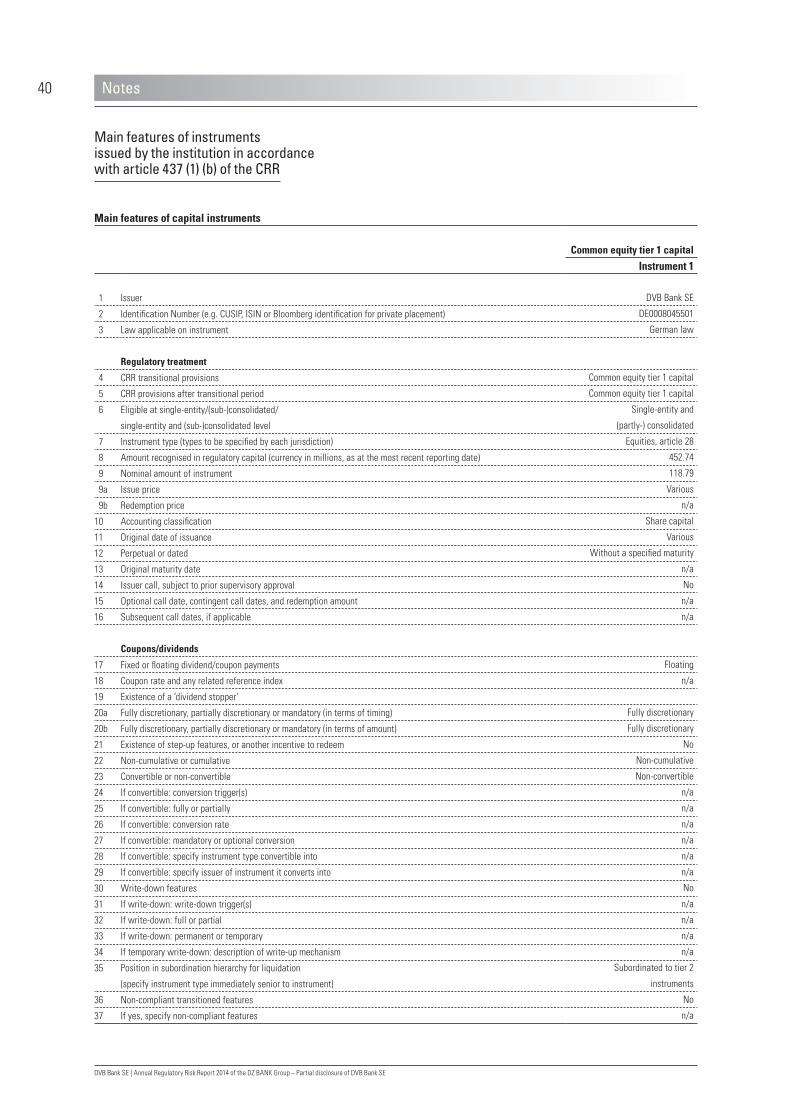

Own funds in accordance with article 437 (1) (b) of the CRR

Please refer to annex A for a description of the main features of the common equity tier 1 and additional tier 1 instruments and tier 2 instruments issued by DVB.

Capital requirements in accordance with article 438 (a) of the CRR

Detailed information regarding the method used to manage economic capital is provided in the section “Capacity to carry and sustain risk/risk capital” on pages 144 to 146 of the report on opportunities and risks in DVB’s Group Annual Report 2014. As at 31 December 2014, DVB’s regulatory capital amounted to a total of €1,352 million (previous year: €1,318 million). DVB’s aggregate risk cover used for economic capital management, also disclosed in the section “Capacity to carry and sustain risk/risk capital” of the report on opportunities and risks of the Group Management Report 2014, amounted to €1,473 million (previous year: €1,546 million). The €73 million decline in the aggregate risk cover reported for 2014 and compared to the end of the previous year, was largely due to higher deferred tax assets, a higher capital buffer, and a gap between expected losses and existing write-downs. Profit retention and higher subordinated liabilities only offset these reducing factors in part.

Capital requirements in accordance with article 438 (c) to (f), 445 and 446 of the CRR

Credit risks

DVB has applied the advanced Internal Ratings Based Approach (IRB Approach or IRBA) to determine capital requirements for its business with vessels, aircraft, rail and road assets since 1 January 2008. The Group’s internal rating systems have been approved in that respect by the German Federal Financial Super-visory Authority (BaFin). All such exposures are classified as ’Corporate’ assets. DVB applied for approval to implement or expand rating systems for the remaining smaller loan portfolios related to aircraft engines and container boxes as well as Group Treasury in the autumn of 2009. Approval was granted as of 1 October 2010. The associated exposures are allocated to the asset classes “Corporates”, “Institutions” or “Sovereign govern-ments”.

DVB currently has no exposures to securitisations.

Own funds and capital requirements

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

17

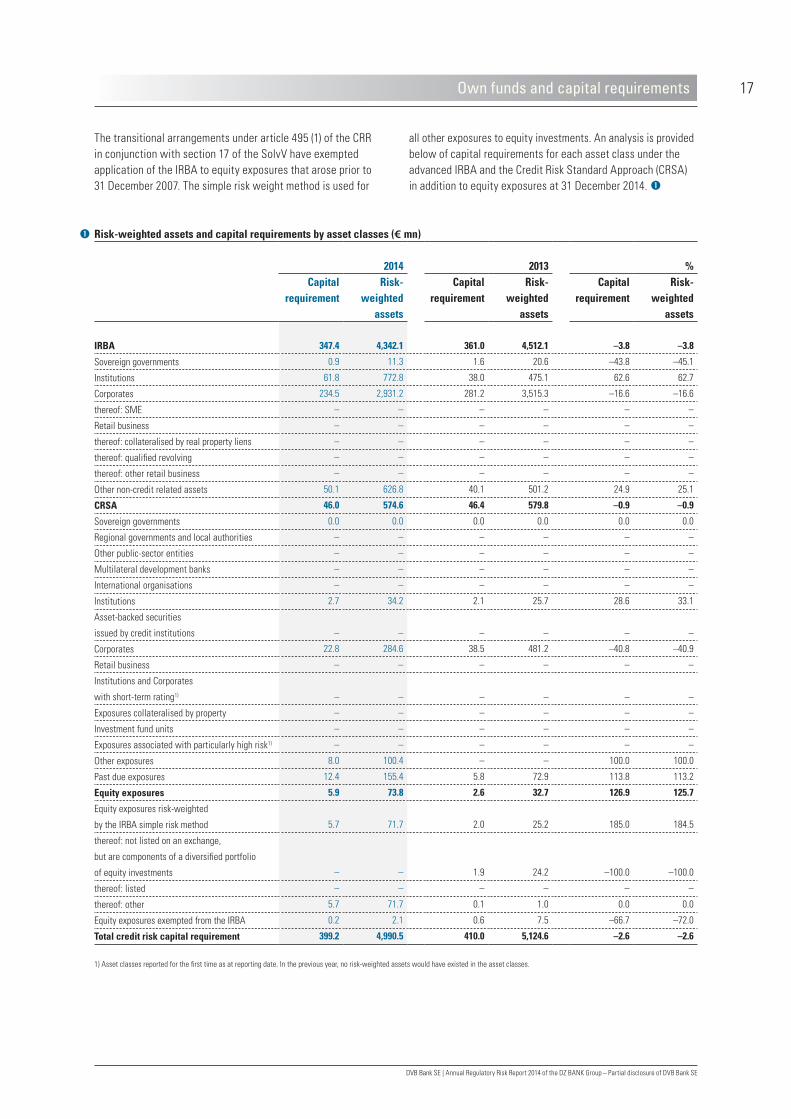

The transitional arrangements under article 495 (1) of the CRR in conjunction with section 17 of the SolvV have exempted application of the IRBA to equity exposures that arose prior to 31 December 2007. The simple risk weight method is used for

all other exposures to equity investments. An analysis is provided below of capital requirements for each asset class under the advanced IRBA and the Credit Risk Standard Approach (CRSA) in addition to equity exposures at 31 December 2014.

Risk-weighted assets and capital requirements by asset classes (€ mn)

2014 2013 %Capital

requirement Risk-

weighted assets

Capital requirement

Risk-weighted

assets

Capital requirement

Risk-weighted

assets

IRBA 347.4 4,342.1 361.0 4,512.1 –3.8 –3.8

Sovereign governments 0.9 11.3 1.6 20.6 –43.8 –45.1

Institutions 61.8 772.8 38.0 475.1 62.6 62.7

Corporates 234.5 2,931.2 281.2 3,515.3 –16.6 –16.6

thereof: SME – – – – – –

Retail business – – – – – –

thereof: collateralised by real property liens – – – – – –

thereof: qualified revolving – – – – – –

thereof: other retail business – – – – – –

Other non-credit related assets 50.1 626.8 40.1 501.2 24.9 25.1

CRSA 46.0 574.6 46.4 579.8 –0.9 –0.9

Sovereign governments 0.0 0.0 0.0 0.0 0.0 0.0

Regional governments and local authorities – – – – – –

Other public-sector entities – – – – – –

Multilateral development banks – – – – – –

International organisations – – – – – –

Institutions 2.7 34.2 2.1 25.7 28.6 33.1

Asset-backed securities

issued by credit institutions – – – – – –

Corporates 22.8 284.6 38.5 481.2 –40.8 –40.9

Retail business – – – – – –

Institutions and Corporates

with short-term rating1) – – – – – –

Exposures collateralised by property – – – – – –

Investment fund units – – – – – –

Exposures associated with particularly high risk1) – – – – – –

Other exposures 8.0 100.4 – – 100.0 100.0

Past due exposures 12.4 155.4 5.8 72.9 113.8 113.2

Equity exposures 5.9 73.8 2.6 32.7 126.9 125.7

Equity exposures risk-weighted

by the IRBA simple risk method 5.7 71.7 2.0 25.2 185.0 184.5

thereof: not listed on an exchange,

but are components of a diversified portfolio

of equity investments – – 1.9 24.2 –100.0 –100.0

thereof: listed – – – – – –

thereof: other 5.7 71.7 0.1 1.0 0.0 0.0

Equity exposures exempted from the IRBA 0.2 2.1 0.6 7.5 –66.7 –72.0

Total credit risk capital requirement 399.2 4,990.5 410.0 5,124.6 –2.6 –2.6

1) Asset classes reported for the first time as at reporting date. In the previous year, no risk-weighted assets would have existed in the asset classes.

Own funds and capital requirements

18

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

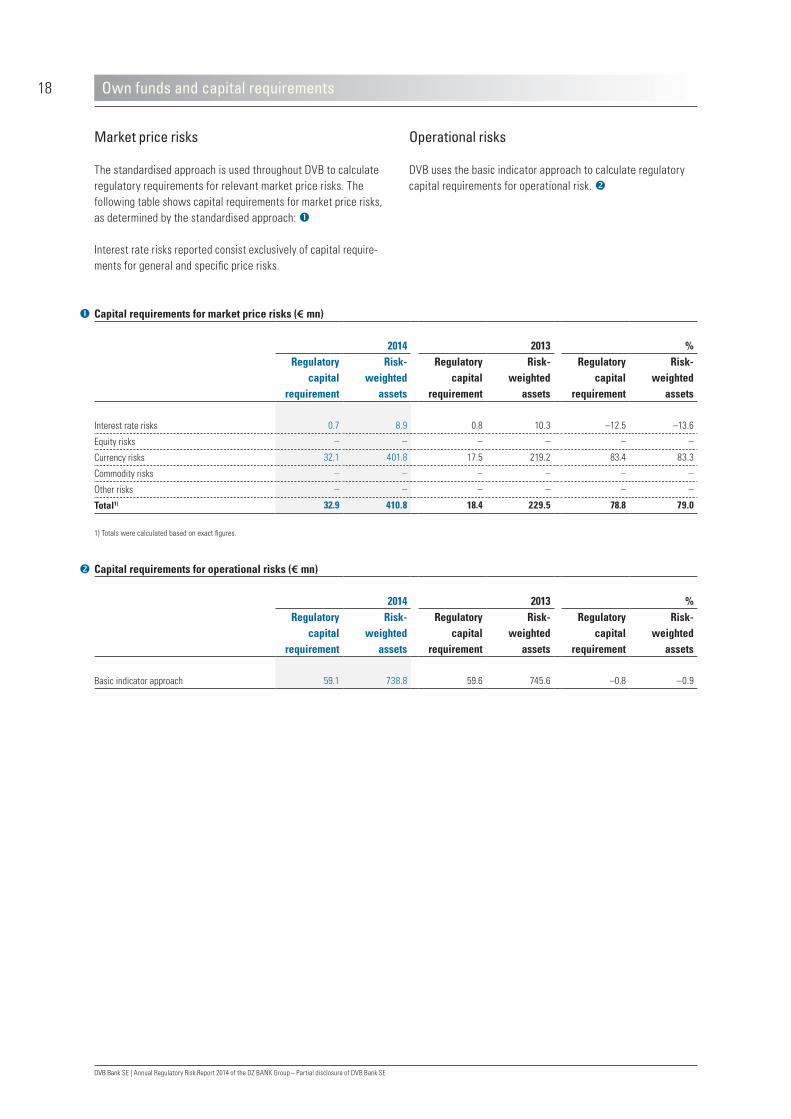

Market price risks

The standardised approach is used throughout DVB to calculate regulatory requirements for relevant market price risks. The following table shows capital requirements for market price risks, as determined by the standardised approach:

Interest rate risks reported consist exclusively of capital require-ments for general and specific price risks.

Operational risks

DVB uses the basic indicator approach to calculate regulatory capital requirements for operational risk.

Capital requirements for market price risks (€ mn)

2014 2013 %Regulatory

capital requirement

Risk-weighted

assets

Regulatory capital

requirement

Risk-weighted

assets

Regulatory capital

requirement

Risk-weighted

assets

Interest rate risks 0.7 8.9 0.8 10.3 –12.5 –13.6

Equity risks – – – – – –

Currency risks 32.1 401.8 17.5 219.2 83.4 83.3

Commodity risks – – – – – –

Other risks – – – – – –

Total1) 32.9 410.8 18.4 229.5 78.8 79.0

1) Totals were calculated based on exact figures.

Capital requirements for operational risks (€ mn)

2014 2013 %Regulatory

capital requirement

Risk-weighted

assets

Regulatory capital

requirement

Risk-weighted

assets

Regulatory capital

requirement

Risk-weighted

assets

Basic indicator approach 59.1 738.8 59.6 745.6 –0.8 –0.9

Own funds and capital requirements

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

19

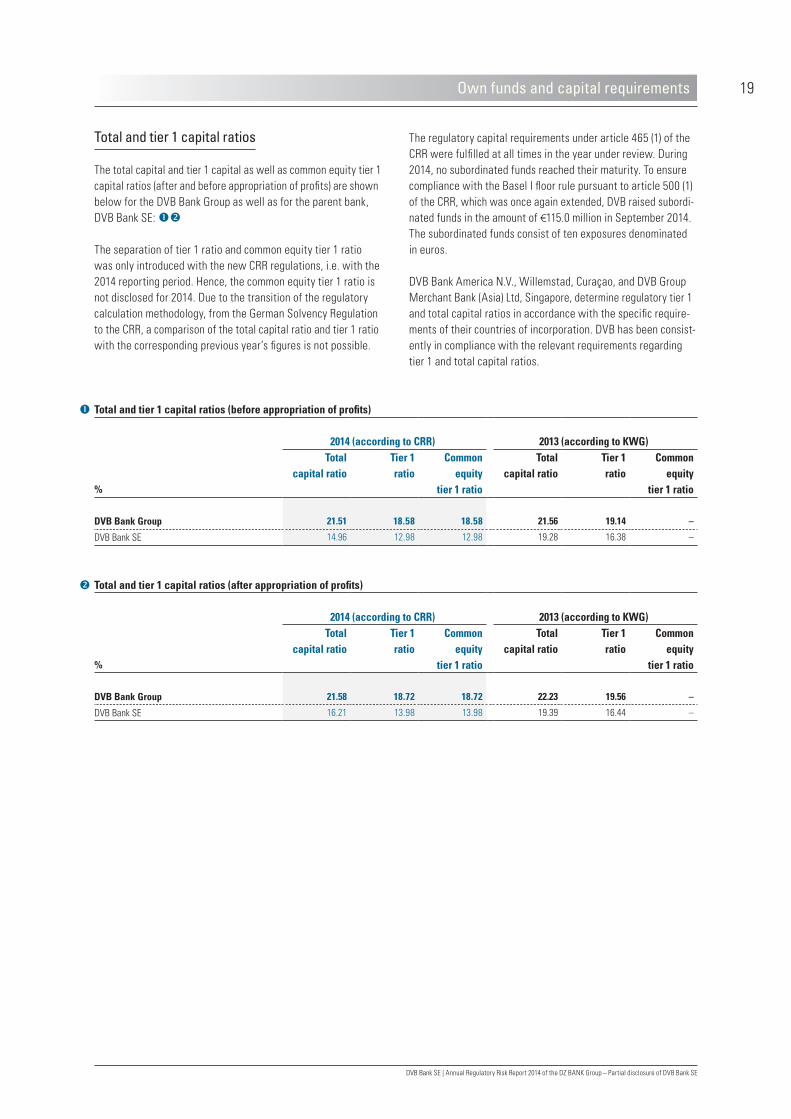

Total and tier 1 capital ratios

The total capital and tier 1 capital as well as common equity tier 1 capital ratios (after and before appropriation of profits) are shown below for the DVB Bank Group as well as for the parent bank, DVB Bank SE:

The separation of tier 1 ratio and common equity tier 1 ratio was only introduced with the new CRR regulations, i.e. with the 2014 reporting period. Hence, the common equity tier 1 ratio is not disclosed for 2014. Due to the transition of the regulatory calculation methodology, from the German Solvency Regulation to the CRR, a comparison of the total capital ratio and tier 1 ratio with the corresponding previous year’s figures is not possible.

The regulatory capital requirements under article 465 (1) of the CRR were fulfilled at all times in the year under review. During 2014, no subordinated funds reached their maturity. To ensure compliance with the Basel I floor rule pursuant to article 500 (1) of the CRR, which was once again extended, DVB raised subordi-nated funds in the amount of €115.0 million in September 2014. The subordinated funds consist of ten exposures denominated in euros.

DVB Bank America N.V., Willemstad, Curaçao, and DVB Group Merchant Bank (Asia) Ltd, Singapore, determine regulatory tier 1 and total capital ratios in accordance with the specific require-ments of their countries of incorporation. DVB has been consist-ently in compliance with the relevant requirements regarding tier 1 and total capital ratios.

Total and tier 1 capital ratios (before appropriation of profits)

2014 (according to CRR) 2013 (according to KWG) %

Total capital ratio

Tier 1 ratio

Common equity

tier 1 ratio

Total capital ratio

Tier 1 ratio

Common equity

tier 1 ratio

DVB Bank Group 21.51 18.58 18.58 21.56 19.14 –

DVB Bank SE 14.96 12.98 12.98 19.28 16.38 –

Total and tier 1 capital ratios (after appropriation of profits)

2014 (according to CRR) 2013 (according to KWG) %

Total capital ratio

Tier 1 ratio

Common equity

tier 1 ratio

Total capital ratio

Tier 1 ratio

Common equity

tier 1 ratio

DVB Bank Group 21.58 18.72 18.72 22.23 19.56 –

DVB Bank SE 16.21 13.98 13.98 19.39 16.44 –

Own funds and capital requirements

20

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Counterparty credit risk

Objectives and principles of credit risk management in accordance with article 435 of the CRR

The objectives and principles on which risk management is based are described in the section “Credit risk” of the report on opportunities and risks on pages 147 to 160 of the Group Annual Report 2014.

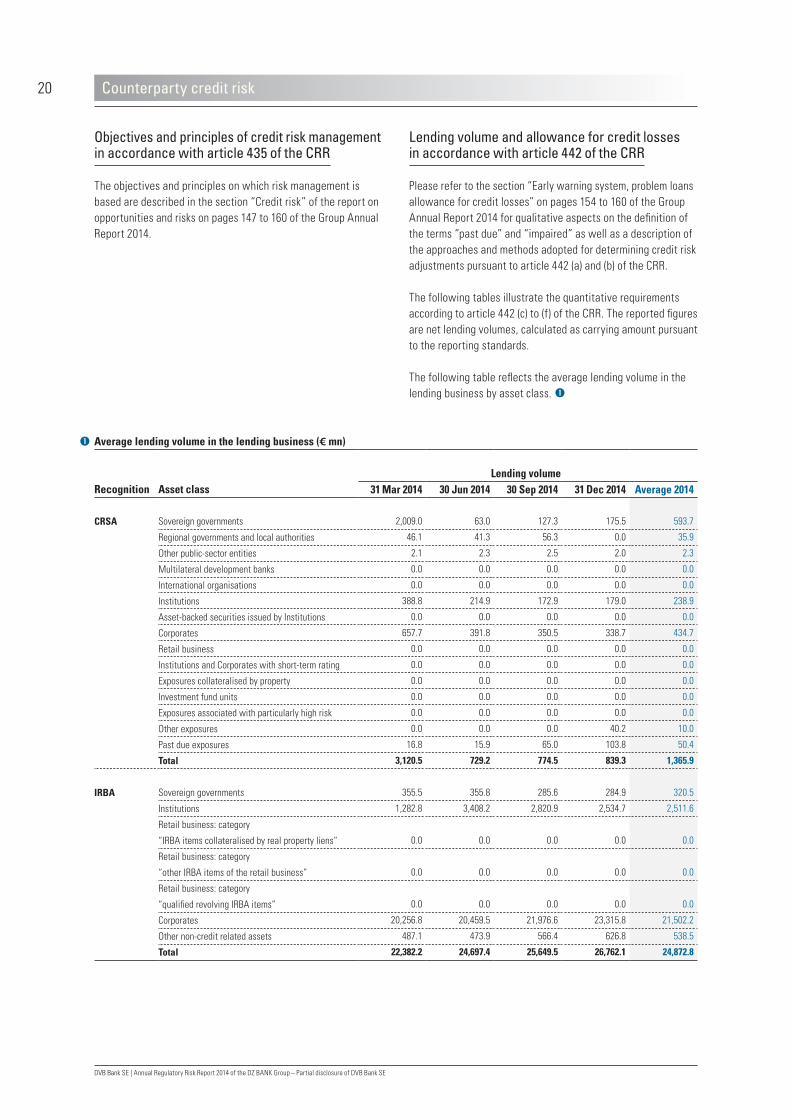

Lending volume and allowance for credit losses in accordance with article 442 of the CRR

Please refer to the section “Early warning system, problem loans allowance for credit losses” on pages 154 to 160 of the Group Annual Report 2014 for qualitative aspects on the definition of the terms “past due” and “impaired” as well as a description of the approaches and methods adopted for determining credit risk adjustments pursuant to article 442 (a) and (b) of the CRR.

The following tables illustrate the quantitative requirements according to article 442 (c) to (f) of the CRR. The reported figures are net lending volumes, calculated as carrying amount pursuant to the reporting standards.

The following table reflects the average lending volume in the lending business by asset class.

Average lending volume in the lending business (€ mn)

Lending volumeReco gnition Asset class 31 Mar 2014 30 Jun 2014 30 Sep 2014 31 Dec 2014 Average 2014

CRSA Sovereign governments 2,009.0 63.0 127.3 175.5 593.7

Regional governments and local authorities 46.1 41.3 56.3 0.0 35.9

Other public-sector entities 2.1 2.3 2.5 2.0 2.3

Multilateral development banks 0.0 0.0 0.0 0.0 0.0

International organisations 0.0 0.0 0.0 0.0 0.0

Institutions 388.8 214.9 172.9 179.0 238.9

Asset-backed securities issued by Institutions 0.0 0.0 0.0 0.0 0.0

Corporates 657.7 391.8 350.5 338.7 434.7

Retail business 0.0 0.0 0.0 0.0 0.0

Institutions and Corporates with short-term rating 0.0 0.0 0.0 0.0 0.0

Exposures collateralised by property 0.0 0.0 0.0 0.0 0.0

Investment fund units 0.0 0.0 0.0 0.0 0.0

Exposures associated with particularly high risk 0.0 0.0 0.0 0.0 0.0

Other exposures 0.0 0.0 0.0 40.2 10.0

Past due exposures 16.8 15.9 65.0 103.8 50.4

Total 3,120.5 729.2 774.5 839.3 1,365.9

IRBA Sovereign governments 355.5 355.8 285.6 284.9 320.5

Institutions 1,282.8 3,408.2 2,820.9 2,534.7 2,511.6

Retail business: category

“IRBA items collateralised by real property liens” 0.0 0.0 0.0 0.0 0.0

Retail business: category

“other IRBA items of the retail business” 0.0 0.0 0.0 0.0 0.0

Retail business: category

“qualified revolving IRBA items” 0.0 0.0 0.0 0.0 0.0

Corporates 20,256.8 20,459.5 21,976.6 23,315.8 21,502.2

Other non-credit related assets 487.1 473.9 566.4 626.8 538.5

Total 22,382.2 24,697.4 25,649.5 26,762.1 24,872.8

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

21Counterparty credit risk

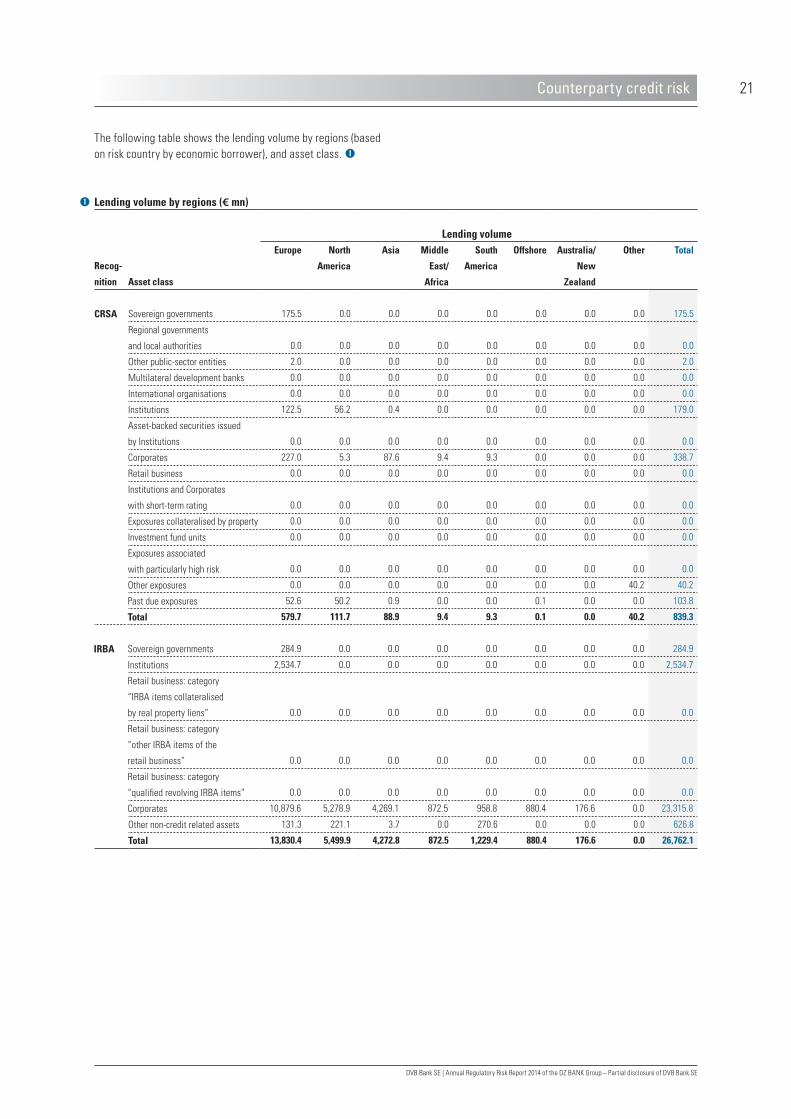

The following table shows the lending volume by regions (based on risk country by economic borrower), and asset class.

Lending volume by regions (€ mn)

Lending volume

Recog-

nition

Asset class

Europe

North

America

Asia

Middle

East/

Africa

South

America

Offshore

Australia/

New

Zealand

Other

Total

CRSA Sovereign governments 175.5 0.0 0.0 0.0 0.0 0.0 0.0 0.0 175.5

Regional governments

and local authorities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other public-sector entities 2.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2.0

Multilateral development banks 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

International organisations 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Institutions 122.5 56.2 0.4 0.0 0.0 0.0 0.0 0.0 179.0

Asset-backed securities issued

by Institutions 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Corporates 227.0 5.3 87.6 9.4 9.3 0.0 0.0 0.0 338.7

Retail business 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Institutions and Corporates

with short-term rating 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Exposures collateralised by property 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Investment fund units 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Exposures associated

with particularly high risk 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other exposures 0.0 0.0 0.0 0.0 0.0 0.0 0.0 40.2 40.2

Past due exposures 52.6 50.2 0.9 0.0 0.0 0.1 0.0 0.0 103.8

Total 579.7 111.7 88.9 9.4 9.3 0.1 0.0 40.2 839.3

IRBA Sovereign governments 284.9 0.0 0.0 0.0 0.0 0.0 0.0 0.0 284.9

Institutions 2,534.7 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2,534.7

Retail business: category

“IRBA items collateralised

by real property liens” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Retail business: category

“other IRBA items of the

retail business” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Retail business: category

“qualified revolving IRBA items” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Corporates 10,879.6 5,278.9 4,269.1 872.5 958.8 880.4 176.6 0.0 23,315.8

Other non-credit related assets 131.3 221.1 3.7 0.0 270.6 0.0 0.0 0.0 626.8

Total 13,830.4 5,499.9 4,272.8 872.5 1,229.4 880.4 176.6 0.0 26,762.1

22

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

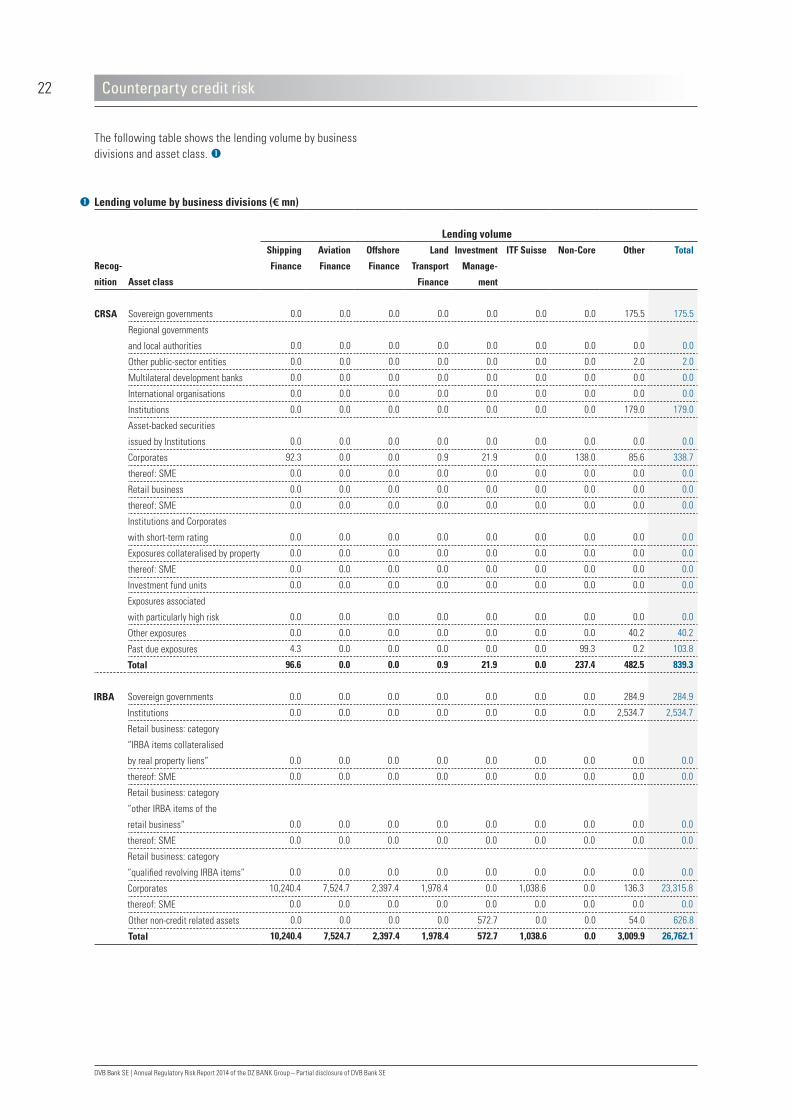

The following table shows the lending volume by business divisions and asset class.

Lending volume by business divisions (€ mn)

Lending volume

Recog-

nition

Asset class

Shipping

Finance

Aviation

Finance

Offshore

Finance

Land

Transport

Finance

Investment

Manage-

ment

ITF Suisse

Non-Core

Other

Total

CRSA Sovereign governments 0.0 0.0 0.0 0.0 0.0 0.0 0.0 175.5 175.5

Regional governments

and local authorities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other public-sector entities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2.0 2.0

Multilateral development banks 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

International organisations 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Institutions 0.0 0.0 0.0 0.0 0.0 0.0 0.0 179.0 179.0

Asset-backed securities

issued by Institutions 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Corporates 92.3 0.0 0.0 0.9 21.9 0.0 138.0 85.6 338.7

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Retail business 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Institutions and Corporates

with short-term rating 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Exposures collateralised by property 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Investment fund units 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Exposures associated

with particularly high risk 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other exposures 0.0 0.0 0.0 0.0 0.0 0.0 0.0 40.2 40.2

Past due exposures 4.3 0.0 0.0 0.0 0.0 0.0 99.3 0.2 103.8

Total 96.6 0.0 0.0 0.9 21.9 0.0 237.4 482.5 839.3

IRBA Sovereign governments 0.0 0.0 0.0 0.0 0.0 0.0 0.0 284.9 284.9

Institutions 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2,534.7 2,534.7

Retail business: category

“IRBA items collateralised

by real property liens” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Retail business: category

“other IRBA items of the

retail business” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Retail business: category

“qualified revolving IRBA items” 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Corporates 10,240.4 7,524.7 2,397.4 1,978.4 0.0 1,038.6 0.0 136.3 23,315.8

thereof: SME 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Other non-credit related assets 0.0 0.0 0.0 0.0 572.7 0.0 0.0 54.0 626.8

Total 10,240.4 7,524.7 2,397.4 1,978.4 572.7 1,038.6 0.0 3,009.9 26,762.1

Counterparty credit risk

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

23

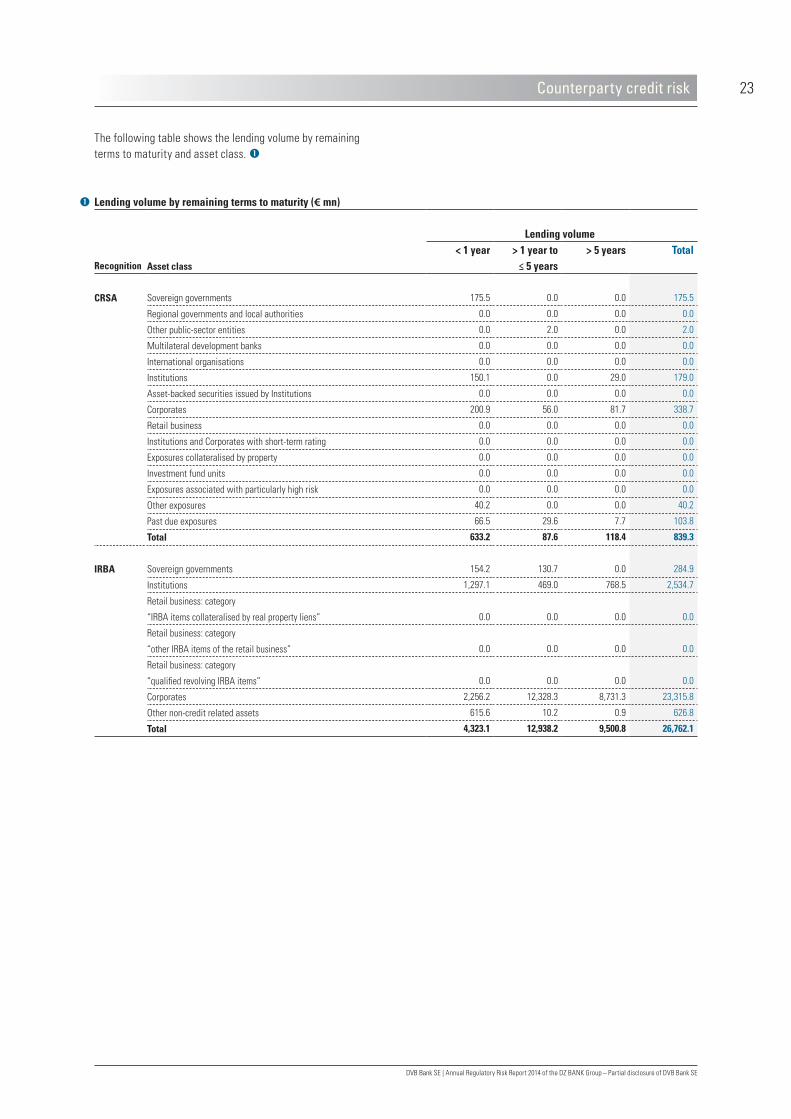

The following table shows the lending volume by remaining terms to maturity and asset class.

Lending volume by remaining terms to maturity (€ mn)

Lending volume

Recognition

Asset class

< 1 year > 1 year to ≤ 5 years

> 5 years Total

CRSA Sovereign governments 175.5 0.0 0.0 175.5

Regional governments and local authorities 0.0 0.0 0.0 0.0

Other public-sector entities 0.0 2.0 0.0 2.0

Multilateral development banks 0.0 0.0 0.0 0.0

International organisations 0.0 0.0 0.0 0.0

Institutions 150.1 0.0 29.0 179.0

Asset-backed securities issued by Institutions 0.0 0.0 0.0 0.0

Corporates 200.9 56.0 81.7 338.7

Retail business 0.0 0.0 0.0 0.0

Institutions and Corporates with short-term rating 0.0 0.0 0.0 0.0

Exposures collateralised by property 0.0 0.0 0.0 0.0

Investment fund units 0.0 0.0 0.0 0.0

Exposures associated with particularly high risk 0.0 0.0 0.0 0.0

Other exposures 40.2 0.0 0.0 40.2

Past due exposures 66.5 29.6 7.7 103.8

Total 633.2 87.6 118.4 839.3

IRBA Sovereign governments 154.2 130.7 0.0 284.9

Institutions 1,297.1 469.0 768.5 2,534.7

Retail business: category

“IRBA items collateralised by real property liens” 0.0 0.0 0.0 0.0

Retail business: category

“other IRBA items of the retail business” 0.0 0.0 0.0 0.0

Retail business: category

“qualified revolving IRBA items” 0.0 0.0 0.0 0.0

Corporates 2,256.2 12,328.3 8,731.3 23,315.8

Other non-credit related assets 615.6 10.2 0.9 626.8

Total 4,323.1 12,938.2 9,500.8 26,762.1

Counterparty credit risk

24

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

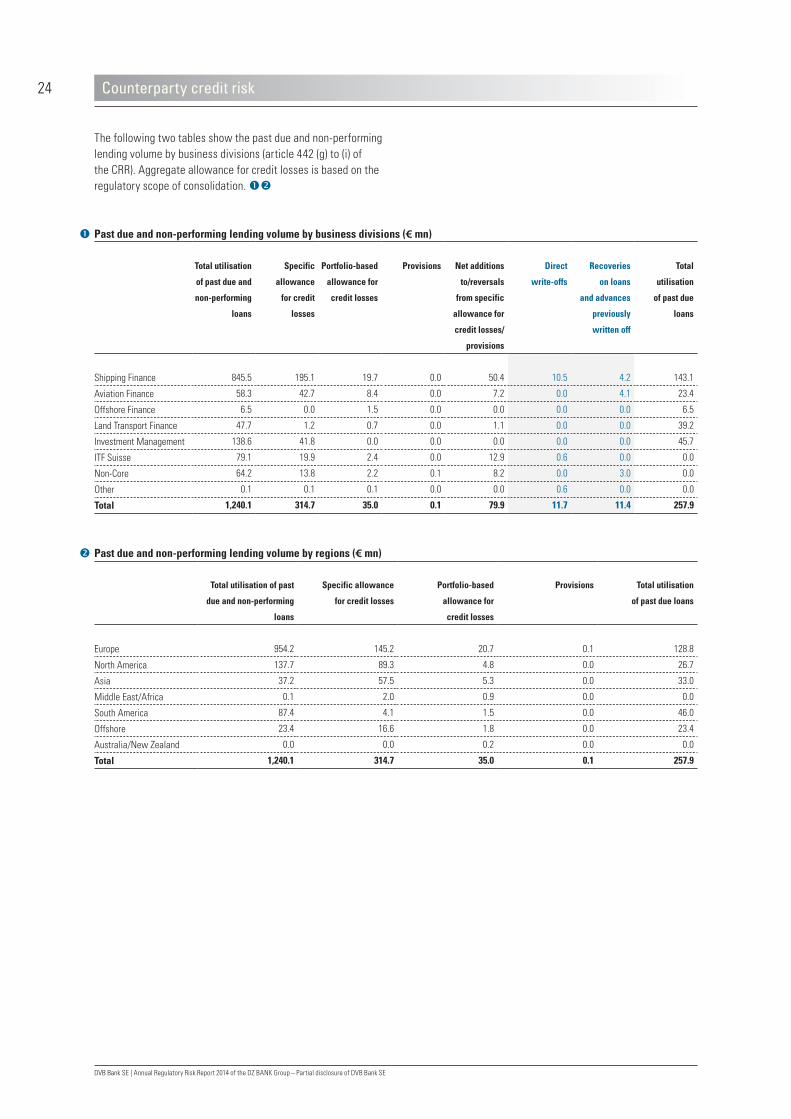

The following two tables show the past due and non-performing lending volume by business divisions (article 442 (g) to (i) of the CRR). Aggregate allowance for credit losses is based on the regulatory scope of consolidation.

Past due and non-performing lending volume by business divisions (€ mn)

Total utilisation

of past due and

non-performing

loans

Specific

allowance

for credit

losses

Portfolio-based

allowance for

credit losses

Provisions

Net additions

to/reversals

from specific

allowance for

credit losses/

provisions

Direct

write-offs

Recoveries

on loans

and advances

previously

written off

Total

utilisation

of past due

loans

Shipping Finance 845.5 195.1 19.7 0.0 50.4 10.5 4.2 143.1

Aviation Finance 58.3 42.7 8.4 0.0 7.2 0.0 4.1 23.4

Offshore Finance 6.5 0.0 1.5 0.0 0.0 0.0 0.0 6.5

Land Transport Finance 47.7 1.2 0.7 0.0 1.1 0.0 0.0 39.2

Investment Management 138.6 41.8 0.0 0.0 0.0 0.0 0.0 45.7

ITF Suisse 79.1 19.9 2.4 0.0 12.9 0.6 0.0 0.0

Non-Core 64.2 13.8 2.2 0.1 8.2 0.0 3.0 0.0

Other 0.1 0.1 0.1 0.0 0.0 0.6 0.0 0.0

Total 1,240.1 314.7 35.0 0.1 79.9 11.7 11.4 257.9

Past due and non-performing lending volume by regions (€ mn)

Total utilisation of past

due and non-performing

loans

Specific allowance

for credit losses

Portfolio-based

allowance for

credit losses

Provisions

Total utilisation

of past due loans

Europe 954.2 145.2 20.7 0.1 128.8

North America 137.7 89.3 4.8 0.0 26.7

Asia 37.2 57.5 5.3 0.0 33.0

Middle East/Africa 0.1 2.0 0.9 0.0 0.0

South America 87.4 4.1 1.5 0.0 46.0

Offshore 23.4 16.6 1.8 0.0 23.4

Australia/New Zealand 0.0 0.0 0.2 0.0 0.0

Total 1,240.1 314.7 35.0 0.1 257.9

Counterparty credit risk

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

25

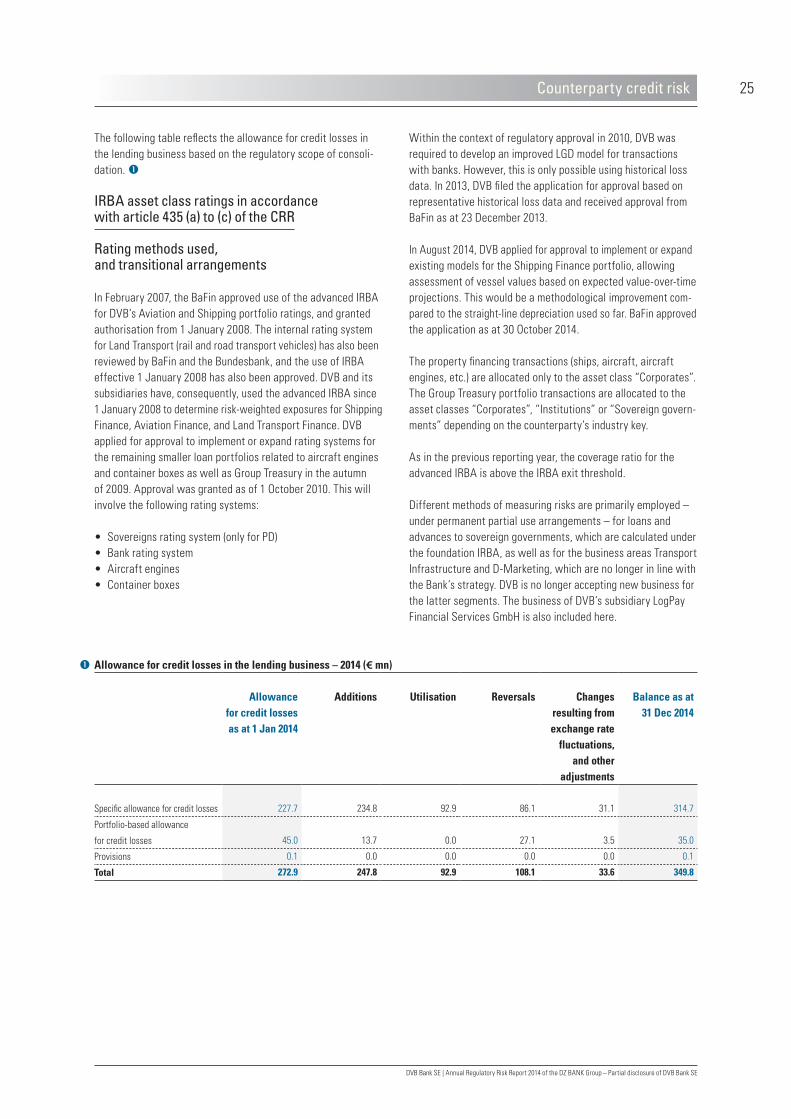

The following table reflects the allowance for credit losses in the lending business based on the regulatory scope of consoli-dation.

IRBA asset class ratings in accordance with article 435 (a) to (c) of the CRR

Rating methods used, and transitional arrangements

In February 2007, the BaFin approved use of the advanced IRBA for DVB’s Aviation and Shipping portfolio ratings, and granted authorisation from 1 January 2008. The internal rating system for Land Transport (rail and road transport vehicles) has also been reviewed by BaFin and the Bundesbank, and the use of IRBA effective 1 January 2008 has also been approved. DVB and its subsidiaries have, consequently, used the advanced IRBA since 1 January 2008 to determine risk-weighted exposures for Shipping Finance, Aviation Finance, and Land Transport Finance. DVB applied for approval to implement or expand rating systems for the remaining smaller loan portfolios related to aircraft engines and container boxes as well as Group Treasury in the autumn of 2009. Approval was granted as of 1 October 2010. This will involve the following rating systems:

• Sovereigns rating system (only for PD)• Bank rating system • Aircraft engines• Container boxes

Within the context of regulatory approval in 2010, DVB was required to develop an improved LGD model for transactions with banks. However, this is only possible using historical loss data. In 2013, DVB filed the application for approval based on representative historical loss data and received approval from BaFin as at 23 December 2013.

In August 2014, DVB applied for approval to implement or expand existing models for the Shipping Finance portfolio, allowing assessment of vessel values based on expected value-over-time projections. This would be a methodological improvement com-pared to the straight-line depreciation used so far. BaFin approved the application as at 30 October 2014.

The property financing transactions (ships, aircraft, aircraft engines, etc.) are allocated only to the asset class “Corporates”. The Group Treasury portfolio transactions are allocated to the asset classes “Corporates”, “Institutions” or “Sovereign govern-ments” depending on the counterparty’s industry key.

As in the previous reporting year, the coverage ratio for the advanced IRBA is above the IRBA exit threshold.

Different methods of measuring risks are primarily employed – under permanent partial use arrangements – for loans and advances to sovereign governments, which are calculated under the foundation IRBA, as well as for the business areas Transport Infrastructure and D-Marketing, which are no longer in line with the Bank’s strategy. DVB is no longer accepting new business for the latter segments. The business of DVB’s subsidiary LogPay Financial Services GmbH is also included here.

Allowance for credit losses in the lending business – 2014 (€ mn)

Allowance for credit losses as at 1 Jan 2014

Additions

Utilisation

Reversals

Changes resulting from exchange rate

fluctuations, and other

adjustments

Balance as at 31 Dec 2014

Specific allowance for credit losses 227.7 234.8 92.9 86.1 31.1 314.7

Portfolio-based allowance

for credit losses 45.0 13.7 0.0 27.1 3.5 35.0

Provisions 0.1 0.0 0.0 0.0 0.0 0.1

Total 272.9 247.8 92.9 108.1 33.6 349.8

Counterparty credit risk

26

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

Counterparty credit risk

The methods used to determine an asset’s horizon value vary from division to division. They include the discounted cash flow method (DCF), the future market value method (FMV), projected depreciation and straight-line depreciation. The asset values calculated by these methods are then reduced by haircuts that are determined at least once a year, as part of the annual vali-dation. In addition, empirical loan loss data is reviewed at least annually and is, consequently, an important element in assuring the reliability of the model’s LGD estimates.

ISDA (International Swaps and Derivatives Association) Master Agreements are concluded with counterparties within the Group Treasury portfolio, i.e. the LGD can only be calculated on the basis of the liquidation scenario. The LGD for these transactions is estimated based on representative historical loss data, with all elements of costs and income being incorporated in the LGD calculation in line with property financings. A 45% LGD is pre-scribed for the Sovereign governments and central banks asset class under regulatory rules.

DVB’s conservative approach to estimating EaD is demonstrated by the application of a 100% credit conversion factor. All drawn and undrawn lines are, consequently, included in exposures. The undrawn lines, however, must be irrevocable, legally binding lending commitments – irrespective of the actual date of draw-down. Transaction-specific credit conversion factors are only applied to loans financing the construction of new vessels, for which drawdowns may only be made on a percentage of com-pletion basis.

The measurement basis for money market and currency trans-actions as well as securities, derivatives and options (EaD) relies on the current positive market value of the financial instrument and the regulatory add-on. The current market value is determined for each transaction using calculation methods prescribed by regulatory bodies.

Additional uses of internal estimates

In addition to determining regulatory capital adequacy, IRM is also used as an integral instrument for the overall management of the entire Bank. For example, the ratings it generates are used for the purposes of lending authorities. Standard risk costs, which are also calculated by the model, are an integral component of the formula used to calculate minimum margins for individual exposures both before and after committing the Bank. Furthermore, they are used to plan specific and portfolio- based allowances for credit losses.

Internal rating system structure

DVB’s internal rating model (IRM) is used to determine risk-weighted exposure for the Corporate asset class. The IRM consists of four modules for the calculation of an exposure’s probability of default (PD), two modules for the estimation of the expected exposure at default (EaD) as well as eight modules for the expected loss given default (LGD). Moreover, DVB uses two additional modules to determine the probability of default related to a bank or a sovereign government (guarantor for prop-erty financings or counterparty within the Group Treasury port-folio).

A multiple-step statistical method based on the “shadow rating approach” is used to determine the rating class of individual counterparties to a transaction. Following an initial approximate classification of the counterparty, a division-specific rating is determined that is subject to change due to qualitative factors (soft factors) and country-specific transfer risk. It is possible to override a final rating by adding a substantiated commentary. All upgrades in ratings must be approved by a body with the relevant authority.

The manner in which a financed project’s stakeholders (guarantors, borrowers, lessees/charterers) are treated depends on the nature of the specific project’s structure. In these situations, it is normally possible for owners to select either direct loans, guarantee facilities or other types of finance depending on the preferences of lessees or charterers. The structures and ratings described above involving those stakeholders determine the loan’s transaction rating.

In the case of a bank and a sovereign government as a counter-party or guarantor, DVB obtains the rating grade allocated to such counterparty from its parent company DZ BANK AG. This rating grade is subjected to a plausibility check by DVB. The transfer of rating grades has also been reviewed and approved by the BaFin and Deutsche Bundesbank. Both DZ BANK AG modules have had regulatory approval since 2008.

The loss given default (LGD) of a property financing is determined at DVB by weighting three scenarios: liquidation, restructuring or recovery. LGD values for restructurings and recoveries are determined with reference to empirical loan loss data. All ele-ments of costs and income are considered when determining LGD. Considering the given market conditions for the financed objects, the liquidation LGD will be calculated through the IRM.

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

27Counterparty credit risk

Allocation to rating categories

All obligors or consortia of obligors are allocated to either Shipping Finance, Aviation Finance or Land Transport Finance, depending on the specific nature of the transaction or the financed asset. Each of these business divisions has its own rating system – except with respect to leasing companies, which are subject to a separate, cross-divisional rating system. An unambiguous allocation to the appropriate rating system is also ensured in the case of banks or sovereign governments. DVB’s operating systems prevent transactions with counterparties for which no rating has been determined.

CRSA asset class ratings in accordance with article 444 (a) to (d) of the CRR

DVB uses the simple risk weight method in conjunction with the CRSA approach to offset collateral against exposures. The CRSA entails calculating capital requirements exclusively with refer-ence to external risk ratings for claims on sovereign governments and central banks as well as on institutions. Pursuant to article 135 to 141 of the CRR, both asset classes are currently required to be used for the Organisation for Economic Co-operation and Development’s export credit agencies.

The use of external credit ratings is made in accordance with regulatory requirements. DVB does not apply credit ratings of bond issues to rate exposures.

Rating system controls

Credit risk exposure for the entire DVB Group is monitored inde-pendently by Group Risk Management. Group Risk Management’s internal rating responsibilities are:

• conception, implementation and documentation of rating modules;

• ongoing monitoring and consistent application of the rating models;

• review of ratings, and control for (and rectification of) defects in data quality;

• validation and adjustment of rating modules (at least once a year), particularly with respect to the monitoring of the results of its selectivity controls and stability of the rating system.

Group Risk Management’s internal reporting includes reports submitted to DVB Bank SE’s Board of Managing Directors on the findings of its reviews. Group Risk Management submits regular reports on rating results to the Bank’s Board of Managing Direc-tors and Supervisory Board, within the scope of risk reporting.

The LGD model is fine-tuned and validated by Group Risk Manage-ment, with sub sequent reports to the banking supervisory authorities. The suitability of the models is assured at least once a year through the quantitative and qualitative validation of the PD and LGD risk parameters applied within the rating systems. In the case of the PD models for banks and sovereign governments, DZ BANK provides the quantitative validation report on an annual basis so that DVB can provide the qualitative part to form a full report, which is also disclosed to the BaFin.

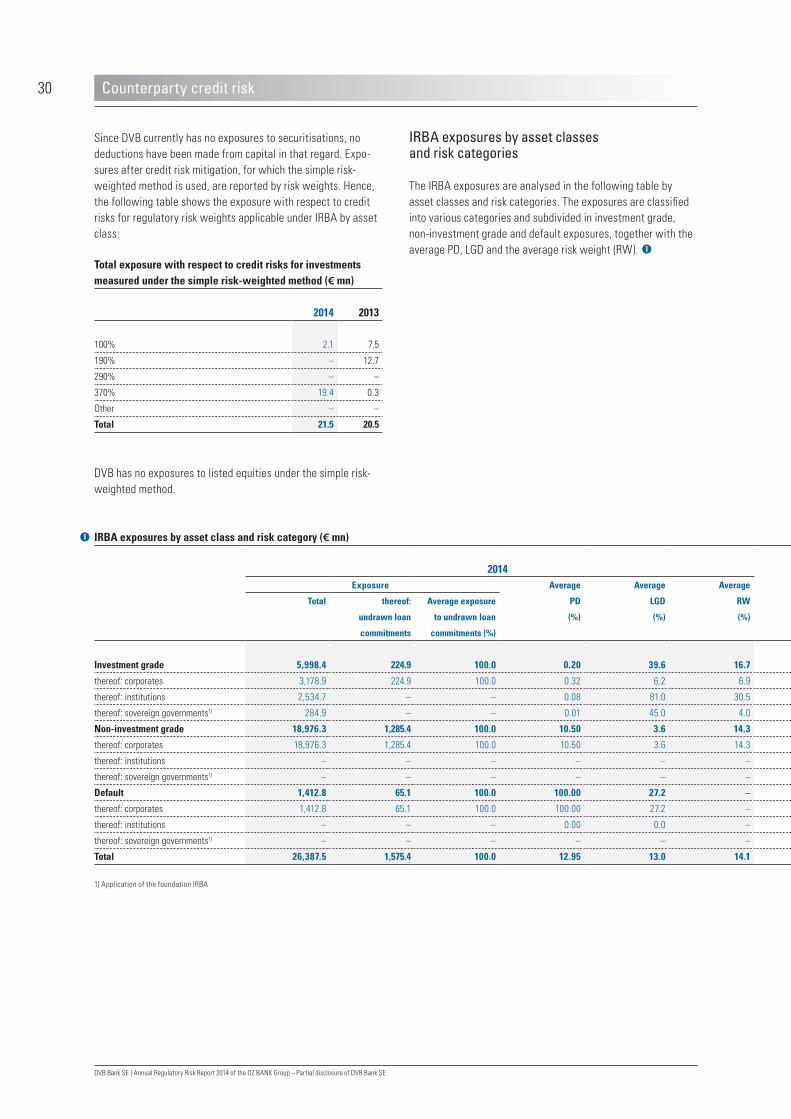

28

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

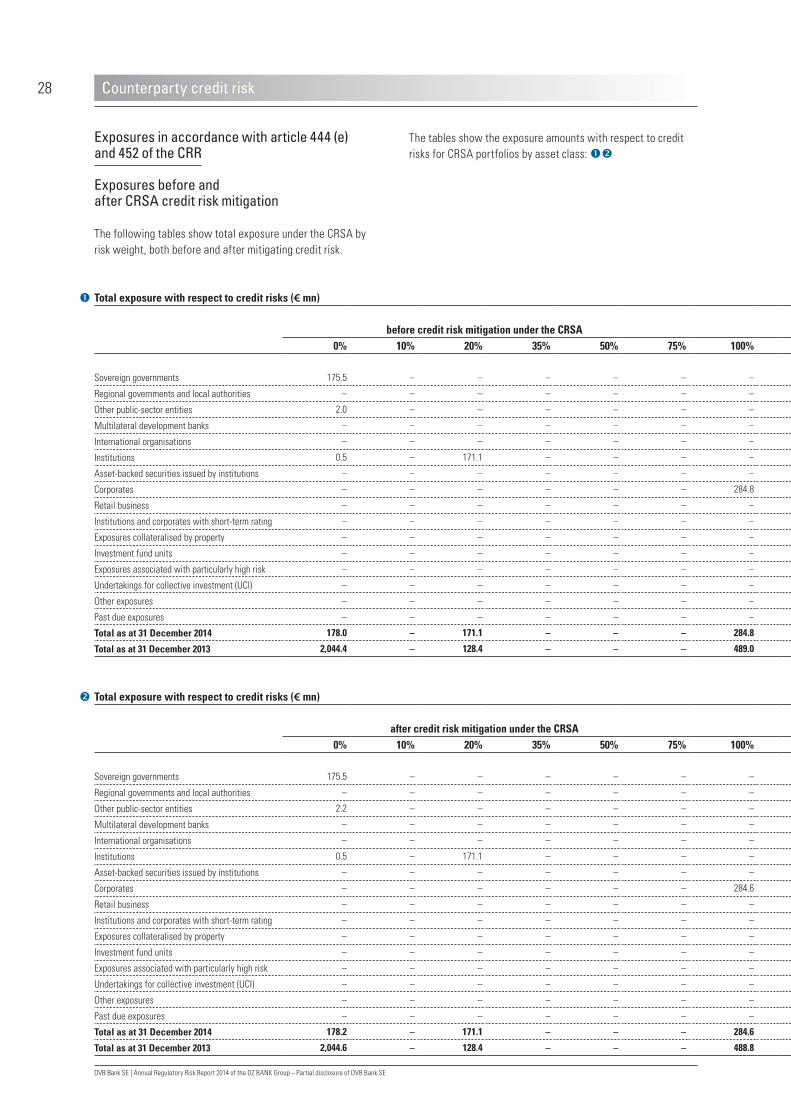

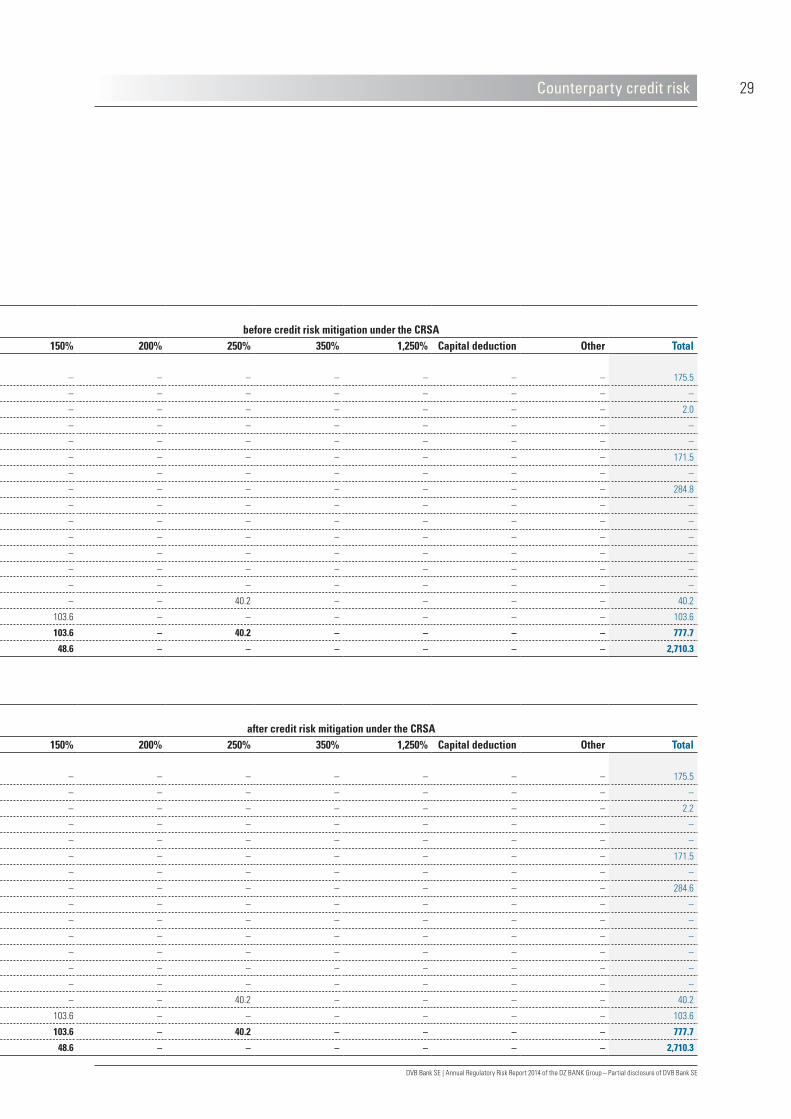

The tables show the exposure amounts with respect to credit risks for CRSA portfolios by asset class:

Exposures in accordance with article 444 (e) and 452 of the CRR

Exposures before and after CRSA credit risk mitigation

The following tables show total exposure under the CRSA by risk weight, both before and after mitigating credit risk.

Total exposure with respect to credit risks (€ mn)

before credit risk mitigation under the CRSA before credit risk mitigation under the CRSA0% 10% 20% 35% 50% 75% 100% 150% 200% 250% 350% 1,250% Capital deduction Other Total

Sovereign governments 175.5 – – – – – – – – – – – – – 175.5

Regional governments and local authorities – – – – – – – – – – – – – – –

Other public-sector entities 2.0 – – – – – – – – – – – – – 2.0

Multilateral development banks – – – – – – – – – – – – – – –

International organisations – – – – – – – – – – – – – – –

Institutions 0.5 – 171.1 – – – – – – – – – – – 171.5

Asset-backed securities issued by institutions – – – – – – – – – – – – – – –

Corporates – – – – – – 284.8 – – – – – – – 284.8

Retail business – – – – – – – – – – – – – – –

Institutions and corporates with short-term rating – – – – – – – – – – – – – – –

Exposures collateralised by property – – – – – – – – – – – – – – –

Investment fund units – – – – – – – – – – – – – – –

Exposures associated with particularly high risk – – – – – – – – – – – – – – –

Undertakings for collective investment (UCI) – – – – – – – – – – – – – – –

Other exposures – – – – – – – – – 40.2 – – – – 40.2

Past due exposures – – – – – – – 103.6 – – – – – – 103.6

Total as at 31 December 2014 178.0 – 171.1 – – – 284.8 103.6 – 40.2 – – – – 777.7

Total as at 31 December 2013 2,044.4 – 128.4 – – – 489.0 48.6 – – – – – – 2,710.3

Total exposure with respect to credit risks (€ mn)

after credit risk mitigation under the CRSA after credit risk mitigation under the CRSA0% 10% 20% 35% 50% 75% 100% 150% 200% 250% 350% 1,250% Capital deduction Other Total

Sovereign governments 175.5 – – – – – – – – – – – – – 175.5

Regional governments and local authorities – – – – – – – – – – – – – – –

Other public-sector entities 2.2 – – – – – – – – – – – – – 2.2

Multilateral development banks – – – – – – – – – – – – – – –

International organisations – – – – – – – – – – – – – – –

Institutions 0.5 – 171.1 – – – – – – – – – – – 171.5

Asset-backed securities issued by institutions – – – – – – – – – – – – – – –

Corporates – – – – – – 284.6 – – – – – – – 284.6

Retail business – – – – – – – – – – – – – – –

Institutions and corporates with short-term rating – – – – – – – – – – – – – – –

Exposures collateralised by property – – – – – – – – – – – – – – –

Investment fund units – – – – – – – – – – – – – – –

Exposures associated with particularly high risk – – – – – – – – – – – – – – –

Undertakings for collective investment (UCI) – – – – – – – – – – – – – – –

Other exposures – – – – – – – – – 40.2 – – – – 40.2

Past due exposures – – – – – – – 103.6 – – – – – – 103.6

Total as at 31 December 2014 178.2 – 171.1 – – – 284.6 103.6 – 40.2 – – – – 777.7

Total as at 31 December 2013 2,044.6 – 128.4 – – – 488.8 48.6 – – – – – – 2,710.3

Counterparty credit risk

DVB Bank SE | Annual Regulatory Risk Report 2014 of the DZ BANK Group – Partial disclosure of DVB Bank SE

29

Total exposure with respect to credit risks (€ mn)