Embed Size (px)

Citation preview

PART 5 Macroeconomic Policy

5.1 Monetary Policy

5.2 Fiscal Policy

The Federal Reserve System

Established by the Federal Reserve Act of 1913

Lender of Last Resort in Financial Crises

Entities

Federal Reserve Banks (12)Board of Governors of the Federal Reserve SystemFederal Open Market CommitteeFederal Advisory Council2800 Member Banks

Aimed at diffusing power, providing checks and balances.

Board of Governors of the Federal Reserve System

Leadership is provided by the Board of Governors:

Seven members headquartered in Washington, D.C.

Appointed by the president and confirmed by the Senate14-year non-renewable term (plus part of another term)

Required to come from different districts

Chairman is chosen from the governors and serves four-yearterm

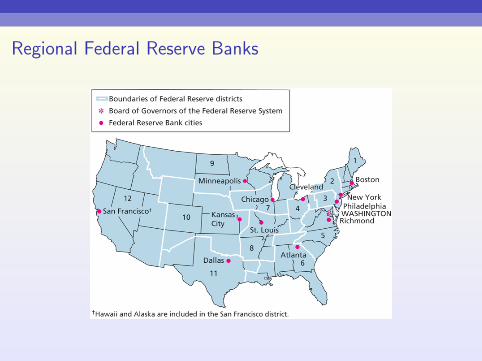

Regional Federal Reserve Banks

Federal Open Market Committee (FOMC)

1. Meets eight times a year (every 6 weeks)

2. Consists of seven members of the Board of Governors, thepresident of the Federal Reserve Bank of New York and thepresidents of four other Federal Reserve banks

3. Chairman of the Board of Governors is also chair of FOMC

4. Issues directives to the trading desk at the Federal ReserveBank of New York

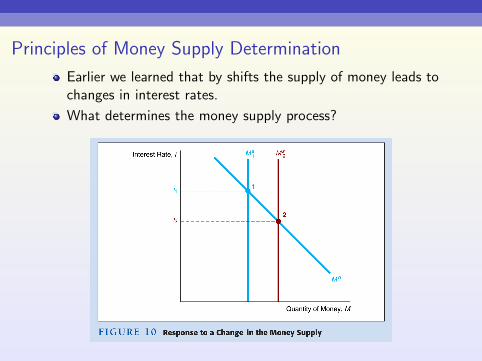

Principles of Money Supply Determination

Earlier we learned that by shifts the supply of money leads tochanges in interest rates.

What determines the money supply process?

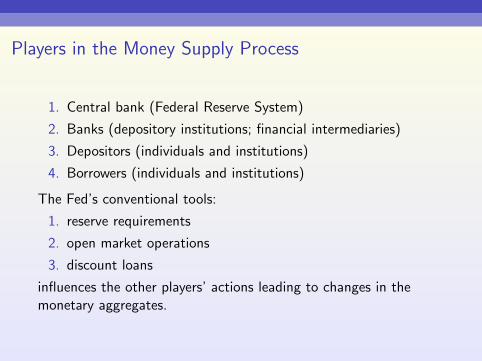

Players in the Money Supply Process

1. Central bank (Federal Reserve System)

2. Banks (depository institutions; financial intermediaries)

3. Depositors (individuals and institutions)

4. Borrowers (individuals and institutions)

The Fed’s conventional tools:

1. reserve requirements

2. open market operations

3. discount loans

influences the other players’ actions leading to changes in themonetary aggregates.

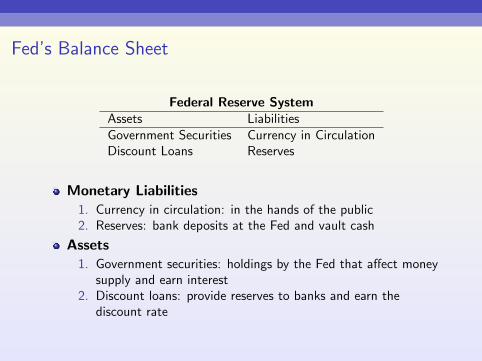

Fed’s Balance Sheet

Federal Reserve SystemAssets LiabilitiesGovernment Securities Currency in CirculationDiscount Loans Reserves

Monetary Liabilities1. Currency in circulation: in the hands of the public2. Reserves: bank deposits at the Fed and vault cash

Assets1. Government securities: holdings by the Fed that affect money

supply and earn interest2. Discount loans: provide reserves to banks and earn the

discount rate

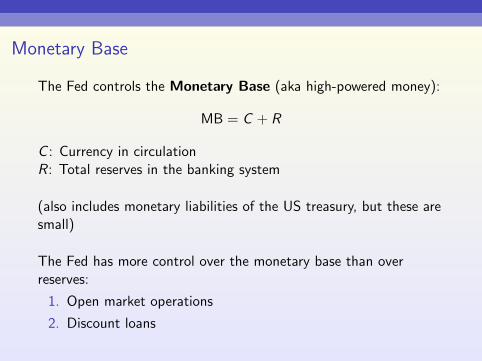

Monetary Base

The Fed controls the Monetary Base (aka high-powered money):

MB = C + R

C : Currency in circulationR: Total reserves in the banking system

(also includes monetary liabilities of the US treasury, but these aresmall)

The Fed has more control over the monetary base than overreserves:

1. Open market operations

2. Discount loans

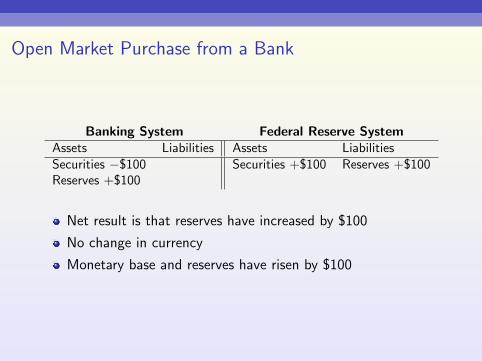

Open Market Purchase from a Bank

Banking System Federal Reserve SystemAssets Liabilities Assets LiabilitiesSecurities −$100 Securities +$100 Reserves +$100Reserves +$100

Net result is that reserves have increased by $100

No change in currency

Monetary base and reserves have risen by $100

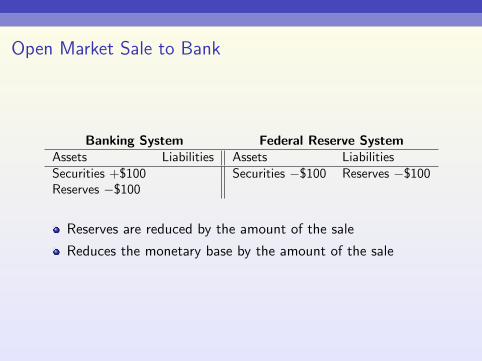

Open Market Sale to Bank

Banking System Federal Reserve SystemAssets Liabilities Assets LiabilitiesSecurities +$100 Securities −$100 Reserves −$100Reserves −$100

Reserves are reduced by the amount of the sale

Reduces the monetary base by the amount of the sale

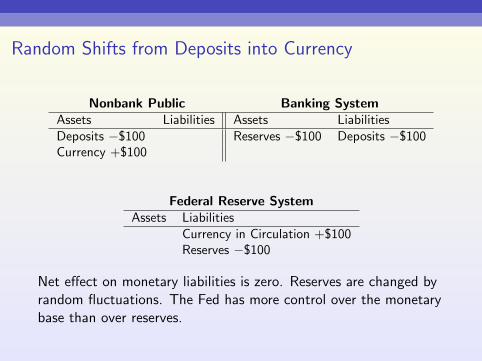

Random Shifts from Deposits into Currency

Nonbank Public Banking SystemAssets Liabilities Assets LiabilitiesDeposits −$100 Reserves −$100 Deposits −$100Currency +$100

Federal Reserve SystemAssets Liabilities

Currency in Circulation +$100Reserves −$100

Net effect on monetary liabilities is zero. Reserves are changed byrandom fluctuations. The Fed has more control over the monetarybase than over reserves.

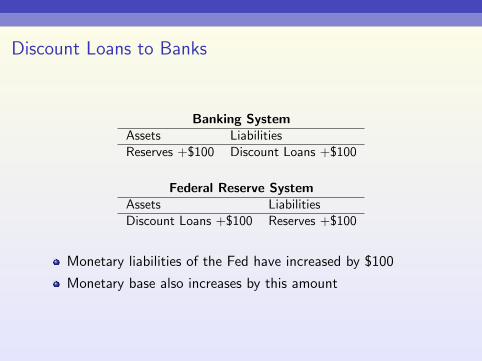

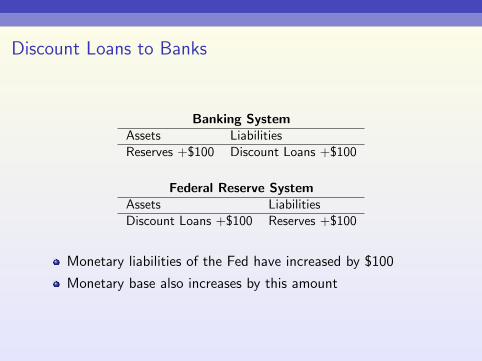

Discount Loans to Banks

Banking SystemAssets LiabilitiesReserves +$100 Discount Loans +$100

Federal Reserve SystemAssets LiabilitiesDiscount Loans +$100 Reserves +$100

Monetary liabilities of the Fed have increased by $100

Monetary base also increases by this amount

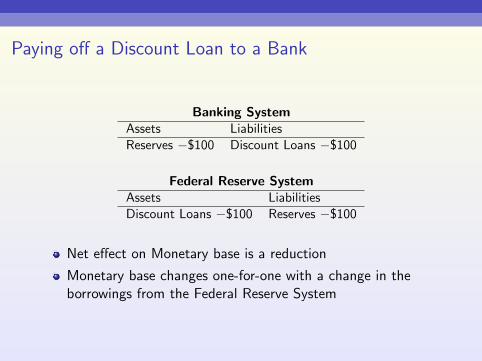

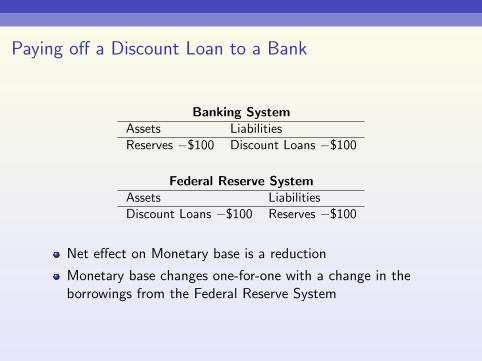

Paying off a Discount Loan to a Bank

Banking SystemAssets LiabilitiesReserves −$100 Discount Loans −$100

Federal Reserve SystemAssets LiabilitiesDiscount Loans −$100 Reserves −$100

Net effect on Monetary base is a reduction

Monetary base changes one-for-one with a change in theborrowings from the Federal Reserve System

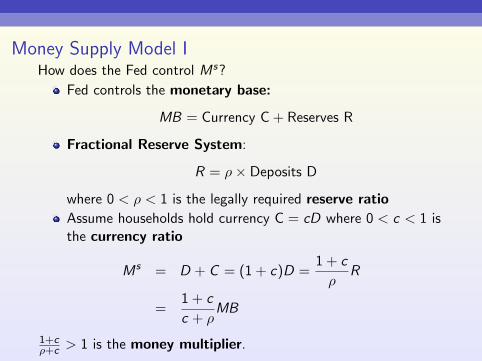

Money Supply Model IHow does the Fed control Ms?

Fed controls the monetary base:

MB = Currency C + Reserves R

Fractional Reserve System:

R = ρ× Deposits D

where 0 < ρ < 1 is the legally required reserve ratio

Assume households hold currency C = cD where 0 < c < 1 isthe currency ratio

Ms = D + C = (1 + c)D =1 + c

ρR

=1 + c

c + ρMB

1+cρ+c > 1 is the money multiplier.

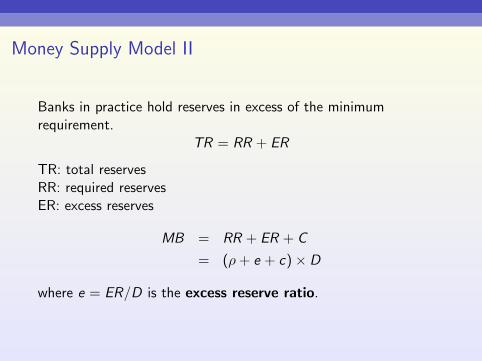

Money Supply Model II

Banks in practice hold reserves in excess of the minimumrequirement.

TR = RR + ER

TR: total reservesRR: required reservesER: excess reserves

MB = RR + ER + C

= (ρ+ e + c)× D

where e = ER/D is the excess reserve ratio.

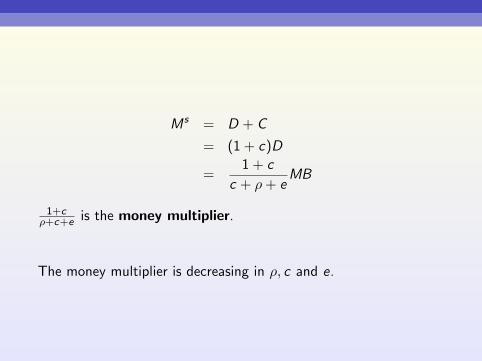

Ms = D + C

= (1 + c)D

=1 + c

c + ρ+ eMB

1+cρ+c+e is the money multiplier.

The money multiplier is decreasing in ρ, c and e.

The excess reserves ratio e is negatively related to the marketinterest rate Ri.e. R ↑→ e ↓→ money multiplier ↑

Reserves do not pay any interest, so R is the opportunity costof holding reserves.

The excess reserves ratio e is positively related to expecteddeposit outflowsi.e. D outflows ↑→ e ↑→ money multiplier ↓

Reserves provide insurance against losses due to depositoutflows.

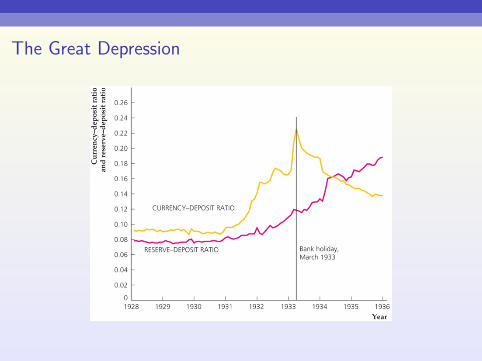

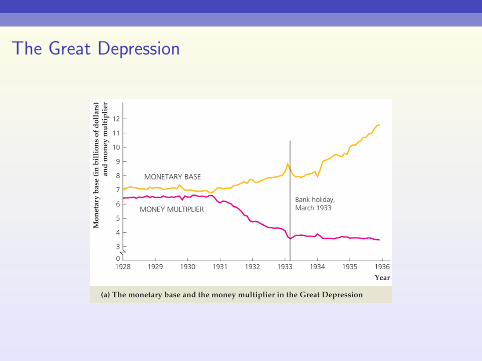

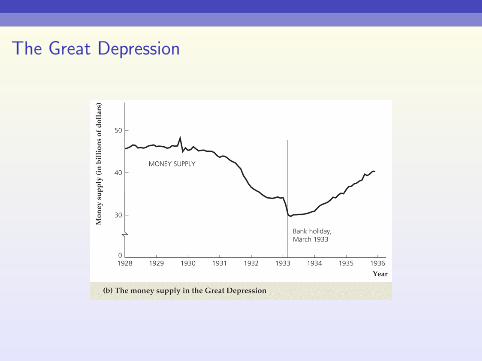

The Great Depression

The Great Depression

The Great Depression

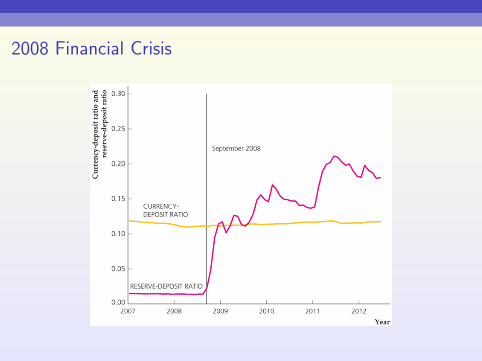

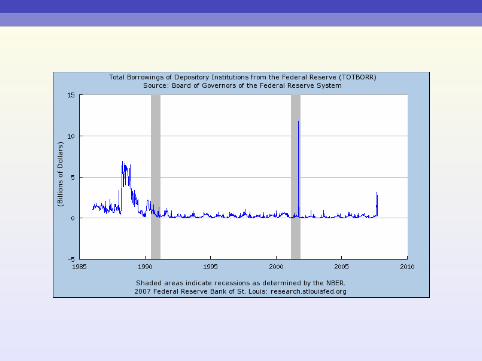

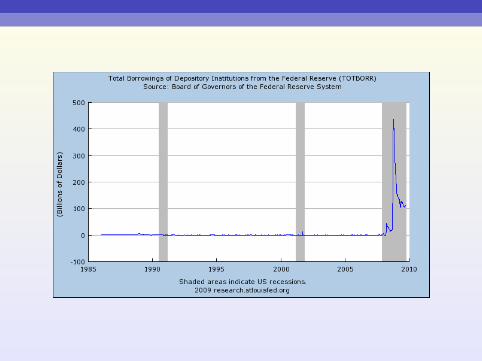

2008 Financial Crisis

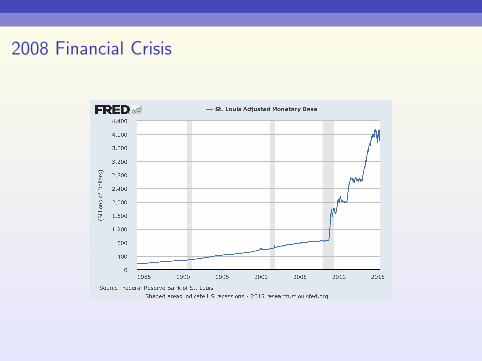

2008 Financial Crisis

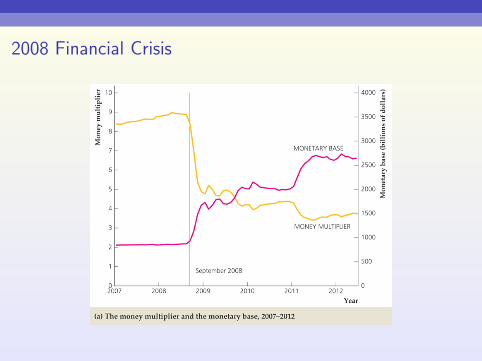

2008 Financial Crisis

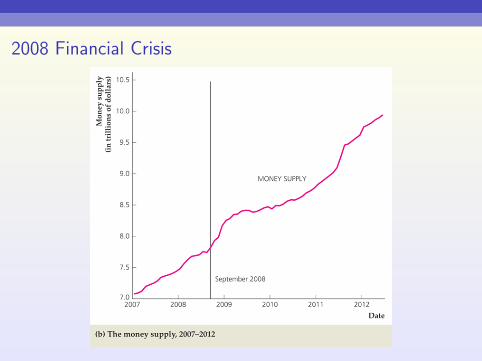

2008 Financial Crisis

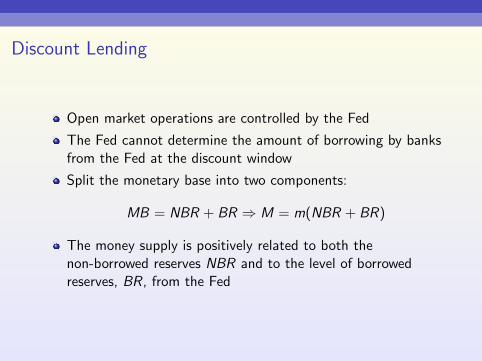

Discount Lending

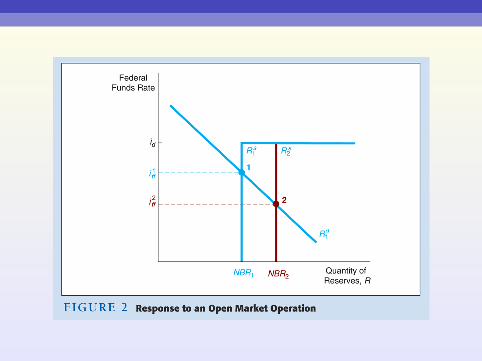

Open market operations are controlled by the Fed

The Fed cannot determine the amount of borrowing by banksfrom the Fed at the discount window

Split the monetary base into two components:

MB = NBR + BR ⇒ M = m(NBR + BR)

The money supply is positively related to both thenon-borrowed reserves NBR and to the level of borrowedreserves, BR, from the Fed

Discount Loans to Banks

Banking SystemAssets LiabilitiesReserves +$100 Discount Loans +$100

Federal Reserve SystemAssets LiabilitiesDiscount Loans +$100 Reserves +$100

Monetary liabilities of the Fed have increased by $100

Monetary base also increases by this amount

Paying off a Discount Loan to a Bank

Banking SystemAssets LiabilitiesReserves −$100 Discount Loans −$100

Federal Reserve SystemAssets LiabilitiesDiscount Loans −$100 Reserves −$100

Net effect on Monetary base is a reduction

Monetary base changes one-for-one with a change in theborrowings from the Federal Reserve System

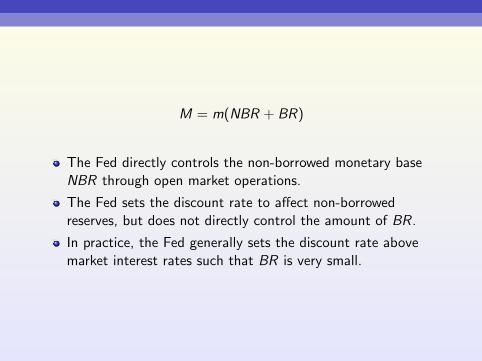

M = m(NBR + BR)

The Fed directly controls the non-borrowed monetary baseNBR through open market operations.

The Fed sets the discount rate to affect non-borrowedreserves, but does not directly control the amount of BR.

In practice, the Fed generally sets the discount rate abovemarket interest rates such that BR is very small.

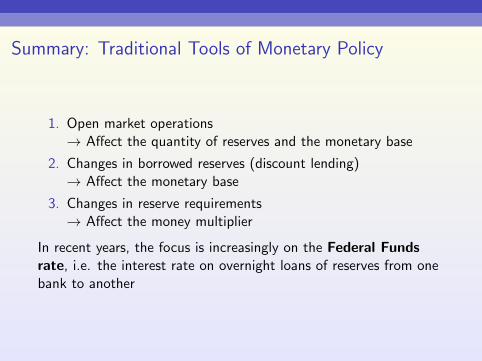

Summary: Traditional Tools of Monetary Policy

1. Open market operations→ Affect the quantity of reserves and the monetary base

2. Changes in borrowed reserves (discount lending)→ Affect the monetary base

3. Changes in reserve requirements→ Affect the money multiplier

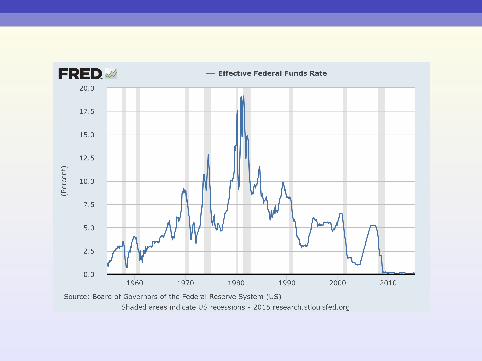

In recent years, the focus is increasingly on the Federal Fundsrate, i.e. the interest rate on overnight loans of reserves from onebank to another

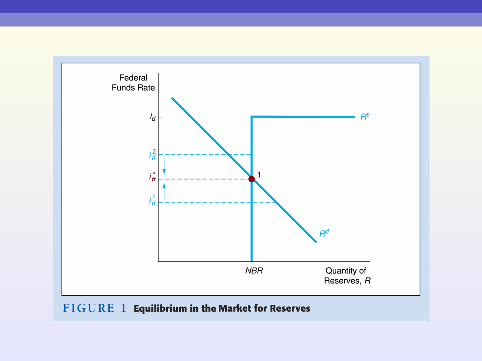

Market for ReservesDemand for Reserves:

Two components: required and excess reserves

TRd = RR + ER

The price is the interest rate that could have been earned, i.e. thefunds rate iff

As iff ↓, the opportunity cost falls and ER ↑→ TRd ↑ → Downwardsloping demand curve

Supply of Reserves

Two components: non-borrowed and borrowed reserves

TRs = NBR + BR

Cost of borrowing from the Fed is the discount rate id .

If iff < id , banks will not borrow and supply curve is vertical

If iff > id , banks can borrow at id , and re-lend at iff , the supplycurve is horizontal (perfectly elastic) at id .

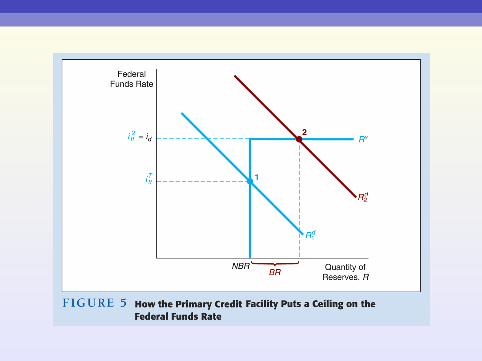

In 2008, the Federal Reserve Board announced that it would beginpaying interest on depository institutions’ reserve balances.

Interest on reserves

provides a floor on the federal funds rate

allows better control of excess reserves when it begins toremove monetary policy stimulus in the future