Embed Size (px)

Citation preview

partpart

44

PowerPoint Presentation by Charlie CookPowerPoint Presentation by Charlie Cook

Copyright Copyright © © 2003 South-Western College Publishing.2003 South-Western College Publishing. All rights reserved.All rights reserved.

Management Management Teams, Teams, Organizational Organizational Forms, and Forms, and Strategic Strategic AlliancesAlliances

1010

The New VentureBusiness Plan

12e

Copyright © by South-Western College Publishing. All rights reserved. 10–2

Looking AheadLooking AheadLooking AheadLooking Ahead

After studying this chapter, you should be able to:

1. Describe the characteristics and value of a strong management team.

2. Explain the common legal forms of organization used by small businesses.

3. Identify factors to consider in choosing among the primary legal forms of organization.

4. Describe the unique features and restrictions of specialized organizational forms such as limited partnerships, S corporations, and limited liability companies.

Copyright © by South-Western College Publishing. All rights reserved. 10–3

Looking Ahead (cont’d)Looking Ahead (cont’d)Looking Ahead (cont’d)Looking Ahead (cont’d)

5. Explain the nature of strategic alliances and their uses in small businesses.

6. Describe the effective use of boards of directors and advisory councils.

7. Explain how different forms of organization are taxed by the federal government.

Copyright © by South-Western College Publishing. All rights reserved. 10–4

The Management TeamThe Management TeamThe Management TeamThe Management Team

• Management team:–Consists of managers and other key persons who

give a company its general direction

• Characteristics of a Strong Management Team–Capable of securing the resources needed to

make business a success–Reassures investors about the their investment

and the continuity of business–Diversity of talent makes the team stronger than

an individual entrepreneur

Copyright © by South-Western College Publishing. All rights reserved. 10–5

The Management Team (cont’)The Management Team (cont’)The Management Team (cont’)The Management Team (cont’)

• Building a Management team:–Competencies required depends on type of

businessCombination of education and experienceRequires achieving a balance of skills and

competence in functional areas

–Designing a management structure that defines relationships and responsibilities

• Outside professional support:–Supplements the skills of a management team–Active board of directors can counsel and guide

Copyright © by South-Western College Publishing. All rights reserved. 10–6

Common Formsof LegalOrganization

Subchapter SCorporation

SoleProprietorship

Partnership

Corporation

Regular CCorporation

Limited Liability Company

LimitedPartnership

GeneralPartnership

Fig 10.1

Legal Forms Legal Forms of of

OrganizationOrganization

Legal Forms Legal Forms of of

OrganizationOrganization

Copyright © by South-Western College Publishing. All rights reserved. 10–7

Legal Forms of Ownership (cont’d)Legal Forms of Ownership (cont’d)Legal Forms of Ownership (cont’d)Legal Forms of Ownership (cont’d)

• Sole Proprietorship–A business owned by one person–Disadvantages

Unlimited personal liabilityNo tax free benefitsDeath/incapacity of owner terminates business

–AdvantagesOwnership of the company name and assets may

be transferred.There is generally no registration or filing fee.Freedom from interference

Copyright © by South-Western College Publishing. All rights reserved. 10–8

Sole ProprietorshipSole ProprietorshipSole ProprietorshipSole Proprietorship

• Sole Proprietorship–A business owned by one person

• Advantages–Receives all of the firm’s profits.–Holds title to all of the firm’s assets–Can easily sell or transfer ownership of the

company name and assets.–Requires no registration or filing fee.–Has absolute freedom from interference by other

stakeholders.

Copyright © by South-Western College Publishing. All rights reserved. 10–9

Sole Proprietorship (cont’d)Sole Proprietorship (cont’d)Sole Proprietorship (cont’d)Sole Proprietorship (cont’d)

• Disadvantages–Bears all business risk.–Is subject to all claims of creditors.–Has unlimited personal liability for business–Receives no tax free benefits as an employee–Death/incapacity of owner terminates business–Is limited to the proprietor’s personal capital.–is taxed on business income as personal income.

Copyright © by South-Western College Publishing. All rights reserved. 10–10

The Partnership OptionThe Partnership OptionThe Partnership OptionThe Partnership Option

• Partnership–A legal entity formed by two or more co-owners to

carry on a business for profit.

• Partner Qualifications–Required: of legal age to contract–Desired: Honest, healthy, capable, and compatible

• Questions about Partnership Formation–What is our business concept?–How are we going to structure ownership?–Why do we need each other?–How do our lifestyles differ?

Copyright © by South-Western College Publishing. All rights reserved. 10–11Fig 10.2

Sharing Workload

Sharing FinancialBurden

Sharing EmotionalBurden

Procuring ExecutiveTalent

Companionship

InterpersonalConflicts

Dilution of Equity

Dissatisfactionwith Partner

Absence of OneClear Leader

Frustration of NotCalling Own Shots

Advantages Disadvantages

The The Advantages Advantages

and and Disadvantages Disadvantages

of of PartnershipsPartnerships

The The Advantages Advantages

and and Disadvantages Disadvantages

of of PartnershipsPartnerships

Copyright © by South-Western College Publishing. All rights reserved. 10–12

Partnership TermsPartnership TermsPartnership TermsPartnership Terms

• Articles of Partnership–A document that states explicitly the rights and

duties of partners.

• Agency Power–The ability of any one partner

to legally bind (e.g., borrow money) the other partners.

Copyright © by South-Western College Publishing. All rights reserved. 10–13

The C Corporation OptionThe C Corporation OptionThe C Corporation OptionThe C Corporation Option

• Corporation–A business organization that exists as a legal

entity and provides limited liability for its owners.

• Legal Entity–A business organization that is recognized by the

law as having a separate legal existence (“artificial being”); can be sued, hold property, incur debt.

• C Corporation–An ordinary, or regular, corporation chartered by

the state and taxed by the federal government as a separate legal entity.

Copyright © by South-Western College Publishing. All rights reserved. 10–14

Corporate Charter: Articles of IncorporationCorporate Charter: Articles of IncorporationCorporate Charter: Articles of IncorporationCorporate Charter: Articles of Incorporation

• Name of company• Formal statement of

formation• Type of Business• Location• Duration• Classes and

preferences of stock• Number and par value

of authorized shares

• Voting privileges for each class of stock

• Names of incorporators and directors

• Capital stockholders• Statement of limited

liability for stockholders• Statement of directors’

powers

Copyright © by South-Western College Publishing. All rights reserved. 10–15

Comparison of Legal Forms of OrganizationComparison of Legal Forms of OrganizationComparison of Legal Forms of OrganizationComparison of Legal Forms of Organization

Sole proprietorship

General partnership

Corporation

Form oforganizationpreferred

Minimum requirements;generally no registrationor filing fee

Minimum requirements; generally no registration orfiling fee; written partnershipagreement not legally requiredbut strongly suggested

Most expensive and greatestrequirements; filing fees; compliance with state regulations for corporations

Proprietorship orgeneral partnership

Unlimited liability

Unlimited liability

Liability limited to investmentin company

Corporation

Limited to proprietor’spersonal capital

Limited to partner’sability and desire tocontribute capital

Usually the most attractive form forraising capital

Corporation

Form ofOrganization

Initial OrganizationalRequirements and Costs

Liability ofOwners

Attractiveness forRaising Capital

Copyright © by South-Western College Publishing. All rights reserved. 10–16

Rights and Legal Status of StockholdersRights and Legal Status of StockholdersRights and Legal Status of StockholdersRights and Legal Status of Stockholders

• Stock Certificate–A document specifying the number of shares of

stock owned by a shareholder

• Pre-emptive Right–The right of stockholders to buy new shares of

stock before they are offered to the public.

• Legal Status–Ownership provides control over the firm.–Ownership limits liability to investment in the firm.–Ownership can be transferred without affecting

the firm’s operations

Copyright © by South-Western College Publishing. All rights reserved. 10–17

Choosing an Organizational FormChoosing an Organizational FormChoosing an Organizational FormChoosing an Organizational Form

• Factors that affect the choice of the firm’s structure:–Initial organizational costs and requirements–Limited versus unlimited liability for the owners–Continuity of business–Transferability of ownership–Management control–Attractiveness for raising equity capital–Income taxes

Copyright © by South-Western College Publishing. All rights reserved. 10–18

Specialized Forms of OrganizationSpecialized Forms of OrganizationSpecialized Forms of OrganizationSpecialized Forms of Organization

• Limited Partnership Structure–General partner—active in the business,

personally liable for the debts of the business–Limited partners—not active in the business,

liability limited to investment in business–Income (taxable) or losses—are apportioned to

each partner

Copyright © by South-Western College Publishing. All rights reserved. 10–19

Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)

• S Corporation–Eligibility Requirements

No more than 75 stockholdersAll stockholders must be individualsOnly one class of stock outstandingMust be a domestic corporationMust operate on a calendar year basisNo nonresident alien stockholders

–BenefitsLiability limited to investment in corporationDividends avoid double taxation (corporate and

personal income).

Copyright © by South-Western College Publishing. All rights reserved. 10–20

Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)Specialized Forms of Organization (cont’d)

• Limited Liability Company–A corporation in which stockholders have limited

liability but pay personal income taxes on the business profits.

Copyright © by South-Western College Publishing. All rights reserved. 10–21

Strategic AlliancesStrategic AlliancesStrategic AlliancesStrategic Alliances

• Strategic Alliances–An organizational relationship that links two or

more independent business entities in a common endeavor

–BenefitsReduced cycle times through shared resourcesIncreased performance through synergistic

combinations of financial resources and creativity

–RiskDifficulty in establishing and maintaining alliances

Copyright © by South-Western College Publishing. All rights reserved. 10–22

The Board of DirectorsThe Board of DirectorsThe Board of DirectorsThe Board of Directors

• Board of Directors–The governing body of a corporation, elected by

the stockholders–Inside directors

Board members who work for the firm

–Outside directorBoard members who do not work for the firm

• Duties–Elect the firm’s officers (top management)–Approve management’s plans and policies–Review performance and declare dividends

Copyright © by South-Western College Publishing. All rights reserved. 10–23

The Board of Directors (cont’d)The Board of Directors (cont’d)The Board of Directors (cont’d)The Board of Directors (cont’d)

• Contributions of Board of Directors–Bring knowledge and experience

Review policy decisionsProvide general directionMonitor the firm’s ethical behaviorMediate and resolve disputes among top

management

• Alternative: Advisory Council–Provides advice but does not have the fiduciary

responsibility for the direction of the firm.

Copyright © by South-Western College Publishing. All rights reserved. 10–24

Federal Income Taxes and Organizational Federal Income Taxes and Organizational Form: How Businesses Are TaxedForm: How Businesses Are Taxed

Federal Income Taxes and Organizational Federal Income Taxes and Organizational Form: How Businesses Are TaxedForm: How Businesses Are Taxed

• Sole Proprietorship–Self-employed persons are taxed on their

business incomes at tax rates set for individuals.

• Partnership–The partnership does not pay taxes; allocated

shares of income from partnership are taxed as personal income for each of the partners.

• Corporation–As a separate legal entity, it reports its income and

pays any taxes related to these profits.

Copyright © by South-Western College Publishing. All rights reserved. 10–25

Federal Income Taxes and Organizational Form:Federal Income Taxes and Organizational Form:How Businesses Are TaxedHow Businesses Are Taxed

Federal Income Taxes and Organizational Form:Federal Income Taxes and Organizational Form:How Businesses Are TaxedHow Businesses Are Taxed

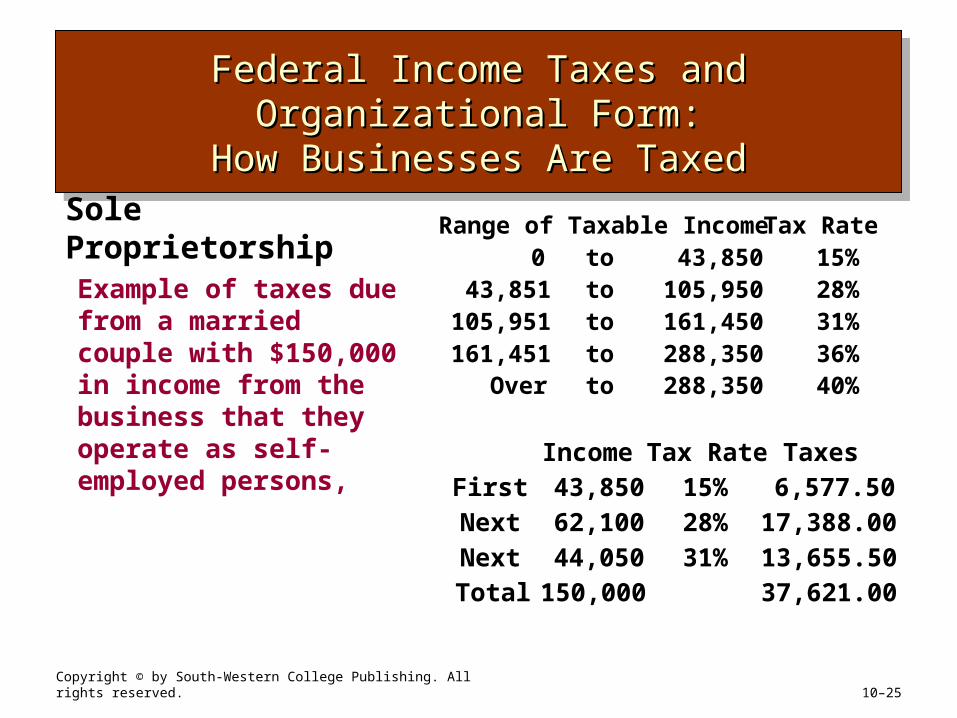

Sole ProprietorshipExample of taxes due from a married couple with $150,000 in income from the business that they operate as self-employed persons,

Tax Rate0 to 43,850 15%

43,851 to 105,950 28%105,951 to 161,450 31%161,451 to 288,350 36%

Over to 288,350 40%

Range of Taxable Income

Income Tax Rate TaxesFirst 43,850 15% 6,577.50 Next 62,100 28% 17,388.00 Next 44,050 31% 13,655.50 Total 150,000 37,621.00

Copyright © by South-Western College Publishing. All rights reserved. 10–26

Federal Income Taxes and Organizational Form:Federal Income Taxes and Organizational Form:How Businesses Are TaxedHow Businesses Are Taxed

Federal Income Taxes and Organizational Form:Federal Income Taxes and Organizational Form:How Businesses Are TaxedHow Businesses Are Taxed

CorporationExample of taxes due from the profits of a corporation. Any profits of the corporation that are distributed to the stockholders are taxed again as personal income.

Range of Taxable Income Tax Rate

$0 to $50,000 15%

$50,001 to $75,000 25%

$75,001 to $100,000 34%

$100,001 to $335,000 39%

Income x Tax Rate= TaxesFirst $50,000 15% $7,500Next $25,000 25% $6,250Next $25,000 34% $8,500Remaining $50,000 39% $19,500Total $150,000 $41,750

Copyright © by South-Western College Publishing. All rights reserved. 10–27

Section 1244 StockSection 1244 StockSection 1244 StockSection 1244 Stock

• Ordinary Income–Income earned in the ordinary course of business,

including any salary

• Capital Gains and Losses–Gains and losses from sale of property that are

not part of the firm’s regular business

• Section 1244 Stock–Special of class stock that allows the owner to

claim an ordinary income tax-deductible loss should the stock become worthless