Embed Size (px)

Citation preview

OFFICIAL STATEMENT DATED JANUARY 24, 2012

PARKING AUTHORITY OF THE TOWNSHIP OF BLOOMFIELDIN THE COUNTY OF ESSEX, NEW JERSEY

$3,530,000 PARKING PROJECT NOTE (TOWNSHIP GUARANTEED, SERIES 2012) (FEDERALLY TAXABLE)

(Noncallable)Project Note Interest Rate: 1.56%

Project Note Re-offering Yield: 1.35%

NEW ISSUE – BOOK ENTRY ONLY

Dated: Date of Delivery

RATING: MIG-1

Maturity: January 31, 2013

Interest on the Project Note (as defined herein) is includable in gross income for federal income tax purposes. Further, in the opinion of Bond Counsel, interest on the Project Note and any gain on the sale thereof are not includable as gross income under the New Jersey Gross Income Tax Act. See “TAX MATTERS” herein.

The $3,530,000 Parking Project Note (Township Guaranteed, Series 2012) (Federally Taxable) (the “Project Note”) shall be issued by the Parking Authority of the Township of Bloomfield (the “Authority”) in the form of one certificate and shall be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). The principal of and interest on the Project Note are payable upon presentation and surrender of the Project Note on its maturity date at TD Bank, National Association, Cherry Hill, New Jersey, which shall act as trustee, registrar and paying agent for the Project Note (the “Trustee”, “Registrar” and “Paying Agent”). Interest shall be computed on the basis of a three hundred sixty (360) day year consisting of twelve (12) months of thirty (30) days each.

The Project Note is issued pursuant to the Parking Authority Law, constituting Chapter 198 of the Pamphlet Laws of 1948 of the State of New Jersey, as amended and supplemented (the “Act”), and a project note resolution of the Authority, duly adopted on April 6, 2004, entitled, “Resolution of the Parking Authority of the Township of Bloomfield Authorizing the Issuance of Not to Exceed $20,000,000 Project Notes”, as amended and supplemented, including by a supplemental resolution of the Authority, duly adopted on December 20, 2011, entitled “Supplemental Resolution Authorizing the Issuance of Not to Exceed $3,600,000 Parking Project Note of the Parking Authority of the Township of Bloomfield”, and by a Certificate of the Executive Director of the Authority dated the date of sale of the Project Note (collectively, the “Resolution”). The Project Note is being issued to finance the current refunding a portion of the principal of the Authority’s 2011 Note (as defined herein) (together with any unspent proceeds of the 2011 Note). See “PURPOSES OF THE PROJECT NOTE” herein.

The Project Note is a direct and general obligation of the Authority, and the full faith and credit of the Authority are pledged to the payment of the principal of and interest on the Project Note. The Project Note shall be secured by a pledge by the Authority of certain funds and accounts, including Revenues (as defined herein) of the Authority. Such pledge, however, is subordinate in all respects to any and all bonds that may be issued by the Authority. The Project Note is further secured by a pledge of the rights of the Authority to receive principal and interest payments from the Township pursuant to Ordinance No. 4-12 of the Township, finally adopted on March 15, 2004, as amended by Ordinance No. 11-10 of the Township, finally adopted on March 7, 2011 (as amended, the “Guaranty Ordinance”). See “SECURITY FOR THE PROJECT NOTE” herein.

THE AUTHORITY HAS NO POWER TO LEVY OR COLLECT TAXES, AND THE PROJECT NOTE SHALL NOT BE DEEMED TO CREATE A DEBT OR A LIABILITY OF THE STATE OF NEW JERSEY (THE “STATE”) OR OF ANY COUNTY OR POLITICAL SUBDIVISION OF THE STATE, OTHER THAN THE AUTHORITY (EXCEPT TO THE EXTENT OF THE OBLIGATION OF THE TOWNSHIP TO MAKE PAYMENTS UNDER THE GUARANTY ORDINANCE) AND DO NOT AND SHALL NOT CREATE OR CONSTITUTE ANY INDEBTEDNESS, LIABILITY OR OBLIGATION OF THE STATE OR OF ANY COUNTY OR POLICTICAL SUBDIVISION OF THE STATE, OTHER THAN THE AUTHORITY (EXCEPT TO THE EXTENT OF THE OBLIGATION OF THE TOWNSHIP TO MAKE PAYMENTS UNDER THE GUARANTY ORDINANCE) EITHER LEGAL, MORAL OR OTHERWISE.

This cover contains certain information for quick reference only. It is not a summary of this Official Statement. Investors must read the entire Official Statement, including the Appendices attached hereto, to obtain information essential to the making of an informed investment decision. The Project Note is offered for delivery when, as and if issued and delivered and received by NW Capital Markets Inc. (the “Underwriter”), subject to the approving legal opinion of McManimon & Scotland, L.L.C., Newark, New Jersey, Bond Counsel to the Authority. Certain legal matters will be passed upon for the Authority by its General Counsel, McManimon & Scotland, L.L.C., Newark, New Jersey and for the Township by its counsel Brian J. Aloia, Esq., Bloomfield, New Jersey. It is expected that the Project Note in definitive form will be available for delivery through DTC on or about January 31, 2012.

TOWNSHIP OF BLOOMFIELD COUNTY OF ESSEX

MAYOR

Raymond McCarthy

TOWNSHIP COUNCIL

Carlos Bernard, Council Member Peggy O’Boyle Dunigan Council Member

Elias Chalet, Council Member Bernard Hamilton, Council Member Nicholas Joanow, Council Member

Michael J. Venezia, Council Member

TOWNSHIP ADMINISTRATOR

Yoshi Manale

TOWNSHIP CLERK

Louise M. Palagano

CHIEF FINANCIAL OFFICER

Robert Renna

GENERAL COUNSEL

Brian J. Aloia, Esq. Bloomfield, New Jersey

INDEPENDENT AUDITOR

Samuel Klein and Company Certified Public Accountants

Newark, New Jersey

PARKING AUTHORITY OF THE TOWNSHIP OF BLOOMFIELD

COMMISSIONERS

John A. Generazio, Chairperson Thomas O. Johnston, Esq., Vice Chairperson

Russ Moserowitz, Secretary Joseph Catalano, Treasurer

Oscar McKee, Commissioner

EXECUTIVE DIRECTOR

Karan Hochman

GENERAL COUNSEL

McManimon & Scotland, L.L.C. Newark, New Jersey

BOND COUNSEL

McManimon & Scotland, L.L.C. Newark, New Jersey

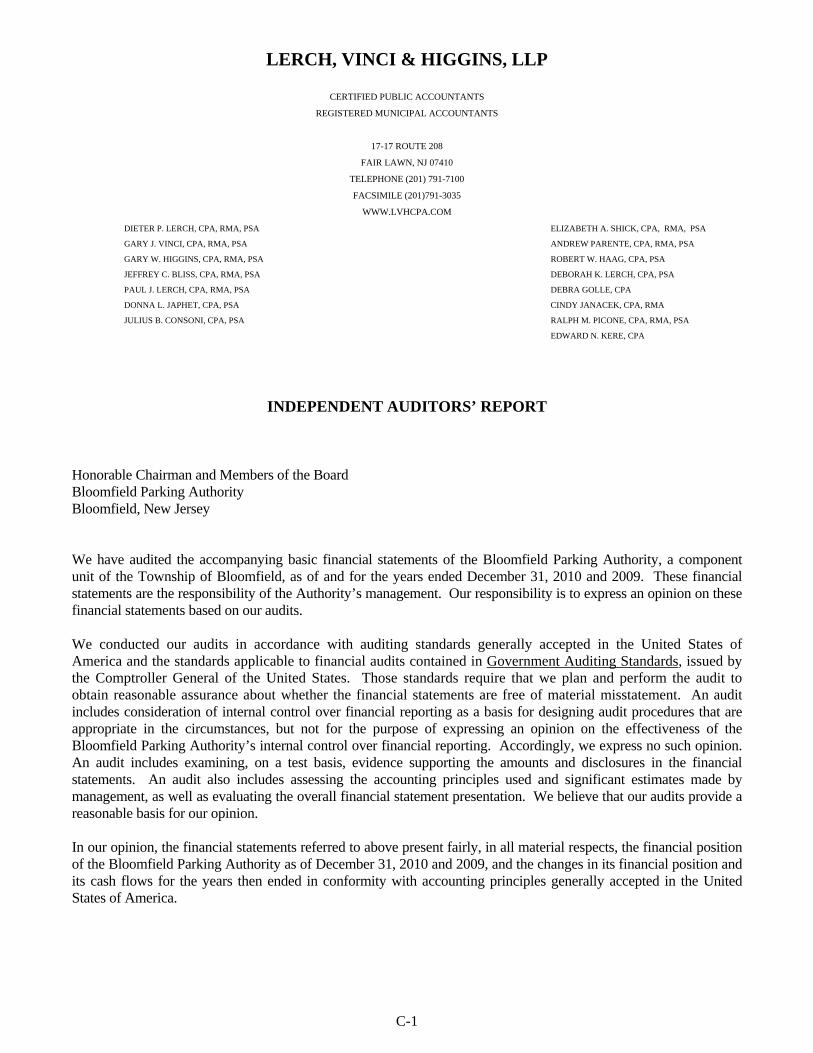

INDEPENDENT AUDITOR

Lerch, Vinci & Higgins, LLP Fair Lawn, New Jersey

FINANCIAL ADVISOR

Acacia Financial Group, Inc. Marlton, New Jersey

No broker, dealer, salesperson or other person has been authorized by the Authority or the Underwriter to give any information or to make any representations with respect to the Project Note other than those contained in this Official Statement, and, if given or made, such information or representations must not be relied upon as having been authorized by the foregoing. The information contained herein has been provided by the Authority and other sources deemed reliable; however, no representation or warranty is made as to its accuracy or completeness and such information is not to be construed as a representation of accuracy or completeness and such information is not to be construed as a representation or warranty by the Underwriter or, as to information from sources other than itself, by the Authority. Certain financial, economic and demographic information concerning the Township is contained in Appendices A and B to this Official Statement. The Authority has not confirmed the accuracy or completeness of information relating to the Township, and the Authority and the Underwriter disclaim any responsibility for the accuracy or completeness thereof. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale hereunder shall, under any circumstances, create any implication that there has been no change in any of the information herein since the date hereof, or the date as of which such information is given, if earlier. References in this Official Statement to laws, rules, regulations, resolutions, agreements, reports and documents do not purport to be comprehensive or definitive. All references to such documents are qualified in their entirety by reference to the particular document, the full text of which may contain qualifications of and exceptions to statements made herein, and copies of which may be inspected at the offices of the Authority during normal business hours. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Project Note in any jurisdiction in which it is unlawful for any person to make such an offer, solicitation or sale. In making an investment decision, investors must rely on their own examination of the Authority and the Township and the terms of the offering, including the merits and risks involved. These securities have not been recommended by any federal or state securities agency or regulatory authority. Furthermore, the foregoing authorities have not confirmed the accuracy or determined the adequacy of this document. Any representation to the contrary is a criminal offense.

i

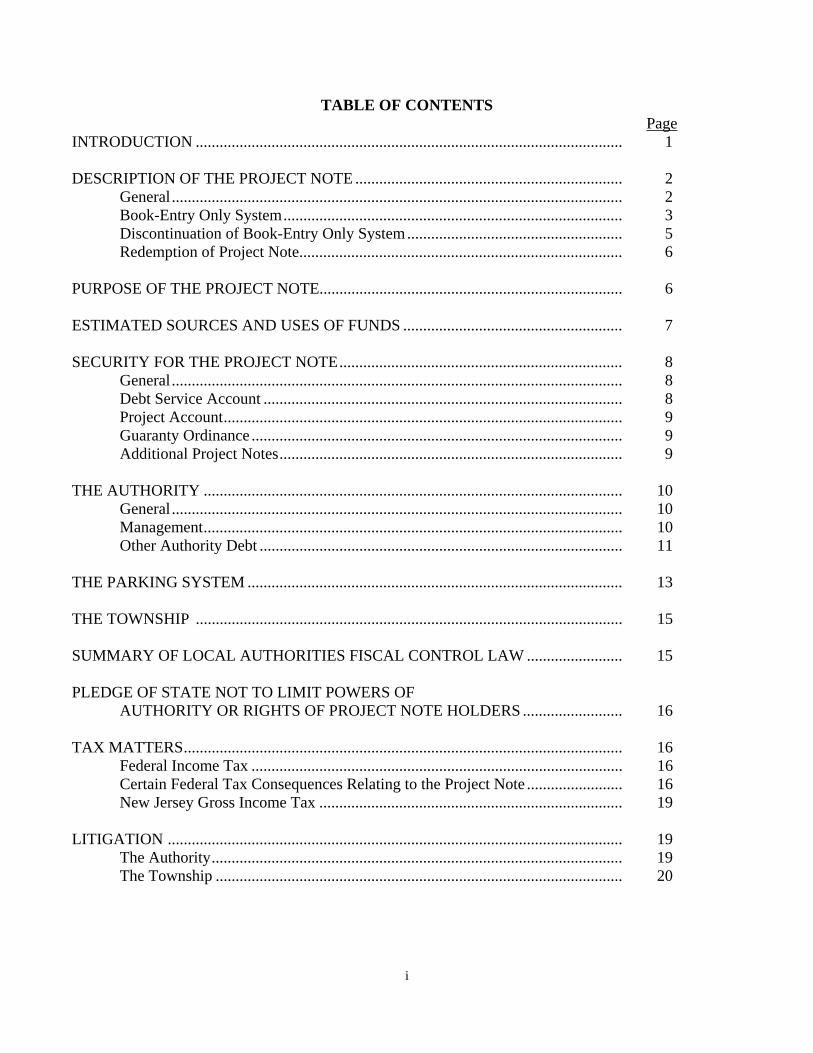

TABLE OF CONTENTS Page INTRODUCTION ........................................................................................................... 1 DESCRIPTION OF THE PROJECT NOTE ................................................................... 2 General ................................................................................................................. 2 Book-Entry Only System ..................................................................................... 3 Discontinuation of Book-Entry Only System ...................................................... 5 Redemption of Project Note................................................................................. 6 PURPOSE OF THE PROJECT NOTE............................................................................ 6 ESTIMATED SOURCES AND USES OF FUNDS ....................................................... 7 SECURITY FOR THE PROJECT NOTE ....................................................................... 8 General ................................................................................................................. 8 Debt Service Account .......................................................................................... 8 Project Account .................................................................................................... 9 Guaranty Ordinance ............................................................................................. 9 Additional Project Notes ...................................................................................... 9 THE AUTHORITY ......................................................................................................... 10 General ................................................................................................................. 10 Management ......................................................................................................... 10 Other Authority Debt ........................................................................................... 11 THE PARKING SYSTEM .............................................................................................. 13 THE TOWNSHIP ........................................................................................................... 15 SUMMARY OF LOCAL AUTHORITIES FISCAL CONTROL LAW ........................ 15 PLEDGE OF STATE NOT TO LIMIT POWERS OF AUTHORITY OR RIGHTS OF PROJECT NOTE HOLDERS ......................... 16 TAX MATTERS .............................................................................................................. 16 Federal Income Tax ............................................................................................. 16 Certain Federal Tax Consequences Relating to the Project Note ........................ 16 New Jersey Gross Income Tax ............................................................................ 19 LITIGATION .................................................................................................................. 19 The Authority ....................................................................................................... 19 The Township ...................................................................................................... 20

ii

SECONDARY MARKET DISCLOSURE...................................................................... 20 The Authority ....................................................................................................... 20 The Township ...................................................................................................... 21 General ................................................................................................................. 23 RATING …… ................................................................................................................. 24 MUNICIPAL BANKRUPTCY ....................................................................................... 24 LEGALITY FOR INVESTMENT .................................................................................. 25 APPROVAL OF LEGAL PROCEEDINGS .................................................................... 25 UNDERWRITING .......................................................................................................... 25 FINANCIAL ADVISOR ................................................................................................. 25 APPENDICES ................................................................................................................. 26 PREPARATION OF OFFICIAL STATEMENT ............................................................ 26 MISCELLANEOUS ........................................................................................................ 27 APPENDIX A DESCRIPTION OF THE TOWNSHIP OF BLOOMFIELD WITH CERTAIN

ECONOMIC AND DEBT INFORMATION APPENDIX B AUDITED FINANCIAL STATEMENTS OF THE TOWNSHIP OF BLOOMFIELD

FOR THE YEARS ENDED DECEMBER 31, 2009, DECEMBER 31, 2008, DECEMBER 31, 2007, DECEMBER 31, 2006 AND DECEMBER 31, 2005 AND INDEPENDENT AUDITOR’S REPORT RELATED THERETO

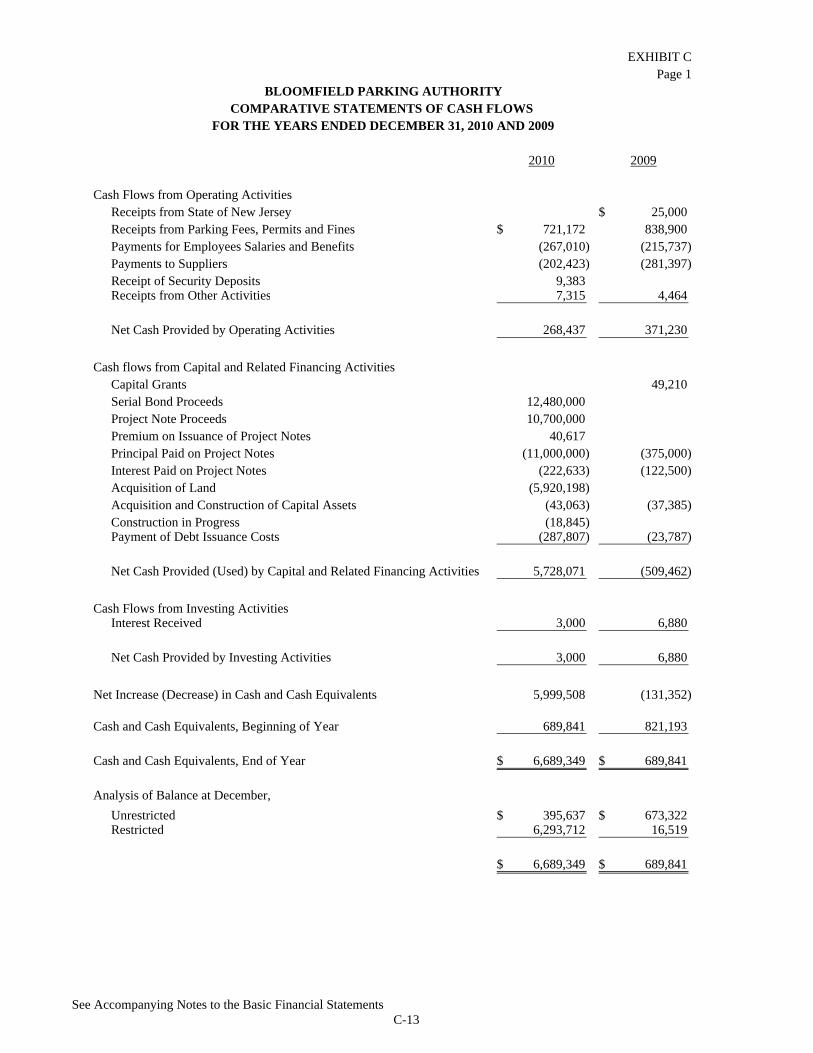

APPENDIX C AUDIT REPORT FOR THE PARKING AUTHORITY OF THE TOWNSHIP OF

BLOOMFIELD FOR THE YEARS ENDED DECEMBER 31, 2010 AND DECEMBER 31, 2009

APPENDIX D SUMMARY OF DEFINITIONS AND CERTAIN PROVISIONS OF THE PROJECT

NOTE RESOLUTION APPENDIX E FORM OF LEGAL OPINION OF BOND COUNSEL

OFFICIAL STATEMENT

PARKING AUTHORITY OF THE TOWNSHIP OF BLOOMFIELD Relating to its

$3,530,000

Principal Amount of Parking Project Note (Township Guaranteed, Series 2012)

(Federally Taxable) (Noncallable)

INTRODUCTION

This Official Statement, which includes the cover page hereof and the Appendices attached

hereto, is furnished by the Parking Authority of the Township of Bloomfield (the “Authority”), a public body corporate and politic of the State of New Jersey (the “State”), to provide certain information relating to the Authority, the Township of Bloomfield, in the County of Essex, New Jersey (the “Township”), the Parking System (as defined herein) located in the Township, and the $3,530,000 principal amount of a Parking Project Note (Township Guaranteed, Series 2012) (Federally Taxable) (the “Project Note”) to be issued by the Authority. The Project Note is issued pursuant to the Parking Authority Law, constituting Chapter 198 of the Pamphlet Laws of 1948 of the State, as amended and supplemented (the “Act”) a project note resolution of the Authority, duly adopted on April 6, 2004, entitled, “Resolution of the Parking Authority of the Township of Bloomfield Authorizing the Issuance of Not to Exceed $20,000,000 Project Notes”, as amended and supplemented, including by a supplemental resolution of the Authority, duly adopted on December 20, 2011, entitled, “Supplemental Resolution Authorizing the Issuance of Not to Exceed $3,600,000 Parking Project Note of the Parking Authority of the Township of Bloomfield”, and by a Certificate of the Executive Director of the Authority dated the date of sale of the Project Note (collectively, the “Resolution”). A description of certain provisions of the Resolution can be found herein in Appendix D under the caption “SUMMARY OF DEFINITIONS AND CERTAIN PROVISIONS OF THE PROJECT NOTE RESOLUTION”. TD Bank, National Association, Cherry Hill, New Jersey has been appointed to serve as trustee, paying agent and registrar for the Project Note (the “Trustee,” “Paying Agent” and “Registrar”). The Project Note is a direct and general obligation of the Authority, and the full faith and credit of the Authority are pledged to the payment of the principal of and interest on the Project Note. The Project Note shall be secured by a pledge by the Authority of certain funds and accounts, including Revenues (as defined herein) of the Authority. Such pledge, however, is subordinate in all respects to any and all bonds that may be issued by the Authority relating to the Parking System. The Project Note is further secured by a pledge of the rights of the Authority to receive principal and interest payments from the Township pursuant to Ordinance No. 4-12 of the Township, finally adopted on March 15, 2004, as amended by Ordinance No. 11-10 of the Township, finally adopted March 7, 2011 (as amended, the “Guaranty Ordinance”). See “SECURITY FOR THE PROJECT NOTE” herein.

- 2 -

THE AUTHORITY HAS NO POWER TO LEVY OR COLLECT TAXES, AND THE PROJECT NOTE SHALL NOT BE DEEMED TO CREATE A DEBT OR A LIABILITY OF THE STATE OR OF ANY COUNTY OR POLITICAL SUBDIVISION OF THE STATE, OTHER THAN THE AUTHORITY (EXCEPT TO THE EXTENT OF THE OBLIGATION OF THE TOWNSHIP TO MAKE PAYMENTS UNDER THE GUARANTY ORDINANCE) AND DO NOT AND SHALL NOT CREATE OR CONSTITUTE ANY INDEBTEDNESS, LIABILITY OR OBLIGATION OF THE STATE, OR OF ANY COUNTY OR POLITICAL SUBDIVISION OF THE STATE, OTHER THAN THE AUTHORITY (EXCEPT TO THE EXTENT OF THE OBLIGATION OF THE TOWNSHIP TO MAKE PAYMENTS UNDER THE GUARANTY ORDINANCE), EITHER LEGAL, MORAL OR OTHERWISE. Copies of the Resolution and the Guaranty Ordinance are on file at the offices of the Authority in Bloomfield, New Jersey and at the principal corporate trust office of the Trustee in Cherry Hill, New Jersey. Reference is made to such documents for the provisions relating to, among other things, the terms of and the security for the Project Note, the custody and application of the proceeds of the Project Note, the rights and remedies of the holders of the Project Note, and the rights, duties and obligations of the Authority, the Township and the Trustee. There follows in this Official Statement brief descriptions of, among other things, the Project Note, the Resolution, the Guaranty Ordinance, the Authority, the Township and the Parking System. Certain demographic and financial information relating to the Township is attached to this Official Statement as Appendices A and B. This information has been furnished by the Township and its auditors, and the Authority has not confirmed the accuracy or completeness of such information relating to the Township and disclaims any responsibility for the accuracy or completeness thereof. Capitalized words and terms which are used herein, which are not ordinarily capitalized and which are not otherwise defined herein, shall have the meanings which are assigned to such words and terms in the Resolution. The summaries of and references to all documents, statutes, reports and other instruments which are referred to herein do not purport to be complete, comprehensive or definitive, and each such summary and reference is qualified in its entirety by reference to such document, statute, report or instrument.

DESCRIPTION OF THE PROJECT NOTE General The Project Note is to be issued in the aggregate principal amount of $3,530,000. The Project Note shall be dated and bear interest from the date of issuance, will mature on the date and in the principal amount which are set forth on the cover page hereof and shall be numbered 2012-1. Upon initial issuance and delivery, the Project Note will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”), which will act as securities depository for the Project Note. The Project Note may be purchased in book-entry form in authorized denominations of $5,000 or any integral multiple of $1,000 in excess thereof through book entries made on the books of DTC.

- 3 -

So long as DTC or its nominee, Cede & Co., is the registered owner of the Project Note, payment of the principal of and interest on the Project Note will be made directly to Cede & Co., as nominee of DTC. Disbursement of such payment to the participants of DTC (“DTC participants”) is the responsibility of DTC and disbursement of such payments to the Beneficial Owners (as defined herein) of the Project Note is the responsibility of the DTC Participants and not the Authority or the Trustee. See “DESCRIPTION OF THE PROJECT NOTE - Book Entry Only System” herein. Book-Entry Only System

The following description of the procedures and record keeping with respect to beneficial ownership interest in the Project Note, payment of principal and interest and other payments on the Project Note to Direct and Indirect Participants (defined below) or Beneficial Owners (defined below), confirmation and transfer of beneficial ownership interests in the Project Note and other related transactions by and between DTC, Direct and Indirect Participants and Beneficial Owners, is based on certain information furnished by DTC to the Authority. Accordingly, the Authority does not make any representations as to the completeness or accuracy of such information. DTC will act as securities depository for the Project Note. The Project Note will be issued as a fully-registered security, registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered certificate will be issued for the Project Note, in the aggregate principal amount of the issue, and will be deposited with DTC.

DTC, the world’s largest securities depository, is a limited-purpose trust company organized under the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law, a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-U.S. equity issues, corporate and municipal debt issues, and money market instruments (from over 100 countries) that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). DTCC is the holding company for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly (“Indirect Participants”). DTC has a Standard & Poor’s rating of AA+. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com.

- 4 -

Purchases of the Project Note under the DTC system must be made by or through Direct Participants, which will receive credits for the Project Note on DTC’s records. The ownership interest of each actual purchaser of the Project Note (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Project Note are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in the Project Note, except in the event that use of the book-entry system for the Project Note is discontinued. To facilitate subsequent transfers, the Project Note deposited by Direct Participants with DTC is registered in the name of DTC’s partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of the Project Note with DTC and its registration in the name of Cede & Co. or such other DTC nominee do not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Project Note; DTC’s records reflect only the identity of the Direct Participants to whose accounts such Project Note is credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers. Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of the Project Note may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Project Note, such as redemptions, tenders, defaults, and proposed amendments to the Project Note documents. For example, Beneficial Owners of the Project Note may wish to ascertain that the nominees holding the Project Note for their benefit have agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them. Redemption notices relating to the Project Note (if any) shall be sent to DTC. If less than all of the Project Note is being redeemed, DTC’s practice is to determine by lot the amount of the interest of each Direct Participant in the Project Note to be redeemed. Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to the Project Note unless authorized by a Direct Participant in accordance with DTC’s MMI Procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the issuer as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.’s consenting or voting rights to those Direct Participants to whose accounts securities are credited on the record date (identified in a listing attached to the Omnibus Proxy).

- 5 -

Redemption proceeds, distributions, and dividend payments on the Project Note will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is to credit Direct Participants’ accounts upon DTC’s receipt of funds and corresponding detail information from the Paying Agent, on payable dates in accordance with their respective holdings shown on DTC’s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in "street name," and will be the responsibility of such Participant and not of DTC nor its nominee, the Paying Agent, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of redemption proceeds, distributions, and dividend payments to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the Authority (through the Paying Agent), disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as depository with respect to the Project Note at any time by giving reasonable notice to the Authority or the Paying Agent. Under such circumstances, in the event that a successor depository is not obtained, the book-entry system shall be discontinued and the Trustee will execute and make available for delivery, a replacement Project Note in the form of a registered certificate.

The Authority may decide to discontinue use of the system of book-entry-only transfers

through DTC (or a successor securities depository). In that event, a certificate will be printed and delivered by the Authority.

The information in this section concerning DTC and DTC’s book-entry system has been

obtained from sources that the Authority believes to be reliable, but the Authority takes no responsibility for the accuracy thereof.

THE PAYING AGENT WILL NOT HAVE ANY RESPONSIBILITY OR OBLIGATION

TO SUCH DTC PARTICIPANTS OR THE PERSONS FOR WHOM THEY ACT AS NOMINEES WITH RESPECT TO THE PAYMENTS TO OR PROVIDING OF NOTICE FOR THE DTC PARTICIPANTS, OR THE INDIRECT PARTICIPANTS, OR BENEFICIAL OWNERS.

SO LONG AS CEDE & CO. IS THE REGISTERED OWNER OF THE PROJECT NOTE,

AS NOMINEE OF DTC, REFERENCES HEREIN TO THE NOTEHOLDERS OR REGISTERED OWNERS OF THE PROJECT NOTE (OTHER THAN UNDER THE CAPTION “TAX MATTERS”) SHALL MEAN CEDE & CO. AND SHALL NOT MEAN THE BENEFICIAL OWNERS OF THE PROJECT NOTE. Discontinuation of Book-Entry Only System If the Authority, in its sole discretion, determines that DTC is not capable of discharging its duties, or if DTC discontinues providing its services with respect to the Project Note at any time, the Authority will attempt to locate another qualified Securities Depository. If the Authority fails to find

- 6 -

such Securities Depository, or if the Authority determines, in its sole discretion, that it is in the best interest of the Authority or that the interest of the Beneficial Owners might be adversely affected if the book-entry only system of transfer is continued (the Authority undertakes no obligation to make an investigation to determine the occurrence of any events that would permit it to make such determination) the Authority shall notify DTC of the termination of the book-entry only system. In the event that the book-entry only system for the Project Note is discontinued, the Authority has, pursuant to the Resolution, provided that upon receipt of the Note certificates from DTC and the Participant information, the Authority will authenticate (or cause to be authenticated) and deliver definitive Project Notes to the holders thereof, and the principal of and interest on the Project Note will be payable and the Project Note may thereafter be transferred or exchanged in the manner described in the Project Note certificates so provided.

Redemption of Project Note

The Project Note is not subject to redemption prior to its stated maturity.

PURPOSE OF THE PROJECT NOTE

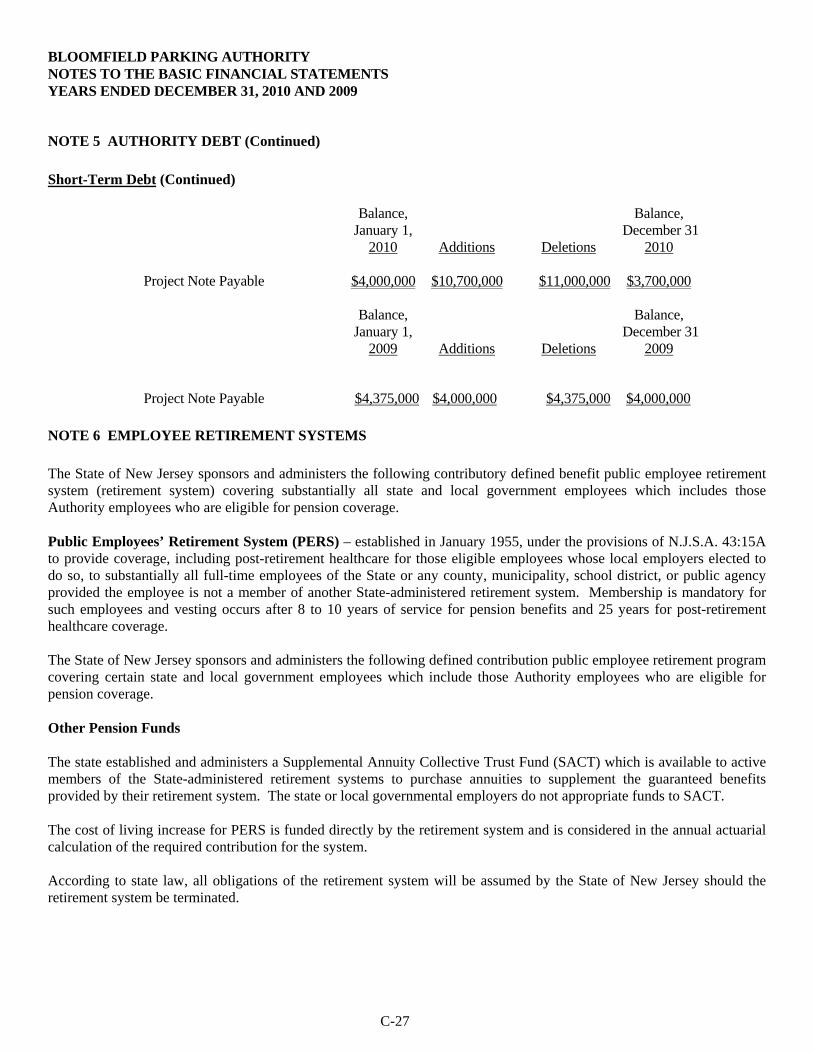

The Project Note is being issued for the purpose of currently refunding a portion of the principal of the Authority’s $3,650,000 Parking Project Note (Township Guaranteed, Series 2011) (Federally Taxable), dated and issued on February 1, 2011 and maturing on February 1, 2012 (the “2011 Note”) (together with any unspent proceeds from the 2011 Note and other available funds).

Proceeds from the sale and issuance of the 2011 Note were used to (i) currently refund the

principal of and interest on the Authority’s $3,700,000 Parking Project Note (Township Guaranteed, Series 2010B) (Federally Taxable), dated and issued on May 14, 2010 and maturing on February 2, 2011 (the “2010B Note”) (together with any unspent proceeds from the 2010B Note and other available funds) and (ii) pay costs and expenses associated with the issuance and delivery of the 2011 Note. Proceeds from the sale and issuance of the 2010B Note were used to (i) currently refund the principal of and interest on the Authority’s $4,000,000 Parking Project Note (Township Guaranteed, Series 2009) (Federally Taxable), dated and issued on May 14, 2009 and maturing on May 14, 2010 (the “2009 Note”) and (ii) pay costs and expenses associated with the issuance and delivery of the 2010B Project Note.

Proceeds from the sale and issuance of the 2009 Note were used to (i) currently refund the

principal of and interest on the Authority’s $4,375,000 Parking Project Note (Township Guaranteed, Series 2007) (Federally Taxable) (the “2007 Note”), (ii) pay certain preliminary or “soft” costs in connection with the design of a parking deck in the Township and (iii) pay costs and expenses associated with the issuance and delivery of the 2009 Note. Proceeds from the sale and issuance of the 2007 Note were used to (i) currently refund the principal of and interest on the Authority’s $5,000,000 Parking Project Note (Township Guaranteed, Series 2006) (Federally Taxable) (the “2006 Note”), (ii) pay certain preliminary or “soft” costs in connection with the design of a parking deck in the Township and (iii) pay costs and expenses associated with the issuance and delivery of the 2007 Note.

- 7 -

Proceeds from the sale and issuance of the 2006 Note were used to (i) currently refund the

principal of and interest on the Authority’s $6,000,000 Parking Project Note (Township Guaranteed, Series 2005) (Federally Taxable) (the “2005 Note”), (ii) pay certain preliminary or “soft” costs in connection with the design of a parking deck in the Township and (iii) pay costs and expenses associated with the issuance and delivery of the 2006 Note. Proceeds from the sale and issuance of the 2005 Note were used to (i) currently refund the principal of and interest on the Authority’s $4,000,000 Parking Project Note (Township Guaranteed, Series 2004A) (Federally Taxable) (the “2004 Note”), (ii) pay certain preliminary or “soft” costs in connection with the design of a parking deck in the Township and (iii) pay costs and expenses associated with the issuance and delivery of the 2005 Note. Proceeds from the sale and issuance of the 2004 Note were used to (i) fund the long term lease of certain parcels of parking property from the Township, (ii) make payment to the Township of certain amounts owed to the Township for the lease of parking employees from the Township and the provision of certain services by the Township to the Authority pursuant to an intra-local agreement between the Authority and the Township, (iii) pay certain start-up costs in connection with the creation and organization of the Authority and (iv) pay costs and expenses associated with the issuance and delivery of the 2004 Note.

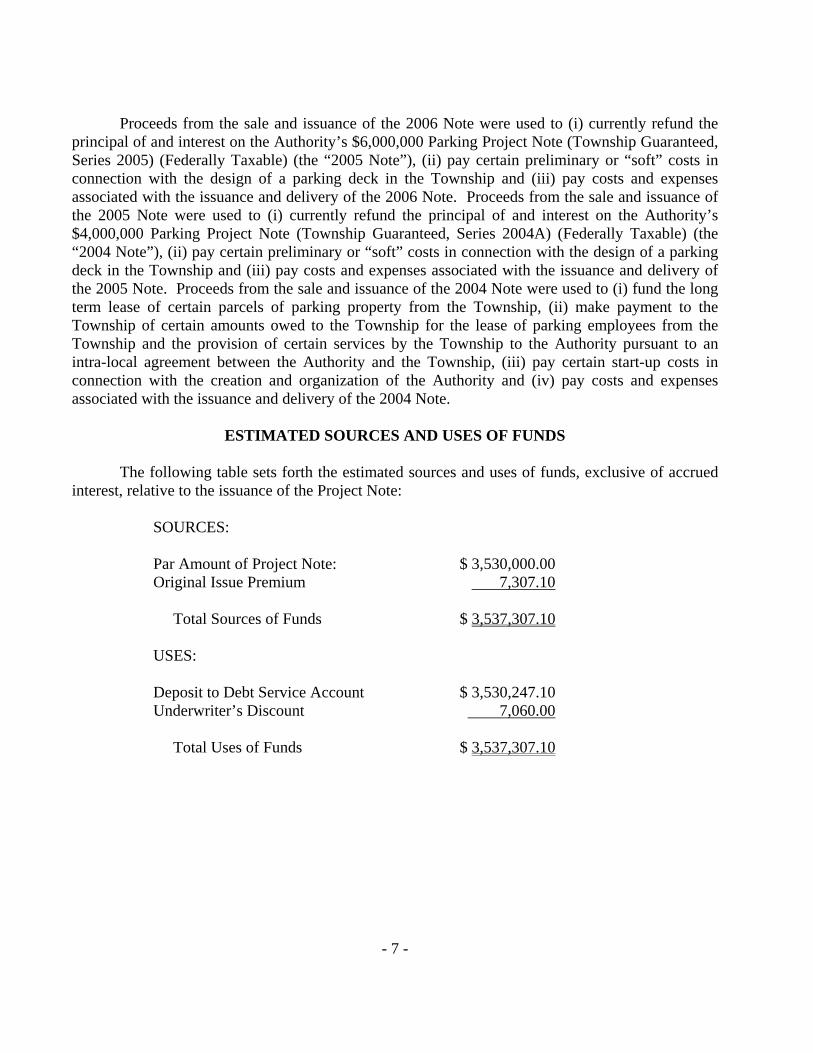

ESTIMATED SOURCES AND USES OF FUNDS

The following table sets forth the estimated sources and uses of funds, exclusive of accrued interest, relative to the issuance of the Project Note:

SOURCES: Par Amount of Project Note: $ 3,530,000.00 Original Issue Premium 7,307.10 Total Sources of Funds $ 3,537,307.10 USES: Deposit to Debt Service Account $ 3,530,247.10 Underwriter’s Discount 7,060.00 Total Uses of Funds $ 3,537,307.10

- 8 -

SECURITY FOR THE PROJECT NOTE General

In order to secure the payment of the Project Note, the Authority covenants and agrees with the holders of the Project Note, and makes provisions which shall be a part of the contract with such holders, that the Authority will, upon receipt of any proceeds of the Project Note, cause the same to be paid, deposited and applied as provided in the Resolution. As security for the due and punctual payment of the principal of and interest on the Project Note and the due and punctual payment and performance of the obligations under the Resolution, the Authority has pledged to the holders of the Project Note, and has granted to the holders thereof a lien on and security interest in (a) all amounts, securities and funds on deposit from time to time in the project account established by the Authority pursuant to the Resolution (the “Project Account”), subject to the application of such amounts, securities and funds in accordance with the provisions of the Resolution; (b) all amounts, securities and funds on deposit from time to time in the debt service account established by the Authority pursuant to the Resolution (the “Debt Service Account”); and (c) all proceeds derived from the issuance and/or sale by the Authority of Additional Project Notes (as defined herein), for the payment of the Project Note in accordance with the covenants and agreements of the Authority contained in the Resolution. Such pledge, however, is subordinate in all respects to any and all bonds that may be issued by the Authority relating to the Parking System. Payment of the principal of and interest on the Project Note is further secured by the assignment and pledge of the Authority’s rights to receive payments from the Township pursuant to the Guaranty Ordinance.

The provisions of the Project Note and the Resolution are deemed to be and do constitute,

contracts by and among the Authority, the Trustee and the holders, from time to time, of the Project Note, and the pledge which is made in the Resolution and the provisions, covenants and agreements which are set forth in the Resolution to be performed by or on behalf of the Authority shall be for the equal benefit, protection and security of the holders of the Project Note.

The Project Note is a direct and general obligation of the Authority, and the full faith and

credit of the Authority are pledged to the payment of the principal of and interest on the Project Note. The Authority has no power to levy or collect taxes. The Project Note is not a debt or liability of the State, the Township or any other political subdivision of the State, other than the Authority (except to the extent of the obligation of the Township to make payments under the Guaranty Ordinance). Neither the members of the Authority nor any person executing the Project Note shall be liable personally thereon by reason of the issuance thereof. Debt Service Account Pursuant to the Resolution, there shall be deposited into the Debt Service Account all moneys, whether constituting fees, rents, charges and other income derived or to be derived by the Authority from or for the operation, use or services of the Parking System (the “Revenues”) or proceeds of Project Notes that may be required or be made available for the payment of the principal of or interest on the Project Note outstanding from time to time. The moneys at any time in the Debt Service Account shall be held and applied solely to the payment and discharge of the principal of

- 9 -

and interest on the Project Note when due and payable. Pending application of the money in said account to such purpose, any moneys therein shall be invested by the Authority in accordance with the Resolution, provided that such investments shall mature in such amounts and at such times as will permit funds to be available for payment of principal of and interest on the Project Note. Project Account Pursuant to the Resolution, all moneys, including Revenues, that may be available and the proceeds of all Project Notes not deposited in the Debt Service Account, shall be deposited in the Project Account. Moneys in the Project Account shall be invested by the Authority in accordance with the Resolution, provided that such investments shall mature in such amounts and at such times as will permit funds to be available when needed to pay the cost of the Project (as defined in the Resolution). Amounts in the Project Account shall be paid out only pursuant to resolution or resolutions of the Authority adopted for application to payment of such costs of the Project. No disbursement shall be made from the Project Account until after the filing with the Chairperson of the Authority of a voucher signed by an Authority officer certifying that such disbursement is necessary to pay part of such disbursement and stating, by general classification, the purpose for which such disbursement is to be made. All moneys in the Project Account are pledged by the Resolution pending their application as provided in this paragraph, to secure the payment of the principal of and interest on the Project Note. Guaranty Ordinance Pursuant to the Guaranty Ordinance, the Township has agreed to fully and unconditionally guaranty the timely payment of the principal of and interest on the Project Note. The full faith and credit of the Township are pledged for the full and punctual performance of said guaranty. Pursuant to the Resolution, all of the rights of the Authority to receive payments from the Township pursuant to the Guaranty Ordinance are assigned and pledged to secure the payment of the principal of and interest on the Project Note. Additional Project Notes Pursuant to the terms of the Resolution, the Authority may, from time to time, issue one or more series of Additional Project Notes for the purposes set forth in the Resolution (the “Additional Project Notes”). Any Additional Project Notes issued by the Authority will be issued on a parity basis, (i.e., of equal rank, without preference, priority or distinction, with the Project Note) and will be entitled to the same pledge of Revenues and other moneys held under the Resolution as applies to the Project Note. Prior to the issuance of any series of Additional Project Notes, the Authority must satisfy certain conditions precedent as set forth in the Resolution.

- 10 -

THE AUTHORITY General

The Authority is a public body corporate and politic of the State, which was created, in accordance with the provisions of the Act, and by an ordinance of the Township, duly adopted on August 4, 2003, as amended by ordinances duly adopted on February 18, 2004 and November 9, 2009. The Authority was created in order to develop a comprehensive and coordinated plan for the development, financing, construction, operation and/or management of the Parking System within the Township. See “THE PARKING SYSTEM” herein.

The Authority has various powers under the Act, including, among others, the following: (1)

to sue and be sued; (2) to enter into leases and contracts and other instruments to carry out its powers; (3) to acquire property by any lawful means, including the exercise of the power of eminent domain with the consent of the Township; (4) to hold, to operate and to administer its property; (5) to issue its bonds and to secure their payment and the rights of holders thereof under one or more resolutions; (6) to enter into contracts with and to accept grants from the Federal government, the State and its political subdivisions or any agency thereof, and any person; (7) to fix, alter, charge and collect rents, rates and other charges, at reasonable rates to be determined exclusively by it, for the use of the facilities and projects of the Authority and for all services sold, furnished or supplied directly or indirectly by the Authority through said facilities and projects, which shall, together with any grants, receipts, contributions or income from other sources, be sufficient to provide for the payment of the expenses of the Authority, repair, maintenance and operation of its facilities and projects, and payment of the principal of and interest on, and any premiums upon the redemption of, its bonds and other obligations, and to fulfill the terms and provisions of any agreements made with the purchasers or holders of any such bonds or other obligations; and (8) to make and to enforce rules and regulations for the management of its business affairs. Management

The Authority is governed by a board consisting of up to five (5) members, each of whom is appointed by the Township Council. Upon expiration of a member's term, such member shall continue to serve until such member has been reappointed or until a successor has been appointed and qualified.

The current members of the Authority and the respective dates of expiration of their terms are set forth below:

Name Position Held Term Expires

John A. Generazio Chairperson December 31, 2012

Thomas O. Johnston, Esq. Vice Chairperson December 31, 2015

Russ Moserowitz Secretary December 31, 2013

Joseph Catalano Treasurer December 31, 2011

- 11 -

Oscar McKee Commissioner December 31, 2014

The daily operation of the Authority is managed by its Executive Director, Karan Hochman.

The Authority's administrative offices are located at 230 Broad Street, Bloomfield, New Jersey 07003.

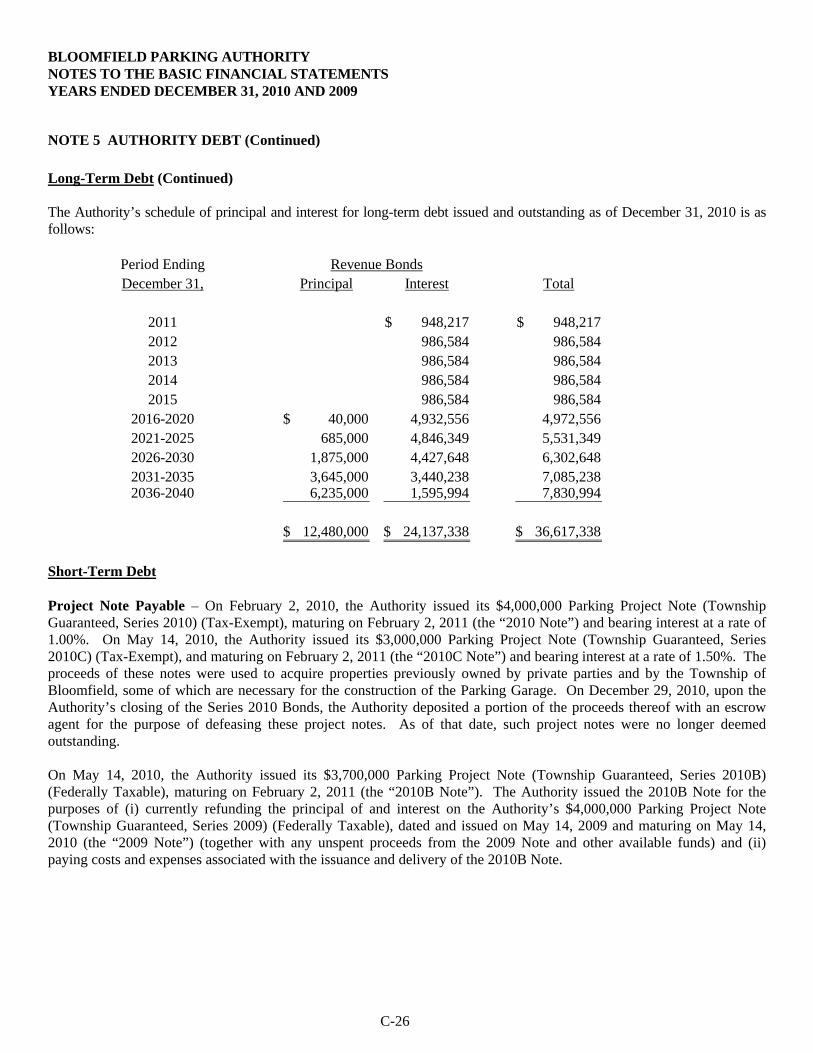

Other Authority Debt

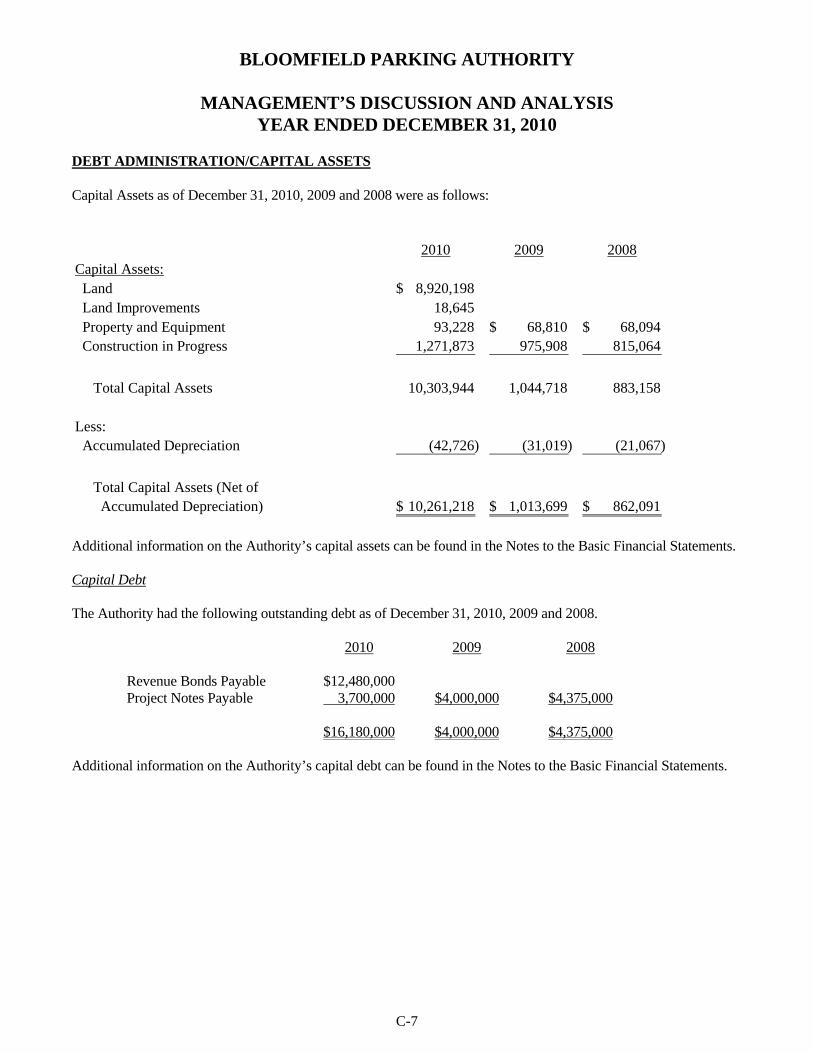

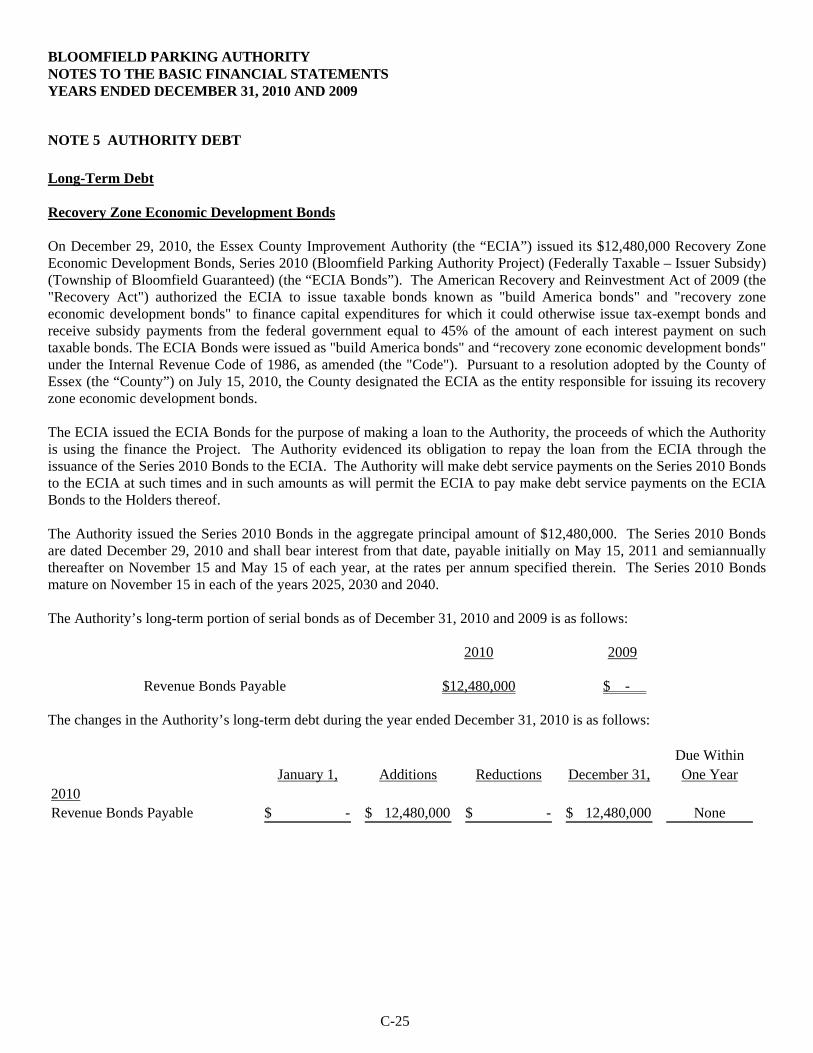

At the present time, the only other outstanding obligations of the Authority are its

$12,480,000 Revenue Bonds (Township Guaranteed, Series 2010D) (the “2010D Bonds”). The 2010D Bonds are dated December 29, 2010, and bear interest, payable initially on May 15, 2011 and semiannually thereafter on November 15 and May 15 of each year at the rates per annum set forth below.

The 2010D Bonds bear interest at the rates, and mature on the dates, in the years and in the amounts as set forth below:

$725,000 7.275% Term Bond Due November 15, 2025

$1,875,000 7.608% Term Bond Due November 15, 2030

$9,880,000 8.008% Term Bond Due November 15, 2040

A portion of the proceeds of the 2010D Bonds were used to defease the Authority’s (i)

$4,000,000 Parking Project Note (Township Guaranteed, Series 2010) (Tax-Exempt) and (ii) $3,000,000 Parking Project Note (Township Guaranteed, Series 2010C) (Tax-Exempt), each of which matured on February 2, 2011. A portion of the proceeds of the 2010D Bonds are also being used to: (A) fund costs associated with the design of, and preliminary constructions costs associated with, the Parking Garage (as defined below); (B) pay capitalized interest on the 2010D Bonds through December 31, 2013; and (C) pay costs associated with the issuance of the 2010D Bonds (collectively, the “2010D Project”). The first sinking fund installment in connection with the 2010D Bonds is due on the Term Bond due November 15, 2025 on November 15, 2019.

The Authority issued the 2010D Bonds to the Essex County Improvement Authority (the

“ECIA”) to evidence the Authority’s obligation to repay a loan from the ECIA in connection with the Parking Garage. On December 29, 2010, the ECIA issued its Recovery Zone Economic Development Bonds, Series 2010 (Bloomfield Parking Authority Project) (Federally Taxable – Issuer Subsidy) (the “ECIA Bonds”), in the aggregate principal amount of $12,480,000, and loaned the proceeds thereof to the Authority to finance the 2010D Project.

The American Recovery and Reinvestment Act of 2009 (the "Recovery Act") authorized the

ECIA to issue taxable bonds known as "build America bonds" and "recovery zone economic development bonds" to finance capital expenditures for which it could otherwise issue tax-exempt bonds and receive subsidy payments from the federal government equal to 45% of the amount of each interest payment on such taxable bonds. The ECIA Bonds were issued as "build America

- 12 -

bonds" and “recovery zone economic development bonds" under the Internal Revenue Code of 1986, as amended (the "Code").

The ECIA made the irrevocable election to have Section 54AA of the Code apply to the

ECIA Bonds so the ECIA Bonds may be "build America bonds" as defined in Code Section 54AA(d). In addition, the ECIA designated the ECIA Bonds, as provided in Code Section 1400U-2(b)(1)(B), as "recovery zone economic development bonds" for purposes of Code Section 1400U-2 in order to receive the refundable credits allowed to issuers pursuant to Code Sections 1400U-2(a) and 6431 with respect to the ECIA Bonds (the "RZEDB Interest Subsidy Payments"). Under applicable law, the RZEDB Interest Subsidy Payments are to be paid by the United States Treasury directly to any issuer of bonds that qualify as "build America bonds" and as "recovery zone economic development bonds" in an amount equal to 45% of the interest payable by such issuer on such bonds on each interest payment date, provided that certain requirements, as described in the Code and related Internal Revenue Service (the "Service") pronouncements, as to the uses and investment of the bond proceeds and other matters, are continuously satisfied by such issuer.

The ECIA covenanted to comply with the requirements of the Code necessary to maintain the

qualification of the ECIA Bonds as "build America bonds" as defined in Code Section 54AA(d) and as "recovery zone economic development bonds" as defined in Code Section 1400U-2(b). In the event that the ECIA does not comply with such requirements, it may be retroactively disqualified from being eligible to receive the RZEDB Interest Subsidy Payments otherwise allowable with respect to the ECIA Bonds from the date of issuance thereof, regardless of the date on which the event causing such disqualification occurs. In order to actually be paid, the RZEDB Interest Subsidy Payment with respect to each interest payment under the ECIA Bonds, the ECIA must file IRS Form 8038-CP not earlier than ninety (90) days nor later than forty-five (45) days prior to each interest payment date with respect to the ECIA Bonds. Also the RZEDB Interest Subsidy Payments are subject to being offset by certain amounts that may, for unrelated reasons, be owed by the ECIA to any agency of the United States. No assurance is given that the United States Treasury will make the RZEDB Interest Subsidy Payments in the amounts to which the ECIA believes it will be entitled, nor that such payments will be made in a timely manner. The RZEDB Interest Subsidy Payments do not constitute a full faith and credit guarantee of the United States and are not pledged to the security of the ECIA Bonds. In addition, the Authority has agreed to comply with the requirements of the Code necessary to maintain the qualification of the ECIA Bonds as "build America bonds" as defined in Code Section 54AA(d) and as "recovery zone economic development bonds" as defined in Code Section 1400U-2(b).

In accordance with the terms of the 2010D Bonds, the Authority is required to make

payments to the ECIA in amounts equal to the debt service on the ECIA Bonds on May 15 and November 15, which dates are 30 days prior to each interest payment date and principal payment date on the ECIA Bonds, after taking into account such funds as may be on deposit with the ECIA from RZEDB Interest Subsidy Payments. Moreover, the Authority’s obligation to make payments under the 2010D Bonds is secured by the Guaranty Ordinance.

- 13 -

THE PARKING SYSTEM

The Authority operates, maintains and manages parking lots located throughout the Township which it owns, as well as a number of other lots and metered parking areas that it leases from the Township. There are presently parking facilities located on the following parcels of land on the Tax Map of the Township: Block 127, Lot 40; Block 127, Lot 43; Block 127, Lot 44; Block 153, Lot 13.01; Block 153, Lot 14; Block 153, Lot 37; Block 225, Lot 1; Block 225, Lot 9; Block 227, Lot 26, Block 228, Lot 1; Block 311, Lot 13; and Block 571, Lot 19 (collectively, the “Authority Owned Parking Facilities”); and Block 153, Lot 15; a portion of Block 245, Lot 4; and a portion of Block 301, Lot 1 (the “Township Owned Parking Facilities” and, together with the Authority Owned Parking Facilities and the on-street parking meters, the “Parking System”). Pursuant to a lease agreement by and between the Authority and the Township, dated as of July 1, 2005, the Authority leased Block 153, Lot 15, a portion of Block 245, Lot 4 and a portion of Block 301, Lot 1 (along with other lots that the Authority has since acquired and which are described above) and the on-street parking meters from the Township. Pursuant to an Ordinance adopted by the Township on November 9, 2009, the Township authorized the sale of all Township Owned Parking Facilities to the Authority and the Authority anticipates acquiring title to the remaining such Facilities in 2012. Revenues collected from the Parking System are not dedicated to the parking facility from which they originate; all revenues are collected for the support of the Parking System as a whole.

Pursuant to the Local Redevelopment and Housing Law, N.J.S.A. 40A:12A-1 et seq. (the

“Redevelopment Law”), the Township designated the properties identified on the Township’s tax maps as Block 228, Lots 1, 4, 5, 7, 8, 10, 11, 13, 14, 15, 16, 17, 18, 19, 21, 24, 27, 28, 29, 30, 31, 33 & 35, and Block 220, Lot 40 (the “Redevelopment Area”) as an “area in need of redevelopment”. On February 7, 2011, the Mayor and Council of the Township (“Mayor and Council”) adopted an ordinance approving and adopting a redevelopment plan, entitled the “Redevelopment Plan for Block 228 and Block 220, Lot 40 Redevelopment Plan Area” (as the same may be amended and supplemented, the “Redevelopment Plan”), for the Redevelopment Area, as well as for portions of the abutting rights-of-way extending to the centerline of the streets surrounding the aforementioned properties, specifically, Lackawanna Place, Washington Street and Glenwood Avenue. On March 7, 2011, the Mayor and Council adopted an ordinance vacating various portions of the Lackawanna Place and Washington Street rights-of-way in the Township, which portions are described in more detail in said ordinance. Upon such vacation, the Authority obtained title to such vacated portions of the rights-of-way.

Bloomfield Center Urban Renewal, LLC (the “Redeveloper”) and the Township have entered

into that certain Redevelopment Agreement, dated March 8, 2011 (the “Redevelopment Agreement”). Pursuant to the Redevelopment Agreement, the Redeveloper will redevelop the portion of the Redevelopment Area consisting of all of Block 228, as well as the aforementioned vacated portions of the Lackawanna Place and Washington Street rights-of-way (collectively, the “Project Site”). In particular, the Redeveloper will redevelop the Project Site by constructing thereon a project (the “Redevelopment Project”) consisting of: (i) (A) approximately 60,000 square feet of retail space, including approximately 10,000 square feet of restaurant space (together, the “Retail Component”), and (B) approximately 224 residential units (the “Residential Component”

- 14 -

and, together with the Retail Component, the “BCUR Project”) on a portion of the Project Site that it will own, by itself or along with a separate developer of the Residential Component (the “BCUR Project Site”); and (ii) an approximately 439 space parking garage (the “Parking Garage”) on a portion of the Project Site that the Authority will own (the “Parking Garage Project Site”).

The Authority currently owns the entire Project Site. The Redeveloper and the Authority

have entered into that certain Land Swap Agreement, dated January 5, 2011, pursuant to which the Authority will subdivide the Project Site to create the BCUR Project Site and the Parking Garage Project Site, then convey the BCUR Project Site to the Redeveloper, and the Authority will retain ownership of the Parking Garage Project Site. Upon its completion, the Parking Garage will become part of the Parking System.

In March 2011, the Redeveloper and the Authority jointly applied to the Planning Board of

the Township (the “Planning Board”) for site plan approval in connection with the Redevelopment Project and for approval to subdivide the Project Site to create the BCUR Project Site and the Parking Garage Project Site (together, the “Redevelopment Project Approvals”). After a public hearing held on April 19 and May 19, 2011, the Planning Board granted the Redevelopment Project Approvals. At this time, the Authority expects that the Township will vacate additional portions of the Lackawanna Place, Washington Street and Glenwood Avenue rights-of-way. The Authority expects to seek amended subdivision approval in order to incorporate these additionally vacated portions of the rights-of-way into the Project Site. The Redeveloper also expects to seek amended site plan approval in connection with the BCUR Project in order to address certain minor modifications to the façade thereof.

Under the terms of a Financial Agreement by and between the Redeveloper and the

Township, dated as of May 10, 2011 (the “Financial Agreement”), the Redeveloper will (i) construct the BCUR Project on the BCUR Project Site and (ii) in lieu of paying property taxes associated with the BCUR Project and the BCUR Project Site, pay to the Township the Annual Service Charge (as defined in the Financial Agreement). Pursuant to the Financial Agreement, the Township has pledged its right to receive the Annual Service Charge to the Authority which has, in turn, pledged the Annual Service Charge to the payment of debt service on the 2010D Bonds.

On March 7, 2011, the Mayor and Council adopted an ordinance directing the special

assessment of a portion of the costs relating to the Parking Garage on the BCUR Project Site. The future owner(s) of the Project Site, therefore, will be obligated to make special assessment payments (the “Special Assessment Payments”) to the Township; such payments, however, will be due only to the extent that such future owner(s) does not pay the Annual Service Charge pursuant to the Financial Agreement. The Township, pursuant to an agreement expected to be entered into by and between the Township and BCUR, intends to pledge its right to receive the Special Assessment Payments to the Authority, which has agreed, in turn, to pledge the Special Assessment Payments to the payment of debt service on the 2010D Bonds.

On August 4, 2011, the Authority and the Redeveloper entered into that certain Parking

Garage Construction Agreement, pursuant to which the Redeveloper and the Authority will design, and the Redeveloper will build, the Parking Garage. Since then, representatives of the Redeveloper and the Authority have been working together to design the Parking Garage, and the Redeveloper

- 15 -

has executed a contract with a residential developer to build the Residential Component. Moreover, in November 2011, the Authority completed the demolition of buildings on the Project Site. The Authority expects construction of the Parking Garage to commence in or before June 2012, and construction of the BCUR Project to follow.

The Authority operates the Parking System with its own employees and personnel supplied

by Standard Parking Corporation, New York, NY (“Standard”) pursuant to a contract between the Authority and Standard originally executed in July 2009 (the “Contract”). Under the Contract, Standard provides personnel to assist Authority employees in the performance of various duties, including the enforcement of parking-related statutes, rules, ordinances and regulations. The original term of the Contract was for one year, from July 2009 to July 2010, and it was renewed at the option of the Authority and Standard, for two additional one-year terms.

On December 20, 2011, the Authority adopted a temporary budget for the first quarter of

fiscal year January 1, 2012 to December 31, 2012. The Authority expects to adopt its budget for the entire fiscal year January 1, 2012 to December 31, 2012 at a meeting scheduled for January 17, 2012.

THE TOWNSHIP

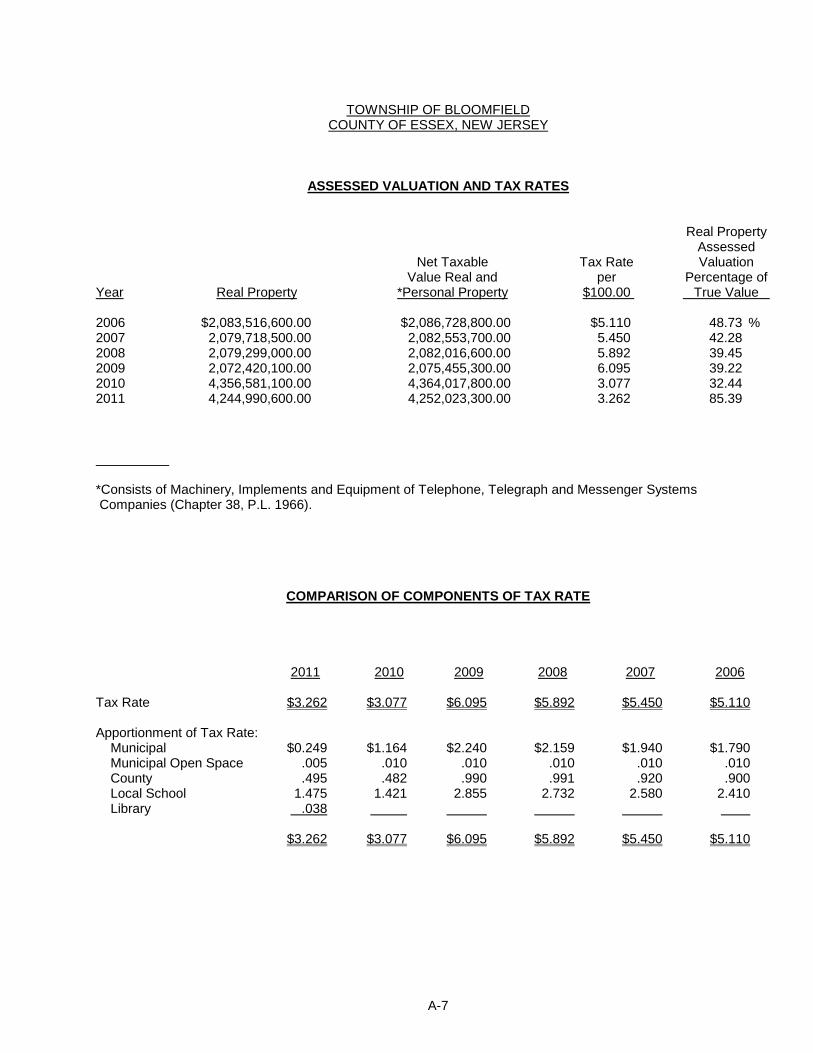

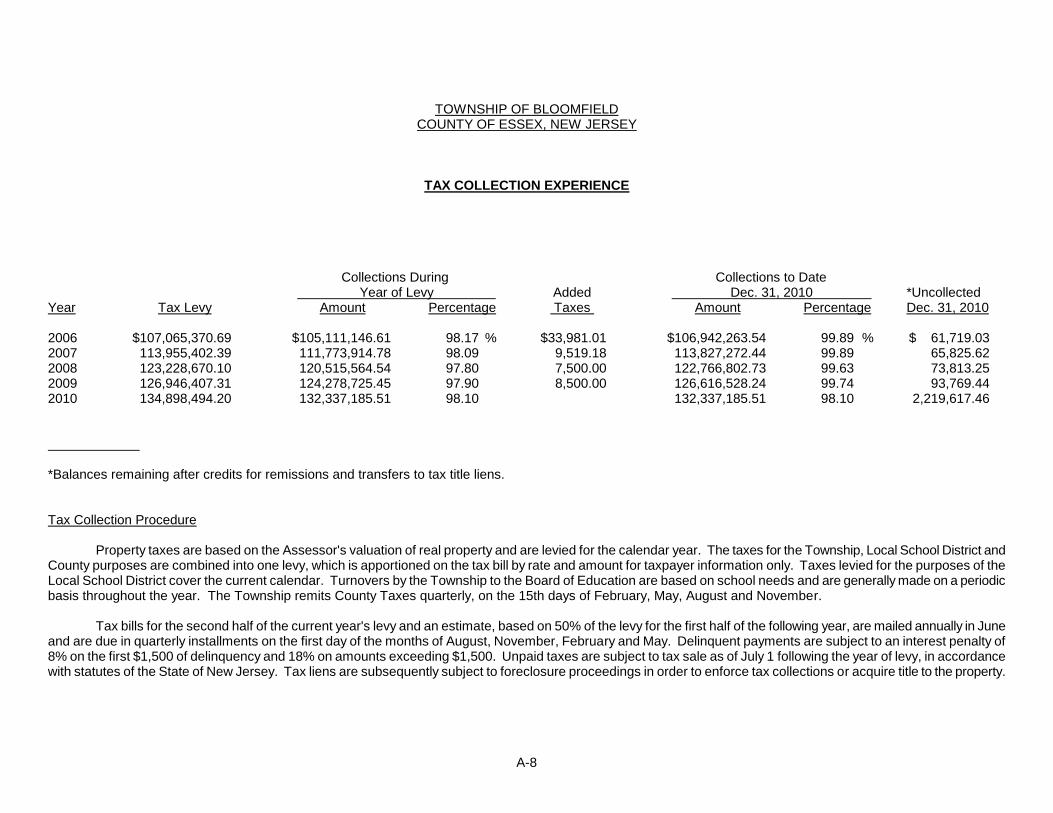

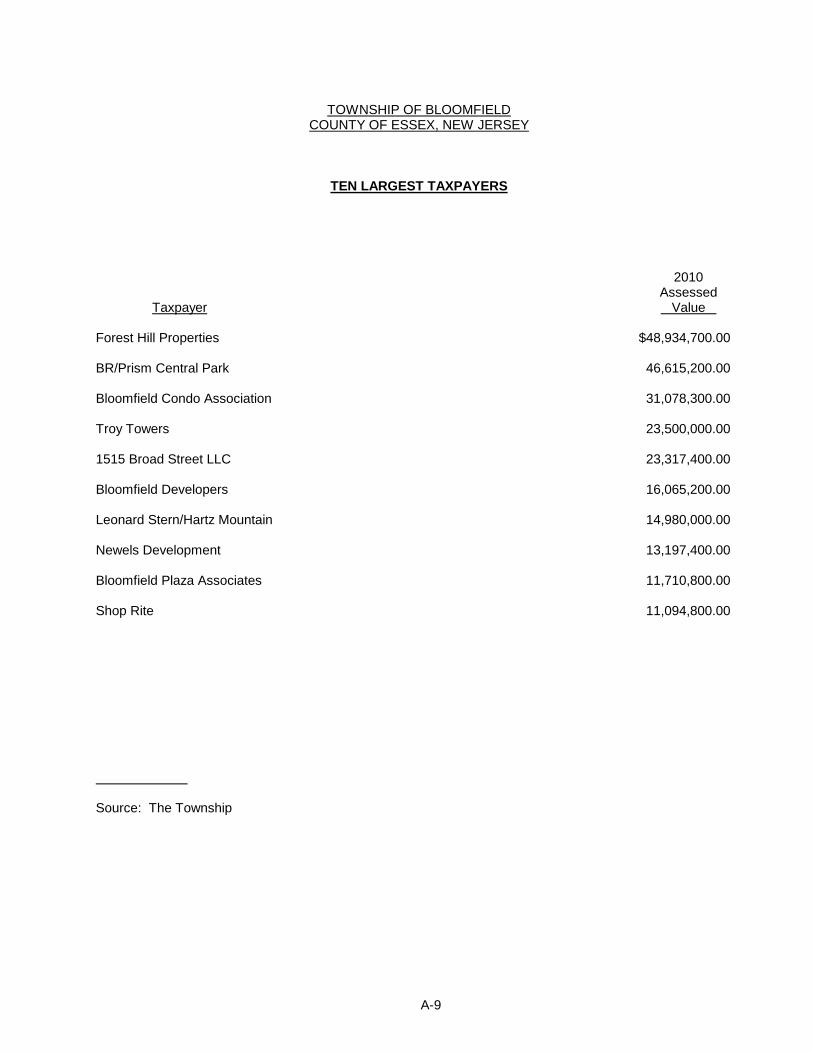

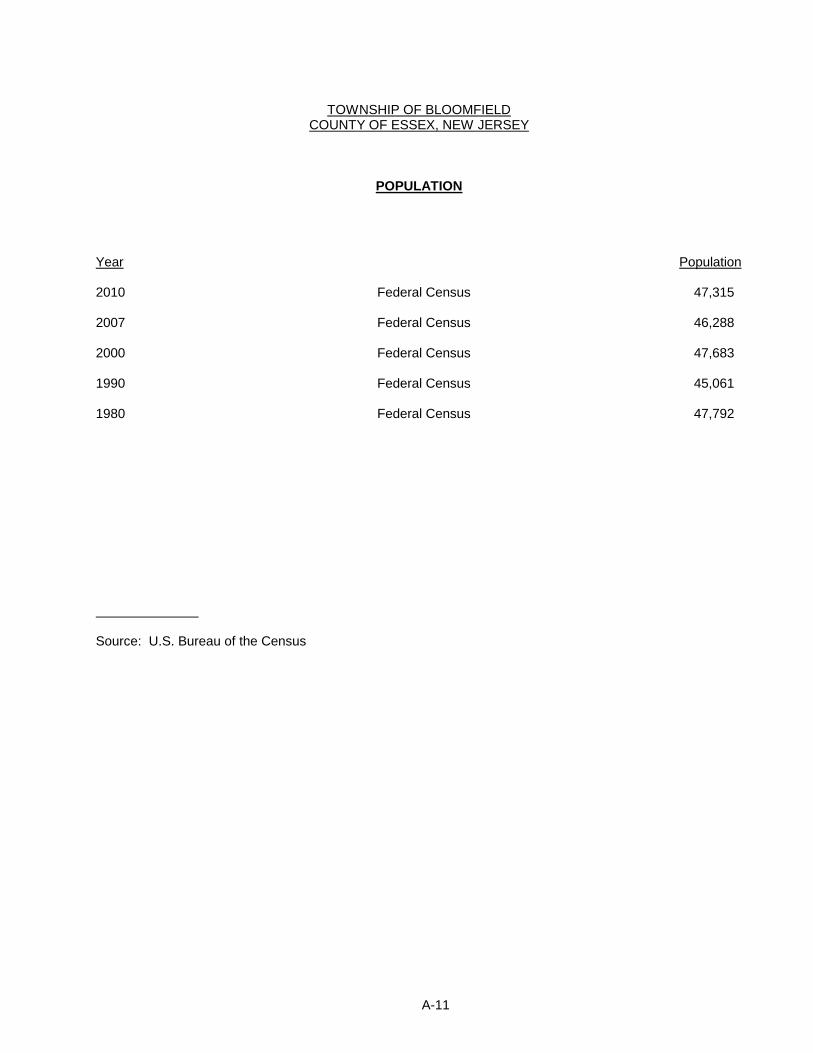

The Township is located in Essex County, New Jersey. The Township has never defaulted in

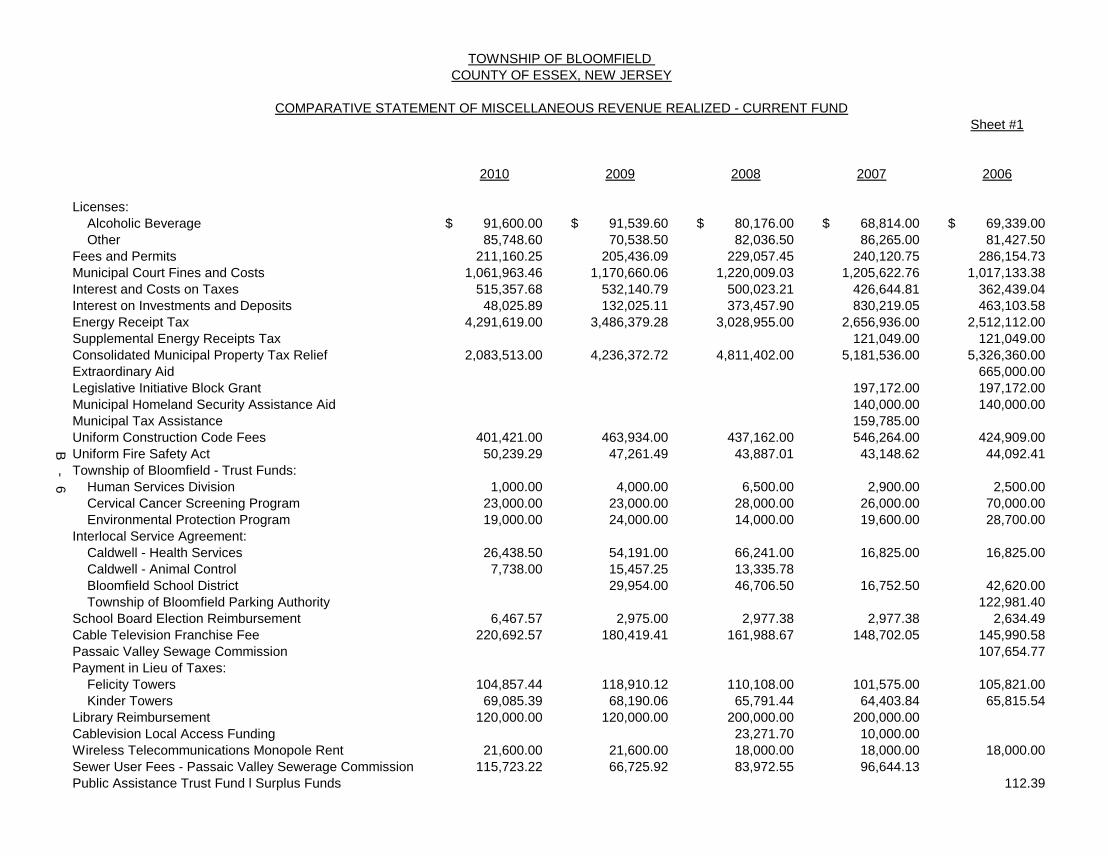

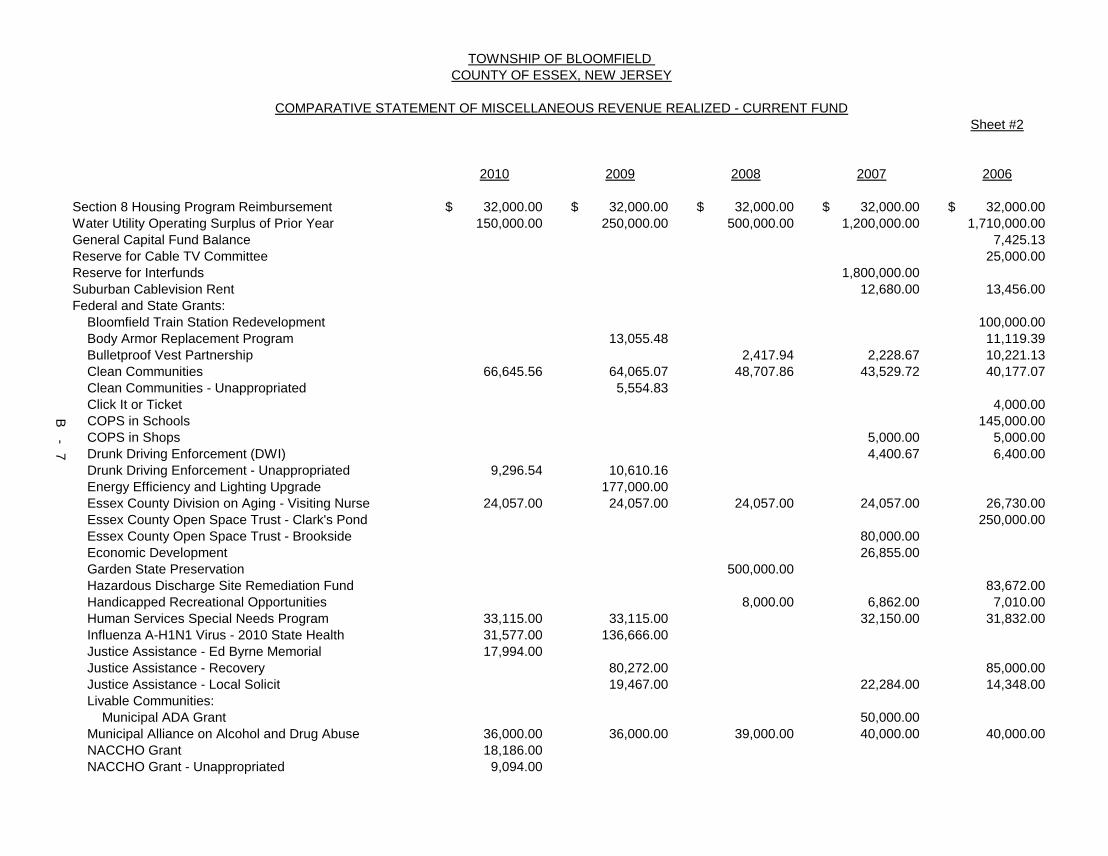

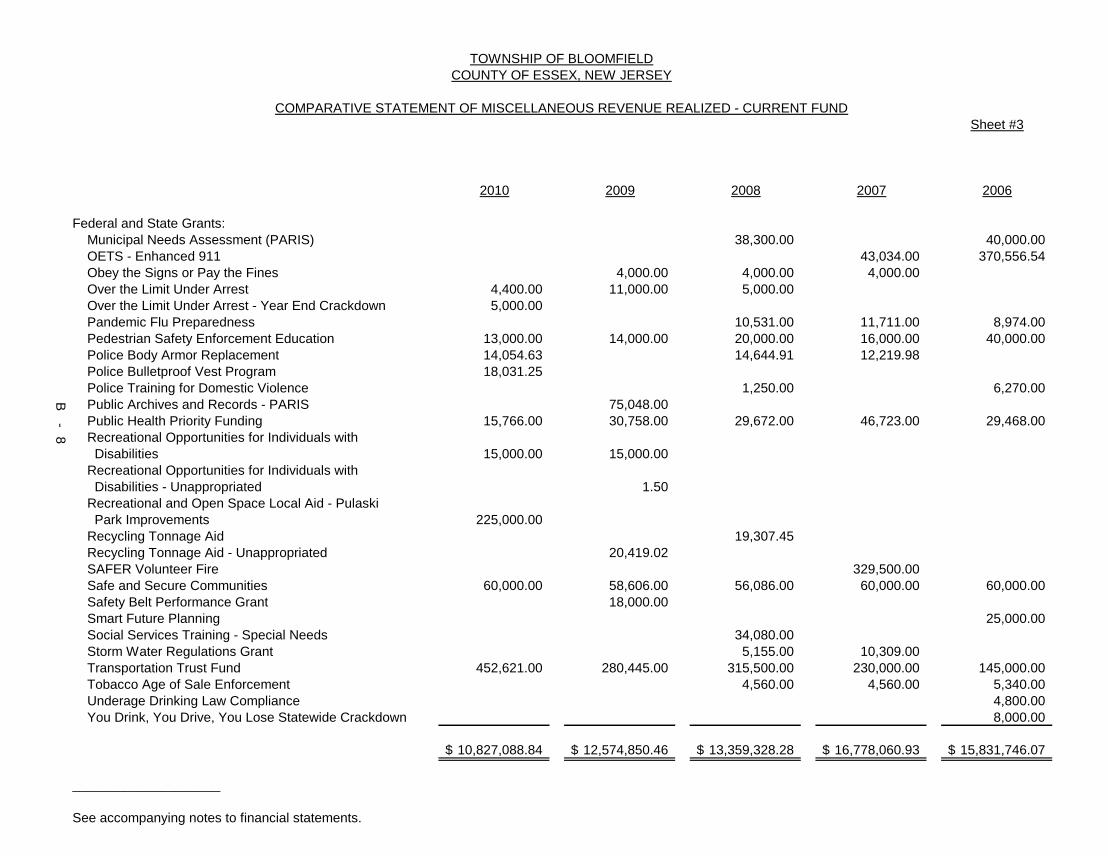

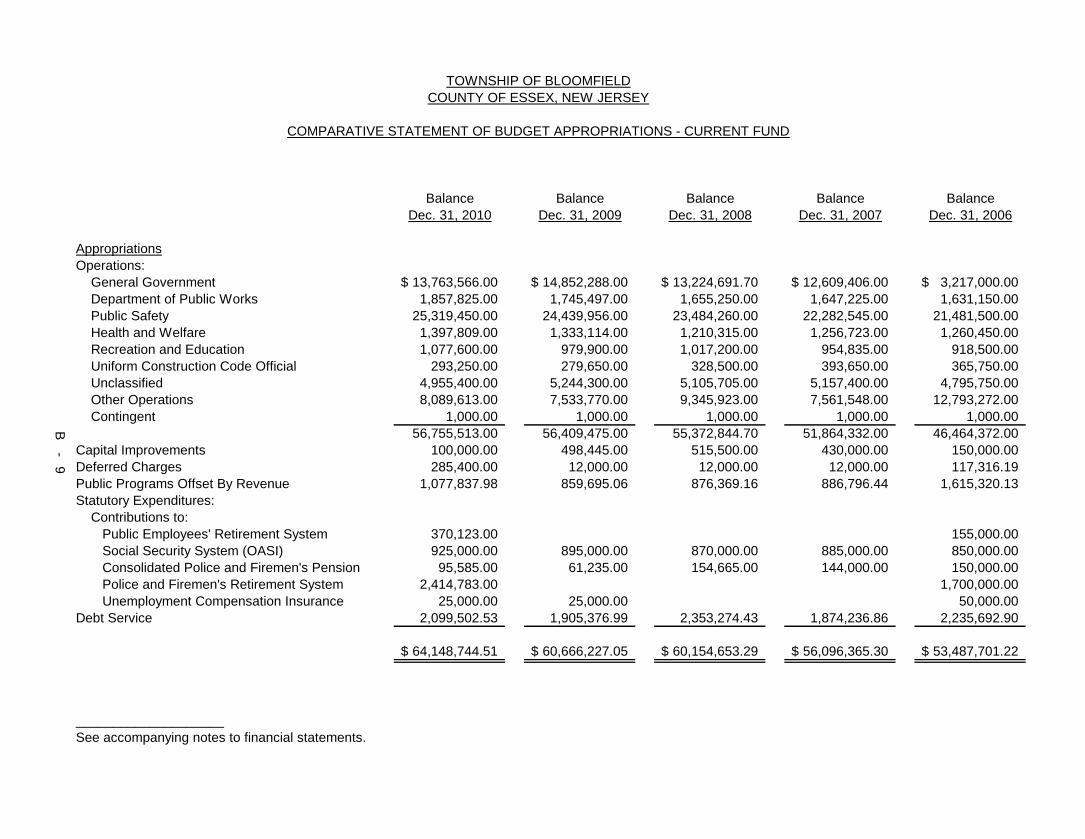

the payment of its general obligation bonds or notes. See Appendices A and B attached hereto for certain general information and selected financial information concerning the Township.

SUMMARY OF LOCAL AUTHORITIES FISCAL CONTROL LAW

The Local Authorities Fiscal Control Law, Chapter 313 of the Pamphlet Laws of 1983 of the

State, became effective on November 24, 1983. This law provides for "State review of project financing of local authorities and for State supervision over the financial operations of local authorities".

The Local Finance Board, in the Division of Local Government Services, Department of

Community Affairs, New Jersey (the "Local Finance Board"), prescribes the procedures for the adoption and execution of annual budgets, and approval must be obtained prior to a budget's adoption. Such budget shall also comply with the terms and provisions of any bond resolutions. On granting approval of a budget, the reasonableness and accuracy of revenue estimates are considered. Such revenue must be sufficient to meet all expenses, including debt service. An annual audit shall be made and completed within four months of the close of a fiscal year by a registered municipal accountant or certified public accountant licensed in the State.

A financing program must be submitted to the Local Finance Board for a hearing and review

prior to implementation. Such review generally focuses on the nature, purpose and scope of the financing, engineering or feasibility studies, terms and provisions of service contracts, bond resolutions, proposed terms and conditions of negotiated sales, and proposed or maximum debt

- 16 -

service and operational funding requirements. Bond anticipation notes or project notes may be issued and renewed pursuant to the provisions of the Local Authorities Fiscal Control Law.

A local authority may not be created unless the Local Finance Board so approves and a local

authority may not be dissolved without providing for payment of all outstanding obligations and without approval by the Local Finance Board.

The Local Finance Board issued positive findings in connection with the issuance of the

original project note by resolution dated March 10, 2004. Pursuant to N.J.S.A. 40A:5A-24, the Authority is required to seek the approval of the Local Finance Board to renew the 2011 Note because more than three years have passed since the issuance of the original note (the 2004 Note). On January 11, 2012, the Local Finance Board, by resolution adopted that date, approved the issuance of the 2012 Note and issued positive findings in connection therewith.

PLEDGE OF STATE NOT TO LIMIT POWERS OF AUTHORITY OR RIGHTS OF PROJECT NOTE HOLDERS

The Act sets forth the pledge and agreement of the State that it will not limit or alter the

rights vested by the Act in the Authority to fulfill the terms of any agreements which have been made with the holders of the Authority's obligations, until such obligations, together with the interest thereon and any premiums upon the redemption thereof, are fully met and discharged.

TAX MATTERS Federal Income Tax Interest on the Project Note is includable in gross income for federal income tax purposes. Certain Federal Tax Consequences Relating to the Project Note

The following is a summary of certain federal income tax consequences of the ownership of the Project Note as of the date hereof. Each prospective investor should consult with its own tax advisor regarding the application of federal income tax laws, as well as any state, local, foreign or other tax laws, to its particular situation. This summary is based on the Code, as well as Treasury Regulations and administrative and judicial rulings and practice. Legislative, judicial and administrative changes may occur, possibly with retroactive effect, that could alter or modify the continued validity of the statements and conclusions set forth herein. This summary is intended as a general explanatory discussion of the consequences of holding the Project Note generally and does not purport to furnish information in the level of detail or with the investor’s specific tax circumstances that would be provided by an investor’s own tax advisor. For example, it generally is addressed only to original purchasers of the Project Note that are “U.S. holders” (as defined below), deals only with the Project Note held as capital assets within the meaning of Section 1221 of the Code and does not address tax consequences to holders that may be relevant to investors subject to special rules. In addition, this summary does

- 17 -

not address alternative minimum tax issues or the indirect consequences to a holder of an equity interest in the Project Note. As used herein, a “U.S. holder” is a “U.S. person” that is a beneficial owner of a Project Note. A non-U.S. investor” is a holder (or beneficial owner) of the Project Note that is not a U.S. person. For these purposes, a “U.S. person” is a citizen or resident of the United States, a corporation or partnership created or organized in or under the laws of the United States or any political subdivision thereof (except, in the case of a partnership, to the extent otherwise provided in Treasury Regulations), an estate the income of which is subject to United States federal income taxation regardless of its source or a trust if (i) a United States court is able to exercise primary supervision over the trust’s administration and (ii) one or more United States persons have the authority to control all of the trust’s substantial decisions.

Market Discount. If a holder purchases the Project Note for an amount that is less than the principal amount of such Project Note, and such difference is not considered to be de minimis, then such discount will represent market discount that ultimately will constitute ordinary income (and not capital gain). Further, absent an election to accrue market discount currently, upon a sale or exchange of the Project Note, a portion of any gain will be ordinary income to the extent it represents the amount of any such market discount that was accrued through the date of sale. In addition, absent an election to accrue market discount currently, the portion of any interest expense incurred or continued to carry a market discount bond that does not exceed the accrued market discount for any taxable year, will be deferred. For federal income tax purposes, a portion of the amount realized on a sale attributed to the Project Note will be treated as accrued interest and thus will be taxed as ordinary income to the seller (and will not be subject to tax in the hands of the buyer).

Market Premium. A purchaser of the Project Note who purchases such Project Note at a cost greater than its then principal amount will be considered to have purchased such Project Note at a market premium. Under Section 171 of the Code, such a purchaser must amortize the amount of such market premium using constant yield principles based on the purchaser’s yield to maturity. Amortizable market premium is generally treated as an offset to interest income, and a reduction in basis under Code Section 1016(a) of the Project Note is required for amortizable bond premium that is applied to reduce interest payments. Purchasers of any Project Note who acquire such Project Note at a premium should consult with their own tax advisors with respect to the determination and treatment of amortizable premium for federal income tax purposes and with respect to state and local tax consequences of owning such Project Note.

Sale or Redemption of the Project Note. A bondowner’s tax basis for the Project Note is the price such owner pays for the Project Note plus amounts of any original issue discount included in income, reduced on account of any payments received (other than “qualified periodic interest” payments) and any amortized premium. Gain or loss recognized on a sale, exchange or redemption of the Project Note, measured by the difference between the amount realized and the Project Note basis as so adjusted, will generally give rise to capital gain or loss if the Project Note is held as a capital asset.

- 18 -

Possible Recognition of Taxable Gain or Loss upon Defeasance of the Project Note.

Defeasance of any Project Note may result in a deemed exchange under Section 1001 of the Code, in which event the holder of such Project Note will recognize taxable gain or loss in an amount equal to the difference between the amount realized from the deemed exchange (less any accrued qualified stated interest which will be taxable as such) and the holder’s adjusted basis in such Project Note.

Backup Withholding. A bondowner may, under certain circumstances, be subject to “backup withholding” at the rate of 31% with respect to interest or original issue discount on the Project Note. This withholding generally applies if the owner of the Project Note (a) fails to furnish the Trustee or other payor with its taxpayer identification number; (b) furnishes the Trustee or other payor an incorrect taxpayer identification number; (c) fails to report properly interest, dividends or other “reportable payments” as defined in the Code; or (d) under certain circumstances, fails to provide the Trustee or other payor with a certified statement, signed under penalty of perjury, that the taxpayer identification number provided is its correct number and that the holder is not subject to backup withholding. Backup withholding will not apply, however, with respect to certain payments made to bondowners, including payments to certain exempt recipients (such as certain exempt organizations) and to certain Nonresidents (as defined below). Owners of the Project Note should consult their tax advisors as to their qualification for exemption from backup withholding and the procedure for obtaining the exemption. The amount of “reportable payments” for each calendar year and the amount of tax withheld, if any, with respect to payments on the Project Note will be reported to the bondowners and to the Internal Revenue Service.

Foreign Bondowners. Under the Code, interest and original issue discount income with respect to the Project Note held by nonresident alien individuals, foreign corporations or other non-United States persons (‘Nonresidents”) generally will not be subject to the 28% United States withholding tax if the Trustee (or other person who would otherwise be required to withhold tax from such payments) is provided with an appropriate statement that the beneficial owner of the Project Note is a Nonresident. The withholding tax may be reduced or eliminated by an applicable tax treaty, if any. Notwithstanding the foregoing, if any such payments are effectively connected with a United States trade or business conducted by a Nonresident bondowner, they will be subject to regular United States income tax, but will ordinarily be exempt from United States withholding tax.

ERISA. The Employees Retirement Income Security Act of 1974, as amended (“ERISA”), and the Code generally prohibit certain transactions between a qualified employee benefit plan under ERISA (an “ERISA Plan”) and persons who, with respect to that plan, are fiduciaries or other “parties in interest” within the meaning of ERISA or “disqualified persons” within the meaning of the Code. All fiduciaries of ERISA Plans, in consultation with their advisors, should carefully consider the impact of ERISA and the Code on an investment in any Project Note.

- 19 -

In all events, all investors should consult their own tax advisors in determining the federal, state, local and other tax consequences to them of the purchase, ownership and disposition of the Project Note.

IRS Circular 230 Disclosure. To ensure compliance with requirements imposed by the IRS, any purchaser of the Project Note is hereby informed that (i) any federal tax advice contained in this offering material (including any attachments) is not intended or written by Bond Counsel to be used, and that it cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer under the Code; (ii) such advice is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by the written advice; and (iii) the taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

New Jersey Gross Income Tax

In the opinion of McManimon & Scotland, L.L.C., Bond Counsel, to be delivered simultaneously with the delivery of the Project Note, under existing law, interest on the Project Note and any gain on the sale thereof are not includable in gross income under the existing New Jersey Gross Income Tax Act.

ALL POTENTIAL PURCHASERS OF THE PROJECT NOTE SHOULD CONSULT WITH THEIR TAX ADVISORS IN ORDER TO UNDERSTAND THE IMPLICATIONS OF THE CODE.

LITIGATION The Authority

In the opinion of the Authority’s General Counsel, McManimon & Scotland, L.L.C., Newark New Jersey, there is no controversy or litigation of any nature now pending or threatened, restraining or enjoining the issuance, sale, execution or delivery of the Project Note, or in any way questioning or affecting the validity of the Project Note or any proceedings of the Authority taken with respect to the issuance or sale thereof. There is no controversy or litigation of any nature now pending or threatened restraining or enjoining the security pledged for the Project Note or the pledge or application of any moneys or security provided for the payment of the Project Note. In August 2011, Bloomfield Joint Venture, a Partnership, Farrand Street Associates, a Partnership, Bloomfield Daval Corp., Bloomfield Transit Village I, LLC, Bloomfield Transit Village II, LLC and Bloomfield Transit Village III, LLC (collectively, the “BJV Plaintiffs”), the owners of certain properties in the area around Block 228 filed a Complaint in Lieu of Prerogative Writs (the “BJV Complaint”) in the Superior Court of New Jersey, Law Division, against the Authority, the Redeveloper and the Planning Board. In the BJV Complaint, the BJV Plaintiffs claim that the Planning Board acted arbitrarily, capriciously and unreasonably in granting the Redevelopment Project Approvals. Specifically, the BJV Plaintiffs allege that the application submitted to the Planning Board improperly included Plaintiff Bloomfield Daval Corp.’s property within the site plan

- 20 -

without its consent, and that the development proposal submitted by the Redeveloper and the Authority failed to provide adequate parking, an adequate traffic plan, and adequate on and off-site loading areas. A trial in this matter is scheduled for March 9, 2012, and the Authority, the Redeveloper and the Planning Board are vigorously defending this matter. The Township To the knowledge of Brian J. Aloia, Esq., Bloomfield, New Jersey (the “Township Attorney”), there is no litigation of any nature now pending or threatened, restraining or enjoining the sale, issuance, execution or delivery of the Project Note, or the levy or collection of any taxes to pay the principal of or the interest on the Project Note, or in any manner questioning the authority or proceedings for the issuance of the Project Note or for the levy or collection of taxes, or contesting the corporate existence or the boundaries of the Township or the title of any of the present officers. Moreover, to the knowledge of the Township Attorney, no litigation is presently pending or threatened that, in the opinion of the Township Attorney, would have a material adverse impact on the financial condition of the Township if adversely decided. A certificate to such effect will be executed by the Township Attorney and delivered to the Underwriter at the closing.

SECONDARY MARKET DISCLOSURE

The Authority

The Authority, pursuant to the requirements of Securities and Exchange Commission (the “SEC”) Rule 15c2-12 (the “Rule”) related to continuing secondary market disclosure, has undertaken to provide for the benefit of the holders of the Project Note and the beneficial owners thereof for as long as the Project Note remain outstanding (unless the Project Note has been wholly defeased):

(a) Annually to the Municipal Securities Rulemaking Board’s Electronic Municipal Market

Access (“EMMA”) system or such other repository designated by the SEC to be an authorized repository for filing secondary market disclosure information, if any, financial information or operating data that is customarily prepared and publicly available consisting of the audited financial statements (or unaudited financial statements if audited financial statements are not then available by the date of filing) of the Authority and the Authority’s most current adopted budget. The audited financial information will be prepared in accordance with accounting principles generally accepted in the United States of America;

(b) As soon as practicable and not in excess of ten (10) business days after the occurrence

of any of the following events, notice to EMMA of the occurrence of any such event: (1) Principal or interest payment delinquencies; (2) Non-payment related defaults, if material; (3) Unscheduled draws on debt service reserves reflecting financial difficulties;

- 21 -

(4) Unscheduled draws on credit enhancements reflecting financial difficulties; (5) Substitution of credit or liquidity providers, or their failure to perform; (6) Adverse tax opinions by the Internal Revenue Service of proposed or final determinations of taxability, Notices of Proposed Issue (IRS Form 5701-TEB) or other material notices or determinations with respect to the tax status of the security, or other material events affecting the tax status of the security;

(7) Modifications to the rights of security holders, if material; (8) Bond calls, if material, and tender offers; (9) Defeasances;

(10) Release, substitution or sale of property securing repayment of the securities, if material; (11) Rating changes; (12) Bankruptcy, insolvency, receivership or similar event of the obligated person; (13) the consummation of a merger, consolidation, or acquisition involving an obligated person or the sale of all or substantially all of the assets of the obligated person, other than in the ordinary course of business, the entry into a definitive agreement to undertake such an action or the termination of a definitive agreement relating to any such actions, other than pursuant to its terms, if material; and (14) Appointment of a successor or additional trustee or the change of name of a trustee, if material. For the purposes of the event identified in subparagraph (12) above, the event is considered