Embed Size (px)

Citation preview

Presented by: Don Washkewicz Chairman, CEO & President

Parker Hannifin CorporationAnnual Shareholders Meeting

October 22, 2008

2

Forward-Looking Statements:Forward-looking statements contained in this and other written and oral reports are made based on known events and circumstances at the time of release, and as such, are subject in the future to unforeseen uncertainties and risks. All statements regarding future performance, earnings projections, events or developments are forward-looking statements. It is possible that the future performance and earnings projections of the company and individual segments may differ materially from current expectations, depending on economic conditions within its mobile, industrial and aerospace markets, and the company's ability to maintain and achieve anticipated benefits associated with announced realignment activities, strategic initiatives to improve operating margins, and growth, innovation and global diversification initiatives. A change in economic conditions in individual markets may have a particularly volatile effect on segment results. Among the other factors which may affect future performance are: changes in business relationships with and purchases by or from major customers or suppliers, including delays or cancellations in shipments or significant changes in financial condition; uncertainties surrounding timing, successful completion or integration of acquisitions; threats associated with and efforts to combat terrorism; uncertainties surrounding the ultimate resolution of outstanding litigation; competitive market conditions and resulting effects on sales and pricing; increases in raw material costs that cannot be recovered in product pricing; the company’s ability to manage costs related to employee retirement and health care benefits and insurance; and global economic factors, including manufacturing activity, air travel trends, currency exchange rates, difficulties entering new markets and general economic conditions such as inflation, interest rates and credit availability. The company makes these statements as of the date of this disclosure, and undertakes no obligation to update them.

3

FY2008 Review

Win Strategy Update

1st Quarter Results – FY2009

Outlook for FY2009

Presentation Agenda

4

FY2008 Results

5

Another Another OutstandingOutstanding

Year!Year!

FY08 Results

6

5th Record Yearin a row !

FY08 Results

7

$12 Billion +

FY08 Record Results - - -

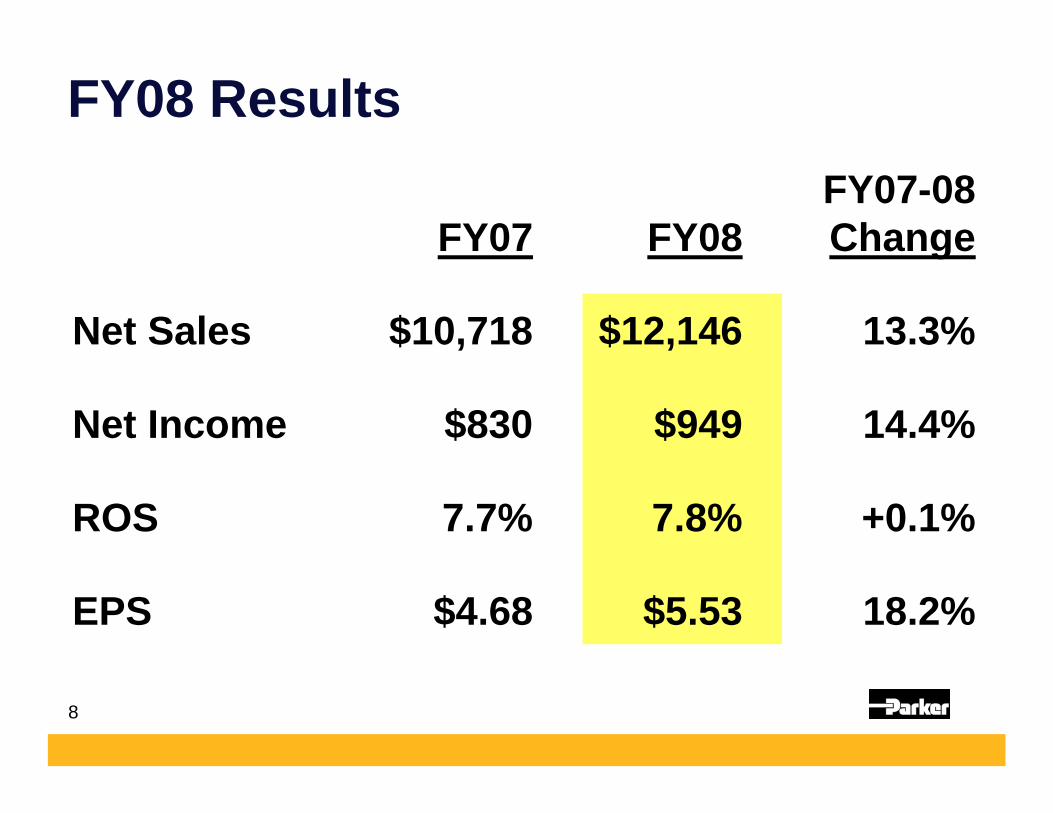

8

FY07-08FY07 FY08 Change

Net Sales $10,718 $12,146 13.3%

Net Income $830 $949 14.4%

ROS 7.7% 7.8% +0.1%

EPS $4.68 $5.53 18.2%

FY08 Results

9

2008 Revenue Growth

2008 Revenue Growth

$10,718

$12,146$511

$373

$544

$10,000

$10,500

$11,000

$11,500

$12,000

$12,500

FY07 Organic StrategicAcquisitions

Currency FY08

$MM

+5%+3%

+5% +13%

10

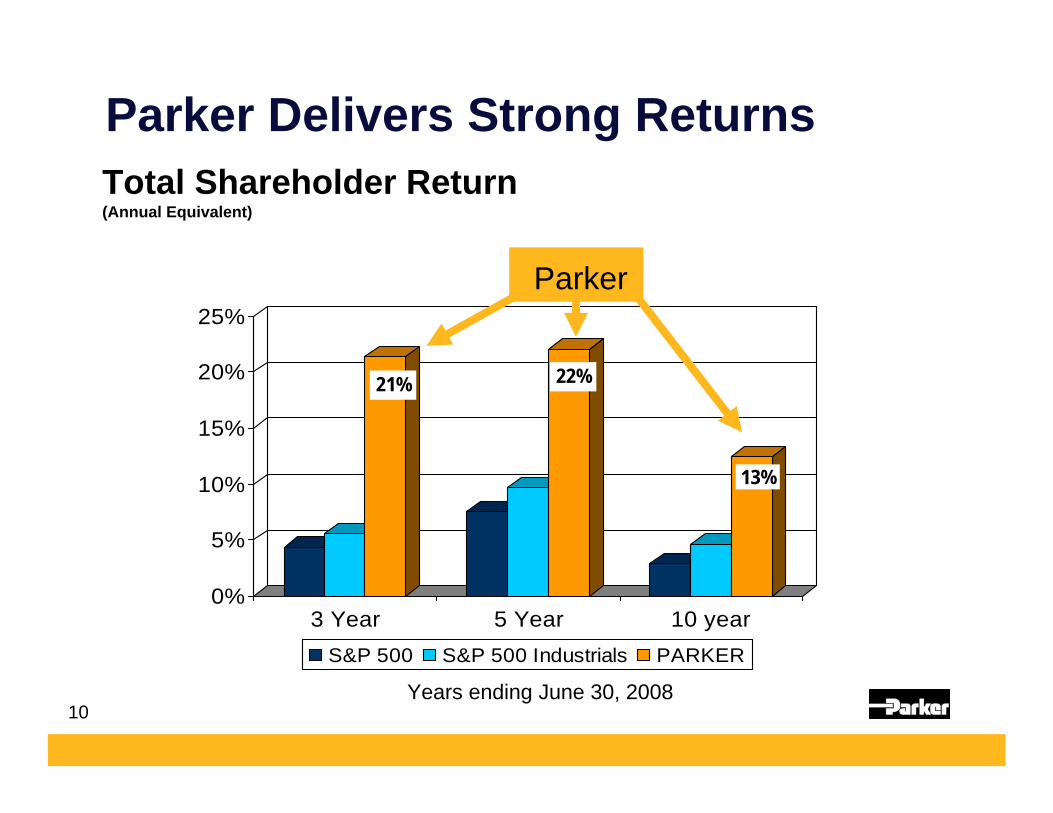

Total Shareholder Return(Annual Equivalent)

Parker Delivers Strong Returns

0%

5%

10%

15%

20%

25%

3 Year 5 Year 10 yearS&P 500 S&P 500 Industrials PARKER

21% 22%

13%

Parker

Years ending June 30, 2008

11

*Among the top 5 longest-running dividendincrease records in the S&P 500 index.

$.00

$.10

$.20

$.30

$.40

$.50

$.60

$.70

$.80

$.90

$1.00

$1.10

57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09

97% Increase in Four Years

52 Consecutive Years of Increased Dividends

12

Records Achieved in FY08

FY08 Results

13

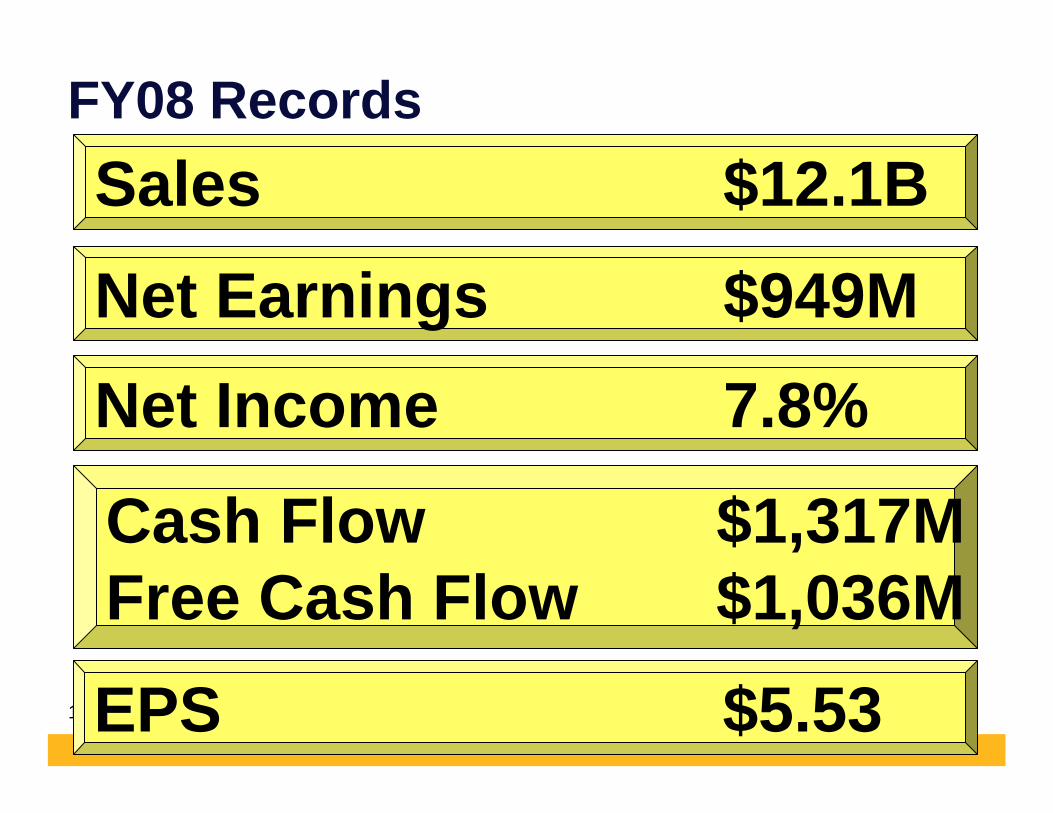

FY08 RecordsSales $12.1B

Net Earnings $949MNet Income 7.8%

Cash Flow $1,317MFree Cash Flow $1,036M

EPS $5.53

14

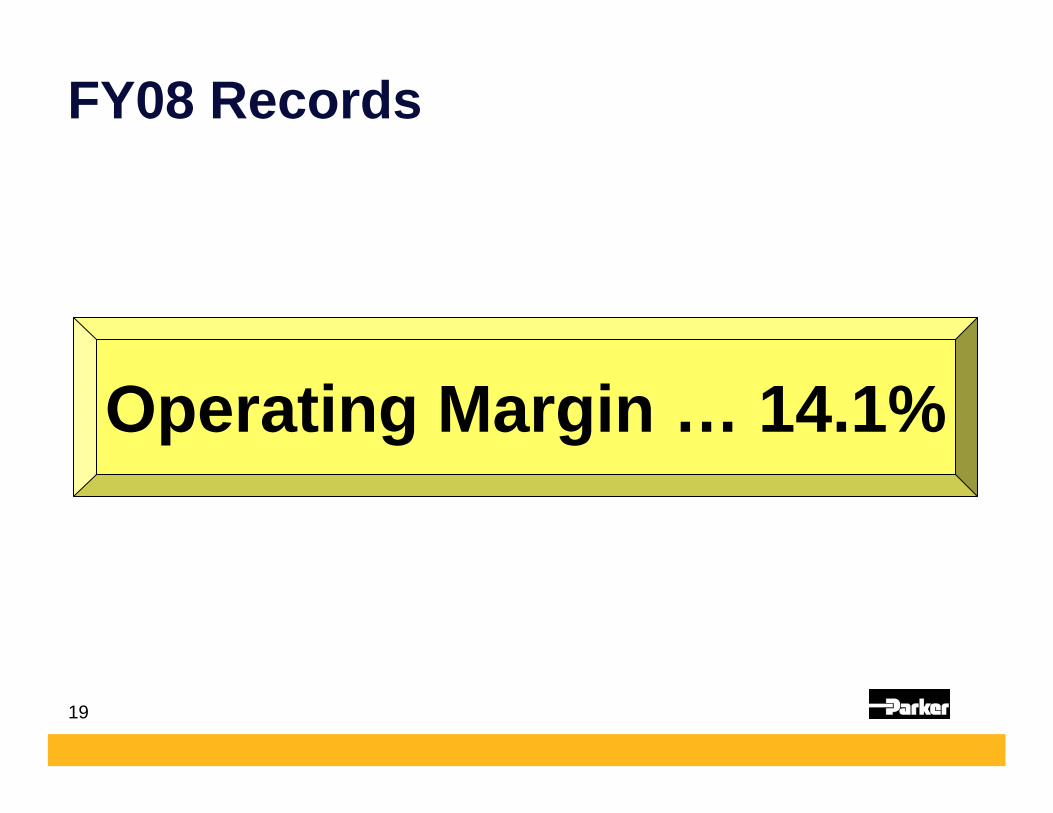

FY08 Records

Operating Margin 14.1%

Ind’l Euro Oper. Margin $15.6%

Productivity $204K

Ind’l Operating Margin 15.1%

Ind’l Int’l Oper. Margin 15.8%

15

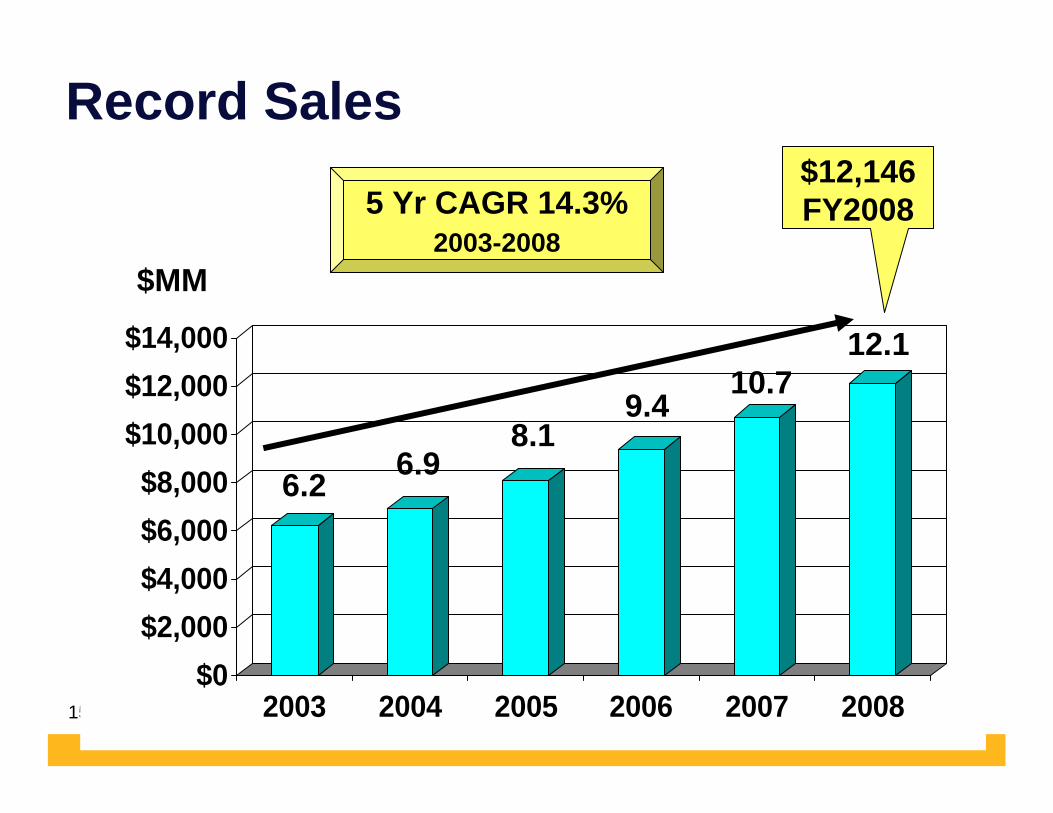

Record Sales

$0$2,000$4,000$6,000$8,000

$10,000$12,000$14,000

2003 2004 2005 2006 2007 2008

5 Yr CAGR 14.3%2003-2008

$12,146FY2008

6.2 6.98.1

$MM

9.410.7

12.1

16

FY08 Long Term Growth

35 Year CAGR Sales = 10.9%

17

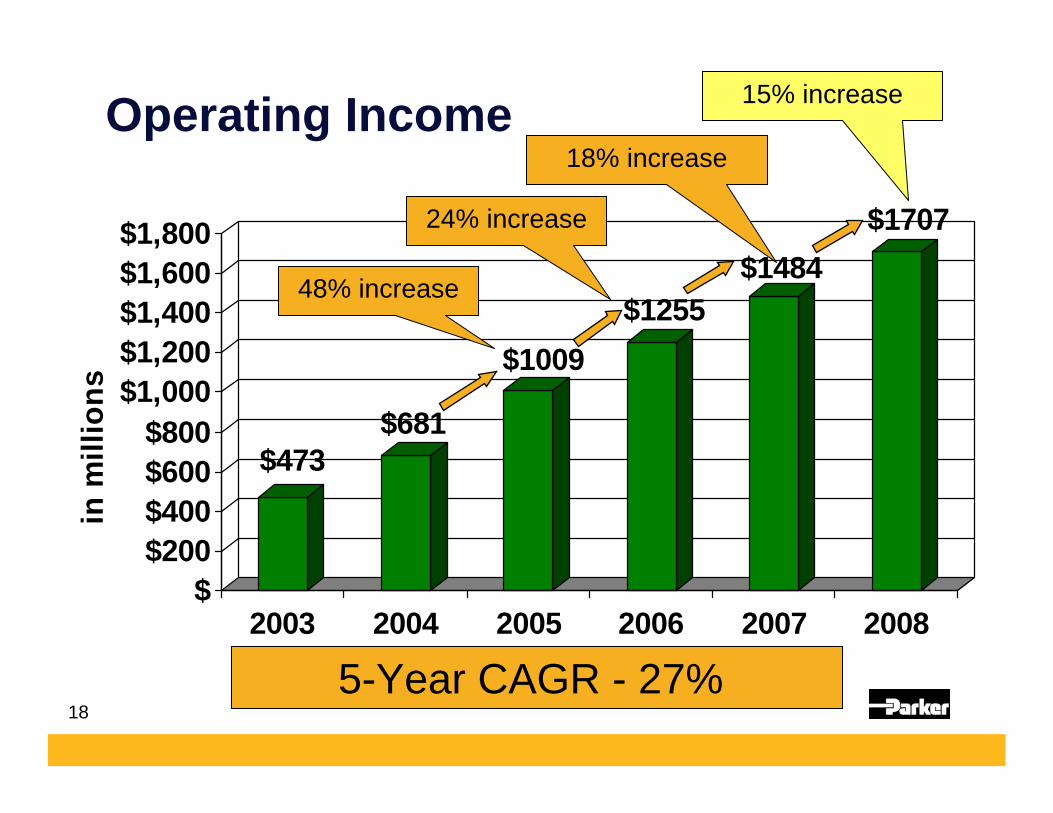

FY08 Records

Operating Income

18

Operating Income

$473$681

$1009$1255

$1484$1707

$$200$400$600$800

$1,000$1,200$1,400$1,600$1,800

in m

illio

ns

2003 2004 2005 2006 2007 2008Fiscal Year

24% increase

18% increase

48% increase

5-Year CAGR - 27%

15% increase

19

FY08 Records

Operating Margin … 14.1%

20

Operating Margin Trend

7.3 7.6

9.9

12.513.4 13.8 14.1

7

9

11

13

15

%

2002 2003 2004 2005 2006 2007 2008

Record

Goal 15%

21

FY08 Records

Cash Flow

22

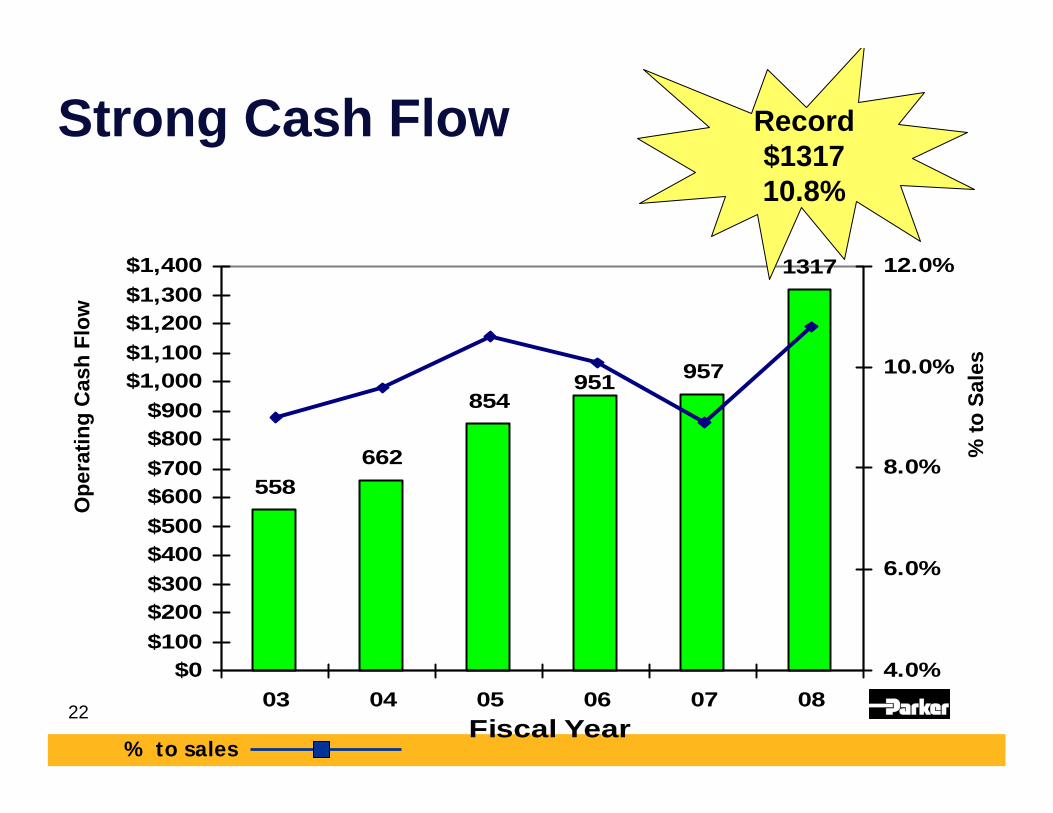

Strong Cash Flow

558662

854957

1317

951

$0$100$200$300$400$500$600$700$800$900

$1,000$1,100$1,200$1,300$1,400

03 04 05 06 07 08Fiscal Year

4.0%

6.0%

8.0%

10.0%

12.0%

% to sales

Ope

ratin

g C

ash

Flow

% to

Sal

es

Record$131710.8%

23

FY08 Records

EPS +18%

24

EPS

$0.75 $1.08$1.86

$2.95 $3.52$4.68

$5.53

0.001.002.003.004.005.006.007.008.00

2002 2003 2004 2005 2006 2007 2008Fiscal Year

$5.53+18%$/Share

40% - 6 Year CAGR

25

Other FY08Accomplishments

26

FY08 Acquisitions

10 Acquisitions$546M

27

FY08 Accomplishments

Strong Balance Sheet

28

Maintained Strong Balance Sheet

Q1 Q2 Q3 Q4

27.2% 29.7% 26.1% 28.3%

2008 Debt to Total Cap

Target 37% Max.

29

FY08 Accomplishments

Entire Company executing Winovation

30

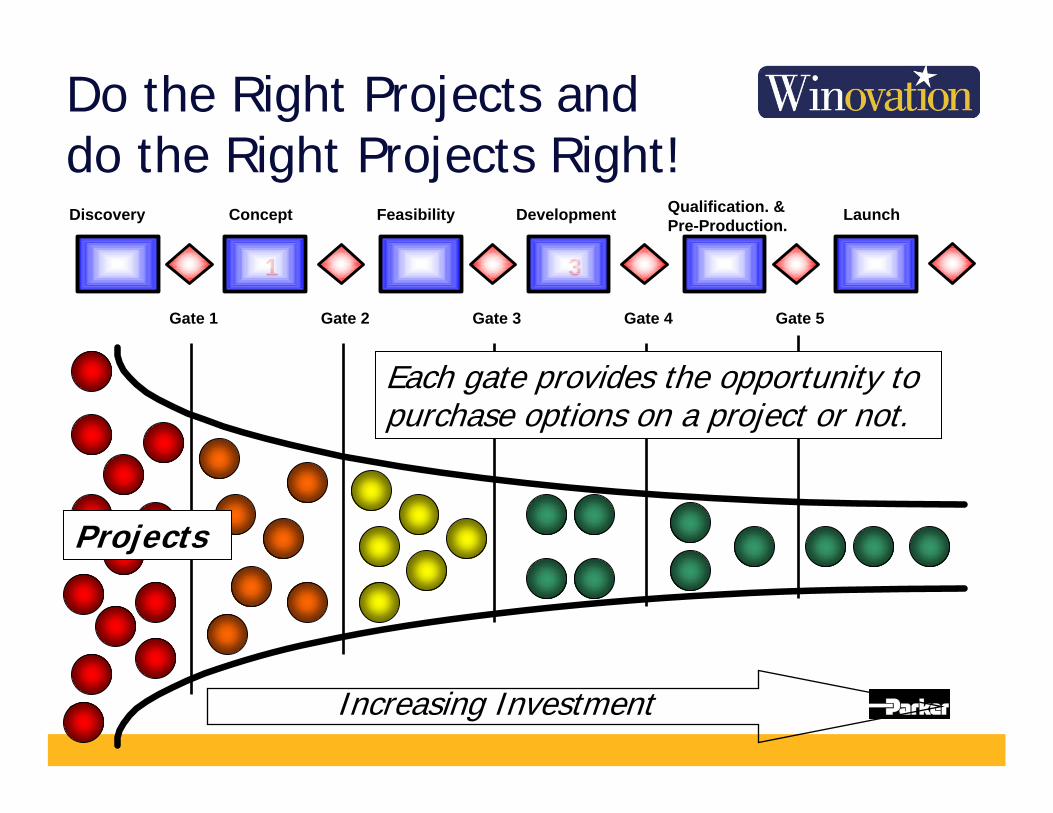

Do the Right Projects and do the Right Projects Right!

1 3

Gate 1 Gate 2 Gate 3 Gate 4 Gate 5

Concept Development LaunchFeasibilityDiscovery Qualification. & Pre-Production.

Increasing Investment

Each gate provides the opportunity to purchase options on a project or not.

Projects

31

Uniquely Positioned to Address Global Challenges

Energy

Water

Disease

Education

Democracy

PopulationPoverty

Food

Environment

Terrorism/War

32

Uniquely Positioned to Address Global Challenges

Energy

Water

Disease

Education

Democracy

PopulationPoverty

Food

Environment

Terrorism/War

33

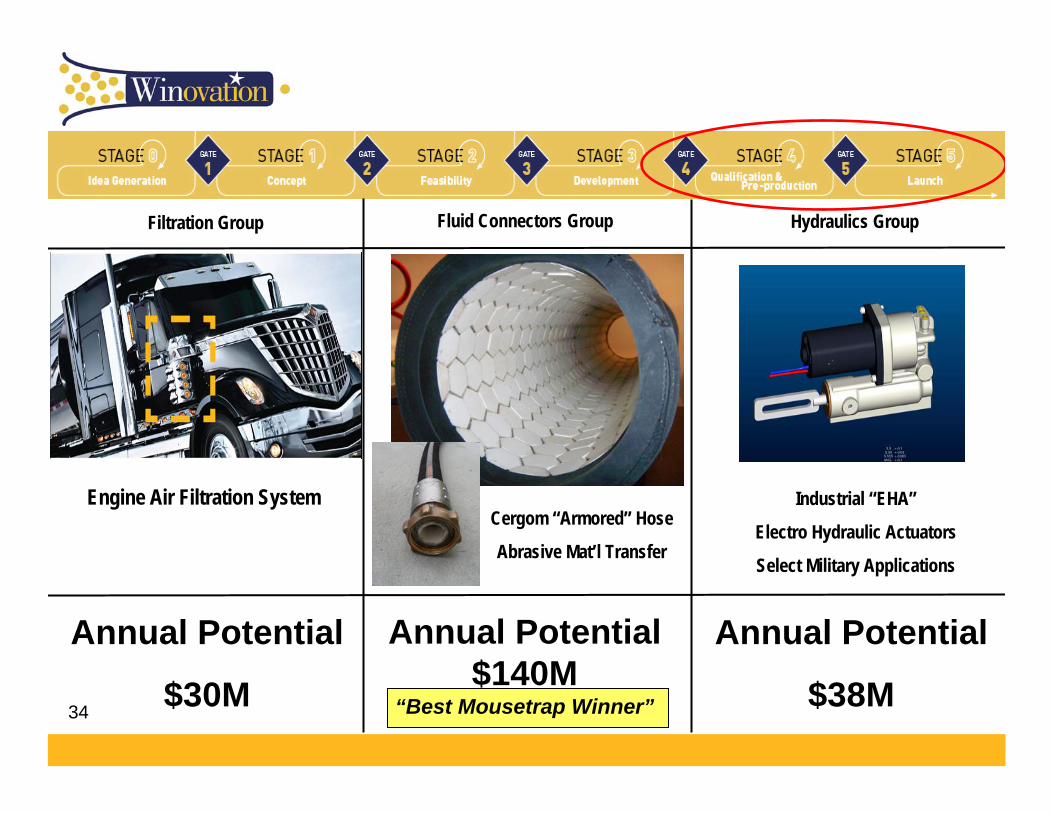

AKT “Solar Scriber” Project

Large format (“Gen8”)

PV Panel Manufacturing System

FWDBoeing 787

Hydraulic Subsystem

Aerospace Group Automation Group Climate & Industrial Controls Group

Lifetime Potential

$1.7B

Annual Potential

$45M

(S)ORIT

Electronic

Refrigerant Control Valve

Annual Potential

$120M

34

Cergom “Armored” Hose

Abrasive Mat’l Transfer

Engine Air Filtration System

Filtration Group Fluid Connectors Group Hydraulics Group

Industrial “EHA”

Electro Hydraulic Actuators

Select Military Applications

Annual Potential

$30M

Annual Potential

$38M

Annual Potential$140M

“Best Mousetrap Winner”

35

3M CFC Free

Metered Dose InhalerFugitive Emissions Valves

Engine Air Filtration System

Instrumentation Group Seal Group

Annual Potential

$5M/year

Annual Potential

$9M

36

Financial Goals

FY2008

37

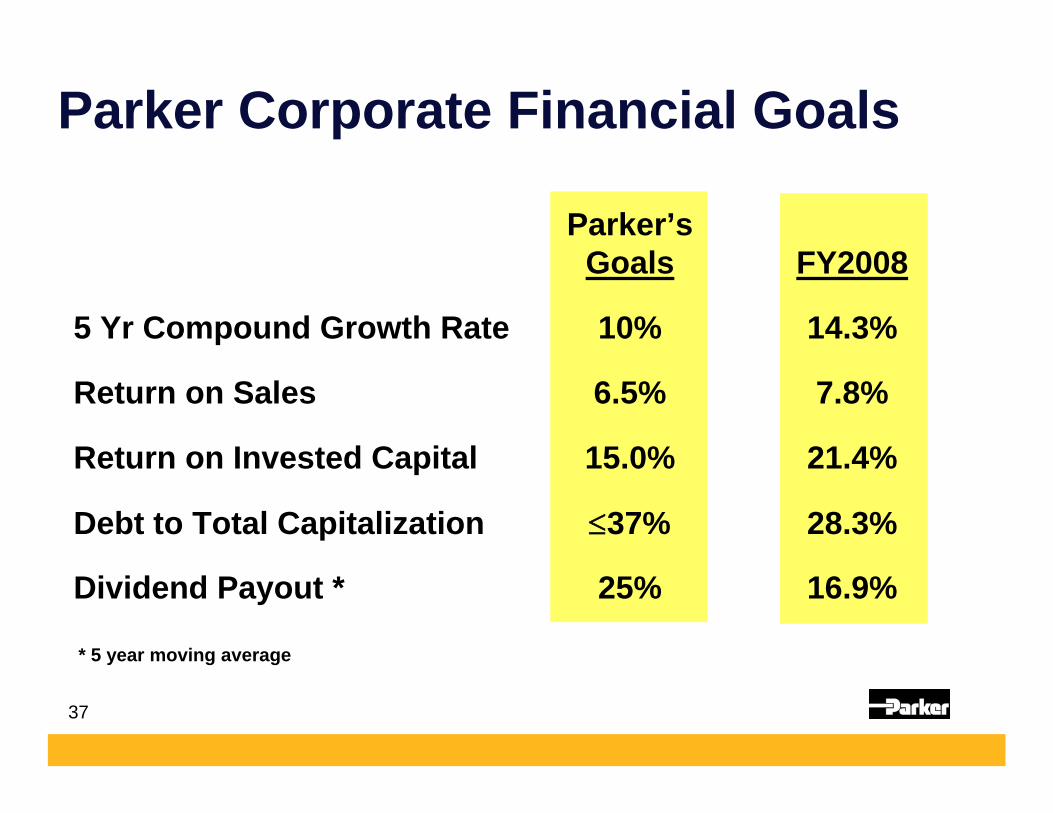

Parker Corporate Financial Goals

Parker’sGoals FY2008

5 Yr Compound Growth Rate 10% 14.3%

Return on Sales 6.5% 7.8%

Return on Invested Capital 15.0% 21.4%

Debt to Total Capitalization ≤37% 28.3%

Dividend Payout * 25% 16.9%

* 5 year moving average

38

FY2008

WIN Strategy

39

Parker’s Win Strategy

Goals #1 PremierCustomer Service

FinancialPerformance

ProfitableGrowth

STRATEGIES

Internal

Acquisitions Globalization♦Delivery of Quality Parts

on Time

♦Value Added Services

♦Best Systems-PHconnect

♦ Suppliers ⇒ STRATEGICPROCUREMENT

♦Operation ⇒ LEAN

♦ Customers ⇒ STRATEGICPRICING

♦ European Initiatives

♦

♦ Innovative Products

♦ Systems Solutions

♦ Strong Distribution

Vision The #1 Motion & Control Company

Empowered Employees

40

What is the “Win Strategy”?

Operational Excellence&

Growth

41

“It’s How We Add Value”

What is the “Win Strategy”?

42

Goals #1 PremierCustomer Service

FinancialPerformance

ProfitableGrowth

STRATEGIES

Internal

Acquisitions Globalization♦Delivery of Quality Parts

on Time

♦Value Added Services

♦Best Systems-PHconnect

♦ Suppliers ⇒ StrategicProcurement

♦Operation ⇒ Lean

♦ Customers ⇒ StrategicPricing

♦ European Initiatives

♦

♦ Innovative Products

♦ Systems Solutions

♦ Strong Distribution

Vision The #1 Motion & Control Company

Empowered Employees

Still our #1 Goal

43

Parker’s Culture

The Customer is #1

44

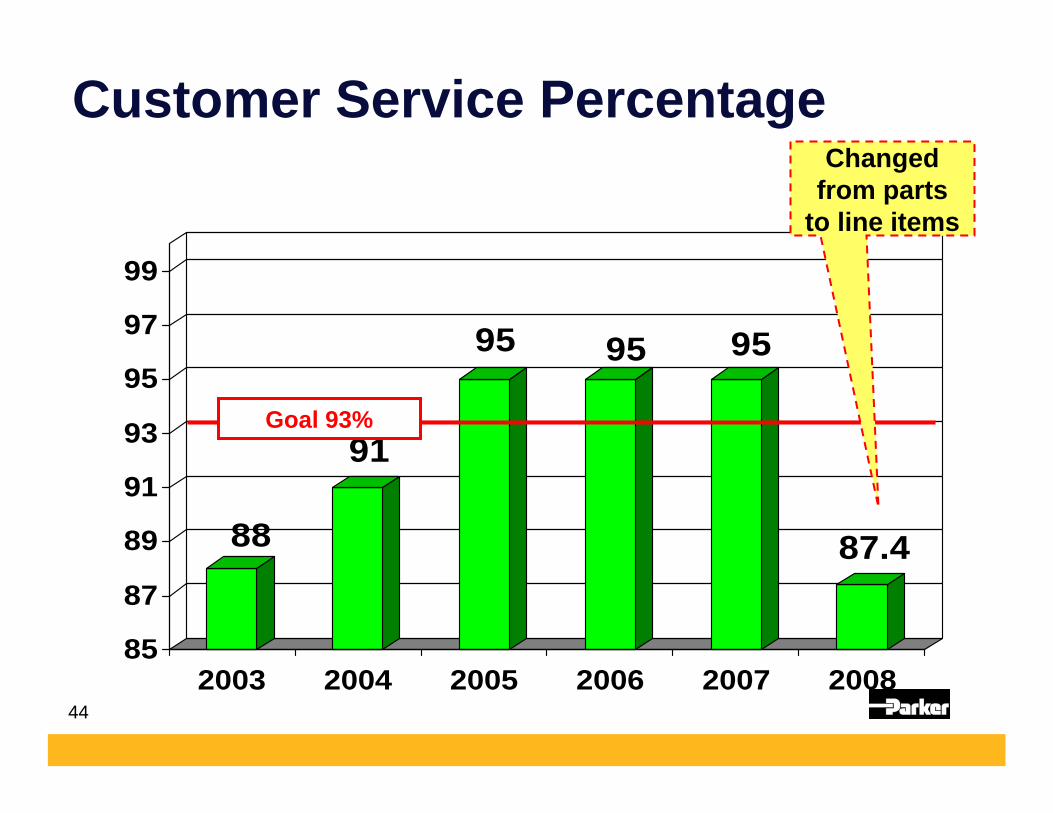

88

91

95 95 95

87.4

85

87

89

91

93

95

97

99

2003 2004 2005 2006 2007 2008

Goal 93%

Customer Service PercentageChanged

from parts to line items

45

Goals #1 PremierCustomer Service

FinancialPerformance

ProfitableGrowth

STRATEGIES

Internal

Acquisitions Globalization♦Delivery of Quality Parts

on Time

♦Value Added Services

♦Best Systems-PHconnect

♦ Suppliers ⇒ STRATEGICPROCUREMENT

♦Operation ⇒ LEAN

♦ Customers ⇒ STRATEGICPRICING

♦ European Initiatives

♦

♦ Innovative Products

♦ Systems Solutions

♦ Strong Distribution

Vision The #1 Motion & Control Company

Empowered Employees

Goal #2

Financial Performance

46

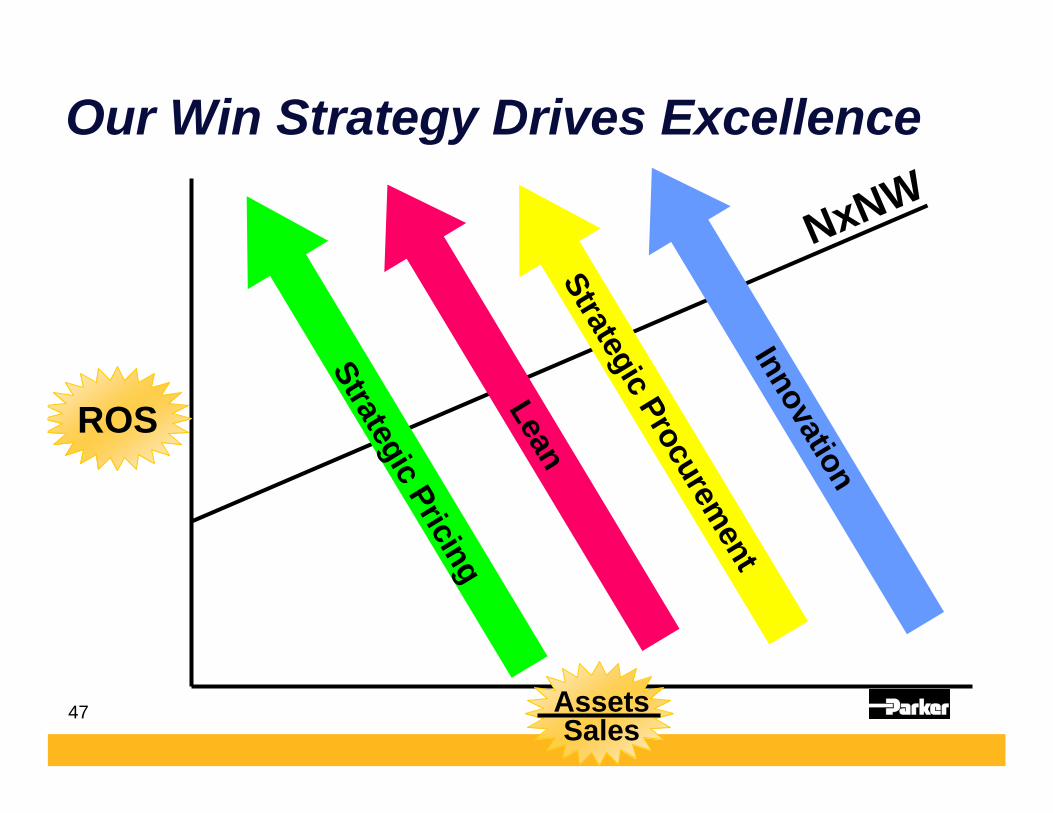

The “Win Strategy” Objective

Maximize ROIC

Returns

Invested Capital

47

Our Win Strategy Drives Excellence

NxNW

Strategic PricingLean

Strategic Procurement

ROS

InnovationInnovation

SalesAssets

48

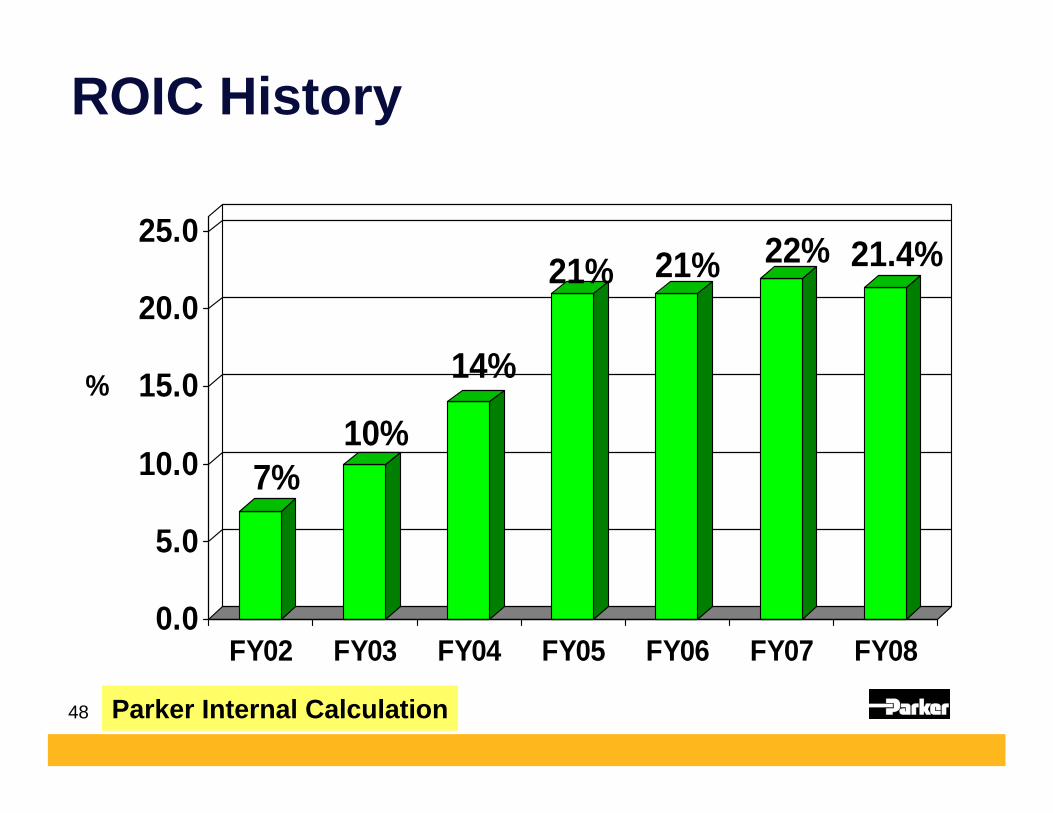

ROIC History

7%10%

14%

21% 21% 22% 21.4%

0.0

5.0

10.0

15.0

20.0

25.0

%

FY02 FY03 FY04 FY05 FY06 FY07 FY08

Parker Internal Calculation

49

12.8%13.6%

14.0%14.7%14.8%

15.5%16.0%

16.5%16.8%

17.7%17.8%17.9%18.0%

20.9%21.4%

23.1%23.9%24.0%24.3%24.5%

27.0%30.7%

31.9%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

Peer JPeer QPeer RPeer PPeer APeer MPeer H

35th PercentilePeer KPeer GPeer I

50th PercentilePeer OPeer L

PARKERPeer EPeer F

75th PercentilePeer CPeer NPeer DPeer BPeer A

Return on Invested Capital %

2008 ROIC versus Peers

21.4%

Parker

50

Lean Metrics

FY2008

51

12.3%13.0%

12.1%12.3%

12.7%13.2%

12.2%

11.8%

12.6%

12.6%13.5%

12.6%

17.7%

17.3%

18.0%

16.9%

19.1%

17.9%

17.1%

16.5%

17.1%16.2%

15.7%

14.0%14.5%

13.5%12.6%

13.4%

15.8%16.8%

15.7% 14.5%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08

Inventory % to Sales

Goal = 10¢

52

125 130 132 135

154168

174189

204

100

120

140

160

180

200

FY00 FY02 FY04 FY06 FY08

ProductivitySales/Employee

000’s

With annualized acquisition volume

Record+8%

53

European Profitability

54

Record

3.1 3.3

7.910.1

11.113.4

15.6

0

2

4

6

8

10

12

14

16

02 03 04 05 06 07 08Fiscal Year

Goal 15%

Ind’l European Operating Margin%

RO

S

55

Goal #3

Goals #1 PremierCustomer Service

FinancialPerformance

ProfitableGrowth

STRATEGIES

Internal

Acquisitions Globalization♦Delivery of Quality Parts

on Time

♦Value Added Services

♦Best Systems-PHconnect

♦ Suppliers ⇒ STRATEGICPROCUREMENT

♦Operation ⇒ LEAN

♦ Customers ⇒ STRATEGICPRICING

♦ European Initiatives

♦

♦ Innovative Products

♦ Systems Solutions

♦ Strong Distribution

Vision The #1 Motion & Control Company

Empowered Employees

Profitable Growth

56

Parker FY08 Global Growth

USA+2%

Germany+17%

Canada-0.6%

United Kingdom+4%

Italy12%

Brazil15%

Sweden+17%

France15%

South Korea+31%

China+34%

57

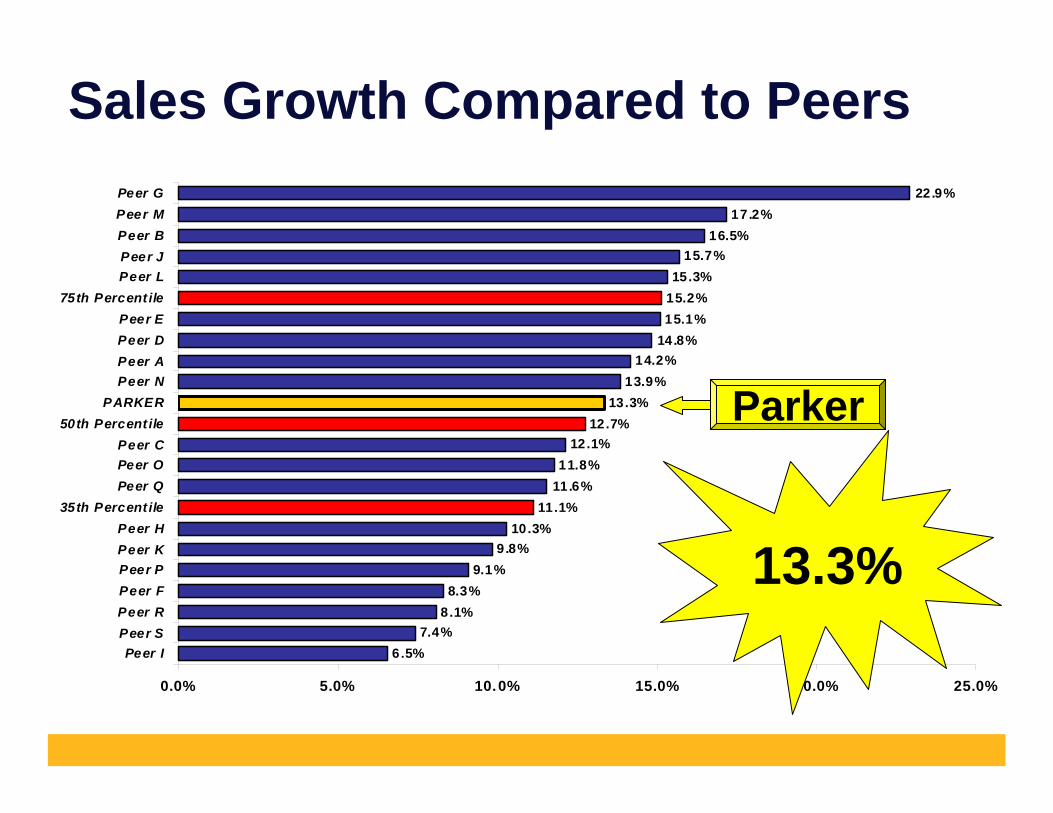

6.5%7.4%

8.1%8.3%

9.1%9.8%

10.3%11.1%

11.6%11.8%

12.1%12.7%

13.3%13.9%

14.2%14.8%15.1%15.2%15.3%

15.7%16.5%

17.2%22.9%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Peer IPeer SPeer RPeer FPeer PPeer KPeer H

35th Percent ilePeer QPeer OPeer C

50th Percent ilePARKER

Peer NPeer APeer DPeer E

75th Percent ilePeer LPeer JPeer BPeer MPeer G

Sales Growth Compared to Peers

Parker

13.3%

58

#1 Market Position

Profitable Growth

59

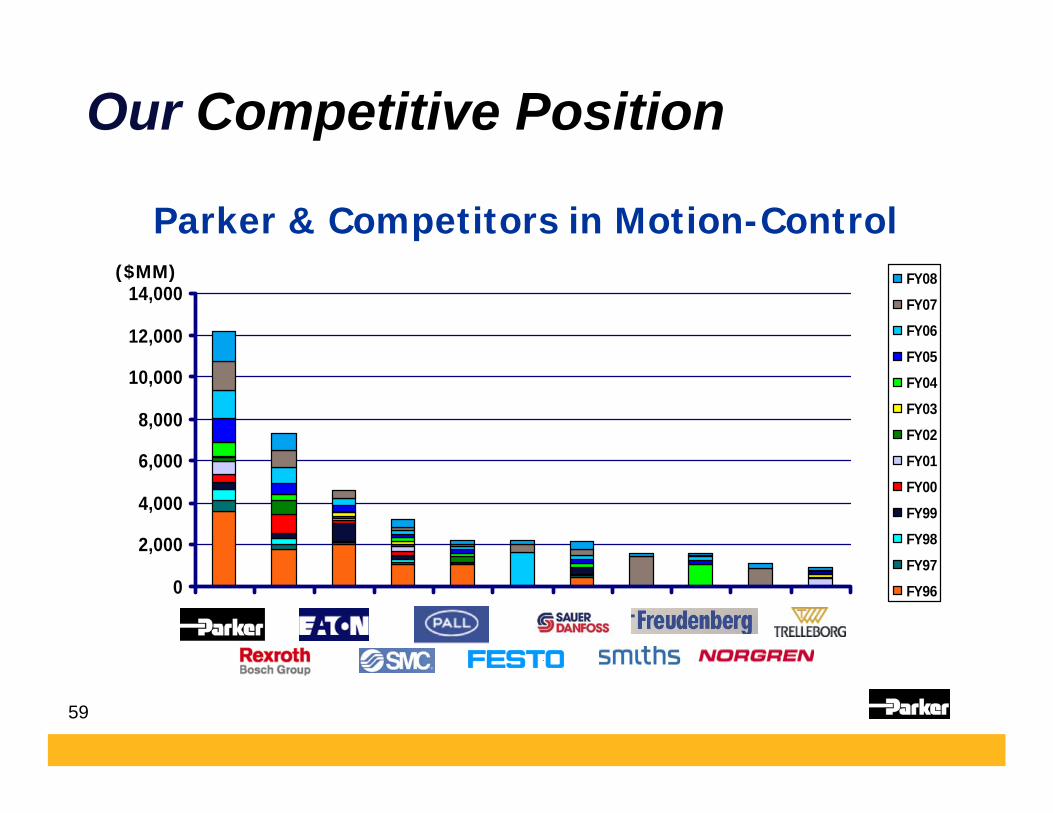

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000FY08FY07FY06FY05FY04FY03FY02FY01FY00FY99FY98FY97FY96

Parker & Competitors in Motion-Control($MM)

Our Competitive Position

60

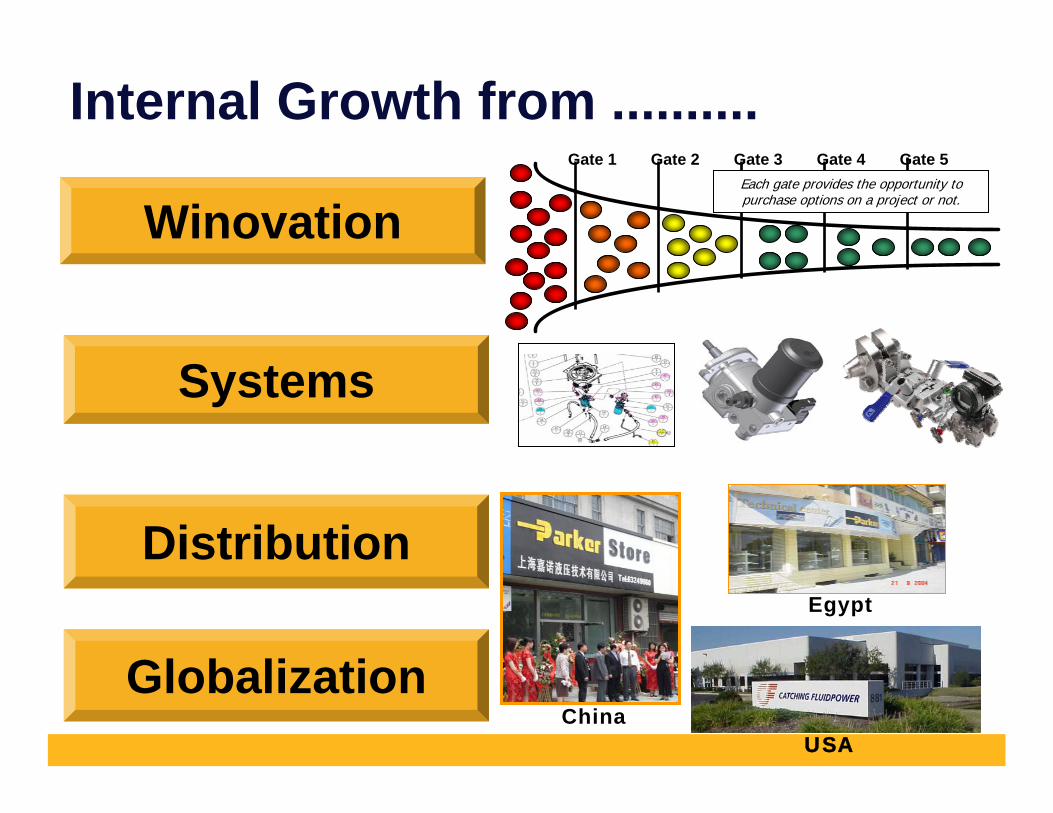

Internal Growth from ..........

Winovation

Systems

Distribution

Gate 1 Gate 2 Gate 3 Gate 4 Gate 5Each gate provides the opportunity to purchase options on a project or not.

ChinaUSA

Egypt

Globalization

61

Globalization

Growth through:

62

Global Growth

• Saudi Arabia• Morocco• Algeria

New Sales Offices FY08

63

Global GrowthEurope-Middle East-Africa

• Russia• Turkey• Dubai• Switzerland

New Sales Companies FY08

64

Asia

Global Growth

65

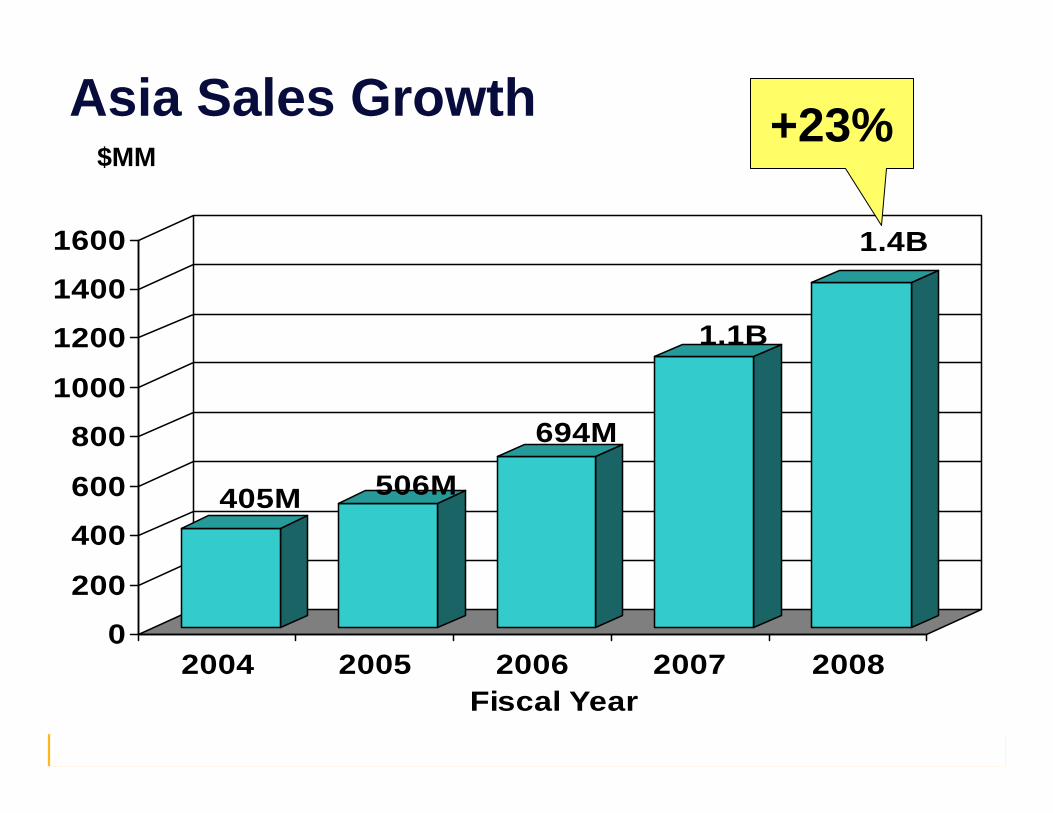

Asia Sales Growth

405M 506M

694M

1.1B

1.4B

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008Fiscal Year

$MM+23%

66

Asia Sales Growth

405M 506M

694M

1.1B

1.4B

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008Fiscal Year

$MM+23%

5 Year CAGR 29%

67

A rendering a year ago!

Global Growth$20M Hydraulic Hose PlantQingdao China

68

Global GrowthFY08 Major AccomplishmentsQingdao China Greenfield Hydraulic Hose Plant

69

Global GrowthShanghai China Filtration

• New leased factory)• 130,000 sq. ft.• Move in: Nov 08• Revenue: $15M in FY09

70

System Engineering Center

Hydraulic Manufacturing

Filtration Manufacturing

Global GrowthKorea: Jangan Factory

71

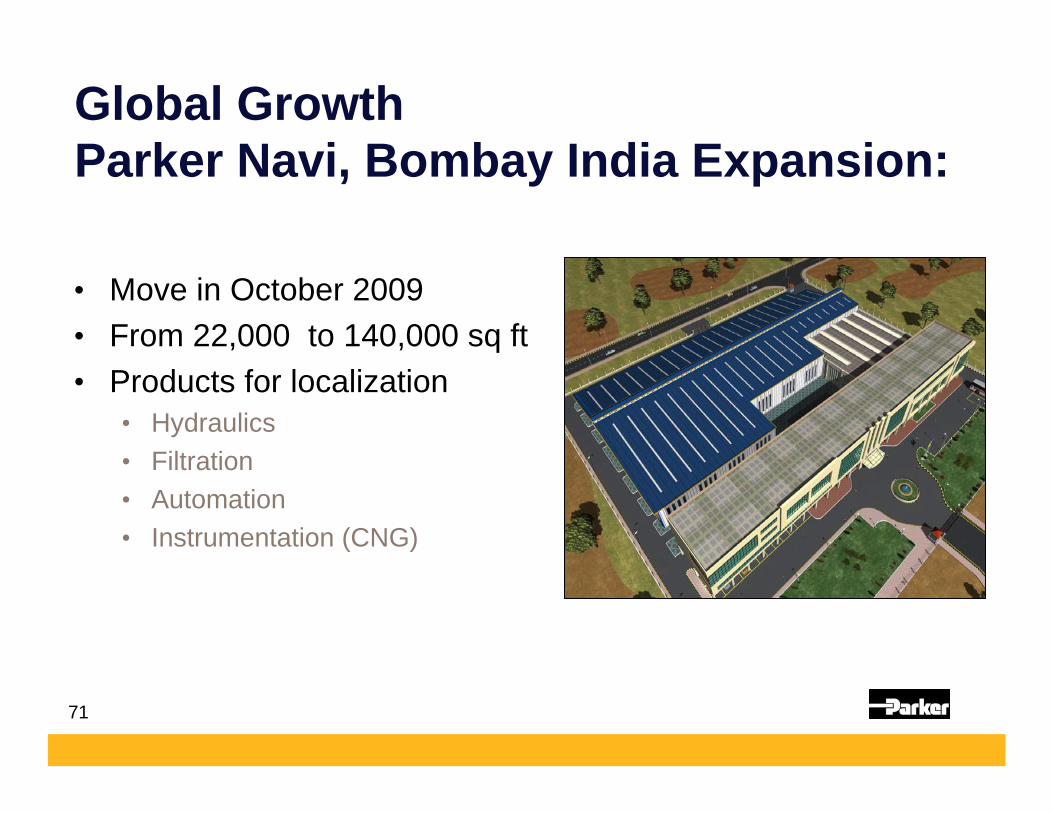

Global GrowthParker Navi, Bombay India Expansion:

• Move in October 2009• From 22,000 to 140,000 sq ft• Products for localization

• Hydraulics• Filtration• Automation• Instrumentation (CNG)

72

Global GrowthParker Rayong Thailand Filtration

Complete (Oct, 2008)

FY09 Sales: $6.6M

90,000 ft2

73

Incubator Update -Low Cost Country

Production

Growth throughStrong Distribution

Profitable Growth

74

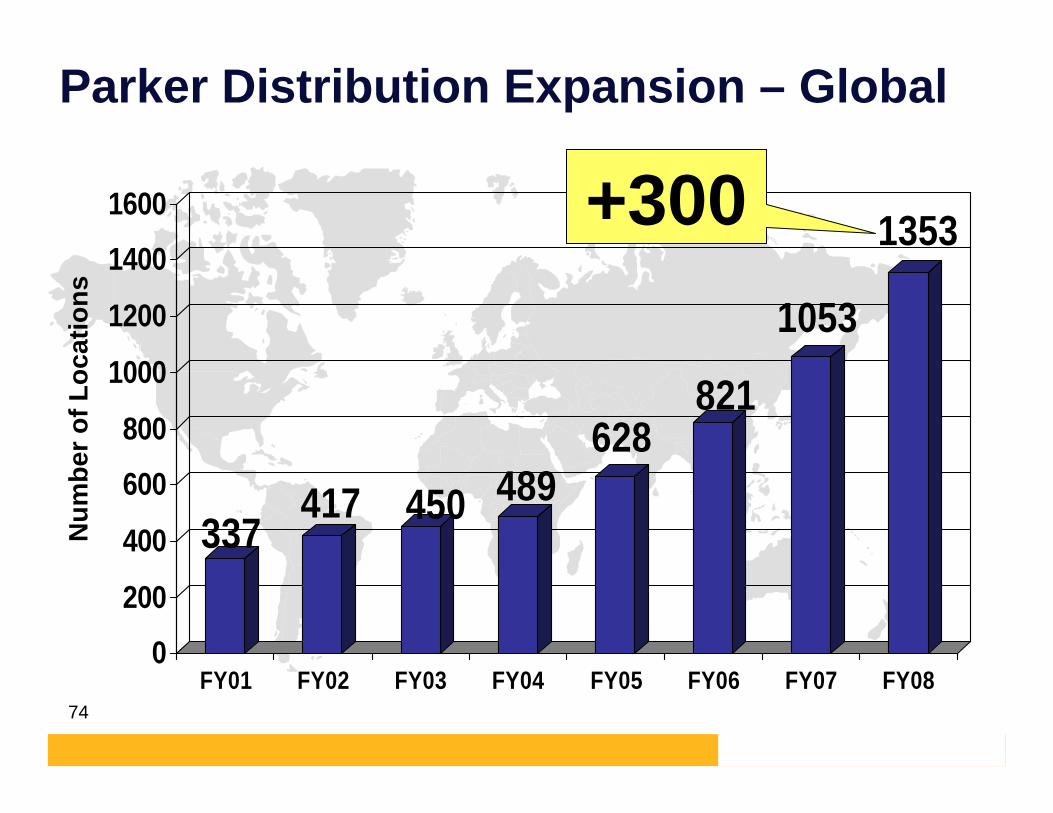

Parker Distribution Expansion – Global

8040

138

212

251

337417 450 489

628821

1053

1353

0

200

400

600

800

1000

1200

1400

1600

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08

+300

Num

ber o

f Loc

atio

ns

75

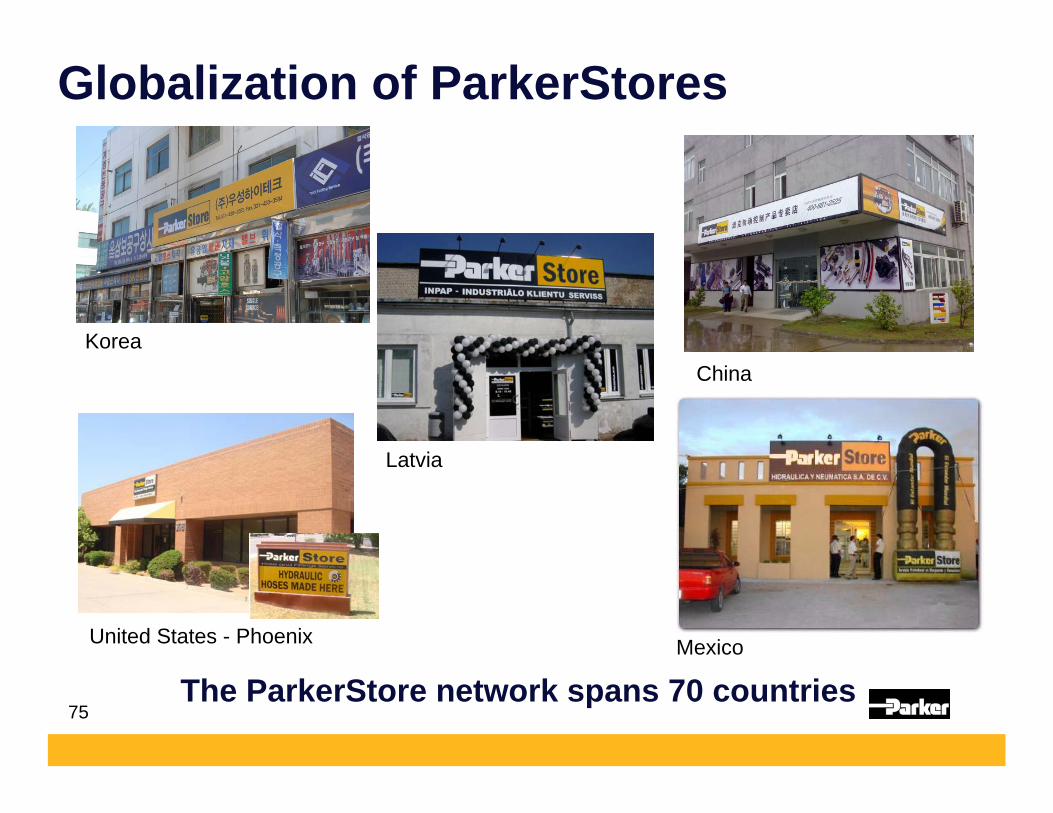

Globalization of ParkerStores

KoreaChina

United States - Phoenix

Latvia

The ParkerStore network spans 70 countriesMexico

76

FY20091st Quarter Results

Fiscal Year 2009

77

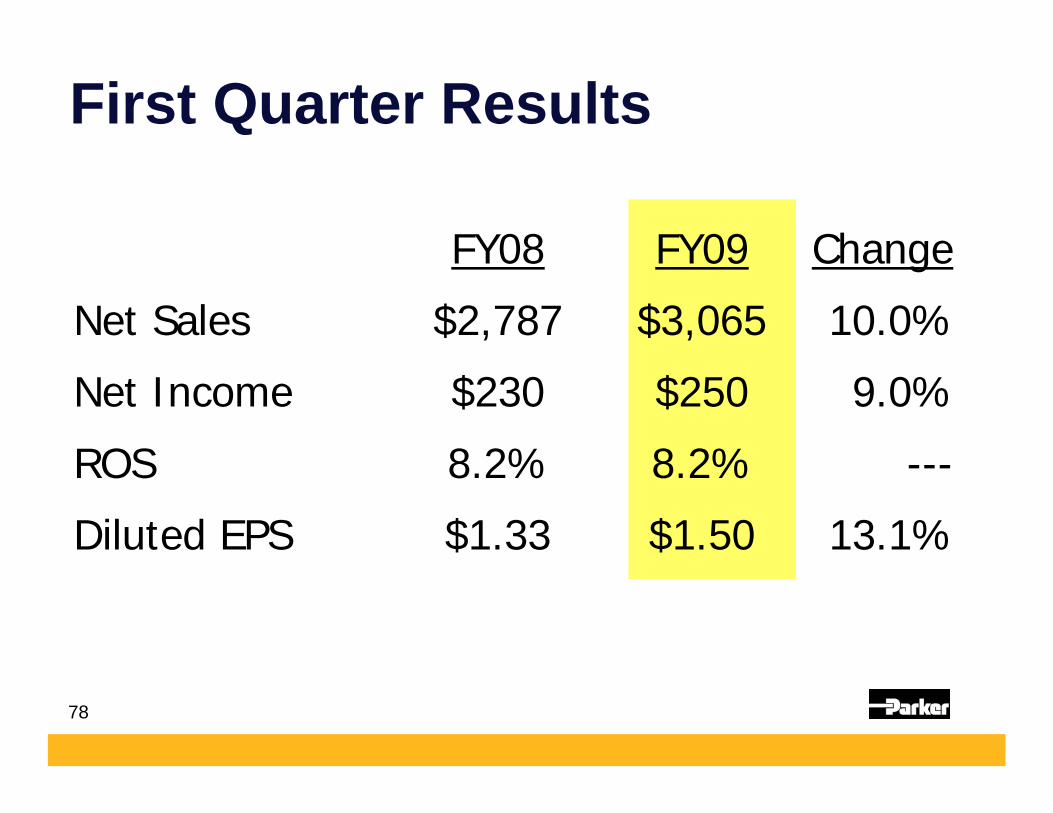

Record Quarter !!

FY09 1st Quarter

78

First Quarter Results

FY08 FY09 Change

Net Sales $2,787 $3,065 10.0%

Net Income $230 $250 9.0%

ROS 8.2% 8.2% ---

Diluted EPS $1.33 $1.50 13.1%

79

FY2009 Outlook

80

Parker’s New Order Rates1st Quarter FY09

Aerospace 9%Industrial North America 2%Industrial International -4%Climate & Industrial Control 5%

Total 1%

81

PMI Last 12 Months

50.049.6

48.6

50.2

43.5

48.3

50.0

48.4

50.7

48.6

50.4 49.9

42

43

44

45

46

47

48

49

50

51

52

53

54

55

Oct Nov Dec Jan '08 Feb Mar Apr May Jun Jul Aug Sep

ISM Index SummaryPrevious Month Comparison

82

0

1

2

3

4

5

6

Federal Reserve Discount Rates

Fed cuts key rateRecession Zone

1.5%

2003 2004 2005 2006 2007 2008

83

Global Economy

84

Global Economy

85

Global Economy

Real GDP growth forecasts

Spring forecast Interim forecastQ1 Q2 Q3 Q4 Apr-08 Sep-08

Germany 1.3 -0.5 -0.2 0.2 1.8 1.8Spain 0.3 0.1 -0.1 -0.3 2.2 1.4France 0.4 -0.3 0.0 0.1 1.6 1.0Italy 0.5 -0.3 0.0 0.1 0.5 0.1Netherlands 0.4 0.0 0.3 0.4 2.6 2.2Euro area 0.7 -0.2 0.0 0.1 1.7 1.3Poland 1.4 1.5 0.7 0.6 5.3 5.4UK 0.3 0.0 -0.2 -0.2 1.7 1.1EU27 0.6 -0.1 0.0 0.1 2.0 1.4

Source: EUThe quarterly figures are working - day and seasonally adjusted, while the annual figures are unadjusted

% year - on - year 2008% quarter - on - quarter 2008

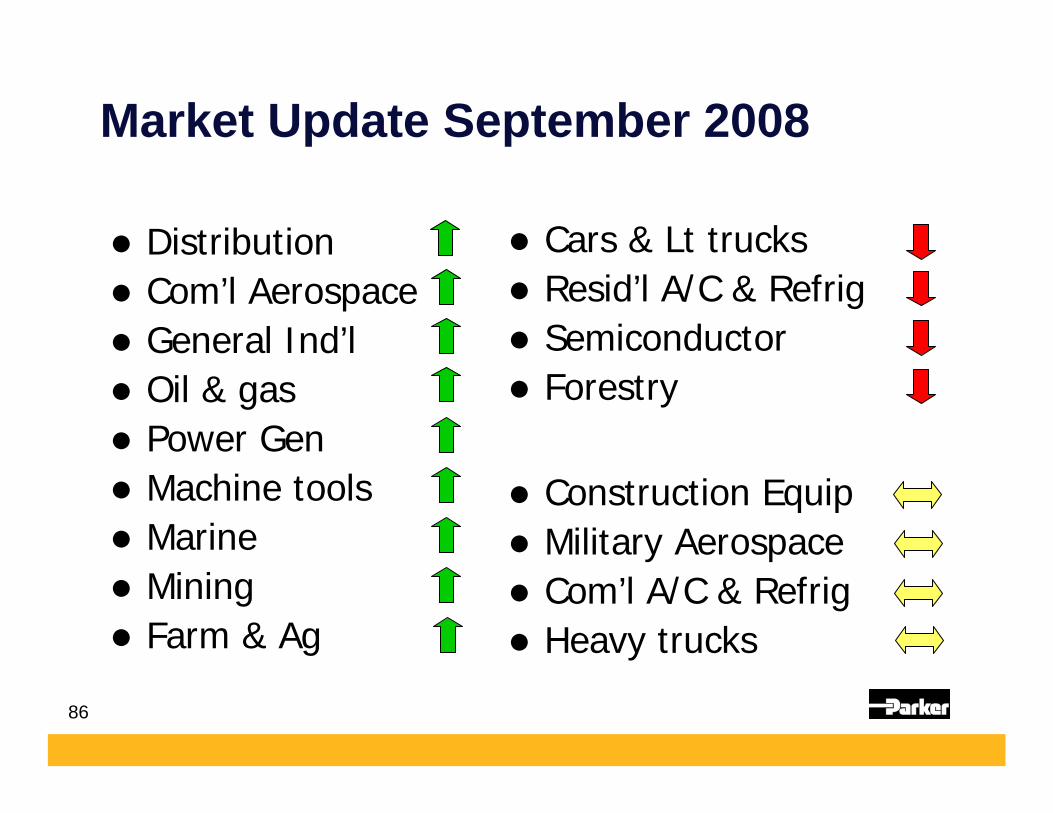

86

DistributionCom’l AerospaceGeneral Ind’l Oil & gasPower GenMachine toolsMarineMiningFarm & Ag

Cars & Lt trucksResid’l A/C & RefrigSemiconductorForestry

Construction EquipMilitary AerospaceCom’l A/C & RefrigHeavy trucks

Market Update September 2008

87

What Does GoodLook Like ?

The Future

88

20% Market Share

Top quartile ROIC

The Premier Diversified Industrial

A/S

ROSNxNW

Top quartile P/E Multiple

10% CAGR

The Future --What does good look like?

89