Embed Size (px)

Citation preview

Pareto Conference – Seadrill Per Wullf, Seadrill Chief Executive Officer

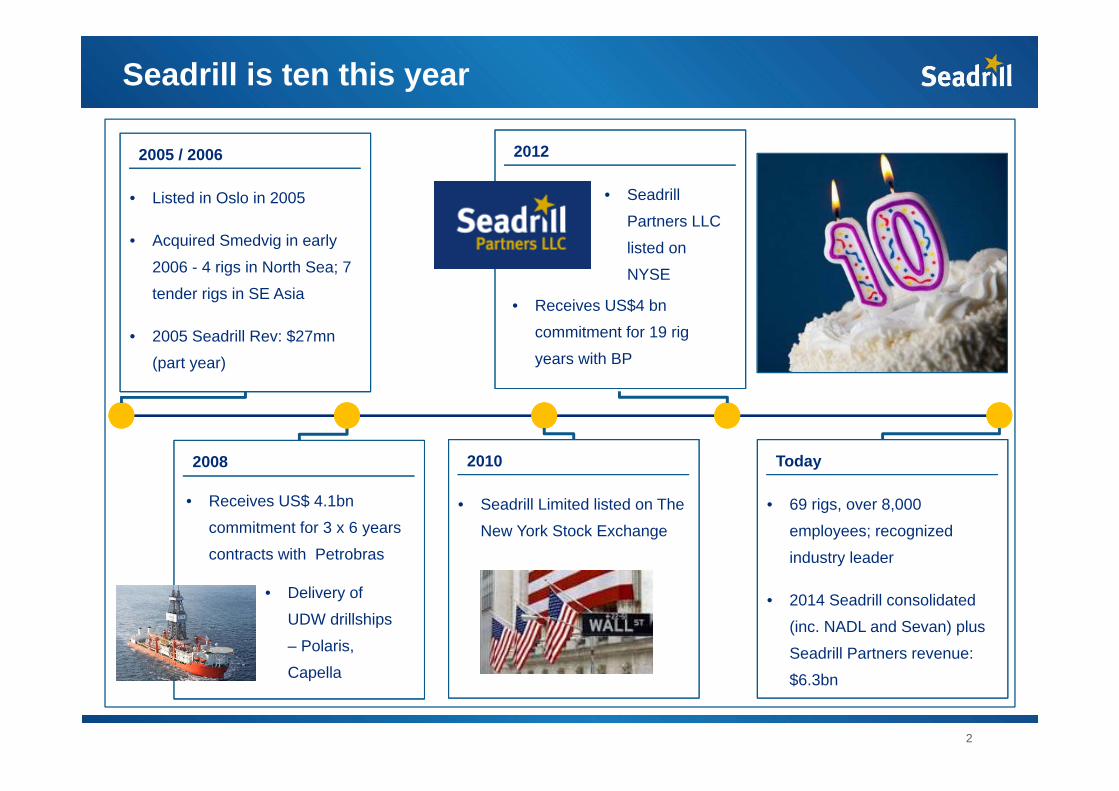

Seadrill is ten this year

• Listed in Oslo in 2005

• Acquired Smedvig in early

2006 - 4 rigs in North Sea; 7

tender rigs in SE Asia

• 2005 Seadrill Rev: $27mn

(part year)

2

2005 / 2006

• Receives US$ 4.1bn

commitment for 3 x 6 years

contracts with Petrobras

2008

• Seadrill Limited listed on The

New York Stock Exchange

2010

• Seadrill

Partners LLC

listed on

NYSE

2012

• Receives US$4 bn

commitment for 19 rig

years with BP

• 69 rigs, over 8,000

employees; recognized

industry leader

• 2014 Seadrill consolidated

(inc. NADL and Sevan) plus

Seadrill Partners revenue:

$6.3bn

Today

• Delivery of

UDW drillships

– Polaris,

Capella

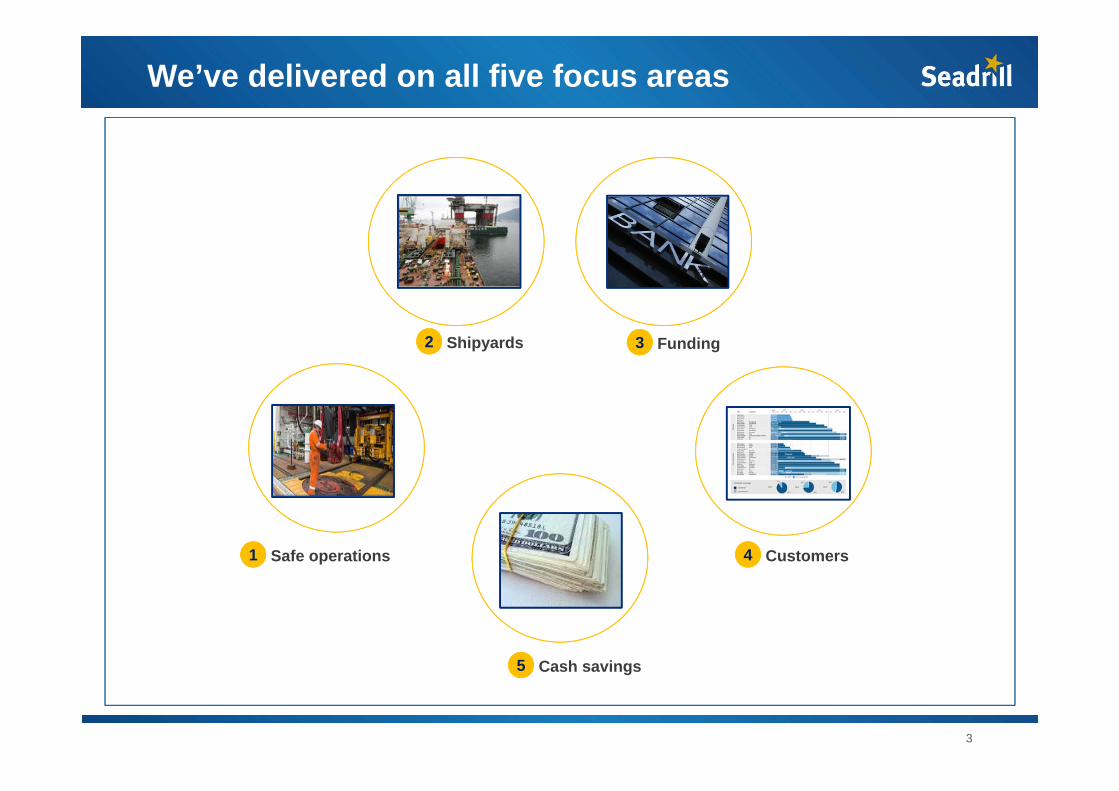

We’ve delivered on all five focus areas

3

Shipyards2 Funding3

Customers4Safe operations1

Cash savings5

Continued focus on safe, efficient operations

4

Safe operations1

Utilization across the fleet has been high…

…and HSE performance solid

• Improved trend in HSE focus areas (YTD Aug versus same period last year)– Hurts - 47%– Dropped Objects - 31%

• Continual improvement of the QHSE management system– Global alignment of HSE Directives– Systematic compliance process (Corporate Audit, Regional and Rig Verification)

• Technical utilization high at 95% YTD August (equal to results same period last year)

• 13 class projects executed YTD all on time and budget

• Four drill ships put in service since August 2014 (West Saturn, West Neptune, West

Jupiter and West Carina); all operating with technical utilization above 96%

* Under Water Survey In Lieu of Drydocking

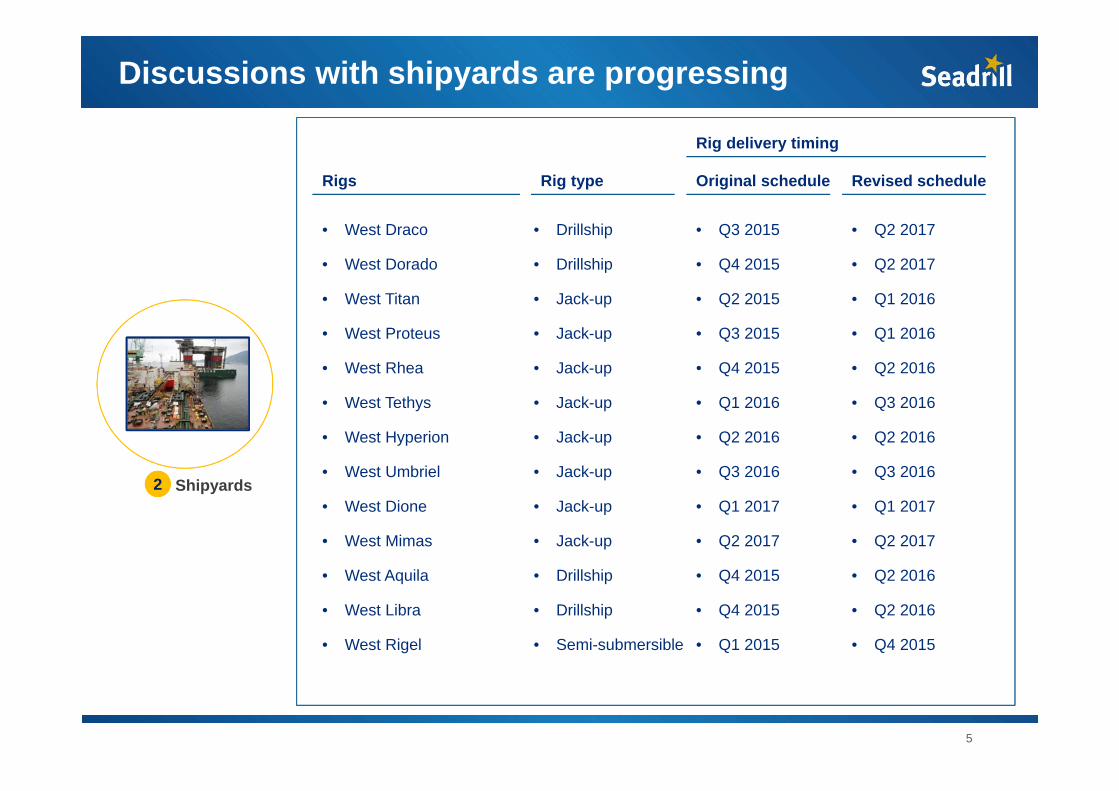

Discussions with shipyards are progressing

5

Shipyards2

Rigs

• West Draco

• West Dorado

• West Titan

• West Proteus

• West Rhea

• West Tethys

• West Hyperion

• West Umbriel

• West Dione

• West Mimas

• West Aquila

• West Libra

• West Rigel

Original schedule

• Q3 2015

• Q4 2015

• Q2 2015

• Q3 2015

• Q4 2015

• Q1 2016

• Q2 2016

• Q3 2016

• Q1 2017

• Q2 2017

• Q4 2015

• Q4 2015

• Q1 2015

Revised schedule

• Q2 2017

• Q2 2017

• Q1 2016

• Q1 2016

• Q2 2016

• Q3 2016

• Q2 2016

• Q3 2016

• Q1 2017

• Q2 2017

• Q2 2016

• Q2 2016

• Q4 2015

Rig delivery timing

Rig type

• Drillship

• Drillship

• Jack-up

• Jack-up

• Jack-up

• Jack-up

• Jack-up

• Jack-up

• Jack-up

• Jack-up

• Drillship

• Drillship

• Semi-submersible

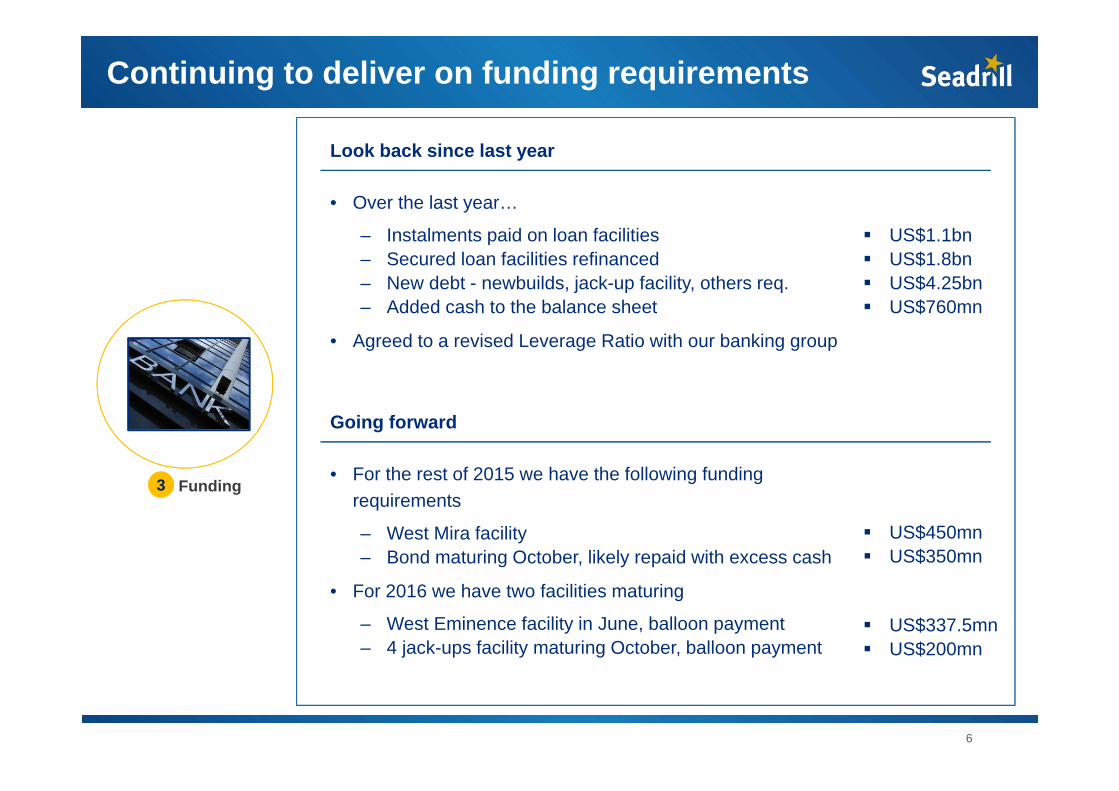

Continuing to deliver on funding requirements

6

Look back since last year

• Over the last year…

– Instalments paid on loan facilities– Secured loan facilities refinanced– New debt - newbuilds, jack-up facility, others req.– Added cash to the balance sheet

• Agreed to a revised Leverage Ratio with our banking group

Funding3

Going forward

• For the rest of 2015 we have the following funding requirements

– West Mira facility – Bond maturing October, likely repaid with excess cash

• For 2016 we have two facilities maturing

– West Eminence facility in June, balloon payment– 4 jack-ups facility maturing October, balloon payment

• xx

US$1.1bn US$1.8bn US$4.25bn US$760mn

• xx

US$450mn US$350mn

• xx

US$337.5mn US$200mn

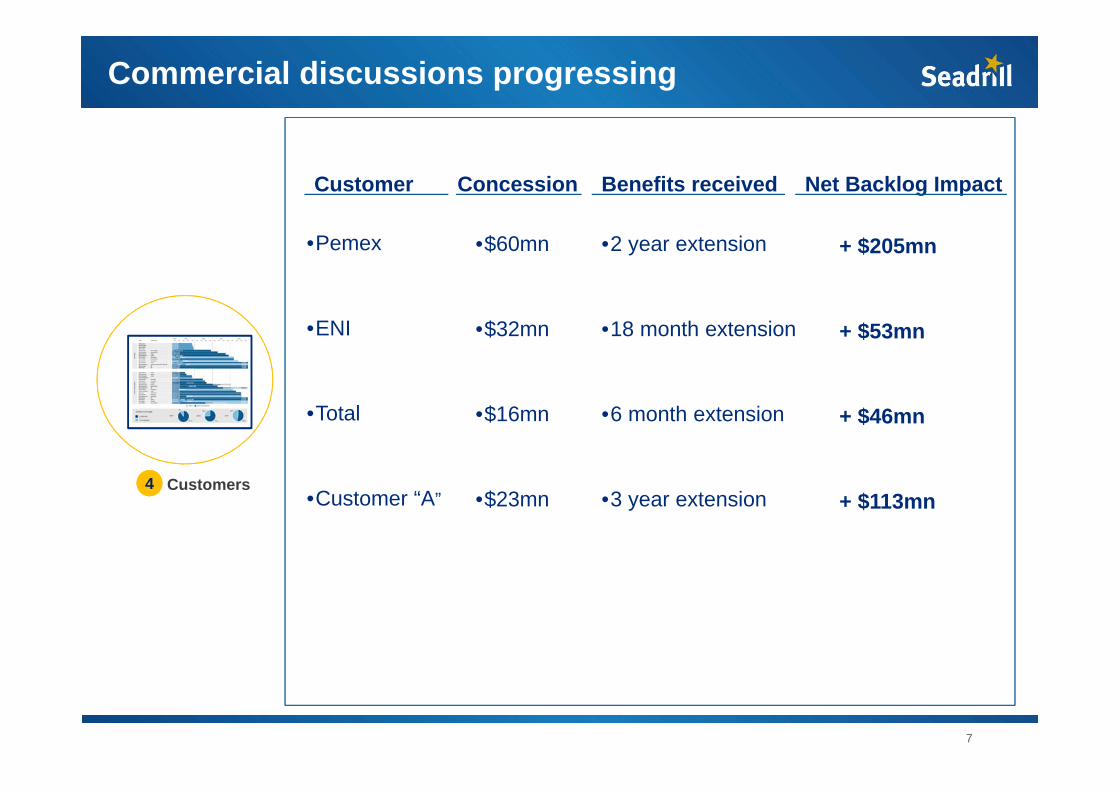

Commercial discussions progressing

7

Customer

•Pemex

•ENI

•Total

•Customer “A”

Concession

•$60mn

•$32mn

•$16mn

•$23mn

Benefits received

•2 year extension

•18 month extension

•6 month extension

•3 year extension

Net Backlog Impact

+ $205mn

+ $53mn

+ $46mn

+ $113mnCustomers4

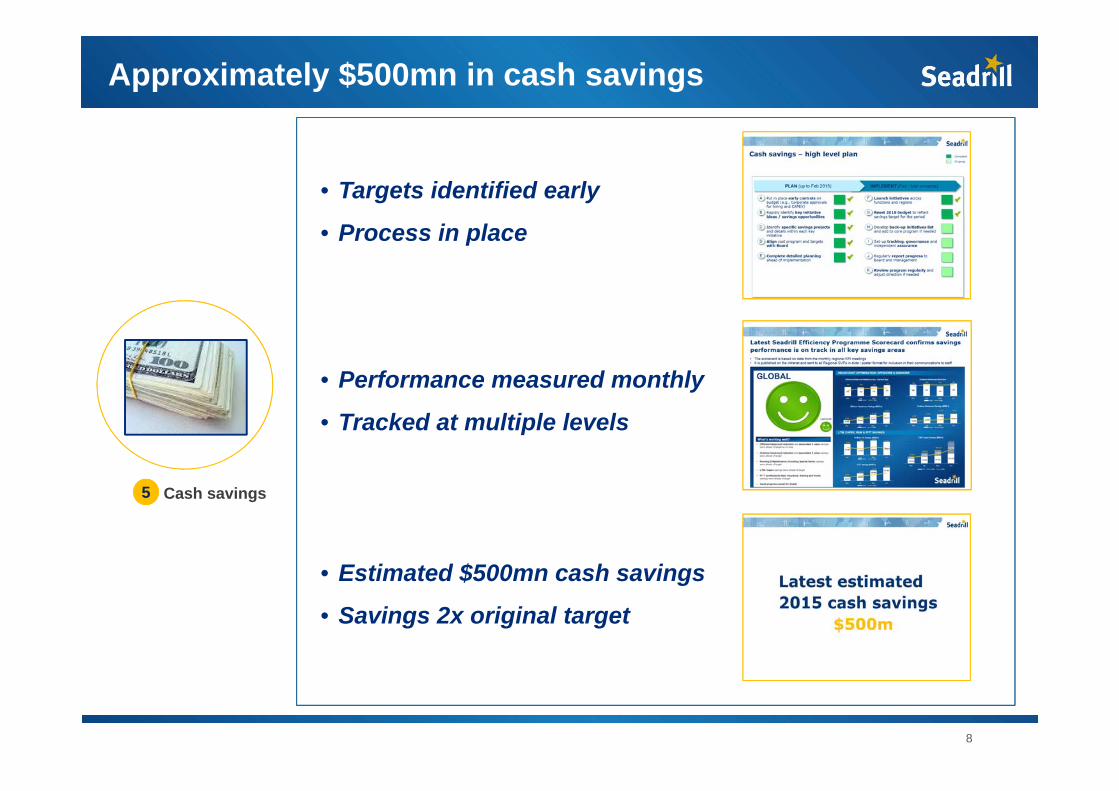

Approximately $500mn in cash savings

8

• Targets identified early

• Process in place

Cash savings5

• Performance measured monthly

• Tracked at multiple levels

• Estimated $500mn cash savings

• Savings 2x original target

9

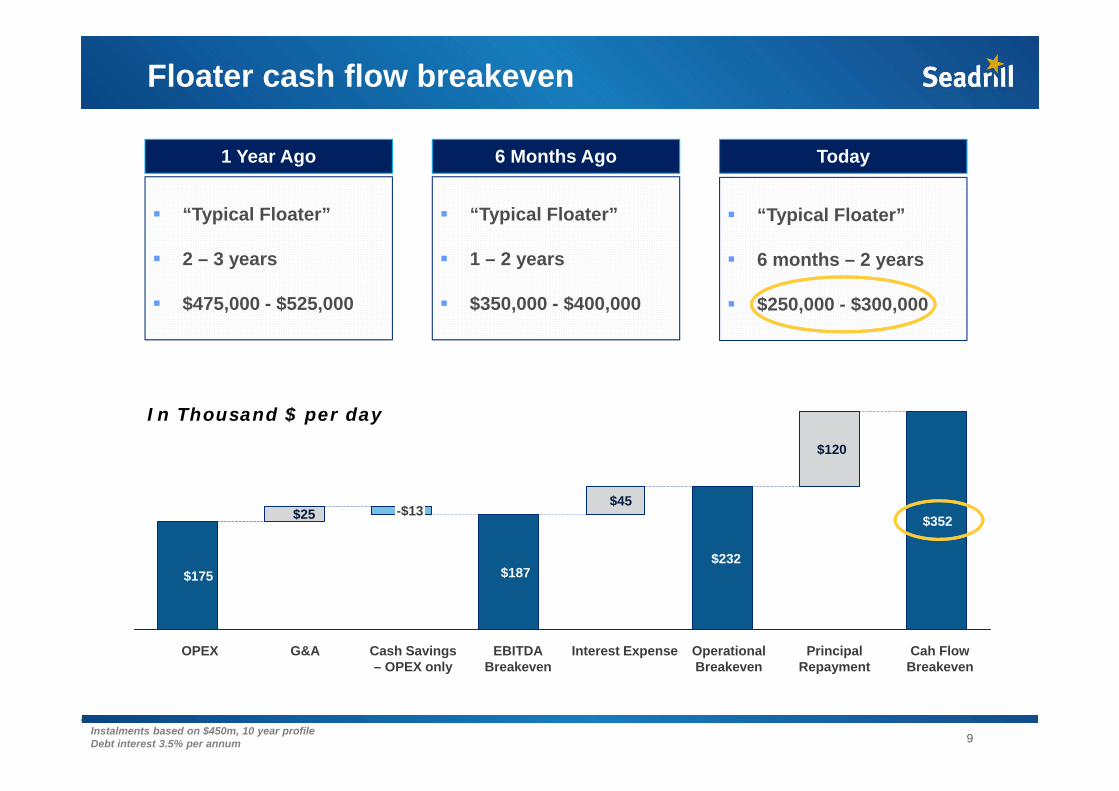

Floater cash flow breakeven

6 Months Ago

“Typical Floater”

1 – 2 years

$350,000 - $400,000

Today

“Typical Floater”

6 months – 2 years

$250,000 - $300,000

1 Year Ago

“Typical Floater”

2 – 3 years

$475,000 - $525,000

Instalments based on $450m, 10 year profileDebt interest 3.5% per annum

$45

Interest Expense

$232

Operational Breakeven

EBITDA Breakeven

$187

Cash Savings – OPEX only

G&A

$25

OPEX

$175

Cah Flow Breakeven

$352

Principal Repayment

$120

-$13

In Thousand $ per day

10

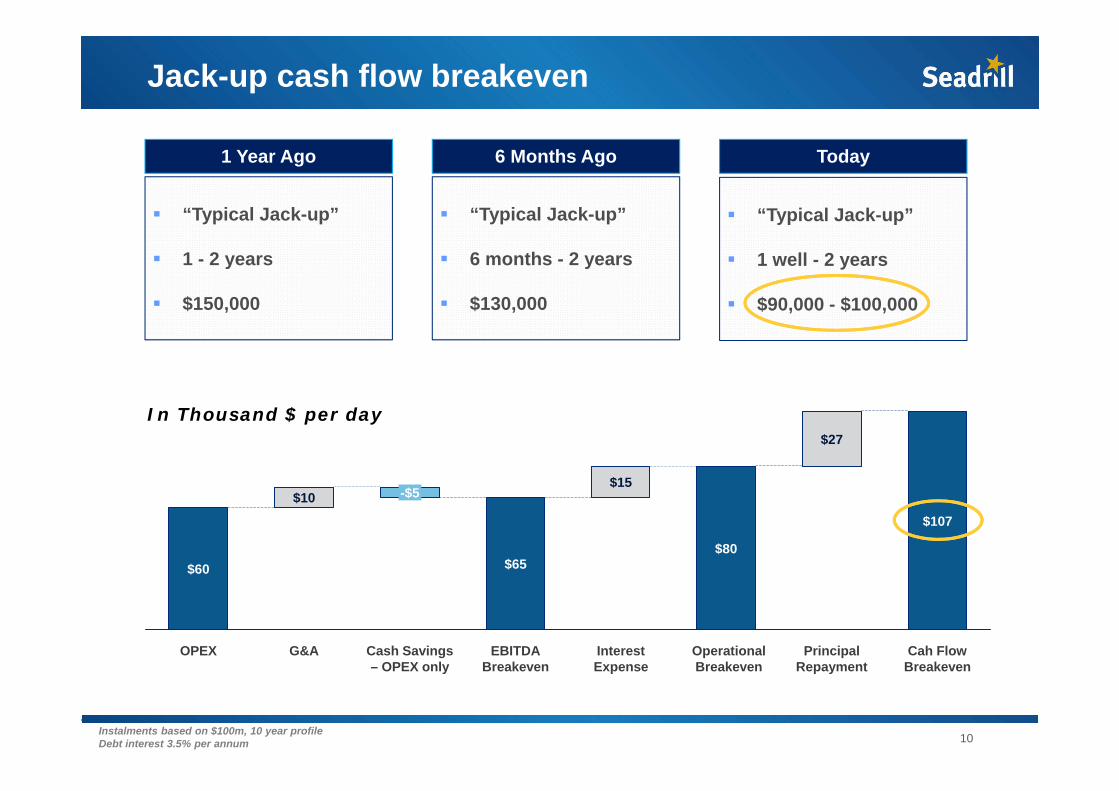

Jack-up cash flow breakeven

6 Months Ago

“Typical Jack-up”

6 months - 2 years

$130,000

“Typical Jack-up”

1 well - 2 years

$90,000 - $100,000

1 Year Ago

“Typical Jack-up”

1 - 2 years

$150,000

Today

Instalments based on $100m, 10 year profileDebt interest 3.5% per annum

In Thousand $ per day

OPEX Principal Repayment

Cah Flow Breakeven

G&A Cash Savings – OPEX only

$60

$10

$65

$15

$80

$107

EBITDA Breakeven

Interest Expense

-$5

$27

Operational Breakeven

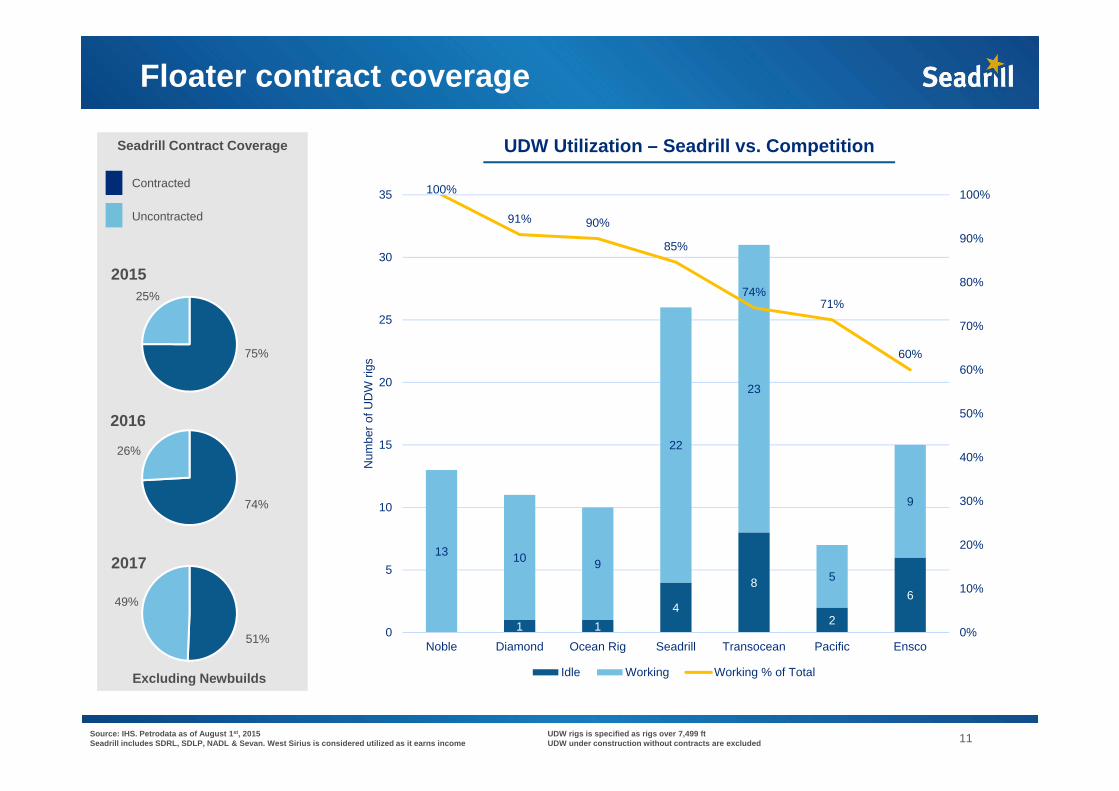

Source: IHS. Petrodata as of August 1st, 2015Seadrill includes SDRL, SDLP, NADL & Sevan. West Sirius is considered utilized as it earns income

UDW rigs is specified as rigs over 7,499 ftUDW under construction without contracts are excluded

We’re having very difficult conversationsFloater contract coverage

44%65%

84%

Seadrill Contract Coverage

Contracted

Uncontracted

2015

2016

2017

75%

25%

74%

26%

51%

49%

UDW Utilization – Seadrill vs. Competition

1 14

8

2

6

13 10 9

22

23

5

9

100%

91% 90%

85%

74%71%

60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

Noble Diamond Ocean Rig Seadrill Transocean Pacific Ensco

Num

ber o

f UD

W ri

gs

Idle Working Working % of TotalExcluding Newbuilds

11

12

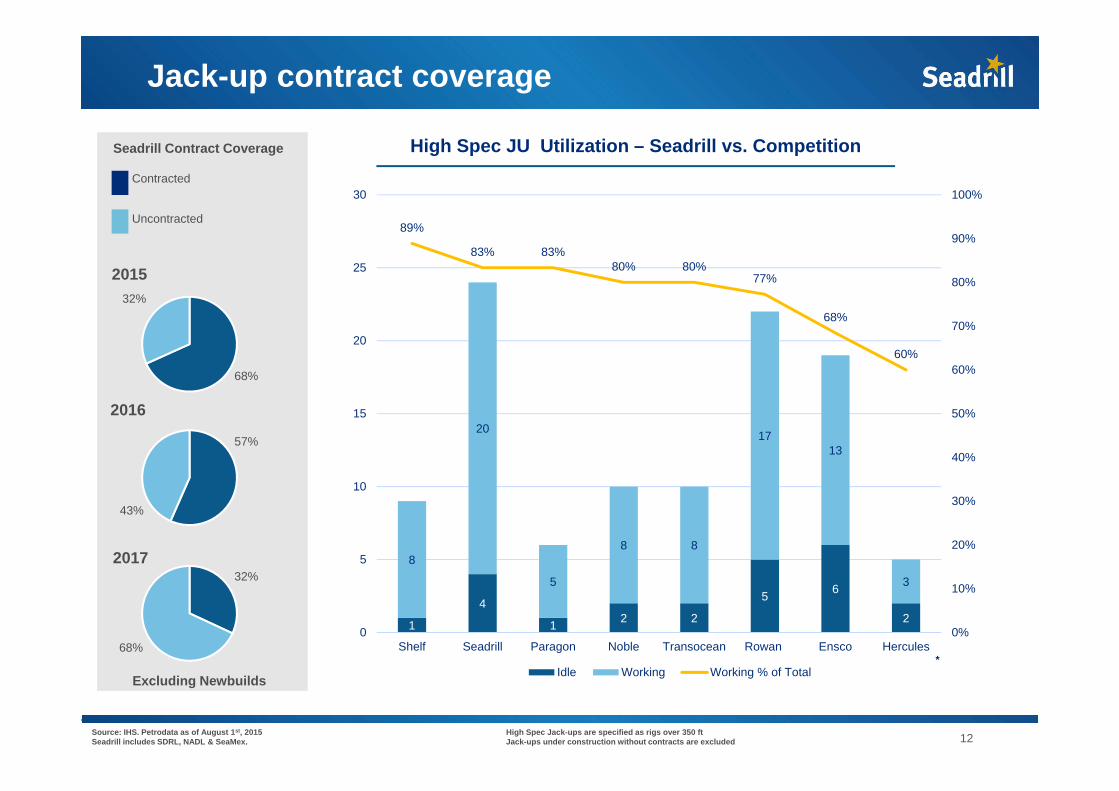

Jack-up contract coverage

44%65%

84%

Seadrill Contract Coverage

Contracted

Uncontracted

2015

2016

2017

High Spec JU Utilization – Seadrill vs. Competition

68%

32%

43%

57%

32%

68%*

1

4

1 2 2

5 6

2

8

20

5

8 8

1713

3

89%

83% 83%80% 80%

77%

68%

60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

Shelf Seadrill Paragon Noble Transocean Rowan Ensco Hercules

Idle Working Working % of Total

Source: IHS. Petrodata as of August 1st, 2015Seadrill includes SDRL, NADL & SeaMex.

High Spec Jack-ups are specified as rigs over 350 ftJack-ups under construction without contracts are excluded

Excluding Newbuilds

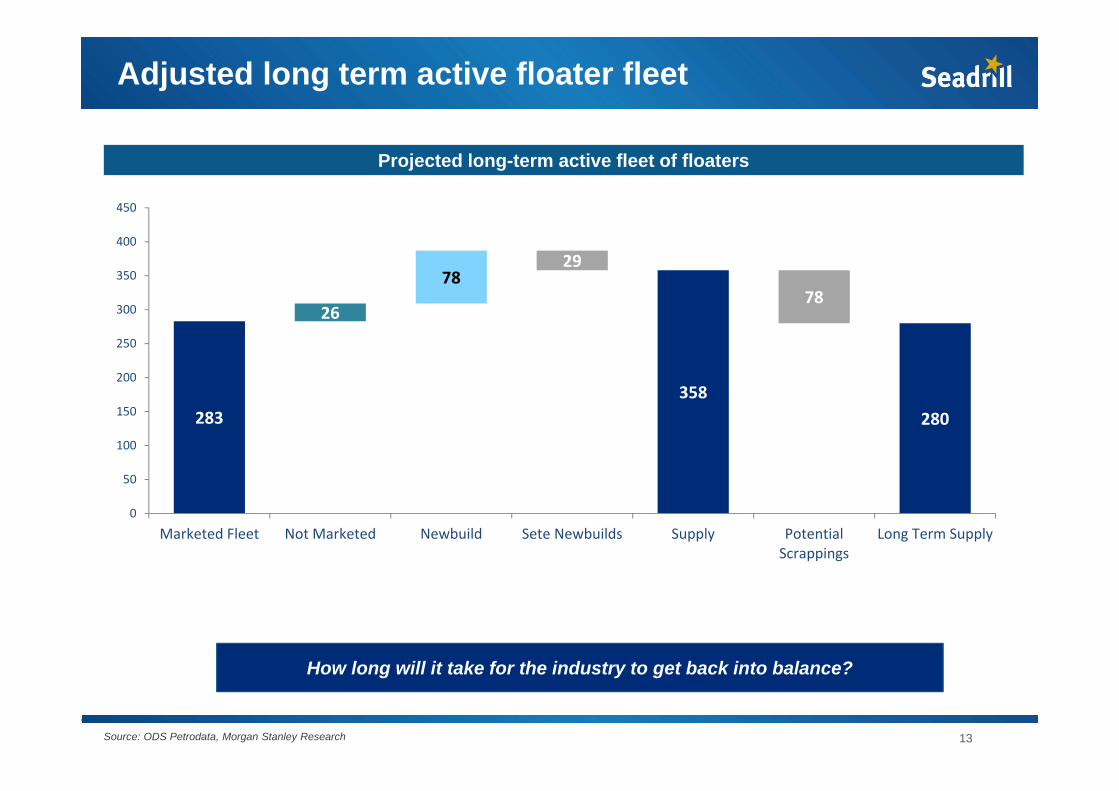

Projected long-term active fleet of floaters

Source: ODS Petrodata, Morgan Stanley Research

Adjusted long term active floater fleet

283 283 280

26

358

7878

29

0

50

100

150

200

250

300

350

400

450

Marketed Fleet Not Marketed Newbuild Sete Newbuilds Supply PotentialScrappings

Long Term Supply

How long will it take for the industry to get back into balance?

13

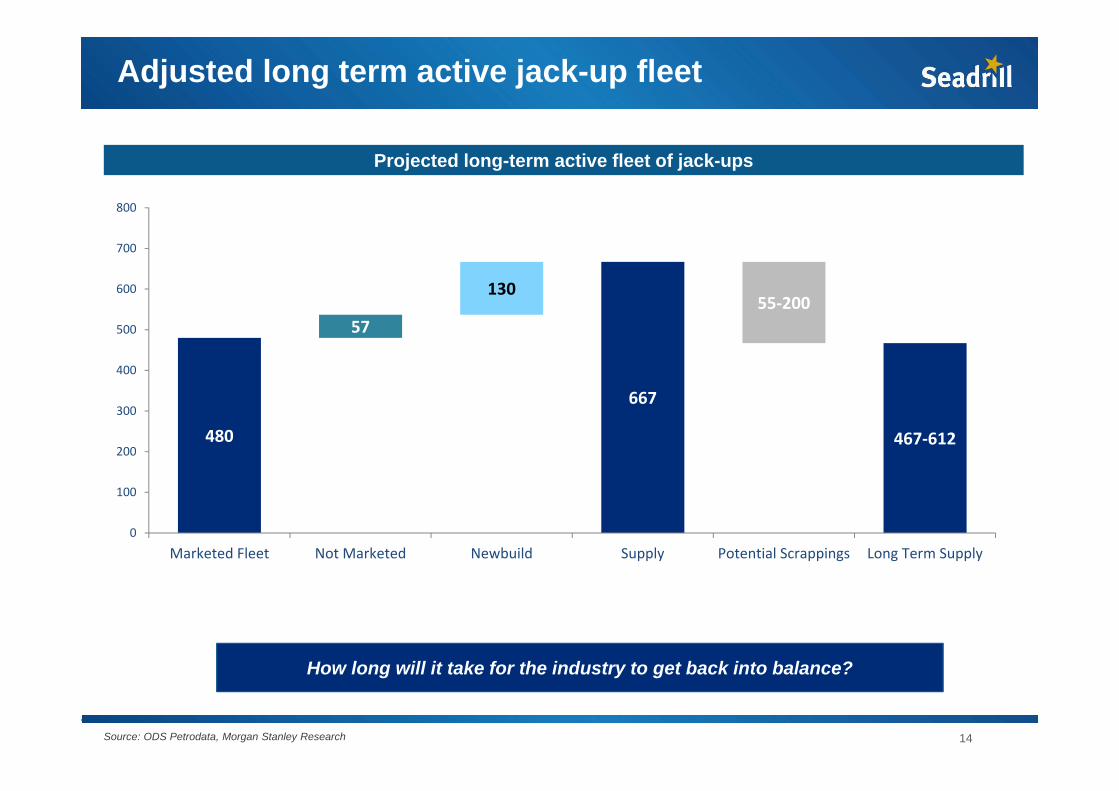

Projected long-term active fleet of jack-ups

Source: ODS Petrodata, Morgan Stanley Research

Adjusted long term active jack-up fleet

480 537467‐612

57

667

55‐200130

0

100

200

300

400

500

600

700

800

Marketed Fleet Not Marketed Newbuild Supply Potential Scrappings Long Term Supply

How long will it take for the industry to get back into balance?

14

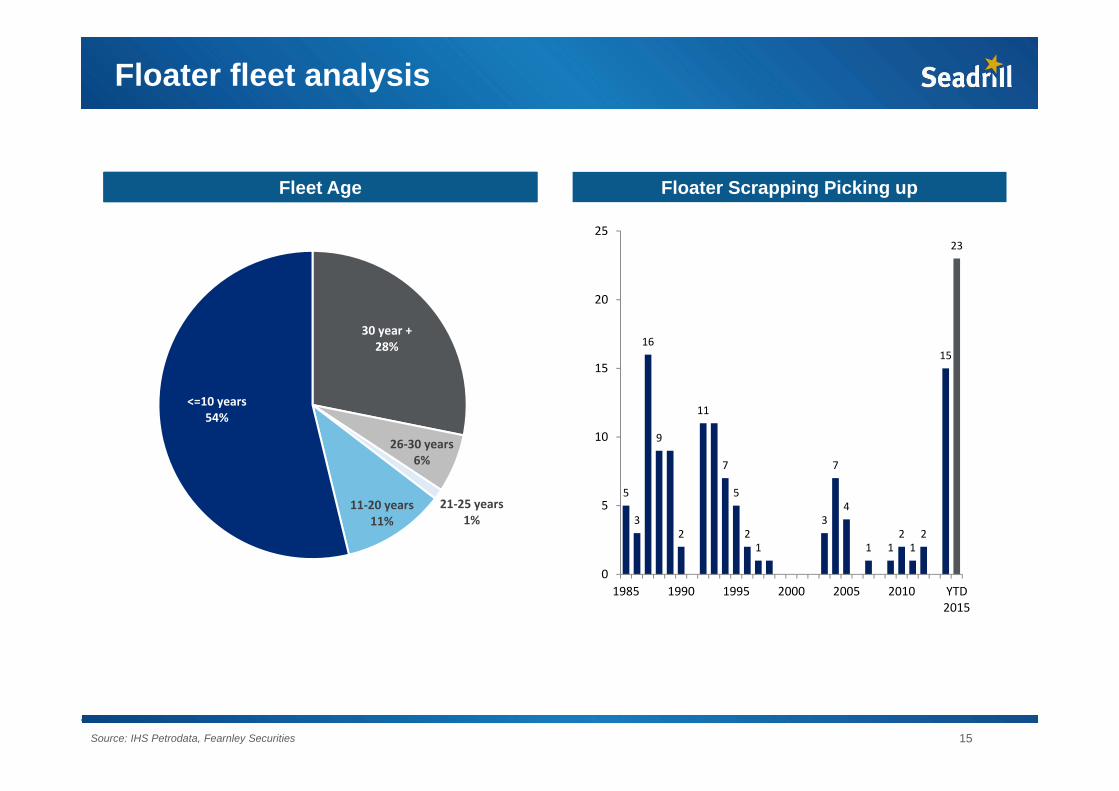

30 year +28%

26‐30 years6%

21‐25 years1%

11‐20 years11%

<=10 years54%

Average floater age today: 17 years

15

Average floater age today: 17 years

Floater fleet analysis

Source: IHS Petrodata, Fearnley Securities

Fleet Age Floater Scrapping Picking up

5

3

16

9

2

11

7

5

21

3

7

4

1 1212

15

23

0

5

10

15

20

25

1985 1990 1995 2000 2005 2010 YTD2015

Average floater age today: 17 years

16

Average floater age today: 17 years

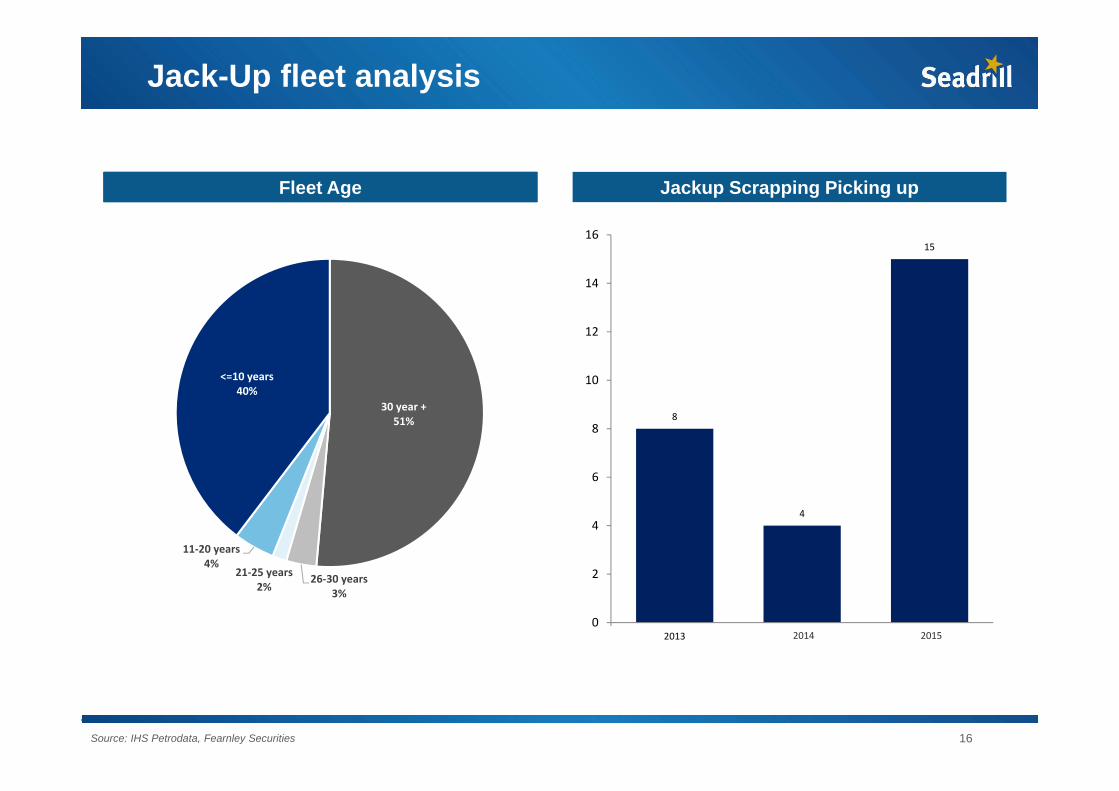

Jack-Up fleet analysis

Source: IHS Petrodata, Fearnley Securities

Fleet Age Jackup Scrapping Picking up

8

4

15

0

2

4

6

8

10

12

14

16

2013 2014 2015

30 year +51%

26‐30 years3%

21‐25 years2%

11‐20 years4%

<=10 years40%

Delivered on the most important actions this year

Conclusion

17

Strengthened the balance sheet

Reset operating costs and saved cash

Negotiated effectively with customers, shipyards, and banks

Consolidation will happen and we will be sitting in the driver’s seat when the industry returns to growth