Embed Size (px)

Citation preview

Papua New Guinea Taxation Review (2013-2015)

Issues Paper No.5: An examination of the advantages and

disadvantages of tax incentives

Prepared by the Taxation Review Committee

12 December 2014

[This page intentionally left blank]

Consultation Process The Tax Review Committee (Committee) is seeking your feedback and comments on this Issues Paper. This and other issues papers will be released throughout 2014 and the first quarter of 2015 and are designed to promote targeted discussion and debate on particular areas subject to Review. Consultation questions are included throughout the paper to guide responses but stakeholders should feel free to raise any issue of relevance.

Feedback in response to this Issues Paper will help to inform the development of the Committee’s draft recommendations to Government, which will be subject to a further round of consultation before being finalized.

To ensure that there is transparency in the consultation process, all submissions are published on the Tax Review website (www.taxreview.gov.pg) unless the submission is by justification, marked ‘CONFIDENTIAL’.

Submissions in response to this paper are due by 13 February 2015.

All submissions should be sent via mail and/or email to:

Head of Secretariat Tax Review Secretariat c/- Department of Treasury PO Box 542, Waigani, NCD

Email: [email protected]

For any other general enquiries, email: [email protected] or call the Tax Review Secretariat on (675) 325 3775 or (675) 325 5977.

Page i

TABLE OF CONTENTS

TABLE OF CONTENTS .......................................................................... I

FOREWORD ...................................................................................... IV

EXECUTIVE SUMMARY ...................................................................... VI

Consultation Questions ............................................................................... vii Overview of Tax Incentives Regime in PNG .................................................... vii The Advantages and Disadvantages of Tax Incentives ..................................... vii Tax Incentives in PNG – Possible Directions for Reform .................................. vii Other issues .................................................................................................... viii

CHAPTER 1: OVERVIEW OF TAX INCENTIVES REGIME IN PNG 1

What are tax incentives? ................................................................................1

Tax Incentives Offered in PNG .....................................................................1 General incentives ............................................................................................. 1 Taxpayer and project-specific incentives ............................................................ 7

Policy framework governing the award of tax incentives in PNG .............8 Compliance with World Trade Organisation obligations ................................. 10

Process for the awarding of tax incentives ................................................ 10

Reporting on and valuation of tax incentives ........................................... 11

CHAPTER 2: THE ADVANTAGES AND DISADVANTAGES OF TAX INCENTIVES 14

Advantages of tax incentives...................................................................... 14

Disadvantages of Tax Incentives ................................................................ 15

Strengths and weaknesses of particular incentives .................................. 18

International experience with tax incentives............................................. 19

CHAPTER 3 – VIEWS FROM CONSULTATION& PRIOR TAX REVIEW .......................................................................................... 21

Comments in relation to the Mining and Petroleum Taxation ................ 21

Page ii

Comments as part of a broader “Blue Sky” consultation ......................... 22 Sector/taxpayer-specific issues ........................................................................ 23 General issues ................................................................................................. 24 Industrial Development (Pioneer Status) Act ................................................... 24 Administrative and legislative framework applying to incentives .................... 25

Consideration of tax incentives in the 2000 Tax Review .......................... 26

CHAPTER 4: TAX INCENTIVES IN PNG – POSSIBLE DIRECTIONS FOR REFORM ................................................................ 27

A whole-of-tax-system approach to incentives ......................................... 28

A Framework for Tax Incentives in PNG .................................................. 30 The process for granting tax incentives ............................................................ 30 The policy basis upon which incentives are granted ........................................ 32 The legislative framework underpinning tax incentives ................................... 34 Ongoing reporting and monitoring of tax incentives ........................................ 35

CHAPTER 5 – OTHER ISSUES ............................................................. 37

Mining and Petroleum Sector ..................................................................... 37

Infrastructure Tax Credit ............................................................................ 37

Research & Development Incentive ........................................................... 40

Pioneer Act................................................................................................... 41

Special Economic Zones.............................................................................. 42

Incentives relating to GST/Import Duties/Excise.................................... 43

Exemptions provided to aid organisations and workers ......................... 43

Project agreements ...................................................................................... 45

ATTACHMENT A: SUMMARY OF GENERAL TAX INCENTIVES OFFERED IN PNG ............................................................................ 46

ATTACHMENT B: SUMMARY OF KEY FINDINGS AND RECOMMENDATIONS FROM THE NATIONAL INVESTMENT POLICY, VOLUME II (1999)............................................................... 66

ATTACHMENT C: VALUE OF INCOME TAX INCENTIVES (2015 BUDGET) ......................................................................................... 73

Page iii

ATTACHMENT D:STRENGTHS AND WEAKNESSES OF DIFFERENT TYPES OF TAX INCENTIVES ............................................. 74

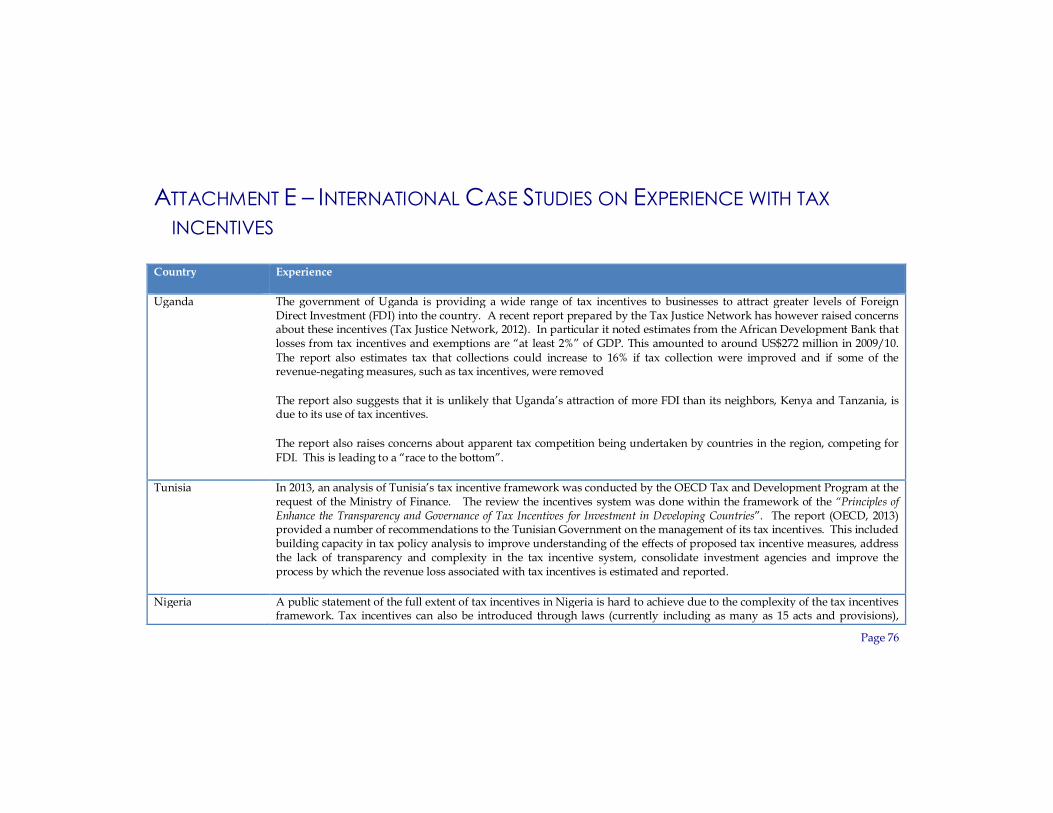

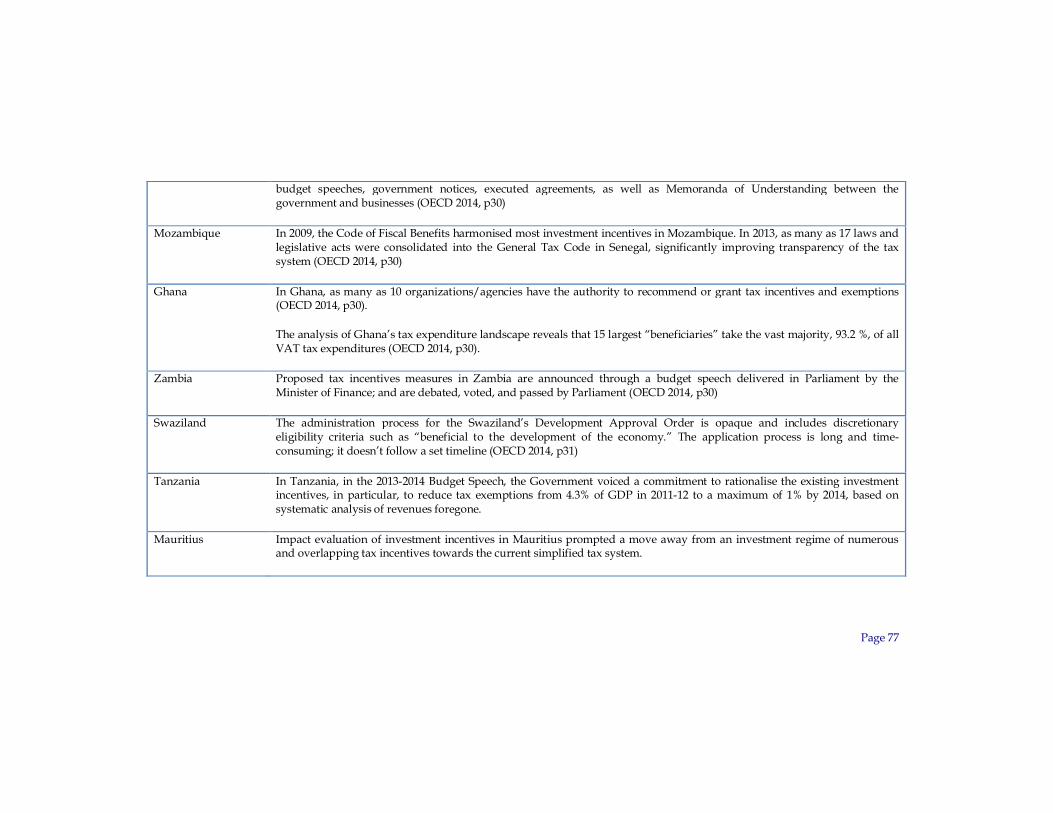

ATTACHMENT E – INTERNATIONAL CASE STUDIES ON EXPERIENCE WITH TAX INCENTIVES.................................................. 76

REFERENCES ................................................................................... 78

ABBREVIATIONS .............................................................................. 80

Page iv

FOREWORD

In 2013, the Government committed to comprehensively review PNG’s revenue regime. The primary reason for the Review is to ensure that it remains relevant, efficient and effective.

Government revenue is critical to funding essential services and infrastructure for Papua New Guinea, to share the benefits of prosperity across families, communities and regions and to lay the foundations for future growth. Consequently, this Review is a high priority of the Government and an important platform of the Government’s economic and fiscal strategy. The last comprehensive taxation review was undertaken in 2000 and given the substantial economic, fiscal and technological developments over the past 14 years, it is timely that another review is undertaken to ensure that the country’s tax system is modern, robust and is able to support the country’s medium and long-term economic and social development objectives. While formally titled a ‘Tax Review’, the Review will consider other sources of revenue, including non-taxation revenues. The terms of reference to the Review have called on the Tax Review Committee to examine the advantages and disadvantages of tax incentives. The Review began this work as part of Issues Paper 3, the Broad Directions Paper. This Issues Paper considers the use of tax incentives in PNG in more detail, providing an overview of the existing regime, highlighting the advantages and limitations of tax incentives and discussing the overall framework in place to guide the awarding and management of incentives. Trying to incentivise certain activities or help particular sectors of the economy to grow can be important public policy goals. However, as is explored in this paper, there are limitations on the ability of the tax system to achieve this. In particular, PNG’s experiences with the research and development incentive and the infrastructure tax credit have highlighted the challenges of implementing or effectively monitoring particular incentives in the absence of sufficient administrative or technical capacity. Whilst tax incentives have their limitations, the overall design of the tax system does play an important role in the economy of a country and can provide significant incentives, and disincentives with respect to certain activities. The rates of personal income taxes, if set too high, can act as a real disincentive to work. Corporate income taxes also need to remain competitive internationally in order to attract foreign investment. Where the tax system itself is acting as a barrier to growth, such as with the challenges that small and medium enterprises face in entering the formal economy, then creative approaches to tax design may be required. Given its terms of reference, this Review provides an opportunity to take a broad view of the tax system, and to the issue of incentives more generally. To the extent that specific tax incentives remain a feature of PNG’s tax system, it is important that these are granted and managed within a clear and transparent framework. However,

Page v

perhaps more importantly, opportunities for more comprehensive and substantive tax reform should be pursued so that, as a whole, the tax system is fairer, simpler and more competitive. Whilst the paper suggests that this should be the ultimate goal for PNG’s tax system, in the short term there is an urgent need to improve the way that tax incentives are managed and, in particular, to more effectively and accurately assess the value of revenues foregone from the incentives. In particular, PNG’s experience with the R&D tax concession highlights a critical need to evaluate the ongoing merit of significant incentives in the tax system, including their ongoing policy rationale and risk to revenue. The Committee looks forward to receiving submissions on this paper and to future engagement with interested stakeholders on the future of Papua New Guinea’s tax system.

Sir Nagora Bogan, KBE Chairman, Tax Review Committee

Page vi

EXECUTIVE SUMMARY

A ‘tax incentive’ is a type of concessional tax treatment used to achieve some type of policy goal – usually the promotion of growth of a particular industry or sector of the economy. A range of different types of tax incentives are used in PNG, resulting in eligible taxpayers paying either less tax that they would have or paying tax later than they would have under ‘standard’ tax rules.

This paper provides an overview of the incentives used in PNG including a number of significant tax incentive measures that are or have been applied in PNG. It highlights that tax incentives have been and continue to be a key feature of PNG’s tax system.

Consistent with the terms of reference for the Review the paper then considers both the advantages and disadvantages of tax incentives. Whilst tax incentives are often implemented in pursuit of good public policy goals, the paper highlights a number of disadvantages of tax incentives, drawing on extensive international experience and writing on the issue.

First and foremost, tax incentives can undermine the tax system’s primary function which is to generate revenue to fund the provision of government services and infrastructure. Treating taxpayers differently also undermines the equity of the tax system and, if poorly targeted, can simply generate an unfair competitive advantage. Of significant concern in the PNG context is the additional complexity that tax incentives can create, placing greater demand on already limited tax administration resources.

International experience, and PNG’s experience with some of its own tax incentive regimes (in particular the R&D incentive), also highlights that incentives are often ineffective in achieving their desired policy outcome or in contributing to economic growth more broadly.

The paper then puts forward, for discussion, a proposed approach for PNG to take on the issue of tax incentives. The central position put forward by the paper is that, rather than focus on sector or industry specific incentives, PNG should focus on creating an overall tax system that is simpler, fairer and more competitive. Such an approach may have a strong impact on ‘incentives’ – for example, a move by PNG to maintain a corporate income tax rate that is internationally competitive is likely to have a far greater impact on attracting foreign investment compared to any sector specific incentive.

Whilst suggesting that such a ‘whole of tax system’ approach should be the goal for PNG, the paper recognises that incentives are likely to remain a feature of PNG’s tax system to some extent. Accordingly the paper puts forward a framework, for discussion, for the management and award of these incentives. The framework includes the process for granting tax incentives, the policy basis on which they are granted, the legislative framework for incentives as well as a framework for the

Executive Summary

Page vii

ongoing reporting and monitoring. Finally the paper suggests that there is an urgent need to adequately assess the value of incentives and to review significant incentives in the law.

Consultation Questions Below are the various consultation questions posed throughout the paper. As noted above, they are intended to act as prompts only and stakeholders should feel free to raise any other related views/issues.

Overview of Tax Incentives Regime in PNG

Question 1.1 – are stakeholders aware of any other tax incentives not captured in the table?

Question 1.2 – do stakeholders agree with the stated purpose of each incentive, as provided for by the Review?

Question 1.3 - are relevant stakeholders able to indicate how individual incentives helped to achieve the stated policy goal?

The Advantages and Disadvantages of Tax Incentives

Question 2-1 – what other advantages do tax incentives have, particularly in the PNG context?

Question 2-2 – what other disadvantages do tax incentives have, particularly in the PNG context?

Question 2-3 – do stakeholders have any other views about the merits of particular types of tax incentives?

Tax Incentives in PNG – Possible Directions for Reform

Question 4.1 – do stakeholders agree that PNG should focus on creating a tax system that is overall simpler, fairer and more competitive?

Question 4.2 – would stakeholders agree to a trade-off between removing existing incentives with other reforms that focused on making the tax system simpler, and more competitive overall?

Question 4.3 – do stakeholders agree that there is a need for a framework to guide the granting and management of tax incentives?

Question 4.4 –should PNG consider formalizing the process for the granting of tax incentives, similar to the process adopted recently in the Solomon Islands?

Executive Summary

Page viii

Question 4.5 – do stakeholders consider that there is a need to create a new body for the carriage and formulation of National Strategic Economic Development Plans in PNG, with part of its role being to ensure that consideration of targeted interventions using the tax system are placed in a broader economic context?

Question 4.6 –what are stakeholder’s views on the proposed principles to guide the award of tax incentives in PNG? Are there any other principles that should be included?

Question 4.7 –do stakeholders consider that there is any merit in amalgamating existing incentives into a single piece of legislation or into a part of existing legislation, such as the income tax act?

Question 4.8 –which Government portfolio is best placed to have ultimate responsibility for tax incentives?

Question 4.9 – do stakeholders agree that the tax incentive report should be given greater prominence in the annual Budget, and include the policy rationale for each incentive? Should a separate report be prepared?

Question 4.10 – how can PNG most simply estimate the value of the tax incentives it provided?

Question 4.11 – do stakeholders agree that the annual report on the value of tax incentives should include the value of any taxpayer of project specific incentive?

Question 4.12 – do stakeholders agree that there needs to be some effort in evaluating the ongoing value of revenue incentives provided in PNG? Which incentives are most in critical need of evaluation?

Other issues

Question 5.1 – do stakeholders agree that, before any decision is taken to substantially change the ITC scheme (including guidelines) an independent, third-party audit of the scheme is requires?

Question 5.2 – for firms that have utilised the enhanced deduction for R&D that was previously available, how did the incentive promote investment in research and development that would not have otherwise occurred? What broader benefits to PNG and the PNG economy did that research and development produce? How might a future R&D concession be framed differently?

Question 5.3 – what value, if any, do the existing research and development incentives (available under section 95) continue to provide?

Question 5.4 – do stakeholders agree that reform of the corporate income tax, with a view to making PNG more attractive to international investment, should focus on a

Executive Summary

Page ix

reduction in overall rates rather than the provision of targeted tax holidays to specific sectors?

Question 5.5 – on what basis should consideration be given to providing exemptions/reductions to GST/Import Duties/Excise?

Question 5.6 – is there value in clarifying, in law, the limitation on tax exemptions available to aid organisations (for example, in clarifying that exemptions apply to the organization and its employees only)?

Question 5.7 – what are stakeholders views about the value of GST exemptions provided for individuals employed in relation to aid projects?

Question 5.8 – should project agreements not include a reference to incentives already available in legislation?

Question 5.9 – do stakeholder’s agree that any provisions in a project agreement purporting to provide tax treatment not generally available under the tax law should be published?

* * * * *

Page 1

CHAPTER 1: OVERVIEW OF TAX INCENTIVES REGIME IN PNG

What are tax incentives? A ‘tax incentive’ is a type of concessional tax treatment (i.e. treatment that is better than the ‘standard’ tax treatment) used to help to achieve a policy outcome. The term ‘incentives’ is usually linked to achieving the policy goal of promoting investment or growth in relation to a particular sector of the economy. However, concessional tax treatment is often provided to achieve broader policy goals (such as encouraging donations to charities). For the purposes of this paper, ‘tax incentive’ is used to describe all concessional tax treatment, regardless of the policy goal being pursued.

There are many ways that the tax system can provide such concessional treatment and usually involves the taxpayer paying less tax or paying tax later than they otherwise would have. The types of tax incentives provided in PNG and elsewhere are described further below.

Tax Incentives Offered in PNG

General incentives

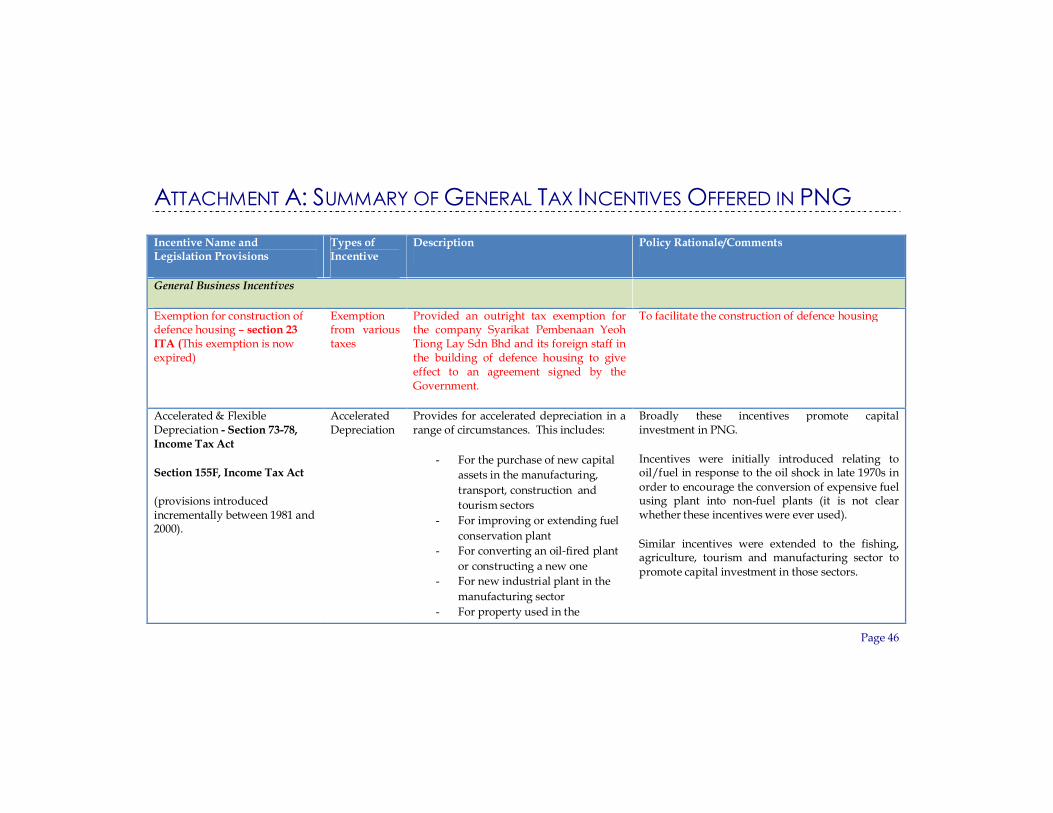

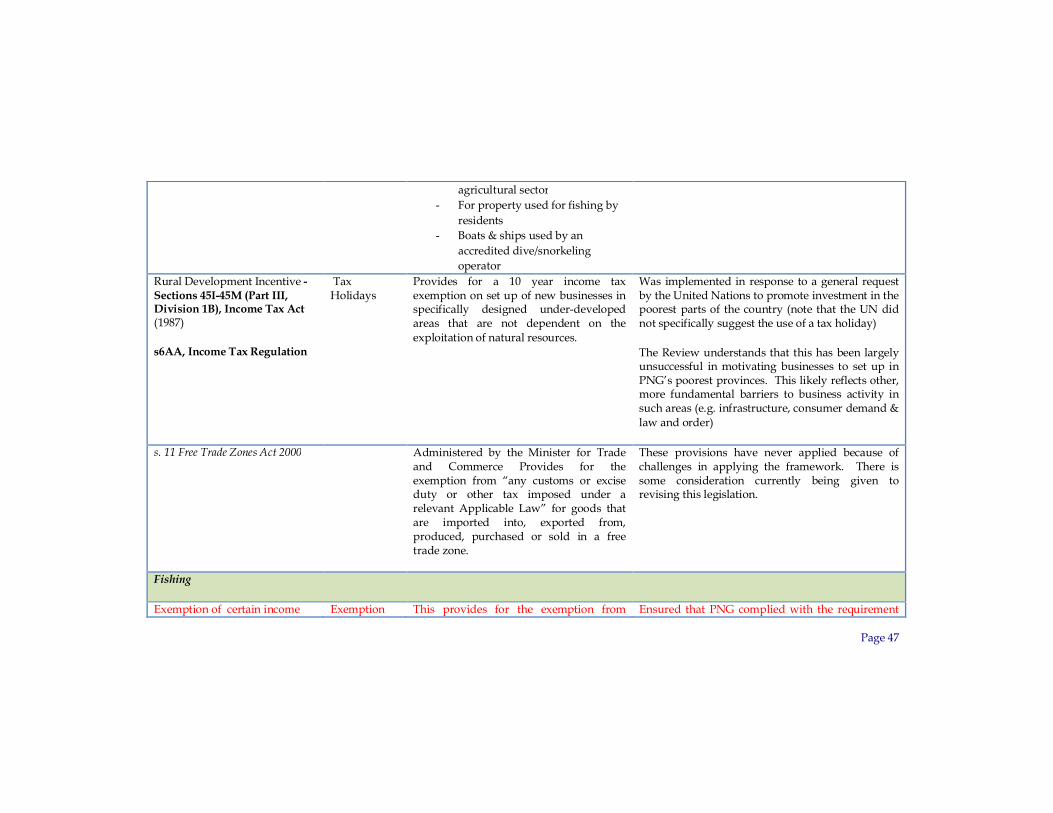

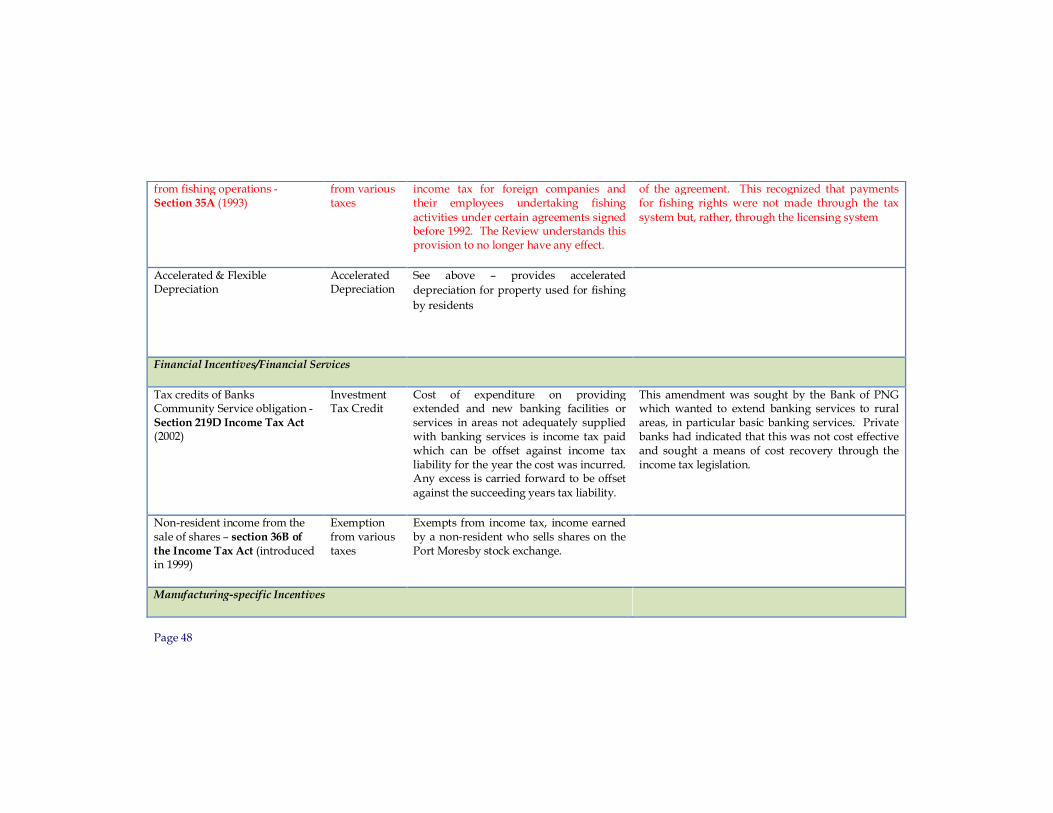

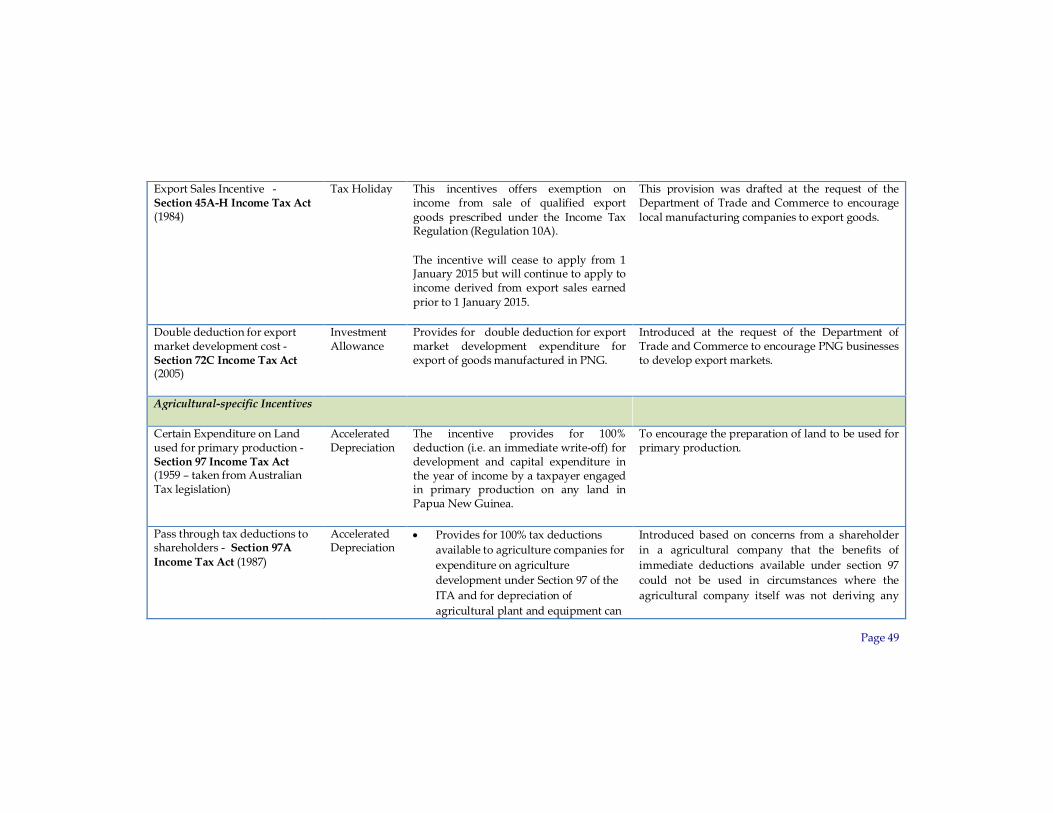

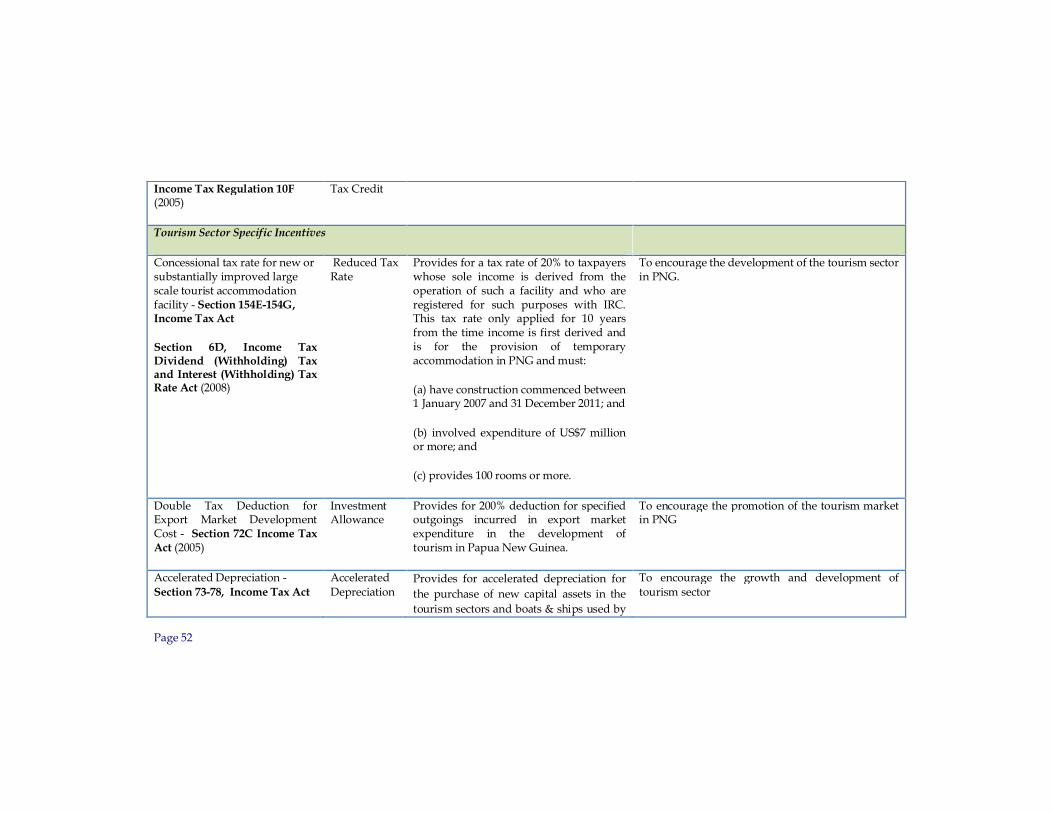

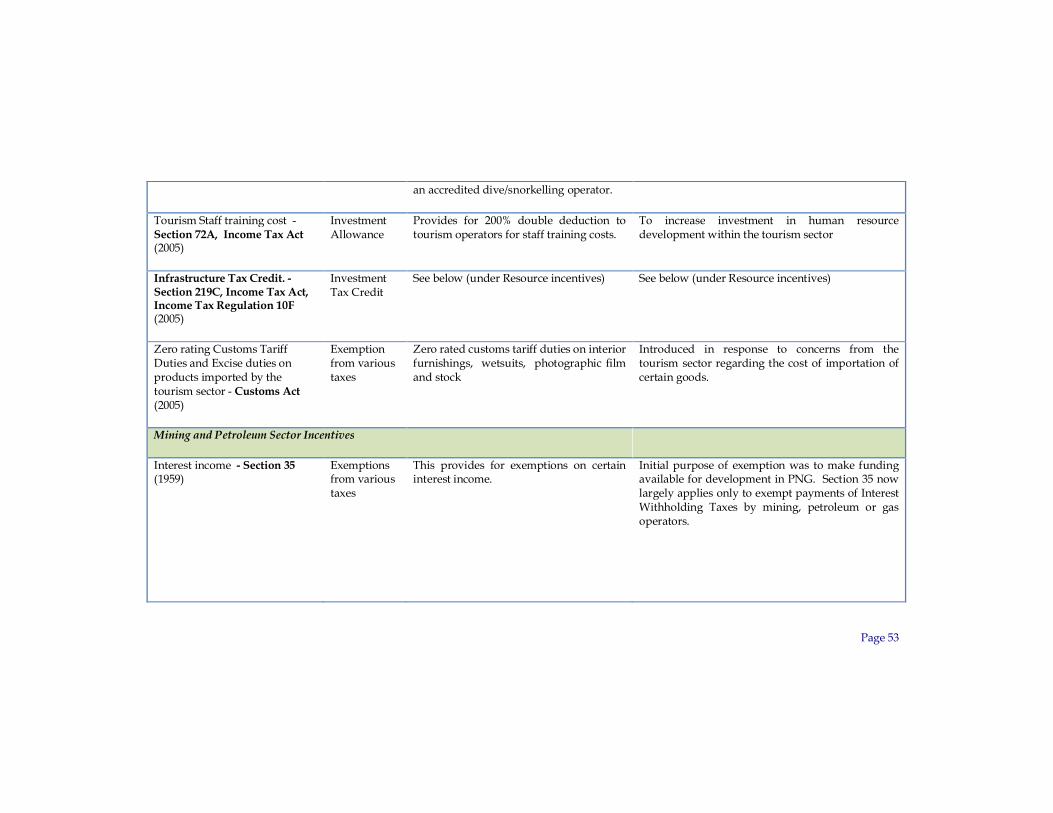

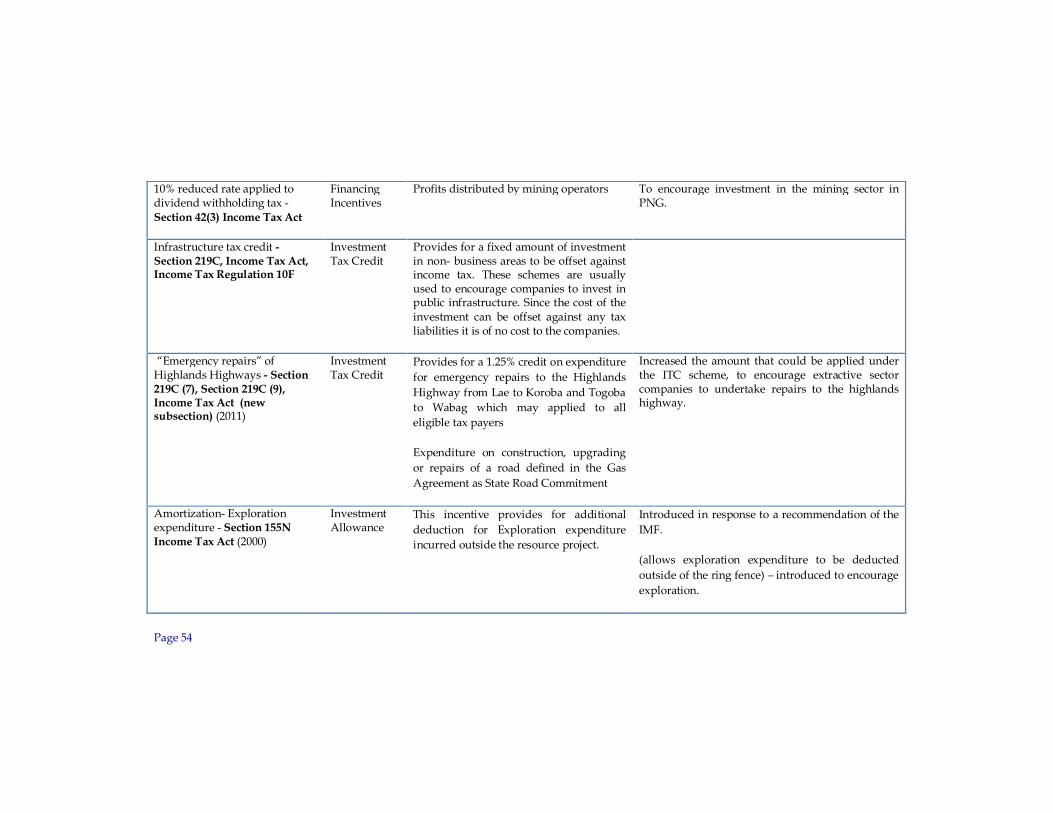

PNG offers a range of incentives. A list of a number of these incentives is found at Attachment A. The table also includes the purpose of each incentive, based on the research and analysis of the Review team.

Question 1.1 – are stakeholders aware of any other tax incentives not captured in the table?

Question 1.2 – do stakeholders agree with the stated purpose of each incentive, as provided for by the Review?

Question 1.3 - are relevant stakeholders able to indicate how individual incentives helped to achieve the stated policy goal?

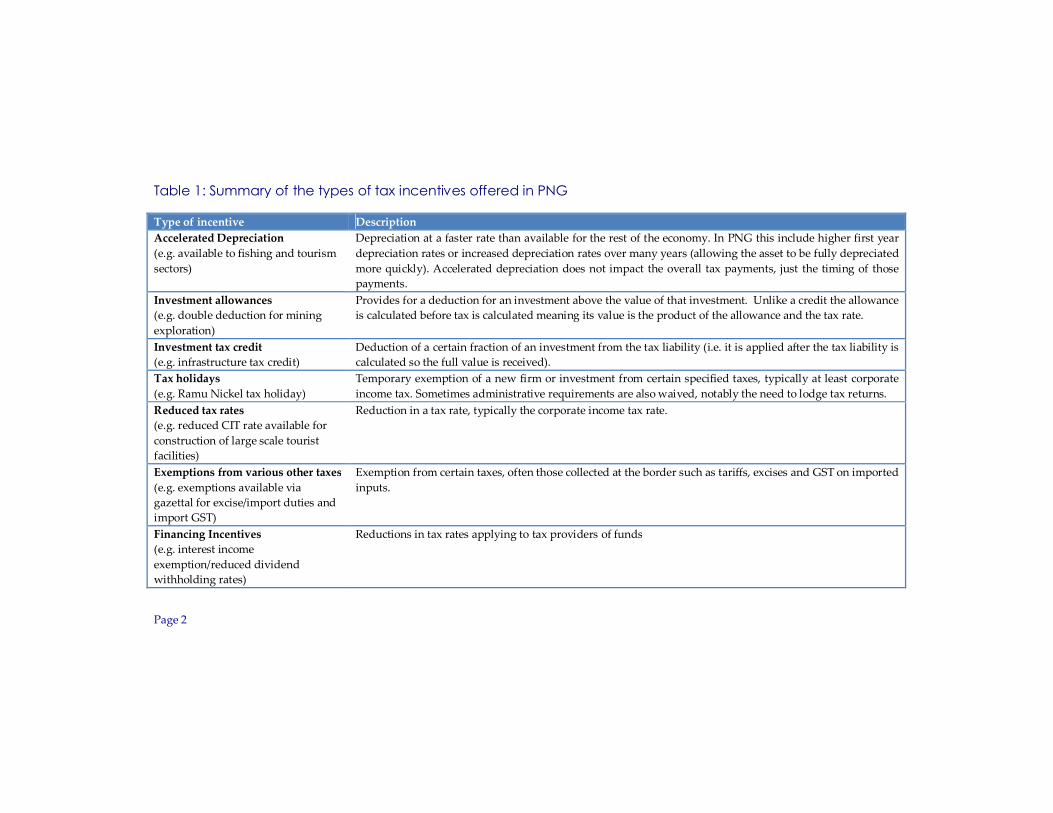

The types of incentives offered are varied and are summarised in the following table.

Page 2

Table 1: Summary of the types of tax incentives offered in PNG

Type of incentive Description Accelerated Depreciation (e.g. available to fishing and tourism sectors)

Depreciation at a faster rate than available for the rest of the economy. In PNG this include higher first year depreciation rates or increased depreciation rates over many years (allowing the asset to be fully depreciated more quickly). Accelerated depreciation does not impact the overall tax payments, just the timing of those payments.

Investment allowances (e.g. double deduction for mining exploration)

Provides for a deduction for an investment above the value of that investment. Unlike a credit the allowance is calculated before tax is calculated meaning its value is the product of the allowance and the tax rate.

Investment tax credit (e.g. infrastructure tax credit)

Deduction of a certain fraction of an investment from the tax liability (i.e. it is applied after the tax liability is calculated so the full value is received).

Tax holidays (e.g. Ramu Nickel tax holiday)

Temporary exemption of a new firm or investment from certain specified taxes, typically at least corporate income tax. Sometimes administrative requirements are also waived, notably the need to lodge tax returns.

Reduced tax rates (e.g. reduced CIT rate available for construction of large scale tourist facilities)

Reduction in a tax rate, typically the corporate income tax rate.

Exemptions from various other taxes (e.g. exemptions available via gazettal for excise/import duties and import GST)

Exemption from certain taxes, often those collected at the border such as tariffs, excises and GST on imported inputs.

Financing Incentives (e.g. interest income exemption/reduced dividend withholding rates)

Reductions in tax rates applying to tax providers of funds

Page 3

In addition, certain fundamental features of PNG’s tax system, such as an absence of taxes on capital gains, can be seen as a significant concession.

As is illustrated in Attachment A, the types of activities trying to be incentivized through the tax system are broad. There has been a particular focus on providing incentives to the manufacturing, tourism, agricultural and extractive sectors. A number of incentives have also been provided to promote the development of areas outside the main urban centres. Similar to other jurisdictions, the tax system has also been used to assist the work of charities and other like non-government organisations.

A number of significant incentives are discussed in more detail below.

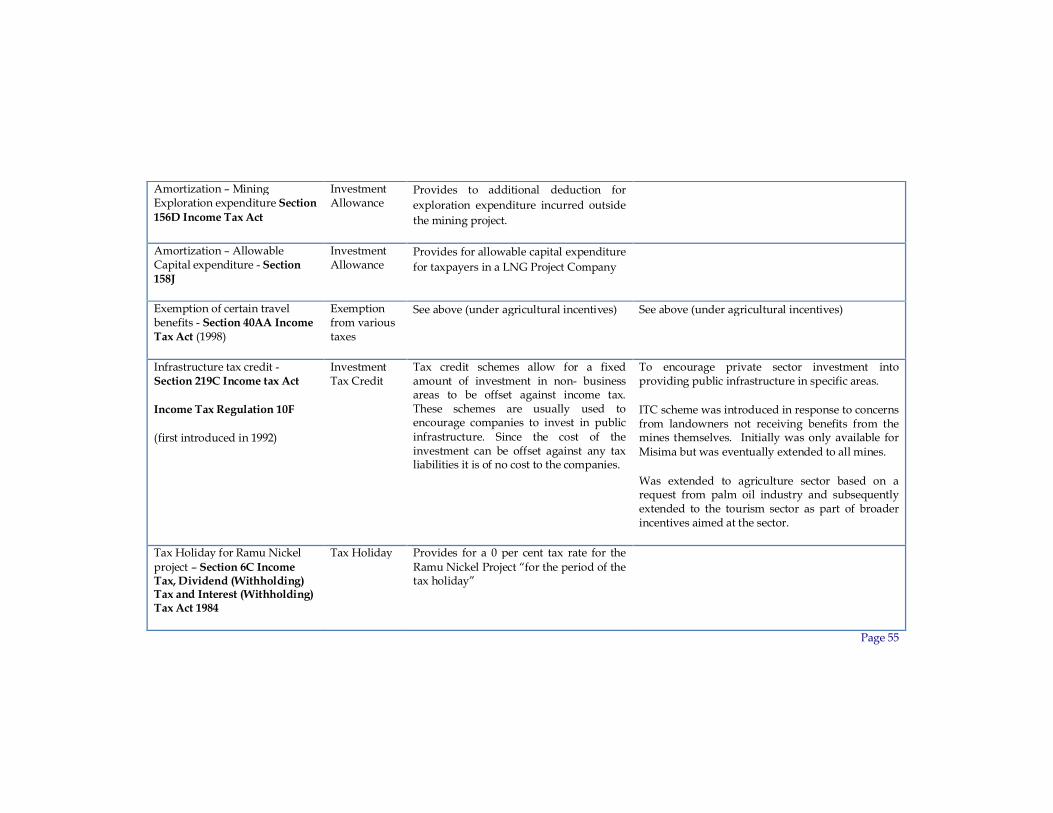

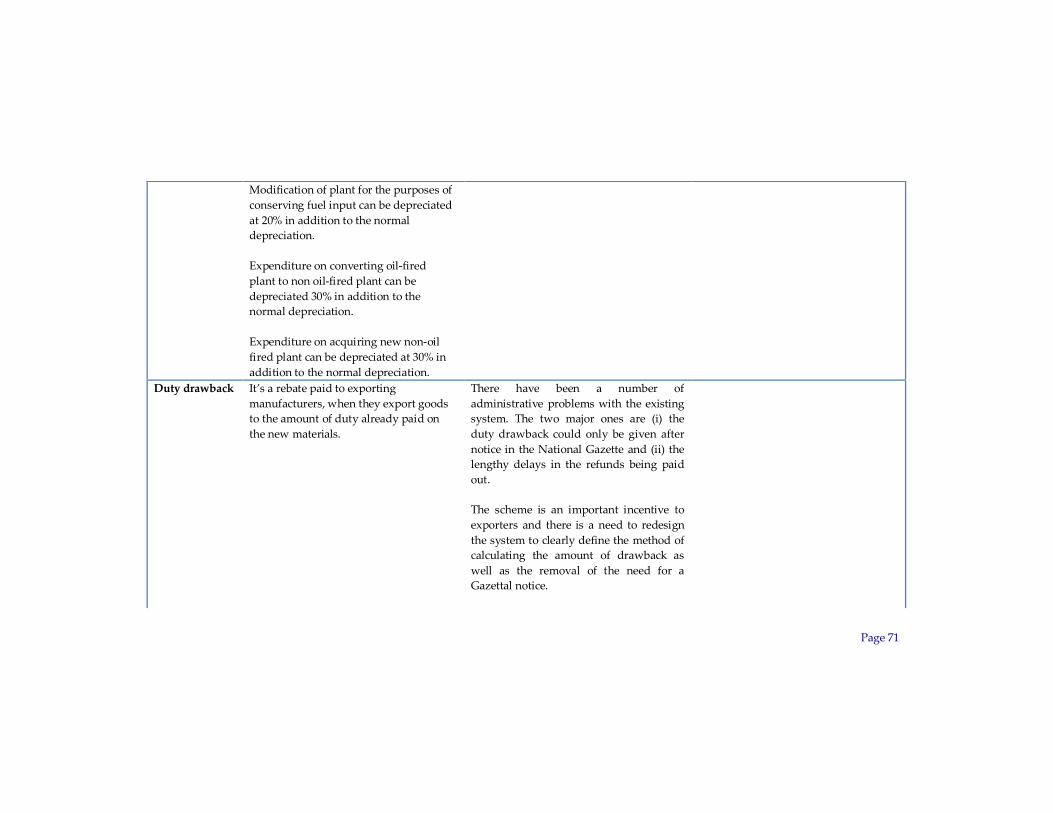

Infrastructure Tax Credit

A discussion on the Infrastructure Tax Credit (ITC) scheme was included in Issues Paper 1, in the context of the Mining and Petroleum Sector.

Under the ITC scheme, eligible companies receive a tax credit for funds expended on approved infrastructure projects – this means that tax payable by the company is reduced by the expenditure and, as a result, there is no cost to the company. The scheme was first introduced in 1992 as a means of utilising mining and petroleum companies as contractors to build infrastructure without the need for an appropriation from Treasury. This would ensure that communities impacted by the resource project would be able to receive tangible benefits from the use extraction of resources in their areas. The scheme recognised both that:

• the National and Provincial Governments lacked the skills and capacity to deliver infrastructure, particularly in remote areas where mining and petroleum activities took place; and

• that resource companies were well placed in these areas to deliver such projects both given their management and construction capacity.

The scheme has undergone a number of changes since its introduction. Key features of the regime are:

• whilst initially only applicable to the mining and petroleum sector, it has subsequently been extended to the tourism and agriculture sectors;

• the amount that can be expended under the scheme in any income year is limited to the lesser of the amount of tax payable or:

- for the mining and petroleum sectors (in general) – to .75 per cent of assessable income;

- for the primary production sector – to 1.5% of assessable income - for the tourism sector – to 1.5% of assessable income.

• companies working on the PNG-LNG project can access an additional 1.25% (making 2% in total);

Page 4

• unused credits can be carried forward for two years; • whilst initially implemented to ensure the delivery of infrastructure in areas

impacted by resource projects, this is not a requirement and “developers are strongly encouraged to undertake projects in parts of the country other than the province or area of impact in which the development is located”;

• whilst initially focused on the construction of infrastructure, the scheme was subsequently extended to maintenance – a response to the recommendations of the 2000 Tax Review.

In addition to the tax credit provisions included in the Income Tax Act (see section 219C) the scheme is governed by the Tax Credit Scheme Guidelines, overseen by the Department of National Planning and Monitoring and last updated in 2001. The guidelines set down the scope of projects that can be funded under the scheme and also the process of having projects approved under the scheme. Efforts are currently underway to update those guidelines, subject to the outcomes of the Tax Review.

Amendments made in 2013 created a new national infrastructure tax credit scheme, allowing projects of national significance to be approved at the discretion of the National Executive Council (NEC) (rather than under the guidelines) with any limits also to be set by NEC. Subsequent amendment were made in the 2014 Budget to remove this aspect of the scheme in response to concerns about the open ended expenditure that it represented. The Review understands that prior to its repeal a number of infrastructure projects in Port Moresby were approved.

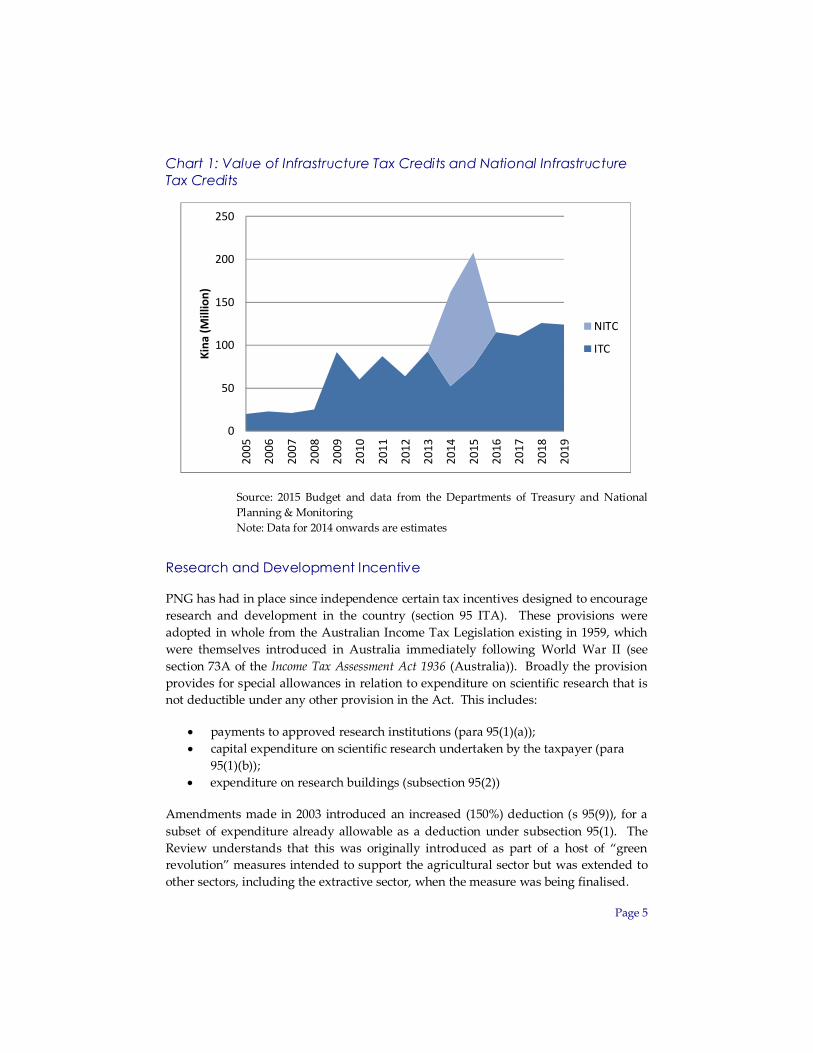

Consistent with recommendations made in the 2000 Tax Review, the value of ITC credits (including projected value) is included in each year’s Budget. This is reflected in Chart 1 below which shows both the ongoing value of the ordinary ITC scheme and the value of projects approved by NEC under the national infrastructure tax credit scheme.

Page 5

Chart 1: Value of Infrastructure Tax Credits and National Infrastructure Tax Credits

Source: 2015 Budget and data from the Departments of Treasury and National Planning & Monitoring Note: Data for 2014 onwards are estimates

Research and Development Incentive

PNG has had in place since independence certain tax incentives designed to encourage research and development in the country (section 95 ITA). These provisions were adopted in whole from the Australian Income Tax Legislation existing in 1959, which were themselves introduced in Australia immediately following World War II (see section 73A of the Income Tax Assessment Act 1936 (Australia)). Broadly the provision provides for special allowances in relation to expenditure on scientific research that is not deductible under any other provision in the Act. This includes:

• payments to approved research institutions (para 95(1)(a)); • capital expenditure on scientific research undertaken by the taxpayer (para

95(1)(b)); • expenditure on research buildings (subsection 95(2))

Amendments made in 2003 introduced an increased (150%) deduction (s 95(9)), for a subset of expenditure already allowable as a deduction under subsection 95(1). The Review understands that this was originally introduced as part of a host of “green revolution” measures intended to support the agricultural sector but was extended to other sectors, including the extractive sector, when the measure was being finalised.

0

50

100

150

200

250

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Kina

(Mill

ion)

NITC

ITC

Page 6

Broadly, the enhanced deduction was for research involving innovation or high degrees of technical risk, undertaken under a plan approved by a Committee. The Committee was to consist of the Commissioner-General as well as two business and two technical experts.

The 2014 Budget removed the 150 percent deduction because of the challenges in administering the highly technical provisions and in obtaining individuals with the necessary skills and experience to effectively assess applications. It was also removed on the basis that the concession had failed to fulfil its policy intent – that is to promote research and development that had broader economic spin-offs where that research would not have been undertaken in the absence of thee concession. The 2014 Budget papers stated that:

While the concept of the R&D incentive is sound, its administration in Papua New Guinea is not feasible at this time. R&D concessions are always difficult to target, and lack of targeting has led to the Government funding R&D expenditures that would have occurred without the R&D tax concession.

Whilst removing the enhanced deduction aspect (i.e. extra 50%) of the regime for expenditure after 1 January 2014, the changes did not remove other concessional aspects of the regime. In addition, there remains the legacy issue of pre January 2014 claims awaiting approval from a Committee that is not currently established. From a tax system perspective these legacy issues are significant – the 2014 Budget noted that these claims represented a K2.4 billion contingent liability - or almost 30% of total Government tax revenue in any given year (based on 2013 amounts). The Review also understands that a significant proportion of the claims relate to research and development undertaken by the oil and gas sector.

Industrial Development (Pioneer Status) Act

Whilst long repealed it is worth noting the Industrial Development (Pioneer Status) Act, given that a number of submissions to the Review have argued for its reinstatement (this is considered further in Chapters 3 & 4 below). Introduced in the 1990s and administered by the then Ministry of Commerce and Industry, the Act provided a five-year corporate income tax holiday to ‘pioneer’ firms investing in manufacturing/pioneering activities in PNG. The Act was repealed in 1999 as part of the Structural Adjustment Program (SAP) for two key reasons1:

• to restore fiscal stability through expanding the tax base; and

• the legislation was in conflict with the Multilateral Trade Agreement on Subsidies

1 See Department of Trade, Commerce & Industry, 2014, ‘Submission to the PNG Tax Review – Re-Introduction of the Industrial Development (Pioneer Status) Act

Page 7

and Countervailing Measures – this was because the Act applied only to a firm that proposed to manufacture goods solely for export which was regarded as a ‘subsidy’ under the agreement.

Free Trade Zone Act

In July 2000, Parliament passed the Free Trade Zone (FTZ) Act 2000 establishing the framework and mechanism for the creation and operation of free trade zone. The purpose of establishing FTZ was to bring investment and to set up processing industries with export and employment creation potential in the less developed border provinces, particularly, Sandown, Western, Gulf and North Solomon’s Province.

Following the enactment of the legislation, it was recognised that having a FTZ in those border provinces would be challenging given the absence of sufficient infrastructure. The Government subsequently decided to develop the concept of a Special Economic Zone, incorporating this into its overall economic development strategy in 2008. The Pacific Marine Industrial Zone in Madang is the first project to be implemented under the SEZ concept.

Tax issues associated with SEZ’s are discussed further in Chapter 5 below.

Taxpayer and project-specific incentives

In addition to the range of general incentives available in the law, PNG has also provided a series of taxpayer-specific or project specific tax incentives.

In the Mining sector this includes the Ramu Nickel Project which was given a 10 year tax holiday. Whilst initially included in the relevant project agreement this incentive was also incorporated into legislation in the Income Tax, Dividend (Withholding) Tax and Interest (Withholding) Tax Act (see section 6C).

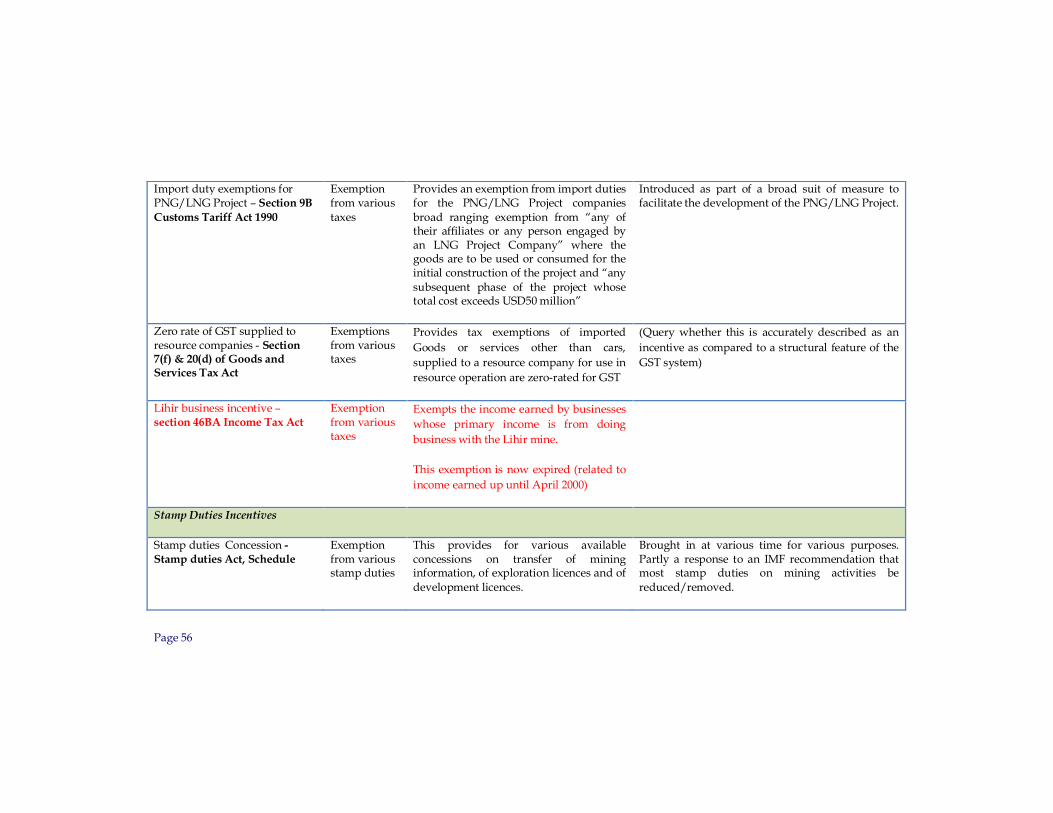

Similarly, the PNG-LNG Project has been granted a series of exemptions that have been prescribed in legislation. This includes, for example, an exemption from import duties provided for under section 9B of the Customs Tariff Act 1990 Customs Tariff Act). Special accelerated depreciation rules are also applicable to the Project (section 158J ITA)

In addition, a number of pieces of tax legislation allow for the Governor General, acting on advice and through a gazettal notice, to provide for an exemption (or reduction) from the relevant tax or duty in specific circumstances. This includes:

• in relation to import duties, under section 9 of the Customs Tariff Act (however exemptions by gazettal cannot be provided in relation to commercial projects);

• in relation to excise, under section 3 of the Excise Tariff Act 1956; • in relation to the Goods and Services Tax (GST), under subsection 25(8) of the

Page 8

GST Act; and • in relation to income tax, a charitable organization can be prescribed under

subsection 25A(3) of the Income Tax Act

The Review team has been unable to identify a comprehensive list of projects or entities that have been provided exemptions or reduced rates under these provisions.

The Review has, however, been able to identify a number of project agreements between PNG and various companies. These agreements include clauses relating to the provision of investment incentives, including tax incentives. In some cases these simply restate the ability of the company to be able to access incentives generally available in the law. In other cases they provide for the company or project to be granted specific incentives such as those that can be made available by gazettal as identified above. Under these agreements the State has an obligation to ensure that the required authorisation for the relevant incentive (for example, gazettal) is put in place.

The Review is aware also that a number of agreements may have been signed with fishing operators, providing valuable fishing licenses in exchange for an undertaking to develop some downstream processing facility (such as a canning facility). Whilst not strictly a tax incentive this can be seen in the same light as a tax incentive (revenue is foregone in exchange for pursuing some other policy goal such as encouraging value adding and downstream processing) particularly given the role that fishing license fees play in the absence of being able to effectively apply the corporate income tax regime to offshore fishing vessels (this was discussed in Issues Paper 2).

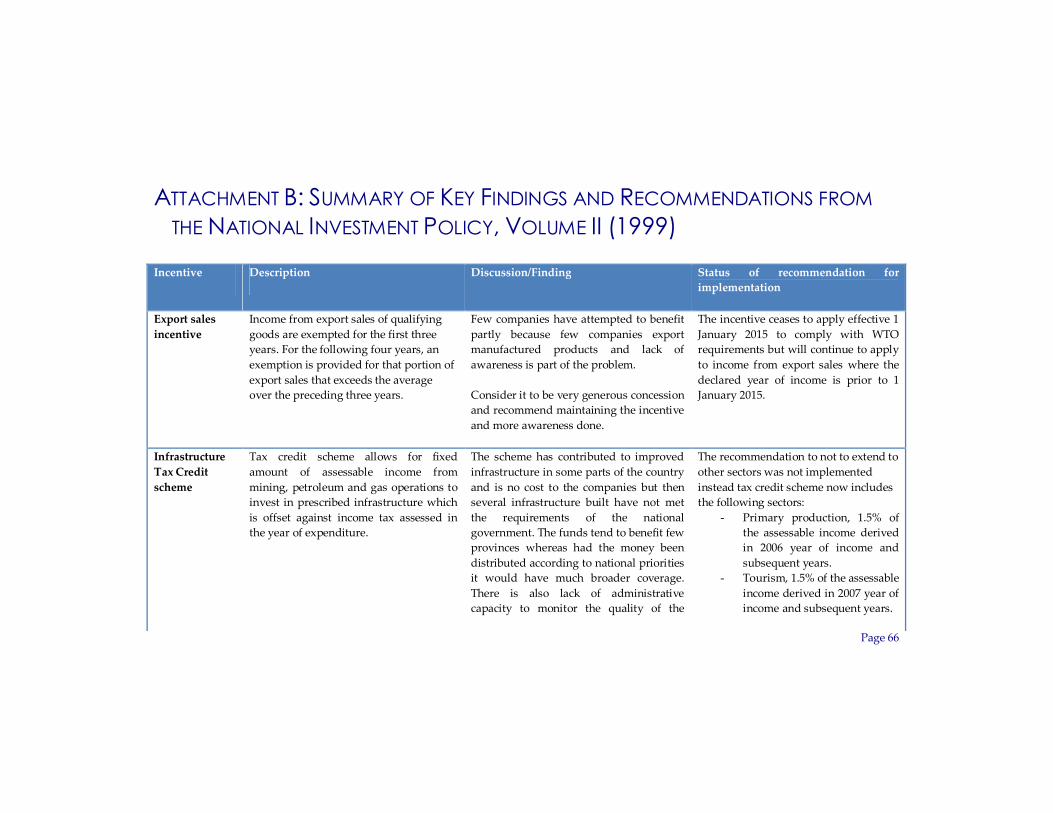

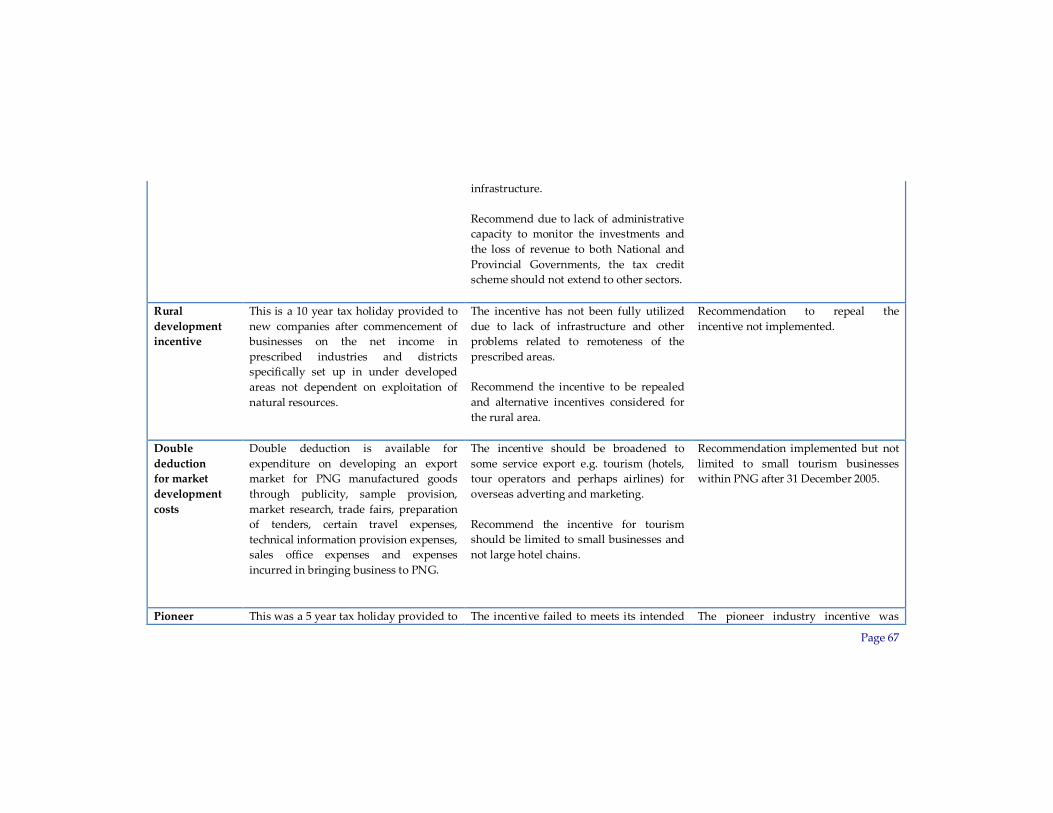

Policy framework governing the award of tax incentives in PNG The Review has been unable to identify any recent, clear overall government policy framework governing the granting of tax incentives in PNG. The closest document is the National Investment Policy (Volume 2), produced by the then Department of Commerce and Industry and approved in 1999. The Review understands that this document continues to be used by the now Department of Trade, Commerce and Industry to guide its work in this area.

Of note, five key points are highlighted by the paper in relation to tax incentives:

• The investment regime must be seen as stable

• Tax incentives should be properly targeted

• Incentives should take into account limitations in administrative capabilities

• Tax holidays do not necessarily encourage investment

Page 9

• The investment regime should have few distortions

The policy notes that “company specific negotiations are seen as the major disincentive to investing in PNG, and should therefore be avoided in favour of the rules based system of incentives”. A number of these themes are again picked up in Chapter 2 below.

As well as providing a high level policy guide, the Policy also represents the most recent attempt to assess the effectiveness of various incentives existing at the time. Findings and recommendations in relation to specific incentives are summarised at Attachment B together with an indication of whether those recommendations were subsequently adopted.

In addition to the National Investment Policy, PNG also has a range of development and fiscal policies that form part of the existing policy framework that could be considered relevant to the provision of incentives. These plans and policies, and their relevance to the tax reform process, were discussed in detail in Issues Paper 3 issued by the Committee. Relevantly, the development plans set forth an ambitious agenda for economic growth and development. In addition the recently published National Strategy for Responsible Sustainable, from the Department of National Planning and Monitoring, seeks to place these development plans on a sustainable footing. This development, to be sustained, needs to be funded in large part through PNG’s revenue system. The cost (in terms of foregone revenue) of tax incentives need to be considered in that context.

The Medium Term Fiscal Strategy specifically considers tax incentives. It identifies the need to ‘restrict taxation exemptions and special arrangements’ with a particular focus on eliminating special tax concessions for all new resource projects.

Sector-specific plans, such as the National Agriculture Development Plan (2007-2016) have also had a role in suggesting tax incentives for particular areas of the economy.

A number of specific incentives in the law also have guidelines that govern their award. As noted above, the Infrastructure Tax Credit is governed by its own guidelines. These guidelines are currently under Review by the Department of National Planning and Monitoring.

The Review also understands that there may be informal policy frameworks guiding the provision of incentives. For example, the Review understands from the Department of Trade, Commerce and Industry, that in the context of project-specific agreements, excise duty exemptions will generally only be provided:

• in relation to machinery during the construction phase of a project;

• where such goods cannot be source locally;

Page 10

• in relation to new of stagnant sectors of the economy; and

• after an assessment of the benefits to be provided by the project, measured against the revenue foregone from the provision of the incentive.

Compliance with World Trade Organisation obligations

One important consideration for PNG, as with all World Trade Organisation (WTO) members, is that any incentives need to be compliant with their WTO obligations. A number of disputes considered by the WTO’s Dispute Settlement Body have confirmed that the principles and rules underlying the WTO (including but not limited to the principle of non-discrimination) can impact a country’s direct and indirect taxes (Daly 2005, p25). With respect to indirect taxes (for example excise) this will be an issue where the tax system provides for different treatment between imported and locally produced products.

Similarly direct tax measures may contravene WTO rules where they discriminate between investors – this could include measures designed to provide assistance for export activities, provide protection against imports or to support domestic production. In PNG, the export sales exemption currently available under the Income Tax Act2 is an example of one such direct tax measure – this tax incentive will cease to apply from 1 January 2015 to ensure that PNG is compliant with its WTO obligations.

Process for the awarding of tax incentives The idea for the provision of a new incentive may arise in a number of different ways. It may arise as part of the general deliberations of Government, as part of a Department’s work in trying to identify a means of assisting a particular group or sector of the economy or through a direct request from a particular taxpayer or sector.

Whichever way the idea for the incentive arises, as the provision of tax incentives requires either the amendment of existing law, or the issuing of a gazettal notice (by the Governor-General acting on advice), the decision to provide a tax incentive is one for Government (through the key decision making body – the National Executive Council (NEC)) and, where amendments to legislation are required, Parliament.

The Government, through the NEC, needs to make a decision on whether to grant an incentive based on the perspective provided by various agencies. These perspectives

2 See attachment for more information. Broadly incentive provides that income from export sales of qualifying goods are exempted for the first three years. For the following four years, an exemption is provided for that portion of export sales that exceeds the average over the preceding three years

Page 11

may be different but equally important in assessing the merits of a particular incentive. Notably:

• the Department of Treasury has overarching policy responsibility for the tax system and for considerations of fiscal sustainability going forward;

• the Department of Trade, Commerce and Industry has responsibility for promoting investment and trade;

• the IRC and Customs have an interest in both the impact of any incentive on the overall revenue system and on its ability to be effectively administered; and

• the Department of National Planning and Monitoring has an interest in the sustainability of the revenue system going forward to fund development.

In addition, particular Departments and agencies will have an interest in incentives relevant to their portfolios (for example, the agencies responsible for the extractive sectors in relation to incentives sought by mining and petroleum companies, or the Department of Foreign Affairs regarding exemptions for international organisations or aid purposes).

However, with the exception of the ITC (which has in place a formal process), there does not appear to be a clear and defined process for relevant Government agencies to come together to assess the merits of particular incentives and provide advice to Government3. This is in contrast to the approach taken in other countries, most recently in the Solomon Islands as discussed further below in Chapter 2 below.

As a result of this, the Review understands that the process for analysing, advising on and ultimately deciding on the provision of tax incentives is often ad hoc which is perhaps reflected in the scope and type of incentives found in PNG (see Attachment A).

Reporting on and valuation of tax incentives As will be discussed in Chapter 4 below, a number of jurisdictions around the world do report the type and cost of their tax incentives. This helps to promote the overall transparency of the tax incentives regime and to provide a clear picture to Government of the revenue consequences of providing the incentive.

3 Although the Review understands that an inter-Departmental working group had previously been established for a similar purpose.

Page 12

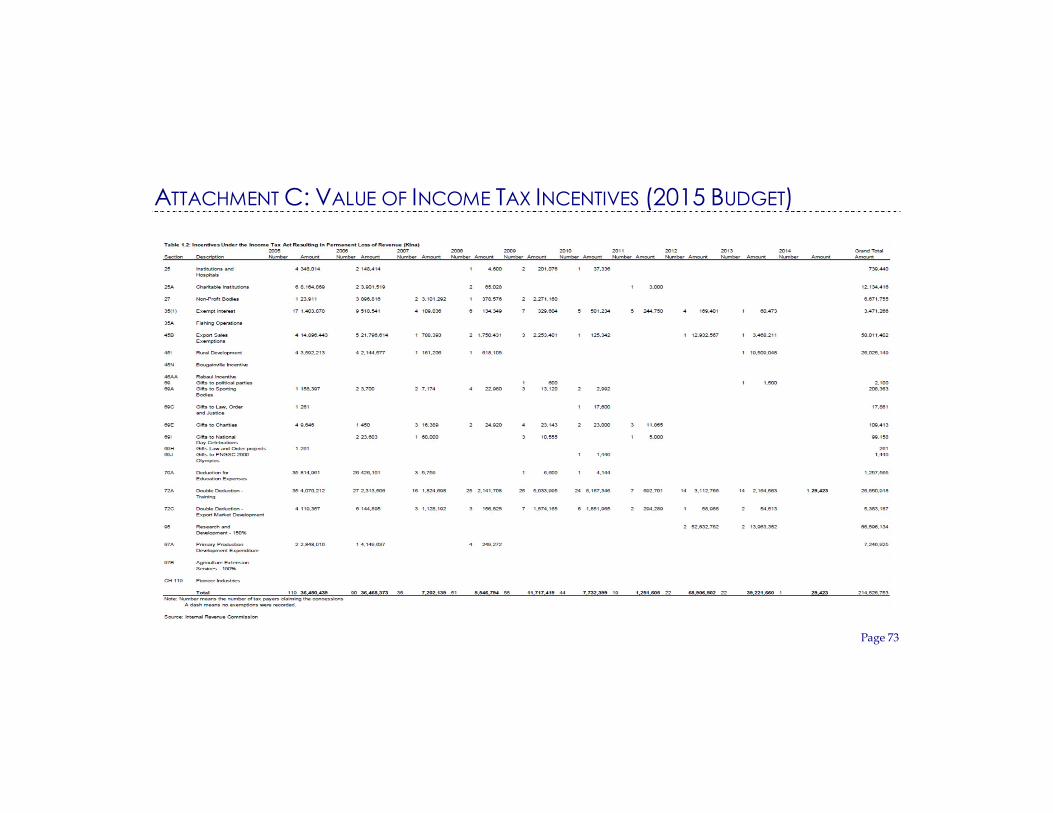

Some limited reporting of incentives is provided for each year as part of PNG’s Budget documents. The recent 2015 Budget, for example, included tables outlining the costs of the infrastructure tax credit scheme, certain incentives provided under the Income Tax Act (both resulting in a permanent loss as well a deferral of revenue) as well as the value of exemptions provided under the Stamp Duties Act.

The table outlining the estimated revenue foregone as a consequence of incentives provided under the income tax law is extracted at Attachment C. It estimates that, since 2005, the value of incentives in terms of revenue foregone is estimated to be K214 million. Much of the information in relation to these is taken from income tax returns4. However, this information is unlikely to reflect the true value of the incentive being provided as it relies on the voluntary disclosure by the relevant taxpayer. The information is also incomplete as it does not include the value of revenue foregone from all incentives available under the income tax law, including those applying to specific taxpayers such as Ramu Nickel Project or the PNG LNG Project (this may reflect restrictions previously imposed by the tax secrecy provisions but which have been addressed as part of changes made in the 2015 Budget).

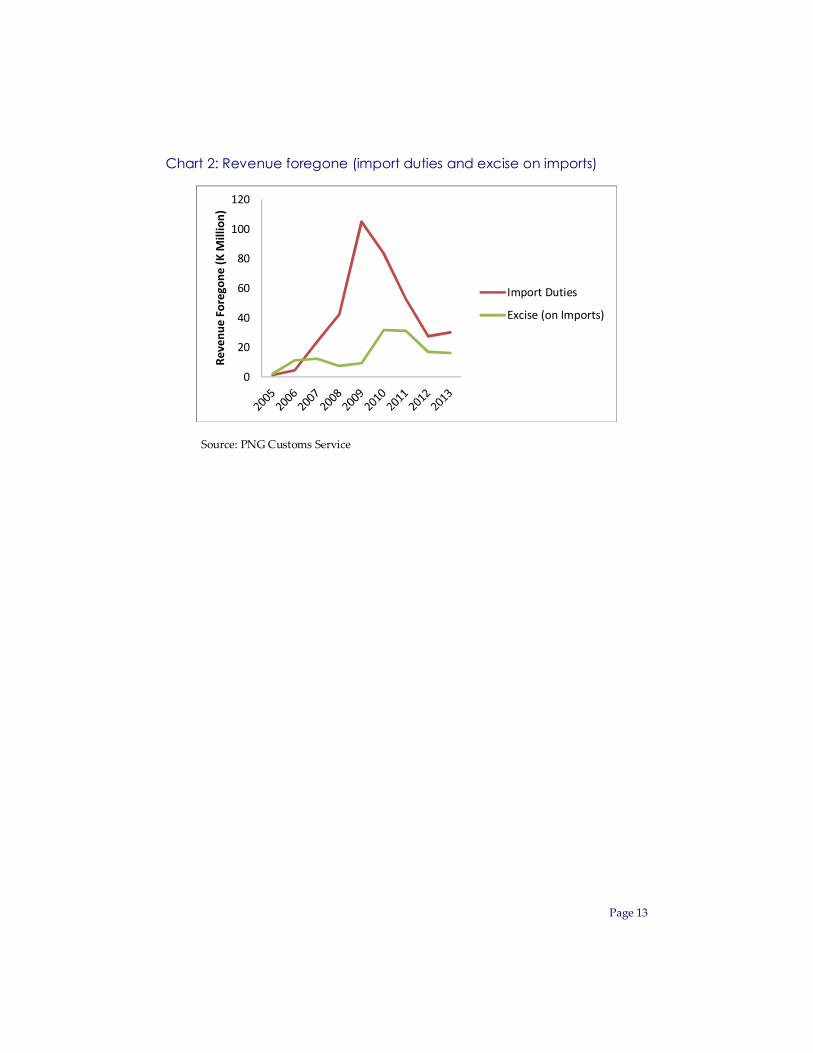

The Review has also obtained some information from PNG Customs Service (PNGCS) regarding the revenue foregone for various exemptions available in relation to the revenue streams that they collect – namely, GST (Import), Import Duties (i.e. tariffs) and Import Excise Duties.

The revenue foregone from GST (Imports) was estimated at K434 million in 2013. However, it would be incorrect to see this as an ‘incentive’ as much of this would relate to exemptions available to natural resource projects. As will be explored further in the issues paper relating to GST, providing an exemption from GST for enterprises engaged wholly in exports (such as extractive companies) is a basic feature of many GST systems. This highlights the importance of distinguishing between tax treatment that is an ‘incentive’ and one that is simply a standard feature of the tax system.

Chart 2 below illustrates the estimated value of revenue foregone from exemptions available for import duties and excise. The large increase in import duty exemptions are a consequence of imports made during the construction phase of the PNG-LNG Project.

4 In particular, see Form C (Company Return), available at http://www.irc.gov.pg/tax_form.html

Page 13

Chart 2: Revenue foregone (import duties and excise on imports)

Source: PNG Customs Service

0

20

40

60

80

100

120

Reve

nue

Fore

gone

(K M

illio

n)

Import Duties

Excise (on Imports)

Page 14

CHAPTER 2: THE ADVANTAGES AND DISADVANTAGES OF TAX INCENTIVES

The terms of reference to the Review specifically request the Tax Review Committee to consider the advantages and disadvantages of tax incentives. Some consideration was given to this in Issues Paper 1 (in that context, incentives specific to the mining and petroleum sector) and in the Broad Directions Paper (Issues Paper 3). The points raised in those papers are expanded on here.

Of note, this paper does not look at the merits of otherwise of incentivising particular activities. In many cases, there are clear justifications for Government trying to find ways of achieving a particular policy outcome (such as helping to grow a particular sector of the economy or encouraging the training of staff). Rather, this paper looks at the role that the tax system can play in this, and the advantages and limitations that it has in playing such a role.

This Chapter also looks at a number of international examples of how other countries have approached tax incentives.

Advantages of tax incentives Many countries, developed and developing alike, use their tax system to incentivise particular activities. There may be a number of reasons for this. This includes:

• Producing broader benefits: Incentives may aim to encourage activities that produce benefits for society that the private market does not fully take into account (“positive externalities”). Incentives for training for research and development are often justified on this basis.

• Increasing competitiveness: Incentives may also be justified on the basis that they make a country more competitive, allowing it to compete for foreign direct investment with its neighbours.

• Compensation for other costs: Tax incentives may also be used to compensate businesses for other costs of doing business in the country such as poor infrastructure, crime problems, corruption, or unnecessary red tape.

Question 2-1 – what other advantages do tax incentives have, particularly in the PNG context?

Page 15

Disadvantages of Tax Incentives Much has been written about the disadvantages of tax incentives and, in particular, the challenges they pose to developing countries such as PNG5. A number of these issues were considered in Issues Papers 1 and 3 released by the Committee.

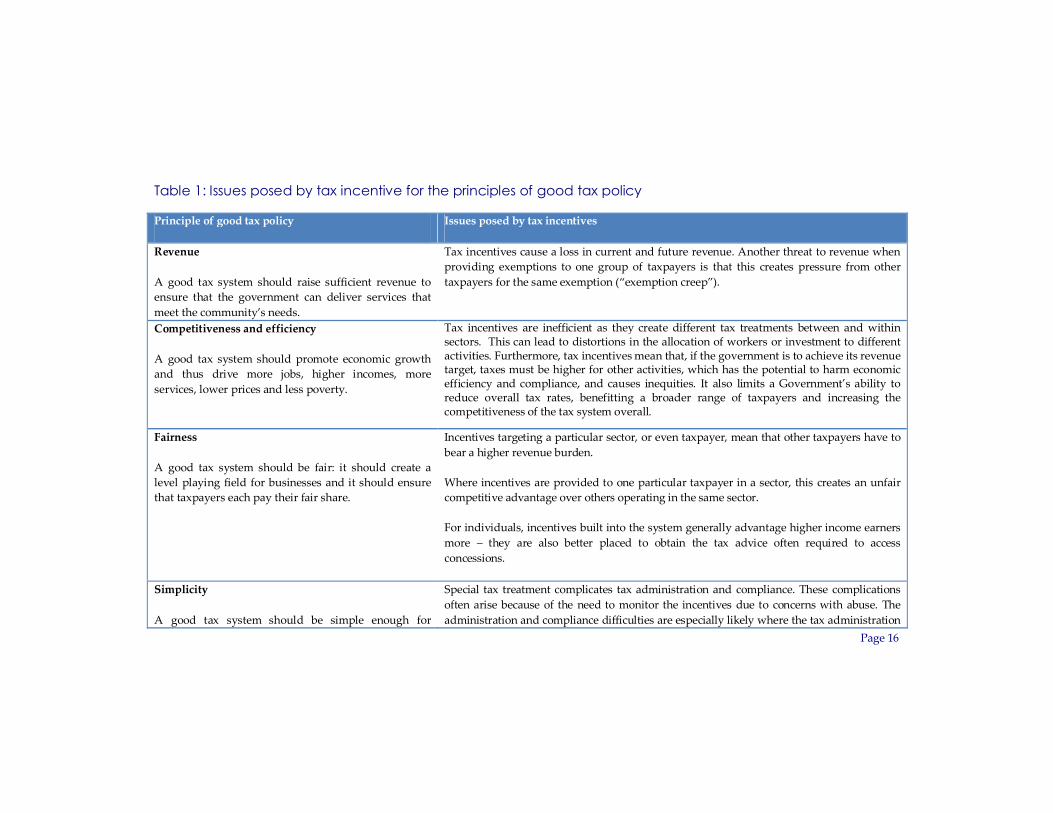

However, it is worth reflecting on these limitations in the context of the broad principles for good tax policy outlined in Issues Paper 3. These are listed in Table 1 on the following page.

In addition to the issues that tax incentives pose in relation to good tax policy principles, there is a very real question as to whether using the tax system is effective in achieving the desired policy goal. As was noted in the National Investment Policy, tax incentives may be redundant as they do not lead to a change (or a limited change) in the intended behaviour, with the incentive simply providing a windfall gain for firms that were going to undertake the activity anyway. This appears to have been the case with the R&D concession.

Where the policy problem trying to be addressed is a non-tax problem then there may be a more direct means of fixing the problem. For example, if the problem is simply the broader cost of doing business, a more direct means of assisting taxpayers is through direct grants – this has the same effect as a tax incentive designed to reduce a tax burden but allows for greater control on costs because overall spending is limited by the budget allocation.

Another example may be the tourism sector. The tax system is unlikely to be a significant reason why tourists do not choose PNG as their holiday destination. Rather this is more likely to relate to issues such as law and order and cost of travel.

There have been a number of international studies undertaken on the value of tax incentives, including with respect to developing countries. The evidence suggests that tax incentives rarely have any significant effect on investments. A recent study of 40 developing countries found that tax incentives had no effect on economic growth and aggregate investment (Klemm & Van Parys, 2009).

5 See a list of references at the end of this Issues Paper

Page 16

Table 1: Issues posed by tax incentive for the principles of good tax policy

Principle of good tax policy Issues posed by tax incentives

Revenue A good tax system should raise sufficient revenue to ensure that the government can deliver services that meet the community’s needs.

Tax incentives cause a loss in current and future revenue. Another threat to revenue when providing exemptions to one group of taxpayers is that this creates pressure from other taxpayers for the same exemption (“exemption creep”).

Competitiveness and efficiency A good tax system should promote economic growth and thus drive more jobs, higher incomes, more services, lower prices and less poverty.

Tax incentives are inefficient as they create different tax treatments between and within sectors. This can lead to distortions in the allocation of workers or investment to different activities. Furthermore, tax incentives mean that, if the government is to achieve its revenue target, taxes must be higher for other activities, which has the potential to harm economic efficiency and compliance, and causes inequities. It also limits a Government’s ability to reduce overall tax rates, benefitting a broader range of taxpayers and increasing the competitiveness of the tax system overall.

Fairness A good tax system should be fair: it should create a level playing field for businesses and it should ensure that taxpayers each pay their fair share.

Incentives targeting a particular sector, or even taxpayer, mean that other taxpayers have to bear a higher revenue burden.

Where incentives are provided to one particular taxpayer in a sector, this creates an unfair competitive advantage over others operating in the same sector.

For individuals, incentives built into the system generally advantage higher income earners more – they are also better placed to obtain the tax advice often required to access concessions.

Simplicity A good tax system should be simple enough for

Special tax treatment complicates tax administration and compliance. These complications often arise because of the need to monitor the incentives due to concerns with abuse. The administration and compliance difficulties are especially likely where the tax administration

Page 17

taxpayers to understand and meet their tax obligations. It should also minimise the administrative costs for government and for the taxpayer.

is also weak.

The inability of PNG to effectively implement the R&D incentive, as highlighted above, is an example of this. Complexity is a particular concern in PNG. Discussions with IRC and PNGCS have confirmed that significant resources need to be devoted to administering incentives.

Tax incentives can also complicate the affairs of taxpayers as it encourages tax planning.

Trust in and accountability of government A good tax system including a reliable tax administration should build trust and confidence in government and should be transparent and encourage greater government accountability and integrity.

Tax incentives can create opportunities for tax abuse and corruption. An example of such abuse can be transfer pricing between related parties to ensure profits are made in exempt activities and deductions in fully taxable activities.

Page 18

It is worth noting also that a recent analysis of the key reform priorities for business conducted by the Institute of National Affairs in conjunction with the Asian Development Bank (INA 2014) confirmed that the top areas of reform from a business perspective were law and order and corruption. Tackling these will involve, amongst other things, a steady revenue base to pursue reforms.

Of note from a revenue perspective:

• Reform of the company tax rate was the fifth in order of priority • Stability of rules was the seventh in order of priority • Subsidy/tariff support was ninth in order of priority • Local level government taxes and rules were tenth in order of priority • The GST was twentieth in order of priority

Question 2-2 – what other disadvantages do tax incentives have, particularly in the PNG context?

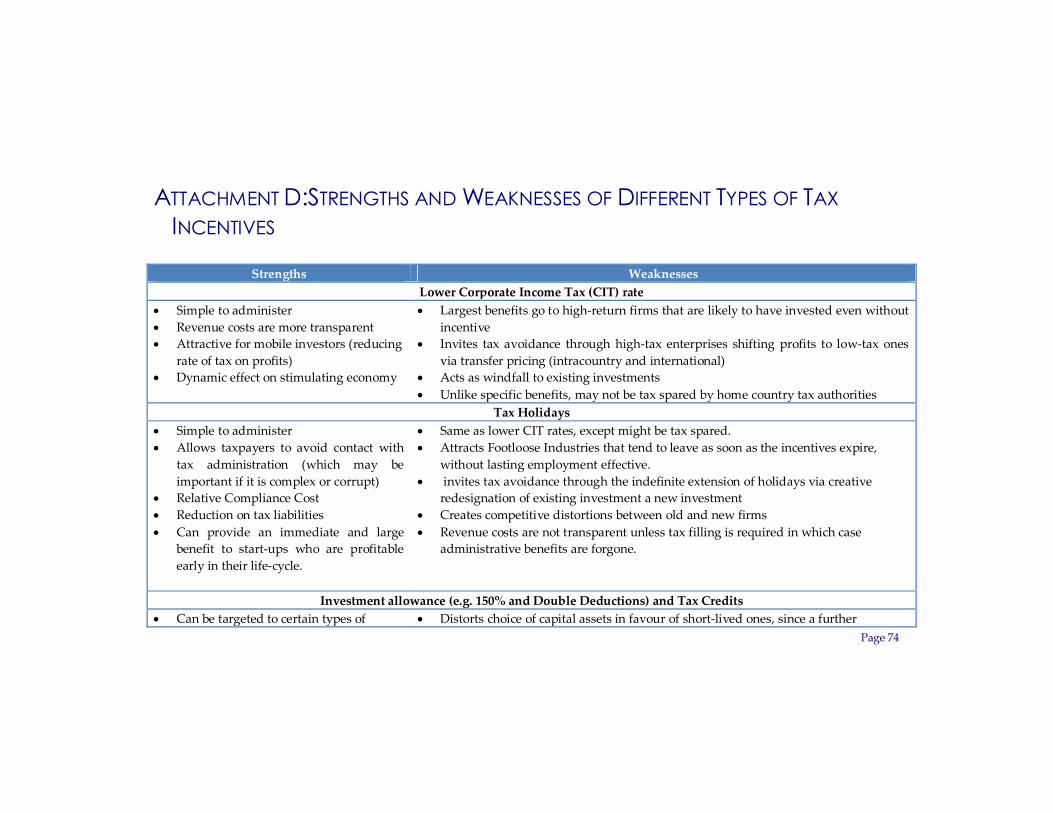

Strengths and weaknesses of particular incentives In addition to the advantages and disadvantages of tax incentives generally, certain types of incentives have particular strengths and weaknesses. A list of these is at Attachment D.

As noted in Issues Paper 1, there are particular concerns around the use of tax holidays. To the extent that they are of any value, they tend to attract footloose firms that leave as soon as the incentive expires, without lasting employment benefits. This was the finding in the National Investment Policy in relation to the 5-year corporate income tax holidays available under the Pioneer Status Act. The Policy found that:

The incentive failed to meets its intended purpose as businesses granted the incentive ceased operating on expiry of the incentive period.

In other circumstances, a tax holiday may actually be of little use in promoting investment in new enterprises which are often unprofitable in the early years and unlikely to benefit from the incentive.

In addition, tax holidays are arguably poorly targeted as they are not generally linked to any level of investment, which is what they are trying to promote. This can be contrasted to other incentives such as accelerated depreciation and investment allowances which, by their nature, require some investment by the taxpayer.

In general accelerated depreciation is the preferred (and least harmful) form of tax incentive. It is less costly for revenue collections than income tax holidays, investment allowances or tax credits and generally provides less scope for tax abuse.

Page 19

As a second-best alternative, investment allowances and investment tax credits are more cost effective than income tax holidays. As indicated above, unlike tax holidays, these credits/allowances require actual investment by the business. They also allow better targeting of particular types of investment, and their fiscal costs are more transparent and easier to control.

The provision of ‘border taxes’ such as import duties, excise and import GST has some drawbacks. If not appropriately targeted they can generate an unfair competitive advantage to those firms receiving the incentive and may be open to abuse or leakage into the domestic economy (with goods being onsold for lower prices or used for purposes other than which the incentive was provided).

Question 2-3 – do stakeholders have any other views about the merits of particular types of tax incentives?

International experience with tax incentives Most countries in the world provide some form of tax incentive. Details on incentives provided in the Asian region, for example, are available on the Asian Development Bank website.6

As noted above, much has also been written about the challenges posed by tax incentives to developing countries in particular and PNG can learn much from the experiences of like countries. This was most recently highlighted in a report to the G20’s Development Working Group which stated that (OECD 2014, p22):

The damage to the revenue base that erodes the resources for the real drivers of investment decisions — infrastructure, education and security — is compounded by the lack of transparency and clarity in the provision, administration, and governance of tax incentives in developing countries.

A recommendation to the G20 for the IMF, OECD, UN and World Bank to develop a report in 2015 to develop a guide on how best to balance investment and public revenue priorities and to estimate the costs of tax incentives should be followed closely in PNG.

Attachment E also contains case studies on tax incentive issues that have arisen in a number of jurisdictions.

Given its proximity, it is worth reflecting in particular on the recent experience in the Solomon Islands.

Prior to changes enacted in 2012, legislation relating to Import Duties, Excise, GST, Income Tax, Sales Tax and Stamp Duties included broad provisions allowing the

6 See the ADB’s Asian Region Integration Centre database (http://aric.adb.org/taxincentives)

Page 20

Commissioner of Taxation to provide exemptions. Changes made in 20127 altered the process by which such exemptions were provided. The changes created a formal “Exemption Committee” whose role it is to provide advice to the Minister (in this case the Minister for Treasury and Finance) where a request has been made for an exemption. The Committee consists of representatives of the revenue administrators, the Ministry of Development Planning and the Ministry of Commerce.

The Committee’s recommendations to the Minister are based on national interest criteria, to be outlined in Regulations. The Minister can only agree to an exemption where recommended by the Committee however the Minister retains the ability to decline an exemption application, even if it is recommended by the committee.

The purpose of the changes was to:

• to combine the pre-existing exemption committees (tax and customs); • provide largely uniform criteria for the assessment of the merits of exemption

applications; • to provide a balance between ministerial discretion and professional

bureaucratic advice; and • to increase levels of transparency and accountability.

7 See the Customs and Excise (Amendment) No. 2 Act 2012 (No. 8 of 2012)

Page 21

CHAPTER 3 – VIEWS FROM CONSULTATION& PRIOR TAX REVIEW

The Tax Review Committee has received a number of comments from interested stakeholders on the issue of tax incentives. This is both in response to specific questions posed in Issues Paper 1 on Mining and Petroleum Taxation as well as part of the broader “Blue Sky” consultation process.

This Chapter provides a summary of these views. It also provides a summary of the comments and recommendations made in relation to tax incentives as part of the 2000 Tax Review.

Comments in relation to the Mining and Petroleum Taxation Issues Paper 1 sought stakeholder’s views on the provision of tax incentives for the mining and petroleum sector and, in particular, asked whether special reductions in the main fiscal rates should not be granted to new mining or petroleum projects.

Stakeholders in the extractives sector largely supported the need for project specific tax incentives, noting that there were peculiarities with the mining and gas sector that justified such incentives. The Chamber of Mines and Petroleum, for example, noted that:

Some flexibility in the resources tax regime is desirable. This is due to the inherent risks and challenges of operating in the resources sector (capital intensive, upfront costs, long project lives, etc)…8

However, there was some support of applying incentives on a sector basis, rather than on a project specific basis. Exxon Mobil stated that:

…incentives could be provided in the petroleum and gas sector as a whole, but not on a project specific basis.9

In particular, Exxon Mobil argued for the need for incentives to encourage high cost exploration.

8 PNG Chamber of Mines and Petroleum 2014, ‘Chamber Submission to the Tax Review Committee on Mining and Petroleum Taxation in PNG’, 30 May 2014, available at www.taxreview.gov.pg/submissions.

9Exxon Mobil, 2014, ‘PNG Tax Review – EMPNG Response to Consultation Questions’, 30 May 2014, available at www.taxreview.gov.pg/submissions.

Page 22

A number of submissions also noted the importance of incentives being used to make marginal projects viable. In the absence of incentives, it is argued, some projects would not proceed or would be delayed. This would be to the detriment of the broader benefits that result from significant investment such as community investment, employment opportunities and the development of infrastructure.

In addition to the feedback received in response to Issues Paper 1, a number of other comments were received as part of the broader consultation process that are relevant to mining and petroleum taxation. Notably, a number of representations raised concerns around the provision of incentives, such as tax holidays, in the mining and petroleum sector. This sentiment was also expressed during the Tax Symposium held in Port Moresby in May. There was a view in a number of submissions that the incentives provided to the sector were ‘unfair’ when compared to the treatment provided to other sectors. One submission stated:

[The] Mineral sector gets favourable treatment like tax breaks and holidays and tax credit schemes, while the non-mineral sector where the bulk of the population lives does not have such favours. Such privileges should be minimal and applies across different sectors. Taxes should be favourable to the non-mineral sector where the bulk of our population is engaged to increase the tax base, encourage wider participation and enable benefits to flow down to our people.10

Some submissions suggested that incentives such as tax holidays and “investment concessions” for the sector should not be entertained. One representation raised a more specific concern – that the exemption from import duties available to the sector for the importation of items such as food meant that locally produced food was uncompetitive and that, as a consequence, local economic development opportunities were lost.

Comments as part of a broader “Blue Sky” consultation In addition to the specific feedback received in response to Issues Paper 1, through its “Blue Sky consultation” and other outreach activities the Review has received a range of other views from stakeholders on tax incentives offered in PNG. Some representations were sector specific and others more general.

10 See BPNG, 2014, ‘Submission to the Tax Review Committee’, available at www.taxreview.gov.pg/submissions.

Page 23

Sector/taxpayer-specific issues

Agriculture

In addition to those comments directed at the incentives provided to the Mining and Petroleum sector, a number of submissions were also received in relation to incentives provided to the agriculture sector (of which, as noted in Chapter 1, there are numerous). PNG Palm Oil Council, for example, argued that the existing incentives were necessary for the sector, as a means of compensating for the higher cost of doing business when compared to competitor countries such as Indonesia and Malaysia11. There was also a call for additional incentives for the sector including:

• broad tax breaks for the sector and allowing the carry back of losses12 • the reactivation of the ‘Green Revolution’ program13 • full (100%) depreciation (in the year of purchase) for all plant, equipment,

machinery and vehicles for those engaged in growing commodity crops14; and • full (100%) depreciation (in the year of purchase) for companies and businesses

involved in manufacturing bee hives, wax foundation15.

Small Business

The need for a tax system that was more favourable to PNG’s small businesses was also raised in a number of submissions. This ranged from outright tax exemptions for a period of time16 to measures that seek to address the high levels of compliance costs being faced by smaller businesses17.

Tourism

In the course of discussions with representatives of the tourism sector, the Review was provided with a 2009 report entitled Review of Tourism Investment Incentives in PNG. Given the number of existing incentives aimed at the tourism sector (as noted in Chapter 1) it is worth noting some of the key findings in the report.

11 See PriceWaterhouseCoopers (on behalf of Palm Oil Industry Association) Submission, 2014, ‘Incentives for the Palm Oil Industry – Submission to the Tax Review Committee’, p. 4 available at www.taxreview.gov.pg/submissions.

12 See Basil, S, 2014, ‘Taxation Review Committee – Public Consultation Presentation’, available at www.taxreview.gov.pg/submissions.

13 Ibid. 14 Ibid. 15Farmers and Settlers Association Inc, 2014, ‘Submission to the PNG Tax Review’ (via email),

available at www.taxreview.gov.pg/submissions. 16 See JAJ & Associates, 2014, ‘Submission to the PNG Tax Review’, 30 April 2014, available at

www.taxreview.gov.pg/submissions. 17 See KPMG, 2014, ‘Submission to the PNG Tax Review’, 15 May 2014, available at

www.taxreview.gov.pg/submissions

Page 24

In particular the report highlights the failure of a number of incentives that were introduced in 2006 (double deduction for marketing expenses, accelerated depreciation for capital investments, tariff and duty exemptions for hospitality related items) to achieve their policy goal of stimulating major new tourism investments.

General issues

A number of stakeholders also raised concerns about the granting of incentives more generally. Some questioned whether incentives had actually been effective, despite their long history in PNG whilst others questioned their fairness, suggesting that any ‘incentives’ should be provided to all businesses18.

In support of the Government’s stated policy, some submissions called for incentives provided at a project or company level to stop being provided and for those, not currently authorised under the Income Tax Law, to be repealed19. The same submission also called for other administrative concessions to be withdrawn, such as exemptions from lodgement of tax returns and documentation and allowing taxpayers to keep books and records in a foreign currency.

Of interest PricewaterhouseCoopers’ submission in response to Issues Paper 2 (Corporate & International Taxation) included the results of a simple survey of around 100 businesses in PNG. Two results from this survey are worth noting. Some 73% of respondents answered in the affirmative when asked whether tax concessions affected their business decision making. However an even higher majority of respondents (some 78%) indicated that they would be willing to forego tax concessions in exchange for a simpler system overall20.

Industrial Development (Pioneer Status) Act

Two submissions to the Review also recommended the re-introduction of the Industrial Development (Pioneer Status) Act which, as noted in Chapter 1, was repealed in 1999. The Department of Trade, Commerce and Industry in particular provided a comprehensive submission to the Review arguing for the reintroduction of the Act to promote investment in the manufacturing sector in PNG21. The submission notes the role of the corporate income tax in influencing the return on capital and hence the

18 See Gabori R, 2014, ‘Submission to the PNG Tax Review’, 25 March 2014, available at www.taxreview.gov.pg/submissions.

19 See Adam Smith International, 2014, ‘Submission to the Tax Review Committee – Recommended Tax Reforms for Papua New Guinea’, April 2014, www.taxreview.gov.pg/submissions

20 See PricewaterhouseCoopers, 2014, ‘Submission: Issues Paper No. 2 – Corporate & International Taxation’, 29 August 2014, available at www.taxreview.gov.pg/submissions

21 See Department of Trade, Commerce & Industry, 2014, ‘Submission to the PNG Tax Review – Re-Introduction of the Industrial Development (Pioneer Status) Act available at www.taxreview.gov.pg/submissions.

Page 25

inflow of international capital. This point was also made in the Committee’s second issues paper on Corporate & International Taxation.

Administrative and legislative framework applying to incentives

A number of submissions raised issues about the way that incentives were granted and administered and the legislative framework that underpins them. A number argued that there did not appear to be a clear policy framework under which the granting of incentives took place and that they simply created an uneven playing field. One submission suggested that incentives needed to be reviewed annually22.

The Department of Trade, Commerce and Industry’s submission also put forward a number of suggestions regarding the legislative framework underpinning incentives. They argue that, consistent with international best practice, all investment incentives should be placed into a single piece of legislation and administered by a single agency. The current system, in which incentives are administered by different agencies and with a different legislative basis, creates a “complex implementation system, non-transparency, possible corrupt practice, ad hoc and unfair or discriminative practices.”

To address this they recommend that existing incentives be codified into a reintroduced Industrial Development Act to be administered by the Department of Trade, Commerce and Industry. This would recognise that:

…the duties, responsibilities and powers of the administration of the investment incentives fall within the jurisdiction of the Ministry of Commerce and Industry or an equivalent body and not the Ministry of Treasury or Revenue collection entities.

One submission raised concerns about the legislative basis on which PNG provides tax exemptions to various aid organisations. It was noted that these exemptions are provided for under specific legislation (notably the Aid Status (Privileges and Immunities) Act) or under specific agreements but without any clear basis in the income tax laws. It was suggested that all exemptions and concessions provided to aid organisations under bilateral agreements and /or aid legislation to be incorporated in PNG tax laws via a new ‘catch–all’ provision23.

A related concern, raised by the PNGCS, was that it was unclear at what point aid-related exemptions ceased where aid-project work had been contracted and sub-contracted out.

22 See Nipuru, F, 2014, ‘Submission to the PNG Tax Review’, available at www.taxreview.gov.pg/submissions.

23 See Deloitte, 2014, ‘Submission to the PNG Tax Review’, 14 May 2014, available at www.taxreview.gov.pg/submissions

Page 26

Consideration of tax incentives in the 2000 Tax Review The issue of tax incentives was also considered as part of the last Tax Review24. The Final Report from that Review highlighted a number of concerns about the extensive use of tax incentives to support activities. Whilst acknowledging that the underlying purpose of the incentive was usually positive, it noted that some were “self-serving and accord benefits to a small sector of the economy rather than benefiting the masses”. Even for those that supported desirable activities it found that:

The main problem is that many categories of tax benefits/incentives are extraordinarily inefficient because much of the revenue given up does little or nothing to advance the targeted activities. In the context of the current tax regime, most of the tax incentives embodied in the present law has (sic) evolved on an ad hoc basis and have yet to be critically analyzed to determine their effectiveness.

With that in mind any new incentives will complicate the tax regime, create opportunities to conduct favored activities only for tax benefit, and add to the feeling that the tax regime is a maze that can profitably be navigated only by those who are well to do or well instructed. Even more so there is the grave risk that the process will feed on itself.

The Review went on to recommend that the recommendations from the National Investment Policy Volume 2 (discussed in Chapter 1) be implemented. Details of recommendations regarding specific incentives, and their status (in terms of implementation) are found at Attachment B.

24 A complete copy of final report from this Review can be found at www.taxreview.gov.pg/publications (see pages 21 & 22 for the discussion on tax incentives)

Page 27

CHAPTER 4: TAX INCENTIVES IN PNG – POSSIBLE DIRECTIONS FOR REFORM

This Chapter brings together the background and issues raised in the previous Chapters and sets forth possible reform directions for tax incentives in PNG. Feedback is sought from stakeholders on these proposed directions and questions are posed throughout this Chapter to guide this feedback.

Before considering possible reform directions it is worth reflecting on the key findings that have arisen from the previous Chapters:

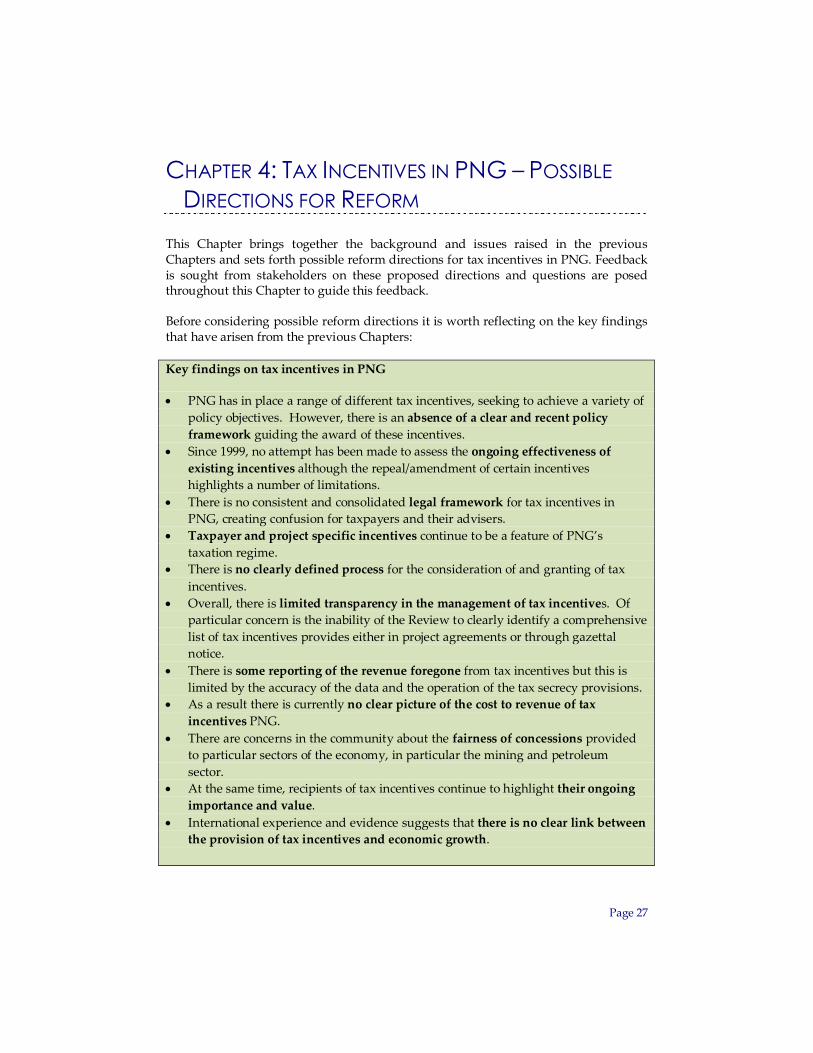

Key findings on tax incentives in PNG

• PNG has in place a range of different tax incentives, seeking to achieve a variety of policy objectives. However, there is an absence of a clear and recent policy framework guiding the award of these incentives.

• Since 1999, no attempt has been made to assess the ongoing effectiveness of existing incentives although the repeal/amendment of certain incentives highlights a number of limitations.

• There is no consistent and consolidated legal framework for tax incentives in PNG, creating confusion for taxpayers and their advisers.

• Taxpayer and project specific incentives continue to be a feature of PNG’s taxation regime.

• There is no clearly defined process for the consideration of and granting of tax incentives.

• Overall, there is limited transparency in the management of tax incentives. Of particular concern is the inability of the Review to clearly identify a comprehensive list of tax incentives provides either in project agreements or through gazettal notice.

• There is some reporting of the revenue foregone from tax incentives but this is limited by the accuracy of the data and the operation of the tax secrecy provisions.

• As a result there is currently no clear picture of the cost to revenue of tax incentives PNG.

• There are concerns in the community about the fairness of concessions provided to particular sectors of the economy, in particular the mining and petroleum sector.

• At the same time, recipients of tax incentives continue to highlight their ongoing importance and value.

• International experience and evidence suggests that there is no clear link between the provision of tax incentives and economic growth.

Page 28

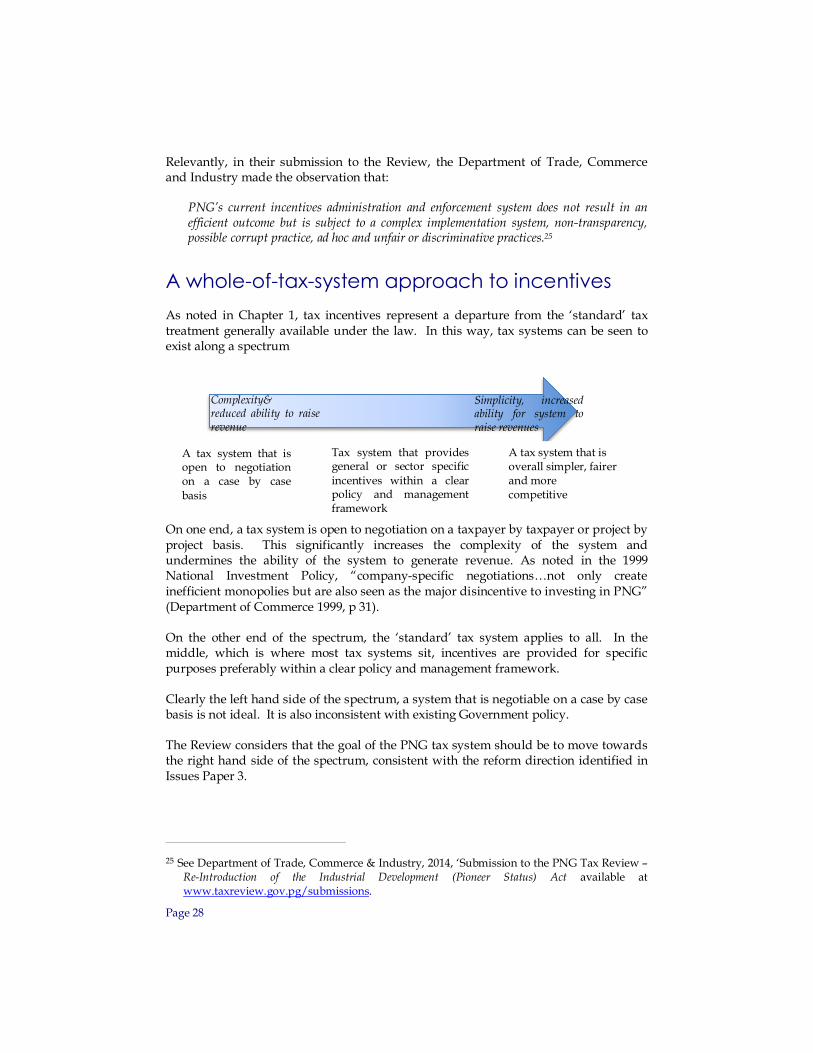

Relevantly, in their submission to the Review, the Department of Trade, Commerce and Industry made the observation that:

PNG’s current incentives administration and enforcement system does not result in an efficient outcome but is subject to a complex implementation system, non-transparency, possible corrupt practice, ad hoc and unfair or discriminative practices.25

A whole-of-tax-system approach to incentives As noted in Chapter 1, tax incentives represent a departure from the ‘standard’ tax treatment generally available under the law. In this way, tax systems can be seen to exist along a spectrum

On one end, a tax system is open to negotiation on a taxpayer by taxpayer or project by project basis. This significantly increases the complexity of the system and undermines the ability of the system to generate revenue. As noted in the 1999 National Investment Policy, “company-specific negotiations…not only create inefficient monopolies but are also seen as the major disincentive to investing in PNG” (Department of Commerce 1999, p 31).

On the other end of the spectrum, the ‘standard’ tax system applies to all. In the middle, which is where most tax systems sit, incentives are provided for specific purposes preferably within a clear policy and management framework.