Embed Size (px)

Citation preview

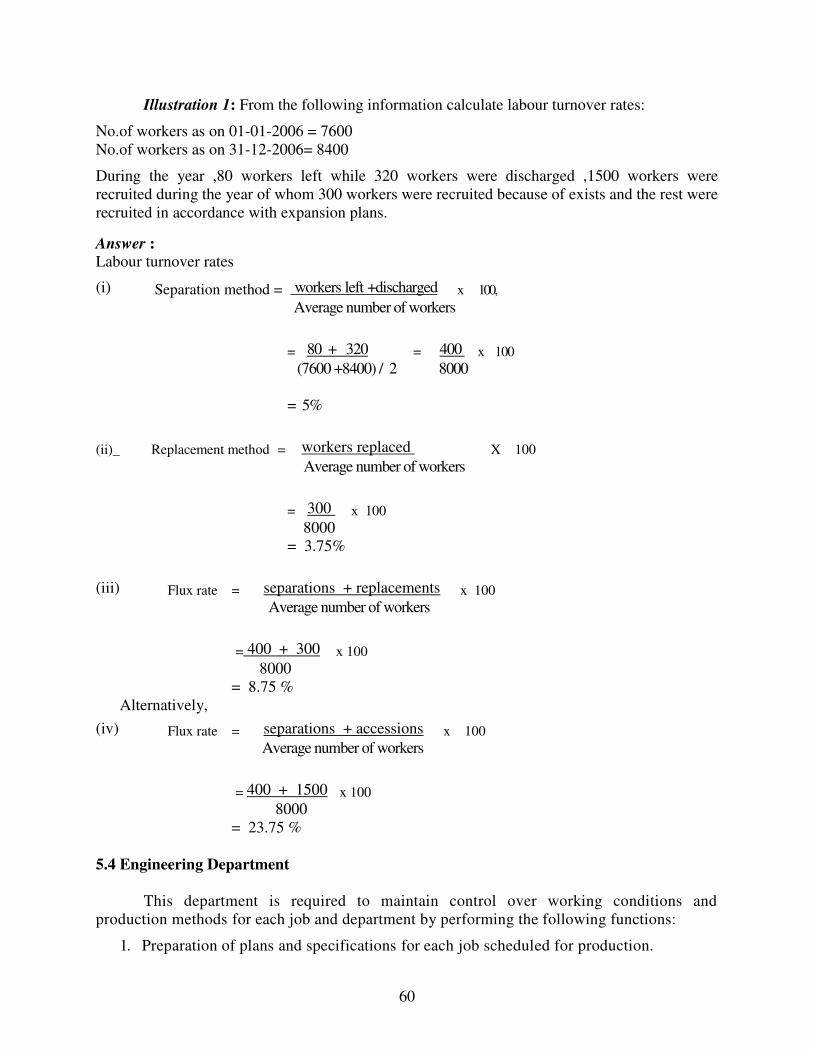

Graduate Course

B.Com (Hons) II Year

Paper IX : Cost Accounting

Contents:

Unit 1

Lesson 1: Cost Accounting: An Overview

Lesson 2: Cost Concepts and Classification

Unit 2

Lesson 3: Accounting for Material Cost

Lesson 4: Pricing & Materials

Unit 3

Lesson 5: Labour Cost

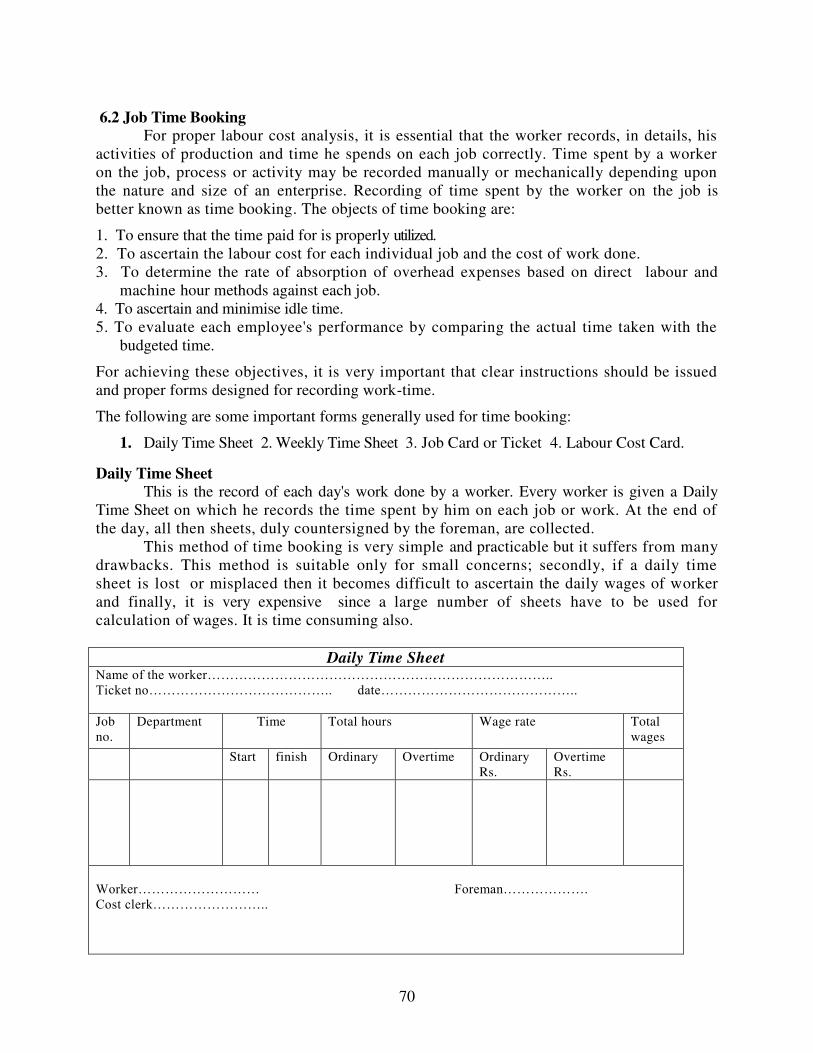

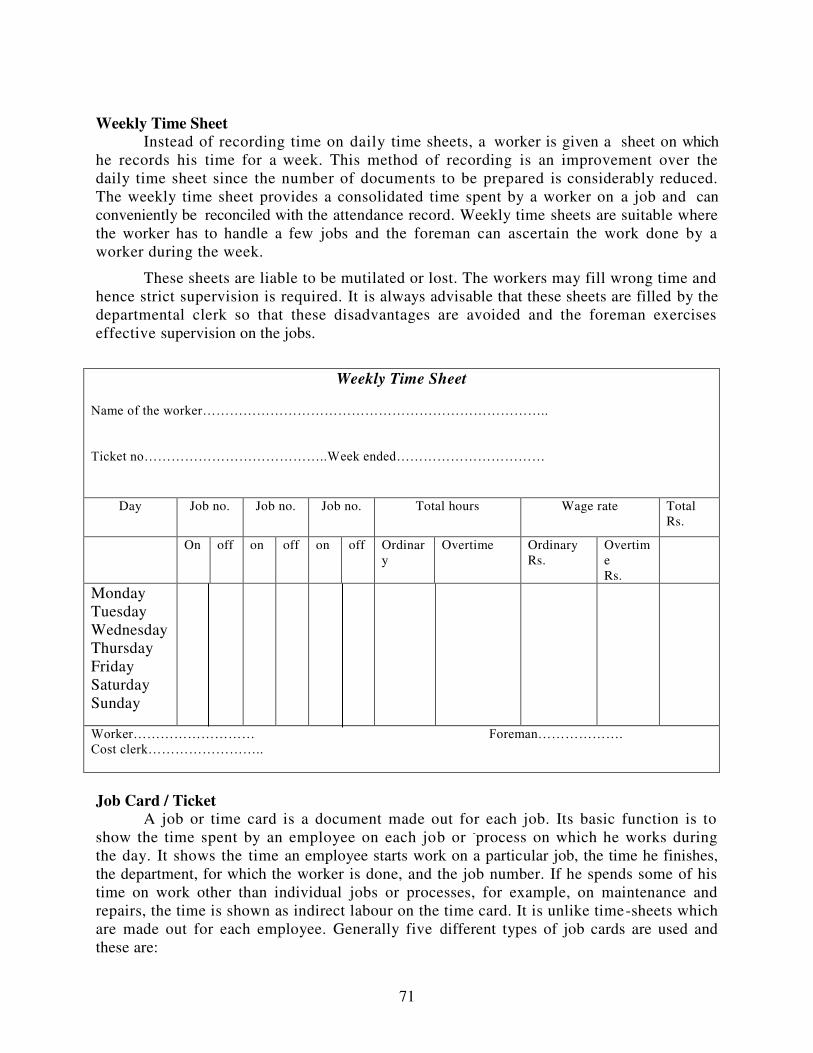

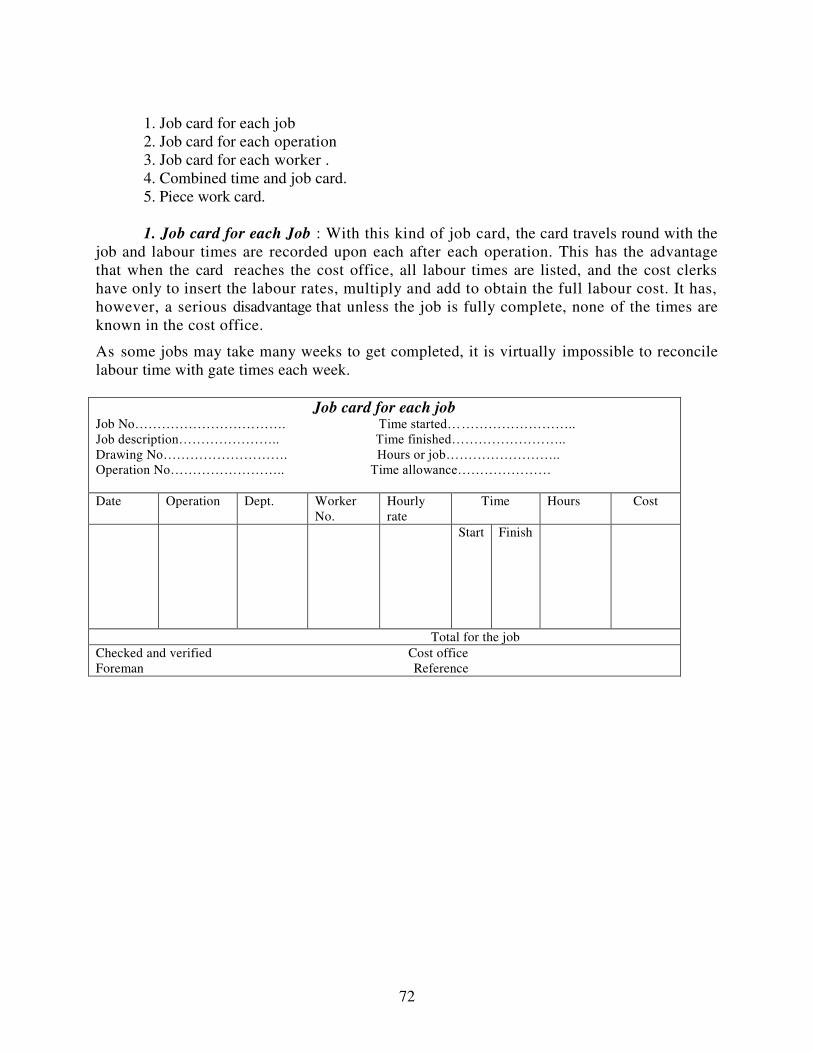

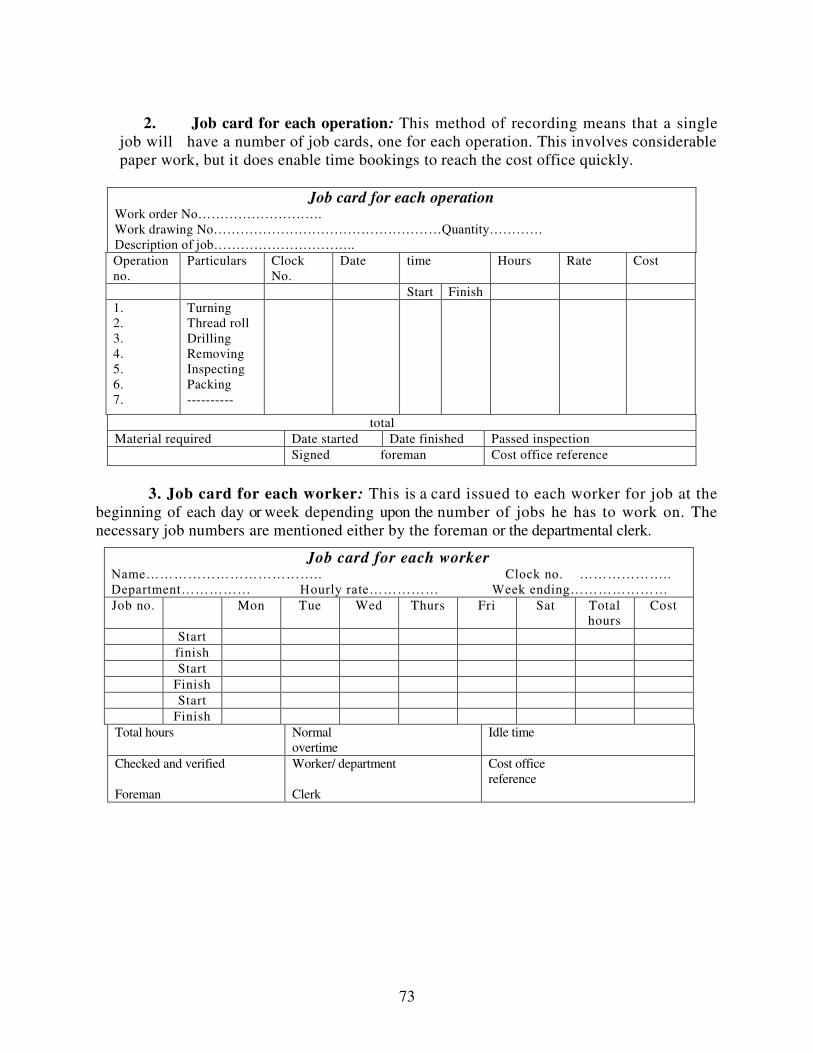

Lesson 6 Time-Keeping and Time Booking

Editor

K.B. Gupta

School of Open Learning University of Delhi

5, Cavalry Lane, Delhi-110007

Session 2007-08 Copies

© School of Open Learning

Published by The Executive Director, School of Open Learning, 5 Cavalry Lane,

University of Delhi, Delhi-110007.

Laser typeset at Computer Centre, School of Open Learning.

Printed at

1

UNIT 1

LESSON 1

COST ACCOUNTING: AN OVERVIEW

Manisha Verma

HansRaj College

University of Delhi

"A business can be hardly successful over the long-run without effective procedures for treating

costs and revenues”

- Peter F. Drucker in Managing the Next Society

Cost accounting has grown into an exciting discipline. Now it is a recognized

feature of modern business life. It’s also the foundation of a firm's internal information

system. Management is seeing costing as the instrument of productivity, profitability,

and efficiency. Its users of information are no longer simply factory enterprises. Today, it

is universally employed and equally touches merchandising and service organizations.

Over the years, cost accounting as a body of principle and practice has matured into cost

management systems with focus on customer satisfaction and maintaining competitive

position.

1.1 Meaning of Costing and Cost Accounting

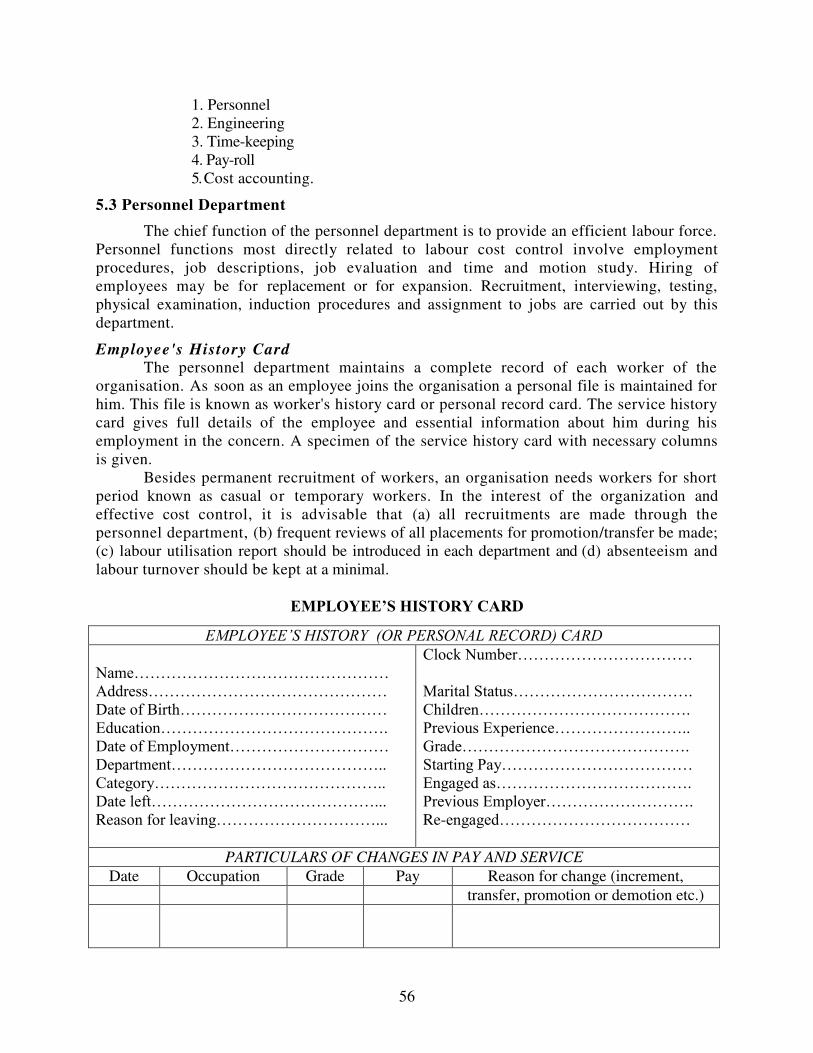

The primary purpose of accounting is to provide financial information relating to

an economic/business activity. It is concerned with measuring, recording, and reporting

financial information by the management to plan and control the activities of a business as

LEARNING OBJECTIVES

After studying this chapter, you should be able to understand

1.1 Meaning of Costing and Cost Accounting

1.2 Objectives of Cost Accounting

1.3 Limitations of Financial Accounting

1.4 Relationship with Financial Accounting

1.5 Differences between Financial Accounting and Cost Accounting

1.6 Advantages of Cost Accounting

1.7 Objections to Cost Accounting

1.8 Costing Methods and Techniques

1.9 Installation of Cost Accounting System

1.10 Practical Difficulties in Installation

1.11 Essentials of a Good System

2

well as by others who provide funds or who have various interests in the operations of an

entity. The accounting system that provides the information to measure product costs and

performance, and control the operations of a firm is called cost accounting.

The Chartered Institute of Management Accountants (CIMA), London has defined costing as,

"the techniques and processes of ascertaining costs.” Wheldon has defined costing as, "the

proper allocation of expenditure and involves the collection of costs for every order, job,

process, service or unit." Thus, costing simply means cost finding by any process or technique. It

consists of principles and rules which are used for determining:

(a) The cost of manufacturing a product, e.g., motor car, furniture, chemical, steel, paper,

etc., and

(b) The cost of providing a service, e.g., electricity, transport, education, etc.

The terms `costing' and `cost accounting' are often used interchangeably. Cost

accounting is a formal system of accounting for costs in the books of account by means of

which costs of products and services are ascertained and controlled.

An authoritative definition of cost accounting has been given by CIMA, London as

follows: "the application of costing and cost accounting principles, methods and techniques

to the science, art and, practice of cost control and the ascertainment of profitability. It

includes the presentation of information derived there from for the purposes of managerial

decision making."

Cost accountancy is thus the science, art and practice of a cost accountant. It is a

science in the sense that it is a body of systematic knowledge which a cost accountant should

possess for the proper discharge of his duties and responsibilities. It is an art as it requires the

ability and skill on the part of a cost accountant in applying the principles of cost

accountancy to various managerial problems like price fixation, cost control, etc. Practice

refers to constant efforts on the part of cost accountant in the field of cost accountancy.

Theoretical knowledge alone would not enable a cost accountant to deal with the various

intricacies involved. He should, thus, have sufficient practical training, and exposure to real life

costing dilemmas.

1.2 Objectives of Cost Accounting

The main objectives of cost accounting are as follows:

1. Ascertainment of cost: The primary objective of cost accounting is to determine the

cost of product manufactured or service rendered i.e. both aggregate cost and unit

product costs. For cost ascertainment, various methods are employed in different

industries like job costing, process costing, operating costing etc.

2. Cost control: Cost accounting aims at improving profitability by controlling and reducing

costs. For this purpose, various specialized techniques like standard costing, budgetary

control, inventory control, value analysis, etc., are used. This objective of cost control

and cost reduction is becoming increasingly important in the present scenario because

of growing competition in the business world.

3

3. Guide for managerial decision making : Cost data provide guidelines for various

managerial decisions like make or buy, keep or replace, accept or reject, continue

or drop a product.

4. Determination of selling price: Cost accounting provides cost information on the basis of

which selling prices of products or services may be fixed.

FINANCIAL ACCOUNTING AND COST ACCOUNTING

Financial accounting aims at presenting a true and fair view of the overall results of

transactions and events which are recorded in the books of accounts in terms of money, and in

accordance with established principles, accounting standards and legal requirements. The

financial statements, comprising the income statement, position statement as well as the funds

flow statement reveal the overall performance and position of the business entity. Such reporting

is hawed on a post mortem examination of past events. Although management has some interest

in the information contained in these statements, the information is of little practical

significance from the point of view of planning, control and decision-making. Cost accounting

was thus evolved to overcome the limitations of financial accounting.

1.3 Limitations of Financial Accounting

In spite of its popularity, financial accounting suffers from the following limitations:

(a) Historical in Nature: Financial accounting is essentially historical in nature. It records

transactions and events which have already occurred. As such, the financial statements

prepared and presented at the end of the accounting period, report on past events as a part

of stewardship function of management. Although, the information is historically

important, it does not provide the management with day-to-day information for

evaluating operational efficiency.

(b) Overall Performance: Financial accounting discloses and reports profitability or

otherwise of the business as a whole. Since it does not classify accounts on the basis of

departments or segments, products, processes and sales territories, it fails to provide

information about costs and profit of these sub-divisions of the organisation.

(c) No Objective Classification: In financial accounting, accounts are classified under two

major groups, viz. personal and impersonal. Such a primary classification made

subjectively, is of little use to management to ascertain costs by products, jobs and

processes.

(d) Distinction between Direct and Indirect Expenses: In the case of financial accounting,

expenses are not classified into direct and indirect, fixed and variable, controllable

and uncontrollable, and assigned to departments, jobs or products. As such, controllable

items of expenses cannot be distinguished from uncontrollable ones for purposes of cost

control and cost reduction.

(e) Material Losses: There being no material control system operating under financial

accounting, there is no safeguard against material losses consequent upon wastage,

pilferage, deterioration and obsolescence of materials.

(f)) Labour Cost Control: In the case of financial accounting, there is no means of comparing

4

the time clocked with the time booked since workers are paid on the basis of hours worked.

Consequently, losses resulting from idle time, evasion of work and loitering cannot be

controlled. Further, labour time is not recorded job-wise. Hence, there is no means of

judging the efficient utilization of labour time and no incentive systems based upon

results can be introduced.

(g) Idle Facilities: Financial accounting does not reveal losses due to idle plant and

equipment. Such losses can neither be analyzed nor controlled.

(h) No Cost Comparison: Financial accounting does not provide data for comparison of

costs of' two periods, two firms, two jobs, departments or processes. As such, it is not

possible to arrive at conclusions regarding the profitability or otherwise of different

products, jobs, departments, processes or sales territories.

(i) Distortion of Trading Results: In financial accounting, the values of closing inventories

are estimated for the purpose of income statement and balance sheet. If the values are

not stated accurately, matching of costs with revenues cannot be done properly.

Consequently, trading results become distorted to the extent of variation in values.

(j) Only Monetary Information: Financial accounting records contain information

relating to transactions and events of a business entity capable of being expressed in terms of

money. There is no place in these records for non monetary information such as quantity of

materials and quality of labour, etc.

(k) Fixation of Product Price: Financial accounting records do not furnish the required

information regarding quantity and costs to enable management to fix the price of

products, jobs and processes or services rendered. Financial accounting also fails to

explain the reason why there is rise or fall in cost of production.

(l) Inventory Levels cannot be fixed: Financial accounting fails to supply the necessary

information to management for fixation of stock levels such as maximum level,

minimum level, ordering level, etc. In the absence of fixation of such levels, investment in

inventories cannot be optimized.

(m) Lack of Data for Decision-making: Decision-making is one of the basic functions of

management of any organisation. However, financial accounting fails to furnish the

required data for such decisions as introduction of a product line, discontinuance of

production of a product or a department, whether to make or buy, equipment

replacement, suitable product-mix, etc.

1.4 Relationship with Financial Accounting

Cost accounting is a branch of accounting in much the same way as financial accounting.

In fact, financial accounting provides the data base for cost accounting. Necessary

information relating to costs is obtained from financial accounting records. As such, cost

accounting and financial accounting are complementary to each other. The similarities

between the two branches of accounting are:

i) Both cost and financial accounting are the branches of accounting.

ii) Both are concerned with recording and reporting accounting

information.

5

iii) Both the sets of accounts use the same basic documents for recording transactions

and events.

iv) Both record transactions and events on the basis of double entry.

v) Both the sets of accounts record information in monetary terms

although cost accounting records contain additional information.

vi) Each of these branches is mutually helpful to the other. While financial accounting

provides basic information for writing up cost records, cost accounting assists

financial accounting in inventory valuation thereby facilitating the preparation of

financial statements.

vii) Both the sets of accounting records furnish the required information to

interested parties.

viii) Each of these branches facilitates performance appraisal in its own way.

ix) Both the sets of accounts are a means of control.

1.5 Differences between the Two

In spite of the above points of similarity between financial and cost accounting, the two

branches of accounting differ from each other in the following respects

(i) Purpose: Financial accounting records disclose profitability or otherwise, i.e., trading

results as well as the financial position of a business. The chief purpose of cost

accounting is to provide detailed cost information to management.

(ii) Nature: Financial accounting is historical in nature. The information provided by the

records is in respect of only monetary transactions and events which have already

occurred and about which nothing can be done. Cost accounting, on the other hand,

focuses not only with past transactions but of the future ones also.

(iii) Legality: Financial accounting is legally necessary, especially in the case of companies.

Even in the case of other forms of business, financial accounting has almost become

mandatory by virtue of the application of other enactments much as the Income Tax Act

and Sales Tax Act. Cost accounting is not legally necessary except for certain specified

industries.

(iv) Reporting: Financial accounting serves the interest of people belonging to different

groups outside the organization such as shareholders, creditors, potential investors, workers,

taxation authorities, financial analyst, government, trade unions. Therefore this branch of

accounting accomplishes only external reporting of financial information. Cost accounting,

however, serves the needs of management and thus accomplishes internal reporting.

(v) Periodicity: Financial accounting reports are prepared on annual basis while cost

accounting reports are prepared on weekly, monthly, quarterly even daily basis

depending on the needs of management.

(vi) Analysis of profit:. Financial accounts reveal the profit or loss of business as a whole

for a particular period. Cost accounts show the detailed cost and profit data for each

product line, department, division, section, process.

6

(vii) Focus: In Financial accounting focus is on recording, classifying and summarizing the

financial transactions .In cost accounting the focus is on cost ascertainment and cost control.

(viii) Format of presenting information: Financial accounting has a single uniform format of

presenting information, i.e., Profit and Loss Account, Balance Sheet and Cash flow

statement Cost accounting has varied forms of presenting cost information which

are tailored to meet the needs of management and thus lacks a uniform format.

(ix) Analysis of cost: In financial accounting, no distinction is made between direct and

indirect costs, fixed and variable costs and controllable and uncontrollable costs. In

cost accounting, costs are distinguished according to their identification with the cost

units (direct and indirect), according to variability (fixed and variable), and

according to responsibility (controllable and uncontrollable costs).

(x) Use of standards: In financial accounting there are no predetermined standards of

cost and performance to evaluate the efficiency of operations as regards the use of

material, labour and overhead facilities. Cost accounting makes the use of standard

costs against which actual costs are compared, variances are calculated and analyzed

into their causes that corrective action may be taken.

1.6 Advantages of Cost Accounting

Cost accounting provides information that is useful to management in planning,

control and decision-making. The main advantages of cost accounting are listed below:

1. It reveals unprofitable activities, losses, and inefficiencies such as wastage of material

in the form of spoilage, excessive scrap, and idle time of labour and idleness of

plant facilities. Management can take steps to check these wastes and losses.

2. It helps the management in fixation of prices. Accurate cost data can be used as a

guide for preparation of quotations and submission of tenders.

3. It provides suitable data and information which helps the management in taking

decisions such as make or buy, shut-down or continue selection of most profitable

product-mix, acceptance or rejection of a special order, introduction of a new product,

etc.

4. Detailed costs of materials, labour and overheads reveal actual and potential sources

of cost saving and reduction.

5. Maintenance of time and job records for workers reveals losses incurred due to idle

time. Such records assist in taking steps to minimize those losses.

6. Centralization of purchasing is facilitated by the use of cost accounting. This results in

economical purchases.

7. A perpetual inventory system which facilitates continuous stock-taking helps in the

preparation of interim profit and loss account.

8. Cost accounting lays the basis of standard costing and budgetary control systems.

These two techniques help the management in cost control. Variance analysis and

comparison of actual performance with budget estimates indicates areas where

economies can be achieved.

7

9. A system of cost accounting provides an independent and reliable check on the

accuracy of financial accounts. A reconciliation is made of the profit as shown by cost

accounts with that shown by financial accounts.

10. Installation of uniform costing enables management to make inter-firm comparisons.

1.7 Objections against Cost Accounting

There are objections raised against the introduction of cost accounting.

(i) It is expensive. A cost accounting system involves recording, classification,

analysis, allocation and apportionment of costs and absorption of overheads which

require considerable amount of clerical work.

(ii) It leads to increase in workload. The results shown by the cost accounts differ

materially from those shown by the financial accounts. Preparation of reconciliation

statements frequently is necessary to verify their accuracy. This leads to unnecessary

increase in work load.

(iii) It is unnecessary. Introduction of costing system itself does not control costs or contribute

to operating efficiency of the concern. It gives management information with which to

control costs. If the management is alert and efficient, it can control costs without the aid

of this system. This is, therefore, unnecessary.

The above arguments are untenable. The basic aim of cost accounting is minimizing costs

by avoiding wastes at all stages therefore it, it will be wrong to call it expensive , infact it is a

profitable investment. Differences between results shown by cost accounts and financial

accounts arise on account of over and under-absorption of overheads, methods of material

pricing used and treatment of other incomes. An integrated system of accounts can help in

elimination of these differences. In this age of competition and globalization costing is not

unnecessary, but must for each manufacturer because he must know the exact cost not only of

each article made but also of each process involved in its production so that he may be in a

position to avoid waste and minimise its cost. It is possible only when proper costing records are

maintained. Hence, it is wrong to say that it is unnecessary.

1.8 Costing Methods and Techniques

Methods: The methods of costing refer to the processes employed in the

ascertainment of costs. Several methods have been designed to suit the needs of different industries

.The methods of costing to be applied in a particular concern depends upon the type and nature of

manufacturing activity. .

1 Job Costing is that form of specific order costing under which each job is treated as a cost

unit and costs are accumulated and ascertained separately for each job. It is applied in

those industries where the goods are manufactured against specific orders as per

customer’s specifications e.g. printing press, repair shop, interior decoration, painting.

2. Contract Costing is that form of specific order costing under which each contract is treated

as a cost unit and costs are accumulated and ascertained separately for each contract e.g.

construction of building, roads, bridges or other construction work..

3. Batch Costing is that form of specific order costing under which each batch is treated as a

cost unit and costs are accumulated and ascertained separately for each batch .It is applied

8

in those industries where the similar articles are produced in definite batches e.g.

readymade garments, toys manufacturing industries, tyres and tubes, spare parts and

components, pharmaceutical industries.

4. Process Costing is a method of costing under which all costs are accumulated for each

stage of production and the cost per unit of product is ascertained at each stage of

production. It is applied in those industries where manufacturing activity is carried

on continuously by means of two or more processes and output of one process

becomes the input of the following process till completion. e.g. paper industries,

chemical industries, textile industries, sugar industries.

5. Unit /Single /Output Costing is applied in those industries where only one product

or a few grades of the same product are produced and production involves only a

single process or operation and production is uniform and continuous and units of

output are identical e.g. cement industry, steel industry, floor mills industry,

bricks making industry.

6. Operating /Service Costing it is used to ascertain the cost of providing services

incase of those undertakings which render services and are not engaged in the

manufacture of tangible products e.g. road transport, railways, airlines, hotels,

hospitals, electricity, cinemas.

7. Multiple /Composite Costing It involves the application of two or more methods of

costing in respect of same product. It is used in industries where number of

components are separately produced and then assembled in a final product e.g.

bicycle, motor cycle, scooter, T.V., air conditioners, cars, refrigerators.

Techniques: The techniques of costing are not alternatives to the methods of costing.

These are the different ways of analyzing and presenting costs for the purpose of

controlling costs or making managerial decisions irrespective of method of costing being

used. Some of the popular techniques of costing are as follows:

1. Standard costing: This is a very valuable technique of controlling cost. In this technique,

standard cost is pre-determined as target of performance, and actual performance is

measured against the standard. The difference between standard and actual costs is

analyzed to know the reasons for the difference so that corrective actions may be taken.

2. Budgetary control: A budget is an expression of a firm's business plan in financial form.

Budgetary control is a technique applied to the control of total expenditure on

materials, wages and overheads by comparing actual performance with the budgeted

performance. Thus, in addition to its use in planning, the budget is a control and co-

ordination of business operations.

3. Marginal costing: In this technique, separation of costs into fixed and variable is of

special interest and importance. This is so because marginal costing regards only

variable costs as the cost of the products. Fixed cost is treated as period cost and no

attempt is made to allocate or apportion these cost to cost centres or cost units. It is

transferred to costing profit and loss account of period. This technique is used to study

the effect on profit of changes in volume of output.

4. Total absorption costing: It is a traditional method of costing whereby total costs (fixed

and variable) are charged to products. This is in complete contrast to marginal costing

9

where only variable costs are charged to products.

5. Uniform costing: It is the practice of using the same costing principles or practices by a

number of firms in the same industry. It helps in inter firm comparisons, fixation of price,

cost reduction and in seeking tax relief or protection from government.

1.9 Installation of Cost Accounting

All cost accounting systems reflect the same principles and purposes, although their

application may vary with circumstances out of necessity. Accordingly, the cost accounting

system proposed to be installed should be designed to suit the nature of the business.

Further, the system should be simple, and the expenses of operating it should be

commensurate with the expected benefits.

The preliminary considerations governing the design and installation of a cost accounting

system are:

(a) Nature of Business: The system sought to be designed and introduced, should suit the

nature of business. Accordingly, it is necessary to be thoroughly acquainted with the

technical aspects and the methods of production. If the business engaged in is the

production of goods, it should further be seen whether it produces a s ingle product

on a mass scale, or a multi-product concern producing more than one product, or a

jobbing type of business, a process type or an assembly unit.

(b) Nature of Organisation: It is equally necessary to study the layout, nature and size

of the organisation. Since the system to be designed should suit the organisation, the

existing types of authority relationship, the number of layers and the extent of

authority and responsibility should also be studied.

(c) Methods and Procedures: The methods of manufacture and the procedures existing for

purchase, receipt, storage and issue of materials, the methods of wage payment, computation

and payment of wages and of arriving at overheads also deserve careful study.

(d) Technical Aspects: Although the cost accountant is not a technical expert, it is

necessary for him to get acquainted with the nature of product, the methods and

stages of production, the operations involved, varieties produced and such other technical

aspects of the business. Since production efficiency depends upon effective production

control, it is equally necessary to know the degree of control exercised over

production.

(e) Management's Expectations and Policies: The cost accounting system to be

designed also depends upon management policy and their expectations from the system.

If, for instance, the management's objective of installing a costing system is only to

ascertain the cost of each product, the cost accounting system should be simple enough

to achieve that objective.

(f) Simplicity: The system to be introduced should be simple and easy to operate. The

operating personnel should be capable of understanding the procedures laid down

for working the system efficiently.

(g) Co-operation and Support of Personnel: No system of cost accounting, however

carefully designed, can be worked successfully without enlisting the co-operation and

support of the personnel involved in the cost accounting process. As such, the

10

system should not be thrust upon them. They should be consulted, their views and

suggestions considered, and they should be made cost conscious and drawn into the

cost accounting process.

(h) Standardization of Forms: Accumulation of cost information necessarily involves

the maintenance of detailed cost records. Since this entails considerable clerical

work, the staff may resent it. It is, therefore, necessary to reduce clerical work to the

minimum. Printed forms should be used and they should be standardized as regards

size and contents with instructions printed.

(i) Accuracy of Data: It is also necessary to determine the degree of accuracy of data to be

supplied by the cost accounting system.

(J) Prompt Reporting: Since a cost accounting system is mainly intended for internal

reporting of cost information, cost data should be made available promptly and

regularly. It is also necessary that the information supplied should be clear, non-

technical and unambiguous. There should be no duplication in reporting the same

information.

(k) Flexibility: The costing system should be flexible and capable of adaptation to changing

circumstances. It requires periodical scrutiny and change to avoid the danger of

becoming obsolete owing to changes and developments in the business.

(l) Reconciliation: Where cost records are maintained independently of financial

records, arrangements should be made for regular reconciliation of the trading result

as revealed by both the set of books.

(m) Cost: It is equally necessary that the cost of installing a system of cost accounting

should be commensurate with the benefits of installation. In other words, the benefits

should not outweigh the cost of installation and operation of the costing system.

1.10 Practical Difficulties in Installation

Apart from technical problems, the practical difficulties which may arise in

connection with the introduction of a cost accounting system are the following:

(a) Lack of Support from Management: In many cases, the costing system is thrust on

the managerial personnel, without consulting them and without explaining the

benefits of the system. It may also happen that the system introduced may not be

supported by the top management, probably because of the expenditure involved. In

either case, the system introduced arouses fear and suspicion in the minds of line

managers. Consequently, they view the system as interference in their work, and are

likely to resist the same. The difficulty may be got over by explaining the benefits

accruing from the system to all those who would be involved in the cost accounting

process and instilling in their minds a sense of co-operation.They should be made

cost conscious by being drawn into the process of designing and installation.

(b) Resistance from the Accounting Staff: The accounting staff may offer resistance to the

introduction of cost accounting on the ground that their work would increase, or that

it is interference in their routine work of accounting. Their resistance may also be due

to their feeling of losing importance with the introduction of cost accounting. Even this

difficulty may easily be overcome by explaining to them the need for cost accounting

11

and assuring, at the same time that their position would not, in any way, be affected.

They should be made to feel that it is absolutely necessary to supplement their

accounting work with cost accounting and that the system would neither increase

their work nor bring about unemployment, but on the contrary, the system would

create more employment opportunities.

(c) Non-co-operation of Operating Personnel: The foremen, supervisory staff and operating

personnel may also offer resistance to the system due to ignorance and suspicion. As

a result, they may not supply the necessary data for the successful working of the cost

accounting system.

To overcome this difficulty, it is necessary to properly educate them. They should be made

aware of the benefits accruing from the system, and should be made cost conscious by

winning their confidence.

(d) Shortage of Trained Staff: At the time of introduction of a suitable system of cost

accounting, the concern may experience non-availability or shortage of trained staff to

handle the, work involved in operating it.

This difficulty need not be an excuse for non-introduction of the system designed. It is

necessary to train the existing staff and introduce the system rather slowly, instead of

thrusting a complete system upon them irrespective of whether or not they are ready to

accept and handle the system.

(e) Cost of Installation: The use of standardized forms necessary for recording and

reporting involves additional expenditure which the concern may not afford.The

design of a system and the details of the methods to be employed will vary widely

according to the nature of each concern. Accordingly, the system should be designed

to suit the concern, and the obtainable results should justify the cost of additional

staff and records involved. Cost-benefit analysis should be made to justify the costs

involved.

1.11 Essentials of a Good System

A suitably designed and an easily workable system of cost accounting should reflect the

following features:

1. The system designed should be appropriate to the organisation structure and

methods of production.

2. It should be capable of achieving the objectives and goals set by the management.

3. The system should be simple enough to be understood by the operating personnel.

4. It should be flexible so as to permit easy adaptability to changed conditions of

business.

5. The reports and statements produced by the system should contain the relevant

information for the intended purpose.

6. The reports and statements produced should be timely, accurate and effective.

12

QUESTIONS

1. “Limitations of financial accounting have made the management realize the importance of cost accounting” Comment.

2. What is cost accounting? Discuss briefly its objectives and advantages?

3. State the main differences between cost accounting and financial accounting?

4. You have been asked to install a costing system in a manufacturing business. What

practical difficulties would you expect and how do you propose to overcome them?

5. “Cost accounting system is neither unnecessary nor expensive rather it is a profitable investment” Comment.

6. What method of costing would you adopt for the following industries? Give reasons

1. Ship building

2. Toy making

3. Oil refinery

4. Sugar

5. Road transport company

13

LESSON 2

COST CONCEPTS AND CLASSIFICATION

Manisha Varma

Hans Raj College

University of Delhi

2.1 Costs vs. Expense and Loss

The term `cost' does not have a definite meaning and its scope is extremely broad and

general. It is, therefore, not easy to define or explain this term without leaving any doubt

concerning its meaning. Cost accountants, economists and others develop the concept of cost

according to their needs because one complete description of `cost' to suit all situations is not

possible.

According to the Oxford Dictionary, cost means "the price paid for something." Some other

definitions of cost are given below:

According to CIMA, London “Cost is the amount of expenditure (actual or notional)

incurred or attributable to a given thing.”

According to WM Harper "A cost is the value of economic resources used as a result of

producing or doing the things coasted."

According to ICWA of India "Cost is a measurement, in monetary terms, of the amount

of resources used for the purpose of production of goods or rendering of services".

Often the terms `cost' and `expense' are used interchangeably. But cost 'should be

distinguished from expense and loss.

Expense is defined as "an expired cost resulting from a productive usage of an

asset." It is that cost which has been applied against revenue of a particular accounting period

in accordance with the principle of matching costs to revenue. In other words, an expense is

that portion of the revenue earning potential of an asset which has been consumed in the

LEARNING OBJECTIVES

After studying this chapter, you should be able to understand

2.1 Costs vs. Expense and Loss

2.2 Cost Classifications

2.3 Elements of Cost

2.4 Items Excluded From Cost Accounts

2.5 Cost Sheet

2.6 Questions

14

generation of revenue. Unexpired or unconsumed part of the cost is recorded as an asset in

the balance sheet. Such an unexpired cost is converted into an expense when it expires while

helping to earn revenue. For example: when a plant is purchased, depreciation on plant

(expired cost) is charged to profit and loss account as an expense and cost of plant

remaining after providing depreciation (unexpired cost) is shown as an asset in the balance

sheet. Every year, depreciation on plant representing expense is debited to profit and loss

account and depreciated value representing unexpired cost is shown in the balance

sheet. Pre-paid insurance is also an example of unexpired cost which is shown in the balance

sheet as an asset.

Loss is defined as "reduction in, a firm's equity other than from withdrawals of capital

for which no compensating value has been received." A loss is an expired cost resulting from the

decline in the service potential of an asset that generated no benefit to the firm. Obsolescence or

destruction of stock by fire are examples of loss.

2.2 Cost Classifications

Classification is the process of grouping costs according to their common

characteristics. It is a systematic placement of like items together according to their common

features.

The principal bases on which costs are classified are:

1. Variability (behavioral classification)

2 Functional areas (functional classification)

3. Responsibility (controllable and uncontrollable costs)

4: Traceability/identifiably (direct and indirect costs)

5. The accounting period charged to revenue (product costs and period costs)

6. Decision-making (relevant and irrelevant costs).

Behavioral Classification

The basis of classification, the behaviour pattern of costs considers how the costs

respond, i.e. change with a given change in the volume of production. While some costs

vary with the change in the quantity of output, others do not. Accordingly, there are

three categories of costs: fixed, variable and semi-variable.

Fixed costs: These are unaffected by variations in the volume of activity. The total

fixed costs remain constant over a relevant range of output, while the fixed cost per unit

varies with the output. Fixed costs have no particular relation to the volume of activity.

These are incurred irrespective of production and sales. These are usually time based. Some

typical examples are rent, insurance, taxes and managerial salaries.

Variable cost: These are the costs which vary in direct proportion to changes in

volume. They increase or decrease in the same proportion in which the output increases or

decreases. The total amount of variable costs tends to change in respect to changes in

production volume, but the variable cost per unit stays at the same level for a considerable

period of time. The examples of such costs are direct material, direct labour, small tools,

commission of salesmen, power.

15

Semi-variable costs: Also known as `mixed costs'. These costs include both a fixed

and a variable component, i.e. these are partly fixed and partly variable. A semi-variable

cost often has a fixed element below which it will not fall at any level of output. The

variable element in semi-variable costs changes either at a constant rate or in lumps. For

example, introduction of an additional shift in the factory will require additional

supervisors and certain costs will increase by steps. In the case of a telephone connection,

there is a minimum rent and beyond a specified number of calls, the charges very

according to the number of calls made. In fact, there is no definite pattern of behaviour of

semi variable costs. The examples of such costs are supervision, maintenance and repairs,

telephone expenses, light and power, depreciation.

Functional Classification

Costs classified according to managerial functions are accumulated according to the

activity performed. The costs of a typical organization may be divided into manufacturing,

marketing, administrative and financing groups.

Manufacturing cost: These are related to the production of an item. These are the sum of

direct materials, direct labour and factory overhead. In other words, these include all the costs

incurred in the factory up to that stage when the goods are ready for dispatch. Examples are:

salaries of factory manager, supervisors and foremen, rent, rates and insurance of the factory,

power and fuel used in the factory, depreciation, maintenance and repairs of building, plant,

machinery tools, etc.

Administrative costs: These include all expenditures incurred in formulating the plans,

directing the organization and controlling the operations. A major portion of these costs are policy

costs which are of fixed nature and, therefore, uncontrollable. These include salaries paid to

management and clerical staff, rent, rates and insurance of general offices, their lighting, heating

and air-conditioning, depreciation of office buildings, furniture, machinery, etc.

Selling and distribution costs: Selling Cost: These are incurred to create and stimulate

demand and to secure orders. These include salaries, commission and traveling expenses of

salesmen and technical representatives and sales managers, advertising, catalogues, price lists, bad

debts and collection charges, cost of market research, etc.

Distribution Cost: These are .the costs incurred in moving the goods from the point of

production to the point of consumption. These include: warehouse expenses, carriage outwards,

depreciation and upkeep of delivery vans, wages of packers, van drivers, etc.

Financing costs: These are costs incurred for raising and using capital, e.g. interest on

loans and debentures, commission or brokerage on issue of shares and debentures, discount on

the issue of shares and debentures, etc.

Controllability Classification

Costs are also classified in terms of responsibility over them. Responsibility carries the

authority of the manager to influence costs-increase or decrease their amount. As such, there

are two groups: Controllable and uncontrollable.

Controllable Costs. Costs are said to be controllable when the amount of the cost incurred

can be influenced by the action of a specified member (manager or supervisor) of an undertaking.

16

Uncontrollable Costs. Costs which cannot be influenced by the action of a specified

member (manager or supervisor) of an undertaking are known as uncontrollable costs.

The distinction between controllable and uncontrollable costs depends upon a point of reference.

An item of cost may be uncontrollable at one level of management but the same item may be

controllable at another level of management. Almost all costs are controllable at some level of

management. Segregation of costs into controllable and uncontrollable categories will help the

management in fixing responsibilities of different executives for unfavourable cost variances. An

executive should be held responsible only for those costs which are under his control.

Manufacturing Classification

Costs are also classified as to when they are charged against revenue. The basis as the

period benefited by the particular cost. This is essential in matching expenses against revenues in

the relevant period. Such a grouping helps management in income measurement for the

preparation of financial statements. Here, two categories are product costs and period costs.

Product Costs. These are the costs directly identified with the product. These are the

cost of goods produced and kept ready for sale. They are direct materials, direct labour, variable

factory overheads. These costs provide no benefit till the product is sold, and are, therefore,

inventoried. When the products are sold, the total product costs are recorded as an expense, and is

called “cost of goods sold”. It is matched against revenue for the period in which

products are sold.

Period Costs. These are not directly related to the product and, therefore, not inventoried.

If the period costs benefit only one accounting period, it is called revenue expenditure. If they

benefit two or more accounting periods, they are treated as assets till they are charged as

expenditure for the relevant years. Normally, expense of fixed nature like depreciation of assets,

insurance premium, rent and rates are treated as fixed costs. These costs represent non-operating

items and are related to passage of time and not to the production and sales of the period.

In a manufacturing organisation all manufacturing costs are regarded as product costs

and non-manufacturing costs are regarded as period cost. In retailing and wholesaling

organisations goods are purchased for resale without changing their basic form. The cost of goods

purchased is regarded as product cost and all other costs such as administration and selling and

distribution are considered to be period costs.

Identification / Traceability Classification.

Costs are classified as direct and indirect costs on the basis of their identification with

particular jobs, products or processes.

Direct Cost: It is a cost which can be directly identified with a product, process or

department. Materials used and labour employed in manufacturing an article or in a particular

process of production, are common examples of direct costs.

Indirect Costs: These costs are not traceable to any particular product, process or

department, but are common to different products, processes or departments. Factory manager's

salary, factory rent, depreciation of machinery, etc., are typical examples of indirect costs.

The distinction between direct and indirect costs depends upon whether or not the cost can

be identified with the activity or other relevant unit. A cost such as the plant superintendent's

salary can be readily identified with the plant and hence is a direct cost of the plant. However, it is

17

an indirect cost of any department within the plant or of any line of product manufactured. Thus

the nature of business and cost unit chosen will determine which are direct and which

are indirect costs Direct costs are allocated whereas indirect costs are apportioned to

different jobs, products or services on a reasonable basis.

Decision-making Classification

For managerial decision-making, costs are -sub-divided under:

(i) Relevant costs and

(ii) Irrelevant costs.

Relevant costs: These are costs which are relevant for decision-making (for the

future) such as differential or incremental costs, opportunity costs, out-of-pocket costs, etc.

Differential Costs: Management is expected to make decisions and in doing so

compares alternatives. In making a decision, management compares the costs of the

alternatives. The costs that remain the same in any case can be disregarded but the

difference in cost between alternatives is relevant to decision-making. A difference in cost

between one course of action and another is differential cost. If a decision results in an

increased cost, the differential cost may be called incremental cost. If the cost is

decreased, the differential cost may be referred to as a decremental cost. A decision in

favour of an alternative is taken only when, the incremental revenue between two levels

of output is greater than differential cost of those levels of activity. This differential cost is

the difference in net costs and benefits between two or more alternative courses of action.

If the selection of an alternative involves changes in variable costs only, marginal cost

and differential costs are the same. However, a decision may involve changes in fixed costs

also.

Opportunity Costs: In choosing between alternative management has to select the

best alternative but in doing so, has to give up the returns that could have been derived

from the rejected alternatives. The sacrifice of a return or benefit from a rejected

alternative is known as the opportunity cost of the alternative accepted. Opportunity cost

are not entered in the accounting records, yet they are used in decision-making. Often

management is confronted with alternatives, each having its advantages.

Out-of-Pocket Costs: An out-of-pocket cost signifies the relevant cash expenditure

which is involved in a particular situation. Manangement decisions are directly affected by

such costs. Thus, an out-of-pocket cost is the present or future cash expenditure connected

with a certain decision which will change according to the nature of the decision made. For

example, if it is proposed to replace the company's delivery trucks by an arrangement to deliver

goods through public carriers, the depreciated value of the truck is irrelevant (being a sunk cost) to

decide upon the proposal. But, the cost of fuel, driver's salary and maintenance expenditure

involved in using the truck should be relevant costs in deciding whether the delivery system

should be change. These are out-of-pocket costs.

Irrelevant costs: These are those which are not pertinent to a decision. These are the

costs that will not be changed by a decision. Because irrelevant costs will not be affected,

they may be ignored in decision-making process. An example of irrelevant cost is that of sunk

cost.

18

Sunk Cost: It is a cost incurred as a result of decision made in the past which

cannot be reversed or altered by any decision in the future. Sunk costs are irrelevant for

decision-making. The written down values of assets previously purchased are sunk costs.

Let us suppose the management of a company is considering the desirability of replacing

an existing machine by a new one. Suppose, an old machine originally costs Rs. 20,000 and

it has been depreciated to the extent of Rs. 15000 so far. If it is scrapped (no value being

realisable on sale) there will be an accounting loss of Rs. 5000. It would be wrong to

recognise this loss as a cost for deciding upon the proposed replacement. The book value of

the existing machine is really a sunk cost and the decision to replace or not to replace the

machine will not make any difference to its undepreciated value. It is irrelevant to the

question of replacing the existing machine. The difference in income which will result from

the installation of new machine and expected return on capital investment should be the

deciding factor.

Other Cost Concepts

Shut down cost: These are the costs which will still be incurred although a plant is

shut down temporarily, e.g. rent, rates, depreciation, maintenance of plant, etc.

Research cost: It is the cost of searching for new or improved products, new

application of materials or new or improved methods of production.

Development cost: It is the cost of the process which begins with the implementation

of the decisions to produce a new/improved product. It ends with the commencement of

production of that product or method. Thus, it is the cost of commercial exploitation of

successful research. Development cost of new products is treated as an item of deferred

expenditure to be spread over a number of years. It is charged to product costs when

production is fully established.

Joint cost: These are the costs incurred up to the point in a given process where

individual products can be identified. Whenever two or more products are produced out of

the same basic raw material or process, the cost of material purchased and processing are

called joint costs. Such costs have to be apportioned to various products on some basis.

2.3 Elements of Cost

A cost is composed of three elements, i.e., material, labour and expense. Each of these

elements may be direct or indirect.

Material Cost: According to CIMA, London, material cost is "the cost of

commodities supplied to an undertaking.” Material cost includes cost of procurement,

freight inwards, taxes, insurance, etc., directly attributable to the acquisition. Trade

discounts, rebates, duty drawbacks, refund on account of modvat, sales tax, etc., are

deducted in determining the cost of material. Materials may be direct or indirect.

Direct materials: Direct material cost is that which can be conveniently identified

with and allocated to cost units. Direct materials generally become a part of the finished

product. For example, cotton used in a textile, clay in bricks, leather in shoes, steel in

machines, cloth in garments, timber in furniture.

Indirect materials: These are those materials which cannot be conveniently

identified with individual cost units. These are minor in importance, such as (i) small

19

and relatively inexpensive items which may become a part of the finished product, e.g.,

pins, screws, nuts and bolts, thread, etc., (ii) those items which do not physically

become a part of the finished products, e.g., coal, lubricating oil and grease, sand paper

used in polishing, soap, etc.

Labour Cost: According to CIMA, London, labour cost is “the cost of remuneration

(wages, salaries, commission ,bonuses etc) of the employees of an undertaking.” It includes

all fringe benefits like P.F.contribution, gratuity, ESI, overtime, incentive bonus, wages for

holidays, idle time etc. Labour may be direct or indirect.

Direct labour cost consists of wages paid to workers directly engaged in converting raw materials

into finished products. These wages can be conveniently identified with a particular product, job

or process. Wages paid to a machine operator, shoe-maker carpenter, weaver, tailor is a

case of direct wages.

Indirect labour: It is of general character and cannot be conveniently identified with a

particular cost unit. In other words, indirect labour is not directly engaged in the production

operations but only to assist or help in production operations. Supervisor, Inspector,

Cleaner, Clerk, Peon, Watchmen are examples of indirect labour.

Expenses: All costs other than material and labour are termed as expenses. According

to CIMA, London. It is defined as “the cost of services provided, to an undertaking and the

notional cost of the use of owned assets.” Expenses may be direct or indirect.

Direct expenses: are those expenses which can be identified with and allocated to

cost centres or units. These are those expenses which are specifically incurred in

connection with a particular job or cost unit. Direct expenses are also known as chargeable

expenses. Hire of special plant for a particular job, Travelling expenses in securing a particular

contract, Cost of patent rights, Experimental costs, Cost of special drawings, designs and

layouts, Job processing charges, Royalty paid in mining, Depreciation or hire of a plant used on a

contract at site are examples of direct costs.

Indirect expenses: All indirect costs, other than indirect materials and indirect labour

costs, are termed as indirect expenses. These cannot be directly identified with a particular job,

process or work order and are common to cost units or cost centres. Rent and rates,

Depreciation, Lighting and power, Advertising, Insurance, and Repairs are examples of indirect

expenses.

Direct material + Direct labour + Direct expenses = Prime Cost

Indirect material + Indirect labour + Indirect expenses = Overhead

Overheads are divided into three groups as follows:

(a) Manufacturing (works, factory or production) overheads: Such indirect expenses

which are incurred in the factory and concerned with the running of the factory or plant are

known as manufacturing overheads. Following are a few items of such expenses: Rent, rates and

insurance of factory premises, power used in factory building, plant and machinery, etc.

(b) Office and Administrative Overheads. These indirect expenses are not related to factory

but they pertain to the management and administration of business. Such expenses are incurred

on the direction and control of an undertaking. Examples are: Office rent, lighting and heating,

postage and telegrams, telephones and other charges, depreciation of office building, furniture

20

and equipment, bank charges, legal charges, audit fee etc.

(c) Selling and Distribution Overheads. Indirect Expenses incurred for marketing of a

commodity, for securing orders for the articles, despatching goods sold, and for making efforts to

find and retain customers, are called selling and distribution overheads. Examples are

advertisement expenses, cost of preparing tenders, travelling expenses, bad debts, collection charges,

warehouse charges, packing and loading charges, carriage outwards, etc.

2.4 Items excluded from Cost Accounts There are certain items which are included in financial accounts but not in cost accounts.

These items fall into three categories:

Appropriation of profits

(i) Appropriation to sinking funds.

(ii) Dividends paid.

(iii) Taxes on income and profits.

(iv) Transfers to general reserves.

(v) Amount written off-goodwill, preliminary expenses, underwriting commission,

discount on debentures issued, expenses on capital issue.

(vi) Capital expenditure specifically charged to revenue.

(vii) Charitable donations.

Matters of pure finance

(a) Purely financial charges:

(i) Losses on sale of investments, buildings, etc.

(ii) Expenses on transfer of company's office.

(iii) Interest on bank loan, debentures, mortgages, etc.

(iv) Penalties and fines.

(v) Losses due to scrapping of machinery.

(vi) Remuneration paid to the proprietor in excess of a fair reward for services rendered.

(b) Purely financial incomes :

(i) Interest received on bank deposits.

(ii) Profits made on the sale of investments, fixed assets, etc.

(iii) Transfer fees received.

(iv) Rent receivable.

(v) Interest, dividends, etc., received on investments.

(vi) Brokerage received.

(vii) Discount, commission received.

Abnormal gains and losses (i) Losses or gains on sale of fixed assets.

(ii) Loss to business property on account of theft, fire or other natural calamities .

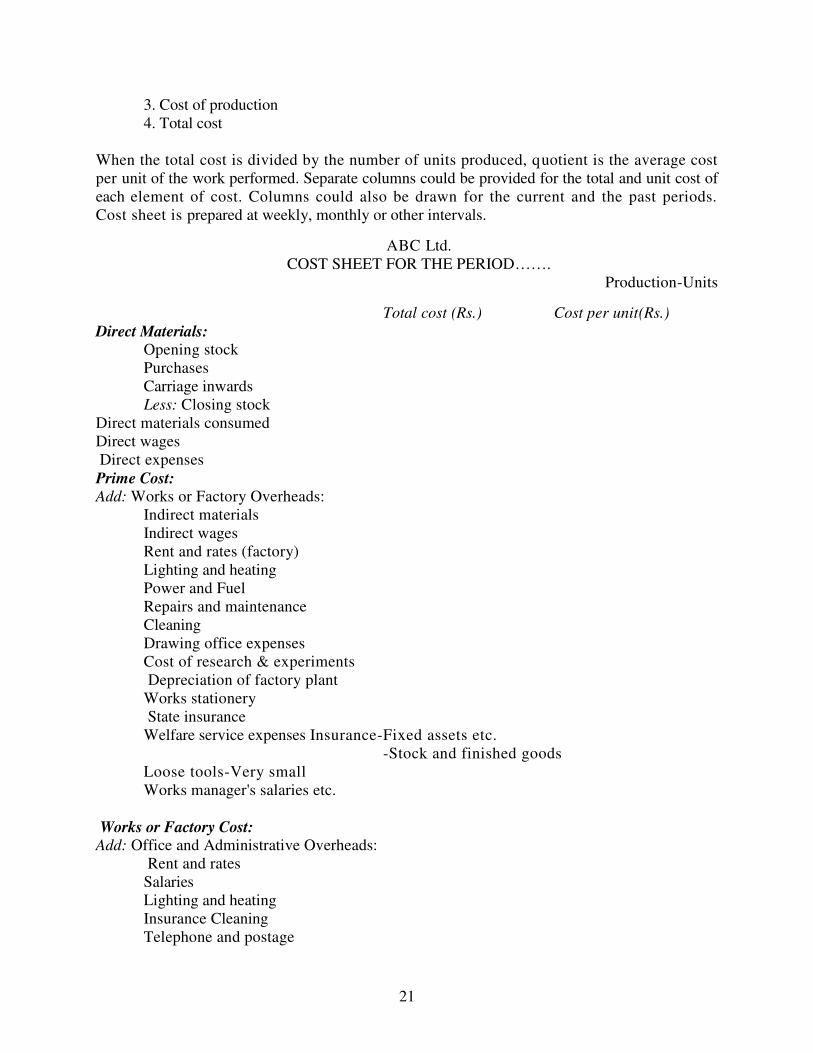

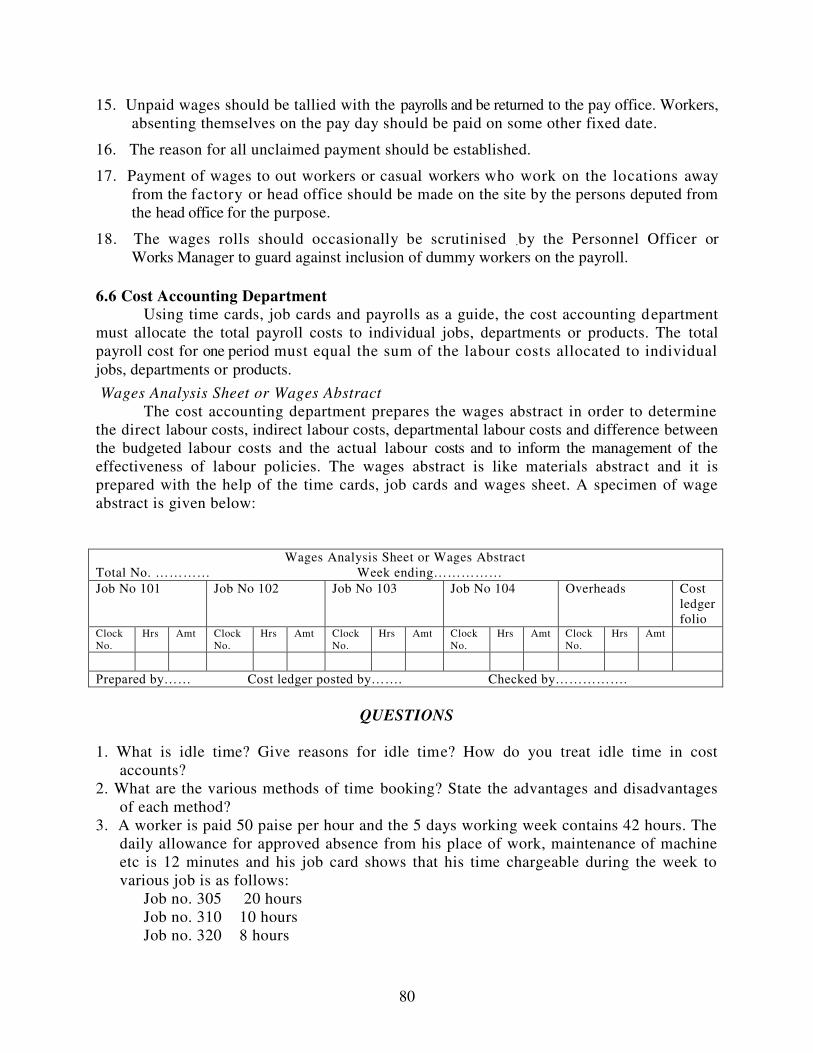

2.5 Cost Sheet

The statement of cost according to element-wise is known as cost sheet. The preparation of

cost-sheet is one of the most important and primary function of cost accounting. The statement discloses

the following:

1. Prime cost

2. Work cost

21

3. Cost of production

4. Total cost

When the total cost is divided by the number of units produced, quotient is the average cost

per unit of the work performed. Separate columns could be provided for the total and unit cost of

each element of cost. Columns could also be drawn for the current and the past periods.

Cost sheet is prepared at weekly, monthly or other intervals.

ABC Ltd.

COST SHEET FOR THE PERIOD……. Production-Units

Total cost (Rs.) Cost per unit(Rs.)

Direct Materials: Opening stock

Purchases

Carriage inwards

Less: Closing stock

Direct materials consumed

Direct wages

Direct expenses

Prime Cost: Add: Works or Factory Overheads:

Indirect materials

Indirect wages

Rent and rates (factory)

Lighting and heating

Power and Fuel

Repairs and maintenance

Cleaning

Drawing office expenses

Cost of research & experiments

Depreciation of factory plant

Works stationery

State insurance

Welfare service expenses Insurance-Fixed assets etc.

-Stock and finished goods

Loose tools-Very small

Works manager's salaries etc.

Works or Factory Cost: Add: Office and Administrative Overheads:

Rent and rates

Salaries

Lighting and heating

Insurance Cleaning

Telephone and postage

22

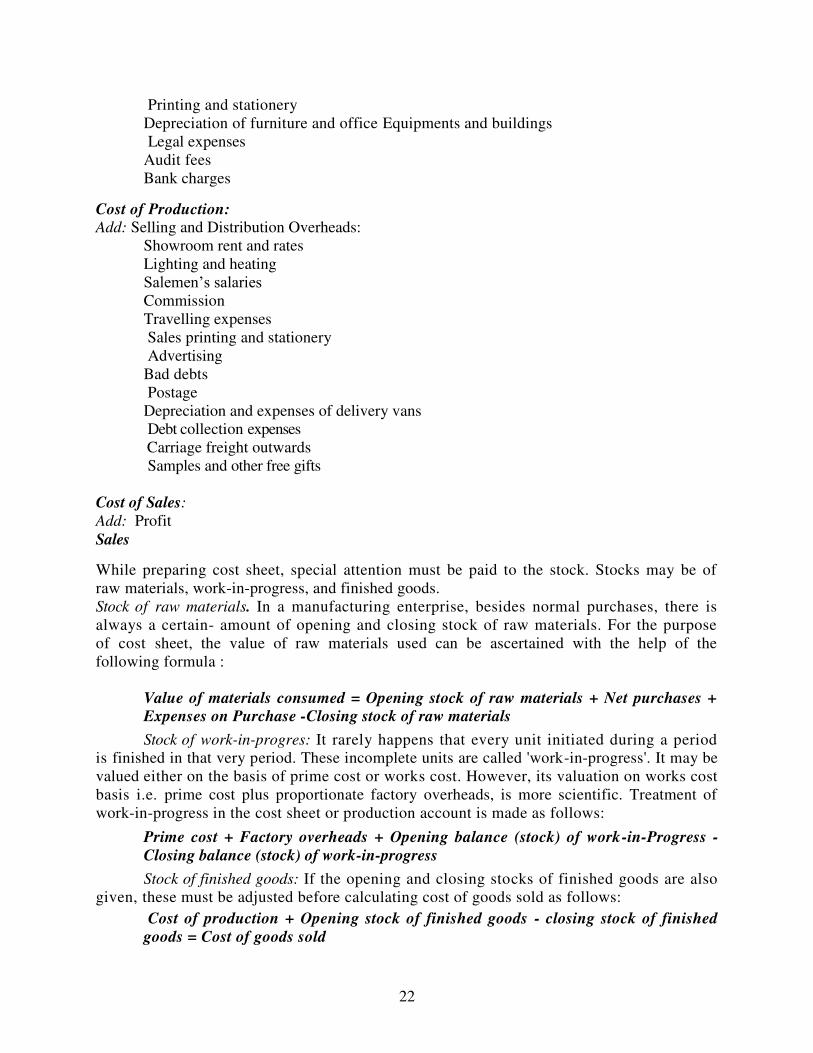

Printing and stationery

Depreciation of furniture and office Equipments and buildings

Legal expenses

Audit fees

Bank charges

Cost of Production: Add: Selling and Distribution Overheads:

Showroom rent and rates

Lighting and heating

Salemen’s salaries

Commission

Travelling expenses

Sales printing and stationery

Advertising

Bad debts

Postage

Depreciation and expenses of delivery vans

Debt collection expenses

Carriage freight outwards

Samples and other free gifts

Cost of Sales:

Add: Profit

Sales

While preparing cost sheet, special attention must be paid to the stock. Stocks may be of

raw materials, work-in-progress, and finished goods.

Stock of raw materials. In a manufacturing enterprise, besides normal purchases, there is

always a certain- amount of opening and closing stock of raw materials. For the purpose

of cost sheet, the value of raw materials used can be ascertained with the help of the

following formula :

Value of materials consumed = Opening stock of raw materials + Net purchases +

Expenses on Purchase -Closing stock of raw materials

Stock of work-in-progres: It rarely happens that every unit initiated during a period

is finished in that very period. These incomplete units are called 'work-in-progress'. It may be

valued either on the basis of prime cost or works cost. However, its valuation on works cost

basis i.e. prime cost plus proportionate factory overheads, is more scientific. Treatment of

work-in-progress in the cost sheet or production account is made as follows:

Prime cost + Factory overheads + Opening balance (stock) of work-in-Progress -

Closing balance (stock) of work-in-progress

Stock of finished goods: If the opening and closing stocks of finished goods are also

given, these must be adjusted before calculating cost of goods sold as follows:

Cost of production + Opening stock of finished goods - closing stock of finished

goods = Cost of goods sold

23

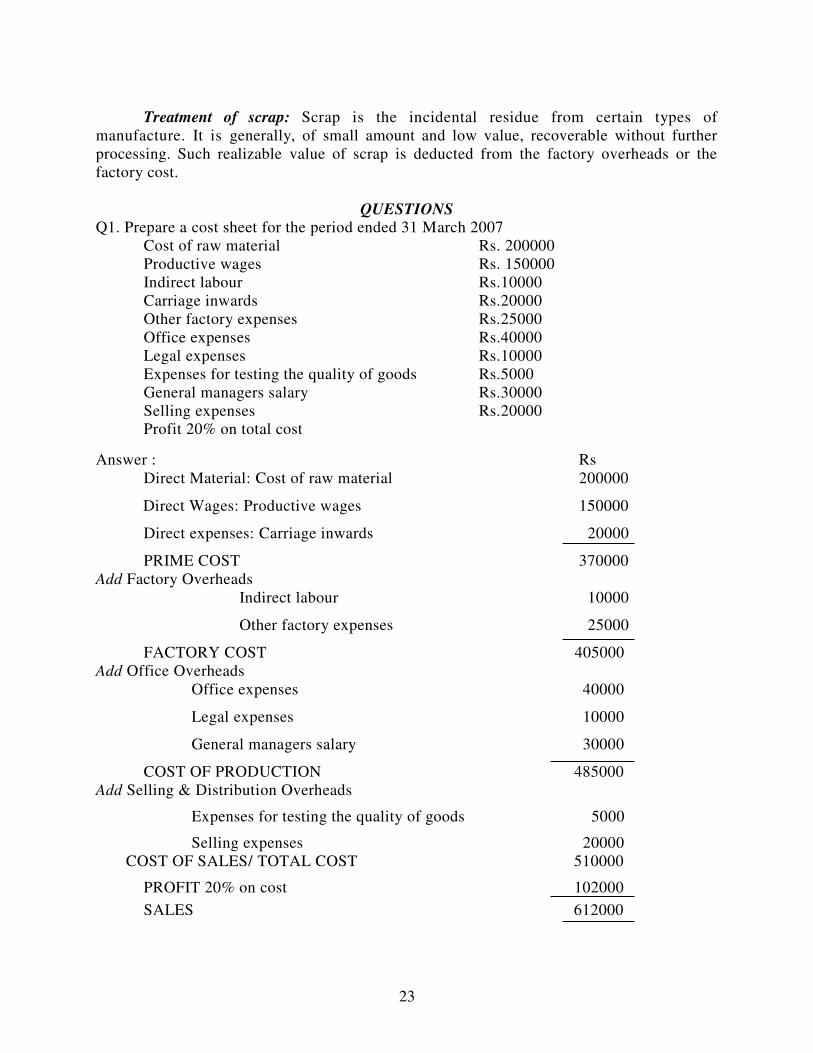

Treatment of scrap: Scrap is the incidental residue from certain types of

manufacture. It is generally, of small amount and low value, recoverable without further

processing. Such realizable value of scrap is deducted from the factory overheads or the

factory cost.

QUESTIONS Q1. Prepare a cost sheet for the period ended 31 March 2007

Cost of raw material Rs. 200000

Productive wages Rs. 150000

Indirect labour Rs.10000

Carriage inwards Rs.20000

Other factory expenses Rs.25000

Office expenses Rs.40000

Legal expenses Rs.10000

Expenses for testing the quality of goods Rs.5000

General managers salary Rs.30000

Selling expenses Rs.20000

Profit 20% on total cost

Answer : Rs

Direct Material: Cost of raw material 200000

Direct Wages: Productive wages 150000

Direct expenses: Carriage inwards 20000

PRIME COST 370000

Add Factory Overheads

Indirect labour 10000

Other factory expenses 25000

FACTORY COST 405000

Add Office Overheads

Office expenses 40000

Legal expenses 10000

General managers salary 30000

COST OF PRODUCTION 485000

Add Selling & Distribution Overheads

Expenses for testing the quality of goods 5000

Selling expenses 20000

COST OF SALES/ TOTAL COST 510000

PROFIT 20% on cost 102000

SALES 612000

24

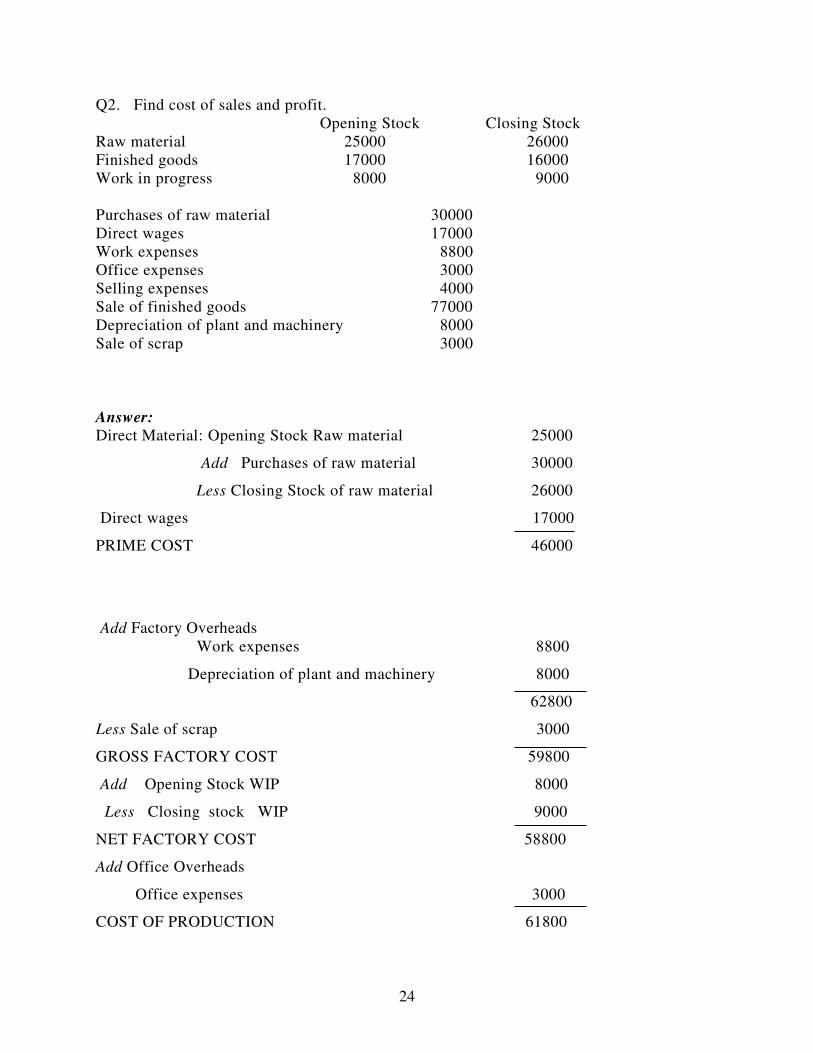

Q2. Find cost of sales and profit.

Opening Stock Closing Stock

Raw material 25000 26000

Finished goods 17000 16000

Work in progress 8000 9000

Purchases of raw material 30000

Direct wages 17000

Work expenses 8800

Office expenses 3000

Selling expenses 4000

Sale of finished goods 77000

Depreciation of plant and machinery 8000

Sale of scrap 3000

Answer:

Direct Material: Opening Stock Raw material 25000

Add Purchases of raw material 30000

Less Closing Stock of raw material 26000

Direct wages 17000

PRIME COST 46000

Add Factory Overheads

Work expenses 8800

Depreciation of plant and machinery 8000

62800

Less Sale of scrap 3000

GROSS FACTORY COST 59800

Add Opening Stock WIP 8000

Less Closing stock WIP 9000

NET FACTORY COST 58800

Add Office Overheads

Office expenses 3000

COST OF PRODUCTION 61800

25

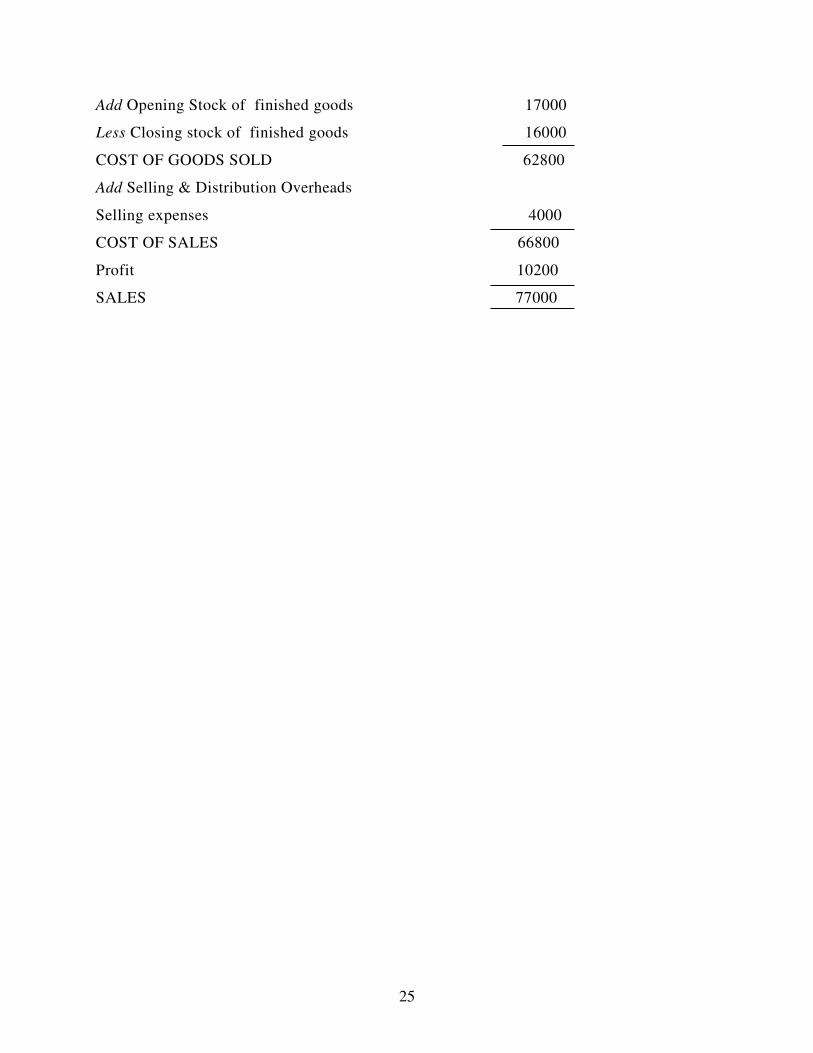

Add Opening Stock of finished goods 17000

Less Closing stock of finished goods 16000

COST OF GOODS SOLD 62800

Add Selling & Distribution Overheads

Selling expenses 4000

COST OF SALES 66800

Profit 10200

SALES 77000

26

UNIT 2

LESSON 3

ACCOUNTING FOR MATERIAL COST

Manisha Verma

Hans Raj College

University of Delhi

A very important component of total cost of production which may be as high as 40% to

60% is the material cost element. Materials are commodities that are used up while rendering a

service or if it is a manufacturing organization then materials gets converted into finished

product. Whatever is the case materials are purchased, stored and issued according to the

requirements of a company. Inorder to prevent the chances of theft, deterioration ,wastage

,shrinkage, spoilage of materials, physical controls will have to be excerised at each stage right

from purchase till the final consumption.

3.1 Meaning of Materials

The term `materials' refer to all commodities supplied to an undertaking. Materials may be

direct or indirect.

Direct materials are those materials which can be conveniently identified with and can be

directly allocated to a particular product, job or process. Examples : timber in furniture, cloth in

garments, milk & cream in ice cream, paper in books, gold/silver in jewellery, bricks & cement in building

construction, steel in machines, leather in shoes.

Indirect materials are those materials which cannot be conveniently identified with and cannot

directly allocated to a particular product, job or process. Examples :

1. Stores used for maintaining machines such as lubricant oil & grease, cotton waste,

consumable stores etc.

2. Stores used by service departments (like power house, boiler house).

LEARNING OBJECTIVES

After studying this chapter, you should be able to understand

3.1 Meaning of Materials

3.2 Material Control

3.3 Inventory Control

3.4 Techniques of Inventory Control

1. ABC Analysis

2. Economic Order Quantity (EOQ)

3. Stock Levels, Minimum Level, Maximum Level, Recorder Level, Reorder Quantity.

4. Inventory Turnover Ratio and review of Slow and Non-moving items.

5. Proper Purchase Procedure

6. Proper Storage Procedure

7. Proper Issue Procedure

8. Two Bin system

9. Use of Perpetual Inventory Records and Continous Stock Verification.

27

3. Materials of small value which can not be conveniently identified with a particular

product, job or process. For example, nails used in furniture, thread used in stitching

garments.

3.2 Material Control

Material Control involves the planning, organising and controlling the procurement, storage

and usage of materials so to as achieve the objectives of efficiency and economy.

Objectives of Material Control

The main objectives of material control are as follows:

1. To avoid the situation of under stocking i.e. to provide continous supply of required materials

so that the activities of production and service departments may not be held up.

2. To avoid the situation of over-stocking i.e. to maintain optimum investment in inventory

considering the operating requirements and financial resources ,so as , to reduce carrying

costs.

3. To ensure the procurement of materials and stores of the required quality at minimum cost

from a reliable source.

4. To minimise the total cost (i.e. ordering costs & carrying costs)

5. To avoid wastages and losses during storage and usage.

6. To maintain proper and upto date records of inventory

7. To provide the required information to the management so as to help the management in

taking inventory decisions.

Essential Requirements of Material Control

The essential requirements of material control are as follows:

1. Proper Co-ordination - There should be proper co-ordination of all departments involved viz.

Purchasing, Receiving, Inspection, Storage, Production, Cost and Finance.

2. Proper Purchase System - There should be proper purchase system to ensure the procurement of

materials and stores of the required quality at minimum cost from a reliable source.

3. Proper Storage System - There should be proper storage system to ensure a place for

everything and everything in its place and avoidance of losses during storage and minimum

storage cost.

4. Proper Issue System - There should be proper system for the issue of materials to ensure that

delivery of materials of the required quality in the required quantity at the required time

upon requisition to the department making requisition.

5. Perpetual Inventory System - There should be perpetual inventory system so as to determine

the quantity and value of each item of materials in stock at any point of time.

6. Continuous Stock Taking System - There should be continuous stock taking system so as to

ensure accuracy of perpetual inventory records.

7. Internal Check System - These should be internal check system so that all transactions

concerning materials are automatically checked.

8. Proper Budgetary Control System - There should be proper budgetary control system to

ensure economy in purchasing and usage of materials and stores.

28

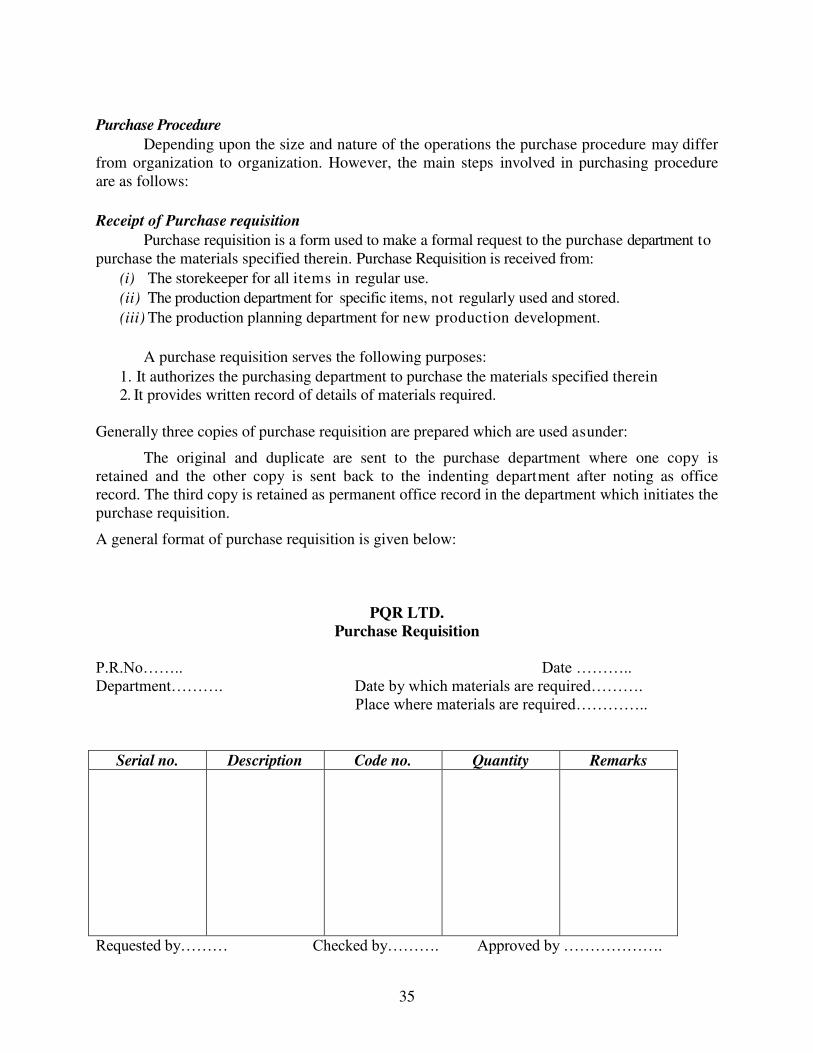

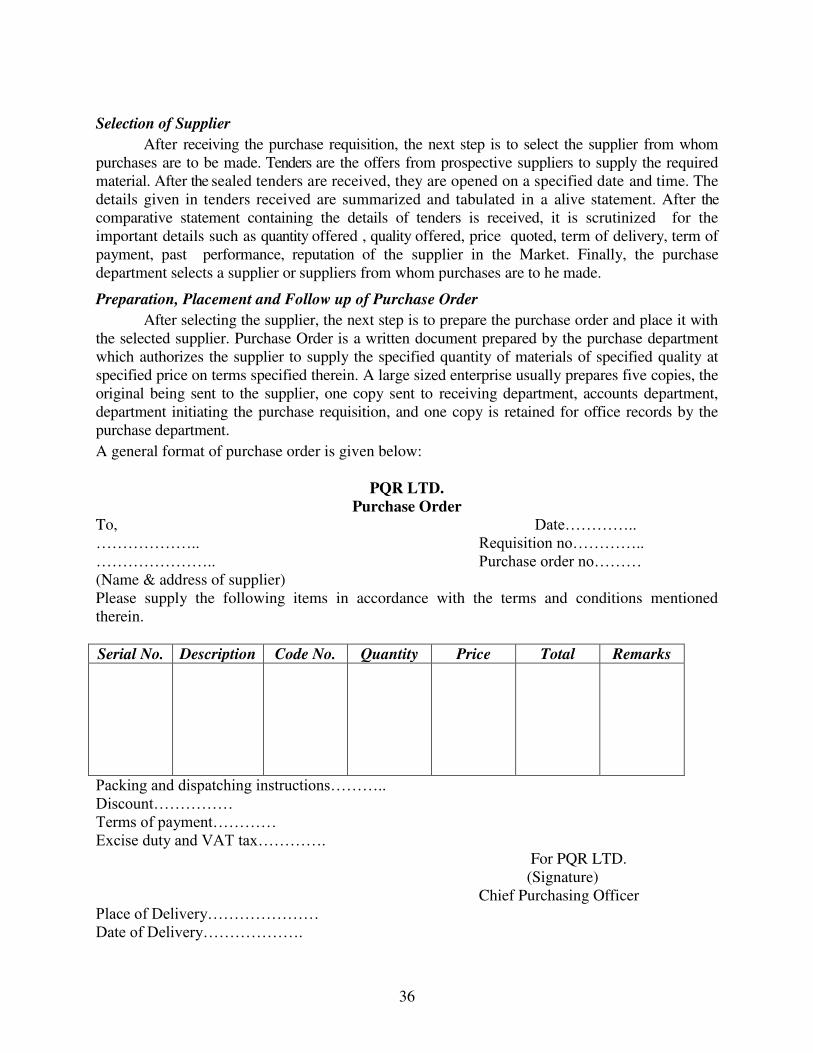

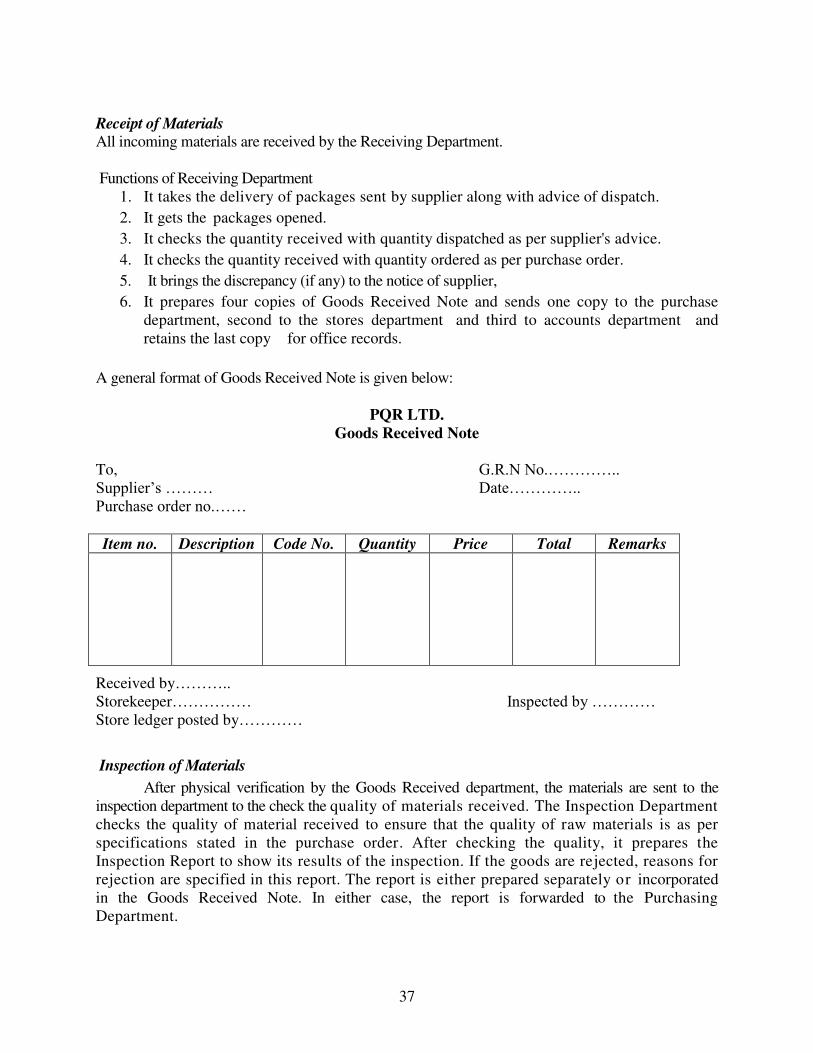

9. Proper Forms - There should be use of proper forms with regard to Purchase Requisition,

Purchase Order, Material Received Note, Material Requisition, Bill of Materials, Material

Returned Note, Material Transfer Note, Bin Card, Stores Card etc.

10. Proper Accounting System - There should be proper accounting system so as to determine the

cost of materials at time of receipt and consumption.

11. Proper Reporting System - These should be proper reporting system to ensure regular

reporting to the management regarding :

(a) Materials purchased (b) Materials issued (c) Materials in hand (d) Slow-moving and

obsolete stock etc.

3.3 Inventory Control

Inventory comprises -

(a) Stock of Raw-materials; (b) Stock of Work-in-progress;

(c) Stock of Finished Goods; and (d) Stock of Stores and Spares

Inventory control involves the planning, organising and controlling the purchase and

storage of inventory so as to ensure the availability of inventory –(a) of the required

quality(b) in the required quantity(c) at the required time(d) at the minimum cost.

3.4 Techniques of Inventory Control

The various techniques of inventory control are as follows:

1. ABC Analysis

2. Economic Order Quantity (EOQ)

3. Stock Levels, Minimum Level, Maximum Level, Recorder Level, Re-order

Quantity.

4. Inventory Turnover Ratio and review of Slow and Non-moving items.

5. Proper Purchase Procedure

6. Proper Storage Procedure

7. Proper Issue Procedure

8. Two Bin system

9. Use of Perpetual Inventory Records and Continous Stock Verification.

ABC analysis

ABC analysis is a system of inventory control. It exercises discriminating control

over different items of stores classified on the basis of the investment involved. It is based

on the principle of management by exception i.e. concentrate more on critical areas than

others.

Usually all items of stores are classified into 3 categories according to their

importance (i.e. their value and frequency of replenishment during a period) as follows:

29

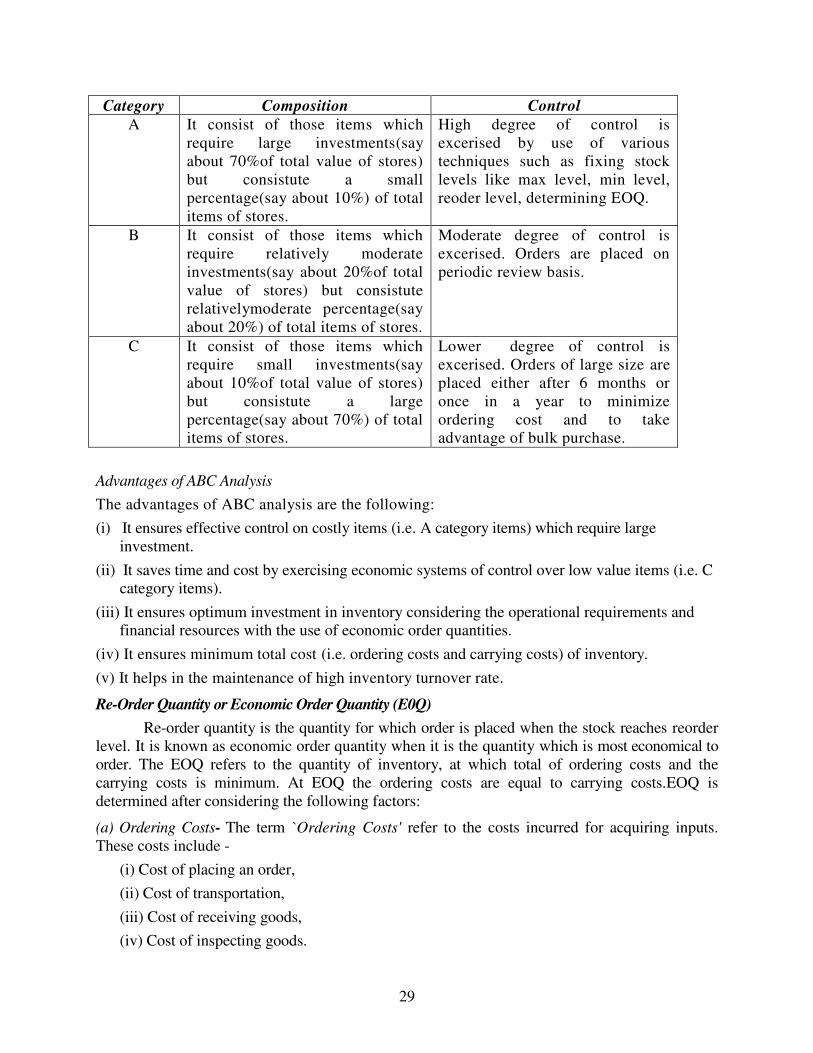

Category Composition Control

A It consist of those items which

require large investments(say

about 70%of total value of stores)

but consistute a small

percentage(say about 10%) of total

items of stores.

High degree of control is

excerised by use of various

techniques such as fixing stock

levels like max level, min level,

reoder level, determining EOQ.

B It consist of those items which

require relatively moderate

investments(say about 20%of total

value of stores) but consistute

relativelymoderate percentage(say

about 20%) of total items of stores.

Moderate degree of control is

excerised. Orders are placed on

periodic review basis.

C It consist of those items which

require small investments(say

about 10%of total value of stores)

but consistute a large

percentage(say about 70%) of total

items of stores.

Lower degree of control is

excerised. Orders of large size are

placed either after 6 months or

once in a year to minimize

ordering cost and to take

advantage of bulk purchase.

Advantages of ABC Analysis

The advantages of ABC analysis are the following:

(i) It ensures effective control on costly items (i.e. A category items) which require large

investment.

(ii) It saves time and cost by exercising economic systems of control over low value items (i.e. C

category items).

(iii) It ensures optimum investment in inventory considering the operational requirements and

financial resources with the use of economic order quantities.

(iv) It ensures minimum total cost (i.e. ordering costs and carrying costs) of inventory.

(v) It helps in the maintenance of high inventory turnover rate.

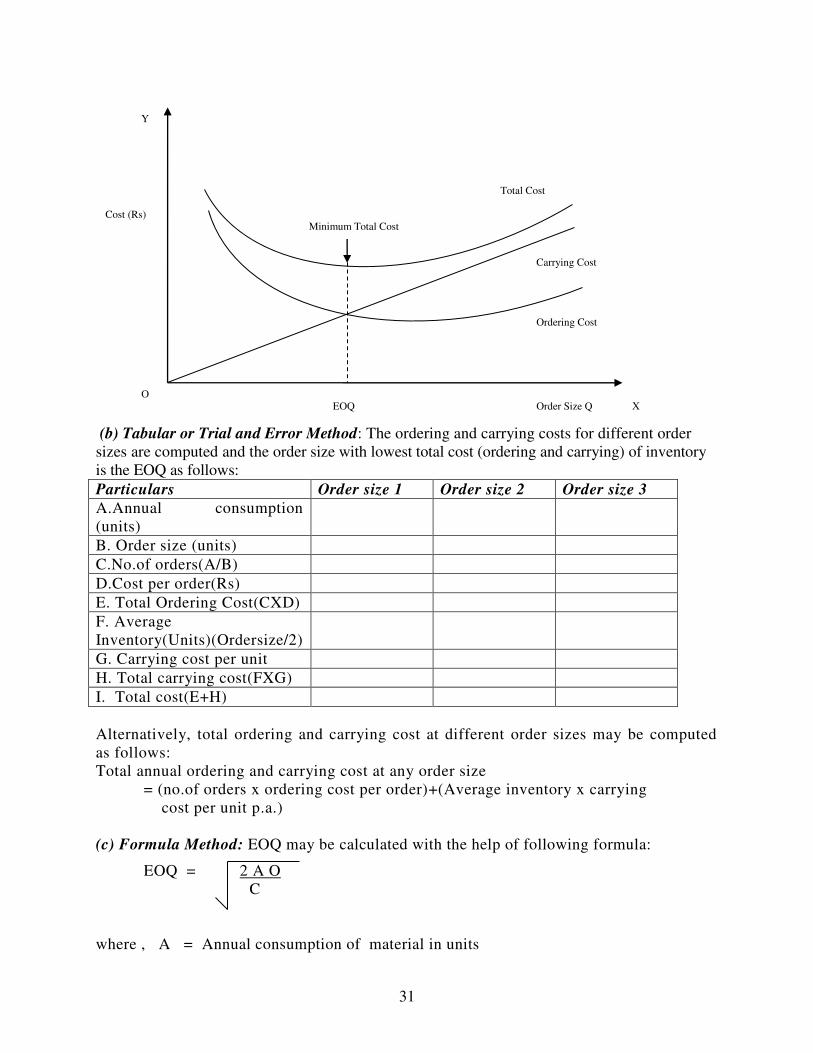

Re-Order Quantity or Economic Order Quantity (E0Q)

Re-order quantity is the quantity for which order is placed when the stock reaches reorder

level. It is known as economic order quantity when it is the quantity which is most economical to

order. The EOQ refers to the quantity of inventory, at which total of ordering costs and the

carrying costs is minimum. At EOQ the ordering costs are equal to carrying costs.EOQ is

determined after considering the following factors:

(a) Ordering Costs- The term `Ordering Costs' refer to the costs incurred for acquiring inputs.

These costs include -

(i) Cost of placing an order,

(ii) Cost of transportation,

(iii) Cost of receiving goods,

(iv) Cost of inspecting goods.

30

There is an inverse relationship between order size and ordering cost.

Larger the order size, Lower the ordering costs because of fewer orders

Smaller the order size , Higher the ordering costs because of more orders

(b) Carrying Costs- The term 'Carrying Costs' refer to the costs incurred in maintaining a given

level of inventory. These costs include

(i) cost of storage space,

(ii) cost of handling materials,

(iii) cost of insurance,

(iv) cost of deterioration or obsolescence,

(v) cost of store staff

There is positive relationship between order size and carrying cost.

Larger the order size, higher the carrying costs because of high average inventory.

Smaller the order size, lower the carrying costs because of low average inventory.

(c) Annual consumption (usage) of inventory: Importance of EOQ

The EOQ technique solves one of the major problems of the inventory management

i.e. the order quantity problem by answering to the question: “How much inventory should

be ordered at a particular point of time?”