Embed Size (px)

Citation preview

Hong Kong – Shanghai Stock

Connect

10 March 2015

Introduction & Welcome

Camille Thommes, Director General, ALFI

Hong Kong – Shanghai

Stock Connect

Addressing Market Feedback

James Fok, Chief of Staff & Head of Group

Strategy, HKEx

Christine Wong, Chief Counsel & Head of

Legal Services Department, HKEx

Shanghai-Hong Kong Stock Connect

Addressing Market Feedback

February / March 2015

The information contained in this document is for general informational purposes only and does not constitute an offer, solicitation or recommendation to buy or sell any securities or to

provide any investment advice or service of any kind. This document is solely intended for distribution to and use by professional investors, including certain United States (“U.S.”)

institutions and other entities in the U.S. that meet specified criteria (see below for additional information for persons in the U.S.). This document is not directed at, and is not intended

for distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Hong Kong

Exchanges and Clearing Limited (“HKEx”), The Stock Exchange of Hong Kong Limited (“SEHK”), Hong Kong Securities Clearing Company Limited (“HKSCC”), Shanghai Stock

Exchange (“SSE”), China Securities Depository and Clearing Corporation Limited (“ChinaClear”) (together, the “Entities”, each an “Entity”) or any of their affiliates, or any of the

companies that they operate, to any registration requirement within such jurisdiction or country.

No section or clause in this document may be regarded as creating any obligation on the part of any of the Entities. Rights and obligations with regard to the trading, clearing and

settlement of securities transactions effected on the SSE and SEHK, including through the Shanghai-Hong Kong Stock Connect (“Stock Connect”), shall depend solely on the

applicable rules of SSE, SEHK, HKSCC and ChinaClear, as well as applicable laws, rules and regulations of Mainland China and Hong Kong.

Currently, access to the Northbound Trading Link of Stock Connect is only available to intermediaries licensed/regulated in Hong Kong; access to the Southbound Trading Link of

Stock Connect is only available to intermediaries licensed/regulated in Mainland China. Direct access to Stock Connect is not available outside Hong Kong and Mainland China.

Although the information contained in this document is obtained or compiled from sources believed to be reliable, none of the Entities guarantee the accuracy, validity, timeliness or

completeness of the information or data for any particular purpose, and the Entities and the companies that they operate shall not accept any responsibility for, or be liable for, errors,

omissions or other inaccuracies in the information or for the consequences thereof. The information set out in this document is provided on an “as is” and “as available” basis and may

be amended or changed in the course of the implementation of Shanghai-Hong Kong Stock Connect. It is not a substitute for professional advice which takes account of your specific

circumstances and nothing in this document constitutes legal advice. HKEx and its subsidiaries shall not be responsible or liable for any loss or damage, directly or indirectly, arising

from the use of or reliance upon any information provided in this document or the presentation given.

ADDITIONAL INFORMATION FOR PERSONS IN THE UNITED KINGDOM: This document is being distributed only to, and is directed only at: (a) persons who have professional

experience in matters relating to investments who fall within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (b) high net

worth entities, and other persons to whom it may otherwise lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as

“relevant persons”). Any person who is not a relevant person should not act or rely on this document or any of its contents.

ADDITIONAL INFORMATION FOR PERSONS IN THE UNITED STATES: The only persons in the U.S. to which this document is intended to be distributed are (i) broker-dealers

registered with the U.S. Securities and Exchange Commission and US institutional investors that in each case qualify as “qualified institutional buyers,” as defined in Rule 144A under

the U.S. Securities Act of 1933, as amended; and (ii) international organisations that are excluded from the definition of “U.S. person” for purposes of Regulation S under such U.S.

Securities Act. This document is distributed to such persons for the sole purpose of generally familiarising such persons with the existence and operations of the Shanghai-Hong Kong

Stock Connect, as well as the types of products that may be traded through Stock Connect. Any securities mentioned in this document are traded on the SEHK or SSE, and neither of

them are registered as national securities exchanges in the United States of America. As such, their services and facilities are not directly available in the United States. The securities

mentioned in this document (i) have not been registered for offer or sale with the U.S. Securities and Exchange Commission or any other governmental authority in the United States,

(ii) have not been approved by any such authority, and (iii) are not subject to U.S. public disclosure requirements.

5

Important Information

Agenda

Update since launch1

Addressing investors’ queries2

Summary3

Appendix4

6

Agenda

Update since launch1

Addressing investors’ queries

Summary3

Appendix4

2

7

What is Shanghai-Hong Kong Stock Connect?

MainlandHong Kong

Regulatory

Co-operation

Note: * SEHK and HKSCC are both wholly-owned subsidiaries of HKEx

Trading LinksSSESEHK*

Clearing & CSD

LinksHKSCC* ChinaClear

8

A mutual market access programme through which Hong Kong and international

investors with access to SEHK and Mainland Chinese investors with access to SSE can

trade and settle shares listed on each other’s market via their existing exchange and

clearing house

Quotas (US$bn)

How Does It Compare to other China Market

Access Schemes?

Exempt individual

quota application?

Exempt lock-ups?

Securities

accessible?

Trading costs2?

Stock Connect is the most flexible and lowest cost route

to access the China onshore market

• Stocks, bonds and warrants traded on exchanges

• Fixed income products traded in interbank bond market

• Funds investing in securities

• Stock index futures

Subset of SSE-listed stocks

(569 names)

$$$ $$$ $

1 Based on research estimates2 According to Standard Chartered, investors without QFII / RQFII quota have to borrow quota at 100-200bps whereas trading cost under Stock Connect is only 10-20bps

QFII RQFII Stock Connect

Approved quota

Utilised quota

551

68

301

49

17

9

48

How Does It Operate?

* Note: Only eligible Mainland investors can participate in Southbound trading

“Home Market” rules

Leverage existing infrastructure

Gross order routing

RMB

Super-clearer model

Regulatory cooperation

A Shares

Order

Routin

g

Cle

ari

ng

& C

SD

Lin

k

SSE

SEHK

So

uth

bo

un

d

Eligible Shares

ChinaClear

No

rthb

ou

nd

Cle

arin

g &

CS

D L

ink

SEHK

Subsidiary

SSE

Subsidiary

Order

Routin

g

HKSCC

Eligible Shares

Hong Kong Shares

EPs/CPs

Mainland

Hong Kong

SSE Members/

ChinaClear

Participants

HK & overseas

investors

Mainland investors*

CSRC

SFC

Re

gu

lato

ry C

oo

pe

rati

on

En

forc

em

en

t Co

op

era

tion

10

Stock Connect brings together two different market structures to facilitate

seamless cross-border trading

What were the Initial Restrictions?

Aggregate Quota

Daily Quota

Stock Eligibility

Investor Eligibility

Northbound Southbound

RMB300bn(~US$48bn)

RMB13bn(~US$2bn)

SSE180 + SSE380

Index constituents

+

Dual-listed A+H shares

No Restrictions

RMB250bn(~US$40bn)

RMB10.5bn(~US$1.7bn)

Hang Seng Large Cap + Mid Cap

Index constituents

+

Dual-listed A+H shares

Retail investors must have min.

RMB500k

Initial restrictions imposed for risk management reasons are expected to be relaxed over time

11

How has it Fared Since Launch?

Total Traded Value(Total Buy + Sell)

Aggregate Quota

Utilised

Average Daily

Traded Value(Daily Buy + Sell)

Average Daily

Traded Value /

Daily Quota

Northbound Southbound

RMB319bn(~US$51bn)

RMB105.7bn

(35.2% of aggregate quota)

RMB5.1bn(~US$0.8bn)

39%

HK$64bn(~US$8bn)

RMB24.4bn

(9.8% of aggregate quota)

HK$1.1bn(~US$0.1bn)

8%

% of Total Market

Turnover0.6% 0.5%

Operations have been smooth and daily quota has been hit only once (Northbound)

12Note: Data for 17 Nov 2014 – 18 Feb 2015

Agenda

13

Update since launch1

Addressing investors’ queries

Summary3

Appendix4

2

What Questions have International Fund Managers

Raised about Stock Connect?

Beneficial

ownership

Enforcement

rights

Asset

segregation

Settlement –

delivery versus

payment

Settlement –

pre-trade

checking

Do investors have beneficial ownership of SSE Securities?

How do investors exercise and enforce their rights as beneficial owners?

Will overseas investors be able to bring legal actions in the Mainland?

What are the asset segregation and reconciliation arrangements?

Can the pre-delivery requirement (from custodian to broker) be avoided?

Is there flexibility to use broker of choice for entry and exit?

Can DVP be achieved?

Overseas fund managers have raised a number of questions on the Stock Connect structure

14

Concerns of International Fund Managers

UCITS Funds 1940 Act Funds

Must entrust assets to depositary for safekeeping

Depositary’s liability not affected by entrusting

assets to a third party for safe-keeping

Trustee must “exercise care and diligence” in

appointing safe-keeping agent

Obligation to maintain “appropriate level of

supervision” over agent

Must maintain legal separation of non-cash assets

held in custody

Legal entitlement to the assets should be assured

Non-US assets may be placed with

“Eligible Foreign Custodians” (Rule 17f-5); and

“Eligible Securities Depositaries” (Rule 17f-7)

“Foreign custody managers” must provide reports

on material change in foreign custody arrangements

Contracts with an Eligible Foreign Custodian must

provide for, inter alia:

Indemnification / insurance;

Free transferability of ownership;

Adequate records identifying the Fund

US and European fund managers’ obligations under relevant laws and regulations are

capable of being met under the Stock Connect structure

15

What is the Role of HKSCC?

Within the Hong Kong Regulatory Framework Under Stock Connect

Recognised Clearing House (RCH) approved by the

Securities & Futures Commission (SFC) under

S37(1) of the Securities & Futures Ordinance (SFO)

Central Securities Depository (CSD) and Securities

Settlement System (SSS) with rules approved by the

SFC

Protected under S45 of SFO from insolvency

clawbacks due to HK participant defaults

Financial Market Infrastructure (FMI) recognised by

SFC, IMF and other international bodies

Complies with CPMI-IOSCO’s Principles for

Financial Market Infrastructures (April 2012)

To be recognised as a “Third Country CCP” under

EMIR

Approved as Special Clearing Participant of

ChinaClear

Responsible for clearing and settling trades

executed via Northbound Trading Link with

ChinaClear for HK participants

Provides Central Securities Depository (CSD)

services to Northbound investors

Holds SSE-listed securities on behalf of Northbound

investors as nominee holder

Role of HKSCC recognised by SFC and CSRC and

embedded in relevant Stock Connect Rules and

Regulations

HKSCC is a CSD, not a custodian/safe-keeping

agent – its participants include Custodian

Participants

HKSCC’s role as a RCH, CSD and nominee are recognised under the

HK regulatory framework and under Stock Connect

16

Holding StructureHKSCC as nominee holder of SSE Securities for investors

17

All A Shares are issued in scripless form

ChinaClear records = electronic registers of

members of issuers

HKSCC holds SSE Securities as nominee

holder for its participants and their clients

All SSE Securities acquired through Northbound

Trading Link are held in HKSCC participants’

CCASS Stock Accounts

HKSCC provides CSD and nominee services to

participants to assert their rights in SSE

Securities through facilitating:

voting;

dividend distribution; and

corporate communications

Investors’ interest in SSE Securities is reflected

in their brokers’ or custodians’ client records

HKSCC has no proprietary interest in SSE

Securities

Indirect holding structure recognised by CPMI-

IOSCO Principles for Financial Market

Infrastructures

Beneficial

Ownership

CP-n’s Client Records

HK investor

HK investor

HK investor

CP-3’s Client Records

HK investor

HK investor

HK investor

CP-2’s Client Records

HK investor

HK investor

HK investor

ChinaClear – electronic ROM

MainlandInvestor-1

MainlandInvestor-2

MainlandInvestor-3

HKSCCOmnibus

a/c

HKSCC CCASS

CP-1 CP-2 CP-3 CP-n

CP-1’s Client Records

HK investor-1

HK investor-2

HK investor-3

Beneficial

Ownership

Who is the shareholder on record? Who owns the shares?

HKSCC is nominee holder for investors

“Although securities shall be recorded in the securities

accounts of the securities holders themselves, if any

of the laws, administrative regulations or the CSRC

rules prescribes that the securities shall be recorded

in the securities accounts of a nominee holder, such

provisions shall prevail.” CSRC’s Administrative Measures for Securities Registration and

Settlement Art 18

“Shares bought by investors through Northbound

trading shall be registered under the name of

HKSCC.” CSRC’s Several Provisions on Shanghai-HK Stock

Connect Art 13

“HKSCC shall open an ordinary RMB SSE share

account under its name and shall hold the securities

held by overseas investors as a nominee holder.” ChinaClear’s Shanghai-HK Stock Connect Implementing Rules Art 6

“Securities registration records issued by ChinaClear

shall be valid evidence of the holding of securities.” ChinaClear’s Registration Rules Art 5

Investors are beneficial owners and have proprietary

interest in SSE Securities

“Investors are entitled in accordance with the law to

the rights and interests in respect of shares

purchased through Shanghai-Hong Kong Stock

Connect.” CSRC’s Several Provisions on Shanghai-HK Stock Connect Art 13

“The holdings of an investor in a listed company

include shares registered under such investor’s name

and shares not registered under such investor’s name

but voting rights in respect of which may be actually

controlled by such investor.” CSRC’s Administrative Measures for Acquisition of Listed

Companies Art 12

“Certification on securities holding of the beneficial

owner issued by the nominee holder constitutes

lawful proof of the beneficial owner’s holding of the

relevant securities.”ChinaClear’s Registration Rules Art 5

HKSCC has no proprietary interest in SSE Securities

(CCASS R824)

HKSCC holds on trust for investors: CA Pacific’s case

No difference to role for HK listed securities

Who is the Owner of SSE Securities?

18

Hong Kong law

No - CA Pacific’s case; shares still belong to investors

Mainland China law

No - investors are real owners of SSE Securities

Recognise HK liquidator of HKSCC, will give effect to HK law

Position

Investors hold SSE Securities through HKSCC and enjoy proprietary rights as shareholders

If HKSCC is insolvent, will SSE Securities form part of its bankruptcy assets for

distribution to its creditors? Acid Test

Not relevant

ChinaClear has no interest in SSE Securities

Post-clearing, ChinaClear acts as securities registration institution

Is bankruptcy of

ChinaClear relevant?

Beneficial

Ownership

19

Do Investors have Beneficial Ownership?

Comparison with QFII/RQFIIs – see slide 30

Obligations to HKSCC participants set out in CCASS Rules and Operational Procedures

Obligation to seek and act on instructions from Participants

Services covering all the above - responsible for collecting and distributing dividends to its

participants, obtaining and consolidating voting instructions and subsequently submitting a

combined single voting instruction to issuers

CCASS Rules and OPs approved by SFC, cannot be amended without SFC approval

HKSCC’s obligations

Voting rights

Rights to call and participate in shareholders’ meetings

Right to propose matters for voting at shareholders’ meetings

Right to subscribe for allocated entitlements

Right to receive dividends and other distributions

Rights that may be

exercised through

HKSCC

“Nominee holders are legally entitled to the relevant rights as securities holders and shall bear

corresponding obligations to the relevant beneficial owners. The beneficial owners shall

exercise their relevant rights through the nominee holders. When nominee holders exercise

the relevant rights as securities holders, they shall consult the beneficial owners in accordance

with the instructions of the beneficial owners and shall not harm the interests of the beneficial

owners.” (ChinaClear Registration Rules Art 5)

Nominee holder’s role

under Mainland China

law

Beneficial owners exercise rights through HKSCC

Beneficial

Ownership

20

How do Investors Exercise Their Rights as

Beneficial Owners?

Action in Mainland courts against listed issuers

Availability of causes of action subject to Mainland China law

Where a cause of action is available:

HKSCC as nominee holder can take legal action as shareholder on record

Mainland law does not specifically provide for or prohibit beneficial owners from taking

legal action directly

BUT there is legal support for beneficial owners to take legal action directly including:

Article 119 of Civil Procedure Law: The plaintiff shall be an individual, legal

person or any other organisation with a direct interest in the case

If an investor can provide evidence to prove that it is the beneficial owner and

has a direct interest, it can bring legal action in Mainland courts in its own name

In Mainland China

Action in Hong Kong courts against HKSCC for failure to perform obligations

HKSCC Participants can directly take action

Investors can directly take action or require HKSCC Participants or intermediaries in custody

chain to take action

In Hong Kong

Beneficial owners can enforce their rights in courts as beneficial owners

Enforcement

Rights

21

How do Investors Enforce Their Rights as

Beneficial Owners?

Article 5 of ChinaClear’s Registration Rules: securities holding of the beneficial owner

issued by the nominee holder constitutes lawful proof of the beneficial owner’s holding of the

relevant securities - this recognises HKSCC’s certification of investor holdings

HKSCC in discussion with ChinaClear on format of certification

Article 3 of CSRC and SFC Joint Announcement on Stock Connect: clearing

arrangements will be subject to the regulations and operational rules of the market where

clearing takes place

If HKSCC and HKSCC Participant’s certification of an investor’s interest as beneficial owner is

acceptable under Hong Kong law, it will be acceptable to Mainland authorities

HKSCC’s assistance in

enforcing rights

Proof of investor’s

holdings

Proposed rule change to confirm position in March 2015

confirm proprietary interests in SSE Securities belong to investors

confirm HKSCC’s commitment to provide assistance to bring legal action

HKSCC

rule amendment

Enforcement

Rights

22

Further Enhancements on Enforcement Rights

Underway

Where an investor decides to bring legal action to enforce its rights in Mainland China, HKSCC

can provide assistance as necessary, including:

providing certification of relevant participant’s and investor’s holdings in SSE Securities

assisting investor in bringing action subject to its statutory duties and satisfaction of

reasonable conditions (e.g. payment of fees and cost upfront and indemnities)

HKSCC will provide assistance to investors if they decide to enforce their rights

Comparison with QFII/RQFIIs – see slide 30

What are the Account Segregation Arrangements?

23

HKSCC holds SSE Securities in omnibus

account as nominee holder for HK Clearing

Participants and their clients

Omnibus account segregated from the

accounts of ChinaClear’s other participants

HKSCC Clearing Participants and Custodian

Participants hold SSE Securities in CCASS

Stock Accounts

Participants can open one or more “sub-

account” (Stock Segregated Accounts) to

segregate clients’ assets

Each participant’s account is segregated from

the accounts of HKSCC’s other participants

Investors’ interest in SSE Securities is

reflected in their brokers’ or custodians’ client

records

HK brokers hold clients’ assets on trust under

HK law

HK brokers regulated by SFC and are

required to keep separate records for each

client

Asset

Segregation

CP-n’s Client Records

HK investor

HK investor

HK investor

CP-3’s Client Records

HK investor

HK investor

HK investor

CP-2’s Client Records

HK investor

HK investor

HK investor

ChinaClear – electronic ROM

MainlandInvestor-1

MainlandInvestor-2

MainlandInvestor-3

HKSCCOmnibus

a/c

HKSCC CCASS

CP-1 CP-2 CP-3 CP-n

CP-1’s Client Records

HK investor-1

HK investor-2

HK investor-3

What are the Reconciliation Procedures to Ensure Accuracy

of Holdings at Different Levels of the Structure?

24

ChinaClear as host CCP & CSD of SSE

SecuritiesProvides daily files on stock movements and stock

balances to HKSCC

HKSCC

Participants

ChinaClear

HKSCC

Reconciliation

procedures

specified in CSD

and Clearing Links

AgreementHKSCC as a participating CCP & CSD of

ChinaClearReconciles daily files provided by ChinaClear against

its own records

Provides daily reports / files on stock movements and

stock balances + enquiry functions to its participants

Reconciliation

procedures

specified in

CCASS Rules

Participants of HKSCCReconcile daily files / reports / enquiry results

provided by HKSCC against their internal records

Major types of share

movements in CCASS

Settlement of Northbound

trades

Share transfers initiated by

brokers/custodians

between their CCASS

Stock Accounts (i.e.

“Settlement Instructions” or

SIs)

Nominee activities (e.g.

bonus share payment)

HKSCC publishes shareholding information per stock per participant

on a daily basis via the HKEx website

Asset

Segregation

Pre-trade CheckingHow does it work today?

25

SSE

CSC

Passed

Pre-trade

Checking

?

Hong Kong

Brokers

Place sell order

Yes

No

Route order to SSE

Reject order

What is Pre-trade checking?

A mechanism to ensure investors will have sufficient

shares to settle their sell trades

Sell orders will be rejected if the investor’s cumulative

sell quantity in that stock for the day is higher than its

stockholdings at market open

Hong Kong brokers are responsible to ensure that they

have in place procedures and systems to prevent their

clients (i.e. investors) from day trading and overselling

of SSE Securities

How to ensure compliance with Pre-trade

checking?

Investors can transfer shares to the selling Hong Kong

brokers on T-1 day, or

Investors can also request their custodians to input

instructions in CCASS to transfer shares to the selling

Hong Kong brokers by 7:30am on T day, for settlement

at 7:45am

Pre-trade

Checking

In order to comply with SSE's pre-trade checking requirements, investors holding shares

with custodians must transfer shares to the execution broker before trading

How does it work?

As an add-on to existing model:

Custodians* upon investors’ requests to open Special Segregated Accounts (SPSA) and CCASS will generate a unique

Investor ID. The SPSAs are for keeping shareholding of investors separately

CCASS will snapshot SSE Securities holdings under custodians’ SPSAs and replicate to CSC to facilitate Pre-trade

Checking

Investors should inform its designated EPs the assigned Investor IDs for Pre-trade Checking when placing sell orders

Custodians transfer shares from the SPSA to the relevant Clearing Participants for settlement (based on investors’

instructions)

Pre-trade CheckingWhat enhancements are we making?

26

SSE

CSC Passed

Pre-trade

Checking

?

Hong Kong Brokers

Place sell order for

institutional investor

Yes

No

Route order to SSE

Reject

order

CCASS

CustodianSPSA 1

SPSA 2

SPSA 3

…

1

3

GCP 1

DCP 1

DCP 2

2

4

1

3

2

4

* Including GCPs who are non-EPs and Custodian Participants of CCASS

Under enhanced model, investors who use custodians only transfer SSE Securities

to Clearing Participants after sell order execution (post-trade delivery)

Pre-trade

Checking

Some brokers and custodians have developed solutions

Delivery versus

Payment

(DVP)

Settlement

Solutions available

A feature of the SSE market

Transferring shares on T and receive cash on T+1

Note HKSCC is a Central Counterparty and guarantees performance

Free of Payment

(FOP)

Settlement

Delivery Versus

Payment

27

Settlement – Delivery Versus Payment

DVP can be provided by brokers or custodians using Model B or Model C where

the broker or custodian will extend credit or make special arrangements with

investors

DVP settlement solutions have been developed by the market

Agenda

28

Update since launch1

Addressing investors’ queries

Summary3

Appendix4

2

Summary

29

Stock Connect is the most flexible and lowest cost way of accessing onshore China equities

Regarding outstanding questions raised by international fund managers:

Do investors have beneficial ownership? YES

Can investors enforce their rights?NO EXPRESS PROHIBITION ON DIRECT

ENFORCEMENT, AND HKSCC WILL ASSIST

WHERE NECESSARY

Are assets properly segregated? YES

Are investors able to avoid pre-trade

transfers?YES, PRE-TRADE CHECKING ENHANCEMENT

EFFECTIVE IN MARCH 2015

Are investors able to achieve DVP? YES, MARKET PARTICIPANTS HAVE

DEVELOPED/ARE DEVELOPING SOLUTIONS

More Information Available on HKEx Website

30

Designated webpage for

Shanghai-Hong Kong Stock

Connect by HKEx

http://www.hkex.com.hk/eng/csm/chinaConnect.asp?LangCode=en

Information Book and FAQ for

Investors and Supplemental

FAQ to fund industry

http://www.hkex.com.hk/eng/market/sec_tradinfra/chinaconnect/investorinfo.htm

http://www.hkex.com.hk/eng/newsconsul/hkexnews/2015/Documents/Issues%20concerning%20Shanghai

-Hong%20Kong%20Stock%20Connect.pdf

General Rules of CCASS http://www.hkex.com.hk/eng/rulesreg/clearrules/ccassgr/ccassrule.htm

Note: Chapters 41 and 42 are new chapters specific to Shanghai-Hong Kong Stock Connect

CCASS Operational Procedures http://www.hkex.com.hk/eng/rulesreg/clearrules/ccassop/ccassoptpcd3.htm

Rules of the Exchange http://www.hkex.com.hk/eng/rulesreg/traderules/sehk/exrule.htm

Note: Chapters 14, 14A and 15 are new chapters specific to Shanghai-Hong Kong Stock Connect

CCASS Shareholding search http://www.hkexnews.hk/sdw/search/search_sdw.asp

Note: Provides CCASS shareholding information for the past 12 months, on a per stock per Clearing

Participant basis

Bi-Weekly Investor Newsletter http://www.hkex.com.hk/eng/market/sec_tradinfra/chinaconnect/Newsletter.htm

Note: Regular investor newsletter updates on trading statistics of the programme, trading calendars and

economic data calendars

Agenda

31

Update since launch1

Addressing investors’ queries

Summary3

Appendix4

2

Northbound & Southbound Aggregate Quota Usage

32Source: HKEx, as of 17 Feb 2015

105,7

0

20

40

60

80

100

120

RM

B b

n

Aggregate Quota Usage (17 Nov 14 - 17 Feb 15)Northbound

Quota Limit (RMB300 bn)24,4

0

5

10

15

20

25

30

RM

B b

n

Aggregate Quota Usage (17 Nov 14 - 13 Feb 15)Southbound

Quota Limit (RMB250 bn)

33

Comparison between Stock Connect and

QFII/RQFII Schemes

QFII/RQFII Stock Connect Northbound

CSRC approval Required – QFII/RQFII qualification Not required for investors

SAFE approval Required - Individual quota for each QFII/RQFII Not required – Stock Connect quotas applicable to all investors

HK licensing requirement Required – Type 1/Type 9 SFO licensing Not required for investors, brokers or fund managers

Clearing ChinaClear ChinaClear (host CCP) and HKSCC (participating CCP)

Broker origination China, maximum three brokers each on SSE, SZSE and CFFEX Hong Kong, theoretically unlimited number of brokers

Investment scope Stocks, funds, listed and interbank bonds stock index futures Subset of SSE-listed stocks (569 names) – SSE 180/380 & A+H

Transfer of quota Prohibited No restrictions – not subject to individual quota

Cross-border remittance 1 year lock up (n/a to open-ended funds) and restrictions on fund

repatriation

No restrictions

Block trade Allowed Not allowed – subject to the non-trade transfer exemptions,

generally no SSE off-exchange transactions are allowed.

Currency inflow QFII - USD with onshore conversion ; RQFII - RMB (CNH) RMB (CNH)

Tax Not subject to Business Tax; since 17/11/14, not subject to CGT Not subject to Business Tax and CGT

Pre-trade checking and

settlement method

Pre-trade checking applicable to cash (buyer) and shares (seller)

Delivery of shares on T, payment on T+1

Applicable to shares (seller)

Deliver of shares on T, payment on T+1

Onshore account proprietary client money open-ended fund HKSCC

Account type R/QFII’s own

account

omnibus a/c - R/QFII as

nominee holder for

investors

segregated a/c - R/QFII as

nominee holder for

investors with designation

omnibus account at ChinaClear - HKSCC as nominee holder for

investors

segregated accounts of HK participants at HKSCC

Special status as CSD Not applicable No No Yes

Enforcement right of

investors

Yes, holder on

record

Not holder on record,

R/QFII can sue, no

express prohibition on

direct enforcement

Not holder on record,

R/QFII can sue, no

express prohibition on

direct enforcement

Not holder on record; HKSCC can sue, no express prohibition on

direct enforcement

New Regulations on Stock Connect

Hong Kong Mainland

Amendments to SEHK’s Trading Rules

on SH-HK Stock ConnectCSRC Several Provisions on the Pilot Programme

of SH-HK Stock Connect

Amendments to HKSCC’s Clearing Rules and

Procedures on SH-HK Stock Connect

SSE’s SH-HK Stock Connect Pilot Programme

Provisions

Amendments to SEHK’s Operational Procedures on

Stamp Duty Collection

ChinaClear’s Implementing Rules for Registration,

Depository and Clearing Services under SH-HK

Stock Connect

Amendments to SEHK’s Disciplinary ProceduresMOF, SAT and CSRC Notice on Taxation Policy on

SH-HK Stock Connect

SFC’s FAQ on A-share Rights Issue Prospectuses PBOC & CSRC’s Notice on SH-HK Stock Connect

CSRC’s Filing Requirements for HK Listed Issuers

Making Rights Issues to Mainland Shareholders via

SH-HK Stock Connect 34

Stock Connect Legal Documentation

Four-Party Agreement: SEHK, SSE, HKSCC & ChinaClear

Trading Links Agreement: SEHK, SEHK SPV, SSE & SSE SPV

Clearing Links Agreement: HKSCC & ChinaClear

Other Agreements:

• Northbound order-routing services agreement: SEHK & SEHK SPV

• Clearing agency agreement (Northbound): SEHK SPV & HKSCC

• Clearing agency agreement (Southbound): SSE SPV & ChinaClear

• Clearing Participant Agreement (Northbound): HKSCC as participant of ChinaClear

• Clearing Participant Agreement (Southbound): ChinaClear as participant of HKSCC

• Agreements with BOC (HK & Shanghai) re RMB fund flow

Regulatory MOU: SFC & CSRC

35

HKSCC’s role: CSD, custodian or safe-keeping agent?

36

CPMI-IOSCO’s description:

A CSD provides securities accounts, central safe-keeping services, and asset services,

which may include the administration of corporate actions and redemptions.

A CSD can hold securities in physical form or in dematerialised form. The activities of a

CSD may vary depending on whether it operates in a jurisdiction with a direct or an indirect

holding arrangement or a combination of both.

An indirect holding system employs a multi-tiered arrangement for the custody and transfer

of ownership of securities in which investors are identified only at the level of their

custodian or intermediary.

In many countries, a CSD also operates a securities settlement system which enables

securities to be transferred and settled by book entry according to a set of predetermined

multilateral rules.

What is a CSD?

Yes, the indirect nominee holding structure is recognised by CPMI-IOSCO’s Principles

Is nominee holder’s

role consistent with

CSD’s functions?

CSD, not custodian or “safe-keeping agent”

HKSCC complies with CPMI-IOSCO’s Principles on Financial Market Infrastructures

Regulated by SFC and recognised by IMF

Will be subject to HK’s resolution regime for financial market infrastructures

HKSCC’s role

HKSCC acts as a CSD; nominee holder’s role is consistent with its CSD functions

Panel Shanghai and Hong

Kong Stock Connect

Martin DobbinsSenior Vice President, Managing Director,

State Street Bank Luxembourg,

and Chairman of ABBL/ ALFI Depositary Forum

Panel Shanghai and Hong

Kong Stock Connect

Yvan De LaurentisHead of Depositary and Fiduciary Services,

BNP Paribas Securities Services

Sonia BiraschiGeneral Manager, State Street Bank Luxembourg

Hermann BeythanPartner, Linklaters LLP

Johan SchreuderManaging Director, Investec Asset Management, Lux.

Introduction

Yvan De Laurentis, Head of Depositary and Fiduciary Services,

BNP Paribas Securities Services

Agenda

1. Introduction

2. Timeline

3. Which Stock Connect models exist?

4. Stock Connect as of today

5. Benefits of Stock Connect

6. Matters for consideration

7. Future outlook

8. An asset manager case-study

9. Q&A from the audience

40

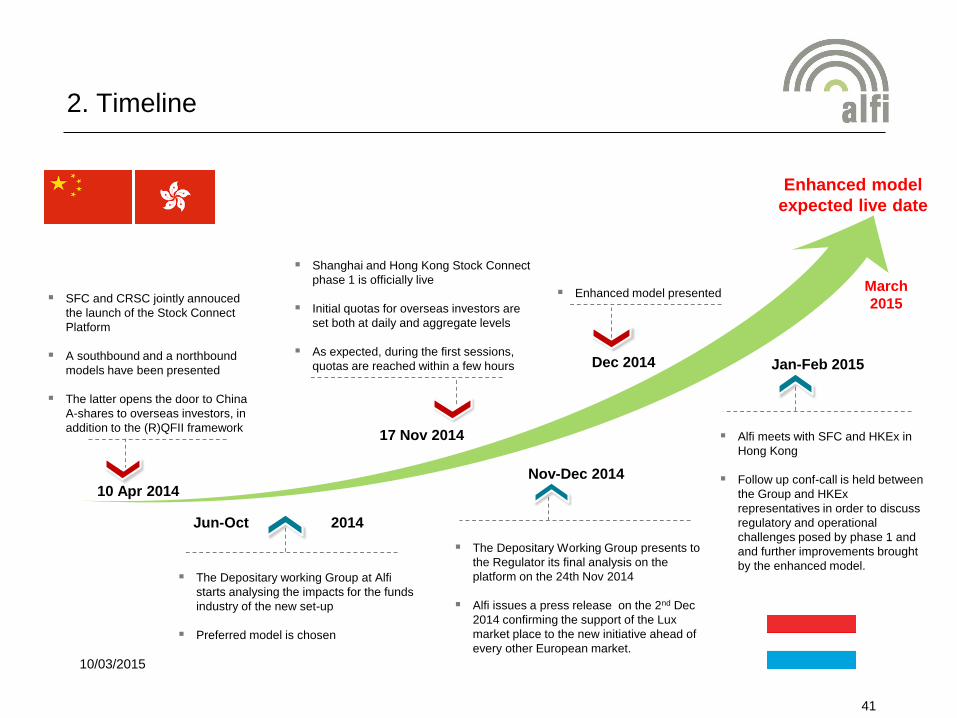

2. Timeline

March

2015

17 Nov 2014

Shanghai and Hong Kong Stock Connect

phase 1 is officially live

Initial quotas for overseas investors are

set both at daily and aggregate levels

As expected, during the first sessions,

quotas are reached within a few hours

10 Apr 2014

SFC and CRSC jointly annouced

the launch of the Stock Connect

Platform

A southbound and a northbound

models have been presented

The latter opens the door to China

A-shares to overseas investors, in

addition to the (R)QFII framework

Jun-Oct 2014

The Depositary working Group at Alfi

starts analysing the impacts for the funds

industry of the new set-up

Preferred model is chosen

Nov-Dec 2014

The Depositary Working Group presents to

the Regulator its final analysis on the

platform on the 24th Nov 2014

Alfi issues a press release on the 2nd Dec

2014 confirming the support of the Lux

market place to the new initiative ahead of

every other European market.

Enhanced model

expected live date

Dec 2014

Enhanced model presented

Jan-Feb 2015

Alfi meets with SFC and HKEx in

Hong Kong

Follow up conf-call is held between

the Group and HKEx

representatives in order to discuss

regulatory and operational

challenges posed by phase 1 and

and further improvements brought

by the enhanced model.

10/03/2015

41

3. Which Stock Connect Models exist?

Depositary affiliated or

non affiliated to sub custodian

and/or broker

HK Sub custodian &

GCPCSDCC

China

Securities depositary and

clearing corporation

Limited

(“ChinaClear”)

Account

1 “jumbo” HKSCC

Nominee account

Sub-custody

Depository omnibus or by

sub-fund

Account

Sub-Fund

Segregation – client assets

segregated from proprietary

assets & daily reconciliation

(verbal confirmation only for

HKSCC to CSDCC) Broker type 4 & DCP

Not affiliated to HK sub custodian & depositary

Other GCP

Broker Account @ GCP

multiple client a/c

HK

SC

C

Ho

ng

Ko

ng

se

cu

rities c

lea

ring

co

mp

an

y

Account

HK Sub custodian with

multiple sub omnibus

accounts that segregate

securities by product:

- proprietary assets

- brokerage assets

- HK sub-custody assets

- Stock Connect assets

- etc

Account

DCP = broker 4

account

Account

GCP / Broker 3

account

Broker Account @ GCP

Broker 1 account

Broker type 1 Affiliated to HK sub

custodian &/or

depositary

Model 1 – Standard market practice model (Agency Broker Model)

Broker type 2Not affiliated to HK sub

custodian &/or

depositary

Broker Account @ GCP

Broker 2 account

Broker type 3Not affiliated to HK sub

custodian &/or

depositary

1

1

1

1

1

Most common

set-ups

Not supported

for Lux

domiciled funds

42

3. Which Stock Connect Models exist?

Model 2 – Single broker solution (Broker affiliated to sub-custodian which acts as GCP)

Depositary affiliated or

non affiliated to sub custodian

and/or broker

HK Sub custodian &

GCP

CSDCCChina

Securities depositary and

clearing corporation

Limited

(“ChinaClear”)

Account

1 “jumbo” HKSCC

Nominee account

Sub-custody

Depository omnibus or by

sub-fund

Account

Sub-Fund

HK

SC

C

Ho

ng

Ko

ng

se

cu

rities

cle

arin

g c

om

pa

ny

Broker Account @ GCP

Broker 1 account

Broker type 1Affiliated to sub

custodian HK &/or

depositary

Note:

HK sub custodian offering model 2 may also offer model 1.

Account

HK Sub custodian with

multiple sub omnibus

accounts that segregate

securities by product:

- proprietary assets

- brokerage assets

- HK sub-custody assets

- Stock Connect assets

- etc

Segregation – client assets

segregated from proprietary

assets & daily reconciliation

(verbal confirmation only for

HKSCC to CSDCC)

1

1

1

1

HK

Common

set-up

OMNIBUS

43

3. Which Stock Connect Models exist?

Model 3 – Multiple external brokers with sub-custodian acting as GCP

Depositary affiliated or

non affiliated to sub custodian

and/or broker

HK Sub custodian &

GCP

CSDCCChina

Securities depositary and

clearing corporation

Limited

(“ChinaClear”)

Account

1 “jumbo” HKSCC

Nominee account

Sub-custody

Depository omnibus or by

sub-fund

Account

Sub-FundH

KS

CC

Broker Account @ GCP

Broker 1 account

Broker type 1Affiliated to HK sub

custodian HK &/or

depositary

Broker type 2Not affiliated to HK sub

custodian & depositary

Broker Account @ GCP

Broker 2 account

Brokers to give up their self

clearing license and for the HK

sub custodian to act as GCP

Account

HK Sub custodian with

multiple sub omnibus

accounts that segregate

securities by product:

- proprietary assets

- brokerage assets

- HK sub-custody assets

- Stock Connect assets

- etc

Segregation – client assets

segregated from proprietary

assets & daily reconciliation

(verbal confirmation only for

HKSCC to CSDCC)

1

11

1

2

2

Common

set-up

Note:

HK sub custodian offering model 2 may also offer model 1.44

Stock Connect as of today

Sonia Biraschi, General Manager, State Street Bank Luxembourg

Quota Information – Northbound – 9 March 2015

Quota usage

(RMB) (%)

Aggregate Quota - Opening Balance 190,268 Mio 63%

Daily quota balance (as of 15:01) 12,335 Mio 94%

Turnover – Northbound – 9 March 2015 (15:55)

RMB

Buy and Sell Trades 3,823 Mio

Buy Trades 2,206 Mio

Sell Trades 1,617 Mio

Source: Hong Kong Exchanges and Clearing Limited (HKEx)

4. Stock Connect as of today

46

4. Stock Connect as of today

1. Where are we?

Live on Stock Connect

Regulatory filing with CSSF completed and awaiting approval

Interest raised and starting Stock Connect project

No interest raised

2. Which interest?

Asset managers following passive and active investment strategies

Mainly UCITS and also non UCITS & segregated accounts

Different investment weightings (from 100% to below 5%)

Mix of RQFII and Stock Connect or RQFII/Stock Connect on stand alone basis

New versus existing UCITS with different base currencies (e.g. EUR, USD, RMB)

Different share classes (e.g. EUR, USD, GBP, RMB)

47

Benefits of Stock Connect

Hermann BeythanPartner, Linklaters LLP

5. Benefits of Stock Connect

1. RQFII brought greater flexibility compared to QFII

2. Stock Connects brings even greater flexibility in terms of

a. Market access

no need to request a quota

b. Time to market

few weeks versus 6 months to start investing into China A shares

c. Liquidity of the investment

possibility to enter/exit the market at any time

d. Investment strategies

possibility to rebalance portfolio easily (asset allocation)

49

Matters for consideration

Yvan De Laurentis, Head of Depositary and Fiduciary Services,

BNP Paribas Securities Services

6. Matters for consideration

1. Counterparty risk vis-à-vis the broker

the operating model for trading on the Shanghai and Hong Kong stock

Connect Platform foresees a pre-trade delivery of the shares in T-1 to the

broker account

2. Role of HKSCC in the custody chain

CSD, market infrastructure and/or sub-custodian

3. Enforcement of rights of the nominee holder

the PRC law authorizes only recognized beneficial owners to bring

legal actions into Chinese courts

4. Market liquidity

the authorities have set a quota mechanism, both at daily and

aggregate level, for SSE securities traded through the Stock

Connect platform

51

Future outlook

Sonia Biraschi, General Manager, State Street Bank Luxembourg

7. Future Outlook – Phase 2 of the Platform

1. Stock Connect Phase 2 enhancements

Creation of Special Segregated Accounts (SPSA) and unique Investor ID

Multiple broker model

Some considerations

Settlement process and counterparty risk

Single sided settlement process

2. Shenzhen-HK Connect expansion with potential launch in Q3 2015

3. Short selling of China Stock Connect securities(new circular posted 26 Feb - to be analysed)

53

An asset manager

case-study

Johan Schreuder, Managing Director,

Investec Asset Management, Luxembourg

8. An Asset Manager Case-study

1. Daily and aggregate quotas

2. Pre-funded purchasing

3. Beneficial ownership

4. T-1 delivery on sale

5. Risk disclosure

55

Thank You!

![[COVER] - HKEX](https://img.pdfslide.us/doc/110x75/62741b1e74c6e036e9016d7c/cover-hkex.jpg)