Embed Size (px)

Citation preview

Cost of Living

Comments on The Finance Supplementary (Second Amendment) Bill,

2019

408, Continental Trade Centre, Block8, Clifton, Karachi 75600, PakistanKarachi - Lahore - Islamabad

https://goo.gl/LFiWyx https://goo.gl/QDM4ZM

IMF Devaluation

In�ation

BudgetDe�cit

CADe�cit

Diminishing Revenues

DecliningGDP Growth

Low FEReserves

SoaringDebt

Discount Rate Hike

ECONOMIC CRISIS

Second Finance Amendment Bill, 2019 | Comments

CONTENTS

Prologue

Pakistan Economic Overview 1 - 8

Proposed amendments in Income Tax Ordinance, 2001 9 - 14

Proposed amendments in Sales Tax Act, 1990 15 - 16

Proposed amendments in Federal Excise Act, 2005 17

Proposed amendments in Customs Act, 1969 18 - 21

Second Finance Amendment Bill, 2019 | Comments

Prologue:

These comments give an overview of the country’s economy for the period July 2018 to December 2018 and

the important changes which are proposed through the Finance Supplementary (Second Amendment) Bill

2019 (“The bill”) tabled before the Parliament on January 23, 2019. This is the third amendment being

introduced during fiscal year 2018-19. The country is suffering of severe economic crisis and through these

amendments, government is trying to reinforce the confidence of economy and provide a breathing vent to

business community.

The instant commentary contains comments on the amendments proposed in the bill 2018; through the

Income Tax Ordinance, 2001 (“ITO”); the Sales Tax Act, 1990 (“STA”), the Federal Excise Act, 2005 (“FED”)

and Customs Act, 1969 (“CA”)

The amendments proposed through these laws are intended to be effective, once the Bill is passed by the

Parliament in its present form or with some amendments and would therefore be effective thereafter, unless

otherwise indicated.

This commentary is intended to provide general guidance to our clients and other readers on the important

changes proposed to be brought through the Bill and should not be construed as an expert advice relating

to a particular matter. For assessing the impact of proposed changes, reference should be made to the

appropriate wording to the relevant law, notifications issued thereunder and judgment given by the Courts.

This Memorandum has been prepared exclusively for the use of our staff, clients and intended readers based

on public information available with us till the time of giving it for printing. This Memorandum should not be

published or printed in any manner without seeking a written consent from us.

It should be noted that the instant commentary is our interpretation of the changes proposed in the bill. Our

comments in this commentary should not be construed as definite and should therefore, be used only as a

guidance.

Warm Regards TOLA ASSOCIATES Wednesday, 23 January 2019

Page | 1

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

Preamble:

For Pakistan, 2018 marked by economic instability. From lows of 2012 to record breaking performance graduated over last five years, it is under pressure again chiefly due to widening trade deficit owing to huge import bills, resulting mounting of current account deficit (“CAD”) and devaluation of Pak Rupee.

The economy did not fare well in 2018. Acceleration halted and the economic challenges were aggravated in the second half. The PTI government’s negotiated bilateral inflows averted a sovereign default and offered space for maneuverability to fix disruptive factors.

As end of 2018, all global economic forecasters have revised down the expected economic performance of the country citing shrinking foreign exchange reserves and a high debt burden among other factors. The World Bank, International Monetary Fund (IMF) and the Asian Development Bank have brought down the GDP growth forecast by two to three per cent. Reputable credit rating agencies Moody’s and Fitch Ratings have downgraded Pakistan to the lower end of the highly speculative grade.

It is appropriate to identify the missteps that changed the future perception from highly optimistic at the start of 2018 to moderately doubtful by its close. It will, however, be more relevant at this moment to pinpoint factors that can influence the economic course going forward.

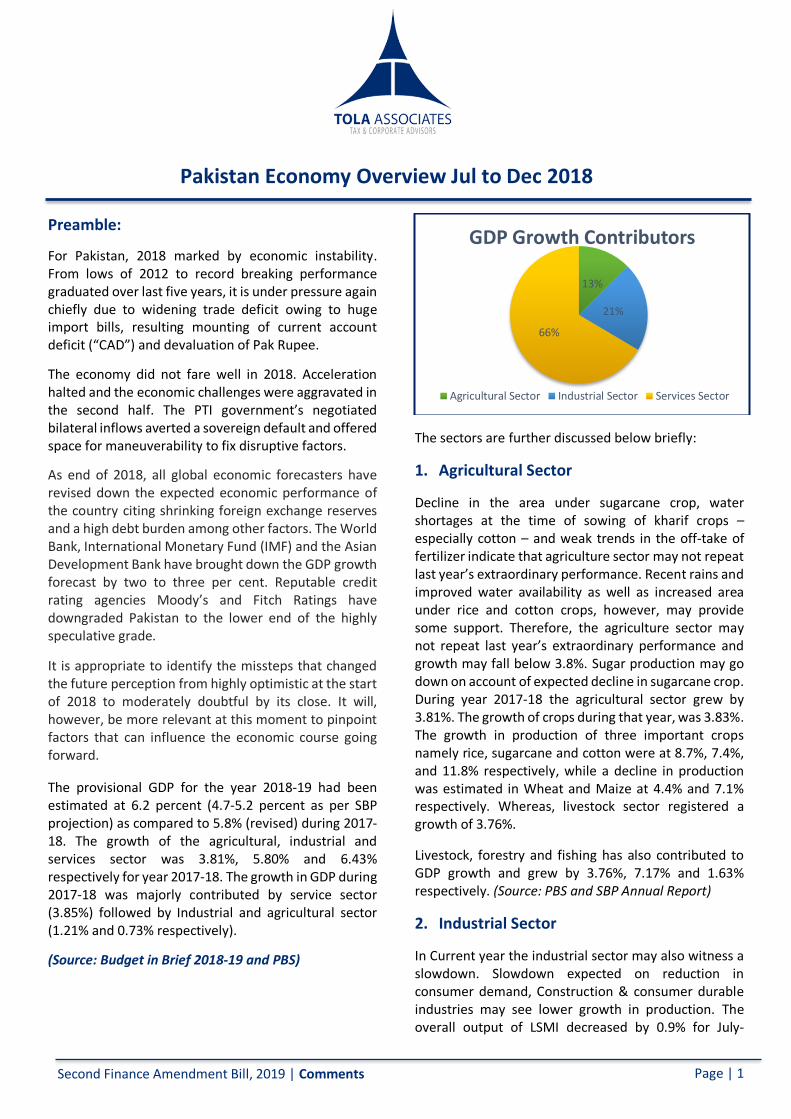

The provisional GDP for the year 2018-19 had been estimated at 6.2 percent (4.7-5.2 percent as per SBP projection) as compared to 5.8% (revised) during 2017-18. The growth of the agricultural, industrial and services sector was 3.81%, 5.80% and 6.43% respectively for year 2017-18. The growth in GDP during 2017-18 was majorly contributed by service sector (3.85%) followed by Industrial and agricultural sector (1.21% and 0.73% respectively).

(Source: Budget in Brief 2018-19 and PBS)

The sectors are further discussed below briefly:

1. Agricultural Sector

Decline in the area under sugarcane crop, water shortages at the time of sowing of kharif crops – especially cotton – and weak trends in the off-take of fertilizer indicate that agriculture sector may not repeat last year’s extraordinary performance. Recent rains and improved water availability as well as increased area under rice and cotton crops, however, may provide some support. Therefore, the agriculture sector may not repeat last year’s extraordinary performance and growth may fall below 3.8%. Sugar production may go down on account of expected decline in sugarcane crop. During year 2017-18 the agricultural sector grew by 3.81%. The growth of crops during that year, was 3.83%. The growth in production of three important crops namely rice, sugarcane and cotton were at 8.7%, 7.4%, and 11.8% respectively, while a decline in production was estimated in Wheat and Maize at 4.4% and 7.1% respectively. Whereas, livestock sector registered a growth of 3.76%.

Livestock, forestry and fishing has also contributed to GDP growth and grew by 3.76%, 7.17% and 1.63% respectively. (Source: PBS and SBP Annual Report)

2. Industrial Sector

In Current year the industrial sector may also witness a slowdown. Slowdown expected on reduction in consumer demand, Construction & consumer durable industries may see lower growth in production. The overall output of LSMI decreased by 0.9% for July-

13%

21%

66%

GDP Growth Contributors

Agricultural Sector Industrial Sector Services Sector

Page | 2

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

November 2018-19 compared to July-November 2017-2018, the production in Jul-Nov 2018-19 as compared to Jul-Nov 2017-18 has significantly decreased in Pharmaceuticals, Coke & Petroleum Products, Iron & Steel Products and Electronics while it has increased in Fertilizers and Paper & Board. During year 2017-18the overall industrial sector showed an increase of 5.80. The mining and quarrying sector grew by 3.04%. The large-scale manufacturing sector showed an increase of 6.24%. Major contributors to this growth were cement (12%), tractors (44.7%), trucks (24.41%) and petroleum products (10.26%). Electricity and gas sub sector showed growth of 1.84% while the construction activity increased by 9.13%. (Source: PBS)

3. Services Sector

Slower growth in industrial and agriculture sectors will also affect performance of the services sector. During year 2017-18 the services sector showed a growth of 6.43%. Wholesale and retail trade sector grew at a rate of 7.51% which is dependent on the output of agriculture and manufacturing and imports. Agriculture increased by 3.81%, Manufacturing increased by 5.80% and imports increased by 17%. Transport, storage and communication sector grew at a rate of 3.58%. Finance and insurance sector showed an overall increase of 6.13%, General government services grew by 11.42%. It is mainly driven by the increase in salaries and the inflation. Other private services also contributed positively. (Source: PBS)

4. Historical GDP growth rates

Pakistan has been successful in achieving consistently increasing growth rates during last six fiscal years.

5. GDP – A Geographical Comparison

A comparison of growth with other countries of region shows Pakistan’s growth has been consistent as compared to India and Sri Lanka. The GDP growth of India has been stagnant for last three years, whereas,

Pakistan’ GDP growth has shown improvements.

(www.data.worldbank.org)

Pakistan India Bangladesh

Sri Lanka

2013 3.70 6.40 6.00 3.40

2014 4.10 7.40 6.30 5.00

2015 4.00 8.20 6.80 5.00

2016 4.70 7.10 7.20 4.50

2017 5.20 6.70 7.10 3.10

2018 5.50 7.40 7.00 4.00

Est. 2019 4.0 7.80 7.00 4.50

GDP Size ($ in Billion) (2018)

306.9 2690 286.27 92.5

Tax To GDP ratio (2013)

11.18 10.99 8.96 10.49

(IMF, World Economic Outlook, Database, Oct 2018)

(IMF, World Economic Outlook, Database, Oct 2018)

6. Inflation

Average inflation for 2018-19, targeted at 6.0 percent (6.5-7.5 percent as per SBP) higher than 3.9% recorded in 2017-18. Increase in gas tariffs, import duties and excise duties further add to inflation both directly and indirectly. Period-wise analysis shows CPI slightly increased to 6.05 percent for July-December 2018-19

6.20

3.684.04 4.05

4.715.36

5.80

0.36

2.58

3.62 3.84

4.99

0

1

2

3

4

5

6

7

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017R

2018E

2019T

Pakistan GDP Growth

PMLN PPPP PMLQ

4.1 44.7

5.2 5.5

4.0

7.27.6 7.6 7.6 7.3

7.8

6.01 6.066.55

7.05 6.9 7.0

4.9 4.8 55 4.8 4.5

2014 2015 2016 2017 2018 2019 PE

Pakistan India Bangladesh Sri Lanka

Page | 3

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

compared to 3.75 percent in July-December 2017-18. Average SPI during at July-December 2018-19, was at 2.06 percent as against 1.33 percent in July-December 2017-18. Similarly, average WPI stood at 11.58 percent in the same period compared to 1.96 percent last year.

2014-

15 2015-

16 2016-

17 2017-

18 2018-

19

CPI 4.81 2.64 4.01 3.78 6.2

SPI 1.86 1.27 1.42 0.96 2.0

WPI 0.03 -1.5 3.79 2.7 12.1

(Source: PBS)

7. GDP at Current Market Prices

GDP at current market prices has also been computed and stands at Rs. 34,396 billion for 2017-18. This shows a growth of 7.6% over Rs. 31,963 billion for 2016-17. The per capita income is calculated to be Rs. 180,204 for 2017-18. Whereas, per capita income during 2016-17 was Rs. 162,230 based on provisional figures of Population Census 2017 held in March 2017. The revised series of per capita income will be compiled after finalization of 6th Housing and Population Census result.

2017-18 (Revised)

2018-19 Target

GDP at CMP (Rs Billion)

34,396 38,388

Inflation (in %) 4.50 6.00

Investment and Savings (% of GDP)

Total Investment 16.40 17.20

National Savings 12.10 13.30

Foreign Savings (External Resource)

4.40 3.80

(Source: PBS and Budget in Brief 2018-19)

8. Foreign Investment in Pakistan

The foreign investment in Pakistan for period July-December 2018 (provisional) stood at $899.5 million as compared to $ 3950.1 million July-December 2017(Revised) showing a decrease of $3,050 million a decrease of 77.2%. (Source: SBP)

4.81

2.644.01 3.78

6.2

1.86 1.27 1.42 0.962.0

0.03-1.5

3.79 2.7

12.1

2014-15 2015-16 2016-17 2017-18 2018-19

CPI SPI WPI

34,396

38,388

32,000

34,000

36,000

38,000

40,000

2017-18 2018-19 PE

Real GDP (Rs. Bn)

Real GDP (Rs. Bn)

3,050

899.5 -

2,000

4,000

July - Dec 2017 (Revised) July - Dec 2018 (PE)

Foreign Investment ($ in Million)

Foreign Investment ($ in Million)

4.5 6.0

-

2.0

4.0

6.0

8.0

2017-18 (Revised) 2018-19 PE

Inflation

Inflation

Page | 4

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

9. Broad Money (M2):

Stocks at end June

2018

Flows FY17

Flows FY18

Monetary Impact

since 1st

July to

11-01-2019

12-01-2018

(Rs. In Million)

Currency

in

Circulation

4,387,828 577,531 476,513 316,181 172,796

Other

Deposits

with SBP

26,962 3,936 4,270 449 -71

Total

Demand

and Time

Deposits

including

RFCDs

11,582,372

1,174,562

935,497

141,215 67,809

Broad

Money

(M2)

15,997,162 1,756,029 1,416,280 457,844 240,534

Growth 13.69% 9.71% 2.86% 1.65%

(Source: SBP)

Money supply, during 1st July 2018 to 11th January 2019, increased by Rs. 673,195 million (4.62%), which stood at Rs. 4,387,828 million at 30th June 2018. During similar previous periods, money supply increased by Rs. 172,796 (290%).

(Source: SBP)

10. Net Government Sector borrowing

Net Government Borrowing was Rs. 671 billion during July 2018 to 11th January 2019, which was Rs. 349 billion for the similar previous periods. The Government borrowings were majorly utilized to support budgetary deficit (Rs. 772 billion) while maintaining lending position in commodity operations (Rs. 102 billion).

July to 11th January 2018

July to 12th January 2017

(Rs. In Million)

Borrowing for Budgetary Support*

772,593 371,960

Commodity Operations

(102,602) (23,946)

Others 1,167 1,880

Net Government Sector Borrowing

671,158 349,895

(Source: SBP)

11. Credit to Non-Government Sector

Credit to non-government sector during 1st July 2018 to 11th January 2019 was higher at at Rs. 639,373 million in comparison with similar periods of previous year (Rs. 288,057 million). Rs. 496 million credit to Private sector while Rs. 142 million were provided to public sector enterprises.

-100,000

0

100,000

200,000

300,000

400,000

500,000

Jul - 11 Jan '19 Jul - 12 Jan '18

Monetary Impact

Total Demand and Time Deposits including RFCDs

Other Deposits with SBP

Currency in Circulation

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

Jul - 11 Jan '19 Jul - 12 Jan '18

Net Government Sector Borrowing

Others

Page | 5

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

July to 11th January 2019

July to 11th January

2018

(Rs. In Million)

Credit to Private Sector

495,702 201,899

Credit to Public Sector Enterprises (PSEs)

142,094 285,712

PSEs special Account-Debt Repayment with SBP

0 0

Credit to NBFIs 1,577 446

Credit to Non-Government Sector

639,373 288,057

(Source: SBP)

(Source: SBP)

12. Foreign Exchange Reserves

Foreign exchange reserves, as on 11th January 2019 were down to $ 13.5 billion (18%) as compared to last years’ (end of June 2018) $ 16.4 billion. Private banking reserves seen a rise of 33%% from last year (end of June 2018), whereas, government reserves were 4% increase.

January 2019 June 2018

($ In Million)

Government Reserves 6,901 9,789

Private Banking reserves

6,588 6,618

Total 13,489 16,407

(Source: SBP)

(Source: SBP)

13. Regional Currency Comparison

USD parity with Pakistani Rupee took a hike of 26% as compared to its values in December 2017. USD parity with PKR remained bit consistent during past years with the exception of recent devaluation during Last six months.

USD Parity with

As on PKR Chinese

Yuan Bangladeshi

Taka Indian Rupee

Jan-19 139.75 6.79 82.26 71.28

Dec-18 139.85 6.87 82.25 69.71

Dec-17 110.70 6.51 82.69 63.87

Dec-16 104.40 6.95 78.92 67.92

Dec-15 104.75 6.49 78.25 66.15

Dec-14 100.55 6.21 77.93 63.04

Dec-13 105.40 6.05 77.67 61.80

(Source: SBP)

14. Balance of Payments:

The current account deficit for July-December 2018-19 stood at $7,983 million compared to $ 8,353 million in July-December 2017-18 indicating slight improvement

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Jul - 11 Jan '19 Jul - 12 Jan '18

Credit to Non Government Sector

Credit to NBFIs

PSEs special Account-Debt Repayment with SBP

Credit to Public Sector Enterprises (PSEs)

Credit to Private Sector

0

5,000

10,000

15,000

20,000

11 Jan 2019 30 Jun 2018

Foreign Exchange Reserves

Government Reserves Private Banking reserves

Page | 6

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

in current account deficit which stood at 5.4 percent of GDP compared to 5.2 percent last year. Trade deficit during the first six months of 2018-19 stood at $17.4 billion with exports of $14.4 billion and imports of $31.9 billion. The Export during the period slightly decline by $ 36 million (0.25%) and imports decrease by $ 62 million (0.2%).

July -Dec 2019

July -Dec 2018

$ Million

Exports 14,439 14,475

Imports 31,936 31,998

Trade Balance -17,497 -17,503

Current Account Deficit (CAD) 7,983 8,353

CAD % of GDP 5.4 5.2

(source: SBP)

15. Workers’ Remittances

Workers’ remittances amounted to $10.58 billion in July-December 2018-19 compared with US$ 9.68 billion during same period last year registering an increase of 10 percent. The total liquid foreign exchange reserves stood at $ 13.5 billion on 11th January 2019.

16. Outlook for 2018-19

Amid growing risk on external sector, the government did succeed in managing to get critical dollar inflows from friendly nations. The secured breathing space

better positioned the country’s economic managers to bargain with the IMF regarding conditions that are perceived to be unduly harsh and politically costly.

Besides mitigating risks to the external sector, the dollar injection from China and Saudi Arabia, and promised budgetary support from the UAE, did earn the new government some trust in the country.

The projection of key economic indicators and service sector as per various sources is presented in below table. The services sector is projected to expand by 5.1 percent in FY19 compared with 6.4 percent in FY18. Agriculture sector growth is projected to normalize at 3.5 percent after a growth rate of 3.8 percent in FY18. The industry sector is projected to grow at 5.0 percent in FY19 compared with 5.8 percent in FY18. However, continued growth in services and industry is expected to support a recovery in overall growth to 5.2 percent in FY20.

Target Sector 2018-19 Target

GDP 3 – 4.5%

Trade Deficit 29 bn

Dollar Exchange Rate 145 – 150

Inflation 7.7 – 8.9%

Per Capita GDP Growth Rate 2.2%

Current Account balance (% of GDP) -5%

Agriculture Growth 3.5%

Industrial Sector Growth 5%

Service Sector Growth 5.1%

(Source: Topline Securities, Taurus Securities, ADB, IMF and WB)

As per recent IMF review, Macroeconomic stability gains have been eroding, putting the outlook at risk. Growth is expected to moderate to 4pc in 2019, and slow to about 3pc in the medium-term. It projected a slight rise in the unemployment ratio. The current account balance is forecast at negative 5.3pc for 2019 compared to negative 4.1pc for 2017 and negative 5.9pc in 2018.

i. Fiscal Policy: Public investment spending at the federal and provincial levels is expected to be scaled down and an increase in revenue collection

14,475 14,439

17,503 17,497

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

July-Dec 2018 July-Dec 2019

$ Billion

Exports Trade Balance

Page | 7

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

is projected through tax-base expansion and other administrative measures. Fiscal consolidation is, in turn, expected to improve debt dynamics, but the public debt-to-GDP ratio is expected to remain at around 70 percent of GDP until FY20—the debt burden benchmark for emerging markets

ii. Monetary Policy: The State Bank of Pakistan (SBP) ramped up its benchmark interest rate by a more-than-expected 150 basis points to 10 percent in December 2018 citing it would persist rising inflation and elevated fiscal deficit, but it is likely to put a further dent in economic growth, which has already trimmed to little over 4 percent for the fiscal 2019, as one percent increase in discount rate will add half a percent of GDP in fiscal deficit, resultantly 0.7 budget deficit goes up.

iii. Inflation: The increase in prices will be driven by exchange-rate pass-through to domestic prices and a moderate increase in international oil prices

iv. CPEC Impact on Socio Economic Conditions

2019 is also expected to be the year for foreign investments in Pakistan. CPEC shall be entering its second phase that shall be more focused on trade and industry, moving on from infrastructure. This shall play a pivotal role in terms of technology and skills transfer to our economy. Multi-national companies from sectors ranging from automobiles, telecommunications, energy, electronics and others have also expressed their interest to invest in Pakistan.

Devaluation – a recipe to economic stability or economic disaster?

Amidst the current currency devaluation fiasco, there are two different types of opinions which came on the scene. Economists and Pakistani analyst have been quoted saying that the current situation of national currency would not cause any panic in the market. In fact, the self-correcting mechanism of demand and supply would balance the prevailing market system.

However, on the other hand some analysts have warned that the Pakistani currency is still over-valued and would continue to fall. The bail-out from International Monetary Funds (IMF) due to widening gap in current account deficit would pull Pakistan in further debt and discourage potential investment. The continued borrowing would also trigger further imbalance turning the Pakistani economy fragile.

The Mitigating Factors

Besides the above, the following steps taken recently may offset the negative outlook of the economy and external pressures:

• China agrees to almost double its imports from Pakistan In November, Beijing agreed to increase its imports from Pakistan to $2.2 billion by end of 2018-19 from the existing level of $1.2bn and to $3.2bn by end of next fiscal year.

• Currency swap arrangement (CSA) In May 2018, the currency swap arrangement (CSA) between the SBP and the People’s Bank of China (PBOC) was extended for a period of 3 years in respective local currencies. Further Both the central banks agreed to increase the CSA amount from CNY (Chinese Yuan) 10 billion to CNY 20bn and from Rs165bn to Rs351bn. The currency swap arrangement facilitates traders to do business with each other in local currency instead of the US dollar.

• Rs82bn plan launched to reduce rural poverty The Ministry of National Food Security and Research (MNFSR) in December unveiled a Rs82 billion plan for the agriculture sector, with the aim of enhanced crop yield, improved water efficiency, livestock and fisheries development, and creation of agro-markets with the overall objective of uplifting small farmers and reducing rural poverty. The comprehensive plan will be implemented within two to three years.

Page | 8

Pakistan Economy Overview Jul to Dec 2018

Second Finance Amendment Bill, 2019 | Comments

• Pakistan’s ‘Doing Business’ ranking up 11 notches In November 2018, the World Bank issued the ‘Doing Business Report: Training for Reform 2019’. It showed that Pakistan improved its ranking by 11 points, moving from 147th to 136th position.

Pakistan made starting a business easier by introducing the online one-stop registration system; replaced several forms for incorporation with a single application; and established an information exchange mechanism between the Securities and Exchange Commission of Pakistan (SECP) and Federal Board of Revenue (FBR). Further progress in this ranking will definitely help in economic turnaround.

Page | 9

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

1. Tax on undistributed reserves – Section 5A

It was made necessary through FA 1999 for listed companies with free reserves of more than 40% of their paid-up capital to distribute at least 50% of their taxed profits as cash dividend.

Vide finance act 2017 tax at 7.5% was charged on every public company other than a scheduled bank or a modaraba, that derives profit for a tax year but does not distribute at least 40% of its after-tax profits within six months of the end of the tax year through cash or bonus shares.

FA 2018 reduced the tax rate from 7.5% to 5%. FA 2018 also reduced the threshold of 40% reserves to 20% reserves.

The bill proposes to limit the application of this tax till tax year 2019 only.

Imposition of tax for not distributing profits is against the reinvestment business model of corporations. Amendment would result in decline of the tax revenue in short run, however, the same will reap higher tax revenues in longer run due to reinvestment and expansion in tax base.

2. Carryforward of loss on disposal of Securities

– Section 37A

Currently loss on disposal of securities is allowed to be set off against gains on disposal of any other securities chargeable to tax under ITO. Carryforward of such losses is not allowed.

The bill proposes that any loss sustained on disposal of any security which could not be setoff in tax year 2019, or any subsequent tax year, the same shall be available to be carryforward for next three years to be adjusted against gain on disposal of any security chargeable to tax under ITO.

3. Income of Federal Government – Section 49

Currently, proviso to subsection (4) of section 49 provides that income from sale of spectrum license by Pakistan Telecommunication Authority (“PTA”) on behalf of the Federal Government (“FG”) after 01-03-

2014 shall be treated as income of FG and not PTA. This has effect that such income from sale of spectrum license by PTA will be exempt from Income Tax.

The bill propose that renewal of spectrum licenses too by PTA shall be treated as income of FG i.e. the same shall be exempt from income tax.

4. Special Procedures for Small Traders and

Shopkeepers – Section 99B

Vide Income Tax (Third Amendment) Act, 2016 (also termed as ‘Voluntary tax Compliance Scheme’), a new section 99A along with Ninth Schedule was inserted to provide small traders and shopkeepers option to be assessed as per Ninth Schedule or be assessed in normal manner.

Ninth Schedule provides taxation on basis of working capital and turnover for tax years 2015 to 2018.

For tax year 2019 and onwards, the bill proposes to empower the FG to notify special procedures for such small traders and shopkeepers, so that further procedures for their assessment, return filing etc. may be notified.

Finance Minister, in his speech in National Assembly stated that such procedures will be notified for Islamabad initially and then will be notified for rest of the Pakistan, if successful.

5. Provisional Assessment – Concealed Offshore

Asset – Section 123

Where a concealed asset of a person is impounded by any government agency which, in the opinion of the Commissioner, was acquired from any taxable income, the commissioner has power to pass a provisional assessment order before making a final assessment. However, the Commissioner shall finalize the provisional assessment as soon as practicable.

The bill proposes that where any “offshore asset” is discovered, the Commissioner may issue a provisional assessment order before issuing a final assessment order for the last completed tax year of the person. For example, if an offshore asset is discovered in Tax Year 2019, tax year 2018 will be provisionally assessed.

Page | 10

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

6. Minimum Tax on Imports – Section 148

Section 148 provides that the tax required to be collected from a person under section 148 shall be minimum tax for a tax year on the import of─

edible oil;

packing material; and

plastic raw material imported by an industrial

undertaking falling under PCT headings 39.01 to

39.12.

FA 2018 made addition in the list uch that tax required to be deducted under section 148 on import of goods where goods are sold in the same condition as they were when imported; shall also be minimum tax, i.e. tax deducted at import stage of commercial importers were brought under normal tax regime from fixed tax regime.

The bill proposes to reverse the above amendment. The proposal is introduced to address issues of commercial importers who were under threat of audits consequent to amendment vide FA 2018. However, the proposal is against the principle of tax equity.

7. Filing of Monthly Statement – Monthly to Semi

Annually – Section 165

Section 165 requires every withholding agent to file a withholding statement on monthly basis. The bill proposes that the statement may be filed on semi annually instead of monthly basis.

The dates for filing of statements have been proposed to be 31st July and 31st January for half years ended on 30th June and 31st December, respectively.

However, the commissioner has also been empowered to require the taxpayer to furnish the statement for any period.

8. Restriction on purchase of certain assets –

section 227C

FA 2018 imposed restriction on non-filer on first registration of new motor vehicles. The restriction was

also imposed on acceptance or processing of any application for registering, recording or attesting transfer of any immovable property valuing more than Rs. 5 million in the name of a non-filer.

Finance Supplementary (Amendment) Act 2018 introduced following exceptions to the restrictions:

motorcycle having engine capacity of less than 200 cc, motorcycle-rickshaw, agricultural tractor or any other motor vehicle having engine capacity of less than 200 cc;

a person holding a Pakistan origin card or a national identity card for overseas Pakistani who produces a certificate from a scheduled bank of receipt of foreign exchange remitted from outside Pakistan through normal banking channels during a period of sixty days prior to the date of booking, registration or purchase of motor vehicle or, in case of immovable property, prior to the date of registering, recording, or attesting transfer; or

a legal heir acquiring immovable property in inheritance.

The bill proposes to add following further exceptions to the general restriction:

locally manufactured motor vehicle having engine capacity not exceeding 1300 cc; or

a person holding a Pakistan origin card or a national identity card for a non-resident Pakistani having international passport who produces a certificate from a scheduled bank of receipt of foreign exchange remitted from outside Pakistan through normal banking channels during a period of sixty days prior to the date of booking, registration or purchase of motor vehicle or, in case of immovable property, prior to the date of registering, recording, or attesting transfer; or

The relaxation in registration of motor vehicles has been compensated by a proposal of exponential increase in advance tax on registration of motor vehicles by non-filers.

Page | 11

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

9. Collection of tax by stock exchange – Section

233A

Section 233A provides that tax at 0.02% shall be collected by stock exchange on sale and purchase of share. Vide FA 2018, the tax so collected was made adjustable.

The bill now proposes to omit section 233A with effect from 01-02-2019. It is a positive proposal which will kick start trading activity at stock exchange.

10. Super Tax - Section 4B

A super tax was levied, for tax year 2015, vide Finance Act 2015 (“FA-15”) for every banking company and every other company whose taxable profits exceeded Rs.500 million. The super tax was charged in the backdrop of Military operation ‘Zarb-e-Azb’ for rehabilitation of Temporarily Displaced Persons (“TDPs”). The tax was levied at 4% for Banking Companies and at 3% for others. The tax was continued till tax year 2017.

The super tax was continued till tax year 2020, however the rate of such tax is reduced by 1% each year. For banking companies, the rate for tax year 2018 was 0% whereas, for tax years 2019, 2020 and 2021; the rates were 4%, 3% and 2% respectively.

The bill proposes that for banking companies, the rates for 2018 to 2021 may be 4%. Whereas, for other companies, the rate for tax year 2020 is proposed to be reduced to 0% from 1%.

It may be noted here that banking companies have filed their returns for tax year 2018, wherein, they have not paid super tax as per current provisions. The change in super tax rates from 0% to 4% may lead to litigations.

11. Advance Tax on import of mobile phones -

Section 148, Part II, First Schedule

The bill proposes to charge advance tax on import of mobile phones by any person as under:

S. No.

C & F Value of Mobile Phone

(in USD)

Tax (in Rs.)

1. Up to 30 70

2. Exceeding 30 and Up to 100

730

3. Exceeding 100 and Up to 200

930

4. Exceeding 200 and Up to 350

970

5. Exceeding 350 and Up to 500

3,000

6. Exceeding 500 5,200

A clarification would be required whether these mobile

phones also attract recently introduced baggage rules

for the purpose of customs duty and registration of

mobile phones at international airports.

12. No advance tax on Cash Withdrawal and

Banking Transactions on Filers - Section 231A,

231AA - Division VI, Part IV, First Schedule

On cash withdrawals exceeding Rs. 50,000, advance tax at 0.3% and 0.6% is charged for filers and non-filers, respectively. Moreover, on banking transactions exceeding Rs. 25,000 advance tax at 0.3% and 0.6% is also charged for filers and non-filers, respectively

The bill proposes to waive such advance tax on cash withdrawals from filers. The proposal may result in less revenue collections. Also, desired increase in tax net would be minimal as non-filers already absorb this advance tax in their costs.

13. Advance tax on functions and gatherings -

Section 236D - Division XI, Part IV, First

Schedule

Currently advance tax on functions and gatherings is 5%. Whereas, the rate of functions of marriage in a marriage hall, marquee, hotel, restaurant, commercial lawn, club, a community place or any other place used for such purpose shall be higher of 5% or 20,000 per function.

Page | 12

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

the above limit of Rs. 20,000 has been proposed to be reduced to Rs. 5,000 in case of total function area is less than 500 square yards.

14. Advance tax on registration of Private Motor

Vehicles - Section 231B - Division VII, Part IV,

First Schedule

The bill proposes to increase advance tax at the time of registering of private motor vehicles as under:

Current Proposed

S/N Engine

Capacity For Filers

Tax Rate for Non-

filers

Tax Rate for Non-

Filers

1 Upto 850cc Rs.7500 Rs.10,000 Rs.15000

2 851cc to 1000cc

Rs.15,000 Rs.25,000 Rs.37500

3 1001cc to 1300cc

Rs.25,000 Rs.45,000 Rs.60,000

4 1301cc to 1600cc

Rs.50,000 Rs.100,000 Rs.150,000

5 1601cc to 1800cc

Rs.75,000 Rs.150,000 Rs.200,000

6 1801cc to 2000cc

Rs.100,000 Rs.200000 Rs.300,000

7 2001cc to 2500cc

Rs.150000 Rs.300,000 Rs.450,000

8 2501cc to 3000cc

Rs.200000 Rs.400000 Rs.600,000

9 Above 3001cc Rs.250,000 Rs.450,000 Rs.675,000

15. Exemption from total income under Second

Schedule Part I

1. The bill proposes that that any income derived by following institutions shall be exempt from income tax:

(i) National Disaster Risk Management Fund

(ii) Deposit Protection Corporation established under sub-section (1) of section 3 of Deposit Protection Corporation Act 2016 (Act XXXVII of 2016)

2. Clause (126I) provides exemption from tax on profits and gains derived from industrial undertaking set up by 31st December 2016 and engaged in the manufacture of plant, machinery, equipment and items with dedicated use for generation of renewable energy from sources like solar and wind for a period of five years beginning from first day of July 2015. The bill proposes to introduce a new provision after clause (126I) has been proposed to be inserted through which the benefit of exemption from tax on profit and gains can also be obtained by industrial undertaking set up between 1st March 2019 and the 30th June 2023 for a period of five years from the date of industrial set up.

We understand that the exemption granted on profits and gains do not have any economic benefit to industrial undertaking unless tax benefit on minimum tax/turnover under Section 113 of ITO and Alternate Corporate Tax (ACT) under Section 113C of ITO is also offered for same period.

16. Reduction in tax liability under Second

Schedule Part III

1. Section 59B provides group relief (surrender of

tax losses) whereby a subsidiary company may

surrender its assessed losses (excluding capital

losses) for the tax year other than brought

forward losses and capital losses in favor of its

holding company or its subsidiary company or

any other subsidiary of the holding company.

The holding company shall directly hold share

capital of the subsidiary company as under:

(i) One of company in group is listed in

Pakistan (55% or more)

(ii) None of company in group is listed in

Pakistan (75% or more)

The loss surrendered by subsidiary company may be

claimed by holding company or a subsidiary

company up to the holding percentage of holding

Page | 13

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

company against business income of holding or

subsidiary in the tax year and subsequent two years.

The bill proposes to insert a new clause (17) through

which the company can claim reduction in tax on

dividend if the recipient of dividend company, for

the tax year, has surrendered loss or received loss

from company distributing dividend to the extent of

percentage of ordinary shareholding, the recipient

of dividend has in the company.

We suggest review of proposed amendments and it

will be beneficial if the position prior to 2016 may

be restored.

17. Exemption from specific provision – Second

Schedule, Part IV

1. Clause 11A of Second Schedule Part IV provides the exemption from minimum tax. The bill proposes exemption from minimum tax on following institutions:

(i) National Disaster Risk Management Fund

(ii) Deposit Protection Corporation established under sub-section (1) of section 3 of Deposit Protection corporation Act 2016 (Act XXXVll of 2016

2. The bill has proposed to introduce a new clause 38D through which the exemption from withholding of tax on profit on debt under Section 151 & withholding of tax on payment for goods, services and contracts under section 153 of ITO has been proposed to the National Disaster Risk Management Fund.

3. The bill proposes to insert a new clause 81A after clause 81 through which the exemption from furnishing of monthly withholding statement under clause (a) of sub-section (1) of section 165 has been proposed to the banking companies for furnishing of information of taxes collected and deducted on cash withdrawal from a bank under section 231A and

tax deducted on profit on debt under section 151 of ITO.

4. The bill, after clause 95, proposes to insert a new clause 95A through which the exemption from advance tax at the time of sale by auction under section 236A has been proposed in respect of auction of franchise rights to participating teams in a national or international league organized by any board or other organization established by the Government in Pakistan for the purposes of controlling' regulation or encouraging major games and sports recognized by the Government with effect from the first day of July' 2019.

The proposal is positive for promotion of sports in the country, however, FBR may lose revenues on auction of new franchise teams of Pakistan Sports League by Pakistan Cricket Board.

5. The bill proposes a new clause 101A through which the exemption from withholding tax on cash withdrawal under Section 231A of ITO has been proposed for Pak Rupee account holders if the deposits in accounts are solely made from foreign remittance credited directly to the account.

The bill proposes to introduce a new clause

(111) through which the exemption from Super

Tax chargeable under section 4B has been

proposed on income of banking company

earned under Rule 7D, 7E, 7F of the Seventh

Schedule of ITO inserted vide the bill.

18. Amendments in Seventh Schedule

1. 7D Reduced rate of tax for additional advances to micro, small and medium enterprise

After Rule 7C new Rule 7D has been proved to be inserted through which a reduce rate of 20% has been proposed on interest income earned by banking company on additional advances to

Page | 14

Amendments in Income Tax Ordinance, 2001

Second Finance Amendment Bill, 2019 | Comments

micro, small and medium enterprises for tax year 2020 to 2023.

We suggest that large commercial banks should be restricted to advance loans to only micro finance banks, instead of advancing loans to micro, small and medium enterprises. Without such restriction, the micro finance banking industry will be swallowed by large banking corporations.

2. 7E Reduced rate of tax for additional advances to low cost housing finance

A new Rule 7E has been proposed to be inserted through which a reduce rate of 20% has been proposed on interest income earned by banking company on low cost housing finance for tax year 2020 to 2023.

3. 7F Reduced rate of tax for additional advances

as Farm credit

A new Rule 7F has been inserted through which a reduce rate of 20% has been proposed on interest income earned by banking company on additional advances to Farm Credit in Pakistan for tax year 2020 to 2023.

Page | 15

Amendments in Sales Tax Act, 1990

Second Finance Amendment Bill, 2019 | Comments

1. Payment of refund through Promissory notes

Section 67(A)

Through this bill It is proposed that a new section shall be inserted in the Sales Tax Act,1990 whereby the sales tax refunds payable under the Sales Tax Act,1990 may be paid through promissory note instead of paying sales tax through cheque to State Bank of Pakistan through the procedure defined in the 10 Schedule to the Sales Tax Act,1990.

2. 10th SCHEDULE (Payment of refund through

Promissory Note)

The Government has taken a good initiative and relief for the exporters whose refunds amounting to almost Rs 250 million were stuck with the Government. The Government itself is cash strapped and is unable to give the sales tax refunds to the exporters. By issuing promissory notes the Government will have to bear the cost of 10% payable to the holder of promissory note. At this moment it is not clear weather this scheme is perpetual or for future refunds arising in the years to come. We feel that a similar scheme should be introduced for the pending refunds of Income Tax.

The Bill proposes the insert the following schedule to the Sales Tax Act,1990.

The promissory notes shall be issued by the Note Office in lieu of sales tax refunds as found admissible under the sales Tax Act, 1990, to the refund claimants. The promissory notes will be printed by Pakistan Security Printing Corporation with security features and in the form as the Board may determine.

The maturity period of the promissory notes will be three years from the date of issuance and promissory notes shall be issued in multiples of one hundred thousand Rupees. The promissory note will bear annual simple profit at ten per cent and shall be redeemable after the period of maturity. The promissory notes will only be redeemable before maturity if the Board allows the same along with profit payable at the time of redemption.

Furthermore, these notes will be traded freely in the country's secondary markets and approved security for

calculating the statutory liquidity reserve. In addition to that notes will be accepted by the banks as collateral.

There will be no compulsory deduction of Zakat against the promissory notes and sahib-e-nisab may pay Zakat voluntarily according to Shariah.

3. Transfer of notes

The notes shall be transferable only in the manner provided hereunder: -

a. lt shall be transferable by endorsement and delivery like a promissory note Payable to order;

b. No endorsement of a note shall be valid unless made by the signature of the holder or his duly constituted attorney or representative inscribed on the back of the note itself;

c. No writing on a note shall be valid for the purpose of negotiation if such writing purports to transfer only a part of the amount denominated by the note;

d. The note office may decline to accept a note endorsed in blank for any purpose unless the endorsement in blank is converted into that in full before presentation.

e. Payment on redemption will be made when a note becomes due for payment, it shall be presented at the note office by the holder. On redemption, the profit on the notes shall be paid along with the face value, in the form of a crossed cheque drawn on the State Bank of Pakistan.

In case a promissory note is lost, stolen, destroyed, mutilated or destroyed either Wholly or in part the same procedure as laid out in respect of the promissory note in the Public Debt Rules, 1946 shall be followed. ln case of an executant being unable to write the procedure as provided in the Public Debt Rules, 1946, shall be followed.

4. Sixth Schedule

Following items are proposed to be included in sixth

schedule

Page | 16

Amendments in Sales Tax Act, 1990

Second Finance Amendment Bill, 2019 | Comments

S.No Description Tariff Heading Proposed Tax Rate

117

Appliances and items required for colostomy procedures as specified in Chapter 99 of the First Schedule to The Custom Act, 1969 subject to the same conditions specified therein

99.25 Exempt

150.

Plant and machinery excluding consumer durable goods and office equipment as imported by greenfield industries, intending to manufacture taxable goods, during their construction and installation period subject to conditions noted below and issuance of exemption certificate by the Commissioner Inland Revenue having jurisdiction: -

Conditions:

a. The importer is registered under the Act on or after the first day of July 2019; and

b. The industry is not established by splitting up or reconstruction or reconstitution of an undertaking already in existence or by transfer of machinery or plant from another industrial undertaking ln Pakistan

Chapter 84 and 85 Exempt

5. 9TH SCHEDULE

S# Description Sales Tax on

import or local supply

Sales Tax (chargeable at

the time of registration if IMEI number

by CMO’s)

Sales Tax on supply (payable at the time of supply by CMO)

2 Cellular mobile phones or satellite phones to be charged on the basis of import value pe set, or equivalent value in rupees in case of supply by the manufacturer, at the rate as indicated against each category: -

-

A. Not exceeding US$ 30 - -

B. Exceeding US$ 30 but not exceeding US$ 100 Rs. 150 Rs. 150

C. Exceeding US$ 100 but not exceeding US$ 200 Rs. 1,470 Rs. 1,470

D. Exceeding US$ 200 but not exceeding U$ 350 Rs. 1,870 Rs. 1,870

E. Exceeding US$ 350 but not exceeding US$500 Rs. 1,930 Rs. 1,930

F. Exceeding US$ 500 Rs. 6,000 Rs. 6,000

Rs. 10,300 Rs. 10,300

Page | 17

Amendments in Federal Excise Act, 2005

Second Finance Amendment Bill, 2019 | Comments

The Bill proposes to amend the federal excise duty on the luxury cars and SUV having engine capacity of more than

3000 cc as under: -

S. No Description Heading / sub

headings Rate of Duty

55A Imported motor cars, SUVS and other motor vehicles

of cylinder capacity of 3000cc or above. Principally

designed for the transport of persons (other than

those of headings 87.02), including station wagons

and racing cars of cylinder capacity of 3000cc or

above

87.03 Thirty percent ad

valorem

55B Locally manufactured or assembled moto cars' SUVS

and other motor vehicles of cylinder capacity of

1800cc or above, principally designed for the

transport of Persons (other than those of headings

87.02), including start on wagons and racing cars of

cylinder capacity of 1800cc or above

87.03 Ten percent ad val.

Page | 18

Amendments in Customs Act, 1969

Second Finance Amendment Bill, 2019 | Comments

1. Amendments in Customs Act, 1969

The Bill Proposed the amendment in the rate of customs duty in respect of the following items covered

under SRO 1125:

S. No

Description PCT Code Existing Rate of

Customs Duty (%)

Reduce Rate of

Customs Duty (%)

(Proposed)

Conditions

1 Footwear Sector: lf imported by manufacturers of Footwear, registered under the Sales Tax Act, 1990

(i) Toluene 2902.3000 3% 3%

(ii) Butanone (methyl ethyl ketone) 2914.1200 3% 3%

(iii) Other 3207.1090 3% 3% (iv) Other 3208.1090 20% 20%

(v) Other 3208.9090 20% 20%

(vi) Mould release preparations 3403.9910 3% 3%

(vii) Shoe adhesives 3506.9110 16% 16%

(viii) Other 3506.9190 16% 16%

(ix) Shoe lasts 3926.9060 20% 16%

(x) Other 4005.1090 11% 11%

(xi) Other 4005.9900 11% 11%

(xii) Machinery for making or repairing footwear

8453.2000 3% 0%

(xiii) Parts 8477.9000 3% 0%

(xiv) injection or compression types 8480.7100 3% 0%

2 Tanners: lf imported by Tanners, registered under the Sales Tax Act, 1990

(i) Formic acid 2915.1100 20% 16%

(ii) Other 2915.1290 3% 3%

(iii) Other 2933.9990 11% 11%

(iv) Synthetic organic tanning substances 3202 1000 3% 3% (v) Other 3202.9090 11% 11%

(vi) Basic dyes and preparations based thereon

3204.1300 3% 3%

(vii) Other 3204.9000 20% 16%

(viii) Of a kind used in the Paper or like industries

3809.9200 16% 11%

(ix) Of a kind used in the leather or like industries

3809.9300 16% 11%

(x) Acrylic binders 3906.9020 16% 20%

(xi) Polyurethanes 3909.5000 3% 0%

(xii) Machinery for preparing, tanning or working hides, skins or leather

8453.1000 3% 0%

(xiii) Parts 8453.9000 3% 0% 3 Leather Sector:

Page | 19

Amendments in Customs Act, 1969

Second Finance Amendment Bill, 2019 | Comments

(i) Magnesium oxide 2519.9010 3% 0% lf imported by Manufacturers of Leather sector, registered under the Sales Tax Act, 1990

(ii) Other 2836.9990 3% 0%

(iii) Sodium formate 2915.1210 3% 0%

(iv) Tanning substances, tanning preparations based on chromium sulphate

3202.9010 20% 20%

(v) Disperse dyes and preparations based thereon

3204.1100 16% 16%

(vi) Stamping foils 3212.1000 16% 11%

(vii) Of a kind used in the leather or like industries

3403.1110 20% 16%

(viii) Of a kind used in the leather or like industries including fat liquors

3403.9110 20% 16%

4 Gloves: lf imported by Manufacturers of Gloves, registered under the Sales Tax Act, 1990

(i) Latex 4002.1100 3% 0%

(ii) Other 4002.1900 3% 0%

(iii) Other 4016.1090 20% 5%

(iv) Machines for reeling, unreeling, folding, cutting or pinking textile fabrics

8451.5000 3% 0%

(v) Other 8452.2900 3% 0%

(vi) Other 8477.3090 3% 0% (vii) Buttons 9606.2920 16% 20%

(viii) Other 9606.2990 16% 20%

6 Furniture: lf imported by Manufacturers of Furniture, registered under the Sales Tax Act, 1990

Other 8465.9190 3% 0%

7 Ceramics: lf imported by Manufacturers registered under the Sales Tax Act, 1990

(i) Verifiable enamels and glazes, engobes (slips) and similar Preparations

3207.2000 11% 3%

(ii) Containing by weight more than 50 % of graphite or other carbon or of a mixture of these Products

6903.1000 11% 3%

(iii) Other 6903.2090 11% 3%

8 Diapers/ Sanitary Napkins: lf imported by Manufacturers of diapers/sanitary napkins registered under the Sales Tax Act, 1990, subject to annual quota determination and verification by the input Output Co-efficient Organization (IOCO) and certification by the Engineering Development Board.

(i) Other 3506.9190 11% 5%

(ii) Other 3906.9090 11% 5%

(iii) Of polymers of ethylene 3920.1000 20% 16%

(iv) Of other Plastics 3921.1900 20% 16%

(v) Of polymers of ethylene 3923.2100 20% 5%

(vi) Weighing not more than 25 g/m 2 5603.1100 16% 11%

(vii) Weighing more than 25 g/m2 but not more than 70 g/m2

5603.9200 20% 16%

(viii) Weighing more than 70 g/m 2 but not more than 150 g/m 2

5603.9300 16% 11%

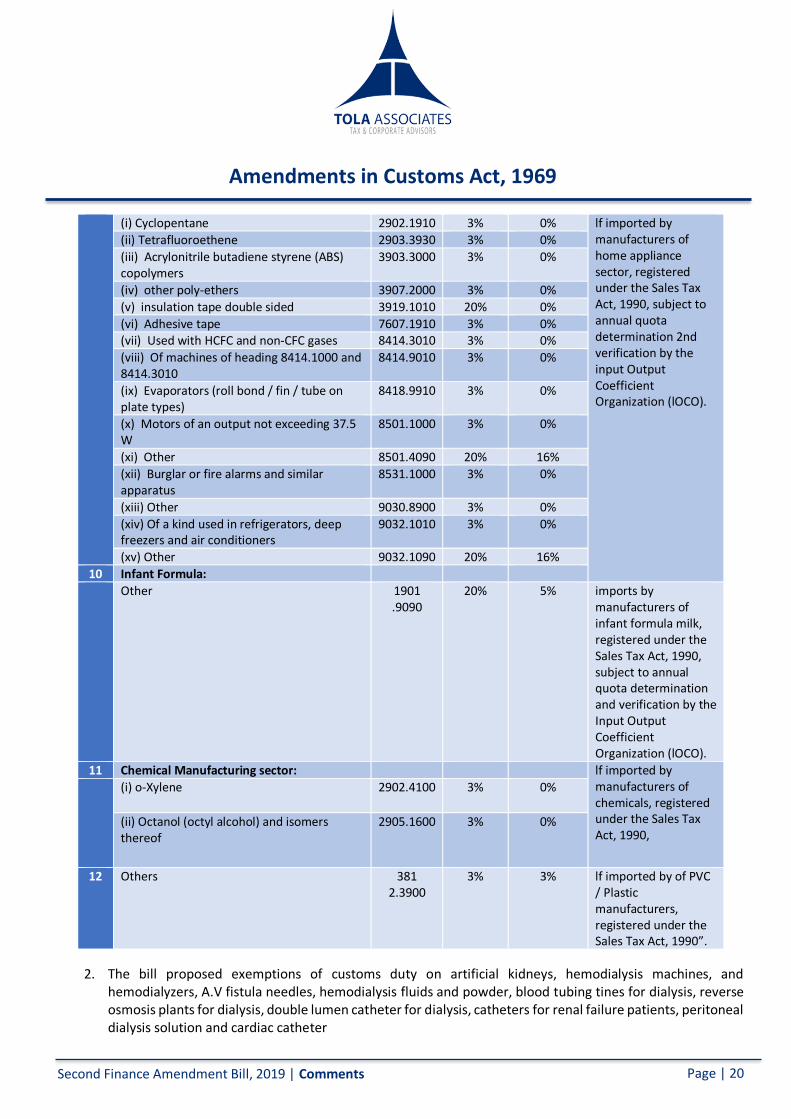

9 Home Appliance Sector:

Page | 20

Amendments in Customs Act, 1969

Second Finance Amendment Bill, 2019 | Comments

2. The bill proposed exemptions of customs duty on artificial kidneys, hemodialysis machines, and hemodialyzers, A.V fistula needles, hemodialysis fluids and powder, blood tubing tines for dialysis, reverse osmosis plants for dialysis, double lumen catheter for dialysis, catheters for renal failure patients, peritoneal dialysis solution and cardiac catheter

(i) Cyclopentane 2902.1910 3% 0% lf imported by manufacturers of home appliance sector, registered under the Sales Tax Act, 1990, subject to annual quota determination 2nd verification by the input Output Coefficient Organization (lOCO).

(ii) Tetrafluoroethene 2903.3930 3% 0%

(iii) Acrylonitrile butadiene styrene (ABS) copolymers

3903.3000 3% 0%

(iv) other poly-ethers 3907.2000 3% 0%

(v) insulation tape double sided 3919.1010 20% 0%

(vi) Adhesive tape 7607.1910 3% 0% (vii) Used with HCFC and non-CFC gases 8414.3010 3% 0%

(viii) Of machines of heading 8414.1000 and 8414.3010

8414.9010 3% 0%

(ix) Evaporators (roll bond / fin / tube on plate types)

8418.9910 3% 0%

(x) Motors of an output not exceeding 37.5 W

8501.1000 3% 0%

(xi) Other 8501.4090 20% 16%

(xii) Burglar or fire alarms and similar apparatus

8531.1000 3% 0%

(xiii) Other 9030.8900 3% 0%

(xiv) Of a kind used in refrigerators, deep freezers and air conditioners

9032.1010 3% 0%

(xv) Other 9032.1090 20% 16%

10 Infant Formula:

Other 1901 .9090

20% 5% imports by manufacturers of infant formula milk, registered under the Sales Tax Act, 1990, subject to annual quota determination and verification by the Input Output Coefficient Organization (lOCO).

11 Chemical Manufacturing sector: lf imported by manufacturers of chemicals, registered under the Sales Tax Act, 1990,

(i) o-Xylene 2902.4100 3% 0%

(ii) Octanol (octyl alcohol) and isomers thereof

2905.1600 3% 0%

12 Others 381 2.3900

3% 3% lf imported by of PVC / Plastic manufacturers, registered under the Sales Tax Act, 1990”.

Page | 21

Amendments in Customs Act, 1969

Second Finance Amendment Bill, 2019 | Comments

3. The bill proposes zero duty on items and appliances of Ostomy use including base plate, stoma wafer, Falange,

stoma powder, plastic clips, liquid washers and wipes, night drainage bag, cystoscope, lithotripter, colposcope,

sigmoidoscope, laparoscope and other.

Note:

Regulatory duties on various raw material items have been adjusted (increase/decrease), which will be notified

through various SROs subsequently.

TOLA ASSOCIATESTAX & C ORPO RATE AD V ISORS

408, Continental Trade CentreBlock 8, Clifton, Karachi 75600, PakistanTel: +92 21 3530 3294-6, Fax +92 21 3530 3293eMail: [email protected]: www.tolaassociates.com

Other offices:

144, 1st Floor, Street No. 82, Sector E-11/2 FECHSIslamabad 44000, PakistanTel: +92 51 835 1551, Fax: +92 51 835 1552

202-E, 2nd Floor Sadiq Plaza69 The Mall Road, Lahore, PakistanTel: +92 42 3628 0403, Fax: +92 42 3628 0402