Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

11 November 2010Asia Pacific/Pakistan

Equity ResearchEnergy

Pakistan Energy Sector ASSUMING COVERAGE

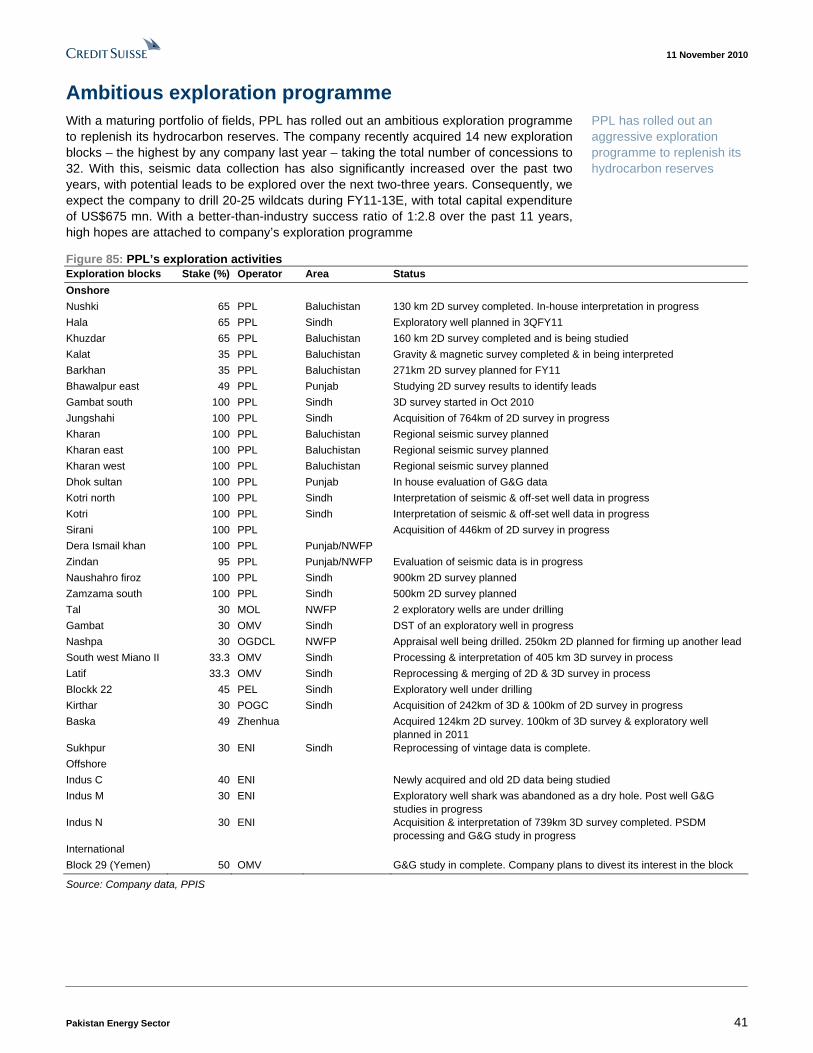

To ride on rising power tariffs Figure 1: Tariffs will cover 92% of electricity generation costs by June 2011

0

2

4

6

8

10

12

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

1QFY

11

FY11

Consumer tariff Avg generation costPRs/Kw

Source: Company data, Credit Suisse estimates

■ Tides are turning against circular debt: Circular debt (inter-corporate debt) has blemished the return profile of Pakistan Energy stocks over the past two years. The problem arose when the cash-starved government kept electricity prices below cost recovery levels and delayed payments of subsidies, thus forcing companies to cut payouts. But now, as power tariffs play catch up with electricity generation costs, we believe the circular debt is nearing a conclusion. Hence, we expect energy stocks to gradually return to their historical payout ratios from FY11.

■ Tariffs to increase to cover 92% of costs by June 2011: Having twice missed the deadline to eliminate power subsidies, the IMF has refused to release the remaining tranches of US$3.4 bn under the Stand-By Agreement. The government is now expected to play by IMF’s suggestions and hike tariffs in FY11. Press reports also suggest another 17% tariff hike.

■ Cheapest in the region: Pakistan energy sector companies are among the region’s cheapest. With dividend payments due to gradually normalise from FY11, we expect energy stocks to move to their historical valuation multiples.

■ PSO, PPL and HUBCO top picks: We assume coverage of the Pakistan Energy sector with an OVERWEIGHT; we have OUTPERFORM ratings on PPL (TP PRs246), PSO (TP PRs381) and OGDC (TP PRs 173). We also initiate coverage of Hub Power Company with OUTPERFORM (TP PRs 49). PSO, PPL and HUBCO are trading at a 50-70% discount to regional valuation multiples and are 12-40% below their average P/E, with dividend yields in the range of 5.4-15%.

Research Analysts Raza Rawjani 65 6212 3035

11 November 2010

Pakistan Energy Sector 2

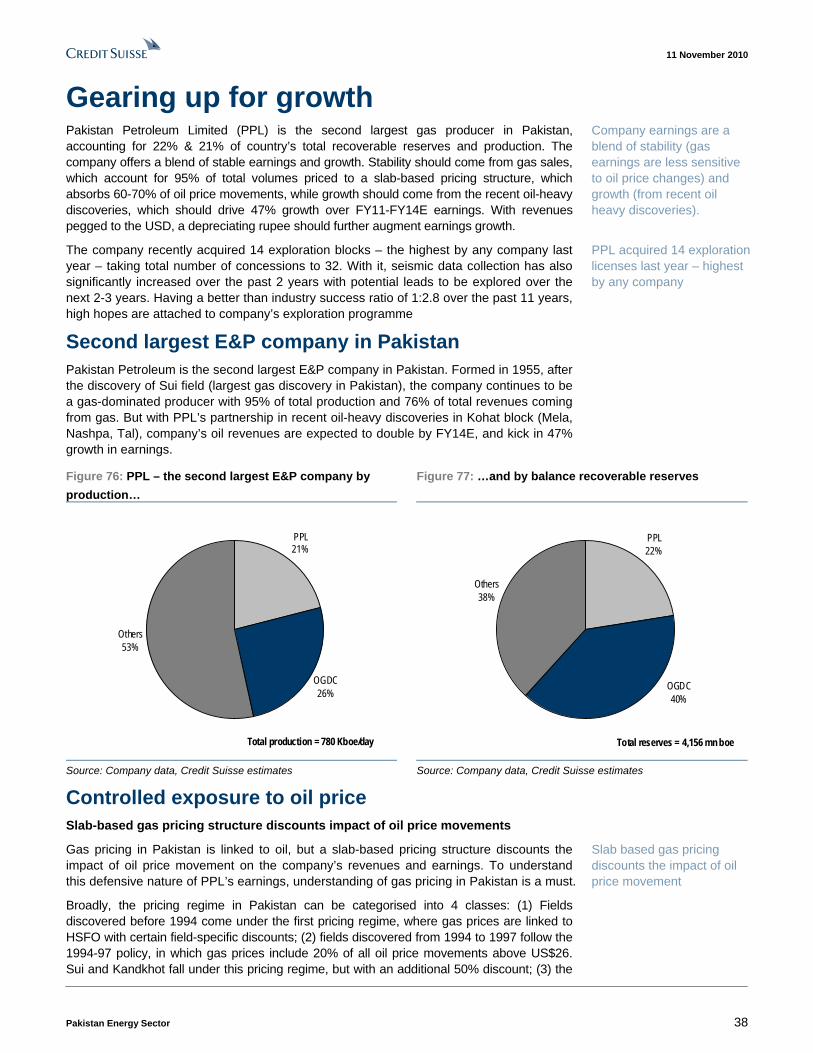

Focus charts and tables Figure 2: Pakistan energy sector’s company profiles Figure 3: Tariffs can rise further; tariffs higher in 2003

Company Profile OGDC Oil & Gas Development Co. (OGDC) is the largest E&P

company in Pakistan accounting for 26% of total production, 40% of reserves (1.6 bn boe) and 35% of awarded acreage.

PPL Pakistan Petroleum is the 2nd largest gas producer in Pakistan accounting for 24% of total gas production and reserves. Recently, the company has increased its exploration activities to replenish its reserves.

PSO Pakistan State Oil (PSO) is the largest OMC in Pakistan, having a market share of 70%.

HUBCO Hub Power Co. (HUBCO), which received the deal of decade award in 1999, is a 1200 MW IPP. Two new projects, a 214 MW oil fired IPP and 84MW hydro IPP are also in pipeline.

0.000

0.002

0.004

0.006

0.008

0.010

0.012

0.014

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

1QFY

11

FY11

E

(%)Tariffs as % age GDP per capita were higher in 2003 than what theywill be in 2011

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: Net circular debt during the past two years Figure 5: Div. yields to rise after circular debt resolution

-

50

100

150

200

250

Oct-0

8

Mar-0

9

Jun-0

9

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov-0

9

Dec-0

9

Jan-1

0

Feb-

10

Mar-1

0

Apr-1

0

July-

10

Sept-

10

PRs bn1st TFC of PRs80bn 2nd TFC of PRs 80bn

+ Auto. Tariff adjustments start

Tariffs increased 18%

Tariffs increased 6%Tariffs increased 12% Tariffs increased 7.6%

-

5

10

15

20

25

FY08 FY09 FY10 FY11E FY12E FY13E

PSO PPL OGDC HUBC

%

Source: Company data Source: Company data, Credit Suisse estimates

Figure 6: Valuation matrix Mkt cap Share price Upside P/E (x) P/B (x) ROE (%) Div. yield (%) (US$ mn) Rating current target (%) FY11E FY12E FY11E FY12E FY11E FY12E FY11E FY12E

PPL.KA 1,741 O 193.0 246 27 7.3 7.1 2.3 2.0 35 30 5.7 7.3PSO.KA 1,007 O 281.7 381 35 5.2 4.3 1.3 1.1 28 29 6.7 16.3HPWR.KA 742 O 33.5 49 46 6.2 4.9 1.3 1.2 21 25 14.9 16.9OGDC.KA 7,337 O 158.1 173 9 10.4 9.6 3.4 2.9 37 33 3.9 6.3Source: Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 3

To ride on rising power tariffs Circular debt blemished the return profile of Pakistan energy stocks as it dented the payout profiles of most companies. But now, as power tariffs play catch up with electricity generation costs, we believe circular debt is past its tipping point and is finally dwindling toward its end. Thus, we expect energy stocks to gradually return to their historical payout ratios starting FY11.

Likely resolution of circular debt in FY11 Since Pakistan’s participation in the IMF programme, electricity tariffs have increased 58% and now cover for 75% of all generation costs. With the IMF insisting upon sealing the gap between electricity tariffs and generation costs and with fiscal health of the government too fragile to carry on with electricity subsidies, we believe the government is left with no option but to increase electricity tariffs in FY11 by 15-20%. This should: 1) restrict accumulation of fresh circular debt to manageable levels, 2) limit electricity differentials in FY11 to PRs130 bn – almost half of that in FY10, 3) bring tariffs to a level where they cover 90-95% of all generation costs by June FY11, and 4) ensure long-term sustainability of the sector. Pakistan’s intention of entering into another IMF programme once the current one ends puts further pressure on the government to abide by IMF’s conditions of eliminating electricity subsidies by FY11. The whole scenario benefits the energy sector the most as improving cash flows due to higher tariffs will allow resumption of routine operations and bring back the high payouts.

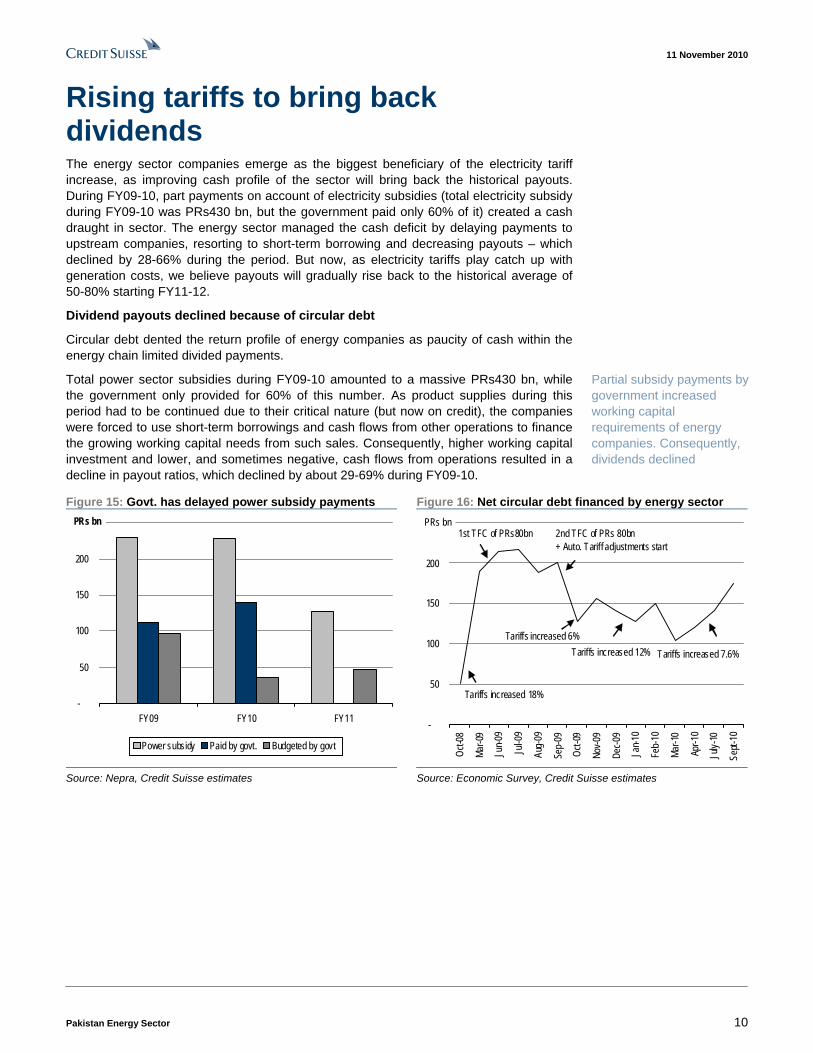

Rising tariffs to bring back dividends The energy sector companies emerge as the biggest beneficiary of the electricity tariff increase, as improving cash profile of the sector will bring back the historical payouts. During FY09-10, part payments on account of electricity subsidies (the total electricity subsidy during FY09-10 was PRs430 bn, but the government paid only 60% of it) created a cash draught in sector. The energy sector managed the cash deficit by delaying payments to upstream companies, resorting to short-term borrowing and decreasing payouts – which declined by 28-66% during the period. But now, as electricity tariffs play catch up with generation costs, we believe payouts will gradually rise back to the historical average of 50-80% starting FY11-12.

Assuming coverage with an OVERWEIGHT We assume coverage of the Pakistan energy sector with an OVERWEIGHT stance and with OUTPERFORM ratings on PPL (revised target price of PRs 246), PSO (revised target price of PRs381) and OGDC (a revised target price of PRs173). We also initiate coverage of Hub Power Company with an OUTPERFORM rating (target price PRs 49). Pakistan energy sector companies are among the cheapest in the region. During FY09-10, absence of high payouts was the restraining factor for the sector to trace back to historical valuation multiples. As the dividend payments gradually normalise from FY11, we expect energy stocks to move to their historical valuation multiples.

PSO, PPL and HUBCO are our top picks Our top picks in the the sector are PSO, PPL and HUBCO. The stocks are trading at 50-70% discount to regional valuation multiples and 12-40% below their average P/Es, with dividend yields in the range of 5.4-15%.

Increase in electricity tariffs to restrict circular debt growth in FY11

Energy companies emerge as the biggest beneficiary of these tariff hikes as improving cash flows of the sector will make space for routine operations and higher payouts

Assuming coverage with OVERWEIGHT. PSO, PPL and HUBCO are our top picks

11 November 2010

Pakistan Energy Sector 4

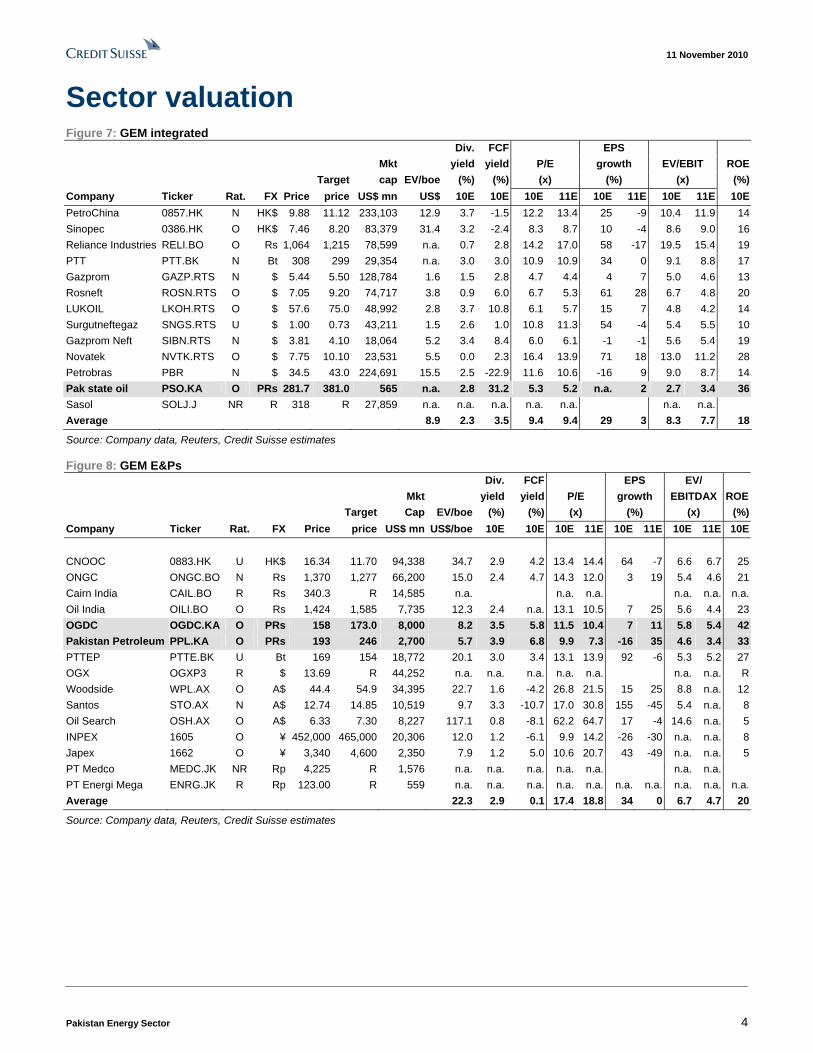

Sector valuation Figure 7: GEM integrated Div. FCF EPS Mkt yield yield P/E growth EV/EBIT ROE Target cap EV/boe (%) (%) (x) (%) (x) (%)Company Ticker Rat. FX Price price US$ mn US$ 10E 10E 10E 11E 10E 11E 10E 11E 10EPetroChina 0857.HK N HK$ 9.88 11.12 233,103 12.9 3.7 -1.5 12.2 13.4 25 -9 10.4 11.9 14Sinopec 0386.HK O HK$ 7.46 8.20 83,379 31.4 3.2 -2.4 8.3 8.7 10 -4 8.6 9.0 16Reliance Industries RELI.BO O Rs 1,064 1,215 78,599 n.a. 0.7 2.8 14.2 17.0 58 -17 19.5 15.4 19PTT PTT.BK N Bt 308 299 29,354 n.a. 3.0 3.0 10.9 10.9 34 0 9.1 8.8 17Gazprom GAZP.RTS N $ 5.44 5.50 128,784 1.6 1.5 2.8 4.7 4.4 4 7 5.0 4.6 13Rosneft ROSN.RTS O $ 7.05 9.20 74,717 3.8 0.9 6.0 6.7 5.3 61 28 6.7 4.8 20LUKOIL LKOH.RTS O $ 57.6 75.0 48,992 2.8 3.7 10.8 6.1 5.7 15 7 4.8 4.2 14Surgutneftegaz SNGS.RTS U $ 1.00 0.73 43,211 1.5 2.6 1.0 10.8 11.3 54 -4 5.4 5.5 10Gazprom Neft SIBN.RTS N $ 3.81 4.10 18,064 5.2 3.4 8.4 6.0 6.1 -1 -1 5.6 5.4 19Novatek NVTK.RTS O $ 7.75 10.10 23,531 5.5 0.0 2.3 16.4 13.9 71 18 13.0 11.2 28Petrobras PBR N $ 34.5 43.0 224,691 15.5 2.5 -22.9 11.6 10.6 -16 9 9.0 8.7 14Pak state oil PSO.KA O PRs 281.7 381.0 565 n.a. 2.8 31.2 5.3 5.2 n.a. 2 2.7 3.4 36Sasol SOLJ.J NR R 318 R 27,859 n.a. n.a. n.a. n.a. n.a. n.a. n.a.Average 8.9 2.3 3.5 9.4 9.4 29 3 8.3 7.7 18

Source: Company data, Reuters, Credit Suisse estimates

Figure 8: GEM E&Ps Div. FCF EPS EV/ Mkt yield yield P/E growth EBITDAX ROE Target Cap EV/boe (%) (%) (x) (%) (x) (%)Company Ticker Rat. FX Price price US$ mn US$/boe 10E 10E 10E 11E 10E 11E 10E 11E 10E CNOOC 0883.HK U HK$ 16.34 11.70 94,338 34.7 2.9 4.2 13.4 14.4 64 -7 6.6 6.7 25ONGC ONGC.BO N Rs 1,370 1,277 66,200 15.0 2.4 4.7 14.3 12.0 3 19 5.4 4.6 21Cairn India CAIL.BO R Rs 340.3 R 14,585 n.a. n.a. n.a. n.a. n.a. n.a.Oil India OILI.BO O Rs 1,424 1,585 7,735 12.3 2.4 n.a. 13.1 10.5 7 25 5.6 4.4 23OGDC OGDC.KA O PRs 158 173.0 8,000 8.2 3.5 5.8 11.5 10.4 7 11 5.8 5.4 42Pakistan Petroleum PPL.KA O PRs 193 246 2,700 5.7 3.9 6.8 9.9 7.3 -16 35 4.6 3.4 33PTTEP PTTE.BK U Bt 169 154 18,772 20.1 3.0 3.4 13.1 13.9 92 -6 5.3 5.2 27OGX OGXP3 R $ 13.69 R 44,252 n.a. n.a. n.a. n.a. n.a. n.a. n.a. RWoodside WPL.AX O A$ 44.4 54.9 34,395 22.7 1.6 -4.2 26.8 21.5 15 25 8.8 n.a. 12Santos STO.AX N A$ 12.74 14.85 10,519 9.7 3.3 -10.7 17.0 30.8 155 -45 5.4 n.a. 8Oil Search OSH.AX O A$ 6.33 7.30 8,227 117.1 0.8 -8.1 62.2 64.7 17 -4 14.6 n.a. 5INPEX 1605 O ¥ 452,000 465,000 20,306 12.0 1.2 -6.1 9.9 14.2 -26 -30 n.a. n.a. 8Japex 1662 O ¥ 3,340 4,600 2,350 7.9 1.2 5.0 10.6 20.7 43 -49 n.a. n.a. 5PT Medco MEDC.JK NR Rp 4,225 R 1,576 n.a. n.a. n.a. n.a. n.a. n.a. n.a.PT Energi Mega ENRG.JK R Rp 123.00 R 559 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Average 22.3 2.9 0.1 17.4 18.8 34 0 6.7 4.7 20

Source: Company data, Reuters, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 5

Circular debt resolution in FY11 Since Pakistan’s participation in the IMF programme, electricity tariffs have increased 58% and now cover for 75% of all generation costs. With the IMF insisting upon sealing the gap between electricity tariffs and generation costs, and with fiscal health of the government too fragile to carry on with electricity subsidies, we believe the government is left with no option but to increase electricity tariffs in FY11 by 15-20%. This should: 1) restrict accumulation of fresh circular debt to manageable levels, 2) limit electricity differentials in FY11 to PRs130 bn – almost half of that in FY10, 3) bring tariffs to a level where they cover 90-95% of all generation costs by June FY11, and 4) ensure long-term sustainability of the sector. Pakistan’s intention of entering into another IMF programme once the current one ends puts further pressure on the government to abide by IMF’s conditions of eliminating electricity subsidies by FY11. The whole scenario benefits the energy sector the most as improving cash flows due to higher tariffs will allow resumption of routine operations and bring back the high payouts.

What is circular debt? Circular debt is basically inter-company debt within the Pakistan energy sector that accrued as a result of electricity tariffs being kept below cost recovery levels. It started with the government’s inability to finance electricity subsidy; this inability trickled down the entire energy chain in the form of partial and delayed payments to electricity producers and fuel suppliers. Now, the repayment of working capital financing is also linked to it.

Pakistan is among the few developing countries that have a high percentage of electricity generated from gas and fuel oil (more than 60%). Gas to the power sector is provided through the use of indigenous deposits (gas is explored by E&P companies and transmitted by gas distribution companies), while nearly 75% of fuel oil is imported (oil marketing companies import fuel oil for power generation). Hence, a high percentage of electricity generation cost is linked to oil price.

This gas and fuel oil is sold to power generation companies (government-owned as well as independent power producers, or IPPs), which in turn sell their output to a central body –the Central Power Purchasing Authority (CPPA) – at the rate negotiated in the power purchasing agreement. The purchase of this electricity and the negotiated price is both guaranteed by the government. In almost all cases, the negotiated price is basically cost plus pricing, where the power producer is guaranteed a fixed return on his investment along with payments of all costs. Costs for a power generation company are basically fuel costs (90%-plus) and O&M costs. Hence, it is obvious that a power producer can only make fuel supply payments if it is promptly reimbursed by the government for such payments.

The government, after buying electricity from these companies, notifies a consumer price based on its social, political and economic objectives, and sells electricity to consumers through several government-owned distribution companies (Discos). Traditionally, the government has always notified tariffs below generation costs, but the difference has been relatively miniscule and hence easier to finance.

However, more recently, the difference between the notified price and generation cost widened to about 33% of generation costs, and, as a result, the government had to finance a large stock of the subsidy, which in FY10 is estimated to be around PRs230 bn (US$2.7 bn) or about 1.58% of GDP.

Multiple facets of circular debt

Circular debt is a compound of many problems.

Circular debt is basically inter-corporate debt that has accrued because electricity tariffs are below cost recovery levels, while government is delaying subsidy payments

As more than 60% of electricity in Pakistan is produced from gas or oil, when electricity tariffs did not increase in line with the rise in oil prices, it burdened the government with massive subsidies

And delayed/partial payment of subsidies by a cash-strapped government forced downstream companies to delay payments to upstream companies

11 November 2010

Pakistan Energy Sector 6

The principal problem is government’s inability to finance electricity subsidy payments. The government has traditionally subsidised electricity tariffs. However, the quantum of subsidies rose when the oil price spiked in FY07-08. Any benefits of the oil price plunge that followed were limited due to rupee depreciation. The government, which was already running high twin account deficits, found it difficult to finance the increased subsidies. Consequently, payments to electricity producers got delayed and resulted in a cash draught in the entire energy chain.

The second problem is the incapacity of electricity distribution companies to collect bills. Distribution companies have had a hard time in collecting payments from other government bodies and from certain geographical locations. Though it is a relatively small problem, but accumulation of unpaid bills from such customers compounded the problem in FY08-09.

Figure 9: Recovery rates for distribution companies IESCO LESCO GEPCO FESCO MEPCO PESCO HESCO QESCORecovery rate (%) 96 92 96 97 95.8 85 59.8 58Market share (%) 10 19 8 11 13 11 7 6

Source: Nepra

Another problem is that distribution companies have high transmission and distribution (T&D) losses. T&D losses in Pakistan are around 22%. Although a certain part of these losses is theft, but underinvestment, poor infrastructure and infrequent maintenance are also to be blamed.

Figure 10: Transmission and distribution losses in Pakistan IESCO LESCO GEPCO FESCO MEPCO PESCO HESCO QESCO KESCT&D loss (%) 11 13 11 11 18 38 35 20 36Market share (%) 10 19 8 11 13 11 7 6 13

Source: Nepra

The last problem is more structural. Pakistan has high dependence on furnace oil for its electricity needs, which tends to increase the electricity generation cost. This has to shift to cheaper alternatives in the long run.

IMF is pushing for elimination of electricity subsidies Pakistan has already missed the revised deadline of August 2010 to eliminate subsidies

Pakistan has now twice missed the deadline set by the IMF for eliminating electricity subsidies.

Initially, Pakistan had committed to the IMF to remove electricity tariff subsidies by June 2009. But fearing that the price increase will be politically too costly, the government backed out of the agreement and negotiated a year extension of this deadline (new deadline was August 2010).

However, even after a 32% increase in electricity tariffs, the government was unable to achieve cost recovery, and missed the second deadline of August 2010 as well.

As a result, pressure from IMF has escalated and disbursement of further loan tranches has been deferred

The IMF has now adopted a stricter stance for the government after most of the FY10 policy targets were missed (fiscal deficit was 6.3% as against a target of 5.1%, net borrowing from SBP was PRs44 bn versus a target of zero net borrowing, non resolution of circular debt, value added tax was not imposed). Along with this, the international lender has also delayed the disbursement of the fifth loan tranche (disbursement was originally planned in August 2010) and has informed the government that it will need to show material progress with respect to the implementation of Value Added Tax and resolution of circular debt, before Pakistan’s case can be pursued further.

Factors responsible for rise of circular debt: (i) delay in subsidy payments from government, (ii) high bad debts, (iii) high T&D losses, and (iv) high dependence on furnace oil for electricity needs

Pakistan has now twice missed the deadline for eliminating electricity subsidies. IMF may not allow further relaxations

As a result, the IMF has now adopted a stricter stance and delayed the disbursement of further loan tranches

11 November 2010

Pakistan Energy Sector 7

IMF has set tough pre-conditions for the disbursement of next loan tranche

The IMF has set completion of following energy sector targets/reforms as pre-conditions before its board can consider Pakistan’s case:

■ Material progress towards elimination of circular debt and electricity subsidy

■ Empowering NEPRA (National Electric Power Regulatory Authority) to notify electricity tariffs on the basis of full cost recovery

■ Completion of consumer classification survey and fuel efficiency audits

■ Dissolution of Pakistan Electric Power Company (PEPCO)

■ Corporatisation of power sector and engagement of private sector managers to run state-owned entities.

Government has assured the IMF of resolution of circular debt in FY11 – may have to intensify efforts to satisfy IMF’s concerns

The encouraging news is that the government has shown genuine seriousness in reforming the power sector and in eliminating subsidies (government has to be credited for increasing tariffs by 58% in two years). Likewise, even in the recent policy-level talks with the IMF, the government has reiterated its intention to resolve circular debt and has committed to eliminate the electricity subsidy and complete all other power sector reforms in FY11.

We believe that the government will have to abide by IMF’s targets this time, as several external assistance programs and, to some extent, interim political stability are linked to IMF’s favourable review of the economy (currently measured in terms of disbursement of next loan tranche). Also, given the government’s intention of signing up for another IMF programme, and the fact that it twice missed the deadline for achieving full cost recovery, further put pressure on the government to take the difficult political decision of increasing the electricity tariffs.

Previous IMF targets achieved by the government

■ Pakistan raised electricity tariffs by 18% in November 2008, which was a pre-condition to enter into the IMF programme. Prior to this, tariffs had already been increased twice by a cumulative 19%. Electricity tariffs were also raised 1% in February 2009.

■ An SPV, Power holding (Pvt) Ltd, was created to assume all of power sector’s liabilities. The SPV, on the back of a government guarantee, floated two TFCs of a cumulative amount of PRs160 bn (US$2 bn). The cash raised was used to assume the existing circular debt stock of the industry. This eliminated about 50% of the total circular debt stock outstanding at that time.

■ Nepra (National Electric Power Regulatory Authority), which was only mandated to calculate electricity tariffs based on full cost recovery, was given the power to notify adjustments in electricity tariffs caused by variances in fuel prices or by changes in electricity generation mix. We estimate that this measure helped in recovering PRs40 bn of generation costs in FY10

■ Another round of electricity tariffs hikes was implemented in FY10, whereby tariffs were increased by another 27.7%. While the government did not exactly follow IMF’s schedule, the end target was achieved.

■ Effective 1 October 2010, electricity tariffs were further hiked by 2%. The same day, PEPCO was also dissolved, to pave way for the eventual deregulation and corporatisation of the power sector.

In recent meetings with IMF, government has assured of resolving circular debt by FY11 by increasing tariffs and by implementing structural reforms

11 November 2010

Pakistan Energy Sector 8

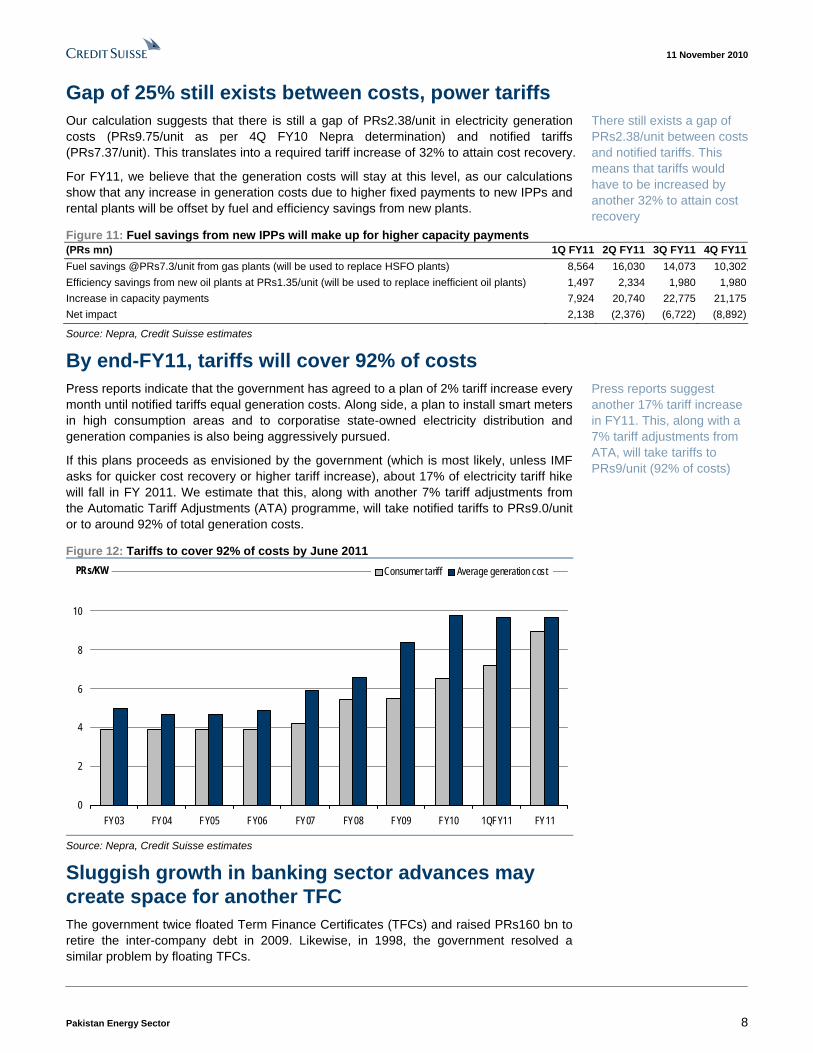

Gap of 25% still exists between costs, power tariffs Our calculation suggests that there is still a gap of PRs2.38/unit in electricity generation costs (PRs9.75/unit as per 4Q FY10 Nepra determination) and notified tariffs (PRs7.37/unit). This translates into a required tariff increase of 32% to attain cost recovery.

For FY11, we believe that the generation costs will stay at this level, as our calculations show that any increase in generation costs due to higher fixed payments to new IPPs and rental plants will be offset by fuel and efficiency savings from new plants.

Figure 11: Fuel savings from new IPPs will make up for higher capacity payments (PRs mn) 1Q FY11 2Q FY11 3Q FY11 4Q FY11Fuel savings @PRs7.3/unit from gas plants (will be used to replace HSFO plants) 8,564 16,030 14,073 10,302Efficiency savings from new oil plants at PRs1.35/unit (will be used to replace inefficient oil plants) 1,497 2,334 1,980 1,980Increase in capacity payments 7,924 20,740 22,775 21,175Net impact 2,138 (2,376) (6,722) (8,892)

Source: Nepra, Credit Suisse estimates

By end-FY11, tariffs will cover 92% of costs Press reports indicate that the government has agreed to a plan of 2% tariff increase every month until notified tariffs equal generation costs. Along side, a plan to install smart meters in high consumption areas and to corporatise state-owned electricity distribution and generation companies is also being aggressively pursued.

If this plans proceeds as envisioned by the government (which is most likely, unless IMF asks for quicker cost recovery or higher tariff increase), about 17% of electricity tariff hike will fall in FY 2011. We estimate that this, along with another 7% tariff adjustments from the Automatic Tariff Adjustments (ATA) programme, will take notified tariffs to PRs9.0/unit or to around 92% of total generation costs.

Figure 12: Tariffs to cover 92% of costs by June 2011

0

2

4

6

8

10

12

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 1QFY11 FY11

Consumer tariff Average generation costPRs/KW

Source: Nepra, Credit Suisse estimates

Sluggish growth in banking sector advances may create space for another TFC The government twice floated Term Finance Certificates (TFCs) and raised PRs160 bn to retire the inter-company debt in 2009. Likewise, in 1998, the government resolved a similar problem by floating TFCs.

There still exists a gap of PRs2.38/unit between costs and notified tariffs. This means that tariffs would have to be increased by another 32% to attain cost recovery

Press reports suggest another 17% tariff increase in FY11. This, along with a 7% tariff adjustments from ATA, will take tariffs to PRs9/unit (92% of costs)

11 November 2010

Pakistan Energy Sector 9

Our Pakistan bank sector analyst believes that the current high interest rate scenario will lead to subdued growth in advances and make banks invest more into government treasuries. This scarcity of investment avenues can likely pave way for another power sector TFC, which will offer banks higher return than other investment options.

Tariffs as a percentage of per-capita GDP higher in 2003 We calculate that even after a proposed 20-25% increase in power tariffs, tariffs as a percentage of GDP per capita will be lower than they were in 2003 because total inflation during the period rose by about 105%, while tariffs during the period grew only by 72%.

Figure 13: Tariffs can rise further; tariffs higher in 2003 Figure 14: Power tariff increase has lagged inflation

0.000

0.002

0.004

0.006

0.008

0.010

0.012

0.014

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

1QFY

11

FY11

E

(%)Tariffs as %age GDP per capita were higher in 2003 than what theywill be in 2011

-

20

40

60

80

100

120

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10

Cumulative inc in CPI Cumulative inc in power tariffs

Source: Economic survey, Credit Suisse estimates Source: Economic survey, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 10

Rising tariffs to bring back dividends The energy sector companies emerge as the biggest beneficiary of the electricity tariff increase, as improving cash profile of the sector will bring back the historical payouts. During FY09-10, part payments on account of electricity subsidies (total electricity subsidy during FY09-10 was PRs430 bn, but the government paid only 60% of it) created a cash draught in sector. The energy sector managed the cash deficit by delaying payments to upstream companies, resorting to short-term borrowing and decreasing payouts – which declined by 28-66% during the period. But now, as electricity tariffs play catch up with generation costs, we believe payouts will gradually rise back to the historical average of 50-80% starting FY11-12.

Dividend payouts declined because of circular debt

Circular debt dented the return profile of energy companies as paucity of cash within the energy chain limited divided payments.

Total power sector subsidies during FY09-10 amounted to a massive PRs430 bn, while the government only provided for 60% of this number. As product supplies during this period had to be continued due to their critical nature (but now on credit), the companies were forced to use short-term borrowings and cash flows from other operations to finance the growing working capital needs from such sales. Consequently, higher working capital investment and lower, and sometimes negative, cash flows from operations resulted in a decline in payout ratios, which declined by about 29-69% during FY09-10.

Figure 15: Govt. has delayed power subsidy payments Figure 16: Net circular debt financed by energy sector

-

50

100

150

200

250

FY09 FY10 FY11

Power subsidy Paid by govt. Budgeted by govt

PRs bn

-

50

100

150

200

250

Oct-0

8

Mar-0

9

Jun-0

9

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov-0

9

Dec-0

9

Jan-1

0

Feb-

10

Mar-1

0

Apr-1

0

July-

10

Sept-

10

PRs bn1st TFC of PRs80bn 2nd TFC of PRs 80bn

+ Auto. Tariff adjustments start

Tariffs increased 18%

Tariffs increased 6%Tariffs increased 12% Tariffs increased 7.6%

Source: Nepra, Credit Suisse estimates Source: Economic Survey, Credit Suisse estimates

Partial subsidy payments by government increased working capital requirements of energy companies. Consequently, dividends declined

11 November 2010

Pakistan Energy Sector 11

Working capital investments increased due to circular debt

Figure 17: Trade receivables and payables for PSO Figure 18: Trade receivables and payables for OGDC

-

20

40

60

80

100

120

140

160

180

4qFy

06

2qFy

07

4qFy

07

2qFy

08

4qFy

08

2qFy

09

4qFy

09

2qFy

10

4qFy

10

Trade receivables Trade payables

PRs bn

-102030405060708090

100

4qFy

06

2qFy

07

4qFy

07

2qFy

08

4qFy

08

2qFy

09

4qFy

09

2qFy

10

4qFy

10

Trade receivables Trade payables

PRs bn

Source: Company data Source: Company data

Figure 19: Trade receivables and payables for PPL Figure 20: Trade receivables and payables for HUBCO

-

5

10

15

20

25

30

35

40

4qFy

06

2qFy

07

4qFy

07

2qFy

08

4qFy

08

2qFy

09

4qFy

09

2qFy

10

4qFy

10

Trade receivables Trade payables

PRs bn

-

10

20

30

40

50

60

70

80

4qFy

06

2qFy

07

4qFy

07

2qFy

08

4qFy

08

2qFy

09

4qFy

09

2qFy

10

4qFy

10

Trade receivables Trade payables

PRs bn

Source: Company data Source: Company data

Power sector reforms to improve energy sector’s cash flows FY11 and FY12 should be better years for the energy sector because:

■ Tariffs have increased 58% over the past two years and now cover 76% of the generation costs. Whereas in the beginning of FY10, tariffs only covered 57% of the generation costs.

■ The government plans to increase tariffs by another 17% in FY11 and implement other structural reforms in sector. With the proposed tariff increase, FY11 subsidy will be around PRs130 bn – much lower than PRs230 bn in FY09 and FY10.

■ Per unit generation cost is also expected to come down due to better water availability, allowing for optimal hydel generation. Moreover, with some of the energy conservation/gas curtailment measures expected to continue throughout the year, abundant supply of gas will be available for power generation, thereby limiting the use of costlier fuels.

Power sector reforms and 58% tariff increases brought over the past two years will restrict circular debt growth and will make space for routine operations and higher payouts

11 November 2010

Pakistan Energy Sector 12

■ Court cases against electricity tariff hikes have been resolved; this should further augment cash flows.

■ The mechanism of the ATA (tariffs are monthly adjusted for fuel price and fuel mix changes) will prevent reoccurrence of circular debt of such magnitude.

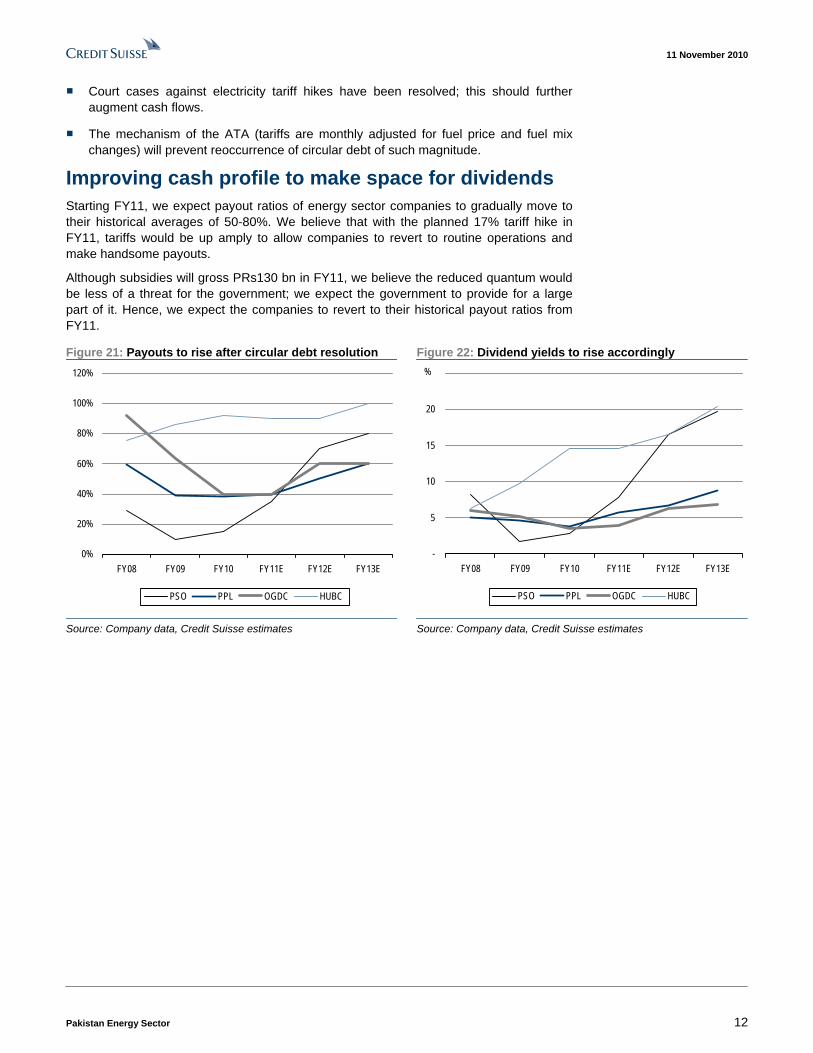

Improving cash profile to make space for dividends Starting FY11, we expect payout ratios of energy sector companies to gradually move to their historical averages of 50-80%. We believe that with the planned 17% tariff hike in FY11, tariffs would be up amply to allow companies to revert to routine operations and make handsome payouts.

Although subsidies will gross PRs130 bn in FY11, we believe the reduced quantum would be less of a threat for the government; we expect the government to provide for a large part of it. Hence, we expect the companies to revert to their historical payout ratios from FY11.

Figure 21: Payouts to rise after circular debt resolution Figure 22: Dividend yields to rise accordingly

0%

20%

40%

60%

80%

100%

120%

FY08 FY09 FY10 FY11E FY12E FY13E

PSO PPL OGDC HUBC

-

5

10

15

20

25

FY08 FY09 FY10 FY11E FY12E FY13E

PSO PPL OGDC HUBC

%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 13

Assuming coverage with an OVERWEIGHT We assume coverage of the Pakistan energy sector with an OVERWEIGHT stance and with OUTPERFORM ratings on PPL (revised target price of PRs 246), PSO (revised target price of PRs381) & OGDC (revised target price of PRs 173) We also initiate coverage of Hub Power Company with an OUTPERFORM rating (target price PRs 49). Pakistan energy sector companies are among the cheapest in the region. During FY09-10, absence of high payouts restrained the sector to trace back their historical valuation multiples. With the dividend payments expected to normalise from FY11, we expect energy stocks to return to their historical valuation multiples.

Valuation methodology We have used average historical multiples to value Pakistan energy sector companies. Specifically, we have used historical dividend yields to value downstream companies, as prices for downstream companies appear to be more responsive to dividends than to earnings. For upstream companies, we use the historical price-to-earning ratio.

In coming up with a target multiple, we have not included the valuation multiples after June 2008, as it was from July 2008 that the problem of circular debt started affecting the energy companies and dented the valuation multiples.

We value downstream companies on dividend yield

We value downstream companies on dividend yields as prices for downstream companies historically appear to be more responsive to dividend payouts.

Pakistan State Oil

Based on a target yield of 8.54%, our December 2011 target price for PSO is PRs381. Our target dividend yield of 8.54% is the average of forward dividend yields from July 1998 to June 2008.

Figure 23: PSO’s valuation matrix Target P/E at Div yield EV/EBITDA EPS DPS Target price (TP) target price at target price at target price FY11 FY12 FY11 FY12 D/Y Dec-11 FY11 FY12 FY11 FY12 FY11 FY12PSO 54 66 19 46 8.5 381 7.07 5.81 4.95 12.05 4.14 3.39

Source: Company data, Credit Suisse estimates

Figure 24: Forward dividend yield for PSO Figure 25: Forward P/E for PSO

-

2

4

6

8

10

12

14

16

18

20

Jul-9

7

Jul-9

8

Jul-9

9

Jul-0

0

Jul-0

1

Jul-0

2

Jul-0

3

Jul-0

4

Jul-0

5

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

(%)

Target D/Y = 8.54

Avg D/Y = 8.09

0

2

4

6

8

10

12

14

16

18

20

Jul-9

7

Jul-9

8

Jul-9

9

Jul-0

0

Jul-0

1

Jul-0

2

Jul-0

3

Jul-0

4

Jul-0

5

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0P/E

Average PE = 8.4x

Source: Bloomberg, Credit Suisse estimates Source: Bloomberg, Credit Suisse estimates

We have valued Pakistan’s energy sector on historical multiples

We value PSO with a target dividend yield of 8.54% with December 2011 target price of PRs381

11 November 2010

Pakistan Energy Sector 14

Hub Power Company

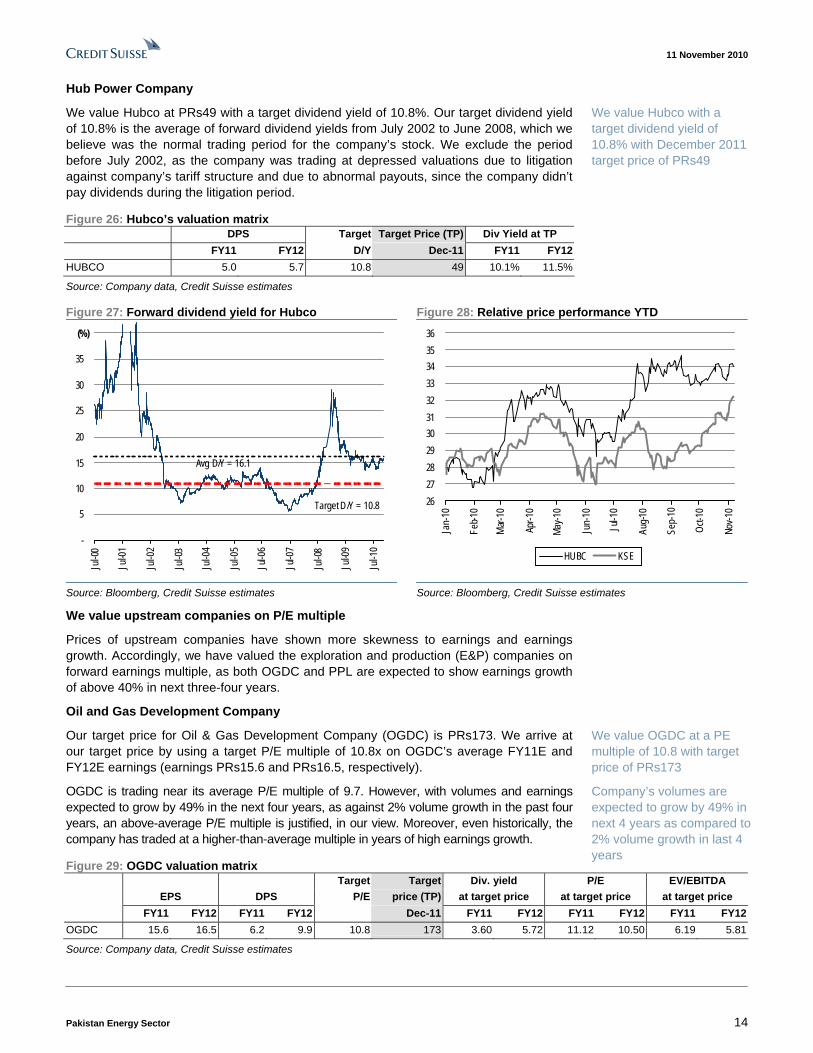

We value Hubco at PRs49 with a target dividend yield of 10.8%. Our target dividend yield of 10.8% is the average of forward dividend yields from July 2002 to June 2008, which we believe was the normal trading period for the company’s stock. We exclude the period before July 2002, as the company was trading at depressed valuations due to litigation against company’s tariff structure and due to abnormal payouts, since the company didn’t pay dividends during the litigation period.

Figure 26: Hubco’s valuation matrix DPS Target Target Price (TP) Div Yield at TP FY11 FY12 D/Y Dec-11 FY11 FY12 HUBCO 5.0 5.7 10.8 49 10.1% 11.5%

Source: Company data, Credit Suisse estimates

Figure 27: Forward dividend yield for Hubco Figure 28: Relative price performance YTD

-

5

10

15

20

25

30

35

40

Jul-0

0

Jul-0

1

Jul-0

2

Jul-0

3

Jul-0

4

Jul-0

5

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

(%)

Avg D/Y = 16.1

Target D/Y = 10.8

2627282930313233343536

Jan-

10

Feb-1

0

Mar-

10

Apr-1

0

May-1

0

Jun-

10

Jul-1

0

Aug-1

0

Sep-

10

Oct-1

0

Nov-1

0

HUBC KSE

Source: Bloomberg, Credit Suisse estimates Source: Bloomberg, Credit Suisse estimates

We value upstream companies on P/E multiple

Prices of upstream companies have shown more skewness to earnings and earnings growth. Accordingly, we have valued the exploration and production (E&P) companies on forward earnings multiple, as both OGDC and PPL are expected to show earnings growth of above 40% in next three-four years.

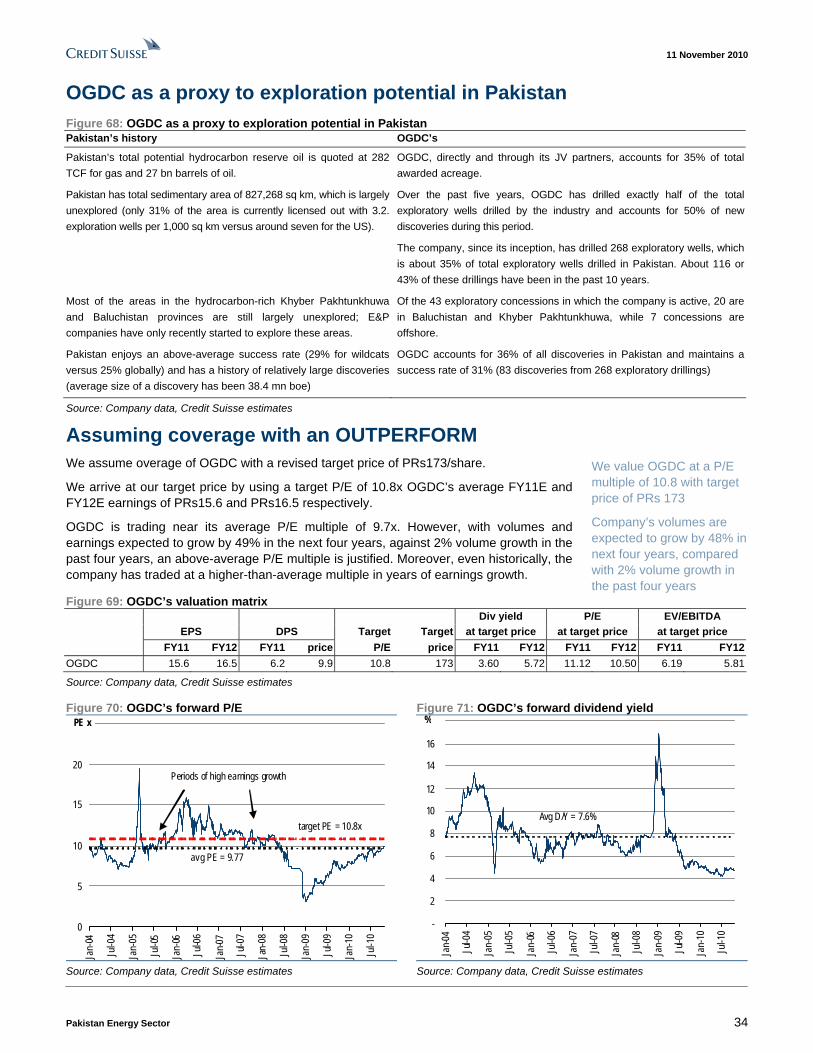

Oil and Gas Development Company

Our target price for Oil & Gas Development Company (OGDC) is PRs173. We arrive at our target price by using a target P/E multiple of 10.8x on OGDC’s average FY11E and FY12E earnings (earnings PRs15.6 and PRs16.5, respectively).

OGDC is trading near its average P/E multiple of 9.7. However, with volumes and earnings expected to grow by 49% in the next four years, as against 2% volume growth in the past four years, an above-average P/E multiple is justified, in our view. Moreover, even historically, the company has traded at a higher-than-average multiple in years of high earnings growth.

Figure 29: OGDC valuation matrix Target Target Div. yield P/E EV/EBITDA EPS DPS P/E price (TP) at target price at target price at target price FY11 FY12 FY11 FY12 Dec-11 FY11 FY12 FY11 FY12 FY11 FY12OGDC 15.6 16.5 6.2 9.9 10.8 173 3.60 5.72 11.12 10.50 6.19 5.81

Source: Company data, Credit Suisse estimates

We value Hubco with a target dividend yield of 10.8% with December 2011 target price of PRs49

We value OGDC at a PE multiple of 10.8 with target price of PRs173

Company’s volumes are expected to grow by 49% in next 4 years as compared to 2% volume growth in last 4 years

11 November 2010

Pakistan Energy Sector 15

Figure 30: OGDC forward P/E Figure 31: OGDC forward dividend yield

0

5

10

15

20

25

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-0

7

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

PE x

target PE = 10.8x

avg PE = 9.77

Periods of high earnings growth

-

2

4

6

8

10

12

14

16

18

Jan-0

4

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

%

Avg D/Y = 7.6%

Source: Bloomberg, Credit Suisse estimates Source: Bloomberg, Credit Suisse estimates

Pakistan Petroleum Limited

We assume coverage of PPL with a revised target price of PRs246. With earnings expected to grow 64% over the next four years, we shift our valuation methodology to P/E multiple-based valuation. We use a target P/E of 9.2x (average historical P/E) on average earnings for FY11E and FY12E (add avg EPS) to value PPL.

Figure 32: PPL’s valuation matrix Target Div P/E EV/EBITDAX price yield at at at EPS DPS - FY11 Target (TP) target price target price target price FY11 FY12 FY11 FY12 P/E Dec-11 FY11 FY12 FY11 FY12 FY11 FY12 PPL 26.4 27.0 11 14 9.2 246 4.48 5.70 9.32 9.09 4.64 4.42

Source: Company data, Credit Suisse estimates

Figure 33: Historical forward P/E multiple for PPL Figure 34: Historical forward P/E multiple for PPL

0

2

4

6

8

10

12

14

16

18

20

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-0

7

Jul-0

7

Jan-

08

Jul-0

8

Jan-0

9

Jul-0

9

Jan-

10

Jul-1

0

PE x

target PE = 9.2x

avg PE = 8.2x

-

2

4

6

8

10

12

14

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-0

8

Jul-0

8

Jan-

09

Jul-0

9

Jan-1

0

Jul-1

0

%

average D/Y = 5.4%

Source: Bloomberg, Credit Suisse estimates Source: Bloomberg, Credit Suisse estimates

We value PPL at a P/E of 9.2x, with target price of PRs246

The company’s earnings are expected to grow 64% over the next four years

11 November 2010

Pakistan Energy Sector 16

Asia Pacific / PakistanOil & Gas Refining & Marketing

Pakistan State Oil Company Ltd (PSO.KA / PSO PA)

ASSUMING COVERAGE

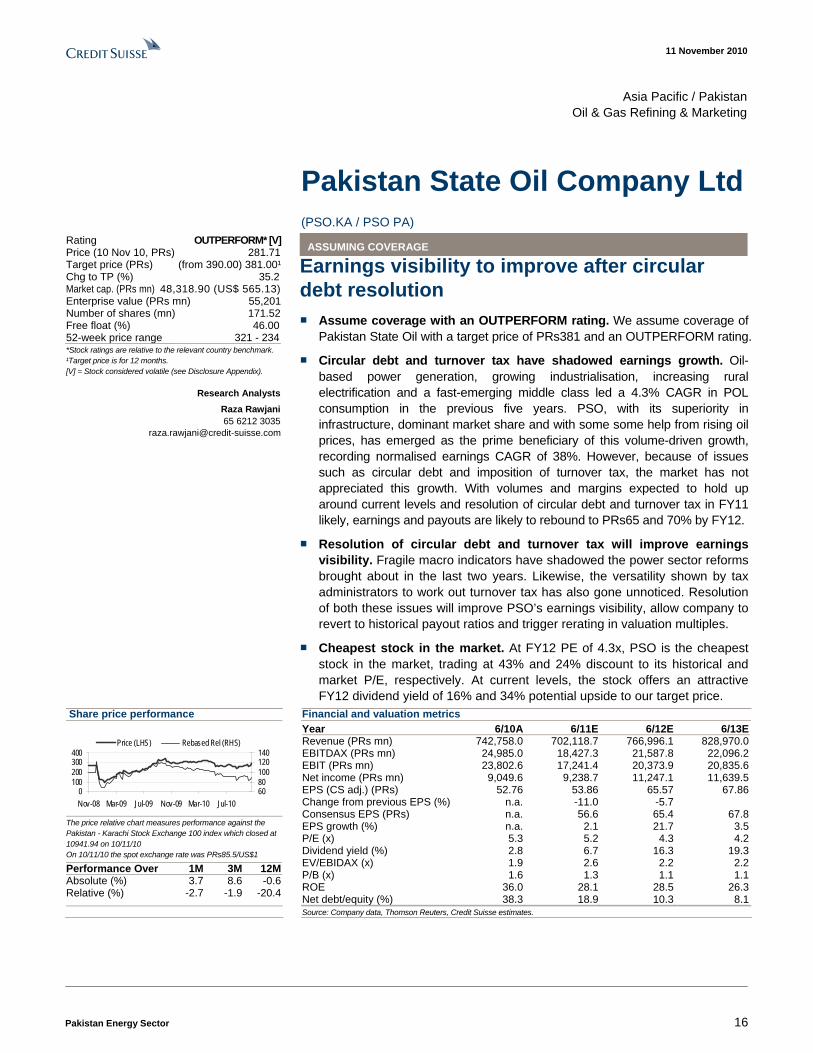

Earnings visibility to improve after circular debt resolution ■ Assume coverage with an OUTPERFORM rating. We assume coverage of

Pakistan State Oil with a target price of PRs381 and an OUTPERFORM rating.

■ Circular debt and turnover tax have shadowed earnings growth. Oil-based power generation, growing industrialisation, increasing rural electrification and a fast-emerging middle class led a 4.3% CAGR in POL consumption in the previous five years. PSO, with its superiority in infrastructure, dominant market share and with some some help from rising oil prices, has emerged as the prime beneficiary of this volume-driven growth, recording normalised earnings CAGR of 38%. However, because of issues such as circular debt and imposition of turnover tax, the market has not appreciated this growth. With volumes and margins expected to hold up around current levels and resolution of circular debt and turnover tax in FY11 likely, earnings and payouts are likely to rebound to PRs65 and 70% by FY12.

■ Resolution of circular debt and turnover tax will improve earnings visibility. Fragile macro indicators have shadowed the power sector reforms brought about in the last two years. Likewise, the versatility shown by tax administrators to work out turnover tax has also gone unnoticed. Resolution of both these issues will improve PSO’s earnings visibility, allow company to revert to historical payout ratios and trigger rerating in valuation multiples.

■ Cheapest stock in the market. At FY12 PE of 4.3x, PSO is the cheapest stock in the market, trading at 43% and 24% discount to its historical and market P/E, respectively. At current levels, the stock offers an attractive FY12 dividend yield of 16% and 34% potential upside to our target price.

Share price performance

0100200300400

Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-106080100120140

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the Pakistan - Karachi Stock Exchange 100 index which closed at 10941.94 on 10/11/10 On 10/11/10 the spot exchange rate was PRs85.5/US$1

Performance Over 1M 3M 12M Absolute (%) 3.7 8.6 -0.6 Relative (%) -2.7 -1.9 -20.4

Financial and valuation metrics

Year 6/10A 6/11E 6/12E 6/13ERevenue (PRs mn) 742,758.0 702,118.7 766,996.1 828,970.0EBITDAX (PRs mn) 24,985.0 18,427.3 21,587.8 22,096.2EBIT (PRs mn) 23,802.6 17,241.4 20,373.9 20,835.6Net income (PRs mn) 9,049.6 9,238.7 11,247.1 11,639.5EPS (CS adj.) (PRs) 52.76 53.86 65.57 67.86Change from previous EPS (%) n.a. -11.0 -5.7Consensus EPS (PRs) n.a. 56.6 65.4 67.8EPS growth (%) n.a. 2.1 21.7 3.5P/E (x) 5.3 5.2 4.3 4.2Dividend yield (%) 2.8 6.7 16.3 19.3EV/EBIDAX (x) 1.9 2.6 2.2 2.2P/B (x) 1.6 1.3 1.1 1.1ROE 36.0 28.1 28.5 26.3Net debt/equity (%) 38.3 18.9 10.3 8.1

Source: Company data, Thomson Reuters, Credit Suisse estimates.

*Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months. [V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts Raza Rawjani 65 6212 3035

Rating OUTPERFORM* [V] Price (10 Nov 10, PRs) 281.71 Target price (PRs) (from 390.00) 381.00¹ Chg to TP (%) 35.2 Market cap. (PRs mn) 48,318.90 (US$ 565.13) Enterprise value (PRs mn) 55,201 Number of shares (mn) 171.52 Free float (%) 46.00 52-week price range 321 - 234

11 November 2010

Pakistan Energy Sector 17

Earnings visibility to improve after circular debt resolution Oil-based power generation, growing industrialisation, increasing rural electrification and a fast-emerging middle class led a 4.3% CAGR in POL consumption in the previous five years. PSO, with its superiority in infrastructure, dominant market share and a some help from rising oil prices, has emerged as the prime beneficiary of this volume-driven growth, recording normalised earnings CAGR of 38%. However, because of issues such as circular debt and imposition of turnover tax, the market has not appreciated this growth. With volumes and margins expected to hold up around current levels and resolution of circular debt and turnover tax expected in FY11, earnings and payouts are likely to rebound to PRs65 and 70% by FY12

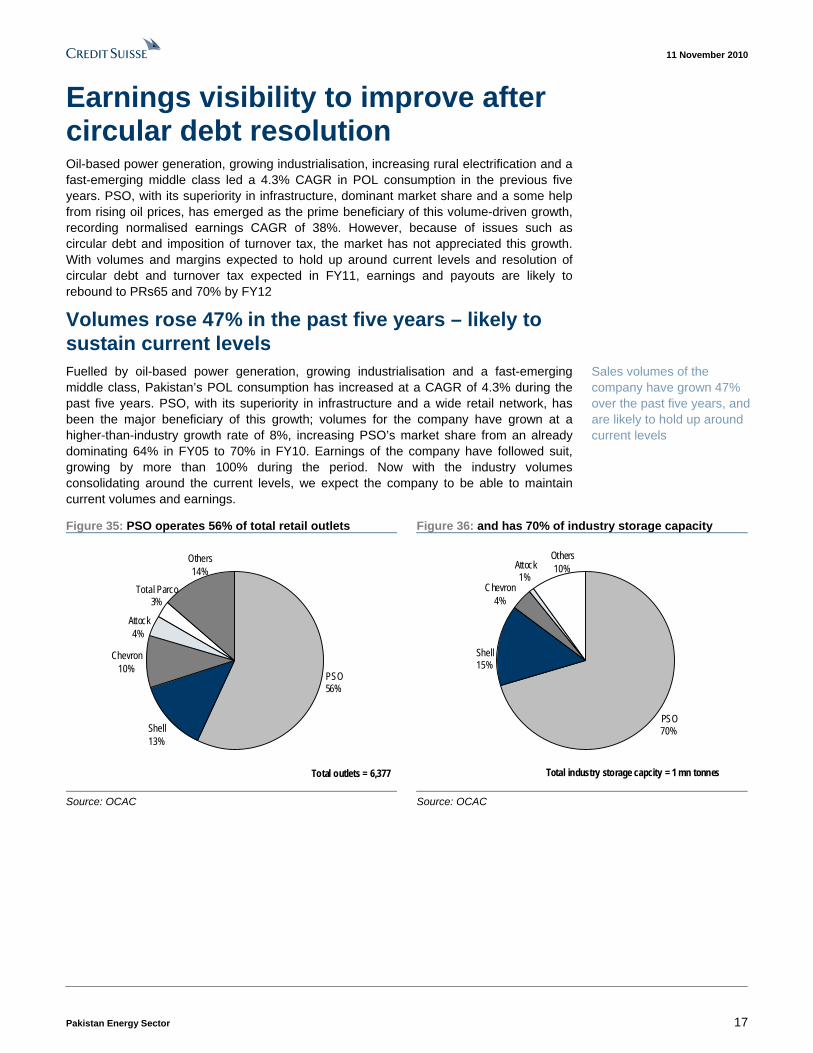

Volumes rose 47% in the past five years – likely to sustain current levels Fuelled by oil-based power generation, growing industrialisation and a fast-emerging middle class, Pakistan’s POL consumption has increased at a CAGR of 4.3% during the past five years. PSO, with its superiority in infrastructure and a wide retail network, has been the major beneficiary of this growth; volumes for the company have grown at a higher-than-industry growth rate of 8%, increasing PSO’s market share from an already dominating 64% in FY05 to 70% in FY10. Earnings of the company have followed suit, growing by more than 100% during the period. Now with the industry volumes consolidating around the current levels, we expect the company to be able to maintain current volumes and earnings.

Figure 35: PSO operates 56% of total retail outlets Figure 36: and has 70% of industry storage capacity

PSO56%

Shell13%

Chevron10%

Others14%

Total Parco3%

Attock4%

Total outlets = 6,377

PSO70%

Attock1%

Others10%

Chevron4%

Shell15%

Total industry storage capcity = 1 mn tonnes

Source: OCAC Source: OCAC

Sales volumes of the company have grown 47% over the past five years, and are likely to hold up around current levels

11 November 2010

Pakistan Energy Sector 18

Figure 37: PSO handles 70% of total industry volumes… Figure 38: …and sells 85-88% of total furnace oil

-

5

10

15

20

25

FY08 FY09 FY10 FY11E FY12E FY13E

Industry PSO

mn tonnes

-

2

4

6

8

10

12

FY08 FY09 FY10 FY11E FY12E FY13E

Industry PSO

mn tonnes

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

High oil prices have increased absolute margins; expect reduced policy overhang Owing to the rising oil prices, PSO’s absolute per tonne gross margins have increased at 21% CAGR over the past three years – from PRs1,042/t in FY07 to PRs1,828/t in FY10. This is despite the fact that the government has routinely intervened to keep the margins of regulated products in check. However, going forward, further negative intervention by the government is unlikely, as: (i) the government in its last policy change has fixed OMC margins in rupee terms for all regulated products and (ii) current margins as a percentage of ex refinery price are at, or near, their lowest levels.

In our model, we have assumed a 7% cut in PSO’s gross margin over FY11 due to increased competition in the de-regulated product segment and recent policy change for the regulated product segment. But we believe that the current margins in the regulated product segments are unsustainable and will be revised upwards in the due course of time. Hence, we model that margins will grow at rupee depreciation rate after FY12.

Figure 39: Per tonne gross margin for PSO is at its peak Figure 40: Regulated product margins are at/near bottom

-200400600800

1,0001,2001,4001,6001,8002,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

Gross margin per tonne

0%

1%

2%

3%

4%

5%

6%

7%

8%

3QFY06 2QFY07 1QFY08 4QFY08 3QFY09 2QFY10 1QFY11

Mogas HOBC HSD

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Rising oil prices have increased the company’s gross margins by 75% over the past three years

We expect 7% decline in margins in FY11 due to increased competition and revision in regulated product margins

11 November 2010

Pakistan Energy Sector 19

Core earnings have increased 1.5 times, but remain underappreciated due to low payouts The massive growth in volumes and margins has had a multiplier effect on earnings, which, as a result, has increased 1.5x over the past three years to PRs72/share (FY10 normalised earnings). But this growth has been underappreciated by the market due to issues of circular debt and imposition of 1% turnover tax, which have resulted in declining payouts.

Figure 41: Normalised EPS has doubled in past three years…

Figure 42: …but payouts have declined due to circular debt

-

10

20

30

40

50

60

70

80

FY04 FY05 FY06 FY07 FY08 FY09 FY10

Normalised EPS Dividends

PRs/share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

FY04 FY05 FY06 FY07 FY08 FY09 FY10

Source: Company data Source: Company data

Circular debt is basically inter-company debt within the Pakistan energy sector, which has accrued as a result of electricity tariffs being kept below cost recovery levels. This in turn has resulted in a cash draught in energy sector due to non payment of subsidies by the government. Turnover tax on the other hand is the minimum tax that any company has to pay. For PSO, this means an effective tax rate in the range of 45-50%.

Figure 43: Work capital investments have increased due to circular debt

Figure 44: Resolution of turnover tax will decrease effective tax rate

-20

-15

-10

-5

0

5

10

15

20

25

30

4qFy

06

2qFy

07

4qFy

07

2qFy

08

4qFy

08

2qFy

09

4qFy

09

2qFy

10

4qFy

10

PRs bn+ve value shows investmentinto working capital

0%

10%

20%

30%

40%

50%

60%

FY11E FY12E FY13E FY14E FY15E

Effective tax rate Effective tax rate if 1% turnover tax is applied

Source: Company data Source: Company data, Credit Suisse estimates

Due to volume and margin increase, core earnings have increased 1.5 times

11 November 2010

Pakistan Energy Sector 20

Turnover tax near resolution, circular debt resolution is next; payouts should increase Although a formal notification is awaited, press reports suggest that the government has already approved the reduction in turnover tax to 0.5% for all companies having sales greater than PRs1 bn. We believe this measure will improve earnings visibility of the company in the near term and will also reduce the policy overhang and uncertainty over company’s rock-solid earning profile. Additionally, a likely reversal of PRs16/share in tax expense will further increase FY11 earnings.

Now the only looming issue hindering company’s stock price growth is circular debt. But, as discussed earlier, circular debt will be less of a concern after FY11 because: (i) the government is determined to eliminate electricity subsidies and has already committed to the IMF to carry out reforms in the electricity sector, (ii) current tariffs cover 75% of generation costs versus 67% in FY10, and (iii) by FY11, electricity tariffs are expected to increase by another 17% and cover 92% of electricity generation costs.

We believe that with resolution of both these issues, earnings visibility of PSO’s should improve. Also higher cash flows as a result of circular debt resolution will allow company to resume routine operations and revert to historical payout ratios.

Assuming coverage with an OUTPERFORM We assume coverage of Pakistan State Oil with a revised target price of PRs381.

With resumption of normal payouts the biggest catalyst for the company’s stock price, we shift our valuation methodology and value PSO at a target dividend yield of 8.5%.

Figure 45: PSO valuation matrix Target P/E at Div yield at EV/EBITDA at EPS DPS Target price (TP) target price target price target price FY11 FY12 FY11 FY12 D/Y Dec-11 FY11 FY12 FY11 FY12 FY11 FY12PSO 54 66 19 46 8.5 381 7.07 5.81 4.95 12.05 4.14 3.39

Source: Credit Suisse estimates

The company is currently trading at 24% discount to market P/E of 7x. Furthermore, the stock price of the company has also lagged the market in recent times due to issues of circular debt and turnover tax, and at current price offers 34% return to our target price.

Figure 46: Change from previous estimates New estimates Previous estimates Rating TP EPS FY11E EPS FY12E Rating TP EPS FY11E EPS FY12EPSO O 381 53.9 65.6 O 390 60.5 69.5

Source: Credit Suisse estimates

Press reports indicate that the government has approved the reduction in turnover tax for large-size companies

We expect circular debt resolution in FY11; this will increase earnings visibility, which was lacking in previous years

We value PSO with a target dividend yield of 8.54%, with target price of PRs 407

11 November 2010

Pakistan Energy Sector 21

Risks Adverse oil price movements can lower company margins

As prices of petroleum products move broadly in line with oil prices, adverse oil price movements can cause product prices to decrease, which can decrease company margins on de-regulated products. Likewise, lower oil prices may even prompt the government to lower margins on regulated products.

Furthermore, adverse oil price movements can also result in inventory losses for the company.

Rapid rupee depreciation

Since the company normally gets 14 days of credit period from international suppliers, a rapid rupee depreciation can result in high exchange losses for the company.

Circular debt may not get resolved

The company has been among the worst affected entities because of circular debt. Hence if the resolution of circular debt prolongs, company’s earnings and payouts will continue to suffer until circular debt gets resolved.

Government may not exempt OMCs from turnover tax

Under the current tax regime, PSO is liable to pay taxes at a rate of 1% of its net revenues. If the company does not get an exemption from this regime, effective tax rate for the company will increase to 45-50% from the current 35%.

Regulatory risk

Prices and OMC margins for certain petroleum products are notified by the government. Hence, there is a risk that the government, in order to meet its political and social objectives, may revise margins of regulated products in a way which is detrimental to the company.

Political risks

The government of Pakistan is the majority owner of PSO. Hence, as a majority shareholder, the government may pursue some of its macroeconomic and social activities through the company. As a result, the company can engage in certain activities which may not be based purely on commercial considerations.

11 November 2010

Pakistan Energy Sector 22

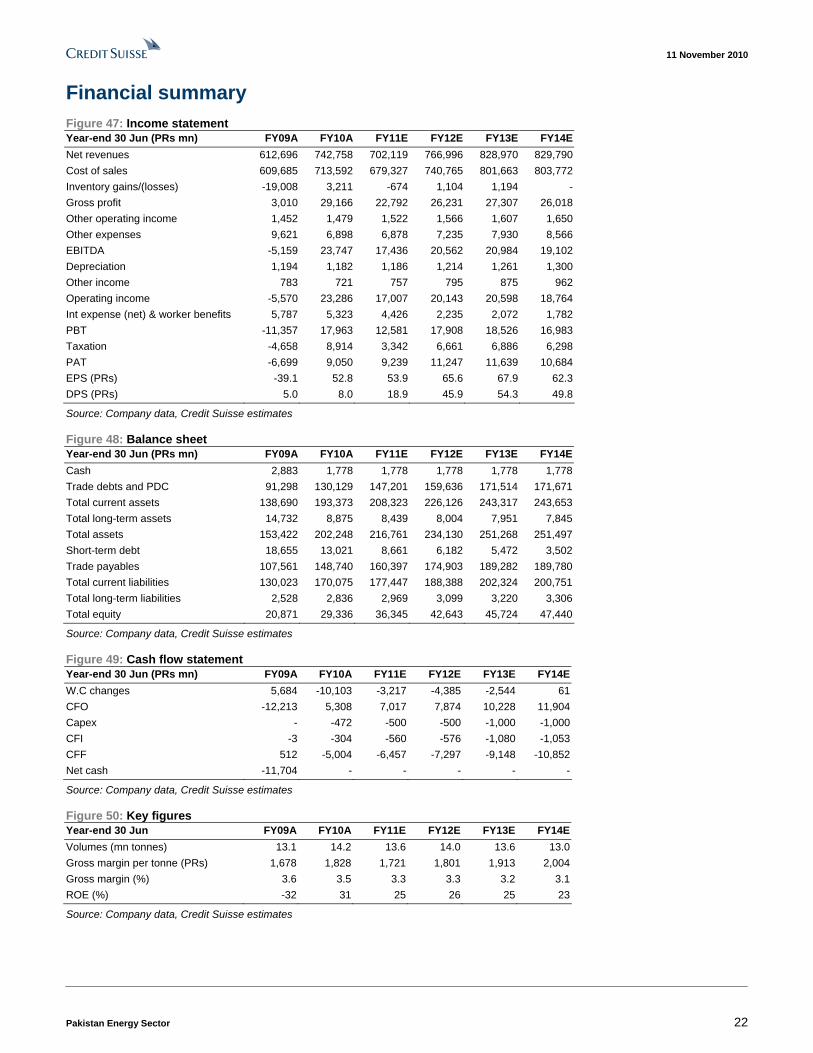

Financial summary Figure 47: Income statement Year-end 30 Jun (PRs mn) FY09A FY10A FY11E FY12E FY13E FY14E Net revenues 612,696 742,758 702,119 766,996 828,970 829,790 Cost of sales 609,685 713,592 679,327 740,765 801,663 803,772 Inventory gains/(losses) -19,008 3,211 -674 1,104 1,194 - Gross profit 3,010 29,166 22,792 26,231 27,307 26,018 Other operating income 1,452 1,479 1,522 1,566 1,607 1,650 Other expenses 9,621 6,898 6,878 7,235 7,930 8,566 EBITDA -5,159 23,747 17,436 20,562 20,984 19,102 Depreciation 1,194 1,182 1,186 1,214 1,261 1,300 Other income 783 721 757 795 875 962 Operating income -5,570 23,286 17,007 20,143 20,598 18,764 Int expense (net) & worker benefits 5,787 5,323 4,426 2,235 2,072 1,782 PBT -11,357 17,963 12,581 17,908 18,526 16,983 Taxation -4,658 8,914 3,342 6,661 6,886 6,298 PAT -6,699 9,050 9,239 11,247 11,639 10,684 EPS (PRs) -39.1 52.8 53.9 65.6 67.9 62.3 DPS (PRs) 5.0 8.0 18.9 45.9 54.3 49.8

Source: Company data, Credit Suisse estimates

Figure 48: Balance sheet Year-end 30 Jun (PRs mn) FY09A FY10A FY11E FY12E FY13E FY14E Cash 2,883 1,778 1,778 1,778 1,778 1,778 Trade debts and PDC 91,298 130,129 147,201 159,636 171,514 171,671 Total current assets 138,690 193,373 208,323 226,126 243,317 243,653 Total long-term assets 14,732 8,875 8,439 8,004 7,951 7,845 Total assets 153,422 202,248 216,761 234,130 251,268 251,497 Short-term debt 18,655 13,021 8,661 6,182 5,472 3,502 Trade payables 107,561 148,740 160,397 174,903 189,282 189,780 Total current liabilities 130,023 170,075 177,447 188,388 202,324 200,751 Total long-term liabilities 2,528 2,836 2,969 3,099 3,220 3,306 Total equity 20,871 29,336 36,345 42,643 45,724 47,440

Source: Company data, Credit Suisse estimates

Figure 49: Cash flow statement Year-end 30 Jun (PRs mn) FY09A FY10A FY11E FY12E FY13E FY14EW.C changes 5,684 -10,103 -3,217 -4,385 -2,544 61CFO -12,213 5,308 7,017 7,874 10,228 11,904Capex - -472 -500 -500 -1,000 -1,000CFI -3 -304 -560 -576 -1,080 -1,053CFF 512 -5,004 -6,457 -7,297 -9,148 -10,852Net cash -11,704 - - - - -

Source: Company data, Credit Suisse estimates

Figure 50: Key figures Year-end 30 Jun FY09A FY10A FY11E FY12E FY13E FY14EVolumes (mn tonnes) 13.1 14.2 13.6 14.0 13.6 13.0Gross margin per tonne (PRs) 1,678 1,828 1,721 1,801 1,913 2,004Gross margin (%) 3.6 3.5 3.3 3.3 3.2 3.1ROE (%) -32 31 25 26 25 23

Source: Company data, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 23

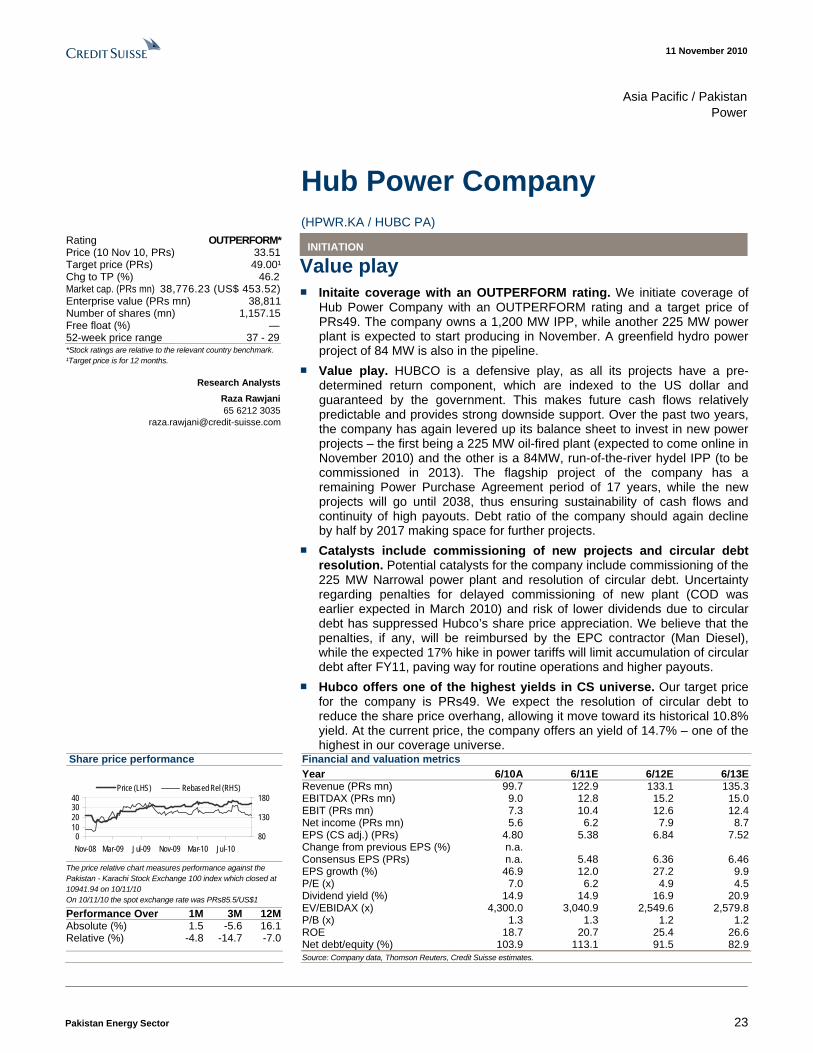

Asia Pacific / PakistanPower

Hub Power Company (HPWR.KA / HUBC PA)

INITIATION

Value play ■ Initaite coverage with an OUTPERFORM rating. We initiate coverage of

Hub Power Company with an OUTPERFORM rating and a target price of PRs49. The company owns a 1,200 MW IPP, while another 225 MW power plant is expected to start producing in November. A greenfield hydro power project of 84 MW is also in the pipeline.

■ Value play. HUBCO is a defensive play, as all its projects have a pre-determined return component, which are indexed to the US dollar and guaranteed by the government. This makes future cash flows relatively predictable and provides strong downside support. Over the past two years, the company has again levered up its balance sheet to invest in new power projects – the first being a 225 MW oil-fired plant (expected to come online in November 2010) and the other is a 84MW, run-of-the-river hydel IPP (to be commissioned in 2013). The flagship project of the company has a remaining Power Purchase Agreement period of 17 years, while the new projects will go until 2038, thus ensuring sustainability of cash flows and continuity of high payouts. Debt ratio of the company should again decline by half by 2017 making space for further projects.

■ Catalysts include commissioning of new projects and circular debt resolution. Potential catalysts for the company include commissioning of the 225 MW Narrowal power plant and resolution of circular debt. Uncertainty regarding penalties for delayed commissioning of new plant (COD was earlier expected in March 2010) and risk of lower dividends due to circular debt has suppressed Hubco’s share price appreciation. We believe that the penalties, if any, will be reimbursed by the EPC contractor (Man Diesel), while the expected 17% hike in power tariffs will limit accumulation of circular debt after FY11, paving way for routine operations and higher payouts.

■ Hubco offers one of the highest yields in CS universe. Our target price for the company is PRs49. We expect the resolution of circular debt to reduce the share price overhang, allowing it move toward its historical 10.8% yield. At the current price, the company offers an yield of 14.7% – one of the highest in our coverage universe.

Share price performance

010203040

Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-1080

130

180Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the Pakistan - Karachi Stock Exchange 100 index which closed at 10941.94 on 10/11/10 On 10/11/10 the spot exchange rate was PRs85.5/US$1

Performance Over 1M 3M 12M Absolute (%) 1.5 -5.6 16.1 Relative (%) -4.8 -14.7 -7.0

Financial and valuation metrics

Year 6/10A 6/11E 6/12E 6/13ERevenue (PRs mn) 99.7 122.9 133.1 135.3EBITDAX (PRs mn) 9.0 12.8 15.2 15.0EBIT (PRs mn) 7.3 10.4 12.6 12.4Net income (PRs mn) 5.6 6.2 7.9 8.7EPS (CS adj.) (PRs) 4.80 5.38 6.84 7.52Change from previous EPS (%) n.a. Consensus EPS (PRs) n.a. 5.48 6.36 6.46EPS growth (%) 46.9 12.0 27.2 9.9P/E (x) 7.0 6.2 4.9 4.5Dividend yield (%) 14.9 14.9 16.9 20.9EV/EBIDAX (x) 4,300.0 3,040.9 2,549.6 2,579.8P/B (x) 1.3 1.3 1.2 1.2ROE 18.7 20.7 25.4 26.6Net debt/equity (%) 103.9 113.1 91.5 82.9

Source: Company data, Thomson Reuters, Credit Suisse estimates.

*Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months.

Research Analysts Raza Rawjani 65 6212 3035

Rating OUTPERFORM* Price (10 Nov 10, PRs) 33.51 Target price (PRs) 49.00¹ Chg to TP (%) 46.2 Market cap. (PRs mn) 38,776.23 (US$ 453.52) Enterprise value (PRs mn) 38,811 Number of shares (mn) 1,157.15 Free float (%) — 52-week price range 37 - 29

11 November 2010

Pakistan Energy Sector 24

Value play HUBCO is a defensive play, as all its projects have a pre-determined return component, which are indexed to the US dollar and guaranteed by the government. This makes future cash flows relatively predictable and provides strong downside support. Over the past two years, the company has again levered up its balance sheet to invest in new power projects – the first being a 225 MW oil-fired plant (expected to come online in November 2010) and the other is a 84MW, run-of-the-river hydel IPP (to be commissioned in 2013). The flagship project of the company (a 1,200 MW oil-fired power plant) has a remaining Power Purchase Agreement period of 17 years, while the new projects will go until 2038, thus ensuring sustainability of cash flows and continuity of high payouts. Debt ratio of the company should again decline by half by 2017 making space for future projects.

Predictable cash flows limit downside Like all IPPs in Pakistan, Hub Power Company has a predetermined return component for all its power projects; this makes cash flows predictable and provides downside support. The payments made to the company under this structure are: (1) independent of capacity utilisation, (2) defined in US dollars (3) indexed to the US CPI (only for company’s flagship 1,200 MW power project), and (4) are guaranteed by the government. Almost all other costs incurred by the company, including fuel costs and O&M costs are passed through. Even the debt assumed by company for financing power projects is passed through.

Figure 51: Annual projected return per share for Hub Power Company IPPs

-

2

4

6

8

10

12

14

16

18

20

FY 20

11

FY 20

13

FY 20

15

FY 20

17

FY 20

19

FY 20

21

FY 2

023

FY 20

25

FY 20

27

FY 20

29

FY 20

31

FY 20

33

FY 2

035

FY 20

37

PRs/share

Hubco 1,200 MW plantPayments indexed to US CPI & US$Project ends 2027

Hubco 214 MW Narrowl plantPayments indexed to US$Project ends 2035

Hubco 84 MW Hydro IPPPayments indexed to US$Project ends 2038

Source: PPIB, Credit Suisse estimates

New projects to contribute to dividends from 2014 We expect the contributions from the new projects (Narrowal and Laraib) to start reflecting in dividends from FY14.

Hubco Narrowal Project

The Narrowal project is expected to achieve commercial operations date (COD) in November 2010. However, we do not see the project to contribute toward final dividends until FY14, as the ROE component of the tariff structure will first be used to make the interest and principal repayments (25% equity component of the project has been raised as debt on company’s balance sheet). Hence, dividend contributions from the Narrowal project will be back-loaded.

Hubco has predetermined return component, which is indexed to USD and guaranteed by the government. Thus, cash flows are easier to predict

The company has levered its balance sheet to invest into new projects. We expect contribution from new projects to start from FY14

11 November 2010

Pakistan Energy Sector 25

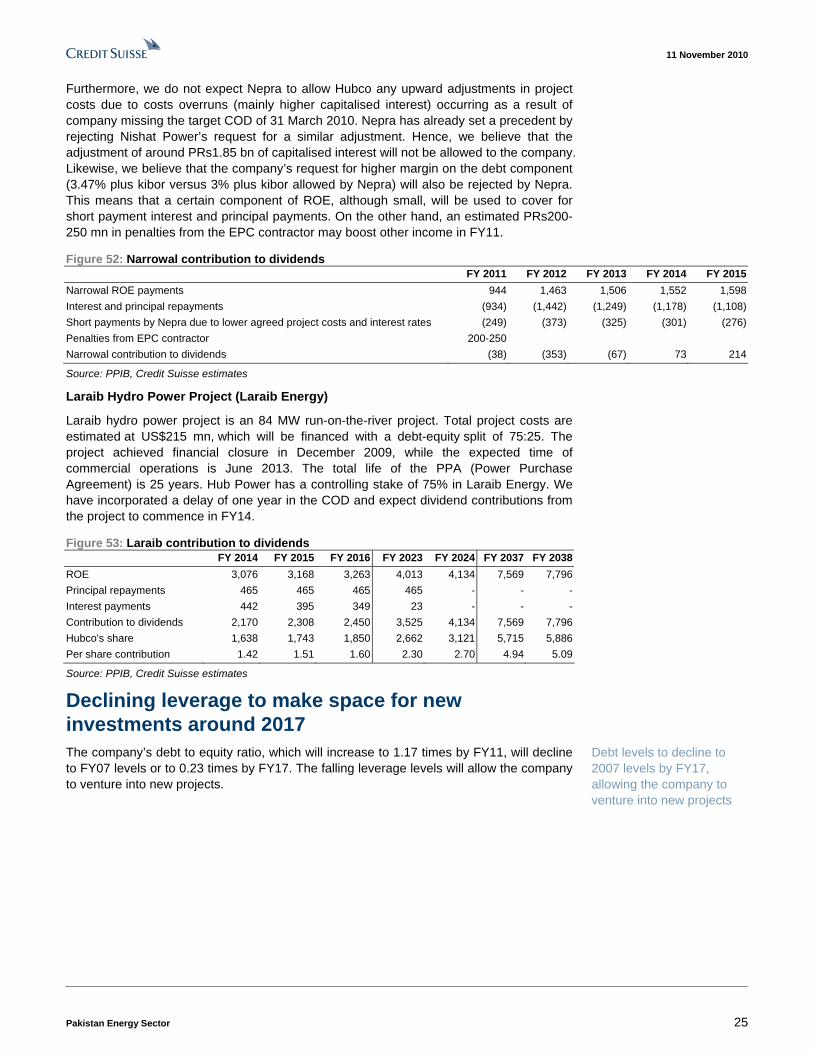

Furthermore, we do not expect Nepra to allow Hubco any upward adjustments in project costs due to costs overruns (mainly higher capitalised interest) occurring as a result of company missing the target COD of 31 March 2010. Nepra has already set a precedent by rejecting Nishat Power’s request for a similar adjustment. Hence, we believe that the adjustment of around PRs1.85 bn of capitalised interest will not be allowed to the company. Likewise, we believe that the company’s request for higher margin on the debt component (3.47% plus kibor versus 3% plus kibor allowed by Nepra) will also be rejected by Nepra. This means that a certain component of ROE, although small, will be used to cover for short payment interest and principal payments. On the other hand, an estimated PRs200-250 mn in penalties from the EPC contractor may boost other income in FY11.

Figure 52: Narrowal contribution to dividends FY 2011 FY 2012 FY 2013 FY 2014 FY 2015Narrowal ROE payments 944 1,463 1,506 1,552 1,598Interest and principal repayments (934) (1,442) (1,249) (1,178) (1,108)Short payments by Nepra due to lower agreed project costs and interest rates (249) (373) (325) (301) (276)Penalties from EPC contractor 200-250 Narrowal contribution to dividends (38) (353) (67) 73 214

Source: PPIB, Credit Suisse estimates

Laraib Hydro Power Project (Laraib Energy)

Laraib hydro power project is an 84 MW run-on-the-river project. Total project costs are estimated at US$215 mn, which will be financed with a debt-equity split of 75:25. The project achieved financial closure in December 2009, while the expected time of commercial operations is June 2013. The total life of the PPA (Power Purchase Agreement) is 25 years. Hub Power has a controlling stake of 75% in Laraib Energy. We have incorporated a delay of one year in the COD and expect dividend contributions from the project to commence in FY14.

Figure 53: Laraib contribution to dividends FY 2014 FY 2015 FY 2016 FY 2023 FY 2024 FY 2037 FY 2038 ROE 3,076 3,168 3,263 4,013 4,134 7,569 7,796 Principal repayments 465 465 465 465 - - - Interest payments 442 395 349 23 - - - Contribution to dividends 2,170 2,308 2,450 3,525 4,134 7,569 7,796 Hubco's share 1,638 1,743 1,850 2,662 3,121 5,715 5,886 Per share contribution 1.42 1.51 1.60 2.30 2.70 4.94 5.09

Source: PPIB, Credit Suisse estimates

Declining leverage to make space for new investments around 2017 The company’s debt to equity ratio, which will increase to 1.17 times by FY11, will decline to FY07 levels or to 0.23 times by FY17. The falling leverage levels will allow the company to venture into new projects.

Debt levels to decline to 2007 levels by FY17, allowing the company to venture into new projects

11 November 2010

Pakistan Energy Sector 26

Figure 54: Declining leverage will make space for new projects in FY17-18

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000FY

99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Debt D/E (RHS)

New Projects

PRs mn (x)

Source: Credit Suisse estimates

Dividends have held up despite circular debt The company has been able to manage its mounting circular debt receivables by withholding payments of its fuel supplier (PSO.KA) and through higher short-term borrowings (Figure 57). Consequently, dividends have not suffered as they have in the case of upstream companies. Furthermore, a rising tariff structure has also supported dividend payouts.

Figure 55: Dividends have held up Figure 56: Increased debt and payable days have financed circular debt

-

1

2

3

4

5

6

7

8

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FCF/share DPS

PRs/share

(8,000)

(3,000)

2,000

7,000

12,000

17,000

22,000

27,000

FY08 FY09 FY10

Chng in payables Chng in ST debt Chng in receivables

PRs mn

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Initiate coverage with an OUTPERFORM We initiate coverage of Hub Power Company with a target price of PRs49 and an OUTPERFORM rating. The company is currently trading at a FY11 dividend yield of 14.9%.

We value Hubco at PRs49 with a target dividend yield of 10.8%. Our target dividend yield of 10.8% is the average of forward dividend yields from July 2002 to June 2008, which we believe was the normal trading period for the stock. We exclude the period before July

Hubco has financed delayed payments from government by delaying payments to fuel suppliers and by assuming short-term debt. Hence, dividends have not suffered

We value Hubco with a target dividend yield of 10.8%, with target price of PRs49

11 November 2010

Pakistan Energy Sector 27

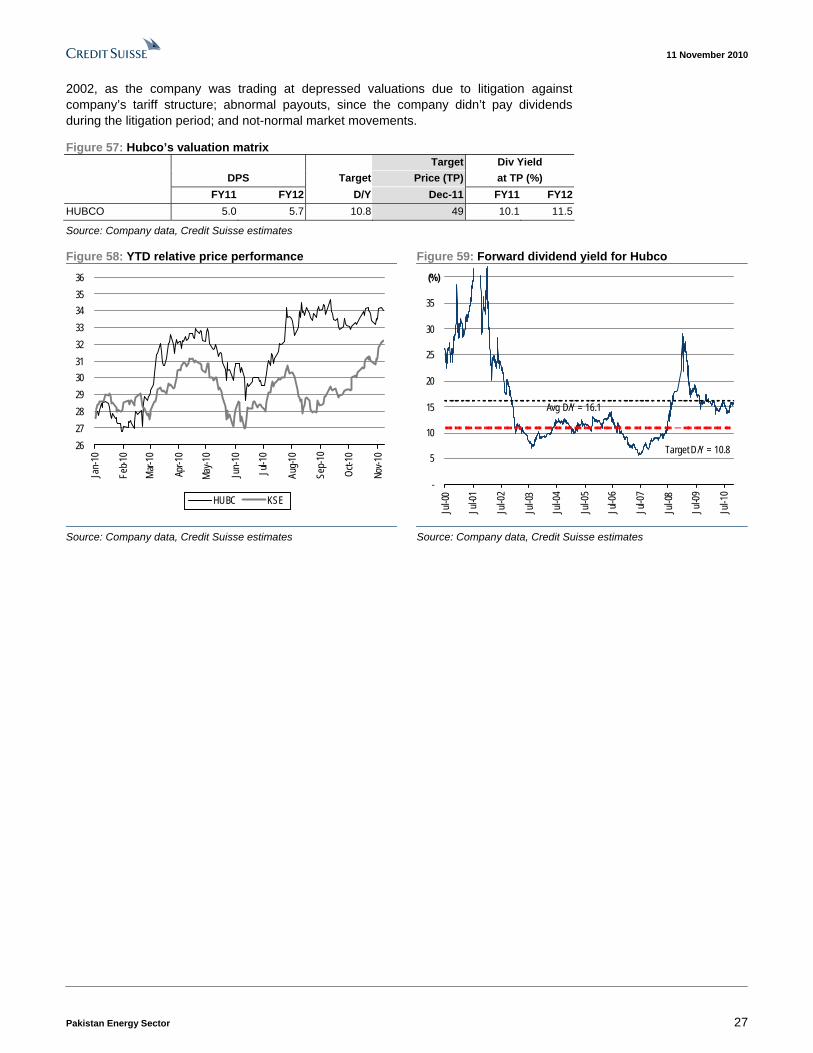

2002, as the company was trading at depressed valuations due to litigation against company’s tariff structure; abnormal payouts, since the company didn’t pay dividends during the litigation period; and not-normal market movements.

Figure 57: Hubco’s valuation matrix Target Div Yield DPS Target Price (TP) at TP (%) FY11 FY12 D/Y Dec-11 FY11 FY12 HUBCO 5.0 5.7 10.8 49 10.1 11.5

Source: Company data, Credit Suisse estimates

Figure 58: YTD relative price performance Figure 59: Forward dividend yield for Hubco

2627282930313233343536

Jan-

10

Feb-1

0

Mar-

10

Apr-1

0

May-1

0

Jun-

10

Jul-1

0

Aug-1

0

Sep-

10

Oct-1

0

Nov-1

0

HUBC KSE

-

5

10

15

20

25

30

35

40

Jul-0

0

Jul-0

1

Jul-0

2

Jul-0

3

Jul-0

4

Jul-0

5

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

(%)

Avg D/Y = 16.1

Target D/Y = 10.8

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 28

Risks Revision in power purchase agreement

The government may unilaterally revise the power purchase agreement in a way which can hurt future earnings. Possible amendments can be lower tariffs or removal of USD indexation.

Imposition of income tax

Company’s earnings are currently exempt from paying income tax. However, the government may force the company to pay income tax in the future.

Delay in new projects

There is a possibility that the new projects the company is working on may not materialise in time. As a result, the company may have to pay certain penalties to PPIB.

No growth beyond current projects

The company’s flagship project has a remaining project life of 17 years, while the new projects of the company will go until 2038. Beyond this, the company has not announced any projects.

Circular debt may not get resolved

Circular debt has affected the company’s operations and payout capacity to a certain extent. Hence, a delay in the circular debt resolution can result in lower payouts.

11 November 2010

Pakistan Energy Sector 29

Financial summary Figure 60: Income statement Year-end 30 Jun (PRs mn) FY 2009 FY 2010 FY 2011E FY 2012E FY 2013E PRs/USD 78 84 89 93 95 Revenue 82,784 99,694 122,898 133,140 135,337 Op. costs 74,995 90,309 109,643 117,340 119,668 Gross profit 7,789 9,385 13,255 15,800 15,669 EBITDA 7,446 9,018 12,751 15,209 15,031 Depreciation 1,709 1,721 2,339 2,651 2,658 EBIT 5,737 7,296 10,412 12,558 12,373 Financial charges 2,095 1,794 4,279 4,731 3,746 PAT 3,781 5,556 6,223 7,916 8,697 EPS (PRs) 3.27 4.80 5.38 6.84 7.52 Adj. EPS (PRs) 2.42 3.95 3.54 4.02 4.69 DPS (PRs) 3.3 5.0 5.0 5.7 7.0

Source: Company data, Credit Suisse estimates

Figure 61: Balance sheet Year-end 30 Jun (PRs mn) FY 2009 FY 2010 FY 2011E FY 2012E FY 2013ECash 1,034 809 1,000 1,000 1,000 Trade debts 46,629 66,712 84,322 74,109 62,890 Other current assets 3,964 2,937 4,446 4,627 4,735 Fixed assets 38,559 52,237 51,643 50,044 48,060 Total assets 90,186 122,696 141,411 129,780 116,685 Trade payable 41,992 55,606 67,075 57,567 47,719 Short-term debt 3,582 6,744 8,217 6,513 8,162 Long-term debt 12,320 25,100 27,059 23,793 20,527 Other liabilities 2,759 5,364 8,746 9,860 6,865 Equity 29,532 29,881 30,314 32,046 33,413

Source: Company data, Credit Suisse estimates

Figure 62: Cash flow statement Year-end 30 Jun (PRs mn) FY 2009 FY 2010 FY 2011E FY 2012E FY 2013E EBITDA 7,446 9,018 12,751 15,209 15,031 Working capital changes 7,516 (5,181) (8,053) (3,052) (5,479) CFO 14,963 3,837 4,699 12,157 9,552 Capex (5,668) (13,453) (1,032) (126) (130) CFI (6,181) (14,817) (2,150) (1,004) (604) Change in LT debt 4,049 12,780 1,959 (3,266) (3,266) Change in ST debt (9,745) 3,161 1,474 (1,704) 1,649 Dividends (2,716) (5,194) (5,791) (6,184) (7,330) CFF (8,412) 10,748 (2,358) (11,154) (8,948) Net cash 370 (231) 191 - -

Source: Company data, Credit Suisse estimates

Figure 63: Ratio analysis Ratios (%) FY 2009 FY 2010 FY 2011E FY 2012E FY 2013EGross margin 9 9 11 12 12EBITDA margin 9 9 10 11 11Net margin 5 6 5 6 6Debt to equity (x) 0.54 1.07 1.16 0.95 0.86 Debt to assets (x) 0.18 0.26 0.25 0.23 0.25

Source: Company data, Credit Suisse estimates

11 November 2010

Pakistan Energy Sector 30

Asia Pacific / PakistanOil & Gas Exploration & Production

Oil & Gas Development Company (OGDC.KA / OGDC PA)

ASSUMING COVERAGE

Belated volume resurgence ■ Assume coverage with an OUTPERFORM rating. We are assuming

coverage of OGDC with a revised target price of 173 and an OUTPERFORM rating.

■ Production growth finally materialising. Oil and Gas Development Co. (OGDC) is all set for a volume renaissance during FY11-14E, whereby total production of the company will increase 49%, underpinning a similar increase in earnings. The growth will be driven by the homecoming of the long-awaited development projects in Qadirpur, Uch, Sinjhoro and Kunar Pasakhi deep fields. Once online, these projects will add incremental 32 mn boe to total production. The growth story is further augmented by the surge in production from Mela, Nashpa and Tal fields. Full production potential of these discoveries is expected in FY11-15E – when total production from these fields should nearly double to 9 mn boe in FY15 from 5 mn boe in FY10.

■ Catalysts. Resolution of circular debt, commencement of production from development projects and improvement of security situation in potential exploration areas are key catalyst for the company..