Embed Size (px)

Citation preview

TABLE OF CONTENTS

PAGE

TOP STRATEGIES FOR ENERGY INTELLIGENCE

lnsresearch.com

CONNECT:

TOP STRATEGIES FOR ENERGY INTELLIGENCE

lnsresearch.com

TABLE OF CONTENTS

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Section 1: Mega-Trends Drive the Need for Energy Intelligence . . . . . . . . . . . . . . 5

Section 2: Individual Company Responses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Section 3: Market Drivers for Energy Management . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Section 4: Challenges with Energy Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Section 5: Strategies for a Successful Energy Intelligence Solution . . . . . . . . . . 22

Section 6: Actionable Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Executive Summary

4

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

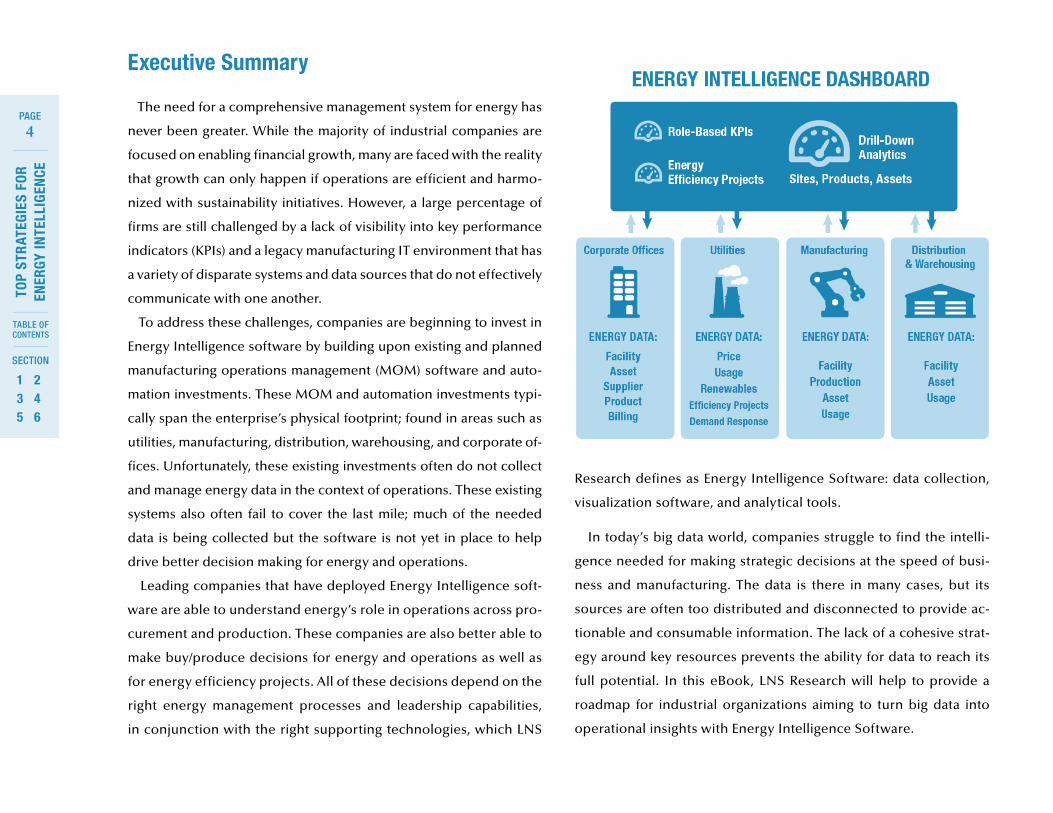

The need for a comprehensive management system for energy has

never been greater. While the majority of industrial companies are

focused on enabling financial growth, many are faced with the reality

that growth can only happen if operations are efficient and harmo-

nized with sustainability initiatives. However, a large percentage of

firms are still challenged by a lack of visibility into key performance

indicators (KPIs) and a legacy manufacturing IT environment that has

a variety of disparate systems and data sources that do not effectively

communicate with one another.

To address these challenges, companies are beginning to invest in

Energy Intelligence software by building upon existing and planned

manufacturing operations management (MOM) software and auto-

mation investments. These MOM and automation investments typi-

cally span the enterprise’s physical footprint; found in areas such as

utilities, manufacturing, distribution, warehousing, and corporate of-

fices. Unfortunately, these existing investments often do not collect

and manage energy data in the context of operations. These existing

systems also often fail to cover the last mile; much of the needed

data is being collected but the software is not yet in place to help

drive better decision making for energy and operations.

Leading companies that have deployed Energy Intelligence soft-

ware are able to understand energy’s role in operations across pro-

curement and production. These companies are also better able to

make buy/produce decisions for energy and operations as well as

for energy efficiency projects. All of these decisions depend on the

right energy management processes and leadership capabilities,

in conjunction with the right supporting technologies, which LNS

Research defines as Energy Intelligence Software: data collection,

visualization software, and analytical tools.

In today’s big data world, companies struggle to find the intelli-

gence needed for making strategic decisions at the speed of busi-

ness and manufacturing. The data is there in many cases, but its

sources are often too distributed and disconnected to provide ac-

tionable and consumable information. The lack of a cohesive strat-

egy around key resources prevents the ability for data to reach its

full potential. In this eBook, LNS Research will help to provide a

roadmap for industrial organizations aiming to turn big data into

operational insights with Energy Intelligence Software.

Executive Summary

SECTION 1

Mega-Trends Drive the Need for Energy Intelligence

6

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

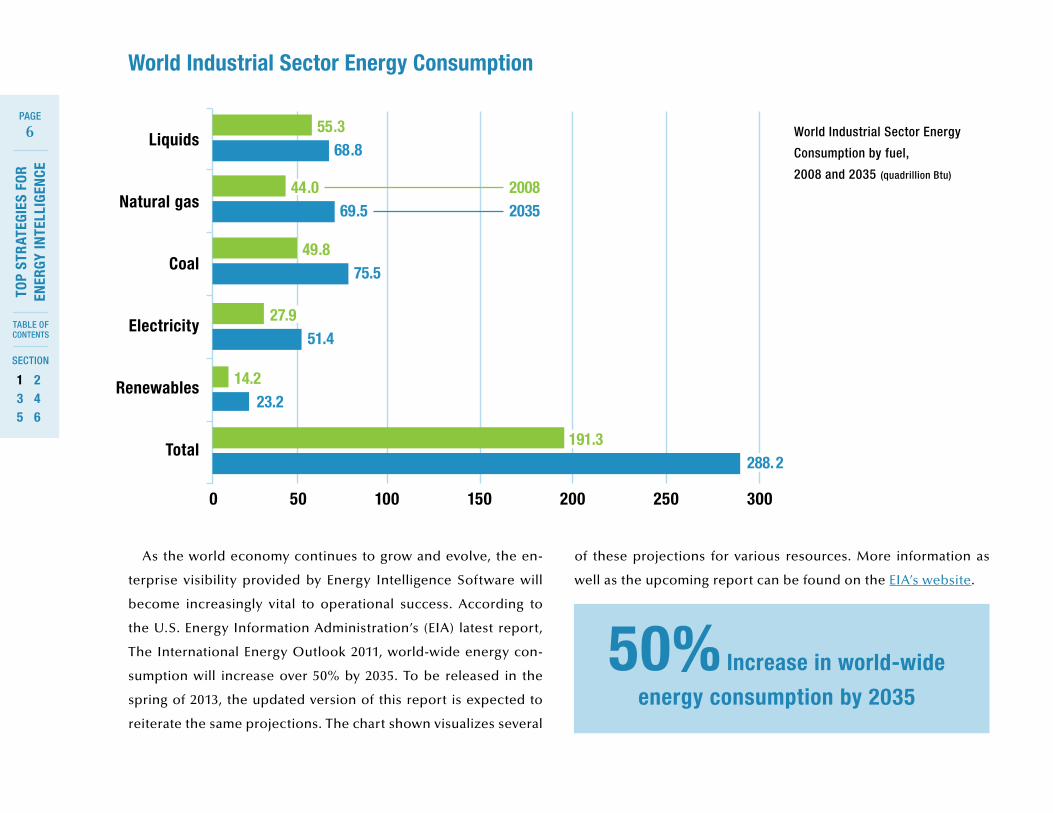

World Industrial Sector Energy Consumption

As the world economy continues to grow and evolve, the en-

terprise visibility provided by Energy Intelligence Software will

become increasingly vital to operational success. According to

the U.S. Energy Information Administration’s (EIA) latest report,

The International Energy Outlook 2011, world-wide energy con-

sumption will increase over 50% by 2035. To be released in the

spring of 2013, the updated version of this report is expected to

reiterate the same projections. The chart shown visualizes several

of these projections for various resources. More information as

well as the upcoming report can be found on the EIA’s website.

50% Increase in world-wide

energy consumption by 2035

Liquids

Natural gas

Coal

Electricity

Renewables

Total

0 50 100 150 200 250 300

55.368.8

44.0 200869.5 2035

49.875.5

27.951.4

14.223.2

191.3288. 2

World Industrial Sector Energy

Consumption by fuel,

2008 and 2035 (quadrillion Btu)

7

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

ExxonMobil’s The Outlook for Energy: A view to 2040 puts the impact of population growth on the industrial sector

into perspective. It says:

“Energy demand in developing nations (Non-OECD) will rise 65% by 2040 compared to 2010, reflecting

growing prosperity and expanding economies. Overall, global energy demand will grow 35%, even with

significant efficiency gains, as the world’s population expands from about 7 billion people today to nearly

9 billion people by 2040, led by growth in Africa and India.”

The business case for improved energy management in the indus-

trial space has never been stronger. At the macroeconomic level,

the world continues to move toward cleaner and cheaper sources

of energy. Correspondingly, the overall consumption of energy in

the industrial space is continuing to grow at a rate that business

executives cannot ignore.

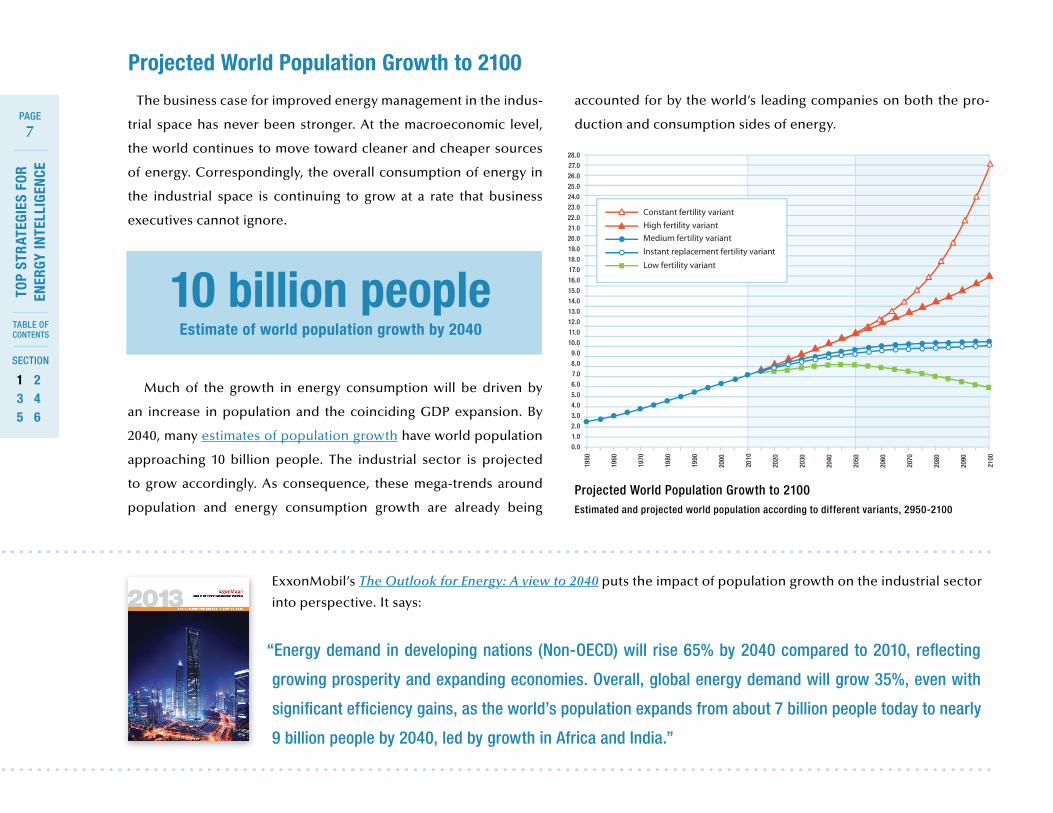

Much of the growth in energy consumption will be driven by

an increase in population and the coinciding GDP expansion. By

2040, many estimates of population growth have world population

approaching 10 billion people. The industrial sector is projected

to grow accordingly. As consequence, these mega-trends around

population and energy consumption growth are already being

Projected World Population Growth to 2100

10 billion peopleEstimate of world population growth by 2040

28.0

27.0

26.0

25.0

24.0

23.0

22.0

21.0

20.0

19.0

18.0

17.0

16.0

15.0

14.0

13.0

12.0

11.0

10.0

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

2060

2070

2080

2090

2100

Constant fertility variant

High fertility variantMedium fertility variant

Instant replacement fertility variant

Low fertility variant

Projected World Population Growth to 2100Estimated and projected world population according to different variants, 2950-2100

accounted for by the world’s leading companies on both the pro-

duction and consumption sides of energy.

8

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

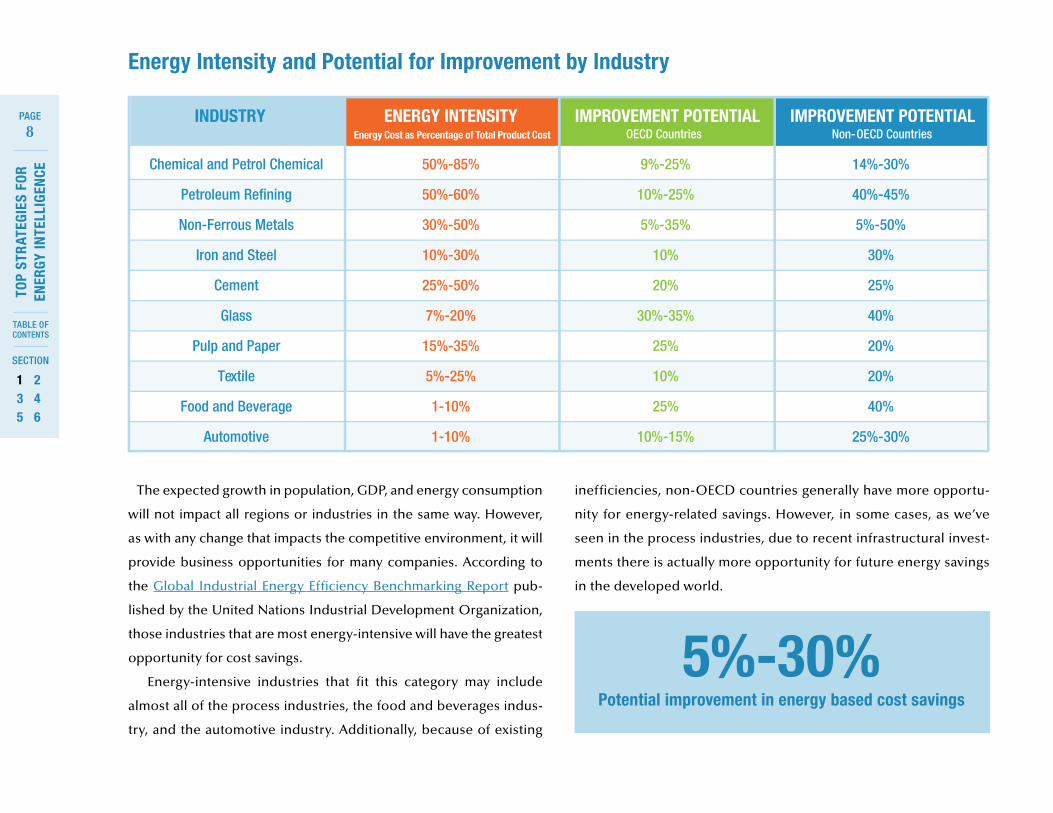

Energy Intensity and Potential for Improvement by Industry

50%-85%

50%-60%

30%-50%

10%-30%

25%-50%

7%-20%

15%-35%

5%-25%

1-10%

1-10%

ENERGY INTENSITY

Chemical and Petrol Chemical

Petroleum Refining

Non-Ferrous Metals

Iron and Steel

Cement

Glass

Pulp and Paper

Textile

Food and Beverage

Automotive

INDUSTRY

9%-25%

10%-25%

5%-35%

10%

20%

30%-35%

25%

10%

25%

10%-15%

IMPROVEMENT POTENTIALOECD Countries

14%-30%

40%-45%

5%-50%

30%

25%

40%

20%

20%

40%

25%-30%

IMPROVEMENT POTENTIALNon-OECD Countries

The expected growth in population, GDP, and energy consumption

will not impact all regions or industries in the same way. However,

as with any change that impacts the competitive environment, it will

provide business opportunities for many companies. According to

the Global Industrial Energy Efficiency Benchmarking Report pub-

lished by the United Nations Industrial Development Organization,

those industries that are most energy-intensive will have the greatest

opportunity for cost savings.

Energy-intensive industries that fit this category may include

almost all of the process industries, the food and beverages indus-

try, and the automotive industry. Additionally, because of existing

inefficiencies, non-OECD countries generally have more opportu-

nity for energy-related savings. However, in some cases, as we’ve

seen in the process industries, due to recent infrastructural invest-

ments there is actually more opportunity for future energy savings

in the developed world.

5%-30% Potential improvement in energy based cost savings

Energy Cost as Percentage of Total Product Cost

SECTION 2

Individual Company Responses

“10

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

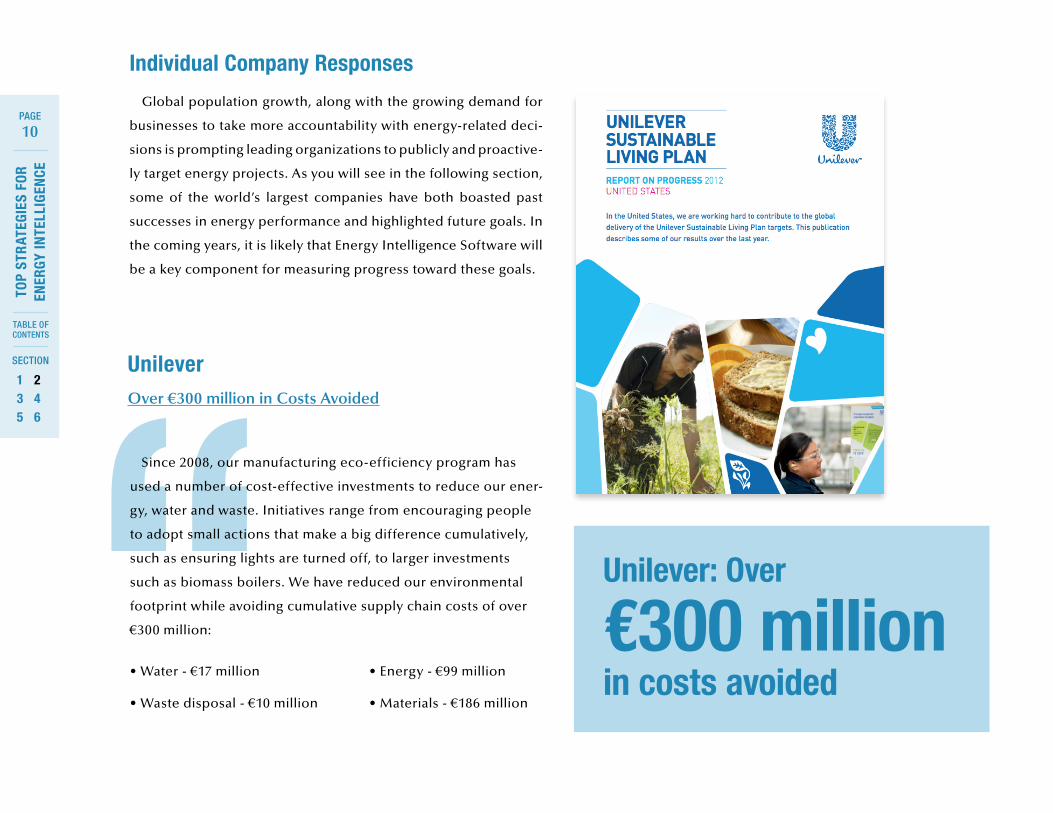

Since 2008, our manufacturing eco-efficiency program has

used a number of cost-effective investments to reduce our ener-

gy, water and waste. Initiatives range from encouraging people

to adopt small actions that make a big difference cumulatively,

such as ensuring lights are turned off, to larger investments

such as biomass boilers. We have reduced our environmental

footprint while avoiding cumulative supply chain costs of over

€300 million:

• Water - €17 million • Energy - €99 million

• Waste disposal - €10 million • Materials - €186 million

Global population growth, along with the growing demand for

businesses to take more accountability with energy-related deci-

sions is prompting leading organizations to publicly and proactive-

ly target energy projects. As you will see in the following section,

some of the world’s largest companies have both boasted past

successes in energy performance and highlighted future goals. In

the coming years, it is likely that Energy Intelligence Software will

be a key component for measuring progress toward these goals.

Individual Company Responses

UnileverOver €300 million in Costs Avoided

Unilever: Over

€300 million

in costs avoided

“

11

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

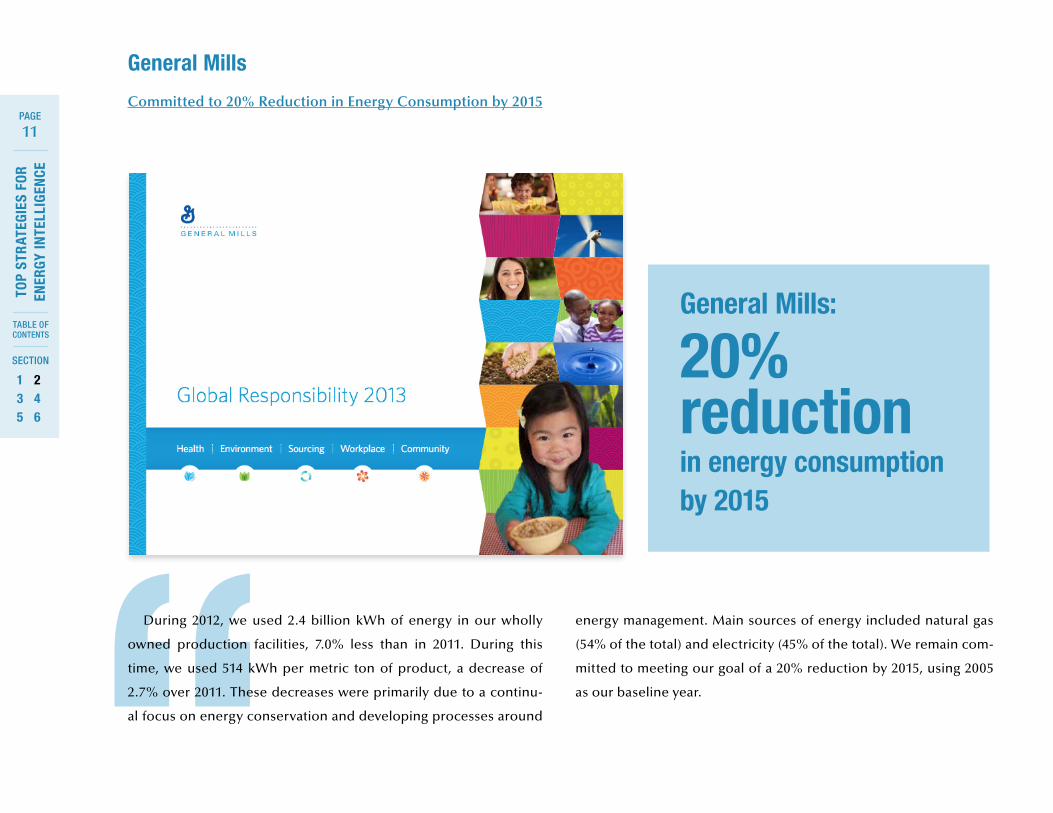

Committed to 20% Reduction in Energy Consumption by 2015

General Mills

General Mills:

20% reduction in energy consumption by 2015

During 2012, we used 2.4 billion kWh of energy in our wholly

owned production facilities, 7.0% less than in 2011. During this

time, we used 514 kWh per metric ton of product, a decrease of

2.7% over 2011. These decreases were primarily due to a continu-

al focus on energy conservation and developing processes around

energy management. Main sources of energy included natural gas

(54% of the total) and electricity (45% of the total). We remain com-

mitted to meeting our goal of a 20% reduction by 2015, using 2005

as our baseline year.

“12

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

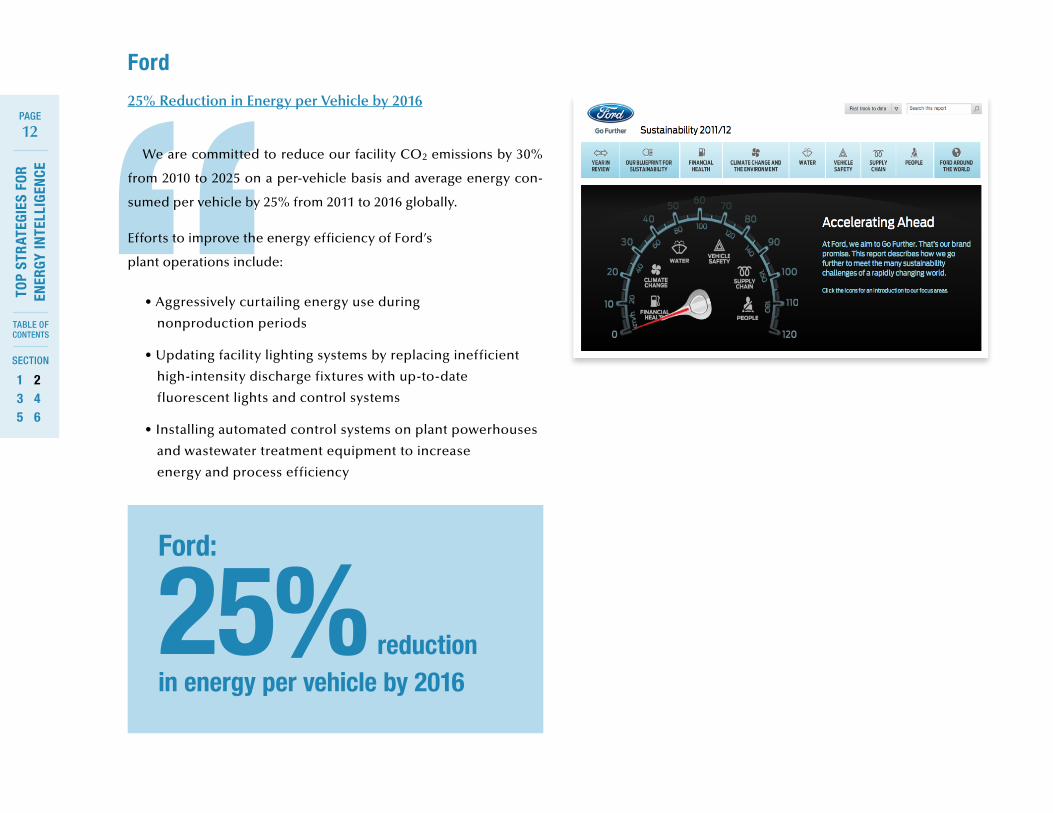

25% Reduction in Energy per Vehicle by 2016

Ford

We are committed to reduce our facility CO2 emissions by 30%

from 2010 to 2025 on a per-vehicle basis and average energy con-

sumed per vehicle by 25% from 2011 to 2016 globally.

Efforts to improve the energy efficiency of Ford’s

plant operations include:

• Aggressively curtailing energy use during

nonproduction periods

• Updating facility lighting systems by replacing inefficient

high-intensity discharge fixtures with up-to-date

fluorescent lights and control systems

• Installing automated control systems on plant powerhouses

and wastewater treatment equipment to increase

energy and process efficiency

Ford:

25% reductionin energy per vehicle by 2016

“13

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

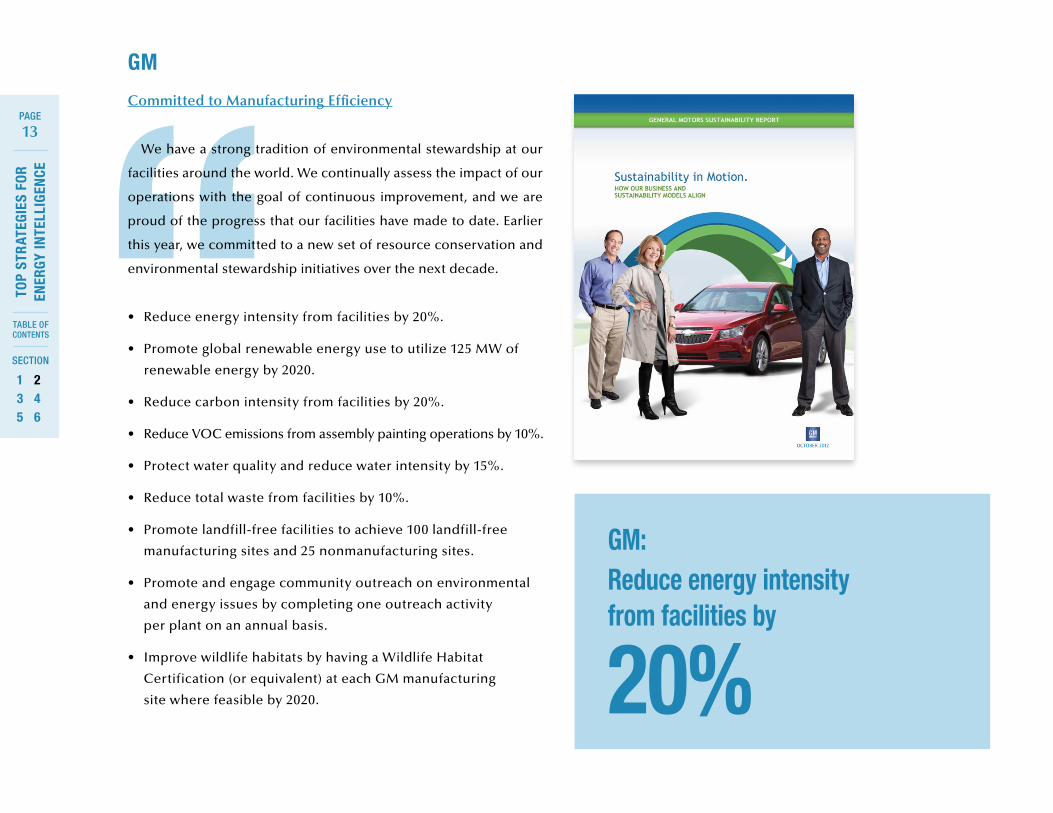

• Reduce energy intensity from facilities by 20%.

• Promote global renewable energy use to utilize 125 MW of

renewable energy by 2020.

• Reduce carbon intensity from facilities by 20%.

• Reduce VOC emissions from assembly painting operations by 10%.

• Protect water quality and reduce water intensity by 15%.

• Reduce total waste from facilities by 10%.

• Promote landfill-free facilities to achieve 100 landfill-free

manufacturing sites and 25 nonmanufacturing sites.

• Promote and engage community outreach on environmental

and energy issues by completing one outreach activity

per plant on an annual basis.

• Improve wildlife habitats by having a Wildlife Habitat

Certification (or equivalent) at each GM manufacturing

site where feasible by 2020.

GM

GM:Reduce energy intensity from facilities by

20%

Committed to Manufacturing Efficiency

We have a strong tradition of environmental stewardship at our

facilities around the world. We continually assess the impact of our

operations with the goal of continuous improvement, and we are

proud of the progress that our facilities have made to date. Earlier

this year, we committed to a new set of resource conservation and

environmental stewardship initiatives over the next decade.

SECTION 3

Market Drivers for Energy Management

15

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

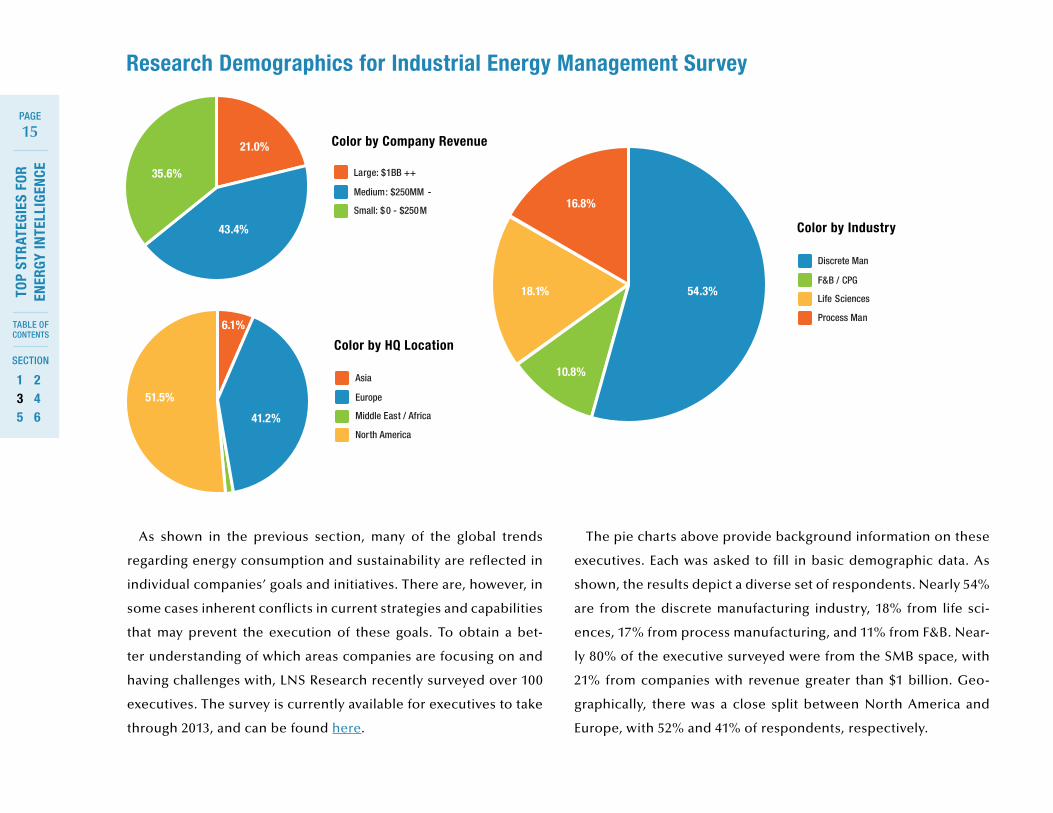

Research Demographics for Industrial Energy Management Survey

The pie charts above provide background information on these

executives. Each was asked to fill in basic demographic data. As

shown, the results depict a diverse set of respondents. Nearly 54%

are from the discrete manufacturing industry, 18% from life sci-

ences, 17% from process manufacturing, and 11% from F&B. Near-

ly 80% of the executive surveyed were from the SMB space, with

21% from companies with revenue greater than $1 billion. Geo-

graphically, there was a close split between North America and

Europe, with 52% and 41% of respondents, respectively.

35.6%

21.0%

43.4%

51.5%

41.2%

6.1%

Large: $1BB ++

Medium: $250MM -

Small: $0 - $250M

Asia

Europe

Middle East / Africa

North America

Discrete Man

F&B / CPG

Life Sciences

Process Man

54.3%18.1%

16.8%

10.8%

Color by HQ Location

Color by Industry

Color by Company Revenue

As shown in the previous section, many of the global trends

regarding energy consumption and sustainability are reflected in

individual companies’ goals and initiatives. There are, however, in

some cases inherent conflicts in current strategies and capabilities

that may prevent the execution of these goals. To obtain a bet-

ter understanding of which areas companies are focusing on and

having challenges with, LNS Research recently surveyed over 100

executives. The survey is currently available for executives to take

through 2013, and can be found here.

16

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

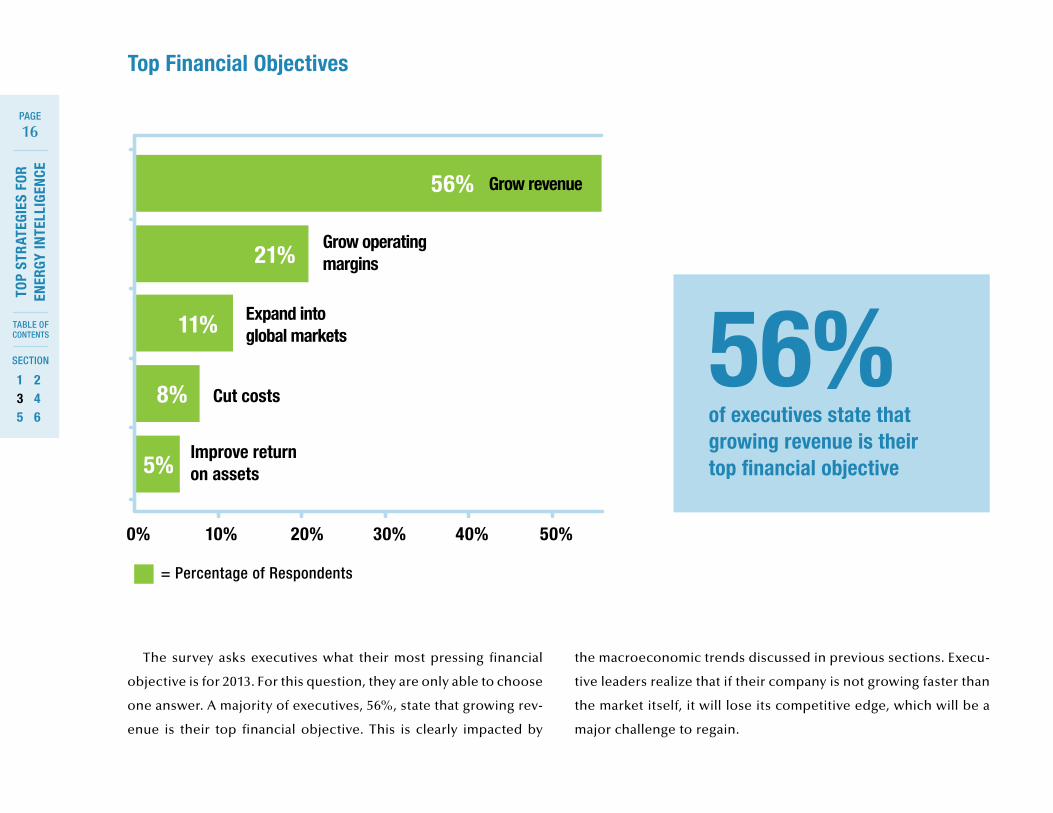

The survey asks executives what their most pressing financial

objective is for 2013. For this question, they are only able to choose

one answer. A majority of executives, 56%, state that growing rev-

enue is their top financial objective. This is clearly impacted by

Top Financial Objectives

= Percentage of Respondents

50%0% 10% 20% 30% 40%

Grow revenue

Grow operatingmargins

Expand into global markets

Improve return on assets

Cut costs

56%

21%

11%

8%

5%

the macroeconomic trends discussed in previous sections. Execu-

tive leaders realize that if their company is not growing faster than

the market itself, it will lose its competitive edge, which will be a

major challenge to regain.

56% of executives state that growing revenue is their top financial objective

17

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

0% 10% 20% 30% 40% 50% 60%

48%

21%

7%

7%

6%

5%

3%

2%

Reduce the total cost of operations

Align energy and operations with corporate sustainability objectives

Meet consumer demands for sustainable products

Ensure regulatory compliance

Reduce carbon emissions

Better communicate performance to stakeholders

Better manage energy supply risk

Reduce water use

Top Objectives for Energy Management

= Percentage of Respondents

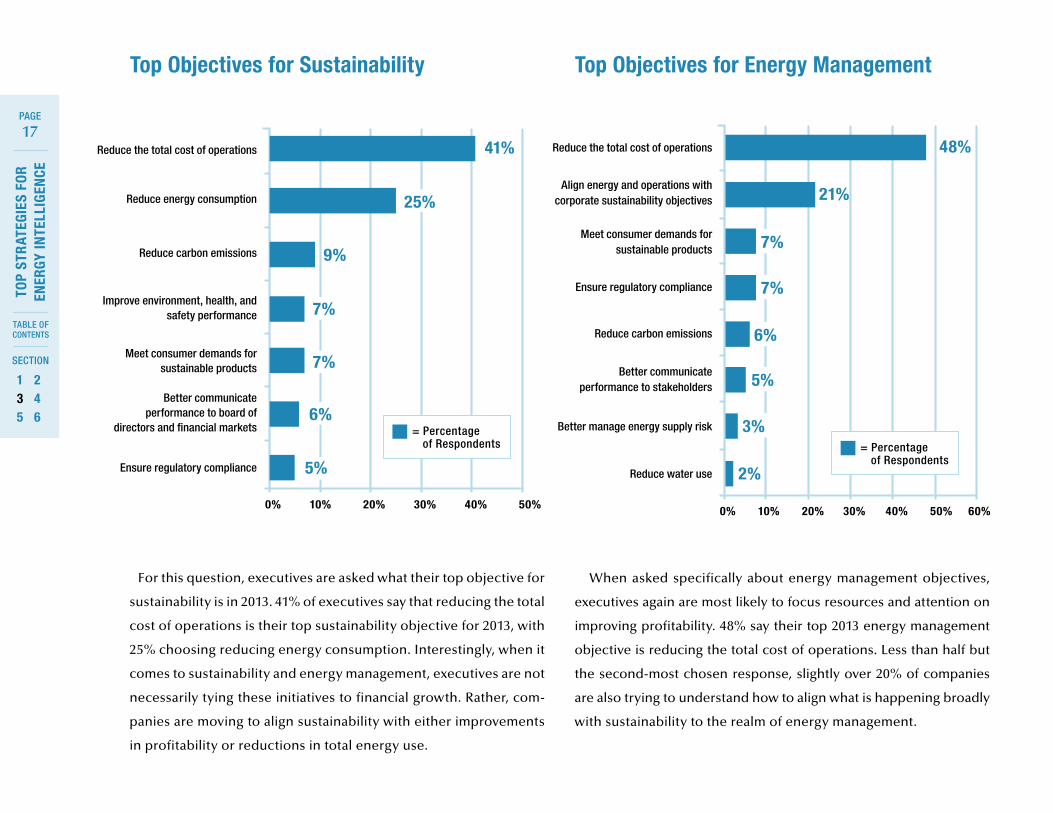

When asked specifically about energy management objectives,

executives again are most likely to focus resources and attention on

improving profitability. 48% say their top 2013 energy management

objective is reducing the total cost of operations. Less than half but

the second-most chosen response, slightly over 20% of companies

are also trying to understand how to align what is happening broadly

with sustainability to the realm of energy management.

For this question, executives are asked what their top objective for

sustainability is in 2013. 41% of executives say that reducing the total

cost of operations is their top sustainability objective for 2013, with

25% choosing reducing energy consumption. Interestingly, when it

comes to sustainability and energy management, executives are not

necessarily tying these initiatives to financial growth. Rather, com-

panies are moving to align sustainability with either improvements

in profitability or reductions in total energy use.

0% 10% 20% 30% 40% 50%

41%

25%

9%

7%

7%

6%

5%

Reduce the total cost of operations

Reduce energy consumption

Reduce carbon emissions

Improve environment, health, and safety performance

Meet consumer demands for sustainable products

Better communicate performance to board of

directors and financial markets

Ensure regulatory compliance

Top Objectives for Sustainability

= Percentage of Respondents

SECTION 4

Challenges with Energy Management

19

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

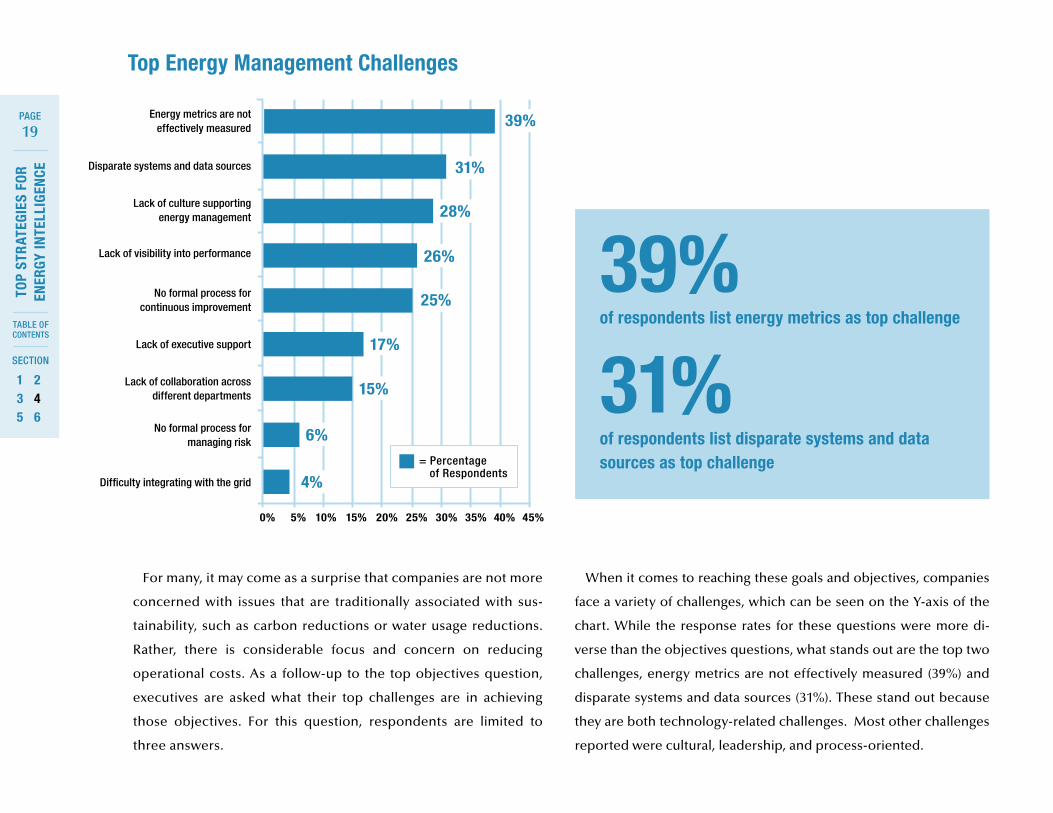

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

39%

25%

26%

28%

31%

17%

15%

4%

6%

Energy metrics are not effectively measured

Disparate systems and data sources

Lack of culture supporting energy management

Lack of visibility into performance

No formal process for continuous improvement

Lack of executive support

Lack of collaboration across different departments

No formal process for managing risk

Difficulty integrating with the grid

For many, it may come as a surprise that companies are not more

concerned with issues that are traditionally associated with sus-

tainability, such as carbon reductions or water usage reductions.

Rather, there is considerable focus and concern on reducing

operational costs. As a follow-up to the top objectives question,

executives are asked what their top challenges are in achieving

those objectives. For this question, respondents are limited to

three answers.

= Percentage of Respondents

Top Energy Management Challenges

When it comes to reaching these goals and objectives, companies

face a variety of challenges, which can be seen on the Y-axis of the

chart. While the response rates for these questions were more di-

verse than the objectives questions, what stands out are the top two

challenges, energy metrics are not effectively measured (39%) and

disparate systems and data sources (31%). These stand out because

they are both technology-related challenges. Most other challenges

reported were cultural, leadership, and process-oriented.

39% of respondents list energy metrics as top challenge

31% of respondents list disparate systems and data sources as top challenge

20

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

DESIGN

PROCURE MAINTAIN SELL

MANUFACTURE DELIVER SERVICE

Energy Efficiencyof Products

Supplier Energy Intensity

Operations Energy Intensity

Supply Chain Energy Intensity

Energy Efficiency of Assets

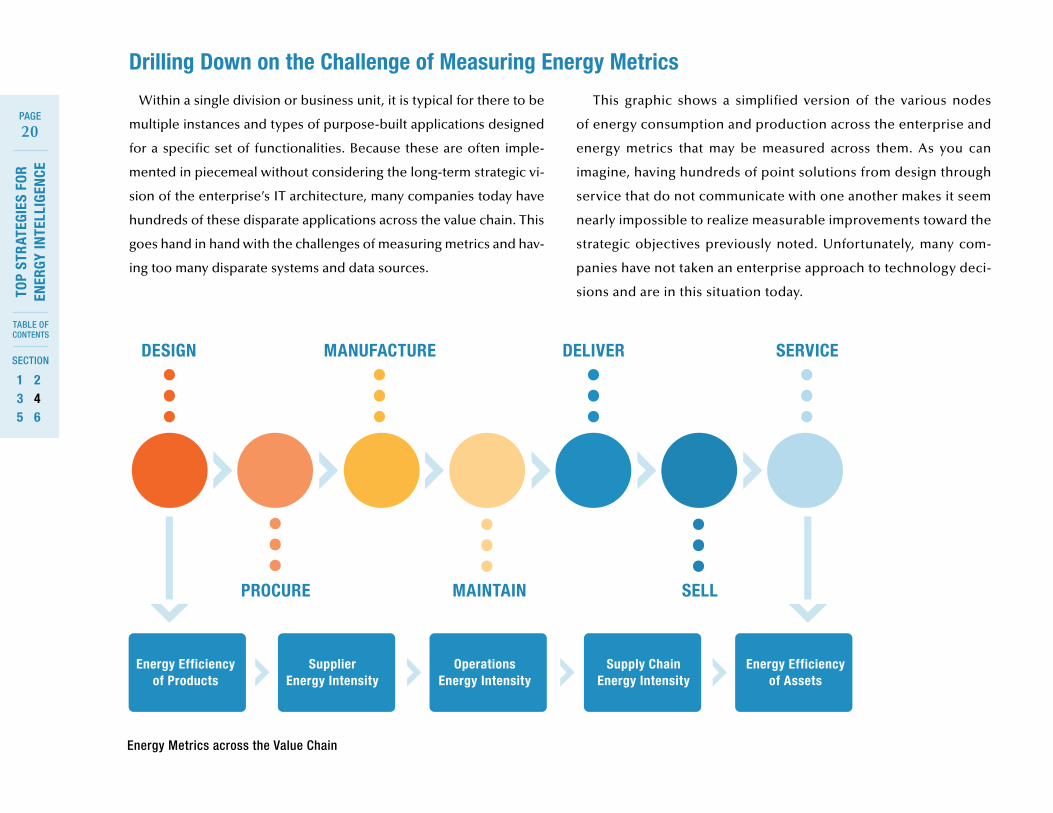

Within a single division or business unit, it is typical for there to be

multiple instances and types of purpose-built applications designed

for a specific set of functionalities. Because these are often imple-

mented in piecemeal without considering the long-term strategic vi-

sion of the enterprise’s IT architecture, many companies today have

hundreds of these disparate applications across the value chain. This

goes hand in hand with the challenges of measuring metrics and hav-

ing too many disparate systems and data sources.

This graphic shows a simplified version of the various nodes

of energy consumption and production across the enterprise and

energy metrics that may be measured across them. As you can

imagine, having hundreds of point solutions from design through

service that do not communicate with one another makes it seem

nearly impossible to realize measurable improvements toward the

strategic objectives previously noted. Unfortunately, many com-

panies have not taken an enterprise approach to technology deci-

sions and are in this situation today.

Energy Metrics across the Value Chain

Drilling Down on the Challenge of Measuring Energy Metrics

21

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

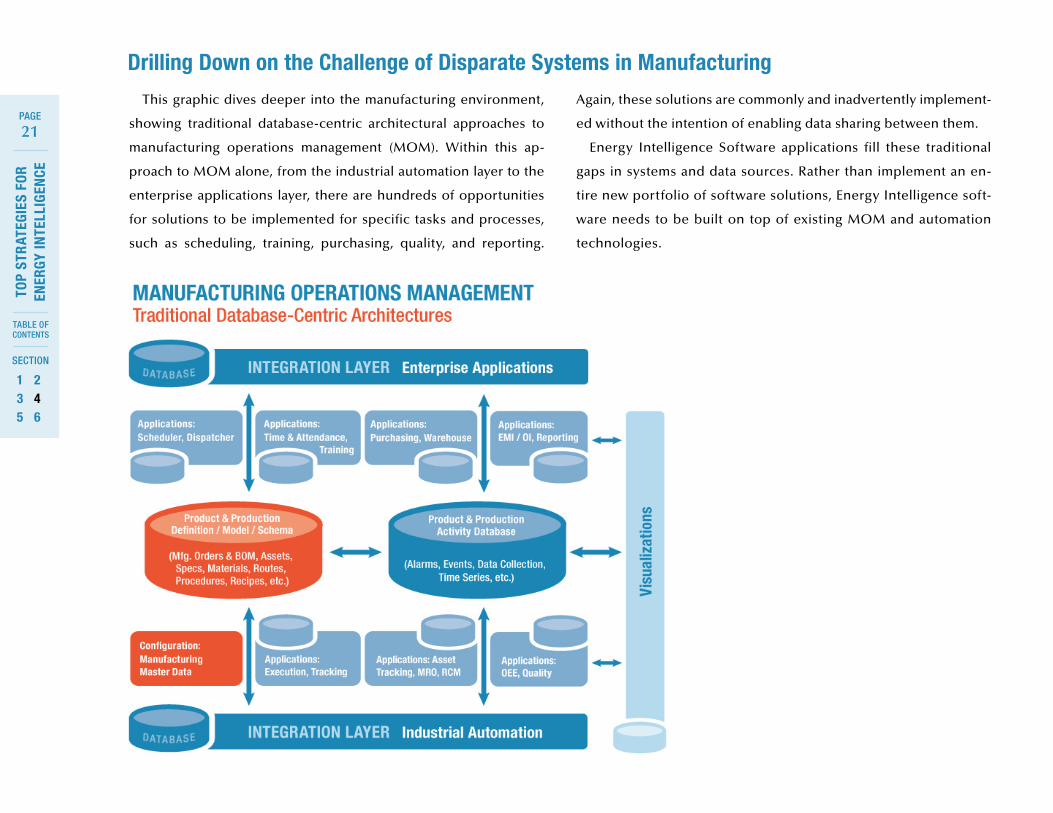

This graphic dives deeper into the manufacturing environment,

showing traditional database-centric architectural approaches to

manufacturing operations management (MOM). Within this ap-

proach to MOM alone, from the industrial automation layer to the

enterprise applications layer, there are hundreds of opportunities

for solutions to be implemented for specific tasks and processes,

such as scheduling, training, purchasing, quality, and reporting.

Again, these solutions are commonly and inadvertently implement-

ed without the intention of enabling data sharing between them.

Energy Intelligence Software applications fill these traditional

gaps in systems and data sources. Rather than implement an en-

tire new portfolio of software solutions, Energy Intelligence soft-

ware needs to be built on top of existing MOM and automation

technologies.

Drilling Down on the Challenge of Disparate Systems in Manufacturing

SECTION 5

Strategies for a Successful Energy Intelligence Solution

23

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

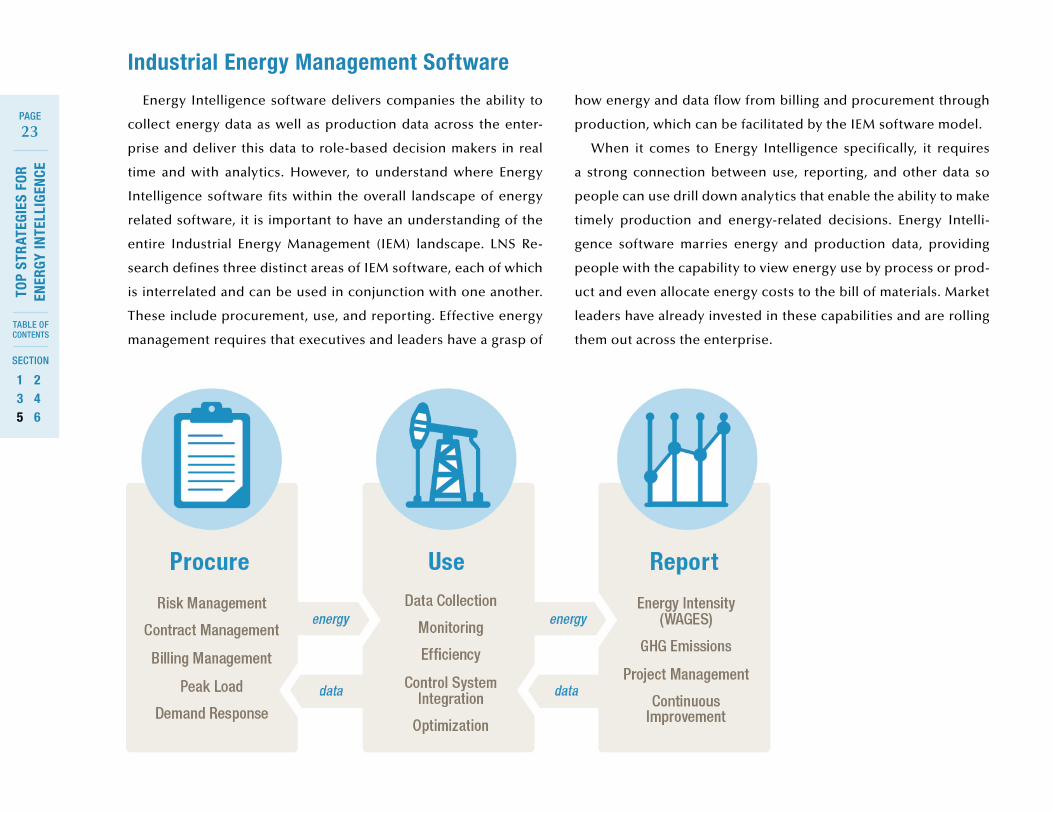

Industrial Energy Management Software

Energy Intelligence software delivers companies the ability to

collect energy data as well as production data across the enter-

prise and deliver this data to role-based decision makers in real

time and with analytics. However, to understand where Energy

Intelligence software fits within the overall landscape of energy

related software, it is important to have an understanding of the

entire Industrial Energy Management (IEM) landscape. LNS Re-

search defines three distinct areas of IEM software, each of which

is interrelated and can be used in conjunction with one another.

These include procurement, use, and reporting. Effective energy

management requires that executives and leaders have a grasp of

how energy and data flow from billing and procurement through

production, which can be facilitated by the IEM software model.

When it comes to Energy Intelligence specifically, it requires

a strong connection between use, reporting, and other data so

people can use drill down analytics that enable the ability to make

timely production and energy-related decisions. Energy Intelli-

gence software marries energy and production data, providing

people with the capability to view energy use by process or prod-

uct and even allocate energy costs to the bill of materials. Market

leaders have already invested in these capabilities and are rolling

them out across the enterprise.

24

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

“Our goal is to create an exciting, viable, profitably growing company for the

good of all of us. We’re continuing to do that by making a full family of best-

in-class vehicles, in terms of quality, and fuel efficiency, and safety and

really smart design – like SYNC® and MyFord® – and of course the very best

value by using our scale worldwide.”

Alan R. Mulally, Ford President and Chief Executive Officer

Leveraging Energy Intelligence software to make measurable

improvements in energy and sustainability-related KPIs requires

more than simply an investment. It should be an organizational issue

that aligns and then optimizes key resources – people, processes, and

technology – in support of the implementation. Without the proper

alignment of these key resources, many organizations are often left

with a costly investment that never reaches its potential ROI. The

following sections intend to discuss the roles of people, process-

es, and technology more in depth.

People Above all, executive backing is required to support and be the

foundation of this initiative. All too often, initiatives such as ener-

gy management or quality management lose momentum because

support from senior leadership is either lacking or tapers off over

time. This backing will act as a catalyst for building an energy-fo-

cused culture and an effective Energy Intelligence implementa-

tion. Those responsible for making energy-related decisions have

to understand the consequences as well as benefits of their ac-

tions in relation to KPIs.

“Executive backing is required to support and be the foundation of energy management initiatives”

25

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

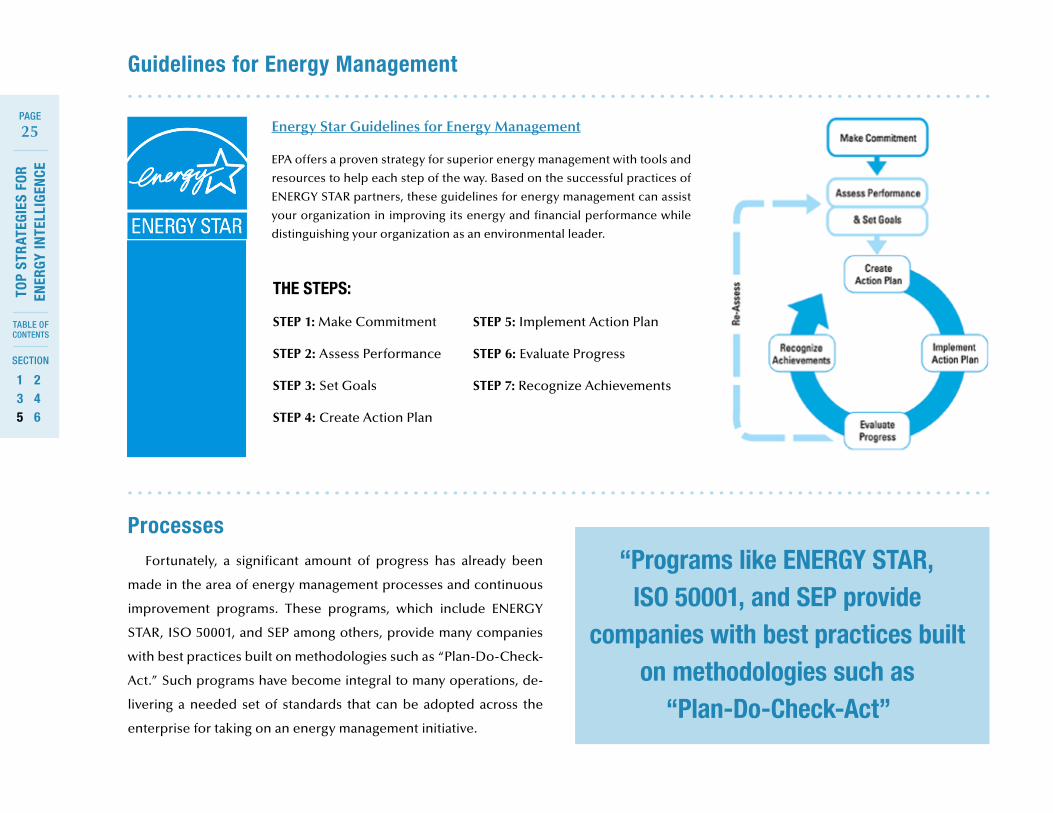

Guidelines for Energy Management

Energy Star Guidelines for Energy Management

EPA offers a proven strategy for superior energy management with tools and

resources to help each step of the way. Based on the successful practices of

ENERGY STAR partners, these guidelines for energy management can assist

your organization in improving its energy and financial performance while

distinguishing your organization as an environmental leader.

Processes Fortunately, a significant amount of progress has already been

made in the area of energy management processes and continuous

improvement programs. These programs, which include ENERGY

STAR, ISO 50001, and SEP among others, provide many companies

with best practices built on methodologies such as “Plan-Do-Check-

Act.” Such programs have become integral to many operations, de-

livering a needed set of standards that can be adopted across the

enterprise for taking on an energy management initiative.

THE STEPS:

STEP 1: Make Commitment

STEP 2: Assess Performance

STEP 3: Set Goals

STEP 4: Create Action Plan

STEP 5: Implement Action Plan

STEP 6: Evaluate Progress

STEP 7: Recognize Achievements

“Programs like ENERGY STAR, ISO 50001, and SEP provide

companies with best practices built on methodologies such as

“Plan-Do-Check-Act”

26

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

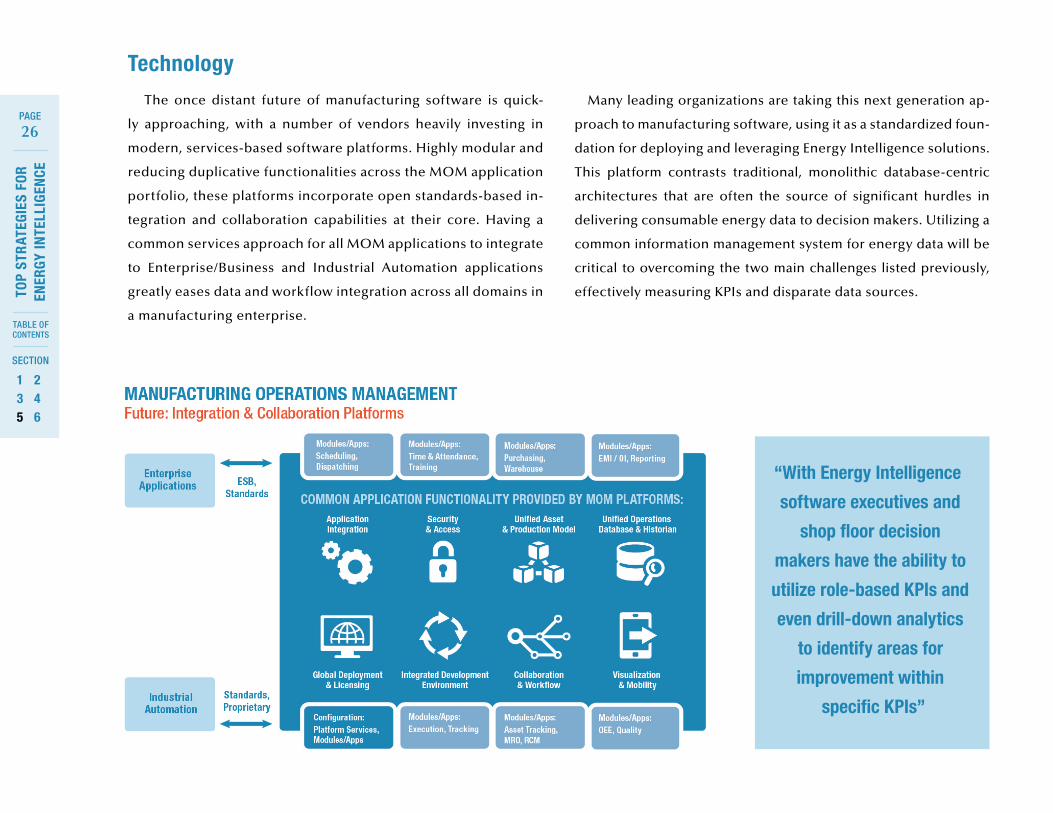

Technology The once distant future of manufacturing software is quick-

ly approaching, with a number of vendors heavily investing in

modern, services-based software platforms. Highly modular and

reducing duplicative functionalities across the MOM application

portfolio, these platforms incorporate open standards-based in-

tegration and collaboration capabilities at their core. Having a

common services approach for all MOM applications to integrate

to Enterprise/Business and Industrial Automation applications

greatly eases data and workflow integration across all domains in

a manufacturing enterprise.

Many leading organizations are taking this next generation ap-

proach to manufacturing software, using it as a standardized foun-

dation for deploying and leveraging Energy Intelligence solutions.

This platform contrasts traditional, monolithic database-centric

architectures that are often the source of significant hurdles in

delivering consumable energy data to decision makers. Utilizing a

common information management system for energy data will be

critical to overcoming the two main challenges listed previously,

effectively measuring KPIs and disparate data sources.

“With Energy Intelligence

software executives and

shop floor decision

makers have the ability to

utilize role-based KPIs and

even drill-down analytics

to identify areas for

improvement within

specific KPIs”

27

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

Undoubtedly, there is a disconnect across many enterprises when it

comes to the diversity of data sources, energy and MOM applications,

and best practices for measuring energy and sustainability KPIs. In

many ways, this disconnect is simply a result of the growing complex-

ities of manufacturing and industrial operations. However, advance-

ments in technology around Energy Intelligence are enabling organi-

zations to turn this disconnect into operational insights that will be key

for retaining and improving a competitive edge over time.

This graphic visualizes the complexities of enterprise data sourc-

es and applications from utilities to manufacturing, distribution and

warehousing, and corporate offices. Energy Intelligence software

standardizes these data sources often with cloud-based technolo-

gies, delivering consumable and actionable information to the met-

rics dashboard. With this solution, executives and decision makers

down to the shop floor have the ability to utilize role-based KPIs and

even drill-down analytics to identify areas for improvement within

those specific KPIs.

The use of role-based KPIs and drill-down analytics is a vital com-

ponent for energy efficiency projects. Without the standardized data

delivered by Energy Intelligence software, efforts and even strategies

for achieving progress toward energy efficiency projects can be too

divided to ever deliver real value. With the use of business intelli-

gence (BI) tools, standardized data can be dissected at a very granu-

lar level to not only measure progress toward energy efficiency proj-

ects, but to quickly assess and make changes to current strategies at

the speed of business and manufacturing.

SECTION 6

Actionable Recommendations

29

TOP

STR

ATEG

IES

FOR

EN

ERGY

INTE

LLIG

ENCE

SECTION

TABLE OF CONTENTS

PAGE

135

246

While more environmentally-conscious decisions will be expected

by stakeholders over time, the operational and financial benefits

of Energy Intelligence software warrant enough evidence to take

action now.

Tips for aligning people with energy initiatives:

• Instill a culture of energy management that starts with senior leadership

• Appoint site-level energy leaders responsible for performance

• Create an internal marketing program to support the initiative

• Put energy metrics on meeting agendas for all levels of management

• Develop cross-functional teams for improvement and education

• Offer incentives for performance improvements in energy metrics

Additional Technology Recommendations

• Energy Intelligence applications need to build on existing IT and automation investments

• Leverage existing next generation investments and roadmaps in MOM if available

• Ensure both energy and production data is collected with sufficient granularity to provide the analytical capabilities for measuring energy intensity of specific products and assets

• Focus on KPI visibility and the connection between energy consumption and production performance to drive a quick ROI

Authors:

Matthew LittlefieldPresident and Principal Analyst

Mike Roberts

Research Associate

Presented by: Distribution made possible by our sponsor:

lnsresearch.com

Connect:

© LNS Research, 2013. All Rights Reserved.